Embed Size (px)

Citation preview

Access to Consumer Finance for Vulnerable Groups: One Size Does Not Fit All

i i Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All i i i

Access to Consumer Finance for Vulnerable Groups:

One Size Does Not Fit All

AFricA cleAn enerGy (Ace)technicAl AssistAnce FAcility (tAF)

iv Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Disclaimer

This report is provided on the basis that it is for the use of the Foreign, Commonwealth and Development Office (FCDO) only. Tetra Tech International Development Ltd will not be bound to discuss, explain or reply to queries raised by any agency other than the intended recipients of this report. Tetra Tech International Development Ltd disclaims all liability to any third party who may place reliance on this report and therefore does not assume responsibility for any loss or damage suffered by any such third party in reliance thereon.

Foreign, Commonwealth and Development Office (FCDO) Africa Clean Energy Technical Assistance Facility

© October 2020

Tetra Tech International Development

This report is produced by the Africa Clean Energy – Technical Assistance Facility (ACE-TAF) and authored by Open Capital Advisors.

w Ace-tAF: Ewan Bloomfield, Joyce DeMucci, Margaret Wanjiku, Pauline Githugu

w open capital Advisors: Aditya Shah, Brian Lang’at, Jonathan Clowes

We also want to thank the following organizations for their participation in consultations and valuable inputs.

w 60 Decibels w Azuri Technologies w CGAP w GSMA w Hello Solar w IFC – Lighting Africa w Lydetco PLC w Mercy Corps w One Acre Fund w PEG w Renewable Energy Association of Zimbabwe w Solar Industry Association of Zambia w Sunny Money w Vitalite Group w Wassha w Widenergy w Zonful

Prosperity House, Westlands Road,P.O. Box 4320, 00100, Nairobi, Kenya.Tel: +254 (0)20 271 0485

Cover page: Power Africa - M-POWER-962 ; Photo credit Power AfricaTitle page: Power Africa in Senegal: MBOUR - SENEGAL: Villagers daily life in a village off grid August 07 2017 near Mbour, Senegal. Photo credit: Xaume Olleros

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All v

C O N T E N T SAbbreviations vi

Executive Summary vii

ChApTEr 1: CONTExT 1

ChApTEr 2: AffOrdAbiliTy ANd ACCESSibiliTy ChAllENgES fOr VulNErAblE grOupS 4

2.1 Accessibility Challenges 4

2.2 AffordabilityChallenges 7

ChApTEr 3: ThE CurrENT STATE Of CONSumEr fiNANCE fOr VulNErAblE COmmuNiTiES 10

3.1 PAYGoModels 10

3.1.1 PAYGoviaMobileMoney 11

3.1.2 PAYGoviaAirtimeCredit 14

3.1.3 PAYGoviaCashCollections 14

3.1.4 ModificationstoPAYGoModels 17

3.2 TheMicro-FinanceInstitution(MFI)Model 19

3.2.1 TheAdvantagesoftheMFIModelforVulnerableGroups 20

3.2.2 TheDisadvantagesoftheMFIModelforVulnerableGroups 20

3.2.3 ModificationstoTheMFIModel 21

3.3 TheRentalModel 22

3.3.1 TheAdvantagesoftheRentalModelforVulnerableGroups 23

3.3.2 TheDisadvantagesoftheRentalModelforVulnerableGroups 24

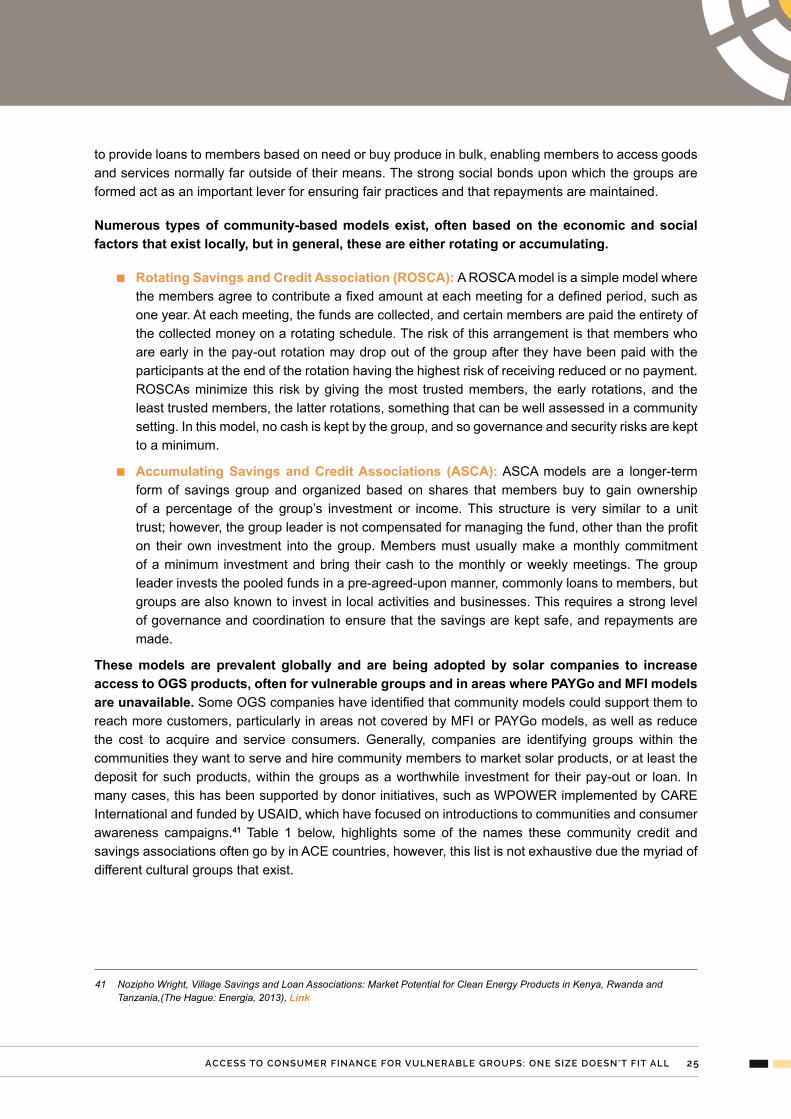

3.4 Community-BasedModels 24

3.4.1 TheAdvantagesofCommunity-BasedModelsforVulnerableCommunities 26

3.4.2 TheDisadvantagesofCommunity-BasedModelsforVulnerableCommunities 26

3.5 OtherConsumerFinanceModels 27

3.5.1 PayrollDeductions 27

3.5.2 RemittanceSupportedModels 28

3.5.3 LaybyModel 29

ChApTEr 4: rECOmmENdATiONS fOr imprOViNg ACCESS TO CONSumEr fiNANCE fOr VulNErAblE grOupS 30

vi Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Abbreviation Definition

CGAP ConsultativeGrouptoAssistthePoor

CTEN CommunityTechnologyEmpowermentNetwork

ESMAP EnergySectorManagementAssistanceProgram

IDcard Identificationcard

IDPs InternallyDisplacedPersons

LED Light-EmittingDiode

MFIs MicrofinanceInstitutions

MNOs MobileNetworkOperators

OGS Off-GridSolar

PAYGo Pay-as-you-go

PAYGrow Pay-as-you-grow

PULSE ProductiveUseLeveragingSolarEnergy

PV PhotoVoltaic

SIM SubscriberIdentificationModule

SMS ShortMessageService

SSA Sub-SaharanAfrica

UNHCR UnitedNationsHighCommissionforRefugees

USD UnitedStatesDollar

USSD UnstructuredSupplementaryServiceData

VAS ValueAddedService

VSLAs VillageSavingsandLoanAssociations

Wp WattPeak

A b b r E V i AT i O N S

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All vi i

E x E C u T i V E S u m m A r y

1 LightingGlobal,VividEconomics,andOpenCapital,2020Off-GridSolarMarketTrendsReports(MTR),(WashingtonDC:InternationalFinanceCorporation,2020),43,

2 Off-GridUtilitiesReportBridgingtheRuralEnergyGapinEmergingMarkets,(London,ShellFoundation,2020),5, 3 LightingGlobal,VividEconomics,andOpenCapital,2020Off-GridSolarMarketTrendsReports(MTR),(WashingtonDC:

InternationalFinanceCorporation,2020),15,

Consumerfinancemechanismshavebeen instrumental in enabling increased access tooff-gridsolar (OGS)products.With the totalpriceofahousehold tier1OGSproductaveragingUSD147andapproximately40%ofSub-SaharanAfricanslivingonlessthanUSD1.25perday,theyareprohibitivelyexpensiveformany.1,2Consumerfinancingmechanismsreducetheupfrontcostoftheseproductsandrequirerelativelysmallregularrepaymentsuntilthecostofthesystem,plusadditionalfeessuchasinterest,ispaidoff.Themostwell-knownconsumerfinancemodelintheOGSsectorismobilemoneyenabledpay-as-you-go(PAYGo)buttraditionalassetfinancing,financingthroughmicrofinanceinstitutions(MFIs),andcommunity-basedmodels,amongothers,allplayaroleinsupportingconsumerstoovercomeaffordabilityconstraintsthroughaccesstoconsumerfinance.

However,thecurrentcoverageofconsumerfinancemodelsisnotuniversal,andsomegroups,particularlyinvulnerablecommunities,areleftun-orunderserved.Despitereducingaffordabilitybarriers,46millionpeoplearestillunabletoaffordOGSproductsthroughconsumerfinancemechanisms.3 Additionally,manyofthe670millionconsumersthataretheoreticallyabletoaffordOGSproductslackthemeanstoaccessthem.MarginalizedandvulnerablegroupsinSub-SaharanAfricasuchaswomen,refugees,andreligiousminoritiesoftenfacethegreatestchallengesinaccessingtheavailableconsumerfinancemodelsduetotheirsocialorfinancialsituation.Figure1providesanoverviewoffourconsumerfinancemechanismsandexampleoftheirrelativeadvantagesanddisadvantagesforvulnerablegroups(amoredetaileddescriptioncanbefoundinChapter3).

