Embed Size (px)

Citation preview

CCHHAAPPTTEERR VV

AANN AAPPPPRRAAIISSAALL OOFF TTHHEE FFIINNAANNCCIIAALL

PPEERRFFOORRMMAANNCCEE OOFF TTHHEE GGDDCCCCBB

–– AA CCAAMMEELL AANNAALLYYSSIISS

125

AN APPRAISAL OF THE FINANCIAL PERFORMANCE OF THE

GDCCB - A CAMEL ANALYSIS

5.1 Introduction:

In this chapter an attempt is made to appraise the financial

performance of the Guntur District Central Co-operative Bank

(GDCCB), during the study period from 2000-01 to 2008-09. Capital

Adequacy, Asset Quality, Management Quality, Earnings and Liquidity

Ratios (CAMEL Model) is used to analyze the financial performance of

the GDCCB.

5.2 Financial Performance of the GDCCB:

As per the parameters indicated by NABARD a Weak

Co-operative Central Bank has been defined as a bank whose bad and

doubtful debts, accumulated losses and other overdues over three

years together, exceed 50 per cent of its Own Funds. The

Government or NABARD takes the Rehabilitation work, for weak bank

with the main emphasis of reviving it from its weak condition to attain

economically viable status over a phase of period.

Table 5.1 presents an analysis of the financial performance of

the GDCCB during the period from 2000-01 to 2008-09. In the light of

the parameters indicated by NABARD, the GDCCB shows that during

the study period, the sum of the Bad & doubtful debts and

accumulated losses had been below 50 percent of the owned funds of

the bank. It is thus evident from the analysis that the GDCCB does

not fell in the category of weak Bank.

126

Table 5.1

Financial Performance of the GDCCB ( in Lakhs)

S.No Item 2000-01 2004-05 2008-09

I Owned Funds

a. Paid up Share Capital 3,395 3,659 4,185

b. Reserve Fund 539 1,121 1,636

c. Total (a+b) 3,934 4,780 5,821

II Erosion in Owned Funds

a. Bad& Doubtful

(Overdues Over 3 Years)

1,097 2,040 366

b. Accumulated Losses - - -

c. Total 1,097 2,040 366

III 50% of Owned funds

i.e 50% of I(c)

1,967

2,390

2,911

IV a. III-II(c) 870 350 2,545

b. Exceeds to III NIL NIL NIL

Source: Annual Reports of the GDCCB

5.3 Financial Performance of the GDCCB - A CAMEL Analysis:

For this purpose a widely accepted analytical model – CAMEL

Analysis is adopted and results are obtained. CAMEL Analysis focuses

on the following parameters.

a) Capital Adequacy Ratios

b) Asset Quality Ratios

c) Management Quality Ratios

d) Earnings Ratios

e) Liquidity Ratios

Annual growth rates were calculated for three phases of banking

operation. CAMEL Model recommended by Padmanbhan working

127

group 1995 has been employed to assess and appraise the financial

performance of GDCCB.

5.3.1 Capital Adequacy Ratios:

Capital adequacy has emerged as one of the major indicators of

the financial health of a banking entity. It is measured as a ratio of

bank’s own capital (new equity, retained earnings, etc.) to its

risk-weighted assets (loans, investments in stock markets, guarantees,

etc). Well adherence to capital adequacy regime does play a vital role

in minimizing the cascading effects of banking and financial sector

crises.

5.3.1.1 Capital to Risk Weighted Assets Ratio (CRAR) of the

GDCCB:

Capital adequacy is an indicator of the financial health of the

banking system. It explains the relation between net capital funds and

risk weighted assets. If the ratio is high, it is good for the organization.

In table 5.2 the ratio is calculated and examined for the data

pertaining to the GDCCB for the study period.

It is calculated by using following formula.

CRAR= (Net Capital Funds/Risk Weighted Assets) ×100

Net Capital Funds=(Paid up Capital+ Reserves+ Profit& Loss A/C (Cr))

- (Accumulated Losses +Short Fall in Provisions)

Risk Weighted Assets=Current Assets+ Investments+ Loans and

Advances.

128

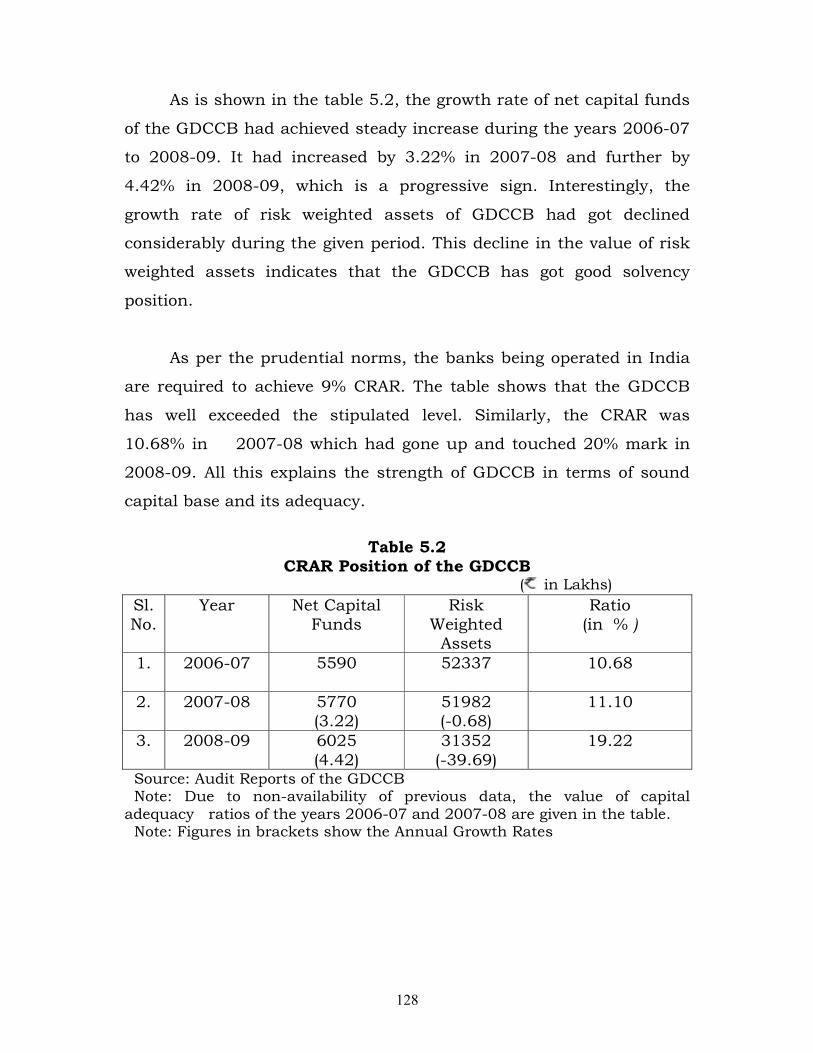

As is shown in the table 5.2, the growth rate of net capital funds

of the GDCCB had achieved steady increase during the years 2006-07

to 2008-09. It had increased by 3.22% in 2007-08 and further by

4.42% in 2008-09, which is a progressive sign. Interestingly, the

growth rate of risk weighted assets of GDCCB had got declined

considerably during the given period. This decline in the value of risk

weighted assets indicates that the GDCCB has got good solvency

position.

As per the prudential norms, the banks being operated in India

are required to achieve 9% CRAR. The table shows that the GDCCB

has well exceeded the stipulated level. Similarly, the CRAR was

10.68% in 2007-08 which had gone up and touched 20% mark in

2008-09. All this explains the strength of GDCCB in terms of sound

capital base and its adequacy.

Table 5.2 CRAR Position of the GDCCB

( in Lakhs) Sl. No.

Year Net Capital Funds

Risk Weighted Assets

Ratio (in % )

1. 2006-07 5590 52337 10.68

2. 2007-08 5770 (3.22)

51982 (-0.68)

11.10

3. 2008-09 6025

(4.42)

31352

(-39.69)

19.22

Source: Audit Reports of the GDCCB Note: Due to non-availability of previous data, the value of capital adequacy ratios of the years 2006-07 and 2007-08 are given in the table. Note: Figures in brackets show the Annual Growth Rates

129

Chart 5.1 CRAR Position of the GDCCB

0

5

10

15

20

Ratio

Ratio 10.68 11.1 19.22

2000-01 2004-05 2008-09

5.3.1.2 Net Non Performing Assets (NPAs) to Net worth Ratio of

the GDCCB:

Another important ratio that indicates the status of capital

adequacy is net NPAs to net worth ratio. It explains the relation

between net non performing assets to net worth of the organization.

Non performing assets means an asset or account of borrower,

which has been classified by a bank or financial institution as

sub-standard, doubtful and loss assets, in accordance with the

directions or guidelines relating to asset classification issued by The

Reserve Bank of India.

Net Worth means, it is permanent liability owned by the

company/firm to the proprietor, partners or share holders. If the net

NPA to Net worth Ratio is less, it indicates that non performing assets

are less and that is good sign for organization.

Net NPA to Net worth Ratio is calculated by using following formula.

Net NPA to Net Worth Ratio= (Net NPAs/Net Worth) ×100

Net NPAs= Gross NPAs – Provisions held in respect of the Non

Performing Assets.

130

Net Worth= Share Capital + Reserves and Surplus

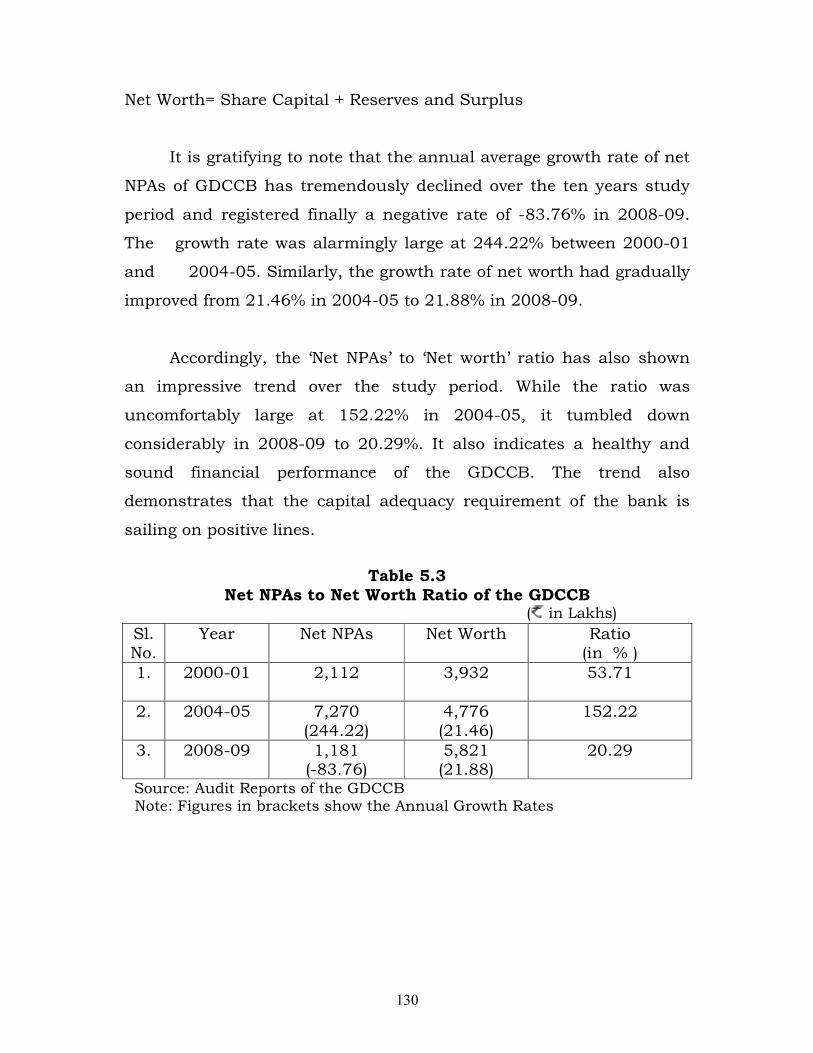

It is gratifying to note that the annual average growth rate of net

NPAs of GDCCB has tremendously declined over the ten years study

period and registered finally a negative rate of -83.76% in 2008-09.

The growth rate was alarmingly large at 244.22% between 2000-01

and 2004-05. Similarly, the growth rate of net worth had gradually

improved from 21.46% in 2004-05 to 21.88% in 2008-09.

Accordingly, the ‘Net NPAs’ to ‘Net worth’ ratio has also shown

an impressive trend over the study period. While the ratio was

uncomfortably large at 152.22% in 2004-05, it tumbled down

considerably in 2008-09 to 20.29%. It also indicates a healthy and

sound financial performance of the GDCCB. The trend also

demonstrates that the capital adequacy requirement of the bank is

sailing on positive lines.

