Embed Size (px)

DESCRIPTION

Bajaj Allianz Limited

Citation preview

MPBIM 1

INTERNSHIP REPORT ON

BAJAJ ALLIANZ LIMITED

Submitted in partial fulfillment of the requirements of the MBA Degree Course of Bangalore University

Submitted By

Annapurna.N.K

Under the Guidance and Supervision Of

Dr.N.S Viswanath

M.P.BIRLA INSTITUTE OF MANAGEMENT Associate Bharatiya Vidya Bhavan

# 43, Race Course Road Bangalore-560001

2004 – 2006

MPBIM 2

EXECUTIVE SUMMARY

What is life insurance �

7KH�+HDG�RU�WKH�EUHDGZLQQHU�RI�WKH�IDPLO\�JHQHUDOO\�VXSSRUWV�WKH�IDPLO\�IRU�WKHLU�EDVLF�QHHGV��VXFK�DV��IRRG��FORWKLQJ��VKHOWHU��E\�EULQJLQJ�LQFRPH�DW�D�UHJXODU�LQWHUYDO��6R�ORQJ�DV�KH�RU�VKH�OLYHV��WKH�LQFRPH� LV�UHFHLYHG�VWHDGLO\��WKH�IDPLO\�LV�VHFXUH��EXW�XQWLPHO\�GHDWK�RU�GLVDELOLW\�RI�WKDW�SHUVRQ�SXWV�WKH�IDPLO\�LQ�D�YHU\�GLIILFXOW�VLWXDWLRQ��DQG�VRPHWLPHV�LQ�VWDUN�SRYHUW\��8QFHUWDLQW\�RI�GHDWK�LV�LQKHUHQW�LQ�KXPDQ�OLIH�� �

�,W�LV�WKH�XQFHUWDLQW\�WKDW�LV�WKH�U LVN��ZKLFK�JLYHV�ULVH�WR�WKH�QHFHVVLW\�IRU�VRPH�IRUP�RI�

SURWHFWLRQ� DJDLQVW� WKH� ILQDQFLDO� ORVV� DULVLQJ� IURP� GHDWK�� ,QVXUDQFH� VXEVWLWXWHV� WKLV�XQFHUWDLQW\�E\�FHUWDLQW\� �

�7KH�SULPDU\�SXUSRVH�RI�/LIH�,QVXUDQFH�LV�WKH�SURWHFWLRQ�RI�WKH�IDPLO\��,QVXUDQFH�LQ�

LWV� YDULRXV�IRUPV�SURWHFWV�DJDLQVW�VXFK�PLVIRUWXQHV�E\�KDYLQJ�WKH�ORVVHV�RI�WKH�XQIRUWXQDWH�IHZ�SDLG�E\�WKH�FRQWULEXWLRQ�RI�WKH�PDQ\�WKDW�DUH�H[SRVHG�WR�WKH�VDPH�ULVN��7KLV�LV�WKH�HVVHQFH�RI�LQVXUDQFH ��WKH�VKDULQJ�RI�ORVVHV�DQG�VXEVWLWXWLRQ�RI�FHUWDLQW\�IRU�XQ FHUWDLQW\��

�The increasing role of IRDA- Insurance Regulatory development authority and

the increasing private players in today’s insurance industry has also been picturised The

project also gives a birds eye view about the present insurance industry and how are the

customers benefited from the changes taken place from past to present in this industry

$� GHWDLOHG� FRPSDQ\� SURILOH� DORQJ�ZLWK� WKH� ILQDQFLDO� KLJKOLJKWV� RI� WKH� SUHYLRXV�DVVHVVPHQW�\HDU�RI�WKH�FRPSDQ\�KDV�DOVR�EHHQ�LQFOXGHG

�¬¬��The project titled “a comparative study of different products in

insurance industry with that of Bajaj Allianz life insurance Company

limited” is undertaken at Bajaj Allianz Life Insurance Company Ltd,

Bangalore.��

MPBIM 3

¬¬��The project is undertaken in order to understand the different

products of different companies and compare them based on

certain parameters.��

¬¬��The main aim of conducting this study is to come out with a

conclusion as to which product of which company is doing best

and from the customers point of view which product is the best for

their investment.��

¬¬��The companies considered for comparison are Bajaj Allianz Life

Insurance Company Ltd, ICICI Prudential and Life Insurance

Corporation of India. The products considered for the project are

endowment plan, unit linked plans and the children plan.��

��

����

MPBIM 4

INDUSTRY PROFILE

MPBIM 5

LIFE INSURANCE IN INDIA INTRODUCTION

With such a large population and the untapped market area of this population Insurance

happens to be a very big opportunity in India. Today it stands as a business growing at

the rate of 15-20 per cent annually. Together with banking services, it adds about 7 per

cent to the country’s GDP .In spite of all this growth the statistics of the penetration of

the insurance in the country is very poor. Nearly 80% of Indian populations are without

Life insurance cover and the Health insurance. This is an indicator that growth potential

for the insurance sector is immense in India. It was due to this immense growth that the

regulations were introduced in the insurance sector and in continuation “Malhotra

Committee” was constituted by the government in 1993 to examine the various aspects

of the industry. The key element of the reform process was Participation of overseas

insurance companies with 26% capital. Creating a more efficient and competitive

financial system suitable for the requirements of the economy was the main idea behind

this reform.

Since then the insurance industry has gone through many sea changes .The competition

LIC started facing from these companies were threatening to the existence of LIC. Since

the liberalization of the industry the insurance industry has never looked back and today

stand as the one of the most competitive and exploring industry in India. The entry of the

private players and the increased use of the new distribution are in the limelight today.

The use of new distribution techniques and the IT tools has increased the scope of the

industry in the longer run.

A BRIEF HISTORY

The origin of insurance is very old .The time when we were not even born; man has

sought some sort of protection from the unpredictable calamities of the nature. The basic

MPBIM 6

urge in man to secure himself against any form of risk and uncertainty led to the origin of

insurance.

