Embed Size (px)

Citation preview

A86045 Accoun,ng and Financial Repor,ng (2013/2014)

Session 10 Inventories and Construc,on

contracts

Paul G. Smith B.A., F.C.A.

SESSION 10 OVERVIEW

A 86045 Accoun,ng and Financial Repor,ng 2

Course Objec,ves -‐ Reminder

A 86045 Accoun,ng and Financial Repor,ng 3

At the end of this course students will be able to: • Read and interpret financial statements of companies applying interna:onal accoun:ng standards

• Iden,fy and evaluate the impact on a companies accounts of alterna:ve accoun:ng methods

• Assess the economic-‐ financial posi:on of a company.

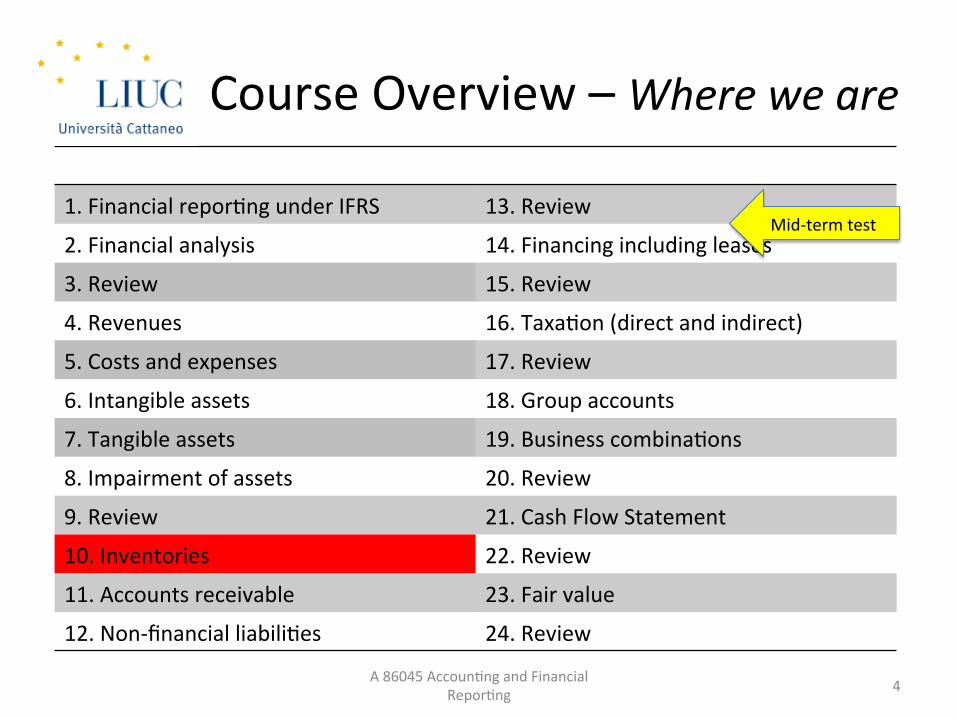

Course Overview – Where we are

A 86045 Accoun,ng and Financial Repor,ng 4

1. Financial repor,ng under IFRS 13. Review

2. Financial analysis 14. Financing including leases

3. Review 15. Review

4. Revenues 16. Taxa,on (direct and indirect)

5. Costs and expenses 17. Review

6. Intangible assets 18. Group accounts

7. Tangible assets 19. Business combina,ons

8. Impairment of assets 20. Review

9. Review 21. Cash Flow Statement

10. Inventories 22. Review

11. Accounts receivable 23. Fair value

12. Non-‐financial liabili,es 24. Review

Mid-‐term test

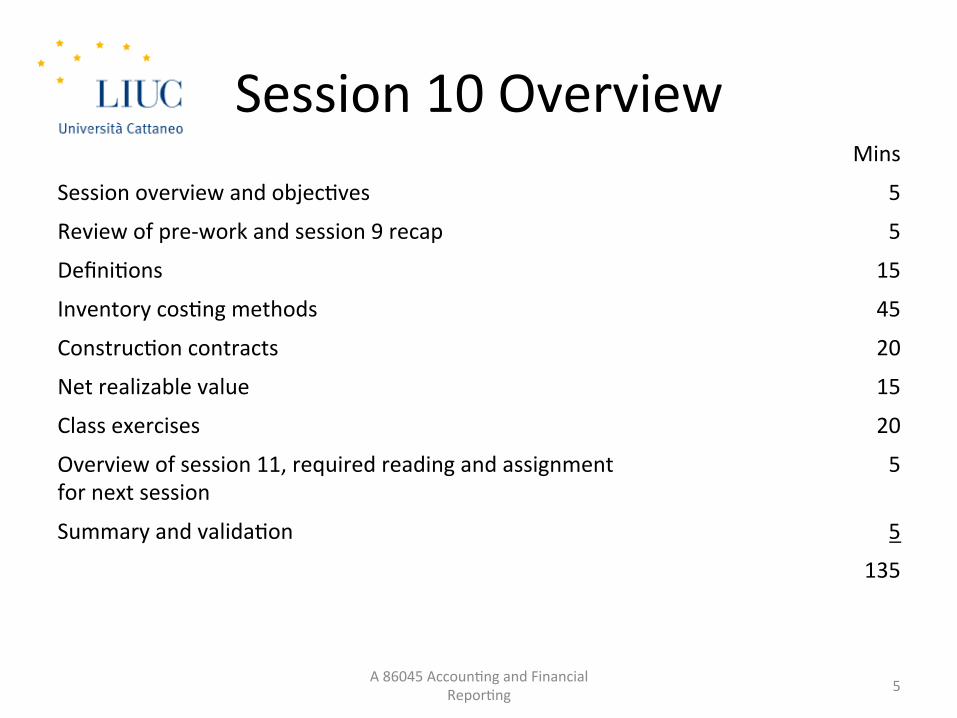

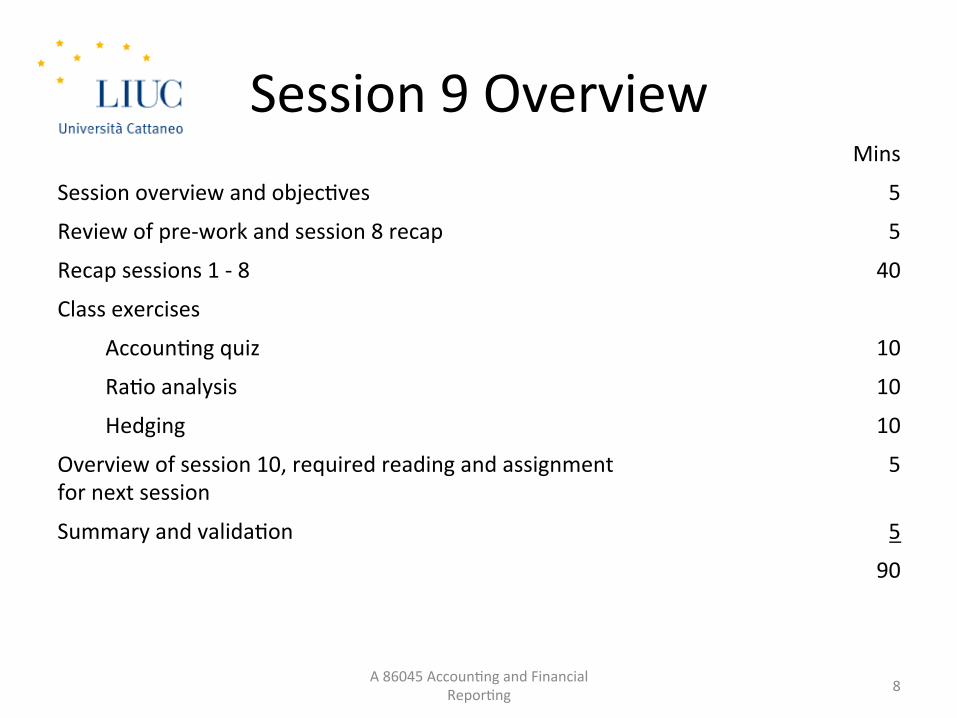

Session 10 Overview Mins

Session overview and objec,ves 5

Review of pre-‐work and session 9 recap 5

Defini,ons 15

Inventory cos,ng methods 45

Construc,on contracts 20

Net realizable value 15

Class exercises 20

Overview of session 11, required reading and assignment for next session

5

Summary and valida,on 5

135

5 A 86045 Accoun,ng and Financial Repor,ng

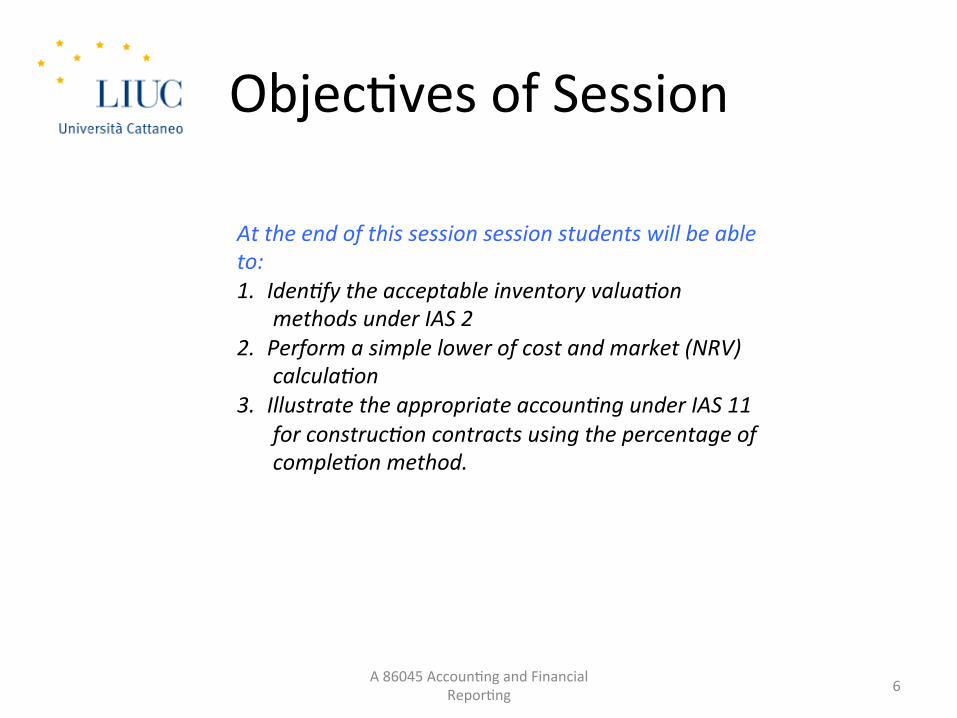

Objec,ves of Session

A 86045 Accoun,ng and Financial Repor,ng 6

At the end of this session session students will be able to: 1. Iden:fy the acceptable inventory valua:on

methods under IAS 2 2. Perform a simple lower of cost and market (NRV)

calcula:on 3. Illustrate the appropriate accoun:ng under IAS 11

for construc:on contracts using the percentage of comple:on method.

SESSION 9 RECAP AND PRE-‐WORK SESSION 10

A 86045 Accoun,ng and Financial Repor,ng 7

Session 9 Overview Mins

Session overview and objec,ves 5

Review of pre-‐work and session 8 recap 5

Recap sessions 1 -‐ 8 40

Class exercises

Accoun,ng quiz 10

Ra,o analysis 10

Hedging 10

Overview of session 10, required reading and assignment for next session

5

Summary and valida,on 5

90

8 A 86045 Accoun,ng and Financial Repor,ng

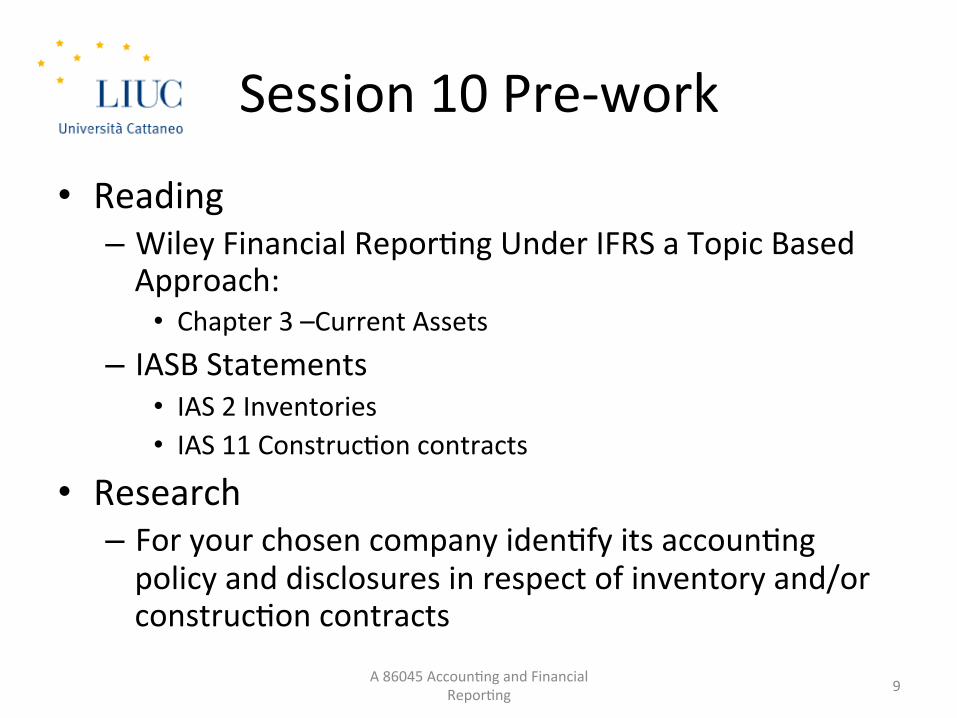

Session 10 Pre-‐work

• Reading – Wiley Financial Repor,ng Under IFRS a Topic Based Approach: • Chapter 3 –Current Assets

