Embed Size (px)

Citation preview

An Assessment of the Pakistan-Sri LankaFree Trade Agreement

April, 2015

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Acknowledgements:

Team Leader: Samir S. AmirLead Researcher: Danish Hyder

Disclaimer: The findings, interpretations and conclusions expressed herein are those of the author(s) and do not necessarily reflect the views of the Board of Directors and Members of the Pakistan Business Council or the companies they represent.

Any conclusions of analysis based on ITC, IDB, CTS, UNCTSD and WEO data are the responsibility of the author(s) and do not necessarily reflect the opinion of the WTO, IMF or UN.

Although every effort has been made to cross-check and verify the authenticity of the data, the Pakistan Business Council does not guarantee the data included in this work. All data and statistics used are correct as of 1 February, 2015, and may be subject to change.

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

The PBC’s Member Companies

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

The PBC’s Member Companies

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

TABLE OF CONTENTSSection 1: A Brief Introduction to Pakistan-Sri Lanka Trade

1.0 The Pakistan Business Council: An Overview ………………………………… .. 08

Executive Summary

2.0 Key Findings ……………………………………………………………………… ...... 09

2.1. Overview of Pak-Sri Lanka potential for trade ……………………………………… 09

2.2. High Potential Trade Item Lists …………………………………………………….… 10

3.0 Recommendations …………………………………………………………….… ...... 11

3.1. Trade Delegations and Single Country Exhibitions ............................................... 11

3.2. Agreement on changes to FTA terms ................................................................... 11

3.3. Greater involvement of businessmen in drafting of FTA ....................................... 11

3.4. Forums for trade dispute resolution ...................................................................... 11

4.0 Study Objective ................................................................................................ 12

5.0 Pakistan Sri Lanka Free Trade Agreement: Brief Introduction ……… ............ 14

5.1. Short Economy Profiles ......................................................................................... 14

5.2. Top Trading Partners ............................................................................................. 16

5.3. Overview of Pak-Sri Lanka Trade ........................................................................... 18

5.4. Overview of Pakistan’s Exports from the World and to Sri Lanka ........................ 21

5.5. Overview of Pakistan’s Imports from the World and from Sri Lanka………… ....... 26

Section 2: Analysis of Pakistan’s Exports to Sri Lanka under FTA

6.0 Prelimanry Analysis of Pakistani Exports to Sri Lanka Under FTA ..................................................................................... 29

6.1 Comparison of Pakistan and India’s Trade with Sri Lanka ................................... 31

7.0 Analysis of Pakistan’s Exports to Sri Lanka ................................................... 33

7.1. TradePotential≥USD10million .......................................................................... 35

7.2. USD5million≤TradePotential<USD10million ................................................. 37

7.3. USD1million≤TradePotential<USD5million .................................................. 39

7.4. High Trade Potential, Favourable CAGR items with tariff advantage over India … 41

7.5. High Trade Potential, Favourable CAGR items that should receive Tariff concessions ….. ................................................................................ 42

7.6. Two digit HS codes with High Trade Potential ...................................................... 45

7.7. Two digit HS codes with High Trade Potential and favourable CAGR values ...... 46

7.8. Comparison with India for high potential Pakistani products ……… .................... 47

7.9. Items on Sri Lanka’s no concession list with Pakistan RCA advantage …… ........ 48

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Section 3: Analysis of Sri Lanka’s Exports to Pakistan under FTA

8.0 Preliminary Analysis of Sri Lankan Exports to Pakistan Under FTA ........................................................................ 51

8.1. Comparison of Sri Lanka and China trade with Pakistan ...................................... 53

9.0 Analysis Of Sri Lanka’s Exports To Pakistan ................................................... 55

9.1. TradePotential≥USD10million…………………………… .................................. 55

9.2. USD5million≤TradePotential<USD10million ................................................. 57

9.3. USD1million≤TradePotential<USD5million .................................................. 58

9.4. USD500,000≤TradePotential<USD1million………. ...................................... 59

9.5. High Trade Potential, Favourable CAGR items that should receive Tariff concessions ….. ............................................................. 60

9.6. Two digit HS codes with High Trade Potential …… ............................................... 61

9.7. Two digit HS codes with High Trade Potential and favourable CAGR values …. .. 62

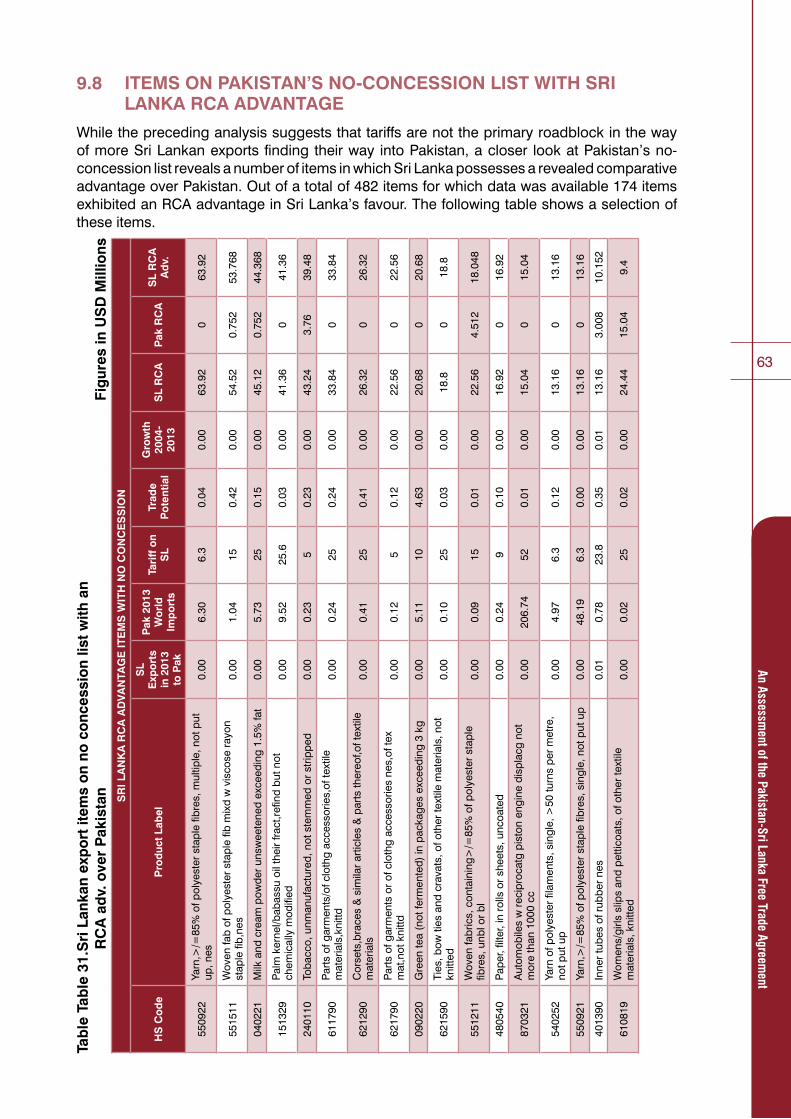

9.8. Items on Pakistan’s no concession list with Sri Lankan RCA Advantage ............. 63

Section 4: Concerns and Recommendations

10.0 General Concerns ............................................................................................ 65

10.1. Lack of interest in Pak-Sri Lanka trade .................................................................. 65

10.2. Unilateral changes made to FTA terms …………………………………………… ... 65

10.3. Insufficient involvement of businessmen in drafting of FTA……………………… .. 66

10.4. Lack of effective trade dispute resolution ……………………………………… ....... 66

11.0 Views of Selected High Potential Pakistani Exporters ................................... 66

11.1. Plastics …………………………………………………………………………………. 66

11.2. Fruits and Vegetables …………………………………………………………… ........ 66

11.3. Articles of Iron and Steel (Pipes) ........................................................................... 67

12.0 Recommendations ........................................................................................... 67

12.1. Trade Delegations and Single Country Exhibitions .............................................. 67

12.2. Increased involvement of businessmen in drafting of FTA ................................... 68

12.3. Discussion before change in FTA terms ............................................................... 68

12.4. Forums for efficient resolution of trade disputes .................................................. 69

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Annexures

Annexure A: List of most exportable product lines ................................................. 71

Table of Pakistani Exports to Sri Lanka .......................................................................... 71

Table of Sri Lankan Exports to Pakistan ......................................................................... 86

Annexure B: List of product lines on no concession lists with high RCA .............. 95

Table of high RCA Pakistani products with no concession................................. ........... 95

Table of high RCA Sri Lankan products with no concession ......................................... 98

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Section 1 A Brief

Introduction to Pakistan-Sri Lanka

Trade

08

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

1.0 THE PAKISTAN BUSINESS COUNCIL: AN OVERVIEW

The Pakistan Business Council (PBC) is a business policy advocacy forum, representing private-sector businesses that have substantial investments in Pakistan’s economy. It was formed in 2005 by 14 (now 47) of Pakistan’s largest enterprises, including multinationals, to allow businesses to meaningfully interact with government and other stakeholders. The Pakistan Business Council is a pan-industry advocacy group. It is not a trade body nor does it advocate for any specific business sector. Rather, its key advocacy thrust is on easing barriers to allow Pakistani businesses to compete in regional and global arenas. The PBC works closely with the relevant government departments, ministries, regulators and institutions, as well as other stakeholders including professional bodies, to develop consensus on major issues which impact the conduct of business in and from Pakistan. The PBC has submitted key position papers and recommendations to the government on legislation and other government policies affecting businesses. It also serves on various taskforces and committees of the Government of Pakistan as well as those of the State Bank, SECP and other regulators with the objective to provide policy assistance on new initiatives and reforms. The PBC conducts research and holds conferences and seminars to facilitate the flow of relevant information to all stakeholders in order to help create an informed view on the major issues faced by Pakistan. The PBC’s Founding Objectives:

• Toprovidefortheformationandexchangeofviewsonanyquestionconnectedwiththeconduct of businesses in and from Pakistan.

•Toconduct,organize,setup,administerandmanagecampaigns,surveys,focusgroups,workshops, seminars and field works for carrying out research and raising awareness in regard to matters affecting businesses in Pakistan.

•Toacquire,collect,compile,analyze,publishandprovidestatistics,dataanalysisandotherinformation relating to businesses of any kind, nature or description and on opportunities for such businesses within and outside Pakistan.

