Embed Size (px)

Citation preview

Corporate Update

FC Research Analyst: Michelle Weerasinghe

SRI LANKA

NESTLÉ LANKA PLC HOLD

NEST.N0000 Mar 2016

Affordability stirs up demand

P/E 31 December 2013 2014 2015 2016E 2017E FY18E

Revenue (LKR mn) 30,913 32,903 35,855 40,337 46,185 53,344

Net Profit (LKR mn) 3,317 3,787 4,124 5,274 6,161 7,680

EPS (LKR) 61.7 70.5 76.8 98.2 114.7 140.3

YoY % Growth 13% 14% 9% 28% 17% 22%

Valuations

PER (x) 32.4 28.4 26.7 20.9 17.9 14.6

PBV (x) 25.5 26.3 24.4 24.1 23.8 23.8

Div Yield (%) 3.0% 3.4% 3.1% 4.7% 5.5% 6.8%

NAVPS 78.5 76.1 84.2 85.1 86.3 86.1

DPS (LKR) 60.0 68.5 64.5 97.2 113.5 138.9

Div Payout 97% 97% 84% 99% 99% 99%

Current Price: LKR 2,000.0 Fair Value: LKR 2,100.0

222150.5

Nestlé Lanka PLC is expected to keep up its growth momentum to achieve an

earnings CAGR of c.23% 2015-2018E. NEST’s margins which expanded due to

the decline in global commodity prices and energy prices is likely to be

maintained amidst the increase in affordability levels of middle income earners

driving NEST’s volumes. Further, an attractive return is expected from exports’

revenue contribution due to the rupee depreciation. NEST’s expensive multiples

sustained by strong growth leads to a fair value of LKR 2,100.0. HOLD

Revenue forecast at 14%: FC Research expects revenue to grow by c.49% in

2015-2018E growing at CAGR of c.14% throughout the period. Prices of Nestlé’s

products fall into the affordability level of Sri Lanka’s growing middle income

earning segment’s rising income (2014 GNI per capita - USD 3,460) leading it to

reach out to a wider group of consumers. Nestlé’s rapidly growing export

contribution (revenue contribution grew to 13% in 2014 from 11% in 2010)

dominated by exports is expected to support revenue further, strengthened by

the rupee depreciation.

GP margin maintained at 42%: FC Research expects to maintain the GP margin

target to reach c.42% by 2016E due to the advantage of lower cost of production.

The slump in global oil prices (WTI -4.26% YTD) and the slowdown in Chinese

economy have further led global commodity prices collapse making a

considerable impact on Nestlé’s raw materials such as wheat (-25% Jan-Nov

2015) and sugar (-2% YTD). Further, a growth in NEST’s volumes due to

economies of scale and price increase in products is further expected amid

increased affordability of consumers.

NEST overall return of 10% for 1 year period: NEST’s strong earnings growth

results in a CAGR of c.23% 2015-2018E. Our target price stands at LKR 2,100.0

providing a return of 10% including a dividend yield of 5%. [LKR 2,067.0 DCF

based, LKR 2,160.0 PER based, 2,021.0 DDM based]

Figure 1: NEST Price Volume Graph

Disclosure on Shareholding:

First Capital Equities (Pvt) Ltd and any of its

affiliates do not hold shares in NEST and will not

trade in this share for the seven trading days

following the issue of this document.

Source: CSE

KEY DATA

Share Price (LKR)

Average Daily Volume (Shares)

Average Daily Turnover (LKR)

53.7

Price Performance (%) 1 mth 3 mths 12mths

NEST 0% -9% -13%

ASPI -5% -12% -15%

90.82%

0.81%

0.64%

0.44%

0.37%

9.18%Estimated Free Float

Major Shareholders as at 31st Dec 2015

Nestle S A

HSBC International Nominees Ltd-SSBT

HSBC International Nominees Ltd-SSL

RBC Investor Services Bank

Ms Neesha Harnam

2,000.00

52w High/Low (LKR) 2,322.00 / 1,984.20

1,699

3,571,329

Issued Share Capital (Shares mn)

Market Capitalisation (LKR mn) 107,451

FC Research

2

“Affordability stirs up demand”

1.0 Introduction

“Local Multinational”: Nestle Lanka PLC is engaged in manufacturing,

marketing, selling and distribution of food and beverage products. It’ local

portfolio of products carry some of the renowned brands in the country

including Nestomalt, Milo, Milkmaid, Nespray and Maggi with 90% of its

products being manufactured at its production facility in Kurunegala.

