Embed Size (px)

Citation preview

Audit Committee Meeting

Teacher Retirement System of Texas 1000 Red River Street, Austin, Texas 78701-2698

December 2016

NOTE: The Board of Trustees (Board) of the Teacher Retirement System of Texas will not consider or act upon any item before the Audit Committee (Committee) at this meeting of the Committee. This meeting is not a regular meeting of the Board. However, because the full Audit Committee constitutes a quorum of the Board, the meeting of the Committee is also being posted as a meeting of the Board out of an abundance of caution.

TEACHER RETIREMENT SYSTEM OF TEXAS BOARD OF TRUSTEES

AND AUDIT COMMITTEE

(Mr. Moss, Chairman; Ms. Charleston; Mr.Corpus; Dr. Gibson; and Ms. Palmer, Committee Members)

All or part of the September 23, 2016, meeting of the TRS Audit Committee and Board of Trustees may be held by telephone or video conference call as authorized under Sections 551.130 and 551.127 of the Texas Government Code. The Board intends to have a quorum physically present at the following location, which will be open to the public during the open portions of the meeting: 1000 Red River, Austin, Texas 78701 in the TRS East Building, 5th Floor, Boardroom.

AGENDA

December 2, 2016 – 9:30 a.m. TRS East Building, 5th Floor, Boardroom

1. Call roll of Committee members

2. Approve minutes of September 23, 2016 Audit Committee meeting – Christopher Moss

3. Receive independent audit reports on audits of the Comprehensive Financial Reports forFiscal Year 2016

A. TRS – Michael Clayton and Kelley Ngaide, State Auditor’s Office (SAO) B. TRS Investment Company (TRICOT) – Bhakti Patel, Grant Thornton

4. Receive review reports for TRS health plan and drug benefit administration for TRS-Careand TRS-ActiveCare – Yimei Zhao; Amy Quertermous, John Meka, Keith Gall, and CarolHamilton, Truven Health Analytics

A. Results overview of TRS-Care and TRS-ActiveCare health plan and drug administration review reports for September 1, 2013 to August 31, 2015

B. Review Report of TRS-Care health plan administration by Aetna for September 1, 2013 to August 31, 2015 and review of TRS-ActiveCare health plan administration by Aetna for September 1, 2014 to August 31, 2015

C. Review Report of TRS-ActiveCare drug benefit administration by Caremark Rx for September 1, 2014 to August 31, 2015

D. Review Report of TRS-Care drug benefit administration by ESI for September 1, 2013 to August 31, 2015

E. Review Report of TRS-Care Employer Group Waiver Plan (EGWP) drug benefit administration by ESI for September 1, 2013 to December 31, 2014

5. Receive Compliance reports – Heather Traeger

6. Receive Internal Audit reportsA. Quarterly Investment Compliance Testing (Agreed-Upon Procedures) – Hugh

Ohn and Heather Traeger B. 403(b) Program Audit – Hugh Ohn

NOTE: The Board of Trustees (Board) of the Teacher Retirement System of Texas will not consider or act upon any item before the Audit Committee (Committee) at this meeting of the Committee. This meeting is not a regular meeting of the Board. However, because the full Audit Committee constitutes a quorum of the Board, the meeting of the Committee is also being posted as a meeting of the Board out of an abundance of caution.

C. Follow-Up Audit on Outstanding Audit Recommendations (Records Management) – Jan Engler and Toma Miller

D. Prior audit and consulting recommendations; and, implementation status of Automation Best Ideas - Amy Barrett, Chris Bailey, and Scot Leith

E. Internal Audit Annual Report – Amy Barrett

7. Discuss or consider Internal Audit administrative reports and matters related to governance, risk management, internal control, compliance violations, fraud, regulatory reviews or investigations, fraud risk areas, audits for the annual internal audit plan, or auditors' ability to perform duties – Christopher Moss and Amy Barrett

TAB 2

December 2016 Board Audit Committee Meeting 1

TEACHER RETIREMENT SYSTEM OF TEXAS AUDIT COMMITTEE MEETING MINUTES

September 23, 2016

The Audit Committee of the Board of Trustees of the Teacher Retirement System of Texas met on September 23, 2016, in the boardroom located on the fifth floor of the TRS East Building offices at 1000 Red River Street, Austin, Texas.

Committee Members present: Mr. Chris Moss, Chair Ms. Karen Charleston Mr. David Corpus Ms. Anita Palmer Other Board Members present: Mr. Joe Colonnetta Mr. John Elliott Mr. David Kelly Ms. Dolores Ramirez Others present: Brian Guthrie, TRS Jan Engler, TRS Ken Welch, TRS Rodrigo Dominguez, TRS Carolina de Onis, TRS Cari Casey, TRS Amy Barrett, TRS Simin Pang, TRS Katrina Daniel, TRS Anandhi Mani, TRS Toma Miller, TRS Lih-Jen Lan, TRS Heather Traeger, TRS Michael Clayton, SAO Hugh Ohn, TRS Kelley Ngaide, SAO Dorvin Handrick, TRS Ted Melina Raab, Texas AFT Dinah Arce, TRS Philip Mullins, TSEU Art Mata, TRS LeRoy DeHaven, TRTA Katherine Farrell, TRS Audit Committee Chair Mr. Moss called the meeting to order at 8:05 a.m.

1. Call roll of Committee members.

Ms. Farrell called the roll. A quorum was present. Dr. Gibson was absent.

2. Consider the approval of the proposed minutes of the July 29, 2016 committee meeting – Committee Chair Mr. Chris Moss.

On a motion by Ms. Palmer, seconded by Ms. Charleston, the proposed minutes for the July 29, 2016 Audit Committee meeting were approved as presented.

December 2016 Board Audit Committee Meeting 2

3. Receive State Auditor’s Office presentation on the planned audit of TRS’ Comprehensive Annual Financial Report for fiscal year 2016 and results of the audit of TRS’ fiscal year 2015 Employer Pension Liability Allocation Schedules – Michael Clayton and Kelley Ngaide, State Auditor’s Office

Ms. Kelly Ngaide informed the committee that the State Auditor expected to release its opinion on the TRS’ financial statements for fiscal year 2016 on November 17. Ms. Ngaide noted the report on internal controls and compliance and other matters will be released at the end of November. She then reviewed new Governmental Accounting Standards Board (GASB) standards that will affect the audit. Mr. Clayton discussed in further detail the liability schedules. He indicated that when GASB 75, that is related to financial reporting of other postemployment benefits (OPEB), comes into play, it will have an effect similar to the 2014 GASB 68. Mr. Clayton noted the OPEB number is going to be a very large number and will probably garner a lot of interest. Mr. Clayton indicated that more guidance regarding the OPEB is expected and indicated there may be additional work required to produce the necessary schedules. Mr. Clayton said TRS staff did a good job with their outreach efforts on the pension liability schedules and it will be key to do that for OPEB as well.

4. Receive final report on the TRS-ActiveCare Open Enrollment Readiness Review and results of TRS Open Enrollment – Amy Barrett, Toma Miller, and Katrina Daniel

Ms. Daniel reported that as the enrollment progressed relatively few issues were seen. Ms. Daniel stated that every time something came up Aetna and WellSystems addressed it. Ms. Daniels indicated there will be a future discussions with Aetna about what went well during open enrollment and work needed to do in the future. Ms. Daniel stated the first full billing cycle is not complete but things have gone well so far. Mr. Greg Wood stated they recognized that just due to size and complexity that there would be some issues. He reported they positioned themselves to react and respond quickly to resolve the unexpected events and the teams performed well. Ms. Daniel concluded the next step is to review with Aetna the issues that came up from the districts during the enrollment process. She then said they would consult with some of the districts to determine what needs to be done for an even better enrollment cycle next year.

5. Receive Investment Compliance reports – Heather Traeger Ms. Barrett provided background as to the distinction between compliance and audit. Ms. Heather Traeger reported on the ethics and fraud monitoring. Ms. Traeger stated that, during the reporting period, her office had looked into four items, three of which had been concluded while one was still pending. Of these items, two were from Benefits, one from Human Resources and one from Legal. Ms. Traeger noted TRS is taking steps to enhance the visibility of the different avenues in which ethics and compliance issues can be raised. Ms. Traeger then reported on the Code of Ethics for Contractors (Code). She reminded the committee that the Board has revised the Code at its June 2016 meeting and put into place new processes for contractors to report any actual or potential conflict of interests. Ms. Traeger noted

December 2016 Board Audit Committee Meeting 3

that there had been three conflict determination requests from contractors, one of which had been withdrawn due to a transaction not moving forward. Ms. Traeger said the Executive Director and General Counsel had determined there was no conflict existed in the two remaining cases.

