Embed Size (px)

Citation preview

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Please refer to the Disclaimers at the end of this Report.

AMBIT INSIGHTS 21 March 2017

DAILY

Updates

Jubilant Foodworks (SELL)

CEO’s checklist for a turnaround

(Click here for detailed note)

Ahluwalia Contracts (NOT RATED)

The storm is over

(Click here for detailed note)

BFSI

Microfinance - Sticky delinquencies to hit earnings

Idea Cellular (SELL)

M&A announced; now comes the hard part

Derivatives

Alpha This Week

An alternative take on the markets

(Click here for detailed note)

Analyst Notes: ITC: Government’s balanced approach on cigarette taxation continues Ritesh Vaidya, CFA, +91 22 3043 3246

The GST Council last week finalised the maximum cess to be implemented on cigarettes at 290% ad valorem or Rs4170 per 1,000 sticks (https://goo.gl/t4NPNg). Based on our understanding, it seems that the dreaded cess on cigarettes could just be a replacement of the current excise duty on cigarettes. The changes in the tax structure for cigarettes under GST could be: a) replacement of 26% VAT currently with a GST of 28%; and b) replacement of the current excise duty with cess. This would keep the GST tax neutral for cigarettes as mentioned by Finance Minister Arun Jaitley. This structure highlights the balance the Government is trying to strike between cigarette tax collections and curbing consumption. Reiterate BUY on ITC. Source: Ambit Capital research

Please refer to our website for complete coverage universe

http://research.ambitcapital.com

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

CEO’s checklist for a turnaround

A new CEO and recent commentary on profitable growth have renewed hope amongst investors. However, the path is not as quick as delivering pizza in 30 minutes. Correcting price value proposition (10% price CAGR over FY11-16) no longer assures margin expansion in sync with SSG. Measures like headcount reduction, while margin accretive, would impair delivery-centric business. Architecture around product, technology and advertisement is at the core of growing customer base, which at 15mn is low despite presence in 260 cities. Own-store model remains Jubilant’s handicap vs successful Domino’s franchisees globally that are asset-light but tech heavy. We would like to see steps on the above by the new management before turning BUYers on a franchise which is struggling but not beyond resurrection. At 43x FY19E EPS, the stock factors 7% SSG over FY18-20E but ignores risks associated with near-term execution and re-building the foundations. Competitive position: STRONG Changes to this position: NEGATIVE Checklist #1 Price drop or product improvement? Lower prices or better products can drive SSG revival but with margin compression; 100bps fall in gross margins needs 250bps in SSG to maintain EBITDA margins. Domino’s offering is rated as mediocre by a large customer base (on Zomato) vs global positioning as value for money proposition. Moreover, in just top 10 cities its pricing faces competition from over 11,000 better dining choices (pizza competitors outnumber Dominos 2:1). Checklist #2 Expanding small user base; headcount cut is short term fix Headcount reduction may boost near-term earnings but compromises delivery experience in the long run. Investments in product (quality), communicating the same and technology (ease of ordering, reducing delivery time) helped the US business in 2010. For Jubilant, given input cost inflation (28% CAGR over FY11-16) and low user base of 15mn, such measures can be margin-dilutive. Checklist #3 Is sub-franchising feasible? Jubilant is perhaps the only sizeable master franchisee that has not sub-franchised. Jubilant expanded in many small towns, with 180 of them having <10 stores. Ramp-up at these locations has been delayed due to higher costs vs lower revenues (lower share of delivery) than stores in major cities. Sub-franchisee model is more viable in smaller towns given franchisee-owned real estate and lower administration costs from family members’ involvement. Growth multiples cannot be ascribed to earnings from cost savings Costs saving measures are a short-term fix and do not warrant valuation re-rating. Re-building this asset-heavy business will take longer than just a couple of quarters and could depress margins. Titan, at 33x FY19E EPS, with an asset-light model has demonstrated agility in product pricing to overcome regulatory disruptions. But Jubilant is constrained by size and cost structure. Our fair value of `879 implies 33x FY19E EPS; SSG over 10% is a key risk to our SELL rating.

COMPANY INSIGHT JUBI IN EQUITY March 21, 2017

Jubilant FoodworksSELL

Consumer Discretionary

Recommendation Mcap (bn): `71/US$1.1 6M ADV (mn): `728.3/US$10.9 CMP: `1,119 TP (12 mths): `879 Downside (%): 22

Flags Accounting: GREEN Predictability: AMBER Earnings Momentum: RED

Catalysts

Further gross margin decline in FY18E given higher cheese cost

FY18E SSG to be capped at 7% given rising competition.

Continued delay in ramp-up of new stores to over 3 years from erstwhile 2.5 years.

Performance (%)

Source: Bloomberg, Ambit Capital Research

60

708090

100110120

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-

16

Aug

-16

Sep-

16

Oct

-16

Nov

-16

Dec

-16

Jan-

17

Feb-

17

JUBI IN SENSEX

Research Analysts

Abhishek Ranganathan, CFA

+ 91 22 3043 3085

Mayank Porwal

+ 91 22 3043 3214 [email protected]

Key financials Year to March FY15 FY16 FY17E FY18E FY19E

Net Revenues (` mn) 20,928 24,380 26,253 30,698 37,260

Operating margin (%) 12.2% 11.4% 9.9% 10.7% 11.3%

Net Profits (` mn) 1,111 1,048 843 1,202 1,721

Diluted EPS (`) 16.9 15.9 12.8 18.3 26.2

RoCE (%) 19% 15% 11% 14% 18%

P/E (x) 66.1 70.2 87.2 61.3 42.3

EV/EBITDA (x) 28.5 26.2 28.1 21.9 16.4

Source: Company, Ambit Capital research

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

The storm is over

Ahluwalia could be a rare turnaround story in the contracting space. Its superior RoE (22% vs 16% median for mid-sized EPCs) and cash conversion (76% vs 63%) after losses in FY13 are a function of steadfast discipline to improve order book quality (more Government, less fixed price projects). A low debt balance sheet (0.3x D/E; 0.9x with customer advances) and ample order book (2x FY19E revenue, consensus) keep it in good stead. With large redevelopment projects in Delhi to be tendered in the next 1-2 years (~Rs400bn) and a possible kicker from affordable housing, opportunities for the larger 6-7 buildings contractors could be large. Valuation of 14x FY19E consensus EPS is in-line with peers despite superior RoE and better cash conversion record. Key risk: Fixed price contracts from NBCC that are too large to address.

Competitive position: MODERATE Changes to this position: STABLE A contractor reborn Ahluwalia’s turnaround post FY13 was due to bidding discipline - the company has materially reduced exposure to private real estate (by 21ppt to 32%) and fixed price contracts and willingness to let revenues decline. A stressed balance sheet (1.3x D/E in FY13), like peers, was led by aggressive growth, investments and a slowing economy. But unlike contracting peers that never recover, Ahluwalia is seemingly a case of a credible turnaround (RoE: 22% vs -30% in FY13), leaving it in good stead of the upcoming opportunities. The buildings space could be the next center of action NBCC’s and CPWD’s ~Rs400bn Delhi redevelopment projects will commence execution in the next 18 months. We believe this would necessitate ordering of Rs70bn-120bn over FY18E. Lower competition due to larger ticket sizes (Rs10bn) could benefit the larger 6-7 domestic contractors. Affordable housing presents a large (Rs250bn) opportunity, though not all of it would be addressable. Order book already provides ample visibility and management expects reducing exposure to private real estate to reduce working capital. Will it be different in Delhi this time? Exuberance of FY04-11 was led by realty boom around Delhi and the slowdown thereafter impacted profits and receivables. Commonwealth Games project is a perfect example of the highs-and-lows. However, with NBCC, a listed, credible, stated-owned company now handling the large development projects, we expect fewer issues with the projects. Valuations in-line with peers Ahluwalia’s current valuation of 14x FY19E consensus EPS is in-line with peer multiples despite superior RoE. Valuations should be looked at in the context of ordering environment (possibly improving) and modest growth expectations (consensus revenue: 15% CAGR). Contractors are a better play on redevelopment projects over NBCC due to the latter’s expensive multiple and inevitable delays that are not yet baked into consensus estimates.

