Embed Size (px)

Citation preview

SORAS...INGABO Y’AMAHINA

2011 Annual Report

ANN

UAL

REPO

RT 2

011

SORAS ASSURANCES GENERALES LTDShare capital: 1.000.000.000 rwandese francsHead office : Boulevard de la Révolution, Kigali

E-mail: [email protected]

ASSURANCES GENERALES LTD

SORAS

L’ASSUREUR RASSURANT

2011 Annual Report

TABLE OF CONTENTS

SORAS...INGABO Y’AMAHINA

2011 Annual Report

Michel MEYFROIDT : Chairman of the Board of Directors

Michel MEYFROIDT is a civil engineer from the Catholic University of Leuven (Belgium), graduated in Commercial and financial sciences from St Aloysius University of Antwerp and INSEAD.From 1974 to 1978 He worked as engineer in the Division of Bridges of SECO company ;From 1978 to 1998, he successively worked as Management Supervisor , Secretary General, Director General in charge of the Sales Department and Deputy Managing Director of Group ROYALE BELGE (Bank and Insurance);From 1999 to 2002, he worked as Director in charge of management of all Fortis Group’s insurance activities at global level ;From 2002 to 2008, he was the CFO of Brussels Airlines Group and since 2008, he is Managing Director. He is also Managing Director of MUPATY s.a., management company ;HE is the Chairman of the Board of Directors of SORAS ASSURANCES GENERALES since June 2010.

Charles MPORANYI : Vice Chairman of the Board of Directors

Charles MPORANYI holds a BA in Enterprise Economy from Fribourg University ;From 1971 to 1982: HE worked with TRAFIPRO Cooperative as Management Assistant, Sales Manager `Administrative Controller;From 1982 to 1984: HE worked as Administrator and Manager of Imprimerie de Kigali ;From 1984 to 2009 : HE worked as Administrator and Manager, Managing Director of Société Rwandaise d’Assurances;Since 2010 : he is the President of SORAS GROUP LTD and Vice Chairman of SORAS ASSURANCES GENERALES LTD.

Marc RUGENERA : Director

Marc RUGENERA holds a BA in Commercial and Financial Sciences and a Masters in Business Engineering from Institut Catholique de Hautes Etudes Commerciales (ICHEC Brussels);From 1980 to 1988, he worked with Rwanda Development Bank as Project Analyst, Head of the Department of SME and Head in charge of Supervision and Assistance to Enterprises;From 1988 to 1992, he worked as Managing Director of the Company for Industry and Trade in Africa;From 1992 to 1997, he was Minister of Finance;From 1997 to 2000, he was Minister of Trade, Industry and Tourism;From 2000 to 2010, he was Managing Director of Société Rwandaise d’Assurances (SORAS S.A.) Since June 2010, he is Managing Director SORAS ASSURANCES GENERALES LTD.

Léon NIESSEN :Director

Léon NIESSEN is a graduate and holds a BA in Mathematics, Master in Business Administration (MBA) from the Institute of Administration and Management (IAG) of the Catholic University of Leuven. He holds a BA in Insurance Accounting and has been awarded various certificates in taxability, Business Law and Accounting. He is a member of the Institute of Chartered Accountants and Tax advisers of Belgium ;He has a proven experience of more than 27years in the field of insurance and management of pension funds with specialization in taxation, information management, management control, accounting and reporting;In 1984, he started his career in VICTOIRE insurance company of SUEZ Group as Head of Computer Department ;In 1987, he worked there as head of Computer Department (Accounting, finance and reinsurance);In 1989, he was appointed Head of the Department of Accounting and Administration for the Group;In 1994, he joined DELOITTE & TOUCHE Belgium where he is responsible for audit and adviser to insurance sector and pension funds;In 2004, he joined, as partner, LANE CLARK & PEACOCK BELGIUM (consulting actuary) where he is also responsible for the sector of insurance and Pension funds;Since 2007, he directly advises insurance companies and pension funds in different countries through existing different operational structures.

BOARD OF DIRECTORS

L’ASSUREUR RASSURANT

2011 Annual Report

Olivier COSTA : DirectorOlivier COSTA is an Electro mechanical Engineer from Brussels Independent University and holds a Master’s degree in Business Administration (MBA) from the University of California in Los Angeles) Faculty of Strategy y and Finance.From 1995 to 1997, He worked as Automobile Engineer at PHILIPS AUTOMOTIVE ELECTRONICS responsible for development of components in Brussels, Paris and Auburn (Indiana)From 1997 to 2000, he worked as Sales Manager at SIEMENS AUTOMOTIVEFrom 2002 to 2003, he was Research Assistant in Corporate Strategy at the University of California in Los AngelesSince 2003, he is an administrator for a Group of companies (BANDAG, RWANDA MOTOR PARTS, CPQ, SECAM, CREAXION, EXPAND, LOGI ONE).

Emmanuel NTAGANDA :Director

Emmanuel NTAGANDA holds a BA in Management sciences from the National University of Rwanda and a degree in post university studies from the Paris-based Centre for Financial Economic and Bank studies (CEFEB)From 1981 to 1992, he worked at Rwanda Development Bank as Project Analyst, Head of the Department in charge ofSupervision and Assistance to Enterprises and Financial ManagerFrom 1992 to 2010, he worked at The Development Bank for Great Lakes Countries (BDEGL) as Head of TreasuryDepartment and Financial Manager FinancierFrom 2002 to 2005, he was the Chairman of the Board of Directors and Member of the Management Committee of Rwanda Commercial Bank.

Faustin NTEZILYAYO : Director

- Faustin NTEZILYAYO holds a PhD in Law from the University of Antwerp, a Master’s degree In tax law from Brussels Independent University and a Master’s in International Businesses, with specialization in International trade policy from Carleton University, Canada.- Since 1986, he taught at the national University of Rwanda and at the School of Finance and Banking (Kigali), and at the University of Ottawa (Canada).- From 1995 to à 1996, he was the legal adviser of the National Bank of Rwanda and senior jurist Expert jurist for private sector development project (MINICOM).- From 1996 to 1999, he was Minister of Justice- From 2000 to 2003, ]he was Vice Governor of the National Bank of Rwanda- From 2003 to 2005, he was the Managing Director of Rwanda Public Utilities Regulatory Agency. Since 2006, he is an independent consultant and Professor in various higher learning institutions Dr Ntezilyayo is lawyer in Kigali Bar Association and member of East African Law SocietyHe resigned from the Board of Directors on 25th november 2011.

