Embed Size (px)

Citation preview

Accounts of the Company Chapter -IXChapter IX

Audit & Auditors Ch t XChapter - X

Books of Accounts Section 128

2013

Main sections in the chapter

Re-opening of Accounts

Financial Statement Section 129

Section 130 es A

ct, 2

Re-opening of Accounts

Voluntary Revision of financial statement Section 131

Section 130

X Com

pani

e

CG to Prescribe Accounting standards

NFRA

Section 133

Section 132

hapt

er –

Im

pany

-C

CG to Prescribe Accounting standards

Financial Statement , Boards Report etcSection 134

Ch

the

Com

Right of members to copies of FS

FS to be filled with ROC

Section 136

Section 137 ount

s of

FS to be filled with ROC

Internal Audit Section 138

Acc

o

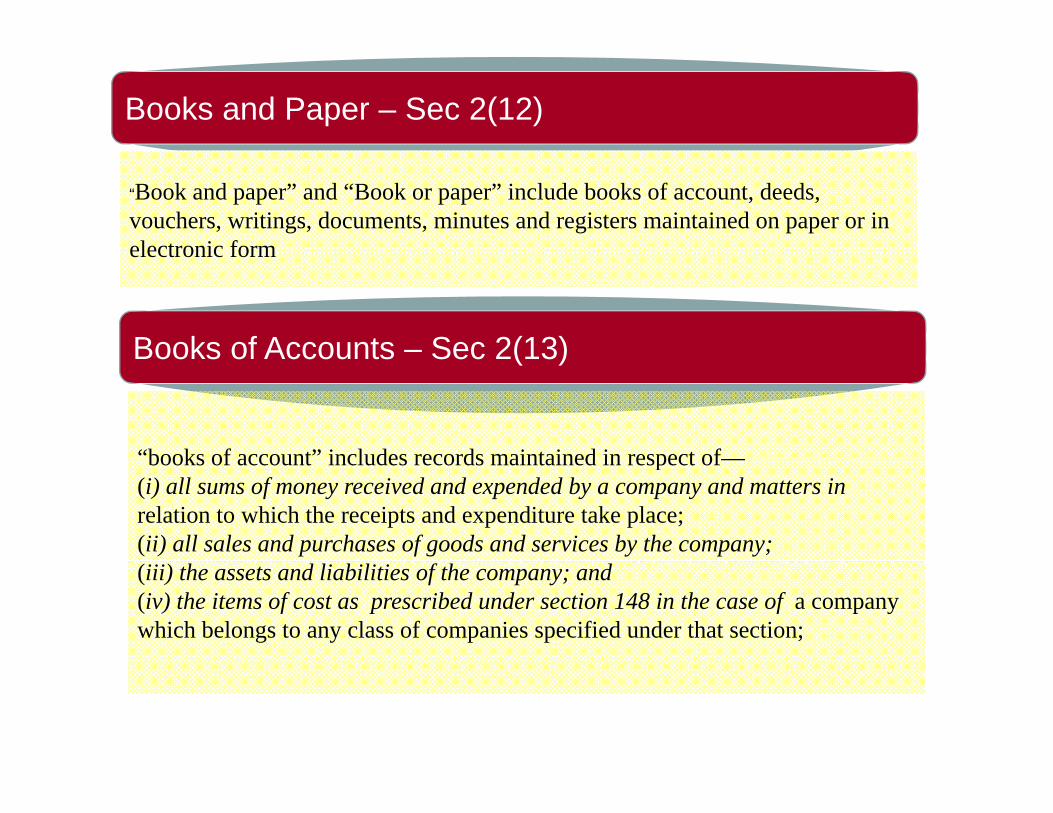

Books and Paper – Sec 2(12)

“Book and paper” and “Book or paper” include books of account, deeds,vouchers, writings, documents, minutes and registers maintained on paper or in electronic form

Books of Accounts – Sec 2(13)

electronic form

Books of Accounts Sec 2(13)

“books of account” includes records maintained in respect ofbooks of account includes records maintained in respect of—(i) all sums of money received and expended by a company and matters inrelation to which the receipts and expenditure take place;(ii) all sales and purchases of goods and services by the company;(iii) the assets and liabilities of the company; and(iv) the items of cost as prescribed under section 148 in the case of a company which belongs to any class of companies specified under that section;

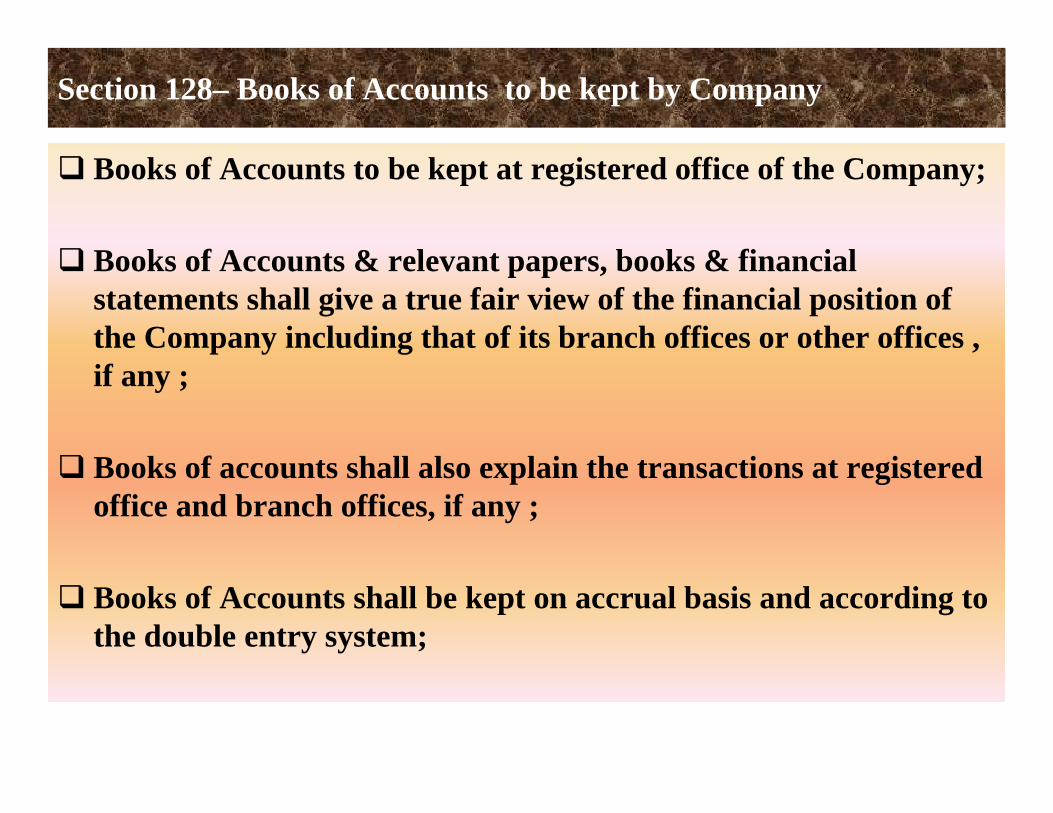

Section 128– Books of Accounts to be kept by Company

Books of Accounts to be kept at registered office of the Company;

B k f A t & l t b k & fi i lBooks of Accounts & relevant papers, books & financial statements shall give a true fair view of the financial position of the Company including that of its branch offices or other offices , if any ;

B k f h ll l l i h i i dBooks of accounts shall also explain the transactions at registered office and branch offices, if any ;

Books of Accounts shall be kept on accrual basis and according to the double entry system;

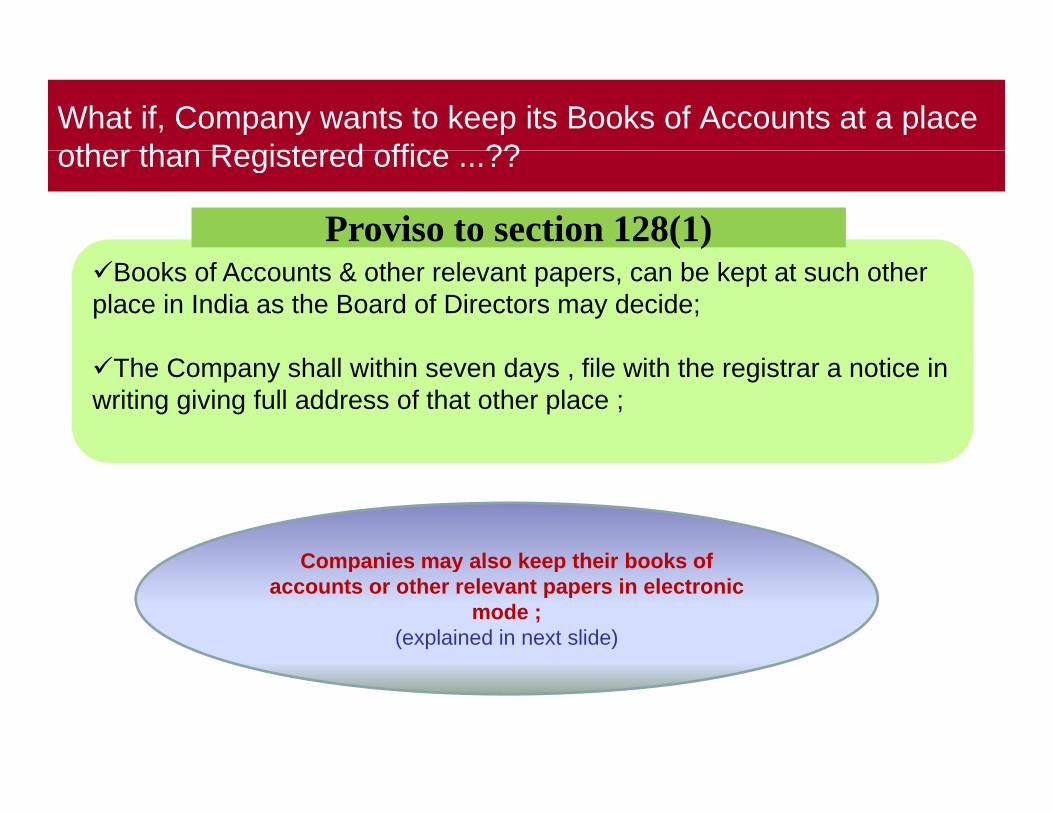

What if, Company wants to keep its Books of Accounts at a place other than Registered office ??other than Registered office ...??

Proviso to section 128(1)Books of Accounts & other relevant papers, can be kept at such other

place in India as the Board of Directors may decide;

The Company shall within seven days , file with the registrar a notice in writing giving full address of that other place ;

Companies may also keep their books ofCompanies may also keep their books of accounts or other relevant papers in electronic

mode ;(explained in next slide)

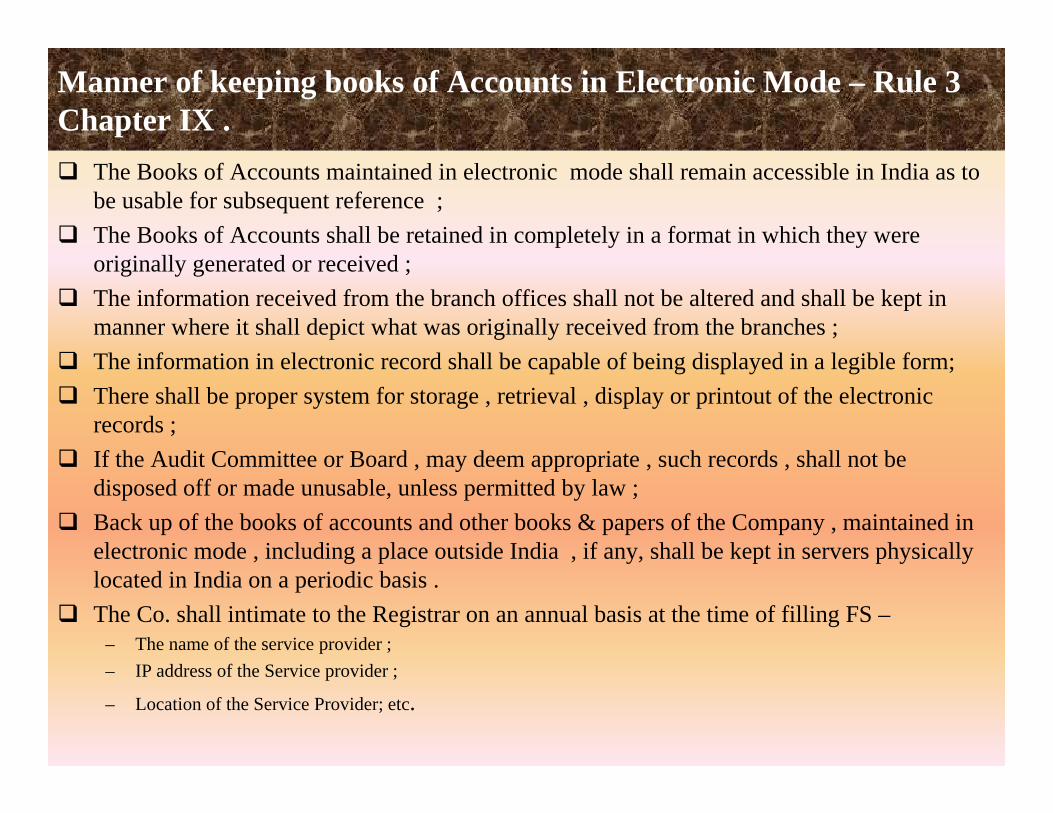

Manner of keeping books of Accounts in Electronic Mode – Rule 3 Chapter IX .

