Embed Size (px)

Citation preview

Acquisition of Acquisition of Seabrook Nuclear Seabrook Nuclear Generating PlantGenerating PlantApril 16, 2002April 16, 2002

Safe Harbor Statement: Any statements made herein about future operating results or other future events are forward-looking statements under the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Actual results may differ substantially from such forward-looking statements. A discussion of factors that could cause actual results or events to vary is contained in FPL Group's 2001 SEC Form 10-K.

2

Forward Statements

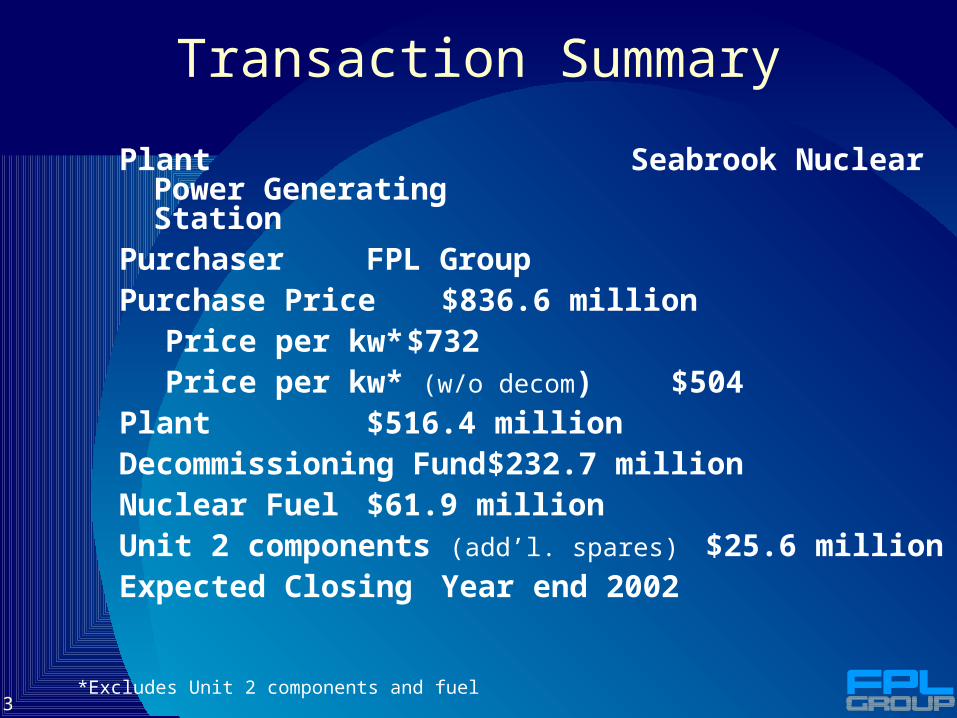

3*Excludes Unit 2 components and fuel

Transaction Summary

Plant Seabrook Nuclear Power GeneratingStation

Purchaser FPL GroupPurchase Price $836.6 million

Price per kw* $732Price per kw* (w/o decom) $504

Plant $516.4 million Decommissioning Fund $232.7 millionNuclear Fuel $61.9 millionUnit 2 components (add’l. spares) $25.6 millionExpected Closing Year end 2002

