Embed Size (px)

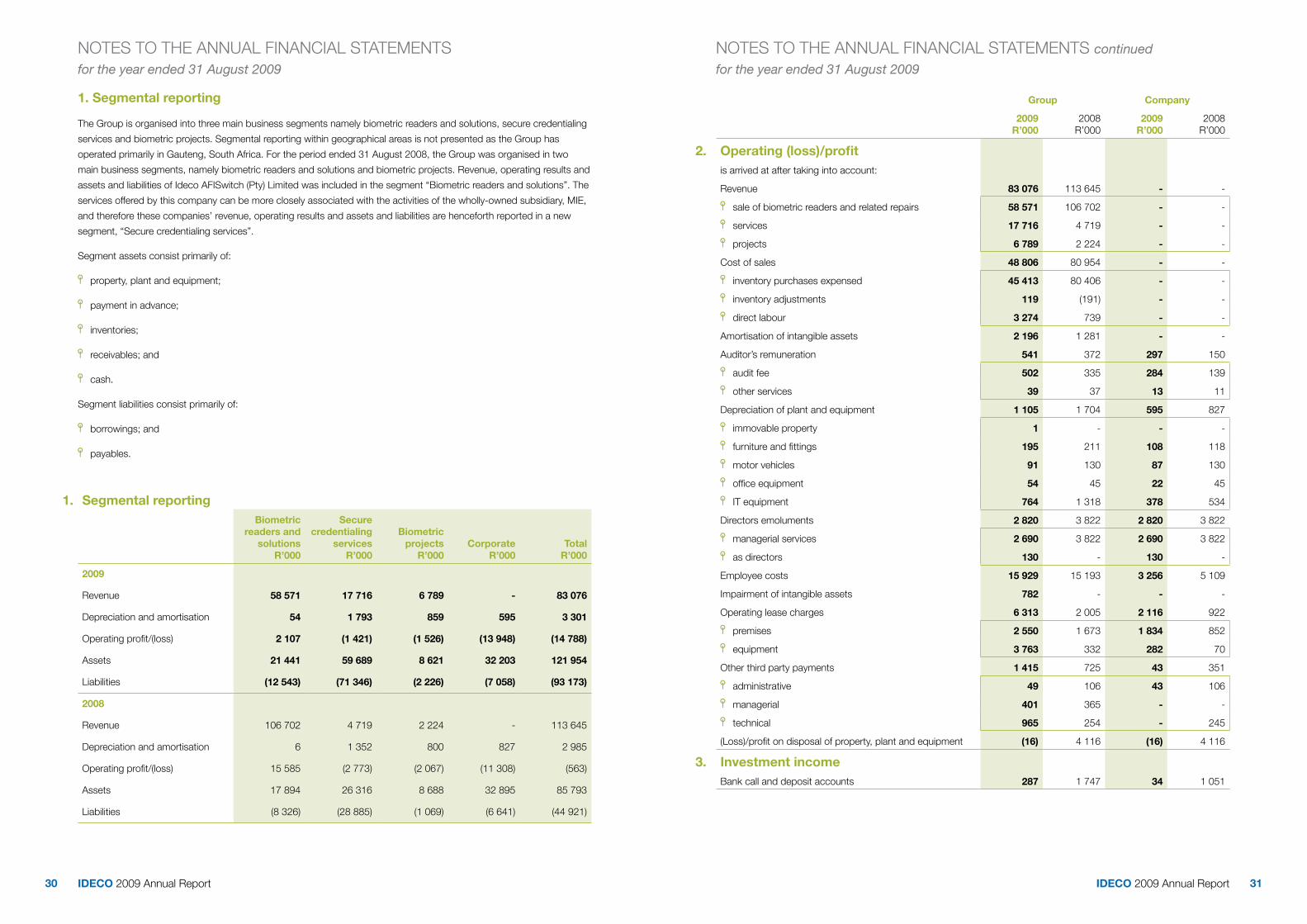

Citation preview

ANNUAL REPORT 2009

Listed on the AltX board of the Johannesburg Securities

Exchange, Ideco Group Limited (IDE) is an established

leader in the application of biometric technology and

southern Africa’s sole distributor of Sagem fingerprint

biometrics.

The Group’s digitisation of The Department of Home

Affairs’ paper-based fingerprint records is still the largest

project of its kind in the world.

Through AFISwitch, Ideco operates South Africa’s only

commercially-available, automated link to the SAPS

criminal record database.

In addition to our extensive work with Government, we

are the world’s largest distributor of Sagem fingerprint

biometrics for access control and time management

solutions.

There are now over 50 000 Sagem fingerprint readers

deployed across southern Africa, securely controlling

workplace access for almost two million people in a

diverse range of professionally-managed, security-

conscious businesses.

Identity Management

The optimum identity management solutions are founded

on technologies that can accurately and consistently

confirm the identity of an individual.

Identity management solutions start by creating a unique

link between an individual and a definitive biometric

characteristic such as a fingerprint. This unique link

then enables continual identification for a wide range of

purposes.

For example, within government, biometrically-empowered

identification can be incorporated in official credentials

such as birth certificates, national ID documents, drivers’

licences, pension and health cards, passports and work-

permits. Amongst law enforcement agencies, fingerprint

biometrics have been used for decades and Ideco works

closely with such organisations in South Africa.

Commercial applications for biometrics are equally diverse.

Fingerprint biometrics are commonly used in large-scale

solutions for workplace access management where they

have an established reputation for far greater security,

accuracy, speed and integrity than traditional PINs, access

cards and passwords.

PROFILE

IDECO 2009 Annual Report 1

Contents Page

Financial highlights 1

Board of directors 2

Group structure 3

Executive chairman’s report 4

Corporate governance 8

Analysis of shareholders 11

Statement of responsibility by the board of directors 12

Statement of compliance by the company secretary 12

Independent auditor of Ideco Group Limited 13

Directors’ report 14

Income statements 16

Balance sheets 17

Statements of changes in equity 18

Cash flow statements 19

Notes to the financial statements 20

Notice of annual general meeting 51

Form of proxy Inserted

IDECO GROUP LIMITEDANNUAL REPORT 2009

FINANCIAL HIGHLIGHTS

2009 2008 2007

R’000 R’000 R’000

Revenue 83 076 113 645 209 471

Operating (loss)/profit (14 788) (563) 31 317

Total assets 121 954 85 793 55 692

Cash and cash equivalents 8 247 (2 792) 26 177

Shareholders’ equity 28 781 40 872 16 589

Number of shares in issue 202 222 222 202 222 222 25 000 000

Weighted average number of shares 202 222 222 127 550 685 25 000 000

Headline (loss)/earnings per share (cents) (5,69) (0,43) 88,84

Basic (loss)/earnings per share (cents) (5,98) 2,35 88,85

Net asset value per share (cents) 14,23 20,21 66,36

IDECO 2009 Annual Report2 IDECO 2009 Annual Report 3

GROUP STRUCTURE

Ideco Biometric Security Solutions (Pty) Limited (“IBSS”)

is the sole supplier of Sagem biometric products in

South Africa. IBSS distributes and supports Sagem’s

fingerprint scanners for access control and time-and-

attendance solutions through its partner network which

covers the entire country.

Ideco Technologies (Pty) Limited delivers large-scale

biometric and identity management projects which

typically range from 12 to 60 months in duration.

Ideco AFISwitch (Pty) Limited operates a system

developed by Ideco to provide automated criminal

background checks to the private sector and members

of the public in terms of an agreement with the South

African Police Service.

Ideco Biometrix (Pty) Limited supplies biometric

equipment to the public sector on contracts

administered by the State Information Technology

Agency and the Electronic Communication Security

Company. This equipment ranges from physical and

logical access control scanners to forensic fingerprint

acquisition stations.

