Embed Size (px)

Citation preview

ANNUAL REPORT

2012

Report and Statement of Accounts for the

Year Ended 31 December 2012

ANNUAL REPORT

2012

Report and Statement of Accounts for the

Year Ended 31 December 2012

© 2013 Bank of JamaicaNethersole Place

KingstonJamaica

Telephone: (876) 922 0750-9Fax: (876) 967 4265

Email: [email protected]: www.boj.org.jm

ISSN 0067 3668

Printed in Jamaica

Mission Statement

The mission of the Bank of Jamaica

is to formulate and implement

monetary and regulatory policies

to safeguard the value of the domestic

currency and to ensure the soundness

and development of the financial system

by being a strong and efficient

organisation with highly motivated

and professional employees

working for the benefit of

the people of Jamaica.

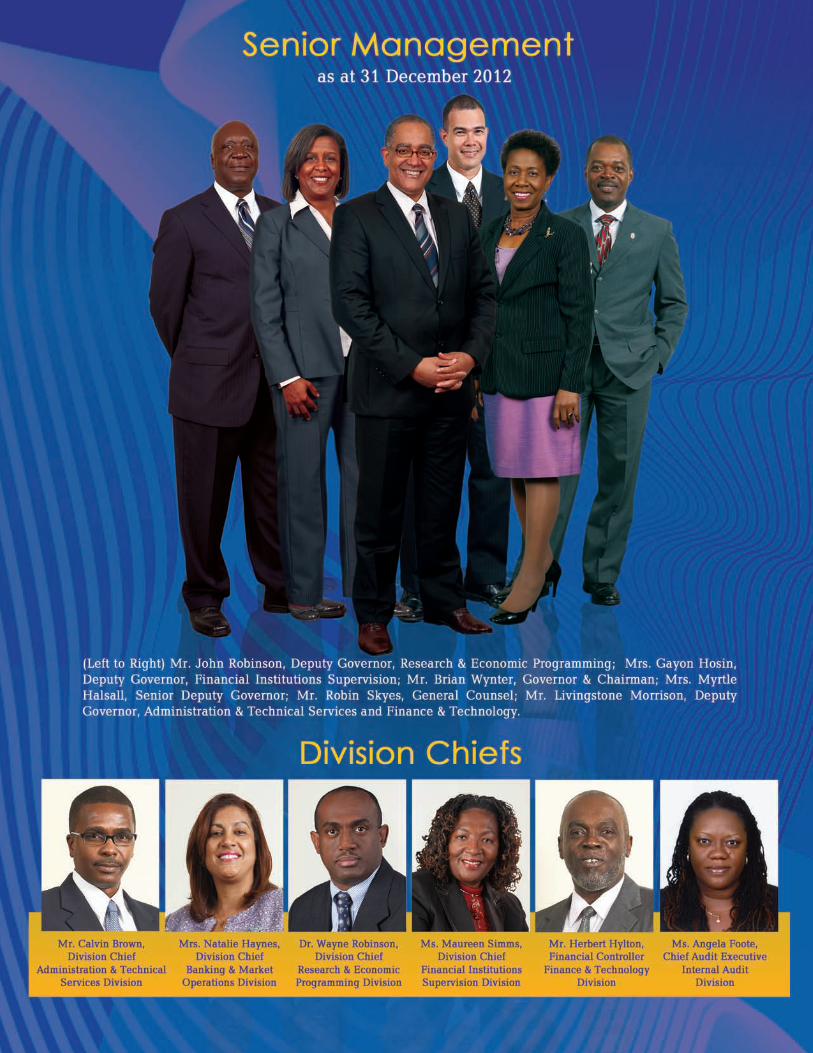

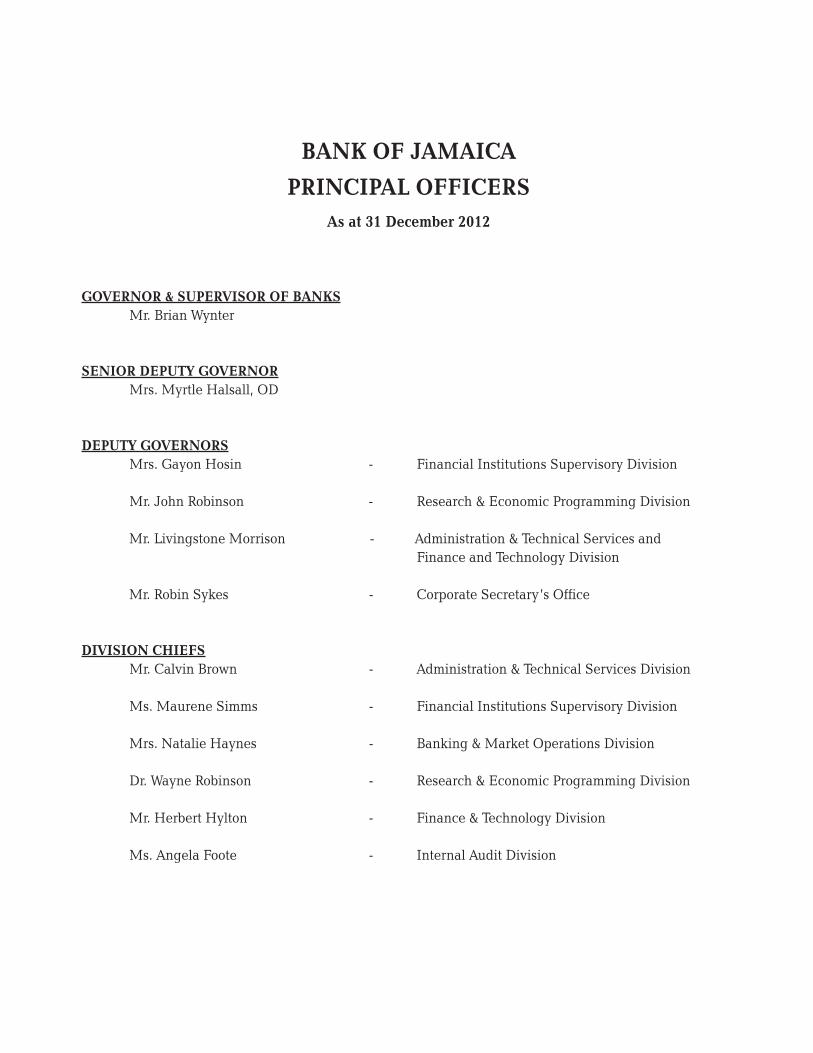

BANK OF JAMAICA

PRINCIPAL OFFICERSAs at 31 December 2012

GOVERNOR & SUPERVISOR OF BANKS Mr. Brian Wynter

SENIOR DEPUTY GOVERNOR Mrs. Myrtle Halsall, OD

DEPUTY GOVERNORS Mrs. Gayon Hosin - Financial Institutions Supervisory Division

Mr. John Robinson - Research & Economic Programming Division

Mr. Livingstone Morrison - Administration & Technical Services and Finance and Technology Division

Mr. Robin Sykes - Corporate Secretary’s Office

DIVISION CHIEFS Mr. Calvin Brown - Administration & Technical Services Division

Ms. Maurene Simms - Financial Institutions Supervisory Division

Mrs. Natalie Haynes - Banking & Market Operations Division

Dr. Wayne Robinson - Research & Economic Programming Division

Mr. Herbert Hylton - Finance & Technology Division

Ms. Angela Foote - Internal Audit Division

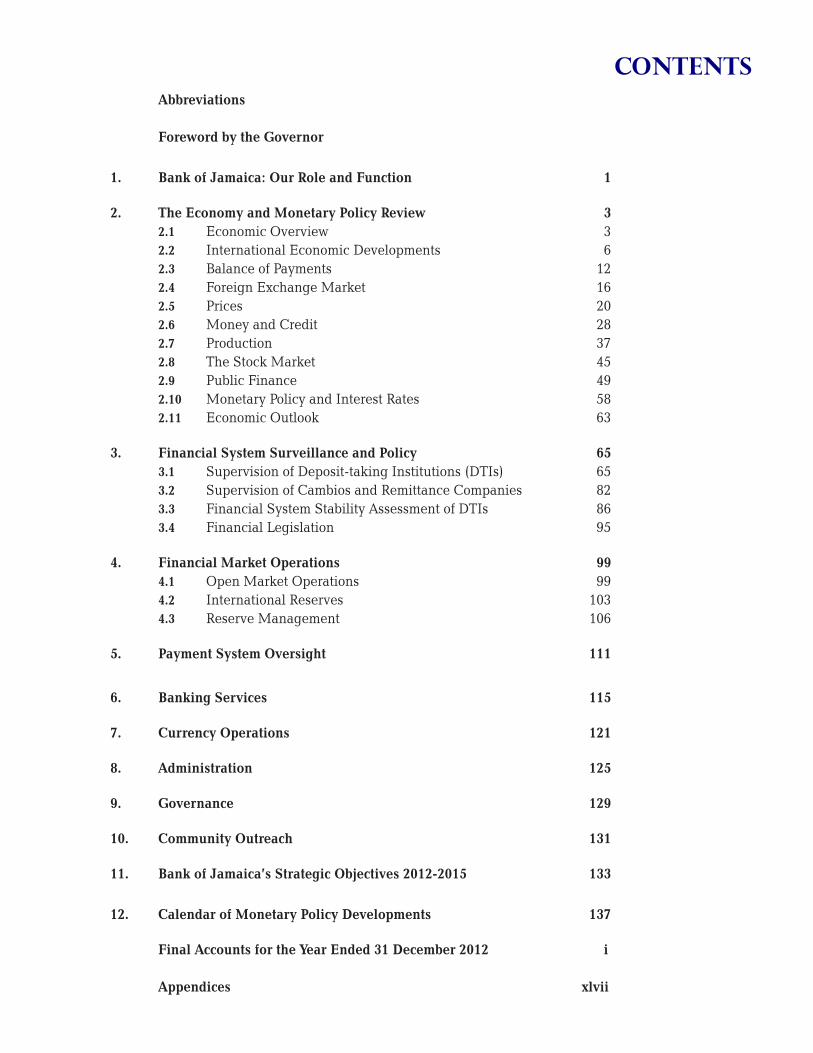

Abbreviations

Foreword by the Governor

1. Bank of Jamaica: Our Role and Function 1

2. The Economy and Monetary Policy Review 32.1 Economic Overview 3 2.2 International Economic Developments 62.3 Balance of Payments 122.4 Foreign Exchange Market 162.5 Prices 202.6 Money and Credit 282.7 Production 372.8 The Stock Market 452.9 Public Finance 492.10 Monetary Policy and Interest Rates 582.11 Economic Outlook 63

3. Financial System Surveillance and Policy 653.1 Supervision of Deposit-taking Institutions (DTIs) 653.2 Supervision of Cambios and Remittance Companies 823.3 Financial System Stability Assessment of DTIs 863.4 Financial Legislation 95

4. Financial Market Operations 99 4.1 Open Market Operations 994.2 International Reserves 1034.3 Reserve Management 106

5. Payment System Oversight 111

6. Banking Services 115

7. Currency Operations 121

8. Administration 125

9. Governance 129

10. Community Outreach 131

11. Bank of Jamaica’s Strategic Objectives 2012-2015 133

12. Calendar of Monetary Policy Developments 137

Final Accounts for the Year Ended 31 December 2012 i Appendices xlvii

CONTENTS

ABBREVIATIONS

ABM Automated Banking MachinesACH Automated Clearing HouseACP African, Pacific and Caribbean (countries)AFI Approved Financial InstitutionAML Anti-money Laundering ARP Average Realized PriceASBA Association of Banking Supervisors of the Americas BCBS Basel Committee on Banking SupervisionBCP Basel Core Principle BIS Bank for International SettlementsBMI Benchmark Investment InstrumentsBN BillionBOE Bank of EnglandBOJ Bank of JamaicaBoJ Bank of JapanBOP Balance of Paymentsbps basis points

CAD Canadian Dollar CAPE Caribbean Advanced Proficiency ExaminationCAR Capital Adequacy RatioCARICOM Caribbean CommunityCCPS Central CounterpartiesCCMB Capital & Credit Merchant BankCD Certificate of DepositCDB Caribbean Development BankCFATF Caribbean Financial Action Task ForceCPC Chief Parliamentary CounselCFT Counter-Financing of TerrorismCGBS Caribbean Group of Banking Supervisorsc.i.f. Cost, insurance and freightCIFTS Customer Inquiry Funds Transfer SystemCOM CommunicationCPI Consumer Price IndexCPI-AF Consumer Price Index excluding Agriculture and FuelCPI-FF Consumer Price Index excluding Food and FuelCRA Credit Reporting ActCRR Cash Reserve RequirementCSD Central Securities DepositoryCTMS Central Treasury Management SystemC&WJCCUL Communications and Other Workers of Jamaica Cooperative Credit Union

Limited

DBJ Development Bank of JamaicaDJIA Dow Jones Industrial IndexDNFBP Designated Non-Financial Businesses & ProffessionsDSGE Dynamic Stochastic General EquilibriumDTI Deposit-taking InstitutionsDVBP Dollar Value of a Basis PointDvP Delivery versus PaymentDVPP Dollar Value of a Percentage Point

