Embed Size (px)

Citation preview

AN EMPIRICAL STUDY ON RELATIONSHIP BETWEEN EXCHANGE RATE AND

SECTORAL INDICES IN BSE

Dr.R.K.Sudhamathi1

& M.Ganeshwari2

1. Dr.R.K.Sudhamathi, Associate Professor, Department of Management,

PSGR Krishnammal College for Women.

2. Ganeshwari.M, PhD Research Scholar , Department of Management,

PSGR Krishnammal College for Women.

Abstract

The present study focuses on the relationship between exchange rate and sectoral

indices listed in Bombay Stock Exchange(BSE) over the period 1.4.2015-31.3.2018. To analyse

the sectoral relationship with exchange rate and vice versa, the ADF test, Johansen

cointergartion, Granger Causality test and Correlation is applied for the study. The study

found that exchange-rate changes have negative effects on some sectors but positive effects on

others. Import intensive sectors like Bank, Auto, FMCG, Metal, infrastructure, IT, Oil& gas,

realty and TECK responded negatively to the weakening rupee. Further, the study suggests

individual and institutional investors to diversify their portfolio and can enjoy with handsome

return from the market.

Keyword:Sectoral indices, Johansen cointergartion, Granger Causality test, portfolio

Introduction

Foreign exchange market stability and stock market growth are the twin economic

objectives that all the country needs to achieve. This is because the financial position of every

economy i.e., both developing and developed country can be assessed from its exchange rate

stability. Stock market price and exchange rates are interconnected directly or indirectly, because

today, world is turning into a global village due to trade liberalization and globalization. For

example, investors i.e., foreign people are busy investing their capital in the stock markets world

over. Hence, in this process international investment is booming quickly and capital is moving

all across the world. The advantagefor these investors is being determined by foreign exchange

rate. Moreover, fluctuation in the exchange rates may bring about uncertainty or otherwise in

these investors. Thus, foreign exchange is the major determinant of stock market fluctuations.

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/197

In the earlier studies, researchers have investigated the impact of exchange rate on all

types of stocks under BSE and NSE.The present study is carried out to know the effectof

Exchange rate on all the sectors listed in BSE. The study will provide insights for investors

regarding the impact of exchange rate fluctuations over each sector.

Review of literature

Existing literature relating to the association between stock prices and exchange rates

shows diverse outlook. An early attempt has been made by (Saadet Kasman,2003) in this area

considered TRY/USD, financial sector index, production sector index, service sector index and

found that a long run relationship exist between only industry sector index with TRY/USD.

(KalimUllah, 2015) analyzed the relationship between both the market in Pakistan and concluded

there exist a bidirectional relationship between PKR/USD and KSE 100 i.e., investors can use

information of one market to predict the other market.

N.S.Nataraja, Ganesh.L and Sunil Kumar (2014) made a slight different study to detect

the impact of CNX Bank NIFTY with INR/USD. He found a negative correlation and Granger

causality test reveals uni -directional relationship between both the variables. Similar study has

been conducted by Uma Shankar Megha(2012) concluded that week rupee rate has significant

positive relationship with stock prices of Infosys and Wipro companies. Nikita Kagalwala

andDivyang Patel(2013) analyzed the relationship between Indian stock exchange and exchange

rate using monthly data and found that there is no or little impact of exchange rate on Indian

stock market.In recent days, economists are giving significance for the study of temporal relation

between exchange rates and stock returns, for theoretical as well as empirical reasons. The

development of any country’s economy is influenced by the changes in the series, stock price

and exchange rate. Also, the relationship between both the rates gives the guidelines in

predicting the future trends for each other by investors.

Data and methodology

To analyse the relationship between exchange rate and sectoral indices, this paper uses

daily data for exchange rate and all the sectors listed in BSE over the period 1.4.2015 –

31.3.2018. The data used for the study is USD/INR and all the 14 sectors listed in BSE

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/198

i.e.,(Auto, Bank, Capital goods, consumer durables, FMCG, healthcare, Infrastructure, IT,

Metal,Oil & Gas, Power, PSU, Realty and TECK) and the data has been collected from NSE and

RBI websites.

The study start by testing stationarity for all the series using Augmented Dickey Fuller (ADF)

test to assess the order of integration of all the series. Further, the study proceed to test for

Granger causality test to find the short run relationship and co-integration between series

integrated to test the long run relationship between both the markets.

Research Gap

Going through various literatures it is found that most of the studies conducted on either

correlation among the stock markets of developed countries or about volatility. A few of them

conducted on sectoral diversification in countries other than India. It is observed that the

researcher hardly found any study of current data belonging to Indian stock market as far as

sectoral diversification is concerned. So it is an attempt to fill the gap.

Objective

The primary objective of the study is to analyse the dynamic relationship between exchange rate

and sectoral indices in long run and short run.

Analysis & Interpretation:

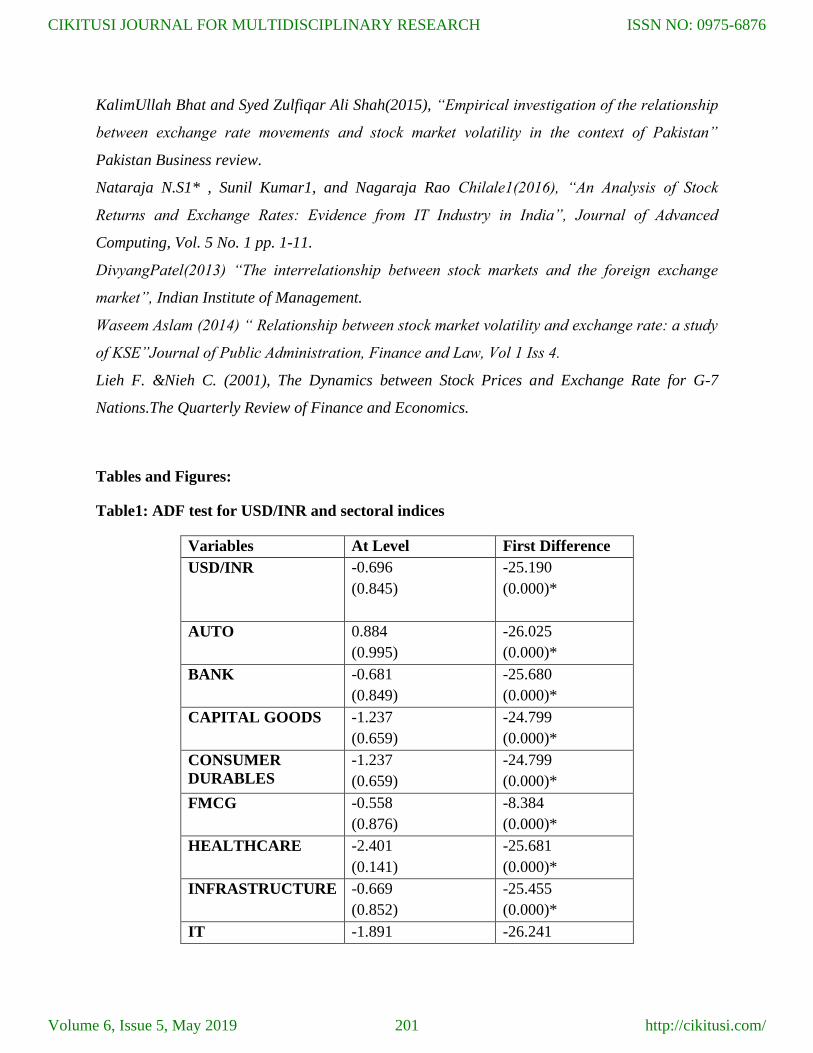

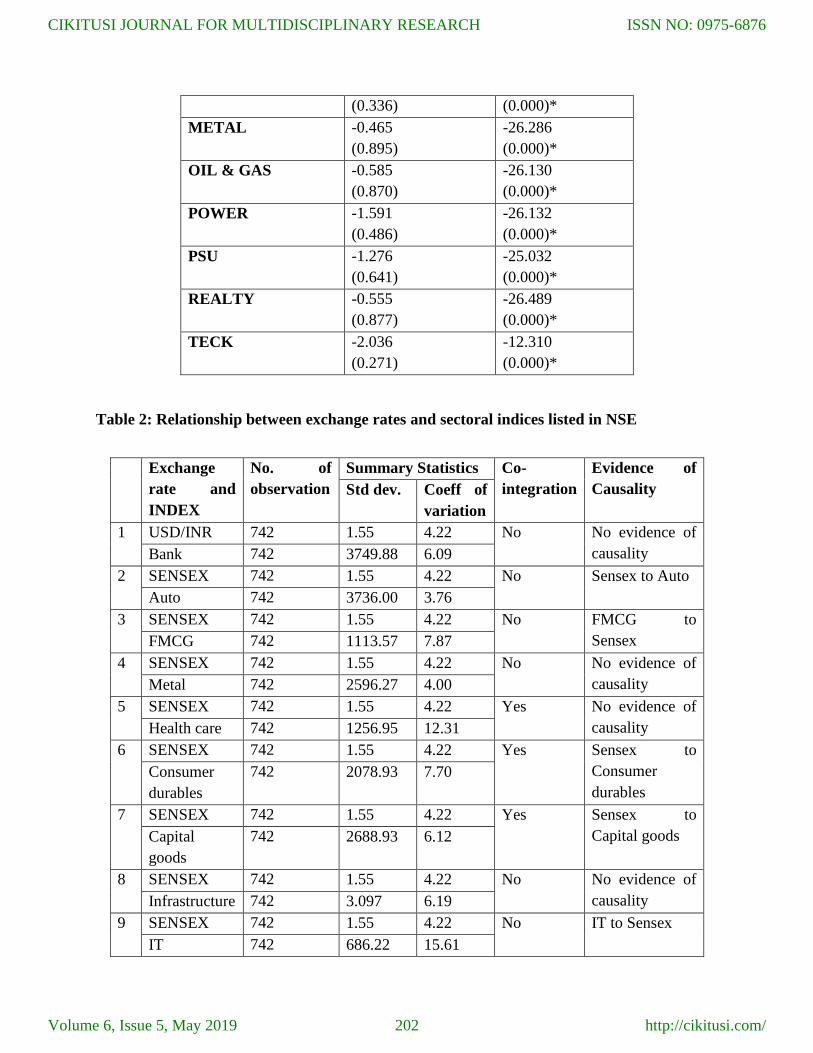

Table1: ADF test for USD/INR and sectoral indices

The above shows the results of ADF test for USD/INR and sectoral indices. The tests

were conducted at level and first difference for three years from April 2015 to March 2018.

Results revealed that at level and level both the variables were found to be greater than 0.05

which confirmed that null hypothesis cannot be rejected at level. It evidenced that the USD/INR

and sectors series was non stationary.

ADF statistics at first difference evidenced that USD/INR and sectoral indices were

found to be stationary since the p value is less than 0.05. Thus, the null hypothesis of non-

stationary are rejected at 1% level of significance.

