Embed Size (px)

Citation preview

REPÚBLICA DE MOÇAMBIQUE

MINISTÉRIO DA AGRICULTURA DIRECÇÃO NACIONAL DE FLORESTAS E FAUNA BRAVIA

FORESTRY ENTREPRENEURSHIP AND JOINT FOREST MANAGEMENT PROJECT

Nordic Development Fund SAVCOR INDUFOR Oy Credit No. 247 Report 6253-10E

May 2005

ACTUAL SITUATION OF THE FOREST INDUSTRY

IN SOFALA, ZAMBEZIA AND CABO DELGADO

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. i

TABLE OF CONTENTS EXECUTIVE SUMMARY ....................................................................................................... iv

1. INTRODUCTION ..............................................................................................................1 1.1 Linkage to National Development programs..............................................................1 1.2 Report Objectives .......................................................................................................2 1.3 Methodology...............................................................................................................3

1.3.1 Study Preparation and Data Collection...............................................................3 1.3.2 Data Processing and Assumptions ......................................................................3

2. ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA ............................4 2.1 Nurseries and Forest Plantations ................................................................................4 2.2 Harvesting...................................................................................................................5

2.2.1 Interviewed Persons and Labor Force ................................................................5 2.2.2 Applied Technology and Logging Capacity.......................................................6 2.2.3 Harvested Species and Their Utilization ............................................................7

2.3 Processing and Marketing of Wood Products ............................................................9 2.3.1 Labor Force and Training ...................................................................................9 2.3.2 Technology and Production Capacity...............................................................10 2.3.3 Products and Their Markets ..............................................................................11

2.4 Investments ...............................................................................................................12 2.4.1 During 1998-2003.............................................................................................12 2.4.2 Planned for 2004-2009 .....................................................................................13

3. ACTUAL SITUATION OF THE FOREST INDUSTRY IN ZAMBEZIA.....................13 3.1 Nurseries and Forest Plantations ..............................................................................13 3.2 Harvesting.................................................................................................................14

3.2.1 Interviewed Persons and Labor Force ..............................................................14 3.2.2 Applied Technology and Logging Capacity.....................................................15 3.2.3 Harvested Species and Their Processing ..........................................................16

3.3 Processing and Marketing of Wood Products ..........................................................17 3.3.1 Labor Force and Training .................................................................................17 3.3.2 Technology and Production Capacity...............................................................18 3.3.3 Products and Their Markets ..............................................................................19

3.4 Investments in Forest Industry..................................................................................21 3.4.1 During 1998-2003.............................................................................................21 3.4.2 Planned for 2004-2009 .....................................................................................22

4. ACTUAL SITUATION OF THE FOREST INDUSTRY IN CABO DELGADO ..........23 4.1 Nurseries and Forest Plantations ..............................................................................23 4.2 Harvesting.................................................................................................................23

4.2.1 Interviewed Persons and Labor Force ..............................................................23 4.2.2 Applied Technology and Logging Capacity.....................................................24 4.2.3 Harvested Species and Their Processing ..........................................................25

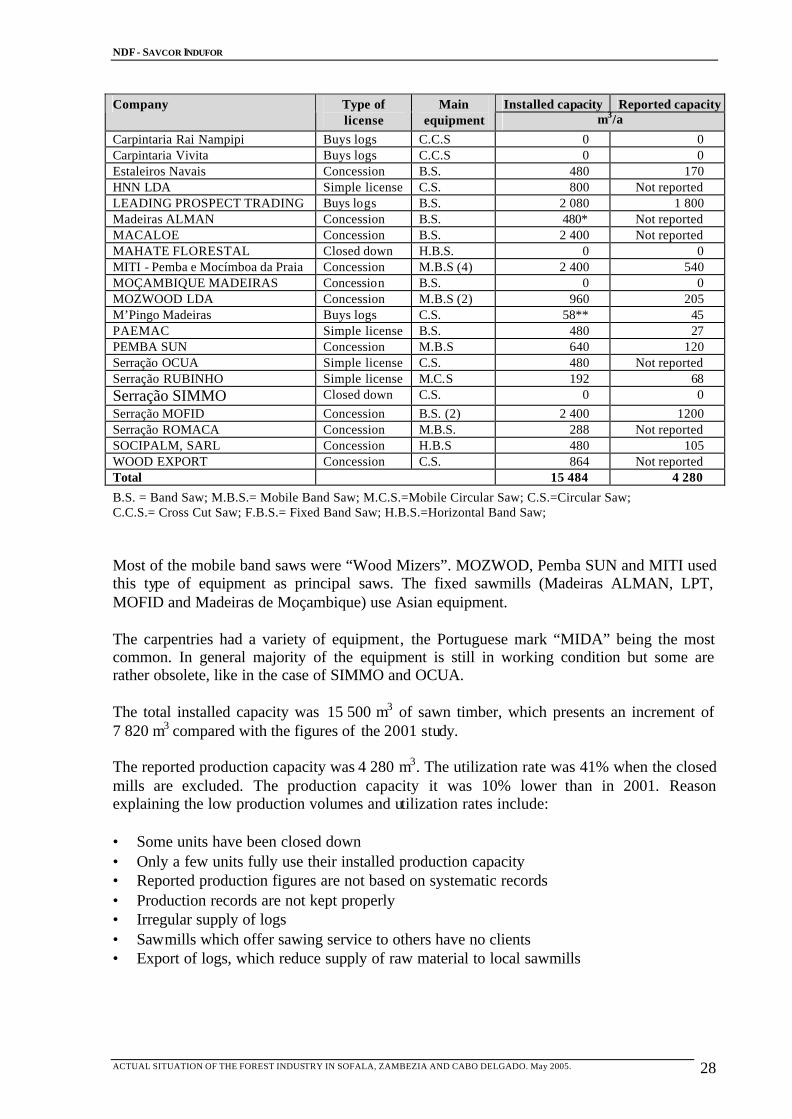

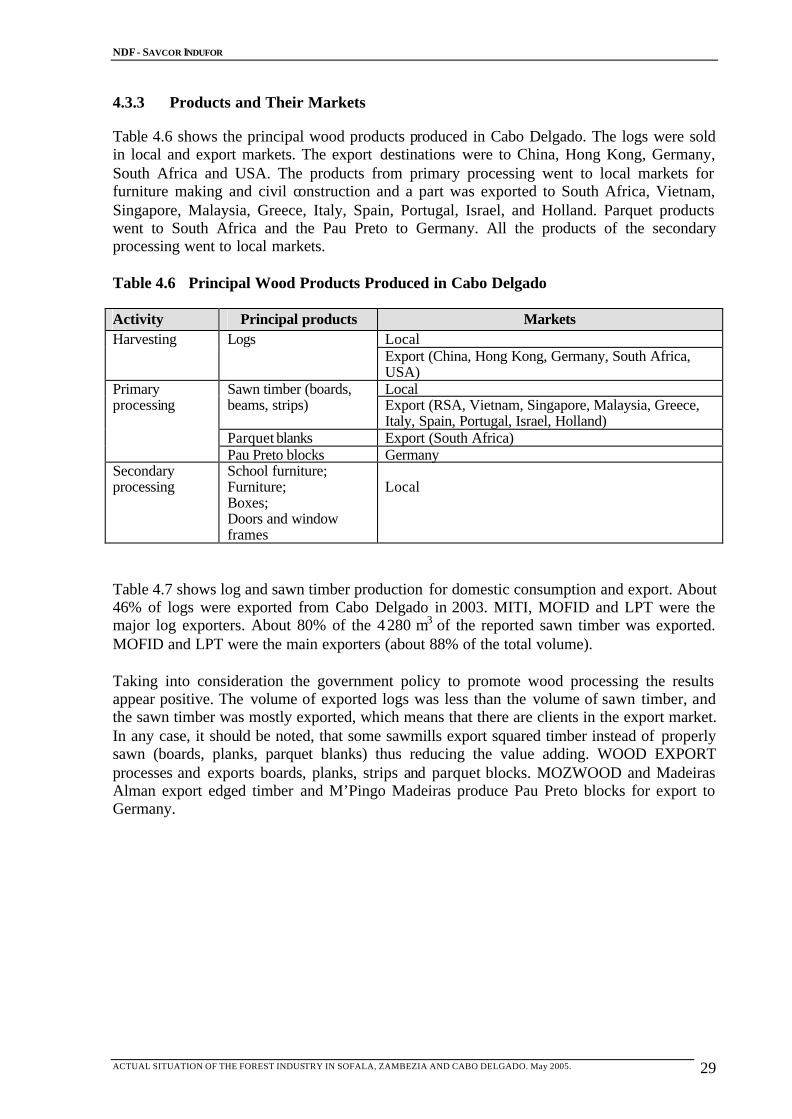

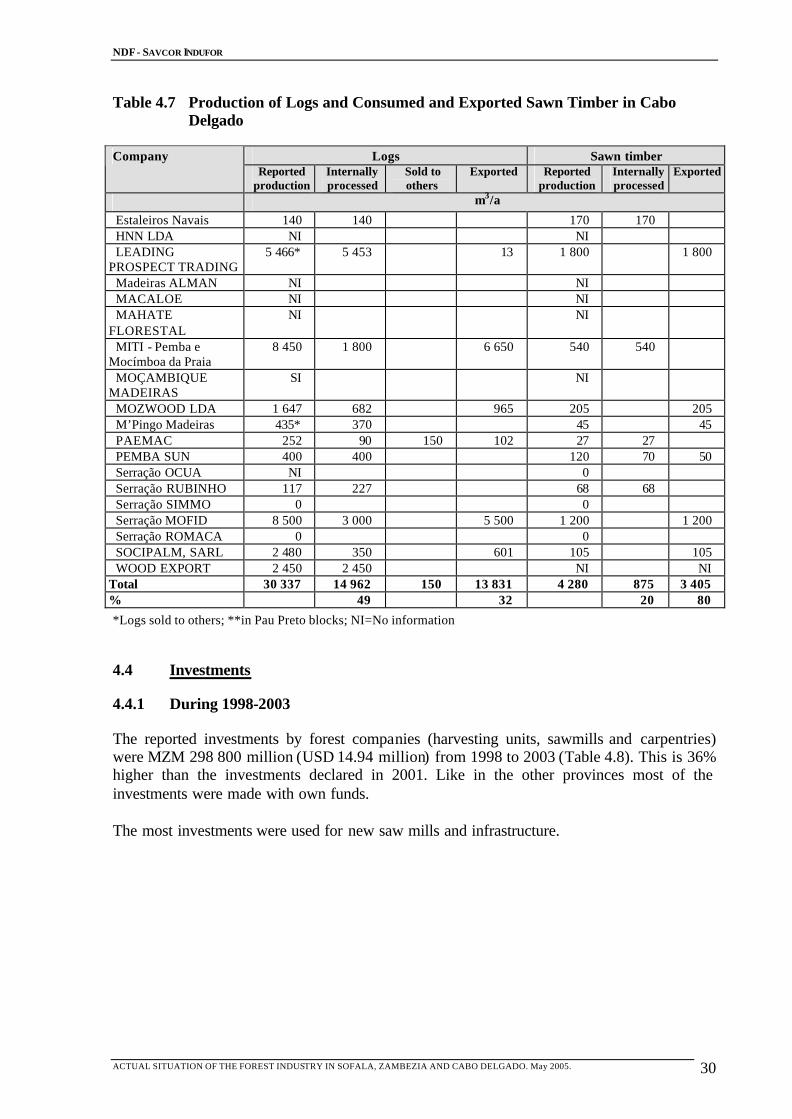

4.3 Processing and marketing .........................................................................................26 4.3.1 Labor Force and Training .................................................................................26 4.3.2 Technology and Production Capacity...............................................................27 4.3.3 Products and Their Markets ..............................................................................29

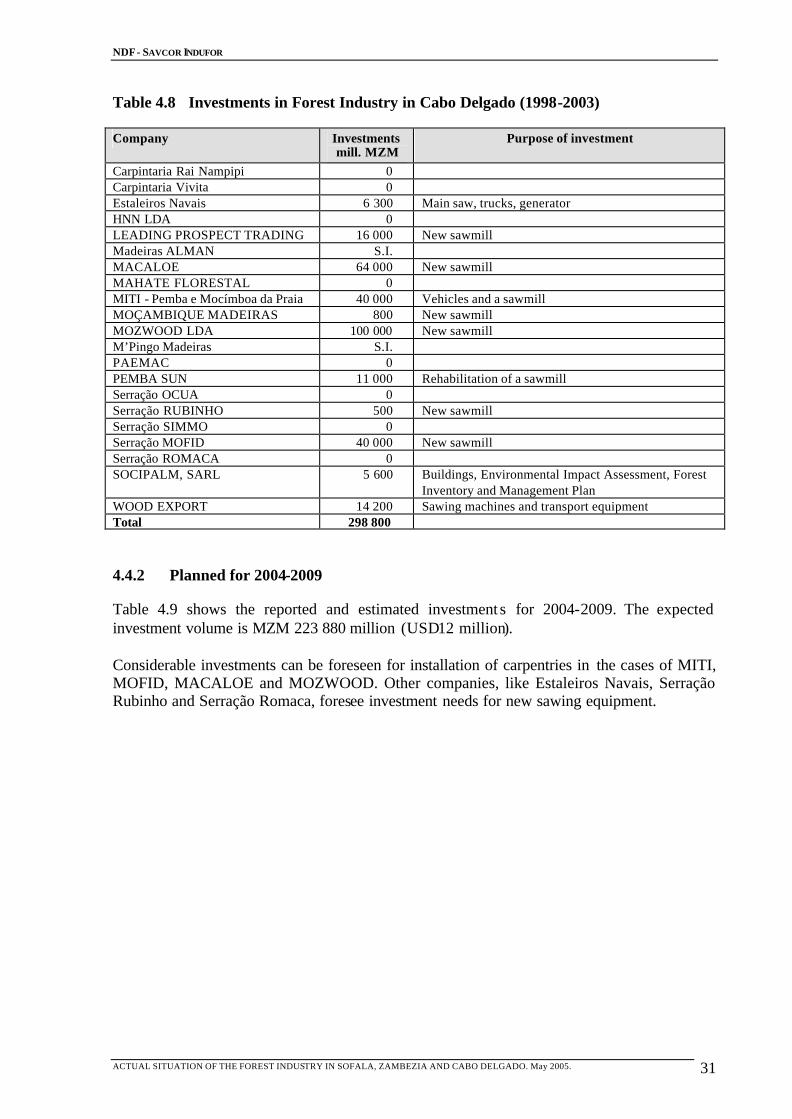

4.4 Investments ...............................................................................................................30 4.4.1 During 1998-2003.............................................................................................30 4.4.2 Planned for 2004-2009 .....................................................................................31

5. ANALYSIS OF THE THREE PROVINCES...................................................................32 5.1 Nurseries and Forest Plantations ..............................................................................32

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. ii

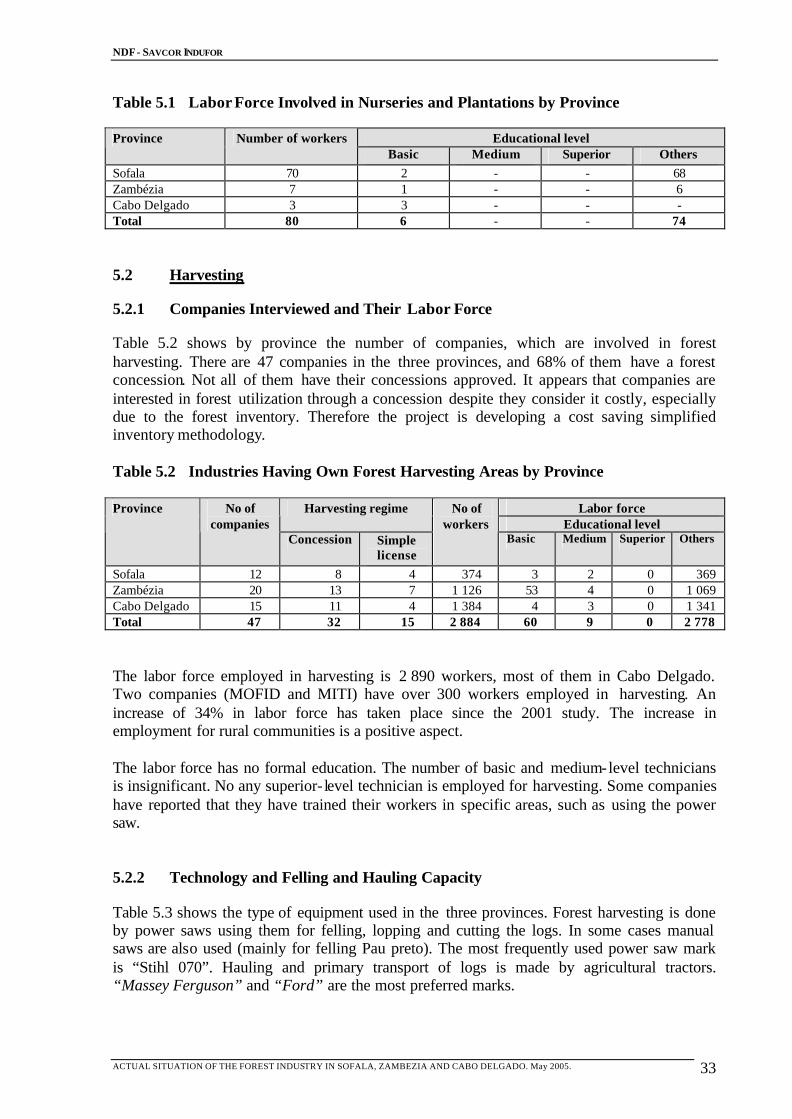

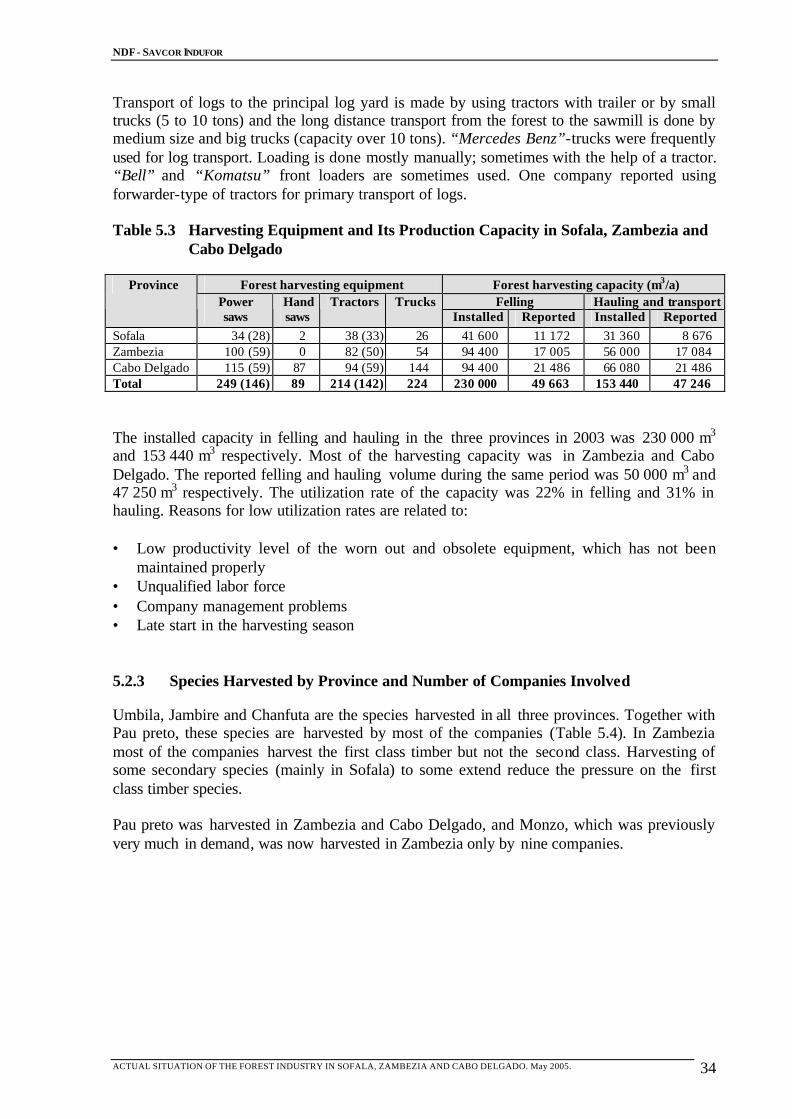

5.2 Harvesting.................................................................................................................33 5.2.1 Companies Interviewed and Their Labor Force ...............................................33 5.2.2 Technology and Felling and Hauling Capacity................................................33 5.2.3 Species Harvested by Province and Number of Companies Involved .............34