Managed Integrity Evaluation (Pty) Limited (“MIE”) is the

leading provider of background and pre-employment

screening services in South Africa. MIE’s verifications

integrate seamlessly with clients’ HR decision-

making process, adhering to published service-level

agreements and adding value by managing risk. The

types of services that MIE provides include: criminal

record checks, credit record checks, motor vehicle

reports, employment verification, education verification,

reference checks, and professional certification

verifications. MIE is a registered Credit Bureau.

Ideco Identity Solutions (Pty) Limited is a newly formed

company specialising in identity management services

in the retail and financial services sectors.

IDECO GROUP LIMITED

IDECO Biometric Security Solutions

(Pty) Limited – 100%

IDECO Technologies (Pty) Limited – 100%

IDECO AFISwitch(Pty) Limited – 100%

IDECO Biometrix(Pty) Limited – 100%

Managed Integrity Evaluation

(Pty) Limited – 100%

IDECO Identity Solutions

(Pty) Limited – 100%

BOARD OF DIRECTORS

Vhonani Mufamadi (41)Executive chairmanBA LLB (Wits)

Vhonani completed his articles with Edward Nathan and

was admitted as an attorney to the High Court in 1991,

but left the legal profession in 1997 to follow several

investment opportunities in consumer goods distribution,

the ICT sector and infra-structure engineering.

He was one of the founding members of Ideco and served

on boards and governing structures of, inter alia, Business

Map, Tiso Group and the University of Witwatersrand.

Malose Kekana (39)Non-executive directorBComm (Witwatersrand)

Malose until recently served as chief executive officer

of the Umsobomvu Youth Fund (UYF). He had several

positions in banking before starting Prodigy Capital,

a private equity fund associated with Prodigy Asset

Management based in Cape Town. After that, he started

Baswa Investment Company to participate in Black

Economic Empowerment Transactions as a youth

investment group.

Malose serves on the Board of the Black Management

Forum Investment, Where he is the Deputy Chair and

chair of the Investment Committee since 1998. He serves

on the Council of the University of Limpopo. He was

appointed onto the Council for the Support of National

Defence which is charged with supporting the National

Reserve Force and the SA National Defence Force.

Ayanda Sisulu-Dunstan (33)Non-executive directorBachelor of Arts (Hons) (Wellesley College, Boston, USA)

Ayanda is a business development director with

responsibility for State Owned Enterprises at Rand

Merchant Bank.

She was previously a fixed income sales trader in

RMB Treasury. Ayanda began her career as a Private

Equity analyst at Brait Capital Partners and has 9 years

investment banking experience.

Rainer Troester (53) (German)Non-executive directorBBA Business Administration, Business Administration (University of Applied Sciences)

During his career he has worked in different management

positions as an employee of Siemens AG and IBM

Germany before founding his own IT technology

consultancy company in 1997.

Since 2002 he has concentrated on biometric business

in European markets. In 2006 his company merged with

idematrix from Switzerland, an established international

biometric identity management solution provider.

HB Aucamp (59)Financial directorBCom (Potch), BCompt (Hons) (Unisa), CA(SA)

After completing his articles, he joined Deloitte in

Bloemfontein as audit manager and qualified as a

chartered accountant in 1979.

After a career as financial manager in the fertilizer industry,

he set up a financial consultancy business and consulted

for various listed and unlisted companies in the fertilizer,

engineering and ICT sectors.

He has been involved with the founders of Ideco since the

early nineties and has advised them on financial matters

before and after formation of the Ideco Group.

IDECO 2009 Annual Report4 IDECO 2009 Annual Report 5

in these sectors was also scaled down. However this

business appears to have stabilised and tracking back to

earlier levels of growth.

Compared to the previous reporting period, where sales

of biometric readers to the public sector comprised 25%

of segmental revenue, sales to the public sector for the

period under review was less than 1% of segmental

revenue. This trend tracked government expenditure

pattern in the sector, and accordingly it is expected to

recover well along with the planned increased government

spending. Many key biometric and related projects

were cancelled by government and are gradually being

reintroduced for implementation. These include the

procurement of fingerprint readers by the police for a

multiplicity of applications; and the introduction of a smart

driver’s license card by the Department of Transport.

Secure credentialing services

This segment provides fingerprint-based criminal record

checks in terms of a long-term agreement with SAPS

as well as background screening services for employers

on existing and prospective employees. The activities of

this segment are conducted in two companies: Ideco

AFISwitch (Pty) Ltd (AFISwitch) - offering criminal record

checks and MIE – offering background screening services.

The AFISwitch results were previously included in the

biometric readers and solutions segment, but AFISwitch’s

activities are more closely related to those of MIE, hence

the re-classification in this new segment.

Revenue from criminal background checks increased by

177% for the year ended 31 August 2009 compared to

the annualised revenue for the eighteen months ended

31 August 2008. This is testimony to the widening rollout

of the AFISwitch infrastructure and service, which will

drive a significant part of the Group’s future growth. The

effective date of the acquisition of MIE as a wholly-owned

subsidiary was on 1 July 2009, and therefore only two

months of that company’s results are included in the

segmental results. MIE has a strong trend of growth and

profitability over the last 21 years of its existence.

Biometric projects

Revenue generated by this segment was 4,5 times higher

than the annualised revenue for the eighteen months

ended 31 August 2008. The main reason for this increase

is the commencement of the five-year contract for the

delivery of drivers licences in Namibia in December 2008.

Financial overview

The operating loss of R563 000 for the eighteen months

ended 31 August 2008 included a once-off profit on the

sale of property of R4,1 million, making the operating

loss from trading activities for that period R3,5 million.

The operating loss of R14,8 million for the year ended

31 August 2009 was therefore effectively R11,3 million

higher than the previous 18 month reporting period. The

major contributing factors to the increase in the operating

loss were the reduced sales of biometric readers in the

government sphere and increased operating costs

Vhonani Mufamadi

Executive chairman

Introduction

Since our listing in 2007 this is our first report covering a

twelve month period of operations. The preceding report

covered a period of eighteen months following the change

of our financial year in August 2007 from the end of

February to the end of August.

The year under review

The difficult trading conditions which, for us, started in late

2008 continued well into 2009. In this time we have seen

poor sales of biometric devices and solutions in both the

private and public sectors. However the decline appears

to have bottomed out as we have been doing business

at a stable level for several months now. We are now

focusing our effort on driving growth back to pre-decline

levels and beyond. The demand for biometric devices

is getting more and more robust; and we are expanding

our criminal background checking service, as well as

acquiring new business for our solutions and services. In

this context the highlight of the year ended August 2009

was the acquisition of the 70% share in Kroll Background

Screening (Pty) Limited, which was not already held by

Ideco and thereby making it a wholly-owned subsidiary of

the Group. The company was renamed Managed Integrity

Evaluation (Pty) Limited (MIE) – thereby returning to its

South African roots when it traded as MIE until 2003.

The Group was also re-organised into three business

segments:

Biometric readers and solutions;

Secure credentialing services and

Biometric projects.

The reorganisation has been implemented to enhance the

Group’s efficiencies in operations.

Biometric readers and solutions

This segment combines the activities of Ideco Biometric

Security Solutions (Pty) Limited (IBSS) and Ideco Biometrix

(Pty) Limited (Ideco Biometrix). IBSS distributes biometric

readers through a partner channel to the private sector,

while Ideco Biometrix supplies such readers directly to

government departments.

The economic downturn resulted in a slow-down of

revenue growth in sales to the private sector, where

the growth rate decreased to 11% compared to the

annualised revenue for the eighteen months ended

31 August 2008. These biometric readers are usually

integrated into security and /or payroll solutions on the

mines, factories, office blocks and residential complexes.

