Embed Size (px)

Citation preview

RECREATION DISTRICT NO. 6 OF ALLEN PARISH

Annual Financial Statements

As of September 30,2006 and for the Year Then Ended

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

itlnl*Release Date

RECREATION DISTRICT NO. 6 OF ALLEN PARISH

Annual Financial StatementsAs of and for the Year Ended September 30. 2006

With Supplemental Information Schedules

CONTENTSPage

independent Auditor's Report 2

Basic Financial Statements

Government-Wide Financial Statements:

Statement of Net Assets 5

Statement of Activities 6

Fund Financial Statements;

Governmental Funds:

Balance Sheet 7

Statement of Revenues, Expenditures, and Changesin Fund Balances 8

Notes to me Financial Statements 10

Required Supplemental Information (Part II)

Budget Comparison Schedule 18

Other Supplemental Schedules

Per Diem Paid Board Members 20

Schedule of Findings 21

Management's Corrective Action Plan (Unaudited) 22

Status of Prior Audit Findings 23

Independent Auditor's

Report on Internal Control Over Financial Reporting and onCompliance and Other Matters Based on an Audit of FinancialStatements Performed in Accordance with Govemmenf AuditingStandards 25

Stutzman & Gates, LLCCertified Public Accountants

MNfc

INDEPENDENT AUDITOR'S REPORT

Board of CommissionersRecreation District No. 6 of Alton ParishAlien Parish Police JuryReeves, Louisiana 70658

r̂ L1!?? audlted ̂ accomPanV'n9 financial statements of the governmental adivitfes and each majorfend of Recreation pistnct No. 6 of Allen Parish, a component unit of the Allen Parish Police Jury, as of and

S?1!!!!̂ !!̂as listed In i toe tabte of contents. These financial statements are the responsibility of Recreation District!£ r̂1 ^8fbhs ma

jna9ement Our responsibility is to express opinions on these financial

statements based on our audit.

We conducted oun audit in accordance with auditing standards generally accepted in the United States ofAmenca and the standards applicable to financial audits contained in Government Auditing Standardsissued by the Comptroller General of the United States. Those standards require thai we plan and performthe audit to obtain reasonable assurance about whether the financial statements are free of materialmtsslatement An audit includes examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includes assessing the accounting principles usedand the significant estimates made by management, as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinions.

in our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities and each major fund of the Recreation DistrictNo. 6 of Allen Parish, as of September 30, 2006, and the respective changes in financial position, thereoffor the year then ended in conformity with accounting principles generally accepted in the United States ofAmerica.

In accordance with Government Auditing Standards, we have also issued our report dated March 1 , 2007.on our consideration of the Recreation District No. 6 of Allen Parish's internal control over financialreporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grantagreements and other matters. ThepurposeofthatreportistodescrlbetttescopeofcMJrt^tingof internalcontrol over financial reporting and compliance and the results of that testing, and not to provide an opinionon the Internal control over financial reporting or on compliance. That report is an integral part of an auditperformed In accordance with Government Auditing Standards and should be considered in assessing theresults of our audit

The budgetary comparison information on page 1 8 is not a required part of the basic financial statementsbut is supplementary information required by accounting principles generally accepted in the United Statesof America. We have applied certain limited procedures, which consisted principally of inquiries ofmanagement regarding the methods of measurement and presentation of the required supplementaryinformation. However, we did not audit the information and express no opinion on it

Recreation District No. 6 of Allen Parish has not presented management's discussion and analysis that theGovernmental Accounting Standards Board has determined is necessary to supplement, although notrequired to be a part of, the basic financial statements.

T

Board of CommissionersPage 2

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the Recreation District No. 6 of Allen Parish's basic financial statements. The other supplementalschedules as listed in the table of contents are presented for purposes of additional analysis and are not arequired part of the basic financial statements. The per diem paid board members and status of prior auditfindings have been subjected to the auditing procedures applied in the audit of the basic financialstatements and, in our opinion, are fairly stated in all material respects in relation to the basic financialstatements taken as a whole. The management's corrective action plan has not been subjected to theauditing procedures applied in the audit of the basic financial statements and, accordingly, we express noopinion on it

, t**f —A^ i i ,"»^

Stutzman & Gates, LLCMarch 1,2007

BASIC FINANCIAL STATEMENTS

-4

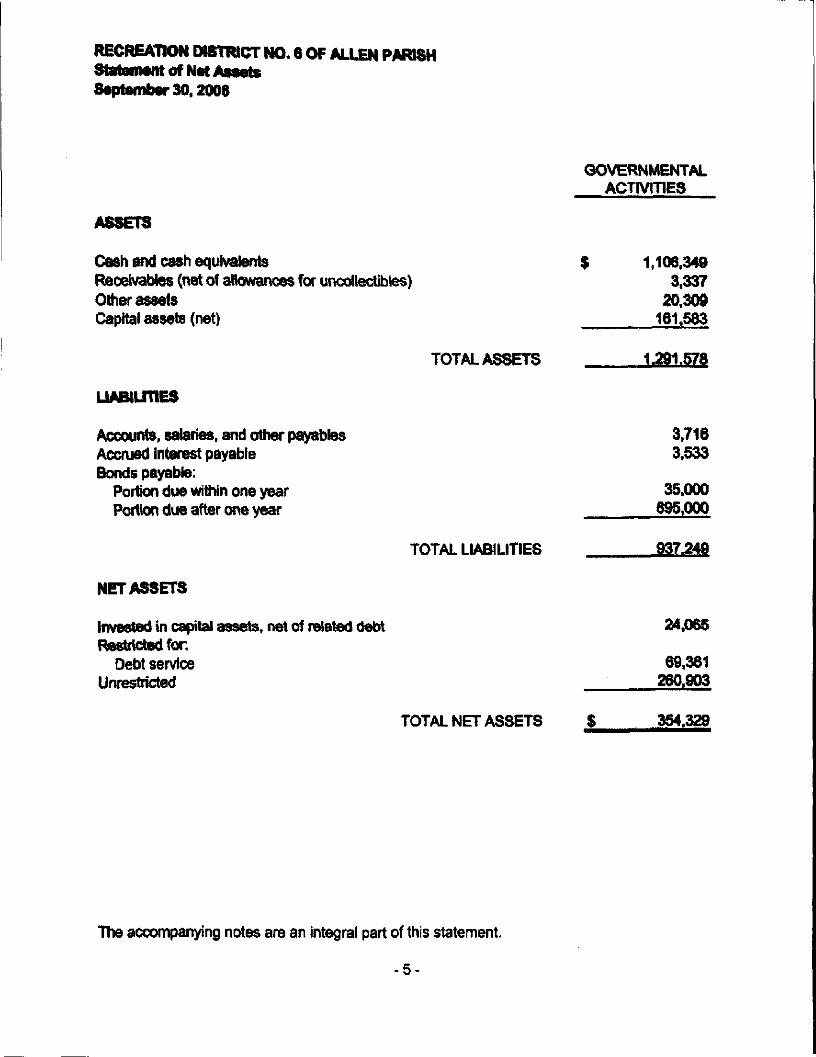

RECREATION DISTRICT NO. 6 OF ALLEN PARISHStatement of Nat AssetsSeptember 30,2006

ASSETS

Cash and cash equivalentsReceivables (net of allowances for uncollectibtes)Other assetsCapital assets (net)

LIABILITIES

Accounts, salaries, and other payabtesAccrued Interest payableBonds payable:

Portion due within one yearPortion due after one year

TOTAL ASSETS

TOTAL LIABILITIES

NET ASSETS

Invested in capital assets, net of related debtRestricted for.

