Embed Size (px)

Citation preview

Technology, Media & Telecommunications Predictions 2011 a

A shared approachto

Adviser and Consultancy Charging

Introduction 2

Generic principles 3

Facilitating Adviser Charging 4

Facilitating Consultancy Charging 7

Core Adviser and Consultancy Charging structures 11

Cooling-off and opt-out 13

Changes to an adviser firm 15

Value Added Tax (VAT) 17

Glossary 1918

Contents

A shared approach to Adviser and Consultancy Charging 1

“ We know extremely well in our industry about the devil being in the detail. And so it is with Adviser Charging and Consultancy Charging. Simple in concept but not without some practical challenges in their application. We therefore very much welcome the initiative taken by this group, comprising of experienced advisers and product providers, in taking the time to work through in detail these important matters. For advisers thinking about how Adviser Charging and Consultancy Charging might work for them in practice, we believe this document should prove to be a very helpful starting point.”

Stephen Gay, Director General, AIFA

“ The ABI supports the RDR which will introduce massive changes for the financial services industry and consumers, including the ban on commission payments for advice and the introduction of Adviser and Consultancy Charging. So we welcome this new guidance as it will help advisers, insurers and others to understand ways in which Adviser and Consultancy Charging can work in practice.”

Maggie Craig, Director of Financial Conduct Regulation, ABI

“ Deloitte is particularly pleased to have facilitated the creation of A shared approach to Adviser and Consultancy Charging. We very much want to see a smooth transition to a post-RDR world and believe the outputs of the project will go a long way to helping both advisers and the wider provider community prepare for the practicalities of the RDR. We hope the publication will act as a framework to underpin core AC and CC facilitation across the industry, without restricting in any way what advisers and providers might wish to offer in addition.”

Gavin Norwod, Partner, Deloitte

A shared approach to Adviser and Consultancy Charging 2

Introduction

The regulatory changes arising from the Retail Distribution Review (RDR) take effect on 31st December 2012. Although many of the regulatory rules and guidance are in place, the industry needs to develop a view as to how certain processes and activities around Adviser Charging (AC) and Consultancy Charging (CC) will operate in practice.

We (AEGON, Friends Life, Legal & General, Prudential and Scottish Life) believe A shared approach to Adviser and Consultancy Charging represents one of the first concrete deliverables around the RDR from the industry, helping to clarify practical issues and core AC and CC functionality. Through a series of workshops and meetings facilitated by Deloitte, we have developed a common approach to facilitating AC and CC through the product by creating a series of high level principles and processes detailed in this document. We have also expressed our views on the core AC and CC charging structure options that we think are likely to be widely available in the market. It will be for advisers to determine when it will benefit their clients to facilitate an AC or CC from the product.

The guide is not intended to restrict in any way the types of AC or CC facilitation providers will offer or how they choose to operate it. Providers will not necessarily offer all the options set out in this document. Instead it aims to ensure all parties involved in an AC or CC arrangement have a common understanding of the activities and processes that underpin it.

We would like to express our sincere thanks to Sesame Bankhall Group for their valuable input throughout the project.

Clarity will continue to emerge in the coming months. However we believe the publication of this document will help the adviser community to move forward towards implementation of AC and CC with increased confidence. We hope all readers will find this document useful in supporting as smooth as possible a transition to RDR.

If you have any questions or would like to discuss the content of this guide, please contact your representative from any of the product providers listed above.

The contents of the pack are owned by the product providers listed above and not Deloitte. The views contained within the document are the views of these providers. Whilst this document has been created in good faith based on our understanding of the regulations as at 16th December, we cannot be held responsible for any inaccuracies or changes in regulations that may render the information contained in this document incorrect.

A shared approach to Adviser and Consultancy Charging 3

Here we provide an overview of the generic principles that we believe will underpin Adviser Charging and Consultancy Charging.