VISIT NOTE AHLU IN EQUITY March 21, 2017

Ahluwalia ContractsNOT RATED

E&C/ Infrastructure

Recommendation Mcap (bn): `22/US$0.3 6M ADV (mn): `21/US$0.3 CMP: `311 TP (12 mths): NA Upside (%): NA

Flags Accounting: RED Predictability: AMBER Earnings Momentum: RED

Performance (%)

Source: Bloomberg, Ambit Capital Research

80 90

100 110 120 130 140

Mar

-16

May

-16

Jun-

16

Aug

-16

Sep-

16

Nov

-16

Dec

-16

Jan-

17

Mar

-17

SENSEX AHLU

Research Analysts

Utsav Mehta, CFA +91 22 3043 3209

Nitin Bhasin

+91 22 3043 3241

Key financials Rs bn Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Revenues 14.5 14.3 9.6 10.6 12.5 EBITDA margin 0.2 (0.3) 0.2 1.1 1.6 PAT (0.5) (0.7) 0.2 0.6 0.8 EPS (Rs) (7.4) (11.4) 3.5 9.6 12.6 RoE -16% -30% 10% 23% 22% RoCE -5% -14% 2% 18% 19% P/E (42) (27) 90 33 25

Source: Company, Ambit Capital research

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

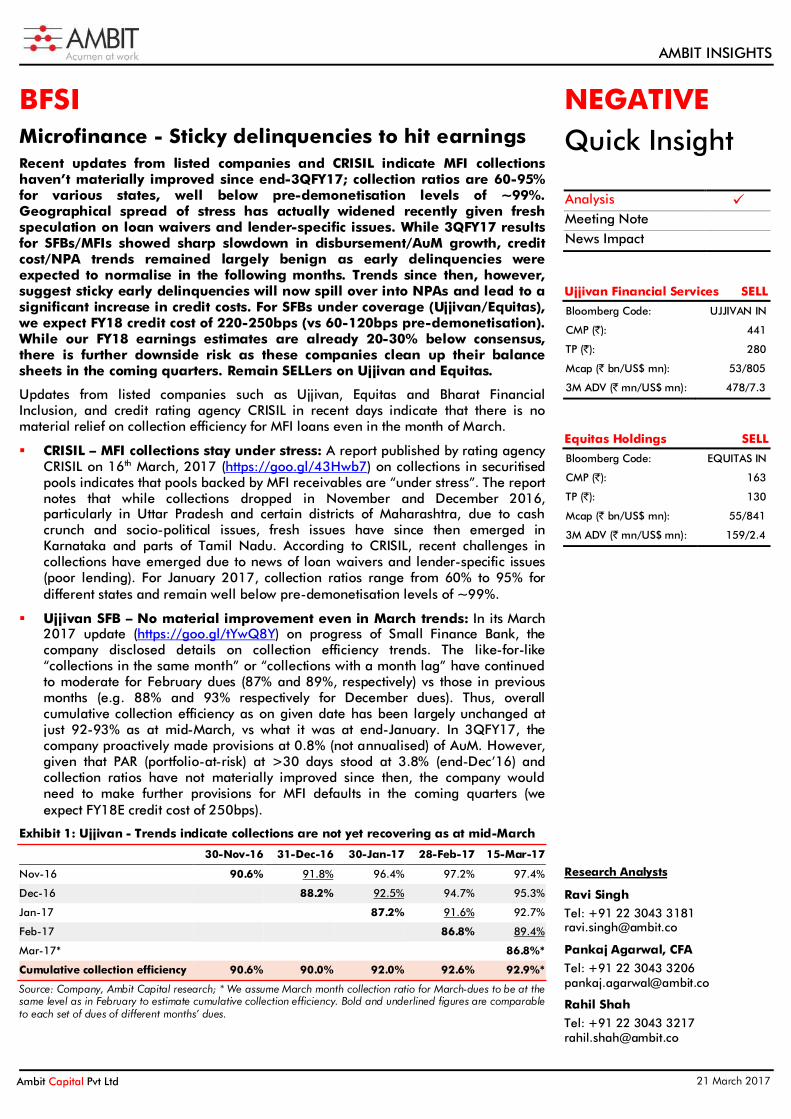

BFSI Microfinance - Sticky delinquencies to hit earnings Recent updates from listed companies and CRISIL indicate MFI collections haven’t materially improved since end-3QFY17; collection ratios are 60-95% for various states, well below pre-demonetisation levels of ~99%. Geographical spread of stress has actually widened recently given fresh speculation on loan waivers and lender-specific issues. While 3QFY17 results for SFBs/MFIs showed sharp slowdown in disbursement/AuM growth, credit cost/NPA trends remained largely benign as early delinquencies were expected to normalise in the following months. Trends since then, however, suggest sticky early delinquencies will now spill over into NPAs and lead to a significant increase in credit costs. For SFBs under coverage (Ujjivan/Equitas), we expect FY18 credit cost of 220-250bps (vs 60-120bps pre-demonetisation). While our FY18 earnings estimates are already 20-30% below consensus, there is further downside risk as these companies clean up their balance sheets in the coming quarters. Remain SELLers on Ujjivan and Equitas.

Updates from listed companies such as Ujjivan, Equitas and Bharat Financial Inclusion, and credit rating agency CRISIL in recent days indicate that there is no material relief on collection efficiency for MFI loans even in the month of March.

CRISIL – MFI collections stay under stress: A report published by rating agency CRISIL on 16th March, 2017 (https://goo.gl/43Hwb7) on collections in securitised pools indicates that pools backed by MFI receivables are “under stress”. The report notes that while collections dropped in November and December 2016, particularly in Uttar Pradesh and certain districts of Maharashtra, due to cash crunch and socio-political issues, fresh issues have since then emerged in Karnataka and parts of Tamil Nadu. According to CRISIL, recent challenges in collections have emerged due to news of loan waivers and lender-specific issues (poor lending). For January 2017, collection ratios range from 60% to 95% for different states and remain well below pre-demonetisation levels of ~99%.

Ujjivan SFB – No material improvement even in March trends: In its March 2017 update (https://goo.gl/tYwQ8Y) on progress of Small Finance Bank, the company disclosed details on collection efficiency trends. The like-for-like “collections in the same month” or “collections with a month lag” have continued to moderate for February dues (87% and 89%, respectively) vs those in previous months (e.g. 88% and 93% respectively for December dues). Thus, overall cumulative collection efficiency as on given date has been largely unchanged at just 92-93% as at mid-March, vs what it was at end-January. In 3QFY17, the company proactively made provisions at 0.8% (not annualised) of AuM. However, given that PAR (portfolio-at-risk) at >30 days stood at 3.8% (end-Dec’16) and collection ratios have not materially improved since then, the company would need to make further provisions for MFI defaults in the coming quarters (we expect FY18E credit cost of 250bps).

Exhibit 1: Ujjivan - Trends indicate collections are not yet recovering as at mid-March

30-Nov-16 31-Dec-16 30-Jan-17 28-Feb-17 15-Mar-17

Nov-16 90.6% 91.8% 96.4% 97.2% 97.4%

Dec-16 88.2% 92.5% 94.7% 95.3%

Jan-17 87.2% 91.6% 92.7%

Feb-17 86.8% 89.4%

Mar-17* 86.8%*

Cumulative collection efficiency 90.6% 90.0% 92.0% 92.6% 92.9%*

Source: Company, Ambit Capital research; * We assume March month collection ratio for March-dues to be at the same level as in February to estimate cumulative collection efficiency. Bold and underlined figures are comparable to each set of dues of different months’ dues.

NEGATIVE Quick Insight

Analysis Meeting Note News Impact

Ujjivan Financial Services SELL Bloomberg Code: UJJIVAN IN

CMP (`): 441

TP (`): 280

Mcap (` bn/US$ mn): 53/805

3M ADV (` mn/US$ mn): 478/7.3

Equitas Holdings SELL Bloomberg Code: EQUITAS IN

CMP (`): 163

TP (`): 130

Mcap (` bn/US$ mn): 55/841

3M ADV (` mn/US$ mn): 159/2.4

Research Analysts

Ravi Singh

Tel: +91 22 3043 3181 [email protected]

Pankaj Agarwal, CFA

Tel: +91 22 3043 3206 [email protected]

Rahil Shah

Tel: +91 22 3043 3217 [email protected]

