Embed Size (px)

Citation preview

AIMR PERFORMANCEPRESENTATION

STANDARDS(AIMR-PPS®)

Amended and Restated as

the AIMR-PPS® Standards,the U.S. and Canadian version of GIPS®

PO Box 3668Charlottesville, VA 22903-0668 USA

Tel: 434-951-5499 • Fax: 434-951-5320E-mail: [email protected]

Internet: www.aimr.org

ASSOCIATION FOR INVESTMENT

MANAGEMENT AND RESEARCH

AIMR-PPS redraft Oct 2001 cover.qxd 10/3/2001 11:10 AM Page 1

CFA®, Chartered Financial Analyst, AIMR-PPS ®, GIPS ®, the Translation of GIPS Logo andCountry Version of GIPS Logo are just a few of the trademarks owned by the Associationfor Investment Management and Research (AIMR®). To view a list of the Association forInvestment Management and Research’s trademarks and a Guide for the Use of AIMR’sMarks, please visit our Web site at www.aimr.org.

AIMR-PPS redraft Oct 2001.fm Page -2 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR®

AIMR-PPS IMPLEMENTATION COMMITTEE2001–2002

CHAIR

James E. Hollis III, CFAStandish Mellon Asset ManagementBoston, Massachusetts

Thomas S. Drumm, CFANeedham, Massachusetts

James L. KermesGlenmede Trust CompanyPhiladelphia, Pennsylvania

Iain W. McAraJ.P. Morgan Investment Management, Inc.New York, New York

Neil E. Riddles, CFAHansberger Global Investors, Inc.Fort Lauderdale, Florida

Douglas S. Rogers, CFADeloitte & Touche Investment Advisers, LLCChicago, Illinois

Derek A. Sasveld, CFABrinson Partners, Inc.Chicago, Illinois

David D. SpauldingThe Spaulding Group, Inc.Somerset, New Jersey

Robert H. Steinbach, CFACommunications Solutions InternationalToronto, Ontario

Karyn D. Vincent, CFACAPS, Inc.Portland, Oregon

Lee N. Price, CFA (observer)Price Performance Measurement Systems, Inc.Palo Alto, California

AIMR STAFF

Jonathan A. BoersmaAlecia L. LicataJessica L. Mann, CFA

INVESTMENT PERFORMANCE COUNCIL (IPC)2001–2002

CHAIR

John C. Stannard, CFAFrank Russell CompanyUnited Kingdom

Yoshiaki AkedaNomura Funds Research and Technologies Co., Ltd.Japan

Carl R. BaconStatproUnited Kingdom

Louis Boulanger, CFAWilliam M. Mercer LimitedNew Zealand

Herbert M. Chain Deloitte & Touche LLPUnited States

Lynn A. Clark Ontario Municipal Employees Retirement SystemCanada

Alain Ernewein France

Bernd R. FischerCommerzbankGermany

David J. GambleBritish Airways Pension Investment ManagementUnited Kingdom

Lesley A. HarveySouth Africa

Brian HendersonThe WM CompanyUnited Kingdom

Willem Hensbergen Lombard Odier Institutional Asset ManagementThe Netherlands

Brian Hersey, CFAWatson Wyatt Investment ConsultingUnited States

AIMR-PPS redraft Oct 2001.fm Page -1 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR®

Jean-François HirschelSociete Generale Asset ManagementFrance

David H. S. HobbsPhillips & DrewUnited Kingdom

James E. Hollis III, CFAStandish Mellon Asset ManagementUnited States

Shigeo IshigakiKPMG Japan (Century Ota Showa & Co.)Japan

Iskander Ismail Amanah SSCM Asset ManagementMalaysia

Todd A. Jankowski, CFAThe Northwestern Mutual Life CompanyUnited States

Carol A. KennedyPantheon GroupUnited Kingdom

Bo KnudsenUnibank A/SDenmark

Yoh KuwabaraChuo Aoyama Audit CorporationJapan

Jörg LillaBHF BankGermany

David M. MacKendrickDM Independent Services Ltd.United Kingdom

Terence V. Pavlic, CFAPavlic Investment Advisors, Inc.United States

Ehsan RahmanWashington Metropolitan Area Transit AuthorityUnited States

Deborah ReidyNational Pensions Reserve FundIreland

Neil E. Riddles, CFAHansberger Global Investors, Inc.United States

Max RothBanque Cantonale VaudoiseSwitzerland

Paul S. Saint-PierreWall Street Realty CapitalUnited States

Maria E. Smith-BreslinSmith Affiliated Capital Corp.United States

Glenn SolomonCogent Investment OperationAustralia

Louise SpencerPricewaterhouseCoopers LLPUnited Kingdom

Cheng Chih SungGovernment of Singapore Investment CorporationSingapore

Ronald J. SurzRoxbury Capital ManagementUnited States

Ad J.C. van den OuwelandRobeco GroupThe Netherlands

Hans-Jörg von EuwJulius Baer Asset Management Ltd.Switzerland

AIMR STAFF

Jonathan A. BoersmaAlecia L. LicataJessica L. Mann, CFA

AIMR-PPS redraft Oct 2001.fm Page 0 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 1

AIMR PERFORMANCE PRESENTATION STANDARDS (AIMR-PPS®)

Amended and Restated asthe AIMR-PPS® Standards, the U.S. and Canadian version of GIPS®

OUTLINE

I. APPLICATION OF THE GIPS STANDARDS AT THE LOCAL LEVEL

A. BACKGROUNDB. AIMR-PPS REQUIREMENTS AND RECOMMENDATIONS DIFFERENT FROM THE GIPS STANDARDSC. GLOBAL INVESTMENT PERFORMANCE STANDARDS INTRODUCTION

II. CONTENT OF THE AIMR-PPS STANDARDS

III. VERIFICATION

APPENDIXES

A. GIPS STANDARDS SAMPLE PRESENTATION B. AIMR-PPS STANDARDS SAMPLE PRESENTATIONSC. AIMR-PPS ADVERTISING GUIDELINESD. GUIDANCE ON VERIFICATION

AIMR-PPS redraft Oct 2001.fm Page 1 Tuesday, October 2, 2001 5:35 PM

2 ©2001, AIMR®

I. APPLICATION OF THE GIPS STANDARDS AT THE LOCAL LEVEL

A. BACKGROUNDThe AIMR Performance Presentation Standards werefirst introduced by the Financial Analysts Federation’sCommittee for Performance Presentation Standards inthe September/October 1987 issue of the FinancialAnalysts Journal. Since that time, the AIMR-PPS stan-dards have been reviewed extensively by members ofthe industry and revised in response to their manycomments and recommendations. The underlyingprinciples of fair representation and full disclosure,however, have remained unchanged.

Since their establishment, the AIMR-PPS standardshave received overwhelming acceptance from the U.S.and Canadian investment industry. Initially, on a glo-bal basis, only a few countries outside North Americaadopted the AIMR-PPS standards to serve as the localperformance standards. Some countries chose toadhere to their own nationally accepted guidelineswhile others had few or no standards for presentinginvestment performance. These practices have limitedthe comparability of performance results from firmsin different countries and have hindered the ability offirms to penetrate markets on a global basis.

Implementing a Global StandardIn 1995, therefore, AIMR recognized the need for oneglobally accepted set of standards for the calculationand presentation of investment performance. AIMRsponsored and funded the Global Investment Perfor-mance Standards (GIPS) Committee to develop andpublish one global standard by which firms calculateand present performance to clients and prospectiveclients. On February 19, 1999, AIMR formallyendorsed the Global Investment Performance Stan-dards as the worldwide standard to calculate andpresent investment performance.

The GIPS standards, based on the underlying princi-ples of fair representation and full disclosure, have beencrafted to meet the needs and capacity of a broad rangeof global markets. Such standards also facilitate compe-tition in the global investment industry by allowingclients and potential clients to make an “apples toapples” comparison of investment advisory firms.

Investment Performance CouncilFollowing approval by the AIMR Board of Governorsin 1999, the GIPS committee’s role and responsibility in

developing the GIPS standards concluded. However,AIMR recognized that effective promotion, implemen-tation, and interpretation of the Standards require anoperational governance structure to meet the ongoingneeds for maintaining and developing high-qualityglobal investment performance standards. To meetthese needs, AIMR established the Investment Perfor-mance Council (IPC) in 2000. The IPC also provides apractical and effective implementation structure for theGIPS standards and encourages wider public partici-pation in an industrywide standard.

The principal goal of the IPC is to have all countriesadopt the GIPS standards as the Standard for invest-ment firms seeking to present historical investmentperformance. As of April 2001, approximately 25countries around the world have adopted or are in theprocess of adopting the GIPS standards or of estab-lishing a local investment performance standard. TheIPC believes the establishment and acceptance of theGIPS standards are vital steps in facilitating the avail-ability of comparable investment performance historyon a global basis. GIPS compliance provides firmswith a “passport” and creates a level playing fieldwhere all firms can compete on equal footing. How-ever, for the GIPS passport to be effective, sponsors ofall country standards must remove or minimizepotential local “barriers to entry” in the form of addi-tional requirements, over and above those found inthe GIPS standards.

The IPC strongly encourages countries without aninvestment performance standard in place to acceptGIPS standards as the local standard and translatethem into the local language when necessary, thuspromoting a “Translation of GIPS” (TG). However, theIPC recognizes that some countries will need to adoptcertain requirements in addition to the GIPS standards,especially when required by specific local regulation orto meet existing, well-established practice. Therefore,to achieve a globally harmonized investment perfor-mance presentation practice, the IPC is promoting a“Country Version of GIPS” (CVG) approach. Underthis approach, countries will adopt the GIPS standardsas their core standards. This core will be supplementedwhere provisions over and above GIPS standards arenecessary, preferably only to satisfy local regulatory orlegal requirements and well-established practices. Anyother differences must be transitioned out of the CVG

AIMR-PPS redraft Oct 2001.fm Page 2 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 3

during a specified period, so that the CVG convergeswith the GIPS standards. In this way, compliance withthe GIPS standards will provide investment managerswith a “right of access” to be considered alongsideinvestment managers who comply with the local stan-dards, thereby allowing all managers to be measuredon equal terms.

The IPC will also develop the GIPS standards asquickly as is practicable into a “gold standard.” Thisgold standard will eventually incorporate many of theregulatory and well-established best practices thatexist in local markets around the world.

