Embed Size (px)

Citation preview

1

SINGLE PREMIUM GROUP ANNUITY

CONTRACT INSTALLATION

&

BENEFIT ADMINISTRATION

GUIDE

.

Annuities Underwritten by:

American General Life Insurance Company Houston, Texas

Questions? Please call: Richard S. Weiss Vice President, Pensions (908) 334-4631 [email protected]

2

American General Life Companies – Pensions

is pleased to provide our

Single Premium Group Annuity Contract Installation

& Benefit Administration Guide

This Guide provides details of our:

Financial Quality

Experience, Capabilities and Services

Contract Installation Process and Timeline

Sample Participant Correspondence

o Welcome Letter o Certificates o Benefit Forms

Sample Group Annuity Contract

3

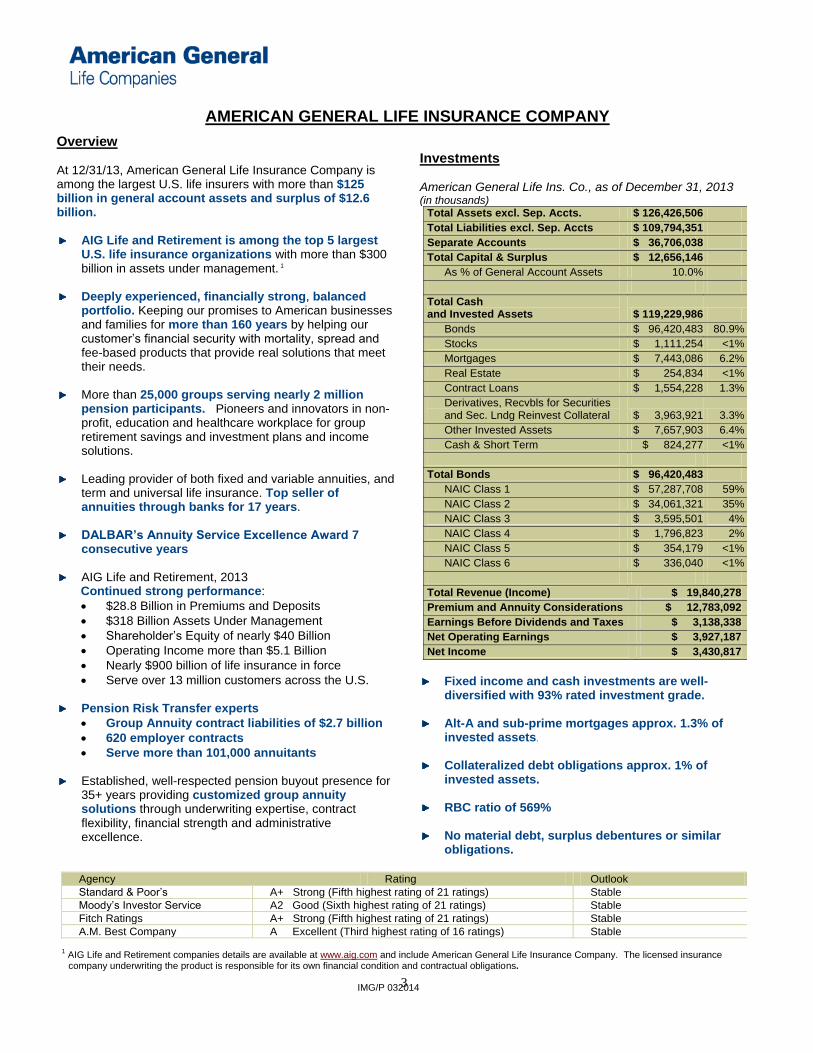

AMERICAN GENERAL LIFE INSURANCE COMPANY

Overview At 12/31/13, American General Life Insurance Company is among the largest U.S. life insurers with more than $125 billion in general account assets and surplus of $12.6 billion.

AIG Life and Retirement is among the top 5 largest U.S. life insurance organizations with more than $300 billion in assets under management. 1

Deeply experienced, financially strong, balanced

portfolio. Keeping our promises to American businesses and families for more than 160 years by helping our customer’s financial security with mortality, spread and fee-based products that provide real solutions that meet their needs.

More than 25,000 groups serving nearly 2 million

pension participants. Pioneers and innovators in non-profit, education and healthcare workplace for group retirement savings and investment plans and income solutions.

Leading provider of both fixed and variable annuities, and

term and universal life insurance. Top seller of annuities through banks for 17 years.

DALBAR’s Annuity Service Excellence Award 7

consecutive years

AIG Life and Retirement, 2013 Continued strong performance:

$28.8 Billion in Premiums and Deposits

$318 Billion Assets Under Management

Shareholder’s Equity of nearly $40 Billion

Operating Income more than $5.1 Billion

Nearly $900 billion of life insurance in force

Serve over 13 million customers across the U.S.

Pension Risk Transfer experts

Group Annuity contract liabilities of $2.7 billion

620 employer contracts

Serve more than 101,000 annuitants

Established, well-respected pension buyout presence for 35+ years providing customized group annuity solutions through underwriting expertise, contract flexibility, financial strength and administrative excellence.

Investments American General Life Ins. Co., as of December 31, 2013 (in thousands)

Total Assets excl. Sep. Accts. $ 126,426,506

Total Liabilities excl. Sep. Accts $ 109,794,351

Separate Accounts $ 36,706,038

Total Capital & Surplus $ 12,656,146

As % of General Account Assets 10.0%

Total Cash and Invested Assets $ 119,229,986

Bonds $ 96,420,483 80.9%

Stocks $ 1,111,254 <1%

Mortgages $ 7,443,086 6.2%

Real Estate $ 254,834 <1%

Contract Loans $ 1,554,228 1.3%

Derivatives, Recvbls for Securities and Sec. Lndg Reinvest Collateral $ 3,963,921 3.3%

Other Invested Assets $ 7,657,903 6.4%

Cash & Short Term $ 824,277 <1%

Total Bonds $ 96,420,483

NAIC Class 1 $ 57,287,708 59%

NAIC Class 2 $ 34,061,321 35%

NAIC Class 3 $ 3,595,501 4%

NAIC Class 4 $ 1,796,823 2%

NAIC Class 5 $ 354,179 <1%

NAIC Class 6 $ 336,040 <1%

Total Revenue (Income) $ 19,840,278

Premium and Annuity Considerations $ 12,783,092

Earnings Before Dividends and Taxes $ 3,138,338

Net Operating Earnings $ 3,927,187

Net Income $ 3,430,817

Fixed income and cash investments are well-

diversified with 93% rated investment grade.

Alt-A and sub-prime mortgages approx. 1.3% of invested assets.

Collateralized debt obligations approx. 1% of

invested assets.

RBC ratio of 569%

No material debt, surplus debentures or similar obligations.

Agency Rating Outlook

Standard & Poor’s A+ Strong (Fifth highest rating of 21 ratings) Stable

Moody’s Investor Service A2 Good (Sixth highest rating of 21 ratings) Stable

Fitch Ratings A+ Strong (Fifth highest rating of 21 ratings) Stable

A.M. Best Company A Excellent (Third highest rating of 16 ratings) Stable

1 AIG Life and Retirement companies details are available at www.aig.com and include American General Life Insurance Company. The licensed insurance company underwriting the product is responsible for its own financial condition and contractual obligations. IMG/P 032014

4

AIG Life and Retirement Services

2013 - Awarded DALBAR’s Annuity Service Award for 7th consecutive year

2012 – PlanSponsor Magazine Best-in-Class Awards for Participant Services (6 categories)

2012 - #4 Annuity Service Call Center Evaluation

2012 - “Very Good” ranking for Client/Investor Statements for 11th consecutive year

2012 - #2 ranking for Producer Website among Life Insurance and Annuity websites for

Financial Professionals

Dalbar's Service Quality Measurement program provides an annual ranking of the level of telephone service being provided by various financial services firms. These rankings are

based on four detailed criteria including the representative's Attitude, the level of

Accommodation, the level of Expertise displayed and how effectively Interruptions to the flow of the call were handled.

Investor Statements are a critical line of communication between financial services

firms and their clients. Dalbar's annual rankings indicate which firms are using this tool most effectively and efficiently to communicate with their clients.

Each quarter Dalbar's WebMonitor team identifies the best-in-class financial services

websites. The rankings below list the industry-leading firms which earned an "Excellent" or

"Very Good" designation for the market segment and time period selected.

5

A Note about Life Insurance Companies and Ratings

Insurance is a highly regulated industry. All insurance companies doing business in the

United States are regulated by state law, and required to maintain enough capital and surplus to

satisfy their obligations to their policy holders. The type and quantity of investments in which

insurance companies may invest surplus capital is also limited by state law.

Each life insurance company is individually responsible for the liabilities associated with the

business that it sells. In addition, each insurer is individually regulated by its state of domicile for

compliance and financial solvency independent of its parent or affiliates. This includes ongoing

financial reporting to the regulator and undergoing periodic financial examination. American

General Life is regulated by the Texas Department of Insurance.

In accordance with state insurance requirements and investment guidelines, an insurer’s

general account is primarily invested in high quality investment grade fixed income securities

(bonds). The investment objective of the general account is to optimize yield, adjusting for credit

risk, liquidity and liability characteristics. State insurance regulations are substantial and are

designed to preserve and enhance the solvency of the general account and to assure that the

contractual obligations to our policy holders are fulfilled. These regulations, along with the

conservative investment requirements, help to safeguard policy holders.

Guarantees provided in an insurer’s annuity contracts and life insurance policies are backed

by its general account. The general account supports only the obligations of the insurer and is not

obligated to support any other businesses, member companies or parent companies.

Independent ratings agencies, such as A.M. Best, Moody’s, Standard & Poor’s and Fitch,

provide opinions on an organization’s ability to meet its financial obligations to its policy holders,

creditors and shareholders. Generally there are two components to ratings — a credit rating and a

financial strength rating. Credit ratings, or long-term debt ratings, are an evaluation by the ratings

agencies of the creditworthiness of an organization and its ability to pay its short- and long-term

debt. Financial strength ratings are an evaluation by the ratings agencies of an insurer’s ability to

meet its obligations to its policy holders. Some insurance organizations may have different ratings

for debt and financial strength.

For more than 160 years, American General Life companies have earned the trust and

confidence of our policyholders and today remains well-capitalized, financially strong and among

the nation’s safest available annuity providers.

6

Experience & Capabilities

COMMITMENT TO GROUP ANNUITIES UNPARALLELED EXPERTISE

Our Pension Risk Transfer team includes more than 40 experienced professionals dedicated exclusively to group annuity underwriting and pricing, product development and contract services, investments, actuarial, risk management, accounting and asset/liability management, new business and in-force client support, including participant administration, legal, IT and financial support and a specialized, stand-alone Pension Annuity Service Center.

AGL’s Pension Annuity Service Center is a fully staffed payment facility located in Wilmington, Delaware and is responsible for all participant and client level services with particular knowledge of pension plan terminations and benefits administration. Many of us have been working together for more than 20 years. Our first pension terminal funding annuity was installed in 1977 and we service several contracts in excess of 5,000 annuitants. In the past 10 years, AIG Life and Retirement has issued pension closeout contracts around the world, more than $1 Billion, in the U.S., Canada and U.K.

AGL considers pension annuity administration a core competency and we do not utilize external administration arrangements. We perform the services as lead administrator for most of our clients and have several contracts in which we “bulk” pay to a client’s trust and perform regular reconciliations and audits. In 2011, we installed a new group annuity block of business of more than $425 million covering multiple plans and contracts and, our largest contract continues to provide direct benefit services to more than 7,800 annuitants.

Your Underwriter is your primary contact and is most familiar with your plan specifications, annuity provisions and benefit calculations, and services required to accurately install your contract. Your Underwriter leads the pricing of data and will remain as your primary contact throughout contract implementation, including writing the Proposal, reconciliation, and drafting of your Contract and participant Certificates.