6. Receive Internal Audit reports A. Quarterly Investment Compliance Testing (Agreed-Upon Procedures) – Hugh

Ohn and Heather Traeger

Mr. Hugh Ohn reported on the results of the quarterly investment compliance testing. Mr. Ohn stated a couple of new areas tested during the quarter were the budget transfers, expenditures and the employees and Trustee annual ethics training. Mr. Ohn noted the results indicated that there were no compliance violations during this time period.

B. Second-Half Test Results of Investment Controls (Tactical Asset Allocation) – Hugh Ohn

Mr. Ohn reported on the results of the semiannual test of IMD controls related to the tactical asset allocations. Also covered were the derivatives instrument that the tactical asset allocation (TAA) group uses to execute their trade. Other IMD groups that provide support for the tactical, TAA portfolios, such as risk group, trading group, and investment operations group were covered. Mr. Ohn reported the results of the audit indicate that management controls are working effectively. Mr. Ohn stated they did recommend putting together written operating procedures for completing the complicated strategies running the models. He said management agrees with this recommendation.

C. Overall Opinion on Investment Management Division Internal Controls –

Hugh Ohn Mr. Ohn noted the opinion issued is similar to opinions in the past two fiscal years. And like the past two years, Mr. Ohn, stated the opinion is expressly based on 28 internal and external audits performed in the past three fiscal years. Mr. Ohn reported that overall IMD controls are effective to ensure that they are achieving their business objectives. Mr. Ohn said this opinion is based on the facts that significant controls are working at IMD as designed. In conclusion, Mr. Ohn remarked that since they had not identified any significant control weaknesses or deficiencies in the past three years, they are planning to deviate from the regularly scheduled audit cycle. Mr. Ohn stated they plan to lightly cover internal public markets as planned but also will try to cover the private markets a bit more.

D. Annual Testing of Benefit Payments (Agreed-Upon Procedures) – Amy

Barrett and Dorvin Handrick Ms. Barrett reported the results from testing benefits are excellent. Only one issue was found, and it was related to the calculation of final average salaries in the member’s favor.

E. Employer Audits – Dinah Arce and Art Mata

Mr. Art Mata reported the employer audit team completed the audits of Socorro ISD and Ysleta ISD, both districts are located in the El Paso area. Mr. Mata stated they audited the March 2016

December 2016 Board Audit Committee Meeting 4

contribution reports for these districts to confirm member eligibility and accuracy of contributions and also tested the census data of all the members. Mr. Mata noted that most of the districts reports were accurate and complete for the same that was tested. However, both districts in the summary reports were incomplete or inaccurate. Mr. Ohn said the statutory minimum report and the employment after retirement report for both districts contained errors. Ms. Dinah Arce reported on the two years that employer audits have been conducted. She noted in total eleven audits have been conducted with seven completed this past year. Ms. Arce reviewed the size of the schools and contributions reported. She said the schools are in the process of making corrections, seven schools having completed the corrections. Ms. Arce noted in the coming year there will be changes to the report in order to streamline it down and initiate efficiencies in order to accommodate the increase in number and to report quickly to schools. Ms. Barbie Pearson reported on the overall recovered or given credit for the whole year in which audits were performed. Audits only look at one month. Ms. Pearson said the net correction was a negative $17,294. New employee contributions made in error was why there was a net payout. In answer to Mr. Kelly’s inquiry, Ms. Barrett and Ms. Pearson said guidance to districts will be given through monthly newsletters and presentations.

7. Receive report on the status of prior audit and consulting recommendations – Amy

Barrett Ms. Amy Barrett reported they are scaling back in terms of what is focused on with the regular employer audits. Ms. Barrett stated they are to focus on what is not understood by the employer and pass along information to benefit reporting for communicating and educating. Ms. Barrett said they are going to do a separate audit to see if more can be done in just employment after retirement. Ms. Barrett said the third area is to develop an audit program for colleges and universities. Ms. Barrett reported on the outstanding audit recommendations as making good progress. The only one issue is in regards to TEAM being implemented in order to wrap that one up on strengthening controls.

8. Consider recommendations to the Board of Trustees – Amy Barrett

A. Proposed revisions to the Internal Audit Charter Ms. Amy Barrett brought forward two revisions to the Internal Audit Charter. Ms. Barrett stated the first change is driven by the Institute of Internal Auditors which have decided that the mission statement for Internal Audit is really a definition of Internal Audit. The Institute also recommended a list of ten principles for Internal Audit. Ms. Barrett recommended the Charter incorporate these changes. The other recommended change is to reflect the responsibility for the hotline to Compliance.

B. Proposed Audit Plan for Fiscal Year 2017

Ms. Amy Barrett noted how the plan was developed through risk assessment, feedback from various groups and interviews with Trustees. Ms. Barrett provided a summary of the plan and the audits that are proposed for the fiscal year 2017. Ms. Barrett reported there is sufficient resources to complete the annual audit plan.

December 2016 Board Audit Committee Meeting 5

On a motion by Mr. Moss, seconded by Mr. Corpus, the Committee unanimously approved to recommend that the Board of Trustees adopt the proposed revisions to the Internal Audit charter as presented by staff and to approve the proposed audit plan for the fiscal year 2017 as presented by staff.

9. Discuss or consider Internal Audit administrative reports and matters related to

governance, risk management, internal control, compliance violations, fraud, regulatory reviews or investigations, fraud risk areas, audits for the annual internal audit plan, or auditors' ability to perform duties – Christopher Moss and Amy Barrett

Ms. Barrett reported that they did get through the annual audit plan last year with all the assurance projects completed. Ms. Barrett noted data analysis activities were not completed. Ms. Barrett reported they met all of the performance measures for last year. Ms. Barrett then took the opportunity to introduce newest members of Audit and inform the Committee about reorganization and promotions within Audit. Without further discussion, the meeting adjourned at 9:55 a.m. APPROVED BY THE AUDIT COMMITTEE OF THE BOARD OF TRUSTEES OF THE TEACHER RETIREMENT SYSTEM OF TEXAS ON THE 2ND DAY OF DECEMBER 2016.

______________________________ _________________ Katherine H. Farrell Date Secretary of the TRS Board of Trustees

TAB 3

TAB 3A

TAB 3B Information regarding this report will be

distributed at the Audit Committee Meeting

TAB 4

TAB 4A

PRESENTATION TITLE >>> NAME FEB-09-15

PRESENTATION FOR THE AUDIT COMMITTEE BY TRUVEN HEALTH ANALYTICS

DECEMBER 2, 2016

Tab 4A

Background of Audited Plans

• Three self-funded plans:• ActiveCare 1-HD

• ActiveCare 2

• ActiveCare Select

• Health Plan Administrator: Aetna

• Pharmacy Benefits Manager: CVSHealth/Caremark

TRS-ActiveCare

• Three self-funded plans:• Care 1

• Care 2

• Care 3

• Health Plan Administrator:Aetna

• Pharmacy Benefits Manager:Express Scripts

TRS-Care

2

TRS Audit Changes

What changes were made?

• Procured a new audit firm:Truven Health Analytics, an IBM Company

• Full Claims Review vs. Sampling only

• Annual audits vs. every two years

• Increased focus on self-insured plans

Why were changes made?

• Truven brings full claim reprocessing, focused testing, and impact analysis based on error characteristics and root causes

• Increased assurance that our venders are implementing plan designs accordingly

• Shortened issue identification and resolution time

• Increased oversight of the self-insured plans and their vendors

3

More errors identified than in previous years is reflective of expanded auditing,

not declining vendor performance.

