Embed Size (px)

Citation preview

The Changing Face of the

Australian Export Coal Industry

Informa

Australian Coal Conference16 & 17 August 2018

Bede Boyle

Coal Ventures & Associates

Contents

The Strategic Context for Recent M&A Activity

1. Demand for Australian High Quality Coals

2. Coal Market Volatility is Driven by China

3. India is now Largest Importer of Australian Metallurgical Coal

4. India Thermal Coal – Complex Domestic & Import Dynamics

5. Convergence of Three Trends is boosting Coal Industry Profits

Restructuring of Australian Export Coal Industry

6. Restructuring of Australian Export Coal Industry

Contents- continued

New Projects Pipeline

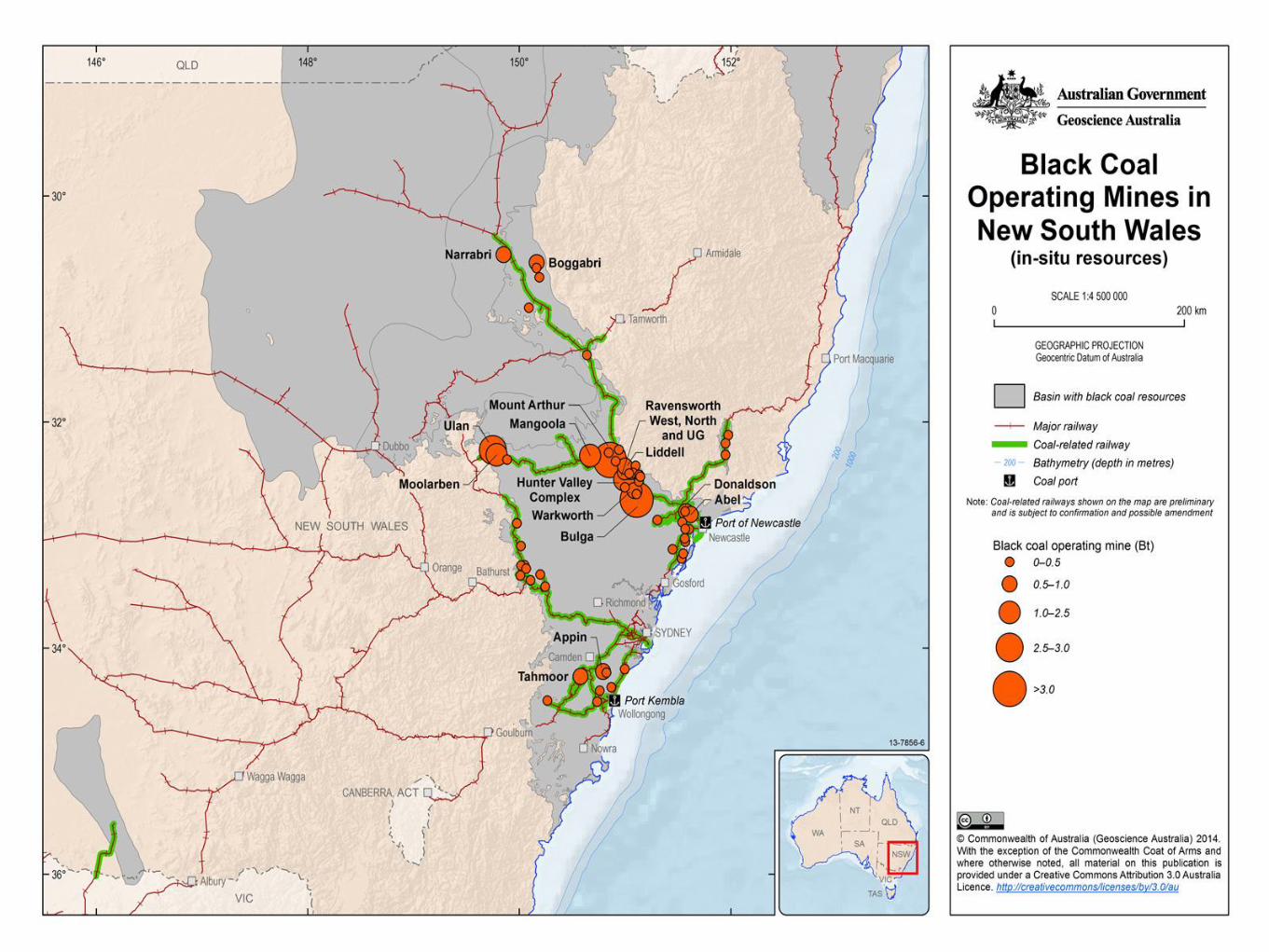

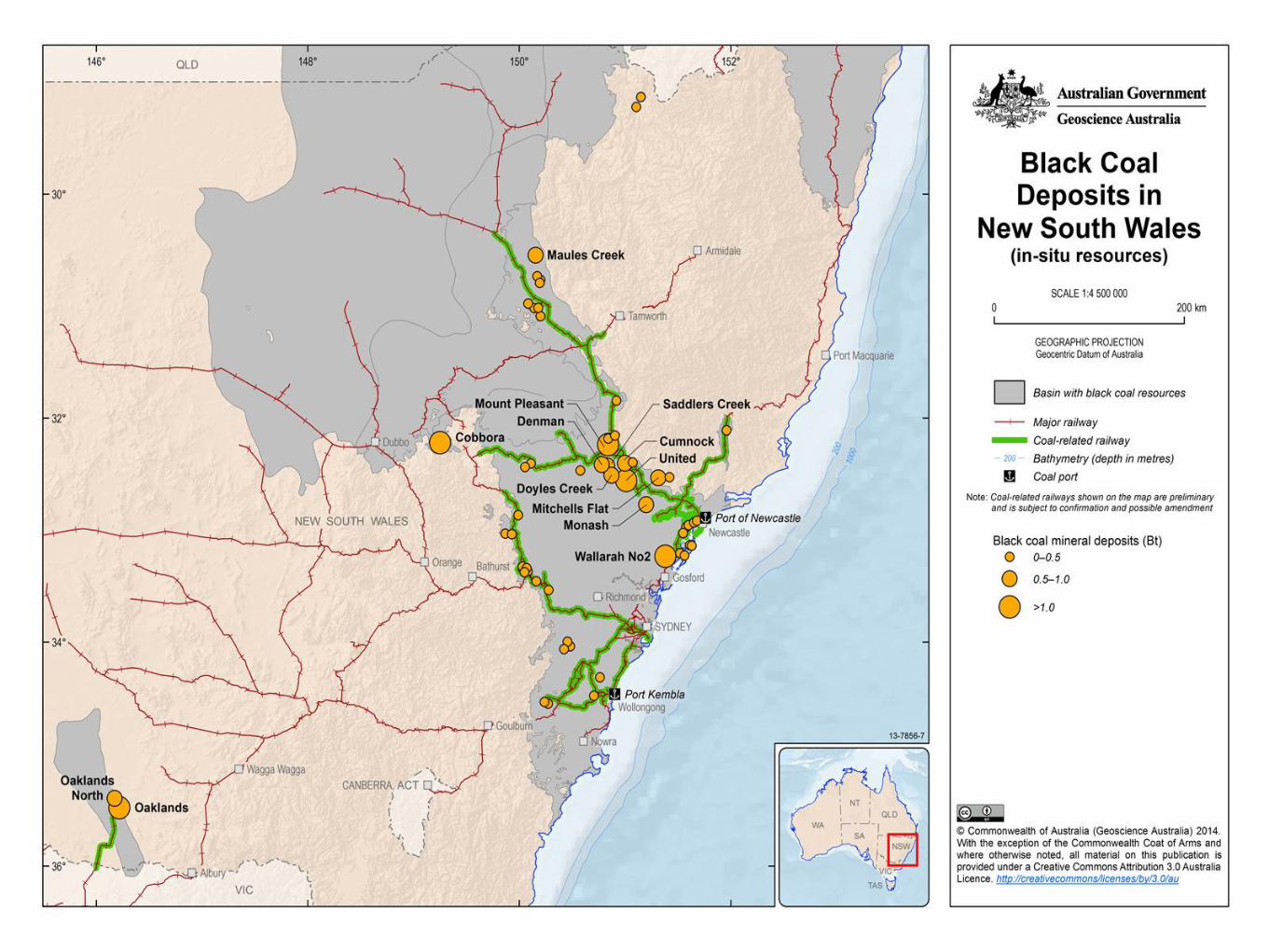

New South Wales

Maps Black Coal Deposits and Operating Mines in NSW

7. NSW Government is creating uncertainty for Investment

8. Timing of NSW Brownfield and New Projects is Uncertain

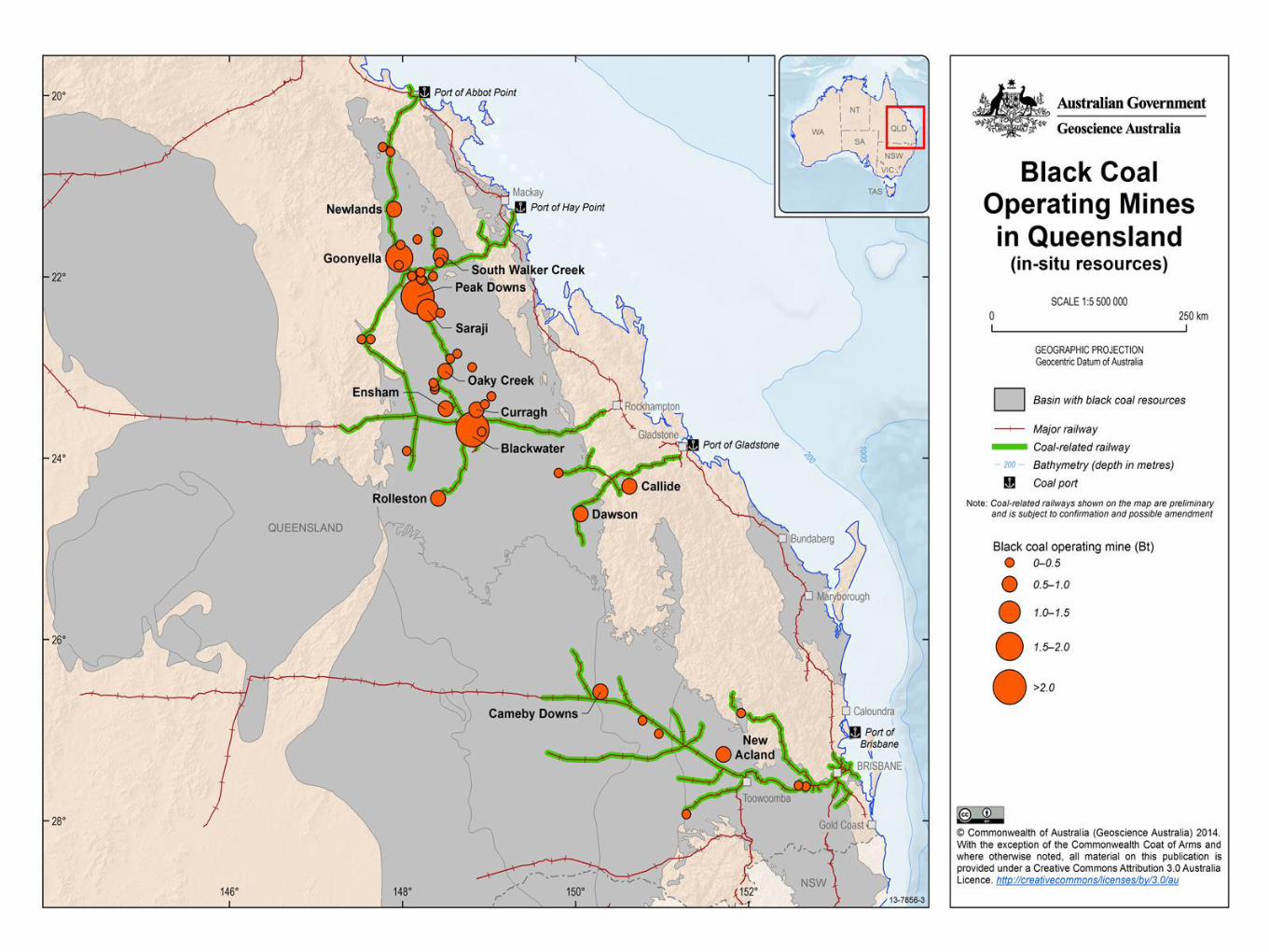

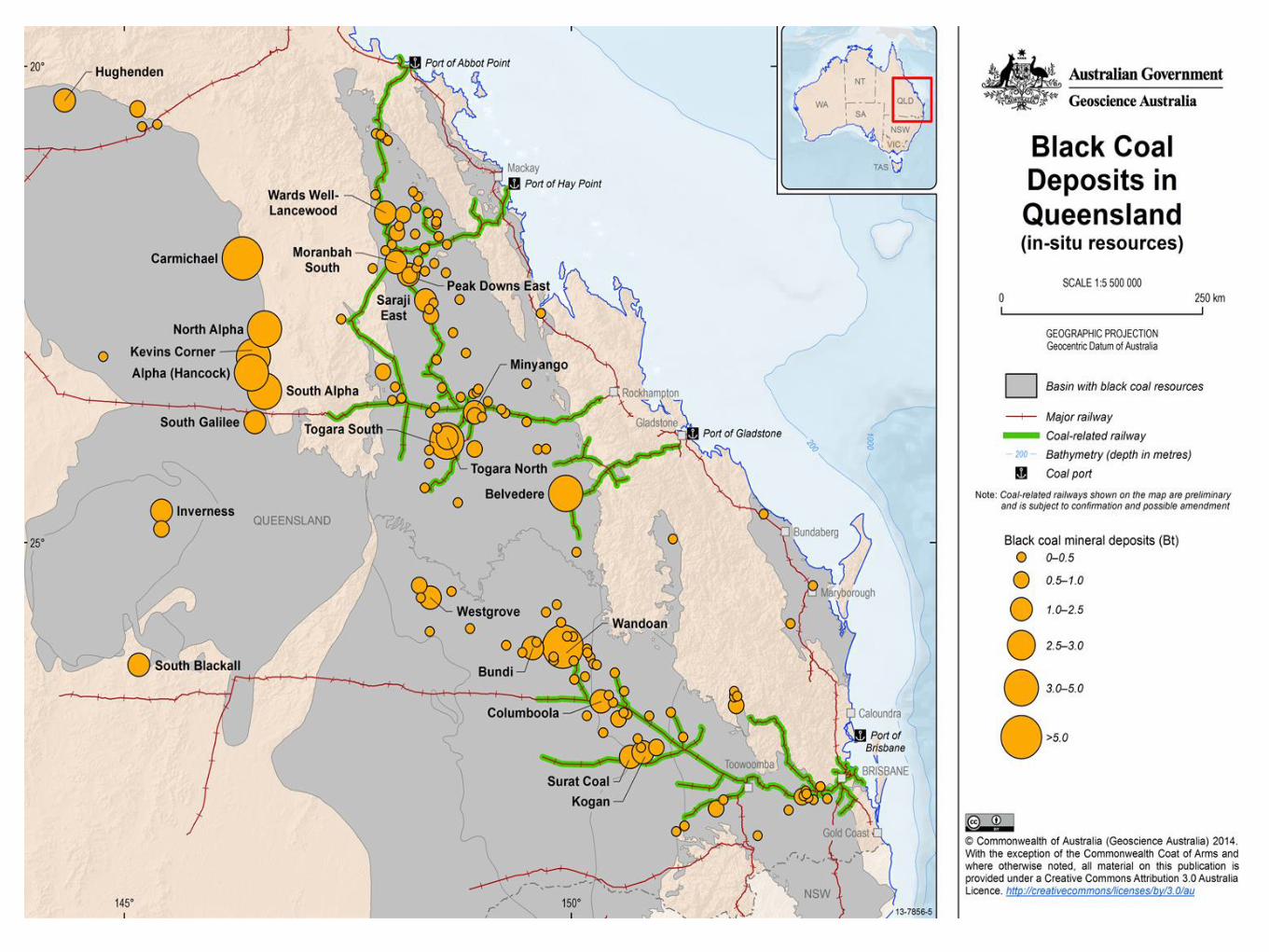

Queensland

Maps Black Coal Deposits and Operating Mines in QLD

9. QLD Metallurgical Coal Project Pipeline

10. Timing of QLD Thermal Coal Projects is Uncertain

11. Inter-port Global linking Australia to China One Belt – One Road

Through Port of Gladstone

12. I-PG Proposed Toowoomba – Gladstone Railway

Potential for link with Surat Basin Coal

13. Coal Ventures & Associates

Contents- continued

The Contents of this presentation are based on three studies

available free on request to [email protected]

1. Australian Export Coal Industry 2018-2027

A Decade of Growth

2. The Changing Face of the Australian Export Coal Industry

M&A Activity is dramatically changing the Face of the Australian

Export Coal Industry

3. Queensland Metallurgical Coal Projects to 2020

And Future Projects Pipeline

With acknowledgement to Marion Hookham Associate Director IHS Energy

1 Demand for Australian High Quality Coals

2018 to 2027 will be a Decade of Growth for Australian Export

Coal Industry. Asia demand pull for Australian high quality coals

for energy security and to drive economic development will

sustain exports of both thermal and metallurgical coals