– IASB Statements • IAS 2 Inventories • IAS 11 Construc,on contracts

• Research – For your chosen company iden,fy its accoun,ng policy and disclosures in respect of inventory and/or construc,on contracts

A 86045 Accoun,ng and Financial Repor,ng 9

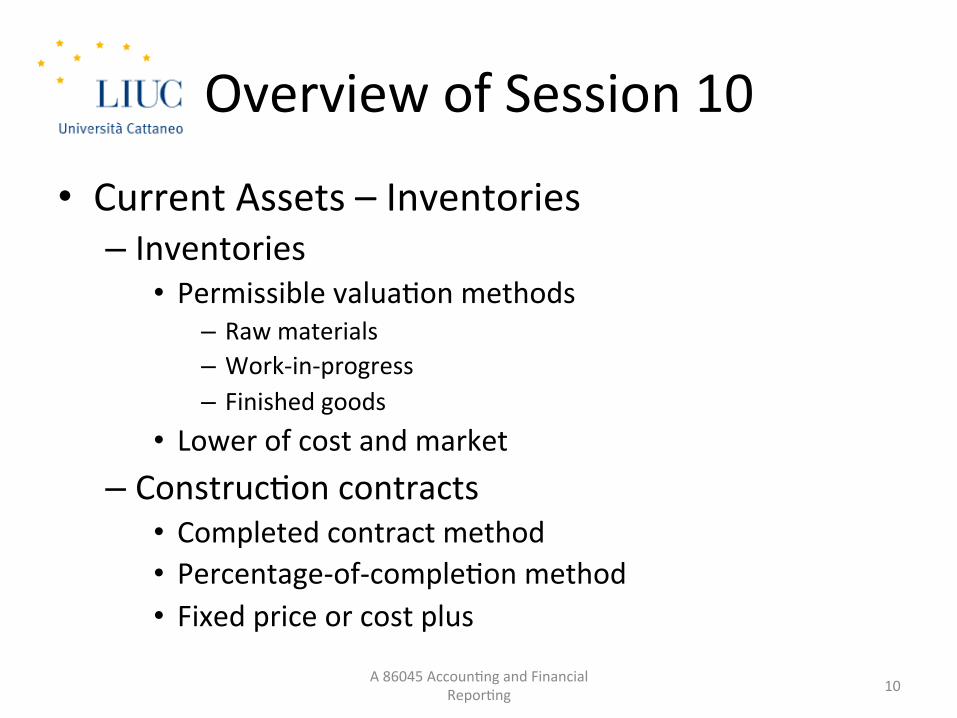

Overview of Session 10

• Current Assets – Inventories – Inventories

• Permissible valua,on methods – Raw materials – Work-‐in-‐progress – Finished goods

• Lower of cost and market – Construc,on contracts

• Completed contract method • Percentage-‐of-‐comple,on method • Fixed price or cost plus

A 86045 Accoun,ng and Financial Repor,ng 10

INVENTORIES

A 86045 Accoun,ng and Financial Repor,ng 11

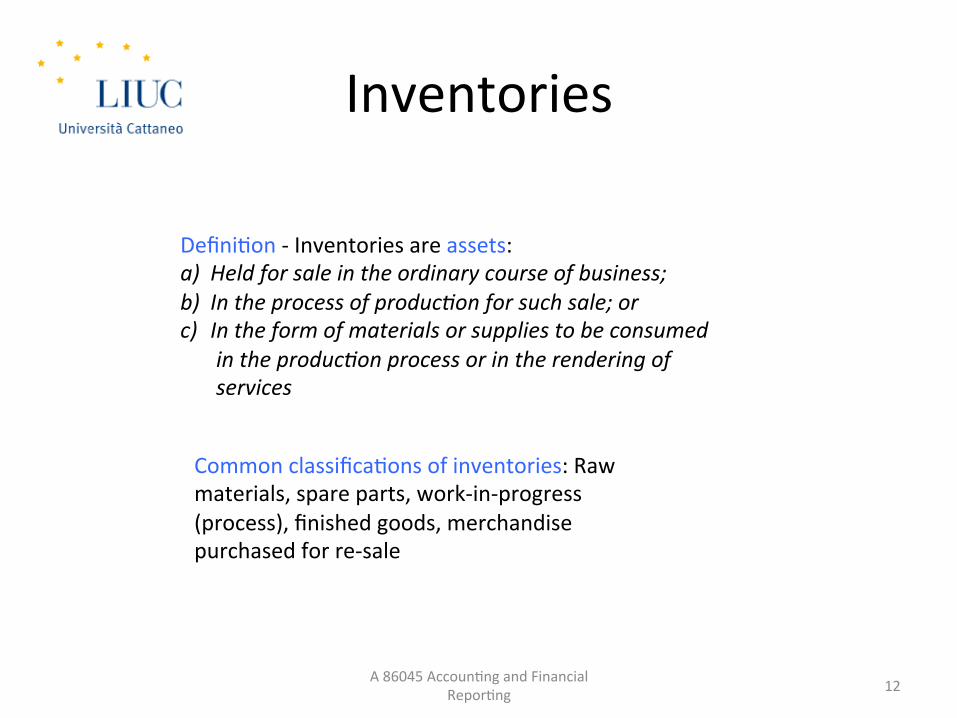

Inventories

A 86045 Accoun,ng and Financial Repor,ng 12

Defini,on -‐ Inventories are assets: a) Held for sale in the ordinary course of business; b) In the process of produc:on for such sale; or c) In the form of materials or supplies to be consumed

in the produc:on process or in the rendering of services

Common classifica,ons of inventories: Raw materials, spare parts, work-‐in-‐progress (process), finished goods, merchandise purchased for re-‐sale

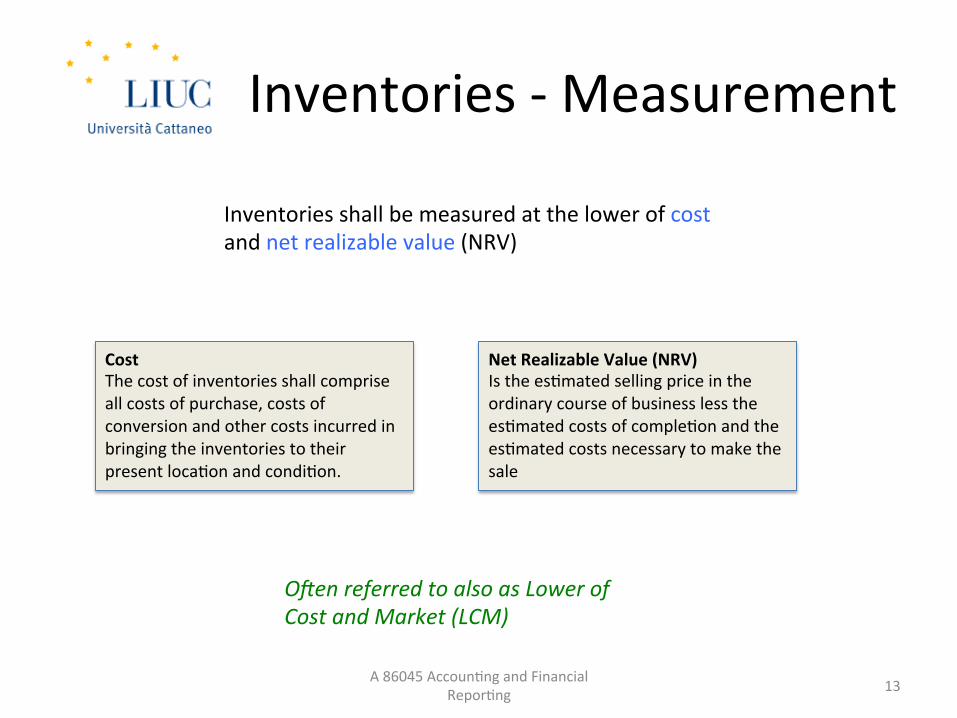

Inventories -‐ Measurement

A 86045 Accoun,ng and Financial Repor,ng 13

Inventories shall be measured at the lower of cost and net realizable value (NRV)

Cost The cost of inventories shall comprise all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present loca,on and condi,on.

Net Realizable Value (NRV) Is the es,mated selling price in the ordinary course of business less the es,mated costs of comple,on and the es,mated costs necessary to make the sale

OMen referred to also as Lower of Cost and Market (LCM)

