Embed Size (px)

Citation preview

Annual Report and Financial Statements

for the year ended 31

March 2015

2

Contents

Board Members, Executive Officers and Professional Advisers 3–4

Statement on Corporate Governance 5–6

Report of the Board of Management 7–9

Auditor’s Report 10–11

Income and Expenditure Account 12

Balance Sheet 13

Cash Flow Statement and notes to the Cash Flow Statement 14–15

Notes to the Financial Statements 16–35

2

Board Members, Executive Officers and Professional AdvisersBoard MembersChair Ms D Rosser

Vice Chair Mr S Kelly

Treasurer and Chair of Audit Committee Mr G Price

Secretary Mr K Protheroe

Other MembersMs S BickertonMr R ChickMs B Gladwyn (appointed November 2014)Mr N Hazelden (appointed July 2014)Ms J Hughes (left September 2014)Ms T Johnson (left January 2015)Mrs J Lewis (left July 2014)Mr H Mehta (appointed January 2015)Mrs K MalekinMr P MaxMr P MilesMr R Smith (left July 2014)

Permitted ObserversMs S Ahmed (appointed April 2015)Mr G Kenning (appointed March 2015)

Executive OfficersChief Executive Mr K Protheroe

Director of Finance & ICT Mr M Potter

Director of Customer and Community Services Mr M Thomas

Development Director Mrs C Lewis

Director of Corporate Services Mrs L Sulley

Registered OfficeTolven CourtDowlais RoadCardiffCF24 5LQ

Area Office50 Meteor StreetAdamsdownCardiffCF24 0HE

3

4

Board Members, Executive Officers and Professional AdvisersProfessional Advisers

Statutory Auditors Haines Watts Wales LLP7 Neptune CourtVanguard WayCardiffCF24 5PJ

Internal AuditorsMazars LLPClifton Down HouseBeaufort BuildingsCliftonBristolBS8 4AN

Principal BankersBarclays Bank plc,1-5 St Davids WaySt Davids CentreCardiffCF10 2DP

Legal AdvisersBlake MorganHugh James L G Williams & Prichard

Registered under the Co-Operative and Community Benefit Societies Act 2014 No. 21667R

Registered by the Welsh Government No. L035

5

Statement on Corporate GovernanceFor the year ended 31 March 2015

Board of Management

The aim is that our Board of Management comprises up to twelve non-executive members, ideally four of whom should be tenant members, and possible additional co-opted members. The Board is responsible for managing the affairs of the Association. Board members are drawn from a wide background bringing together professional, commercial and local experience together with tenant representatives.

The Board is responsible for the Association’s strategy and policy framework. It delegates the day to day management and implementation of that framework to the Chief Executive and other senior executives. The senior executives meet monthly and attend Board meetings.

Meetings

Board members are elected at the Annual General Meeting.

The Board meets eleven times per year (including the Annual General Meeting). Individual meetings are themed to consider substantive matters relating to the Association’s strategic and operational activities.

The Board receives reports and considers policies in respect of the housing management, maintenance and community services functions, financial management and the implementation of the Association’s financial regulations. Reports are also received concerning development activity with regard to the appraisal of projects against the risk management policy and framework, the development programme and the corporate strategy.

The Board considers reports in respect of its employment and legal responsibilities as part of personnel reporting requirements. Board meetings are attended by the Chief Executive, Director of Finance & ICT, Director of Customer & Community Services, Development Director and Director of Corporate Services. Other staff attend Board meetings as required.

The Audit Committee, previously referred to as the Scrutiny Committee until June 2014, comprising five Board members meets four times a year. The Committee is attended by the Chief Executive and the Director of Finance & ICT with other staff attending as required. Representatives of both the internal and external auditors are also in attendance.

The Audit Committee advises the Board on internal audit functions, the effectiveness of internal control functions, performance audit reports and risk. The Audit Committee also reviews selected topics in accordance with a work programme approved by the Board. Directors and Managers responsible for the service area or strategy being scrutinised attend the Committee as required.

The Board considers reports on recommendations arising out of internal/external audit and Welsh Government Regulation inspections/action plans and monitors their implementation against targets set.

Risk management statement

The Association has a formal risk management strategy, which is approved annually by the Board. This stipulates that the Board has ultimate responsibility for risk management.

The strategy determines the processes by which risk is managed. One of the essential elements of this strategy is that a risk matrix is maintained to manage the key risks. The Senior Management team, led by the Chief Executive, has overall responsibility for both risk management and for the maintenance of the risk matrix.

The Board has delegated responsibility for monitoring the risk management processes to the Audit Committee. The Audit Committee receives a report of risk management from the Senior Management Team on a quarterly basis.

6

Statement on Corporate GovernanceFor the year ended 31 March 2015

The Board, through both the direct reporting of risk and the work of the Audit Committee, will monitor how management have managed and mitigated the risks of the Association.

Internal financial control

In meeting its responsibilities for the internal control arrangements, the Board of Management procures internal audit services through Mazars LLP.

A risk-based programme of audits reviewing the system of internal control spanning all aspects of the Association’s activities is agreed annually. The reviews are designed to provide reasonable, but not absolute, assurance regarding the safeguarding of assets, the maintenance of proper accounting records and the reliability of financial information. Mazars have direct and unfettered access to the Chairs of the Audit Committee and the Board.

The Audit Committee reviewed the system of internal controls for the period 1 April 2014 to the date of approval of the financial statements.

The procedures that have been established, which are designed to provide effective internal financial control, are:

• written financial procedures/regulations and delegated authorities;

• comprehensive systems of financial reporting including: annual budgets and monthly management accounts;

• monitoring of the internal financial controls and procedures by the internal auditor whose reports are reviewed by the Audit Committee;

• clearly defined management and reporting structures;

• an annually revised five year corporate strategy incorporating five-year financial forecasts and targets in respect of growth and unit costs;

• an annually revised thirty-year financial forecast – required by, and submitted to the Welsh Government.

7

Report of the Board of ManagementFor the year ended 31 March 2015

The Board of Management presents its report and the audited financial statements for the year ended 31 March 2015

Principal objectives and activities

The principal objectives and activities of the Association are the provision of housing and associated amenities for persons in necessitous circumstances upon terms appropriate to their means.

Board members and senior executives

The Board members and senior executives of the Association who served during the year are set out on page 3. The senior executives hold no interest in the Association’s shares and have no legal status as directors, although they act as executives within authority delegated by the Board.

EmployeesThe strength of the Association lies in the quality and commitment of its employees. Our ability to meet our objectives and commitments to our customers in an efficient and effective manner depends on the contribution of employees throughout the Association.

The Association continues to provide information on its objectives, progress and activities through regular team meetings and staff conferences. The Association provides training programmes focused on the knowledge, skills and teamwork necessary to meet the objectives of the Association.

Review of businessOur financial performance for the year is detailed in the financial statements. The Board of Management considers that the results are satisfactory and indicate the continued growth and financial strength of the Association.

The surplus this year reflects the demanding nature of the financial spending priorities and the predicted medium term financial outlook. During the year we took forward a number of projects as we strived to achieve our six corporate Outcomes, four of which specifically relate to our customers and the communities where work, and involved significant resource commitments. For example:

• we helped 280 people, including 104 families, get a home of their own

• Cardiff Accessible Homes rehoused 161 disabled people

• we built 22 new homes for rent in Penylan ranging from 2 bedroom apartments to 4 bedroom family houses

• we built 6 new homes for sale to provide low-cost home ownership opportunities for people on modest incomes

• commenced construction of a further 44 new homes in Splott and Butetown

• we acquired the strategically important Hamadryad Hospital site; work will commence on 55 new apartments in 2015/16

• we increased the number of our homes that meet the WHQS standard to 99.92%

• we fully completed our planned maintenance programme for 2014/15, involving the installation of 30 new kitchens, 13 showers, 35 electric heating systems and 279 boilers

• we (Communities First, LIFT, Care & Repair and CCHA) secured £863k in additional welfare benefits and savings for people, supported 131 people to get a job and helped another 317 complete skills qualifications

8

Report of the Board of ManagementFor the year ended 31 March 2015

• over 25,000 people made use of the cinema, media suite, services, facilities, activities and training opportunities in our community centres in Butetown, Trowbridge, Tremorfa and Adamsdown

• 2,592 people participated in community projects to improve prosperity, learning and health organised by Communities First

• 540 children were helped to improve their performance at school with Communities First’s help

• our Tenants’ Services Inspectors completed an inspection of our Independent Living Service and commenced an inspection of our reactive repairs service. 156 tenants took part in the consultation – the largest number the TSIs have ever recorded

• we organised 14 community events, where we engaged with 342 tenants

• we continued to work in partnership with Taff and Cadwyn Housing Associations to host the BME contact group, which held 5 events throughout the year

• Care & Repair helped 1,294 people with repairs, maintenance and adaptation works worth £1m. They helped 2,833 people to return safely from hospital, or helped them to remain living at home, by doing small works of improvement to their homes

• Cardiff Accessible Homes completed 170 disability adaptations to peoples’ homes, resulting in the installation of 34 stair lifts, 102 level access showers and 73 jobs to ramp and widen access to homes and rooms

• we provided personal support to 53 tenants to help them to successfully live independently, and helped 34 supported tenants to move on in a positive way

• we completed 121 ‘wellbeing visits’ to older tenants

By prudently planning these demanding commitments we achieved these objectives whilst improving our surplus position and plan to continue to do so in subsequent years.

We fully committed our Social Housing Grant received from the Welsh Government. In the year, the Association received new grants of over £2.13m to build new homes. In total, homes available for rent comprised 2,762 by the end of the financial year.

To enable us to support these activities and our business we maintained our robust financial position. Turnover from rental income was £12.3m reflecting an increase in rents in line with rents guidance issued by the Welsh Government, and the new schemes coming into management.

During the year we completed the draw-down of £6m in new funding via the Welsh Government’s Housing Bond as part of our medium term financial planning. We also maintained the substantial fixed-rate element of our loan portfolio to protect the Association’s longer-term position against the current uncertain economic backdrop.

As a result we declared a surplus of £2,390,000 before transfers from designated and restricted reserves of £239,000. We met all our loan covenants and satisfied the Welsh Government’s regulatory financial viability criteria. The Welsh Government’s judgement in respect of our financial viability was: “Pass – the Association has adequate resources to meet current and future business and financial commitments”.

Changes in fixed assetsDetails of fixed assets are set out in notes 9 to 13 of the financial statements.

Reserves Transfers to and from reserves are set out in note 21.

9

Report of the Board of ManagementFor the year ended 31 March 2015

Statement of Board of Management responsibilitiesThe Board of Management is responsible for preparing the financial statements in accordance with applicable law and United Kingdom Generally Accepted Accounting Practice (GAAP).

The Co-Operative and Community Benefit Societies Act 2014 and registered social housing legislation require the Board of Management to prepare financial statements for each financial year that give a true and fair view of the state of affairs of the Association and of the Income and Expenditure of the Association for that period. In preparing these financial statements, the Board is required to:

• select suitable accounting policies and apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• state whether applicable accounting standards and the Statement of Recommended Practice (Accounting by Registered Housing Associations) have been followed, (subject to any material departures disclosed, and explained in the financial statements);

• prepare the financial statements on a going-concern basis unless it is inappropriate to presume that the Association will continue in business for the foreseeable future.

The Board of Management is responsible for keeping proper accounting records that disclose, with reasonable accuracy at any time, the financial position of the Association and enable it to ensure that the financial statements comply with the relevant legislation. The Board is also responsible for maintaining an adequate system of internal control for safeguarding the assets of the Association and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

As far as the Board of Management is aware:

• there is no relevant audit information of which the Association’s auditors are unaware; and

• the members of the Board of Management have taken all steps that they ought to have taken to make themselves aware of any relevant audit information and to establish that the auditors are aware of that information.

Annual General MeetingThe Annual General Meeting will be held on the 21 July 2015 at St Peter’s Hall, Cardiff. At this meeting, the Association’s 2014/15 Annual Report will be presented for adoption.

AuditorsA resolution to re-appoint Haines Watts Wales LLP as auditors to Cardiff Community Housing Association Limited will be proposed at the Annual General Meeting.

By Order of the Board of Management

Debbie Rosser Chair 24 June 2015

10

Independent Auditor’s Report to the Members of Cardiff Community Housing Association Limited For the year ended 31 March 2015

We have audited the financial statements of Cardiff Community Housing Association Limited (‘the Association’) for the year ended 31st March 2015 which comprise the Income and Expenditure Account, Balance Sheet, the Cash Flow Statement and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice).