4

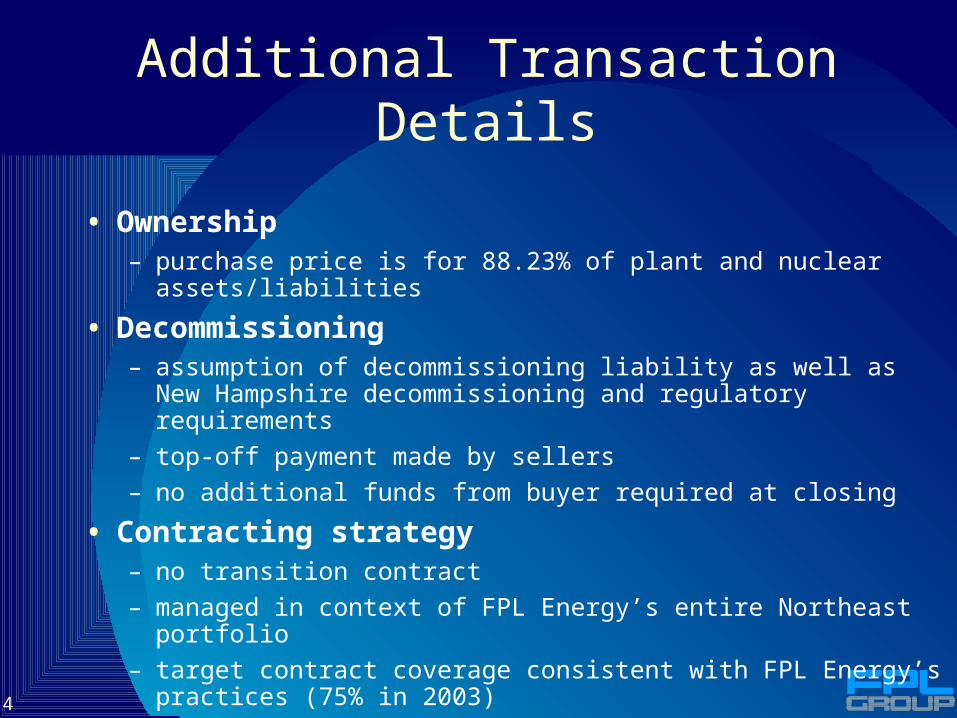

Additional Transaction Details

• Ownership– purchase price is for 88.23% of plant and nuclear assets/liabilities

• Decommissioning– assumption of decommissioning liability as well as New

Hampshire decommissioning and regulatory requirements

– top-off payment made by sellers

– no additional funds from buyer required at closing

• Contracting strategy – no transition contract

– managed in context of FPL Energy’s entire Northeast portfolio

– target contract coverage consistent with FPL Energy’s practices (75% in 2003)

5

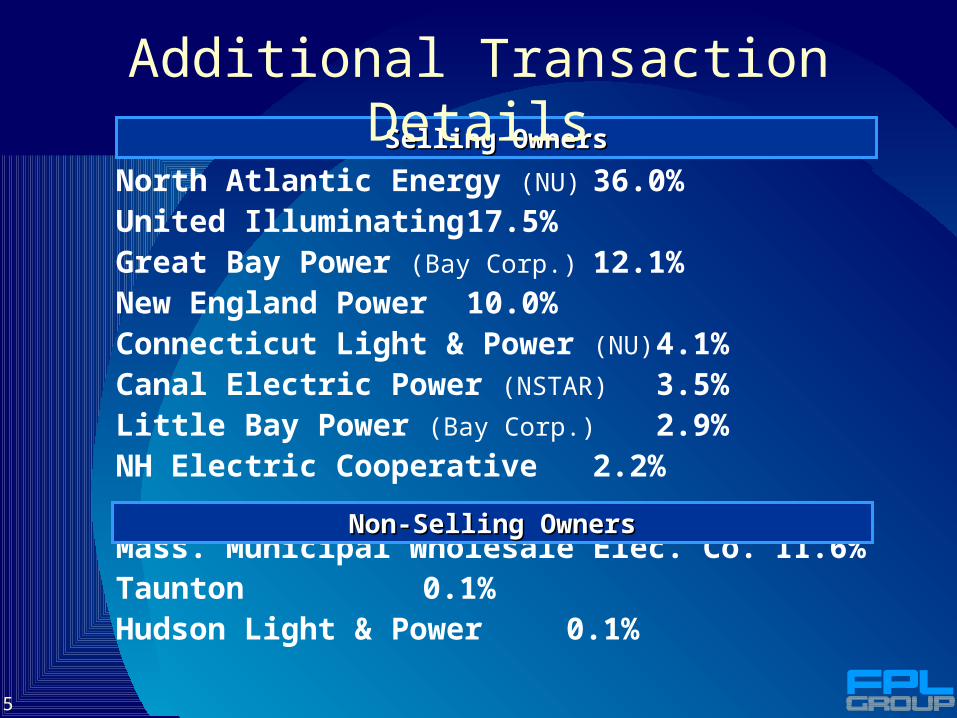

North Atlantic Energy (NU) 36.0%United Illuminating 17.5%Great Bay Power (Bay Corp.) 12.1%New England Power 10.0%Connecticut Light & Power (NU) 4.1%Canal Electric Power (NSTAR) 3.5%Little Bay Power (Bay Corp.) 2.9%NH Electric Cooperative 2.2%

