Embed Size (px)

Citation preview

Annual General Meeting23 November 2018

Forward-Looking Statements

This presentation contains forward-looking statements. These statements have been made by the Directors in good faith based on the information available to them up to the time of the preparation of this presentation. Due to the inherent uncertainties, including both economic and business risk factors underlying such forward-looking information, actual results may differ materially from those expressed or implied by these forward-looking statements. The Directors undertake no obligation to update any forward-looking statements contained in this presentation, whether as a result of new information, future events or otherwise.

2

2018 Highlights

3

2018 Financial Highlights

Dividend

Results ahead

of guidance

Strong contribution

from associates

and joint venture

Strong cash

performance

All percentage movements quoted above are in constant currency4

Operating Profit: +4.6% to €71.2 million

Adjusted EPS: +7.6% to 48.8 cent

Share of PAT: +70% to €7.2 million

Free Cashflow: +74.1% to €56.6 million

Year end debt: €38.4 million

Year end leverage: 0.54x

Final dividend: 17.85 cent

Total dividend: 21.00 cent

Payout ratio: 43%

2018 Operational Highlights

New seed processing and

input formulation facility in Poland

Investment in new operating

capacity for Feed business

Strong businessperformance in

highly challengingseason

Integration of acquisitions completed

in 2018

Agri-Services Digital roll out well advanced

in period

5

2018 Strategic Highlights

Creating the

building blocks for

future growth

First time entry

in Latin AmericaBrazil

Paraná

New and devolved capability organisedon a geographical profit centre basis

