Embed Size (px)

Citation preview

HSBC Bank Malta p.l.c. Annual Report and Accounts 2011

HSBC Bank Malta p.l.c. is a member of the HSBC Group, whose ultimate parent company is HSBC Holdings plc. Headquartered in London, HSBC Holdings plc is one of the largest banking and financial services organisations in the world. The HSBC Group’s international network comprises around 7,500 offices in over 80 countries and territories in Europe, the Asia-Pacific region, the Americas, the Middle East and Africa.

The HSBC Group

HSBC Bank Malta p.l.c.Registered in Malta: number C3177Registered Office and Head Office: 116 Archbishop StreetValletta VLT 1444Malta Telephone: 356 2597 0000Customer Service: 356 2380 2380Facsimile: 356 2380 4923www.hsbc.com.mt

HSBC Holdings plcRegistered Office and Group Management Office:8 Canada SquareLondon E14 5HQUnited KingdomTelephone: 44 020 7991 8888Facsimile: 44 020 7992 4880www.hsbc.com

1

H S B C B A N K M A L T A P . L . C .

Contents

1

2 Chairman’sStatement

5 ChiefExecutiveOfficer’sReview

10 BoardofDirectors

12 FinancialReview

14 ReportoftheDirectors

18 StatementofCompliancewiththePrinciplesofGoodCorporateGovernance

26 RemunerationReport

28 Directors’ResponsibilitiesStatement

29 IncomeStatements

30 StatementsofComprehensiveIncome

31 StatementsofFinancialPosition

32 StatementsofChangesinEquity

34 StatementsofCashFlows

35 NotesontheFinancialStatements

91 IndependentAuditors’ReporttotheMembersofHSBCBankMaltap.l.c.

93 GroupIncomeStatementsandStatementsofComprehensiveIncome:Five-YearComparison

94 GroupStatementsofFinancialPosition:Five-YearComparison

95 GroupStatementsofCashFlows:Five-YearComparison

96 GroupAccountingRatios:Five-YearComparison

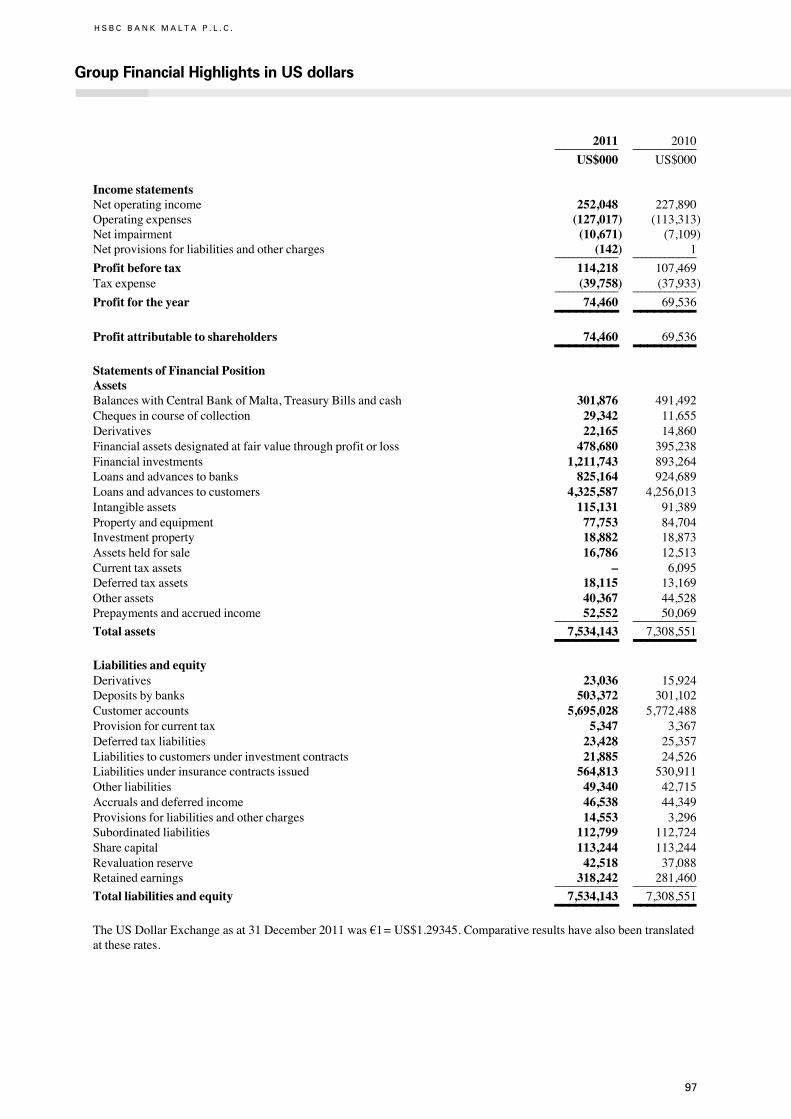

97 GroupFinancialHighlightsinUSdollars

98 BranchesandOffices

2

H S B C B A N K M A L T A P . L . C .

Chairman’s Statement

2

Iampleasedtoadvisethat2011wasagoodyearforHSBC BankMalta p.l.c. during which it delivered asolidperformance inspiteofverychallengingmarketconditions.

Results

Profit before taxation was §88m, representing anincrease of 6% over prior year. On a like for likebasis,excludingone-offitemsin2010and2011,profitbefore taxwas up 1%.Against the current economicbackdrop,theworstinlivingmemory,thisrepresentsacredibleperformanceandwasunderpinnedbypositivecontributionsbyallbusinesslines.

Bybeingprudent,yetproactive,HSBCBankMaltahas managed to navigate successfully through thesetroubledwaters.Particularnoteshouldbetakenoftheexcellentworkduring2011toreduceriskonthebank’sinvestmentportfolio.Thebankhascontinuedtogrowits loan book and retains its position as the leadinginternationalbankinMalta.

Profitattributabletoshareholders increasedby7%to §58m. On the basis of these results the Board isrecommending a final gross ordinary dividend of 7.2centpershare.Togetherwiththeinterimgrossdividendof8.2centpershare(5.3centnetoftax)paidinAugust2011,thetotaldividendfortheyearis15.4cent.

During2011,thenumberofthebank’sshareholdersstoodataround10,400,manyofwhichhaveremainedloyalovertheyears.Astestimonytoourcommitmentto communicate better and more frequently with ourshareholders we launched a new bilingual onlinepublication,L-Azzjonist.Thiseco-friendlypublicationis available in the Investor Relations section of theHSBCBankMaltawebsiteandhasalreadyprovedtobepopularwithinvestorsofthebank.

HSBCBankMaltap.l.c.isasubsidiaryofLondon-basedHSBCHoldingsplc,oneoftheworld’sleadingfinancialservicesorganisations,andremainsthelargestcompany listed on theMalta Stock Exchange with amarketcapitalisationofaround§750m.

Strategy

2011 was the first year of implementing the HSBCgroup approved four-year Medium Term Outlook(MTO). This is the bank’s strategic plan for theperiod 2011-2014 which establishes a clear directionof thebank’sfutureanddevelopmentopportunities inMaltaand thestrategic imperativesneeded toachievesustainablegrowth.

The overall strategy is based on building thebusiness organically and consolidating the bank’smarket position by sustaining its strong domesticfranchise and growing internationally by leveragingitsglobalreachthroughtheHSBCGroup’sworldwidenetwork and internationally recognised brand. Byplaying to its strengths and focusing on its naturalcompetitive advantages as a global organisation, thebankwill seek to capitalise on the increasingmarketopportunitiesandplayaleadingroleinMalta’sgrowthasaninternationalfinancialservicescentre.

During the year under review, the bank hascontinuedtotransformtheorganisationinlinewiththeMTO by focusing on its segmentation strategy in itsprincipal customer groups, generating efficiencies bystreamliningprocessesandoperations,makinggreateruse of Regional Centres of Excellence, investing intechnology and automated channels and deliveringan unrivalled customer experience. Furthermore, thebank has been very active in facilitating cross-bordercommercial activity through its leading internationalbusinessstrategyandplayingamoreactiveroleintheareaofglobalbankingandmarkets.

3

Reflecting customer behavioural trends of lowerteller activity and theneed for continuedproductivityand cost effectiveness, the bank has announced an§11mrestructuringcharge thatwillseea reduction inits staff complement and the closure of six branches.This restructuring is necessary to achieve long-termgoals and will not involve any staff compulsoryredundancies.Displacedemployeeswillberedeployedelsewhere within the organisation or may chooseto apply for a voluntary redundancy/early voluntaryretirementschemethathasbeenmadeavailable.

Against this backdrop, it is worth noting that thebank remains committed to its substantial investmentprogrammeinMalta.During2011thebankimplementedanewstate-of-the-artcorebankingsystemwithacapitalinvestmentof §10m. In addition to this,HSBCMaltacontinues the roll out of its §11m project to upgradeitsbranchnetworkinlinewithGroupglobalstandardsand introduce next-generation ATMs with increasedfunctionalityforgreatercustomerconvenience.

In December the bank sold its card acquiringbusiness to Global Payments Inc. for a considerationof §11m. This is in line with HSBC Group strategyof exiting this part of the business around theworld.GlobalPayments is a recognisedworldwide leader inpayments processing and together with HSBC BankMaltawillcontinuetoprovidecustomerswiththecardacceptanceflexibility,convenience,serviceandsupporttheyneed.ThenewacquiringbusinesswillcontinuetotradeundertheHSBCbrandforthetimebeingandwillbecalledHSBCMerchantServicesLtd.

Corporate Sustainability

ThekeyforHSBCBankMaltaand theHSBCGroupremains long term corporate sustainability. As suchthe bank recognises the importance of continuing itsprogrammeofinvestmentsintheMaltesecommunity.Theprincipalfocusareasare:

•Environment•Education,inparticulardisadvantagedchildren,and•Heritage

The HSBC Malta Foundation is the bank’s mainchannel for corporate sustainability activity. In 2011the Foundation supported a wide range of activitiesaroundMalta.Someofthekeyeventsincluded:

Environment

The afforestation project at Ta˙t Chambray in GozoThe projectwill cost §200,000 and itwill be equallyfinancedbytheFoundationandtheMalteseGovernment.HSBChasbeenasponsoroftheafforestationprojectinMaltafromthestartandhassofarplantedover25,000treesaspartofthisnationalprogramme.

Eco-SchoolsTheHSBCMaltaFoundationhasbeensupportingtheEco-Schools Programme for the past 6 years. Over40,000studentshaveparticipatedinthisprogrammeandsofaratleast20schoolshavesecuredtheInternationalGreenFlagAward,aprestigiousaccreditationfortheirenvironmentalpracticesatschool.

Education

Young EnterpriseHSBChasbeenthesponsoroftheJuniorAchievementYoung Enterprise Malta for the past 11 years. Theprogrammeoffersahigh-qualityeducationprogrammethat teaches students entrepreneurship and businessskillsinapracticalway.

Caritas MaltaTheFoundationisalong-timesupporterofCaritasMaltain running its educational programme in primary andsecondaryschoolswiththeaimofinstillingsoundvaluesandpromotingpreventionagainstsubstanceabuse.

Heritage

Support for Casa Rocca Piccola’s celebration of laceTheFoundationisproudtobeassociatedwithauniqueMalteselacecompetitionheldannuallyatCasaRoccaPiccola inValletta. In2011thecompetitionhonoured58traditionallacemakers,includingfourchildren.

HSBC Malta employees participate in the HSBC Climate Partnership programme as part of HSBC’s long standing commitment to protecting the environment and tackling climate change.

HSBC Malta received FT’s The Banker Award 2011 in recognition for its achievements and best overall performance.

Gozo historical documents HSBC was the main sponsor of an exhibition ofsome 30 historical documents, etchings, plans andphotographs relating to herbs, health and hospitals ofGozoattheNationalArchivesinVictoria.

Throughout the year, in addition to signaturesponsorshipssuchasthosenotedaboveandthebank’sparticipationwithL-Istrina, a large number ofHSBCstaffhavegenerouslygiven their time toworkwithinthecommunity.ItisthisthatmakesHSBC’scorporatesustainabilityworkparticularlyspecial.

Board

During 2011 there was one change to the Board ofDirectors from the majority shareholder. Ms SallyRobsonretiredfromtheHSBCGroupafteralongandsuccessfulcareerinwhichshespentherlastfiveyearsin Malta as a Director, Chief Operating Officer andsubsequentlyChief Technology and ServicesOfficer.MsRobsonwas succeededbyPhilipFarrugiawho isthecurrentChiefTechnologyandServicesOfficerofthebank.

I would like to express my gratitude to AlanRichards who has served as a Director and CEO ofthe bank since 2008. From the beginning of 2012,Mr Richards has been appointed CEO for HSBCIndonesia. I thank Mr Richards for his positivecontribution to thebankover theyears andwishhimevery success in his new position. I also warmlywelcomeMarkWatkinsonasanincomingDirectorandnewCEOof thebank.MrWatkinson joinedus fromHSBC North America and has been with the HSBCGroupfor26years,workinginmanycountriesaroundthe world. I am certain Mr Watkinson will use hisknowledge and significant international experience tocontinuethesuccessofHSBCMalta.

IamfortunatetobetheChairmanofaBoardwhosemembershaveawealthofbothlocalandinternationalknowledge.Collectivelywehavemanaged toprovidethenecessaryleadershipandvisiontosuccessfullyguideour organisation through exceptionally challengingtimes.

The Board comprises myself as Chairman, anexpatriateexecutivedirectorwhoisalsoChiefExecutiveOfficer of thebank, one local executivedirectorwhoalsoservesasChiefTechnologyandServicesOfficer,five prominent non-executive directors who are allMalteseandoneoverseas-baseddirectorwhoisChiefExecutiveOfficer,ContinentalEuropeforHSBC.

I am confident that through the contributions ofits members, the Board will continue to build on itsachievementsandleadthebankforwardinthefuture.

International Recognition

HSBCBankMaltahasbeennamedBankof theYearinMalta for 2011 by the prestigiousFinancialTimesmonthlypublicationTheBanker.

WinningthisinternationalawardisafittingaccoladeforthestrongperformancethebankdeliveredacrossallbusinessareasinspiteofincreasinglydifficultmarketconditionsandisalsoagreattributetotheHSBCteaminMalta.

The well-deserved award also enhances ourcredentials asMalta’s leading local and internationalbank.

Outlook

2012isanticipatedtobeanevenmorechallengingyearthan2011.Theglobalandeurozoneeconomicclimateremainsverydifficultatbest.However,thebankiswellpositioned to tackle the year ahead and remains verymuchopenforbusiness.

I would like to take this opportunity to thank theBoardofDirectors,ManagementandStaffofthebankfortheirhardwork,loyaltyandcommitmentinmaking2011asuccessfulyear.TheHSBCMaltateamremainsthebank’sgreatestassetandkeydifferentiation.

I thankourShareholders for theirongoingsupportand our customers for their continued trust in ourorganisation.

With a clear strategy and a very strong globalparent,IamconfidentthatwecanbuildonourbusinessinMaltain2012.

AlbertMizzi,Chairman 24February2012

Chairman’s Statement (continued)

4

H S B C B A N K M A L T A P . L . C .

5

H S B C B A N K M A L T A P . L . C .

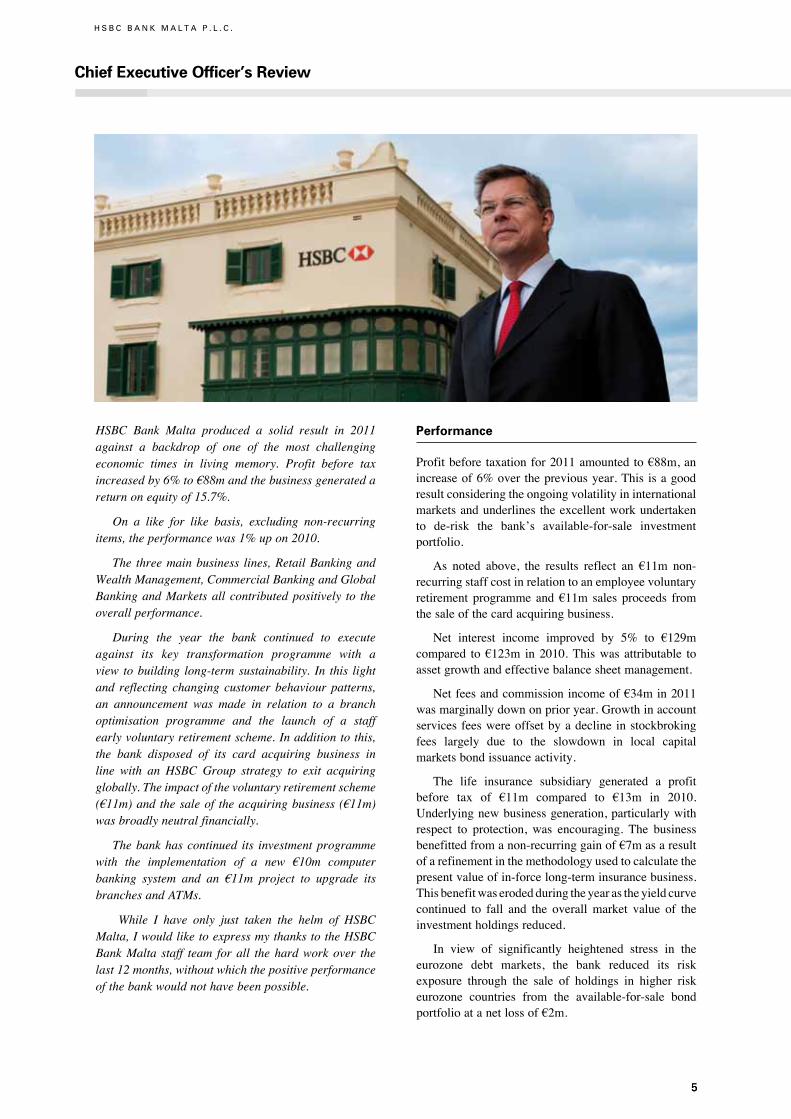

Chief Executive Officer’s Review

HSBC Bank Malta produced a solid result in 2011against a backdrop of one of the most challengingeconomic times in living memory. Profit before taxincreasedby6%to§88mandthebusinessgeneratedareturnonequityof15.7%.

On a like for like basis, excluding non-recurringitems,theperformancewas1%upon2010.

The threemainbusiness lines,RetailBankingandWealthManagement,CommercialBankingandGlobalBankingandMarketsall contributedpositively to theoverallperformance.

During the year the bank continued to executeagainst its key transformation programme with aview tobuilding long-termsustainability. In this lightand reflecting changing customerbehaviourpatterns,an announcement was made in relation to a branchoptimisation programme and the launch of a staffearlyvoluntaryretirementscheme.Inadditiontothis,the bank disposed of its card acquiring business inline with an HSBC Group strategy to exit acquiringglobally.Theimpactofthevoluntaryretirementscheme(§11m)and thesaleof theacquiringbusiness(§11m)wasbroadlyneutralfinancially.

Thebankhascontinued its investmentprogrammewith the implementation of a new §10m computerbanking system and an §11m project to upgrade itsbranchesandATMs.

While I have only just taken the helm of HSBCMalta,IwouldliketoexpressmythankstotheHSBCBankMalta staff team forall thehardworkover thelast12months,withoutwhichthepositiveperformanceofthebankwouldnothavebeenpossible.

Performance

Profitbefore taxationfor2011amountedto§88m,anincreaseof6%over thepreviousyear.This isagoodresultconsideringtheongoingvolatilityininternationalmarketsandunderlines theexcellentworkundertakento de-risk the bank’s available-for-sale investmentportfolio.

As noted above, the results reflect an §11m non-recurringstaffcostinrelationtoanemployeevoluntaryretirement programme and §11m sales proceeds fromthesaleofthecardacquiringbusiness.

Net interest income improved by 5% to §129mcompared to§123m in2010.Thiswas attributable toassetgrowthandeffectivebalancesheetmanagement.

Netfeesandcommissionincomeof§34min2011wasmarginallydownonprioryear.Growthinaccountservicesfeeswereoffsetbyadecline instockbrokingfees largely due to the slowdown in local capitalmarketsbondissuanceactivity.

The life insurance subsidiary generated a profitbefore tax of §11m compared to §13m in 2010.Underlyingnewbusinessgeneration,particularlywithrespect to protection, was encouraging. The businessbenefittedfromanon-recurringgainof§7masaresultofarefinementinthemethodologyusedtocalculatethepresentvalueofin-forcelong-terminsurancebusiness.Thisbenefitwaserodedduringtheyearastheyieldcurvecontinued to fall and the overallmarket value of theinvestmentholdingsreduced.

In view of significantly heightened stress in theeurozone debt markets, the bank reduced its riskexposure through the sale of holdings in higher riskeurozone countries from the available-for-sale bondportfolioatanetlossof§2m.

5

Netotheroperatingincomeincreasedsignificantly,from§5min2010to§24min2011.Therisewasdrivenbytheabovenotedsaleofthecardacquiringbusinessand the non-recurring gain in the Life insurancesubsidiaryrelatingtoamethodologychange.

Operating expenses of §98m were §11m or 12%higher compared to the previous yearwith a cost-to-income ratio of 50.4% compared to 49.7% in 2010.Costsincreasedprincipallyduetothepreviouslynotedemployeevoluntaryretirementprovisionof§11mandduetohighercostsrelatingtoutilities,regulatoryfeesandcompliance.

Ataconsolidatedlevel,netimpairmentsrosefrom§5m to §8m in 2011. This was principally due to a§4mprovisiontakenonGreekGovernmentbondsheldby the Life insurance subsidiary. The Life insurancesubsidiaryexposuretoGreekdebtiscurrentlyminimalandstandsat§2m.

Other than the above exposure and investments inMalteseGovernmentdebt, thegrouphasnoexposuretosouthernEuropeangovernmentdebt.

Thegroup’savailable-for-saleinvestmentsportfolioremainswelldiversifiedandconservative.

At a bank level, while there was a marginaldeterioration in non-performing loans from 4% to5%, in general asset quality remains good and loanimpairments declined to §4m (11 basis points of theoverallloanbook)against§5min2010.

Net loansandadvances to customers increasedby§54m to §3,344m. Mortgage market share remainedstable. Gross new lending to customers amounted to§656mwhichreflects thebank’scontinuedsupport tothelocaleconomy.

Liabilitiesroseby§142mduringtheyearandstoodat§5,458mat theyearend.The increase in liabilitiesreflectedariseinplacementswiththebankandasmallfallincustomerdeposits.

Thebank’sliquiditypositionremainsstrongwithanadvancestodepositsratioof76%,comparedwith74%at31December2010.

The bank strengthened its capital ratio by 140basis points during the year and this now stands at11.6%. This is well in excess of the 8% minimumregulatory requirement. The bank intends tomaintainaconservativeapproachtocapitalandwillcontinuetobuildcapitalwhereappropriate.

Basedon theresults theBoard is recommendingafinalgrossordinarydividendof7.2centpershare.

Retail Banking and Wealth Management

During2011,RetailBankingandWealthManagementcontinued to provide customerswith the high qualityservice and brand experience for which HSBC isrenowned.

The focus in Premier was to deepen existingrelationships with our valued customer base. During2011thenewLifeStageToolwaslaunchedtoprovidecustomers with a user friendly way tomap their lifestages and wealth management needs against theproductsandservicesofferedbyHSBC.Furthermore,anexcitingrangeofnewdiscountsandprivilegesweremadeavailabletoPremiercustomersandbenefitswereextendedtofamilymembers.

Thebank’sFinancialPlanningAdvisorsandPrivateClient Managers have access to an unrivalled rangeof both HSBC and third party investment solutionsincluding life protection and retirement planning. In2011,inviewofthevolatileglobalmarkets,thefocuswasondevelopingstructuredinvestmentproductsthatprovide capital protection to give customers peace ofmind.

HSBC’s Trust business continues to provide ahighly bespoke service to our customer base. Groupreferralsfromotheroverseasofficesremainspositive.

Shareshop provides access to international stockexchanges and facilitates the buying and selling ofbondsandequitiesforourretailcustomers.

The bank remains very active in the domesticmortgage sector and during 2011 saw a growth inbusiness both from first time buyers and those whowerelookingforasecondproperty.

HSBCGlobalAssetManagementMaltahadanothersolid year despite difficult market conditions. Thebusiness registered stable performance in the levelof assets under management driven by institutionalbusinessandretailfunds.

Underlying insurance sales, particularly relatingto protection, were strong. The overall result of thebusiness,however,washamperedbymarketvolatilityonitsinvestmentportfolioalthoughthiswasoffsetbybeneficialchangesinthemethodologyforrecognisingtheemergenceofinsurancemanufacturingprofits.

HSBC Insurance Management Services (Europe)Limitedwasestablishedtocarryoutregulatedinsurancemanagement activities for otherHSBCentities acrossthe wider Group. In addition to support our ownlocal insurance manufacturing business, insuranceadministration services are already being provided toHSBCLife (Europe)LtdoperatingoutofDublinandZurich.

Chief Executive Officer’s Review (continued)

6

H S B C B A N K M A L T A P . L . C .

an important tradingroutebetweenEuropeandNorthAfrica,gaininghugelyfromitslocationwithinEuropeandalsoitsproximitytothekeymarketsoftheMiddleEast.

TwosuccessfulHSBCTradeSummitswereheldinShanghaiandHamburgandwereattendedbyanumberof key customers from Malta with an internationalfocus. Feedback from the events was very positiveandenabledthecustomersconcernedtonetworkwithpotentialclientsandsuppliersfromaroundtheworld.

For thesecondconsecutiveyear,HSBCsponsoredthe European Business Awards. Malta InternationalAirportplc andCamilleriHoldingsLtdwonaRuband’Honneur prize and represented the very best ofMaltesebusinessesattheevent.

For our small and medium local businesses welaunched the Knowledge Centre information facility,a free resource, offering our business customerspracticalinformationtohelprunorstartanewventure.Our Business Banking Direct proposition was alsointroduced to highlight the bank’s online and callcentrecapabilitiesforsmallerbusinesses.

In 2011, a group of bank “business advisors”coached a Young Enterprise team. The youngentrepreneursinvolvedwentontowintheMaltaFinalsandsubsequentlyparticipate in theEuropeanfinals inOslo,Norway.

Global Banking and Markets

Despiteincreasingfinancialstressacrosstheeurozone,GlobalBankingandMarketshascontinued todeliverabove plan results. This has been achieved throughprudent management of the bank’s investments andmarkets risks, whilst also re-positioning all businessunitstoplayaleadingroleindrivingMalta’sgrowthasahubforinternationalfinancialservices.

Fromaninsuranceregulatoryperspective,workonSolvencyIIimplementationcontinueswithsignificantprogressmadeonallaspectsofadoptingthefutureriskbasedmethodologies.

Commercial Banking

TheCommercialBankingbusinessdelivered a strongperformanceduring2011inspiteoftheglobaleconomicheadwinds and political turmoil inNorthAfrica. Thelendingbookremainshealthyandwellsecuredandthe2012pipelineispositive.

Customer service remains a key focus of thecommercialbankingstrategy.Duringtheyearwehaveremained close to our customers to better understandtheir requirements and to provide them with supportwhere necessary in an increasingly challengingeconomicenvironment.

During 2011 we continued to concentrate onthe Leading International Business strategy. This isprovingtobeaverysuccessfulpartofourcommercialbanking business.We have participated in a numberof business delegations and overseas networkingevents leveraging HSBC’s international reach. Apartner support agreementwas signedwith theMaltaChamber of Commerce, Enterprise and Industry tohelpthoseenterpriseswantingtoexpandtheirbusinessinternationally.AnagreementwasalsosignedwiththeMaltese-Chinese Chamber of Commerce to supportentrepreneurs from both countries. This follows thelaunch of theRenminbi trade settlement account thatestablishedHSBCasthefirstbankinMaltatoenableMaltese companies to directly trade in the Chinesecurrency, thus facilitating trade and investment withChinesecounterparts.

