Embed Size (px)

Citation preview

AJ LUCAS GROUP LIMITEDFINANCIAL REPORT

YE

AR

EN

DE

D 3

0 J

UN

E 2

00

8F

or p

erso

nal u

se o

nly

1 Directors’ report

15 income statements

16 statements of recogniseD income anD expense

17 Balance sheets

18 statements of cash flows

19 notes to the financial statements

52 Directors’ Declaration

53 inDepenDent auDitor’s report

54 australian stock exchange aDDitional information

55 Directory

For

per

sona

l use

onl

y

1 LUCAS GROUP

ALLAN CAMPbELL BCom LLB ExECUTIvE ChAIRMAN AND CEO. AGE 52. DIRECTOR SINCE 1995.

After qualifying as a lawyer, Mr Campbell worked for several leading investment banks initially in Australia followed

by ten years in London and New York. During this period he was given responsibility for corporate advisory and

recovery where he gained valuable hands on experience for the turn around of distressed companies.

Mr Campbell acquired Lucas in 1995, commenced the Company on a path and listed the Company on the

Australian Securities Exchange in 1999. Subsequently, he has been responsible for the Company’s strategic

direction and has established its position as one of the leading provider of mining and infrastructure services in

Australia.

IAN STUART-RObERTSON AAIQS ExECUTIvE DIRECTOR. AGE 59. DIRECTOR SINCE 1995.

Mr Stuart-Robertson is a qualified quantity surveyor with nearly 40 years experience in civil and building

construction. He has previously served as a director of several construction companies and been responsible for the

delivery of many major projects. He also has considerable expertise in project cost reporting systems and makes a

vital contribution to the Group in his role as chairman of the tender review committee.

He is also a non-executive director of quantity surveyors, John Hollis & Partners.

ANDREw LUkAS Be NON-ExECUTIvE DIRECTOR. AGE 61. DIRECTOR SINCE 1995.

Mr Lukas is a qualified civil engineer. He joined Lucas in 1975 after working in the engineering and construction of

pipelines in USA and Australia for the Williams group of companies.

He pioneered the development of horizontal directional drilling in Australia and is an authority on this

technology as well as pipelines. He is also a leading proponent of directional drilling in coal seam gas extraction.

He is an executive committee member and past president of the Australian Pipeline Industry Association (APIA),

a director and immediate past president of the International Pipeline and Offshore Contractors Association (IPLOCA).

Mr Lukas was appointed Chief Executive Officer of Sydney Gas Limited on 19 March 2008 following which he

ceased executive duties at AJ Lucas.

MARTIN GREEN FCA INDEPENDENT NON-ExECUTIvE DIRECTOR, ChAIRMAN OF AUDIT COMMITTEE. AGE 63. DIRECTOR SINCE 1999.

Mr Green is a Fellow of the Institute of Chartered Accountants and an official liquidator of the Supreme Court of

NSW. He has been in public practice for 36 years, mainly specialising in business recovery and insolvency. He has

substantial business and finance experience at senior levels.

He is currently a principal at Ferrier Green Krejci Silvia Chartered Accountants, a former honorary director/

treasurer of the National Trust of Australia (NSW) and has served at various times in many public roles and

capacities.

Mr Green also serves as Chairman of the Company’s Audit Committee.

GARRy O’MEALLy BSc Be INDEPENDENT NON-ExECUTIvE DIRECTOR, MEMbER OF AUDIT COMMITTEE. AGE 72. DIRECTOR SINCE 1999.

Mr O’Meally has over 40 years experience in the oil and gas industries, mainly with Australian Gas Light Company

where he served as general manager of AGL Gas Companies and later of AGL Petroleum. He was also general

manager of Queensland and Northern Territory for Santos Limited and has consulted to many energy companies.

He was previously president of the Australian Gas Association, councillor and Queensland chairman of the

Australian Petroleum Production and Exploration Association and an executive manager of the Australian Pipeline

Industry Association. Mr O’Meally’s knowledge of the energy industries has been vitally important in the Group’s

expansion into its coal seam gas activities.

Directors’ reportThe Board of directors have pleasure in presenting their report together with the financial report of AJ Lucas Group Limited (the Company) and the

consolidated entity, being the Company and its controlled entities (the Group), for the year ended 30 June 2008 and the auditor’s report thereon.

DirectorsThe Directors of AJ Lucas Group Limited at any time during or since the end of the financial year are as follows:

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 2

company secretaryMr Nicholas Swan MA, ACA, MBA, was appointed as company secretary on 15 November 2001. He has also served as the company secretary of several

listed public companies as well as of a responsible entity for managed investment schemes.

Directors’ meetingsThe number of directors’ meetings (including meetings of committees of directors) held during the financial year, during the period of each director’s

tenure, and number of such meetings attended by each of the directors is:

Board of Directors audit committeeheld attended held attended

Allan Campbell 12 12 — —

Ian Stuart-Robertson 12 11 — —

Andrew Lukas 12 6 — —

Martin Green 12 12 2 2

Garry O’Meally 12 12 2 2

corporate governance statementThe Board of directors is responsible for the corporate governance of the Group. This statement outlines the main corporate governance practices. Unless

otherwise stated, these practices were in place for the entire year.

bOARD OF DIRECTORSThe directors of the Company are accountable to shareholders for the proper management of the business and affairs of the Company.

The key responsibilities of the Board are to:

• establishandmonitorthecorporatestrategiesoftheCompany;

• ensurepropercorporategovernance;

• monitortheperformanceofmanagement;

• ensurethatappropriateriskmanagementsystems,internalcontrols,reportingsystemsandcomplianceframeworksareinplaceandoperating

effectively;

• monitorfinancialresults;

• approvedecisionsconcerninginvestments,acquisitionsanddividends;and

• complywithreportingandotherrequirementsofthelaw.

The Board’s role and responsibilities are documented in a written Board charter.

COMPOSITION OF ThE bOARDThe constitution of the Company requires between three and ten directors. Currently there are five with a majority non-executives.

Directors are appointed for their industry-specific expertise and commercial acumen. The Board believes that all the directors can make, and do make,

quality and independent judgements in the best interests of the Company. While the chairman is also the chief executive officer, his contribution to the

Company is considered vital to direct the strategy of the Company as well as its management. The directors are able to obtain independent advice at the

expense of the Company.

There is no nomination committee. Instead, the Board assesses the performance of individual directors and the Board as a whole.

EThICAL AND RESPONSIbLE DECISION MAkINGThe Company has a code of conduct to guide the directors and key executives. It includes disclosure of conflicts of interest and use of information not

otherwise publicly known or available. Any director with an interest in matters being considered by the Board must take no part in decisions relating to

those matters.

TRADING IN COMPANy SECURITIESThe Company has a share trading policy prohibiting directors, senior management and their associates from trading in the Company’s securities other

than in certain nominated periods (between two and thirty days following the release of the half yearly and annual results and the annual general

meeting) and at such other times as the Board permits. Such persons must obtain prior approval before conducting any trade.

INTEGRITy IN FINANCIAL REPORTINGThe Board has established an audit committee which provides assistance to the Board in fulfilling its corporate governance and oversight responsibilities

in relation to the Company’s financial reporting, internal control systems, risk management systems, regulatory compliance and external audit.

The committee must have at least two members. All members must be independent non-executive directors. At least one member must have

financial expertise and some members shall have an understanding of the industry in which the Company operates.

The principal roles of the committee are to:

• assesswhethertheaccountingmethodsandstatutoryreportingappliedbymanagementareconsistentandcomplywithaccountingstandardsand

applicablelawsandregulations;

• makerecommendationsontheappointmentoftheexternalauditors,assesstheirperformanceandindependenceandensurethatmanagement

respondstoauditfindingsandrecommendations;

For

per

sona

l use

onl

y

3 LUCAS GROUP

• discusstheadequacyandeffectivenessoftheCompany’sinternalcontrolsystemsandpoliciestoassessandmanagebusinessrisksanditslegal

andregulatorycomplianceprogrammes;and

• ensureeffectivemonitoringoftheCompany’scompliancewithitscodesofconductandBoardpolicystatements.

The audit committee meets with the external auditors at least twice a year. The committee is authorised to seek information from any employee or

external party and obtain legal or other professional advice.

TIMELy AND bALANCED DISCLOSUREThe Company has established policies and procedures designed to ensure compliance with Australian Securities Exchange (ASX) listing rules disclosure

requirements so that investors have equal and timely access to all material information. The Company also posts all information disclosed to the ASX on

its website.