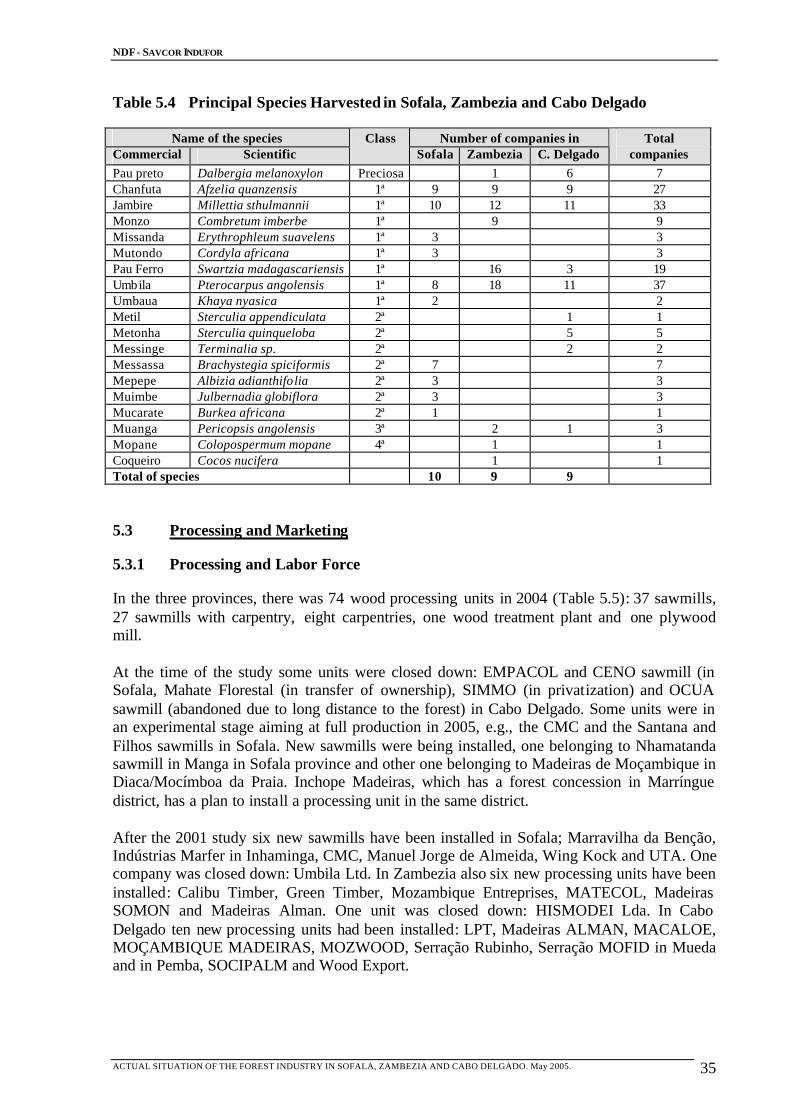

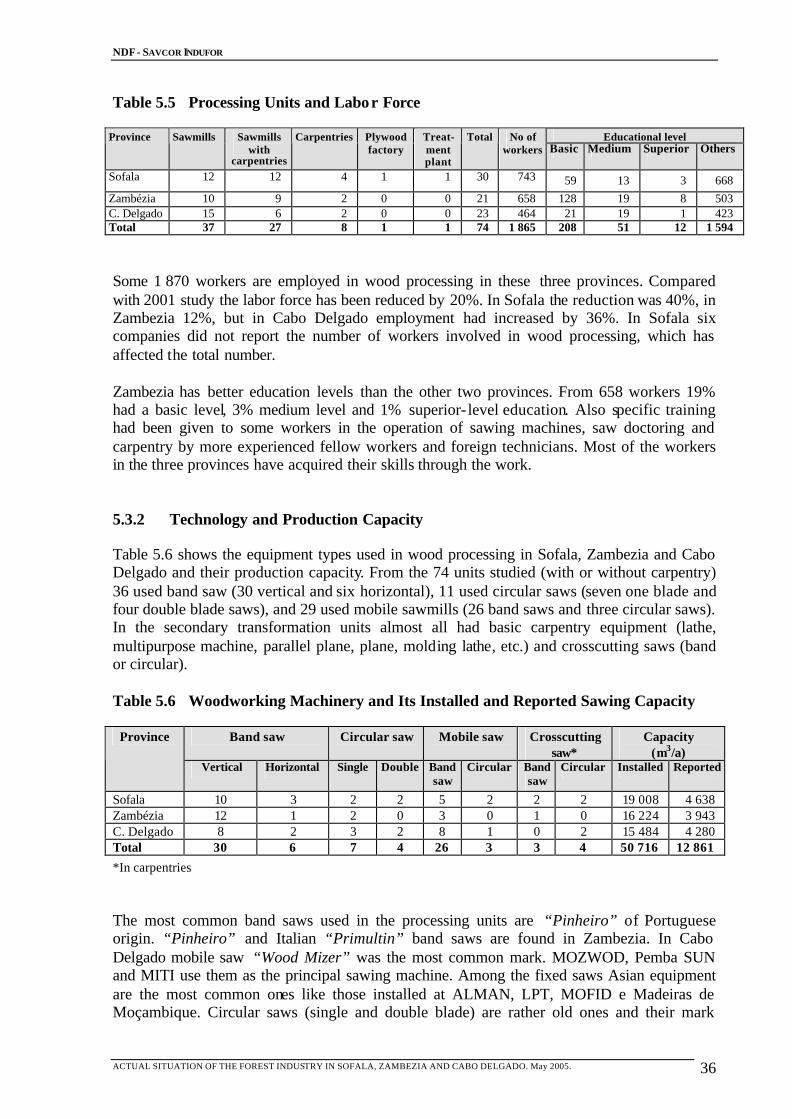

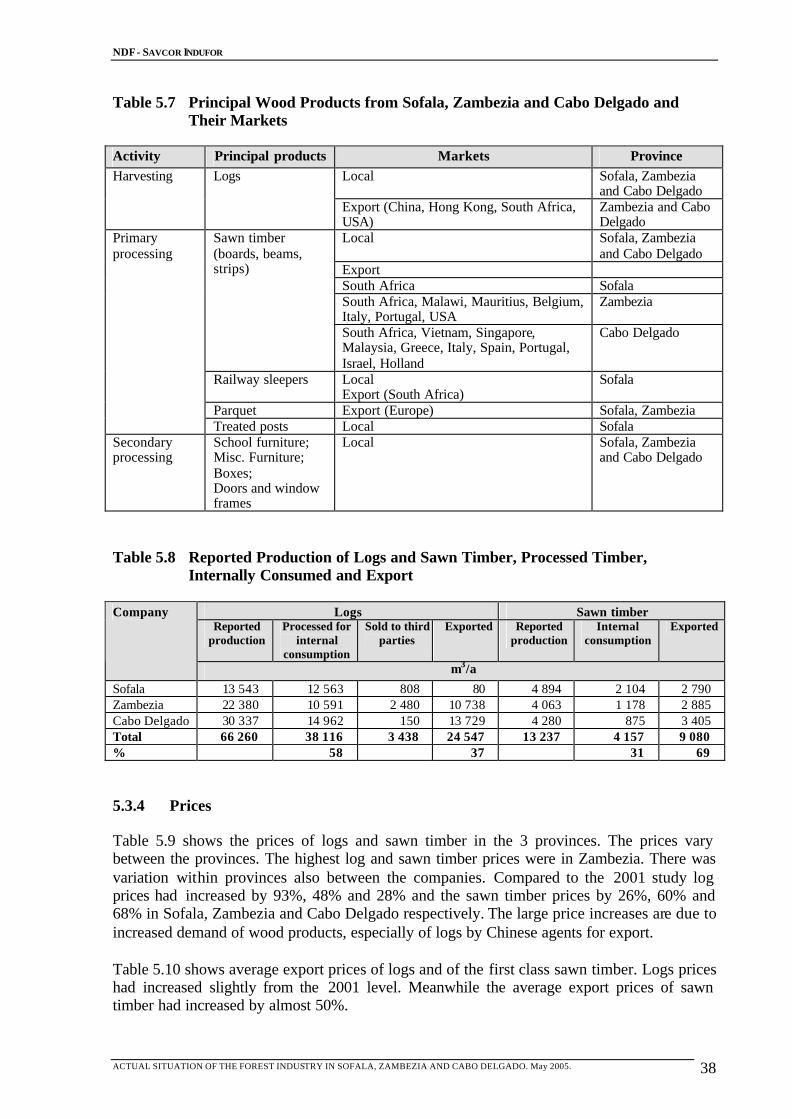

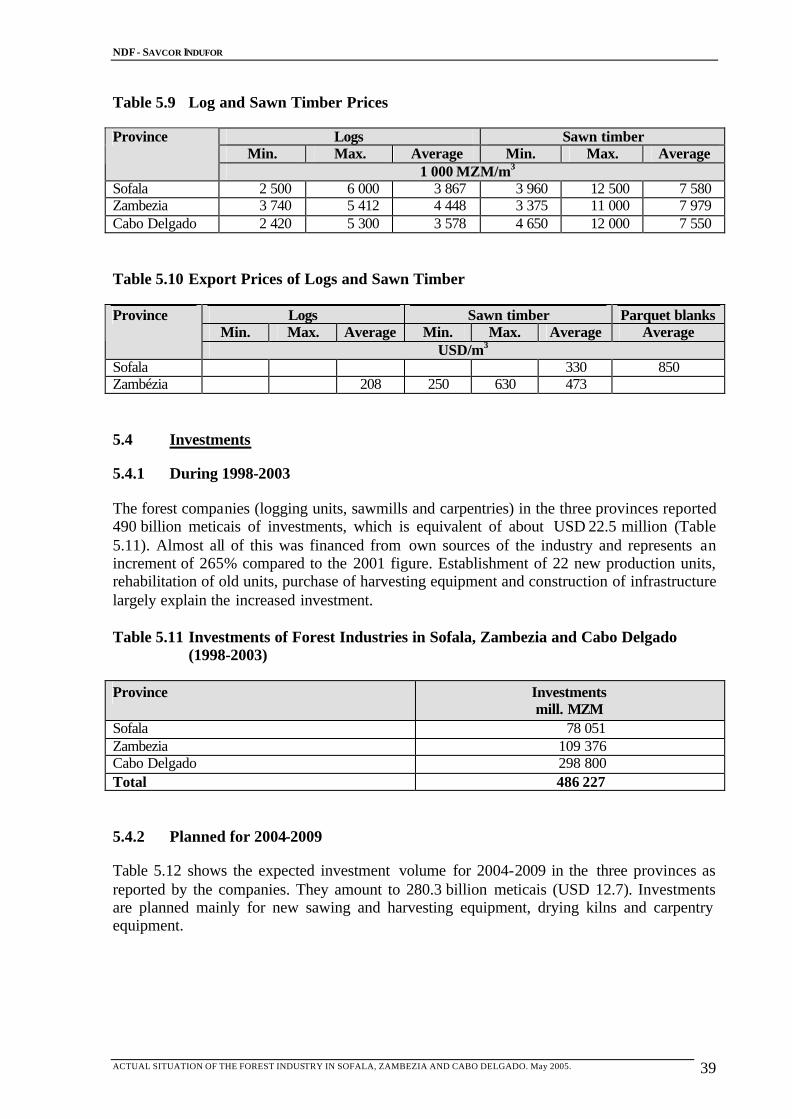

5.3 Processing and Marketing.........................................................................................35 5.3.1 Processing and Labor Force..............................................................................35 5.3.2 Technology and Production Capacity...............................................................36 5.3.3 Marketing..........................................................................................................37 5.3.4 Prices.................................................................................................................38

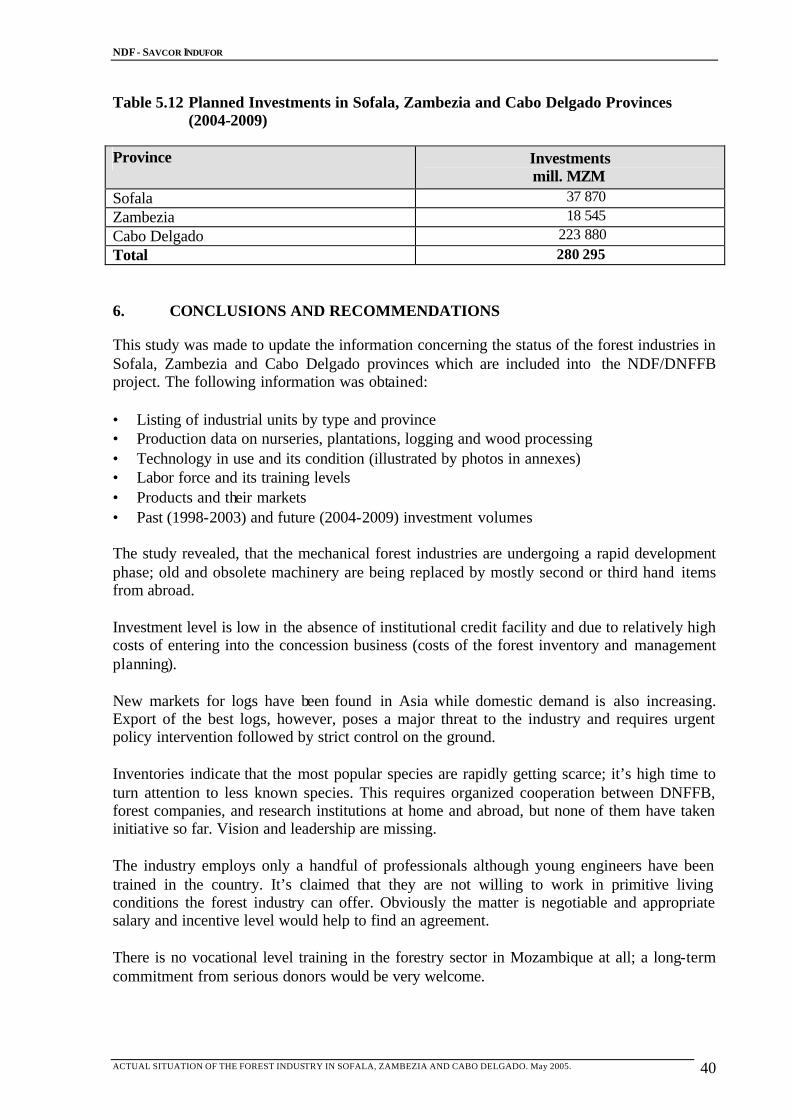

5.4 Investments ...............................................................................................................39 5.4.1 During 1998-2003.............................................................................................39 5.4.2 Planned for 2004-2009 .....................................................................................39

6. CONCLUSIONS AND RECOMMENDATIONS...........................................................40 List of Figures Figure 2.1 Flow of Logs in the Production Chain................................................................8 Figure 3.1 Flow of Logs in the Production Chain in Zambezia .........................................17 Figure 4.1 Flow of Logs in the Production Chain..............................................................26 List of Tables Table 2.1 Produced and Planted Seedlings by Company in Sofala in 2003 ...........................4 Table 2.2 Labor Force Involved in Nurseries and Tree Planting............................................5 Table 2.3 Harvesting Regime, Number of Workers Employed and Training Level of the

Companies ..............................................................................................................6 Table 2.4 Logging Equipment and Harvesting Capacity........................................................7 Table 2.5 Processed Tree Species by Company .....................................................................8 Table 2.6 Wood Processing Industry in Sofala and Its Labor Force ......................................9 Table 2.7 Type of the Equipment and Its Production Capacity............................................11 Table 2.8 Principal Wood Products in Sofala .......................................................................12 Table 2.9 Investments (MZM) in Forest Industries in Sofala Province (1998-2003) ..........12 Table 2.10 Planned Industrial Investments in Sofala Province for the Period 2004-2009.....13 Table 3.1 Labor Force in Forest Nurseries and Plantations ..................................................14 Table 3.2 Harvesting Regime, Number of Workers Employed and Training Level of the

Companies ............................................................................................................14 Table 3.3 Harvesting Equipment and Capacity ....................................................................15 Table 3.4 Principal Species Harvested by Companies in Zambezia .....................................16 Table 3.5 Forest Industry by Type and Its Labor Force by Educational Level in Zambezia18 Table 3.6 Type of Wood Processing Equipment and Sawn Timber Production Capacity...19 Table 3.7 Main Wood Products Produced in Zambezi .........................................................20 Table 3.8 Production of Logs and Sawn Wood for Domestic and Export Markets .............21 Table 3.9 Investments in Forest Industries in Zambezia (1998-2003) .................................22 Table 3.10 Expected Investments in Forest Industries in Zambezia Province (2004-2009) ..23 Table 4.1 Type of License and Training Levels in Logging Industry..................................24 Table 4.2 Equipment Used in Logging and Its Production Capacity ...................................25 Table 4.3 Main Species Harvested by Companies in Cabo Delgado Province ....................26 Table 4.4 Forest Industry by Type and Its Labor Force by Educational Level in Cabo

Delgado .................................................................................................................27 Table 4.5 Type of Equipment Used and Sawn Timber Production Capacity.......................27

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. iii

Table 4.6 Principal Wood Products Produced in Cabo Delgado ..........................................29 Table 4.7 Production of Logs and Consumed and Exported Sawn Timber in Cabo Delgado

..............................................................................................................................30 Table 4.8 Investments in Forest Industry in Cabo Delgado (1998-2003) ............................31 Table 4.9 Investments in Forest Industries in Sofala Province (2004-2009)........................32 Table 5.1 Labor Force Involved in Nurseries and Plantations by Province .........................33 Table 5.2 Industries Having Own Forest Harvesting Areas by Province .............................33 Table 5.3 Harvesting Equipment and Its Production Capacity in Sofala, Zambezia and Cabo

Delgado .................................................................................................................34 Table 5.4 Principal Species Harvested in Sofala, Zambezia and Cabo Delgado..................35 Table 5.5 Processing Units and Labor Force ........................................................................36 Table 5.6 Woodworking Machinery and Its Installed and Reported Sawing Capacity........36 Table 5.7 Principal Wood Products from Sofala, Zambezia and Cabo Delgado and Their

Markets .................................................................................................................38 Table 5.8 Reported Production of Logs and Sawn Timber, Processed Timber, Internally

Consumed and Export...........................................................................................38 Table 5.9 Log and Sawn Timber Prices................................................................................39 Table 5.10 Export Prices of Logs and Sawn Timber ..............................................................39 Table 5.11 Investments of Forest Industries in Sofala, Zambezia and Cabo Delgado (1998-

2003) .....................................................................................................................39 Table 5.12 Planned Investments in Sofala, Zambezia and Cabo Delgado Provinces (2004-

2009) .....................................................................................................................40 List of Annexes Annex 1 Questionnaire Format Annex 2 Company Data from Sofala Annex 3 Company Data from Zambezia Annex 4 Company Data from Cabo Delgado

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. iv

EXECUTIVE SUMMARY The Forestry Entrepreneurship and Joint Forest Management Project started collecting baseline information from forestry sector companies in March 2004. By end of the year all of them (67) were interviewed in the Project provinces: Sofala, Zambezia and Cabo Delgado. The data collection focused on technical and economic aspects of the companies. Also local associations (5) of the forestry sector entrepreneurs, administrators (7) and financial institutions (5) were met and briefed about the project objectives and the opportunities it will offer to them. The data presented in this report was collected during field visits between March and December 2004. The data is structured by province. Conclusions and recommendations follow the same structure as the provincial presentations. The detailed data is presented in by companies Annex 1. The company data is shown in a structured, standard format, which includes basic registration information, species and quantities harvested and processed, principal products and markets, and the main machinery and problems the company management have encountered. An addition, consultants listed some observations and confidential information given by the company owners, which is not included into this report; such as potential investments and credit needs. Entrepreneurs have demonstrated keen interest on the Project, and many of them are anxiously waiting for the launching of its main development instrument – the credit facility – and expecting competitive interest rates. Despite of the rather ramshackle overall status of the industry and of the difficulties to understand the fundamental requirements of sustainability in forest management, the consultants found spirit of entrepreneurship, which can significantly contribute to the poverty alleviation targets of the Project. A major challenge now is to create a true partnership between the parties; the state administration, forest communities, entrepreneurs and the financial institution for the credit line. Key Issues Identified 1. Pressure to continue granting “licencias simples” is high, especially in Cabo Delgado and

Zambezia. This is mainly because the turnover under “licencias simples” is fast and access to cash and credit is easy, provided by Asian buyers when exporting logs than processing them into value added products.