1. The AC agreement is between the client and the adviser firm, not the adviser.

2. The CC agreement is between the employer and the adviser firm, not the adviser.

3. AC/CC taken from pensions can only pay for advice and services on pensions.

4. Providers will communicate to the market the products through which they will facilitate AC and CC, and the AC and CC structures available for these products.

5. Before any AC or CC can be facilitated, the adviser firm and the provider need to re-agree terms of business.

6. AC/CC instructions will capture any initial, ongoing or ad-hoc AC/CC and stipulate that it will be the gross amount (i.e. including VAT). The CC instruction can be at scheme or at individual level.

7. Providers do not require information with regard to AC/CC which they are not facilitating.

8. The provider will comply with AC/CC instructions once validated, in a timely manner.

9. Advisers or employers will communicate services/changes to services being provided to the client or individual, in a timely manner.

10. Advisers will keep their own VAT records for AC/CC. Providers will not keep these records.

Generic principles

A shared approach to Adviser and Consultancy Charging 4

Starting, stopping and amending AC are the core activities that will be involved in facilitating AC.

Here are the core processes that we believe will underpin AC facilitation, and that could be adopted across the industry.

The process flows provide the activities in a step-by-step format. Providers and advisers may not necessarily carry out the process steps in exactly the same order.

Starting an Adviser Charge

Facilitating Adviser Charging

1. Introduction 5. Application2. Needs analysis

6. Provider validation

3. Research

7. Policy set up and confirmation of AC

4. Recommendation

8. Administration of AC

9. Payments to adviser firm

•Advisermeetsclient and they agree services and charging structure (the AC agreement).

•Adviser/clientcompletes product application.

•Adviser/clientcompletes standard AC instruction.

•Advisercarriesout needs analysis.

•Providervalidatesthe instruction.

•Adviserresearches products and AC facilitation options.

•Adviserrequestsillustrations, including impact of AC options.

•Providercompletes new business process for product.

•ProviderconfirmsAC to client and adviser.

•Adviserrecommends product(s) to client.

•ACchargingstructure is agreed.

•Note:Thismayrepresent a variation to the AC agreement.

•Provideradministers the AC within the product.

•Providercreditsadviser firm.

•Remunerationstatement should split commission, AC and CC transactions.

A shared approach to Adviser and Consultancy Charging 5

Stopping and reducing Adviser ChargesThis process applies when providers are instructed to stop or reduce AC. It does not cover situations where AC reduces or stops as a result of contribution or fund variations.

1. Services/AC 2. Illustration request

6. Information to client

3. Client/adviser instruction

7. Information to adviser

4. Provider validation

8. Administration of AC

9. Payments to adviser firm

•Adviserandclient discuss the changes to services and associated AC.

•Provideractsoninstruction.

•Illustrationof impact of amended AC is requestedbythe adviser from the provider (optional).

•Providerinformsclient.

•Providerreceivesthe instruction from either the client or the adviser.

•Providerinformsadviser.

•Providervalidatesthe instruction.

•Provideradministers any remaining AC within the product.

•Providercreditsadviser firm.

•Remuneration Statement should split commission, AC and CC transactions.

5. Amendment of charges

A shared approach to Adviser and Consultancy Charging 6

Increasing an Adviser Charge or applying an ad-hoc Adviser Charge

1. Services/AC5. Amendment of charges

2. Illustration request

6. Information to client

3. Client instruction

7. Information to adviser

4. Provider validation

9. Payments to adviser firm

•Adviserandclient discuss the changes to services and associated AC.

•Provideractsoninstruction.

•Illustrationof impact of amended AC is requestedbytheadviser from the provider.

•Providerinformsclient.

•Theclientconfirms they agree to the increased/ad-hocAC and adviser documents this and sends instruction to provider.

•Note:Theremayor may not be an associated policy alteration.

•Providerinformsadviser.

•Providervalidatesthe instruction.

•Provideradministers the AC within the product.

•Providercreditsadviser firm.

•Remunerationstatement should split commission, AC and CC transactions.

