Embed Size (px)

Citation preview

1

Australia and New Zealand Banking Group Limited

Peter Marriott, Chief Financial Officer

Ross Glasscock, Executive Treasurer, Group Wholesale Funding

Rick Moscati, Executive Treasurer, Balance Sheet Management

Shaun Coughlan, Executive Treasurer Global Money Markets

January 2003

2

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

3

ANZ Group Overview

• One of the four major Australian banks

• Established in 1835

• Full range financial service provider

• Distinctive specialist business strategy – 17 separate businesses

• Assets (as at FYE 2002) A$183.1bn.(US$102.8bn.)

• Market Cap. (as at 31/12/02) A$26.1bn.(US$14.7bn.)

• Tier 1 Capital Ratio 7.9%

• Credit Ratings AA-/Aa3 (Stable)

4

Highlights

• Performing well - record profit of $2,168m *

– EPS Growth 17%– ROE 21.6%– Cost Income ratio 46.0%

• Strong capital position, well provisioned

• Record staff satisfaction – up 16% to 78%

• Exciting Restoring Customer Faith pilot

• Specialised business strategy operating well

• Stretch target for 2003 of 10% EPS growth

* Before gains from “significant transactions”

5

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

6

Building a credible track record

1024 1106

14801747 1870

2168

400

900

1400

1900

2400

1997

1998

1999

2000

2001

2002

$m NPAT21.6

20.219.3

17.215.9

17.6

1012141618202224

1997

1998

1999

2000

2001

2002

% ROE

40

45

50

55

60

65

1997

1998

1999

2000

2001

2002

012345678

Income/Expenses

101171

198100

84

137

0

50

100

150

200

250

1997

1998

1999

2000

2001

2002

Total Shareholder Return$b%

Cost - Income Ratio

7

Leading reputation for disclosure and transparency

• Profit and Loss statements for all 17 Business Units

• Enhanced disclosure on :– Critical accounting policies– Special purpose and off balance sheet vehicles– Deferred acquisition costs, software assets, and deferred income– Accounting for derivates and hedging

• Excellent disclosure on credit quality

• External recognition, including awards for:– Best communication of shareholder value– Best management of continuous disclosure– Best results/analyst briefings

8

Our growth philosophy unchanged – but primary focus on organic out-performance

Organic out-performance

Portfolioreshaping

Transformationalmoves

• Extend specialisation• Restoring Customer Faith• Increase share of wallet• Drive productivity • Revenue growth

materially higher than expense growth

• Take business units to sustainable leadership positions

• Build a range of strategic options

Our targets

• Invest in high growth areas• Build specialist capabilities• Exit weak positions• Risk reduction

• Step changes in positioning• Creating new growth options• Proactively shaping industry

9

Opportunities for growth

Personal Banking• Full rollout Restoring Customer Faith• Expand network in growth locations

• Autonomous customer organisation• Rollout Restoring Customer Faith

Wealth Management • Maintain high investment spending• Lower profit volatility from ING ANZ JV

Institutional & ANZIB • Leverage leading relationship position• Leverage business integration synergies

Corporate & SME• Investment spending budgeted• Leverage business integration synergies

Opportunity Approach

New Zealand

10

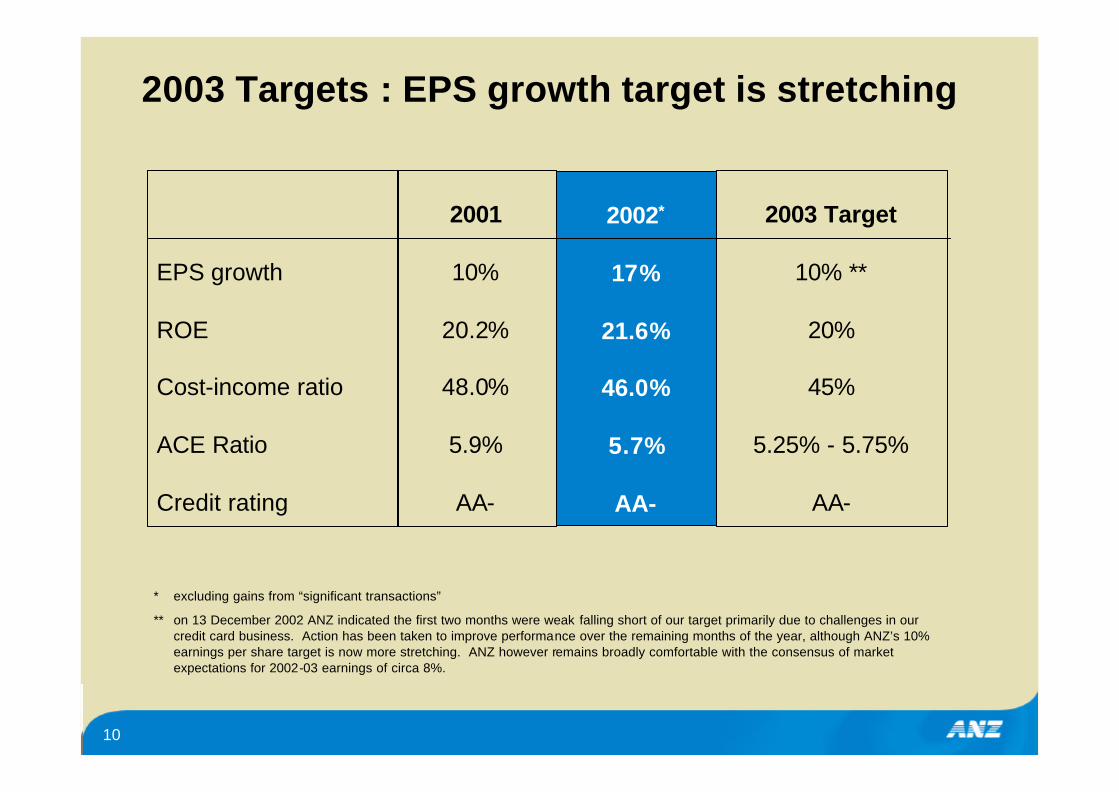

2003 Targets : EPS growth target is stretching

EPS growth

ROE

Cost-income ratio

ACE Ratio

Credit rating

2003 Target

10% **

20%

45%

5.25% - 5.75%

AA-

2001

10%

20.2%

48.0%

5.9%

AA-

2002*

17%

21.6%

46.0%

5.7%

AA-

* excluding gains from “significant transactions”

** on 13 December 2002 ANZ indicated the first two months were weak falling short of our target primarily due to challenges in our credit card business. Action has been taken to improve performance over the remaining months of the year, although ANZ’s 10% earnings per share target is now more stretching. ANZ however remains broadly comfortable with the consensus of market expectations for 2002-03 earnings of circa 8%.

11

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

12

A solid result, driven primarily by revenue growth

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

1870

2001

Interest Income

185 Provisioning (79)

Non Interest Income

223

Expenses(61)

Tax & OEI30 2168

$m

2002

Before one-offs

Significant transactions

154 2322

2002

Tax rate change $79

Tax on higher profit $(49)

13

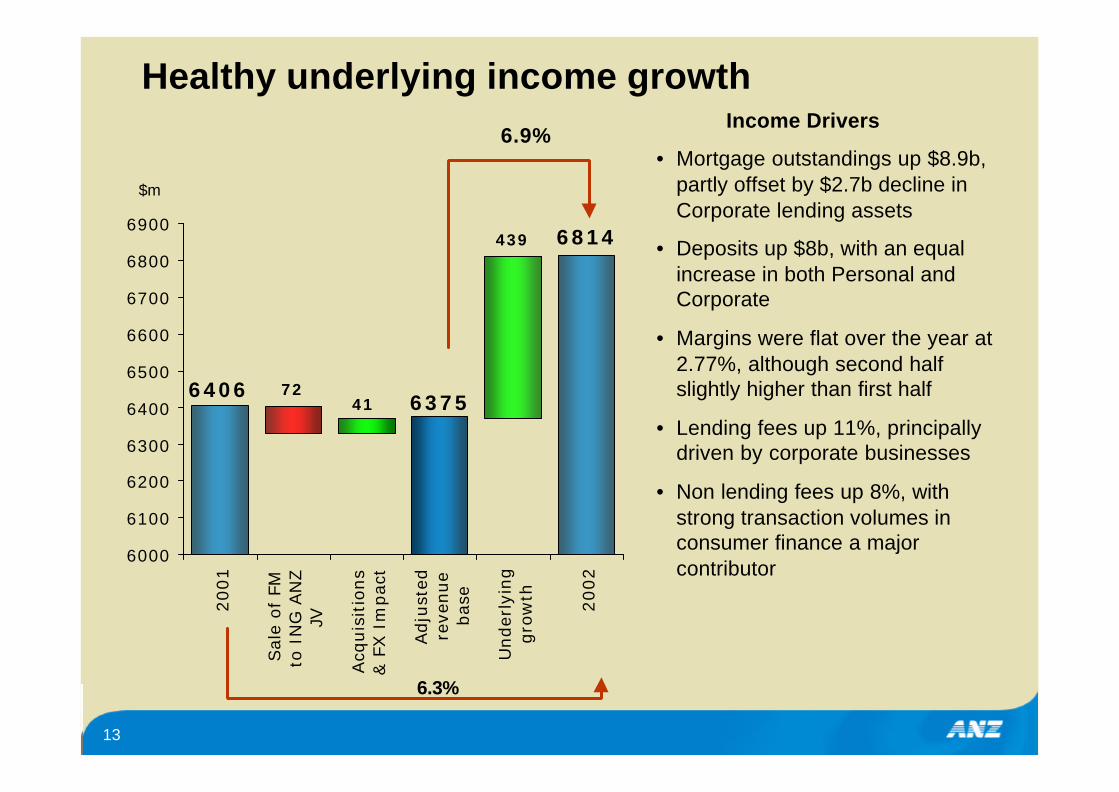

Healthy underlying income growth

64066375

6814

4172

439

6000

6100

6200

6300

6400

6500

6600

6700

6800

69002001

Sale

of

FMto

IN

G A

NZ

JV

Acq

uis

itio

ns

& F

X I

mpact

Adju

sted

reve

nue

bas

e

Under

lyin

ggro

wth

2002

$m

• Mortgage outstandings up $8.9b, partly offset by $2.7b decline in Corporate lending assets

• Deposits up $8b, with an equal increase in both Personal and Corporate

• Margins were flat over the year at 2.77%, although second half slightly higher than first half

• Lending fees up 11%, principally driven by corporate businesses

• Non lending fees up 8%, with strong transaction volumes in consumer finance a major contributor

Income Drivers6.9%

6.3%

14

0 100 200 300

A diversified portfolio performing well

2002 NPAT $m

NPAT increase

NPAT decrease

Prior period NPAT

2nd half NPAT $m

0 100 200 300

Personal Banking AustraliaMortgagesInstitutional BankingTransaction ServicesSmall Med BusinessCorporate BankingPersonal Banking NZConsumer FinanceAsset FinanceForeign ExchangeStructured FinanceGroup TreasuryWealth ManagementCorp Finance & AdvisoryAsia/Pac Personal BankingCapital MarketsING JV/ANZ FM

