Embed Size (px)

Citation preview

ANNUAL FINANCIAL STATEMENTS IN TERMS SECTION 15 OF THE PENSION FUNDS ACT NO 24, 1956

AS AMENDED (PENSION FUNDS ACT)

NAME OF RETIREMENT FUND: SELF ASSURANCE DOMESTIC EMPLOYEES

PROVIDENT FUND

FINANCIAL SERVICES BOARD REGISTRATION NUMBER:

12/8/20527

For the period: 01/07/2013 to 30/06/2014

CONTENTS

Schedule Page

Schedule Page

A Regulatory information 2 G Statement of changes in net

assets and funds 12

B Statement of responsibility by the Board of Fund

4 HA Notes to the financial statements 13

C Statement of responsibility by the principal officer

6 I Report of the independent auditors / Board of Fund (whichever is applicable) to the Registrar of Pension Funds

19

E Report of the Board of Fund 7 IA Investment schedule pertaining to annual financial statements

19

F Statement of net assets and funds

11 IB Assets held in compliance with Regulation 28

22

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

2

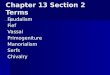

SCHEDULE A REGULATORY INFORMATION

For the period ended 30/06/2014 Registered office of the fund

Postal address: P O Box 829, Wilgeheuwel, 1736 Physical address: A3 Willow Crest Office Estate, Van Hoof Street, Roodepoort, 1724

Financial reporting periods

Current: 01/07/2013 To 30/06/2014 Previous: 01/07/2012 To 30/06/2013

Board of Fund

Full name E-mail address Capacity* Date appointed

Chairperson

Jacobs NG [email protected] Chairman 05/03/2004

Trustees

Jacobs NG [email protected] Independent 17/07/2013

Coomber AR [email protected] Independent 22/09/2008

Lendrum K [email protected] Independent 01/07/2013

Vorster PW [email protected] Independent 17/07/2013

Schedule of meetings held by the Board of Fund in terms of the rules of the fund

Meeting date Place of meeting Quorum (yes/no)

22/08/2013 Brefco (Pty) Ltd Yes

21/11/2013 Brefco (Pty) Ltd Yes

19/02/2014 Brefco (Pty) Ltd Yes

27/03/2014 Brefco (Pty) Ltd Yes

28/05/2014 Brefco (Pty) Ltd Yes

Fund officers

Principal officer

Full name: From Date Postal address:

Physical address: Tel number: Email address

Botha JH 01/09/2010 P O Box 829, Wilgeheuwel,

1736

A3 Willow Crest Office Estate, Van Hoof Street,

Roodepoort

(010) 594-2902 [email protected]

Monitoring Person

Full name: From Date Postal address:

Physical address: Tel number: Email address

Botha JH 01/09/2010 P O Box 829, Wilgeheuwel,

1736

A3 Willow Crest Office Estate, Van Hoof Street,

Roodepoort

(010) 594-2902 [email protected]

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

3

SCHEDULE A (Continue)

REGULATORY INFORMATION

For the period ended 30/06/2014

Professional service providers

Actuary/Valuator

Full name: Postal address: Physical address: Tel number: Email address

Welham RH (Sellems Actuaries)

P O Box 53, Wendywood,

2144

Unit B, Morningside Office Park,

222 Rivonia Road, Morningside

(011) 656-5381 [email protected]

Benefit Administrator

Full name: From Date Postal address: Physical address: Tel number: Reg Number

Brefco (Pty) Ltd 01/05/2010 PO Box 829, Wilgeheuwel,

1736

A3 Willow Crest Office Estate, Van Hoof Street,

Roodepoort

(011) 958-0511 24/218

Investment administrator

Full name: Postal address: Physical address: Tel number: Reg Number

ACSIS Limited PO Box 44604, Claremont,

7735

The Estuaries, 2 Oxbow Crescent,

Century City

(021) 524 4410 26/10/588

Investment advisor

Full name: Postal address: Physical address: Tel number: Reg Number

ACSIS Limited PO Box 44604, Claremont,

7735

The Estuaries, 2 Oxbow Crescent,

Century City

(021) 524 4410 FSP no: 588

Participating Employers

The list of participating employers is available for inspection at the fund’s registered office.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

4

SCHEDULE B STATEMENT OF RESPONSIBILITY BY THE BOARD OF FUND For the period ended 30/06/2014 Responsibilities The Board of Fund hereby confirm to the best of their knowledge and belief that, during the period under review, in the execution of their duties they have complied with the duties imposed by Pension Funds Act legislation and the rules of the fund, including the following: • ensured that proper registers, books and records of the operations of the fund were kept, inclusive of proper

minutes of all resolutions passed by the Board of Fund; • ensured that proper internal control systems were employed by or on behalf of the fund; • ensured that adequate and appropriate information was communicated to the members of the fund,

informing them of their rights, benefits and duties in terms of the rules of the fund; • took all reasonable steps to ensure that contributions, where applicable, were paid timeously to the fund or

reported where necessary in accordance with section 13A and regulation 33 of the Pension Funds Act; • obtained expert advice on matters where they lacked sufficient expertise; • ensured that the rules and the operation and administration of the fund complied with the Pension Funds Act

and all applicable legislation; • ensured that fidelity cover was maintained and that this cover was deemed adequate and in compliance with

the rules of the fund; and • ensured that investments of the fund were implemented and maintained in accordance with the fund’s

investment strategy. With regard to the above, the trustees would like to put on record that certain instances of poor administration and record-keeping prior to April 2010 have subsequently been brought to their attention. As a result, the trustees have concerns about the standard of record-keeping and controls that were in fact implemented, executed and maintained by the then administrator, Self-Assurance Benefit Administrators (Pty) Ltd. The difficulties experienced by the previous administrator relating to the fund, included a high turnover of staff involved with the fund, poor record keeping and poor financial reporting, resulting in a period of uncertainty with regards to the administration of the fund. Refer to notes 8 and 9 of the report of the board of trustees. The board of trustees undertake to adhere to its duties until such time as the matters are finally sorted out. Approval of the annual financial statements The annual financial statements of Self Assurance Domestic Employees Provident Fund are the responsibility of the Board of Fund. The Board of Fund fulfils this responsibility by ensuring the implementation and maintenance of accounting systems and practices adequately supported by internal financial controls. These controls, which are implemented and executed by the fund and/or its benefit administrators, provide reasonable assurance that: • the fund’s assets are safeguarded; • transactions are properly authorised and executed; and • the financial records are reliable. The annual financial statements set out on pages 11 to 18 have been prepared for regulatory purposes in accordance with the Regulatory Reporting Requirements for Retirement Funds in South Africa, the rules of the fund and the Pension Funds Act. • The basis of accounting applicable to retirement funds in South Africa as indicated in the principal

accounting policies contained in the notes to the financial statements on page 13 to 14; • the financial rules of the fund; and • the provisions of the Pension Funds Act in South Africa.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