As the recession entrenched in 2008/2009 expenditure

EXECUTIVE CHAIRMAN’S REPORT

IDECO 2009 Annual Report6 IDECO 2009 Annual Report 7

Other projects and prospects

We have concluded a three year ticketing agreement

with the Bombela Operating Company in charge of

operating the Gautrain service, following the award of

the international tender to us. Ideco won this tender with

its offer of a card ticketing solution on par with similar

services in major cities such as Paris and London. This

award signals industry recognition of Ideco’s solution

offerings and expertise, and further boosts prospects

of growth in the company’s sector of activity – identity

management and related services. In this tender we

offered a solution in partnership with ASK of France,

who supply a wide variety of secure card, document and

border control solutions. Following on the early success

of this partnership, we are exploring extension of our

business cooperation in southern Africa.

The Group’s biometric solutions for specific sectors such

as retail, micro-lending and credit bureaux are gaining

momentum and management is confident that these

sectors will provide solid revenue streams in the near

future. The company is currently negotiating contracts with

specific customers for the use of its technology solutions

in these sectors. These contracts are expected to be

concluded and implementation to commence in the year

to end August 2010.

Ideco has also concluded a memorandum of

understanding with MorphoTrak Incorporated, the USA

subsidiary of Sagem Defence Securité, France to explore

the US market for the establishment of a joint venture

to distribute Sagem biometric scanners in that market.

This follows the successes of the Ideco distribution

model in the South African market which appears to have

good resonance with the access control and time and

attendance market in the USA as well. Ideco’s contribution

to this exploration has been to transfer two of its experts

into the employ of MorphoTrak for a 12 month period.

Initial reports on the viability of the venture are very

promising.

We wish to thank all our stakeholders for their support,

especially our employees who have worked hard and

remained loyal to the Group during this difficult year. We

are also grateful to our suppliers and distribution partners

whose loyalty is critical to our growth and success.

Vhonani MufamadiExecutive chairman

of R4 million for the further rollout of the criminal record

checking service. The bulk of the cost in the rollout

was rental of equipment which is being installed at 350

drivers licence testing stations. Furthermore, the Group

staff complement, excluding the new acquisition, MIE,

increased by approximately 20%, especially in the fields

of research and development and sales. The increase in

staff complement was necessary in gearing for the delivery

of the AFISwitch service and new product research and

development to stay abreast of industry development. An

increase of R3,1 million in finance charges and a reduction

of R1,5 million in investment income resulted in a loss

before tax of R16,8 million compared to a profit before tax

of R2,4 million for the eighteen months ended 31 August

2008.

Property, plant and equipment increased by R3,4 million,

mainly due to the acquisition of MIE, which includes an

unencumbered fixed property of R2,3 million. The big

increase in other non-current assets is mainly as a result

of goodwill on the acquisition of MIE. The increase in

computer software is also mainly due to the acquisition

of MIE, which owns the trademark NQR software used to

check qualifications in the background screening industry.

The right of use of R15,9 million referred to in note 10 in

the consolidated annual financial statements is in respect

of a charge by Sagem Security SA (Pty) Limited (Sagem),

which entitles AFISwitch to make use of the South

African Police Services (SAPS) Automated Fingerprint

Identification System (AFIS). The payment of this amount

is part of AFISwitch’s agreement with SAPS relating to

criminal background checking service. This amount will be

amortised over the remaining period of the agreement with

SAPS.

Inventories mainly consist of biometric readers held in

IBSS – the subsidiary focused on the access control and

time & attendance business. The inventory increased by

about 14%, which was in line with the increased revenue

of the subsidiary.

The major addition to non-current liabilities is the

cumulative redeemable preference shares issued to the

National Empowerment Fund Trust (NEF) to finance the

acquisition of MIE. The dividend rate of the preference

shares is 75% of the prime overdraft rate. The other

non-current liability consists of a bond registered over a

property in Centurion, with an outstanding balance of

R2,6 million.

Trade and other payables increased by R2,6 million, mainly

as a result of the acquisition of MIE.

The other current liabilities consist of an amount of

R24,4 million due to Sagem which was taken over in

respect of the SAPS AFIS referred to above. The balance

of R2,9 million formed part of the MIE transaction and was

repaid in October 2009.

Prospects

Biometric readers and solutions

It is expected that segmental revenue in the private

sector will remain constant until the economic recovery

is well underway. Ideco’s certified partners have however

submitted several proposals to their customers for new

biometric applications in respect of risk management and

cost control, which could make up for the lower revenue

due to the generally poor economic climate.

Ideco has also been appointed as a sub-contractor to

supply biometric components and systems by several

suppliers who are contracted by government for various

security projects. Therefore, management is confident that

stronger sales to the public sector will resume in the year

ending 31 August 2010.

Secure credentialing services

The criminal record checking service, conducted by

AFISwitch, will continue to show strong growth. This

company has commenced the implementation of the

service to the Department of Transport for Professional

Drivers Permits, which constitute approximately 50%

of the service capacity. The installation of background

checking equipment at the 350 testing stations

countrywide has begun and will continue throughout

2010. The agreement concluded in May 2009 for the

management of more than 300 000 identity profiles will

also be implemented during 2010, further providing

predictable annuity revenue flow to the Group.

The acquisition of the remaining 70% of MIE will enhance

the performance of this segment for the year ending 31

August 2010. This will be the first reporting period in which

MIE’s full year results will be included in Ideco’s Group

results. MIE has an excellent profit and revenue growth

history. MIE has gained several new customers and

has also obtained security clearance to do background

screening services for government departments.

Biometric projects

We expect to add a few more projects similar to the

Namibian drivers licence project, as more such project

tenders are adjudicated in 2010 and beyond. Most

governments in the southern African region have issued

tenders for the procurement of various biometric systems

ranging from identity to border control systems. As

biometrics gain wider usage in the world and this region,

Ideco is well positioned to capture a good share of this

business as a recognised leader in the market.

IDECO 2009 Annual Report8 IDECO 2009 Annual Report 9

Audit and risk committee

The audit and risk committee comprises two non-executive directors Mr Malose Kekana (Chairman) and Ms Ayanda Sisulu-Dunstan as well as a representative from the company’s designated adviser, who is an invitee in terms of the JSE Listings Requirements.

The primary responsibility of the committee is to evaluate matters concerning accounting policies, internal controls, auditing, financial reporting, risk management, compliance and reviewing the annual financial statements of the Group prior to board approval. This committee also assists the board with company policies, the structure, size and effectiveness of the board and its committees, and in reviewing the Group’s governance processes. Furthermore, it establishes the formal induction process and ensures that a training and development programme is in place for committee members.

The external auditors attend the meetings and have unlimited access to the chairperson of the committee. The audit committee is responsible for recommending the use of the external auditors for non-audit services. Auditors are appointed annually based on the recommendation of the audit and risk committee.

The audit and risk committee has considered the qualifications and experience of Mr HB Aucamp, the Group’s financial director, and is of the opinion that he is suitably qualified to carry out his duties.

Remuneration committee

A remuneration committee was constituted during the year, consisting of the non-executive directors and Mr Vhonani Mufamadi . The committee is primarily responsible for formulating the remuneration strategy and policies of the Group and the terms and conditions of employment of executive directors and senior executives, whilst the board grants final approval of their recommendations. The committee has not yet had its first meeting, but will meet quarterly in future.

Nomination committee

The Group currently does not have a nomination committee. Nominations to the board are handled by the remuneration committee for the time being.

Company secretary

The Group’s financial director, Mr HB Aucamp, undertakes the duties of company secretary. While it is acknowledged that it is not recommended practice for the company secretary to also be a director of the company, it was considered more of a priority to first enhance the expertise in the finance department. This issue will be addressed when the time is appropriate.

The company secretary provides guidance to the directors on their duties and ensures awareness of all relevant statutory requirements and legislation. All directors have access to the advice and services of the company secretary. Independent professional advice will be arranged for the directors by the company secretary, at the Company’s expense, where it has been requested by the directors.