Debt serviceUnrestricted

TOTAL NET ASSETS

GOVERNMENTALACTIVITIES

1,106.3493.337

20.3091S1.S83

1.291.578

3.7163.533

35.000695.000

937.249

24.065

69,361260.903

354.329

The accompanying notes are an integral part of this statement.

-5-

$8IO ^t

3 £ 8,. CM

l

*O

JQ

oo

& coCD W

H££o

<0 O)C> O

ICD

c 8II^ fg111ill

(A

I

5 r

uj S oa: S u. OO

§u>

c<D

E§o

2 « 2<D 0 ,O

Ss1"O £

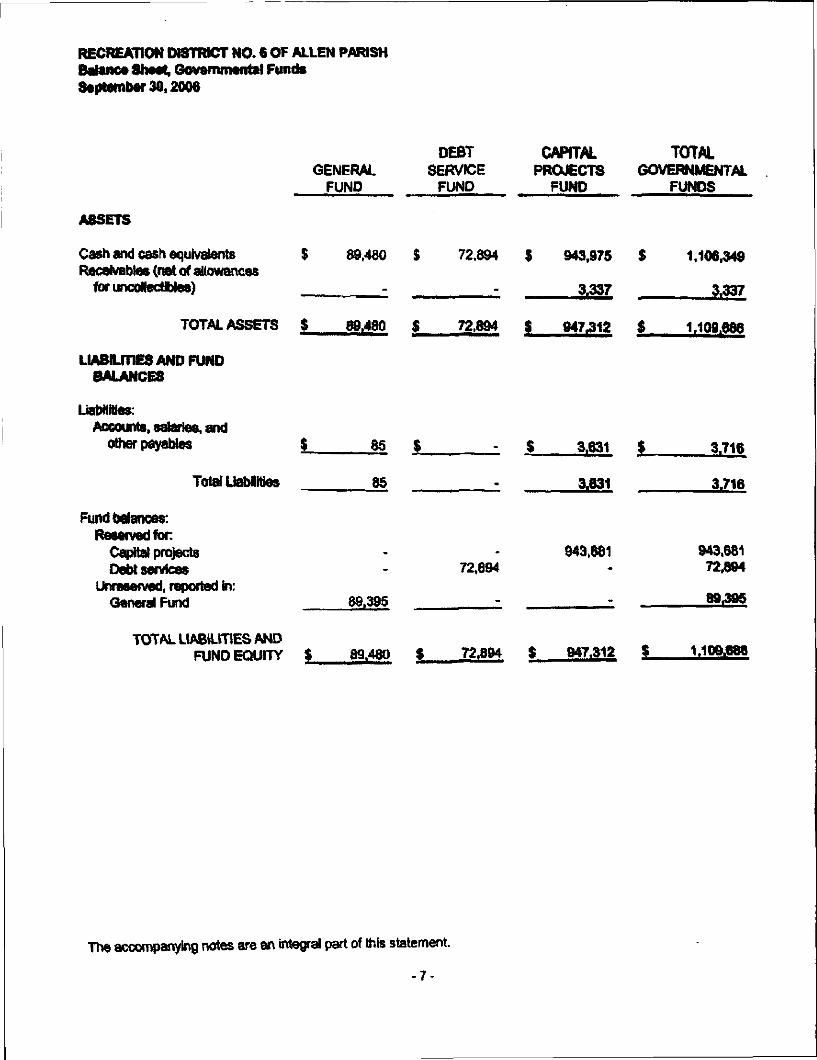

RECREATION DISTRICT NO. € OF ALLEN PARISHBalance Sheet, Governmental Fund*September 30,2006

GENERALFUND

DEBTSERVICE

FUND

ASSETS

Cash and cash equivalentsReceivables (net of allowances

fbruncoRectibies)

89,480 $ 72,894

TOTALASSETS $ 89,480 $ 72.894

LIABILFHES AND FUNDBALANCES

Accounts, salaries, andother payables

Total Uabiities

Fund balances:Reserved for

Capital projectsDebt services

Unreserved, reported in:General Fund

TOTAL LIABILITIES AND

85 $

85

89.395

72,894

$

f

$

CAPITALPROJECTS

FUND

943,975

3.337

947^12

3.631

3.631

943,681

$ 947.312

TOTALGOVERNMENTAL

FUNDS

$ 1,106,349

3T337

S 1.109,686

$ 3.716

3.716

943.68172394

89,395

$ 1.109,686

The accompanying notes are an integral part of this statement.

- 7 -

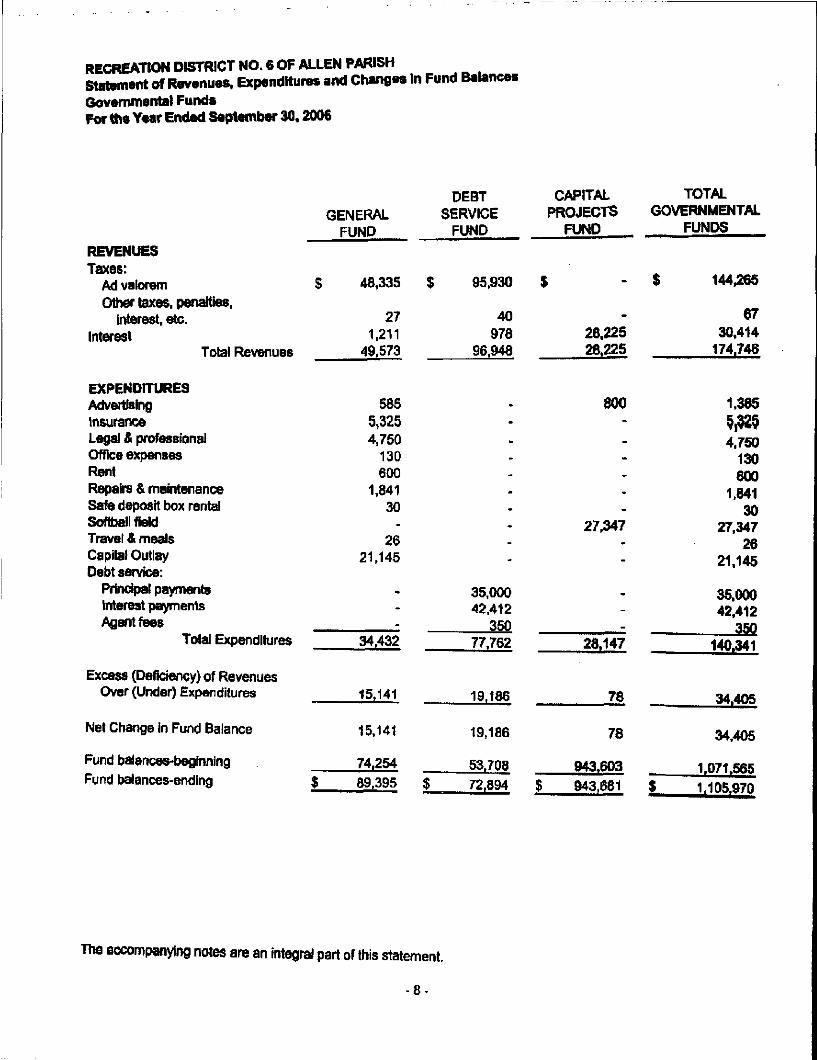

RECREATION DISTRICT NO. 6 OF ALLEN PARISHStatement of Revenues, Expenditure* and Changes In Fund Balances