Audit Results

Good News Report

Vendor performance above industry standards

Affirmation of contractual obligations

4

TRUVEN HEALTH ANALYTICS - TRS AUDITS

• Audit Scope• Medical - Aetna

• TRS-Care (9/1/2013 – 8/31/2015)• TRS-ActiveCare (9/1/2014 – 8/31/2015)

• Rx - Caremark• TRS-ActiveCare (9/1/2014 – 8/31/2015)

• Rx - ESI• TRS-Care - EGWP (9/1/2013 – 12/31/2014)

• TRS-Care - Commercial (9/1/2013 – 8/31/2015)

• Claims Audit, Operational Review, Performance Guarantee Verification

5

TRUVEN HEALTH ANALYTICS – TRS AUDITS

• Audit Methodology - Claims

• Obtain Summary Plan Descriptions (SPD) and other Benefit Documentation

• Develop Benefit Templates Based on SPDs

• Obtain Claims Files From Administrators

• Use Proprietary Software to Re-adjudicate 100% of Claims• Benefit Determinations (Coinsurance, Copayments, Deductibles, etc.)• Industry Standards

Administrator Claim Count Paid

Aetna 9,741,865 $2,654,331,350

Caremark 4,331,150 $333,432,600

ESI - Commercial 5,990,979 $627,162,700

ESI - EGWP 6,164,874 $548,457,201 6

TRUVEN HEALTH ANALYTICS – TRS AUDITS

• Audit Methodology - Claims (continued)

• Group Potential Exceptions Into Various Categories

• Select Claims Samples from Exception Categories

• Test Claims Samples

• Medical - Onsite Audit

• Rx - Reviewed Remotely

• Evaluate Administrator Sample Responses

• Complete 100% Claims Analysis Based on Remaining Sample Exceptions

• “Agree To”

• “Agree to Disagree”7

TRUVEN HEALTH ANALYTICS - TRS AUDITS

• Audit Results, Key Findings and Observations

• Administrators Performing At or Above Acceptable Levels

• Medical – Aetna

• Overall claims findings are within Truven benchmark (1%-2%)• TRS-ActiveCare - 0.04%

• TRS-Care - 0.07%

• Opportunities to clarify benefit intentions• Ineligible Services

• Coinsurance Provisions

8

TRUVEN HEALTH ANALYTICS - TRS AUDITS

• Rx - Caremark

• Overall claims findings of 1.52% of Rx spend are within Truven benchmark (< 2%)

• Opportunities for improvements• Early Refill Claims

• Copayment Application

• Caremark addressing exceptions for VA claims and will reimburse TRS

9

TRUVEN HEALTH ANALYTICS - TRS AUDITS

• Rx - ESI-Commercial• Overall claims findings of 0.96% (FY2014) and 0.65% (FY2015) of Rx spend

are within Truven benchmark (< 2%)

• Opportunities for improvements• Duplicate and Early Refill Claims

• Quantity Limitation Clinical Program

• Rx - ESI-EGWP• Overall claims findings of 0.22% (CY2013) and 0.30% (CY2014) of Rx spend

are within Truven benchmark (< 2%)

• Opportunities for improvements• Early Refill Claims

• Quantity Limitation Clinical Program

10

TAB 4B

Teacher Retirement System of Texas Review of Health Plan Administration by Aetna for September 1, 2013 to August 31, 2015

Plans: TRS-ActiveCare and TRS-Care

Prepared for: Teacher Retirement System of Texas Version F1.0.1 Submitted: September 23, 2016 Submitted by: Truven Health Analytics

©Truven Health Analytics Inc. Proprietary and Confidential Page 4 of 78

1 EXECUTIVE SUMMARY

1.1 Engag ement Overview and Scope The Teacher Retirement System of Texas (TRS) engaged Truven Health Analytics (Truven) to conduct a health claims review to:

Assess the administration of TRS’s self-funded employee health plans by Aetna. Determine if Aetna is in compliance with the terms of the Administrative Services Agreement

(ASA), Summary Plan Description (SPD), and other applicable documents.

This engagement primarily examined Aetna’s claims adjudication accuracy relative to all claims incurred by TRS’s plan members for TRS-Care plans from September 1, 2013 to August 31, 2015 and paid through November 30, 2015 and for TRS-ActiveCare plans from September 1, 2014 to August 31, 2015 and paid through November 30, 2015. In addition, we were engaged to perform an operational review to assess the policies, procedures, and controls that support the administration of TRS’s health plans. The health plans included in the review consist of the following:

TRS-ActiveCare 1-HD Fiscal Year 2015 TRS-ActiveCare 2 Fiscal Year 2015 TRS-ActiveCare Select Fiscal Year 2015 TRS-Care 1 Fiscal Years 2014 and 2015 TRS-Care 2 Fiscal Years 2014 and 2015 TRS-Care 3 Fiscal Years 2014 and 2015

1.2 Claims Review Result s Using our proprietary software, we analyzed 100% of the paid claims incurred by TRS’s members for the review period (for more information about the 100% claims analysis, see Section 2, Engagement Approach).

The proprietary software is designed to process and identify claim exceptions in the following categories:

Payments in compliance with the plan design. This includes plan customized edits to assure that benefits are paid in accordance with the SPD including items such as benefit limits, frequencies and maximums and the appropriate application of deductibles, copayments and coinsurance. The software assures that claims for benefit exclusions (ineligible services) are not paid and that emergency claims are correctly processed for in and out of network providers.

Payments only for eligible members. The software identifies claims paid for inactive members, as well as services paid prior to or after a member’s eligibility dates.

Industry Standard edits. This includes system control edits such as National Correct Coding Initiative edits (NCCI), identification of claims that may be other party liability and coordination of benefits such as Medicare, end stage renal disease (ESRD), subrogation and worker’s compensation, duplicate payments, assistant surgeon payments and anesthesia/surgical reduction claims. NCCI edits also include facility and physician up-coding and unbundling, incidental charges, medically unlikely and never events.

©Truven Health Analytics Inc. Proprietary and Confidential Page 5 of 78

Case Management edits. This includes identification of claims which may benefit from case management and/or utilization review such as high risk obstetrical claims, rehabilitation claims and terminally ill member claims.

Payment Integrity edits. These include the identification of claims which may benefit from additional provider pattern analysis to identify fraud, waste and abuse. Examples of these edits include claims for ambulance trips that had no subsequent claim that same day for an emergency room, diagnosis or CPT conflicts with age or gender, new patient exams when a less expensive established exam should have been billed, incidental services and once in a lifetime services.

Contract review. In addition to the claim exceptions identified by the software algorithms, a sample of claims are reviewed to assure compliance with the provider contract. These represent large dollar claims which are reviewed manually during an onsite visit to assure payment for each service was made in accordance with the provisions of the provider contract.

Exception categories were developed based on rules customized to TRS specific plan benefits described in the SPDs, industry standards for coding, and claims processing best practices (e.g., duplicate claims).

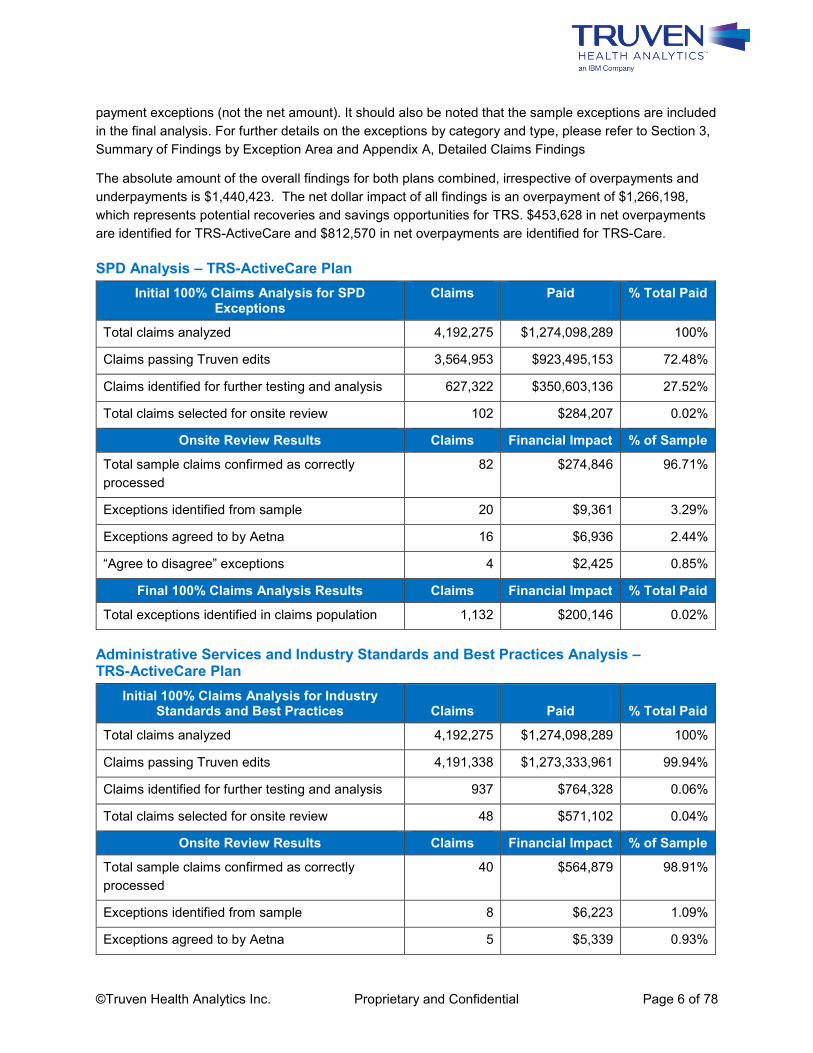

From the population of potential exceptions, we selected a sample of 300 claims for onsite review that consisted of 150 claims for each plan, TRS-ActiveCare and TRS-Care. Of the 300 claims reviewed, we determined during the onsite review that 257 claims were processed and paid correctly. Of the remaining 43 exceptions, Aetna agreed with Truven’s assessment that there was an exception in processing the claim on 33 claims. On the remaining 10 claims, Aetna did not agree, but Truven considers these to be exceptions. Based on these 43 exceptions, Truven determined which types of exceptions represented systemic claims processing exceptions and for these exception categories 100% of the claims identified were considered to be exceptions. This process resulted in the identification of 6,910 claims and $1,440,423 in total exceptions with $1,266,198 in net overpayment exceptions for both plans. The following chart provides the breakdown of total exceptions by plan.