Accountability and audit

Going concern

The consolidated and company annual financial statements contained in this annual report have been prepared on the going concern basis. The directors have reviewed the Group’s budget and cash flow forecast for the year to 31 August 2010. The directors report that on the basis of this review and after making enquiries, they have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. For this reason, the Group continues to adopt the going concern basis in preparing the annual financial statements.

Auditing and accounting

The board is of the opinion that their auditors observe the highest level of business and professional ethics and that their independence is not in any way impaired. The auditors have the right of access to all information or personnel within the Group on any matter necessary to fulfil their duties. The external auditors attend audit and risk committee meetings by invitation.

Internal audit

Due to the present size of the Group, an internal audit function has not been established. This will be implemented accordingly with the Group’s expansion.

Internal control

The Company’s internal controls are designed to provide reasonable assurance to the integrity and reliability of the financial statements and to adequately safeguard, verify and maintain accountability of its assets. These internal controls are achieved through financial controls, operational controls, compliance with laws and regulations and risk management.

The controls and systems are designed to provide reasonable, but not absolute, assurance against misstatement of financial information or loss.

Recommendations made by the Group’s external auditors are being reviewed by the audit and risk committee, and changes to internal controls are being made where necessary.

CORPORATE GOVERNANCE

Ideco Group Limited (“Ideco” or “the Company” or “the Group”) listed on the Alternate Exchange (“AltX”) of the JSE Limited (“JSE”) on 30 October 2007 and is a public company incorporated in South Africa under the provisions of the Companies Act of 1973, as amended (“the Companies Act”).

The Group is committed to the principles established in the Code of Corporate Practices and Conduct as set out in the King II Report on Corporate Governance in South Africa (“the King II Report”), as well as to the Listings Requirements of the JSE.

Ideco is committed to the principles of transparency, integrity and accountability as advocated in the King II Report. In supporting the King II Report, the directors of Ideco recognise the need to conduct the business of the company with integrity and in accordance with generally accepted corporate practices. Therefore, Ideco subscribes to the principles of timeous, honest and objective communications with its stakeholders and the highest standards of ethics in the conduct of its business.

Board composition

Ideco has a unitary board and Mr Vhonani Mufamadi is the executive chairman of Ideco. The board has delegated certain powers to the executive chairman with due regard to the fiduciary responsibility on the one hand, and operational and strategic efficiency on the other, while simultaneously retaining effective control over the company. With a clear distinction between the respective responsibilities at board level, together with the responsibilities as delegated to the executive chairman, a balance of authority is therefore maintained and no one director is able to exercise unfettered decision-making powers.

At the last practicable date, the board of Ideco comprised five directors, with Mr HB Aucamp being the financial director and Mr Vhonani Mufamadi the executive chairman, and the balance and majority being non-executive directors. It is the intention of the group to appoint a non-executive chairman in the near future in order to comply with the King II Report. All of the members of the board of directors demonstrate the necessary caliber and credibility, skills and experience as may be expected from a director of a listed company. Ms Ayanda Sisulu-Dunstan, Mr Malose Kekana and Mr Rainer Troester meet the requirements of the JSE for independent non-executive directors.

Particulars of the directors are set out on page 2. The non-executive directors and the executive directors do not have fixed-term service contracts. In terms of the Company’s articles of association, one-third of directors shall retire from office at the annual general meeting to be

held on 16 April 2010 (or if their number is not a multiple of three then the number nearest to, but not less than one third). Retiring directors shall be eligible for re-election.

The board has a comprehensive system of controls in place to ensure that risks are mitigated and the Group’s objectives are attained. Furthermore, the board, together with senior management define levels of materiality, reviews performance, institute control measure and evaluates and monitors business matters which have an impact on the wellbeing of the Group and its stakeholders.

The board functions within a formal framework with the following terms of reference:

A board charter which sets out the responsibilities of

the board as a whole as well as for individual directors.

A trading policy to regulate the dealings in securities

by directors, directors of major subsidiaries and the

company secretary of Ideco.

A nomination policy detailing procedures for

appointments to the board.

A board charter has been adopted by the board to govern the responsibilities of the directors. Board meetings are scheduled for each quarter but the board may convene any additional meetings that may be considered appropriate or necessary. The board regularly reviews the direction of the Group, strategic issues, major contracts, acquisitions, financing and corporate governance. In addition, the board is also responsible for the relationship management and informative reporting to stakeholders. The board determines key risk areas, defines levels of materiality and ensures performance in all areas of the Group. The board has complete power and control to lead the Group but delegates certain matters with the necessary authority to management.

There were three board meetings during the year, two of which could not be attended by Mr Troester due to overseas commitments. All other directors and the company secretary attended all scheduled board meetings. There was 100% attendance at the four meetings of the audit and risk committee. Representatives from the designated advisor attend all board and audit and

risk committee meetings by invitation.

Board committees

While the board remains accountable and responsible for the performance and affairs of the Company, specific functions and responsibilities have formally been delegated to committees which operate within agreed terms of reference approved by the board. The functions of these committees are described in more detail below.

IDECO 2009 Annual Report10 IDECO 2009 Annual Report 11

Analysis of shareholdings Number of holders

% of total shareholders

Number of shares

% of total issued share capital

1 - 10 000 98 39,04% 515 779 0,26%

10 001 - 100 000 105 41,83% 4 530 549 2,24%

100 001 - 1 000 000 41 16,33% 13 205 958 6,53%

1 000 001 - and more 7 2,79% 183 969 936 90,97%

Totals 251 100,00% 202 222 222 100,00%

Categories of shareholders

Insurance companies 1 0,40% 3 000 000 1,48%

Banks 2 0,80% 3 105 688 1,54%

Collective investment schemes and mutual funds

6 2,39% 4 433 756 2,19%

Trusts 19 7,58% 967 066 0,48%

Pension funds and medical schemes

4 1,59% 455 024 0,23%

Private companies and close corporations

18 7,17% 175 140 876 86,62%

Individuals 201 80,07% 15 119 812 7,47%

Totals 251 100,00% 202 222 222 100,00%

Shareholder spread

Public 242 96,41% 27 348 719 13,52%

Non-public 1 0,40% 1 818 182 0,90%

Directors 7 2,79% 86 005 389 42,53%

Major shareholder 1 0,40% 87 049 932 43,05%

Totals 251 100,00% 202 222 222 100,00%

Major shareholders (5% and more of the shares in issue)

Muvoni Investment Holdings (Pty) Limited

83 762 634 41,42%

Six Sis Limited 87 049 932 43,05%

ANALYSIS OF SHAREHOLDERSRisk management

Effective risk management is integral and extremely important in Ideco’s objective to continuously add value to the business in all areas of the Group’s operations. The board and management are responsible for designing, implementing and monitoring the processes of risk management incorporating it into the daily activities of the Group. The board determines the Group’s tolerance for risk and is responsible for ensuring that the Group has an effective, ongoing process in place that identifies risk factors across the Group, measuring its impact and implement what is necessary to proactively manage these risks.

Share dealings

Ideco has a closed-period policy that requires directors be precluded from dealing in the Group’s shares prior to the release of the Group’s interim and annual results. To ensure that dealings are not carried out at a time when other price sensitive information may be known, directors must at all times obtain permission from the chief executive before dealings in the shares of the Group. Approved dealings in the Group’s shares by directors are disclosed to the JSE and published on the Stock Exchange News Services (SENS). All approved dealings are reported in arrears to the regular meetings of the board. There has been no change in directors’ shareholding between 31 August 2009 and the date of this report.

People and values

Ideco’s goal is to attract and retain, at every level of the company, people who represent the highest standards of excellence and integrity. The Company is dedicated to diversity, fair treatment, mutual respect and trust. Its management practices leadership that teaches, inspires and promotes full participation and career development and encourages open and effective communication.

