Embed Size (px)

Citation preview

Accessing Your Hidden Assets

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 2

Agenda

Defining the asset (establishing a common language)

Selling the asset

Mortgaging the asset

Conclusion

Questions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 3

Disclaimer

Solutions described have been used elsewhere in the last2 years but may not be as effective in the localmarket/regulatory environment

Some solutions may not be available locally or currently

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 4

Assumptions

Local life insurers have significant inforce business

Local regulatory requirements include a level ofconservatism, particularly on mortality and/or persistency

True in almost all jurisdictions

Serves to hide one of the companies biggest assets

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 5

Common Language

Value of Inforce (VIF)

– VIF is the discounted present value of all futurestatutory profits on a block of inforce business

– For the purposes of this presentation VIF does notinclude consumption or release of solvency orrespectability capital

– Only items which contribute to statutory profits areincluded in VIF

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 6

Common Language

Embedded Value (EV)

– EV = VIF + Free Assets

– Free Assets include all capital not included in the VIFreserves

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 7

The Hidden Asset

Almost by definition, VIF is not an admissible asset forsolvency calculations

In many regimes the VIF of inforce business is very largewhen compared to the solvency needs of the companydue to high historical margins

As a rule of thumb, mortality VIF is about 0.1% to 0.5% oftotal sum at risk

Insurers are more and more commonly looking to the VIFto finance organic growth or acquisitions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 8

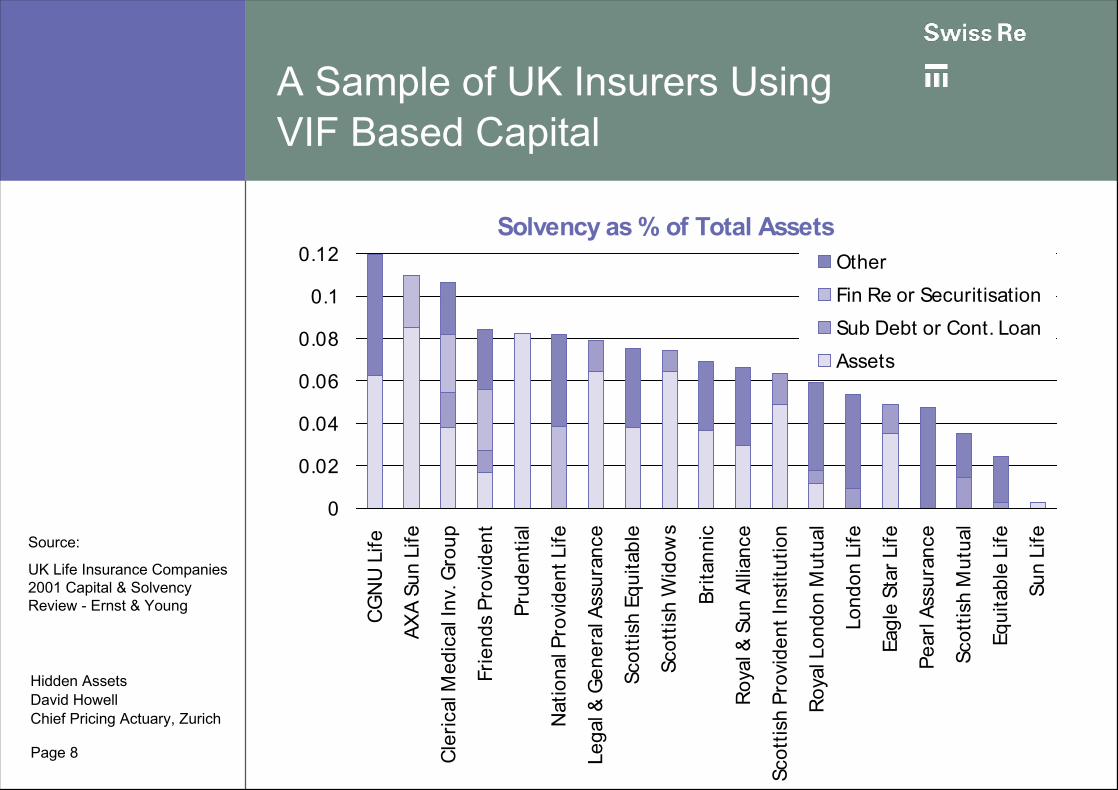

A Sample of UK Insurers UsingVIF Based Capital

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Solvency as % of Total Assets

0

0.02

0.04

0.06

0.08

0.1

0.12

CG

NU

Life

AXA

Sun

Life

Cler

ical

Med

ical

Inv.

