Embed Size (px)

Citation preview

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

#SASFPT17

Building a Bridge between Risk and

Finance to Address IFRS 9 and Stress-

testingMartim Rocha

SAS

Experience your new possible

SAS® FORUM

PORTUGAL 2017

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

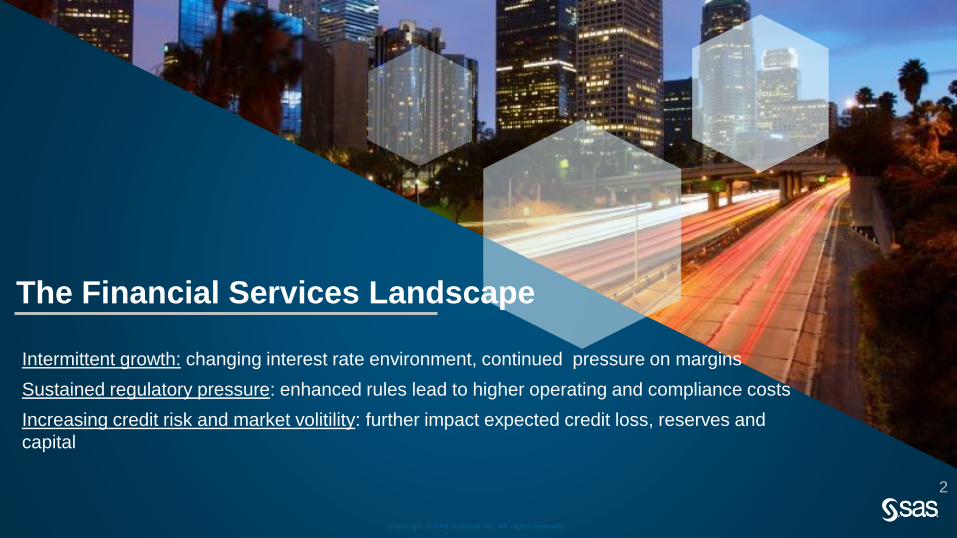

The Financial Services Landscape

Intermittent growth: changing interest rate environment, continued pressure on margins

Sustained regulatory pressure: enhanced rules lead to higher operating and compliance costs

Increasing credit risk and market volitility: further impact expected credit loss, reserves and

capital

2

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

#SASFPT17

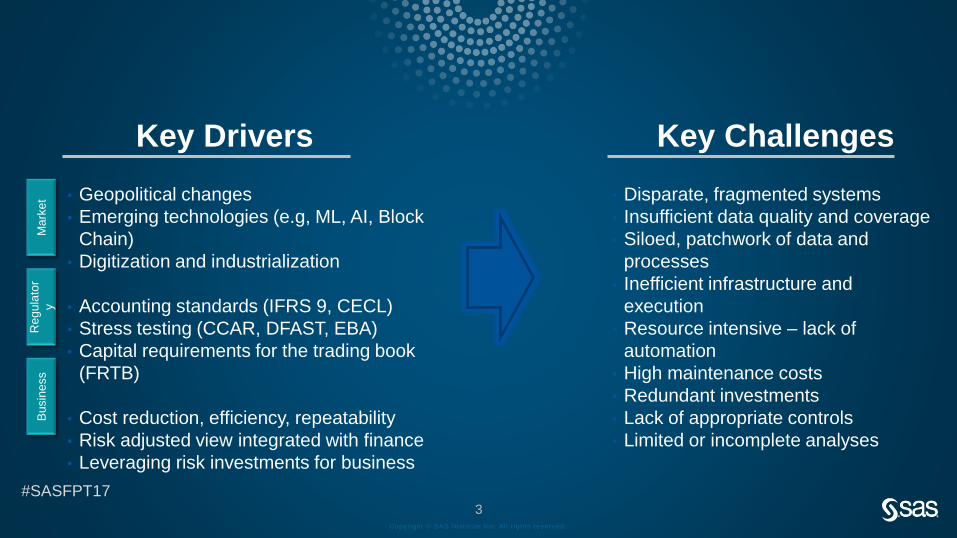

• Geopolitical changes

• Emerging technologies (e.g, ML, AI, Block

Chain)

• Digitization and industrialization

• Accounting standards (IFRS 9, CECL)

• Stress testing (CCAR, DFAST, EBA)

• Capital requirements for the trading book

(FRTB)