SORAS...INGABO Y’AMAHINA

2011 Annual Report

Marc RUGENERA : Managing Director

Marc RUGENERA holds a BA in and Financial Sciences with specialization in Bank and Finances and commercial engineer from Institut Catholique de Hautes Etudes Commerciales (ICHEC Brussels)From 1980 to 1988, he worked with Rwanda Development Bank an Project Analyst, Head of the Department of SME and Head in charge of Supervision and Assistance to Enterprises.From 1988 to 1992, he worked as Managing Director of the Company for Industry and Trade in Africa From 1992 to 1997, he was Minister of FinanceFrom 1997 to 2000, he was Minister of Trade, Industry and TourismFrom 2000 to 2010, he was Managing Director and Administrator Director General of Société Rwandaise d’Assurances (SORAS S.A.)Since June 2010, he is Managing Director of SORAS ASSURANCES GENERALES LTD.

Anastase MBABAJENDE : Director of Production

Anastase MBABAJENDE holds a degree of Technician Engineer in Electronics from UNR; BA in ICT Sciences from the National University of Rwanda and Certified IBM System Administrator of IBM Training Centre, Johannesburg, South Africa. From 1990 to 1994, he worked in the Computer department of Société Rwandaise d’Assurances (SORAS S.A.)From 1994 to 2009, he was Head of the Computer Department at Société Rwandaise d’Assurances (SORAS S.A.)Since 2009, he director of PRODUCTION at SORAS ASSURANCES GENERALES LTD

Joseph NKIKABAHIZI :Director of Finance and AdministrationJoseph NKIKABAHIZI holds a BA in Management from the National University of Rwanda, a degree from Institut Africain des Hautes Etudes Bancaires et Financière of Douala, Cameroon and a certificate in insurance practice policy awarded by ACII- London ;- From 1991 to 1995, he worked as inspector in the Audit Department , Financial Controller in Finance Department of Caisse Centrale de l’Union des Banques Populaires du Rwanda ;- From 1995 to 1996, he worked at Bank of Kigali as Deputy Operation officer and andBranch Manager ;- From 1999 to 2010, he was at Société Nationale d’Assurances du Rwanda (SONARWA) as head of the Section of Miscellaneous Risks , Head of the Department of Accidents and Miscellaneous Risks, Head of the Department of Fire and Miscellaneous Risks, Commercial Inspector and Director of Finance and Asset management from 2005 to 2010.-He is Director of Administration and Finance at SORASASSURANCES GENERALES LTD since May 2010.

Pierre Claver NKULIKIYINKA :Director of Claims and Litigation

Pierre Claver NKULIKIYINKA has graduated in Public Administration from the National University of Rwanda and holds a BA in Law from Kigali Independent University (ULK).From 1994 to 1995, he worked in the Ministry of Public Service as Head of Division of Inspection of Public Service and Disputes litigation.He has been working with Société Rwandaise d’Assurances since 1995; he has held the position of Head of Administrative Department upon recruitment, Head of the Department of Claims and Litigation, since 1996, Commercial Director since 2002 and Director of Claims and Litigation since 2010.

Benjamin MBUNDI :Commercial Director

Benjamin MBUNDI holds a BA in Statistics and Economics from African and Mauritian Institute of Statistics and Applied Economics (IAMSEA) and a Master’s Degree in Business Administration (MBA) awarded by the Maastricht School of Management.- Since 1990, he worked at Société Nationale d’Assurances du Rwanda (SONARWA) as employee and then as Head of the Research and Marketing Department up to 1996. - From 1996 to 2000, he successively held the positions Head Division of Marine , Head of the Moto Division , Head of the Marine, Fire and Miscellaneous Division Risk and then Commercial Director from 2001 to 2010;-He is Commercial Director at SORAS ASSURANCES GENERALES LTD since September 2010.

MANAGEMENT BOARD

L’ASSUREUR RASSURANT

2011 Annual Report

INTERNAL AUDITOR

COMPANY SECRETARY

Vincent UZARAMA:INTERNAL AUDITORVincent UZARAMA holds a BA in Finance from Kigali Institute of Science, Technology and Management (KIST). He also graduated as SuperiorTechnician from the Institute of Public Finance, Faculty of Taxation (ISFP) of Mburabuturo.From 1998 to 2009, he worked at Rwanda Revenue Authority where he held various positions, as Tax Inspector,, Head of the Section of tax inspection, Head of the Division of Tax and Customs investigations, Head of the Division of Accounts of the Expenditure, Head of Audit Division in the Department of Large Taxpayers, and from 2006 to 2009 as Deputy Commissioner in charge of the Department of Small and medium Taxpayers.From January 2010 to June 2010, he worked as independent Consultant in Audit, Accounting and Tax consultancy service.From July 2010 to present day, he works as Head of the Internal Audit Department at SORAS.

Jean Claude HODARI :Company Secretary & Compliance Officer Jean Claude HODARI holds a degree in Laws from the National University of Rwanda and has attended various professional training sessions in Rwanda, United States and in Egypt.From 2000 to 2004: he worked as judge and Vice-president of the Court of First Instance.From 2004 to 2008 : he worked as Chief Prosecutor at the Provincial ;Prosecution and Prosecutor for Intermediate Court From 2008 to à 2010: he worked an employee of the Ministry of Justice responsible for Karongi Access to Justice Center;Since 2011 he is the Corporate Secretary of SORAS GROUP LTD

2011 Annual Report

CHAIRMAN’S STATEMENT.

Dear shareholders’

It is with pleasure that I make this statement about SORAS AG Ltd performance for the year 2011. I will here below, highlight briefly significant development in the business environment that has impacted the performance during 2011.

I am pleased to note that the economy in Rwanda continues to provide an environment of business growth that encourages investors.

The East African Customers Union has created new market dynamics within regional trade and,pursuit of regional integration will create both opportunity and competition in the market.

As a result of stable Rwanda economy,a good performance was achieved this year. In fact, the Gross written premium for the year 2011,amount to Rwf 9.455.830.279 against Rwf 7,399,408,345 in 2010. An increase of 28%.

SORAS AG Ltd achieved a net profit of Rwf 1,529,987,524 . This performance was due to the increase in the turnover, but also by the impact of the IFRS first adoption.

During the 2011 year, a cash payment dividend of Rwf 500 000 000 has been proposed to the shareholder’s annual general meeting.