Gro

up

Frie

nds

Prov

iden

t

Prud

entia

l

Nat

iona

l Pro

vide

nt L

ife

Lega

l & G

ener

al A

ssur

ance

Scot

tish

Equi

tabl

e

Scot

tish

Wid

ows

Brita

nnic

Roya

l & S

un A

llian

ce

Scot

tish

Prov

iden

t Ins

titut

ion

Roy

al L

ondo

n M

utua

l

Lond

on L

ife

Eagl

e St

ar L

ife

Pear

l Ass

uran

ce

Scot

tish

Mut

ual

Equi

tabl

e Li

fe

Sun

Life

Other

Fin Re or Securitisation

Sub Debt or Cont. Loan

Assets

Source:

UK Life Insurance Companies2001 Capital & SolvencyReview - Ernst & Young

Page 9

Agenda

Defining the asset (establishing a common language)

Selling the asset

Mortgaging the asset

Conclusion

Questions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 10

Selling the Asset

Includes everything from traditional reinsurance to sale ofthe life company

Generally raises the highest proportion of VIF

Often creates rating capital (S&P only give credit for 50%VIF)

May be more acceptable to regulators

Possible difference in USGAAP treatment if deemed atrue sale

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 11

Selling the Company

What it is:

– Obvious

When to use it:

– The parent needs capital

– Life insurance (or at least this sub) is a not a corestrategy

– Maximizing the amount of capital raised is importantas sale may realize significant extra value over VIF interms of free assets and franchise value

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 12

Selling a BlockAdmin Re

What it is:

– Admin Re is a popular solution in the US for divestingan under-performing or non-core block of business

– Effectively all responsibility for running off a definedblock is passed to the reinsurer including policyadministration

– Selling to a professional reinsurer protects yourownership of clients

– Expense savings and management focus are oftenkey drivers

– Difficult to pursue in Hong Kong due to the limitedavailability of established TPAs and existing low costbase

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 13

Selling a BlockAdmin Re

When to use it:

– The insurance company needs reliable long termcapital

– Rating capital is an issue

– Legacy product or system issues take adisproportionate amount of time

– Maximizing the effective use of VIF is important as itmay release up to 100% of VIF (if discount rates arerealistic) or more depending on expense assumptions

– Can also be used to sell a whole company when costefficiency is more important than franchise valueHidden Assets

David HowellChief Pricing Actuary, Zurich

Page 14

Sale of Mortality Margins

What it is:

– Most valuation bases require conservativeassumptions to be made about mortality or similarnon-investment risks which implies that a reliablestream of future profits exist

– These future cashflows can be crystallized byreinsuring large blocks of inforce mortality risk atpremium rates just under the valuation assumption

– An initial commission payment compensates thecompany for the loss of the future cashflows

– Can be a very cost effective way of accessing VIFwithout giving up control of the block