Mass. Municipal Wholesale Elec. Co. 11.6%Taunton 0.1%Hudson Light & Power 0.1%

Selling OwnersSelling Owners

Non-Selling OwnersNon-Selling Owners

Additional Transaction Details

6

Governmental Approvals

• Federal Energy Regulatory Commission• Nuclear Regulatory Commission • Federal Trade Commission

or Department of Justice• Environmental Protection Agency • Federal Communications Commission• New Hampshire Nuclear Decommissioning

Finance Committee• New Hampshire Site Evaluation Committee• New Hampshire Department of

Environmental Services• Town of Seabrook

7

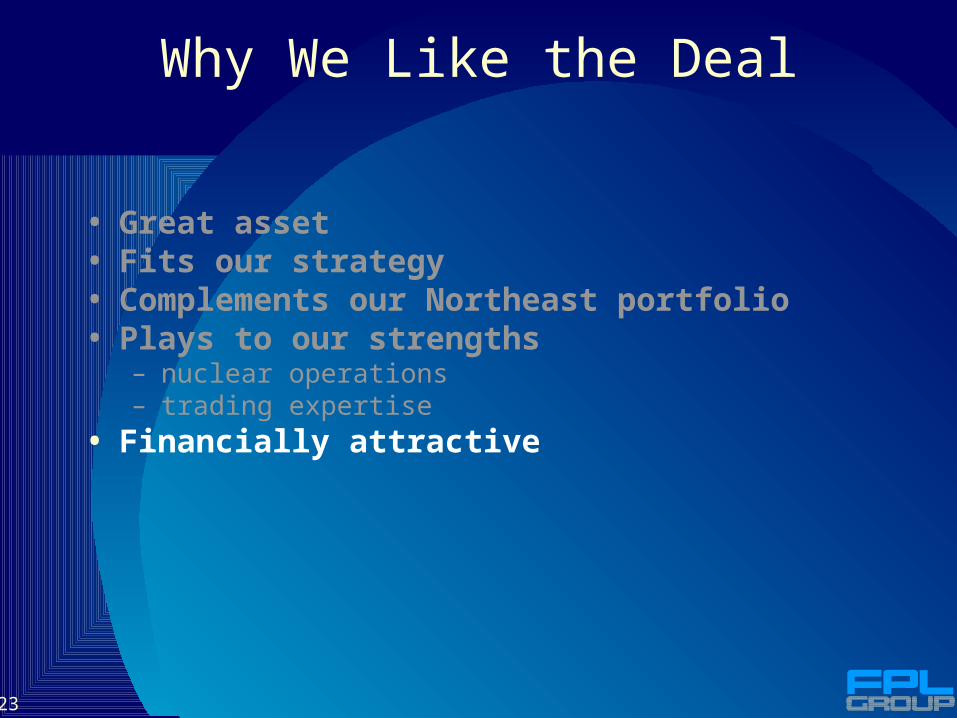

Why We Like the Deal

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive

8

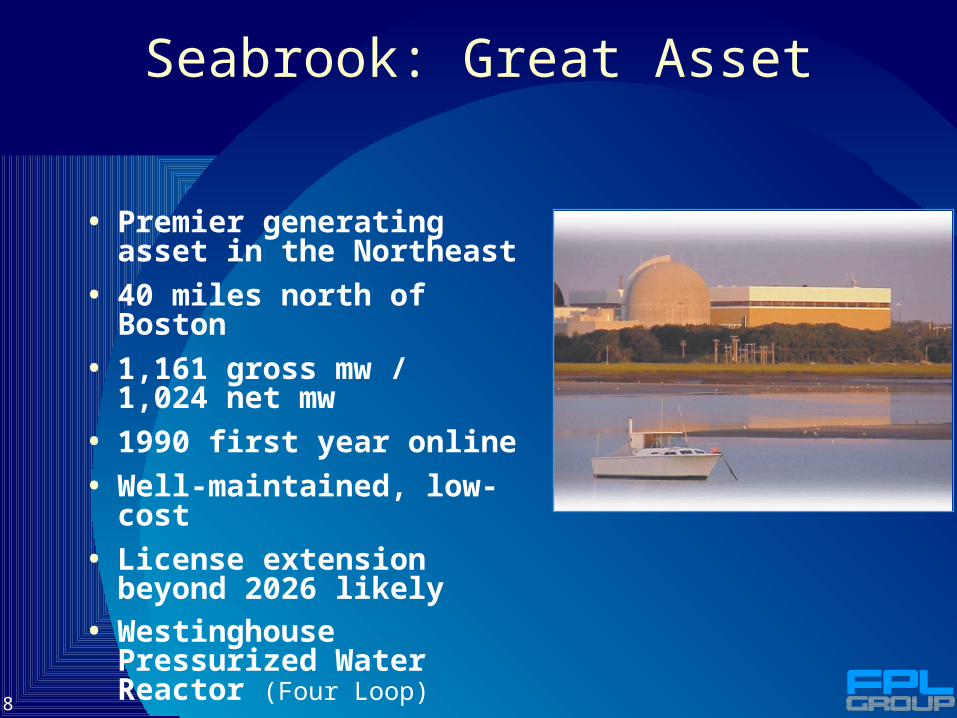

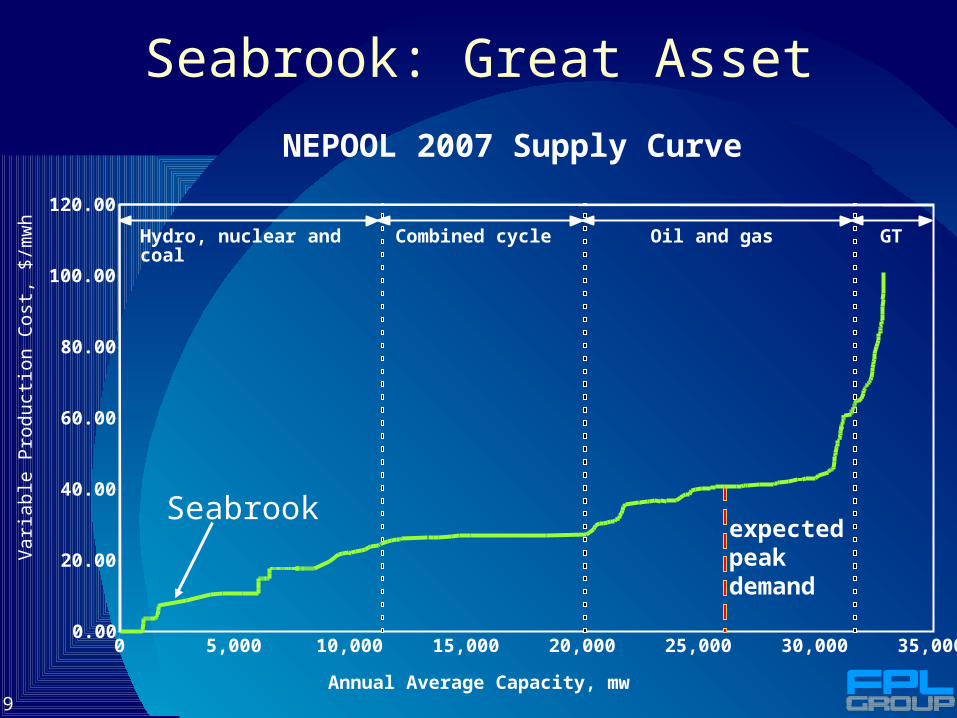

Seabrook: Great Asset

• Premier generating asset in the Northeast

• 40 miles north of Boston

• 1,161 gross mw / 1,024 net mw

• 1990 first year online

• Well-maintained, low-cost

• License extension beyond 2026 likely

• Westinghouse Pressurized Water Reactor (Four Loop)

9

NEPOOL 2007 Supply Curve

0.00

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Annual Average Capacity, mw

Var

iabl

e P

rodu

ctio

n C

ost,

$/m

wh

Hydro, nuclear and coal Combined cycle Oil and gas GT

Seabrookexpected peak demand

Seabrook: Great Asset

10

Why We Like the Deal

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive

11

Major diversified wholesale electric generator Major diversified wholesale electric generator which adds value by actively managing and trading which adds value by actively managing and trading energy commodities in conjunction with our assetsenergy commodities in conjunction with our assets