EBIS Enterprise Business Intelligence SystemECI Export Credit InsuranceEPA Economic Partnership AgreementEU European UnionEWS Early Warning System EXIM National Export-Import Bank of Jamaica

FATCA Foreign Accoount Tax Compliance ActFATF Financial Action Task ForceFed Federal Reserve (US)FIA Financial Institutions ActFID Financial Investigations DivisionFIDA Financial Investigations Division ActFINSTAB Financial Stability DepartmentFISD Financial Institutions Supervisory DivisionFIU Financial Intelligence UnitFNB Food and Non-alcoholic Beveragesf.o.b. Free on boardFRF Fiscal Responsibility FrameworkFSAP Financial Sector Assessment ProgrammeFSC Financial Services CommissionFSSF Financial Sector Support FundFX Foreign ExchangeFY Fiscal Year

GBP Great Britain PoundGCT General Consumption TaxGDP Gross Domestic ProductGFA Gross Foreign AssetsGKMA Greater Kingston Metropolitan AreaGOJ Government of JamaicaGSDA Government Securities Dematerialization Act

HEART Human Employment and Resource TrainingHMF Honourable Minister of FinanceHWEG Housing, Water, Electricity, Gas and Other Fuels

IDB Inter-American Development BankIBRD International Bank for Reconstruction and Development (World Bank)ICBS International Conference of Banking SupervisorsIFC International Finance CorporationIFPAS Inflation Forecast & Policy Assessment SystemIFRS International Financial Reporting StandardsIMAJ Incorporated Master Builders Associations of JamaicaIMF International Monetary FundIMF-SBA International Monetary Fund – Stand-By ArrangementIPCP Index of Primary Commodity PricesIPDF Insurance Policy Discounting FacilityIPI Import Price Index

JBA Jamaica Bankers AssociationJBDC Jamaica Business Development CentreJCCUL Jamaica Cooperative Credit Union LeagueJCSD Jamaica Central Securities DepositoryJDX Jamaica Debt ExchangeJEEP Jamaica Emergency Employment ProgrammeJGA Jamaica Guild of ArtistsJMMB Jamaica Money Market BrokersJNBS Jamaica National Building SocietyJSE Jamaica Stock ExchangeJTB Jamaica Tourist Board

KYC Know Your CustomerLAR Liquid Assets RequirementLIBOR London Inter-bank Offer RateLRS Local Registered StockLTRO Long-Term Refinancing Operations

MaFI Macro-Financial IndexMFIs Multilateral Financial InstitutionsMOF Ministry of Finance MOU Memorandum of UnderstandingMN MillionMPI Micro-prudential IndexMUG Market User Group

NCTVET National Council on Technical and Vocational Education and TrainingNDA Net Domestic AssetsNHT National Housing TrustNIM Net Interest MarginNIR Net International ReservesNOP Net Open Position NPCB National People’s Cooperative Bank of JamaicaNPL Non-Performing LoansNPS National Payment SystemNROCC National Road Operating & Construction Company

OMO Open Market OperationsOMT Outright Monetary TransactionOPBs Other Public BodiesOPEC Organization of Petroleum Exporting CountriesOUC Other Urban Centres

PAYE Pay As You Earn (income tax)PBOC People’s Bank of ChinaPBMA Public Bodies Management and Accountability PCB People’s Cooperative BankPCMB PanCaribbean Merchant Bank PD Primary DealersPDA Primary Dealers AssociationPFMIs Principles for Financial Market InfrastructuresPL Performing LoansPOCA Proceeds of Crime ActPOS Point of SalePPP Production & Productivity Programmepps Percentage pointsPSCA Payments Clearing and Settlement ActPSE Public Sector Entity

R&A Restaurants AccommodationR&C Recreation & CultureRADA The Rural Agricultural Development AgencyREER Real Effective Exchange RateROAA Return on Average AssetsRSP Remittance Service ProviderRTGS Real Time Gross SettlementRWCA Risk Weighted Capital Adequacy

SCT Special Consumption TaxSDR Special Drawing RightsSIFIs Systemically Important Financial InstitutionsSIPS Systemically Important Payments SystemSME Small and Medium Sized EnterprisesSPBS Selected Public BodiesSRC Scientific Research CouncilSSM Special Safeguard MechanismSTATIN Statistical Institute of JamaicaSWIPS System-wide Important Payment System

TCI Trade Credit InsuranceTPA Terrorism Prevention ActTRAN Transport

UK United KingdomUN United NationsUR Unemployment RateUSA United States of AmericaUSD US Dollar

VAT Value Added TaxVMBS Victoria Mutual Building SocietyVR Variable Rate

WASR Weighted Average Selling RateWATBY Weighted Average Treasury Bill YieldWTI West Texas Intermediate (crude oil)WTO World Trade Organization

YOY Year Over Year

FOREWORD by the governor

The Bank continued to operate in a challenging environment character-

ised by uncertainties in both the domestic and international economies.

Within the domestic economy, investor concerns about the nature and

timing of a funding arrangement with the International Monetary Fund

(IMF) resulted in uncertainties in the financial markets. For the global

economy, the protracted fiscal crisis in Europe continued to have a debili-

tating impact on world trade and growth.

In the context of the uncertainty in the domestic economy, there was a

reduction in net private capital inflows which contributed to increased

instability in the foreign exchange market, reflected in a faster pace of depreciation of the exchange rate

relative to 2011. In this regard, the Bank intervened in the foreign exchange market on several occasions and

in the December quarter offered three special variable rate instruments to primary dealers and commercial

banks. The Bank also maintained its policy rate throughout the year in a context where the outlook for inflation

remained within the targeted range.

Inflation for 2012 was 8.0 per cent, relative to 6.0 per cent in 2011. The higher out-turn was against the

background of adverse weather conditions, the implementation of tax measures and an acceleration in the

rate of depreciation of the domestic currency. However, persistently weak domestic demand conditions, lower

crude oil prices and a significant reduction in communication costs moderated the impact of inflationary

impulses. Against the background of weak demand and the uncertainties, the domestic economy is estimated

to have contracted by 0.3 per cent in 2012. This weak demand reflected the impact of increased unemployment,

declining real wages, reduced pace of growth in remittances and deterioration in both consumer and business

sentiments.

In spite of the uncertain environment the financial system remained stable. In particular, deposit-taking

institutions (DTIs) were largely resilient to macro-prudential stress tests due to strong capital positions and

improved loan quality. In relation to credit, interest rate and foreign exchange stress tests, the results showed

that the system was resilient to these hypothetical shocks, with the post shock capital adequacy ratios (CARs)

generally remaining above the 10.0 per cent minimum benchmark. The assessment of the Bank’s macro-

financial index, which assesses the vulnerability of the financial sector to the changes in the macroeconomy,

also reflected an improvement. Similarly, the DTIs generally recorded a better performance in the micro-

prudential index (MiPI) due to improvements in balance sheet and asset quality indicators.

While no new legislation for the financial sector was passed in 2012 , the Bank continued work on developing

and refining bills to effectively carry out its mandate of financial stability. A major focus was the development of

the ‘Omnibus Banking Bill’ for which the Bank released a Consultation Paper on “Proposals for Enhancement

of the Legislative Framework for the Deposit-taking Sector” in December 2012. The proposed legislation will

strengthen the Bank’s oversight of the deposit-taking financial sector and achieve greater conformity with

the Basel Core Principles as well as other global best practice standards. Additionally, the Omnibus Banking

Bill will consolidate the three deposit-taking statutes into a single piece of legislation to provide for easier

updating of the regulatory framework and eliminate existing inconsistencies and arbitrage opportunities.

In an effort to achieve greater financial inclusion and access to financial services, the Bank pursued amend-

ments to Jamaica’s legal and regulatory framework to allow banks to partner with non-bank third parties to

offer banking services, as agents. These amendments will allow banking customers to conduct banking trans-

actions such as cash deposits and withdrawals within certain size limits from third-party locations. Such agent

activities will also enable banking customers to perform a range of other transactions electronically, including

funds transfers between accounts and balance inquiries.

During 2012, the Bank continued to provide banking and payment services to its clients in the most efficient

and secure way. In this regard, the Bank facilitated the training of the Government’s staff and granted them

access to the JamClear Real Time Gross Settlement (RTGS) system. There were efficiency gains from this

training as the Government, the single most significant initiator of large value transactions, was able to create

its own files in the system, taking full responsibility for verifying the accuracy and timeliness of payments.

Further, the Bank lowered the Automated Clearing House value threshold to $3.0 million from $5.0 million as

part of its risk mitigation strategy of having all large value transactions settled in the RTGS. In addition, the

Bank improved the efficiency of its currency operations by using more durable substrates in the production of

four Bank notes. The $1000, $500 and $50 notes were printed on pre- and post-print varnished cotton while

the $100 note was printed on a composite material of protective polyester film layered around a cotton fibre

core known as Hybrid®.

The Bank continued the investment in its human resources in 2012 through exposure to various seminars,

conferences and workshops both locally and abroad. To this end, the training function was re-launched under

the theme “Vision 2015: Targeted Training-Creating a New Generation of Central Bankers”, aimed at creating

a cadre of central bankers equipped to function in several areas of the Bank. With regard to the physical

infrastructure, the Bank intensified its efforts in 2012 to optimize the use of its physical plant and equipment,

advance its energy management programme as well as implement environmentally friendly initiatives. The key

strategies included the development and implementation of Phase 3 of its Energy Management programme

and the completion of the Glass Fenestration System project. Of note, the Bank achieved a reduction of 12.0

per cent in energy consumption which exceeded its projected savings of 5.0 per cent to 10.0 per cent for the

year.

During the year, the Bank continued its outreach programmes, including the School Education Programme

and the Economic Seminar Series. The Bank also hosted the 2nd G. Arthur Brown Memorial Lecture which

was presented by former Prime Minister, the Most Hon P.J. Patterson on the topic “Stimulating the Flow

of Our Creative Potential”. The Bank remains committed to maintain and enhance its current outreach

programmes while being open to the possibility of new projects aimed at adding value to the employee and

visitor experience.

While economic activity was subdued, the year 2012 was special for Jamaica as it marked the country’s 50th

anniversary of independence. In observance of the anniversary, the Bank issued a series of commemorative

banknotes and coins. Additionally, the Bank’s Lunch Hour Concerts highlighted performances that were

selected to display Jamaican talent over the 50 years. As a mark of the country’s achievement at the Olympic

Games, the Bank released gold and silver commemorative coins in honour of the eight athletes who won

individual Olympic gold medals since Jamaica began participating in 1948.

During 2012, the Bank played a key role in negotiations with the IMF for a borrowing programme. The

engagement with the IMF began with the Article IV consultations which set the stage for discussion on a new

borrowing programme. As the lead member of the country’s negotiating team, I want to express my gratitude

for the outstanding service that was delivered by my staff, particularly those who went beyond the call of duty

at great personal sacrifice. At a time when remuneration has been frozen for all staff members it would be

remiss of me not to recognise in words the commitment and hard work of all members of staff. I am also very

grateful for the contributions of members of the Board of Directors of the Bank during this challenging year.

In 2012, there were changes in the composition of the Board of the Bank due to the resignation of some of

its members and appointments to fill the vacancies. Specifically, there were resignations from Dr. Wesley

Hughes, Dr. Celia Brown-Blake, Dr. Nigel Clarke, Mr. Rohan Barnett and Mr. Mark Myers. On behalf of the

Bank, I want to express my gratitude to these persons for their dedicated service and to wish them well in their

future endeavours. I am also pleased to welcome as their replacements, Mr. Devon Rowe, the new Financial

Secretary and ex officio member, Mr. Christopher Bicknell, Dr. Christine Clarke, Dr. Vincent Lawrence, Miss

Janice Holness and Mr. Dennis Morrison.

The Bank recognizes that there will be continuing challenges for the economy in 2013. Foremost among these

is the successful conclusion of an agreement with the IMF and the subsequent adherence to the performance

targets under the medium-term macroeconomic programme. The signing of this agreement is anticipated

to lead to an improvement in Jamaica’s economic environment in 2013 due to reduced uncertainties, The

Board and management of the Bank are confident that with the professionalism and high standards of the

staff, the Bank will be able to confront the challenges of 2013 and beyond. The Bank’s strategic focus in this

regard involves enhancing the monetary policy framework to achieve the inflation objective, strengthening

the Bank’s institutional framework for maintaining financial system stability and aligning the Bank’s human

resources, processes, technology and organizational structure to support the attainment of the Bank’s strategic

objectives. Brian Wynter

GovernorBank of Jamaica

- 1 -

1. Bank of Jamaica: Our Role & Function

Bank of Jamaica (BOJ), established by the

Bank of Jamaica Act (1960), is responsible for

the implementation of sound and consistent

monetary policies, while ensuring financial

system stability through robust supervisory

and regulatory policies. The achievement of

these objectives is critical to the attainment of

sustainable growth in the Jamaican economy.

The two-fold nature of the Bank’s operations is

captured in its mission statement:

The mission of the Bank of Jamaica is to

formulate and implement monetary and

regulatory policies to safeguard the value of the

domestic currency and to ensure the soundness

and development of the financial system by

being a strong and efficient organization with

highly motivated and professional employees

working for the benefit of the people of Jamaica.