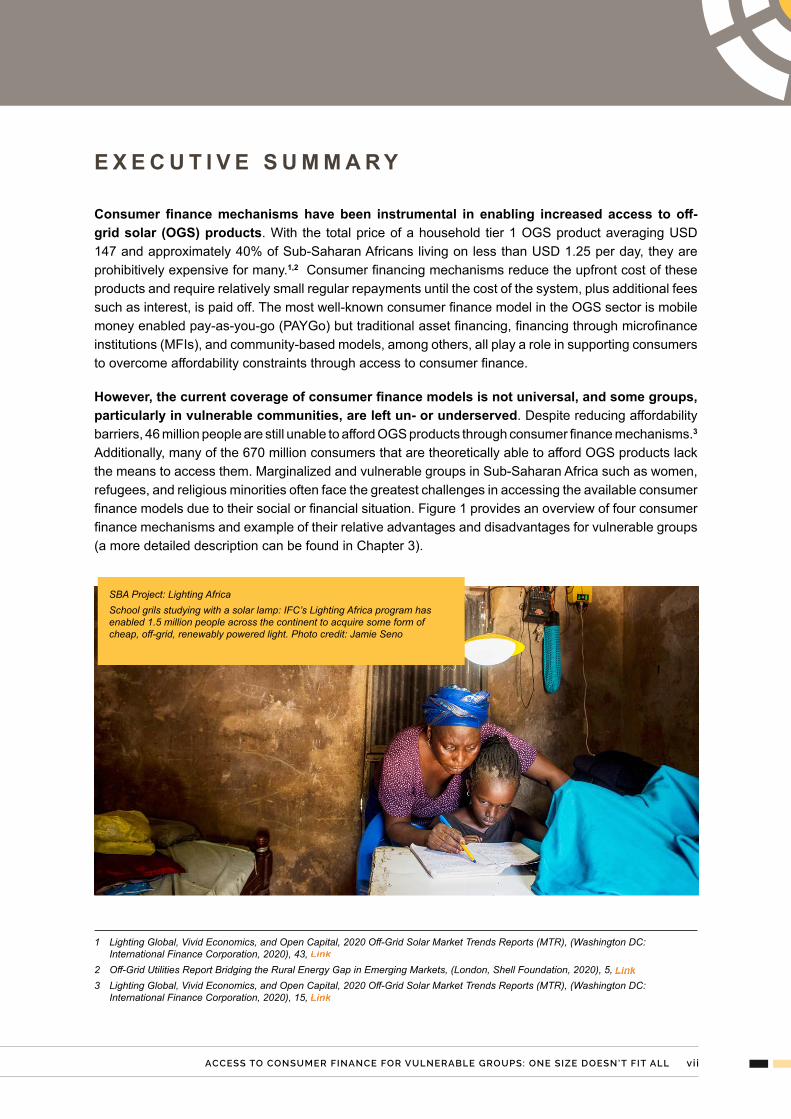

SBAProject:LightingAfricaSchoolgrilsstudyingwithasolarlamp:IFC’sLightingAfricaprogramhasenabled1.5millionpeopleacrossthecontinenttoacquiresomeformofcheap,off-grid,renewablypoweredlight.Photocredit:JamieSeno

vi i i Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

B

rief O

verv

iew

R

egio

ns P

reva

lent

Adv

anta

ges

and

disa

dvan

tage

s of

PAY

Go

mod

els

are

high

ly d

epen

dent

on

the

paym

ent

mec

hani

sm

PAYG

o M

odel

s

mak

es p

erio

dic

repa

ymen

ts

via

mob

ile m

oney

, cas

h,

airti

me

or s

crat

ch c

ards

. If t

he

cons

umer

fails

to m

ake

a re

paym

ent,

the

devi

ce is

re

mot

ely

lock

ed u

ntil

paym

ent

is m

ade.

Par

ticul

arly

stro

ng

pres

ence

in E

ast

Afri

ca, p

artic

ular

ly

Ken

ya, d

ue to

hig

h m

obile

mon

ey

adop

tion

rate

s

M

obile

mon

ey –

Red

uces

the

need

for

phys

ical

infra

stru

ctur

e w

hich

can

in

crea

se a

cces

s in

rura

l or h

ard

to

reac

h ar

eas

Mob

ile m

oney

- P

ositi

vely

con

tribu

tes

to

the

finan

cial

incl

usio

n of

pre

viou

sly

unde

rser

ved

low

-inco

me

earn

ers.

Cas

h - C

ash

colle

ctio

ns d

o no

t req

uire

ac

cess

to b

anki

ng a

nd

tele

com

mun

icat

ion

serv

ices

.

M

obile

mon

ey -

Poo

r mob

ile n

etw

orks

an

d lo

w m

obile

mon

ey p

enet

ratio

n lim

its

the

pote

ntia

l upt

ake

of P

AYG

o vi

a m

obile

mon

ey in

som

e re

gion

s an

d co

untri

es

C

ash

- Cas

h co

llect

ion

limits

con

sum

er

choi

ce o

n re

paym

ent v

alue

s an

d is

mor

e la

bor i

nten

sive

whi

ch c

an in

crea

se c

osts

MFI

Mod

els

An

OG

S co

mpa

ny p

rovi

des

the

prod

uct w

hile

an

MFI

pr

ovid

es c

onsu

mer

fina

ncin

g.

The

cons

umer

mak

es re

gula

r re

paym

ents

to th

e M

FI th

at

will

gen

eral

ly re

poss

ess

the

syst

em if

the

cons

umer

fails

to

repa

y.

Pre

vale

nt in

man

y co

untri

es w

ith lo

wer

m

obile

mon

ey

pene

tratio

n, in

pa

rticu

lar E

thio

pia

and

Nig

eria

Le

nds

itsel

f to

colle

ctiv

e le

ndin

g m

echa

nism

s w

hich

are

ben

efici

al to

vu

lner

able

gro

ups

One

of a

n M

FI's

cor

e co

mpe

tenc

ies

is

the

prov

isio

n an

d se

rvic

ing

of c

onsu

mer

fin

ance

, whi

ch c

an le

ad to

a m

ore

cost

-ef

fect

ive

proc

ess

MFI

s ha

ve re

ceiv

ed fi

nanc

ing

supp

ort

from

dev

elop

men

t par

tner

s ta

rget

ed a

t vu

lner

able

gro

ups

M

FIs

ofte

n ha

ve e

xpen

sive

phy

sica

l in

frast

ruct

ure

and

high

ove

rhea

ds w

hich

ca

n in

crea

se th

e co

st o

f con

sum

er

finan

ce

P

oor M

FI c

over

age

in lo

w p

opul

atio

n de

nsity

are

as li

mits

acc

ess

to s

ervi

ces

MFI

s of

ten

have

stri

ngen

t and

com

plex

cr

edit

chec

ks

Ren

tal M

odel

s

cons

umer

use

s th

e de

vice

for

a se

t tim

e or

unt

il th

e ba

ttery

di

es b

efor

e re

turn

ing

it an

d re

ntin

g a

new

pro

duct

.

Not

able

com

pani

es in

S

ierr

a Le

one

(Mob

ile

Pow

er),

Sen

egal

(S

unny

Mon

ey) a

nd

Tanz

ania

(Was

sha

& Ja

za E

nerg

y)

E

limin

atio

n of

dep

osit

paym

ents

re

duce

s af

ford

abili

ty b

arrie

rs

C

an in

crea

se c

onsu

mer

cho

ice

and

have

add

ition

al b

enefi

ts in

con

sum

er

educ

atio

n

S

olar

kio

sks

can

offe

r add

ition

al

com

mun

ity s

ervi

ces

e.g.

pho

ne

char

ging

, IC

T se

rvic

es, e

tc.

La

ck o

f evi

denc

e re

gard

ing

mod

el’s

vi

abili

ty fo

r lar

ge s

cale

impl

emen

tatio

n \

H

igh

brea

kage

, fau

lt or

non

-ret

urn

rate

s on

rent

ed p

rodu

cts

Lack

of t

rans

fer o

f ow

ners

hip

of p

rodu

cts

Com

mun

ity B

ased

M

odel

s C

omm

unity

sav

ings

and

cr

edit

grou

ps a

re o

ften

form

ed b

y co

mm

on

dem

ogra

phic

s, e

.g. f

arm

ers.

Th

eir g

oal i

s to

incr

ease

fin

anci

al s

tand

ing

of it

s m

embe

rs b

y po

olin

g ca

pita

l to

prov

ide

loan

s or

exp

ensi

ve

item

s.

Whi

le n

ot o

ften

used

fo

r OG

S pr

oduc

ts,

com

mun

ity le

ndin

g m

odel

s ar

e pr

eval

ent

acro

ss S

SA

(Tab

le 1

)

G

roup

s ar

e ve

ry c

omm

on a

mon

g vu

lner

able

com

mun

ities

, wel

l es

tabl

ishe

d an

d tru

sted

.

Sel

f-man

agem

ent f

oste

rs lo

w

adm

inis

trativ

e co

sts

Soc

ial b

onds

ens

ure

rela

tivel

y hi

gh

repa

ymen

t rat

es

Lo

ans

to p

urch

ase

an O

GS

devi

ce m

ay

requ

ire a

larg

er a

mou

nt o

r lon

ger

repa

ymen

t per

iod

than

is g

ener

ally

ty

pica

l The

re is

cur

rent

ly li

ttle-

know

n be

st p

ract

ice

for h

ow th

ese

mod

els

can

be s

cale

d up

eco

nom

ical

ly, p

artic

ular

ly in

ha

rder

to re

ach

area

s

The

OG

S co

mpa

ny p

rovi

des

the

prod

uct a

nd fi

nanc

ing

to

the

cons

umer

. The

con

sum

er

The

OG

S co

mpa

ny re

nts

out

char

ged

batte

ries

or O

GS

prod

ucts

for a

fee.

The

Exam

ples

of A

dvan

tage

s fo

r Vu

lner

able

Com

mun

ities

Ex

ampl

es o

f Dia

dvan

tage

s fo

r Vu

lner

able

Com

mun

ities

Figure1:O

verviewof4consumerfinancemodelsforO

GSproductsinSub-SaharanAfricaandtheirrelativeadvantagesanddisadvantages

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All ix

Giventhehighlyvaryingsocio-economicsituationofvulnerablecommunities,itisclearthereisno“silverbullet”norone-size-fits-allsolution,ratheranumberofrecommendationswhichtogetherimproveaccesstoconsumerfinance.Expandingcoverageofexistingmodelswillrequirestakeholderparticipationatboth themacroandmicro levels to improvecoverageandreducecosts.Newmodelscanbedevelopedorborrowedfromothersectorstoprovideadditionalcoverage,includingthe increased use of remittances or community lending. It is also vital that any recommendationsto improveconsumerfinancing for theendusersarecognisantof the fact thatOGScompaniesaregenerallycommercialentitiesthatneedtomaintainstrongconsumerrepaymentsandlowdefaultratestomeettheirownobligations.Giventhat,thisreportprovidesanumberofrecommendationswhichOGSstakeholderscancometogethertoimplementtoimproveaccessforvulnerablegroups:

Increasing theavailabilityofdisaggregatedenergyaccessdatawillmake iteasier toidentifywhichgroupscurrentlylackaccessandenablethedesignoftargetedconsumerfinance mechanisms. There is currently very limited data available on which vulnerablegroups aremost underserved.This hinders the sectors ability to design consumer financemechanismsand initiativesspecifically tosupport thesegroups.Organizationsor initiativessuchasACETAF,ESMAPand60Decibelsareseekingtofill thisgapbutcouldbegreatlysupportedbyaccesstocompanydata.

Leveraging and engaging community groups and structures as part of consumerfinancemechanismstoreduceOGScompanies’operatingcostsandincreaseconsumerengagement.Vulnerablecommunitiesoftenhavestrongexistingsocialstructuresandtheirowncreditandsavingsassociationswhichcanbothbeleveragedtoboostrepaymentsand

PeterMutai,42,inLugari,KakamegaCountywasamongthefirstmembersofLugariBodaSACCOtoapplyforaloantobuya4Asolarlantern.“The4Ahas4bulbsandcosts8500shillings(USD84)andisenoughformythree-roomedhouse.Onebulbisplacedoutsidetoprovidelightingatnightandforsecuritypurposes,”Mutaisaid.Photocredit:PowerAfrica

x Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

provideconsumerfinance.OGSstakeholderscanconductresearchintothesesocialstructurestoenableconsumerfinanceproviderstoknowhowtoleveragetheminlieuofcollateralandtoimproverepaymentrates.Additionally,communitygroupscanbeengagedandsupportedto provide consumer financing to members for OGS products with the support of OGSdevelopmentpartners.