5

SCHEDULE B (Continue)

STATEMENT OF RESPONSIBILITY BY THE BOARD OF FUND For the period ended 30/06/2014 The following instances of non-compliance with Acts, Legislation, Regulations and Rules, including the provisions of laws and regulations that determine the reported amounts and disclosures in the financial statements came to our attention and were not rectified before the Board of Fund’s approval of the financial statements:

Nature and cause of non-compliance

Possible impact of non-compliance matter on the Fund

Corrective course of action to resolve non-compliance matter

Valuation Reports from 2007 onwards not yet been approved by the FSB

Financial soundness as fund could be underfunded.

The report is to be finalised by the Actuary and then to be submitted to the FSB.

These financial statements: • were approved by the Board of Fund on 26/02/2015; • are to the best of the Board members knowledge and belief certified to be complete and correct; • fairly represent the net assets of the fund at 30 June 2014 as well as the results of its activities for the period

then ended; and • are signed on behalf of the Board of Fund by:

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

6

SCHEDULE C STATEMENT OF RESPONSIBILITY BY THE PRINCIPAL OFFICER For the period ended 30/06/2014

I confirm that for the period under review the Self Assurance Domestic Employees Provident Fund has timeously submitted all regulatory and other returns, statements, documents and any other information as required in terms of the Pension Funds Act and to the best of my knowledge all applicable legislation except for the following (where applicable): I am aware of the following non-submissions:

1. Annual financial statement 2. Valuation reports.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

7

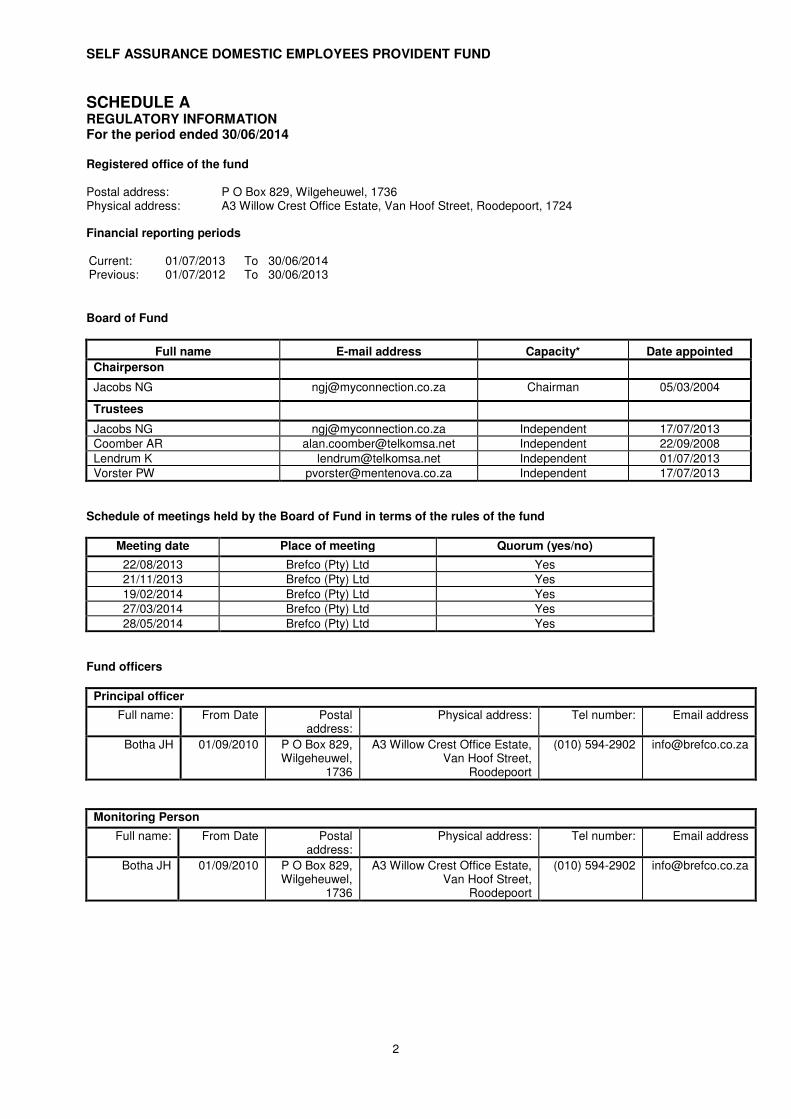

SCHEDULE E

REPORT OF THE BOARD OF FUND For the period ended 30/06/2014 1. DESCRIPTION OF THE FUND

1.1. Type of fund

The Fund is a provident fund and is a defined contribution fund. In terms of regulation 30(2) (t) (ii) of the Regulations to the Pension Funds Act, the umbrella fund is registered as a type A umbrella fund.

1.2. Benefits 1.2.1. Summary in terms of the rules of the fund.

The benefit structure of this Fund is based solely on the accumulation of contributions plus investment income earned from the appropriate investments. The Fund provides lump sum benefits to members of the Fund when they retire or resign from their employer as well as death benefits for their dependants should they die in service. The benefits provided for are: (a) Retirement benefit: Share of Fund (b) Withdrawal benefit: Share of Fund (c) Death benefit: Share of Fund

1.2.2 Unclaimed benefits

1.2.2.1. Strategy of Board of Fund towards unclaimed benefits. In respect of unclaimed benefits, complete records, as prescribed, are maintained as from the date of the benefit was identified as unclaimed. All unclaimed benefits are held in accordance with the default investment portfolio strategy the Board decided.