8. Administration of AC

A shared approach to Adviser and Consultancy Charging 7

Starting, stopping and amending CC are the core activities that will be involved in facilitating CC.

Here are the core processes that we believe will underpin CC facilitation, and that could be adopted across the industry.

The process flows provide the activities in a step-by-step format. They also reflect the involvement of individual members who are the legal owners of the policies. Providers and advisers may not necessarily carry out the process steps in exactly the same order.

Starting a Consultancy Charge

Facilitating Consultancy Charging

1. Introduction 2. Needs analysis 3. Research 4. Recommendation 5. Application

•Advisermeetsemployer and they agree services and charging structure (the CC agreement).

•Advisercarriesout needs analysis.

•Adviserandemployer agree on approach to apportioning of CC across the members.

•Adviserresearches products and CC facilitation options.

•Adviserrequeststerms for the scheme and sample illustrations including impact of CC options (if any).

•Adviserdecideson preferred product.

•Adviserrecommends product to employer.

•Adviserobtains generic illustrations.

•Adviserandemployer agree on scheme set up and CC structure.

•Note:Thismayrequirerefinement to suit employer needs and a variation to the CC agreement.

•Advisercompletes product application.

•Employer/advisercompletes standard CC instruction.

Continued on the next page

A shared approach to Adviser and Consultancy Charging 8

6. Provider validation7. Scheme communications

8. Policy set up and confirmation of CC

9. Administration of CC

10. Payments to adviser firm

•Providervalidatesthe instruction.

•Note:Memberspecific validation may be required.

•Providerprovides joining pack including scheme details, application and illustration.

•Adviser/employer/provider carry out communications and enrolment as agreed.

•Providercompletes new business process for individual policies.

•ProviderconfirmsCC to individuals, employer and adviser.

•Provideradministers the CC within the product.

•Providercreditsadviser firm.

•Remunerationstatement should split commission, AC and CC transactions.

Starting a Consultancy Charge (continued)

A shared approach to Adviser and Consultancy Charging 9

Stopping and reducing Consultancy ChargesThis process applies when providers are instructed to stop or reduce CC. It does not cover situations where CC reduces or stops as a result of contribution or fund variations.

1. Services/CC

6. Amendment of charges

2. Illustration request

7. Information to employer

3. Amendment ofservices

8. Information to individual

4. Employer/adviser instruction

5. Provider validation

9. Information to adviser

10. Administration of CC

11. Payments to adviser firm

•Adviserandemployer discuss the changes to services and associated CC.

•Provideractsoninstruction.

•Illustrationof impact of amended CC is requestedbythe adviser from the provider for the employer (optional).

•Providerinformsemployer.

•Adviser/employerinforms the individual of changes to services.

•Providerinformsindividuals.

•Providerreceivesthe instruction from either employer or adviser.

•Providervalidatesthe instruction.

•Providerinformsadviser.

•Provideradministers any remaining CC within the product.

•Providercreditsadviser firm.

•Remunerationstatement should split commission, AC and CC transactions.

