Embed Size (px)

Citation preview

Newcastle spot price steadies to weak market By John O’Neil The threat of strike action by workers of Colombia’s second largest coal miner Drummond has seen a slight rise in European spot market prices this week. Even if the strike does eventuate, which will reduce Colombia’s coal exports by at least 2.2mt a month, it is unlikely to provide more than a temporary halt to the price slide with Europe seriously oversupplied with coal. Drummond and the union representing the workers Sintramienergética failed to reach an agreement on a new three-year labour agreement by the deadline of July 8. Workers have until July 17 to vote for strike action or seek arbitration although new talks between Drummond and the union will begin on July 11. If Colombia’s supply disruption in March this year as a result of strike action by workers of the country’s largest miner Cerrejón and the ban on Drummond coal shipments is any indication, the possible strike action is unlikely to have any impact on prices in Asia, although it may halt the low volumes of Colombia coal which have recently been leaking into the Asian market, a Brisbane-based trader said. Two prompt physical trades of Newcastle coal were settled on globalCOAL on July 9 – a 75,000t cargo for October delivery at US$77.50/t FOB and 25,000t trade for September delivery at $77/t FOB. With prompt physicals settled in the range of $76.10 to $77/t last week, this week’s trades may indicate the Newcastle spot prices may be “nearing the bottom”, he said. However, a Sydney-based trader said he wasn’t “brave enough to call where the floor in Newcastle prices may be”. The Newcastle globalCOAL trades this week were still at a reasonable discount to the prevailing swap prices, so the spot market could still decline further, he said. Port Waratah Coal Services’ terminals at Newcastle continue to show no signs of reducing export volumes, despite rolling strike action by PWCS workers, a good indication that NSW producers are still pushing coal into an already saturated Asian market. “Large take-or-pay obligations will obscure cash cost limitations on production,” the trader said. “No-one is talking about cutting production yet.” The Brisbane trader said there was plenty of Newcastle coal available to the spot market which could be had for about $76/t FOB or lower but there were few buyers as end users were well stocked. “This is traditionally the quiet period,” he said.

Australian Coal Report

ISSUE 0505 10 July 2013 www.coalportal.com

coalportal. ®com

This week’s Australian Coal Report includes the monthly port statistics

BRIEFSAtrum finds more Canadian coal ASX-listed coal developer Atrum Coal has intersected thick shallow coal seams at its flagship Groundhog Anthracite Project in British Columbia, Canada. A drilling program targeting the s70 seam encountered net coal thickness of 6.8m at a depth of 30.4 to 42.2m depth and a net thickness of 3.4m at depths of 10.65 to 19.1m in the north-west area of the project. Atrum plans to extract a 300kg bulk sample to confirm the product specification at Groundhog which includes premium grade anthracite and premium grade ultra-low volatile PCI for use in steel manufacturing and ferro industries.

Yanzhou lobs take over for Yancoal A year after a local stock exchange listing of its Australian operations, China’s Yanzhou Coal Mining Company is proposing to take them private. The Hong Kong-quoted but Chinese state-controlled Yanzhou has announced an all-paper offer for the 22% of its Australian offshoot it does not control. But both Yanzhou and Yancoal said the proposal - offering securities known as CDIs in Yanzhou - was non-binding and subject to a complex web of scrutiny and approvals. Yancoal said its independent directors would initiate discussions with Yanzhou and seek an independent valuation of the Australian company in a process expected to take several months. Yanzhou said its proposal was worth A$0.91c a share and this represented a 30% premium to recent market quotes. Yancoal shares have lost about 30% of their value since early 2013, in line with a number of quoted Australian coal companies. Yanzhou said a successful takeover would allow the Chinese company to achieve deliver higher efficiency across a “highly integrated business”. Yancoal is one of the most diverse coal producers in Australia, with output of around 16.5mtpa in several met and thermal categories. The proposal has also brought speculation that Yanzhou may seek to list its wider operations on the Australian stock exchange as part of a plan to gain foreign investment clearance for the takeover.

Resgen signs new offtake ASX-listed Resource Generation has simultaneously cancelled a 0.5mt offtake agreement with Indian company Bhushan Steel and signed a new deal with another Indian investor. Resgen is developing the Boikarabelo mine in South Africa’s Waterberg region, due to start in 2015 at 6mtpa output before lifting to 25mt in stage 2.

IHS McCloskey Weekly prices

FOB markers grade 5-Jul-13 28-Jun-13 21-Jun-13 Jun-13High Ash 5,500 5,500kc NAR 67.45 69.20 70.55 71.55

Differential 6,000kc NAR 2.45 2.07 3.88 5.01

Spreads

FOB Spread (Newc/RB) 6,000kc NAR 3.62 3.55 4.65 4.89

FOB Spread (Newc/RB) 5,500kc NAR 0.85 1.30 1.45 1.57

Washspreads

Simple Washspread 6,000kc NAR -9.32 -9.59 -8.24 -7.80

Logistical Washspread 6,000kc NAR -5.32 -5.59 -4.24 -3.80

Logistical washspread assumes $3.50/t washing cost 20% yield loss and $20/t port and rail fees

FOB spread is differential of Newcastle minus Richards Bay, for both 6,000kc NAR and 5,500kc NAR

BRIEFS CONTINUED

Australian Coal Report

Australian Coal Report Issue 0505 10 July 2013 2

With Chinese buyers also most absent from the market for spot market the Newcastle high ash 5,500kc NAR coal, its price is also now falling quite quickly. The Sydney trader said HA 5,500kc coal was now being offered at $66.50/t FOB with little interest from buyers. Further complicating the ability to settle deals is the issue of distressed cargoes with a number of vessels reported off the east coast of China with coal unable to find a home. “Credit constraints in China are forcing Chinese traders to re-offer previously purchased cargoes into the market as they can’t open L/Cs (letters of credit),” the Sydney trader said. The Brisbane trader said most producers and sellers were looking very closely at their Chinese counter parties and were only willing to sell to those they had dealt with previously. To add to Australian producers’ problems, the Newcastle HA 5,500kc NAR coal is coming under increasing price pressure from the domestic product. The spot price of the domestically produced 5,500kc NAR coal at the benchmark Chinese port of Qinhuangdao continues to fall, down RMB 12/t (US$1.95)over the past two weeks, to RMB 581/t($94.70/t) FOB on July 5. A Singapore trader said the price is expected to fall a further RMB 20/t ($3.25/t) over the next several of weeks which would price imported coal out of the Chinese market.