Over half the worlds population is in Asia

1. Demand for Australian High Quality Coals

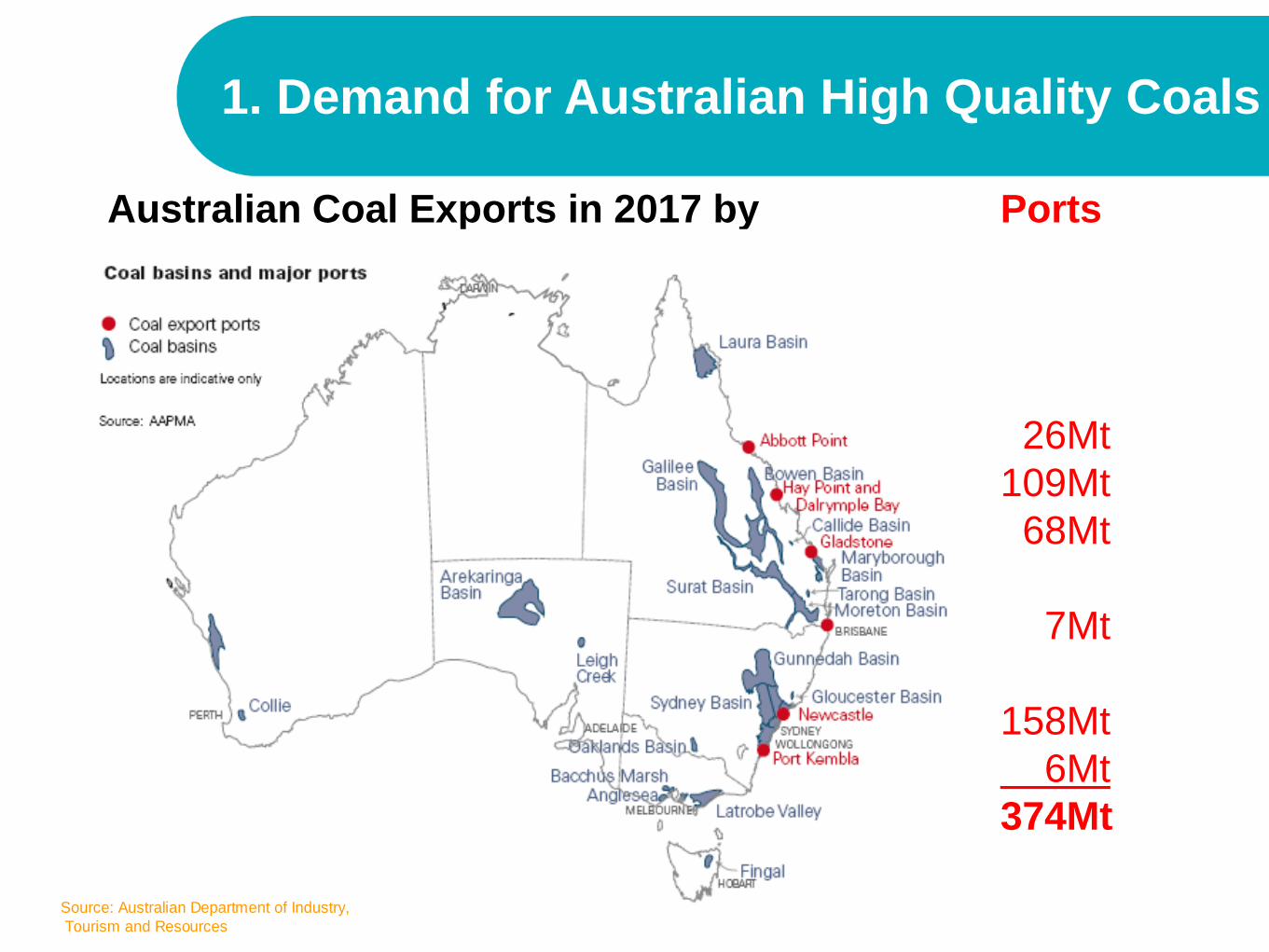

Australian Coal Exports in 2017 by Ports

27Mt 26Mt

109Mt

68Mt

7Mt

158Mt

6Mt

374Mt

Source: Australian Department of Industry,

Tourism and Resources

1 Demand for Australian High Quality Coals

2018 to 2027 will be a Decade of Growth for Australian Export Coal

• Asia demand for Australian Metallurgical and Thermal Coals is

Forecast to increase by 44Mtpa over the next Decade to 2027.

Source: IHS Markit Seaborne Coal Outlook 2017 to 2027

• 130Mtpa Unused Export Terminal Capacity is a key enabler of

Rapid Brownfield Mine Developments in response to Market

Demand for Metallurgical and Thermal Coals

• Metallurgical Coal The IHS Markit forecast 30Mtpa increase in

Metallurgical Coal Exports is underpinned by an expectation of

higher demand from India.

• Thermal Coal The rapid expansion of coal-fired power capacity in

Southeast Asia will drive demand higher in markets including

Taiwan, Thailand, Malaysia, the Philippines and Vietnam.

1 Demand for Australian High Quality Coals

2018 to 2027 will be a Decade of Growth for Australian Export Coal

What is often overlooked is that even in recent years the use of

fossil fuels has grown by even more in aggregate terms than

renewables. The Australian Government Chief Economist advising the

Australian Government in Resources and Energy Quarterly June 2015

that World energy consumption is likely to be one of the defining issues

of the 21st century, particularly the way in which the world

simultaneously addresses climate change and access to energy.

And highlighted in Resources and Energy Quarterly June 2017 that

there were 365 advanced technology coal fired power stations

planned or under construction globally.

In India nearly 100 new coal fired power plants currently under

construction are scheduled to come online by the end of 2018.

1 Demand for Australian High Quality Coals

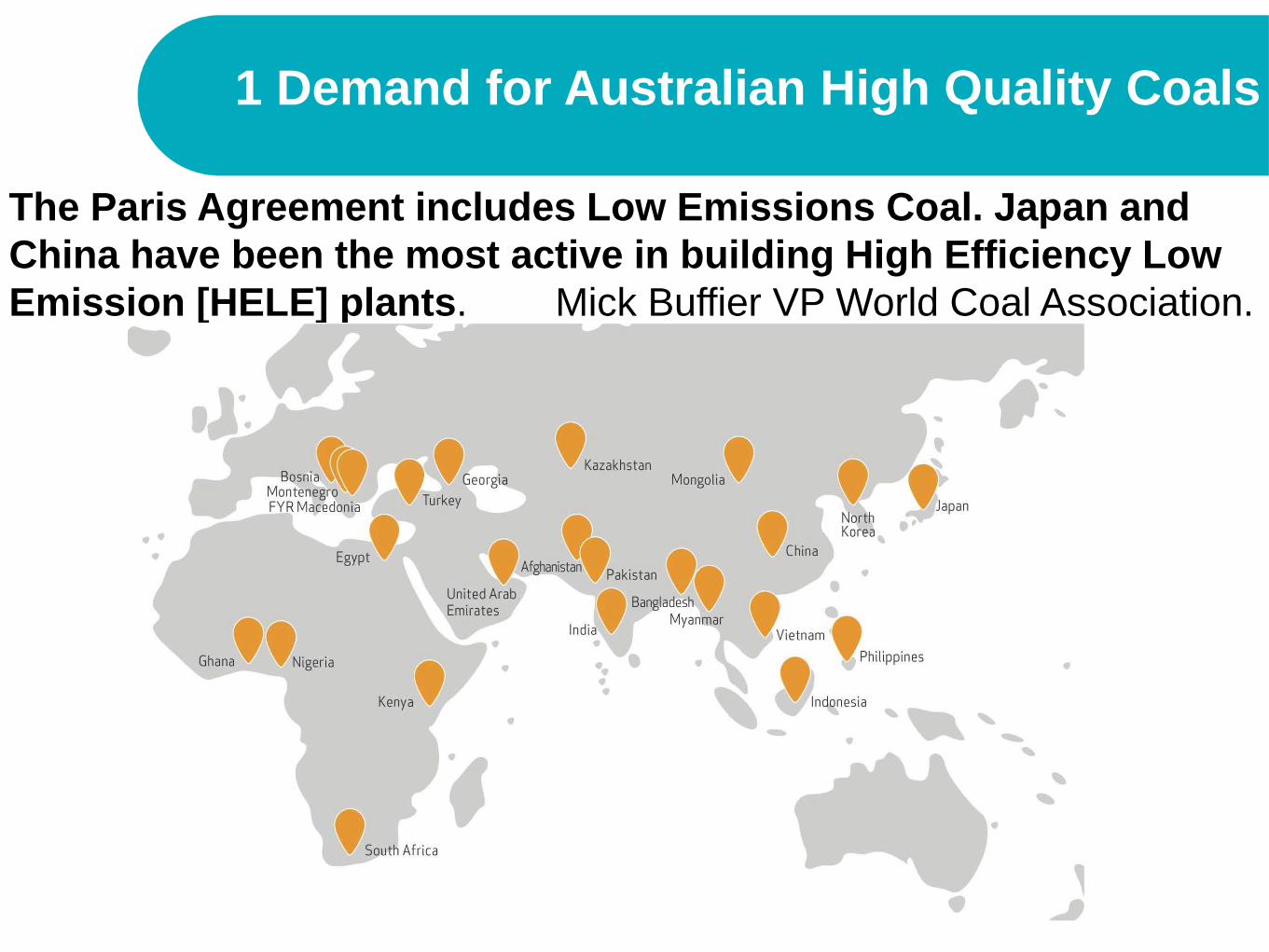

The Paris Agreement includes Low Emissions Coal. Japan and

China have been the most active in building High Efficiency Low

Emission [HELE] plants. Mick Buffier VP World Coal Association.