15

309

241246258 252 256

301290

434242

36 35

4245

40

0

50

100

150

200

250

300

350

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar02

Sep-02

0

10

20

30

40

50

60

70

80ELP adjustmentELP $ELP BP's

Provisioning charge reflects conservative management

ELP Charge$m bp’s • ELP portfolio level

adjustment continued

• reflecting ongoing global economic uncertainty

• calculated as one notch downgrade across GSF portfolio

• Domestic ELP rate declining

• ELP adjustment likely to continue until international defaults stabilise

16

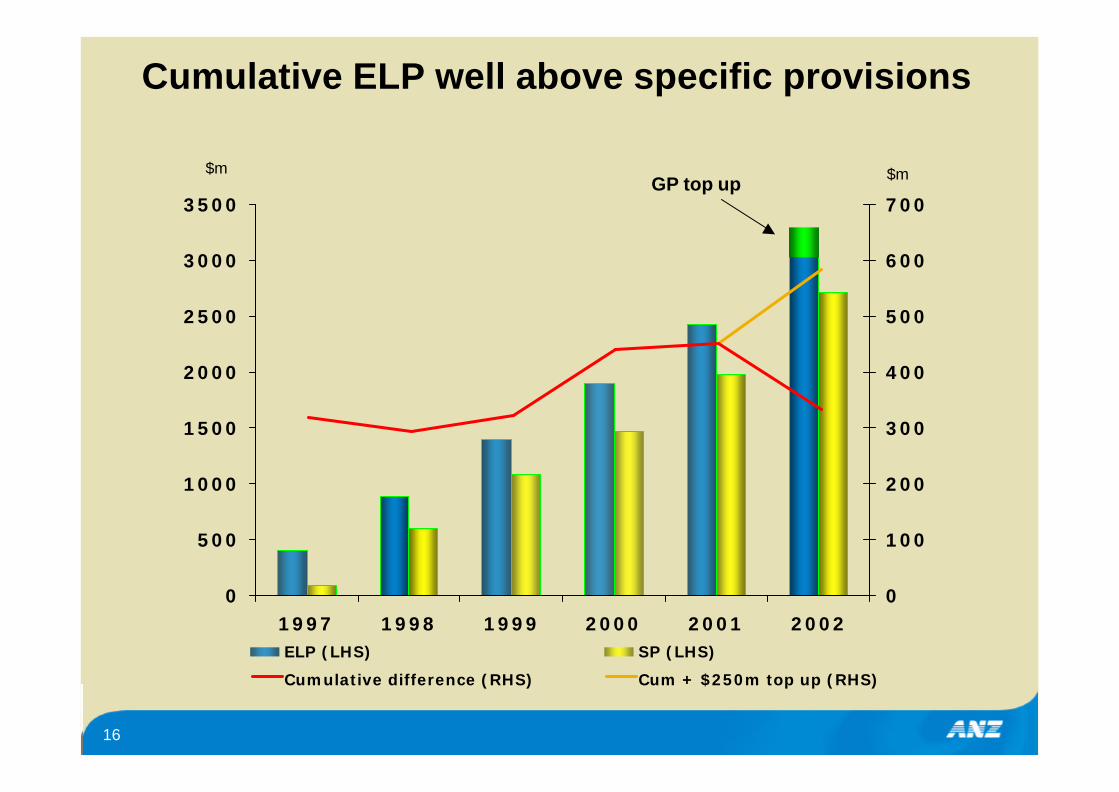

Cumulative ELP well above specific provisions

0

500

1000

1500

2000

2500

3000

3500

1997 1998 1999 2000 2001 20020

100

200

300

400

500

600

700

ELP (LHS) SP (LHS)

Cumulative difference (RHS) Cum + $250m top up (RHS)

GP top up$m $m

17

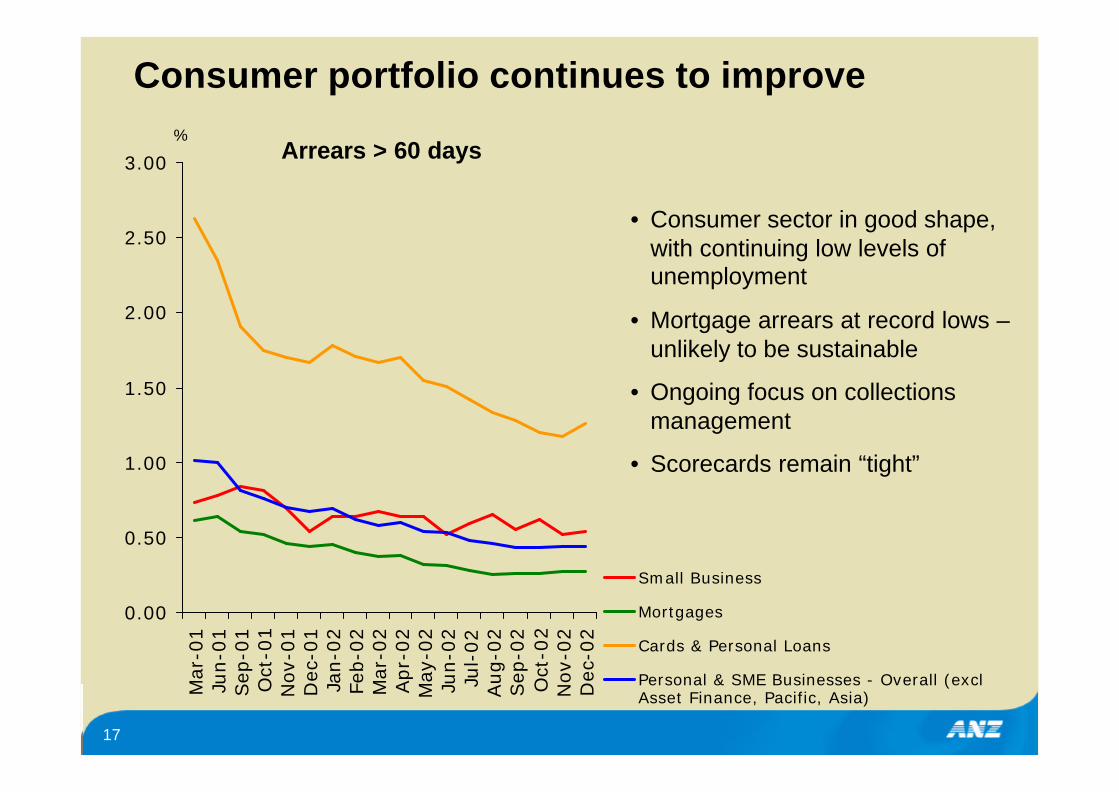

Consumer portfolio continues to improve

Arrears > 60 days%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Mar

-01

Jun-0

1Sep

-01

Oct

-01

Nov-

01

Dec

-01

Jan-0

2Fe

b-0

2M

ar-0

2Apr-

02

May

-02

Jun-0

2Ju

l-02

Aug-0

2Sep

-02

Oct

-02

Nov-

02

Dec

-02

Small Business

Mortgages

Cards & Personal Loans

Personal & SME Businesses - Overall (exclAsset Finance, Pacific, Asia)

• Consumer sector in good shape, with continuing low levels of unemployment

• Mortgage arrears at record lows –unlikely to be sustainable

• Ongoing focus on collections management

• Scorecards remain “tight”

18

Mortgage outlook – slight deterioration

0.000.100.200.300.400.500.600.700.80

Jan-01

May-01

Sep-01

Jan-02

May-02

Sep-02

Jan-03

Home LoanRes Inv Loan

60 day arrears improving%

• ANZ has not allowed FHOG to be the source of minimum equity requirement

• Behavioural scores remain stable

• Scorecards tightened in 2001, resulting in higher quality borrowers

• Unemployment, a key driver of default, continues to trend downwards

• Scenario analysis at 95% confidence suggests loss not exceeding 4-6 bp over next 12 months, compared with ELP of 5 bp

• Based on uncommitted monthly income at time of application, 100% of customers could meet a 1% rise in interest rates, and 97.2% could meet a 2% increase without rearranging affairs

-20

-10

0

10

20

30

40

50

60

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

Sydney

Melbourne

% change House prices well below previous peaks

19

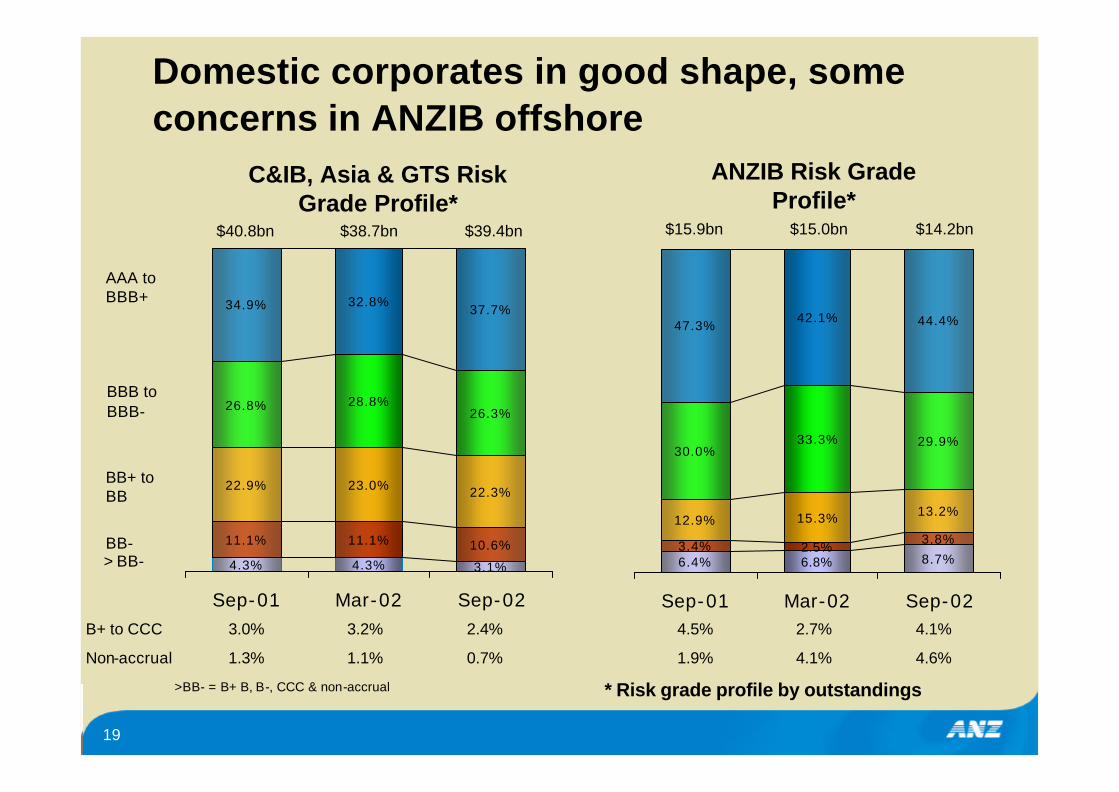

4.3% 4.3% 3.1%

11.1% 11.1% 10.6%

22.9% 23.0% 22.3%

26.8% 28.8%26.3%

37.7%32.8%34.9%

Sep-01 Mar-02 Sep-02

Domestic corporates in good shape, some concerns in ANZIB offshore

>BB- = B+ B, B-, CCC & non-accrual

AAA to BBB+

BBB to BBB-

BB+ to BB

BB-> BB-

$40.8bn $38.7bn

C&IB, Asia & GTS Risk Grade Profile*

B+ to CCC 3.0% 3.2% 2.4% 4.5% 2.7% 4.1%

Non-accrual 1.3% 1.1% 0.7% 1.9% 4.1% 4.6%

$39.4bn

* Risk grade profile by outstandings

6.4% 6.8% 8.7%3.4% 2.5%

3.8%12.9% 15.3% 13.2%

30.0%33.3% 29.9%

44.4%42.1%47.3%

Sep-01 Mar-02 Sep-02

$15.9bn $15.0bn $14.2bn

ANZIB Risk Grade Profile*

20

Specific provisions again impacted by large corporate collapses

0

50

100

150

200

250

300

350

400

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Net specific provisions - $m (LHS)% International SPs (RHS)ELP charge - $m (LHS)