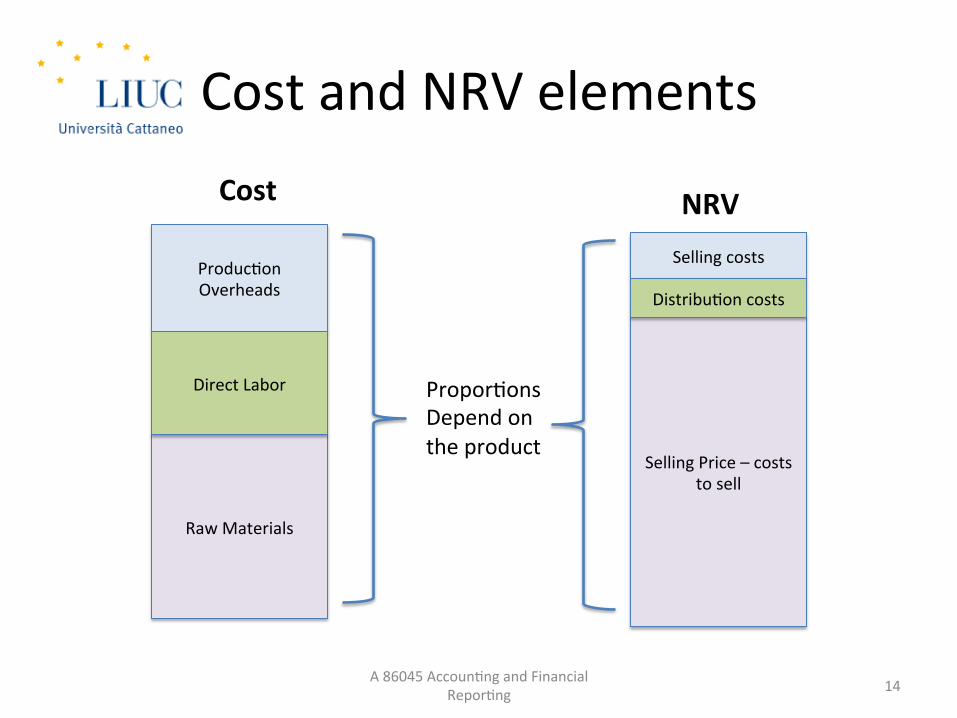

Cost and NRV elements

A 86045 Accoun,ng and Financial Repor,ng 14

Raw Materials

Produc,on Overheads

Direct Labor Propor,ons Depend on the product

Selling Price – costs to sell

Selling costs

Distribu,on costs

Cost NRV

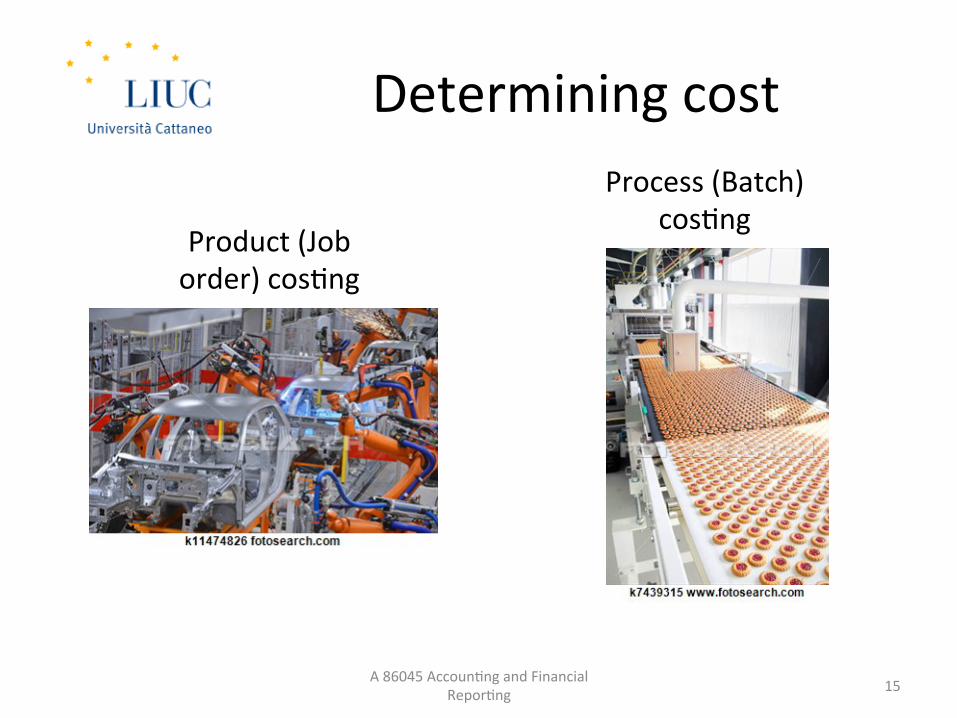

Determining cost

A 86045 Accoun,ng and Financial Repor,ng 15

Product (Job order) cos,ng

Process (Batch) cos,ng

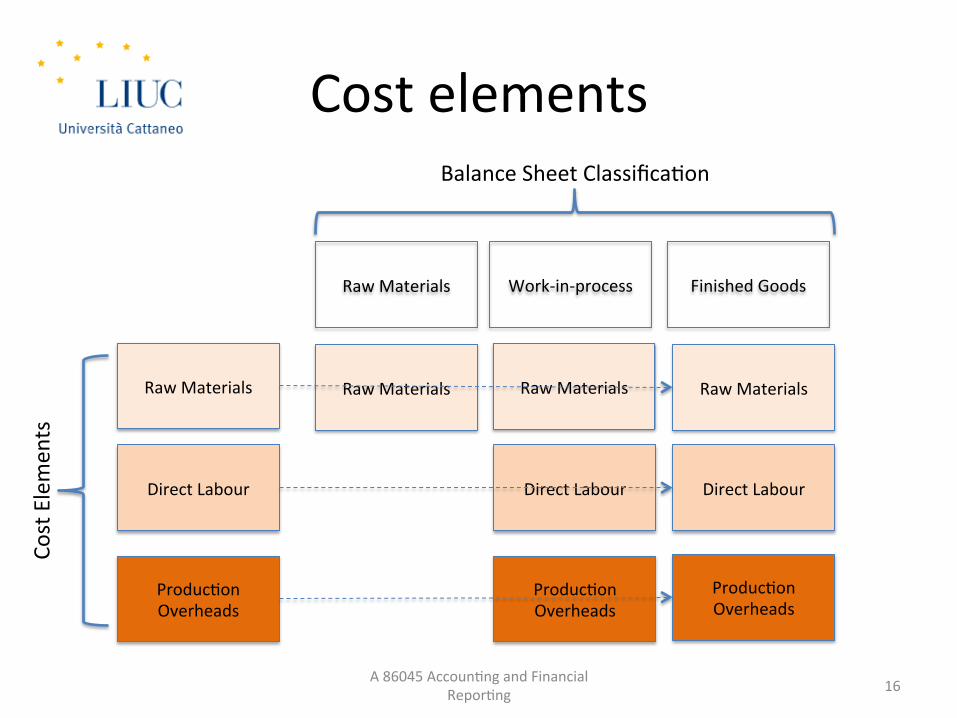

Cost elements

A 86045 Accoun,ng and Financial Repor,ng 16

Raw Materials

Work-‐in-‐process Finished Goods Raw Materials

Direct Labour

Produc,on Overheads

Raw Materials Raw Materials Raw Materials

Direct Labour Direct Labour

Produc,on Overheads

Produc,on Overheads

Balance Sheet Classifica,on

Cost Elemen

ts

Fixed and Variable Costs

A 86045 Accoun,ng and Financial Repor,ng 17

€

Units/ % of capacity u,lized

Sales

Variable costs

Fixed costs

Break-‐even Point

Total Cost

Profit

Loss

COSTING METHODS

A 86045 Accoun,ng and Financial Repor,ng 18

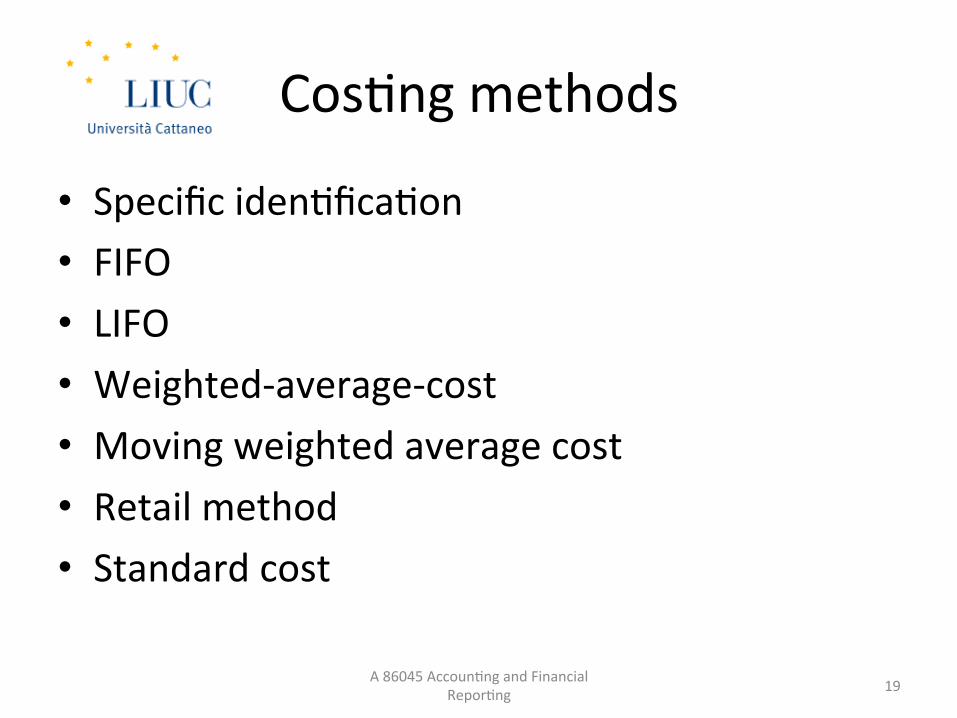

Cos,ng methods

• Specific iden,fica,on • FIFO • LIFO • Weighted-‐average-‐cost • Moving weighted average cost • Retail method • Standard cost

A 86045 Accoun,ng and Financial Repor,ng 19

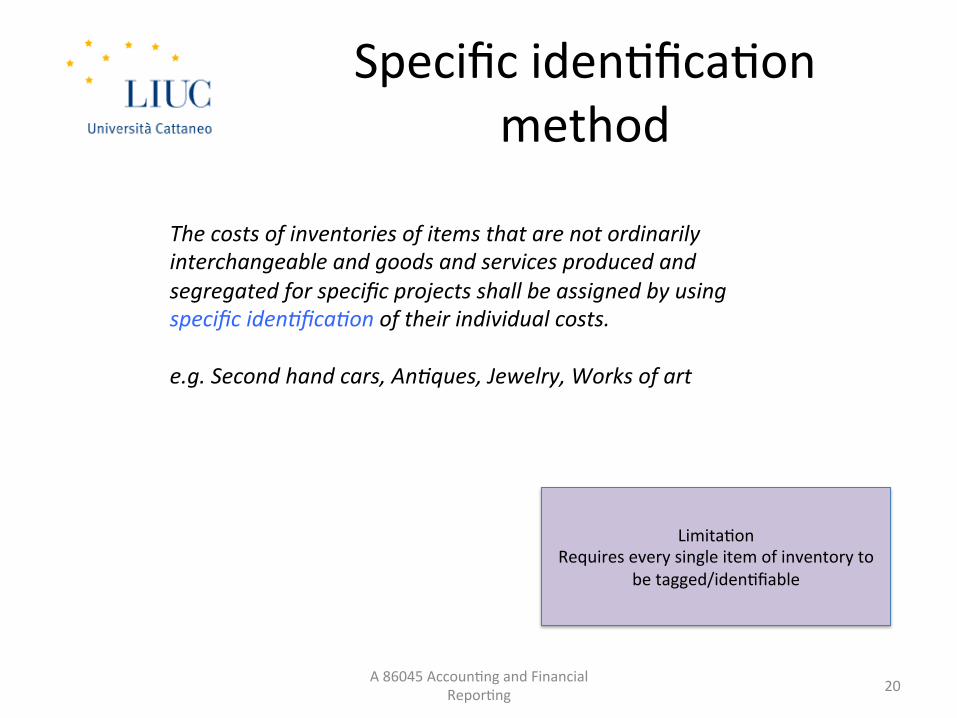

Specific iden,fica,on method

A 86045 Accoun,ng and Financial Repor,ng 20

The costs of inventories of items that are not ordinarily interchangeable and goods and services produced and segregated for specific projects shall be assigned by using specific iden:fica:on of their individual costs. e.g. Second hand cars, An:ques, Jewelry, Works of art

Limita,on Requires every single item of inventory to

be tagged/iden,fiable

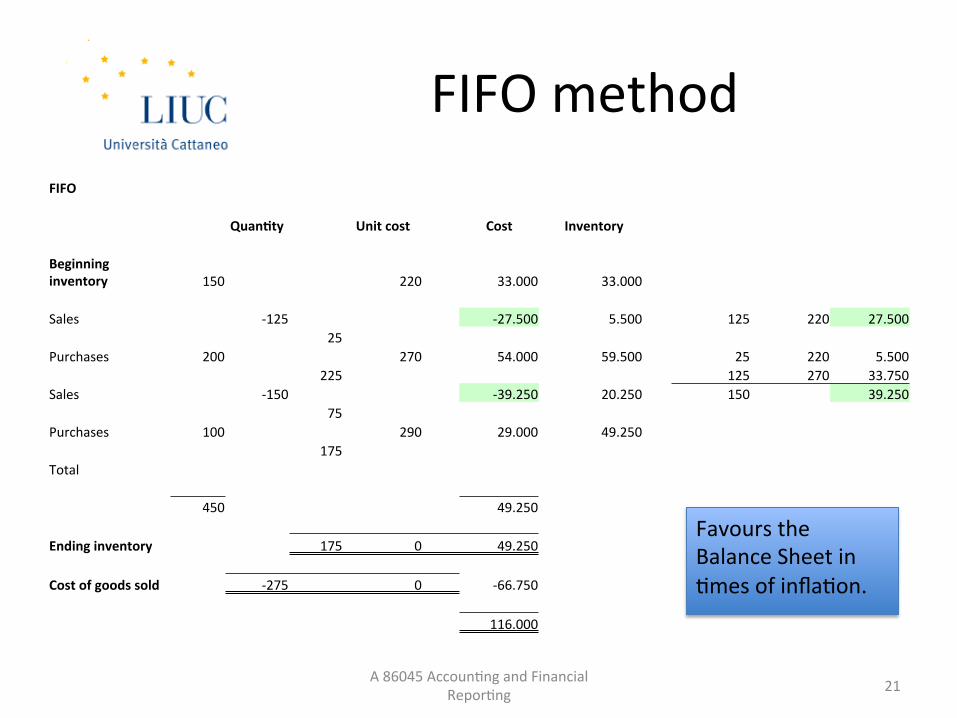

FIFO method

A 86045 Accoun,ng and Financial Repor,ng 21

FIFO

QuanGty Unit cost Cost Inventory

Beginning inventory 150 220 33.000 33.000

Sales -‐125 -‐27.500 5.500 125 220 27.500 25

Purchases 200 270 54.000 59.500 25 220 5.500 225 125 270 33.750

Sales -‐150 -‐39.250 20.250 150 39.250 75

Purchases 100 290 29.000 49.250 175

Total

450 49.250

Ending inventory 175 0 49.250

Cost of goods sold -‐275 0 -‐66.750

116.000

Favours the Balance Sheet in ,mes of infla,on.