Share Price Performance: NEST’s price had been ranging between LKR 2,320-

2,023 during the last 12 month period. Currently it trades at LKR 2,023, a -

12.8% decline in price since March 2015. With an estimated free float of

9.18% NEST has been recognized as an illiquid counter holding 4.17% of the

total market capitalization.

2.0 Revenue to grow at 14% CAGR 2015-18E

2.1 Growth in purchasing power & per capita GNI

GNI to grow at 13%: With the budgetary proposal on increasing the salary of

government sector employees by LKR 10,000 in March 2015 together with

implementation of several other proposals including reduction of energy

prices as well as commodity prices leading to improved purchasing power,

we expect Sri Lanka’s per capita GNI (Gross National Income) to grow at an

annual average of c.13% during 2015-2017E. GNI has grown at 12% CAGR in

2009-2014 and 13% CAGR in 2005-2009 displaying a healthy growth. Sri

Lanka’s GNI per capita in 2014 stands at USD 3,460, well above average South

Asia’s per capita GNI (USD 1,496) and that of lower middle income countries

(USD 2,012).

Figure 2: ASPI vs NEST

Source: FC Research

Figure 3: GNI per capita shows a steady growth compared to South Asian

Region and Lower Middle Income Countries

Source: The World Bank and FC Research Estimates

FC Research

3

“Affordability stirs up demand”

Source: Annual Reports

2.2 Exports continue growth at 15% annually

Exports to strengthen revenue: NEST, the world’s largest exporter of coconut

milk powder is expected to continue to grow its revenue by 15% annually

being in line with its historical trend of 15% CAGR 2010-14. NEST’s exports of

coconut milk powder accounts for a notable 13% of its 2014 revenue, LKR

4.3bn, a shift from 11% in 2010 revenue. Maggi Coconut Milk Powder is solely

developed in Sri Lanka and is now exported to nearly 60 countries across the

world. Despite volatility in coconut prices, Sri Lanka’s coconut milk powder

exports have grown both in value and volumes.

2.3 Negative publicity relating to Maggi noodles controversy

Marketing expense growth to moderate: Marketing expenses grew by

19.3%YoY in 2015 compared to 16.7%YoY in 2014. Going forward it is

expected that these expenses would moderate at c.19% through 2016E-

2017E and c.18% in 2018E.

Increase in marketing expenses in the past: For the past 8 quarters

marketing expenses had been increasing noticeably. For 4Q2015 and 3Q2015

marketing expenses had increased by 37%YoY for each quarter while

marketing to revenue ratio had rocketed to 25% in 4Q2015 from 15% in

1Q2015 due to Maggi noodles controversy in India. In 2015 marketing

expenses had increased by 26%YoY compared to 20% in 2014 and 19% in

2013. The increase in marketing expenses and promotional activities carried

out to gain market consolidation are expected to boost NEST’s revenue from

9% in 2015 to c.13% in 2016E.

Sink in Maggi noodles sales: In June 2015 Nestle India destroyed more than

USD50m worth of Maggi noodles, following a ban imposed by India's food

safety regulator. The regulator stated that tests have found the instant

noodles "unsafe and hazardous" and has accused Nestle of failing to comply

Figure 6: Marketing, Selling and Distribution

Expenses over past 8 quarters

Source: Quarterly Financial Reports

Figure 5: Export Revenue (Maggi Coconut Milk Powder)

2,000

2,500

3,000

3,500

4,000

4,500

LKR

(m

n)

CAGR 15% 2010-14

Figure 4: NEST Revenue Classification

87%

13%

Local Revenue Exports

Source: Annual Report

FC Research

4

“Affordability stirs up demand”

with food safety laws since it found higher-than-allowed levels of lead in

some packets. The negative publicity relating to India’s Maggi Noodles

controversy deemed to have hampered the revenue growth during 2015

compelling NEST to boost their Marketing, Sales and Distribution expenses

affecting the bottom line.