This report is made solely to the Association’s members, as a body corporate, in accordance with the requirements of the Co-Operative and Community Benefit Societies Act 2014, schedule 1 to the Housing Act 1996 and the Accounting Requirements for Social Landlords Registered in Wales - General Determination 2009. Our audit work has been undertaken so that we might state to the Association’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Association and the Association’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of the Board of Management and the auditorAs explained more fully in the Statement of Board of Management’s responsibilities, set out on page 9, the Board of Management is responsible for the preparation of financial statements which give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practice Board’s Ethical standards for Auditors.

We review whether the Board of Management’s statement on internal financial control reflects the Association’s compliance with the Housing for Wales Circular HFW 02/10 “Internal controls and reporting” and we report whether the statement is not inconsistent with the information of which we are aware from our audit of the financial statements. We are not required to form an opinion on the effectiveness of the Association’s corporate governance procedures or its internal financial control.

Scope of the audit of the financial statementsAn audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Association’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the Board of Management; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the Board of Management report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Independent Auditor’s Report to the Members of Cardiff Community Housing Association Limited For the year ended 31 March 2015

11

Opinion on internal controlIn our opinion, with respect to the Board of Management’s statement on internal financial control:

• the Board of Management has provided the disclosures required by the Circular and the statement is not inconsistent with the information of which we are aware from our audit work on the financial statements.

Opinion on financial statementsIn our opinion the financial statements:

• give a true and fair view of the state of the Association’s affairs as at 31st March 2015 and of its income and expenditure for the year then ended;

• have been properly prepared in accordance with the Co-Operative and Community Benefit Societies Act 2014, schedule 1 to the Housing Act 1996 and the Accounting Requirements for Social Landlords Registered in Wales - General Determination 2009.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the following matters where the Co-Operative and Community Benefit Societies Act 2014 require us to report to you if, in our opinion:

• a satisfactory system of control over transactions has not been maintained; or

• the Association has not kept proper accounting records; or

• the financial statements are not in agreement with the books of account; or

• we have not received all the information and explanations we need for our audit.

Haines Watts Wales LLP Statutory Auditor7 Neptune CourtVanguard WayCardiffCF24 5PJ

12

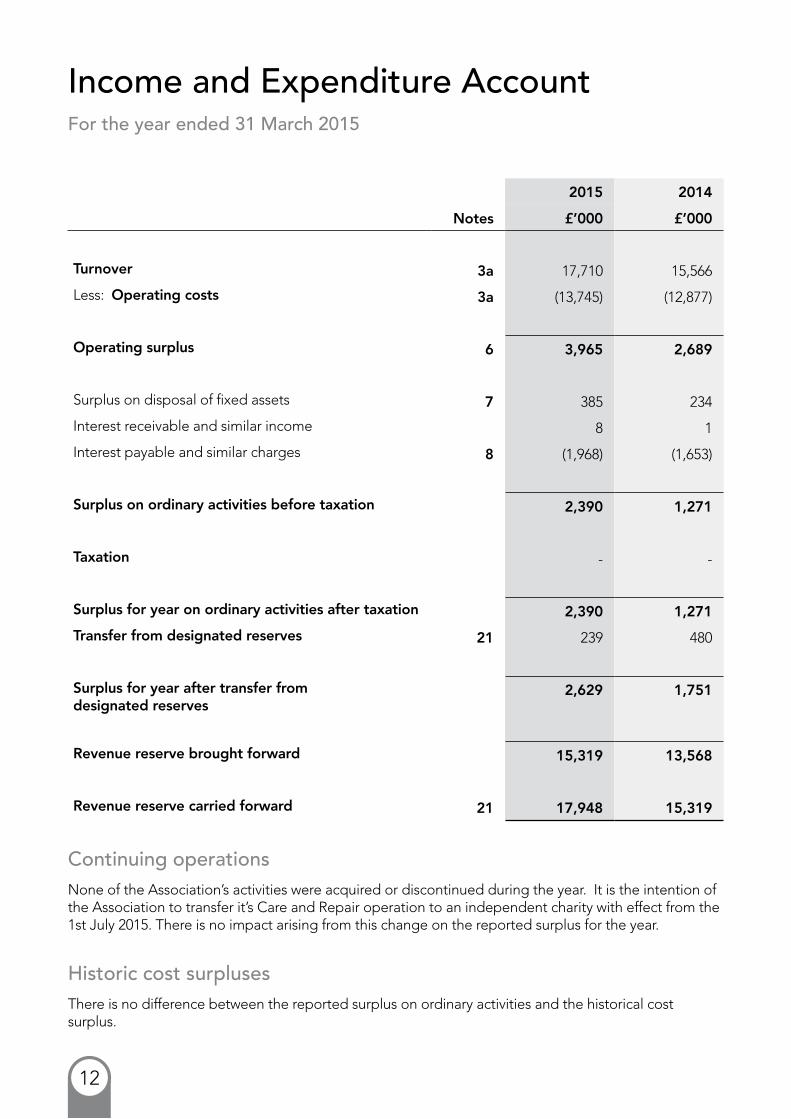

Income and Expenditure AccountFor the year ended 31 March 2015

2015 2014

Notes £’000 £’000

Turnover 3a 17,710 15,566

Less: Operating costs 3a (13,745) (12,877)

Operating surplus 6 3,965 2,689

Surplus on disposal of fixed assets 7 385 234

Interest receivable and similar income 8 1

Interest payable and similar charges 8 (1,968) (1,653)

Surplus on ordinary activities before taxation 2,390 1,271

Taxation - -

Surplus for year on ordinary activities after taxation 2,390 1,271

Transfer from designated reserves 21 239 480

Surplus for year after transfer from designated reserves

2,629 1,751

Revenue reserve brought forward 15,319 13,568

Revenue reserve carried forward 21 17,948 15,319

Continuing operationsNone of the Association’s activities were acquired or discontinued during the year. It is the intention of the Association to transfer it’s Care and Repair operation to an independent charity with effect from the 1st July 2015. There is no impact arising from this change on the reported surplus for the year.

Historic cost surplusesThere is no difference between the reported surplus on ordinary activities and the historical cost surplus.

13

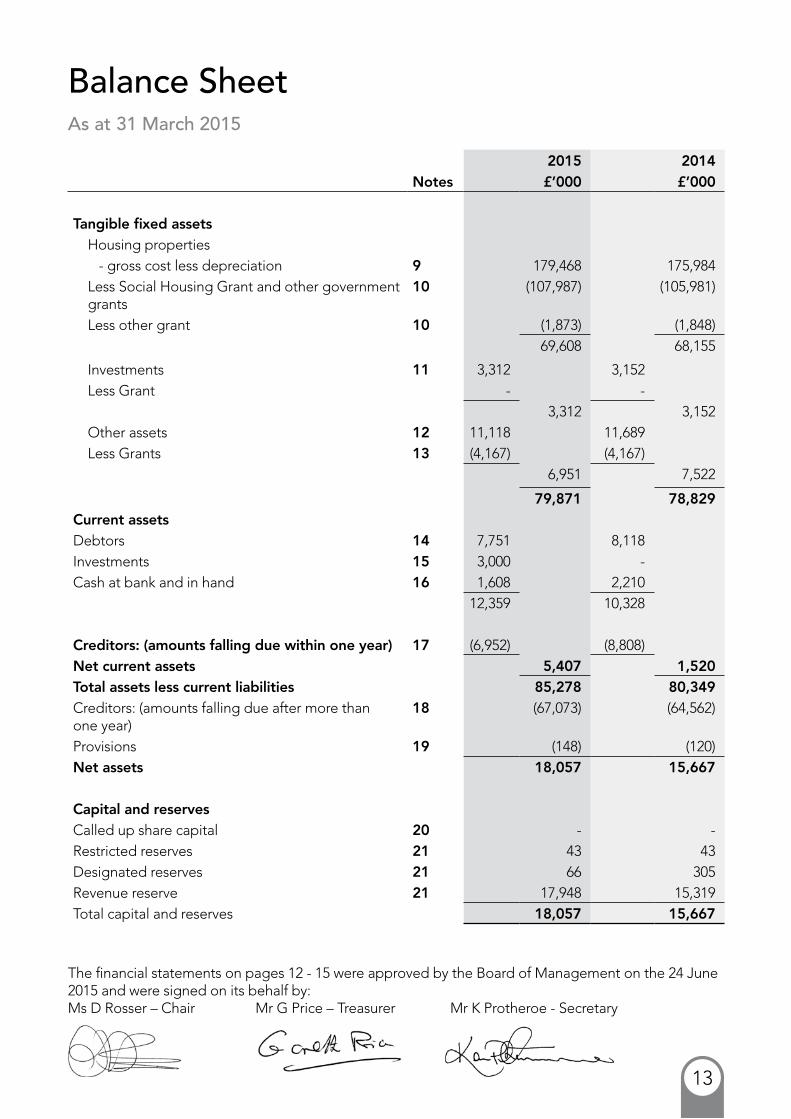

Balance SheetAs at 31 March 2015

2015 2014Notes £’000 £’000

Tangible fixed assets Housing properties - gross cost less depreciation 9 179,468 175,984 Less Social Housing Grant and other government grants

10 (107,987) (105,981)

Less other grant 10 (1,873) (1,848) 69,608 68,155

Investments 11 3,312 3,152 Less Grant - - 3,312 3,152 Other assets 12 11,118 11,689 Less Grants 13 (4,167) (4,167)

6,951 7,522

79,871 78,829Current assetsDebtors 14 7,751 8,118Investments 15 3,000 -Cash at bank and in hand 16 1,608 2,210

12,359 10,328

Creditors: (amounts falling due within one year) 17 (6,952) (8,808)Net current assets 5,407 1,520Total assets less current liabilities 85,278 80,349Creditors: (amounts falling due after more than one year)

18 (67,073) (64,562)

Provisions 19 (148) (120)Net assets 18,057 15,667

Capital and reservesCalled up share capital 20 - -Restricted reserves 21 43 43Designated reserves 21 66 305Revenue reserve 21 17,948 15,319Total capital and reserves 18,057 15,667

The financial statements on pages 12 - 15 were approved by the Board of Management on the 24 June 2015 and were signed on its behalf by: Ms D Rosser – Chair Mr G Price – Treasurer Mr K Protheroe - Secretary

14

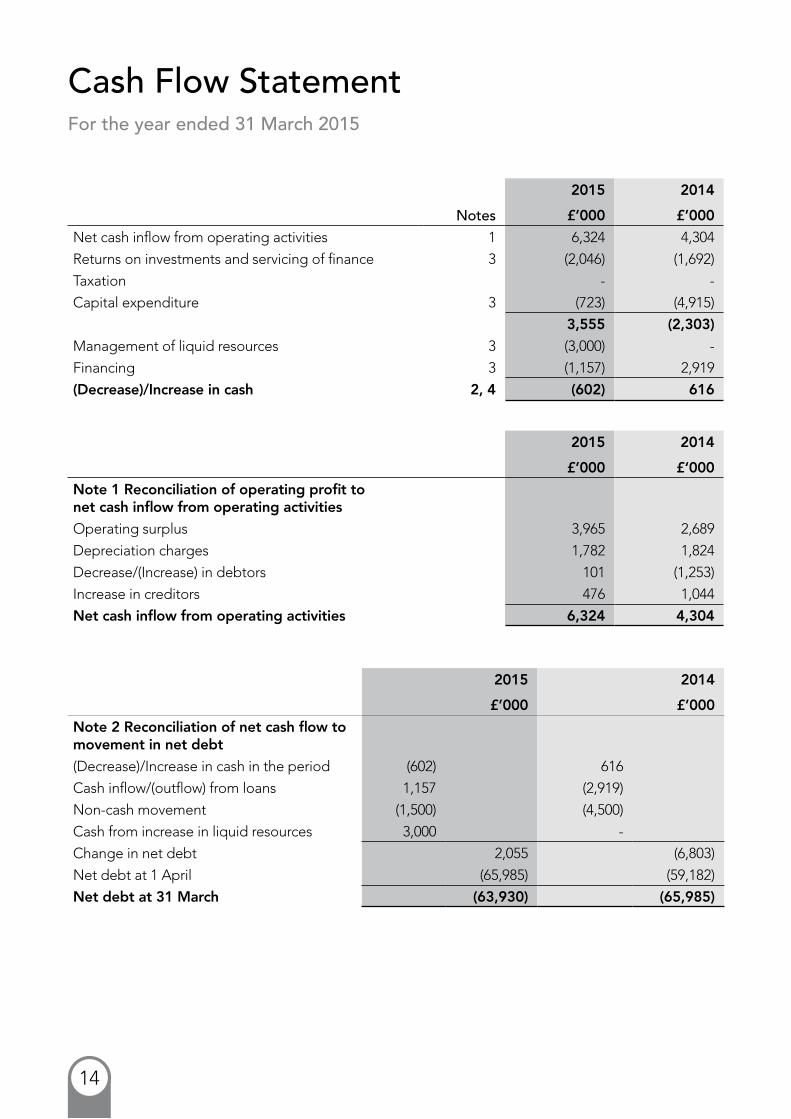

2015 2014

Notes £’000 £’000

Net cash inflow from operating activities 1 6,324 4,304

Returns on investments and servicing of finance 3 (2,046) (1,692)