The Books of Accounts maintained in electronic mode shall remain accessible in India as to be usable for subsequent reference ;The Books of Accounts shall be retained in completely in a format in which they were originally generated or received ;The information received from the branch offices shall not be altered and shall be kept in manner where it shall depict what was originally received from the branches ;Th i f ti i l t i d h ll b bl f b i di l d i l ibl fThe information in electronic record shall be capable of being displayed in a legible form;There shall be proper system for storage , retrieval , display or printout of the electronic records ;If the Audit Committee or Board may deem appropriate such records shall not beIf the Audit Committee or Board , may deem appropriate , such records , shall not be disposed off or made unusable, unless permitted by law ;Back up of the books of accounts and other books & papers of the Company , maintained in electronic mode , including a place outside India , if any, shall be kept in servers physically , g p , y, p p y ylocated in India on a periodic basis .The Co. shall intimate to the Registrar on an annual basis at the time of filling FS –

– The name of the service provider ;– IP address of the Service provider ;

– Location of the Service Provider; etc.

Section 128– Books of Accounts to be kept by Company

The books of accounts shall remain open for inspection by directors of the Company or such other place , during business hours ;I ti f b k f t f th b idi f thInspection of books of accounts of the subsidiary of the company , shall only be done by a person authorised in this behalf by a resolution of the Board of directors ;The books of accounts relating to a period not less than eight preceding financial years , shall be kept in good order ;P l f i Offi i d f l d hi i h llPenalty for contravention : Officer in default under this section shall be punishable with imprisonment for a term which may extend to one year or with a fine minimum of 50,000 and maximum of 5 lakhs .y

“Officer in default for this section” ; managing director, the whole-time director in charge of finance, the Chief Financial Officer or any other person of a company charged by the Board with the duty of complying with the provisions of this section

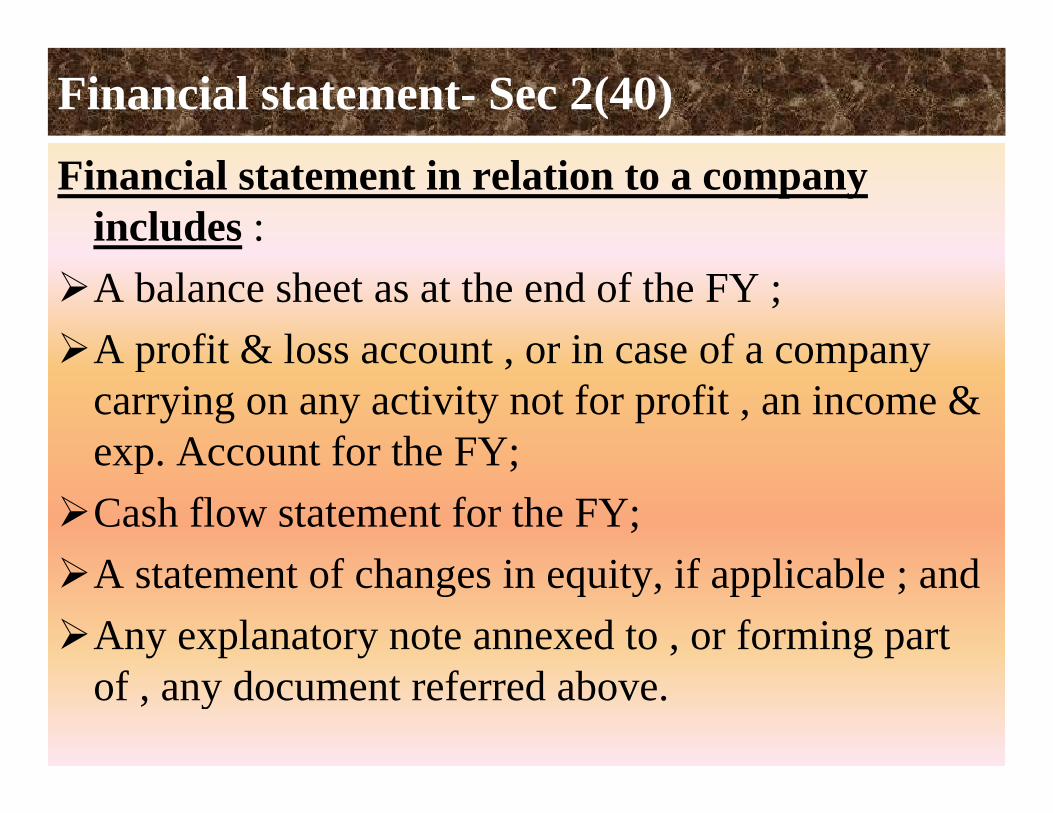

Financial statement- Sec 2(40)

Financial statement in relation to a company includes : A balance sheet as at the end of the FY ;A profit & loss account or in case of a companyA profit & loss account , or in case of a company carrying on any activity not for profit , an income & exp Account for the FY;exp. Account for the FY;Cash flow statement for the FY;A f h i i if li bl dA statement of changes in equity, if applicable ; andAny explanatory note annexed to , or forming part of , any document referred above.

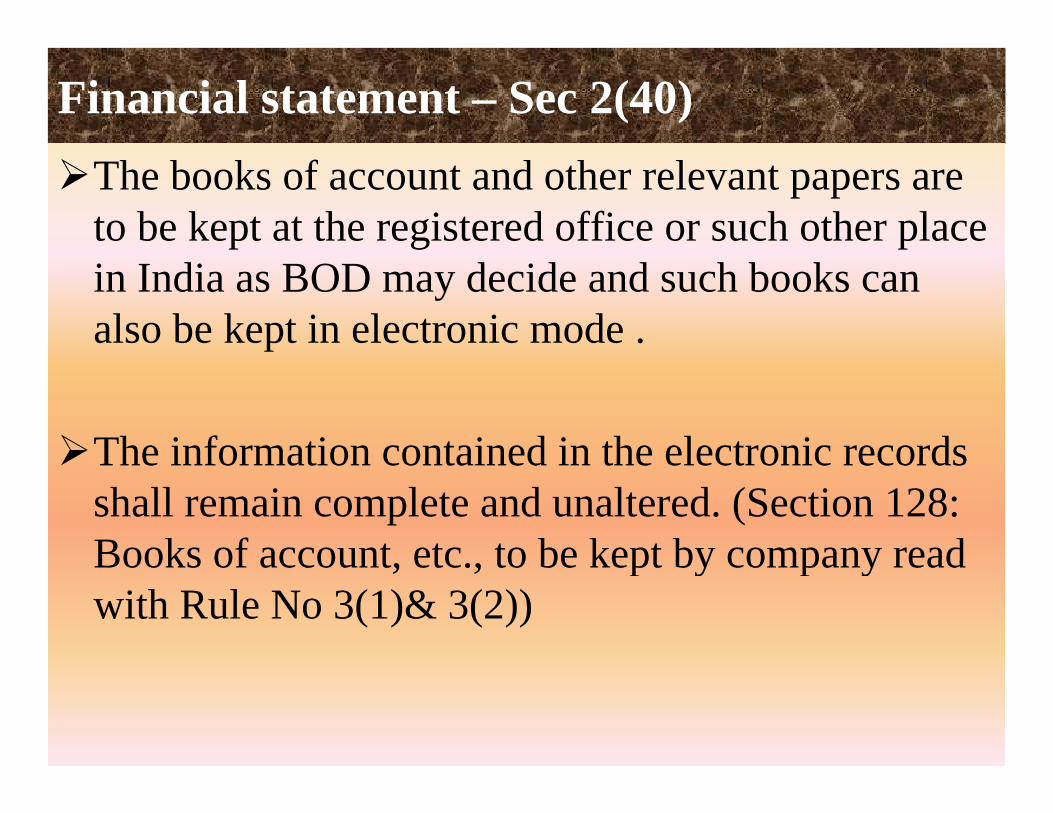

Financial statement – Sec 2(40) The books of account and other relevant papers are to be kept at the registered office or such other place in India as BOD may decide and such books can also be kept in electronic mode .

The information contained in the electronic recordsThe information contained in the electronic records shall remain complete and unaltered. (Section 128: Books of account etc to be kept by company readBooks of account, etc., to be kept by company read with Rule No 3(1)& 3(2))

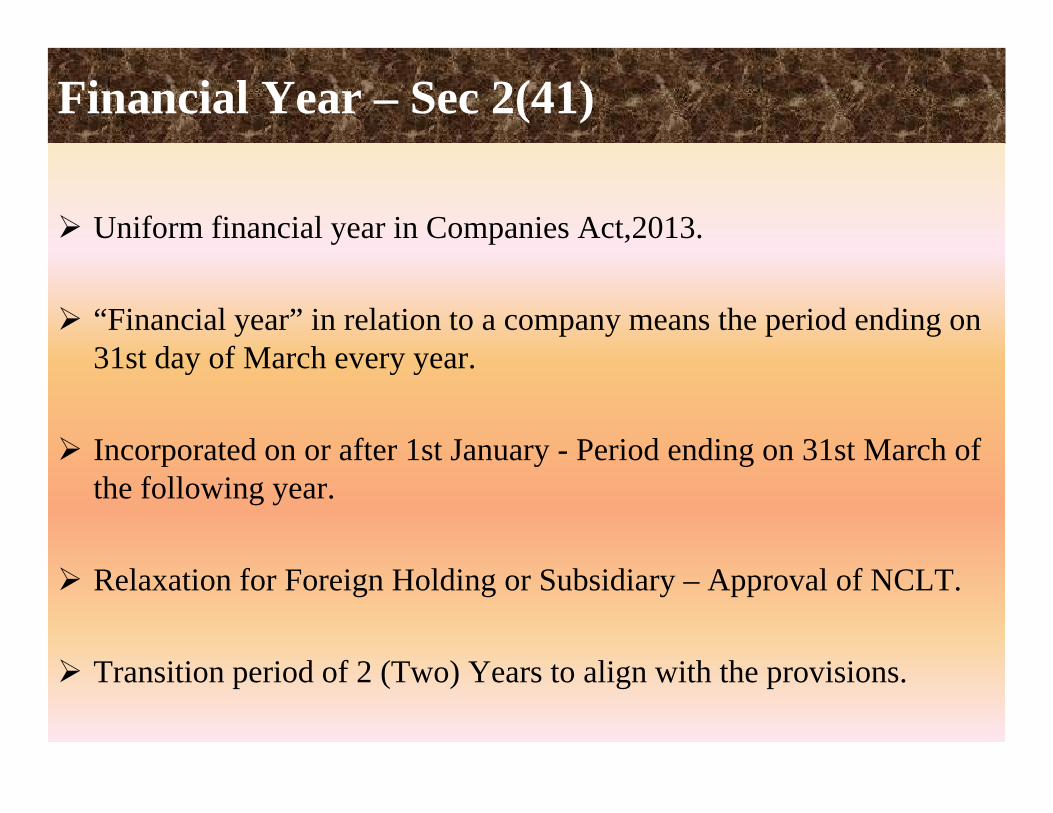

Financial Year – Sec 2(41)

Uniform financial year in Companies Act,2013.

“Financial year” in relation to a company means the period ending on 31st day of March every year31st day of March every year.

Incorporated on or after 1st January - Period ending on 31st March ofIncorporated on or after 1st January Period ending on 31st March of the following year.

Relaxation for Foreign Holding or Subsidiary – Approval of NCLT.

T i i i d f 2 (T ) Y li i h h i iTransition period of 2 (Two) Years to align with the provisions.