Table 5.3 Net NPAs to Net Worth Ratio of the GDCCB

( in Lakhs)

Sl. No.

Year Net NPAs Net Worth Ratio (in % )

1. 2000-01 2,112 3,932 53.71

2. 2004-05 7,270 (244.22)

4,776 (21.46)

152.22

3. 2008-09 1,181 (-83.76)

5,821 (21.88)

20.29

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

131

Chart 5.2 Net NPAs to Net worth Ratio of the GDCCB

0

50

100

150

200

Ratio

Ratio 53.71 152.22 20.29

2000-01 2004-05 2008-09

5.3.2 Asset Quality Ratios:

Asset quality signifies the degree of financial strength of and

risks in a bank’s assets, mainly loans and investments. The

maintenance of asset quality is a fundamental feature of banking. A

broad evaluation of asset quality is one of the most important

components in assessing the current situation and future viability of a

bank.

Under CAMEL Model of analysis, the asset quality ratios

command significant recognition. Some of the important Asset Quality

ratios are adopted for analyzing the data of the GDCCB.

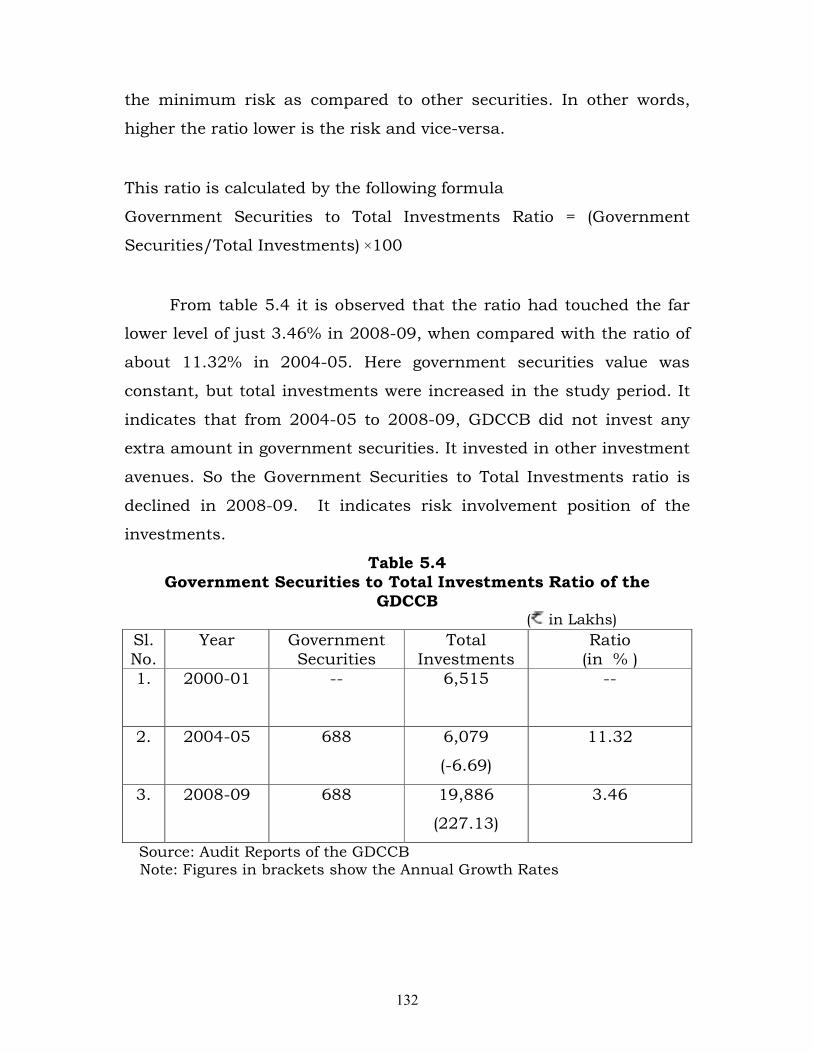

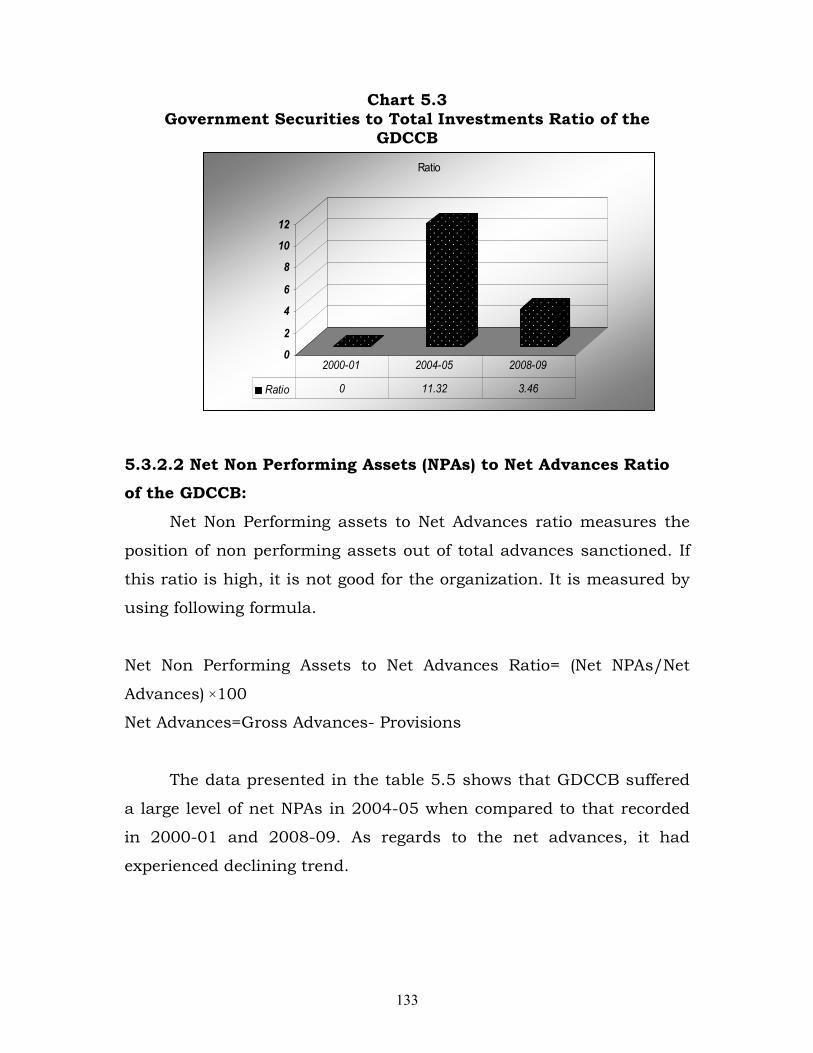

5.3.2.1 Government Securities to Total Investments Ratio of the

GDCCB:

Government securities to total investments ratio measures the

risk involved in total investments. Government securities are deemed

to be the risk free securities and thus it is generally believed that

higher proportion of this kind of securities in total investment carry

132

the minimum risk as compared to other securities. In other words,

higher the ratio lower is the risk and vice-versa.

This ratio is calculated by the following formula

Government Securities to Total Investments Ratio = (Government

Securities/Total Investments) ×100

From table 5.4 it is observed that the ratio had touched the far

lower level of just 3.46% in 2008-09, when compared with the ratio of

about 11.32% in 2004-05. Here government securities value was

constant, but total investments were increased in the study period. It

indicates that from 2004-05 to 2008-09, GDCCB did not invest any

extra amount in government securities. It invested in other investment

avenues. So the Government Securities to Total Investments ratio is

declined in 2008-09. It indicates risk involvement position of the

investments.

Table 5.4 Government Securities to Total Investments Ratio of the

GDCCB ( in Lakhs)

Sl. No.

Year Government Securities

Total Investments

Ratio (in % )

1. 2000-01 -- 6,515 --

2. 2004-05 688 6,079

(-6.69)

11.32

3. 2008-09 688 19,886

(227.13)

3.46

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

133

Chart 5.3 Government Securities to Total Investments Ratio of the

GDCCB

0

2

4

6

8

10

12

Ratio

Ratio 0 11.32 3.46

2000-01 2004-05 2008-09

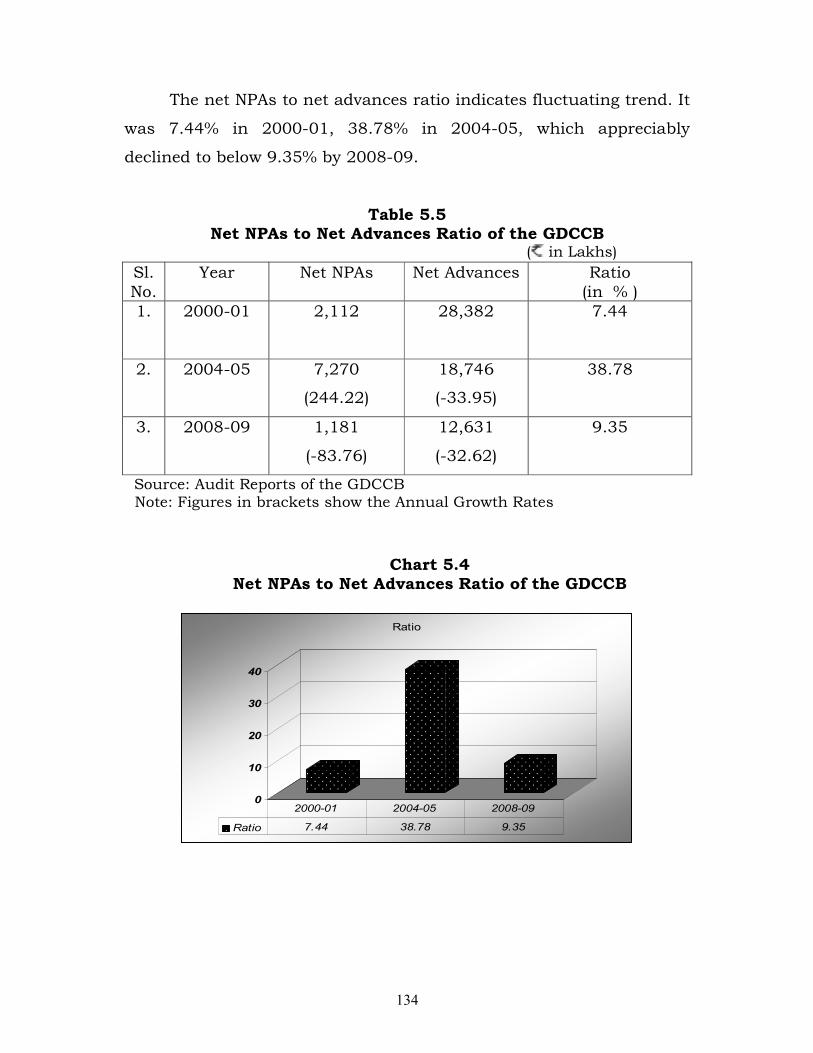

5.3.2.2 Net Non Performing Assets (NPAs) to Net Advances Ratio

of the GDCCB:

Net Non Performing assets to Net Advances ratio measures the

position of non performing assets out of total advances sanctioned. If

this ratio is high, it is not good for the organization. It is measured by

using following formula.

Net Non Performing Assets to Net Advances Ratio= (Net NPAs/Net

Advances) ×100

Net Advances=Gross Advances- Provisions

The data presented in the table 5.5 shows that GDCCB suffered

a large level of net NPAs in 2004-05 when compared to that recorded

in 2000-01 and 2008-09. As regards to the net advances, it had

experienced declining trend.

134

The net NPAs to net advances ratio indicates fluctuating trend. It

was 7.44% in 2000-01, 38.78% in 2004-05, which appreciably

declined to below 9.35% by 2008-09.

Table 5.5 Net NPAs to Net Advances Ratio of the GDCCB

( in Lakhs)

Sl.

No.

