Embed Size (px)

Citation preview

1 | P a g e

Agriculture and Food Industry Opportunities

in Japan & China

June 2015

2 | P a g e

CONTENTS

JAPAN ................................................................................................................................. 3

SUMMARY OF THE OPPORTUNITIES .......................................................................................................... 3

INDUSTRY PROSPECTS.................................................................................................................................. 3

MARKET OVERVIEW .................................................................................................................................... 12

CHINA .............................................................................................................................. 15

SUMMARY OF THE OPPORTUNITIES ........................................................................................................ 15

INDUSTRY PROSPECTS................................................................................................................................ 15

SHANGHAI AGRICULTURE AND FOOD ....................................................................................................... 26

MARKET OVERVIEW .................................................................................................................................... 29

3 | P a g e

Japan

I. Summary of Opportunities Opportunities exist for a range of agricultural products, in particular, processed and consumer ready

food products. For U.S. companies to tap into this dynamic market, they should be aware of several key

factors affecting food purchase trends. These factors are: a rapidly aging population, diversification of

eating habits, emphasis on high quality, increasing demand for convenience, and food safety concerns.

II. Industry Prospects

Opportunities

The United States remained Japan‘s top supplier of agricultural products, with a 24 percent market

share in 2013. However, China, Australia, Canada, Thailand, and Brazil have grown as strong competitors

for the United States. In CY 2013, U.S. farm, forestry, and fishery exports to Japan fell slightly from

$15.09 billion to $13.8 billion. However, much of that was due to the decline in feeds and fodders

caused by the 2012 drought in the United States. In that same period, consumer ready products grew

about 2 percent, from $6.25 billion to $6.36 billion, driven mainly by beef, dairy products, and tree nuts.

In 2012, the value of Japan’s consumer food and beverage market-- food retail and food service sector

combined-- was valued at around $812 billion. For complete agricultural statistics, please visit the web

site of the USDA‘s Foreign Agricultural Service at http://www.fas.usda.gov/data.

Opportunities exist for a range of agricultural products, in particular, processed and consumer ready

food products. For U.S. companies to tap into this dynamic market, they should be aware of several key

factors affecting food purchase trends. These factors are: a rapidly aging population, diversification of

eating habits, emphasis on high quality, increasing demand for convenience, and food safety concerns.

Exporters interested in the Japanese market should make note that three of the biggest annual food

related trade shows in Japan and all of Asia are: Foodex Japan, Supermarket Trade Show, and

International Food Ingredients & Additives Exhibition and Conference (IFIA) Japan.

Japan‘s population is aging faster than any other country in the world. According to Japan‘s National

Institute of Population and Social Security Research, by 2020, 29.2 percent of the population will be over

65 years of age. Coupled with the fact that Japanese life expectancy is the highest in the world, there is a

strong demand for "healthy foods." Such concepts as "functional foods" are well understood, and many

products certified by the Ministry of Health, Labor and Welfare as FOSHU (Food for Specific Health Use)

are commonly consumed. Food products that offer health benefits, such as lowering cholesterol, or

containing a high level of antioxidants have a marketing advantage in Japan. Local supermarkets already

carry an assortment of functional foods such as energy drinks, bars, and snacks containing dried fruit

and nuts, offering to provide nutritional health benefits. In addition, consumers are able to purchase

boxed meals supporting specific dietetic programs. Catering to the elderly and institutional markets –

cafeterias, schools, and hospitals – food preparers are increasingly serving ready-to-eat meals while

4 | P a g e

trying to preserve the appearance of traditional dishes. For example, when serving deboned fish dishes,

the meat is reshaped and presented in the form of a fish.1

Planet Retail notes that household sizes are shrinking, and the single-person household is becoming

more common. This may act as a positive shock to the industry, as single-person households are more

likely to dine out than families.

The aging population also brings demand for certain products, specifically in the realm of health and

wellness. Products aimed at enhancing the nutritional and health value of foods, while still offering

quality, taste and innovation, will appeal to Japanese consumers who want to increase their longevity

and improve their health. These products will come with higher prices, likely for lower volume, but will

most likely not offset the overall decline in value that is expected to occur in the Japanese food market.2

Since the 1960's, the Japanese diet has become dramatically westernized. Rice and tofu-based products

have been replaced by meat and dairy as the main source of protein. For example, per capita protein

consumption of rice fell from 32 percent in 1960 to 12.4 percent in 2010 while per capita protein

consumption of meat went from five percent in 1960 to 18.3 percent in 2010. Per capita protein

consumption for dairy products also increased from 2.5 percent in 1960 to 9.5 percent in 2010. In

addition to the popularity of western food, food trends have recently become more complex. Various

ethnic foods are also becoming popular and are often combined with Japanese cuisine creating "fusion"

foods. In addition, to “fusion” foods restaurants, there are also more authentic ethnic food restaurants

that cater to the broadening Japanese palate. Hence, to satisfy demand for non-traditional foods,

restaurants are seeking a wider variety of international food ingredients. Another aspect of

diversification is the trend of "individual eating", or convenience foods. Because of the busy, fast paced

lifestyle of modern Japanese, it has become less common for all family members to eat together.

"Individualization" of eating makes convenience an essential factor. Microwave (or semi-prepared) food

and Home Meal Replacement (HMR) cuisine has become an indispensable part of life and are sold in

supermarkets, restaurants and convenience stores such as 7-Eleven and Lawson‘s that are now found all

over Japanese cities.

In response to rising household demand for home delivery and increasing activity of online food sales,

the food delivery system in Japan is also expanding. Over the last three years, home delivery has

become very popular. Today, local supermarkets have staff specifically dedicated to handle home

deliveries. Similarly, hotels offer weekly and monthly menus that consumers can order via telephone or

internet; food service companies are now offering delivery services as well.

While economic stagnation and declining income have made people more price-conscious than in the

past, quality continues to be a crucial factor in food purchasing decisions. Food safety continues to be an

important consideration for most Japanese consumers, who are more sensitive to perceived risk than

the average American consumer. Following global trends, Japanese consumers have a renewed interest

in maintaining health and wellbeing, including healthier diets consisting of fresh fruits and vegetables.

Yet another developing trend is the growing number of males cooking at home. As more women have

joined the labor market and delayed marriage; and the rate of divorce among male-retirees increases,

5 | P a g e

more males are forced to prepare meals for themselves. As a result, there has been a surge in cooking

classes catering to male audiences who then need ingredients to prepare their meals. Men joining the

ranks of women visiting supermarkets in search for new food items will likely widen the target audience

and opportunities for market development.

The retail sector remains the focus of U.S. investment in Japan‘s food industry. In 2008, Seiyu became a

wholly-owned subsidiary of Wal-Mart. Prior to that; Seiyu was the third largest Japanese supermarket in

terms of food sales. Currently, Seiyu‘s sales ranking cannot be confirmed as the company is no longer

listed. Similarly, Costco appears to be doing very well in Japan. Since opening its first location in this

market in 1999, Costco has expanded their operation to eighteen warehouses located throughout Japan,

and is planning to open one more in summer 2014.3

FAS Osaka reports there are recent trends of burgeoning growth for private brands, healthy foods,

ecofriendly or energy saving foods (typically as frozen foods), market consolidation for greater

efficiency, and new retail ideas to meet new demands. Energy efficient foods (frozen foods - bento

dashi), prepared foods (Home Meal Replacements), and desserts have all seen a strong market growth.

Healthy or functional foods continue to be important. Japanese food manufacturers seek quality

ingredients and conveniently prepared semi-processed foods that can reduce costs. Specifically,

indications are that there is good potential in the market for pork, surimi, roe and urchin, processed

fruits and vegetables, soybean, fruit, tree nuts, wheat, and health and functional foods.4

Food Industries

Fish and Seafood

Trends

Fish and seafood volume sales started to decline again in 2013, with demand declining by 60,000

tonnes or so, equivalent to a 2% decline in volume. While this may have appeared to be

disappointing following growth in 2012, it is evidence that the Japanese market has corrected itself

and normalised following Fukushima. Volume sales increased by 1% in 2012. However, this positive

performance is misleading as it followed a huge 8% decline in 2010 on the back of consumer

concerns over contaminated fish in the wake of Fukushima.