• Cost reduction, efficiency, repeatability

• Risk adjusted view integrated with finance

• Leveraging risk investments for business

• Disparate, fragmented systems

• Insufficient data quality and coverage

• Siloed, patchwork of data and

processes

• Inefficient infrastructure and

execution

• Resource intensive – lack of

automation

• High maintenance costs

• Redundant investments

• Lack of appropriate controls

• Limited or incomplete analyses

3

Key Drivers Key Challenges

Bu

sin

ess

Re

gu

lato

r

yM

ark

et

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

4

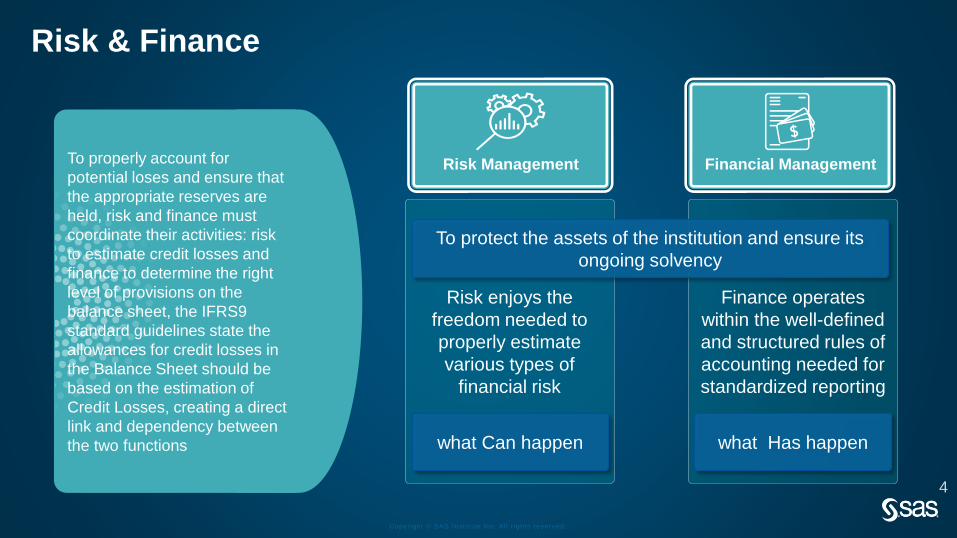

To properly account for

potential loses and ensure that

the appropriate reserves are

held, risk and finance must

coordinate their activities: risk

to estimate credit losses and

finance to determine the right

level of provisions on the

balance sheet, the IFRS9

standard guidelines state the

allowances for credit losses in

the Balance Sheet should be

based on the estimation of

Credit Losses, creating a direct

link and dependency between

the two functions

Risk Management

Risk enjoys the

freedom needed to

properly estimate

various types of

financial risk

Financial Management

Finance operates

within the well-defined

and structured rules of

accounting needed for

standardized reporting

Risk & Finance

To protect the assets of the institution and ensure its

ongoing solvency

what Can happen what Has happen

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

SAS RISK FOCUS AREAS

Enterprise

Stress TestingCCAR/DFAST/EBA

Credit Scoring

PD/LGD/EAD

Regulatory Risk

ManagementRWA/FRTB/IRRBB

Expected Credit

Loss IFRS9/CECL

Model Risk

ManagementTRIM/SR 11-7

6

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

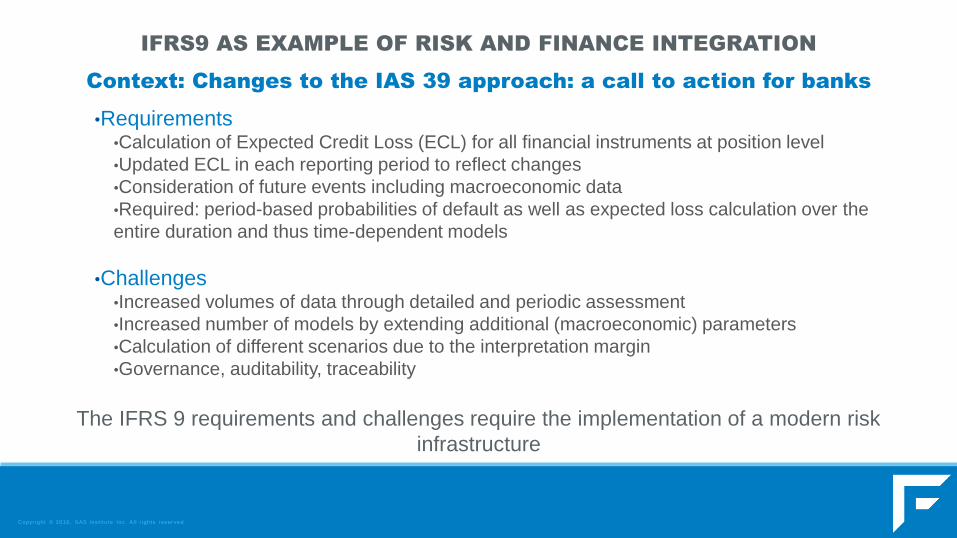

•Requirements•Calculation of Expected Credit Loss (ECL) for all financial instruments at position level

•Updated ECL in each reporting period to reflect changes

•Consideration of future events including macroeconomic data

•Required: period-based probabilities of default as well as expected loss calculation over the

entire duration and thus time-dependent models

•Challenges•Increased volumes of data through detailed and periodic assessment

•Increased number of models by extending additional (macroeconomic) parameters

•Calculation of different scenarios due to the interpretation margin

•Governance, auditability, traceability

The IFRS 9 requirements and challenges require the implementation of a modern risk