Enhanced Group services and functional leadership

Geographical diversification

Seasonality balance

Building international scale

Appointment of new CFO

Appointment of CEO Continental Europe

Appointment of CEO Latin America

6

Business Overview & Strategy

7

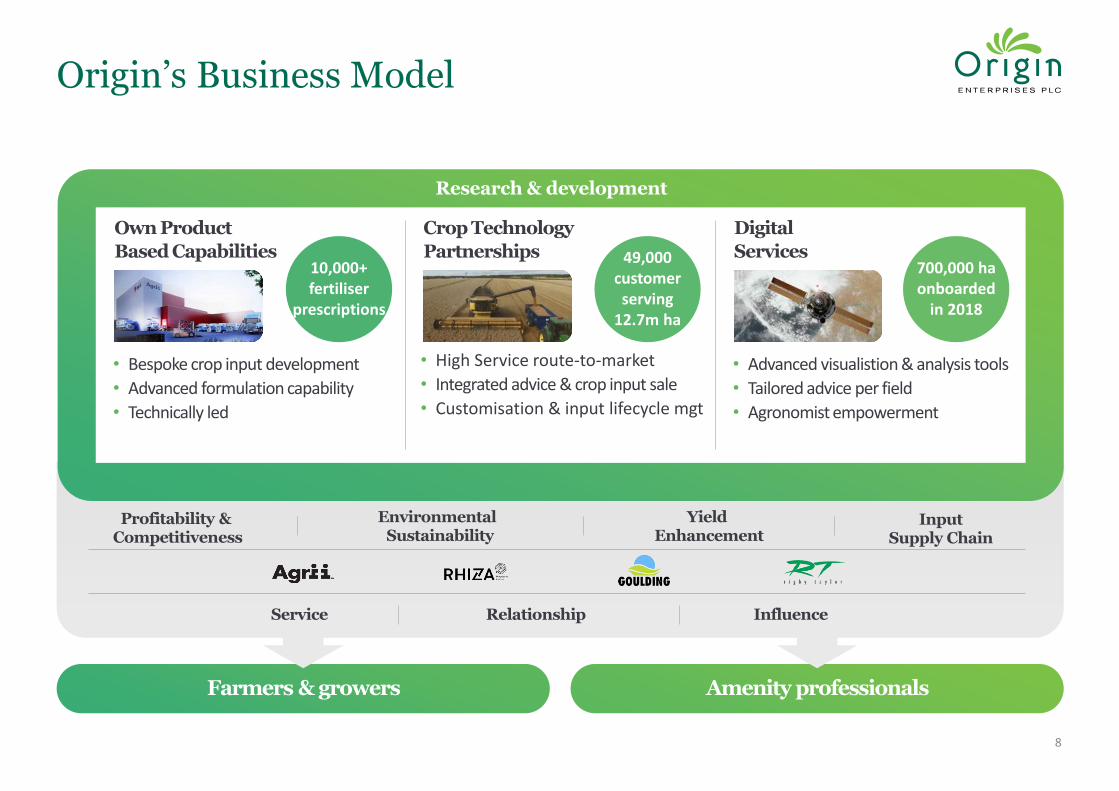

Research & development

Origin’s Business Model

8

Crop Technology

Partnerships

Digital

Services

Own Product

Based Capabilities 49,000customerserving

12.7m ha

700,000 haonboarded

in 2018

10,000+fertiliser

prescriptions

• Advanced visualistion & analysis tools

• Tailored advice per field

• Agronomist empowerment

• Bespoke crop input development

• Advanced formulation capability

• Technically led

• High Service route-to-market

• Integrated advice & crop input sale

• Customisation & input lifecycle mgt

Amenity professionalsFarmers & growers

EnvironmentalSustainability

Profitability &Competitiveness

Input Supply Chain

Yield Enhancement

InfluenceService Relationship

The Strategic Context for Farming & FoodMacro Trends

9

Productivity and Yield Gaps

Regulation and Escalating Cost of Innovation

Increasing Farm Professionalisation

Consolidation

Climate Change and Environmental

Stewardship

Digital Agriculture and Greater Technology

Enablement

Populationgrowth

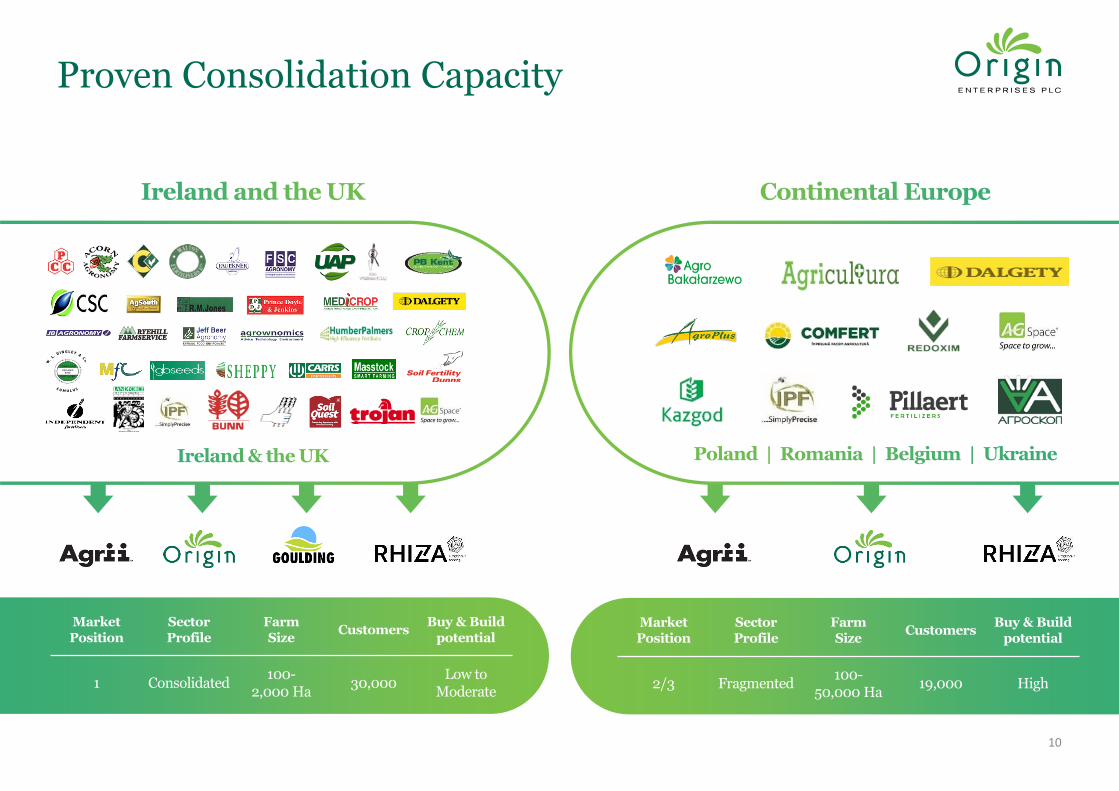

Proven Consolidation Capacity

10

MarketPosition

SectorProfile

FarmSize

CustomersBuy & Build

potential

1 Consolidated100-

2,000 Ha30,000

Low to Moderate

MarketPosition

SectorProfile

FarmSize

CustomersBuy & Build

potential

2/3 Fragmented100-

50,000 Ha19,000 High

Latin America

Primary producers

• Increasing professionalisation• Increasing intensification and farm consolidation