Provisions$m Single

customers2nd half Specific

Provisions by size

• Only 4 customers with specific provisions greater than $10m

< $5m

$5m - $10m

$10m - $20m

$20m - $50m

1customer

1customer

>$100m2

customers

21

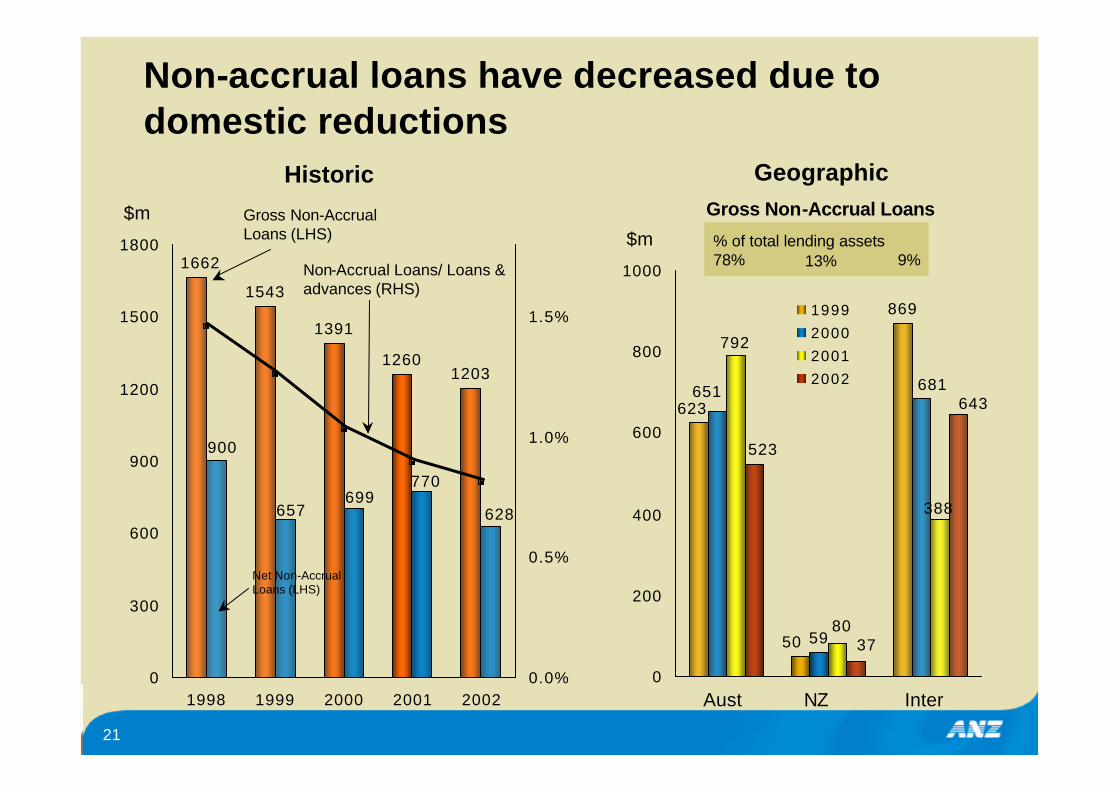

869

5950

623651 681

388

80

792

523

37

643

0

200

400

600

800

1000

1999

2000

2001

2002

1543

1391

12601203

1662

628

770699

657

900

0

300

600

900

1200

1500

1800

1998 1999 2000 2001 20020.0%

0.5%

1.0%

1.5%

Non-accrual loans have decreased due to domestic reductions

Gross Non-Accrual Loans (LHS)

Net Non-Accrual Loans (LHS)

$m

Non-Accrual Loans/ Loans & advances (RHS)

Historic

Aust InterNZ

GeographicGross Non-Accrual Loans

$m9%78%

% of total lending assets13%

22

Offshore SCCLs now in place

60%

100%

Australia/New Zealand OffShore Corporates

Comparative SCCL Customer Limits

25%

75%

100%

80%

> 100%Security

< 100%Security

Lending type SCCL % for offshore Corporates (excl. GSF)

indicative based on BBB- grading

Direct Exposure(Including on and Off Balance sheet)

Indirect or Contingent Exposure

Market Related

Exposures

Capped at AUD 300m

Capped at AUD 100m

GSF Direct Exposures capped at AUD 450m for > 100% Security and AUD 200m for < 100% Security

23

Overall - provisioning levels strong

0.96

0.82

0.90

1.06

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

ANZSep 02

CBAJun 02

NABSep 02

WBCSep 02

GP/RWA’s%

0

20

40

60

80

100

120

140

160

180

200

ANZ

Austra

liaCan

ada

Germany Fra

nce UK

%Provisions/Non Accrual

Loans

Source: CSFB

24

3.25%

3.75%

4.25%

4.75%

5.25%

5.75%

6.25%

ANZ NAB CBA WBC*

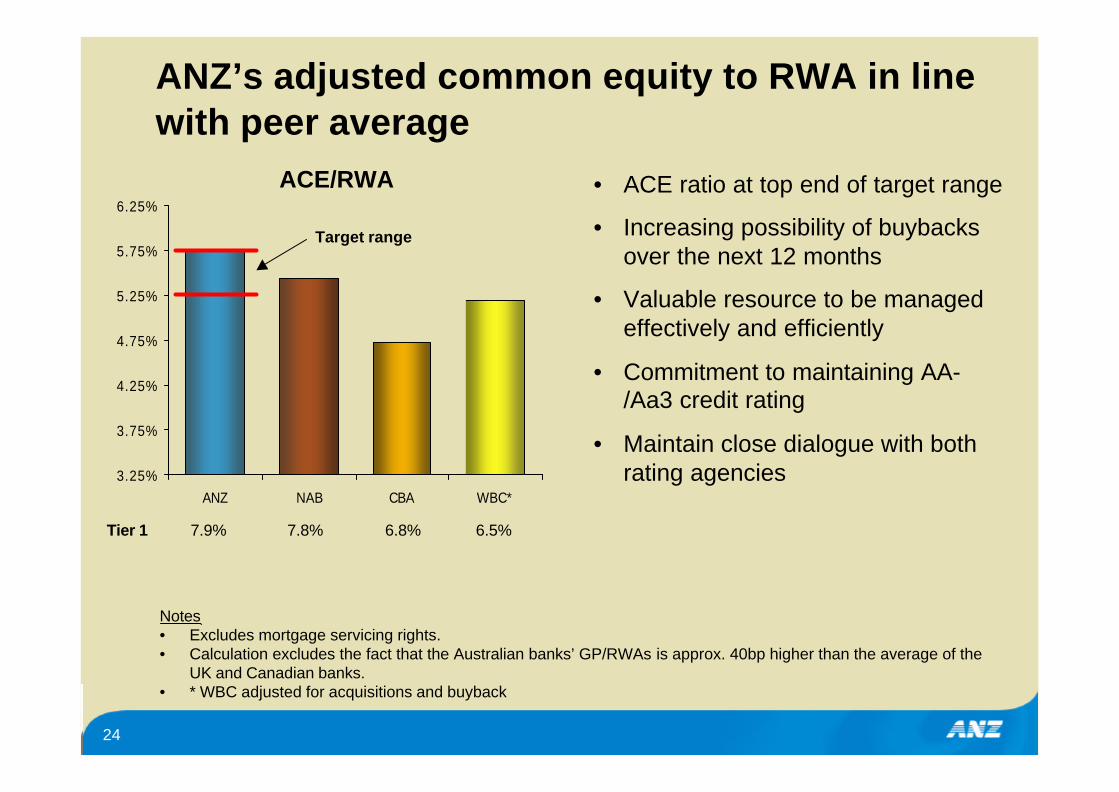

ANZ’s adjusted common equity to RWA in line with peer average

Notes• Excludes mortgage servicing rights.• Calculation excludes the fact that the Australian banks’ GP/RWAs is approx. 40bp higher than the average of the

UK and Canadian banks.• * WBC adjusted for acquisitions and buyback

Target range

• ACE ratio at top end of target range

• Increasing possibility of buybacks over the next 12 months

• Valuable resource to be managed effectively and efficiently

• Commitment to maintaining AA-/Aa3 credit rating

• Maintain close dialogue with both rating agencies

ACE/RWA

Tier 1 7.9% 7.8% 6.8% 6.5%

25

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

26

Determining the term debt funding requirement

• Importance of stable funding base

• Analysed domestic and offshore peer group

• Businesses required to meet a self funding ratio – CFI (customer to total funding)

• Wholesale funding ratio – TFI (term wholesale funding to term lending)

• Securitisation as a balance sheet tool

Customer Funding Indicator

50%

55%

60%

65%

Sep-2000 Sep-2001 Mar-2002 Jun-2002 Sep-2002

CFI Minimum

Term Funding Indicator

0%

5%

10%

15%

20%

Sep-1996

Sep-1997

Sep-1998

Sep-1999

Sep-2000

Sep-2001

Sep-2002

TFI Minimum

27

Term wholesale funding objectives

• Maintain continued access to major international debt capital markets

• Continue diversification by markets, investors, currency and structures

• Promote recognition of the ANZ’s credit credentials through regular debt investor presentations

• Periodic benchmark issues

• Build liquid yield curves

• Promote transparency of issuance

28

The strategy to date has worked

• Highest penetration of € investors of any of our domestic peers

• Diverse investor base

• Strong correlation between successfully executed public issuance and reverse enquiries received

• Most proactive of Australian major banks to regularly update domestic and offshore debt investors

• Access during difficult market conditions

• Credit line availability

• Rating agencies focus on liability management

29

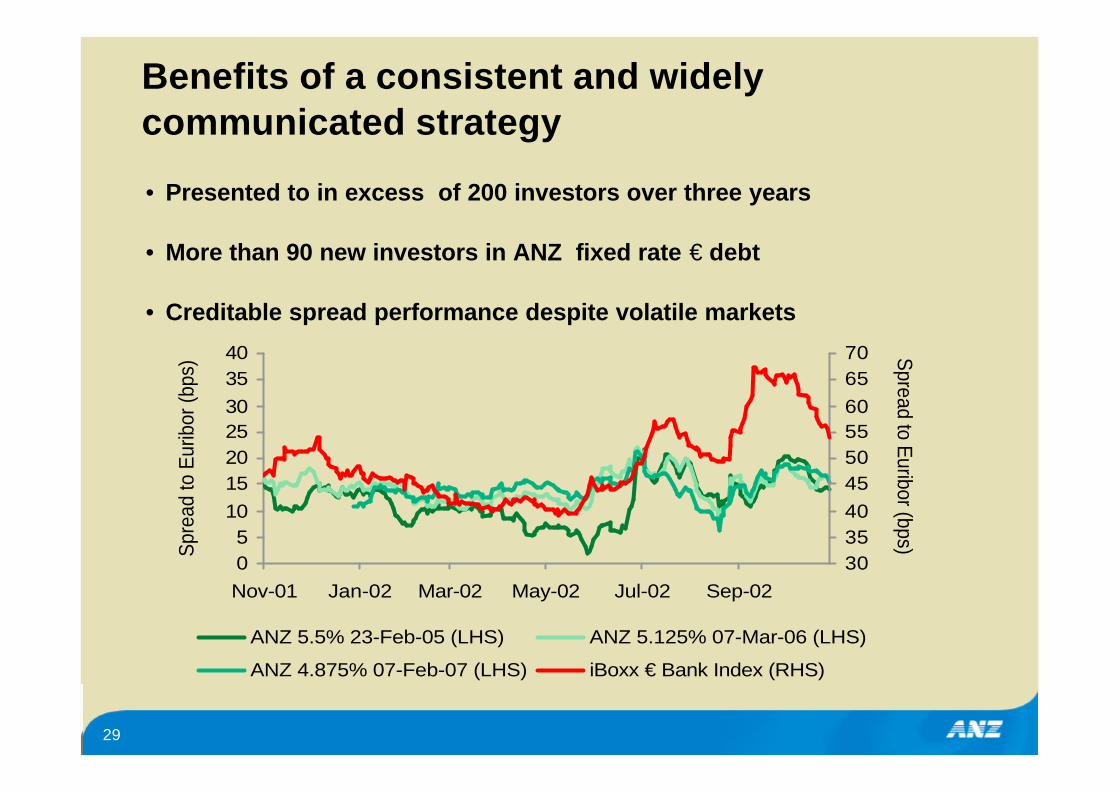

Benefits of a consistent and widely communicated strategy

• Presented to in excess of 200 investors over three years

• More than 90 new investors in ANZ fixed rate € debt

• Creditable spread performance despite volatile markets

05

10152025303540

Nov-01 Jan-02 Mar-02 May-02 Jul-02 Sep-02

Spre

ad to

Eur

ibor

(bps

)

303540455055606570 Spread to Euribor (bps)

ANZ 5.5% 23-Feb-05 (LHS) ANZ 5.125% 07-Mar-06 (LHS)

ANZ 4.875% 07-Feb-07 (LHS) iBoxx € Bank Index (RHS)

