Embed Size (px)

Citation preview

© 2016 IHS Markit. All Rights Reserved.© 2016 IHS Markit. All Rights Reserved.

Proactive PositioningSeeking Opportunity in a Low Growth Environment

AUTOMOTIVE

Mike Jackson, Senior Executive, North America, Vehicle Production Forecasting +1-248-465-2833, [email protected]

19 October, 2016 | Tokyo

© 2016 IHS Markit

Contents

North America Production Outlook

Product Mix: Cars, SUVs, Trucks

Market Dynamics

OEM Reviews

Summary

Contents

© 2016 IHS Markit. All Rights Reserved.

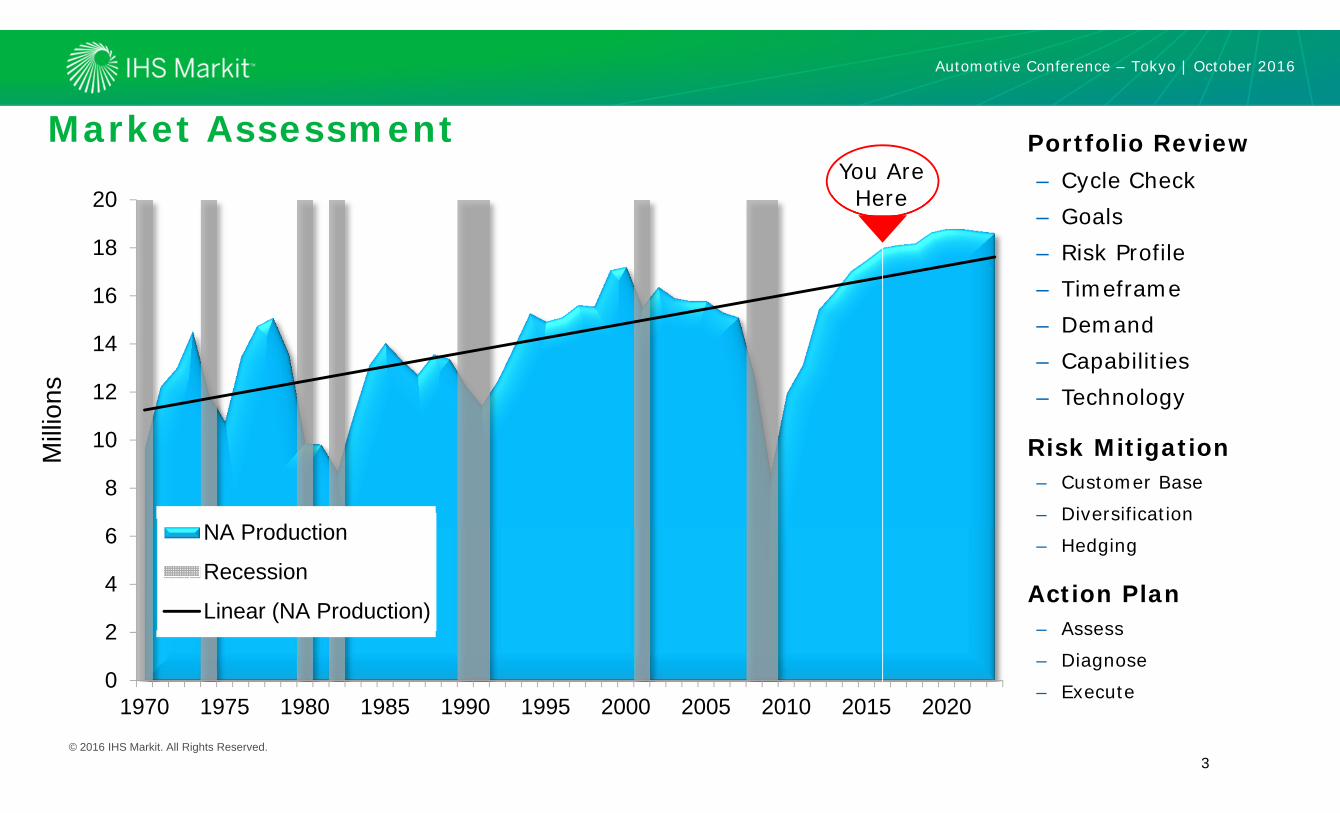

0

2

4

6

8

10

12

14

16

18

20

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Mill

ions

NA Production

Recession

Linear (NA Production)

Market Assessment Portfolio Review– Cycle Check– Goals– Risk Profile– Timeframe– Demand– Capabilities– Technology

Risk Mitigation– Customer Base

– Diversification

– Hedging

Action Plan– Assess

– Diagnose

– Execute

You Are Here

3

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit. All Rights Reserved.

L

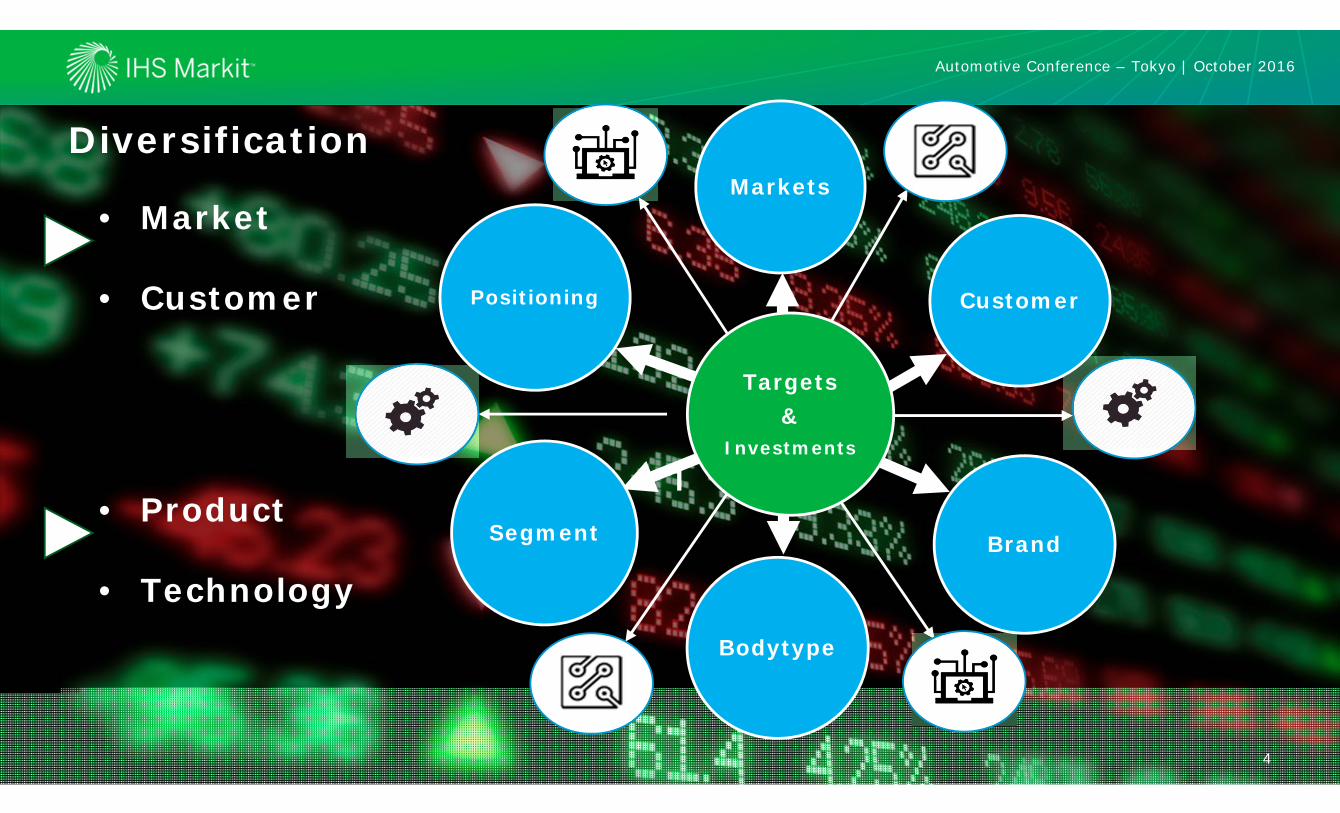

Diversification

Targets&

Investments

Markets

Customer

Brand

Bodytype

Segment

Positioning

• Market

• Customer

• Product

• Technology

4

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit. All Rights Reserved.