2. Only a few companies have fully met all the legal requirements needed for a forest concession. The new government is facing challenging decisions when reconsidering what to do with uncompleted concession applications and the prevailing tax and other exemptions.

3. High cost and low utility value of the Management Plan continue to be a major obstacle according to the opinion of the concession holders. Rethinking is needed on the forest concession strategy. Especially the inventory methods and costs, and timing of the approval process of the concession application appear to require adjustments.

4. Although only a half of the installed sawing capacity is utilized, in some areas the sustainably harvestable volume1 is being exceeded. The pressure for over-harvesting falls especially on the most well known commercial species, such as Pau Ferro (Swarzia madagascarencis), Pau Preto (Dalbergia melanoxylon), Panga Panga/Jambire (Millettia stuhlmannii), Chanfuta (Afzelia guanzensis), Umbila (Pterocarpus angolensis), Missanda

1 When the latest available forest inventory figures of Saket from year 1994 are used as reference.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. v

(Erythropleum suavoelens), Messassa (Brachystegia spp.), Monzo (Combretum imbembe), Muanga (Afromosia angolensis), and Umbaua (Khaya nyasica).

5. Other important development issues include (i) involvement of the local communities in the concession management, and (ii) entrepreneurs’ limited knowledge of the market situation.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 1

1. INTRODUCTION

1.1 Linkage to National Development programs

The Government of Mozambique (GoM) started economic restructuring in 1987. The aim has been to revitalize the production and increase benefits to individuals. This has led to profound reforms, especially improving the business environment of the private sector. GoM removed import restrictions as well as subsidies and the import tariffs were simplified. Several parastatals have been privatized, including in the banking sector. These measures resulted in an impressive economic growth, as an average over 10% during the final years of the 1990s. The growth of the GDP, however, dropped in year 2000 to 2.1% due to serious floods but continued to grow reaching 15% in year 2001, 9% in 2002 and 7.1% in 20032. In relative terms the contribution of the forestry sector to GDP varied between 3.1% and 3.9% during the period of 1996-20013. Despite the progress, Mozambique continues to be one of the poorest countries in the world. Almost 70% of the population live in absolute poverty4. In order to reduce poverty GoM adopted a comprehensive and integrated action plan for reduction of absolute poverty “Plano de Acção para a Redução da Pobreza Absoluta (PARPA)”. Rapid growth is an essential to reduce poverty on medium and long-term basis. The strategy incorporates policies to create proper environment to stimulate investments and to increase productivity to reach average GDP growth of 8%5. PARPA recognize employment and entrepreneurship as the engines of socio-economic development. Private initiatives of the citizens are recognized as crucially important in the poverty reduction strategy. The program states that “the private initiatives include individual producers and their families (as micro-scale economic units being increasingly important in agro-silvi-pasture, handicraft and informal urban businesses) called micro, small and medium enterprises”. PARPA 2000-2005 defines the principal objectives in the forestry sector as follows: “…to continue facilitating communities, the private sector and other producers in the forestry sector…paying sufficient attention to the long-term sustainability of the use of natural resources”. Direct reference to the forest sector is made in the Agricultural Development Programme (PROAGRI)6, in the PARPA section, related with rural development. The overall goal of PROAGRI is to achieve environmentally sustainable and equitable growth in rural areas so that poverty is reduced and food security improved. PROAGRI will approach this objective through a set of investments and activities designed to (i) reform MADER in order to make it more efficient and effective ; (ii) support the execution of MADER’s activities in the country; and (iii) harmonies donor support to agricultural development and establish systematically greater Mozambican “ownership” of the projects. Four sub-components, (institutional support, conservation areas, community programs and production management) have been identified by PROAGRI for the forestry and wildlife sector for 1998-2002. It has been difficult to find funding for the production management7. The existing

2 World Bank, http://www.worldbank.org/afr/mz/ctry_brief.htm 3 DNFFB, 2003. Contribution of the forestry sector to the national economy. 4 PARPA, 2001. Action Plan for Reduction of Absolute Poverty. 5 PARPA, 2001. Action Plan for Reduction of Absolute Poverty. 6 PROAGRI is a sectoral programme implemented by Mozambique’s Ministry of Agriculture and Rural Development, which receive financial support from several donors. 7 NDF/MADER, 2001. Forestry Entrepreneurship and Joint Forest Management Project.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 2

sawmills and carpentries are in great majority technically obsolete with low efficiency in using raw materials. The processed wood products are of low quality and of little commercial value8. The outputs of production management in PROAGRI are defined as (i) establishment of permanent production forest estate, (ii) development of forest concession management, and (iii) improvement of forest products utilization and product value. In this spirit, and within the frame of the PROAGRI, Nordic Development Fund (NDF) and the Government of Mozambique signed a loan agreement to assist SMEs operating in the forestry sector. The Forestry Entrepreneurship and Joint Forest Management Project was formulated to mobilize the needed assistance. The overall objective of this Project is poverty mitigation, thus directly contributing to PARPA. The Project aims at improving conditions for sustainable forest management and increasing the productive forest area in the long run. The loan agreement between GoM ands NDF is EUR 7.4 million and includes four components: (1) institution building, (includes the credit facility) (2) development of SMEs (3) sustained forest management by concession holders and communities (4) capacity building The Project started in 2004 and will last until 2007. About EUR 3.3 million have been allocated as credit to be granted for SMEs in the forestry sector for their modernization. Provinces of Sofala, Zambezia and Cabo Delgado were selected as pilot areas based on the following criteria: • Having adequate forest resources • Having entrepreneurs capable in harvesting, transport, sawing, carpentry and other value

adding production • Existence of other projects and organizations, which could help the Project in marketing,

training, credit management, etc. This document presents the actual state of the small and medium size forest industries in the 3 pilot provinces. The data partially updates the previous study done in 20019. 1.2 Report Objectives

This base line study aims at finding out the actual situation of the forest industries in the Project provinces; Sofala, Zambezia and Cabo Delgado. The specific information includes: • Industrial units organized by province and by type • Data on tree nurseries, plantations, logging, and processing technology • Technology applied • Data on sales and investments

8 Chitará, 2003. Instrumento para a promoção do investimento privado na indústria florestal moçambicana. MADER/DNFFB. 9 Eureka, 2001. Inquérito à indùstria madereira.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 3

• Labor force and its training • Products and their marketing • Investment volumes 1.3 Methodology

1.3.1 Study Preparation and Data Collection

A study questionnaire was prepared in consultation with the staff of DNFFB (Annex 1). The questionnaire was piloted first in three timber production units in Maputo province in order to test and improve it. Information was collected from 30 wood processing units in Sofala, 21 in Zambezia and 23 in Cabo Delgado. Most of them were sawmills with or without carpentries, or independent carpentries. Consultant visited every wood procession unit, which was registered at Provincial Forest Services (SPFFBs), and the owner or his representative was interviewed. Due to time constraint small carpentries scattered in the provinces were not visited. 1.3.2 Data Processing and Assumptions

The collected data, which includes production, harvesting, primary and secondary processing, investments, labor force, its training, and used technology, was processed for the final report. For calculation of the installed logging capacity it was assumed tha t 160 days (8 months)/ year were actually worked and by using a manual saw 4 m3 of logs were cut/day and 10 m3/day by using power saw. Hauling capacity of an agricultural tractor as well as of the transport capacity of the trucks was assumed to be 7 m3/day/tractor or /truck. The above figures were obtained from an earlier study. Eureka (2001) reports, that daily production of a logging gang vary from 1 to 4 m3 /day when manual saw is used and from 3 to 10 m3/day when power saw is used. The hauling capacity vary between 10 to 40 m3/day if the average distance is 500 m. The lowest installed capacities were assumed to be 1 m3/day/manual saw, 3 m3 /day/power saw, 5 m3/day/hauling tractor and truck. Fath [ref.?] measured productivity in five companies in Gaza, Sofala, Zambézia, Nampula and Cabo Delgado in 2002, and found that in Gaza 2.86 m3 of Mecruse was cut by manual saw per day and Muroto in Nampula 16.25 m3/day by power saw. Average daily felling by power saw was 10 m3/day when the average distance between trees was 70 m and the harvested volume was 2 m3/ha of Umbila and Mucarala in Sofala, Zambézia, and Cabo Delgado provinces. Hauling capacity varied from 7 m3/day in Sofala (Umbila) and Zambezia (Murroto) to 18 m3 /day in Cabo Delgado (Umbila). In this study the number of power saws and tractors effectively used was taken into consideration to avoid overestimation. It was noticed that some companies had a big number of equipment (power saws, manual saws and tractors), of which a part was used and the other was kept in reserve to replace broken ones. In cases when information was not supplied the consultants made their own estimates.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 4

The production capacity in the sawmills was calculated based on the actually operational equipment. The same method was used as Eureka in 2001 assuming that there are 160 working days/year, the supply of the raw material is regular and that the main saw determines the production quantity. The company representatives reported the actual produc tion volumes sawn per day by the main saw. The declared production capacity was established as an average produced during the last three years in cases the data existed. The results of the study were compared with those of Eureka from year 2001 to analyze the industrial development in the study provinces. 2. ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA

2.1 Nurseries and Forest Plantations

From the 25 companies interviewed in Sofala only seven produce seedlings of native species for reforestation. Five of them have a forest concession, one simple license and one is producing seedlings in cooperation with local community where the nurseries are located. These are very low figures taking into consideration that almost 50% of the companies operate a concession, the management plan of which should include reforestation activities. Table 2.1 shows the number of produced and planted seedlings. Table 2.1 Produced and Planted Seedlings by Company in Sofala in 2003

Company Type of license

Number of produced seedlings

Number of

planted seedlings

Planted area (ha)

Planted species

Carpintaria Marravilha da Benção

Simple license

5 100 40 Chanfuta, Jambire, Umbila

Companhia de Madeiras de Moçambique

Concession (28 852 ha)

562 Chanfuta (11%), Jambire (10%), Mutondo (2%) and Umbila (77%).

Indústria Madeireira de Moçambique

Concession (23 000 ha)

750 630 10 Chanfuta, Jambire Messassa, Mutondo, Umbila

Indústrias Marfer Concession (49 561 ha)

2 800 Chanfuta, Jambire, Umbila,

Moçambique Florestal

Concession (20 000 ha)

1 500 Chanfuta(17%), Jambire(53%), Muimbe (15%) and Missanda (15%)

Serração Mezimbite * 25 000 Chanfuta, Muanga, Pau-preto and Umbila

TCT – Indústrias Florestais

Concession (24 821 ha)

8 000-10 000 36 000 Chanfuta, Jambire and Mutondo

Total Note: * Buys raw material from communities With the exception of TCT sawmill in Mezimbite the number of seedlings produced in nurseries and planted is very low. Majority of the companies (72%) have not engaged at all in reforestation. Anyhow, there has been some progress compared to the 2001 study when only TCT produced seedlings and carried out reforestation.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 5

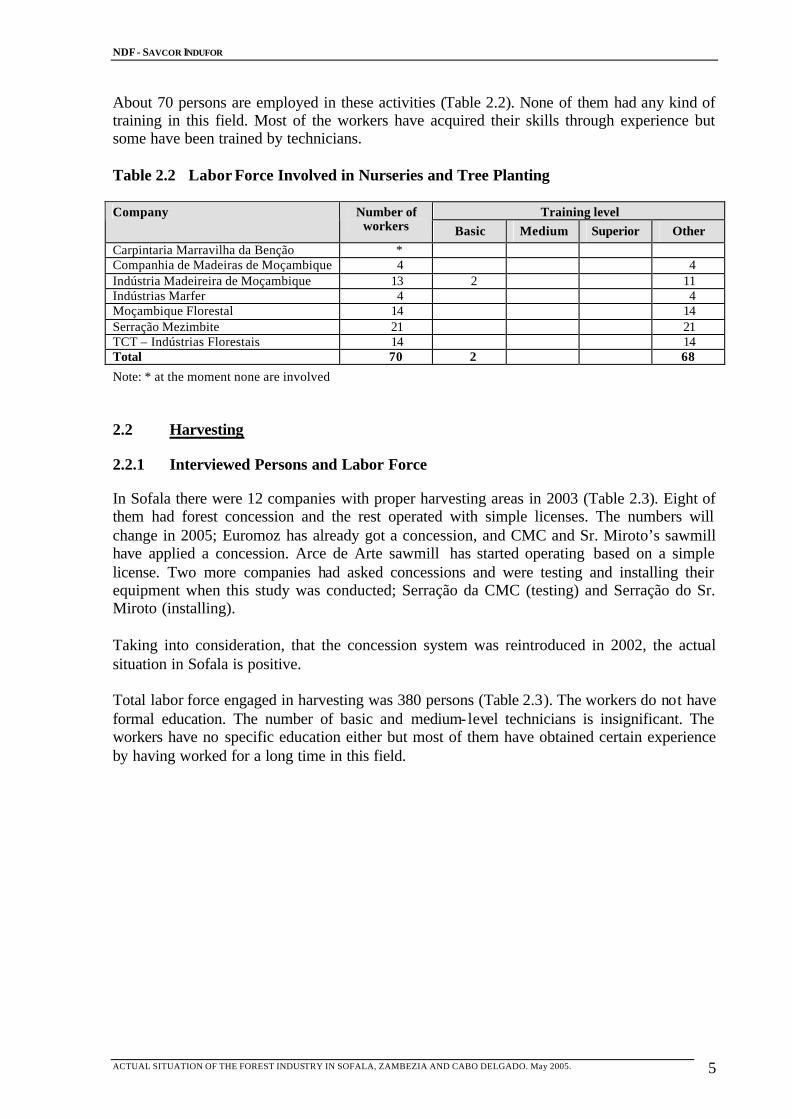

About 70 persons are employed in these activities (Table 2.2). None of them had any kind of training in this field. Most of the workers have acquired their skills through experience but some have been trained by technicians. Table 2.2 Labor Force Involved in Nurseries and Tree Planting

Training level Company Number of workers Basic Medium Superior Other

Carpintaria Marravilha da Benção * Companhia de Madeiras de Moçambique 4 4 Indústria Madeireira de Moçambique 13 2 11 Indústrias Marfer 4 4 Moçambique Florestal 14 14 Serração Mezimbite 21 21 TCT – Indústrias Florestais 14 14 Total 70 2 68

Note: * at the moment none are involved 2.2 Harvesting

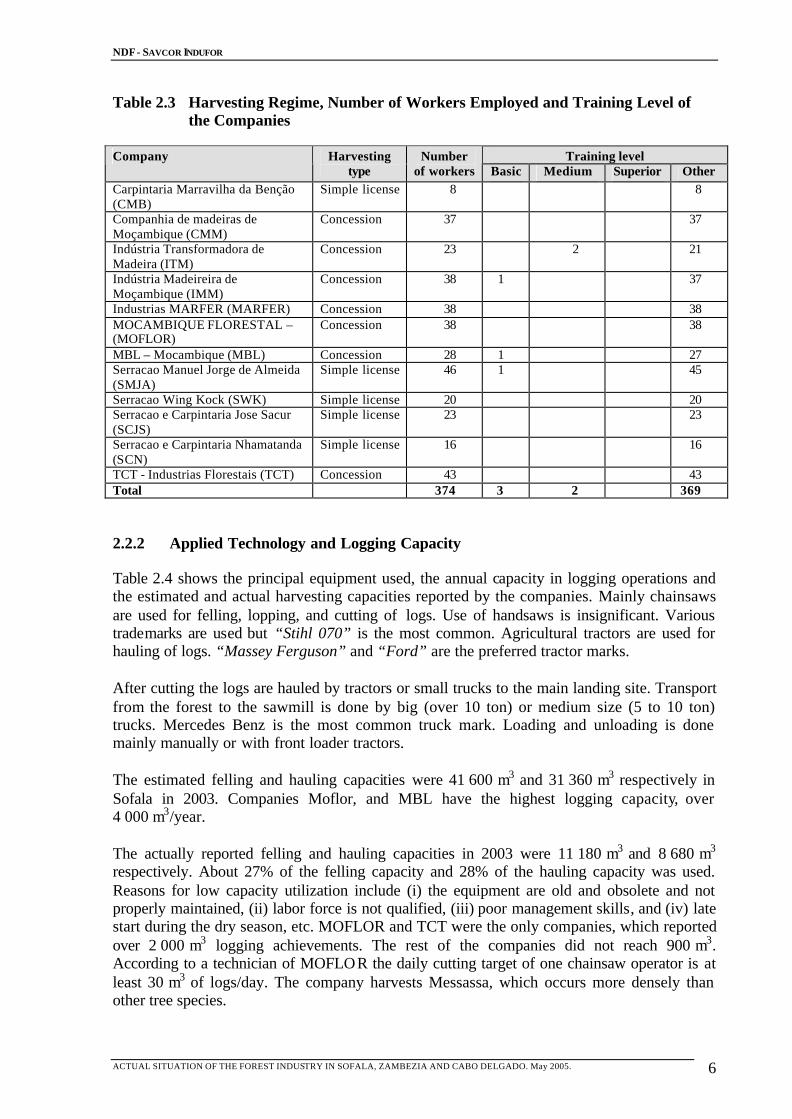

2.2.1 Interviewed Persons and Labor Force

In Sofala there were 12 companies with proper harvesting areas in 2003 (Table 2.3). Eight of them had forest concession and the rest operated with simple licenses. The numbers will change in 2005; Euromoz has already got a concession, and CMC and Sr. Miroto’s sawmill have applied a concession. Arce de Arte sawmill has started operating based on a simple license. Two more companies had asked concessions and were testing and installing their equipment when this study was conducted; Serração da CMC (testing) and Serração do Sr. Miroto (installing). Taking into consideration, that the concession system was reintroduced in 2002, the actual situation in Sofala is positive. Total labor force engaged in harvesting was 380 persons (Table 2.3). The workers do not have formal education. The number of basic and medium-level technicians is insignificant. The workers have no specific education either but most of them have obtained certain experience by having worked for a long time in this field.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 6