While confidence has returned to the fish and seafood industry, the underlying long term trend of

year on year declines returned in 2013 due to the evolving Japanese diet and population ageing as

well as decline. While much has been made of the Japanese return to normality and ‘business as

usual’, the heavy decline posted by molluscs and cephalopods cannot be ignored as there is a

suspicion that domestic molluscs (many of which are filter feeders and grazers) will show the highest

level of contamination, with concerns over safety living on.

The Japanese are rightly famed for their high per capita consumption of fish and sea food, which

was reported at just under 33kg in 2013, almost seven times greater than that of a typical US

consumer for example. While fish and sea food is still central to the Japanese diet, per capita

consumption has fallen from close to 40kg in 2007, thus illustrating the influence of demographics

and the internationalisation of the Japanese diet.

6 | P a g e

While ageing and population decline have taken their toll on fish volume sales, the younger

generation is perhaps more culinary adventurous than the baby boomers and often looks to ready

meals and consumer food service, with fish consumption amongst under 30 year-olds being

significantly lower than within older generations. Many younger consumers are reported to be

lacking the skills to prepare and cook fish and sea food themselves - a situation which threatens the

long term future of the industry, at least in the domestic context.

Also fish and seafood is often perceived negatively amongst many younger consumers as it tends to

smell, which Japanese typically have a low tolerance for, and can be tricky to prepare as it involves

gutting and cleaning at home. However, it is possible that a health inspired boom may have the

potential to rekindle consumer interest in the area, although this appears unlikely without a major

change in the modernisation of how fish and seafood is sold and packaged in retailers.

The number of fishery workers declined during the review period while the workforce in this area is

also ageing. For example, in 2007 there were 204,000 people working in the fishery industry, with

men aged 65-years-old and above accounting for 37% of this number. In addition, there are

considerable concerns that a shortage of young fishery workers over the forecast period will result

in a decline in the number of fisheries in Japan.

Those buying fish and seafood in Japan continued to tighten their budgets towards the end of the

review period, with low-priced products such as cheaper imported fish and seafood gaining share as

a result. In addition, consumers shifted from pricier seasonal but fresh fish and seafood to cheaper

non-seasonal products sold in frozen formats.

Due to the poor economic situation in Japan, pricing remains an important consideration for many

consumers. This is evident in both retail and foodservice operations. Within sushi fast food, 100 yen

kaitenzushi outfits such as Kura continue to trade well while higher end and especially mid-price tier

establishments continue to be squeezed by consumers’ reluctance to spend due to the on-going

economic downturn.

Molluscs and cephalopods, squid, octopus and cuttlefish are very common in the Japanese diet but

have been less commonly seen on the menu since 2012. Consumers at home find these products

messy and troublesome to prepare and squid, with its associated high levels of cholesterol, has

proved to be less popular with its core older consumer group, who are on the whole trying to keep

their cholesterol levels down.

Crustaceans, prawns, crabs and shrimp are still common items. However, like squid, prawns and

shrimp have suffered from being associated with high cholesterol as well as being prohibitively

expensive, especially for larger specimens. The fact that crabs are also a popular seasonal favourite

but also command a high price also impacted sales during the recession.

The importance of the Japanese food service sector for fish consumption is highlighted by the fact

that it accounted for 48% of fish volume sales in 2013. This figure has increased slightly since 2007,

which is interesting as the number of sushi outlets has actually declined by 25% over the last 20

years. Part of the reason for this contradictory pattern has been the scaling up of the Japanese food

service sector and the increasing mechanisation of sushi outlets in particular, which have seen

average prices decline by 30% over the same period – a fact which highlights how sushi is now highly

accessible and more akin to fast food.

7 | P a g e

Prospects

During the forecast period, fish and seafood sales are expected to continue to decline, with the area

having a projected constant 2014 price value CAGR of -3%. The prospect of a sales tax hike in 2014 is

likely to do little to help the area as fish still tends to be relatively expensive in comparison to some

meats such as chicken or pork. Also, with ‘Abenomics’ leading to a weakening of the Japanese yen in

a bid to boost exports, imports are likely to become more expensive – a development which will

likely lead to a noticeable increase in prices of fish and seafood imports when combined with the

rise in sales tax.

There is expected to be growing global demand for fish and seafood and an increase in prices for

these products during the forecast period, particularly in China and Western Europe. This will be due

to increased consumer awareness of healthy foods in these countries. These trends will negatively

impact Japan's status as the leading global importer of fish and seafood. In addition, the on-going

decline in global fish stocks is also a source of concern. Furthermore, Japanese companies are

struggling to secure supplies of popular fish and seafood products such as tuna and salmon due to

being outbid by foreign companies.

In terms of retail fish and seafood sales, without significant efforts to modernise, fish sales will

continue to decline for the foreseeable future, not least due to the declining population (1% yearly

over review period). In addition, the rapid ageing of the population and the propensity for older

people to require less in the way of calorie intake will also count against fish and seafood

consumption, in line with other areas.

PACKAGED FOOD

Increased sales of premium products support the growth in packaged food

GDP growth was only slightly positive during 2014, due in part to the slow growth in wages among

Japanese households and increases in the price of products. The Japanese yen continued to become

weaker during 2014, due to the effects of Abenomics, the economic policy implemented by the

Japanese government. Many multinational companies have benefited from Abenomics and continued to

improve their performance during 2014. However, the benefits received by multinational companies

have not yet filtered down to small and medium sized Japanese companies. As a result, most Japanese

households have not yet benefited from increases in wages and household budgets.

Despite the less than impressive GDP growth packaged food experienced approximately 2% value

growth, accelerating from less than 1% growth in 2013, due to the increase in unit price across packaged

food. Unit prices increased due to the VAT rise, increases in the cost of ingredients and rising sales of

premium products. The tax rise was implemented in April 2014, with VAT increasing from 5% to 8%. The

cost of ingredients for manufacturing packaged food, such as milk, flour and fruit, increased during

2014, due to the weakness of the Japanese yen and a decline in domestic production. The increase in

unit prices was also caused by growth in sales of premium products, due to their popularity among the

growing number of seniors in the Japanese population who tend to look for quality over quantity.

8 | P a g e

Manufacturers have been reluctant to increase the unit prices of existing products, as they are aware

that Japanese consumers are sensitive to price and they can easily switch to a rival’s products or trade

down to more reasonable options, such as private label products in the economy segment. As a result,

manufacturers have increasingly launched new premium products with added value, such as offering

better taste with exclusive ingredients and greater convenience, as the high unit prices of premium

products which provide better flavour are more readily accepted by consumers.

Manufacturers’ strategies to sell more premium products were successful during 2014. Companies

offered a range of premium products across a wide range of packaged food categories, and effectively

captured the interest of consumers through effective marketing and promotional campaigns.

Manufacturers primarily targeted seniors for premium products, as there are a growing number of

seniors in the Japanese population and manufacturers are aware that many of them prefer quality over

quantity, and they do not mind paying more for better products.

The decline in the number of new born babies caused an increase in the proportion of old people in the

population. As a result, manufacturers have been shifting their focus of product development from

children to seniors across a wide range of products. For example, traditionally, manufacturers used to

develop and market confectionery products primarily targeted at children. However, manufacturers are

increasingly developing confectionery targeted at retired seniors, such as premium chocolate products

with selected ingredients and products that emphasise the health benefits of cacao to consumers. Also,

leading players in baby food have forayed into the convalescence market by utilising their know-how in

baby food, in light of the growing ageing population and the potential of the convalescence industry.

Health benefits drives sales

Japanese consumers became more health conscious over the review period. This was due to the start of

the metabolic syndrome checking system in 2008. The metabolic syndrome checking system is

mandatory for people aged 40 and over. Metabolic syndrome is a condition that is associated with age

and obesity, and which vastly increases the chances of developing lifestyle diseases such as diabetes and

cardiovascular disease. By starting the mandatory check-ups, the government aimed to raise people’s

awareness of lifestyle diseases and improve early prevention. Due to greater awareness of their health

conditions, increasing numbers of Japanese consumers are working out more regularly. They are also

paying greater attention to their dietary habits and are more concerned about the amount of fat and

sugar they consume.