The HSBC Trade Connections quarterly forecastanticipates that trade inMalta will continue to growover thenext12months.Malta isexpected toremain

7

HSBC Bank Malta together with the the British High Commission Malta hosted an event for British Foreign Secretary Rt Hon. William Hague to meet members of local British Business Forum during a one-day visit to Malta on his way to Libya.

8

H S B C B A N K M A L T A P . L . C .

Overall, theGlobalBanking andMarkets businesshas become an important contributor to the bank’sbottomlineandplaysapivotalroleintheimplementationofourstrategy.

Technology and Services

During2011webroughttofruitionvarioustechnologicaland services projects with the aim of enhancingcustomerexperience,improvingoperationalefficiency,andreducingoperationalcosts.

Thebiggestsingleinitiativein2011wastheupgradeofourcorebankingcomputersystemwithaninvestmentofover§10m.ThisnewHSBCGroupsystemenabledus to standardise our banking systems, our processesand our products to meet the ever-changing needs ofour customers, and to make it easier for them to dobusiness with the bank from anywhere in the world.The implementation of this project was carried outseamlesslyandefficientlywithoutaffectingthenormaldailyservicestoourcustomers.

Investmentswerealsomadeinworkflowprocessesand imaging systems, whilst further standardisedprocessesweremigratedtoGroupandRegionalCentresof Excellence, thereby enabling the bank to improveinternalefficiencyandfreemoreresourcesforutilisationinmoreprofitableareas.

We have continued our branch refurbishingprogrammeandcompletedanotherfivebranchestoaddtothefourrenovatedin2010.ThesebranchesarenowinlinewiththehighestHSBCGroupstandardsaroundtheworldandreflectthechangingbehaviourpatternofourcustomerswhoincreasinglylookformortgageandwealth management advice in branches but prefer totransacteitheronlineorthroughoneofourcallcentres.

InkeepingwithHSBCGroup’spolicyofpro-activerisk management, the Global Markets team sold thebank’sinvestmentsinperipheralEuropeandebtduringthe year. The current book of high quality assets hasbenefittedfromtheanticipated‘flight toquality’.Thishas resulted in a positive adjustment to reserves. Theadoptionofaprudentinvestmentapproachandtheuseof sophisticated risk management techniques boostednetinterestincomein2011.

TheGlobalMarkets teamhas seena40% increasein foreignexchangeactivity as it leverages theHSBCGroup’sglobalnetworktoprovidebestinclassservicestoourinternationalcorporateandinstitutionalcustomers.Wehavealsoseenasignificantincreaseinthesalesofcapitalprotected investmentproducts, tailored tomeetour retail customers’ needs, in partnershipwithRetailBankingandWealthManagement.HSBCStockbrokerscontinues to be the largest broker on theMalta StockExchange.

InordertosupportthegrowthofthefinancialservicessectorinMaltaandtoprovideanattractivepropositiontofinancialinstitutionssettinguporrelocatingtoMalta,we established a dedicated Financial Institutions teamduring the year. The team is comprised of both localandinternationalstaffandoffersmarketleadingadviceand services. Coupled with this initiative the fundadministration and custody business was restructuredtodrivehigher customer service levels and toprepareforanincreasinglychallenginginternationalregulatoryenvironment.

HSBC Securities Services (HSS) made goodprogressduring theyearandgeneratedaprofitbeforetaxof§1.5m.HSSremainsakeyarea for investment.Wehavelaunchedagovernanceprogrammetooverseea number of significant initiatives to enhance theinternationalpropositionofthebusiness.

Chief Executive Officer’s Review (continued)

HSBC Malta is investing §11 million to upgrade its branches and ATMs. The new branches are designed to give more privacy and space to customers visiting HSBC to plan their financial future and manage their wealth.

9

Outlook

TheMaltese economy has performed reasonablywellover the last twelvemonths and showed considerableresiliencesincetheglobaltroublesbeganinlate2008.The economy has registered above-average EU andeurozone GDP growth in both 2010 and 2011. Thebankingsystemremainsrobustandtheeconomyhasnotsufferedfromahousingorsovereigndebtcrisis.

GDPgrowthislikelytoremainpositivein2012butlowerthan2011.Thecontinuedtravailsoftheeurozoneand economic uncertainty will weigh on confidence.Bank and domestic corporate profitabilitywill remainunder pressure and companies will focus on drivingoperational efficiencies and sustainable costs savingswhile real growth is hard to achieve. Nevertheless,we remain cautiously optimistic as the key banksin the market remain well capitalised and open forbusiness,touristnumberscontinuetogrow,thehousingmarket while soft has not declined significantly, thelocal regulatory atmosphere is pro-business and realgrowth and opportunity is seen asMalta develops itsinternationalfinancialservicesplatform.

HSBCBankMalta remainswellpositioned for thechallengingyearahead.Thebalancesheetisstrong,thestrategy is clear and key transformation programmesarewellunderway.Thefocuswillremainoninvestinginour local franchise and leveragingour internationalcompetitive advantage through our parent, HSBCHoldings, one of the world’s largest and strongestfinancialorganisations.

MarkWatkinson,ChiefExecutiveOfficer24February2012

A Commercial Banking Contact Centre wasestablished during the year to provide a high qualityand efficient telephone service to our commercialcustomers.

Another important initiative was the upgrade andincreaseofourATMnetworkacrosstheisland.Atotalof 14next-generationATMswere installed invariouslocalities, offering instant value for cash deposits tocustomers, with cheque deposit functionality to beprovidedlaterin2012.

Customerbehaviourischanging.During2011telleractivityinourbranchnetworkdroppedby14%whilsttheuseofInternetBankingincreasedby13%andcardusageatpointofsaleby11%.Itis,therefore,importantthatwecontinuetoinvestinprovidingmoreandbetterself-service facilities to satisfy the changing needs ofourcustomers.

Asaresultofbetterpropertymanagement,thebankdisposed of vacant freehold and leasehold propertiesincluding a significant part of its ex-Head Office inRepublicStreet,Valletta.

People

Our people remain our greatest strength and it needsto be recognised that only through our talented andprofessionalworkforcecouldourgoodresults in2011havebeenachieved.

During2011wesignednewCollectiveAgreementsthatprovideforimprovedworkingconditions,benefitsandopportunitiesforallstaff.

Wecontinuetoinvestinourpeoplethroughtraining,professionaldevelopmentandtalentmanagement.

A number of staff benefitted from overseasprogrammesrunbytheHSBCGroupandwecontinueto look for and promote international attachment/secondmentopportunitiesforkeytalent.

AsInotedearlier,duringtheyearthebankannouncedanearlyvoluntaryretirementschemeforitsemployeesas part of the continued transformation programmeof the business. Such programmes remain entirelyvoluntarybutattheoptionofthebank.

In 2012 we will continue to introducemore staff-related initiatives and invest to maintain the higheststandardsofprofessionalism.

10

H S B C B A N K M A L T A P . L . C .

Board of Directors

10

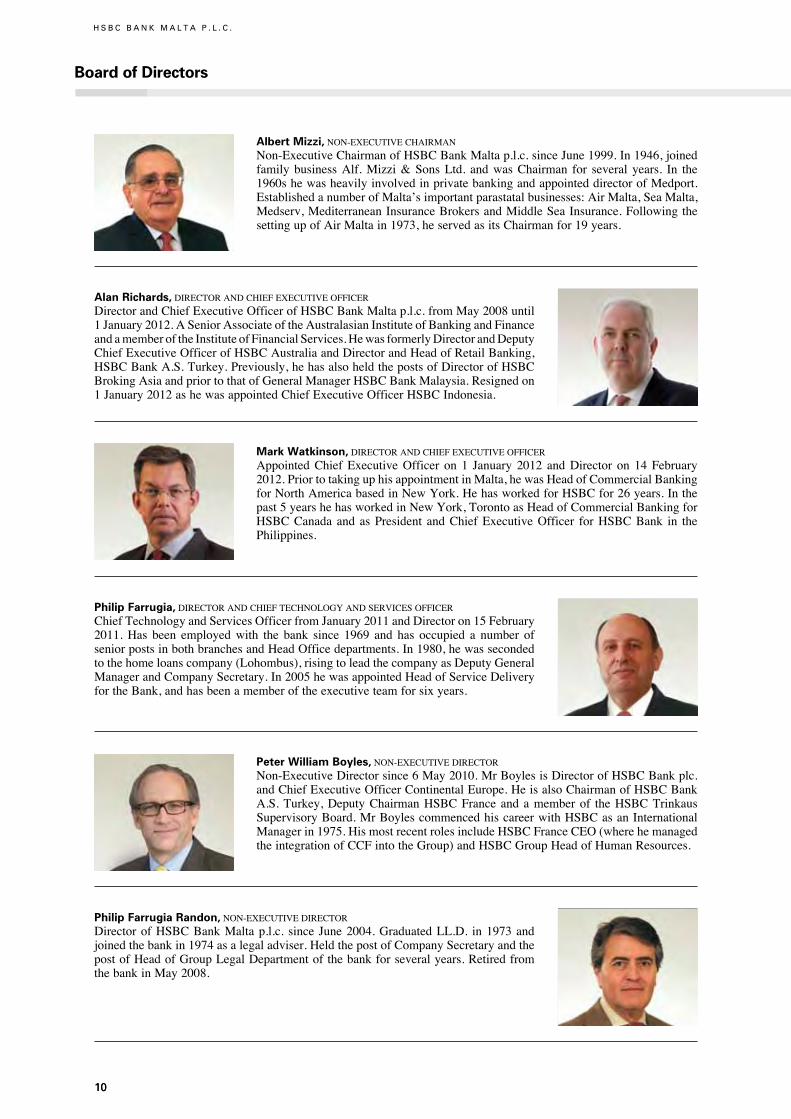

Albert Mizzi,NON-EXECUTIVECHAIRMAN

Non-ExecutiveChairmanofHSBCBankMaltap.l.c.sinceJune1999.In1946,joinedfamily businessAlf.Mizzi&SonsLtd. andwasChairman for several years. In the1960shewasheavilyinvolvedinprivatebankingandappointeddirectorofMedport.EstablishedanumberofMalta’simportantparastatalbusinesses:AirMalta,SeaMalta,Medserv,MediterraneanInsuranceBrokersandMiddleSeaInsurance.FollowingthesettingupofAirMaltain1973,heservedasitsChairmanfor19years.

Mark Watkinson,DIRECTORANDCHIEFEXECUTIVEOFFICERAppointedChiefExecutiveOfficer on 1 January 2012 andDirector on 14February2012.PriortotakinguphisappointmentinMalta,hewasHeadofCommercialBankingforNorthAmericabasedinNewYork.HehasworkedforHSBCfor26years.Inthepast5yearshehasworkedinNewYork,TorontoasHeadofCommercialBankingforHSBCCanada and asPresident andChiefExecutiveOfficer forHSBCBank in thePhilippines.

Peter William Boyles,NON-EXECUTIVEDIRECTORNon-ExecutiveDirectorsince6May2010.MrBoylesisDirectorofHSBCBankplc.andChiefExecutiveOfficerContinentalEurope.HeisalsoChairmanofHSBCBankA.S.Turkey,DeputyChairmanHSBCFranceandamemberof theHSBCTrinkausSupervisoryBoard.MrBoylescommencedhiscareerwithHSBCasanInternationalManagerin1975.HismostrecentrolesincludeHSBCFranceCEO(wherehemanagedtheintegrationofCCFintotheGroup)andHSBCGroupHeadofHumanResources.

Alan Richards,DIRECTORANDCHIEFEXECUTIVEOFFICERDirectorandChiefExecutiveOfficerofHSBCBankMaltap.l.c.fromMay2008until1January2012.ASeniorAssociateoftheAustralasianInstituteofBankingandFinanceandamemberoftheInstituteofFinancialServices.HewasformerlyDirectorandDeputyChiefExecutiveOfficerofHSBCAustraliaandDirectorandHeadofRetailBanking,HSBCBankA.S.Turkey.Previously,hehasalsoheldthepostsofDirectorofHSBCBrokingAsiaandpriortothatofGeneralManagerHSBCBankMalaysia.Resignedon1January2012ashewasappointedChiefExecutiveOfficerHSBCIndonesia.

Philip Farrugia,DIRECTORANDCHIEFTECHNOLOGYANDSERVICESOFFICERChiefTechnologyandServicesOfficerfromJanuary2011andDirectoron15February2011.Has been employedwith the bank since 1969 and has occupied a number ofseniorpostsinbothbranchesandHeadOfficedepartments.In1980,hewassecondedtothehomeloanscompany(Lohombus),risingtoleadthecompanyasDeputyGeneralManagerandCompanySecretary.In2005hewasappointedHeadofServiceDeliveryfortheBank,andhasbeenamemberoftheexecutiveteamforsixyears.

Philip Farrugia Randon,NON-EXECUTIVEDIRECTORDirectorofHSBCBankMaltap.l.c. since June2004.GraduatedLL.D. in1973andjoinedthebankin1974asalegaladviser.HeldthepostofCompanySecretaryandthepostofHeadofGroupLegalDepartmentofthebankforseveralyears.RetiredfromthebankinMay2008.

11

Charles John Farrugia,NON-EXECUTIVEDIRECTORDirectorofHSBCBankMaltap.l.c.sinceNovember2004.Joinedthebankin1975.Was appointedChiefDealer in 1995,Group Senior TreasuryManager in 1999 andManagingDirectorofHSBCStockbrokers(Malta)Limitedin2001.HeldthepostofHeadofGlobalBanking andMarkets ofHSBCBankMalta p.l.c. for several years.RetiredfromthebankJanuary2010.

Saviour sive Sonny Portelli,NON-EXECUTIVEDIRECTORAppointedDirector ofHSBCBankMalta p.l.c. on9October 2006.MrPortelli is aseniorMaltesebusinessmanwhoiscurrentlytheChairmanofTheMaltaCouncilforEconomicandSocialDevelopment.MrPortellihadanearlycareerintheMaltaCivilServicewhichhelefttojointheTouristSector.BesidesbeingaMarketingSpecialisthesitsasnon-executivedirectorontheboardsofvariousMaltesecompanies.

