Embed Size (px)

Citation preview

ASIAN DEVELOPMENT BANK PCR: PHI 19178

PROJECT COMPLETION REPORT

ON THE

SECOND MANILA PORT PROJECT(Loan No. 875-PHI)

IN THE

PHILIPPINES

September 1997

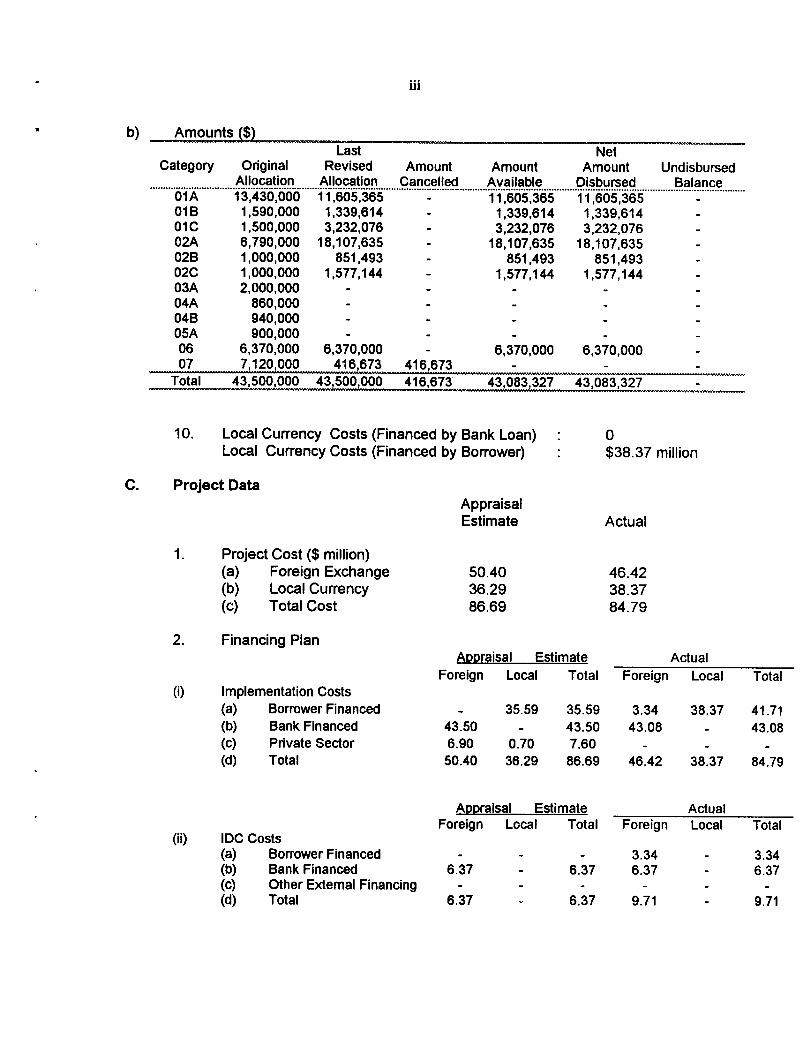

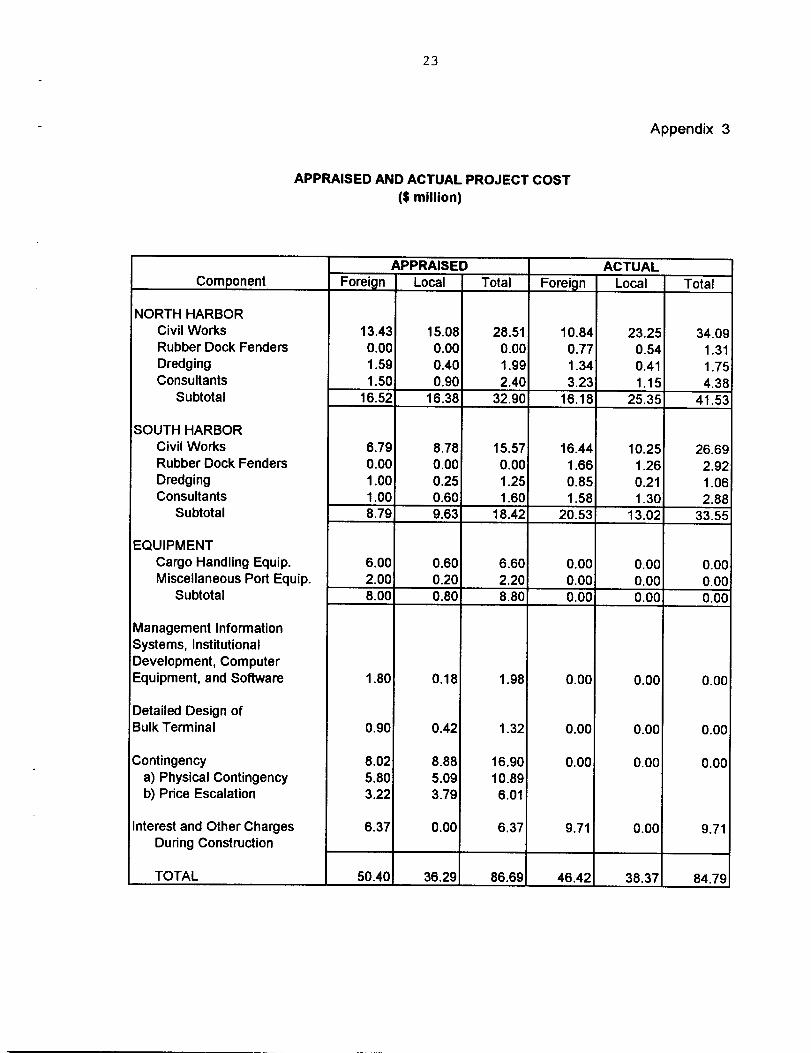

P1.00$1.00 I

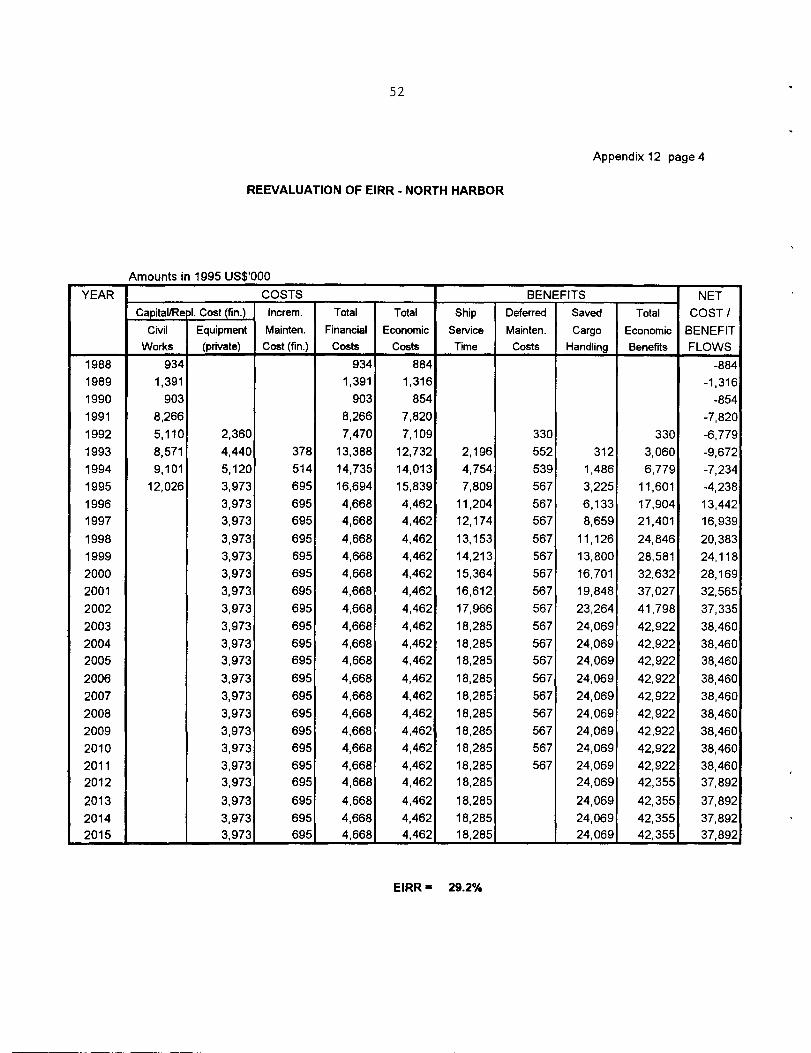

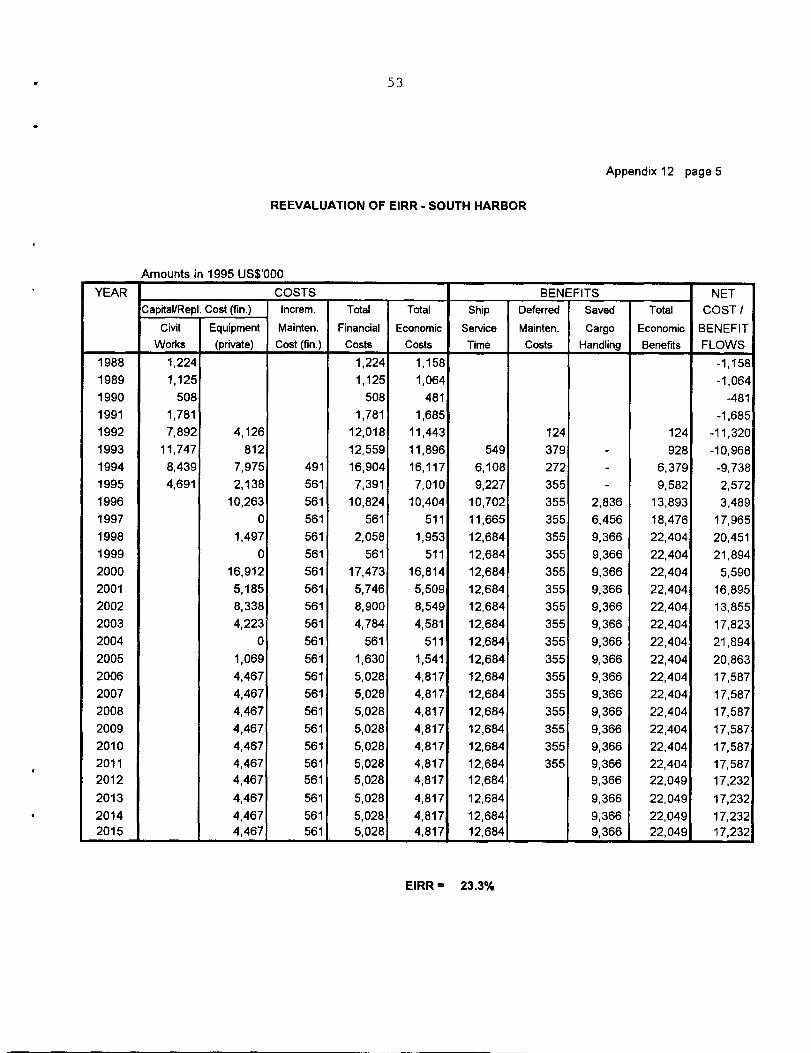

CAGRCPACSCEIRRFIRRIACSRRICBIDCMICTMISNHOGCCO&MPPAPPARROROSHTA

IDead Weight TonGross Registered TonTwenty-foot Equivalent Unit

DWTGRTTEU

CURRENCY EQUIVALENTS

Currency Unit - Philippine Peso (P)

At Appraisal At Project Completion$0. 048 $0.038P20.73 P26.21

ABBREVIATIONS

Compound Annual Growth RateCebu Port AuthorityConsultants Selection CommitteeEconomic Internal Rate of ReturnFinancial Internal Rate of ReturnInteragency Committee on Squatter Removal and RelocationInternational Competitive BiddingInterest and Other Charges During ConstructionManila International Container TerminalManagement Information SystemNorth HarborOffice of the Government Corporate CounselOperation & MaintenancePhilippine Ports AuthorityProject/Program Performance Audit ReportRoll-on-roll-offSouth HarborTechnical Assistance

WEIGHTS AND MEASURES

NOTES

(I) The fiscal year (FY) of the Government ends on 31 December.(ii) In this Report, "$" refers to US dollars.(iii) In this Report, "ton" refers to "metric ton" unless otherwise noted.

CONTENTS

Page

BASIC DATA il-v

MAPS

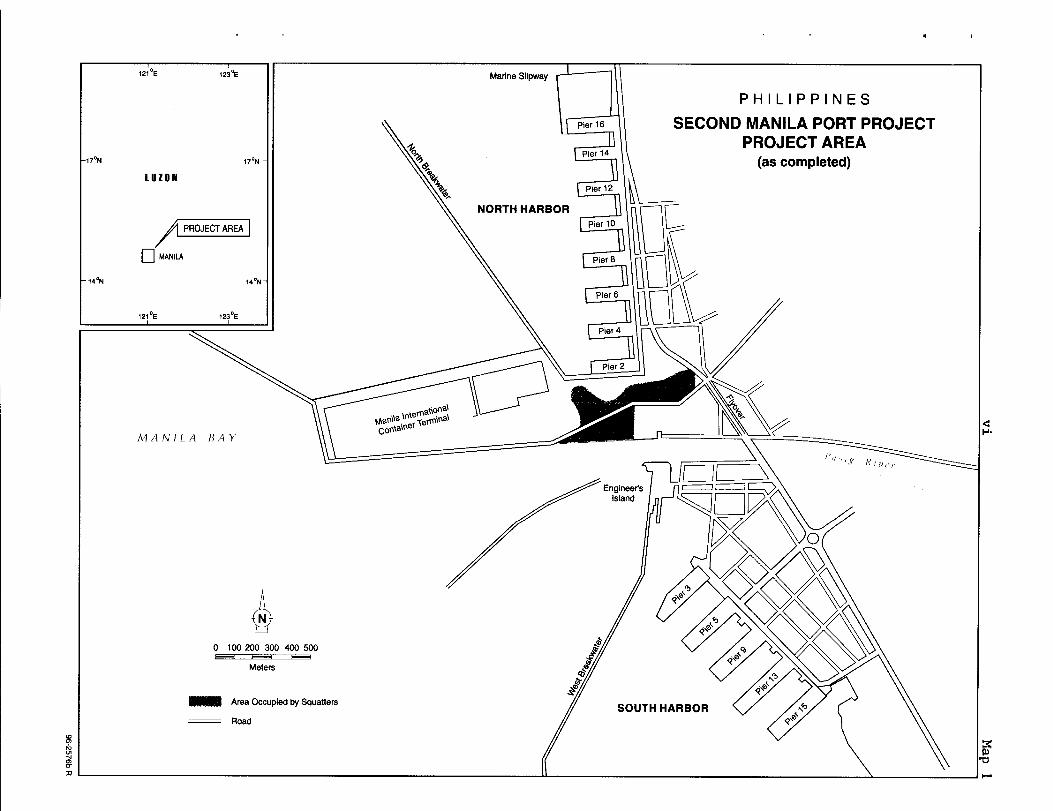

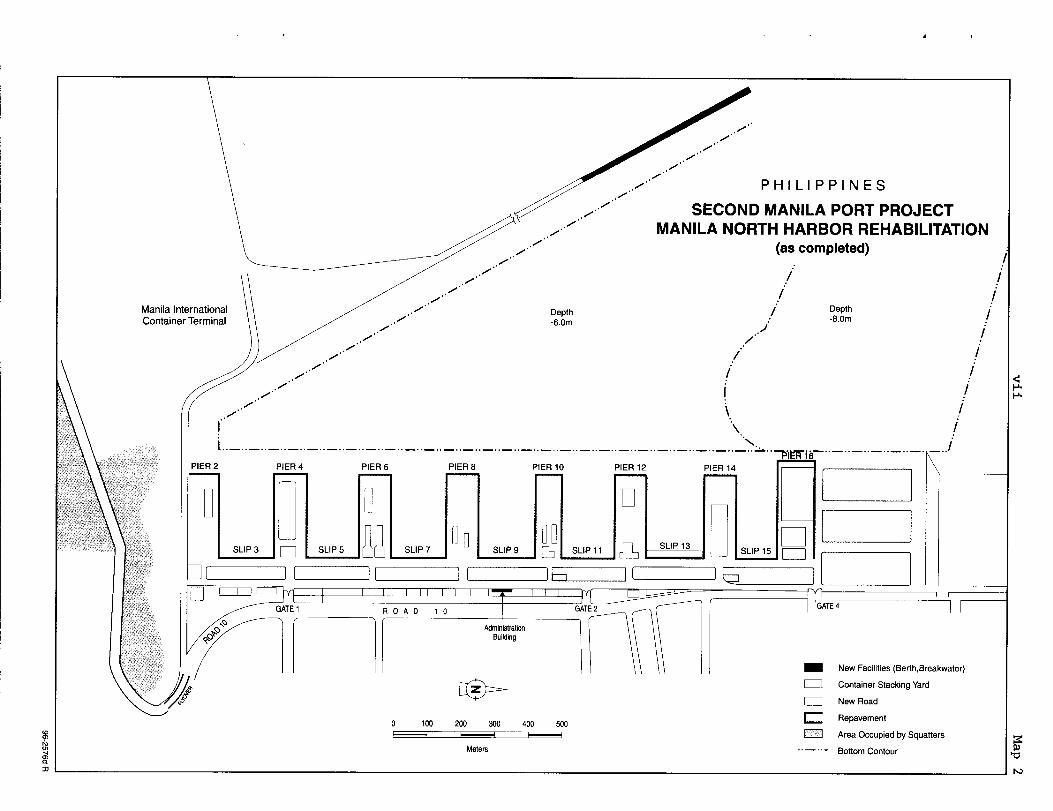

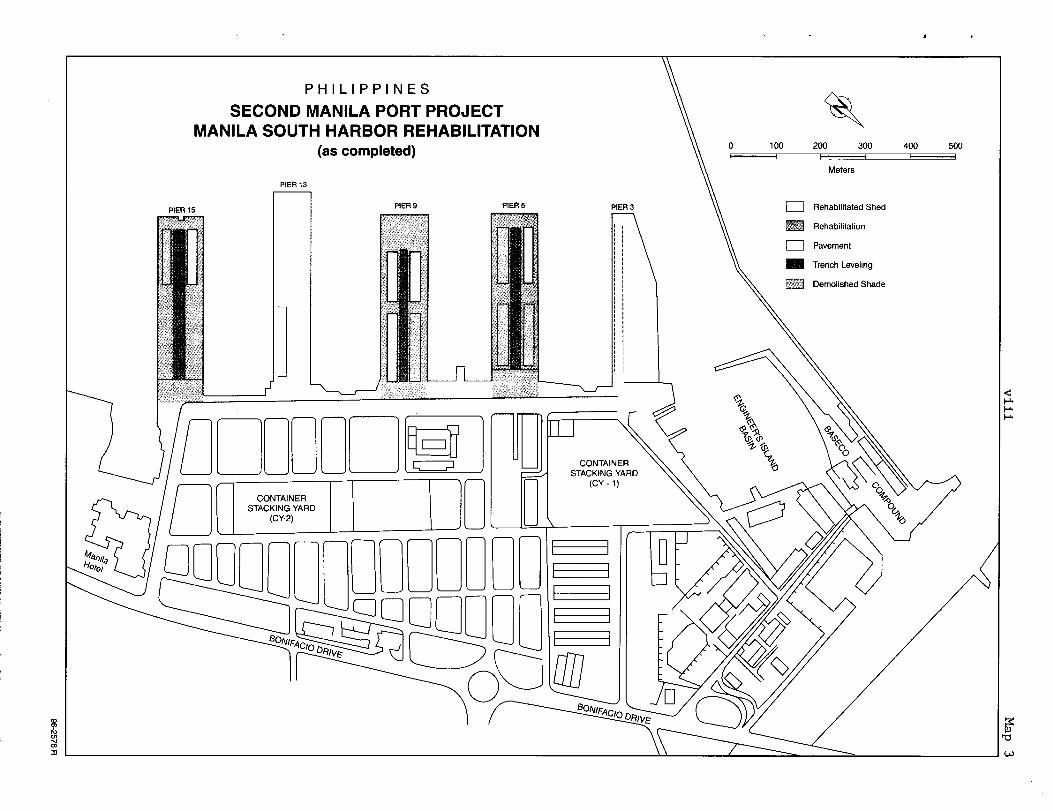

Map 1 Project Area viMap 2 Manila North Harbor Rehabilitation viiMap 3 Manila South Harbor Rehabilitation viii