AIMR-PPS Standards as a Country Version of GIPSIn early 1999, AIMR took the first step in movingtoward a global investment performance standard bysignificantly revising the requirements of the AIMR-PPS standards to bring them in line with the GIPSstandards. AIMR has now taken the next step byredrafting the AIMR-PPS standards into the CVGformat and restating them here as the U.S. andCanadian version of the GIPS standards. Accordingto the IPC’s global strategy, AIMR is the countrysponsor for the AIMR-PPS standards, the U.S. andCanadian version of the GIPS standards.

Because the GIPS standards are based on theAIMR-PPS standards, redrafting the AIMR-PPS stan-dards into the CVG format was primarily a reorgani-zation of the existing provisions, with only a fewsubstantive changes. AIMR hopes that this redraft ofthe AIMR-PPS standards will set an example of howcountries or regions with existing standards can movetoward one global standard by incorporating the GIPSstandards as the core of the local standard with mini-mal additional provisions only as necessary to satisfythe country-specific requirements (well-establishedpractice or regulation). The AIMR-PPS standards nowincorporate all the GIPS requirements and recommen-dations. The full text of the GIPS standards is con-tained in Section II of this document. Several additionsto the GIPS provisions will apply in the United Statesand Canada to represent well-established practices,and firms must observe them in addition to all GIPSrequirements in order to claim compliance with theAIMR-PPS standards. These minimal additions arenoted in the text of the provisions (Section II) in italicsas well as summarized in the AIMR-PPS Introductionin Section I.B. AIMR-PPS Requirements and Recom-mendations Different from GIPS.

The AIMR-PPS standards will automatically incorpo-rate future developments to the GIPS standards, par-ticularly those provisions affecting technical areas thatare currently addressed in the AIMR-PPS standardsbut not yet addressed in the GIPS standards (e.g., realestate and venture capital).

B. AIMR-PPS SPECIFIC REQUIREMENTS AND RECOMMENDATIONS DIFFERENT FROM THE GIPS STANDARDS

Although the AIMR-PPS standards incorporate all ofthe core GIPS requirements and recommendations,additional provisions apply to the AIMR-PPS stan-dards by nature of well-established practices. Firmsclaiming compliance with the GIPS standards mustalso satisfy the following AIMR-PPS specific require-ments in order to claim compliance with the AIMR-PPSstandards. These additions are included in the body ofthe AIMR-PPS provisions (Section II) as notations thatare italicized.

The following provisions of the AIMR-PPS standardsserve to supplement or modify existing GIPS require-ments and/or recommendations.

RequirementsSection II.4.A.2. Under the GIPS standards, firms mustdisclose the total firm assets for each period presented.Prior to the redraft of the AIMR-PPS standards, firmswere not required to disclose this information. There-fore, it is necessary to clarify that under the redraftedAIMR-PPS standards, firms must disclose total firmassets for each period retroactively.

Section II.4.A.13. Under the GIPS standards, firms arerequired to disclose whether the presentation conformswith local laws and regulations that differ from GIPSrequirements and the manner in which the local stan-dards conflict with the GIPS standards. According toexisting interpretations of the AIMR-PPS standards,firms must disclose whether the presentation conformsto local laws and regulations that differ from the AIMR-PPS requirements. The GIPS provision is modifiedslightly to require firms to disclose whether local lawsand regulations conflict with the AIMR-PPS standards.

Section II.4.A.14. The GIPS standards do not have an“effective date.” Instead, the GIPS standards requirefirms to initially have at least five years of compliantperformance history, and for any performance pre-sented for periods prior to January 1, 2000, that doesnot comply with the GIPS standards, firms must

AIMR-PPS redraft Oct 2001.fm Page 3 Tuesday, October 2, 2001 5:35 PM

4 ©2001, AIMR®

disclose the period of non-compliance and how thepresentation is not in compliance with the GIPS stan-dards. The AIMR-PPS standards have four effectivedates for compliance, which are provided in the AIMR-PPS Introduction, Section I.B. Under the AIMR-PPSstandards, when firms present performance results forperiods prior to the applicable effective dates of theAIMR-PPS standards that do not comply with theAIMR-PPS standards, they must disclose the periodsof non-compliance and how the presentation is not incompliance with the AIMR-PPS standards.

Section II.4.A.16. and II.4.B.3. Under the GIPS stan-dards, firms are recommended to disclose the feeschedule (see Section II.4.B.3). The AIMR-PPS stan-dards require firms to disclose the fee schedule. Toclaim compliance with the AIMR-PPS standards, thepresentation must disclose the firm’s fee scheduleappropriate to the presentation.

Section II.5.A.1.(a). AIMR-PPS standards have a morestringent requirement regarding the length of the his-torical record of performance that must be shown. TheGIPS standards require firms to present 5 years (ini-tially, building up to 10 years) whereas the AIMR-PPSstandards require 10 years. Firms claiming compliancewith the AIMR-PPS standards must present 10 yearsof performance history (or since firm inception ifinception is less than 10 years).

Section II.5.A.1.(c). Both the AIMR-PPS standards andthe GIPS standards require firms to present the numberof portfolios and amount of assets in the composite andthe percentage of the firm’s total assets represented bythe composite at the end of each period. However,prior to the redraft of the AIMR-PPS standards, firmscould choose when to calculate these figures (e.g.,beginning or end of period). The redrafted AIMR-PPSstandards now retroactively require (for all periodsafter January 1, 1997) firms to provide the number ofportfolios and amount of assets in the composite andthe percentage of the firm’s total assets represented bythe composite at the end of each period. Prior to Janu-ary 1, 1997, firms may choose to report these figures asof the beginning of the period or as of the end of theperiod, as long as the method prior to January 1, 1997,is consistently followed and disclosed.

Section II.5.A.1.(e). Firms must use the approvedAIMR-PPS “Compliance Statement” as provided inSection I.B of the AIMR-PPS Introduction in order toclaim compliance with the AIMR-PPS standards.

Section II.5.A.2. Under the GIPS standards, firms maylink non-GIPS-compliant performance to their compli-ant history so long as firms meet the disclosurerequirements of Section II.4 and no non-compliantperformance is presented for periods after January 1,2000. Firms claiming compliance with the AIMR-PPSstandards and wishing to also claim GIPS compliancemust note the potential historical differences betweenthe AIMR-PPS and GIPS standards and disclose thosedifferences. (See Section I.B. AIMR-PPS and GIPSStandards for a discussion of the historical differ-ences.) The effective dates of compliance and retroac-tive compliance guidelines for the AIMR-PPSstandards are also provided below.

Section II.5.A.8. The GIPS standards do not have aspecific requirement to prohibit firms from restatingcomposite results following a change in the firm’sorganization. The AIMR-PPS standards include arequirement that firms may not restate compositeresults following changes in a firm’s organization.

Additional AIMR-PPS SectionsBy implementing the CVG approach, the AIMR-PPSstandards have adopted the GIPS standards as the coreprinciples (subject to minor differences noted in italics).Sections II.1 through II.5 reflect the basic elementsinvolved in presenting performance information: InputData, Calculation Methodology, Composite Construc-tion, Disclosures, and Presentation and Reporting. TheAIMR-PPS standards also consist of four additionalsections (II.6 through II.9) that address the calculationand presentation of performance for alternative assetcategories (e.g., real estate, venture and private place-ments, wrap-fee accounts, and after-tax returns). Theseadditional sections have been imported from the pre-vious version of the AIMR-PPS standards with nochanges (except for minor changes made to require-ments II.8.A.2 and II.8.A.3 to clarify the wrap-feerequirements). However, they will be changed to con-form to the GIPS standards over time as guidelines inthese technical areas are developed and adopted by theIPC and AIMR.

VerificationSection III. Verification. The GIPS standards containone level of Verification, whereas Verification underthe AIMR-PPS standards has previously consisted oftwo levels: Level I (firmwide verification) and Level II(verification of a specific composite). To encourage theconvergence of the AIMR-PPS standards and the GIPS

AIMR-PPS redraft Oct 2001.fm Page 4 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 5

standards, Section III. Verification only contains theLevel I (GIPS) verification procedures. Level I (GIPS)verification focuses on firmwide compliance by con-firming that an investment firm has complied with allthe composite construction requirements on a firmwidebasis and that the firm’s processes and procedures aredesigned to calculate and present performance resultsin compliance with the AIMR-PPS standards.

The redrafted AIMR-PPS standards also serve as theinitial steps to creating only one level of verification inthe United States and Canada by eliminating as ofJanuary 1, 2003, “Level II (composite) verification” asan accepted form of verification. Instead, like the GIPSstandards, an investment management firm maychoose to have a further, more extensive, specificallyfocused examination or performance audit of a spe-cific composite presentation. After January 1, 2003,firms will not be able to make the claim that a partic-ular composite has been “verified” but can claim thatthe composite returns have been examined or audited.Until January 1, 2003, the previous Level II verificationprocedures have been retitled “Performance Examina-tion (Level II)” and have been redrafted to focus on theneed for the verifier to conduct and report on a LevelI verification prior to issuing a Performance Examina-tion (Level II) report.

Additional guidance for issuing and using a Level Iverification report as well as the procedures for con-ducting a Performance Examination (Level II) is pro-vided in Appendix D Verification Guidance. ThisAppendix serves to provide the U.S. and Canadianverification industry with guidance and to providemore clear and workable performance examinationprocedures.

AIMR-PPS and GIPS StandardsFirms currently wishing to comply with the GIPS stan-dards must be able to meet all of the GIPS requirements,including a five-year compliant historical record. As ofJanuary 1, 2002, all firms that claim compliance withthe AIMR-PPS standards will also have a minimum offive years of GIPS-compliant history (or compliant his-tory since firm inception) and can therefore claim com-pliance with the GIPS standards. However, beforeasserting their GIPS claim, firms must consider that theGIPS standards include a disclosure requirement thatstates any performance presented prior to January 1,2000, that does not comply with the GIPS standardsmust be disclosed and firms must explain how thepresentation is not in compliance with the GIPS stan-

dards (Section II.4.A.14). From a calculation perspec-tive, the AIMR-PPS and the GIPS standards are thesame for all performance results for periods after Jan-uary 1, 1997. However, for performance results forperiods prior to 1997, two potential issues exist underthe AIMR-PPS standards that could result in perfor-mance reporting that adheres to the AIMR-PPS stan-dards but does not meet the GIPS requirements andwould warrant the additional GIPS disclosure:

• Disclosures: Under the GIPS standards, firms arerequired to disclose the number of portfolios andamount of assets in the composite and the percent-age of the firm’s total assets represented by thecomposite as of the end of the period. Under theAIMR-PPS standards, firms must disclose thesefigures as of the end of the period for all periodsafter January 1, 1997, but prior to 1997, firms canchoose when to make these disclosures (beginningor end of period) under the AIMR-PPS standards.