1 Demand for Australian High Quality Coals

2018 to 2027 will be a Decade of Growth for Australian Export Coal

Coal will be Critical in Powering up Southeast Asia

• Southeast Asia energy demand grows by 67% to 2040.

• Of 650 million people in Southeast Asia, 250m rely on biomass for

cooking and 65m have no electricity.

“Coal is expected to be the largest growth of energy in S-E Asia”

“Coal-fired power plants double in capacity to 160GW”

“Reflects…relative affordability …and ample availability of resources”

Coal will drive India’s Economic Growth with Coal Generating

Capacity more than Doubling

• India Electricity demand grows 5% pa over the next 25 years

• Coal generation capacity more than doubles

• Renewables increase significantly in mix (x10)

Source: (IEA) Southeast Asia Energy Outlook 2017

2. Coal Market Volatility is Driven by China

China coal imports are small margin on very large domestic base

In 2017 China imported 70Mt of metallurgical coal and 188Mt thermal

coal which totals only 7% of China production of 3.7billion t.

China 2016-2020 plan will lift production from 3.7billion t in 2016 to

3.9billion t in 2020.

China costs have risen sharply due to labour and transport costs

and in 2018 the Chinese government has conflicting objectives:

Firstly to close unsafe coal mines which will decrease production and

Secondly to lower prices to domestic users by increasing production.

How these conflicting China Government policies are implemented will

determine China Domestic Prices and impact Import Prices.

The government’s targeted range for China 5,500kcal Domestic FOB

Mine Sales is RMB500- 570/t (US$72.67-US82.85/t). However, in

October 2017 FOB Qinhuangdao Price hit RMB735/t (US$112.23/t)

3. India is now Australia’s Largest

Market for Metallurgical Coal

Make in India Campaign was launched by

Prime Minister Modi in 2014 and is already

transforming India into a Global design and

manufacturing Hub.

In 2015 India was the top destination globally for foreign direct

investment, surpassing the United States of America as well as

the People's Republic of China with US$63billion in FDI. International

companies including Apple, Ford, General Electric, Sandvik and VW

are establishing major manufacturing facilities in India.

Metallurgical Coal

India is dependent on 50Mtpa imported coking coal to meet its needs.

• Domestic coking coal is poor quality

15%-18% Ash and has poor coking properties.

• Target imports will reach 90Mtpa to support increased

steelmaking capacity. [G Edwards, Australian Coal Conference July 2017]

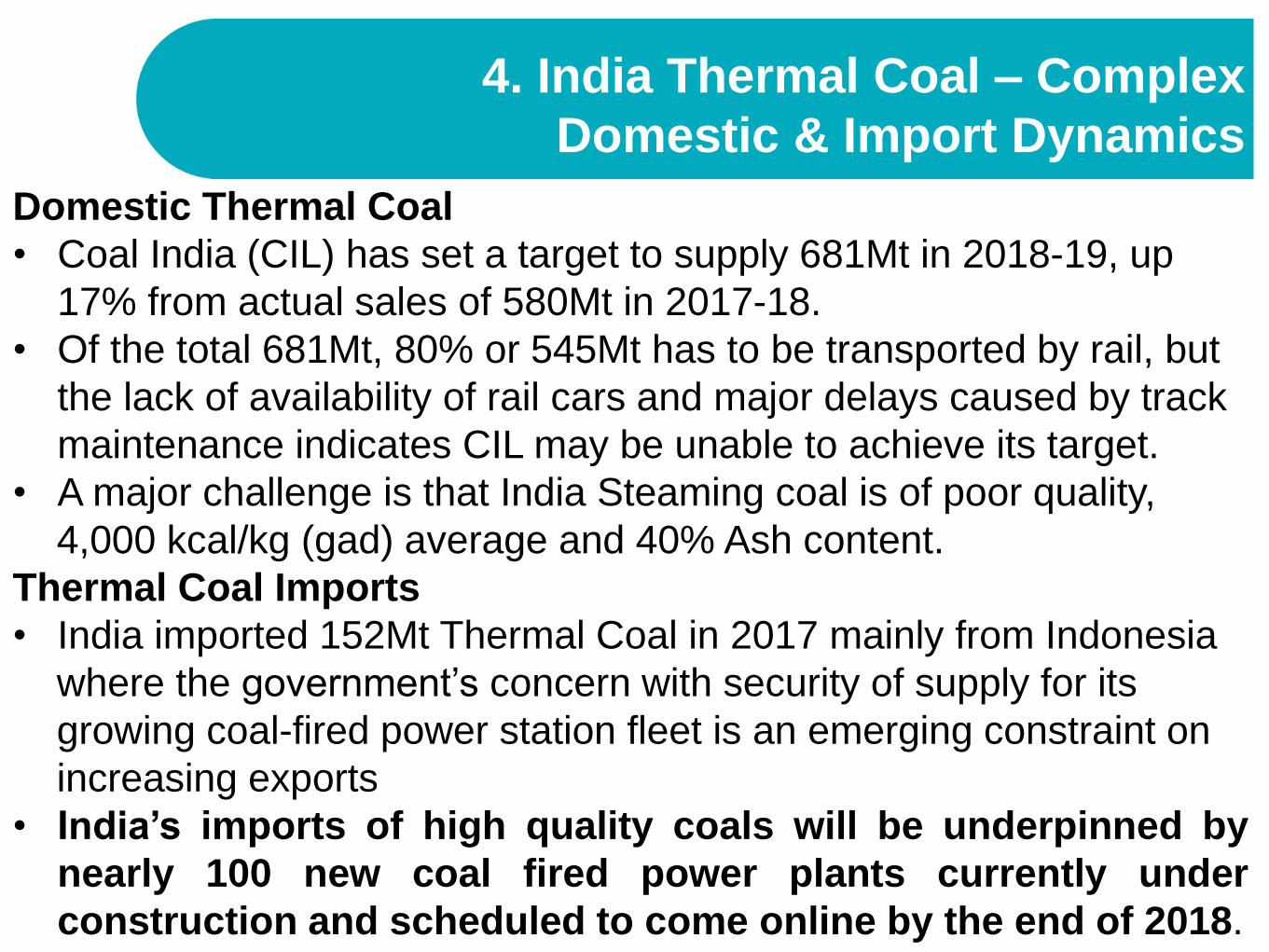

4. India Thermal Coal – Complex

Domestic & Import Dynamics

Domestic Thermal Coal

• Coal India (CIL) has set a target to supply 681Mt in 2018-19, up

17% from actual sales of 580Mt in 2017-18.

• Of the total 681Mt, 80% or 545Mt has to be transported by rail, but

the lack of availability of rail cars and major delays caused by track

maintenance indicates CIL may be unable to achieve its target.

• A major challenge is that India Steaming coal is of poor quality,

4,000 kcal/kg (gad) average and 40% Ash content.

Thermal Coal Imports

• India imported 152Mt Thermal Coal in 2017 mainly from Indonesia

where the government’s concern with security of supply for its

growing coal-fired power station fleet is an emerging constraint on

increasing exports

• India’s imports of high quality coals will be underpinned by

nearly 100 new coal fired power plants currently under

construction and scheduled to come online by the end of 2018.

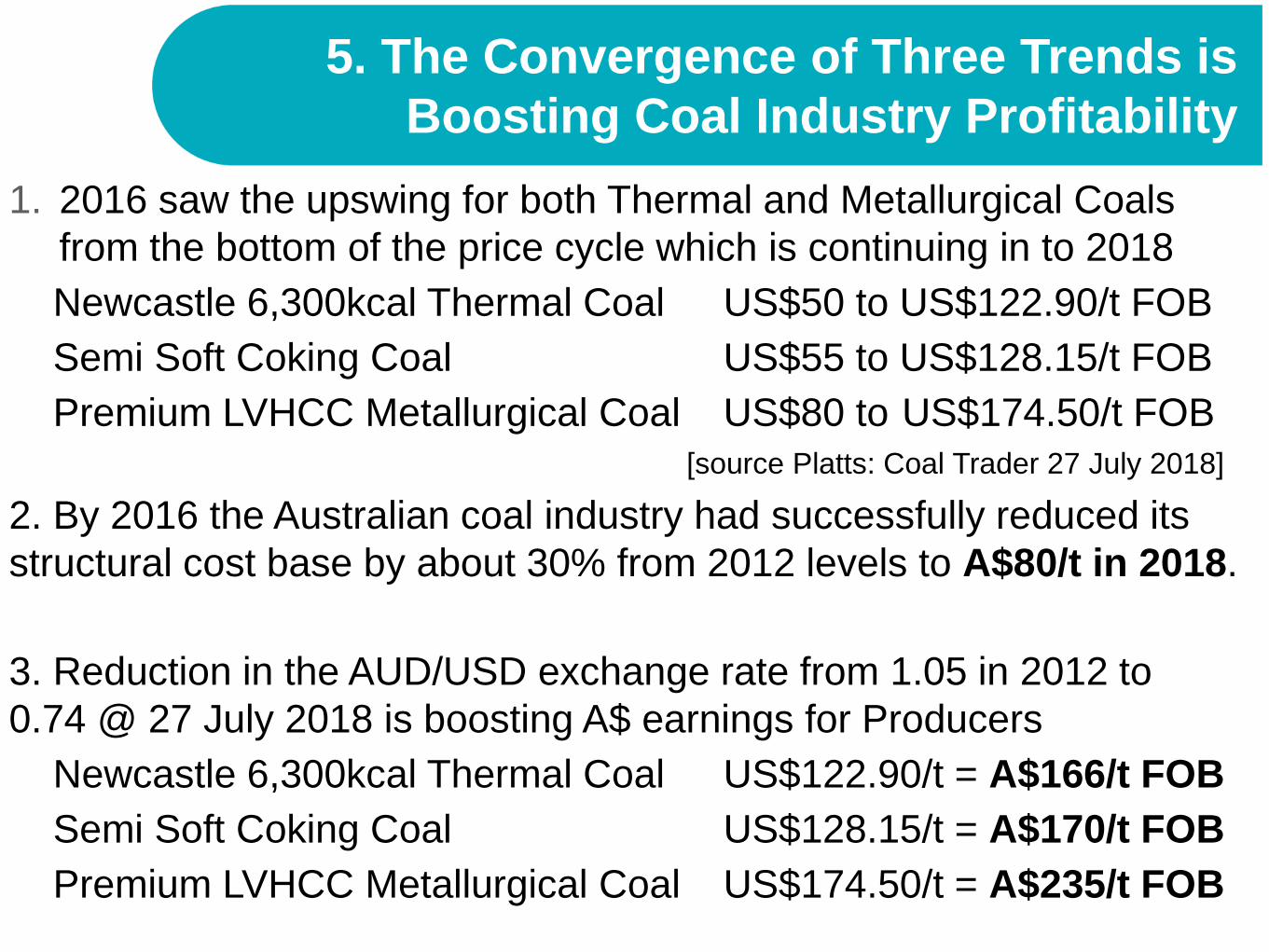

5. The Convergence of Three Trends is

Boosting Coal Industry Profitability

1. 2016 saw the upswing for both Thermal and Metallurgical Coals

from the bottom of the price cycle which is continuing in to 2018

Newcastle 6,300kcal Thermal Coal US$50 to US$122.90/t FOB

Semi Soft Coking Coal US$55 to US$128.15/t FOB

Premium LVHCC Metallurgical Coal US$80 to US$174.50/t FOB

[source Platts: Coal Trader 27 July 2018]

2. By 2016 the Australian coal industry had successfully reduced its

structural cost base by about 30% from 2012 levels to A$80/t in 2018.