I. PROJECT DESCRIPTION 1

EVALUATION OF IMPLEMENTATION

A. Project Components 2B. Implementation Arrangements 3C. Project Costs 3D. Project Schedule 4E. Engagement of Consultants and Procurement of Goods and Services 5F. Performance of Consultants, Contractors, and Suppliers 5G. Conditions and Covenants 6H. Disbursements 6I. Environmental Impact 7J. Performance of the Borrower and the Executing Agency 7K. Performance of the Bank 9

Ill. EVALUATION OF INITIAL PERFORMANCE AND BENEFITS

A. Traffic Reevaluation 9B. Financial Performance of PPA 11C. Financial Reevaluation of the Project 120. Economic Reevaluation of the Project 13E. Attainment of Benefits 14

IV. CONCLUSIONS AND RECOMMENDATIONS

A. Conclusions 14B. Recommendations 15

APPENDIXES 17

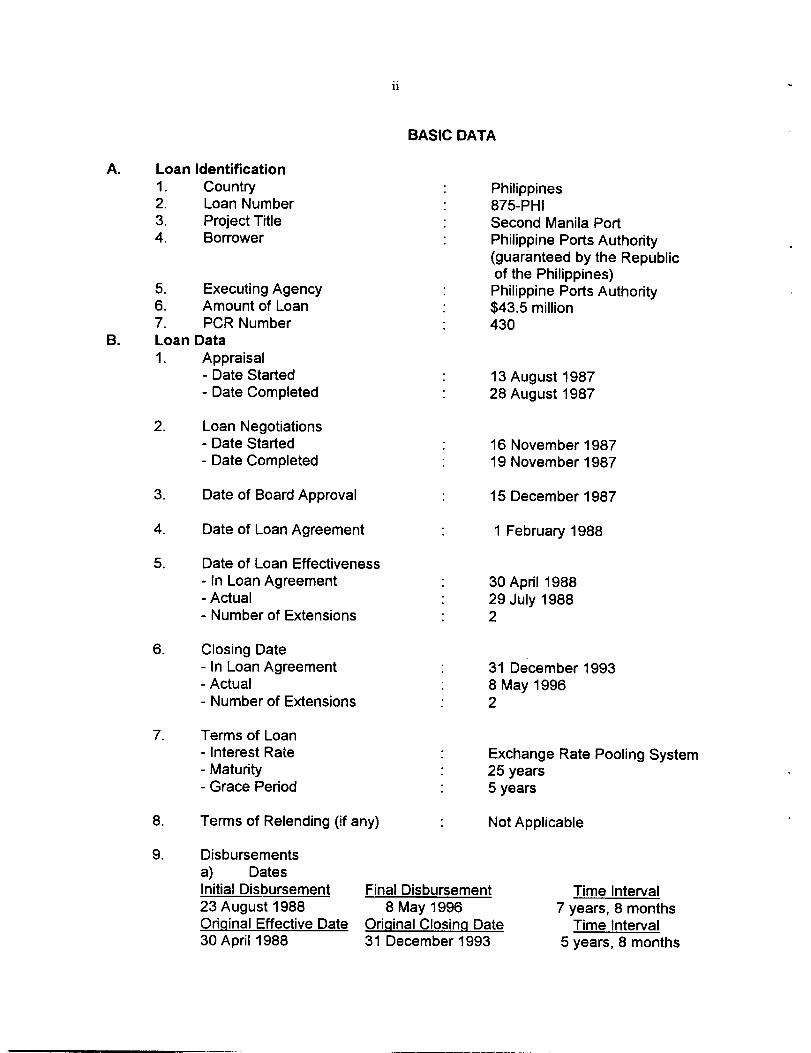

A. Loan Identification1. Country2. Loan Number3. Project Title4. Borrower

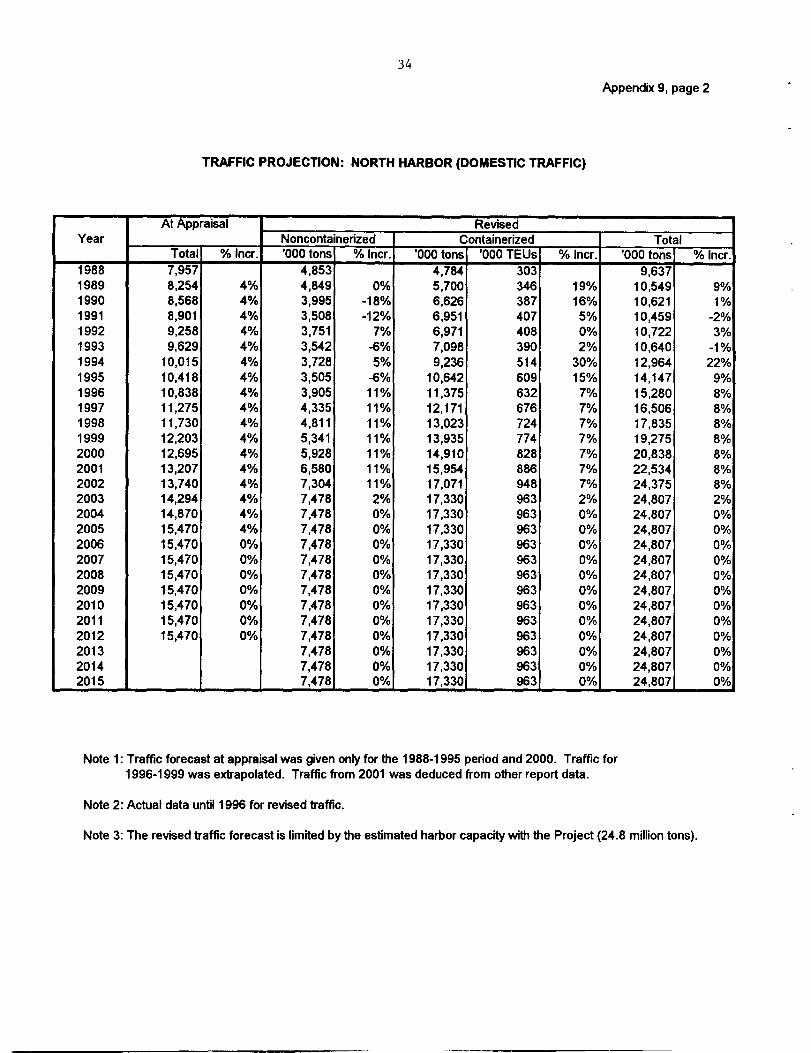

Philippines875-PHISecond Manila PortPhilippine Ports Authority(guaranteed by the Republicof the Philippines)

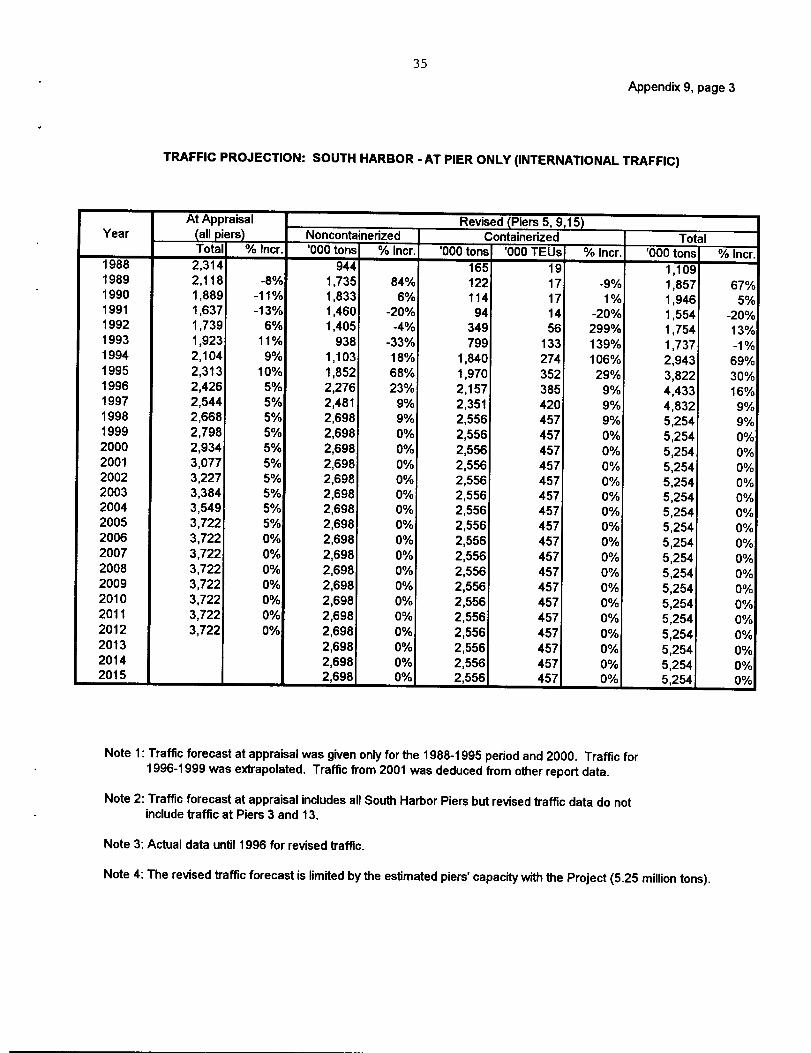

11

BASIC DATA

5. Executing Agency : Philippine Ports Authority6. Amount of Loan : $43.5 million7. PCR Number : 430

B. Loan Data1. Appraisal

- Date Started 13 August 1987- Date Completed : 28 August 1987

2. Loan Negotiations- Date Started : 16 November 1987- Date Completed : 19 November 1987

3. Date of Board Approval : 15 December 1987

4. Date of Loan Agreement : 1 February 1988

5. Date of Loan Effectiveness- In Loan Agreement : 30 April 1988- Actual : 29 July 1988- Number of Extensions : 2

6. Closing Date- In Loan Agreement : 31 December 1993-Actual : 8May 1996- Number of Extensions : 2

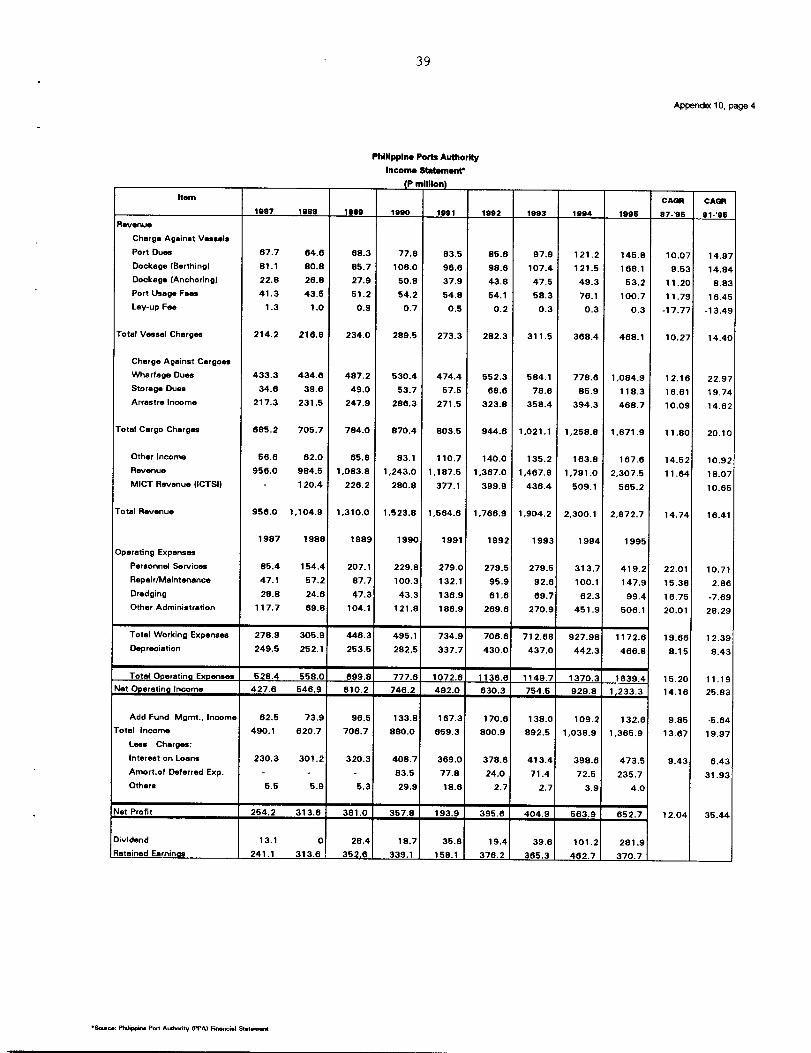

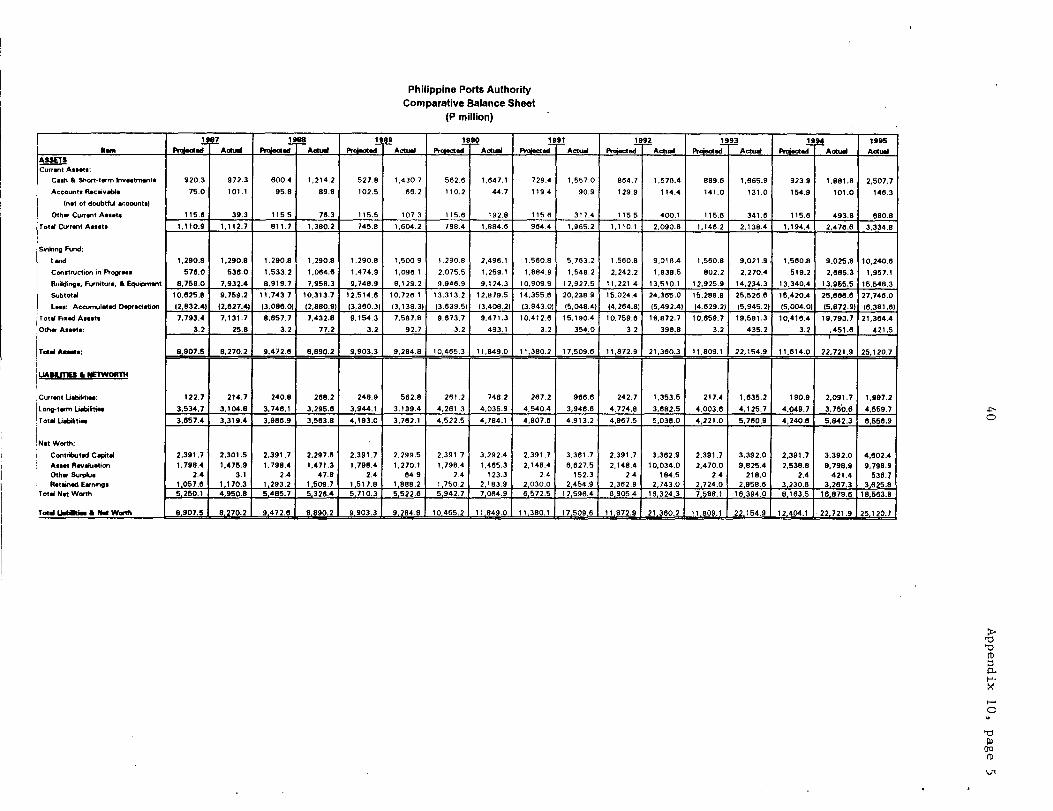

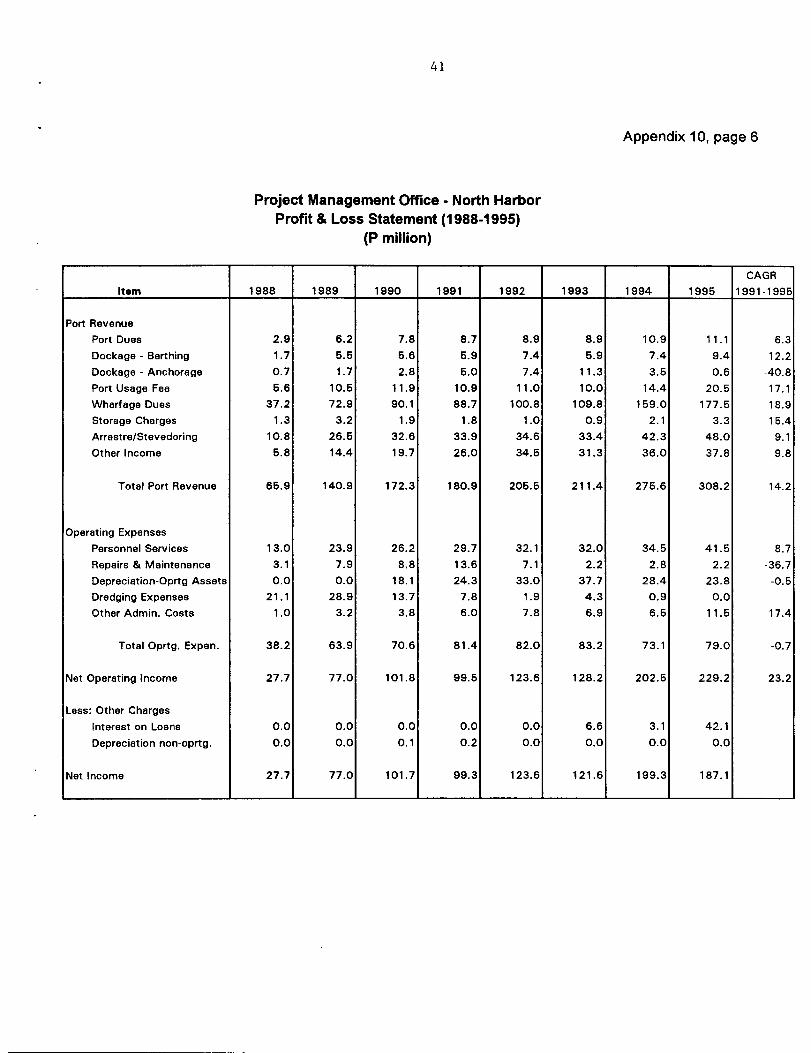

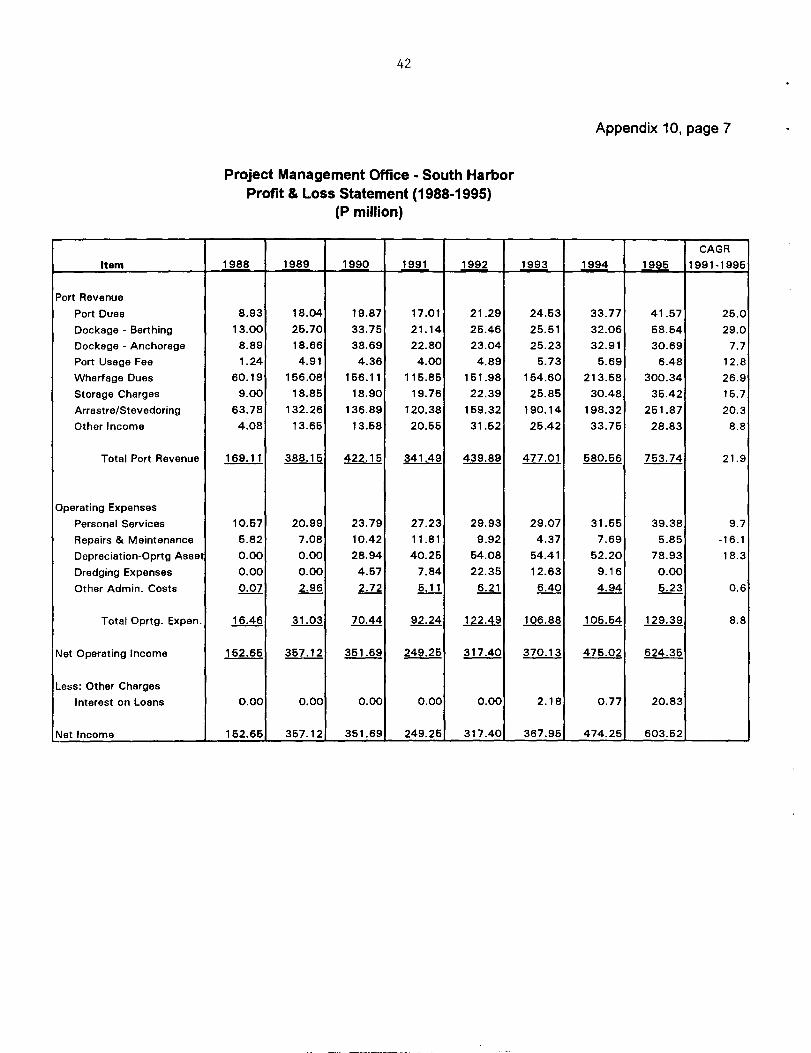

7. Terms of Loan- Interest Rate Exchange Rate Pooling System- Maturity 25 years- Grace Period : 5 years

8. Terms of Relending (if any) : Not Applicable

9. Disbursementsa) DatesInitial Disbursement Final Disbursement ___________23 August 1988 8 May 1996Orig inal Effective Date Ori ginal Closing Date ___________30 April 1988 31 December 1993