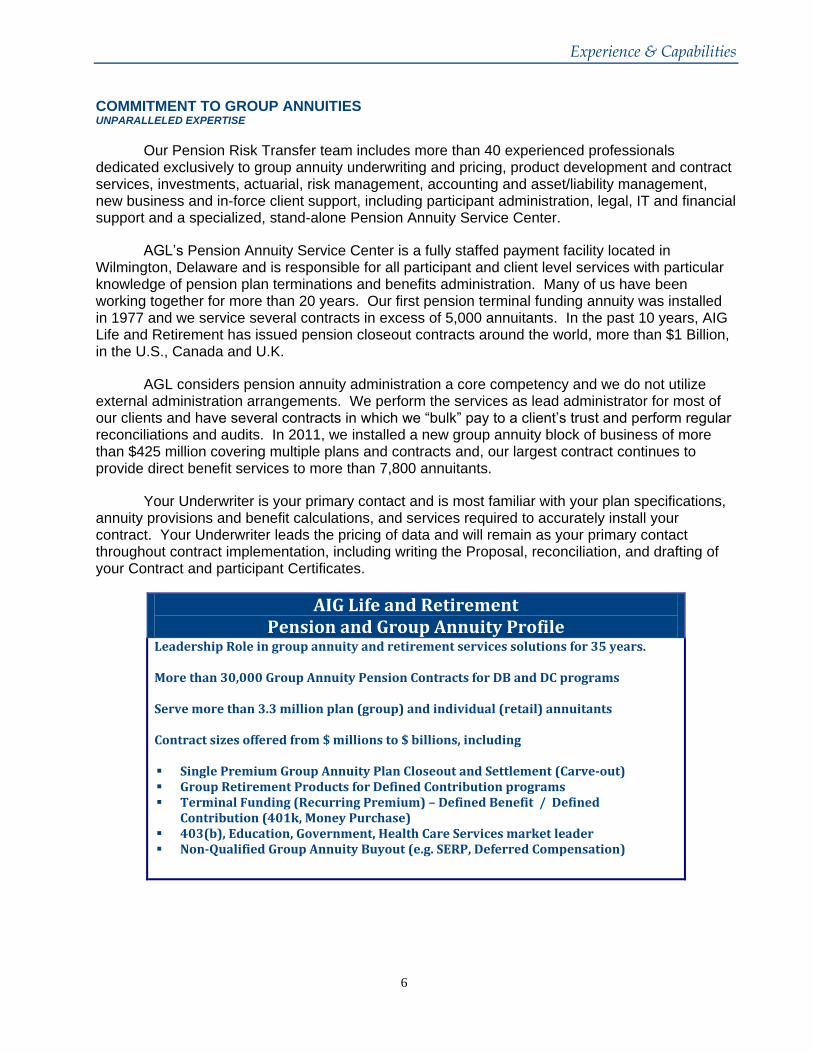

AIG Life and Retirement Pension and Group Annuity Profile

Leadership Role in group annuity and retirement services solutions for 35 years. More than 30,000 Group Annuity Pension Contracts for DB and DC programs Serve more than 3.3 million plan (group) and individual (retail) annuitants Contract sizes offered from $ millions to $ billions, including Single Premium Group Annuity Plan Closeout and Settlement (Carve-out) Group Retirement Products for Defined Contribution programs Terminal Funding (Recurring Premium) – Defined Benefit / Defined

Contribution (401k, Money Purchase) 403(b), Education, Government, Health Care Services market leader Non-Qualified Group Annuity Buyout (e.g. SERP, Deferred Compensation)

7

Experience & Capabilities

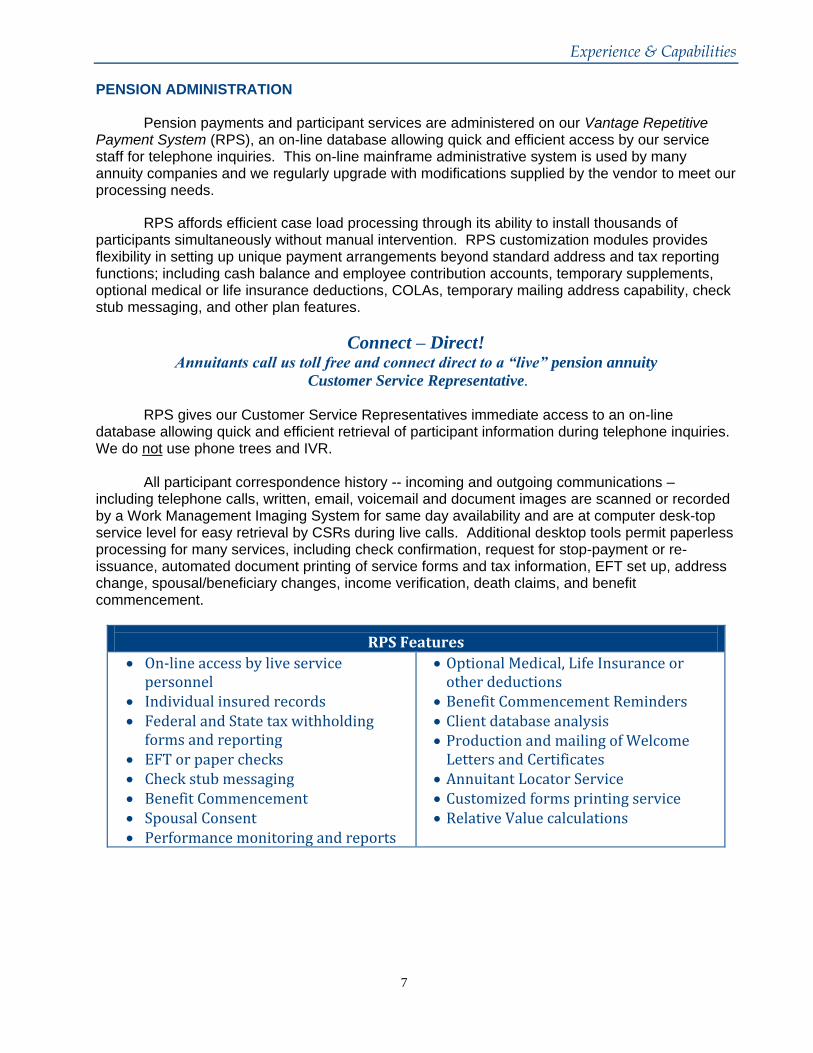

PENSION ADMINISTRATION Pension payments and participant services are administered on our Vantage Repetitive Payment System (RPS), an on-line database allowing quick and efficient access by our service staff for telephone inquiries. This on-line mainframe administrative system is used by many annuity companies and we regularly upgrade with modifications supplied by the vendor to meet our processing needs.

RPS affords efficient case load processing through its ability to install thousands of participants simultaneously without manual intervention. RPS customization modules provides flexibility in setting up unique payment arrangements beyond standard address and tax reporting functions; including cash balance and employee contribution accounts, temporary supplements, optional medical or life insurance deductions, COLAs, temporary mailing address capability, check stub messaging, and other plan features.

Connect – Direct! Annuitants call us toll free and connect direct to a “live” pension annuity

Customer Service Representative. RPS gives our Customer Service Representatives immediate access to an on-line database allowing quick and efficient retrieval of participant information during telephone inquiries. We do not use phone trees and IVR.

All participant correspondence history -- incoming and outgoing communications – including telephone calls, written, email, voicemail and document images are scanned or recorded by a Work Management Imaging System for same day availability and are at computer desk-top service level for easy retrieval by CSRs during live calls. Additional desktop tools permit paperless processing for many services, including check confirmation, request for stop-payment or re-issuance, automated document printing of service forms and tax information, EFT set up, address change, spousal/beneficiary changes, income verification, death claims, and benefit commencement.

RPS Features

On-line access by live service personnel

Individual insured records Federal and State tax withholding

forms and reporting EFT or paper checks Check stub messaging Benefit Commencement Spousal Consent Performance monitoring and reports

Optional Medical, Life Insurance or other deductions

Benefit Commencement Reminders Client database analysis Production and mailing of Welcome

Letters and Certificates Annuitant Locator Service Customized forms printing service Relative Value calculations

8

Experience & Capabilities

INSURED SERVICES

Annuitants receive an introductory Welcome Letter and Data Verification form before their first monthly annuity payment. The letter introduces our company and provides the names, addresses, and telephone numbers of our Administration staff. Data Verification allows us to identify and resolve data discrepancies with you early in the contract installation process.

Our Pension Annuity Service Center in Wilmington, Delaware is the annuitant service point for annuitant benefit services. Contract holder (and their advisors) client services are provided by your Underwriter. Regular or on-going participant information requests may be made to your Underwriter or we can assign a dedicated CSR to provide periodic participant data reports related to your contract.

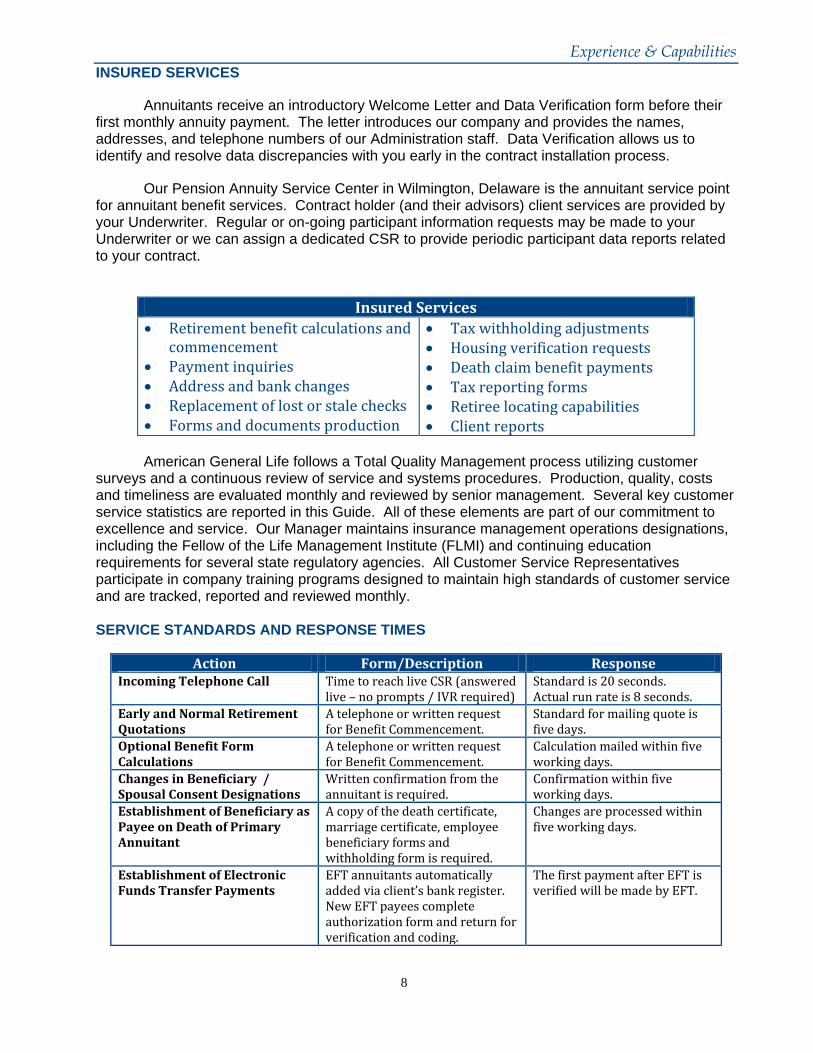

Insured Services Retirement benefit calculations and

commencement Payment inquiries Address and bank changes Replacement of lost or stale checks Forms and documents production

Tax withholding adjustments Housing verification requests Death claim benefit payments Tax reporting forms Retiree locating capabilities Client reports

American General Life follows a Total Quality Management process utilizing customer

surveys and a continuous review of service and systems procedures. Production, quality, costs and timeliness are evaluated monthly and reviewed by senior management. Several key customer service statistics are reported in this Guide. All of these elements are part of our commitment to excellence and service. Our Manager maintains insurance management operations designations, including the Fellow of the Life Management Institute (FLMI) and continuing education requirements for several state regulatory agencies. All Customer Service Representatives participate in company training programs designed to maintain high standards of customer service and are tracked, reported and reviewed monthly.

SERVICE STANDARDS AND RESPONSE TIMES

Action Form/Description Response Incoming Telephone Call Time to reach live CSR (answered

live – no prompts / IVR required) Standard is 20 seconds. Actual run rate is 8 seconds.

Early and Normal Retirement Quotations

A telephone or written request for Benefit Commencement.

Standard for mailing quote is five days.

Optional Benefit Form Calculations

A telephone or written request for Benefit Commencement.

Calculation mailed within five working days.

Changes in Beneficiary / Spousal Consent Designations

Written confirmation from the annuitant is required.

Confirmation within five working days.

Establishment of Beneficiary as Payee on Death of Primary Annuitant

A copy of the death certificate, marriage certificate, employee beneficiary forms and withholding form is required.

Changes are processed within five working days.

Establishment of Electronic Funds Transfer Payments

EFT annuitants automatically added via client’s bank register. New EFT payees complete authorization form and return for verification and coding.

The first payment after EFT is verified will be made by EFT.