Broad Based Black Economic Empowerment (BBBEE)

Ideco is an equal opportunity employer and there is no distinction on the basis of ethnic origin or gender or any other manner.

Employment equity

Ideco is committed to maintaining a balanced workforce that reflects the demographic realities within South Africa, and in line with governmental guidelines prescribed in this regard.

IDECO 2009 Annual Report12 IDECO 2009 Annual Report 13

INDEPENDENT AUDITOR’S REPORT

To the members of Ideco Group Limited

We have audited the consolidated annual financial statements and annual financial statements of Ideco Group Limited,

which comprise the consolidated and separate balance sheets as at 31 August 2009, and the consolidated and separate

income statements, the consolidated and separate statements of changes in equity and consolidated and separate cash

flow statements for the year then ended, and a summary of significant accounting policies and other explanatory notes,

and the directors’ report, as set out on pages 14 to 50.

Directors’ responsibility for the financial statements

The company’s directors are responsible for the preparation and fair presentation of these financial statements in

accordance with International Financial Reporting Standards, and in the manner required by the Companies Act of South

Africa. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation

and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error;

selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the

circumstances.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in

accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements

and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material

misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial

statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of

material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the

auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements

in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing

an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of

accounting principles used and the reasonableness of accounting estimates made by management, as well as evaluating

the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion

Opinion

In our opinion, these financial statements present fairly, in all material respects, the consolidated and separate financial

position of Ideco Group Limited as at 31 August 2009, and its consolidated and separate financial performance and

consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting

Standards, and in the manner required by the Companies Act of South Africa.

BDO South Africa Incorporated

Per: J R Roberts

Registered Auditor

26 February 2010

13 Wellington Road, Parktown, 2193

STATEMENT OF RESPONSIBILITY BY THE BOARD OF DIRECTORS

The directors are responsible for the preparation and fair presentation of the consolidated annual financial statements and

annual financial statements of Ideco Group Limited, comprising the balance sheets at 31 August 2009, and the income

statements, the statements of changes in equity and cash flow statements for the period then ended, and the notes

to the financial statements, which include a summary of significant accounting policies and other explanatory notes, in

accordance with International Financial Reporting Standards and in the manner required by the Companies Act of South

Africa.

The directors acknowledge that they are ultimately responsible for the system of internal financial control established

by the group and place considerable importance on maintaining a strong control environment. To enable the directors

to meet these responsibilities, the board of directors sets standards for internal control aimed at reducing the risk of

error or loss in a cost effective manner. The standards include the proper delegation of responsibilities within a clearly

defined framework, effective accounting procedures and adequate segregation of duties to ensure an acceptable level

of risk. These controls are monitored throughout the group and all employees are required to maintain the highest

ethical standards in ensuring the Group’s business is conducted in a manner that all reasonable circumstances is above

reproach. The focus of risk management in the Group is on identifying, assessing, managing and monitoring all known

forms of risk across the Group.

While operating risk control cannot be fully eliminated, the Group endeavours to minimise it by ensuring that appropriate

infrastructure, control systems and ethical behaviour are applied and managed within pre-determined procedures and

constraints.

The directors are of the opinion, based on the information and explanations given by management that the system of

internal control provides reasonable assurance that the financial records may be relied on for the preparation of the

financial statements. However, any system of internal financial control can provide only reasonable, and not absolute,

assurance against material misstatement or loss.

The directors have reviewed the Group’s cash flow forecast for the year to 31 August 2010 and, in light of this review and

the current financial position, they are satisfied that the group has or has access to adequate resources to continue in

operational existence for the foreseeable future.

The external auditors are responsible for independently reviewing and reporting on the consolidated annual financial

statements. The consolidated financial statements have been examined by the group’s external auditors and their report

is presented on page 13.

APPROVAL OF ANNUAL FINANCIAL STATEMENTS

The consolidated annual financial statements and annual financial statements of Ideco Group Limited, for the year ending

31 August 2009 set out on pages 14 to 50 were approved by the board of directors on 26 February 2010 and are signed

on its behalf by:

V Mufamadi AX Sisulu-Dunstan

Executive chairman Non-executive director

STATEMENT OF COMPLIANCE BY THE COMPANY SECRETARY

In terms of the Companies Act, No 61 of 1973 (as amended) (“the Act”), I certify that, to the best of my knowledge, the

company has lodged with the Registrar of Companies all such returns as are required of a public company in terms of

the Act and that all such returns are true, correct and up to date.

HB Aucamp

Company secretary

IDECO 2009 Annual Report14 IDECO 2009 Annual Report 15

special resolution passed by the shareholders of Ideco in

general meeting. No exchange control or other restrictions

exist in respect of the borrowing powers of the Group.

Dividends

No dividends have been declared to members during the

year (2008: Rnil)

Special Resolutions

Ideco Group Limited passed the following special

resolution in the twelve months to 31 August 2009:

General authority to repurchase issued shares

Post balance sheet events

During September 2009 Ideco Group Limited acquired a

25% share in a new biometric venture offering biometric

solutions to the health industry.

The repayment of the amount of R24,4 million due to

Sagem Security SA (Pty) Limited as detailed in note 20

has been rescheduled during November 2009. Of this

amount, R12,7 million is now repayable in March 2010

and the balance of R11,7 million is payable in four equal

instalments from 15 September 2010 to 15 December

2010. No interest will accrue on the outstanding amount.

Other than the above, the directors are not aware of any

post balance sheet events that require comment.

Bankers

The Group bankers are Absa Bank Limited.

Directors

The directors in office at the date of this report are:

V Mufamadi

HB Aucamp

A X Sisulu-Dunstan

M F Kekana

R Troester (German)

Secretary

HB Aucamp

Refer to corporate information on page 56.

Auditors

BDO South Africa Incorporated will continue in office in

accordance with section 270(2) of the Companies Act.

Subsidiaries

Details of the Company’s subsidiaries are set out in note 9

of these financial statements.

The group has also formed a new wholly-owned

subsidiary, Ideco Identity Solutions (Pty) Limited that will

specialise in identity management services and solutions

specifically aimed at the financial services and retail

sectors of the economy.

Acquisition of subsidiary (formerly an associate)

With effect from 1 July 2009, the group acquired the

70% of the issued share capital of MIE, not already held

by Ideco, for nil consideration. This transaction has been

accounted for using the purchase method of accounting.

The acquisition was effected by way of a share re-

purchase by MIE, which re-purchase was financed by

issuing cumulative redeemable preference shares to the

value of R40,6 million to the National Empowerment Fund

Trust.

Refer to note 28 for further details of this acquisition.

The directors have pleasure in submitting their second

report and consolidated annual financial statements and

annual financial statements of Ideco Group Limited for the

year ended 31 August 2009.

Business activities

Ideco Group Limited is an investment holding company

with investments in wholly–owned subsidiaries providing

fingerprint–solutions and logical access control, large

scale Automated Fingerprint Identification Systems (AFIS)

solutions, fingerprint scanning activities, as well as secure

credentialing services to employers.

The operating results and state of affairs of the company

are fully set out in the consolidated group annual financial

statements and do not in our opinion require any further

comment.

General review of operations

Net loss of the Group was R12,1 million (2008 profit R3,0

million), after a tax credit of R4,7 million (2008: tax credit

R0,6 million).

Going concern

The consolidated annual financial statements have been

prepared on the basis of accounting policies applicable

to a going concern. This basis presumes that funds will

be available to finance future operations and that the

realisation of assets and settlement of liabilities, contingent

obligations and commitments will occur in the ordinary

course of business.