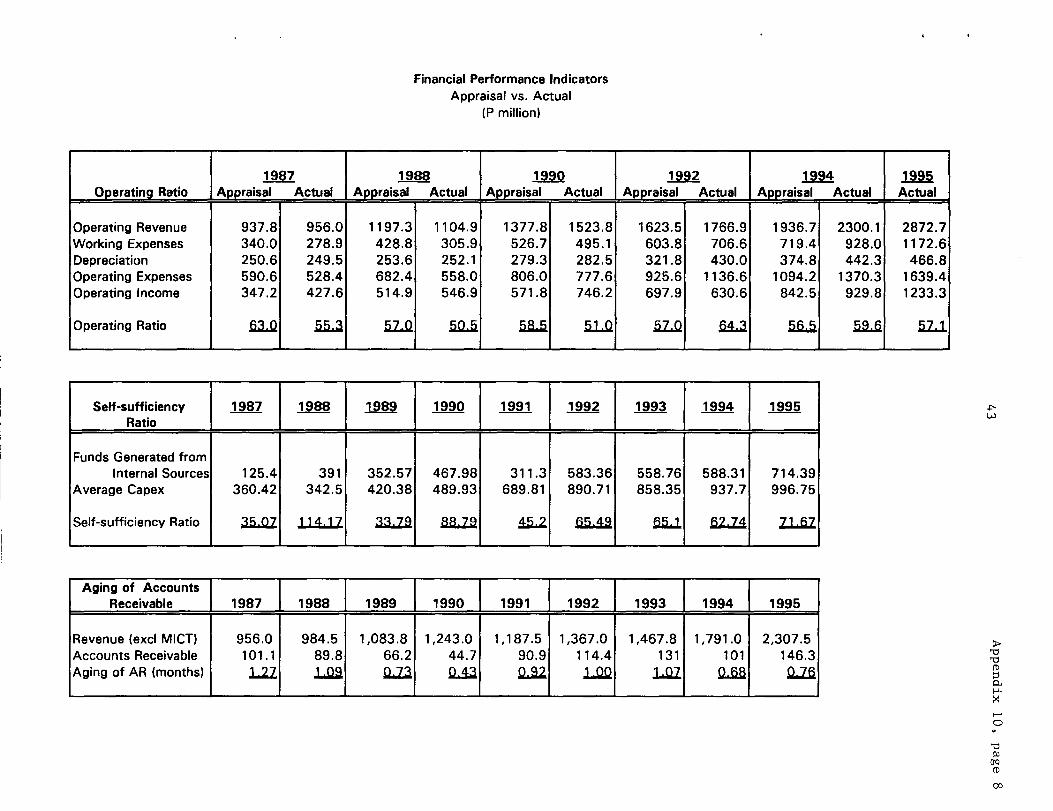

Time Interval7 years, 8 months

Time Interval5 years, 8 months

Total

41.7143.08

84.79

- 3,34

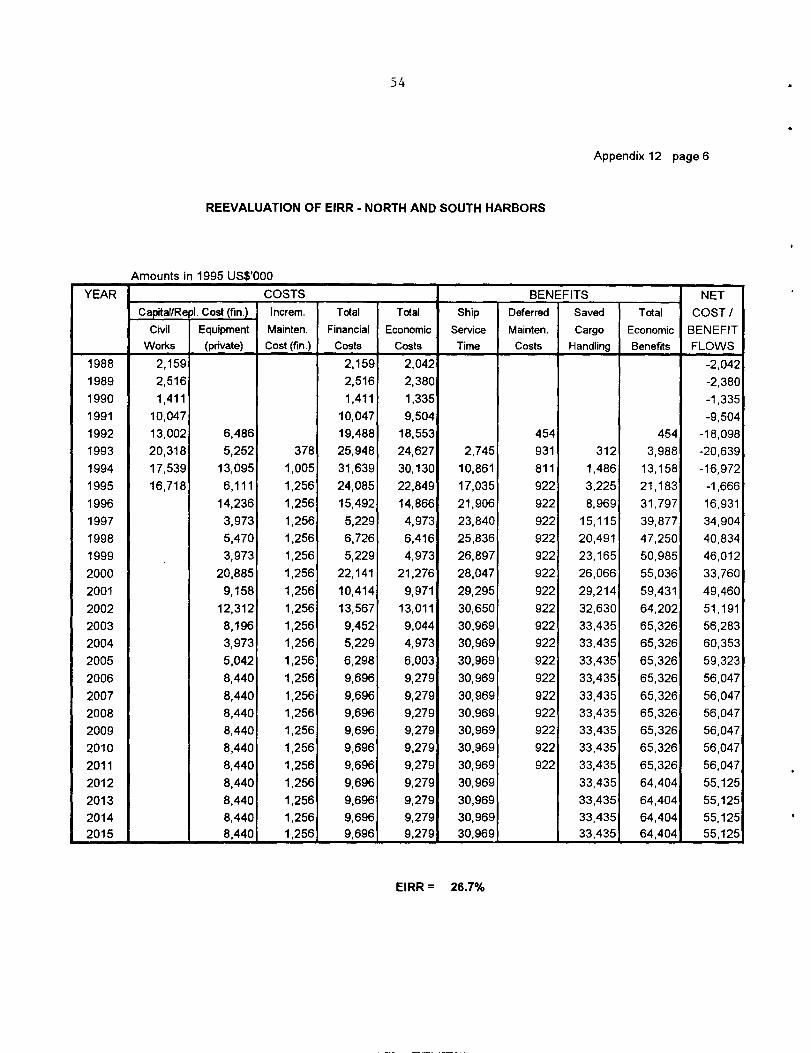

6.37 6.37

6.37 9.71

- 3.34- 6.37

- 9.71

111

b) Amounts ($)Last Net

Category Original Revised Amount Amount Amount UndisbursedAllocation Allocation Cancelled Available Disbursed Balance

O1A 13,430,000 11,605,365 - 11,605,365 11,605,365 -OIB 1,590,000 1,339,614 - 1,339,614 1,339,614 -O1C 1,500,000 3,232,076 - 3,232,076 3,232,076 -02A 6,790,000 18,107,635 - 18,107,635 18,107,635 -02B 1,000,000 851,493 - 851,493 851,493 -02C 1,000,000 1,577,144 - 1,577,144 1,577,144 -03A 2,000,000 - - - - -04A 860,000 - - - - -04B 940,000 - - - - -05A 900,000 - - - - -06 6,370,000 6,370,000 - 6,370,000 6,370,000 -07 7,120,000 416,673 416,673 - - -

Total 43,500,000 43,500,000 416,673 43,083,327 43,083,327 -

10. Local Currency Costs (Financed by Bank Loan)Local Currency Costs (Financed by Borrower)

C. Project DataAppraisalEstimate

0$38.37 million

Actual

1. Project Cost ($ million)(a) Foreign Exchange

50.40

46.42(b) Local Currency

36.29

38.37(C) Total Cost

86.69

84.79

2. Financing PlanAøDraisal Estimate Actual

Foreign Local Total Foreign Local(i) Implementation Costs

(a) Borrower Financed - 35.59 35.59 3.34 38.37(b) Bank Financed

43.50 - 43.50 43.08 -(c) Private Sector

6.90 0.70 7.60 - -(d) Total

50.40 36,29 86.69 46.42 38.37

ADpraisal Estimate ActualForeign Local Total Foreign Local

(ii) IDC Costs(a) Borrower Financed - -(b) Bank Financed 6.37 -(C) Other External Financing - -(d) Total 6.37

Total

4

Project ScheduleAppraisalEstimate Actual

iv

Cost Breakdown by ProjectComponents

North Harbor(a) Civil Works(b) Dredging(C) Consulting Services

South Harbor(d) Civil Works(e) Dredging(f) Consulting Services

(g) Equipment(h) MIS Development(i) Bulk Terminal Detailed

Design

(j) Contingencies(k) IDC

Total

Appraisal Estimate ActualForeign Local Total Foreign Local Total

13.43 15.08 28.51 11.61 23.79 35.40

1.59 0.40 1.99 1.34 0.41 1.75

1.50 0.90 2.40 3.23 1.15 4.38

6.79 8.78 15.57 18.10 11.51 29.61

1.00 0.25 1.25 0.85 0.21 1.06

1.00 0.60 1.60 1.58 1.30 2.88

8.00 0.80 8.80 - - -

1.80 0.18 1.98 - - -

0.90 0.42 1.32 - - -

8.02 8.88 16.90 - - -

6.37 - 6.37 9.71 - 9.71

50.40 36.29 86.68 46.42 38.37 84.79

(a) Date of Contracts with Consultants- North Harbor Jan 1988- South Harbor Jan 1988

(b) Completion of Engineering Design Sep 1988

(C) Civil Works Contracts- Date of Award

- North Harbor Jun 1989- South Harbor Jun 1989

- Completion of Work- North Harbor Jun 1992- South Harbor Jun 1992

(d) Equipment and Supplies a- First procurement Jul 1988- Last procurement Dec 1992

(e) Start of Operations- North Harbor Jan 1993

May 1988May 1988

Dec 1988

Mar 1991Jul 1991

Dec 1995May 1994

I

Jan 1996

a Component was canceled.

Type of Mission No. ofPersons

Person-days Specializationof Members a

Date

3

455

957

1122

162

142

62

8I

6I

21

42

6I

31

34

47

V

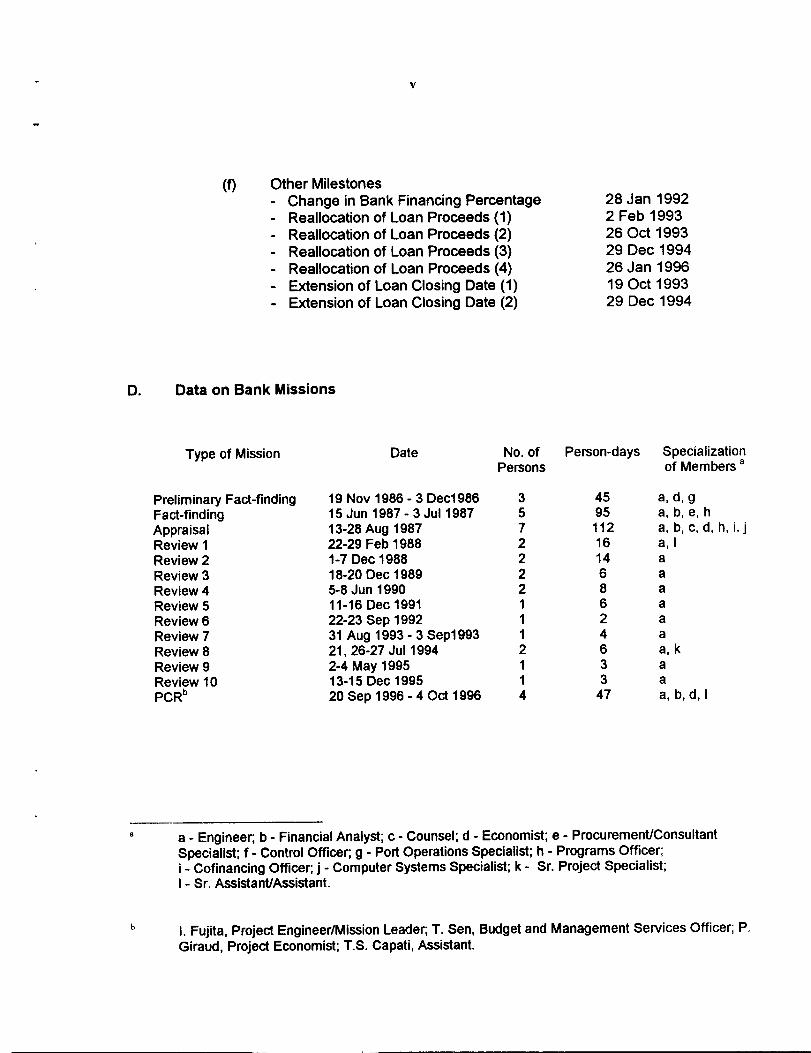

(f) Other Milestones- Change in Bank Financing Percentage- Reallocation of Loan Proceeds (1)- Reallocation of Loan Proceeds (2)- Reallocation of Loan Proceeds (3)- Reallocation of Loan Proceeds (4)- Extension of Loan Closing Date (I)- Extension of Loan Closing Date (2)

28 Jan 19922 Feb 199326 Oct 199329 Dec 199426 Jan 199619 Oct 199329 Dec 1994

D. Data on Bank Missions

Preliminary Fact-findingFact-findingAppraisalReview IReview 2Review 3Review 4Review 5Review 6Review 7Review 8Review 9Review 10PCRb

19 Nov 1986-3 Dec198615 Jun 1987-3Jul 198713-28 Aug 198722-29 Feb 19881-7 Dec 198818-20 Dec 19895-8 Jun 199011-16 Dec 199122-23 Sep 199231 Aug 1993-3 Sep199321, 26-27 Jut 19942-4 May 199513-15 Dec 199520 Sep 1996 - 4 Oct 1996

a, d, ga, b, e, ha, b, c, d, h, i.a, I

aaa, kaaa, b, d, I

a - Engineer; b - Financial Analyst; c - Counsel; d - Economist; e - Procurement/ConsultantSpecialist; f - Control Officer; g - Port Operations Specialist; h - Programs Officer;- Cofinancing Officer, j - Computer Systems Specialist; k - Sr. Project Specialist;- Sr. Assistant/Assistant.

I. Fujita, Project Engineer/Mission Leader; T. Sen. Budget and Management Services Officer; P.Giraud, Project Economist; T.S. Capati, Assistant.

123°C

17°N -I

LUZON

PROJECT AREA

[11 MANILA

-14°N

MANILA BAY

Io 100200300400500- - -

Meters

Area Occupied by Squatters

Road

11

C,a

/

/

SOUTH HARBOR

EngineeIsland

1g

Marine Slipway

PHILIPPINES

Pier 16 SECOND MANILA PORT PROJECTPROJECT AREA

Pier 14 1

\ (as completed)

pier 12

NORTH HARBOR pIer 10

Pier 8

pier6

er2

nati0afl1atnteTlnal

Conta I-I.

II

I/

/I

/I

I/

Depth-BOrn

(31-4C,

PHILIPPINES

SECOND MANILA PORT PROJECTMANILA NORTH HARBOR REHABILITATION

(as completed)

•1

\\ IManila International \ \ Depth /Container Terminal \ \ -6Om

J

PIER 2 PIER 4 PIER 6 PIER 8 PIER 10 PIER 12 PIER 14 ] _______________

____________ _____________________________________________________

____________

____LI__ __ __E 1 1

SLIP 3 ri SLIP 5 SLIP 7 SLIP 9 SLIP 11 SLIP 13 ______________

Ii 11 II 1b II ii

GATE 2_____________________________________________________ L__-- [iE

GATE1 ROAD 10

-i r

Ad.5r

New Facilities (Berth,Breaater)

Lull Container Slacking Yard

L New Road

[ Repavement0 100 200 300 400 500E•" Area Occupied by Squatters

Meters - - - - Bottom Contour

I-'I-'

0 100 200 300 400 500I_I

Meters

UII

PIER 9 PIER 5PIER15 I PIER 3 Rehabilitated Shed

Rehabilitation

Pavement

Trench Leveling

Demolished Shade

-J.

Ii

CONTAINERSTACKING YARD

(CV - 1)

ii

N)

0)

PHILIPPINESSECOND MANILA PORT PROJECT

MANILA SOUTH HARBOR REHABILITATION(as completed)

PIER 13

_Em 1[1(CY2) _L ___

CONTAINER

ISTACKINGYARD I

urn

(-))

I. PROJECT DESCRIPTION

1. The principal objective of the Project was to facilitate improvements in cargohandling productivity, and thereby to reduce cargo handling costs for port users, byrehabilitating North and South Harbors. An additional objective was to develop the institutionalcapacity of the Philippine Ports Authority (PPA) by assisting it to develop effective financial andmanagerial systems.

2. The Project was in line with the Mid-Term Development Plan of the Governmentfor 1987-1992, the main objective of which for the port sector was to rehabilitate port facilities.As Manila is by far the largest market and focal point for distribution in the Philippines, theGovernment placed top priority on rehabilitating Manila Port. The Project focused on therehabilitation of dilapidated port facilities at North and South Harbors with a small expansion ofport facilities at North Harbor by reclaiming slip 17 and constructing three deepwater berthswith sufficient back-up area for a roll-on-roll-off (RORO) ship terminal; passenger terminal; andcontainer stacking yard. The modest scope of the Project reflected the economic uncertaintiesof the country at the time of Project formulation and processing, which necessitated theadoption of conservative demand forecasts for port traffic. Taking into account the uncertaineconomic environment, the Project as formulated 1 is considered to have been appropriate.During Project implementation, however, the Philippine economy started rebounding and porttraffic increased much faster than expected at appraisal.

3. A loan of $43.5 million was approved on 15 December 1987 to finance part ofthe foreign exchange cost of the Project. The loan became effective on 29 July 1988 after twoextensions. The Project was completed at the end of 1995, with almost all the facilities at NorthHarbor, and major parts of the facilities at South Harbor rehabilitated; it helped to support thehigh economic growth of the country starting in 1994. The Project was formulated withflexibility, and several changes occurring in its scope during implementation were handledpromptly. Some of the components were deleted from the scope; savings from these deletionswere utilized to finance the cost increase of civil works. The loan was closed on 8 May 1996after two extensions, with all disbursements having been completed. Key events associatedwith the Project are given in chronological order in Appendix 1.

The North Harbor component was regarded as the first phase of the development of the Harbor, and thesecond phase was to build a domestic container terminal, which so far has not materialized. Instead, thereis a new port development project currently ongoing north of the Harbor as a part of an industrial parkdevelopment using private financing, known as the Smoky Mountain Development Project.

2

II. EVALUATION OF IMPLEMENTATION

A. Project Components

4. The Project comprised five components: (i) Part A, rehabilitation of NorthHarbor, (ii) Part B, rehabilitation of South Harbor, (iii) Part C, provision of Cargo HandlingEquipment and Miscellaneous Port Equipment, (iv) Part D, Management and InformationSystems (MIS) Development and Institutional Strengthening, and (v) Part E, Detailed Designfor a Bulk Terminal. Among these five components, Parts A and B were the core of the Projectwith the largest share of the cost (more than 80 percent of the base cost). For the other threecomponents, investment or technical assistance (TA) from sources other than PPA wasenvisaged concurrently with, or prior to, the Bank loan. This included investment from privateterminal operators for Part C; a grant from the Government of Singapore for Part D 1 ; and afeasibility study from bilateral financial institutions for Part E. The Loan Agreement includedrelevant clauses to flexibly respond to possible changes during Project implementation.

5. Details of changes in the Bank-financed Project scope are provided in Appendix2. Only the first two components (rehabilitation of North and South Harbors) were retained as:(i) PPA made other arrangements for miscellaneous port equipment expected to be financedby the Bank under Part C; (ii) PPA decided to use the loan proceeds from the World Bank forthe MIS under Part D, rather than grant money from the Singapore Government; and (iii)based on a study financed by the United States Agency for International Development, PPAdecided to adopt the build-operate-transfer modality for the bulk terminal under Part E. Thesurplus loan proceeds derived from these deletions2 were used to increase financing for PartsA and B. During Project implementation some modifications were made to Parts A and B toreflect site conditions, port user's views, and changes in traffic demand after Projectformulation. These modifications included converting pier 5 in South Harbor into a containerterminal, and deleting the RORO facilities from the North Harbor component. As containerpenetration has been higher than expected at both the harbors and there are no RORO shipsthat require special facilities for loading/unloading RORO cargoes, these changes areconsidered to be appropriate.