• Appropriate Treatment of Accrued Income:According to the GIPS standards, in both thenumerator and denominator, the market values offixed-income securities must include accruedincome for all periods. Prior to January 1, 1997, theAIMR-PPS standards did not specify that firmsmust accrue income in both the beginning andending market values (numerator and denomina-tor) for performance calculations.

Effective Dates for ComplianceThe AIMR Performance Presentation Standards,amended and restated as the AIMR-PPS Standards,the U.S. and Canadian version of GIPS, were adoptedby the AIMR Board of Governors on May 20, 2001. Tofacilitate the transition to the revised Standards,firms claiming compliance with the AIMR-PPS stan-dards will have until December 31, 2001 to satisfy thenew requirements resulting from the revision. Theimplementation date of the revised Standards is Jan-uary 1, 2002. On this date, the restated Standards willfully replace the previous version of the Standardsand any performance presentations created on orafter January 1, 2002, must comply with the revisedAIMR-PPS standards.

The GIPS standards were adopted without an effectivedate for compliance. Because the AIMR-PPS standardspreceded the GIPS standards, it was necessary todevelop effective dates for compliance with the AIMR-PPS standards to allow firms to build a compliant trackrecord and develop the infrastructure necessary to

AIMR-PPS redraft Oct 2001.fm Page 5 Tuesday, October 2, 2001 5:35 PM

6 ©2001, AIMR®

comply while promoting the importance and rele-vance of standards. For an investment firm to claimcompliance with the AIMR-PPS standards, the firmmust meet the following historical effective dates:

• From January 1, 1993, all of the firm’s actual dis-cretionary fee-paying nontaxable portfolios solelyinvested in U.S. and/or Canadian investmentsmust be presented in composites that adhere to theAIMR-PPS standards.

• From January 1, 1994, all of the firm’s actualdiscretionary fee-paying portfolios invested innon-U.S. and/or non-Canadian investments(“international portfolios”) and taxable portfo-lios (both U.S., Canadian and international) mustbe presented in composites that adhere to theAIMR-PPS standards.

• From July 1, 1995, all of the firm’s actual discretion-ary fee-paying portfolios meeting the definition ofa wrap-fee account must be presented in compos-ites that adhere to the AIMR-PPS standards.

• From January 1, 1997, all of the firm’s compositesand performance presentations must includeaccrued income in both the beginning and endingmarket values for performance calculations.

Clarification, Guidance and Interpreta-tion of the AIMR-PPS StandardsFirms that claim compliance with the AIMR-PPS stan-dards must understand all the requirements and rec-ommendations of the AIMR-PPS standards, includingany updates, reports, or clarifications published bythe AIMR-PPS Implementation Committee or theInvestment Performance Council, including the mostrecent version of the AIMR Performance PresentationStandards Handbook. All clarification and updateinformation will be made available to the public viathe AIMR Web site (www.aimr.org/standards/) andmust be considered when determining a firm’s claimof compliance.

Once the AIMR-PPS standards are endorsed by the IPCas a CVG, the IPC will become the responsible body forinterpreting, clarifying, and expanding the GIPS stan-dards (which are the core of the AIMR-PPS standards).The AIMR-PPS Implementation Committee will onlyinterpret and expand the AIMR-PPS standards toaddress U.S. and Canadian issues (e.g., after-tax per-formance reporting).

Firm Policies and ProceduresImplicit in an investment firm’s claim of compliance isthe need for the firm to document, in writing, its poli-

cies and procedures used in establishing and maintain-ing compliance with all the applicable requirements ofthe AIMR-PPS standards. Documented policies andprocedures will not only aid firms in their ongoingmaintenance of compliance but will also benefit bothverifiers and regulators in examining a firm’s claim ofcompliance with the AIMR-PPS standards.

AIMR-PPS Advertising GuidelinesThe ability to advertise performance results is essen-tial to every investment adviser. AIMR recently devel-oped the AIMR-PPS Advertising Guidelines to allowfirms to claim compliance with the AIMR-PPS stan-dards and present limited or no performance informa-tion in an advertisement as long as the firm adheres tothe Guidelines. The Guidelines require that firmspresent certain information that is a subset of theinformation required by the AIMR-PPS standards.Alternatively, firms can claim compliance with thestandards without presenting any performance infor-mation. AIMR anticipates that the IPC will use theAIMR-PPS Advertising Guidelines as a base todevelop similar guidance to allow firms to advertisetheir claim of compliance with the GIPS standards.

AIMR-PPS Claim of ComplianceOnce a firm has met all of the required elements of theAIMR-PPS standards, the firm may use the following“Compliance Statement” on a performance presenta-tion that meets all of the requirements of the Standardsto indicate that the presentation is in compliance withthe AIMR-PPS standards:

[Insert name of firm] has prepared and pre-sented this report in compliance with the Perfor-mance Presentation Standards of the Associationfor Investment Management and Research(AIMR-PPS®), the U.S. and Canadian version ofthe Global Investment Performance Standards(GIPS®). AIMR has not been involved in thepreparation or review of this report.

The AIMR-PPS Claim of Compliance statement canonly be made on a presentation that fully adheres tothe requirements of the AIMR-PPS standards. Firmswishing to claim compliance with both the AIMR-PPSand the GIPS standards must include the AIMR-PPSCompliance Statement as well as the GIPS ComplianceStatement set out in the GIPS Introduction in SectionI.C.17 of this document.

Retroactive ComplianceThe AIMR-PPS standards require that firms report,at a minimum, ten years of investment performance

AIMR-PPS redraft Oct 2001.fm Page 6 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 7

(or performance since the inception of the firm ifinception is less than ten years) to claim compliancewith the Standards. The record prior to the January1, 1993, implementation date of the Standards neednot be restated for a firm to claim compliance as longas the firm follows the guidelines of retroactive com-pliance. However, firms must present 10 years ofannual performance (assuming inception is at leastten years ago) in order to satisfy the requirements ofthe AIMR-PPS standards.

Firms with records or performance calculations forperiods prior to the applicable effective date(s) that arenot in conformance with the AIMR-PPS standards canstill claim compliance with the AIMR-PPS standardsif certain conditions are met. To claim compliance, thefirm has three options:

• restate its historical performance numbers inaccordance with the AIMR-PPS standards;

• restate its historical performance in accordancewith the Relaxed Retroactive Standards,explained in the paragraphs below, for retroactivecompliance; or

• use its nonconforming historical performance anddisclose specifically when and how the perfor-mance is not in compliance.

The first option is the desired approach. For the secondoption, under the Relaxed Retroactive guidelines forcompliance prior to January 1, 1993, two relaxationsare allowed:• Portfolios and composites may be valued on an

annual basis as a maximum. Valuation periods forboth portfolios and composites may be as long asone year (although if cash flows were significantduring the year, valuations should be done morefrequently). To qualify for inclusion in a compositethat is valued annually, a portfolio must have beenunder management according to a strategy appro-priate to the composite for at least one year.

• Accrual accounting need not be applied.

For the third option, if a firm claims compliance withthe AIMR-PPS standards but the performance recordprior to the applicable effective date is not in compli-ance and the non-compliance periods are linked toperiods that are in compliance, the firm must:• disclose that the full record is not in compliance,• identify the non-compliance periods, and• explain exactly how the non-compliance periods

are out of compliance.

In any case, the performance record after the applica-ble effective dates must adhere fully to the require-ments of the AIMR-PPS standards.

AIMR-PPS redraft Oct 2001.fm Page 7 Tuesday, October 2, 2001 5:35 PM

8 ©2001, AIMR®

C. GLOBAL INVESTMENT PERFORMANCE STANDARDS INTRODUCTION

The IPC’s standardized CVG approach requires that CVGsinclude the GIPS Introduction in its entirety with no addi-tions or modifications. The following section contains thefull text of the GIPS Introduction as adopted by the AIMRBoard of Governors on February 19, 1999.

All references made to GIPS below are relevant to the AIMR-PPS standards as well (except where highlighted in italics).

1. INTRODUCTION

PREAMBLE—WHY IS A GLOBAL STANDARD NEEDED?1. The financial markets and the investment man-

agement industry are becoming increasingly glo-bal in nature. Given the variety of financial entitiesand countries involved, this globalization of theinvestment process and the exponential growth ofassets under management demonstrate the needto standardize the calculation and presentation ofinvestment performance.

2. Prospective clients and asset managers will bene-fit from an established standard for investmentperformance measurement and presentation thatis recognized worldwide. Investment practices,regulation, performance measurement, andreporting of performance results vary consider-ably from country to country. Some countries haveguidelines that are widely accepted within theirborders, and others have few recognized stan-dards for presenting investment performance.

3. Requiring investment managers to adhere to per-formance presentation standards will help assureinvestors that the performance information is bothcomplete and fairly presented. Firms in countrieswith minimal presentation standards will be ableto compete for business on an equal footing withfirms from countries that have more developedstandards. Firms from countries with establishedpractices will have more confidence of being fairlycompared to “local” firms when competing forbusiness in countries that have not previouslyadopted performance standards.

4. Both prospective and existing clients of invest-ment firms will benefit from a global investmentperformance standard by having a greater degreeof confidence in the performance numbers pre-sented by the firms. Performance standards that

are accepted in all countries enable all investmentfirms to measure and present their investmentperformance so that clients can readily compareinvestment performance among firms.

VISION STATEMENT5. A global investment performance standard leads

to readily accepted presentations of investmentperformance that (1) present performance resultswhich are readily comparable among investmentmanagers, without regard to geographic location,and (2) facilitate a dialogue between investmentmanagers and their prospective clients about thecritical issues of how the manager achieved per-formance results and future investment strategies.

OBJECTIVES6. To obtain worldwide acceptance of a standard for

the calculation and presentation of investmentperformance in a fair, comparable format that pro-vides full disclosure.