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

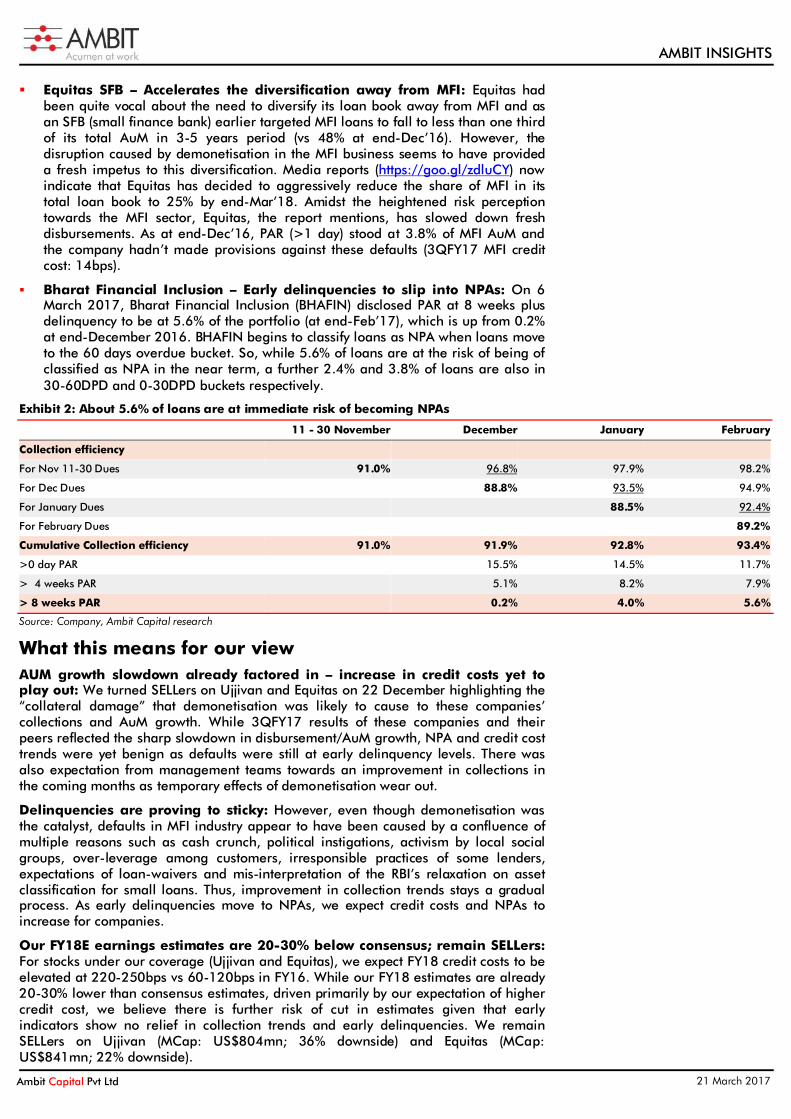

Equitas SFB – Accelerates the diversification away from MFI: Equitas had been quite vocal about the need to diversify its loan book away from MFI and as an SFB (small finance bank) earlier targeted MFI loans to fall to less than one third of its total AuM in 3-5 years period (vs 48% at end-Dec’16). However, the disruption caused by demonetisation in the MFI business seems to have provided a fresh impetus to this diversification. Media reports (https://goo.gl/zdluCY) now indicate that Equitas has decided to aggressively reduce the share of MFI in its total loan book to 25% by end-Mar’18. Amidst the heightened risk perception towards the MFI sector, Equitas, the report mentions, has slowed down fresh disbursements. As at end-Dec’16, PAR (>1 day) stood at 3.8% of MFI AuM and the company hadn’t made provisions against these defaults (3QFY17 MFI credit cost: 14bps).

Bharat Financial Inclusion – Early delinquencies to slip into NPAs: On 6 March 2017, Bharat Financial Inclusion (BHAFIN) disclosed PAR at 8 weeks plus delinquency to be at 5.6% of the portfolio (at end-Feb’17), which is up from 0.2% at end-December 2016. BHAFIN begins to classify loans as NPA when loans move to the 60 days overdue bucket. So, while 5.6% of loans are at the risk of being of classified as NPA in the near term, a further 2.4% and 3.8% of loans are also in 30-60DPD and 0-30DPD buckets respectively.

Exhibit 2: About 5.6% of loans are at immediate risk of becoming NPAs

11 - 30 November December January February

Collection efficiency

For Nov 11-30 Dues 91.0% 96.8% 97.9% 98.2%

For Dec Dues 88.8% 93.5% 94.9%

For January Dues 88.5% 92.4%

For February Dues 89.2%

Cumulative Collection efficiency 91.0% 91.9% 92.8% 93.4%

>0 day PAR 15.5% 14.5% 11.7%

> 4 weeks PAR 5.1% 8.2% 7.9%

> 8 weeks PAR 0.2% 4.0% 5.6%

Source: Company, Ambit Capital research

What this means for our view AUM growth slowdown already factored in – increase in credit costs yet to play out: We turned SELLers on Ujjivan and Equitas on 22 December highlighting the “collateral damage” that demonetisation was likely to cause to these companies’ collections and AuM growth. While 3QFY17 results of these companies and their peers reflected the sharp slowdown in disbursement/AuM growth, NPA and credit cost trends were yet benign as defaults were still at early delinquency levels. There was also expectation from management teams towards an improvement in collections in the coming months as temporary effects of demonetisation wear out.

Delinquencies are proving to sticky: However, even though demonetisation was the catalyst, defaults in MFI industry appear to have been caused by a confluence of multiple reasons such as cash crunch, political instigations, activism by local social groups, over-leverage among customers, irresponsible practices of some lenders, expectations of loan-waivers and mis-interpretation of the RBI’s relaxation on asset classification for small loans. Thus, improvement in collection trends stays a gradual process. As early delinquencies move to NPAs, we expect credit costs and NPAs to increase for companies.

Our FY18E earnings estimates are 20-30% below consensus; remain SELLers: For stocks under our coverage (Ujjivan and Equitas), we expect FY18 credit costs to be elevated at 220-250bps vs 60-120bps in FY16. While our FY18 estimates are already 20-30% lower than consensus estimates, driven primarily by our expectation of higher credit cost, we believe there is further risk of cut in estimates given that early indicators show no relief in collection trends and early delinquencies. We remain SELLers on Ujjivan (MCap: US$804mn; 36% downside) and Equitas (MCap: US$841mn; 22% downside).

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

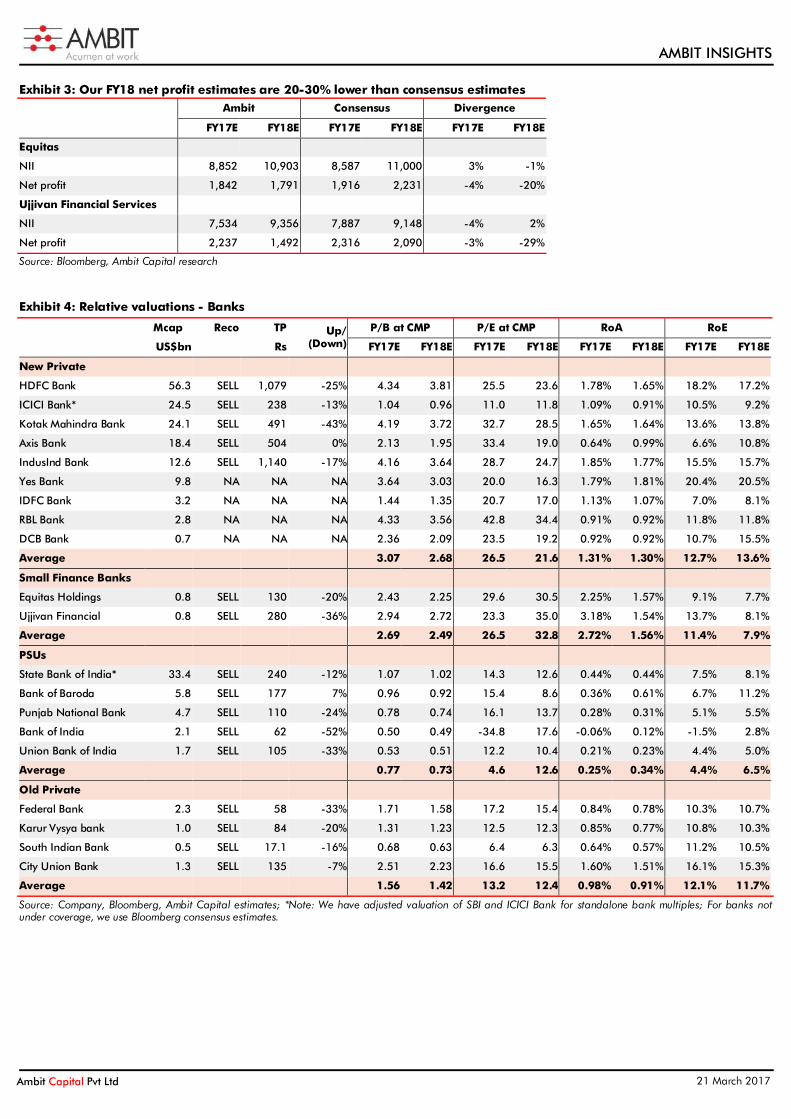

Exhibit 3: Our FY18 net profit estimates are 20-30% lower than consensus estimates

Ambit Consensus Divergence

FY17E FY18E FY17E FY18E FY17E FY18E

Equitas NII 8,852 10,903 8,587 11,000 3% -1%

Net profit 1,842 1,791 1,916 2,231 -4% -20%

Ujjivan Financial Services NII 7,534 9,356 7,887 9,148 -4% 2%

Net profit 2,237 1,492 2,316 2,090 -3% -29%

Source: Bloomberg, Ambit Capital research

Exhibit 4: Relative valuations - Banks

Mcap Reco TP Up/ (Down)