6. During Project processing, there were disagreements among the shippingcompanies as to whether common passenger facilities were desirable. Thus, it was agreed thatthe passenger facilities at North Harbor would be constructed only if further discussions withinshipping companies resulted in a clear consensus about the desirability of such facilities.Eventually, PPA deleted the passenger facilities from the North Harbor component 2 as it didnot succeed in obtaining the concurrence of the shipping lines to use them.

At the time of appraisal, the World Bank was processing its Provincial Ports Project (Loan No. 2823-PHI)under which an MIS component was also considered.During Project implementation, PPA changed the basic planning concept of the passenger facilities fromtwo separate one-storey buildings to a large-scale passenger terminal with elevated passenger corridors,that would segregate passenger flow from cargo flow and other associated traffic. The proposal was turneddown by the Bank, as no feasibility study was made available, and it was doubtful whether the shippinglines would agree to the common use of such terminal.

3

B. Implementation Arrangements

7. PPA was the Borrower and the Executing Agency for the loan, which wasguaranteed by the Government of the Philippines. During Project implementation, there wereno delays in the provision of counterpart funds, which had been a major problem duringimplementation of the first Manila Port Project (Loan No. 412-PHI). PPA established a ProjectOffice to supervise the day-to-day implementation and coordination of the Project. The ProjectOffice was headed by an experienced full-time Project Director under whom two ProjectManagers, one each for the South and North Harbors, were assigned. The Project Directorchanged twice during implementation, but this had little effect, as one of the two ProjectManagers succeeded to the position to maintain continuity. The Bank approved, in September1987, advance action and retroactive financing up to $1.6 million for dredging and forconsulting services which helped timely implementation of the Project.

8. Civil works, except dredging, were contracted through International CompetitiveBidding (ICB) under two separate contracts, one each for the North and South Harborscomponents. Dredging was undertaken by PPA through force account, as the dredgingquantity was not large enough to attract an international contractor, and PPA's dredgingequipment had proved to be sufficient to carry out dredging in a cost-effective manner (seepara. 17). Rehabilitation of pier 3 in South Harbor was deleted from the scope, as it wasfinanced by the private operator who had been awarded the operational franchise for 15 yearsin 1992. While the procurement of rubber fenders was originally included in the civil workscontracts, this was carried out separately to ensure the timely availability of the goods to thecontractors; this arrangement is considered to be appropriate.

C. Project Costs

9. At appraisal, the total cost of the Project was estimated at $86.69 millionequivalent (inclusive of taxes and duties amounting to $2.8 million), of which $50.40 million, orabout 58 percent, was the foreign exchange cost, including $6.37 million of interest and othercharges during construction (IDC). Local currency costs were estimated at $36.29 millionequivalent, or about 42 percent. The cost estimates for North Harbor were based on theAppraisal Mission's review of the study financed by Bank TA, 1 while the costs for SouthHarbor were based on the Appraisal Mission's review of the findings of a feasibility studyfunded by Japan International Cooperation Agency. The cost estimates included a physicalcontingency allowance of 20 percent for the civil works, 10 percent for equipment, and 5percent for consulting services and price escalation. Because of uncertainty associated withthe nature of the works, particularly the lack of "as-built" drawings of the existing facilities, thephysical contingency allowance of 20 percent for civil works was considered to be appropriate,but even that proved to be inadequate (see para. 11).

10. Although the actual Project cost was $84.79 million ($46.42 million in foreignexchange and $38.37 million equivalent in local currency costs), about $2 million less than theappraisal estimate, the cost of rehabilitating the North and South Harbors increasedconsiderably except for dredging. The final civil works cost of the North Harbor component was$35.40 million against the appraisal estimate of $28.51 million; consulting services costs were$4.38 miflion against $2.40 million; and dredging was $1.75 million against $1.99 million. Thecivil works cost of the South Harbor rehabilitation component was $29.61 million against the

TA No. 842-PHI: Second Manila Port, for $75000, approved on 12 January 1987.

4

appraisal estimate of $15.57 million; consulting services costs were $2.88 million against $1.60million; and dredging was $1.06 million against $1.25 million (see Appendix 3).

11. The significant increase in the civil works cost of South Harbor (90 percent) wasattributable mainly to (i) conversion of pier 5 into a container wharf, which required majorstructural strengthening; (ii) more advanced detenoration of the facilities than expected atappraisal, which required more material and labor inputs (the most deteriorated pier 13 wasdeleted from the Project scope); and (iii) additional works (e.g., leveling the quay floor by fillingthe lower basin) identified during detailed design. Though lower than that in South Harbor, theoverrun in civil works costs for North Harbor of 24 percent over the appraisal estimateexceeded the physical contingencies of 20 percent. The significant increase in consultingservices cost reflects the longer than expected length of assignment (7.5 years against 5 yearsfor the North Harbor component, and 7 years against 5 years for the South Harborcomponent), and a major increase in the foreign exchange cost for the North Harborconsultants (the contract was awarded to a Japanese company payable in yen, whichappreciated significantly from $1=Y160 in 1989 to $1=Y100-110 from 1997 onward).

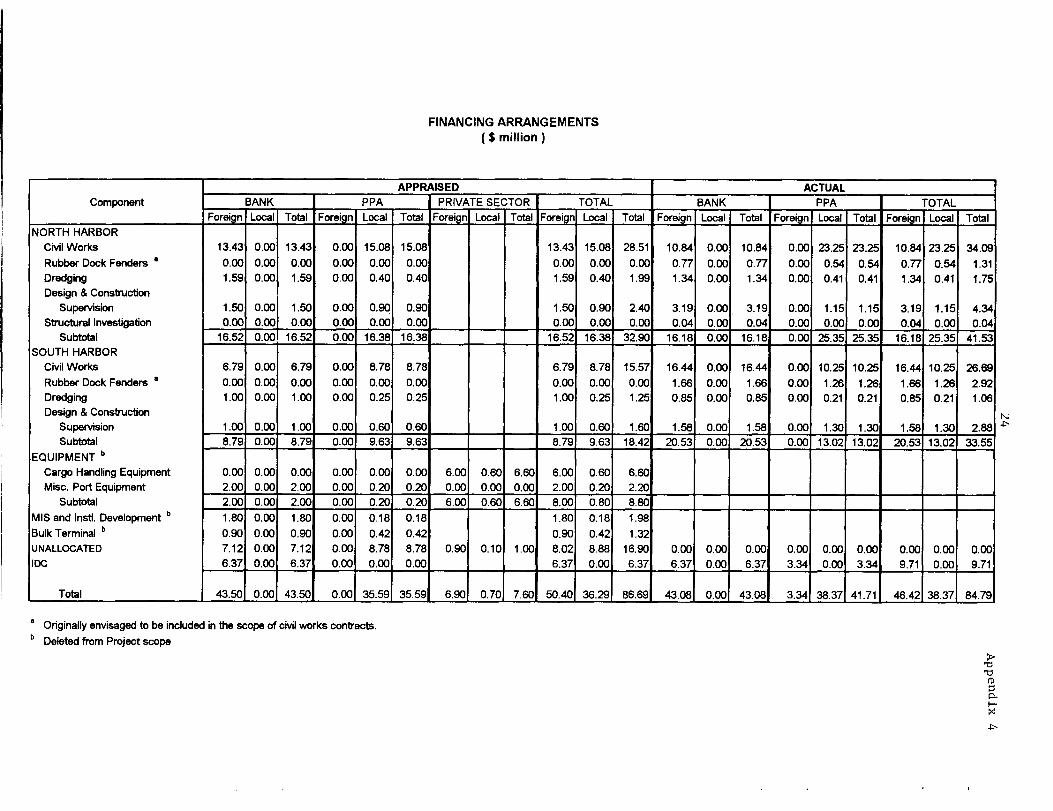

12. The final Project cost was, however, accommodated within the appraisalestimate by utilizing surplus loan proceeds from the deleted components and contingencies.The foreign exchange cost borne by PPA was the excess of IDC over the amount providedunder the loan. Actual Bank financing was $0.42 million less than the appraisal estimate.These loan savings were cancelled (see Appendix 4).

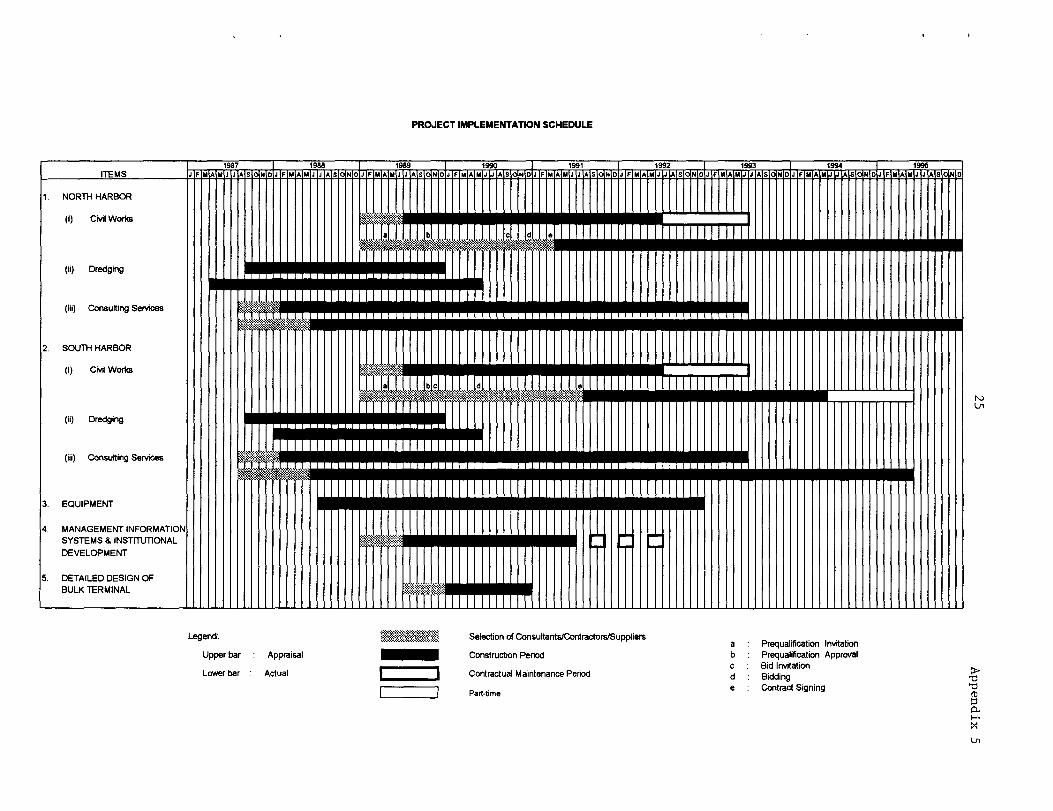

D. Project Schedule

13. The Project was expected to be implemented over a five-and-half year period,including the warranty period, beginning in September 1987 when the dredging workscommenced. Civil works for the two harbors were expected to commence in July 1989.Project facilities were expected to become fully operational in late 1992, and the warrantyperiod was to end in mid-1993.

14. The Project schedules at appraisal and as actually implemented are shown inAppendix 5. The Project was delayed more than two years, mainly because of protractedprocedures within the Government to award civil works contracts. Prequalification proceduresprogressed smoothly starting in May 1989 and ending in November 1989. Bidding followedright after prequalification. While bids for the civil works contract for South Harbor wereopened in May 1990, the contract was awarded and signed only in July 1991. This delayoccurred because of a claim by one of the losing bidders 1 and a dispute between theGovernment and the winning bidder on the contract terms, which took one year to settle. Achange in the chairman of the Prequalification, Biddings and Awards Committee alsocontributed to the delay. For North Harbor, bid invitation was withheld for seven months due tothe Government's intention to introduce private financing for the Project. This wassubsequently abandoned, and the bids were called in September 1990. The contract for NorthHarbor was awarded in March 1991.

15. The Project encountered several engineering problems that delayedconstruction. At South Harbor, the state of deterioration of the port structures was worse than

The fourth lowest bidder offered a 15 percent discount (after discount, the bidder would have been thelowest bidder), but with a bond of only one day validity.

5

expected at appraisal. At North Harbor, extremely weak soil conditions at slip 17 and thecollapse of slip 13 (see para. 18) led to delays. The actual construction period for SouthHarbor was 2 years and 7 months (two piers were deleted from the Project scope, and onepier required extensive work to convert it into container berths). The North Harbor componentwas implemented in 4 years and 9 months. The appraisal schedule envisaged completion ofboth in three years. The loan was closed on 8 May 1996 after two extensions, about 2 yearsand 4 months later than the appraisal estimate.

E. Engagement of Consultants and Procurement of Goods and Services

16. Details of the contract packages are provided in Appendix 6. There were threeadditional contracts, two for the procurement of rubber fenders through ICB (Contracts 1-A and4-A) and one for consulting services for structural investigation through direct appointment(Contract 3-A). Six contracts were deleted from the Project scope, because of the reasonsmentioned in para. 5, for the procurement of (i) miscellaneous equipment (Contract 7); (ii)computer equipment and software (Contract 9); and (iii) consulting services for design andimplementation of part of the computerized MIS (Contract 8); strengthening PPA's institutionalcapability to improve its MIS (Contract 10); providing advice on port management andoperations (Contract 11); and detailed design of the bulk terminal (Contract 12). The remainingcontracts were implemented as envisaged at appraisal.

17. Separating the procurement of rubber fenders from the civil works contracts($1.31 million for North Harbor and $2.92 million for South Harbor, both through ICB) wasappropriate to ensure timely provision of the goods to the contractors. The dredging of thebasins, slips, and approach channels at North and South Harbors was conducted under forceaccount because (i) the estimated cost of contracts of $1.99 million and $1.25 million was toosmall to attract international contractors due to mobilization costs; (ii) local contractors did nothave appropriate dredging equipment; and (iii) PPA had the appropriate equipment toundertake the dredging in a cost-effective manner, and such dredging was urgently required tofacilitate timely implementation of the Project. The actual dredging cost was around $1 percubic meter, which was comparable with the international price at the time. This arrangementwas appropriate.

F. Performance of Consultants, Contractors and Suppliers

18. The performance of the consultants, contractors and suppliers is evaluated asgenerally satisfactory. The consultants and the contractor engaged for North Harbor were notresponsible for the collapse of slip 13,1 as the results of the investigation conducted after theincident showed that (i) the method and quality of predesign investigation and design ofrehabilitation were satisfactory; (ii) the quality of civil works was satisfactory; (iii) slip 13 was theonly structure where tie-wires had been installed originally instead of tie-rods to hold backsheet piles, and the tie-wires had insufficient strength for the purpose; and (iv) it was notpossible to detect the deficiency beforehand. The failure of the pier was caused by fragilityresulting from the extensive deterioration of the original structure, triggered by the stacking ofheavy cargo.

19. As the Project was implemented while port operations were taking place, closecoordination of the construction with port operations was required. Because six operators were

There has recently been a second incidence of collapse, at pier 15 in South Harbor. ( see para. 30).

6

handling cargo in North Harbor, coordination with these operators was extremely complicatedand time consuming. The consultants and the contractor cooperated with PPA in coordinatingwith the cargo handlers, and well-planned construction methods were followed to minimizedisruptions to port operations.

G. Conditions and Covenants

20. As shown in Appendix 7, compliance by the Executing Agency with the loancovenants was generally satisfactory except for (i) timely acquisition of land for the Project,and (ii) the formation of the Cebu Port Authority (CPA) without prior consultation with the Bank.The major problem encountered during implementation of the first Manila Port Project hadbeen PPA's lack of access to counterpart funds. To avoid this problem, relevant clauses werestipulated in the Loan Agreement, and there were no delays in the provision of counterpartfunds. PPA maintained a good financial position: its operating ratio and self-financing ratiowere satisfactory during Project implementation (see para. 49). In line with the loan covenants,PPA also revalued its fixed assets and revised tariffs, both of which were essential to maintainthe financial viability of the Project (see paras. 46 and 50).

21. Relocation of 1,400 squatter families from slip 17 of North Harbor wassuccessfully carried out through joint efforts of Government agencies concerned (InteragencyCommittee on Squatter Removal and Relocation; IACSRR). The second step was phasedrelocation of 7,000 squatter families from the southern end of North Harbor. After completionof the relocation of about 100 families, a temporary restraining order was issued. DespiteIACSRR's efforts to resolve the issue, the relocation was suspended for a long period, and therelocation site was occupied by other squatters, which further complicated the issue.Consequently, two minor components -- the construction of a part of the container yard at Slip0 and the associated link road to the Manila International Container Terminal access road --were deleted from the Project scope (Appendix 2).

22. CPA was created by the Government in September 1992, and its operationsstarted in 1996 despite opposition by PPA. Although CPA's assets constituted about 18percent of PPA's total assets in 1995, its operations mainly concern domestic cargo andpassengers, which generate only modest revenues. The separation will not seriously affectPPA's financial performance (see paras. 51 and 52).

H. Disbursements

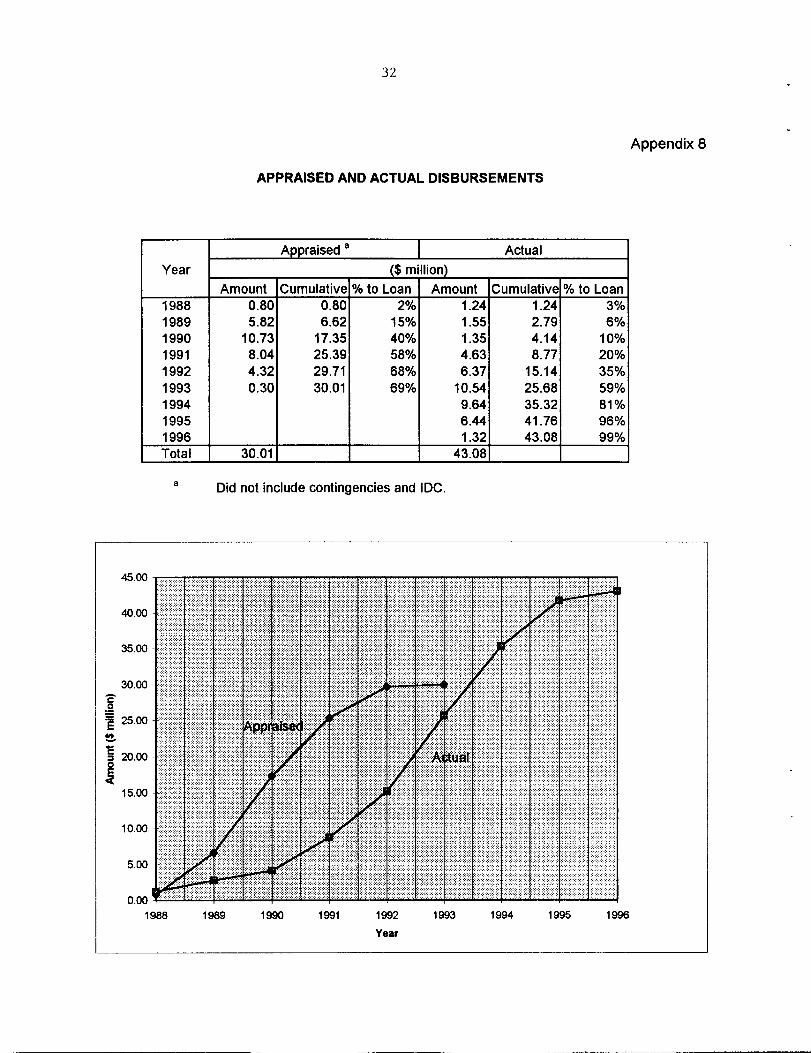

23. Disbursements amounted to $43.08 million out of the loan of $43.50 million, or99 percent. The remaining $0.42 million was canceled. There were three cancellations ofProject components: (i) Part C, $2 million to procure various items of equipment; (ii) Part D,$1.80 million to provide consulting services for MIS and institutional development; and (iii) PartE, $0.90 million to provide consulting services for detailed design of a bulk terminal. The totalsavings of $4.7 million, together with the unallocated amount of $6.37 million, were utilized tofinance the increased cost of civil works and consulting services under Parts A and B(rehabilitation of North and South Harbors). Disbursements were made over 7 years and 8months, starting in August 1988 and ending in May 1996. This compares with the 5 years and8 months estimated at appraisal. Submission of withdrawal applications was generally timely(see Appendix 8).