The further penetration of the health and wellness trend supported growth in sales of products with

health benefits over the review period, such as yoghurt, olive oil and muesli. Despite minimal increases

in income and the tax rise implemented in 2014, many Japanese consumers do not mind paying more in

order to gain health benefits from food and improve their health. For example, yoghurt continued to

grow, registering 6% current value growth in 2014. This growth was mainly driven by greater awareness

of the health benefits of yoghurt. This was aided by TV programmes that reported the scientific research

that identified the health benefits of yoghurt, in addition to it improving stomach conditions, such as its

effectiveness for the prevention of influenza, norovirus infection and hay fever. Olive oil also

9 | P a g e

demonstrated strong growth over the review period, with a 6% CAGR. Olive oil has been found to have

health benefits, such as improving the profile of fats contained in the blood and preventing blood-

related diseases, and has become particularly popular among seniors, who value its health benefits.

In response to the health and wellness trend, manufacturers have been changing the production

processes of existing products to enable them to make products that have better health effects. For

example, deep frying in oil was the usual process used by manufacturers to produce pouch instant

noodles. However, manufacturers have been increasing the range of pouch instant noodles which are

not deep fried.

Convenience is key

As in other developed countries, household sizes are decreasing in Japan. According to Euromonitor

International’s Countries and Consumers’ data, the number of households with four persons or more

declined by 8% between 2009 and 2014, while single-person households increased by 8% and two-

person households increased by 7% over the same period. In 2014, single-person households accounted

for 33% of total households and two-person households accounted for 28%. These were significant

increases compared to 1995, when the share of single-person households was only 26%, and that of

two-person households 23%. According to the Ministry of Health, Labour and Welfare, dual-income

households increased from 51% of total households in 2002 to 57% in 2012, as more females continued

to work after marriage.

The increase in small-sized families, combined with the increase of working females, meant Japanese

consumers came to spend less time on preparing meals. Whilst single-person households consider it a

burden to cook for just one person, working females tend not to cook at home due to their busy

lifestyles. Consumers have tended to avoid cooking at home, instead purchasing cooked meals from

convenience stores, supermarkets and fast food operators. According to Euromonitor International’s

Consumer Foodservice data, convenience stores fast food registered 9% current value growth in 2013.

The busier lifestyles of Japanese consumers have impacted the packaged food market, especially instant

noodles and ready meals, which are considered as convenient in saving time. For example, prepared

salads demonstrated a 5% CAGR in value terms over the review period. Although salads are considered

healthy, preparing salads from scratch require consumers to purchase a wide range of ingredients.

Therefore, busy small-sized households have come to appreciate the convenience of prepared salads,

which contain various types of vegetables and enable consumers to prepare salads in single servings.

IMPULSE AND INDULGENCE PRODUCTS – KEY TRENDS AND DEVELOPMENTS

Trends

Impulse and indulgence products grew by 1% in value terms in 2014, following declines in 2012 and

2013. Although volume sales registered a further decline, value sales growth was positive due to

increases in unit prices. This was mainly because of the VAT increase from 5% to 8% in April 2014, as

well as the growing popularity of premium products among consumers. Gum, sweet and savoury

snacks and unpackaged/artisanal cakes experienced declines, while all other categories experienced

positive growth.

10 | P a g e

Ice cream registered the strongest current value growth in impulse and indulgence products in 2014,

supported by growth in sales of single-portion ice cream. Over the review period, manufacturers

successfully established ice cream as a frozen dessert and increased consumption among all age

groups, while ice cream was previously consumed mostly by children. Single-portion ice cream

became particularly popular as Japanese consumers like to try out different flavours and explore

new products. Growth in sales was also supported by increased sales of premium ice cream,

specifically products targeted at seniors and other adults who value quality over quantity.

Small packet sizes continue to become more popular, due to growth in the number of single-person

households who can only consume a small amount of impulse and indulgence food each time. There

has been growth in the number of both seniors and young adults living by themselves. Small packet

sizes are also becoming popular as they are portable and can be consumed on a single occasion.

MEAL SOLUTIONS – KEY TRENDS AND DEVELOPMENTS

Trends

Meal solutions continued to grow in 2014, by 2% in value terms. All of the meal solutions categories

demonstrated positive growth. The growth of meal solutions, such as ready meals, soup, frozen

processed food and chilled processed food, was supported by growth in the number of consumers

who are looking for convenient solutions for meals and desserts that enable them to save time.

Japanese consumers are becoming increasingly busy, with an increase in the number of female

adults who continue to work after marriage and after having children.

Ready meals demonstrated the strongest current value growth of 4% in 2014. Ready meals are

typically more expensive than preparing one’s own meals from raw ingredients. However, there are

more consumers who prefer to pay more for saving time, due to busier lifestyles and the increased

number of women who continue to work after marriage and having children. Furthermore, there is

also growth in the number of single females and males who do not get married. These consumers, in

particular, value the convenience of ready meals as they often need to work for long hours and have

little time to prepare meals.

Soup recorded a 3% growth rate in value terms in 2014, due to its convenience and health benefits.

Soup has an important role in Japanese people’s diets. Traditionally, Japanese consumers cook miso

soup or some other type of traditional Japanese soup every morning with rice and fish fillet, as soup

can be quickly and easily prepared, and is a convenient option. As Japanese consumers have come

to lead busier lives, more are preparing soup from packaged soup products. Packaged soup products

are especially useful for working men and women living in single households, as they only consume

a small amount of soup when they make it, and soup products that come with measured servings

are particularly convenient.

At the same time that many people are looking for convenience, the number of consumers who

engage in home cooking has been increasing, due to the emergence of the health and wellness

trend, and growth in the number of consumers who like to save money by reducing their frequency

of eating out. Home cooking is an attractive option for health-conscious consumers, as it enables

them to choose their own ingredients and helps them ensure that they eat healthy and safe food.

The increasing popularity of home cooking drove growth in sauces, dressings and condiments in

2014, with 2% value growth.

11 | P a g e

NUTRITION/STAPLES – KEY TRENDS AND DEVELOPMENTS

Trends

Nutrition/staples demonstrated 1% growth in current value terms in 2014. Growth was stronger in

2014 than in 2013, driven by breakfast cereals, meal replacement, and yoghurt and sour milk

products.

Breakfast cereals demonstrated the fastest growth in nutrition/staples in 2014, with a 12% value

increase, primarily due to the rising popularity of granola. Granola is muesli baked until crisp, which

is typically consumed with a variety of toppings, such as yoghurt, honey, syrup and fruit. Before

granola became popular, eating cereals for breakfast was not common, as Japanese consumers

preferred the taste of rice and bread, which can be eaten in a variety of ways. However, granola

became popular and is recognized as an attractive replacement for rice and bread for breakfast, due

to promotional efforts by manufacturers suggesting eating granola with yoghurt. Granola has health

benefits, such as improvement in digestion, skin condition and reduction in body fat.

Rice declined by 2% in value terms in 2014. Rice remains the most popular staple among Japanese

consumers, due to its strong penetration in Japanese culture. Traditionally, Japanese people have

been accustomed to eating rice three times a day at every meal. However, there has been a clear

shift from rice to other staples, such as bread and pasta, among Japanese consumers. Those in the

younger generations, in particular, have become more interested in Western diets.

Olive oil experienced 11% growth in value terms in 2014. Consumer awareness of the health

benefits of olive oil has increased, such as improving the profile of fats contained in the blood and

preventing blood-related diseases, which are particularly appealing to elderly consumers. The health

benefits of olive oil have been widely promoted by television programmes, which supported the

better understanding and further penetration of such products among Japanese consumers.5

On 28 June, 2013, the CAA (Consumers Affair Agency) announced the new food labeling law, which went

into force on 1 April, 2015. The regulation was comprised with 3 items: unification of the food labeling

control, enforcement of food labeling and making a new category of health foods.

1. Unification of the food labeling control

Originally, food labeling in Japan is under the control of three ministries, MHLW (Ministry of Health,

Labour and Welfare), MAFF (Ministry of Agriculture, Forestry and Fisheries) and MOF (Ministry of

Finance), while the new regulation authorizes CAA as the only competent authority of food labeling.

