Embed Size (px)

DESCRIPTION

Aviation Finance

Citation preview

EAS431

Aviation Finance

Seminar 1

Understanding Financing Requirements

- Prediction of Air Traffic Growth• Depends on GDP Growth (2:1) and Real cost of Air Travel

- Capacity Growth • (Number of Seats, Efficient use, airborne Time, Flying

Speed)

- Numbers of Aircraft • Size of Aircraft

- Retirements (30 years life span)

Understanding Financing Requirements

Understanding Financing Requirements

Understanding Financing Requirements

CyclicalityFinancing needs to be fairly conservative

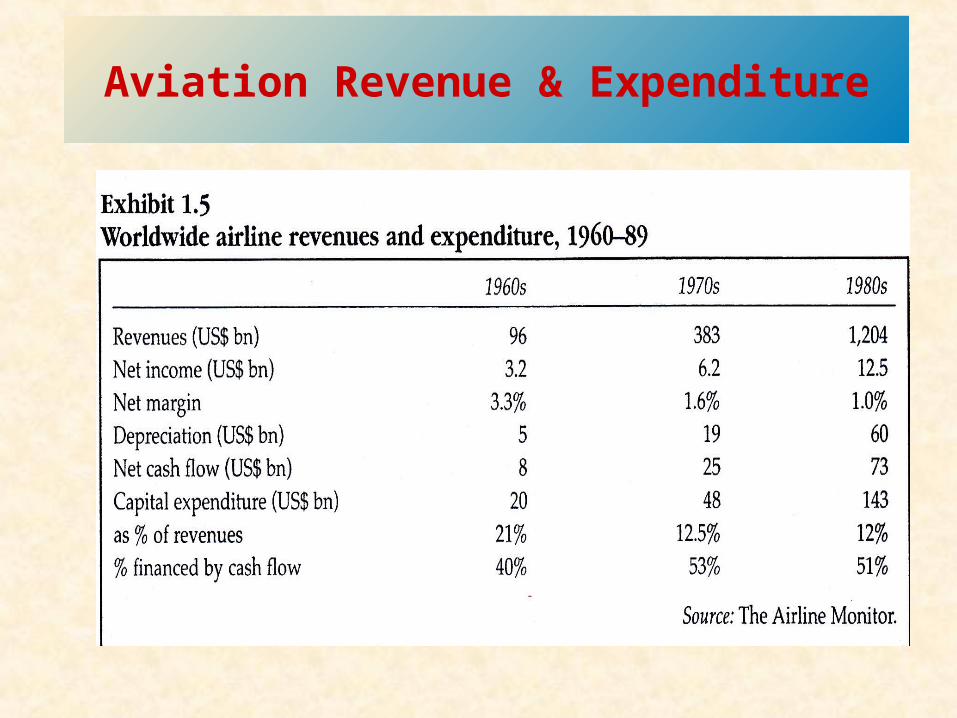

Aviation Revenue & Expenditure

Aviation Revenue & Expenditure

Financing Methods

Market Demand Fluctuations, Tax Funding

Residual Value Risk

Residual Value Risk

External Shock factors & Profitability

• GDP growth• War & terrorism (e.g. Iraq, Sept 11)• Environmental – Volcanic Eruption• Uncertain Fuel Prices

- hedging- Fuel Tanking- Fuel Surcharges to Passengers

External Shock factors & Profitability

• Asian currency crisis• Epidemic (Sars, Bird Flu)• Capital Intensive – Large Fixed Assets

– Low Cost Carriers• Govt vs Private

– National Strategic Economic Key Assets– Air transport Access

The Balance Sheet

Balance Sheet

Income Statement

Balance Sheet

2003 2002 2003 2002Cash 696 58 A/P 307 303

A/R 956 992 N/P 26 119

Inventory 301 361 Other CL 1,662 1,353Other CA 303 264 Total CL 1,995 1,775Total CA 2,256 1,675 LT Debt 843 1,091