Bank of Jamaica conducts monetary policy

with the aim of achieving inflation in line with

that of our major trading partners. While not

operating an explicit inflation targeting regime,

on BOJ’s recommendation, the inflation target

range for the current fiscal year is announced

by the Minister of Finance at the beginning

of each year. In formulating monetary policy

to achieve this target, the Bank takes into

consideration all prevailing and prospective

developments in the macro economy, fiscal

operations, external sector as well as relevant

market information. A decision to change the

stance of monetary policy can be reflected in a

number of adjustments. These include changes

in the rates paid on the Bank’s certificates of

deposit and adjustments to the liquid asset and

cash reserve ratios.

In fulfilling its mandate to maintain financial

system stability, the BOJ has supervisory and

regulatory oversight of commercial banks and

other licensed deposit-taking institutions.

The BOJ routinely monitors institutions’

compliance with all the relevant legislation

and regulations to ensure the highest level of

prudence and integrity in the management

of such organizations. The Bank’s overall

responsibility for financial stability is supported

by micro- and macro-prudential assessments,

which are underpinned by the results from

early warning systems and risk models.

The Bank’s responsibilities also include:

• oversightoftheoperationofthepayments

system and the foreign exchange market;

• theissueandredemptionofcurrency;

• the provision of banking services to the

Government and commercial banks

as well as fiscal agency services to the

Government; and

•management of the external reserves of

Jamaica.

- 3 -

2. The Economy & Monetary Policy Review

2. The Financial Systemthese inflationary impulses was, however,

moderated by a reduction in crude oil prices,

lower communication cost and generally weak

demand conditions.

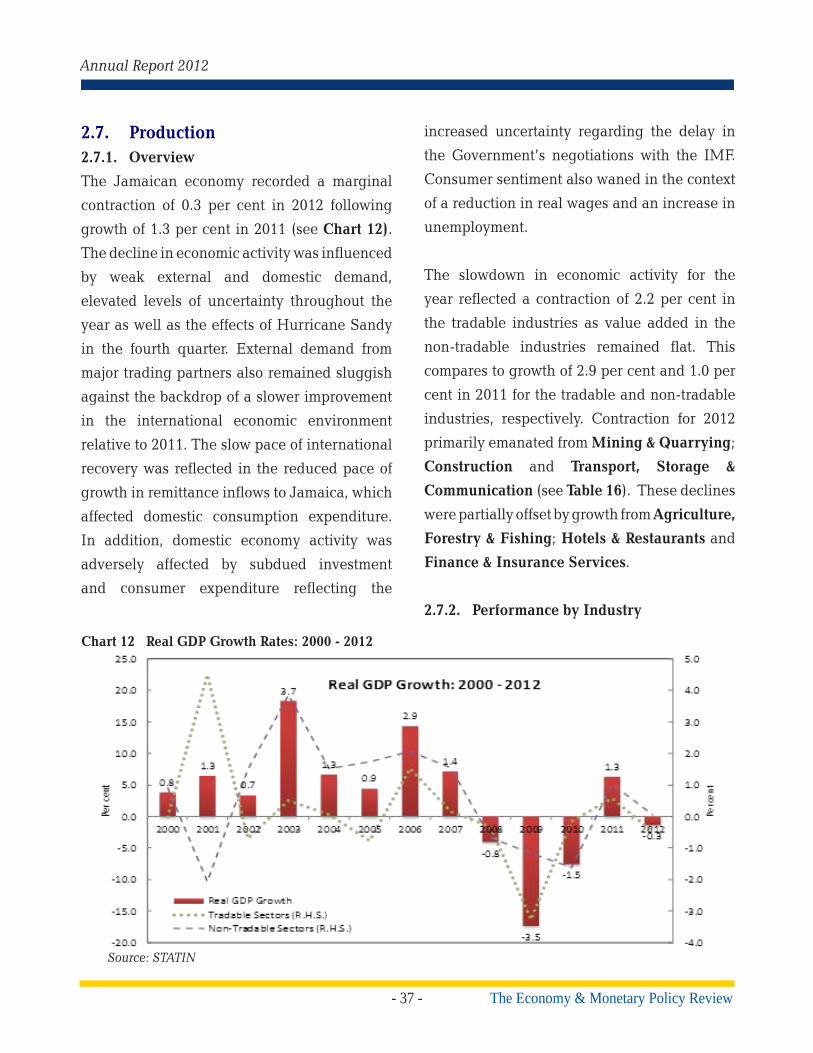

The Jamaican economy recorded an estimated

marginal contraction of 0.3 per cent in 2012,

following growth of 1.3 per cent in 2011. The

decline in economic activity was influenced by

weak external and domestic demand, elevated

levels of uncertainty throughout the year as well

as the effects of adverse weather conditions.

External demand from major trading partners

remained sluggish against the backdrop of

slower growth in the world economy relative

to 2011. Consumer demand was also adversely

affected by a reduction in real wages, an

increase in unemployment and a reduced

pace of growth in remittances. In addition,

uncertainty about the Government’s pending

agreement with the IMF had an adverse impact

on investor sentiment.

The decline in economic activity for the year

reflected a contraction in the tradable industries,

as value added in the non-tradable industries

remained flat. The contraction for 2012 was

primarily reflected in Mining & Quarrying,

Construction and Transport, Storage &

Communication. However, there was a partly

offsetting impact from growth in Agriculture,

Forestry & Fishing, Hotels & Restaurants and

Finance & Insurance Services.

2.1. Economic OverviewThe Bank of Jamaica (BOJ) maintained

its monetary policy stance in 2012 in the

context of continued weak domestic demand

which tempered the impact of inflationary

impulses as well as uncertainties within the

local and international economies. Within the

domestic economy, uncertainty surrounding

the timing and content of an agreement with

the International Monetary Fund (IMF) on

a new medium-term economic programme

contributed to instability in the foreign

exchange market and delays in investment

projects. Uncertainty in the global economy

was largely related to developments in the Euro

Area and its impact on international financial

and commodity markets.

Headline inflation, as measured by the point-

to-point change in the All Jamaica Consumer

Price Index (CPI), was 8.0 per cent for 2012,

relative to 6.0 per cent for 2011. The outturn

for 2012 was influenced by the implementation

of tax measures announced in the FY2012/13

budget as well as shortages in the supplies

of several agriculture items, due to the

impact of drought conditions in the first half

of the year and the passage of Hurricane

Sandy in October. Inflationary pressures also

emanated from a rise in international grains

prices and the pass-through of exchange rate

depreciation during the year. The impact of

- 4 -The Economy & Monetary Policy Review

Bank of Jamaica

money supply (M3J) decelerated to 0.6 per

cent from 10.5 per cent in 2011 and was well

below the average growth of 8.7 per cent for the

last five years. This marginal increase in 2012,

occurred in the context of the contraction of the

domestic economy, declining real incomes and

marked deceleration in remittance inflows to

Jamaica.

Jamaica’s balance of payments is estimated

to have improved in 2012, largely reflecting

a reduction in the value of imports associated

with weak global and domestic demand

conditions. The weakness in the global economy

contributed to a decline in some commodity

prices, particularly crude oil. In this regard,

the current account deficit is estimated to have

narrowed to 12.7 per cent of GDP from 14.6

per cent in 2011. This improvement reflected

a narrowing in the deficits on the Goods and

Income sub-accounts, the impact of which was

partly offset by lower surpluses on the Services

and Current Transfers sub-accounts. Net

Private and Official Investment inflows were

insufficient to finance the deficits on the capital

and current accounts. Consequently, the NIR

of the Bank fell by US$840.5 million to US$1

125.6 million at end-2012, with gross reserves

representing 13.2 weeks of projected goods and

services imports.

During the period April to December 2012,

public sector performance was affected by the

weak domestic economy which was exacerbated

by uncertainty related to an agreement with

The foreign exchange market in 2012 was

characterized by periods of heightened demand

and reduced private capital and official inflows

relative to 2011. The reduction in inflows was

associated with the uncertainties among the

public surrounding the finalisation of a new

medium-term programme and the adequacy of

the net international reserves (NIR). Against

this background, the Jamaica Dollar reflected

a point-to-point depreciation of 6.9 per cent

against the US dollar for 2012, relative to

depreciation of 0.9 per cent for 2011.

Interest rates on the Bank’s 30-day Certificate

of Deposit (CD) and overnight instrument were

maintained at 6.25 per cent and 0.25 per cent,

respectively, throughout 2012. Additionally,

the domestic cash reserve and liquid assets

requirements were maintained at 12.0 per cent

and 26.0 per cent, respectively. However, in

the context of excess Jamaica Dollar liquidity,

the Bank introduced three variable rate

instruments which were offered to Primary

Dealers and commercial banks between 31

October and 05 November 2012.

In the context of these developments, the

monetary base expanded by 6.5 per cent for

2012, relative to 7.8 per cent for 2011, and

largely reflected net currency issue. The

expansion in the monetary base was facilitated

by an increase in the net domestic assets of the

Central Bank as there was a decline in the NIR.

Concurrent with the slower expansion in the

monetary base, growth in broad Jamaica Dollar

- 5 -

Annual Report 2012

The Economy & Monetary Policy Review

the IMF. This delay resulted in the non-

receipt of some loan and grant flows from

multilateral financial institutions, which led to

postponement of project spending, particularly

by public bodies, consolidating to a build-up in

surplus balances by these entities by end-2012.

With respect to Central Government, revenues

grew by 4.7 per cent for the period, relative to

growth of 6.1 per cent for the corresponding

period in 2011. As a consequence of the

lower revenues, expenditure was curtailed

as the Central Government sought to meet

its fiscal deficit and primary surplus targets

for FY2012/13. In addition, in the context of

the investor uncertainty, the Government was

unable to extend the maturity profile of the debt

stock and increase the proportion of fixed rate

issues, consistent with the debt strategy.

Jamaica’s economic environment is anticipated

to improve in 2013 in the context of reduced

uncertainties consequent on the signing of an

IMF agreement as well as continued global

growth. The economy is expected to expand

in the range of 0.5 per cent to 1.5 per cent in

2013, in contrast to the contraction in 2012.

Most industries are expected to grow in 2013

with the major contributors being Agriculture,

Forestry & Fishing, Construction and Mining

& Quarrying. However, despite the overall

expected expansion in output, domestic

demand conditions are anticipated to remain

weak due to significant fiscal consolidation.

Notwithstanding the relatively weak demand

conditions, headline inflation for 2013 could

exceed the rate recorded in 2012 in the context

of higher import prices and further exchange

rate pass-through. In that context, the Bank will

continue to manage inflation expectations to

obtain the objectives outlined in the medium-

term macroeconomic programme.

- 6 -The Economy & Monetary Policy Review

Bank of Jamaica

2.2. International Economic

Developments

2.2.1. Overview

Global growth continued to decelerate in 2012

reflecting weak economic activity in most

advanced and emerging market economies.

In particular, the impact of austerity measures

in the Euro Area, stemming from the region’s

sovereign debt crisis, resulted in a contraction in

economic activity in that economy for the year.

As a result, some Euro Area economies were

characterized by heightened unemployment

rates and reduced consumer spending during

the year. This had spill-over effects on the

United Kingdom (UK) as well as some emerging

markets such as China. However, there was

increased domestic demand in the USA.

During 2012, a number of central banks in both

advanced and emerging market economies

implemented additional expansionary

monetary policy measures in an attempt to spur

growth. In spite of the expansionary monetary

policies, global inflation decelerated in the

context of continued weak demand and lower

commodity prices.