Major diversified wholesale electric generator Major diversified wholesale electric generator which adds value by actively managing and trading which adds value by actively managing and trading energy commodities in conjunction with our assetsenergy commodities in conjunction with our assets

Fits FPL Energy’s Strategy

Seabrook

• Clean• Diverse fuel sources • Build critical mass in key regions• Dispatch diversity• Low-cost• Operating control and majority ownership

12 Percentages may not add to 100% due to rounding

FPL Energy Fuel Source Diversity

Current

Pro forma w/Seabrook 12/31/02

Pro forma w/Seabrook 2004

Gas 46% 46% 59%

Wind 28% 24% 21%

Hydro 7% 5% 3%

Oil 15% 9% 7%

Other 5% 3% 2%

Nuclear 0% 13% 9%

100% 100% 100%

TOTAL mw 5,063 7,976 11,588

13Percentages may not add to 100% due to rounding

FPL Energy Regional Diversity

Northeast 28% 38% 26%

Central &Mid West

35% 29% 37%

Mid-Atlantic& Southeast

20% 13% 21%

West 16% 20% 16%

100% 100% 100%

TOTAL mw 5,063 7,976 11,588

Current

Pro forma w/Seabrook 12/31/02

Pro forma w/Seabrook 2004

14

Why We Like the Deal

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive

15

Complements FPL Energy’s Northeast Portfolio

Hydro (29)

Oil (3)

RISEP

Bellingham

Sayreville

Seabrook

Bayswater

Ebensburg

Montgomery Co.

Marcus Hook 50Marcus Hook 750

Birch

In operationUnder construction

16

ProjectMaine Hydro 373Maine Oil 755Bellingham 148Sayreville 148Pennsylvania assets 75 Current Total 1,497

RISEP (mid ‘02)535Bayswater (mid ‘02) 54Seabrook (end ‘02) 1,024Marcus Hook 750 (mid ‘04) 744 Pro Forma Total 3,854