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 15

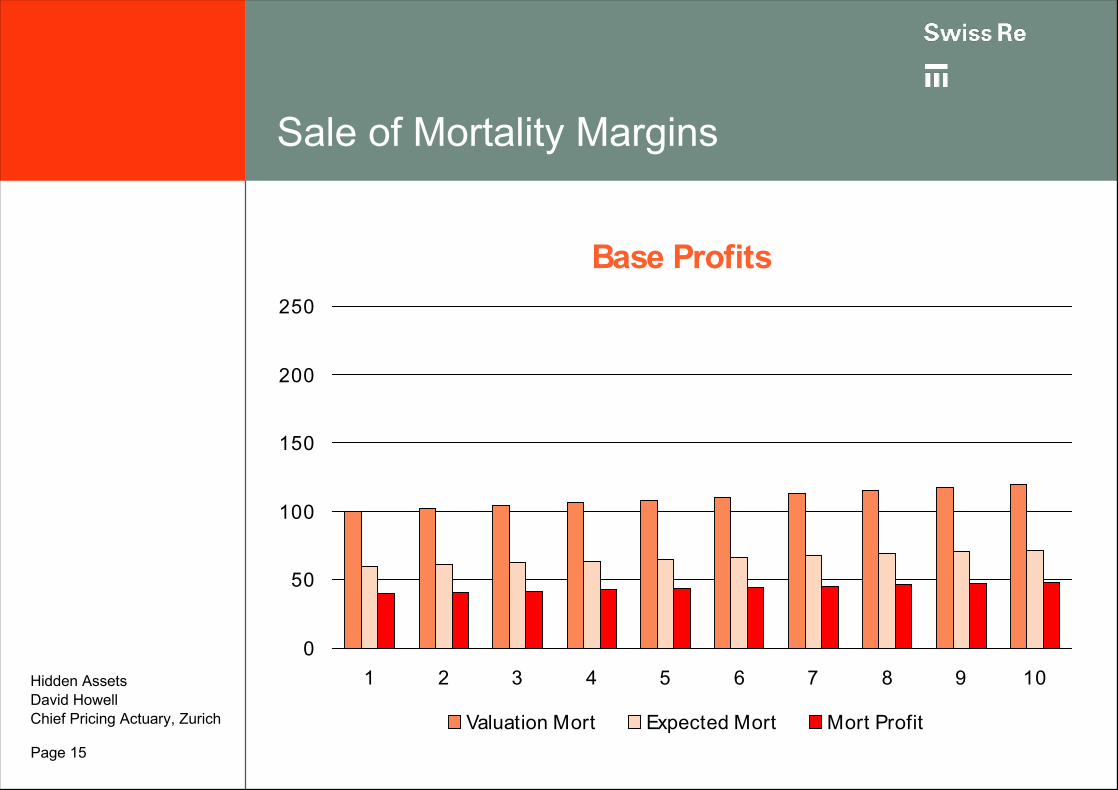

Sale of Mortality Margins

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Base Profits

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10

Valuation Mort Expected Mort Mort Profit

Page 16

Sale of Mortality Margins

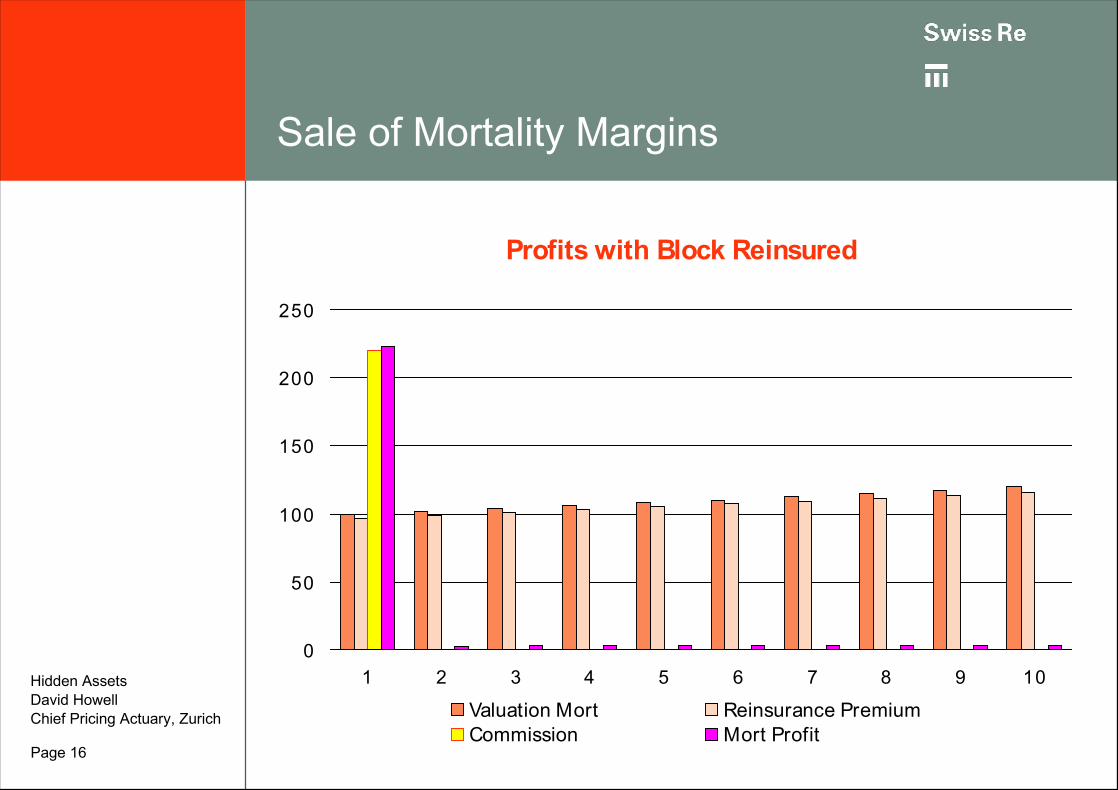

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Profits with Block Reinsured