1.2.3 Beneficiary benefits

As there are no benefits for any beneficiaries of a former member the Board of Funds have not adopted a strategy towards beneficiaries.

1.3. Contributions

1.3.1. Description in terms of the rules of the Fund.

1.3.1.1. Members’ contributions. Members are not required to contribute to the Fund. Contributions ceased in March 2011

1.3.1.2. Employers’ contributions.

The employers contribute at various rates as specified in the Rules of the Fund. Contributions ceased in March 2011

1.4. Rules/ amendments

1.4.1. Revised rules / Consolidated rules: All rule amendments are available for inspection at the fund’s registered office.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

8

SCHEDULE E (continue)

REPORT OF THE BOARD OF FUND For the period ended 30/06/2014 2. INVESTMENTS

2.1. Investment strategy

The investment strategy of the fund is set by the board of trustees after taking due consideration of the advice of the fund’s investment and other professional advisors. This investment strategy complies with the provisions of regulation 28 of the Pension Funds Act in South Africa. The investments are managed according to the following principles: 2.1.1. General

All investments are made with ACSIS Ltd.

2.1.2. Individual members choice The Fund does not offer any individual member an option of the investments products the fund invested with.

2.1.3. Unclaimed benefits

Unclaimed benefits are held in the Fund.

2.1.4. Surplus apportionment There is no surplus apportionment allocation. A nil surplus apportionment was submitted and approved by the Financial Service Board on the 25

th May 2006.

2.1.5. Reserve accounts

There are no reserve accounts

2.2. Management of investments

The Fund’s investments consist of managed portfolios with ACSIS Ltd. All investment administrators have complete discretion as to the composition of their share of the portfolio within the boundaries allowed by the Pension Funds Act in South Africa. The board of trustees meets at regular intervals to discuss investment policy and to monitor the asset allocation and performance of the investment administrators against the investment strategy of the fund. Investment managers deduct their fees from the assets of the fund under their administration on a basis agreed by the trustees. .

3. MEMBERSHIP

Active members

Numbers at beginning of period 92 Withdrawals (9) Retirements (2)

Numbers at end of period 81

Number at end of period (South African citizen) * 81 Number at end of period (non- South African citizen) 0

*Note: The Fund does not have the citizenship details for these members; therefor all were classified as South African citizens.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

9

SCHEDULE E (continue)

REPORT OF THE BOARD OF FUND For the period ended 30/06/2014

4. ACTUARIAL VALUATION

The last statutory valuation of the Fund was prepared as at 30 June 2004, the surplus apportionment date of the Fund. This valuation was prepared by I.J. Minnaar, employed by Clemans, Murfin & Rolland at the time, and revealed no surplus to be apportioned to stakeholders in terms of the Pension Funds Act. The Registrar registered the Funds’ nil surplus submission on 25 May 2006. The next statutory valuation of the Fund is due as at 30 June 2007 and is in the process of being completed.

5. SURPLUS APPORTIONMENT OR NIL SCHEME

The Fund does not have a surplus apportionment scheme as envisaged by Section 15B(1) of the Act as it has no surplus to be apportioned. The NIL surplus apportionment scheme was approved by the Registrar on the 25th of May 2006.

6. HOUSING LOAN FACILITIES

No loan facilities were made available by the Fund during the period under review.

7. INVESTMENTS IN PARTICIPATING EMPLOYERS

During the period under review, no investment in any participating employer was held by the Fund. 8. SIGNIFICANT MATTERS

8.1 Prior to 1st May 2010 Self-Assurance Benefit Administrators (Pty) Ltd was the appointed benefit

administrator for the fund. The Trustees would like to place on record that instances of poor administration and record-keeping were brought to their attention. As a result, the Trustees had concerns about the standard of record-keeping and controls that were in fact implemented and executed and maintained by the then administrator, Self-Assurance Benefit Administrators. The difficulties experienced by the previous administrator relating to the fund included a high turnover of staff involved with the Fund, poor record keeping and poor financial reporting. All of these factors contributed to a period of uncertainty with regards to the administration of the Fund.

8.2 In early 2010 Self-Assurance Benefit Administrators advised the Fund that they were unable to

continue with the on-going administration. The Fund then appointed Brefco (Pty) Ltd:

a) to verify the fund’s records and data from 30 June 2007 being the last submitted and accepted audited financial statements, and

b) to deal with the day to day administration of the Fund. 8.3 Due to administrative issues encountered with the Fund’s previous administrators, Self Assurance

Benefit Administrators, the Fund was unable to verify the accuracy and completeness of Fund member credits at the beginning of the year. The trustees decided that the values per the audited financial statements at 30 June 2007 were the most accurate values to use as the opening balances.

8.4 During the review of the current financial period the trustees found that there was significant

supporting documentation missing from the Funds previous administrators, Self Assurance Benefit Administrators (Pty) Ltd, inter alia (a) No employer contributions/remittances could be provided. The collections were operated via a

debit order system and the previous administrator made changes to the monthly contributions when communicated or advised by the employer. All contributions updated to the member record agreed to the amount received in the bank.

(b) No supporting returns could be provided to the trustees for compliance with the South African Reserve Bank D.427 requirements.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

10

SCHEDULE E (continue)

REPORT OF THE BOARD OF FUND For the period ended 30/06/2014

8.5 Due to the lack of documentation and the various changes in administration, the trustees took a

prudent decision to verify member’s fund records as each financial year is processed. This resulted in member’s benefits being paid on a partial basis, with a final agterskot payment to be made after the completion of all the prospective year end audits.

8.6 Risk premiums and administration charges – The Fund has accounted for administration fees on the

basis of actual contributions received and banked into the Fund’s bank account. This actual contribution has been allocated in the fund’s accounting records as contributions received. The trustees are of the opinion that this matter is dealt with appropriately and has no significant impact on the financial status of the fund.