The insurance came to India from UK; with the establishment of the Oriental Life

Insurance Corporation in 1818.The Indian life insurance company act 1912 was the first

statutory body that started to regulate the life insurance business in India. By 1956 about

154 Indian, 16 foreign and 75 provident firms were been established in India. Then the

central government took over these companies and as a result the LIC was formed. Since

then LIC has worked towards spreading life insurance and building a wide network

across the length and the breath of the country. After the liberalization the entrance of

foreign players has added to the competition in market.the

IMPACT OF LIBERALIZATION

The introduction of private players in the industry has added to the colors in the dull

Industry . The initiatives taken by the private players are very competitive and have given

Immense competition to the on time monopoly of the market LIC. Since the advent of the

private players in the market the industry has seen new and innovative steps taken by the

players in this sector. The new players have improved the service quality of the

Insurance. As a result LIC down the years have seen the declining phase in its career. The

market share was distributed among the private players. Though LIC still holds the 75%

of the insurance sector but the upcoming natures of these private players are enough to

give more competition to LIC in the near future. LIC market share has decreased from

95% (2002-03) to 81 %( 2004-05).The following companies has the rest of the market

share of the insurance industry

Objectives and Advantages of Life Insurance

1. Protection against risk of untimely death

Life Insurance is a product, which offers protection against risk of death. In case of

death, the full sum assured is made available under a life assurance policy, whereas

under other savings schemes, the total accumulated savings alone will be available.

MPBIM 7

2. Protection during old age

Life Insurance can also be used as a means of saving for one’s future. There are a

number of Life Insurance policies, which in addition to life cover also provide the

means of investing one’s income. The sum as per the policy will be received only

after a period of time. This amount thus provides for old age.

3. Forced Savings

Life insurance brings about forced savings. Payment of life insurance premiums is

compulsory and becomes a habit. Savings in other schemes can be easily withdrawn

and may be used for less worthy purposes. Termination of a life insurance policy by

the policyholder usually results in a substantial loss in benefits under the policy to the

policyholder. One is thus encouraged to save and keep one’s policy alive.

4. Educational requirements and charity

In certain cases, the object of insurance may be to serve as security to educational

funds in respect of loans advanced for educational purposes or to provide donations to

charitable institutions like hospitals & schools.

5. Nomination and Assignment

The Life insured can name the person or persons to whom the policy moneys would

be payable in the event of his death. The proceeds of a Life Insurance policy can be

protected against the claims of the creditors of the Life Insured by effecting a valid

assignment of the policy. The beneficiaries are fully protected from creditors except

to the extent of any interest in the policy retained by the insured.

6. Marketability and suitability for borrowing

After a period of 3 years, if the policyholder finds that he is unable to continue

payment of premiums he can surrender a policy for a cash sum. A life insurance

policy is acceptable as a security for a commercial loan.

7. Loans from the Insurance Company

A policyholder can take a loan from his insurance company against the security of his

life insurance policy provided the terms of his policy allow for such a loan. This loan

can be taken usually after a period of 3 years from commencement of the policy and

is a percentage of it’s surrender value.

MPBIM 8

8. Investment options

The unit linked products give comprehensive insurance solutions that cater to an

individual’s dual needs of earning potentially high returns as well as stay insured for

life. Thus there is an option to invest money in products that combine the best of

insurance and investment. In a volatile market conditions it is possible to secure both

as one can hedge the investments with safer investment vehicles that provide a

diversified portfolio.

8. Tax benefits

• The Indian Income Tax Act provides tax concessions to the policyholder both

on payment of premium and on the maturity amount.

• Under Section 88 , the Tax benefits on premium paid by an individual for life

insurance policies on his own life\on the life of spouse\children-minor or

major, including married daughters, can be summed as under:-

Income Tax

Section

Gross Annual Salary Tax Savings

< Rs 1.5 lakh Rs. 12,000 on investments

of Rs. 60,000

Rs 1.5 lakh- Rs. 5

lakh

Rs.10,500 on investments

of Rs. 70,000

Section 88

> Rs. 5 lakh Nil

Section 80CCC

(Pension Plans)

Across all income

slabs

Upto Rs. 3,000 saved on

investment of Rs. 10,000

Section 80D

(Critical Illness

Riders)

Across all income

slabs

Upto Rs. 3,000 saved on

Investment of Rs. 10,000.

• Under Section 10(10D), any sum received under a Life Insurance Policy

(excluding sums received under a Keyman Insurance Policy) including bonus

on such policy is fully exempt from tax(provided the premium payable does

not exceed 20% of the actual capital sum assured)

MPBIM 9

• However the above tax calculations are subject to changes as per the Finance

Act governed from time to time. The customer has to be advised that he

should consult his tax advisor on taxation issues.

9. Protection to wife and children

Under Section 6 of the Married Women’s Property Act if a married man takes a

policy of life insurance on his own life and expresses on the face of it to be for the

benefit of his wife, or of his wife and children, or any of them, then it shall be

deemed to be a trust for the benefit of his wife, or his wife and children, or any of

them, according to the interest so expressed, and shall not, so long as any object

of trust remains, be subject to the control of the husband; or to his creditors, or

form part of his estate. An insurance policy taken by a married man in the

above manner is ideal way to protect the interest of his wife and children,

even after his untimely death .

Tax Benefits of Life Insurance

The following tax benefits applicable to policyholders

Under Income Tax Act,1961

An individual or HUF can claim rebate on the insurance premium paid for self, spouse

and children (including dependent children), under section 88 of Income Tax Act.

The premiums paid towards Retirement Plan upto Rs.10,000, will qualify for deduction

from taxable income under sec. 80CCC of the Income Tax Act

Money received under a Life Insurance Policy

As per section 10(10D) of the Income Tax Act,1961, any sum received under a life

insurance policy including bonus declared or paid do not form part of taxable Income. To

put it simply, it is exempt from tax. However, monies received under keyman insurance

policy are not covered under section 10(10D).

MPBIM 10

Under Wealth Tax Act

Insurance premium paid as well as surrender value of Insurance policy do not form part

of chargeable wealth. For the same no wealth tax is attracted when the policy is in force.