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10

Valuation Mort Reinsurance PremiumCommission Mort Profit

Page 17

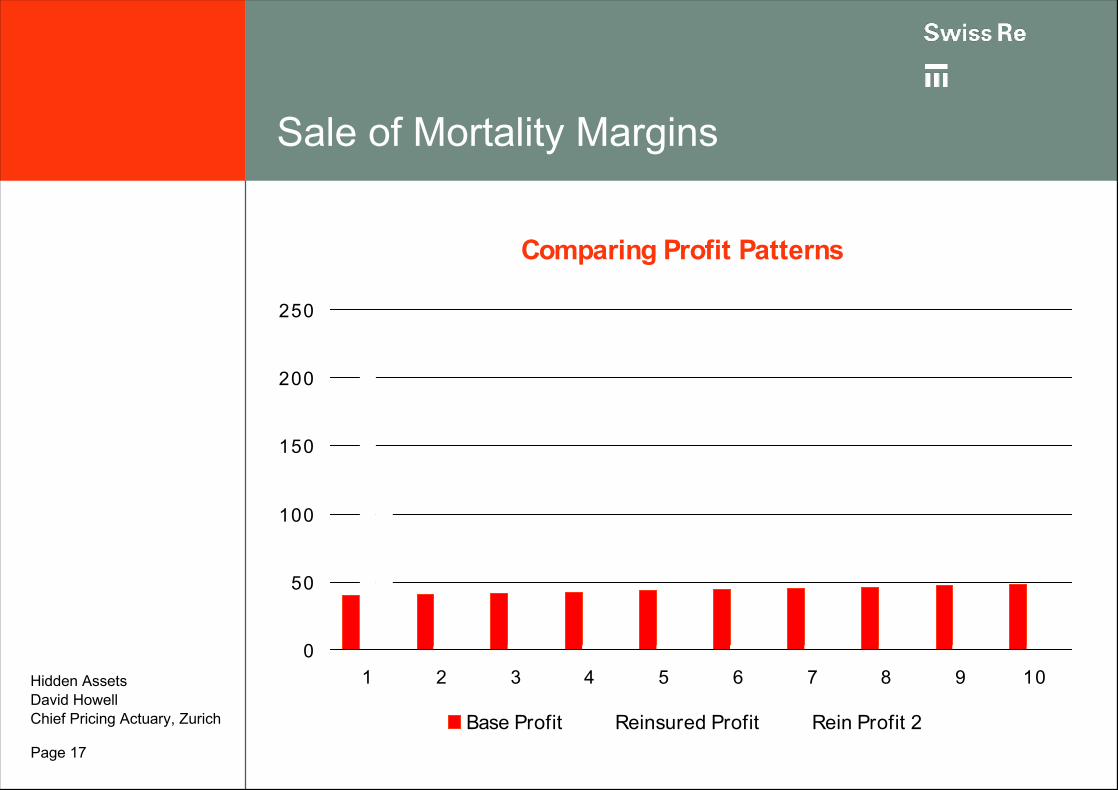

Sale of Mortality Margins

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Comparing Profit Patterns

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10

Base Profit Reinsured Profit Rein Profit 2

Page 18

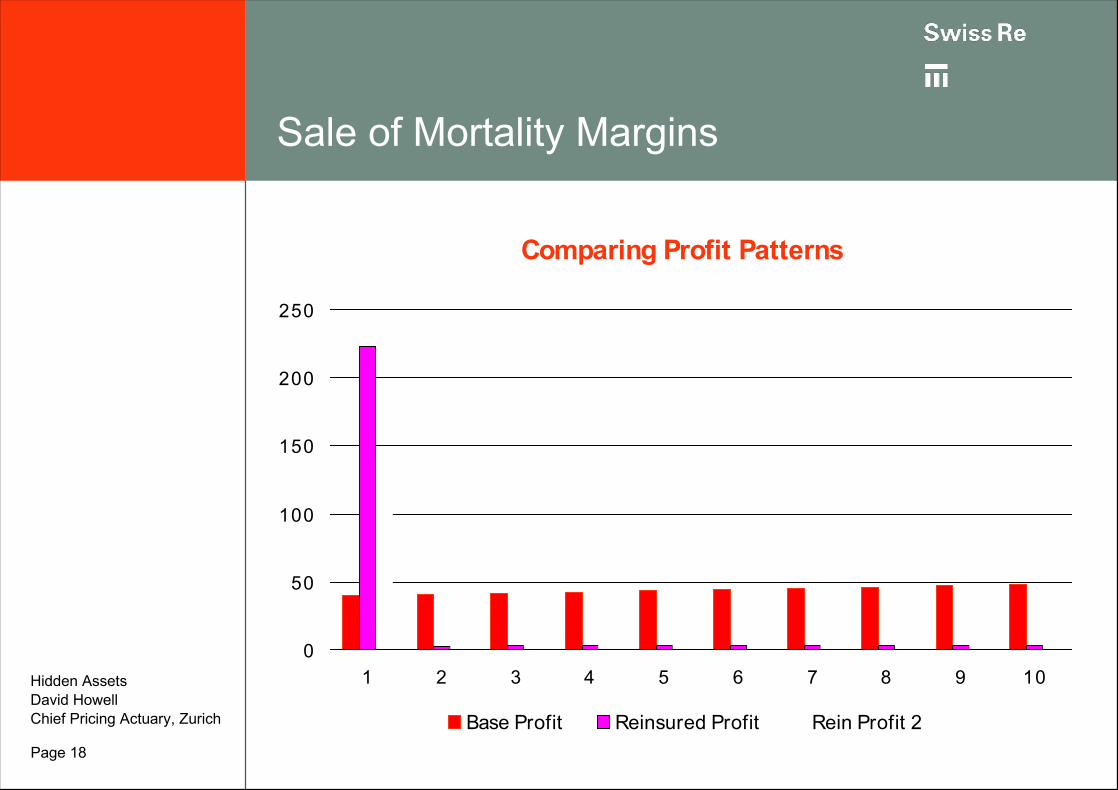

Sale of Mortality Margins

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Comparing Profit Patterns

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10

Base Profit Reinsured Profit Rein Profit 2

Page 19

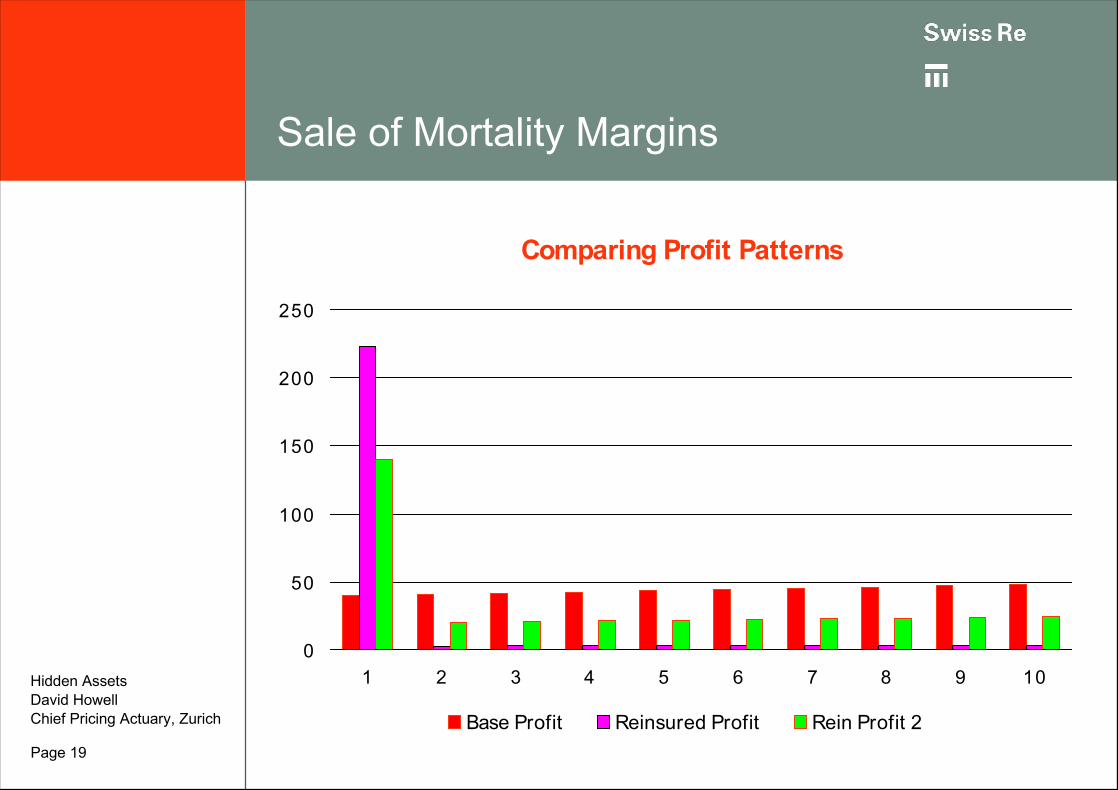

Sale of Mortality Margins

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Comparing Profit Patterns

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10

Base Profit Reinsured Profit Rein Profit 2

Page 20

Sale of Mortality Margins

Isn’t this giving away profit?

– This depends on how profit is defined

– On a pure dollars/euros/pounds of cashflow basis“Yes” but the profit emerges earlier and so can beinvested

– On an EV or RoC basis this method frequentlyincreases profits as a specialist reinsurer is morecapital efficient in managing mortality risk

– How is the increase in financial stability and strategicoptions valued?

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 21

What about the credit risk?

Insurer Credit Risk

