Embed Size (px)

Citation preview

Appendix AChapter 2

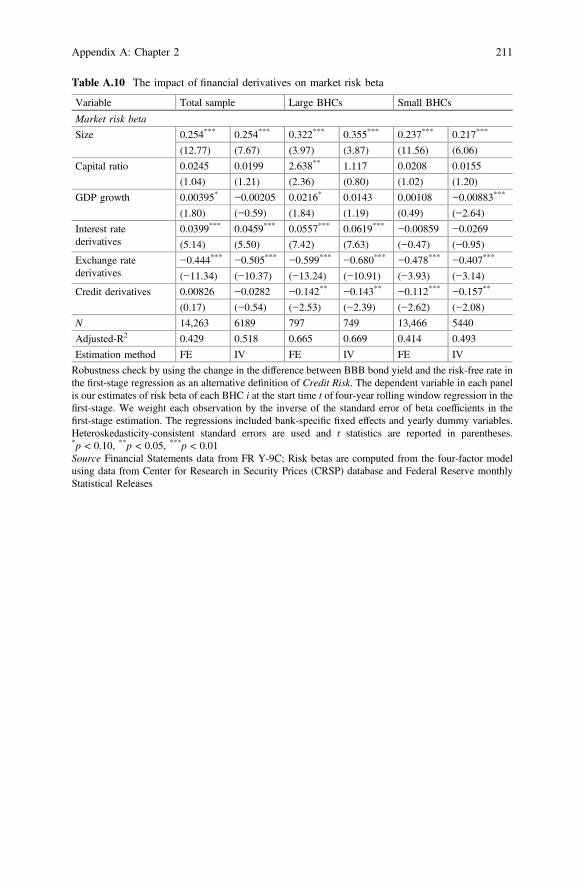

See Tables A.1, A.2, A.3, A.4, A.5, A.6, A.7, A.8, A.9 and A.10.

© Shanghai Jiao Tong University Press and Springer Nature Singapore Pte Ltd. 2018S. Li, Financial Institutions in the Global Financial Crisis,https://doi.org/10.1007/978-981-10-7440-0

177

Table A.1 Diagnostic tests of instruments used in IV regression in Table 2.8

Totalsample

LargeBHCs

SmallBHCs

Panel A: Interest rate risk betas

Weak-instrument-robustinference:

Anderson-RubinWald test (p-value)

23.45***

(0.000)12.46***

(0.0060)13.16**

(0.011)

Underidentification test Kleibergen-Paap rkLM statistic(p-value)

40.26***

(0.000)42.130***

(0.000)31.29***

(0.000)

Weak identification test Cragg-DonaldWald F statistic

2942.68*** 457.639*** 1751.21***

Kleibergen-PaapWald rk F statistic

34.48*** 33.96*** 41.66***

Panel B: Exchange rate risk beta

Weak-instrument-robustinference:

Anderson-RubinWald test (p-value)

39.51***

(0.000)32.50***

(0.000)14.97***

(0.002)

Underidentification test Kleibergen-Paap rkLM statistic(p-value)

82.61***

(0.000)72.71***

(0.000)13.65***

(0.003)

Weak identification test Cragg-DonaldWald F statistic

1684.93*** 219.89*** 1605.38***

Kleibergen-PaapWald rk F statistic

36.845*** 37.65*** 16.45***

Panel C: Credit risk beta

Weak-instrument-robustinference:

Anderson-RubinWald test (p-value)

19.45***

(0.000)32.71***

(0.000)12.64**

(0.012)

Underidentification test Kleibergen-Paap rkLM statistic(p-value)

33.20***

(0.000)35.88***

(0.000)20.21***

(0.001)

Weak identification test Cragg-DonaldWald F statistic

1.4e+04*** 3938.86*** 2119.16***

Kleibergen-PaapWald rk F statistic

150.687*** 218.270*** 44.36***

*p < 0.10, **p < 0.05, ***p < 0.01

178 Appendix A: Chapter 2

Tab

leA.2

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas

Variable

Total

BHCs

Large

BHCs

SmallBHCs

Pan

elA:Interestrate

risk

beta

(foreign

expo

sure

asinstrumentvariab

le)

Interestmargin

4.54

2***

0.78

4−8.46

7***

8.02

8**

8.51

5*21

8.4*

*4.19

3***

−0.06

26−1.79

5

(6.26)

(0.44)

(−2.73

)(1.99)

(1.95)

(2.53)

(5.85)

(−0.03

)(−1.56

)

C&Iloans

−0.38

52.22

0**

8.88

8***

12.20*

**14

.09*

**0.13

8−0.80

0**

0.69

90.59

3

(−0.99

)(2.26)

(3.60)

(4.11)

(4.35)

(0.14)

(−2.09

)(0.73)

(0.67)

Mortgageloans

0.12

90.75

45.30

9***

9.00

0***

9.66

2***

0.33

50.05

040.19

50.14

8

(0.54)

(1.20)

(3.52)

(3.92)

(4.07)

(0.51)

(0.22)

(0.32)

(0.29)

Other

loans

−1.55

2***

−1.34

614

.05*

**5.13

9**

5.60

8**

0.85

6−1.65

7***

−3.81

1***

1.09

4*

(−3.22

)(−1.09

)(3.56)

(2.05)

(2.03)

(1.24)

(−3.70

)(−3.18

)(1.94)

Dom

estic

depo

sits

−0.86

1***

1.78

7***

1.97

8***

1.61

51.01

1−0.24

9−1.58

0***

0.38

10.05

31

(−3.34

)(3.08)

(2.75)

(0.95)

(0.57)

(−0.49

)(−6.41

)(0.66)

(0.17)

GAPratio

−0.00

693

−0.00

453

−0.02

45**

*0.00

158

0.00

516

−0.00

199*

−0.02

74−0.10

6**

−0.08

68**

(−1.57

)(−0.92

)(−5.49

)(0.29)

(0.88)

(−1.80

)(−1.16

)(−2.14

)(−2.37

)

Size

0.64

1***

0.91

7***

4.32

3***

1.04

8**

1.16

3***

0.01

230.47

4***

0.42

6***

0.16

0

(10.41

)(5.78)

(3.95)

(2.58)

(2.81)

(0.19)

(8.65)

(3.05)

(1.26)

Capitalratio

0.09

522.94

3***

6.95

1***

4.49

63.66

5−2.88

50.04

171.20

90.13

8

(0.86)

(3.57)

(2.92)

(1.08)

(0.74)

(−1.45

)(0.69)

(1.46)

(0.24)

GDPgrow

th−0.00

625

−0.00

0173

0.00

539

0.02

610.02

830.00

529

−0.01

17**

−0.03

99***

0.00

146

(−1.28

)(−0.01

)(0.51)

(1.12)

(1.17)

(0.57)

(−2.36

)(−2.97

)(0.14)

Interestrate

derivativ

es0.11

6***

0.14

6***

1.12

7*0.09

62**

*0.10

6***

0.01

26*

0.15

7***

0.20

0***

0.15

5

(4.50)

(4.60)

(1.88)

(3.29)

(3.10)

(1.96)

(2.99)

(2.93)

(1.64)

L.interestrate

risk

beta

0.03

611.08

0***

0.25

6*

(1.04)

(81.24

)(1.80)

(con

tinued)

Appendix A: Chapter 2 179

Tab

leA.2

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N11

,795

4367

3866

754

719

725

11,041

3648

3169

Adjusted-R2

0.19

90.13

80.47

30.47

40.19

10.06

67

AR(1)

0.00

80.00

00.01

4

AR(2)

0.67

60.20

60.43

6

HansenJstatistic

(p-value)

3.27

(0.514

)2.67

(0.103

)4.04

(0.401

)

Pan

elB:Excha

ngerate

risk

beta

(interestrate

expo

sure

asinstrumentvariab

le)

Assetsin

foreigncurrencies

−0.62

1−1.78

10.02

26−4.41

6***

−4.01

9***

0.77

84.86

4***

3.87

5***

−0.55

8

(−0.61

)(−1.56

)(0.05)

(−3.74

)(−3.19

)(0.99)

(4.88)

(3.15)

(−1.06

)

Foreignexchange

depo

sits

1.08

9*−0.30

3−0.27

9−1.52

8−2.11

6*0.15

81.45

0**

−1.49

80.22

0

(1.73)

(−0.34

)(−0.32

)(−1.44

)(−1.80

)(0.11)

(1.98)

(−1.22

)(0.24)

Size

−0.13

4***

−0.26

5***

0.19

9*0.16

40.11

40.18

1−0.11

8**

−0.21

2**

0.22

0*

(−2.69

)(−3.49

)(1.65)

(1.20)

(0.83)

(0.41)

(−2.23

)(−2.36

)(1.73)

Capitalratio

−0.04

05−0.32

30.25

6−2.40

6−2.80

50.28

3−0.04

99−0.16

30.29

0

(−0.78

)(−0.79

)(1.00)

(−1.15

)(−1.18

)(0.09)

(−0.87

)(−0.45

)(1.04)

GDPgrow

th0.01

69**

*0.01

69**

−0.00

514

0.02

570.01

740.01

720.01

69**

*0.02

32***

−0.01

07

(3.15)

(2.24)

(−0.72

)(1.41)

(0.92)

(0.83)

(3.04)

(2.84)

(−1.39

)

Exchang

erate

derivativ

es0.54

5***

0.65

8***

0.15

5***

0.72

1***

0.83

7***

0.14

50.79

1***

0.92

0***

0.13

0***

(6.31)