infrastructure

IFRS9 AS EXAMPLE OF RISK AND FINANCE INTEGRATION

Context: Changes to the IAS 39 approach: a call to action for banks

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

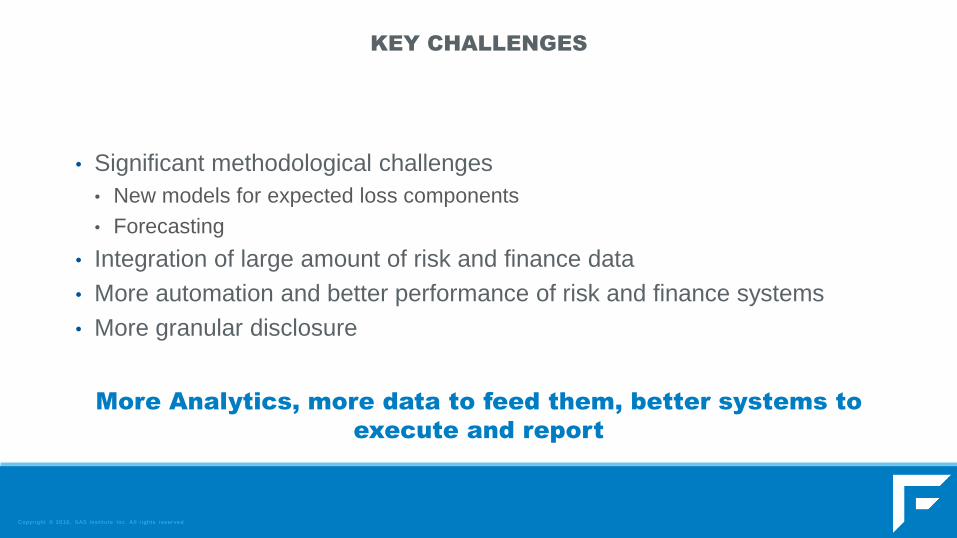

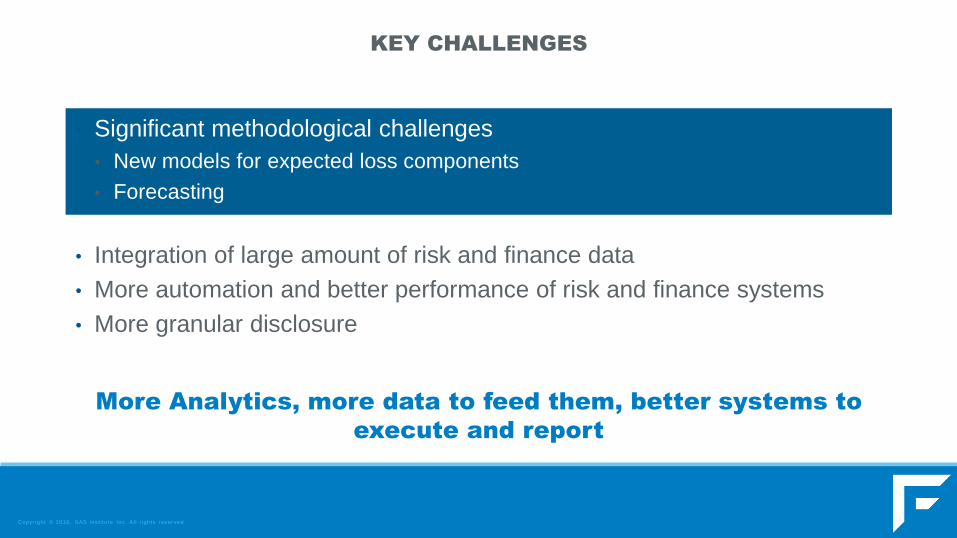

KEY CHALLENGES

• Significant methodological challenges

• New models for expected loss components

• Forecasting

• Integration of large amount of risk and finance data

• More automation and better performance of risk and finance systems

• More granular disclosure

More Analytics, more data to feed them, better systems to

execute and report

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

8

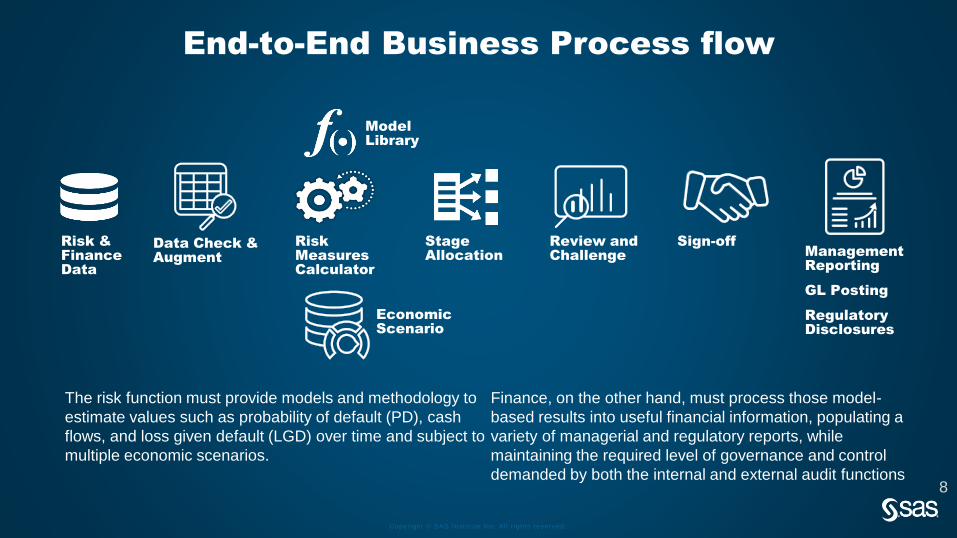

The risk function must provide models and methodology to

estimate values such as probability of default (PD), cash

flows, and loss given default (LGD) over time and subject to

multiple economic scenarios.

Finance, on the other hand, must process those model-

based results into useful financial information, populating a

variety of managerial and regulatory reports, while

maintaining the required level of governance and control

demanded by both the internal and external audit functions

End-to-End Business Process flow

Risk & Finance Data

Model Library

Risk Measures Calculator

Management Reporting

GL Posting

Regulatory Disclosures

Stage Allocation

Review and Challenge

Sign-offData Check & Augment

Economic Scenario

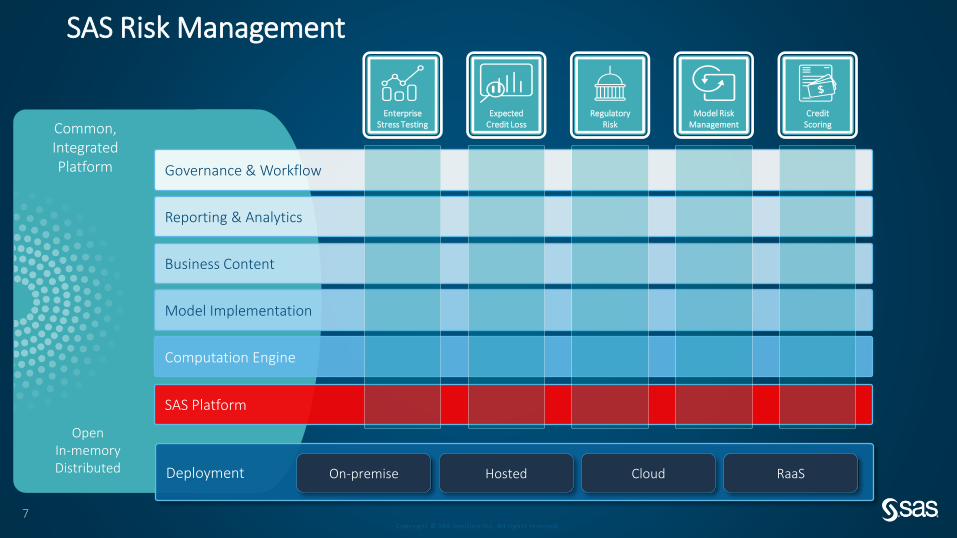

Copyright © SAS Inst itute Inc. A l l r ights reserved.