5146201732 34

201926

2021North American Production

5

189 LAUNCH EVENTS

+9.4M+.8M +.6M

+10.2M1

5.8

15

.81

5.3

15

.11

2.6

8.6

11

.9 13

.1 15

.41

6.2

17

.01

7.5

18

.01

8.1

18

.21

8.6

18

.81

8.8

18

.71

8.6

0.0

4.0

8.0

12.0

16.0

20.0

2004 2008 2012 2016 2020

Mill

ion

s

5

Automotive Conference – Tokyo | October 2016

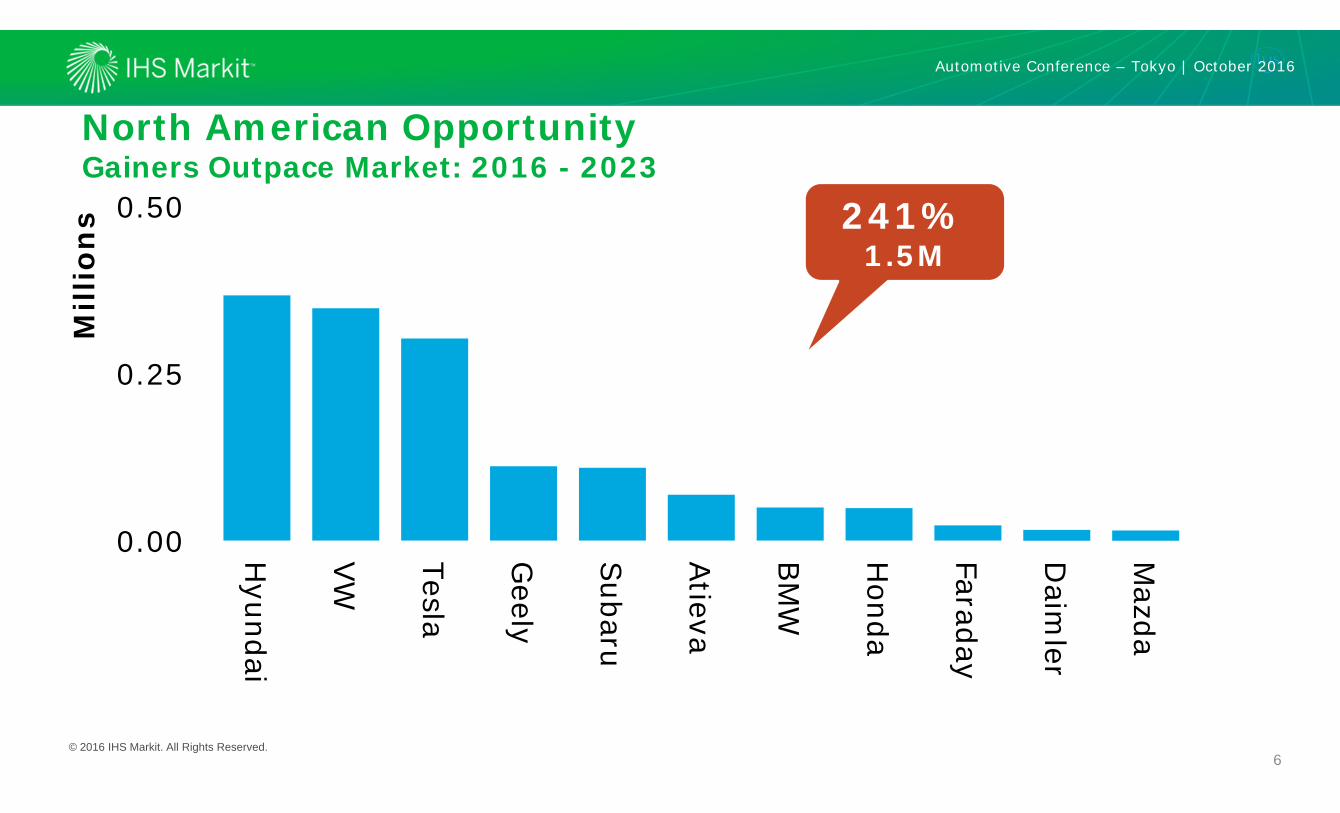

© 2016 IHS Markit. All Rights Reserved.6

0.00

0.25

0.50

Hyundai

VW

Tesla

Geely

Subaru

Atieva

BM

W

Honda

Faraday

Daim

ler

Mazda

Mill

ion

sNorth American OpportunityGainers Outpace Market: 2016 - 2023

241%1.5M

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

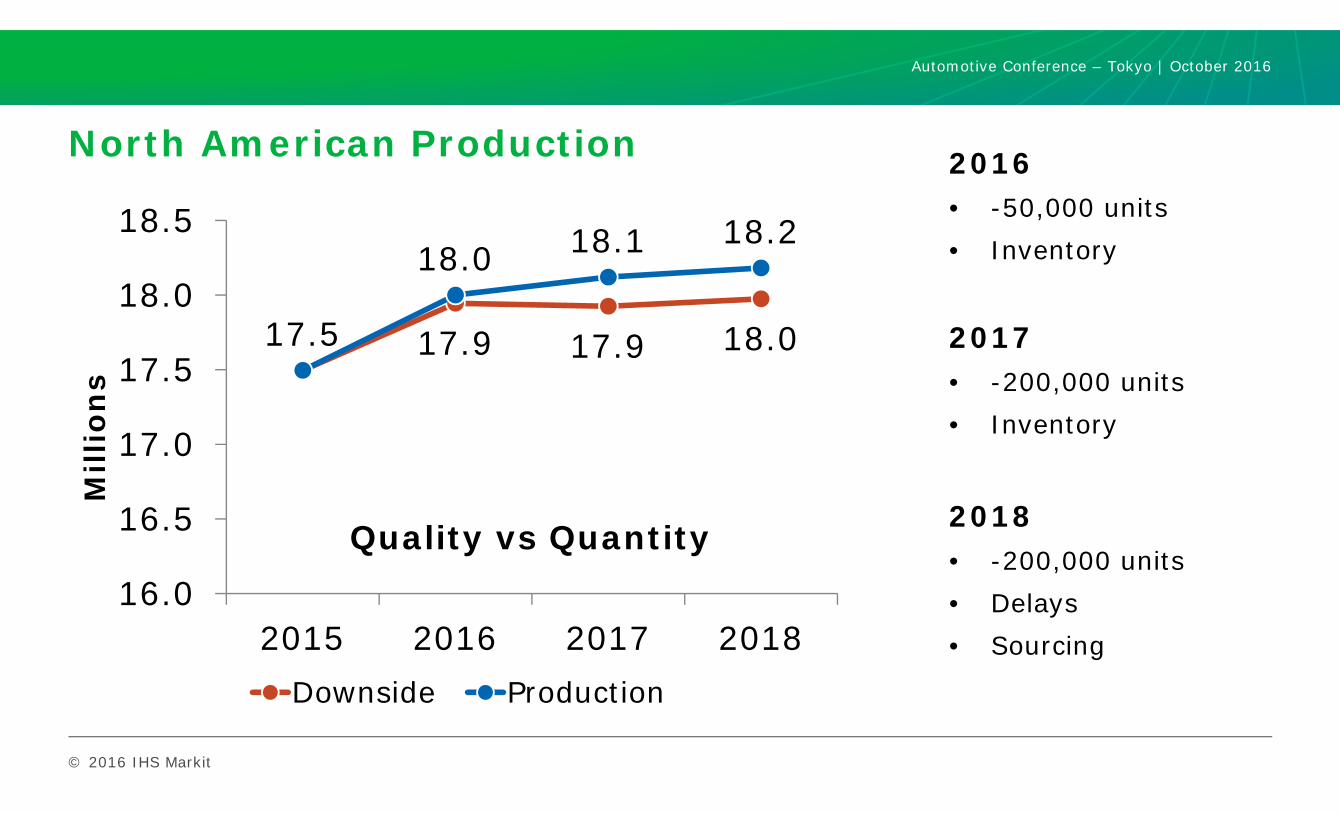

North American Production

17.9 17.9 18.017.5

18.0 18.1 18.2

16.0

16.5

17.0

17.5

18.0

18.5

2015 2016 2017 2018

Mill

ion

s

Downside Production

2016• -50,000 units• Inventory

2017• -200,000 units• Inventory

2018• -200,000 units• Delays• Sourcing

Quality vs Quantity

Automotive Conference – Tokyo | October 2016

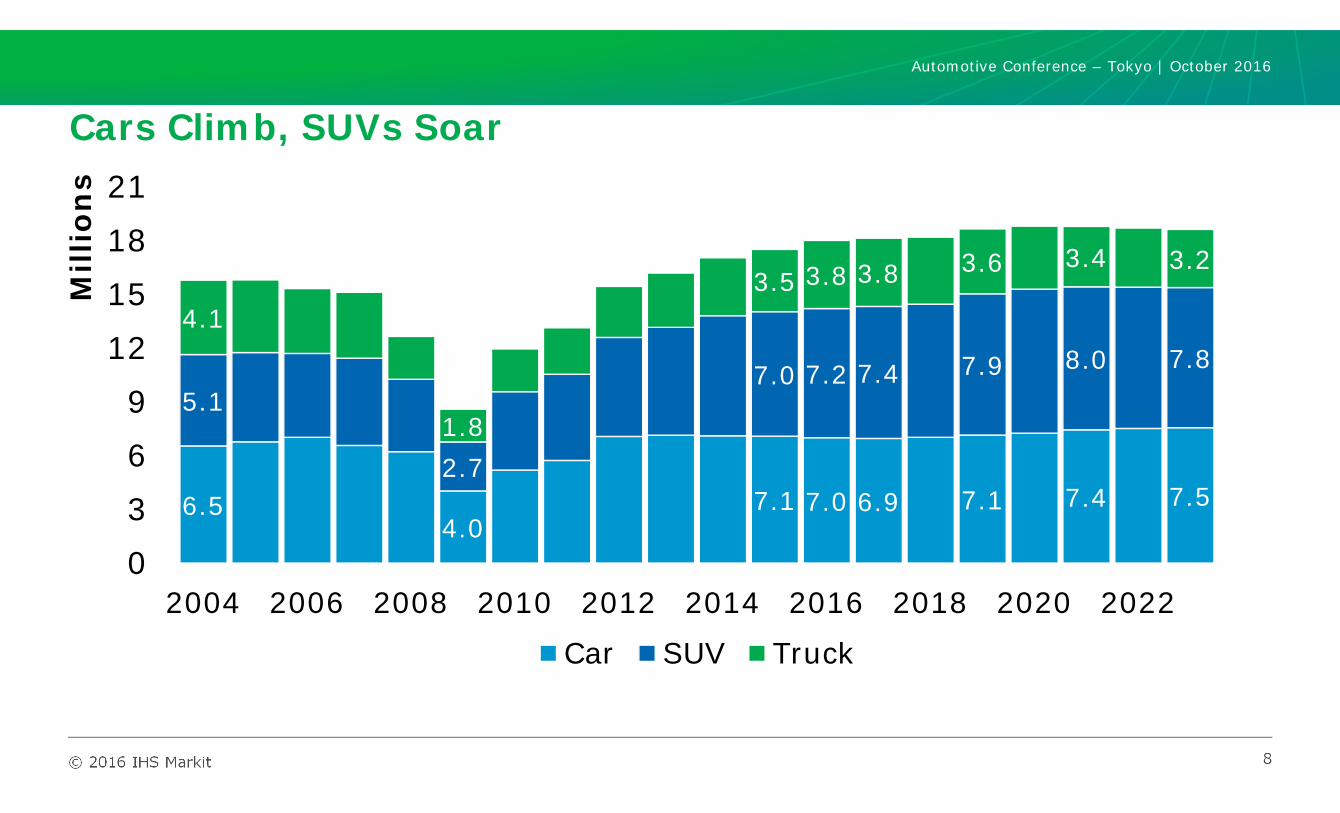

© 2016 IHS Markit 8

6.54.0

7.1 7.0 6.9 7.1 7.4 7.5

5.1

2.7

7.0 7.2 7.4 7.9 8.0 7.84.1

1.8

3.5 3.8 3.8 3.6 3.4 3.2

0

3

6

9

12

15

18

21

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Mill

ion

s

Car SUV Truck

Cars Climb, SUVs Soar

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

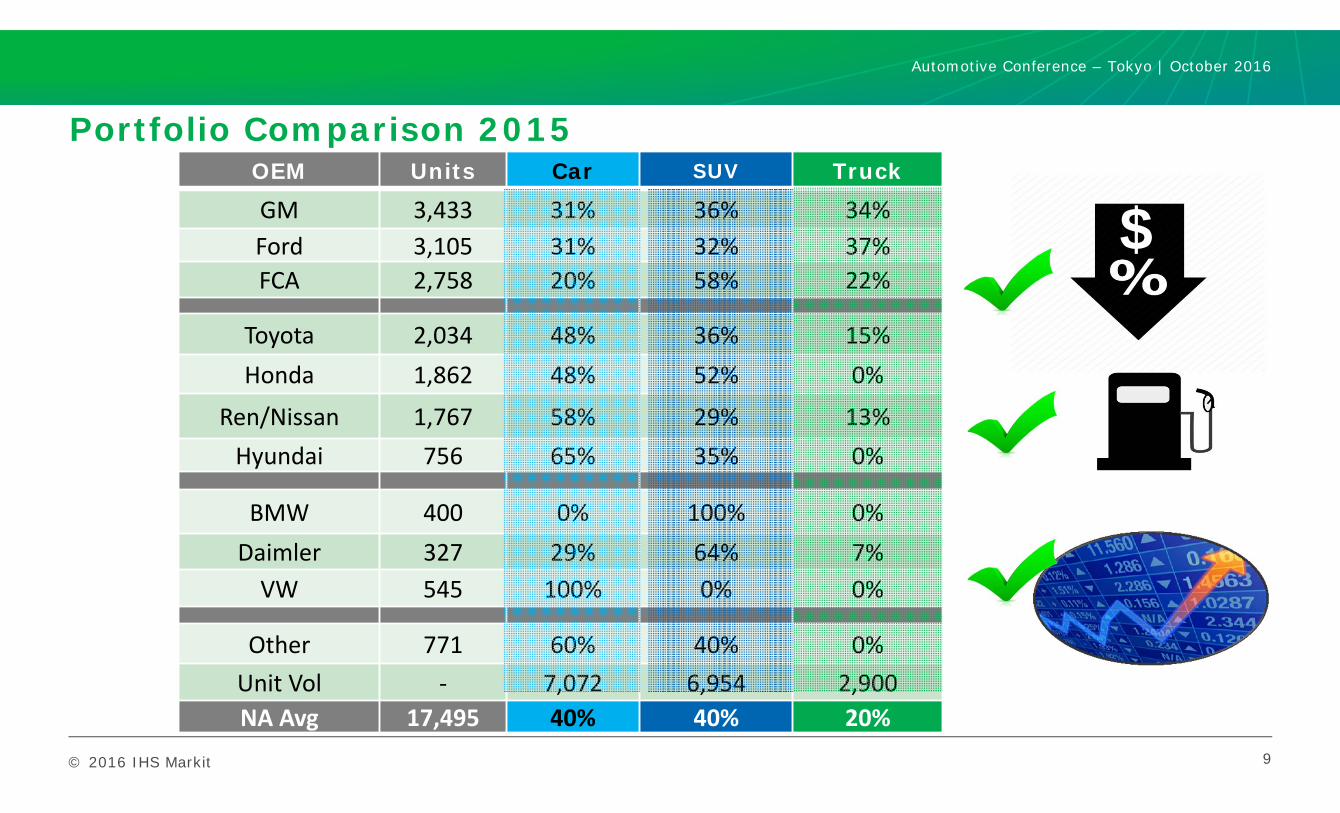