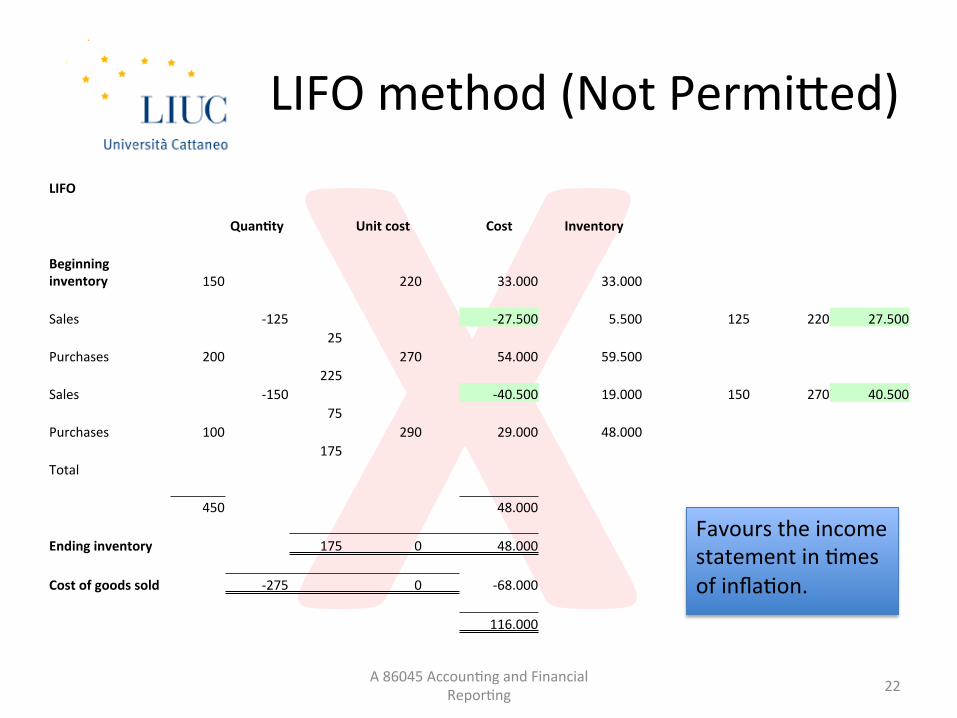

X LIFO

QuanGty Unit cost Cost Inventory

Beginning inventory 150 220 33.000 33.000

Sales -‐125 -‐27.500 5.500 125 220 27.500 25

Purchases 200 270 54.000 59.500 225

Sales -‐150 -‐40.500 19.000 150 270 40.500 75

Purchases 100 290 29.000 48.000 175

Total

450 48.000

Ending inventory 175 0 48.000

Cost of goods sold -‐275 0 -‐68.000

116.000

LIFO method (Not Permiged)

A 86045 Accoun,ng and Financial Repor,ng 22

Favours the income statement in ,mes of infla,on.

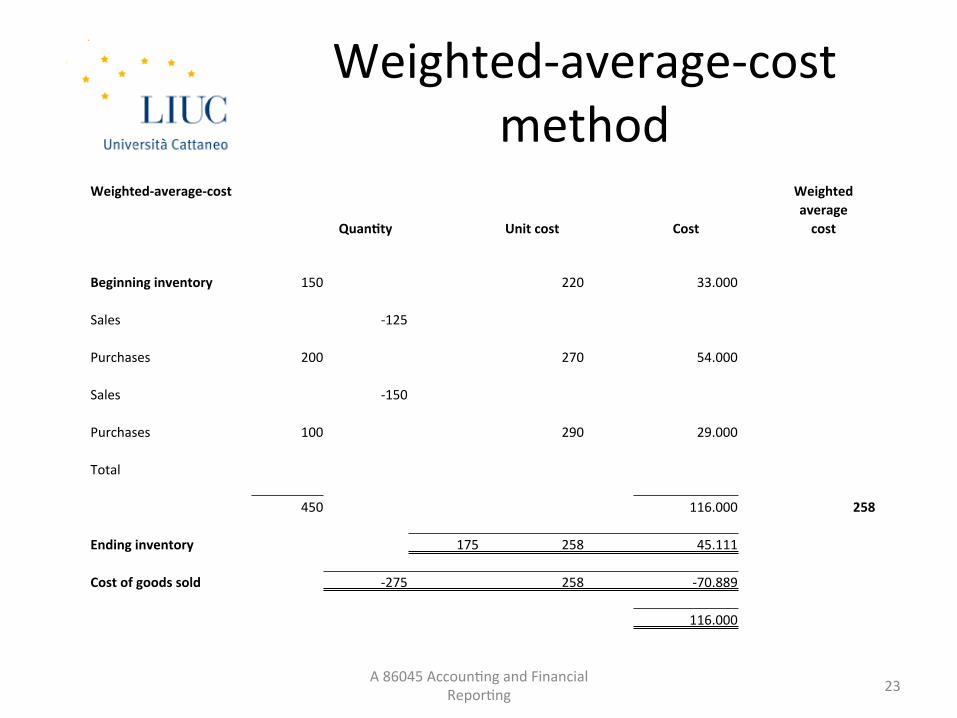

Weighted-‐average-‐cost method

A 86045 Accoun,ng and Financial Repor,ng 23

Weighted-‐average-‐cost Weighted average

QuanGty Unit cost Cost cost

Beginning inventory 150 220 33.000

Sales -‐125

Purchases 200 270 54.000

Sales -‐150

Purchases 100 290 29.000

Total

450 116.000 258

Ending inventory 175 258 45.111

Cost of goods sold -‐275 258 -‐70.889

116.000

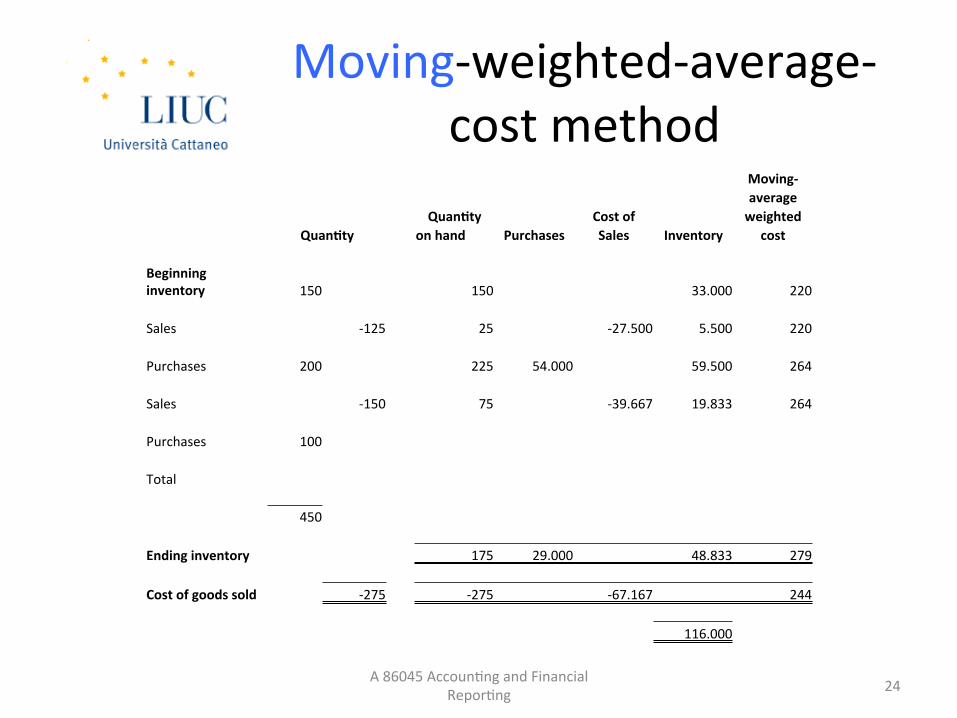

Moving-‐weighted-‐average-‐cost method

A 86045 Accoun,ng and Financial Repor,ng 24

Moving-‐ average

QuanGty Cost of weighted QuanGty on hand Purchases Sales Inventory cost

Beginning inventory 150 150 33.000 220

Sales -‐125 25 -‐27.500 5.500 220

Purchases 200 225 54.000 59.500 264

Sales -‐150 75 -‐39.667 19.833 264

Purchases 100

Total

450

Ending inventory 175 29.000 48.833 279

Cost of goods sold -‐275 -‐275 -‐67.167 244

116.000

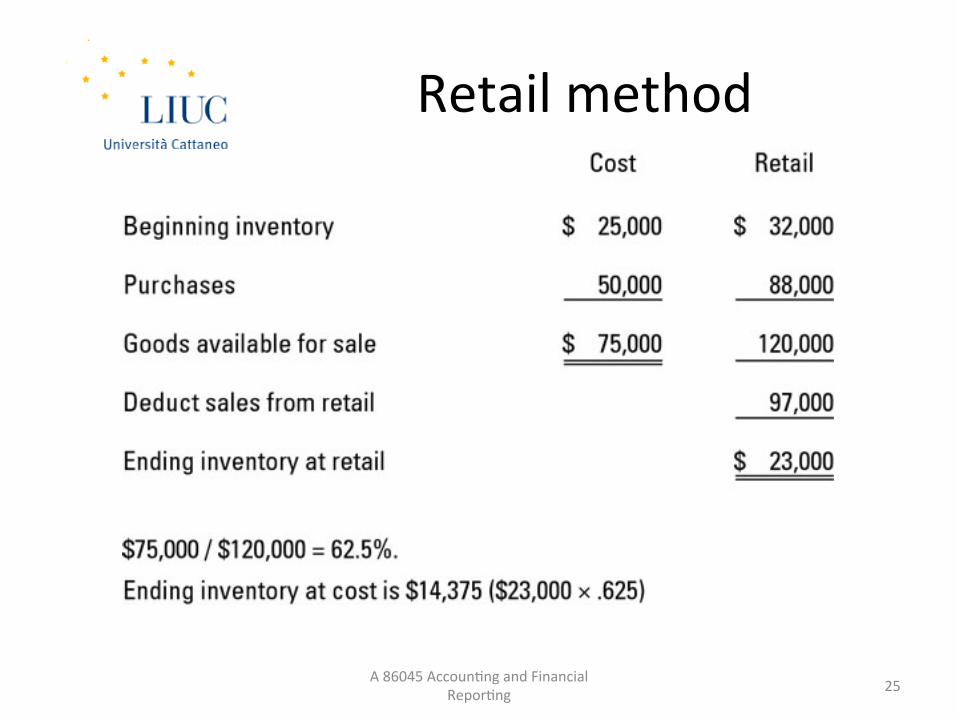

Retail method

A 86045 Accoun,ng and Financial Repor,ng 25

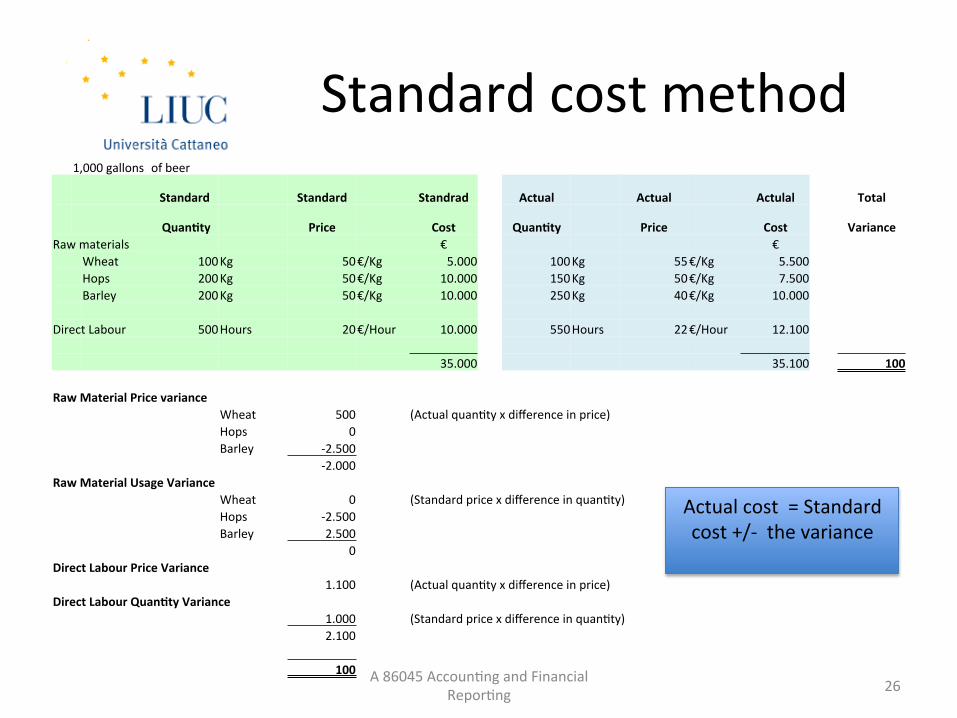

Standard cost method

A 86045 Accoun,ng and Financial Repor,ng 26

1,000 gallons of beer

Standard Standard Standrad Actual Actual Actulal Total

QuanGty Price Cost QuanGty Price Cost Variance Raw materials € €

Wheat 100 Kg 50 €/Kg 5.000 100 Kg 55 €/Kg 5.500 Hops 200 Kg 50 €/Kg 10.000 150 Kg 50 €/Kg 7.500 Barley 200 Kg 50 €/Kg 10.000 250 Kg 40 €/Kg 10.000

Direct Labour 500 Hours 20 €/Hour 10.000 550 Hours 22 €/Hour 12.100

35.000 35.100 100

Raw Material Price variance Wheat 500 (Actual quan,ty x difference in price) Hops 0 Barley -‐2.500