2.2.2. Output

The pace of economic growth in the global

economy is estimated to have moderated to 3.2

per cent in 2012, following an expansion of 3.9

per cent in 2011. This outturn reflected slower

growth rates in both advanced and developing

economies. In particular, advanced economies

recorded growth of 1.3 per cent in 2012, relative

to an expansion of 1.6 per cent in 2011 while

growth for the developing countries slowed to

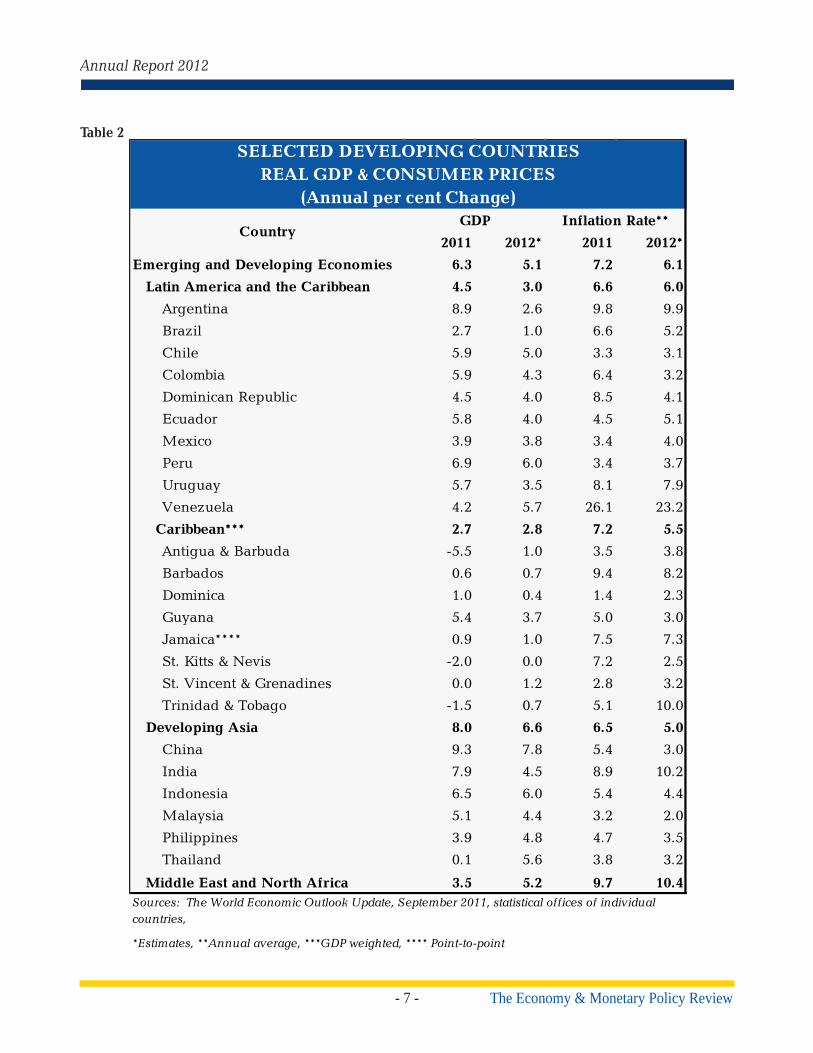

5.1 per cent from 6.3 per cent in 2011 (see Table

1 & Table 2). Among the larger developing

economies, China recorded the fastest output

growth in 2012, albeit at a slower rate (see

Table 2).

Table 1

2011 2012* 2011 2012* 2011 2012* 2011 2012*

Advanced Economies 1.6 1.3 7.9 8.0 2.7 2.0 n/a n/a

of which

USA 1.8 2.2 9.0 8.2 3.1 2.0 0.0 - 0.25 0.0 - 0.25

UK 0.9 -0.2 8.0 8.1 4.5 2.7 0.5 0.5

Euro Area 1.4 -0.4 10.2 11.2 2.7 2.3 1.0 0.75

Canada 2.6 2.0 7.5 7.3 2.9 1.8 1.0 1.0

Japan -0.6 2.0 4.6 4.5 -0.3 0.0 0.1 0.1

Source: IMF World Economic Outlook Update: September 2011; January 2012 , International Labour Office, statistical agencies of individual countries

*Estimates ** Annual average *** End-of-period

INDUSTRIAL ECONOMIESReal GDP, Consumer Prices and Unemployment Rates

(Annual percentage change and per cent of labour force)

Country GDPUnemployment

RateInflation Rate**

Central Bank Target

Interest Rates***

- 7 -

Annual Report 2012

The Economy & Monetary Policy Review

Table 2

2011 2012* 2011 2012*

Emerging and Developing Economies 6.3 5.1 7.2 6.1

Latin America and the Caribbean 4.5 3.0 6.6 6.0

Argentina 8.9 2.6 9.8 9.9

Brazil 2.7 1.0 6.6 5.2

Chile 5.9 5.0 3.3 3.1

Colombia 5.9 4.3 6.4 3.2

Dominican Republic 4.5 4.0 8.5 4.1

Ecuador 5.8 4.0 4.5 5.1

Mexico 3.9 3.8 3.4 4.0

Peru 6.9 6.0 3.4 3.7

Uruguay 5.7 3.5 8.1 7.9

Venezuela 4.2 5.7 26.1 23.2

Caribbean*** 2.7 2.8 7.2 5.5

Antigua & Barbuda -5.5 1.0 3.5 3.8

Barbados 0.6 0.7 9.4 8.2

Dominica 1.0 0.4 1.4 2.3

Guyana 5.4 3.7 5.0 3.0

Jamaica**** 0.9 1.0 7.5 7.3

St. Kitts & Nevis -2.0 0.0 7.2 2.5

St. Vincent & Grenadines 0.0 1.2 2.8 3.2

Trinidad & Tobago -1.5 0.7 5.1 10.0

Developing Asia 8.0 6.6 6.5 5.0

China 9.3 7.8 5.4 3.0

India 7.9 4.5 8.9 10.2

Indonesia 6.5 6.0 5.4 4.4

Malaysia 5.1 4.4 3.2 2.0

Philippines 3.9 4.8 4.7 3.5

Thailand 0.1 5.6 3.8 3.2

Middle East and North Africa 3.5 5.2 9.7 10.4Sources: The World Economic Outlook Update, September 2011, statistical offices of individual countries,

*Estimates, **Annual average, ***GDP weighted, **** Point-to-point

SELECTED DEVELOPING COUNTRIESREAL GDP & CONSUMER PRICES

(Annual per cent Change)

CountryGDP Inflation Rate**

- 8 -The Economy & Monetary Policy Review

Bank of Jamaica

Growth among the advanced economies

was constrained by the impact of various

austerity measures implemented by European

governments in an effort to contain the region’s

sovereign debt crisis. However, the impact

of these measures was partially offset by

improvements in consumption and investment

expenditure associated with additional

monetary easing in the Euro Area, the USA and

Japan. Economic growth in Japan recovered in

2012, following the impact of the natural disaster

in the preceding year. For the developing

countries, growth in economic output continued

to decelerate due to the impact of weak global

demand which negatively influenced external

trade. Notwithstanding the overall outturn, the

Middle East and North Africa region recorded

an increase in output to 5.2 per cent in 2012

from 3.5 per cent in 2011. This reflected the

impact of export-led growth in the context of

higher oil prices in the first half of the year.

2.2.3. Monetary Policy

The central banks of selected advanced

economies maintained an expansionary

monetary policy stance in 2012 in an effort to

counter the effects of weak demand conditions

that characterized the year. In the USA, for

example, the Federal Reserve Board (Fed)

extended its “Operation Twist” programme,

involving the purchase of Treasury securities

to end-2012 from June 2012. It also launched

a third round of quantitative easing (QE3) in

September 2012, which involved the monthly

purchase of US$40 billion of mortgage-backed

securities for an unlimited period. Following

the launch of QE3 the Fed increased its

monthly purchase of Treasury securities by

US$45 billion in December 2012 in an effort to

maintain downward pressures on longer-term

interest rates. In order to reduce uncertainty

regarding its monetary policy stance, the Fed

pledged to maintain target interest rates within

the range of 0.0 per cent to 0.25 per cent until

the unemployment rate fall below 6.5 per cent

and projected inflation for one and two years

ahead, remaining below 2.5 per cent.

Similarly, the European Central Bank (ECB)

employed a second round of Longer-Term

Refinancing Operations (LTRO) in February

2012, lowered its target interest rates in

July and implemented Outright Monetary

Transactions (OMT) in September. The Bank

of England (BoE) also increased the size of its

asset purchase programme by £100.0 billion to

£375.0 billion in 2012 but halted its third round

of quantitative easing as it shifted its focus to

the Funding for Lending scheme. In an effort

to achieve an inflation target of 1.0 per cent,

the Bank of Japan (BoJ) also expanded its asset

purchase programme; by approximately ¥46.0

trillion to ¥101.0 trillion during 2012.

The central banks of some large emerging

market countries also employed monetary

easing in 2012. This was primarily effected

through the reduction in policy rates. In

particular, the People’s Bank of China (PBoC),

in May 2012 lowered the reserve requirement

- 9 -

Annual Report 2012

The Economy & Monetary Policy Review

for deposit-taking financial institutions by 50

bps to 20.0 per cent for large banks and 18.0 per

cent for small banks. The PBoC later reduced

its benchmark lending rate by 56 bps to 6.0 per

cent in July 2012. The Reserve Bank of India

reduced its target repo rate by 50 bps to 8.0 per

cent while the Central Bank of Brazil lowered

its Selic rate by 325 bps to 7.25 per cent. These

monetary policy initiatives were implemented

in an effort to inject additional liquidity into the

financial system. Conversely, the Central Bank

of the Russian Federation tightened monetary

policy in September 2012, by increasing its

policy rate by 25 bps to 8.25 per cent in an effort

to curb inflationary pressures.

2.2.4. Global Inflation

Global inflation decelerated in 2012. For the

advanced economies, the annual average

inflation rate decelerated to 2.0 per cent in 2012

from 2.7 per cent in 2011. The same measure of

inflation among the developing countries also

fell by 1.1 percentage points to 6.1 per cent in

2012 (see Table 1 & Table 2). The deceleration

reflected a decline in overall commodity prices.

In particular, the prices of non-fuel commodities

fell during the year while there was a significant

moderation in the rate of increase in energy

costs. These price movements were mainly

associated with weak demand conditions in both

advanced and emerging market economies.

However, significantly lower fuel prices in the

second half of the year partly offset the impact

of higher prices in the first half of 2012.

2.2.5. Selected Exchange Rates

Selected international currencies such as the

Euro, Canadian dollar, Great Britain Pound and

the Japanese Yen all depreciated against the

US dollar (USD) during the year (see Table 3).

The depreciation of these currencies primarily

reflected the impact of the slowdown in global

economic activity stemming from uncertainties

in the Euro Area throughout the year. However,

there was a strengthening of the Euro in the

last quarter of 2012 due to the impact of the

implementation of debt sustainability measures

in Greece. In addition, the concerns regarding

Table 3

2011 2012 2011 2012

Canadian Dollar 1.01 1.00 4.2 -1.0

Japanese Yen/1 79.73 79.83 -9.0 0.1

Great Britain Pound 1.60 1.59 3.7 -0.6

Euro 1.39 1.29 4.9 -7.2

Source: Bloomberg

1. Expressed as local currency per unit of US dollars (in accordance with international convention)

Annual Per cent Change

Advanced Economies: Exchange Rates(Annual Average)

US Dollars per Unit of National Currency

- 10 -The Economy & Monetary Policy Review

Bank of Jamaica

the finalisation of the US 2013 fiscal budget

led to a weakening of the USD against selected

currencies in the final quarter of the year.

2.2.6. Commodity Markets

Commodity prices generally declined in 2012,

relative to the previous year, in the context of

lower demand associated with global economic

weakness, particularly during the second half

of the year. Additionally, increased supplies

of some commodities, amid record production

in key-producing regions, had a dampening

impact on prices. In this regard, the IMF’s Index

of Primary Commodity Prices (IPCP) registered

a decline of 3.1 per cent in 2012 relative to an

increase of 26.3 per cent in 2011 (see Table 4).

The decline in the IPCP reflected a contraction

in Non-fuel Commodities, the impact of which

was partly offset by a mild expansion in Energy.

Lower Non-fuel Commodities primarily

reflected reduced prices for Industrial Inputs,

including agricultural raw materials and

metals. The marginal increase in Energy

reflected higher prices during the first half of

the year, associated with geo-political tensions.

The impact was largely offset by the effects of

weak global demand on prices in the second

half of the year.

Table 4

2011 2012/1

All Primary Commodities 26.3 - 3.1

1. Non-fuel Commodities 17.8 - 9.8

1.1 Edibles 19.4 - 3.7

(a) Food 19.7 - 1.8

(b) Beverages 16.6 - 18.6

1.2 Industrial Inputs 16.4 - 15.5(a) Agricultural Raw Materials 22.7 - 12.6

(b) Metals 13.5 - 16.8

2. Energy 31.8 0.7

Petroleum/2 31.6 1.0

(a) WTI 19.6 - 1.0

(b) Brent 39.3 0.9

(c) Dubai 35.8 2.7

SUMMARY OF WORLD COMMODITY PRICESAnnual Average Per Cent Change

Source: IMF1/ Provisional2/ Simple Average of West Texas Intermediate (WTI), Brent and Dubai Crude oil prices

- 11 -

Annual Report 2012

The Economy & Monetary Policy Review

In terms of Non-Fuel Commodities, there was a

decline of 3.7 per cent gggin the price of Edibles,

compared with a rise of 19.4 per cent in 2011. The

outturn was mainly attributed to a 18.6 per cent

contraction in Beverages in 2012, compared to

growth of 16.6 per cent in the previous year (see

Table 4). Downward price movements largely

reflected a 31.3 per cent fall in the price of Arabica

coffee due to record production in Brazil, the

world’s largest producer. The fall in the sub-index

was also exacerbated by a sharp decline of 20.2

per cent in cocoa prices, given increased supplies

from the top producer, Ivory Coast.

Food prices declined by 1.8 per cent in 2012,

compared to an increase of 19.7 per cent in 2011.

Despite the impact of extreme drought conditions

on the prices of US soybeans and corn, price

declines emanating from increased global supplies

of other commodities including sugar, pork and

fish resulted in an overall decline in this category.

In 2012, the price of Industrial Inputs fell by

15.5 per cent, in contrast to an increase in the

preceding year. The outturn reflected declines in

both agricultural raw materials and metals. With

regard to metals, a deceleration in the pace of

activity in the manufacturing sectors of the Euro

Area and China contributed to the downward

trend in prices, particularly aluminium. In this

context, aluminium prices recorded a decline of

15.7 per cent, compared to a rise of 10.2 per cent

in 2011.