– If the initial commission is paid in cash atcommencement the reinsurer will be exposed tomaterial credit risk

– This credit risk will have an associated cost and maylimit the capital that can be raised

– Cost can be reduced and capital availability increasedby credit risk mitigants such as trusts and paymentoffsets

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 22

What about the credit risk?

Reinsurer Credit Risk

– If the initial commission is paid in cash atcommencement there is little or no reinsurance creditrisk

– If other structures are used then the choice ofreinsurer becomes even more important than thenormal structuring skills and competitiveness issues

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 23

What about policyholderpersistency risk?

Reinsurers are generally adverse to taking large amountsof policyholder persistency risk and hence it is expensiveto reinsure

This risk is affected by the day to day management andmarketing activities of the insurer

The majority of persistency risk can be structured out ofthe treaty such that it is retained by the insurer

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 24

Sale of Mortality Margins

When to use it:

– The insurance company needs reliable long termcapital

– Rating capital is an issue

– Admin efficiency is already high

– Maximizing the effective use of VIF is important as itmay release up to 100% of mortality VIF (if discountrates are realistic)

– A stable stream of future margins are desirable(achieved by setting reinsurance premiums less thanvaluation assumptions)Hidden Assets

David HowellChief Pricing Actuary, Zurich

Page 25

Sale of All Margins

Effective sale of NB is the norm for term business in theUS and UK

– Generally level premium and high initial commission

– Sale of total mortality and persistency margin on 80-90% of the business

– This is not the high premium and high profitcommission type of reinsurance more commonly donein Continental Europe and Asia

– Doesn’t fit easily with the others topics in thispresentation as it is generally applied to NB

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 26

Agenda

Defining the asset (establishing a common language)

Selling the asset

Mortgaging the asset

Conclusion

Questions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 27

Mortgaging the Asset

In all forms this consists of taking a loan against securedagainst the VIF

Major differences lie in how the capital in loaned and whothe lender is

Rarely raises more than 50% of VIF, if that

Generally does not generate any ratings capital

Requires detailed knowledge of regulations and possiblydiscussions with regulators

Credit analysis can is very thorough and may seemintrusive

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 28

Financial Reinsurance (Fin Re)

What it is:

– Fin Re is the provision of capital via a reinsurancetreaty with minimal insurance risk transfer