A shared approach to Adviser and Consultancy Charging 10

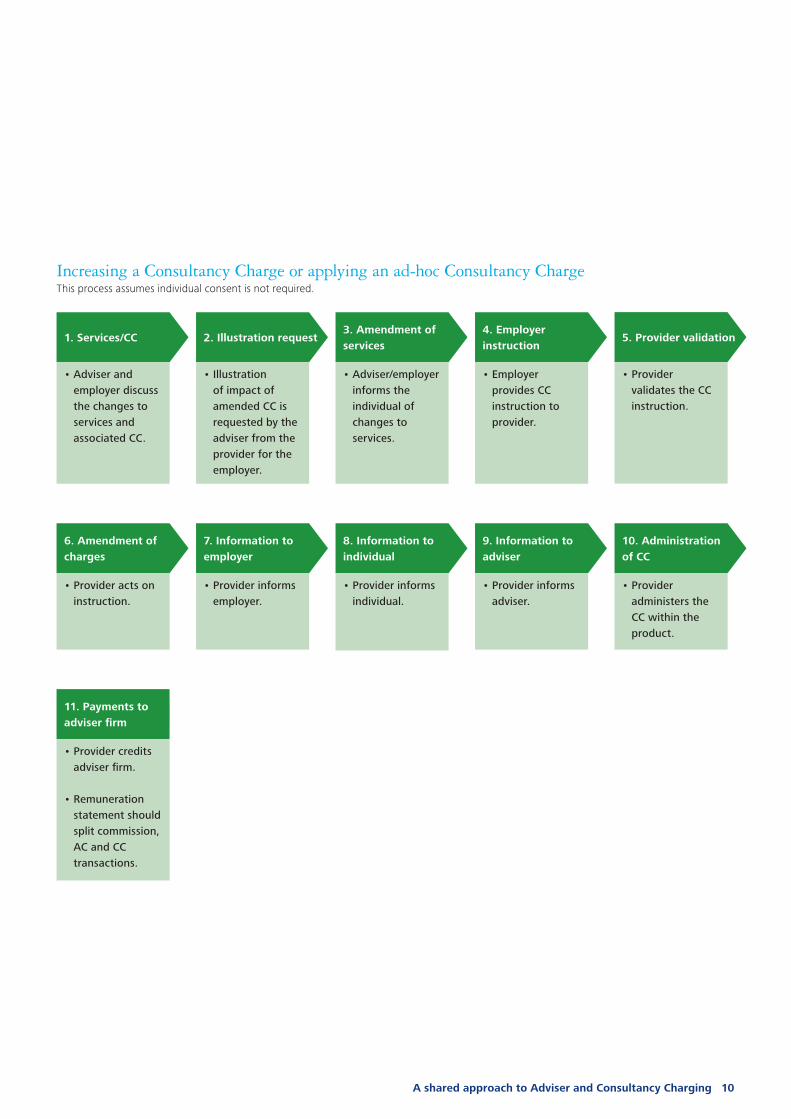

Increasing a Consultancy Charge or applying an ad-hoc Consultancy ChargeThis process assumes individual consent is not required.

1. Services/CC

6. Amendment of charges

2. Illustration request

7. Information to employer

3. Amendment ofservices

8. Information to individual

4. Employer instruction

5. Provider validation

9. Information to adviser

10. Administration of CC

11. Payments to adviser firm

•Adviserandemployer discuss the changes to services and associated CC.

•Provideractsoninstruction.

•Illustrationof impact of amended CC is requestedbytheadviser from the provider for the employer.

•Providerinformsemployer.

•Adviser/employerinforms the individual of changes to services.

•Providerinformsindividual.

•Employerprovides CC instruction to provider.

•Providervalidates the CC instruction.

•Providerinformsadviser.

•Provideradministers the CC within the product.

•Providercreditsadviser firm.

•Remunerationstatement should split commission, AC and CC transactions.

A shared approach to Adviser and Consultancy Charging 11

Initial Ongoing Ad-hoc

Gross singlecontribution andtransfer value

1.£and/or%ofgrosssinglecontribution or transfer value (one-off payment).

1.£and/or%offunds.2.Frequencymonthlyasdefault.

1.£and/or%offund(one-offpayment).

Gross regular contribution

1.£and/or%ofgrossregularcontributions.

2.Period:instalmentsover 1-24months(Note:Ifthetermof the product is 12 months for example, the spread would be a maximum of 12 months).*

1.£and/or%offundsand/or%ofgross regular contributions.

2.Frequencymonthlyasdefault.

1.£and/or%offund(one-offpayment).

Here we set out the core AC and CC charging structures, which we believe are likely to be offered by the provider community. Different providers are likely to offer different options. But when an adviser firm is agreeing on an AC or CC structure with a client, they will want to do so with confidence that the provider they ultimately select is likely to be able to facilitate that structure.