CLEAR COMMUNICATION wITh ShAREhOLDERSThe Company has a communications strategy to promote effective communication with shareholders. The company secretary has been nominated

as the person responsible for communications with the ASX. This role includes responsibility for ensuring compliance with the continuous disclosure

requirements in the ASX listing rules.

RISk IDENTIFICATION AND MANAGEMENTThe Board has established policies on risk management. The systems of internal financial controls have been determined by senior management and

are designed to provide reasonable but not absolute protection against fraud, material mis-statement or loss. The chief executive officer and chief

financial officer provide representation to the audit committee and the Board on the risk management, compliance and control systems for the Group.

ENCOURAGE ENhANCED PERFORMANCEThe performance of committees, individual directors and key executives is evaluated regularly by the Board.

There has been no formal performance evaluation of the Board, directors or committees during the reporting period. The Board informally evaluates

its performance and that of the individual directors and committees on a regular basis. The Board believes that the individuals on the Board have made

quality and independent judgements in the best interests of the Company on all relevant issues during the reporting period. There has been a formal

performance evaluation of all key executives (other than the executive directors) during the reporting period.

RECOGNISE ThE INTERESTS OF ALL STAkEhOLDERSThe Company has established various codes of conduct to guide compliance with legal and other obligations to stakeholders and the community at

large. These include ethical and work standards, employment practices including occupational health and safety and employment opportunities, and

environmental protection. The Company’s compliance and that of its employees is monitored through internal review.

principal activitiesAJ Lucas Group is a diversified infrastructure and mining services and construction group specialising in providing services to the water and wastewater,

oil and gas, resources and property sectors.

The Group has in excess of 1,100 employees and a client base principally comprising State and local governments and major corporations.

The Group is structured into three principal business segments:

Drilling: Australia’s foremost provider of drilling services to the coal and coal seam gas industries for the degasification of coal mines and the recovery

and commercialisation of coal seam gas and associated services. The Group is also the market leader in the trenchless installation of conduits and pipes

using horizontal directional drilling.

Pipelines: Australia’s market-leading provider for the engineering and installation of pipelines including hydrostatic testing.

Construction and infrastructure: provision of construction and civil engineering services together with facilities management.

review anD results of operations OvERvIEw OF ThE CONSOLIDATED ENTITyThe consolidated entity recorded a net profit of $13,468,000 (2007: $6,396,000). A summary of the results is set out in the following table:

Summary of financial results

2008$’000

2007$’000

Total revenue 424,301 216,369EBITDA 37,412 14,907EBIT 25,961 5,941Profit before tax 20,408 4,178Net profit attributable to members 13,468 6,396Total assets 229,899 150,948Net assets 65,160 30,438

Basic earnings per share 24.5¢ 11.9 ¢

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 4

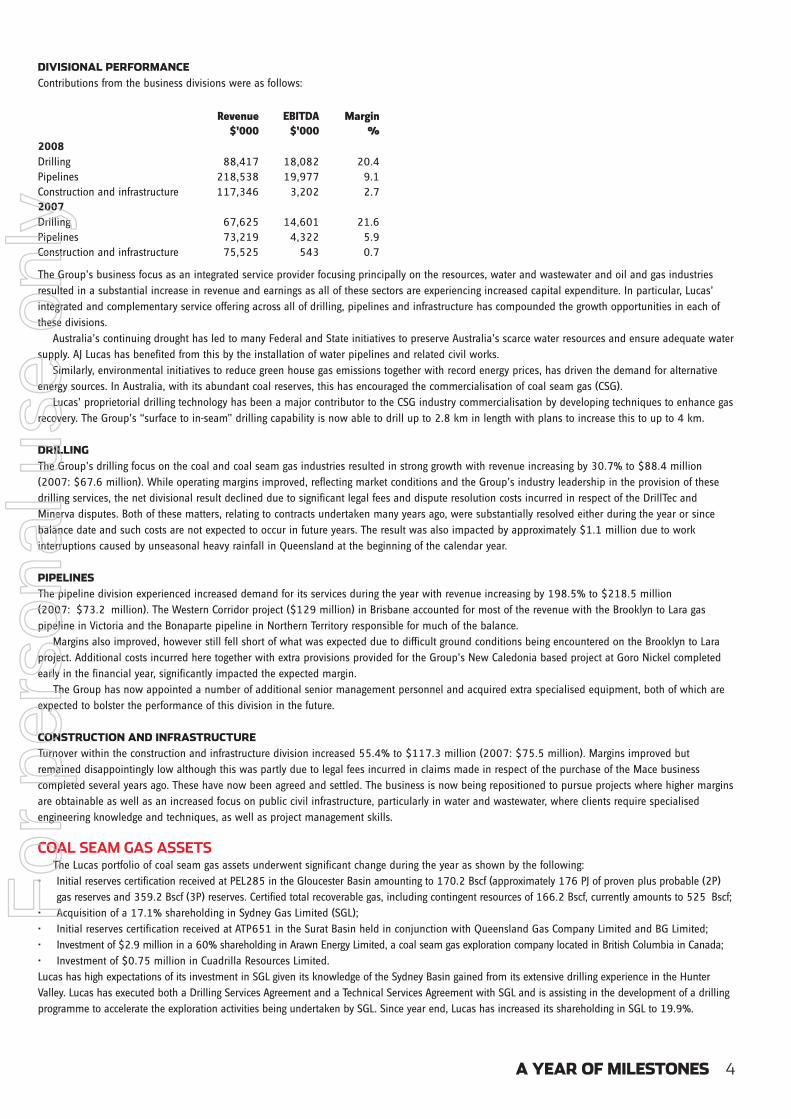

DIvISIONAL PERFORMANCEContributions from the business divisions were as follows:

revenue $’000

eBitDa $’000

margin %

2008Drilling 88,417 18,082 20.4Pipelines 218,538 19,977 9.1Construction and infrastructure 117,346 3,202 2.72007Drilling 67,625 14,601 21.6Pipelines 73,219 4,322 5.9Construction and infrastructure 75,525 543 0.7

The Group’s business focus as an integrated service provider focusing principally on the resources, water and wastewater and oil and gas industries

resulted in a substantial increase in revenue and earnings as all of these sectors are experiencing increased capital expenditure. In particular, Lucas’

integrated and complementary service offering across all of drilling, pipelines and infrastructure has compounded the growth opportunities in each of

these divisions.

Australia’s continuing drought has led to many Federal and State initiatives to preserve Australia’s scarce water resources and ensure adequate water

supply. AJ Lucas has benefited from this by the installation of water pipelines and related civil works.

Similarly, environmental initiatives to reduce green house gas emissions together with record energy prices, has driven the demand for alternative

energy sources. In Australia, with its abundant coal reserves, this has encouraged the commercialisation of coal seam gas (CSG).

Lucas’ proprietorial drilling technology has been a major contributor to the CSG industry commercialisation by developing techniques to enhance gas

recovery. The Group’s “surface to in-seam” drilling capability is now able to drill up to 2.8 km in length with plans to increase this to up to 4 km.

DRILLING The Group’s drilling focus on the coal and coal seam gas industries resulted in strong growth with revenue increasing by 30.7% to $88.4 million

(2007: $67.6 million). While operating margins improved, reflecting market conditions and the Group’s industry leadership in the provision of these

drilling services, the net divisional result declined due to significant legal fees and dispute resolution costs incurred in respect of the DrillTec and

Minerva disputes. Both of these matters, relating to contracts undertaken many years ago, were substantially resolved either during the year or since

balance date and such costs are not expected to occur in future years. The result was also impacted by approximately $1.1 million due to work

interruptions caused by unseasonal heavy rainfall in Queensland at the beginning of the calendar year.

PIPELINESThe pipeline division experienced increased demand for its services during the year with revenue increasing by 198.5% to $218.5 million

(2007: $73.2 million). The Western Corridor project ($129 million) in Brisbane accounted for most of the revenue with the Brooklyn to Lara gas

pipeline in Victoria and the Bonaparte pipeline in Northern Territory responsible for much of the balance.

Margins also improved, however still fell short of what was expected due to difficult ground conditions being encountered on the Brooklyn to Lara

project. Additional costs incurred here together with extra provisions provided for the Group’s New Caledonia based project at Goro Nickel completed

early in the financial year, significantly impacted the expected margin.

The Group has now appointed a number of additional senior management personnel and acquired extra specialised equipment, both of which are

expected to bolster the performance of this division in the future.