Year Net NPAs Net Advances Ratio

(in % )

1. 2000-01 2,112 28,382 7.44

2. 2004-05 7,270

(244.22)

18,746

(-33.95)

38.78

3. 2008-09 1,181

(-83.76)

12,631

(-32.62)

9.35

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.4 Net NPAs to Net Advances Ratio of the GDCCB

0

10

20

30

40

Ratio

Ratio 7.44 38.78 9.35

2000-01 2004-05 2008-09

135

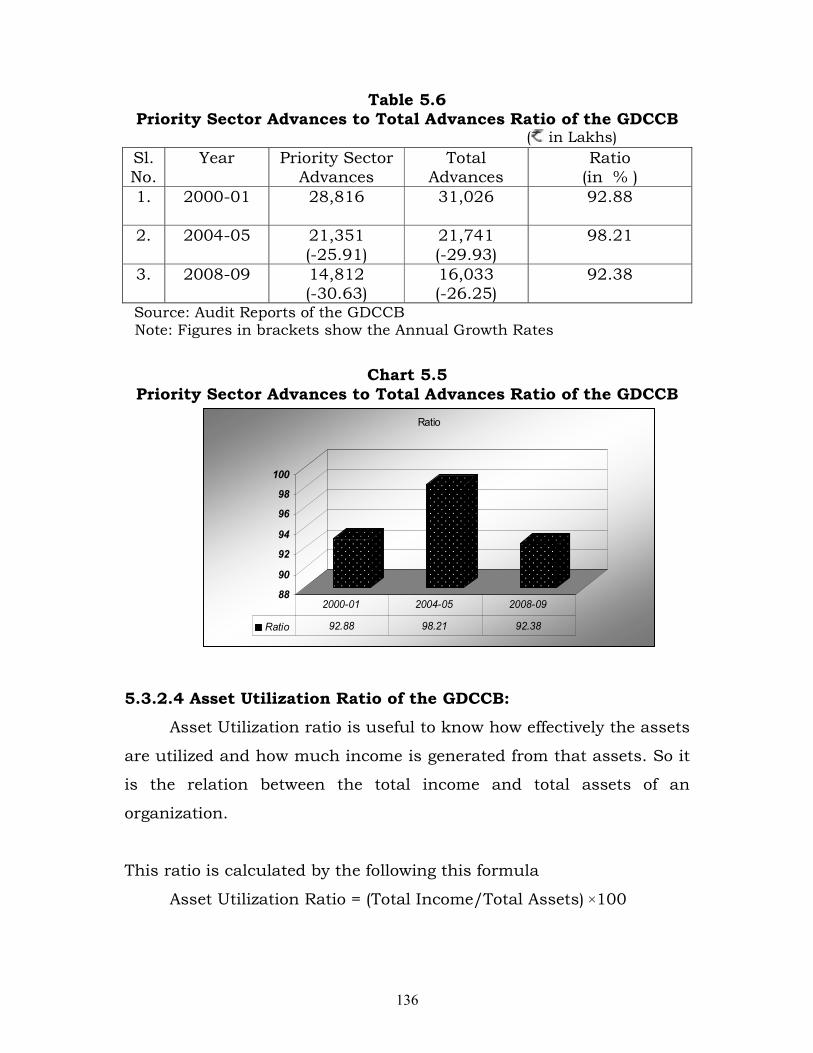

5.3.2.3 Priority Sector Advances to Total Advances Ratio of the

GDCCB:

Priority sector advances to Total Advances Ratio helps to know

the importance that the bank is giving to priority sector and how

amount is sanctioned to that sector out of total advances. If this ratio

is high, it indicates the bank is giving more amounts for priority

sector. Priority sector advances includes advances given to agriculture,

small scale industries, housing finance, self employment education

loans, self help Groups etc.,

This ratio is calculated by the following this formula

Priority Sector Advances to Total Advances Ratio = (Priority Sector

Advances/Total Advances) ×100

The growth rate of priority sector advances by GDCCB had

shown a negative trend, showing -30.63% in 2008-09, while it had

shown an ascending trend up to 2004-05. As regards the total

advances also the same trend is observed. It had shown decreasing

trend with -29.93% in 2004-05 again declined to –26.25% in 2008-09.

Though the ratio of priority sector advances to total advances

has been fluctuating, i.e., 92.88% in 2000-01, 98.21% in 2004-05,

and 92.38% in 2008-09, it has been considerably and appreciably

large.

136

Table 5.6 Priority Sector Advances to Total Advances Ratio of the GDCCB

( in Lakhs)

Sl. No.

Year Priority Sector Advances

Total Advances

Ratio (in % )

1. 2000-01 28,816 31,026 92.88

2. 2004-05 21,351

(-25.91)

21,741

(-29.93)

98.21

3. 2008-09 14,812 (-30.63)

16,033 (-26.25)

92.38

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.5

Priority Sector Advances to Total Advances Ratio of the GDCCB

88

90

92

94

96

98

100

Ratio

Ratio 92.88 98.21 92.38

2000-01 2004-05 2008-09

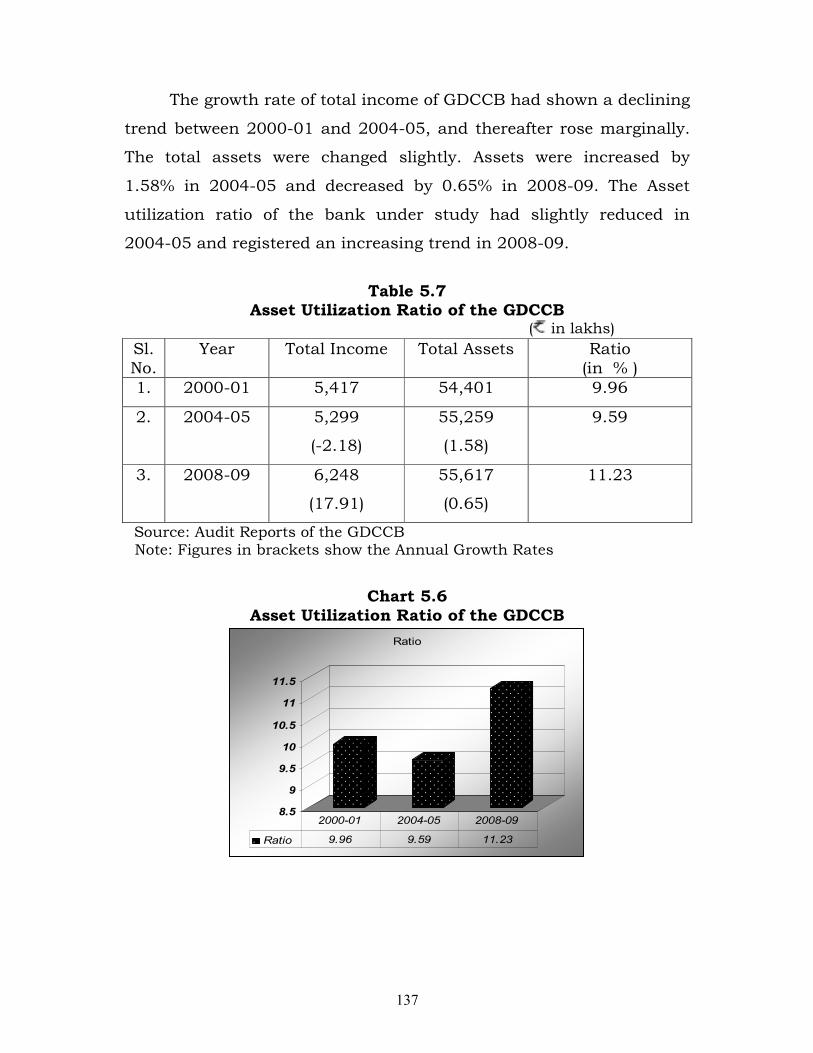

5.3.2.4 Asset Utilization Ratio of the GDCCB:

Asset Utilization ratio is useful to know how effectively the assets

are utilized and how much income is generated from that assets. So it

is the relation between the total income and total assets of an

organization.

This ratio is calculated by the following this formula

Asset Utilization Ratio = (Total Income/Total Assets) ×100

137

The growth rate of total income of GDCCB had shown a declining

trend between 2000-01 and 2004-05, and thereafter rose marginally.

The total assets were changed slightly. Assets were increased by

1.58% in 2004-05 and decreased by 0.65% in 2008-09. The Asset

utilization ratio of the bank under study had slightly reduced in

2004-05 and registered an increasing trend in 2008-09.

Table 5.7 Asset Utilization Ratio of the GDCCB

( in lakhs)

Sl. No.

Year Total Income Total Assets Ratio (in % )

1. 2000-01 5,417 54,401 9.96

2. 2004-05 5,299

(-2.18)

55,259

(1.58)

9.59

3. 2008-09 6,248

(17.91)

55,617

(0.65)

11.23

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.6

Asset Utilization Ratio of the GDCCB

8.5

9

9.5

10

10.5

11

11.5

Ratio

Ratio 9.96 9.59 11.23

2000-01 2004-05 2008-09

138

5.3.3 Management Quality Ratios:

Management efficiency is another vital component of the CAMEL

model that ensures the survival and growth of a bank. It is the

management which sets vision and goals for the organization and

ensures that it achieves them. In the process of achieving their goals,

management takes certain crucial decisions depending on its risk

perception. Hence, analysts and investors use this parameter to

evaluate management efficiency as to assign premium to better

managed banks and discount to poorly managed ones.

While the other factors of CAMEL model can be quantified fairly

easily from current financial statements, management quality is a

somewhat elusive and subjective measure, yet one that is crucial to

institutional success. As management quality is inextricably tied to a

bank’s success or failure, it is important to develop and improve

methods of grading management efficacy. Besides this, the banking

sector reforms also reinforce the need to improve productivity of the

banks through appropriate measures which aim at reducing the

operating cost and improving the profitability of the banks.

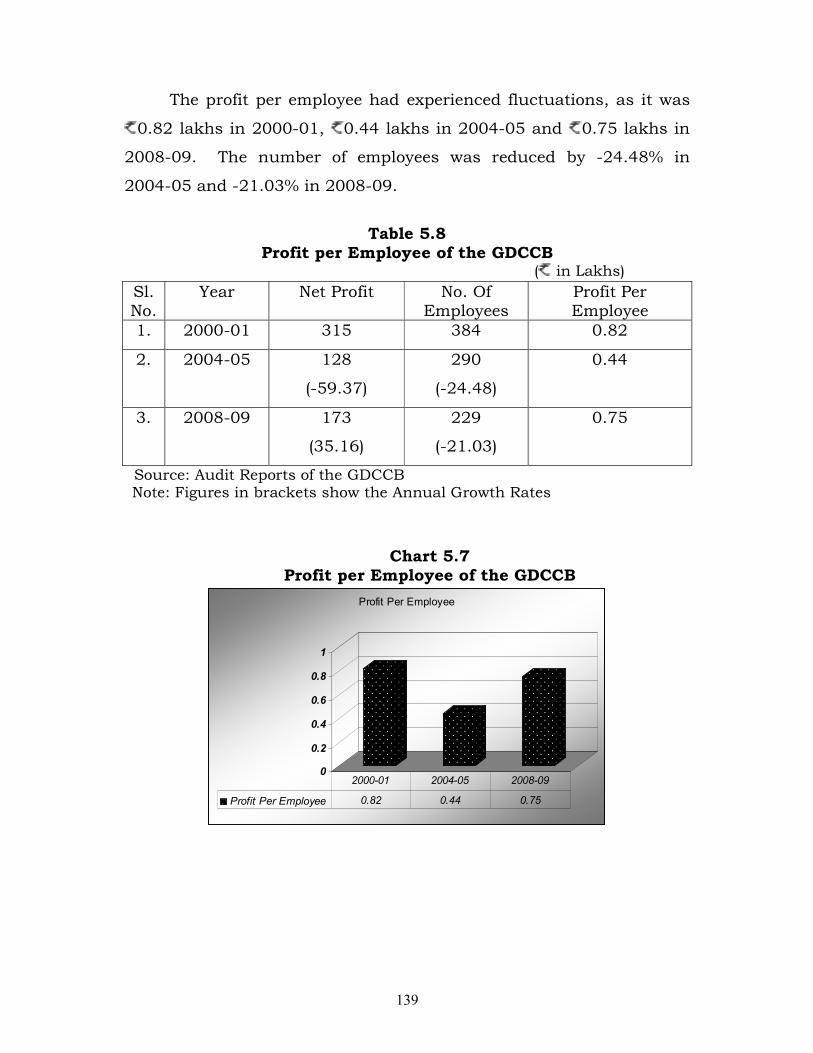

5.3.3.1 Profit per Employee of the GDCCB:

Net profit per employee is the amount of profit earned per an

employee. The range of profit determines the quality of management.

Higher the quality of management, higher the profits per employee.

It calculated by the following this formula

Profit per Employee of GDCCB= (Net Profit/No. of Employees)

139

The profit per employee had experienced fluctuations, as it was

0.82 lakhs in 2000-01, 0.44 lakhs in 2004-05 and 0.75 lakhs in

2008-09. The number of employees was reduced by -24.48% in

2004-05 and -21.03% in 2008-09.

Table 5.8

Profit per Employee of the GDCCB ( in Lakhs)

Sl. No.

