Embed Size (px)

Citation preview

1

Compliance & Ethics Institute

604 Auditing for Corruption in Emerging Markets:Applying fraud detection skills to reduce corruption

October 14, 2012

Copyright © 2011 Deloitte Development LLC. All rights reserved.1 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

“At any given moment, there is a certain percentage of the population that’s up to no good.”

J. Edgar Hoover

2

Copyright © 2011 Deloitte Development LLC. All rights reserved.2 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

1. Compare and Contrast - Fraud vs. Corruption

2. Corruption Environment in Key Emerging Markets

3. How to leverage Fraud Detection and Fraud Auditing

Discussion Contents

Compare and Contrast Fraud vs. Corruption

3

Copyright © 2011 Deloitte Development LLC. All rights reserved.4 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

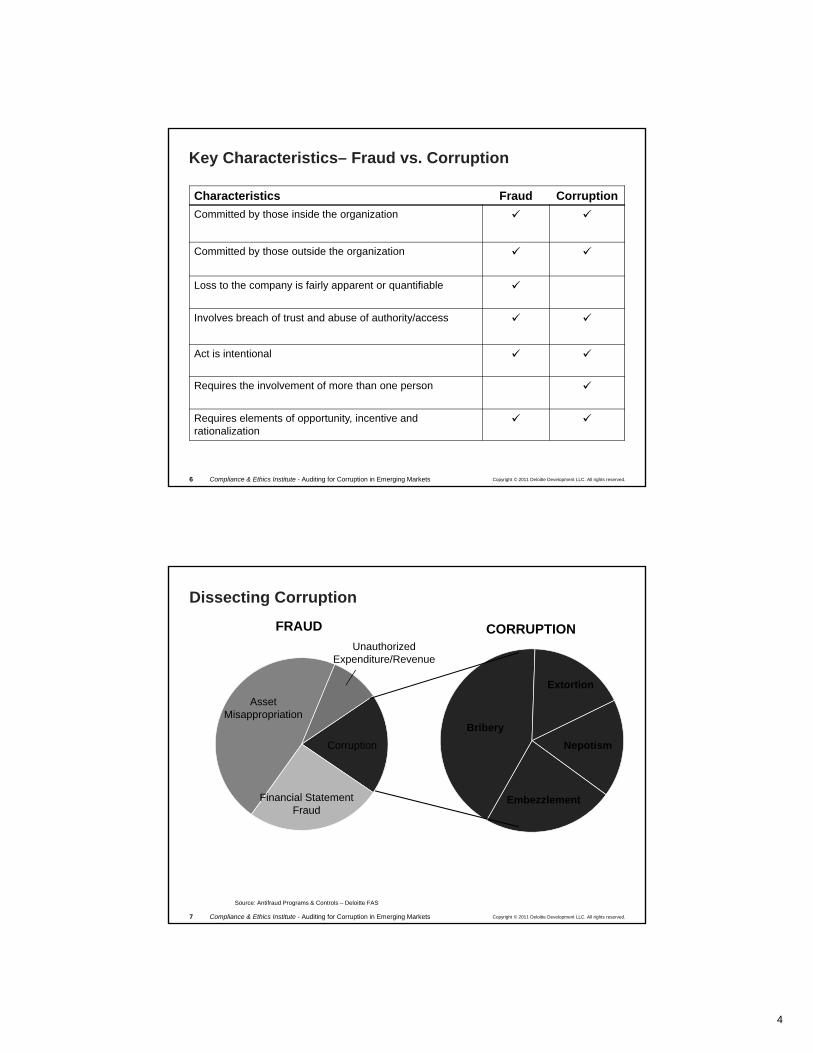

Fraud vs. Corruption

Fraud:Deriving undue benefit by bypassing some controls or bending some rules. Fraud schemes are used to commit corrupt activities.

• Asset Misappropriation

• Financial statement irregularities

• Unauthorized Expenditures

• Unauthorized Revenue

• Corruption

Copyright © 2011 Deloitte Development LLC. All rights reserved.5 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Fraud vs. Corruption

Corruption:Takes place in the form of providing illicit benefits; subset of fraud; harder to find; narrower scope than fraud.