Table 2.3 Harvesting Regime, Number of Workers Employed and Training Level of the Companies

Training level Company Harvesting type

Number of workers Basic Medium Superior Other

Carpintaria Marravilha da Benção (CMB)

Simple license 8 8

Companhia de madeiras de Moçambique (CMM)

Concession 37 37

Indústria Transformadora de Madeira (ITM)

Concession 23 2 21

Indústria Madeireira de Moçambique (IMM)

Concession 38 1 37

Industrias MARFER (MARFER) Concession 38 38 MOCAMBIQUE FLORESTAL – (MOFLOR)

Concession 38 38

MBL – Mocambique (MBL) Concession 28 1 27 Serracao Manuel Jorge de Almeida (SMJA)

Simple license 46 1 45

Serracao Wing Kock (SWK) Simple license 20 20 Serracao e Carpintaria Jose Sacur (SCJS)

Simple license 23 23

Serracao e Carpintaria Nhamatanda (SCN)

Simple license 16 16

TCT - Industrias Florestais (TCT) Concession 43 43 Total 374 3 2 369 2.2.2 Applied Technology and Logging Capacity

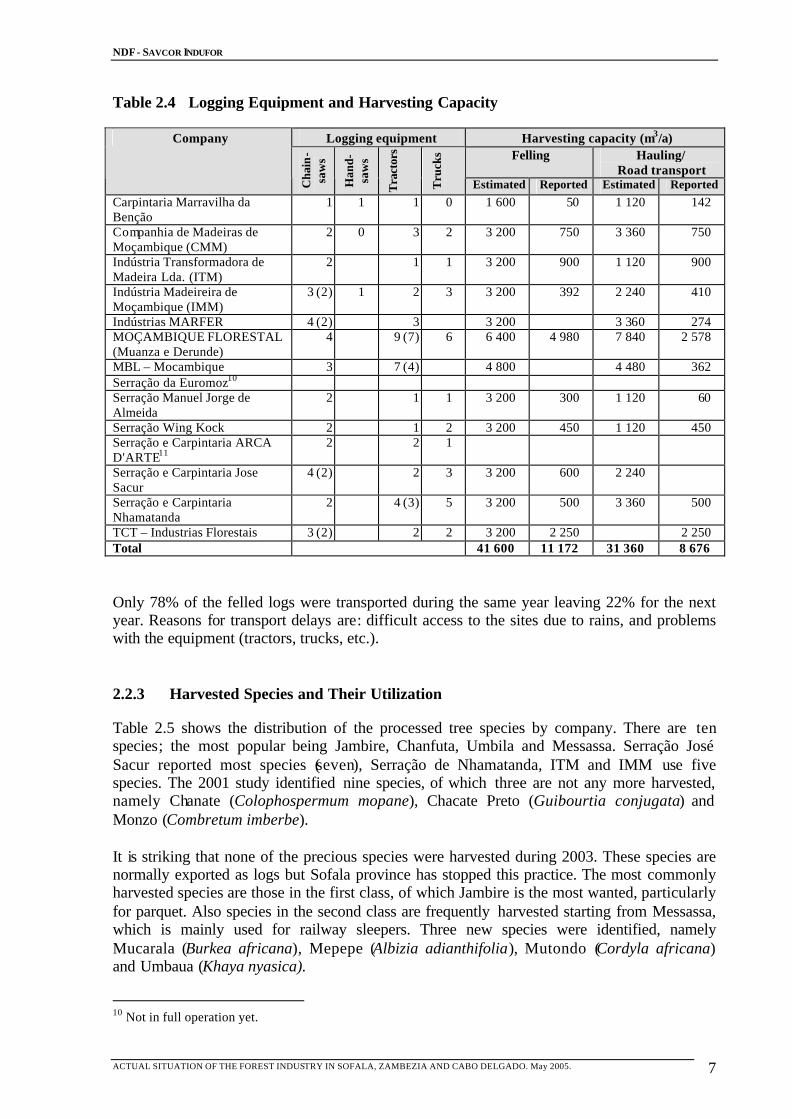

Table 2.4 shows the principal equipment used, the annual capacity in logging operations and the estimated and actual harvesting capacities reported by the companies. Mainly chainsaws are used for felling, lopping, and cutting of logs. Use of handsaws is insignificant. Various trademarks are used but “Stihl 070” is the most common. Agricultural tractors are used for hauling of logs. “Massey Ferguson” and “Ford” are the preferred tractor marks. After cutting the logs are hauled by tractors or small trucks to the main landing site. Transport from the forest to the sawmill is done by big (over 10 ton) or medium size (5 to 10 ton) trucks. Mercedes Benz is the most common truck mark. Loading and unloading is done mainly manually or with front loader tractors. The estimated felling and hauling capacities were 41 600 m3 and 31 360 m3 respectively in Sofala in 2003. Companies Moflor, and MBL have the highest logging capacity, over 4 000 m3/year. The actually reported felling and hauling capacities in 2003 were 11 180 m3 and 8 680 m3

respectively. About 27% of the felling capacity and 28% of the hauling capacity was used. Reasons for low capacity utilization include (i) the equipment are old and obsolete and not properly maintained, (ii) labor force is not qualified, (iii) poor management skills, and (iv) late start during the dry season, etc. MOFLOR and TCT were the only companies, which reported over 2 000 m3 logging achievements. The rest of the companies did not reach 900 m3. According to a technician of MOFLOR the daily cutting target of one chainsaw operator is at least 30 m3 of logs/day. The company harvests Messassa, which occurs more densely than other tree species.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 7

Table 2.4 Logging Equipment and Harvesting Capacity

Logging equipment Harvesting capacity (m3/a) Felling Hauling/

Road transport

Company

Cha

in-

saw

s

Han

d-sa

ws

Tra

ctor

s

Tru

cks

Estimated Reported Estimated Reported Carpintaria Marravilha da Benção

1 1 1 0 1 600 50 1 120 142

Companhia de Madeiras de Moçambique (CMM)

2 0 3 2 3 200 750 3 360 750

Indústria Transformadora de Madeira Lda. (ITM)

2 1 1 3 200 900 1 120 900

Indústria Madeireira de Moçambique (IMM)

3 (2) 1 2 3 3 200 392 2 240 410

Indústrias MARFER 4 (2) 3 3 200 3 360 274 MOÇAMBIQUE FLORESTAL (Muanza e Derunde)

4 9 (7) 6 6 400 4 980 7 840 2 578

MBL – Mocambique 3 7 (4) 4 800 4 480 362 Serração da Euromoz10 Serração Manuel Jorge de Almeida

2 1 1 3 200 300 1 120 60

Serração Wing Kock 2 1 2 3 200 450 1 120 450 Serração e Carpintaria ARCA D'ARTE11

2 2 1

Serração e Carpintaria Jose Sacur

4 (2) 2 3 3 200 600 2 240

Serração e Carpintaria Nhamatanda

2 4 (3) 5 3 200 500 3 360 500

TCT – Industrias Florestais 3 (2) 2 2 3 200 2 250 2 250 Total 41 600 11 172 31 360 8 676 Only 78% of the felled logs were transported during the same year leaving 22% for the next year. Reasons for transport delays are: difficult access to the sites due to rains, and problems with the equipment (tractors, trucks, etc.). 2.2.3 Harvested Species and Their Utilization

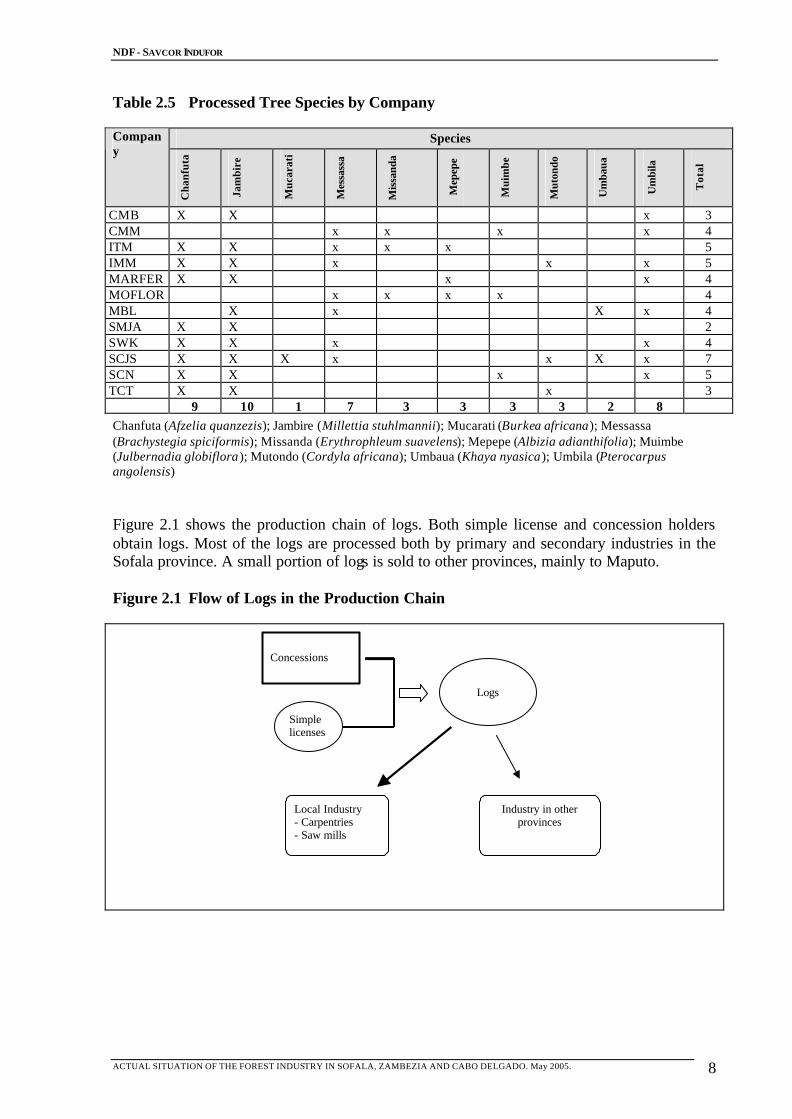

Table 2.5 shows the distribution of the processed tree species by company. There are ten species; the most popular being Jambire, Chanfuta, Umbila and Messassa. Serração José Sacur reported most species (seven), Serração de Nhamatanda, ITM and IMM use five species. The 2001 study identified nine species, of which three are not any more harvested, namely Chanate (Colophospermum mopane), Chacate Preto (Guibourtia conjugata) and Monzo (Combretum imberbe). It is striking that none of the precious species were harvested during 2003. These species are normally exported as logs but Sofala province has stopped this practice. The most commonly harvested species are those in the first class, of which Jambire is the most wanted, particularly for parquet. Also species in the second class are frequently harvested starting from Messassa, which is mainly used for railway sleepers. Three new species were identified, namely Mucarala (Burkea africana), Mepepe (Albizia adianthifolia), Mutondo (Cordyla africana) and Umbaua (Khaya nyasica).

10 Not in full operation yet.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 8

Table 2.5 Processed Tree Species by Company

Species Company

Cha

nfut

a

Jam

bire

Muc

arat

i

Mes

sass

a

Mis

sand

a

Mep

epe

Mui

mbe

Mut

ondo

Um

baua

Um

bila

Tot

al

CMB X X x 3 CMM x x x x 4 ITM X X x x x 5 IMM X X x x x 5 MARFER X X x x 4 MOFLOR x x x x 4 MBL X x X x 4 SMJA X X 2 SWK X X x x 4 SCJS X X X x x X x 7 SCN X X x x 5 TCT X X x 3

9 10 1 7 3 3 3 3 2 8 Chanfuta (Afzelia quanzezis); Jambire (Millettia stuhlmannii); Mucarati (Burkea africana); Messassa (Brachystegia spiciformis); Missanda (Erythrophleum suavelens); Mepepe (Albizia adianthifolia); Muimbe (Julbernadia globiflora); Mutondo (Cordyla africana); Umbaua (Khaya nyasica); Umbila (Pterocarpus angolensis) Figure 2.1 shows the production chain of logs. Both simple license and concession holders obtain logs. Most of the logs are processed both by primary and secondary industries in the Sofala province. A small portion of logs is sold to other provinces, mainly to Maputo. Figure 2.1 Flow of Logs in the Production Chain

Concessions

Simple licenses

Logs

Local Industry - Carpentries - Saw mills

Industry in other provinces

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 9

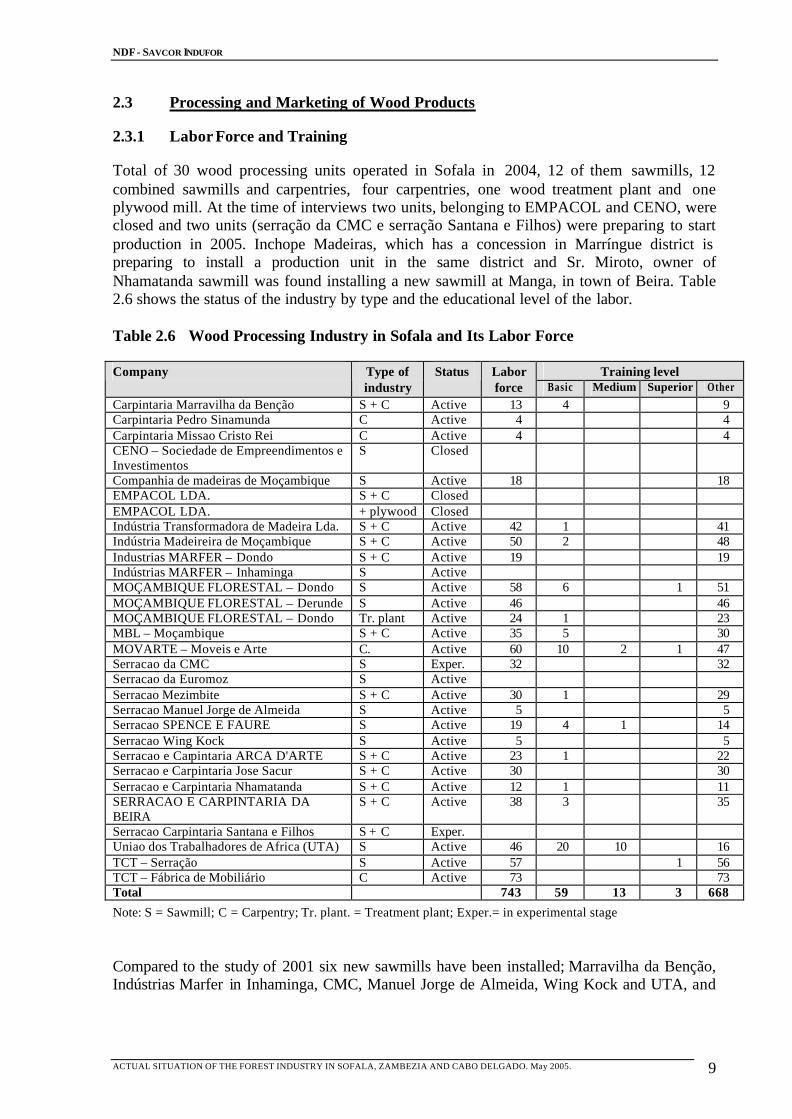

2.3 Processing and Marketing of Wood Products

2.3.1 Labor Force and Training

Total of 30 wood processing units operated in Sofala in 2004, 12 of them sawmills, 12 combined sawmills and carpentries, four carpentries, one wood treatment plant and one plywood mill. At the time of interviews two units, belonging to EMPACOL and CENO, were closed and two units (serração da CMC e serração Santana e Filhos) were preparing to start production in 2005. Inchope Madeiras, which has a concession in Marríngue district is preparing to install a production unit in the same district and Sr. Miroto, owner of Nhamatanda sawmill was found installing a new sawmill at Manga, in town of Beira. Table 2.6 shows the status of the industry by type and the educational level of the labor. Table 2.6 Wood Processing Industry in Sofala and Its Labor Force

Training level Company Type of industry

Status Labor force Basic Medium Superior Other

Carpintaria Marravilha da Benção S + C Active 13 4 9 Carpintaria Pedro Sinamunda C Active 4 4 Carpintaria Missao Cristo Rei C Active 4 4 CENO – Sociedade de Empreendimentos e Investimentos

S Closed

Companhia de madeiras de Moçambique S Active 18 18 EMPACOL LDA. S + C Closed EMPACOL LDA. + plywood Closed Indústria Transformadora de Madeira Lda. S + C Active 42 1 41 Indústria Madeireira de Moçambique S + C Active 50 2 48 Industrias MARFER – Dondo S + C Active 19 19 Indústrias MARFER – Inhaminga S Active MOÇAMBIQUE FLORESTAL – Dondo S Active 58 6 1 51 MOÇAMBIQUE FLORESTAL – Derunde S Active 46 46 MOÇAMBIQUE FLORESTAL – Dondo Tr. plant Active 24 1 23 MBL – Moçambique S + C Active 35 5 30 MOVARTE – Moveis e Arte C. Active 60 10 2 1 47 Serracao da CMC S Exper. 32 32 Serracao da Euromoz S Active Serracao Mezimbite S + C Active 30 1 29 Serracao Manuel Jorge de Almeida S Active 5 5 Serracao SPENCE E FAURE S Active 19 4 1 14 Serracao Wing Kock S Active 5 5 Serracao e Carpintaria ARCA D'ARTE S + C Active 23 1 22 Serracao e Carpintaria Jose Sacur S + C Active 30 30 Serracao e Carpintaria Nhamatanda S + C Active 12 1 11 SERRACAO E CARPINTARIA DA BEIRA

S + C Active 38 3 35

Serracao Carpintaria Santana e Filhos S + C Exper. Uniao dos Trabalhadores de Africa (UTA) S Active 46 20 10 16 TCT – Serração S Active 57 1 56 TCT – Fábrica de Mobiliário C Active 73 73 Total 743 59 13 3 668

Note: S = Sawmill; C = Carpentry; Tr. plant. = Treatment plant; Exper.= in experimental stage Compared to the study of 2001 six new sawmills have been installed; Marravilha da Benção, Indústrias Marfer in Inhaminga, CMC, Manuel Jorge de Almeida, Wing Kock and UTA, and

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 10

one (Umbila Lda.) has been closed. Four sawmills and two old carpentries were not included in the 2001 study although they were operating that time. Number of workers directly employed in wood processing is 743. Of them only 59 have basic education, 13 medium, and three higher- level education. Although most of the workers have acquired certain experience they have not received any formal training. 2.3.2 Technology and Production Capacity

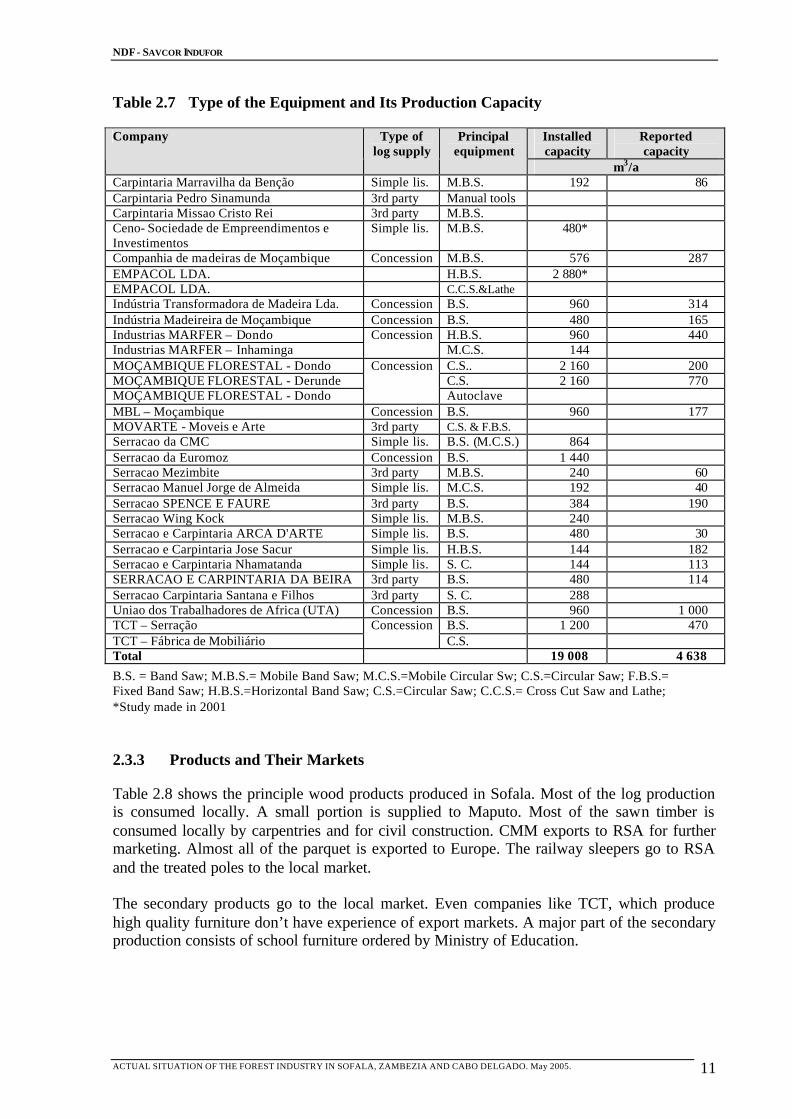

Table 2.7 shows the type of equipment used in wood processing in Sofala and their capacity. Of 24 sawmills (with or without carpentry), 13 used band saw (ten vertical and three horizontal), four circular saws (two one-blade and two two-blade saws) and seven are mobile sawmills (five mobile band saws and two circular saws). At the secondary processing units almost all have basic equipment for carpentry (lathe, multipurpose machine, parallel plane, plane, molding lathe, etc.) and a circular or a band saw. One small carpentry unit located in Marríngue use manual tools for wood processing.