9

Experience & Capabilities

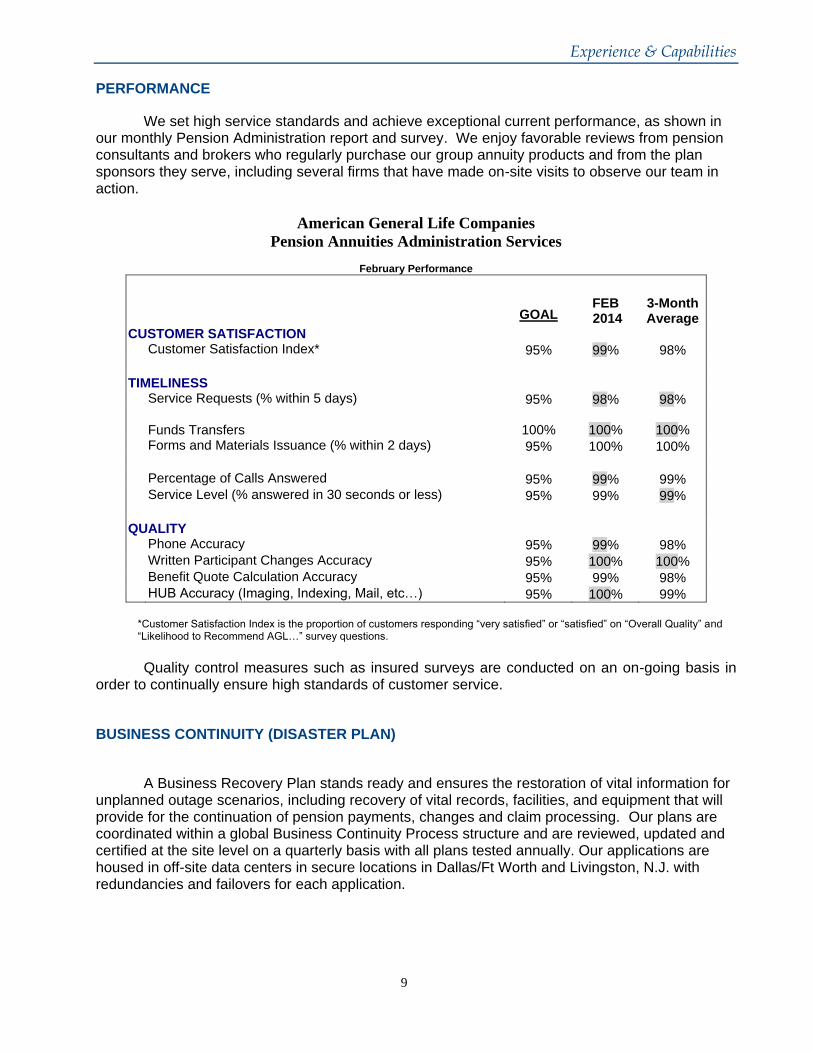

PERFORMANCE

We set high service standards and achieve exceptional current performance, as shown in our monthly Pension Administration report and survey. We enjoy favorable reviews from pension consultants and brokers who regularly purchase our group annuity products and from the plan sponsors they serve, including several firms that have made on-site visits to observe our team in action.

American General Life Companies

Pension Annuities Administration Services

February Performance

GOAL FEB 2014

3-Month Average

CUSTOMER SATISFACTION Customer Satisfaction Index* 95% 99% 98%

TIMELINESS Service Requests (% within 5 days) 95% 98% 98%

Funds Transfers 100% 100% 100% Forms and Materials Issuance (% within 2 days) 95% 100% 100% Percentage of Calls Answered 95% 99% 99% Service Level (% answered in 30 seconds or less) 95% 99% 99%

QUALITY Phone Accuracy 95% 99% 98% Written Participant Changes Accuracy 95% 100% 100% Benefit Quote Calculation Accuracy 95% 99% 98% HUB Accuracy (Imaging, Indexing, Mail, etc…) 95% 100% 99%

*Customer Satisfaction Index is the proportion of customers responding “very satisfied” or “satisfied” on “Overall Quality” and “Likelihood to Recommend AGL…” survey questions.

Quality control measures such as insured surveys are conducted on an on-going basis in order to continually ensure high standards of customer service.

BUSINESS CONTINUITY (DISASTER PLAN)

A Business Recovery Plan stands ready and ensures the restoration of vital information for

unplanned outage scenarios, including recovery of vital records, facilities, and equipment that will provide for the continuation of pension payments, changes and claim processing. Our plans are coordinated within a global Business Continuity Process structure and are reviewed, updated and certified at the site level on a quarterly basis with all plans tested annually. Our applications are housed in off-site data centers in secure locations in Dallas/Ft Worth and Livingston, N.J. with redundancies and failovers for each application.

10

Experience & Capabilities

A short term disruption of less than 2 days may be handled by either: (i) temporarily

suspending normal operations until the emergency has ended. We would update the toll-free numbers with a message informing the participants that “Today Friday, Month/Date, our office is closed. We will reopen Monday, Month/Date at 8:00 A.M. EST. Please call back then so we can assist you.” or (ii) providing CSR with laptop that is pre-loaded with software that accepts re-routed incoming telephone calls to our toll-free number. For disruptions that last more than 2 days, we maintain a contract with SunGard in Philadelphia to relocate staff and services. From this site, we can access phone systems, work stations and software applications for the continuation of participant services. [Note: In Q1 2014, we successfully tested and implemented our BCP disaster recovery, using our off-site facilities.] Similarly, we have Service Level Agreements in place with IT support teams to ensure that planned upgrades and maintenance activities occur after normal business hours and are tested before and after implementation.

11

Experience & Capabilities

REFERENCES, PENSION PLAN CONTRACT BUYOUTS

DB PLANS

Client: Joy Technologies Mark A. Harder, CEBS Benefits Specialist Joy Global Tel: 414-670-7357

Kevin Tschudy Employee Benefits Supervisor Joy Global Tel: 414-670-7418

Aimee Foreman, PHR Employee Benefit Analyst Joy Global Tel: 414-670-7632

Client: Equitable Resources Mary C. Krejsa, Benefits and Compensation Specialist (pronounced “cray-sah”) EQT Corporation 625 Liberty Avenue, Suite 1700, Pittsburgh, PA 15222-3111 412-553-5782 (Office) [email protected] Client: Unova, Inc. - now called Intermec, Inc. Paula Bauert Director, Treasury and Assistant Treasurer Intermec, Inc. 6001 36th Avenue West Everett WA 98203 Tel +1 425 265 2485 [email protected]

Client: Biogen Kelly Ashton Carlson Manager, Benefits Biogen Idec 14 Cambridge Center Cambridge, MA 02142 617-679-2849 (direct) [email protected]

DC PLANS AGL administers several group annuity contracts for money purchase plan and 401(k) plan terminations and operates several innovative distribution platforms, including pioneering the Retirement Income Annuity option program with The Vanguard Group, and specialty group annuity marketers and plan sponsors.

Please call for references in cases of DC plan termination.

12

Contract Installation

WORKING WITH YOUR UNDERWRITER

Your Underwriter has been studying your plan provisions and data and asking detailed questions so that we can deliver a well-crafted Proposal and Quote. Our experience pricing and administering group annuity contracts has earned American General Life Companies a well-respected reputation for producing outstanding, detailed offers for unique and complex contracts that demand both accurate communication to plan sponsors and excellent administration to plan participants. Your Underwriter works directly with you, the plan sponsor, and competently leads our pricing, administration, and IT teams through the post-sale contract installation steps.

Please see the next page for your customized Contract Implementation Timeline. Installation of the complete data file and direct payment of benefits depends on timely receipt of complete, accurate, and timely census information. Data Requirements are included in our Proposal Placement Documents and are included in this Annuity Guide. Payment Records are compared to the priced annuity Census and a full accounting reconciliation of premium, containing individual participant data and premium adjustments, is reported to you and your consultant.

Payment Records are verified and formatted for automated entry into RPS to implement contract installation, CSR (“Customer Service Representatives”) Case Profile training and to facilitate participant servicing, including mailing of Welcome Letters, telephone inquiries and monthly benefit payments. Pension Administration staff specialize in group annuity contracts and are cross-trained for resource allocation during peak periods and prepare a production-based IT environment dedicated to verifying and loading participant records, modifying system capabilities with any contract-specific requirements, and production and mailing of Welcome Letters. There will be a small spike in telephone calls following the mailing of your employer notification letter, our Welcome Letter, certificates, and annual tax forms during which calls are managed through overflow call routing to full-time Pension Administration employees within our Pension Annuity Service Center. All CSRs and employees receive training on new contracts prior to our first mailing of Welcome Letters. We do not use IVR (no prompts required to reach “live” CSR). We can provide customized messages solely to your annuitants.

During non-peak times, cross-trained customer service staff dedicated solely to our group pension closeout contracts perform a broad range of related annuity contract services other than responding to incoming telephone calls, including form requests, stop payment, stale and re-issue check requests, death claim notifications and processing, address change and EFT set-up, income verification, beneficiary changes, QDROs, tax reporting changes and related forms, all under the direction of an IT, Legal or Senior Manager.

At any time during your contract, you may contact us Pension Administration and make a

written request for data about the status of contract participants.

13

Contract Installation

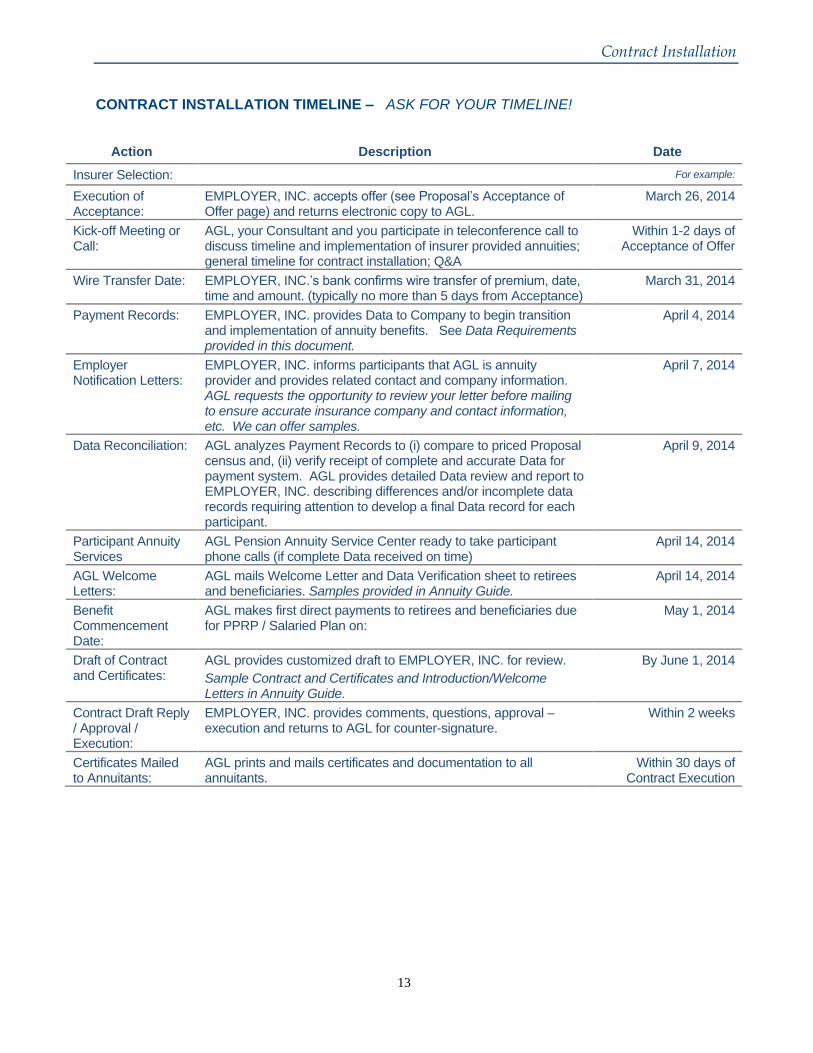

CONTRACT INSTALLATION TIMELINE – ASK FOR YOUR TIMELINE!

Action Description Date

Insurer Selection: For example:

Execution of Acceptance:

EMPLOYER, INC. accepts offer (see Proposal’s Acceptance of Offer page) and returns electronic copy to AGL.

March 26, 2014

Kick-off Meeting or Call:

AGL, your Consultant and you participate in teleconference call to discuss timeline and implementation of insurer provided annuities; general timeline for contract installation; Q&A

Within 1-2 days of Acceptance of Offer

Wire Transfer Date: EMPLOYER, INC.’s bank confirms wire transfer of premium, date, time and amount. (typically no more than 5 days from Acceptance)

March 31, 2014

Payment Records: EMPLOYER, INC. provides Data to Company to begin transition and implementation of annuity benefits. See Data Requirements provided in this document.

April 4, 2014

Employer Notification Letters:

EMPLOYER, INC. informs participants that AGL is annuity provider and provides related contact and company information. AGL requests the opportunity to review your letter before mailing to ensure accurate insurance company and contact information, etc. We can offer samples.

April 7, 2014

Data Reconciliation: AGL analyzes Payment Records to (i) compare to priced Proposal census and, (ii) verify receipt of complete and accurate Data for payment system. AGL provides detailed Data review and report to EMPLOYER, INC. describing differences and/or incomplete data records requiring attention to develop a final Data record for each participant.

April 9, 2014

Participant Annuity Services

AGL Pension Annuity Service Center ready to take participant phone calls (if complete Data received on time)

April 14, 2014

AGL Welcome Letters:

AGL mails Welcome Letter and Data Verification sheet to retirees and beneficiaries. Samples provided in Annuity Guide.

April 14, 2014

Benefit Commencement Date:

AGL makes first direct payments to retirees and beneficiaries due for PPRP / Salaried Plan on:

May 1, 2014

Draft of Contract and Certificates:

AGL provides customized draft to EMPLOYER, INC. for review.

Sample Contract and Certificates and Introduction/Welcome Letters in Annuity Guide.