(5.80)

(4.83)

(6.84)

(6.07)

(1.54)

(5.29)

(4.19)

(4.40)

L.exchange

rate

risk

beta

0.97

3***

1.68

6***

0.98

1***

(10.95

)(3.80)

(10.61

)

N11

,803

4416

3926

759

728

707

11,044

3688

3219

Adjusted-R2

0.16

50.20

60.40

40.40

80.16

00.19

3(con

tinued)

180 Appendix A: Chapter 2

Tab

leA.2

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

AR(1)

0.00

00.00

30.00

0

AR(2)

0.44

50.11

00.81

6

HansenJstatistic

(p-value)

0.55

2(0.75

9)2.52

(0.640

)1.05

(0.789

)

Pan

elC:Creditrisk

beta

(interestrate

expo

sure

asinstrumentvariab

le)

Marketliq

uidity

−0.51

1***

−0.41

6***

−0.08

91−0.25

3−0.43

8*−1.51

1−0.51

8***

−0.43

7***

0.14

6

(−9.38

)(−5.21

)(−1.24

)(−1.11

)(−1.95

)(−1.00

)(−9.23

)(−5.25

)(1.32)

Fund

ingliq

uidity

−0.38

8***

−0.63

6***

0.01

39−1.56

2***

−1.59

5***

−8.24

4−0.34

6**

−0.52

7***

−0.07

80

(−2.94

)(−4.04

)(0.14)

(−3.59

)(−3.74

)(−0.88

)(−2.48

)(−3.06

)(−0.63

)

Non

-perform

ingLoans

−4.71

7***

−2.99

6***

−0.34

5−11

.42*

**−12

.56*

**6.64

1−4.26

9***

−1.42

5***

0.46

4

(−11

.39)

(−6.01

)(−1.03

)(−7.45

)(−8.53

)(0.09)

(−10

.17)

(−2.94

)(1.39)

Loancharge-offs

−5.92

2***

−4.30

8*−0.24

4−17

.73*

**−23

.56*

**49

.66

−3.87

8*−0.60

90.24

1

(−2.68

)(−1.83

)(−0.24

)(−3.13

)(−5.17

)(0.30)

(−1.65

)(−0.26

)(0.21)

Loanloss

prov

isions

6.48

8***

4.77

5**

0.32

812

.56*

**16

.69*

**−49

.98

5.59

2***

2.44

52.61

1**

(3.19)

(2.08)

(0.30)

(2.70)

(3.92)

(−0.25

)(2.60)

(1.06)

(2.18)

Size

0.04

96**

*−0.01

80−0.02

060.20

7***

0.27

8***

0.00

968

0.06

58**

*0.00

813

−0.00

276

(2.83)

(−0.68

)(−0.69

)(4.14)

(6.01)

(0.02)

(3.60)

(0.28)

(−0.07

)

Capitalratio

−0.00

646

−0.04

000.11

7**

2.16

2***

1.72

8**

−0.36

7−0.00

130

0.04

620.11

7

(−0.69

)(−0.46

)(1.97)

(3.03)

(2.17)

(−0.09

)(−0.11

)(0.53)

(1.39)

GDPgrow

th0.00

617*

**0.00

622*

*0.00

583*

*0.01

61**

0.01

64**

−0.01

870.00

520*

**0.00

454

0.00

836*

*

(3.40)

(2.27)

(2.09)

(2.41)

(2.54)

(−1.14

)(2.80)

(1.58)

(2.02)

Creditderivativ

es0.07

61**

*0.07

46***

0.02

57**

0.10

3***

0.09

48**

*0.01

110.07

08*

0.10

20.04

26***

(4.73)

(4.37)

(2.23)

(5.88)

(5.71)

(0.11)

(1.76)

(1.40)

(2.75)

(con

tinued)

Appendix A: Chapter 2 181

Tab

leA.2

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

L.creditrisk

beta

−0.65

4***

0.33

20.90

6***

(−6.96

)(1.24)

(7.87)

N10

,984

4152

3705

697

667

646

10,287

3485

3059

Adjusted-R2

0.16

30.21

60.59

40.62

00.14

90.16

8

AR(1)

0.00

00.02

0.00

0

AR(2)

0.78

90.26

70.40

8

HansenJstatistic

(p-value)

2.02

(0.364

)10

.18(0.17

9)0.15

(0.928

)

Estim

ationmetho

dFE

IVGMM

FEIV

GMM

FEIV

GMM

PanelA

isusingforeignexpo

sure

asinstrumentvariable,w

hile

PanelBandPanelCareusinginterestrate

expo

sure

asinstrumentvariable.T

hedependent

variable

ineach

Panelisou

restim

ates

ofrisk

beta

ofeach

BHCiatthe

starttim

eto

ffou

r-year

rolling

windo

wregression

inthefirst-stage.Weweigh

teach

observationby

theinverseof

thestandard

errorof

betacoefficientsin

thefirst-stageestim

ation.

The

regression

sinclud

edbank

-specificfixedeffectsandyearly

dummyvariables.Heteroskedasticity

-con

sistentstandard

errors

areused

andtstatisticsarerepo

rted

inparentheses.

* p<0.10

,**p<0.05

,*** p

<0.01

Source

Financialstatementsdatafrom

FRY-9C;R

iskbetasarecompu

tedfrom

thefour-factormod

elusingdatafrom

CenterforResearchin

Security

Prices

(CRSP

)database

andFederalReserve

mon

thly

Statistical

Releases

182 Appendix A: Chapter 2

Tab

leA.3

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas

Variable

Total

BHCs

Large

BHCs

SmallBHCs

Pan

elA:Interestrate

risk

beta

(basisexpo

sure

asinstrumentvariab

le)

Interestmargin

4.54

2***

0.51

3−0.27

28.02

8**

7.14

794

.64*

*4.19

3***

−0.09

4314

.11*

**

(6.26)

(0.29)

(−0.14

)(1.99)

(1.61)

(2.67)

(5.85)

(−0.05

)(4.01)

C&Iloans

−0.38

52.25

7**

1.48

912

.20*

**14

.23*

**−0.19

5−0.80

0**

0.69

0−2.40

4

(−0.99

)(2.29)

(1.42)

(4.11)

(4.31)

(−0.19

)(−2.09

)(0.72)

(−1.56

)

Mortgageloans

0.12

90.69

60.40

09.00

0***

9.51

7***

−0.08

690.05

040.19

5−0.45

8

(0.54)

(1.10)

(0.65)

(3.92)

(4.00)

(−0.11

)(0.22)

(0.32)

(−0.94

)

Other

loans

−1.55

2***

−1.23

21.74

55.13

9**

5.73

1**

0.58

7−1.65

7***

−3.82

7***

−0.39

9

(−3.22

)(−0.98

)(1.62)

(2.05)

(2.01)

(0.72)

(−3.70

)(−3.19

)(−0.32

)

Dom

estic

depo

sits

−0.86

1***

1.69

6***

−0.07

071.61

50.67

4−0.14

1−1.58

0***

0.39

5−0.45

6

(−3.34

)(2.93)

(−0.18

)(0.95)

(0.37)

(−0.32

)(−6.41

)(0.68)

(−0.88

)

GAPratio

−0.00

693

−0.00

453

−0.02

38**

*0.00

158

0.00

511

−0.00

127

−0.02

74−0.10

6**

0.22

7

(−1.57

)(−0.93

)(−3.38

)(0.29)

(0.88)

(−0.88

)(−1.16

)(−2.13

)(0.90)

Size

0.64

1***

0.92

4***

0.34

81.04

8**

1.20

9***

−0.03

090.47

4***

0.42

9***

0.57

8***

(10.41

)(5.80)

(1.15)

(2.58)

(2.86)

(−0.30

)(8.65)

(3.07)

(2.80)

Capitalratio

0.09

522.90

9***

−0.09

424.49

63.97

5−3.57

50.04

171.22

00.14

3

(0.86)

(3.54)

(−0.13

)(1.08)

(0.78)

(−1.56

)(0.69)

(1.47)

(1.13)

GDPgrow

th−0.00

625

−0.00

0947

0.00

529

0.02

610.02

540.00

307

−0.01

17**

−0.03

97***

−0.00

0912

(−1.28

)(−0.08

)(0.51)

(1.12)

(1.05)

(0.33)

(−2.36

)(−2.95

)(−0.08

)

Interestrate

derivativ

es0.11

6***

0.14

6***

0.51

5*0.09

62**

*0.10

4***

0.01

07**

0.15

7***

0.20

0***

0.22

6**

(4.50)

(4.60)

(1.65)

(3.29)

(3.11)

(2.19)

(2.99)

(2.92)

(2.37)

L.interestrate

risk

beta

0.18

31.07

8***

0.54

1***

(0.61)

(77.96

)(2.99)

(con

tinued)

Appendix A: Chapter 2 183

Tab

leA.3

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N11

,795

4348

3837

754

706

725

11,041

3642

3169

Adjusted-R2

0.19

90.13

60.47

30.47

10.19

10.06

66

AR(1)

0.00

00.00

00.00

0

AR(2)

0.97

80.20

00.06

8

HansenJstatistic

(p-value)

2.79

(0.646

)3.05

(0.09)

9.52

2(0.05

)

Pan

elB:Excha

ngerate

risk

beta

(basisexpo

sure

asinstrumentvariab

le)

Assetsin

foreigncurrencies

−0.62

1−1.09

70.28

7−4.41

6***

−4.00

9***

1.12

24.86

4***

4.77

3***

−0.55

0

(−0.61

)(−0.96

)(0.57)