Plan Claim Exceptions Total Payment

Exceptions Net Overpayment

% of Total Paid as

Exceptions

TRS-ActiveCare 2,161 $521,967 $453,628 0.04%

TRS-Care 4,749 $918,456 $812,570 0.07%

Total 6,910 $1,440,423 $1,266,198 0.05%

1.3 Result s by Plan The sample results were analyzed by plan. The 300 claim sample contained 150 claims each from both the TRS-ActiveCare plans and the TRS-Care plans. For the TRS-ActiveCare plans there was an exception rate of 0.05% of paid dollars reviewed, while the TRS-Care plans had an exception rate of 0.07% of paid dollars reviewed. Both plans performed well when compared to audits of other third party administrators.

These results include claims that were both overpaid and underpaid by Aetna. The dollar figures shown for the exceptions reflect the combined total of overpayment and underpayment dollar amounts of the

©Truven Health Analytics Inc. Proprietary and Confidential Page 6 of 78

payment exceptions (not the net amount). It should also be noted that the sample exceptions are included in the final analysis. For further details on the exceptions by category and type, please refer to Section 3, Summary of Findings by Exception Area and Appendix A, Detailed Claims Findings

The absolute amount of the overall findings for both plans combined, irrespective of overpayments and underpayments is $1,440,423. The net dollar impact of all findings is an overpayment of $1,266,198, which represents potential recoveries and savings opportunities for TRS. $453,628 in net overpayments are identified for TRS-ActiveCare and $812,570 in net overpayments are identified for TRS-Care.

SPD Analysis – TRS-ActiveCare Plan Initial 100% Claims Analysis for SPD

Exceptions Claims Paid % Total Paid

Total claims analyzed 4,192,275 $1,274,098,289 100%

Claims passing Truven edits 3,564,953 $923,495,153 72.48%

Claims identified for further testing and analysis 627,322 $350,603,136 27.52%

Total claims selected for onsite review 102 $284,207 0.02%

Onsite Review Results Claims Financial Impact % of Sample

Total sample claims confirmed as correctly processed

82 $274,846 96.71%

Exceptions identified from sample 20 $9,361 3.29%

Exceptions agreed to by Aetna 16 $6,936 2.44%

“Agree to disagree” exceptions 4 $2,425 0.85%

Final 100% Claims Analysis Results Claims Financial Impact % Total Paid

Total exceptions identified in claims population 1,132 $200,146 0.02%

Administrative Services and Industry Standards and Best Practices Analysis – TRS-ActiveCare Plan

Initial 100% Claims Analysis for Industry Standards and Best Practices Claims Paid % Total Paid

Total claims analyzed 4,192,275 $1,274,098,289 100%

Claims passing Truven edits 4,191,338 $1,273,333,961 99.94%

Claims identified for further testing and analysis 937 $764,328 0.06%

Total claims selected for onsite review 48 $571,102 0.04%

Onsite Review Results Claims Financial Impact % of Sample

Total sample claims confirmed as correctly processed

40 $564,879 98.91%

Exceptions identified from sample 8 $6,223 1.09%

Exceptions agreed to by Aetna 5 $5,339 0.93%

©Truven Health Analytics Inc. Proprietary and Confidential Page 7 of 78

“Agree to disagree” exceptions 3 $884 0.15%

Final 100% Claims Analysis Results Claims Financial Impact % Total Paid

Total exceptions identified in claims population 1,030 $321,821 0.03%

SPD Analysis – TRS-Care Plan Initial 100% Claims Analysis for SPD

Exceptions Claims Paid % Total Paid

Total claims analyzed 5,549,590 $1,380,233,060 100%

Claims passing Truven edits 5,423,870 $1,292,230,130 93.62%

Claims identified for further testing and analysis 125,720 $88,002,930 6.38%

Total claims selected for onsite review 97 $175,784 0.01%

Onsite Review Results Claims Financial Impact % of Sample

Total sample claims confirmed as correctly processed

87 $173,602 98.76%

Exceptions identified from sample 10 $2,182 1.24%

Exceptions agreed to by Aetna 7 $1,795 1.02%

“Agree to disagree” exceptions 3 $386 0.22%

Final 100% Claims Analysis Results Claims Financial Impact % Total Paid

Total exceptions identified in claims population 3,542 $351,935 0.03%

Administrative Services and Industry Standards and Best Practices Analysis – TRS-Care Plan

Initial 100% Claims Analysis for Industry Standards and Best Practices Claims Paid % Total Paid

Total claims analyzed 5,549,590 $1,380,233,060 100%

Claims passing Truven edits 5,548,922 $1,378,441,219 99.87%

Claims identified for further testing and analysis 668 $1,791,841 0.13%

Total claims selected for onsite review 53 $912,891 0.07%

Onsite Review Results Claims Financial Impact % of Sample

Total sample claims confirmed as correctly processed

48 $909,909 99.67%

Exceptions identified from sample 5 $2,982 0.33%

Exceptions agreed to by Aetna 5 $2,982 0.33%

“Agree to disagree” exceptions - - 0.00%

Final 100% Claims Analysis Results Claims Financial Impact % Total Paid

©Truven Health Analytics Inc. Proprietary and Confidential Page 8 of 78

Total exceptions identified in claims population 1,207 $566,521 0.04%

1.4 Review Conclus ion s Based on the results of this review and our prior audit experience with other administrators, we determined Aetna is performing at an above-average level. Our experience is that, on an overall basis, the total dollars identified as exceptions range between 1% to 2% of the total dollars analyzed. The results of this review were that 0.05% of the total dollars analyzed were identified as exceptions. Unless specifically noted in the findings sections of this report, claims met the plan specific and industry standards for proper claims adjudication.

The results of our operational review indicated that generally Aetna has the proper organizational structure and processes in place to support your account. However, there were two observations made regarding Aetna processes for overpayment reporting and claims turnaround time. These observations will be discussed in detail in the Operational Review Observation section of this report.

Although performance was above-average there are several opportunities for improvement that would result in both short-term and long-term savings to TRS. Those opportunities are highlighted below.

1.5 Summ ary of Findin gs Aetna reported that approximately 84% of TRS-Care claims and approximately 87% of TRS-ActiveCare claims are auto-adjudicated, which is within and slightly above the industry average of 80% to 85%. Auto-adjudicated claims pass through all system edits, and benefits are then calculated based on the plan design features programmed in the system without claims examiner intervention. Therefore, any exceptions attributed to a discrepancy in the interpretation or loading of the benefits would impact all similar claims.

The following charts provide information on the overall review findings from a financial perspective.

SPD Exceptions – TRS-ActiveCare Plan

Exception Category Net Findings Over-

payment Under-

payment Total

Findings % of Total

100 Percent Coverage ($1,086) - $1,086 $1,086 0.5%

Coinsurance Application $7,201 $15,684 $8,483 $24,168 12.1%

Copayment Application $9,867 $34,467 $24,600 $59,067 29.5%

Ineligible Services $107,308 $107,308 - $107,308 53.6%

Visit Limitation $8,517 $8,517 - $8,517 4.3%

Grand Total $131,807 $165,977 $34,170 $200,146 100.0%

©Truven Health Analytics Inc. Proprietary and Confidential Page 9 of 78

Administrative Services and Industry Standards and Best Practices Exceptions – TRS-ActiveCare Plan

Exception Category Net Findings Over-

payment Under-

payment Total

Findings % of Total

Contract Review $4,726 $4,726 - $4,726 1.5%

Eligibility $884 $884 - $884 0.3%

Duplicate Claim Payment $260,752 $260,752 - $260,752 81.0%

Surgery Payments $55,459 $55,459 - $55,459 17.2%

Grand Total $321,821 $321,821 - $321,821 100.0%

SPD Exceptions – TRS-Care Plan

Exception Category Net Findings Over-

payment Under-

payment Total

Findings % of Total

100 Percent Coverage ($187) - $187 $187 0.1%

Coinsurance Application $197,748 $245,473 $47,725 $293,198 83.3%

Copayment Application ($4,328) $703 $5,031 $5,734 1.6%

Ineligible Services $41,577 $41,577 - $41,577 11.8%

Visit Limitation $11,239 $11,239 - $11.239 3.2%

Grand Total $246,049 $298,992 $52,943 $351,935 100.0%

Administrative Services and Industry Standards and Best Practices Exceptions – TRS-Care Plan

Exception Category Net Findings Over-

payment Under-

payment Total

Findings % of Total

Duplicate Claim Payment $444,132 $444,132 - $444,132 78.4%

Surgery Payments $122,389 $122,389 - $122,389 21.6%

Grand Total $566,521 $566,521 - $566,521 100.0%

For further details on the exceptions by category and type, please refer to Section 3, Summary of Findings by Exception Area and Appendix A, Detailed Claims Findings.