FPL Energy Assets inthe Northeast

Oil 20%

Natural Gas 44%

Nuclear 27%Hydro 10%

Other 1%

Net MW

Totals may not add due to rounding

17

Why We Like the Deal

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive

18

FPL Group Nuclear Portfolio

Net mwReactor

Type

Turkey Point 3 693 PWR

Turkey Point 4 693 PWR

St. Lucie 1 839 PWR

St. Lucie 2 714 PWR

Total 2,939

Seabrook 1,024 PWR

Pro forma Total 3,963

• FPL is an experienced operator of PWRs

• Seabrook expands nuclear portfolio by more than 30%

19

Top-Tier Nuclear Performance

Data Source: Institute of Nuclear Power Operators (INPO) U.S. sites

2001 WANO Performance IndexAll U.S. Sites

0

20

40

60

80

100

Turkey Point 4 3 St. Lucie 2 1

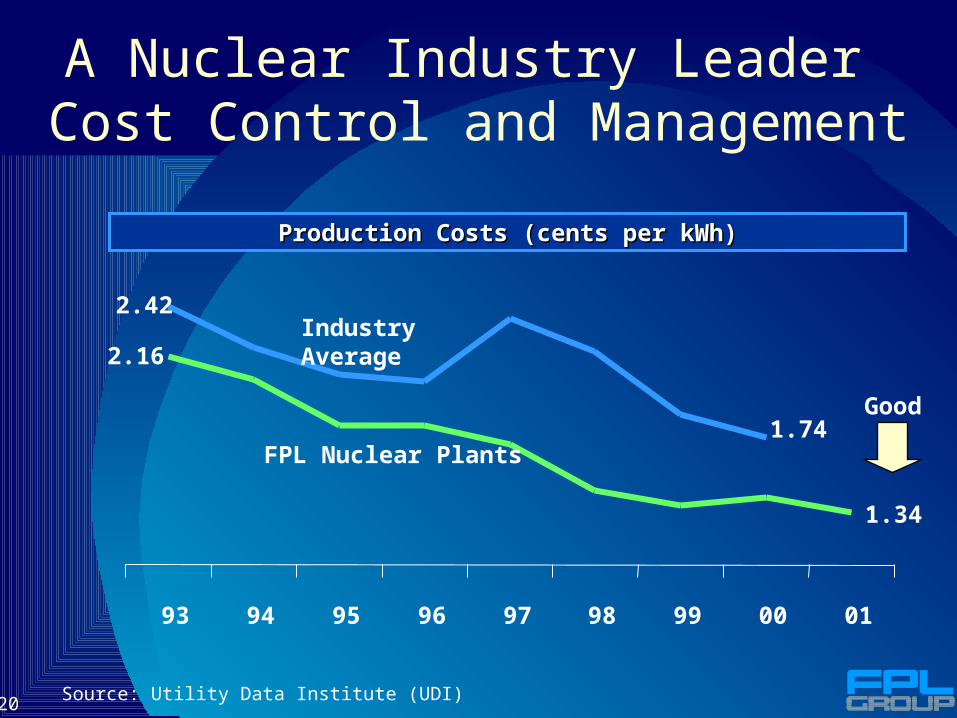

20

Production Costs (cents per kWh)Production Costs (cents per kWh)

1.74

2.42

2.16

1.34

93 94 95 96 97 98 99 00 01

Industry Average

FPL Nuclear Plants

Source: Utility Data Institute (UDI)