7

24. Terms of reference of the consultants engaged for the detailed design andconstruction supervision included a clause to review and update the Project cost estimate,including its breakdown into foreign exchange and local currency costs. As a result, it wasfound that the foreign exchange cost for South Harbor was higher than for North Harbor, andratios were adjusted for disbursement purposes for South Harbor from 40 percent 60 percent,and for North Harbor from 52 percent to 35 percent, without changing the total amount offoreign exchange costs.

I. Environmental Impact

25. There was no significant environmental impact due to the Project. Because ofconstruction of a container yard at North Harbor, containers are now stacked inside the portarea rather than on the roads, as was done in the past. Through the clean-up and realignmentof facilities as well as introduction of proper garbage collecting systems, the Project hascontributed to an improved working environment within the port. Drainage constructed as partof the Project has reduced flooding, thus contributing to the improvement.

26. Although the procurement of garbage collection equipment envisaged underPart C was dropped from the Project scope, in 1992 PPA entered into a new arrangement withthe municipality through which garbage was collected from inside the port area under contract.PPA is also an active member of a new joint program for the environmental protection ofManila Bay wherein the various agencies cooperate to clean and maintain the bay. 1 This is animportant step forward to improve the port's environment.

J. Performance of the Borrower and the Executing Agency

27. PPA was both the Borrower and the Executing Agency for t e Project. Theperformance of PPA was generally satisfactory: (i) there was no delay in 1 ie provision ofcounterpart funds; (ii) communications with the Bank were timely; (iii) implementationarrangements were well established and maintained; and (iv) the conditions and covenantsstipulated in the Loan Agreement were generally complied with.

28. During Project implementation, the Government introduced institutional andorganizational changes in the port sector, including (i) promoting private sector participation inport operations and investment (PPA extended the contract for terminal operations with theprivate operator from 3 years to 15 years, to make it more commensurate with the investmentby the private operator); (ii) coordinating development plans and works between the port andthe city; and (iii) streamlining PPA port systems. Item (i) is in line with the Loan Agreement, anditems (ii) and (iii) are in conformity with the key issues noted in the Bank's ProjectPerformance Audit Report (PPAR) for Loan No. 412-PHI: Manila Port Project.2

29. There were, however, some issues that needed careful monitoring and analysisby the Government and the Bank. One of these issues was the creation of CPA, despiteopposition by PPA. While this move was a part of the Government's decentralization policy,

Known as Manila Bay Clean-up Campaign." Agencies concerned include the Department of Environmentand Natural Resources as the lead agency, Philippine Coast Guard, PPA, City of Manila, and variousprivate organizations and individual volunteers.Circulated to the Board in September 1994.

8

no proper analysis of the implications was carried out, nor was the Bank consulted, althoughthe Loan Agreement required this.

30. Another issue was the failure of two of the rehabilitated facilities: slip 13 ofNorth Harbor and a part of pier 15 of South Harbor. A part of slip 13 collapsed in September1994, one year after rehabilitation. Although the failure was due to a deficiency in the originalwharf structure, the continuous stacking of unusually heavy container cargoes triggered thefailure. While PPA engineers were aware of the likely risks and requested the operational unitto take counter measures, there was a lack of proper communications between theengineering and operational units of PPA. After the incident, both units had intensivediscussions, and PPA introduced loading limitations on cargo handling operations, taking intoaccount the design strength of the structures. However, the collapse of a part of pier 15occurred in June 1997, three years after rehabilitation, casts some doubt on the effectivenessof enforcement of these limitations. The cause of the collapse is still under investigation at thetime of writing this Report. While it is most probable that stacking of heavy cargo (almost threetimes heavier than the design load of the pier) buckled the supporting steel monotube piles,some of the piles were found to be unrehabilitated and may not have been able to providetheir design capacity.

31. The MIS component was deleted from the Project because PPA decided to usepart of a World Bank loan for the purpose rather than the Singapore Government grant. Underthe World Bank financing, a master plan of the PPA computer systems was developed and,following the master plan, PPA and the private operators in Manila Port have graduallydeveloped a computerized MIS system through their own resources. The system has on-lineconnections to port traffic data collected by the South Harbor operator and the ManilaInternational Container Terminal (MICT) operator, which allows PPA to monitor and supervisethe operations and management of South Harbor and MICT. However, the system has noaccess to North Harbor and to ports other than Manila Port. To improve the efficient andeffective management of its operations, the MIS needs to be enhanced by PPA.

32. PPA maintained close consultation with private port operators and port users,which facilitated smooth implementation of the Project. The deletion of the common userpassenger terminal at North Harbor is considered appropriate; it was agreed during processingthat the passenger terminal would be built only if the operators wanted it. As no consensuswas reached during implementation, it was not built.

33. PPA, in cooperation with other Government agencies concerned, hasintroduced new traffic regulations in and around North Harbor. Jeepneys, taxis, and tricyclesare not allowed to enter the port area. Shanties along each side of R-101 have beendemolished, and there are now three lanes in each direction. This, coupled with theconstruction of the collector roads within the port, has improved port traffic flows dramatically,thus enhancing the efficiency of port operations.

The radial road running along the coastline of Manila Bay.

9

K. Performance of the Bank

34. During Project implementation, changes in Project scope and associatedmatters became necessary because of various reasons: (i) traffic demand surged after Projectformulation; (ii) conditions justifying some of the Project components did not materialize; and(iii) the Government decided to promote more private sector involvement in the port sector.Whenever the need for change arose, the Bank examined the matter and took appropriateaction. The Bank gave timely and relevant technical advice to PPA for the resolution ofproblems encountered during Project implementation.

III. EVALUATION OF INITIAL PERFORMANCE AND BENEFITS

A. Traffic Reevaluation

35. The Project has been reevaluated based on actual port traffic and revised trafficforecasts over the anticipated Project life. At appraisal, very conservative traffic forecasts weremade because (i) the economy of the country had experienced deep recession between 1982and 1985, which resulted in a decline of port traffic at Manila; and (ii) the Project wasprocessed immediately after the political events in 1986, a period of economic uncertainty.Actually, the economy of the country rebounded, showing strong growth particularly from 1994onward.

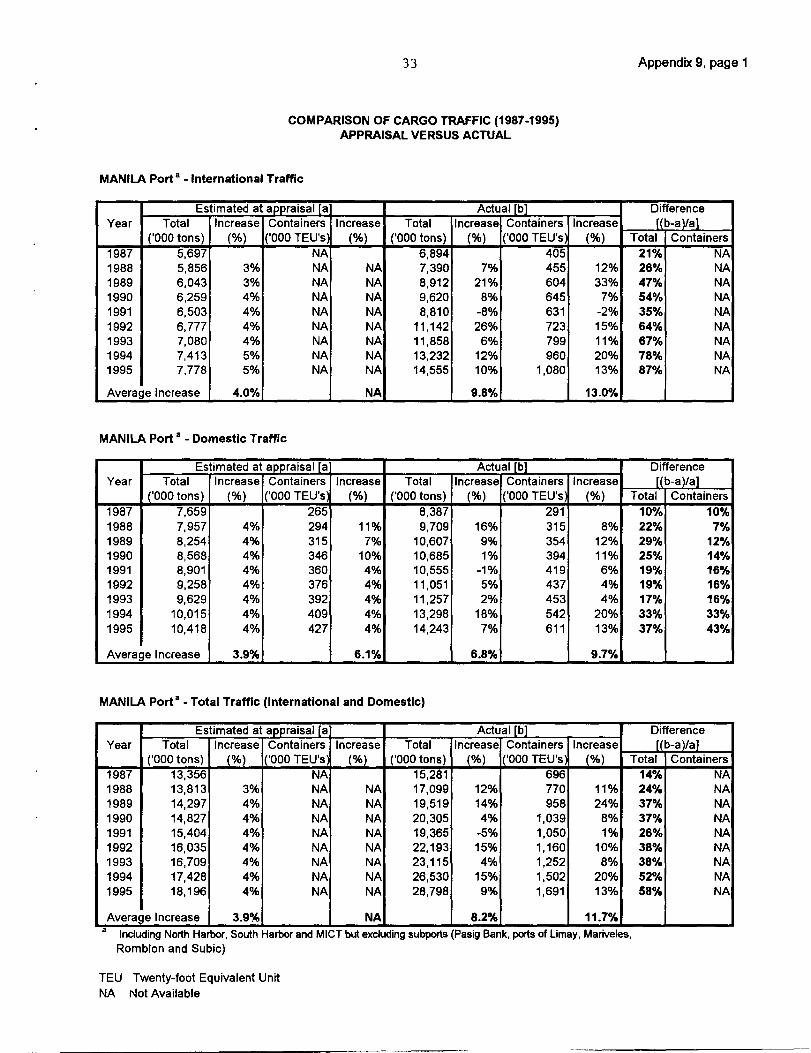

36. A comparison of the appraisal forecast with actual traffic from 1987 to 1995 indicates aclear divergence. Manila Port 1 traffic has increased much faster than expected during the pastnine years in terms of cargo, passengers, ship calls, and average cargo volume handled pership. Data have been compared on the same basis as at appraisal: (i) traffic handled over allof the piers at South Harbor, but excluding traffic at anchorage; and (ii) total traffic at NorthHarbor, at pier and anchorage. Comparison tables are provided in Appendix 9.

1. International Traffic

37. At appraisal, the international cargo traffic at Manila Port was expected toincrease from 5.7 million tons in 1987 to 7.8 million tons in 1995, equivalent to a 4.0 percentaverage annual growth rate. The traffic actually grew at an average rate of 9.8 percent perannum to reach 14.6 million tons in 1995, 87 percent higher than forecast at appraisal.

38. The international cargo traffic is handled at South Harbor and MId. In 1986,78.4 percent of total international cargo traffic was handled at South Harbor. At appraisal, itwas expected that this share would decrease to less than half in the 1990s (particularly, theshare of container traffic was anticipated to decrease sharply from about 60 percent to 15percent) due to the completion of Phase II of MICT. The actual share of international cargo atSouth Harbor did not decrease as expected and has stabilized at around 60 percent since1991. While there was no forecast provided at appraisal for international container traffic, thishas increased at an average annual growth rate of 13 percent to reach 1,080,000 twenty-footequivalent units (TEUs) in 1995, of which South Harbor handled around 30 percent.

For this analysis, Manila Port includes North Harbor, South Harbor, and MICT but excludes subports(Pasig Bank, private and municipal ports of Limay, Marivelles, Romblon, and Subic). During the last 10years, about 40 percent of the total cargo traffic and 5 percent of the total passenger traffic of Manila PortDistrict Office area have been handled through these subports.

10

39. The number of international ship calls increased from 2,232 in 1987 to 3,864 in1995. The average international ship size increased from about 8,400 gross registered tons(GRT) in 1987 to about 10,300 GRT in 1995, an increase of 23 percent over the period. Theaverage international cargo volume handled per ship also increased by 22 percent, fromaround 3,100 tons per ship call in 1987 to about 3,800 tons per ship call in 1995.

2. Domestic Traffic

40. Domestic cargo traffic through Manila Port is handled mainly at North Harbor.1At appraisal, domestic cargo was forecast to increase from 7.7 million tons in 1987 to 10.4million tons in 1995, equivalent to a 3.9 percent average annual growth rate. The domesticcargo traffic actually increased at an average of 6.8 percent per annum to reach 14.2 milliontons in 1995, 37 percent higher than forecast at appraisal.

41. At appraisal, domestic container traffic was projected to increase from 265,000TEUs in 1987 to 427,000 TEUs in 1995, equivalent to a 6.1 percent average annual growthrate. The domestic container traffic actually increased at an average growth rate of 9.7percent per annum to reach 611,000 TEUs in 1995, 43 percent more than expected atappraisal.

42. The number of domestic ship calls increased from 5,099 in 1987 to 6,538 in1995. The average ship size nearly doubled from 1,900 gross registered tons (GRT) in 1987to 3,600 GRT in 1995. However, the average domestic cargo volume handled per shipincreased by only 32 percent, from around 1,600 tons per ship call in 1987 to about 2,200 tonsper ship call in 1995. This shows a trend towards using bigger ships calling at severaldomestic ports rather than small ships making return trips between two ports.

3. Revised Traffic Forecast (1996-2015)

43. In 1996, traffic grew at about 16 percent over 1995 traffic at South Harbor (9percent for container traffic and 23 percent for noncontainerized cargo traffic). At NorthHarbor, traffic grew by about 8 percent (7 percent for containerized and 11 percent fornoncontainerized cargo). Revised traffic forecasts are based on the following assumptions:

(i) International Traffic. A 9 percent annual growth has been assumed forboth container and non containerized cargo traffic until 2000, after which thegrowth rate should progressively decrease to 5 percent, which is close to theaverage long-term international maritime traffic growth expected in the ASEANregion. Taking into account productivity improvements due to the Project and toadditional equipment investment made by the private sector, the capacity ofpiers 5, 9, and 15, which were the only ones rehabilitated under the Project, hasbeen estimated at about 5.3 million tons; this is expected to be reached in 1998.The traffic increase attributable to the Project has been limited to this level in theeconomic and financial analyses.

Over the past decade, about 1 percent of the total domestic cargo traffic of Manila Port has been handledat South Harbor and MICT.

11

(ii) Domestic Traffic. An 8 percent growth rate has been assumed fordomestic traffic (7 percent for container traffic and 11 percent for non-containerized cargo traffic). The capacity of piers 2-18, which were rehabilitatedunder the Project, has been estimated at about 24.8 million tons; this isexpected to be reached in 2003. Traffic handled at North Harbor has beenlimited to this level for the economic and financial analyses.

44. At appraisal, the average economic asset life of the Project was estimated at 20years from the start-up year, planned to be 1993. The project period considered for evaluationwas therefore 1988-2012. The same average economic asset life has been retained for theProject reevaluation. The Project was fully operational in January 1996, so the Project periodconsidered for reevaluation, including the implementation period, is 1988-2015.

45. The Project reevaluation is based on the total traffic at North Harbor, but only onthe traffic handled at piers 5, 9, and 15 of South Harbor, because piers 3 and 13 were deletedfrom the Project scope. It is assumed that no traffic has been directly generated by the Projectimprovements or put off by the increase in charges. The Project has allowed traffic growth totake place only in Manila, within the limits of its incremental capacity. The revised trafficforecasts are provided in Appendix 9, along with the traffic forecast at appraisal.

B. Financial Performance of PPA

46. PPA, in general, and both North and South Harbors at Manila Port, in particular,have experienced significant increases in revenues over the last several years that are wellabove the appraisal estimates. This is attributable to higher than expected traffic growth andtariff increases. The overall operating expenses of PPA have increased almost in proportion tothe revenue increases, primarily due to substantial increases in personnel costs and otheradministrative expenses. The increase in operating expenses at South Harbor has been lowerthan the overall rate of PPA, and the operating expenses at North Harbor have evendecreased (for details, see Appendix 10).

47. The overall financial performance has been better than that anticipated atappraisal. While PPA's operating ratios have not improved significantly, the profits and cashgeneration have been quite substantial. The operations of North and South Harbors andMICT have been very profitable and continue to subsidize the operations of several smallerports. Analysis of the financial statements indicates that the increased liquidity and soundfinancial position of PPA should enable it to meet all its financial obligations including debt-service requirements. Starting in 1994, PPA has been required to pay half of its net income ofthe previous year as a dividend to the Government. This will restrict PPA's cash build-up,which could severely affect its expansion plans and ability to finance such investments frominternally generated funds. PPA is requesting a reconsideration of the payment of dividends tothe Government. Comparative financial performance indicators are presented in Appendix 10.

48. While the financial reporting of PPA seems adequate at the aggregate level,costing by pier or Project component, or by cost center, is not available. This is aconsequence of the delay in implementing the computerized MIS system and the differentoperations not being linked to the main office by local area networks.

12

49. Based on the financial performance indicators, PPA has complied with thefinancial covenants agreed upon at appraisal. Operating ratios were maintained below thecovenanted maximum of 65 percent, while self-financing ratios (computed in accordance withthe appraisal method) were substantially higher than the minimum 30 percent required.

50. Asset revaluation was last carried out in June 1991 and led to a substantialupward valuation in land and other assets of PPA from 1992. As a result of asset revaluation,PPA was required to pay real estate taxes of P80 million in 1993, increasing to P155 million in1994 and 1995. No revaluation was undertaken in 1996 pending the outcome of PPA'sappeal against payment of real estate taxes and in anticipation that further upward adjustmentin asset values may lead to an additional real estate tax burden.

51. In 1992, the Government established CPA, which includes Cebu Port and someother minor ports in Cebu Island. Existing assets and related liabilities of the Port ManagementOffice at Cebu were transferred to CPA and separated from PPA in January 1996. Thetransfer of assets worth P4.5 billion was equivalent to about 18 percent of PPA's total assets in1995.

52. The creation of CPA may be viewed as a positive step in promoting regionaldevelopment in the province of Cebu and is expected to improve integration and coordinationof planning, development, and operation of ports within its territorial jurisdiction. Cebu Port'sshare of the country's cargo volume is about 10 percent against its asset share of 18 percent.The port has a distinct nature of being a domestic distribution center, domestic cargorepresenting about 90 percent of the total cargo volume (compared with less than 60 percentfor PPA). This indicates that the revenue contribution of the port to PPA would be much lessthan its asset share. Since this trend is likely to continue in the future, the financial implicationof the separation is not serious for PPA. The present deficit of CPA will continue until CPAincreases its tariffs for domestic cargo and attracts more international cargo.

C. Financial Reevaluation of the Project

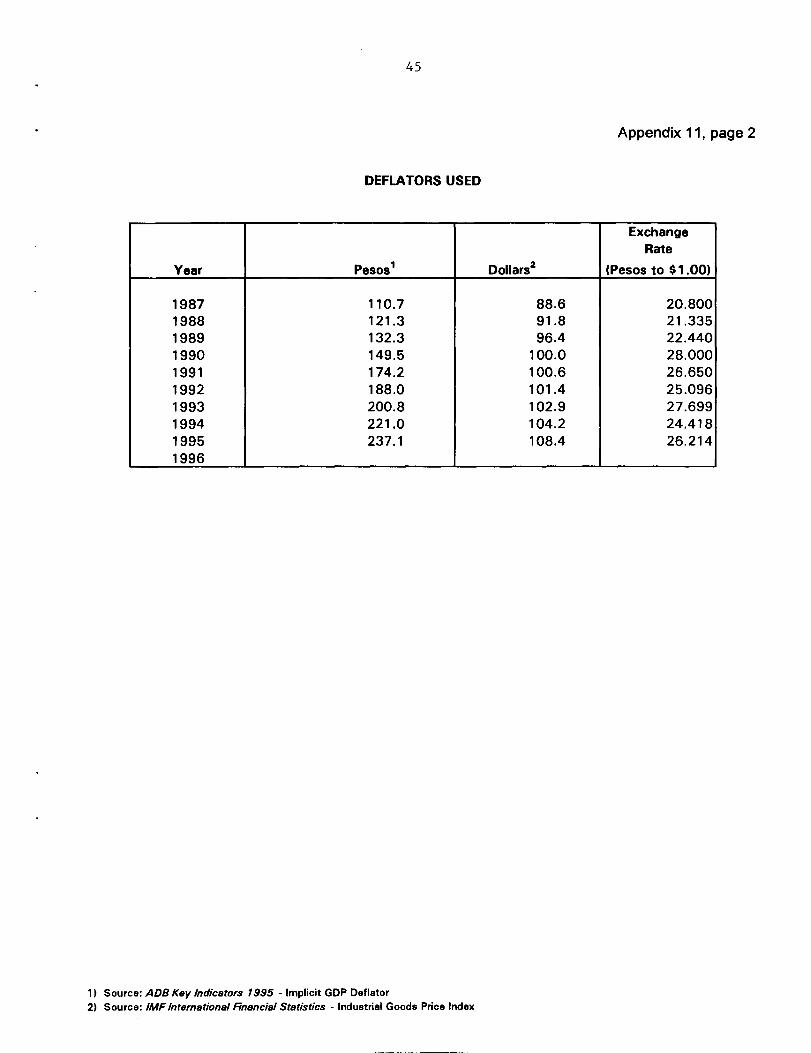

53. The methodology of "with" and "without" the Project comparison used atappraisal has also been followed in recalculating the financial internal rate of return (FIRR).The underlying assumptions at appraisal have been verified and updated using the actualperformance of Manila Port (for details see Appendix 11).