On maturity of policy the amount received , if it remains in cash on March 31 of the

succeeding year, will form part of chargeable wealth.

Under Gift Tax Act

Gift Tax Act has been abolished and is no longer applicable. Accordingly, gifts are not

normally taxable. However, there are clubbing provisions in Income Tax Act(Sec 64),

which make gifts taxable in certain circumstances.

THE VARIOUS LIFE INSURERS ENTERED INDIA IN THE FOLLOWING

YEARS

Sl.No. Date of Reg. NAME OF THE COMPANY

1 23.10.2000 HDFC Standard Life Insurance Co. Ltd.

2 15.11.2000 Max New York Life Insurance Co. Ltd

3 24.11.2000 ICICI Prudential Life Insurance Co.Ltd

4 10.01.2001 OM Kotak Mahindra Life Insurance

5 31.01.2001 Birla Sun Life Insurance Co. Ltd

MPBIM 11

6 12.02.2001 Tata AIG Life Insurance Co. Ltd

7 30.03.2001 SBI Life Insurance Co.Ltd

8 02.08.2001 ING Vysya Life Insurance Co. Ltd

9 03.08.2001 Allianz Bajaj Life Insurance Co. Ltd

10 06.08.2001 MetLife India Insurance Co. Ltd

11 03.01/2002 AMP SANMAR Assurance Co. Ltd

12 14.05.2002 Aviva Life Insurance Co. Ltd

13 06.02.2004 Sahara India Insurance Co. Ltd

MARKET SHARE (%) OF THE PRIVATE INSURANCE PLAYERS IN THE

INDIA.

S.NO Company Premium Premium

market

share%

Growth rate

Up to FEB

2005

Up to FEB

2005

Up to FEB 2005

1 Bajaj Allianz 49405.12 2.86 333.50

2 ING Vysya 9684.14 .56 114.39

3 AMP Sanmar 8247.45 0.48 292.72

MPBIM 12

4 SBI Life 39603.33 2.29 240.90

5 Tata AIG 25283.08 1.46 76.96

6 HDFC Standard 33533.73 1.94 123.53

7 ICICI Prudential 115465.48 6.69 100.06

8 Birla Sunlife 48454.48 2.81 95.76

9 Aviva 14980.78 0.87 152.40

10 Kotak Mahindra 14398.02 0.83 106.85

11 Max New York 18260.76 1.06 73.61

12 Met Life 4555.62 0.26 149.18

13 Sahara Life 35.23 0.00 0.00

Private 381907.65 22.12 129.20

GRAND TOTAL 813014.01 2534287.67 7527698 26260468 100.00 100.00

MPBIM 13

MARKET SHARE OF LIC AND PVT INSURERS BASED ON POLICY

COLLECTED IN THE YEAR 2004-2005

0

MARKET SHARE BASED ON POLICY COLLECTED

LIC , 91.50%

PVT INSURERS, 8.50%

MPBIM 14

bajaj allianz13%

AMP sanmar2%

icici pru27%

Sahara0%HDFC

9% kotak

3%

Birla Sunlife9%

Max New York10%

Metlife2%

SBI life6%

ING vysya5%

Aviva 4%

Tata aig10%

MPBIM 15

bajaj allianz15%

AMP sanmar2%

icici pru29%

Sahara0%

HDFC9%

kotak7%

Birla Sunlife11%

Max New York4%

Metlife1%

SBI life9%

ING vysya5%

Aviva 3%

Tata aig5%

The Role and Functions of IRDA in the Insurance Industry

The Insurance regulation In India, Insurance regulation in India started with the

passage of the Life Insurance Companies act 1912, and provided Fund Act, 1912. The

first comprehensive legislation was introduced with the Insurance Act. 1938, which strict

state control over insurance business in the country under the supervision of the

controller of insurance. The important functions of the IRDA as per the IRDA act 1999

include the following. Licensing and regulating the insurance sector any acting as an

independent and regulatory body. Specifying requisite qualifications, code of conduct and

practical training for insurance intermediaries and agents. Protecting the interest of the

policyholders in matters concerning assigning of policy, settlement of claims etc.

MPBIM 16

Regulating investments of funds by insurance companies. Calling for information

from undertaking, conducting enquiries and investigation including audit of insurers and

other organization connected with the insurance business. Regulating maintenance of

margins of solvency of the insurer. Adjudication of disputes between insurers and

intermediaries.

Supervising the functioning of the tariff Advisory Committee. Promoting efficiency in

the conduct of insurance sector.

Insurance, apart from acting as an important financial instrument for risk cover, it

is also a major instrument for mobilization of long terms savings. The savings part of

insurance has channeled efficiently into long-term investments and would play a greater

role in funding the infrastructure projects with long gestation periods . in the liberalized

scenario , IRDA will have to play a crucial role towards meeting the Long – term

solvency of insurance companies, should also promote competition among them..

(c) Specifying requisite qualifications, code of conduct and practical training for

intermediary or insurance intermediaries and agents;

(d) Specifying the code of conduct for surveyors and loss assessors;

(e) Promoting efficiency in the conduct of insurance business;

(f) Promoting and regulating professional organizations connected with the insurance and

re-insurance business;

(g) Levying fees and other charges for carrying out the purposes of this Act;

(h) calling for information from, undertaking inspection of, conducting enquiries and

investigations including audit of the insurers, intermediaries, insurance intermediaries

and other organizations connected with the insurance business;

(I) control and regulation of the rates, advantages, terms and conditions that may be

offered by insurers in respect of general insurance business not so

Controlled and regulated by the Tariff Advisory Committee under section 64U of the

Insurance Act, 1938 (4 of 1938);

MPBIM 17

(j) Specifying the form and manner in which books of account shall be maintained and

statement of accounts shall be rendered by insurers and other insurance intermediaries;

(k) Regulating investment of funds by insurance companies;

(l) Regulating maintenance of margin of solvency;

(m) Adjudication of disputes between insurers and intermediaries or insurance

intermediaries;

(n) Supervising the functioning of the Tariff Advisory Committee;

(o) Specifying the percentage of premium income of the insurer to finance schemes for

promoting and regulating professional organizations referred to in clause (f);

(p) Specifying the percentage of life insurance business and general insurance business to

be undertaken by the insurer in the rural or social sector; and

(q) Exercising such other powers as may be prescribed

MPBIM 18

COMPANY PROFILE

MPBIM 19

Since you will be paying premiums for years to come, you don't want your insurance

company to disappear before you or your family receives the benefit. It is worth asking

how long the company has been in business, how many life insurance policies they

manage and their credit rating. In most cases, you will get a better deal from the smaller

life insurance companies, but you just need to be more careful to research them and make

sure they are stable. Bajaj Allianz is sure to one such life insurance company

Bajaj Allianz life insurance Company limited is a joint venture between two companies.