3. Reduction in the AUD/USD exchange rate from 1.05 in 2012 to

0.74 @ 27 July 2018 is boosting A$ earnings for Producers

Newcastle 6,300kcal Thermal Coal US$122.90/t = A$166/t FOB

Semi Soft Coking Coal US$128.15/t = A$170/t FOB

Premium LVHCC Metallurgical Coal US$174.50/t = A$235/t FOB

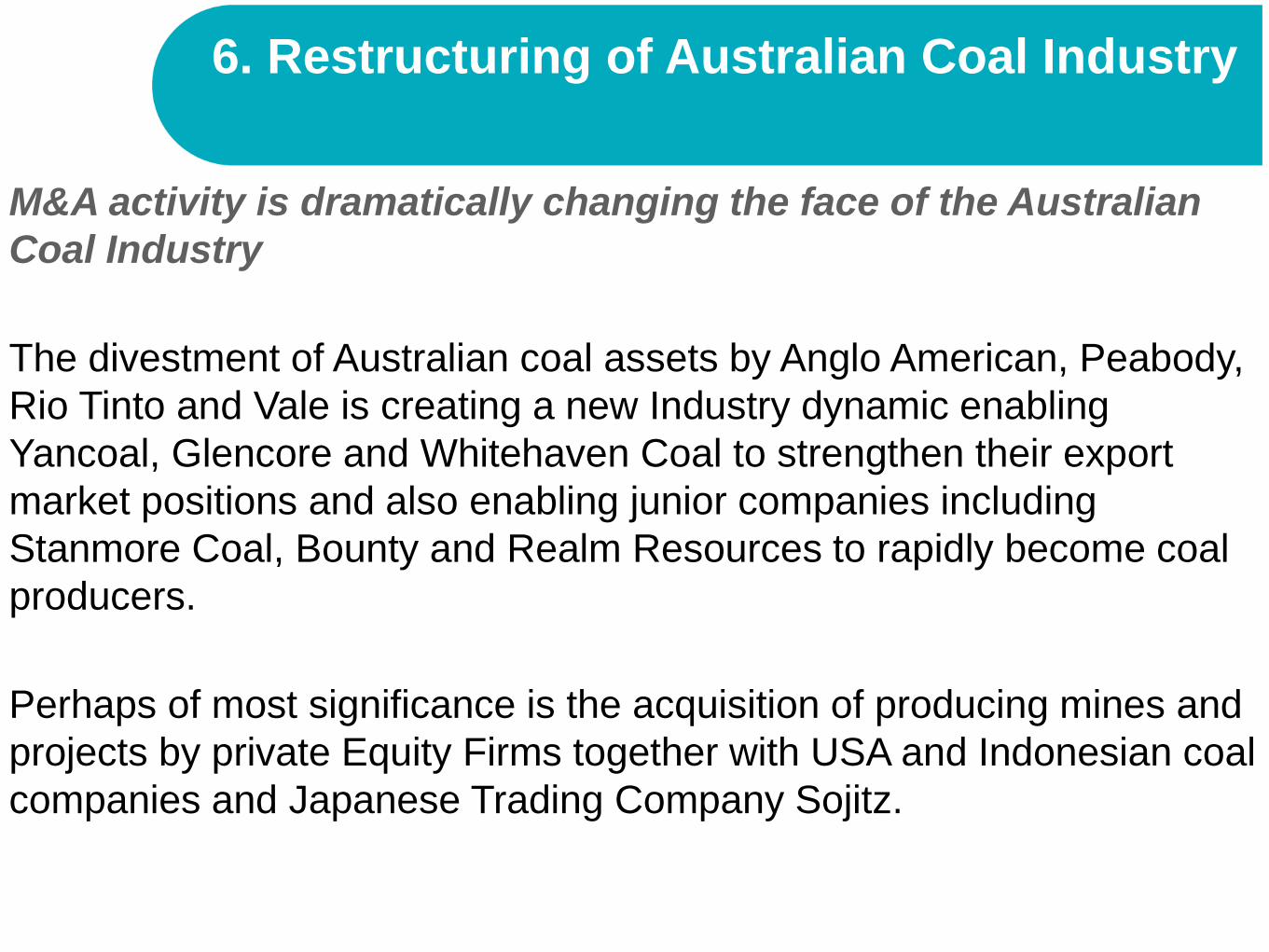

6. Restructuring of Australian Coal Industry

M&A activity is dramatically changing the face of the Australian

Coal Industry

The divestment of Australian coal assets by Anglo American, Peabody,

Rio Tinto and Vale is creating a new Industry dynamic enabling

Yancoal, Glencore and Whitehaven Coal to strengthen their export

market positions and also enabling junior companies including

Stanmore Coal, Bounty and Realm Resources to rapidly become coal

producers.

Perhaps of most significance is the acquisition of producing mines and

projects by private Equity Firms together with USA and Indonesian coal

companies and Japanese Trading Company Sojitz.

