Embed Size (px)

Citation preview

ALM and pricing of life insurance products

Vladimír KrejčíPrague, 1 April 2004

Main tasks of ALM

Investment strategy

Product design and pricing

Capital and risk management

Product design and pricing

Design Passing the investment risk to clients Possibility to hedge the risk borne by

shareholders

Pricing (profit testing) Reasonable assumptions about

Future yields Discount rate

Let‘s start – question 1

Does profitability of a life insurance product depend on investment strategy?

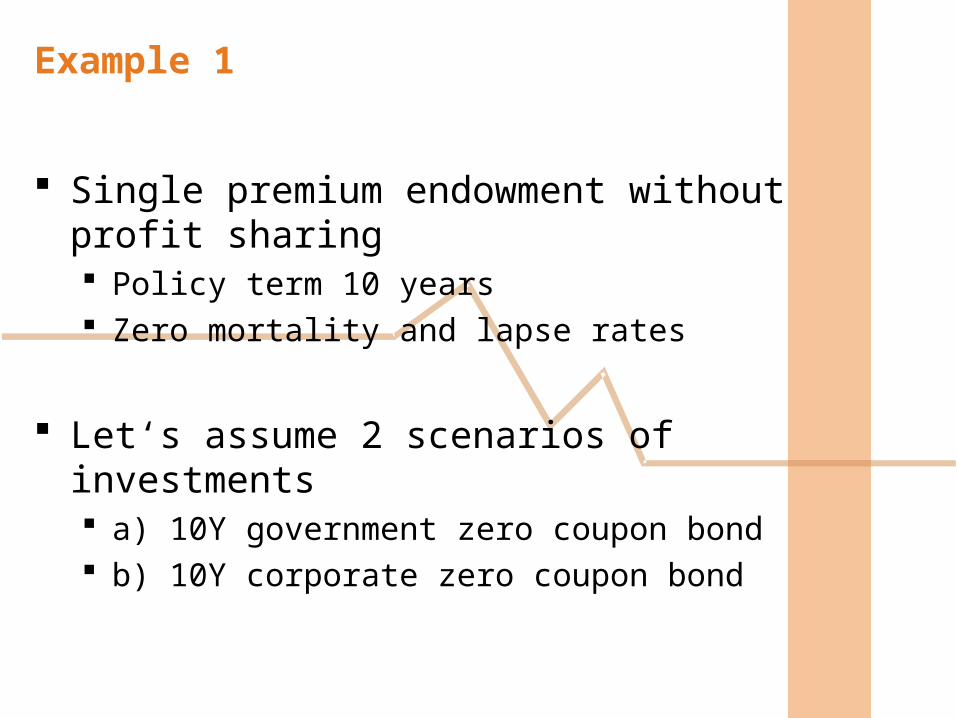

Example 1

Single premium endowment without profit sharing Policy term 10 years Zero mortality and lapse rates

Let‘s assume 2 scenarios of investments a) 10Y government zero coupon bond b) 10Y corporate zero coupon bond