(−3.74

)(−3.08

)(1.50)

(4.88)

(4.04)

(−1.07

)

Foreignexchange

depo

sits

1.08

9*−0.50

7−0.08

54−1.52

8−2.44

3**

0.05

501.45

0**

−1.71

00.44

6

(1.73)

(−0.56

)(−0.09

)(−1.44

)(−2.01

)(0.03)

(1.98)

(−1.36

)(0.45)

Size

−0.13

4***

−0.28

0***

0.23

8**

0.16

40.09

590.06

77−0.11

8**

−0.22

6**

0.25

4**

(−2.69

)(−3.62

)(1.98)

(1.20)

(0.69)

(0.18)

(−2.23

)(−2.46

)(1.97)

Capitalratio

−0.04

05−0.20

50.23

0−2.40

6−2.83

5−0.17

9−0.04

99−0.16

20.25

8

(−0.78

)(−0.47

)(0.83)

(−1.15

)(−1.17

)(−0.07

)(−0.87

)(−0.44

)(0.90)

GDPgrow

th0.01

69**

*0.01

61**

−0.00

738

0.02

570.01

880.01

530.01

69**

*0.02

24***

−0.01

30

(3.15)

(2.10)

(−1.01

)(1.41)

(0.99)

(0.81)

(3.04)

(2.72)

(−1.65

)

Exchang

erate

derivativ

es0.54

5***

0.67

8***

0.15

3***

0.72

1***

0.85

7***

0.11

00.79

1***

0.93

4***

0.13

5***

(6.31)

(5.81)

(4.97)

(6.84)

(5.95)

(1.35)

(5.29)

(4.15)

(4.62)

L.exchange

rate

risk

beta

0.99

3***

1.50

8***

0.98

7***

(10.89

)(4.49)

(10.63

)

N11

,803

4354

3841

759

711

682

11,044

3643

3159

Adjusted-R2

0.16

50.20

30.40

40.40

40.16

00.19

3(con

tinued)

184 Appendix A: Chapter 2

Tab

leA.3

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

AR(1)

0.00

00.00

20.00

0

AR(2)

0.47

20.12

80.84

7

HansenJstatistic

(p-value)

0.86

4(0.64

9)2.94

(0.568

)1.29

(0.731

)

Pan

elC:Creditrisk

beta

(foreign

expo

sure

asinstrumentvariab

le)

Marketliq

uidity

−0.51

1***

−0.44

0***

−0.11

1−0.25

3−0.43

9*−0.26

2−0.51

8***

−0.46

2***

0.11

4

(−9.38

)(−5.48

)(−1.49

)(−1.11

)(−1.95

)(−0.05

)(−9.23

)(−5.54

)(1.11)

Fund

ingliq

uidity

−0.38

8***

−0.66

3***

0.02

33−1.56

2***

−1.60

1***

13.62*

*−0.34

6**

−0.54

7***

−0.05

00

(−2.94

)(−4.04

)(0.23)

(−3.59

)(−3.76

)(2.14)

(−2.48

)(−3.04

)(−0.40

)

Non

-perform

ingloans

−4.71

7***

−3.14

7***

−0.53

2−11

.42*

**−12

.54*

**−39

.84

−4.26

9***

−1.57

0***

0.26

6

(−11

.39)

(−6.25

)(−1.62

)(−7.45

)(−8.51

)(0.77)

(−10

.17)

(−3.22

)(0.86)

Loancharge-offs

−5.92

2***

−4.50

1*−0.20

0−17

.73*

**−23

.53*

**−41

.29

−3.87

8*−0.74

30.16

5

(−2.68

)(−1.94

)(−0.20

)(−3.13

)(−5.16

)(−1.19

)(−1.65

)(−0.32

)(0.14)

Loanloss

prov

isions

6.48

8***

4.96

0**

0.19

312

.56*

**16

.65*

**80

.36*

*5.59

2***

2.57

02.68

5**

(3.19)

(2.20)

(0.18)

(2.70)

(3.91)

(2.65)

(2.60)

(1.14)

(2.23)

Size

0.04

96**

*−0.00

257

−0.01

400.20

7***

0.27

7***

−0.39

00.06

58**

*0.02

640.00

147

(2.83)

(−0.10

)(−0.47

)(4.14)

(5.99)

(−0.72

)(3.60)

(0.92)

(0.03)

Capitalratio

−0.00

646

−0.01

330.13

7**

2.16

2***

1.72

0**

−33

.11*

−0.00

130

0.07

350.08

67

(−0.69

)(−0.15

)(2.19)

(3.03)

(2.16)

(−1.81

)(−0.11

)(0.86)

(1.16)

GDPgrow

th0.00

617*

**0.00

609*

*0.00

570*

*0.01

61**

0.01

64**

−0.06

770.00

520*

**0.00

437

0.00

701*

(3.40)

(2.22)

(2.04)

(2.41)

(2.54)

(−1.63

)(2.80)

(1.52)

(1.73)

Creditderivativ

es0.07

61**

*0.07

34**

*0.02

43**

*0.10

3***

0.09

61**

*0.99

8***

0.07

08*

0.10

10.04

47***

(4.73)

(4.33)

(2.62)

(5.88)

(5.77)

(3.75)

(1.76)

(1.41)

(3.32)

(con

tinued)

Appendix A: Chapter 2 185

Tab

leA.3

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

L.creditrisk

beta

−0.70

3***

0.06

580.90

2***

(−7.37

)(0.19)

(7.65)

N10

,984

4121

3664

697

667

646

10,287

3454

3018

Adjusted-R2

0.16

30.21

90.59

40.62

00.14

90.16

9

AR(1)

0.00

00.00

10.00

0

AR(2)

0.83

40.48

20.12

8

HansenJstatistic

(p-value)

0.46

0(0.79

5)6.91

(0.938

)1.51

(0.470

)

Estim

ationmetho

dFE

IVGMM

FEIV

GMM

FEIV

GMM

PanelA

andPanelB

areusingbasisexpo

sure

asinstrumentv

ariable,whilePanelC

isusingforeignexpo

sure

asinstrumentv

ariable.The

depend

entv

ariablein

each

Panelisou

restim

ates

ofrisk

betaof

each

BHCiatthe

starttim

eto

ffou

r-year

rolling

windo

wregression

inthefirst-stage.Weweigh

teachob

servationby

theinverseof

thestandard

errorof

beta

coefficients

inthefirst-stageestim

ation.

The

regression

sinclud

edbank

-specificfixedeffectsandyearly

dummy

variables.Heteroskedasticity

-con

sistentstandard

errors

areused

andtstatisticsarerepo

rted

inparentheses.

* p<0.10

,**p<0.05

,*** p

<0.01

Source

FinancialS

tatementsdatafrom

FRY-9C;R

iskbetasarecompu

tedfrom

thefour-factormod

elusingdatafrom

CenterforResearchin

Security

Prices

(CRSP

)database

andFederalReserve

mon

thly

Statistical

Releases

186 Appendix A: Chapter 2

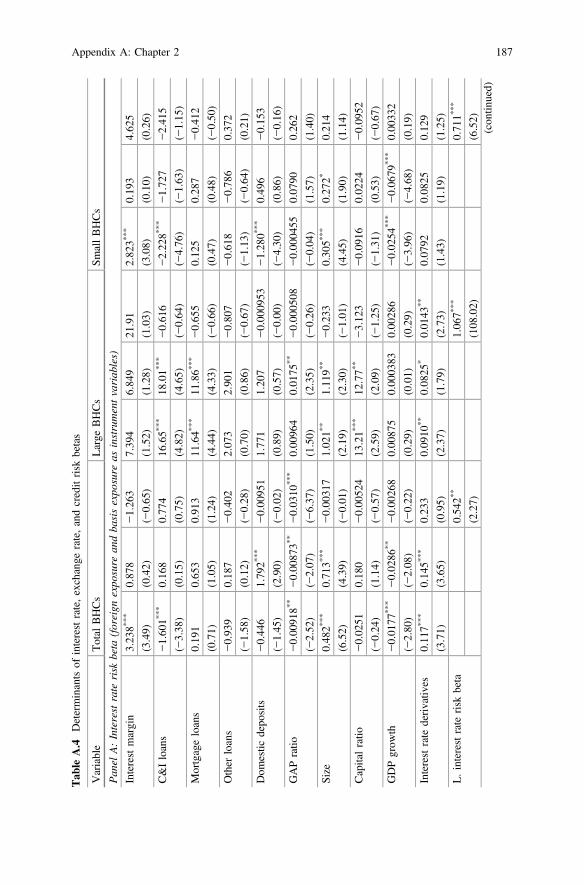

Tab

leA.4

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas

Variable

Total

BHCs

Large

BHCs

SmallBHCs

Pan

elA:Interestrate

risk

beta

(foreign

expo

sure

andba

sisexpo

sure

asinstrumentvariab

les)

Interestmargin

3.23

8***

0.87

8−1.26

37.39

46.84

921

.91

2.82

3***

0.19

34.62

5

(3.49)

(0.42)

(−0.65

)(1.52)

(1.28)

(1.03)

(3.08)

(0.10)

(0.26)

C&Iloans

−1.60

1***

0.16

80.77

416

.65*

**18

.01*

**−0.61

6−2.22

8***

−1.72

7−2.41

5

(−3.38

)(0.15)

(0.75)

(4.82)

(4.65)

(−0.64

)(−4.76

)(−1.63

)(−1.15

)