•TopromoteandfacilitatetheintegrationofbusinessesinPakistanintotheworldeconomyand to encourage the development and growth of Pakistani multinationals.

• TointeractwithGovernmentsintheeconomicdevelopmentofPakistanandtofacilitate,foster and further the economic, social and human resource development of Pakistan.

The PBC is a Section 42 not-for-profit Company Limited by Guarantee. Its working is overseen by a Board of Directors elected every three years by the Membership with the Board being headed by a Non-Executive Chairman. The day-to-day operations of the PBC are run by a professional secretariat headed by a full-time, paid CEO.

More information on the PBC, its members, and its workings, can be found on its website: www.pbc.org.pk

09

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Executive Summary

2.0 KEY FINDINGS

2.1. OVERVIEW OF PAK-SRI LANKA TRADE AND POTENTIAL FOR GROWTH

Pakistan and Sri Lanka signed a Free Trade Agreement in July 2002 and it became operational in June 2005. The terms of the FTA were comprehensive and granted 100% immediate concession to major Pakistani exports such as cotton and cement and major Sri Lankan exportssuchasrubberandcoconutproducts.By2010bothcountrieswererequiredtohaveremoved tariffs on all items barring those listed in their respective no-concession lists or those facing Tariff Rate Quotas (TRQ).

Top Pakistani exports to Sri Lanka include cotton products, cement, refined sugar and potatoes. Top Sri Lankan exports to Pakistan include vegetable products, rubber, fibreboard and coconut products. Pakistan’s exports to Sri Lanka grew from USD 154 million in 2004 to USD 316 million in 2013, but Pakistan could only claim 1.7% of total Sri Lankan imports from the world in 2013. Sri Lanka’s exports to Pakistan grew from USD 46 million to USD 63 million between 2004 and 2013, and Sri Lanka claimed only 0.14% of total Pakistani imports from the world in 2013.

Fig.1 Pakistan-Sri Lanka trade numbers 2004-2013

Trade between the two countries has shown lacklustre growth despite the FTA. Both countries claim significant market shares in precious few exports to the other. Trade has continued in roughly the same mix of products that existed prior to the FTA and most tariff lines continue toreportzerotrade.ThisisinstarkcontrasttoSriLanka’straderelationswithcountriessuchas India and China, wherein significant and fast-paced growth has occurred.

This Study suggests that fledgling Pakistan-Sri Lanka trade relations cannot be blamed on a paucity of opportunities or lack of potential for trade. Both countries produce goods that have healthy markets in the partner country. The FTA is comprehensive and offers full concession on a variety of important exports. Sri Lanka is currently in a period of reconstruction following the conclusion of long-lasting political conflict and is growing its status as a prime tourist destination. Moreover, Pakistan and Sri Lanka have strong political ties and the goodwill between them is part of what led Pakistan to sign its first free trade agreement with Sri Lanka. Considerable potential remains dormant, and this Study attempts to flesh out the specifics of thispotentialandsuggestwaystoremoveobstructionstoitsrealization.

134.715153.662

177.595

208.573 216.72 216.963

283.87

347.722

300.904316.382

45.6659.18

70.9759.79 66.22 55.79 53.37 61.13

83.4163.52

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US

D M

ILLI

ONS

Pakistan's Trade with Sri Lanka

Exports

Imports

10

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

2.2. HIGH POTENTIAL TRADE ITEMS

This Study identifies export items at the 6 digit HS code level which, based on certain favourable metrics, are poised to effectively drive the growth of trade between Pakistan and Sri Lanka. The metrics used are those of trade potential and Compound Annual Growth Rate (CAGR) values. Trade potential represents the extent to which trade can theoretically be increased with another country, and therefore provides an idea of the scope for trade expansion. A CAGR value for growth in, say, exports of an item over a certain period gives us the rate at which the exports would have grown if they grew smoothly, and therefore can function as a rough indicator of a growth trend. If, for a product X, trade potential is high, and the CAGR values of its total world exports by the exporting country and its total world imports by the importing country are high, it can be said that the exporting country is a significant and growing producer and the importing country is a significant and growing consumer of product X. This Study identifies items that exhibit this combination of favourable metrics, but a low or negative CAGR value for their trade between Pakistan and Sri Lanka, suggesting that certain generally positive trends have failed to encompass the Pak-Sri Lanka trade relation.

This further suggests that once the Pak-Sri Lanka specific obstruction to trade is removed, tradecanbeincreasedquicklybyharnessingthepositivetrends.Investigationintotheissuesfaced in Pak-Sri Lanka trade give us some idea of what these obstructions might be.

The following are selected Pakistani export items with high trade potential and favourable CAGR values. Out of the total trade potential of around USD 1.7 billion for the items surveyed at the 6 digit level, USD 500 million is concentrated in items with favourable CAGR values.

Table 1. Pakistani products that have high trade potential and encouraging CAGR values

HS CODES WITH HIGH TRADE POTENTIAL AND FAVOURABLE CAGR VALUES

HS Code Product Label Total Trade Potential in High CAGR Items in USD millions

Number of high potential/CAGR items at 6 digit HS code

73 Articles of iron or steel 53 3

39 Plastics and articles thereof. 34 11

85 Electrical,electronicequipment 29 6

62Articles of apparel and clothing accessories, not knitted or crocheted.

16 3

The following are selected Sri Lankan export item HS codes with high potential and favourable CAGR values at the 6 digit HS code level. Out of the total trade potential of around USD 1 billion for the items surveyed at the 6 digit level, USD 880 million is concentrated in items with favourable CAGR values.

Table 2. Sri Lankan products that have high trade potential and encouraging CAGR values

HS CODES WITH HIGH TRADE POTENTIAL AND HIGH CAGR VALUES

HS Code Product Label Total Trade Potential in High CAGR Items in USD millions

Number of high potential/CAGR items at 6 digit HS code

09 Coffee, tea, mate and spices 316 2

85 Electrical,electronicequipment 75 13

40 Rubber and articles thereof 40 6

21 Miscellaneous edible preparations 31 2

These tables suggest that a lack of trade potential is not the primary impediment to better Pakistan-Sri Lanka trade relations.

11

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

3.0 RECOMMENDATIONS

The major impediment to healthier trade relations between Pakistan and Sri Lanka seems to be disengagement between the countries’ business men as well as their policy makers. This could be due to misconceptions regarding Sri Lanka’s potential as a market for Pakistani goods and the resulting lack of interest in trade with the country. This suggests that the unrealizedpotentialthisStudyidentifiesremainsunrealizedlargelybecauseneithercountryviews the other as a priority market despite an abundance of opportunities. This is evinced by the lack of regular trade delegations and single country exhibitions, which leads to weak ties between the business communities of the two countries, thereby making it difficult to jump-start trade within neglected high potential items. While there are specific items which can be put forward to be considered for further concessions, by and large the FTA terms themselves are comprehensive and do not seem to be in need of any serious amendments.

3.1 TRADE DELEGATIONS AND SINGLE COUNTRY EXHIBITIONS

Trade delegations and single country exhibitions must be held regularly in order to lay the groundwork for stronger ties between the two countries’ business communities, as well as to raise awareness regarding the significant potential that lies in Pak-Sri Lanka trade. One of the major complaints voiced by Pakistani exporters to Sri Lanka is that a lack of interaction with their Sri Lankan counterparts impedes the identification of further opportunities for business in either country and prevents existing partnerships from being deepened. The granting of arrival visas by both sides would be a significant step towards facilitating the kind of interaction requiredtoboosttrade. 3.2 AGREEMENT ON CHANGES TO FTA TERMS

Any changes in tariffs, para-tariffs or no-concession lists that conflict with the terms of the FTA must be discussed by both countries before being brought into effect. There are instances of unilateral changes made by both Pakistan and Sri Lanka that have undermined the spirit of theFTAandconsequentlyseriouslydisruptedbusinessdealingsbetweenthetwocountrieswithin products such as broom corn and steel pipes. Problematic changes such as these will likely become less common as trade between Pakistan and Sri Lanka becomes more significant.

3.3 GREATER INVOLVEMENT OF BUSINESSMEN IN REVIEW OF THE FTA

Industrialists and exporters should have greater involvement in the drafting of future FTAs and the review of this existing FTA. A commonly voiced complaint was that an FTA can only be maximally advantageous if it takes into account the variegated and interwoven issues and concerns of different sectors affected by the FTA. In other words, an item-byitem discussion involving stakeholder is thought to be necessary.

3.4 FORUMS FOR TRADE DISPUTE RESOLUTION

Forums must be set up for the efficient arbitration of trade disputes. Disputes arise with regularity and end up unaddressed due to the lack of efficient mechanisms for their resolution. This has acted as an additional disincentive to trade between Pakistan and Sri Lanka, as the dangerofadelayedresolutionornoresolutionhasresultedinmorefrequentcasesoffraud.

12

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

4.0 STUDY OBJECTIVES

The decade following the signing of the Pakistan-Sri Lanka Free Trade Agreement has witnessed low growth in trade between the two countries. This is particularly troubling becauseinadditiontohavingstrongpoliticaltiesandcomprehensiveFTAtermstocapitalizeon, both countries also seem to possess markets for the other’s major export goods. The primary aim of this Study is to estimate the potential for bilateral trade between Pakistan and Sri Lanka and recommend means for achieving the same. We therefore start by identifying:

a) Items possessing high potential for export from Pakistan to Sri Lanka b) Items possessing high potential for export from Sri Lanka to Pakistan

Sources of Data

The data for this study has been drawn from ITC Trademap for the period ended 2013 , which bases its data on UN Comtrade, maintained by the United Nations Statistics Division (UNSD). AnyquarterlyandmonthlydataisdrawnbyTrademapfromnationalandregionalsources.AlltariffvaluesareequivalentadvaloremtariffsdrawnfromTrademapunlessotherwisenoted.

Methodology

This study provides a list of items at the 6-digit HS code level that exhibit high trade potential, with items possessing favourable CAGR metrics highlighted.