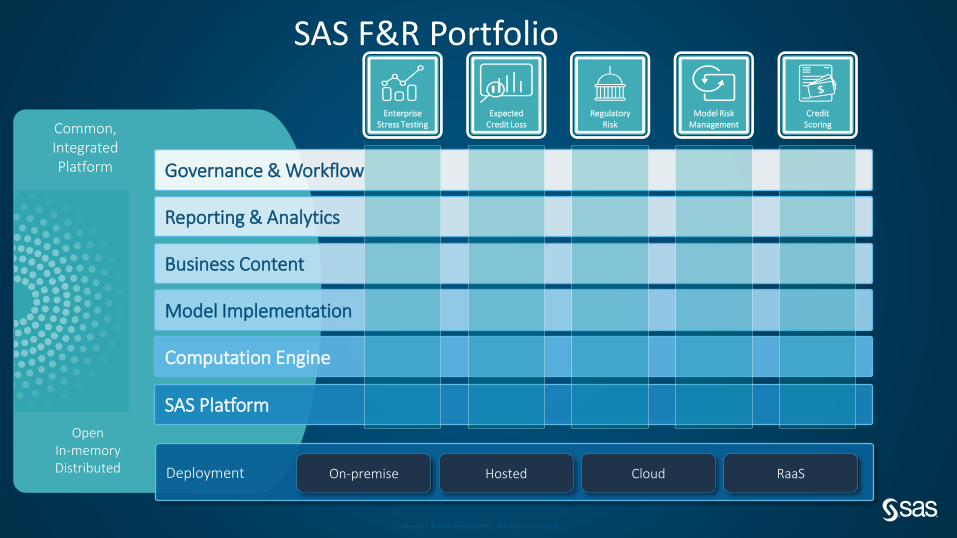

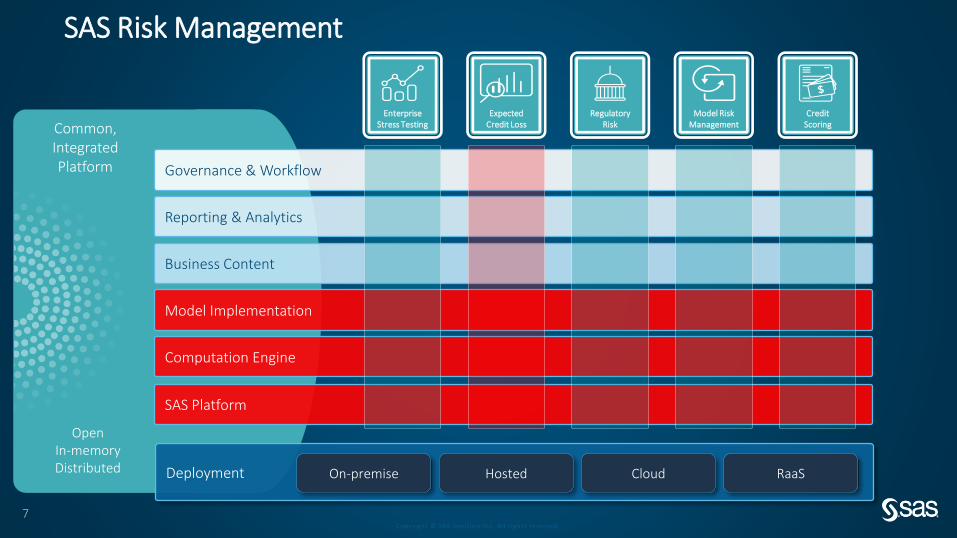

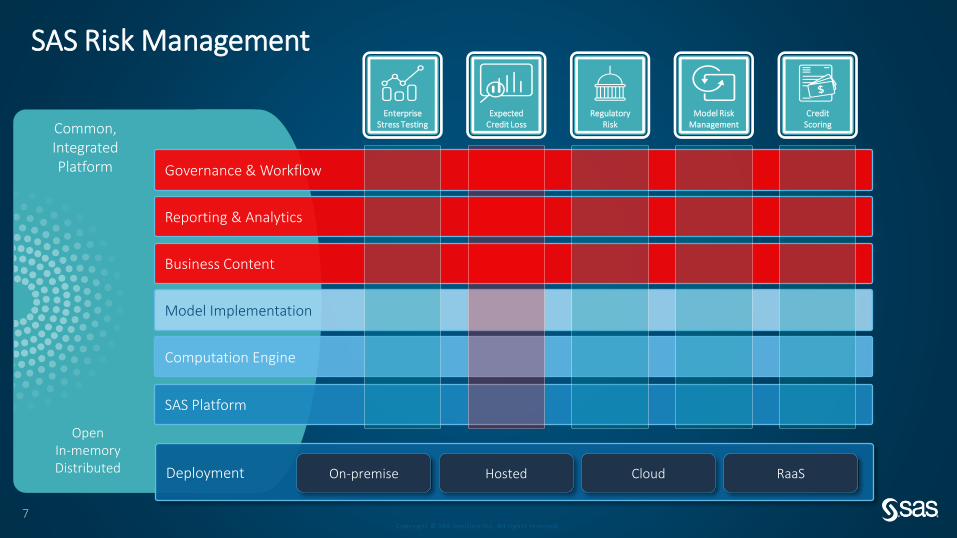

OpenIn-memoryDistributed

Common, Integrated Platform

Reporting & Analytics

Business Content

SAS Platform

Computation Engine

Governance & Workflow

Model Implementation

SAS F&R Portfolio

Deployment On-premise Hosted Cloud RaaS

Enterprise Stress Testing

Expected Credit Loss

Regulatory Risk

Model Risk Management

Credit Scoring

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

KEY CHALLENGES

• Significant methodological challenges

• New models for expected loss components

• Forecasting

• Integration of large amount of risk and finance data

• More automation and better performance of risk and finance systems

• More granular disclosure

More Analytics, more data to feed them, better systems to

execute and report

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

#SASFPT17

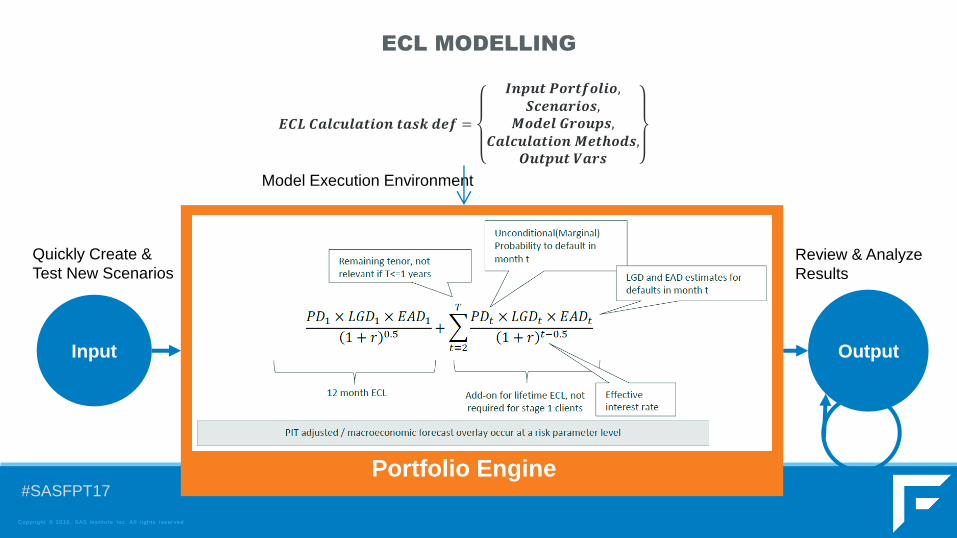

Review & Analyze

Results

Model Execution Environment

Quickly Create &

Test New Scenarios

ECL MODELLING

𝑬𝑪𝑳 𝑪𝒂𝒍𝒄𝒖𝒍𝒂𝒕𝒊𝒐𝒏 𝒕𝒂𝒔𝒌 𝒅𝒆𝒇 =

𝑰𝒏𝒑𝒖𝒕 𝑷𝒐𝒓𝒕𝒇𝒐𝒍𝒊𝒐,𝑺𝒄𝒆𝒏𝒂𝒓𝒊𝒐𝒔,

𝑴𝒐𝒅𝒆𝒍 𝑮𝒓𝒐𝒖𝒑𝒔,𝑪𝒂𝒍𝒄𝒖𝒍𝒂𝒕𝒊𝒐𝒏 𝑴𝒆𝒕𝒉𝒐𝒅𝒔,

𝑶𝒖𝒕𝒑𝒖𝒕 𝑽𝒂𝒓𝒔

Input Output

Portfolio Engine

Copyright © SAS Inst itute Inc. A l l r ights reserved.

OpenIn-memoryDistributed

Common, Integrated Platform

Reporting & Analytics

Business Content

SAS Platform

Computation Engine

Governance & Workflow

Model Implementation

SAS Risk Management

7

Deployment On-premise Hosted Cloud RaaS

Enterprise Stress Testing

Expected Credit Loss

Regulatory Risk

Model Risk Management

Credit Scoring

Copyright © SAS Inst itute Inc. A l l r ights reserved.

Scenario Management

EXPLORER DESIGNER

Define/Load scenario

Scenario library

Change scenarios

Scenario Enrichment, model Risk Factors from Base Scenarios

Export scenarios

Copyright © SAS Inst itute Inc. A l l r ights reserved.