Year Net Profit No. Of Employees

Profit Per Employee

1. 2000-01 315 384 0.82

2. 2004-05 128

(-59.37)

290

(-24.48)

0.44

3. 2008-09 173

(35.16)

229

(-21.03)

0.75

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.7

Profit per Employee of the GDCCB

0

0.2

0.4

0.6

0.8

1

Profit Per Employee

Profit Per Employee 0.82 0.44 0.75

2000-01 2004-05 2008-09

140

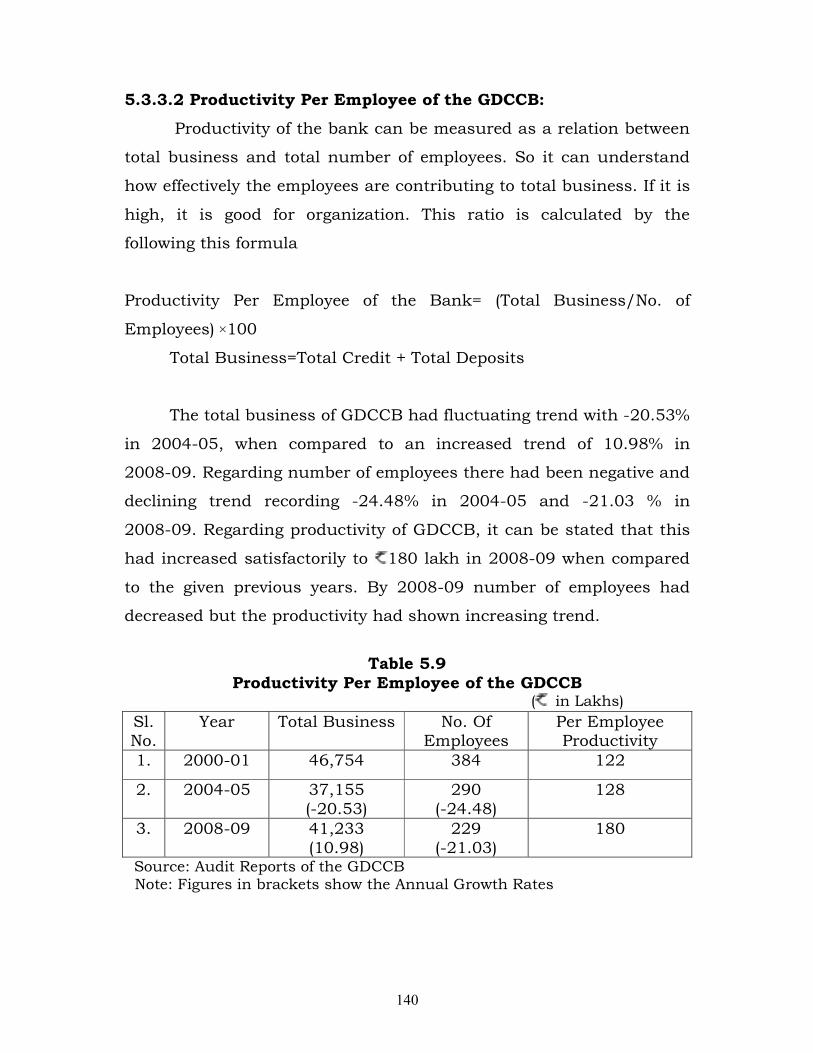

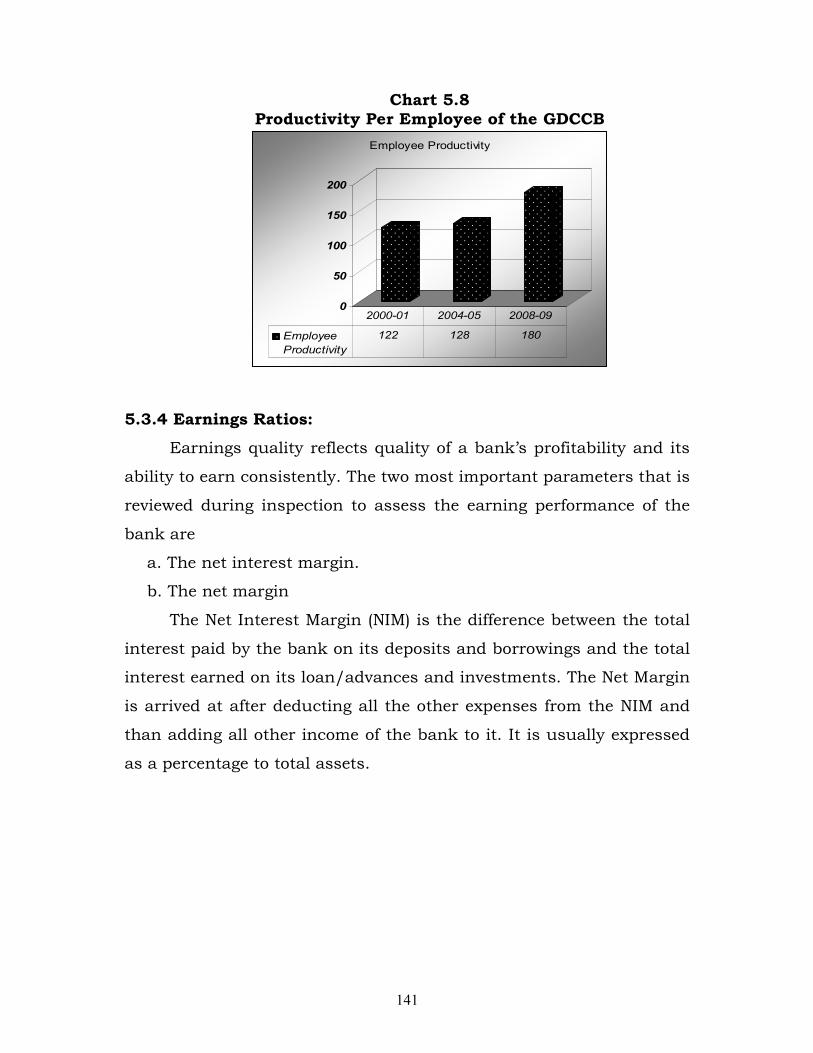

5.3.3.2 Productivity Per Employee of the GDCCB:

Productivity of the bank can be measured as a relation between

total business and total number of employees. So it can understand

how effectively the employees are contributing to total business. If it is

high, it is good for organization. This ratio is calculated by the

following this formula

Productivity Per Employee of the Bank= (Total Business/No. of

Employees) ×100

Total Business=Total Credit + Total Deposits

The total business of GDCCB had fluctuating trend with -20.53%

in 2004-05, when compared to an increased trend of 10.98% in

2008-09. Regarding number of employees there had been negative and

declining trend recording -24.48% in 2004-05 and -21.03 % in

2008-09. Regarding productivity of GDCCB, it can be stated that this

had increased satisfactorily to 180 lakh in 2008-09 when compared

to the given previous years. By 2008-09 number of employees had

decreased but the productivity had shown increasing trend.

Table 5.9

Productivity Per Employee of the GDCCB ( in Lakhs) Sl. No.

Year Total Business No. Of Employees

Per Employee Productivity

1. 2000-01 46,754 384 122

2. 2004-05 37,155 (-20.53)

290 (-24.48)

128

3. 2008-09 41,233 (10.98)

229 (-21.03)

180

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

141

Chart 5.8 Productivity Per Employee of the GDCCB

0

50

100

150

200

Employee Productivity

Employee

Productivity

122 128 180

2000-01 2004-05 2008-09

5.3.4 Earnings Ratios:

Earnings quality reflects quality of a bank’s profitability and its

ability to earn consistently. The two most important parameters that is

reviewed during inspection to assess the earning performance of the

bank are

a. The net interest margin.

b. The net margin

The Net Interest Margin (NIM) is the difference between the total

interest paid by the bank on its deposits and borrowings and the total

interest earned on its loan/advances and investments. The Net Margin

is arrived at after deducting all the other expenses from the NIM and

than adding all other income of the bank to it. It is usually expressed

as a percentage to total assets.

142

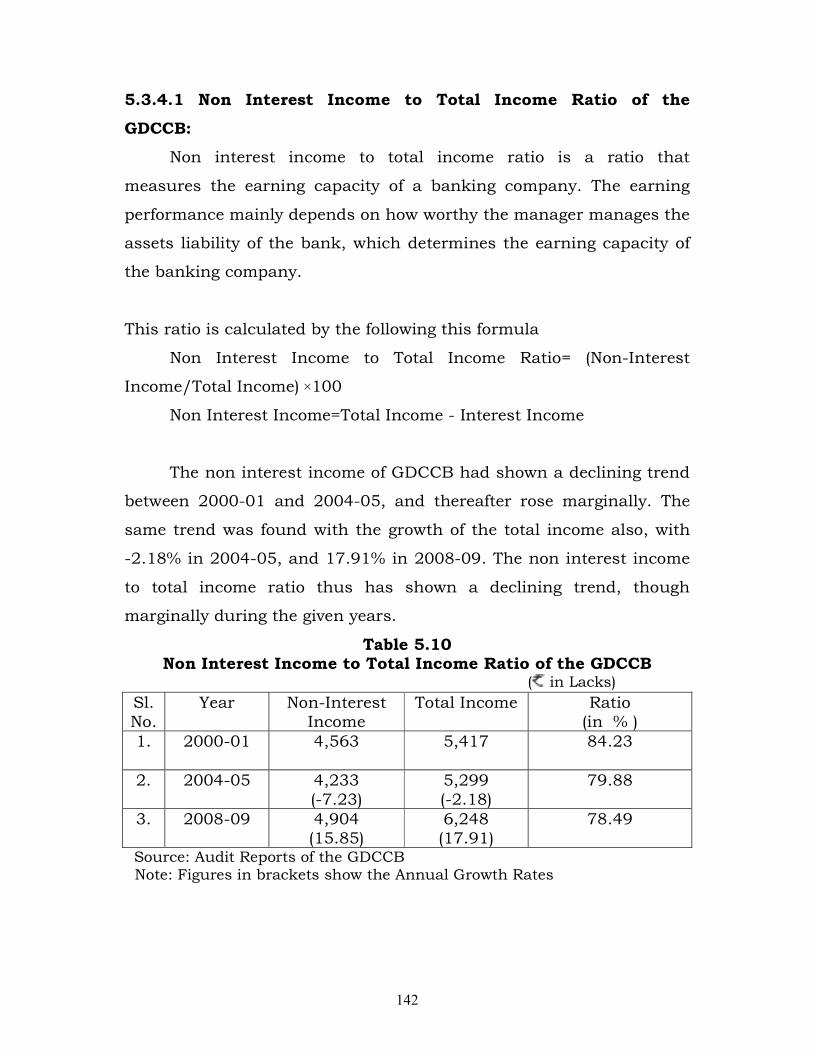

5.3.4.1 Non Interest Income to Total Income Ratio of the

GDCCB:

Non interest income to total income ratio is a ratio that

measures the earning capacity of a banking company. The earning

performance mainly depends on how worthy the manager manages the

assets liability of the bank, which determines the earning capacity of

the banking company.

This ratio is calculated by the following this formula

Non Interest Income to Total Income Ratio= (Non-Interest

Income/Total Income) ×100

Non Interest Income=Total Income - Interest Income

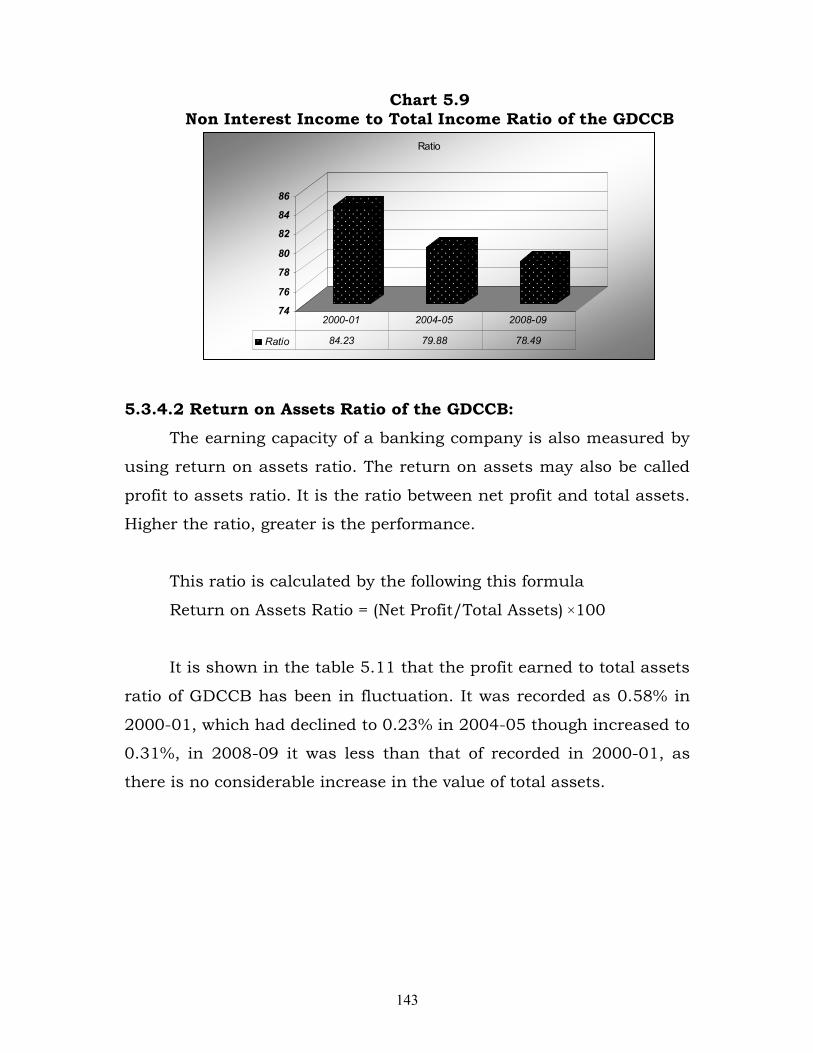

The non interest income of GDCCB had shown a declining trend

between 2000-01 and 2004-05, and thereafter rose marginally. The

same trend was found with the growth of the total income also, with

-2.18% in 2004-05, and 17.91% in 2008-09. The non interest income

to total income ratio thus has shown a declining trend, though

marginally during the given years.