On the good governance side, the Board of Directors of SORAS S.A. convened four times during 2011:

- On 25th march 2011, items on the agenda of the Board Meeting included examination of the Report of the General Meeting of Shareholders of the year 2010, adoption of the annual audited accounts for the year 2010, convening of the ordinary General Meeting .

- 18th may 2011, the Board of Directors approved the financial statement as at 31st March 2011; the Board of Directors approved the financial statement as at 31stJune 2011; the PRIMA 2000 budget refurbishment, the Human Resources policy and the human resources internal rules;

- 25th november 2011, the Board of Directors approved the financial statement as at 31st september 2011 and the 2012 budget;

The ordinary General meeting convened two times during the year 2011:

- On 25th march 2011, the ordinary General Meeting approved the 2010 annual financial statements, the annual audited accounts for the year 2010 and the approbation of profit and total comprehensive income for the year 2010.

- A second ordinary General Meeting convened on 30th august 2011 and reviewed its decision to sale the PRIMA 2000 residence but to rent it to GENIMMO after refurbishment;

- ordinary General Meeting appointed GPO and Partners as external auditor for a period of one the year 2011.

SORAS...INGABO Y’AMAHINA

L’ASSUREUR RASSURANT

2011 Annual Report

L’ASSUREUR RASSURANT

CONCLUSION

We anticipate that the market place will become increasingly competitive in the coming years.

We shall improve efficiency of our business and be more customer friendly oriented to meet our customer expectations.

We thank our loyal customers for their confidence to work closely with the company during the year.

We thank our shareholders for their continued trust and confidence in the company.

Thanks also to all staff for their hard work, commitment and loyalty, without which this performance and growth would not have been possible. We hope we will all strive to deliver in the same spirit in 2012 and beyond.

Michel Meyfroidt.

Chairman.

SORAS...INGABO Y’AMAHINA

2011 Annual Report

MANAGEMENT’S STATEMENTBUSINESS ENVIRONMENT.

Throughout financial year 2011, Rwanda’s economy evolved in a more conducive environment both on national and international level compared with year 2010 which characterized by deep recession brought about by the global financial crisis, fuel and food high prices and high inflation in the region.

Despite those challenges, the national economy achieved a growth rate of 8,8% , mainly due to good performances in practically all the sectors with growths of 8,2% in the agricultural sector, 15% in the industrial sector and 7,2% in the sector of the services.The agricultural sector recorded a sustainable growth during these three last years Agriculture due to the ongoing investments under the crop intensification program (CIP) through the provision of fertilizers and improved seeds, land consolidation and increased irrigated areas.

The growth in the secondary industry was especially carried by under sector construction industry whose contribution to the GDP increased by 22, %, the mines with an increase of 15,5% and manufacturing industry with a growth of 6,8%;

The growth was also stimulated by the recovery in the sector of the services, particularly, under sector banks and insurances with 10,6% of growth, communication and transport sector (+5,6%) and by wholesale and of detail (4,9%).

With regard to external trade, exports were dominated by tea, coffee and minerals and increased b y 52.8% in value and 48.4 % in volume, while imports increased too by 17.3% in value and 12.1% in volume.

The imports were dominated by raw materials with 46% of the total volume, followed by the foods with 34%, the fuels and lubrifiants(16,5%) and equipment with 12,1%.

The balance of payments released a positive balance of 120,3 million USD at at the end of December 2011.

Although the rate of inflation is increased during the year 2011, it could be maintained on reasonable levels compared to the other countries of the area, due to efective monetary policy and tax effective, with the stability of the exchange rate and a performance in agricultural production.

Inflation in Rwanda has been increasing over the year 2011 but maintained at moderate levels despite global and regional high inflationary pressures.

This relatively better performance is explained by the improved food production,

efficient management of the monetary policy, a stable exchange rate which limited the pass-through of imported inflation to domestic market and a good coordination of fiscal and monetary policies.

Annual headline inflation stood at 5.6 percent in 2011 after 2.3 percent in 2010.

Increase in the level of liquidity in the banking sector led to resumption of credit in favor of the private sector which increased by 28.4 %against a drop of 11.1% in 2010.

Interest rates required by the banking sector on deposits slightly increased from 6.84% in December 2010 to 7.17% in December 2011 while borrowing rates were fluctuating between 15.63% and 17.04%.

The insurance sector achieved good performances with total assets which went up from 128 Billion Rwanda Francs as at 31/12/2010 to 143.7 Billion Rwanda Francs as at 31/12/2011, which represents an increase of 12.5%.