Buildingtheevidencebaseforgovernments,MNOsandfinancialinstitutionstoincreasecoverageofenablinginfrastructuretomanycurrentlyexcludedvulnerablegroups.Manyvulnerable communitiesarenot coveredbymobilenetworksor don’t haveaccess toMFIsbranchesduetotheperceptionoflowdemand.DevelopmentpartnersandOGScompaniescan provide evidence for demand for such services and can come together to lobby suchorganizationstoprovidetheinfrastructurerequired.

Supportinitiativeslookingatformalizingremittancesasameansofprovidingenergyaccesstovulnerablecommunities.Moneysenthomebymigrantsasremittancescompeteswithinternationalaidasoneofthelargestfinancialinflowstodevelopingcountriesyetremainsa highly informal process. There has been some work to formalize this process and useremittancefundstopayforOGSproducts,suchasBBOXX’spartnershipwithShellFoundation.However,furthersupport inthisareafundedbydevelopmentpartnerscouldunlockawholenewcustomerbaseandensuremorereliablefinancesbyassessingthewiderfeasibilityandimpactofsuchmodels,andtherolevariousstakeholderswouldneedtoplayinscalingitup.

Providesupporttoscaleandtestrentalmodelstotargetspecificvulnerablecommunitiesdueto its lowerfinancialbarrier toentry.Rentalmodels,suchassolar librariesorsolarkiosks,haveenabledconsumerstoregularlygainaccesstoenergywithoutrequiringsignificantupfront costswhichactasabarrier inotherconsumerfinancemechanisms.Thismodel isregaining traction in recent years through companies such asSunnyMoney,Mobile PowerandJazaEnergy.Additionaltechnicalassistanceandfinancialsupporttoexpandthismodeluptoscalecouldprovideaccesstothosethatcurrentlycannotaffordotherformsofconsumerfinance.

PhilipsAfricaRoadshowFootballeventDaresSalaamPictureby:RobVerbeek-Philips

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All xi

Support companies to run pilot studies on the impact of varying consumer financetermsonconsumeraccess,affordability,repaymentanddefaultrates.WhileanumberofOGScompaniesarecurrentlyexperimentingwithfinance terms, there remainsvery littleconsensusinthesectoronwhichapproachhasthegreatestimpactonincreasingaccessforvulnerable communities.OGSdevelopment partners could supportOGScompanies to runpilots todeterminewhichfinancing termsaremosteffective inengagingvulnerablegroupswhilealsoensuringstrongrepayments.

Incorporateconsumerinsuranceintoconsumerfinancemechanismstosupportthosemostatriskofeconomicshocks.Insuranceagainsteconomicshocks,suchasthedeathof the breadwinner, can cover the remaining payments to bemade to theOGS companywiththehouseholdnolongerbeingliable.SuchinsurancepartnershipscanbearrangedbyOGScompaniesforaround1%oftheendconsumerproductpriceandcouldhugelybenefitvulnerablegroupsthataremoresusceptibletosucheconomicshocks.Developmentpartnerscouldsupport thescaleupof this initiativethroughresearchonits impact, thefacilitationofmarketlinkagesandinitialde-riskingforinsurancecompanies.

IncreasesectorfocusontheprovisionofconsumerfinanceforsmallerOGSproducts.TheOGSsectorhasseenadramaticshift towardsselling largersystemsover the last fewyearsascompaniesseek tobecomeprofitable.Thisshift leads to lower incomeandmorevulnerableconsumersbeingunabletoaffordOGSproducts.Whilesomecompaniesdooffersmaller systems through consumer financing, to further support vulnerable communities toaccessOGSproducts,consumersneedmoreoptionstoaccesslessexpensiveproductsthatmeettheirenergyneedswithintheirspendinglimit.

Thisreportexaminestheroleofconsumerfinanceinservingvulnerablegroupsbyaddressingfourkeyobjectives:

Identifying vulnerable groups and explaining the affordability and accessibilitychallenges they face.This report identifies the social andeconomic characteristicswhichtypify underserved vulnerable groups and how these present affordability and accessibilitybarrierstoconsumerfinanceforOGSproducts.

Illustratingtheadvantagesandshortcomingsofexistingconsumerfinancemodelsinaddressingthechallengesofvulnerablegroups.Whilecurrentconsumerfinancemodelshavemade great strides in improving access, this report will dig deeper into their specificadvantagesanddisadvantagesforvulnerablegroups.

Examiningthemodificationsimplementedbycompaniesinaddressingshortcomingsof existing consumer finance models. This report highlights attempts made to extendconsumerfinancetoagreaternumberofconsumersandproviders.

Providing recommendations to increase access to consumer finance for vulnerablecommunities.Basedonthesefindings,thisreporthighlightsstepswhichOGSstakeholderscantaketoincreaseaccesstoconsumerfinanceforvulnerablecommunities.

xi i Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 1

Despiteglobalelectrificationefforts,approximately840millionpeoplestilllackaccesstoelectricityin2020,about70%ofwhomliveinSub-SaharanAfrica(SSA)andmanythatare regardedas themost vulnerable in society.4 Between2010and2019, electrification

efforts helped improveSub-SaharanAfrica’s total electricity rates fromapproximately 30% to43%.5

However,therearediscrepanciesacrosssocialgroupsandgeographies.ForexampleinSSA,80%ofpeoplelackingaccesstoelectricityareconcentratedinruralareas,while89%ofrefugeesandinternallydisplacedpersons(IDPs)livingincampshavetier0electricityaccess.6,7Thoseindividualslocatedinremote,ruralsettingsfacechallengessuchasinadequatesourcesofincomeandpoorinfrastructurethatleadtoaconstrainedabilitytoaffordconventionalsourcesofelectricityandwhichalsodiscourageselectricityprovidersfromservingthemduetothehighcostofdoingso.Vulnerablegroupsarethemostlikelytofacethesechallenges,whichareoftencompoundedbyadditionalbarriersduetotheirsocio-economicsituation,whichpreventsthemgainingaccesstoelectricity.

Decreasing component costs havehelpedpushoff-grid solar (OGS) as a viable solution formanyunelectrifiedpopulations,but thesecost reductionsareslowing,andproductsarestillunaffordableformany.Thedecreaseinthepriceoflithium-ionbatteries,solarPVpanels,andLEDbulbshascontributedtothe improvedaffordabilityofoff-gridsolarproducts.9However,withthetotalpriceofahouseholdtier1OGSproductstillaveragingUSD147andwithapproximately40%ofSub-SaharanAfricanslivingonlessthanUSD1.25perday,OGSproductsarestillprohibitivelyexpensiveformanylow-incomeearners.10,11Withcostsexpectedtoleveloffinthecomingyears,thetotalpricewillcontinuetoremainoutofreachformostofthispopulation.

Consumer financing can increase the affordability of OGS products, but access to formalfinancingoptionshasbeen limited,particularly forvulnerablegroups.Formalfinancial serviceproviderssuchascommercialbankshavelimitedpresenceinruralareasbecauseofthelowmarket

4 MorePeopleHaveAccesstoElectricityThanEverBefore,butWorldisFallingShortofSustainableEnergyGoals,WorldBank,May22, 2019,

5 NiravPatel,FigureoftheWeek:ElectricityaccessinAfrica,Brookings,March29,2019,6 AcceleratingSDG7AchievementPolicyBrief01AchievingUniversalAccesstoElectricity,IEAUNDP&IRENA,7 JohannaLehneet.al,EnergyServicesforrefugeesanddisplacedpeople,EnergyStrategyReviews,8 SolarLightsandtheExtremePoorinOff-GridUganda,Energypedia,9 2020Off-GridSolarMarketTrendsReports(MTR),2020,66,10 2020Off-GridSolarMarketTrendsReports(MTR),2020,43,11 Off-GridUtilitiesReportBridgingtheRuralEnergyGapinEmergingMarkets,2020,5,

ThedefinitionofvulnerablegroupsWhile there isnosingledefinitionofavulnerablegroup, this reportdefinesvulnerablegroupsascommunitieswhicharegenerallylivinginastateofentrenchedenergypovertyduetotheirsocio-economicsituationandlackofaccesstoenablinginfrastructure.They are generally characterized by constrained financial resources or the unavailability of marketinteractionsnecessaryfortheparticipationinmarketbasedoffgridenergysolutions.8

Context 1

2 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

potential associated with low-income levels and limited economies of scale, creating high costs toservecustomers.Additionally,even inareaswherefinancial institutionsarepresent, theyhavebeenreluctanttolendforenergyproductsbecauseoftheirlimitedunderstandingofOGStechnologiesandthepotentialunknownprofitabilityoflendingforOGSproducts.Thisisfurthercompoundedbythelackofcredithistoryandlimitedaccesstocollateralthatcharacterizesmanywithoutenergyaccess.

Consumerfinancingmodelssuchaspay-as-you-go(PAYGo)havehelpedincreaseaffordability,driving the rapidgrowthof theoff-gridsolarsector,andaccelerating futuregrowth.Between2018 to 2019 alone, themarket value of off-grid PAYGo sales grew from USD 164million to 217million,indicatingagrowingmarketdemandforfinancingoptions.12,13 Consumerfinancingmechanismstheoreticallyenablea670-million-personaddressablemarket,ofthe716millionpeoplethatlackelectricityinSub-SaharanAfricaandAsia-Pacific.14,15 Theuptakeof instalmentdrivenmulti-lightproductshasundoubtedlybeenpropelledbythesuccessofmobilemoneyinSSA.Networkcoveragehasspikedwithover700+millionconnectionsintheregion,withpositivetrendsalsonotedregardingthedecreaseofmobilephonecostswhicharekeyfactorsinimprovingtheaccessibilityofconsumerfinancingmodelssuchasPAYGo.16

Despitethissignificantprogress,notall670millionconsumersthatcanaffordOGSproductscanaccessconsumerfinancingmechanisms,particularlyvulnerablegroupsthatarelimitedbytheirspecificsocio-economicsituation.WhiletheavailabilityofconsumerfinanceforOGSproductshasgrownrapidlyoverthelastdecadethroughtheriseofmobilephoneownershipandmobilemoney,andtheincreasedengagementofmicrofinanceinstitutions(MFIs)inthesector,thecoverageofthesemechanisms isnotuniversal, leavingmanyconsumersunable toaffordanOGSproduct.Consumerfinance is often particularly hard to access for people in deep rural areas or vulnerable groups astheyareseenaslessattractivecustomersbyconsumerfinanceprovidersduetolowincomesorthehighcostofservingthem.Whilenotdocumented,itisthereforehighlylikelythatthetruefigurefortheserviceablemarketissignificantlysmallerthanthe670-million-personaddressablemarket,althoughbyexactlyhowmuchisnotcurrentlyknown.

12 GOGLA,GlobalOff-GridSolarMarketReport:Semi-AnnualSalesandImpactData,2018,13 GOGLA,GlobalOff-GridSolarMarketReport:Semi-AnnualSalesandImpactData,2019,14 2020OffGridSolarMarketTrendsReport(MTR),2020,15,15 Thisassumesaccesstoamulti-lightsolarproduct,paidinmonthlyinstalmentswiththeconsumersavingforuptothreemonthsfor

the deposit.16 RoxannaElliott,MobilePhonePenetrationThroughoutSub-SaharanAfrica,July82019,

DefinitionofOGSConsumerFinanceThis report defines consumer finance as a loan to a consumer used to finance anOGSproduct,allowingaconsumertopurchaseaproductovertime,whichtheywouldotherwisenotbeabletoiftheyhadtopaythefullcostupfront.Financingtypicallyinvolvesthebreakdownof the totalOGSproduct cost intoadownpaymentandsubsequent instalmentpayments.Thismakestheproductmoreaffordabletoend-usersbyspreadingpaymentsacrossapre-determinedperiod.Atthesametime,consumerfinancingincludesadditionalfees,suchasinterestpayments,whichdriveupthetotalOGSproductcosttheconsumerpaysover-timecomparedtobuyingthesystemoutrightinoneupfrontpayment.Theseextrafeesareduetoincreasedcoststoservicetheloanandtheincreasedriskofnon-payment.