Governmental FundsFor the Year Ended September 30,2006

REVENUESTaxes:

Ad valoremOther taxes, penalties,

interest, etc.Interest

Total Revenues

EXPENDITURESAdvertisingInsuranceLegal & professionalOffice expensesRentRepairs & maintenanceSafe deposit box rentalSoftball fieldTravel & mealsCapital OutlayDebt service:

Principal paymentsInterest paymentsAgent fees

Total Expenditures

Excess (Deficiency) of RevenuesOver (Under) Expenditures

Net Change in Fund Balance

Fund balances-beginningFund balances-ending

GENERALFUND

$ 48,335

271,211

49,573

5855,3254,750

130600

1,84130

-26

21,145

---

34t432

15,141

15,141

74.254$ 89,395

DEBTSERVICE

FUND

$ 95,930

40978

96,948

---------

35,00042,412

35077.762

19,186

19,186

53,708$ 72.894

CAPITALPROJECTS

FUND

$

-

28.22528,225

800-

-.---

27,347.

-

--.

28.147

78

78

943,603

$ 943,681

TOTALGOVERNMENTAL

FUNDS

$ 144,265

6730,414

174.746

1.385

w4.750

130600

1.84130

27.34726

21,145

35,00042,412

35°140,341

34.405

34,405

1.071.565$ 1.105^970

Tne accompanying notes are an Integral part of this statement.

NOTES TO THE FINANCIAL STATEMENTS

- 9-

RECREATION DISTRICT NO. 6 OF ALLEN PARISH

Notes to the Financial StatementsAs of and for the Year Ended September 30,2006

INTRODUCTION

Recreation District No. 6 of Allen Parish was created by the Allen Parish Police Jury on September 18,2000 under the authority conferred by Article VI, Section 19 of the Constitution of the State of Louisiana of1974, Sections 4562 to 4566, both inclusive of TiUe 33 of the Louisiana Revised Statutes of 1950 (R.S.33:4562-33:4566). The District was created to provide recreational facilities for the citizens of Ward Threeof Allen Parish. The Distik* is gowmed by five commissioners v^^Police Jury and maybe be compensated by a per diem of $10 per meeting attended, not to exceed twelvemeetings per year As of September 30,2006, the cornmlssionere have chosen not to be paid any perdiem. The District encompasses all of Ward Three of Allen Parish and has approximately 2,500 citizens.As of September 30,2006, the District has no employees. The District is in the process of developing therecreation complex and when it is completed it will offer a wide range of recreational facilities to thecitizens,

GASB Statement No. 14, Tte Reporting Entity, established criteria for determining the governmentalreporting entity and component units that should be included within the reporting entity. Under provisionsof this Statement, the Recreation District No. 6 of Alien Parish is considered a component unit of the MienParish Police Jury, As a component unit, the accompanying financial statements we included within thereporting of the primary government, either blended into those financial statements or separately reportedas discrete component units.

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The government-wide financial statements (i.e., the statement of net assets and the statement of changesin net assets) report information on all of the nonffduciary activities of the Recreation District No. 6 of AllenParish. For the most part the effect of interfutvj activity has been removed from these statements.Governmental activities, which normally are supported by taxes and intergovernmental revenues, wereported separately from business-type activities, which rely to a significant extent on fees and charges forsupport

The statement of activities demonstrates the degree to which the direct expenses of a given function orsegment are offset by program revenues. Direct expenses are those that are dearly identifiable with aspecific function or segment Program revenues include 1) changes to customers or applicants whopurchase, use or directly benefit from goods, services, or privileges provided by a given function orsegment and 2) grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular function or segment Taxes and other items not property Included amongprogram revenues are reported instead as general revenues.

Separate financial statements are provided for governmental funds and proprietary funds. All individualgovernmental funds and individual enterprise funds are reported as separate columns in the fund finandalstatements.

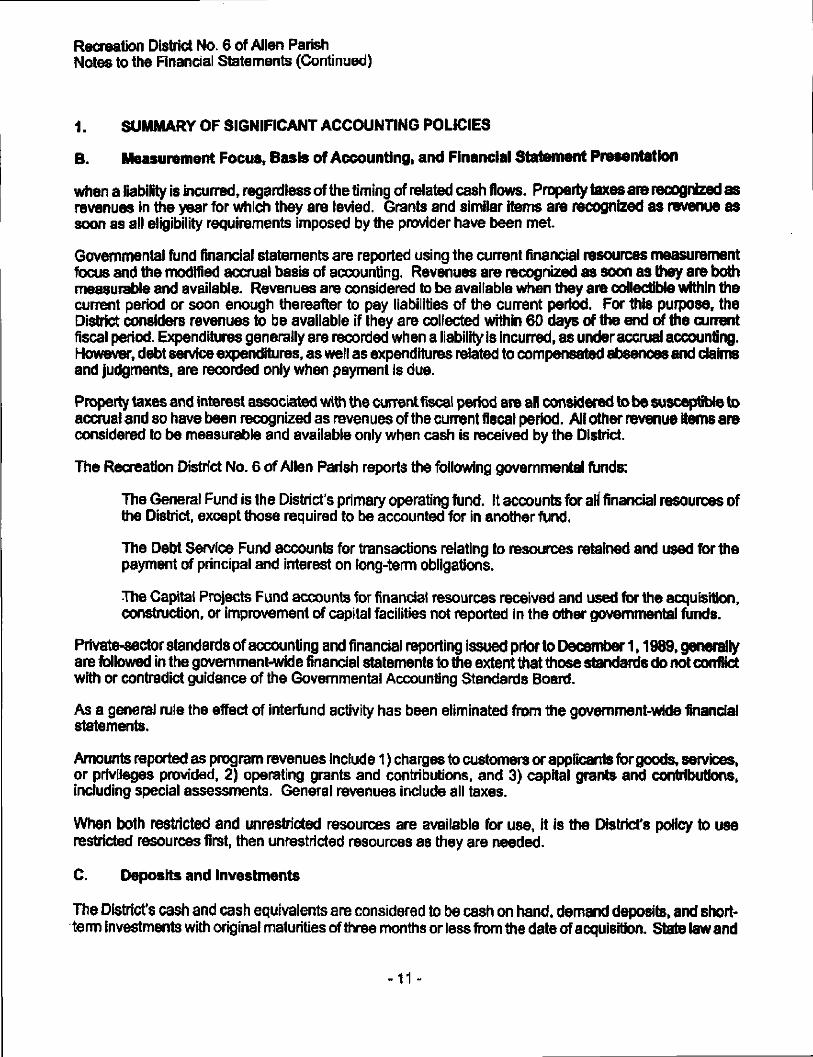

6. Measurement Focus, Basis of Accounting, and Financial Statement Presentation

The government-wide financial statements are reported using the economic resources measurement!̂and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded

-10-

Recreation District No 6 of Allen ParishNotes to the Financial Statements (Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

B. Measurement Focus, Basis of Accounting, and Financial Statement Presentation

when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized asrevenues in the year for which they are levied. Grants and similar items are recognized as revenue assoon as all eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial resources measurementfocus and the modified accrual basis of accounting. Revenues are recognized as soon as they are bothmeasurable and available. Revenues are considered to be available when they are collectible within thecurrent period or soon enough thereafter to pay liabilities of the current period. For this purpose, theDistrict considers revenues to be available if they are collected within 60 days of the end of the currentfiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting.[However, debt service expenditures, as well as expenditures related to compensated absences and claimsand judgments, are recorded only when payment is due.