Table 5.10 Non Interest Income to Total Income Ratio of the GDCCB

( in Lacks)

Sl. No.

Year Non-Interest Income

Total Income Ratio (in % )

1. 2000-01 4,563 5,417 84.23

2. 2004-05 4,233 (-7.23)

5,299 (-2.18)

79.88

3. 2008-09 4,904 (15.85)

6,248 (17.91)

78.49

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

143

Chart 5.9 Non Interest Income to Total Income Ratio of the GDCCB

74

76

78

80

82

84

86

Ratio

Ratio 84.23 79.88 78.49

2000-01 2004-05 2008-09

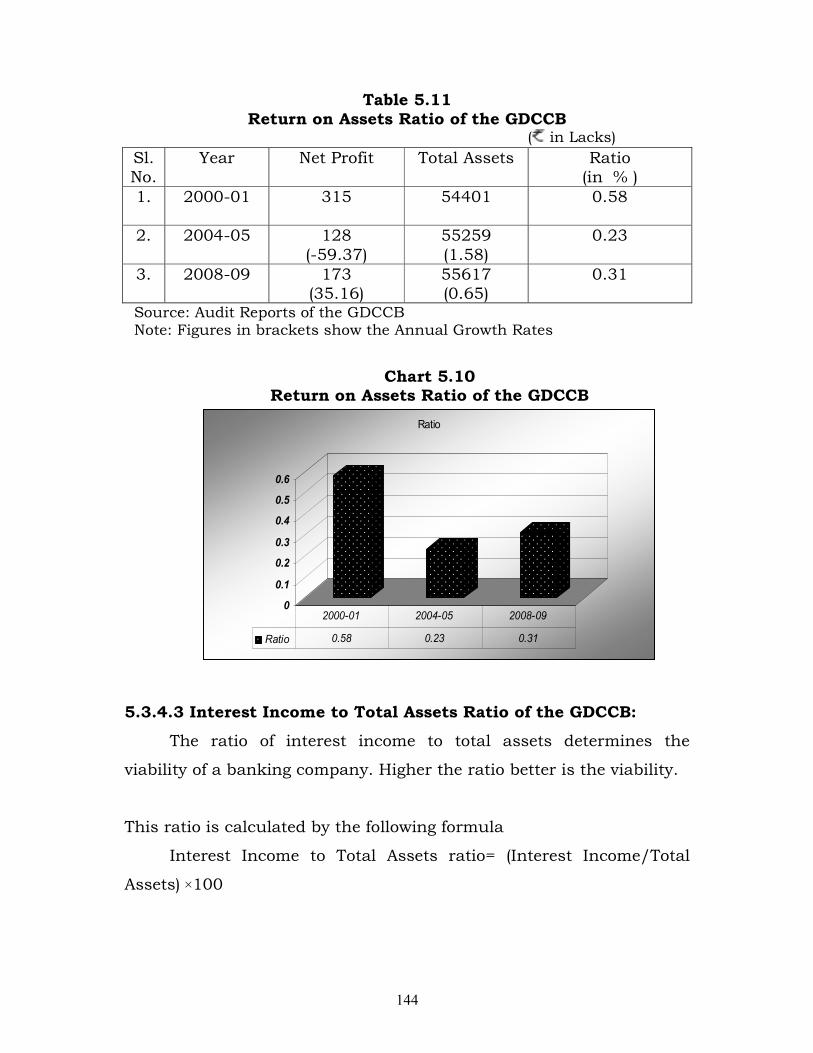

5.3.4.2 Return on Assets Ratio of the GDCCB:

The earning capacity of a banking company is also measured by

using return on assets ratio. The return on assets may also be called

profit to assets ratio. It is the ratio between net profit and total assets.

Higher the ratio, greater is the performance.

This ratio is calculated by the following this formula

Return on Assets Ratio = (Net Profit/Total Assets) ×100

It is shown in the table 5.11 that the profit earned to total assets

ratio of GDCCB has been in fluctuation. It was recorded as 0.58% in

2000-01, which had declined to 0.23% in 2004-05 though increased to

0.31%, in 2008-09 it was less than that of recorded in 2000-01, as

there is no considerable increase in the value of total assets.

144

Table 5.11 Return on Assets Ratio of the GDCCB

( in Lacks)

Sl. No.

Year Net Profit Total Assets Ratio (in % )

1. 2000-01 315 54401 0.58

2. 2004-05 128

(-59.37)

55259

(1.58)

0.23

3. 2008-09 173 (35.16)

55617 (0.65)

0.31

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.10

Return on Assets Ratio of the GDCCB

0

0.1

0.2

0.3

0.4

0.5

0.6

Ratio

Ratio 0.58 0.23 0.31

2000-01 2004-05 2008-09

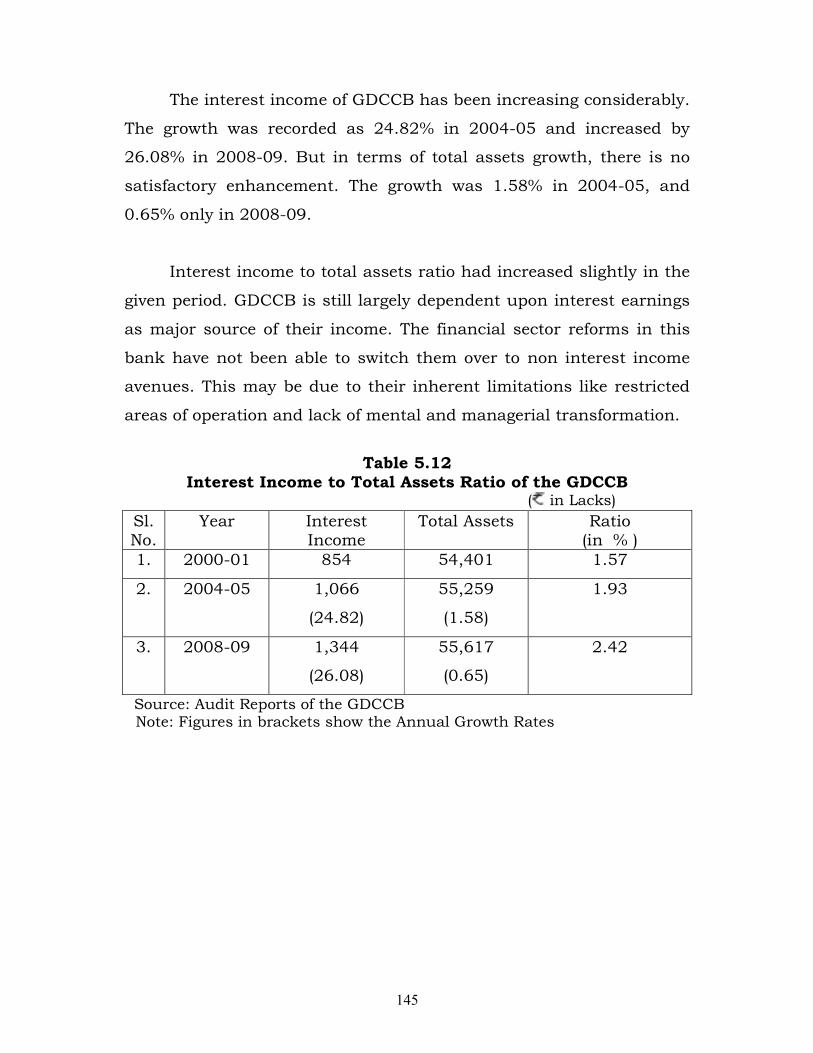

5.3.4.3 Interest Income to Total Assets Ratio of the GDCCB:

The ratio of interest income to total assets determines the

viability of a banking company. Higher the ratio better is the viability.

This ratio is calculated by the following formula

Interest Income to Total Assets ratio= (Interest Income/Total

Assets) ×100

145

The interest income of GDCCB has been increasing considerably.

The growth was recorded as 24.82% in 2004-05 and increased by

26.08% in 2008-09. But in terms of total assets growth, there is no

satisfactory enhancement. The growth was 1.58% in 2004-05, and

0.65% only in 2008-09.

Interest income to total assets ratio had increased slightly in the

given period. GDCCB is still largely dependent upon interest earnings

as major source of their income. The financial sector reforms in this

bank have not been able to switch them over to non interest income

avenues. This may be due to their inherent limitations like restricted

areas of operation and lack of mental and managerial transformation.

Table 5.12

Interest Income to Total Assets Ratio of the GDCCB ( in Lacks)

Sl. No.

Year Interest Income

Total Assets Ratio (in % )

1. 2000-01 854 54,401 1.57

2. 2004-05 1,066

(24.82)

55,259

(1.58)

1.93

3. 2008-09 1,344

(26.08)

55,617

(0.65)

2.42

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

146

Chart 5.11

Interest Income to Total Assets of the GDCCB

0

0.5

1

1.5

2

2.5

Ratio

Ratio 1.57 1.93 2.42

2000-01 2004-05 2008-09

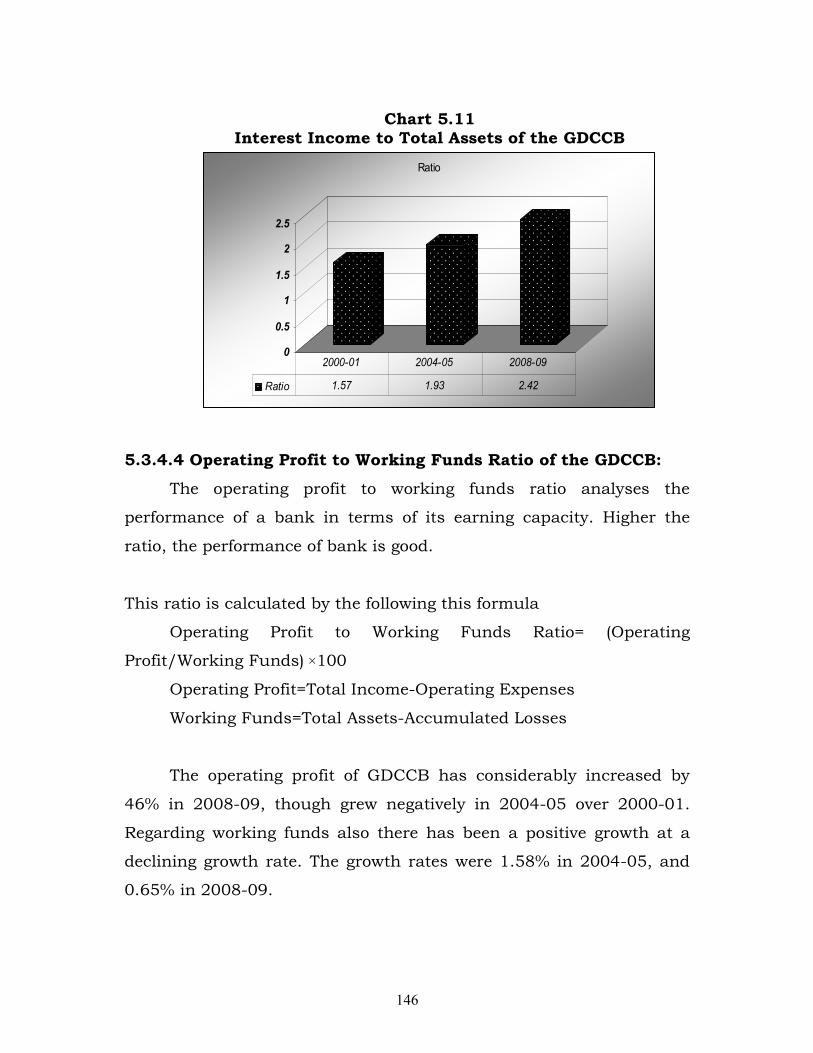

5.3.4.4 Operating Profit to Working Funds Ratio of the GDCCB:

The operating profit to working funds ratio analyses the

performance of a bank in terms of its earning capacity. Higher the

ratio, the performance of bank is good.