30

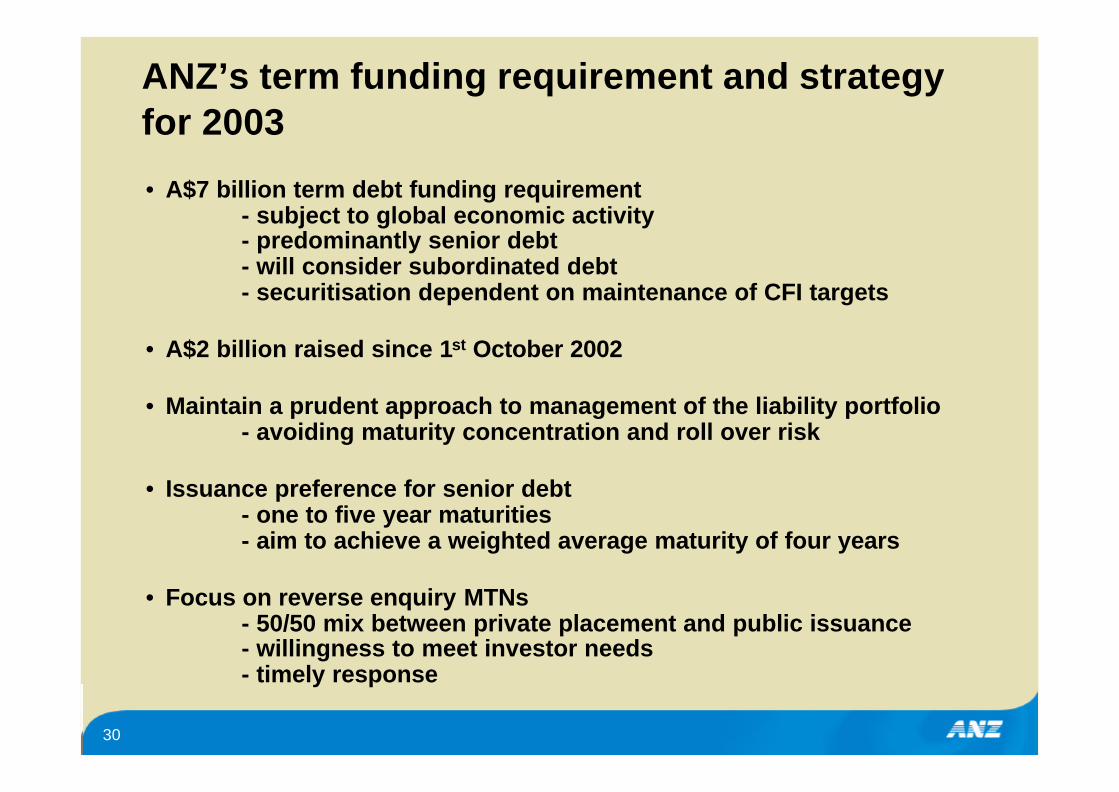

ANZ’s term funding requirement and strategy for 2003

• A$7 billion term debt funding requirement- subject to global economic activity- predominantly senior debt- will consider subordinated debt- securitisation dependent on maintenance of CFI targets

• A$2 billion raised since 1st October 2002

• Maintain a prudent approach to management of the liability portfolio- avoiding maturity concentration and roll over risk

• Issuance preference for senior debt- one to five year maturities- aim to achieve a weighted average maturity of four years

• Focus on reverse enquiry MTNs- 50/50 mix between private placement and public issuance- willingness to meet investor needs- timely response

31

Achievable, based on previous experienceFinancial Year 2001

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AUD USD HKDGBP JPY EUR

Financial Year 2002

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AUD USD HKD GBPEUR NOK SGD NZDCAD

Pub

licP

rivat

e

Pub

licP

rivat

e

32

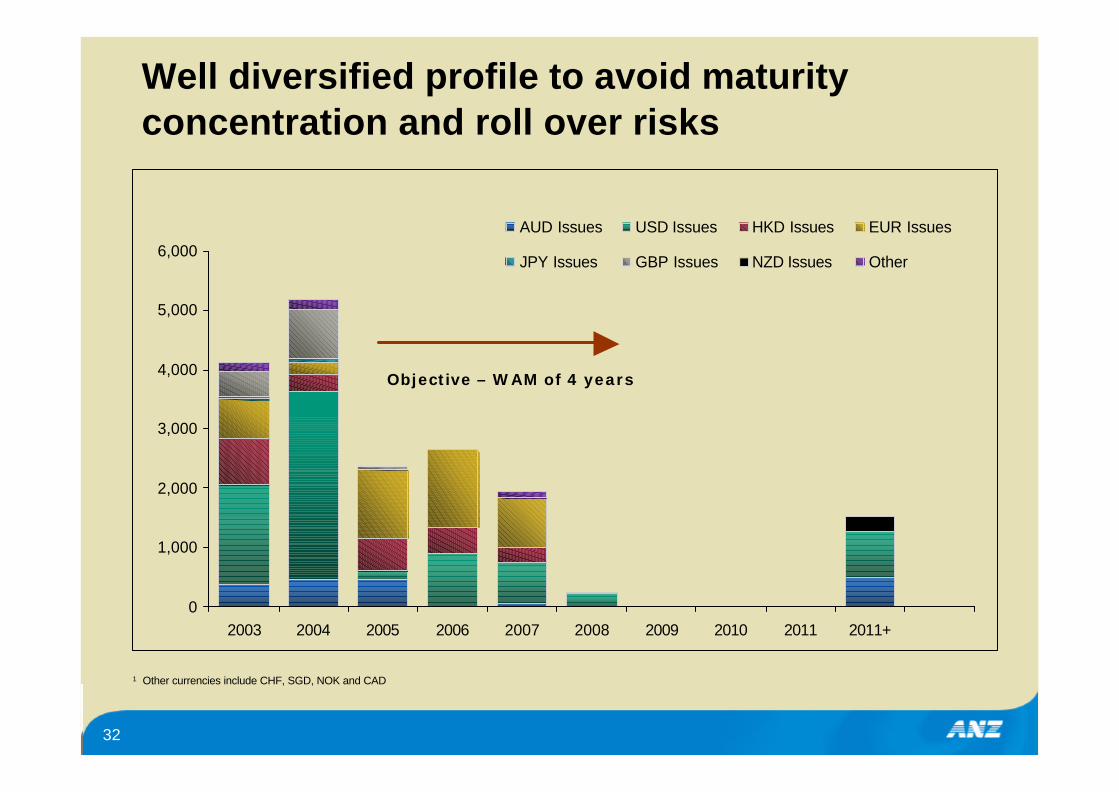

Well diversified profile to avoid maturity concentration and roll over risks

0

1,000

2,000

3,000

4,000

5,000

6,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2011+

AUD Issues USD Issues HKD Issues EUR Issues

JPY Issues GBP Issues NZD Issues Other

1 Other currencies include CHF, SGD, NOK and CAD

Objective – WAM of 4 years

33

Potential to issue Lower Tier II

• Opportunity to restructure capital composition

• Underweight Lower Tier II relative to domestic peer group

• Amortisation of subordinated debt portfolio under APRA guidelines

• Last issued Lower Tier II in Europe in 1997

Capital ratios

0%

5%

10%

Tier 2 2.78% 4.58% 3.76% 3.72%

Hybrid 0.97% 0.49% 1.08% 0.36%

ACE 5.74% 4.73% 5.37% 4.80%

ANZ CBA NAB WBC

Adjusted Common Equity

3%

4%

5%

6%

ANZ CBA NAB WBC SGB

Average (excl. ANZ)

34

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

35

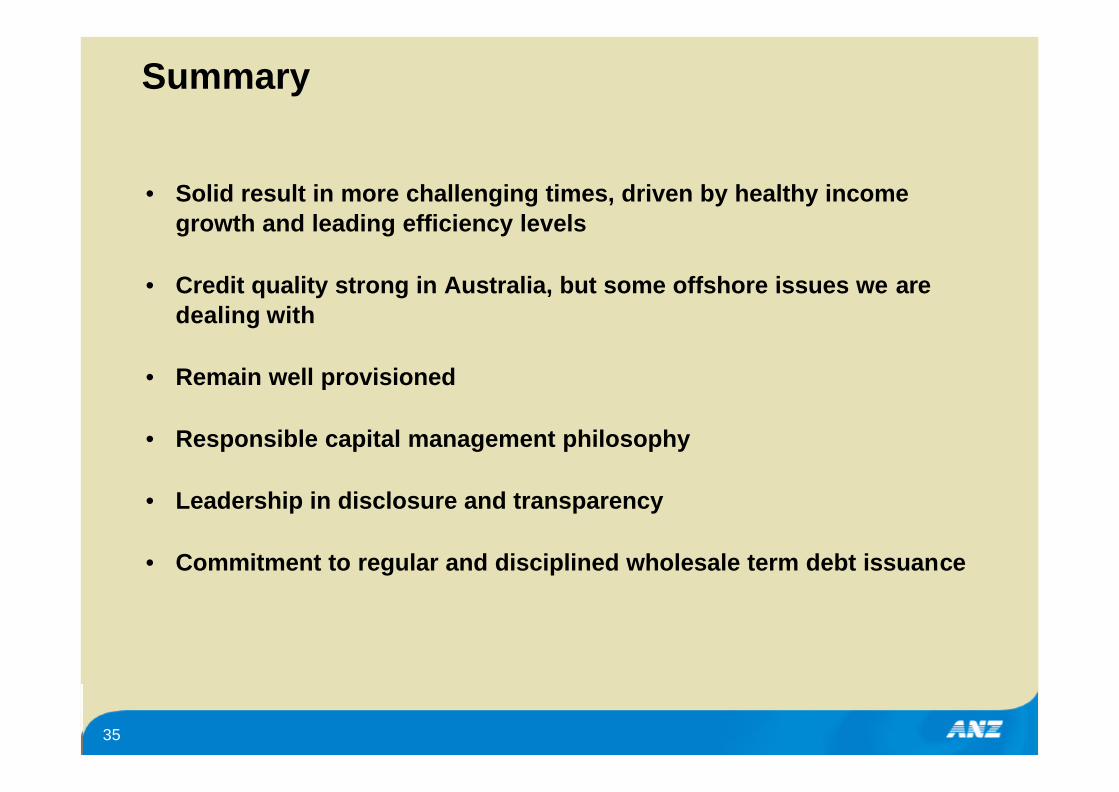

Summary

• Solid result in more challenging times, driven by healthy incomegrowth and leading efficiency levels

• Credit quality strong in Australia, but some offshore issues we are dealing with

• Remain well provisioned

• Responsible capital management philosophy

• Leadership in disclosure and transparency

• Commitment to regular and disciplined wholesale term debt issuance

36

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular

investor. These should be considered, with or without professional advice when deciding if an investment is appropriate.

For further information visit

www.anz.comor contact

Philip GentryHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4091 e-mail: [email protected]