2. Enforcement of food labeling

Besides, according to the new legislation, all foods should be labeled according to the enforced law

after transitional periods: 6 months for fresh foods and 5 years for the other foods. All processed foods

and additives should be labeled calories and contents of proteins, lipids, carbohydrates and sodium.

The labeling system of “health food” is also improved. In Japanese “health foods”, there are three

categories: Food for Special Dietary Uses, FOSDU, Food for Specified Health Uses, FOSHU, and “the

others”. FOSDU and FOSHU are allowed to be labeled with health claim after sever approval process

12 | P a g e

similar for medicines. But, “the others” are not allowed to indicate any health claims even if they have

some data to support the claims".

3. Making a new category of health foods

CAA creates a new category, Food with Function Claims, from “the other” health foods. They are not

necessary to get the CAA approvals but to report to the CAA with data supporting the health claims on

manufacturers’ risk.6

III. Market Overview As the world’s fourth-largest buyer of American products and the world’s third-largest economy, Japan,

among the most dynamic and advanced countries in the world, is a market that should be considered by

all American exporters. Japan is a technology powerhouse, a proving ground for consumer goods and

services, and in the social and commercial vanguard of developed market demographics. Further,

Japanese companies are also major investors in the United States, and as a result Japan sees dozens of

visits by senior U.S. state and city officials annually. While the reasons U.S. firms engage with Japan are

diverse, the strategic and tactical importance of the Japanese market is critical not only for their

business in Japan, but in the United States and third-country markets as well.

Japan continues to enjoy attention in the business news this year owing to a variety of factors, including

the strong performance of the Japanese stock

market in 2013, continued brighter business and

consumer sentiment, a yen that has seemingly

stabilized at a level sharply lower than that of recent

years, and the apparent end of stubborn deflation.

The new economic policies linked to these

developments are known collectively as

“Abenomics”-- a three pronged strategy of bold

monetary loosening, fiscal stimulus centered on

infrastructure spending, and growth-oriented

structural reform. While the implications and

ultimate success of this strategy in reigniting long-

term growth in Japan are uncertain, it has drawn

considerable attention from U.S. businesses.

The U.S., Japan and ten other countries are

negotiating the Trans-Pacific Partnership (TPP). With

Japan’s participation, its members would account for

nearly 40 percent of World GDP. Moreover, the

liberalization expected to be required of TPP member countries may play an important role in

promoting the domestic economic reforms likely to be called for under “Abenomics.” As of May 2014,

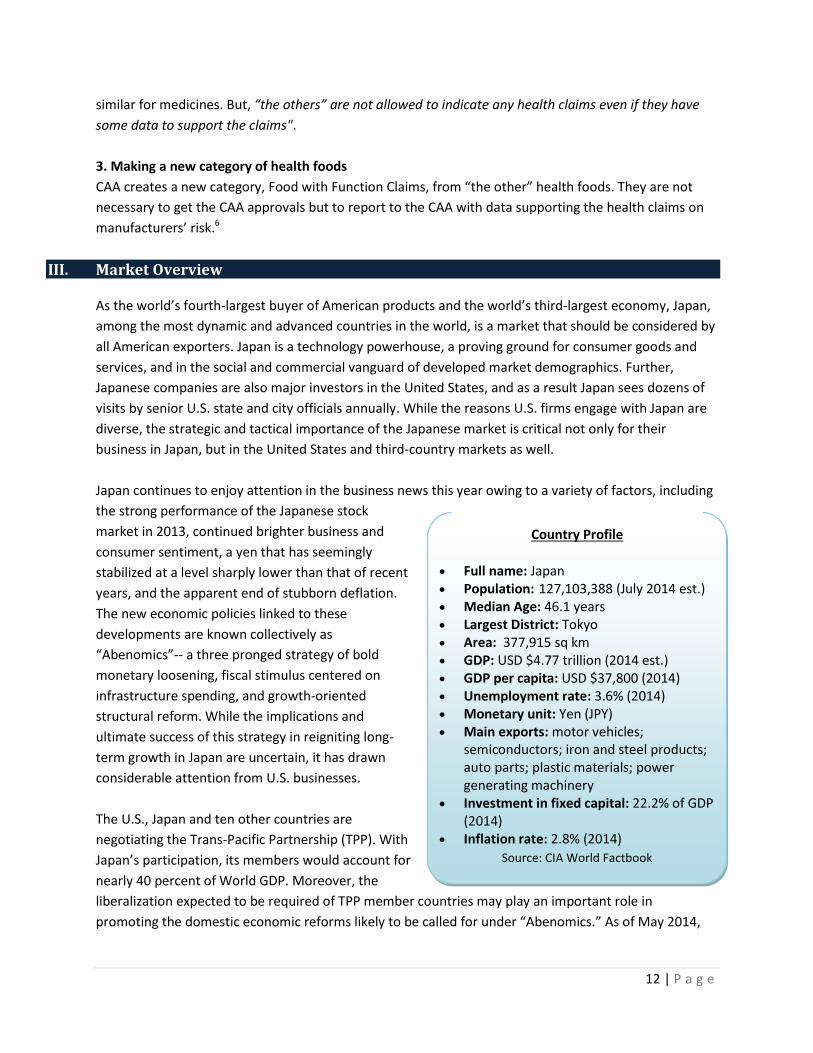

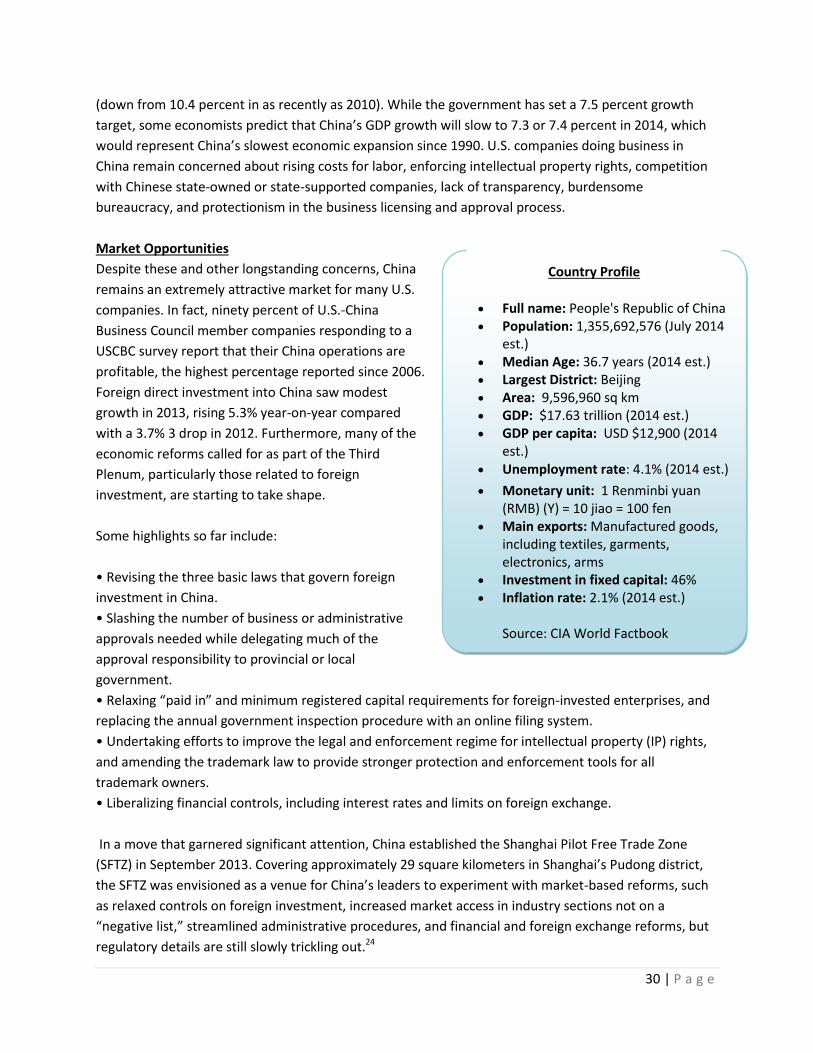

Country Profile

Full name: Japan Population: 127,103,388 (July 2014 est.) Median Age: 46.1 years Largest District: Tokyo Area: 377,915 sq km GDP: USD $4.77 trillion (2014 est.) GDP per capita: USD $37,800 (2014) Unemployment rate: 3.6% (2014) Monetary unit: Yen (JPY) Main exports: motor vehicles;

semiconductors; iron and steel products; auto parts; plastic materials; power generating machinery

Investment in fixed capital: 22.2% of GDP (2014)

Inflation rate: 2.8% (2014)

Source: CIA World Factbook

13 | P a g e

the U.S.-Japan TPP talks have been proceeding vigorously, with most topics already or nearly agreed

upon.