Coal exports grow 10.7%By John O’Neil

In the first six months of 2013, Australian’s coal export volume grew by 10.7% or 32.3mt to 334.1mt, despite coal prices being much lower than those of the previous financial year. Queensland’s contribution to the total was 180.1mt, up 9.2% year-on-year, while NSW exported 154mt of coal, an increase of 12.5% y-o-y supported by increased capacity at both the Port Waratah Coal Services (PWCS) and the Newcastle Coal Infrastructure Group (NCIG) terminals at Newcastle. The largest increase in export volume, apart from the expanded NCIG terminal, came from Dalrymple Bay Coal Terminal (DBCT)

which shipped 62.4mt of coal in FY2012-13, an 11.5mt increase on FY2011-12 when the Bowen Basin mines were still recovering from the rains and floods of December 2010 and early 2011. DBCT’s FY2012-13 throughput was just

short of its FY record of 63.4mt achieved in FY2009-10. The 85mtpa capacity terminal operated at 73% of its nominal capacity during the financial year just passed. The BMA-operated Hay Point Coal Terminal (HPCT) exported 34.1Mt of coal in FY2012-13, an increase of 2.1mt, but short of 36.3mt exported in FY2009-10 - the previous time when Queensland was relatively free of severe weather events. The 44mtpa HPCT operated at 77% of its nominal capacity in FY2012-13. The Adani-owned Abbot Point Coal Terminal (APCT) increased its export volume by 4.1mt y-o-y to 17.7mt. The previous highest volume was 16.9mt in FY2009-10 but the terminal has since doubled its capacity from 25mtpa to 50mtpa which was available for all of FY2012-13.

Resgen and special investment vehicle Valu Investments Pte. Ltd have entered into a 20-year export coal offtake contract for 1mtpa once production starts at the Boikarabelo mine. Once stage 2 production kicks off, the volume increases to 2mtpa. Valu will also conduct feasibility studies for the development of both a 200MW power station and a 1200MW coal-fired power station adjacent to the Boikarabelo mine. Resgen has granted Valu the right to own, build and operate both power stations as an independent project. Indian company CESC has pulled out of its option to explore setting up a power plant but will still take coal under an earlier offtake agreement.

New Age coking coal potential in Scotland Washability test work on coal extracted from the first drill hole at ASX-listed New Age Exploration’s Lochinvar metallurgical coal project in Southern Scotland indicates the potential for a low ash and low phosphorus metallurgical coal with good yields. The maximum fluidity of these coals is high and could provide a suitable blend for coals of lower reactivity, the company said.

Abbot Point deadline extended Federal environment minister Mark Butler has extended the deadline for assessing plans to expand Abbot Point coal terminal near Bowen in North Queensland, according to ABC News. The July 9 deadline has been extended for a further month. In a statement Butler said he needed more time to consider the project’s potential impacts and hear the views of interested parties, particularly those who had concerns about the effects of dredging and dumping 3 cubic metres of spoil out to sea. “It is not unusual to have short extensions for the assessment of large and complex projects like this one,” he said. “The initial statutory timeframe for federal assessment applies equally to all projects, whether it’s a small housing development or a larger project like this.” Mr Butler said a decision could be made before August 9 if he was satisfied with the information put to him by interested parties.

Algae.Tec signs biodiesel deal Algae.Tec has contracted with Biodiesel Industries Australia (BIA), to refine algal oil from its carbon capture and biofuels production facility alongside the 2640MW Bayswater coal-fired power station near Sydney. The oil, to be produced from the Algae.Tec facility planned for 2014 at the Macquarie Generation power station, will be refined by BIA then used locally by mining and industry in the Hunter region. BIA MD Andrew Hill said the company produced biodiesel for clients including Caltex, local councils, and the mining industry. “We have long considered algae to be the Holy Grail for biofuels, so we are pleased to see this new algae to biofuels development happening just up the road at MacGen,” he said.

The largest increase in export volume, apart from the expanded NCIG terminal, came from Dalrymple Bay Coal Terminal (DBCT) which shipped 62.4mt of coal in FY2012-13.

Australian Coal Report

Australian Coal Report Issue 505 10 July 2013

The combined throughput of Gladstone’s RG Tanna and Barney Point terminals declined 2.5mt y-o-y to 57.3mt in FY2012-13 as a result of the closure of the Blackwater and Moura rail systems earlier in 2013 because of track damage and flooding. The combined 76mtpa capacity terminals still managed to achieve 75% efficiency. Exports from the New Hope’s Queensland Bulk Handling (QBH) facility at the Port of Brisbane declined marginally from 8.7m in FY2011-12 to 8.6mt in FY2012-13. Exports for both years were impacted by the closure of the Western rail line due to washouts on the Toowoomba Ranges which prevent coal being transported from the Surat Basin for several weeks in January 2013 and several months from January 2012. However, the 10mtpa capacity terminal was able operate

at 86% of its nominal capacity in FY2012-13. In NSW, Port Waratah Coal Services increased exports by 6.2mt y-o-y in FY2012-13 to 108.5mt supported by a nameplate capacity increase from 113mtpa

to 133mtpa. Of the total exports, 85% or 92.5mt was thermal coal and the remaining 16mt was semi soft coking coal. Weak coal demand meant PWCS wasn’t able to take full advantage of the 20mtpa capacity expansion and the combined Kooragang and Carrington terminals operated at only 82% of their combined nominal capacity. NCIG also benefited from a nameplate capacity expansion which increased from 30mtpa to 53mtpa in July 2012. NCIG’s exports have grown from 20.1mt in FY2011-12 to 32.3mtpa in FY2012-13. Port Kembla Coal Terminal (PKCT) throughput fell by 1.3mt in FY2012-13 to 13.2mt mainly due to adverse weather conditions which closed the port of several occasions and electric and mechanical problems with the shiploader. The 18mtpa PKCT operated at 73% of its nominal capacity and exported 8.2mt of coking coal and 5mt of thermal coal in FY2012-13.