CONSTRUCTION AND INFRASTRUCTURETurnover within the construction and infrastructure division increased 55.4% to $117.3 million (2007: $75.5 million). Margins improved but

remained disappointingly low although this was partly due to legal fees incurred in claims made in respect of the purchase of the Mace business

completed several years ago. These have now been agreed and settled. The business is now being repositioned to pursue projects where higher margins

are obtainable as well as an increased focus on public civil infrastructure, particularly in water and wastewater, where clients require specialised

engineering knowledge and techniques, as well as project management skills.

coal seam gas assetsThe Lucas portfolio of coal seam gas assets underwent significant change during the year as shown by the following:

• InitialreservescertificationreceivedatPEL285intheGloucesterBasinamountingto170.2Bscf(approximately176PJofprovenplusprobable(2P)

gasreservesand359.2Bscf(3P)reserves.Certifiedtotalrecoverablegas,includingcontingentresourcesof166.2Bscf,currentlyamountsto525 Bscf;

• Acquisitionofa17.1%shareholdinginSydneyGasLimited(SGL);

• InitialreservescertificationreceivedatATP651intheSuratBasinheldinconjunctionwithQueenslandGasCompanyLimitedandBGLimited;

• Investmentof$2.9millionina60%shareholdinginArawnEnergyLimited,acoalseamgasexplorationcompanylocatedinBritishColumbiainCanada;

• Investmentof$0.75millioninCuadrillaResourcesLimited.

Lucas has high expectations of its investment in SGL given its knowledge of the Sydney Basin gained from its extensive drilling experience in the Hunter

Valley. Lucas has executed both a Drilling Services Agreement and a Technical Services Agreement with SGL and is assisting in the development of a drilling

programme to accelerate the exploration activities being undertaken by SGL. Since year end, Lucas has increased its shareholding in SGL to 19.9%.

For

per

sona

l use

onl

y

5 LUCAS GROUP

At Gloucester Basin, exploration activity continues with a number of pilot production wells now in testing with gas flow rates recently averaging in

excess of 1 million cubic feet per day. The project has been awarded Major Project Status in New South Wales and commercialisation initiatives are

well underway, including work on a pipeline to Hexham. Lucas expects to be shipping gas to market by end 2009/beginning 2010.

The Lucas Group also expanded its exploration activities in unconventional hydrocarbons overseas to Canada and Europe, through its investments in

Arawn Energy and Cuadrilla Resources. The Group has a very positive view on the prospects for unconventional hydrocarbons, particularly shale gas in

Europe and, to this end, has taken formative steps to position itself in this sector.

investments for future performanceThe consolidated entity acquired plant and equipment totalling $34,818,000 (2007: $15,810,000) during the year including $11,221,000 from the

purchase of the Capricorn Weston Drilling Group. The capital expenditure largely reflects substantial investment in additional capacity to sustain the

rapid growth of the Group’s drilling and pipeline activities.

In August 2008, the Group completed the acquisition of Mitchell Drilling for a purchase consideration of $150 million. Mitchell Drilling is the largest

specialist drilling company for the coal seam gas industry in Queensland and complements Lucas Drilling’s coal seam gas market position in New South

Wales. The combined entity has 88 rigs making the Group the largest provider of drilling services to the coal and coal seam gas industries in Australia.

review of financial conDitionCAPITAL STRUCTUREThe Company’s capital structure is managed in a manner to maximise the return to shareholders subject to consideration of the financing risk of the

business and the cash flows generated from operations. No shares were issued by the Company during the year other than arising from the conversion

of convertible notes, the exercise of management rights, and deferred consideration for the acquisition of McDermott Drilling Pty Limited.

Subsequent to year end, the Company has purchased the business of Mitchell Drilling for $150 million. This was funded out of an institutional

placement of $29.5 million, a $15 million equity placement to the vendor, deferred consideration of $15 million and the balance from bank

borrowings. At the same time, all of the Group’s borrowing facilities were renegotiated and their terms extended.

CASh FLOwS FROM OPERATIONSNet cash flow generated from operations during the year amounted to $50,070,000, a 420% increase over the previous year (2007: $9,602,000). The

increased cash flow reflects the change in business mix to a greater proportion of higher margin drilling work and the growth in Group consolidated

revenue.

IMPACT OF LEGISLATION AND OThER ExTERNAL REqUIREMENTSThere were no changes in environmental or other legislative requirements during the year that have significantly impacted the results or operations of

the Group.

DiviDenDsDividends paid or declared by the Company since the end of the previous year were:

DeclareD anD paiD During the year 2008

cents

per share

total amount $’000

franked/

unfranked

Date of

paymentFinal 2007 2.5 1,362 100% franked 28 Sept 2007Interim 2008 3.5 1,911 100% franked 28 Mar 2008

3,273

DeclareD after enD of year

After the balance sheet date, the directors have declared a 2008 final ordinary dividend as follows:

cents per share

total amount $’000

franked/ unfranked

Date of payment

4.5 3,038 15% franked 29 Sept 2008

The financial effect of this dividend has not been brought to account in the financial statements for the year ending 30 June 2008 and will be

recognised in the 2009 financial report.

state of affairsIn the opinion of the Directors, there were no significant changes in the state of affairs of the Group during the financial year under review.

environmental regulations anD native titleAs infrastructure engineers, meeting stringent environmental and land use regulations, including native title issues, are an important element of our

work. Lucas is committed to identifying environmental risks and engineering solutions to avoid, minimise or mitigate them. We work closely with all

levels of government, landholders, Aboriginal land councils and other bodies to ensure our activities have minimal or no effect on land use and areas

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 6

of environmental, archaeological or cultural importance. One of the key benefits of directional drilling is its ability to avoid or substantially mitigate

environmental impact.

Group policy requires all operations to be conducted in a manner that will preserve and protect the environment.

At PEL285 in the Gloucester Basin, the Group holds together with its joint venture partner, two bore licence certificates under the Water Act 1912, for

the drainage of water from the production wells.

The directors are not aware of any significant environmental incidents, or breaches of environmental regulations during or since the end of the year.

events subsequent to reporting DateOn 23 July 2008, the Company purchased the business of Mitchell Drilling, the largest specialist drilling company for the coal seam gas industry in

Queensland. The purchase price of $150 million was funded by a $15 million equity placement to the vendor, with the balance out of an equity

placement to institutional shareholders of $29.5 million, deferred consideration of $15 million and increased borrowing facilities. At the same time, the

Group’s bank facilities have been renegotiated and their terms extended.

Subsequent to year-end, the directors have declared a final ordinary dividend of 4.5¢ per share, franked to 15%.

Other than these matters, there has not arisen in the interval between the end of the financial year and the date of this report any item, transaction

or event of a material or unusual nature likely, in the opinion of the directors of the Company, to affect significantly the operations of the Group, the

results of those operations, or the state of affairs of the Group, in future financial years.

likely DevelopmentsThe Group has successfully established itself as the leading service provider in each of its chosen activities. Its strategy of being an integrated service

provider to the resources water and wastewater, oil and gas and property sectors presents many opportunities to leverage its service offering.

The coal seam gas industry is expected to experience significant growth in preparation for the proposed export of LNG through Gladstone, AJ Lucas

is the only company with the full service capability to provide technical services, drilling and management services, well head completions, work overs,

well services, gas gathering systems through to pipelines to market. This gives the Group a significant strategic advantage over all its competitors. The

acquisition of Mitchell Drilling strengthens this capability through adding additional capacity, customer contacts, drilling expertise and management

depth. The Group will continue to invest in additional plant and equipment to provide it with the extra capacity to service the expected increase in

demand from the coal seam gas producers.

The complementary nature of the Group’s activities will also be drawn upon to undertake civil works for the infrastructure works to be undertaken

by the pipeline division. Partnering with selected entities through joint ventures and alliances, and the development and application of innovative

technology and practices, are expected to create opportunities to apply the Group’s civil works expertise.

The Group also intends to restructure its coal seam gas interests to provide investor transparency to their underlying value. The form of this

restructuring is yet to be determined but will relieve the Group of any direct funding obligation, in particular in respect to Gloucester Basin, as the

investment projects move into their commercialisation stage.

The Group will however, continue to investigate direct investment opportunities in the water and wastewater sectors, initially based on the water

being produced from the dewatering of coal seam gas properties where the Group is drilling. The Group will also pursue investment opportunities in

unconventional hydrocarbons (shale gas), sustainable energies (geothermal and tidal) and other technologies being developed to reduce green house

gas emissions by carbon geosequestration.

Further information about likely developments in the operations of the Group and the expected results of those operations in future financial years

has not been included in this report because disclosure of the information would be likely to result in unreasonable prejudice to the Group.

other DisclosuresUNISSUED ShARES UNDER RIGhTS OR OPTIONSAt the date of this report, unissued shares of the Company under rights or options are:

Expiry date exercise price number of shares28 May 2009 — 24,00030 June 2010 — 369,18330 June 2010 — 369,18326 November 2011 $1.10 550,00031 August 2012 — 1,119,06323 November 2012 $2.11 250,000

All rights and options expire on the earlier of their expiry date, termination of the employee’s employment and cessation of the officer’s service.