Intuitively, trade potential is the theoretical extent to which trade of a given item can be expanded, which suggests the actual scope for growth in trade of that item. It is given by the followingequation:

Trade Potential

=Min (Pakistan’s exports to the world of X,Sri Lanka’s imports from the world of X)

-Pakistan’s current exports to Sri lanka of X

For instance, if Pakistan exports USD 500 million worth of cement to the world, and Sri Lanka imports USD 300 million worth of cement from the world, and Pakistan exports USD 40 million worth of cement to Sri Lanka, then trade potential is USD 260 million, since Pakistan has the capacity to export USD 260 million worth of cement to Sri Lanka given Sri Lanka’s import requirements.

The Compound Annual Growth Rate (CAGR) is the geometric mean of the individual annual growth rates during a period. It gives you the growth rate that would have gotten your initial value to your final value had the value grown smoothly over the relevant period. It is given by:

If the CAGR for Pakistan’s world exports of a good is high, and the CAGR for Sri Lanka’s world imports of that good is high, but the CAGR for export of that good from Pakistan to Sri Lanka is low or negative, the item has been highlighted, since the removal of an obstruction that is potentially specific to Pakistan-Sri Lanka relations can jump-start trade of the good between the two countries.

1 2013 was the last year for which complete data was available.

13

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Furthermore, the revealed comparative advantage has been calculated for items on either country’s no concession list to bring attention to items that may be worth considering for further concessions. Revealed comparative advantage is given by:

RCA indicates the relative efficiency of a country in exporting a particular good.

14

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

5.0 PAKISTAN SRI LANKA FREE TRADE AGREEMENT (PSLFTA)

The Pakistan-Sri Lanka Free Trade agreement (PSLFTA) was signed in July 2002 and became operationalfrom12thJune2005.TheFTArequiredbothcountriestoachievezerotariffsona range of items during a certain time-frame. Pakistan granted 100% immediate concession on 206 items at the 6-digit HS level whereas Sri Lanka granted 100% immediate concession on 102 items at the same level. Pakistan’s no concession list ran to 540 items at the 6 digit level while Sri Lanka’s no concession list ran to 697 items, which were cut down to 607 items inApril2013.Furthermore,PakistangrantedSriLankaadutyfreetariffratequota(TRQ)ontea products as well as another TRQ at 35% margin of preference on the MFN rate on various clothing items. Sri Lanka reciprocated by granting Pakistan a duty free TRQ on long grain Basmati riceandpotatoes.Thetermsof theFTArequiredPakistantophaseout tariffsonitems not on its no-concession list by 2008, while Sri Lanka had till 2010 to do the same. Major Pakistani exports that Sri Lanka granted full concession to include cotton, apparel, knitted fabrics and cement. Major Sri Lankan exports granted full concession by Pakistan include rubber, coconut products and vegetable products.

Table 3. Summary of Pak-Sri Lanka FTA terms

Tariff Reduction Pakistan Sri Lanka

100% immediate concession 206 items 102 items

Tariff-phasing out period 3 years 5 years

Sensitive List 540 607 (amended in 2013)

Rules of OriginDirect Value Addition (DVA) is 35% of FOB value. If parts of an input originate from a contracting country, minimum aggregate content must be 35% with minimum domestic input content being 25%.

The most recent year for which comprehensive trade data was available was 2013 and therefore the tariff concessions granted to Sri Lankan import items by the Federal Board of Revenue in April 2014 have not been taken into account.

5.1 SHORT ECONOMY PROFILES

The GDP Average Annual Growth Rate (AAGR) in Sri Lanka averaged 6.59% from 2003 until 2014, whereas Pakistan’s GDP AAGR for the same period was 11.11%

Fig. 2 GDP Growth rates of Pakistan and Sri Lanka

From 2004 to 2013 Sri Lanka’s total trade with the world grew by 110% whereas Pakistan’s trade grew by 120%. However, since the FTA was fully implemented in 2010, Sri Lanka’s trade has grown by 35% whereas Pakistan’s trade has grown by only 17%. Both Pakistan and Sri

0

50

100

150

200

250

2003 2005 2007 2009 2011 2013

US

D B

ILLI

ON

S

GDP Annual Growth

Sri Lanka GDP

Pakistan GDP

-2.5

-2

-1.5

-1

-0.5

02003 2005 2007 2009 2011

US

D B

ILLI

ONS

Trade Deficit Growth Rate

Sri Lanka Trade Balance

Pakistan Trade Balance

15

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Lanka have had negative trade balances over the period 2004-2013, with the Sri Lankan trade imbalance increasing by 232% and the Pakistani trade balance increasing by 308% during this time.

Fig. 3 Pakistan and Sri Lanka’s balances of trade

0

50

100

150

200

250

2003 2005 2007 2009 2011 2013

US

D B

ILLI

ON

S

GDP Annual Growth

Sri Lanka GDP

Pakistan GDP

-2.5

-2

-1.5

-1

-0.5

02003 2005 2007 2009 2011

US

D B

ILLI

ONS

Trade Deficit Growth Rate

Sri Lanka Trade Balance

Pakistan Trade Balance

16

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

5.2 TOP TRADING PARTNERS

Pakistan’s exports have continued to be dominated by the US over the past few years, whereas exports to China have grown over three times since 2007 to make it Pakistan’s second largest export destination in 2013. Both Afghanistan and the UK have shown healthy growth as export markets for Pakistani products over this period though the UAE has fallen off by a small amount.

Table 4. Pakistan’s top five export destinations Figures in USD Billions

Pakistan Export Partner 2007 2008 2009 2010 2011 2012 2013

USA 3.85 3.65 3.22 3.67 3.84 3.67 3.75

China 0.61 0.73 1.00 1.44 1.68 2.62 2.65

United Arab Emirates 2.11 2.01 1.54 1.83 1.92 2.87 1.78

Afghanistan 0.84 1.45 1.37 1.68 2.66 2.10 2.00

United Kingdom 0.97 1.00 0.94 1.11 1.26 1.25 1.43

The UAE has emerged as Pakistan’s major origin of imports over the period under consideration, and while imports from the rest of the top five import partners showed overall growth during this time, Saudi imports fell by a small amount.

Table 5. Pakistan’s top five origins of imports Figures in USD Billions

Pakistan Import Partner 2007 2008 2009 2010 2011 2012 2013

United Arab Emirates 2.77 3.78 3.35 5.25 6.82 7.21 7.75

China 4.16 4.74 3.78 5.25 6.47 6.69 6.63

Kuwait 1.85 3.44 1.80 2.61 3.89 4.21 3.95

Saudi Arabia 4.01 5.95 3.50 3.84 4.67 4.28 3.85

Malaysia 1.16 1.69 1.61 2.05 2.73 2.13 1.92

Sri Lanka’s exports have flowed primarily to the EU and the US over the past few years, with the US gradually gaining importance as an export destination until 2013 when it was only 4.6% lower than exports to the EU. India has held on to a distant third place in the top Sri Lankan import partners and has shown little growth as a market for Sri Lankan goods between 2007 and 2013.

Table 6. Sri Lanka’s top five export destinations Figures in USD Billions

Sri Lanka Export Partner 2007 2008 2009 2010 2011 2012 2013

EU 2.39 2.49 2.33 2.53 2.80 2.94 2.69

USA 1.98 1.89 1.59 1.77 2.14 2.12 2.57

India 0.52 0.42 0.33 0.47 0.52 0.60 0.54

Russia 0.20 0.22 0.19 0.24 0.28 0.26 0.28

United Arab Emirates 0.21 0.26 0.21 0.25 0.30 0.23 0.24

India has been Sri Lanka’s major source of imports over this period, though China has asserted itself as a serious competitor for the Sri Lankan market by more than doubling its exports to the country since 2007. The table suggests that the Sri Lankan market for foreign goods is healthy and growing, and this should be a guiding idea in assessing Pakistan’s fledgling trade relationship with the country.

17

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Table 7. Sri Lanka’s top five origins of import Figures in USD Billions

Sri Lanka Import Partner 2007 2008 2009 2010 2011 2012 2013

India 2.59 2.84 1.72 3.31 4.45 3.81 4.75

China 1.39 1.63 1.57 1.99 2.99 3.00 3.44

Singapore 0.83 0.99 0.76 1.20 1.33 1.56 1.96

EU 1.17 1.19 1.00 1.22 1.56 1.49 1.38

United Arab Emirates 0.37 0.46 0.30 0.34 0.81 1.29 1.22

18

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

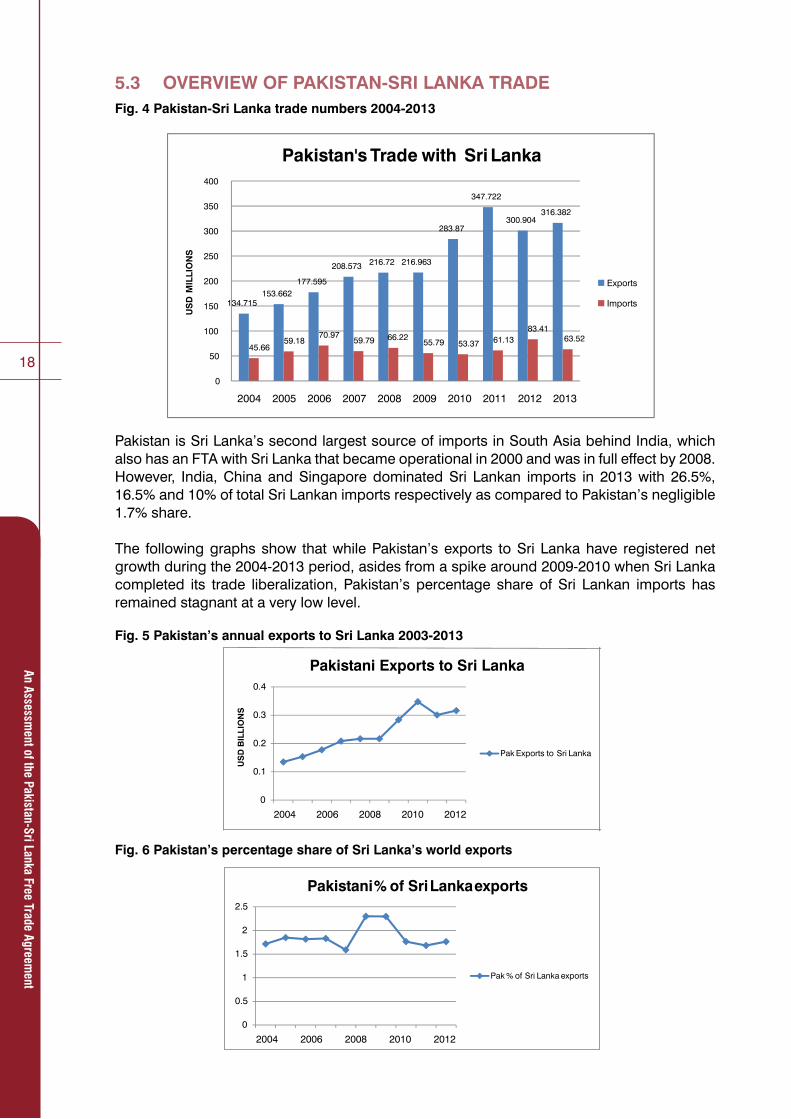

5.3 OVERVIEW OF PAKISTAN-SRI LANKA TRADEFig. 4 Pakistan-Sri Lanka trade numbers 2004-2013

Pakistan is Sri Lanka’s second largest source of imports in South Asia behind India, which also has an FTA with Sri Lanka that became operational in 2000 and was in full effect by 2008. However, India, China and Singapore dominated Sri Lankan imports in 2013 with 26.5%, 16.5% and 10% of total Sri Lankan imports respectively as compared to Pakistan’s negligible 1.7% share.