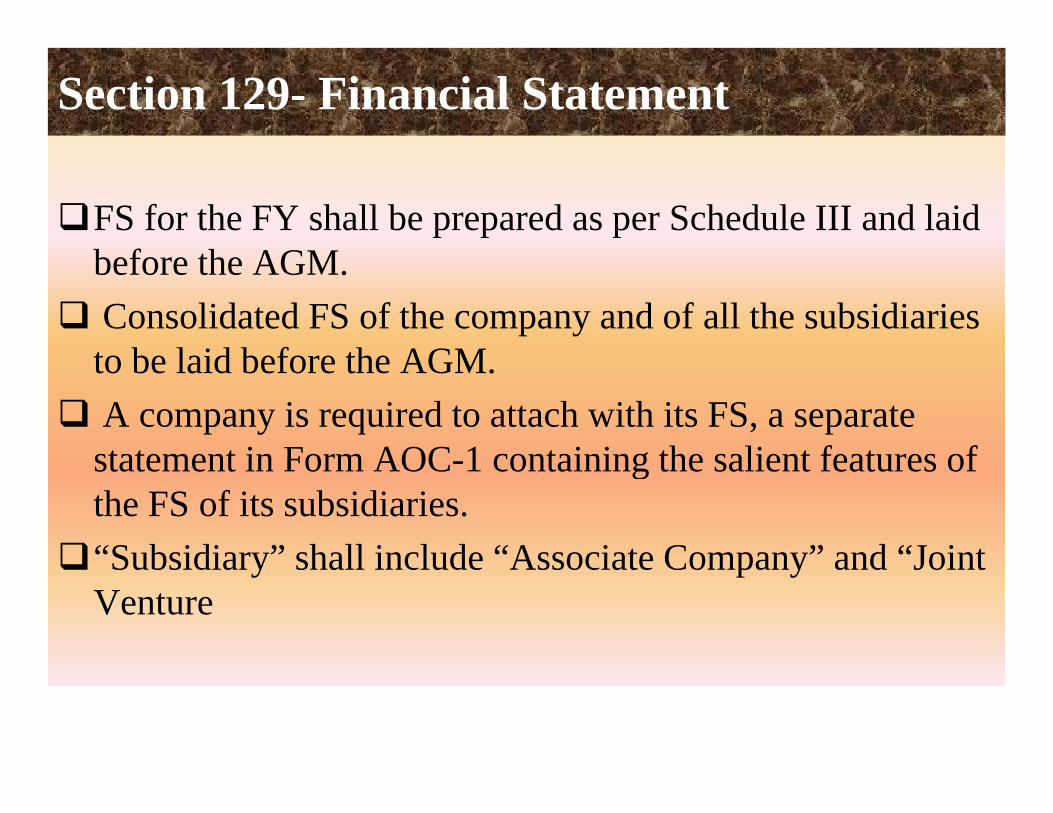

Section 129- Financial Statement

FS for the FY shall be prepared as per Schedule III and laid b f th AGMbefore the AGM.Consolidated FS of the company and of all the subsidiaries t b l id b f th AGMto be laid before the AGM.A company is required to attach with its FS, a separate statement in Form AOC 1 containing the salient features ofstatement in Form AOC-1 containing the salient features of the FS of its subsidiaries.“Subsidiary” shall include “Associate Company” and “JointSubsidiary shall include Associate Company and Joint Venture

Schedule III of Companies Act, 2013S h d l III f th C i A t 2013 i R i d S h d l VI f th C iSchedule III of the Companies Act 2013, is same as Revised Schedule VI of the Companies Act, 1956 except that it contains general instructions for preparation of Consolidated Financial Statements (CFS) of Company and its subsidiaries, as the same has been mandated by the new Act.yIf company is required to prepare CFS, i.e., consolidated balance sheet and consolidated statement of profit and loss, the company shall mutatis mutandis follow the requirements of Schedule III.In addition, the CFS shall disclose the information as per the requirements specified in the applicable Accounting Standards including:– Profit or loss attributable to “minority interest” and to owners of the parent in the

statement of profit and loss shall be presented as allocation for the periodstatement of profit and loss shall be presented as allocation for the period.– “Minority interests” in the balance sheet within equity shall be presente separately from

the equity of the owners of the parent.All subsidiaries associates and joint ventures (whether Indian or foreign) will be coveredAll subsidiaries, associates and joint ventures (whether Indian or foreign) will be covered under CFS.An entity shall disclose the list of subsidiaries or associates or joint ventures which have not been consolidated in the consolidated financial statements along with the reasons of not consolidating.Schedule III of the Act, does not have format for the Cash Flow Statemen and Statement for Changes in Equity

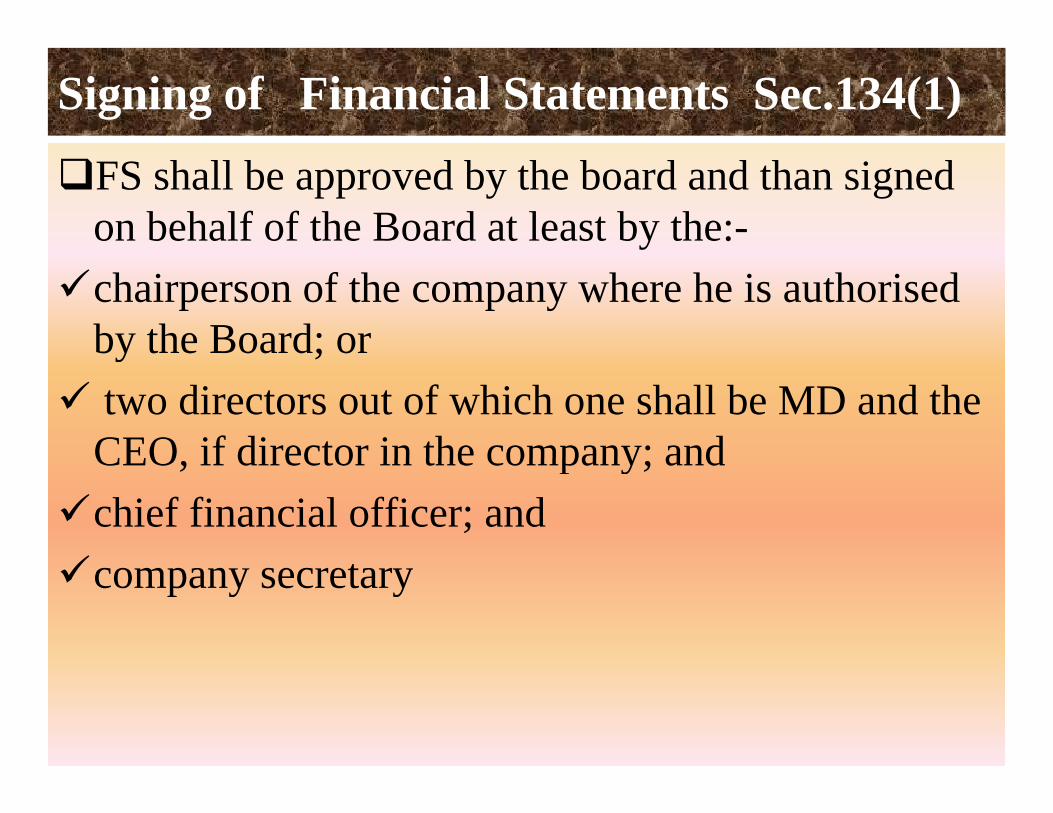

Signing of Financial Statements Sec.134(1)

FS shall be approved by the board and than signed on behalf of the Board at least by the:-chairperson of the company where he is authorised by the Board; ory ;two directors out of which one shall be MD and the CEO if director in the company; andCEO, if director in the company; andchief financial officer; andcompany secretary

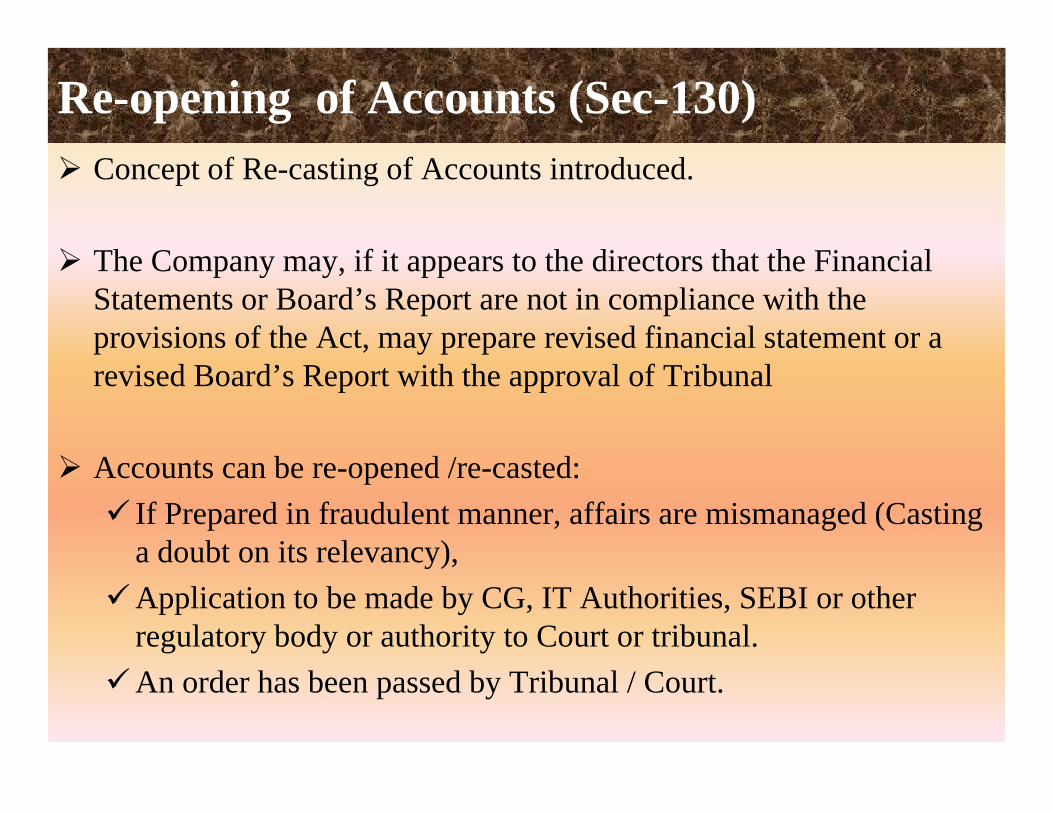

Re-opening of Accounts (Sec-130)Concept of Re-casting of Accounts introduced.

Th C if it t th di t th t th Fi i lThe Company may, if it appears to the directors that the Financial Statements or Board’s Report are not in compliance with the provisions of the Act, may prepare revised financial statement or a revised Board’s Report with the approval of Tribunal

A b d / dAccounts can be re-opened /re-casted: If Prepared in fraudulent manner, affairs are mismanaged (Casting a doubt on its relevancy),a doubt on its relevancy), Application to be made by CG, IT Authorities, SEBI or other regulatory body or authority to Court or tribunal. An order has been passed by Tribunal / Court.

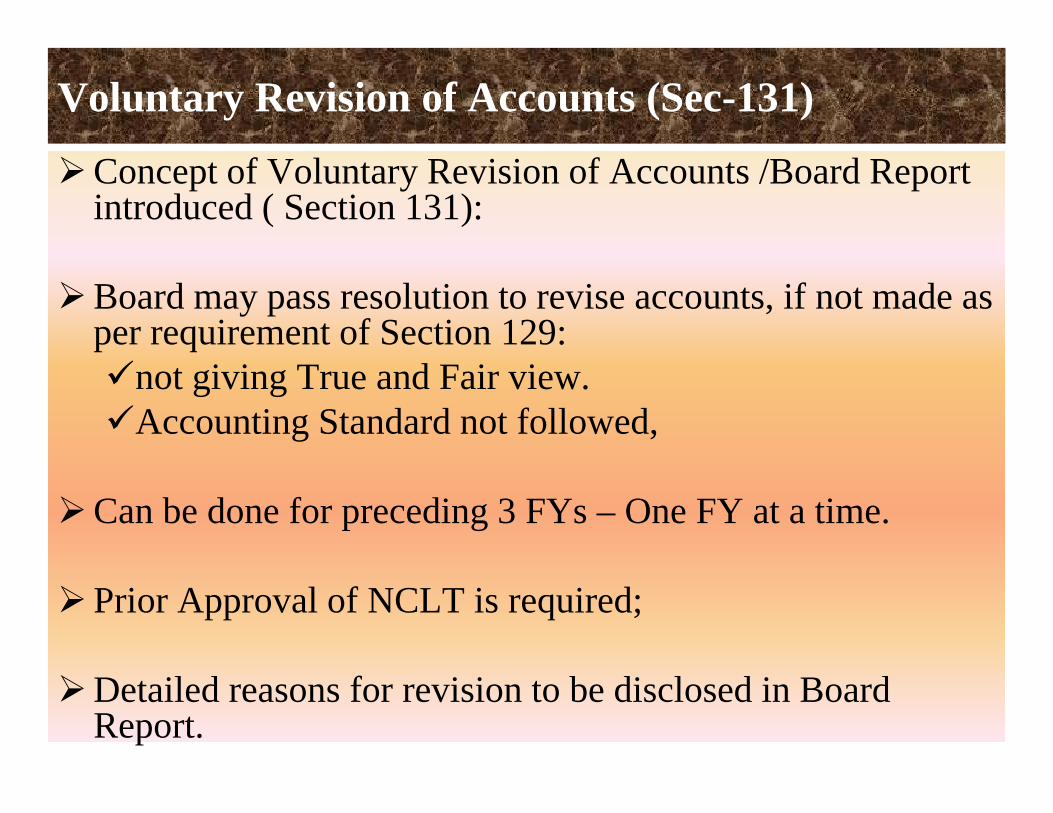

Voluntary Revision of Accounts (Sec-131)

Concept of Voluntary Revision of Accounts /Board Report introduced ( Section 131):

Board may pass resolution to revise accounts, if not made as per requirement of Section 129:

not giving True and Fair view.Accounting Standard not followed,

Can be done for preceding 3 FYs – One FY at a time.

Prior Approval of NCLT is required;

Detailed reasons for revision to be disclosed in Board Report.