37

Outline

1. Group Overview

2. Strategy and Business Overview

3. Financial/Operating Performance Overview

4. Term Debt Funding Strategy

5. Summary

6. Supplementary Information

38

Additional information on strategy

39

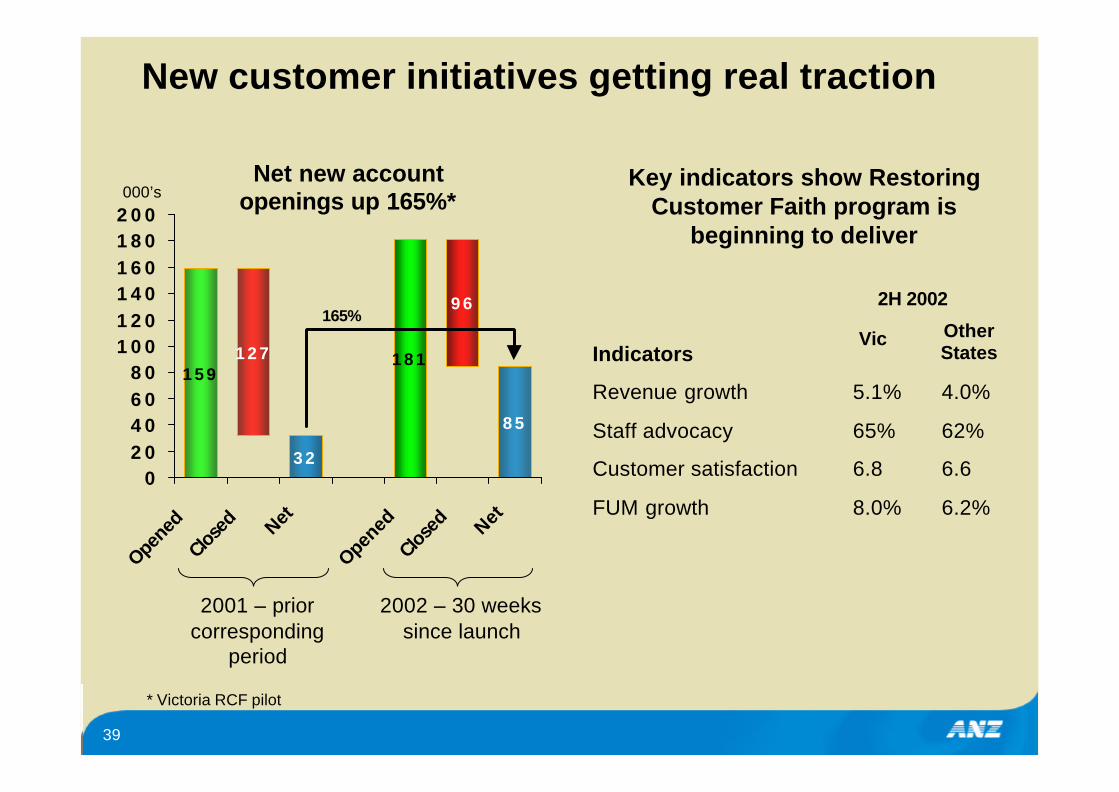

New customer initiatives getting real traction

32

85

127

96

159181

020406080

100120140160180200

Opene

d

Close

d Net

Opene

d

Close

d Net

2001 – prior corresponding

period

2002 – 30 weeks since launch

Net new account openings up 165%*000’s

Indicators

Revenue growth 5.1% 4.0%

Staff advocacy 65% 62%

Customer satisfaction 6.8 6.6

FUM growth 8.0% 6.2%

Vic Other States

2H 2002

Key indicators show Restoring Customer Faith program is

beginning to deliver

165%

* Victoria RCF pilot

40

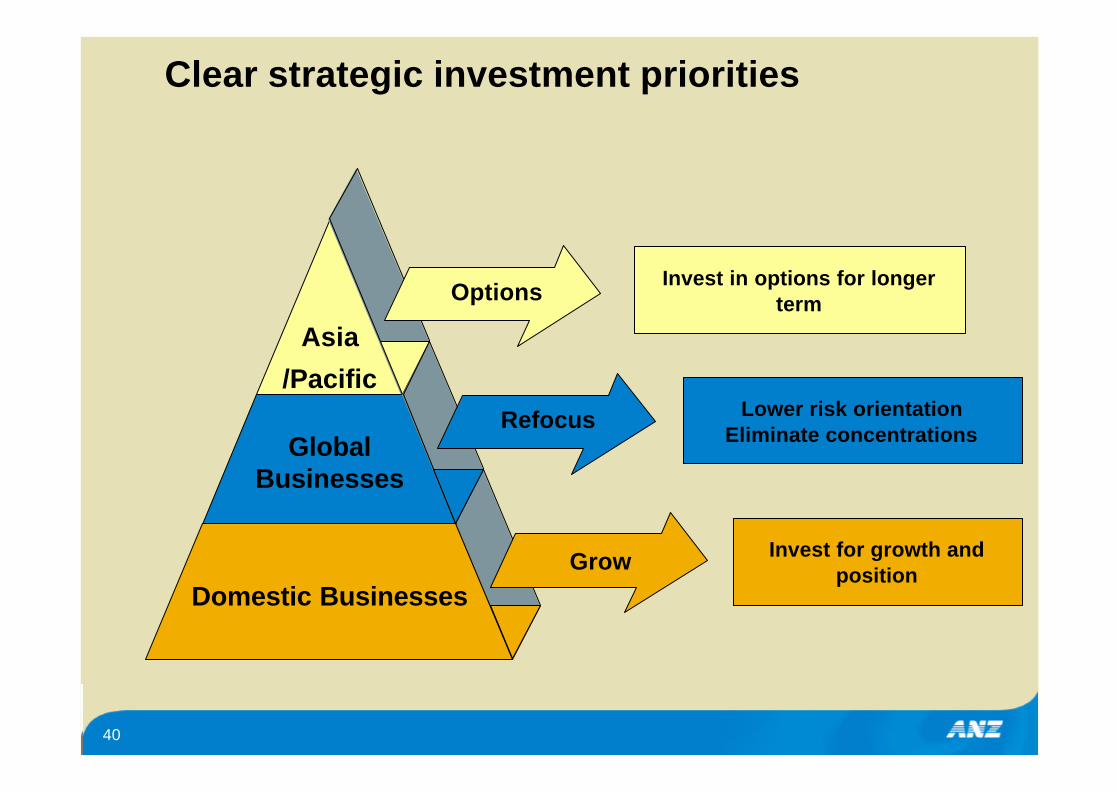

Clear strategic investment priorities

Asia

/Pacific

Global Businesses

Domestic Businesses

Options

Refocus

Invest in options for longer term

Lower risk orientation Eliminate concentrations

Invest for growth and position

Grow

41

0

10

20

30

40

50

ANZ CBA NAB WBC

Consumer portfolio – significant opportunity for ANZ in domestic markets

Share of Customers*

Wallet Share*

Priorities

• Deliver on promise of Restoring Customer Faith

• Improve community perceptions

• Deliver on ING ANZ JV

• Continue product innovation

• Utilise CRM capabilities

• Target market share growth of 1% pa in key markets

0

10

20

30

40

50

60

ANZ CBA NAB WBC

%

%

* source: Roy Morgan Research

42

-10

-5

0

5

10

15

1990

1992

1994

1996

1998

2000

2002

2004

2006

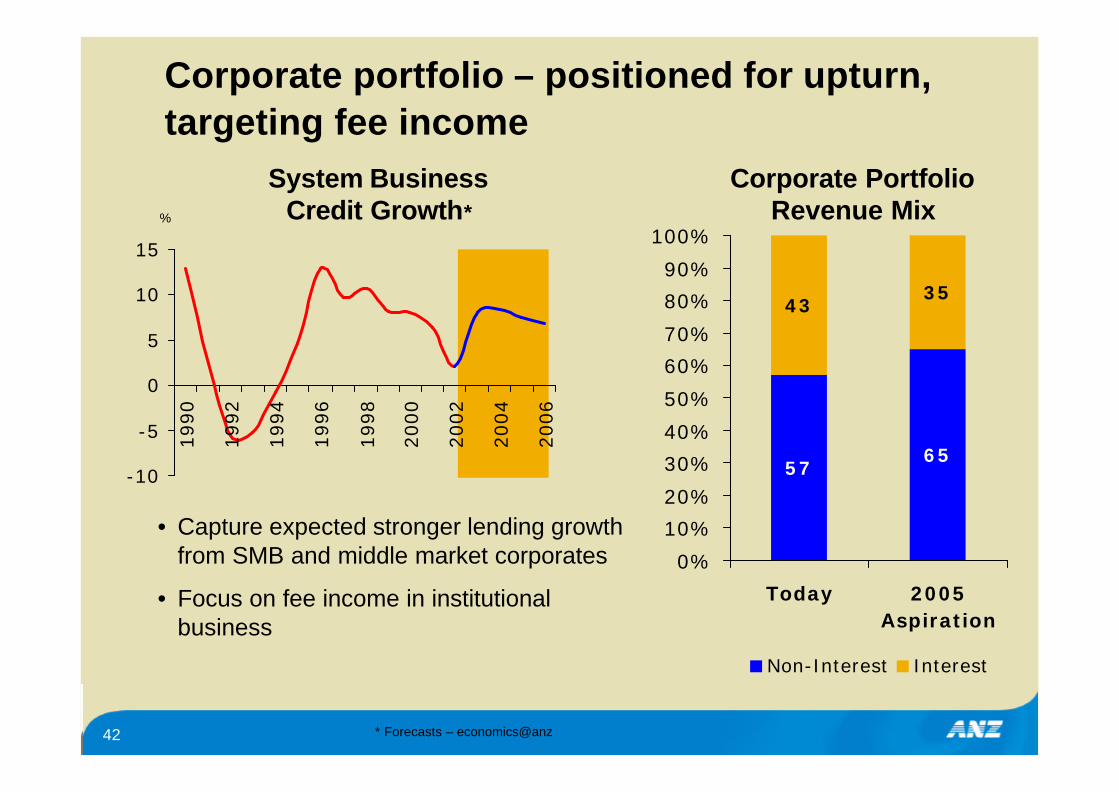

Corporate portfolio – positioned for upturn, targeting fee income

System Business Credit Growth*

5765

4335

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Today 2005Aspiration

Non-Interest Interest

Corporate Portfolio Revenue Mix

• Capture expected stronger lending growth from SMB and middle market corporates

• Focus on fee income in institutional business

%

* Forecasts – economics@anz

43

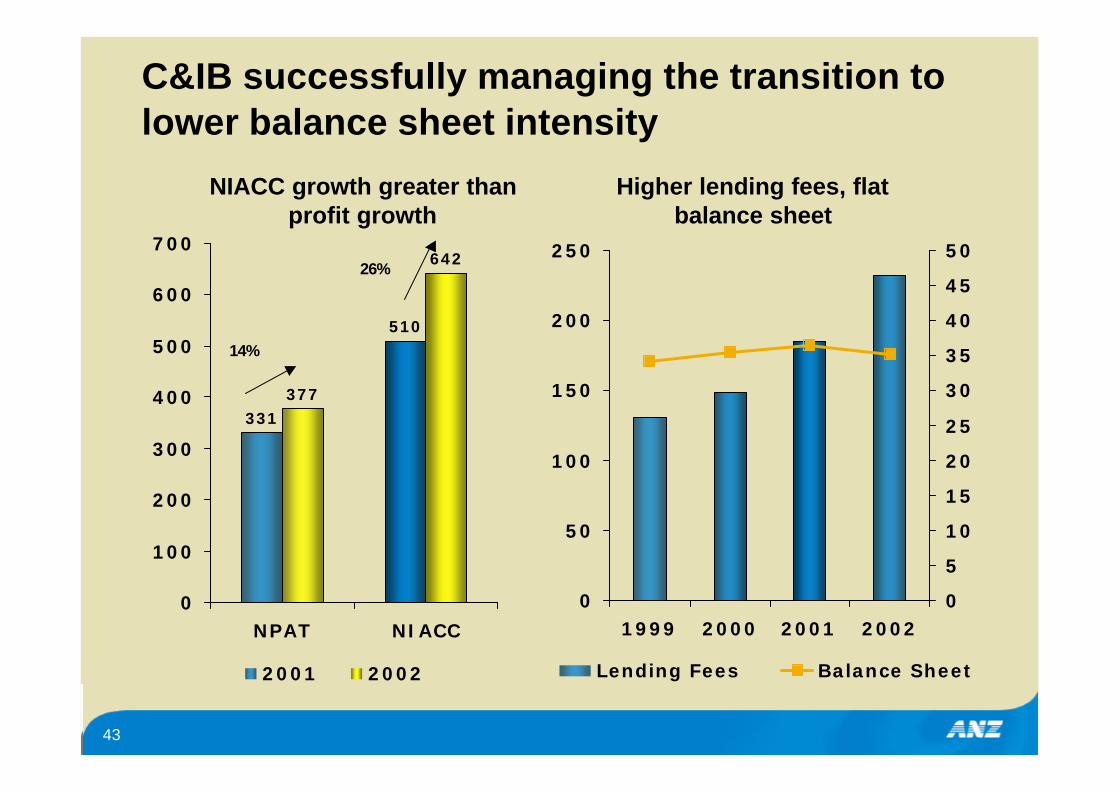

C&IB successfully managing the transition to lower balance sheet intensity

331

510

377

642

0

100

200

300

400

500

600

700

NPAT NIACC

2001 2002

14%

26%

0

50

100

150

200

250

1999 2000 2001 20020

5

10

15

20

25

30

35

40

45

50

Lending Fees Balance Sheet

Higher lending fees, flat balance sheet

NIACC growth greater than profit growth

44

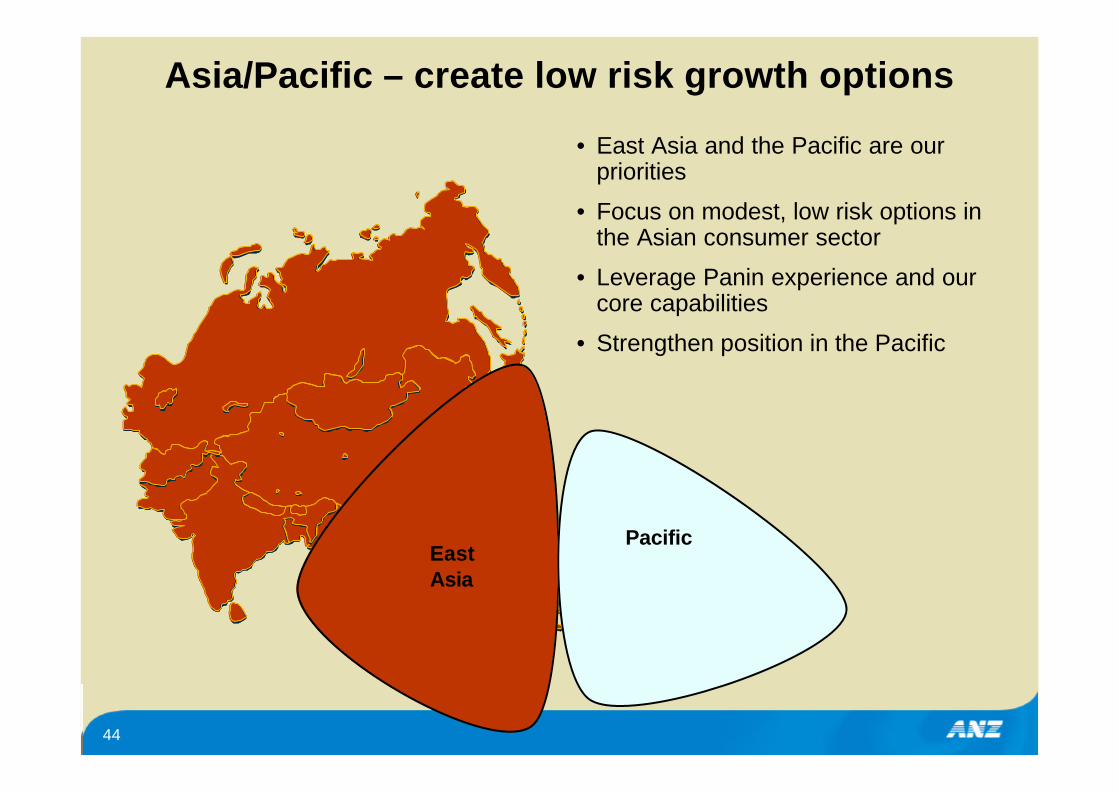

Asia/Pacific – create low risk growth options

• East Asia and the Pacific are our priorities

• Focus on modest, low risk options in the Asian consumer sector

• Leverage Panin experience and our core capabilities

• Strengthen position in the Pacific