Table 2: Relationship between exchange rates and sectoral indices listed in NSE

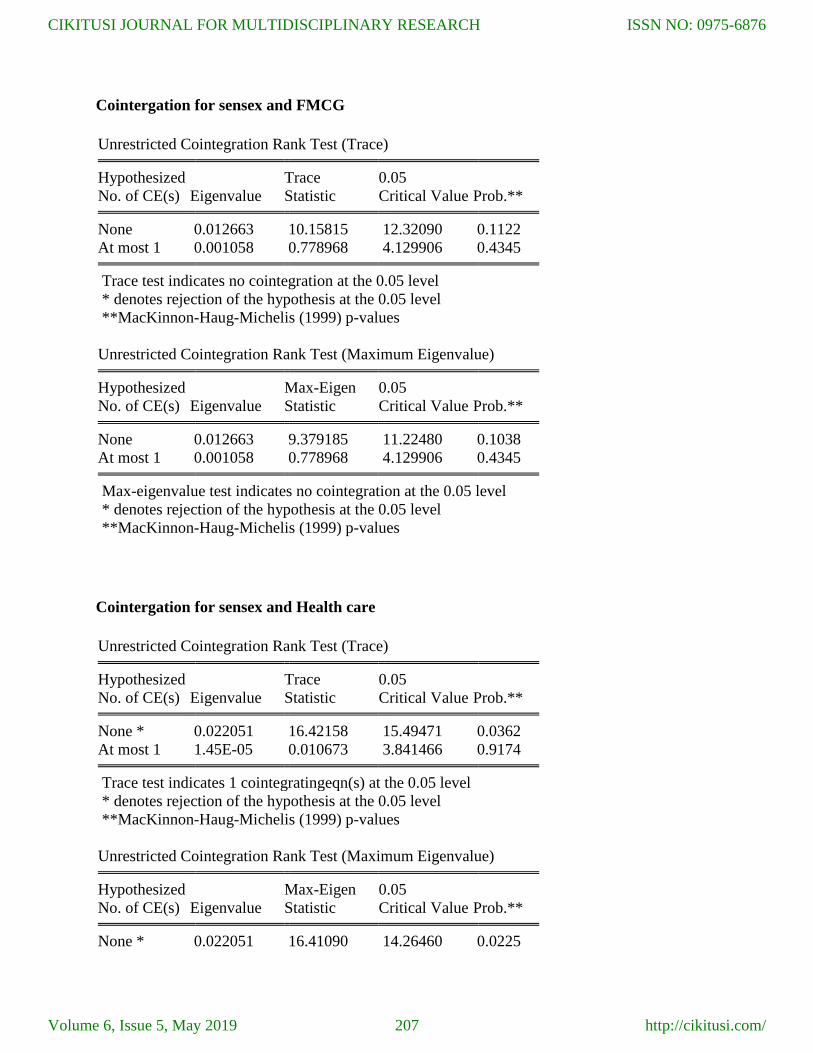

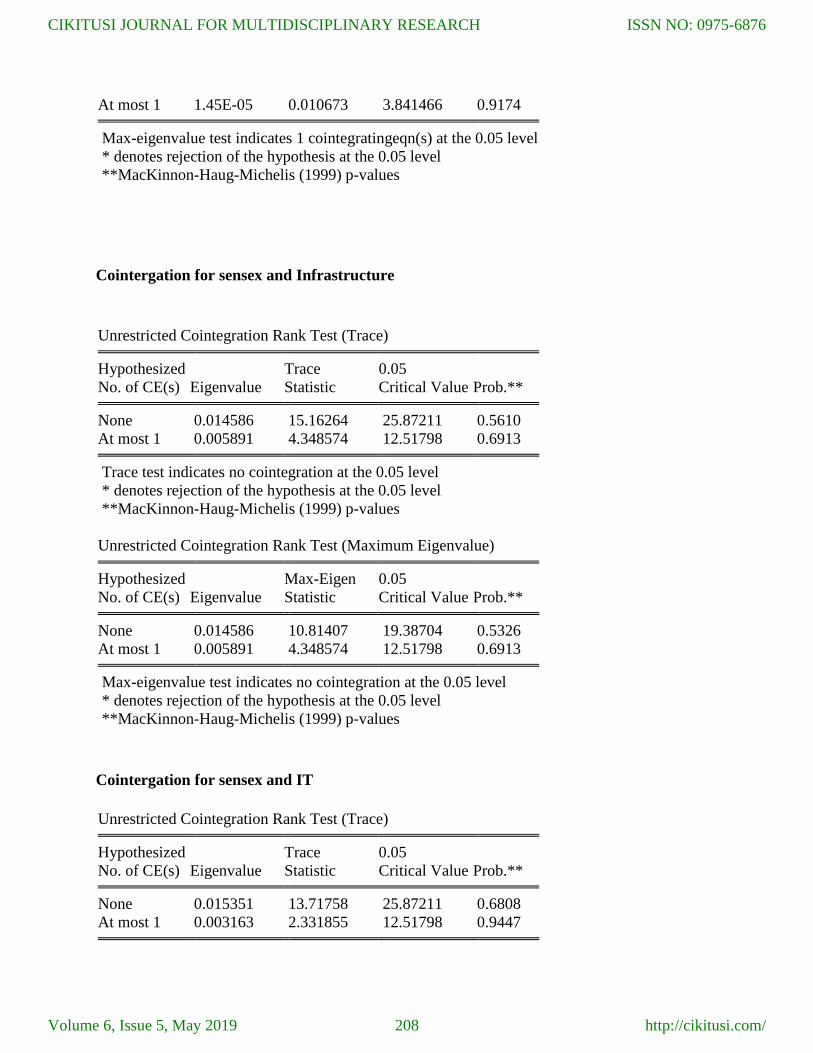

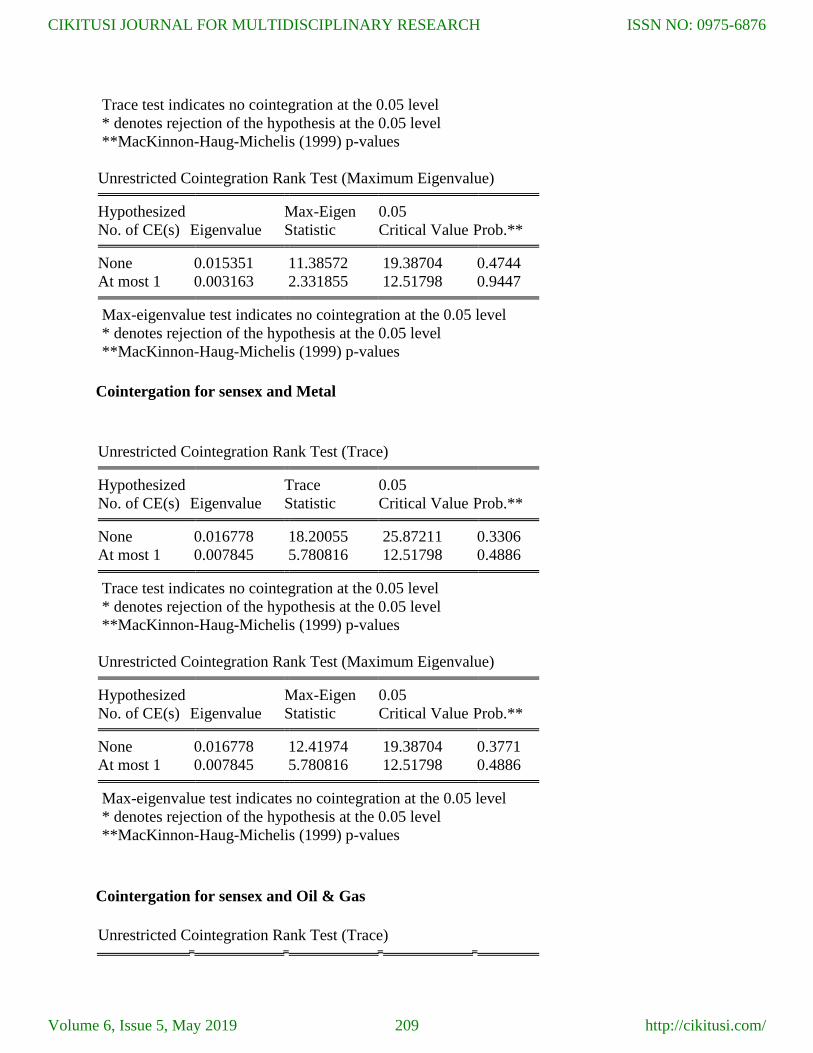

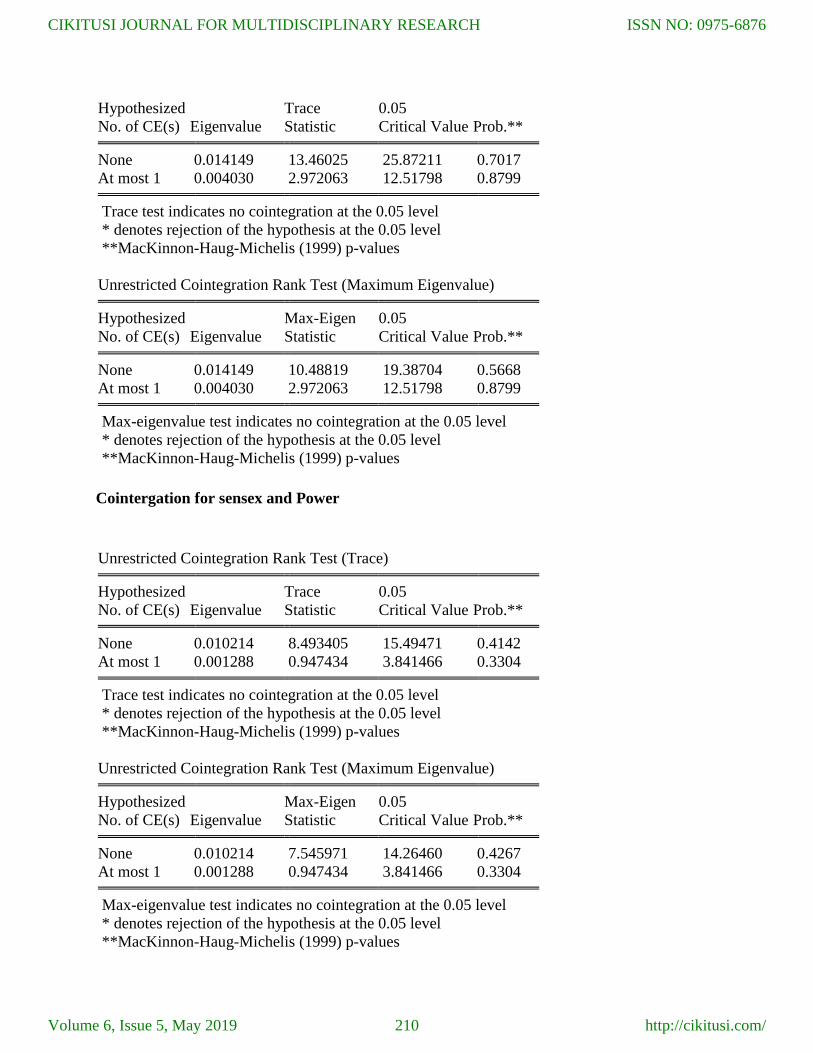

From the above table, Co-integration test reveals that out of 14 industry sectors identified

only Capital goods, consumer durables, Healthcare and realty sectors were found to have long

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/199

run relationship with exchange rate. Granger causality test reveals that sectors like Auto, FMCG,

consumer durables, capital goods IT, Oil& Gas, TECK and realty sectors were found to have

short run relationship with exchange rate.