L’ASSUREUR RASSURANT

2011 Annual Report

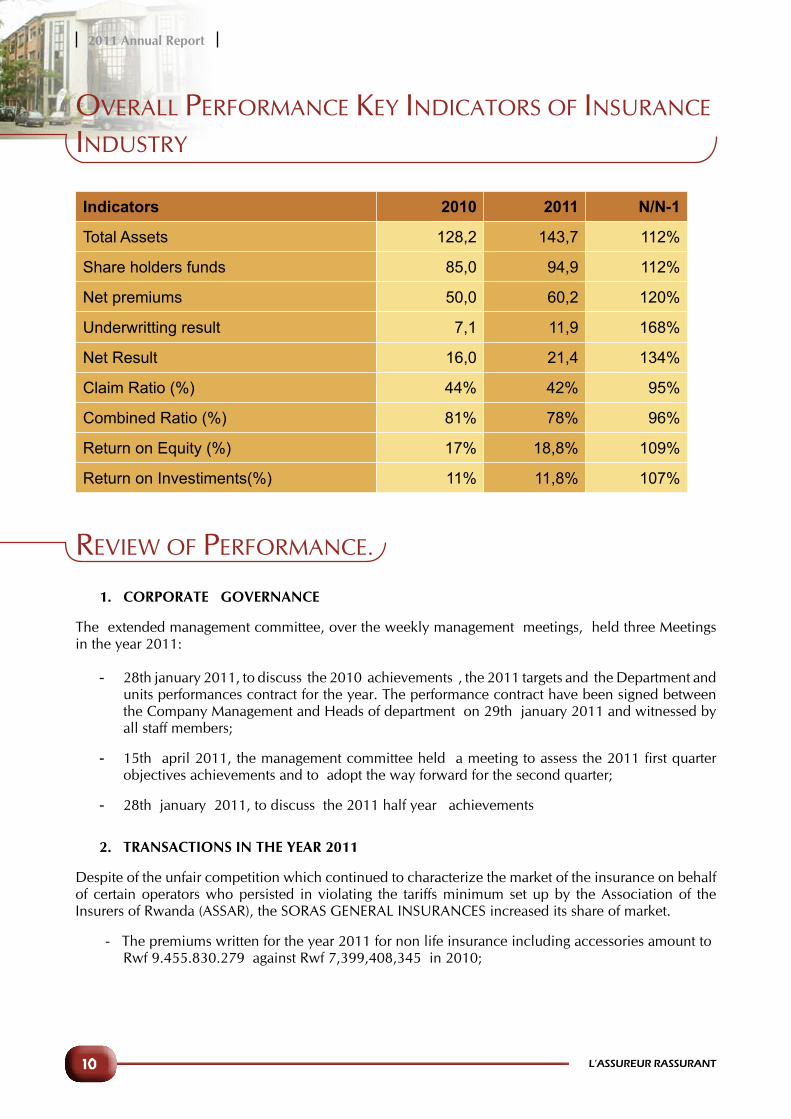

OVERALL PERFORMANCE KEY INDICATORS OF INSURANCE

INDUSTRY

Indicators 2010 2011 N/N-1

Total Assets 128,2 143,7 112%

Share holders funds 85,0 94,9 112%

Net premiums 50,0 60,2 120%

Underwritting result 7,1 11,9 168%

Net Result 16,0 21,4 134%

Claim Ratio (%) 44% 42% 95%

Combined Ratio (%) 81% 78% 96%

Return on Equity (%) 17% 18,8% 109%

Return on Investiments(%) 11% 11,8% 107%

REVIEW OF PERFORMANCE.

1. CORPORATE GOVERNANCE

The extended management committee, over the weekly management meetings, held three Meetings in the year 2011:

- 28th january 2011, to discuss the 2010 achievements , the 2011 targets and the Department and units performances contract for the year. The performance contract have been signed between the Company Management and Heads of department on 29th january 2011 and witnessed by all staff members;

- 15th april 2011, the management committee held a meeting to assess the 2011 first quarter objectives achievements and to adopt the way forward for the second quarter;

- 28th january 2011, to discuss the 2011 half year achievements

2. TRANSACTIONS IN THE YEAR 2011

Despite of the unfair competition which continued to characterize the market of the insurance on behalf of certain operators who persisted in violating the tariffs minimum set up by the Association of the Insurers of Rwanda (ASSAR), the SORAS GENERAL INSURANCES increased its share of market.

- The premiums written for the year 2011 for non life insurance including accessories amount to Rwf 9.455.830.279 against Rwf 7,399,408,345 in 2010;

SORAS...INGABO Y’AMAHINA

2011 Annual Report

- The other income including the investment income amount of Rwf 1,200,424,653 compared with Rwf 943,636,810 in 2010;

- The claims incurred amounted to Rwf 3,271,070,648 in 2010 against Rwf 3,714,671,754 in 2011;

- The management cost total Rwf 2,243,715,274 in 2010 against Rwf 3.469,317,529 in 2011;

- The profit before tax is Rwf 2.037.359.882 in 2011 and amounts to Rwf 662,717,053 2010, while the net profit was 1.529.987.524 at end of 2011.

1. PROSPECTS FOR THE YEAR 2012.

The monetary policy and tax will aim at the consolidation of the assets by privileging economic macro stability despite of the risks due to the crisis of the debt and the inflationary pressures which persist.

The growth rate of the economy is projected to 7,6% while inflation should be contained

to 7,5% at at the end of December 2012.

In the insurance industry, the National Bank of Rwanda intends to finalize the bills on the insurance contract and the compulsory insurances.

The SORAS GENERAL INSURANCES Ltd projects to achieve a turnover in increase of 15% compared to that of the year 2011.

All the operational Departments and services signed with the company the performance contracts which will be evaluated quarterly to adopt the strategies for the achievement of fixed objectives.

The year 2012 will be also that of the finalization, the adoption and the installation of various policy documents necessary to the management of the Company but also those required by the Regulator.

It is mainly different procedure manuals, investments policy document, the IT policy document ,training policy document , the policy of provisioning as well as business continuity program.

During the year 2012, the Company will shift completely from the former software AIMS which appeared to be non performing towards the new technical software NOVANET. This process will be followed by the installation of certain applications by extranet at some of our partners, Brokers, Banks, corporate customers, in order to draw a competitive advantage from it.

The SORAS GENERAL INSURANCES will also acquire a new accounting software SAGE 100 which should enable us to have reliable Financial statements on time.

Once all these reforms completed, we should look for ISO certification as well as company notation by rating companies.

L’ASSUREUR RASSURANT

2011 Annual Report

TURNOVER PATTERNS OVER YEARS

YEAR MOTO PREMIUMS IRDT PREMIUMS MEDICAL PREMIUM TOTAL PREMIUM %(N/N-1)

2001 579,309,337 244,050,576 823,359,913 98%

2002 541,193,674 279,410,070 820,603,744 100%

2003 810,609,684 380,077,786 1,190,687,470 145%

2004 1,013,990,628 466,736,739 1,480,727,367 124%

2005 1,188,688,041 545,014,163 1,733,702,204 117%

2006 1,029,624,366 712,067,704 144,933,138 1,886,625,208 109%

2007 1,325,140,410 1,211,323,413 488,143,166 3,024,606,989 160%

2008 1,989,177,051 1,251,299,477 1,060,823,119 4,301,299,647 142%

2009 2,820,867,815 1,501,276,104 1,328,983,080 5,651,126,999 131%

2010 3,146,028,502 2,117,787,432 2,135,592,411 7,399,408,345 131%

2011 3,719,425,155 2,558,951,416 3,177,453,708 9,455,830,279 128%

SORAS...INGABO Y’AMAHINA

2011 Annual Report

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2011

Directors’ Responsibilities and Approval

The directors are required in terms of the Companies Act of Rwanda to maintain adequate accounting

records and are responsible for the content and integrity of the financial statements and related

financial information included in this report.

It is their responsibility to ensure that the financial statements fairly present the state of affairs of the

company as at the end of the financial year and the results of its operations and cash flows for the

period then ended, in conformity with International Financial Reporting Standards.

The external auditors are engaged to express an independent opinion on the financial statements.

The financial statements are prepared in accordance with International Financial Reporting Standards

and are based upon appropriate accounting policies consistently applied and supported by reasonable

and prudent judgments and estimates.

The directors acknowledge that they are ultimately responsible for the system of internal financial

control established by the company and place considerable importance on maintaining a strong

control environment.