This is not intended to limit the number of structures that can be offered by anyone, but to ensure there is a certain level of consistency between provider and adviser approaches to ensure smooth facilitation of AC/CC to benefit advisers, clients and providers.

The options documented are not exhaustive, and providers may offer one or more of these charge types and others as they deem appropriate.

Pensions (including drawdown)

Core Adviser and Consultancy Charging structures

Notes:•Furtheroptionsforongoingchargesincludeflexibilityofstartdate,enddate,frequency(e.g.quarterly,yearly),inadvanceorarrearsand

escalation of £ amounts. An option for regular contribution Initial charges defined at scheme level is escalation of £ amount.•ForCCwithinascheme,differentcategoriesofmembermaybesubjecttodifferentCCstructuresandlevels.•Thefollowingappliestoallboxes:Withdeductionoptions,theminimumstandardistoprovideoneofthefollowingoptions: (a) deduct from contribution before asset purchase; or (b) cancellation of asset. •CCcanonlybeagreeduponandappliedforbyanemployerfortheiremployees.•TheoptiontoapplyadditionalAC,withindividualmemberconsent,maybeofferedtomembersofaschemewithCC.•Whenreceiveinstructions,actinatimelymanner,i.e.fordeductiondate.•Providersmayofferoneormoreofeachofthesetypeofcharges.

*Instalments over a period of time greater than 24 months could also be an option.

A shared approach to Adviser and Consultancy Charging 12

Notes:•Furtheroptionsforongoingchargesincludeflexibilityofstartdate,enddate,frequency(e.g.quarterly,yearly),inadvanceorarrearsand

escalation of £ amounts.•Thefollowingappliestoallboxes:Theminimumstandardistoprovideoneofthefollowingoptions: (a) deduct from contribution before asset purchase; (b) cancellation of asset; or (c) facilitation outside of the product. •Whenreceiveinstructions,actinatimelymanner,i.e.fordeductiondate.•Providersmayofferoneormoreofeachofthesetypeofcharges.•Regularcontributionsandtransfervaluedonotapplytoinvestmentbonds.

*Instalments over a period of time greater than 24 months could also be an option.

Initial Ongoing Ad-hoc

Singlecontribution and transfer value

1.£and/or%ofsinglecontributionor transfer value (one-off payment).

1.£and/or%offunds.2.Frequencymonthlyasdefault.

1.£and/or%offund(one-offpayment).

Regular contribution

1.£and/or%ofregularcontributions.

2.Period:instalmentsover 1-24months(Note:Ifthetermof the product is 12 months for example, the spread would be a maximum of 12 months).*

1.£and/or%offundsand/or%ofregular contributions.

2.Frequencymonthlyasdefault.

1.£and/or%offund(one-offpayment).

Initial Ongoing Ad-hoc

1.£and/or%ofannuitypurchaseprice(one-off payment).

Default assumption is none.* Default assumption is none.*

Collective investments (e.g. Equity ISAs) and investment bonds

Annuities

Notes:* An investment annuity may offer a chance for ongoing advice in the same style as pensions, with flexibility of start date, frequency (e.g. quarterly, yearly) and escalation of £ amounts.

A shared approach to Adviser and Consultancy Charging 13

On cancellation within the cooling-off period, the FSA will allow refunds to the client to be either net or gross of AC/CC.

The FSA also recently made changes to its COBS rules to reflect pension reforms and automatic enrolment. A scheme used for automatic enrolment will offer all members an opt-out facility instead of cancellation rights. But under opt-out, DWP legislation stipulates that the individual must receive a return of their full contributions – i.e. without any deduction for AC/CC.

It is likely that different providers will take different approaches on both cancellation and opt-out. For cancellation, they may also vary their approach between products. Here we set out some common principles that providers might follow and explain the implications of different approaches.

Adviser firms should also make it clear in their AC/CC agreement with clients what will happen to agreed AC/CC on cancellation – in particular, if the client is still liable to pay this and if not, the mechanisms to follow to have it repaid.