7. To ensure accurate and consistent investmentperformance data for reporting, record keeping,marketing, and presentation.

8. To promote fair, global competition among invest-ment firms for all markets without creating barriersto entry for new firms.

9. To foster the notion of industry self-regulation ona global basis.

OVERVIEW10. The Global Investment Performance Standards

(GIPS) have several key characteristics:

a. GIPS are ethical standards for investmentperformance presentation to ensure fair rep-resentation and full disclosure of an invest-ment firm’s performance history.

b. GIPS exist as a minimum worldwide stan-dard where local or country-specific law, reg-ulation, or industry standards may not existfor investment performance measurementand/or presentation.

c. GIPS require managers to include all actualfee-paying, discretionary portfolios in com-posites defined according to similar strategyand/or investment objective and requirefirms to show GIPS-compliant history for aminimum of five years, or since inception ofthe firm or composite if in existence less than

AIMR-PPS redraft Oct 2001.fm Page 8 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 9

five years. The AIMR-PPS standards requirethat a firm report ten years of annual investmentperformance (or since firm inception if inceptionis less than ten years).

d. GIPS require firms to use certain calculationand presentation methods and to make certaindisclosures along with the performancerecord.

e. GIPS rely on the integrity of input data. Theaccuracy of input data is critical to the accu-racy of the performance presentation. Forexample, benchmarks and compositesshould be created/selected on an ex antebasis, not after the fact.

f. GIPS consist of guidelines that firms arerequired to follow in order to claim compli-ance. The adoption of other elements of GIPSis recommended for firms to achieve bestpractice in performance presentation.

g. GIPS apply to the presentation of investmentperformance of assets managed on behalf ofa third party.

h. GIPS should be applied with the goal of fulldisclosure and fair representation of invest-ment performance. Meeting the objective offull and fair disclosure is likely to requiremore than compliance with the minimumrequirements of GIPS. If an investment firmapplies GIPS in a performance situation thatis not addressed specifically by the standardsor is open to interpretation, disclosures otherthan those required by GIPS may be neces-sary. To fully explain the performanceincluded in a presentation, firms are encour-aged to present all relevant supplementalinformation.

i. In cases in which applicable local or country-specific law or regulation conflicts with GIPS,the Standards require firms to comply withthe local law or regulation and make fulldisclosure of the conflict.

j. GIPS do not address every aspect of perfor-mance measurement, valuation, attribution,or coverage of all asset classes. GIPS willevolve over time to address additionalaspects of investment performance. Certainrecommended elements in GIPS may becomerequirements in the future.

SCOPE11. Application of GIPS. Investment management

firms from any country may come into compliancewith GIPS. Compliance with GIPS will facilitate afirm’s participation in the investment manage-ment industry on a global level.

12. Definition of a Firm. GIPS must be applied on afirmwide basis. A firm may define itself as:

a. an entity registered with the appropriatenational regulatory authority overseeing theentity’s investment management activities;or

b. an investment firm, subsidiary, or divisionheld out to clients or potential clients as adistinct business unit (e.g., a subsidiary firmor distinct business unit managing privateclient assets may claim compliance for itselfwithout its parent organization being in com-pliance);

c. (until January 1, 2005) all assets managed toone or more base currencies (for firms man-aging global assets).

When presenting investment performance in compli-ance with GIPS, an investment management firm muststate how it defines itself as a “firm.”

13. Historical Performance Record.

a. A firm is required to present, at a minimum,five years of annual investment performancethat is compliant with GIPS. If the firm orcomposite has been in existence less thanfive years, firms must present performancesince the inception of the firm or composite.The AIMR-PPS standards require that a firmreport ten years of annual investment perfor-mance (or since firm inception if inception is lessthan ten years).

b. After a firm presents five years of complianthistory, firms must present additional annualperformance up to ten years. For example,after a firm presents five years of complianthistory, the firm must add an additional yearof performance each year so that after fiveyears of claiming compliance, the firm pre-sents a ten-year performance record.

c. A firm may link a non-GIPS-compliant per-formance record to their compliant history solong as no non-compliant performance is

AIMR-PPS redraft Oct 2001.fm Page 9 Tuesday, October 2, 2001 5:35 PM

10 ©2001, AIMR®

presented for periods after January 1, 2000,and the firm discloses the periods of non-compliance and explains how the presenta-tion is not in compliance with GIPS. AfterJanuary 1, 2002, firms that meet the requirementsof the AIMR-PPS standards also meet all therequirements of the GIPS standards and can there-fore claim compliance with GIPS. However, priorto asserting their GIPS claim, firms must considerthat GIPS includes a disclosure requirement thatstates any performance presented prior to January1, 2000, that does not comply with the GIPSstandards must be disclosed and firms mustexplain how the presentation is not in compliancewith GIPS (Section II.4.A.14). For a discussion ofthe possible historical differences between theAIMR-PPS and GIPS standards, see Section I.BAIMR-PPS and GIPS Standards.

Nothing in this section shall prevent firms from imme-diately presenting more than five years of perfor-mance results.

COMPLIANCE14. Requirements. Firms must meet all the require-

ments set forth in GIPS to claim compliance withGIPS. Although GIPS requirements must be metimmediately by a firm claiming compliance, thefollowing requirements do not go into effect untila future date:

a. Portfolios must be valued at least monthly forperiods beginning January 1, 2001.

b. Time-weighted rates of return adjusted forcash flows are required. Firms must use time-weighted rates of return adjusted for daily-weighted cash flows for periods beginningJanuary 1, 2005.

c. For periods beginning January 1, 2010, firmswill likely be required to value portfolios onthe date of any external cash flow.

d. Firms must use trade-date accounting forperiods beginning January 1, 2005.

e. Accrual accounting must be used for divi-dends (as of the ex dividend date) for periodsbeginning January 1, 2005.

Until these future requirements become effective,these provisions should be considered recommenda-tions. Firms are encouraged to implement theserequirements prior to their effective date. To ease com-pliance with GIPS when the future requirements take

effect, firms should design performance software toincorporate these future requirements.

15. Compliance Check. Firms must take all steps nec-essary to ensure that they have satisfied all of therequirements of GIPS before claiming compliancewith GIPS. Firms are strongly encouraged to per-form periodic internal compliance checks andimplement adequate business controls on allstages of the investment performance process—from data input to presentation material—toensure the validity of compliance claims.

16. Third-Party Performance Measurement andComposite Construction. GIPS recognize the roleof independent third-party performance measur-ers and the value they can add to the firm’sperformance-measurement activities. Wherethird-party performance measurement is an estab-lished practice or is available, firms are encour-aged to use this service as it applies to theinvestment firm. Similarly, where the practice is toallow third parties to construct composites forinvestment firms, firms can use such compositesin a GIPS-compliant presentation only if the com-posites comply with GIPS.

17. Claim of Compliance. Once a firm has met all ofthe required elements of GIPS, the firm may usethe following “Compliance Statement” to indicatethat the performance presentation is in compli-ance with GIPS:

[Insert name of firm] has prepared andpresented this report in compliancewith the Global Investment Perfor-mance Standards (GIPS®).

In order to claim compliance with the AIMR-PPSstandards, firms must use the following Claim of Com-pliance Statement:

[Insert name of firm] has prepared and pre-sented this report in compliance with thePerformance Presentation Standards of theAssociation for Investment Managementand Research (AIMR-PPS®), the U.S. andCanadian version of the Global InvestmentPerformance Standards (GIPS®). AIMRhas not been involved in the preparation orreview of this report.

If the performance presentation does not meet allof the requirements of GIPS, firms cannot repre-sent that the performance presentation is “in

AIMR-PPS redraft Oct 2001.fm Page 10 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 11

compliance with the Global Investment Perfor-mance Standards except for . . . .” Statementsreferring to the calculation methodology used ina presentation as being “in accordance (or com-pliance) with the Global Investment PerformanceStandards” are prohibited except when appliedto the performance of a single, existing client.

18. Sample Presentation. A sample presentation,shown in Appendix A, provides an example ofwhat a compliant performance presentation couldlook like, including disclosures.

RELATIONSHIP OF GIPS WITH COUNTRY-SPECIFIC LAWS, REGULATIONS, AND INDUSTRY STANDARDS19. GIPS fill the void where no country standards

exist. Regulators and investment organizationsworldwide are strongly encouraged to recognizeand adopt GIPS as the performance presentationstandard applicable to their constituencies. If thereis a need for country-specific guidelines that gobeyond GIPS, regulators and organizations areencouraged to develop and implement suchguidelines to augment, but not conflict with, GIPS.Regulators are urged to supervise country compli-ance with GIPS and any country-specific stan-dards that may exist.

20. Where existing laws, regulations, or industry stan-dards already impose performance presentationstandards, firms are strongly encouraged to com-ply with GIPS in addition to those local require-ments. Compliance with applicable law orregulation does not necessarily lead to compliancewith GIPS. When complying with GIPS and local

law or regulation, firms must disclose any locallaws and regulations that conflict with GIPS. TheAIMR-PPS standards require firms to disclose whetherthe presentation conforms with local laws and regula-tions that differ from AIMR-PPS requirements and themanner in which the local standards conflict with theAIMR-PPS standards.

21. The establishment of GIPS will minimize the com-plexities that result with the existing contingentreciprocity agreements among organizations withtheir own standards. Organizations are encour-aged to recognize GIPS rather than establish“country-to-country” reciprocity agreements forcountry-specific standards. When a country orgroup establishes local performance presentationstandards, such standards should incorporate allof the required elements of the GIPS and state thatcompliance with GIPS is equivalent to compliancewith the local standards.

22. As required by the IPC, countries with existingstandards must specifically acknowledge GIPS para-graph 21 (above) by including the following “right ofaccess” statement to emphasize that firms that areGIPS-compliant but not in compliance with the CVG(e.g. AIMR-PPS) are permitted to compete withmanagers that comply with the CVG in managersearches, and so on.

Right of Access statement:

“A GIPS-compliant firm is permitted to present itsGIPS-compliant investment performance in any mar-ket and should receive full consideration alongside aninvestment firm that claims compliance with theAIMR-PPS standards.”