Property taxes and interest associated with the current fiscal period are all considered to be susceptible toaccrual and so have been recognized as revenues of the current fiscal period. All other revenue items areconsidered to be measurable and available only when cash is received by the District.

The Recreation District No. 6 of Allen Parish reports the following governmental funds:

The General Fund is the District's primary operating fund. It accounts for all financial resources ofthe District, except those required to be accounted for in another fund.

The Debt Service Fund accounts for transactions relating to resources retained and used for thepayment of principal and interest on long-term obligations.

The Capital Projects Fund accounts for financial resources received and used for the acquisition,construction, or improvement of capital facilities not reported in the other governmental funds.

Private-sector standards of accounting and financial reporting issued prior to December 1,1989, generallyare followed in the government-wide financial statements to the extent that those standards do not conflictwith or contradict guidance of the Governmental Accounting Standards Board.

As a general rule the effect of interfund activity has been eliminated from the government-wide financialstatements.

Amounts reported as program revenues include 1) charges to customers or applicants for goods, services,or privileges provided, 2) operating grants and contributions, and 3) capital grants and contributions,including special assessments. General revenues include all taxes.

When both restricted and unrestricted resources are available for use, it is the District's policy to userestricted resources first, then unrestricted resources as they are needed.

C. Deposits and Investments

The District's cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition. State law and

-11-

Recreation District Ho. 6 of Allen ParishNotes to the Financial Statements (Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

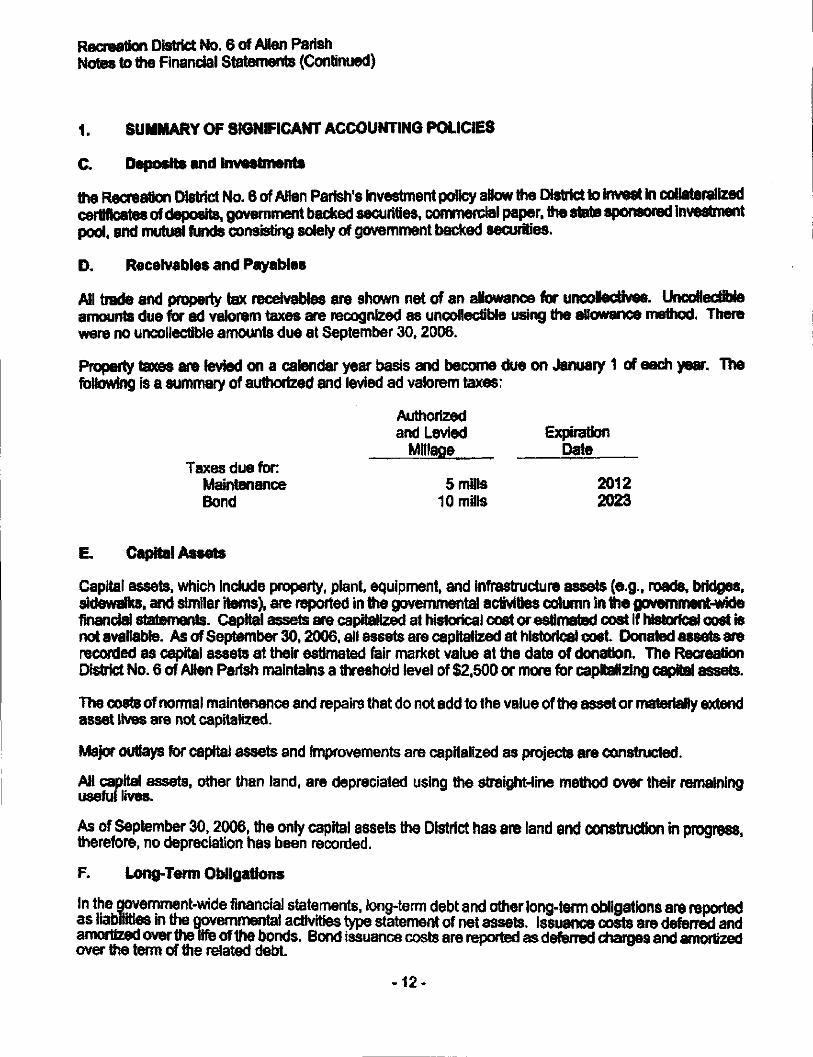

C. Deposit* and Investments

the Recreation District No. 6 of Allen Parish's investment policy allow the District to invest In coilateraHzadcertificates of deposits, government backed securities, commercial paper, the state sponsored Investmentpool, am! mutual funds consisting solely of government backed securities.

D. Receivables and Payable*

Ail trade and property tax receivables are shown net of an allowance for unoofectives. UncoHectibteamounts due for ad valorem taxes are recognized as uncollectible using the allowance method. Therewere no uncollectible amounts due at September 30,2006.

Property taxes are levied on a calendar year basis and become due on January 1 of each year. Thefollowing fs a summary of authorized and levied ad valorem taxes:

Authorizedand Levied

Miffaae

5 mills10 mills

ExpirationDate

20122023

Taxes due forMaintenanceBond

E, Capital Assets

Capital assets, which include property, plant, equipment, and infrastructure assets (e.g., roads, bridges,sidewalks, and similar items), are reported in the governmental activities column In the government-widefinancial statements. Capital assets are capitalized at historical cost or estimated cost if historical cost isnot available. As of September 30,2006, alt assets are capitalized at historical cost. Donated assets arerecorded as capital assets at their estimated fair market value at the date of donation. The RecreationDistrict No. 6 of Allen Parish maintains a threshold level of $2,500 or more for capitalizing capital assets.

The costs of normal maintenance and repairs that do not add to the value of the asset or materially extendasset lives are not capitalized.

Major outlays for capital assets and improvements are capitalized as projects are constructed.

All capital assets, other than land, are depreciated using the straight-line method over their remaininguseful lives.

As of September 30,2006, the only capital assets the District has are land and construction in progress,therefore, no depreciation has been recorded.