Taxation - -

Capital expenditure 3 (723) (4,915)

3,555 (2,303)

Management of liquid resources 3 (3,000) -

Financing 3 (1,157) 2,919

(Decrease)/Increase in cash 2, 4 (602) 616

2015 2014

£’000 £‘000

Note 1 Reconciliation of operating profit to net cash inflow from operating activities

Operating surplus 3,965 2,689

Depreciation charges 1,782 1,824

Decrease/(Increase) in debtors 101 (1,253)

Increase in creditors 476 1,044

Net cash inflow from operating activities 6,324 4,304

2015 2014

£’000 £’000

Note 2 Reconciliation of net cash flow to movement in net debt

(Decrease)/Increase in cash in the period (602) 616

Cash inflow/(outflow) from loans 1,157 (2,919)

Non-cash movement (1,500) (4,500)

Cash from increase in liquid resources 3,000 -

Change in net debt 2,055 (6,803)

Net debt at 1 April (65,985) (59,182)

Net debt at 31 March (63,930) (65,985)

Cash Flow Statement For the year ended 31 March 2015

15

Cash Flow Statement For the year ended 31 March 2015

2015 2014

£’000 £’000

Note 3 Gross cash flows

Returns on investments and servicing of finance

Interest received 8 1

Interest paid (2,054) (1,693)

(2,046) (1,692)

Capital expenditure

Payments to acquire tangible fixed assets (5,925) (6,805)

Social Housing Grant received 3,783 1,681

Receipts from sale of tangible fixed assets 1,394 88

Capital Grants received/(repaid) 25 121

(723) (4,915)

Management of liquid resources

Investments made (14,000) -

Investments redeemed 11,000 -

(3,000) -

Financing

Issue of ordinary share capital - -

Housing loans received 2,476 4,000

Housing loans repaid (3,633) (1,081)

(1,157) 2,919

At 1 April 2014

Cash flows

Other changes

At 31 March 2015

£’000 £’000 £’000 £’000

Note 4 Analysis of changes in net debt

Cash at bank and in hand 2,210 (602) - 1,608

Loans due within one year (3,633) 3,633 (1,465) (1,465)

Loans due after one year (64,562) (2,476) (35) (67,073)

Current asset investments - 3,000 - 3,000

Net Debt (65,985) 3,555 (1,500) (63,930)

16

1. Legal status

The Association is registered under the Co-Operative and Community Benefit Societies Act 2014 and is a registered social landlord. The Association has adopted charitable rules.

2. Accounting policies

Introduction and accounting basis

The principal accounting policies of the Association are set out in the paragraphs below. These financial statements are prepared under the historical cost convention and have been prepared in accordance with applicable Accounting Standards and Statements of Recommended Practice in the United Kingdom and in particular with the Statement of Recommended Practice - Accounting by Registered Social Landlords updated in 2010, and the Accounting Requirements for Social Landlords Registered in Wales – General Determination 2009.

Turnover (note 3(b))

Turnover represents rent and service income receivable less voids, income from properties leased to the City and County of Cardiff and various grants receivable from Supporting People and others. Grants receivable are recognised as income when the terms and conditions of the grant are met. Turnover also includes income relating to the costs of assets under construction built for third parties.

Fixed assets

Capitalisation of housing properties (note 9)

Properties - Initial Costs. Housing properties are measured at cost which includes only those costs which are directly attributable. Apart from land costs, contract payments, architect’s fees etc., certain internal costs are also capitalised. These internal costs relate to costs directly attributable to bringing an asset into management, together with incremental costs incurred by the Association that would have been avoided if the asset had not been acquired. In practice this includes only the internal staff costs directly attributable in bringing a scheme into management but not

associated overheads. Expenditure on abortive schemes is written off to revenue in the year the scheme is deemed abortive. Lifts are treated as a separate class of asset. The accounting for mixed development follows a similar basis.

Properties - Additional Costs. Expenditure relating to planned maintenance or improvement will only be capitalised if it results in an increase to the economic performance of the asset. If the expenditure only maintained the asset’s performance or arrested its decline in performance, it cannot be capitalised. To increase an asset’s performance, expenditure must result in one or more of the following occurring:

• increased rental income

• a reduction in future maintenance costs

• a significant extension to the life of the property

Impairment Review - Properties should not be shown at an amount exceeding their recoverable amount. The Association checks annually for any indication of impairment by reference to:

• trends in the rate of voids and letting of stock

• advice from external valuers regarding their expectations of the value of stock.

Where there is any indication of impairment, a full review is carried out.

Capitalisation of interest (note 8)

Interest on capital borrowed to enable the financing of each development is capitalised, to the extent that it accrues in respect of the period of the development, in accordance with the Statement of Recommended Practice - Accounting by Registered Social Landlords 2010. In such instances, the development activities are demonstrably in progress. The capitalisation of interest represents either:

a fair proportion of interest on borrowings of the Association as a whole; or

interest on borrowings specifically financing the development programme or scheme.

Notes to the Financial Statements

17

Notes to the Financial Statements

The amount of interest capitalised during the period is disclosed in a note to the accounts as a deduction from total interest payable in the period. The interest capitalised is based on the average cost of borrowing, except where a specific loan facility is used to fund the development, in which case the interest on the specific loan is used.

Should any development become abortive, the capitalised interest is written-off and charged to the income and expenditure account in the year the development is aborted.

Depreciation (notes 9 and 12)

Depreciation is charged on a straight line basis using the historic cost of property components after deduction of grants. Where a housing property comprises two or more major components with substantially different useful economic lives, each component is accounted for separately and depreciated over its individual useful economic life.

The following lives are to be used in relation to new properties built or acquired:

• Modern purpose built houses 150 years

• Modern purpose built flats 100 years

• Older refurbished houses 100 years

• Older refurbished flats 50 years

Other Components

• Doors 30 years

• Bathrooms 27 years

• Boilers 15 years

• Boiler plant 25 years

• Electrical heating 15 years

• Kitchens 25 years

• Flat roofs 65 years

• Windows 30 years

Freehold land and housing properties in the course of construction are not depreciated.

The assets are depreciated on the straight-line basis and the residual value of the asset relates solely to the cost of the land held in the balance sheet.

The only exception to this policy relates to the lifts at various locations which are to be depreciated over 25 years. The depreciable amount relates to the mechanical part of the lift and excludes the lift shaft.

Other fixed assets (note 12)

The Board of Management has determined the cost of the office premises, excluding land, to be depreciated at a rate of 2% of cost per annum.

Office fittings, furnishings and telephone equipment are depreciated at a rate of 10% of original cost per annum.

Motor vehicles are depreciated at a rate of 25% per annum on a reducing balance basis.

Computer and other electronic equipment is depreciated within a range of rates of 16.67% - 25% of cost per annum.

Assets for which a service charge is made to tenants

The Rent Officer has determined a range of capitalisation periods for fittings and furnishings for which a service charge can be levied on tenants. These periods range from 25 years for lifts (4% per annum) to 8 years for appliances (12.5% per annum).

Social Housing Grants (Housing Association Grants) (notes 10 and 23)

Housing Association Grants (HAG) were historically made by the former Welsh Office and were utilised to reduce the amount of mortgage-loan in respect of an approved scheme to the amount which it was estimated could be serviced by the net annual income of the scheme.

18

Notes to the Financial Statements

The 1988 Housing Act introduced HAG as a fixed percentage of the approved scheme cost. In 1996 this grant was renamed Social Housing Grant (SHG). SHG that is wholly pre-determined is referred to in the financial statements as “fixed SHG”. SHG is now awarded by the Welsh Government.

These grants are received from central government agencies and local authorities and are offset against the cost of housing properties on the face of the balance sheet. The Companies Act 1985 requires tangible fixed assets to be included at purchase price or production cost, less any provision for depreciation or diminution in value. However, this requirement conflicts with the generally accepted accounting principles for Registered Social Housing Providers set out in the Statement of Recommended Practice (SORP): Accounting by Registered Social Housing Providers. The purpose of grants is to subsidise the capital cost of affordable housing. Accordingly, management consider it necessary to adopt the accounting treatment set out in the SORP to give a true and fair view.

The amount of SHG is calculated on the qualifying cost of the scheme in accordance with instructions issued from time to time by the Welsh Government. The grants are paid directly to the lending authority and are reflected in the accounts of the Association either: when the payment has been made and the relevant mortgage loan reduced or when fixed SHG has been claimed from the lending authority.

SHG received at the end of the year has been allocated over the aggregate cost of development. Any SHG in advance included in the creditors is the net of SHG receivable in respect of the units in development less the total costs capitalised in respect of those units.

SHG is recycled under certain circumstances; primarily following the sale of a property, but is normally restricted to net proceeds of sale. Work to existing housing properties is generally treated as repairs and charged to the income and expenditure account. Where works are for the purpose of improvement then that expenditure is capitalised in housing properties. SHG is matched to the category of expenditure within the income

and expenditure account or balance sheet as appropriate. Surplus SHG may be repayable to the Welsh Government in circumstances where it is not possible to recycle grant funding on new developments.

Fixed Asset Investments (note 11)

The Rent to Mortgage scheme was introduced by S.108 of the Leasehold Reform, Housing and Urban Development Act 1993 and ceased on 18th July 2005 under S.190 of the Housing Act 2005. The scheme provided a number of secure tenants with the statutory right to purchase part of their property, with the remaining portion retained by the Association. The Association made one sale under this legislation during 2002/03. This scheme ended during the year on the sale of the property in question.

The accounting treatment adopted follows that of Homebuy as outlined in the SORP updated 2010. Thus the Association’s share of the property is shown as a fixed asset investment at gross cost in the balance sheet with the grant from the Welsh Government being recognised separately.

Grant is abated to the extent that the proceeds from the sale of the property are lower than the historic cost. In such circumstances this abatement is shown as a contingent liability (see note 23). Any future increase/decrease in the value of the property will reduce/increase the abatement.

19

Notes to the Financial Statements

Low-Cost Home Ownership (note 11)

From 2004/05 the Association has embarked on the sale of particular properties through Low-Cost Home Ownership (LCHO). These sales have been undertaken without SHG funding. Under the LCHO scheme the purchaser pays the Association a specified proportion of the market value of the property with the remaining proportion of the value funded through a loan from the Association. Interest is not paid during the life of the loan. Rather, when the property is sold the Association receives the equivalent proportion of the gross receipt as repayment of the loan plus interest. Thus, the interest rate is not known until the time of sale. In addition, the market value of the property may be below that prevailing at the time of the sale. In such circumstances the Association receives an amount that is lower than the loan initially provided.

All assets under construction, whether for resale or not, are shown in the balance sheet as assets under construction. On completion of the asset, the asset is transferred to fixed asset investments, but only if the asset has been designated for resale. If SHG from the Welsh Government has been received against these properties, this is recognised separately (see note 11). Once these assets have been sold the full asset value is disposed of. As a consequence, only the loan from the Association to the tenant remains within the balance sheet after sale. These loans are also held within fixed asset investments at their original cost.

Long-term contracts

The Association, on occasion, provides management services in respect of the procurement and construction of developments for other social housing providers. These contracts can extend over more than one accounting period. In accordance with SSAP 9 and UITF 40 the accounting treatment in respect of long-term contracts is therefore adopted. This requires that where the outcome of a contract can be assessed with reasonable certainty, even though it is not complete, then part of the surplus attributable to the work performed at

the accounting date should be included in the Income and Expenditure account for the year. Where it is not possible to assess the degree of surplus with any certainty, the turnover and cost recognised should be equal; the effect being to recognise surplus on that contract. Full provision is made for all known or anticipated expenditure on individual contracts; taking a prudent view of future claims income immediately at the point when such expenditure is foreseen.