Good

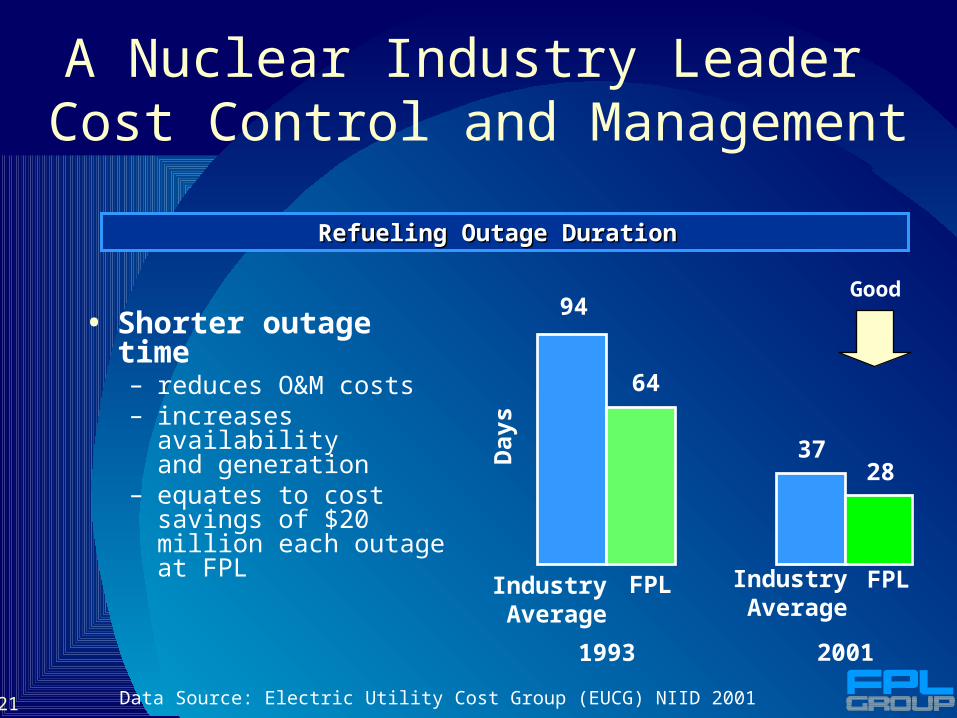

A Nuclear Industry Leader Cost Control and Management

21

Refueling Outage Duration Refueling Outage Duration

Data Source: Electric Utility Cost Group (EUCG) NIID 2001

Good

Day

s

94

37

64

28

1993 2001

Industry Average

FPL Industry Average

FPL

A Nuclear Industry Leader Cost Control and Management

• Shorter outage time– reduces O&M costs– increases availability

and generation– equates to cost savings

of $20 million each outage at FPL

22

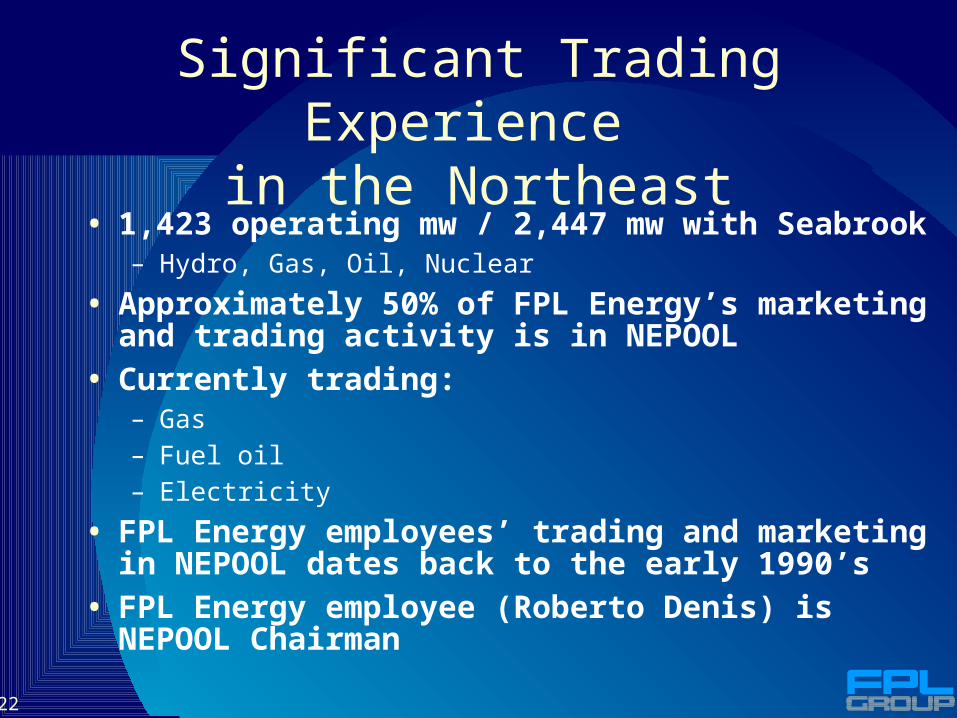

Significant Trading Experience in the Northeast

• 1,423 operating mw / 2,447 mw with Seabrook– Hydro, Gas, Oil, Nuclear

• Approximately 50% of FPL Energy’s marketing and trading activity is in NEPOOL

• Currently trading:– Gas– Fuel oil– Electricity

• FPL Energy employees’ trading and marketing in NEPOOL dates back to the early 1990’s