AIMR-PPS redraft Oct 2001.fm Page 11 Tuesday, October 2, 2001 5:35 PM

12 ©2001, AIMR®

II. CONTENT OF THE AIMR-PPS STANDARDS

(Amended and Restated asthe AIMR-PPS Standards, the U.S. and Canadian Version of GIPS)

OUTLINE

Provisions of the AIMR-PPS and Global Investment Performance Standards*

1. Input Data

2. Calculation Methodology

3. Composite Construction

4. Disclosures

5. Presentation and Reporting

Additional AIMR-PPS Provisions For Alternative Asset Categories

6. Real Estate

7. Venture and Private Placements

8. Wrap-Fee Accounts

9. After-Tax Performance

*The GIPS Provisions above have been supplemented or modified with additional AIMR-PPS requirements andrecommendations. The additions are highlighted in italics in this section and are summarized in the AIMR-PPSIntroduction Section I.B.

AIMR-PPS redraft Oct 2001.fm Page 12 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 13

Provisions of the AIMR-PPS and Global Investment Performance Standards

All references made to GIPS below are relevant to theAIMR-PPS standards as well (except where indicatedby italics).

GIPS is divided into five sections that reflect the basicelements involved in presenting performance informa-tion: Input Data, Calculation Methodology, CompositeConstruction, Disclosures, and Presentation andReporting.

1. Input Data: Consistency of input data is critical toeffective compliance with GIPS and establishesthe foundation for full, fair, and comparableinvestment performance presentations. The Stan-dards provide the blueprint for a firm to follow inconstructing this foundation.

2. Calculation Methodology: Achieving compara-bility among investment management firms’ per-formance presentations requires uniformity inmethods used to calculate returns. The Standardsmandate the use of certain calculation methodol-ogies (e.g., performance must be calculated usinga time-weighted total-rate-of-return method).

3. Composite Construction: A composite is anaggregation of a number of portfolios into a singlegroup that represents a particular investmentobjective or strategy. The composite return is theasset-weighted average of the performance resultsof all the portfolios in the composite. Creatingmeaningful, asset-weighted composites is criticalto the fair presentation, consistency, and compa-rability of results over time and among firms.

4. Disclosures: Disclosures allow firms to elaborateon the raw numbers provided in the presentationand give the end user of the presentation theproper context in which to understand the perfor-

mance results. To comply with GIPS, firms mustdisclose certain information about their perfor-mance presentation and the calculation methodol-ogy adopted by the firm. Although somedisclosures are required of all firms, others arespecific to certain circumstances and thus may notbe applicable in all situations.

5. Presentation and Reporting: After constructingthe composites, gathering the input data, calcu-lating returns, and determining the necessary dis-closures, the firm must incorporate thisinformation in presentations based on the guide-lines set out in GIPS for presenting the investmentperformance results. No finite set of guidelinescan cover all potential situations or anticipatefuture developments in investment industrystructure, technology, products, or practices.When appropriate, firms have the responsibilityto include in GIPS-compliant presentations infor-mation not covered by the Standards.

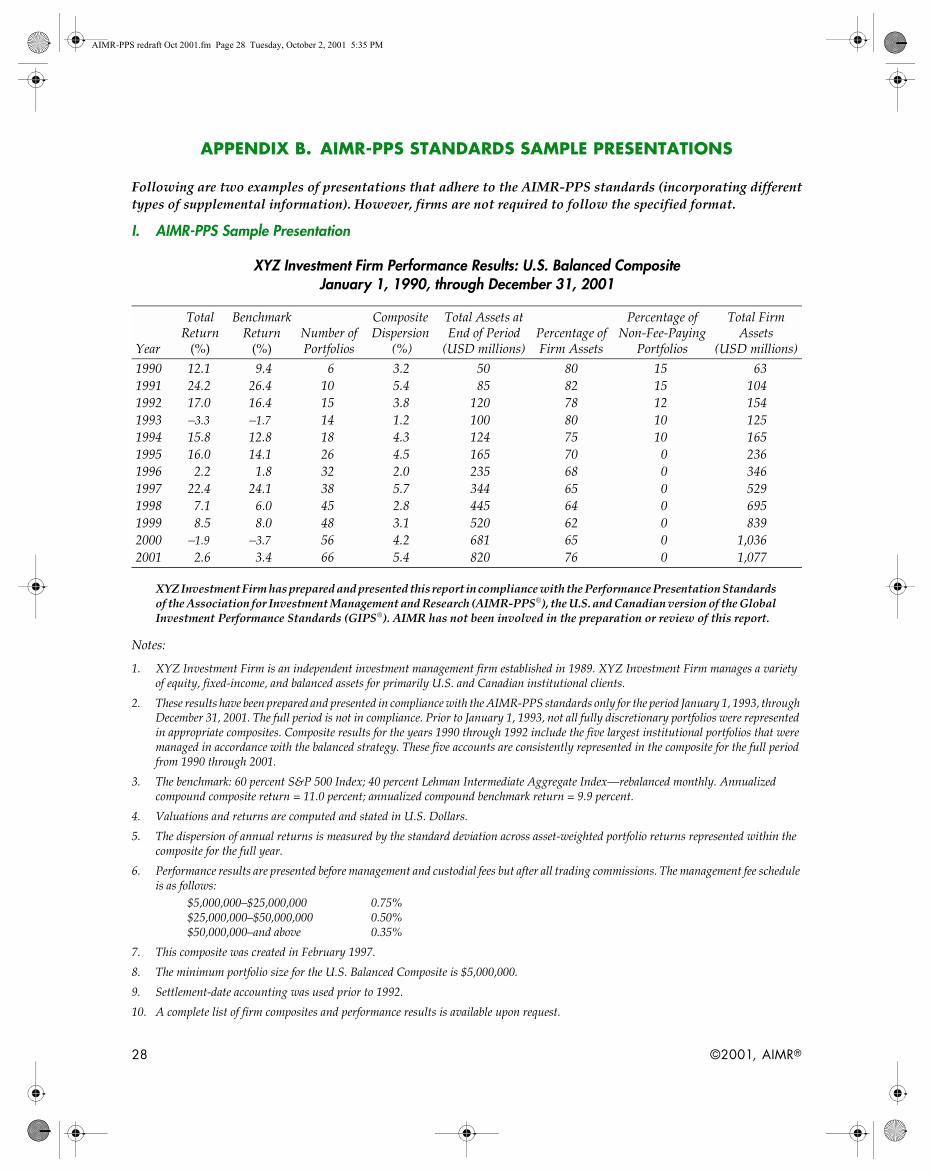

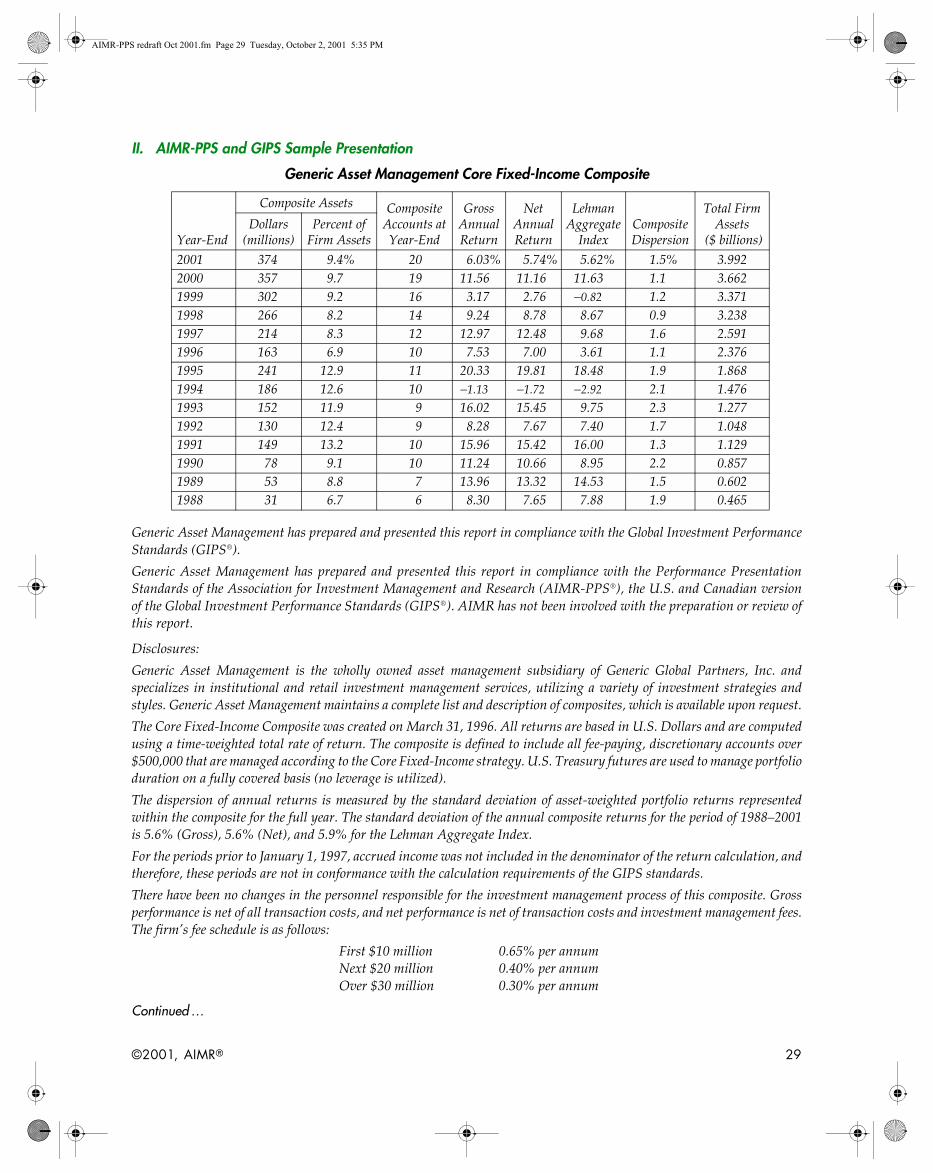

The Standards for each section are divided betweenrequirements, listed first in each section, and recom-mended guidelines. Firms must follow the requiredelements of GIPS to claim compliance with GIPS. Firmsare strongly encouraged to adopt and implement therecommendations to ensure that the firm fully adheresto the spirit and intent of GIPS. An example of a GIPS-compliant presentation for a single composite isincluded in Appendix A. Examples of AIMR-PPS-compliant presentations are also provided in Appendix B.