The services provided by the Association are charged out with the purpose to recover only the cost of the provision of the service. The surplus on these services is taken as zero and the transfer to turnover therefore, equals the amount recorded as cost of sales (see note 3a).

The amount by which turnover exceeds payments received on account is shown separately under debtors as amounts recoverable under contracts, and is a classification specific to long-term contracts (see note 14).

Treasury policy

The Association’s treasury policy is concerned with the effective control of the risks associated with the management of its cash flows, banking, money market and capital market transactions, and the pursuit of optimum performance consistent with those risks. In respect of monies borrowed, interest payable is minimised within a balanced loan portfolio aimed at reducing exposure to interest rate variability, whilst investments aim to maximise return whilst minimising risk.

Pensions

The Association participates in the Social Housing Pension Scheme. Retirement benefits to employees of the Association are funded by contributions from all participating employees and employers in the scheme. Payments are made to a fund operated by the Pensions Trust: an independent Trust providing superannuation benefits to employees of voluntary organisations. These payments are made in accordance with periodic calculations by consulting actuaries and

20

Notes to the Financial Statements

are based on pension costs applicable across the various participating associations taken as a whole.

In addition, staff are able to make additional voluntary contributions (AVCs) into the Pension Trust’s Growth Plan in respect of their pension through the Association. The Association does not make any financial contribution towards this element of the staff member’s pension.

The Association also contributes to a defined contribution scheme run by Standard Life. This scheme was inherited from Adamsdown Housing Association in 1996 when CCHA was formed from the merger of the Adamsdown and Moors Housing Associations. Scheme membership within CCHA is declining as members leave. The scheme is not open to new members. The provisions of FRS 17 “Retirement Benefits” have been adopted. The expected cost of pensions to the Association is charged to the Income & Expenditure account, spreading the cost of pensions over the service lives of employees.

Major repairs/WHQS and other designated reserves (note 21)

The major repairs/WHQS designated reserve was created to fund the works required to achieve WHQS compliance on our housing stock. During 2015/16 we are completing a stock condition survey of all properties to identify the future cost of maintaining our housing stock. The ongoing use of this reserve is under review pending implementation of the Housing SORP 2014.

In addition to the Major Repairs/WHQS designated reserve, the Association maintains a designated reserve for the replacement of certain items of capital equipment in managed properties for which a service charge is made.

In 2004/05 the Housing Association Property Mutual reduced insurance cover on certain properties from 35 to 20 years. The monies the Association received in recompense have been set aside in a designated reserve to contribute to future claims against the properties concerned.

In 2007/08 the Association established a designated reserve for the Care and Repair Agency. In 2014/15 the balance on the reserve has been transferred the Revenue Reserve pending the creation of the Agency as an independent charity on the 1st July 2015.

Restricted reserves (note 21)

During 2004/05 the Association received a donation of Tremorfa Hall. Its use is restricted to activities beneficial to the social sustainability of the area, and as such in accordance with the SORP updated 2008, a transfer was made to restricted reserves equivalent to the value of the property.

Apportionment of management expenses

Direct employees administration and operating costs have been apportioned to the relevant activities on the basis of costs of the staff to the extent that they are directly engaged in each of the activities and such activities rightfully attract overhead cost.

Taxation

CCHA is not liable for Corporation Tax due to its charitable status. The Association accounts for its Value Added Tax (VAT) within its appropriate cost structures to the extent that it is not recoverable.

Lease obligations

Rentals paid under lease obligations are charged to the income and expenditure account under the accruals basis. Where an asset is created under a finance lease this will be recorded in the Association’s balance sheet.

21

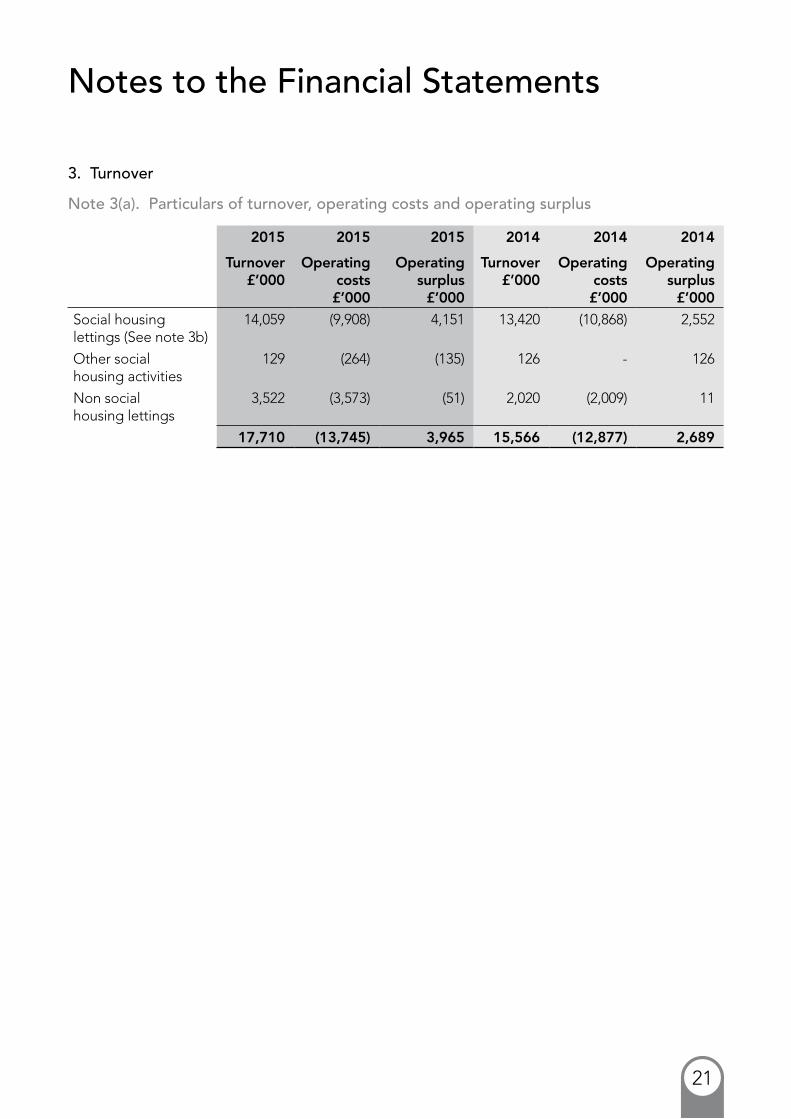

Notes to the Financial Statements

3. Turnover

Note 3(a). Particulars of turnover, operating costs and operating surplus

2015 2015 2015 2014 2014 2014

Turnover £’000

Operating costs £’000

Operating surplus

£’000

Turnover £’000

Operating costs £’000

Operating surplus

£’000

Social housing lettings (See note 3b)

14,059 (9,908) 4,151 13,420 (10,868) 2,552

Other social housing activities

129 (264) (135) 126 - 126

Non social housing lettings

3,522 (3,573) (51) 2,020 (2,009) 11

17,710 (13,745) 3,965 15,566 (12,877) 2,689

22

Notes to the Financial Statements

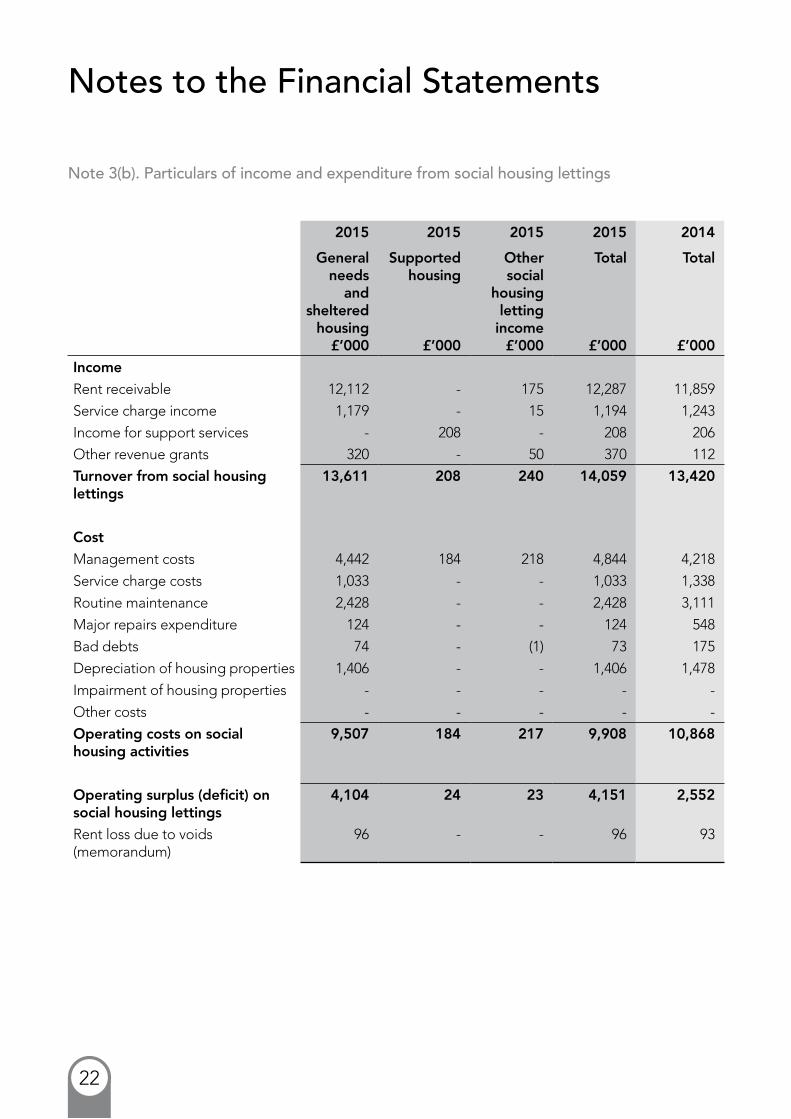

Note 3(b). Particulars of income and expenditure from social housing lettings

2015 2015 2015 2015 2014

General needs

and sheltered

housing £’000

Supported housing

£’000

Other social

housing letting

income £’000

Total

£’000

Total

£’000

Income

Rent receivable 12,112 - 175 12,287 11,859

Service charge income 1,179 - 15 1,194 1,243

Income for support services - 208 - 208 206

Other revenue grants 320 - 50 370 112

Turnover from social housing lettings

13,611 208 240 14,059 13,420

Cost

Management costs 4,442 184 218 4,844 4,218

Service charge costs 1,033 - - 1,033 1,338

Routine maintenance 2,428 - - 2,428 3,111

Major repairs expenditure 124 - - 124 548

Bad debts 74 - (1) 73 175

Depreciation of housing properties 1,406 - - 1,406 1,478

Impairment of housing properties - - - - -

Other costs - - - - -

Operating costs on social housing activities

9,507 184 217 9,908 10,868

Operating surplus (deficit) on social housing lettings

4,104 24 23 4,151 2,552

Rent loss due to voids (memorandum)