George Brancaleone,COMPANYSECRETARY

CompanySecretaryofHSBCBankMaltap.l.c. since June2004. Joined thebank in1980andgraduatedLL.D.in1988.CompanySecretaryofvariousHSBCsubsidiariesinMaltasince2001.PresentlyholdsthepostofSeniorManageratAudit,ComplianceandLegalDepartmentofHSBCBankMaltap.l.c.

Peter Paul Testaferrata Moroni Viani,NON-EXECUTIVEDIRECTORNon-ExecutiveDirectorofHSBCBankMaltap.l.c.sinceMarch2001.HoldsvariousexecutivepositionsanddirectorshipswithintheTestaferrataGroupofcompanies.

James Dunbar Cousin,NON-EXECUTIVEDIRECTORAppointed Director of the Bank on 1 April 2009. Joined Barclays Bank D.C.O. in1968.OccupiedvariousmanagerialroleswithinthebranchnetworkofMid-MedBankLtd. Subsequently, he occupied the roles of Executive Manager and later Head ofCommercialBankingofthebank.MrDunbarCousinretiredfromthebankattheendof2008.

12

H S B C B A N K M A L T A P . L . C .

Financial Review

Summary of Financial Performance

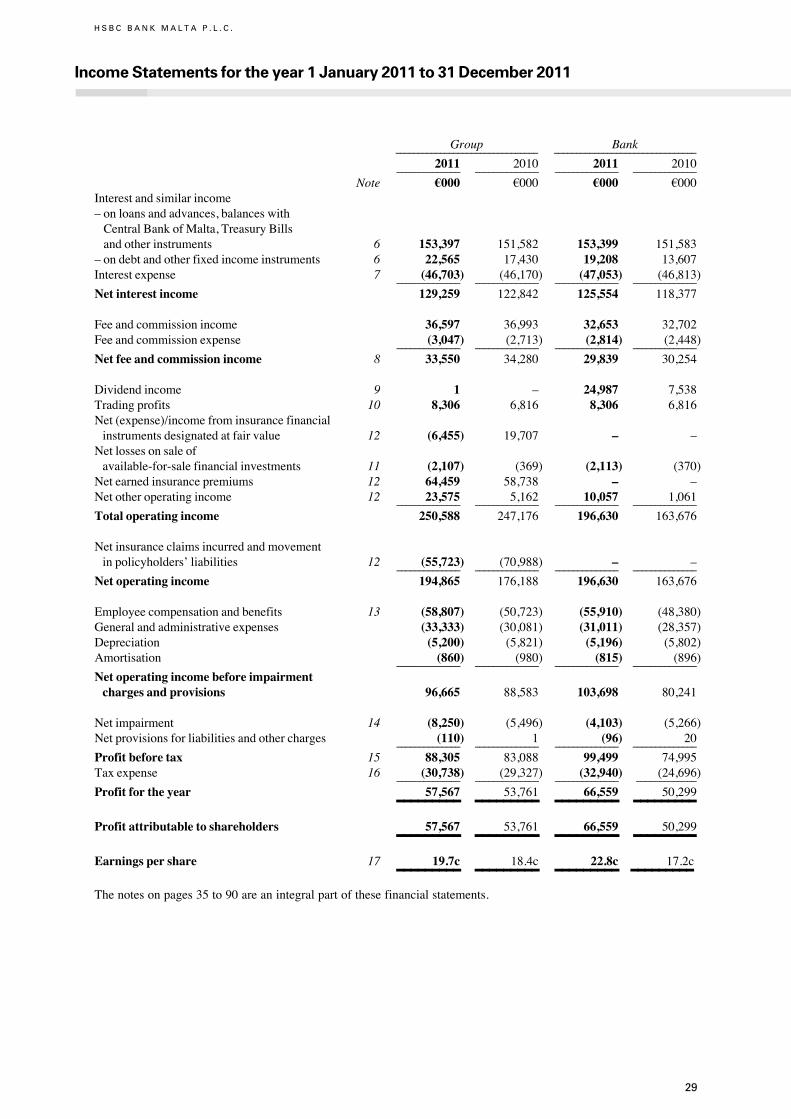

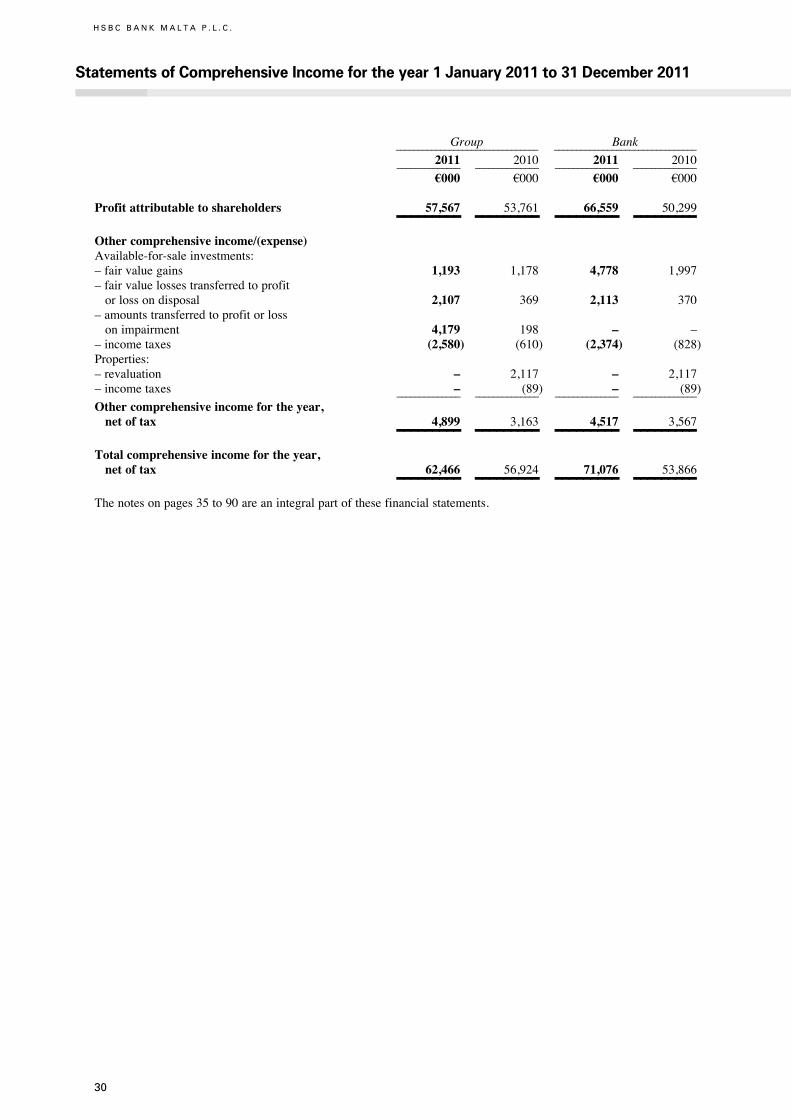

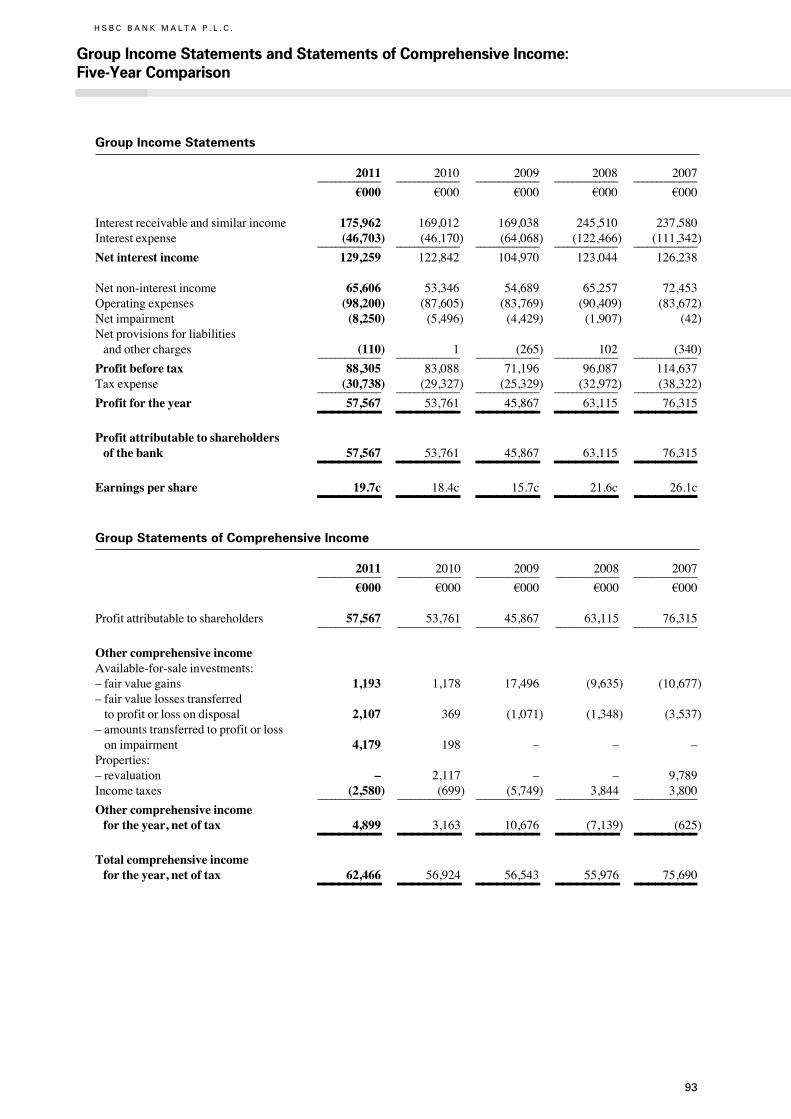

Group profitAgainst a backdrop of very challenging economicconditionsinEurope,HSBCBankMaltap.l.c.deliveredagoodperformancein2011.Thereportedprofitbeforetaxof§88mincreasedby6%,or§5mcomparedto2010drivenprimarilybyanimprovedlevelofrevenues.

Profit attributable to shareholders was §58m, anincreaseof§4moverprioryearfigure.

Netoperatingincomeof§195mincreasedby§19mcompared with §176m in 2010. Net interest incomeincreasedby§6mto§129m.

Operating expenses were §98m, an increase of§11m over prior year but this included restructuringcostsof§11m.

Thegroup’scosttoincomeratiois50.4%comparedtoaprioryearratioof49.7%.

Shareholder ratiosEarningspershareof19.7centcomparedto18.4centforthesameperiodin2010,withthepre-taxreturnonshareholders’ funds at 24.1% compared to 24.9% in2010.

The Directors propose a final gross dividend of7.2 cent per share. This follows on the gross interimdividendof8.2centpaidinAugust2011.

Net interest incomeNetinterestincomeimprovedby5%to§129mcomparedto §123m last year attributable to asset growth andeffectivebalancesheetmanagement.However,liabilitymargins remain under pressure given the low interestrateenvironment.

Non-interest incomeNon-interestincomeincreasedsignificantlyfrom§53min 2010 to §66m in 2011 benefiting from net gainsof §10m arising from the sale of our card acquiringbusiness toGlobalPayments Incand increase in lifeinsurancepresentvalueofin-forcelong-terminsurancebusiness. Underlying performance of the bank’s corebusinessremainedsatisfactorygiventhevolatilemarketconditionswith investmentactivity impactedbyweakinvestorsentiment.

Netfeesandcommissionincomeof§34min2011was marginally down on 2010. Growth in accountservicesfeeswereoffsetbyadecline instockbrokingfees largely due to the slow-down in local capitalmarketsbondissuanceactivity.

Trading profits of §8m increased by 22% or §1mcomparedto§7min2010duetogoodgrowthinforeignexchangevolumes.

The second half of 2011 was dominated bythe continuing volatility in the global markets andspecificallythesignificantdeteriorationintheeurozonesovereign crisis.Thebank anticipated this in the firsthalf of the year and positioned the balance sheet tosignificantlyreducemarketriskatanetlossof§2masat31December2011.

The life insurance subsidiary generated a profitbefore tax of §11m compared to §13m in 2010.Underlying new business performance generationparticularlywithrespecttoprotectionwasencouraging.The business benefited from a non-recurring gain of§7m as a result of a refinement in the methodologyusedtocalculatethepresentvalueofin-forcelong-terminsurancebusiness.Thisbenefitwaserodedduringtheyearas theEuroswapcurvecontinuedtofallandtheoverallmarketvalueofinvestmentholdingsreduced.

Operating expensesOperatingexpensesof§98mwere§11mor12%highercompared to the previous yearwith a cost to incomeratio of 50.4% compared to 49.7% in 2010. Costsincreased,principallyduetostaffvoluntaryretirementscheme provision of §11m reported in Employeecompensation and benefits and due to higher costsrelatingtoutilitiesandcompliancecosts.

General and administrative expenses increased by§3m to §33m as a result of investment in channelmigration,offshoring,improvingsystemsaswellasthecostofhigherutilitiesandcompliancecosts.

Depreciation and amortisation charges of §6mdecreasedby§0.7mcomparedtothepreviousyear.

Net impairment Netimpairmentof§8mincludedanimpairmentof§4mrelating to the available-for-sale Greek governmentbondsheldbytheLifeinsurancesubsidiary.

At a bank level, while there was a marginaldeteriorationinnon-performingloansfrom4%to5%,thegeneralassetqualityremainsgoodandimpairmentsdeclinedto§4m(11basispointsofoverallloanbook)against§5min2010.

Impairment reversals contributed §5m toprofitability.Newimpairmentallowancesof§7mwereraisedandbaddebtwrite-offsof§1mwereeffected.

13

TaxationThe2011effectiverateoftaxwas34.8%percent.Taxexpensefor2011amountedto§31m.