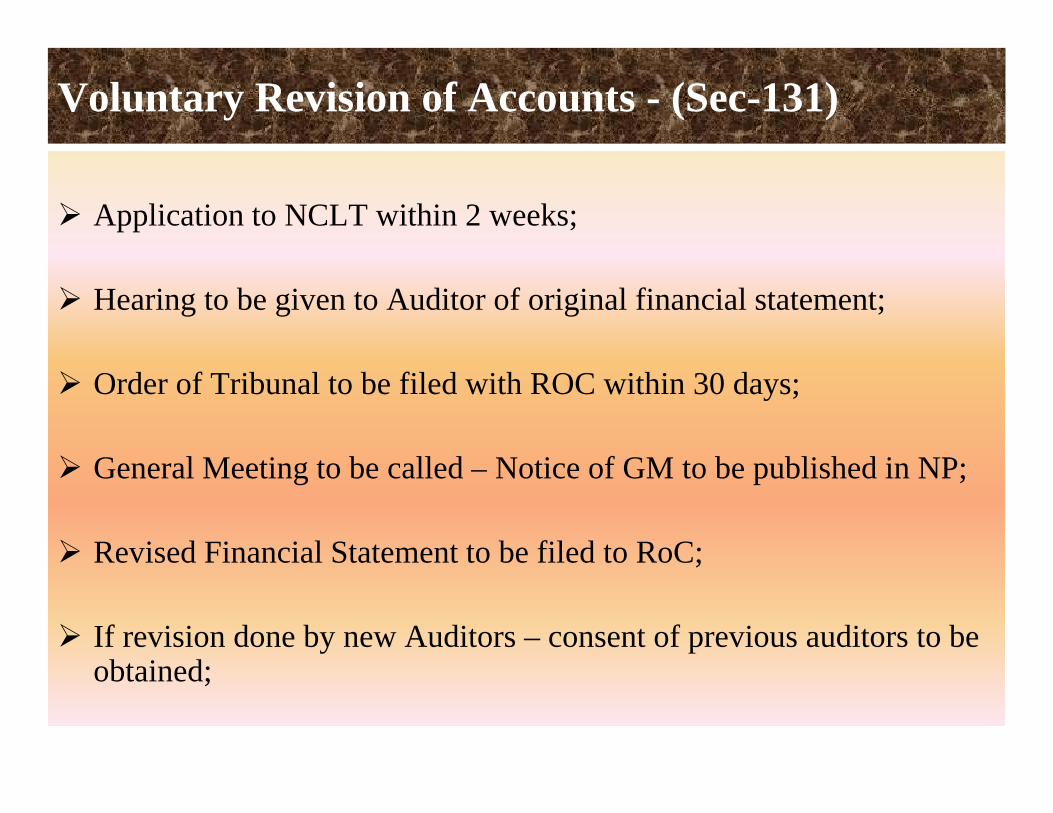

Voluntary Revision of Accounts - (Sec-131)

Application to NCLT within 2 weeks;

Hearing to be given to Auditor of original financial statement;

Order of Tribunal to be filed with ROC within 30 days;

G l M i b ll d N i f GM b bli h d i NPGeneral Meeting to be called – Notice of GM to be published in NP;

Revised Financial Statement to be filed to RoC;Revised Financial Statement to be filed to RoC;

If revision done by new Auditors – consent of previous auditors to be bt i dobtained;

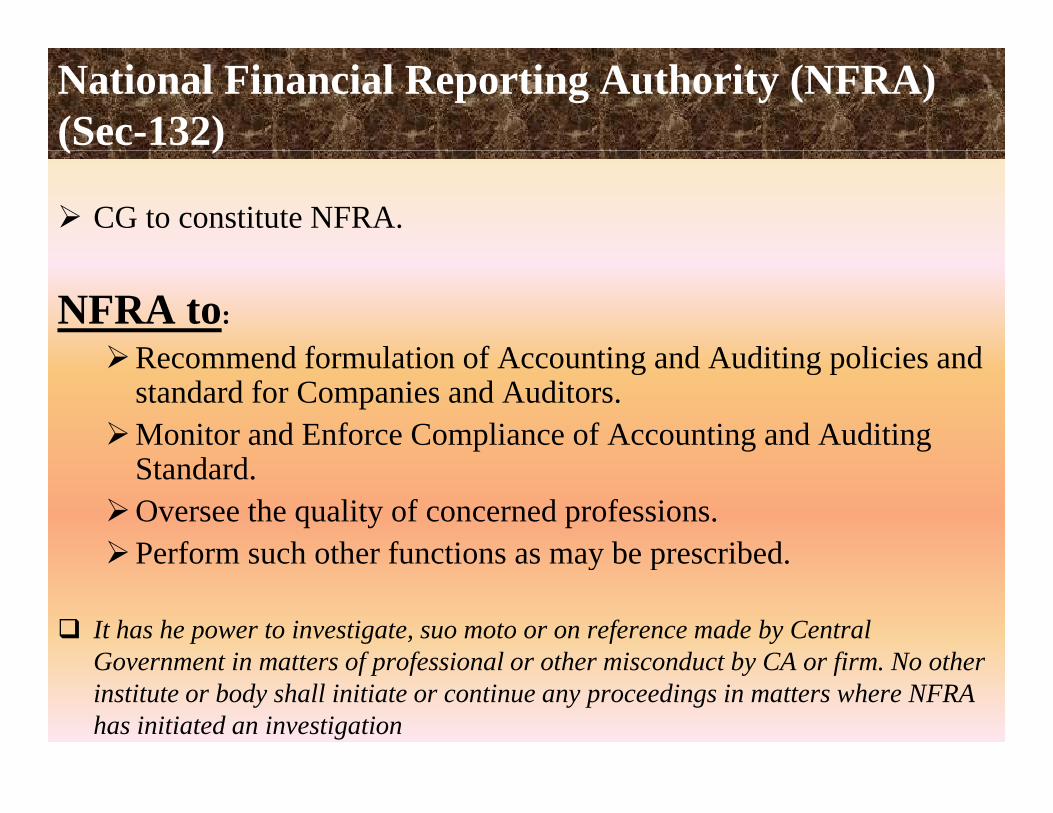

National Financial Reporting Authority (NFRA)(Sec-132)( )

CG to constitute NFRA.

NFRA to:

Recommend formulation of Accounting and Auditing policies andRecommend formulation of Accounting and Auditing policies and standard for Companies and Auditors. Monitor and Enforce Compliance of Accounting and Auditing S d dStandard. Oversee the quality of concerned professions. Perform such other functions as may be prescribed.Perform such other functions as may be prescribed.

It has he power to investigate, suo moto or on reference made by Central Government in matters of professional or other misconduct by CA or firm No otherGovernment in matters of professional or other misconduct by CA or firm. No other institute or body shall initiate or continue any proceedings in matters where NFRA has initiated an investigation

National Financial Reporting Authority (NFRA) (Sec-132)(Sec 132)Powers of NFRA:

Investigate Company / Professionals.Investigate Company / Professionals.Order discovery or production of books of accounts Summon or enforce attendanceOrder inspection of books, registers, other documentsIssue commission for examination of witness or documentsImpose penalty – 1 Lac or 5 times fees received / 10 L or 10 timesImpose penalty 1 Lac or 5 times fees received / 10 L or 10 timesDebarring members from doing practice.

Orders passed by NFRA are appealable to Appellate Authority. NFRA to prepare its Annual Report and Accounts of NFRA shall be subject to CAG Audit.

Section 133 – CG to prescribe Accounting Standards :CG ib A ti St d dCG may prescribe Accounting Standards or any

addendum to it with the recommendation of the ICAIICAI.

NFRA ill l b C lt d dNFRA will also be Consulted and ;

Accounting Standards to be prescribed with after examination of the recommendations made by th NFRAthe NFRA

Director Responsibility statement &Board of Directors Reportp

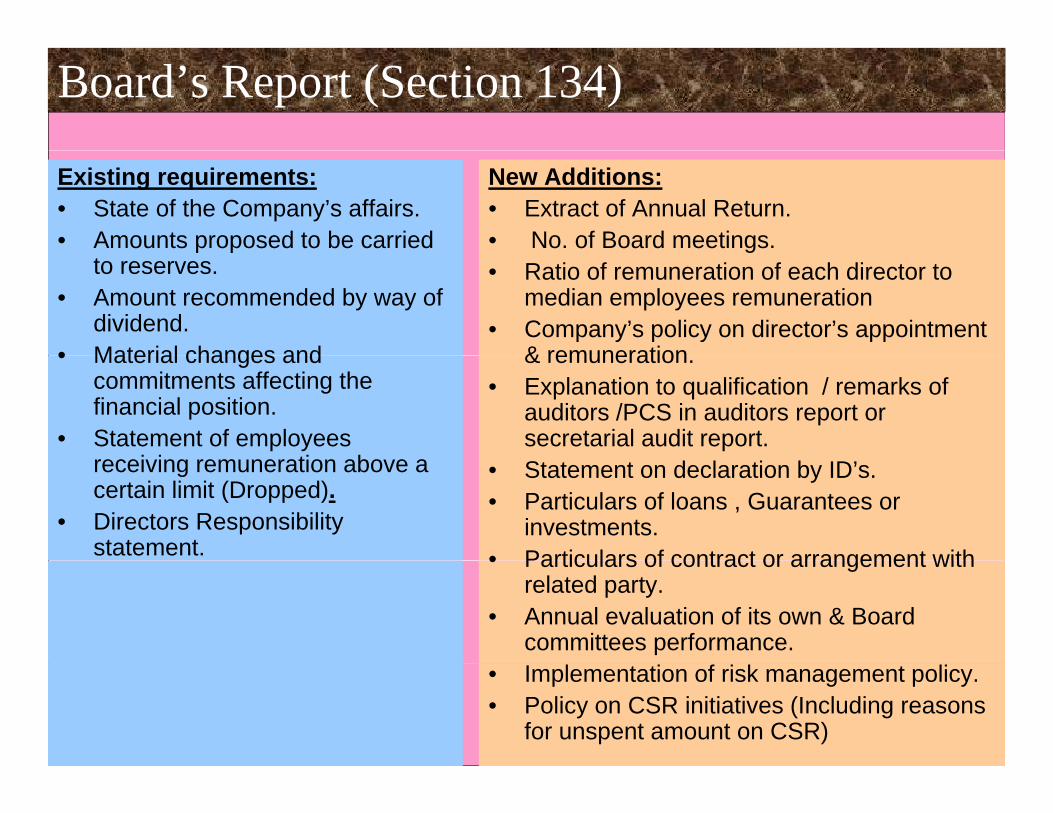

Board’s Report (Section 134)

Existing requirements:• State of the Company’s affairs.• Amounts proposed to be carried

New Additions:• Extract of Annual Return.• No. of Board meetings.

to reserves.• Amount recommended by way of

dividend.• Material changes and

g• Ratio of remuneration of each director to

median employees remuneration• Company’s policy on director’s appointment

& remuneration• Material changes and commitments affecting the financial position.

• Statement of employees i i ti b

& remuneration.• Explanation to qualification / remarks of

auditors /PCS in auditors report or secretarial audit report.

receiving remuneration above a certain limit (Dropped).

• Directors Responsibility statement.

• Statement on declaration by ID’s.• Particulars of loans , Guarantees or

investments.• Particulars of contract or arrangement with• Particulars of contract or arrangement with

related party.• Annual evaluation of its own & Board

committees performance.• Implementation of risk management policy.• Policy on CSR initiatives (Including reasons

for unspent amount on CSR)

Directors Responsibility statement ( Sec 134(5) )

A li bl tiPrudent judgment and Proper and sufficient

C f th i tApplicable accounting Standards duly followed ,

With explanations for Material departures.

Estimates made so as To give true & fair

View of the state of Affairs of the Co.

Care for the mainte-Nance of adequate Accounting records& safeguarding of

Assets

Annual accounts Prepared on going

Concern basis

Adequate Internal Financial controls, In case of listed Co.