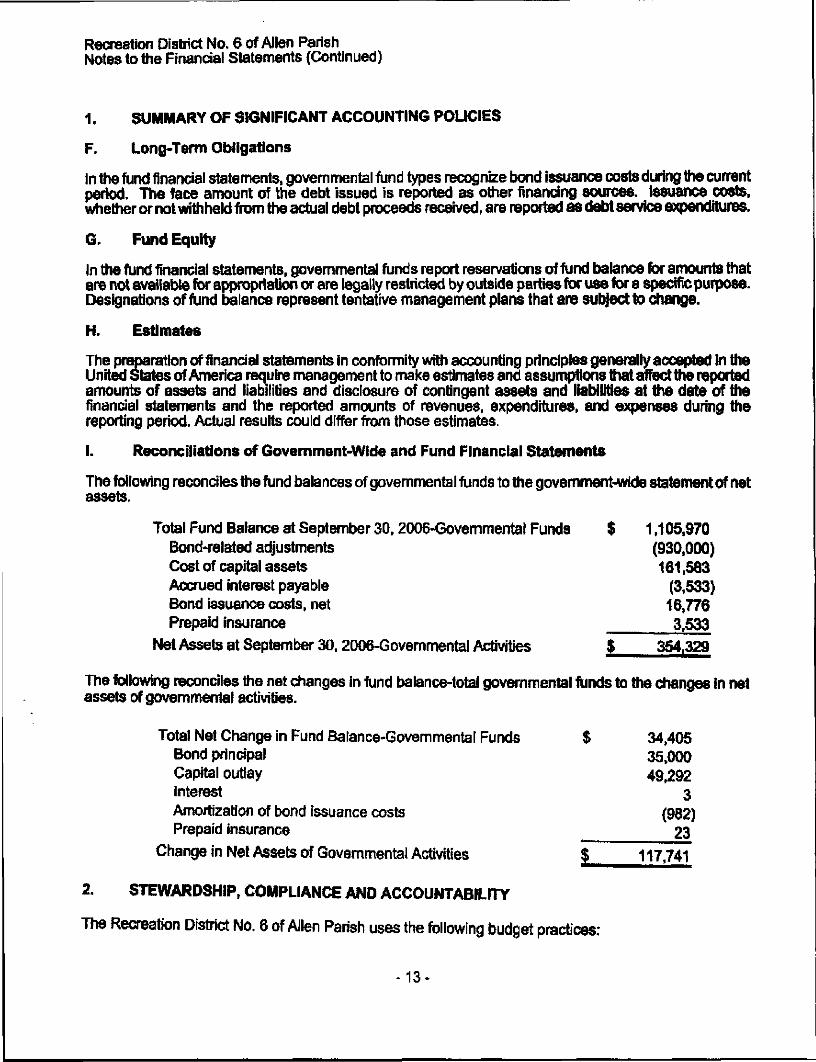

F. Long-Term Obligations

In the government-wide financial statements, long-term debt and other long-term obligations are reportedas liabilities in the governmental activities type statement of net assets, issuance costs are deferred andamortized over the life of the bonds. Bond issuance costs are reported as deferred charges and amortizedover the term of the related debt

-12-

Recreation District No. 6 of Allen ParishNotes to the Financial Statements (Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

F. Long-Term Obligations

In the fund financial statements, governmental fund types recognize bond issuance costs during the currentperiod. The face amount of the debt issued is reported as other financing sources, issuance costs,whether or not withheld from the actual debt proceeds received, are repotted as debt service expenditures.

G. Fund Equity

In the fund financial statements, governmental funds report reservations of fund balance for amounts thatare not available for appropriation or are legally restricted by outside parties for use for a specific purpose.Designations of fund balance represent tentative management plans that are subject to change.

H. Estimates

The preparation of financial statements In conformity with accounting principles generally accepted in theUnited slates of America require management to make estimates and assumptions that affect the reportedamounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of thefinancial statements and the reported amounts of revenues, expenditures, and expenses during thereporting period. Actual results could differ from those estimates.

1. Reconciliations of Government-Wide and Fund Financial Statements

The following reconciles the fund balances of governmental funds to the government-wide statement of netassets.

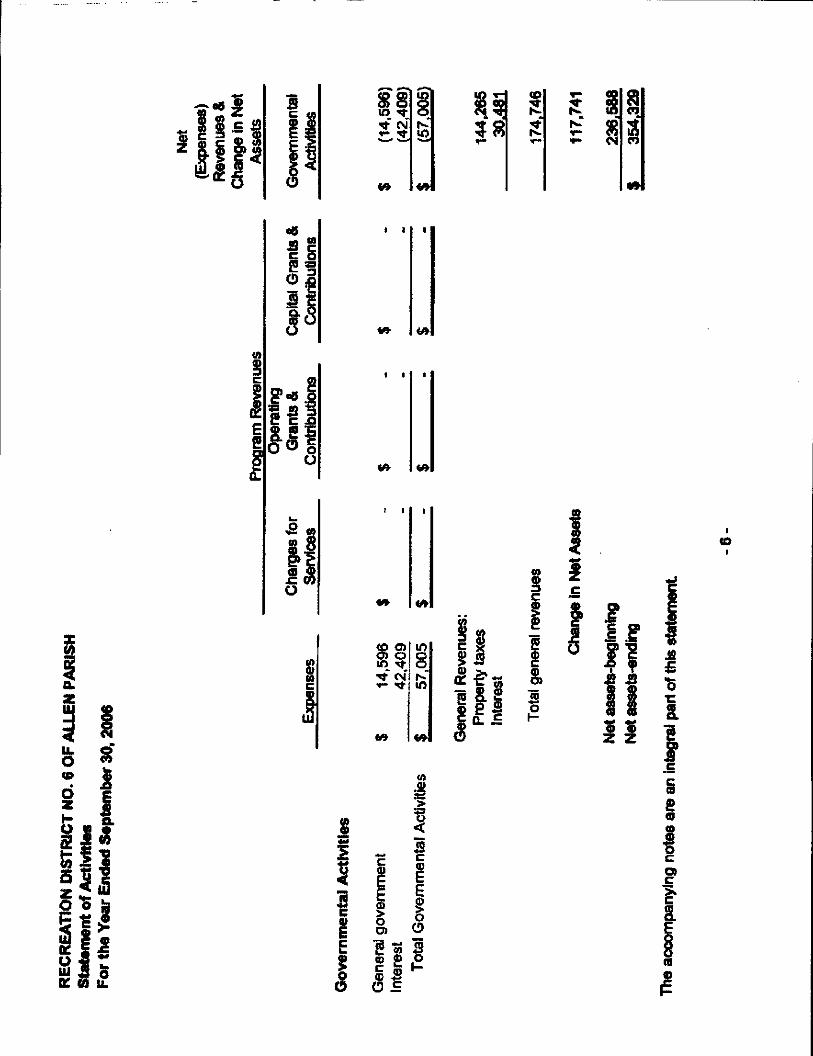

Total Fund Balance at September 30f 2006-Govemmental Funds $ 1,105,970Bond-related adjustments (930,000)Cost of capital assets 161,583Accrued interest payable (3,533)Bond issuance costs, net 16,776Prepaid insurance 3,533

Net Assets at September 30,2006-Governmental Activities $ 354,329

The following reconciles the net changes in fund balance-total governmental funds to the changes in netassets of governmental activities.

Total Net Change in Fund Balance-Governmental Funds $ 34,405Bond principal 35,000Capital outlay 49,292Interest 3Amortization of bond issuance costs (982)Prepaid insurance 23

Change in Net Assets of Governmental Activities $ 117,741

2. STEWARDSHIP, COMPLIANCE AND ACCOUNTABILITY

The Recreation District No. 6 of Allen Parish uses the following budget practices;

-13-

Recreation District No. 6 of Allen ParishNotes to the Financial Statements (Continued)

2. STEWARDSHIP, COMPLIANCE AND ACCOUNTABILITY

A budget is adopted on a basis consistent with generally accepted accounting principles. Anannual appropriated budget is adopted for the General Fund. All annual appropriations lapse atfiscal year end.

On or before the last meeting of each year, the budget is prepared by fund, function, and activityand includes information on the past year, current year estimates, and requested appropriations forthe next fiscal year.