The following graphs show that while Pakistan’s exports to Sri Lanka have registered net growth during the 2004-2013 period, asides from a spike around 2009-2010 when Sri Lanka completed its trade liberalization, Pakistan’s percentage share of Sri Lankan imports hasremained stagnant at a very low level.

Fig. 5 Pakistan’s annual exports to Sri Lanka 2003-2013

Fig. 6 Pakistan’s percentage share of Sri Lanka’s world exports

134.715153.662

177.595

208.573 216.72 216.963

283.87

347.722

300.904316.382

45.6659.18

70.9759.79 66.22

55.79 53.37 61.1383.41

63.52

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US

D M

ILLI

ON

S

Pakistan's Trade with Sri Lanka

Exports

Imports

Fig. 5 Pakistan’s annual exports to Sri Lanka 2003-2013

Fig. 6 Pakistan’s percentage share of Sri Lanka’s world exports

0

0.1

0.2

0.3

0.4

2004 2006 2008 2010 2012

US

D B

ILLI

ON

S

Pakistani Exports to Sri Lanka

Pak Exports to Sri Lanka

0

0.5

1

1.5

2

2.5

2004 2006 2008 2010 2012

Pakistani % of Sri Lanka exports

Pak % of Sri Lanka exports

Fig. 5 Pakistan’s annual exports to Sri Lanka 2003-2013

Fig. 6 Pakistan’s percentage share of Sri Lanka’s world exports

0

0.1

0.2

0.3

0.4

2004 2006 2008 2010 2012

US

D B

ILLI

ON

S

Pakistani Exports to Sri Lanka

Pak Exports to Sri Lanka

0

0.5

1

1.5

2

2.5

2004 2006 2008 2010 2012

Pakistani % of Sri Lanka exports

Pak % of Sri Lanka exports

19

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

In 2004 Pakistani exports to Sri Lanka were USD 154 million, which was 1.15% of total Pakistani exports and 2.8% of Sri Lankan imports. By 2013 they were USD 316 million, which was 1.26% of total Pakistani exports and 1.7% of Sri Lankan imports. It is therefore clear that the period over which the FTA gradually came into effect Pakistan’s absolute level of exports to Sri Lanka increased by 105% but its share of Sri Lanka’s total imports actually fell, which is cause for concern since Pakistan’s share of the Sri Lankan import goods market was very small to begin with.

For comparison, India, Sri Lanka’s other FTA partner, had exports to Sri Lanka of USD 1.4 billion in 2004, which were 17.8% of Sri Lanka’s total imports and by 2013 exports were USD 4.8 billion, and 26.5% of Sri Lanka’s total imports. So, prima facie, India was able to better capitalizeonitsFTAwithSriLankathanPakistanwasonthePSLFTA.

On the other hand, Sri Lanka’s exports to Pakistan were USD 46 million (0.83% of Sri Lankan exports) in 2004 and USD 63 million (0.63% of Sri Lankan exports) in 2013. So Pakistan has remained an insignificant export destination for Sri Lankan products during the period the FTA has come into effect. Sri Lanka’s exports to India were USD 333 million (6.1% of Sri Lankan exports) in 2004 and USD 515 million (5.15 % of Sri Lankan exports) in 2013, suggesting that while there is a significant absolute rise in exports to India, Sri Lankan exports are finding other priority markets or have been unable to overcome India’s significant non-tariff barriers. It should be kept in mind, however, that while the current state of trade between Sri Lanka and Pakistan is not entirely encouraging, both are markets for the other’s primary exports. Pakistan is an important export market for tea, which is a top Sri Lankan export item, and it is also a significant importer of copra and rubber, which are also important Sri Lankan exports. Sri Lanka is an important market for textile products, machinery and pharmaceuticals along with other products that Pakistan records significant exports of. Therefore a more fruitful trading partnership seems to lie within reach for the two countries.

Table 8. Pakistan and India’s exports to Sri Lanka in 2004 and 2013

2004 2013

Pakistani Exports to Sri Lanka 154 million 316 million

Indian Exports to Sri Lanka 1.4 billion 4.8 billion

Table 9. Pakistan and India’s imports from Sri Lanka in 2004 and 2013

2004 2013

Pakistani Imports from Sri Lanka 46 million 63 million

Indian Imports from Sri Lanka 313 million 515 million

20

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

The following graphs show that Sri Lanka’s major trade partners exhibited aggressive growth not just in absolute exports but also in their share of the Sri Lankan market during 2004-2013, whereas Pakistan remained a bit player in the Sri Lankan market.

Fig. 7 Composition of Sri Lanka’s total imports by country of origin

Fig. 8 Sri Lankan world imports by partner country percentage shares

It should be noted that Pakistan has been a major trading partner of Sri Lanka’s in the past: in 1990 Pakistan accounted for 27.6% of Sri Lanka’s imports from SAARC countries (South Asian Association for Regional Cooperation), and for 45.8% of Sri Lanka’s exports to the same region. However, the FTA does not seem to have done enough to counteract the falling off of Pakistan-Sri Lanka trade relations since their heyday.

Fig. 7 Composition of Sri Lanka’s total imports by country of origin

Fig. 8Sri Lankan world imports by partner country percentage shares

0

1

2

3

4

5

2004 2006 2008 2010 2012

US

D B

ILLI

ON

S

Sri Lankan Import Composition by Import origin

Pak Exports

India Exports

China Exports

Singapore Exports

0

5

10

15

20

25

30

2004 2006 2008 2010 2012

Trade Partner Percentage Share in Sri Lankan Imports

Pak % Share

India % Share

China % share

Singapore % share

Fig. 7 Composition of Sri Lanka’s total imports by country of origin

Fig. 8Sri Lankan world imports by partner country percentage shares

0

1

2

3

4

5

2004 2006 2008 2010 2012

US

D B

ILLI

ON

S

Sri Lankan Import Composition by Import origin

Pak Exports

India Exports

China Exports

Singapore Exports

0

5

10

15

20

25

30

2004 2006 2008 2010 2012

Trade Partner Percentage Share in Sri Lankan Imports

Pak % Share

India % Share

China % share

Singapore % share

21

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

5.4 OVERVIEW OF PAKISTAN’S EXPORTS TO THE WORLD AND TO SRI LANKA

Pakistan’s export mix has remained consistent over the period 2007-2013, with cotton, textile products and cereals dominating. High growth in a number of export items is worth noting- export of cereals grew by 75%, salt, sulphur etc. by 187%, sugar exports grew over 900% and pearls and precious stones grew by 260%.

Table 9. Pakistan’s world exports 2007-2013 Figures in USD MillionsPAKISTAN’S EXPORTS TO THE WORLD

HS Code Product labelExported value in

2007

Exported value in

2008

Exported value in

2009

Exported value in

2010

Exported value in

2011

Exported value in

2012

Exported value in

2013

52 Cotton 3,440 3,596 3,204 4,013 5,097 5,226 5,334

63Other made textile articles, sets, worn clothing etc

3,179 3,146 2,918 3,285 3,570 3,285 3,685

10 Cereals 1,244 2,508 1,823 2,280 2,807 2,061 2,181

61Articles of apparel, accessories, knit or crochet

1,851 1,888 1,681 1,982 2,239 2,006 2,105

62Articles of apparel, accessories, not knit or crochet

1,371 1,361 1,206 1,462 1,775 1,694 1,855

42Articles of leather, animal gut, harness, travel goods

692 767 578 619 681 674 744

25Salt, sulphur, earth, stone, plaster, lime and cement

252 601 563 514 571 714 723

17 Sugars and sugar confectionery 61 239 112 88 67 254 634

41Raw hides and skins (other than fur skins) and leather

392 383 270 416 468 457 530

27Mineral fuels, oils, distillation products, etc

994 1,230 715 1,203 1,312 331 527

39 Plastics and articles thereof 187 296 306 408 544 521 450

71Pearls, precious stones, metals, coins, etc

120 240 479 590 469 1,634 437

8 Edible fruit, nuts, peel of citrus fruit, melons 125 145 203 254 311 348 434

55 Manmade staple fibres 386 285 300 511 606 449 418

22 Beverages, spirits and vinegar 156 231 122 187 273 173 364

90Optical, photo, technical, medical, etc apparatus

241 280 257 261 302 319 348

22

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

The table on the following page is suggestive with regards to the importance of Pakistani imports to Sri Lanka. A number of top Pakistani exports to Sri Lanka registered significant growthinabsolutetermsduring2004-2013,thoughthisislargelyaconsequenceofverylowexport numbers in 2004 to begin with. While several exports exhibit this unarguably positive trajectory, growth in percentage shares of the Sri Lankan market suggests that the trend was not strong enough to carve out a space for Pakistan as a significant Sri Lankan trade partner. In other words, most Pakistani export items held onto only a marginal presence in Sri Lanka’s import market during this period. Notable exceptions to this were cotton (18.6%), raw hides (28.4%), milling products (21.5%) and sugar (12%), which all managed to capture a major part of their respective markets. On the other hand, market share in HS 63 (other textile articles) and HS 03 (fish, crustaceans etc.) dropped significantly from 68% and 13% to 24% and 4% respectively of total Sri Lankan imports.2

2The most recent year for which comprehensive trade data was available was 2013 and therefore the tariff concessions granted to Sri Lankan import items by the Federal Board of Revenue in April 2014 have not been taken into account in this report.