By June 1, 2014

Contract Draft Reply / Approval / Execution:

EMPLOYER, INC. provides comments, questions, approval – execution and returns to AGL for counter-signature.

Within 2 weeks

Certificates Mailed to Annuitants:

AGL prints and mails certificates and documentation to all annuitants.

Within 30 days of Contract Execution

14

Contract Installation

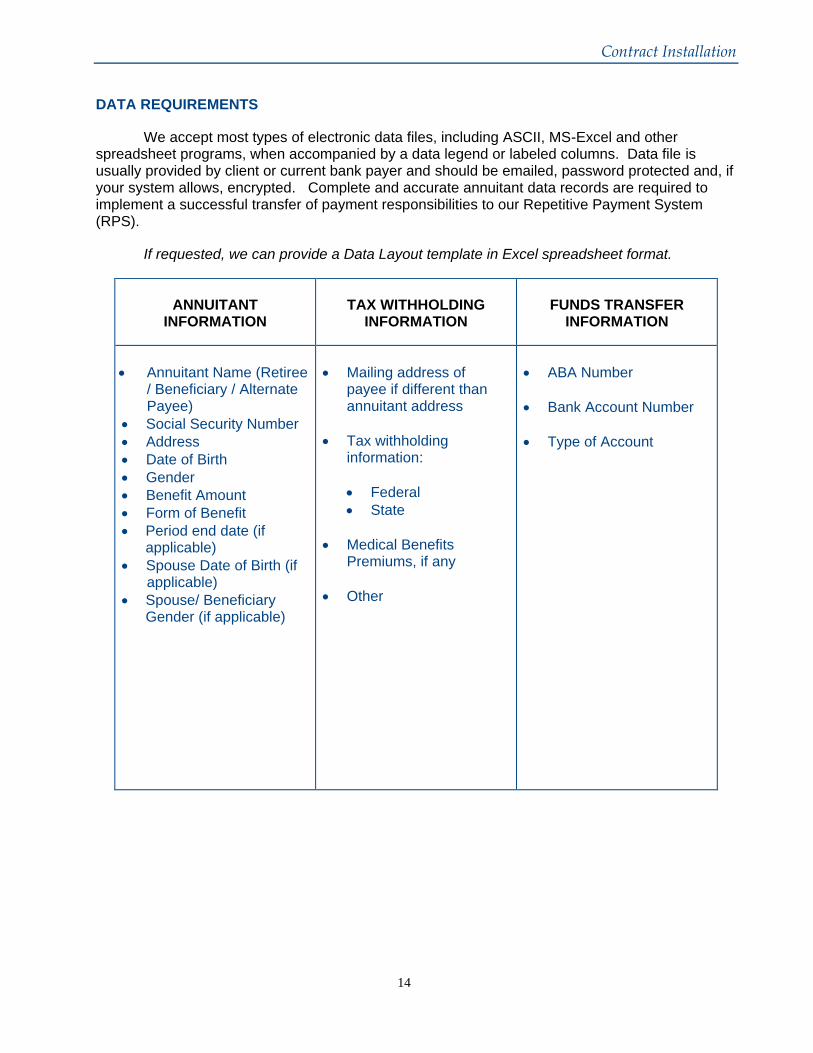

DATA REQUIREMENTS

We accept most types of electronic data files, including ASCII, MS-Excel and other spreadsheet programs, when accompanied by a data legend or labeled columns. Data file is usually provided by client or current bank payer and should be emailed, password protected and, if your system allows, encrypted. Complete and accurate annuitant data records are required to implement a successful transfer of payment responsibilities to our Repetitive Payment System (RPS).

If requested, we can provide a Data Layout template in Excel spreadsheet format.

ANNUITANT

INFORMATION

TAX WITHHOLDING

INFORMATION

FUNDS TRANSFER

INFORMATION

Annuitant Name (Retiree / Beneficiary / Alternate Payee)

Social Security Number

Address

Date of Birth

Gender

Benefit Amount

Form of Benefit

Period end date (if applicable)

Spouse Date of Birth (if applicable)

Spouse/ Beneficiary Gender (if applicable)

Mailing address of payee if different than annuitant address

Tax withholding information:

Federal

State

Medical Benefits Premiums, if any

Other

ABA Number

Bank Account Number

Type of Account

15

Contract Installation

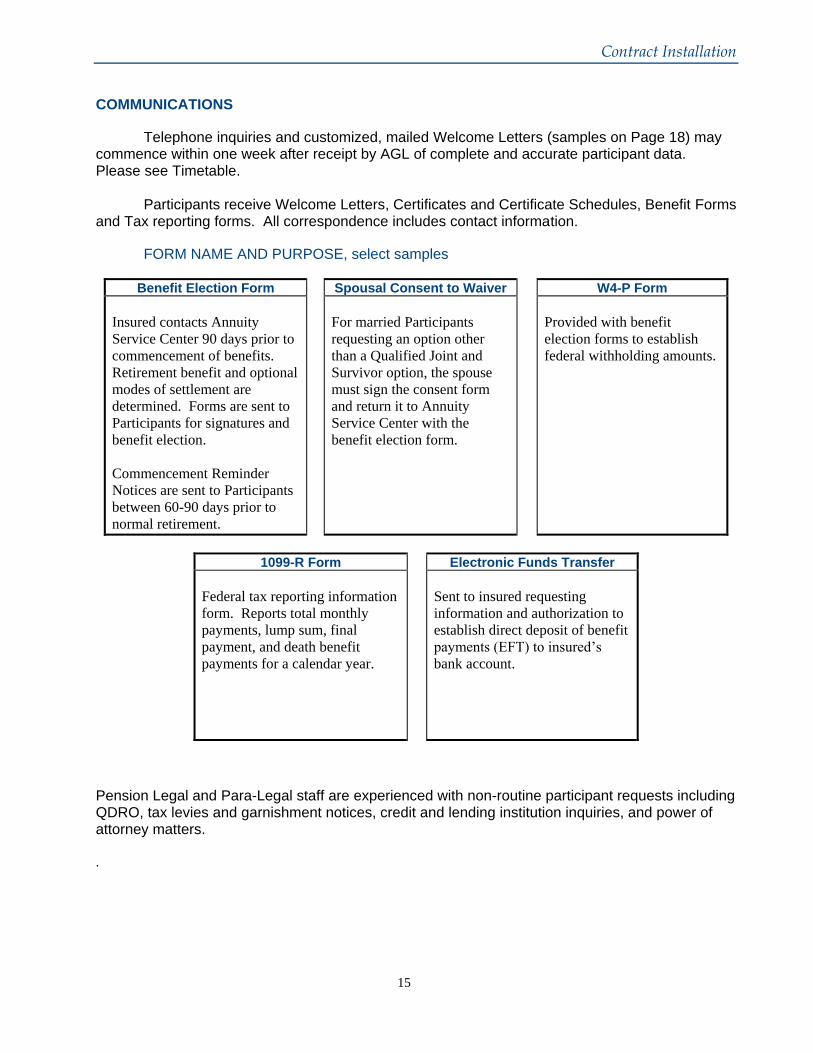

COMMUNICATIONS

Telephone inquiries and customized, mailed Welcome Letters (samples on Page 18) may commence within one week after receipt by AGL of complete and accurate participant data. Please see Timetable.

Participants receive Welcome Letters, Certificates and Certificate Schedules, Benefit Forms and Tax reporting forms. All correspondence includes contact information.

FORM NAME AND PURPOSE, select samples

Benefit Election Form Spousal Consent to Waiver W4-P Form

Insured contacts Annuity

Service Center 90 days prior to

commencement of benefits.

Retirement benefit and optional

modes of settlement are

determined. Forms are sent to

Participants for signatures and

benefit election.

Commencement Reminder

Notices are sent to Participants

between 60-90 days prior to

normal retirement.

For married Participants

requesting an option other

than a Qualified Joint and

Survivor option, the spouse

must sign the consent form

and return it to Annuity

Service Center with the

benefit election form.

Provided with benefit

election forms to establish

federal withholding amounts.

1099-R Form Electronic Funds Transfer

Federal tax reporting information

form. Reports total monthly

payments, lump sum, final

payment, and death benefit

payments for a calendar year.

Sent to insured requesting

information and authorization to

establish direct deposit of benefit

payments (EFT) to insured’s

bank account.

Pension Legal and Para-Legal staff are experienced with non-routine participant requests including QDRO, tax levies and garnishment notices, credit and lending institution inquiries, and power of attorney matters. .

16

Contract Installation

MAIL DATES FOR INSURED CHECKS Paper checks are mailed approximately eight days prior to the due date to allow for sufficient postal delivery time. Check issue dates are adjusted as necessary to assure delivery by the first of the month. Participants are encouraged to enroll in our EFT program to avoid possible mailing delays. Monthly paper confirmation statements are not provided when payment is through EFT. VERIFICATION OF PARTICIPANTS’ YEARS OF SERVICE Length of service of Active Participants, where applicable to contract provisions, must be verified by the employer. SMALL BENEFITS If monthly annuity payments are less than $50, we may make payments less frequently than monthly, and will make these payments in an aggregate amount not later than the first day of the period to which the payment applies. MISSING / LOCATING PARTICIPANTS Benefit Commencement Reminder mailings are sent:

Six months prior to normal retirement date

Each year past normal retirement date

Age 70½ until 75 Returned mail triggers attempts to locate participant address / telephone / email using search utilities, including Thomson Reuters Clear and other commercial services (e.g., Equifax, Google for obituaries and survivors). We search our files (documents previously received) for telephone numbers, Power of Attorney, spouse / beneficiary information. Death notifications through monthly Death Master File Match Process or responses from Commencement Reminder mailings triggers:

First Letter to annuitant, if undeliverable: o Address search, as above o Locate and contact family members/ beneficiary(ies)

Second Letter, 31st day

Third Letter, 61st day, if no confirmation of receipt and no beneficiary located

Escheatment rules begin, if no response or identification of benefit owner

If we discover a death or find alternate addresses, we send a letter asking them to contact us so we can verify that we have located the correct person and/or relative. POWER OF ATTORNEY Pension Administration requires a copy of the legal documents naming the guardian or legal representative in the event of an insured’s incapacity. CONTRACTS AND CERTIFICATES After the contract is signed, each insured is provided with a certificate describing his or her benefits. Samples of these documents are included at the end of this guide.

17

Contract Installation

PARTICIPANT CONTACT INFORMATION

American General Life Companies Pension Administration Department P.O. Box 1834 Wilmington, DE 19899-1834

Office Hours: 8:00 AM - 5:00 PM (ET)

Participant Toll Free Access: (800) 842-3068

Email:

Employer Direct Dial: (302) 575-5225 Stephanie Dooley, VP

Facsimile: (302) 427-8951

18

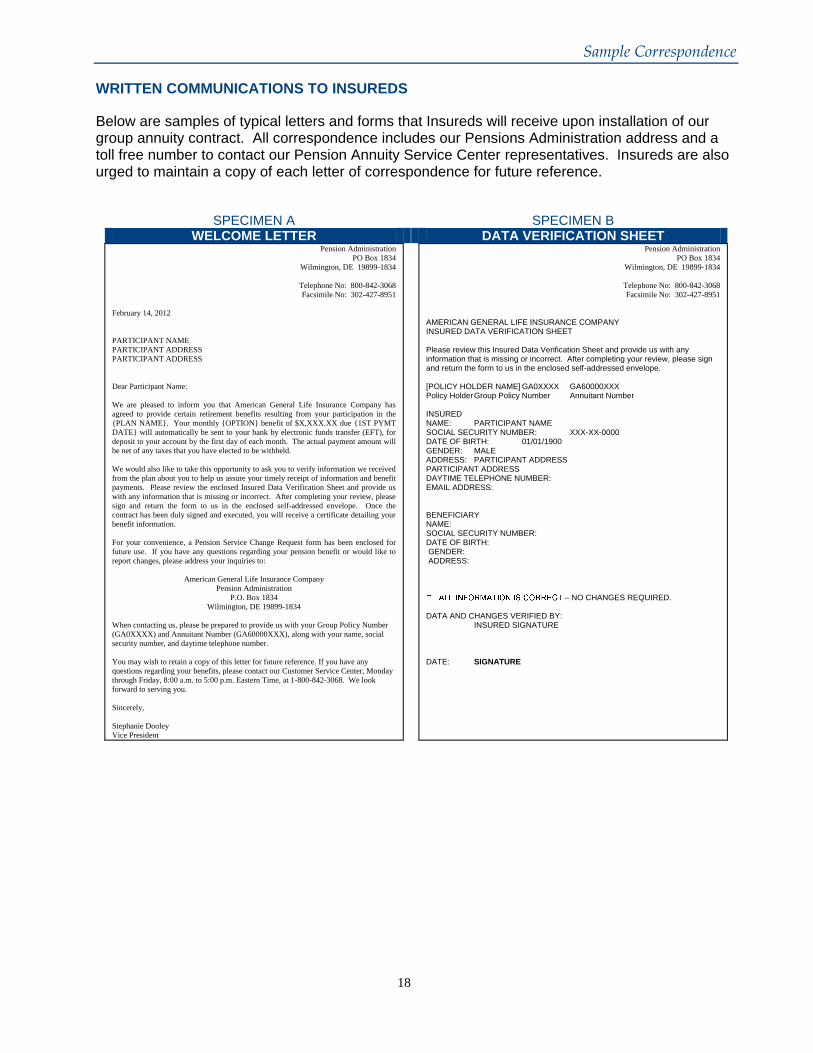

Sample Correspondence

WRITTEN COMMUNICATIONS TO INSUREDS

Below are samples of typical letters and forms that Insureds will receive upon installation of our group annuity contract. All correspondence includes our Pensions Administration address and a toll free number to contact our Pension Annuity Service Center representatives. Insureds are also urged to maintain a copy of each letter of correspondence for future reference.