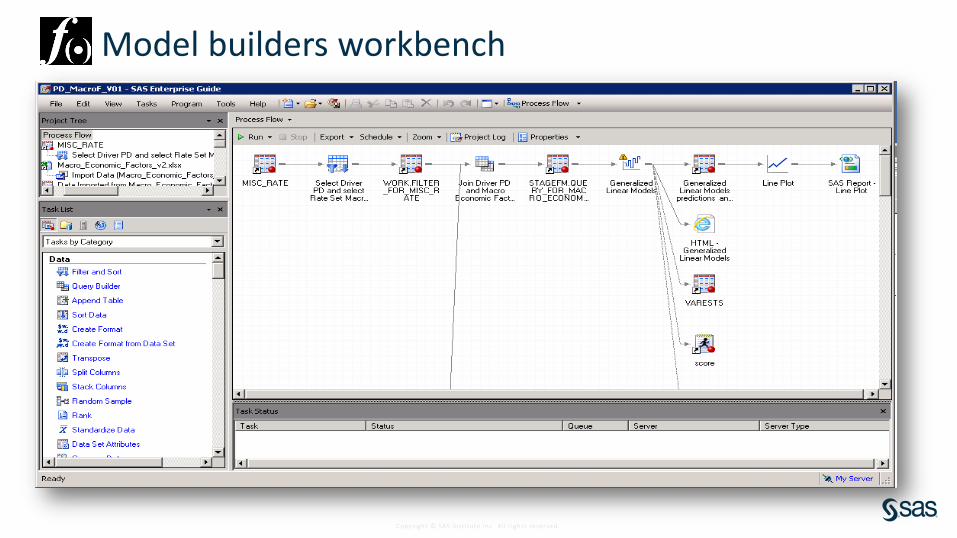

Model builders workbench

Copyright © SAS Inst itute Inc. A l l r ights reserved.

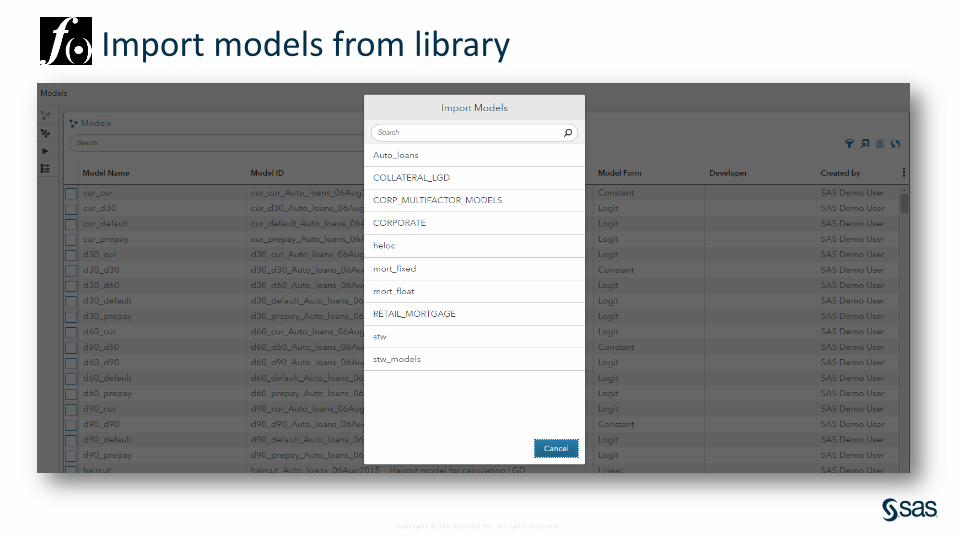

Import models from library

Copyright © SAS Inst itute Inc. A l l r ights reserved.

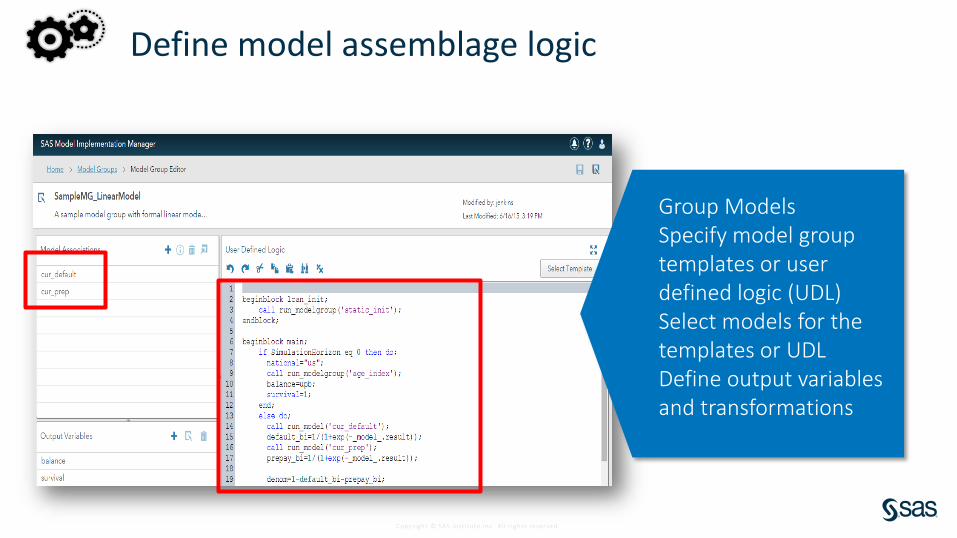

Define model assemblage logic

Group ModelsSpecify model group templates or user defined logic (UDL)Select models for the templates or UDLDefine output variables and transformations

Copyright © SAS Inst itute Inc. A l l r ights reserved.

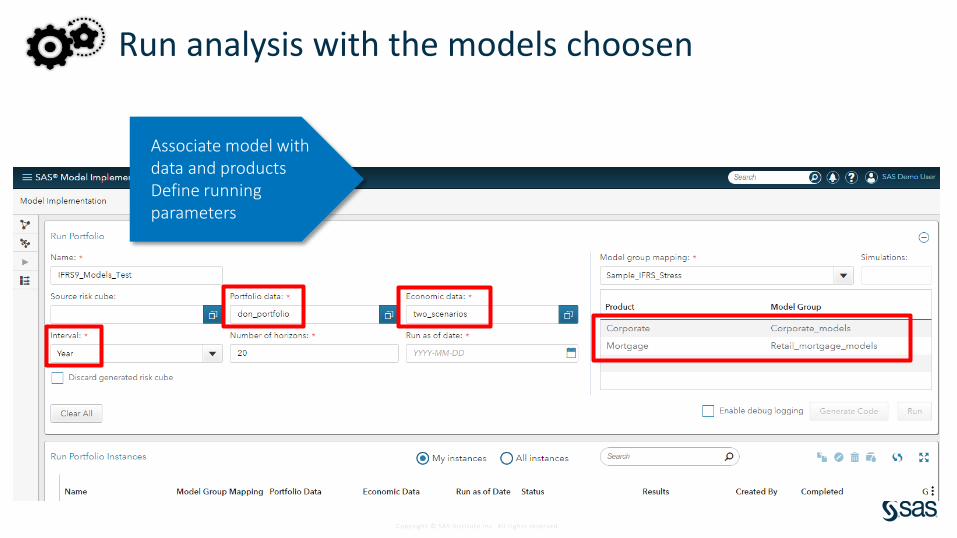

Run analysis with the models choosen

Associate model with data and productsDefine running parameters

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

KEY CHALLENGES

• Significant methodological challenges

• New models for expected loss components

• Forecasting

• Integration of large amount of risk and finance data

• More automation and better performance of risk and finance systems

• More granular disclosure

More Analytics, more data to feed them, better systems to

execute and report

Copyright © SAS Inst itute Inc. A l l r ights reserved.