PacificEast Asia

45

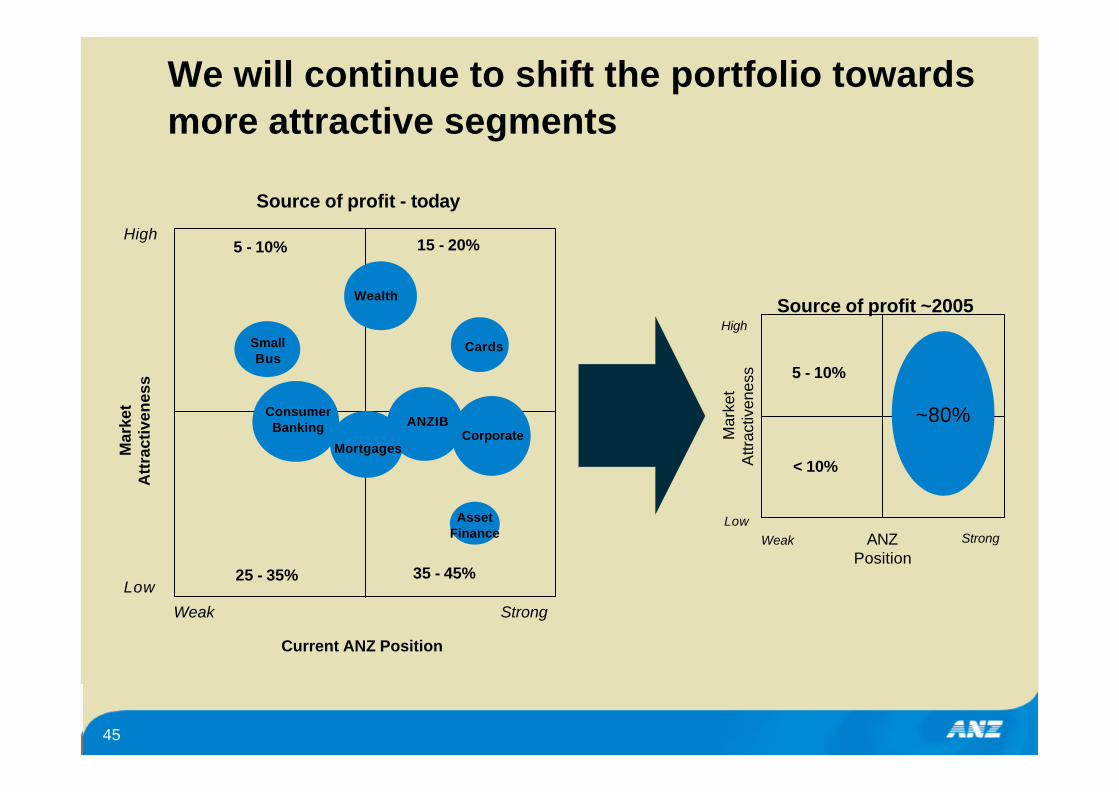

We will continue to shift the portfolio towards more attractive segments

Weak Strong

Low

High

Mar

ket

Att

ract

iven

ess

Current ANZ Position

Wealth

Cards

ConsumerBanking

SmallBus

ANZIBCorporate

AssetFinance

Mortgages

15 - 20%

35 - 45%25 - 35%

5 - 10%

Source of profit - today

< 10%

5 - 10%

Source of profit ~2005

~80%

ANZPosition

High

LowWeak Strong

Mar

ket

Attr

activ

enes

s

46

Additional information on results

47

0 200 400 600 800

A diversified portfolio performing well

Personal Customers

Corporate Businesses

ANZIB

Mortgages

Small Med Business

Consumer Finance

Asset Finance

Group Treasury

47

61

23

10

27

50

10

49

573

527

311

246

157

149

102

124

9%

13%

8%

4%

21%

51%

11%

65%

2002 NPAT Change from 2001

2002 NPAT $m

2002 NPAT increase

2002 NPAT decrease

2001 NPAT

48

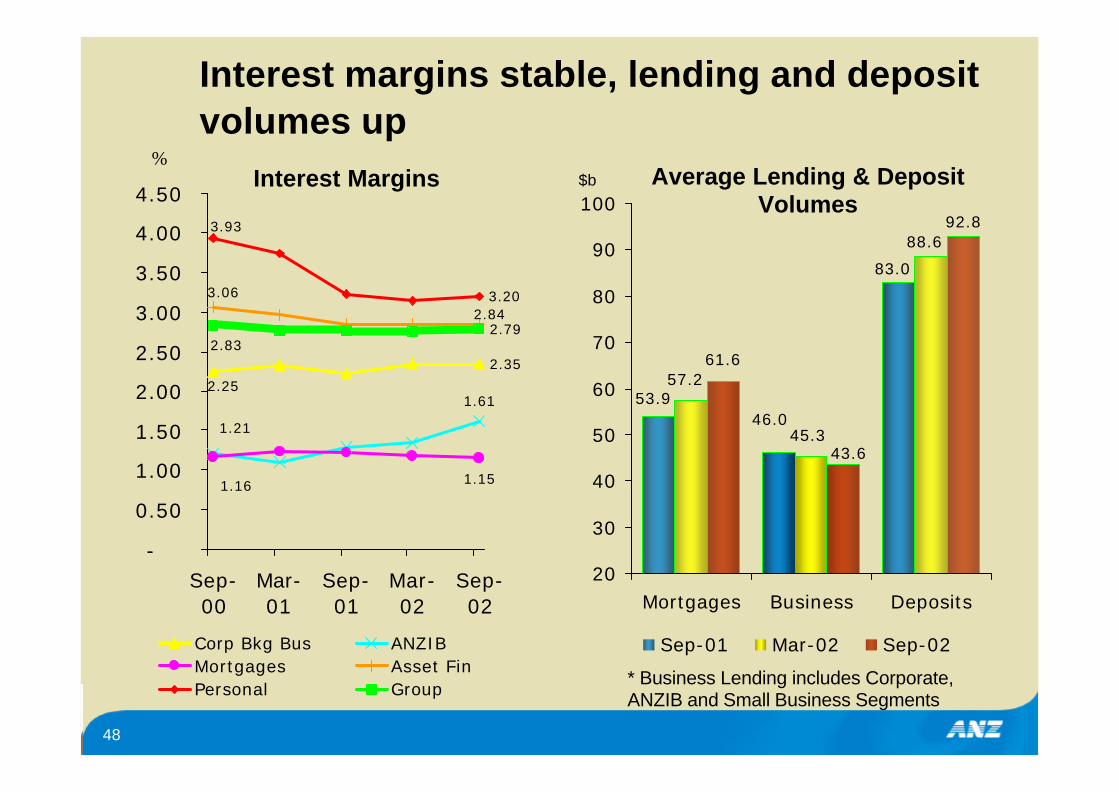

2.35

1.61

1.15

3.20

2.79

2.25

1.21

1.16

2.84

3.06

3.93

2.83

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Corp Bkg Bus ANZIBMortgages Asset FinPersonal Group

Interest margins stable, lending and deposit volumes up

%Interest Margins

92.8

53.9

83.0

46.0

57.2

88.6

45.3

61.6

43.6

20

30

40

50

60

70

80

90

100

Mortgages Business Deposits

Sep-01 Mar-02 Sep-02

Average Lending & Deposit Volumes

$b

* Business Lending includes Corporate, ANZIB and Small Business Segments

49

1000

1200

1400

1600

1800

2000

2200Sep

-97

Mar

-98

Sep

-98

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

40

45

50

55

60

65

70

ExpensesCost Income RatioPeer Average CTI*

Cost income ratio on track to meet target of 45

$m CTI (%)

45.5

• Peer average impacted by funds management acquisitions

• $31m expense reduction from sold businesses

• Effective half on half cost growth of 1.8%

• We will invest more in growth areas, particularly personal businesses

• 2000 $361m restructuring provision fully utilised, ongoing $60m+ charge likely

* Source: CSFB

50

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

1H 01 2H 01 1H 02 2H 02

We will continue to carefully manage cost growth relative to revenue growth

Underlying cost growth trending upward • Balancing earnings

outcomes with investment in growth

• “Surplus” earnings targeted for investment

• Cost-income ratio to trend downward

+

• Higher amortisation and depreciation

• Increasing growth investment

51

Underlying expense growth of 2.3%

3153

3081

3092

20

72

31

3000

3020

3040

3060

3080

3100

3120

3140

31602001

ING

AN

Z J

V

Acq

uis

itio

ns

& F

X I

mpact

Adju

sted

Under

lyin

gG

row

th

2002 A

dj

2.3%

$m

• Computer expenses increased by 16%, reflecting:

• depreciation and amortisation charges up 30%

• software purchases up 28%

2%

52

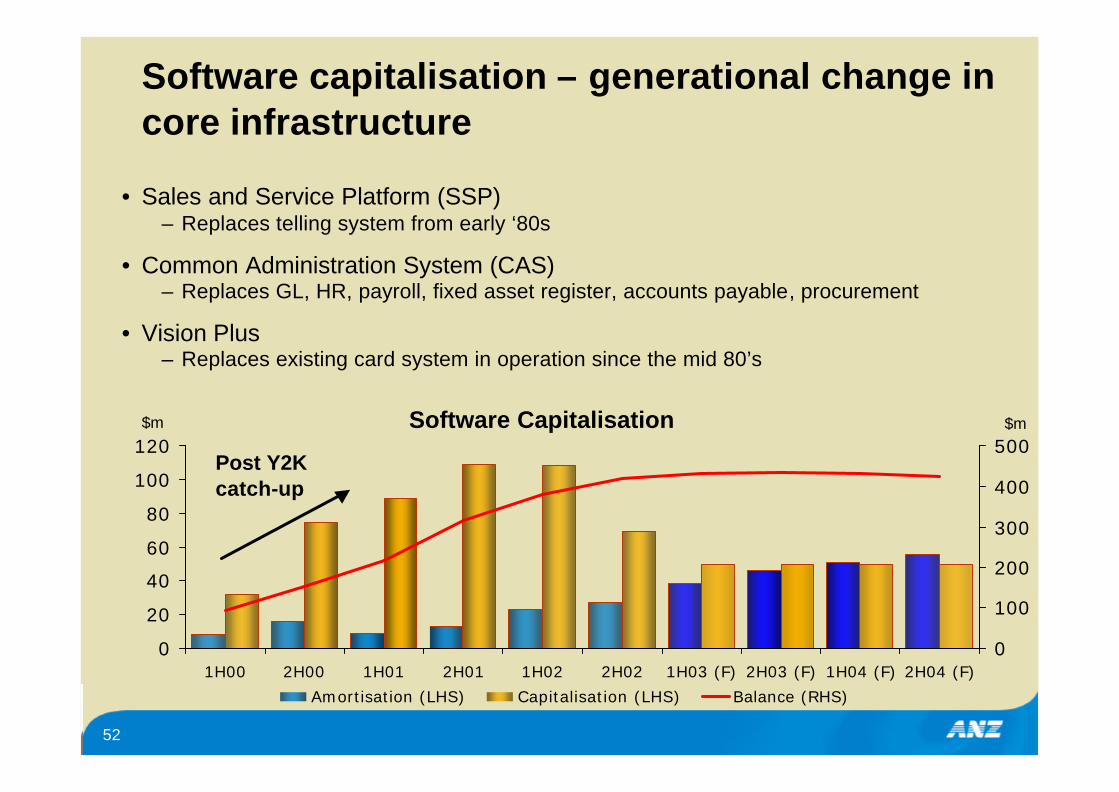

0

20

40

60

80

100

120

1H00 2H00 1H01 2H01 1H02 2H02 1H03 (F) 2H03 (F) 1H04 (F) 2H04 (F)0

100

200

300

400

500

Amortisation (LHS) Capitalisation (LHS) Balance (RHS)

Software capitalisation – generational change in core infrastructure

• Sales and Service Platform (SSP)– Replaces telling system from early ‘80s

• Common Administration System (CAS)– Replaces GL, HR, payroll, fixed asset register, accounts payable, procurement

• Vision Plus – Replaces existing card system in operation since the mid 80’s

$m $mSoftware Capitalisation

Post Y2K catch-up

53

Additional credit quality information

54

House prices – unemployment a key driver

-20

-10

0

10

20

30

40

50

60

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

-3

-2

-1

0

1

2

3

4

5

Sydney House PricesChange in Unemployment

-20

-10

0

10

20

30

40

50

60

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

-8

-6

-4

-2

0

2

4

6

Sydney House Prices

Change in Mortgage Rate

Sydney house prices v change in unemployment

Sydney house prices v change in interest rates

Ch

ang

e in S

ydn

ey Ho

use P

rices (%)

Ch

ang

e in S

ydn

ey Ho

use P

rices (%)

Ch

ang

e in N

SW

un

emp

loym

ent (in

verted scale)

Ch

ang

e in m

ortg

age rates (in

verted scale)

55

4

6

8

10

12

14

16

18

90 92 94 96 98 00 02 044

5

6

7

8

9

10

11

12

90 92 94 96 98 00 02 04

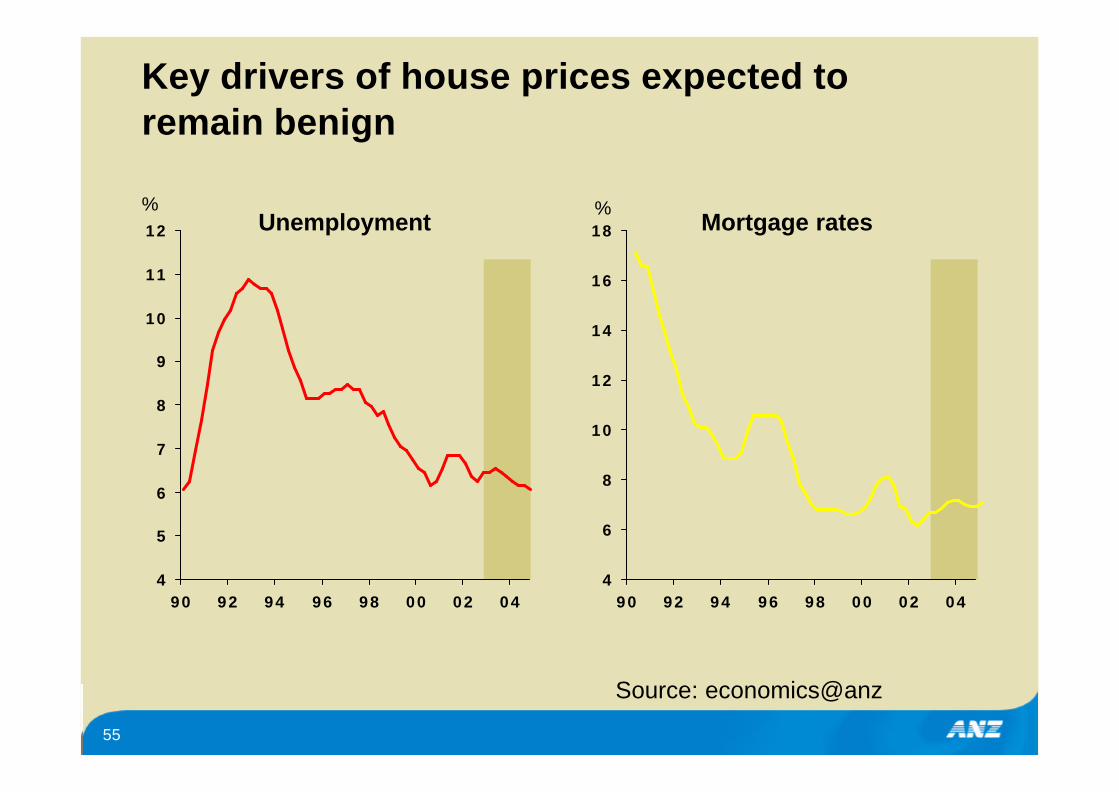

Key drivers of house prices expected to remain benign

Unemployment Mortgage rates% %

Source: economics@anz

56

0 50 100 150

ConsumerFinance

CBB

Asset Finance

GSF

Personal

Mortgages

SME

CF&A

GFX

0

50

100

150

200

250

300

350

400

GFX

CF&A SM

E

Mortg

ages

Perso

nal B

ankin

g GSF

Asset F

inance CB

B CF

SPELP

0

20

40

60

80

100

120

140

160

180

GFX

CF&A SM

E

Mortg

ages

Perso

nal B

ankin

g GSF

Asset Fina

nce CB

B CF

SP

ELP

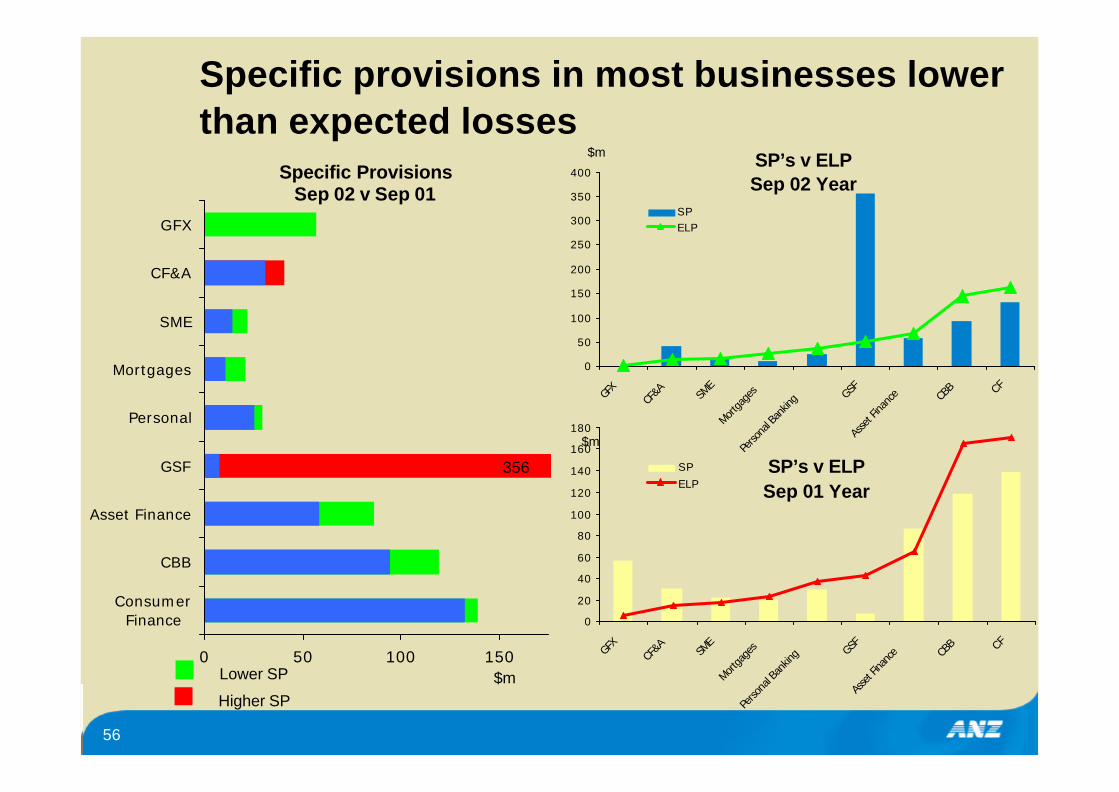

Specific provisions in most businesses lower than expected losses

SP’s v ELPSep 02 Year

SP’s v ELPSep 01 Year

$m

$m

Specific Provisions Sep 02 v Sep 01

$mLower SP

Higher SP

356

57

New non-accruals dominated by 2 large customers over each of the past 2 years

GeographicNew Non-Accrual Loans$m

1,029

931

1,3571,285

1,395

0

300

600

900

1,200

1,500

1998 1999 2000 2001 20020.0%

0.5%

1.0%

1.5%

HistoricNew Non-Accrual Loans (LHS)

New Non-Accrual Loans/Loans & advances (RHS)

2 Customers

2 Customers

0

100

200

300

400

500

600

700

800

900

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

Aust/NZ UK/US Asia Other Inter

$m

58

Fallen Angels phenomenon continues

March 2001 ratings for Full Year 2002 new non accrual loans

• Speed of collapse difficult to model

• We continue to diversify the portfolio

• SCCL’s further reduced and refined

B4%

BB1%

CCC9%

BBB + to BBB-86%

59

6.7%0.8%

8.7%

21.2%

62.6%

Sep-02

Global telecommunications portfolio in reasonable shape

50%

12%

35%

3%

Aust/NZ (97.6% Investment Grade)

Americas (69.3% Investment Grade)

UK/Europe (71.1% Investment Grade)

Asia (34.5% Investment Grade)

Exposure by geography

83.8% investment grade

Telco Risk Grade Profile*

4.8% $0.3bNon Accrual

1.9% $0.1bB+ to CCC

$5.5bTotal Limits (AUD)

AAA to BBB+

BBB to BBB-

BB+ to BBBB->BB-

>BB- = B+ B, B-, CCC & non-accrual*Risk grade profile by limits

$3.4b

$1.2b

$0.5b

$0.4b

49

4

3

# of customers

60

8%1%

24%

21%

46%

Sep-02

Global energy portfolio – some issues, but containable

Global Energy Portfolio*

AAA to BBB+

BBB to BBB-

BB+ to BB

BB-

>BB-16%

36%

16%

32%

Sep-02

US Energy Portfolio

>BB- = B+ B, B-, CCC & non-accrual

(AUDm)Total Limits $9.6bn $2.2bnB+ to CCC 4.8% $0.46b 12.2% $0.27bNon Accrual 3.2% $0.3b 4.0% $0.09b

Exposure by geography

53%

25%

9%

9%4%

Aust/NZ (77.5% Inv Grade)

Americas (43.5% Inv Grade)

UK/Europe (64.6% Inv Grade)

Asia (61.0% Inv Grade)