4

Copyright © 2011 Deloitte Development LLC. All rights reserved.6 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Characteristics Fraud Corruption

Committed by those inside the organization

Committed by those outside the organization

Loss to the company is fairly apparent or quantifiable

Involves breach of trust and abuse of authority/access

Act is intentional

Requires the involvement of more than one person

Requires elements of opportunity, incentive and rationalization

Key Characteristics– Fraud vs. Corruption

Copyright © 2011 Deloitte Development LLC. All rights reserved.7 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Dissecting Corruption

Source: Antifraud Programs & Controls – Deloitte FAS

Asset Misappropriation

Financial Statement Fraud

Corruption

Bribery

Extortion

Nepotism

Embezzlement

Unauthorized Expenditure/Revenue

FRAUD CORRUPTION

5

Corruption Environment in Key Emerging Markets

Copyright © 2011 Deloitte Development LLC. All rights reserved.9 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Emerging Markets

6

Copyright © 2011 Deloitte Development LLC. All rights reserved.10 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

High Risk Markets for Corruption – 2011

Copyright © 2011 Deloitte Development LLC. All rights reserved.11 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Emerging Market Corruption RisksWhile emerging markets can present opportunities to access new customers and resources, they also bring significant integrity and corruption risks

• Travel, gifts and entertainment• Use of agents, consultants, distributors and other third parties• Bids & tenders• Contracting• Expense reports• Commission payments• Discounts/Rebates• Donations• Political contributions• Customs payments

Corruption – High Risk Areas and Red Flags

7

Copyright © 2011 Deloitte Development LLC. All rights reserved.12 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