1.6 Except ion Categories Compared to Industry Bench marks

The following chart compares Aetna’s experience for the identified exception categories to that of other Health Plans (Benchmark Error Rate). The error rate identified on the Aetna claims is well below that of other commercial and government health plans audited by Truven.

©Truven Health Analytics Inc. Proprietary and Confidential Page 10 of 78

Benchmarks – TRS-ActiveCare Plan

Exception Category Benchmark Error Rate

Aetna Error Rate Aetna Score

100 Percent Coverage 1.70% 0.001% Below average error rate

Coinsurance Application 4.14% 0.003% Below average error rate

Copayment Application 4.28% 0.017% Below average error rate

Ineligible Services 0.35% 0.004% Below average error rate

Visit Limitation 0.11% 0.012% Below average error rate

Duplicate Claims Payment 0.03% 0.007% Below average error rate

Surgery Payments 0.07% 0.003% Below average error rate

Benchmarks – TRS-Care Plan

Exception Category Benchmark Error Rate

Aetna Error Rate Aetna Score

100 Percent Coverage 1.70% 0.003% Below average error rate

Coinsurance Application 4.14% 0.11% Below average error rate

Copayment Application 4.28% 0.002% Below average error rate

Ineligible Services 0.35% 0.10% Below average error rate

Visit Limitation 0.11% 0.006% Below average error rate

Duplicate Claims Payment 0.03% 0.007% Below average error rate

Surgery Payments 0.07% 0.006% Below average error rate

1.7 Recommendations Request and review financial and claim impact analyses for all “Agreed To” exceptions and other

exceptions where Aetna was not properly adjudicating claims according to the SPD language. Where applicable, recoveries should be pursued.

Work with Aetna to clarify the intent of all the plan design features identified as exceptions, with particular focus on non-covered (ineligible) services. Further clarifying language in the SPD related to ineligible services may be helpful. For services which are typically excluded but where approval for payment may be provided on an exception basis, a prior authorization requirement may be appropriate.

Aetna should address the issues identified that are related to the correct application of member liability such as coinsurance and copayment to assure that members are assessed the correct amount and that claims are paid correctly for claims that require coinsurance as well as claims that are covered at 100%.

©Truven Health Analytics Inc. Proprietary and Confidential Page 11 of 78

Aetna should institute edits in the claims processing system to assure chiropractic visits are paid only up to the specified limit.

There were two claims with procedural issues identified which did not have a financial impact but where a change is recommended. When allowed charges are assigned to multiple lines of a claim record or when a claim is processed for an outdated code, the allowed amount should be assigned only to lines for procedure codes representing covered services. This would allow editing software to better identify true errors and eliminate false positive results.

1.8 Aetna’s Response We recognize that the type of audit performed by Truven selects samples based on what they consider a high probability of being paid in error rather than as a statistical sampling. This type of audit is not a measure of overall quality or indicative of any trends. Details for all errors identified and overpayment recovery status are found in the sections below along with the service center responses. We have completed a thorough root cause analysis of all the agreed upon errors and educational feedback has been provided to ensure a thorough understanding of the impact of the errors identified. All affected claims have been referred for reprocessing with the exception of those claims that would result in member responsibility.

Aetna takes these audit results very seriously and recognizes that there is always room for improvement. We continue to focus on continuous quality review through the development of additional system enhancements, as well as conducting focused and refresher training sessions with Claim Benefit Specialists. These steps are vital to our success in quality improvement and are outlined as they relate to this audit in the action plan portion of our report.

TAB 4C

Teacher Retirement System of Texas Review of Drug Benefit Administration by Caremark Rx for September 1, 2014 to August 31, 2015

Plan: TRS-ActiveCare

Prepared for: Teacher Retirement System of Texas Submitted: November 17, 2016 Submitted by: Truven Health Analytics

©Truven Health Analytics Inc. Proprietary and Confidential Page 4 of 41

1 EXECUTIVE SUMMARY

1.1 Engagement Ov ervi ew The Teacher Retirement System of Texas (TRS) engaged the services of Truven Health Analytics (Truven) to conduct a pharmacy claims review to assess Caremark Rx’s (Caremark's) administration of TRS’s self-funded pharmacydrug plans and determine if Caremark complies with the terms of the administrative agreement. This engagement encompassed an audit of Caremark to assess the accuracy and appropriateness of its fiduciary responsibility as the plan’s administrative agent including the prescription adjudication process, compliance with pricing agreements, contract terms, and review of quality control procedures. Truven performed an electronic audit of all claims adjudicated by Caremark from September 1, 2014 through August 31, 2015.

The pharmacy drug plans included in this review consist of the following:

TRS-ActiveCare 1 HD Fiscal Year 2015 TRS-ActiveCare 2 Fiscal Year 2015 TRS-Active Select Network Fiscal Year 2015

1.2 Claim s Review Scope Truven analyzed 100% of TRS’s claims incurred by TRS’s plan participants during the audit period and selected a sample of 160 claims for testing and review from Fiscal Year 2015. The sample was selected based on various exception areas identified in the population of claims processed during the audit period. These exception areas were based on standard administrative rules such as quantity limits, ample day supply, co-payments, and eligibility specific to the plan benefits described in the contract and other benefit documents

1.3 Audit Concl usions The sample claims were reviewed based on Caremark’s responses, and 25 exceptions were identified. We evaluated all 4,331,150 claims during the audit period based on Caremark’s responses and identified $5,055,126 in net payment exceptions. The following chart compares the total net cost of all exceptions identified by this audit against the total cost of TRS’s entire claims population.

Overall Audit Results Paid

Total cost of all employee prescription drug claims $333,432,600

Total cost of claims sampled (detail Claims Sample Results) $25,573

Total net exceptions identified in claims sample (detail Claims Sample Results) $746

Total net cost of all exceptions identified from the analysis of TRS’s entire claims population (based on the attributes and root causes of Truven’s claims sample findings)

$5,055,126

Additional discount shortfall using TRS’s contracted rates for mail and retail and specialty drugs (TRS previously received $7.1M based on Caremark’s reconciliation.)

$53,829

©Truven Health Analytics Inc. Proprietary and Confidential Page 5 of 41

The financial impact of all claim exceptions identified through this audit are net overpayments of $5,055,126 representing 1.52% of TRS’s total prescription drug plan spend. This includes approximately $5,430,000 in overpayments identified for early refills, which represents a future cost savings opportunity. This overpayment amount was primarily offset by underpayments found in the copayment category. Based on the results of the audit, we have several recommendations that we believe, if implemented, would improve the overall claims processing accuracy rate and could result in savings to TRS.

1.4 Summ ary of Key Find ings and Observ ation s & Recommendati ons

The following summarizes our key findings and observations and recommendations based on the results of the audit

1.4.1 Key Findings and Observations Discount Analysis: Based on our discount analysis, we determined that Caremark did not meet

the guarantee on all specialty claims. We have determined that claims were processed at a lower discount rate than indicated in TRS’s contract resulting in a shortfall of $53,829.

Copayment application: Claims were processed at copays other than outlined in the contract. Claims processed at Veteran Affair’s pharmacies and Retail 90 claims caused the majority of the copayment exceptions. According to Caremark, they are reviewing claims that adjudicated with the incorrect copayment during the impact period and will reimburse TRS at the conclusion of the audit.

Early Refill: Claims were filled outside of early refill parameters set in the contract. The majority of the findings were for retail claims that were filled prior to the plan design utilization of 75%.

Gender Conflicts: Although the results were minimal, we found instances where prescriptions were filled that conflicted with the member’s gender. A gender-specific edit is not in place in the plan design.

1.4.2 Recommendations TRS previously accepted Caremark's payment of $7,112,399 for not meeting contractual

obligations for discounts for mail and retail claims. Truven recommends TRS continue to work with Caremark to reconcile the specialty discount shortfall identified during this audit.

We recommend that TRS work with Caremark to resolve the copayment issues identified in the audit. Furthermore, we recommend TRS work with Caremark to determine if the Dispense as Written (DAW) penalty program is in line with client intentions.

A discussion of early refill parameters should be undertaken between Caremark and TRS. Specific parameters should be outlined in detail and agreed upon to ensure early refills occur for valid reasons such as vacation overrides, dosage changes or lost medication.