Bajaj Auto and Allianz AG.

Allianz Group's Indian life insurance joint venture has changed its name to Bajaj

Allianz Life insurance from Allianz Bajaj life insurance (Bombay), Aug 4, 2004

Allianz AG

��Worlds largest insurance company by revenue –Rs520353cr (euro96.9billion)

��World wide 2nd by gross written premiums-Rs477930cr (euro 89 billion)

��3rd largest assets under management (AUM) and largest amongst insurance

companies

��11th largest corporation in the world

��50% of globe business from life insurance, close to 60 million lives insured

globally

��Established in 1890, 110 years of insurance expertise

��More then 70 countries,173750 employees worldwide

��Insurance to almost half of the fortune 500 companies

Bajaj auto

��One of the largest 2 and 3 wheeler manufacturers in the world

��21 million + vehicles on the road across the globe

��Managing fund of over Rs5200cr

MPBIM 20

��Bajaj auto finance one of the largest companies in India

��Rs5934cr turnover and profits after tax of 732cr in 2004-05

Bajaj allianz life insurance

��The fastest growing private life insurance company in India, with a growth rate of

380%

��Have sold over 650000 policies to satisfied customers

��Is back by a network of 400 offices spanning the country

��Ranked second among private life insurance companies in India

�� Assets under management Rs936 cr

��Shareholder capital base of Rs267cr

��Product tailored to suit your needs

��Decentralized organization structure for faster response

��Wide reach to serve you better-a national wide network of 400 branches

��Specialized departments for banc assurance, corporate agency and group business

��Well networked customer care centers (CCCs) with state of art IT systems

��Highest standard of customer service and simplified claims process in the industry

��Website to provide all assistance and information on products and services, online

buying and online renewals.

��Toll-free number to answer all your queries, accessible from anywhere in the

country and a strong tele-marketing and direct marking team

��Swift and easy claim settlement process

��Accelerated growth

Vision

• To be the first choice insurer for customers.

• To be the preferred employer for staff in the insurance industry.

• To be the number one insurer for creating shareholder value

MPBIM 21

Mission

As a responsible, customer focused market leader, we will strive to understand the

insurance needs of the consumers and translate it into affordable products that deliver

value for money.

The Bajaj Allianz Difference

• Business strategy aligned to clients' needs and trends in Indian and global economy /

industry

• Internationally experienced core team, majority with local background

• Fast, decentralised decision making

• Long-term commitment to market and clients

Underwriting

Our underwriting philosophy focuses on:

• Understanding the customer's needs

• Underwriting what we understand

• Meeting the customer's requirements

• Ensuring optimal coverage at lowest cost

claimsPhilosophy

The Bajaj Allianz team follows a service that aims at taking the anxiety out of claims

processing. We pride ourselves on a friendly and open approach. We are focused towards

providing you a hassle free and speedy claims processing.

Our claims philosophy is to:

•Be flexible and settle fast

•Ensure no claim file to be seen by more than 3 people

• Check processes regularly against the global Allianz OPEX (Operational

Excellence)methodology

Sold over 1 million since inception.

MPBIM 22

Customer Orientation:

At Bajaj Allianz, our guiding principles are customer service and client satisfaction. All

our efforts are directed towards understanding the culture, social environment and

individual insurance requirements - so that we can cater to all your varied needs.

Experience And Expert Servicing Team

We are driven by a team of experienced people who understand Indian risks and are

supported by the necessary international expertise required to analyse and assess them.

Superior Technology

• In order to ensure speedy and accurate processing of your needs, we have

established world class technology, with renowned insurance software, which

networks all our offices and intermediaries

• Using the Web, policies can be issued from any office across the country for retail

products

• Unique, user friendly software developed to make the process of issue of policies

and

claims settlement simpler (e.g. online insurance of marine policy certificate)

Unique Forms of Risk Cover

• Special PA cover for Amarnath Yatris

• Housing loan cover for people, who are suddenly unemployed

• Film insurance

• Event management cover

MPBIM 23

• Sports & Entertainment Insurance Package

Risk Management – Our Expertise

Our service methodology is tried, tested and Proven the world over and involves:

• Risk identification: Inspections

• Risk analysis: Portfolio review and gap analysis

• Risk retention

• Risk Transfer: To an insurer as well as reinsurer (as required)

• Creation of need based products

• Ongoing dialogue and proactivity

COMPANY PRODUCTS

“Insurance is a contract between two parties whereby one party called

insurer undertakes the risk in exchange for a fixed amount of money on the

happening of a certain event.”

1. CASH GAIN

People needs for insurance protection will vary at different stages of life.

Sometimes, they may need to release a part of their savings from insurance commitments

and utilize it for other pressing needs. The Bajaj Allianz Cashgain is ideal for those who

want to reap and enjoy the benefits of their life insurance policy at regular intervals

during their lifetime.

Bajaj Allianz Cashgain is a specially designed plan that offers a host of additional

benefits you may choose to develop a sound financial portfolio for your family. Among

the many unique benefits, the most significant is the Family Income Benefit (FIB) that

sustains the family by compensating the loss of regular income due to death or permanent

disability.