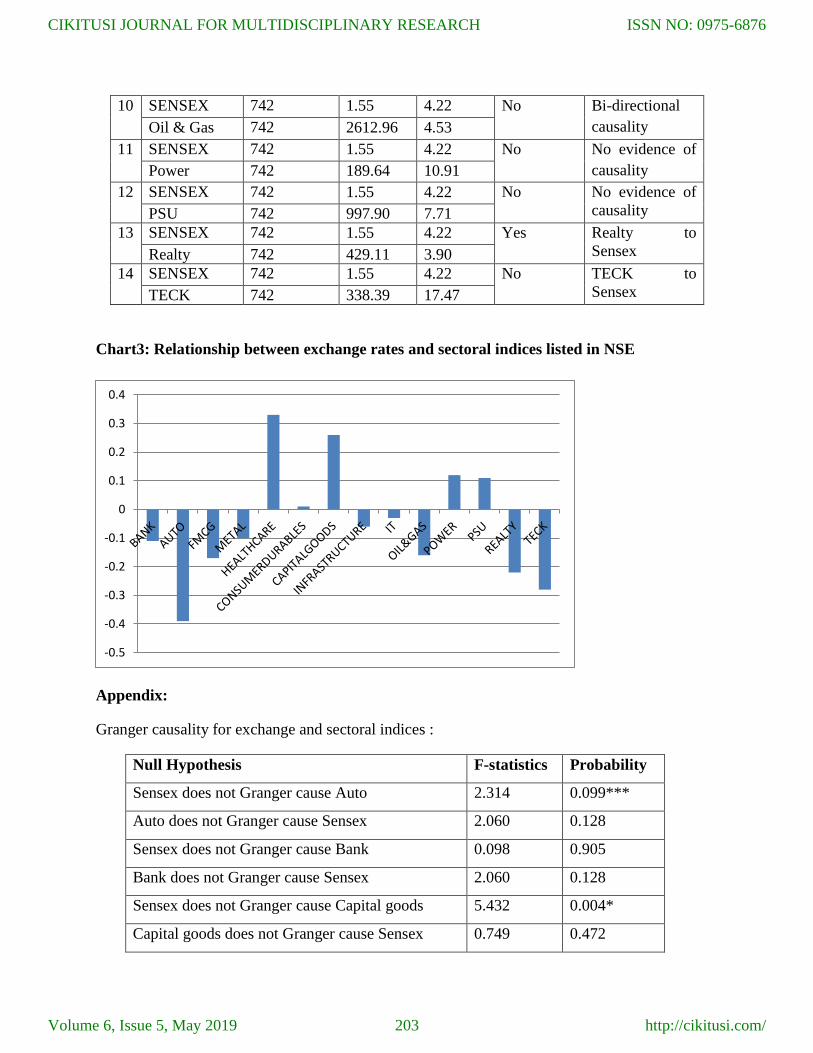

Chart1: Relationship between exchange rates and sectoral indices listed in NSE

From the above chart, it is found that health care, capital goods, consumer durables, Power, PSU

are positively correlated with USD/INR. Most of the import extensive sectors like Bank, Auto,

FMCG, Metal, infrastructure, IT, Oil& gas, realty and TECK are negatively correlated with

USD/INR. These sectors respond negatively to weakening of rupee.

Conclusion

The knowledge of the stock market structure is important for both investors and portfolio

managers to invest rationally. The present paper is focused on analysis the relationship between

exchange rate and sectoral indices listed in BSE. The study found that different sectors

responded differently to the change in exchange rate fluctuations. Exchange-rate changes have

negative effects on some sectors but positive effects on others. Import intensive sectors like

Bank, Auto, FMCG, Metal, infrastructure, IT, Oil& gas, realty and TECK responded negatively

to the weakening rupee. All other sectors were found to be positively correlated with the

appreciating rupee during 2015 to 2018 and thus testifying differing effects of exchange rate

changes on the performance of stock indices across different sectors. The implication of the

result may help individual and institutional investors to diversify their portfolio and can enjoy

with handsome return from the market.

Biblography:

Saadetkasman(2003), “The relationship between exchange rates and Stock prices: A causality

analysis” Celal Bayar University.

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/200

KalimUllah Bhat and Syed Zulfiqar Ali Shah(2015), “Empirical investigation of the relationship

between exchange rate movements and stock market volatility in the context of Pakistan”

Pakistan Business review.

Nataraja N.S1* , Sunil Kumar1, and Nagaraja Rao Chilale1(2016), “An Analysis of Stock

Returns and Exchange Rates: Evidence from IT Industry in India”, Journal of Advanced

Computing, Vol. 5 No. 1 pp. 1-11.

DivyangPatel(2013) “The interrelationship between stock markets and the foreign exchange

market”, Indian Institute of Management.

Waseem Aslam (2014) “ Relationship between stock market volatility and exchange rate: a study

of KSE”Journal of Public Administration, Finance and Law, Vol 1 Iss 4.

Lieh F. &Nieh C. (2001), The Dynamics between Stock Prices and Exchange Rate for G-7

Nations.The Quarterly Review of Finance and Economics.