We recommend a gender-specific edit be considered as a future cost savings opportunity to ensure proper Drug Utilization Review (DUR), plan deductibles, maximum out of pockets, and that potential fraud is addressed.

©Truven Health Analytics Inc. Proprietary and Confidential Page 6 of 41

A discussion of plan excluded products should be undertaken between Caremark and TRS to ensure they are in line with client intentions. Specific parameters should be outlined in detail.

TAB 4D

=

Teacher Retirement System of Texas Review of Drug Benefit Administration By Express Scripts Inc.

For September 1, 2013 to August 31, 2015

Plan: TRS-Care Prepared for: Teacher Retirement System of Texas Submitted: November 18, 2016 Submitted by: Truven Health Analytics

1 EXECUTIVE SUMMARY

1.1 Engagement Overview The Teacher Retirement System of Texas (TRS) engaged the services of Truven Health Analytics (Truven) to conduct a pharmacy claims review to assess Express Scripts, Inc.'s (ESI’s) administration of TRS’s self-funded prescription drug plans and determine if ESI complies with the terms of the administrative agreement. This engagement encompassed an audit of ESI to assess the accuracy and appropriateness of its fiduciary responsibility as the plan’s administrative agent including the prescription adjudication process, compliance with pricing agreements, contract terms, and review of quality control procedures. Truven performed an electronic audit of all claims adjudicated by ESI from September 1, 2013 through August 31, 2015.

The prescription drug plans included in this review consist of the following:

TRS-Care 2 Fiscal Years 2014 and 2015 TRS-Care 3 Fiscal Years 2014 and 2015 TRS-Care 1 Fiscal Years 2014 and 2015

1.2 Claims Review Scope Truven analyzed 100% of TRS’s claims incurred by TRS’s plan participants during the audit period and selected a sample of 38 claims for the fiscal plan year 2014 for testing and review and a sample of 21 claims for testing and review for fiscal plan year 2015. The sample was selected based on various exception areas identified in the population of claims processed during the audit period. These exception areas were based on standard administrative rules such as quantity limits, ample day supply, co-payments, and eligibility specific to the plan benefits described in the contract and other benefit documents.

1.3 Audit Conclusions The sample claims were reviewed based on ESI’s responses. We evaluated all 2,929,964 claims during the audit period FY2014 based on ESI’s responses and identified $2,838,401 in potential overpayments. We evaluated all 3,061,015 claims during the audit period FY2015 based on ESI’s responses and identified $2,172,991 in potential overpayments.

The following charts compare the total cost of all exceptions identified by this review against the total cost of the TRS’s entire claims population.

Fiscal Plan Year 2014 Overall Audit Results Paid

Total cost of all employee prescription drug claims for FY2014 $294,423,834

Total cost of claims sampled $44,653

Total exceptions identified in claims sample (detail Claims Sample Results) $2,375

Total cost of potential claims exceptions identified from the 100% analysis of the entire claims population for FY2014 (based on the attributes and root causes of Truven’s sample findings)

$2,838,401

The financial impact of all claims exceptions identified through this review for FY2014 is potential overpayments of $2,838,401 representing 0.96% of TRS’s total prescription drug plan spend. The financial impact of all exceptions is below our industry standard threshold of < 2%. Based on the results of our review, we have several recommendations that we believe, if implemented, would improve the overall claims processing accuracy rate and could result in savings to TRS.

Fiscal Plan Year 2015 Overall Audit Results Paid

Total cost of all employee prescription drug claims for FY2015 $332,738,866

Total cost of claims sampled $6,030

Total exceptions identified in claims sample (detail Claims Sample Results) $837

Total cost of potential claims exceptions identified from the 100% analysis of the entire claims population for FY2015 (based on the attributes and root causes of Truven’s claims sample findings)

$2,172,991

The financial impact of all claims exceptions identified through this review for FY2015 is potential overpayments of $2,172,991 representing 0.65% of TRS’s total prescription drug plan spend. The financial impact of all exceptions is below our industry standard threshold of < 2%. Based on the results of our review, we have several recommendations that we believe, if implemented, would improve the overall claims processing accuracy rate and could result in savings to TRS.

1.4 Summary of Key Findings and Observations & Recommendations

The following summarizes our key findings and observations and recommendations based on findings identified in the entire TRS claims population.

1.4.1 Key Findings and Observations Benefit Plan Administration:

o Duplicate Claims and Early Refill: Duplicate claims were filled for the same drug on the same day. Also, claims were filled prior to the refill utilization parameters set in the contract.

o Quantity Limitations: Claims were filled prior to quantity limit parameters set in the contract. ESI noted the “first fill at mail” logic as the reason for the claims being filled outside of plan parameters. Truven disagrees with this logic. Quantity limitations are set up based on the recommended daily dose from the Food and Drug Administration (FDA) for certain drugs. These parameters are designed to be a cost savings opportunity for TRS.

1.4.2 Recommendations Benefit Plan Administration:

o Duplicate Claims and Early Refills: We recommend TRS work with ESI to reconcile claims

processed outside of plan utilization parameters. In addition, a discussion of early refill and duplicate drug parameters should be undertaken between ESI and TRS. Specific parameters should be outlined in detail and agreed to. This should be discussed as a future cost savings opportunity.

o Quantity Limitations: We recommend TRS work with ESI to reconcile claims processed outside of plan parameters. In addition, a discussion of quantity limitations should be undertaken between ESI and TRS. Specific parameters should be outlined and agreed to. This should be discussed as a future cost savings opportunity.

TAB 4E

Teacher Retirement System of Texas Review of EGWP Drug Benefit Administration by Express Scripts, Inc.

for September 1, 2013 to December 31, 2013 and January 1, 2014 to December 31, 2014 Plan: TRS-Care Prepared for: Teacher Retirement System of Texas Submitted: November 18, 2016 Submitted by: Truven Health Analytics

©Truven Health Analytics Inc. Proprietary and Confidential Page 4 of 37

1 EXECUTIVE SUMMARY

1.1 Engag ement Overview The Teacher Retirement System of Texas (TRS) engaged the services of Truven Health Analytics (Truven) to conduct a pharmacy claims review to assess Express Scripts, Inc.'s (ESI’s) administration of TRS’s self-funded prescription drug Employer Group Waiver Plan (EGWP) and determine if ESI complies with the terms of the administrative agreement. This engagement encompassed an audit of ESI to assess the accuracy and appropriateness of its fiduciary responsibility as the plan’s administrative agent including the prescription adjudication process, compliance with pricing agreements, contract terms, and review of quality control procedures. Truven performed an electronic audit of all claims adjudicated by ESI from September 1, 2013 through December 31, 2014.

The prescription drug plans included in this review consist of the following:

TRS-Care 2 Calendar Years 2013 (September – December) and 2014 TRS-Care 3 Calendar Years 2013 (September – December) and 2014

1.2 Claims Review Scope Truven analyzed 100% of TRS’s claims incurred by TRS’s plan participants during the audit period and selected a sample of 45 claims for the short plan year 2013 (September 1, 2013 through December 31, 2013) for testing and review and a sample of 41 claims for testing and review for calendar year 2014. The sample was selected based on various exception areas identified in the population of claims processed during the audit period. These exception areas were based on standard administrative rules such as quantity limits, ample day supply, co-payments, and eligibility specific to the plan benefits described in the contract and other benefit documents.

1.3 Audit Conclusi ons The sample claims were reviewed based on ESI’s responses, and various exceptions were identified. We evaluated all 1,475,803 claims during the audit period for the short plan year 2013 and all 4,689,071 claims for calendar year 2014. Based on ESI’s responses, we identified $272,965 as potential overpayments for the short plan year 2013 and $1,289,904 was identified as potential overpayments for calendar year 2014. The following charts compares the total cost of all exceptions identified by this audit against the total cost of TRS’s entire claims population.

1.4 Short Pla n Year 2013 Overall Audit Results Paid

Total cost of all employee prescription drug claims for SPY2013 $121,667,137

Total cost of claims sampled $21,125

Total dollar errors/exceptions identified in claims sample $941

Total cost of potential claim exceptions identified from the 100% analysis of the entire claims population for SPY2013 (based on the attributes and root causes of Truven’s sample findings)

$272,965

©Truven Health Analytics Inc. Proprietary and Confidential Page 5 of 37

The financial impact of all potential exceptions identified is overpayments of $272,965, representing 0.22% of TRS’s total prescription drug spend for EGWP for the short plan year 2013. The financial impact of all exceptions is below our industry standard threshold of < 2%. Based on the results of our review, we have several recommendations that we believe, if implemented, would improve the overall claims processing accuracy rate and could result in savings to TRS.