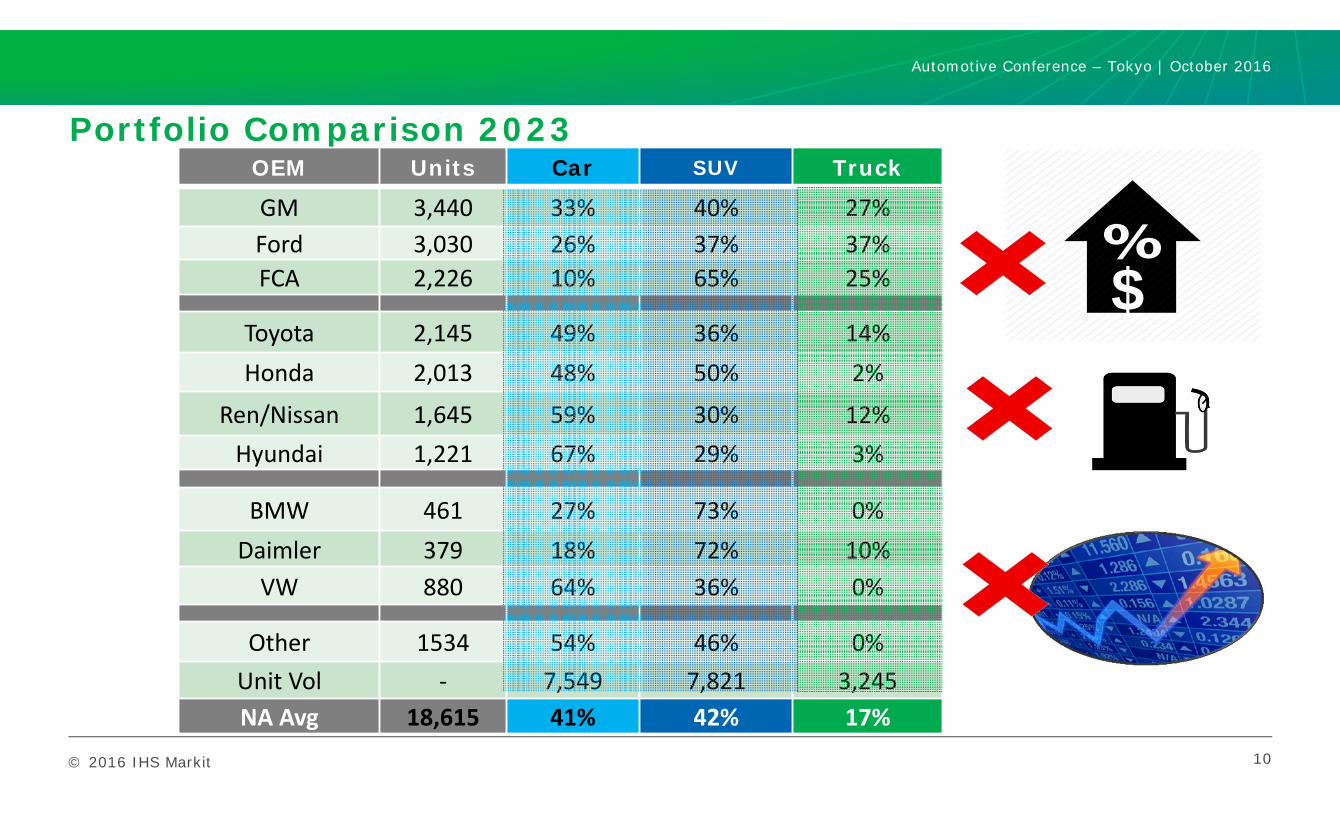

Portfolio Comparison 2015

9

OEM Units Car SUV Truck

GM 3,433 31% 36% 34%Ford 3,105 31% 32% 37%FCA 2,758 20% 58% 22%

Toyota 2,034 48% 36% 15%Honda 1,862 48% 52% 0%

Ren/Nissan 1,767 58% 29% 13%Hyundai 756 65% 35% 0%

BMW 400 0% 100% 0%Daimler 327 29% 64% 7%VW 545 100% 0% 0%

Other 771 60% 40% 0%Unit Vol ‐ 7,072 6,954 2,900NA Avg 17,495 40% 40% 20%

$

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Portfolio Comparison 2023

10

OEM Units Car SUV Truck

GM 3,440 33% 40% 27%Ford 3,030 26% 37% 37%FCA 2,226 10% 65% 25%

Toyota 2,145 49% 36% 14%Honda 2,013 48% 50% 2%

Ren/Nissan 1,645 59% 30% 12%Hyundai 1,221 67% 29% 3%

BMW 461 27% 73% 0%Daimler 379 18% 72% 10%VW 880 64% 36% 0%

Other 1534 54% 46% 0%Unit Vol ‐ 7,549 7,821 3,245NA Avg 18,615 41% 42% 17%

$

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

ContentsPresentation Name / Month 2016

North American Production Outlook

Product Profiles: Cars, SUVs, Trucks

Market Dynamics

OEM Reviews

Summary

© 2016 IHS Markit

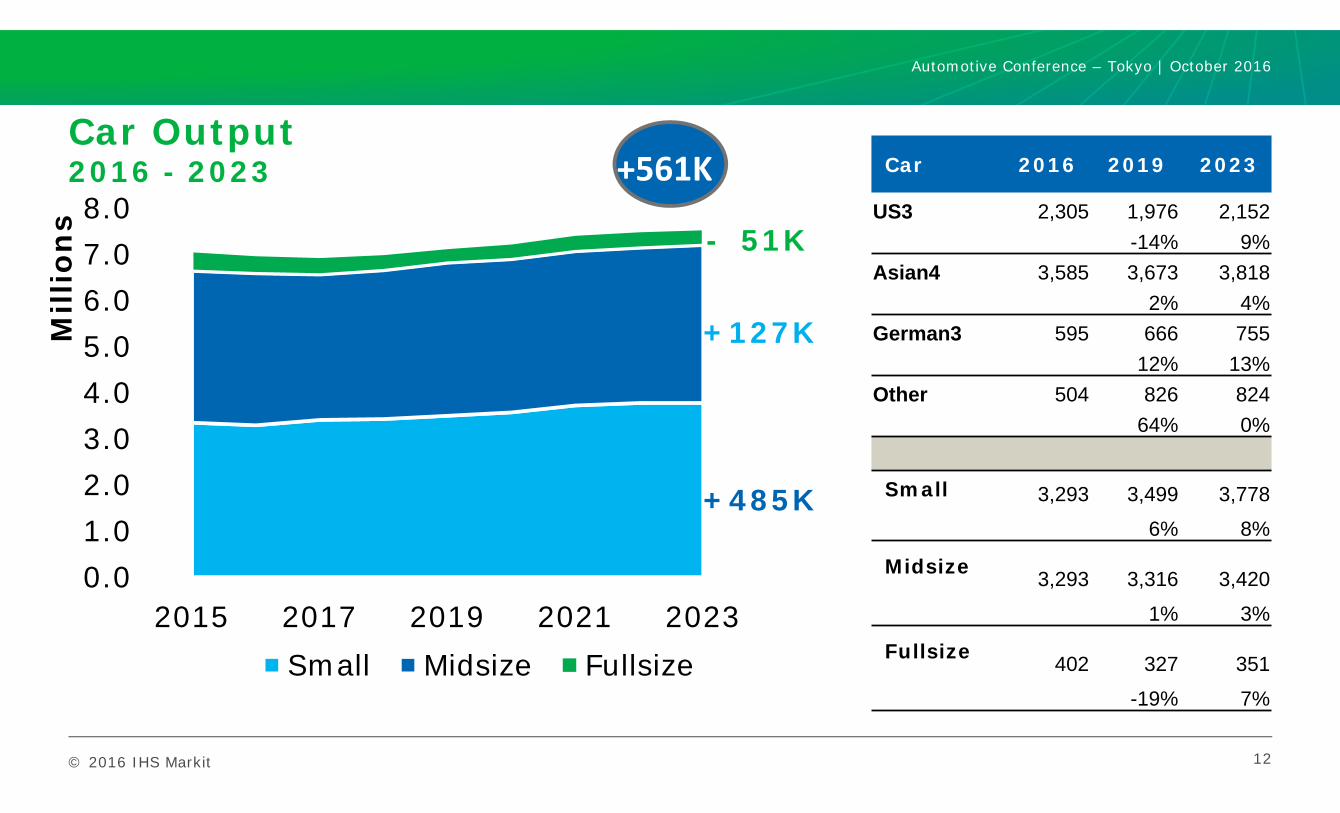

Car Output2016 - 2023

12

0.01.02.03.04.05.06.07.08.0

2015 2017 2019 2021 2023

Mill

ion

s

Small Midsize Fullsize

Car 2016 2019 2023

US3 2,305 1,976 2,152 -14% 9%

Asian4 3,585 3,673 3,818 2% 4%

German3 595 666 755 12% 13%

Other 504 826 824 64% 0%

Small 3,293 3,499 3,778

6% 8%

Midsize 3,293 3,316 3,420

1% 3%

Fullsize 402 327 351

-19% 7%

+485K

+127K

- 51K

+561K