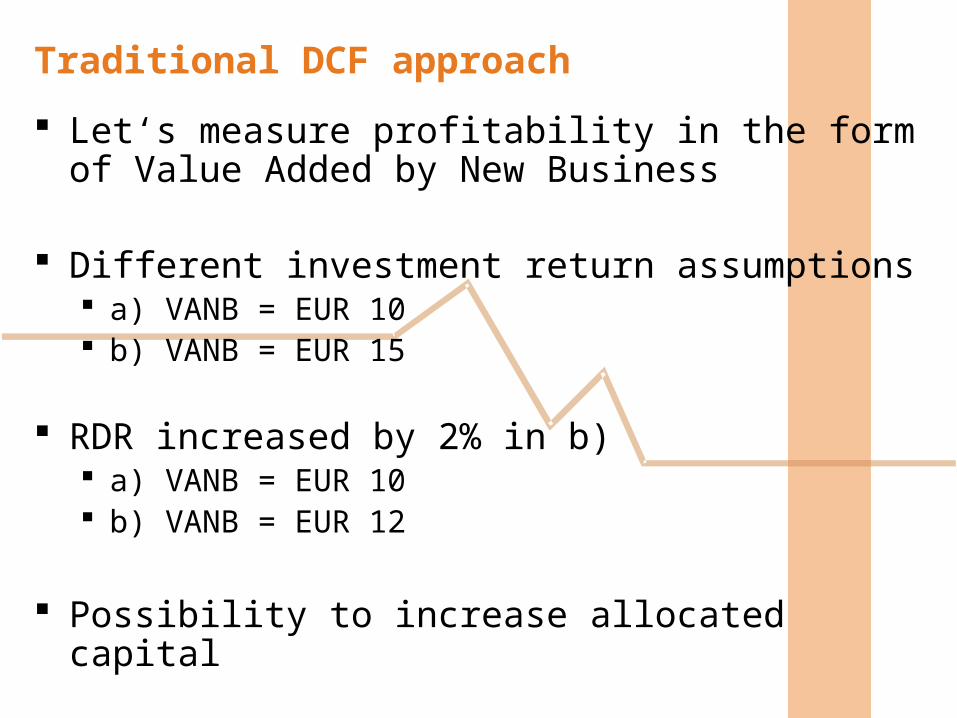

Traditional DCF approach

Let‘s measure profitability in the form of Value Added by New Business

Different investment return assumptions a) VANB = EUR 10 b) VANB = EUR 15

RDR increased by 2% in b) a) VANB = EUR 10 b) VANB = EUR 12

Possibility to increase allocated capital

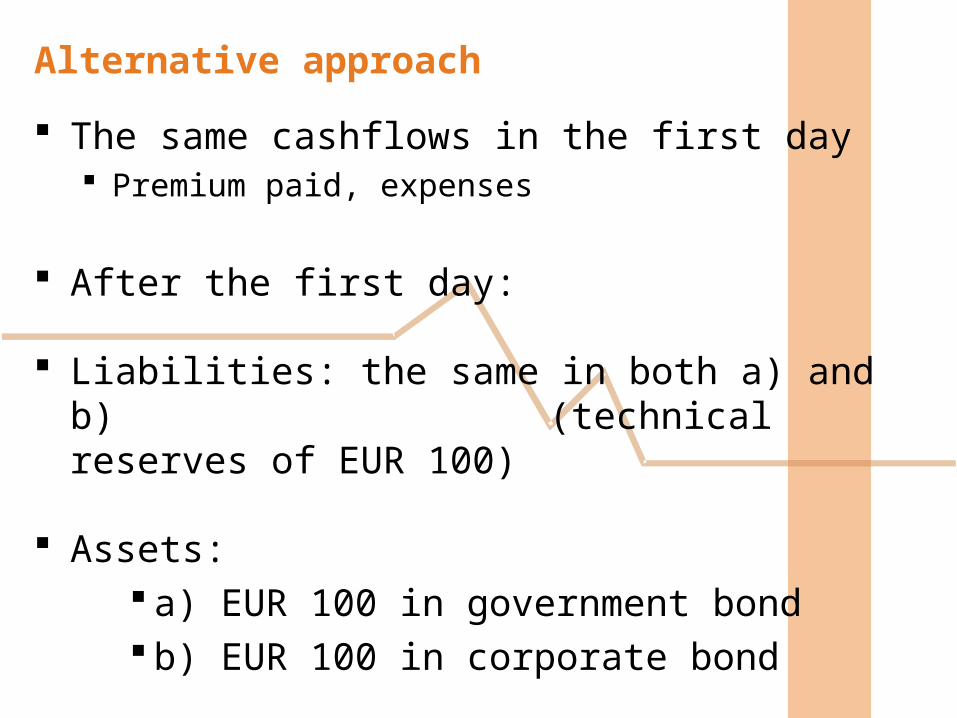

Alternative approach

The same cashflows in the first day Premium paid, expenses

After the first day:

Liabilities: the same in both a) and b)(technical reserves of EUR

100)

Assets: a) EUR 100 in government bond b) EUR 100 in corporate bond

Alternative approach

In other words:

„We do not invest risk free and therefore our yields will be higher than risk free.“

Risky investment strategy increases the profit potential You can make more profits if you are good

(succesful, lucky)

But it increases the loss potential as well „…our yields will be probably higher…“

=> it does not increase market value

Does profitability of this life insurance product depend on investment strategy?

Traditional DCF

YES

Alternative approach

NO

What approach is more appropriate?

Question 2

Is market value the appropriate measure?

Why do we have different PV? Information, investment horizon, risk attitude

What decisions are we willing to base on our PV?