Middle East (98.0% Inv Grade)

$4.5b

$2.0b

$2.3b

$0.8b

*Risk grade profile by limits

$0.7b

$0.36b

$0.8b

$0.36b

7812

5

# of customers

265

2

# of customers

61

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

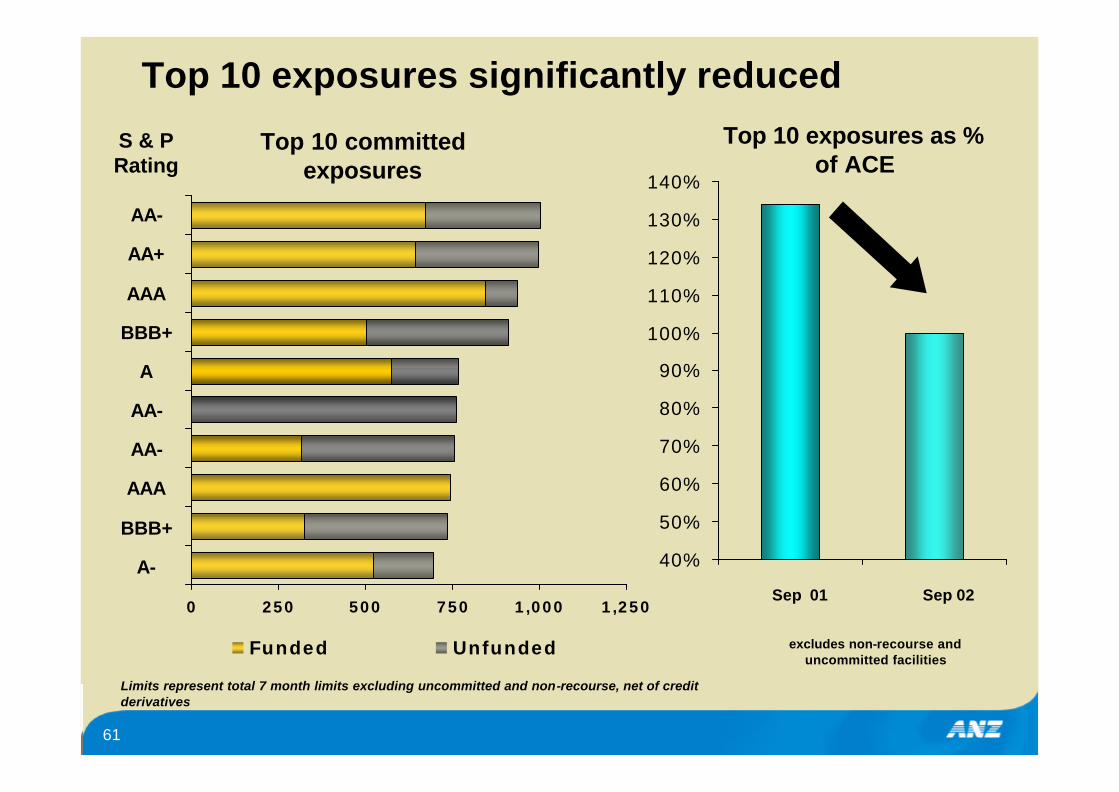

Top 10 exposures significantly reduced

Top 10 committed exposures

Top 10 exposures as % of ACE

Sep 01 Sep 02

Limits represent total 7 month limits excluding uncommitted and non-recourse, net of credit derivatives

excludes non-recourse and uncommitted facilities

0 250 500 750 1,000 1,250

Funded Unfunded

S & P Rating

AA-

AA+

AAA

BBB+

A

AA-

AA-

AAA

BBB+

A-

62

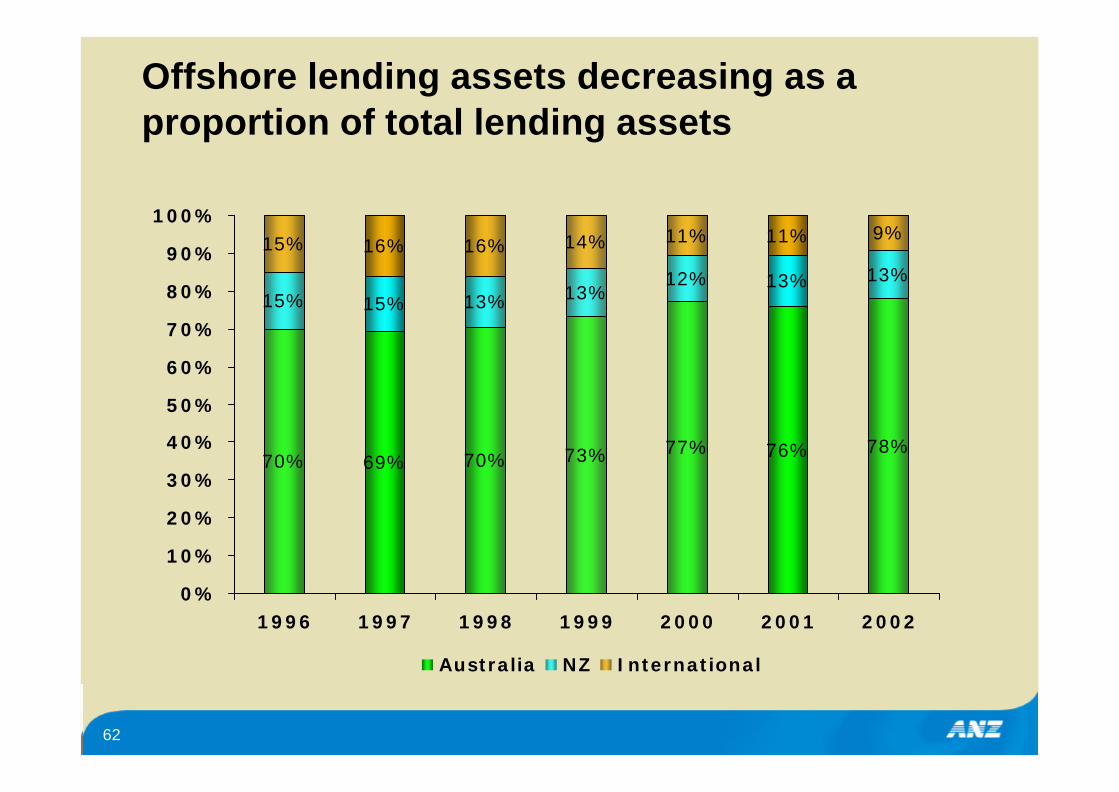

Offshore lending assets decreasing as a proportion of total lending assets

70% 69% 70% 73% 77% 76% 78%

15% 15% 13% 13%12% 13% 13%

15% 16% 16% 14% 11% 11% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996 1997 1998 1999 2000 2001 2002

Australia NZ International

63

Increased industry diversification

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Co

mm

erc

ial

Pro

pert

y

Man

ufa

ctu

rin

g

Reta

il T

rad

e

Fin

an

ce -

Ban

ks

Wh

ole

sale

Tra

de

Ag

ricu

ltu

re

Bu

sin

ess

Serv

ices

Fin

an

ce -

Oth

er

Cu

ltu

ral

& R

ec

serv

ices

Acc

om

m,

Pu

bs,

Clu

bs

Tra

nsp

ort

&S

tora

ge

Oth

er

1993 2002

% of Group Lending Assets(Aust/NZ)

Policy Cap

64

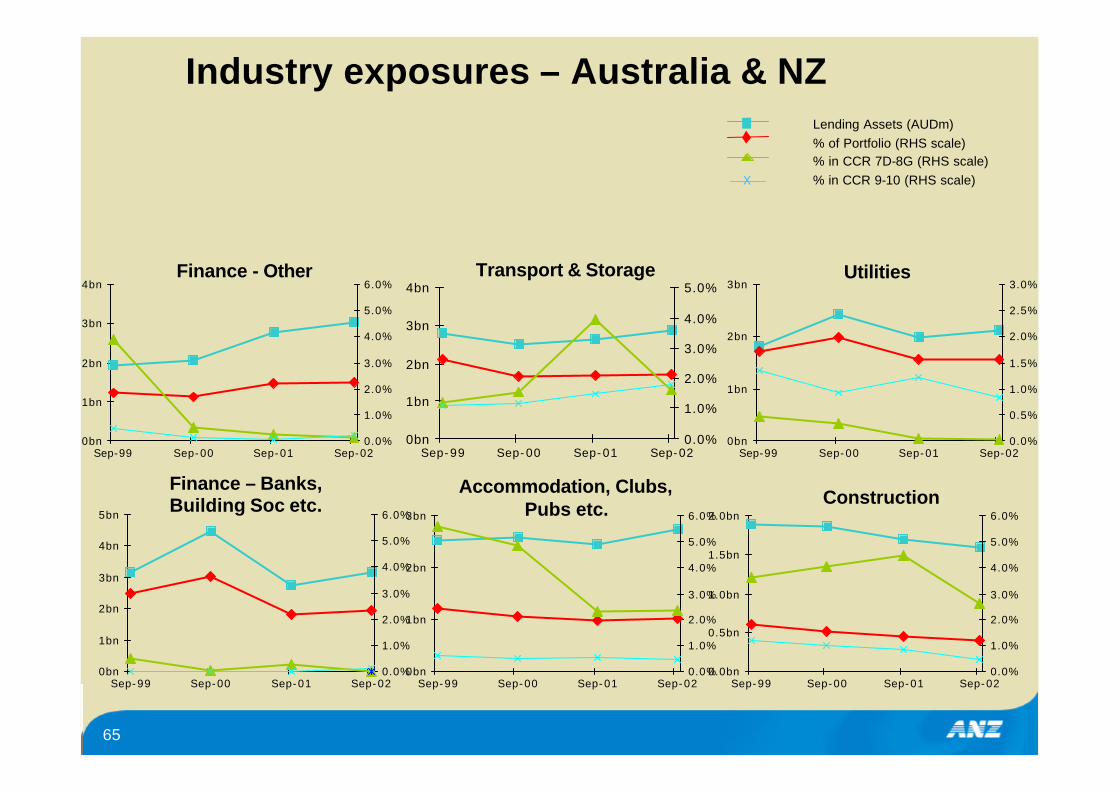

Industry exposures – Australia & NZ

0.0bn

0.5bn

1.0bn

1.5bn

2.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0.0bn

0.5bn

1.0bn

1.5bn

2.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.0bn

0.2bn

0.4bn

0.6bn

0.8bn

1.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0.0bn

0.2bn

0.4bn

0.6bn

0.8bn

1.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.0bn

0.5bn

1.0bn

1.5bn

2.0bn

2.5bn

3.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

5.0%

10.0%

15.0%

Health & Community Services

Mining

Cultural & Recreational Services

Personal & Other Services

Forestry & Fishing

Communication Services

0.0bn

0.2bn

0.4bn

0.6bn

0.8bn

1.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%10.0%

Lending Assets (AUDm)% of Portfolio (RHS scale)% in CCR 7D-8G (RHS scale)% in CCR 9-10 (RHS scale)x

65

Industry exposures – Australia & NZ

0bn

1bn

2bn

3bn

4bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0bn

1bn

2bn

3bn

4bn

5bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Finance - Other

Finance – Banks, Building Soc etc.

0bn

1bn

2bn

3bn

4bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0bn

1bn

2bn

3bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Transport & Storage

Accommodation, Clubs, Pubs etc.

0bn

1bn

2bn

3bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0.0bn

0.5bn

1.0bn

1.5bn

2.0bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Utilities

Construction

Lending Assets (AUDm)% of Portfolio (RHS scale)% in CCR 7D-8G (RHS scale)% in CCR 9-10 (RHS scale)x

66

Industry exposures – Australia & NZ

0bn

2bn

4bn

6bn

8bn

10bn

12bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0bn

2bn

4bn

6bn

8bn

10bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Real Estate Operators & Dev.

Manufacturing

0bn

2bn

4bn

6bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0bn

2bn

4bn

6bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Retail Trade

Wholesale Trade

0bn

1bn

2bn

3bn

4bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0bn

1bn

2bn

3bn

4bn

Sep-99 Sep-00 Sep-01 Sep-020.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Agriculture

Business Services

Lending Assets (AUDm)% of Portfolio (RHS scale)% in CCR 7D-8G (RHS scale)% in CCR 9-10 (RHS scale)x