Proper systems toEnsure complianceWith all applicable

Laws

Additional Responsibility statement

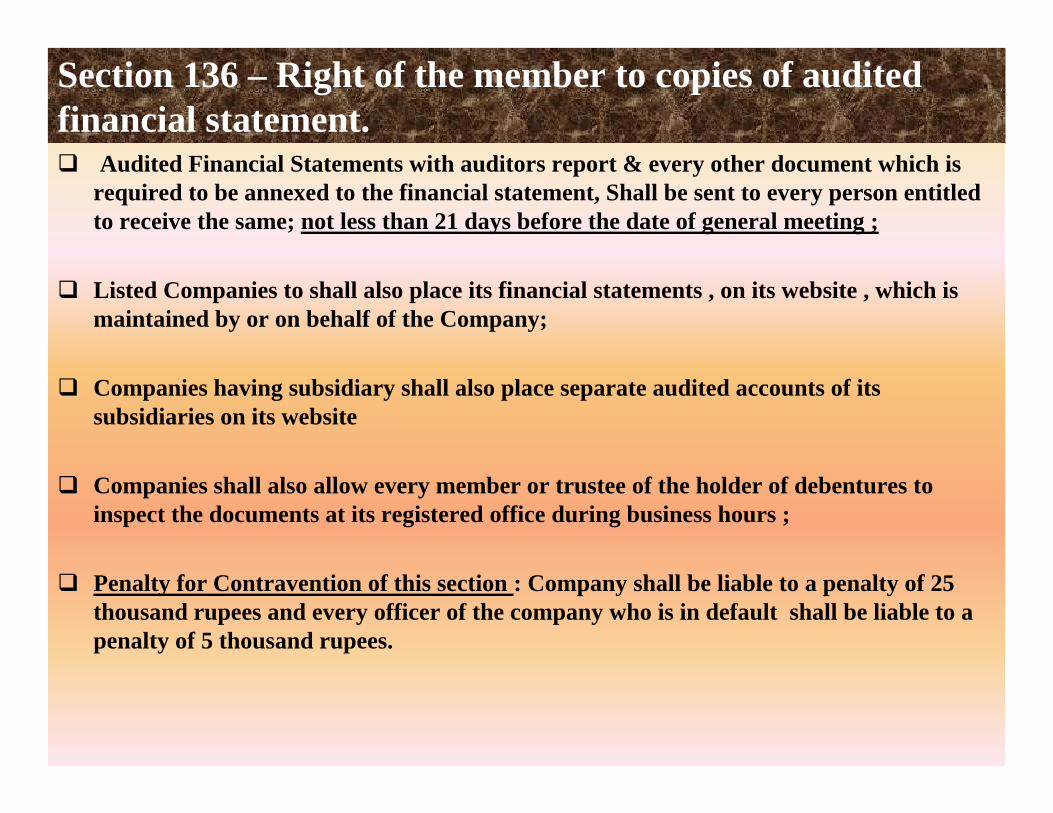

Section 136 – Right of the member to copies of audited financial statement.

Audited Financial Statements with auditors report & every other document which is required to be annexed to the financial statement, Shall be sent to every person entitled to receive the same; not less than 21 days before the date of general meeting ;

Listed Companies to shall also place its financial statements , on its website , which is maintained by or on behalf of the Company;

Companies having subsidiary shall also place separate audited accounts of its subsidiaries on its website

Companies shall also allow every member or trustee of the holder of debentures to inspect the documents at its registered office during business hours ;

Penalty for Contravention of this section : Company shall be liable to a penalty of 25 thousand rupees and every officer of the company who is in default shall be liable to a penalty of 5 thousand rupees.

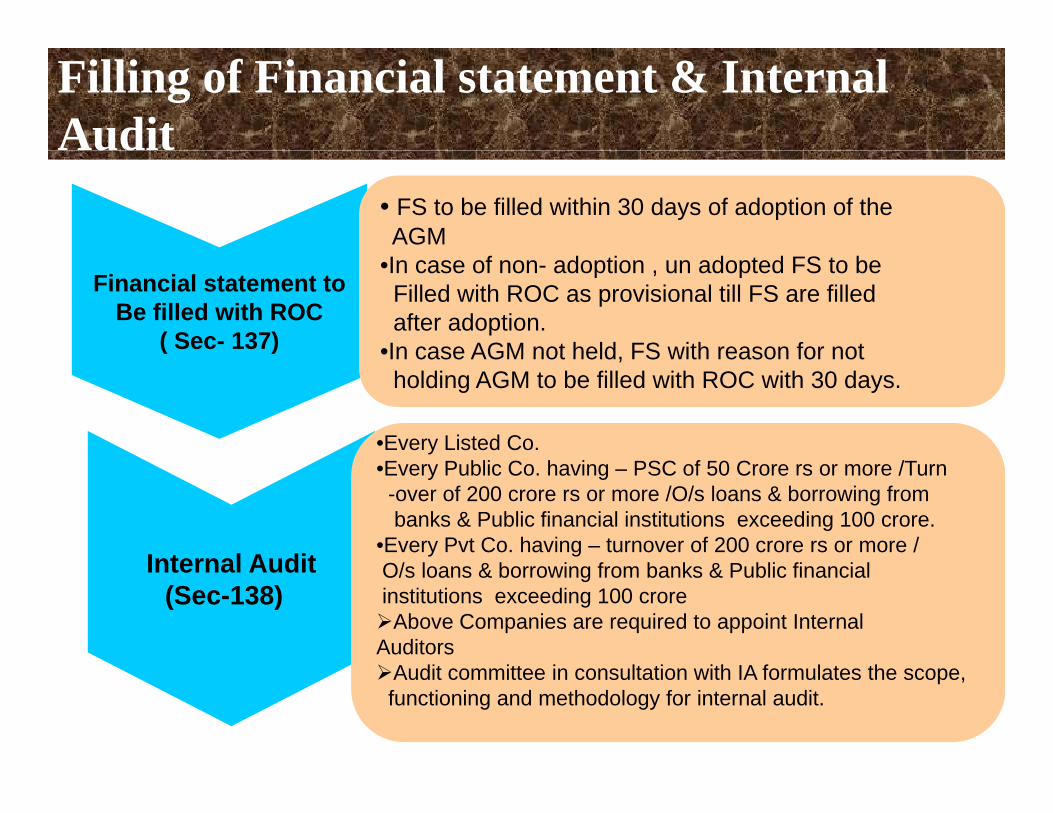

Filling of Financial statement & Internal Audit ud

• FS to be filled within 30 days of adoption of the AGM

Financial statement toBe filled with ROC

( Sec- 137)

•In case of non- adoption , un adopted FS to be Filled with ROC as provisional till FS are filled after adoption.

•In case AGM not held FS with reason for notIn case AGM not held, FS with reason for not holding AGM to be filled with ROC with 30 days.

•Every Listed Co.

Internal Audit

•Every Public Co. having – PSC of 50 Crore rs or more /Turn-over of 200 crore rs or more /O/s loans & borrowing from banks & Public financial institutions exceeding 100 crore.

•Every Pvt Co. having – turnover of 200 crore rs or more /Internal Audit

(Sec-138)O/s loans & borrowing from banks & Public financialinstitutions exceeding 100 croreAbove Companies are required to appoint Internal

Auditors Audit committee in consultation with IA formulates the scope,functioning and methodology for internal audit.

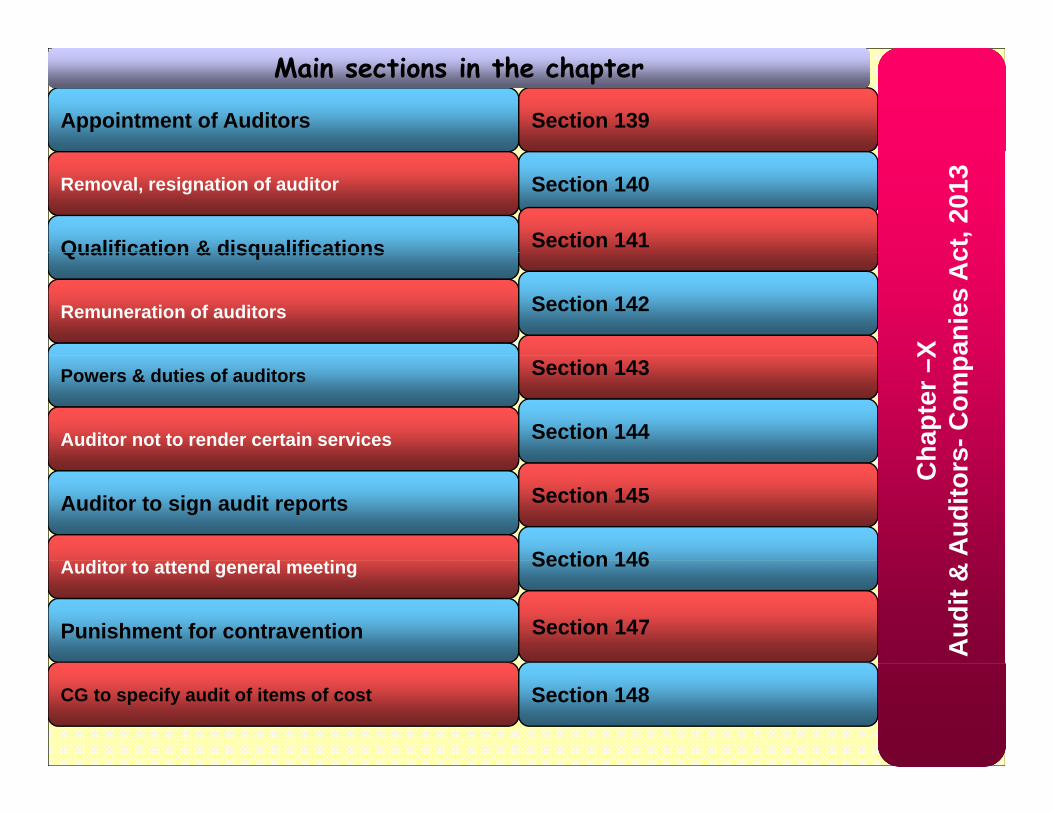

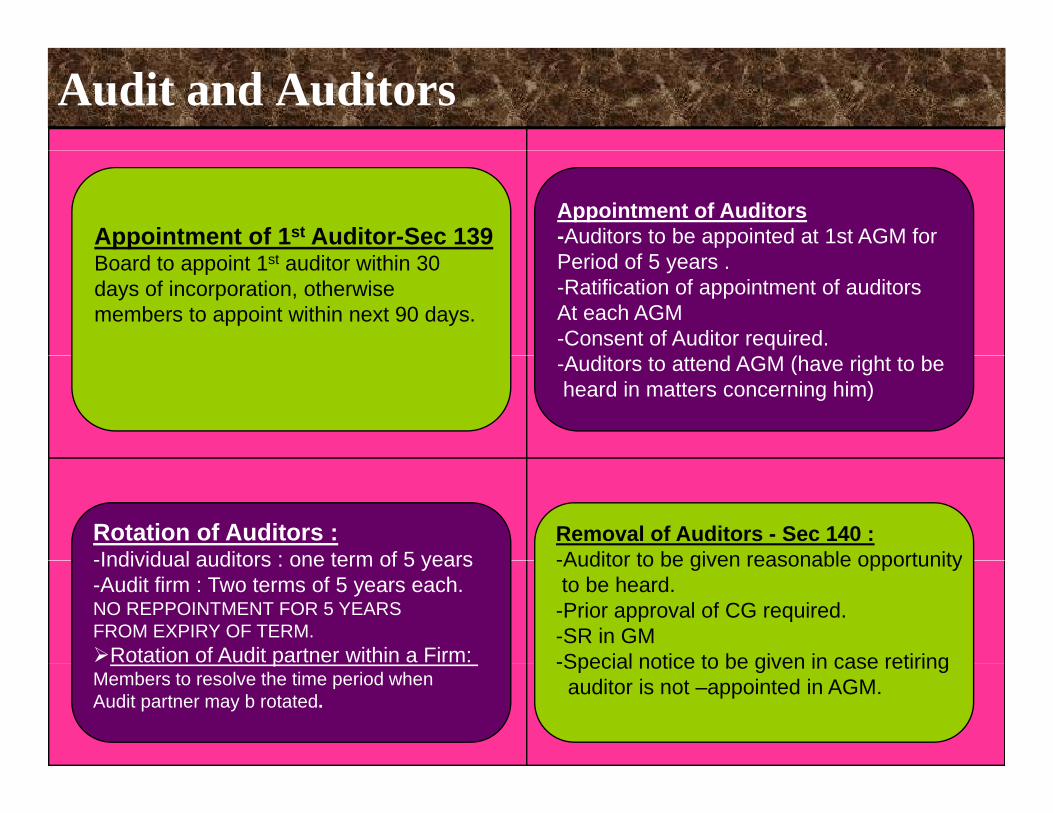

Appointment of Auditors Section 139

Main sections in the chapter

Removal, resignation of auditor Section 140

Qualification & disqualifications Section 141 ct, 2

013

Qualification & disqualifications

Remuneration of auditors Section 142

X anie

s A

c

Powers & duties of auditors

Auditor not to render certain services

Section 143

Section 144

hapt

er –

Xs-

Com

p

Auditor to sign audit reports

A dit t tt d l ti

Section 145

Section 146

Ch

Aud

itors

Auditor to attend general meeting

Punishment for contravention Section 147

Section 146

Aud

it &

CG to specify audit of items of cost Section 148

Audit and Auditors

Appointment of 1st Auditor-Sec 139Appointment of Auditors-Auditors to be appointed at 1st AGM for

Board to appoint 1st auditor within 30 days of incorporation, otherwise members to appoint within next 90 days.

Period of 5 years .-Ratification of appointment of auditors At each AGM-Consent of Auditor required.

G (-Auditors to attend AGM (have right to beheard in matters concerning him)

Rotation of Auditors :-Individual auditors : one term of 5 years

Removal of Auditors - Sec 140 :-Auditor to be given reasonable opportunity-Individual auditors : one term of 5 years

-Audit firm : Two terms of 5 years each.NO REPPOINTMENT FOR 5 YEARS FROM EXPIRY OF TERM.

Rotation of Audit partner within a Firm:

-Auditor to be given reasonable opportunityto be heard.-Prior approval of CG required.-SR in GM-Special notice to be given in case retiringp

Members to resolve the time period when Audit partner may b rotated.