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

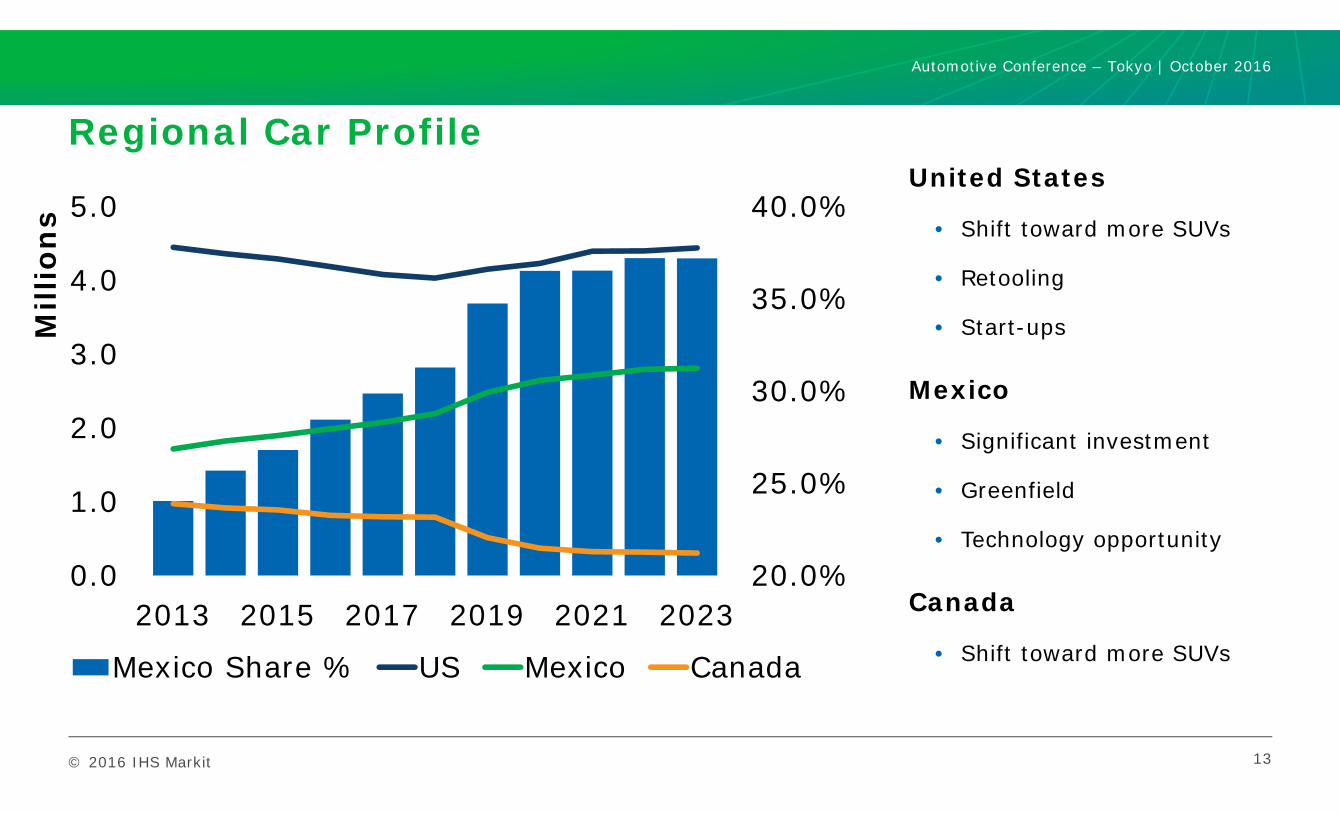

Regional Car Profile

13

20.0%

25.0%

30.0%

35.0%

40.0%

0.0

1.0

2.0

3.0

4.0

5.0

2013 2015 2017 2019 2021 2023

Mill

ion

s

Mexico Share % US Mexico Canada

United States

• Shift toward more SUVs

• Retooling

• Start-ups

Mexico

• Significant investment

• Greenfield

• Technology opportunity

Canada

• Shift toward more SUVs

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

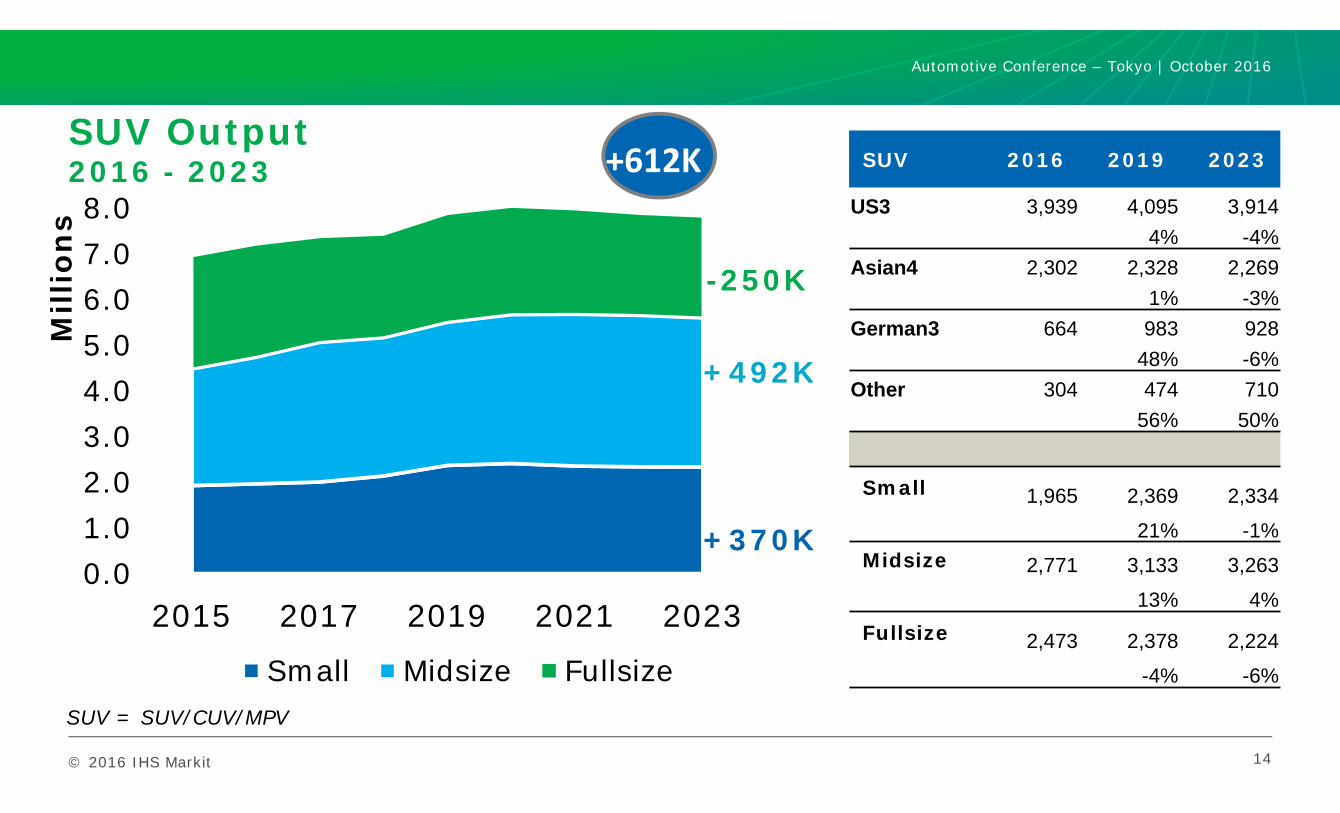

SUV Output2016 - 2023

14

0.01.02.03.04.05.06.07.08.0

2015 2017 2019 2021 2023

Mill

ion

s

Small Midsize Fullsize

SUV 2016 2019 2023

US3 3,939 4,095 3,914 4% -4%

Asian4 2,302 2,328 2,269 1% -3%

German3 664 983 928 48% -6%

Other 304 474 710 56% 50%

Small 1,965 2,369 2,334

21% -1%Midsize 2,771 3,133 3,263

13% 4%Fullsize 2,473 2,378 2,224

-4% -6%

+612K

+370K

+492K

-250K

SUV = SUV/CUV/MPV

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

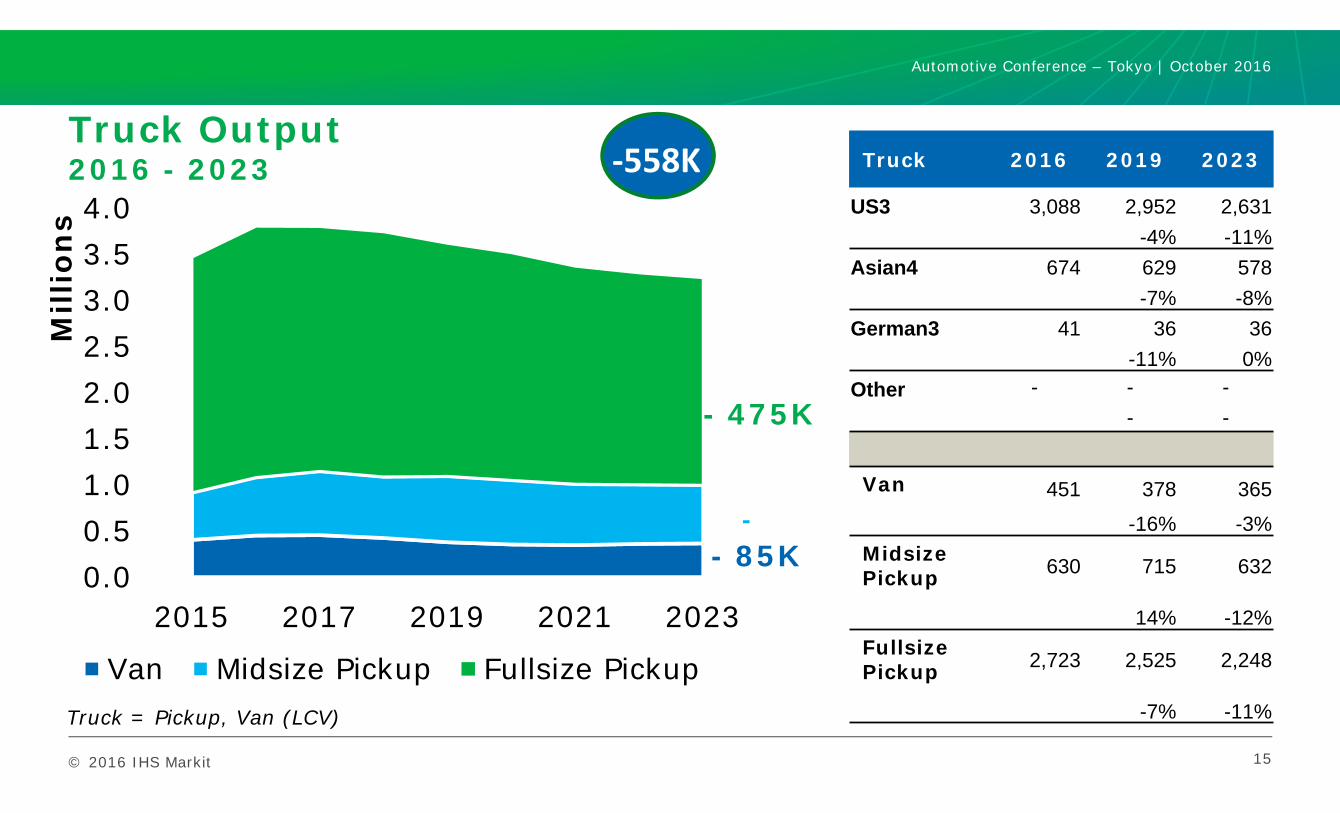

Truck Output2016 - 2023

15

0.00.51.01.52.02.53.03.54.0

2015 2017 2019 2021 2023

Mill

ion

s

Van Midsize Pickup Fullsize Pickup

Truck 2016 2019 2023

US3 3,088 2,952 2,631 -4% -11%

Asian4 674 629 578 -7% -8%

German3 41 36 36 -11% 0%

Other - - -- -

Van 451 378 365

-16% -3%Midsize Pickup 630 715 632

14% -12%FullsizePickup 2,723 2,525 2,248

-7% -11%

‐558K

- 85K-

- 475K

Truck = Pickup, Van (LCV)