GVK Hancock push eco-friendly coal By Jack Saunders/John O’Neil Indonesian miner, Adaro, did a great job marketing the environmental benefits of its low-ash, low-sulphur coals when launched to market a few years ago. Now, GVK-Hancock is doing something similar and pointing out the benefits of the Galilee basin coal it is developing for export. Working with GVK, leading Australian coal power researcher Lindsay Juniper, has written a paper demonstrating how both the environment and power station performance can be improved by utilising better quality and relatively cleaner burning coals. Global trends have increasingly moved to lower qualities, increasing the volume of pollutants from coal burning and to reverse the trend in coal quality deterioration a new, large volume source is required. Juniper claims one of the best credentialed prospects for replacing China’s high ash, low rank domestic coal with high rank, low ash imported coal is the Galilee Basin.

3

BRIEFS CONTINUED “BIA is playing a key role to accelerate the transition to biofuels in the region.” BIA was established in 2003 and is refining up to 17m million litres a year.

Carabella upgrades Bluff resources ASX-listed coal explorer Carabella Resources has updated the JORC resource estimate for the Bluff project in Queensland’s Bowen Basin from 18.2mt to 21mt. There has been a 70% increase in indicated resources from 6.6mt to 11.2mt. An exploration target in the range 3.4mt – 24mt has also been identified. The PCI project is 20km east of Blackwater and adjacent to the Gladstone rail line.

Aviva shareholders approve Mmamantswe Aviva Corporation shareholders have voted in favour of selling the 1.3bt Mmamantswe coal project to African Energy Resources for A$3.5m cash. This satisfies the final condition for the Mmamantswe project acquisition by African Energy. Aviva told the ASX Sentient Executive GP IV Ltd, acting for Sentient Global Resources Fund IV, L.P. would now subscribe for a further $3.5m of African Energy shares at $0.12 each. “On completion, African Energy will have secured the full rights to 3.8bt of coal in Botswana and maintained its working capital at approximately $6m,” Aviva said. “At conclusion, Sentient will own approximately 17.4% of the issued shares in African Energy and will be the single largest shareholder.”

Strategy to attract more women to resources Queensland Education Minister John-Paul Langbroek has launched a strategy to increase female participation in the resources sector. “The resource sector is one of the state government’s four pillars and a key Queensland industry that has traditionally experienced difficulty engaging and retaining female workers,” he said during a visit to the Myne Start simulated underground mine in Mackay. “That’s why the government is contributing $100,000 annually over three years to support the Women in Resources Sector Strategy, to attract and retain female workers in the industry. “The strategy funds the Queensland Resources Council to deliver the Women in Mining and Resources Queensland (WIMARQ) Women’s Mentoring Program that involves four months of face-to-face training each year to develop the skills of 20 mentors and 20 mentees.”

Less regulation creates jobs - ACA The Australian Coal Association has welcomed the federal coalition’s commitment to reduce regulation and boost productivity as a positive step to encourage investment and drive jobs in the coal industry. “The industry welcomes the coalition’s commitment to reduce Australia’s red and green tape,” said CEO Dr Nikki Williams. “We’ve seen regulations steadily increase in Australia. Extra regulation brings higher costs and delays in project approvals, which in turn deters investors and threatens Australian jobs.”

NCIG also benefited from a nameplate capacity expansion which increased from 30mtpa to 53mtpa in July 2012.

Chris Hartley, general manager marketing GVK Hancock said: “We have been banging on for years about coal quality impacts on power station boiler efficiency. As quality improves less coal is needed to be mined, less coal needs to be transported to exporting ports, less coal needs to be transported from destination ports to the power stations and less coal needs to be burnt. All of these contribute to a better environmental outcome. Hartley said coal with ash content above 20% caused power stations to emit more particulate matter into the atmosphere than if they used a lower ash coal. “The higher the level of impurities, the less the energy content in the coal and the higher the volume consumed to achieve required power station outputs. “Substituting low rank, high ash Chinese domestic coal with high rank, low ash Australian alternatives such as those planned to be exported from the Galilee Basin will result in less emissions in terms of actual particulates per tonne burnt. As well it will allow lower tonnages to be transported and burnt to achieve equivalent power station output,” he said. Hartley contends coal pricing has not moved in relation to the real, embedded value in individual coals, if one considers the impact the coal has on all of the purchase, transportation and utilisation costs involved in producing a unit of electricity. “This is achieved by measuring the coal’s ‘value-in-use’. This calculates the impact of coal properties on the technical performance of the coal and their influence on costs within the power station including costs that relate to mitigation of any environmental impacts.” Measuring value-in-use is achieved by modelling which simulates the performance of a modern super-critical power plant. “Such modelling measures the impact of coal properties on the utilisation performance of the coal and the subsequent impact on costs within the power station,” he said. “These can be compared with the costs incurred by simulating the burning of other coals to estimate their values relative to each other.” “Here, we compared a medium rank, export quality bituminous coal, such as that from the Galilee Basin, with a domestically produced low rank, high ash, high moisture coal that might be used in a Chinese power plant. “Thus, if the cost of Chinese coal delivered to the plant stockpile was US$40/t (say), then the electricity generator could afford to pay up to US$88/t for the high rank, low ash coal without exceeding his current cost of electricity production with

the Chinese coal. “When comparing the costs of electricity generation using a low rank coal with that of a high rank, low ash coal, the value-in-use price difference is greater than the pro rata difference in price based solely on energy content, meaning the poorer quality coal is generally being over-priced.” Hartley said this distortion could be seen in the price of poor quality Indonesian coal. “The market price for the Indonesian 4,700kc is about US$67/t using the price per unit of energy, but if you use a value-in-use analysis, you should be paying about $42/t,” he said. Hartley admits that it is an uphill battle to change what he describes as “a fairly ingrained mindset in the industry” towards the value-in-use price analysis, particularly among power generators which have separate purchasing units. “We are trying to get companies which buy coal for electricity generation not to think in dollars per unit of energy but the cost per unit of electricity,” he said. “China’s five largest utilities have separate companies – one which buys the coal and the other which generates the electricity. For the coal purchasing company, their KPI is all about buying the cheapest coal available.”