Net FA 3,138 3,358 C/S 2,556 2,167

Total Assets

5,394 5,033 Total Liab. & Equity

5,394 5,033

Numbers in millions

Income Statement

Revenues 5,000

Cost of Goods Sold 2,006

Expenses 1,740

Depreciation 116

EBIT 1,138

Interest Expense 7

Taxable Income 1,131Taxes 442

Net Income 689

EPS 3.61

Dividends per share 1.08

Numbers in millions, except EPS & DPS

Sources and Uses

• Sources– Cash inflow – occurs when we “sell” something– Decrease in asset account (Sample B/S)

• Accounts receivable, inventory, and net fixed assets– Increase in liability or equity account

• Accounts payable, other current liabilities, and common stock

• Uses– Cash outflow – occurs when we “buy” something– Increase in asset account

• Cash and other current assets– Decrease in liability or equity account

• Notes payable and long-term debt

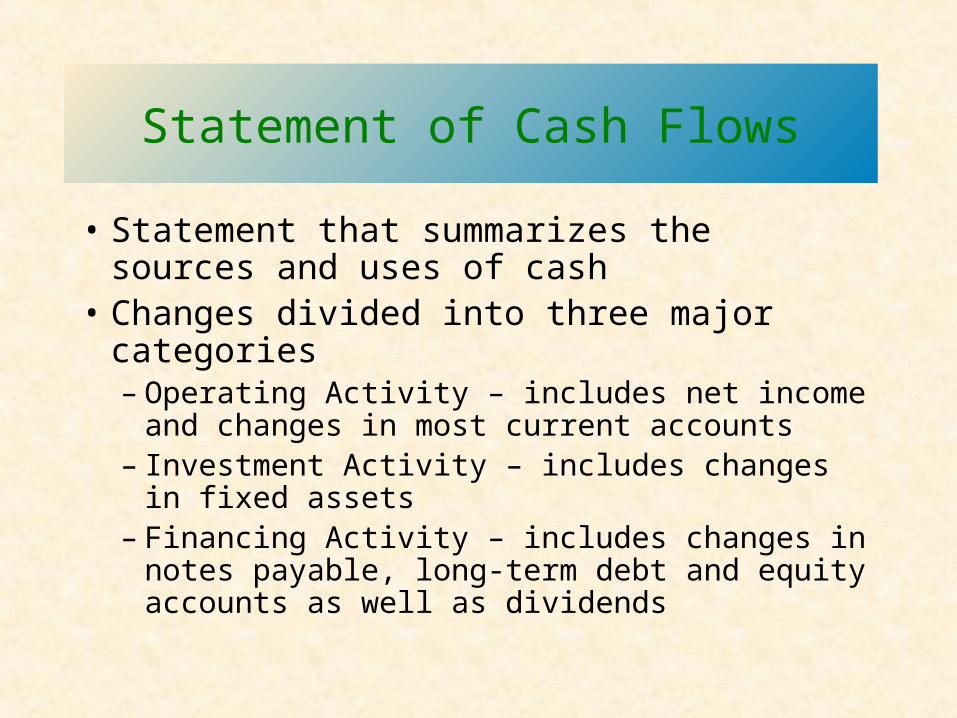

Statement of Cash Flows

• Statement that summarizes the sources and uses of cash

• Changes divided into three major categories– Operating Activity – includes net income and

changes in most current accounts– Investment Activity – includes changes in fixed

assets– Financing Activity – includes changes in notes

payable, long-term debt and equity accounts as well as dividends

Statement of Cash Flows

Cash, beginning of year 58 Financing Activity

Operating Activity Decrease in Notes Payable -93

Net Income 689 Decrease in LT Debt -248

Plus: Depreciation 116 Decrease in C/S (minus RE) -94

Decrease in A/R 36 Dividends Paid -206

Decrease in Inventory 60 Net Cash from Financing -641

Increase in A/P 4 Net Increase in Cash 638

Increase in Other CL 309 Cash End of Year 696

Less: Increase in CA -39

Net Cash from Operations 1,175

Investment Activity

Sale of Fixed Assets 104

Net Cash from Investments 104

Numbers in millions

What is business risk?