1.5 Calendar Year 2014 Overall Audit Results Paid

Total cost of all employee prescription drug claims CY 2014 $426,790,064

Total cost of claims sampled $38,572

Total dollar errors/exceptions identified in claims sample $878

Total cost of potential claims exceptions identified from the 100% analysis for the entire claims population for CY 2014 (based on the attributes and root causes of Truven’s sample findings)

$1,289,904

The financial impact of all potential exceptions identified through this review is overpayments of $1,289,904 representing 0.30% of TRS’s total prescription drug spend for EGWP for calendar year 2014. The financial impact of all exceptions is below our industry standard threshold of < 2%. Based on the results of our review, we have several recommendations that we believe, if implemented, would improve the overall claims processing accuracy rate and could result in savings to TRS.

1.6 Summ ary of Key Findin gs and Obser vations & Recommendations

The following summarizes our key findings and observations and recommendations based on the findings identified in the entire TRS claims population.

1.6.1 Key Findings and Observations Benefit Plan Administration:

Quantity Limitations: Claims exceeded quantity limitation parameters set in the contract. Quantity limitations are designed to be a cost savings opportunity for TRS. After further review of all information provided by ESI, we do not agree that ESI has provided sufficient documentation to support the claims being refilled early and exceeding the plan limitations in the contract.

Duplicate Claims and Early Refills: Claims were processed prior to the plan’s utilization contractual parameters. ESI stated that TRS has contractual language that allows members prescriptions to be refilled if member has less than 21 days supply on hand at mail. Truven disagrees with this rule being applied to claims in which member obtain 30 days supply of medication at mail. This rule would allow claims filled at mail for a 30-day supply to be refilled at 30% utilization. Truven has spoken with TRS and obtained confirmation that the rule stating members can obtain refill when member has less than 21-day supply on hand was intended for claims filled for a 90-day supply of medication.

©Truven Health Analytics Inc. Proprietary and Confidential Page 6 of 37

Recommendations Benefit Plan Administration:

Quantity Limitations: We recommend TRS work with ESI to reconcile claims processed outside of plan parameters. In addition, a discussion of quantity limitations should be undertaken between ESI and TRS. Specific parameters should be outlined and agreed to. This should be discussed as a future cost savings opportunity.

Duplicate Claims and Early Refill: We recommend TRS work with ESI to reconcile claims processed outside of plan utilization parameters. In addition, a discussion of early refill and duplicate drug parameters should be undertaken between ESI and TRS. Specific parameters should be outlined in detail and agreed to. This should be discussed as a future cost savings opportunity.

TAB 5

The information for this agenda item is confidential.

TAB 6

TAB 6A

QUARTERLY INVESTMENT COMPLIANCE TESTING INVESTMENT POLICY STATEMENT (IPS), SECURITIES LENDING POLICY (SLP), PERFORMANCE INCENTIVE PAY (PIP) PLAN, WIRE

TRANSFER PROCEDURES, AND ETHICS POLICIES CALENDAR QUARTER ENDED SEPTEMBER 30, 2016, EXCEPT AS NOTED

Legend: Red - Significant to TRS Orange - Significant to Business Objectives Yellow - Other Reportable Exception Green - Positive Test Result/ No Exception

November 15, 2016 Project #17-302

1. Board Reports All required information is reported to the TRS Board of Trustees

2. Investment Selection and Approval Investments made are within delegated limits and established selection criteria

3. Other (IPS, SLP, PIP, wire transfers, other reporting) Risk limits are followed for other investment programs and activities

4. Ethics Policies Ethics filing and reporting requirements are met

Management Responses

Management Assertions

Test Results

Compare Board reports to IPS requirements

Trace sample information included in Board reports to supporting documentation

Obtain evidence of monitoring of the securities lending agent and the program performance

Verify wire transfers are authorized and supported

Test accuracy of Internal Public Markets PIP calculations for the quarter ended 6/30/2016.

Obtain senior management disclosure about known compliance violations

Obtain evidence that financial disclosures were made to the Texas Ethics Commission

Obtain evidence that financial service providers filed annual disclosure statements on conflicts of interest

Trace investments approved by the Internal Investment Committee (IIC) to supporting documentation

Compare approval limits of new investments with IPS

Obtain evidence that Placement Agent Questionnaires (PAQs) were received prior to investing

N/A

Business Objectives

Business Risks

Agreed-Upon Procedures

Board is not informed of key investment decisions or critical information

Risks exceed Board-established tolerances or management policies and procedures

All required information is reported to the Board

Programs are within risk limits and activities follow established policies and procedures

N/A

Ethics policy requirements are not completed or filed

Ethics policies and requirements are being followed

Approvals and fundings exceed delegated limits

Approvals and fundings are within delegated limits and made for qualified managers

All requirements of the IPS, SLP, PIP, and wire transfer procedures were met

N/A N/A

All ethics filing and reporting requirements tested were met

All reporting requirements were met

Documentation provided support for the reports tested

All investments tested were in compliance with approval limits

PAQs were obtained for all investments tested

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 1

November 15, 2016 Carolina de Onis, TRS General Counsel Subject: Report on Independent Testing of Compliance We have completed the Quarterly Investment Compliance Testing for the quarter ended September 30, 2016, as included in the Fiscal Year 2017 Audit Plan. The scope of this engagement included the requirements of the Investment Policy Statement (IPS), Securities Lending Policy (SLP), Employee Ethics Policy, Board of Trustees Ethics Policy, Code of Ethics for Contractors, Wire Transfer Procedures, and Performance Incentive Pay (PIP) Plan. We performed the procedures that were agreed to by the TRS Legal Services division. These procedures include tests that supplement the current compliance monitoring procedures performed by State Street and the Chief Compliance Officer. This agreed-upon procedures engagement was performed in accordance with generally accepted government auditing standards contained in the Government Auditing Standards issued by the Comptroller General of the United States. The sufficiency of the agreed-upon procedures performed is solely the responsibility of the specified users of the report. Consequently, we make no representations regarding the sufficiency of the procedures described in Appendix A either for the purpose for which this report has been requested or for any other purpose. Our testing procedures and results are included in Appendix A. Internal Control Structure We were not engaged to and did not perform an examination of the internal controls nor the operating effectiveness pertaining to the subject areas tested. Accordingly, we do not express an opinion on the suitability of the design of internal controls nor the operating effectiveness of the subject areas tested. Had we performed additional procedures, or had we made an examination of the system of internal control, other matters might have come to our attention that would have been reported to you. This report relates only to the procedures specified below and does not extend to the internal control structure. This report is intended solely for information and use by TRS management, the Board of Trustees, and oversight agencies, and is not intended to be and should not be used by anyone other than those specified parties. However, this report is a matter of public record and its distribution is not limited.

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 2

* * * * * We express our appreciation to management and key personnel of the Investment Management Division, Investment Accounting, and Legal Services for their cooperation and professionalism shown to us during this quarterly testing. _____________________________ _______________________________ Amy Barrett, CIA, CPA, CISA Hugh Ohn, CFA, CPA, CIA, FRM Chief Audit Executive Director of Investment Audit Services _____________________________ Rodrigo Dominguez Internal Auditor

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 3

APPENDIX A

AGREED-UPON PROCEDURES AND RESULTS

STEP #

OBJ. # TEST PURPOSE TEST DESCRIPTION TEST RESULT MANAGEMENT RESPONSE

1 1 IPS Article 1.7a - 1.7o – Obtain evidence that all requirements were reported to Board of Trustees. Quarterly reporting requirements include investment performance, asset class exposures, and external investments under consideration. Semi-annual reports include outstanding derivatives, leverage, and liquidity positions, and risk limits

Obtain all information required to be reported to Board of Trustees and compare to reporting requirements per Investment Policy Statement (IPS)test

Information required to be reported to Board of Trustees complied with IPS requirements.

No response required

2 2 IPS Article 2.6 – Verify that Investment Management Division (IMD) evaluated hedge fund classification

Select sample of approved investments in hedge funds and external managers

Obtain analysis indicating whether each investment is hedge fund or not. If analysis is unavailable, inconclusive, or erroneous, report that result

For any analysis requiring Board approval of classification, obtain Board minutes to test whether approval was obtained

Each of approved investments in hedge funds and external managers tested had analysis indicating whether investment was a hedge fund or not. No Board approval was required.

No response required

3 2 IPS Article 2.7a – Verify that the Internal Investment Committee (IIC) approved all private and relevant public markets fund investments

For the private and public markets funds approved during the quarter, obtain existence of IIC approval

Inquire with Director of External Public Markets whether portfolios were adjusted for the purposes of rebalancing or adjusting risks

If funds added, test if such additional investments or allocations did not exceed 2% of Hedge Fund

IIC approval existed for all funds approved during the quarter. Funds added to previously approved investments or purposes of rebalancing or adjusting risk did not exceed 2% of associated portfolios.