Tables and Figures:

Table1: ADF test for USD/INR and sectoral indices

Variables At Level First Difference

USD/INR -0.696

(0.845)

-25.190

(0.000)*

AUTO 0.884

(0.995)

-26.025

(0.000)*

BANK -0.681

(0.849)

-25.680

(0.000)*

CAPITAL GOODS -1.237

(0.659)

-24.799

(0.000)*

CONSUMER

DURABLES

-1.237

(0.659)

-24.799

(0.000)*

FMCG -0.558

(0.876)

-8.384

(0.000)*

HEALTHCARE -2.401

(0.141)

-25.681

(0.000)*

INFRASTRUCTURE -0.669

(0.852)

-25.455

(0.000)*

IT -1.891 -26.241

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/201

(0.336) (0.000)*

METAL -0.465

(0.895)

-26.286

(0.000)*

OIL & GAS -0.585

(0.870)

-26.130

(0.000)*

POWER -1.591

(0.486)

-26.132

(0.000)*

PSU -1.276

(0.641)

-25.032

(0.000)*

REALTY -0.555

(0.877)

-26.489

(0.000)*

TECK -2.036

(0.271)

-12.310

(0.000)*

Table 2: Relationship between exchange rates and sectoral indices listed in NSE

Exchange

rate and

INDEX

No. of

observation

Summary Statistics Co-

integration

Evidence of

Causality Std dev. Coeff of

variation

1 USD/INR 742 1.55 4.22 No No evidence of

causality Bank 742 3749.88 6.09

2 SENSEX 742 1.55 4.22 No Sensex to Auto

Auto 742 3736.00 3.76

3 SENSEX 742 1.55 4.22 No FMCG to

Sensex FMCG 742 1113.57 7.87

4 SENSEX 742 1.55 4.22 No No evidence of

causality Metal 742 2596.27 4.00

5 SENSEX 742 1.55 4.22 Yes No evidence of

causality Health care 742 1256.95 12.31

6 SENSEX 742 1.55 4.22 Yes Sensex to

Consumer

durables

Consumer

durables

742 2078.93 7.70

7 SENSEX 742 1.55 4.22 Yes Sensex to

Capital goods Capital

goods

742 2688.93 6.12

8 SENSEX 742 1.55 4.22 No No evidence of

causality Infrastructure 742 3.097 6.19

9 SENSEX 742 1.55 4.22 No IT to Sensex

IT 742 686.22 15.61

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/202

Chart3: Relationship between exchange rates and sectoral indices listed in NSE

Appendix:

Granger causality for exchange and sectoral indices :

Null Hypothesis F-statistics Probability

Sensex does not Granger cause Auto 2.314 0.099***

Auto does not Granger cause Sensex 2.060 0.128

Sensex does not Granger cause Bank 0.098 0.905

Bank does not Granger cause Sensex 2.060 0.128

Sensex does not Granger cause Capital goods 5.432 0.004*

Capital goods does not Granger cause Sensex 0.749 0.472

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

10 SENSEX 742 1.55 4.22 No Bi-directional

causality Oil & Gas 742 2612.96 4.53

11 SENSEX 742 1.55 4.22 No No evidence of

causality Power 742 189.64 10.91

12 SENSEX 742 1.55 4.22 No No evidence of

causality PSU 742 997.90 7.71

13 SENSEX 742 1.55 4.22 Yes Realty to

Sensex Realty 742 429.11 3.90

14 SENSEX 742 1.55 4.22 No TECK to

Sensex TECK 742 338.39 17.47

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/203

Sensex does not Granger cause FMCG 0.319 0.726

FMCG does not Granger cause Sensex 3.941 0.019*

Sensex does not Granger cause Consumer durables 5.432 0.004*

Consumer durables does not Granger cause Sensex 0.749 0.472

Sensex does not Granger cause IT 0.820 0.440

IT does not Granger cause Sensex 2.748 0.064**

Sensex does not Granger cause Oil & Gas 3.629 0.027*

Oil & Gas does not Granger cause Sensex 3.935 0.020*

Sensex does not Granger cause Power 2.261 0.104

Power does not Granger cause Sensex 0.522 0.593

Sensex does not Granger cause PSU 2.147 0.117

PSU does not Granger cause Sensex 1.375 0.253

Sensex does not Granger cause Realty 1.296 0.274

Realty does not Granger cause Sensex 3.048 0.048**

Sensex does not Granger cause TECK 1.299 0.273

TECK does not Granger cause Sensex 2.571 0.077***

*1% level of significance;

**5% level of significance;

***10% level of significance

Johansen Cointergation test

Cointergationfor sensex and auto

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.007090 5.667352 12.32090 0.4777

At most 1 0.000585 0.430874 4.129906 0.5750

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/204

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.007090 5.236478 11.22480 0.4446

At most 1 0.000585 0.430874 4.129906 0.5750

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and bank

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.003197 2.695685 12.32090 0.8840

At most 1 0.000460 0.338879 4.129906 0.6230

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.003197 2.356805 11.22480 0.8802