The rights or options do not entitle the holders to participate in any share issue of the Company.

ShARES ISSUED ON ExERCISE OF RIGhTSDuring or since the end of the financial year, the Company issued ordinary shares as result of the exercise of rights:

number of sharesamount paid

on each share474,333 $Nil

There were no amounts unpaid on the shares issued.

For

per

sona

l use

onl

y

7 LUCAS GROUP

Directors’ shareholDings anD other interestsThe relevant interest of each director and their director-related entities in the shares and options over shares issued by the Company, as notified by the

directors to the Australian Securities Exchange in accordance with Section 205G(1) of the Corporations Act 2001, at the date of this report are:

ordinary shares

options issued under management

rights planAllan Campbell 10,140,083 360,000Ian Stuart-Robertson 1,386,750 220,000Andrew Lukas 6,204,833 220,000Martin Green 125,000 —Garry O’Meally 219,180 —

inDemnification anD insurance of officers anD auDitorsINDEMNIFICATIONThe Company has agreed to indemnify all directors and officers of the Company against all liabilities including expenses to another person or entity

(other than the Company or a related body corporate) that may arise from their position as directors or officers of the Group, except where the liability

arises out of conduct involving a lack of good faith.

No indemnity has been provided to the auditors of the Company.

INSURANCE PREMIUMSSince the end of the previous financial year, the Company has paid premiums in respect of Directors’ and Officers’ liability and legal expenses insurance

contracts for the year ended 30 June 2008 and, since the end of the financial year, the Company has paid or agreed to pay premiums in respect of

Directors’ and Officers’ insurance for the year ending 30 June 2009.

non-auDit servicesDuring the year, KPMG, the Company’s auditor, has performed certain other services in addition to their statutory duties.

The Board has considered the non-audit services provided during the year by the auditor and in accordance with written advice provided by

resolution of the audit committee, is satisfied that the provision of those non-audit services during the year by the auditor is compatible with, and did

not compromise, the auditor independence requirements of the Corporations Act 2001 for the following reasons:

• allnon-auditservicesweresubjecttothecorporategovernanceproceduresadoptedbytheCompanyandhavebeenreviewedbytheaudit

committeetoensuretheydonotimpacttheintegrityandobjectivityoftheauditor;and

• thenon-auditservicesprovideddonotunderminethegeneralprinciplesrelatingtoauditorindependenceassetoutinAPES110‘CodeofEthics

for Professional Accountants’, as they did not involve reviewing or auditing the auditor’s own work, acting in a management or decision-making

capacity for the Company, acting as an advocate for the Company or jointly sharing risks and rewards.

Payments to the auditor of the Company, KPMG, and its related practices for non-audit services provided during the year, as set out in note 5 in the

notes to the financial statements, amounted to $353,701 (2007: $92,939).

leaD auDitor’s inDepenDence DeclarationThe Lead auditor’s independence declaration is set out on page 14 and forms part of the Directors’ Report for the financial year ended 30 June 2008.

rounDing offThe Company is of a kind referred to in ASIC 98/100 dated 10 July 1998 and, in accordance with that Class Order, amounts in the Directors’ Report

and the financial report are rounded off to the nearest thousand dollars, unless otherwise stated.

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 8

remuneration report - auDiteDThis remuneration report, which forms part of the Directors’ Report, outlines the remuneration policy for directors and senior management of the

Company and the Group.

REMUNERATION PhILOSOPhy The key principle of the Company’s executive remuneration policy is to set remuneration at a level that will attract and retain qualified and experienced

personnel and motivate and reward them to achieve strategic objectives and improve business results.

Remuneration is structured to reward employees for increasing shareholder value. This is achieved by providing a fixed remuneration component

together with short and long term performance-based incentives.

Through creating goal congruence between directors, executives and shareholders, it is hoped to maximise shareholder value.

AJ Lucas aims to set fixed annual remuneration at market median levels for jobs of comparable size and responsibility using established job

evaluation methods and to provide incentives to enable top performers to be remunerated at the upper end of the market, subject always to the

performance of the Group.

The aim of the incentive plans is to drive performance to successfully implement annual business plans and increase shareholder value.

The remuneration for executives and staff is reviewed annually, using a formal performance appraisal process and market data derived from

independent surveys of people with similar competencies and responsibilities.

REMUNERATION STRUCTURERemuneration packages include a mix of fixed and variable remuneration and short and long-term incentives.

FIxED REMUNERATIONFixed remuneration consists of base remuneration which is calculated on a total cost basis and includes any fringe benefit tax charges related to

employee benefits including motor vehicles as well as employer contributions to superannuation.

INCENTIvE bASED REMUNERATIONIncentive based remuneration includes short-term and long-term incentives and is designed to reward executive directors and senior executives for

meeting or exceeding their financial objectives.

All incentive remuneration is subject to the Group achieving certain performance criteria including most importantly a minimum level of profit.

Subject to these performance criteria being met, the short-term incentives (STI) may be received as cash or ordinary shares in the Company subject to a

minimum percentage being taken in shares. The STI shares vest in equal tranches at the end of each of the first and second year after being granted.

The long-term incentive (LTI) is only available to be taken in ordinary shares and vests after three years subject to the recipient still being employed

by the Group at that time.

RELATIONShIP OF REMUNERATION TO COMPANy PERFORMANCEIn considering the Group’s performance and benefits for shareholder wealth, executive management has regard to the following indices in respect of the

current financial year and the previous two financial years.

30 Jun 2008 30 Jun 2007 30 Jun 2006

Revenue ($’000) $424,301 $216,369 $171,232

Net profit attributable to equity holders of the Company ($’000) $13,468 $6,396 $3,030

Earnings per share 24.5¢ 11.9¢ 5.9¢Dividend per share 6.0¢ 0.0¢ 0.0¢Share price at balance date $6.27 $2.00 $0.87Share price appreciation 314% 230% (32.6)%

The overall level of key management personnel compensation takes into account the performance of the Group over a number of years. Over the past

four years, the Group’s profit from ordinary activity after income tax has grown at an average rate per annum of over 79%. During the same period, the

average increase in key management’s compensation has grown by approximately 12% per annum.

For

per

sona

l use

onl

y

9 LUCAS GROUP

Details of the nature and amount of each major element of remuneration of each director of the Company and each of the five named highest paid

executives of the Company and Group and other key management personnel are as per the table set out below:

ShORT-TERMPOST

EMPLOyMENTShARE bASED

PAyMENTSproportion of remuneration performance

related %

Value of options and rights as proportion of remuneration

%

salary/ fees

$

cash Bonus

$

non-monetary benefits (1)

$

total

$

superannuation benefits

$

Value of options and rights (2)

$

total

$Executive directors

Allan Campbell2008 425,000 — — 425,000 — 58,483 483,483 — 12.1

2007 393,883 — — 393,883 — 12,476 406,359 — 3.1

Ian Stuart-Robertson2008 336,711 — — 336,711 20,271 36,455 393,437 — 9.32007 252,554 — 12,138 264,692 20,271 7,486 292,449 — 2.6

Non-executive directors

Andrew Lukas (3) 2008 172,915 — 23,972 196,887 12,176 36,455 245,518 14.82007 254,255 — 4,440 258,695 21,345 7,486 287,526 — 2.6

Martin Green2008 45,000 — — 45,000 — — 45,000 — —2007 45,000 — — 45,000 — 40,500 85,500 — 47.4

Garry O’Meally2008 45,000 — — 45,000 — — 45,000 — —2007 45,000 — — 45,000 — 40,500 85,500 — 47.4

Executive officersIan RedfernGeneral Manager Construction

2008 303,183 — — 303,183 26,143 132,823 462,149 21.8 28.72007 249,327 — 5,693 255,020 12,686 10,000 277,706 — 3.6

Kevin LesterGeneral Manager Pipelines

2008 286,020 — 24,021 310,041 19,782 85,674 415,498 14.6 20.62007 268,665 111,167 968 380,800 18,620 — 399,420 27.8 —

Mark Summergreene (4) 2008 232,737 — — 232,737 21,906 78,822 333,465 16.7 23.6Chief Financial Officer 2007 219,914 37,381 6,629 263,924 16,503 — 280,427 13.3 —Brian Burden Chief Estimator

2008 228,211 — — 228,211 18,021 77,108 323,340 16.7 23.72007 203,252 — 2,257 205,509 17,062 — 222,571 — —

Brett Tredinnick 2008 199,057 — 7,978 207,035 17,810 70,185 295,030 16.8 23.8General Manager, Drilling

Mark Tonkin

General Manager

2008 218,548 — — 218,548 17,223 50,341 286,112 11.1 17.62007 181,355 — 1,844 183,199 16,200 — 199,399 — —

FormerTim Herlihy (4)

Chief Financial Officer

2007 104,415 — 20,261 124,676 10,000 — 134,676 — —

OThER bENEFITSThe remuneration policy provides that directors and senior executives may obtain loans from the Group. All such loans are made at commercial rates

and therefore do not represent a benefit to the recipient or attract fringe benefit tax. No loan amounts have been written down as the balances are

considered fully collectible.