High-level options for cooling-off

Refunds can either be gross or net of AC or CC

1. Refund clients investments gross of AC or CC.

If providers choose to follow this approach, they can either:

(a) delay deducting AC/CC from the policy and paying it to the adviser until the cooling-off period has ended; or

(b) reclaim paid AC/CC from the adviser.

2. Refund clients investments net of AC or CC.

Here, it will be for the adviser and client to agree whether the adviser should refund the AC or CC to the client. This should be covered in their AC/CC agreement.

Key principles

While different providers will adopt different approaches, and possibly vary these between products, the following principles should apply:

1. The right to cancel and how the refund will be calculated will be communicated to individuals in pre-sale documentation such as Key Features.

2. Pension transfer payments should be refunded in full to the ceding scheme and any AC/CC reclaimed from the adviser.

3. Providers will inform the adviser of all cancellations promptly.

4. If any ongoing (in addition to initial) AC/CC is paid during the cooling-off period, it will be treated the same as initial.

Cooling-off and opt-out

A shared approach to Adviser and Consultancy Charging 14

High-level options for opt-out from automatic enrolment

Refunds must be gross of AC or CC. Providers will either:

(a) delay deducting AC/CC from the policy and paying it to the adviser until the opt-out period has ended; or

(b) reclaim paid AC/CC from the adviser.

Key principles

While different providers will adopt different approaches, the following principles should apply:

1. The right to opt-out will be communicated by the provider and pre-sale documentation will make it clear that on opt-out, the client will get a refund of their full contributions.

2. Providers will inform the adviser of all opt-outs promptly.

3. If any ongoing (in addition to initial) AC/CC is paid during the opt-out period, it will be treated the same as initial.

A shared approach to Adviser and Consultancy Charging 15

There are a range of scenarios under which there could be a change to an adviser firm and a number of these are considered below.

This is a complex area which will result in providers adopting different approaches. The approaches taken will depend on their own internal risk and due diligence procedures.

Please note: This is for AC and CC only, not commission.

Changes to an adviser firm

Question Answer

1. What if the adviser firm sells their client contracts and database to another firm?

If the adviser firm (regulated entity) is selling part or all of the client contracts and database (with the same terms and services continuing to apply), the provider may need to check (depending on theirownrisk/complianceandduediligenceprocesses)thelegalsaleandpurchaseagreementtoensure that they could deal with the purchasing firm in relation to the clients documented in the agreement.OncevalidatedtheprovidershouldnotnecessarilyneedtostopthecurrentAC/CCinstructions and start a new one, but simply redirect the current instruction to the new adviser firm. Twocommunicationswouldberequired:onefromthe‘new’andonefromthe‘old’adviserfirm to the client (who is the employer when referring to a CC) to explain the change of adviser. The provider would also inform the client once they have validated the agreement (not to seek agreement but to advise of the change). The Provider would also write to individuals to inform then of the change in relation to CC transfers. If a client rejects the change in adviser firm, the charge would be stopped and the provider would inform the client and the adviser firms.

2. What if the adviser firm has a change in shareholders or partners?

TheprovidercancontinuetofacilitatetheAC/CCaspreviouslyinstructed.

3. What if the adviser firm has a change in legal status (i.e. Limited company to Limited Liability Partnership)?

Provider’sapproachwilldependontheirownrisk/complianceandduediligenceprocesses.

4. What are the implications of multiple advisers related to a policy?

Where the advisers are from the same firm, there are no problems as the client agreement is with the adviser firm, not the specific individuals.

There will be situations where multiple adviser firms will be receiving AC and CC simultaneously. Providers must exercise caution to ensure they do not breach the Data Protection Act.

Continued on the next page

A shared approach to Adviser and Consultancy Charging 16

Question Answer

5. What if the adviser firm loses regulatory permissions? What happens to future payments of AC and CC?”

Where AC is being paid to remunerate the adviser for ongoing services, loss of regulatory permission is very likely (but not certain) to mean these agreed ongoing services cannot be provided and future AC payments should stop. Provider firms will become aware of an intermediary firm losing authorisation through data supplied by the FSA. Where this happens, provider firms will need to contact the adviser firm to confirm whether or not ongoing AC can continue. If ongoing AC is to stop, future deductions from the policy will also stop.