PAKISTAN’S EXPORTS TO THE WORLD

HS Code Product labelExported value in

2007

Exported value in

2008

Exported value in

2009

Exported value in

2010

Exported value in

2011

Exported value in

2012

Exported value in

2013

03Fish, crustaceans, molluscs,aquaticinvertebrates nes

161 218 193 231 261 292 333

07Edible vegetables and certain roots and tubers

73 46 86 120 259 188 249

11Milling products, malt, starches, inulin, wheat gluten

110 24 22 47 368 263 227

95 Toys, games, sports requisites 211 226 172 212 225 219 221

23

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Tab

le 1

0. P

akis

tani

imp

ort

s’ s

har

e o

f th

eir

mar

ket

in S

ri L

anka

Fi

gur

es in

US

D M

illio

ns

PA

KIS

TAN

’S S

HA

RE

OF

SR

I LA

NK

AN

IMP

OR

TS

HS

Co

de

Pro

duc

t La

bel

Exp

ort

s to

Sri

La

nka

2004

Sri

Lan

ka’s

im

po

rts

fro

m

wo

rld

200

4

% s

har

e o

f to

tal

Sri

Lan

kan

imp

ort

s

Exp

ort

s to

Sri

La

nka

2013

Sri

Lan

ka’s

im

po

rts

fro

m

wo

rld

201

3

% s

har

e o

f to

tal

Sri

Lan

kan

imp

ort

s

Ch

ang

e in

ex

po

rts

Ch

ang

e in

%

shar

e o

f S

ri

Lank

an Im

po

rts

Eq

uiva

lent

ad

va

lore

m t

ariff

ap

plie

d b

y S

ri L

anka

to

P

akis

tan

52C

otto

n60

527

11.5

0%10

254

918

.60%

427.

20

25S

alt,

sulp

hur,

eart

h,

ston

e, p

last

er, l

ime

and

cem

ent

097

0%45

587

7.70

%45

7.6

0.6

10C

erea

ls21

262

8.20

%38

355

10.7

0%16

2.5

6.9

17S

ugar

s an

d su

gar

conf

ectio

nery

212

81.

50%

3528

912

%33

10.4

12.3

07E

dibl

e ve

geta

bles

an

d ce

rtai

n ro

ots

and

tube

rs5

845.

80%

1828

66.

20%

130.

414

.9

30P

harm

aceu

tical

pr

oduc

ts5

103

5.20

%17

330

5.30

%12

0.1

0.2

73A

rtic

les

of ir

on o

r st

eel

414

03.

10%

1537

03.

90%

100.

92.

3

60K

nitte

d or

cro

chet

ed

fabr

ic2

343

0.50

%5

620

0.80

%3

0.3

0

03Fi

sh, c

rust

acea

ns,

molluscs,aquatic

inve

rteb

rate

s ne

s6

4113

.50%

511

74%

-1-9

.54.

5

11M

illin

g pr

oduc

ts, m

alt,

star

ches

, inu

lin, w

heat

gl

uten

07

0.10

%4

1921

.50%

421

.40.

6

41R

aw h

ides

and

ski

ns

(oth

er th

an fu

rski

ns)

and

leat

her

09

2.40

%4

1528

.40%

425

.90.

6

39P

last

ics

and

artic

les

ther

eof

627

92.

10%

459

50.

60%

-2-1

.52.

3

22B

ever

ages

, spi

rits

and

vine

gar

018

0%3

535.

60%

35.

681

.5

52C

otto

n60

527

11.5

0%10

254

918

.60%

427.

20

25S

alt,

sulp

hur,

eart

h,

ston

e, p

last

er, l

ime

and

cem

ent

097

0%45

587

7.70

%45

7.6

0.6

10C

erea

ls21

262

8.20

%38

355

10.7

0%16

2.5

6.9

24

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

PA

KIS

TAN

’S S

HA

RE

OF

SR

I LA

NK

AN

IMP

OR

TS

HS

Co

de

Pro

duc

t La

bel

Exp

ort

s to

Sri

La

nka

2004

Sri

Lan

ka’s

im

po

rts

fro

m

wo

rld

200

4

% s

har

e o

f to

tal

Sri

Lan

kan

imp

ort

s

Exp

ort

s to

Sri

La

nka

2013

Sri

Lan

ka’s

im

po

rts

fro

m

wo

rld

201

3

% s

har

e o

f to

tal

Sri

Lan

kan

imp

ort

s

Ch

ang

e in

ex

po

rts

Ch

ang

e in

%

shar

e o

f S

ri

Lank

an Im

po

rts

Eq

uiva

lent

ad

va

lore

m t

ariff

ap

plie

d b

y S

ri L

anka

to

P

akis

tan

17S

ugar

s an

d su

gar

conf

ectio

nery

212

81.

50%

3528

912

%33

10.4

12.3

07E

dibl

e ve

geta

bles

an

d ce

rtai

n ro

ots

and

tube

rs5

845.

80%

1828

66.

20%

130.

414

.9

30P

harm

aceu

tical

pr

oduc

ts5

103

5.20

%17

330

5.30

%12

0.1

0.2

73A

rtic

les

of ir

on o

r st

eel

414

03.

10%

1537

03.

90%

100.

92.

3

60K

nitte

d or

cro

chet

ed

fabr

ic2

343

0.50

%5

620

0.80

%3

0.3

0

03Fi

sh, c

rust

acea

ns,

molluscs,aquatic

inve

rteb

rate

s ne

s6

4113

.50%

511

74%

-1-9

.54.

5

11M

illin

g pr

oduc

ts, m

alt,

star

ches

, inu

lin, w

heat

gl

uten

07

0.10

%4

1921

.50%

421

.40.

6

41R

aw h

ides

and

ski

ns

(oth

er th

an fu

rski

ns)

and

leat

her

09

2.40

%4

1528

.40%

425

.90.

6

39P

last

ics

and

artic

les

ther

eof

627

92.

10%

459

50.

60%

-2-1

.52.

3

22B

ever

ages

, spi

rits

and

vine

gar

018

0%3

535.

60%

35.

681

.5

25

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

The following table is suggestive with regards to Sri Lanka’s importance to Pakistan as a destination for its exports. Items such as pharmaceutical products (10%), articles of iron and steel (8%) and knitted or crotched fabric (16%) are among the few Pakistani export categories that rely significantly on Sri Lankan demand. The table shows that several major exports to Sri Lanka have actually shrunk in their importance as sources of export revenue for Pakistan during 2004-2013, one example being edible vegetables which fell from 12% of Pakistan’s total exports of the item to 7%. Several top Pakistani exports to Sri Lanka account for less than 1% of those items’ total exports by Pakistan, such as raw hides and plastics.

Table 11. Sri Lanka’s share in world exports of Pakistani items Figures in USD Millions

SRI LANKA’S SHARE OF PAKISTAN’S EXPORTS

HS Code Product LabelExports to Sri Lanka

2004

Exports to world

2004

% Share of total world

exports

Exports to Sri Lanka 2013

Exports to world

2013

% Share of total world

exports

Change in % share

52 Cotton 60 2,979 2% 102 5,334 1.90% -0.1

25Salt, sulphur, earth, stone, plaster, lime and cement

0 44 0.10% 45 723 6.30% 6.2

10 Cereals 21 683 3.10% 38 2,181 1.70% -1.4

17 Sugars and sugar confectionery 2 107 1.80% 35 634 5.50% 3.6

07Edible vegetables and certain roots and tubers

5 40 12.10% 18 249 7.10% -5

30 Pharmaceutical products 5 57 9.40% 17 169 10.30% 0.9

73 Articles of iron or steel 4 55 7.80% 15 180 8.10% 0.3

60 Knitted or crocheted fabric 2 179 1% 5 33 16.10% 15.1

03Fish, crustaceans, molluscs,aquaticinvertebrates nes

6 114 4.90% 5 333 1.40% -3.5

11Milling products, malt, starches, inulin, wheat gluten

0 53 0% 4 227 1.80% 1.8

41Raw hides and skins (other than furskins) and leather

0 286 0.10% 4 530 0.80% 0.7

39 Plastics and articles thereof 6 165 3.50% 4 450 0.80% -2.7

22 Beverages, spirits and vinegar 0 29 0% 3 364 0.80% 0.8

08 Edible fruit, nuts, peel of citrus fruit, melons 2 107 1.60% 3 434 0.60% -1

09 Coffee, tea, mate and spices 1 16 5.90% 2 77 3.10% -2.8

63Other made textile articles, sets, worn clothing etc

6 2,353 0.20% 2 3,685 0.10% -0.2

61Articles of apparel, accessories, knit or crochet

2 1,665 0.10% 2 2,105 0.10% 0

87 Vehicles other than railway, tramway 1 37 2.80% 2 74 2.50% -0.3

55 Manmade staple fibres 1 111 0.70% 2 418 0.40% -0.3

85 Electrical, electronic equipment 1 66 1.20% 1 115 0.80% -0.4

26

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

5.5 OVERVIEW OF PAKISTAN’S IMPORTS FROM THE WORLD AND FROM SRI LANKA

Major Pakistani imports from the world that registered significant percentage increases include mineral fuels (45%), animal and vegetable fats (34%), and printed books and newspapers (95%).Itemswhoseimportsfellduringthisperiodincludeelectronicequipment(-29%),vehiclesotherthanrailways(-15%)andtramwaysandfertilizers(-23%).