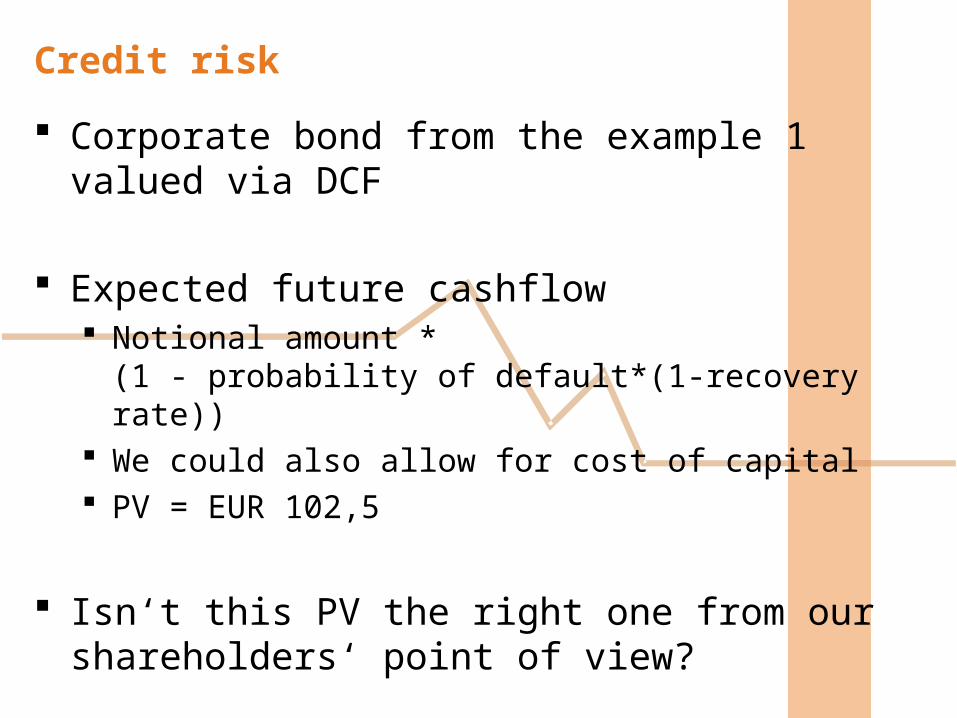

Credit risk

Corporate bond from the example 1 valued via DCF

Expected future cashflow Notional amount * (1

- probability of default*(1-recovery rate)) We could also allow for cost of capital PV = EUR 102,5

Isn‘t this PV the right one from our shareholders‘ point of view?

Why is the market price different?

What factors we did not allow for?

Market can expect different probability of default

Potential downgrades

Volatility of credit spreads

Market can have different cost of capital

Investors are risk averse

How did the market arrive at the price?

Supply / Demand consensus of market participants

Who are market participants? Banks, insurance companies, investment funds, …

Komercni banka, CSOB, Ceska sporitelna, Ceska pojistovna, ING, Deutsche bank, Morgan Stanley, Meril Lynch, Bank of America, Credit Lyonais, …

Very well educated, trained and experienced teams

Very well informed teams – equally informed

Efficient market

Stock markets

Forward on stocks – what is the forward price? Expected yield (arbitrage) Risk free yield

Stock returns over a long horizon

Sentiment, trends, bull/bear markets

Interest rates risk, duration mismatch

What do we estimate?

Macroeconomic development Decisions of billions of people all around the

world Estimate of these decisions by thousands of

analysts and market players Sentiment, media, psychology, hedging

Time horizon

Why is our PV different than market value?

Do we have better know how?

Are we better informed?

Are the markets efficient?

Do we really have arguments for the PV we have calculated?

Why is our PV different than market value? We do not have better information, so …

…our shareholders have to be differently risk averse than the market… do we know their utility function that well?

…or not interested in short term results what about if the investment strategy

reports high losses and we say these are only temporary?

Is market value the appropriate measure for us?

What decision are we willing to base on our PV?

What decisions are we willing to base on our PV?

Purchase of particular security

Investment strategy

Liability product design and pricing

Summary

Is market value the appropriate measure for valuation of life insurance liabilities?

Does profitability of this life insurance product depend on investment strategy?

A practical problem

A practical problem

Profit in life insurance is a small sum of

Large positive numbers Premium income, investment income

Large negative numbers Claims, expenses

It is very difficult to adjust the discount rate to particular investment assumptions

The problem – cont.

The smaller the profit, the bigger the problem

Low interest rate environment Lower margins are relatively more sensitive to

changes in investment income

Products with profit sharing Change in profit sharing Change in company‘s margin

Do we have market evidence for use of the traditional EV in M&A?

Suggested solution

EV with risk free investment returns and risk free discount

Do we know to evaluate the mortality, lapse, expense, … risks?

Risk free EV can be some comparative basis – the traditional EV should not be higher (negative value of mortality, lapse, expense, … risks)

Suggestion 2

EV with cashflow specific discount rates

Products with profit sharing

Short introduction

What about products with profit sharing?

Risky investment strategy increases the profitability (compared to risk free strategy) if you pass to clients more risks and less profits

If you pass to clients more profits than risks then: The riskier investments, the lower

profitability

What about products with profit sharing?

How to compare the passed profits and risks? Contingent claims valuation methods

Low interest rate environment Very low expected profit sharing rates Limited space for passing the risk (= losses) Simple estimate on passing more profits/risk may

be possible