(i) Without the Project. The vessel and cargo handling capacity ofboth North and South Harbors at the piers would gradually decline because offrequent repair and maintenance work. This would lead to a decline in revenue,while operation and maintenance (O&M) costs would continue to escalate. Witha reduced capacity, port users would incur higher costs arising from doublehandling of cargo associated with servicing vessels at anchorage.

ii) With the Project. The construction of three deepwater berths atNorth Harbor and the capacity of the facilities would be maintained or expandedbecause of conversion of pier 5, South Harbor, into a container terminal. While

13

there would be additional O&M costs estimated at 1.5 percent of the capitalcost, these would be significantly lower than the O&M costs in the "without" theProject case.

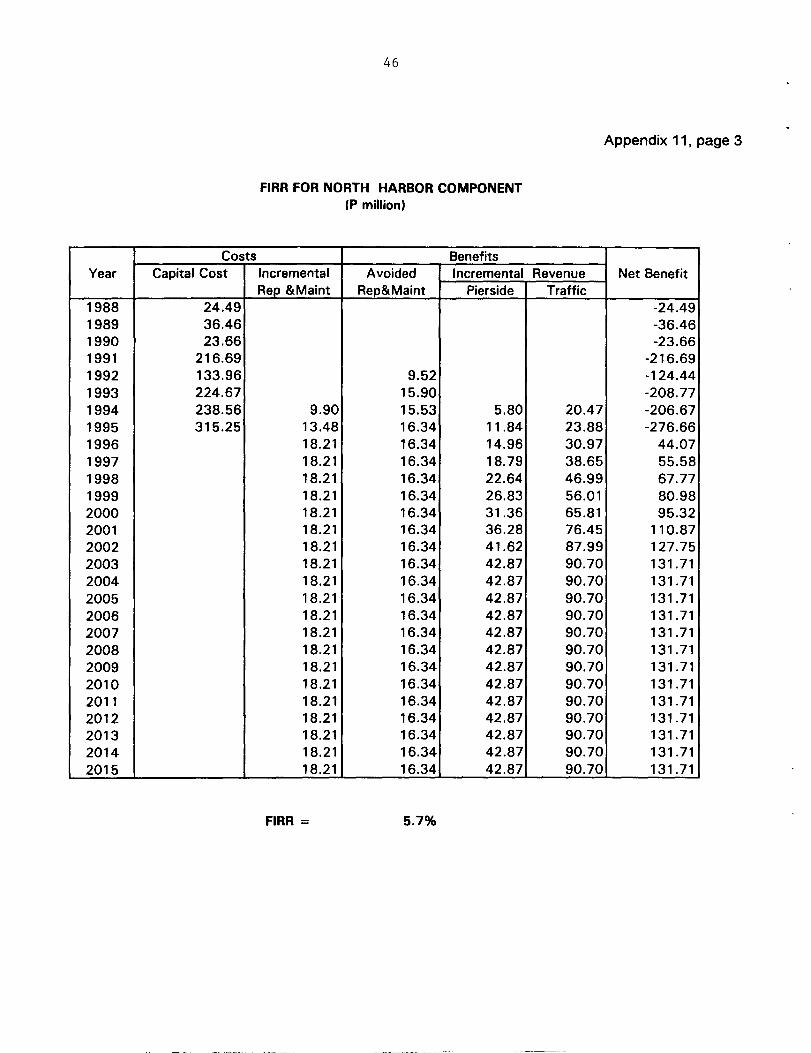

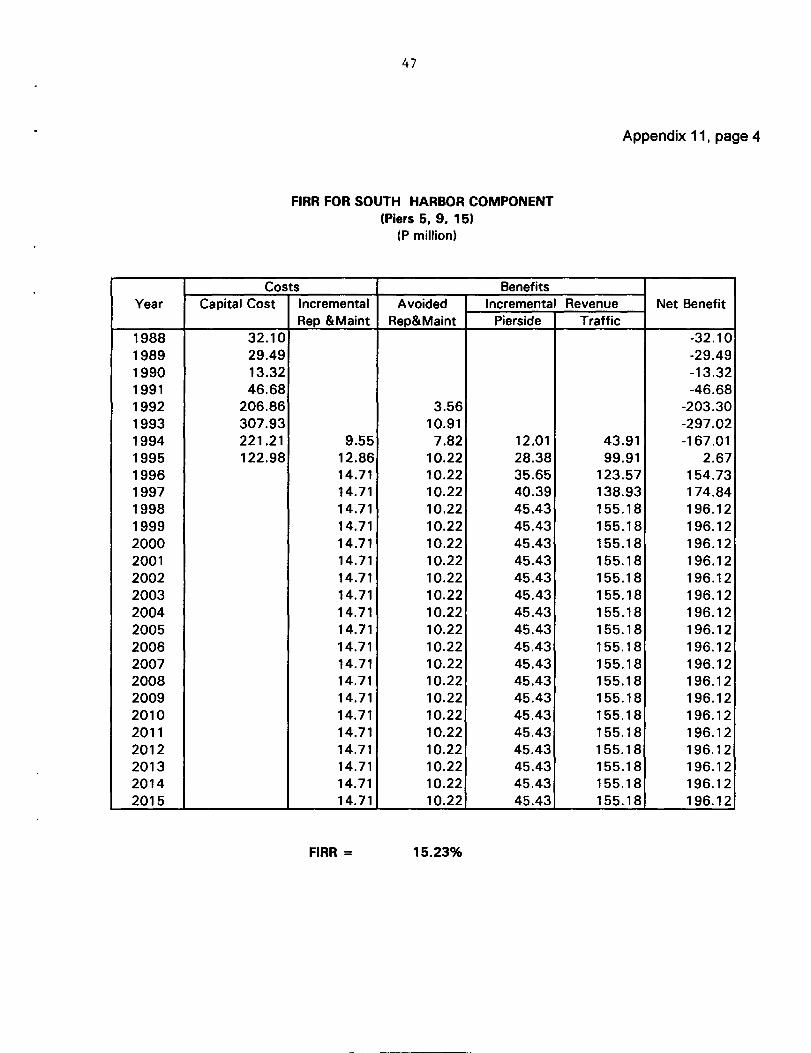

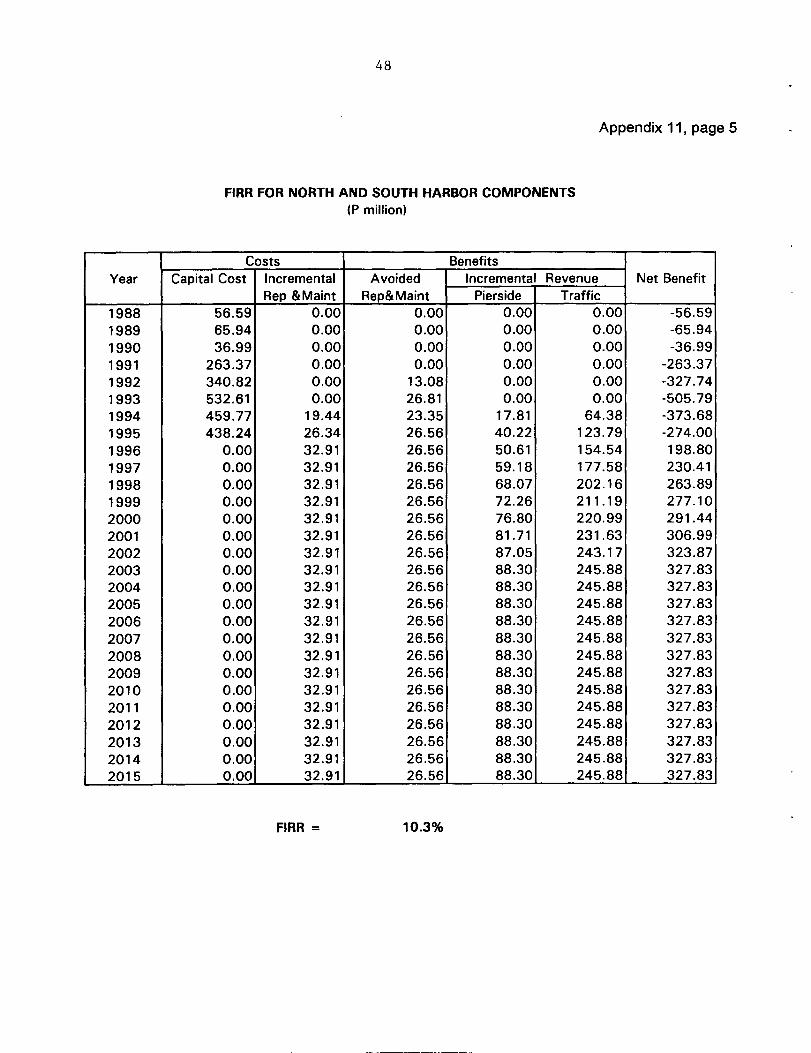

54. Incremental benefits and costs for South Harbor have been adjusted to reflectonly revenues and costs attributable to the Project piers (5, 9, and 15). Based on theseassumptions, the FIRRs recalculated separately for North and South Harbors and for theProject as whole are 5.7 percent, 15.2 percent, and 10.3 percent, respectively compared withthe appraisal estimates of 9.2 percent, 11.9 percent, and 10.4 percent, respectively.

D. Economic Reevaluation of the Project

55. The Project has been reevaluated on the basis of a "with" and "without" theProject comparison, using slightly different assumptions from those used at appraisal

(i) Without the Project. The uneven working surface of the piers and thevery poor condition of existing equipment would lead to worsening cargohandling operations and increasing ship turnaround times. Facilities at Northand South Harbors would continue to deteriorate, resulting in higher O&Mcosts. The limited container stacking capacity at North Harbor would require off-pier handling (at anchorage) at higher cost after the pier capacity is reached.

(ii) With the Project. The rehabilitated piers will allow better operatingconditions and will attract investment in new and replacement equipment byprivate operators, thus improving cargo handling productivity and reducing shipturnaround times. O&M costs at the rehabilitated structure will be reduced.Additional container yard area and better container handling efficiency willreduce the requirement for off-pier handling. Capacity will be reached in 1998at South Harbor and in 2003 at North Harbor, avoiding additional costs forexcess cargo, which would have been handled at anchorage from 1995 withoutthe Project. Although a reduction in the share of South Harbor cargo handled atanchorage could be expected with the Project before the piers reach capacity, ithas not been quantified as a benefit. The reduction in equipment O&M costsand the extension of the economic life of the equipment, which could beexpected from the improvement of pier working surfaces, has also not beenquantified as a benefit.

56. The economic costs and benefits in the "with" and "without" the Project caseshave been reevaluated for the Project as a whole, and for the North and South Harborcomponents separately. The economic internal rates of return (EIRRs) are estimated at 26.7percent for the whole Project, 29.2 percent for North Harbor, and 23.3 percent for SouthHarbor (see Appendix 12). These rates are higher than those estimated at appraisal (15.7percent, 15.4 percent, and 16.2 percent, respectively), due mainly to higher traffic growth thanexpected at appraisal.

14

E. Attainment of Benefits

57. Although the whole Project was completed only at the end of 1995, parts of itwere completed and put into operation before this date. South Harbor rehabilitation wascompleted by mid-1994, and rehabilitation of piers 2-16 at North Harbor was graduallycompleted from mid-1992 to the end of 1994. Private operators signed operation concessioncontracts in 1991 and immediately started to provide new cargo handling equipment. Based ondiscussions with the Manila Port District Office and Port Management Offices at South andNorth Harbors, and on analysis of port data and operational indicators, it is clear that some ofthe expected benefits were attained before the Project was fully completed:

(i) Before Project implementation, the average ship turnaround timewas about 124 hours at South Harbor and 78 hours at North Harbor. In 1995,the average turnaround time had been reduced to about 102 hours at SouthHarbor and 60 hours at North Harbor, an improvement of 22 and 18 hours,respectively, per ship call. The average waiting time stayed reasonably low at 4hours per call at South Harbor and less than 1 hour per call at North Harbor.

(ii) The consolidated profit and loss statements of Manila Port DistrictOffice in 1991 and 1995, that is, immediately before and after Projectimplementation, show a reduction of P23 million in repair and maintenanceexpenses for South and North Harbors combined.

(iii) The cargo volume handled at South Harbor (Piers 5, 9, and 15)was about 1.1 million tons in 1988, which increased to 3.8 million tons in 1995.Similarly, the cargo volume handled at North Harbor increased from 9.6 milliontons to 14.1 million tons over the same period. Sharp increases in cargovolumes were recorded in 1994, when the major Project facilities were put inoperation. This reflects the resumed economic growth of the country, which,without the restored and expanded port capacity under the Project, would havebeen diverted elsewhere.

IV. CONCLUSIONS AND RECOMMENDATIONS

A. Conclusions

58. After various changes in scope, the Project was completed successfully. BothNorth and South Harbors have been rehabilitated, which helped accommodate the rapidincrease of cargo volume starting in 1994. Without the Project, there would have been acontinuing series of wharf collapses, which would have hindered port operations, causing abottleneck of cargo movement.

59. Despite the rapid increase of cargo volume, traffic flows in and around the porthave been improved, particularly at North Harbor, because of construction of collector roads

15

within the port area, together with the proper introduction of traffic regulations. This has alsocontributed to improved port operations.

60. The changes in Project scope are considered appropriate. During Projectprocessing, there were stilt unknown factors and uncertainties, and, accordingly, possibilitiesfor changes in scope were envisaged, and allowed for in the loan documents. Because of thisflexibility, there were no significant delays resulting from such changes. While Parts C, D, andE were deleted from the Project scope, they were implemented, or are being implemented,under other schemes including investment by the private sector. The loan savings from thedeletions were utilized to finance the cost increase in the rehabilitation works under Part A andB.

61. Private sector participation in the port substantially increased during theimplementation period. The extension of the operational contract from 3 years to 15 yearsenabled the South Harbor operator to invest more in facilities and equipment, particularly forcontainers, thereby reducing PPA's financial burden. Moreover, this created competition withinthe port for international containers, thus promoting higher efficiency of the port.

62. PPA has proved itself to be a sound and sustainable organization. Thearrangement that made PPA both the Executing Agency and the Borrower worked well. Therewere no problems in the provision of local counterpart funds , which is often observed in otherprojects in the country, and delays in implementation were significantly reduced in comparisonwith the Manila Port Project. The initial operation of the facilities indicates that the benefitsexpected at appraisal have either been attained already or will be attained. The FIRR for theProject is estimated at 10.3 percent and the EIRR at 26.7 percent. The Project is, therefore,considered to be generally successful.

B. Recommendations

1. General

63. Experience with the Project confirms the difficulties associated withrehabilitating existing facilities as opposed to constructing new ones. Rehabilitation of oldstructures is usually associated with the non-availability of as-built drawings; difficulties inaccurately determining the structural condition; and accordingly, difficulties in determining theappropriate methods and scope of rehabilitation. Because of these factors, higher contingencyallowances should be provided for both costs and completion times for such projects ascompared with those for new ones.

2. Project- Related

64. PPA needs to remind the port operators continuously that the facilities havebeen rehabilitated to their original design strength only and cannot accommodate excess cargoweight. PPA also needs to improve enforcement of the load limitation determined by structuralinvestigation and analysis, with proper supervision and monitoring, so as to avoid any furthercollapse of the structures.

16

65. The squatter issue at Manila Port continues to be an obstacle for future portdevelopment and its management and operations, as well as an aesthetic concern to the maingateway of the country's capital city. This is a highly political issue and may need a long timeto resolve. While the scope of possible actions by PPA is limited, PPA, as the owner of theport, should prevent further sprawl of the squatter area.

66. The PPAR may be prepared in 1999 when the Project facilities at South Harborreach their capacity, and the newly constructed container terminal at North Harbor will be in fulloperation.

17

APPENDIXES

Number Title Page Cited On(page, para.)

1

2

3

4

5

6

7

8

9

10

11

12

Major Events in Project Implementation

Changes in Project Components

Appraised and Actual Project Cost

Financing Arrangements

Project Implementation Schedule

Contract Packages

CompJiance with Loan Covenants

Appraised and Actual Disbursements

Comparison of Cargo Traffic (1 987-1995)

Financial Performance of PPA

Financial Reevaluation of the Project

Economic Reevaluation of the Project

18

1,3

22

2, 5

23

3, 10

24

4,12

25

4,14

26

5,16

27

6,20

32

6,23

33

9,36

36

11,46

44

12,53

49

13,56

18

Appendix 1, page 1

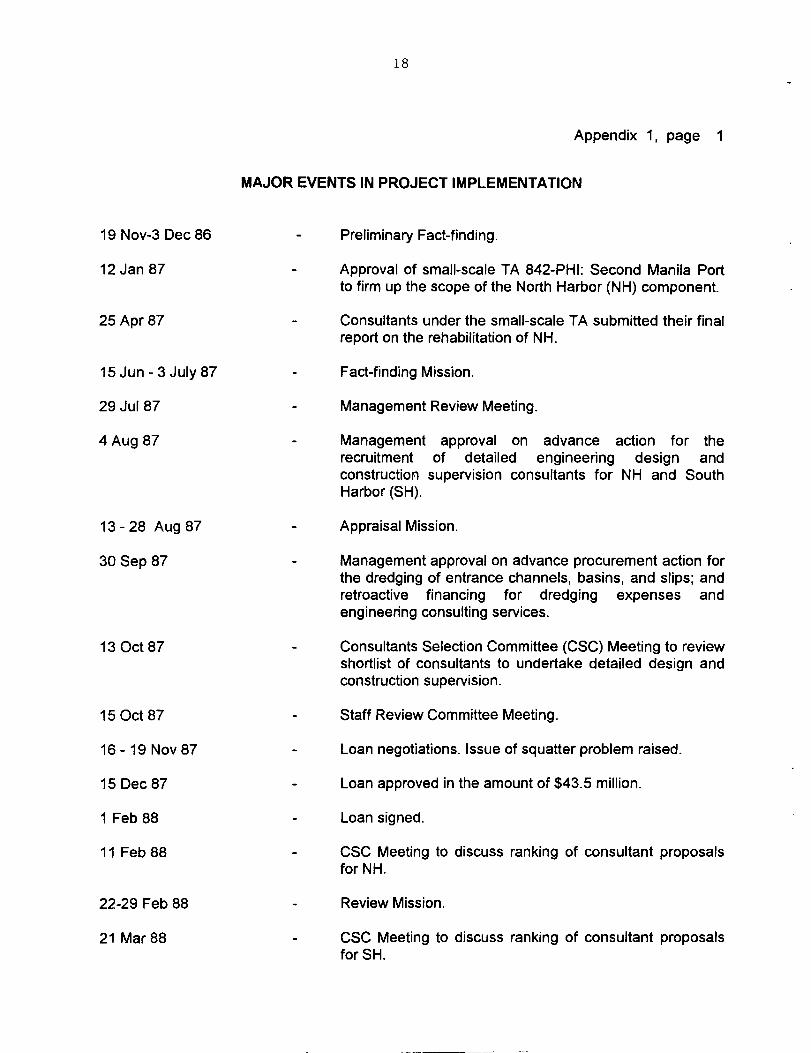

MAJOR EVENTS IN PROJECT IMPLEMENTATION

19 Nov-3 Dec86

12 Jan 87

25Apr87

l5Jun-3July87

29 Jul 87

4 Aug 87

13-28 Aug87

30 Sep 87

13 Oct87

15Oct87

16- 19 Nov87

15 Dec87

1 Feb 88

11 Feb88

22-29 Feb 88

21 Mar88

- Preliminary Fact-finding.