With respect to Energy, crude oil prices, as

measured by the West Texas Intermediate (WTI)

benchmark, fell by 1.0 per cent to average

US$94.21 per barrel (bbl.) in 2012. The decline in

fuel prices was broadly influenced by an overall

reduction in fuel demand associated with the

weak global economy. In addition, high US crude

oil inventories tempered fuel prices throughout

the year. Price movements were affected by the

adverse developments to confidence during the

latter half of 2012. These developments included an

intensification of the sovereign debt and banking

crises in the Euro Area. Uncertainties regarding

the outcome of the US elections and the 2013

fiscal budget negotiations also played a role. The

impact of these developments on crude oil prices

was partly offset by the effects of geo-political

tensions largely associated with uncertainty

surrounding crude oil supplies, following the

implementation of sanctions by the West against

Iran. Furthermore, the implementation of stimulus

measures by the major central banks contributed

to upward adjustments in oil prices.

- 12 -The Economy & Monetary Policy Review

Bank of Jamaica

2.3. Balance of Payments

2.3.1. Overview

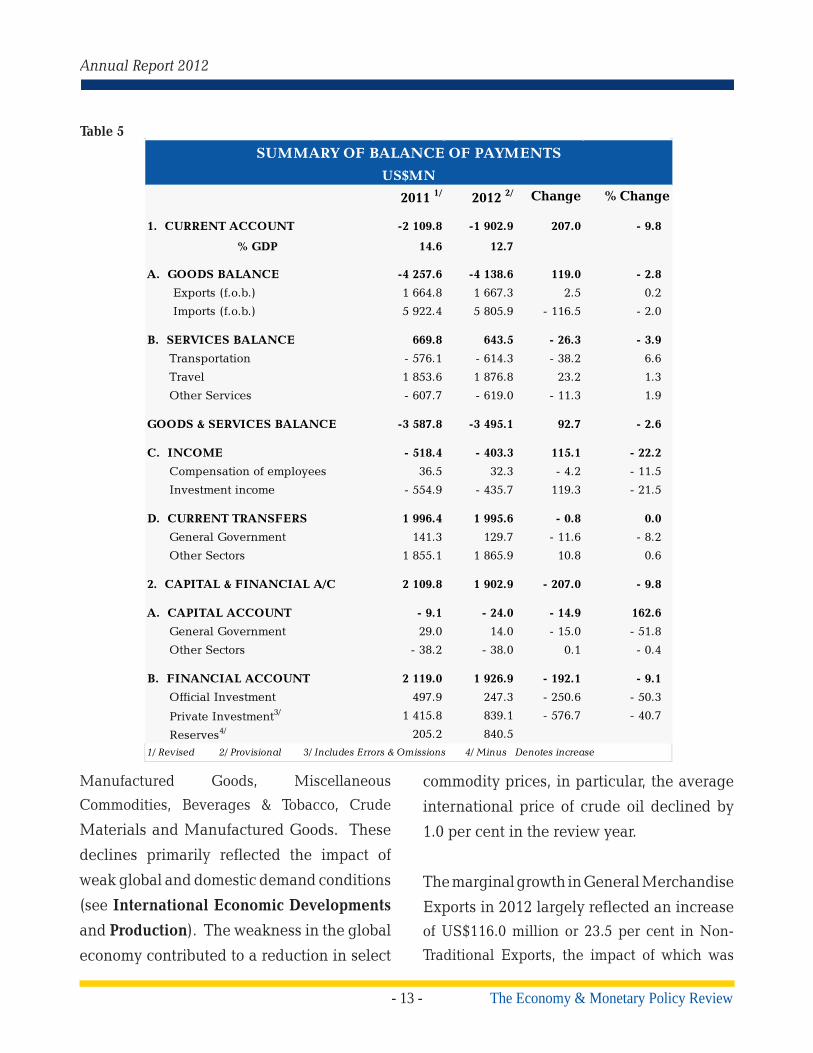

Provisional data indicate that Jamaica’s

balance of payments (BOP) improved in 2012,

largely reflecting a reduction in the value

of imports associated with weak global and

domestic demand conditions. The weakness

in the global economy contributed to a decline

in select commodity prices, particularly oil

(see International Economic Developments

and Production). The current account deficit

for the year is estimated to have narrowed by

US$207.0 million to US$1 902.9 million or 12.7

per cent of GDP relative to 2011 (see Chart 1 and

Table 5). This improvement reflected declines

in the deficits on the Goods and Income sub-

accounts, the impact of which was partly offset

by reductions in the surpluses on the Services

and Current Transfers sub-accounts.

Net Private and Official Investment inflows

were insufficient to finance the deficits on the

capital and current accounts. Consequently,

the NIR of the Bank fell by US$840.5 million

to US$1 125.6 million at end-2012, with gross

reserves representing 13.2 weeks of projected

goods and services imports.

2.3.2. Merchandise Trade

In 2012, the merchandise trade deficit narrowed

by US$119.0 million relative to the deficit for

2011 (see Table 5). This improvement was

mainly driven by a decline of US$116.5 million

or 2.0 per cent in the value of imports (f.o.b.)

and a marginal increase of US$2.5 million or

0.2 per cent in earnings from exports.

The estimated contraction in imports was due

primarily to a reduction of US$113.0 million

or 4.6 per cent in spending on Mineral Fuels.

There were also declines in all other categories

of imports, with the exception of Miscellaneous

Chart 1

9.9

15.9

20.4

9.3 7.0

14.612.7

0.0

5.0

10.0

15.0

20.0

25.0

2006 2007 2008 2009 2010 2011 2012

Per c

ent o

f GDP

Year

Jamaica: Current Account Deficit to GDP

- 13 -

Annual Report 2012

The Economy & Monetary Policy Review

Manufactured Goods, Miscellaneous

Commodities, Beverages & Tobacco, Crude

Materials and Manufactured Goods. These

declines primarily reflected the impact of

weak global and domestic demand conditions

(see International Economic Developments

and Production). The weakness in the global

economy contributed to a reduction in select

commodity prices, in particular, the average

international price of crude oil declined by

1.0 per cent in the review year.

The marginal growth in General Merchandise

Exports in 2012 largely reflected an increase of US$116.0 million or 23.5 per cent in Non-

Traditional Exports, the impact of which was

Table 5

2011 1/ 2012 2/ Change % Change

1. CURRENT ACCOUNT -2 109.8 -1 902.9 207.0 - 9.8

% GDP 14.6 12.7

A. GOODS BALANCE -4 257.6 -4 138.6 119.0 - 2.8

Exports (f.o.b.) 1 664.8 1 667.3 2.5 0.2

Imports (f.o.b.) 5 922.4 5 805.9 - 116.5 - 2.0

B. SERVICES BALANCE 669.8 643.5 - 26.3 - 3.9

Transportation - 576.1 - 614.3 - 38.2 6.6

Travel 1 853.6 1 876.8 23.2 1.3

Other Services - 607.7 - 619.0 - 11.3 1.9

GOODS & SERVICES BALANCE -3 587.8 -3 495.1 92.7 - 2.6

C. INCOME - 518.4 - 403.3 115.1 - 22.2

Compensation of employees 36.5 32.3 - 4.2 - 11.5

Investment income - 554.9 - 435.7 119.3 - 21.5

D. CURRENT TRANSFERS 1 996.4 1 995.6 - 0.8 0.0

General Government 141.3 129.7 - 11.6 - 8.2

Other Sectors 1 855.1 1 865.9 10.8 0.6

2. CAPITAL & FINANCIAL A/C 2 109.8 1 902.9 - 207.0 - 9.8

A. CAPITAL ACCOUNT - 9.1 - 24.0 - 14.9 162.6

General Government 29.0 14.0 - 15.0 - 51.8

Other Sectors - 38.2 - 38.0 0.1 - 0.4

B. FINANCIAL ACCOUNT 2 119.0 1 926.9 - 192.1 - 9.1

Official Investment 497.9 247.3 - 250.6 - 50.3

Private Investment3/ 1 415.8 839.1 - 576.7 - 40.7

Reserves4/ 205.2 840.5

SUMMARY OF BALANCE OF PAYMENTS

1/ Revised 2/ Provisional 3/ Includes Errors & Omissions 4/ Minus Denotes increase

US$MN

- 14 -The Economy & Monetary Policy Review

Bank of Jamaica

partly offset by a decline in alumina exports.

With regard to Non-Traditional Exports, the

increase largely reflected higher receipts from

chemicals, primarily ethanol. Lower alumina

export earnings reflected a contraction of

11.0 per cent in export volumes as well as a

decline of 8.5 per cent in the average realised

price (ARP) of the commodity. The decline in

export volumes resulted from reduced capacity

utilisation at the JAMALCO alumina plant

which experienced production problems during

the first half of the year.

2.3.3. Services

Net earnings from Services declined by an

estimated 3.9 per cent to US$643.5 million in

2012, this reflecting increases in the deficits

on Transportation and Other Services. The

widening of the deficit on the Transportation

sub-account mainly reflected lower gross

inflows by US$59.2 million, relative to 2011,

due to declining activity at the country’s

ports. With regard to the Other Services the

worsening in the deficit was due largely to an

increase of US$10.8 million or 1.2 per cent in

payments for Insurance and Other Business

Services. The impact of the worsened deficits

in Transportation and Other Services was

partly offset by growth of 1.3 per cent in net

travel inflows relative to 2011 (see Table 5).

This improvement primarily reflected a rise of

1.8 per cent in stop-over visitor arrivals and

an expansion of 17.4 per cent in cruise visitor

arrivals.

2.3.4. Income

For 2012, the deficit on the income sub-account

narrowed by US$115.1 million or 22.2 per

cent to US$403.3 million. This improvement

principally reflected a decline of US$80.4

million or 71.9 per cent in the imputed profit

repatriated by the direct investment companies

and a fall of US$40.1 million or 8.6 per cent in

interest payments by the Central Government.

The impact of this improvement was partly

offset by a decline of US$4.2 million or 11.5 per

cent in Compensation of Employees, resulting

from higher outflows from foreigners working

in Jamaica (see Table 5).

2.3.5. Current Transfers

The surplus on the Current Transfers sub-

account fell marginally in 2012, reflecting a

decline of US$11.6 million or 8.2 per cent in

Government Grants, the impact of which was

partly offset by growth of US$10.8 million or

0.6 per cent in net Private Transfers. Of note,

Gross Private Transfer inflows increased by 0.8

per cent for 2012, relative to the expansion of

2.5 per cent in 2011. The slower pace of growth

in private inflows may have been influenced

by weakness in major developed countries as

well as institutional changes in the remittance

industry during the year.

2.3.6. Capital and Financial Account

The deficit on the Capital Account expanded by

US$14.9 million to US$24.0 million for 2012,

while the surplus on the Financial Account

narrowed by US$192.1 million to US$1 926.9

- 15 -

Annual Report 2012

The Economy & Monetary Policy Review

million. This deterioration in the Financial

Account largely reflected respective declines

of US$576.7 million and US$250.6 million in

net Private and Official Investment inflows (see

Table 5).

The decline in Net Official Investments

stemmed from a fall of US$623.1 million in

gross official inflows (see Table 6). Lower

Official inflows were largely underpinned

by a reduction of US$445.5 million in Other

Assistance, which was related to the government

not accessing the international market in 2012.

In addition, there was a decline of US$177.6

million in Project Loans, following exceptional

disbursements in 2011. The impact of these

weaker inflows was partly offset by a decline in

Gross Official Outflows, which was related to a

lower level of amortization of government debt

as well as a reduction in trade suppliers’ credit.

Net private and official investments were insuf-

ficient to finance the deficits on the capital and

current accounts. As a result, the NIR of the

Bank fell by US$840.5 million to US$1125.6

million at end-2012. Gross Foreign Assets at

end-2012 were valued at US$1 980.80 million,

representing 13.2 weeks of projected goods and

services imports.