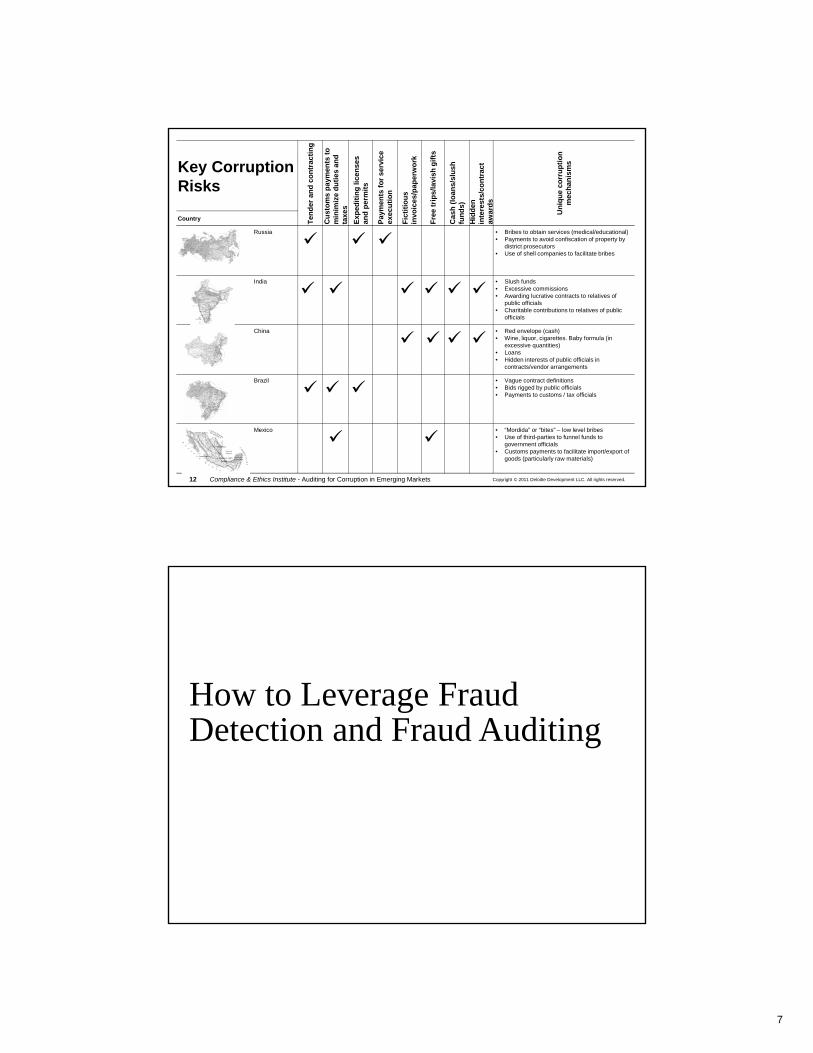

Critical success factorsKey Corruption Risks

Ten

der

and

co

ntr

acti

ng

Cu

sto

ms

pay

men

ts t

o

min

imiz

e d

uti

es a

nd

ta

xes

Exp

edit

ing

lice

nse

s an

d p

erm

its

Pay

men

tsfo

r se

rvic

e ex

ecu

tio

n

Fic

titi

ou

sin

voic

es/p

aper

wo

rk

Fre

etr

ips/

lavi

sh g

ifts

Cas

h(l

oan

s/sl

ush

fu

nd

s)

Hid

den

in

tere

sts/

con

trac

t aw

ard

s

Un

iqu

eco

rru

pti

on

m

ech

anis

ms

Country

1 Russia

• Bribes to obtain services (medical/educational)• Payments to avoid confiscation of property by

district prosecutors• Use of shell companies to facilitate bribes

India

• Slush funds• Excessive commissions• Awarding lucrative contracts to relatives of

public officials• Charitable contributions to relatives of public

officials

China

• Red envelope (cash)• Wine, liquor, cigarettes. Baby formula (in

excessive quantities)• Loans• Hidden interests of public officials in

contracts/vendor arrangements

Brazil

• Vague contract definitions• Bids rigged by public officials• Payments to customs / tax officials

Mexico

• “Mordida” or “bites” – low level bribes• Use of third-parties to funnel funds to

government officials• Customs payments to facilitate import/export of

goods (particularly raw materials)

How to Leverage Fraud Detection and Fraud Auditing

8

Copyright © 2011 Deloitte Development LLC. All rights reserved.14 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