To enable the directors to meet these responsibilities, the board sets standards for internal control

aimed at reducing the risk of error or loss in a cost effective manner.

The standards include the proper delegation of responsibilities within a clearly defined framework,

effective accounting procedures and adequate segregation of duties to ensure an acceptable level of

risk.

These controls are monitored throughout the company and all employees are required to maintain

the highest ethical standards in ensuring the company’s business is conducted in a manner that in all

reasonable circumstances is above reproach.

The focus of risk management in the company is on identifying, assessing, managing and monitoring

all known forms of risk across the company.

While operating risk cannot be fully eliminated, the company endeavors to minimize it by ensuring

that appropriate infrastructure, controls, systems and ethical behavior are applied and managed within

predetermined procedures and constraints.

The directors are of the opinion, based on the information and explanations given by management,

that the system of internal control provides reasonable assurance that the financial records may be

relied on for the preparation of the financial statements.

L’ASSUREUR RASSURANT

2011 Annual Report

However, any system of internal financial control can provide only reasonable, and not absolute,

assurance against material misstatement or loss.

The directors have reviewed the company’s cash flow forecast for the year to December 31, 2012 and,

in the light of this review and the current financial position, they are satisfied that the company has or

has access to adequate resources to continue in operational existence for the foreseeable future.

The external auditors are responsible for independently reviewing and reporting on the company’s

financial statements. The financial statements have been examined by the company’s external auditors

and their report is presented on pages 15 to 16.

The financial statements set out on pages 17 to 19, which have been prepared on the going concern

basis, were approved by the board on 28th march 2012 and were signed on its behalf by:

Director Director

SORAS...INGABO Y’AMAHINA

2011 Annual Report

INDEPENDENT AUDITORS’ REPORT

To the member of SORAS ASSURANCES GENERALES Ltd;

Report on the Financial Statements

We have audited the financial statements of SORAS ASSURANCES GENERALES Ltd, which comprise the statement of financial position as at December 31, 2011, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes, as set out on pages 17 to 29.

Directors’ Responsibility for the Financial Statements

The company’s directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and in the manner required by the Companies Act of Rwanda.

This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error.

In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.

An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

L’ASSUREUR RASSURANT

2011 Annual Report

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of SORAS ASSURANCES GENERALES Ltd as at December 31, 2011, and its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards, and in the manner required by the Companies Act of Rwanda.

Report on Other Legal and Regulatory Requirements

As required by the Rwandan Companies Act we report to you, based on our audit the following:

• We have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit;

• In our opinion proper books of account have been kept by the company, so far as appears from our examination of those books;

• The company’s Statement of Financial Position and Statement of Comprehensive Income are in agreement with the books of account.

• We also noted other matters involving internal control and its operation that we have reported to the management of SORAS ASSURANCES GENERALES Ltd in a separate letter ; and

• The audit team members do not have any interest, loans to or from this client or any related entity or any significant shareholder, officer or director thereof.

GPO Partners Rwanda Ltd

Patrick GASHAGAZAPartner 28th march 2012.

SORAS...INGABO Y’AMAHINA

2011 Annual Report

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2011

2011 2010Note(s) RWF RWF

RetraitéAssets Non-Current AssetsInvestment property 1 4,152,072,856 4,217,978,774Property, plant and equipment 2 3,976,341,560 3,931,039,928Intangible assets 3 219,157,242 241,362,465Investments in subsidiaries 4 913,091,498 913,091,498

Investments in associates 5 600,000,000 219,000,000

Other financial assets 6 4,165,214,693 1,159,636,205Other non current assets 732,673 732,673

14,026,610,522 10,682,841,543Current AssetsLoans to group companies 7 804,702,678 517,800,192Trade and other receivables 8 2,456,296,681 2,681,381,595Inventories 42,769,716 37,241,944Cash and cash equivalents 9 1,305,053,890 1,356,180,963

4,608,822,965 4,592,604,694Total Assets 18,635,433,487 15,275,446,237

Equity and LiabilitiesEquity Share capital 10 1,000,000,000 1,000,000,000Reserves 5,492,164,805 5,492,164,805Retained income 11 1,416,039,901 -113,947,622

7,908,204,706 6,378,217,183LiabilitiesNon-Current LiabilitiesDeferred tax 12 2,130,530,806 2,138,887,877Curent Liabilities Current tax payable 439,879,673 127,955,592Trade and other payables 13 1,383,028,772 746,958,579Provisions 14 6,773,789,530 5,883,427,006

8,596,697,975 6,758,341,177Total Liabilities 10,727,228,781 8,897,229,054Total Equity and Liabilities 18,635,433,487 15,275,446,237

The financial statements together with explanatory notes set out on pages 17 to 29 were approved by the Board of Directors on 28th march 2012 and were signed on its

Board Chairman Director

L’ASSUREUR RASSURANT

2011 Annual Report

Financial Statements for the year ended December 31, 2011

Statement of Comprehensive Income

2011 2010Notes RWF RWF

Income Gross premiums written 9,455,830,279 7,399,408,345 Premiums ceded to reinsurers (2,094,695,390) (1,559,591,308)Net premiums written 7,361,134,889 5,839,817,037 Change in gross provision for unearned premiums (745,156,163) (590,110,995)

Reinsurers’ share of change in provision for unearned premiums 518,567,425 0

(226,588,738) (590,110,995)Net earned premiums 15 7,134,546,151 5,249,706,042

Other income Investment return 569,730,318 540,570,397 Other income 630,694,335 403,066,413 1,200,424,653 943,636,810 RNet revenue 8,334,970,804 6,193,342,852 Expenses Insurance claims (4,163,737,060) (3,432,834,396)Insurance claims recoverable from reinsurers 476,307,916 636,431,181

Increase/Decrease of insurance claims provision (27,242,610) (474,667,433)

Net insurance claims (3,714,671,754) (3,271,070,648) Other underwriting and corporate expenses: Other underwriting operating expenses (3,284,322,799) (2,259,554,551)Loss on disposal of financial assets (184,994,729) 0 Total other underwriting and corporate expenses (Refer to page 25) (3,469,317,528) (2,259,554,551)

Total expenses (7,183,989,282) (5,530,625,199)Fair value adjustments 16 703,798,631 0(Loss)/Profit before tax 1,854,780,153 662,717,653 Income tax 17 (324,792,629) (776,664,674)(Loss)/Profit for the year 1,529,987,524 (113,947,021)