- Approval of small-scale TA 842-PHI: Second Manila Portto firm up the scope of the North Harbor (NH) component.

- Consultants under the small-scale TA submitted their finalreport on the rehabilitation of NH.

- Fact-finding Mission.

- Management Review Meeting.

- Management approval on advance action for therecruitment of detailed engineering design andconstruction supervision consultants for NH and SouthHarbor (SH).

- Appraisal Mission.

- Management approval on advance procurement action forthe dredging of entrance channels, basins, and slips; andretroactive financing for dredging expenses andengineering consulting services.

- Consultants Selection Committee (CSC) Meeting to reviewshortlist of consultants to undertake detailed design andconstruction supervision.

- Staff Review Committee Meeting.

- Loan negotiations. Issue of squatter problem raised.

- Loan approved in the amount of $43.5 million.

- Loan signed.

- CSC Meeting to discuss ranking of consultant proposalsfor NH.

- Review Mission.

- CSC Meeting to discuss ranking of consultant proposalsforSH.

19

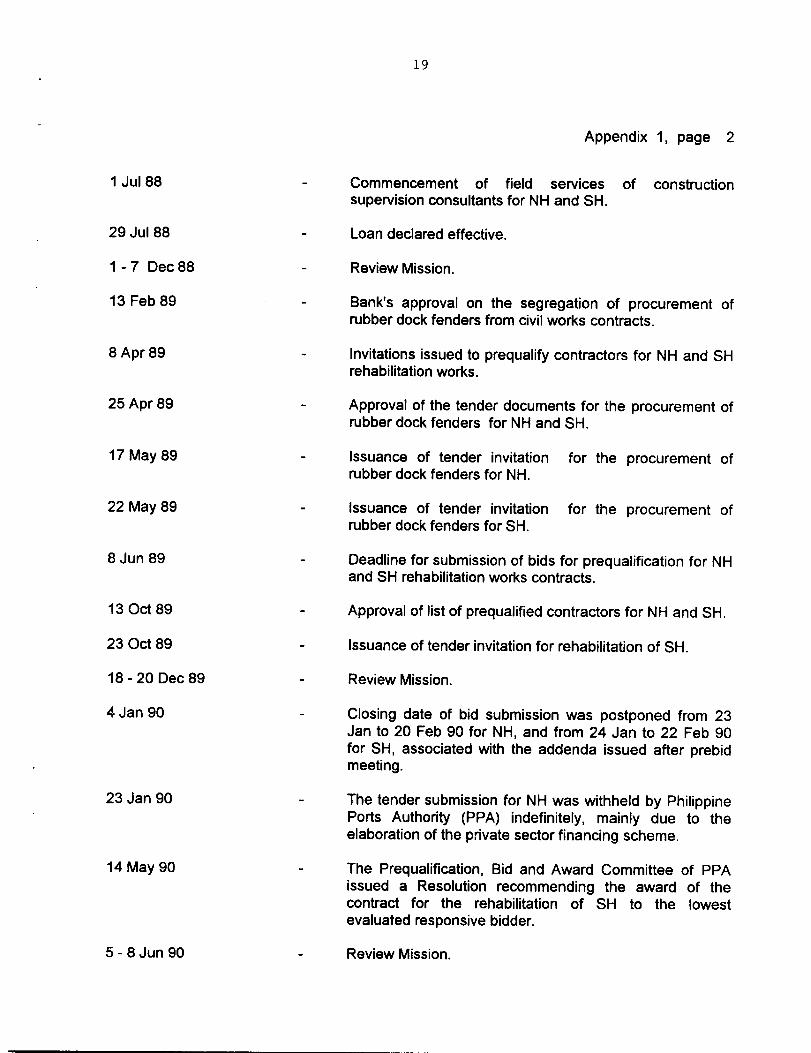

Appendix 1, page 2

1 Jul 88

29 Jul 88

1-7 Dec88

13 Feb 89

8Apr89

25Apr89

17 May89

22 May 89

8 Jun 89

13 Oct89

23 Oct 89

18-20 Dec89

4Jan90

23 Jan 90

14 May 90

5 - 8 Jun 90

- Commencement of field services of constructionsupervision consultants for NH and SH.

- Loan declared effective.

- Review Mission.

- Bank's approval on the segregation of procurement ofrubber dock fenders from civil works contracts.

- Invitations issued to prequalify contractors for NH and SHrehabilitation works.

- Approval of the tender documents for the procurement ofrubber dock fenders for NH and SH.

- Issuance of tender invitation for the procurement ofrubber dock fenders for NH.

- Issuance of tender invitation for the procurement ofrubber dock fenders for SH.

- Deadline for submission of bids for prequalification for NHand SH rehabilitation works contracts.

- Approval of list of prequalified contractors for NH and SH.

- Issuance of tender invitation for rehabilitation of SH.

- Review Mission.

- Closing date of bid submission was postponed from 23Jan to 20 Feb 90 for NH, and from 24 Jan to 22 Feb 90for SH, associated with the addenda issued after prebidmeeting.

- The tender submission for NH was withheld by PhilippinePorts Authority (PPA) indefinitely, mainly due to theelaboration of the private sector financing scheme.

- The Prequalification, Bid and Award Committee of PPAissued a Resolution recommending the award of thecontract for the rehabilitation of SH to the lowestevaluated responsive bidder.

- Review Mission.

20

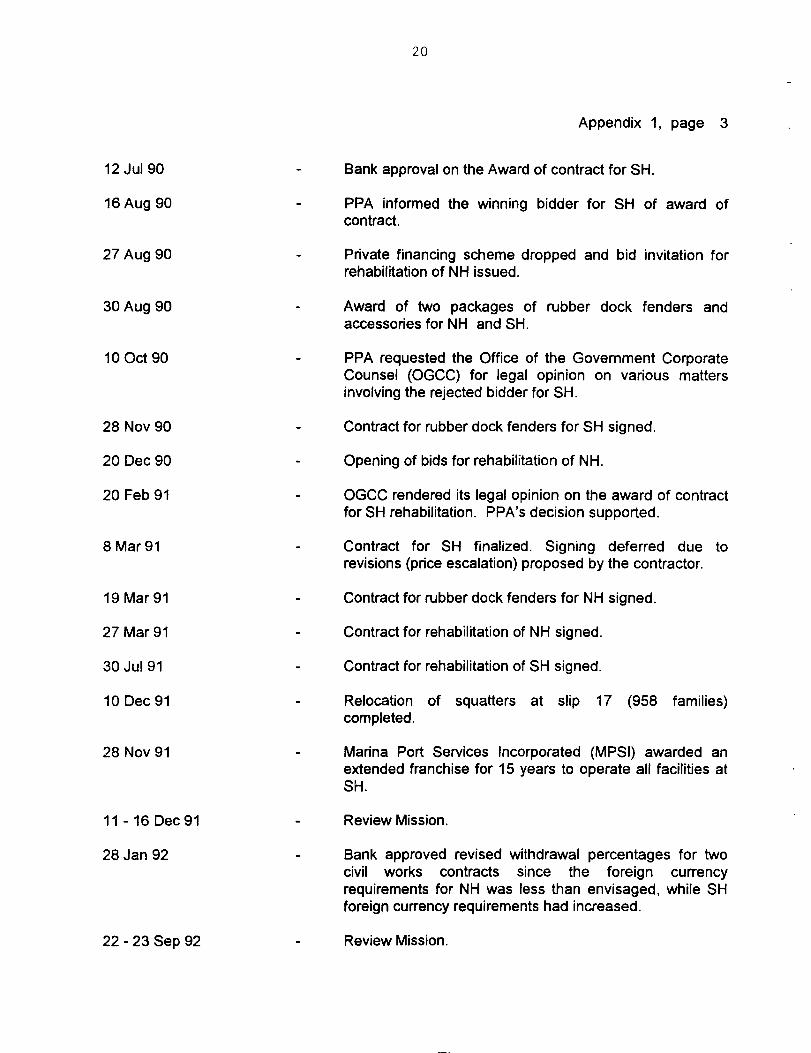

Appendix 1, page 3

12 Jul 90

16 Aug 90

27Aug90

30 Aug 90

10Oct90

28 Nov 90

20 Dec 90

20 Feb 91

8Mar91

19Mar91

27Mar91

30 Jul 91

10 Dec91

28 Nov 91

11- 16Dec91

28 Jan 92

22 - 23 Sep 92

- Bank approval on the Award of contract for SH.

- PPA informed the winning bidder for SH of award ofcontract.

- Private financing scheme dropped and bid invitation forrehabilitation of NH issued.

- Award of two packages of rubber dock fenders andaccessories for NH and SH.

- PPA requested the Office of the Government CorporateCounsel (OGCC) for legal opinion on various mattersinvolving the rejected bidder for SH.

- Contract for rubber dock fenders for SH signed.

- Opening of bids for rehabilitation of NH.

- OGCC rendered its legal opinion on the award of contractfor SH rehabilitation. PPA's decision supported.

- Contract for SH finalized. Signing deferred due torevisions (price escalation) proposed by the contractor.

- Contract for rubber dock fenders for NH signed.

- Contract for rehabilitation of NH signed.

- Contract for rehabilitation of SH signed.

- Relocation of squatters at slip 17 (958 families)completed.

- Marina Port Services Incorporated (MPSI) awarded anextended franchise for 15 years to operate all facilities atSH.

- Review Mission.

- Bank approved revised withdrawal percentages for twocivil works contracts since the foreign currencyrequirements for NH was less than envisaged, while SHforeign currency requirements had increased.

- Review Mission.

21

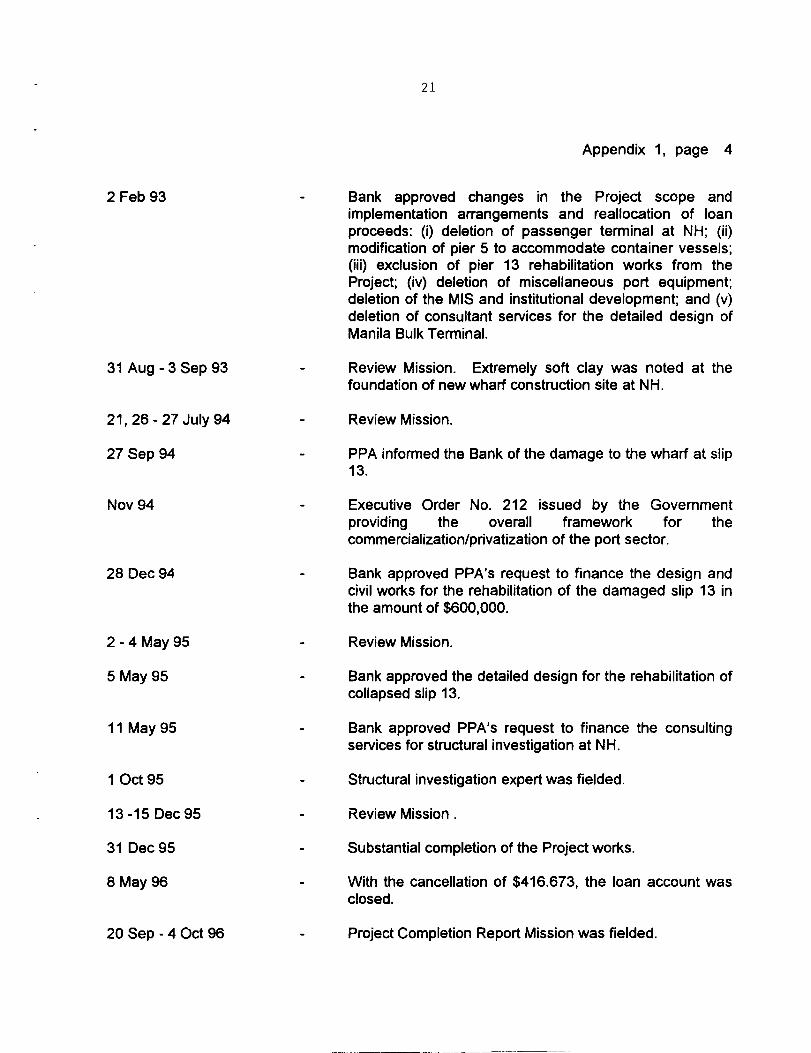

Appendix 1, page 4

2 Feb 93

31 Aug - 3 Sep 93

21,26- 27July94

27 Sep 94

Nov 94

28 Dec 94

2 - 4 May 95

5 May 95

11 May95

1Oct95

13-15 Dec95

31Dec95

8May96

20 Sep - 4 Oct 96

Bank approved changes in the Project scope andimplementation arrangements and reallocation of loanproceeds: (i) deletion of passenger terminal at NH; (ii)modification of pier 5 to accommodate container vessels;(iii) exclusion of pier 13 rehabilitation works from theProject; (iv) deletion of miscellaneous port equipment;deletion of the MIS and institutional development; and (v)deletion of consultant services for the detailed design ofManila Bulk Terminal.

Review Mission. Extremely soft clay was noted at thefoundation of new wharf construction site at NH.

Review Mission.

PPA informed the Bank of the damage to the wharf at slip13.

- Executive Order No. 212 issued by the Governmentproviding the overall framework for thecommercialization/pnvatization of the port sector.

- Bank approved PPA's request to finance the design andcivil works for the rehabilitation of the damaged slip 13 inthe amount of $600,000.

- Review Mission.

- Bank approved the detailed design for the rehabilitation ofcollapsed slip 13.

- Bank approved PPA's request to finance the consultingservices for structural investigation at NH.

- Structural investigation expert was fielded.

- Review Mission.

- Substantial completion of the Project works.

- With the cancellation of $416.673, the loan account wasclosed.

- Project Completion Report Mission was fielded.

22

Appendix 2

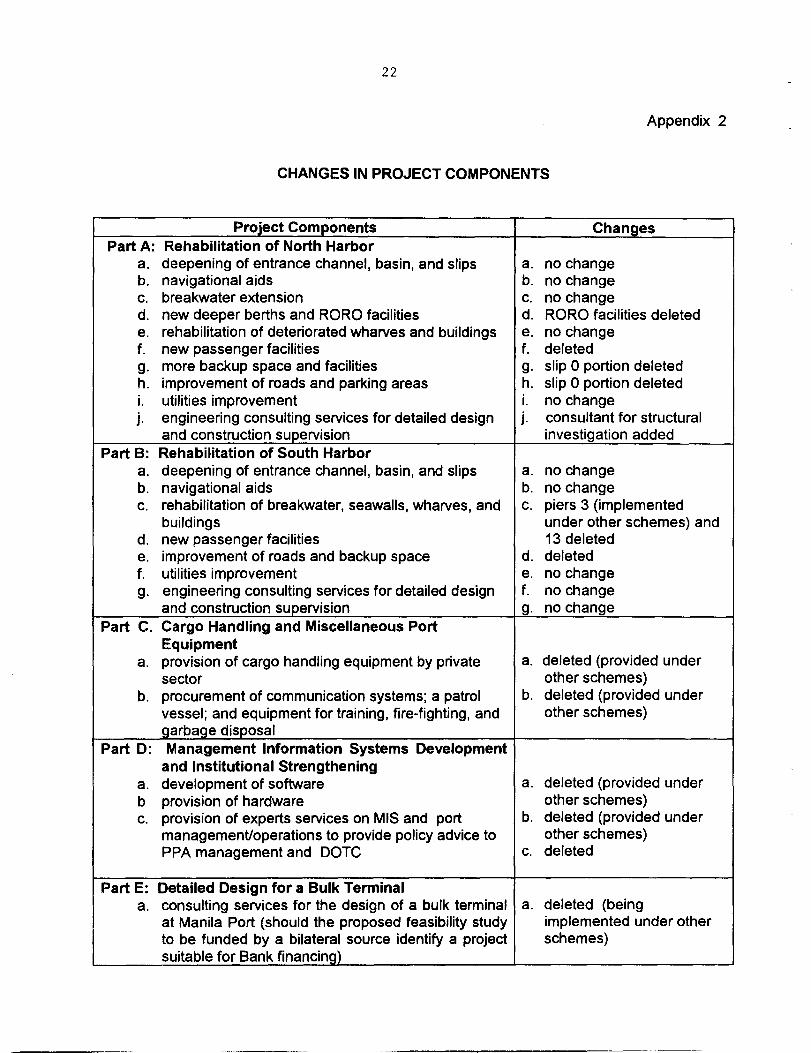

CHANGES IN PROJECT COMPONENTS

Project Components ChangesPart A: Rehabilitation of North Harbor

a. deepening of entrance channel, basin, and slips a. no changeb. navigational aids b. no changec. breakwater extension c. no changed. new deeper berths and RORO facilities d. RORO facilities deletede. rehabilitation of deteriorated wharves and buildings e. no changef. new passenger facilities f. deletedg. more backup space and facilities g. slip 0 portion deletedh. improvement of roads and parking areas h. slip 0 portion deletedi. utilities improvement i. no changej. engineering consulting services for detailed design j . consultant for structural

and construction supervision investigation addedPart B: Rehabilitation of South Harbor

a. deepening of entrance channel, basin, and slips a. no changeb. navigational aids b. no changec. rehabilitation of breakwater, seawalls, wharves, and c. piers 3 (implemented

buildings under other schemes) andd. new passenger facilities 13 deletede. improvement of roads and backup space d. deletedf. utilities improvement e. no changeg. engineering consulting services for detailed design f. no change

and construction supervision g. no changePart C. Cargo Handling and Miscellaneous Port

Equipmenta. provision of cargo handling equipment by private a. deleted (provided under

sector other schemes)b. procurement of communication systems; a patrol b. deleted (provided under

vessel; and equipment for training, fire-fighting, and other schemes)

garbage_disposal ___________________________Part D: Management Information Systems Development

and Institutional Strengtheninga. development of software a. deleted (provided underb provision of hardware other schemes)c. provision of experts services on MIS and port b. deleted (provided under

management/operations to provide policy advice to other schemes)PPA management and DOTC c. deleted

Part E: Detailed Design for a Bulk Terminala. consulting services for the design of a bulk terminal a. deleted (being

at Manila Port (should the proposed feasibility study implemented under otherto be funded by a bilateral source identify a project schemes)suitablefor Bank financing) __________________________-

23

Appendix 3

APPRAISED AND ACTUAL PROJECT COST($ million)

______APPRAISED______ _______ ACTUAL _______Component Foreign Local Total Foreign Local Total

NORTH HARBORCivil Works 13.43 15.08 28.51 10.84 23.25 34.09Rubber Dock Fenders 0.00 0.00 0.00 0.77 0.54 1.31Dredging 1.59 0.40 1.99 1.34 0.41 1.75Consultants 1.50 0.90 2.40 3.23 1.15 4.38

Subtotal 16.52 16.38 32.90 16.18 25.35 41.53

SOUTH HARBORCivil Works 6.79 8.78 15.57 16.44 10.25 26.69Rubber Dock Fenders 0.00 0.00 0.00 1.66 1.26 2.92Dredging 1.00 0.25 1.25 0.85 0.21 1.06Consultants 1.00 0.60 1.60 1.58 1.30 2.88

Subtotal 8.79 9.63 18.42 20.53 13.02 33.55

EQUIPMENTCargo Handling Equip. 6.00 0.60 6.60 0.00 0.00 0.00Miscellaneous Port Equip. 2.00 0.20 2.20 0.00 0.00 0.00

Subtotal 8.00 0.80 8.80 0.00 0.00 0.00

Management InformationSystems, InstitutionalDevelopment, ComputerEquipment, and Software 1.80 0.18 1.98 0.00 0.00 0.00

Detailed Design ofBulklerminal 0.90 0.42 1.32 0.00 0.00 0.00

Contingency 8.02 8.88 16.90 0.00 0.00 0.00a) Physical Contingency 5.80 5.09 10.89b) Price Escalation 3.22 3.79 6.01

Interest and Other Charges 6.37 0.00 6.37 9.71 0.00 9.71DuringConstruction _________ ________ ________ _________

TOTAL 50.40 36.29 86.69 46.42 38.37 84.79

FINANCING ARRANGEMENTS

($ million)

_______________ APPRAISED _______________ ________________ ACTUAL _______________Component ____ BANK ____ PPA PRIVATE SECTOR TOTAL ____ BANK ____ PPA ____ TOTAL