SERvICE AGREEMENTS All executive directors and senior executives are employed under a standard AJ Lucas contract. The service contract outlines the components of

remuneration but does not prescribe how remunerations levels are modified year to year. Remuneration levels are reviewed every year to take into

account cost of living changes, any change in the scope of the role performed and any changes required to meet the principles of the remuneration

policy.

The service contracts are unlimited in term. All contracts can be terminated without notice by the Company with compensation, if any, payable to the

employee in accordance with the law or by negotiated agreement.

NON-ExECUTIvE DIRECTORS The remuneration of the non-executive directors, currently each $45,000 per annum, is determined by the Board within the aggregate amount

approved by shareholders. No additional remuneration is paid for serving on any sub-committee of the Board.

In recognition that the amount of the individual fees paid to non-executive directors is less than generally paid to persons in such roles in

comparable sized companies, the Company has in the past periodically awarded them shares under its Deferred Share Plan. Such shares vest from the

date of issue but cannot be disposed of until the earlier of 10 years from the date of issue or the date their service with AJ Lucas ceases.

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 10

Details of the nature and amount of each major element of remuneration of each director of the Company and each of the five named highest paid

executives of the Company and Group and other key management personnel are as per the table set out below:

ShORT-TERMPOST

EMPLOyMENTShARE bASED

PAyMENTSproportion of remuneration performance

related %

Value of options and rights as proportion of remuneration

%

salary/ fees

$

cash Bonus

$

non-monetary benefits (1)

$

total

$

superannuation benefits

$

Value of options and rights (2)

$

total

$Executive directors

Allan Campbell2008 425,000 — — 425,000 — 58,483 483,483 — 12.1

2007 393,883 — — 393,883 — 12,476 406,359 — 3.1

Ian Stuart-Robertson2008 336,711 — — 336,711 20,271 36,455 393,437 — 9.32007 252,554 — 12,138 264,692 20,271 7,486 292,449 — 2.6

Non-executive directors

Andrew Lukas (3) 2008 172,915 — 23,972 196,887 12,176 36,455 245,518 14.82007 254,255 — 4,440 258,695 21,345 7,486 287,526 — 2.6

Martin Green2008 45,000 — — 45,000 — — 45,000 — —2007 45,000 — — 45,000 — 40,500 85,500 — 47.4

Garry O’Meally2008 45,000 — — 45,000 — — 45,000 — —2007 45,000 — — 45,000 — 40,500 85,500 — 47.4

Executive officersIan RedfernGeneral Manager Construction

2008 303,183 — — 303,183 26,143 132,823 462,149 21.8 28.72007 249,327 — 5,693 255,020 12,686 10,000 277,706 — 3.6

Kevin LesterGeneral Manager Pipelines

2008 286,020 — 24,021 310,041 19,782 85,674 415,498 14.6 20.62007 268,665 111,167 968 380,800 18,620 — 399,420 27.8 —

Mark Summergreene (4) 2008 232,737 — — 232,737 21,906 78,822 333,465 16.7 23.6Chief Financial Officer 2007 219,914 37,381 6,629 263,924 16,503 — 280,427 13.3 —Brian Burden Chief Estimator

2008 228,211 — — 228,211 18,021 77,108 323,340 16.7 23.72007 203,252 — 2,257 205,509 17,062 — 222,571 — —

Brett Tredinnick 2008 199,057 — 7,978 207,035 17,810 70,185 295,030 16.8 23.8General Manager, Drilling

Mark Tonkin

General Manager

2008 218,548 — — 218,548 17,223 50,341 286,112 11.1 17.62007 181,355 — 1,844 183,199 16,200 — 199,399 — —

FormerTim Herlihy (4)

Chief Financial Officer

2007 104,415 — 20,261 124,676 10,000 — 134,676 — —

Amounts disclosed for remuneration of key management persons exclude insurance

premiums of $18,595 (2007: $22,884) paid by the Group in respect of directors’

and officers’ liability insurance contracts which cover current and former directors and

officers of the Company and its controlled entities, This amount has not been allocated

to the individuals covered by the insurance policy as the directors believe that no

reasonable basis for such allocation exists.

(1) Non-monetary benefits comprise benefits subject to FBT.

(2) The fair value of the options has been calculated using a Black-Scholes pricing

model and allocated to each reporting period evenly over the period from grant

date to vesting date. The value disclosed is the portion of the fair value of the rights

allocated to this reporting period.

The following factors and assumptions were used in determining the fair value of

options and rights issued during the year on grant date:

Grant date 24 Nov 2006 31 Aug 2007 23 Nov 2007Expiry date 24 Nov 2011 31 Aug 2012 23 Nov 2012Share price on grant date $1.08 $2.11 $3.40Exercise price $1.10 — $2.11Volatility 44% 49% - 56% 51%Risk free interest rate 5.7% 6.2% - 6.3% 6.4%Dividend yield 4.8% 2.8% 2.2%Fair value per options or rights $0.25 $1.88 - $2.05 $1.70

(3) Mr Lukas ceased to serve as an executive of the Company on 19 March 2008 and

became a non-executive director from that date.

(4) Mr Herlihy resigned on 31 December 2006.

Mr Summergreene was appointed Chief Financial Officer in his place from 1

January 2007.

For

per

sona

l use

onl

y

11 LUCAS GROUP

RIGhTS AND OPTIONS OvER EqUITy INSTRUMENTS GRANTED AS COMPENSATION Details of rights and options that were granted to each key management person that vested during the reporting period are as follows:

grant date

number of options or

rights granted during 2008

fair value per option or

right at grant date

$

exercise price

per option or right

$

expiry date

number of

options or rights vested during

2008DirectorsAS Campbell 23 Nov 2007 110,000 1.70 2.11 23 Nov 2012 110,000I Stuart-Robertson 23 Nov 2007 70,000 1.70 2.11 23 Nov 2012 70,000AJ Lukas 23 Nov 2007 70,000 1.70 2.11 23 Nov 2012 70,000ExecutivesI Redfern 31 Aug 2007 34,239 2.05 — 30 Jun 2010 34,239

31 Aug 2007 34,239 1.97 — 30 Jun 2011 —31 Aug 2007 61,333 1.88 — 31 Aug 2012 —

K Lester 31 Aug 2007 20,543 2.05 — 30 Jun 2010 20,54331 Aug 2007 20,543 1.97 — 30 Jun 2011 —31 Aug 2007 48,271 1.88 — 31 Aug 2012 —

M Summergreene 31 Aug 2007 18,900 2.05 — 30 Jun 2010 18,90031 Aug 2007 18,900 1.97 — 30 Jun 2011 —31 Aug 2007 44,409 1.88 — 31 Aug 2012 —

B Burden 31 Aug 2007 18,489 2.05 — 30 Jun 2010 18,48931 Aug 2007 18,489 1.97 — 30 Jun 2011 —31 Aug 2007 43,444 1.88 — 31 Aug 2012 —

B Tredinnick 31 Aug 2007 16,829 2.05 — 30 Jun 2010 16,28931 Aug 2007 16,829 1.97 — 30 Jun 2011 —31 Aug 2007 39,544 1.88 — 31 Aug 2012 —

M Tonkin 31 Aug 2007 10,742 2.05 — 30 Jun 2010 10,74231 Aug 2007 10,742 1.97 — 30 Jun 2011 —31 Aug 2007 35,869 1.88 — 31 Aug 2012 —

grant date

number of

options granted during 2007

fair value per option at

grant date $

exercise price

per options $

expiry date

number of

options vested during 2007

DirectorsAS Campbell 24 Nov 2006 250,000 0.25 1.10 24 Nov 2011 —AJ Lukas 24 Nov 2006 150,000 0.25 1.10 24 Nov 2011 —I Stuart-Robertson 24 Nov 2006 150,000 0.25 1.10 24 Nov 2011 —

During the financial year, 250,000 options over unissued ordinary shares in the Company were issued to the executive directors as approved by

shareholders at the 2007 Annual General Meeting. These options vest immediately on grant but may not be exercised prior to the third anniversary of

the grant date. No options or rights have been granted since the end of the financial year.