SORAS...INGABO Y’AMAHINA

2011 Annual Report

Financial Statements for the year ended December 31, 2011

Statement of Changes in Equity

Share capital

RWF

Revaluation reserve

RWF

Other

RWF

Total reserves

RWF

Retained income

RWF

Total equity

RWFBalance at January 01, 2010Total comprehensive income for the year

1,000,000,000

-

-

5,522,919,108

-

(30,754,303)

-

5,492,164,805

(662,717,052)

(113,947,622)

337,282,948

5,378,217,183

Result for 2010 before IFRS adoption

- - - -662,717,052 662,717,052

Total changes - 5,522,919,108 (30,754,303) 5,492,164,805 548,769,430 6,040,934,235Balance at January 01, 2011Total comprehensive income for the year

1,000,000,000

-

5,522,919,108

-

(30,754,303)

-

5,492,164,805

-

(113,947,622)

1,529,987,523

6,378,217,183

1,529,987,523

Total changes - - - - 1,529,987,523 1,529,987,523

Balance at January 01, 2012

1,000,000,000 5,522,919,108 (30,754,303) 5,492,164,805 1,416,039,901 7,908,204,706

Financial Statements for the year ended December 31, 2011Statement of Cash Flows.

2011Note(s) F RW

Cash generated from operations 18 2,973,253,914 Tax paid 19 (34,963,081)Net cash from operating activities 2,954,568,594Cash flows from investing activitiesPurchase of property, plant and equipment (215,697,219)Sale of property, plant and equipment 2,415,000 Purchase of other intangible assets (82,764,131)Proceeds from loans from group companies (230,843,597)Investment in quoted shares (2,301,779,857)Deposits (5,527,772)Purchase of other Property Plant and equipmentsInterest Income 46,662,096 Dividends received 129,107,576 Net cash from investing activities (2,658,427,904)Cash flows from financing activitiesProceeds on share issueFinance costs (16,267,761)Rounding adjustments (2)Acquisition of additional shares in associates and subsidiaries (331,000,000)Net cash from financing activities (347,267,763)Total cash movement for the year (51,127,073)Cash at the beginning of the year 1,356,180,963 Total cash at end of the year 1,305,053,890

L’ASSUREUR RASSURANT

2011 Annual Report

Financial Statements for the year ended December 31, 2011 Accounting Policies

1. Presentation of Financial Statements

The financial statements have been prepared in accordance with International Financial Reporting Standards, and the Companies Act of Rwanda. The financial statements have been prepared on the historical cost basis, and incorporate the principal accounting policies set out below.

They are presented in Rwanda Francs.

These accounting policies are consistent with the previous period, except for the changes set out in note 20 First-time adoption of International Financial Reporting Standards. 1.1 Investment property

Investment property is recognized as an asset when, and only when, it is probable that the future economic benefits that are associated with the investment property will flow to the enterprise, and the cost of the investment property can be measured reliably.

Investment property is initially recognized at cost. Transaction costs are included in the initial measurement.

Costs include costs incurred initially and costs incurred subsequently to add to, or to replace a part of, or service a property. If a replacement part is recognized in the carrying amount of the investment property, the carrying amount of the replaced part is derecognised.

1.2 Intangible assets

An intangible asset is recognized when:

- it is probable that the expected future economic benefits that are attributable to the asset will flow to the entity; and

- the cost of the asset can be measured reliably.

Intangible assets are initially recognized at cost.

Expenditure on research (or on the research phase of an internal project) is recognized as an expense when it is incurred.

An intangible asset arising from development (or from the development phase of an internal project) is recognized when:

- it is technically feasible to complete the asset so that it will be available for use or sale;

- there is an intention to complete and use or sell it;

- there is an ability to use or sell it;

- it will generate probable future economic benefits;

- there are available technical, financial and other resources to complete the development

SORAS...INGABO Y’AMAHINA

2011 Annual Report

and to use or sell the asset;

- the expenditure attributable to the asset during its development can be measured reliably.

Intangible assets are carried at cost less any accumulated amortization and any impairment losses.

1.3 Investments in subsidiaries

Investments in subsidiaries are carried at cost less any accumulated impairment. The cost of an investment in a subsidiary is the aggregate of:

- the fair value, at the date of exchange, of assets given, liabilities incurred or assumed, and equity instruments issued by the company; plus

- any costs directly attributable to the purchase of the subsidiary.

An adjustment to the cost of a business combination contingent on future events is included in the cost of the combination if the adjustment is probable and can be measured reliably.

1.4 Investments in associates.

An investment in an associate is carried at cost less any accumulated impairment.

1.5 Financial instruments.

Initial recognition and measurement

Financial instruments are recognized initially when the company becomes a party to the contractual provisions of the instruments.

The company classifies financial instruments, or their component parts, on initial recognition as a financial asset, a financial liability or an equity instrument in accordance with the substance of the contractual arrangement.

Financial instruments are measured initially at fair value, except for equity investments for which a fair value is not determinable, which are measured at cost and are classified as available-for-sale financial assets.

For financial instruments which are not at fair value through profit or loss, transaction costs are included in the initial measurement of the instrument. Regular way purchases of financial assets are accounted for at settlement date.

1.6. Loans to (from) group companies

These include loans to and from holding companies, subsidiaries, joint ventures and associates and are recognized initially at fair value plus direct transaction costs.

Loans to group companies are classified as loans and receivables.

Loans from group companies are classified as financial liabilities measured at amortised cost.

L’ASSUREUR RASSURANT

2011 Annual Report

1.7. Loans to shareholders, directors, managers and employees

These financial assets are classified as loans and receivables.

1.8. Receivables

Receivables are initially measured at fair value, and are subsequently measured at amortised cost, using the effective interest rate method. 1.9. Payables

The payables debts are initially measured at fair value, and are then evaluated at the cost amortized by using the method of the effective rate.

1.10. Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, and other short-term highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. These are initially and subsequently recorded at fair value.

1.11. Deferred tax assets and liabilities

A deferred tax liability is recognized for all taxable temporary differences, except to the extent that the deferred tax liability arises from the initial recognition of an asset or liability in a transaction which at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

A deferred tax asset is recognized for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilized. A deferred tax asset is not recognized when it arises from the initial recognition of an asset or liability in a transaction at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

A deferred tax asset is recognized for the carry forward of unused tax losses and unused tax credits to the extent that it is probable that future taxable profit will be available against which the unused tax losses and unused tax credits can be utilized.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

1.12. Tax expenses

Current and deferred taxes are recognized as income or an expense and included in profit or loss for the period, except to the extent that the tax arises from:

- a transaction or event which is recognized, in the same or a different period, to other comprehensive income, or

- a business combination.