Table 12. Pakistan’s imports from the world 2007-2013 Figures in USD Millions

PAKISTAN’S IMPORTS FROM THE WORLD

HS Code Product labelImported value in

2007

Imported value in

2008

Imported value in

2009

Imported value in

2010

Imported value in

2011

Imported value in

2012

Imported value in

2013

% change in

Imports

27Mineral fuels, oils, distillation products, etc

8,350 14,054 8,838 11,399 14,860 15,947 15,247 45.2

84 Machinery, nuclear reactors, boilers, etc 3,262 3,924 3,120 2,953 2,951 3,060 3,058 -6.7

85 Electrical, electronic equipment 3,448 3,782 2,619 2,442 2,430 2,752 2,682 -28.6

29 Organic chemicals 1,570 1,761 1,518 1,721 2,213 2,038 2,016 22.1

15Animal,vegetable fats and oils, cleavage products, etc

1,301 1,880 1,412 1,852 2,589 2,313 1,980 34.3

72 Iron and steel 1,543 1,629 1,683 1,695 1,680 1,848 1,841 16.2

39 Plastics and articles thereof 1,281 1,360 1,185 1,458 1,679 1,501 1,570 18.4

87 Vehicles other than railway, tramway 1,419 1,184 969 1,308 1,502 1,596 1,238 -14.6

52 Cotton 918 1,209 498 831 909 684 1,047 12.3

89Ships, boats and other floating structures

573 183 399 839 527 544 981 41.6

49Printed books, newspapers, pictures etc

42 78 44 46 33 137 858 95.1

30 Pharmaceutical products 374 433 539 498 534 598 675 44.6

31 Fertilizers 748 729 805 648 1,028 908 606 -23.4

38 Miscellaneous chemical products 393 450 503 555 588 549 583 32.7

55 Manmade staple fibres 280 339 345 505 681 539 532 47.3

54 Manmade filaments 339 315 344 516 703 530 527 35.7

07Edible vegetables and certain roots and tubers

288 305 430 507 562 595 500 42.3

73 Articles of iron or steel 388 622 480 425 387 409 486 20.2

12Oil seed, oleagic fruits, grain, seed, fruit, etc, nes

501 380 459 628 691 616 479 -4.7

40 Rubber and articles thereof 342 365 292 413 536 464 460 25.7

A cursory glance at the table below suggests that Sri Lanka is not a major origin of imports for Pakistan, with the exception of vegetable plaiting materials whose Sri Lankan imports account for 69% of all Pakistani imports of the product. This is also the only HS code that has registered any significant growth in its share of Pakistani imports since 2004, growing its share from 31% to 69%. Several top Sri Lankan imports account for less than 1% of total Pakistani imports of those products, including edible vegetables and manmade filaments.

27

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Table 13. Sri Lanka’s share in Pakistan’s total world imports Figures in USD Millions

SRI LANKA’S SHARE OF PAKISTAN’S IMPORTS

HS Code Product Label

Pak Imports from SL

2004

Pak Imports

from world 2004

% Share in Pakistani Imports

Pak Imports from SL

2013

Pak Imports

from world 2013

% Share in Pakistan’s

imports

Change in % share

14Vegetable plaiting materials, vegetable products nes

4 12 31% 17 25 69.20% 38.2

40 Rubber and articles thereof 13 218 5.80% 11 460 2.50% -3.3

44 Wood and articles of wood, wood charcoal 3 54 4.80% 9 110 7.90% 3.1

09 Coffee, tea, mate and spices 7 251 2.60% 7 385 1.80% -0.8

8 Edible fruit, nuts, peel of citrus fruit, melons 4 50 7.40% 6 133 4.30% -3.1

07Edible vegetables and certain roots and tubers

0 106 0% 4 500 0.80% 0.8

54 Manmade filaments 0 156 0.10% 2 527 0.30% 0.2

12Oil seed, oleagic fruits, grain, seed, fruit, etc, nes

11 269 4% 1 479 0.30% -3.7

53Vegetable textile fibres nes, paper yarn, woven fabric

1 32 1.70% 1 51 1.80% 0.1

47Pulp of wood, fibrous cellulosic material, waste etc

0 46 0% 1 107 0.50% 0.5

48

Paper and paperboard, articles of pulp, paper and board

0 225 0.10% 1 441 0.10% 0

62Articles of apparel, accessories, not knit or crochet

0 5 0.60% 1 22 2.40% 1.8

87 Vehicles other than railway, tramway 0 769 0% 0 1,238 0% 0

39 Plastics and articles thereof 1 714 0.10% 0 1,570 0% -0.1

38 Miscellaneous chemical products 0 340 0.10% 0 583 0.10% 0

15Animal,vegetable fats and oils, cleavage products, etc

0 798 0.10% 0 1,980 0% -0.1

61Articles of apparel, accessories, knit or crochet

0 5 0.80% 0 25 1.20% 0.4

76 Aluminium and articles thereof 0 139 0.10% 0 195 0.10% 0

69 Ceramic products 0 62 0% 0 101 0.20% 0.2

55 Manmade staple fibres 0 149 0.20% 0 532 0% -0.2

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Section 2 Analysis of

Pakistan’s Exports to Sri Lanka under

FTA

29

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

6.0 PRELIMINARY ANALYSIS OF PAKISTANI EXPORTS TO SRI LANKA UNDER FTA

At the 2-digit HS code level 16 of the top 20 items registered net growth over the 2004-2013 period. The major growth items were cotton, which showed an increase of over USD 41 million, and HS 25 (salt, sulphur etc.), which showed an increase of over USD 45 million, albeit from a very low initial level of exports. Other major Pakistani exports to Sri Lanka include cereals and sugar products. Four 2-digit HS code items experienced a net reduction in exports, with the steepest reduction hitting HS 63 (other made textiles), which fell by over 3 million dollars.

Table 14. Pakistan’s major exports to Sri Lanka Figures in USD Millions

PAKISTAN'S EXPORTS TO SRI LANKA

HS Code Product label Value in 2004

Value in 2013 Growth

Equivalent ad valorem tariff applied

by Sri Lanka to Pakistan

52 Cotton 60 102 42 0

25 Salt, sulphur, earth, stone, plaster, lime and cement 0 45 45 0.6

10 Cereals 21 38 16 6.9

17 Sugars and sugar confectionery 2 35 33 12.3

07 Edible vegetables and certain roots and tubers 5 18 13 14.9

30 Pharmaceutical products 5 17 12 0.2

73 Articles of iron or steel 4 15 10 2.3

60 Knitted or crocheted fabric 2 5 3 0

03 Fish,crustaceans,molluscs,aquaticinvertebrates nes 6 5 -1 4.5

11 Milling products, malt, starches, inulin, wheat gluten 0 4 4 0.6

41 Raw hides and skins (other than furskins) and leather 0 4 4 0.6

39 Plastics and articles thereof 6 4 -2 2.3

22 Beverages, spirits and vinegar 0 3 3 81.5

08 Edible fruit, nuts, peel of citrus fruit, melons 2 3 1 8.8

09 Coffee, tea, mate and spices 1 2 1 1.6

63 Other made textile articles, sets, worn clothing etc 6 2 -4 0

61 Articles of apparel, accessories, knit or crochet 2 2 0 0

87 Vehicles other than railway, tramway 1 2 1 15.8

55 Manmade staple fibres 1 2 1 0

85 Electrical,electronicequipment 1 1 0 2.7

An analysis at the 6 digit HS code level further highlights the worrying state of Pakistan-Sri Lanka trade relations over the past decade. Out of a total of 3502 items at full concession for exports from Pakistan, a mere 308 (8.8%) items showed net growth in the 2004-2013 period. 2952 (84.3%) full concession items exhibited no growth during this period, and the remaining 242 (6.9%)items showed a fall in exports. Furthermore, 3121 (89%) items at full concession showed0exportsin2013,and2934(83.7%)itemsalsoshowedzeroexportsin2004.Thissuggests that little diversification of exports has been achieved during the FTA period.

Full concession items accounted for around USD 94 million of exports to Sri Lanka in 2004 and for around USD 214 million in 2013, showing a growth by 129%. However, the extent to

30

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

whichthetermsoftheFTAcontributedtothisgrowthrequiresfurtheranalysis.

Out of a total of 568 items at no concession (including the items granted partial concessions in the form of TRQs) for which data was available, only 53 (9.3%) items showed net growth. 469 (82.3%) items registered no growth whereas the remaining 46 (8.1%) items fell in exports. 501 (88%)of these items reportedno exports in 2013, and 471(83%)items reported zeroexports in 2004.

Non-concession items accounted for around USD 34 million of exports to Sri Lanka in 2004 and around USD 70 million in 2013, indicating a growth of 51%. Tariff information was not available for 74 items at the 6-digit code HS level. These items accounted for about USD 6 million of total exports to Sri Lanka in 2013.

Table 15. Pakistani export items with positive, negative or zero growth in exports to Sri Lanka

Positive Growth Items

Negative Growth Items

Zero Growth Items

Full Concession Items 8.8% 6.9% 84.3%

No Concession Items 9.3% 8.1% 82.3%

Fig.8 Pakistani export items to Sri Lanka categorized by positive, negative and zero growthFig.8 Pakistani export items to Sri Lanka categorized by positive, negative and zero growth

0

500

1000

1500

2000

2500

3000

3500

Full Concession Items No Concession Items

Pakistani Export Items to Sri Lanka by Growth

Positive Growth Items

Negative Growth Items

No Growth Items

Num

ber

of

Exp

ort

Item

s

31

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

6.1 COMPARISON OF PAKISTAN & INDIA’S TRADE WITH SRI LANKA

India has emerged as Sri Lanka’s major source of imports and has outperformed Pakistan despite the fact that both countries have signed FTAs with Sri Lanka. A finer-grained comparison of India and Pakistan’s exports to Sri Lanka is necessary to better understand the challenges Pakistan faces with regards to its trade relationship with Sri Lanka.

The total list of Pakistani exports with available data at the 6 digit code comes out to 4070 items.TotalexportstoSriLankafortheseitemsreportedbyPakistanequalaroundUSD292million (this is different from the total reported exports due to missing data for some exports). India’s total exports for these same items amount to around USD 4.7 billion.

India outperforms Pakistan in exports to Sri Lanka in 2834 items on this list of 4070 items, whereas Pakistan outperforms India in a mere 134 items.