-‐2.000 Raw Material Usage Variance

Wheat 0 (Standard price x difference in quan,ty) Hops -‐2.500 Barley 2.500

0 Direct Labour Price Variance

1.100 (Actual quan,ty x difference in price) Direct Labour QuanGty Variance

1.000 (Standard price x difference in quan,ty) 2.100

100

Actual cost = Standard cost +/-‐ the variance

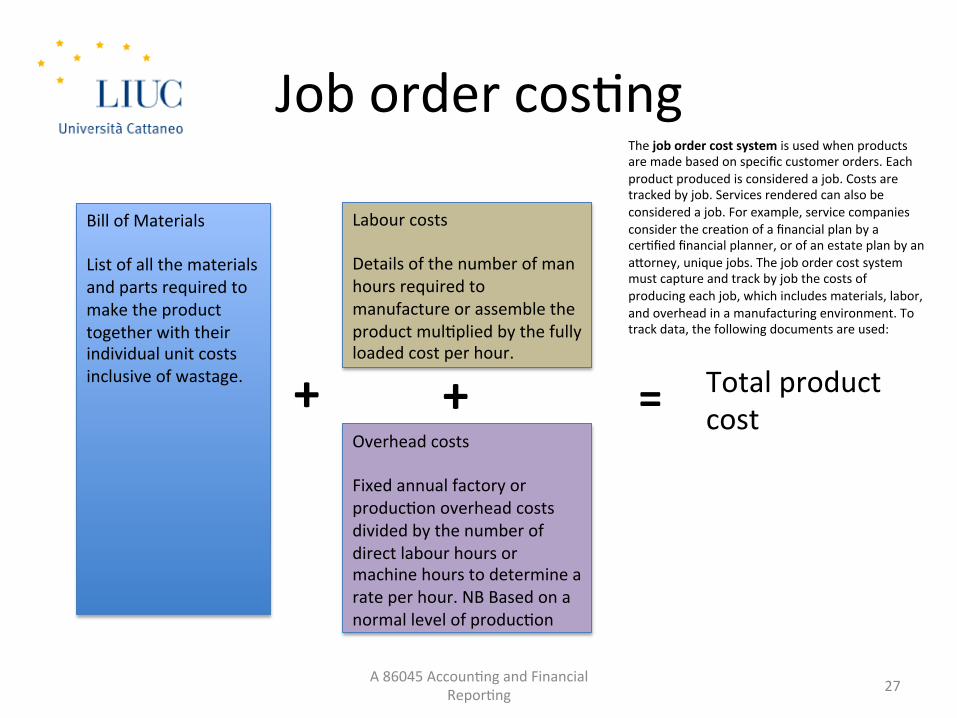

Job order cos,ng

A 86045 Accoun,ng and Financial Repor,ng 27

Bill of Materials List of all the materials and parts required to make the product together with their individual unit costs inclusive of wastage.

Labour costs Details of the number of man hours required to manufacture or assemble the product mul,plied by the fully loaded cost per hour.

Overhead costs Fixed annual factory or produc,on overhead costs divided by the number of direct labour hours or machine hours to determine a rate per hour. NB Based on a normal level of produc,on

+ + = Total product cost

The job order cost system is used when products are made based on specific customer orders. Each product produced is considered a job. Costs are tracked by job. Services rendered can also be considered a job. For example, service companies consider the crea,on of a financial plan by a cer,fied financial planner, or of an estate plan by an agorney, unique jobs. The job order cost system must capture and track by job the costs of producing each job, which includes materials, labor, and overhead in a manufacturing environment. To track data, the following documents are used:

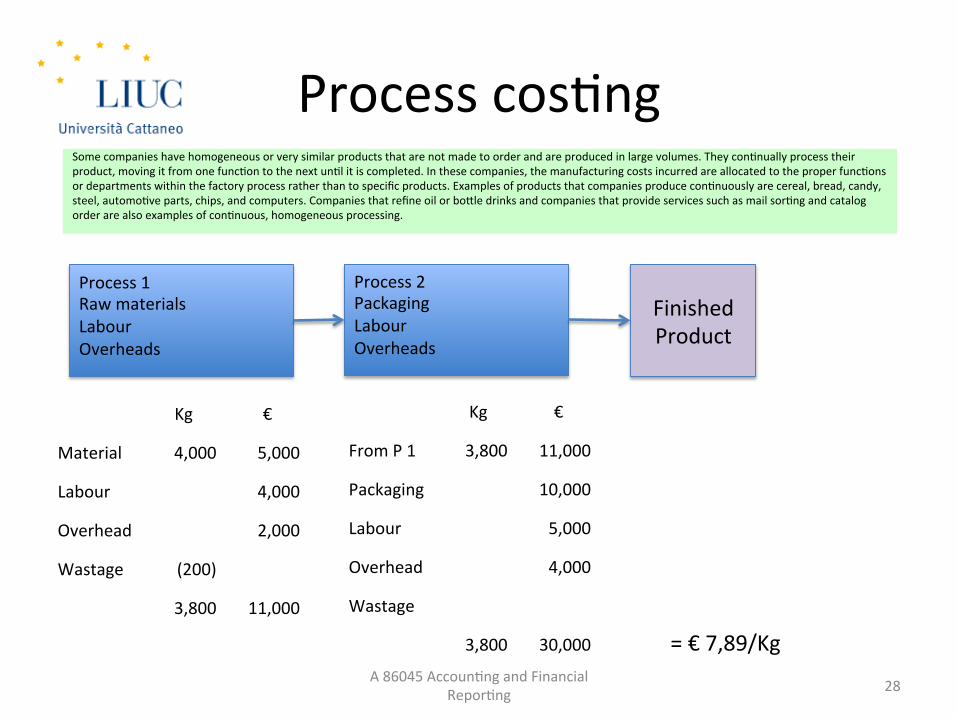

Process cos,ng

A 86045 Accoun,ng and Financial Repor,ng 28

Process 1 Raw materials Labour Overheads

Process 2 Packaging Labour Overheads

Finished Product

Kg €

Material 4,000 5,000

Labour 4,000

Overhead 2,000

Wastage (200)

3,800 11,000

Kg €

From P 1 3,800 11,000

Packaging 10,000

Labour 5,000

Overhead 4,000

Wastage

3,800 30,000 = € 7,89/Kg

Some companies have homogeneous or very similar products that are not made to order and are produced in large volumes. They con,nually process their product, moving it from one func,on to the next un,l it is completed. In these companies, the manufacturing costs incurred are allocated to the proper func,ons or departments within the factory process rather than to specific products. Examples of products that companies produce con,nuously are cereal, bread, candy, steel, automo,ve parts, chips, and computers. Companies that refine oil or bogle drinks and companies that provide services such as mail sor,ng and catalog order are also examples of con,nuous, homogeneous processing.

CONSTRUCTION CONTRACTS

A 86045 Accoun,ng and Financial Repor,ng 29

Construc,on contracts

A 86045 Accoun,ng and Financial Repor,ng 30

Defini,on –a construc:on contract is a contract specifically nego,ated for the construc,on of an asset or combina,on of assets that are closely interrelated or interdependent in terms of their design, technology and func,on or their ul,mate purpose or use.

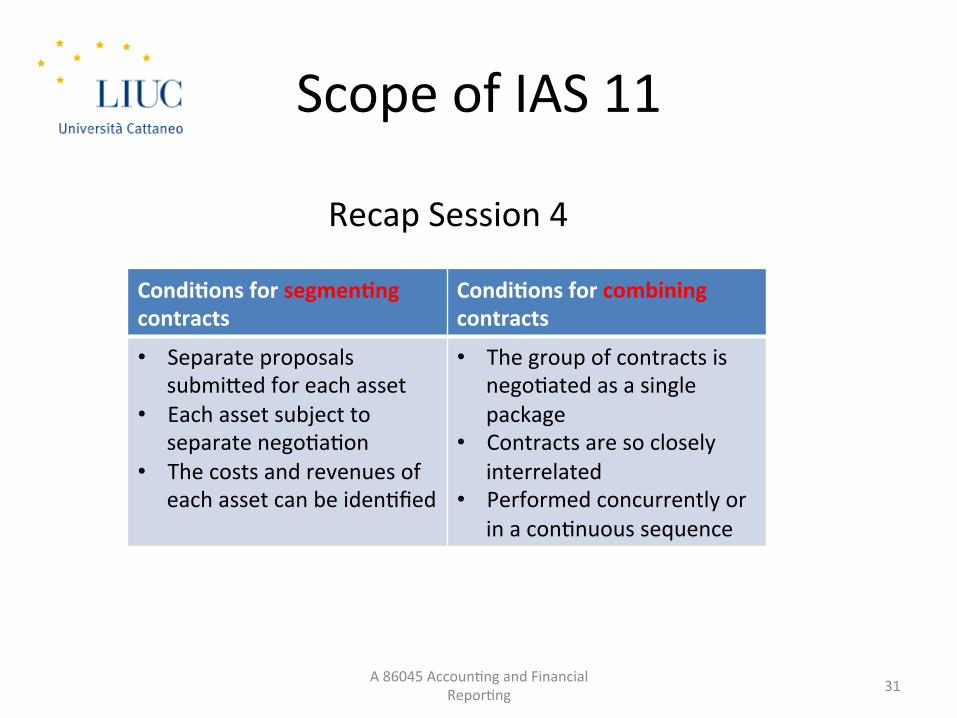

Scope of IAS 11

A 86045 Accoun,ng and Financial Repor,ng 31

CondiGons for segmenGng contracts

CondiGons for combining contracts

• Separate proposals submiged for each asset

• Each asset subject to separate nego,a,on

• The costs and revenues of each asset can be iden,fied

• The group of contracts is nego,ated as a single package

• Contracts are so closely interrelated

• Performed concurrently or in a con,nuous sequence

Recap Session 4

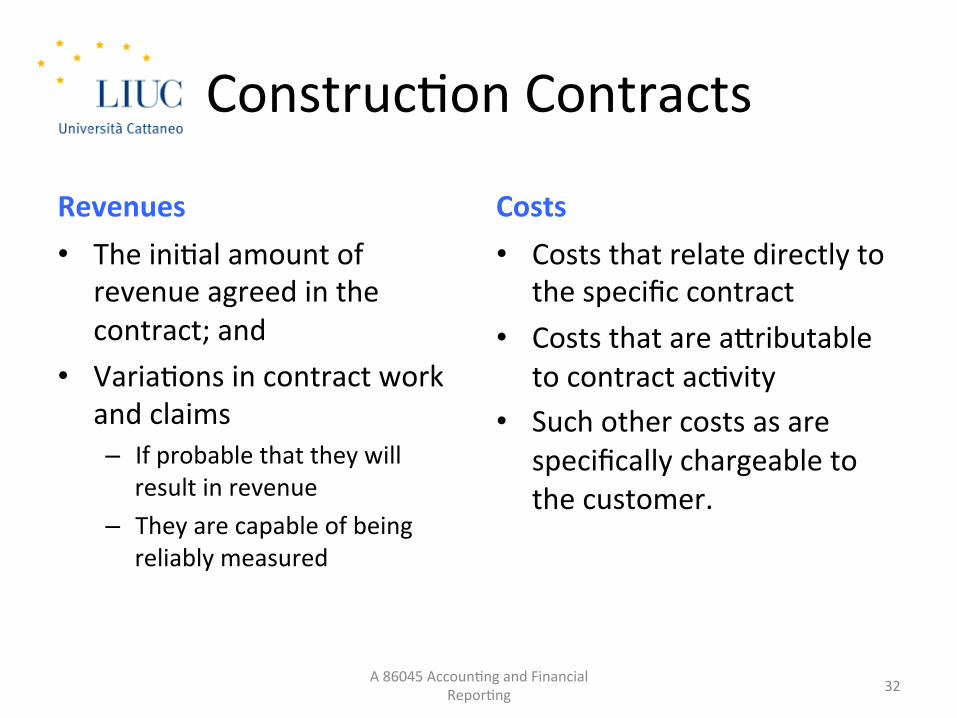

Construc,on Contracts

Revenues • The ini,al amount of

revenue agreed in the contract; and

• Varia,ons in contract work and claims – If probable that they will

result in revenue – They are capable of being

reliably measured

Costs • Costs that relate directly to

the specific contract • Costs that are agributable

to contract ac,vity • Such other costs as are

specifically chargeable to the customer.