96 - - 96 93

23

Notes to the Financial Statements

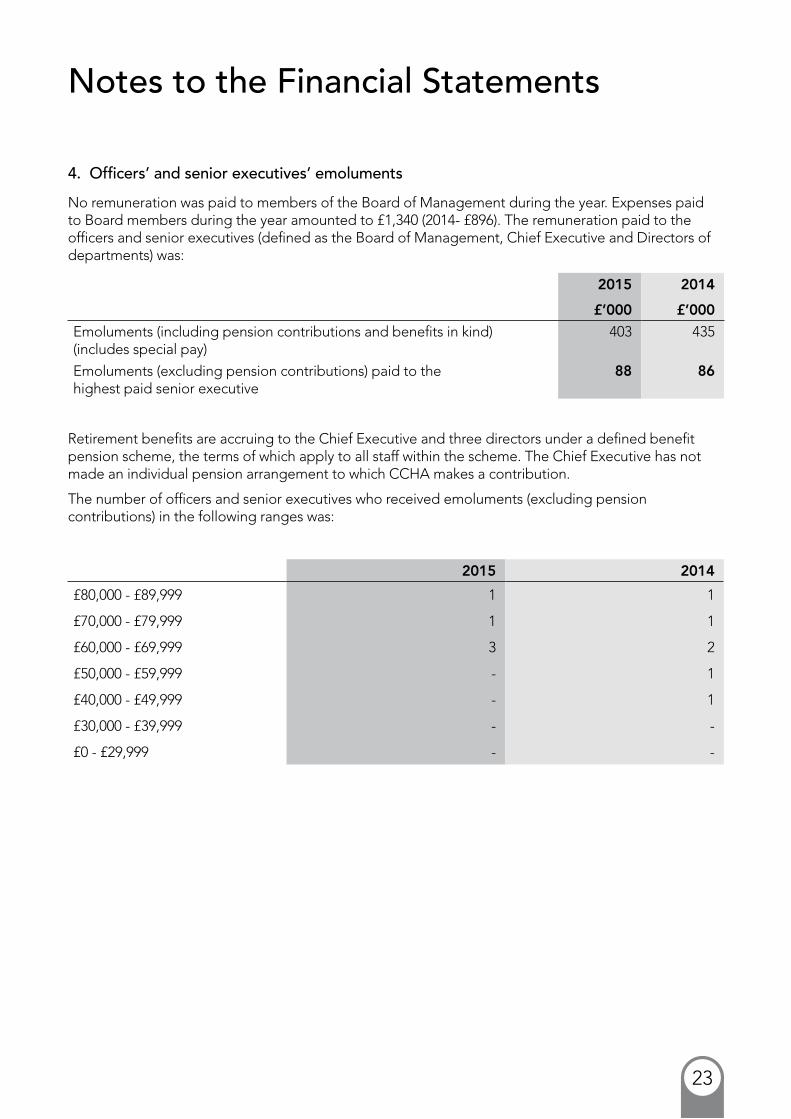

4. Officers’ and senior executives’ emoluments

No remuneration was paid to members of the Board of Management during the year. Expenses paid to Board members during the year amounted to £1,340 (2014- £896). The remuneration paid to the officers and senior executives (defined as the Board of Management, Chief Executive and Directors of departments) was:

2015 2014

£’000 £’000

Emoluments (including pension contributions and benefits in kind) (includes special pay)

403 435

Emoluments (excluding pension contributions) paid to the highest paid senior executive

88 86

Retirement benefits are accruing to the Chief Executive and three directors under a defined benefit pension scheme, the terms of which apply to all staff within the scheme. The Chief Executive has not made an individual pension arrangement to which CCHA makes a contribution.

The number of officers and senior executives who received emoluments (excluding pension contributions) in the following ranges was:

2015 2014

£80,000 - £89,999 1 1

£70,000 - £79,999 1 1

£60,000 - £69,999 3 2

£50,000 - £59,999 - 1

£40,000 - £49,999 - 1

£30,000 - £39,999 - -

£0 - £29,999 - -

24

Notes to the Financial Statements

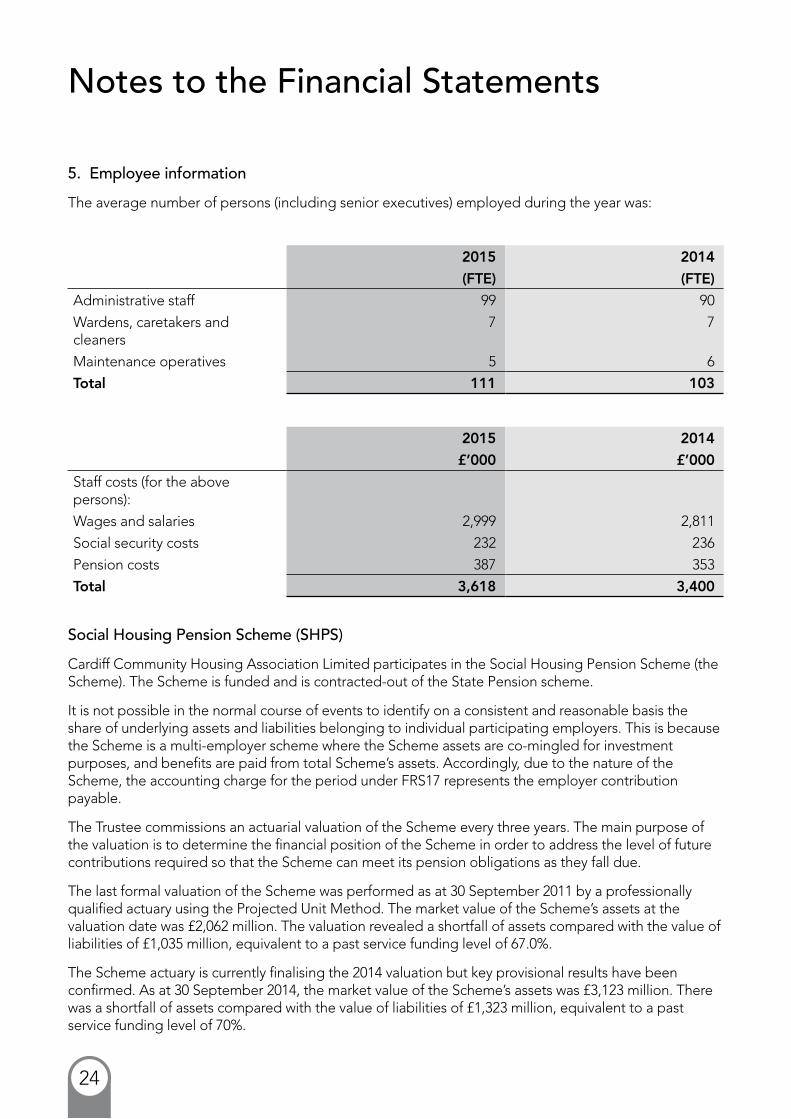

5. Employee information

The average number of persons (including senior executives) employed during the year was:

2015 2014

(FTE) (FTE)

Administrative staff 99 90

Wardens, caretakers and cleaners

7 7

Maintenance operatives 5 6

Total 111 103

2015 2014

£’000 £’000

Staff costs (for the above persons):

Wages and salaries 2,999 2,811

Social security costs 232 236

Pension costs 387 353

Total 3,618 3,400

Social Housing Pension Scheme (SHPS)

Cardiff Community Housing Association Limited participates in the Social Housing Pension Scheme (the Scheme). The Scheme is funded and is contracted-out of the State Pension scheme.

It is not possible in the normal course of events to identify on a consistent and reasonable basis the share of underlying assets and liabilities belonging to individual participating employers. This is because the Scheme is a multi-employer scheme where the Scheme assets are co-mingled for investment purposes, and benefits are paid from total Scheme’s assets. Accordingly, due to the nature of the Scheme, the accounting charge for the period under FRS17 represents the employer contribution payable.

The Trustee commissions an actuarial valuation of the Scheme every three years. The main purpose of the valuation is to determine the financial position of the Scheme in order to address the level of future contributions required so that the Scheme can meet its pension obligations as they fall due.

The last formal valuation of the Scheme was performed as at 30 September 2011 by a professionally qualified actuary using the Projected Unit Method. The market value of the Scheme’s assets at the valuation date was £2,062 million. The valuation revealed a shortfall of assets compared with the value of liabilities of £1,035 million, equivalent to a past service funding level of 67.0%.

The Scheme actuary is currently finalising the 2014 valuation but key provisional results have been confirmed. As at 30 September 2014, the market value of the Scheme’s assets was £3,123 million. There was a shortfall of assets compared with the value of liabilities of £1,323 million, equivalent to a past service funding level of 70%.

25

Notes to the Financial Statements

Growth plan

The Association has one employee participating in the Pension Trusts growth plan as an AVC investment option. This is a multi-employer pension plan which is in most respects a money purchase arrangement but with some guarantees. The Association does not pay any contributions to the growth plan.

Following legislative changes in the Occupational Pension Schemes (Employer Debt on Withdrawal) Regulation 2005 there is a potential debt on the employer, which under the trustees’ policy applies to employers with pre-October 2001 liabilities in the plan and would be due should the employer cease to participate in the plan or the plan winding up. Whilst the amounts of debt can be volatile over time, depending on factors such as investment performance and financial conditions at the time of the cessation event, the Association has been notified by the Pensions Trust that the estimated employer debt on withdrawal from the plan based on the financial position of the plan as at 30th September 2012 was £13,851 (see Contingent Liabilities Note 23).

Standard Life scheme

The Association also participates in a defined contribution pension scheme in respect of certain staff members who transferred from Adamsdown Housing Association Limited. The assets of the scheme are held separately from those of the Association in an independently administered fund. The pensions cost charge included an amount of £5,568 (2013-14 - £5,522) which represents contributions payable by the Association to the fund. There were no outstanding or prepaid contributions as of the balance sheet date.

6. Operating surplus

The operating surplus is stated after charging:

2015 2014

£’000 £’000

Depreciation 1,782 1,824

Capital works written off to revenue

- -

Auditors remuneration

– in their capacity as auditors

17 17

– in respect of other services

- -

Rent losses from bad debts

73 175

7. Profit & loss on sale of fixed assets

2015 2014

£’000 £’000

Sales of property under right to buy/right to acquire/rent to mortgage legislation and LCHO sales

898 421

Less: Cost of sale

(513) (187)

Total 385 234

26

Notes to the Financial Statements

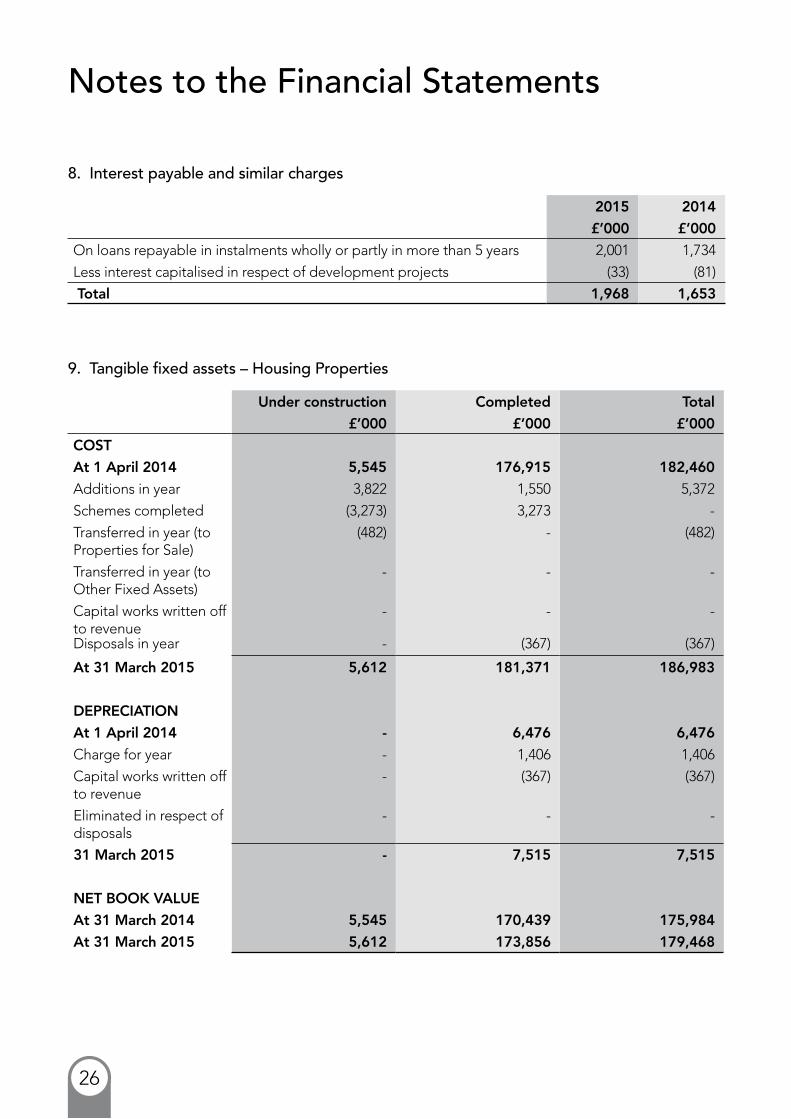

8. Interest payable and similar charges

2015 2014

£’000 £’000

On loans repayable in instalments wholly or partly in more than 5 years 2,001 1,734

Less interest capitalised in respect of development projects (33) (81)

Total 1,968 1,653

9. Tangible fixed assets – Housing Properties

Under construction Completed Total

£’000 £’000 £’000

COST

At 1 April 2014 5,545 176,915 182,460

Additions in year 3,822 1,550 5,372

Schemes completed (3,273) 3,273 -

Transferred in year (to Properties for Sale)

(482) - (482)