• FPL Energy employee (Roberto Denis) is NEPOOL Chairman

23

Why We Like the Deal

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive

24

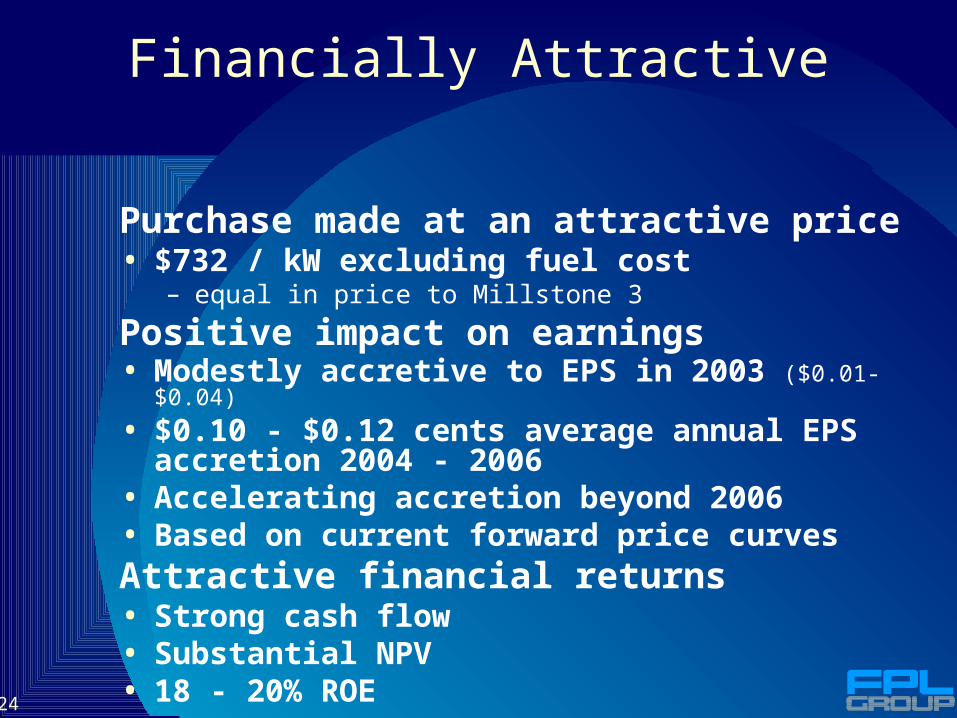

Financially Attractive

Purchase made at an attractive price• $732 / kW excluding fuel cost

– equal in price to Millstone 3

Positive impact on earnings• Modestly accretive to EPS in 2003 ($0.01-$0.04)

• $0.10 - $0.12 cents average annual EPS accretion 2004 - 2006

• Accelerating accretion beyond 2006• Based on current forward price curvesAttractive financial returns• Strong cash flow• Substantial NPV• 18 - 20% ROE

25

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

Unit Uprate OperationalImprovements

License Renewal

NP

V U

psi

de

Po

ten

tial

$40 - $50

$280 - $330

$80 - $120

Substantial Value Creation Potential

$ millions

26

Financing Consistent with FPL Group Plan

• Strong commitment to credit quality

• Target 50% / 50% debt / equity ratio

• Initially financed via a combination of:– $200-300 million equity issuance in 2003 in

conjunction with acquisition

– short-term borrowings

• Opportunistically access capital markets for take-out of short-term financing

27

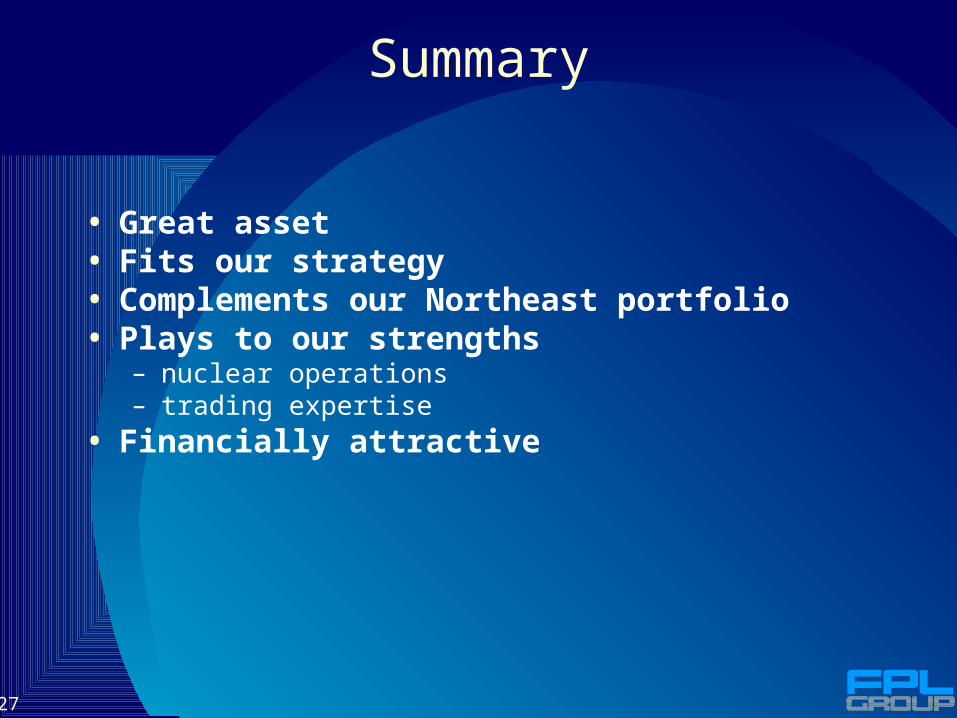

Summary

• Great asset• Fits our strategy• Complements our Northeast portfolio• Plays to our strengths

– nuclear operations– trading expertise

• Financially attractive