OpenIn-memoryDistributed

Common, Integrated Platform

Reporting & Analytics

Business Content

SAS Platform

Computation Engine

Governance & Workflow

Model Implementation

SAS Risk Management

7

Deployment On-premise Hosted Cloud RaaS

Enterprise Stress Testing

Expected Credit Loss

Regulatory Risk

Model Risk Management

Credit Scoring

Copyright © SAS Inst itute Inc. A l l r ights reserved.

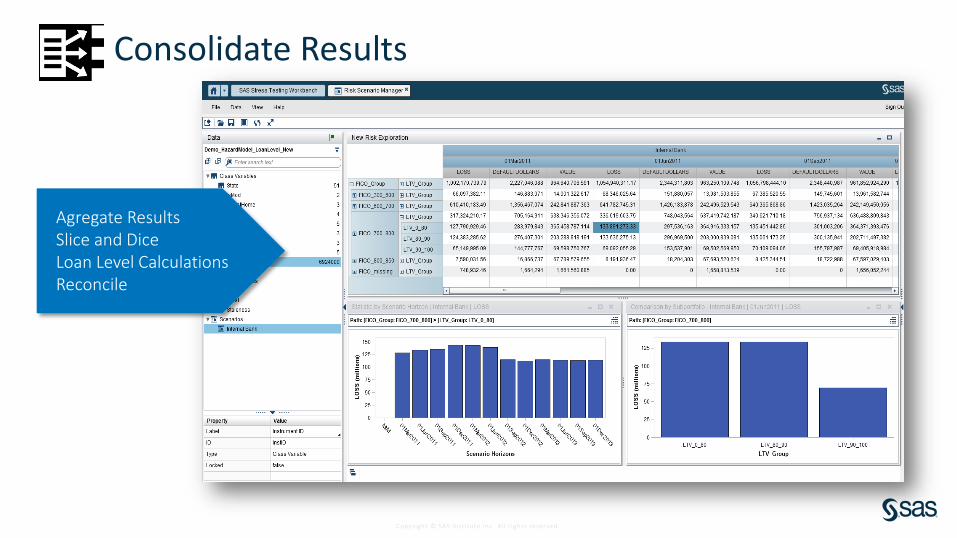

Agregate ResultsSlice and DiceLoan Level Calculations Reconcile

Consolidate Results

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

#SASFPT17

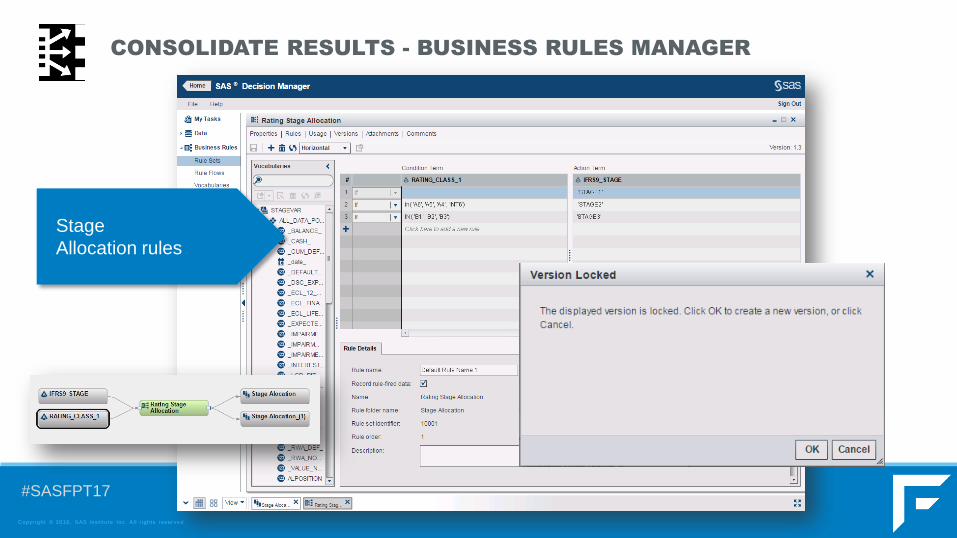

CONSOLIDATE RESULTS - BUSINESS RULES MANAGER

Stage

Allocation rules

Copyr i g ht © 2016, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

#SASFPT17

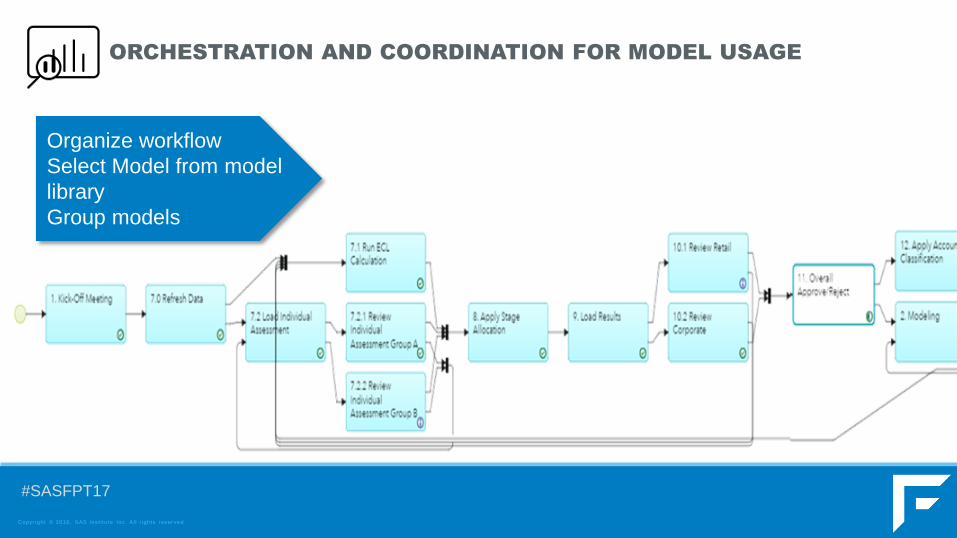

ORCHESTRATION AND COORDINATION FOR MODEL USAGE

Organize workflow

Select Model from model

library

Group models

Copyright © SAS Inst itute Inc. A l l r ights reserved.