Transferred in year (to Other Fixed Assets)

- - -

Capital works written off to revenue

- - -

Disposals in year - (367) (367)

At 31 March 2015 5,612 181,371 186,983

DEPRECIATION

At 1 April 2014 - 6,476 6,476

Charge for year - 1,406 1,406

Capital works written off to revenue

- (367) (367)

Eliminated in respect of disposals

- - -

31 March 2015 - 7,515 7,515

NET BOOK VALUE

At 31 March 2014 5,545 170,439 175,984

At 31 March 2015 5,612 173,856 179,468

27

Notes to the Financial Statements

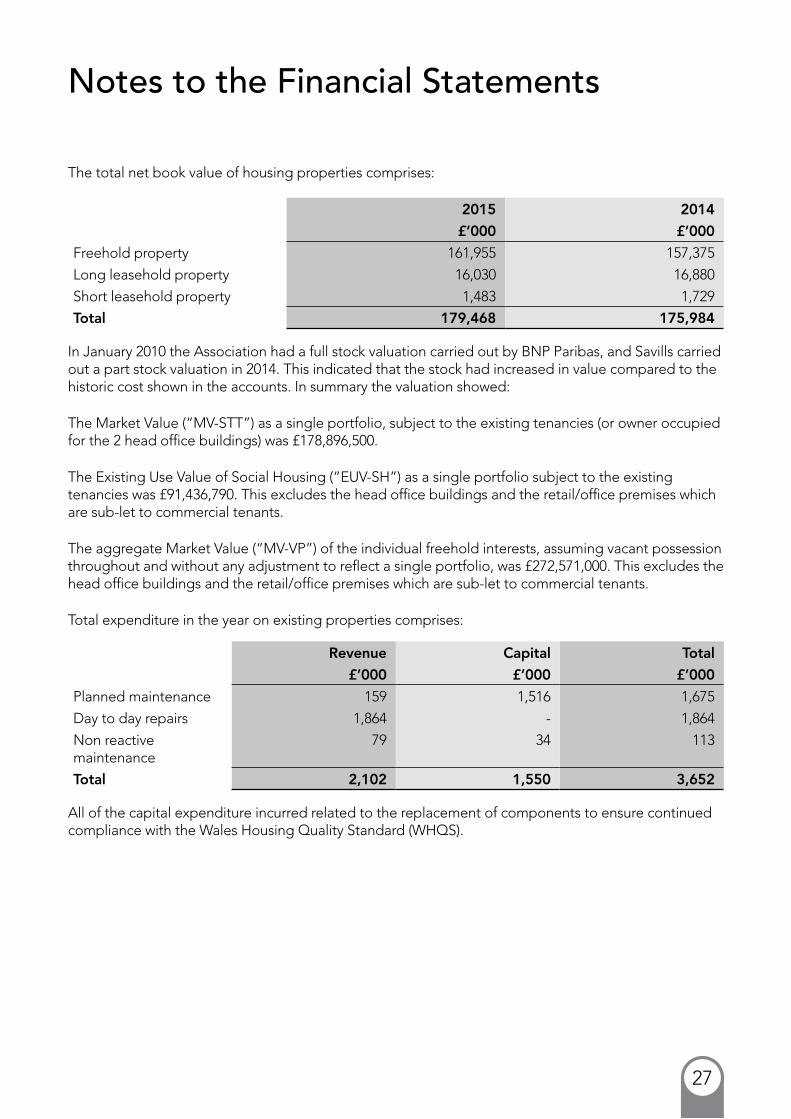

The total net book value of housing properties comprises:

2015 2014

£’000 £’000

Freehold property 161,955 157,375

Long leasehold property 16,030 16,880

Short leasehold property 1,483 1,729

Total 179,468 175,984

In January 2010 the Association had a full stock valuation carried out by BNP Paribas, and Savills carried out a part stock valuation in 2014. This indicated that the stock had increased in value compared to the historic cost shown in the accounts. In summary the valuation showed:

The Market Value (“MV-STT”) as a single portfolio, subject to the existing tenancies (or owner occupied for the 2 head office buildings) was £178,896,500.

The Existing Use Value of Social Housing (“EUV-SH”) as a single portfolio subject to the existing tenancies was £91,436,790. This excludes the head office buildings and the retail/office premises which are sub-let to commercial tenants.

The aggregate Market Value (“MV-VP”) of the individual freehold interests, assuming vacant possession throughout and without any adjustment to reflect a single portfolio, was £272,571,000. This excludes the head office buildings and the retail/office premises which are sub-let to commercial tenants.

Total expenditure in the year on existing properties comprises:

Revenue Capital Total

£’000 £’000 £’000

Planned maintenance 159 1,516 1,675

Day to day repairs 1,864 - 1,864

Non reactive maintenance

79 34 113

Total 2,102 1,550 3,652

All of the capital expenditure incurred related to the replacement of components to ensure continued compliance with the Wales Housing Quality Standard (WHQS).

28

Notes to the Financial Statements

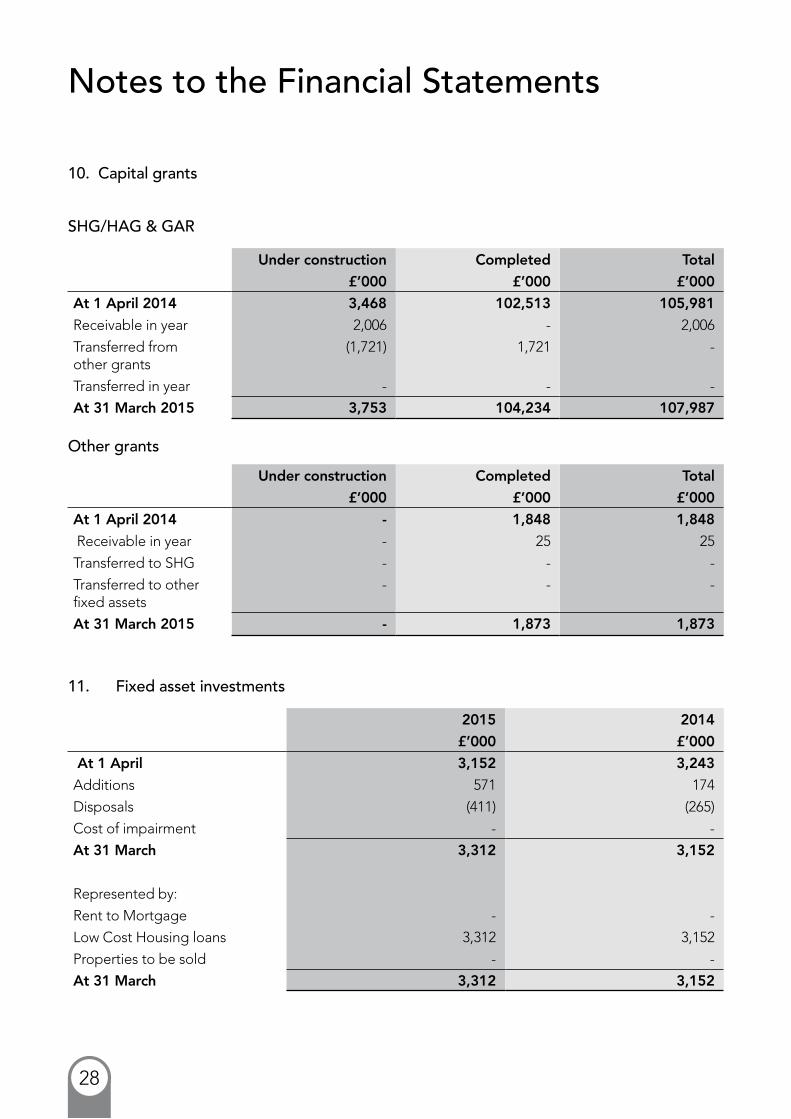

10. Capital grants

SHG/HAG & GAR

Under construction Completed Total

£’000 £’000 £’000

At 1 April 2014 3,468 102,513 105,981

Receivable in year 2,006 - 2,006

Transferred from other grants

(1,721) 1,721 -

Transferred in year - - -

At 31 March 2015 3,753 104,234 107,987

Other grants

Under construction Completed Total

£’000 £’000 £’000

At 1 April 2014 - 1,848 1,848

Receivable in year - 25 25

Transferred to SHG - - -

Transferred to other fixed assets

- - -

At 31 March 2015 - 1,873 1,873

11. Fixed asset investments

2015 2014

£’000 £’000

At 1 April 3,152 3,243

Additions 571 174

Disposals (411) (265)

Cost of impairment - -

At 31 March 3,312 3,152

Represented by:

Rent to Mortgage - -

Low Cost Housing loans 3,312 3,152

Properties to be sold - -

At 31 March 3,312 3,152

29

Notes to the Financial Statements

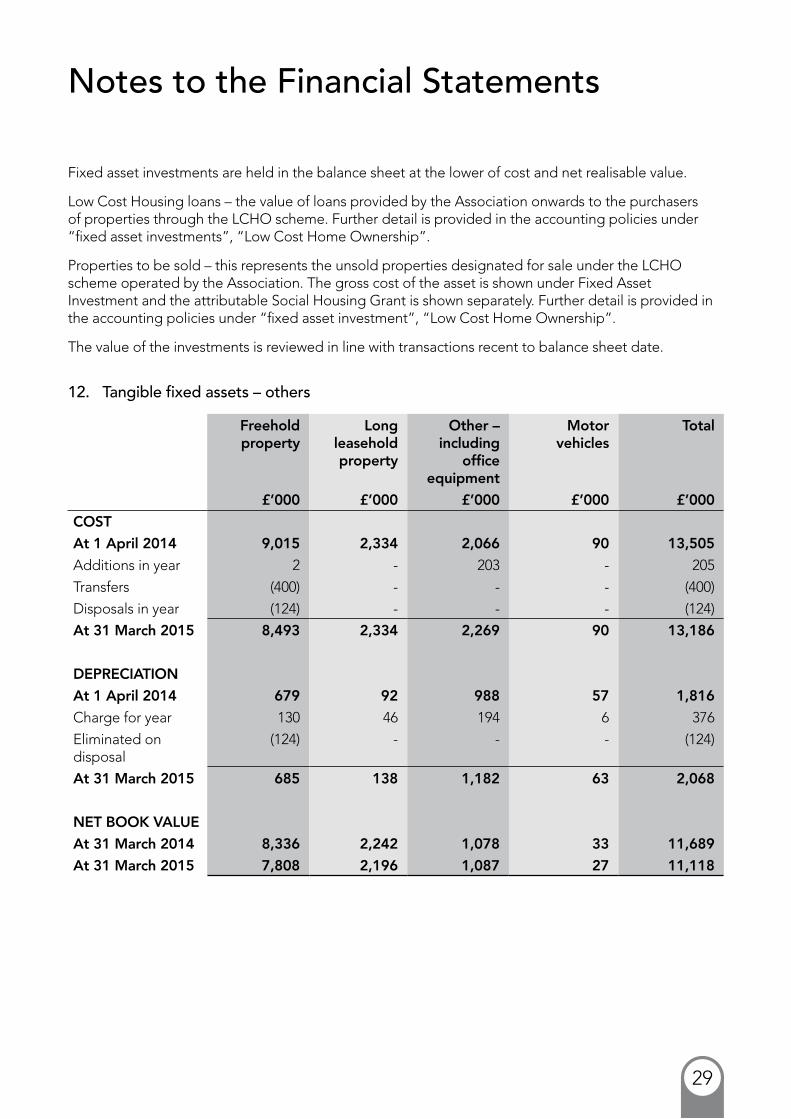

Fixed asset investments are held in the balance sheet at the lower of cost and net realisable value.

Low Cost Housing loans – the value of loans provided by the Association onwards to the purchasers of properties through the LCHO scheme. Further detail is provided in the accounting policies under “fixed asset investments”, “Low Cost Home Ownership”.

Properties to be sold – this represents the unsold properties designated for sale under the LCHO scheme operated by the Association. The gross cost of the asset is shown under Fixed Asset Investment and the attributable Social Housing Grant is shown separately. Further detail is provided in the accounting policies under “fixed asset investment”, “Low Cost Home Ownership”.

The value of the investments is reviewed in line with transactions recent to balance sheet date.