This ratio is calculated by the following this formula

Operating Profit to Working Funds Ratio= (Operating

Profit/Working Funds) ×100

Operating Profit=Total Income-Operating Expenses

Working Funds=Total Assets-Accumulated Losses

The operating profit of GDCCB has considerably increased by

46% in 2008-09, though grew negatively in 2004-05 over 2000-01.

Regarding working funds also there has been a positive growth at a

declining growth rate. The growth rates were 1.58% in 2004-05, and

0.65% in 2008-09.

147

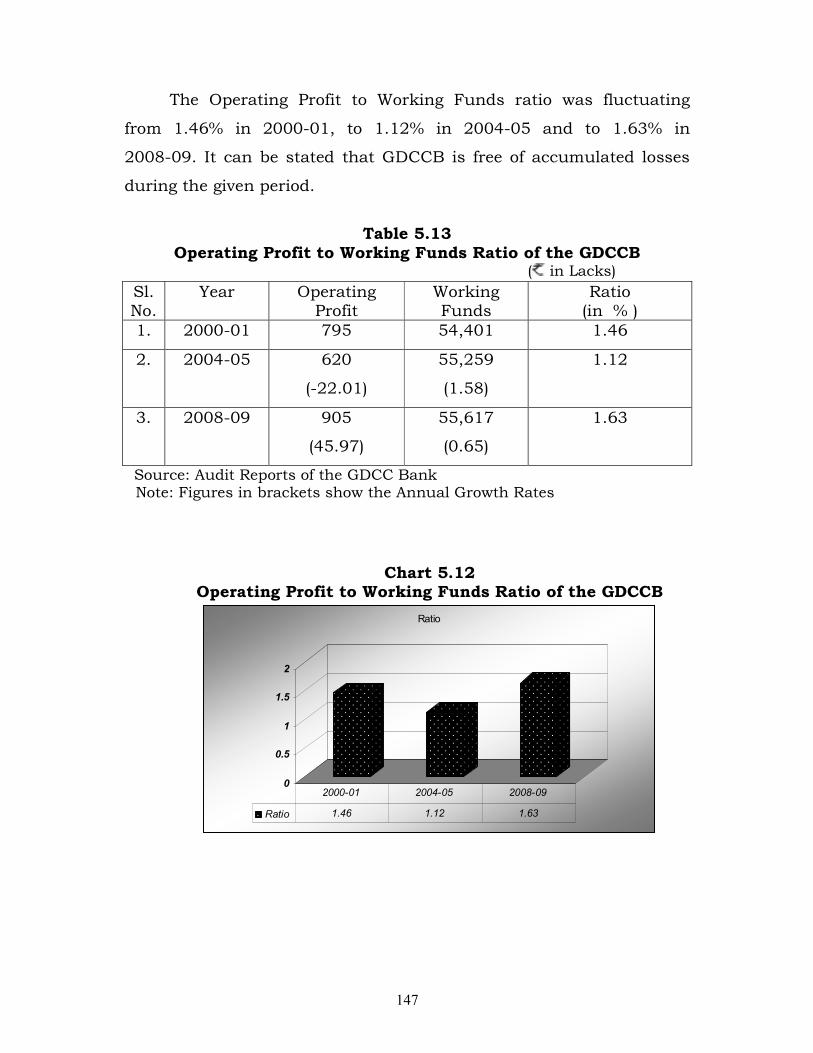

The Operating Profit to Working Funds ratio was fluctuating

from 1.46% in 2000-01, to 1.12% in 2004-05 and to 1.63% in

2008-09. It can be stated that GDCCB is free of accumulated losses

during the given period.

Table 5.13

Operating Profit to Working Funds Ratio of the GDCCB ( in Lacks)

Sl. No.

Year Operating Profit

Working Funds

Ratio (in % )

1. 2000-01 795 54,401 1.46

2. 2004-05 620

(-22.01)

55,259

(1.58)

1.12

3. 2008-09 905

(45.97)

55,617

(0.65)

1.63

Source: Audit Reports of the GDCC Bank Note: Figures in brackets show the Annual Growth Rates

Chart 5.12 Operating Profit to Working Funds Ratio of the GDCCB

0

0.5

1

1.5

2

Ratio

Ratio 1.46 1.12 1.63

2000-01 2004-05 2008-09

148

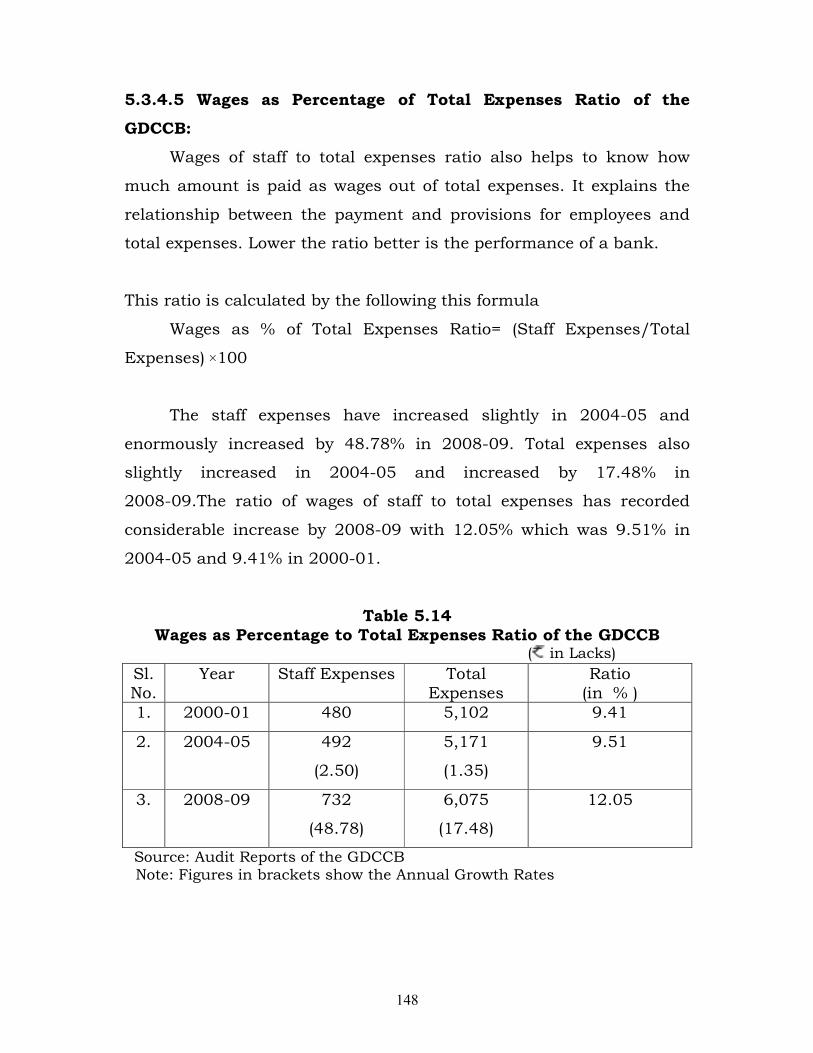

5.3.4.5 Wages as Percentage of Total Expenses Ratio of the

GDCCB:

Wages of staff to total expenses ratio also helps to know how

much amount is paid as wages out of total expenses. It explains the

relationship between the payment and provisions for employees and

total expenses. Lower the ratio better is the performance of a bank.

This ratio is calculated by the following this formula

Wages as % of Total Expenses Ratio= (Staff Expenses/Total

Expenses) ×100

The staff expenses have increased slightly in 2004-05 and

enormously increased by 48.78% in 2008-09. Total expenses also

slightly increased in 2004-05 and increased by 17.48% in

2008-09.The ratio of wages of staff to total expenses has recorded

considerable increase by 2008-09 with 12.05% which was 9.51% in

2004-05 and 9.41% in 2000-01.

Table 5.14 Wages as Percentage to Total Expenses Ratio of the GDCCB

( in Lacks)

Sl. No.

Year Staff Expenses Total Expenses

Ratio (in % )

1. 2000-01 480 5,102 9.41

2. 2004-05 492

(2.50)

5,171

(1.35)

9.51

3. 2008-09 732

(48.78)

6,075

(17.48)