The directors have reviewed the cash flow projections

for the year ending 31 August 2010, which are based

on new contracts being implemented, current projects

and historical trend analysis. Based on these cash flow

projections, the directors are satisfied that the going

concern principle is the correct accounting policy to be

applied by the Group.

Authorised and issued share capital

There were no changes to the share capital during the

year ended 31 August 2009. Details of the share capital

are set out in note 16 of the financial statements.

Directors’ shareholdings

As at 31 August 2009, the present directors held a total

of 86 005 389 ordinary shares in the Company. Details of

their shareholdings are set out in note 27 to these financial

statements.

Borrowing powers

The directors’ borrowing powers have not been exceeded

since Ideco’s incorporation and may only be varied by

DIRECTORS’ REPORT for the year ended 31 August 2009

IDECO 2009 Annual Report16 IDECO 2009 Annual Report 17

INCOME STATEMENTSfor the year ended 31 August 2009

Group Company

Notes

Year ended 31 Aug 2009

R’000

18 months ended

31 Aug 2008 R’000

Year ended 31 Aug 2009

R’000

18 months ended

31 Aug 2008 R’000

Revenue 2 83 076 113 645 - -

Cost of sales 2 (48 806) (80 954) - -

Gross profit 34 270 32 691 - -

Other operating income 166 4 406 6 805 18 510

Operating expenses (49 224) (37 660) (14 753) (16 818)

Operating (loss)/profit 2 (14 788) (563) (7 948) 1 692

Investment income 3 287 1 747 34 1 051

Finance costs 4 (4 359) (1 213) (900) (1 065)

Share of profit of associated company

5 2 023 2 463 2 023 2 463

(Loss)/profit before tax (16 837) 2 434 (6 791) 4 141

Taxation credit 6 4 746 562 2 172 90

(Loss)/profit attributable to ordinary shareholders

(12 091) 2 996 (4 619) 4 231

Basic (loss)/earnings per share (cents)

7 (5,98) 2,35

BALANCE SHEETSat 31 August 2009

Group Company

Notes2009

R’0002008

R’0002009

R’0002008

R’000

ASSETS

Non-current assets 76 415 51 069 30 629 26 940

Property, plant and equipment 8 10 210 6 828 5 770 6 276

Investments in subsidiaries 9 - - 21 098 *

Investment in associate 5 - 19 075 - 19 075

Intangible assets 10 58 724 23 337 1 500 1 500

Deferred tax 11 7 481 1 829 2 261 89

Current assets 45 539 30 389 19 146 44 176

Inventories 12 12 704 11 136 - -

Loans to subsidiaries 9 - - 17 572 43 260

Trade and other receivables 13 23 894 18 955 1 265 628

Cash and cash equivalents 14 8 598 12 9 2

Taxation receivable 343 286 300 286

Non-current assets held for sale 15 - 4 335 - 282

Total assets 121 954 85 793 49 775 71 398

EQUITY AND LIABILITIES

Equity

Share capital 16 1 1 1 1

Share premium 16 21 286 21 286 21 286 21 286

Retained income 7 494 19 585 436 5 055

Shareholders’ equity 28 781 40 872 21 723 26 342

Non-current liabilities 43 357 2 639 2 396 2 639

Long-term borrowings 17 2 396 2 639 2 396 2 639

Deferred tax 11 361 - - -

Cumulative redeemable preference shares

18 40 600 - - -

Current liabilities 49 816 42 282 25 656 42 417

Loans from subsidiaries 9 - - 20 990 38 127

Taxation payable 325 392 - -

Trade and other payables 19 20 257 17 687 1 206 1 314

Current portion of long-term borrowings

17 238 172 238 172

Bank overdraft 14 351 2 804 351 2 804

Other current liabilities 20 27 291 21 227 2 871 -

Provisions 21 1 354 - - -

Total equity and liabilities 121 954 85 793 49 775 71 398

* less than R1 000

IDECO 2009 Annual Report18 IDECO 2009 Annual Report 19

STATEMENTS OF CHANGES IN EQUITY for the year ended 31 August 2009

Ordinary share capital

R’000

Share premium

R’000

Retained earnings

R’000Total

R’000

Group

Balance at 1 March 2007 * * 16 589 16 589

Issue of shares 1 21 286 - 21 287

Profit for the period 2 996 2 996

Balance at 31 August 2008 1 21 286 19 585 40 872

Balance at 1 September 2008 1 21 286 19 585 40 872

Loss for the year (12 091) (12 091)

Total changes - - (12 091) (12 091)

Balance at 31 August 2009 1 21 286 7 494 28 781

Company

Balance at 1 March 2007 * * 824 824

Issue of shares 1 21 286 - 21 287

Profit for the period 4 231 4 231

Balance at 31 August 2008 1 21 286 5 055 26 342

Balance at 1 September 2008 1 21 286 5 055 26 342

Loss for the year (4 619) (4 619)

Total changes - - (4 619) (4 619)

Balance at 31 August 2009 1 21 286 436 21 723

* less than R1 000

CASH FLOW STATEMENTSfor the year ended 31 August 2009

Group Company

Notes2009

R’0002008

R’0002009

R’0002008

R’000

Cash utilised by operations 26.1 (11 652) (5 687) (8 082) (811)

Investment income 287 1 747 34 1 051

Finance costs (4 359) (1 213) (900) (1 065)

Dividends paid - (5 000) - (5 000)

Taxation paid 26.2 (541) (16 887) (14) (1 767)

Net cash from operating activities

(16 265) (27 040) (8 962) (7 592)

Cash flows from investing activities

Proceeds from disposal of property, plant and equipment

2 1 8 498 - 8 498

Acquisition of property, plant and equipment

2 (1 552) (9 903) (105) (9 666)

Acquisition: cash in subsidiary 28 20 093 - - -

Investment in associated company - (16 612) - (16 612)

Investment in intellectual property - (1 500) - (1 500)

Acquisition of computer software (1 725) (4 731) - -

Acquisition of right of use - (18 387) - -

Non-current assets held for sale 4 335 (3 635) 282 (282)

Net cash from investing activities 21 152 (46 270) 177 (19 562)

Cash flows from financing activities

Issue of share capital - 21 287 - 21 287

(Decrease)/increase in long-term borrowings

(177) 2 811 (177) 2 811

Movement in related party loans - (719) 8 551 (11 540)

Movement in other current liabilities 6 329 20 962 2 871 -

Net cash from financing activities

6 152 44 341 11 245 12 558

Net increase/(decrease) in cash and cash equivalents

11 039 (28 969) 2 460 (14 596)

Cash and cash equivalents at the beginning of the year

14 (2 792) 26 177 (2 802) 11 794

Cash and cash equivalents at the end of the year

14 8 247 (2 792) (342) (2 802)

IDECO 2009 Annual Report20 IDECO 2009 Annual Report 21

Ideco Group Limited (the “Company”) is a company

domiciled in South Africa. The consolidated financial

statements of the Company as at and for the year

ended 31 August 2009 comprise the Company and its

subsidiaries (together referred to as the “Group”).

The principle accounting policies adopted in the

preparation of the financial statements are set out below.

Statement of compliance

The consolidated financial statements have been prepared

in accordance with International Financial Reporting

Standards (“IFRS”) and its interpretations adopted by the

International Accounting Standards Board (“IASB”), the

JSE Listings Requirements and the Companies Act of

South Africa.

Basis of preparation

The consolidated annual financial statements are prepared

on the historical cost basis, adjusted by the fair value of

certain assets and liabilities.

The accounting policies set out below have been applied

consistently to all periods presented in these consolidated

financial statements and have been applied consistently

by Group entities.

The financial statements are presented in Rands which

is the Company’s functional and Group’s presentation

currency, and all values are rounded to the nearest

thousand (R’000’s) except when otherwise indicated.