The proposed budget is presented to the District's Board of Commissioners for review. The boardholds a public hearing and may add to, subtract from, or change appropriations, but may notchange the form of the budget. Any changes in the budget must be within the revenues andreserves estimated.

Expenditures may not legally exceed budgeted appropriations by more than five percent. Therewere no amendments to the original budget during the year.

3. CASH AND CASH EQUIVALENTS

At September 30,2006. the Recreation District No. 6 of Allen Parish has cash and cash equivalents (bookbalances) totaling $1,106,348 as follows:

Demand deposits $Interest-bearing demand deposits 171,512Time deposits 934,837Other -

Total $ 1,106,349

These deposits are stated at cost, which approximates market. Under state lawt these deposits (or theresulting bank balances) must be secured by federal deposit insurance or the pledge of securities ownedby the fiscal agent bank. The market value of the pledged securities plus the federal deposit insurancemust at all times equal the amount on deposit with the fiscal agent. These securities are held in the nameof the pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties.

At September 30,2006, the Recreation District No. 6 of Allen Parish has $1,106,349 in deposits (collectedbank balances). These deposits are secured from risk by $300,000 of federal deposit insurance and$806,349 of pledged securities held by the custodial bank in the name of the fiscal agent bank (GASBCategory 3).

Even though the pledged securities are considered uncollateralized (Category 3) under the provisions ofGASB Statement 3, R.S. 39:1229 imposes a statutory requirement on the custodial bank to advertise andsell the pledged securities within 10 days of being notified by the District that the fiscal agent has failed topay deposited funds upon demand.

-14-

Recreation District No. 6 of Allen ParishNotes to the Financial Statements (Continued)

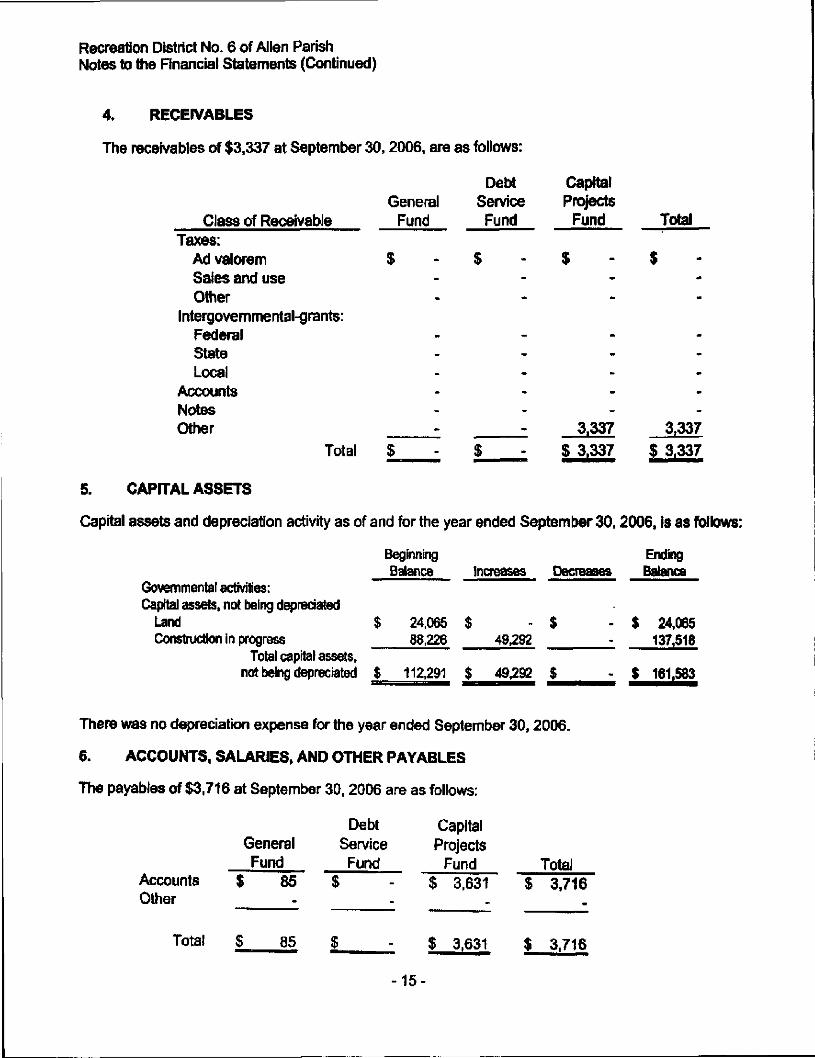

4* RECEIVABLES

The receivables of $3,337 at September 30,2006, are as follows:

GeneralClass of Receivable Fund

Taxes:Ad valorem $Sales and useOther

Intergovernmental-grants:FederalStateLocal

AccountsNotesOther

Total $

Debt CapitalService ProjectsFund Fund

$ - $

3,337

$ - $ 3,337

Total

$

3t337

$ 3,337

5. CAPITAL ASSETS

Capital assets and depredation activity as of and for the year ended September 30.2006, is as follows:

Beginning EndingBalance increases Decreases Balance

Governmental activities:Capital assets, not being depreciated

Land $ 24,065 $ - $ - $ 24,065Construction in progress 88,226 48,292 -_ 137,518

Total capital assets,not being depreciated $ 112.291 $ 49.292 $ $ 161,583

There was no depreciation expense for the year ended September 30,2006.

6. ACCOUNTS, SALARIES, AND OTHER PAYABLES

The payables of $3,716 at September 30, 2006 are as follows:

Debt CapitalGeneral Service ProjectsFund Fund Fund Total

Accounts $ 85 $ - $ 3,631 $ 3,716Other -

Total $ 85 $ - $ 3.631 $ 3.716

-15-

Recreation District No. 6 of Allen ParishMotes to the Financial Statements (Continued)