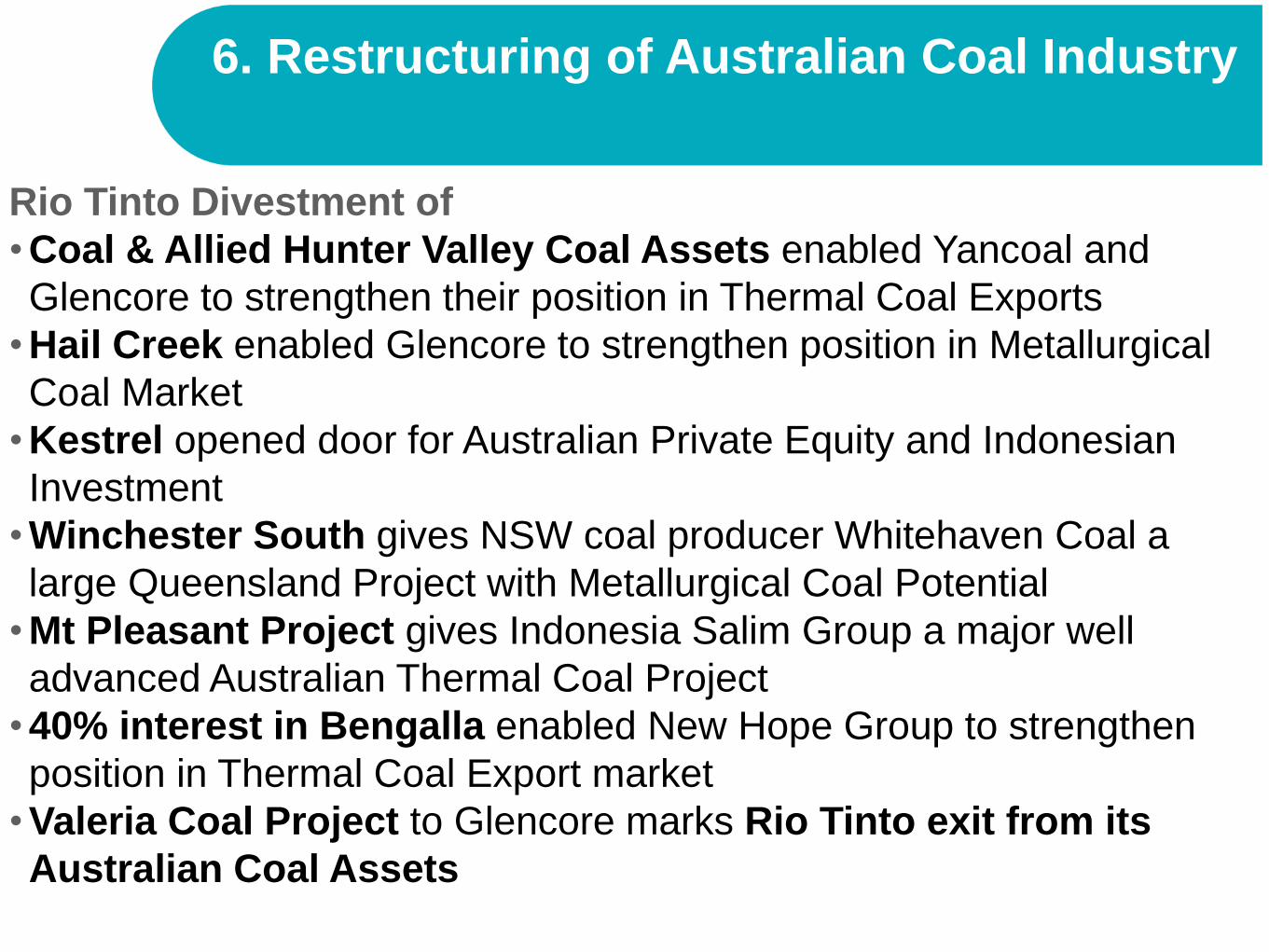

6. Restructuring of Australian Coal Industry

Rio Tinto Divestment of

• Coal & Allied Hunter Valley Coal Assets enabled Yancoal and

Glencore to strengthen their position in Thermal Coal Exports

• Hail Creek enabled Glencore to strengthen position in Metallurgical

Coal Market

• Kestrel opened door for Australian Private Equity and Indonesian

Investment

• Winchester South gives NSW coal producer Whitehaven Coal a

large Queensland Project with Metallurgical Coal Potential

• Mt Pleasant Project gives Indonesia Salim Group a major well

advanced Australian Thermal Coal Project

• 40% interest in Bengalla enabled New Hope Group to strengthen

position in Thermal Coal Export market

• Valeria Coal Project to Glencore marks Rio Tinto exit from its

Australian Coal Assets

6. Restructuring of Australian Coal Industry

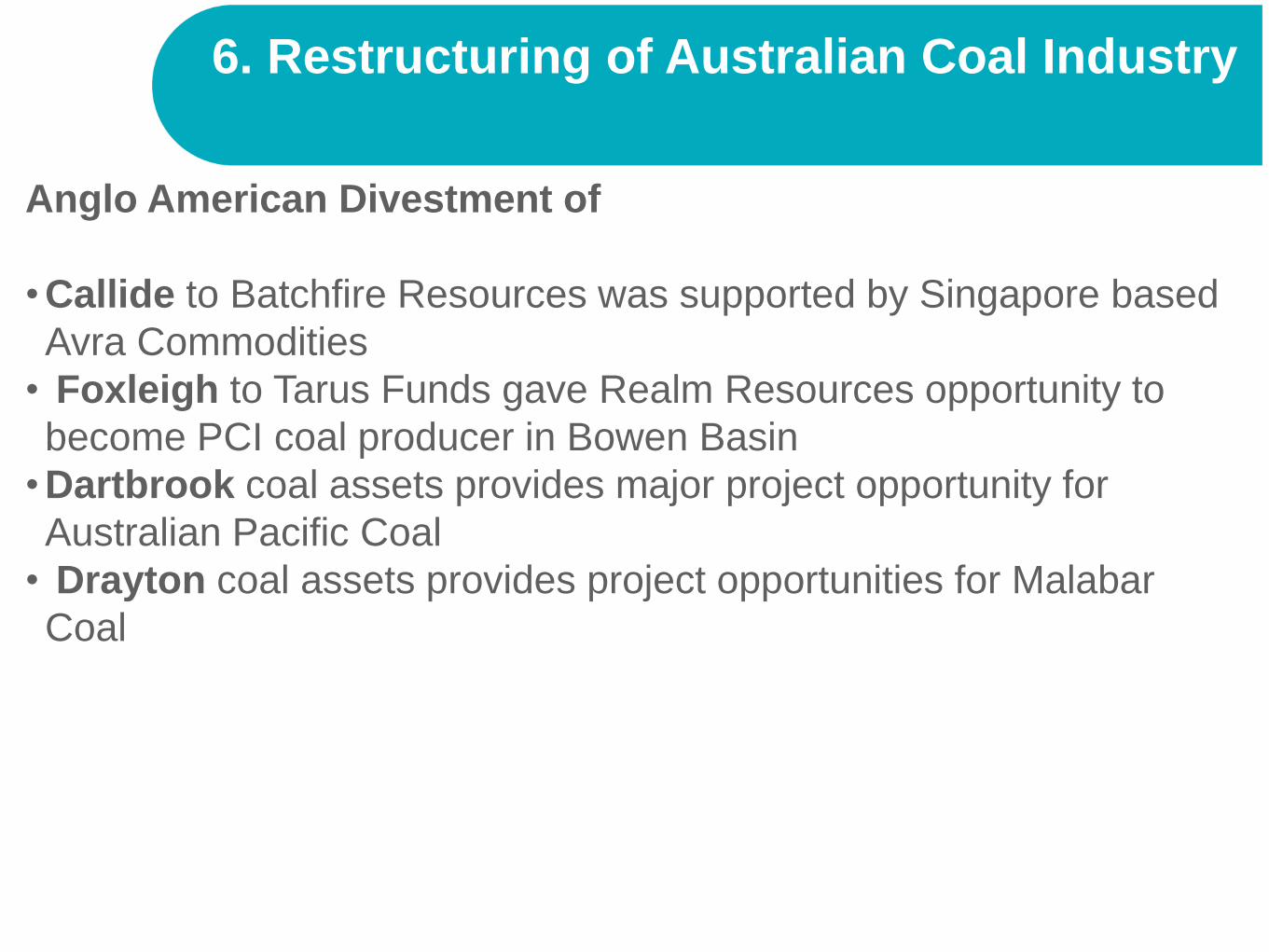

Anglo American Divestment of

• Callide to Batchfire Resources was supported by Singapore based

Avra Commodities

• Foxleigh to Tarus Funds gave Realm Resources opportunity to

become PCI coal producer in Bowen Basin

• Dartbrook coal assets provides major project opportunity for

Australian Pacific Coal

• Drayton coal assets provides project opportunities for Malabar

Coal

6. Restructuring of Australian Coal Industry

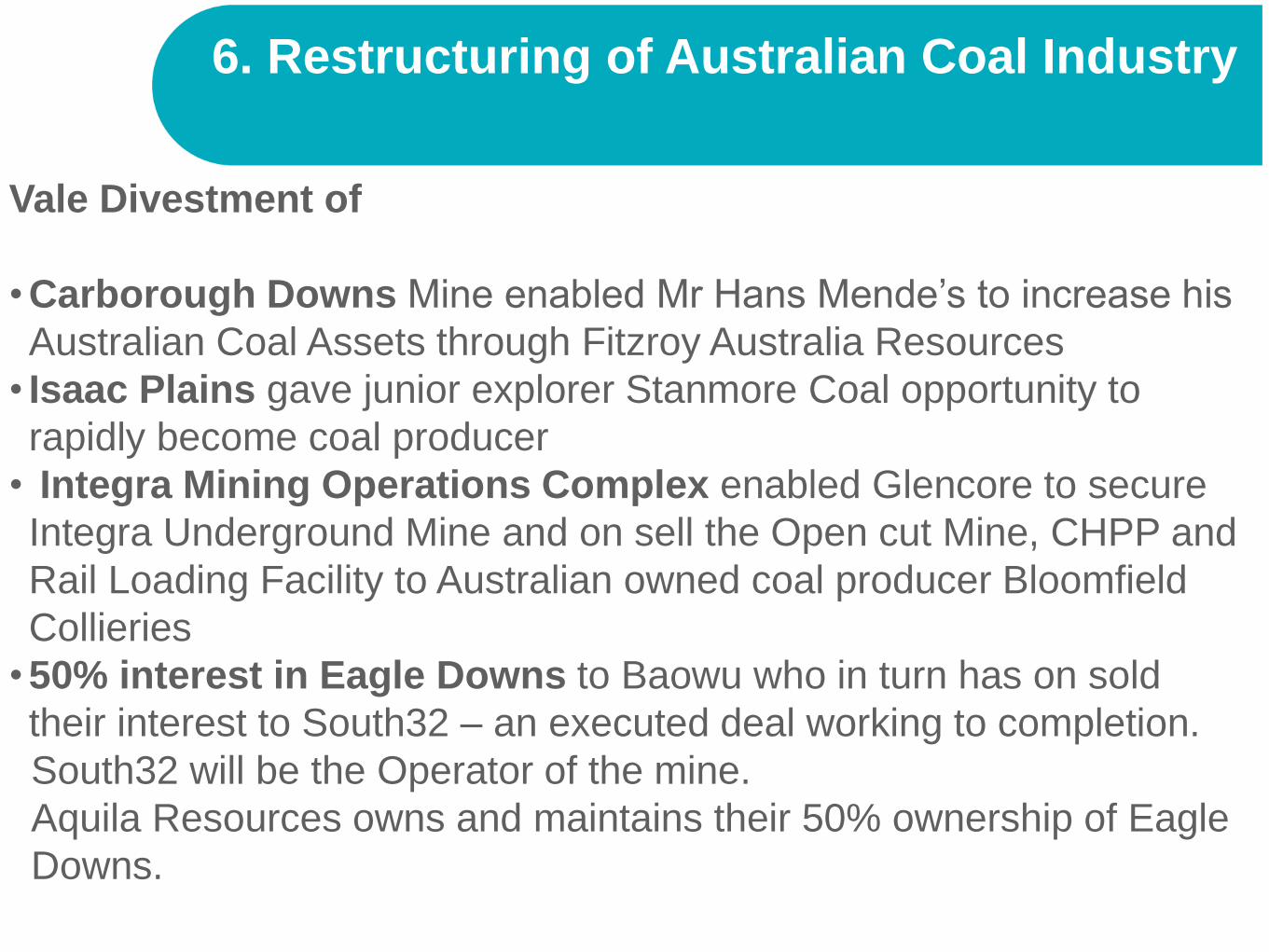

Vale Divestment of

• Carborough Downs Mine enabled Mr Hans Mende’s to increase his

Australian Coal Assets through Fitzroy Australia Resources

• Isaac Plains gave junior explorer Stanmore Coal opportunity to

rapidly become coal producer

• Integra Mining Operations Complex enabled Glencore to secure

Integra Underground Mine and on sell the Open cut Mine, CHPP and

Rail Loading Facility to Australian owned coal producer Bloomfield

Collieries

• 50% interest in Eagle Downs to Baowu who in turn has on sold

their interest to South32 – an executed deal working to completion.

South32 will be the Operator of the mine.

Aquila Resources owns and maintains their 50% ownership of Eagle

Downs.