-Special notice to be given in case retiring auditor is not –appointed in AGM.

Section 141 : Eligibility , Qualification & Disqualifications of auditors

Eligibility & Qualification of Auditors He should be Chartered Accountant ;

Incase of a firm where majority of partners practising in India are qualified for appointment as aforesaid may be appointed by its firmqualified for appointment as aforesaid may be appointed by its firm name, to be auditor of a company

Wh fi LLP i i t d dit th l th tWhere a firm or LLP is appointed as auditor ; then only the partners who are Chartered Accountants shall be authorized to act and sign on behalf of the firm..

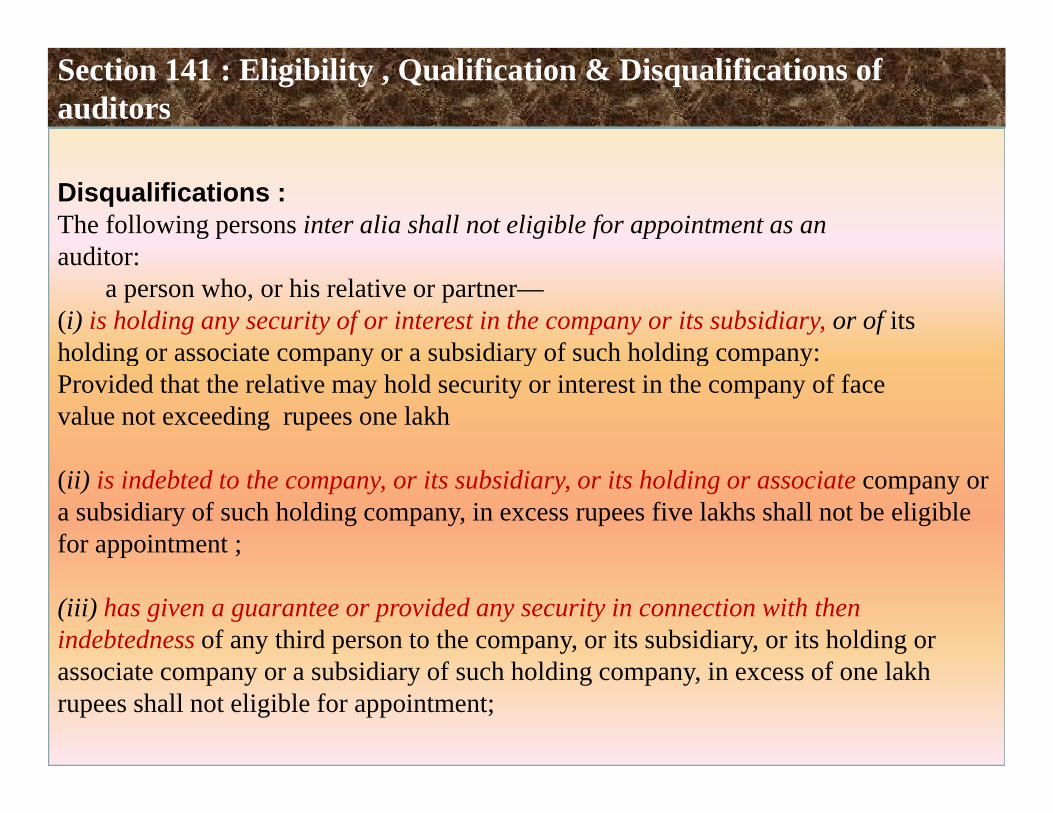

Section 141 : Eligibility , Qualification & Disqualifications of auditors

Disqualifications : The following persons inter alia shall not eligible for appointment as ana ditor:auditor:�� a person who, or his relative or partner—(i) is holding any security of or interest in the company or its subsidiary, or of its holding or associate company or a subsidiary of such holding company:holding or associate company or a subsidiary of such holding company:Provided that the relative may hold security or interest in the company of facevalue not exceeding rupees one lakh

(ii) is indebted to the company, or its subsidiary, or its holding or associate company or a subsidiary of such holding company, in excess rupees five lakhs shall not be eligible for appointment ;

(iii) has given a guarantee or provided any security in connection with then indebtedness of any third person to the company, or its subsidiary, or its holding or

i b idi f h h ldi i f l khassociate company or a subsidiary of such holding company, in excess of one lakhrupees shall not eligible for appointment;

Section 141 : Eligibility , Qualification & Disqualifications of auditors

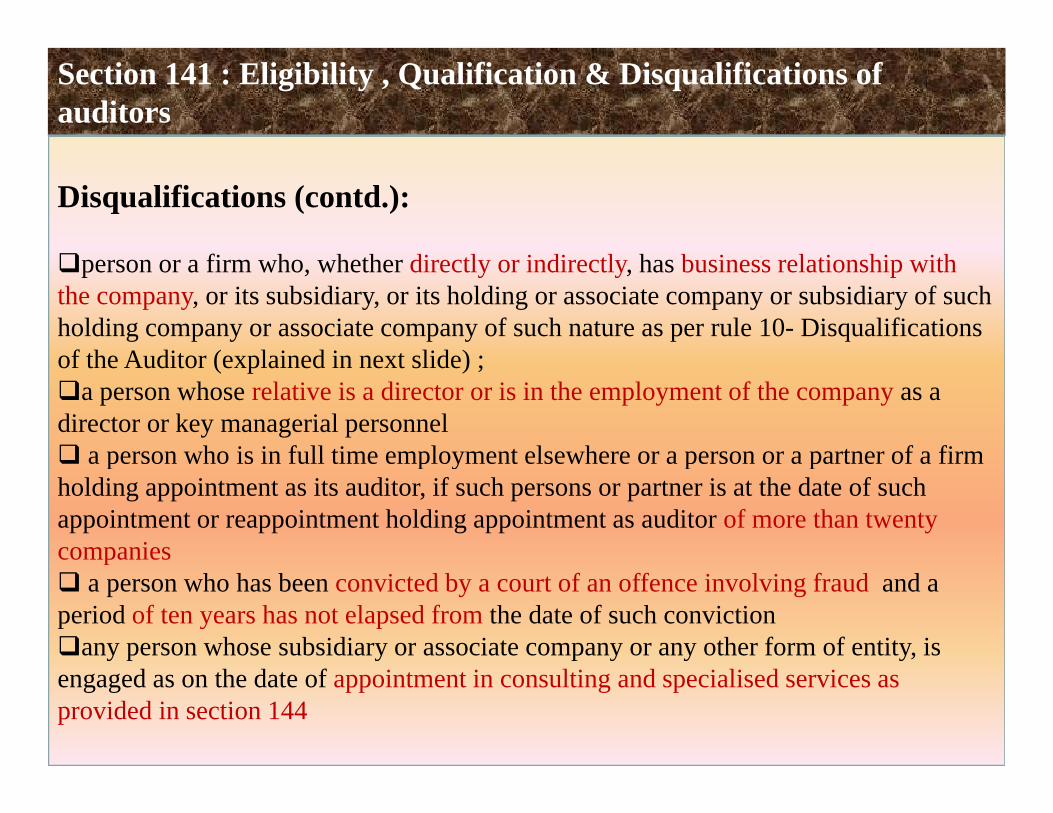

Disqualifications (contd.):

person or a firm who, whether directly or indirectly, has business relationship with the company, or its subsidiary, or its holding or associate company or subsidiary of such holding company or associate company of such nature as per rule 10- Disqualifications

f th A dit ( l i d i t lid )of the Auditor (explained in next slide) ;a person whose relative is a director or is in the employment of the company as a

director or key managerial personnela person who is in full time employment elsewhere or a person or a partner of a firma person who is in full time employment elsewhere or a person or a partner of a firm

holding appointment as its auditor, if such persons or partner is at the date of such appointment or reappointment holding appointment as auditor of more than twenty companiesp

a person who has been convicted by a court of an offence involving fraud and a period of ten years has not elapsed from the date of such conviction

any person whose subsidiary or associate company or any other form of entity, is engaged as on the date of appointment in consulting and specialised services as provided in section 144

Section 141 : Eligibility , Qualification & Disqualifications of auditors

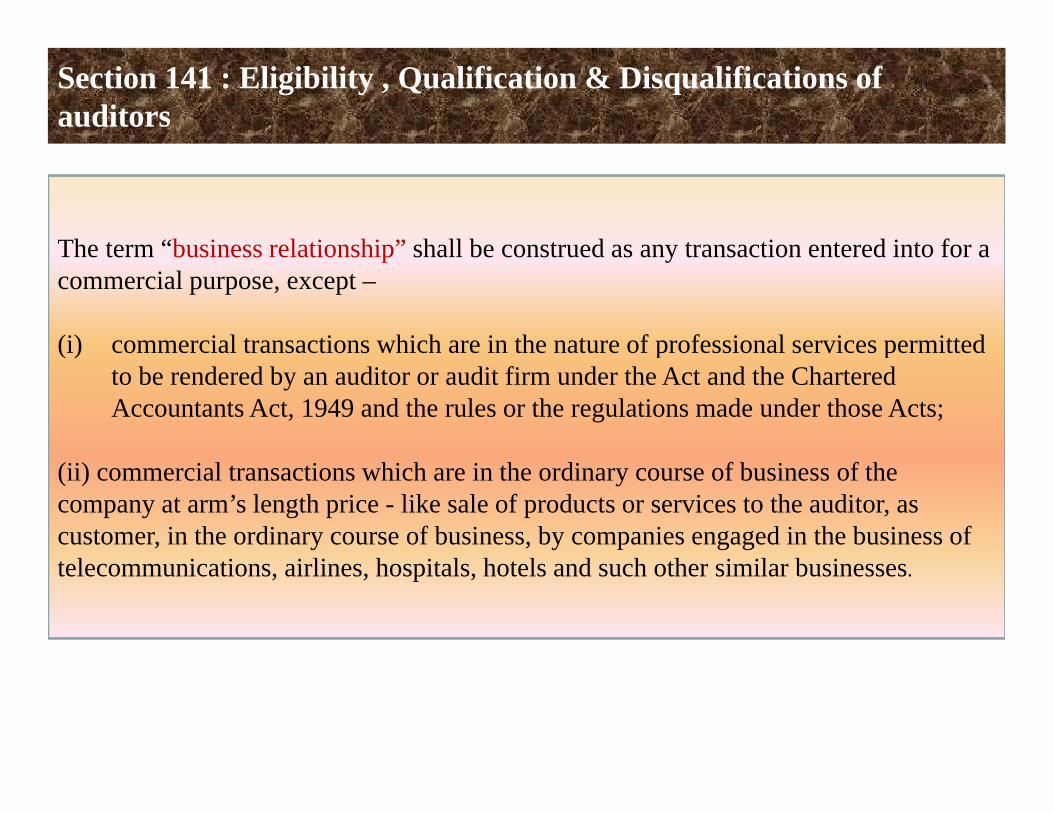

The term “business relationship” shall be construed as any transaction entered into for aThe term business relationship shall be construed as any transaction entered into for a commercial purpose, except –

(i) commercial transactions which are in the nature of professional services permitted ( ) p pto be rendered by an auditor or audit firm under the Act and the Chartered Accountants Act, 1949 and the rules or the regulations made under those Acts;

(ii) commercial transactions which are in the ordinary course of business of the company at arm’s length price - like sale of products or services to the auditor, as customer, in the ordinary course of business, by companies engaged in the business of t l i ti i li h it l h t l d h th i il b itelecommunications, airlines, hospitals, hotels and such other similar businesses.

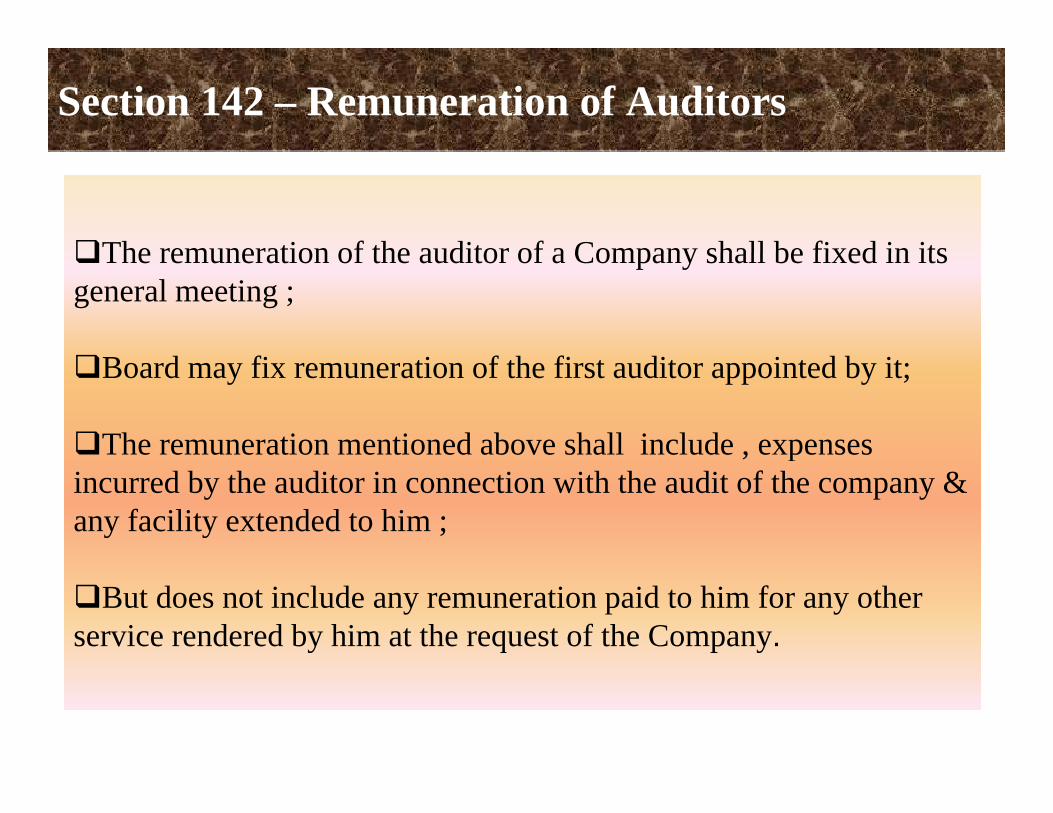

Section 142 – Remuneration of Auditors

The remuneration of the auditor of a Company shall be fixed in itsThe remuneration of the auditor of a Company shall be fixed in its general meeting ;

Board may fix remuneration of the first auditor appointed by it;

The remuneration mentioned above shall include , expenses , pincurred by the auditor in connection with the audit of the company & any facility extended to him ;

But does not include any remuneration paid to him for any other service rendered by him at the request of the Company.