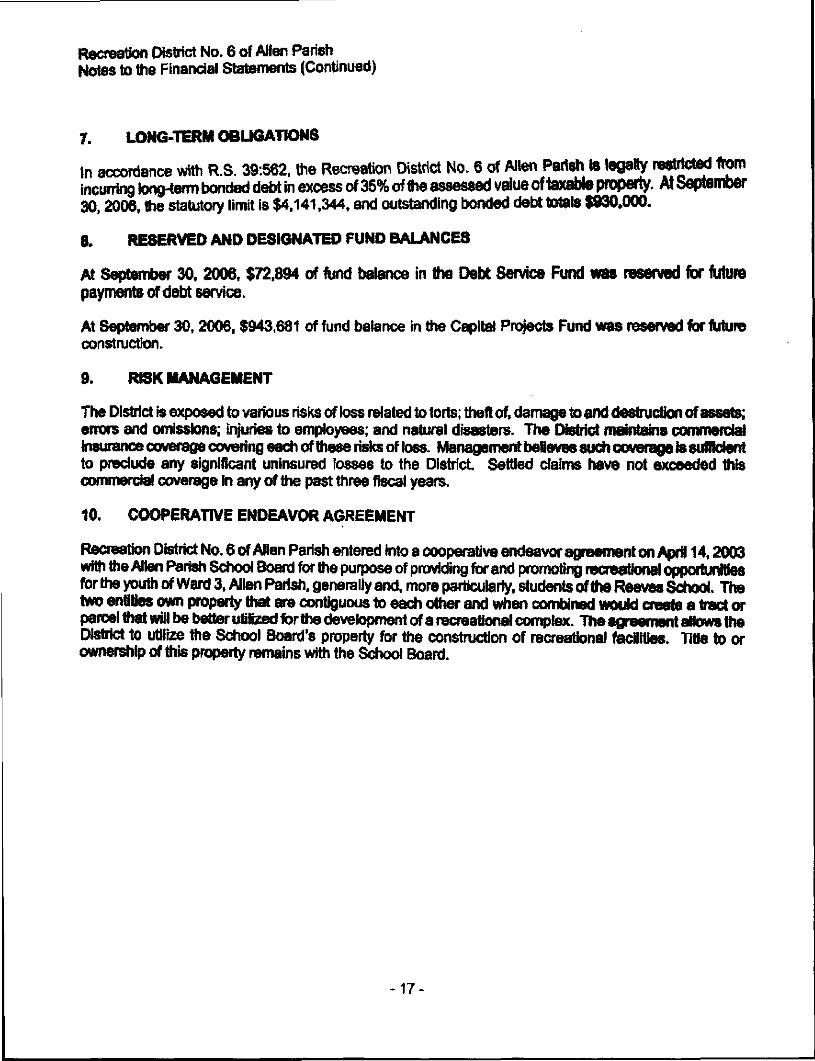

7. LONG-TERM OBLIGATIONS

is a summary of the long-term obligation transactions for the year ended September 30,

Long-term obligations at Beginning of YearAdditionsDeductions

Long-term obligations at End of Year

Bonded Debt$ 965,000

35.000

$ 930.000

The following Is a summary of the current (due in one year or less) and the long-term (due in more than oneyear) portions of long-term obligations as of September 30,2006.

BondedDebt

Current portionLong-term portion

Total

$ 35.000895,000

$ 930.000

All District bonds outstanding at September 30, 2006, for $930,000, are general obligation bonds withmaturities from 2007 to 2023 and interest rates from .10% to 7.0%. Bond principal and interest payable inthe next fiscal year are $35,000 and $42,045, respectively. The individual issues are as follows:

BondInterest

OflginaJIssue RateFinal Payment Interest to

MaturityPrinidpal

OutstandingFundingSource

General ObligationBonds, Series 2003 $ 1,015,000 Up to 7% March 1,2023 $ 557,945 $ 930.000

Ad valoremtaxes

Ail principal and interest requirements are funded in accordance with Louisiana law by the annual advalorem tax levy on taxable property within the District. At September 30, 2006. the Recreation District No,6 of Allen Parish has accumulated $72.894 In the debt service funds for future debt requirements. Thebonds are due as follows:

Year EndingSeptember 30,

2007200820092010

2011-20152016-20202021-2023

Total

PrincipalPayments

$ 35,00035,00040,00040,000

245,000310,000225.000

$ 930,000

InterestPayments

$ 42,04541,21440,10338,743

159,71397,19018,691

$ 437,699

Total$ 77,045

76.21480,10378.743

404,713407.190243,691

$ 1.367,699

-16

Recreation District No. 6 of Allen ParishHoles to the Financial Statements (Continued)

7. LONG-TERM OBLIGATIONS

In accordance with R.S. 39:562, the Recreation District No. 6 of Alton Parish is legally mMMd tornincurring long-term bonded debt in excess of 35% of the assessed value of taxable property. At September30.2006, the statutory limit is $4.141,344, and outstanding bonded debt totals $930.000.

8. RESERVED AND DESIGNATED FUND BALANCES

At September 30, 2006, $72,894 of fund balance in the Debt Service Fund was reserved for futurepayments of debt service.

At September 30,2006, $943,681 of fund balance in the Capitol Projects Fund was reserved for futureconstruction.

9. RISK MANAGEMENT

The District & exposed to various risks of loss related to torts; theft of, damage to and destruction of assets;errors and omissions; injuries to employees; and natural disasters. The District maintains commercialinsurance coverage covering each of these risks of loss, f̂anagernent believes such coverage is suftWe^to preclude any significant uninsured Tosses to the District Settled claims have not exceeded thiscommercial coverage in any of the past three fiscal years.

10. COOPERATIVE ENDEAVOR AGREEMENT

Recreation District No. 6 of Allen Parish entered Into a cooperative endeavor agreement on April 14,

tor the youth erf Ward 3, Allen Paiteh, generally and, more particularly, students of toe Reeves School, Tfcetwo entities own property that are contiguous to eachother and when comWned would create a tract orparcel that will be better utilized for the development of a recreational complex. The agreement aHows theDistrict to utilize the School Board's property for the construction of recreational facilities. Title to orownership of this property remains with the School Board.

17-

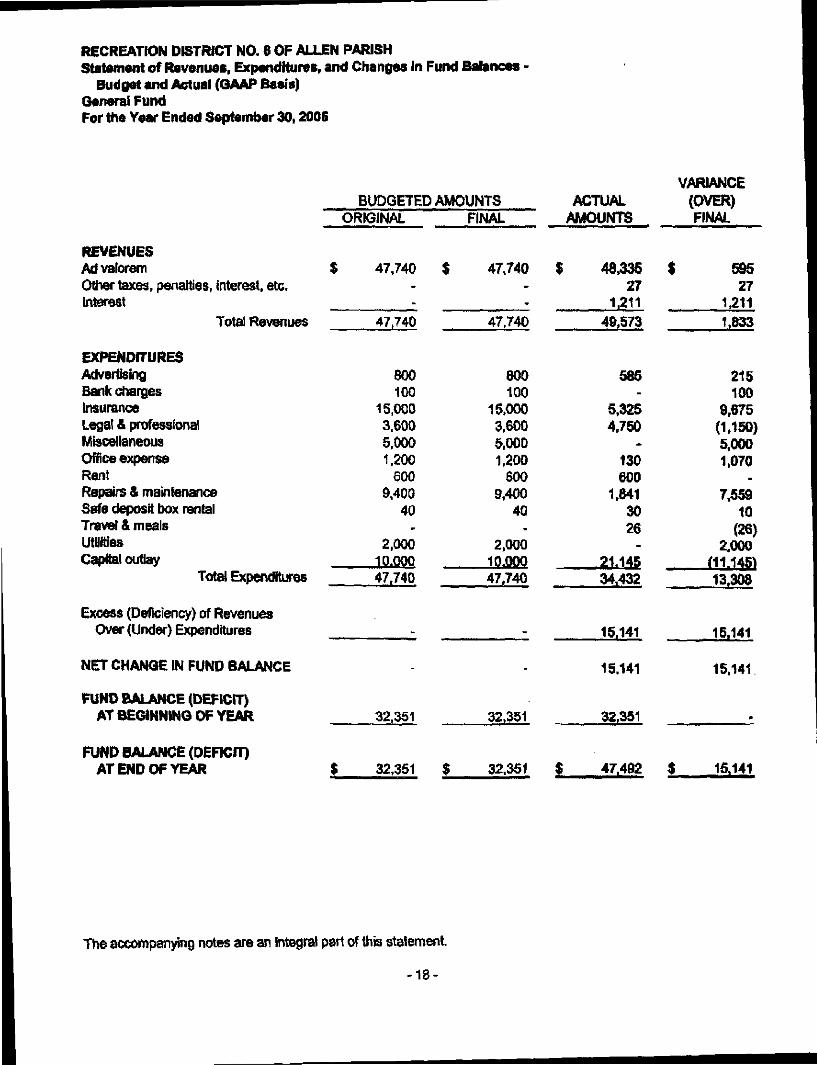

RECREATION DISTRICT NO. 6 OF ALLEN PARISHStatement of Revenues, Expenditures, and Changes In Fund Balances