3.0 GP margin maintained at 42%

Margin to be maintained at 42%: NEST recorded a GP Margin of 42% in

4Q2015. We expect NEST’s margins to be maintained at the same level

(c.42%) by 2016E through 2018E from 40% in 2015 with growing economies

of scales and possible increases in prices due to affordability level of

consumers.

3.1 Exploiting the declining trend in commodity prices

Declining Food Index unlikely to rise: Food and Agriculture Organization of

the UN (FAO) Global Food Price Index fell 29% by end of January 2016

continuing the decline since April 2014. UN FAO the four year slump in world

food prices is unlikely to recover in the near future provided continuity in high

production and low energy costs in the industry.

Figure 8: UN FAO’s Global Food Index

Figure 7: GP margins

GP Margins are

expected to be

maintained at

c.42% 2016E-

2018E

Source: Annual Reports and FC Research estimates

Source: FAO

FC Research

5

“Affordability stirs up demand”

Figure 9: Global Wheat Prices

Figure 9: Global Raw Sugar Prices

Source: OECD

Source: FAO

Figure 10: Global Raw Sugar Prices

Source: OECD

Figure 11: Local Retail Fresh Milk Prices

Source: Dept. of Animal Production and Health

FC Research

6

“Affordability stirs up demand”

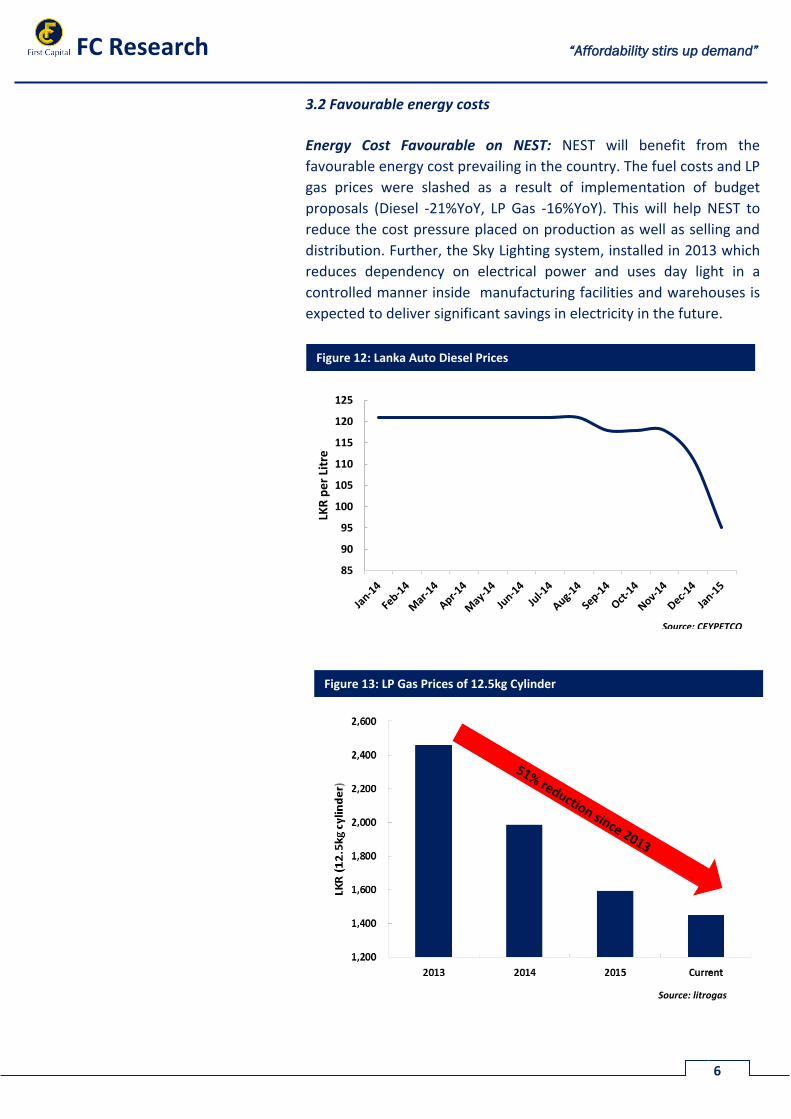

3.2 Favourable energy costs

Energy Cost Favourable on NEST: NEST will benefit from the

favourable energy cost prevailing in the country. The fuel costs and LP

gas prices were slashed as a result of implementation of budget

proposals (Diesel -21%YoY, LP Gas -16%YoY). This will help NEST to

reduce the cost pressure placed on production as well as selling and

distribution. Further, the Sky Lighting system, installed in 2013 which

reduces dependency on electrical power and uses day light in a

controlled manner inside manufacturing facilities and warehouses is

expected to deliver significant savings in electricity in the future.

85

90

95

100

105

110

115

120

125

LKR

pe

r Li

tre

Figure 12: Lanka Auto Diesel Prices

Figure 13: LP Gas Prices of 12.5kg Cylinder

Source: litrogas

Source: CEYPETCO

FC Research

7

“Affordability stirs up demand”

5.0 Expensive multiples but high growth

Expensive multiples sustained by high growth: NEST’s revenue is

expected to grow 2015E-18E CAGR of c.14% given the expected

increase in demand for NEST’s products while cost savings are to be

achieved by favourable energy costs and commodity prices. Hence FC

Research target price for NEST stands at LKR 2,100.0 The target price

of LKR 2,100.0 is based on the average price of LKR 2,067.0 via DCF

valuations, LKR 2,160.0 via PER based valuations and LKR 2,021.0 via

DDM based valuations.