Mortgageloans

0.19

10.65

30.91

311

.64*

**11

.86*

**−0.65

50.12

50.28

7−0.41

2

(0.71)

(1.05)

(1.24)

(4.44)

(4.33)

(−0.66

)(0.47)

(0.48)

(−0.50

)

Other

loans

−0.93

90.18

7−0.40

22.07

32.90

1−0.80

7−0.61

8−0.78

60.37

2

(−1.58

)(0.12)

(−0.28

)(0.70)

(0.86)

(−0.67

)(−1.13

)(−0.64

)(0.21)

Dom

estic

depo

sits

−0.44

61.79

2***

−0.00

951

1.77

11.20

7−0.00

0953

−1.28

0***

0.49

6−0.15

3

(−1.45

)(2.90)

(−0.02

)(0.89)

(0.57)

(−0.00

)(−4.30

)(0.86)

(−0.16

)

GAPratio

−0.00

918*

*−0.00

873*

*−0.03

10**

*0.00

964

0.01

75**

−0.00

0508

−0.00

0455

0.07

900.26

2

(−2.52

)(−2.07

)(−6.37

)(1.50)

(2.35)

(−0.26

)(−0.04

)(1.57)

(1.40)

Size

0.48

2***

0.71

3***

−0.00

317

1.02

1**

1.11

9**

−0.23

30.30

5***

0.27

2*0.21

4

(6.52)

(4.39)

(−0.01

)(2.19)

(2.30)

(−1.01

)(4.45)

(1.90)

(1.14)

Capitalratio

−0.02

510.18

0−0.00

524

13.21*

**12

.77*

*−3.12

3−0.09

160.02

24−0.09

52

(−0.24

)(1.14)

(−0.57

)(2.59)

(2.09)

(−1.25

)(−1.31

)(0.53)

(−0.67

)

GDPgrow

th−0.01

77**

*−0.02

86**

−0.00

268

0.00

875

0.00

0383

0.00

286

−0.02

54**

*−0.06

79***

0.00

332

(−2.80

)(−2.08

)(−0.22

)(0.29)

(0.01)

(0.29)

(−3.96

)(−4.68

)(0.19)

Interestrate

derivativ

es0.11

7***

0.14

5***

0.23

30.09

10**

0.08

25*

0.01

43**

0.07

920.08

250.12

9

(3.71)

(3.65)

(0.95)

(2.37)

(1.79)

(2.73)

(1.43)

(1.19)

(1.25)

L.interestrate

risk

beta

0.54

2**

1.06

7***

0.71

1***

(2.27)

(108

.02)

(6.52)

(con

tinued)

Appendix A: Chapter 2 187

Tab

leA.4

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N14

,128

6154

5476

792

744

762

13,336

5410

4714

Adjusted-R2

0.10

60.06

330.46

00.46

10.09

850.02

09

AR(1)

0.01

40.00

00.00

0

AR(2)

0.73

60.23

70.48

7

HansenJstatistic

(p-value)

11.74

(0.228

)0.02

00(0.990

)2.40

2(0.493

)

Pan

elB:Excha

ngerate

risk

beta

(interestrate

expo

sure

andba

sisexpo

sure

asinstrumentvariab

les)

Assetsin

foreign

currencies

−0.57

0−1.81

9−0.11

3−5.00

7***

−4.76

0***

0.78

54.95

4***

3.89

6***

−1.55

5*

(−0.55

)(−1.47

)(−0.23

)(−4.14

)(−3.60

)(1.07)

(5.02)

(2.78)

(−1.72

)

Foreignexchange

depo

sits

0.82

00.37

00.54

10.04

23−0.50

40.37

10.59

5−0.78

91.30

8

(1.30)

(0.42)

(0.76)

(0.04)

(−0.42

)(0.33)

(0.78)

(−0.65

)(0.98)

Size

−0.04

34−0.12

5*0.19

1*0.15

00.06

71−0.06

43−0.03

05−0.09

100.28

2**

(−0.96

)(−1.76

)(1.95)

(1.16)

(0.53)

(−0.20

)(−0.64

)(−1.12

)(2.40)

Capitalratio

0.00

0939

−0.01

070.00

0230

−3.26

0*−3.34

1−1.06

6−0.00

229

−0.00

811

0.00

0709

(0.06)

(−0.84

)(0.18)

(−1.67

)(−1.52

)(−0.38

)(−0.16

)(−0.78

)(0.52)

GDPgrow

th0.00

678

0.01

25*

−0.00

423

−0.00

0443

−0.00

947

0.00

457

0.00

886*

0.02

24***

−0.01

15

(1.38)

(1.89)

(−0.56

)(−0.02

)(−0.50

)(0.17)

(1.75)

(3.17)

(−1.33

)

Exchang

erate

derivativ

es0.60

0***

0.69

6***

0.14

9***

0.69

3***

0.79

4***

0.05

300.82

6***

0.90

8***

0.10

1***

(6.66)

(5.74)

(4.31)

(6.36)

(5.44)

(1.23)

(4.82)

(3.68)

(3.08)

L.exchange

rate

risk

beta

1.12

3***

1.21

8***

1.23

7***

(13.03

)(5.48)

(5.80)

N14

,136

6155

5474

797

749

717

13,339

5406

4757

Adjusted-R2

0.18

90.24

00.44

10.46

30.18

20.21

7(con

tinued)

188 Appendix A: Chapter 2

Tab

leA.4

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

AR(1)

0.00

00.00

60.00

0

AR(2)

0.11

20.19

60.03

3

HansenJstatistic

(p-value)

0.55

8(0.906

)5.55

4(0.35

2)16

.33

(0.003

)

Pan

elC:Creditrisk

beta

(interestrate

expo

sure

andforeignexpo

sure

asinstrumentvariab

les)

Marketliq

uidity

−0.13

4***

−0.12

8***

−0.00

696

0.33

4***

0.31

5***

0.22

8−0.13

9***

−0.16

5***

0.05

87

(−4.98

)(−2.99

)(−0.23

)(3.39)

(3.07)

(0.97)

(−5.07

)(−3.70

)(1.41)

Fund

ingliq

uidity

−0.18

1***

−0.21

6**

−0.00

0983

−1.09

3***

−1.11

5***

0.61

6*−0.16

2***

−0.11

4−0.12

4***

(−3.25

)(−2.41

)(−0.03

)(−4.37

)(−4.53

)(2.05)

(−2.82

)(−1.15

)(−2.60

)

Non

-perform

ingloans

−1.87

1***

−0.95

0***

0.06

22−6.24

1***

−6.63

7***

9.03

4***

−1.85

8***

−0.76

5***

0.22

0*

(−9.93

)(−4.75

)(0.59)

(−7.14

)(−7.25

)(2.86)

(−9.98

)(−4.24

)(1.95)

Loancharge-offs

−1.71

0−2.78

3**

−0.35

3−12

.41*

**−16

.16*

**−9.12

1**

−0.88

5−1.38

40.04

07

(−1.48

)(−2.34

)(−0.79

)(−3.21

)(−4.95

)(−2.18

)(−0.75

)(−1.17

)(0.08)

Loanloss

prov

isions

3.85

7***

3.79

5***

0.37

78.54

5**

10.24*

**20

.35*

*3.34

6***

2.54

8**

0.43

4

(3.91)

(3.54)

(0.83)

(2.38)

(3.02)

(2.34)

(3.34)

(2.43)

(0.95)

Size

−0.00

759

−0.01

97−0.03

49**

*0.09

67**

*0.12

7***

−0.07

35−0.00

185

−0.01

16−0.02

15

(−0.80

)(−1.31

)(−3.88

)(3.55)

(4.19)

(−1.59

)(−0.19

)(−0.73

)(−1.50

)

Capitalratio

0.00

266

−0.00

214

0.00

0250

0.76

2*0.46

2−1.00

00.00

499

0.00

207

0.00

0422

(0.42)

(−0.59

)(0.60)

(1.95)

(0.92)

(−0.84

)(0.57)

(0.48)

(0.80)

GDPgrow

th0.00

0603

0.00

214

0.00

183

−0.00

224

−0.00

339

−0.00

0924

0.00

114

0.00

447*

**0.00

133

(0.72)

(1.44)

(1.51)

(−1.03

)(−1.46

)(−0.22

)(1.33)

(2.73)

(1.05)

Creditderivativ

es0.01

260.01

770.00

741

0.05

79**

*0.05

85**

*0.07

090.01

83**

0.00

597

0.00

497*

(1.16)

(1.40)

(1.19)

(5.36)

(5.24)

(0.66)

(2.26)

(0.63)

(1.76)

(con

tinued)

Appendix A: Chapter 2 189

Tab

leA.4

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

L.creditrisk

beta

−0.35

4***

2.37

9**

0.80

0***

(−3.85

)(2.78)

(9.60)

N13

,359

5934

5307

737

707

685

12,622

5227

4622

Adjusted-R2

0.08

090.07

720.56

40.58

50.09

190.10

4

AR(1)

0.00

00.04

10.00

0

AR(2)

0.14

80.24

60.10

0

HansenJstatistic

(p-value)

2.93

2(0.402

)2.35

5(0.50

2)0.46

1(0.927

)

Estim

ationmetho

dFE

IVGMM

FEIV

GMM

FEIV

GMM

Rob

ustnesscheckby

usingthechange

inthedifference

betweenBBBbo

ndyieldandtherisk-freeratein

thefirst-stageregression

asan

alternativedefinitio

nof

CreditRisk.PanelA

isusingforeignexpo

sure

andcreditexpo

sure

asinstrumentvariables,PanelBisusinginterestrate

expo

sure

andcreditexpo

sure

asinstrumentvariables,andPanelCisusinginterestrate

expo

sure

andforeignexpo

sure

asinstrumentvariables.The

depend

entvariable

ineach

Panelisou

restim

ates

ofrisk

betaof

each

BHCiatthe

starttim

eto

ffou

r-year

rolling

windo

wregression

inthefirst-stage.Weweigh

teachob

servationby

theinverseof

thestandard

errorof

beta

coefficients

inthefirst-stageestim

ation.