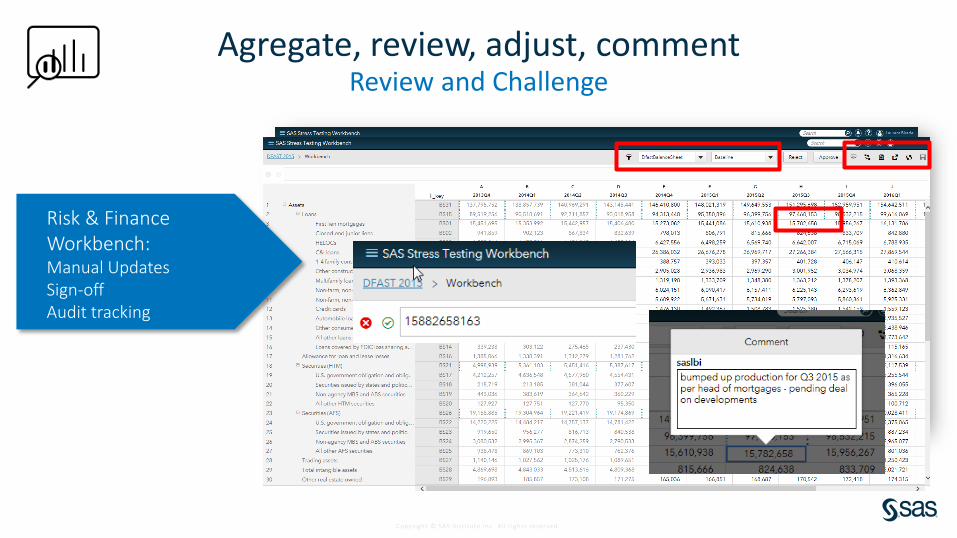

Agregate, review, adjust, commentReview and Challenge

Risk & Finance Workbench:Manual UpdatesSign-offAudit tracking

Copyright © SAS Inst itute Inc. A l l r ights reserved.

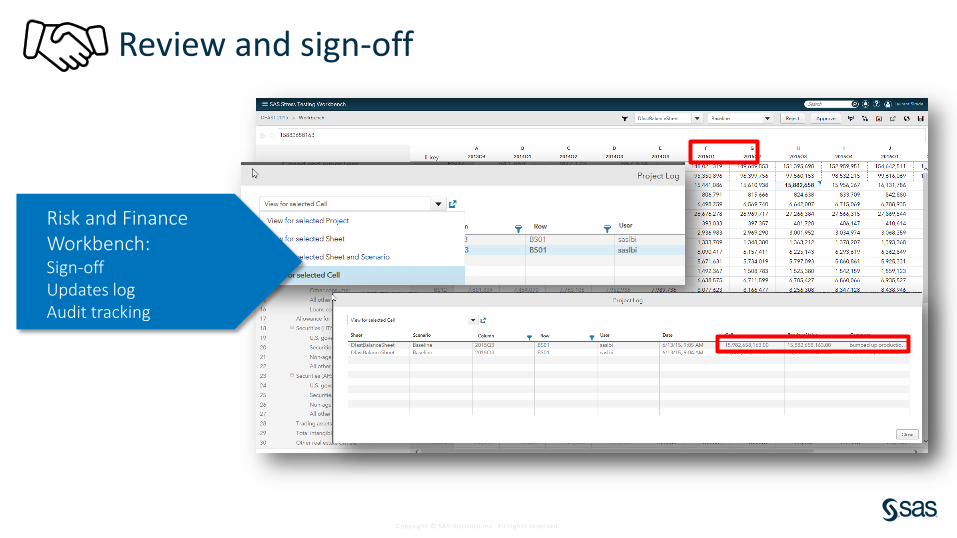

Review and sign-off

Risk and Finance Workbench:Sign-offUpdates logAudit tracking

Copyright © SAS Inst itute Inc. A l l r ights reserved.

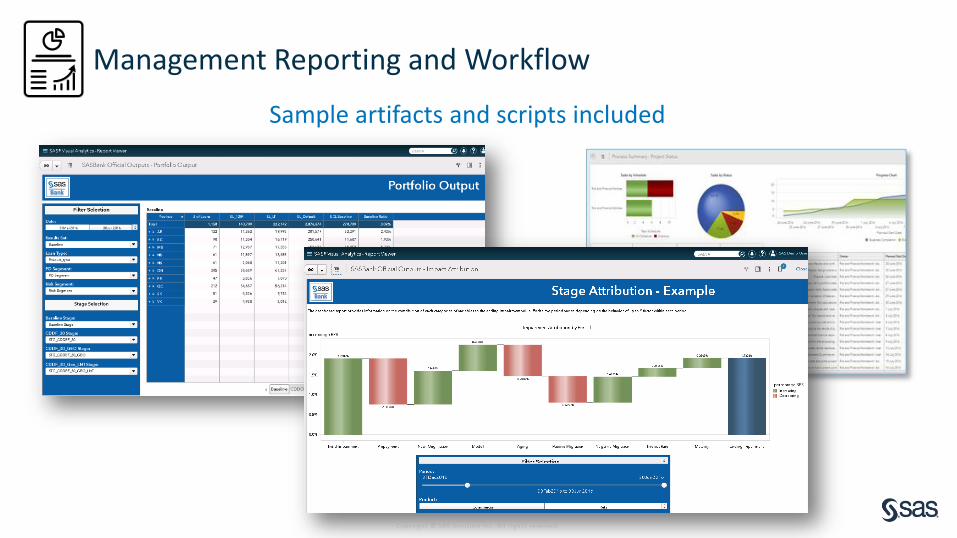

Sample artifacts and scripts included

Management Reporting and Workflow

Copyright © SAS Inst itute Inc. A l l r ights reserved.

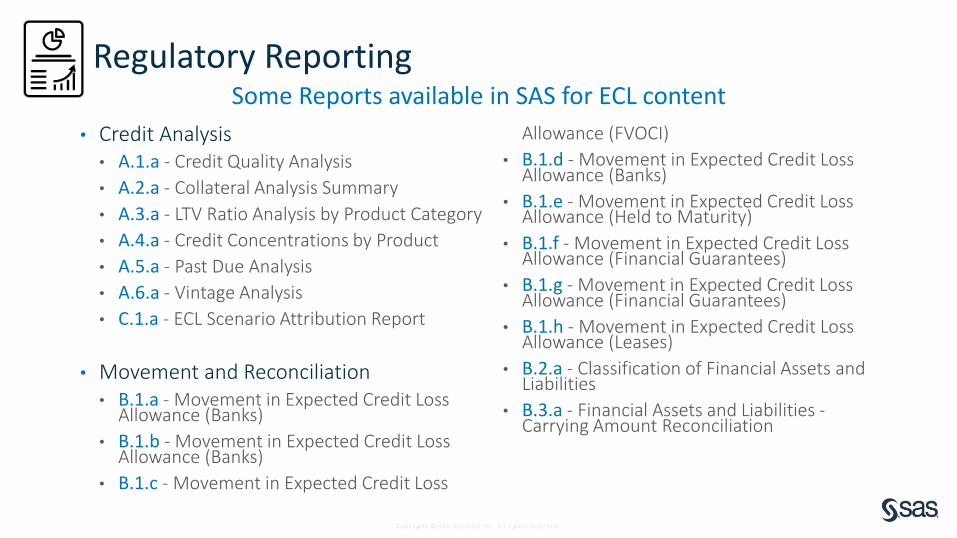

Some Reports available in SAS for ECL content

• Credit Analysis• A.1.a - Credit Quality Analysis

• A.2.a - Collateral Analysis Summary

• A.3.a - LTV Ratio Analysis by Product Category

• A.4.a - Credit Concentrations by Product

• A.5.a - Past Due Analysis

• A.6.a - Vintage Analysis

• C.1.a - ECL Scenario Attribution Report

• Movement and Reconciliation• B.1.a - Movement in Expected Credit Loss

Allowance (Banks)