12.05

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

149

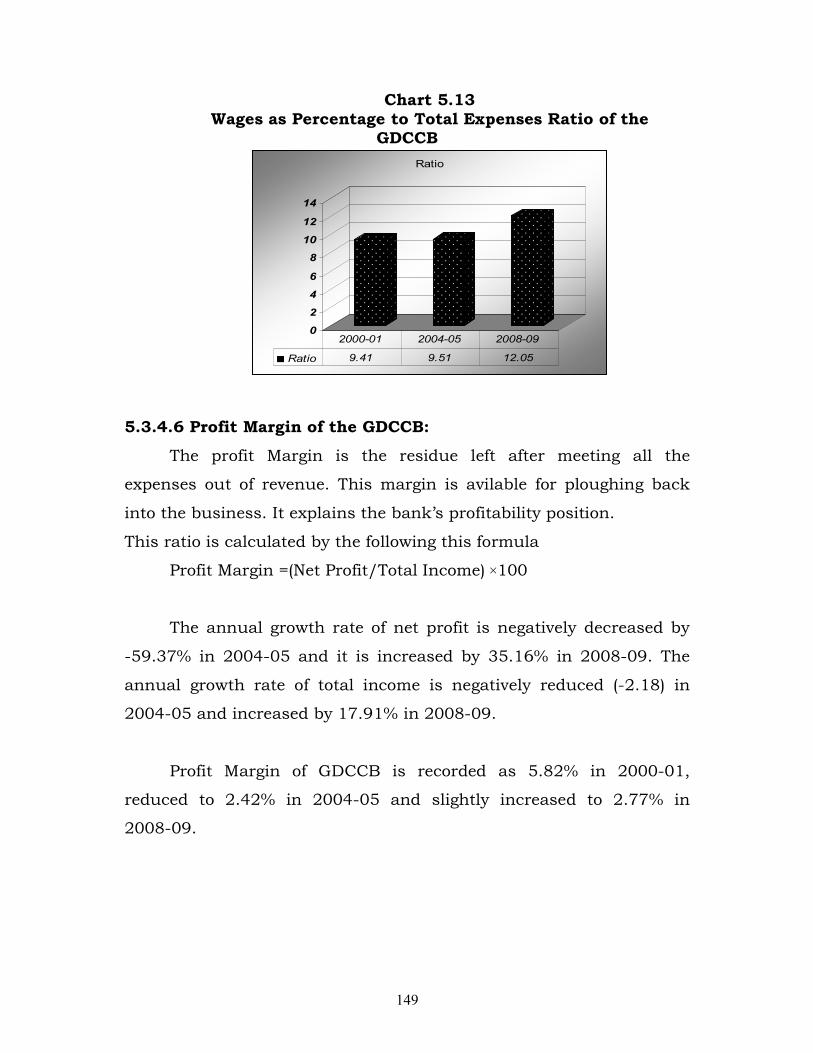

Chart 5.13 Wages as Percentage to Total Expenses Ratio of the

GDCCB

0

2

4

6

8

10

12

14

Ratio

Ratio 9.41 9.51 12.05

2000-01 2004-05 2008-09

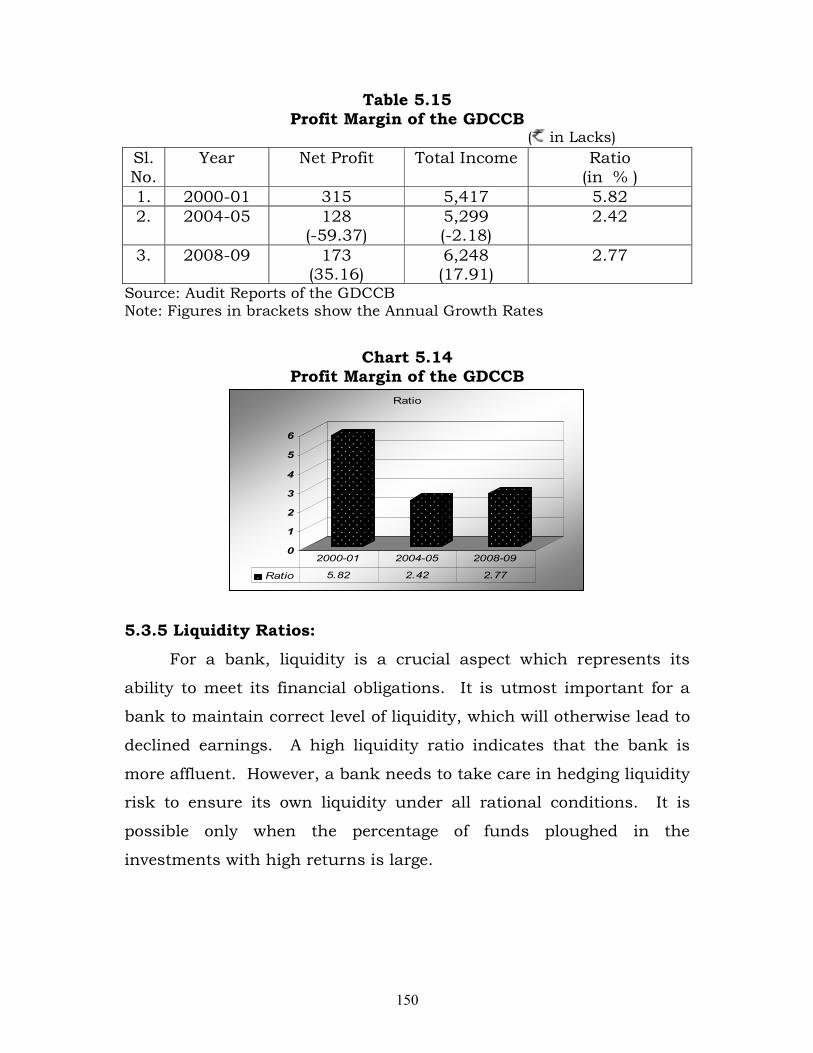

5.3.4.6 Profit Margin of the GDCCB:

The profit Margin is the residue left after meeting all the

expenses out of revenue. This margin is avilable for ploughing back

into the business. It explains the bank’s profitability position.

This ratio is calculated by the following this formula

Profit Margin =(Net Profit/Total Income) ×100

The annual growth rate of net profit is negatively decreased by

-59.37% in 2004-05 and it is increased by 35.16% in 2008-09. The

annual growth rate of total income is negatively reduced (-2.18) in

2004-05 and increased by 17.91% in 2008-09.

Profit Margin of GDCCB is recorded as 5.82% in 2000-01,

reduced to 2.42% in 2004-05 and slightly increased to 2.77% in

2008-09.

150

Table 5.15 Profit Margin of the GDCCB

( in Lacks)

Sl. No.

Year Net Profit Total Income Ratio (in % )

1. 2000-01 315 5,417 5.82

2. 2004-05 128 (-59.37)

5,299 (-2.18)

2.42

3. 2008-09 173 (35.16)

6,248 (17.91)

2.77

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.14

Profit Margin of the GDCCB

0

1

2

3

4

5

6

Ratio

Ratio 5.82 2.42 2.77

2000-01 2004-05 2008-09

5.3.5 Liquidity Ratios:

For a bank, liquidity is a crucial aspect which represents its

ability to meet its financial obligations. It is utmost important for a

bank to maintain correct level of liquidity, which will otherwise lead to

declined earnings. A high liquidity ratio indicates that the bank is

more affluent. However, a bank needs to take care in hedging liquidity

risk to ensure its own liquidity under all rational conditions. It is

possible only when the percentage of funds ploughed in the

investments with high returns is large.

151

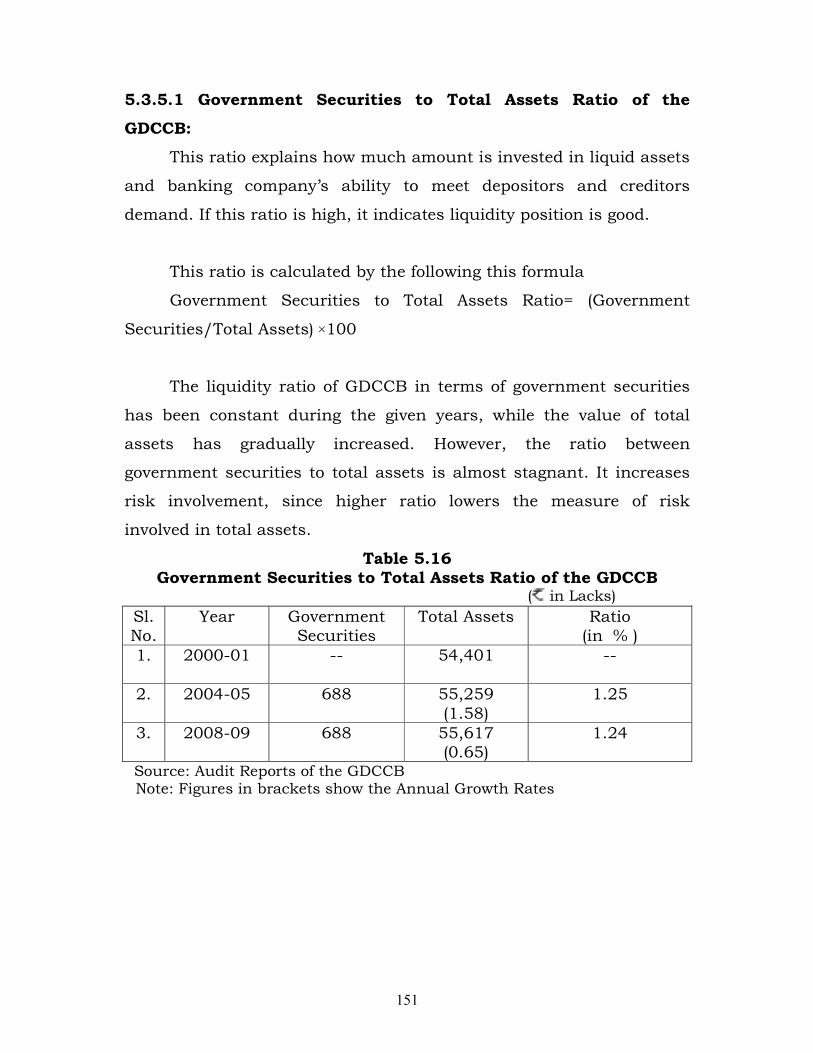

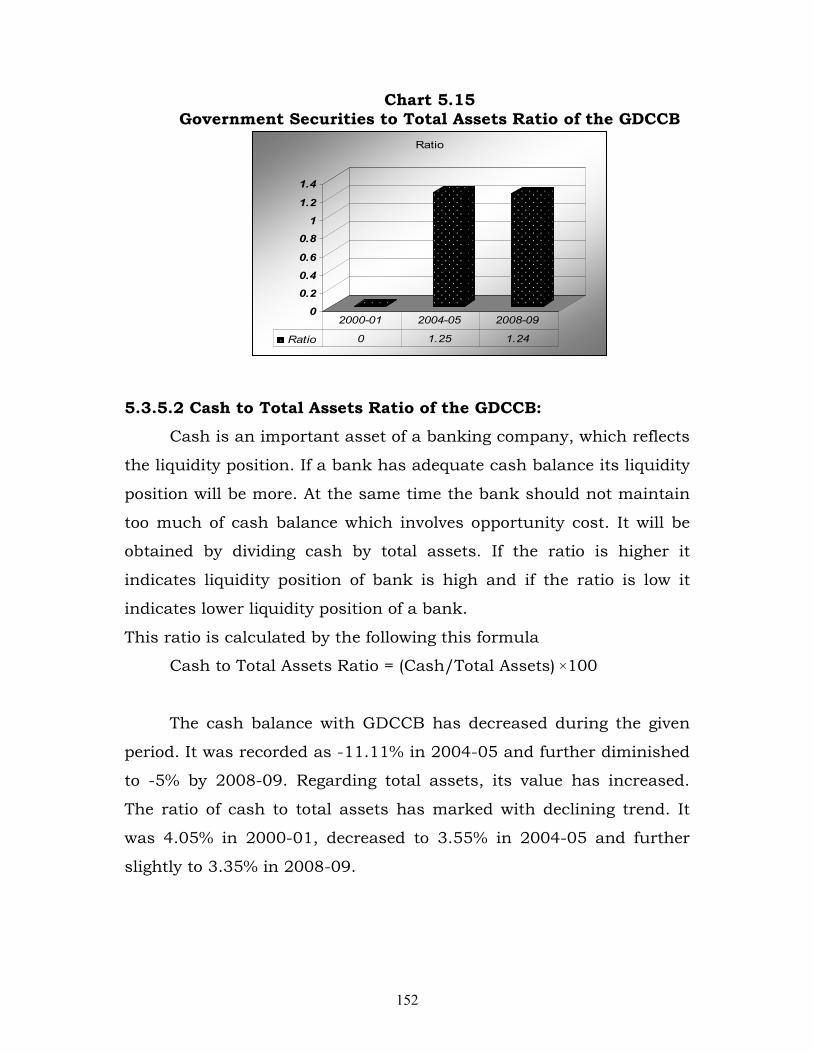

5.3.5.1 Government Securities to Total Assets Ratio of the

GDCCB:

This ratio explains how much amount is invested in liquid assets

and banking company’s ability to meet depositors and creditors

demand. If this ratio is high, it indicates liquidity position is good.

This ratio is calculated by the following this formula

Government Securities to Total Assets Ratio= (Government

Securities/Total Assets) ×100

The liquidity ratio of GDCCB in terms of government securities

has been constant during the given years, while the value of total

assets has gradually increased. However, the ratio between

government securities to total assets is almost stagnant. It increases

risk involvement, since higher ratio lowers the measure of risk

involved in total assets.

Table 5.16 Government Securities to Total Assets Ratio of the GDCCB

( in Lacks)

Sl. No.

Year Government Securities

Total Assets Ratio (in % )

1. 2000-01 -- 54,401 --

2. 2004-05 688 55,259

(1.58)

1.25

3. 2008-09 688 55,617 (0.65)

1.24

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

152

Chart 5.15 Government Securities to Total Assets Ratio of the GDCCB

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Ratio

Ratio 0 1.25 1.24

2000-01 2004-05 2008-09

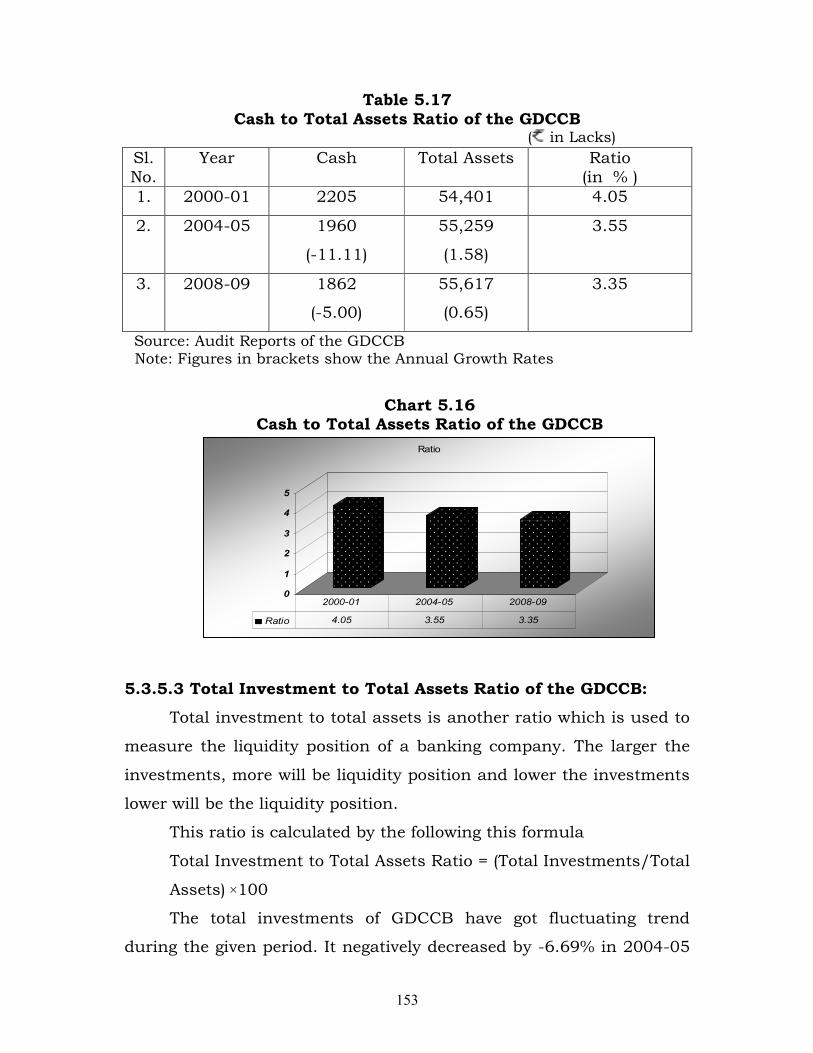

5.3.5.2 Cash to Total Assets Ratio of the GDCCB:

Cash is an important asset of a banking company, which reflects

the liquidity position. If a bank has adequate cash balance its liquidity

position will be more. At the same time the bank should not maintain

too much of cash balance which involves opportunity cost. It will be

obtained by dividing cash by total assets. If the ratio is higher it

indicates liquidity position of bank is high and if the ratio is low it

indicates lower liquidity position of a bank.