No response required

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 4

STEP #

OBJ. # TEST PURPOSE TEST DESCRIPTION TEST RESULT MANAGEMENT RESPONSE

IPS Article 2.7g – Verify funds added to previously approved investments for purposes of rebalancing or adjusting risk did not exceed 2% of associated portfolios

Portfolio, External Manager Portfolio, or Other Absolute Return Portfolio (as appropriate) per investment on a monthly basis

Obtain documentation from IMD staff supporting rebalancing analytics.

4 2 IPS Article 7 – Obtain evidence that new investments in emerging managers meet requirements

Test sample of approved investments to verify: Each is independent private investment

management firm with less than $2 billion Each has a performance track record as a firm of

less than 5 years, or both TRS commitment did not exceed 40% of fund

size

There were no emerging manager investments during the testing period.

No response required

5 2 IPS Article 12 - Obtain evidence of existence of placement agent questionnaire (PAQ) for each new investment selected for testing and test for inclusion in summary report to the Board

For each investment selected for testing, verify that IMD obtained responses to the questionnaire

Obtain evidence that IMD compiled responses to the questionnaires and reported all results to the Board at least semi-annually

Each investment tested had a completed questionnaire and was included in the summary report to the Board.

No response required

6 2 IPS Appendix B – Obtain evidence that investments approved are within policy limits

Select sample of approved investments and obtain tearsheet for each, observe the approved amounts are within authorized limits a) Initial allocation – .50% b) Additional or follow-on – 1% c) Total Manager Limits – 3% d) Total limit each manager organization – 6%

Obtain documentation from IMD staff that supports the calculations of the authorized limits

Inquire if any “Special Investment Opportunities” were made for the quarter

For the sample investments tested, no manager or partner organization exceeded the authorized limits and documentation existed for IMD staff calculations of authorized limits. There were no Special Investment Opportunities.

No response required

7 3 Quarterly Compliance Certification – Obtain evidence that all known

Confirm with the Chief Compliance Officer that she has received compliance certification from IMD profit center managers, Legal Investment

Obtained confirmation from the Chief Compliance Officer. No compliance

No response required

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 5

STEP #

OBJ. # TEST PURPOSE TEST DESCRIPTION TEST RESULT MANAGEMENT RESPONSE

compliance violations have been reported by IMD managers and Investment Legal staff

staff, and CIO regarding any known compliance violations occurred during the testing period

exceptions were identified as a result of the quarterly compliance certification.

8 3 Wire Transfers – Verify wire transfers are authorized and properly supported

Obtain wire transfer reports for testing period, select sample of wire transfers, and test that supporting documentation, including manager authorizations, exists for each

All wire transfers tested were properly authorized and correct amounts were wired.

No response required

9 3 Securities Lending Policy – Obtain evidence that IMD staff monitored the progress of the securities lending program and performance of lender

Obtain evidence for the following securities lending policy requirements: Sec. 3.1. Securities eligible for lending Sec. 3.3 Collateral received

TRS loaned only eligible securities. All collateral received was cash or government securities.

No response required

10 3 Performance Incentive Pay Plan (PIP) – Verify that investment performance results used in quarterly Internal Public Markets (IPM) portfolio matches data from TRS financial applications and custodian bank and that the excess return calculations for individual portfolio managers and sector managers are correct

Trace quarterly IPM individual component calculation spreadsheet to TRS financial performance application data and TRS custodian bank data.

Test whether employee assignments were approved by Senior Director in TRS IPM prior to quarter start by obtaining approval email from Senior Director in TRS IPM to Investment Operations Performance Analyst. If any assignment changes are included in the approval, compare the approved changes to the assignments in the quarterly IPM individual component calculation spreadsheet.

Test whether formulas in the quarterly IPM individual component calculation spreadsheet are correct by recalculating investment return totals by portfolio manager and sector manager, and comparing total investment returns to returns provided by the TRS Custodian Bank.

There were no data, employee assignment, or formula errors included in the quarterly IPM individual component calculation spreadsheet. Thus, excess return calculations for individual portfolio managers and sector managers for the IPM portfolio were correct for the quarter ended June 30, 2016.

No response required

11 4 Employee Ethics Policy – Obtain evidence that the

Obtain evidence that the TRS Executive Director filed a personal financial statement with the

The Executive Director’s 2015 personal financial statement was filed with the

No response required

TRS Internal Audit November 15, 2016 Quarterly Investment Compliance Testing Page 6

STEP #

OBJ. # TEST PURPOSE TEST DESCRIPTION TEST RESULT MANAGEMENT RESPONSE

Executive Director filed a personal financial statement with the Texas Ethics Commission

Texas Ethics Commission for the year ended December, 31, 2015. Ensure that that the filing was made prior to the April 30th deadline.

Texas Ethics Commission. The document was dated prior to the April 30th deadline.

12 4 Code of Ethics for Contractors – Obtain evidence that all TRS brokers, financial advisors, and financial service providers filed annual disclosure statements with TRS General Counsel.

Sec. III.B. Obtain evidence that all TRS brokers, financial advisors, and financial service providers complied with the Code of Ethics for Contractors by filing annual disclosure statements with the TRS General Counsel. Annual filing deadline is April 30th.

All TRS brokers, financial advisors, and financial service providers filed required annual disclosure statements by the due date.

No response required

Note: Testing procedures for the Investment Policy Statement (IPS), Securities Lending Policy (SLP), Employee Ethics Policy, Code of Ethics for Contractors, and Wire Transfer Procedures are for the activities for the quarter ended September 30, 2016. Testing procedures for the Performance Incentive Pay Plan are for the quarter ended June 30, 2016.

TAB 6B

AUDIT OF TRS ADMINISTRATION OF 403(b) PROGRAM November 18, 2016

TRS Internal Audit Department

Project #: 17-601

Companies not meeting certification criteria included in TRS company list

Products not meeting qualification criteria included in TRS product list

Uncertified companies selling products to participants

No or delayed referral on complaints received

No investigation of complaints by regulatory agencies

TRS not informed of complaint resolution

TRS not taking proper action based on resolution

Fee caps not established Fee caps established not

competitive Product fees charged

exceeding the fee caps 403(b) fees collected by

TRS are credited to other funds

Fees collected are used for non-403(b) expenses

Board adoption of fee caps Use of consultant for market

studies on investment product fees

Administration cost analysis 403(b) program budget Financial report on 403(b)

program 403(b) expense monitoring

Financial strength checks completed by Texas Department of Insurance

TRS staff’s company checks on State Securities Board website

Certification and qualification forms required

Publication of certified companies and qualified products on TRS website

Board adoption of fee caps Administration cost analysis 403(b) program budget Financial report on 403(b)

program

Financial strength checks TRS staff’s company

checks Certification and

qualification forms required annual demonstration by

providers

Management controls are operating effectively. However, controls related to determining administration cost for fee-setting purposes could be improved.

Management controls are operating effectively. However, controls related to annual demonstration of provider’s qualifications could be improved.

Require records of provider’s verification of license and qualification as part of annual demonstration

Start tracking the cost of program administration for fee-setting purpose

Will consider this recommendation as part of administrative rule review

TRS rules and polices on complaint reporting

Records of complaints received and referred maintained

Quarterly reporting requirement from Texas Department of Insurance

Records of complaints received and referred maintained

Quarterly reporting requirement from Texas Department of Insurance

Management controls are operating effectively to achieve business objective.

None

NA

Legend of Results: Red - Significant to TRS Orange - Significant to Business Objectives Yellow - Other Reportable Issue Green - Positive Finding or No Issue

Business Objectives

Business Risks

Management Controls

Results

Recommended Actions

Management Responses

Ensure that fee caps of investment products are competitive to the market and that TRS fees to investment companies reflect administration costs

Controls Tested

Maintain lists of certified 403(b) companies and products that meet the requirements of governing laws and rules

Refer complaints received to appropriate regulatory agencies and ensure that they are properly addressed

Agrees – Has already begun tracking staff time to capture the cost of administration

TRS Internal Audit November 18, 2016 Audit of TRS Administration of 403(b) Program Page 1

November 18, 2016 Audit Committee, Board of Trustees Brian Guthrie, Executive Director

EXECUTIVE SUMMARY We have completed the audit of the 403(b) Program, as included in the Fiscal Year 2017 Audit Plan. Primary business objectives related to TRS’ administration of the 403(b) Program are as follows:

To maintain lists of qualified 403(b) companies and products that meet the requirements of governing laws and TRS rules

To refer complaints received to appropriate regulatory agencies and ensure that they are properly addressed

To ensure that fee caps of investment products are competitive as compared to the market and that TRS fees to investment companies reflect administrative costs