P/B at CMP P/E at CMP RoA RoE

US$bn Rs FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E

New Private

HDFC Bank 56.3 SELL 1,079 -25% 4.34 3.81 25.5 23.6 1.78% 1.65% 18.2% 17.2%

ICICI Bank* 24.5 SELL 238 -13% 1.04 0.96 11.0 11.8 1.09% 0.91% 10.5% 9.2%

Kotak Mahindra Bank 24.1 SELL 491 -43% 4.19 3.72 32.7 28.5 1.65% 1.64% 13.6% 13.8%

Axis Bank 18.4 SELL 504 0% 2.13 1.95 33.4 19.0 0.64% 0.99% 6.6% 10.8%

IndusInd Bank 12.6 SELL 1,140 -17% 4.16 3.64 28.7 24.7 1.85% 1.77% 15.5% 15.7%

Yes Bank 9.8 NA NA NA 3.64 3.03 20.0 16.3 1.79% 1.81% 20.4% 20.5%

IDFC Bank 3.2 NA NA NA 1.44 1.35 20.7 17.0 1.13% 1.07% 7.0% 8.1%

RBL Bank 2.8 NA NA NA 4.33 3.56 42.8 34.4 0.91% 0.92% 11.8% 11.8%

DCB Bank 0.7 NA NA NA 2.36 2.09 23.5 19.2 0.92% 0.92% 10.7% 15.5%

Average 3.07 2.68 26.5 21.6 1.31% 1.30% 12.7% 13.6%

Small Finance Banks

Equitas Holdings 0.8 SELL 130 -20% 2.43 2.25 29.6 30.5 2.25% 1.57% 9.1% 7.7%

Ujjivan Financial 0.8 SELL 280 -36% 2.94 2.72 23.3 35.0 3.18% 1.54% 13.7% 8.1%

Average 2.69 2.49 26.5 32.8 2.72% 1.56% 11.4% 7.9%

PSUs

State Bank of India* 33.4 SELL 240 -12% 1.07 1.02 14.3 12.6 0.44% 0.44% 7.5% 8.1%

Bank of Baroda 5.8 SELL 177 7% 0.96 0.92 15.4 8.6 0.36% 0.61% 6.7% 11.2%

Punjab National Bank 4.7 SELL 110 -24% 0.78 0.74 16.1 13.7 0.28% 0.31% 5.1% 5.5%

Bank of India 2.1 SELL 62 -52% 0.50 0.49 -34.8 17.6 -0.06% 0.12% -1.5% 2.8%

Union Bank of India 1.7 SELL 105 -33% 0.53 0.51 12.2 10.4 0.21% 0.23% 4.4% 5.0%

Average 0.77 0.73 4.6 12.6 0.25% 0.34% 4.4% 6.5%

Old Private

Federal Bank 2.3 SELL 58 -33% 1.71 1.58 17.2 15.4 0.84% 0.78% 10.3% 10.7%

Karur Vysya bank 1.0 SELL 84 -20% 1.31 1.23 12.5 12.3 0.85% 0.77% 10.8% 10.3%

South Indian Bank 0.5 SELL 17.1 -16% 0.68 0.63 6.4 6.3 0.64% 0.57% 11.2% 10.5%

City Union Bank 1.3 SELL 135 -7% 2.51 2.23 16.6 15.5 1.60% 1.51% 16.1% 15.3%

Average 1.56 1.42 13.2 12.4 0.98% 0.91% 12.1% 11.7%

Source: Company, Bloomberg, Ambit Capital estimates; *Note: We have adjusted valuation of SBI and ICICI Bank for standalone bank multiples; For banks not under coverage, we use Bloomberg consensus estimates.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

Idea Cellular M&A announced; now comes the hard part Idea-Vodafone outlined significant synergy benefits due to reduced fixed overheads and capex savings. Idea now has adequate spectrum to take on competition. By securing the right to acquire 9.5% stake in MergeCo at Rs130/share (21% discount to price implied by synergy fructification), Idea’s promoters have retained skin in the game, also benefiting minority shareholders. To achieve synergies, the MergeCo will have to weather continued competitive pressures from Jio and Airtel. Also, synergies are protracted; full run-rate of cost and capex synergies (Rs140bn per annum) will start showing only in the fourth full year after the completion of the merger. We remain SELLers on Idea given history of over-optimism on synergy benefits by global telco managements (US, Indonesia etc). We incorporate 20% of management’s estimate of net synergy benefits (Rs670bn) in FY20, upgrading our TP by a significant 50% to Rs90/share.

Complex transaction; towerco divestiture key to deleveraging

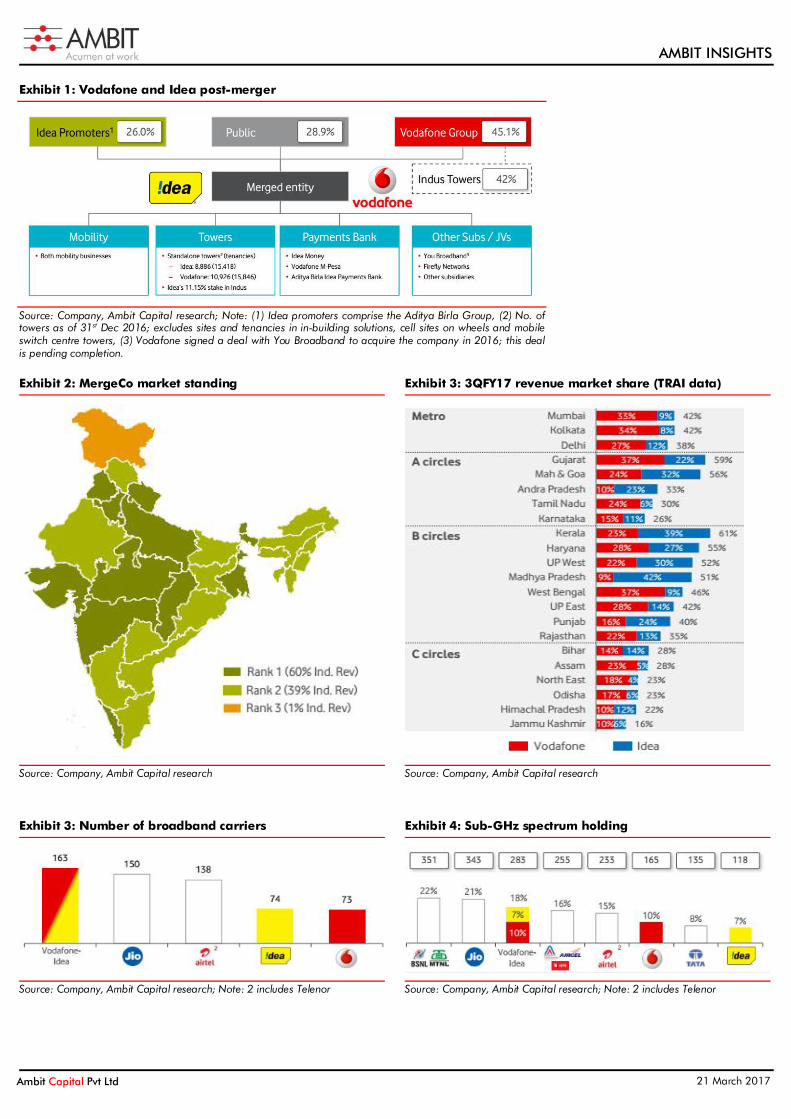

Vodafone will combine its India subsidiary (excluding 42% stake in Indus Towers) with Idea Cellular.

Immediately after the merger, Vodafone will receive 50% stake in MergeCo (3.63bn shares). Concurrent with the deal completion, Vodafone will transfer 4.9% stake in MergeCo to Idea promoters for Rs38.74bn (implying Rs110/share).

Ownership of MergeCo: 45.1% by Vodafone, 26% by Aditya Birla Group and 28.9% by Idea’s minority shareholders.

Idea’s promoters have the option of acquiring 9.5% MergeCo stake from Vodafone’s promoters within three years of the merger at Rs130/share. Fructification of this transaction would equalise the shareholding of Idea and Vodafone promoters in the MergeCo.

Following completion of three years after merger, if equalisation of shareholding of Idea and Vodafone promoters hasn’t been achieved, then Idea can commit to buying up to 9.5% stake in MergeCo from Vodafone’s promoters at market price. In the four years after merger, Vodafone’s promoters can’t sell shares reserved for Idea promoters.

If the Idea and Vodafone promoters’ shareholding doesn’t equalise at the end of year four following the merger, then Vodafone will sell down MergeCo shares to achieve equalisation over a five-year period.

The merged entity will have net debt of Rs1,079bn; 4.4x net debt to trailing 12-month (TTM) EBITDA, which the company hopes to reduce to 4.1x after tower divestitures (Idea’s stake in Indus). Thus, deleveraging of tower assets – comprising (a) 8,886 of Idea’s own towers, (b) 10,926 of Vodafone’s own towers, (c) Idea’s 11.15% stake in Indus towers implying 13,608 towers – is critical for the MergeCo. We believe this could present an interesting opportunity for Bharti Infratel to consolidate the Indian towerco market and correct its capital structure.