SPECIMEN A SPECIMEN B WELCOME LETTER DATA VERIFICATION SHEET

Pension Administration

PO Box 1834

Wilmington, DE 19899-1834

Telephone No: 800-842-3068

Facsimile No: 302-427-8951

February 14, 2012

PARTICIPANT NAME

PARTICIPANT ADDRESS

PARTICIPANT ADDRESS

Dear Participant Name:

We are pleased to inform you that American General Life Insurance Company has

agreed to provide certain retirement benefits resulting from your participation in the

{PLAN NAME}. Your monthly {OPTION} benefit of $X,XXX.XX due {1ST PYMT

DATE} will automatically be sent to your bank by electronic funds transfer (EFT), for

deposit to your account by the first day of each month. The actual payment amount will

be net of any taxes that you have elected to be withheld.

We would also like to take this opportunity to ask you to verify information we received

from the plan about you to help us assure your timely receipt of information and benefit

payments. Please review the enclosed Insured Data Verification Sheet and provide us

with any information that is missing or incorrect. After completing your review, please

sign and return the form to us in the enclosed self-addressed envelope. Once the

contract has been duly signed and executed, you will receive a certificate detailing your

benefit information.

For your convenience, a Pension Service Change Request form has been enclosed for

future use. If you have any questions regarding your pension benefit or would like to

report changes, please address your inquiries to:

American General Life Insurance Company

Pension Administration

P.O. Box 1834

Wilmington, DE 19899-1834

When contacting us, please be prepared to provide us with your Group Policy Number

(GA0XXXX) and Annuitant Number (GA60000XXX), along with your name, social

security number, and daytime telephone number.

You may wish to retain a copy of this letter for future reference. If you have any

questions regarding your benefits, please contact our Customer Service Center, Monday

through Friday, 8:00 a.m. to 5:00 p.m. Eastern Time, at 1-800-842-3068. We look

forward to serving you.

Sincerely,

Stephanie Dooley

Vice President

Pension Administration

PO Box 1834

Wilmington, DE 19899-1834

Telephone No: 800-842-3068

Facsimile No: 302-427-8951

AMERICAN GENERAL LIFE INSURANCE COMPANY INSURED DATA VERIFICATION SHEET Please review this Insured Data Verification Sheet and provide us with any information that is missing or incorrect. After completing your review, please sign and return the form to us in the enclosed self-addressed envelope. [POLICY HOLDER NAME] GA0XXXX GA60000XXX Policy Holder Group Policy Number Annuitant Number INSURED NAME: PARTICIPANT NAME SOCIAL SECURITY NUMBER: XXX-XX-0000 DATE OF BIRTH: 01/01/1900 GENDER: MALE ADDRESS: PARTICIPANT ADDRESS PARTICIPANT ADDRESS DAYTIME TELEPHONE NUMBER: EMAIL ADDRESS: BENEFICIARY NAME: SOCIAL SECURITY NUMBER: DATE OF BIRTH: GENDER: ADDRESS:

– NO CHANGES REQUIRED. DATA AND CHANGES VERIFIED BY: INSURED SIGNATURE DATE: SIGNATURE

19

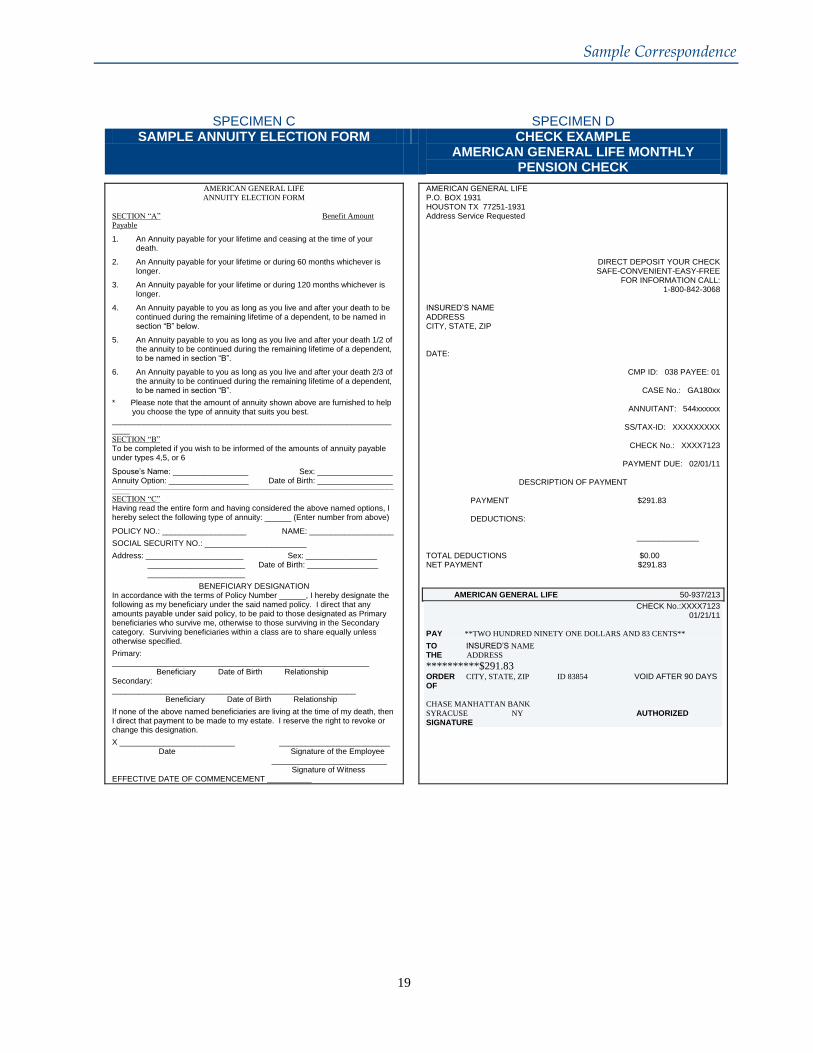

Sample Correspondence

SPECIMEN C SPECIMEN D SAMPLE ANNUITY ELECTION FORM CHECK EXAMPLE

AMERICAN GENERAL LIFE MONTHLY PENSION CHECK

AMERICAN GENERAL LIFE

ANNUITY ELECTION FORM

SECTION “A” Benefit Amount

Payable

1. An Annuity payable for your lifetime and ceasing at the time of your death.

2. An Annuity payable for your lifetime or during 60 months whichever is longer.

3. An Annuity payable for your lifetime or during 120 months whichever is longer.

4. An Annuity payable to you as long as you live and after your death to be continued during the remaining lifetime of a dependent, to be named in section “B” below.

5. An Annuity payable to you as long as you live and after your death 1/2 of the annuity to be continued during the remaining lifetime of a dependent, to be named in section “B”.

6. An Annuity payable to you as long as you live and after your death 2/3 of the annuity to be continued during the remaining lifetime of a dependent, to be named in section “B”.

* Please note that the amount of annuity shown above are furnished to help you choose the type of annuity that suits you best. ___________________________________________________________________ SECTION “B”

To be completed if you wish to be informed of the amounts of annuity payable under types 4,5, or 6

Spouse’s Name: _________________ Sex: _________________ Annuity Option: __________________ Date of Birth: _________________ _______________________________________________________________________________________________________________________________________

SECTION “C”

Having read the entire form and having considered the above named options, I hereby select the following type of annuity: ______ (Enter number from above)

POLICY NO.: ___________________ NAME: ___________________

SOCIAL SECURITY NO.: _______________________

Address: ______________________ Sex: ________________ ______________________ Date of Birth: ________________ ______________________

BENEFICIARY DESIGNATION In accordance with the terms of Policy Number ______, I hereby designate the following as my beneficiary under the said named policy. I direct that any amounts payable under said policy, to be paid to those designated as Primary beneficiaries who survive me, otherwise to those surviving in the Secondary category. Surviving beneficiaries within a class are to share equally unless otherwise specified.

Primary: __________________________________________________________ Beneficiary Date of Birth Relationship Secondary: _______________________________________________________ Beneficiary Date of Birth Relationship

If none of the above named beneficiaries are living at the time of my death, then I direct that payment to be made to my estate. I reserve the right to revoke or change this designation.

X __________________________ _________________________ Date Signature of the Employee __________________________ Signature of Witness EFFECTIVE DATE OF COMMENCEMENT __________

AMERICAN GENERAL LIFE P.O. BOX 1931 HOUSTON TX 77251-1931 Address Service Requested

DIRECT DEPOSIT YOUR CHECK SAFE-CONVENIENT-EASY-FREE

FOR INFORMATION CALL: 1-800-842-3068

INSURED’S NAME ADDRESS CITY, STATE, ZIP DATE:

CMP ID: 038 PAYEE: 01

CASE No.: GA180xx

ANNUITANT: 544xxxxxx

SS/TAX-ID: XXXXXXXXX

CHECK No.: XXXX7123

PAYMENT DUE: 02/01/11

DESCRIPTION OF PAYMENT

PAYMENT $291.83 DEDUCTIONS: ______________ TOTAL DEDUCTIONS $0.00 NET PAYMENT $291.83

AMERICAN GENERAL LIFE 50-937/213

CHECK No.:XXXX7123 01/21/11

PAY **TWO HUNDRED NINETY ONE DOLLARS AND 83 CENTS**

TO INSURED’S NAME THE ADDRESS

**********$291.83

ORDER CITY, STATE, ZIP ID 83854 VOID AFTER 90 DAYS OF CHASE MANHATTAN BANK SYRACUSE NY AUTHORIZED SIGNATURE

20

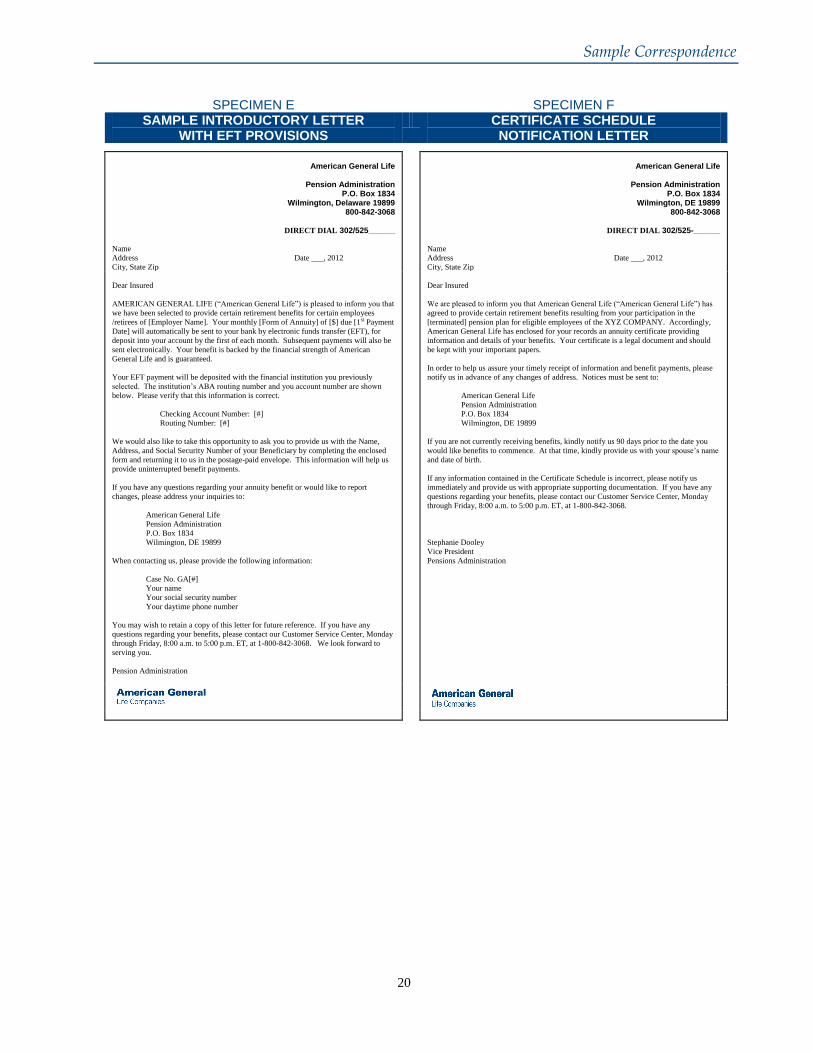

Sample Correspondence

SPECIMEN E SPECIMEN F SAMPLE INTRODUCTORY LETTER

WITH EFT PROVISIONS CERTIFICATE SCHEDULE

NOTIFICATION LETTER

American General Life

Pension Administration

P.O. Box 1834 Wilmington, Delaware 19899

800-842-3068

DIRECT DIAL 302/525______

American General Life

Pension Administration

P.O. Box 1834 Wilmington, DE 19899

800-842-3068

DIRECT DIAL 302/525-______

Name

Address

City, State Zip

Date ___, 2012 Name

Address

City, State Zip

Date ___, 2012

Dear Insured

AMERICAN GENERAL LIFE (“American General Life”) is pleased to inform you that

we have been selected to provide certain retirement benefits for certain employees

/retirees of [Employer Name]. Your monthly [Form of Annuity] of [$] due [1st Payment

Date] will automatically be sent to your bank by electronic funds transfer (EFT), for

deposit into your account by the first of each month. Subsequent payments will also be

sent electronically. Your benefit is backed by the financial strength of American

General Life and is guaranteed.