Budget and Actual (GAAP Basis)General FundFor the Year Ended September 30,2006

REVENUESAd valoremOther taxes, penalties, interest, etc.Interest

Total Revenues

EXPENDITURESAdvertisingBank chargesInsuranceLegal & professionalMiscellaneousOffice expenseRentRepairs & maintenanceSafe deposit box rentalTravel & mealsUtilitiesCapital outlay

Total Expenditures

Excess (Deficiency) of RevenuesOver (Under) Expenditures

NET CHANGE IN FUND BALANCE

FUND BALANCE (DEFICIT)AT BEGINNING OF YEAR

FUND BALANCE (DEFICIT)AT END OF YEAR

BUDGETED AMOUNTSORIGINAL

$ 47,740--

47,740

800100

15,0003,6005,0001,200

6009,400

40-

2,00010.0QQ47,740

FINAL

$ 47J40--

47,740

800100

15,0003,6005,0001,200

8009,400

40-

2,0001Q-PQO47740

ACTUALAMOUNTS

$ 48,33527

1,21149,573

585-

5,3254,750

*130600

1,8413026-

21.14534,432

15,141

VARIANCE(OVER)FINAL

$ 59527

1,211

1,833

215100

9,675(1,150)5,0001,070

-7,559

10(26)

2.000(11.145)13.308

15,141

32,351

32,351 $ 32.351

15.141

32,351

47,492 $

15,141

15,141

The accompanying notes are an integral part of this statement

-18-

OTHER SUPPLEMENTAL SCHEDULES

-19-

Recreation District No. 6 of Alton Parish

PER DIEM PAID BOARD MEMBERS

September 30,2006

PER DIEM PAID BOARD MEMBERS

As provided by Louisiana Revised Statute 38:1794, the board members may receive $10 per diem for eachregular and special meeting attended but shall not be paid for more than twelve meetings In each year.However, at this time the District is not paying per diem.

-20-

RECREATION DISTRICT NO, 6 OF ALLEN PARISHSupplemental Information ScheduleSchedule of FindingsFor the Year Ended September 30,2006

We have audited the financial statements of the Recreation District No. 6 of Allen Parish as of and for theyear ended September 30,2006, and have issued our report dated March 1,2007. We conducted ouraudit in accordance with auditing standards generally accepted in the United States of America and thestandards applicable to financial audits contained in Government Auditing Standards, issued by tieComptroller General of the United States. Our audit of the financial statements as of September 30,2006resulted in an unqualified opinion.

Section I - Summary of Auditor's Results

Financial Statements

Type of auditor's report issued: Unqualified

a. Report on Internal Control and Compliance Material to the Financial Statements

Internal Control

Material weakness(es) identified?

Reportable condition(s) identifiedthat are not considered to bematerial weaknesses?

Noncompliance material to financialstatements noted?

X Yes

Yes

Yes

No

X None reported

X No

Section 11 - Financial Statement Findings

2006-11/C (Material weakness) Segregation of duties:Because of the lack of a large staff, more specifically accounting personnel, there is a problem withsegregation of duties necessary for proper controls. One person is currently performing the function ofpreparing disbursements in the journals, and posting to the general ledger. We do note that this situation isinherent to most entities of this type and is difficult to solve due to the funding limitations of the District. Werecommend that the commissioners take an active interest in the review of all of the financial information.This was also a prior year finding.

21 -

RECREATION DISTRICT NO. 6 OF ALLEN PARISHSupplemental Information ScheduleManagemenf s Corrective Action Plan (Unaudited)

Section Mntemal Control and Compliance Material to the Financial Statements:

2006*1 i/C (Ongoing finding) Segregation of duties:

This is an ongoing finding that cannot be corrected due to the lack of financial resources.

Contact person - Waylin Bertrand, President

-22-

RECREATION DISTRICT NO. 6 OF ALLEN PARISHSupplemental Information ScheduleStatus of Prior Audit Findings

Section 1 - Internal Control and Compliance Material to the Financial Statements:

2005-1IIC (Ongoing finding) Segregation of duties:

Corrective action taken * Due to the Jack of sufficient financial resources, this finding cannot be resolved.See 2006-1 l/C.

-23-

INDEPENDENT AUDITOR'S REPORT SECTION

-24-

Stutzman & Gates, LLCCertified Public Accountants

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING ANDON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITHGOVERNMENT AUDITING STANDARDS

Board of CommissionersRecreation District No. 6 of Allen ParishAllen Parish Police JuryReeves, Louisiana

We have audited the accompanying financial statements of the governmental activities and each majorfund of Recreation District No. 6 of Allen Parish, as of and for the year ended September 30, 2006, whichcollectively comprise the Recreation District No. 6 of Allen Parish's basic financial statements and haveissued our report thereon dated March 1, 2007. We conducted our audit in accordance with auditingstandards generally accepted in the United States of America and the standards applicable to financialaudits contained in Government Auditing Standards, issued by the Comptroller General of the UnitedStates.

internal Control Over Financial Reporting

in planning and performing our audit, we considered Recreation District No. 6 of Allen Parish's internalcontrol over financial reporting in order to determine our auditing procedures for the purpose of expressingour opinions on the financial statements and not to provide an opinion on the internal control over financialreporting. However, we noted certain matters involving the internal control over financial reporting and itsoperation that we consider to be reportable conditions. Reportable conditions involve matters coming toour attention relating to significant deficiencies in the design or operation of the internal control overfinancial reporting that in our judgment, could adversely affect Recreation District No. 6 of Allen Parish'sabiiity to initiate, record, process, and report financial data consistent with the assertions of management inthe financial statements. Reportable conditions are described in the accompanying schedule of findings asitem 2006-1 I/C,

A material weakness is a reportable condition in which the design or operation of one or more of theinternal control components does not reduce to a relatively low level the risk that restatements caused byerror or fraud in amounts that would be material in relation to the financial statements being audited mayoccur and not be detected within a timely period by employees in the normal oourse of performing theirassigned functions. Our consideration of the internal control over financial reporting would not necessarilydisclose all matters in the internal control that might be reportable conditions and, accordingly, would notnecessarily disclose all reportable conditions that are also considered to be material weaknesses.However, of the reportable conditions described above, we consider item 2006-1 I/C to be a materialweakness.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Recreation District No. 6 of Allen Parish'sfinancial statements are free of material misstatement, we performed tests of its compliance with certainprovisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have adirect and material effect on the determination of financial statement amounts. However, providing anopinion on compliance with those provisions was not an objective of our audit, and accordingly, we do notexpress such an opinion. The results of our tests disclosed no instances of noncompliance or other

521 M *" Sfree* * KfrMfer, l*ui&f* 70649 - (337? 738-2 1tM

Board of CommissionersPage 2

matters that are required to be reported under Government Auditing Standards.

This report is intended solely for the information and use of management the Board of Commissioners, theAlien Parish Police Jury, and the Legislative Auditor and is not intended to be and should not be used byanyone other than these specified parties. Under Louisiana Revised Statute 24:513, this report isdistributed by the Legislative Auditor as a public document.

Stutzman & Gates, LLCMarch 1,2007