ExERCISE OF RIGhTS AND OPTIONS GRANTED AS COMPENSATIONDuring the reporting period, the following shares were issued on the exercise of rights and options previously granted as compensation to key

management persons:

2008 2007number

of sharesamount paid

$/sharenumber

of sharesamount paid

$/shareDirectorsAS Campbell — — 83,333 —AJ Lukas — — 83,333 —ExecutivesK Lester 180,000 — — —

There are no amounts unpaid on the shares issued as a result of the exercise of the rights or options.

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 12

ANALySIS OF ShARE-bASED PAyMENTS GRANTED AS REMUNERATION Details of the vesting profile of the options and rights granted as remuneration to each director of the Company and each of the named executives is

detailed below:

options and rights

granted Vested in year

forfeited in

year 1

financial years in which

options or rights vest

Value yet to vest

number Date min2 max3

Directors % % $ $AS Campbell 250,000 24 Nov 2006 — — 2010 — 1,292,500

110,000 23 Nov 2007 100 — 2008 — —I Stuart-Robertson 150,000 24 Nov 2006 — — 2010 — 775,500

70,000 23 Nov 2007 100 — 2008 — —AJ Lukas 150,000 24 Nov 2006 — — 2010 — 775,500

70,000 23 Nov 2007 100 — 2008 — —

Company and consolidated entity executives

I Redfern 34,239 31 Aug 2007 100 — 2008 — —34,239 31 Aug 2007 — — 2009 — 214,67961,333 31 Aug 2007 — — 2010 — 384,558

K Lester 20,543 31 Aug 2007 100 — 2008 — —20,543 31 Aug 2007 — — 2009 — 128,80548,271 31 Aug 2007 — — 2010 — 302,659

M Summergreene 18,900 31 Aug 2007 100 — 2008 — —18,900 31 Aug 2007 — — 2009 — 118,50344,409 31 Aug 2007 — — 2010 — 278,444

B Burden 18,489 31 Aug 2007 100 — 2008 — —18,489 31 Aug 2007 — — 2009 — 115,92643,444 31 Aug 2007 — — 2010 — 272,394

B Tredinnick 16,829 31 Aug 2007 100 — 2008 — —16,829 31 Aug 2007 — — 2009 — 105,51839,544 31 Aug 2007 — — 2010 — 241,671

M Tonkin 10,742 31 Aug 2007 100 — 2008 — —10,742 31 Aug 2007 — — 2009 — 67,35235,869 31 Aug 2007 — — 2010 — 224,899

(1) The % forfeited in the year represents the reduction from the maximum number of options available to vest due to the performance hurdle not

being achieved.

(2) The minimum value of options and rights yet to vest is $nil as the performance criteria may not be met and consequently the right may not vest.

(3) The maximum value of options and rights yet to vest is not determinable as it depends on the market price of shares of AJ Lucas Group on the ASX

on the date the option or rights is exercised. The maximum values presented above are based on the closing share price at 30 June 2008 of $6.27

less the exercise price.

For

per

sona

l use

onl

y

13 LUCAS GROUP

ANALySIS OF MOvEMENTS IN OPTIONS AND RIGhTS The movement during the reporting period, by value, of options and rights over ordinary shares of the Company held by each Company director and

each of the named executives is detailed below:

(i) granted in year

$

(ii) Value of options and rights exercised in year

$

(iii) lapsed in year

$DirectorsAS Campbell 187,000 — —I Stuart-Robertson 119,000 — —AJ Lukas 119,000 — —

— —

ExecutiveI Redfern 252,947 — —K Lester 173,332 360,000 —M Summergreene 159,467 — —B Burden 156,001 — —B Tredinnick 141,995 — —M Tonkin 110,617 — —

(i) The value of options and rights is their fair value calculated at grant date using a Black-Scholes pricing model. The total value of the options and

rights is included in the table above. This amount is allocated to remuneration over the vesting period.

(ii) The value of the options and rights is calculated as the market price of the Company’s shares on the Australian Securities Exchange as at close of

trading on the date the options or rights were exercised after deducting the price paid to exercise the options and rights.

(iii) The value of the options and rights that lapsed during the year represents the benefits foregone and is calculated at the date of the option or right

lapses using a Black-Scholes pricing model assuming the performance hurdle has not been met. No options or rights lapsed in the year.

Signed in accordance with a resolution of the directors pursuant to s.298 (2) of the Corporations Act 2001.

Allan Campbell, Director

Dated at Sydney, this 25th day of September 2008.

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 14

leaD auDitor’s inDepenDence Declaration unDer section 307c of the corporations act 2001To the directors of AJ Lucas Group Limited

I declare that, to the best of my knowledge and belief, in relation to the audit for the financial year ended 30 June 2008 there have been:

• nocontraventionsoftheauditorindependencerequirementsassetoutintheCorporationsAct2001inrelationtotheaudit;and

• nocontraventionsofanyapplicablecodeofprofessionalconductinrelationtotheaudit.

KPMG

Neil Cameron Smith

Partner

Sydney

25 September 2008

For

per

sona

l use

onl

y

15 LUCAS GROUP

aJ lucas group limiteD anD its controlleD entities

income statements for the year enDeD 30 June 2008The accompanying notes are an integral part of these consolidated financial statements.

consolidated company

note2008

$’0002007

$’0002008

$’0002007

$’000Revenue 2 424,301 216,369 1,500 —

Total revenue 424,301 216,369 1,500 —

Material costs (124,587) (65,779) — —

Sub-contractor costs (116,734) (75,272) — —

Employee expenses (80,627) (34,707) — —

Plant and other construction costs (55,404) (16,380) — —

Depreciation and amortisation expenses 4 (11,451) (8,966) — —

Debt recovery and legal costs (6,500) (3,615) — —

Impairment of assets 4 — (3,422) — (1,786)

Profit on acquisition of business 30 — 2,723 — —

Other expenses (3,037) (5,010) (93) (620)

Results from operating activities 25,961 5,941 1,407 (2,406)

Financial income 3 1,322 781 6,591 386

Financial expenses 3 (6,875) (2,544) (5,078) (1,055)

Net financing (costs)/income 3 (5,553) (1,763) 1,513 (669)

Profit/(loss) before income tax 20,408 4,178 2,920 (3,075)

Income tax (expense)/benefit 6 (6,940) 2,218 799 1,866

Profit/(loss) attributable to equity holders of the company 24 13,468 6,396 3,719 (1,209)

Earnings per share:

Basic earnings per share (cents) 7 24.5 11.9

Diluted earnings per share (cents) 7 24.0 11.8

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 16

statements of recogniseD income anD eXpense for the year enDeD 30 June 2008The accompanying notes are an integral part of these consolidated financial statements.

consolidated company

note2008

$’0002007

$’0002008

$’0002007

$’000Exchange differences on translation of foreign operations 24 274 306 — —

Income and expense recognised directly in equity 274 306 — —

Profit/(loss) for the year 24 13,468 6,396 3,719 (1,209)

Total recognised income and expense for the year 24 13,742 6,702 3,719 (1,209)

For

per

sona

l use

onl

y

17 LUCAS GROUP

balance sheets as at 30 June 2008The accompanying notes are an integral part of these consolidated financial statements.

consolidated company

note2008

$’0002007

$’0002008

$’0002007

$’000Current assets

Cash and cash equivalents 8 16,612 18,222 5,519 13,512

Trade and other receivables 9 56,912 28,261 6,064 4,189

Construction work in progress 10 40,685 53,418 — —

Other 11 1,717 435 184 —

Total current assets 115,926 100,336 11,767 17,701

Non-current assets

Trade and other receivables 9 — — 49,889 31,795

Property, plant and equipment 12 55,986 30,921 — —

Investments 13 26,156 63 26,879 1,260

Exploration assets 14 4,100 6,175 — —

Intangible development assets 15 15,452 1,046 — —

Other intangible assets 16 12,279 6,805 2,061 2,061

Deferred tax assets 17 — 5,602 8,405 10,126

Total non-current assets 113,973 50,612 87,234 45,242

Total assets 229,899 150,948 99,001 62,943

Current liabilities

Trade and other payables 18 83,074 66,319 632 84

Interest-bearing loans and borrowings 19 19,996 10,706 4,500 —

Income tax payable 20 114 75 — —

Provisions 21 8,550 2,702 — —

Total current liabilities 111,734 79,802 5,132 84

Non-current liabilities

Trade and other payables 18 — — 29,361 16,217

Interest-bearing loans and borrowings 19 51,036 37,181 18,226 24,188

Deferred tax liabilities 17 1,221 — — —

Provisions 21 748 3,527 — —

Total non-current liabilities 53,005 40,708 47,587 40,405Total liabilities 164,739 120,510 52,719 40,489