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 3

Figure2:TheoreticalaccesstoOGSproductsthroughconsumerfinancingmechanisms(nottoscale)

Whilesubsidiesareexpectedtohelpbridgesomeofthisgapforthemostvulnerable,thereisanopportunity to increaseaccessibilityandaffordabilityofcommercialconsumerfinance toaccelerateenergyaccess.Bothdemandandsupplysidesubsidiesarerecognizedasviableavenueswhichpolicymakerscanusetoreachuniversalaccessofelectricityandsupportvulnerablecommunities.They achieve this by closing affordability gaps for end userswhowould otherwise not afford solarproducts as investigated by the Achieving Dual Goals: Universal Energy Access and SustainableMarkets report.17However,wecannot relyonsubsidiesalone to support vulnerablegroups.Furthereffortsneedtobemadetomovetheneedleregardingaffordabilityandaccessibilitybyanalysingandrestructuringconsumerfinancemodels.WhilemodelssuchasPAYGoandMFIpartnershipshavebeendeployedtothewidergeneralpublic,refiningtheirintrinsiccharacteristicstosuittheneedsofvulnerablecommunitiescanfurthercontributetoimprovedaccessibilityforindividualswhowouldotherwiseremainunserved.

17 AfricaCleanEnergy,Demand-SideSubsidiesinOff-GridSolar:AToolforAchievingUniversalEnergyAccessandSustainableMarkets,

Electrifiedpopulation670millionunelectrifiedpeoplethatcan

theoreticallyaffordatier1OGSproductviaconsumerfinance

Unelectrifiedandcan affordandaccessOGSproducts via consumerfinance

Unelectrifiedandcanaffordbutnot

accessOGSproducts throughconsumer

finance

46millionunelectrifiedpeoplethatcannotanaffordOGSproduct

Women’sgroupsWomenmakeup50%ofthepopulationinSSAbutoftenlackthesameopportunitiesasmenduetotraditionalgenderroles.

Religiousminorities27%ofSSA’spopulationareregardedasIslamiccommunitiesinclinedtopracticeIslamicfinance.

Refugees&IDPs26%oftheworld’srefugeepopulationresidesinAfricaandapproximately12millionpersonsareinternallydisplaced.

Theelderlyanddisabled80+millionpeoplelivewithdisabilitiesinSSAwithelderlypopulationprojectedtoreach+60millionby2025.

Nomadiccommunities30–40millionnomadsareestimatedtoexistglobally.

60%ofAfrica’spopulationisengagedinsmallholderfarmingasananchoreconomicactivity.

Subsistence&smallholderfarmers

PotentiallyvulnerablegroupsthatmaylackaccesstoOGSconsumerfinance

Atheoreticalbreakdownofthemarketcanbeseeninfigure2.

4 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

While affordability and accessibility challenges exist for all consumers, these areparticularly acute to vulnerable groups. Consumer finance models have enabled agreaternumberofconsumerstoaccessOGSproductsbyreducingtheupfrontcostsand

enablingsmallerrepaymentstobemadeovertime.However,withPAYGoonlycontributingto24%ofaffiliatesales(affiliatesalesarethosemadebyGOGLAmembersorsalesofLightingGlobalQualityVerified products) or 5.6% of tier 1 sales consumer financingmechanisms are still not widespreadlimitingconsumerfinancingaccesstopurchaseOGSproducts.18Inaddition,whileconsumerfinancemight be theoretically affordable, for many the deposits and repayments are still prohibitively highwhenaccountingforconsumerwillingnesstopay.Vulnerablegroupsareparticularlyatriskfrombeingexcludedfromconsumerfinanceduetotheadditionaluniquechallengestheyfaceontopofthecommonchallengesthataffectallconsumergroups.Uniquechallengesattributabletoaspecificvulnerablegroup,furthercompoundtheaccessibilityandaffordabilitychallengesandarediscussedinmoredetailbelow.

2.1ACCESSIBILITYCHALLENGES

Accessibility is defined as the availability of ameansor opportunity to successfully accessconsumer financing to acquireOGSproducts. This is important becausewhile consumersmaytheoretically have access to OGS products, challenges such as poor supporting infrastructure, anunfavourableenablingenvironment,stringentcreditchecks,lowliteracylevels,andpreviousnegativeexperiencesmake it practically challenging and consequently limit the opportunities to successfullyaccessconsumerfinance.Manyofthesechallengesareaffectnumerouscustomers,includingvulnerablegroups,andareexploredinmoredetailbelow.

Many consumers lack access to the supporting infrastructure required for most consumerfinancemodels.Supportingpaymentinfrastructure,transportandlastmiledistributionnetworksarenecessary for the effective delivery of consumer financing. For instance, a lack of mobile networkcoverageandunavailable,ordistantlylocatedmobilemoneyagentsmaymeanconsumersareunabletomakepaymentsorforceexistingcustomerstodelayorcompletelymisspayments.Eveninareaswithmobilemoneyagents,theavailabilityorlackthereof,ofa‘float’(amonetarybalanceamobilemoneyagentrequirestoholdtobeabletoconductanymobilemoneytransactions)canlimitaccessanduseofmobilemoney.Additionally,poorqualitytransportinfrastructurecanmakeitdifficultandtimeconsumingforcustomers toaccessamobilemoneyagentorabankingbranch.This isespeciallychallenging,whenMFIs have one branch to cover a vast region. It alsomakes it challenging for companies toconduct installations and providemaintenance services pushing companies to decide that reachingthesecustomersdoesnotrepresentaviableeconomicchoice.

Theenablingenvironment isnot always favourable for thedeploymentof consumerfinanceandcanhaveanoutweighedimpactonvulnerablegroups.Governmentpoliciescaninhibitaccesstoconsumerfinanceduetopoorlydefinedpropertyrightstoassets,suchaslandorcattle.Thiscan

18 LightingGlobal,Off-GridSolarMarketTrendsReport(Washington,DC:IFC,2020),

Affordability and Accessibility Challenges for Vulnerable Groups 2

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 5

particularlyimpactwomen,whereacombinationofcustomsandlawsrestricttheirabilitytoownandmanage land.Additionally, beingcompliantwithgovernment regulations,whichvarydramatically bycountry,canpreventcertainconsumerfinancemodelsfromtakingofforincreasethecostofdeliveringconsumerfinance.Forexample,government regulations inNigeriahave,Wrmanyyears,preventedmobilemoneyfrombeingwidelyadopteddespiteincreasingeffortstochangethis.19

OGScompaniesarepushingtowardsbecomingmorediscerningwiththecustomerstheyselltoastheyseektoshoreuptheirfinances,potentiallyexcludingviablecustomers.GiventheOGSindustry’srecentpushtowardsprofitability,inpartdrivenbyinvestordemands,OGScompanies’havebecomeandcontinuetobemoreselectivewithwhomtheysellto.Forcompaniesthatassessconsumercreditworthiness,creditchecksarebecomingmorestringenttoprotectportfolioquality.ThisisespeciallytrueofMFIswhoserigidcreditchecksandrepaymenttermscomparedtothoseofPAYGocompaniesmay constrict the ability to onboard new customers.20 Credit history is anothermajor challenge asconsumerslacktheformaldocumentationorassetsrequired.Thislimitsaccesstothefewwhomeetassessmentrequirements,excludingthosethathavelower-incomeandlackassetsforcollateral.

Lowliteracyandeducationlevelscreateagapinconsumer’sunderstandingoftheirrightsandhowtoaccessconsumerfinancemodels.InKenya,10%morewomen(26%)areilliteratethanmen(16%),with thegap increasing to 17%betweenwomen (38%)andmen (21%) inUganda.21 These challengesextendtoothervulnerablegroupssuchasrefugees.Forinstance,inBidiBidi,thesecondlargestrefugeecampintheworldlocatedinNorthernUganda,areportbyGSMAfoundthat25%ofsurveyrespondentswereunabletoreadorwriteinanylanguage.22Thistrendextends,notsurprisingly,todigitalliteracywhere59%ofmobileusersindicatedtheyhadsomestrugglesusingmobilephoneswithwomenand theelderlydisproportionatelyaffected.23Low literacy impacts theabilityofpotentialcustomerstocomfortablyengageOGSservicesastheymaynotunderstandthedocumentstheysignandclausestheyagreetoandmayfinditdifficulttoeffectivelyfollowthroughonpaymentobligationssuchasthoserelatedtomobilemoney.

Communitieswhosemembers suffer fromnegative experiences in engagingOGSconsumerfinancingcanpersuadeothersnot toaccessconsumerfinanceforOGSproducts. It iswidelyaccepted thatOGSfinancingexposesmany individuals todebtobligations thatplacesanadditionalfinancialburdenonalreadystrainedincomes.Whilesomearguethatflexiblepaymentsaredesignedtosubstituteforpre-existinglightingexpenditures,thekeydifferenceisthatthelatterisnotobligatoryand therefore has no additional impact on the individuals if it is notmade. In the face of extendedperiodsofnon-payment,customerscanhave theirsystemsrepossessedorbe facedwithadditionalfinancialpenaltiescausingsignificantembarrassmentandstress,bothfinancialandmental.Inaddition,otherfactorssuchasunscrupulousandfraudulentagentbehaviourandpoor-qualityproductsandaftersalesservicecanalsosignificantlyimpactcustomerexperience.Iftheseexperiencesaresharedwidelyamongcommunitymembers, this canserve todeterotherpotential customers fromengagingOGSconsumerfinancing.

19 KanikaSaigal,“RegulatorsgivemobilemoneyinNigeriaaboost”Euromoney,January10,2019,20 DanielWaldronetal,ATaleofTwoSisters,Microfinance&PAYGoInstitutions(WashingtonDC:CGAP-WorldBank,2019),21 MarkButtweiler,“TheImpactofEqualEducation:SolutionstotheGenderDisparityinSub-SaharanAfricanSchools,”Guest

Articles,NextBillion,May2,2019,22 GSMA,TheDigitalLivesofRefugees,(London,UK:GSMA,2019),28,23 GSMA,TheDigitalLivesofRefugees,(London,UK:GSMA,2019),28,

6 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Ontopofthesecommonchallengesimpactingaccessibility,vulnerablegroupsoftenfacespecificchallengesduetotheirsocio-economicsituation.

Refugeecampsareahubofdifferentculturesandlanguages,raisingchallengesconcerningcommunicationandeaseofdoingbusiness.Languagebarriersmaylimittheeffectivenesswithwhichcompanyemployeessuchassalesagentsorcallcentre employees, engagewith refugees going as far as inhibiting any potentialengagement.Thisisbecausebothpartiesmayfearthatlimitedcommunicationcanleadtotransactionaldifficulties.Forthosecompaniesandrefugeesthatdoengage,the engagement can be a source of frustration as both parties try tomeet theirobligations.

Refugeesmay lackappropriate identificationnecessary toaccessavarietyof servicessuchasfinancial and telecommunicationservices.Crossborderrefugeeslackrelevanthostcountryidentificationmakingitchallengingforthemtoopenabankormobilemoneyaccountorevenbuyasimcard.