Available as:

MPBIM 24

• Bajaj Allianz Cashgain Economy: The basic package

• Bajaj Allianz Cashgain Gold: With double protection

• Bajaj Allianz Cashgain Diamond: With triple protection

• Bajaj Allianz Cashgain Platinum: With quadruple protection

A Uniform Life Cover

Besides giving you regular Cash Benefits, this plan takes care of your life

insurance needs also. On death during the term of policy, the following would be paid

irrespective of the Cash Benefits already paid:

• Bajaj Allianz Cashgain Economy: Sum Assured + Bonuses

• Bajaj Allianz Cashgain Gold: Double Sum Assured + Bonuses

• Bajaj Allianz Cashgain Diamond: Triple Sum Assured + Bonuses

• Bajaj Allianz Cashgain Platinum: Quadruple Sum Assured + Bonuses

Choice of Terms

Keeping your convenience in mind, we offer you the widest range of terms: 15,

20, 25 and 30 years.

Additional Protection for you and your family

You have the option to add the following additional benefits, providing total

protection against uncertainties.

Family Income Benefit (FIB) - The Ultimate Protection - For Your Loved Ones

You can select the unique Family Income Benefit from Bajaj Allianz that ensures

total financial protection for your loved ones. In case of death or accidental total

permanent disability, a guaranteed monthly income of 1% of the sum assured (12% per

MPBIM 25

annum) is paid till the end of the policy term or at least for a period of 10 years,

whichever is higher. Moreover, all future premiums are waived.

Comprehensive Accident Protection

This benefit provides comprehensive cover in case of an accident. It comprises of:

Accidental Death Benefit

Accidents are always sudden and sometimes fatal. You can't lessen the emotional

shock, but you can certainly soften the financial one. Bajaj Allianz Accidental Death

Benefit gives the loved ones something to start with after the permanent loss of income

by paying an amount equal to the Sum Assured..

Accidental Permanent Total/Partial Disability Benefit

Accidents are unpredictable, and so are the consequences. They may lead to a

disability - partial or total. This Benefit provides a financial cushion against such

misfortunes. You will get 50% of the Sum Assured in case of partial disability and 100%

in case of total disability. (Subject to a maximum of Rs. 25,00,000/- for partial and Rs.

50,00,000/- for total disability under all policies with Bajaj Allianz taken together).

Waiver of Premium Benefit

An accident may lead to permanent total disability, limiting one’s ability to earn.

Bajaj Allianz Waiver of Premium benefit is a helping hand when one needs it most. It

waives off all future premiums while keeping the valuable life insurance cover alive, thus

enabling you to live up to your commitments.

Critical Illness Benefit (CI)

Some illnesses are critical. They not only alter one’s life's pattern but also result

in a financial drain. Bajaj Allianz Critical Illness Benefit softens the impact on the family

by paying out the Critical Illness Benefit under the plan immediately, while other policy

MPBIM 26

benefits continue (excluding Hospital Cash Benefit). We cover 11 critical illnesses. You

have the flexibility of choosing Critical Illness cover up to the basic Sum Assured

selected by you (Minimum Rs.50, 000).

Hospital Cash Benefit (HC)

The worry of settling hospital bills (room charges) adds to the trauma of

hospitalization. Bajaj Allianz Hospital Cash Benefit reduces this financial burden and

helps recovery with peace of mind.

Flexibility in Coverage

At Bajaj Allianz, we believe in offering benefits and not just products. We realize

that you are unique and your needs for insurance vary with time. We therefore offer you

the flexibility of inclusion of coverage or exclusion of coverage at each policy

anniversary, subject to conditions relating to such inclusions and exclusion.

You have the flexibility to change your package and move to a package that

provides lower protection at each policy anniversary (premiums would be adjusted

accordingly). “Comprehensive Accident Protection” can be included and excluded at

each policy anniversary. Family Income Benefit, Critical Illness Benefit and Hospital

Cash Benefit can be taken at inception only. FIB, CI & HC can be reduced or excluded

subsequently at any policy anniversary. Once reduced or excluded, they cannot be

increased or included subsequently.

Increase in risk coverage

Every added responsibility in your life calls for increase in your risk cover. We

provide you the option to increase coverage upto 50% of the basic Sum Assured on each

of the following happy moments in life.

• Marriage

• The birth of first child

MPBIM 27

• The birth of second child

This additional coverage is not subject to underwriting. The option should be

exercised within 90 days of the occurrence of the said event.

2. SAVE CARE ECONOMY

As the breadwinner of the family you shoulder several responsibilities. Your

spouse's welfare, your children's education, buying a house or a car - you have a lot to

think about, everyday. Bajaj Allianz, believe that the security and growth of your hard

earned money should not add to these.

Which is why Bajaj Allianz has created the “Bajaj Allianz Save Care Economy -

Single Premium”-the 10-year Single Premium version of our popular product “Save Care

Economy”? It is an ideal plan for a one-time lump sum investment that provides for

savings with high risk-cover.

The "Bajaj Allianz Save Care Economy - SP", is a Single Premium investment

plan for 10 years that also participates in the profits of the company. The highlights of

this plan are:

Minimum Guaranteed Return up to 3.54% (depending on age at entry).

The Minimum Guaranteed Amount (Sum Assured) would grow further by way of

compounded annual bonuses.

A high risk-cover of up to 142% (depending on age at entry) of the sum invested

from the beginning of the policy term as a financial safety net to provide for

unpredictable adversities.

Eligible for Tax Benefits under Section 88 and Section 10 (10 D) of the Income

Tax Act.

At Maturity you will receive the Sum Assured (Minimum Guaranteed Amount)

along with the accrued bonuses.

MPBIM 28

Death Benefit: In case of death during the term of the plan, the nominee will be

paid the Sum Assured (Minimum Guaranteed Amount) plus accrued bonuses. In case of

death of a minor (below age 7), the death benefit will be the surrender value or Single

Premium whichever is higher.

3. INVESTGAIN

It takes only a moment to make promises and a lifetime to keep them. Keeping

promises made to your loved ones is not just a responsibility, but a commitment that you

have to live up to. When you promise to see your family through thick and thin you need

to make sure that you have planned for all the eventualities that may befall on them. You

need to be prepared that even if there ever is an instance that you are not there with them

you have saved enough to see them through their entire life. We understand this need,

which is why we have developed Bajaj Allianz’s InvestGain, the plan that helps you in

saying "My family, May you always be happy!”