Current tax and deferred taxes are charged or credited to other comprehensive income if the tax relates to items that are credited or charged, in the same or a different period, to other comprehensive income.

Current tax and deferred taxes are charged or credited directly to equity if the tax relates to items that are credited or charged, in the same or a different period, directly in equity.

SORAS...INGABO Y’AMAHINA

2011 Annual Report

1.13. Impairment of assets

The company assesses at each end of the reporting period whether there is any indication that an asset may be impaired. If any such indication exists, the company estimates the recoverable amount of the asset.

Irrespective of whether there is any indication of impairment, the company also:

- tests intangible assets with an indefinite useful life or intangible assets not yet available for use for impairment annually by comparing its carrying amount with its recoverable amount. This impairment test is performed during the annual period and at the same time every period;

- tests goodwill acquired in a business combination for impairment annually.

If there is any indication that an asset may be impaired, the recoverable amount is estimated for the individual asset. If it is not possible to estimate the recoverable amount of the individual asset, the recoverable amount of the cash-generating unit to which the asset belongs is determined.

The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs to sell and its value in use.

If the recoverable amount of an asset is less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. That reduction is an impairment loss.

1.14. Employeebenefitsandshort-termemployeebenefits

The cost of short-term employee benefits, (those payable within 12 months after the service is rendered, such as paid vacation leave and sick leave, bonuses, and non-monetary benefits such as medical care), are recognized in the period in which the service is rendered and are not discounted.

The expected cost of compensated absences is recognized as an expense as the employees render services that increase their entitlement or, in the case of non- accumulating absences, when the absence occurs.

The expected cost of profit sharing and bonus payments is recognized as an expense when there is a legal or constructive obligation to make such payments as a result of past performance.

1.5 Provisions and contingencies

Provisions are recognized when:

- the company has a present obligation as a result of a past event;

- it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation; and

- a reliable estimate can be made of the obligation.

The amount of a provision is the present value of the expenditure expected to be required to settle the obligation.

L’ASSUREUR RASSURANT

2011 Annual Report

1.16. Revenue

Revenue from the sale of goods is recognized when all the following conditions have been satisfied:

- the company has transferred to the buyer the significant risks and rewards of ownership of the goods;- the company retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold; - the amount of revenue can be measured reliably;- it is probable that the economic benefits associated with the transaction will flow to the company; and

- the costs incurred or to be incurred in respect of the transaction can be measured reliably.

1.17. Turnover

Turnover comprises of sales to customers and service rendered to customers. Turnover is stated at the invoice amount and is exclusive of value added taxation.

1.18. Translation of foreign currencies

Foreign currency transactions

A foreign currency transaction is recorded, on initial recognition in RWF, by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the date of the transaction. At the end of the reporting period:

- foreign currency monetary items are translated using the closing rate;- non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction; and- non-monetary items that are measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

Exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous financial statements are recognized in profit or loss in the period in which they arise.

SORAS...INGABO Y’AMAHINA

2011 Annual Report

Financial Statements for the year ended December 31, 2011

Notes to the Financial Statements

1. Investment property

Rapprochement des Immeubles de placement - 2011 Opening balance Depreciation Total

Investment property 4,217,978,774 (65,905,918) 4,152,072,856

Reconciliation of investment property - 2010

Investment property

Opening balance

4,283,884,692

Depreciation

(65,905,918)

Total

4,217,978,774

2. Property, plant and equipment

2011 2010

Property Cost/valuation Accumulated depreciation Carrying value Cost/valuation Accumulated

depreciation Carrying value

Land 606,038,725 606,038,725 606,038,725 606,038,725Buildings 3,247,820,401 (141,271,223) 3,106,549,178 3,175,240,371 (70,269,817) 3,104,970,554Motor vehicles 297,481,470 (223,313,408) 74,168,062 269,981,470 (199,011,581) 70,969,889Office equipment 553,223,738 (461,831,956) 91,391,782 528,975,757 (444,349,467) 84,626,290IT equipment 83,563,332 (56,581,374) 26,981,958 80,817,526 (66,114,636) 14,702,890Apartment materials 42,919,866 (31,311,009) 11,608,857 42,919,866 (29,079,833) 13,840,033Other property, plant and equipment

350,676,845 (291,073,847) 59,602,998 307,168,386 (271,276,839) 35,891,547

Total 5,181,724,377 -1,205,382,817 3,976,341,560 5,011,142,101 -1,080,102,173 3,931,039,928

3. Intangible assets

2011 2010

Property Cost/valuation Accumulated depreciation Carrying value Cost/valuation Accumulated

depreciation Carrying value

AIMS software 225,745,247 (102,948,570) 122,796,677 199,004,030 - 199,004,030Novanet and sage pastel under development

88,444,343 - 88,444,343 32,421,429 - 32,421,429

Research and develop-ment costs

54,498,854 (46,582,632) 7,916,222 54,837,787 (44,900,781) 9,937,006

Total 368,688,444 (149,531,202) 219,157,242 286,263,246 (44,900,781) 241,362,465

L’ASSUREUR RASSURANT

2011 Annual Report

4. Investments in subsidiaries:

Name of company 2011Carrying amount

2010Carrying amount

Agaseke bank Ltd 913,091,498 913,091,498

The carrying amounts of subsidiaries are shown net of impairment losses.

5. Investments in associates:

Name of company 2011Carrying amount

Carrying amount 2010

GENIMMO 600,000,000 600,000,000

6.OtherfinancialassetsFair value information

Financial assets at fair value through profit or loss are recognised at fair value, which is therefore equal to their carrying amounts.

The company has not reclassified any financial assets from cost or amortised cost to fair value, or from fair value to cost or amortised cost during the current or prior year.