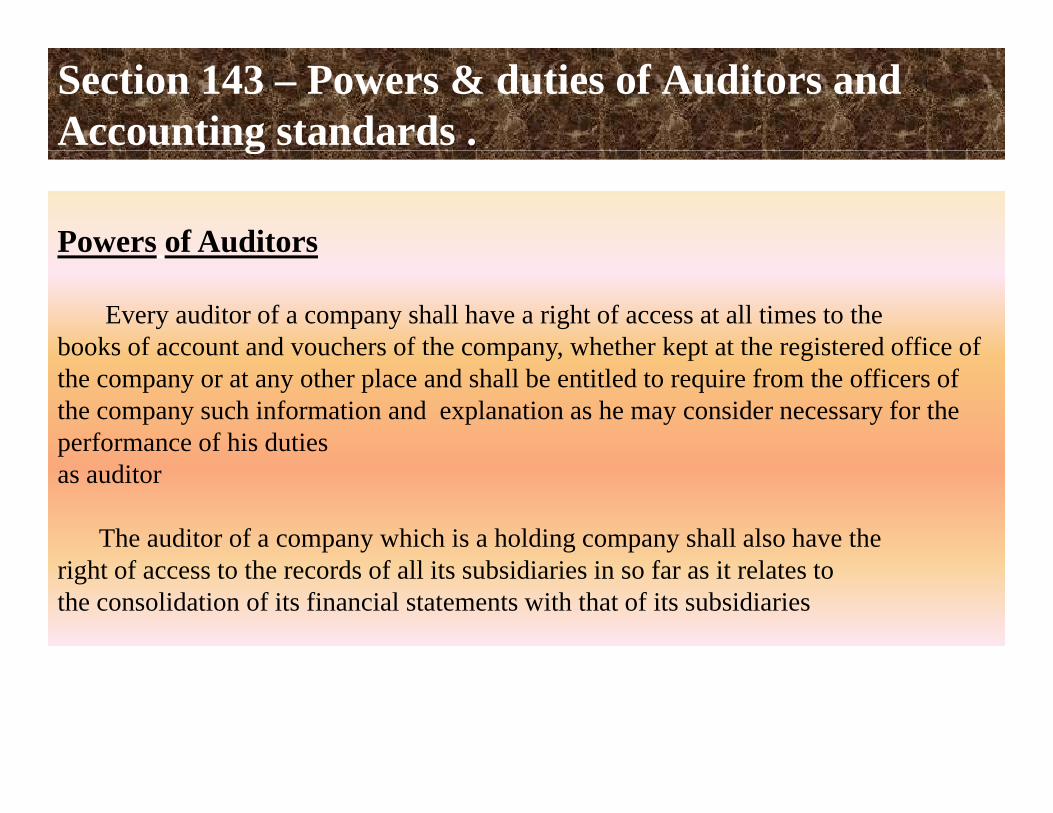

Section 143 – Powers & duties of Auditors and Accounting standards .g

Powers of Auditors

�� Every auditor of a company shall have a right of access at all times to thebooks of account and vouchers of the company, whether kept at the registered office of boo s o accou a d vouc e s o e co pa y, w e e ep a e eg s e ed o ce othe company or at any other place and shall be entitled to require from the officers of the company such information and explanation as he may consider necessary for the performance of his dutiesas auditor

��The auditor of a company which is a holding company shall also have thei h f h d f ll i b idi i i f i lright of access to the records of all its subsidiaries in so far as it relates to

the consolidation of its financial statements with that of its subsidiaries

Section 143 – Powers & duties of Auditors and Accounting standardsg

Reporting Requirements

Matters to be stated in Auditor’s Report:

(a) whether he has sought and obtained all the information and explanations which to ( ) g pthe best of his knowledge and belief were necessary for the purpose of his audit and if not, the details thereof and the effect of such information on the financial statements(b) whether, in his opinion, proper books of account as required by law have been kept by the company so far as appears from his examination of those books and proper returns adequate for the purposes of his audit have been received from branches not visited by him( ) h th th t th t f b h ffi f th dit d b(c) whether the report on the accounts of any branch office of the company audited by a person other than the company’s auditor has been sent to him and the manner in which he has dealt with it in preparing his report(d) whether the company’s balance sheet and profit and loss account dealt with in the(d) whether the company s balance sheet and profit and loss account dealt with in the report are in agreement with the books of account and returns;

Section 143 – Powers & duties of Auditors and Accounting standardsg

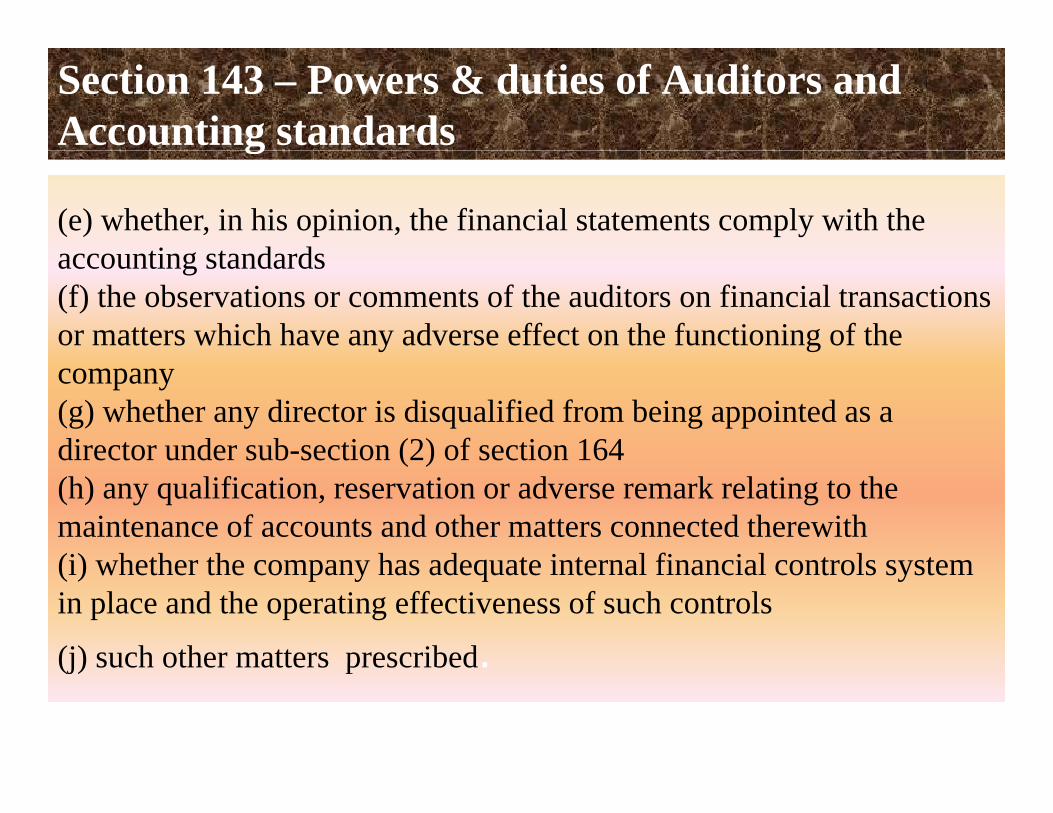

(e) whether, in his opinion, the financial statements comply with the ti t d daccounting standards

(f) the observations or comments of the auditors on financial transactions or matters which have any adverse effect on the functioning of the company(g) whether any director is disqualified from being appointed as a director under sub-section (2) of section 164director under sub section (2) of section 164(h) any qualification, reservation or adverse remark relating to the maintenance of accounts and other matters connected therewith(i) hether the compan has adeq ate internal financial controls s stem(i) whether the company has adequate internal financial controls system in place and the operating effectiveness of such controls

(j) such other matters prescribed.(j) such other matters prescribed.

Section 143 – Powers & duties of Auditors and Accounting standards

Reporting Requirements (Contd.):

g

Matters to be stated in Auditor’s ReportThe auditor shall also report on Whether the company has disclosed

the effect if any of pending litigations on its financial position in itsthe effect, if any, of pending litigations on its financial position in its financial statement ;

Wh th th h d i i f f bl l ifWhether the company has made provision for foreseeable losses, if any, onlong term contracts including derivative contracts ;

Whether there has been delay in depositing money into the InvestorEducation and Protection Fund by the company;Education and Protection Fund by the company;

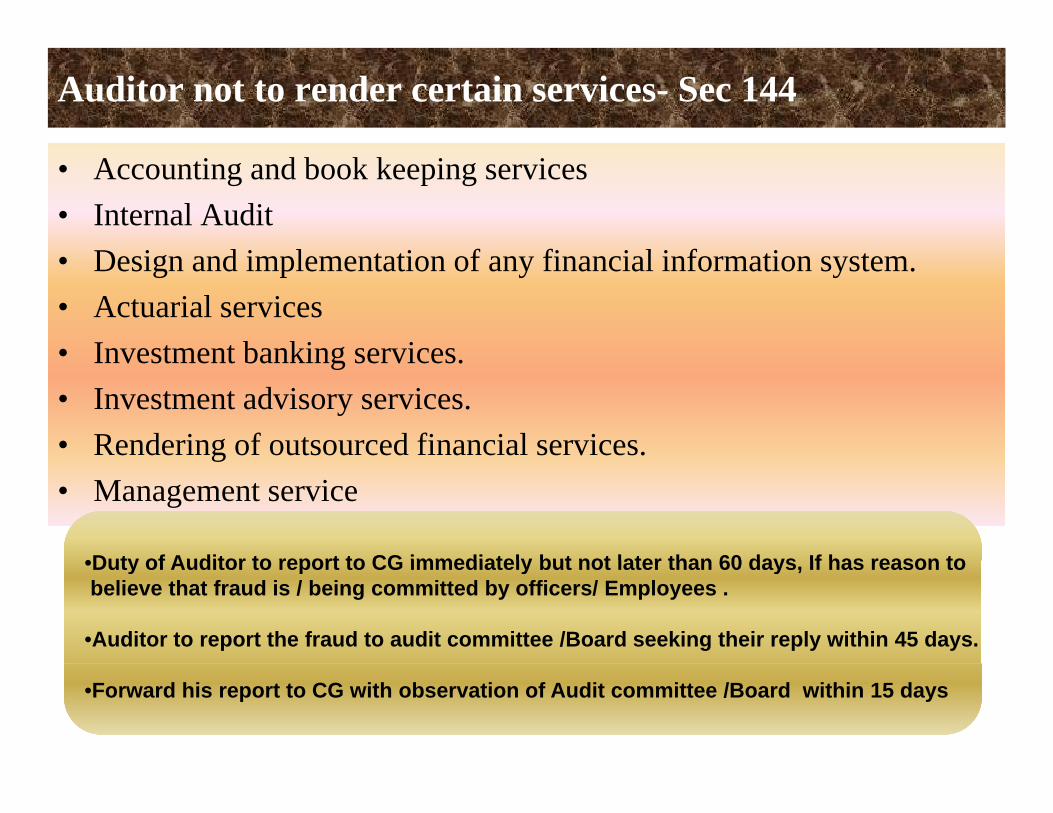

Auditor not to render certain services- Sec 144

• Accounting and book keeping services• Internal Audit

D i d i l t ti f fi i l i f ti t• Design and implementation of any financial information system.• Actuarial services• Investment banking services• Investment banking services.• Investment advisory services.• Rendering of outsourced financial services.g• Management service

•Duty of Auditor to report to CG immediately but not later than 60 days If has reason to•Duty of Auditor to report to CG immediately but not later than 60 days, If has reason to believe that fraud is / being committed by officers/ Employees .