A 86045 Accoun,ng and Financial Repor,ng 32

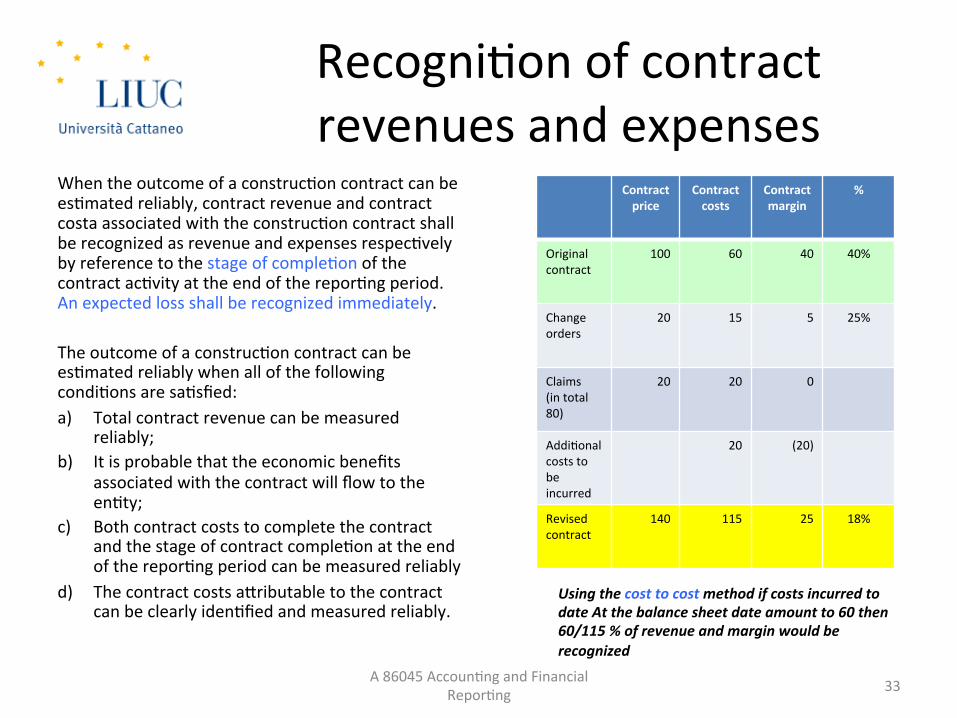

Recogni,on of contract revenues and expenses

When the outcome of a construc,on contract can be es,mated reliably, contract revenue and contract costa associated with the construc,on contract shall be recognized as revenue and expenses respec,vely by reference to the stage of comple,on of the contract ac,vity at the end of the repor,ng period. An expected loss shall be recognized immediately. The outcome of a construc,on contract can be es,mated reliably when all of the following condi,ons are sa,sfied: a) Total contract revenue can be measured

reliably; b) It is probable that the economic benefits

associated with the contract will flow to the en,ty;

c) Both contract costs to complete the contract and the stage of contract comple,on at the end of the repor,ng period can be measured reliably

d) The contract costs agributable to the contract can be clearly iden,fied and measured reliably.

Contract price

Contract costs

Contract margin

%

Original contract

100 60 40 40%

Change orders

20 15 5 25%

Claims (in total 80)

20 20 0

Addi,onal costs to be incurred

20 (20)

Revised contract

140 115 25 18%

A 86045 Accoun,ng and Financial Repor,ng 33

Using the cost to cost method if costs incurred to date At the balance sheet date amount to 60 then 60/115 % of revenue and margin would be recognized

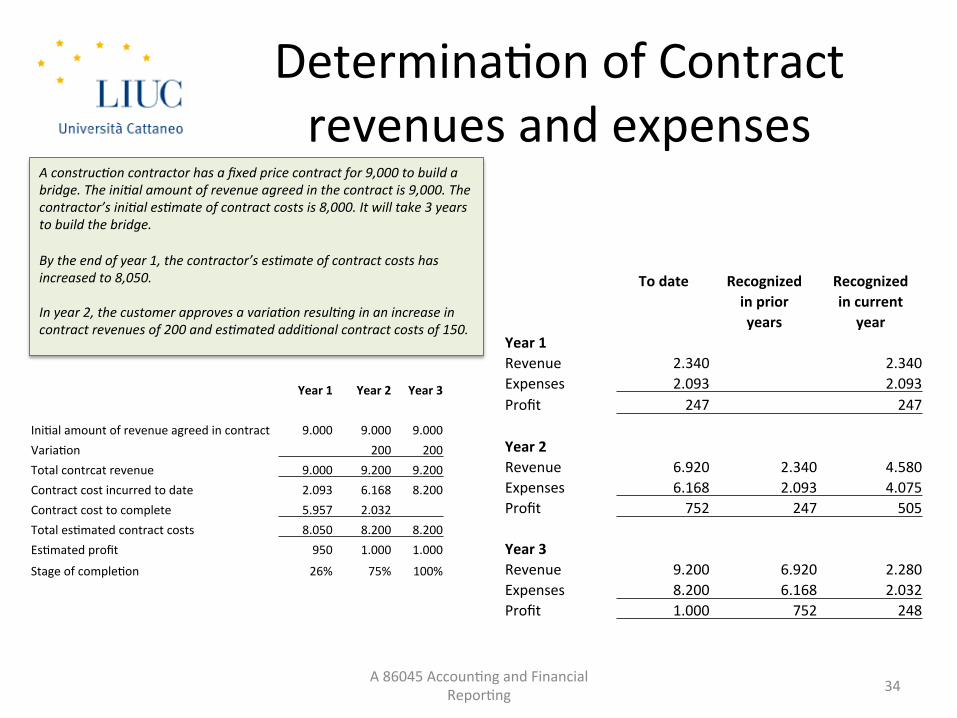

Determina,on of Contract revenues and expenses

A 86045 Accoun,ng and Financial Repor,ng 34

Year 1 Year 2 Year 3

Ini,al amount of revenue agreed in contract 9.000 9.000 9.000 Varia,on 200 200 Total contrcat revenue 9.000 9.200 9.200 Contract cost incurred to date 2.093 6.168 8.200 Contract cost to complete 5.957 2.032 Total es,mated contract costs 8.050 8.200 8.200 Es,mated profit 950 1.000 1.000

Stage of comple,on 26% 75% 100%

To date Recognized Recognized in prior in current years year

Year 1 Revenue 2.340 2.340 Expenses 2.093 2.093 Profit 247 247

Year 2 Revenue 6.920 2.340 4.580 Expenses 6.168 2.093 4.075 Profit 752 247 505

Year 3 Revenue 9.200 6.920 2.280 Expenses 8.200 6.168 2.032 Profit 1.000 752 248

A construc:on contractor has a fixed price contract for 9,000 to build a bridge. The ini:al amount of revenue agreed in the contract is 9,000. The contractor’s ini:al es:mate of contract costs is 8,000. It will take 3 years to build the bridge. By the end of year 1, the contractor’s es:mate of contract costs has increased to 8,050. In year 2, the customer approves a varia:on resul:ng in an increase in contract revenues of 200 and es:mated addi:onal contract costs of 150.

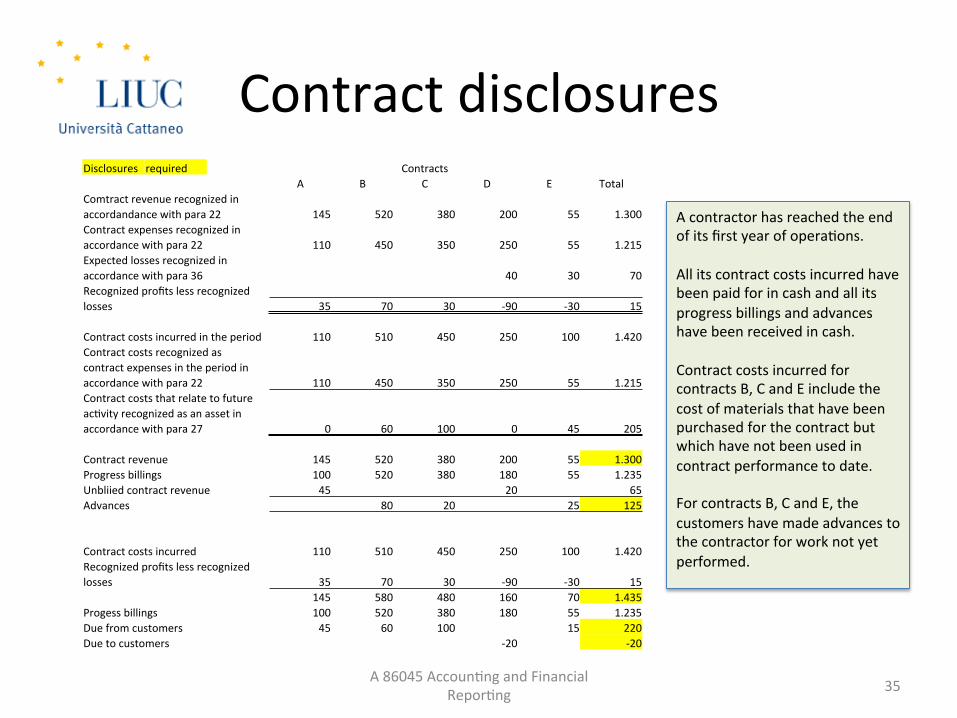

Contract disclosures

A 86045 Accoun,ng and Financial Repor,ng 35

Disclosures required Contracts A B C D E Total

Comtract revenue recognized in accordandance with para 22 145 520 380 200 55 1.300 Contract expenses recognized in accordance with para 22 110 450 350 250 55 1.215 Expected losses recognized in accordance with para 36 40 30 70 Recognized profits less recognized losses 35 70 30 -‐90 -‐30 15

Contract costs incurred in the period 110 510 450 250 100 1.420 Contract costs recognized as contract expenses in the period in accordance with para 22 110 450 350 250 55 1.215 Contract costs that relate to future ac,vity recognized as an asset in accordance with para 27 0 60 100 0 45 205

Contract revenue 145 520 380 200 55 1.300 Progress billings 100 520 380 180 55 1.235 Unbliied contract revenue 45 20 65 Advances 80 20 25 125

Contract costs incurred 110 510 450 250 100 1.420 Recognized profits less recognized losses 35 70 30 -‐90 -‐30 15

145 580 480 160 70 1.435 Progess billings 100 520 380 180 55 1.235 Due from customers 45 60 100 15 220 Due to customers -‐20 -‐20

A contractor has reached the end of its first year of opera,ons. All its contract costs incurred have been paid for in cash and all its progress billings and advances have been received in cash. Contract costs incurred for contracts B, C and E include the cost of materials that have been purchased for the contract but which have not been used in contract performance to date. For contracts B, C and E, the customers have made advances to the contractor for work not yet performed.