While Japan has made significant steps toward economic healing following the tragic combined

earthquake, tsunami, and nuclear incident of March 2011, lasting changes on various levels remain

noticeable, including idled nuclear power plants. In particular, greater levels of manufacturing by

Japanese companies outside of Japan, increased fuel imports and a weakening yen have turned Japan’s

multi-decade trade surplus into a trade deficit.

Japan remains the world‘s third-largest economy, after the United States and China, with a GDP of

almost $6 trillion. Japan is the fourth-largest export market for U.S. goods and services, and our fourth-

largest trading partner overall. In 2013 the U.S. exported $65 billion in goods to Japan. The United States

runs a persistent trade deficit with Japan in merchandise, and a surplus in services.

Japan is the second-largest foreign investor in the United States, with a cumulative investment of

approximately $310 billion.

During 2013 the Japanese yen weakened appreciably and is currently near 5- year lows against the

dollar. Even so, U.S. products remain competitive in Japan.

Japan's large government debt, which totals over 200 percent of GDP, and an aging and shrinking

population are major challenges confronting the economy, but the latter can also present opportunities

for U.S. companies.

In 2013 the top exporters to Japan were China, the United States, Australia, Saudi Arabia, South Korea,

the UAE, and Indonesia. The top importers from Japan were China, the United Sates, South Korea,

Taiwan, and Hong Kong.

The United States-Japan alliance is a cornerstone of U.S. security interests in Asia and is fundamental to

regional stability and prosperity. The U.S.-Japan alliance continues to be based on shared vital interests

and values. These include stability in the Asia-Pacific region, the preservation and promotion of political

and economic freedoms, support for human rights and democratic institutions, and securing of

prosperity for the people of both countries and the international community as a whole. Japan is one of

the world‘s most prosperous and stable democracies.

Market Challenges

The degree of difficulty in penetrating the Japanese market depends on the product or service involved.

Key variables include the degree of local or third-country competition, the number of regulatory hurdles

to be overcome, and cultural factors such as language (both spoken and written), service and quality

expectations, and business practices. Tariffs on most imported goods into Japan are low. However,

cultural, regulatory, or other non-tariff barriers exist that can make market entry difficult. These can

14 | P a g e

include Japanese import license requirements, restricted or prohibited imports, temporary entry of

goods, certifications, standards, labeling requirements, etc.

Market Opportunities

U.S. companies wishing to enter the Japanese market should consider hiring a reputable, well-

connected agent or distributor, and cultivating business contacts through frequent personal visits.

Japan‘s business culture attaches a high degree of importance to personal relationships, and these take

time to establish and nurture. Patience and repeated follow-up are typically required to clinch a deal.

The nature and pace of dealmaking in Japan are quite different from those in the United States. U.S.

business executives are advised to retain a professional interpreter, as many Japanese executives and

decision-makers do not speak English or prefer to speak Japanese.7

15 | P a g e

China

IV. Summary of the Opportunities China remains an extremely attractive market for many U.S. companies. In fact, ninety percent of U.S.-

China Business Council member companies responding to a USCBC survey report that their China

operations are profitable, the highest percentage reported since 2006. Foreign direct investment into

China saw modest growth in 2013, rising 5.3% year-on-year compared with a 3.7% 3 drop in 2012.

Furthermore, many of the economic reforms called for as part of the Third Plenum, particularly those

related to foreign investment, are starting to take shape

V. Industry Prospects

Opportunities

The United States Department of Agriculture, through the Foreign Agricultural Service (FAS), operates

six offices in the People‘s Republic of China for the purpose of expanding exports of U.S. agriculture,

fishery, and forestry products. U.S. agricultural, fishery, and forestry exports to China from January to

December 2013 reached a new high of $29.4 billion, up 3 percent from 2012. China is the largest U.S.

overseas market for agriculture, fish, and forestry exports. Although exports have traditionally been

dominated by soybeans ($13.4 billion) and cotton ($2.2 billion), declining exports of these products in

2013 were more than offset by a boom in exports of higher value products, most notably distiller’s dried

grains with solubles (DDGS - an animal feed) ($1.4 billion) and dairy products ($706 million).

These figures underline a shift in Chinese agricultural imports away from products for processing and re-

export, to finished products for consumption at home. Overall imports of U.S. consumer-oriented food

products increased by 15% in 2013, to end at over $3 billion. Even stronger export growth was seen for

inputs into China’s burgeoning animal husbandry sector. In addition to DDGS, exports of alfalfa hay

jumped 66% to hit $234 million, and 2013 saw the U.S.’ first commercial exports of sorghum to China.

Key consumer trends over the past year have highlighted, in addition to growth in animal husbandry,

consumer food safety concerns, and e-commerce. The former has been a driving factor for imports,

which are seen as being more heavily inspected and generally safer than local products. The impact has

been particularly strong for dairy products, especially those for children, and food ingredients for

Chinese manufacturers seeking to avoid problems with locally sourced ingredients.

E-commerce was the other major trend for food imports, as growth rates for e-commerce far exceeded

those for any other sales format. This is also being affected by consumer 93 concerns over food safety:

in general, e-commerce products are seen as more authentic and safer than those purchased through

traditional stores. Logistics for ecommerce matured, with products as delicate as fresh cherries from the

U.S. and live seafood being promoted and shipped through these channels quite successfully.

16 | P a g e

Due to the changing regulatory environment in China, U.S. exporters are advised to carefully check

import regulations. Individuals and enterprises interested in exporting U.S. agriculture, fishery, and

forestry commodities to China should contact the FAS offices as well as USDA Cooperator organizations.

Exporters of U.S. agricultural commodities should also review the FAS website

(http://www.fas.usda.gov), which features general information about trade shows and other

promotional venues to showcase agricultural products, FAS-sponsored promotional efforts, export

financing and assistance, and a directory of registered suppliers and buyers of agricultural, fishery, and

forestry goods in the United States and abroad. The Animal Plant Health Inspection Service also

operates an office in Beijing.

Best Prospects:

Animal Feed

Hides and Skins

Dairy Products

Fish and Fish Products

Processed Food Products

Tree Nuts

Soybeans

Fresh Fruit

Wood and Wood Products8

It is clear China’s increased wealth has led to an increase in consumption of imported food and

agricultural products. Chinese imports of U.S. food and agricultural products increased from US$12.1

billion in 2008 to US$25.8 billion in 2013. That represented an increase of 114% and China remains the

largest export market for agricultural products. Despite of differences in business culture and

uncertainly about import requirements, U.S. exporters will find that this expanding economy continues

to create business opportunities.

In 2013, U.S. exports of consumer oriented food products to China increased 15% and totaled a new

record high of over US$3 billion. China now ranks as the 5th largest market for consumer ready food

products from the U.S. Top processed food products exported to China in 2013 included cooked and

prepared shellfish (cuttlefish, crab, lobster), concentrated milk, whey protein, other processed food,

ingredients and beverage bases, other prepared/preserved meats, soybean oil, french fries,

lactose/syrup, wine and chocolate (cocoa paste and chocolate candy).