9. SUBSEQUENT EVENTS

No subsequent events to report on.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

11

SCHEDULE F STATEMENT OF NET ASSETS AND FUNDS At 30/06/2014

Notes Current period

R Previous period

R

ASSETS

Non-curent assets 1,894,579 1,658,756

Investments (including investment and owner occupied properties)

1 1,894,579 1,658,756

Current assets 42,866 279,555

Cash at bank 42,866 279,555

Total assets 1,937,445 1,938,311 FUNDS AND LIABILITIES

Members’ funds and surplus account 1,261,808 1,353,994

Members’ individual accounts 1,261,330 1,353,994 Amounts to be allocated 10 478 0

Total funds and reserves 1,261,808 1,353,994 Non-current liabilities 139,680 123,600

Provisions 6.1 139,680 123,600

Current liabilities 535,957 460,717

Benefits payable 2 9,277 9,277 Accounts payable 3 526,680 451,440

Total funds and Liabilities 1,937,445 1,938,311

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

12

SCHEDULE G STATEMENT OF CHANGES IN NET ASSETS AND FUNDS For the period ended 30/06/2014

Notes

Members’ individual accounts Total Total

Accumulated funds Current period Previous

period R R R

Net investment income 4 241,665 241,665 297,591 Less: Administration expenses 5 (103,836) (103,836) (100,461) Net income before transfers and benefits

137,829 137,829 197,130

Transfers and benefits Benefits 2 (230,015) (230,015) (125,827)

Net income after transfers and benefits

(92,186) (92,186) 71,303

Funds and reserves Balance at beginning of period 1,353,994 1,353,994 1,282,691

Balance at end of period 1,261,808 1,261,808 1,353,994

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

13

SCHEDULE HA NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014 PRINCIPAL ACCOUNTING POLICIES The following are the principal accounting policies used by the fund, which are consistent with those of the previous period.

PURPOSE AND BASIS OF PREPARATION OF FINANCIAL STATEMENTS The annual financial statements are prepared in accordance with Regulatory Reporting Requirements for Retirement Funds in South Africa, the rules of the fund and the provisions of the Pension Funds Act in South Africa. The financial statements are prepared on the historical cost and going concern bases, modified by the valuation of financial instruments and investment properties to fair value, and the revaluation of property, plant and equipment to market value. FINANCIAL INSTRUMENTS • Measurement

• Financial instruments include cash and bank balances, investments, housing loans, receivables and accounts payable.

• Financial instruments are initially measured at cost as of trade date, which includes transaction costs. Subsequent to initial recognition, these instruments are measured as set out below.

• Investments

Investments are measured at fair value. The fair value of marketable securities is calculated by reference to the applicable Stock Exchange quoted selling prices at the close of business on the statement of funds and net assets date.

• Collective Investment Schemes

Investments are measured at fair value. The fair value of marketable securities is calculated by reference to the applicable insurer, investment manager or the Stock Exchange quoted selling prices at the close of business on the statement of funds and net assets date.

• Housing loans

The fund did not grant any guarantees for loans or any direct housing loans to its members in terms of Section19(5) of the Pension Fund Act.

• Other Income Not applicable.

• Insurance policies Insurance policies linked to listed investments are valued at fair value and are therefore equivalent to market value of the underlying assets as certified by the Insurer concerned.

• Accounts receivable Accounts receivable are stated at realisation value.

• Cash and cash equivalents Cash and cash equivalents are measured at fair value.

• Accounts payable Accounts payable are stated at the actual amounts due.

PROVISIONS Provisions are brought into account for known obligation as a result of past events, for which it will be required to settle the obligation. A reliable estimate has been made of the amount of the obligation. CONTRIBUTIONS Contributions are brought to account on the accrual basis.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

14

SCHEDULE HA (continue) NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014 PRINCIPAL ACCOUNTING POLICIES - CONTINUE

DIVIDEND INCOME, INSURANCE POLICY INCOME, INTEREST AND RENTALS • Interest is recognised when it is determined that such income will accrue to the fund. • Insurance policy income and dividends are recognised when declared by the insurer. • Gains and losses on investments are recognised during the period in which the change arises.

TRANSFERS TO AND FROM THE FUND Transfers to or from the fund are recognised on approval being granted by the Financial Services Board as required in terms of Section 14 and 13B of the Pension Funds Act. Individual transfers are recognised when the individual member’s transfer is received or paid. End Principal Accounting