6. Restructuring of Australian Coal Industry

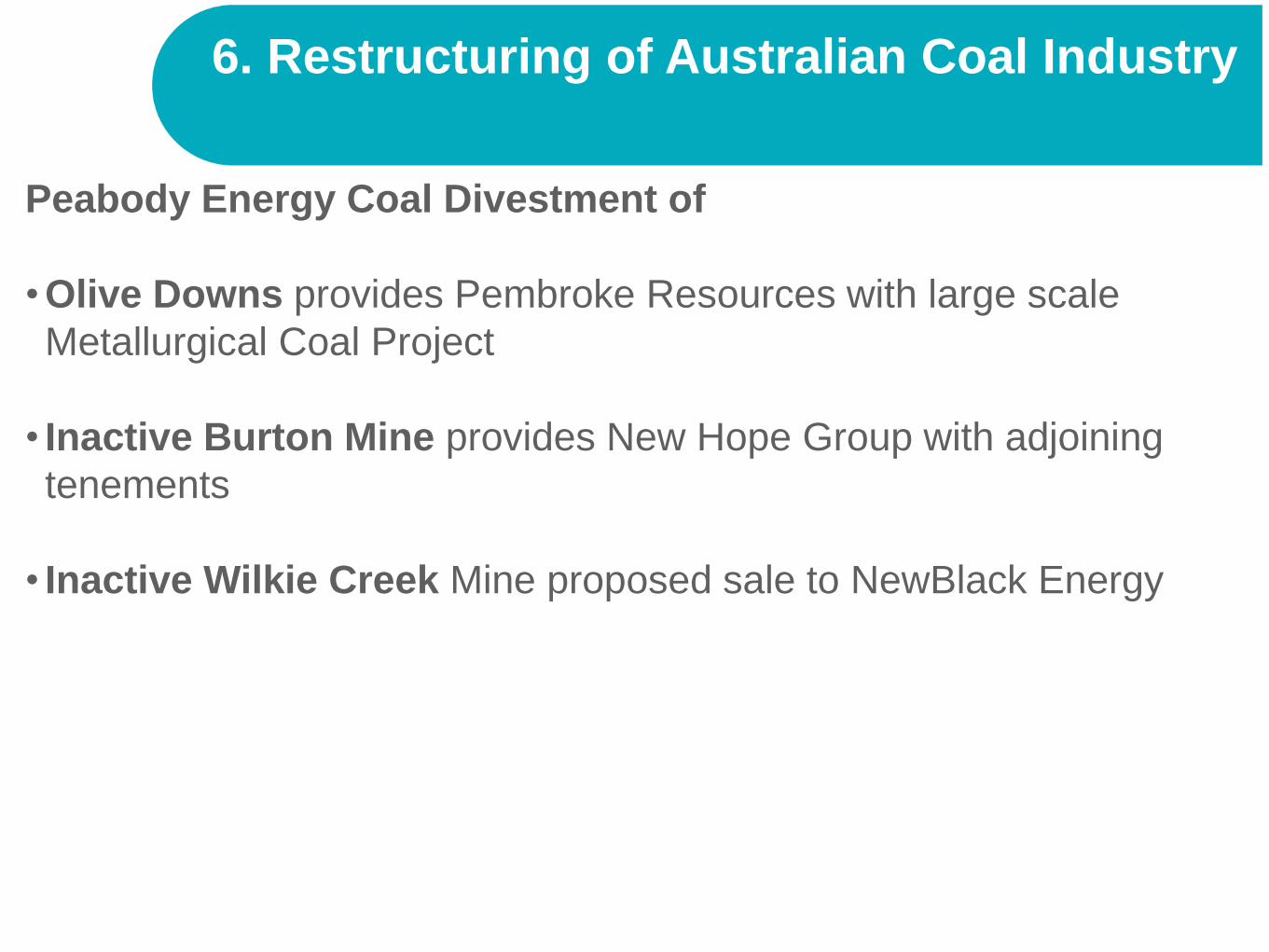

Peabody Energy Coal Divestment of

• Olive Downs provides Pembroke Resources with large scale

Metallurgical Coal Project

• Inactive Burton Mine provides New Hope Group with adjoining

tenements

• Inactive Wilkie Creek Mine proposed sale to NewBlack Energy

6. Restructuring of Australian Coal Industry

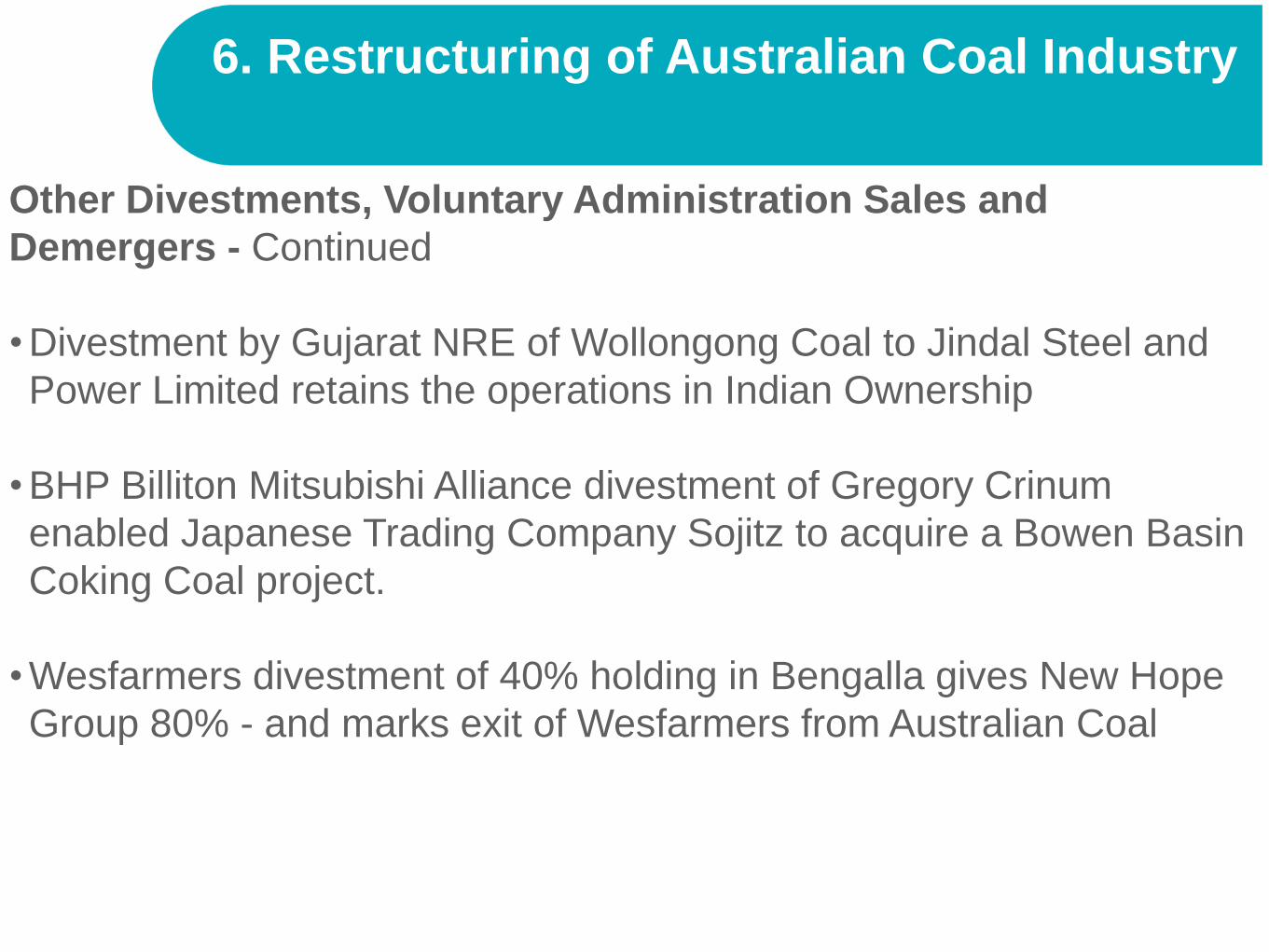

Other Divestments, Voluntary Administration Sales and

Demergers

• Wesfarmers sale of Curragh coal mine to US Coronado Coal Group

established Coronado in Australian Export Coal Industry

• Glencore divestment of Tahmoor Mine enabled GFG Alliance to

become Australia’s only fully integrated steel producer

• Caledon Coal Voluntary Administration provided opportunity for junior

company Bounty Mining to become coal producer

• Cockatoo Coal administration provided investment opportunity for US

based private equity Liberty Mutual Holdings

• BHP Billiton Demerger formed South 32 – Illawarra Metallurgical Coal

NSW

6. Restructuring of Australian Coal Industry

Other Divestments, Voluntary Administration Sales and

Demergers - Continued

• Divestment by Gujarat NRE of Wollongong Coal to Jindal Steel and

Power Limited retains the operations in Indian Ownership

• BHP Billiton Mitsubishi Alliance divestment of Gregory Crinum

enabled Japanese Trading Company Sojitz to acquire a Bowen Basin

Coking Coal project.

• Wesfarmers divestment of 40% holding in Bengalla gives New Hope

Group 80% - and marks exit of Wesfarmers from Australian Coal

6. Restructuring of Australian Coal Industry

However there are emerging Investment Risks with both mining

companies and mining service contractors entering

administration.

1. China state owned Caledon Coal went into administration following

closure of Cook Colliery with large inflow of water into longwall.

2. Failure of Caledon Coal exacerbated the failure of Bandanna

Energy with around 11Mt of 27Mt WICET capacity entitlements

defaulted on to potentially require Restructuring of $4.3bn debt.

3. India Gujarat NRE owned Wollongong Coal stopped production at

Wongawilli Mine with its mining services provider Delta SBD

entering administration in May 2017.

7. NSW Government is creating

Uncertainty for Investment

The costly and torturous path with community and political

impediments to exploration and development of new coal

mines in NSW is creating uncertainty for investors.

BHP Caroona The NSW Government made the unprecedented

move in 2016 to buyback Caroona licence from BHP for $220

million, after strident community and political opposition to the

project.

The concession had been acquired by BHP from the state

government in 2006 for $100m, with the company having invested

over a decade in exploration and development approval processes.

7. NSW Government is creating

Uncertainty for Investment

Shenhua Watermark Shenhua acquired the Watermark exploration

license for A$300m in 2008 through a NSW Government tender.

In July 2017 the Government reached agreement with Shenhua to

refund Shenhua A$262m from the original amount of A$300m in

return for 51.4% of the land area within the license which overlapped

prime agricultural land in the Liverpool Plains.

Chairman of Shenhua Australia Liu Xiang said “Shenhua will continue

to progress its Watermark Coal Mine on the remainder of EL7223 in

line with the planning approvals from both the State of NSW and

Commonwealth Government respectively in 2015.”[ source Australian Coal Report 12 July 2017]

These impediments are stimulating interest in the comparative

economic advantages of producing mines with Development and

Environmental Approvals in place such as Yancoal / Glencore

acquisition of Rio Tinto Coal & Allied Hunter Valley Operations.

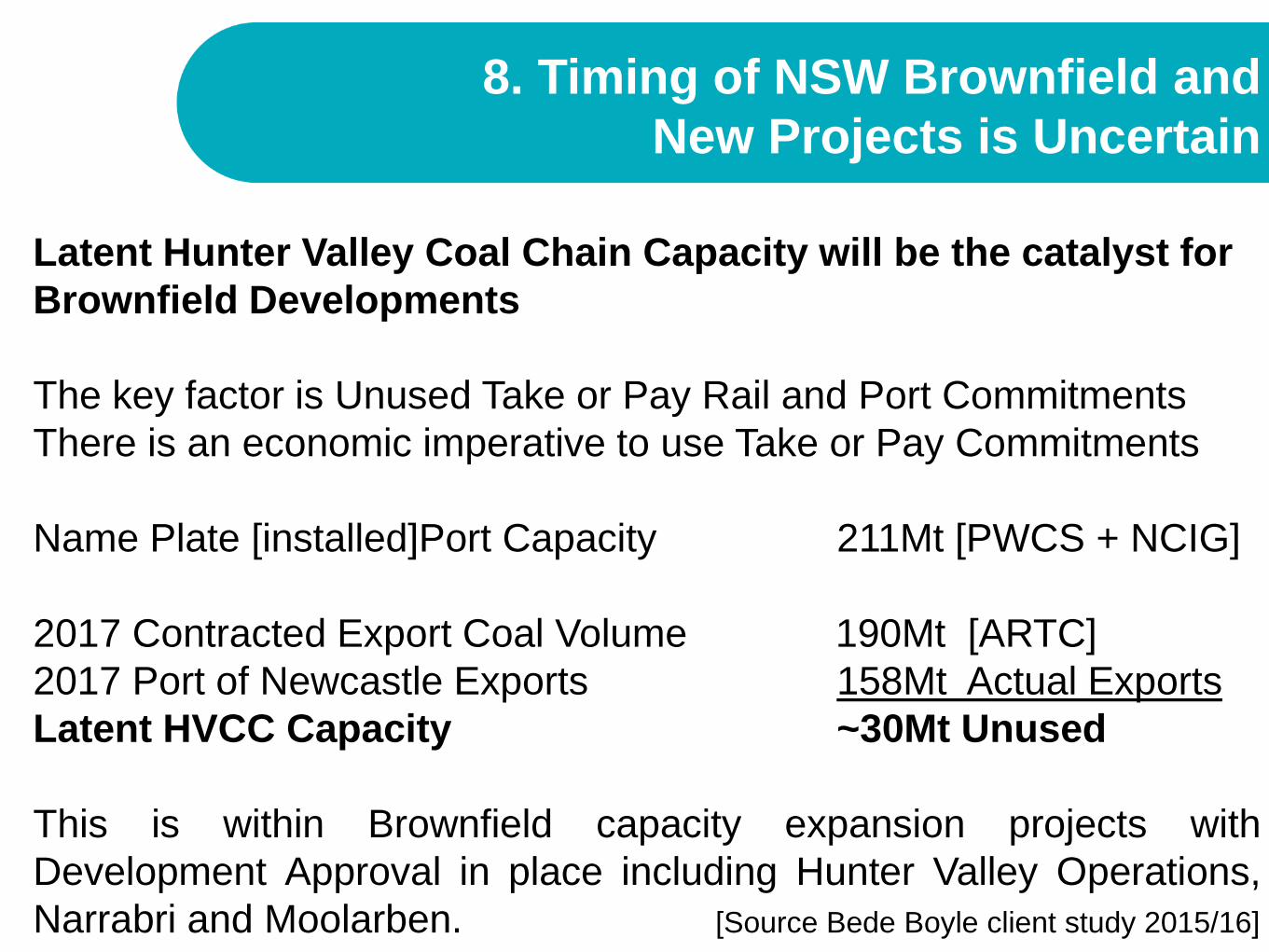

8. Timing of NSW Brownfield and

New Projects is Uncertain

Latent Hunter Valley Coal Chain Capacity will be the catalyst for

Brownfield Developments

The key factor is Unused Take or Pay Rail and Port Commitments

There is an economic imperative to use Take or Pay Commitments

Name Plate [installed]Port Capacity 211Mt [PWCS + NCIG]

2017 Contracted Export Coal Volume 190Mt [ARTC]

2017 Port of Newcastle Exports 158Mt Actual Exports

Latent HVCC Capacity ~30Mt Unused

This is within Brownfield capacity expansion projects with

Development Approval in place including Hunter Valley Operations,

Narrabri and Moolarben. [Source Bede Boyle client study 2015/16]

8. Timing of NSW Brownfield and

New Projects is Uncertain

Brownfield Expansion Projects will precede any financial

commitment to new projects.

In the Hunter – Gloucester Coal Basins some producers can

beneficiate coal to capture the ~ A$7 price margin for Semi Soft

Coking Coal and may commit to CHPP upgrading projects in 2018.

Also the +A$70/tonne price differential between Newcastle Thermal

6,300kcal and High Ash 5,500kcal may be the trigger for upgrading

coal washing circuits in 2018 to capture higher prices for 6,300kcal.

8. Timing of NSW Brownfield and

New Projects is Uncertain

Australian Pacific Coal (APC), has formed a joint venture partnership

with US privately owned investor and miner Stella Natural Resources

(SNR) for the development of the shuttered Dartbrook mine acquired

by APC from Anglo American in 2017.

Stella will pay A$20m for a 50% share in the project which is currently

permitted as a 6Mtpa underground longwall mine. APC acquired 83.3%

interest in the project from Anglo American for $25m in May 2017.

Marubeni also sold its 16.7% interest in Dartbrook to APC for A$5m.

APC and SNR will finalise a bankable development plan with plans to

restart underground mining operations in the March quarter of 2019.

SNR will be the exclusive manager and marketer for the joint venture.