Although GIPS may be translated into many lan-guages, if a discrepancy arises between the differentversions of the standards, the English version of GIPSis controlling.

AIMR-PPS redraft Oct 2001.fm Page 13 Tuesday, October 2, 2001 5:35 PM

14 ©2001, AIMR®

Additional AIMR-PPS Provisions For Alternative Asset Categories

The following four sections (6–9) contain additionalrequirements and recommendations for firms to followwhen presenting the performance results of AdditionalAsset Categories in compliance with the AIMR-PPS stan-dards. These sections are reproduced exactly from the pre-vious version of the AIMR-PPS standards with no changes(except for minor changes made to requirements II.8.A.2and II.8.A.3 to clarify the wrap-fee requirements). As theGIPS standards are developed to address these alternativeasset categories, these sections will be changed to conformto the new GIPS guidelines.

6. Real Estate: Because of its unique characteristics,particularly the lack of a readily verifiable secondarymarket to determine asset values, real estate perfor-mance presentation guidelines warrant separate treat-ment. This section provides guidelines for calculatingand presenting the performance results of real estateinvestments.

7. Venture and Private Placements: AIMR recognizesthat there are difficulties inherent in applying therequirements of the AIMR-PPS standards to invest-ments in venture and private placements. AIMR devel-oped this section to recognize the special requirementsof these different asset classes within the overall ethicalframework of the standards.

8. Wrap-Fee Accounts: Firms must follow the require-ments in this section when reporting performanceresults on wrap-fee accounts in compliance with theAIMR-PPS standards. For purposes of the AIMR Per-formance Presentation Standards, the definition of awrap account is the same as the U.S. Securities andExchange Commission’s definition of a wrap-fee pro-gram: “a program [account] under which any client ischarged a specified fee or fees not based directly upontransactions in a client’s account for investment advi-sory services (which may include portfolio managementor advice concerning the selection of other investmentadvisers) and execution of client transactions.”

9. After-Tax Performance: Currently, firms are recom-mended to present performance results after the effectsof taxes. If firms are reporting performance after-taxresults in compliance, they must follow the require-ments in this section. The objective of these guidelinesis to provide additional information that will help pro-spective clients to assess results in a meaningful waywhen considering the tax implications of the invest-ment. The After-Tax Subcommittee of the AIMR-PPSImplementation Committee is currently working torevise the required and recommended elements of theafter-tax provisions.

AIMR-PPS redraft Oct 2001.fm Page 14 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 15

1. Input Data

1.A. Requirements

1.A.1. All data and information necessary tosupport a firm’s performance presen-tation and to perform the required cal-culations must be captured andmaintained.

1.A.2. Portfolio valuations must be based onmarket values (not cost basis or bookvalues).

1.A.3. Portfolios must be valued at least quar-terly. For periods beginning January 1,2001, portfolios must be valued at leastmonthly. For periods beginning Janu-ary 1, 2010, it is anticipated that firmswill be required to value portfolios onthe date of any external cash flow.

1.A.4. Firms must use trade-date accountingfor periods beginning January 1, 2005.

1.A.5. Accrual accounting must be used forfixed-income securities and all otherassets that accrue interest income.

1.A.6. Accrual accounting must be used fordividends (as of the ex dividend date)for periods beginning January 1, 2005.

1.B. Recommendations

1.B.1. Sources of exchange rates should bethe same for the composite and thebenchmark.

2. Calculation Methodology

2.A. Requirements

2.A.1. Total return, including realized andunrealized gains plus income, must beused.

2.A.2. Time-weighted rates of return thatadjust for cash flows must be used.Periodic returns must be geometricallylinked. Time-weighted rates of returnthat adjust for daily-weighted cashflows must be used for periods begin-ning January 1, 2005. Actual valua-tions at the time of external cash flowswill likely be required for periodsbeginning January 1, 2010.

2.A.3. In both the numerator and the denom-inator, the market values of fixed-income securities must includeaccrued income.

2.A.4. Composites must be asset weightedusing beginning-of-period weightingsor another method that reflects bothbeginning market value and cashflows.

2.A.5. Returns from cash and cash equiva-lents held in portfolios must beincluded in total-return calculations.

2.A.6. Performance must be calculated afterthe deduction of all trading expenses.

2.A.7. If a firm sets a minimum asset level forportfolios to be included in a compos-ite, no portfolios below that asset levelcan be included in that composite.

2.B. Recommendations

2.B.1. Returns should be calculated net ofnon-reclaimable withholding taxes ondividends, interest, and capital gains.Reclaimable withholding taxes shouldbe accrued.

2.B.2. Performance adjustments for externalcash flows should be treated in a con-sistent manner. Significant cash flows(i.e., 10 percent of the portfolio orgreater) that distort performance (i.e.,plus or minus 0.2 percent for theperiod) may require portfolio revalua-tion on the date of the cash flow (orafter investment) and the geometriclinking of subperiods. Actual valua-tions at the time of any external cashflows will likely be required for peri-ods beginning January 1, 2010.

3. Composite Construction

3.A. Requirements

3.A.1. All actual fee-paying discretionaryportfolios must be included in at leastone composite.

3.A.2. Firm composites must be definedaccording to similar investment objec-tives and/or strategies.

AIMR-PPS redraft Oct 2001.fm Page 15 Tuesday, October 2, 2001 5:35 PM

16 ©2001, AIMR®

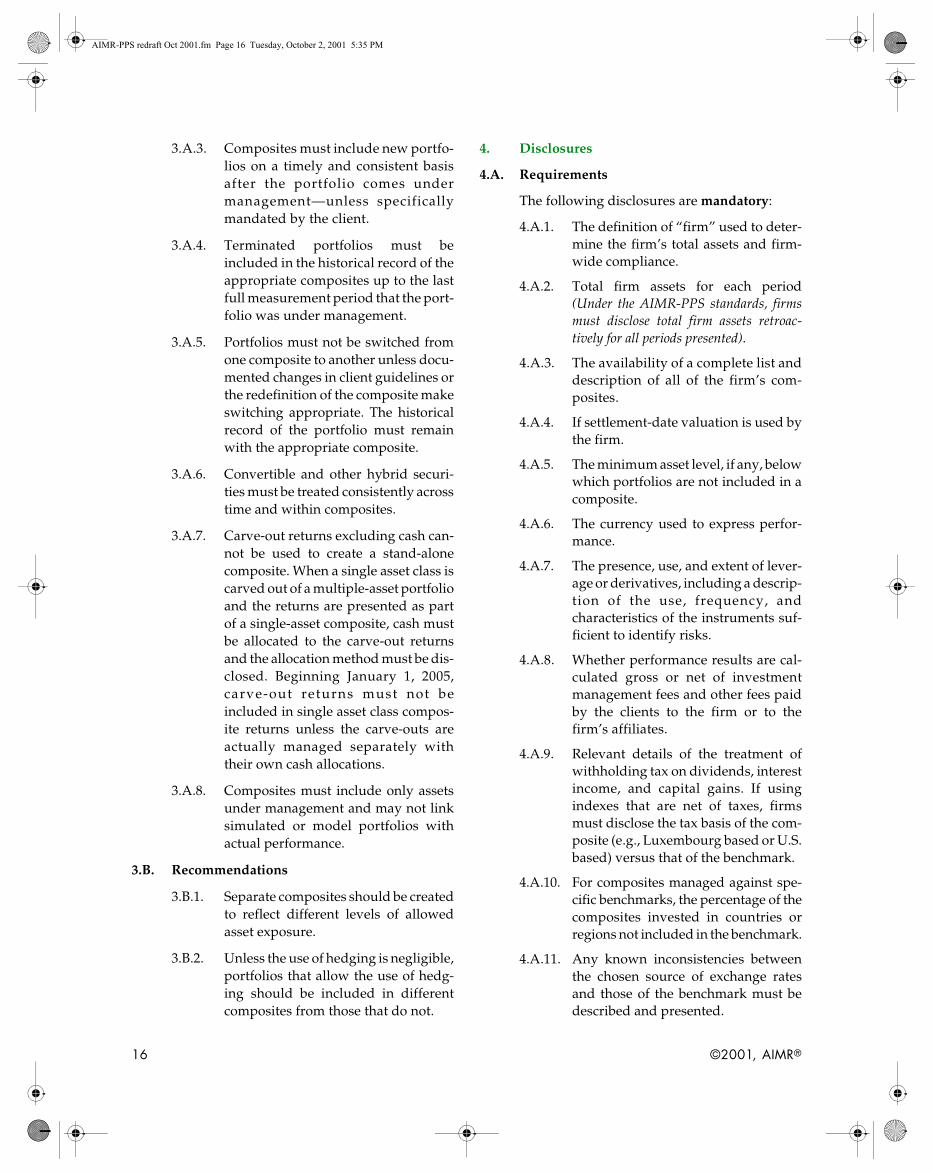

3.A.3. Composites must include new portfo-lios on a timely and consistent basisafter the portfolio comes undermanagement—unless specificallymandated by the client.

3.A.4. Terminated portfolios must beincluded in the historical record of theappropriate composites up to the lastfull measurement period that the port-folio was under management.

3.A.5. Portfolios must not be switched fromone composite to another unless docu-mented changes in client guidelines orthe redefinition of the composite makeswitching appropriate. The historicalrecord of the portfolio must remainwith the appropriate composite.

3.A.6. Convertible and other hybrid securi-ties must be treated consistently acrosstime and within composites.

3.A.7. Carve-out returns excluding cash can-not be used to create a stand-alonecomposite. When a single asset class iscarved out of a multiple-asset portfolioand the returns are presented as partof a single-asset composite, cash mustbe allocated to the carve-out returnsand the allocation method must be dis-closed. Beginning January 1, 2005,carve-out returns must not beincluded in single asset class compos-ite returns unless the carve-outs areactually managed separately withtheir own cash allocations.

3.A.8. Composites must include only assetsunder management and may not linksimulated or model portfolios withactual performance.

3.B. Recommendations

3.B.1. Separate composites should be createdto reflect different levels of allowedasset exposure.

3.B.2. Unless the use of hedging is negligible,portfolios that allow the use of hedg-ing should be included in differentcomposites from those that do not.

4. Disclosures

4.A. Requirements

The following disclosures are mandatory:

4.A.1. The definition of “firm” used to deter-mine the firm’s total assets and firm-wide compliance.