12. Tangible fixed assets – others

Freehold property

Long leasehold property

Other – including

office equipment

Motor vehicles

Total

£’000 £’000 £’000 £’000 £’000

COST

At 1 April 2014 9,015 2,334 2,066 90 13,505

Additions in year 2 - 203 - 205

Transfers (400) - - - (400)

Disposals in year (124) - - - (124)

At 31 March 2015 8,493 2,334 2,269 90 13,186

DEPRECIATION

At 1 April 2014 679 92 988 57 1,816

Charge for year 130 46 194 6 376

Eliminated on disposal

(124) - - - (124)

At 31 March 2015 685 138 1,182 63 2,068

NET BOOK VALUE

At 31 March 2014 8,336 2,242 1,078 33 11,689

At 31 March 2015 7,808 2,196 1,087 27 11,118

30

Notes to the Financial Statements

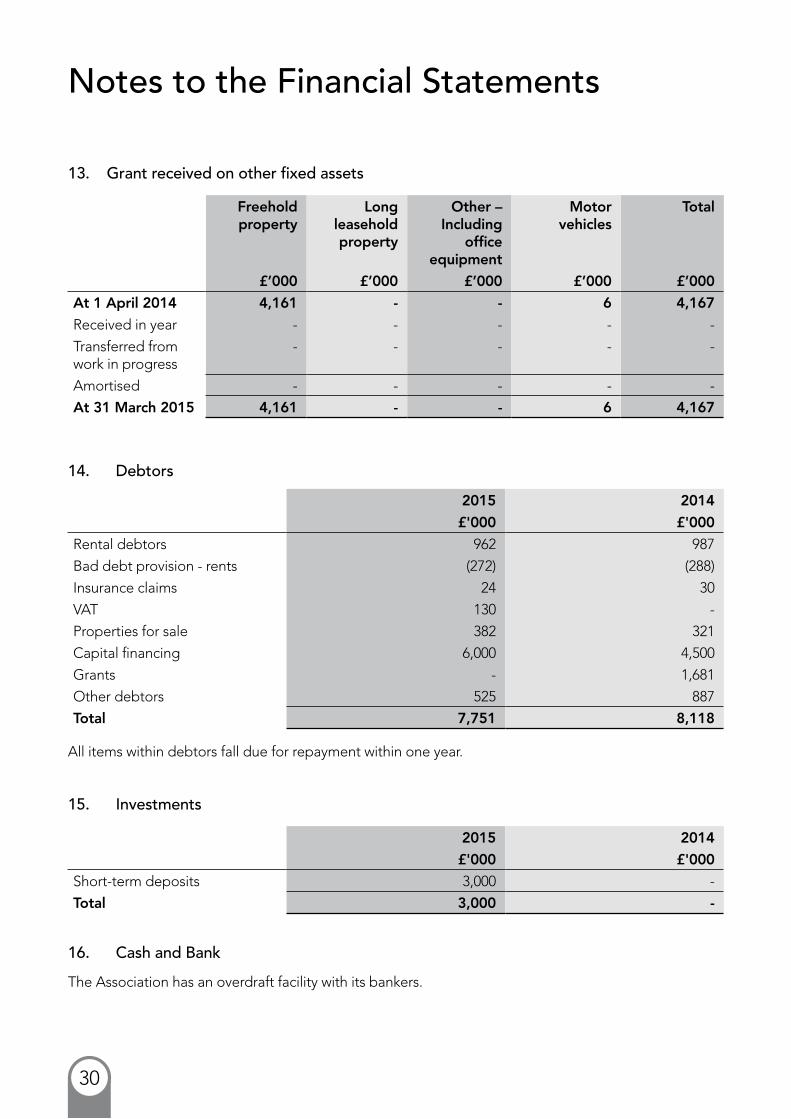

13. Grant received on other fixed assets

Freehold property

Long leasehold property

Other – Including

office equipment

Motor vehicles

Total

£’000 £’000 £’000 £’000 £’000

At 1 April 2014 4,161 - - 6 4,167

Received in year - - - - -

Transferred from work in progress

- - - - -

Amortised - - - - -

At 31 March 2015 4,161 - - 6 4,167

14. Debtors

2015 2014

£'000 £'000

Rental debtors 962 987

Bad debt provision - rents (272) (288)

Insurance claims 24 30

VAT 130 -

Properties for sale 382 321

Capital financing 6,000 4,500

Grants - 1,681

Other debtors 525 887

Total 7,751 8,118

All items within debtors fall due for repayment within one year.

15. Investments

2015 2014

£'000 £'000

Short-term deposits 3,000 -

Total 3,000 -

16. Cash and Bank

The Association has an overdraft facility with its bankers.

31

Notes to the Financial Statements

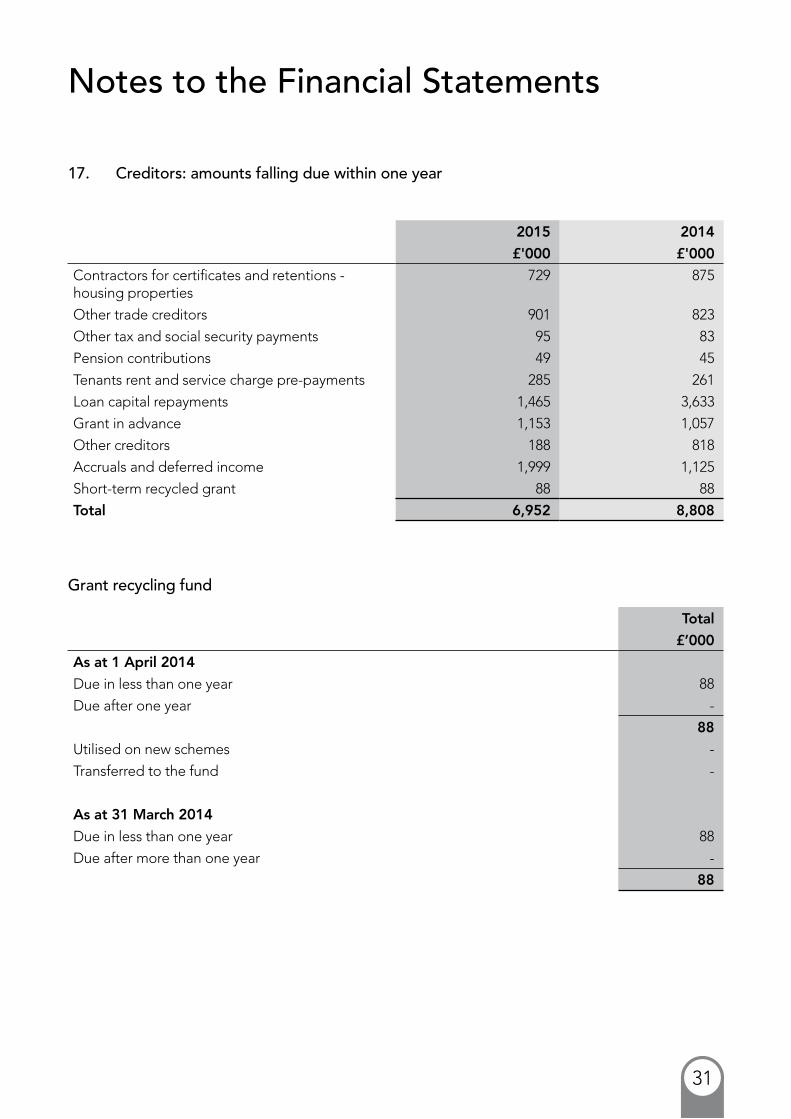

17. Creditors: amounts falling due within one year

2015 2014

£'000 £'000

Contractors for certificates and retentions - housing properties

729 875

Other trade creditors 901 823

Other tax and social security payments 95 83

Pension contributions 49 45

Tenants rent and service charge pre-payments 285 261

Loan capital repayments 1,465 3,633

Grant in advance 1,153 1,057

Other creditors 188 818

Accruals and deferred income 1,999 1,125

Short-term recycled grant 88 88

Total 6,952 8,808

Grant recycling fund

Total

£’000

As at 1 April 2014

Due in less than one year 88

Due after one year -

88

Utilised on new schemes -

Transferred to the fund -

As at 31 March 2014

Due in less than one year 88

Due after more than one year -

88

32

Notes to the Financial Statements

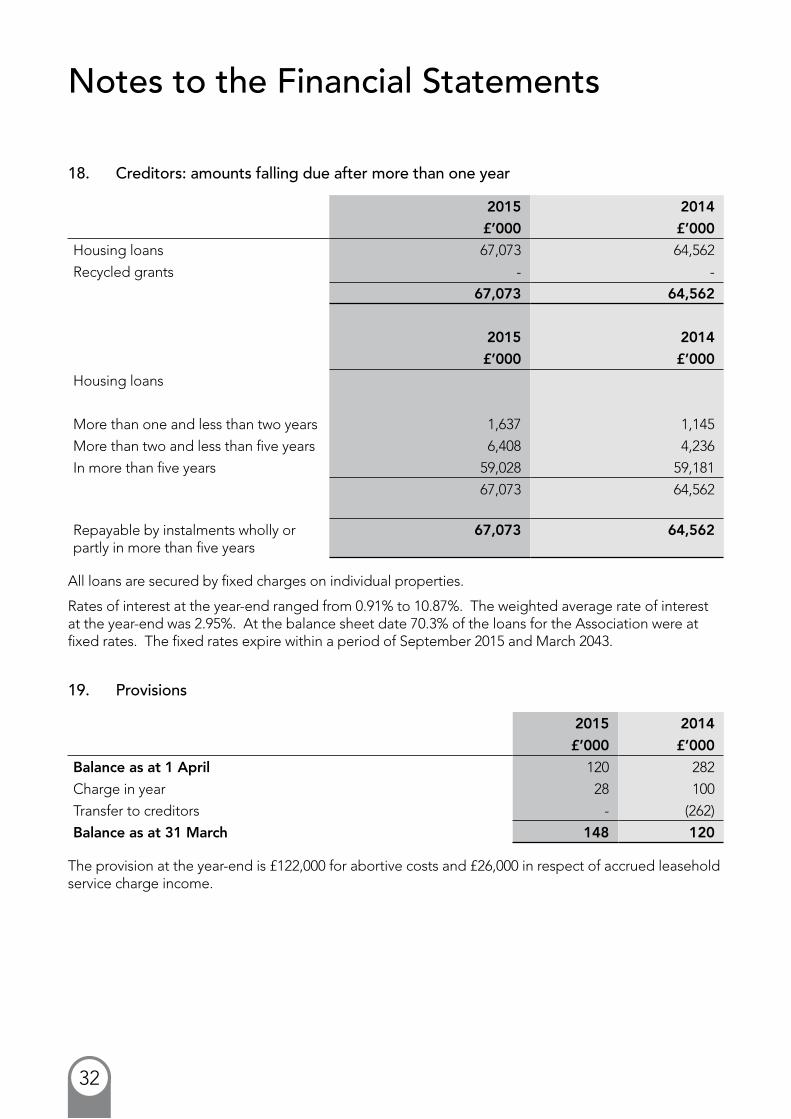

18. Creditors: amounts falling due after more than one year

2015 2014

£’000 £’000

Housing loans 67,073 64,562

Recycled grants - -

67,073 64,562

2015 2014

£’000 £’000

Housing loans

More than one and less than two years 1,637 1,145

More than two and less than five years 6,408 4,236

In more than five years 59,028 59,181

67,073 64,562

Repayable by instalments wholly or partly in more than five years

67,073 64,562

All loans are secured by fixed charges on individual properties.

Rates of interest at the year-end ranged from 0.91% to 10.87%. The weighted average rate of interest at the year-end was 2.95%. At the balance sheet date 70.3% of the loans for the Association were at fixed rates. The fixed rates expire within a period of September 2015 and March 2043.

19. Provisions

2015 2014

£’000 £’000

Balance as at 1 April 120 282

Charge in year 28 100

Transfer to creditors - (262)

Balance as at 31 March 148 120

The provision at the year-end is £122,000 for abortive costs and £26,000 in respect of accrued leasehold service charge income.