Most of the band saws used in Sofala are “Pinheiros”. The circular saws (one or double blade) are rather old and worn out, and their manufacturer was not possible to recognize. Mobile band sawmills are relatively new “Wood Mizers” and circular saws are “Petersons”. The carpentries have a variety of equipment of various marks. In general, a majority of the equipment are still useable although many are obsolete. The installed sawn wood production capacity was 19 000 m3/year in the province or 2 000 m3

more than in the previous study from year 2001. This results from new industries, which have started their production. The reportedly produced quantity was 4 638 m3, which is only 25% of the estimated production capacity. The reported sawn timber production was very low; an average daily production was 2 m3 only. UTA was the only company, which reached the level of 6 m3/day. Compared to the figures reported in 2001, about 60% reduction has taken place. The reasons, which explain a low volume and value of the production include: • Some of the units have been closed down • Some units are still being established and will enter into production in 2005 • Many units are obsolete with very low production capacity • Accurate value registers are not kept systematically • Supply of the raw material is irregular • Saw milling services are hired out, and most of the time the equipment remain idle due to

lack of clients.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 11

Table 2.7 Type of the Equipment and Its Production Capacity

Installed capacity

Reported capacity

Company Type of log supply

Principal equipment

m3/a Carpintaria Marravilha da Benção Simple lis. M.B.S. 192 86 Carpintaria Pedro Sinamunda 3rd party Manual tools Carpintaria Missao Cristo Rei 3rd party M.B.S. Ceno- Sociedade de Empreendimentos e Investimentos

Simple lis. M.B.S. 480*

Companhia de madeiras de Moçambique Concession M.B.S. 576 287 EMPACOL LDA. H.B.S. 2 880* EMPACOL LDA. C.C.S.&Lathe Indústria Transformadora de Madeira Lda. Concession B.S. 960 314 Indústria Madeireira de Moçambique Concession B.S. 480 165 Industrias MARFER – Dondo H.B.S. 960 440 Industrias MARFER – Inhaminga

Concession M.C.S. 144

MOÇAMBIQUE FLORESTAL - Dondo C.S.. 2 160 200 MOÇAMBIQUE FLORESTAL - Derunde C.S. 2 160 770 MOÇAMBIQUE FLORESTAL - Dondo

Concession

Autoclave MBL – Moçambique Concession B.S. 960 177 MOVARTE - Moveis e Arte 3rd party C.S. & F.B.S. Serracao da CMC Simple lis. B.S. (M.C.S.) 864 Serracao da Euromoz Concession B.S. 1 440 Serracao Mezimbite 3rd party M.B.S. 240 60 Serracao Manuel Jorge de Almeida Simple lis. M.C.S. 192 40 Serracao SPENCE E FAURE 3rd party B.S. 384 190 Serracao Wing Kock Simple lis. M.B.S. 240 Serracao e Carpintaria ARCA D'ARTE Simple lis. B.S. 480 30 Serracao e Carpintaria Jose Sacur Simple lis. H.B.S. 144 182 Serracao e Carpintaria Nhamatanda Simple lis. S. C. 144 113 SERRACAO E CARPINTARIA DA BEIRA 3rd party B.S. 480 114 Serracao Carpintaria Santana e Filhos 3rd party S. C. 288 Uniao dos Trabalhadores de Africa (UTA) Concession B.S. 960 1 000 TCT – Serração B.S. 1 200 470 TCT – Fábrica de Mobiliário

Concession C.S.

Total 19 008 4 638

B.S. = Band Saw; M.B.S.= Mobile Band Saw; M.C.S.=Mobile Circular Sw; C.S.=Circular Saw; F.B.S.= Fixed Band Saw; H.B.S.=Horizontal Band Saw; C.S.=Circular Saw; C.C.S.= Cross Cut Saw and Lathe; *Study made in 2001 2.3.3 Products and Their Markets

Table 2.8 shows the principle wood products produced in Sofala. Most of the log production is consumed locally. A small portion is supplied to Maputo. Most of the sawn timber is consumed locally by carpentries and for civil construction. CMM exports to RSA for further marketing. Almost all of the parquet is exported to Europe. The railway sleepers go to RSA and the treated poles to the local market. The secondary products go to the local market. Even companies like TCT, which produce high quality furniture don’t have experience of export markets. A major part of the secondary production consists of school furniture ordered by Ministry of Education.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 12

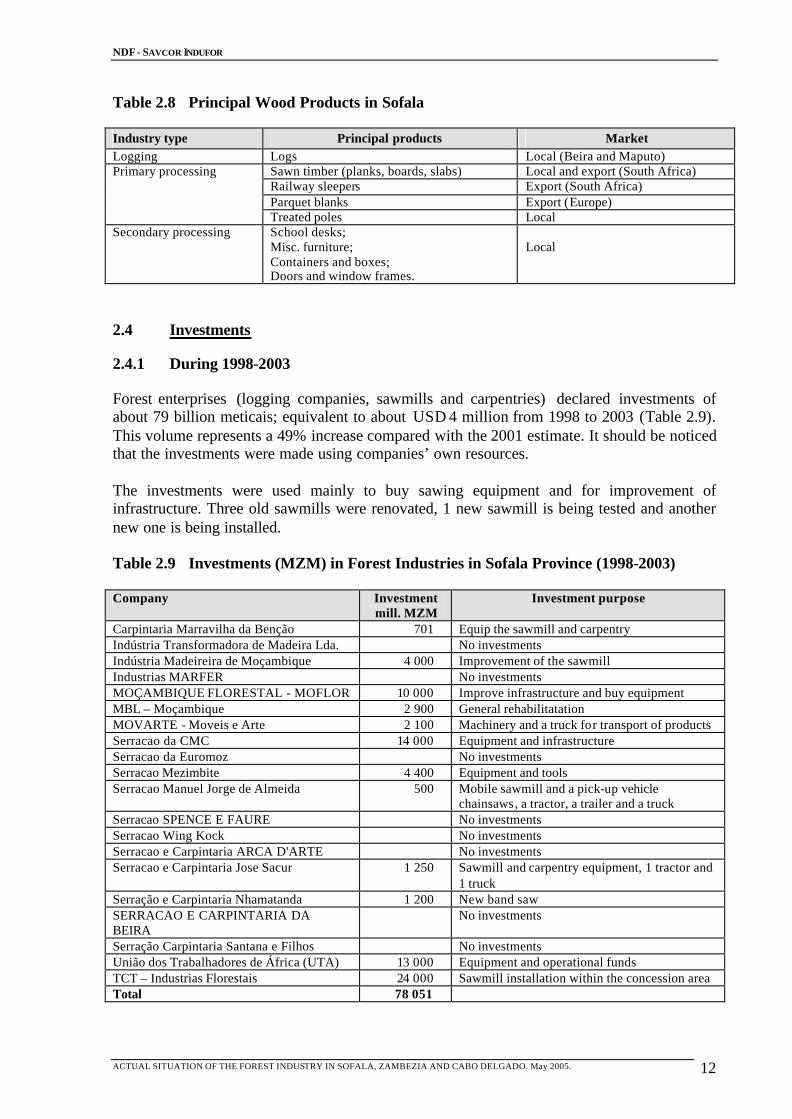

Table 2.8 Principal Wood Products in Sofala

Industry type Principal products Market Logging Logs Local (Beira and Maputo)

Sawn timber (planks, boards, slabs) Local and export (South Africa) Railway sleepers Export (South Africa) Parquet blanks Export (Europe)

Primary processing

Treated poles Local Secondary processing School desks;

Misc. furniture; Containers and boxes; Doors and window frames.

Local

2.4 Investments

2.4.1 During 1998-2003

Forest enterprises (logging companies, sawmills and carpentries) declared investments of about 79 billion meticais; equivalent to about USD 4 million from 1998 to 2003 (Table 2.9). This volume represents a 49% increase compared with the 2001 estimate. It should be noticed that the investments were made using companies’ own resources. The investments were used mainly to buy sawing equipment and for improvement of infrastructure. Three old sawmills were renovated, 1 new sawmill is being tested and another new one is being installed. Table 2.9 Investments (MZM) in Forest Industries in Sofala Province (1998-2003)

Company Investment mill. MZM

Investment purpose

Carpintaria Marravilha da Benção 701 Equip the sawmill and carpentry Indústria Transformadora de Madeira Lda. No investments Indústria Madeireira de Moçambique 4 000 Improvement of the sawmill Industrias MARFER No investments MOÇAMBIQUE FLORESTAL - MOFLOR 10 000 Improve infrastructure and buy equipment MBL – Moçambique 2 900 General rehabilitatation MOVARTE - Moveis e Arte 2 100 Machinery and a truck for transport of products Serracao da CMC 14 000 Equipment and infrastructure Serracao da Euromoz No investments Serracao Mezimbite 4 400 Equipment and tools Serracao Manuel Jorge de Almeida 500 Mobile sawmill and a pick-up vehicle

chainsaws, a tractor, a trailer and a truck Serracao SPENCE E FAURE No investments Serracao Wing Kock No investments Serracao e Carpintaria ARCA D'ARTE No investments Serracao e Carpintaria Jose Sacur 1 250 Sawmill and carpentry equipment, 1 tractor and

1 truck Serração e Carpintaria Nhamatanda 1 200 New band saw SERRACAO E CARPINTARIA DA BEIRA

No investments

Serração Carpintaria Santana e Filhos No investments União dos Trabalhadores de África (UTA) 13 000 Equipment and operational funds TCT – Industrias Florestais 24 000 Sawmill installation within the concession area Total 78 051

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 13

2.4.2 Planned for 2004-2009

Table 2.10 shows investment plans for the period of 2004-2009 by the interviewed companies. The total volume is 38 billion meticais or USD 1.9 million. All companies could not quantify their investment forecasts although they were interested to invest in their production units. Most likely investment targets were a kiln, eucalyptus plantation and logging equipment. Some companies with obsolete equipment showed interest in new machinery. Table 2.10 Planned Industrial Investments in Sofala Province for the Period 2004-2009

Company Investments mill. MZM

Investment purpose

Carpintaria Marravilha da Benção 250 New infrastructure Indústria Transformadora de Madeira Lda. 2 000* Eucalyptus plantation, logging equipment Indústria Madeireira de Moçambique 11 000 Kiln, modernization of the production process Industrias MARFER 1 200* A new main saw MOÇAMBIQUE FLORESTAL – MOFLOR

1 200* A new main saw

MBL – Moçambique 1 000* Installing a sawmill within the concession area MOVARTE - Moveis e Arte 1 000 Industrial plane, parallel plane, compressor,

welding machine Serracao da CMC Serracao da Euromoz Serracao Mezimbite 12 000 School for carpenters Serracao Manuel Jorge de Almeida 2 000 Logging equipment Serracao SPENCE E FAURE 800* Saw milling and saw doctoring equipment Serracao Wing Kock 2 000 Logging equipment Serracao e Carpintaria ARCA D'ARTE Serracao e Carpintaria Jose Sacur 1 000* Mobile saw mill and carpentry equipment Serracao e Carpintaria Nhamatanda 1 200* A new saw mill SERRACAO E CARPINTARIA DA BEIRA

Serracao Carpintaria Santana e Filhos 1 000 A kiln and rehabilitation of the sawmill Uniao dos Trabalhadores de Africa (UTA) TCT - Industrias Florestais 220 Furniture factory equipment Total 37 870 3. ACTUAL SITUATION OF THE FOREST INDUSTRY IN ZAMBEZIA

3.1 Nurseries and Forest Plantations

Only two of the 21 companies in Zambezia had forest nurseries and plantations. Mozambique Enterprises Lda. (MEL) has started with a small nursery bed of 150 Chanfuta seedlings aimed for enrichment planting. J. Domingos Marques (JDM) sawmill also has a small experimental nursery with Pau-ferro, Umbila, Chanfuta and Panga-panga. This company has planted 80 ha of Eucalyptus saligna aiming at sawnwood production. Only seven workers are involved with this activity (Table 3.1). JDM company has one forest technician but the workers do not have any forestry training.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 14

Table 3.1 Labor Force in Forest Nurseries and Plantations

Training level Company No. of workers Basic Medium Superior Others

Mozambique Enterprises Lda. 2 2 Empresa J. Domingos Marques 5 1 4 Total 7 1 6 3.2 Harvesting

3.2.1 Interviewed Persons and Labor Force

Table 3.2 shows the 20 companies, which at the time of the interview were active in harvesting. 13 of them had a forest concession and the rest a simple license. About 65% of the companies in Zambezia had a forest concession, either already approved or in the process. There are 1 130 workers, of which 5% had basic education, 0.4% medium-level education, and the rest (95%) were without formal education. There are no higher- level technicians involved in logging. Six companies informed that their power saw operators have received some technical training, the impact of which has been positive. Table 3.2 Harvesting Regime, Number of Workers Employed and Training Level of

the Companies

Training level Company Harvesting type

Number of workers Basic Medium Superior Others

Calibo Timber Concession 17 17 Carpintaria da Educação (EMACADE) Simple license 18 2 1 15 CARPINTARIA MECANICA DE MOCUBA

Simple license 20 20

CARPINTARIA PICA-PAU Simple license 11 1 10 DANMO TTC Concession 54 6 52 Empresa J. Domingos Marques Concession 132 3 129 Grupo MADAL Concession 217 3 1 214 GREEN TIMBER Concession 50 10 40 Indústria e Carpintaria Sotomane Simple license 15 2 13 Madeiras de Mocuba Simple license 36 2 34 Mozambique Entreprises Lda (MEL) Concession 65 65 Madeiras da Zambezia Concession 40 40 MATECOL Concession 17 2 15 Serração António Alexandrino Simple license 28 1 27 Serração Empresa de Madeiras SOMON Simple license 30* 30 Serração Madeiras Ali Ossene Concession 118 118 Serração Reunidas da Zambézia Concession 70 7 63 Serração da Zambézia Concession 150 10 2 138 Sociedade Moveis Licungo Concession 8 3 5 SOCIEDADE INDUSTRIAL DA MADEIRA

Concession 30 1 29

Total 1 126 53 4 1 069

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 15

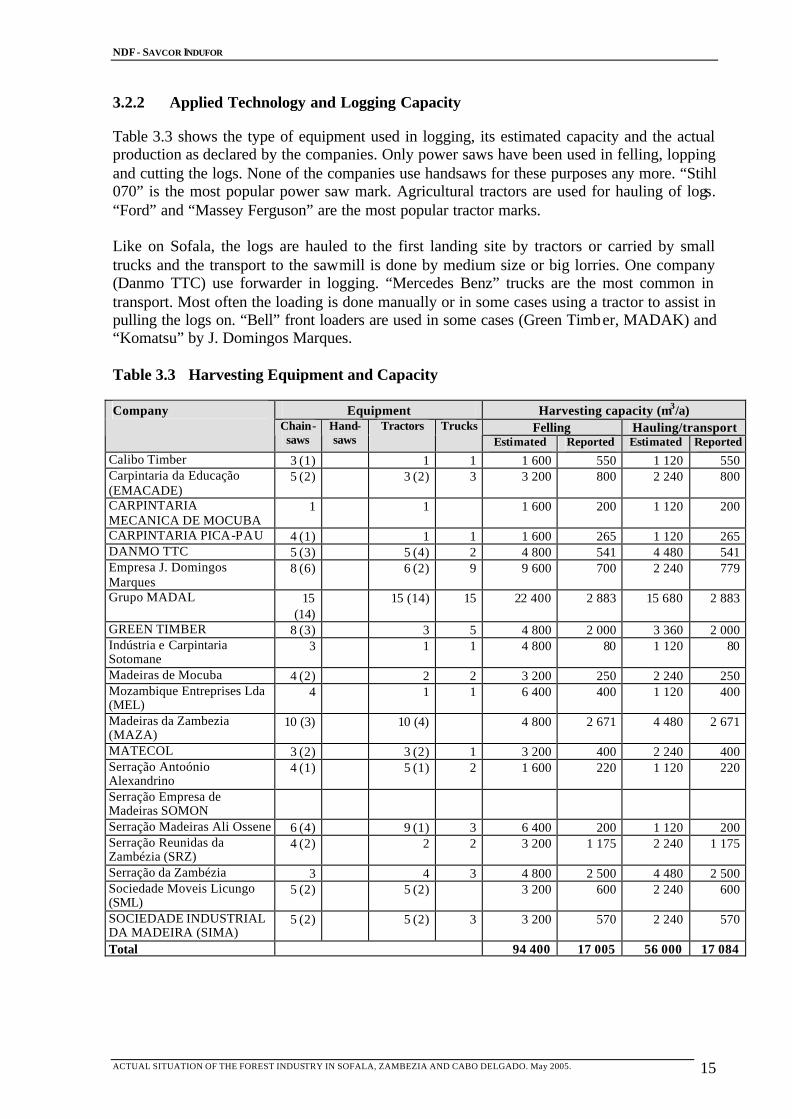

3.2.2 Applied Technology and Logging Capacity

Table 3.3 shows the type of equipment used in logging, its estimated capacity and the actual production as declared by the companies. Only power saws have been used in felling, lopping and cutting the logs. None of the companies use handsaws for these purposes any more. “Stihl 070” is the most popular power saw mark. Agricultural tractors are used for hauling of logs. “Ford” and “Massey Ferguson” are the most popular tractor marks. Like on Sofala, the logs are hauled to the first landing site by tractors or carried by small trucks and the transport to the sawmill is done by medium size or big lorries. One company (Danmo TTC) use forwarder in logging. “Mercedes Benz” trucks are the most common in transport. Most often the loading is done manually or in some cases using a tractor to assist in pulling the logs on. “Bell” front loaders are used in some cases (Green Timber, MADAK) and “Komatsu” by J. Domingos Marques. Table 3.3 Harvesting Equipment and Capacity