Fig 9. Comparison of the levels of Pakistan and India’s exports to Sri Lanka

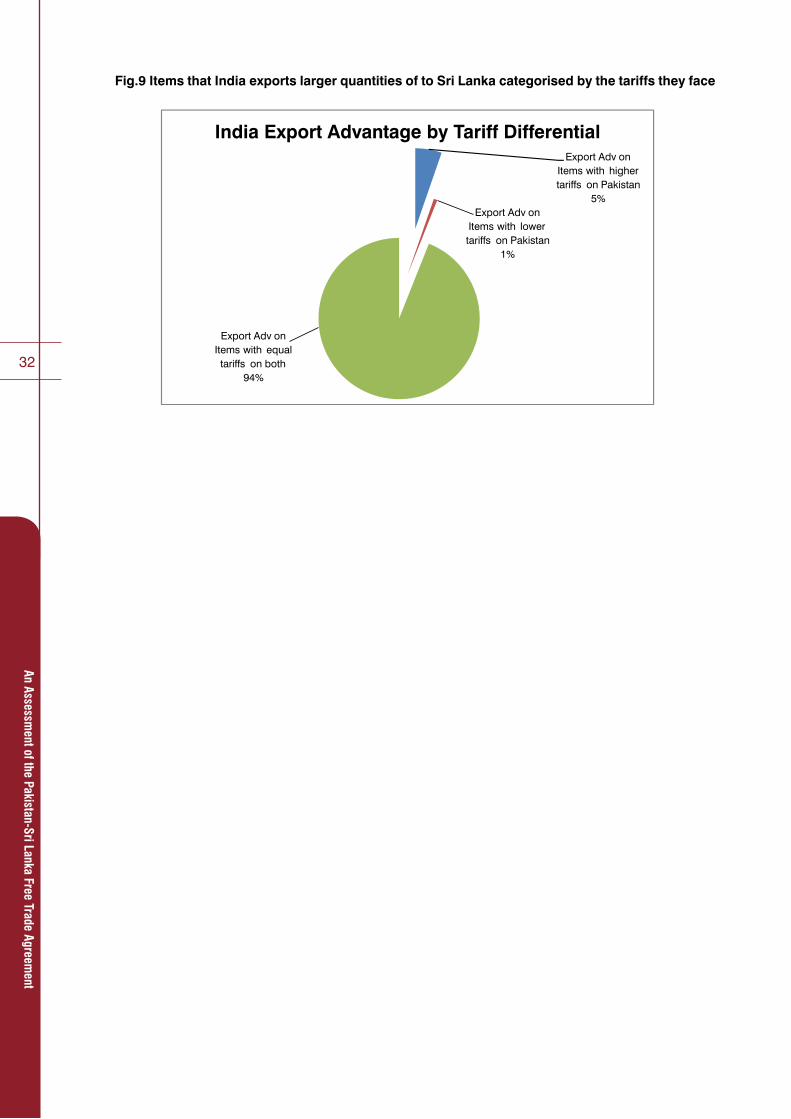

India has a tariff advantage over Pakistan in 21 of the items with available data. India’s export value for these 21 items exceeds Pakistan’s export value for them by around USD 32 million, which is a mere 0.7% of the total export value differential India has over Pakistan. This suggests that India’s superior performance with regards to Sri Lanka is likely not primarily a result of its tariff advantages over Pakistan.

The 308 items on which Pakistan has a tariff advantage on India also report higher total Indian exports to Sri Lanka by an amount of USD 230 million. This reasserts the fact that differences in tariffs are not the primary factor in India’s relatively stronger trade relation with Sri Lanka, since even in cases where Pakistan enjoys higher concessions from Sri Lanka India is able to outperform it.

Items with higher Indian exports

70%

Items with higher Pakistani exports

3%

Items with equal exports

27%

Pakistan and India Exports to Sri Lanka at 6 digit HS code

32

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

Fig.9 Items that India exports larger quantities of to Sri Lanka categorised by the tariffs they face

Export Adv on Items with higher tariffs on Pakistan

5%

Export Adv onItems with lowertariffs on Pakistan

1%

Export Adv on Items with equal tariffs on both

94%

India Export Advantage by Tariff Differential

Fig.9 Items that India exports larger quantities of to Sri Lanka categorised by the tariffs they face

33

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

7.0 ANALYSIS OF PAKISTAN’S EXPORTS TO SRI LANKA

We will now attempt to pinpoint those Pakistani export items to Sri Lanka at the 6 digit HS codelevelthatrequirethemostattentionandhavethehighestpotentialtobeturnedaroundbecause of certain favourable metrics associated with them.

Wewillconsider itemswith tradepotentialhigher thanorequal to1milliondollars.Tradepotential is given by:

Trade Potential therefore gives us a rough picture of the extent to which trade can theoretically be increased for any given item. For example, if Pakistan exports USD 490 million worth of sugar to the world, and Sri Lanka imports USD 260 million worth of sugar from the world, and Pakistan sells USD 30 million worth of sugar to Sri Lanka, Pakistan’s trade potential in this case is (USD 260 million-USD 30 million) USD 230 million.

TofurtherhelpzeroinonhighpotentialitemswewilltakeintoconsiderationtheCompoundAnnual Growth Rates (CAGR) for Pakistan’s exports to Sri Lanka, Sri Lanka’s imports from the world and Pakistan’s exports to the world. The CAGR is the geometric mean of the individual annual growth rates during a period. It gives you the growth rate that would have gotten your initial value to your final value had the value grown smoothly over the relevant period.

If the CAGR for Sri Lanka’s imports of a product X from the world is high, and the CAGR of Pakistan’s exports to the world of product X is similarly high, but the CAGR for Pakistan’s exports of product X to Sri Lanka is relatively low or negative, there is reason to think that somebarrieruniquetoPak-SriLankatraderelationsisimpedingexportsofproductXtoSriLanka. This information coupled with the trade potential for product X can give us a good idea ofwhichitemsrequireurgentattentionduetotheircurrentlywastedpotential.Theexportsof these items to Sri Lanka may be boosted by removing a non-tariff barrier such as a lack of awareness among exporters or prohibitively complex regulations that stand in the way of allowingPakistantocapitalizeontheafore-mentionedpositivetrendsvis-à-visSriLanka.TheCAGR values can also be used to pinpoint those products that are already performing well as Pakistani exports to Sri Lanka.

WecanzeroinevenfurtheronhighpotentialitemsifweconsiderSriLanka’stariffratesonIndia, Sri Lanka’s other South Asian FTA partner, in conjunction with the afore-mentioned metrics. So products that exhibit high trade potential, high-potential CAGR values and a Pakistani tariff advantage over India are particularly deserving of attention. Such items have been compiled into a table later in the report.

Thelistofhighpotentialitemsisorganizedbytradepotentialindescendingorderwithhighpotential CAGR value items highlighted in blue. The total trade potential for items with trade potential exceeding USD 1 million is USD 1.728 billion. Out of a total of these 275 items, 123 or about 45% show high potential CAGR values. These items show a collective trade potential of USD 548 million and so 30% of total trade potential of all items under consideration is concentrated in high CAGR items. In other words, this potential of USD 545 million lies in items that are growing as Pakistani exports to the world and as Sri Lankan imports from the world.

34

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

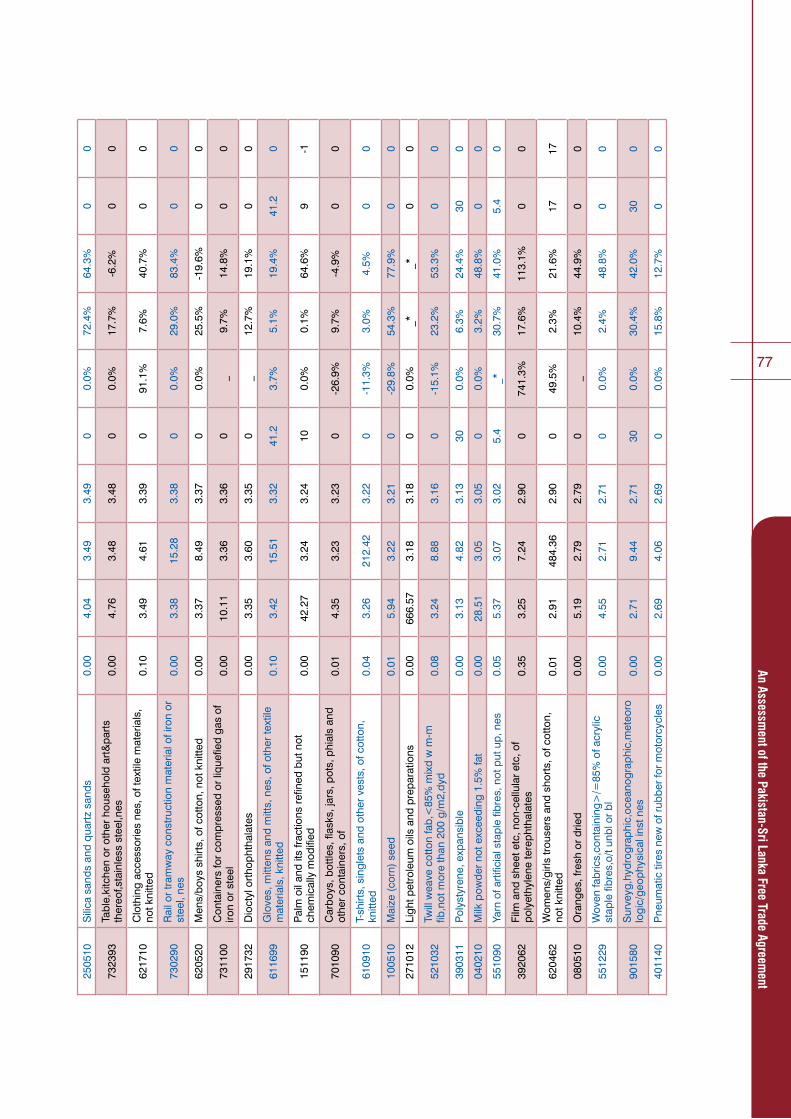

This overview suggests that there is a wealth of items that have experienced favourable trends in their supply and demand by Pakistan and Sri Lanka respectively, and yet these trends have conspicuously failed to encompass the trade relationship between the two countries. 21 of the 275 items have a tariff advantage on India, whereas 242 items show no difference in tariffs imposed on India and Pakistan by Sri Lanka.

Only selected items from the total list of 275 are listed in the following tables.