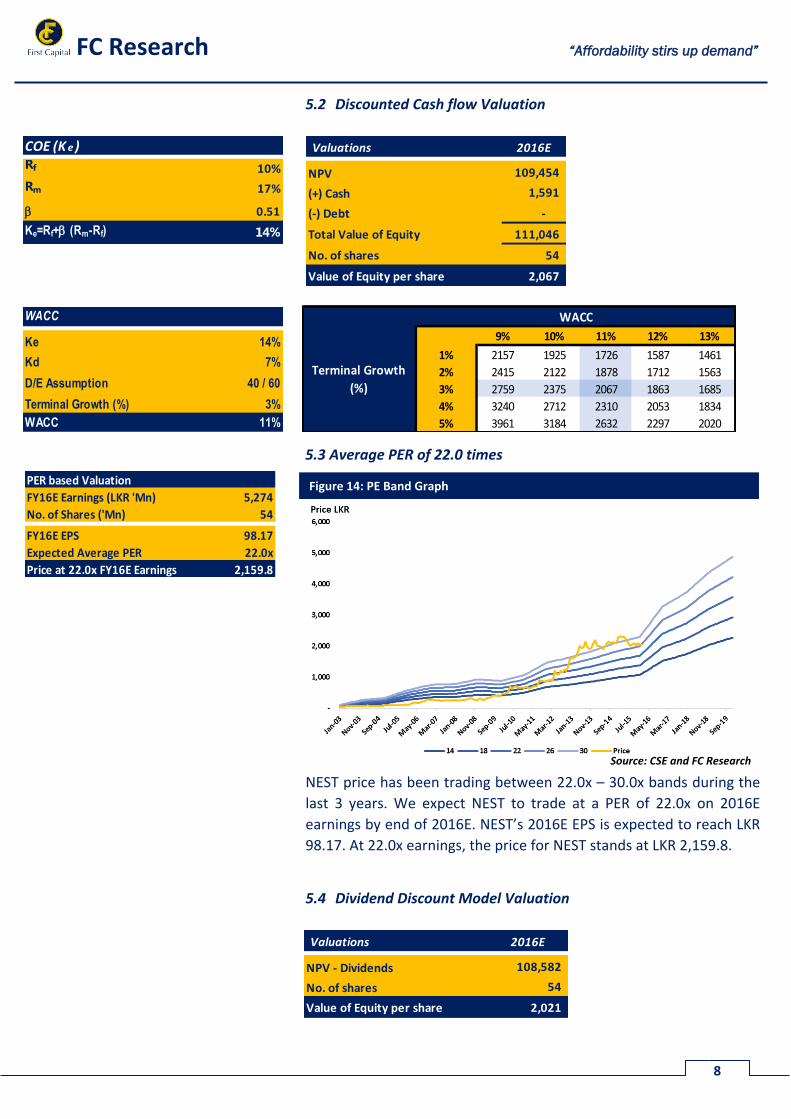

5.1 Fair Value of LKR 2,100.0

We have obtained the target price of LKR 2,100.0 by rounding off the

value calculated by applying the DCF, DDM and PER techniques.

Expected NEST price for FY16E

DCF Valuation based target price 2,066.9

PER based target price 2,159.8

DDM based target price 2,021.0

Average Target Price 2,082.6

Return

Target Price 2,100.0

Current Price 2,000.0

Capital Gain (LKR) 100.0

Dividend FY16E (LKR) 97.2

Capital Gain % 5%

Dividend Yield % 5%

Total Return % 10%

P/E 31 December 2013 2014 2015 2016E 2017E FY18E

Revenue (LKR mn) 30,913 32,903 35,855 40,337 46,185 53,344

Net Profit (LKR mn) 3,317 3,787 4,124 5,274 6,161 7,680

EPS (LKR) 61.7 70.5 76.8 98.2 114.7 140.3

YoY % Growth 13% 14% 9% 28% 17% 22%

Valuations

PER (x) 32.4 28.4 26.7 20.9 17.9 14.6

PBV (x) 25.5 26.3 24.4 24.1 23.8 23.8

Div Yield (%) 3.0% 3.4% 3.1% 4.7% 5.5% 6.8%

NAVPS 78.5 76.1 84.2 85.1 86.3 86.1

DPS (LKR) 60.0 68.5 64.5 97.2 113.5 138.9

Div Payout 97% 97% 84% 99% 99% 99%

FC Research

8

“Affordability stirs up demand”

5.2 Discounted Cash flow Valuation

5.3 Average PER of 22.0 times