The

regression

sinclud

edbank

-specificfixedeffectsandyearly

dummyvariables.

Heteroskedasticity

-con

sistentstandard

errors

areused

andtstatisticsarerepo

rted

inparentheses.

* p<0.10

,**p<0.05

,**

* p<0.01

Source

FinancialS

tatementsdatafrom

FRY-9C;R

iskbetasarecompu

tedfrom

thefour-factormod

elusingdatafrom

CenterforResearchin

Security

Prices

(CRSP

)database

andFederalReserve

mon

thly

Statistical

Releases

190 Appendix A: Chapter 2

Tab

leA.5

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas

Variable

Total

BHCs

Large

BHCs

SmallBHCs

Pan

elA:Interestrate

risk

beta

(foreign

expo

sure

asinstrumentvariab

le)

Interestmargin

3.23

8***

1.01

9−1.28

27.39

48.17

0−12

.24*

**2.82

3***

0.16

0−2.72

9*

(3.49)

(0.49)

(−0.66

)(1.52)

(1.56)

(−3.59

)(3.08)

(0.08)

(−1.75

)

C&Iloans

−1.60

1***

0.21

80.85

916

.65*

**17

.86*

**−0.90

1−2.22

8***

−1.61

71.03

0

(−3.38

)(0.20)

(0.84)

(4.82)

(4.71)

(−0.94

)(−4.76

)(−1.51

)(0.90)

Mortgageloans

0.19

10.72

80.97

711

.64*

**11

.97*

**0.45

20.12

50.31

60.69

8

(0.71)

(1.17)

(1.34)

(4.44)

(4.40)

(0.74)

(0.47)

(0.53)

(1.31)

Other

loans

−0.93

90.15

8−0.41

72.07

32.76

80.77

8−0.61

8−0.61

00.21

3

(−1.58

)(0.11)

(−0.29

)(0.70)

(0.85)

(1.10)

(−1.13

)(−0.49

)(0.30)

Dom

estic

Deposits

−0.44

61.79

1***

−0.08

311.77

11.48

40.05

85−1.28

0***

0.41

9−0.09

06

(−1.45

)(2.89)

(−0.19

)(0.89)

(0.71)

(0.12)

(−4.30

)(0.73)

(−0.20

)

GAPratio

−0.00

918*

*−0.00

844*

*−0.03

18**

*0.00

964

0.01

77**

0.00

177

−0.00

0455

0.07

75−0.09

46**

(−2.52

)(−2.00

)(−5.92

)(1.50)

(2.38)

(1.23)

(−0.04

)(1.54)

(−2.07

)

Size

0.48

2***

0.72

3***

−0.02

141.02

1**

1.07

6**

0.12

90.30

5***

0.29

5**

0.09

80

(6.52)

(4.42)

(−0.05

)(2.19)

(2.25)

(1.36)

(4.45)

(2.02)

(0.59)

Capitalratio

−0.02

510.18

3−0.00

434

13.21*

**12

.32*

*−1.65

3−0.09

160.02

47−0.00

254

(−0.24

)(1.14)

(−0.48

)(2.59)

(2.07)

(−0.77

)(−1.31

)(0.58)

(−0.42

)

GDPgrow

th−0.01

77**

*−0.02

71**

−0.00

192

0.00

875

0.00

546

0.00

816

−0.02

54**

*−0.06

76***

−0.00

622

(−2.80

)(−1.98

)(−0.16

)(0.29)

(0.17)

(0.73)

(−3.96

)(−4.66

)(−0.42

)

Interestrate

derivativ

es0.11

7***

0.14

4***

0.19

70.09

10**

0.08

27*

0.01

35**

0.07

920.08

220.21

6

(3.71)

(3.63)

(1.01)

(2.37)

(1.78)

(2.73)

(1.43)

(1.18)

(0.51)

l.interestrate

risk

beta

0.59

4**

1.07

3***

0.73

8**

(2.30)

(148

.99)

(2.03)

(con

tinued)

Appendix A: Chapter 2 191

Tab

leA.5

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N14

,128

6173

5505

792

757

762

13,336

5416

4711

Adjusted-R2

0.10

60.06

450.46

00.46

30.09

850.02

11

AR(1)

0.01

30.00

00.03

5

AR(2)

0.78

50.26

20.47

8

HansenJstatistic

(p-value)

10.57

(0.227

)0.02

32(0.879

)3.05

6(0.880

)

Pan

elB:Excha

ngerate

risk

beta

(interestrate

expo

sure

asinstrumentvariab

le)

Assetsin

foreign

currencies

−0.57

0−1.80

6−0.31

6−5.00

7***

−4.67

4***

0.41

74.95

4***

3.88

9***

1.67

7**

(−0.55

)(−1.48

)(−0.67

)(−4.14

)(−3.64

)(0.63)

(5.02)

(2.79)

(2.54)

Foreignexchange

depo

sits

0.82

00.36

70.34

10.04

23−0.37

60.34

00.59

5−0.79

30.18

2

(1.30)

(0.42)

(0.49)

(0.04)

(−0.31

)(0.38)

(0.78)

(−0.66

)(0.15)

Size

−0.04

34−0.12

2*0.15

20.15

00.08

43−0.12

4−0.03

05−0.09

02−0.28

2***

(−0.96

)(−1.75

)(1.56)

(1.16)

(0.67)

(−0.33

)(−0.64

)(−1.13

)(−2.64

)

Capitalratio

0.00

0939

−0.00

971

0.00

0339

−3.26

0*−3.26

2−1.67

5−0.00

229

−0.00

700

0.00

334

(0.06)

(−0.79

)(0.27)

(−1.67

)(−1.50

)(−0.50

)(−0.16

)(−0.69

)(1.20)

GDPgrow

th0.00

678

0.01

24*

−0.00

367

−0.00

0443

−0.01

100.00

446

0.00

886*

0.02

24***

−0.00

277

(1.38)

(1.88)

(−0.50

)(−0.02

)(−0.59

)(0.17)

(1.75)

(3.19)

(−0.51

)

Exchang

erate

derivativ

es0.60

0***

0.69

8***

0.15

5***

0.69

3***

0.80

5***

0.05

610.82

6***

0.90

1***

0.12

3**

(6.66)

(5.85)

(4.17)

(6.36)

(5.61)

(0.82)

(4.82)

(3.69)

(2.02)

L.exchange

rate

risk

beta

1.09

8***

1.27

9***

−0.66

1***

(13.36

)(4.80)

(−5.04

)

N14

,136

6221

5565

797

766

742

13,339

5455

4823

Adjusted-R2

0.18

90.24

10.44

10.46

70.18

20.21

7(con

tinued)

192 Appendix A: Chapter 2

Tab

leA.5

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

AR(1)

0.00

00.00

90.00

0

AR(2)

0.10

60.18

70.32

6

HansenJstatistic

(p-value)

0.33

1(0.847

)5.15

4(0.27

2)2.14

6(0.342

)

Pan

elC:Creditrisk

beta

(interestrate

expo

sure

asinstrumentvariab

le)

Marketliq

uidity

−0.13

4***

−0.11

7***

−0.00

539

0.33

4***

0.31

5***

0.19

4−0.13

9***

−0.15

4***

0.06

65

(−4.98

)(−2.73

)(−0.18

)(3.39)

(3.07)

(0.81)

(−5.07

)(−3.45

)(1.65)

Fund

ingliq

uidity

−0.18

1***

−0.18

7**

0.00

368

−1.09

3***

−1.11

5***

0.67

6**

−0.16

2***

−0.08

53−0.12

2**

(−3.25

)(−2.12

)(0.11)

(−4.37

)(−4.53

)(2.25)

(−2.82

)(−0.88

)(−2.53

)

Non

-perform

ingLoans

−1.87

1***

−0.93

6***

0.07

86−6.24

1***

−6.63

7***

8.00

2**

−1.85

8***

−0.75

1***

0.25

0**

(−9.93

)(−4.69

)(0.75)

(−7.14

)(−7.25

)(2.38)

(−9.98

)(−4.16

)(2.17)

Loancharge-offs

−1.71

0−2.74

6**

−0.33

1−12

.41*

**−16

.16*

**−8.33

5*−0.88

5−1.35

6−0.02

19

(−1.48

)(−2.30

)(−0.73

)(−3.21

)(−4.95

)(−1.94

)(−0.75

)(−1.15

)(−0.05

)

Loanloss

Prov

isions

3.85

7***

3.75

4***

0.34

58.54

5**

10.24*

**18

.11*

*3.34

6***

2.51

6**

0.49

8

(3.91)

(3.49)

(0.74)

(2.38)

(3.02)

(2.10)

(3.34)

(2.39)

(1.09)

Size

−0.00

759

−0.02

69*

−0.03

61**

*0.09

67**

*0.12

7***

−0.07

46−0.00

185

−0.01

95−0.02

59*

(−0.80

)(−1.77

)(−4.09

)(3.55)