Speciality nutrition

• Second stage application dedicated to professional holdings

Speciality inputs – growing market

• US$1.7bn in 2016• US$2.2bn in 2021

Brazil – Market Overview

Global Player

0

5

10

15

20

25

30

35

40

0

50

100

150

200

250

20

01

/02

20

03

/04

20

05

/06

20

07

/08

20

09

/10

20

11

/12

20

13

/14

20

15

/16

20

17

/18

E

Production (million t)

Planted area (million ha)

Fertiliser (million t)

Grain Production, planted area and fertiliser consumption

2.42.5 2.6

3.0 3.13.3

3.4 3.23.7

Yield (t/ha)

> 2x Total area of UK

+22% from 2015/2016

Available to be converted into crop land

+30% from 15 years ago

Croplandarea (m ha)

Grain production (m tons)

Pasture land (m ha)

Soya yield(1,000 t/ha)

59

228

198

3.3

% Global Trade

21%

44%

31%

75%

Corn

Sugar

Coffee

FCOJ

Source: CONAB, Rabobank, IBGE

39%Soy

Fertiliser(million t)(millions)

11

#2Export

#1Export

#1Export

#1Export

#2Export

#3Production

#1Production

#1Production

#1Production

#2Production

Latin America

Crop input development

• Leading developer and manufacturer of high value nutrition and speciality inputs

• Paraná state based

• Supplies Brazil and export market

Crop services

• Leading provider of agronomy services, inputs and crop handling / marketing services

• Paraná state based

Main crops

• Soy beans• Corn

Customers

1,200Turnover

€28.4mEBITDA

€9.3mSales Force

60

Customers

4,000EBITDA

€4.3m

Turnover

€88.2mSales Force

65Market: Branded Retail Market: Direct Farm Distribution

• Sugar Cane• Wheat

• Farm size – 100 – 1,000 ha2

• Two crops per year• Fragmented market• Well capitalised primary producers• Favourable logistics to export

19,5

86

17,8

38

3,4

11

24

,83

5

20

,94

2

4,1

34

SoybeanCornWheat

2016/17

2026/27

+ 17%+ 21%

+ 27%

Paraná State

200,000km2

> 2x total areaof Ireland

Source: CONAB, Rabobank, IBGE

Brazil Investment

12

Paraná Production Forecast – Million tns

Group StrategyBuilding Sustainable Value

13

Our VisionTo be the leading and trusted

partner of choice to the farmers,

growers and amenity professionals we serve

Our PurposeTo deliver innovative crop manage-

ment systems to enhance the profitability

and sustainability of our customers’ enterprises

People & Organisation

Development of new and

evolved leadership teams

Improved accountabilities

and autonomy to execute

growth agenda

Scale

Concentrate on target

geographies with long term

growth potential

Build complementary

product based &

distribution capabilities

Market Focus

Prioritise customisation &

localisation of service

Leverage operating model

through investments in

digital & agronomic

capabilities

Portfolio Positioning

Maintain differentiated

position as specialist

route-to-market for crop

technologies

Optimise Group portfolio

through balanced business

and geographical

diversification

Investment Proposition

Market leading

positions with developed routes-to-

market

Consistent & maintainable

cash generation

Favourable long term

market fundamentals

Long term customer & supplier

partnerships

Industryleading R&D and technical

excellence

Strongbalance

sheet with flexibility for

M&A

Diversified geographic & business portfolio

Balanced organic growth,

international expansionand M&A potential

Well positioned to embrace Digitisation

of Agri-Services

974 531 82 6

14

Summary

15

Summary

16

Improving on-farm sentiment may be challenged in the UK by the uncertain nature of Brexit and its timing

Favourable start to FY 2019 with good demand and positive contribution from Latin America

Well positioned to capitalise on scalable and diversified business platform

Resilient 2018 business performance in challenging trading conditions

www.originenterprises.com

4-6 Riverwalk, Citywest Business Campus, Dublin 24, IrelandT: +353 1 5634900 F: +353 1 5634916