Idea’s has got the better of the two; spectrum and skin in the game!

The merger solves two objectives: (a) giving Idea a new lease of life by making available incremental spectrum, and (b) allowing Vodafone PLC to de-consolidate its India operations and create a strong market leader which is self-sustaining. Whilst Vodafone has scored by getting Idea to agree on a merger ratio based on Idea’s undisturbed share price of Rs72.5/share, Idea has managed to bargain for the right of acquiring 9.5% of MergeCo from Vodafone at Rs130/share, a 21% discount to implied price assuming 100% synergy benefits. Idea’s promoters have retained skin in the game and can benefit from upside on fructification of synergies; this would also benefit minority shareholders.

SELL Quick Insight Analysis Meeting Note News Impact

Stock Information Bloomberg Code: IDEA IN

CMP (Rs): 98

TP (Rs): 90

Mcap (Rs bn/US$ mn): 352/5,377

3M ADV (Rs mn/US$ mn): 3,062/46.8

Stock Performance (%)

1M 3M 12M YTD

Absolute (10) 33 (4) 32

Rel. to Sensex (13) 21 (23) 21

Source: Bloomberg, Ambit Capital research

Ambit Estimates (Rs mn)

FY17E FY18E FY19E

Revenues 368 394 429

EBITDA 103 100 113

EPS (Rs) (2.3) (5.8) (3.1)

Source: Bloomberg, Ambit Capital research

Research Analyst

Vivekanand Subbaraman, CFA [email protected] Tel: +91 22 3043 3261

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

FY18 outlook remains clouded due to Jio

Whilst outlining aggressive cost synergies from the merger, both Idea and Vodafone continued to paint a gloomy picture of sector revenue growth in FY18. The same remains challenged owing to Jio’s gargantuan revenue market share aspirations, which continue to hurt incumbent telcos and pressure sector revenue.

Best case scenario is getting synergy benefits in FY20

Both managements outlined the following areas of synergies:

Network and IT

1 The single biggest synergy element is rationalisation of combined site requirements by over 20% following network consolidation.

2 Avoidance of duplicate 4G network expansion and upgrades; re-deployment of overlapping equipment.

3 Material long-term IT investments due to infrastructure sharing and system combination.

Customer services and acquisition

1 Integration of service centres, back offices and distribution efficiencies.

2 Scale efficiencies with service partners.

3 Reduced rotational churn owing to lower market activity – whilst managements didn’t elaborate on their brand strategy, they mentioned that they will persist with the two brands ‘Idea’ and ‘Vodafone’ given complementary strengths across several markets.

Other fixed overheads; reduced combined marketing costs and streamlining of overlapping activities.

The transaction is subject to regulatory approvals, including Telecom Ministry, Competition Commission (anti-trust authority) and shareholder approvals. The managements expect the transaction to be completed in calendar year 2018. Until the completion of the transaction, both entities will operate on a ‘business as usual’ manner and will continue to fund the asset; both Idea and Vodafone have agreed on specific terms for the same. Thus, the two companies will be able to work towards achieving synergies only in 2019; hence, the stated net NPV of merger synergies will be applicable in FY20. Moreover, given the protracted nature of synergy benefits, the managements guided the same would fructify four years after completion of merger. We believe that there is limited visibility of the same. Operating cost synergy guidance is ~15% of current operating expenditure of the merged entity.

Where do we go from here?

Unarguably, the merger gives Idea and Vodafone a new lease of life as it gives them a comprehensive spectrum footprint. That said, there are complications regarding integration of large telcos, particularly in a challenging 22-circle market like India. Recent examples of regional telecom mergers (XL Axiata-Axis in Indonesia) show that synergies are challenging to achieve due to regulatory risks and competitive pressures. Thus, we incorporate 20% of management’s NPV guidance of synergy benefits in FY20, resulting in a 50% upgrade to our target price for Idea to Rs90/share. Our estimates for Idea Cellular exclude Vodafone’s pro-forma financials.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

Exhibit 1: Vodafone and Idea post-merger

Source: Company, Ambit Capital research; Note: (1) Idea promoters comprise the Aditya Birla Group, (2) No. of towers as of 31st Dec 2016; excludes sites and tenancies in in-building solutions, cell sites on wheels and mobile switch centre towers, (3) Vodafone signed a deal with You Broadband to acquire the company in 2016; this deal is pending completion.

Exhibit 2: MergeCo market standing

Source: Company, Ambit Capital research

Exhibit 3: 3QFY17 revenue market share (TRAI data)

Source: Company, Ambit Capital research

Exhibit 3: Number of broadband carriers

Source: Company, Ambit Capital research; Note: 2 includes Telenor

Exhibit 4: Sub-GHz spectrum holding

Source: Company, Ambit Capital research; Note: 2 includes Telenor

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

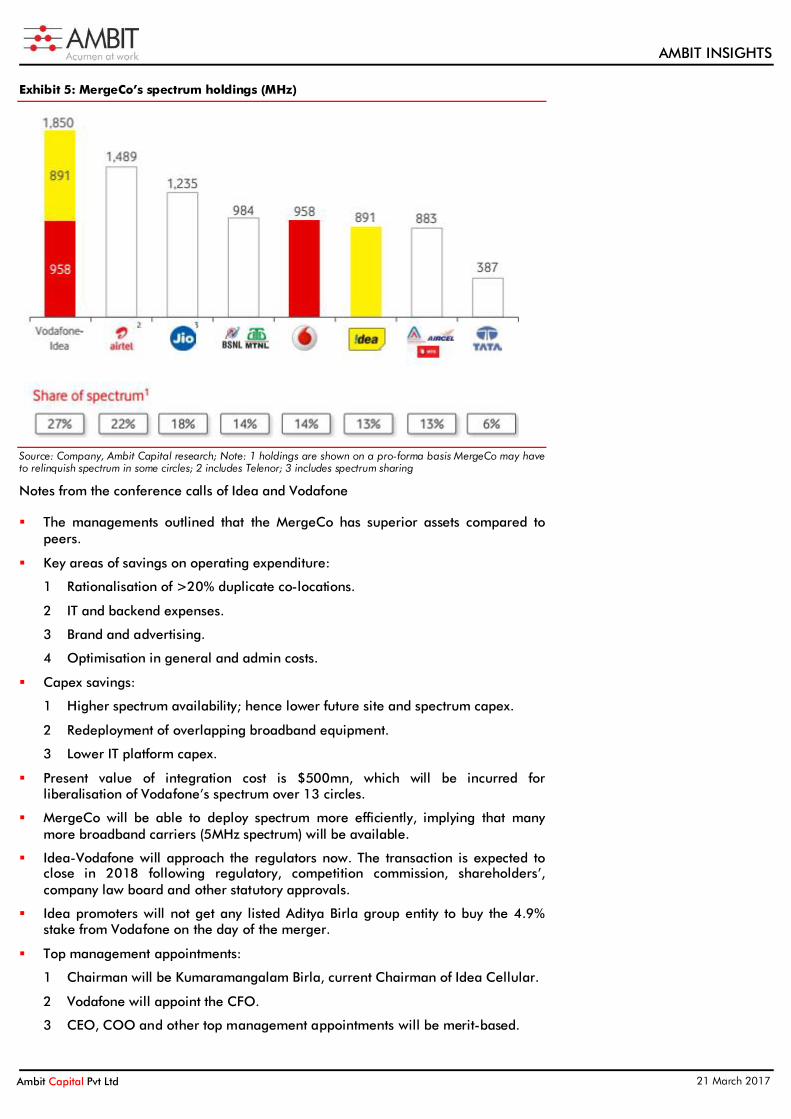

Exhibit 5: MergeCo’s spectrum holdings (MHz)

Source: Company, Ambit Capital research; Note: 1 holdings are shown on a pro-forma basis MergeCo may have to relinquish spectrum in some circles; 2 includes Telenor; 3 includes spectrum sharing

Notes from the conference calls of Idea and Vodafone

The managements outlined that the MergeCo has superior assets compared to peers.

Key areas of savings on operating expenditure:

1 Rationalisation of >20% duplicate co-locations.

2 IT and backend expenses.

3 Brand and advertising.

4 Optimisation in general and admin costs.

Capex savings:

1 Higher spectrum availability; hence lower future site and spectrum capex.

2 Redeployment of overlapping broadband equipment.

3 Lower IT platform capex.

Present value of integration cost is $500mn, which will be incurred for liberalisation of Vodafone’s spectrum over 13 circles.

MergeCo will be able to deploy spectrum more efficiently, implying that many more broadband carriers (5MHz spectrum) will be available.

Idea-Vodafone will approach the regulators now. The transaction is expected to close in 2018 following regulatory, competition commission, shareholders’, company law board and other statutory approvals.