Source: Australian Coal Report 8 August 2018

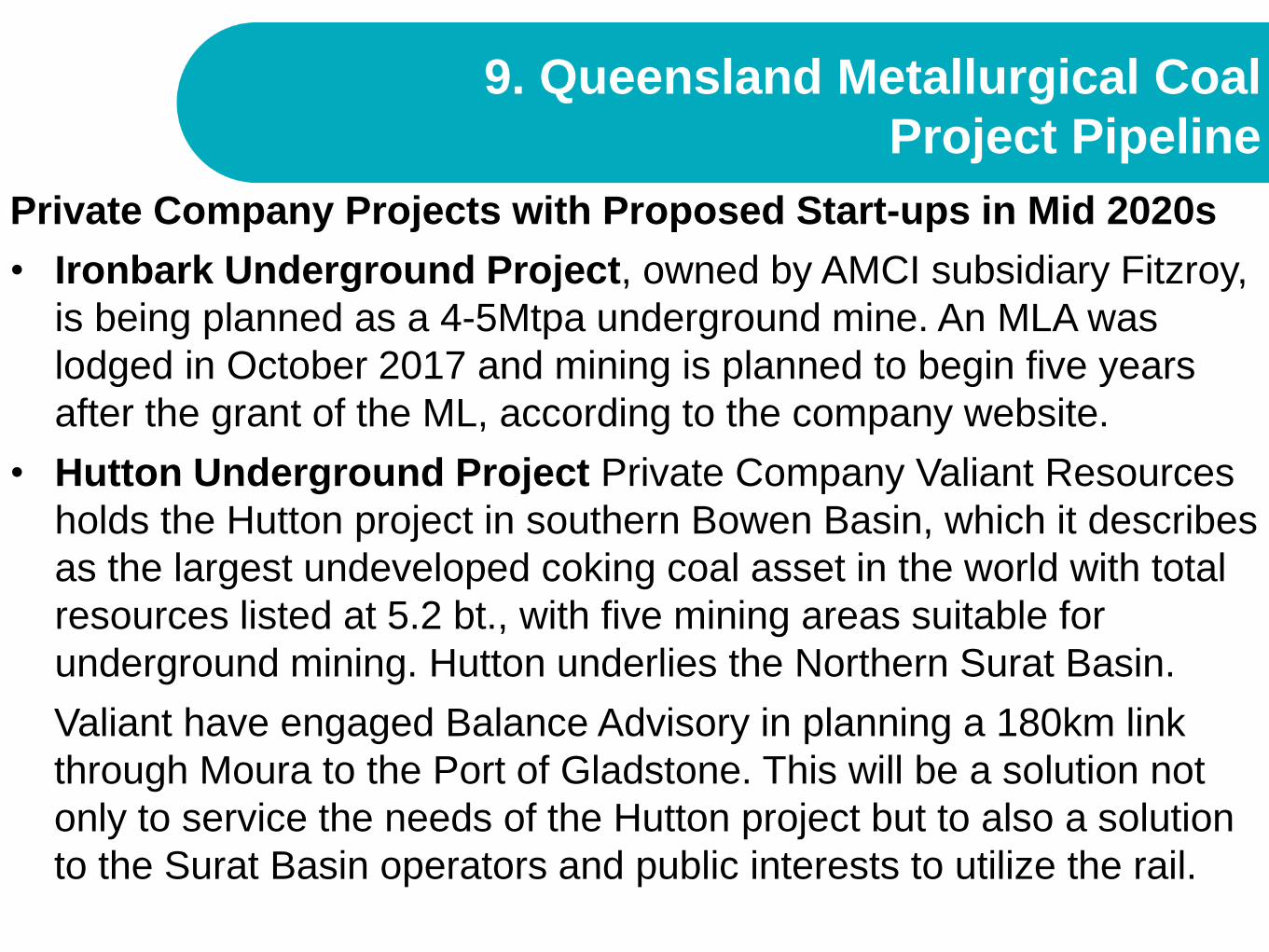

9. Queensland Metallurgical Coal

Project Pipeline

Queensland Metallurgical Coal Project Pipeline could add 15Mt of

New Capacity by 2020

Metallurgical coal is a non-substitutable raw material in the production

of steel from iron ore and Australia’s metallurgical coal export earnings

are expected to have reached a record $38 billion in 2017–18.

2018 will see about 5Mt of new coking coal capacity in Queensland.

Between 2018 and 2020, an estimated 15Mt of new coking coal

supply could come from Queensland if near-term plans for projects

are realized to respond to market demand especially from India.

9. Queensland Metallurgical Coal

Project Pipeline

New Mine Capacity in 2018

• Isaac Plains East Open Cut Mine Stanmore Coal is progressing

its future plans for 1.2Mtpa Isaac Plains East Mine

• Cook Underground Mine Reopened ASX-listed Bounty Mining is

ramping up production of hard coking coal from the

recommissioned Cook mine with the first shipment to Chinese

customers through Gladstone in June. The mine is expected to

produce up to 2.2 mt/y of ROM coal within 12 months.

• Wilton Fairhill Open Cut Japanese trading house Sojitz, plans to

resume mining up to 2Mtpa at the previously mothballed Gregory

Crinum mine which it bought from BHP Billiton Mitsubishi Alliance

• Baralaba North Open Cut Mine Reopening The previously shut

Baralaba mine is currently being developed for mining to resume at

an estimated run rate of 2 to 3Mtpa

9. Queensland Metallurgical Coal

Project Pipeline

Near term projects likely to go ahead by 2020

Isaac Plains East Underground Project Stanmore is on track

to launch production of 1.4Mtpa bord and pillar operation in 2020.

Bluff Carabella Resources was bought out in 2014 by Beijing China

Kingho Energy, through its subsidiary Wealth Mining, who is

progressing development of the 1.2Mtpa PCI Bluff project.

Olive Downs South Pembroke Resources proposed 14Mtpa Olive

Downs South PCI project has a planned start-up of 2020.

Eagle Downs Underground Project is equally 50/50 owned by Aquila

and South32 who will be mine operator. No timelines have been made

public regarding resumption of development. IHS assumes new coal

only available by 2022, at the earliest.

9. Queensland Metallurgical Coal

Project Pipeline

Planned Expansion / Life Extension Projects

Anglo American is on a major drive to optimise production at its

existing mines.

Moranbah/Grosvenor complex planned increase in production around

25% which would add about 1.8Mtpa of production.

Moranbah South 50/50 joint venture project between Anglo American

and Exxaro. Anglo is busy securing environmental approvals for the

project initially scoped on a dual longwall configuration producing

around 18Mtpa.

German Creek operation another two years of production is expected

from the Grasstree mine at which point replacement tonnage must be

developed. The Aquila deposit will be developed as a 5Mtpa thin seam

longwall mine.

9. Queensland Metallurgical Coal

Project Pipeline

Private Company Projects with Proposed Start-ups in Mid 2020s

• Ironbark Underground Project, owned by AMCI subsidiary Fitzroy,

is being planned as a 4-5Mtpa underground mine. An MLA was

lodged in October 2017 and mining is planned to begin five years

after the grant of the ML, according to the company website.

• Hutton Underground Project Private Company Valiant Resources

holds the Hutton project in southern Bowen Basin, which it describes

as the largest undeveloped coking coal asset in the world with total

resources listed at 5.2 bt., with five mining areas suitable for

underground mining. Hutton underlies the Northern Surat Basin.

Valiant have engaged Balance Advisory in planning a 180km link

through Moura to the Port of Gladstone. This will be a solution not

only to service the needs of the Hutton project but to also a solution

to the Surat Basin operators and public interests to utilize the rail.

9. Queensland Metallurgical Coal

Project Pipeline

Other Advanced Queensland Metallurgical Coal Projects

• Dysart East Coal Project India’s Bengal Energy

• Baralaba South Cockatoo Coal

• South Styx Coal Styx Coal

• Colton New Hope Group

• Teresa Coal Project United Mining Group

• Springsure Coal Project Terracom

• Grovesnor West Project Carabella Resources

• Karin Basin Vitrinite

• Minyango Coal Project Caledon Resources

• Jellinbah Mine Extension Bowen Basin Coal

• New Lenton New Hope Group

• Currah Extension Wesfarmers

• Sarum Xstrata

• Cooroorah and Hillalong Bowen Coking Coal

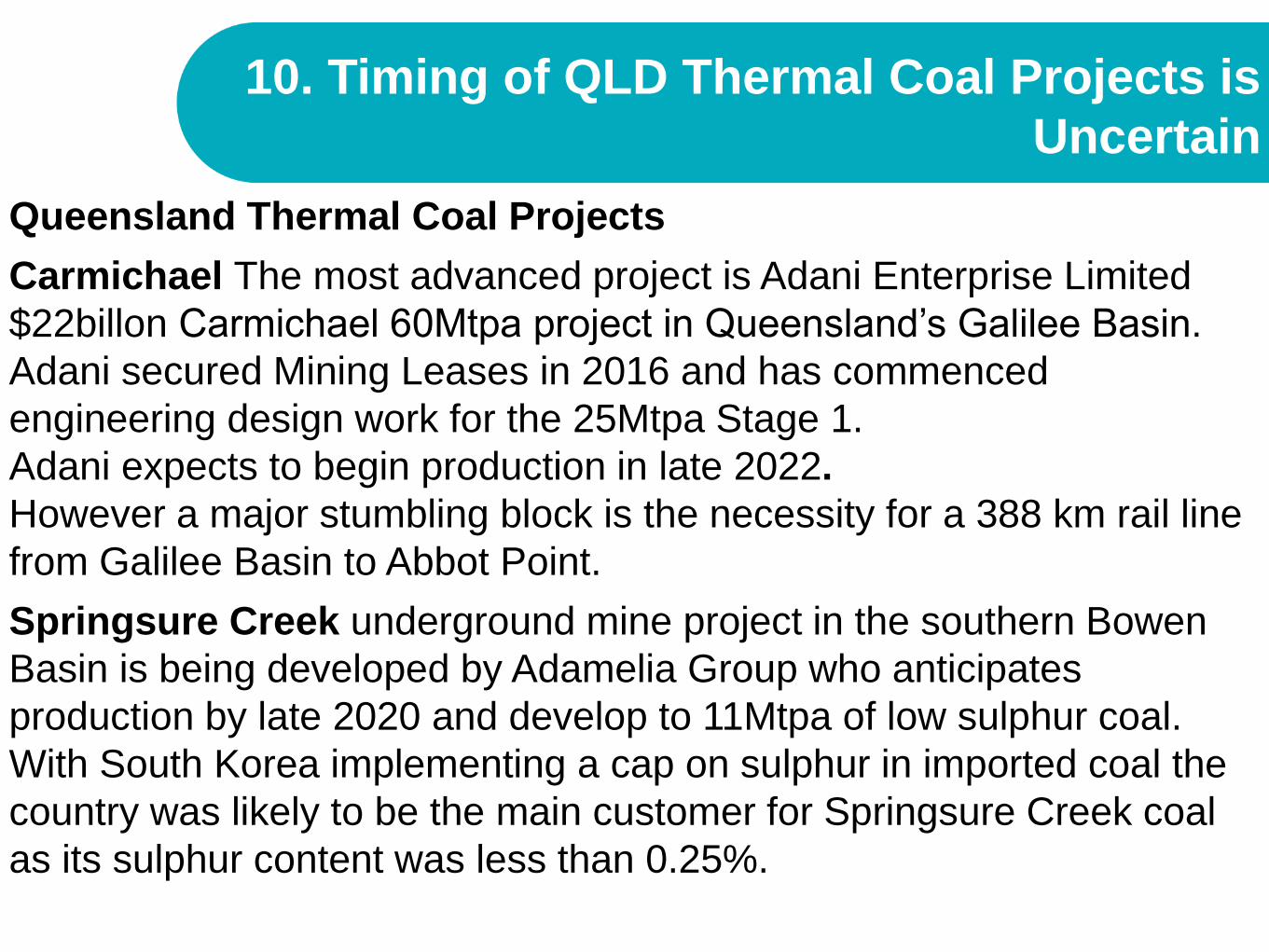

10. Timing of QLD Thermal Coal Projects is

Uncertain

Queensland Thermal Coal Projects

Carmichael The most advanced project is Adani Enterprise Limited

$22billon Carmichael 60Mtpa project in Queensland’s Galilee Basin.

Adani secured Mining Leases in 2016 and has commenced

engineering design work for the 25Mtpa Stage 1.

Adani expects to begin production in late 2022.

However a major stumbling block is the necessity for a 388 km rail line

from Galilee Basin to Abbot Point.

Springsure Creek underground mine project in the southern Bowen

Basin is being developed by Adamelia Group who anticipates

production by late 2020 and develop to 11Mtpa of low sulphur coal.

With South Korea implementing a cap on sulphur in imported coal the

country was likely to be the main customer for Springsure Creek coal

as its sulphur content was less than 0.25%.

10. Timing of QLD Thermal Coal Projects is

Uncertain

Queensland Thermal Coal Projects continued

Taroborah underground longwall project of Chinese owned Shenhuo

International. The company has recently conducted a bankable

feasibility study (BFS) for a single longwall operation capable of

producing around 4.5Mtpa of product coal with potential start up

around 2021-22.

Wandoan 25Mtpa project in the Surat Basin was put on hold by

Glencore after work on the proposed 214 km Surat Basin rail line

linking to the Port of Gladstone was suspended following a fall in

global thermal coal prices.