Your EFT payment will be deposited with the financial institution you previously

selected. The institution’s ABA routing number and you account number are shown

below. Please verify that this information is correct.

Checking Account Number: [#]

Routing Number: [#]

We would also like to take this opportunity to ask you to provide us with the Name,

Address, and Social Security Number of your Beneficiary by completing the enclosed

form and returning it to us in the postage-paid envelope. This information will help us

provide uninterrupted benefit payments.

If you have any questions regarding your annuity benefit or would like to report

changes, please address your inquiries to:

American General Life

Pension Administration

P.O. Box 1834

Wilmington, DE 19899

When contacting us, please provide the following information:

Case No. GA[#]

Your name

Your social security number

Your daytime phone number

You may wish to retain a copy of this letter for future reference. If you have any

questions regarding your benefits, please contact our Customer Service Center, Monday

through Friday, 8:00 a.m. to 5:00 p.m. ET, at 1-800-842-3068. We look forward to

serving you.

Pension Administration

Dear Insured

We are pleased to inform you that American General Life (“American General Life”) has

agreed to provide certain retirement benefits resulting from your participation in the

[terminated] pension plan for eligible employees of the XYZ COMPANY. Accordingly,

American General Life has enclosed for your records an annuity certificate providing

information and details of your benefits. Your certificate is a legal document and should

be kept with your important papers.

In order to help us assure your timely receipt of information and benefit payments, please

notify us in advance of any changes of address. Notices must be sent to:

American General Life

Pension Administration

P.O. Box 1834

Wilmington, DE 19899

If you are not currently receiving benefits, kindly notify us 90 days prior to the date you

would like benefits to commence. At that time, kindly provide us with your spouse’s name

and date of birth.

If any information contained in the Certificate Schedule is incorrect, please notify us

immediately and provide us with appropriate supporting documentation. If you have any

questions regarding your benefits, please contact our Customer Service Center, Monday

through Friday, 8:00 a.m. to 5:00 p.m. ET, at 1-800-842-3068.

Stephanie Dooley

Vice President

Pensions Administration

21

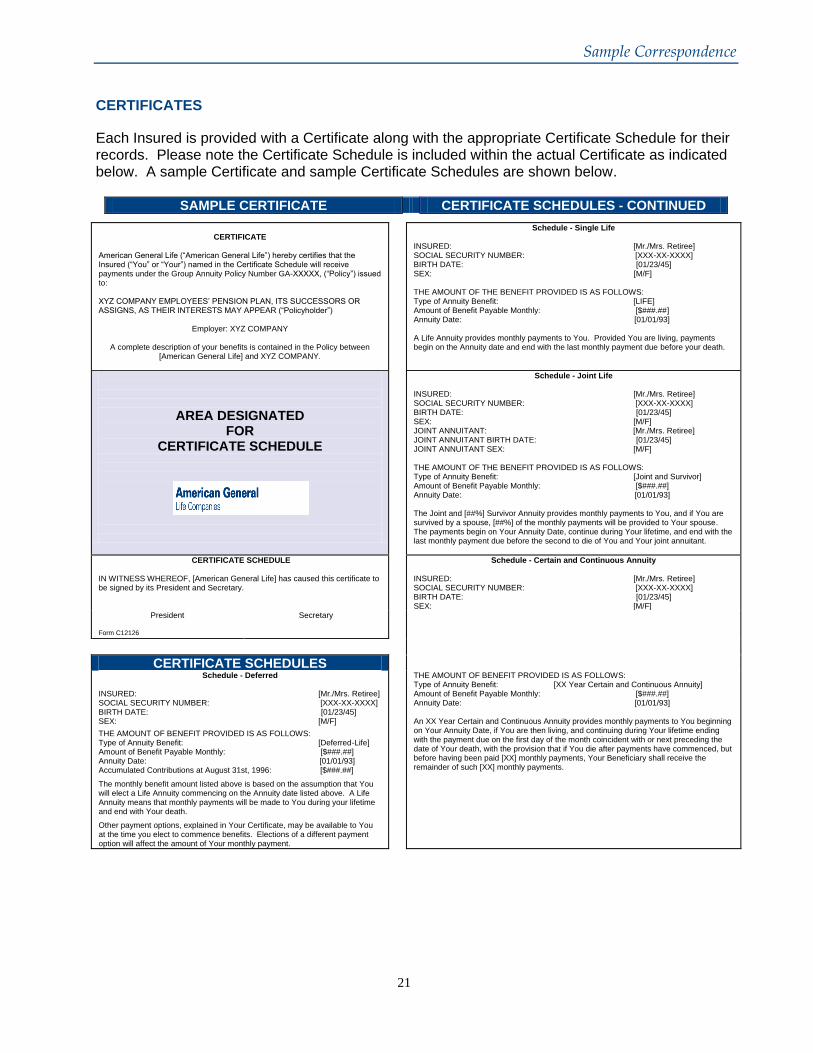

Sample Correspondence

CERTIFICATES

Each Insured is provided with a Certificate along with the appropriate Certificate Schedule for their records. Please note the Certificate Schedule is included within the actual Certificate as indicated below. A sample Certificate and sample Certificate Schedules are shown below.

SAMPLE CERTIFICATE CERTIFICATE SCHEDULES - CONTINUED

CERTIFICATE

American General Life (“American General Life”) hereby certifies that the Insured (“You” or “Your”) named in the Certificate Schedule will receive payments under the Group Annuity Policy Number GA-XXXXX, (“Policy”) issued to: XYZ COMPANY EMPLOYEES’ PENSION PLAN, ITS SUCCESSORS OR ASSIGNS, AS THEIR INTERESTS MAY APPEAR (“Policyholder”)

Employer: XYZ COMPANY

A complete description of your benefits is contained in the Policy between [American General Life] and XYZ COMPANY.

Schedule - Single Life INSURED: [Mr./Mrs. Retiree] SOCIAL SECURITY NUMBER: [XXX-XX-XXXX] BIRTH DATE: [01/23/45] SEX: [M/F] THE AMOUNT OF THE BENEFIT PROVIDED IS AS FOLLOWS: Type of Annuity Benefit: [LIFE] Amount of Benefit Payable Monthly: [$###.##] Annuity Date: [01/01/93] A Life Annuity provides monthly payments to You. Provided You are living, payments begin on the Annuity date and end with the last monthly payment due before your death.

AREA DESIGNATED FOR

CERTIFICATE SCHEDULE

Schedule - Joint Life INSURED: [Mr./Mrs. Retiree] SOCIAL SECURITY NUMBER: [XXX-XX-XXXX] BIRTH DATE: [01/23/45] SEX: [M/F] JOINT ANNUITANT: [Mr./Mrs. Retiree] JOINT ANNUITANT BIRTH DATE: [01/23/45] JOINT ANNUITANT SEX: [M/F] THE AMOUNT OF THE BENEFIT PROVIDED IS AS FOLLOWS: Type of Annuity Benefit: [Joint and Survivor] Amount of Benefit Payable Monthly: [$###.##] Annuity Date: [01/01/93] The Joint and [##%] Survivor Annuity provides monthly payments to You, and if You are survived by a spouse, [##%] of the monthly payments will be provided to Your spouse. The payments begin on Your Annuity Date, continue during Your lifetime, and end with the last monthly payment due before the second to die of You and Your joint annuitant.

CERTIFICATE SCHEDULE

IN WITNESS WHEREOF, [American General Life] has caused this certificate to be signed by its President and Secretary.

Schedule - Certain and Continuous Annuity INSURED: [Mr./Mrs. Retiree] SOCIAL SECURITY NUMBER: [XXX-XX-XXXX] BIRTH DATE: [01/23/45] SEX: [M/F]

President

Form C12126

Secretary

CERTIFICATE SCHEDULES

Schedule - Deferred INSURED: [Mr./Mrs. Retiree] SOCIAL SECURITY NUMBER: [XXX-XX-XXXX] BIRTH DATE: [01/23/45] SEX: [M/F]

THE AMOUNT OF BENEFIT PROVIDED IS AS FOLLOWS: Type of Annuity Benefit: [Deferred-Life] Amount of Benefit Payable Monthly: [$###.##] Annuity Date: [01/01/93] Accumulated Contributions at August 31st, 1996: [$###.##]

The monthly benefit amount listed above is based on the assumption that You will elect a Life Annuity commencing on the Annuity date listed above. A Life Annuity means that monthly payments will be made to You during your lifetime and end with Your death.

Other payment options, explained in Your Certificate, may be available to You at the time you elect to commence benefits. Elections of a different payment option will affect the amount of Your monthly payment.

THE AMOUNT OF BENEFIT PROVIDED IS AS FOLLOWS: Type of Annuity Benefit: [XX Year Certain and Continuous Annuity] Amount of Benefit Payable Monthly: [$###.##] Annuity Date: [01/01/93] An XX Year Certain and Continuous Annuity provides monthly payments to You beginning on Your Annuity Date, if You are then living, and continuing during Your lifetime ending with the payment due on the first day of the month coincident with or next preceding the date of Your death, with the provision that if You die after payments have commenced, but before having been paid [XX] monthly payments, Your Beneficiary shall receive the remainder of such [XX] monthly payments.

Policy Form XXXXXXX

Sample Contract

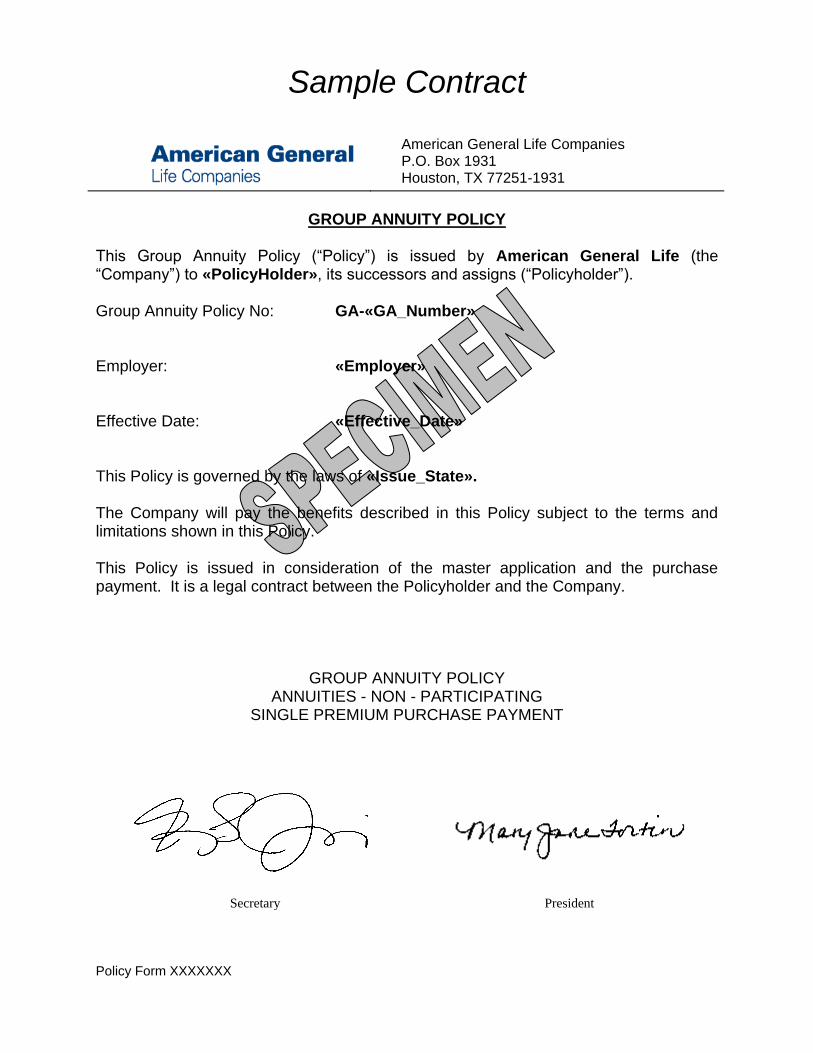

American General Life Companies P.O. Box 1931 Houston, TX 77251-1931

GROUP ANNUITY POLICY

This Group Annuity Policy (“Policy”) is issued by American General Life (the “Company”) to «PolicyHolder», its successors and assigns (“Policyholder”). Group Annuity Policy No: GA-«GA_Number» Employer: «Employer»

Effective Date: «Effective_Date» This Policy is governed by the laws of «Issue_State». The Company will pay the benefits described in this Policy subject to the terms and limitations shown in this Policy. This Policy is issued in consideration of the master application and the purchase payment. It is a legal contract between the Policyholder and the Company.