IEC commits to power Tanzania and MalawiBy Jack Saunders In 2011 the International Monetary Fund (IMF) listed five eastern African nations (Uganda, Rwanda, Mozambique, Tanzania and Malawi) as being among the world’s fastest growing countries during 2005 to 2010. Two of them – Tanzania and Malawi – are united in their intention to exploit their considerable coal reserves to provide the power to fuel the growth needed to break the chains of poverty holding back their people. Some 36% of Tanzania’s population live below the poverty line while Malawi’s proportion is 53%. Tanzania has just revised its estimates of its coal reserves up to 5bt from 1.5bt. Malawi’s budding coal exploration program has already identified five coalfields with estimated reserves of 20mt and 750mt of probable reserves.

Australian Coal Report

Australian Coal Report Issue 0505 10 July 2013 4

BANDANNA SELLS EQUITY IN WICET HOLDINGSQueensland coal developer Bandanna Energy has added to its cash reserves by selling its preference equity in the WICET Holdings (WIPS), the developer of the Wiggins Island Export Coal Terminal (WICET) at Gladstone Bandanna made a net gain of $6m after initially investing S41m in WIPS in September 2011 as part of the funding required to begin construction of the $2.5b WICET Stage 1 project. Bandanna’s sale of the WIPS equity to a global infrastructure investor will not impact its 4mtpa port allocation for the Springsure Creek project in the 27mtpa capacity WICET Stage 1. Bandanna will also maintain its 14% shareholding in the Stage 1 development which is expected to begin exporting first coal in early 2015. Funds raised from the sale increases Bandanna’s cash reserves to $121m, of which $23m is committed as security

against infrastructure contracts. Part of the funds will be applied to the mining lease approval process for the Springsure Creek project in the Bowen Basin, as well as land acquisition and compensation, and further optimisation studies to further reduce the project’s capital and operating costs, Bandanna managing director Michael Gray said. “With port construction now more than 60% complete, Bandanna Energy considers that those funds would be better applied directly towards continued progress of development of Springsure Creek,” he said. “The investment in WICET preference equity by the acquiring party, a global infrastructure investor, demonstrates the investment market’s understanding and confidence that WICET Stage 1 will facilitate the growth of Queensland’s coal export market in line with our forecasts for an increase in the demand for Queensland thermal coal by 2015.”

Australian Coal Report

5Australian Coal Report Issue 0505 10 July 2013

Sydney-based ASX-listed Intra Energy (IEC) has established a growing footprint in the two countries and has already forged memorandums of understanding with both governments to develop coal-fired power stations. The mining junior has two coal mining projects on the go – Tancoal in Tanzania and Malcoal in Malawi – and another project – Tanzacoal – in the development stage. IEC’s flagship thermal coal project is the Ngaka mine, owned 70% by Tancoal and 30% by the state-owned National Development Company, which has an operating capacity of 0.36mtpa out of JORC resources of 423mt. The company’s marketing wing has been working overtime lining up sales contracts in Tanzania, Uganda and Kenya which in turn will significantly lower the production cost per tonne. While the price to customers on the coast is elastic to Richards Bay pricing, prices to inland customers are inelastic. Product from Ngaka attracts about A$54/t at the mine gate and production costs are targeted to fall from #35/t to $25/t once production is ramped up to full capacity and haul road improvements are finalised. Industrial demand for coal is growing about 20% a year. A bankable power purchase agreement (PPA) with Tanzanian power utility TANESCO will allow IEC to sponsor a US$400m

mine-mouth power station, expected to provide 200MW, scalable via modular additions, beginning in early 2018. The government is keen to get away from the

heavy weighting of hydropower in its generation profile and recognises coal-fired generation is a reliable and affordable base load source that is not subject to climate-driven variability. IEC and TANESCO are close to finalising the PPA which ensures payments for power produced will be paid in US dollars and are guaranteed by governments or other guarantors such as the World Bank, African Development Bank or export credit agencies. Meanwhile in Malawi the Nkhachira coal project, 90% owned by Malcoa and 10% by a local entrepreneur, is operational and is expected to produce 0.045mt of coal in 2013-14. As IEC moves from a contract mining arrangement to its own controlled process capacity will be lifted to 0.15mtpa significantly reducing the cost of production. Three size fractions are sold by the mine (fines, mids and coarse) and sales currently average US$70-75/t at the mine gate while production costs come in at $40/t which should go down to $25/t once the company introduces new mining equipment. IEC plots industrial coal demand in Malawi at 0.12 to 0.15mtpa while markets in Zambia are estimated to take a further 0.24mtpa. An MOU with the Malawi government will allow IEC to sponsor the 120MW Pamodzi coal-fired power plant which will be fuelled by a mix of Malawian coal and product barged across Lake Malawi from the Tancoal mine in south-west Tanzania. The company is conducting a bankable feasibility study of the project and aims to have the plant operational by early 2017. IEC is also negotiating a PPA with the power utility, Electricity Supply Corporation of Malawi, hoping to finalise it before the end of this year.

Progress on all fronts has been streamlined thanks to the company’s strong engagement with both the Tanzanian and Malawian governments allowing IEC to emerge as an eastern and central African integrated mine-power operator. IEC recently contracted consultants Optimine to undertake, with IEC’s own staff, a strategic resource review of the company’s portfolio of coal resources. Key targets include the delineation of reserves at Ngaka, delineation of a maiden resource in Malawi and the expansion of sales and production of industrial coal.