China has attracted a growing level of interest from other countries and has signed or is negotiating

bilateral trade pacts with many of its neighbors. Third country competition comes in two distinct areas:

commodity-type products such as frozen meat, poultry, seafood and fresh fruit, and western-style niche

products such as canned and prepared foods and ethnic cuisines, and ingredients. Competition in the

fresh and frozen meat, fruit and vegetables arena, as well as dairy, comes primarily from Pacific Rim

neighbors, including Thailand, New Zealand, Australia, Canada, and Chile, as well as South Africa and

17 | P a g e

Brazil. Competition for western-style prepared foods is much more global, with competitors playing to

their strengths in individual products such as olive oil, wine, pasta and pasta sauces. Currently the U.S.

remains the largest single exporter of consumer oriented food to China, and is the only exporter with a

presence in most categories.9

Food Industries

Seafood Industry

China's huge aquaculture industry produces scallops, shrimp, mussels, snapper, tilapia, turbot, flounder,

abalone and clams, as well as the ubiquitous carp. In 2005, China's aquaculture industry harvested 30

million tones of seafood products, almost two-thirds of the world's total. While wild fisheries remain

under significant constraint, there is no control over aquaculture expansion, although expansion is

expected to slow down as priorities shift to increasing productivity and efficiency. Low production costs,

government support and a population that prefers to purchase live seafood are major reasons for the

growth of China's aquaculture industry. As a result, aquaculture operators are constantly looking for

new technology in order to improve production efficiencies which can be also advantageous for U.S.

firms.10

China's aquatic production in 2012 is forecast at 58 million tons, up four percent from 2011, due to gains

in aquaculture growth as wild catch production remains stagnant. Fishery production challenges include:

slowing investment, environmental concerns and coastal development limiting resources for

aquaculture expansion, scarce resources restrain growth for wild catch numbers, and processing (with

imported material) for re-export facing rising production costs and loss of competitivity. Rising affluence

is raising domestic demand for alternative protein sources, including aquatic products, but weak

overseas economic conditions challenge export growth.

In recent years, China’s seafood industry has become exhausted due to overfishing and contaminated

waters. In an attempt to control the deterioration of the country’s fisheries, the Chinese government

issued a new regulation in 2006, stating that by the end of 2010, the total number of fishing boats will

be capped at 30,000. This creates great business opportunities and higher margins for imported

seafood.11

Total aquatic trade value is expected to rise to an estimated $27 billion in 2012 from $25.8 billion last

year and produce a $10 billion surplus. US exports to China of aquatic products increased to $945 million

in the first ten months of 2012, up 1.6 percent over the same period in the previous year. China’s

aquatic exports to the United States climbed to $2.3 billion in the first ten months of 2012. Imports for

domestic consumption face high import duties and value added tax. Prospects remain strong for US

salmon, frozen fish and fish meal.12

Examining China as an importing country, it is expected that Russia remains its largest supplier of

seafood products, distantly followed by the United States and Japan. Nowadays, the U.S. is China’s

18 | P a g e

second largest seafood exports source. The growing popularity and demand for fish and shellfish in the

last decade is illustrated by a rapid growth of seafood exports from the U.S. between the years 2000-

2010. Currently the total value of seafood exported to China from the U.S. is over 7 times higher than in

the 1990s.

When examining the most prevalent seafood commodities being exported from the U.S. to China, frozen

products have a strong presence at the top of the list. In 2013, the top 3 exported commodities included

frozen flat fish, frozen cuttle fish and squid, and frozen crabs. Moreover, frozen herring, sole and lobster

were also near the top of the list. Despite the export rankings, Chinese consumers prefer to buy live and

fresh aquatic products, including fish, crabs, clams and others. This is particularly true for consumers in

coastal provinces in East and South China, who either purchase seafood products in retail, fish market or

they order in restaurants – preferably live products. This results in a promising outlook for those looking

to export live seafood products, especially lobster and crab.13

Overall China has become a seafood superpower and is playing a significant role in the global business

not only as the largest consumer, but also producer, exporter and importer of seafood products in the

world, representing nearly 40 percent of total global production based on China Customs data.

According to the most recent statistics by China’s Ministry of Agriculture (MOA), China exported 2.72

million tons of fish and seafood products worth $13.45 billion in the first three quarters of 2012,

respectively, a 4.4-percent decrease in volume and an 8-percent increase value. In the first nine months

of 2012, China imported 1.79 million tons of fish and seafood products, worth $3.92 billion, a 4-percent

increase in volume, but an 8-percent decrease in value compared to the same period last year.14

As a result of the economic progress and the structural change of the Chinese society, a new consumer

group of seafood is emerging: China's growing population of young and sophisticated consumers -

located primarily in the major cities - is willing to purchase imported seafood products, in part for their

status but also because imported seafood is believed to be of higher quality, coming from a cleaner

environment.

Secondly, while the preference overall is still for live fish , a growing number of young adults are eating

out and shopping for semi-prepared convenience products in supermarkets due to the hectic pace of

modern life. A test demonstration held in several Shanghai supermarkets in 2006 showed that Chinese

consumers liked and would purchase frozen and sauced seafood products although they also found that

the sauces would have to be reformulated to meet specific regional tastes.15

Thirdly, a large amount of the U.S. exported seafood product is further processed for re-export purpose

in China. For the non-processed products, they are mostly high-value products and are introduced

mainly through HRI (Hotel Restaurants Institutional) foodservice sector in upscale hotels and

restaurants.

The growing number of foreign retailers operating in China is providing more opportunities to promote

branded items to young and affluent workers who now seem to prefer shopping at supermarkets

instead of the traditional fish markets. Carrefour (France), Jusco (Japan), Metro (Germany), and Wal-

19 | P a g e

Mart (USA) are the largest foreign supermarket chains operating in China at present, but domestic

retailers such as Wu-Mart are beginning to follow suit. In general, rapid consolidation of the domestic

retail sector in China is leading to new opportunities for U.S. seafood sales to consumers, especially in

major eastern centers where income levels are higher. China's food service industry continues to offer

the best prospects for live U.S. seafood items.16

PACKAGED FOOD

Packaged food registers healthy sales growth in 2014

Despite a slowdown in China’s economic growth in the last two years of the review period, packaged

food continues to project healthy current value growth in 2014. Sales are benefiting from consumers’

willingness to trade-up to premium products in areas such as baby food, dairy, chocolate confectionery

and oils and fats. Due to growing health consciousness, a growing number of consumers are meanwhile

spending more heavily on healthier and more nutritious packaged food or products that aid weight loss,

such as meal replacement slimming, yoghurt and breakfast cereals.

Healthy packaged food continues to gain popularity in China

The government and many major manufacturers of packaged food are investing in consumer education

campaigns to highlight the importance of healthy eating habits. This is resulting in numerous high-

visibility marketing and education campaigns competing for consumers’ attention. As a result,

consumers’ awareness of the importance of a healthy diet is boosting the consumption of healthy

packaged food, especially products featuring fortified or naturally healthy ingredients. Meanwhile,

manufacturers are reacting to the emerging health and wellness trend by introducing new products with

lower sugar, fat or salt levels or that are preservative free.

Consumers continue to trade up despite slowing economic growth

China saw real GDP growth slow in the last three years of the review period. While 2008-2011 saw

annual growth of 9-10%, growth slowed to below 8% annually in 2012 and 2013. 2014 is meanwhile

expected to see growth of just 7%. This was due to moderating domestic demand, slower investment

and the growing risks of a deep adjustment in real estate prices.

However, urban household incomes grew faster than GDP during the review period, including 2014.

Many consumers thus traded up to premium or higher-quality packaged food within a number of

product categories, including chocolate confectionery, baby food, dairy and ice cream, despite weaker

economic growth. This trend in turn contributed to unit prices rising above the level of inflation for most

product areas in packaged food in 2014. Consumers are increasingly opting for higher-priced products in

their search for better product quality and flavour, alongside higher nutritional value. This trend is also

being encouraged by consumers becoming increasingly health conscious. Consumers are also

increasingly cautious about the ingredients in the packaged food they consume, due to a number of

food safety scandals towards the end of the review period.

In response to these trends, many leading manufacturers focused on the development of new value-

added or premium products. For example, Bright Dairy & Food launched long life/UHT Momchilovtsi

yoghurt in 2009, with this dominating sales of plain spoonable yoghurt by the end of the review period

20 | P a g e

with 51% value share in 2014. In order to capture a share of dynamic long life/UHT yoghurt, Inner

Mongolia Mengniu meanwhile launched Just Yoghurt in this product area in May 2013, with this being

followed by Inner Mongolia Yili’s Ambpoeial in December 2013. These long life/UHT yoghurt brands are

similar in price positioning, packaging, shelf-life and size. However, there are some differences in

positioning. Longevity is the main focus for Momchilovtsi, which is available in two flavours of plain and

strawberry. Just Yoghurt is meanwhile positioned as additive-free, pure, natural and healthy and only

available in plain yoghurt. Ambpoeial is in contrast promoted on the basis of its higher protein content

in comparison to standard plain spoonable yoghurt.