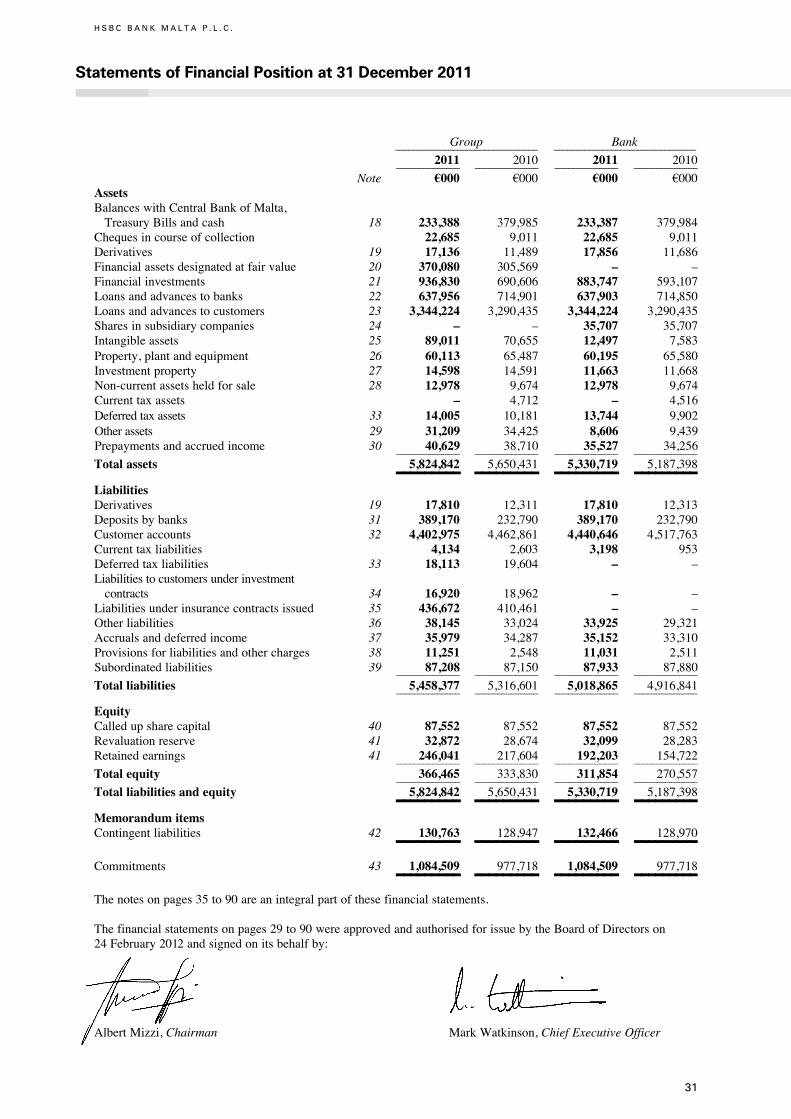

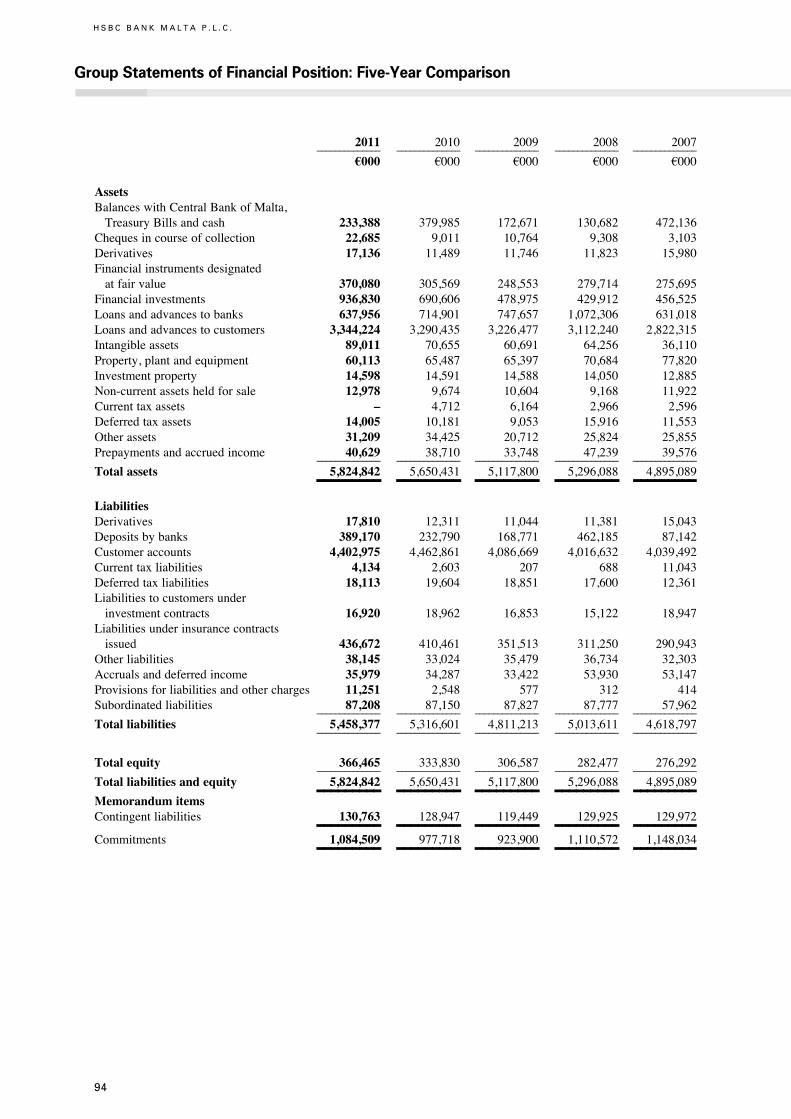

AssetsTotal assetsamounted to§5,825m,3%higher thanat31December2010.Themainincreaseswerereportedin debt securities investments as part of the bank’sliquiditymanagement.

BalanceswithCentralBankofMalta,TreasuryBillsandcashholdingsreducedfromaprioryearendlevelof§380mtoayearendlevelof§233m.

Net loansandadvances tocustomers increasedby§54m to §3,344m supportedmainly by growth in thepersonalsector.

The bank’s liquidity position remains strong withadvances todeposit ratioof76%comparedwith74%at31December2010.

The balance sheet remains well diversified andconservative with negligible exposure to sovereigndebtintheperipheraleurozonecountriesfollowingthesaleofholdings in thehigher risk eurozonecountriesduring2011.

The available-for-sale investment portfolioincreasedby§246mto§937m.Afairvaluegainof§1mwasreportedduringtheyear.Themark-upwascreditedtorevaluationreserve,netoftax.

Life insurance business assets, are primarilydesignated as financial assets at fair value throughprofit or loss. This portfolio increased by §64m to§370mfromaprioryearendlevelof§306m.

LiabilitiesTotal liabilities increased by §142m to §5,458m atyearend.The increase in liabilities reflecteda rise inplacementswiththebankandasmallfallincustomerliabilities.

Customer deposits of §4,403mas at 31December2011reducedby§60mcomparedto31December2010reflecting the levels of volatility of deposits from theinstitutionalsector.Retaildepositswerebroadlystabledespite continuing competitive pressures for depositsincludingfromlocalgovernmentbondissuances.

Funds undermanagement by the group reached ayearendclosinglevelof§694million.

Liabilities under insurance contracts issuedincreasedby§26mduringtheyeartoreachayearendlevelof§437m.

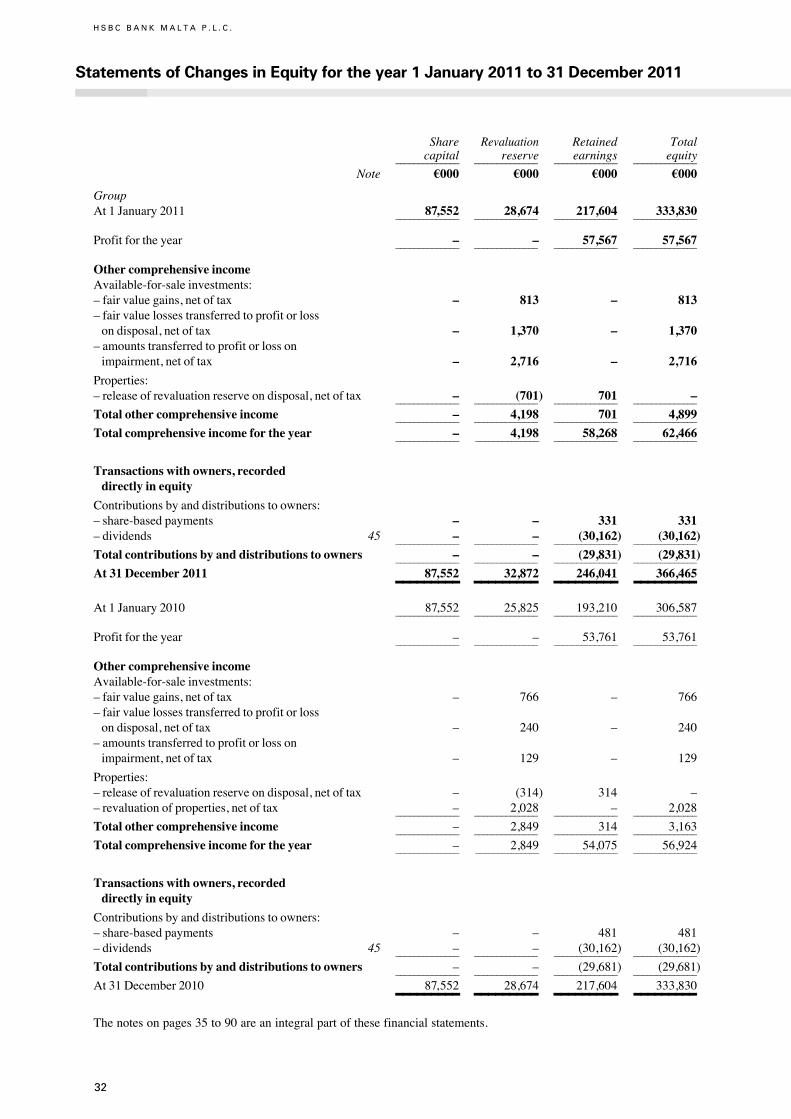

Shareholders’ fundsEquity totaled §366m at year end following dividendpaymentsof§30mduring2011.

The number of shareholders as at 31 December2011stoodat10,366.

Thecapitaladequacyratioat11.6%iswellaboveregulatorycapitalrequirements.

14

H S B C B A N K M A L T A P . L . C .

Report of the Directors

Results for 2011

Thegroup reportedaprofitonordinaryactivitiesbefore taxof§88mfor theyearunder review.Thegroup’sprofitattributabletoshareholdersofthebankwas§58m.

Agrossinterimordinarydividendof8.2centwaspaidon24August2011.TheDirectorshaveproposedagrossfinaldividendof7.2centperordinaryshare.Thefinaldividendwillbepayabletoshareholdersonthebank’sregisterasat19March2012.

Furtherinformationabouttheresultsisprovidedinthegroupincomestatementandthestatementofcomprehensiveincomeonpages29and30.

Principal activities

Principal activities of parent companyThebankisauthorisedtocarryonthebusinessofbankingunder theBankingAct,1994asacredit institution.It isalsoanauthoriseddealerintermsoftheExchangeControlActandalicensedfinancialintermediaryintermsoftheFinancialMarketsAct,1990.ThebankalsoholdsCategory3andCategory4InvestmentServiceslicensesissuedbytheMaltaFinancialServicesAuthorityintermsoftheInvestmentServicesAct,1994.Theselicensesauthorisethebanktoprovidebothinvestmentservicestothirdpartiesandtrusteeorcustodianservicesforcollectiveinvestmentschemes.

Thebankprovidesacomprehensiverangeofbankingandfinancialrelatedservices.

Thegrouphadthefollowingsubsidiariesat31December2011:HSBCLifeAssurance(Malta)Ltd,HSBCGlobalAssetManagement(Malta)Limited,HSBCSecuritiesServices(Malta)Limited,HSBCStockbrokers(Malta)LimitedandHSBCInsuranceManagementServices(Europe)Limited.

Principal activities of subsidiariesHSBCLifeAssurance (Malta)Ltd is authorised by theMaltaFinancial ServicesAuthority to carry on business ofinsurance inMaltaunder the InsuranceBusinessAct,1998.HSBCBankMaltap.l.c. isenrolledasa tied insuranceintermediaryforHSBCLifeAssurance(Malta)LtdundertheInsuranceIntermediariesAct2006.On28April2011,HSBC Life established a new subsidiary HSBC InsuranceManagement Services (Europe) Limited with the mainobjectiveofprovidingoperationalsupporttoHSBCGroupInsuranceCompanies.IthasalreadyenteredintotwoformalagreementsfortheprovisionofinsuranceoperationalandadministrativeservicestoHSBCLifeAssurance(Malta)LtdandHSBCLife(Europe)LtdbasedinDublin.Beyondthesetwoinitialappointments,thiscompanywillbemarketedwithintheHSBCGroupasaCentreofExcellenceforInsuranceOperationalsupportandadministrativeservicesseekingsimilarappointmentsfromotherGroupInsuranceCompanies.

HSBCGlobalAssetManagement (Malta)Limited is the investmentmanagementarmof thebank. Itmanagesarangeofdomesticand international funds,specialising in thedevelopmentofstructuredcapitalsecured investmentsproducts,andintheprovisionof tailor-madediscretionaryportfoliomanagementservices.ThecompanyoffersbothOpenandCloseendedtypesoffundsandinvestments.

HSBCSecuritiesServices(Malta)LimitedislicensedundertheInvestmentServicesAct,1994anditsmainbusinessactivityistheprovisionoffundadministrationservicestoproprietaryandthirdpartyinvestmentfunds.Italsoprovidesbackofficesupport toHSBCBankMaltap.l.c. in thedistributionof thirdparty investment funds through thebanknetwork.

HSBC Stockbrokers (Malta) Limited is a member of the Malta Stock Exchange and is regulated under theInvestment ServicesAct, 1994 by theMalta Financial ServicesAuthority. The company is principally engaged inprovidingstockbrokingbusinessontheMaltaStockExchangeandtoarrange/supportthelistingofstocksandsharesontheExchange.