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 16

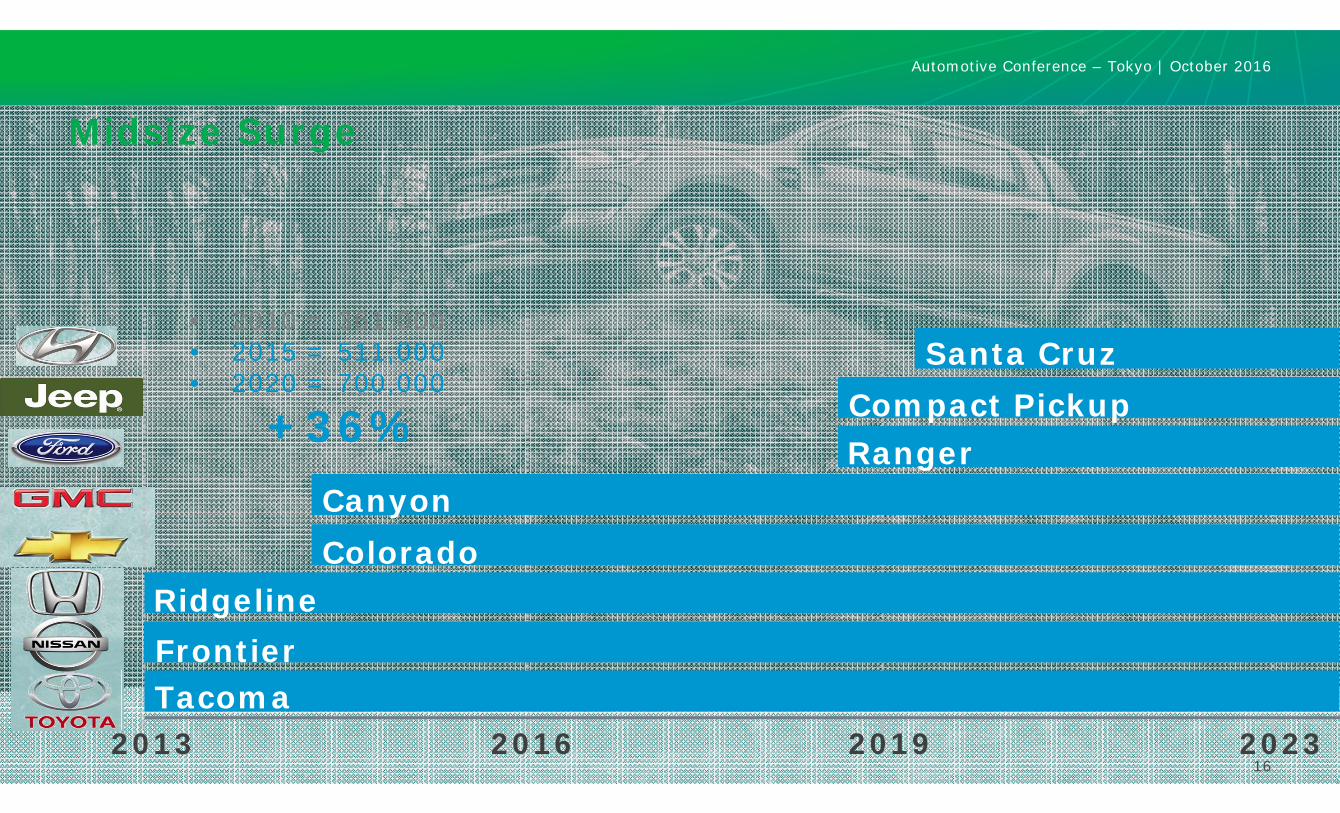

Midsize Surge

• 2010 = 361,000• 2015 = 511,000• 2020 = 700,000

+36%

2013 20232016 2019

RangerCompact Pickup

Santa Cruz

CanyonColorado

RidgelineFrontierTacoma

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

ContentsPresentation Name / Month 2016

North American Production Outlook

Product Profiles: Cars, SUVs, Trucks

Market Dynamics

OEM Reviews

Summary

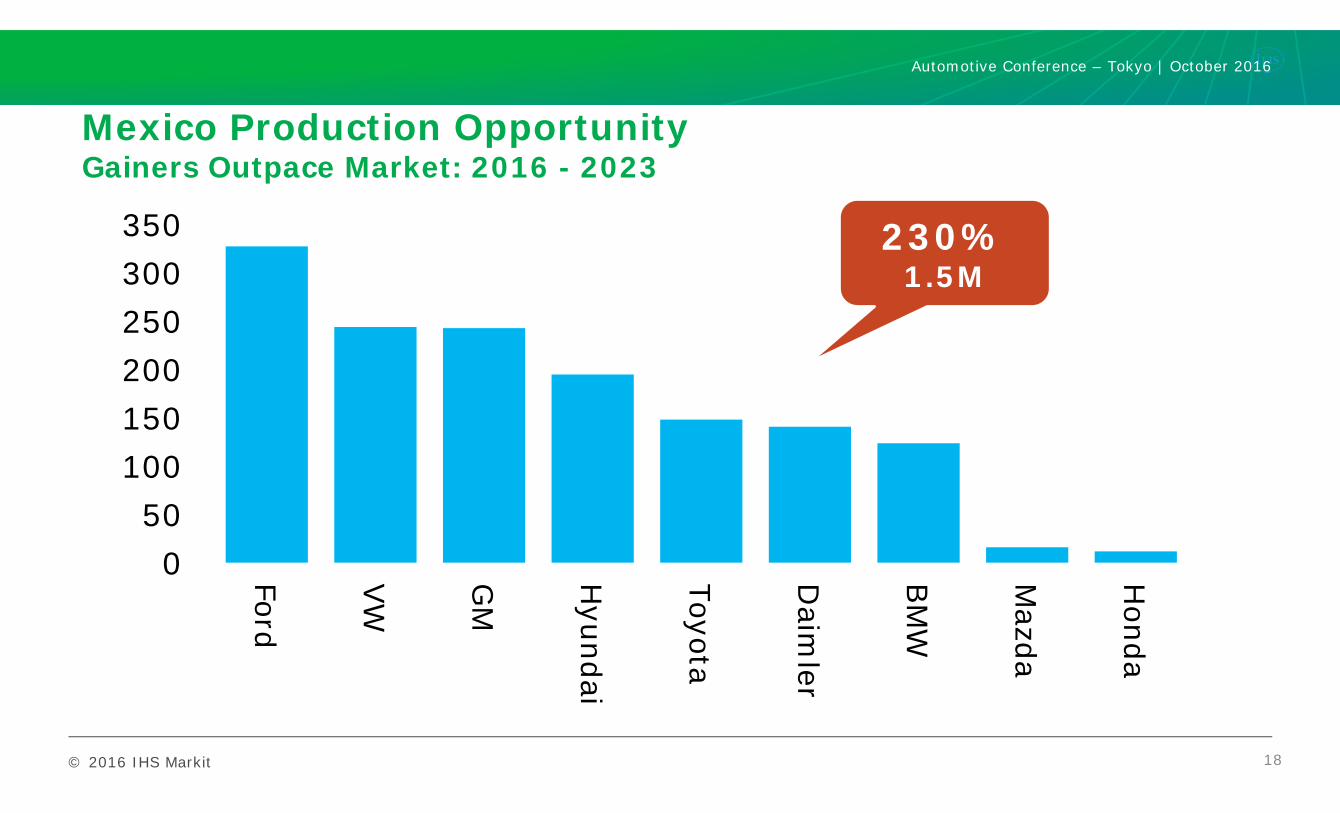

© 2016 IHS Markit 18

050

100150200250300350

Ford

VW

GM

Hyundai

Toyota

Daim

ler

BM

W

Mazda

Honda

Mexico Production OpportunityGainers Outpace Market: 2016 - 2023

230%1.5M

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

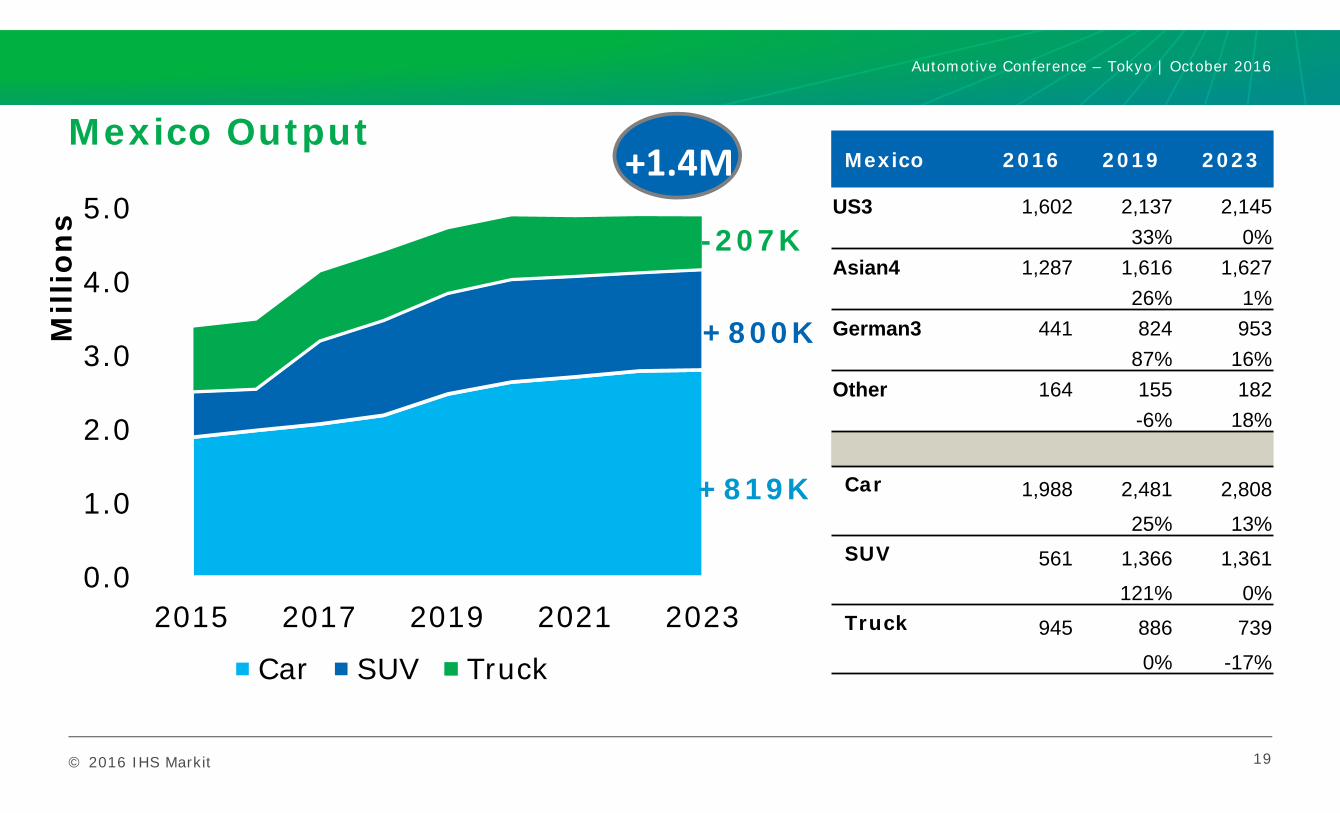

Mexico Output

19

0.0

1.0

2.0

3.0

4.0

5.0

2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

Mexico 2016 2019 2023

US3 1,602 2,137 2,145 33% 0%

Asian4 1,287 1,616 1,627 26% 1%

German3 441 824 953 87% 16%

Other 164 155 182 -6% 18%

Car 1,988 2,481 2,808

25% 13%SUV 561 1,366 1,361

121% 0%Truck 945 886 739

0% -17%

+819K

+800K

-207K

+1.4M

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 20

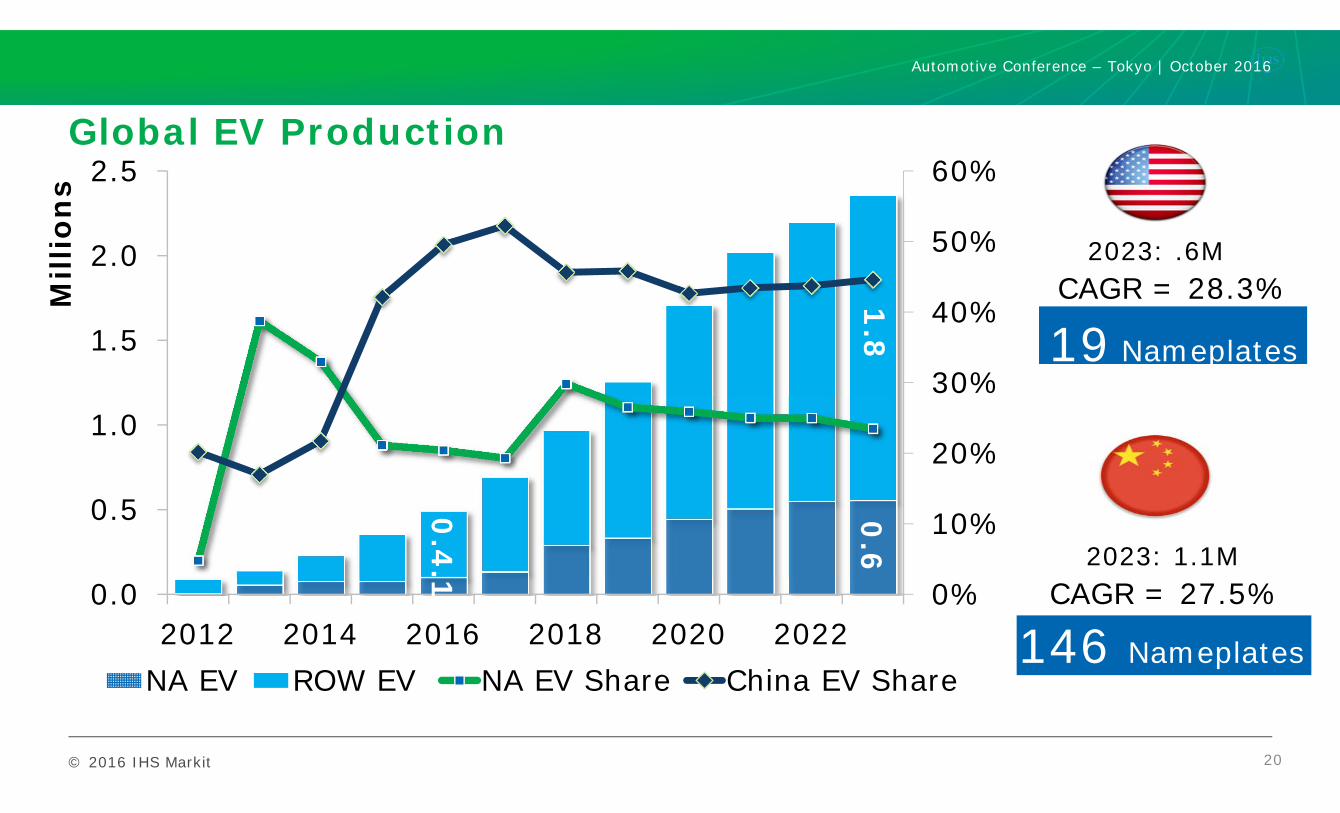

Global EV Production

0.0

.1

0.6

0.4

1.8

0%

10%

20%

30%

40%

50%

60%

0.0

0.5

1.0

1.5

2.0

2.5

2012 2014 2016 2018 2020 2022

Mill

ion

s

NA EV ROW EV NA EV Share China EV Share

CAGR = 27.5%2023: 1.1M

CAGR = 28.3%2023: .6M

19 Nameplates

146 Nameplates

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 21

Disruptive

ToyotaHondaNissanFordBMW

VolkswagenChevrolet

AudiLexusMazda

© 2016 IHS Markit

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

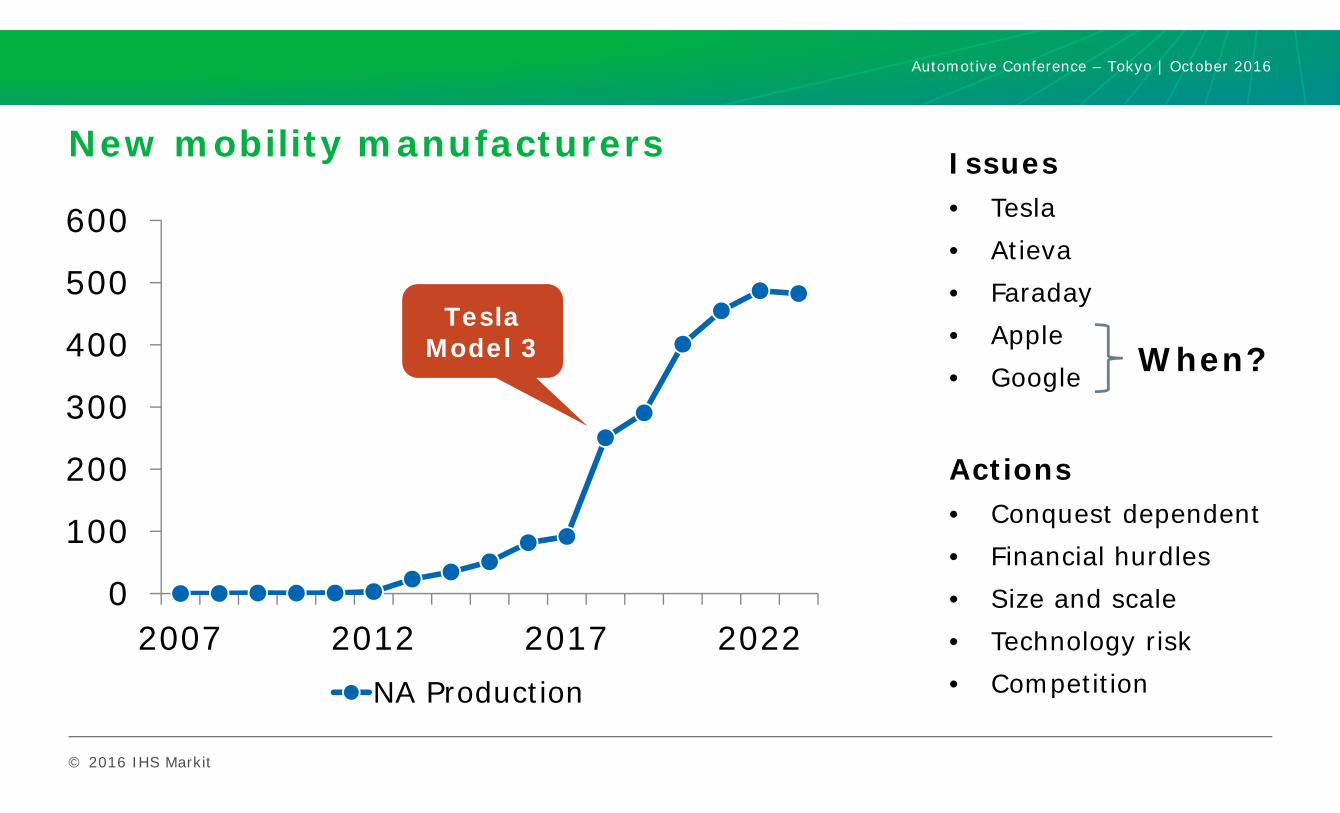

New mobility manufacturers

0

100

200

300

400

500

600

2007 2012 2017 2022NA Production

TeslaModel 3

Issues• Tesla• Atieva• Faraday• Apple• Google

Actions• Conquest dependent• Financial hurdles• Size and scale• Technology risk• Competition

When?