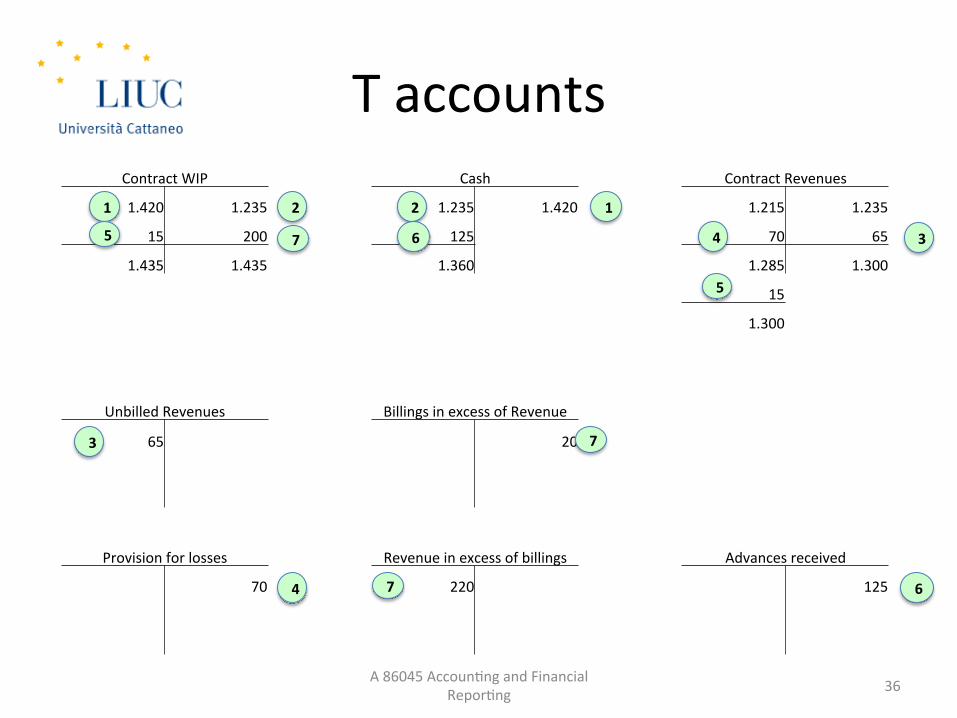

T accounts

A 86045 Accoun,ng and Financial Repor,ng 36

Contract WIP Cash Contract Revenues

1.420 1.235 1.235 1.420 1.215 1.235

15 200 125 70 65

1.435 1.435 1.360 1.285 1.300

15

1.300

Unbilled Revenues Billings in excess of Revenue

65 20

Provision for losses Revenue in excess of billings Advances received

70 220 125

1 122

3

3

4

4

5

5

6

67

7

7

NET REALIZABLE VALUE

A 86045 Accoun,ng and Financial Repor,ng 37

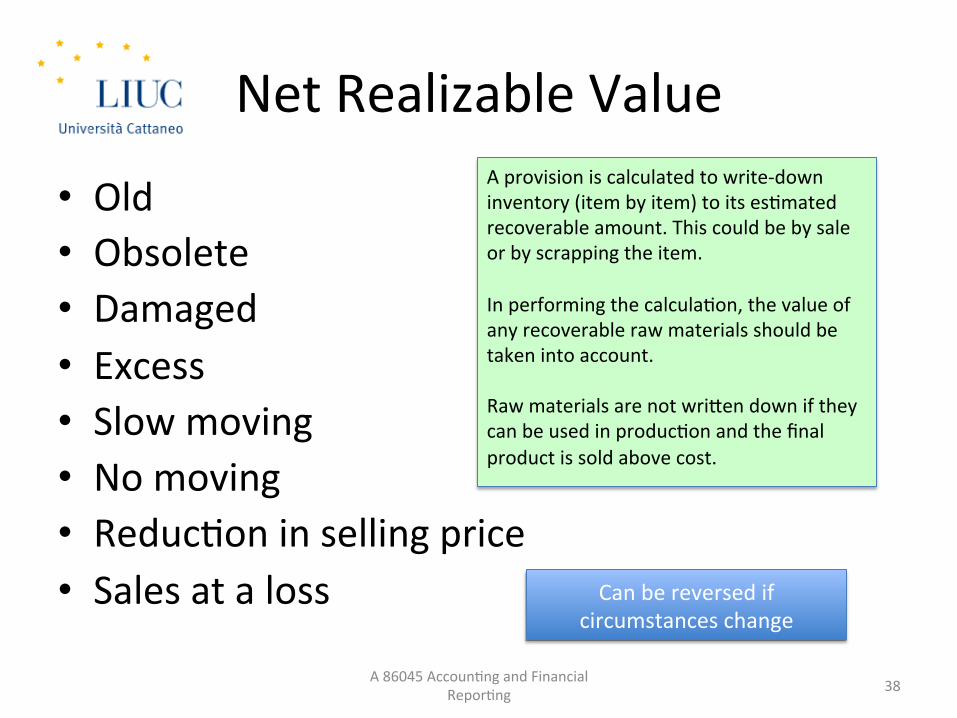

Net Realizable Value

• Old • Obsolete • Damaged • Excess • Slow moving • No moving • Reduc,on in selling price • Sales at a loss

A 86045 Accoun,ng and Financial Repor,ng 38

A provision is calculated to write-‐down inventory (item by item) to its es,mated recoverable amount. This could be by sale or by scrapping the item. In performing the calcula,on, the value of any recoverable raw materials should be taken into account. Raw materials are not wrigen down if they can be used in produc,on and the final product is sold above cost.

Can be reversed if circumstances change

CLASS EXERCISE/EXAMPLES Source IAS 36 Illustra,ve Examples

A 86045 Accoun,ng and Financial Repor,ng 39

Class exercise-‐ construc,on contract

A 86045 Accoun,ng and Financial Repor,ng 40

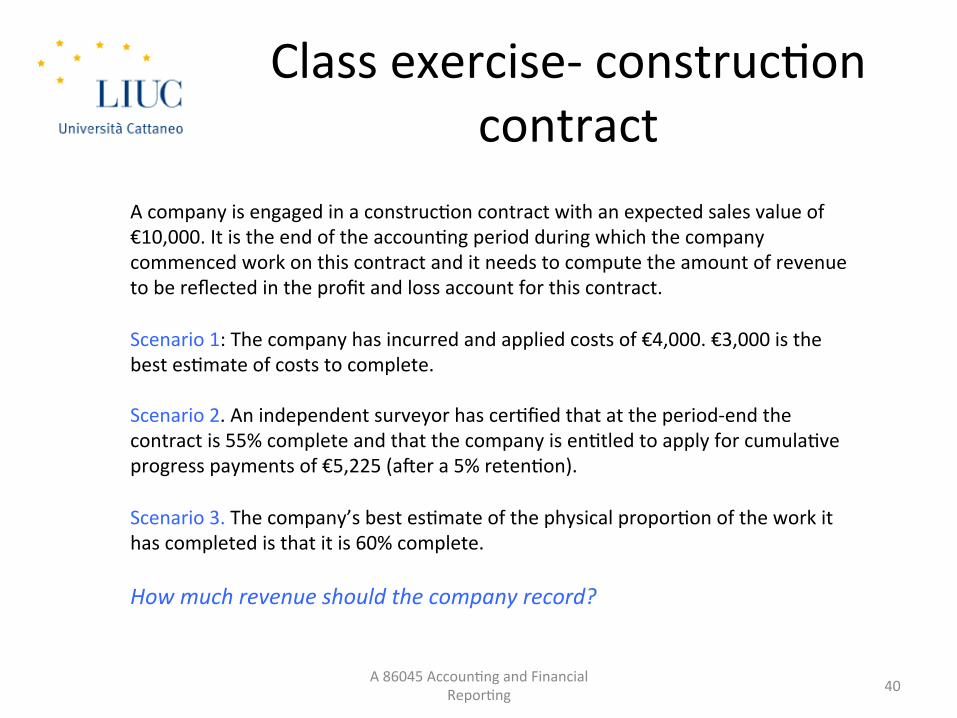

A company is engaged in a construc,on contract with an expected sales value of €10,000. It is the end of the accoun,ng period during which the company commenced work on this contract and it needs to compute the amount of revenue to be reflected in the profit and loss account for this contract. Scenario 1: The company has incurred and applied costs of €4,000. €3,000 is the best es,mate of costs to complete. Scenario 2. An independent surveyor has cer,fied that at the period-‐end the contract is 55% complete and that the company is en,tled to apply for cumula,ve progress payments of €5,225 (aner a 5% reten,on). Scenario 3. The company’s best es,mate of the physical propor,on of the work it has completed is that it is 60% complete. How much revenue should the company record?

Class exercise cont’d

A 86045 Accoun,ng and Financial Repor,ng 41

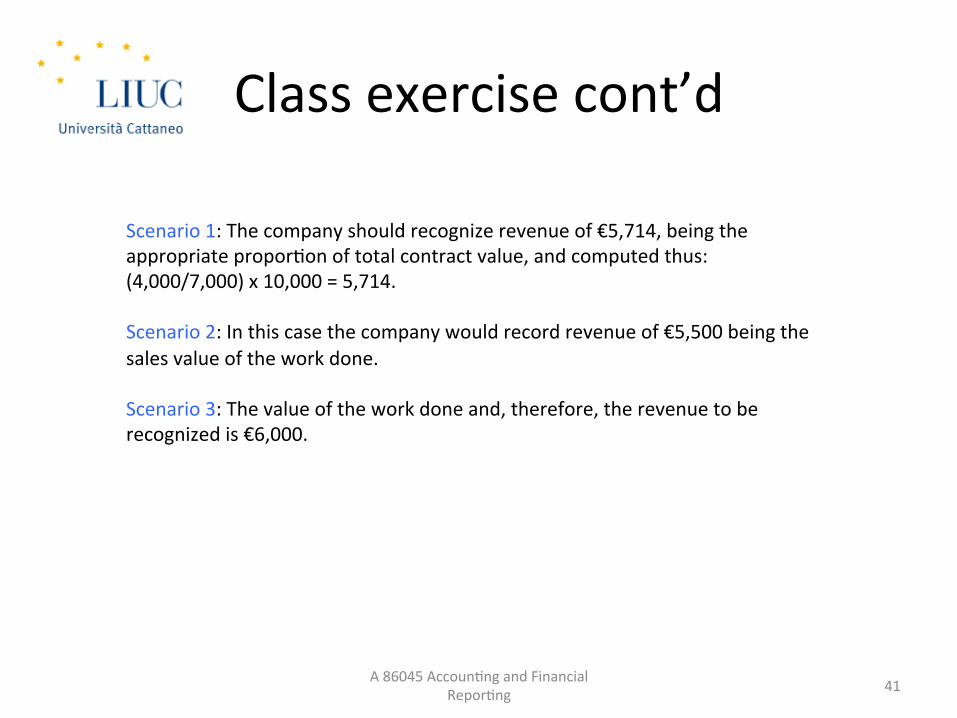

Scenario 1: The company should recognize revenue of €5,714, being the appropriate propor,on of total contract value, and computed thus: (4,000/7,000) x 10,000 = 5,714. Scenario 2: In this case the company would record revenue of €5,500 being the sales value of the work done. Scenario 3: The value of the work done and, therefore, the revenue to be recognized is €6,000.

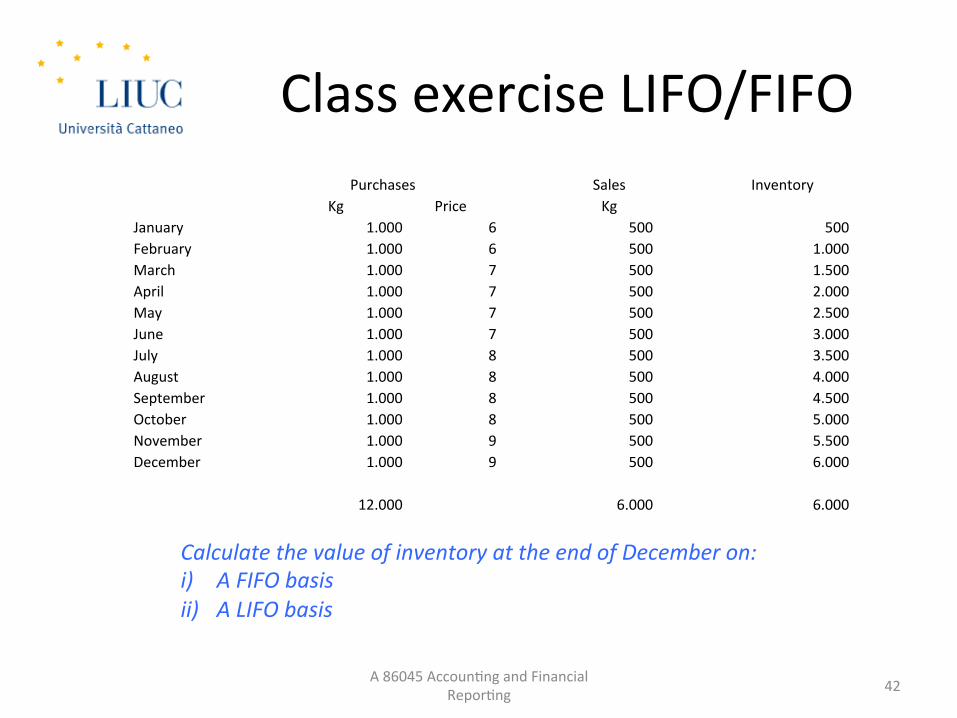

Class exercise LIFO/FIFO

A 86045 Accoun,ng and Financial Repor,ng 42

Purchases Sales Inventory Kg Price Kg

January 1.000 6 500 500 February 1.000 6 500 1.000 March 1.000 7 500 1.500 April 1.000 7 500 2.000 May 1.000 7 500 2.500 June 1.000 7 500 3.000 July 1.000 8 500 3.500 August 1.000 8 500 4.000 September 1.000 8 500 4.500 October 1.000 8 500 5.000 November 1.000 9 500 5.500 December 1.000 9 500 6.000

12.000 6.000 6.000

Calculate the value of inventory at the end of December on: i) A FIFO basis ii) A LIFO basis

Class exercise cont’d

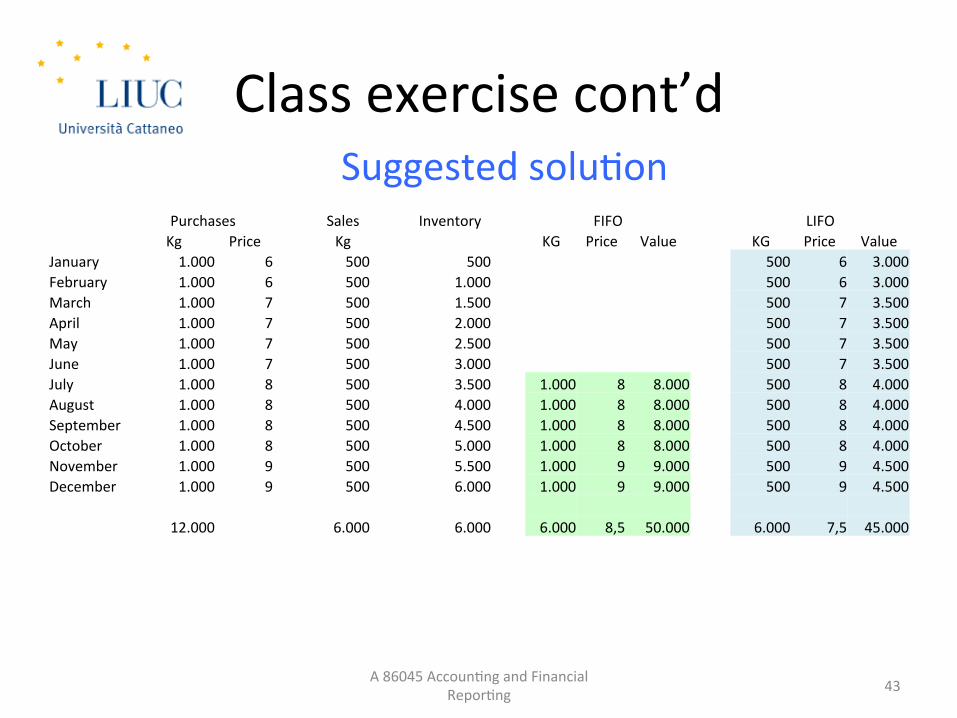

A 86045 Accoun,ng and Financial Repor,ng 43

Purchases Sales Inventory FIFO LIFO Kg Price Kg KG Price Value KG Price Value

January 1.000 6 500 500 500 6 3.000 February 1.000 6 500 1.000 500 6 3.000 March 1.000 7 500 1.500 500 7 3.500 April 1.000 7 500 2.000 500 7 3.500 May 1.000 7 500 2.500 500 7 3.500 June 1.000 7 500 3.000 500 7 3.500 July 1.000 8 500 3.500 1.000 8 8.000 500 8 4.000 August 1.000 8 500 4.000 1.000 8 8.000 500 8 4.000 September 1.000 8 500 4.500 1.000 8 8.000 500 8 4.000 October 1.000 8 500 5.000 1.000 8 8.000 500 8 4.000 November 1.000 9 500 5.500 1.000 9 9.000 500 9 4.500 December 1.000 9 500 6.000 1.000 9 9.000 500 9 4.500