NEST price has been trading between 22.0x – 30.0x bands during the

last 3 years. We expect NEST to trade at a PER of 22.0x on 2016E

earnings by end of 2016E. NEST’s 2016E EPS is expected to reach LKR

98.17. At 22.0x earnings, the price for NEST stands at LKR 2,159.8.

5.4 Dividend Discount Model Valuation

Figure 14: PE Band Graph

Source: CSE and FC Research

Ke 14%

Kd 7%

D/E Assumption 40 / 60

Terminal Growth (%) 3%

WACC 11%

WACC

2067 9% 10% 11% 12% 13%

1% 2157 1925 1726 1587 1461

2% 2415 2122 1878 1712 1563

3% 2759 2375 2067 1863 1685

4% 3240 2712 2310 2053 1834

5% 3961 3184 2632 2297 2020

WACC

Terminal Growth

(%)

PER based Valuation

FY16E Earnings (LKR 'Mn) 5,274

No. of Shares ('Mn) 54

FY16E EPS 98.17

Expected Average PER 22.0x

Price at 22.0x FY16E Earnings 2,159.8

Valuations 2016E

NPV - Dividends 108,582

No. of shares 54

Value of Equity per share 2,021

Valuations 2016E

NPV 109,454

(+) Cash 1,591

(-) Debt -

Total Value of Equity 111,046

No. of shares 54

Value of Equity per share 2,067

COE (K e )Rf 10%

Rm 17%

0.51

Ke=Rf+ (Rm-Rf) 14%

FC Research

9

“Affordability stirs up demand”