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

ContentsPresentation Name / Month 2016

North American Production Outlook

Product Profiles: Cars, SUVs, Trucks

Market Dynamics

OEM Reviews

Summary

© 2016 IHS Markit

0.00.51.01.52.02.53.03.54.0

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

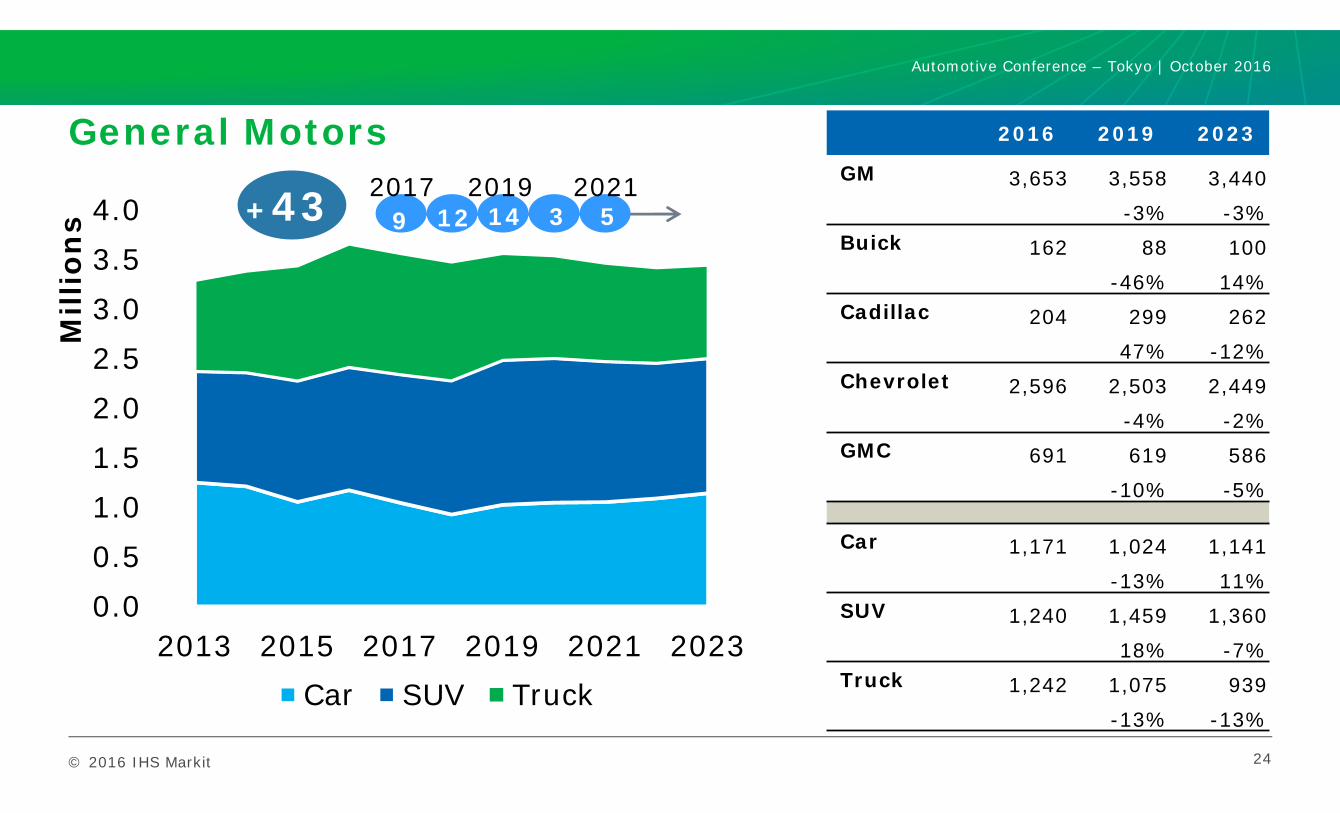

General Motors

24

2016 2019 2023

GM 3,653 3,558 3,440 -3% -3%

Buick 162 88 100 -46% 14%

Cadillac 204 299 262 47% -12%

Chevrolet 2,596 2,503 2,449 -4% -2%

GMC 691 619 586 -10% -5%

Car 1,171 1,024 1,141-13% 11%

SUV 1,240 1,459 1,36018% -7%

Truck 1,242 1,075 939-13% -13%

+43 9 12 14 3 52017 2019 2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

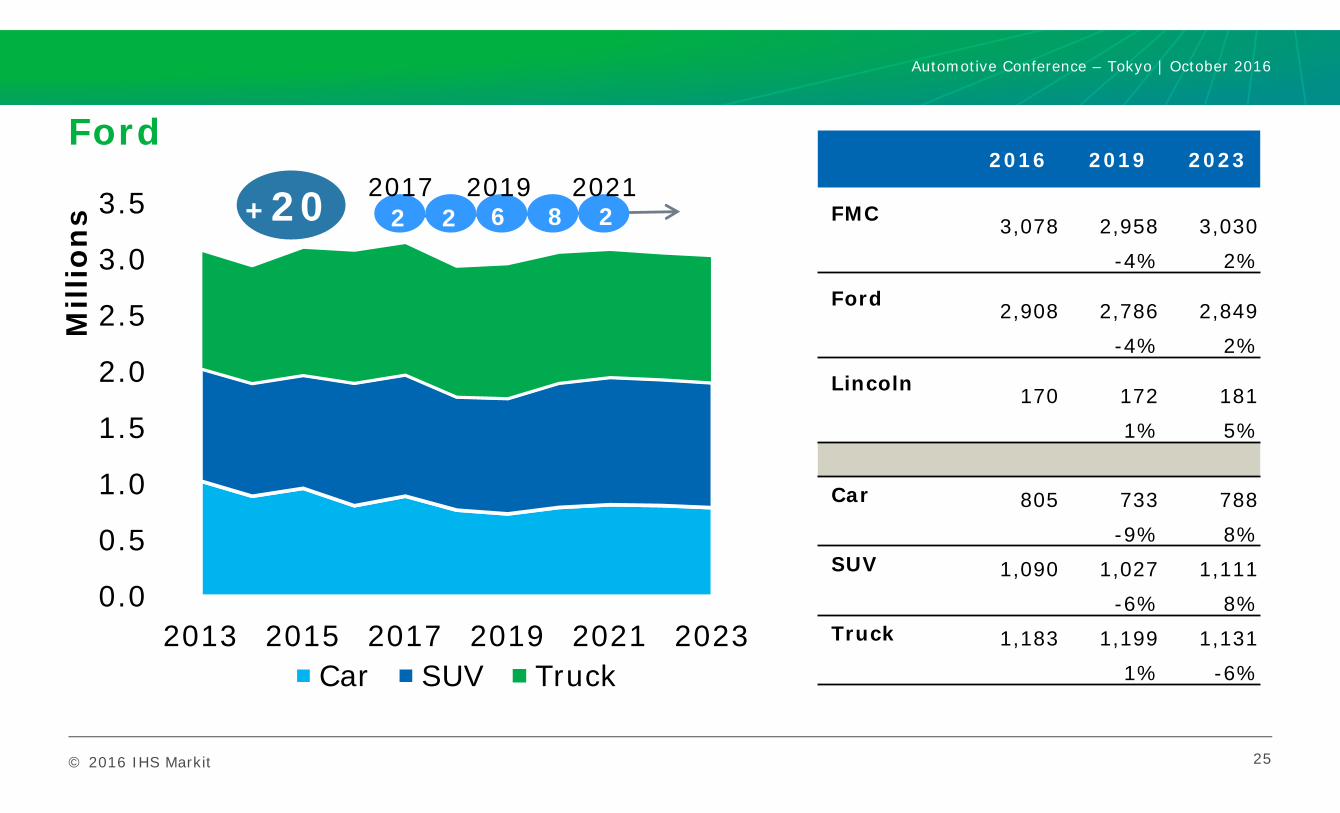

Ford

25

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

FMC 3,078 2,958 3,030 -4% 2%

Ford 2,908 2,786 2,849 -4% 2%

Lincoln 170 172 181 1% 5%

Car 805 733 788-9% 8%

SUV 1,090 1,027 1,111-6% 8%

Truck 1,183 1,199 1,1311% -6%

2 2 6 8 22017 2019 2021

+20

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

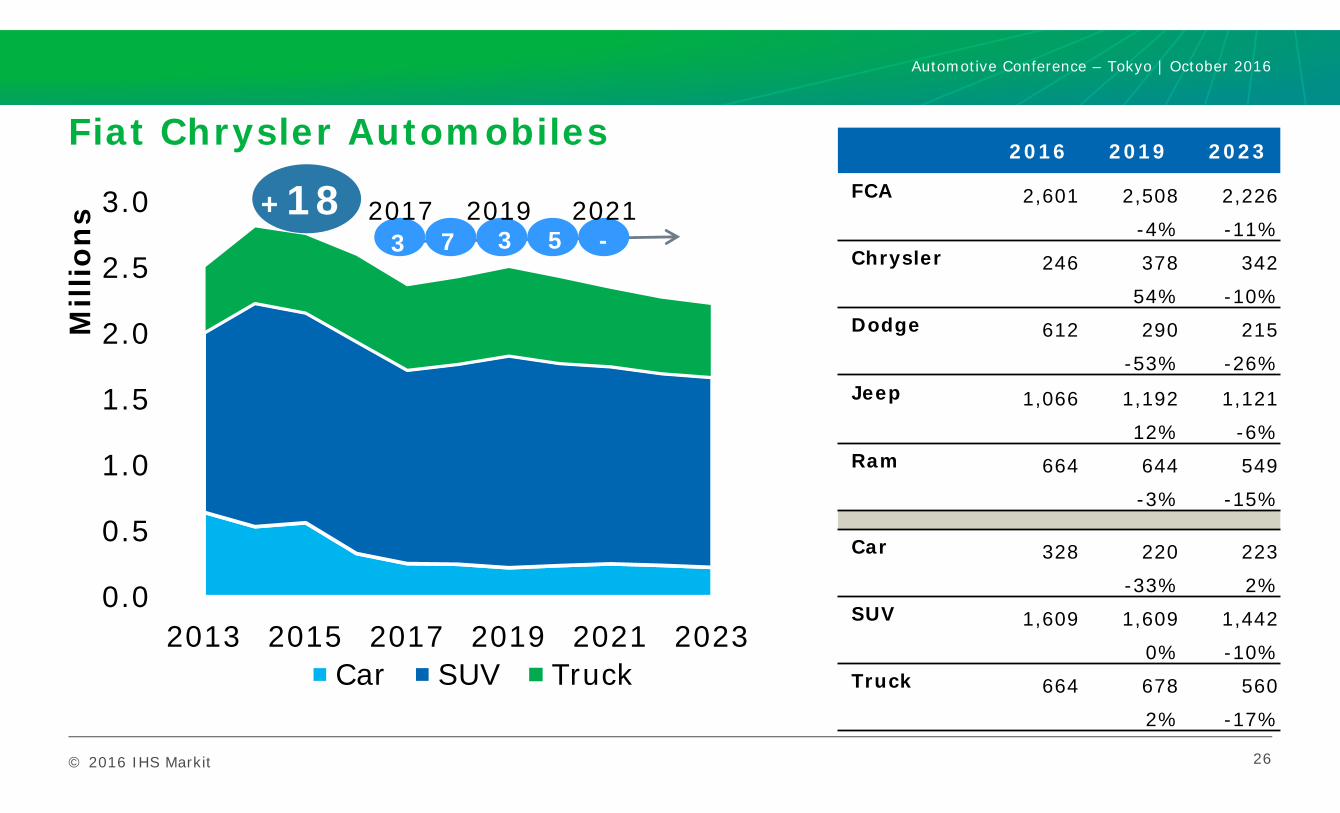

Fiat Chrysler Automobiles

26

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

FCA 2,601 2,508 2,226

-4% -11%Chrysler 246 378 342

54% -10%Dodge 612 290 215

-53% -26%Jeep 1,066 1,192 1,121

12% -6%Ram 664 644 549

-3% -15%

Car 328 220 223

-33% 2%SUV 1,609 1,609 1,442

0% -10%Truck 664 678 560

2% -17%

+183 7 3 5 -

2017 2019 2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

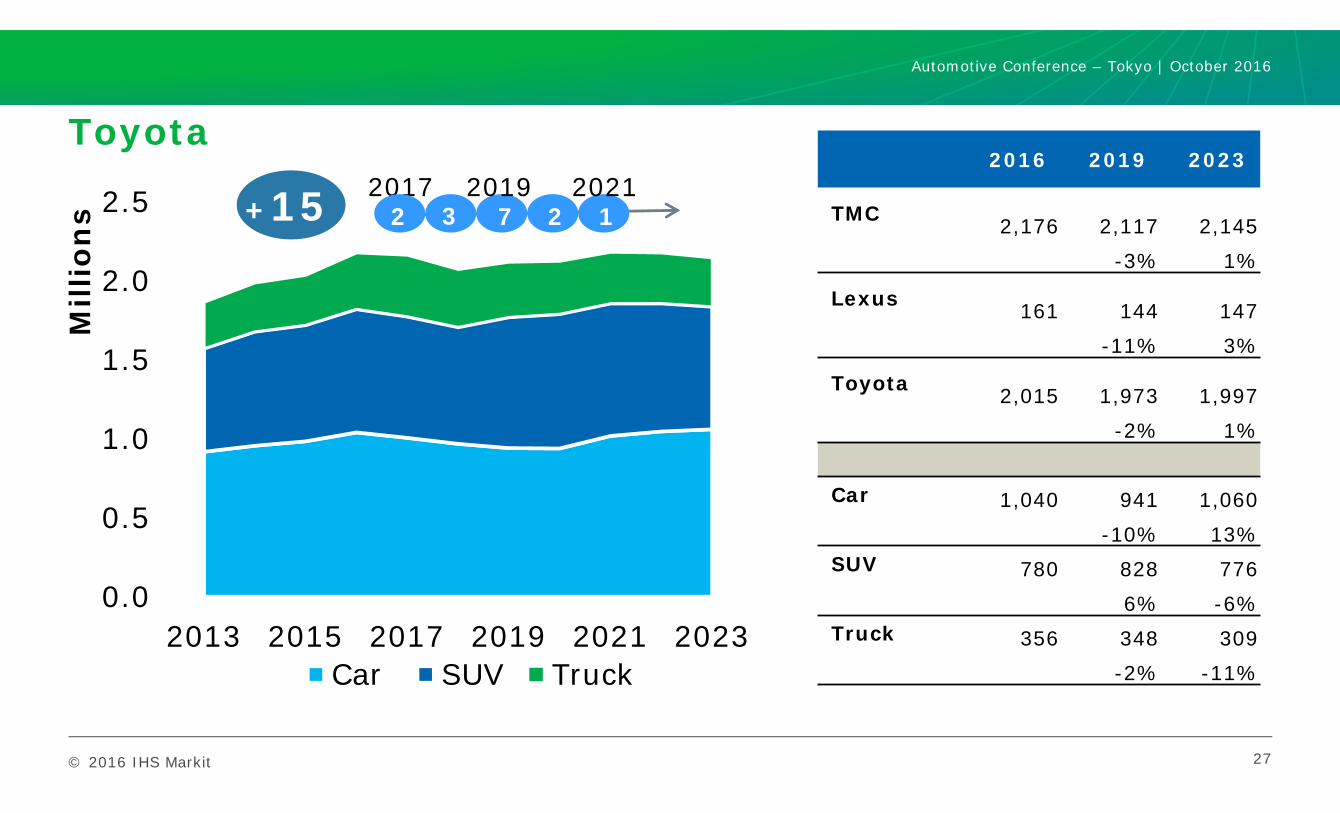

Toyota

27

0.0

0.5

1.0

1.5

2.0

2.5

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

TMC 2,176 2,117 2,145 -3% 1%

Lexus 161 144 147 -11% 3%

Toyota 2,015 1,973 1,997 -2% 1%

Car 1,040 941 1,060-10% 13%

SUV 780 828 7766% -6%

Truck 356 348 309-2% -11%

20172 3 7 2

20191

2021+15

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

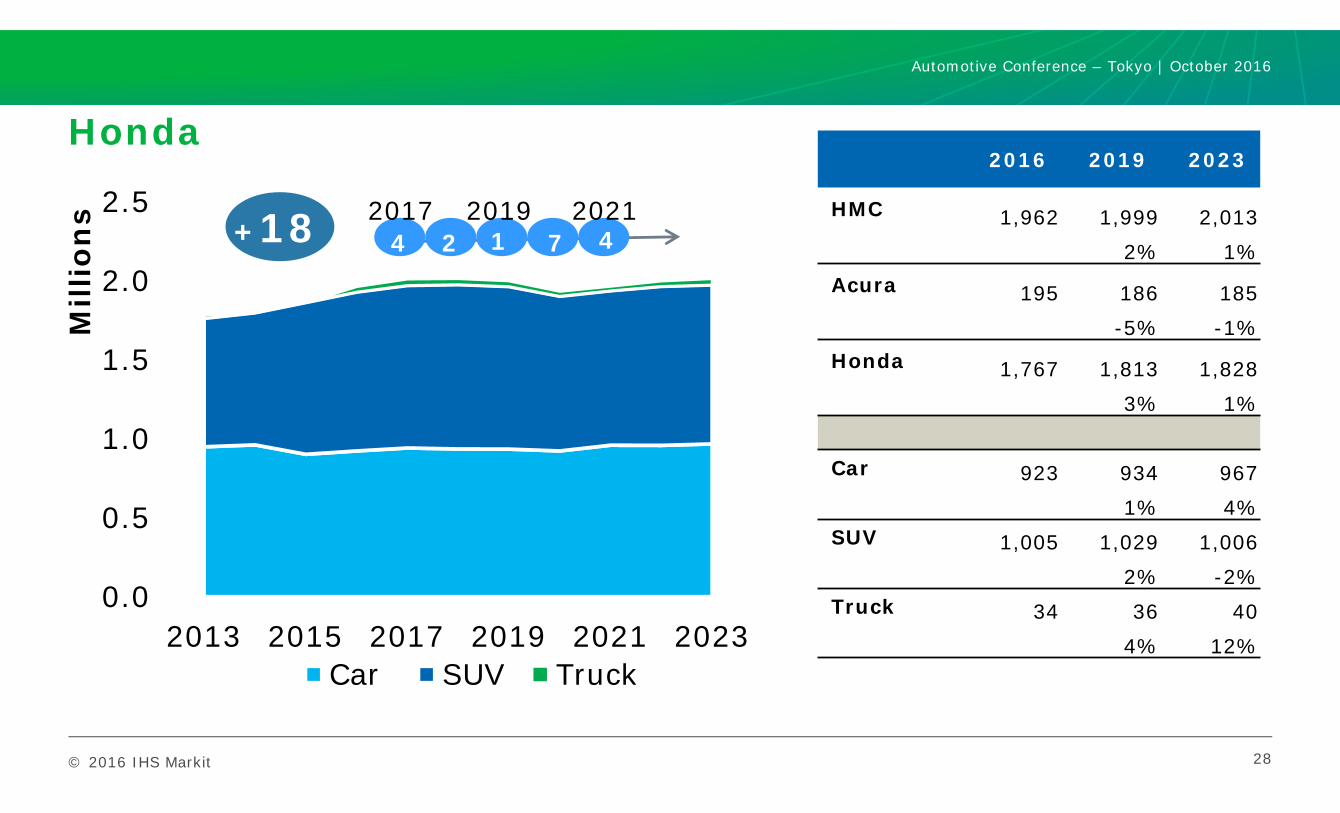

Honda

28

0.0

0.5

1.0

1.5

2.0

2.5

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

HMC 1,962 1,999 2,013 2% 1%

Acura 195 186 185 -5% -1%