(4.19)

(−1.63

)(−0.19

)(−1.22

)(−1.85

)

Capitalratio

0.00

266

−0.00

247

0.00

0238

0.76

2*0.46

2−1.05

30.00

499

0.00

172

0.00

0400

(0.42)

(−0.67

)(0.57)

(1.95)

(0.92)

(−0.91

)(0.57)

(0.41)

(0.75)

GDPgrow

th0.00

0603

0.00

223

0.00

192

−0.00

224

−0.00

339

0.00

0253

0.00

114

0.00

451*

**0.00

152

(0.72)

(1.51)

(1.61)

(−1.03

)(−1.47

)(0.06)

(1.33)

(2.78)

(1.23)

Creditderivativ

es0.01

260.01

800.00

754

0.05

79**

*0.05

85**

*0.00

933*

0.01

83**

0.00

937

0.00

483*

(1.16)

(1.42)

(1.19)

(5.36)

(5.24)

(2.03)

(2.26)

(0.95)

(1.67)

(con

tinued)

Appendix A: Chapter 2 193

Tab

leA.5

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

L.creditrisk

beta

−0.35

3***

2.06

0**

0.79

9***

(−3.81

)(2.36)

(9.76)

N13

,359

5971

5357

737

707

685

12,622

5264

4672

Adjusted-R2

0.08

090.07

770.56

40.58

50.09

190.10

4

AR(1)

0.00

00.05

70.00

0

AR(2)

0.12

10.26

60.14

1

HansenJstatistic

(p-value)

3.29

0(0.193

)2.05

5(0.56

1)0.41

5(0.813

)

Estim

ationmetho

dFE

IVGMM

FEIV

GMM

FEIV

GMM

Rob

ustnesscheckby

usingthechange

inthedifference

betweenBBBbo

ndyieldandtherisk-freeratein

thefirst-stageregression

asan

alternativedefinitio

nof

CreditR

isk.PanelA

isusingforeignexpo

sure

asinstrumentv

ariable,whilePanelB

andPanelC

areusinginterestrateexpo

sure

asinstrumentv

ariable.The

depend

entvariable

ineach

Panelisou

restim

ates

ofrisk

beta

ofeach

BHCiat

thestarttim

etof

four-yearrolling

windo

wregression

inthefirst-stage.

We

weigh

teach

observationby

theinverseof

thestandard

errorof

beta

coefficients

inthefirst-stageestim

ation.

The

regression

sinclud

edbank

-specificfixed

effectsandyearly

dummyvariables.Heteroskedasticity

-con

sistentstandard

errors

areused

andtstatisticsarerepo

rted

inparentheses.*p

<0.10

,**p

<0.05

,*** p

<0.01

Source

FinancialS

tatementsdatafrom

FRY-9C;R

iskbetasarecompu

tedfrom

thefour-factormod

elusingdatafrom

CenterforResearchin

Security

Prices

(CRSP

)database

andFederalReserve

mon

thly

Statistical

Releases

194 Appendix A: Chapter 2

Tab

leA.6

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas

Variable

Total

BHCs

Large

BHCs

SmallBHCs

Pan

elA:Interestrate

risk

beta

(foreign

expo

sure

asinstrumentvariab

le)

Interestmargin

3.23

8***

0.88

0−1.09

77.39

46.87

022

.92

2.82

3***

0.19

3−29

.45*

*

(3.49)

(0.43)

(−0.53

)(1.52)

(1.28)

(1.37)

(3.08)

(0.10)

(−1.99

)

C&Iloans

−1.60

1***

0.16

61.13

216

.65*

**17

.99*

**−0.76

7−2.22

8***

−1.72

5−1.74

8

(−3.38

)(0.15)

(1.21)

(4.82)

(4.64)

(−0.71

)(−4.76

)(−1.63

)(−0.88

)

Mortgageloans

0.19

10.65

21.07

611

.64*

**11

.84*

**−0.82

00.12

50.28

7−0.05

78

(0.71)

(1.05)

(1.56)

(4.44)

(4.33)

(−0.72

)(0.47)

(0.48)

(−0.07

)

Other

loans

−0.93

90.18

70.27

32.07

32.88

8−0.84

6−0.61

8−0.78

70.49

8

(−1.58

)(0.12)

(0.22)

(0.70)

(0.85)

(−0.64

)(−1.13

)(−0.64

)(0.27)

Dom

estic

depo

sits

−0.44

61.79

2***

−0.00

0112

1.77

11.22

60.01

49−1.28

0***

0.49

7−0.45

2

(−1.45

)(2.90)

(−0.00

)(0.89)

(0.58)

(0.04)

(−4.30

)(0.86)

(−0.42

)

GAPratio

−0.00

918*

*−0.00

873*

*−0.02

96**

*0.00

964

0.01

75**

−0.00

0466

−0.00

0455

0.07

900.20

2

(−2.52

)(−2.07

)(−7.42

)(1.50)

(2.36)

(−0.26

)(−0.04

)(1.57)

(1.45)

Size

0.48

2***

0.71

3***

0.24

01.02

1**

1.11

6**

−0.24

70.30

5***

0.27

2*0.23

0

(6.52)

(4.38)

(0.81)

(2.19)

(2.30)

(−0.98

)(4.45)

(1.90)

(1.12)

Capitalratio

−0.02

510.18

0−0.00

290

13.21*

**12

.77*

*−3.45

0−0.09

160.02

24−0.01

98

(−0.24

)(1.14)

(−0.30

)(2.59)

(2.09)

(−1.33

)(−1.31

)(0.53)

(−0.10

)

GDPgrow

th−0.01

77**

*−0.02

86**

0.00

0267

0.00

875

0.00

0190

0.00

176

−0.02

54**

*−0.06

79***

0.00

890

(−2.80

)(−2.08

)(0.02)

(0.29)

(0.01)

(0.17)

(−3.96

)(−4.68

)(0.49)

Interestrate

derivativ

es0.11

7***

0.14

4***

0.29

9*0.09

10**

0.08

03*

0.01

35**

0.07

920.08

340.15

6

(3.71)

(3.63)

(1.75)

(2.37)

(1.75)

(2.27)

(1.43)

(1.20)

(1.48)

L.interestrate

risk

beta

0.42

1**

1.06

8***

0.72

6***

(2.15)

(99.45

)(6.57)

(con

tinued)

Appendix A: Chapter 2 195

Tab

leA.6

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N14

,128

6154

5476

792

744

762

13,336

5410

4714

Adjusted-R2

0.10

60.06

330.46

00.46

10.09

850.02

09

AR(1)

0.01

20.00

00.00

0

AR(2)

0.60

60.14

90.64

2

HansenJstatistic

(p-value)

12.70

(0.241

)0.20

4(0.651

)2.47

8(0.649

)

Pan

elB:Excha

ngerate

risk

beta

(basisexpo

sure

asinstrumentvariab

le)

Assetsin

foreign

currencies

−0.57

0−1.16

5−0.09

98−5.00

7***

−4.64

7***

0.70

94.95

4***

4.66

5***

1.74

5***

(−0.55

)(−0.97

)(−0.21

)(−4.14

)(−3.50

)(0.97)

(5.02)

(3.75)

(2.95)

Foreignexchange

depo

sits

0.82

00.21

20.50

80.04

23−0.68

90.45

90.59

5−0.95

40.37

9

(1.30)

(0.24)

(0.70)

(0.04)

(−0.56

)(0.43)

(0.78)

(−0.79

)(0.31)

Size

−0.04

34−0.13

1*0.18

1*0.15

00.06

61−0.11

3−0.03

05−0.09

48−0.30

1***

(−0.96

)(−1.84

)(1.84)

(1.16)

(0.52)

(−0.34

)(−0.64

)(−1.16

)(−2.83

)

Capitalratio

0.00

0939

−0.00

753

0.00

0281

−3.26

0*−3.34

1−0.62

5−0.00

229

−0.00

716

0.00

317

(0.06)

(−0.64

)(0.23)

(−1.67

)(−1.51

)(−0.22

)(−0.16

)(−0.70

)(1.19)

GDPgrow

th0.00

678

0.01

20*

−0.00

450

−0.00

0443

−0.00

910

0.00

485

0.00

886*

0.02

20***

−0.00

343

(1.38)

(1.81)

(−0.60

)(−0.02

)(−0.48

)(0.18)

(1.75)

(3.11)

(−0.67

)

Exchang

erate

derivativ

es0.60

0***

0.71

6***

0.15

0***

0.69

3***

0.82

3***

0.03

090.82

6***

0.90

5***

0.12

1**

(6.66)

(5.84)

(4.30)

(6.36)

(5.53)

(0.54)

(4.82)

(3.63)

(1.99)

L.exchange

rate

risk

beta

1.11

9***

1.15

9***

−0.68

6***

(13.06

)(4.81)

(−5.14

)

N14

,136

6160

5480

797

749

717

13,339

5411

4763

Adjusted-R2

0.18

90.23

80.44

10.46

20.18

20.21

6(con

tinued)

196 Appendix A: Chapter 2

Tab

leA.6

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

AR(1)

0.00

00.01

30.00

0

AR(2)

0.11

50.18

00.30

0

HansenJstatistic

(p-value)

0.10

9(0.947

)5.36

0(0.252

)0.35

9(0.836

)

Pan

elC:Creditrisk

beta

(foreign

expo

sure

asinstrumentvariab

le)