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

15

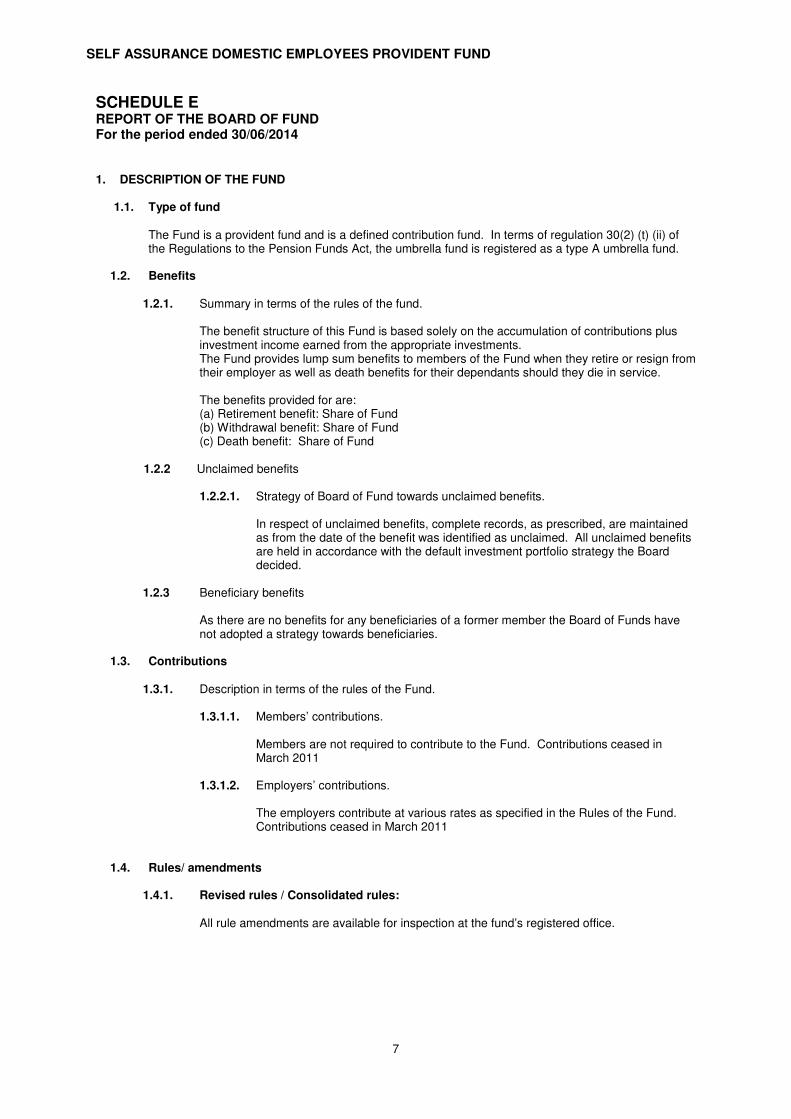

SCHEDULE HA (continue) NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014 1. Investments

1.1. Investment summary

A B A + B Local Foreign Total Total

Current period Previous period

R R R R

Insurance policies 1,485,409 409,170 1,894,579 1,658,756

Total investments 1,485,409 409,170 1,894,579 1,658,756

2. Benefits

2.1. Benefits – current members

A B D A+B+C-D-E

At beginning of

period Benefits for

current period Payments At end of period R R R R

Lump sums on retirements 0 101,977 (101,977) 0 Full benefit 101,977 (101,977)

Lump sums before retirement 9,277 128,038 (128,038) 9,277 Withdrawal benefits 9,277 128,038 (128,038) 9,277

TOTAL (8.1) 9,277 230,015 (230,015) 9,277

Benefits approved - current

Benefits approved - previous

Benefits for current period (B)) 230,015 125,827

Statement of changes in net assets and funds 230,015 125,827

3. Accounts payable

Current period

R

Previous period R

Admin fees due to administrators 526,680 451,440

Total accounts payable 526,680 451,440

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

16

SCHEDULE HA (continue) NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014 4. Net investment income

Current period R

Previous period R

Income from investments (9,944) (8,630)

Interest 5,842 15,731

Adjustment to fair value (provide details) 245,767 290,490 Sub-Total 251,609 306,221

Less: Expenses incurred in managing investments (9,944) (8,630) Total 241,665 297,591

Current Period

Previous Period

Details Adjusted fair Value R R Revaluation of Investments 245,767 290,490

Total Adjustment to fair value 290,490 290,490

5. Administration expenses

Notes Current period

R Previous period

R

Actuarial fees 16,080 16,080 Administration fees 79,739 75,338 Fidelity Insurance 2,750 2,750 Levies 4,617 3,992 Other 5.1 158 121 Board of Fund expenses 5.2 492 2,180 Total 103,836 100,461

5.1. Other

Current Period Previous Period

Details of Other admin expenses R R

Bank Charges 158 121

Total other income 158 121

5.2. Board of Fund expenses Current period

R Previous period

R

Trustees payments 492 2,180

Total Board of Fund expenses 492 2,180

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

17

SCHEDULE HA (continue) NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014

6. Provisions

6.1. Provisions Current Period Previous Period

Prior period adjustment R R

Provision for actuarial fees 139,680 123,600

Total Provisions 139,680 123,600

7. Risk management policies

• SOLVENCY RISK Continuous monitoring by the Board takes place to ensure that appropriate assets are held where the funds obligation to members is dependent upon the performance of specific portfolio assets and that a suitable match of assets exists for all other liabilities.

• CREDIT RISK The Board monitors receivable balances on an on-going basis with the result that the fund’s exposure to bad debts is not significant. An appropriate level of provision is maintained.

• LEGAL RISK Legal risk is the risk that the fund will be exposed to contractual obligations which have not been provided for. Legal representatives of the fund monitor the drafting of contracts to ensure that rights and obligations of all parties are clearly set out.

• CASH FLOW RISK The board of trustees agreed an amount with the administrators that should be kept in the bank account to meet the fund’s cash flows requirements. If the agreed amount is insufficient, the administrator must disinvest to meet the required cash flow.

• CURRENCY RISK

The fund’s exposure to currency risk is mainly in respect of foreign investments made on behalf of members of the fund for the purpose of seeking desirable international diversification of investments.

• LIQUIDITY RISK The fund’s liabilities are backed by appropriate assets and it has significant liquid resources.

• MARKET RISK Market risk is the risk that the value of a financial instrument will fluctuate as a result of changes in market prices of market interest rates.

• INVESTMENTS Investments in insurance policies are valued at fair value as certified by the insurer. Investments are managed with the aim of maximising the fund’s returns while limiting risk to acceptable levels within the framework of statutory requirements. Continuous monitoring takes place to ensure that appropriate assets are held where the liabilities are dependent upon the performance of specific portfolios of assets and that a suitable match of assets exists for all non–market related liabilities.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

18

SCHEDULE HA (continue) NOTES TO THE FINANCIAL STATEMENTS For the period ended 30/06/2014 8. Promised retirement benefits As a defined contribution fund, the fund in association with the principal and participating employers provides the members a course to save towards retirement. The fund liability to the promised retirement benefit is limited to the member’s equitable share of his/her share of fund. The member’s share of fund is the member’s retirement contributions plus the net return earned from the appropriate investment. 9. Related party transactions Fund’s expenses to the value of R The following transactions between the participating employer and the fund occurred during the period The participating employer made contributions to the fund for members’ retirement and towards the

fund’s expenses to the value of 0 And 0 Respectively

10. Amounts to be allocated Current period

R Previous period

R

Investment return to be allocated 478 0

Total amounts to be allocated 478 0

- o O o -

End of Schedule HA

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

19

SCHEDULE I REPORT OF THE BOARD OF FUND TO THE REGISTRAR OF PENSION FUNDS IN TERMS OF SECTION 15 IN RESPECT OF SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FOR THE PERIOD ENDED 30 JUNE 2014 The Board of Fund confirms that, to the best of their knowledge and belief, having made such inquiries as they considered necessary for the purpose of appropriately informing themselves

1:

1. Investment statements were obtained from the investment manager/insurer.

2. Bank reconciliations were performed and reconciling items on the bank reconciliations for the bank accounts of the fund were cleared.