– Charges are defined in terms of a percentage of thecapital supplied

– Usually backed out by ratings agencies in assessingcapital

– Broadly separated into cash and non-cash

– Availability has dropped and price increaseddramatically in the last 24 months

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 29

-20

0

20

40

60

80

100

120

Assets Liabilities

Capital Financing

Before After

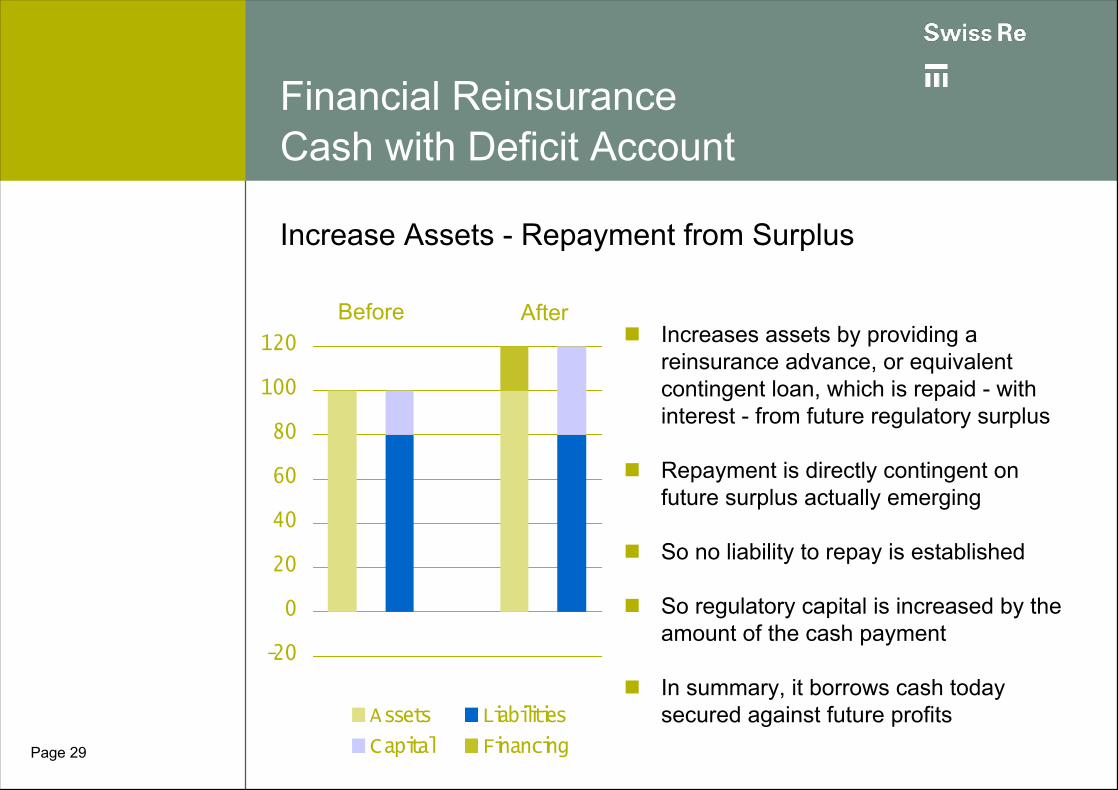

Financial ReinsuranceCash with Deficit Account

Increases assets by providing areinsurance advance, or equivalentcontingent loan, which is repaid - withinterest - from future regulatory surplus