Table 6

20111/ 20122/ ChangeGROSS OFFICIAL INFLOWS 1 670.5 1 047.5 - 623.1

Project Loan 310.1 132.5 - 177.6

Other Assistance 1 360.4 915.0 - 445.5

GROSS OFFICIAL OUTFLOWS 1 172.6 800.2 - 372.4

Government Direct 690.1 569.4 - 120.7

Bank of Jamaica 177.0 66.0 - 110.9

OtherOfficial 305.6 164.8 - 140.8

NET OFFICIAL INVESTMENTS 497.9 247.3 - 250.61/ Revised2/ Provisional

OFFICIAL INVESTMENT FLOWS (US$MN)

- 16 -The Economy & Monetary Policy Review

Bank of Jamaica

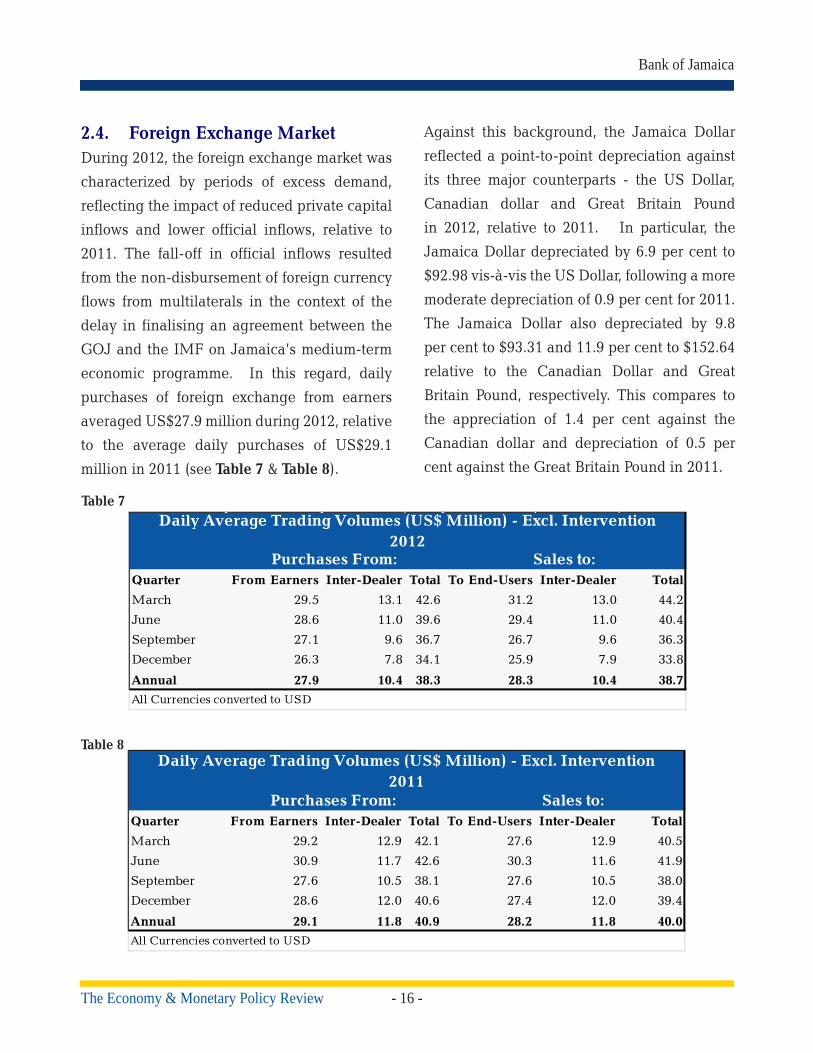

2.4. Foreign Exchange Market During 2012, the foreign exchange market was

characterized by periods of excess demand,

reflecting the impact of reduced private capital

inflows and lower official inflows, relative to

2011. The fall-off in official inflows resulted

from the non-disbursement of foreign currency

flows from multilaterals in the context of the

delay in finalising an agreement between the

GOJ and the IMF on Jamaica’s medium-term

economic programme. In this regard, daily

purchases of foreign exchange from earners

averaged US$27.9 million during 2012, relative

to the average daily purchases of US$29.1

million in 2011 (see Table 7 & Table 8).

Against this background, the Jamaica Dollar

reflected a point-to-point depreciation against

its three major counterparts - the US Dollar,

Canadian dollar and Great Britain Pound

in 2012, relative to 2011. In particular, the

Jamaica Dollar depreciated by 6.9 per cent to

$92.98 vis-à-vis the US Dollar, following a more

moderate depreciation of 0.9 per cent for 2011.

The Jamaica Dollar also depreciated by 9.8

per cent to $93.31 and 11.9 per cent to $152.64

relative to the Canadian Dollar and Great

Britain Pound, respectively. This compares to

the appreciation of 1.4 per cent against the

Canadian dollar and depreciation of 0.5 per

cent against the Great Britain Pound in 2011.

Table 7

Quarter From Earners Inter-Dealer Total To End-Users Inter-Dealer Total

March 29.5 13.1 42.6 31.2 13.0 44.2

June 28.6 11.0 39.6 29.4 11.0 40.4

September 27.1 9.6 36.7 26.7 9.6 36.3

December 26.3 7.8 34.1 25.9 7.9 33.8

Annual 27.9 10.4 38.3 28.3 10.4 38.7

Daily Average Trading Volumes (US$ Million) - Excl. Intervention 2012

Purchases From: Sales to:

All Currencies converted to USD

Table 8

Quarter From Earners Inter-Dealer Total To End-Users Inter-Dealer Total

March 29.2 12.9 42.1 27.6 12.9 40.5

June 30.9 11.7 42.6 30.3 11.6 41.9

September 27.6 10.5 38.1 27.6 10.5 38.0

December 28.6 12.0 40.6 27.4 12.0 39.4

Annual 29.1 11.8 40.9 28.2 11.8 40.0

Daily Average Trading Volumes (US$ Million) - Excl. Intervention 2011

Purchases From: Sales to:

All Currencies converted to USD

- 17 -

Annual Report 2012

The Economy & Monetary Policy Review

In the March 2012 quarter, foreign exchange

market conditions were stable in the context of

fairly ample US Dollar supply. In this regard,

earner inflows averaged US$29.5 million daily

compared with average daily earner inflows of

US$29.2 million for the corresponding quarter

in 2011. However, daily average sales to

end users increased to US$31.2 million from

US$27.6 million for the March 2011 quarter.

Consequently, the weighted average sale rate

(WASR) depreciated by 0.8 per cent in the

March quarter, albeit the slowest quarterly pace

of adjustment in the currency for the calendar

year.

By the middle of the June quarter, market

conditions were adversely affected by the

protracted negotiations between the GOJ

and the IMF on the country’s medium-term

economic programme. This was manifested in

a reduction in earner supply to a daily average

of US$28.6 million from US$30.9 million for

the June 2011 quarter, while average daily

sales was relatively unchanged. Against this

background, the Jamaica Dollar depreciated

by 1.6 per cent in the June 2012 quarter,

relative to a fairly moderate depreciation of

0.2 per cent for the corresponding period in

2011. For the first half of 2012, the Jamaica

Dollar therefore depreciated by 2.4 per cent,

compared with depreciation of 0.1 per cent for

the corresponding period in 2011.

Market conditions remained overwrought

during the second half of 2012, given the

uncertainty about the country’s fiscal outlook.

In particular, there were concerns about the

financing plans for the GOJ Eurobond that was

due to mature in the September quarter. In this

context, the Jamaica Dollar recorded a faster

pace of depreciation, relative to the first half

of the year. The point-to-point depreciation

was 4.6 per cent relative to the first half of the

year, reflecting depreciation of 1.4 per cent and

3.3 per cent for the September and December

quarters, respectively.

The sharp depreciation in the WASR during

the second half of the year coincided with a

trend decline in foreign currency inflows from

earners. In particular, per diem inflows from

earners fell to an average of US$26.7 million for

the second half of the year from an average of

US$29.1 million for the first half of 2012. This

tightening in US dollar supply during the year

was also manifested in the progressive decline

in inter-dealer transactions (see Table 7 & Table

8). Similarly the average per diem sales to end

users fell to US$26.3 million for the second half

of the year from US$30.3 million for the first

half.

In the context of the instability in the foreign

market during the year, the Bank intervened on

several occasions. This resulted in net foreign

currency sale of US$524.6 million, in contrast

to net foreign currency purchase of US$331.3

million for 2011 (see Chart 2). Whilst the

Bank’s frequency of intervention was moderate

during the March quarter, there was a marked

- 18 -The Economy & Monetary Policy Review

Bank of Jamaica

increase the June and September quarters.

This increase was necessitated by the market’s

adverse reaction to the continued delay in ar-

riving at agreement with the IMF. Against this

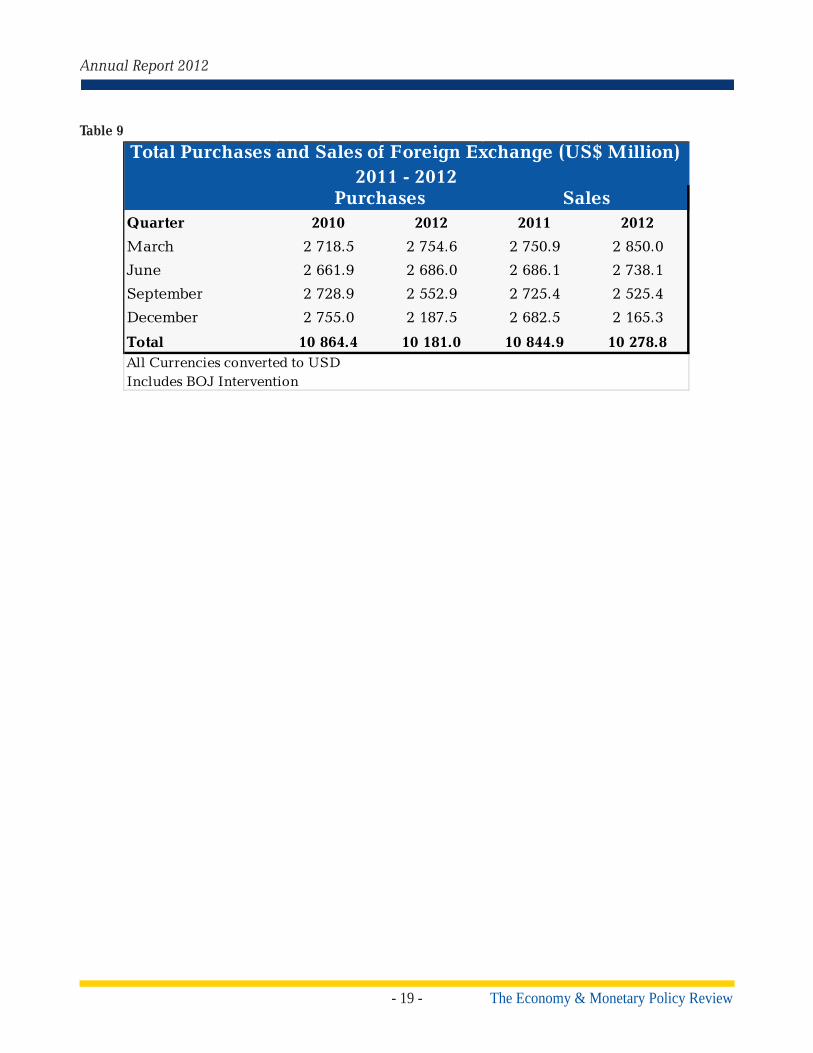

background, total purchases and sales report-

ed by authorized foreign currency traders de-

clined to US$10 181.0 million and US$10 278.8

million, respectively, during 2012 from US$10

864.4 million and US$10 844.9 million, for

2011 (see Table 9). Concurrently, the share of

inter-dealer trades as a per cent of total trades

declined to 26.8 per cent for 2012 from 29.4 per

cent for 2011.

Chart 2 Bank of Jamaica: Foreign Exchange Market Intervention (Spot Market) 2012

The distribution of market activity between the

main intermediaries i.e. authorized dealers and

cambios, shifted marginally for 2012, although

authorised dealers remained the dominant in-

termediary. In this regard, for 2012, the author-

ized dealers’ market share as a percentage of

total foreign exchange sales declined to 54.3

per cent from 62.6 per cent for 2011. In contrast,

there was an increase in cambios’ market share

to 45.7 per cent from 37.4 per cent in 2011.