Equipment Harvesting capacity (m3/a) Felling Hauling/transport

Company Chain- saws

Hand-saws

Tractors Trucks Estimated Reported Estimated Reported

Calibo Timber 3 (1) 1 1 1 600 550 1 120 550 Carpintaria da Educação (EMACADE)

5 (2) 3 (2) 3 3 200 800 2 240 800

CARPINTARIA MECANICA DE MOCUBA

1 1 1 600 200 1 120 200

CARPINTARIA PICA-PAU 4 (1) 1 1 1 600 265 1 120 265 DANMO TTC 5 (3) 5 (4) 2 4 800 541 4 480 541 Empresa J. Domingos Marques

8 (6) 6 (2) 9 9 600 700 2 240 779

Grupo MADAL 15 (14)

15 (14) 15 22 400 2 883 15 680 2 883

GREEN TIMBER 8 (3) 3 5 4 800 2 000 3 360 2 000 Indústria e Carpintaria Sotomane

3 1 1 4 800 80 1 120 80

Madeiras de Mocuba 4 (2) 2 2 3 200 250 2 240 250 Mozambique Entreprises Lda (MEL)

4 1 1 6 400 400 1 120 400

Madeiras da Zambezia (MAZA)

10 (3) 10 (4) 4 800 2 671 4 480 2 671

MATECOL 3 (2) 3 (2) 1 3 200 400 2 240 400 Serração Antoónio Alexandrino

4 (1) 5 (1) 2 1 600 220 1 120 220

Serração Empresa de Madeiras SOMON

Serração Madeiras Ali Ossene 6 (4) 9 (1) 3 6 400 200 1 120 200 Serração Reunidas da Zambézia (SRZ)

4 (2) 2 2 3 200 1 175 2 240 1 175

Serração da Zambézia 3 4 3 4 800 2 500 4 480 2 500 Sociedade Moveis Licungo (SML)

5 (2) 5 (2) 3 200 600 2 240 600

SOCIEDADE INDUSTRIAL DA MADEIRA (SIMA)

5 (2) 5 (2) 3 3 200 570 2 240 570

Total 94 400 17 005 56 000 17 084

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 16

The estimated logging and transport capacity of the forest operators were 94 400 m3 and 56 000 m3 respectively in Zambezia province in 2003. Twelve companies had their logging capacity over 2 000 m3/a. MADAL, MAZA, DANMO TTC and Serração Zambézia all had a harvesting capacity more than 4 000 m3 /a. The reported felling and hauling capacity was 17 000 m3. Equipment utilization rate in felling was 19% and in hauling 31%. Reasons for low rates have been already pointed out in Chapter 2.2.2. 3.2.3 Harvested Species and Their Processing

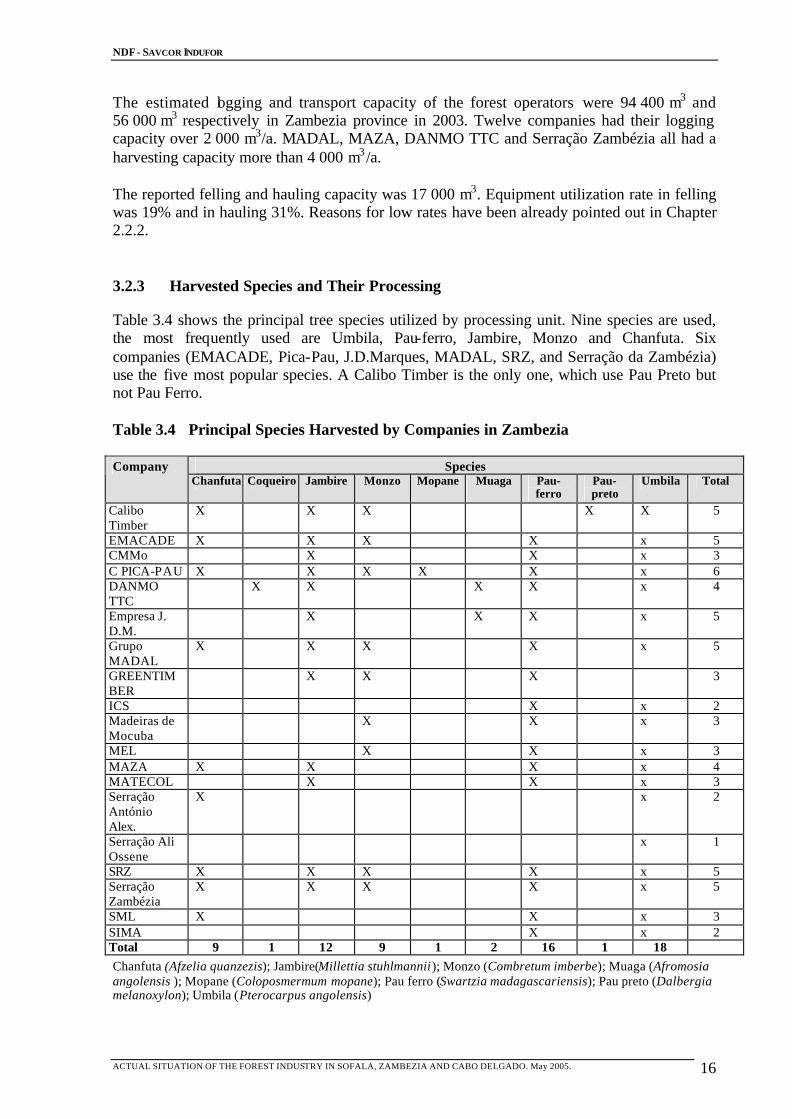

Table 3.4 shows the principal tree species utilized by processing unit. Nine species are used, the most frequently used are Umbila, Pau-ferro, Jambire, Monzo and Chanfuta. Six companies (EMACADE, Pica-Pau, J.D.Marques, MADAL, SRZ, and Serração da Zambézia) use the five most popular species. A Calibo Timber is the only one, which use Pau Preto but not Pau Ferro. Table 3.4 Principal Species Harvested by Companies in Zambezia

Species Company Chanfuta Coqueiro Jambire Monzo Mopane Muaga Pau-

ferro Pau-preto

Umbila Total

Calibo Timber

X X X X X 5

EMACADE X X X X x 5 CMMo X X x 3 C PICA-PAU X X X X X x 6 DANMO TTC

X X X X x 4

Empresa J. D.M.

X X X x 5

Grupo MADAL

X X X X x 5

GREENTIMBER

X X X 3

ICS X x 2 Madeiras de Mocuba

X X x 3

MEL X X x 3 MAZA X X X x 4 MATECOL X X x 3 Serração António Alex.

X x 2

Serração Ali Ossene

x 1

SRZ X X X X x 5 Serração Zambézia

X X X X x 5

SML X X x 3 SIMA X x 2 Total 9 1 12 9 1 2 16 1 18 Chanfuta (Afzelia quanzezis); Jambire(Millettia stuhlmannii); Monzo (Combretum imberbe); Muaga (Afromosia angolensis ); Mopane (Coloposmermum mopane); Pau ferro (Swartzia madagascariensis); Pau preto (Dalbergia melanoxylon); Umbila (Pterocarpus angolensis)

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 17

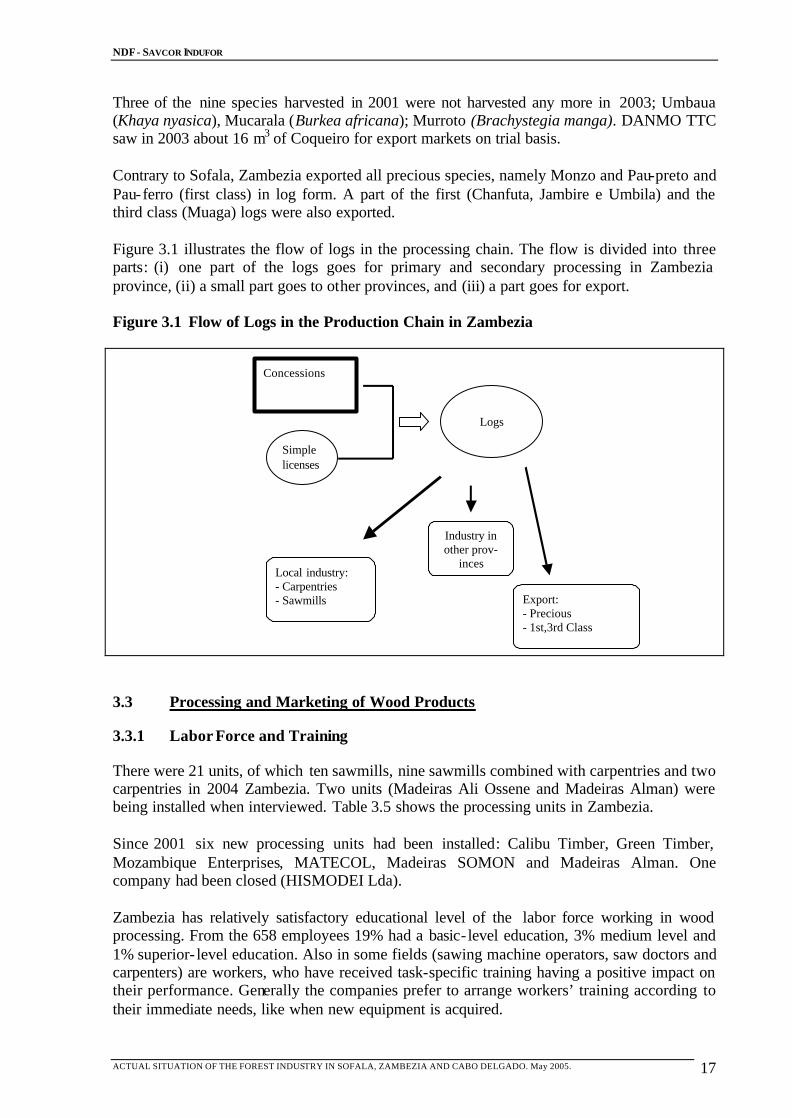

Three of the nine species harvested in 2001 were not harvested any more in 2003; Umbaua (Khaya nyasica), Mucarala (Burkea africana); Murroto (Brachystegia manga). DANMO TTC saw in 2003 about 16 m3 of Coqueiro for export markets on trial basis. Contrary to Sofala, Zambezia exported all precious species, namely Monzo and Pau-preto and Pau-ferro (first class) in log form. A part of the first (Chanfuta, Jambire e Umbila) and the third class (Muaga) logs were also exported. Figure 3.1 illustrates the flow of logs in the processing chain. The flow is divided into three parts: (i) one part of the logs goes for primary and secondary processing in Zambezia province, (ii) a small part goes to other provinces, and (iii) a part goes for export. Figure 3.1 Flow of Logs in the Production Chain in Zambezia

Concessions

Simple licenses

Logs

Local industry: - Carpentries - Sawmills

Industry in other prov-

inces

Export: - Precious - 1st,3rd Class

3.3 Processing and Marketing of Wood Products

3.3.1 Labor Force and Training

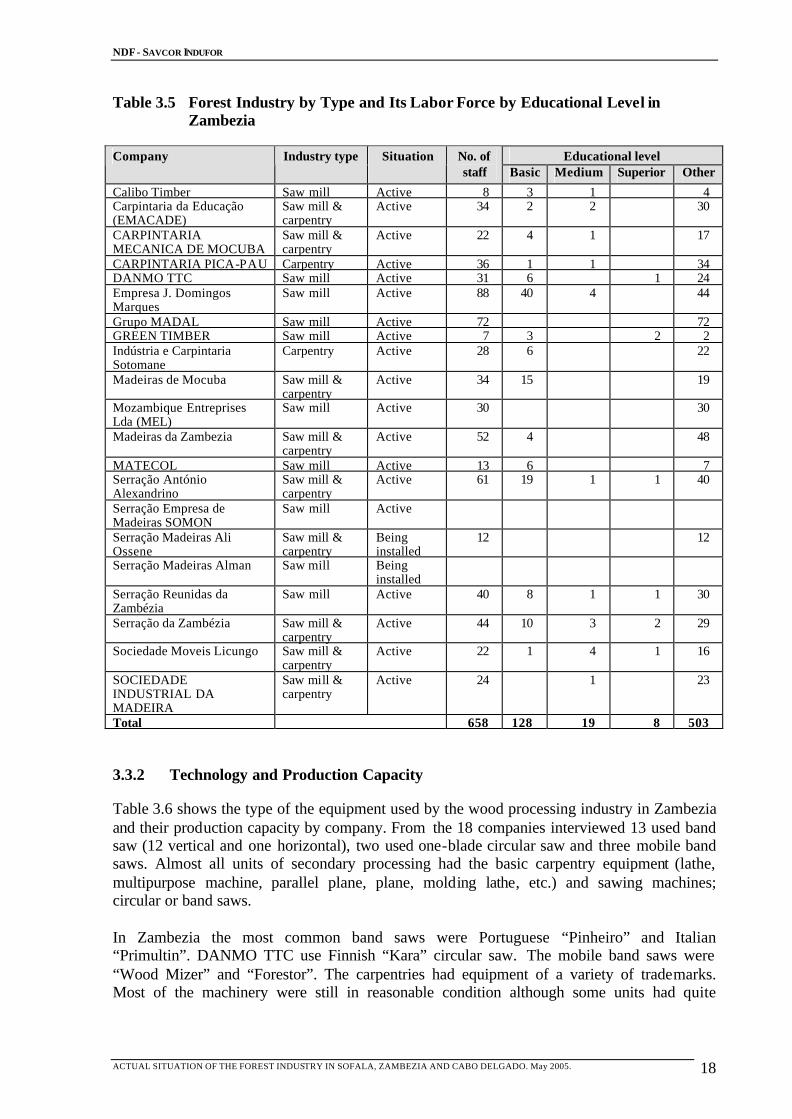

There were 21 units, of which ten sawmills, nine sawmills combined with carpentries and two carpentries in 2004 Zambezia. Two units (Madeiras Ali Ossene and Madeiras Alman) were being installed when interviewed. Table 3.5 shows the processing units in Zambezia. Since 2001 six new processing units had been installed: Calibu Timber, Green Timber, Mozambique Enterprises, MATECOL, Madeiras SOMON and Madeiras Alman. One company had been closed (HISMODEI Lda). Zambezia has relatively satisfactory educational level of the labor force working in wood processing. From the 658 employees 19% had a basic- level education, 3% medium level and 1% superior- level education. Also in some fields (sawing machine operators, saw doctors and carpenters) are workers, who have received task-specific training having a positive impact on their performance. Generally the companies prefer to arrange workers’ training according to their immediate needs, like when new equipment is acquired.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 18

Table 3.5 Forest Industry by Type and Its Labor Force by Educational Level in Zambezia

Educational level Company Industry type Situation No. of staff Basic Medium Superior Other

Calibo Timber Saw mill Active 8 3 1 4 Carpintaria da Educação (EMACADE)

Saw mill & carpentry

Active 34 2 2 30

CARPINTARIA MECANICA DE MOCUBA

Saw mill & carpentry

Active 22 4 1 17

CARPINTARIA PICA-PAU Carpentry Active 36 1 1 34 DANMO TTC Saw mill Active 31 6 1 24 Empresa J. Domingos Marques

Saw mill Active 88 40 4 44

Grupo MADAL Saw mill Active 72 72 GREEN TIMBER Saw mill Active 7 3 2 2 Indústria e Carpintaria Sotomane

Carpentry Active 28 6 22

Madeiras de Mocuba Saw mill & carpentry

Active 34 15 19

Mozambique Entreprises Lda (MEL)

Saw mill Active 30 30

Madeiras da Zambezia Saw mill & carpentry

Active 52 4 48

MATECOL Saw mill Active 13 6 7 Serração António Alexandrino

Saw mill & carpentry

Active 61 19 1 1 40

Serração Empresa de Madeiras SOMON

Saw mill Active

Serração Madeiras Ali Ossene

Saw mill & carpentry

Being installed

12 12

Serração Madeiras Alman Saw mill Being installed

Serração Reunidas da Zambézia

Saw mill Active 40 8 1 1 30

Serração da Zambézia Saw mill & carpentry

Active 44 10 3 2 29

Sociedade Moveis Licungo Saw mill & carpentry

Active 22 1 4 1 16

SOCIEDADE INDUSTRIAL DA MADEIRA

Saw mill & carpentry

Active 24 1 23

Total 658 128 19 8 503 3.3.2 Technology and Production Capacity

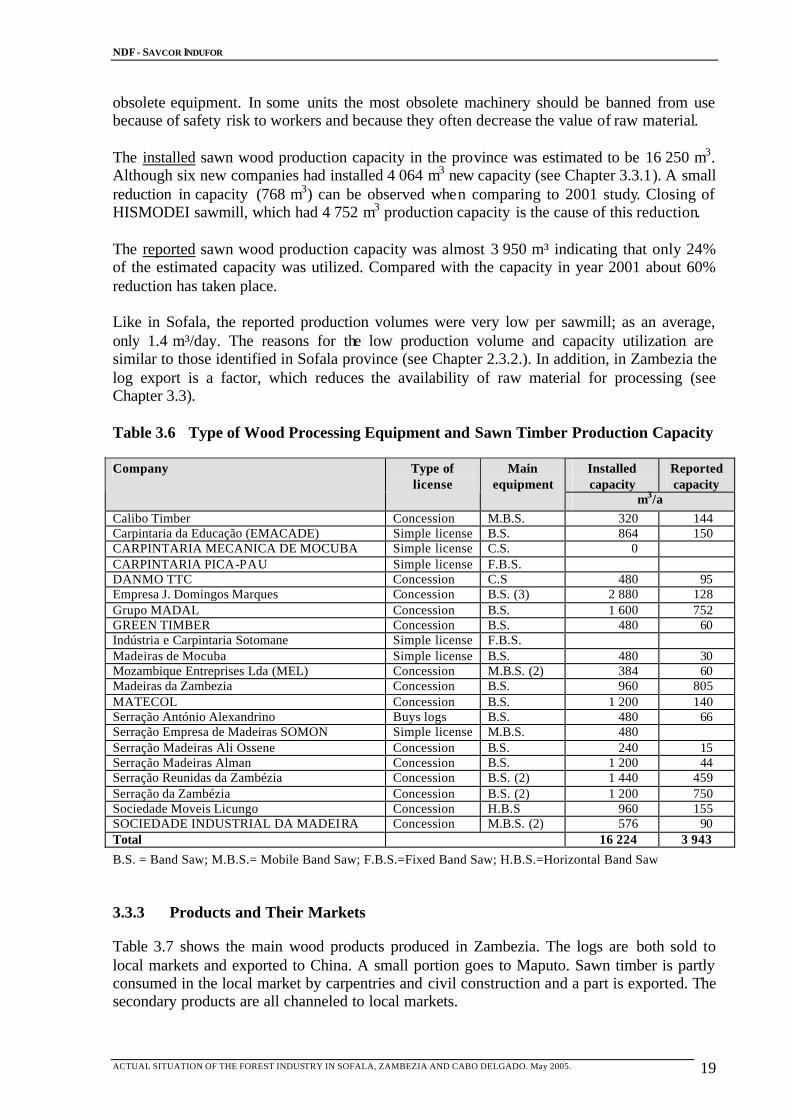

Table 3.6 shows the type of the equipment used by the wood processing industry in Zambezia and their production capacity by company. From the 18 companies interviewed 13 used band saw (12 vertical and one horizontal), two used one-blade circular saw and three mobile band saws. Almost all units of secondary processing had the basic carpentry equipment (lathe, multipurpose machine, parallel plane, plane, molding lathe, etc.) and sawing machines; circular or band saws. In Zambezia the most common band saws were Portuguese “Pinheiro” and Italian “Primultin”. DANMO TTC use Finnish “Kara” circular saw. The mobile band saws were “Wood Mizer” and “Forestor”. The carpentries had equipment of a variety of trademarks. Most of the machinery were still in reasonable condition although some units had quite