Logistical difficulties and bureaucracies can delay and hamper access forOGScompanies.Theorganizationalsetupofrefugeecampsmaymakeitdifficult,cumbersome, and time consuming for companies to enter these markets, whothereforechoosetoentermarketsthathavelowerbarrierstoentry.

WomenaretraditionallylesseconomicallyempoweredthanmenduetotraditionalrolesassignedtowomenandthepatriarchalnatureofmanyAfricansocieties.As men inruralcommunitiesare likely toworkoutdoors, theymaynotstronglyperceivethehouseholdneedforanOGSproduct.Ontheotherhand,womenareresponsibleforhouseholdchoressuchascooking,cleaningandforlookingafterthechildrenandtherefore,intheabsenceofaccesstoenergy,aredisproportionatelyaffected.Genderrolesalso likely impactmobile phoneownershipwithwomen13% less likely toownaphonewith this trendreplicatedwithinrefugeesettings, increasing thebarriersandwideningtheconsumerfinanceaccessgap.24,25

Assetownershipand incomecanbeachallenge forwomen inmanycontexts,eitherduetoa lackofopportunitiesorduetosocietalnormslimitingwomen’ssocialstandingandcreatingagenderpaygap. Inextremecases,womencanbeentirelypreventedfromassetownershiporreceivinganincome.AnoveralltrendisseenacrossAfrica,withwomenmuchlesslikelytoownassetsandwealthcomparedtomen(13% forwomenvs. 36% formen).26 Additionally, in somecountrieswith significantgenderdifferences,womenareatleast11%lesslikelytoownamobilephone,preventingthemfromaccessingmobilemoney.27

24 GSMA,TheMobileGenderGapReport,(London,UK:2020),9,25 GSMA,TheDigitalLivesofRefugees,(London,UK:GSMA,2019),38,26 WorldBank,“GenderGapsinPropertyOwnershipinSub-SaharanAfrica”,(WorldBankGroup,WashingtonDC,2018),27 GSMA,“TheMobileGenderGapReport2019”,(GSMA,London,2019),

Refugeesandinternallydisplacedpeople

Women

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 7

28 Hystra,“PricingQualityCostDriversAndValueAddInTheOff-GridSolarSector,2020,

Some communities prescribe to faiths that detail the kind of financialtransactionsmembersmayengagein.ConventionalMFIsoperateaninterest(riba)model,which they chargeon the loan theyextend to consumers.This isagainsttheIslamictenets,andassuch,manyMuslimcommunitiesabstainfromborrowingfromthetraditionalmicrofinanceservices,whichisagainsttheSharī’ah.

Nomadic communities often live in very remote locations and theymay lackregularaccesstopaymentinfrastructure.ThenumberofnomadicpeopleinAfricaisunclear,butitisestimatedthatthereare30-40millionnomadsglobally.Themajorityarelow-incomehouseholdsthatrelyonpastoralorhunter-gatherpracticesandmaylackaccesstoeducation.Thisnomadicexistencemakesaccesstotheinfrastructurerequiredforconsumerfinancemechanismsevenmorechallengingduetothelackofconsistentcoverageofthisacrossthecontinent.

2.2AFFORDABILITYCHALLENGES

Affordabilityistheabilityofcustomerstopaytheupfrontdepositandmaketheregularpaymentstheyareobligedtomakeaspertheproduct’sfinancingterms.While670millionconsumerswithoutaccesstoelectricitycanaffordOGSproducts,thismaynotbereflectiveofrealityasaffordabilityneedstoincludeboththeabilityandwillingnesstopay.WhileOGSisconsideredattractivebymanycustomergroups,ifnotall,customerscandifferinthevaluetheyassigntotheproductsandthereforetheamounttheyarewilling topay.While theymayvaryacrossandwithina customer segment, gapsbetweenwhatcustomersarewilling topayandwhat theycanpayarecommonwithin the targetmarkets forOGSaspotentialconsumershavecompetingfinancialdemands.VulnerablegroupsinparticularmayassignlessvaluetoanOGSdevicesastheyuselimitedincomeonfoodoreducationandarealsoverysensitivetoexpenseandincomeshockswhichmayleadtotheneedtocutbackonenergyexpenditure.

Despite the success of consumer finance models, affordability remains a major challengethatlimitstheabilityofconsumerstoaccessOGSproducts.OGSsystemsandtheirassociateddistributioncostsarerelativelyhigh,meaningthatevenwithconsumerfinancingmodelsinplace,therearestillmanylow-incomeconsumersforwhichtheregularrepaymentsrequired,letalonetheupfrontdeposit,isunaffordable.Thisaffordabilityissueisfurthercompoundedbythefactthatthereisacostassociatedwithprovidingconsumerfinance,which ispassedonto theconsumer.This results in theconsumerpayingmoreovertimethantheywouldiftheywereabletopurchasetheproductupfront.InthecaseofaPAYGodrivenmodel,thiscanbe25%ormoreofthetotalend-consumerprice.28Commonaffordabilitychallengesaffectingallcustomers,includingvulnerablegroupsarepresentedbelow.

Highdepositsactasthemaincostbarrierforlow-incomehouseholdsasitisgenerallythesinglelargestpaymentthattheymakefortheirOGSsystems.Duetorequiringsomefinancialsecurity,mostconsumerfinancingmodelsrequireanupfrontdeposit tobemade.Thehigherthedeposit, thefewerconsumersthatwillbeabletoaffordit,andthelongeritwilltakeforotherstosaveuptherequired

Religiousminorities

Nomadiccommunities

8 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

amount.Thetimetakentosaveupforthedepositwillcandetermanyfromdoingso,particularlyastheyare likely tostillbespendingonkeroseneorother traditional fuelswhilesaving,somethingnotaccountedforinmanyaffordabilitycalculations.Additionally,thelongertheysaveforthedeposit?thehigherthechancetheywillneedtousethosesavingstocoverothereconomicshockssuchasanillnessinthefamily,droughtorjobloss.

Repaymentperiodsaregenerallynomorethan24monthsduetothefinancialburdenandrisklongerrepaymentshaveonfinanceproviders,whichpushesupmonthlyrepaymentamounts. The longer theperiodoverwhicha consumer canpay for anOGSproduct, the lower their regularrepaymentswillgenerallybe,butthehighertheoverallcosttheypay.Lowerregularrepaymentsarebeneficialtoend-consumersandmayallowthemtoaccesslargersystemsthattheyotherwisemightnotbeabletoafford.However,verylongrepaymentperiodsaregenerallynotofferedduetothehigherriskofdefaultstheypresentandthegreaterstrainoncashflowsforthecreditprovider.

The total cost of a system, and consequently the deposit and repayment amounts, are stillrelativelyhighacrosstheOGSsectorbecauseofthecostofdeliveringsuchmechanisms:

Thehighcostofcollectingpaymentsincreasestheendpriceofproductsascompaniestransfer these costs to the consumer. In a PAYGo model, global system for mobilecommunication (GSM) integration costs are about USD 10 on the high end, while there areadditionalcostsassociatedwithSMSreminders,dataanalyticsteams,callcentres,etc.Inacashcollectionmodel,thecostsassociatedcanbeevenhigherduetothelabourintensivenessoffacetofacevisitsrequiringalargeworkforce.

Providersofconsumercreditwillspreadtheriskofdefaultsandslowrepaymentratesacrosstheconsumerbase.MostprovidersofconsumerfinanceintheOGSsectorhaveasinglepassorfailcreditassessmentforaparticularproduct.Thismeansthatlower-incomeconsumersandthosethataredeemedtobeofhigherriskofdefaultingbutstillpassthecreditassessmentaccessproductsunder thesame termsas lower risk consumers.This increases thefinancialburdenonconsumersascompaniescovertheirrisksfromtheseconsumersbyincreasingthedepositandmonthlyrepaymentsforall.

InvestordemandsandtheforeigncurrencynatureoffinancingavailabletoOGScompaniesinfluencesthedurationandtotalcostofOGSproducts. Investorsthatprovidenon-patientcapitalarelikelytoprovidefinancingtermsinlinewiththeriskprofileoftheOGStargetmarketcustomers.Theborrowingratesofferedcanthereforebehighandfordurationsthatareunlikelytoexceed2to3years.Incorporatingthetimetakentoorder,receive,andsellproducts,andcollectrepaymentshighlightsthelimitedflexibilitythatOGScompaniescanoffercustomersintermsoftotalcostandtermdurationsastheyneedtostartrepayingtheirownfinanciers.Tocompoundthealreadylimitedflexibilityfurther,theforeigncurrencynatureofmostfinancingofferedtoOGScompaniesexposestheircashflowstosignificantforeigncurrencyrisksforcingthemtofactorintherisksintotheirpricing.Inadditiontothegeneraleconomicandpoliticaldynamicsthatinfluenceforeign exchange fluctuations, the presence ofCOVID-19 this year has furtherworsened theoutlookforsomecurrencies.Forexample,theZambianKwachasawitsvaluedepreciate31.5%between1stMarchand19thSeptember2020.29

29 Note:CurrencyratesobtainedfromXe.com

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 9

Ontopofthesecommonchallengesimpactingaffordability,vulnerablegroupsoftenfacespecificaffordabilitychallengesduetotheirsocio-economicsituation.

Smallholder and subsistence farmers experience seasonal income highlycorrelated with crop harvesting patterns. Most farmer incomes are tied to theirharvest periods, experiencing periods of high cash flows at the time of harvest andlowcashflowsintheperiodsbetween.Thefluctuationincashflowsisworseiffarmersaregrowing lowvaluecropswithonly1harvestcycle in theyearandhavenoothersupplementalincome.

Limitedaccesstomarketlinkageslimittheabilitytomaximizefarmerearnings. Smallholderfarmers,especiallythosethatstayinremoteareasmayrelyonmiddlemenorbrokerstoselltheirproduce.Brokersaggregateproduceinanareaandorganizethetransportforallproducetobiggertowncentres,providingaconvenientoptionthroughwhichsmallholderfamerscanoffloadtheirharvest.Theabsenceofappropriatestoragefacilities(coldstorageorotherwise),thepotentialcostsassociatedwithseekingtheirownbuyers,thethreatofproducespoilageandofanincreaseinsupplyandthereforeadropinprices,areallreasonswhyfarmersmaychoosetoselltoabrokeratamuchcheaperpricenegatively impactingtheirearnings.Theearningscanbefurthercompoundediftheharvest for thatperiodwaspoor limiting the total incomeearnedby farmersandsubsequentlynegativelyimpactingtheirabilitytospendongoodssuchasoff-gridsolar.

RefugeesandIDPshavelimitedincome,forcingthemtocarefullyconsidertheirspending.Refugeecampsdonotprovidemanyemploymentopportunities.Whilesomerefugeesmayreceiveremittancesandothersmightengageinsmallbusinessesmostrelyonsupportfromcampmanagerswithsomealsotradingtheirfoodhandoutsforalittlemorecash.Thelimitedincomeforcesthemtomakeseriouschoicesthatleavenoroomforotherexpendituresconsideredunnecessary.

In balancing their household and income generating activities, women-ledhouseholds may earn lower incomes. As previously mentioned, women areresponsiblefornotonlycookingandcleaningthehousebutalsofor lookingafterthechildren.Forsinglemothers,thereisanaddedburdenoftheneedtoearnanincomeforthehousehold.Thisrequireswomentoallocatetheirtimebetweenthetwosetsofactivitiesandthuslimitingtheincometheycanearn.