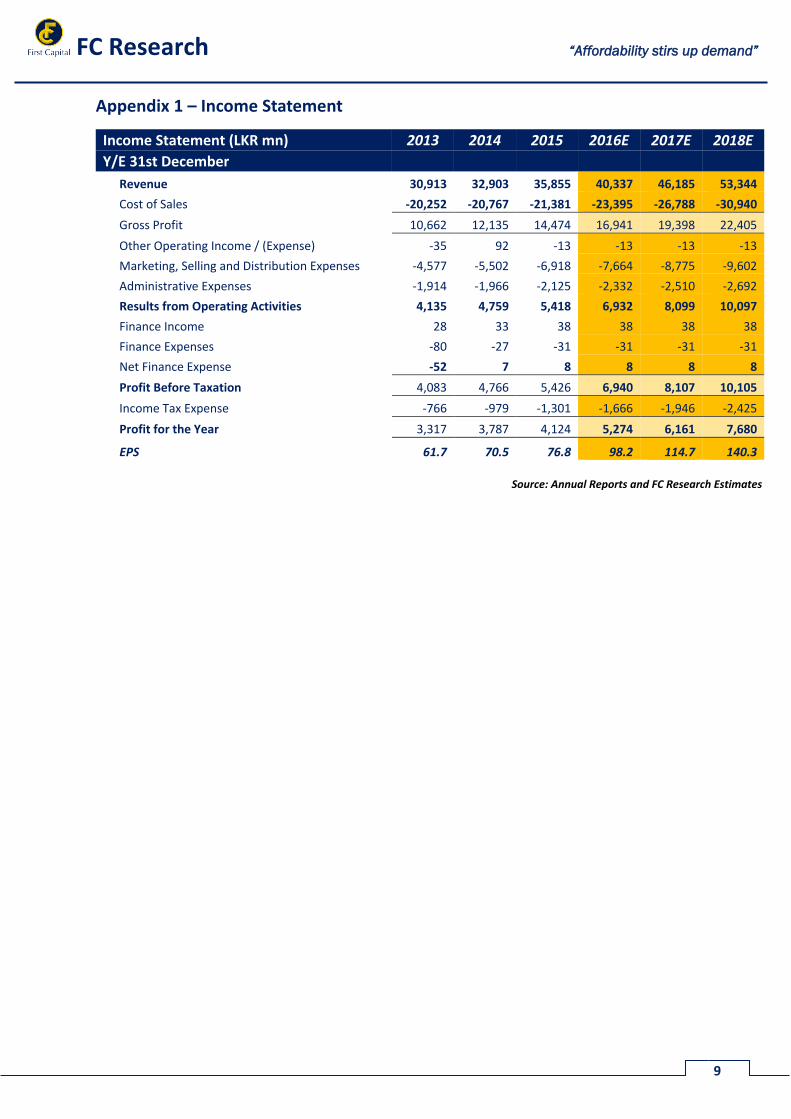

Appendix 1 – Income Statement

Income Statement (LKR mn) 2013 2014 2015 2016E 2017E 2018E

Y/E 31st December

Revenue 30,913 32,903 35,855 40,337 46,185 53,344

Cost of Sales -20,252 -20,767 -21,381 -23,395 -26,788 -30,940

Gross Profit 10,662 12,135 14,474 16,941 19,398 22,405

Other Operating Income / (Expense) -35 92 -13 -13 -13 -13

Marketing, Selling and Distribution Expenses -4,577 -5,502 -6,918 -7,664 -8,775 -9,602

Administrative Expenses -1,914 -1,966 -2,125 -2,332 -2,510 -2,692

Results from Operating Activities 4,135 4,759 5,418 6,932 8,099 10,097

Finance Income 28 33 38 38 38 38

Finance Expenses -80 -27 -31 -31 -31 -31

Net Finance Expense -52 7 8 8 8 8

Profit Before Taxation 4,083 4,766 5,426 6,940 8,107 10,105

Income Tax Expense -766 -979 -1,301 -1,666 -1,946 -2,425

Profit for the Year 3,317 3,787 4,124 5,274 6,161 7,680

EPS 61.7 70.5 76.8 98.2 114.7 140.3

Source: Annual Reports and FC Research Estimates

FC Research

10

“Affordability stirs up demand”