GROUP ANNUITY POLICY ANNUITIES - NON - PARTICIPATING

SINGLE PREMIUM PURCHASE PAYMENT

Secretary President

Policy Form XXXXXXX DRAFT

2

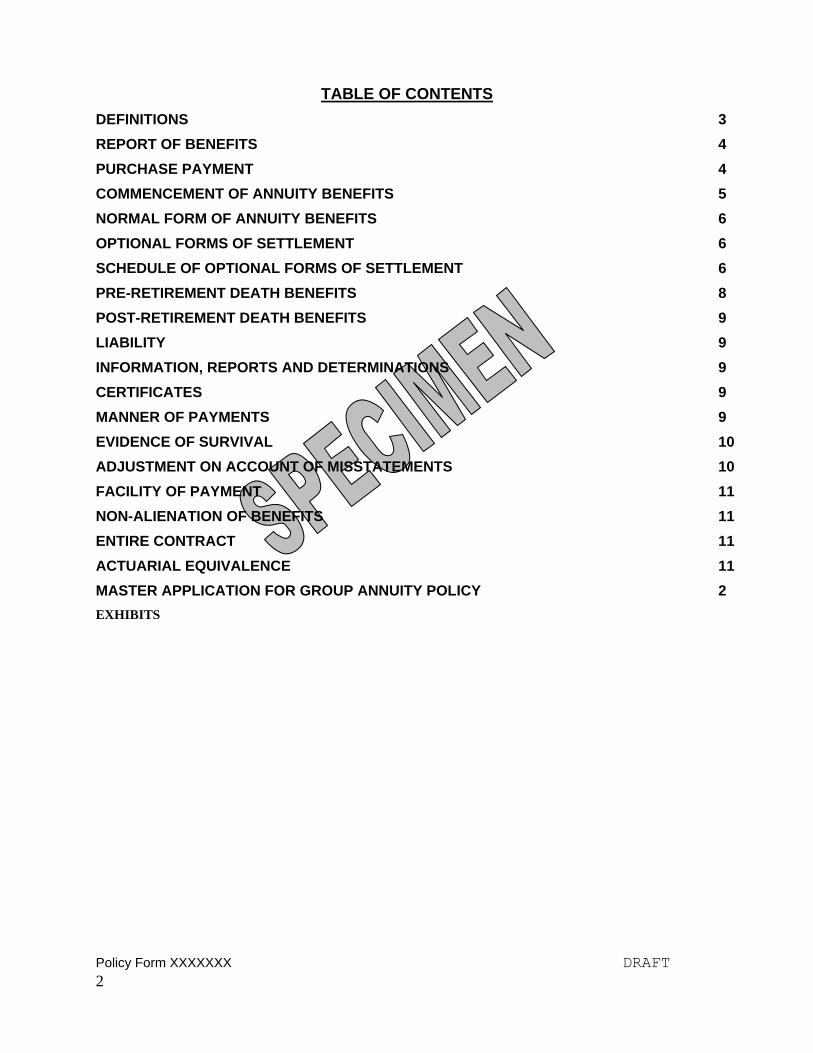

TABLE OF CONTENTS

DEFINITIONS 3

REPORT OF BENEFITS 4

PURCHASE PAYMENT 4

COMMENCEMENT OF ANNUITY BENEFITS 5

NORMAL FORM OF ANNUITY BENEFITS 6

OPTIONAL FORMS OF SETTLEMENT 6

SCHEDULE OF OPTIONAL FORMS OF SETTLEMENT 6

PRE-RETIREMENT DEATH BENEFITS 8

POST-RETIREMENT DEATH BENEFITS 9

LIABILITY 9

INFORMATION, REPORTS AND DETERMINATIONS 9

CERTIFICATES 9

MANNER OF PAYMENTS 9

EVIDENCE OF SURVIVAL 10

ADJUSTMENT ON ACCOUNT OF MISSTATEMENTS 10

FACILITY OF PAYMENT 11

NON-ALIENATION OF BENEFITS 11

ENTIRE CONTRACT 11

ACTUARIAL EQUIVALENCE 11

MASTER APPLICATION FOR GROUP ANNUITY POLICY 2

EXHIBITS

Policy Form XXXXXXX DRAFT

3

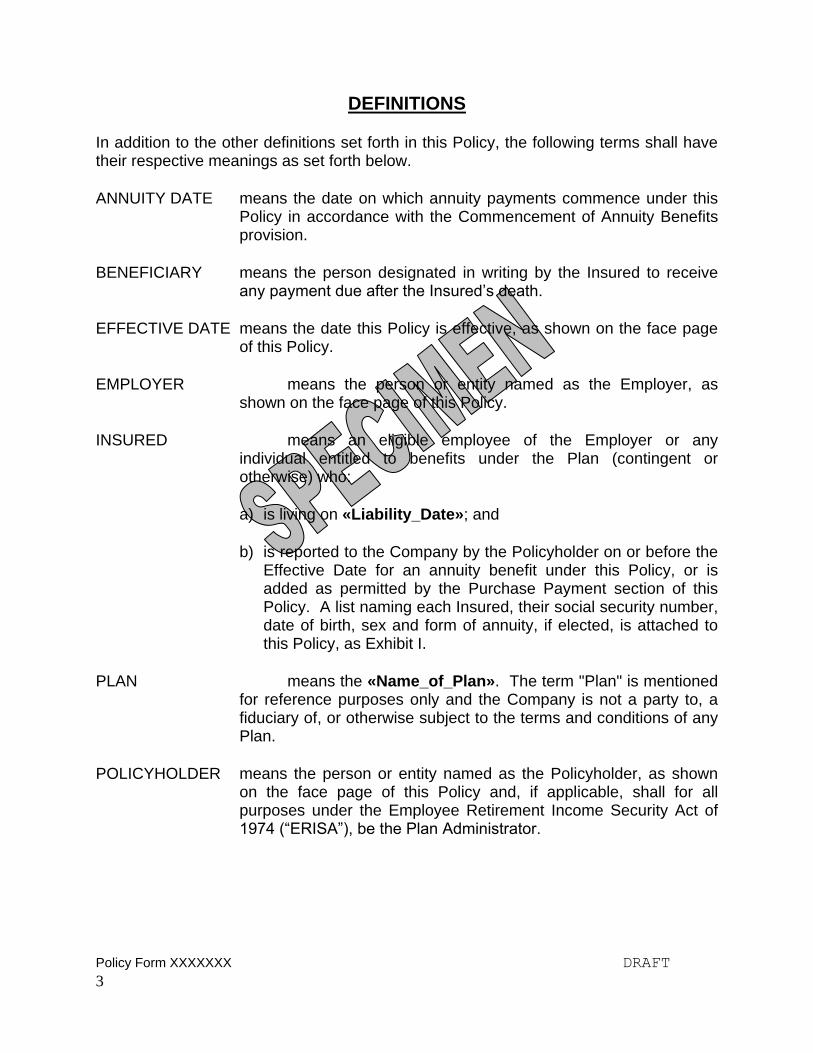

DEFINITIONS

In addition to the other definitions set forth in this Policy, the following terms shall have their respective meanings as set forth below.

ANNUITY DATE means the date on which annuity payments commence under this Policy in accordance with the Commencement of Annuity Benefits provision.

BENEFICIARY means the person designated in writing by the Insured to receive any payment due after the Insured’s death.

EFFECTIVE DATE means the date this Policy is effective, as shown on the face page of this Policy.

EMPLOYER means the person or entity named as the Employer, as shown on the face page of this Policy.

INSURED means an eligible employee of the Employer or any individual entitled to benefits under the Plan (contingent or otherwise) who:

a) is living on «Liability_Date»; and

b) is reported to the Company by the Policyholder on or before the Effective Date for an annuity benefit under this Policy, or is added as permitted by the Purchase Payment section of this Policy. A list naming each Insured, their social security number, date of birth, sex and form of annuity, if elected, is attached to this Policy, as Exhibit I.

PLAN means the «Name_of_Plan». The term "Plan" is mentioned for reference purposes only and the Company is not a party to, a fiduciary of, or otherwise subject to the terms and conditions of any Plan.

POLICYHOLDER means the person or entity named as the Policyholder, as shown on the face page of this Policy and, if applicable, shall for all purposes under the Employee Retirement Income Security Act of 1974 (“ERISA”), be the Plan Administrator.

Policy Form XXXXXXX DRAFT

4

REPORT OF BENEFITS

On or before «Liability_Date», the Policyholder must report to the Company the following information:

a) the name, sex, date of birth, and social security number of each Insured eligible for retirement benefits;

b) the amount and form of each Insured's annuity, if such form has been elected; and

c) the Insured’s Annuity Date and/or Normal Retirement Date, as applicable.

PURCHASE PAYMENT

The Policyholder must make the Purchase Payment, shown in the Master Application attached hereto, to the Company on or before the Effective Date. After the Effective Date, the Policyholder may request the following, subject to the approval of the Company:

a) the addition or deletion of Insureds eligible for annuity benefits; and

b) modification of the amount of an annuity benefit, the forms of available benefits, or any other provisions with respect to an Insured that were misstated in the information given to the Company under the Report of Benefits above.

If the Company approves such a request and additional premium is due, the Policyholder must make the additional premium payment to the Company on a date and in an amount determined by the Company.

If the Company approves such a request and the premium is determined to be less than the amount already paid, the Company will refund the difference to the Policyholder.

The amount of the Net Purchase Payment shown in the Master Application is based on the census data in Exhibit I.

Policy Form XXXXXXX DRAFT

5

COMMENCEMENT OF ANNUITY BENEFITS

For Immediate Insureds, shown on the attached Exhibit I, annuity benefits payable under this Policy will commence on «Commencement_Date».

All other Insureds may commence benefits at age 65, the Insured’s normal retirement date (“Normal Retirement Date”).

Insureds shown on Exhibit I may commence benefits at an early retirement date (“Early Retirement Date”) if the Insured has attained age «Early_Age» and «Early_Service» years of credited service. Insureds’ monthly benefits will be reduced by xx of 1% for each month by which the Early Retirement Date precedes age XX, and by xx of 1% for each additional month prior to age XX.

Insureds may defer the commencement of benefits beyond the Normal Retirement Date to a late retirement date (“Late Retirement Date”). The monthly annuity benefit payable beginning on the Late Retirement Date will be [increased by Actuarial Equivalence to reflect the Late Retirement Date][the same as that payable at the Normal Retirement Date. Backpayments will be made from the Normal Retirement Date to the actual date of commencement.] If no election is made, annuity benefits must commence not later than April 1 of the calendar year following the later of the year of the Insured’s retirement or the year of the Insured’s attainment of age 70 ½.

If, after any benefit becomes due, the Company is unable to authorize or continue payment because the identity or whereabouts of the Insured cannot be ascertained, the Company shall give written notice to such Insured addressed to the Insured’s last known address, as shown by the records of the Company. The benefit payable to the Insured shall continue to be held until the earlier of (a) the date the Insured entitled to the benefit makes application therefore, or (b) the fifth anniversary of the date benefits could otherwise commence to such Insured. For purposes of any applicable escheat laws, the Insured will be deemed to have died prior to the Annuity Date.

If the Company, by making a reasonably diligent effort, cannot locate the Insured within the time described above, the amount payable to such Insured shall be forfeited. Should the Insured subsequently make application for benefits, the amount so forfeited shall be paid to the Insured by the Company. [Undistributed Employee Contributions remaining on deposit with the Company will be subject to any applicable escheat laws after the Annuity Date, if unclaimed. Lump Sum Death Benefits will be subject to any applicable escheat laws after the Annuity Date, if unclaimed.]

In order to commence a benefit an Insured must:

a) retire from the service of the Employer; and

b) notify the Company, in writing on a form acceptable to the Company, of the month on which the annuity benefits are to commence.

Policy Form XXXXXXX DRAFT

6

NORMAL FORM OF ANNUITY BENEFITS

The Normal Form of Annuity Benefit for an unmarried Insured is the accrued monthly benefit, commencing at the Normal Retirement Date and payable for the life of the Insured. The Normal Form of Annuity Benefit for a married Insured is a Qualified Joint and 50% Survivor Annuity (“QJSA”), based on the Insured's accrued benefit, reduced by Actuarial Equivalence factors, unless the QJSA option is waived by the Insured and such waiver is consented to, in writing, by the Insured's spouse. The spouse's consent must be witnessed by an authorized representative of the Policyholder or by a notary public. The requirement of spousal consent described above supersedes any rules regarding options contained in this Policy, and the Insured’s ability to alter any Beneficiary or form of benefits after such consent shall be limited by the terms of the consent.