Honda 1,767 1,813 1,828 3% 1%

Car 923 934 9671% 4%

SUV 1,005 1,029 1,0062% -2%

Truck 34 36 404% 12%

+18 4 2 1 7 42017 2019 2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

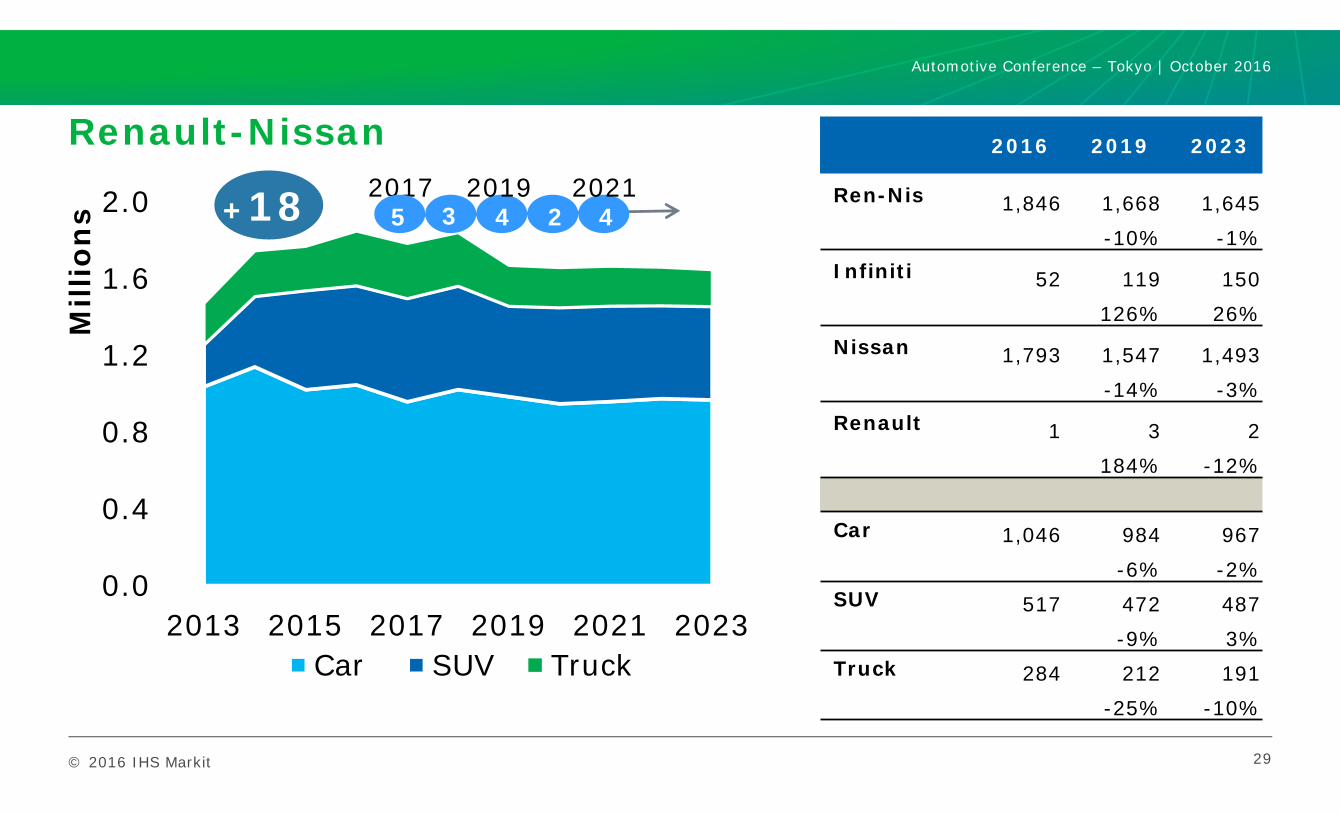

Renault-Nissan

29

0.0

0.4

0.8

1.2

1.6

2.0

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

Ren-Nis 1,846 1,668 1,645 -10% -1%

Infiniti 52 119 150 126% 26%

Nissan 1,793 1,547 1,493 -14% -3%

Renault 1 3 2 184% -12%

Car 1,046 984 967-6% -2%

SUV 517 472 487-9% 3%

Truck 284 212 191-25% -10%

+18 20175 3 4 2

20194

2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

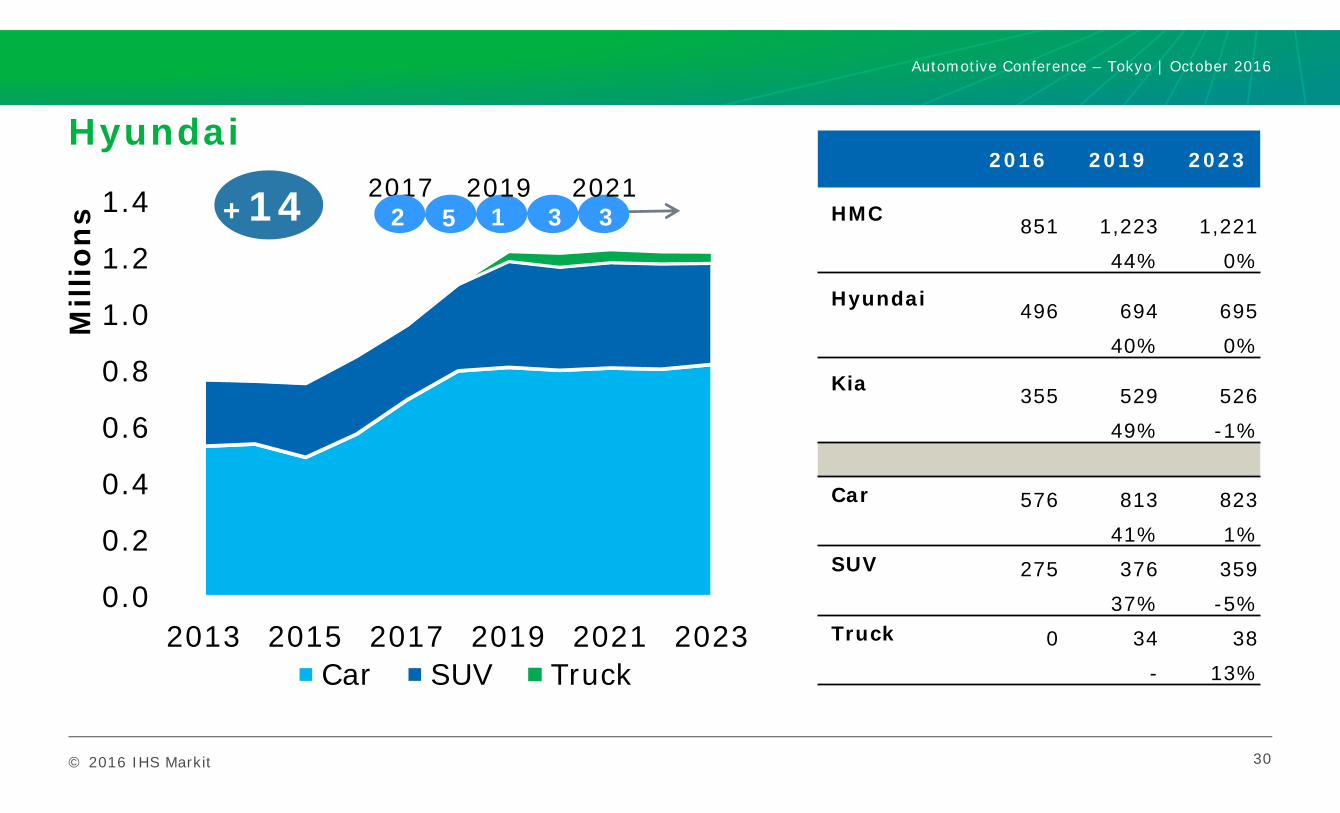

Hyundai

30

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

HMC 851 1,223 1,221 44% 0%

Hyundai 496 694 695 40% 0%

Kia 355 529 526 49% -1%

Car 576 813 82341% 1%

SUV 275 376 35937% -5%

Truck 0 34 38- 13%

+14 20172 5 1 3

20193

2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

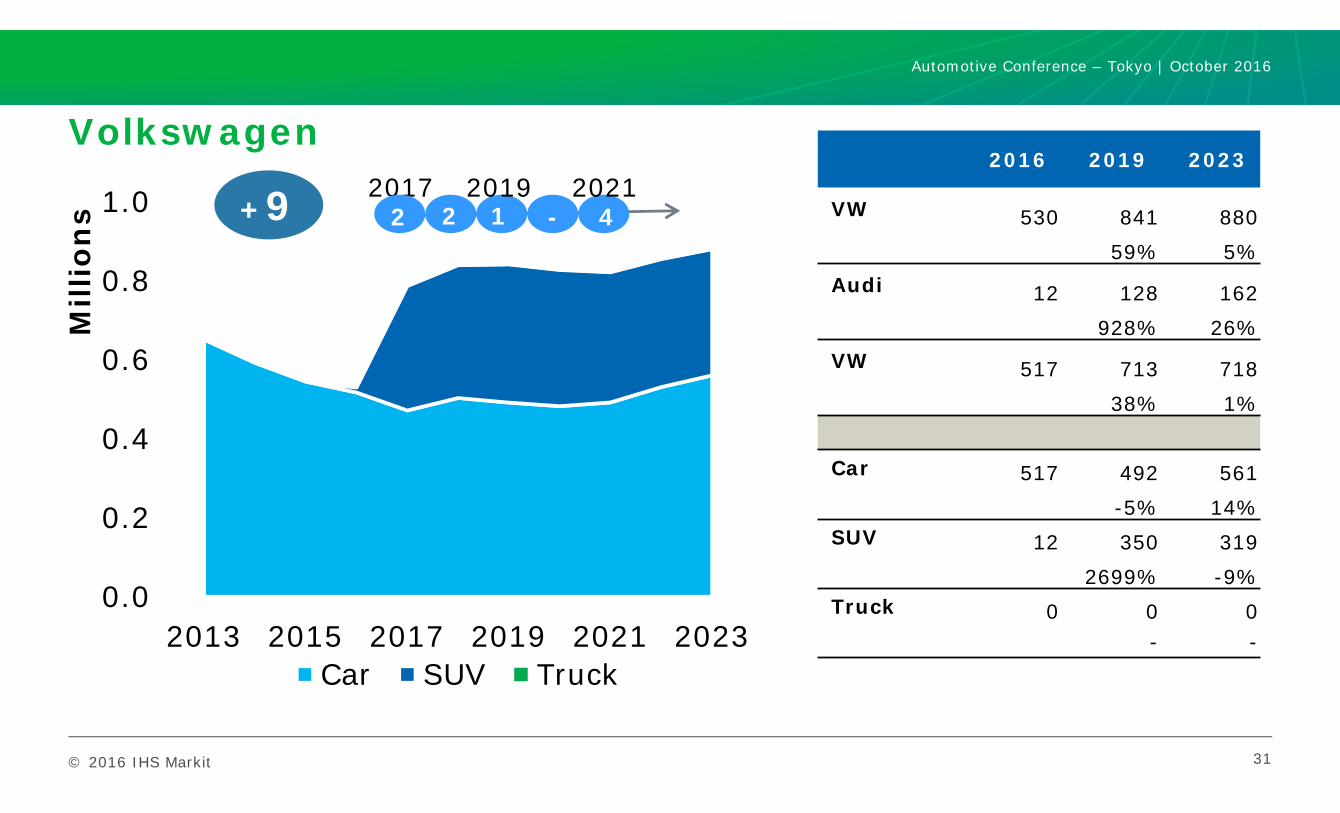

Volkswagen

31

0.0

0.2

0.4

0.6

0.8

1.0

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

VW 530 841 880 59% 5%

Audi 12 128 162 928% 26%

VW 517 713 718 38% 1%

Car 517 492 561-5% 14%

SUV 12 350 3192699% -9%

Truck 0 0 0- -

+9 20172 2 1 -

20194

2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

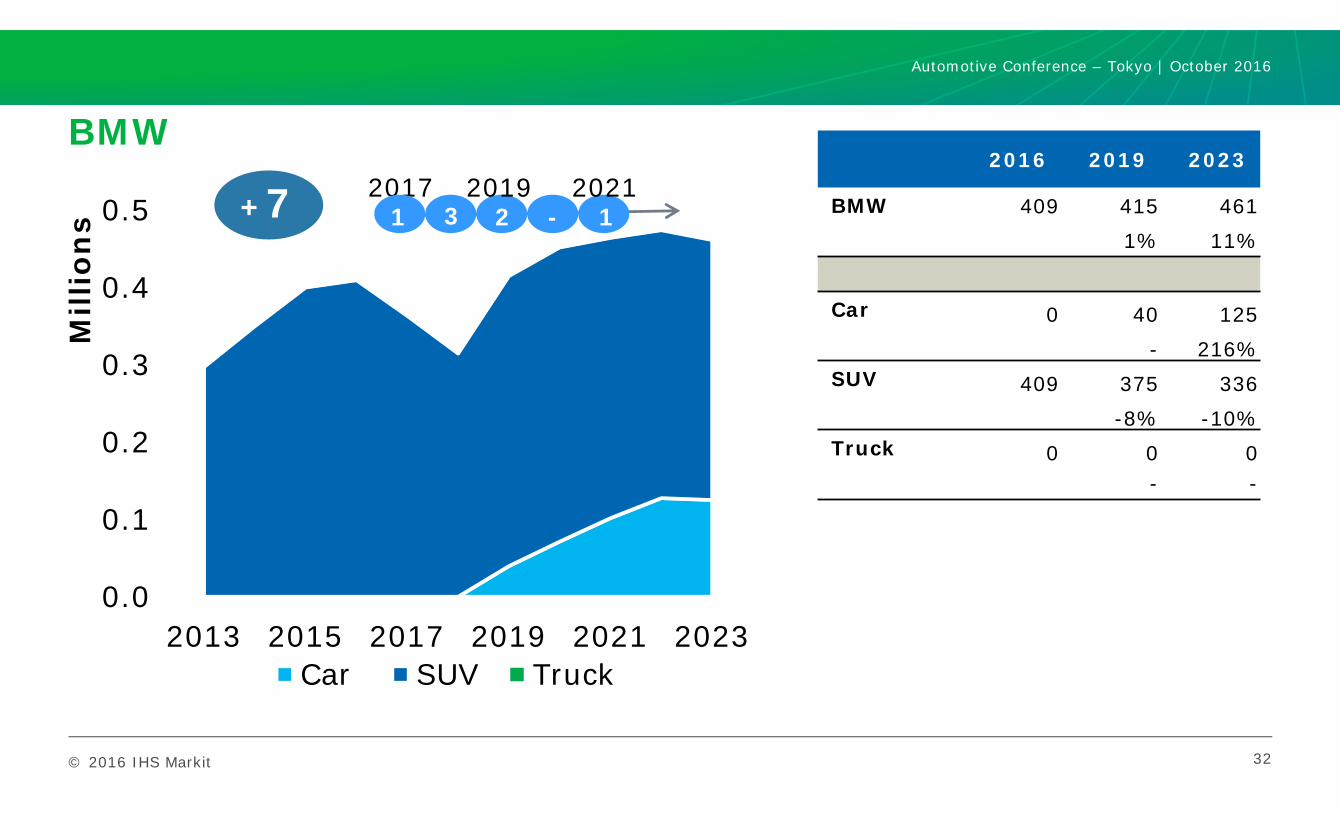

BMW

32

0.0

0.1

0.2

0.3

0.4

0.5

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

BMW 409 415 4611% 11%

Car 0 40 125- 216%

SUV 409 375 336-8% -10%

Truck 0 0 0- -

+7 20171 3 2 -

20191

2021

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

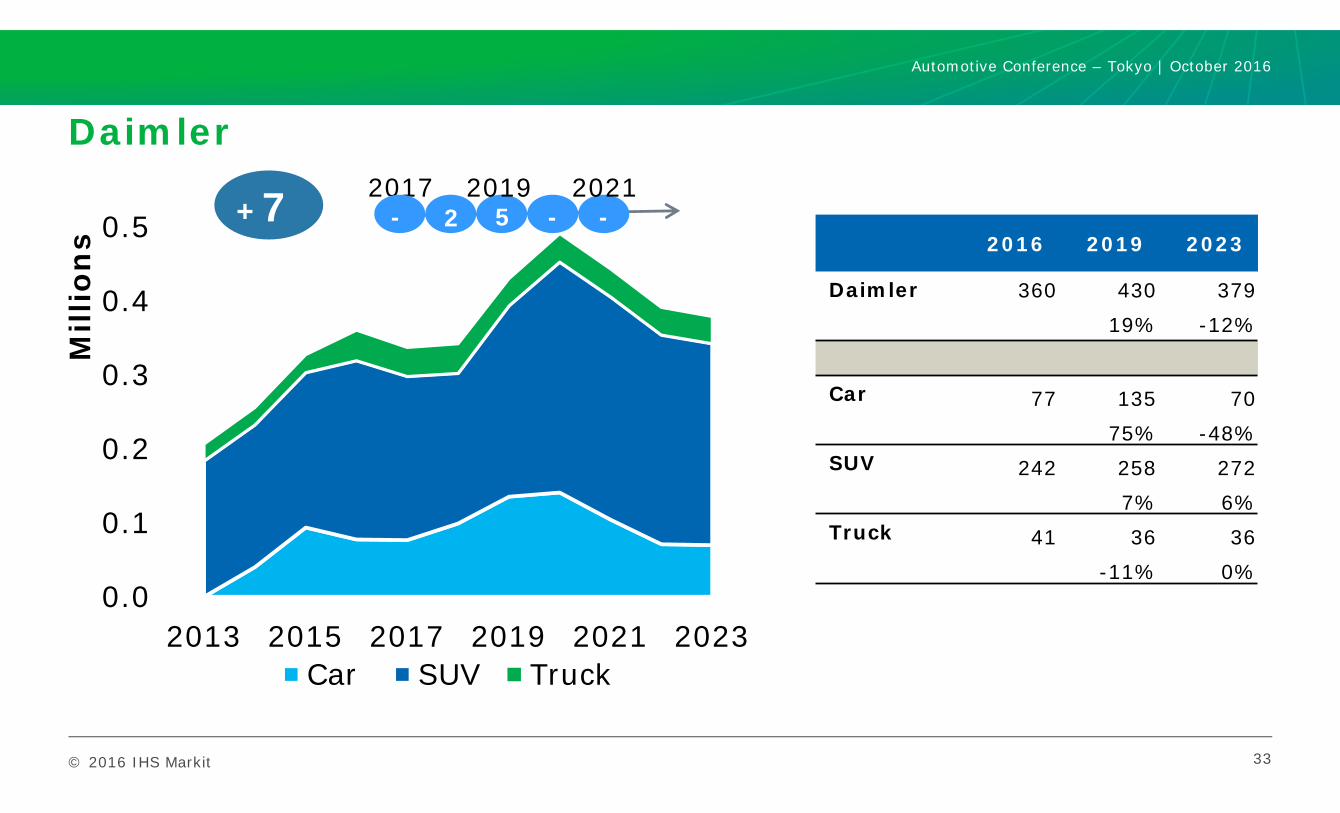

Daimler

33

0.0

0.1

0.2

0.3

0.4

0.5

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

2016 2019 2023

Daimler 360 430 37919% -12%

Car 77 135 7075% -48%

SUV 242 258 2727% 6%

Truck 41 36 36-11% 0%

+7 2017- 2 5 -

2019-

2021

Automotive Conference – Tokyo | October 2016

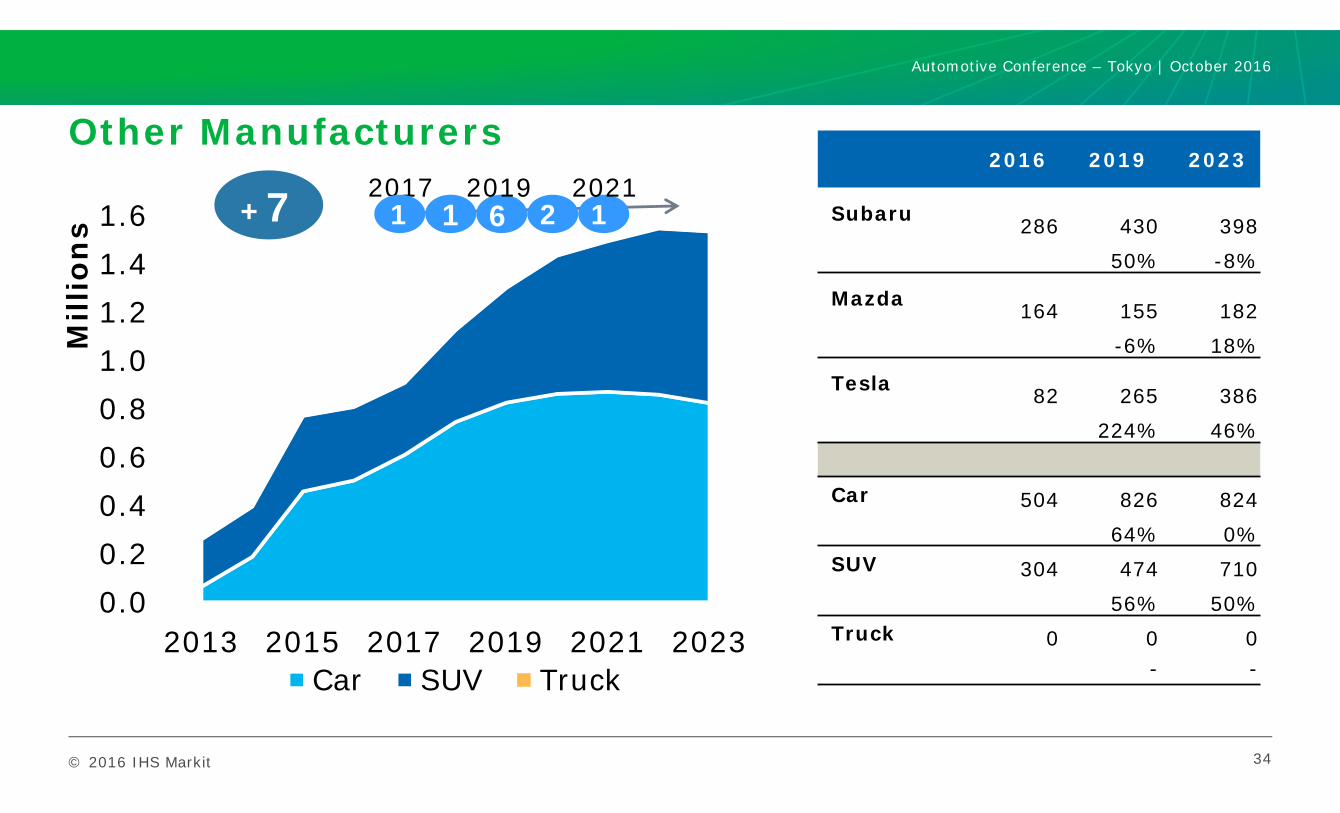

© 2016 IHS Markit 34

0.00.20.40.60.81.01.21.41.6

2013 2015 2017 2019 2021 2023

Mill

ion

s

Car SUV Truck

Other Manufacturers2016 2019 2023