Source: Australian Coal Report 18 July 2018

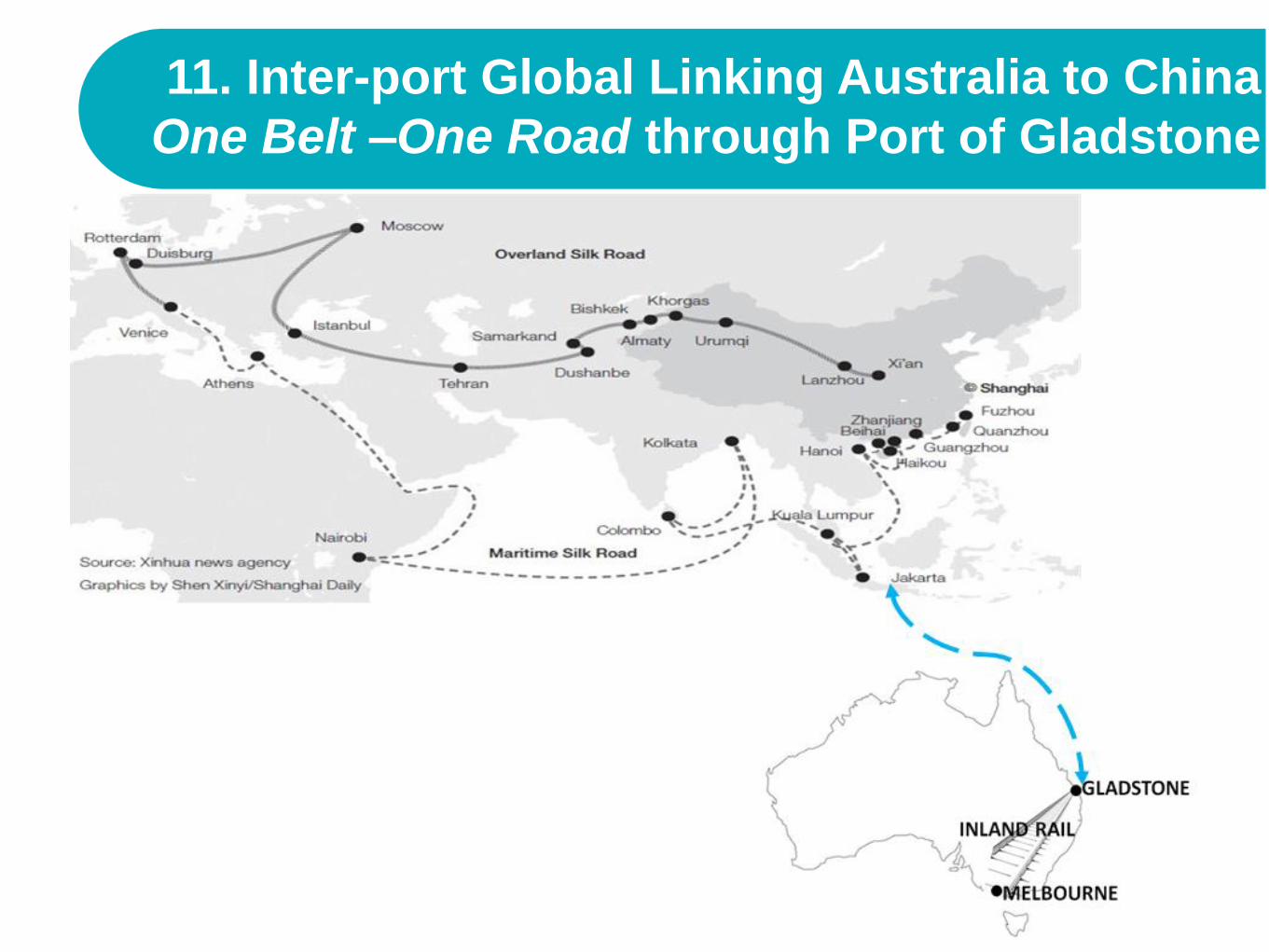

11. Inter-port Global Linking Australia to China

One Belt –One Road through Port of Gladstone

TOOWOOMBAOAKEY

CAIRNS

CHARLEVILLE

STANTHORPE

GLADSTONE PORT GATEWAY

CALLIOPE

WESTGATE

WYANDRA

CUNNAMULLA

QUILPIE

LONGREACH

SOUTH WESTERN

RAIL SYSTEM

CENTRAL WESTERN

RAIL SYSTEM

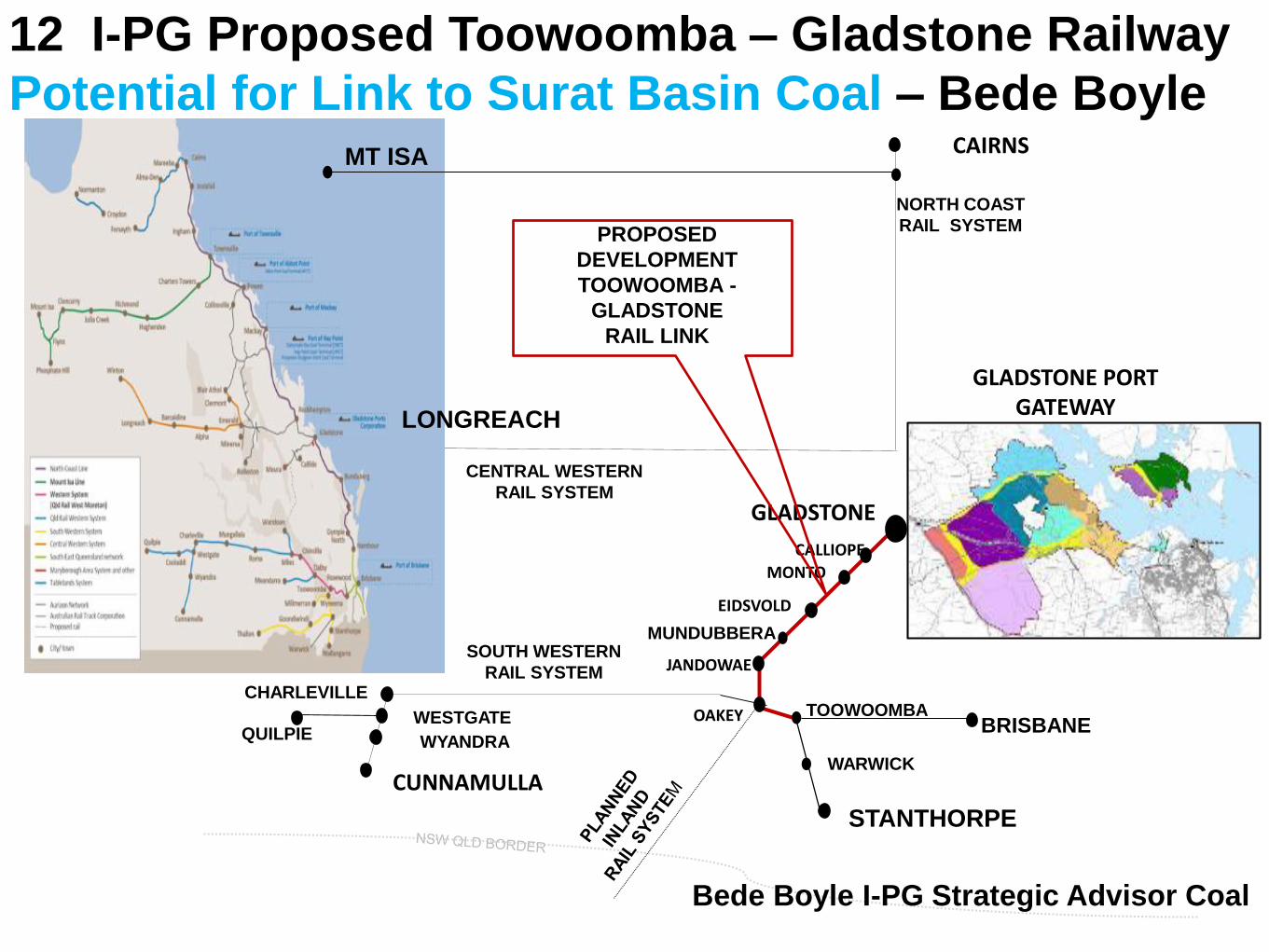

12 I-PG Proposed Toowoomba – Gladstone Railway

Potential for Link to Surat Basin Coal – Bede Boyle

BRISBANE

JANDOWAE

MONTO

GLADSTONE

EIDSVOLD

Bede Boyle I-PG Strategic Advisor Coal

NORTH COAST

RAIL SYSTEM

MUNDUBBERA

WARWICK

PROPOSED

DEVELOPMENT

TOOWOOMBA -

GLADSTONE

RAIL LINK

MT ISA

13. Coal Ventures & Associates

CVA was formed by George Edwards and Bede Boyle with

Hanbury Capital Limited and GEOS Mining to provide Expert

Advice and Support for Coal Acquisitions and Divestments in

Australia and Internationally

George Edwards has been involved with coal for some 50 years and

has part owned and operated three export coal mines since starting up

his own companies 30 years ago.

He has over 100 clients worldwide and is involved in

• Feasibility Studies - JORC Evaluations and Valuations (VALMIN)

• Project and Mine Asset Sales and Purchases, and

• Coal Sales and Purchases.

George was Director Marketing with Coal & Allied,

Chief Executive in Australia for Consolidation Coal Company of USA,

Chairman and GM of Gollin Wallsend Coal Company Limited.

George is currently Director of Atrum Coal.

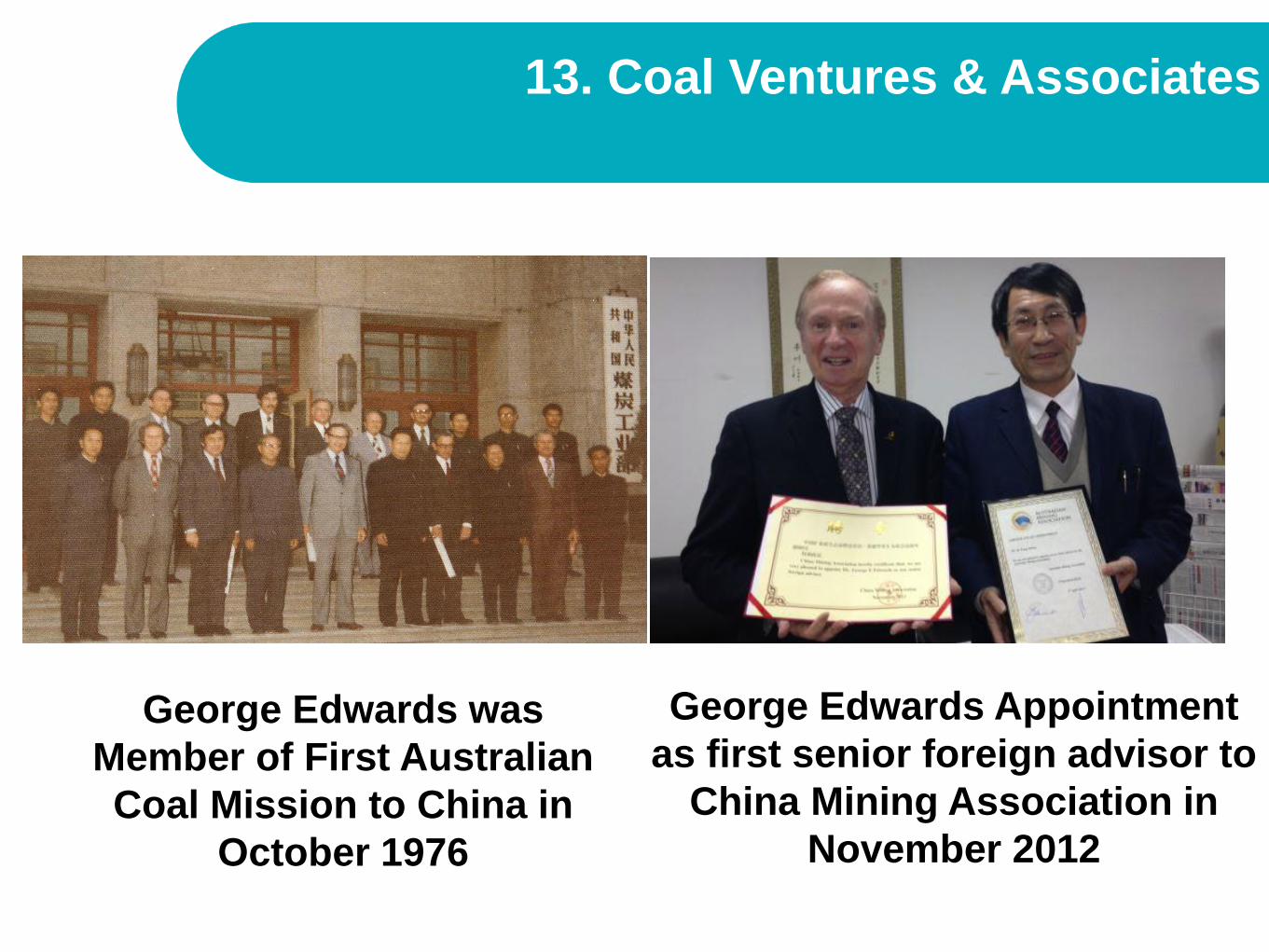

13. Coal Ventures & Associates

George Edwards was

Member of First Australian

Coal Mission to China in

October 1976

George Edwards Appointment

as first senior foreign advisor to

China Mining Association in

November 2012

13. Coal Ventures & Associates

Bede Boyle is a Strategic Advisor to the Australian Coal Industry and

Investors since 1994 on Acquisitions, Divestments and Project

Developments. He was Manager Technical Services with Coal & Allied.

Powercoal

FreightCorp