Business review

Areviewofthebusinessofthebankanditssubsidiariesduringtheyearunderreviewandanindicationoflikelyfuturedevelopmentsaregiveninthe‘ChiefExecutiveOfficer’sReview’onpages5to9.

Shareholder Register Information

Directors’interestinthesharecapitalofthecompanyorinrelatedcompaniesat31December2010:

AlbertMizzi 8,000sharesSavioursiveSonnyPortelli 4,860sharesPhilipFarrugiaRandon 6,400shares

MrCharlesJohnFarrugiahasanon-beneficialinterestof7,511,587ordinarysharesinHSBCBankMaltap.l.c.through the shareholding held by Amalgamated Investments Sicav p.l.c. and a non-beneficial interest of 15,000ordinarysharesthroughtheshareholdingheldbyIndustrialManagementLtd.

MrPeterPaulTestaferrataMoroniVianihasabeneficialinterestof58,800ordinarysharesinHSBCBankMaltap.l.c.throughtheshareholdingofTestaferrataMoroniViani(Holdings)Limited,40,000ordinarysharesthroughtheshareholdingofCappsLtd, 40,000ordinary shares through the shareholdingofVianiLimited and5,000ordinarysharesthroughtheshareholdingofSalesandLettingLimited.

Healsohasanon-beneficialinterestof130,680ordinarysharesinHSBCBankMaltap.l.c.throughtheshareholdingofSantumasShareholdingsp.l.c.underCustodianshipHSBCBankMaltap.l.c.

TherewerenochangestoDirectors’interestfrom31December2010to31January2011.

Shareholdersholdingfivepercent(5%)ormoreoftheequitycapitalat31January2011:

HSBCEuropeB.V. 70.03%

Numberofshareholdersat31January2011:

Oneclassofshares 10,434shareholders(Allshareshaveequalvotingrights)

15

Transactions in own shares

Thebankholdsunitsinamutualfundwhichinvestsinthebank’sshares.Duringtheyear,thebankindirectlyacquired25,838additionalownsharesbringingthetotalnumberofsharesindirectlyheldat31December2011to61,455.

Shareholder Register Information pursuant to Listing Rule 5.64

HSBCBankMaltap.l.c.(the‘bank’)authorisedsharecapitalis§141,000,000.Theissuedandfullypaidupcapitalis§87,552,000dividedinto291,840,000OrdinarySharesofanominalvalueof30.0centeach.Theissuedsharecapitalconsistsofoneclassofordinaryshareswithequalvotingrightsattachedandfreelytransferable.

HSBCEuropeB.V.holds70.03%ofthebank’sshares.

Thelargestsingleshareholderofthebank,provideditholdsatleastthirtythreepercent(33%)oftheordinaryissuedsharecapitalofthebank,shallbeentitledtoappointtheChairmanfromamongsttheDirectorsappointedorelectedtotheBoard.

Everyshareholderowningelevenpercent(11%)oftheordinaryissuedsharecapital,shallbeentitledtoappointoneDirectorforeachandeveryelevenpercent(11%)oftheordinaryissuedsharecapitalofthebankownedbysuchshareholder.AnyfractionalshareholdingnotsoutilisedintheappointmentofDirector(s)shallbeentitledtoparticipateinthevotingfortheelectionoffurtherDirectors.

There isanAchievementShares scheme inexistencewherebyemployees in theGCB3gradeandhighercanbeawardedsharesinHSBCHoldingsplc,dependingontheirperformance.Shareawardswillbereleasedtotheindividualafter3years,providedtheparticipantremainscontinuouslyemployedwithintheGroup.Duringthe3-yearperiodtheemployeehasnovotingrightswhatsoever.

TherulesgoverningtheappointmentofBoardmembersarecontainedinArticles77to80ofthebank’sArticlesofAssociation.AnextraordinaryresolutionapprovedbytheshareholdersinthegeneralmeetingisrequiredtoamendtheArticlesofAssociation.

ThepowersoftheDirectorsareoutlinedinArticles73,74and85ofthebank’sArticlesofAssociation.IntermsofArticle12ofthesaidArticlesofAssociation,thebankmay,subjecttotheprovisionsoftheCompaniesAct1995,acquireorholdanyofitsshares.

TheCollectiveAgreement regulates redundancies,early retirement, resignationor terminationofemploymentofemployees.TherearenocontractsbetweenthebankandtheDirectorsonthebank’sBoard.

Itisherebydeclaredthat,asat31December2011,therequirementspursuanttoListingRules5.64.7and5.64.10didnotapplytothebank.

Shareholder Register Information

Directors’interestinthesharecapitalofthecompanyorinrelatedcompaniesat31December2011:

AlbertMizzi 8,000sharesPhilipFarrugiaRandon 6,400sharesSavioursiveSonnyPortelli 4,700shares

MrCharles JohnFarrugiahasanon-beneficial interestof7,511,587ordinary shares inHSBCBankMaltap.l.c.throughtheshareholdingheldbyAmalgamatedInvestmentsSicavp.l.c.andanon-beneficialinterestof15,000ordinarysharesthroughtheshareholdingheldbyIndustrialManagementLtd.

MrPeterPaulTestaferrataMoroniVianihasabeneficialinterestof58,800ordinarysharesinHSBCBankMaltap.l.c. throughtheshareholdingofTestaferrataMoroniViani(Holdings)Limited,40,000ordinarysharesthroughtheshareholdingofTestaferrataMoroniVianiLimited,40,000ordinarysharesthroughtheshareholdingofVianiLimitedand5,000ordinarysharesthroughtheshareholdingofSalesandLettingLimited.

Shareholder Register Information

Directors’interestinthesharecapitalofthecompanyorinrelatedcompaniesat31December2010:

AlbertMizzi 8,000sharesSavioursiveSonnyPortelli 4,860sharesPhilipFarrugiaRandon 6,400shares

MrCharlesJohnFarrugiahasanon-beneficialinterestof7,511,587ordinarysharesinHSBCBankMaltap.l.c.through the shareholding held by Amalgamated Investments Sicav p.l.c. and a non-beneficial interest of 15,000ordinarysharesthroughtheshareholdingheldbyIndustrialManagementLtd.

MrPeterPaulTestaferrataMoroniVianihasabeneficialinterestof58,800ordinarysharesinHSBCBankMaltap.l.c.throughtheshareholdingofTestaferrataMoroniViani(Holdings)Limited,40,000ordinarysharesthroughtheshareholdingofCappsLtd, 40,000ordinary shares through the shareholdingofVianiLimited and5,000ordinarysharesthroughtheshareholdingofSalesandLettingLimited.

Healsohasanon-beneficialinterestof130,680ordinarysharesinHSBCBankMaltap.l.c.throughtheshareholdingofSantumasShareholdingsp.l.c.underCustodianshipHSBCBankMaltap.l.c.

TherewerenochangestoDirectors’interestfrom31December2010to31January2011.

Shareholdersholdingfivepercent(5%)ormoreoftheequitycapitalat31January2011:

HSBCEuropeB.V. 70.03%

Numberofshareholdersat31January2011:

Oneclassofshares 10,434shareholders(Allshareshaveequalvotingrights)

Report of the Directors (continued)

16

H S B C B A N K M A L T A P . L . C .

Healsohasanon-beneficialinterestof130,680ordinarysharesinHSBCBankMaltap.l.c.throughtheshareholdingofSantumasShareholdingsp.l.c.underCustodianshipofHSBCBankMaltap.l.c.

TherewerenochangestoDirectors’interestfrom31December2011to31January2012.

Shareholdersholdingfivepercent(5%)ormoreoftheequitycapitalat31January2012:

HSBCEuropeB.V. 70.03%

Numberofshareholdersat31January2012:

Oneclassofshares 10,356shareholders(Allshareshaveequalvotingrights)

Number of shareholders analysed by range 16Fe31January20122009 ___________________________________________

Rangeofshareholding Totalshareholders Shares

1–500 2,146 661,035501–1,000 1,619 1,312,5271,001–5,000 4,148 10,460,5225,001andover 2,443 279,405,916 ___________________________________________

Total Shareholding 10,356 291,840,000 Standard licence conditions

In accordancewithSLC7.35of the InvestmentServicesRulesFor InvestmentServicesProviders regulatedby theMaltaFinancialServicesAuthority,licenseholdersarerequiredtoincludeintheDirectors’Reportbreachesofstandardlicenseconditions.Accordingly,theDirectorsconfirmthatnobreachesofthestandardlicenceconditionsandnootherbreachofregulatoryrequirements,whichweresubjecttoadministrativepenaltyorregulatorysanctionwerereported.

Board of Directors

TheDirectorswhoservedduringtheyearandafteryearendareasfollows:

AlbertMizzi(Chairman) PhilipFarrugiaRandonAlanRichards(resignedon1January2012) CharlesJohnFarrugiaMarkWatkinson(appointedon14February2012) PeterPaulTestaferrataMoroniVianiSallyRobson(resignedon9February2011) SavioursiveSonnyPortelliPhilipFarrugia(appointedon15February2011) JamesDunbarCousinPeterWilliamBoyles

Senior management

Asat31December2011,theseniormanagementofthegroupwascomposedofthefollowing:

MarkWatkinson ChiefExecutiveOfficer(appointedon1January2012)AlanRichards ChiefExecutiveOfficer(resignedon1January2012)PhilipFarrugia ChiefTechnologyandServicesOfficerChrisBond HeadofGlobalBankingandMarketsMichelCordina HeadofCommercialBankingPaulSteel HeadofRetailBankingandWealthManagementJosephineMagri ChiefFinancialOfficerStewartLuscott-Evans ChiefRiskOfficerMarkSims HeadofHumanResourcesJohnSammut HeadofAudit,ComplianceandLegalJosephBorg HeadofITJamesHewitson ManagingDirectorHSBCLifeAssurance(Malta)LtdBrianTortell HeadofMarketingPeterCalleya HeadofCapitalManagementandPlanningFrancoAloisio HeadofCommunications

17

Auditors

KPMGhaveexpressedtheirwillingnesstocontinueinoffice.AresolutionproposingthereappointmentofKPMGasauditorsofthebankwillbesubmittedattheforthcomingAnnualGeneralMeeting.

Going Concern

AsrequiredbyListingRule5.62,upondueconsiderationofthebank’sprofitabilityandstatementoffinancialposition,capitaladequacyandsolvency,theDirectorsconfirmthebank’sabilitytocontinueoperatingasagoingconcernfortheforeseeablefuture.

Statement by the Directors pursuant to Listing Rule 5.70.1

Pursuant to Listing Rule 5.70.1 there were no material contracts to which the bank, or anyone of its subsidiaryundertakings,waspartytoandinwhichanyoneoftheDirectorswasdirectlyorindirectlyinterested.

Statement by the Directors pursuant to Listing Rule 5.68

We,theundersigned,declarethattothebestofourknowledge,thefinancialstatementspreparedinaccordancewiththerequirementsofInternationalFinancialReportingStandardsasadoptedbytheEUgiveatrueandfairviewoftheassets,liabilities,financialpositionandprofitorlossofthebankanditssubsidiariesincludedintheconsolidationtakenasawholeandthatthisreportincludesafairreviewofthedevelopmentandperformanceofthebusinessandthepositionofthebankanditssubsidiariesincludedintheconsolidationtakenasawhole,togetherwithadescriptionoftheprincipalrisksanduncertaintiesthattheyface.

SignedonbehalfoftheBoardon24February2012by:

AlbertMizzi,Chairman MarkWatkinson,ChiefExecutiveOfficer

18

H S B C B A N K M A L T A P . L . C .

PursuanttotheMaltaFinancialServicesAuthorityListingRules,HSBCBankMaltap.l.c.(the‘bank’)asacompanywhoseequitysecuritiesarelistedonaregulatedmarketendeavourstoadopttheCodeofPrinciplesofGoodCorporateGovernance (the ‘Principles’) embodied inAppendix 5.1 toChapter 5 of theListingRules. The bank is obliged intermsofListingRule5.94toprepareareportexplaininghowithascompliedwiththeprovisionsof thesaidCode.ThebankherebyincludesaStatementdividedintwosections:thefirstpartdetailingtheeffectivemeasuresadoptedbythebanktoensurecompliancewiththePrinciplesandthesecondpartexplainingthereasonsbehindinstancesofnon-compliance.

Although the Principles are not mandatory, the Board of Directors (the ‘Board’) of the bank believes in theiradoption, and has endorsed them except where there exist particular circumstances that warrant non-adherencethereto.TheBoardbelievesthatadherencetothePrincipleshasbeenandwillremainatoppriorityforthebankandconsidersittobearesponsibilitywhichstartswiththeBoardandpermeatesdownthroughoutthebank.TheBoardisproudofthefactthatthebankhasagoodcorporategovernanceframeworkthatensuresthatdirectorsworkcollectivelythroughaneffectiveBoard,overseethemanagementofthebusiness,setthetonefromthetop,ensuretheintegrityoffinancialreporting,setariskmanagement framework for thebankandcommunicatewithshareholders.TheBoardfirmlybelievesthatadherencetothePrinciplesiscrucialtoensuremoretransparentgovernancestructures,increasedaccountabilityandimprovedrelationswithinthemarketwhichshouldenhancemarketintegrityandconfidence.

Compliance with the Code

Principle 1: The BoardThe bank is headed by an effective Board which leads and controls the bank. All the Directors, individually andcollectively, are of the appropriate calibre, with the necessary skills and experience to assist them in providingleadership,integrityandjudgementindirectingthebank.Theintegrity,honestyanddiligenceoftheDirectorsguaranteethatthebankadherestoHSBCGroup’shighethicalbusinessvalues.

Boardmembersareaccountablefortheirperformanceandthatoftheirdelegates.Besideshavingabroadknowledgeofthebank’sbusinesstheyarealsoconversantwiththestatutoryandregulatoryrequirementsregulatingthisbusiness.

TheBoarddetermines thebank’sstrategicaimsandorganizationalstructuresandregularlyreviewsmanagementperformance.Itensuresthatthebankhastheappropriatefinancialandhumanresourcestomeetitsobjectives.