Trends – sales to foodservice

Foodservice volume sales of packaged food were impacted by the Chinese government’s stricter

controls over the use of public funds for dining out since 2013. Public funds used to entertain

government officials and their guests notably contributed significantly to foodservice sales in China

over the review period. However, the impact of stricter controls over public spending on consumer

foodservice has been counterbalanced by a number of positive factors. Rising disposable income

levels, busier consumer lifestyles and growing urbanisation all supported foodservice volume sales

growth for packaged food at the end of the review period. Consequently, many major product areas

continued to see growth largely in line with review period CAGRs in 2014, including soy based

sauces, chilled processed meat and rice.

Chilled processed meat and soup saw the fastest foodservice volume growth in 2014 over the

previous year, with sales in each product area rising by 12%. In addition to a small sales base, chilled

processed meat is favoured by chefs, as it is regarded as fresher and more flavoursome in

comparison to frozen processed meat. With growing income levels, consumers are also increasingly

focused on quality, encouraging more consumer foodservice operators to shift from frozen

processed meat to chilled processed meat. Soup meanwhile grew from an extremely low sales base,

with sales reaching only around 300 tonnes in 2014. Growth was driven by outlets catering to time-

pressed workers' demand for affordable and quick snacks, with instant soup accounting for all sales.

Foshan Haitian saw a strong performance in foodservice volume sales of packaged food in 2014,

over the previous year. The company benefited from its wide product portfolio in sauces, dressings

and condiments, particularly in widely-used soy based sauces where it offers a wide range. The

company offers premium, standard and economy soy based sauces, thus catering to a wide range of

foodservice outlets in terms of price positioning.

Multinationals are also strong in foodservice volume sales of packaged food, however. Nestlé is

particularly strong in foodservice sales of sauces, dressings and condiments, with its Maggi brand

enjoying high brand awareness among foodservice outlets. In addition, the company also offers

soup to foodservice customers. Domestic players however have a stronger position in lower-priced

and mid-priced foodservice outlets, due to offering more competitive pricing.

21 | P a g e

IMPULSE AND INGULGENCE PRODUCTS – KEY TRENDS AND DEVELOPMENTS

Trends

Impulse and indulgence products posted rapid current value growth in 2014 despite weaker

economic growth towards the end of the review period. Thanks to a general rise in disposable

income levels during the review period, consumers continue to view these products as affordable

luxuries. Growth is also being supported by consumers’ increasing sophistication and growing

exposure to foreign brands via the internet. These trends are increasing consumers' willingness to

try out a wider range of brands in impulse and indulgence products. Impulse and indulgence

products thus saw 10% current value growth in 2014, with this being similar to the growth seen in

2013.

Among the major product areas in impulse and indulgence products, unpackaged/artisanal cakes is

expected to register the strongest current value growth. This product area is benefiting from

consumers' increasingly hectic lifestyles and rising disposable incomes, encouraging stronger

impulse purchases. In addition, unpackaged/artisanal cakes is benefiting strongly from rapid

expansion for both chained and independent bakeries across China, with outlets in this channel

competing aggressively through innovation and a strong focus on quality.

Independent small groceries remains the major distribution channel for impulse and indulgence

products. This is chiefly due to the channel having a wide presence across the country and thus

offering convenient locations for impulse purchases. However, independent small grocers lost value

share to modern grocery retailers such as hypermarkets and supermarkets at the end of the review

period. This was linked to ongoing outlet volume expansion for these channels, alongside their

convenience, wide product ranges and attractive price promotions.

In terms of packaging formats, folding carton packs are increasingly popular in impulse and

indulgence products, particularly in biscuits. This packaging format is gaining share because it

protects biscuits from crushing, being increasingly used by leading manufacturers such as Mondelez.

Small individual packs are also gaining popularity, because these can be easily carried and stored

and are also viewed as offering greater freshness.

The current value unit price of most impulse and indulgence products is set to rise above the level of

inflation in 2014. This trend will be due to consumers trading up in search of greater quality, flavour

and product safety. Many consumers are also attracted to premium impulse and indulgence

products as a signifier of status, especially when giving gifts. An increase in the costs of raw

materials such as cocoa, sugar and dairy also helped to boost the average unit price of impulse and

indulgence products in 2014.

22 | P a g e

MEAL SOLUTIONS – KEY TRENDS AND DEVELOPMENTS

Trends

A growing number of consumers are facing busy lifestyles, with long working hours and commutes.

As a result, many are opting for choose meal solutions instead of cooking from scratch, with this

trend being encouraged by busy daily routines and increasing disposable income levels. This trend is

strongest among working adults, particularly those in single-person households. Frozen dumplings

are for example popular as a quick and simple meal and are regarded as offering a greater degree of

nutrition in comparison to alternatives such as instant noodles.

With rising disposable income levels during the review period, growing urbanisation and increasingly

busy lifestyles, meal solutions saw slightly stronger growth towards the end of the review period.

Stronger growth towards the end of the review period was also linked to consumers' growing

acceptance of convenient packaged food. In comparison to consumer foodservice, meal solutions

are meanwhile not only cheaper but are also regarded by many consumers as being more hygienic

and convenient.

Dessert mixes and soup saw the highest current value growth in meal solutions in 2014 over the

previous year, with both product areas growing by over 13%. Strong growth was partly due to a

relatively low sales base. In addition, instant soup and dessert mixes proved increasingly popular as

between-meal snacks and light lunches towards the end of the review period. These products are

particularly popular among office workers looking for convenience and weight-conscious young

women seeking low-calorie snacks.

Modern grocery retailers are the most important distribution channels for meal solutions, with

supermarkets and hypermarkets being particularly important. This is partly due to the major

consumer group for meal solutions being time-pressed urban consumers. In addition, chilled

processed and frozen processed food require cold storage and distribution, offering supermarkets

and hypermarkets a strong advantage. Convenience stores are also gaining value share, thanks to

offering convenient locations to hungry consumers buying on impulse.

There was also a growing focus on convenience in packaging in meal solutions towards the end of

the review period. Subo Foods for example launched instant soup packed in cups, enabling

consumers to easily make a cup of soup anytime and anywhere if they have access to boiling water.

Unit prices rose slightly above the level of inflation for most product areas in meal solutions in 2014

over the previous year. This was mainly due to rising production and distribution costs. Raw

materials and labour cost notably increased, while players are also increasingly investing in building

up regional logistics centres in order to speed up their distribution. In order to maintain profits,

many players are thus focusing on higher-quality or value-added products, with these being largely

welcomed by an increasingly affluent consumer base.

Chilled processed food is expected to see the strongest growth in the forecast period in meal

solutions with over 8% value CAGR at constant 2014 prices. This will be linked to rising disposable

income levels and a growing focus on food safety. As a result, consumers are expected to trade up

to packaged products in chilled processed meat and the leading brands, while chilled ready meals

23 | P a g e

will benefit from an increasingly affluent and busy consumer base being willing to pay more for

convenience. Many will also opt for chilled ready meals rather than consumer foodservice due to

believing the former to be safer and more hygienic.

Manufacturers are expected to strengthen their logistics and distribution systems over the forecast

period, with a strong focus on improving cold chain systems. Players are keen to further expand

their distribution across China and into lower-tier cities. Players are also expected to focus on

quality and health, with ready meals for example likely to see the launch of more low-fat and low-

calorie options.