AC for initial advice can be spread over a time-period for regular premium policies. If an adviser firmlosesauthorisationduringthattime-period,thereisnoregulatoryrequirementthatfutureinstalments should cease, as these are paying for advice previously given. The AC Instruction given to the provider firm will have made clear if AC is for initial advice or in respect of ongoing services.

CC is agreed with the employer for services which are not necessarily subject to regulated activities. It will be for the adviser and employer to decide if agreed services are affected by the loss of regulatory permissions and to instruct the provider accordingly. Where provider firms become aware of an adviser firm losing authorisation through data supplied by the FSA, they should contact the adviser firm to confirm whether or not ongoing CC should continue.

6. What if an adviser moves between adviser firms?

The AC agreement is not with the adviser, but between the adviser firm and the client. There should be no change to the AC unless the client provides an instruction to stop the previous AC and an instruction to start a new AC.

7. What happens if the client changes their adviser firm?

AnewAC/CCinstructionwillberequiredfromtheclient.

8. What if a new adviser firm (servicing agent) requests detail of payments made from a policy to a previous adviser firm (agent)?

The provider should obtain authority from the client to disclose payment information to the new adviser firm. The transaction history could then be provided.

Continued from previous page

A shared approach to Adviser and Consultancy Charging 17

Value Added Tax (VAT)

When there are changes to the applicable rate of VAT this could lead to a significant volume of work across the industry and potential client confusion. We have sought a practical solution to this in order to ensure fairness to the client, whilst enabling an efficient operational process across the parties involved.

There are three example scenarios where VAT can change:

1. VAT itself changes (this will follow the principles stated below).

2. VAT status of a service provided changes (this would follow some of the steps in increasing or reducing an AC or CC process).

3. VAT status of the adviser changes because they go above or drop below VAT threshold (this would follow some of the steps in increasing or reducing an AC or CC process).

Proposedprinciples:

1. Initial provider statements/declarations to clients should include robust wording around VAT changes where the adviser wants to have the authority to instruct that changes in relation to VAT are to be made by the provider automatically, without having to validate the instruction.

2. Advisers should be able to provide information in an industry standard format, to providers on applicable VAT changes for any client affected at the policy level on which the providers can act to make changes to AC or CC.