•Auditor to report the fraud to audit committee /Board seeking their reply within 45 days.

•Forward his report to CG with observation of Audit committee /Board within 15 days

Sec- 145 : Auditor to sign Audit Reports

The Auditor shall sign the auditor’s report or certify any other document of the Company;The auditors shall also make qualifications ,observations or comments on the financial

i hi h h d ff h f i i f hmatters or transactions , which have any adverse effect on the functioning of the company mentioned in auditor’s report ;

Auditor’s report shall be read before the Company in general meeting ;Auditor’s report shall be open for inspection by any member of the Company .

Sec 146 : Auditor to attend AGM

Notice of general meeting shall be forwarded to auditor of the Company;If t t d A dit h ll tt d th ti hi lf th h hi th i dIf not exempted , Auditor shall attend the meeting himself or through his authorised

representative , who shall also be qualified to be an auditor ;Auditor’s shall also have a right to be heard at General Meeting , on any part of the business

which concerns him as the auditor.

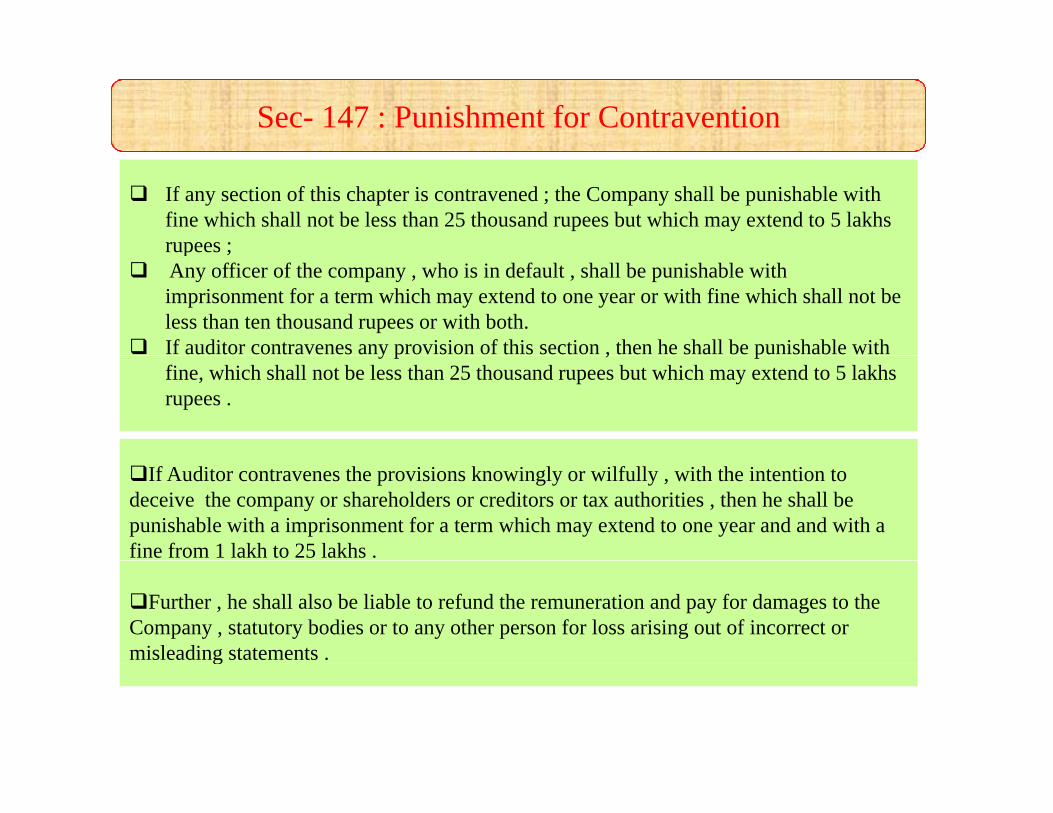

Sec- 147 : Punishment for Contravention

If any section of this chapter is contravened ; the Company shall be punishable with fine which shall not be less than 25 thousand rupees but which may extend to 5 lakhsrupees ;p ;Any officer of the company , who is in default , shall be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than ten thousand rupees or with both.If auditor contravenes any provision of this section , then he shall be punishable with y p , pfine, which shall not be less than 25 thousand rupees but which may extend to 5 lakhsrupees .

If Auditor contravenes the provisions knowingly or wilfully , with the intention to deceive the company or shareholders or creditors or tax authorities , then he shall be punishable with a imprisonment for a term which may extend to one year and and with a fine from 1 lakh to 25 lakhs .

Further , he shall also be liable to refund the remuneration and pay for damages to the Company , statutory bodies or to any other person for loss arising out of incorrect or misleading statements .g

Companies Act,2013

ACCOUNTS AND AUDIT

Financial Statements

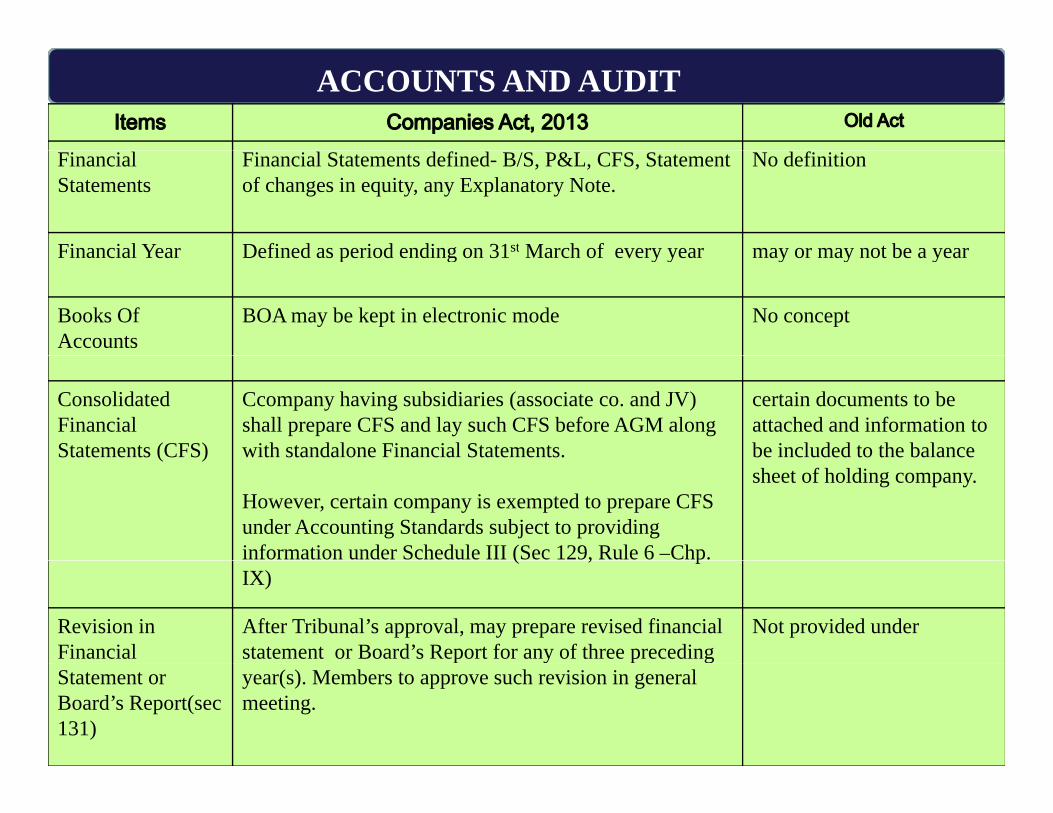

Financial Statements defined- B/S, P&L, CFS, Statement of changes in equity, any Explanatory Note.

No definition

Financial Year Defined as period ending on 31st March of every year may or may not be a yearFinancial Year Defined as period ending on 31 March of every year may or may not be a year

Books Of Accounts

BOA may be kept in electronic mode No concept

ConsolidatedFinancial Statements (CFS)

Ccompany having subsidiaries (associate co. and JV) shall prepare CFS and lay such CFS before AGM along with standalone Financial Statements.

certain documents to be attached and information to be included to the balance ( )

However, certain company is exempted to prepare CFS under Accounting Standards subject to providing information under Schedule III (Sec 129, Rule 6 –Chp.

sheet of holding company.

( , pIX)

Revision in Financial

After Tribunal’s approval, may prepare revised financial statement or Board’s Report for any of three preceding

Not provided under

Statement or Board’s Report(sec 131)

p y p gyear(s). Members to approve such revision in general meeting.

ACCOUNTS AND AUDIT

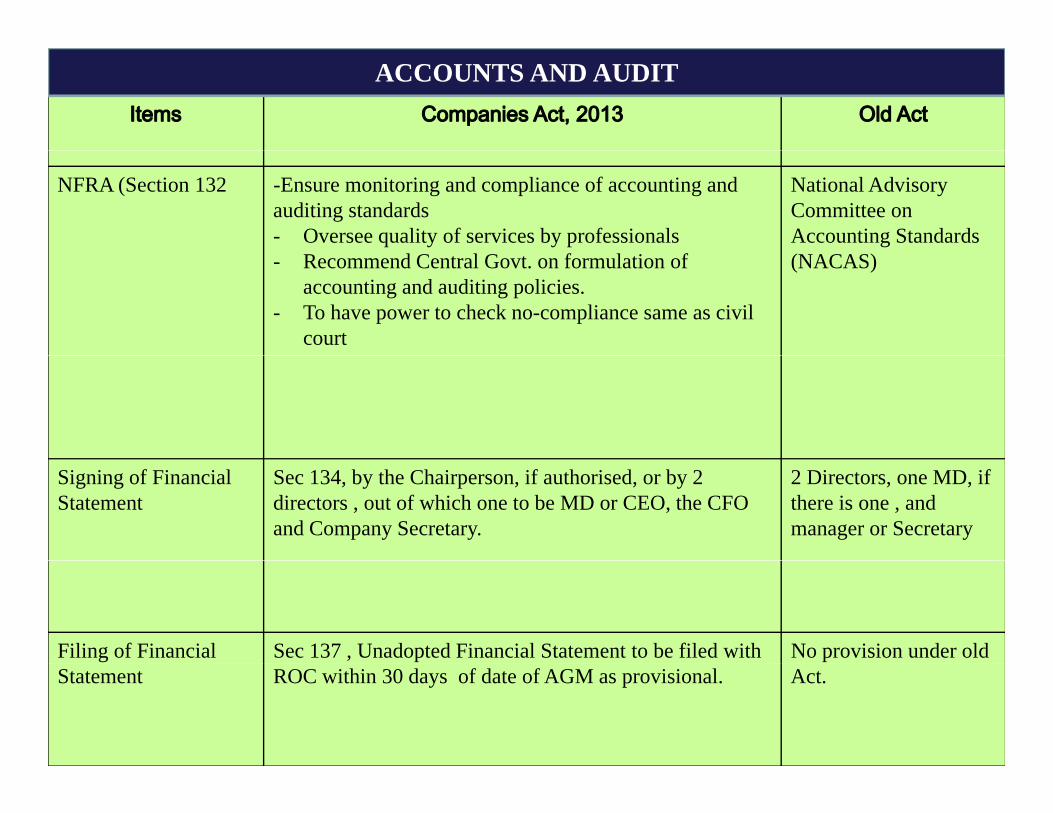

NFRA (Section 132 -Ensure monitoring and compliance of accounting and auditing standards- Oversee quality of services by professionals

National Advisory Committee on Accounting Standards

- Recommend Central Govt. on formulation of accounting and auditing policies.

- To have power to check no-compliance same as civil court

(NACAS)

Signing of Financial Statement

Sec 134, by the Chairperson, if authorised, or by 2 directors , out of which one to be MD or CEO, the CFO and Company Secretary.

2 Directors, one MD, if there is one , and manager or Secretary

Filing of Financial Sec 137 , Unadopted Financial Statement to be filed with No provision under old Statement ROC within 30 days of date of AGM as provisional. Act.

ACCOUNTS AND AUDIT

Internal Audit Section 138- Prescribed Companies to appoint Internal auditor to conduct internal audit of functions and activities.

No provision under companies act 1956, Required under CARO

Appointment of Auditors Section 139- to be appointed till the conclusion of 6th AGM ,- Appointment to be ratified by members at every AGM- Listed Company or other prescribed companies not to appoint

1) An individual as auditor for more than 5 consecutive year. 2) A dit fi f th 2 t f 5 ti

- Section 224- Appointment at AGM

every year- No provision for

i t t f 2t2) Audit firm for more than 2 terms of 5 consecutive years- Every Company to comply with this provision within 3 years

from date of commencement of Act.

appointment for 2terms of 5 consecutive years

Power and duties of Section 143 Auditors to report additionally on: Section 227 provides forPower and duties of Auditors

Section 143, Auditors to report additionally on:-Effect of pending litigations on its financial position in FinancialStatement- Report to Central Government , any offense involving Fraud

likely to materially effect the company.C h d i l fi i l l d

Section 227 provides for the powers and duties of auditors

- Company has adequate internal financial control systems and operating effectiveness of such controls.

End of Presentation ..!!

Thank You for your Attention..!!