Net assets 65,160 30,438 46,282 22,454

Equity

Issued capital 24 54,037 30,655 54,118 30,736

Reserves 24 2,236 1,091 — —

Retained earnings/(accumulated losses) 24 8,887 (1,308) (7,836) (8,282)

Total equity 24 65,160 30,438 46,282 22,454

aJ lucas group limiteD anD its controlleD entities

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 18

statements of cash flows for the year enDeD 30 June 2008The accompanying notes are an integral part of these consolidated financial statements.

consolidated company

note2008

$’0002007

$’0002008

$’0002007

$’000Cash flows from operating activities

Cash receipts from customers 450,877 200,553 66 —

Cash payments to suppliers and employees (394,407) (187,970) (277) (100)

Cash generated from operations 56,470 12,583 (211) (100)

Interest received 547 60 465 —

Income taxes paid (72) (497) — —

Interest and other costs of finance paid (6,875) (2,544) (4,112) (1,172)

Net cash from operating activities 29(b) 50,070 9,602 (3,858) (1,272)

Cash flows from investing activities

Proceeds from sale of plant and equipment 1,018 457 — —

Payment for investment in other entities (27,858) — (25,243) —

Loans to controlled entities — — (8,574) —

Repayment of loans by controlled entities — — — 5,532

Payments for plant and equipment (21,472) (5,953) — —

Exploration and evaluation expenditure (12,513) (2,676) — —

Loans to related entity (1,578) (1,608) (1,578) (1,608)

Repayment of loan to related entity 292 — 263 —

Acquisition of subsidiary net of cash acquired (9,993) (3,198) — —

Net cash from investing activities (72,104) (12,978) (35,132) 3,924

Cash flows from financing activities

Proceeds of borrowings -other 41,690 4,004 22,626 —

Repayment of borrowings - other (6,413) (147) — —

Loans from controlled entities — — 13,144 —

Deferred payment for acquistion (625) _ — —

Dividends paid (3,273) _ (3,273) —

Proceeds from issue of convertible notes — 24,188 — 24,188

Repayment of convertible notes (1,500) (10,000) (1,500) (10,000)

Payment of finance lease liabilities (4,659) (3,521) — —

Net cash from financing activities 25,220 14,524 30,997 14,188

Net increase/(decrease) in cash and cash equivalents 3,186 11,148 (7,993) 16,840

Cash and cash equivalents at beginning of the year 12,559 1,411 13,512 (3,328)

Cash and cash equivalents at end of the year 29(a) 15,745 12,559 5,519 13,512

For

per

sona

l use

onl

y

19 LUCAS GROUP

notes to the financial statements

Page Note content19 1 Significant accounting policies

25 2 Segment reporting

26 3 Financial income and expense

26 4 Other expenses

26 5 Auditor’s remuneration

27 6 Income tax

27 7 Earnings per share

28 8 Cash and cash equivalents

28 9 Trade and other receivables

28 10 Construction work in progress

28 11 Other current assets

29 12 Property, plant and equipment

29 13 Investments

29 14 Exploration assets

30 15 Intangible development assets

30 16 Other intangible assets

31 17 Deferred tax assets and liabilities

33 18 Trade and other payables

33 19 Interest-bearing loans and liabilities

35 20 Current tax liabilities

36 21 Provisions

36 22 Operating leases

36 23 Employee benefits

38 24 Capital and reserves

39 25 Financial instruments

44 26 Interests in joint ventures

45 27 Consolidated entities

45 28 Contingencies

46 29 Reconciliation of cash flows from operating activities

47 30 Acquisition of subsidiary

48 31 Key management personnel disclosures

50 32 Non-key management personnel disclosures

51 33 Deed of cross guarantee

51 34 Events subsequent to balance date

1. significant accounting policies

AJLucasGroupLimited(the‘Company’)isacompanydomiciledin

Australia. The address of the Company’s registered office is 157 Church

Street Ryde, NSW 2112. The consolidated financial report of the Company

for the financial year ended 30 June 2008 comprises the Company and

itssubsidiaries(togetherreferredtoasthe‘Group’)andtheGroup’s

interest in associates and jointly controlled entities. The Group is primarily

involved in construction, civil engineering and commercialisation of coal

seam gas reserves (see note 2).

The accounting policies set out below have been applied consistently

to all periods presented in these consolidated financial statements, and

have been applied consistently by all entities in the Group.

Certain comparative amounts have been reclassified to conform with

the current year’s presentation.

STATEMENT OF COMPLIANCEThe financial report is a general purpose financial report which has

been prepared in accordance with Australian Accounting Standards

(‘AASBs’)(includingAustralianInterpretations)adoptedbytheAustralian

AccountingStandardsBoard(‘AASB’)andtheCorporationsAct2001.The

consolidated financial report of the Group and the financial report of the

CompanycomplywithInternationalFinancialReportingStandards(‘IFRSs’)

and interpretations adopted by the International Accounting Standards

Board(‘IASB’).

The financial statements were approved by the Board of Directors on

25 September 2008.

bASIS OF MEASUREMENTThe consolidated financial statements have been prepared on the

historical cost basis.

FUNCTIONAL AND PRESENTATION CURRENCyThe financial report is presented in Australian dollars which is the

Company’s functional currency and the functional currency of the majority

of the Group. The Company is of a kind referred to in ASIC Class Order

98/100 dated 10 July 1998 (updated by CO 05/641 effective 28 July

2005 and CO 06/51 effective 31 January 2006) and in accordance with

that Class Order, amounts in the financial report and Director’s Report

have been rounded off to the nearest thousand dollars, unless otherwise

stated.

USE OF ESTIMATES AND JUDGMENTSThe preparation of financial statements requires management to make

judgements, estimates and assumptions that affect the application of

accounting policies and the reported amount of assets, liabilities, income

and expenses. Actual results may differ from these estimates. Estimates

and underlying assumptions are reviewed on an ongoing basis. Revisions

to accounting estimates are recognised in the period in which the estimate

is revised and in any future periods affected.

In particular, information about significant areas of estimation

uncertainty and critical judgements in applying accounting policies that

have the most significant effect on the amount recognised in the financial

statements are described in the following notes:

• Note10–constructionworkinprogress

• Note15-intangibledevelopmentassets

• Note16–otherintangibleassets

• Note21–provisions

bASIS OF CONSOLIDATIONASSOCIATES: Associates are those entities in which the Group has

significant influence, but not control, over the financial and operating

For

per

sona

l use

onl

y

A yEAR OF MILESTONES 20

policies. Significant influence is presumed to exist when the Group holds

between 20 and 50 percent of the voting power of another entity.

Associates are accounted for using the equity method (equity

accounted investees) and are initially recognised at cost. The Group’s

investment includes goodwill identified on acquisition, net of any

accumulated impairment losses. The consolidated financial statements

include the Group’s share of income and expenses and equity movements

of equity accounted investees, after adjustments to align the accounting

policies with those of the Group, from the date that significant influence

commences to the date that significant influence ceases. Where the

Group’s share of losses exceeds its interest in an equity accounted

investee, the carrying amount of that interest (including any long-term

investments) is reduced to nil and the recognition of further losses is

discontinued except to the extent that the Group has an obligation or has

made payments on behalf of the investee.

SUbSIDIARIES: Subsidiaries are entities controlled by the Group.

Control exists when the Company has the power, directly or indirectly, to

govern the financial and operating policies of an entity so as to obtain

benefits from its activities. In assessing control, potential voting rights that

presently are exercisable or convertible are taken into account. The financial

statements of subsidiaries are included in the consolidated financial

statements from the date that control commences until the date that control

ceases. The accounting policies of subsidiaries have been changed when

necessary to align them with the policies adopted by the Group.

JOINTLy CONTROLLED OPERATIONS, ASSETS AND ENTITIES: The interest of the Company and of the Group in joint ventures and jointly

controlled assets are brought to account by recognising in its financial

statements the assets it controls, the liabilities that it incurs, the expenses

it incurs and its share of income that it earns from the sale of goods or

services by the joint venture.

TRANSACTIONS ELIMINATED ON CONSOLIDATION: Intragroup

balances, and any unrealised gains and losses or income and expenses

arising from intragroup transactions, are eliminated in preparing

the consolidated financial statements. Unrealised gains arising from

transactions with equity accounted investees are eliminated against the

investment to the extent of the Group’s interest in the investee. Unrealised

losses are eliminated in the same way as unrealised gains, but only to the

extent that there is no evidence of impairment.