Available as:

• Bajaj Allianz Investgain Economy: The basic package

• Bajaj Allianz Investgain Gold: With double protection

• Bajaj Allianz Investgain Diamond: With triple protection

• Bajaj Allianz Investgain Platinum: With quadruple protection All these

packages participate in the profits of the company by way of bonuses, and therefore,

grow with time

Family income benefit

You can select the unique Family Income Benefit from Bajaj Allianz that ensures

total financial protection for your loved ones. In case of death or accidental total

permanent disability, a guaranteed monthly income of 1% of the sum assured (12% per

annum) is paid till the end of the policy term or at least for a period of 10 years,

whichever is higher. Moreover, all future premiums are waived.

MPBIM 29

Popular Products: Endowment Assurance (Participating) and Money Back

(Participating). More than 80% of the life insurance business is from these products.

4. UNIT LINKED INSURANCE POLICY

The thumb rule for buying insurance is that your insurance needs are minimal in

your early earning years, increase with added responsibilities (Marriage, children, loans

etc.) and taper off by the time you retire. It is difficult to find a single insurance plan that

can take care of all your changing requirements in life – additional protection, more

money to invest, sudden requirement of cash or a steady post-retirement income.

With Bajaj Allianz UnitGain, you can invest in one life insurance plan that can

take care of all your changing requirements throughout your life. This plan has been

designed to provide you with maximum flexibility, so that you do not have to worry

about your changing needs.

Bajaj Allianz UnitGain offers the unique option of combining the protection of

life insurance with the attractive prospects of investing in securities. You can choose the

investment funds you want to invest your money, providing you with an opportunity to

have a direct stake in the performance of the financial markets. You also benefit from

attractive tax advantages and can protect your loved ones against unfortunate events.

• Unit Gain Plus : A Unit Linked Plan

Bajaj Allianz Unit Gain Plus offers the unique option of combining the

protection of life insurance with the attractive prospects of investing in

securities. Customers have the choice of 6 investment funds with flexible

investment management; they can change funds at any time. Customers also

benefit from attractive tax advantages and unmatched flexibility -to match

their changing needs. And the advantage of low fund management & fund

administration costs.

MPBIM 30

• Unit Gain Plus SP : A Single Premium Unit Linked Plan

This plan enables the customers to protect their loved ones, while making

their money grow faster with the advantage of low fund management & fund

administration costs. It provides the customers the option of allocating 98% of

the single premium to purchase units in any/all of the 6 funds available with

company

• Unit Gain : A Unit Linked Plan

This amazingly flexible unit linked life insurance plan provides the

customers the opportunity to participate in market linked returns while

enjoying the valuable benefits of life insurance

• Unit Gain SP : A Single Premium Unit Linked Plan

This plan enables the customers to protect their loved ones, while making

their money grow faster. It provides them the option of allocating 100% of the

Single Premium to purchase units in any/all of the 6 funds available with

company.

• Lifelong Gain Plan : Unit Linked Whole Life Plan

This is the perfect plan to take care of ongoing and future family expenses like

debts, expenses on children, living expenses, etc. It can also take care of unforeseen

expenses like accidents, illnesses, hospitalization, etc. and provides customers family

with a safety net. It provides whole life protection with only 10 or 15 years of

contributions. Guaranteed Survival Benefits @3% are available under this policy.

Guaranteed Survival Benefits that pays 3% of the Sum Assured every year after the

premium payments are over

SUITABILITY

MPBIM 31

This policy is a long-term market linked total protection plan. The plans offer

protections for life at the same time allows the policyholder to get market linked

returns. It is a single product combining the benefits of both an investment product and

insurance plan. This apart, the product offers a lot of flexibility.

DIFFERENT FUNDS

EQUITY INDEX

The investment objective of this fund is to provide capital appreciation

through investment in equities. The plan is expected to match the returns given

by NIFTY Index of the National Stock Exchange. This fund will invest at least

85% in equities and maximum 15% in debt and cash.

EQUITY PLUS FUND

The investment objective of this fund is to provide capital appreciation

through investment in selected equity stocks that have the potential for high

capital appreciation. The fund will invest at least 85% in equities and maximum

15% in debt and cash

DEBT PLUS FUND

The objective of this fund is to provide accumulation of income through

investment in high quality fixed income securities like G-securities and corporate

debt rates AA and above. This fund is invested fully in debt instrument and

money market instrument.

BALANCE PLUS FUND

This fund is a fund of funds. The objective of this fund is to provide a

balanced investment between long-term capital appreciation and current income

through investment in the units of our equity and debt funds. The balanced fund

will invest 30% to 50% in the equity index fund and 50% to 70% debt fund.

MPBIM 32

CASH PLUS FUND

The investment objective of this plan is to have a fund that guarantees

invested capital through investments in liquid money market and short term

instruments like commercial papers, certificate of deposits, money market mutual

funds, bank F.D’s etc. The price of unit in this fund is gu aranteed not to go down.

100% of this fund will be invested in money market instruments. The price of the

units in this fund is guaranteed never to go down.

FOCUSED SALES NETWORK

Bajaj Allianz Life Insurance Company

Banc assurance Group and Alternate Channel

Agency Channel

Branches

Satellite Satellite

Standard Chartered Bank

Syndicate Bank

Centurion Bank

Cosmos Bank

Jankalyan Sahakari Bank

Jijamata Sahakari Co-op Bank

Satellite

Group Employee Benefit

Corporate Agency

Franchisee

Brokers

MPBIM 33

The overall premium target is broken down as follows by distribution channel:

FP + SP ANNUAL(crores)

AGENCY 1,827

BANCASSURANCE 650

ALTERNATE CHANNELS 523

RENEWALS 500

TOTAL 3500

AGENCY CHANNEL:

ÖÖ��Currently the company has some 300 offices made up of 68 branches and

about 239 satellite offices.

ÖÖ��The company will continue with the same hub and spoke structure, but will

increase the number of branches to 100 and satellites to 300.