Repayment is directly contingent onfuture surplus actually emerging

So no liability to repay is established

So regulatory capital is increased by theamount of the cash payment

In summary, it borrows cash todaysecured against future profits

Increase Assets - Repayment from Surplus

Page 30

Financial ReinsuranceCashless with Virtual Capital

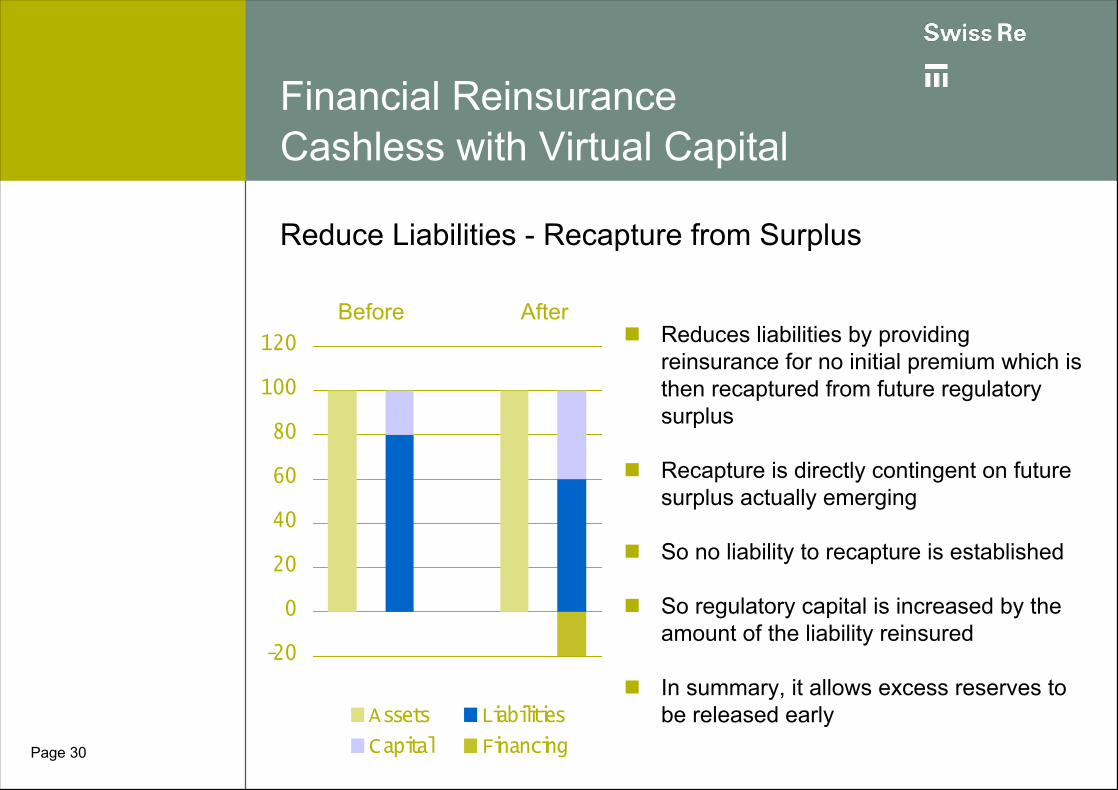

Reduces liabilities by providingreinsurance for no initial premium which isthen recaptured from future regulatorysurplus

Recapture is directly contingent on futuresurplus actually emerging

So no liability to recapture is established

So regulatory capital is increased by theamount of the liability reinsured

In summary, it allows excess reserves tobe released early

-20

0

20

40

60

80

100

120

Assets Liabilities

Capital Financing

Before After

Reduce Liabilities - Recapture from Surplus

Page 31

Financial Reinsurance (Fin Re)

When to use it:

– Capital need is short term and fairly predictable

– Ratings capital is not an issue

– The amount of VIF available is stable and largecompared to the capital need

– Best used by financially strong companies as thiskeeps costs and regulatory problems down

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 32

Securitisation

What it is:

– Securitisation is effectively cash based Fin Re wherethe reinsurance is supplied by the capital markets

Additional Issues:

– Credit assessment much more public

– May accept longer payback period than reinsurers

– Reinsurance wrap may make placement easier

– Only major life insurance securitisation to date is NPIin the UK

– Current markets may not respond positivelyHidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 33

Subordinated Debt

What it is:

– Issuance of highly subordinated long term (usuallyperpetual) sub debt

Issues:

– Key factor is local regulation

– Regulation changes have made this a popular optionin the UK in 1999-2001

– Current markets may restrict attractiveness

– Common intra-group structure (contingent loan)Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 34

Agenda

Defining the asset (establishing a common language)

Selling the asset

Mortgaging the asset

Conclusion

Questions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 35

Points to Consider

Is the available VIF big enough to address your needs orat least make a material contribution to it?

Is the need just for regulatory capital or does ratingscapital need to be considered as well?

Is the capital need short term or long term?

Is the capital needed in the life company or its parent?

Is stabilizing future results be a beneficial side effect?

What solutions are available in your market?

Tax? Key driver or obstacle for many deals.

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

Page 36

Agenda

Defining the asset (establishing a common language)

Selling the asset

Mortgaging the asset

Conclusion

Questions

Hidden AssetsDavid HowellChief Pricing Actuary, Zurich

![ASC Hidden Assets[1]](https://img.pdfslide.net/doc/110x75/577d2ae61a28ab4e1eaa6679/asc-hidden-assets1.jpg)

![Reinkowski Hidden Believers Hidden Apostates[1]](https://img.pdfslide.net/doc/110x75/577cdfdb1a28ab9e78b2245d/reinkowski-hidden-believers-hidden-apostates1.jpg)