The Company applies the accounting policies adopted

by the Group. These accounting policies have been

applied consistently to all periods presented in these

financial statements, except in relation to the adoption

of the new IFRS 7, “Financial Instruments: Disclosures”,

the amendments to IAS 1, “Presentation of Financial

Statements” and the new IFRIC 10, “Interim Financial

Reporting and Impairment”, during the year. Adoption

of these revised standards and interpretations did not

have any effect on the financial performance or position

of the Company. They did however give rise to additional

disclosures, including in some cases, revisions to

accounting policies.

Critical accounting estimates and judgements

The preparation of financial statements in conformity

with IFRS requires management to make judgements,

estimates and assumptions that affect the application of

policies and reported amounts of assets and liabilities,

income and expenses.The resulting accounting estimates

and judgements can, by definition, only approximate the

actual result.

The estimates and underlying assumptions are reviewed

on an ongoing basis. Revisions to accounting estimates

are recognised in the period in which the estimate is

revised if the revision affects only that period, or in the

period of the revision and future periods, if the revision

affects both current and future periods.

The assumptions and estimates that have the potential

to cause a material adjustment to the carrying amount

of assets and liabilities within the next financial year are

discussed below.

Estimate of level of provision required for obsolete stock and doubtful debts

The Group estimates the level of provision required for

obsolete stock and doubtful debts on an ongoing basis

based on historical experience as well as other specific

relevant factors. A comparison between provision

and actual loss incurred is performed to assess the

reasonableness of provisions.

Estimate of taxation

The Group is subject to income tax. Corporate and

deferred taxation calculations have been determined on

the basis of prior year assessed computation adjusted for

changes in taxation legislation in the year. No significant

new transactions have been entered into in the year which

requires specific additional estimates or judgements to

be made. The Group recognises the net future benefit

related to deferred income tax assets to the extent that

it is probable that the deductible temporary differences

will reverse in the foreseeable future. Assessing the

recoverability of the deferred income tax assets requires

the Group to make estimates related to expectations of

future taxable income. Estimates of future taxable income

are based on forecast cash flows from operations and

the application of existing tax laws. To the extent that

future cash flows and taxable income differ significantly

from estimates, the ability of the Group to realise the net

deferred taxation assets recorded at the balance sheet

date could be impacted. Additionally future changes in

taxation laws in which the Group operates could limit the

ability of the Group to obtain taxation deductions in future

periods.

ACCOUNTING POLICIES for the year ended 31 August 2009

Basis of consolidation

The consolidated financial statements reflect the

financial results of the Group. All financial statements

are consolidated with similar items on a line by line basis

except for investments in associates, which are included in

the Group’s results as set out below.

Subsidiaries

Subsidiaries are those entities over whose financial and

operating policies the Group has the power to exercise

control, so as to obtain benefits from their activities. In

assessing control, potential voting rights that are currently

exercisable are taken into account.

Where an investment in a subsidiary is acquired or

disposed of during the financial year its results are

included from, or to, the date control commences or

ceases.

The Company’s investment in subsidiaries is accounted for

at cost, less accumulated impairment losses.

All companies in the Group maintain consistent accounting

policies and have the same year–end.

Associates

The financial results of associates are included in the

Group’s results according to the equity method from

acquisition date until the disposal date.

Under this method, subsequent to the acquisition date,

the Group’s share of profits or losses of associates is

charged to the income statement as equity accounted

earnings and its share of movements in equity reserves

is recognised in the statement of changes in equity. All

cumulative post-acquisition movements in the equity of

associates are adjusted against the cost of the investment.

When the Group’s share of losses in associates equals

or exceeds its interest in those associates, the Group

does not recognise further losses, unless the Group

has incurred a legal or constructive obligation or made

payments on behalf of those associates to make good any

losses.

The share of retained earnings and reserves of associates

is generally determined from the latest audited financial

statements of the associate, but, in some instances, un-

audited financial statements are used.

Where a Group entity transacts with an associate of the

Group, un-realised profits and losses are eliminated to the

extent of the Group’s interest in the respective associate.

Any excess of the cost of acquisition over the Group’s

share of the net fair value of the identifiable assets,

liabilities and contingent liabilities of the associate

recognised at the date of acquisition is recognised as

goodwill. The goodwill is included within the carrying

amount of the investment and is assessed for impairment

as part of the investment. Any excess of the Group’s share

of the net fair value of the identifiable assets, liabilities

and contingent liabilities over the cost of acquisition,

after reassessment, is recognised immediately in profit

or loss. Any impairment of goodwill relating to associates

is charged to the income statement as part of equity

accounted earnings of those associates and the carrying

value of the group’s share of the underlying assets of

associates is written down to its estimated recoverable

amount in accordance with the accounting policy on

impairment.

The company’s investment in an associate is carried at

cost less any accumulated impairment.

Distributions received from the associate reduce the

carrying amount of the investment.

All intra–group transactions and balances, and any

unrealised income and expenses arising from the

intra–group transactions, are eliminated in preparing the

consolidated financial statements.

In respect of associates, unrealised gains and losses

are eliminated to the extent of the Group’s interest in

these entities. Unrealised gains and losses arising from

transactions with associates are eliminated against the

investment in the associate.

Business combinations

The purchase method of accounting is used to account

for the acquisition of businesses by the Group. A

business may comprise an entity, group of entities or an

unincorporated operation including its operating assets

and associated liabilities.

The cost of an acquisition is measured as the fair value of

the assets given, equity instruments issued and liabilities

incurred or assumed at the date of exchange, plus costs

directly attributable to the acquisition.

Identifiable assets acquired and liabilities and contingent

liabilities assumed in a business combination are

measured initially at their fair values at the acquisition date,

irrespective of the extent of any minority interest.

ACCOUNTING POLICIES continued for the year ended 31 August 2009

IDECO 2009 Annual Report22 IDECO 2009 Annual Report 23

ACCOUNTING POLICIES continued for the year ended 31 August 2009

The fair values of the identifiable assets and liabilities are

determined by reference to the market values of those or

similar items or by discounting expected future cash flows

using market participation assumptions.

The excess of the cost of acquisition over the fair value of

the group’s share of the identifiable net assets acquired is

recorded as goodwill. If the cost of acquisition is less than

the fair value of the net assets of the business acquired,

the difference is recognised directly in the income

statement.

Foreign currency transactions

Foreign currency transactions are translated to the

respective functional currencies of Group entities at the

rates of exchange ruling at the dates of the transactions.

Balances on monetary assets and liabilities outstanding

on foreign transactions at the end of the financial year are

translated to the functional currency at the rates ruling at

that date. Gains or losses on translation are recognised in

the income statement.

Non–monetary assets and liabilities that are measured in

terms of historical cost in a foreign currency are translated

using the exchange rate at the date of the transaction.

Non–monetary assets and liabilities denominated in foreign

currencies that are stated at fair value are translated to

Rands at the foreign exchange rates ruling at the dates the

fair value was determined.

Segmental reporting

A segment is a distinguishable component of the Group

that is engaged in providing products or services (primary

segment) within different geographical areas (secondary

segment) which are subject to risks and returns which

are different from those of other segments. The basis

of segment reporting is representative of the internal

structure used for management reporting.

Segment results, assets and liabilities include items

directly attributable to a segment as well as those that can

be allocated on a reasonable basis.

Revenue recognition

Revenue is recognised net of indirect taxes, rebates and

trade discounts and consist primarily of the sale of goods.

Revenue is recognised only when it is probable that the

economic benefits associated with a transaction will flow

to the Group and the amount of revenue can be measured

reliably. No revenue is recognised if there are significant

uncertainties regarding the recovery of the consideration

due, associated costs or the possible return of goods, and

continuing managerial involvement with the goods.