Note: All CAGR values are calculated for the period 2004-2013. CAGR values have only been calculated if there are at least 3 consecutive years of recorded exports and at least one year of recorded exports within the period 2010-2013. This is so that the numbers used are recent and consistent enough to be suggestive of future trends. “_” indicates that these requirementsarenotmet,or in thecaseofnon-CAGRvalues,unavailabilityofdata. “_*”indicates that while export numbers were reported in 2013, the years before did not meet therequirements.Asaresult thisgenerally indicatesveryspottyand/or lowgrowthinthatparticular item and therefore the item should be considered to have not performed well in termsofexportstothecountryunderconsideration.Avalueprecededby“*”indicatesthatwhile there were no recorded exports in 2013, the previous years’ numbers met the afore-mentionedrequirementsforcalculatingaCAGR.ItshouldbenotedthatCAGRvaluesfurnisha suggestive but imprecise picture of growth trends, since very volatile growth cannot be represented accurately using measures such as CAGR or AAGR (Annual Average Growth Rate).

35

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

7.1 TRADEPOTENTIAL≥USD10MILLION

38% of all items with trade potential exceeding USD 10 million exhibit encouraging CAGR values. Total trade potential in this bracket is USD 978 million, a very high value owing to the lack of several major Pakistani exports to Sri Lanka for which Sri Lanka has significant demand. Items with trade potential values exceeding USD 10 million and high potential CAGR values include HS 730890 (structures and parts of structures), HS 901890 (instruments used in medical sciences), and HS 870190 (wheeled tractors).

Tab

le 1

6. P

akis

tani

exp

ort

item

s to

Sri

Lan

ka w

ith h

igh

CA

GR

item

s h

igh

ligh

ted

Fig

ures

in U

SD

Mill

ions

TRADEPOTENTIAL≥USD10MILLION

HS

Co

de

Pro

duc

t La

bel

Pak

201

3 E

xpo

rt t

o

SL

SL

2013

W

orl

d

Imp

ort

Pak

201

3 W

orl

d

Exp

ort

Trad

e P

ote

ntia

lTa

riff

on

Pak

Pak

-SL

CA

GR

SL

Imp

ort

C

AG

RP

ak E

xpo

rt

CA

GR

Tari

ff o

n In

dia

2523

29P

ortla

nd c

emen

t nes

44.4

431

2.28

506.

6626

7.84

043

.50%

27.8

0%37

.60%

0

1701

99R

efin

ed s

ugar

, in

solid

form

, ne

s34

.39

257.

2448

7.78

222.

857.

5_

9.50

%48

.00%

14.9

3004

90M

edic

amen

ts n

es, i

n do

sage

9.41

73.4

827

9.61

64.0

70

12.4

0%14

.20%

9.10

%0

7308

90S

truc

ture

s&pa

rts

of

structures,i/s(exprefabbldgs

of h

eadg

no.

9406

)0.

0046

.56

50.1

146

.56

00.

00%

9.20

%27

.60%

1.3

8517

12Te

leph

ones

for

cellu

lar

netw

orks

mob

ile te

leph

ones

or

for

othe

r w

irele

0.00

44.3

810

6.25

44.3

80

0.00

%7.

10%

-1.2

0%0

9018

90In

stru

men

ts a

nd a

pplia

nces

us

ed in

med

ical

or

vete

rinar

y sc

ienc

es, n

es0.

2334

.90

296.

8134

.66

01.

30%

5.60

%7.

90%

0

5208

39W

oven

fabr

ics

of

cotton,>/=85%,notmore

than200g/m2,dyed,nes

3.40

46.2

638

.00

34.6

00

8.70

%21

.20%

6.70

%0

8701

90W

heel

ed tr

acto

rs n

es0.

7628

.37

33.9

527

.61

02.

90%

7.20

%17

.90%

0

8414

51Fa

ns: t

able

,roo

f etc

w a

sel

f-co

nt e

lec

mtr

of a

n ou

tput

nt

excd

g 12

5W0.

0817

.98

36.1

617

.89

025

.20%

13.6

0%12

.50%

0

2106

90Fo

od p

repa

ratio

ns n

es0.

0128

.56

17.4

717

.46

13.5

-17.

30%

12.2

0%7.

00%

13.4

6203

42Mens/boystrousersand

shor

ts, o

f cot

ton,

not

kni

tted

0.03

16.0

465

3.12

16.0

10

9.30

%21

.60%

8.30

%0

5209

42D

enim

fabr

ics

of

cotton,>/=85%,morethan

200g/m2

23.4

638

.80

495.

9415

.34

073

.80%

3.10

%28

.10%

0

8507

10Le

ad-a

cid

elec

tric

ac

cum

ulat

ors

of a

kin

d us

d f

star

tg p

isto

n en

gine

s0.

0015

.32

20.3

215

.32

300.

00%

14.4

0%51

.30%

30

5209

39W

oven

fabr

ics

of

cotton,>/=85%,morethan

200g/m2,dyed,nes

1.25

127.

0416

.48

15.2

30

63.4

0%0.

90%

41.0

0%0

36

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

TRADEPOTENTIAL≥USD10MILLION

HS

Co

de

Pro

duc

t La

bel

Pak

201

3 E

xpo

rt t

o

SL

SL

2013

W

orl

d

Imp

ort

Pak

201

3 W

orl

d

Exp

ort

Trad

e P

ote

ntia

lTa

riff

on

Pak

Pak

-SL

CA

GR

SL

Imp

ort

C

AG

RP

ak E

xpo

rt

CA

GR

Tari

ff o

n In

dia

5208

59W

oven

fabr

ics

of

cotton,>/=85%,notmore

than200g/m2,printed,nes

0.24

38.9

314

.54

14.3

00

-14.

60%

25.7

0%-1

5.80

%0

5211

42D

enim

fabr

ics

of c

otto

n,

<85%mixedwithm-mfib,

morethan200g/m2

1.61

15.7

551

.54

14.1

40

20.3

0%23

.10%

5.00

%0

2401

10To

bacc

o, u

nman

ufac

ture

d,

not s

tem

med

or

strip

ped

0.00

56.2

013

.11

13.1

175

0.00

%5.

10%

41.9

0%75

3903

19P

olys

tyre

ne n

es0.

1513

.20

53.6

813

.05

0-2

43.0

0%9.

30%

23.8

0%0

5205

11Cottonyarn,>/=85%,single

,uncombd,>/=714.29dtex,

nt p

ut u

p0.

5513

.56

155.

4513

.01

018

.20%

-8.9

0%6.

50%

0

37

An Assessment of the Pakistan-Sri Lanka Free Trade Agreem

ent

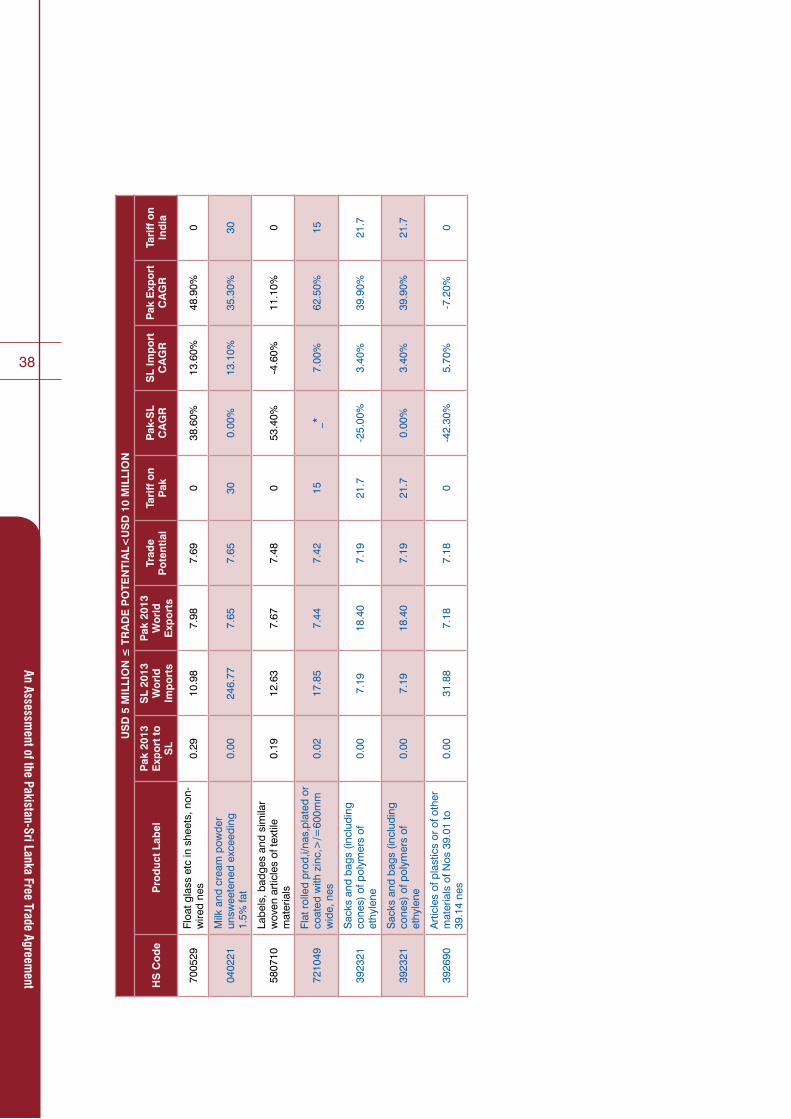

7.2 USD5MILLION≤TRADEPOTENTIAL<USD10MILLION

45% of all items in this category show high potential CAGR values. Total trade potential in this category is USD 341.9 million.

Tab

le 1

7. P

akis

tani

exp

ort

item

s to

Sri

Lan

ka w

ith h

igh

CA

GR

item

s h

igh

ligh

ted

Fig

ures

in U

SD

Mill

ions

USD5MILLION≤TRADEPOTENTIAL<USD10MILLION

HS

Co

de

Pro

duc

t La

bel

Pak

201

3 E

xpo

rt t

o

SL

SL

2013

W

orl

d

Imp

ort

s

Pak

201

3 W

orl

d

Exp

ort

s

Trad

e P

ote

ntia

lTa

riff

on

Pak

Pak

-SL

CA

GR

SL

Imp

ort

C

AG

RP

ak E

xpo

rt

CA

GR

Tari

ff o

n In

dia

2301

20Fl

our,m

eal&

pelle

t of

fish,crust,mol/othaqua

inve

rt,u

nfit

hum

an c

ons

0.11

9.75

16.9

89.

640

-9.7

0%5.

40%

161.

20%

0

3208

90P

aint

s &

varn

i bas

ed o

n po

lym

ers

diss

olv

in a

non

-aqueoussolvnes

0.00

12.1

99.

439.

4320

0.00

%15

.20%

73.3

0%20