2011 2010

Listed shares 2,977,574,739 344,710,151

Unlisted shares 1,187,639,954 814,926,054

TOTAL 4,165,214,693 1,159,636,205

7. Loans to (from) group companies

2011 2010

Soras group 722,816,540 500,820,989

Genimmo 8,848,046 00

Soras vie 73,038,092 16,979,203

TOTAL 804,702,678 517,800,191

8. Trade and other receivables

2011

Trade receivables 1,040,126,872 1,585,998,392

Staff advance - 3,657,961

Prepayments 32,030,080 44,938,928

Suspens account 68,732,766 18,284,590

Share of reinsurers and coinsurers in technical provisions 1,253,674,151 882,227,664

Receivable from coinsurers 61,732,812 80,529,642

Total 2,456,296,681 2,681,381,595

SORAS...INGABO Y’AMAHINA

2011 Annual Report

9. Cash and cash equivalents

Cash on hand 59,478,926 26,735,294

Bank balances 683,123,281 542,967,129

Short-term deposits 561,969,248 681,969,248

Internal transfers cash 482,435 104,509,292

1,305,053,890 1,356,180,963

10. Share capital

2011 2010

Authorised100,000 Ordinary shares of 10,000 each 1,000,000,000 1,000,000,000

11. Retained income

Opening balance (113,947,622) 662,717,052

Retreatment - (662,717,052)

Profit / Loss 1,529,987,523 (113,947,622)

1,416,039,901 (113,947,622)

12. Deferred tax

Accounting net book value of buildings 7,864,660,944 7,928,988,250

Tax base of buildings 762,891,590 799,361,992

Taxable temporarly defference 7,101,769,355 7,129,626,258

Difference due to revaluation 5,350,696,640 5,350,696,640

Difference due to different depreciation rate and method 1,751,072,715 1,778,929,618

Deferred tax on revaluation reserves 1,605,208,992 1,605,208,992

Deferred tax due to difference in depreciation rate and method 525,321,814 533,678,885

Deferred tax as at 31st December 2,130,530,806 2,138,887,877

Deferred tax as at 1st January 2,138,887,877 0

Movement in Deferred tax (8,357,071) 2,138,887,877

Income statement (8,357,071) 533,678,885

Other comprehensive income 0 1,605,209,192

Deferred tax as at 31st December 2,130,530,806 2,138,887,877

13. Trade and other payables

2011 2010

Trade payables 585,703,833 334,895,534

National social security fund 28,808,538 23,194,054

Other payables 700,911,126 382,877,605

Road maintenance fund 29,307,451 27,898,863

Accrued expense 17,684,014

Payable to coinsurers 20,613,810 -21,907,477

TOTAL 1,383,028,772 746,958,579

L’ASSUREUR RASSURANT

2011 Annual Report

14. Provisions

Opening balance Additions TotalProvision for unearned premium 1,951,870,299 745,156,163 2,697,026,462

Provision for outstanding claims 3,931,556,707 145,206,361 4,076,763,068

5,883,427,006 890,362,524 6,773,789,530

15. Net earned premiums

Income 2011 2010

Gross premiums written 9,455,830,279 7,399,408,345

Premiums ceded to reinsurers (2,094,695,390) (1,559,591,308)

Net premiums written 7,361,134,889 5,839,817,037

Change in gross provision for unearned premiums (745,156,163) (590,110,995)

Reinsurers’ share of change in provision for unearned premiums 518,567,425 0

(226,588,738) (590,110,995)

Net earned premiums 7,134,546,151 5,249,706,042

16. Fair value adjustment

Gain on revaluation of quoted shares in BRALIRWA 901,999,566 -

Loss on revaluation of quoted shares in BRITAK (198,200,935) -

703,798,631 -

17. Income tax

Profit before tax 1,854,780,153

Deductions

Dividends received (104,969,236)

Fair value adjustment on quoted shares Bralirwa (901,999,566)

Total 847,811,351

Add Back

None deductible expenses (staff insurance) 23,999,710

Directors's fees 6,500,000

Telephone 20% 6,129,826

Depreciation adjustment 27,856,903

Fair value adjustment on quoted shares Bitak 198,200,935

Total additions 262,687,374

Taxable Income 1,110,498,725

Income tax @ 30% 333,149,700

Deferred tax movement (8,357,071)

Income tax expense 324,792,629

SORAS...INGABO Y’AMAHINA

2011 Annual Report

18. Cash generated from operations

Profit before taxation 1,854,780,152

Adjustments for:

Depreciation and amortization 282,913,790

Profit on sale of assets (2,415,000)

Dividends received (129,107,576)

Interest received (46,662,096)

Fair value adjustments (703,798,631)

Movements in provisions 890,362,524

Movements in operating lease assets and accruals

Trade and other receivables 499,530,505

Trade and other payables 327,660,246

Cash generated from operations 2,973,263,914

19. Tax paid

Local tax (59,446,724)

Current tax for the year recognized in profit or loss (324,792,629)

Other taxes 349,276,272

(34,963,081)

The Network’s development

The network is being extended by : - New members recruited with very strict regard to the criteria laid down in our professional charter- New companies set up by existing members of the network- Partnership treaties with companies in different African regions

PartnershipsAgreements have already been concluded with : - The South African Group Global Alliance represented in Angola, Ghana and Mozambique

- One of Nigeria’s major companies, Leadway Assurance Ltd.- Discussions are on-going with one of East Africa’s leading insurance groups

Projected for 2010- The creation of new companies in West Africa - A partnership agreement in South Africa

N° Countries Companies

1 ALGERIA SALAMA ASSURANCES

2 ANGOLA ANGOLA SEGUROS INSURANCE(GLOBAL ALLIANCE subsidiary)

3 BENIN L’AFRICAINE DES ASSURANCES

4 BURKINA FASO SONAR IARD

5 BURUNDI BICOR

6 CAMEROON ACTIVA ASSURANCES

7 CONGO BRAZZAVILLE ASSURANCE GENERALE DU CONGO (AGC)

8 DEMOCRATIC RER of the CONGO ASSURANCE GENERAIE DU CONGO (AGC)

9 IVORY COAST LA LOYALE ASSURANCES

10 GABON ASSINCO

11 GHANA ACTIVA INSURANCE GHANA

12 EQUATORIAL GUINEA l’AFRICAINE DES ASSURANCES

13 KENYA JUBILEE

14 MADAGASCAR ARO

15 MOROCCO RMA WATANYA

16 MAURITANIA N.A.S.R.

17 MOZAMBIQUE GLOBAL ALLIANCE SEGUROS

18 NIGER LA NIGERIENNE DASSURANCES ETDE REASSURANCES (N.LA.)

19 NIGERIA LEADWAY

20 UGANDA JUBILEE

21 RWANDA SORAS

22 SAO TOME & PRINCIPE GLOBAL ALLIANCE SAO TOME & PRINCIPE

23 SENEGAL SALAMA ASSURANCES

24 TANZANIA JUBILEE

25 CHAD SAFAR

26 TOGO FIDELIA ASSURANCES

27 TUNISIA COMAR

Mem

ber o

f the

Glo

busN

etw

ork