- 19 -

Annual Report 2012

The Economy & Monetary Policy Review

Table 9

Quarter 2010 2012 2011 2012

March 2 718.5 2 754.6 2 750.9 2 850.0

June 2 661.9 2 686.0 2 686.1 2 738.1

September 2 728.9 2 552.9 2 725.4 2 525.4

December 2 755.0 2 187.5 2 682.5 2 165.3

Total 10 864.4 10 181.0 10 844.9 10 278.8

Total Purchases and Sales of Foreign Exchange (US$ Million) 2011 - 2012

Purchases Sales

All Currencies converted to USD Includes BOJ Intervention

- 20 -The Economy & Monetary Policy Review

Bank of Jamaica

2.5. Prices

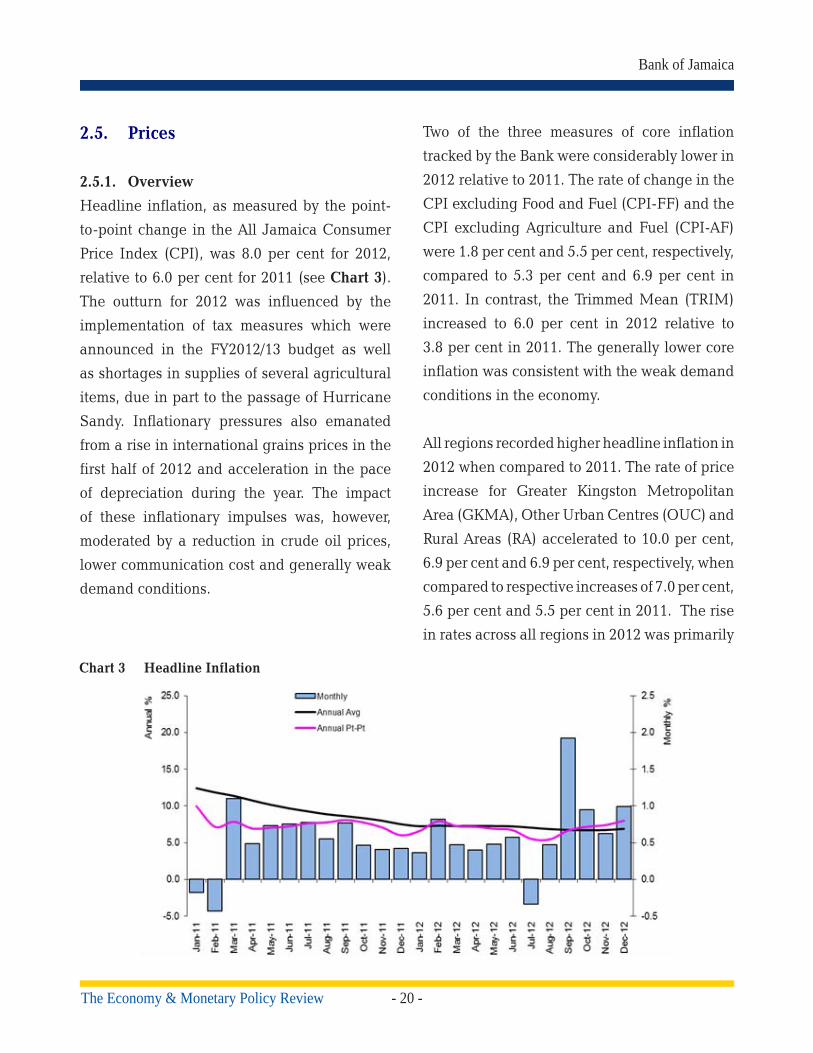

2.5.1. Overview

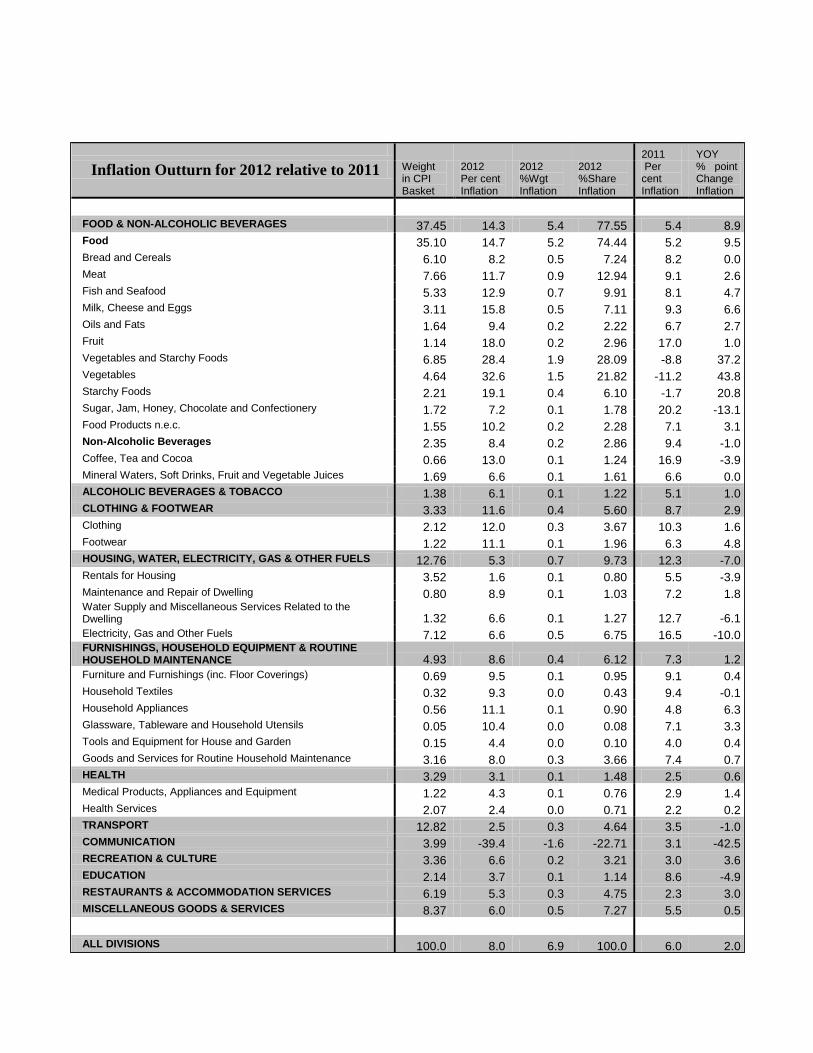

Headline inflation, as measured by the point-

to-point change in the All Jamaica Consumer

Price Index (CPI), was 8.0 per cent for 2012,

relative to 6.0 per cent for 2011 (see Chart 3).

The outturn for 2012 was influenced by the

implementation of tax measures which were

announced in the FY2012/13 budget as well

as shortages in supplies of several agricultural

items, due in part to the passage of Hurricane

Sandy. Inflationary pressures also emanated

from a rise in international grains prices in the

first half of 2012 and acceleration in the pace

of depreciation during the year. The impact

of these inflationary impulses was, however,

moderated by a reduction in crude oil prices,

lower communication cost and generally weak

demand conditions.

Two of the three measures of core inflation

tracked by the Bank were considerably lower in

2012 relative to 2011. The rate of change in the

CPI excluding Food and Fuel (CPI-FF) and the

CPI excluding Agriculture and Fuel (CPI-AF)

were 1.8 per cent and 5.5 per cent, respectively,

compared to 5.3 per cent and 6.9 per cent in

2011. In contrast, the Trimmed Mean (TRIM)

increased to 6.0 per cent in 2012 relative to

3.8 per cent in 2011. The generally lower core

inflation was consistent with the weak demand

conditions in the economy.

All regions recorded higher headline inflation in

2012 when compared to 2011. The rate of price

increase for Greater Kingston Metropolitan

Area (GKMA), Other Urban Centres (OUC) and

Rural Areas (RA) accelerated to 10.0 per cent,

6.9 per cent and 6.9 per cent, respectively, when

compared to respective increases of 7.0 per cent,

5.6 per cent and 5.5 per cent in 2011. The rise

in rates across all regions in 2012 was primarily

Chart 3 Headline Inflation

- 21 -

Annual Report 2012

The Economy & Monetary Policy Review

reflected in Food & Non-Alcoholic Beverages

(FNB), Restaurants & Accommodation Services

Source: STATIN

18.8

8.6

16.6

5.0

10.6

3.8

2.4

30.4

4.3

2.0

4.9

8.0

FNB

ATB

CF

HWEG

FHERM

HLTH

TRAN

COM

R&C

ED

R&A

MIS

11.4

3.7

7.6

6.3

2.3

2.5

1.3

34.8

1.0

16.0

3.9

2.7

%Inflation (2012) GKMA Change (yoy %ppt)

12.1

6.4

10.6

4.9

9.0

2.4

2.1

40.1

6.7

5.1

6.2

6.5

FNB

ATB

CF

HWEG

FHERM

HLTH

TRAN

COM

R&C

ED

R&A

MIS

8.3

0.0

1.0

6.6

2.2

0.9

2.3

43.3

1.6

3.7

2.8

0.7

%Inflation (2012) OUC Change (yoy %ppt)

12.2

4.5

9.0

5.8

6.7

3.0

2.4

46.9

8.2

5.3

5.3

4.3

FNB

ATB

CF

HWEG

FHERM

HLTH

TRAN

COM

R&C

ED

R&A

MIS

7.4

0.3

1.4

8.0

0.1

0.1

1.0

48.9

6.2

3.8

2.2

0.7

%Inflation (2012) RA Change (yoy %ppt)

Blue bars = positive and Red bars = negative

Chart 4 Annual Inflation & YOY Change by Region

(R&A) and Recreation & Culture (R&C) (see

Chart 4 & Appendix A).

- 22 -The Economy & Monetary Policy Review

Bank of Jamaica

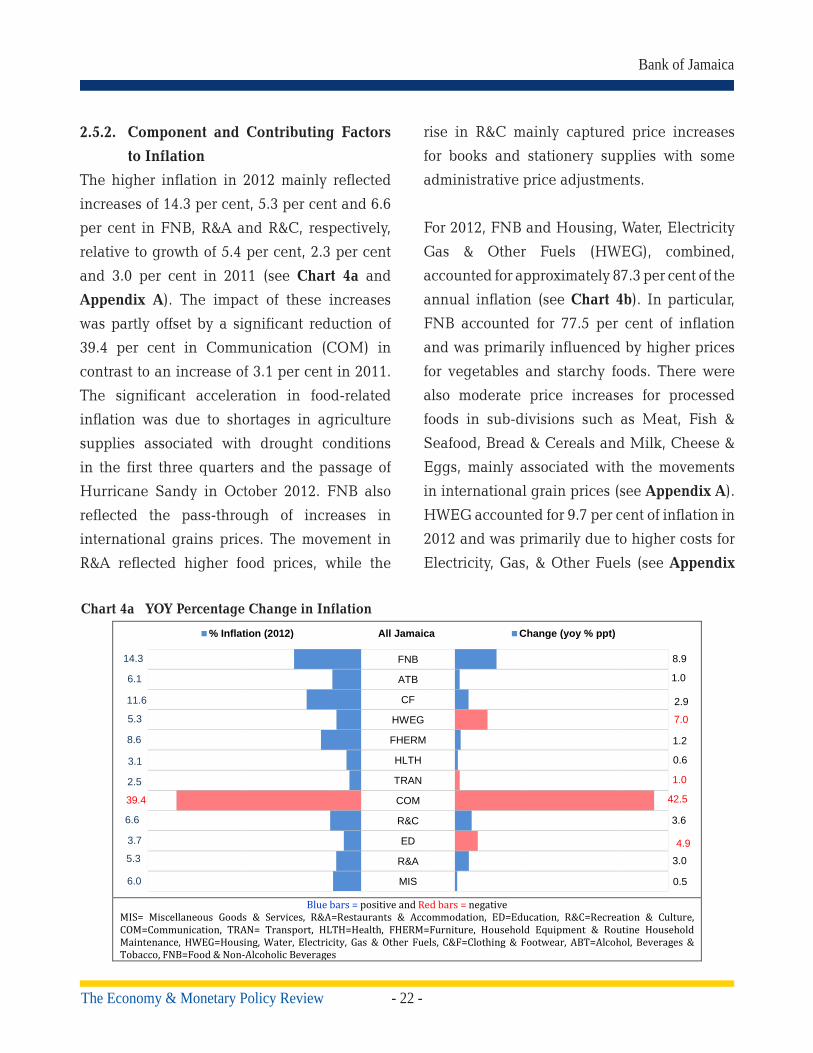

2.5.2. Component and Contributing Factors

to Inflation

The higher inflation in 2012 mainly reflected

increases of 14.3 per cent, 5.3 per cent and 6.6

per cent in FNB, R&A and R&C, respectively,

relative to growth of 5.4 per cent, 2.3 per cent

and 3.0 per cent in 2011 (see Chart 4a and

Appendix A). The impact of these increases

was partly offset by a significant reduction of

39.4 per cent in Communication (COM) in

contrast to an increase of 3.1 per cent in 2011.

The significant acceleration in food-related

inflation was due to shortages in agriculture

supplies associated with drought conditions

in the first three quarters and the passage of

Hurricane Sandy in October 2012. FNB also

reflected the pass-through of increases in

international grains prices. The movement in

R&A reflected higher food prices, while the

rise in R&C mainly captured price increases

for books and stationery supplies with some

administrative price adjustments.