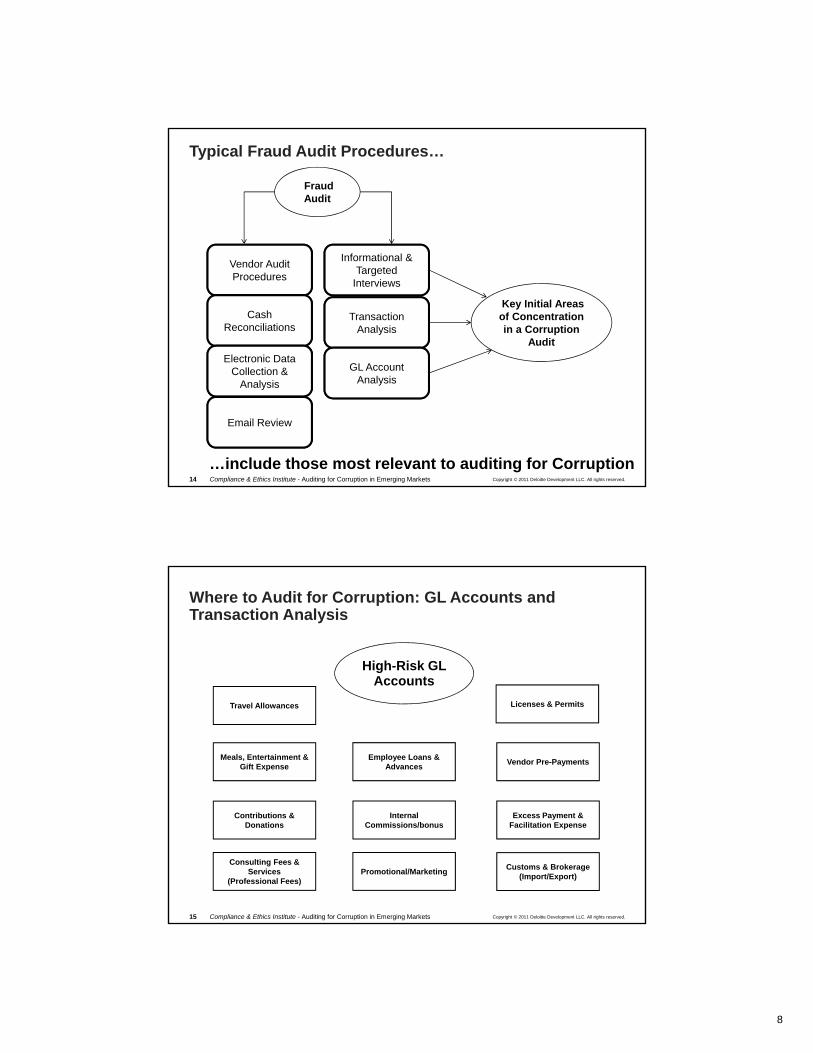

Typical Fraud Audit Procedures…

Vendor Audit Procedures

Cash Reconciliations

Electronic Data Collection &

Analysis

Email Review

Informational & Targeted

Interviews

Transaction Analysis

GL Account Analysis

Fraud Audit

…include those most relevant to auditing for Corruption

Key Initial Areas of Concentration in a Corruption

Audit

Copyright © 2011 Deloitte Development LLC. All rights reserved.15 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Where to Audit for Corruption: GL Accounts and Transaction Analysis

High-Risk GL Accounts

Employee Loans & Advances

Licenses & Permits

Vendor Pre-Payments

Contributions & Donations

Excess Payment & Facilitation Expense

Internal Commissions/bonus

Meals, Entertainment & Gift Expense

Travel Allowances

Promotional/MarketingConsulting Fees &

Services(Professional Fees)

Customs & Brokerage(Import/Export)

9

Copyright © 2011 Deloitte Development LLC. All rights reserved.16 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Corruption Audit Interviews – Who should be involved?

CFOInternational

FinanceOperations

Supply Chain

MarketingGlobal Sales

Human Resources

IT/Systems

Internal Audit

Compliance

Accounting

Corporate Development

Real EstateTax/

Treasury

Purchasing

Copyright © 2011 Deloitte Development LLC. All rights reserved.17 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Internal Audit Approach – Integrating Leading Practices to Reduce the Risk of Corruption and Fraud

• Compliance generally driving process with minimal or no internal audit input

• Not doing stand-alone FCPA audits or FCPA risk assessments

• Internal audit not trained to detect FCPA violations

• Proactive testing, if any, is not risk based and often includes random selections

• FCPA policies do not adequately identify internal audit’s role

• Dedicated and properly trained audit team focused on FCPA

• Structured risk assessment and gap analysis

• Marriage of compliance, legal, and audit

• Stand-alone FCPA reviews

• Testing of high-risk locations on at least a rotating basis

• Use of electronic data anomaly tools to identify and test high risk transactions

• Regular, open communication channel with Legal and Compliance in order to have timelyinformation on potential risk areas and to assist Legal/Compliance and/or adjust internal audit projects to address such risk areas

10

Copyright © 2011 Deloitte Development LLC. All rights reserved.18 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