33

Notes to the Financial Statements

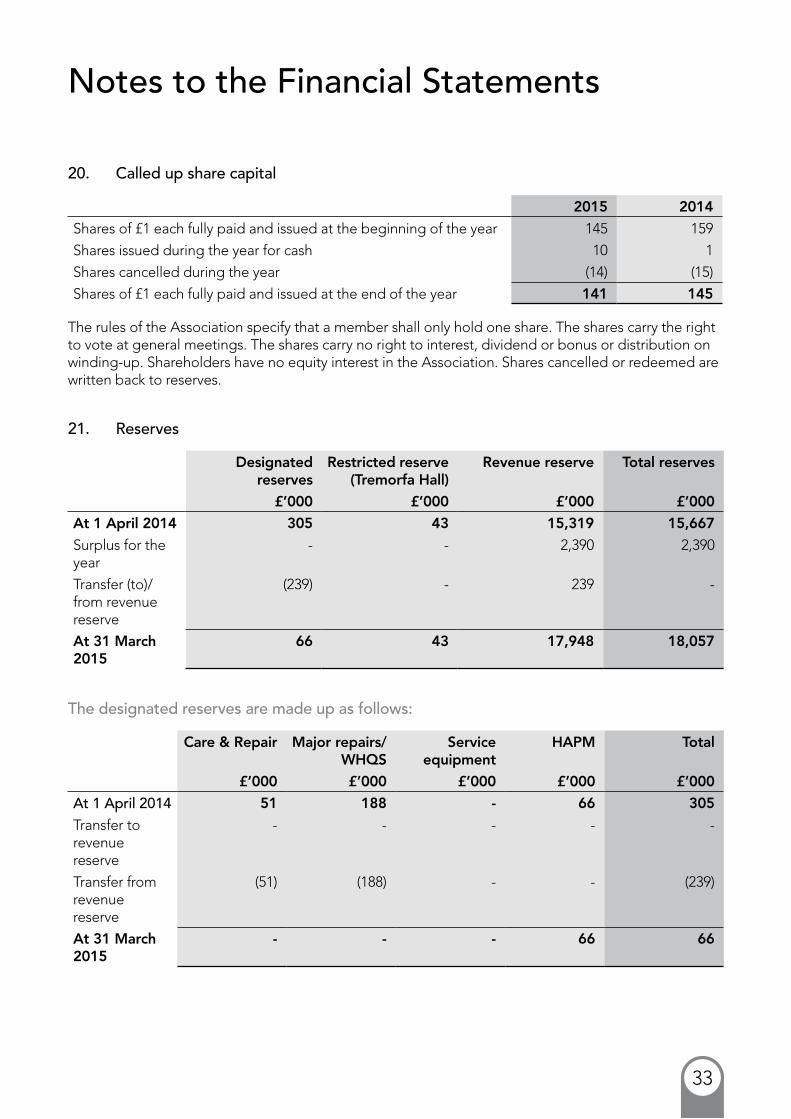

20. Called up share capital

2015 2014

Shares of £1 each fully paid and issued at the beginning of the year 145 159

Shares issued during the year for cash 10 1

Shares cancelled during the year (14) (15)

Shares of £1 each fully paid and issued at the end of the year 141 145

The rules of the Association specify that a member shall only hold one share. The shares carry the right to vote at general meetings. The shares carry no right to interest, dividend or bonus or distribution on winding-up. Shareholders have no equity interest in the Association. Shares cancelled or redeemed are written back to reserves.

21. Reserves

Designated reserves

Restricted reserve (Tremorfa Hall)

Revenue reserve Total reserves

£’000 £’000 £’000 £’000

At 1 April 2014 305 43 15,319 15,667

Surplus for the year

- - 2,390 2,390

Transfer (to)/from revenue reserve

(239) - 239 -

At 31 March 2015

66 43 17,948 18,057

The designated reserves are made up as follows:

Care & Repair Major repairs/ WHQS

Service equipment

HAPM Total

£’000 £’000 £’000 £’000 £’000

At 1 April 2014 51 188 - 66 305

Transfer to revenue reserve

- - - - -

Transfer from revenue reserve

(51) (188) - - (239)

At 31 March 2015

- - - 66 66

34

Notes to the Financial Statements

The Tremorfa Hall restricted reserve is in respect of a donation of the hall to CCHA from the Tremorfa Hall Committee in 2004/05. The use of the property is restricted to activities beneficial to the social sustainability of the area and as such, in accordance with the Statement of Recommended Practice Update 2005, a transfer has been made to restricted reserves equivalent to the value of the property.

The HAPM reserve arose following the reduction in insurance cover in 2004/05 for certain properties from 35 years to 20 years by the Housing Association Property Mutual. In recompense the Association received some £66,000 which has been placed in a designated reserve to contribute to future claims against the properties concerned.

The Care & Repair reserve has been transferred to the revenue reserve pending the creation of the Agency as an independent charity on the 1st July 2015.

The WHQS reserve has been fully utilised during the year. The ongoing use of this reserve is under review pending implementation of the Housing SORP 2014.

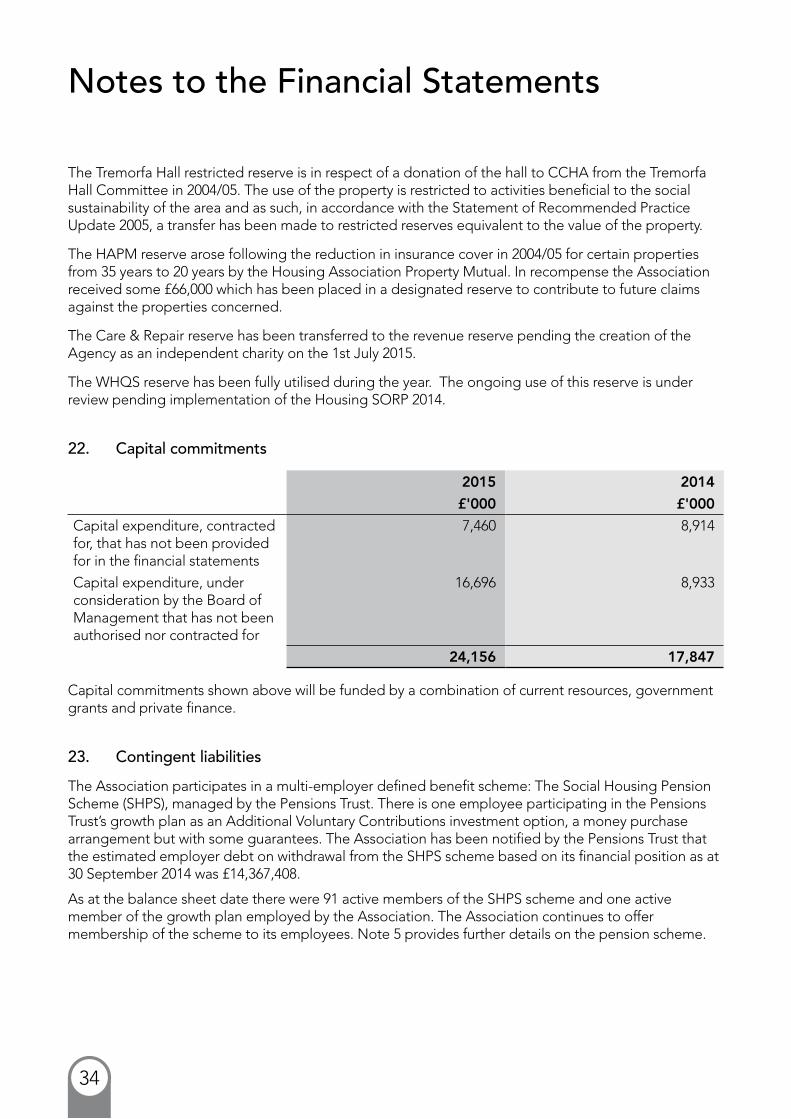

22. Capital commitments

2015 2014

£'000 £'000

Capital expenditure, contracted for, that has not been provided for in the financial statements

7,460 8,914

Capital expenditure, under consideration by the Board of Management that has not been authorised nor contracted for

16,696 8,933

24,156 17,847

Capital commitments shown above will be funded by a combination of current resources, government grants and private finance.

23. Contingent liabilities

The Association participates in a multi-employer defined benefit scheme: The Social Housing Pension Scheme (SHPS), managed by the Pensions Trust. There is one employee participating in the Pensions Trust’s growth plan as an Additional Voluntary Contributions investment option, a money purchase arrangement but with some guarantees. The Association has been notified by the Pensions Trust that the estimated employer debt on withdrawal from the SHPS scheme based on its financial position as at 30 September 2014 was £14,367,408.

As at the balance sheet date there were 91 active members of the SHPS scheme and one active member of the growth plan employed by the Association. The Association continues to offer membership of the scheme to its employees. Note 5 provides further details on the pension scheme.

35

Notes to the Financial Statements

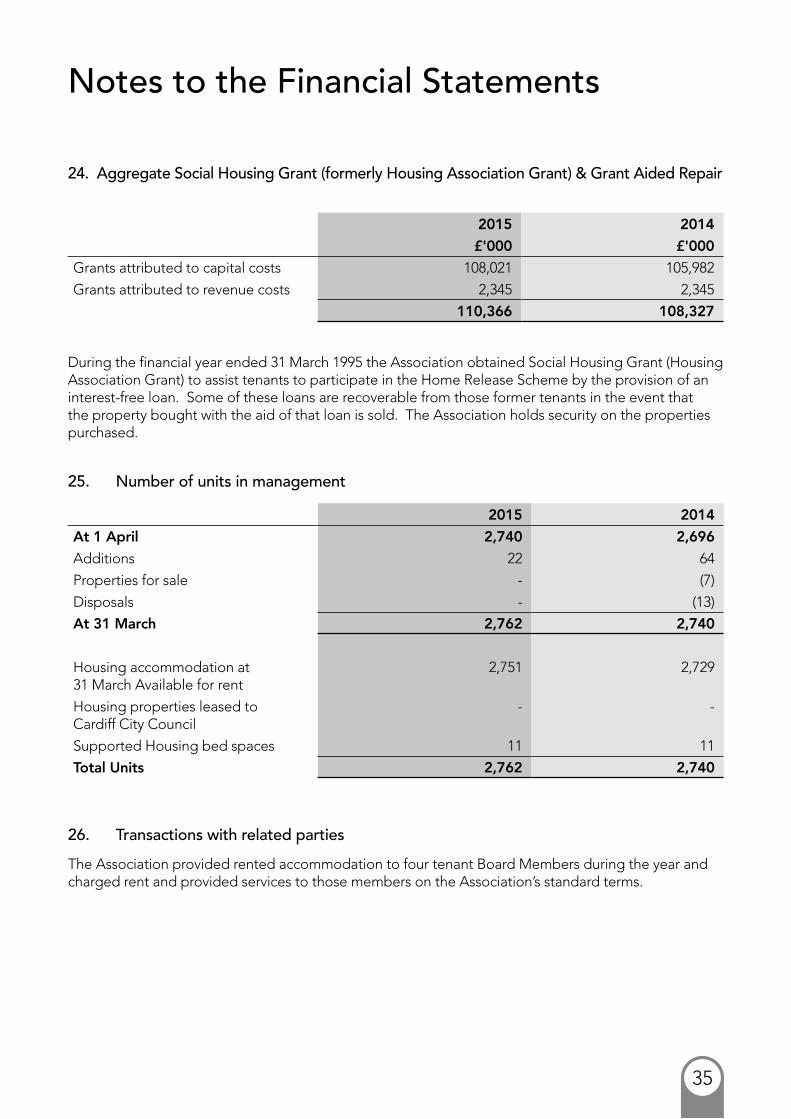

24. Aggregate Social Housing Grant (formerly Housing Association Grant) & Grant Aided Repair

2015 2014

£'000 £'000

Grants attributed to capital costs 108,021 105,982

Grants attributed to revenue costs 2,345 2,345

110,366 108,327

During the financial year ended 31 March 1995 the Association obtained Social Housing Grant (Housing Association Grant) to assist tenants to participate in the Home Release Scheme by the provision of an interest-free loan. Some of these loans are recoverable from those former tenants in the event that the property bought with the aid of that loan is sold. The Association holds security on the properties purchased.

25. Number of units in management

2015 2014

At 1 April 2,740 2,696

Additions 22 64

Properties for sale - (7)

Disposals - (13)

At 31 March 2,762 2,740

Housing accommodation at 31 March Available for rent

2,751 2,729

Housing properties leased to Cardiff City Council

- -

Supported Housing bed spaces 11 11

Total Units 2,762 2,740

26. Transactions with related parties

The Association provided rented accommodation to four tenant Board Members during the year and charged rent and provided services to those members on the Association’s standard terms.

Cardiff Community Housing Association Tolven Court Dowlais Road Cardiff CF24 5LQ

Tel 029 2046 8490 Fax 029 2046 8444

Callaghan House 50 Meteor Street Adamsdown Cardiff CF24 0HE

[email protected] www.ccha.org.uk Created by Carrick – carrickcreative.co.uk