Theelderlyanddisabledlackemploymentopportunitieswhichcansignificantlyhinder their ability to pay. Elderly and disabled persons are identified as high-riskgroupsbymanygovernmentsacrossSSA.Forexample,inKenya,themostvulnerablein thesegroupsareeligible toaccessgovernment support programmessuchas theNationalCashTransferProgram.Thisisduetotheirlimitedemploymentopportunitiesaswellassocietalchallengescommontothesegroups,suchasalackofsupportnetworkandeducation.ThiscausessignificantchallengesintheirabilitytoaffordOGSproductsthroughconsumerfinancemechanisms.

Smallholderandsubsistence

farmers

Refugeesandinternally

displacedpeople

Women

Elderlyanddisabled

10 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

Currently available consumer financemechanisms have alreadymade strides towardsbetter serving and increasing energy access for vulnerable groups. PAYGo and MFImodelshaveexpandedrapidlyinthelastdecadeandenabledaccesstoconsumerfinancefor

millionsofconsumers.Theirrapidexpansionhasinlargepartbeenpossibleduetotherapidgrowthofmobilemoneyacross thecontinentand theever-increasingcoverageofMFInetworks.Now, inabid to further increaseaccessibilityandcreate reliable repayments,OGScompaniesaredevelopingmodifications to these already existing consumer financemodels taking advantage of local marketnuancesandconsumercharacteristicsaffectingpurchasingpower.Inaddition,otherconsumerfinancemechanisms,includingrentalmodelsandcommunitymodels,havethepotentialtoincreaseaccessforalargernumberofconsumers,includingvulnerablecommunities.

However, consumer finance mechanisms are generally driven by OGS companies’ need toincreaseprofitabilityandimprovesustainabilitymeaningfocusonvulnerablegroupsisoftenstilllimited.Whileavarietyoftoolsandstrategieshavebeenimplemented,theyunderstandablyalloperatewithinthemarginsofincreasingcompanyprofitabilityandensuringtheyarecommerciallysustainable.Aspreviouslydiscussed,vulnerablegroupsaretoalargeextentdifficulttoserveduetouncertaintiessurrounding theirability to repayand thehighercosts to reach them. It is thereforeunderstandablethatOGScompanieshavetodategenerallyfocusedonserving“low-hanging-fruit”customersthataremorefinanciallyattractiveoreasiertoreach.Thismeansthatexistingconsumerfinancemechanisms,andthemodificationsbeingmadetothembyOGScompanies,aregenerallynotspecificallytailoredtobetterservingvulnerablecommunities,leavingthemperpetuallyunderserved.Despitethis,manyoftheimprovementsbeingmadetoconsumerfinancearebeneficialtovulnerablegroupsandareexaminedinmoredetailbelow.

3.1PAYGoMODELS

ThePAYGomodelisoneofthemostusedconsumerfinancingmodelsinSub-SaharanAfrica. WhilemanyassociatePAYGowithmobilemoney,numerousvariationsofthePAYGoconsumerfinancemodelexist.Despite this,all themodelsgenerallysharesomecommon factors. Initially,acustomerwill go throughacreditassessment.This isoftenvery limitedandmaynot require thecustomer toprovideanyphysicalproofofincome,expenditure,orassets,norprovideanycollateral.Iftheconsumerpassesabasiccredit/backgroundcheckwhichvariesbycompany,theythenpayadepositcoveringapercentageofthetotalproductprice(generally10-30%ofthetotalcost).Theconsumerthenmakesongoingregularpaymentstoenablethemtounlockthedeviceforasetperiod,potentiallyasshortasonadailybasis,viaapre-determinedpaymentmechanism(mobilemoney,airtime,cash,etc.).Iftheconsumerdoesnotmakearepayment,theproductisremotelylockeduntilthenextpaymentismade.RemotelockingprovidesreasonableassurancethatOGSconsumerswillregularlypayasafailuretodosowillleadtotheshutdownofthesystempendingfurtherpayment.WhilethePAYGomodeldoesnotprecluderepossessionofsystemsonnon-payment,inreality,theremotelockingfunctionalitymeansOGScompaniesonlydosoinextremecasesasconsumerscangolongperiodsbetweenrepaymentsduringwhichtimetheycan’tusethesystem.

The Current State of Consumer Finance for Vulnerable Groups 3

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 11

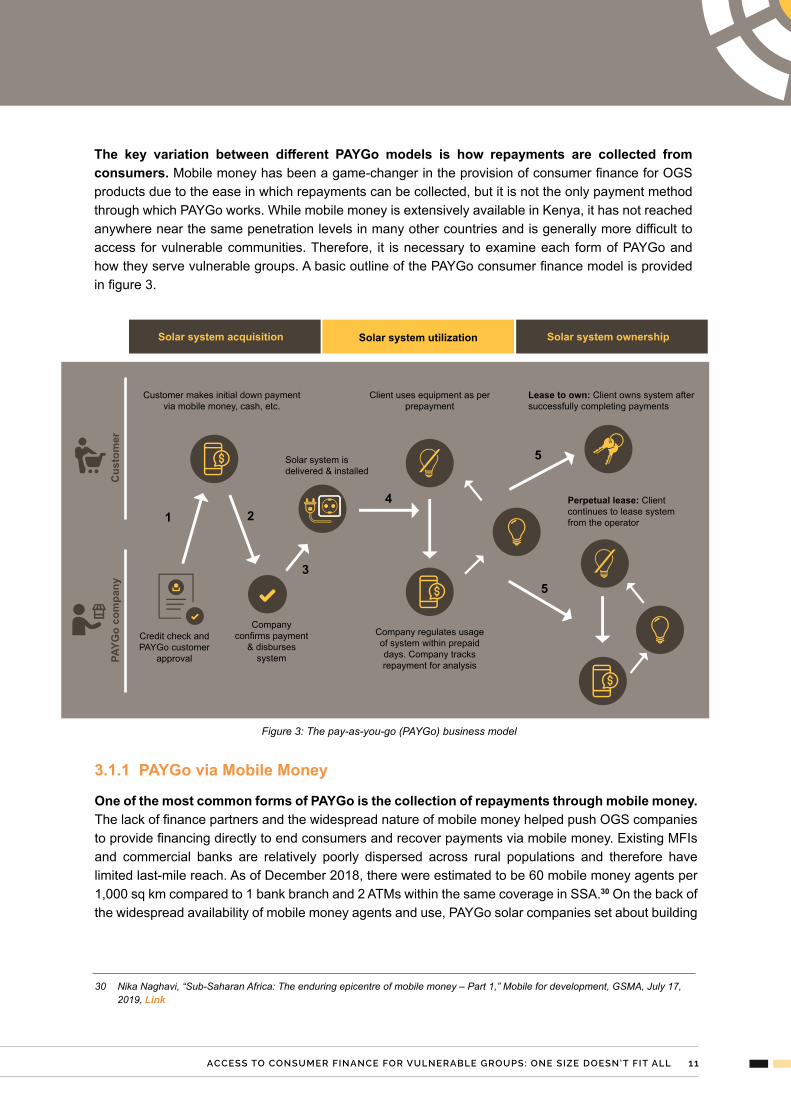

The key variation between different PAYGo models is how repayments are collected fromconsumers.Mobilemoneyhasbeenagame-changerintheprovisionofconsumerfinanceforOGSproductsduetotheeaseinwhichrepaymentscanbecollected,butitisnottheonlypaymentmethodthroughwhichPAYGoworks.WhilemobilemoneyisextensivelyavailableinKenya,ithasnotreachedanywherenearthesamepenetrationlevelsinmanyothercountriesandisgenerallymoredifficulttoaccess forvulnerablecommunities.Therefore, it isnecessary toexamineeach formofPAYGoandhowtheyservevulnerablegroups.AbasicoutlineofthePAYGoconsumerfinancemodelisprovidedinfigure3.

3.1.1PAYGoviaMobileMoney

OneofthemostcommonformsofPAYGoisthecollectionofrepaymentsthroughmobilemoney. ThelackoffinancepartnersandthewidespreadnatureofmobilemoneyhelpedpushOGScompaniestoprovidefinancingdirectlytoendconsumersandrecoverpaymentsviamobilemoney.ExistingMFIsand commercial banks are relatively poorly dispersed across rural populations and therefore havelimitedlast-milereach.AsofDecember2018,therewereestimatedtobe60mobilemoneyagentsper1,000sqkmcomparedto1bankbranchand2ATMswithinthesamecoverageinSSA.30Onthebackofthewidespreadavailabilityofmobilemoneyagentsanduse,PAYGosolarcompaniessetaboutbuilding

30 NikaNaghavi,“Sub-SaharanAfrica:Theenduringepicentreofmobilemoney–Part1,”Mobilefordevelopment,GSMA,July17,2019,

Figure3:Thepay-as-you-go(PAYGo)businessmodel

SolarsystemutilizationSolarsystemacquisition SolarsystemownershipSolarsystemutilization

CreditcheckandPAYGocustomer

approval

Companyconfirmspayment

&disbursessystem

Companyregulatesusageofsystemwithinprepaiddays.Companytracksrepaymentforanalysis

Perpetuallease: Client continuestoleasesystemfromtheoperator

Solarsystemisdelivered&installed

Cus

tom

er

PAYG

ocompany

1 2

3

4

5

5

Customermakesinitialdownpaymentviamobilemoney,cash,etc.

Clientusesequipmentasperprepayment

lease to own:Clientownssystemaftersuccessfullycompletingpayments

12 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

theirownnetworksorpartneringwithotherdistributorsengagedinlast-miledistributiontoreachtheirtargetcustomers.Consumersareabletomaketheirregularrepaymentsviamobilemoney,whichwilleitherautomaticallyunlocktheOGSsystemorprovidetheconsumerwithacodethattheycantypeintothedevicetounlockitforthenumberofdaysforwhichtheyhavepaid.TheubiquityofthismodelhasledtomobilemoneybecomingoneofthemostcommonpaymentmethodsandalmostsynonymouswithPAYGoitself.

3.1.1.1TheadvantagesofPAYGoviamobilemoneyforvulnerablegroups

Mobilemoneyreducestheneedforphysicalinfrastructurewhichcanincreaseaccessinruralor hard to reach areas. The implementation ofmobilemoney payments has led to the increasedcoverageforOGSconsumersinareaswhereaccessmayhavepreviouslybeenunavailable.Limitedphysicalinteractionbetweenbothpartiesisrequired,withpaymentsmadeandacknowledgedviaremotesystems.ThismeansOGScompaniesdonotrequirestafftobenearitscustomerstocollectpayments,somethingthatisparticularlychallenginginhardtoreachareasandoftenacharacteristicofvulnerablegroups.Additionally, theability topay remotelycanbehugelybeneficial tonomadiccommunitiesorthosethattravelforseasonalworkthatareunlikelytohaveconsistentaccesstophysicalinfrastructure.

Accesstomobilemoneyisincreasingonthebackofimprovementsinmobilenetworkcoverage,combinedwithadecreaseinmobilephonecostsandactiontoincreaseaccessforvulnerablegroups.ContinuedinvestmentsintotelecommunicationsinfrastructurehavehelpedimprovenetworkcoverageacrossSSA.Thishasinpartbeendrivenbythedevelopmentcommunities’ambitiontoprovidecoverageforvulnerablecommunitiesthathavetodatebeenunderserved.Inaddition,therehasbeenaninfluxofcheaphandsetsfromIndiaandChinaandalargernumberofdevelopmentprogrammesfocusedonmobilephoneownership,suchasthosebyUNHCRinrefugeesettings.Thesefactorshavehelpedboostvulnerablegroupsaccesstomobilemoneyacrossmanycountries,particularlyinthosewhosegovernmentshavealsoenabledthisgrowththroughsupportiveregulations,anditisexpectedthatitsadoptionwillcontinuetogrowinthefuture.