• B.1.b - Movement in Expected Credit Loss Allowance (Banks)

• B.1.c - Movement in Expected Credit Loss

Allowance (FVOCI)

• B.1.d - Movement in Expected Credit Loss Allowance (Banks)

• B.1.e - Movement in Expected Credit Loss Allowance (Held to Maturity)

• B.1.f - Movement in Expected Credit Loss Allowance (Financial Guarantees)

• B.1.g - Movement in Expected Credit Loss Allowance (Financial Guarantees)

• B.1.h - Movement in Expected Credit Loss Allowance (Leases)

• B.2.a - Classification of Financial Assets and Liabilities

• B.3.a - Financial Assets and Liabilities -Carrying Amount Reconciliation

Regulatory Reporting

Copyright © SAS Inst itute Inc. A l l r ights reserved.

OpenIn-memoryDistributed

Common, Integrated Platform

Reporting & Analytics

Business Content

SAS Platform

Computation Engine

Governance & Workflow

Model Implementation

SAS Risk Management

7

Deployment On-premise Hosted Cloud RaaS

Enterprise Stress Testing

Expected Credit Loss

Regulatory Risk

Model Risk Management

Credit Scoring

Copyright © SAS Inst itute Inc. A l l r ights reserved.

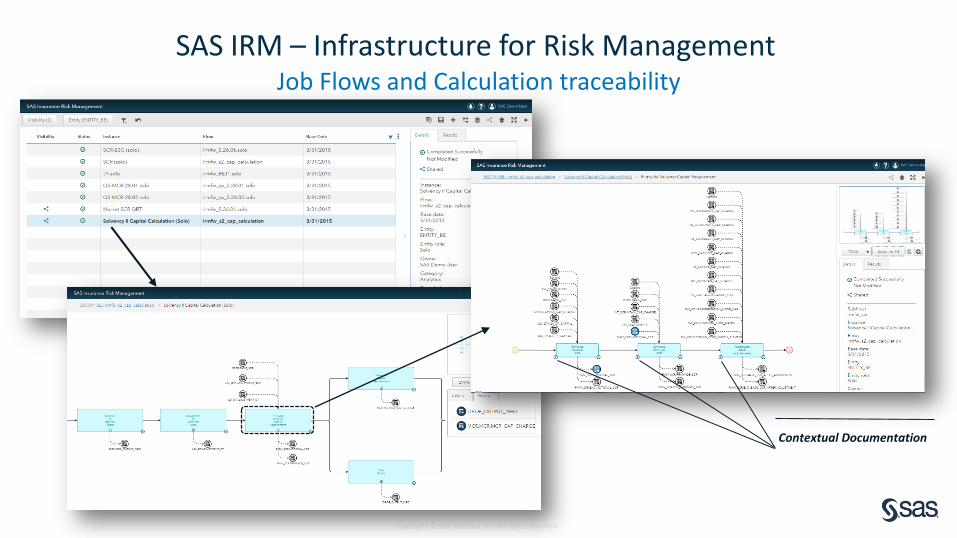

SAS IRM – Infrastructure for Risk ManagementJob Flows and Calculation traceability

Contextual Documentation

Copyright © SAS Inst itute Inc. A l l r ights reserved.

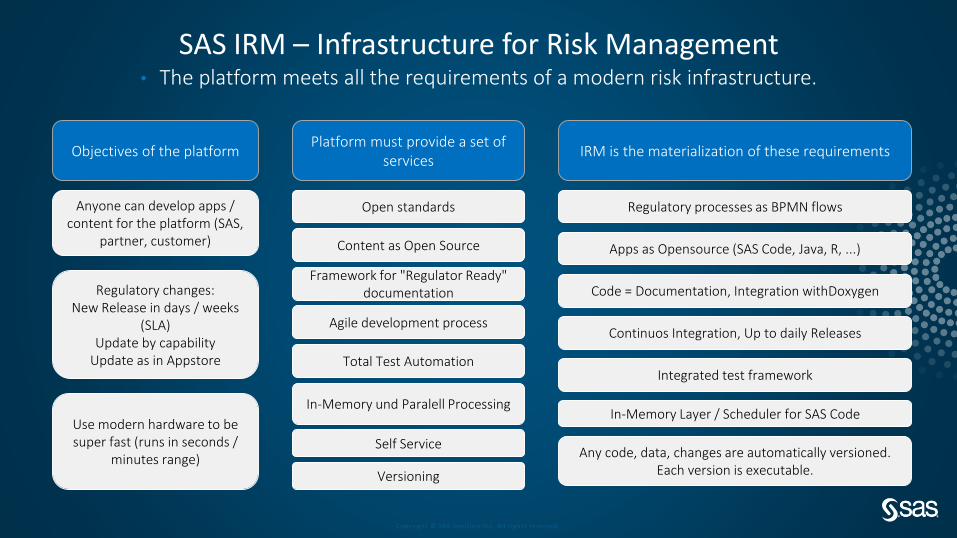

Platform must provide a set of services

Open standards

Content as Open Source

Framework for "Regulator Ready" documentation

Objectives of the platform

Anyone can develop apps / content for the platform (SAS,

partner, customer)

Agile development process

Total Test Automation

Regulatory changes:New Release in days / weeks

(SLA)Update by capability

Update as in Appstore

Use modern hardware to be super fast (runs in seconds /

minutes range)

In-Memory und Paralell Processing

IRM is the materialization of these requirements

Regulatory processes as BPMN flows

Apps as Opensource (SAS Code, Java, R, ...)

Code = Documentation, Integration withDoxygen

Continuos Integration, Up to daily Releases

Integrated test framework

In-Memory Layer / Scheduler for SAS Code

Self Service

Versioning

Any code, data, changes are automatically versioned. Each version is executable.

SAS IRM – Infrastructure for Risk Management• The platform meets all the requirements of a modern risk infrastructure.

Copyright © SAS Inst itute Inc. A l l r ights reserved.

30

Traditionally risk and finance groups within a bank operate separately.

Challenge of the new IFRS 9 and CECL regulation, however, requires the two groups to collaborate much more closely.

Risk and finance traditionally use separate and dedicated IT applications

In order to efficiently manage the IFRS9 and CECL process both functions should share the same IT application.

Banks need a solution that provides an integrated, scalable, and controlled risk and finance platform to enable those collaborations.

Even more, these two groups can work together easily to see how different business assumptions might affect a bank’s financials and create the best strategy for the bank.

Copyright © SAS Inst i tute Inc. Al l r ights reserv ed.

#SASFPT17

OBRIGADO