3. All Members were invested in one portfolio and switches between portfolios did not apply and paragraphs 3.1 to 3.5 are not applicable.

4. The transactions in the member account per the unaudited annual financial statements were made in terms of the registered rules of the Fund and/or the Act.

5. The Rules of the Fund do not permit any reserve accounts therefore paragraph 5.1 and 5.2 are not applicable

6. The Fund did not have any investments in accordance with the terms of section 19(4) of the Act.

7. The Fund does not provide any housing loans and therefore paragraph 7.1 to 7.2 are not applicable

8. The Fund does not provide any guarantees for housing loans and therefore paragraph 8.1 to 8.2 are not applicable

9. Loans were not granted and/or investments were not made as prohibited in terms of section 19(5B).

10. Contributions –

10.1. There were no contributions due during the period.

10.2. The Fund did not have any amounts disclosed as arrear contributions at year-end.

10.3. The relevant steps as prescribed in terms of regulation 33 have been complied with in the recovery of arrear contributions.

11. Benefits – 11.1. The benefits have been paid in accordance with the rules of the Fund. 11.2. The Fund did not re-insure any death benefits and the recovery of death benefits is not applicable. 11.3. The benefits that comply with the definition of “unclaimed benefits” in the Act were classified as

unclaimed.

12. The Fund does not pay any Pensions and Annuities and therefor paragraphs 12.1 to 12.5 are not applicable.

13. The Fund did not have any Section 14 transfers and therefor paragraphs 13.1 to 13.5 are not applicable

14. Fidelity insurance cover was in place throughout the year ended 30 June 2014.

1 Notes:

• Delete where not applicable.

• Exceptions should be disclosed.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

20

SCHEDULE I (continue) REPORT OF THE BOARD OF FUND TO THE REGISTRAR OF PENSION FUNDS IN TERMS OF SECTION 15 IN RESPECT OF SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FOR THE PERIOD ENDED 30 JUNE 2014

15. Financial soundness –

15.1. Per the most recent statutory valuation signed and submitted by the valuator as at 30 June 2004, the Fund was in a sound financial position. The valuation at 30 June 2007 is currently being finalised.

15.2. As the Fund was in a sound financial position no scheme had been approved by the Registrar and had not been implemented.

16. Regulation 28

16.1. We have reviewed Annexure B to Schedule I (“the Annexure”), Assets of the Fund held in Compliance with Regulation 28 of the Act of SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT set out on pages 20 to 22.

In our opinion, the Annexure does represents, in all material respects, the assets of the fund in compliance with Regulation 28.

16.2. Regulation 28 compliant certificates for investments in collective investment schemes were obtained from the relevant registered collective investment scheme manager and the certificate states that the collective investment scheme is Regulation 28 complaint.

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

21

SCHEDULE IA – INVESTMENT SCHEDULE At 30/06/2014

Investments

Notes Direct Investments

Compliant Investments

Total Local Total Foreign

Total percentage foreign exposure

TOTAL as per Regulation 28 (Schedule IB)

Note L

R R R R R % R

Cash (including cash at bank) A 42,866 42,866 42,866 0 0.00% 42,866

Insurance Policies : 0 1,894,579 1,894,579 1,485,409 409,170 21.60% 1,894,579

- Linked Policies L 0 1,894,579 1,894,579 1,485,409 409,170 21.60% 1,894,579

TOTAL INVESTMENTS 42,866 1,894,579 1,937,445 1,528,275 409,170 21.12% 1,937,445

A CASH

Instrument

Fair value Previous Period

R R

Local Notes and coins, any balance or deposit in an account held with a South African bank List issuers/entities which exceeds 5% of total assets

Standard Bank of SA Ltd 42,866 279,555

TOTAL CASH 42,866 279,555

L CERTIFIED REGULATION 28 COMPLIANT INVESTMENTS

Instrument Local or Foreign

R Fair value

R Previous Period

R

Linked Policies – reg28(8)(b)(ii) 1,894,579 1,894,579 1,658,756

Local 1,894,579 1,894,579 1,658,756

List issuers/entities which exceeds 5% of total assets 1,894,579 1,894,579 1,658,756

ACSIS Strategy 1%-3% 1,894,579 1,894,579 1,658,756

N INVESTMENTS NOT DISCLOSED

Investment manager/CIS/ Insurer responsible for not providing information on investment(s)/portfolio

Fair value R Previous Period R Reasons (provide details)

ACSIS Strategy 1%-3% 54,129 0 It is excluded in terms of sub regulation 8b of Regulation 28 because the fund is less than 5% of the total NAV of the pension fund and we receive a certificate(attached) from Prudential stating that the fund is Reg28 compliant and thus no need to look through to the individual instruments held by the fund.”

54,129 0

P RECONCILIATION BETWEEN THE INVESTMENTS IN SCHEDULE H2 AND SCHEDULE IA

Cash at bank Compliant investments

Total

Cash 42,866 42,866

Insurance Policies 1,894,579 1,894,579 TOTAL INVESTMENTS 42,866 1,894,579 1,937,445

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

22

SCHEDULE IB ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014

Fair value R A Total assets (Schedule IA -Total investments) 1,937,445 B1 Less: Reg 28 compliant investments

(certificate received from issuing entity):- 0

B.1.1 Collective Investment Schemes (Reg 28(8)(b)(i)) 0 B.1.2 Linked Policies (Reg 28(8)(b)(ii)) 0 B.1.3 Non-Linked policies (Reg 28(8)(b)(iii)) 0 B.1.4 Entity regulated by FSB (Reg 28(8)(b)(iv)) 0

B2 Less: Reg 28 Excluded investments 0

B.2.1 Insurance Policies ( Reg 28(3)(c)) 0 C Less: Investments not disclosed /data not available for disclosure [Refer

Schedule IAN] (54,129)

D TOTAL ASSETS for REGULATION 28 DISCLOSURE 1,883,316

Max % or SARB max limit

per issuer, entity or instrume

nt

1 CASH 100% 395,916 21.02%

1.1 Notes, deposits, money market instruments issued by a South African Bank, margin accounts, settlement accounts with an exchange and Islamic liquidity management financial instruments 100% 390,855 20.75%