Mobilemoneytransactionseliminatecash-basedriskssuchasfraudandhighcollectioncostswhichmaybemoreprevalentinvulnerablecommunities.Mobilemoneyreducesthelikelihoodoffraudasthesystemsareequippedtoperformthousandsoftransactionssafelyandsecurely.Additionally,collectionviamobilemoneyreducestheneedforfieldstafftomanuallycollectcashfromordistributevoucherstoconsumers,whichreduceacompany’soverheadcosts,whichcanultimatelyreducethecostoffinancingfortheconsumer.Thesechallengesarelikelytobemorepronouncedinvulnerablecommunitiesthatmaysufferfromsecuritychallengesorareparticularlyremoteandhardtoreach.

PAYGoviamobilemoneypaymentspositivelycontributestothefinancialinclusionofpreviouslyunderservedlow-incomeearners.ThedemandforOGSsystemshasledtoanincreaseintheadoptionofmobilemoneyservices.Thishasdriven theuseofdigitalfinanceservicesby low-incomegroupsandcollectivelycontributedtoimprovedfinancialinclusioninemergingmarketssuchasSub-SaharanAfrica.31Additionally,duetotheeaseinwhichmobilemoneydatacanbecollected,somecompaniesareabletopassdataontonationalcreditbureaustobuildconsumers’creditscoresandenablethem

31 USAIDGlobalDevelopmentLab,Pay-As-YouGoSolarasaDriverofFinancialInclusion,(WashingtonDC:USAID,2017),

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 13

toaccessadditionalservicesinthefuture.Thisisparticularlybeneficialtovulnerablecommunitiesthatwouldotherwisehavelimitedabilitytobuildupacredithistoryduetoalackofviablefinanceoptions.

RepaymentsviamobilemoneycaneasilybeanalysedenablingOGScompaniestoidentifygoodcustomersthatcanbuildacredithistorytoaccessmoreproductsorservices.OGScompaniescanusecustomerpaymentdata tohelpbuildacredithistory foreachcustomer, therebyhelping toidentify the best customers. Upgrades offered to these customersmay include improving to largerlightingsystemsorofferingappliances.ThisisnotonlybeneficialtothecustomerbutalsoincreasethecustomertheirlifetimevaluewiththeOGScompany.Inaddition,companieslikeFenixuserepaymentdatatoofferfinancingproductssuchasschoolloanstotheircustomers.Thisensuresthatconsumersaretreatedontheirownmeritsbasedontheirindividualrepaymentperformance,enablingvulnerableconsumerstoprovetheircreditworthinessandincreasinglyaccessnewproductsandserviceswhichwouldotherwisebeoutofreach.

3.1.1.2ThedisadvantagesofPAYGoviamobilemoneyforvulnerablegroups

PoormobilenetworksandlowmobilemoneypenetrationlimitsthepotentialuptakeofPAYGoviamobilemoney in some regions and countries. Despitemobile network coverage expandingdramaticallyoverthepasttwodecadesacrossSSA,therearestillruralareasinwhichnetworkcoverageisnon-existent,makingrepaymentviamobilemoneyimpossible.ThiscanparticularlyimpactvulnerablegroupsthatoftenliveinareaswheremobilenetworkcoverageislowduetorelativelylowdemandorgeographicalinaccessibilitymeaningMNOsdonotwanttoprovideservicesintheseareasastheydonotseeitasbeingfinanciallyworthwhile.

Low literacy and education levels negatively impact the adoption of mobile money amongvulnerable communities and may limit the ability to understand payment obligations. Manyvulnerablegroupssufferfromlowlevelsofliteracyandfinancialliteracy.ThelackoffacetofacecontactandneedtouseamobilephonemaydiscouragecustomersfrompurchasingPAYGoproducts,andforthosethatdopurchasetheproducts,alackofunderstandingmayleadtocustomersfindingthemselvescontinuously in arrears and without access, hindering the seamless customer experience initiallyintendedbyOGScompanies.

Some marginalized groups are unable to access mobile money services due to a lack ofdocumentation. Inmanycountries, consumers requirean IDcard toaccessaSIMcardormobilemoney services.Formanyrefugees,IDPs,undocumentedpeople,orothervulnerablegroups,itisnotpossibletoprovidethis,whichhinderstheirabilitytoaccessmobileaccountsandhencemobilemoney.

Pooragentnetworkcoverage insomeareasmaycausepaymentpainpoints forconsumersduetotheneedtotravellongdistancestomakepayments.Mobilemoneyrequiresthepresenceofmobilemoneyagentsthatcollectdepositsandenablewithdrawals.Thesearelessavailableindeepruralareas,wherevulnerablecommunitiesareoftenlocated,duetothelogisticalchallengesassociatedwith theirmanagement and a lack of demand.This can result in customers needing to travel longdistances tomakedepositswhichmaydeter themfrompurchasingoff-gridsolarproducts.ThishasbeenthecaseintheEnergyandCashPlusprojectinKenya,wherealackofmobilemoneyagentshascreatedadditionalcostsforprojectbeneficiariesastheymustpayfortransporttoaccesstherequiredservices.

14 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

3.1.2PAYGoviaAirtimeCredit

In thePAYGovia airtimemodel, consumersmake their repayments through thepurchaseofairtimecredit.Thismodelcloselyalignswiththemobilemoneyenabledmodel;however,itdoesnotrequireconsumerstohaveamobilemoneyaccountbutonlyamobilephoneandapre-paidSIM.Inthismodel,thecustomerstop-uptheirmobileairtime,thesamebalancetheyusetomakephonecallsorbuydatabundles.CustomersthenusetheUSSDmenuorsendanSMStorequestthatpartoftheircreditisusedtopayfortheirOGSsystems,andtheMNOdeductsthisfromtheiraccount.TheMNOnotifiestheOGScompanythatthenremotelyunlocksthecustomer’sOGSsystemorsendsthemacodesothattheycanunlocktheirsystemthemselves.

3.1.2.1TheadvantagesofPAYGoviaairtimeforvulnerablegroups

ThePAYGoviaairtimemodelremovesbarriersspecificallyassociatedwiththeneedforamobilemoneyaccountandaccesstoanagentnetwork.Consumersonlyrequireamobilephoneandnotamobilemoneyaccountinthismodel,andhenceit ispotentiallyaccessibletoafargreaternumberofuserswheremobilemoney isunavailable.Additionally, consumersaregenerally familiarwith theconceptofpurchasingairtimeandhencemaybemorecomfortablewith theprocess,particularlyasmobilemoneyagentsareoftennotverycommon in ruralareaswhileairtime retailersaregenerallyavailableandaccessibleforconsumers.Thisisparticularlyadvantageousforvulnerablecommunitiesthatmayhaveamobilephoneandbefamiliarwithtopupsbutarelesslikelytohaveaccesstomobilemoney.

3.1.2.2ThedisadvantagesofPAYGoviaairtimeforvulnerablegroups

In addition to theneed tohaveamobilephone, thePAYGovia airtimemodelhasadditionaltechnical and partnership related challenges not faced in themobilemoney enabledmodel. Vulnerablecommunitiesstillfaceaccesschallengesduetotheirreducedaccesstomobilephonesandpoornetworkcoverage.Additionally, touseairtimeforrepayments,OGScompaniesrequireamuchcloserpartnershipwithanMNOandisfarmorereliantontheirsupporttoenableandprocesspayments.Touseairtime,acompanyneedstobeapprovedbyanMNOasaValueAddedService(VAS)vendor.Paymentsaremadetoandrecordedbythemobileoperator,andtheOGScompanythenneedstobeinstantlynotifiedaboutthepaymenttobeabletounlockthesysteminreal-time.ThislevelofintegrationandpaymenttrustrequiresadeeppartnershipandsupportbetweentheMNOandOGScompanyandcanpushupcostsduetorevenuesharearrangementsbetweentheOGScompanyandtheMNO.Whilethismodelwasmorecommonprior to thewidespreadavailabilityofmobilemoneyand itspotentialbenefits, it has not gained significant prominence in recent years, in part due to the technical andoperationalchallengesinvolvedintheOGScompany/MNOpartnershipandtheriseofmobilemoneysupersedingthispaymentmechanism..

3.1.3PAYGoviaCashCollections

CashcollectionsfromlocalagentsisanothermeansthroughwhichpaymentsforPAYGocanbecollected.Inthismodel,consumersarevisitedbyafieldagentoftheOGScompanytopayincashtounlocktheirsystemforasetperiod.UnlikethemobilemoneyorairtimeenabledPAYGoinwhichconsumersareoftenabletomakeapaymentforaperiodasshortasoneday,thecashcollectionmodel

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 15

generally requires thataconsumerpays foraminimumof twoweeksata timedue to the logisticalchallengesassociatedwithregularlyvisitingacustomer.Uponreceivingthepayment,thefieldofficerupdates theOGS company’s systems via their mobile device/app so that the OGS device can beunlocked remotely or via sending an unlock code to the consumer.Thismodel leansmore closelytowardsthetypicalMFImodeloffieldcollectionsbyruralagentsbutleveragessomeofthebenefitsofPAYGowithremotelocking,reducingtheneedforrepossessions.

3.1.3.1TheadvantagesofPAYGoviacashcollectionsforvulnerablegroups

PAYGoviacashcollectionsdoesnotrequiretheconsumertohaveaccesstoanybankingormobileservice.UnlikepreviouslymentionedPAYGomodels, cash collectiononly requires that theconsumerhasaccesstocashtoenablethemtomakerepayments.Neitherdoesitrequireanetworkofmobilemoneyagentswithinproximityoftheconsumer.Inthisway,itismoreinclusivethanmobilemoneyorairtimeenabledmodels,particularlyformarginalizedgroupsthatmightlackaccesstosuchservicesandinwhichcashisoftentheonlyformofmoneyavailable.

Early,butlimited,evidenceindicatesthatcashcollectionmodelsinmarketswithlowerlevelsofmobilemoneypenetrationmayhaveahigherrepaymentandlowerdefaultrate.32GreenlightPlanethaspilotedacashcollectionmodelinNigeriaduetothelowrateofmobilemoneyinthecountryand the lackof suitablealternativeconsumerfinancingmodels.While thesepilotsarestill ongoing,repaymentsbyconsumerstakingpartinthecashcollectionmodelaresignificantlyhigherthanthosethatwereusingmobilemoney.Whilethereasonforthisisnotyetfullyclear,thefactthatconsumersareremindedtopaythroughaphysicalvisitfromacollectionagentlikelyplaysapartinconditioningthemtomakerepayments.ThiscouldbebeneficialinincreasingrepaymentratesamongstvulnerablecommunitiesthatOGScompaniesmightotherwiseviewasbeingtooriskytoserveduetotheirhighercreditrisk.