The Board delegates specific responsibilities to a number of committees, notably the Audit Committee, theRemunerationCommittee,theExecutiveCommittee,theAssetandLiabilityManagementCommittee,theGroupRiskManagementCommitteeandtheCreditRiskManagementCommittee.

FurtherdetailinrelationtotheCommitteesandtheresponsibilitiesoftheirrespectiveboardscanbefoundunderPrinciple8ofthisStatement.

Principle 2: Chairman and Chief Executive OfficerThepositionoftheChairmanandthatoftheChiefExecutiveOfficerareoccupiedbydifferentindividuals.ThereisacleardivisionofresponsibilitiesbetweentherunningoftheboardandtheChiefExecutiveOfficer’sresponsibilityin managing the bank’s business. This separation of roles of the Chairman and Chief Executive Officer avoidsconcentrationofauthorityandpowerinoneindividualanddifferentiatesleadershipoftheboardfromtherunningofthebusiness.

The Chairman exercises independent judgement even though he is appointed by the majority shareholder. HeleadstheBoard,setstheagendaandensuresthattheDirectorsreceiveprecise,timelyandobjectiveinformationandat the same time ensures effective communication with shareholders. During Board meetings, he leads the Boardandencourages active engagementby all boardmembers for thediscussionof complexandcontentious issues andstimulatesconstructivechallengeofseniormanagement.

On the other hand, the Chief Executive Officer is Chairman of most of the Board Committees and subsidiarycompanies.Hismainroleandresponsibilityistoexecuteagreedstrategyandmanagethebusiness.

Statement of Compliance with the Code of Principles of Good Corporate Governance

19

Principle 3: Composition of the Board TheBoardconsidersthatthesizeoftheBoardisthemostappropriatetoensureaneffectivemanagementandoversightoverthebank’soperationsasdemonstratedthroughouttheyears.

TheBoardiscomposedofindividualswhohavearangeofskills,competence,knowledgeandexperiencethatenablethemtofulfiltheirrolesdiligentlyandarecapableofunderstandingandfullyappreciatingthebusinessriskissuesandkeyperformanceindicators.

InlinewithPrinciple3,theBoardiscomposedofanon-executiveChairman,twoexecutiveDirectors,threenon-executiveDirectorsandthreeindependentnon-executiveDirectors.

Theindependentnon-executiveDirectorsarethefollowing:

MrSavioursiveSonnyPortelli

MrPeterPaulTestaferrataMoroniViani

MrJamesDunbarCousin

IndeterminingtheindependenceorotherwiseofitsDirectors,theBoardhasconsidered,interalia,theprinciplesrelatingtoindependenceembodiedinthecode,theGroup’sownpracticeaswellasgeneralgoodpracticeprinciples.

TheBoardconsidersthat thefact thatoneof theDirectorsisaformeremployeeof thebankandtheotherhasasignificantbusiness relationshipwith thebankdonotundermine the saidDirectors’ ability to exercise independentjudgementwhenconsideringtheissuesbroughtbeforetheBoard.Moreover,thesetwoDirectorswerenominatedbytheminorityshareholders.

IntermsofPrinciple3.4eachnon-executiveDirectorhasconfirmedinwritingtotheBoardthatheundertook:

a)tomaintaininallcircumstanceshisindependenceofanalysis,decisionandaction;

b)nottoseekoracceptanyunreasonableadvantagesthatcouldbeconsideredascompromisinghisindependence;and

c)toclearlyexpresshisoppositionintheeventthathefindsthatadecisionoftheBoardmayharmthebank.

Principle 4: The Responsibilities of the BoardTheBoardconcentratesprimarilyonstrategy,policysetting,businessplansandfinancialinformation.Itreviewsandevaluatescorporatestrategy,majoroperationalandfunctionalplans,riskpolicyandfinancialperformanceobjectives.Italsomonitorsimplementationofsuchobjectivesandcorporateperformancewithintheparametersofallrelevantlaws,regulationsandcodesofbestpractice.Theboardensuresthatabalanceismaintainedbetweenenterpriseandcontrol.

TheBoard’sinformedassessmentofmanagement’sperformanceresultsfromaclearinternalandexternalreportingsystem. The Board continuously assesses and monitors the bank’s present and future operations, opportunities,threatsandrisksintheexternalenvironmentandcurrentandfuturestrengthsandweaknesses.Theevaluationofthemanagement’simplementationofcorporatestrategyandfinancialobligationsisbasedontheuseofkeyperformanceindicators enabling the bank to adopt expedient corrective measures. These key business risks and performanceindicatorsarebenchmarkedagainstindustrynormssoastoensurethatthebank’sperformanceiseffectivelyevaluated.

TheBoardensuresthatthebankhasappropriatepoliciesandproceduresinplacethatguaranteethatthebankanditsemployeesmaintainthehigheststandardsofcorporateconductandcompliancewiththeapplicablelaws,regulations,businessandethicalstandards.

20

H S B C B A N K M A L T A P . L . C .

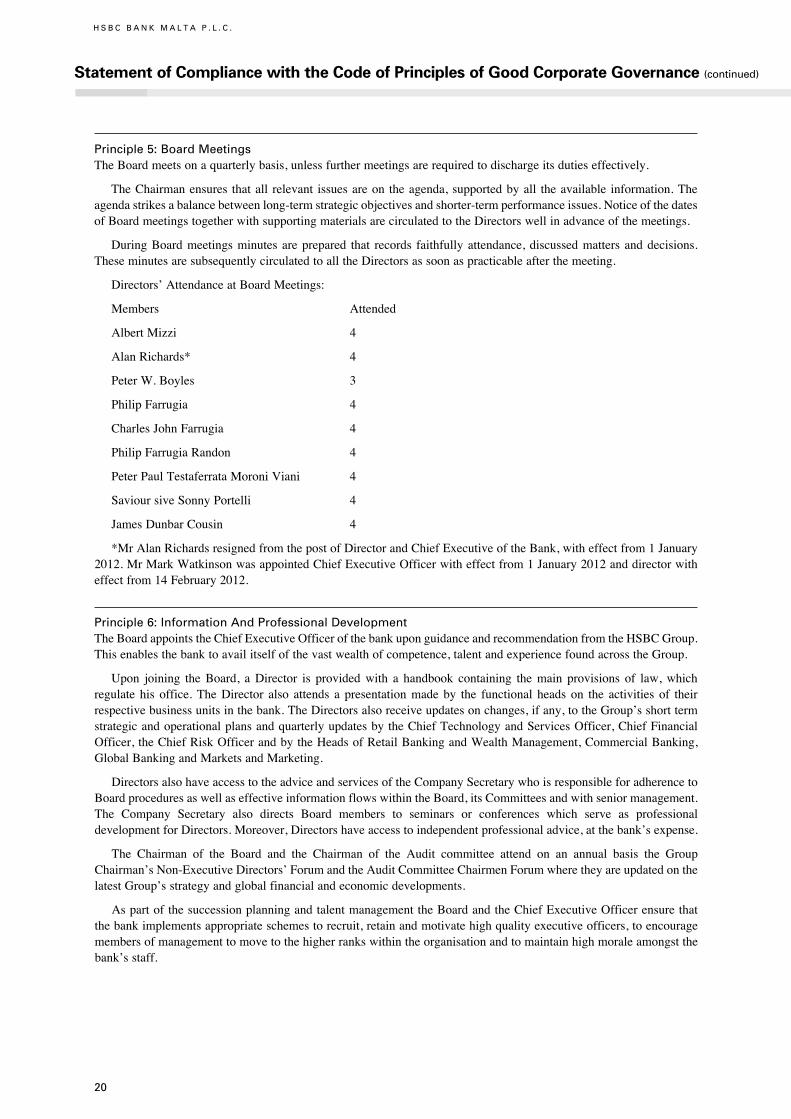

Principle 5: Board MeetingsTheBoardmeetsonaquarterlybasis,unlessfurthermeetingsarerequiredtodischargeitsdutieseffectively.

TheChairmanensures thatall relevant issuesareon theagenda,supportedbyall theavailable information.Theagendastrikesabalancebetweenlong-termstrategicobjectivesandshorter-termperformanceissues.NoticeofthedatesofBoardmeetingstogetherwithsupportingmaterialsarecirculatedtotheDirectorswellinadvanceofthemeetings.

DuringBoardmeetingsminutesareprepared that records faithfullyattendance,discussedmatters anddecisions.TheseminutesaresubsequentlycirculatedtoalltheDirectorsassoonaspracticableafterthemeeting.

Directors’AttendanceatBoardMeetings:

Members Attended

AlbertMizzi 4

AlanRichards* 4

PeterW.Boyles 3

PhilipFarrugia 4

CharlesJohnFarrugia 4

PhilipFarrugiaRandon 4

PeterPaulTestaferrataMoroniViani 4

SavioursiveSonnyPortelli 4

JamesDunbarCousin 4

*MrAlanRichardsresignedfromthepostofDirectorandChiefExecutiveoftheBank,witheffectfrom1January2012.MrMarkWatkinsonwasappointedChiefExecutiveOfficerwitheffectfrom1January2012anddirectorwitheffectfrom14February2012.

Principle 6: Information And Professional DevelopmentTheBoardappointstheChiefExecutiveOfficerofthebankuponguidanceandrecommendationfromtheHSBCGroup.Thisenablesthebanktoavailitselfofthevastwealthofcompetence,talentandexperiencefoundacrosstheGroup.

Upon joining theBoard, aDirector is providedwith a handbook containing themain provisions of law,whichregulate his office.TheDirector also attends a presentationmade by the functional heads on the activities of theirrespectivebusinessunitsinthebank.TheDirectorsalsoreceiveupdatesonchanges,ifany,totheGroup’sshorttermstrategicandoperationalplansandquarterlyupdatesbytheChiefTechnologyandServicesOfficer,ChiefFinancialOfficer,theChiefRiskOfficerandbytheHeadsofRetailBankingandWealthManagement,CommercialBanking,GlobalBankingandMarketsandMarketing.

DirectorsalsohaveaccesstotheadviceandservicesoftheCompanySecretarywhoisresponsibleforadherencetoBoardproceduresaswellaseffectiveinformationflowswithintheBoard,itsCommitteesandwithseniormanagement.The Company Secretary also directs Board members to seminars or conferences which serve as professionaldevelopmentforDirectors.Moreover,Directorshaveaccesstoindependentprofessionaladvice,atthebank’sexpense.

The Chairman of the Board and the Chairman of the Audit committee attend on an annual basis the GroupChairman’sNon-ExecutiveDirectors’ForumandtheAuditCommitteeChairmenForumwheretheyareupdatedonthelatestGroup’sstrategyandglobalfinancialandeconomicdevelopments.

AspartofthesuccessionplanningandtalentmanagementtheBoardandtheChiefExecutiveOfficerensurethatthebankimplementsappropriateschemestorecruit,retainandmotivatehighqualityexecutiveofficers,toencouragemembersofmanagementtomovetothehigherrankswithintheorganisationandtomaintainhighmoraleamongstthebank’sstaff.

Statement of Compliance with the Code of Principles of Good Corporate Governance (continued)

21

Principle 7: Evaluation of the Board PerformanceTheBoardundertookanevaluationofitsownperformance,theChairman’sperformanceandthatofitsCommittees.TheBoarddidnotappointanadhoccommitteetocarryoutthisperformanceevaluationbuttheevaluationexercisewasconductedthroughaBoardEffectivenessQuestionnairebytheCompanySecretaryinliaisonwiththeChairmanmodelledonaBoardEffectivenessQuestionnaireusedbytheGroup.

AlthoughnomaterialchangesresultedfromananalysisoftheresponsestothisBoardEffectivenessQuestionnairecertainminorchangeswereimplementedinordertoincreasetheBoard’seffectiveness.

Principle 8: CommitteesThe Board delegates specific responsibilities to Committees, which operate under their respective formal terms ofreference.TheBoardhasestablishedthefollowingCommittees:

Audit CommitteeTheAuditCommitteemetfivetimesduringthisyear.ItsTermsofReferencewereoriginallymodelledmainlyontherecommendationsintheCadburyReport,theUKWalkerReviewandarecompliantwiththeListingRules.ThisyeartheseTermsofReferencehavebeenamendedinordertoincreasetheAuditCommittee’soversightonriskfactors.

TheprimarypurposeofthisCommitteeistoprotecttheinterestsofthebank’sshareholdersandassisttheDirectorsinconductingtheirroleeffectivelysothatthebank’sdecision-makingcapabilityandtheaccuracyofitsreportingandfinancialresultsaremaintainedatahighlevelatalltimes.

TheAuditCommitteealsoscrutinisesandapprovesrelatedpartytransactions.Itconsidersthematerialityandthenatureoftherelatedpartytransactioncarriedoutbythebanktoensurethatthearms’lengthprincipleisadheredtoatalltimes.

ThemembersoftheAuditCommitteeareMessrsSavioursiveSonnyPortelli(Chairman)andPeterPaulTestaferrataMoroni Viani who are independent non-executive directors and Dr Philip Farrugia Randon LL.D. who is a non-executivedirector.ExecutivesofthebankareinvitedtoattendanyofthemeetingsasdirectedbytheCommittee.TheChiefExecutiveOfficer,theChiefTechnologyandServicesOfficer,theChiefRiskOfficerandarepresentativeoftheexternalauditorsattendthemeetings.InlinewithListingRule5.131,theHeadofInternalAuditisalwayspresentforitsmeetingsandhasarightofdirectaccesstotheChairmanoftheCommitteeatalltimes.TheHeadofContinentalEuropeGroupAuditsometimesattendsthesemeetings.

MrSavioursiveSonnyPortelliwasappointedbytheBoardasthedirectorwhoisindependentandcompetentinaccountingand/orauditingintermsofListingRule5.117onthebasisthathehasalonganddistinguishedcareerinbothpubliccompaniesandprivateenterprise.Presently,MrPortelliisalsoChairmanoftheMaltaCouncilforEconomicand Social Development.Mr Portelli has served on the Bank’s Board of Directors since October 2006 where hiscontributionshavedemonstratedthatheishighlycompetentinaccountingandaucourantwithaccountingstandardsandpracticesandthathealsopossessesthequalitiesandexperiencerequiredtodischargehisdutiesasChairmanofthisCommittee.