4.A.2. Total firm assets for each period(Under the AIMR-PPS standards, firmsmust disclose total firm assets retroac-tively for all periods presented).

4.A.3. The availability of a complete list anddescription of all of the firm’s com-posites.

4.A.4. If settlement-date valuation is used bythe firm.

4.A.5. The minimum asset level, if any, belowwhich portfolios are not included in acomposite.

4.A.6. The currency used to express perfor-mance.

4.A.7. The presence, use, and extent of lever-age or derivatives, including a descrip-tion of the use, frequency, andcharacteristics of the instruments suf-ficient to identify risks.

4.A.8. Whether performance results are cal-culated gross or net of investmentmanagement fees and other fees paidby the clients to the firm or to thefirm’s affiliates.

4.A.9. Relevant details of the treatment ofwithholding tax on dividends, interestincome, and capital gains. If usingindexes that are net of taxes, firmsmust disclose the tax basis of the com-posite (e.g., Luxembourg based or U.S.based) versus that of the benchmark.

4.A.10. For composites managed against spe-cific benchmarks, the percentage of thecomposites invested in countries orregions not included in the benchmark.

4.A.11. Any known inconsistencies betweenthe chosen source of exchange ratesand those of the benchmark must bedescribed and presented.

AIMR-PPS redraft Oct 2001.fm Page 16 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 17

4.A.12. Whether the firm has included any non-fee-paying portfolios in compositesand the percentage of composite assetsthat are non-fee-paying portfolios.

4.A.13. The AIMR-PPS standards require thatfirms disclose whether the presentation con-forms with local laws and regulations thatdiffer from AIMR-PPS requirements andthe manner in which the local standardsconflict with the AIMR-PPS standards.(GIPS requirement: Whether the pre-sentation conforms with local laws andregulations that differ from GIPSrequirements and the manner in whichthe local standards conflict with GIPS.)

4.A.14. The effective dates for AIMR-PPS compli-ance are provided in the AIMR-PPS Intro-duction, Section I.B. For any performancepresented for periods prior to the applicableeffective dates, the period of non-complianceand how the presentation is not in compli-ance with the AIMR-PPS standards.(GIPS requirement: For any perfor-mance presented for periods prior toJanuary 1, 2000, that does not complywith GIPS, the period of non-compliance and how the presentationis not in compliance with GIPS.)

4.A.15. When a single asset class is carved outof a multiple-asset portfolio and thereturns are presented as part of asingle-asset composite, the methodused to allocate cash to the carve-outreturns.

4.A.16. The AIMR-PPS standards require firmsto disclose the firm’s fee schedule(s) appro-priate to the presentation (GIPS recom-mendation: firms should disclose thefee schedule appropriate to the pre-sentation, see Section II.4.B.3 below).

4.B. Recommendations

The following disclosures are recommended:

4.B.1. The portfolio valuation sources andmethods used by the firm.

4.B.2. The calculation method used by thefirm.

4.B.3. The AIMR-PPS standards require thatfirms disclose the fee schedule appropriateto the presentation (See Section II.4.A.16).(GIPS recommendation: When gross-of-fee performance is presented, thefirm’s fee schedule[s] appropriate tothe presentation.)

4.B.4. When only net-of-fee performance ispresented, the average weighted man-agement and other applicable fees.

4.B.5. Any significant events within the firm(such as ownership or personnelchanges) that would help a prospectiveclient interpret the performance record.

5. Presentation and Reporting

5.A. Requirements

5.A.1. The following items must be reported:

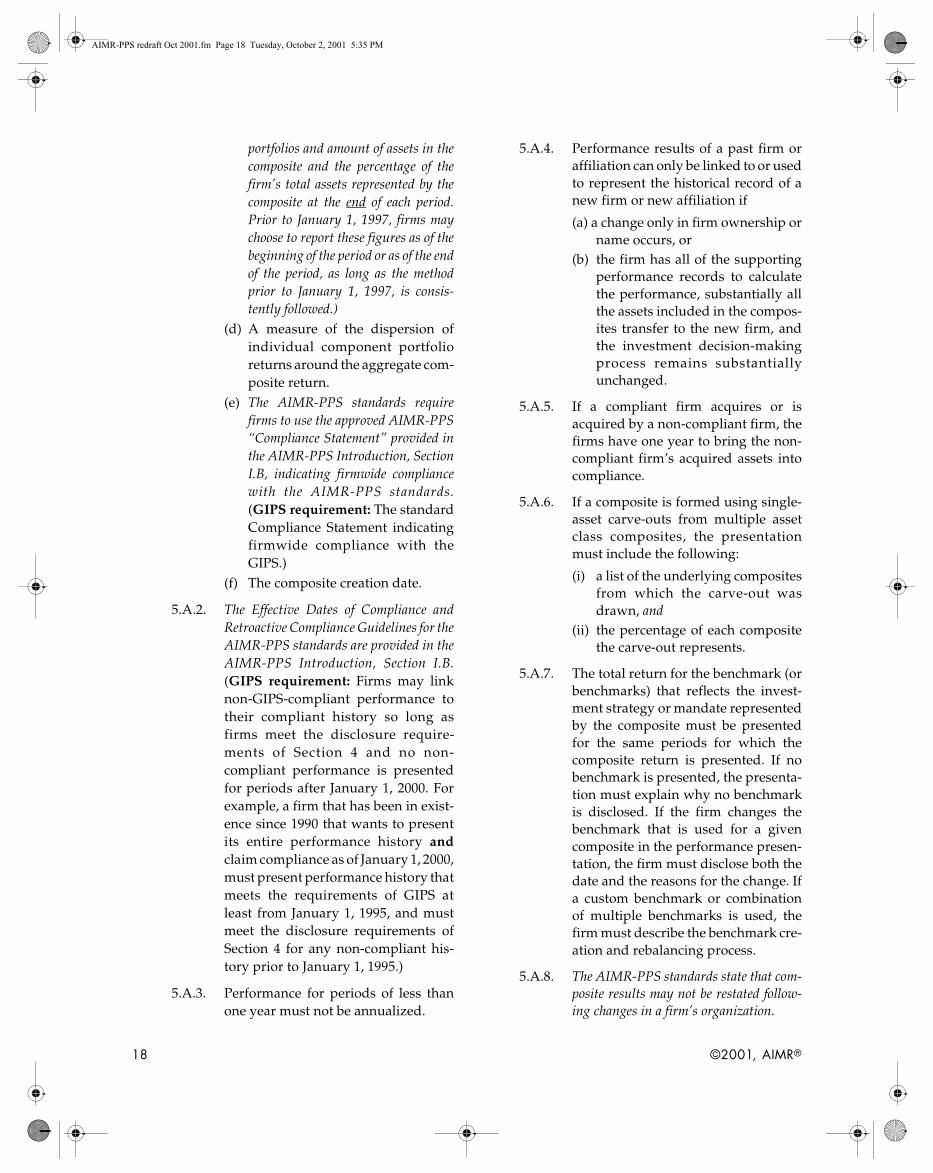

(a) The AIMR-PPS standards requirefirms to present, at a minimum, tenyears of annual performance history.See Introduction, Section I.B, for adiscussion on the Effective Dates andRetroactive Compliance. (GIPSrequirement: At least five years ofperformance [or a record for theperiod since firm inception, ifinception is less than five years]that is GIPS compliant. After pre-senting five years of performance,firms must present additionalannual performance up to 10 years.[For example, after a firm presentsfive years of compliant history, thefirm must add an additional yearof performance each year so thatafter five years of claiming compli-ance, the firm presents a 10-yearperformance record.])

(b) Annual returns for all years. (c) The number of portfolios and

amount of assets in the compositeand the percentage of the firm’stotal assets represented by thecomposite at the end of eachperiod. (For all periods after January1, 1997, the AIMR-PPS standardsrequire firms to provide the number of

AIMR-PPS redraft Oct 2001.fm Page 17 Tuesday, October 2, 2001 5:35 PM

18 ©2001, AIMR®

portfolios and amount of assets in thecomposite and the percentage of thefirm’s total assets represented by thecomposite at the end of each period.Prior to January 1, 1997, firms maychoose to report these figures as of thebeginning of the period or as of the endof the period, as long as the methodprior to January 1, 1997, is consis-tently followed.)

(d) A measure of the dispersion ofindividual component portfolioreturns around the aggregate com-posite return.

(e) The AIMR-PPS standards requirefirms to use the approved AIMR-PPS“Compliance Statement” provided inthe AIMR-PPS Introduction, SectionI.B, indicating firmwide compliancewith the AIMR-PPS standards.(GIPS requirement: The standardCompliance Statement indicatingfirmwide compliance with theGIPS.)

(f) The composite creation date.

5.A.2. The Effective Dates of Compliance andRetroactive Compliance Guidelines for theAIMR-PPS standards are provided in theAIMR-PPS Introduction, Section I.B.(GIPS requirement: Firms may linknon-GIPS-compliant performance totheir compliant history so long asfirms meet the disclosure require-ments of Section 4 and no non-compliant performance is presentedfor periods after January 1, 2000. Forexample, a firm that has been in exist-ence since 1990 that wants to presentits entire performance history andclaim compliance as of January 1, 2000,must present performance history thatmeets the requirements of GIPS atleast from January 1, 1995, and mustmeet the disclosure requirements ofSection 4 for any non-compliant his-tory prior to January 1, 1995.)

5.A.3. Performance for periods of less thanone year must not be annualized.

5.A.4. Performance results of a past firm oraffiliation can only be linked to or usedto represent the historical record of anew firm or new affiliation if

(a) a change only in firm ownership orname occurs, or

(b) the firm has all of the supportingperformance records to calculatethe performance, substantially allthe assets included in the compos-ites transfer to the new firm, andthe investment decision-makingprocess remains substantiallyunchanged.

5.A.5. If a compliant firm acquires or isacquired by a non-compliant firm, thefirms have one year to bring the non-compliant firm’s acquired assets intocompliance.

5.A.6. If a composite is formed using single-asset carve-outs from multiple assetclass composites, the presentationmust include the following:

(i) a list of the underlying compositesfrom which the carve-out wasdrawn, and

(ii) the percentage of each compositethe carve-out represents.