3.1.3.2ThedisadvantagesofPAYGoviacashcollectionsforvulnerablegroups

The cash collectionmodel ismore labour-intensive than other PAYGomodels, requiring anextensivenetworkoffieldagentstocollectrepaymentsandpotentiallyleadingtohighercosts. Anextensivenetworkoffieldagentsisrequiredtocollectpaymentsincashwithasinglefieldagentonlyabletomanage100-120customers.Thesefieldagentswillneedtobehiredandtrainedatarapidrateasnewcustomersareacquired,whichwillbecostly.Additionally,fieldagentswillneedtoreceivefinancialcompensationfortravelandmakingcollections,whichwilladdtotheoverallcostofthemodel.Finally, theOGScompany requireshighlysophisticatedprocessesandsystems toensure theycanmanagethenetworkoffieldagentsandensuretheyarevisitingtheappropriatecustomerstocollectrepayments.Developmentandmaintenancecostsofsuchprocessesandsystemsarelikelytobehigh.Thesehighercostswillbepassedontoconsumers,potentiallymakingthemunaffordableforvulnerablecommunities.

The cash collection model limits consumer choice regarding repayment values and canpotentiallyleavethemwithoutaccesstopowerforextendedperiods.Duetothelabour-intensivenatureofthecashcollectionmodel,repaymentperiodsgenerallyneedtobelongertoreducetheneed

32 GreenlightPlanet,GreenlightPlanetNigeriaPilotlearnings:2017-2019,(Kenya:GreenlightPlanet,2019),

16 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

toconduct regular visits toconsumers.This reduces theconsumer’schoiceandability topay forashorterperiodwhenfundsareconstrained.Additionally,itpotentiallyincreasestheriskofnon-paymentasconsumersneedtobereliedontosaveupfundsforalongerperiodoftime,whichleavesthemopentofinancialshocksthatmightrequiretheuseofthosefunds.Thesechallengesarefarmorelikelytoimpactvulnerableconsumers thathave lower incomesandaremoresusceptible tofinancialshockslimitingtheirabilitytomakelargerrepayments.

Box1:TheuseofScratchCardsorVouchers

In this model, the consumer purchases a scratch card or voucher via any paymentmechanism from a local agent that then allows them to unlock their device. In additiontosharingadvantageswith thecashcollectionmodel, theconsumerhasmorechoiceover thelengthoftimetheyunlockthesystem.AnadvantageofthePAYGoviascratchcardsandvouchersmodel isthattheconsumerhasmorechoiceoverhowlongtheywanttounlockthesystemforbypurchasing thecorrespondingcard fromanagent in the localcommunity.However, insuchamodel theOGScompany facessignificant logistical challenges inprintingscratchcardsandvouchersanddistributing these to vendors in the communitieswhere their products arebeingused.Thiswilladdcostswhichwillultimatelybepassedontothecustomer.

TwoM-POWERcustomersusingtheirphonesoutsidetheirwelllithome.CreditstoMathieuYoungforOffGrid:Electric.Photocredit:PowerAfrica

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 17

3.1.4ModificationstoPAYGoModelsCompaniesaremodifyingelementsofthePAYGoconsumerfinanceprocesstofurtherincreaseaccess forall consumergroups.WitheachPAYGomodel currently implementedhaving inherentlimitationsinservingsomegroups,manycompanieshavetakenstepstoimplementtweakstomakethemodelmorefavourabletoconsumersegmentsexperiencingaffordabilityoraccessibilityconstraints.However, these modifications are generally not specifically tailored to vulnerable groups but aredesignedwithafocusonincreasingoverallconsumernumbersandfinancialperformance,i.e.improvingrepaymentanddefaultrates.Inaddition,manyofthesemodificationsarestillwithintrialphases,anditremainstobeseenwhetherthesewillbeeffectiveinimprovingaccesstoconsumerfinancewhilestillbeingfinanciallyviableforOGScompanies.

Varyingtheupfrontdeposit:SomeOGScompanieshaveexperimentedwith loweringorevenremovalofupfrontdepositstoeliminateaffordabilitybarriersforconsumers.Thedepositisgenerallythelargestbarriertoaffordabilityofaproductasitwilloftenrequireaconsumertosaveupforseveralmonthstomeetthecost.Duringthistime,consumers,particularlythosemostvulnerableones,canbe subject to financial shockswhich causes them toneed touse the savings.The loweringoreliminationofdepositsremovesthissavingbarrierforconsumersmeaningtheyonlyneedtomaketheregularrepaymentcosts.However,whilethisapproachmayattractmorecustomers,itcomeswithsignificantfinancialrisktotheOGScompanyasitnegativelyimpactscash-flowbyremovingcashreceivedforthedeposit.Additionally,aconsumer’sabilitytoprovideadepositcanbeseenasanindicationthattheycanmaketheregularrepayments,soitsremovalmaynegativelyimpactrepaymentanddefaultratesascompanieshavelessinsightintoaconsumer’sfinancesandtheconsumerthemselveshaslessskininthegamesomaybemorelikelytodefault.

Extensionoralterationsofrepaymenttermdurations:Somecompanieshavelongerrepaymenthorizons, leadingto lowerregularrepaymentamounts, toattractconsumersandmakepaymenttermsmorefavourabletovulnerablegroups.Whiletheregularrepaymentsarenotthemainbarriertoaconsumer’sabilitytoaffordaconsumerfinancemechanism,itdoesplayafactorintheirdecisionmakingprocessaslowerregularrepaymentswillleavemoremoneyavailableforothernecessities.Whilelongerrepaymenttermsmaybeattractivetotheconsumerithassomesignificantchallenges.Firstly,itwouldresultinreducedcashflowsfortheOGScompany.Secondly,itincreasesoperationalcostsastheloanneedstobeservicedoveralongertime.Finally,itmayincreasetheriskofdefaultduetothelengthoftimeoverwhichtheconsumerispayingwhichincreasestheriskofexternalfinancialshocksorrepaymentfatigue.ThesefactorswouldlikelyultimatelyleadtoahigheroverallrepaymentcostfortheconsumerastheOGScompanymitigatesitsrisksbyincreasingprices.

Box2:Thepay-as-you-grow(PAYGrow)repaymentstructure

InaPAYGrowmodel,anOGSsupplieralignstheconsumerfinancingmodelwithseasonalincome. The PAYGrowmodel aligns closely with the traditional PAYGomodel with the abilitytoremotelymonitor theOGSproductandreceivepaymentsviamobilemoney.However,whilethePAYGomodelrequiresdailyorweeklypayments,thePAYGrowmodelonlyrequiresperiodicrepaymentsthatarealignedtoseasonalincome.WhilenotyetcommonintheOGSsector,ithasattractedattention in theagriculturalPULSEsector,where incomeishighlyseasonalbasedonharvestcycles.Forexample,SunCulture–alocalsupplierofsolarirrigationequipmentandhomelighting–hasofferedthismodeltofarmersinKenya.

18 Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All

33 SteveWiggins,LeapingandLearning:LinkingSmallholderFarmerstoMarkets(London,UnitedKingdom,2013),

Aligning repayments to seasonal income can increase accessibility to consumer financingmodels.Consumerswithseasonalincomeareoftensmallholderandsubsistencefarmersthathaveahigherperceivedlevelofcreditriskduetoirregularincome,lowerlevelsofeducationandfinancialliteracy, aswell as the risk of crop failure. This can prevent them from accessingmore traditionalconsumerfinancemechanismsdue tobeingunable topass thecreditassessmentorbeingunableto keep up with monthly payments, an issue which is at least partially overcome in a PAYGrowmodel.Additionally,aPAYGrowmodelprovidesthepossibilityoflinkingrepaymentstoseasonalcropperformancethroughremotemonitoring,allowingforvariablepaymentamountstomatchconsumerincome.

PAYGrowmodelsarelimitedtofewsectorsandprovidehigherrisktofinanceproviders,whichcandriveupoverallcosts.ThePAYGrowmodelismostlylimitedtotheagriculturesectorduetothespecific characteristicof seasonal incomes.While thenumberof smallholder farmers is significant,withapotentialmarketof67million forsolarwaterpumpsalone, this limits thePAYGrowmodel tobeinganichemechanismratherthanauniversalmodel.Additionally,thePAYGrowmodelislikelytobemoreexpensivetofinanceanddifficulttomanageforOGScompaniesduetotheirregularnatureofrepaymentscausingcashflowproblemsandpotentiallylongrepaymentperiods.Thesehigherriskswillpushupthecostsofthemodel,whichwillultimatelybepassedontotheconsumer.

Supportingconsumersavings:Supportingcustomerstosaveuptothenecessaryrepaymentthresholdhelpsavoidallocationof income toother competingneeds.SomeOGScompanieshavedevelopedsavingtoolsandmechanismssuchaselectronicwalletsforconsumerssothattheycansetasideperiodic incometomakerepaymentsfor theirSHS.ThismeanscustomersthatmaystruggletosavefortheirregularrepaymentshaveameanstodosowhileringfencingmoneytorepaytheSHSsystemratherthanitbeingspentonotherdemands.However,thiscouldpotentiallybeconsideredasdepositmobilisationandattracttheattentionofCentralBankersorotherfinancialregulators.

Incomegenerationsupport:SomeOGScompaniesprovidelocalizedmarketopportunitiestopotentialcustomersfortheirproducehelpingtoboosttheirabilitytomakerepaymentsorpurchaseproducts upfront.Despite over 80%of food production activities inSub-SaharanAfrica beinggeneratedfromsubsistencefarming,manylacktheadequateinfrastructureandcapacitytolocateareadymarketfortheircrops.33OGScompanieshavebeenobservedtoprovidemarketlinkagestofarmersinexchangeforaportionoftheirearningsbeingearmarkedforSHSrepayments.

Protection against loss of income:Some OGS companies have partnered with insurancecompaniestointroduceinsuranceagainstdefaultintheeventofdeathorillnessofahousehold’sprimaryincomeearner.Suchinitiativesarerelativelynewinthesector,butcompaniessuchasZonfulandZuwahaveimplementedsuchsystemsinZimbabweandMalawi,respectively.Thisisnotonlybeneficialtotheconsumerthatisprotectedagainstfurthereconomicshockcausedbythelossofelectricityintheeventofthelossofthebreadwinner,butalsolowersacompany’sdefaultrate.Duetotherelativenascencyofthisinitiativeinthesector,moredataisrequiredtoassesstheoverallimpactonanOGScompany’sfinancesandinsupportingconsumerprotection.

Box2:Thepay-as-you-grow(PAYGrow)repaymentstructure(Continued)

Access to consumer FinAnce For VulnerAble Groups: one size Doesn’t Fit All 19

3.2 THEMICRO-FINANCEINSTITUTION(MFI)MODEL

MFIsprovideconsumerfinancing forOGSproducts inmanySub-SaharanAfricanandAsiancountries.Thismodel isveryprevalent inmarketswheremobilemoneyhas relatively low levelsofpenetration,suchasNigeriaandEthiopia.AnOGScompanymayengageanMFItoprovideconsumerfinancing on their behalf, or an MFI may engage an off-grid solar company to provide their OGSproductstotheirexistingconsumers. However,someMFIs,suchastheBaobabGroupinSenegal,havespunoutseparatesisterOGScompaniesratherthanpartneringwithanexistingOGSprovider.AnMFIloanapprovalprocessusuallyincludesathoroughcreditassessmentcheckandtheneedforcollateraloraguarantor.Onapprovalandprovisionofadeposit,theMFIwillprovidetheproducttotheconsumerdirectlyor transfer fundsdirectly toaretailer toprovidetheOGSdeviceto theconsumer.Post-installation,subsequentpaymentsarecollectedaccordingtoapre-agreedpaymentschedulewiththeMFImanagingprocess.