NUTRITION/STAPLES – KEY TRENDS AND DEVELOPMENTS

Trends

The government continued to strongly promote healthy living concepts to the Chinese population

throughout the review period with a variety of campaigns. Legislation was also adjusted to better

ensure health, with a growing number of local governments for example banning the sale of loose

oils and fats and encouraging consumers to opt for packaged products instead. A number of food

safety scandals during the review period also increased consumers' food safety concerns. There was

for example strong media coverage towards the end of 2013 of a scandal involving unpackaged rice,

with samples being found to contain excessive levels of the heavy metal cadmium. Consumers are

thus increasingly health-conscious and focused on food safety. Manufacturers also increasingly

focused on health towards the end of the review period, both in terms of marketing and with new

product development such as Inner Mongolia Mengniu's Mengniu Just Yoghurt, launched in

November 2013.

Nutrition/staples recorded slightly lower current value growth in 2014 in comparison to the review

period CAGR. This was largely due to maturity for product categories such as noodles and oils and

fats. Growth was however maintained by growing health-consciousness, with milk, cheese and

yoghurt notably benefiting from being viewed as healthy. Consumers are notably increasingly

interested in the digestive health benefits offered by probiotic yoghurt, with many consumers

believing that these products can aid weight loss. Yoghurt thus saw striking current value growth of

19% in 2013 over the previous year. Cheese meanwhile saw the strongest current value growth

within nutrition/staples at 25% in 2014, partly due to a low sales base but also due to growing

consumer interest in Western-style cuisine.

Meal replacement also saw strong current value growth in 2014 over the previous year with an

increase of 24%. Consumers are leading increasingly sedentary lifestyles, partly due to their daily

schedules becoming more hectic and leaving little time to exercise. However, consumers are

simultaneously becoming more focused on achieving a slim and healthy appearance due to their

increasing exposure to international beauty trends. There was thus growing interest in meal

replacement slimming, which is viewed as a more convenient way of losing weight rather than

spending time exercising.

There were numerous packaging innovations in nutrition/staple in 2014. Shaped liquid cartons are

for example becoming a popular packaging format for yoghurt. Since the success of Momchilovtsi,

launched by Bright Dairy & Food Co Ltd in 2009, Inner Mongolia Mengniu and Inner Mongolia Yili

24 | P a g e

also launched spoonable yoghurt in this packaging format, respectively launching Just Yoghurt and

Ambpoeial Greek Yoghurt in November 2013 and April 2014. In prepared baby food, Beijing Huiliduo

meanwhile launched Huiliduo in 25g thin wall plastic containers in April 2014. Compared with more

traditional 113g glass bottles, this range targets impulse consumption. Smaller pack sizes also

minimise the chance of product wastage, as fruits can oxidise when not used sufficiently quickly in

113g glass bottles. In baby formula, Abbott Nutrition meanwhile introduced SmartLock packaging

for HDPE containers towards the end of the review period. SmartLock offers a one-click lock on the

cap that is safe and convenient to use, enabling parents to prepare milk formula powder with just

one hand.

In 2014, raw material costs for dairy and wheat-based products continued to rise in China, with this

inflating unit prices. A premiumisation trend is also resulting in many consumers trading up, with

this trend being further encouraged by strong marketing support for premium brands such as

Bright's Momchilovtsi, Inner Mongolia Mengniu's Deluxe and Inner Mongolia Yili's Satine. Meal

replacement saw the biggest increase in unit price in 2014 over the previous year in

nutrition/staples, due to smaller manufacturers increasing their investment in advertising and

expanding distribution. Many of these smaller players passed increased costs on to Chinese

consumers by increasing selling prices.

Products specifically targeted at children are expected to become a key focus of new product

development in nutrition/staples in the forecast period. Players will be keen to capitalise on Chinese

parents paying more attention to food quality and safety, with child-specific products likely to

encourage consumers to trade up during the forecast period. In drinking milk products, there were

numerous child-specific launches towards the end of the review period such as Inner Mongolia

Mengniu's Mengniu Banana Milk and Mengniu Future Star Organic Milk in January 2014 and

Fonterra's Anchor Children in September 2014. Similar launches are likely in the forecast period. In

cheese, more brands targeting aiming children are meanwhile being imported such as Bongrain's

Milkana Bangbang Cheese.

In wheat-based products such as noodles, breakfast cereals and bread, child-specific products are

also expected to gain share in the forecast period. Towards the end of the review period Kemen

Noodle for example launched Kemen Children Noodles, with this fortified with minerals to help

children’s healthy development. Functional ingredients, a focus on quality and safety and attractive

packaging designs are expected to continue to characterise child-specific nutrition/staples in the

forecast period.

Nutrition/staples is expected to see value growth at constant 2014 prices over the forecast period,

although at a slower rate than the growth witnessed over the review period. Ongoing growth will be

supported by increasing disposable income levels and the combined efforts of the government and

media to encourage consumers to opt for healthier and safer products. Meanwhile, the

government's relaxation of China's one-child policy is also expected to boost the consumer base and

sales of baby food in the forecast period.

Consumer health consciousness will shape sales of nutrition/staples in the forecast period. Some

consumers are expected to cut back on products such as rice and oils and fats, due to these being

perceived as high in carbohydrates and calories. However, the impact of this trend will be

counterbalanced by consumers' growing focus on food safety. Due to food scandals being covered

25 | P a g e

intensively by the Chinese media, more consumers are expected to shift from unpackaged rice and

oils to packaged products, especially in lower-tier cities. As a result, oils and fats and rice will

continue to see value growth in the forecast period, seeing 6% and 12% value CAGRs at constant

2014 prices.

Manufacturers are also expected to introduce smaller pack sizes in nutrition/staples in the forecast

period. This will be in response to consumers' increasingly hectic lifestyles, with consumers thus

becoming less likely to purchase large bulk packs for home cooking. Manufacturers will also be able

to offer smaller pack sizes at higher unit prices, thus increasing their profit margins. Young urban

consumers are particularly showing a preference for small packs in everyday essentials such as rice

and oils and fats, to avoid keeping packs stored for long periods of time and also due to space

constraints. Breakfast cereals and noodles are meanwhile set to see the growing popularity of

single-cup packs in the forecast period, due to these offering considerable convenience.

Cheese is expected to continue to see the strongest sales growth in nutrition/staples in the forecast

period, with an impressive value CAGR of 19%. Growth will partly be linked to a relatively low sales

base but will primarily be driven by consumers' growing interest in Western-style food. Cheese is

expected to see particularly strong sales growth in major cities, where pizza and burger consumer

foodservice is burgeoning and encouraging more consumers to cook similar food at home. However,

as cold chain networks improve there will also be widening distribution for cheese across China in

the forecast period.

The unit price of nutrition/staples is expected to continue to increase above the level of inflation

over the forecast period. This will partly be due to consumers trading up to premium or higher-

quality products in search of greater nutritional value, flavour and product safety, especially in dairy

and baby food. Hikes in raw material costs such for product areas such as oils and fats and dairy will

however also increase the unit price of nutrition/staples in the forecast period.17

Alcohol

Alcohol is gaining popularity in China. Northern Chinese are more likely to consume alcohol than

Southern Chinese, as the climate is much colder in the North. Women in China generally do not

consume alcohol.

China is experiencing growth in the health and wellness, alcohol and tobacco and retail sectors,

resulting from increased urbanization and Western influence.18

China's craft brewing niche has made considerable steps in recent years. The country is already the

world's biggest beer market, with consumption recently reaching 50 billion liters annually. But signs

are growing that Chinese tastes are evolving past mass-produced lagers to the kind of innovative,

higher-quality brews favored by connoisseurs elsewhere in the world. According to Forbes, for instance,

the number of brewpubs in Shanghai alone has doubled since 2010.19

According to U.S. Brewers Association (BA), in 2013, U.S. craft beer exports to China reached 505,206

liters worth $1.15 million (FOB based). With an estimated growth of 30 percent by value, in 2014, it

could reach $1.48 million.

26 | P a g e

With a proactive three-year market promotional plan, U.S. craft beer exports to China could have a year-

on-year growth of 50 percent and reach an annual sale of $5 million by 2017. On an optimistic side,

should the growth reach 100 percent, annual sales could be $12 million by 2017.

Such optimistic market outlooks are based on the below facts:

China is the world’s largest beer producer and consumer; but its domestic beer production

growth slows down and the market of mass-production beers is becoming saturated

Given continued growth of income, Chinese beer consumers pursue better quality and various

flavors; therefore, imported beers, particularly those from Europe, are getting popular