Tenders Korea East-West Power (EWP) has issued three term requirements and one spot tender for various power plants with a deadline for offers of July 12. In the spot tender, EWP is seeking 0.28mt of 4,600kc NAR min material for its Dangjin Power Plant for delivery in August and September. The first of the term tenders calls for 0.28mt of 5,100kc NAR min coal in the first year, with shipment in September and October, and a further 0.14mt in each of years two to five of the contract, through to October 2017, on a fixed price FOB basis. Under the second term tender, EWP is again calling for 5,100kc NAR min product in the same quantities and time frame as the first tender, with the difference to the earlier tender being the requirement for prices on a premium number US$ or discount number US$ against globalCOAL’s Newcastle index, based on a 6,000 NAR basis, FOB only. The final term requirement covers 3,800kc NAR material on a FOB basis, with the need for 0.14mt in the first year of the contract and 0.28mt in each of year two to five of the agreement which will run to October 2017. Karnataka Power Corporation Limited (KPCL) has invited bids for supplying 1.5mt of imported steam coal for blending purpose at their Raichur facility in central India. The selected supplier should supply the coal over 12 months. The scope of the work includes arranging for dispatch of coal from coal mines abroad to the unloading port in India and unloading the coal. The supplier would be required to facilitate and cooperate with third party sampling and analysis of imported coal at loading port and unloading port. South Korea’s generators have launched a joint tender for 0.7mt of low c.v. coal for delivery from September to November, 2013 with deadline for offers of July 16. Issued by Korea Midland Power (Komipo) on behalf of the five utilities, the tender outlines a requirement for 4,600kc NAR min material in 10 panamax shipments destined for the Boryeong, Yeonghung, Samcheonpo, Taean, Hadong and Dangjin power plants. Material with a total max moisture of 28%, max ash content of 17% and max sulphur content of 1% is being sought. Taiwan’s Formosa Plastics Group (FPG) has issued two more tenders for bituminous coal, bringing total new solicitations this week to 0.67mt. Closing date for all tonnage is July 15. The latest two tenders separately call for 0.2mt and 0.3mt of minimum 5,850kc GAR material for delivery in August and September this year. They are unusual for FPG - calling for delivery to Houshi port, Zhangzhou, China, with offers allowable in US$ or remimbi. The specs allow ash up to 22%, with panamax vessels specified. The tenders were issued Tuesday along with two other tenders separately reported by McCloskey’s Newswire and seeking 0.3mt of minimum 6,000kc GAR material and 40,000t of minimum 5,500kc GAR product for August/September delivery.

As IEC moves from a contract mining arrangement to its own controlled process capacity will be lifted to 0.15mtpa significantly reducing the cost of production.

Coal Chain Australia

6Australian Coal Report Issue 0505 10 July 2013

NEWCASTLE VESSEL QUEUE NEWCASTLE

14

24

Test

4

WEEKLY LOADING RATES NEWCASTLE (Mt)

1

1.5

2

2.5

3

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

Mt

Newcastle weekly loading rates

loading rates current port capacity

0

0.5

0.8

1.0

1.2

1.4

Source: HVCCC

0.00

0.50

1.00

1.50

2.00

0.00

0.50

1.00

1.50

2.00

2.50

Test

0.000.00

t shipped closing stock portSource:PWCS

WEEKLY THROUGHPUT NEWCASTLE (Mt)

PORT WRAPDALRYMPLE BAYThe Dalrymple Bay Coal Terminal (DBCT) throughput for the week ending July 8 was 1.506mt, an increase of 0.068mt week-on-week. The 85mtpa terminal operated at 92% of its nominal weekly capacity. In July 2012, DBCT had an average weekly throughput of 0.844mt. Coal stocks at July 8 were 0.564mt, a decrease of 0.117mt w-o-w, and only about half the volume required for the most efficient operation of the terminal. DBCT received on average 21 trains per day, a fall of two trains per day w-o-w. DBCT normally receives 24-27 trains per day when it is operating at its maximum potential. The DBCT ship queue decreased by four vessels w-o-w to 12 vessels as at July 9, with 10 vessels with coal available at the mines, unchanged from last week. The optimal number of vessels in DBCT’s ship queue is about 20 vessels. Shiploader 1 will be out of operation until July 19, shiploader 2 will be closed from July 11 to August 17 and shiploader 3 will be out of action from July 16 to 18, all for planned maintenance, according to ISS. A site-wide power outage is also planned on July 18 for 14 hours. GLADSTONEThe Port of Gladstone had a throughput of 1.405mt for the week ending July 7, an increase of 0.128mt week-on-week. The RG Tanna and Barney Point coal terminals with a combined nameplate capacity of 76mtpa operated 96% of their nominal weekly capacity. In July 2012, the Gladstone coal terminals had an average weekly throughput of 1.098mt. The volume of coal railed to the Port of Gladstone was 1.278mt, a decline of 0.204mt w-o-w. Coal stocks at the port also declined, down 0.16mt w-o-w to 2.4mt. Gladstone requires coal stocks of 2-3mt for the optimal performance of the terminals. As at July 10, the Gladstone ship queue had 21 vessels, an increase of four vessels w-o-w, with nine of the vessels having coal available at the port. A further 13 vessels are expected to arrive at Gladstone during the course of the week with one of the vessels currently having coal available. PORT KEMBLAThe Port Kembla Coal Terminal (PKCT) had a throughput of 0.31mt for the week ending July 9. The 18mtpa terminal operated at 90% of its nominal weekly capacity. In July 2012, PKCT had an average weekly throughput of 0.234mt. Coals stocks at PKCT were 0.34mt, down0.074mt week-on-week, with a ship queue of two vessels, a decline of two vessels w-o-w.