Idea promoters will not get any listed Aditya Birla group entity to buy the 4.9% stake from Vodafone on the day of the merger.

Top management appointments:

1 Chairman will be Kumaramangalam Birla, current Chairman of Idea Cellular.

2 Vodafone will appoint the CFO.

3 CEO, COO and other top management appointments will be merit-based.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

The companies have agreed to keep the respective businesses adequately funded till the merger fructifies.

Spectrum needs for the MergeCo are limited over the next five years.

The two entities expect the MergeCo to be self-sustaining following deleveraging from the sale of tower assets.

Vodafone will be de-consolidating the India business from its parent balance sheet. It will have achieved listing of its India entity following the merger.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

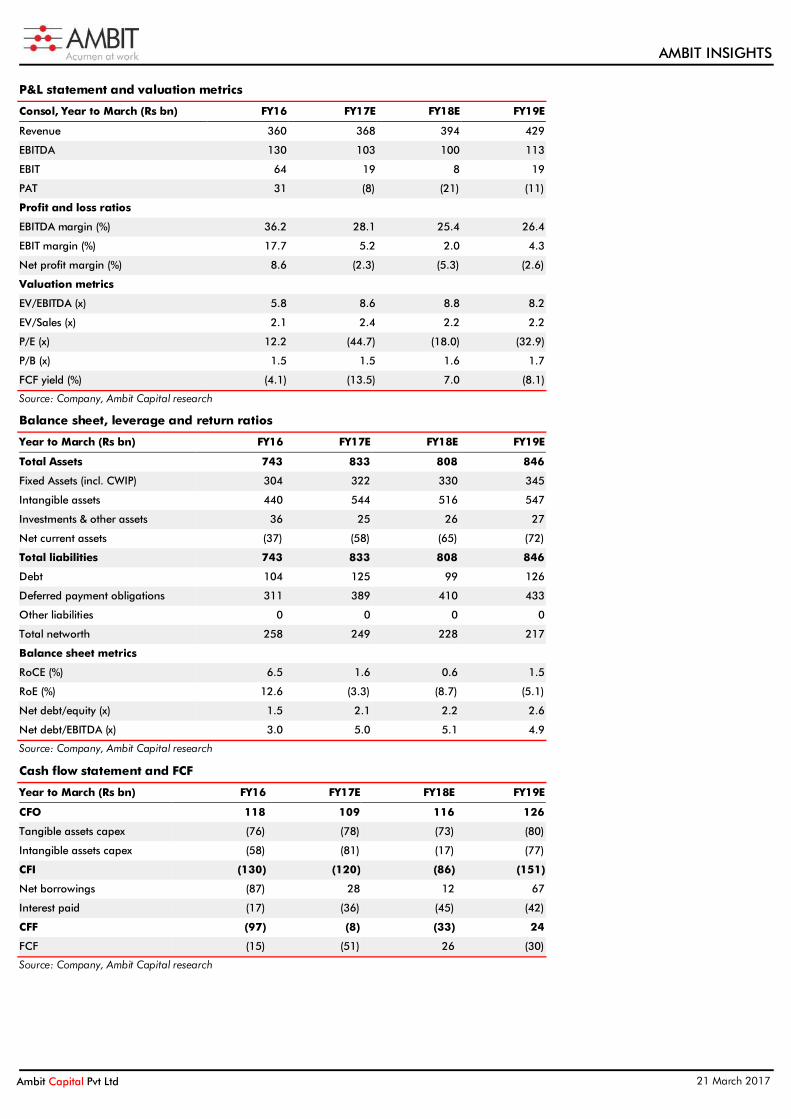

P&L statement and valuation metrics

Consol, Year to March (Rs bn) FY16 FY17E FY18E FY19E

Revenue 360 368 394 429

EBITDA 130 103 100 113

EBIT 64 19 8 19

PAT 31 (8) (21) (11)

Profit and loss ratios

EBITDA margin (%) 36.2 28.1 25.4 26.4

EBIT margin (%) 17.7 5.2 2.0 4.3

Net profit margin (%) 8.6 (2.3) (5.3) (2.6)

Valuation metrics

EV/EBITDA (x) 5.8 8.6 8.8 8.2

EV/Sales (x) 2.1 2.4 2.2 2.2

P/E (x) 12.2 (44.7) (18.0) (32.9)

P/B (x) 1.5 1.5 1.6 1.7

FCF yield (%) (4.1) (13.5) 7.0 (8.1)

Source: Company, Ambit Capital research

Balance sheet, leverage and return ratios

Year to March (Rs bn) FY16 FY17E FY18E FY19E

Total Assets 743 833 808 846

Fixed Assets (incl. CWIP) 304 322 330 345

Intangible assets 440 544 516 547

Investments & other assets 36 25 26 27

Net current assets (37) (58) (65) (72)

Total liabilities 743 833 808 846

Debt 104 125 99 126

Deferred payment obligations 311 389 410 433

Other liabilities 0 0 0 0

Total networth 258 249 228 217

Balance sheet metrics

RoCE (%) 6.5 1.6 0.6 1.5

RoE (%) 12.6 (3.3) (8.7) (5.1)

Net debt/equity (x) 1.5 2.1 2.2 2.6

Net debt/EBITDA (x) 3.0 5.0 5.1 4.9

Source: Company, Ambit Capital research

Cash flow statement and FCF

Year to March (Rs bn) FY16 FY17E FY18E FY19E

CFO 118 109 116 126

Tangible assets capex (76) (78) (73) (80)

Intangible assets capex (58) (81) (17) (77)

CFI (130) (120) (86) (151)

Net borrowings (87) 28 12 67

Interest paid (17) (36) (45) (42)

CFF (97) (8) (33) 24

FCF (15) (51) 26 (30)

Source: Company, Ambit Capital research

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

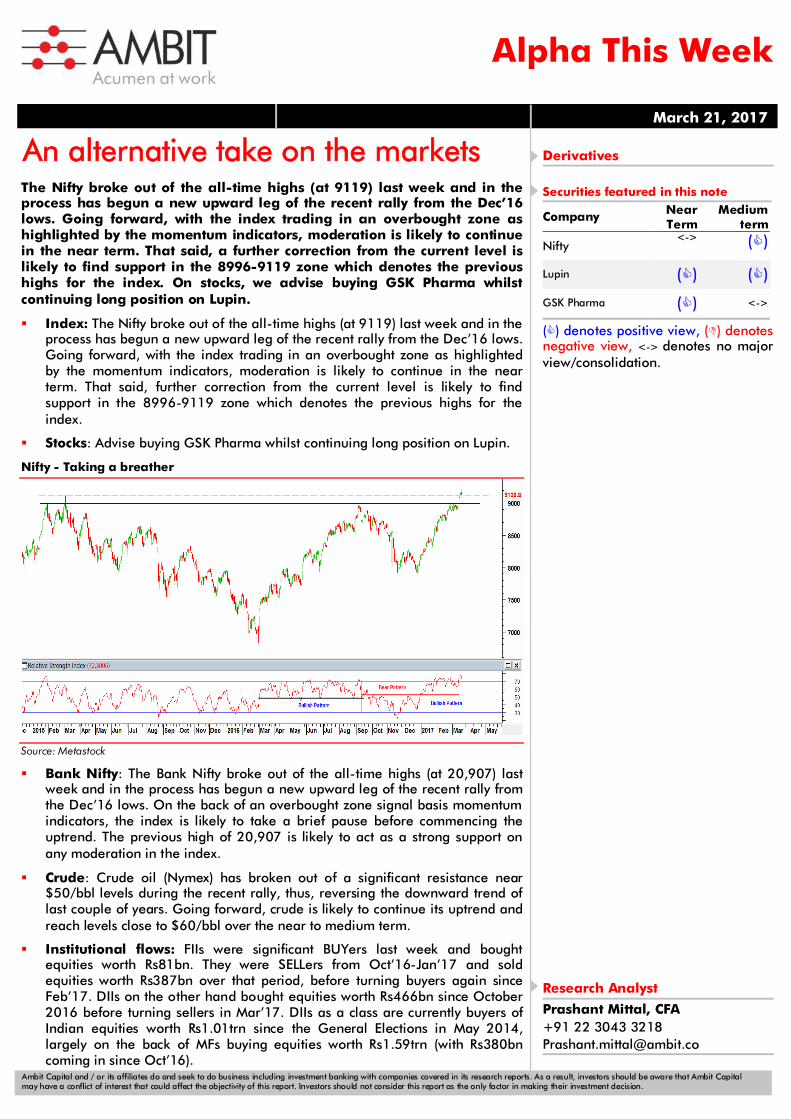

Alpha This Week

March 21, 2017

Derivatives

Securities featured in this note

Company Near Term

Medium term

Nifty <-> ()

Lupin () ()

GSK Pharma () <->

() denotes positive view, () denotes negative view, <-> denotes no major view/consolidation. Research Analyst

Prashant Mittal, CFA +91 22 3043 3218 [email protected]

An alternative take on the markets 17th Sept 2013 The Nifty broke out of the all-time highs (at 9119) last week and in the process has begun a new upward leg of the recent rally from the Dec’16 lows. Going forward, with the index trading in an overbought zone as highlighted by the momentum indicators, moderation is likely to continue in the near term. That said, a further correction from the current level is likely to find support in the 8996-9119 zone which denotes the previous highs for the index. On stocks, we advise buying GSK Pharma whilst continuing long position on Lupin.