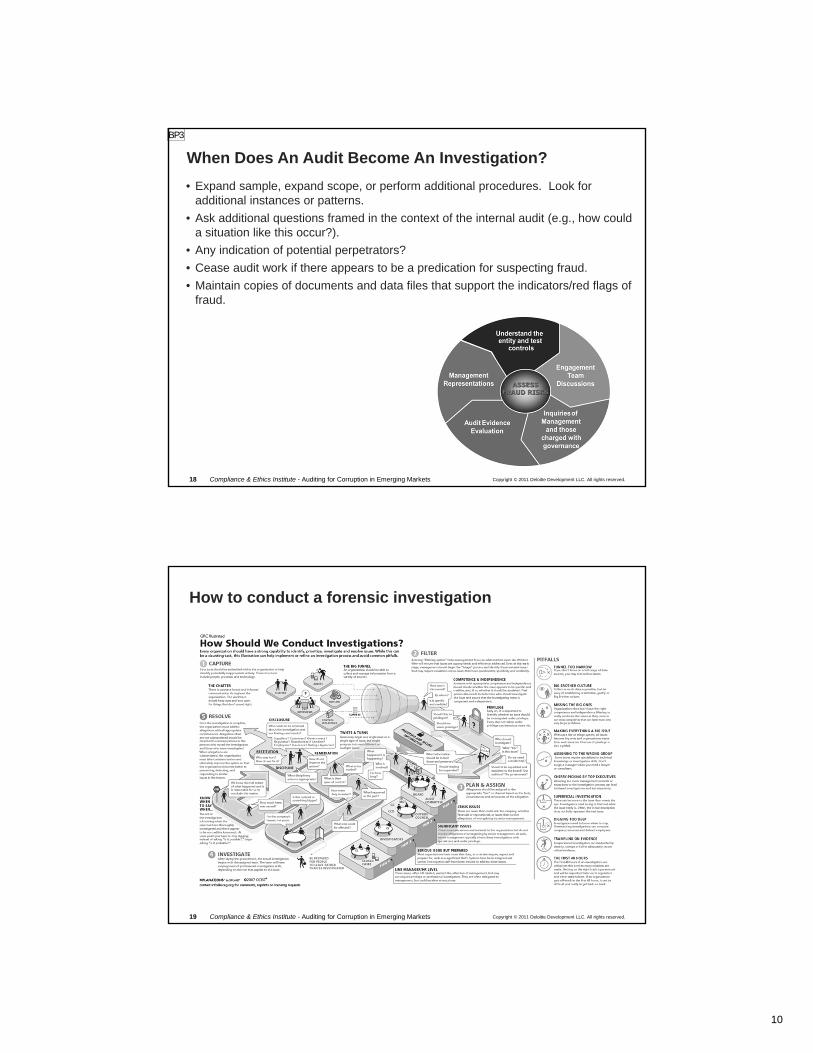

When Does An Audit Become An Investigation?

• Expand sample, expand scope, or perform additional procedures. Look for additional instances or patterns.

• Ask additional questions framed in the context of the internal audit (e.g., how could a situation like this occur?).

• Any indication of potential perpetrators?

• Cease audit work if there appears to be a predication for suspecting fraud.

• Maintain copies of documents and data files that support the indicators/red flags of fraud.

BP3

Copyright © 2011 Deloitte Development LLC. All rights reserved.19 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

How to conduct a forensic investigation

Slide 19

BP3 If you added a picture it isn't showing up in the bottom right corner.Pollard, William, 9/18/2012

11

Questions

Copyright © 2011 Deloitte Development LLC. All rights reserved.21 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

Leading Today’s Presentation

Bill PollardPartnerDeloitte Financial Advisory Services LLP+1 (312) 486 [email protected]

Bill is a partner in the Forensic & Dispute Services practice of Deloitte Financial Advisory Services LLP in Chicago. He has managed and conducted a broad range of forensic accounting and corporate investigations for public and private companies, government agencies and private individuals. He has spent almost two decades providing financial advisory services to clients in the manufacturing, construction, governmental, insurance, and not-for-profit industries, among others. The engagements have involved complex financial accounting related matters, including corporate investigations, accounting restatements, SEC investigations, white collar crimes and litigation support, as well as consulting with clients on FCPA compliance, fraud controls and anti-fraud programs.

Vito GiovingoSenior ManagerDeloitte Financial Advisory Services LLP+1 (312) 486 [email protected]

Vito Giovingo is a senior manager in the Forensic & Dispute Services group of Deloitte Financial Advisory Services LLP in Chicago. He has extensive experience providing forensic investigation and global anti-corruption consulting services to clients in a variety of industries including retail, manufacturing, life sciences, financial services, and technology. Vito has conducted investigations of allegations of bribery and corruption, including conducting interviews, reading witness documentation, and analyzing financial books and records. He has also assisted companies with pre-acquisition due diligence procedures related to anti-corruption in addition to providing assistance with corporate compliance program development and enhancement. Vito also has experience conducting financial fraud investigations, financial statement restatements and bankruptcy claims administration for clients in various industries.

12

Copyright © 2011 Deloitte Development LLC. All rights reserved.22 Compliance & Ethics Institute - Auditing for Corruption in Emerging Markets

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, eachof which is a legally separate and independent entity. As used in this document, “Deloitte” means Deloitte & ToucheLLP and Deloitte Financial Advisory Services LLP, which are separate subsidiaries of Deloitte LLP. Please seewww.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its memberfirms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and itssubsidiaries.

Copyright © 2008 Deloitte Development LLC. All rights reserved