Port Waratah Coal Services (PWCS) terminals at the Port of Newcastle had a throughput of 2.465mt for the week ending July 9, an increase of 0.208mt week-on-week. The combined 133mtpa capacity Carrington and Kooragang terminals operated at 97% of their nominal weekly capacity. In July 2012, PWCS had an average weekly throughput of 2.245mt. PWCS’s shiploading month to date annualised rate was 128.9mt and YTD annualised rate of 108.29mt. PWCS has a shiploading target of 136.9mt for 2013. The PWCS ship queue had 20 vessels, an increase of seven vessels w-o-w, with three vessels off shore with all coal assembled at the port. The optimal number of vessels in PWCS’s ship queue is 20-23 vessels. The average forecast wait time for vessels in the queue is 5.72 day, up from 3.28 days of the previous week. The Hunter Valley Coal Chain Coordinator (HVCCC) estimates PWCS’s ship queue will have 10 vessels at the end of July based on current terminal demand, a decline of three vessels from its estimate of the prior week. July’s nominations for PWCS are currently 10.8mt. The HVCCC estimates PWCS’s ship queue will have 12 vessels at the end of August. PWCS has been notified of the arrival of 32 vessels to load 2.898mt, up from 24 vessels of the previous week. Forward nominations generally number about 20 vessels.PWCS coal stocks were at 1.262mt, down 0.233mt w-o-w, and approaching the normal levels of 1-1.2mt. Meanwhile, the NCIG ship queue has three vessels, an increase of two vessels w-o-w, with an average forecast waiting time of 3.3 days, up from 2.6 days of the previous week.

Coal Chain Australia

0

20

40

60

80

100

Ve

sse

ls

Coal ships waiting by Port (Australia)Hay Point Gladstone Dalrymple Bay Newcastle

COAL SHIPS WAITING BY PORT (AUSTRALIA)

LOAD PORT VESSEL DWT DISCHARGE PORT LOAD DATE Ld/Dis.Terms US$/t SHIPPER

Port Kembla Polaris TBN 140,000 Youngheung 21/30 Jul 45000C/30000C 12.94 Kepco

Newcastle Lansing TBN 70,000 Hualien/Hoping 18/24 Jul 25000C/24000C 11.65 Castleton

Richards Bay Cape Mercury 150,000 India 10/20 Jul Scale/40000C 14.10 not reported

Samarinda D'Amico TBN 70,000 Dahej 1/8 Jul 10000C/30000C 9.30 Libra

SE Kalimantan Navios Titan 65,000 Dahej 3/10 Jul 10000C/30000C 9.30 Libra

Mobile TBN 70,000 Hamburg 25 Jul - 10 Aug 25000C/30000C 15.00 Salzgitter

WEEKLY SHIPPING

14-May-13 21-May-13 28-May-13 4-Jun-13 11-Jun-13 18-Jun-13 25-Jun-13 2-Jul-13 9-Jul-13

Newcastle 22 26 20 21 12 21 21 14 21

Gladstone 12 16 20 18 12 16 21 17 21

Dalrymple Bay 19 26 28 23 21 21 16 18 13

Hay Point 9 5 5 5 3 2 4 2 3

SOURCE: ISS

Australian Coal Report Issue 0505 10 July 2013

Australian Coal Report is copyrighted © 2013 by Energy Publishing Pty Ltd. Information published is considered accurate and reliable, but no responsibility or liability will be accepted for any error or omission. www.coalportal.com Distribution to nonsubscribers is a breach of copyright. Tel +61-7-3020-4000 Fax: +61-7-3102-9151 | Editor: Marian Hookham Email: [email protected]

7

SOURCE: SSY

Coal Chain Australia

8Australian Coal Report Issue 0505 10 July 2013

Vessel Route US$/tonne Vessel Route US$/tonne

Cape Gladstone/Qingdao 10.00 Post Panamax Gladstone/Qingdao 12.50

150,000Mt (10%) Newcastle/Qingdao 11.10 90,000Mt (10%) Newcastle/Qingdao 14.00

Vancouver/Qingdao 11.30 Vancouver/Qingdao 14.40

RBCT/Qingdao 14.40 Brisbane/Kaohsiung (Taiwan) 12.10

Gladstone/Krishnapatnam (India) 11.80 Gladstone/Krishnapatnam (India) 14.80

RBCT/Krishnapatnam 13.10

Mini Cape Brisbane/Kaohsiung (Taiwan) 13.10 Panamax Gladstone/Qingdao 12.80

110,000Mt (5%) Gladstone/Krishnapatnam (India) 15.20 70,000Mt (10%) Newcastle/Qingdao 14.00