Marketliq

uidity

−0.13

4***

−0.12

7***

−0.01

640.33

4***

0.31

4***

0.07

54−0.13

9***

−0.16

5***

−0.02

28

(−4.98

)(−2.98

)(−0.53

)(3.39)

(3.06)

(0.44)

(−5.07

)(−3.69

)(−0.70

)

Fund

ingliq

uidity

−0.18

1***

−0.21

0**

−0.00

533

−1.09

3***

−1.12

1***

0.09

74−0.16

2***

−0.10

7−0.01

02

(−3.25

)(−2.34

)(−0.16

)(−4.37

)(−4.55

)(0.42)

(−2.82

)(−1.08

)(−0.29

)

Non

-perform

ingloans

−1.87

1***

−0.95

7***

0.04

87−6.24

1***

−6.62

3***

−6.95

3−1.85

8***

−0.77

3***

0.04

00

(−9.93

)(−4.76

)(0.46)

(−7.14

)(−7.23

)(−0.96

)(−9.98

)(−4.26

)(0.38)

Loancharge-offs

−1.71

0−2.84

0**

−0.27

0−12

.41*

**−16

.13*

**−3.45

7−0.88

5−1.45

5−0.03

64

(−1.48

)(−2.38

)(−0.61

)(−3.21

)(−4.94

)(−0.44

)(−0.75

)(−1.23

)(−0.08

)

Loanloss

prov

isions

3.85

7***

3.86

0***

0.24

58.54

5**

10.21*

**9.85

93.34

6***

2.63

0**

0.03

64

(3.91)

(3.59)

(0.54)

(2.38)

(3.01)

(0.93)

(3.34)

(2.50)

(0.08)

Size

−0.00

759

−0.02

15−0.03

29**

*0.09

67**

*0.12

6***

−0.13

1***

−0.00

185

−0.01

38−0.02

94***

(−0.80

)(−1.43

)(−3.77

)(3.55)

(4.16)

(−2.94

)(−0.19

)(−0.87

)(−2.96

)

Capitalratio

0.00

266

−0.00

282

0.00

0247

0.76

2*0.45

4−2.37

8*0.00

499

0.00

123

0.00

0314

(0.42)

(−0.72

)(0.59)

(1.95)

(0.90)

(−2.01

)(0.57)

(0.32)

(0.64)

GDPgrow

th0.00

0603

0.00

215

0.00

158

−0.00

224

−0.00

342

0.00

158

0.00

114

0.00

448*

**0.00

183

(0.72)

(1.44)

(1.32)

(−1.03

)(−1.48

)(0.64)

(1.33)

(2.73)

(1.35)

Creditderivativ

es0.01

260.01

790.00

864*

0.05

79**

*0.05

97**

*0.15

6***

0.01

83**

0.00

601

0.01

15***

(1.16)

(1.42)

(1.69)

(5.36)

(5.36)

(4.01)

(2.26)

(0.65)

(3.13)

L.creditrisk

beta

−0.38

1***

0.08

10**

−0.43

6***

(−4.05

)(2.73)

(−3.48

)(con

tinued)

Appendix A: Chapter 2 197

Tab

leA.6

(con

tinued)

Variable

Total

BHCs

Large

BHCs

SmallBHCs

N13

,359

5941

5316

737

707

685

12,622

5234

4631

Adjusted-R2

0.08

090.07

710.56

40.58

50.09

190.10

3

AR(1)

0.00

00.05

40.00

0

AR(2)

0.13

70.42

70.32

4

HansenJstatistic

(p-value)

0.03

0(0.985

)2.73

4(0.987

)0.59

4(0.743

)

Estim

ationmetho

dFE

IVGMM

FEIV

GMM

FEIV

GMM

Rob

ustnesscheckby

usingthechange

inthedifference

betweenBBBbo

ndyieldandtherisk-freeratein

thefirst-stageregression

asan

alternativedefinitio

nof

CreditRisk.

PanelA

andPanelB

areusingbasisexpo

sure

asinstrumentvariable,while

PanelC

isusingforeignexpo

sure

asinstrumentvariable.The

depend

entvariable

ineach

Panelisou

restim

ates

ofrisk

beta

ofeach

BHCiat

thestarttim

etof

four-yearrolling

windo

wregression

inthefirst-stage.

We

weigh

teach

observationby

theinverseof

thestandard

errorof

beta

coefficients

inthefirst-stageestim

ation.

The

regression

sinclud

edbank

-specificfixed

effectsandyearly

dummyvariables.Heteroskedasticity

-con

sistentstandard

errors

areused

andtstatisticsarerepo

rted

inparentheses.

* p<0.10

,** p

<0.05

,*** p

<0.01

Source

FinancialS

tatementsdatafrom

FRY-9C;R

iskbetasarecompu

tedfrom

thefour-factormod

elusingdatafrom

CenterforResearchin

Security

Prices

(CRSP

)database

andFederalReserve

mon

thly

Statistical

Releases

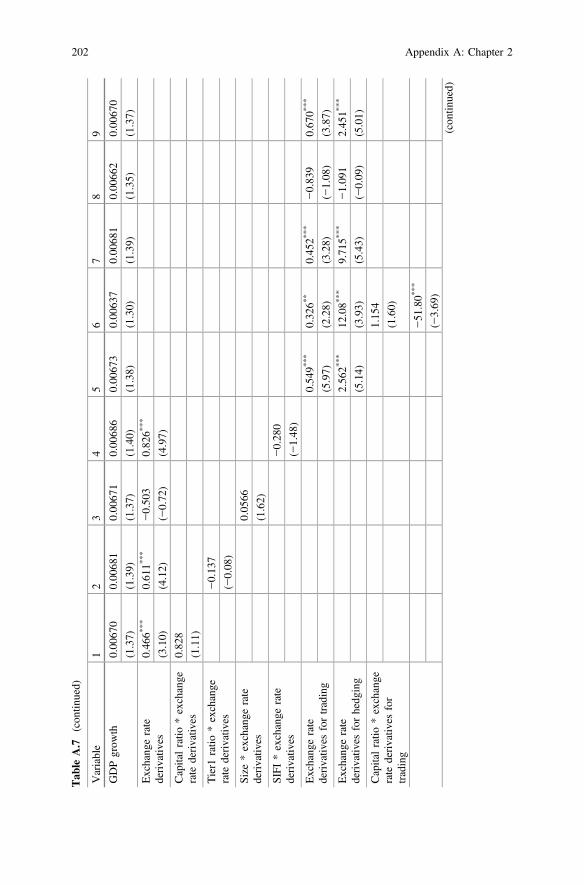

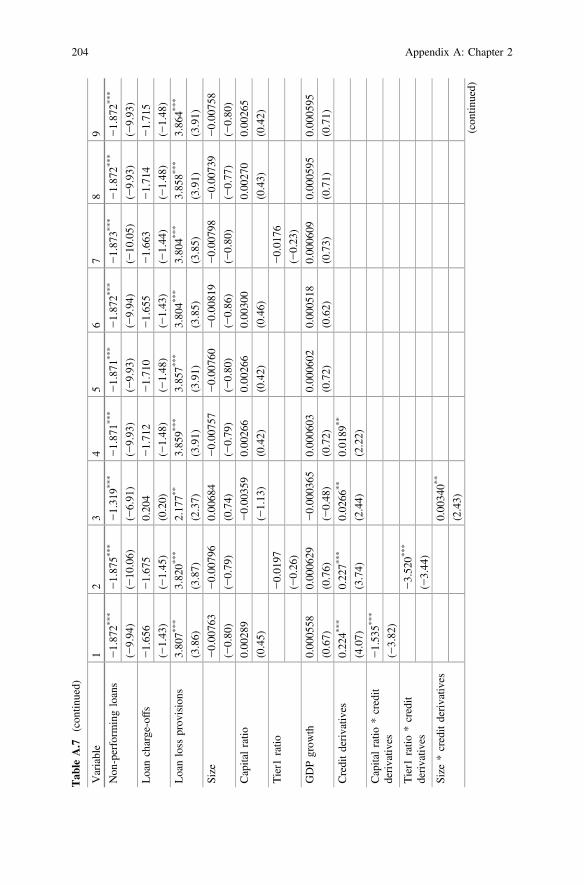

198 Appendix A: Chapter 2

Tab

leA.7

Determinantsof

interestrate,exchange

rate,andcreditrisk

betas,andinteractionterm

s

Variable

12

34

56

78

9

Pan

elA:Interestrate

risk

beta

Interestmargin

3.08

9***

1.55

3**

3.24

2***

3.24

4***

3.15

1***

3.00

2***

1.56

5**

3.08

6***

3.12

3***

(3.33)

(2.01)

(3.50)

(3.50)

(3.40)

(3.23)

(2.03)

(3.33)

(3.37)

C&Iloans

−1.57

7***

−0.77

0**

−1.60

8***

−1.60

9***

−1.55

2***

−1.53

2***

−0.68

6**

−1.53

0***

−1.58

2***

(−3.33

)(−2.29

)(−3.40

)(−3.40

)(−3.28

)(−3.24

)(−2.04

)(−3.24

)(−3.36

)

Mortgageloans

0.22

3−0.13

40.19

50.19

00.21

80.25

1−0.14

70.27

10.22

2

(0.83)

(−0.67

)(0.72)

(0.70)

(0.81)

(0.93)

(−0.74

)(1.00)

(0.83)

Other

loans

−1.00

7*−0.44

8−0.95

8−0.93

6−0.89

6−0.97

2−0.34

6−0.88

1−0.77

7

(−1.70

)(−1.13

)(−1.62

)(−1.58

)(−1.51

)(−1.64

)(−0.89

)(−1.48

)(−1.32

)