Index: The Nifty broke out of the all-time highs (at 9119) last week and in the process has begun a new upward leg of the recent rally from the Dec’16 lows. Going forward, with the index trading in an overbought zone as highlighted by the momentum indicators, moderation is likely to continue in the near term. That said, further correction from the current level is likely to find support in the 8996-9119 zone which denotes the previous highs for the index.

Stocks: Advise buying GSK Pharma whilst continuing long position on Lupin.

Nifty - Taking a breather

Source: Metastock

Bank Nifty: The Bank Nifty broke out of the all-time highs (at 20,907) last week and in the process has begun a new upward leg of the recent rally from the Dec’16 lows. On the back of an overbought zone signal basis momentum indicators, the index is likely to take a brief pause before commencing the uptrend. The previous high of 20,907 is likely to act as a strong support on any moderation in the index.

Crude: Crude oil (Nymex) has broken out of a significant resistance near $50/bbl levels during the recent rally, thus, reversing the downward trend of last couple of years. Going forward, crude is likely to continue its uptrend and reach levels close to $60/bbl over the near to medium term.

Institutional flows: FIIs were significant BUYers last week and bought equities worth Rs81bn. They were SELLers from Oct’16-Jan’17 and sold equities worth Rs387bn over that period, before turning buyers again since Feb’17. DIIs on the other hand bought equities worth Rs466bn since October 2016 before turning sellers in Mar’17. DIIs as a class are currently buyers of Indian equities worth Rs1.01trn since the General Elections in May 2014, largely on the back of MFs buying equities worth Rs1.59trn (with Rs380bn coming in since Oct’16).

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

Institutional Equities Team Saurabh Mukherjea, CFA CEO, Ambit Capital Private Limited (022) 30433174 [email protected] Pramod Gubbi, CFA Head of Equities (022) 30433124 [email protected]

Research Analysts

Name Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Home Building (022) 30433241 [email protected] Aadesh Mehta, CFA Banking / Financial Services (022) 30433239 [email protected] Abhishek Ranganathan, CFA Retail / Consumer Discretionary (022) 30433085 [email protected] Anuj Bansal Consumer (022) 30433122 [email protected] Aditi Singh Economy / Strategy (022) 30433284 [email protected] Ashvin Shetty, CFA Automobiles / Auto Ancillaries (022) 30433285 [email protected] Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected] Deepesh Agarwal, CFA Power Utilities / Capital Goods (022) 30433275 [email protected] Dhiraj Mistry, CFA Consumer (022) 30433264 [email protected] Gaurav Khandelwal, CFA Automobiles / Auto Ancillaries (022) 30433132 [email protected] Girisha Saraf Home Building (022) 30433211 [email protected] Karan Khanna, CFA Strategy (022) 30433251 [email protected] Mayank Porwal Retail / Consumer Discretionary (022) 30433214 [email protected] Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected] Paresh Dave, CFA Healthcare (022) 30433212 [email protected] Parita Ashar, CFA Cement / Metals / Aviation (022) 30433223 [email protected] Prashant Mittal, CFA Strategy / Derivatives (022) 30433218 [email protected] Rahil Shah Banking / Financial Services (022) 30433217 [email protected] Ravi Singh Banking / Financial Services (022) 30433181 [email protected] Ritesh Gupta, CFA Oil & Gas / Chemicals / Agri Inputs (022) 30433242 [email protected] Ritesh Vaidya, CFA Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected] Sagar Rastogi Technology (022) 30433291 [email protected] Sudheer Guntupalli Technology (022) 30433203 [email protected] Sumit Shekhar Economy / Strategy (022) 30433229 [email protected] Utsav Mehta, CFA E&C / Infrastructure (022) 30433209 [email protected] Vivekanand Subbaraman, CFA Media / Telecom (022) 30433261 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7886 2740 [email protected] Dharmen Shah India / Asia (022) 30433289 [email protected] Dipti Mehta India (022) 30433053 [email protected] Krishnan V India / Asia (022) 30433295 [email protected] Nityam Shah, CFA Europe (022) 30433259 [email protected] Punitraj Mehra, CFA India / Asia (022) 30433198 [email protected] Shaleen Silori India (022) 30433256 [email protected]

Singapore

Praveena Pattabiraman Singapore +65 6536 0481 [email protected] Shashank Abhisheik Singapore +65 6536 1935 [email protected]

USA / Canada

Ravilochan Pola – CEO Americas +1(646) 793 6001 [email protected] Hitakshi Mehra Americas +1(646) 793 6002 [email protected] Achint Bhagat, CFA Americas +1(646) 793 6752 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected] Sharoz G Hussain Production (022) 30433183 [email protected] Jestin George Editor (022) 30433272 [email protected] Richard Mugutmal Editor (022) 30433273 [email protected] Nikhil Pillai Database (022) 30433265 [email protected]

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

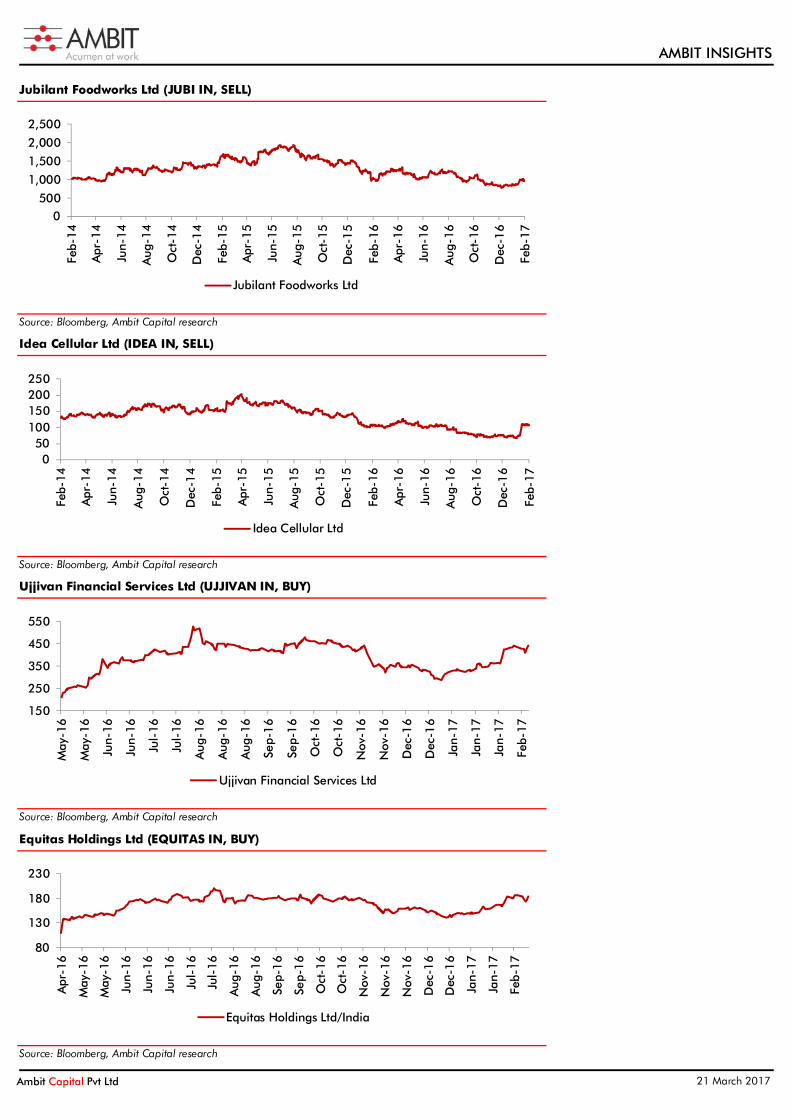

Jubilant Foodworks Ltd (JUBI IN, SELL)

Source: Bloomberg, Ambit Capital research

Idea Cellular Ltd (IDEA IN, SELL)

Source: Bloomberg, Ambit Capital research

Ujjivan Financial Services Ltd (UJJIVAN IN, BUY)

Source: Bloomberg, Ambit Capital research

Equitas Holdings Ltd (EQUITAS IN, BUY)