ÖÖ��The number of STMs a branch or a satellite can have will be between 2 and

8.

ÖÖ��Underwriting and processing of business will continue at the branch level.

ÖÖ��The branches will continue to support the bancassurance and alternate

channels for underwriting and processing of business, as well as offer the

office infrastructure for the other channels staff to operate from.

BANCASSURANCE:

The company has some 6 bank tie ups these will be managed by the bancassurance

team.following are the banks with which the company has tied up:

1. Syndicate bank.

2. Centurion bank.

3. Standard chartered bank.

4. indusland ind bank.

MPBIM 34

ALTERANATE CHANNELS:

The focus will be corporate agency, franchise, brokers, worksite marketing, NRI

business, HNI business, group business and rural

social business

ORGANISATION STRUCTURE OF SALES AGENCY

MPBIM 35

BANK-ASSURANCE/ALTERNATE CHANNEL

CEO

CFO

HOD SALES

ZONAL MANAGER

REGIONAL MANAGER

SENIOR BRANCH MANAGER

BRANCH MANAGER

ASSISTANT BRANCH MANAGER

SALES MANAGER

CONSULTANTS. / AGENTS

MPBIM 36

CEO

CFO

HOD SALES

AREA MANAGER

DEPUTY MANAGER

FINANCIAL SERVICE\PLANNING CONSULTANTS

MPBIM 37

FINANCIAL HIGHLIGHTS YEAR 2004-2005

Particulars 2004-05

Rs. Million

2003-04

Rs.

Million

2002-03

Rs. Million

2001-02

(11 Months)*

Rs. Million

Gross Written Premium 8,560.7 4,798 2,998 1,420

Net Written Premium 4,792.9 2,864 1,808 841

Net Earned Premium 3,709.2 2,306 1,541 98

Net Incurred Claims (2,263.3) (1,542) (1,072) (127)

Net Commissions 419.4 231 155 128

Management Expenses (1,455.9) (984) (689) (370)

Underwriting Results 409.4 11 (33) (271)

Income from Investments 388.8 285 207 143

Others 28.6 22 (3) (5)

Profit Before Tax 769.6 318 171 (133)

Provision for Tax (298.7) (101) (75) 37

Profit After Tax 470.9 217 96 (96)

Claim's Ratio 61% 67% 70% 130%

Commission Ratio -11% -10% -10% -130%

Management Expenses Ratio 40% 42% 43% 376%

Combined Ratio 90% 99% 102% 376%

Return on Equity 34% 20% 9% -9%

Shareholder's Equity 1,824.1 1,380 1,095 997

Assets Under Management 5835.5 3,486 2,709 1,688

Number of Employees 924 480 306 141

MPBIM 38

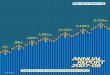

GROWTH OF BAJAJ ALLIANZ LIFE INSURANCE CO

Fiscal year No of policies sold in FY GWP in FY

2001-2002 (6months) 21376 Rs 7cr

2002-2003 115965 Rs69cr

2003-2004 186443 Rs221cr

2004-2005 288189 Rs1002cr

0

50000

100000

150000

200000

250000

300000

2001-2002(6months)

2003-2004

policies sold in Rs

MPBIM 39

0

200

400

600

800

1000

1200

2001-2002(6months)

2002-2003 2003-2004 2004-2005

GWP in cr

¾�Assets under management Rs936 cr

¾�Shareholder capital base of Rs267cr

¾�Product tailored to suit your needs

¾�Decentralized organization structure for faster response

¾�Wide reach to serve you better-a national wide network of 400 branches

¾�Specialized departments for banc assurance, corporate agency and group business

¾�Well networked customer care centers (CCCs) with state of art IT systems

¾�Highest standard of customer service and simplified claims process in the industry

¾�Website to provide all assistance and information on products and services, online

buying and online renewals.

¾�Toll-free number to answer all your queries, accessible from anywhere in the

country and a strong tele-marketing and direct marking team

¾�Swift and easy claim settlement process

LIFE TRACK OF BAJAJ ALLIANZ LIFE INSURANCE COMPANY LTD

Objectives Of The Company For The Year 2004-05:

• to be one of the top 3 private life insurers in terms of gross premium and achieve

a premium target of more than Rs 750 crs.

MPBIM 40

• To be one of the top 2 companies in terms of profitability.

• To be more customer focused and reduce complexity.

The Company’s Major Achievements In The Last Financial Year Are:

• Number 2 amongst the private insurers in terms of new business premium, up to

February 2005.

• Gross premium achieved over Rs 1000crs GWP

• 300 + offices, 2700 + STM’s and 45000 + ICs

• 190 MDRTs , 9COTs

• 6 bancassurance tieups

• intermediaries including franchisees and corporate agents over 400.

• A full basket of products approved.

The Company’s Objectives For The Year 2005-06

• To be one of the top 2 private life insurers in terms of premium and profitability

• Achieve a minimum premium target of Rs 3500 crs(with less than 30% single

premium)each office to look at growing the business from 2004-05levels by

350% to 400%

• Improve customer service at all levels.

• Conduct business in an ethical manner.

THE KEY INITIATIVES THE COMPANY PLANS TO TAKE IN THIS QUARTER

INCLUDE THE FOLLOWING:

¬¬��Increase branch numbers to 100 and satellite offices to 300.

¬¬��Increase STM strength to3500 and IC strength to 50000

¬¬��Products for filing and approval women’s plan, health, tactful and revised ULIP

¬¬��Metro city strategy- increase number of branches in metro cities.

¬¬��Target 5 banks/coop banks for tie ups.

MPBIM 41

¬¬��Increase franchisee and corporate agents tie up.

¬¬��Group and broker team to be strengthened.

¬¬��Tactful team to be setup.

¬¬��NRI and HNI teams to be set up to focus on these areas.

¬¬��Online system to incorporate renewals, switches and withdrawals.

¬¬��Finalization of accounts for 2004-2005

¬¬��Recruitment of training head and trainers for branches

MPBIM 42

THE VARIOUS RESPONSIBILITIES AND THE WORK CARRIED OUT IN THE

BANGALORE BRANCH OFFICE

1. Bangalore is the area office.

2. There are different channels namely bancassurance, retail banking, agents and

agency managers headed by respective managers.