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 19

obsolete equipment. In some units the most obsolete machinery should be banned from use because of safety risk to workers and because they often decrease the value of raw material. The installed sawn wood production capacity in the province was estimated to be 16 250 m3. Although six new companies had installed 4 064 m3 new capacity (see Chapter 3.3.1). A small reduction in capacity (768 m3) can be observed when comparing to 2001 study. Closing of HISMODEI sawmill, which had 4 752 m3 production capacity is the cause of this reduction. The reported sawn wood production capacity was almost 3 950 m³ indicating that only 24% of the estimated capacity was utilized. Compared with the capacity in year 2001 about 60% reduction has taken place. Like in Sofala, the reported production volumes were very low per sawmill; as an average, only 1.4 m³/day. The reasons for the low production volume and capacity utilization are similar to those identified in Sofala province (see Chapter 2.3.2.). In addition, in Zambezia the log export is a factor, which reduces the availability of raw material for processing (see Chapter 3.3). Table 3.6 Type of Wood Processing Equipment and Sawn Timber Production Capacity

Installed capacity

Reported capacity

Company Type of license

Main equipment

m3/a Calibo Timber Concession M.B.S. 320 144 Carpintaria da Educação (EMACADE) Simple license B.S. 864 150 CARPINTARIA MECANICA DE MOCUBA Simple license C.S. 0 CARPINTARIA PICA-PAU Simple license F.B.S. DANMO TTC Concession C.S 480 95 Empresa J. Domingos Marques Concession B.S. (3) 2 880 128 Grupo MADAL Concession B.S. 1 600 752 GREEN TIMBER Concession B.S. 480 60 Indústria e Carpintaria Sotomane Simple license F.B.S. Madeiras de Mocuba Simple license B.S. 480 30 Mozambique Entreprises Lda (MEL) Concession M.B.S. (2) 384 60 Madeiras da Zambezia Concession B.S. 960 805 MATECOL Concession B.S. 1 200 140 Serração António Alexandrino Buys logs B.S. 480 66 Serração Empresa de Madeiras SOMON Simple license M.B.S. 480 Serração Madeiras Ali Ossene Concession B.S. 240 15 Serração Madeiras Alman Concession B.S. 1 200 44 Serração Reunidas da Zambézia Concession B.S. (2) 1 440 459 Serração da Zambézia Concession B.S. (2) 1 200 750 Sociedade Moveis Licungo Concession H.B.S 960 155 SOCIEDADE INDUSTRIAL DA MADEIRA Concession M.B.S. (2) 576 90 Total 16 224 3 943

B.S. = Band Saw; M.B.S.= Mobile Band Saw; F.B.S.=Fixed Band Saw; H.B.S.=Horizontal Band Saw 3.3.3 Products and Their Markets

Table 3.7 shows the main wood products produced in Zambezia. The logs are both sold to local markets and exported to China. A small portion goes to Maputo. Sawn timber is partly consumed in the local market by carpentries and civil construction and a part is exported. The secondary products are all channeled to local markets.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 20

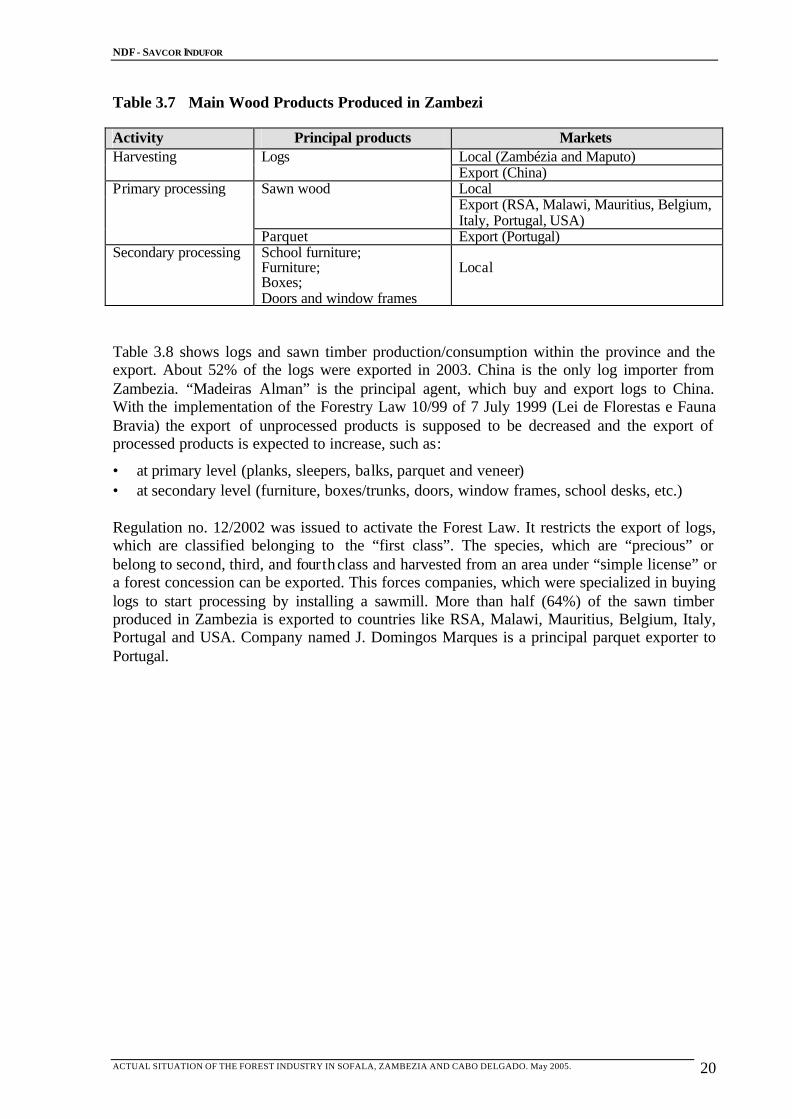

Table 3.7 Main Wood Products Produced in Zambezi

Activity Principal products Markets Local (Zambézia and Maputo) Harvesting Logs Export (China) Local Sawn wood Export (RSA, Malawi, Mauritius, Belgium, Italy, Portugal, USA)

Primary processing

Parquet Export (Portugal) Secondary processing School furniture;

Furniture; Boxes; Doors and window frames

Local

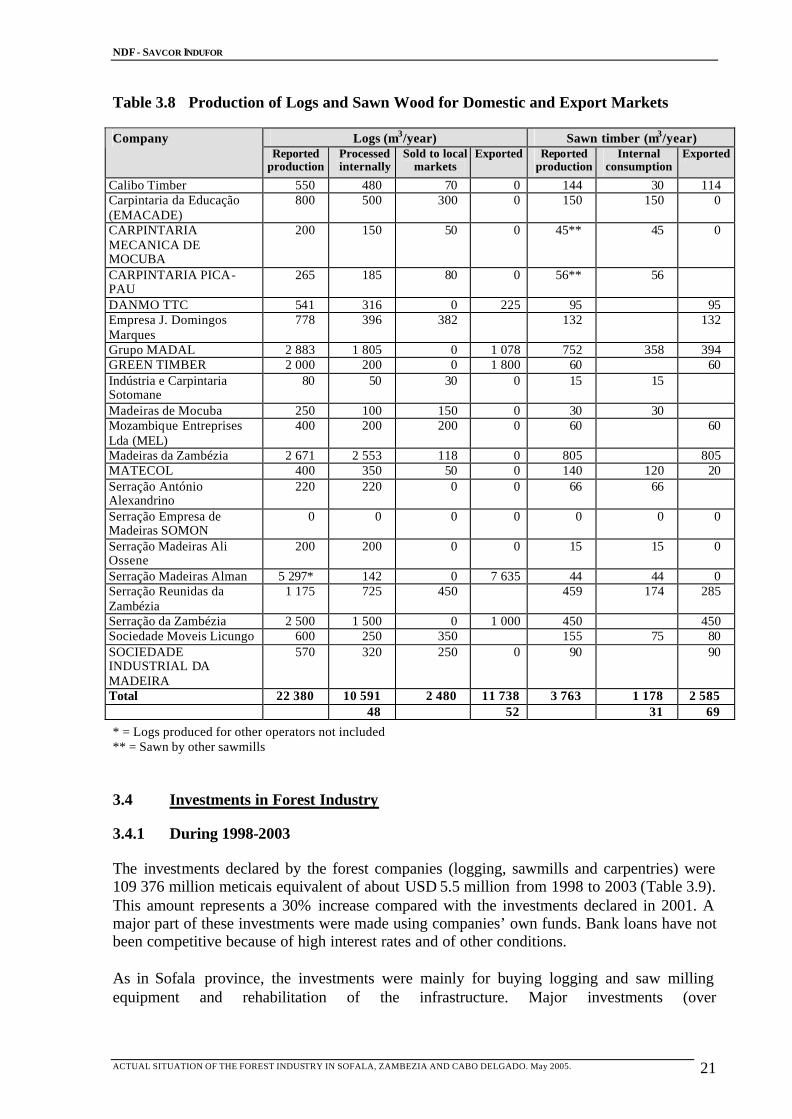

Table 3.8 shows logs and sawn timber production/consumption within the province and the export. About 52% of the logs were exported in 2003. China is the only log importer from Zambezia. “Madeiras Alman” is the principal agent, which buy and export logs to China. With the implementation of the Forestry Law 10/99 of 7 July 1999 (Lei de Florestas e Fauna Bravia) the export of unprocessed products is supposed to be decreased and the export of processed products is expected to increase, such as:

• at primary level (planks, sleepers, balks, parquet and veneer) • at secondary level (furniture, boxes/trunks, doors, window frames, school desks, etc.) Regulation no. 12/2002 was issued to activate the Forest Law. It restricts the export of logs, which are classified belonging to the “first class”. The species, which are “precious” or belong to second, third, and fourth class and harvested from an area under “simple license” or a forest concession can be exported. This forces companies, which were specialized in buying logs to start processing by installing a sawmill. More than half (64%) of the sawn timber produced in Zambezia is exported to countries like RSA, Malawi, Mauritius, Belgium, Italy, Portugal and USA. Company named J. Domingos Marques is a principal parquet exporter to Portugal.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 21

Table 3.8 Production of Logs and Sawn Wood for Domestic and Export Markets

Logs (m3/year) Sawn timber (m3/year) Company Reported

production Processed internally

Sold to local markets

Exported Reported production

Internal consumption

Exported

Calibo Timber 550 480 70 0 144 30 114 Carpintaria da Educação (EMACADE)

800 500 300 0 150 150 0

CARPINTARIA MECANICA DE MOCUBA

200 150 50 0 45** 45 0

CARPINTARIA PICA-PAU

265 185 80 0 56** 56

DANMO TTC 541 316 0 225 95 95 Empresa J. Domingos Marques

778 396 382 132 132

Grupo MADAL 2 883 1 805 0 1 078 752 358 394 GREEN TIMBER 2 000 200 0 1 800 60 60 Indústria e Carpintaria Sotomane

80 50 30 0 15 15

Madeiras de Mocuba 250 100 150 0 30 30 Mozambique Entreprises Lda (MEL)

400 200 200 0 60 60

Madeiras da Zambézia 2 671 2 553 118 0 805 805 MATECOL 400 350 50 0 140 120 20 Serração António Alexandrino

220 220 0 0 66 66

Serração Empresa de Madeiras SOMON

0 0 0 0 0 0 0

Serração Madeiras Ali Ossene

200 200 0 0 15 15 0

Serração Madeiras Alman 5 297* 142 0 7 635 44 44 0 Serração Reunidas da Zambézia

1 175 725 450 459 174 285

Serração da Zambézia 2 500 1 500 0 1 000 450 450 Sociedade Moveis Licungo 600 250 350 155 75 80 SOCIEDADE INDUSTRIAL DA MADEIRA

570 320 250 0 90 90

Total 22 380 10 591 2 480 11 738 3 763 1 178 2 585 48 52 31 69

* = Logs produced for other operators not included ** = Sawn by other sawmills 3.4 Investments in Forest Industry

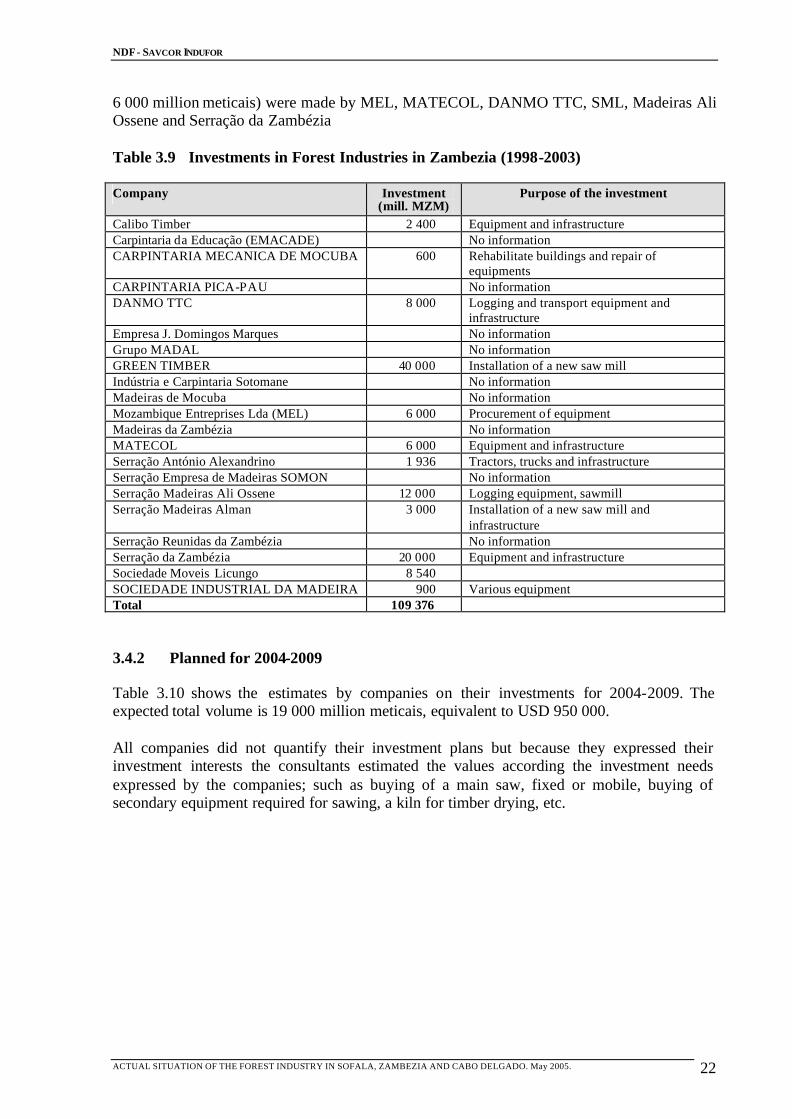

3.4.1 During 1998-2003

The investments declared by the forest companies (logging, sawmills and carpentries) were 109 376 million meticais equivalent of about USD 5.5 million from 1998 to 2003 (Table 3.9). This amount represents a 30% increase compared with the investments declared in 2001. A major part of these investments were made using companies’ own funds. Bank loans have not been competitive because of high interest rates and of other conditions. As in Sofala province, the investments were mainly for buying logging and saw milling equipment and rehabilitation of the infrastructure. Major investments (over

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 22

6 000 million meticais) were made by MEL, MATECOL, DANMO TTC, SML, Madeiras Ali Ossene and Serração da Zambézia Table 3.9 Investments in Forest Industries in Zambezia (1998-2003)

Company Investment (mill. MZM)

Purpose of the investment

Calibo Timber 2 400 Equipment and infrastructure Carpintaria da Educação (EMACADE) No information CARPINTARIA MECANICA DE MOCUBA 600 Rehabilitate buildings and repair of

equipments CARPINTARIA PICA-PAU No information DANMO TTC 8 000 Logging and transport equipment and

infrastructure Empresa J. Domingos Marques No information Grupo MADAL No information GREEN TIMBER 40 000 Installation of a new saw mill Indústria e Carpintaria Sotomane No information Madeiras de Mocuba No information Mozambique Entreprises Lda (MEL) 6 000 Procurement of equipment Madeiras da Zambézia No information MATECOL 6 000 Equipment and infrastructure Serração António Alexandrino 1 936 Tractors, trucks and infrastructure Serração Empresa de Madeiras SOMON No information Serração Madeiras Ali Ossene 12 000 Logging equipment, sawmill Serração Madeiras Alman 3 000 Installation of a new saw mill and

infrastructure Serração Reunidas da Zambézia No information Serração da Zambézia 20 000 Equipment and infrastructure Sociedade Moveis Licungo 8 540 SOCIEDADE INDUSTRIAL DA MADEIRA 900 Various equipment Total 109 376 3.4.2 Planned for 2004-2009

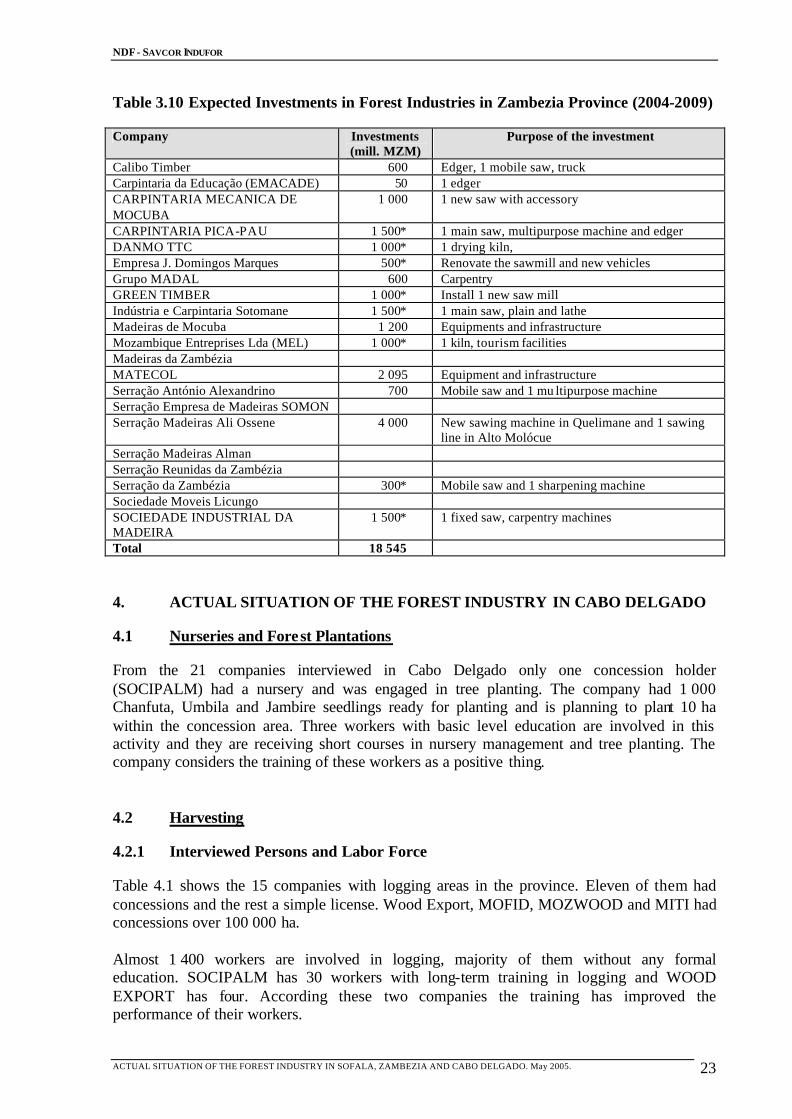

Table 3.10 shows the estimates by companies on their investments for 2004-2009. The expected total volume is 19 000 million meticais, equivalent to USD 950 000. All companies did not quantify their investment plans but because they expressed their investment interests the consultants estimated the values according the investment needs expressed by the companies; such as buying of a main saw, fixed or mobile, buying of secondary equipment required for sawing, a kiln for timber drying, etc.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 23