Gladstone/Qingdao 13.20 Balikpapan/Qingdao 8.10

Newcastle/Qingdao 15.10 Lyttelton/Qingdao (62k) 17.80

Supramax Gladstone/Krishnapatnam (India) 20.80 Vancouver/Qingdao 14.60

50,000Mt (10%) Taboneo/Krishnapatnam 11.60 RBCT/Qingdao 16.60

Taboneo/Qingdao 11.60 Gladstone/Krishnapatnam (India) 15.50

Vancouver/Qingdao 20.60 RBCT/Krishnapatnam 14.20

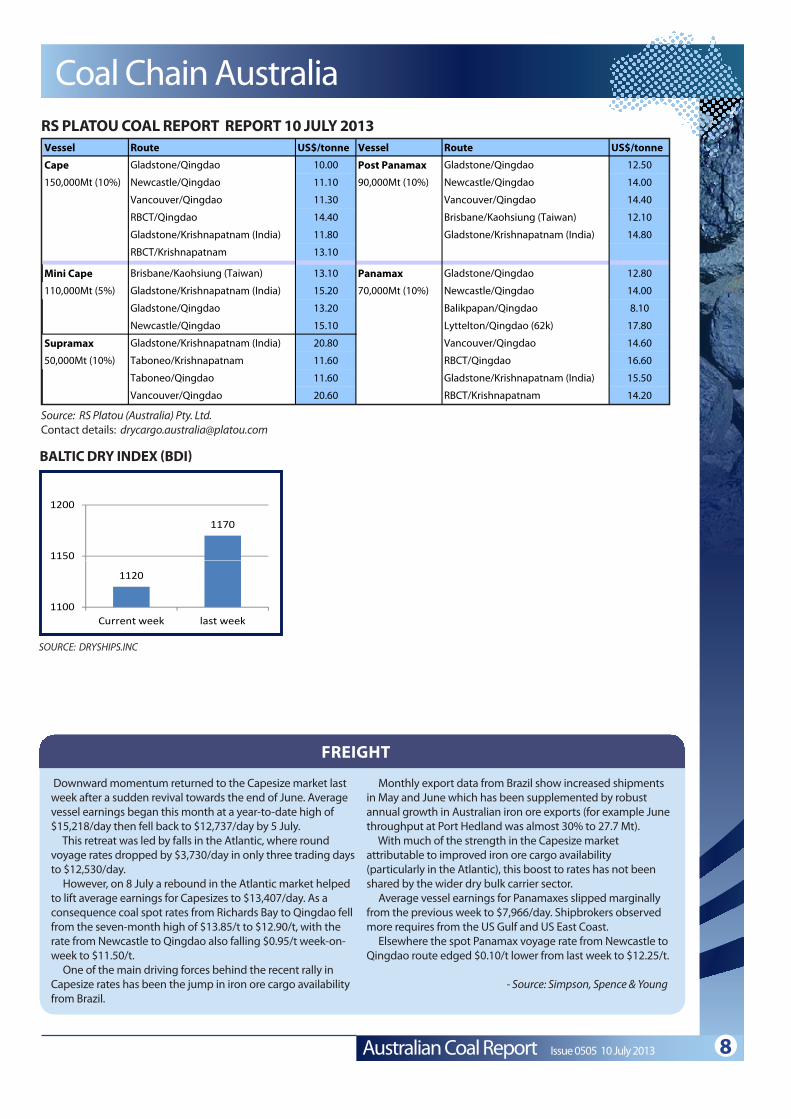

RS PLATOU COAL REPORT REPORT 10 JULY 2013

BALTIC DRY INDEX (BDI)

1170

1150

1200

Chart Title

1120

1100

1150

Current week last week

SOURCE: DRYSHIPS.INC

Source: RS Platou (Australia) Pty. Ltd. Contact details: [email protected]

FREIGHT

Downward momentum returned to the Capesize market last week after a sudden revival towards the end of June. Average vessel earnings began this month at a year-to-date high of $15,218/day then fell back to $12,737/day by 5 July. This retreat was led by falls in the Atlantic, where round voyage rates dropped by $3,730/day in only three trading days to $12,530/day. However, on 8 July a rebound in the Atlantic market helped to lift average earnings for Capesizes to $13,407/day. As a consequence coal spot rates from Richards Bay to Qingdao fell from the seven-month high of $13.85/t to $12.90/t, with the rate from Newcastle to Qingdao also falling $0.95/t week-on-week to $11.50/t. One of the main driving forces behind the recent rally in Capesize rates has been the jump in iron ore cargo availability from Brazil.

Monthly export data from Brazil show increased shipments in May and June which has been supplemented by robust annual growth in Australian iron ore exports (for example June throughput at Port Hedland was almost 30% to 27.7 Mt). With much of the strength in the Capesize market attributable to improved iron ore cargo availability (particularly in the Atlantic), this boost to rates has not been shared by the wider dry bulk carrier sector. Average vessel earnings for Panamaxes slipped marginally from the previous week to $7,966/day. Shipbrokers observed more requires from the US Gulf and US East Coast. Elsewhere the spot Panamax voyage rate from Newcastle to Qingdao route edged $0.10/t lower from last week to $12.25/t. - Source: Simpson, Spence & Young

Coal Chain Australia

Australian Coal Report Issue 0384 February 2011 5

Coal Chain Australia - monthly

9

2

4

6

8

10

12

Newcastle monthly shipments (Mt)

0

2

Shipments Port Capacity

MONTHLY THROUGHPUT (MT) NEWCASTLE

Top 4 Export Destinations in June

GLADSTONEMONTHLY THROUGHPUT (MT)

2

4

6

Newcastle monthly shipments (Mt)

0

Shipments Port Capacity

Top 4 Export Destinations in June

Destination Total m-o-m %

Variation

China 1,666,279 65.11%

Japan 1,652,228 1.42%

India 1,162,492 67.98%

Korea 809,578 67.98%

Throughput at the Port of Waratah Coal Services (PWCS) operated Newcastle coal terminals in June 2013 was 9.314mt, an increase of 0.871mt month-on-month. In June 2012, PWCS had a throughput of 9.153mt. The Kooragang and Carrington terminals with a combined nominal capacity of 133mtpa operated at 84% of their monthly throughput capacity in June. PWCS shiploading finished the month at an annualised rate of 113.32mt and YTD annualised rate of 107.26mt. PWCS has a shiploading target of 136.9mt for 2013. As at June 30, the PWCS ship queue had 13 vessels, a decrease of four vessels from the end of May. Coal stocks at the end of June were 1.59mt, an increase 0.422mt m-o-m and above the 1-1.2mt minimum requirement for the most efficient operation of the terminals. PWCS’s total coal exports to Japan decreased by 0.15mt m-o-m to 4.36mt although thermal coal exports were up 0.1mt to 3.96mt but coking coal exports were down 0.25mt to 0.4mt in June. Surprisingly exports to China increased by 1.27mt m-o-m to 2.61mt, accounting for 28.22% of PWCS’s total exports for the month. It was also the highest volume exported to China since the record breaking 2.95mt shipped in December 2012. The June total included 2.43mt of thermal coal, up 1.09mt m-o-m, and 0.18mt of coking coal. Coal exports to Korea from PWCS in June were down 0.35mt m-o-m to 0.8mt of thermal coal. Taiwan shipments increased by 0.1mt to 0.99mt, including 0.89mt of thermal coal, up 0.34mt m-o-m, and 0.1mt of coking coal, down 0.25mt. Meanwhile, NCIG shipped 2.489mt of coal through the Port of Newcastle in June, down 0.655mt on the previous month. NCIG with a nominal throughput of 53mtpa operated at about 60% of capacity. In June 2012, NCIG shipped 2.269mt of coal.