Appendix 2 – Balance Sheet

Balance Sheet (LKR mn) 2013 2014 2015 2016E 2017E 2018E

As at 31st December

ASSETS

Non-Currrent Assets

Property, Plant and Equipment 4,572 5,209 5,477 5,570 5,551 5,435

Capital Work-in-Progress 238 206 144 144 144 144

4,810 5,415 5,621 5,713 5,695 5,579

Current Assets

Inventories 2,604 2,953 3,322 2,420 2,771 3,201

Trade and Other Receivables 2,101 1,816 2,107 2,420 2,771 3,201

Amounts Due from Related Parties 228 305 204 204 204 204

Cash and Cash Equivalents 788 283 868 1,591 1,197 1,448

5,720 5,356 6,501 6,636 6,943 8,053

Total Assets 10,530 10,771 12,122 12,349 12,638 13,632

EQUITY AND LIABILITIES

Equity

Stated Capital 537 537 537 537 537 537

Retained Earnings 3,678 3,551 3,984 4,037 4,099 4,176

4,216 4,088 4,522 4,574 4,636 4,713

Non-Current Liabilities

Retirement Benefit Obligations 469 515 522 522 522 522

Deferred Tax Liabilities 460 641 699 699 699 699

929 1,156 1,222 1,222 1,222 1,222

Current Liabilities

Trade and Other Payables 2,975 3,765 4,137 4,211 4,286 4,950

Amounts Due to Related Parties 800 749 714 714 714 714

Income Tax Payable 619 706 942 1,043 1,195 1,448

Dividends Payable 88 103 137 137 137 137

Bank Overdrafts 904 205 448 448 448 448

Total Current Liabilities 5,385 5,527 6,379 6,553 6,781 7,698

Total Liabilities 6,314 6,683 7,600 7,775 8,002 8,919

Total Equity and Liabilities 10,530 10,771 12,122 12,350 12,638 13,632

NAVPS

78.5

76.1

84.2

85.1

86.3

86.1

Source: Annual Reports and FC Research Estimates

FC Research

11

“Affordability stirs up demand”

Appendix 3 – Cash flow Statement

Cash flow Statement (LKR mn) 2013 2014 2015 2016E 2017E 2018E Y/E 31st December Cash Flow from Operating Activities

Profit Before Taxation 4,083 4,766 5,426 6,940 8,107 10,105

Adjustments for;

Depreciation 540 548 603 657 668 666

Amortisation 11 0 0 0 0 0

Impairment of Fixed Assets 5 11 0 0 0 0 (Gain) / Loss on Sale of Property, Plant and Equipment 2 -47 -31 0 0 0

Amortisation of Staff Loan Interest 17 17 18 0 0 0

Interest Expense 80 25 31 31 31 31

Interest Income -28 -33 -29 -38 -38 -38

Provision for Obsolete Inventories 40 -8 0 0 0 0

Inventory Written Off 173 160 120 0 0 0

Provision for Impairment of Trade Receivables 6 11 8 0 0 0

Provision for Retirement Benefit Obligations 100 162 99 0 0 0

Net Fair Value Loss on Derivatives 0 1 0 0 0 0

Operating Profit Before Working Capital Changes 5,030 5,612 6,243 7,590 8,767 10,763

Working Capital Changes

(Increase) / Decrease in Inventories -944 -500 -462 902 -351 -430

(Increase) in Trade and Other Receivables -321 196 -197 -313 -351 -430

Increase / (Decrease) in Trade and Other Payables 801 738 310 74 75 664

Cash Generated From Operations 4,565 6,046 5,894 8,252 8,140 10,568

0 0 0 0 0 0

Interest Paid -80 -25 -31 -31 -31 -31

Income Tax Paid -474 -692 -1,000 -1,565 -1,793 -2,172

Retirement Benefit Obligations Paid -108 -181 -115 0 0 0

Net Cash Flows Generated from Operating Activities 3,903 5,147 4,110 6,657 6,317 8,365

Cash Flow from Investing Activities

Purchase of Property, Plant and Equipment -530 -1,166 -813 -750 -650 -550 Proceeds from Sale of Property, Plant and Equipment 66 49 35 0 0 0