This ratio is calculated by the following this formula

Cash to Total Assets Ratio = (Cash/Total Assets) ×100

The cash balance with GDCCB has decreased during the given

period. It was recorded as -11.11% in 2004-05 and further diminished

to -5% by 2008-09. Regarding total assets, its value has increased.

The ratio of cash to total assets has marked with declining trend. It

was 4.05% in 2000-01, decreased to 3.55% in 2004-05 and further

slightly to 3.35% in 2008-09.

153

Table 5.17 Cash to Total Assets Ratio of the GDCCB

( in Lacks)

Sl. No.

Year Cash Total Assets Ratio (in % )

1. 2000-01 2205 54,401 4.05

2. 2004-05 1960

(-11.11)

55,259

(1.58)

3.55

3. 2008-09 1862

(-5.00)

55,617

(0.65)

3.35

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.16

Cash to Total Assets Ratio of the GDCCB

0

1

2

3

4

5

Ratio

Ratio 4.05 3.55 3.35

2000-01 2004-05 2008-09

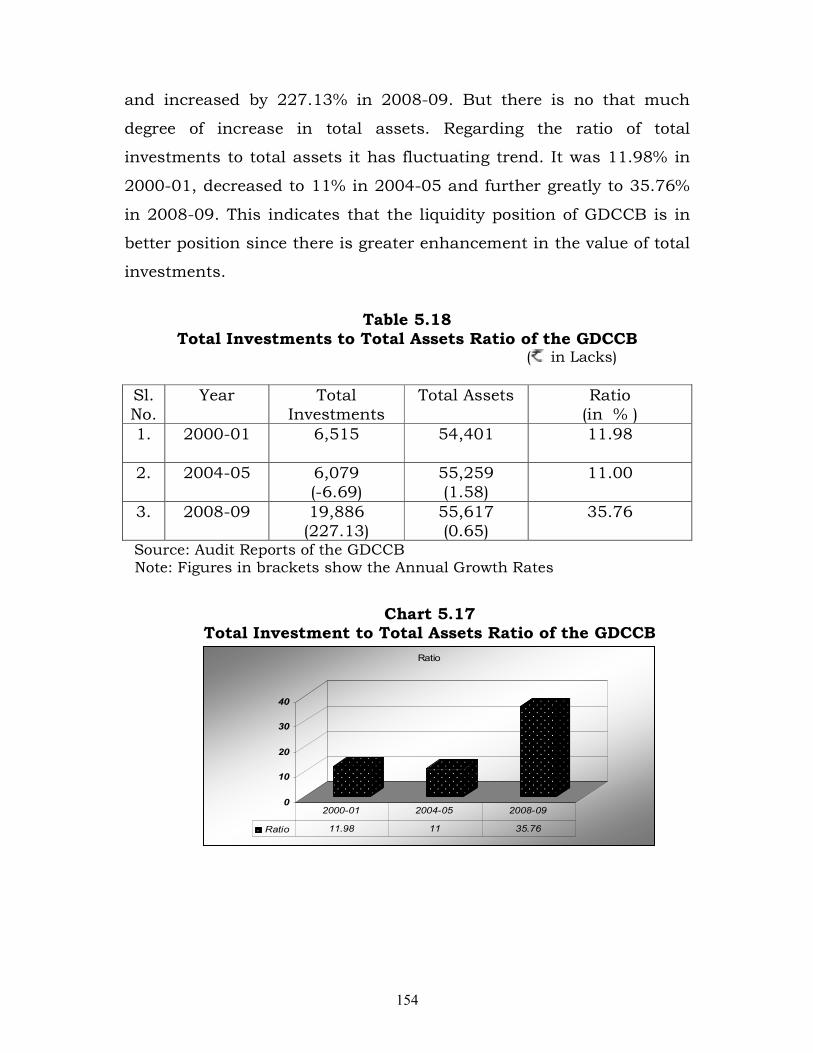

5.3.5.3 Total Investment to Total Assets Ratio of the GDCCB:

Total investment to total assets is another ratio which is used to

measure the liquidity position of a banking company. The larger the

investments, more will be liquidity position and lower the investments

lower will be the liquidity position.

This ratio is calculated by the following this formula

Total Investment to Total Assets Ratio = (Total Investments/Total

Assets) ×100

The total investments of GDCCB have got fluctuating trend

during the given period. It negatively decreased by -6.69% in 2004-05

154

and increased by 227.13% in 2008-09. But there is no that much

degree of increase in total assets. Regarding the ratio of total

investments to total assets it has fluctuating trend. It was 11.98% in

2000-01, decreased to 11% in 2004-05 and further greatly to 35.76%

in 2008-09. This indicates that the liquidity position of GDCCB is in

better position since there is greater enhancement in the value of total

investments.

Table 5.18

Total Investments to Total Assets Ratio of the GDCCB ( in Lacks)

Sl. No.

Year Total Investments

Total Assets Ratio (in % )

1. 2000-01 6,515 54,401 11.98

2. 2004-05 6,079 (-6.69)

55,259 (1.58)

11.00

3. 2008-09 19,886 (227.13)

55,617 (0.65)

35.76

Source: Audit Reports of the GDCCB Note: Figures in brackets show the Annual Growth Rates

Chart 5.17

Total Investment to Total Assets Ratio of the GDCCB

0

10

20

30

40

Ratio

Ratio 11.98 11 35.76

2000-01 2004-05 2008-09

155

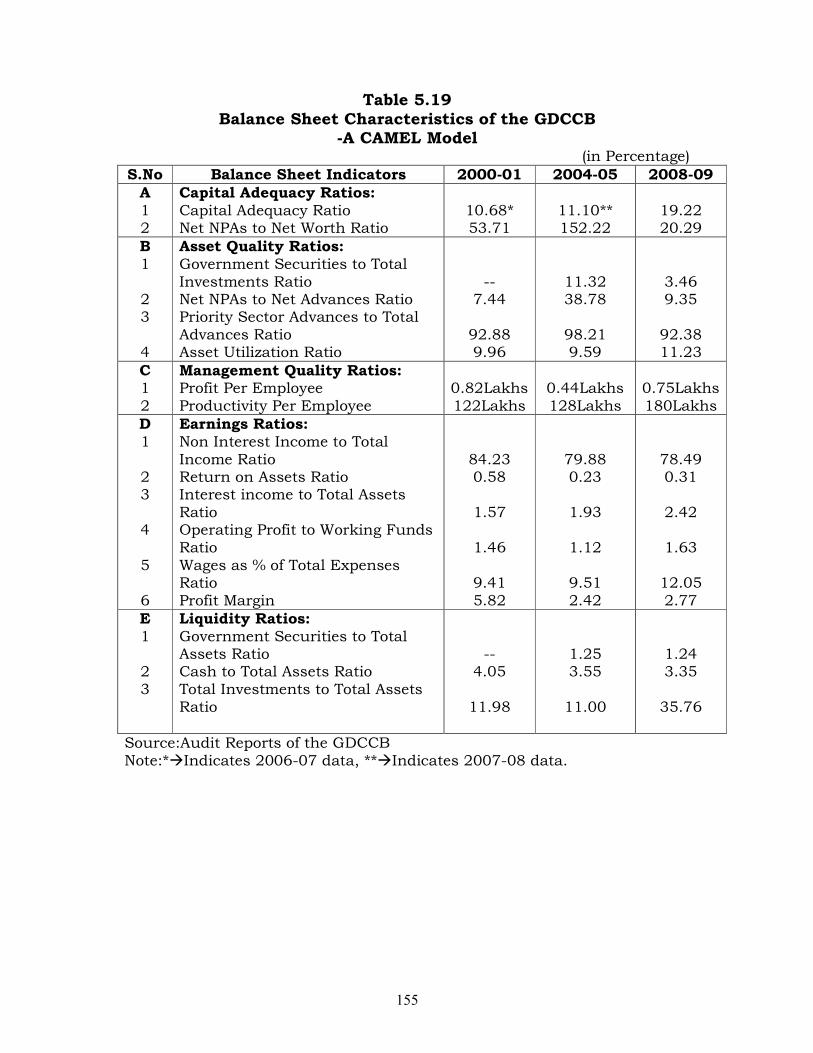

Table 5.19 Balance Sheet Characteristics of the GDCCB

-A CAMEL Model (in Percentage)

S.No Balance Sheet Indicators 2000-01 2004-05 2008-09

A 1 2

Capital Adequacy Ratios: Capital Adequacy Ratio Net NPAs to Net Worth Ratio

10.68* 53.71

11.10** 152.22

19.22 20.29

B 1 2 3 4

Asset Quality Ratios: Government Securities to Total Investments Ratio Net NPAs to Net Advances Ratio Priority Sector Advances to Total Advances Ratio Asset Utilization Ratio

--

7.44

92.88 9.96

11.32 38.78

98.21 9.59

3.46 9.35

92.38 11.23

C 1 2

Management Quality Ratios: Profit Per Employee Productivity Per Employee

0.82Lakhs 122Lakhs

0.44Lakhs 128Lakhs

0.75Lakhs 180Lakhs

D 1 2 3 4 5 6

Earnings Ratios: Non Interest Income to Total Income Ratio Return on Assets Ratio Interest income to Total Assets Ratio Operating Profit to Working Funds Ratio Wages as % of Total Expenses Ratio Profit Margin

84.23 0.58

1.57

1.46

9.41 5.82

79.88 0.23

1.93

1.12

9.51 2.42

78.49 0.31

2.42

1.63

12.05 2.77

E 1 2 3

Liquidity Ratios: Government Securities to Total Assets Ratio Cash to Total Assets Ratio Total Investments to Total Assets Ratio

--

4.05

11.98

1.25 3.55

11.00

1.24 3.35

35.76

Source:Audit Reports of the GDCCB Note:*�Indicates 2006-07 data, **�Indicates 2007-08 data.

156

5.4 Findings:

� According to the parameters indicated by NABARD, in the case

of the GDCCB, the sum of the Bad&Doubtful Debts and

Accumulated Losses has been below the 50 percent mark of the

owned funds. It is evident from the analysis that the financial

position of the GDCCB is better.

� As per the prudential norms, the banks being operated in India

are required to achieve 9% CRAR. It shows that the GDCCB has

well exceeded the stipulated level. Similarly, the CRAR was

10.68% in 2007-08 which has gone up and touched 20% mark

in 2008-09. All this explains the strength of GDCCB in terms of

sound capital base and its adequacy.

� Employee productivity of GDCCB, it can be stated that this is

increased satisfactorily to 180 lakhs in 2008-09 when

compared to the given previous years. By 2008-09 number of

employees had decreased but the productivity ratio has shown

increasing trend.

� The interest income of GDCCB has been increasing

considerably. The growth was recorded as 24.82% in 2004-05

and increased by 26.08% in 2008-09. Interest income to total

assets ratio is increasing slightly in the given period. GDCCB is

still largely dependent upon interest earnings as major source of

their income.

157

� The staff expenses were increased slightly in 2004-05 and

enormously increased by 48.78% in 2008-09. Total expenses

also slightly increased in 2004-05 and increased by 17.48% in

2008-09.The ratio of wages of staff to total expenses has

recorded considerable increase by 2008-09 with 12.05% which

was 9.51% in 2004-05 and 9.41% in 2000-01.

� Profit Margin of GDCCB is recorded as 5.82% in 2000-01,

reduced to 2.42% in 2004-05 and slightly increased to 2.77% in

2008-09. The profit margin of the GDCCB has increased

significantly in the post liberlization era.

� Regarding the ratio of total investments to total assets it has

fluctuating trend. It was 11.98% in 2000-01, decreased to 11%

in 2004-05 and further greatly to 35.76% in 2008-09. It

indicates that the liquidity position of GDCCB is in better

position since there is greater enhancement in the value of total

investments.

![8365 programacao semana_de_eng._florestal[1]](https://img.pdfslide.net/doc/110x75/5563ed8dd8b42a0a288b49b3/8365-programacao-semanadeengflorestal1.jpg)