(a) Notes and coins, any balance or deposit in an account held with a South African bank 25% 345,181 18.33% (b) A money market instrument issued by a South African bank including an Islamic

liquidity management financial instrument 25% 45,434 2.41% (c) Any positive net balance in a margin account with an exchange 25% 240 0.01%

1.2 Balances or deposits, money market instruments issued by a foreign bank including Islamic liquidity management financial instruments 5,061 0.27%

(a) Any balance or deposit held with a foreign bank 5% 4,346 0.23% (b) Any balance or deposit held with an African bank 5% 18 0.00% (c) A money market instrument issued by a foreign bank including an Islamic liquidity

management financial instrument 5% 697 0.04%

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

23

SCHEDULE IB (continue) ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014

Max % or

SARB max

limit

per issuer,

entity or

instrument

2 DEBT INSTRUMENTS INCLUDING ISLAMIC DEBT

INSTRUMENTS

100% or 75%

696,484 36.98%

2.1 Inside the Republic 75/100% 694,296 36.87% (a) Debt instruments issued by, and loans to, the government of the

Republic, and any debt or loan guaranteed by the Republic

100%

291,136 15.46% 75% 10% (b) Debt instruments issued or guaranteed by the government of a foreign

country

75%

2,294 0.12% (c) Debt instruments issued or guaranteed by a South African Bank

against its balance sheet:

75%

162,332 8.62% (c)(i) Listed on an exchange with an issue market capitalisation of R20 billion or

more, or an amount or conditions as prescribed

75% 25%

150,338 7.98% (c)(ii) Listed on an exchange with an issuer market capitalisation of between R2

billion and R20 billion, or an amount or conditions as prescribed

75% 15%

11,994 0.64% (d) Debt instruments issued or guaranteed by an entity that has equity

listed on an exchange, or debt instruments issued or guaranteed by a

public entity under the Public Finance Management Act, 1999 (Act No.

1 of 1999) as prescribed:-

50%

137,818 7.32%

(d)(i) Listed on an exchange 50% 10% 137,818 7.32%

(e) Other debt instruments: 25% 100,716 5.35%

(e)(i) Listed on an exchange 25% 5% 100,443 5.33% (e)(ii) Not listed on an exchange 15% 5% 273 0.01%

2.2 Foreign 2,188 0.12% (b) Debt instruments issued or guaranteed by the government of a foreign

country

143 0.01% (d) Debt instruments issued or guaranteed by an entity that has equity

listed on an exchange

152 0.01%

(d)(ii) Not listed on an exchange 152 0.01% (e) Other debt instruments 1,893 0.10%

(e)(i) Listed on an exchange 31 0.00% (e)(ii) Not listed on an exchange 1,862 0.10%

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

24

SCHEDULE IB (continue) ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014

Max % or

SARB max

limit

per issuer,

entity or

instrument

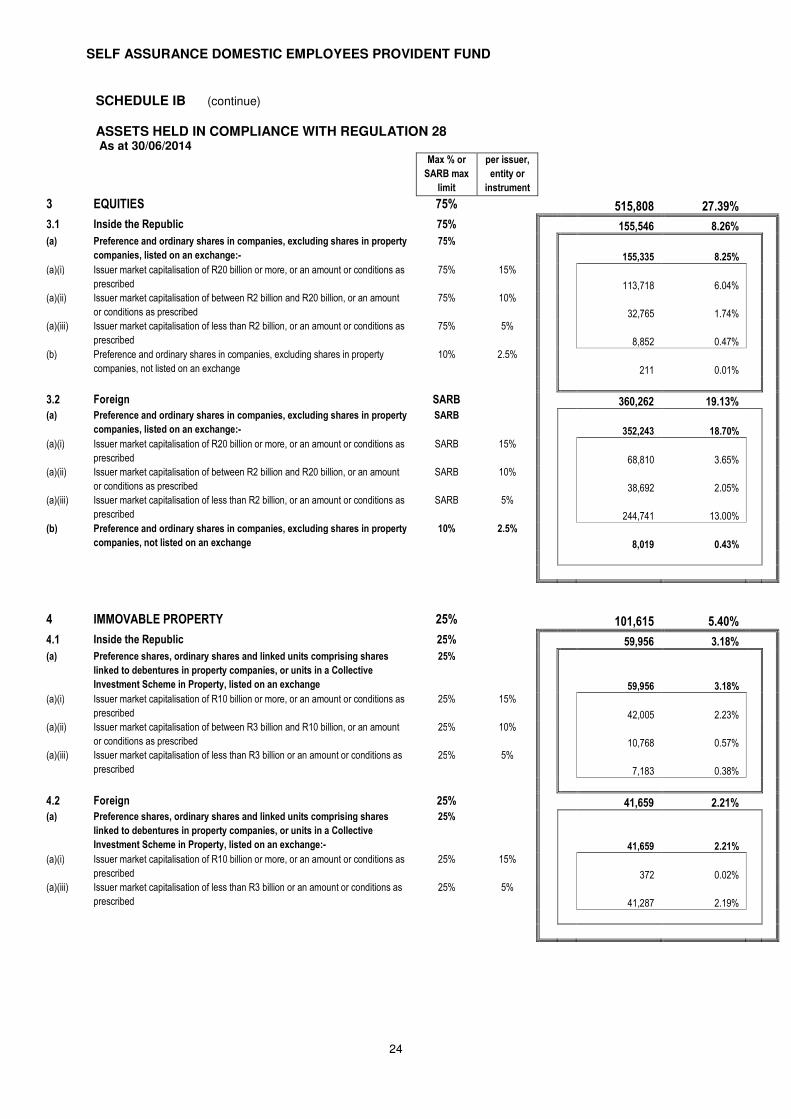

3 EQUITIES 75% 515,808 27.39%

3.1 Inside the Republic 75% 155,546 8.26%

(a) Preference and ordinary shares in companies, excluding shares in property

companies, listed on an exchange:-

75%

155,335 8.25%

(a)(i) Issuer market capitalisation of R20 billion or more, or an amount or conditions as