Table 3.10 Expected Investments in Forest Industries in Zambezia Province (2004-2009)

Company Investments (mill. MZM)

Purpose of the investment

Calibo Timber 600 Edger, 1 mobile saw, truck Carpintaria da Educação (EMACADE) 50 1 edger CARPINTARIA MECANICA DE MOCUBA

1 000 1 new saw with accessory

CARPINTARIA PICA-PAU 1 500* 1 main saw, multipurpose machine and edger DANMO TTC 1 000* 1 drying kiln, Empresa J. Domingos Marques 500* Renovate the sawmill and new vehicles Grupo MADAL 600 Carpentry GREEN TIMBER 1 000* Install 1 new saw mill Indústria e Carpintaria Sotomane 1 500* 1 main saw, plain and lathe Madeiras de Mocuba 1 200 Equipments and infrastructure Mozambique Entreprises Lda (MEL) 1 000* 1 kiln, tourism facilities Madeiras da Zambézia MATECOL 2 095 Equipment and infrastructure Serração António Alexandrino 700 Mobile saw and 1 mu ltipurpose machine Serração Empresa de Madeiras SOMON Serração Madeiras Ali Ossene 4 000 New sawing machine in Quelimane and 1 sawing

line in Alto Molócue Serração Madeiras Alman Serração Reunidas da Zambézia Serração da Zambézia 300* Mobile saw and 1 sharpening machine Sociedade Moveis Licungo SOCIEDADE INDUSTRIAL DA MADEIRA

1 500* 1 fixed saw, carpentry machines

Total 18 545 4. ACTUAL SITUATION OF THE FOREST INDUSTRY IN CABO DELGADO

4.1 Nurseries and Forest Plantations

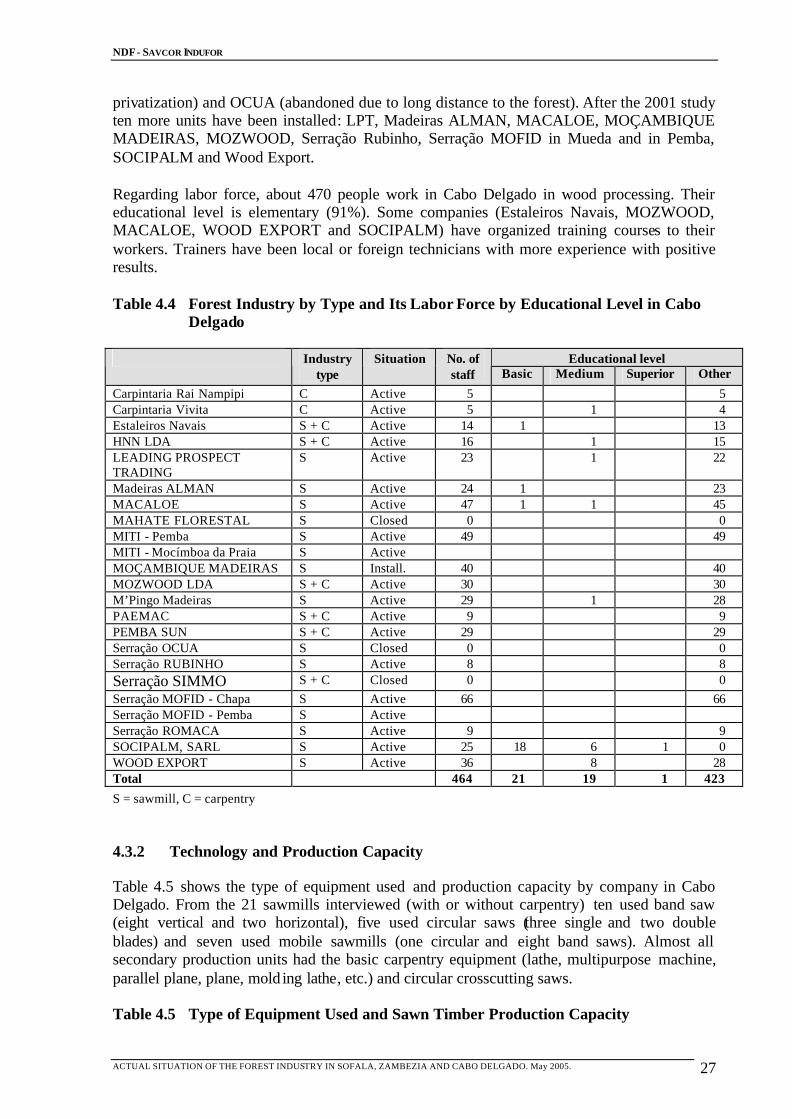

From the 21 companies interviewed in Cabo Delgado only one concession holder (SOCIPALM) had a nursery and was engaged in tree planting. The company had 1 000 Chanfuta, Umbila and Jambire seedlings ready for planting and is planning to plant 10 ha within the concession area. Three workers with basic level education are involved in this activity and they are receiving short courses in nursery management and tree planting. The company considers the training of these workers as a positive thing. 4.2 Harvesting

4.2.1 Interviewed Persons and Labor Force

Table 4.1 shows the 15 companies with logging areas in the province. Eleven of them had concessions and the rest a simple license. Wood Export, MOFID, MOZWOOD and MITI had concessions over 100 000 ha. Almost 1 400 workers are involved in logging, majority of them without any formal education. SOCIPALM has 30 workers with long-term training in logging and WOOD EXPORT has four. According these two companies the training has improved the performance of their workers.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 24

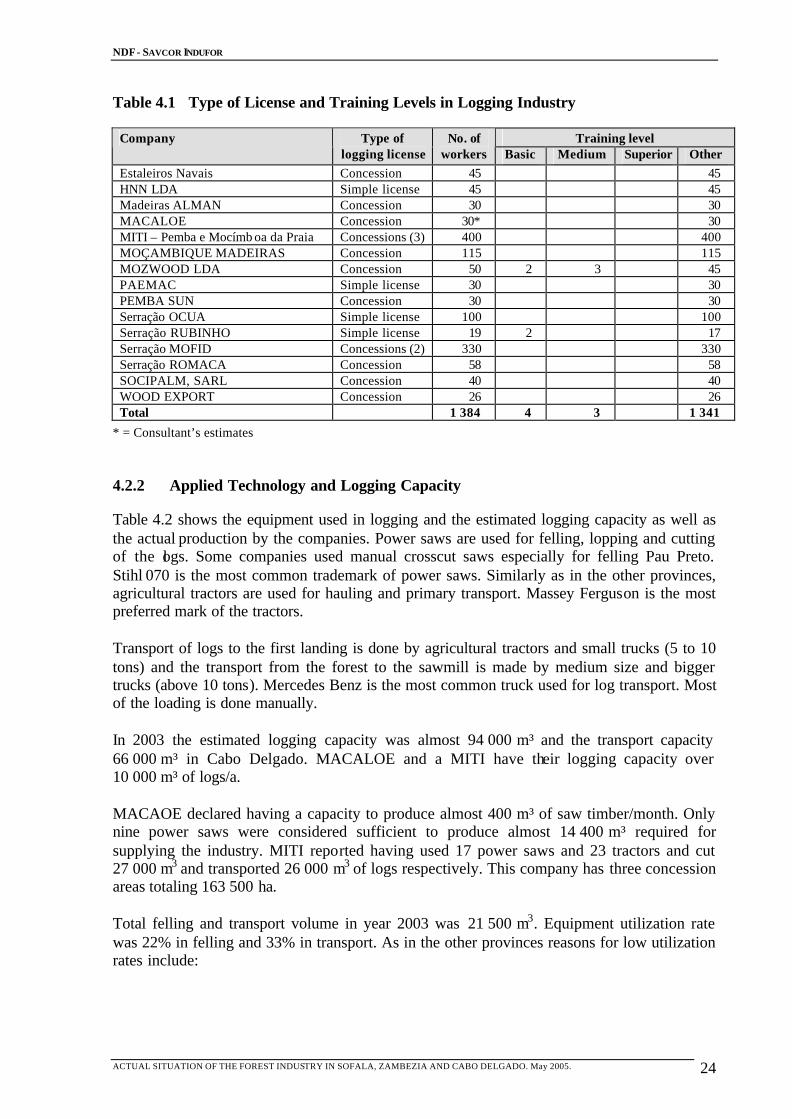

Table 4.1 Type of License and Training Levels in Logging Industry

Training level Company Type of logging license

No. of workers Basic Medium Superior Other

Estaleiros Navais Concession 45 45 HNN LDA Simple license 45 45 Madeiras ALMAN Concession 30 30 MACALOE Concession 30* 30 MITI – Pemba e Mocímb oa da Praia Concessions (3) 400 400 MOÇAMBIQUE MADEIRAS Concession 115 115 MOZWOOD LDA Concession 50 2 3 45 PAEMAC Simple license 30 30 PEMBA SUN Concession 30 30 Serração OCUA Simple license 100 100 Serração RUBINHO Simple license 19 2 17 Serração MOFID Concessions (2) 330 330 Serração ROMACA Concession 58 58 SOCIPALM, SARL Concession 40 40 WOOD EXPORT Concession 26 26 Total 1 384 4 3 1 341

* = Consultant’s estimates 4.2.2 Applied Technology and Logging Capacity

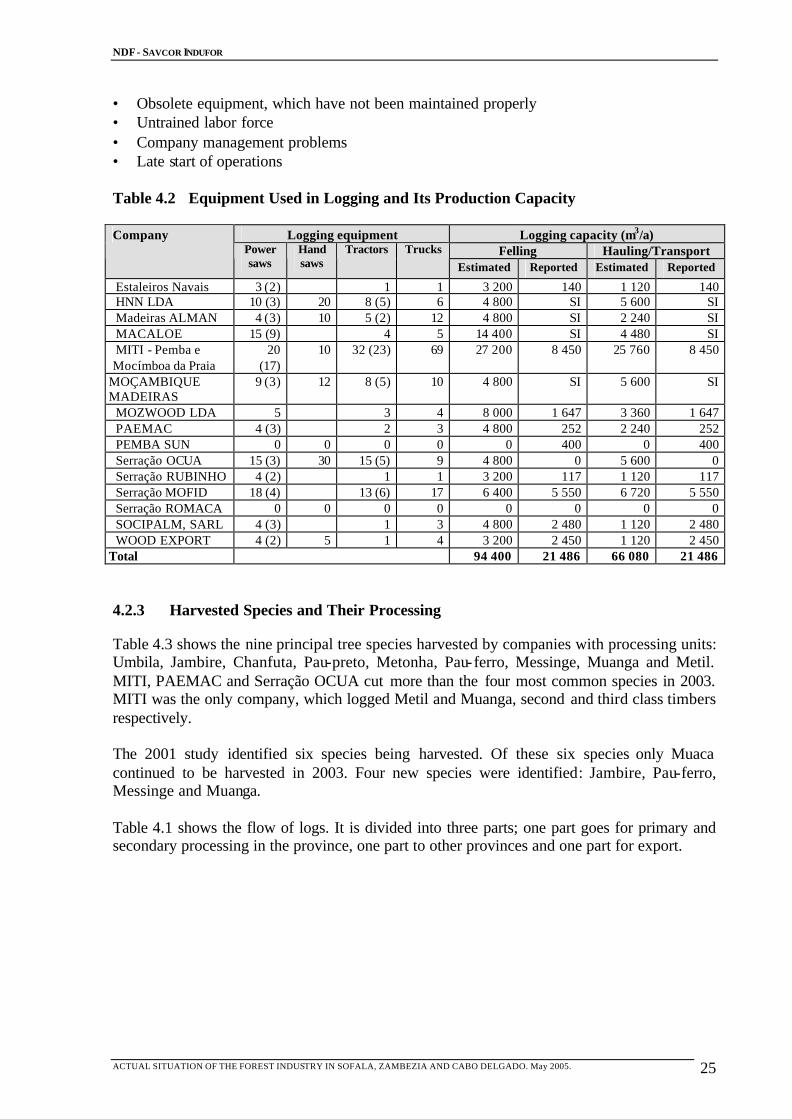

Table 4.2 shows the equipment used in logging and the estimated logging capacity as well as the actual production by the companies. Power saws are used for felling, lopping and cutting of the logs. Some companies used manual crosscut saws especially for felling Pau Preto. Stihl 070 is the most common trademark of power saws. Similarly as in the other provinces, agricultural tractors are used for hauling and primary transport. Massey Ferguson is the most preferred mark of the tractors. Transport of logs to the first landing is done by agricultural tractors and small trucks (5 to 10 tons) and the transport from the forest to the sawmill is made by medium size and bigger trucks (above 10 tons). Mercedes Benz is the most common truck used for log transport. Most of the loading is done manually. In 2003 the estimated logging capacity was almost 94 000 m³ and the transport capacity 66 000 m³ in Cabo Delgado. MACALOE and a MITI have their logging capacity over 10 000 m³ of logs/a. MACAOE declared having a capacity to produce almost 400 m³ of saw timber/month. Only nine power saws were considered sufficient to produce almost 14 400 m³ required for supplying the industry. MITI reported having used 17 power saws and 23 tractors and cut 27 000 m3 and transported 26 000 m3 of logs respectively. This company has three concession areas totaling 163 500 ha. Total felling and transport volume in year 2003 was 21 500 m3. Equipment utilization rate was 22% in felling and 33% in transport. As in the other provinces reasons for low utilization rates include:

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 25

• Obsolete equipment, which have not been maintained properly • Untrained labor force • Company management problems • Late start of operations Table 4.2 Equipment Used in Logging and Its Production Capacity

Logging equipment Logging capacity (m3/a) Felling Hauling/Transport

Company Power saws

Hand saws

Tractors Trucks Estimated Reported Estimated Reported

Estaleiros Navais 3 (2) 1 1 3 200 140 1 120 140 HNN LDA 10 (3) 20 8 (5) 6 4 800 SI 5 600 SI Madeiras ALMAN 4 (3) 10 5 (2) 12 4 800 SI 2 240 SI MACALOE 15 (9) 4 5 14 400 SI 4 480 SI MITI - Pemba e Mocímboa da Praia

20 (17)

10 32 (23) 69 27 200 8 450 25 760 8 450

MOÇAMBIQUE MADEIRAS

9 (3) 12 8 (5) 10 4 800 SI 5 600 SI

MOZWOOD LDA 5 3 4 8 000 1 647 3 360 1 647 PAEMAC 4 (3) 2 3 4 800 252 2 240 252 PEMBA SUN 0 0 0 0 0 400 0 400 Serração OCUA 15 (3) 30 15 (5) 9 4 800 0 5 600 0 Serração RUBINHO 4 (2) 1 1 3 200 117 1 120 117 Serração MOFID 18 (4) 13 (6) 17 6 400 5 550 6 720 5 550 Serração ROMACA 0 0 0 0 0 0 0 0 SOCIPALM, SARL 4 (3) 1 3 4 800 2 480 1 120 2 480 WOOD EXPORT 4 (2) 5 1 4 3 200 2 450 1 120 2 450

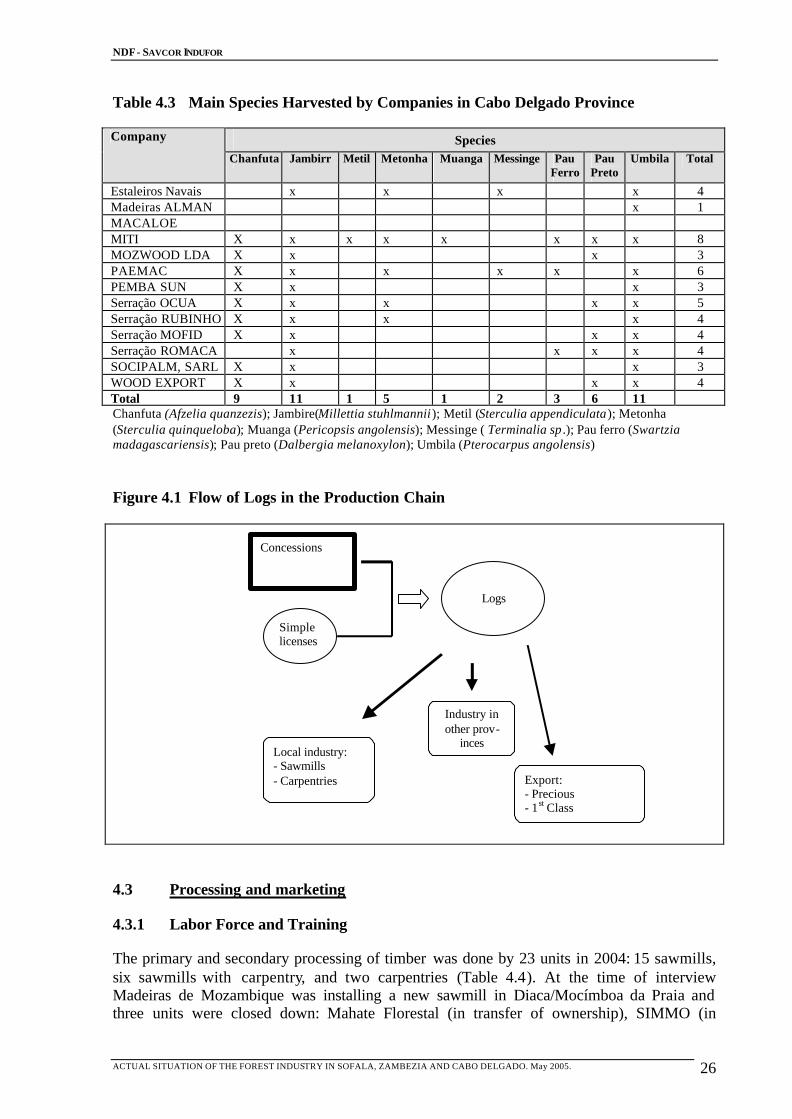

Total 94 400 21 486 66 080 21 486 4.2.3 Harvested Species and Their Processing

Table 4.3 shows the nine principal tree species harvested by companies with processing units: Umbila, Jambire, Chanfuta, Pau-preto, Metonha, Pau-ferro, Messinge, Muanga and Metil. MITI, PAEMAC and Serração OCUA cut more than the four most common species in 2003. MITI was the only company, which logged Metil and Muanga, second and third class timbers respectively. The 2001 study identified six species being harvested. Of these six species only Muaca continued to be harvested in 2003. Four new species were identified: Jambire, Pau-ferro, Messinge and Muanga. Table 4.1 shows the flow of logs. It is divided into three parts; one part goes for primary and secondary processing in the province, one part to other provinces and one part for export.

NDF - SAVCOR INDUFOR

ACTUAL SITUATION OF THE FOREST INDUSTRY IN SOFALA, ZAMBEZIA AND CABO DELGADO. May 2005. 26

Table 4.3 Main Species Harvested by Companies in Cabo Delgado Province

Species Company

Chanfuta Jambirr Metil Metonha Muanga Messinge Pau Ferro

Pau Preto

Umbila Total