• Uncertainty about future operating income (EBIT), i.e., how well can we predict operating income?

• Note that business risk does not include financing effects.

Probability

EBITE(EBIT)0

Low risk

High risk

What determines business risk?

Uncertainty about demand (sales)

• Uncertainty about output prices

• Uncertainty about costs

• Operating leverage

What is operating leverage, and how does it affect a firm’s business risk?

• Operating leverage is the use of fixed costs rather than variable costs.

• If most costs are fixed, hence do not decline when demand falls, then the firm has high operating leverage.

Effect of Operating Leverage

• More operating leverage leads to more business risk, for then a small sales decline causes a big profit decline.

Sales

$ Rev.TC

FC

QBE Sales

$ Rev.

TCFC

QBE

} Profit

Using Operating Leverage

• Typical situation: Can use operating leverage to get higher E(EBIT), but risk also increases.

Probability

EBITL

Low operating leverage

High operating leverage

EBITH

What is financial leverage?Financial risk?

• Financial leverage is the use of debt and preferred stock.

• Financial risk is the additional risk concentrated on common stockholders as a result of financial leverage.

Business Risk vs. Financial Risk

• Business risk depends on business factors such as competition, product liability, and operating leverage.

• Financial risk depends only on the types of securities issued.– More debt, more financial risk.– Concentrates business risk on stockholders.

An Example:Illustrating Effects of Financial Leverage

• Two firms with the same operating leverage, business risk, and probability distribution of EBIT.

• Only differ with respect to their use of debt (capital structure).

Firm U Firm L No debt $10,000 of 12% debt $20,000 in assets $20,000 in assets 40% tax rate 40% tax rate

Firm U: Unleveraged

Economy Bad Average Good Probability 0.25 0.50 0.25 EBIT $2,000 $3,000 $4,000 Interest 0 0 0 EBT $2,000 $3,000 $4,000 Taxes (40%) 800 1,200 1,600 NI $1,200 $1,800 $2,400