The QJSA provides monthly benefits beginning on the Insured’s Annuity Date and ending with the payment due on the first day of the calendar month in which the death of the second to die of the Insured and the Insured’s spouse occurs. The amount of the Insured’s monthly benefit shown on Exhibit I and the Actuarial Equivalence factors will be used to determine the amount of the QJSA benefit. QJSA payments will be made to the Insured, if living, and after the Insured’s death, to the Insured’s spouse. The QJSA monthly payment to the spouse will be 50% of the Insured’s monthly payment.

OPTIONAL FORMS OF SETTLEMENT

Prior to the Insured’s Annuity Date, an Insured may elect in writing, on a form acceptable to the Company, one of the Optional Forms of Settlement set forth in the Schedule of Optional Forms of Settlement. The benefit amount under each Optional Form of Settlement is the Actuarial Equivalent of the Insured’s Life Annuity.

Any election of an Optional Form of Settlement may be revoked or changed by the Insured at any time before a payment is made. No election, revocation, or change shall be effective until the Company receives the necessary information and documentation.

SCHEDULE OF OPTIONAL FORMS OF SETTLEMENT

1. LIFE ANNUITY

The Life Annuity provides monthly payments to the Insured. Payments begin on the Insured’s Annuity Date and end with the payment due on the first day of the calendar month in which the Insured’s death occurs.

2. JOINT AND SURVIVOR ANNUITY

The Joint and Survivor Annuity provides monthly payments. Payments begin on the Insured’s Annuity Date and end with the payment due on the first day of the calendar

Policy Form XXXXXXX DRAFT

7

month in which the death of the second to die of the Insured and the joint annuitant occurs. Payments will be made to:

a) the Insured, while living; and

b) after the death of the Insured, to the joint annuitant, if then living. The amount of each monthly payment to the joint annuitant will be the percentage of the Insured’s monthly annuity payment elected by the Insured (50% or 100%).

An Insured may elect the Joint and Survivor Annuity, subject to the following conditions:

a) The Insured must designate on the option election form the joint annuitant as well as the percentage (50% or 100%) of the monthly annuity payment to be made to the joint annuitant after the Insured’s death.

b) Due proof of the joint annuitant’s age must be received by the Company no later than the Insured’s Annuity Date.

c) If the joint annuitant dies before this annuity form becomes effective, the election shall be revoked and the Life Annuity option assumed. Except as provided in the Pre-Retirement Death Benefits provision, if an Insured dies before this annuity form becomes effective, the joint annuitant shall not be entitled to receive any annuity payments under this Policy. If the joint annuitant dies while this annuity form is effective, the Insured’s annuity payments shall not change as to amount.

d) The consent of the joint annuitant shall not be required for any change or revocation, unless specifically required in the Normal Form of Annuity Benefits section of this Policy.

3. CERTAIN AND CONTINUOUS ANNUITY

The Certain and Continuous Annuity provides monthly payments to the Insured. Payments begin on the Insured’s Annuity Date and end with the payment due on the first day of the calendar month in which the Insured's death occurs. Provided, however, that if the Insured dies after payments have commenced, but before having been paid a total of 60, 120, or 180 monthly payments (as elected by the Insured), then payments will continue to the Insured's Beneficiary for the remainder of such period. For Immediate Insureds, the end of such certain period is the Certain Period End Date, as shown on Exhibit I. The Insured may change the named Beneficiary, in writing, at any time prior to the Insured’s death.

Policy Form XXXXXXX DRAFT

8

4. LUMP SUM

An Insured may elect to receive a lump sum payment equal to the accrued benefit calculated as described below. The lump sum payment amount will be calculated using an interest rate equal to the lesser of

(i) 7 ½%, or

(ii) whichever of the following is applicable:

(A) the applicable interest rate (as defined below) if the vested Accrued Benefit (using such rate) is not in excess of $25,000; and

(B) an interest rate equal to 120% of the applicable interest rate (as defined below) if the vested present value of the Accrued Benefit exceeds $25,000 (as determined under sub clause (A)). In no event shall the present value determined using the rate prescribed by sub clause (B) be less than $25,000.

“Applicable Interest Rate” for this purpose shall mean the interest rate, which would be used (as of the date of distribution) by the Pension Benefit Guaranty Corporation for purposes of determining the present value of a lump sum distribution on plan termination.

PRE-RETIREMENT DEATH BENEFITS

If an Insured dies prior to the Insured’s Annuity Date, no death benefit will be payable except as follows:

A Qualified Pre-Retirement Survivor Annuity (“QPSA”) will be provided to an Insured’s spouse, provided the Insured’s spouse survives the Insured. The QPSA benefit will be equal to 50% of the monthly annuity benefit the Insured would have received had the Insured, if already terminated from the Employer, survived to their earliest retirement age (or if the Insured were employed by the Employer at the time of death, had the Insured separated from service on the date of death, and survived to the earliest retirement age), and had on such date elected to commence benefits in the form of a QJSA.

The benefit will be payable for the life of the spouse, commencing on the later of: (a) the first day of the month following the Insured's date of death, or (b) the first day of the month following the Insured's earliest retirement age, or at a later date as elected by the spouse.

Policy Form XXXXXXX DRAFT

9

POST-RETIREMENT DEATH BENEFITS

If an Insured dies after the Insured’s Annuity Date, benefit continuation will be determined by the form of benefit in effect for the Insured.

LIABILITY

The liability of the Company for the payment of benefits for each Insured is limited to the payment of the annuity benefits and is subject to:

a) the receipt of the purchase payment for such benefits as described in Purchase Payment; and

b) any applicable adjustments as defined in Adjustment on Account of Misstatements.

INFORMATION, REPORTS AND DETERMINATIONS

The Policyholder will supply the Company with any additional information reasonably necessary for the Company to determine its obligations under this Policy. The Company relies on the information, reports and determinations made by the Policyholder.

The following applies to any such reports or determinations:

a) they must be conclusive for the purposes of this Policy; and

b) they may be made by the Employer on behalf of the Policyholder.

CERTIFICATES

Each Insured will be issued a certificate. These certificates will show:

a) the Insured's name and social security number;

b) the benefits for each Insured; and

c) to whom benefits will be payable.

MANNER OF PAYMENTS

Policy Form XXXXXXX DRAFT

10

[Direct Payments

The Company shall make annuity payments by check or electronic funds transfer (EFT). If monthly annuity payments are less than $50, the Company reserves the right to make payments less frequently than monthly, and will make these payments in an aggregate amount not later than the first day of the period to which the payment applies. The responsibility for tax reporting, including production of Form 1099-R and any other required forms, for recipients of the monthly annuity payments made by the Company will be that of the Company.]

[Bulk Reimbursement

The Company shall make annuity payments by reimbursing the Policyholder in bulk by wire transfer prior to the end of each month. The Policyholder will supply the Company with a listing each month, which details any change in the bulk wire amount. The responsibility for tax reporting, including production of Form 1099-R and any other required forms, for recipients of the monthly annuity payments will be that of the Plan payor.]

EVIDENCE OF SURVIVAL

The Company retains the right to require due proof of any payee's survival when an annuity benefit payment is contingent upon survival of the payee. Further, the payee, for himself, his heirs and successors, represents that by negotiation of the Company’s payment that the payee upon whose survival the payment is contingent is living on the date any such benefit payment is due.

ADJUSTMENT ON ACCOUNT OF MISSTATEMENTS

If a person named as an Insured in the Report of Benefits dies before «Liability_Date», no benefit for that person will be payable under this Policy. The Policyholder may request the portion of the Purchase Payment made for such person be:

a) returned in cash, with interest; or

b) disposed of in any other manner agreed upon in writing by the Policyholder and the Company.

The Policyholder has 180 days after the Effective Date to make such requests.

If any other fact on which the Purchase Payment was based has been misstated for any Insured, the amount of benefit payments or the portion of the Purchase Payment will be changed based on the correct fact as determined by the Company. Overpayments by the Company will be deducted from future payments due the Insured. Underpayments by the Company will be paid to the Insured in a lump sum. The Company will not be

Policy Form XXXXXXX DRAFT

11

liable for payment of a benefit in excess of that which would be payable on the basis of the true facts and Purchase Payments actually received.

FACILITY OF PAYMENT

If the payee of any payment provided by this Policy is legally adjudged to be incapable or incompetent, the Company will make payments to the legally appointed guardian or other authorized legal representative of such payee. Such payments shall constitute a full discharge of the obligation of the Company to the extent thereof.

NON-ALIENATION OF BENEFITS

No benefit payable under this Policy may be assigned, alienated, or encumbered by the payee. No benefit shall in any way be subject to any legal process that would subject the benefit to the payment of any claim against the payee

The preceding sentence shall also apply to the creation, assignment, or recognition of a right to any benefit payable with respect to an Insured pursuant to a domestic relations order unless such order is determined by the Company or the Policyholder to be a Qualified Domestic Relations Order.

ENTIRE CONTRACT

This Policy, together with the Master Application, and any attached papers, constitutes the entire contract between the Company and the Policyholder. No endorsements, alteration, or waiver of any provisions of this Policy shall be valid unless made in writing by the Company and signed by a duly authorized officer of the Company.

ACTUARIAL EQUIVALENCE

Actuarial Equivalence shall be determined using the [1983 Group Annuity Table] on a [unisex basis using 75% male and 25% female] and an interest rate of [7½%].

Policy Form XXXXXXX DRAFT

2

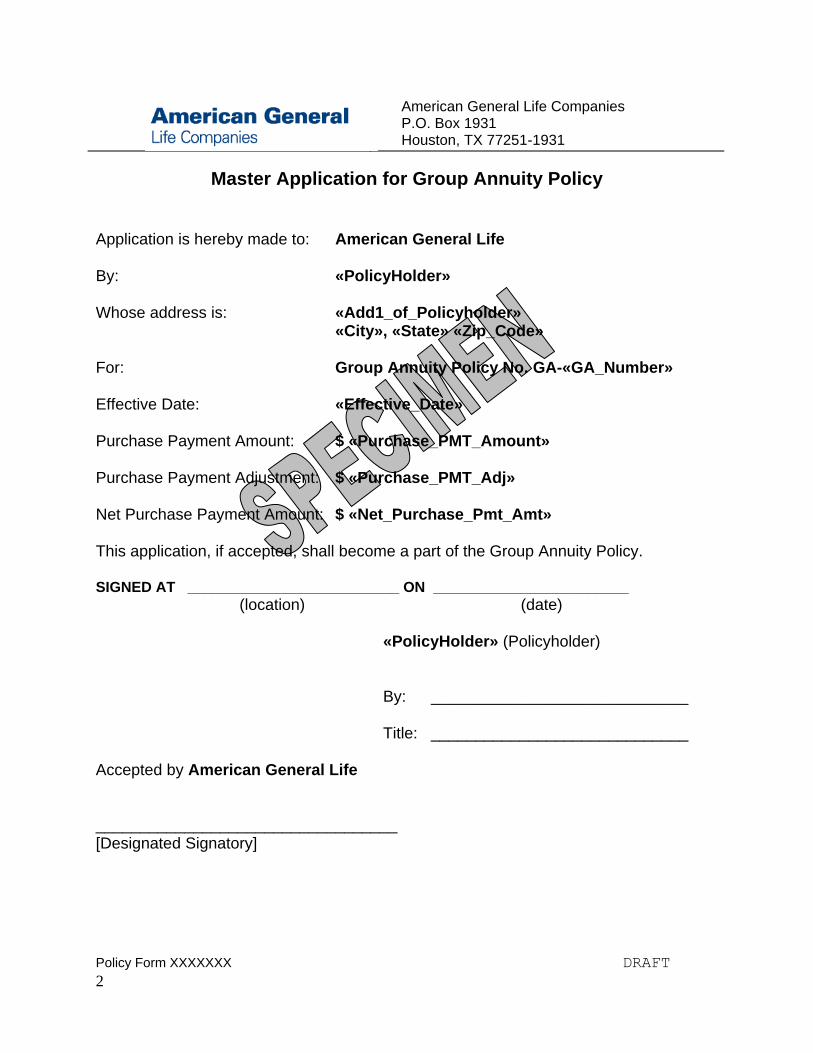

American General Life Companies P.O. Box 1931 Houston, TX 77251-1931

Master Application for Group Annuity Policy

Application is hereby made to: American General Life By: «PolicyHolder» Whose address is: «Add1_of_Policyholder» «City», «State» «Zip_Code» For: Group Annuity Policy No. GA-«GA_Number» Effective Date: «Effective_Date» Purchase Payment Amount: $ «Purchase_PMT_Amount» Purchase Payment Adjustment: $ «Purchase_PMT_Adj» Net Purchase Payment Amount: $ «Net_Purchase_Pmt_Amt» This application, if accepted, shall become a part of the Group Annuity Policy. SIGNED AT __________________________ ON ________________________

(location) (date) «PolicyHolder» (Policyholder) By: _____________________________ Title: _____________________________

Accepted by American General Life __________________________________ [Designated Signatory]