___________________________ Foreign Local Total Foreign Local Total Local Total Local Total Foreign Local Total Foreign Local Total Foreign Local TotalNORTH HARBOR

CMI Works 13.43 0.00 13.43 0.00 15.08 15.08 13.43 15.08 28.51 10.84 0.00 10.84 0.00 23.25 23.25 10.84 23.25 34.09

Rubber Dock Fenders ' 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.77 0.00 0.77 0.00 0.54 0.54 0.77 0.54 1.31Dredging 1.59 0.00 1.59 0.00 0.40 0.40 1.59 0.40 1.99 1.34 0.00 1.34 0.00 0.41 0.41 1.34 0.41 1.75Design & Construction

Supervision 1.50 0.00 1.50 0.00 0.90 0.90 1.50 0.90 2.40 3.19 0.00 3.19 0.00 1.15 1.15 3.19 1.15 4.34Structural Investigation 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.04 0.00 0.04 0.00 0.00 0.00 0.04 0.00 0.04

Subtotal 16.52 0.00 16.52 0.00 16.38 16.38 16.52 16.38 32.90 16.18 0.00 16.18 0.00 25.35 25.35 16.18 25.35 41.53SOUTH HARBOR

Civil Works 6.79 0.00 6.79 0.00 8.78 8.78 6.79 8.78 15.57 16.44 0.00 16.44 0.00 10.25 10.25 16.44 10.25 26.69Rubber Dock Fenders ' 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 1.66 0.00 1.66 0.00 1.26 1.26 1.66 1.26 2.92Dredging 1.00 0.00 1.00 0.00 0.25 0.25 1.00 0.25 1.25 0.85 0.00 0.85 0.00 0.21 0.21 0.85 0.21 1.06Design & Construction

Supervision 1.00 0.00 1.00 0.00 0.60 0.60 1.00 0.60 1.60 1.58 0.00 1.58 0.00 1.30 1.30 1.58 1.30 2.88Subtotal 8.79 0.00 8.79 0.00 9.63 9.63 8.79 9.63 18.42 20.53 0.00 20.53 0.00 13.02 13.02 20.53 13.02 33.55

EQUIPMENT b

Cargo Handling Equipment 0.00 0.00 0.00 0.00 0.00 0.00 6.00 0.60 6.60 6.00 0.60 6.60Misc. Port Equipment 2.00 0.00 2.00 0.00 0.20 0.20 0.00 0.00 0.00 2.00 0.20 2.20 _____ _____ _____

Subtotal 2.00 0.00 2.00 0.00 0.20 0.20 6.00 0.60 6.60 8.00 0.80 8.80 _____ _____ _____

MIS and lnstl. Development b 1.80 0.00 1.80 0.00 0.18 0.18 1.80 0.18 1.98

Bulk Terminal b 0.90 0.00 0.90 0.00 0.42 0.42 0.90 0.42 1.32UNALLOCATED 7.12 0.00 7.12 0.00 8.78 8.78 0.90 0.10 1.00 8.02 8.88 16.90 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00bC 6.37 0.00 6.37 0.00 0.00 0.00 6.37 0.00 6.37 6.37 0.00 6.37 3.34 0.00 3.34 9.71 0.00 9.71

Total 43.50 0.00 43.50 0.00 35.59 35.59 6.90 0.70 7.60 50.40 36.29 86.69 43.08 0.00 43.08 3.34 38.37 41.71 46.42 38.37 84.79

Originally envisaged to be included in the scope of civil works contracts.

Deleted from Project scope

-N

26

Appendix 6

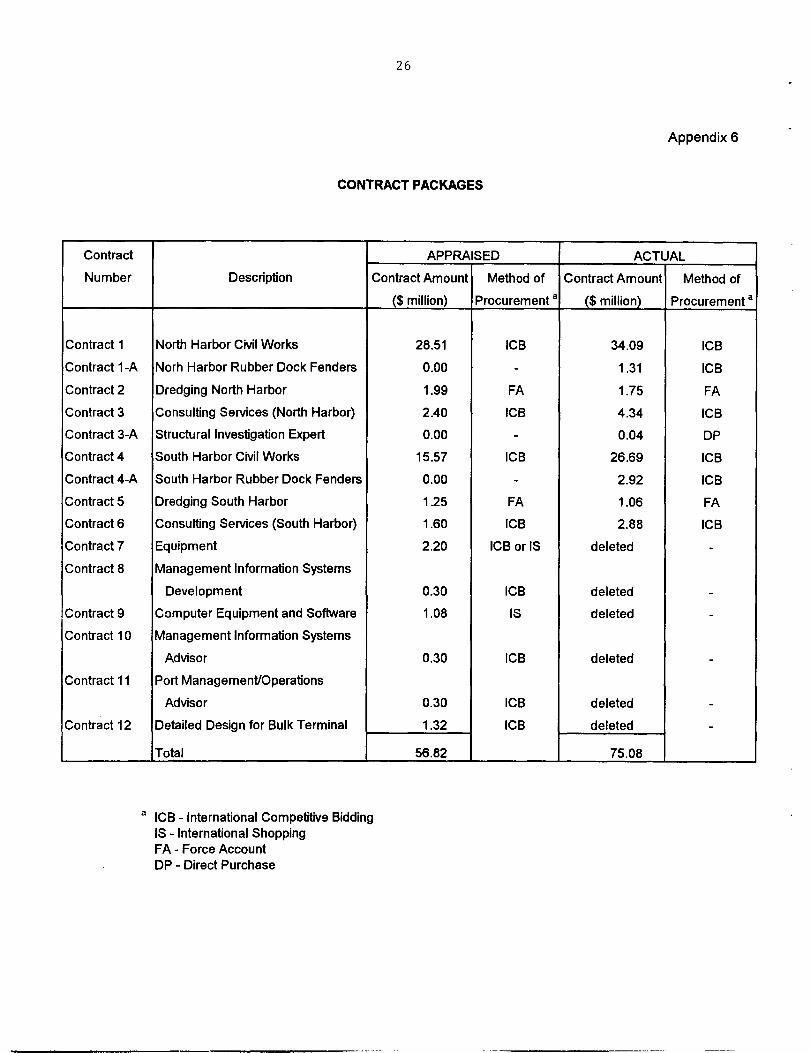

CONTRACT PACKAGES

Contract APPRAISED ACTUAL

Number Description Contract Amount Method of Contract Amount Method of

_____________ ________________________________ ($ million) Procurement amillion) Procurement a

Contract 1 North Harbor Civil Works 28.51 ICB 34.09 ICB

Contract 1-A Norh Harbor Rubber Dock Fenders 0.00 - 1.31 ICB

Contract 2 Dredging North Harbor 1.99 FA 1.75 FA

Contract 3 Consulting Services (North Harbor) 2.40 1GB 4.34 ICB

Contract 3-A Structural Investigation Expert 0.00 - 0.04 DP

Contract 4 South Harbor CMI Works 15.57 ICB 26.69 ICB

Contract 4-A South Harbor Rubber Dock Fenders 0.00 - 2.92 ICB

Contract 5 Dredging South Harbor 1 .25 FA 1.06 FA

Contract 6 Consulting Services (South Harbor) 1.60 ICB 2.88 ICB

Contract 7 Equipment 2.20 ICB or IS deleted -

Contract 8 Management Information Systems

Development 0.30 ICB deleted -

Contract 9 Computer Equipment and Software 1.08 IS deleted -

Contract 10 Management Information Systems

Advisor 0.30 ICB deleted -

Contract 11 Port Management/Operations

Advisor 0.30 ICB deleted -

Contract 12 Detailed Design for Bulk Terminal 1.32 1GB deleted -

____________ Total 56.82 ___________ 75.08 ____________

a ICB - International Competitive BiddingIS - International ShoppingFA - Force AccountDP - Direct Purchase

Reference to

Status ofLoan Agreement

Compliance

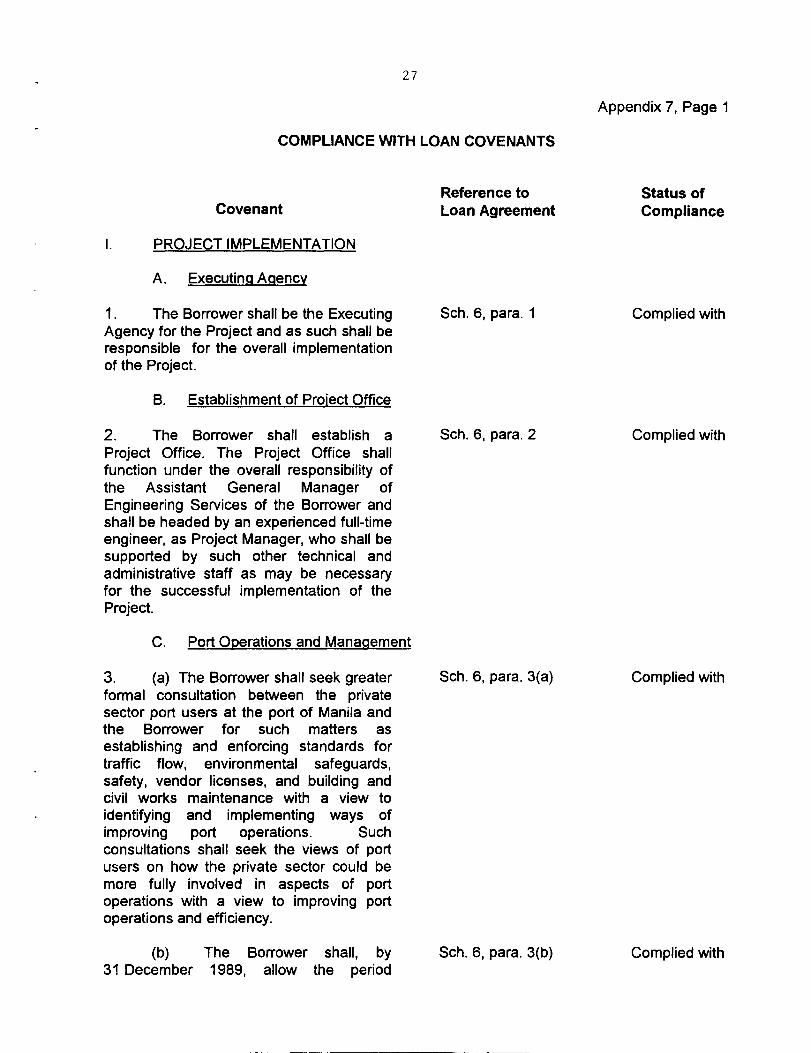

Sch. 6, para. 1

Complied with

Sch. 6, para. 2

Complied with

Sch. 6, para. 3(a)

Complied with

27

Appendix 7, Page 1

COMPLIANCE WITH LOAN COVENANTS

Covenant

PROJECT IMPLEMENTATION

A. Executing Agency

1. The Borrower shall be the ExecutingAgency for the Project and as such shall beresponsible for the overall implementationof the Project.

B. Establishment of Prolect Office

2. The Borrower shall establish aProject Office. The Project Office shallfunction under the overall responsibility ofthe Assistant General Manager ofEngineering Services of the Borrower andshall be headed by an experienced full-timeengineer, as Project Manager, who shall besupported by such other technical andadministrative staff as may be necessaryfor the successful implementation of theProject.

C. Port Operations and Management

3. (a) The Borrower shall seek greaterformal consultation between the privatesector port users at the port of Manila andthe Borrower for such matters asestablishing and enforcing standards fortraffic flow, environmental safeguards,safety, vendor licenses, and building andcivil works maintenance with a view toidentifying and implementing ways ofimproving port operations. Suchconsultations shall seek the views of portusers on how the private sector could bemore fully involved in aspects of portoperations with a view to improving portoperations and efficiency.

(b) The Borrower shall, by Sch. 6, para. 3(b) Complied with31 December 1989, allow the period

A. General

4. Except as the Bank and the Section 4.10Borrower shall otherwise agree, theBorrower shall not sell or otherwise disposeof any of its assets, except in the ordinarycourse of its business.

B. Revaluation of Fixed Assets

28

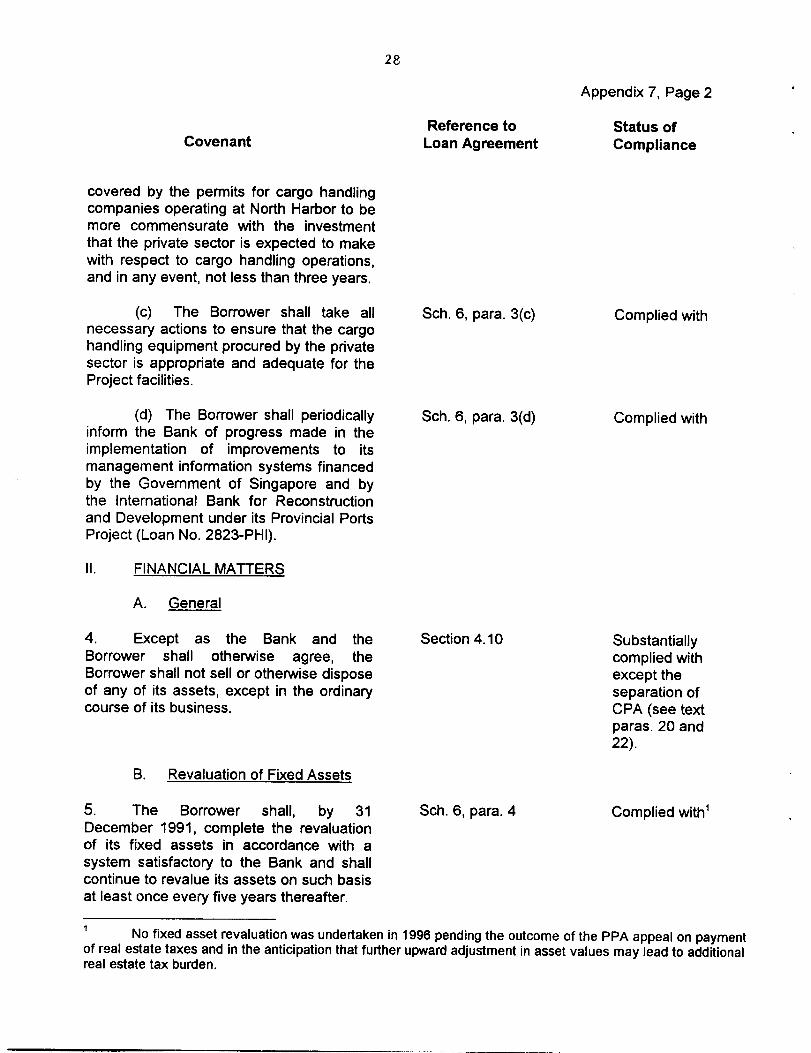

Appendix 7, Page 2

Reference to

Status ofCovenant

Loan Agreement

Compliance

covered by the permits for cargo handlingcompanies operating at North Harbor to bemore commensurate with the investmentthat the private sector is expected to makewith respect to cargo handling operations,and in any event, not less than three years.

(c) The Borrower shall take all Sch. 6, para. 3(c)necessary actions to ensure that the cargohandling equipment procured by the privatesector is appropriate and adequate for theProject facilities.

Complied with

(d) The Borrower shall periodicallyinform the Bank of progress made in theimplementation of improvements to itsmanagement information systems financedby the Government of Singapore and bythe International Bank for Reconstructionand Development under its Provincial PortsProject (Loan No. 2823-PHI).

II. FINANCIAL MATTERS

5. The Borrower shall, by 31December 1991, complete the revaluationof its fixed assets in accordance with asystem satisfactory to the Bank and shallcontinue to revalue its assets on such basisat least once every five years thereafter.

Sch. 6, para. 3(d) Complied with

Substantiallycomplied withexcept theseparation ofCPA (see textparas. 20 and22).

Sch. 6, para. 4 Complied with1

No fixed asset revaluation was undertaken in 1996 pending the outcome of the PPA appeal on paymentof real estate taxes and in the anticipation that further upward adjustment in asset values may lead to additionalreal estate tax burden.

9. The Borrower shall commence, or Sch. 6, para. 8(b)cause to be commenced, within 12 monthsof the Effective Date, a study to carry outan in-depth review of the Borrower'srevenue structure.

F. Financial Statements

29

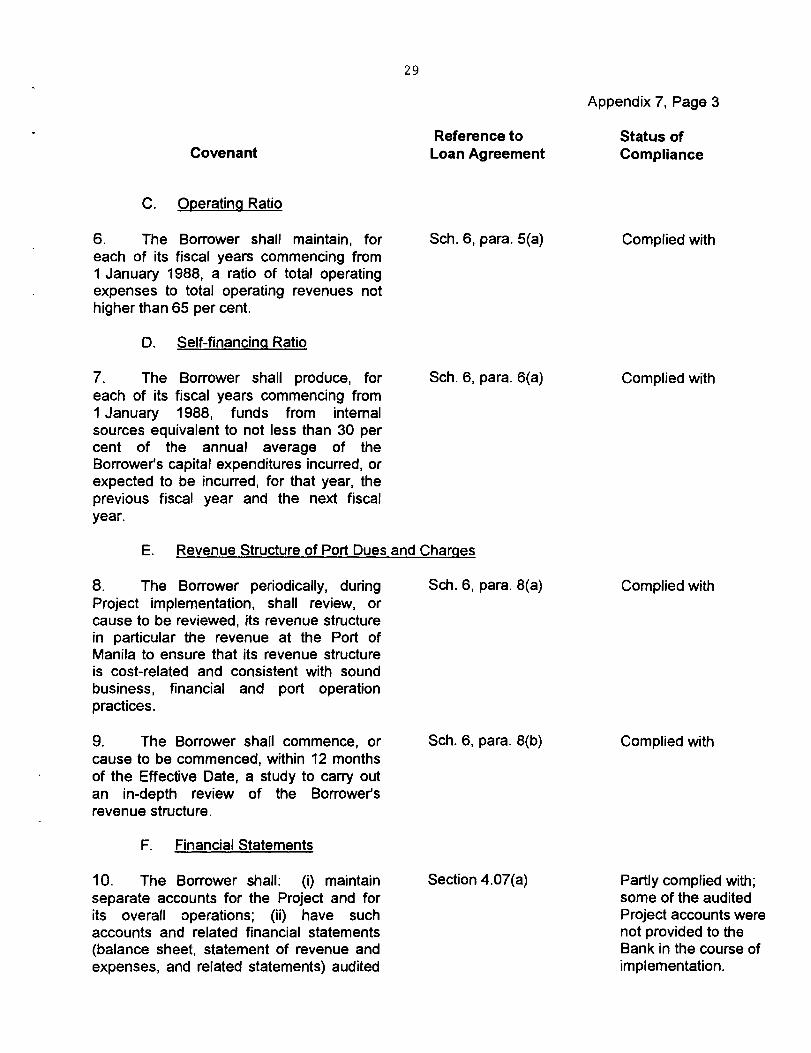

Appendix 7, Page 3

Reference to

Status ofCovenant

Loan Agreement

Compliance

C. Operating Ratio

6. The Borrower shall maintain, for Sch. 6, para. 5(a)each of its fiscal years commencing from1 January 1988, a ratio of total operatingexpenses to total operating revenues nothigher than 65 per cent.

0. Self-financing Ratio

Complied with

7. The Borrower shall produce, foreach of its fiscal years commencing from1 January 1988, funds from internalsources equivalent to not less than 30 percent of the annual average of theBorrower's capital expenditures incurred, orexpected to be incurred, for that year, theprevious fiscal year and the next fiscalyear.

Sch. 6, para. 6(a) Complied with

E. Revenue Structure of Port Dues and Charges

Sch. 6, para. 8(a)

Section 4.07(a)

8. The Borrower periodically, duringProject implementation, shall review, orcause to be reviewed, its revenue structurein particular the revenue at the Port ofManila to ensure that its revenue structureis cost-related and consistent with soundbusiness, financial and port operationpractices.

10. The Borrower shall: (i) maintainseparate accounts for the Project and forits overall operations; (ii) have suchaccounts and related financial statements(balance sheet, statement of revenue andexpenses, and related statements) audited

Complied with

Complied with

Partly complied with;some of the auditedProject accounts werenot provided to theBank in the course ofimplementation.