Firm L: Leveraged

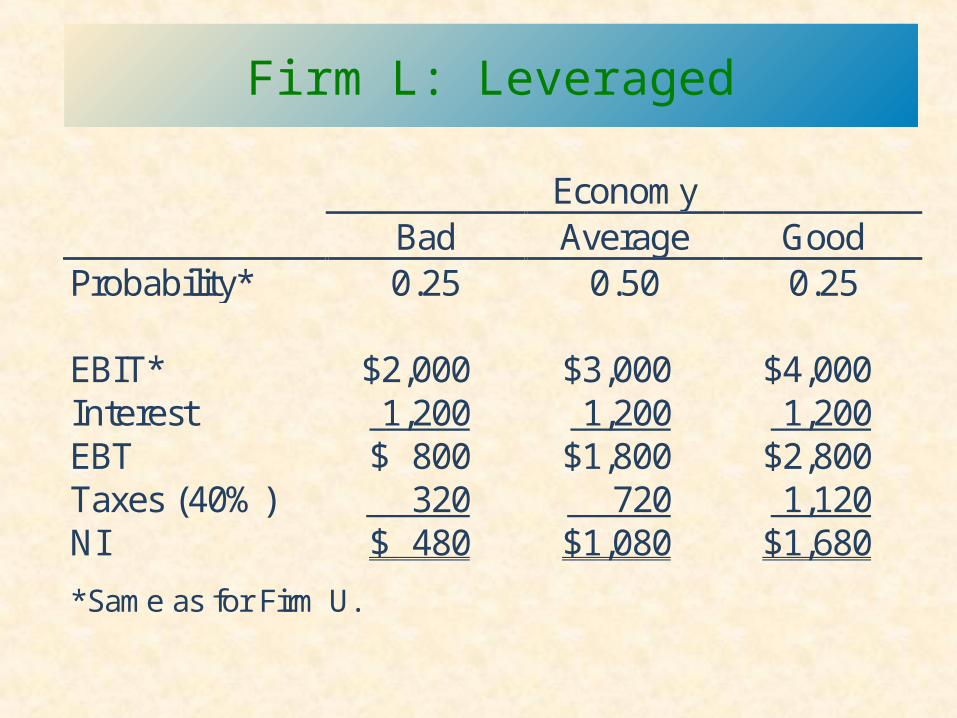

Economy Bad Average Good Probability* 0.25 0.50 0.25 EBIT* $2,000 $3,000 $4,000 Interest 1,200 1,200 1,200 EBT $ 800 $1,800 $2,800 Taxes (40%) 320 720 1,120 NI $ 480 $1,080 $1,680 *Same as for Firm U.

Ratio Comparison Between Leveraged and Unleveraged Firms

Firm U Bad Average Good BEP 10.0% 15.0% 20.0% ROE 6.0 9.0 12.0 TIE Firm L Bad Average Good BEP 10.0% 15.0% 20.0% ROE 4.8 10.8 16.8 TIE 1.67× 2.50x 3.30x

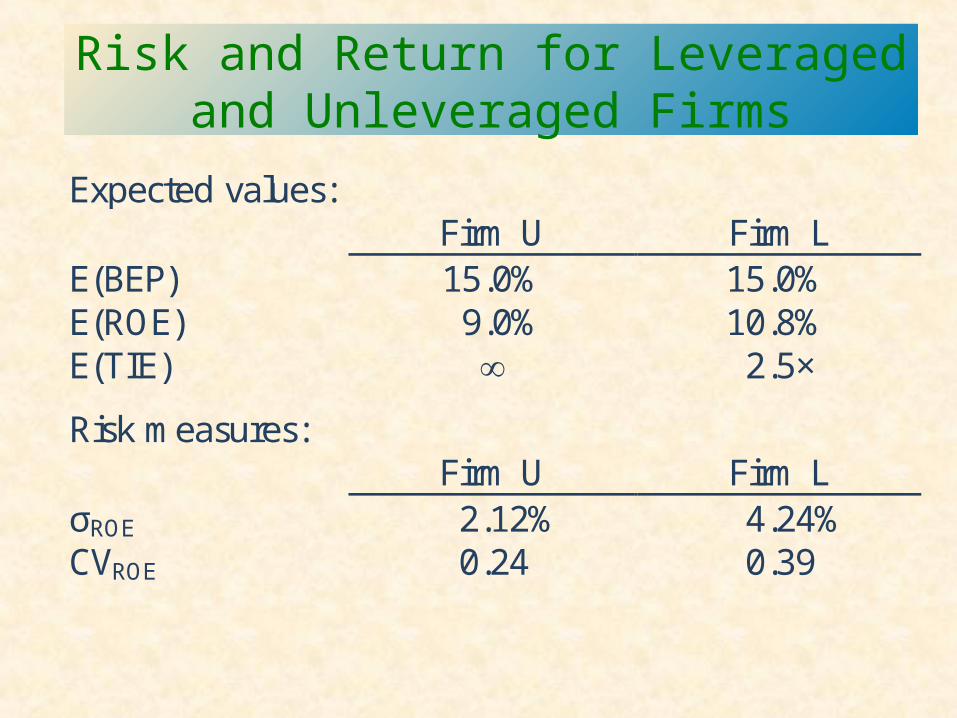

Risk and Return for Leveraged and Unleveraged Firms

Expected values: Firm U Firm L E(BEP) 15.0% 15.0% E(ROE) 9.0% 10.8% E(TIE) 2.5× Risk measures: Firm U Firm L σROE 2.12% 4.24% CVROE 0.24 0.39