At most 1 0.000460 0.338879 4.129906 0.6230

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

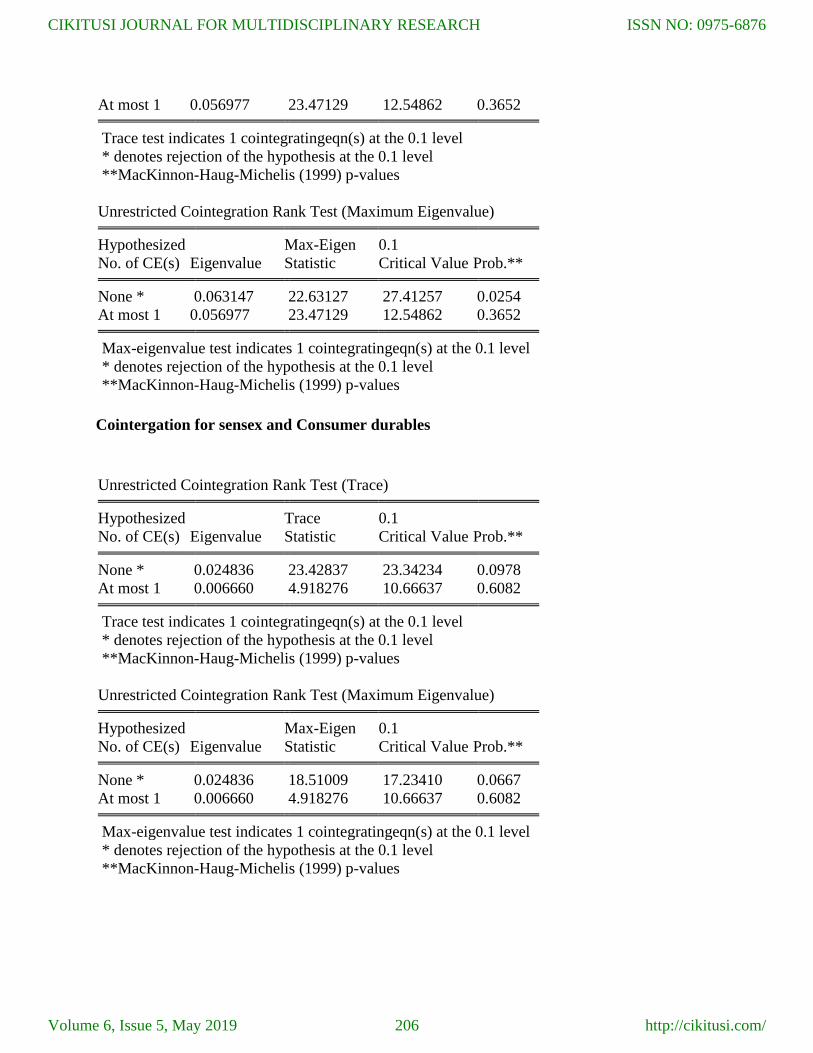

Cointergation for sensex and Capital goods

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.1

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.063147 22.63127 27.41257 0.0254

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/205

At most 1 0.056977 23.47129 12.54862 0.3652

Trace test indicates 1 cointegratingeqn(s) at the 0.1 level

* denotes rejection of the hypothesis at the 0.1 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.1

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.063147 22.63127 27.41257 0.0254

At most 1 0.056977 23.47129 12.54862 0.3652

Max-eigenvalue test indicates 1 cointegratingeqn(s) at the 0.1 level

* denotes rejection of the hypothesis at the 0.1 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Consumer durables

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.1

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.024836 23.42837 23.34234 0.0978

At most 1 0.006660 4.918276 10.66637 0.6082

Trace test indicates 1 cointegratingeqn(s) at the 0.1 level

* denotes rejection of the hypothesis at the 0.1 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.1

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.024836 18.51009 17.23410 0.0667

At most 1 0.006660 4.918276 10.66637 0.6082

Max-eigenvalue test indicates 1 cointegratingeqn(s) at the 0.1 level

* denotes rejection of the hypothesis at the 0.1 level

**MacKinnon-Haug-Michelis (1999) p-values

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/206

Cointergation for sensex and FMCG

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.012663 10.15815 12.32090 0.1122

At most 1 0.001058 0.778968 4.129906 0.4345

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.012663 9.379185 11.22480 0.1038

At most 1 0.001058 0.778968 4.129906 0.4345

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Health care

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.022051 16.42158 15.49471 0.0362

At most 1 1.45E-05 0.010673 3.841466 0.9174

Trace test indicates 1 cointegratingeqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.022051 16.41090 14.26460 0.0225

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/207

At most 1 1.45E-05 0.010673 3.841466 0.9174

Max-eigenvalue test indicates 1 cointegratingeqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Infrastructure

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.014586 15.16264 25.87211 0.5610

At most 1 0.005891 4.348574 12.51798 0.6913

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.014586 10.81407 19.38704 0.5326

At most 1 0.005891 4.348574 12.51798 0.6913

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and IT

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.015351 13.71758 25.87211 0.6808

At most 1 0.003163 2.331855 12.51798 0.9447

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/208

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.015351 11.38572 19.38704 0.4744

At most 1 0.003163 2.331855 12.51798 0.9447

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Metal

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.016778 18.20055 25.87211 0.3306

At most 1 0.007845 5.780816 12.51798 0.4886

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.016778 12.41974 19.38704 0.3771

At most 1 0.007845 5.780816 12.51798 0.4886

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Oil & Gas

Unrestricted Cointegration Rank Test (Trace)

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/209

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.014149 13.46025 25.87211 0.7017

At most 1 0.004030 2.972063 12.51798 0.8799

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.014149 10.48819 19.38704 0.5668

At most 1 0.004030 2.972063 12.51798 0.8799

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and Power

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.010214 8.493405 15.49471 0.4142

At most 1 0.001288 0.947434 3.841466 0.3304

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.010214 7.545971 14.26460 0.4267