Subaru 286 430 398 50% -8%

Mazda 164 155 182 -6% 18%

Tesla 82 265 386 224% 46%

Car 504 826 82464% 0%

SUV 304 474 71056% 50%

Truck 0 0 0- -

20171 1 6 2

20191

2021+7

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

ContentsPresentation Name / Month 2016

North American Production Outlook

Product Profiles: Cars, SUVs, Trucks

Market Dynamics

OEM Reviews

Summary

© 2016 IHS Markit

Summary: Proactive Positioning

• Mitigate Risk: Lower Growth Leads to Higher Risk Behavior

• Take Calculated Risks Over A Set Investment Horizon

• Proactively manage business portfolio; transition ahead of inflection point

• Audit: Align Future Strategy with Core Capabilities and Risk Profile

• Increased launch and investment activity at reduced volumes – drives a profit squeeze

• Leverage: Seize Sound Opportunities to Grow As Market Stress Rises• Window of Opportunity to take action as market maintains momentum

• Diversification: Requires Global Perspective• Embrace global opportunities to develop expertise; Chinese OEMs & Suppliers are actively working to

make inroads, offering risk and reward

Automotive Conference – Tokyo | October 2016

IHS MarkitTM COPYRIGHT NOTICE AND DISCLAIMER © 2016 IHS Markit.

No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS Markit. Content reproduced or redistributed with IHS Markit permission must display IHS Markit legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions and analyses that are based upon it, and to the extent permitted by law, IHS Markit shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially from forecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at your own risk. IHS Markit and the IHS Markit logo are trademarks of IHS Markit.

IHS Markit Customer Care:[email protected]: +1 800 IHS CARE (+1 800 447 2273)Europe, Middle East, and Africa: +44 (0) 1344 328 300Asia and the Pacific Rim: +604 291 3600

Thank You!

![Build Systems with autoconf, automake and libtool [updated]](https://img.pdfslide.net/doc/110x75/5554ac4fb4c905fd608b5276/build-systems-with-autoconf-automake-and-libtool-updated.jpg)