Dom

estic

depo

sits

−0.43

5−0.62

5***

−0.48

2−0.45

5−0.35

3−0.34

9−0.56

2**

−0.42

2−0.34

7

(−1.41

)(−2.69

)(−1.57

)(−1.48

)(−1.15

)(−1.13

)(−2.45

)(−1.37

)(−1.13

)

GAPratio

−0.00

950*

**−0.00

951*

**−0.00

926*

*−0.00

917*

*−0.00

850*

*−0.00

896*

*−0.00

777*

*−0.00

699*

−0.01

04***

(−2.61

)(−2.64

)(−2.54

)(−2.52

)(−2.32

)(−2.44

)(−2.14

)(−1.84

)(−2.70

)

Size

0.47

4***

0.33

1***

0.47

1***

0.48

0***

0.49

5***

0.48

7***

0.33

5***

0.48

0***

0.49

5***

(6.44)

(6.63)

(6.37)

(6.50)

(6.71)

(6.53)

(6.79)

(6.52)

(6.70)

Capitalratio

−0.03

93−0.02

63−0.02

53−0.02

27−0.03

79−0.02

32−0.02

18

(−0.40

)(−0.26

)(−0.24

)(−0.22

)(−0.38

)(−0.22

)(−0.21

)

Tier1

ratio

1.23

9*1.71

9***

(1.87)

(2.74)

GDPgrow

th−0.01

71**

*−0.02

52***

−0.01

78**

*−0.01

76**

*−0.01

81**

*−0.01

75**

*−0.02

39**

*−0.01

79***

−0.01

76***

(−2.71

)(−4.98

)(−2.81

)(−2.79

)(−2.87

)(−2.77

)(−4.74

)(−2.83

)(−2.78

)

Interestrate

derivativ

es−0.20

0***

−0.12

5***

−0.14

00.09

40

(−2.99

)(−3.26

)(−0.61

)(1.61)

(con

tinued)

Appendix A: Chapter 2 199

Tab

leA.7

(con

tinued)

Variable

12

34

56

78

9

Capitalratio

*interest

rate

derivativ

es2.58

5***

(4.62)

Tier1

ratio

*interestrate

derivativ

es3.48

5***

(4.55)

Size

*interestrate

derivativ

es0.01

24

(1.09)

SIFI

*interestrate

derivativ

es0.02

63

(0.39)

Interestrate

derivativ

esfortrading

0.10

4***

−0.20

4***

−0.15

8***

−0.57

4**

−0.16

2***

(3.33)

(−3.02

)(−4.05

)(−2.45

)(−3.35

)

Interestrate

derivativ

esforhedg

ing

0.37

4***

−0.04

721.40

5***

−2.76

80.46

2***

(3.24)

(−0.08

)(3.45)

(−1.64

)(4.21)

Capitalratio

*interest

rate

derivativ

esfor

trading

2.52

6***

(4.40)

Capitalratio

*interest

rate

derivativ

esfor

hedg

ing

3.13

5

(0.69)

Tier1

ratio

*interestrate

derivativ

esfortrading

3.75

2***

(4.66)

Tier1

ratio

*interestrate

derivativ

esforhedg

ing

−10

.12*

*

(−2.18

)(con

tinued)

200 Appendix A: Chapter 2

Tab

leA.7

(con

tinued)

Variable

12

34

56

78

9

Size

*interestrate

derivativ

esfortrading

0.03

22***

(2.76)

Size

*interestrate

derivativ

esforhedg

ing

0.19

2*

(1.82)

SIFI

*interestrate

derivativ

esfortrading

0.28

5***

(4.72)

SIFI

*interestrate

derivativ

esforhedg

ing

−0.90

8*

(−1.68

)

N14

,128

17,375

14,128

14,128

14,132

14,132

17,379

14,132

14,132

Adjusted-R2

0.10

80.10

90.10

60.10

60.10

60.10

80.11

10.10

70.10

7

Pan

elB:Excha

ngerate

risk

beta

Assetsin

foreign

currencies

−0.59

7−0.50

8−0.56

5−0.69

0−0.64

6−2.14

3*−1.74

5*−0.67

3−0.81

3

(−0.57

)(−0.49

)(−0.54

)(−0.65

)(−0.61

)(−1.94

)(−1.67

)(−0.62

)(−0.75

)

Foreignexchange

depo

sits

0.90

90.80

81.05

9*0.95

30.93

61.16

9*1.13

6*1.25

2**

1.00

7

(1.46)

(1.29)

(1.66)

(1.51)

(1.49)

(1.93)

(1.85)

(1.96)

(1.60)

Size

−0.04

46−0.04

73−0.04

90−0.04

21−0.04

90−0.05

08−0.05

75−0.05

70−0.04

92

(−0.98

)(−1.01

)(−1.07

)(−0.93

)(−1.08

)(−1.12

)(−1.23

)(−1.25

)(−1.08

)

Capitalratio

0.00

0231

0.00

0389

0.00

0867

0.00

0743

0.00

0472

0.00

0028

60.00

0746

(0.02)

(0.03)

(0.06)

(0.05)

(0.03)

(0.00)

(0.05)

Tier1

ratio

−0.20

0−0.37

4

(−0.47

)(−0.87

)(con

tinued)

Appendix A: Chapter 2 201

Tab

leA.7

(con

tinued)

Variable

12

34

56

78

9

GDPgrow

th0.00

670

0.00

681

0.00

671

0.00

686

0.00

673

0.00

637

0.00

681

0.00

662

0.00

670

(1.37)

(1.39)

(1.37)

(1.40)

(1.38)

(1.30)

(1.39)

(1.35)

(1.37)

Exchang

erate

derivativ

es0.46

6***

0.61

1***

−0.50

30.82

6***

(3.10)

(4.12)

(−0.72

)(4.97)

Capitalratio

*exchange

rate

derivativ

es0.82

8

(1.11)

Tier1

ratio

*exchange

rate

derivativ

es−0.13

7

(−0.08

)

Size

*exchange

rate

derivativ

es0.05

66

(1.62)

SIFI

*exchange

rate

derivativ

es−0.28

0

(−1.48

)

Exchang

erate

derivativ

esfortrading

0.54

9***

0.32

6**

0.45

2***

−0.83

90.67

0***

(5.97)

(2.28)

(3.28)

(−1.08

)(3.87)

Exchang

erate

derivativ

esforhedg

ing

2.56

2***

12.08*

**9.71

5***

−1.09

12.45

1***

(5.14)

(3.93)

(5.43)

(−0.09

)(5.01)

Capitalratio

*exchange

rate

derivativ

esfor

trading

1.15

4

(1.60)

−51

.80*

**

(−3.69

)(con

tinued)

202 Appendix A: Chapter 2

Tab

leA.7

(con

tinued)

Variable

12

34

56

78

9

Capitalratio

*exchange

rate

derivativ

esfor

hedg

ing

Tier1

ratio

*exchange

rate

derivativ

esfor

trading

0.99

6

(0.63)

Tier1

ratio

*exchange

rate

derivativ

esfor

hedg

ing

−99

.96*

**

(−4.38

)

Size

*exchange

rate

derivativ

esfortrading

0.07

09*

(1.81)

Size

*exchange

rate

derivativ

esforhedg

ing

0.21

5

(0.29)

SIFI

*exchange

rate

derivativ

esfortrading

−0.17

1

(−0.85

)

SIFI

*exchange

rate

derivativ

esforhedg

ing

2.61

8

(0.91)

N14

,136

14,135

14,136

14,136

14,136

14,136

14,135

14,136

14,136

Adjusted-R2

0.18

90.18

90.18

90.18

90.18

90.19

10.19

10.19

00.19

0

Pan

elC:Creditrisk

beta

Marketliq

uidity

−0.13

2***

−0.13

2***

−0.13

0***

−0.13

4***

−0.13

4***

−0.13

1***

−0.13

2***

−0.13

3***

−0.13

4***

(−4.91

)(−4.92

)(−4.94

)(−4.98

)(−4.98

)(−4.90

)(−4.91

)(−4.96

)(−4.98

)

Fund

ingliq

uidity

−0.18

4***

−0.18

3***

−0.10

8**

−0.18

1***

−0.18

2***

−0.18

7***

−0.18

5***

−0.18

1***

−0.18

1***

(−3.29

)(−3.28

)(−2.16

)(−3.24

)(−3.25

)(−3.35

)(−3.30

)(−3.24

)(−3.24

)(con

tinued)

Appendix A: Chapter 2 203

Tab

leA.7

(con

tinued)

Variable

12

34

56

78

9

Non

-perform

ingloans

−1.87

2***

−1.87

5***

−1.31

9***

−1.87

1***

−1.87

1***

−1.87

2***

−1.87

3***

−1.87

2***

−1.87

2***

(−9.94

)(−10

.06)

(−6.91

)(−9.93

)(−9.93

)(−9.94

)(−10

.05)

(−9.93

)(−9.93

)

Loancharge-offs

−1.65

6−1.67

50.20

4−1.71

2−1.71

0−1.65

5−1.66

3−1.71

4−1.71

5

(−1.43

)(−1.45

)(0.20)

(−1.48

)(−1.48

)(−1.43

)(−1.44

)(−1.48

)(−1.48

)

Loanloss

prov

isions

3.80

7***

3.82

0***

2.17

7**

3.85

9***

3.85

7***

3.80

4***

3.80

4***

3.85

8***

3.86

4***

(3.86)