3. The same principles apply for a decrease in VAT.

A shared approach to Adviser and Consultancy Charging 18

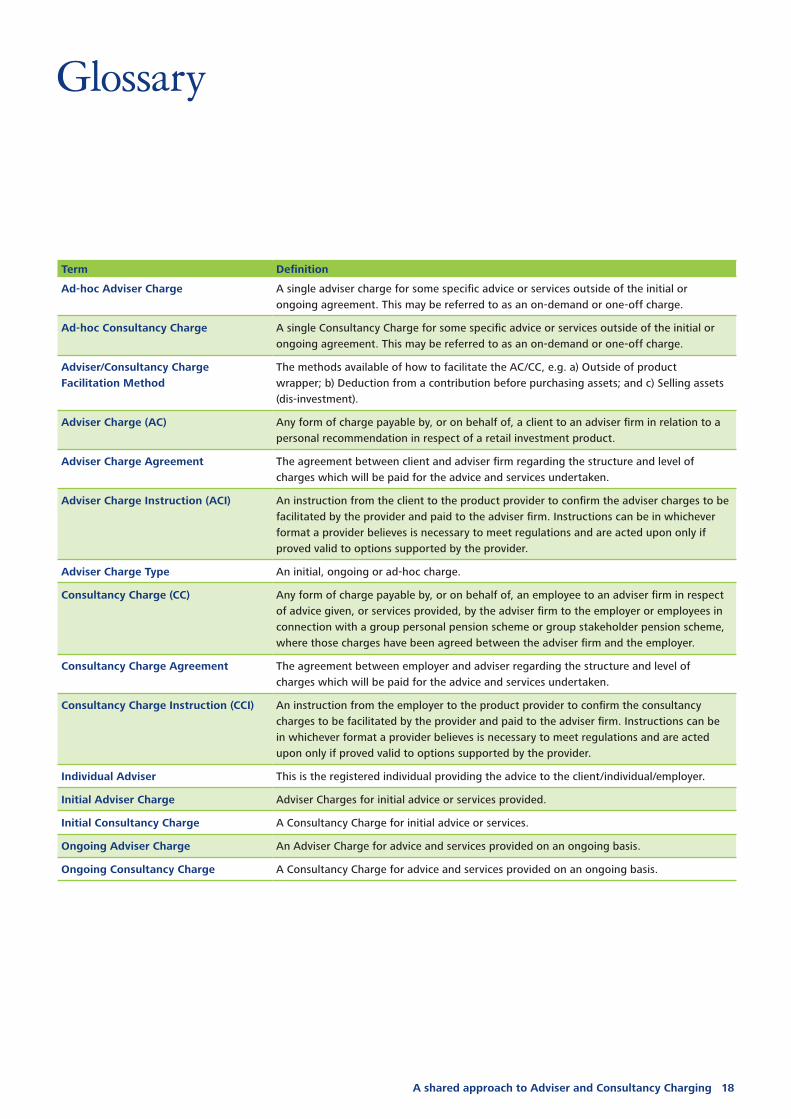

Glossary

Term Definition

Ad-hoc Adviser Charge A single adviser charge for some specific advice or services outside of the initial or ongoing agreement. This may be referred to as an on-demand or one-off charge.

Ad-hoc Consultancy Charge A single Consultancy Charge for some specific advice or services outside of the initial or ongoing agreement. This may be referred to as an on-demand or one-off charge.

Adviser/Consultancy Charge Facilitation Method

ThemethodsavailableofhowtofacilitatetheAC/CC,e.g.a)Outsideofproductwrapper; b) Deduction from a contribution before purchasing assets; and c) Selling assets (dis-investment).

Adviser Charge (AC) Any form of charge payable by, or on behalf of, a client to an adviser firm in relation to a personal recommendation in respect of a retail investment product.

Adviser Charge Agreement The agreement between client and adviser firm regarding the structure and level of charges which will be paid for the advice and services undertaken.

Adviser Charge Instruction (ACI) An instruction from the client to the product provider to confirm the adviser charges to be facilitated by the provider and paid to the adviser firm. Instructions can be in whichever format a provider believes is necessary to meet regulations and are acted upon only if proved valid to options supported by the provider.

Adviser Charge Type An initial, ongoing or ad-hoc charge.

Consultancy Charge (CC) Any form of charge payable by, or on behalf of, an employee to an adviser firm in respect of advice given, or services provided, by the adviser firm to the employer or employees in connection with a group personal pension scheme or group stakeholder pension scheme, where those charges have been agreed between the adviser firm and the employer.

Consultancy Charge Agreement The agreement between employer and adviser regarding the structure and level of charges which will be paid for the advice and services undertaken.

Consultancy Charge Instruction (CCI) An instruction from the employer to the product provider to confirm the consultancy charges to be facilitated by the provider and paid to the adviser firm. Instructions can be in whichever format a provider believes is necessary to meet regulations and are acted upon only if proved valid to options supported by the provider.

Individual Adviser Thisistheregisteredindividualprovidingtheadvicetotheclient/individual/employer.

Initial Adviser Charge Adviser Charges for initial advice or services provided.

Initial Consultancy Charge A Consultancy Charge for initial advice or services.

Ongoing Adviser Charge An Adviser Charge for advice and services provided on an ongoing basis.

Ongoing Consultancy Charge A Consultancy Charge for advice and services provided on an ongoing basis.