prescribed

75% 15%

113,718 6.04% (a)(ii) Issuer market capitalisation of between R2 billion and R20 billion, or an amount

or conditions as prescribed

75% 10%

32,765 1.74% (a)(iii) Issuer market capitalisation of less than R2 billion, or an amount or conditions as

prescribed

75% 5%

8,852 0.47%

(b) Preference and ordinary shares in companies, excluding shares in property

companies, not listed on an exchange

10% 2.5%

211 0.01%

3.2 Foreign SARB 360,262 19.13% (a) Preference and ordinary shares in companies, excluding shares in property

companies, listed on an exchange:-

SARB

352,243 18.70%

(a)(i) Issuer market capitalisation of R20 billion or more, or an amount or conditions as

prescribed

SARB 15%

68,810 3.65% (a)(ii) Issuer market capitalisation of between R2 billion and R20 billion, or an amount

or conditions as prescribed

SARB 10%

38,692 2.05% (a)(iii) Issuer market capitalisation of less than R2 billion, or an amount or conditions as

prescribed

SARB 5%

244,741 13.00% (b) Preference and ordinary shares in companies, excluding shares in property

companies, not listed on an exchange

10% 2.5%

8,019 0.43%

4 IMMOVABLE PROPERTY 25% 101,615 5.40%

4.1 Inside the Republic 25% 59,956 3.18%

(a) Preference shares, ordinary shares and linked units comprising shares

linked to debentures in property companies, or units in a Collective

Investment Scheme in Property, listed on an exchange

25%

59,956 3.18%

(a)(i) Issuer market capitalisation of R10 billion or more, or an amount or conditions as

prescribed

25% 15%

42,005 2.23% (a)(ii) Issuer market capitalisation of between R3 billion and R10 billion, or an amount

or conditions as prescribed

25% 10%

10,768 0.57% (a)(iii) Issuer market capitalisation of less than R3 billion or an amount or conditions as

prescribed

25% 5%

7,183 0.38%

4.2 Foreign 25% 41,659 2.21% (a) Preference shares, ordinary shares and linked units comprising shares

linked to debentures in property companies, or units in a Collective

Investment Scheme in Property, listed on an exchange:-

25%

41,659 2.21%

(a)(i) Issuer market capitalisation of R10 billion or more, or an amount or conditions as

prescribed

25% 15%

372 0.02% (a)(iii) Issuer market capitalisation of less than R3 billion or an amount or conditions as

prescribed

25% 5%

41,287 2.19%

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

25

SCHEDULE IB (continue) ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014

5 COMMODITIES 10% 1,651 0.09%

5.1 Inside the Republic 10% 1,651 0.09%

(a) Kruger Rands and other commodities on an exchange, including exchange

traded commodities

10%

1,651 0.09%

(a)(ii) Other commodities 5% 5% 1,651 0.09%

8 HEDGE FUNDS, PRIVATE EQUITY FUNDS AND ANY OTHER

ASSET NOT REFERRED TO IN THIS SCHEDULE

25%

171,842 9.12%

8.1 Inside the Republic 25% 171,842 9.12%

(a) Hedge fund 25% 171,835 9.12%

(a)(ii) Hedge funds 25% 10% 171,835 9.12%

(c) Other assets not referred to in this schedule and excluding a hedge fund or

private equity fund

7 0.00%

TOTAL ASSETS – REGULATION 28 1,883,316 100.00%

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

26

SCHEDULE IB (continue) ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014 INVESTMENT SUMMARY (REGULATION 28)

Local Percentage of Fair value

Foreign (Excluding Africa)

Percentage of Fair value Africa Total

Percentage of Fair value

R % R % R R %

1 Balances or deposits, money market instruments issued by a bank including Islamic liquidity management financial instruments 390,855 20.17% 5,061 0.27% 18 395,916 20.44%

2 Debt instruments including Islamic debt instruments 694,296 35.84% 2,188 0.11% 0 696,484 35.95%

3 Equities 155,546 8.03% 360,262 18.59% 0 515,808 26.62%

4 Immovable property 59,956 3.09% 41,659 2.15% 0 101,615 5.24%

5 Commodities 1,651 0.09% 0 0.00% 0 1,651 0.09%

8 Hedge Funds, private equity funds and any other assets not referred to in this schedule 171,842 8.87% 0 0.00% 0 171,842 8.87%

9 Fair value of assets to be excluded in terms of sub-regulations3(c ) and (8)(b) of Regulation 28 54,129 2.79% 0 0.00% 0 54,129 2.79%

TOTAL (equal to the fair value of assets) 1,528,275 78.88% 409,170 21.11% 18 1,937,445 100%

BREACHES IN TERMS OF SUB REGULATION 3 OF REGULATION 28

Total (Inside & Foreign)

Percentage of Fair value

Regulation 28 limits

R %

Asset Limits in terms of sub regulation 3(f)

Other debt instruments not listed 11,994 0.62%

Equities not listed 8,230 0.42%

Hedge funds , Private Equity funds and other assets 171,842 8.87%

TOTAL 192,066 9.91% 35%

Asset Limits in terms of sub regulation 3(g)

Equities not listed 8,230 0.42%

TOTAL 8,230 0.42% 15%

Asset Limits in terms of sub-regulation 3(h)

Cash and deposits with a South African Bank 345,181 17.82%

Debt instruments guaranteed by a South African Bank 162,332 8.38%

TOTAL 507,513 26.19% 25%

SELF ASSURANCE DOMESTIC EMPLOYEES PROVIDENT FUND

27

SCHEDULE IB (continue) ASSETS HELD IN COMPLIANCE WITH REGULATION 28 As at 30/06/2014 BREACHES IN TERMS OF SUB REGULATION 3 OF REGULATION 28 NOTES: 1 Credit balance in current accounts must be included in item 1.

2 If the investments exceed the limit per institution/company/individual and no exemption has been obtained, the details below must be completed for each institution/company/individual in each category of assts.

Investments in institution/company/individual

Item % of Fair Value Fair Value ( R)

ACSIS Limited

Item 8 - Hedge funds , Private Equity funds

and other assets 8.87% 171,842