As Chairman of the Audit Committee Mr Portelli attends the Group’s annual Audit Committee Chairmen’sForum.ThisprovidestheChairmanwiththelatestupdatesonkeyconsiderations,prioritiesandchallengesfacingtheCommittee.

IntermsofListingRule5.127.7,theAuditCommitteeisresponsiblefordevelopingandimplementingapolicyontheengagementoftheexternalauditortosupplynon-auditservices.SinceHSBCHoldingsplcisaSecuritiesExchangeCommission(SEC)registeredcompany,non-auditservicesprovidedbytheexternalauditorareregulatedintermsoftheSECrules.

Remuneration Committee (REMCO)TheRemunerationCommitteeisdealtwithundertheRemunerationReportonpages26and27,whichalsoincludestheRemunerationStatementintermsofCodeProvisions8.A.3and8.A.4.

Executive Committee (EXCO)TheExecutiveCommitteemeets on amonthly basis to oversee the overall day-to-daymanagement of the bank inaccordancewith such policies and directions as theBoardmay from time to time determine. TheChief ExecutiveOfficerchairsthisCommitteewhichiscomposedoftheChiefTechnologyandServicesOfficertogetherwiththetopmanagementofthebank.

22

H S B C B A N K M A L T A P . L . C .

Statement of Compliance with the Code of Principles of Good Corporate Governance (continued)

Asset And Liability Management Committee (ALCO)ThisCommitteereviewsthefinancialrisksofthegroupinMaltaandensurestheirprudentmanagement:interestraterisk,liquidityandfundingrisk,foreignexchangerisk,capitalsolvency,marketsectorriskandcountryrisk.Furthermore,ALCOmonitors the external environment andmeasures the impact on profitability of factors such as interest ratevolatility,marketliquidity,exchangeratevolatility,monetaryandfiscalpoliciesandcompetitorbanksactivity.

TheChiefExecutiveOfficer has primary responsibility for ensuring efficient development of asset and liabilitymanagement. Membership consists of senior executives with responsibility for the following functions: corporatebanking,retailbanking,treasury,financialcontrol,marketing,andcredit.TheALCO,whichischairedbytheChiefExecutiveOfficeranddeputisedbytheChiefTechnologyandServicesOfficer,meetsonceamonth.

Credit Risk Management CommitteeThiscommitteereviewsthecreditriskmanagementissuesofthegroupinMalta.ItmeetsonamonthlybasisandischairedbytheChiefExecutiveOfficer.Membershipconsistsofseniorexecutiveswithresponsibilityforthefollowingfunctions: credit and riskmanagement, corporatebanking, retail banking, treasury, consumer finance and audit andcompliance.

Group Risk Management CommitteeThisCommitteereviewstheoperationalrisksofthegroupinMalta:theidentification,measurement,monitoringandcontrollingoperationalbusinessrisksanddeterminesandagreesstrategiesandpoliciestomitigatetheserisks.

ThisCommitteewhichmeetsonaquarterlybasisischairedbytheChiefRiskOfficerandiscomposedoftheChiefTechnologyandServicesOfficer,theChiefRiskOfficer,theHeadofAudit,ComplianceandLegal,HeadofSecurityandFraudandbyotherBusinessandFunctionalHeadsandManagingDirectorsofsomeoftheSubsidiaryCompanies.

Principles 9 and 10: Relations With Shareholders And With The Market, and Institutional ShareholdersThebankmaintainsongoingcommunicationwithitsshareholdersandthemarketonitsstrategyandperformanceinordertoenhancetrustandconfidenceinthebank.Duringtheperiodunderreviewthebankhasissuedvariouscompanyannouncementsandmedia releases toexplainongoingcorporatedevelopmentsandmaterialeventsand transactionswhichhavetakenplaceandtheirimpactonthefinancialpositionofthebank.

TheprincipalcontactwithshareholderstakesplacethroughtheAnnualGeneralMeeting(furtherdetailisprovidedunder the section regardingGeneralMeetings) and ExtraordinaryGeneralMeetings when necessary. Furthermore,communicationwithshareholderstakesplacethroughtheAnnualReportandAccountsbeingsenttoeveryshareholder,whicharephysicallydeliveredtotheshareholdersandwhichcanbeaccessedbyshareholdersthroughthebank’swebsite,primarilytheInvestorRelations’section,andaspecificperiodicalshareholderpublicationentitled“L-Azzjonist”.

Thebankalsoholdsmeetingsforstockbrokers,financialintermediariesandthemediatoexplainthesalientfeaturesoftheinterimandannualfinancialresults.

The bankmaintains an open channel of communicationwith its shareholders through the Company SecretarialOfficeandthroughtheHeadofCommunications.

TheChairmanensures that theviewsofshareholdersarecommunicated to theBoardasawhole.Moreover, theChairmanarrangesforallDirectorstoattendtheAnnualGeneralMeetingandfortheChairmenoftheAuditCommitteeandtheRemunerationCommitteetobeavailabletoanswerquestions.Theconductofthemeetingisconducivetovaliddiscussionandappropriatedecisionmaking.

In termsof thebank’sArticlesofAssociation theDirectorsshallon the requisitionofmembersof thecompanyholdingnotlessthanone-tenthofthepaidupsharecapitalproceeddulytoconveneanExtraordinaryGeneralMeetingofthebank.MinorityshareholdersarenotprohibitedfromformallypresentinganissuetotheBoardofDirectors.

23

Principle 11: Conflicts of InterestsDirectorsareawarethattheirprimaryresponsibilityisalwaystoactintheinterestofthebankanditsshareholdersasawholeirrespectiveofwhoappointedthemtotheBoard.Thisentailsthattheyavoidconflictsofinterestatalltimesandthattheirpersonalinterestsnevertakeprecedenceoverthoseofthebankanditsshareholders.

Byvirtueofthebank’sArticlesofAssociationadirectorisboundnottovoteataBoardmeetingonanycontractorarrangementoranyotherproposalinwhichhehasamaterialinterest,eitherdirectlyorindirectly.

OnjoiningtheBoardandregularlythereafter,DirectorsareinformedandremindedoftheirobligationsondealinginsecuritiesofthebankwithintheparametersoflawandtheListingRules.AproperprocedureofreportingadvancenoticestotheChairmanbyadirectorwhointendstodealinthebank’sshareshasbeenendorsedbytheBoardinlinewiththePrinciples,theListingRulesandtheinternalcodeofdealing.

Principle 12: Corporate SustainabilityHSBC’sCorporateSustainability(CS)activitiestakeplacewithinthecontextoftheGroupwidestrategy.InMaltathebankfulfilstheGroup’sCSstrategyprimarilythroughtheHSBCMaltaFoundation.

ThischaritableFoundationiscommittedtoinvestinginthelocalcommunityandlookstobringaboutlastingbenefittosociety.Itdealswithissuesthatconcernthepublicingeneralbysupervisingprojectsinrelationtodisadvantagedchildren,theenvironmentandMalta’snationalheritage.TheseactivitieshaveasignificantimpactonalargemajorityofMaltesecitizenswhichshowsthebank’sstrongcommitmenttowardssocialinvestment.

Non-Compliance with the Code

Principle 4 (Code Provision 4.2.7)CodeProvision4.2.7.recommends“thedevelopmentofasuccessionpolicyforthefuturecompositionoftheBoardofDirectorsandparticularlytheexecutivecomponentthereof,forwhichtheChairmanshouldholdkeyresponsibility”.

InviewofthefactthatappointmentofDirectorsisamatterreservedexclusivelytothebank’sshareholders(exceptwhere theneedarises to fillacasualvacancy) thebankdoesnotconsider itappropriate toadoptsuchasuccessionpolicy.However,asexplainedunderPrinciple6 thebankcontinuestopursueanactivesuccessionpolicyforseniorexecutive positions, especially by seeking to post local senior staff members abroadwithin the Group in order toenhancetheirinternationalbankingexperience.

Principle 8B (Nomination Committee)TheMemorandumofAssociationofthebankspecificallyregulatestheappointmentofDirectors.TheBoardconsistsofnotmorethannineDirectorswhoareappointed/electedbytheshareholders.Unlessappointedforashorterorlongerperiodbutnotexceedingthreeyears,aDirectorshallholdofficefromtheendofoneAnnualGeneralMeetingtotheendofthenext.Everyshareholderowning11%oftheordinarysharecapitalisentitledtoappointoneDirectorforeach11%shareholding.ThemajorityshareholderthereforehastherighttoappointsixDirectors.Furthermore,anyexcessfractional shareholdingnot soutilisedmaybeused toparticipate in thevoting for theelectionof furtherDirectors.Shareholderswhoownless than11%of theordinarysharecapitalparticipate in theelectionof theremaining threeDirectors.

Thelargestsingleshareholder(subjecttoaminimum33%holdingoftheordinaryissuedsharecapitalofthebank),is entitled to appoint aChairman fromamongst theDirectors appointedor elected to theBoard.Everypoll for theelectionofDirectorsisoverseenbythebank’sexternalauditors.

Withinthiscontext,theBoarddoesnotdeemitnecessarytoappointaNominationCommittee.

Principle 9 (Code Provision 9.2)This Code Provision recommends the bank to have in place a mechanism to resolve conflicts between minorityshareholdersandcontrollingshareholders.Althoughthebankdoesnothavesuchmechanisminplacethereisongoingopendialoguebetweenthebank’sseniormanagementandthenon-executivesdirectorstoensurethatnosuchconflictsarise.

24

H S B C B A N K M A L T A P . L . C .

Statement of Compliance with the Code of Principles of Good Corporate Governance (continued)

Internal Control

TheBoardisultimatelyresponsibleforthebank’ssystemofinternalcontrolandforreviewingitseffectiveness.Suchproceduresaredesignedtomanageratherthantoeliminatetheriskoffailure,toachievebusinessobjectivesandcanonlyprovidereasonableandnotabsoluteassuranceagainstmaterialerror,lossesorfraud.

Thebankhasdelegatedspecific,clearandunequivocalauthoritytotheChiefExecutiveOfficertomanageactivitiesofthebankwithinthelimitssetbyit.Functional,operatingandfinancialreportingstandardsareapplicablewithinallentitiesoftheHSBCGroup.Thesearesupplementedbyoperatingstandardssetbythebank’smanagement,asrequired.

Systemsandproceduresareinplaceinthebanktoidentify,controlandtoreportonthemajorrisksincludingcredit,changesinthemarketpricesoffinancialinstruments,liquidity,operationalerrorandfraud.ExposuretotheserisksismonitoredbytheAssetandLiabilityManagementCommittee,CreditRiskManagementCommitteeandbytheGroupRiskManagementCommittee.

Comprehensiveannual financialplansareprepared, reviewedandapprovedby theBoard.Resultsaremonitoredand reports on progress comparedwith plan are preparedmonthly. Financial accounting and reporting and certainmanagementreportingstandardshavebeenestablished.Centralisedfunctionalcontrolisexercisedoverallcomputersystemdevelopmentsandoperations.Commonsystemsareemployedwherepossibleforsimilarbusinessprocesses.

Responsibilitiesforfinancialperformanceagainstplansandforcapitalexpenditure,creditexposuresandmarketriskexposuresaredelegatedwithlimitstolinemanagement.Inaddition,functionalmanagementinthebankhasbeengiventheresponsibilitytoimplementHSBCpolicies,proceduresandstandardsintheareasoffinance;legalandregulatorycompliance;internalaudit;humanresources;creditrisk;marketrisk;operationalrisk;computersystemsandoperations;propertymanagement;andforcertainHSBCGroupbusinessandproductlines.

TheChiefRiskOfficerisresponsibleforthemanagementofspecificriskswithintheBankincludingcreditriskinthewholesaleandretailportfolios,marketsriskandoperationalrisk.RisksaremonitoredviaregularRiskManagementCommitteesandthroughreportingtotheExecutiveCommitteeandtheBoard.

Theinternalauditfunctionmonitorscompliancewithpoliciesandstandardsandtheeffectivenessofinternalcontrolstructureswithinthebankanditssubsidiaries.Theworkoftheinternalauditfunctionfocusesonareasofgreatestriskasdeterminedbyariskmanagementapproach.

Thebank’sComplianceDepartmentensuresthatHSBCBankMaltagroupanditsemployeesmaintainthehigheststandards of corporate conduct including compliancewith all the local and international regulatory obligations andHSBCGroupethicalstandardsandregulations.

ThroughtheAuditCommittee,theBoardreviewstheprocessesandprocedurestoensuretheeffectivenessofthesystemofinternalcontrolofthebankanditssubsidiaries,whicharemonitoredbyinternalaudit.

Listing Rule 5.97.5TheinformationrequiredbythisListingruleisfoundintheDirectors’Reportonpages14to17.

25

General Meetings

TheGeneralMeetingisthehighestdecisionmakingbodyofthebank.AGeneralMeetingiscalledbytwenty-onedays’noticeanditisconductedinaccordancewiththeArticlesofAssociationofthebank.

TheAnnualGeneralMeetingdealswithwhatistermedas“ordinarybusiness”,namelythereceivingoradoptionof theannual financial statements, thedeclarationof adividend, theappointmentof theBoard (whichmayormaynotinvolveanelection),theappointmentoftheexternalauditorsandthegrantoftheauthoritytotheBoardtofixtheexternal auditors’ emoluments.Otherbusinesswhichmaybe transactedat aGeneralMeetingwill bedealtwith asSpecialBusiness.

Allshareholdersregistered in theshareholders’Registeron therecorddateasdefined in theListingRules,havetheright toattend,participateandvote in theGeneralMeeting.Ashareholderorshareholdersholdingnot less than5%innominalvalueofallthesharesentitledtovoteattheGeneralMeetingmayrequestthebanktoincludeitemsontheagendaofaGeneralMeetingand/ortabledraftresolutionsforitemsincludedintheagendaofageneralmeeting.Suchrequestsaretobereceivedbythebankatleastfortysixdaysbeforethedatesetfortherelativegeneralmeeting.