The Port of Gladstone exported 5.798mt of coal in June, an increase of 0.449mt month-on-month and the best performance since December 2011. The RG Tanna and Barney Point coal terminals with a combined throughput capacity of 76mtpa operated at 92% of the nominal monthly capacity. In June 2012, Gladstone exported 5.122mt of coal. China just nudged out Japan as the largest recipient of coal from Gladstone with 1.666mt, an increase of 0.376mt m-o-m. Coal exports to Japan in June were 1.652mt, a fall of 0.228mt m-o-m. India was Gladstone’s third largest market with 1.162mt, an increase of 0.172mt m-o-m. Gladstone’s ship queue at the end of June had 19 vessels, an increase of five vessels m-o-m.

Destination Total m-o-m %

Variation

Japan 4,356,174 -3.43%

China 2,608,933 94.01%

Taiwan 989,347 10.73%

S. Korea 803,401 -30.07%

SOURCE: GLADSTONE PORTS CORPORATION

SOURCE: PWCS

Australian Coal Report Issue 0505 10 July 2013

Coal Chain Australia

Australian Coal Report Issue 0384 February 2011 5

Coal Chain Australia - monthly

10

2

4

6

8

Newcastle monthly shipments (Mt)

0

2

Shipments Port Capacity

MONTHLY THROUGHPUT (MT) DALRYMPLE BAY

HAY POINT

MONTHLY THROUGHPUT (MT)

1

2

3

4

Newcastle monthly shipments (Mt)

0

1

Shipments Port Capacity

PORT KEMBLA

0.50

1.00

1.50

2.00

Newcastle monthly shipments (Mt)

0.00

0.50

Shipments Port Capacity

MONTHLY THROUGHPUT (MT)

The BHP Mitsubishi Alliance (BMA) operated Hay Point Coal Terminal (HPCT) exported 4.137mt of coal in June, a monthly export volume that hasn’t been bettered since September 2007. Throughput was up 1.061mt on the May volume. The 44mtpa capacity terminal operated at 113% of its nominal monthly capacity. In June 2012, HPCT exported 2.68mt of coal. Shiploader 2 is expected to be out of operation until August 12 for planned maintenance.

The Dalrymple Bay Coal Terminal (DBCT) had a throughput of 5.65mt in June, an increase of 0.06mt month-on-month and the best performance so far in 2013. The 85mtpa capacity terminal operated at 80% of its nominal throughput capacity. In June 2012, DBCT exported 4.252mt of coal. Coal stocks at the end of June were 0.534mt, down 0.07mt at the end of May and only about half the volume required for the most efficient operation of the terminal. DBCT received an average 19 trains per day in June, about the same number of trains per day as in May. The DBCT ship queue had 18 vessels at the end of June, a decrease of nine vessels m-o-m. The vessels had an average turn time of 14.52 days during the month compared with YTD average turn time of 14.55 days. In June, 47 vessels arrived to load 5.048mt of coal. At the beginning of this month, DBCT expected 34 vessels to arrive in July to load 3.263mt of coal.

Port Kembla Coal Terminal (PKCT) exported 1.072mt of coal in June, a fall of 0.04mt month-on-month. Exports included 0.677mt of coking coal and 395mt of thermal coal. In the latter part of the month, Port Kembla was closed for several days due to heavy swells and shiploading was restricted because of an electrical problem with a shiploader. The 18mtpa capacity terminal operated at 71% of its nominal monthly capacity. In June 2012, PKCT exported 1.493mt of coal. China was the largest importer of coal from Port Kembla with 0.441mt of coking coal followed by India which imported 0.223mt of coal including 0.132mt of coking coal and 0.091mt of thermal coal. PKCT exported 0.111mt of coal to Japan in June.

SOURCE: PORT KEMBLA COAL TERMINAL SOURCE: PORT OF HAY POINT

SOURCE: DBCT

Top 4 Export Destinations in June

Destination Total m-o-m %

Variation

China 440,780 143.71%

India 222,845 -29.39%

Japan 123,492 -59.99%

Taiwan 86,413 n/a

Australian Coal Report Issue 0505 10 July 2013

Coal Chain Australia

Australian Coal Report Issue 0384 February 2011 5

Coal Chain Australia - monthly

11

MONTHLY THROUGHPUT (MT)

0.50

1.00

1.50

2.00

2.50

Newcastle monthly shipments (Mt)

0.00

0.50

Shipments Port Capacity

ABBOT POINT BRISBANE

MONTHLY THROUGHPUT (MT)

0.50

1.00

Newcastle monthly shipments (Mt)

0.00

Shipments Port Capacity

Ports

Nominal

Capacity

(Mtpa)

Jun-13 M-O-M % Y-O-Y % YTD total Annualised

QUEENSLAND

Dalrymple Bay 85 5,649,690 1 33 31,011,837 68,737,895

Gladstone 76 5,797,810 8 13 27,731,842 70,540,022

Hay Point 44 4,137,475 35 54 18,368,051 50,339,279

Abbot Point 50 1,676,749 -11 83 9,868,246 20,400,446

Brisbane 10 939,945 57 38 4,144,550 11,435,998

NEW SOUTH WALES

PWCS 133 9,314,000 10 2 53,191,969 113,320,333

NCIG 30 2,489,932 -21 10 16,392,793 30,294,173

Port Kembla 18 1,092,652 -2 -28 6,155,814 13,293,933

total 31,098,253 7 17 166,865,102 378,362,078

The Adani owned Abbot Point Coal Terminal (APCT) had a throughput of 1.677mt in June, a decrease of 0.241mt month-on-month. The 50mtpa capacity terminal operated at 40% of its nominal monthly capacity. In June 2012, APCT exported 0.917mt of coal. At the end of June, APCT had six vessels in its ship queue, an increase of four vessels m-o-m, according to ISS.

The New Hope Corporation-owned Queensland Bulk Handling (QBH) coal facility at the Port of Brisbane exported 0.94mt of coal in June, an increase of 0.343mt month-on-month. The 10mtpa capacity terminal operated at 113% of its nominal monthly throughput capacity. In June 2012, QBH exported 0.679mt of coal.

MONTHLY ANNUALISED RATES (MT)

SOURCE: ABBOT POINT TERMINAL SOURCE: PORT OF BRISBANE

SOURCE: PORTS OF QUEENSLAND AND NEW SOUTH WALES

Australian Coal Report Issue 0505 10 July 2013