5.A.7. The total return for the benchmark (orbenchmarks) that reflects the invest-ment strategy or mandate representedby the composite must be presentedfor the same periods for which thecomposite return is presented. If nobenchmark is presented, the presenta-tion must explain why no benchmarkis disclosed. If the firm changes thebenchmark that is used for a givencomposite in the performance presen-tation, the firm must disclose both thedate and the reasons for the change. Ifa custom benchmark or combinationof multiple benchmarks is used, thefirm must describe the benchmark cre-ation and rebalancing process.

5.A.8. The AIMR-PPS standards state that com-posite results may not be restated follow-ing changes in a firm’s organization.

AIMR-PPS redraft Oct 2001.fm Page 18 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 19

5.B. Recommendations

5.B.1. The following items should beincluded in the composite presenta-tion or disclosed as supplementalinformation:

(a) composite performance gross ofinvestment management fees andcustody fees and before taxes(except for non-reclaimable with-holding taxes),

(b) cumulative returns for compositeand benchmarks for all periods,

(c) equal-weighted means and medianreturns for each composite,

(d) volatility over time of the aggre-gate composite return, and

(e) inconsistencies among portfolioswithin a composite in the use ofexchange rates.

5.B.2. Relevant risk measures—such as vola-tility, tracking error, beta, modifiedduration, etc.—should be presentedalong with total return for both bench-marks and composites.

6. Real Estate

6.A. Requirements

6.A.1. Real estate must be valued through anindependent appraisal at least once everythree years unless client agreements stateotherwise.

6.A.2. Real estate valuations must be reviewed atleast quarterly.

6.A.3. Component returns for participating orconvertible mortgages must be allocated asfollows:

(a) basic cash interest to income return,(b) contingent interest (current receiv-

able) to income return,(c) basic accrued interest (deferred) to

income return,(d) additional contingent interest

(deferred, payable at maturity, pre-payment, or sale) to appreciationreturn,

(e) return that is currently payable fromoperations to income return, and

(f) all other sources of income that aredeferred or realizable in the future tothe appreciation component.

6.A.4. Returns from income and capital appreci-ation must be presented in addition to totalreturn.

6.A.5. The performance presentation must dis-close:

(a) the absence of independent appraisals,(b) the source of the valuation and the

valuation policy,(c) total fee structure and its relationship

to asset valuation,(d) the return formula and accounting

policies for such items as capitalexpenditures, tenant improvements,and leasing commissions,

(e) the cash distribution and retentionpolicy,

(f) whether the returns are: • based on audited operating

results, • exclude any investment expense

that may be paid by the investors,or

• include interest income fromshort-term cash investments orother related investments,

(g) the cash distribution and retentionpolicies with regard to income earnedat the investment level.

6.B. Recommendations

6.B.1. Income earned at the investment levelshould be included in the computation ofincome return regardless of the investor’saccounting policies for recognizing incomefrom real estate investments.

6.B.2. Equity ownership investment strategiesshould be presented separately.

6.B.3. When presenting the components of totalreturn, recognition of income at the invest-ment level, rather than at the operatinglevel, is preferred.

AIMR-PPS redraft Oct 2001.fm Page 19 Tuesday, October 2, 2001 5:35 PM

20 ©2001, AIMR®

7. Venture and Private Placements

7.A. Requirements

7.A.1. All discretionary pooled funds of fundsand separately managed portfolios must beincluded in composites defined by vintageyear (i.e., the year of fund formation andfirst takedown of capital).

7.A.2. For general partners:

(a) Cumulative internal rate of return(IRR) must be presented since inceptionof the fund and be net of fees, expenses,and carry to the general partner.

(b) IRR must be calculated based on cash-on-cash returns plus residual value.

(c) Presentation of return informationmust be in a vintage-year format.

7.A.3. For general partners, the performance pre-sentation must disclose:

(a) changes in the general partner sinceinception of fund,

(b) type of investment, and(c) investment strategy.

7.A.4. For intermediaries and investment advi-sors:

(a) For separately managed accounts andcommingled fund-of-funds struc-tures, cumulative IRR must be pre-sented since inception of the fund andbe net of fees, expenses, and carry tothe general partners but gross ofinvestment advisory fees unless net offees is required to meet applicable reg-ulatory requirements.

(b) Calculation of IRR must be based onan aggregation of all the appropriatepartnership cash flows into one IRRcalculation—as if from one invest-ment.

(c) The inclusion of all discretionarypooled fund-of-funds and separatelymanaged portfolios in composites mustbe defined by vintage year.

7.A.5. For intermediaries and investment advisors,the performance presentation must disclose:

(a) the number of portfolios and fundsincluded in the vintage-year composite,

(b) composite assets,

(c) composite assets in each vintage yearas a percentage of total firm assets(discretionary and nondiscretionarycommitted capital), and

(d) composite assets in each vintage yearas a percentage of total private equityassets.

7.B. Recommendations

7.B.1. General partners:

(a) Industry guidelines should be usedfor valuation of venture capitalinvestments,

(b) Valuation should be either cost ordiscount to comparables in the publicmarket for buyout, mezzanine, dis-tressed, or special situation invest-ments, and

(c) IRR should be calculated net of fees,expenses, and carry without publicstocks discounted and assuming stockdistributions were held.

7.B.2. Net cumulative IRR (after deduction ofadvisory fees and any other administrativeexpenses or carried interest) should be cal-culated for separately managed accounts,managed accounts, and commingled fund-of-funds structures.

7.B.3. For general partners, the following shouldbe disclosed:

(a) gross IRR (before fees, expenses, andcarry), which should be used at thefund and the portfolio level, as supple-mental information,

(b) the multiple on committed capital netof fees and carry to the general partners,

(c) the multiple on invested capital grossof fees and carry,

(d) the distribution multiple on paid-incapital net of fees to the general part-ners, and

(e) the residual multiple on paid-in capi-tal net of fees and carry to the limitedpartners.

7.B.4. For intermediaries and investment advi-sors, the number and size should be dis-closed in terms of committed capital ofdiscretionary and nondiscretionary con-sulting clients.

AIMR-PPS redraft Oct 2001.fm Page 20 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 21

8. Wrap-Fee Accounts

8.A. Requirements

8.A.1. Wrap-fee performance must be shown netof all fees charged directly or indirectly tothe account (unless transaction expensescan be determined and deducted).

8.A.2. When a firm includes portfolios as part ofa wrap-fee composite that do not meet thewrap-fee definition, the firm must disclosefor each year presented:

(a) the dollar amount of the non-wrap-feeportfolios represented and

(b) the fee deducted, which should be thehighest applicable wrap fee.

8.A.3. Pure gross-of-fees performance may onlybe presented as supplemental information(in addition to the required net-of-fees per-formance). Such supplemental informa-tion must disclose:

(a) fees,(b) investment style, and(c) the information that “pure” gross-of-

fees return does not include transac-tion costs.

8.B. Recommendations

8.B.1. Wrap-fee portfolios should be grouped inseparate composites from “non-wrapped”composites.

9. After-Tax Performance

Following are provisions that apply to firms that wish toshow after-tax performance results in compliance with theAIMR-PPS standards. Currently, firms are only recom-mended to present after-tax performance.

9.A. Requirements

9.A.1. For after-tax composites:

(a) Taxes must be recognized in the sameperiod as when the taxable eventoccurred.

(b) Taxes on income and realized capitalgains must be subtracted from resultsregardless of whether taxes are paidfrom assets outside the account orfrom account assets.

(c) The maximum federal income taxrates appropriate to the portfoliosmust be assumed.

(d) The return for after-tax compositesthat hold both taxable and tax-exemptsecurities must be adjusted to an after-tax basis rather than being “grossedup” to a taxable equivalent.

(e) Calculation of after-tax returns fortax-exempt bonds must include amor-tization and accretion of premiums ordiscounts.

(f) Taxes on income are to be recognizedon an accrual basis.

9.A.2. The performance presentation must dis-close:

(a) for composites of taxable portfolios, thecomposite assets as a percentage oftotal assets in taxable portfolios(including nondiscretionary assets)managed according to the same strat-egy for the same type of client,

(b) the tax rate assumptions if perfor-mance results are presented aftertaxes, and

(c) both client average and manageraverage performance if adjustmentsare made for nondiscretionary cashwithdrawals.

9.B. Recommendations

9.B.1. Portfolios should be grouped by tax rate.

9.B.2. Portfolios may be grouped by vintage year,or similar proxy, to group portfolios withsimilar amounts of unrealized capital gains.

9.B.3. Cash-basis accounting is to be used ifrequired by applicable law.

9.B.4. Calculations should be adjusted for non-discretionary capital gains.

9.B.5. Benchmark returns should be calculatedusing the actual turnover in the bench-mark index, if available; otherwise, anapproximation is acceptable.

9.B.6. If returns are presented before taxes, a totalrate of return for the composite should bepresented without adjustment for tax-exempt income to a pretax basis.

AIMR-PPS redraft Oct 2001.fm Page 21 Tuesday, October 2, 2001 5:35 PM

22 ©2001, AIMR®

9.B.7. If returns are presented after taxes, client-specific tax rates may be used for each port-folio (but composite performance should bebased on the same tax rate for all clients inthe composite).

9.B.8. The following presentations should bemade for composites:

(a) beginning and ending market values,(b) contributions and withdrawals,(c) beginning and ending unrealized

capital gains,

(d) realized short-term and long-termcapital gains,

(e) taxable income and tax-exemptincome,

(f) the accounting convention used forthe treatment of realized capital gains(e.g., highest cost, average cost, lowestcost, FIFO, LIFO), and

(g) the method or source for computingafter-tax benchmark return.

AIMR-PPS redraft Oct 2001.fm Page 22 Tuesday, October 2, 2001 5:35 PM

©2001, AIMR® 23

III. VERIFICATION

All references made to GIPS below are relevant to theAIMR-PPS standards and references to verificationare relevant to Level I Verification as well. Additionalguidance on verification, including the procedures forconducting a Performance Examination (Level II), isavailable in Appendix D.

The primary purpose of verification is to establish thata firm claiming compliance with GIPS has adhered tothe standards. Verification will also increase theunderstanding and professionalism of performance-measurement teams and consistency of presentationof performance results.

The verification procedures attempt to strike a bal-ance between ensuring the quality, accuracy, andrelevance of performance presentations and mini-mizing the cost to investment firms of independentreview of performance results. Investment firmsshould assess the benefits of improved internal pro-cesses and procedures, which are as significant as themarketing advantages of verification.