Interest Received 10 16 11 38 38 38

Net Cash Flows Used in Investing Activities -455 -1,101 -767 -712 -612 -512

Cash Flow from Financing Activities

Dividends Paid -2,890 -3,853 -3,001 -5,222 -6,100 -7,603

Net Cash Flows Used in Financing Activities -2,890 -3,853 -3,001 -5,222 -6,100 -7,603

Net Decrease in Cash and Cash Equivalents 559 193 342 724 -395 251

Cash and Cash Equivalents at the Beginning of the Year -675 -116 77 419 1,143 748

Cash and Cash Equivalents at the End of the Year -116 77 419 1,143 748 999

Bank Overdrafts -904 -205 -448 -448 -448 -448

Cash in Hand and Balances with Bank 788 283 868 1,591 1,197 1,448

Source: Annual Reports and FC Research Estimates

347 1/1, Dr. Colvin R. De Silva Mawatha,

Colombo 2

Sales Desk: +94 11 2145 000

Fax: +94 11 2145 050

HEAD OFFICE BRANCHES

347 1/1, Matara Negombo

Dr. Colvin R. De Silva Mawatha, No. 24, 1/3, 2nd Floor, No.72A, 2/1,

Colombo 2 Lakshman Cooray Building, Old Chilaw Road,

Anagarika Dharmapala Mw, Negombo

Sales Desk: +94 11 2145 000 Matara

Fax: +94 11 2145 050 Tel: +94 41 2237 636 Tel: +94 31 2233 299

SALES BRANCHES

CEO Jaliya Wijeratne +94 71 5329 602 Negombo

Priyanka Anuruddha +94 76 6910 035

Colombo Priyantha Wijesiri +94 76 6910 036

Damian Le Grand +94 77 7383 237

Nishantha Mudalige +94 76 6910 041 Matara

Isuru Jayawardana +94 76 7084 953 Sumeda Jayawardana +94 76 6910 038

Anushka Buddhika +94 77 9553 613

Kapila Weerasinghe +94 71 5329 615

Gamini Hettiarachchi +94 76 6910 039

Thushara Abeyratne +94 76 6910 037

RESEARCH

Dimantha Mathew +94 11 2145 016 Amanda Lokugamage +94 11 2145 015

Atchuthan Srirangan +94 11 2145 017 Michelle Weerasinghe +94 11 2145 018

FIRST CAPITAL GROUP

HEAD OFFICE BRANCHES

No. 2, Deal Place, Matara Kurunegala Kandy

Colombo 3 No. 24, 1/3, 2nd Floor, No. 6, 1st Floor, No.213-215,

Tel: +94 11 2576 878 Lakshman Cooray Building, Union Assurance Building, Peradeniya Road,

Anagarika Dharmapala Mawatha, Rajapihilla Mawatha, Kandy

Matara Kurunegala

Tel: +94 41 2222 988 Tel: +94 37 2222 930 Tel: +94 81 2236 010

Disclaimer:This Review is prepared and issued by First Capital Equities (Pvt) Ltd. and is based on information available in the public domain, internally developed and other sources believed

to be correct. Although all reasonable care has been taken to ensure that the contents of this document are accurate, First Capital Equities (Pvt) Ltd and its Directors and

employees, are not responsible for its accuracy, usefulness and reliability and disclaim liability for any loss suffered by the use of information contained herein.

First Capital Equities (Pvt) Ltd may act as a Broker in the investments which are the subject of this document or any related investments and may have acted on or have used the

information contained in this document, or the research or analysis on which it is based, before its publication.

First Capital Equities (Pvt) Ltd

![2015 / 16...Southampton FC Stoke City FC Sunderland AFC Swansea City AFC Tottenham Hotspur FC [London ] Watford FC West Bromwich Albion FC West Ham United FC [London ] …](https://img.pdfslide.net/doc/110x75/6147d88ca830d0442101b33e/2015-16-southampton-fc-stoke-city-fc-sunderland-afc-swansea-city-afc-tottenham.jpg)