12.000 6.000 6.000 6.000 8,5 50.000 6.000 7,5 45.000

Suggested solu,on

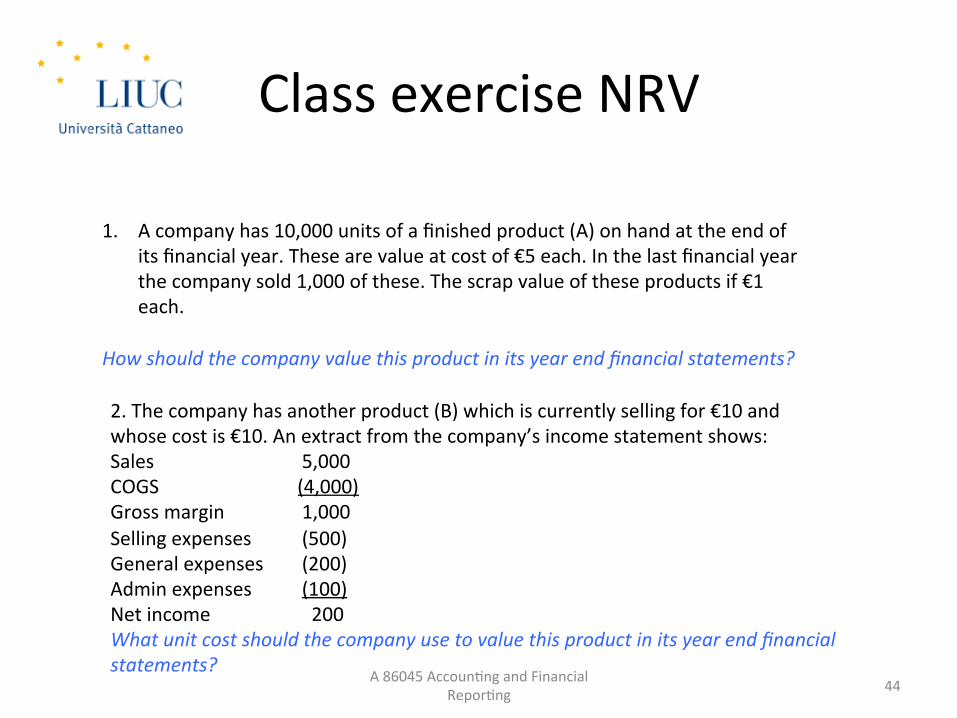

Class exercise NRV

A 86045 Accoun,ng and Financial Repor,ng 44

1. A company has 10,000 units of a finished product (A) on hand at the end of its financial year. These are value at cost of €5 each. In the last financial year the company sold 1,000 of these. The scrap value of these products if €1 each.

How should the company value this product in its year end financial statements?

2. The company has another product (B) which is currently selling for €10 and whose cost is €10. An extract from the company’s income statement shows: Sales 5,000 COGS (4,000) Gross margin 1,000 Selling expenses (500) General expenses (200) Admin expenses (100) Net income 200 What unit cost should the company use to value this product in its year end financial statements?

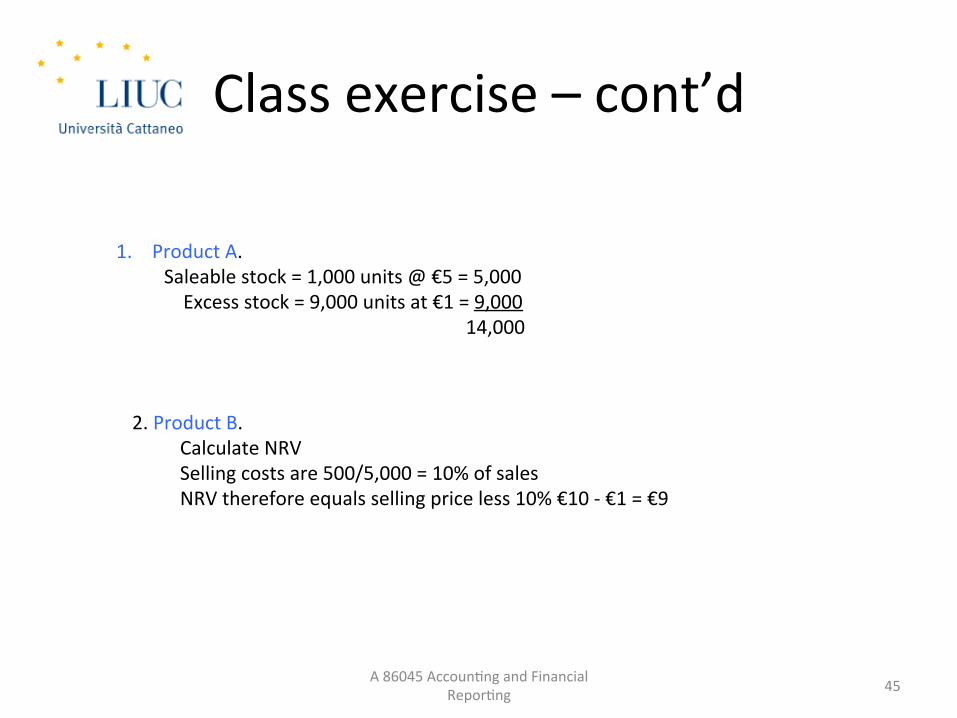

Class exercise – cont’d

A 86045 Accoun,ng and Financial Repor,ng 45

1. Product A. Saleable stock = 1,000 units @ €5 = 5,000 Excess stock = 9,000 units at €1 = 9,000 14,000

2. Product B. Calculate NRV Selling costs are 500/5,000 = 10% of sales NRV therefore equals selling price less 10% €10 -‐ €1 = €9

OVERVIEW, REQUIRED READING AND ASSIGNMENT FOR NEXT SESSION

A 86045 Accoun,ng and Financial Repor,ng 46

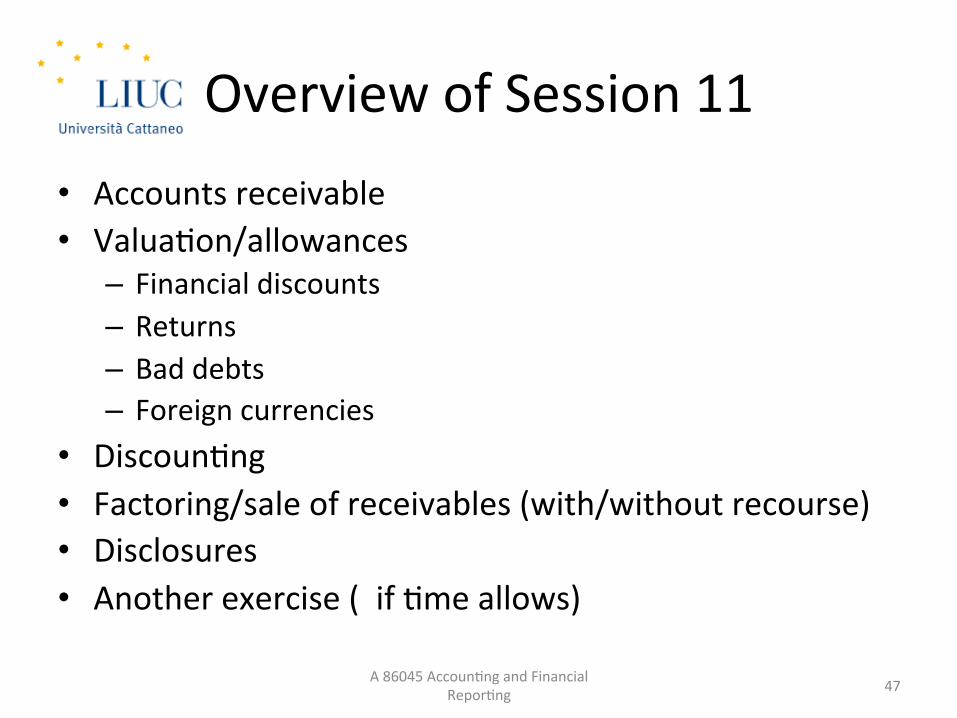

Overview of Session 11

A 86045 Accoun,ng and Financial Repor,ng 47

• Accounts receivable • Valua,on/allowances – Financial discounts – Returns – Bad debts – Foreign currencies

• Discoun,ng • Factoring/sale of receivables (with/without recourse) • Disclosures • Another exercise ( if ,me allows)

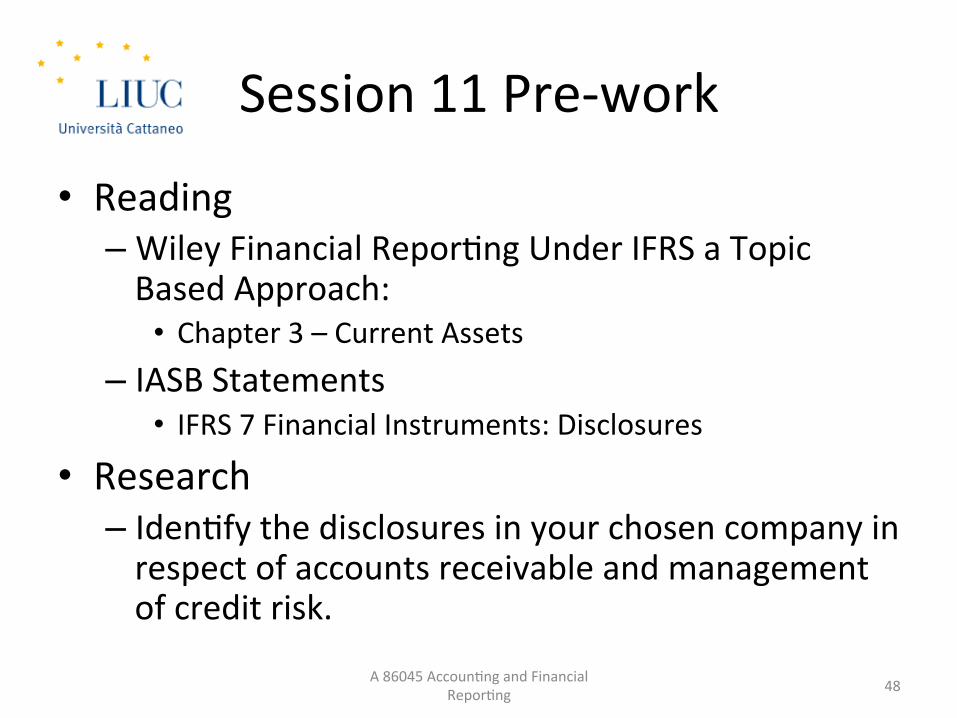

Session 11 Pre-‐work

• Reading – Wiley Financial Repor,ng Under IFRS a Topic Based Approach: • Chapter 3 – Current Assets

– IASB Statements • IFRS 7 Financial Instruments: Disclosures

• Research – Iden,fy the disclosures in your chosen company in respect of accounts receivable and management of credit risk.

A 86045 Accoun,ng and Financial Repor,ng 48

SUMMARY AND VALIDATION

A 86045 Accoun,ng and Financial Repor,ng 49

Summary of Session 10

A 86045 Accoun,ng and Financial Repor,ng 50

• Inventories and Construc,on contracts • Lower of cost and NRV • Cost elements (materials, labour, overheads) • Cos,ng methods (FIFO, LIFO, WAC etc.) • Contract accoun,ng • NRV • Exercises (contracts, LIFO/FIFO, NRV)

Session 10 Valida,on

A 86045 Accoun,ng and Financial Repor,ng 51

• What are inventories? • Define Net Realizable Value (NRV) • What is included in cost? • Which cos,ng method is not allowed for IFRS? • What indicators might suggest that a NRV test might be required?

• When should construc,on contracts be aggregated?