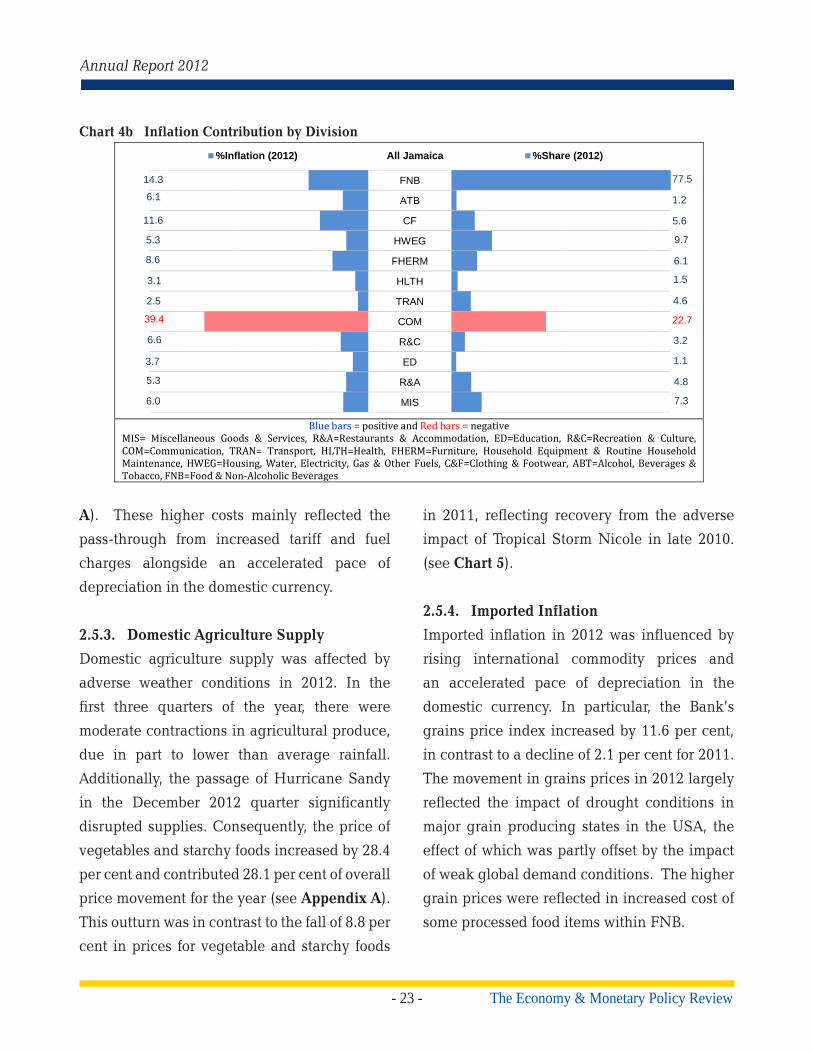

For 2012, FNB and Housing, Water, Electricity

Gas & Other Fuels (HWEG), combined,

accounted for approximately 87.3 per cent of the

annual inflation (see Chart 4b). In particular,

FNB accounted for 77.5 per cent of inflation

and was primarily influenced by higher prices

for vegetables and starchy foods. There were

also moderate price increases for processed

foods in sub-divisions such as Meat, Fish &

Seafood, Bread & Cereals and Milk, Cheese &

Eggs, mainly associated with the movements

in international grain prices (see Appendix A).

HWEG accounted for 9.7 per cent of inflation in

2012 and was primarily due to higher costs for

Electricity, Gas, & Other Fuels (see Appendix

14.3

6.1

11.6

5.3

8.6

3.1

2.5

39.4

6.6

3.7

5.3

6.0

FNB

ATB

CF

HWEG

FHERM

HLTH

TRAN

COM

R&C

ED

R&A

MIS

8.9

1.0

2.9

7.0

1.2

0.6

1.0

42.5

3.6

4.9

3.0

0.5

% Inflation (2012) All Jamaica Change (yoy % ppt)

Blue bars = positive and Red bars = negative

MIS= Miscellaneous Goods & Services, R&A=Restaurants & Accommodation, ED=Education, R&C=Recreation & Culture, COM=Communication, TRAN= Transport, HLTH=Health, FHERM=Furniture, Household Equipment & Routine Household Maintenance, HWEG=Housing, Water, Electricity, Gas & Other Fuels, C&F=Clothing & Footwear, ABT=Alcohol, Beverages & Tobacco, FNB=Food & Non-Alcoholic Beverages

Chart 4a YOY Percentage Change in Inflation

- 23 -

Annual Report 2012

The Economy & Monetary Policy Review

14.3

6.1

11.6

5.3

8.6

3.1

2.5

39.4

6.6

3.7

5.3

6.0

FNB

ATB

CF

HWEG

FHERM

HLTH

TRAN

COM

R&C

ED

R&A

MIS

77.5

1.2

5.6

9.7

6.1

1.5

4.6

22.7

3.2

1.1

4.8

7.3

%Inflation (2012) All Jamaica %Share (2012)

Blue bars = positive and Red bars = negative

MIS= Miscellaneous Goods & Services, R&A=Restaurants & Accommodation, ED=Education, R&C=Recreation & Culture, COM=Communication, TRAN= Transport, HLTH=Health, FHERM=Furniture, Household Equipment & Routine Household Maintenance, HWEG=Housing, Water, Electricity, Gas & Other Fuels, C&F=Clothing & Footwear, ABT=Alcohol, Beverages & Tobacco, FNB=Food & Non-Alcoholic Beverages

Chart 4b Inflation Contribution by Division

A). These higher costs mainly reflected the

pass-through from increased tariff and fuel

charges alongside an accelerated pace of

depreciation in the domestic currency.

2.5.3. Domestic Agriculture Supply

Domestic agriculture supply was affected by

adverse weather conditions in 2012. In the

first three quarters of the year, there were

moderate contractions in agricultural produce,

due in part to lower than average rainfall.

Additionally, the passage of Hurricane Sandy

in the December 2012 quarter significantly

disrupted supplies. Consequently, the price of

vegetables and starchy foods increased by 28.4

per cent and contributed 28.1 per cent of overall

price movement for the year (see Appendix A).

This outturn was in contrast to the fall of 8.8 per

cent in prices for vegetable and starchy foods

in 2011, reflecting recovery from the adverse

impact of Tropical Storm Nicole in late 2010.

(see Chart 5).

2.5.4. Imported Inflation

Imported inflation in 2012 was influenced by

rising international commodity prices and

an accelerated pace of depreciation in the

domestic currency. In particular, the Bank’s

grains price index increased by 11.6 per cent,

in contrast to a decline of 2.1 per cent for 2011.

The movement in grains prices in 2012 largely

reflected the impact of drought conditions in

major grain producing states in the USA, the

effect of which was partly offset by the impact

of weak global demand conditions. The higher

grain prices were reflected in increased cost of

some processed food items within FNB.

- 24 -The Economy & Monetary Policy Review

Bank of Jamaica

In contrast to the movement in grains prices,

there was a decline of 10.5 per cent in the

West Texas Intermediate crude (WTI) oil price,

relative to the increase of 10.5 per cent in 2011

(see Chart 6). Consistent with the decline in

international oil price, there were lower rates of

increase in the cost of fuel and energy related

products. These were reflected in lower rates

of movements in TRAN and HWEG relative to

2011.

The exchange rate between the Jamaica Dollar

and the US Dollar depreciated by 6.9 per cent

for 2012. This compares with depreciation of

0.9 per cent for end-2011. This depreciation

resulted in some pass-through to prices and

was mainly reflected within HWEG and FNB.

The acceleration in the pace of depreciation

during the year was influenced by uncertainties

surrounding negotiations between the GOJ

and the IMF for a new borrowing programme.

2.5.5. Administered and Other Price

Adjustments

During the June 2012 quarter, the tax base

was widened to incorporate a variety of basic

food items that were previously tax-exempt or

zero rated. In addition, there were increased

fees for motor vehicle licences, fitness and

registration. The inflationary impact from these

Chart 5 Average Supplies of Agriculture Produce (2011 - 2012)

2011

Yellow Yam

Irish Potato

Ripe Plantains

Sweet Potato

Dasheen

Carrot

Cabbage

Red Peas

Tomato (Plummie)

Escallion & Thyme

Callaloo

Pumpkin

Lettuce

Star

ches

Vege

tabl

es

Actual Avg. of previous 5-years 2012

52.0

71.8

-15.5

3.1

-4.6

-22.0

-1.7

6.8

9.6

-7.2

-22.0

6.3

-29.2

Actual (%)

Source: RADA

- 25 -

Annual Report 2012

The Economy & Monetary Policy Review

AVG EOP AVG EOP AVG EOPWTI Prices Grain Prices Exchange Rate

2011 95.12 98.58 371.78 355.89 86.07 86.602012 94.21 88.27 380.87 397.115 88.97 92.982011 (yoy%) 19.6 10.5 25.1 -2.1 -1.6 0.92012 (yoy%) -1.0 -10.5 2.4 11.6 3.4 7.4

-10

0

10

20

30

40

50

60

70

80

-50

0

50

100

150

200

250

300

350

4002011

2012

2011 (yoy%)

2012 (yoy%)

Chart 6 Trends in WTI Crude Oil & BOJ Grains Index

Source: Bloomberg & STATIN

tax measures was mainly reflected in FNB and

TRAN. Price increases arising from these tax

measures were highest for dairy products, fish

& seafood and meats, which accounted for

30.0 per cent of the movement in CPI during

the year. Price increases arising from these

tax measures were highest for dairy products,

fish & seafood, and meats which accounted

for 30.0 per cent of the movement in the CPI

during the year. The impact of these impulses

was tempered by a reduction in the GCT rate to

16.5 per cent from 17.5 per cent.

Other price changes also contributed to inflation

pressures throughout 2012. Specifically, he

Incorporated Master Builders Association of

Jamaica (IMAJ) effected an average increase

of 5.0 per cent in wages for artisans in February

2012, which was reflected within HWEG. This

followed an average increase of 10.0 per cent

in 2011. Also, in September 2012, there was

an increase of 11.1 per cent in the National

Minimum Wage, which was reflected in

Furniture, Household Equipment & Routine

Household Maintenance.

2.5.6. Demand and Supply Conditions

Some short-term indicators of domestic

demand reflected mixed results throughout

the year. These indicators include PAYE

receipts and the values of debit & credit card

transactions, imports and non-business loans.

In real terms, PAYE receipts and imports

reflected declines of 3.5 per cent and 3.7 per

cent, respectively, relative to increases of 7.5

per cent and 4.7 per cent in 2011. In contrast,

in real terms, the values of debit and credit

card transactions and non-business loans

increased by 2.9 per cent and 14.8 per cent,

respectively, following growth of 5.2 per cent

and 3.0 per cent for 2011. The mixed outturn

for 2012 indicates overall weak demand in the

domestic economy (see Chart 7).

- 26 -The Economy & Monetary Policy Review

Bank of Jamaica

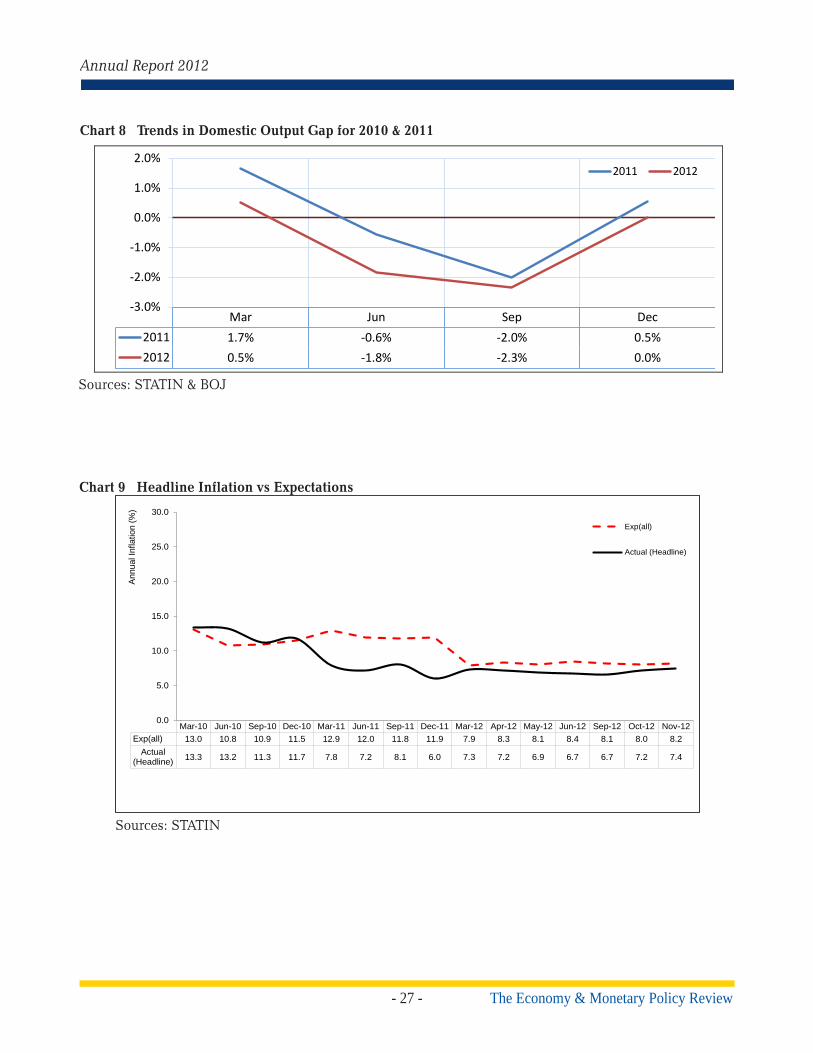

The Bank estimates that Jamaica’s output gap

widened in 2012 as business activity slowed

amid sluggish demand conditions (see Chart 8).

The resulting excess capacity among industrial

suppliers, combined with weakened domestic

demand had a moderating impact on inflation.

2.5.7. Inflation Expectations

The Bank’s survey of inflation expectations

indicated that the average expected annual

inflation among businesses for 2012 was 8.1

per cent, in line with the actual outturn of

8.0 per cent for the year (see Chart 9). This

expectation was also substantially below the

average of 11.9 per cent that was anticipated

for 2011. The result for 2012 reflected a general

downward adjustment in business expectations

as inflationary pressures subsided within the

low demand environment.

Chart 7 Average Supplies of Agriculture Produce (2010-2011)

Sources: MOF, JETS, STATIN, BOJ

A

15

20

25

30

35

40

45

50

55D

ec-0

7

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

J$ m

illio

n de

flate

d

Real PAYE

Polynomial Trend

B

80

100

120

140

160

180

200