At most 1 0.001288 0.947434 3.841466 0.3304

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/210

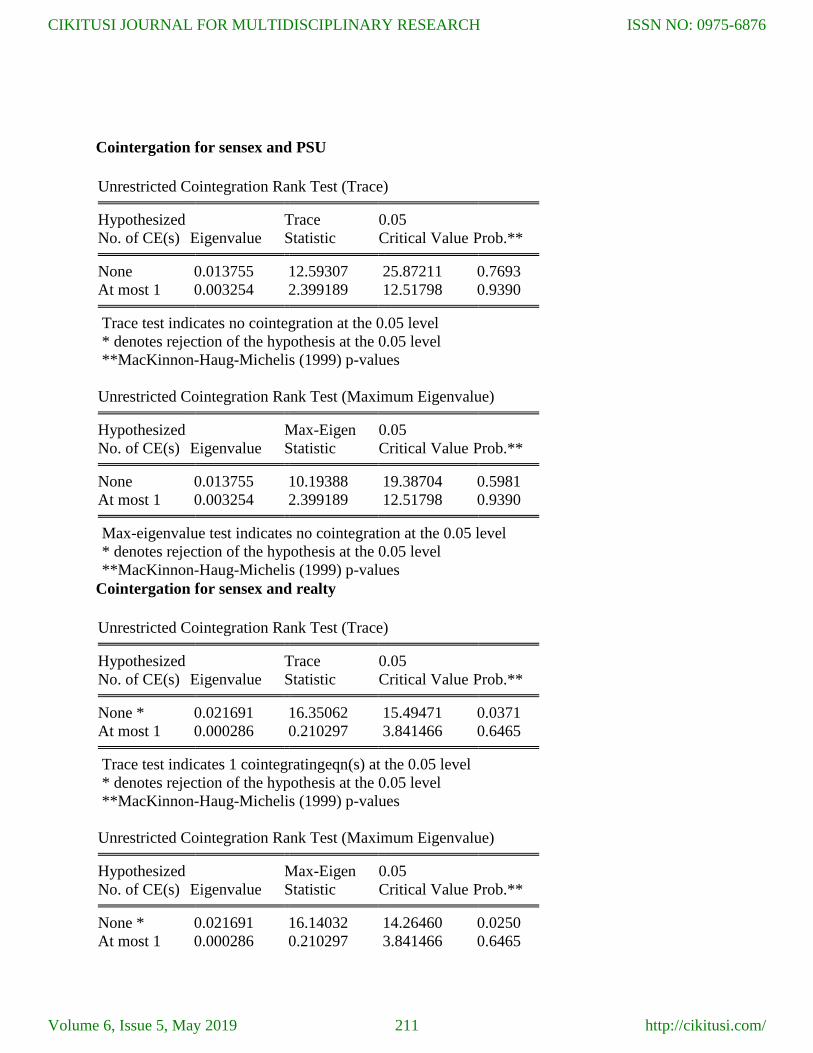

Cointergation for sensex and PSU

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.013755 12.59307 25.87211 0.7693

At most 1 0.003254 2.399189 12.51798 0.9390

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.013755 10.19388 19.38704 0.5981

At most 1 0.003254 2.399189 12.51798 0.9390

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Cointergation for sensex and realty

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.021691 16.35062 15.49471 0.0371

At most 1 0.000286 0.210297 3.841466 0.6465

Trace test indicates 1 cointegratingeqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.021691 16.14032 14.26460 0.0250

At most 1 0.000286 0.210297 3.841466 0.6465

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/211

Max-eigenvalue test indicates 1 cointegratingeqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

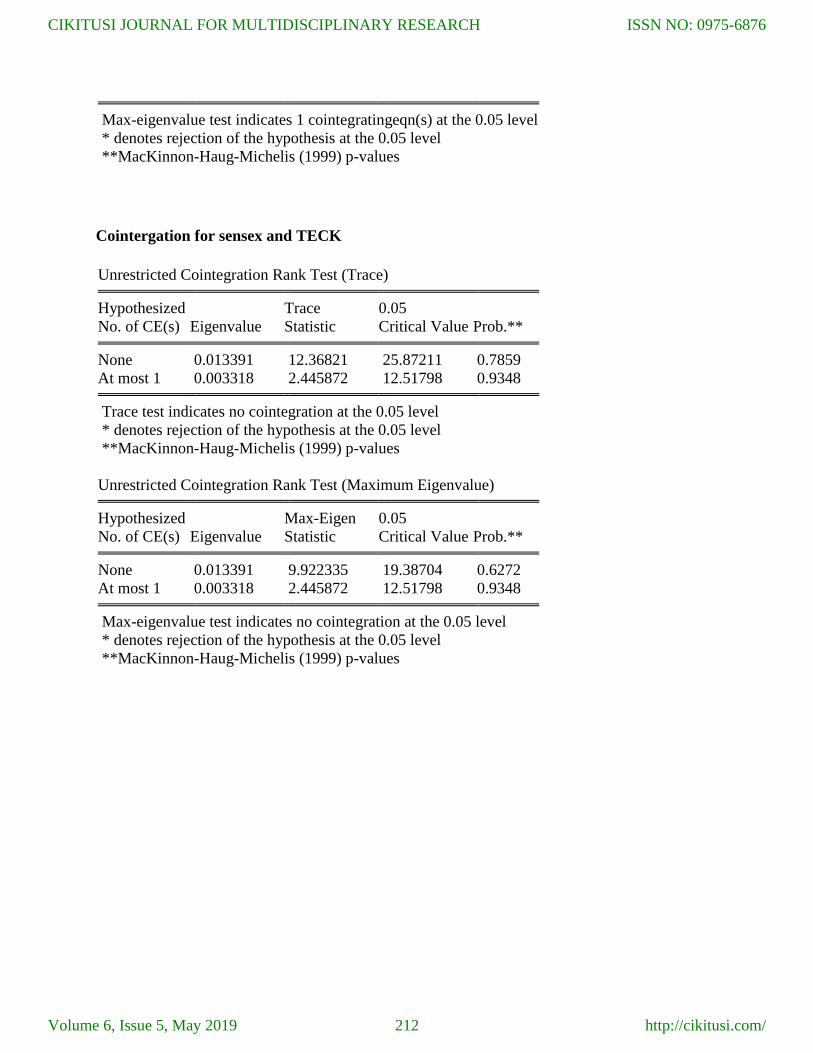

Cointergation for sensex and TECK

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.013391 12.36821 25.87211 0.7859

At most 1 0.003318 2.445872 12.51798 0.9348

Trace test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None 0.013391 9.922335 19.38704 0.6272

At most 1 0.003318 2.445872 12.51798 0.9348

Max-eigenvalue test indicates no cointegration at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

CIKITUSI JOURNAL FOR MULTIDISCIPLINARY RESEARCH

Volume 6, Issue 5, May 2019

ISSN NO: 0975-6876

http://cikitusi.com/212