Revenue arising from the sale of goods is recognised

when the significant risks and rewards of ownership of the

goods have passed to the buyer. Revenue from the sale

of goods is measured at the fair value of the consideration

received or receivable, net of returns, trade discounts

and volume rebates and after eliminating sales within the

Group.

Investment income

Dividends

Dividends are recognised when the right to receive

payment is established, with the exception of dividends

on preference share investments which are recognised on

a time proportion basis, using the effective interest rate

method, in the period to which they relate.

Interest

Interest income is recognised in profit or loss as it accrues

using the effective interest rate method.

Exchange gains

Gains and losses on foreign currency transactions are

reported in profit or loss on a net basis and are included

under finance income.

Finance costs

Finance costs comprise interest payable on borrowings

calculated on the principal outstanding using the effective

interest rate method and is recognised in profit or loss

when it is incurred.

Taxation

The income tax expense comprises current and deferred

tax. The income tax expense is recognised in profit or loss

to the extent that it relates to items recognised directly in

equity, in which case it is recognised in equity.

Current taxation comprises taxation payable calculated

on the basis of the expected taxable income for the year,

using the taxation rates enacted or substantively enacted

at the balance sheet date, and any adjustment of taxation

payable for previous years.

Deferred taxation is provided using the balance sheet

liability method based on temporary differences.

Temporary differences are differences between the

carrying amounts of assets and liabilities for financial

reporting purposes and their tax base. Deferred taxation is

recognised profit or loss except to the extent that it relates

to a transaction that is recorded directly in equity or a

business combination that is an acquisition. The amount

of deferred taxation provided is based on the expected

manner of realisation or settlement of the carrying amount

of assets and liabilities using taxation rates enacted

or substantively enacted at the balance sheet date. A

deferred taxation asset is recognised to the extent that

it is probable that future taxable profits will be available

against which the associated unused taxation losses and

deductible temporary differences can be utilised. Deferred

taxation assets are reduced to the extent that it is no

longer probable that the related taxation benefit will be

realised.

Deferred taxation is not recognised for the following

temporary differences:

The initial recognition of goodwill;

The initial recognition of assets and liabilities in a

transaction that is not a business combination and that

affects neither accounting nor taxable profit; and

Differences relating to investments in subsidiaries to the

extent that the timing of the reversal is controlled by the

Group and it is probable that they will not reverse in the

foreseeable future.

Deferred tax assets and liabilities are offset, if a legally

enforceable right exists to set off current tax assets against

current income tax liabilities and the deferred income taxes

relate to the same taxable entity and the same taxation

authority.

Secondary taxation on companies (STC) is recognised in

the year dividends are declared, net of dividends received.

A deferred tax asset is recognised on unutilised STC

credits when it is probable that such unutilised STC credits

will be utilised in the future.

Dividends payable

Dividends payable and any STC pertaining thereto are

recognised in the period in which such dividends are

declared.

Lease assets

Finance leases

Leases in which the Group assume substantially all the

risks and rewards of ownership are classified as finance

leases.

Property, plant and equipment subject to finance lease

agreements are capitalised at the lower of their fair value

and the present value of the minimum lease payments

and the corresponding liability to the lessor is raised.

Lease payments are allocated using the effective interest

rate method to determine the lease finance cost, which

is charged against operating profit, and the capital

repayment, which reduces the liability to the lessor. These

assets are treated on the same basis as the property, plant

and equipment owned by the Group and is subject to

impairment losses.

Operating leases

Other leases, which do not transfer substantially all the

risks and rewards of ownership, are treated as operating

leases with lease payments charged against operating

income. Payment made under operating leases is charged

against income on a straight–line basis over the period of

the lease, irrespective of the payment terms.

Non-current assets held for sale

Non-current assets and disposal groups are classified

as held for sale if their carrying amount will be recovered

principally through a sale transaction rather than

continuing use. This condition is regarded as met only

when the sale is highly probable and the asset (or disposal

group) is available for immediate sale in its present

condition. Management must be committed to the sale,

which should be expected to qualify for recognition

as a completed sale within one year from the date of

classification.

Property, plant and equipment

Property, plant and equipment are recorded at cost, less

accumulated depreciation and impairment losses.

Cost includes expenditure that is directly attributable to

the acquisition of the asset. Purchased software that is

integral to the functionality of the related equipment is

capitalised as part of that equipment.

Land is not depreciated. Buildings, plant and equipment

are depreciated on the straight–line method over their

expected useful lives to an estimated residual value.

Leased assets are depreciated over the shorter of the

lease term and their useful lives. The current estimated

useful lives are generally:

ACCOUNTING POLICIES continued for the year ended 31 August 2009

IDECO 2009 Annual Report24 IDECO 2009 Annual Report 25

Buildings 50 years

Furniture and fixtures 6 years

Motor vehicles 5 years

Office equipment 5 years

Computer equipment 3 years

Where the carrying amount of an asset is greater than its

estimated recoverable amount (i.e. the higher of value in

use and net fair value less costs to sell) it is written down

immediately to its recoverable amount.

The cost of replacing part of an item of property, plant

and equipment is recognised in the carrying amount of

the item if it is probable that the future economic benefits

embodied within the property, plant and equipment will

flow to the Group and its cost can be measured reliably.

The costs of the day–to–day servicing of property, plant

and equipment are recognised in profit or loss as incurred.

Where parts of an item of property, plant and equipment

have different useful lives, they are accounted for as

separate items (major components) of property, plant and

equipment. Residual values, methods of depreciation

and useful lives of property, plant and equipment are

reassessed, and adjusted if appropriate, at each financial

year–end. Depreciation of an item of property, plant and

equipment begins when it is available for use and ceases

at the earlier of the date it is classified as held for sale or

the date that it is derecognised.

An item of property, plant and equipment is derecognised

upon disposal or when no future economic benefits are

expected from its use or disposal. Gains and losses

on derecognition of property, plant and equipment are

determined by reference to their carrying amount and the

net disposal proceeds and are taken to profit or loss in the

year the asset is derecognised.

Intangible assets

Intangible assets are stated at cost less accumulated

amortisation and impairment losses. Intangible assets are

amortised on a straight–line basis over their estimated

useful lives.

Amortisation is recognised in profit or loss on a straight–

line basis over the estimated useful lives of intangible

assets from the date that they are available for use. The

current estimated useful lives of intangible assets are as

follows:

Computer software 2 years

Intellectual property rights 5 years

Right of use 15 years

Trademark 15 years

The right of use is in respect of a 15 year agreement

with the South African Police Service for access to their

fingerprint database to perform automated criminal

background checks to the private sector and members of

the public.

The estimated useful life and amortisation method are

reviewed at the end of each reporting period, with the

effect of any changes in estimate being accounted for on a

prospective basis.

Goodwill

Goodwill is initially measured at cost, being the excess of

the business combination over the company’s interest of

the net fair value of the identifiable assets, liabilities and

contingent liabilities. Subsequently goodwill is carried at

cost less any accumulated impairment.

For the purpose of impairment testing, cash generating

units to which goodwill has been allocated are tested

for impairment annually, or more frequently when there

is an indication that the unit may be impaired. If the

recoverable amount of the cash generating unit is less

than the carrying amount of the unit, the impairment loss

is allocated first to reduce the carrying amount of any

goodwill allocated to the unit and then to other assets of

the unit pro-rata on the basis of the carrying amount of

each asset in the unit. An impairment loss recognised is

not reversed in a subsequent period.

The excess of the company’s interest in the net fair value

of the identifiable assets, liabilities and contingent liabilities

over the cost of the business combination is immediately

recognised in profit or loss. Internally generated goodwill is

not recognised as an asset.

Impairment of assets

Financial assets

A financial asset is assessed at each reporting date to

determine whether there is any objective evidence that it is

impaired. A financial asset is considered to be impaired if

objective evidence indicates that one or more events have

had a negative effect on the estimated future cash flows of