Source: Bloomberg, Ambit Capital research

0500

1,000

1,500

2,000

2,500

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb-

16

Apr

-16

Jun-

16

Aug

-16

Oct

-16

Dec

-16

Feb-

17

Jubilant Foodworks Ltd

050

100150200250

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb-

16

Apr

-16

Jun-

16

Aug

-16

Oct

-16

Dec

-16

Feb-

17Idea Cellular Ltd

150

250

350

450

550

May

-16

May

-16

Jun-

16

Jun-

16

Jul-

16

Jul-

16

Aug

-16

Aug

-16

Aug

-16

Sep-

16

Sep-

16

Oct

-16

Oct

-16

Nov

-16

Nov

-16

Dec

-16

Dec

-16

Jan-

17

Jan-

17

Jan-

17

Feb-

17

Ujjivan Financial Services Ltd

80

130

180

230

Apr

-16

May

-16

May

-16

Jun-

16

Jun-

16

Jun-

16

Jul-

16

Jul-

16

Aug

-16

Aug

-16

Sep-

16

Sep-

16

Oct

-16

Oct

-16

Nov

-16

Nov

-16

Nov

-16

Dec

-16

Dec

-16

Jan-

17

Jan-

17

Feb-

17

Equitas Holdings Ltd/India

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

Explanation of Investment Rating

Investment Rating Expected return (over 12-month)

BUY >10%

SELL <10%

NO STANCE We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NOT RATED We do not have any forward looking estimates, valuation or recommendation for the stock POSITIVE We have a positive view on the sector and most of stocks under our coverage in the sector are BUYs

NEGATIVE We have a negative view on the sector and most of stocks under our coverage in the sector are SELLs

Disclaimer This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases, in printed form.

Additional information on recommended securities is available on request.

Disclaimer

1. AMBIT Capital Private Limited (“AMBIT Capital”) and its affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio Manager, Merchant Banker and Depository Participant registered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI.

2. AMBIT Capital makes best endeavours to ensure that the research analyst(s) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to be reliable. However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information, opinions, views expressed in this Research Report are those of the research analyst as at the date of this Research Report which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

3. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. If you are dissatisfied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital or its affiliates shall not be responsible and/ or liable for any direct/consequential loss howsoever directly or indirectly, from any use of this Research Report.

4. If this Research Report is received by any client of AMBIT Capital or its affiliate, the relationship of AMBIT Capital/its affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

5. This Research Report is issued for information only and the 'Buy', 'Sell', or ‘Other Recommendation’ made in this Research Report such should not be construed as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securities and should not be intended or treated as a substitute for necessary review or validation or any professional advice. Recipients should consider this Research Report as only a single factor in making any investment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

6. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole or in part, for any purpose. Neither this Research Report nor any copy of it may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons), Canada or Japan or to any resident thereof. The distribution of this Research Report in other jurisdictions may be strictly restricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

7. Ambit Capital Private Limited is registered as a Research Entity under the SEBI (Research Analysts) Regulations, 2014. SEBI Reg.No.- INH000000313.

Conflict of Interests

8. In the normal course of AMBIT Capital’s business circumstances may arise that could result in the interests of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with the interest of another client. AMBIT Capital makes best efforts to ensure that conflicts are identified and managed and that clients’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services.

9. AMBIT Capital and/or its affiliates may from time to time have or solicit investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same.

Additional Disclaimer for Canadian Persons

10. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities and/or to provide advice with respect to securities. 11. AMBIT Capital's head office or principal place of business is located in India. 12. All or substantially all of AMBIT Capital's assets may be situated outside of Canada. 13. It may be difficult for enforcing legal rights against AMBIT Capital because of the above. 14. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2

Canada. 15. Name and address of AMBIT Capital's agent for service of process in the Province of Québec is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada.

Additional Disclaimer for Singapore Persons 16. This Report is prepared and distributed by Ambit Capital Private Limited and distributed as per the approved arrangement under Paragraph 9 of Third Schedule of Securities and Futures Act (CAP 289)

and Paragraph 11 of the First Schedule to the Financial Advisors Act (CAP 110) provided to Ambit Singapore Pte. Limited by Monetary Authority of Singapore. 17. This Report is only available to persons in Singapore who are institutional investors (as defined in section 4A of the Securities and Futures Act (Cap. 289) of Singapore (the “SFA”).” Accordingly, if a

Singapore Person is not or ceases to be such an institutional investor, such Singapore Person must immediately discontinue any use of this Report and inform Ambit Singapore Pte. Limited.

Additional Disclaimer for UK Persons 18. All of the recommendations and views about the securities and companies in this report accurately reflect the personal views of the research analyst named on the cover. No part of this research

analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst in this research report. This report may not be reproduced, redistributed or copied in whole or in part for any purpose.

19. This report is a marketing communication and has been prepared by Ambit Capital Pvt Ltd of Mumbai, India (“Ambit”) and has been approved in the UK by Ambit Capital (UK) Limited (“ACUK”) solely for the purposes of section 21 of the Financial Services and Markets Act 2000. Ambit is regulated by the Securities and Exchange Board of India and is registered as a Research Entity under the SEBI (Research Analysts) Regulations, 2014. ACUK is regulated by the UK Financial Services Authority and has registered office at C/o Panmure Gordon & Co PL, One New Change, London, EC4M9AF.

20. In the UK, this report is directed at and is for distribution only to persons who (i) fall within Article 19(1) (persons who have professional experience in matters relating to investments) or Article 49(2)(a) to (d) (high net worth companies, unincorporated associations etc) of the Financial Services and Markets Act 2000 (Financial Promotions) Order 2005 (as amended) or (ii) are professional customers or eligible counterparties of ACUK (all such persons together being referred to as "relevant persons"). This report must not be acted on or relied upon by persons in the UK who are not relevant persons.

21. Neither Ambit nor ACUK is a US registered broker-dealer. Transactions undertaken in the US in any security mentioned herein must be effected through a US-registered broker-dealer, in conformity with SEC Rule 15a-6.

22. Neither this report nor any copy or part thereof may be distributed in any other jurisdictions where its distribution may be restricted by law and persons into whose possession this report comes should inform themselves about, and observe, any such restrictions. Distribution of this report in any such other jurisdictions may constitute a violation of UK or US securities laws, or the law of any such other jurisdictions.

23. This report does not constitute an offer or solicitation to buy or sell any securities referred to herein. It should not be so construed, nor should it or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. The information in this report, or on which this report is based, has been obtained from publicly available sources that Ambit believes to be reliable and accurate. However, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research. It has also not been independently verified and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties.

24. The information or opinions are provided as at the date of this report and are subject to change without notice. The information and opinions provided in this report take no account of the investors’ individual circumstances and should not be taken as specific advice on the merits of any investment decision. Investors should consider this report as only a single factor in making any investment decisions. Further information is available upon request. No member or employee of Ambit or ACUK accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of this report or its contents.

25. The value of any investment made at your discretion based on this Report, or income therefrom, maybe affected by changes in economic, financial and/or political factors and may go down as well as go up and you may not get back the original amount invested. Some securities and/or investments involve substantial risk and are not suitable for all investors.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 21 March 2017

26. Ambit and its affiliates and their respective officers directors and employees may hold positions in any securities mentioned in this Report (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). Ambit and ACUK may from time to time render advisory and other services to companies referred to in this Report and may receive compensation for the same.

27. Ambit and its affiliates may act as a market maker or risk arbitrator or liquidity provider or may have assumed an underwriting commitment in the securities of companies discussed in this Report (or in related investments) or may sell them or buy them from clients on a principal to principal basis or may be involved in proprietary trading and may also perform or seek to perform investment banking or underwriting services for or relating to those companies.

28. Ambit and ACUK may sell or buy any securities or make any investment which may be contrary to or inconsistent with this Report and are not subject to any prohibition on dealing. By accepting this report you agree to be bound by the foregoing limitations. In the normal course of Ambit and its affiliates’ business, circumstances may arise that could result in the interests of Ambit conflicting with the interests of clients or one client’s interests conflicting with the interest of another client. Ambit makes best efforts to ensure that conflicts are identified, managed and clients’ interests are protected. However, clients/potential clients of Ambit should be aware of these possible conflicts of interests and should make informed decisions in relation to Ambit services.

Disclosures 29. The analyst (s) has/have not served as an officer, director or employee of the subject company. 30. There is no material disciplinary action that has been taken by any regulatory authority impacting equity research analysis activities. 31. All market data included in this report are dated as at the previous stock market closing day from the date of this report. 32. Ambit and/or its associates have actual/beneficial ownership of 1% or more in the securities of DCB Bank Limited. Ambit and/or its associates have received compensation for investment

banking/merchant banking/brokering services from HDFC Bank Ltd in the past 12 months.

Analyst Certification Each of the analysts identified in this report certifies, with respect to the companies or securities that the individual analyses, that (1) the views expressed in this report reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly dependent on the specific recommendations or views expressed in this report. © Copyright 2017 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor. 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 | Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com