FOREIGN CURRENCyFOREIGN CURRENCy TRANSACTIONS: Transactions in foreign

currencies are translated to the respective functional currencies of the

Group’s entities at exchange rates at the dates of the transactions.

Monetary assets and liabilities denominated in foreign currencies at the

reporting date are retranslated to the functional currency at the foreign

exchange rate at that date. The foreign currency gain or loss on monetary

items is the difference between amortised cost in the functional currency

at the beginning of the period, adjusted for effective interest and payments

during the period, and the amortised cost in foreign currency translated

at the exchange rate at the end of the period. Non-monetary assets and

liabilities denominated in foreign currencies that are measured at fair

value are retranslated to the functional currency at the exchange rate at

the date that the fair value was determined. Foreign currency differences

arising on retranslation are recognised in profit or loss.

FOREIGN OPERATIONS: The assets and liabilities of foreign operations

are translated to Australian dollars at exchange rates at the reporting date.

The income and expenses of foreign operations are translated to Australian

dollars at exchange rates at the dates of the transactions.

Foreign currency differences are recognised directly in equity. Since 1

January 2004, the Group’s date of transition to AASBs, such differences

havebeenrecognisedintheforeigncurrencytranslationreserve(‘FCTR’).

When a foreign operation is disposed of, in part or in full, the relevant

amount in the FCTR is transferred to profit or loss.

Foreign exchange gains and losses arising from a monetary item

receivable from or payable to a foreign operation, the settlement of which

is neither planned nor likely in the foreseeable future, are considered to

form part of the net investment in a foreign operation and are recognised

directly in equity in the FCTR.

FINANCIAL INSTRUMENTSNON-DERIvATIvE FINANCIAL INSTRUMENTS: Non-derivative

financial instruments comprise trade and other receivables, cash and cash

equivalents, loans and borrowings, and trade and other payables.

Non-derivative financial instruments are recognised initially at fair

value plus, for instruments not at fair value through profit or loss, any

directly attributable transaction costs. Subsequent to initial recognition,

non-derivative financial instruments are measured as described below.

A financial instrument is recognised if the Group becomes a party

to the contractual provisions of the instrument. Financial assets are

derecognised if the Group’s contractual rights to the cash flows from

the financial assets expire or if the Group transfers the financial asset

to another party without retaining control or substantially all risks and

rewards of the asset. Regular way purchases and sales of financial assets

are accounted for at trade date, i.e., the date that the Group commits itself

to purchase or sell the asset. Financial liabilities are derecognised if the

Group’s obligations specified in the contract expire or are discharged or

cancelled.

Cash and cash equivalents comprise cash balances and call deposits.

Bank overdrafts that are repayable on demand and form an integral part of

the Group’s cash management are included as a component of cash and

cash equivalents for the purpose of the statement of cash flows.

Non-derivative financial instruments are measured at amortised cost

using the effective interest method, less any impairment losses.

available-for-sale financial assets

The Group’s investments in equity securities are classified as available-

for-sale financial assets. Subsequent to initial recognition, they are

measured at fair value and changes therein, other than impairment

losses are recognised directly in a separate component of equity. When

an investment is derecognised, the cumulative gain or loss in equity is

transferred to profit or loss.

COMPOUND FINANCIAL INSTRUMENTS: Compound financial

instruments issued by the Group comprise convertible notes that can be

converted to share capital at the option of the holder, and the number of

shares to be issued does not vary with changes in their fair value.

The liability component of a compound financial instrument is

recognised initially at the fair value of a similar liability that does not

have an equity conversion option. The equity component is recognised

initially at the difference between the fair value of the compound financial

instrument as a whole and the fair value of the liability component. Any

directly attributable transaction costs are allocated to the liability and

equity components in proportion to their initial carrying amounts.

Subsequent to initial recognition, the liability component of a

compound financial instruments is measured at amortised cost using the

effective interest method, unless it is designated at fair value through profit

or loss. The equity component of a compound financial instruments is not

remeasured subsequent to initial recognition.

For

per

sona

l use

onl

y

21 LUCAS GROUP

Interest, dividends, losses and gains relating to the financial liability

are recognised in the profit or loss. Distributions to the equity holders are

recognised against equity, net of any tax benefit.

ShARE CAPITALOrdinary shares: Incremental costs directly attributable to issue of

ordinary shares and share options are recognised as a deduction from

equity, net of any related income tax benefit.

Dividends: Dividends are recognised as a liability in the period in

which they are declared.

LEASED ASSETSLeases in terms of which the Group assumes substantially all the risks

and rewards of ownership are classified as finance leases. Upon initial

recognition, the leased asset is measured at an amount equal to the lower

of its fair value and the present value of the minimum lease payments.

Subsequent to initial recognition, the asset is accounted for in accordance

with the accounting policy applicable to that asset.

Other leases are operating leases and the leased assets are not

recognised on the Group’s balance sheet.

REvENUESERvICES RENDERED: Revenue from services rendered is recognised

in the income statement in proportion to the stage of completion of the

transaction at the balance sheet date. The stage of completion is assessed

by reference to surveys of work performed.

CONSTRUCTION CONTRACTS: Contract revenue includes the initial

amount agreed in the contract plus any variations in contract work, claims

and incentive payments to the extent that it is probable that they will

result in revenue and can be measured reliably. As soon as the outcome

of a construction contract can be estimated reliably, contract revenue and

expenses are recognised in the income statement in proportion to the

stage of completion of the contract.

The stage of completion is assessed by reference to an assessment

of total labour hours and other costs incurred to date as a percentage of

estimated total costs for each contract, unless an alternative measurement

method provides a more accurate indication of the stage of completion.

When the outcome of a construction contract cannot be estimated

reliably, contract revenue is recognised only to the extent of contract costs

incurred that are likely to be recoverable. An expected loss on a contract is

recognised immediately in the income statement.

ASSET SALES: The net proceeds of asset sales are recognised at the

date an unconditional contract of sale is signed.

The gain or loss on disposal is calculated as the difference between the

carrying amount of the asset at the time of disposal and the net proceeds

on disposal and is recognised in other income.

LEASE PAyMENTSPayments made under operating leases are recognised in the income

statement on a straight-line basis over the term of the lease.

Minimum lease payments made under finance leases are apportioned

between the finance expense and the reduction of the outstanding liability.

The finance expense is allocated to each period during the lease term so

as to produce a constant periodic rate of interest on the remaining balance

of the liability.

FINANCE INCOME AND ExPENSESFinance income comprises interest income on funds invested, dividend

income and foreign currency gains that are recognised in the income

statement. Interest income is recognised as it accrues, using the effective

interest method. Dividend income is recognised in profit or loss on the

date that the Group’s right to receive payment is established, which in the

case of quoted securities is the ex-dividend date.

Finance expenses comprise interest expense on borrowings, unwinding

of the discount on provisions and deferred consideration, foreign currency

losses and impairment losses recognised on financial assets that are

recognised in the income statement. All borrowing costs are recognised in

the income statement using the effective interest method.

INCOME TAxIncome tax in the income statement comprises current and deferred tax.

Income tax is recognised in the income statement except to the extent

that it relates to items recognised directly in equity, in which case it is

recognised in equity.

Current tax is the expected tax payable on the taxable income for the

year, using tax rates enacted or substantially enacted at the balance sheet

date, and any adjustment to tax payable in respect of previous years.

Deferred tax is recognised using the balance sheet liability method,

providing for temporary differences between the carrying amounts of

assets and liabilities for financial reporting purposes and the amounts

used for taxation purposes. The following temporary differences are

not provided for: the initial recognition of goodwill and other assets or

liabilities that affect neither accounting nor taxable profit, and differences

relating to investments in subsidiaries to the extent that they will probably

not reverse in the foreseeable future. Deferred tax is measured at the tax

rates that are expected to be applied to the temporary differences when

they reverse, based on the laws that have been enacted or substantially

enacted by the reporting date. Deferred tax assets and liabilities are offset

if there is a legally enforceable right to offset current tax liabilities and

assets, and they relate to income taxes levied by the same authority on the

same taxable entity, or on different tax entities, but they intend to settle

current tax liabilities and assets on a net basis or their tax assets and

liabilities will be realised simultaneously.

A deferred tax asset is recognised only to the extent that it is probable

that future taxable profits will be available against which the asset can be

utilised. Deferred tax assets are reduced to the extent that it is no longer

probable that the related tax benefit will be realised.

Additional income taxes that arise from the distribution of dividends

are recognised at the same time as the liability to pay the related dividend

is recognised.

TAx CONSOLIDATION: The Company and its wholly-owned Australian

resident entities have formed a tax-consolidated group and are therefore