3. Primary responsibility of all the channels is to meet the targets set by the head

office.

4. Policy logins are done here.

5. Underwriting and medical checkups are done here.

6. After the preliminary verification policies are sent to head office for issuance.

7. Training is also held for the newly appointed employees.

8. Certificate for selling insurance is given once employees clear the IRDA exam.

MPBIM 43

MICROSCOPIC STUDY

MPBIM 44

PROJECT TITLE:

“A COMPARATIVE STUDY OF INSURANCE PRODUCTS OF BAJAJ

ALLIANZ LIFE INSURANCE COMPANY WITH COMPITITORS”

PRODUCTS FOR COMPARISON

• UNIT LINKED PLAN

• CHILDREN PLAN

• ENDOWMENT PLAN

COMPANIES FOR THE COMPARISON:

MPBIM 45

• BAJAJ ALLIANZ LIFE INSURANCE COMPANY

• ICICI PRUDENTIAL

• LIFE INSURANCE CORPORATION (LIC)

UNIT LINKED PLANS:

Most insurers in the year 2004 have started offering at least a few unit-linked plans. Unit-

linked life insurance products are those where the benefits are expressed in terms of

number of units and unit price. They can be viewed as a combination of insurance and

mutual funds.

The number of units that a customer would get would depend on the unit price when he

pays his premium. The daily unit price is based on the market value of the underlying

assets (equities, bonds, government securities, et cetera) and computed from the net asset

value.

The advantage of unit-linked plans is that they are simple, clear, and easy to understand.

Being transparent the policyholder gets the entire upside on the performance of his fund.

Besides all the advantages they offer to the customers, unit-linked plans also lead to an

efficient utilization of capital.

Unit-linked products are exempted from tax and they provide life insurance. Investors

welcome these products as they provide capital appreciation even as the yields on

government securities have fallen below 6 per cent, which has made the insurers slash

payouts.

According to the IRDA, a company offering unit-linked plans must give the investor an

option to choose among debt, balanced and equity funds. If you opt for a unit-linked

endowment policy, you can choose to invest your premiums in debt, balanced or equity

plans.

If you choose a debt plan, the majority of your premiums will get invested in debt

securities like gilts and bonds. If you choose equity, then a major portion of your

MPBIM 46

premiums will be invested in the equity market. The plan you choose would depend on

your risk profile and your investment need.

The ideal time to buy a unit-linked plan is when one can expect long-term growth ahead.

This is especially so if one also believes that current market values (stock valuations) are

relatively low.

So if you are opting for a plan that invests primarily in equity, the buzzing market could

lead to windfall returns. However, should the buzz die down, investors could be left

stung.

If one invests in a unit-linked pension plan early on, say when one is 25, one can afford to

take the risk associated with equities, at least in the plan's initial stages. However, as one

approaches retirement the quantum of returns should be subordinated to capital

preservation. At this stage, investing in a plan that has an equity tilt may not be a good

idea.

Considering that unit-linked plans are relatively new launches, their short history does

not permit an assessment of how they will perform in different phases of the stock

market. Even if one views insurance as a long-term commitment, investments based on

performance over such a short time span may not be appropriate.

Particulars/

Name Of The

Company

ICICI Prudential Bajaj Allianz Life

Insurance Co,Ltd

LIC

Name of the

policy

LIFE TIME 11 UNIT GAIN

PLUS

BIMA PLUS

Min age of

entry

0 0 12

Max age of

entry

60 60 55

Min premium

yearly

18,000 15,000

MPBIM 47

yearly

Term Choice rests with the

customer with a min

premium payment for 10

yrs

Choice rests with

the customer with

a min premium

payment for 3 yrs

10yrs

Sum assured Min SA is Rs 1,00,000.

Max SA is Rs 50,00,000.

Min SA is 5 times

of the premium.

Max SA is as per

the age ie 125

times of the

premium . SA can

be increased or

decreased.

Maximum up to

2lakhs

Maturity

benefit

Any time after 4th yrs

contribution 100% of the

surrender value is

avaliable

Anytime after

payment of 3 full

yrs premiums,

can withdraw

100% of the fund

value or the SA

whichever is

higher.

Fund value of

the units along

with maturity

bonus at 5% of

the SA

Death benefit Higher of SA or value of

units. The value of units

will be treated as the

death benefit if the life

assured is less than 7 yrs

of age or more than 70 yrs

of age.

Higher of SA or

value of units.

The value of units

will be treated as

death benefit if

the life assured is

less than 7 years

of age and more

than 70 yrs of age.

Death benefit

during the first

6 months-30%

of the SA +value

of units, next

6months-60% of

the SA+ value of

units .death

after 1st year –

SA +value of

units. Death

during the 10th

yr-105%of the

SA+ value of

MPBIM 48

units. Death

during the 10th

yr-105%of the

SA+ value of

units

Withdrawal

benefit

Partial withdrawal is

available from the 3rd

year onwards. 100%

surrender value is

available after 4th yrs

contribution.

Partial or

complete

withdrawal is

available after 3rd

yr contribution.

Withdrawal

allowed after 1

year.

Flexibility to

increase or

decrease the

premium

The max decrease in

premiums can be upto

20%of the initial

premium chosen at the

time of the inception of

the policy. There is no

limit for increasing the

premium. This can be

done with or without

increase in the SA

Flexibility to raise

the premium is

available with or

without increase

in the SA. The SA

can be even

decreased. The

premiums cannot

be reduced.

Not avaliable

Investment

options

Maximiser, Balancer,

protector & preserver.

Equity Index,

Equity Plus, Debt

Plus, Balanced

Plus, Cash Plus,

Mid cap

Balanced,

Secured &

Risk

Increase/

decrease of

death benefit

Available. Any increase of

SA is subjected to

underwriting

SA can be

increased without

any medical test

every 3rd year

upto 4 times. The

increase would be

25% of the

original SA or Rs

1, 00,000 which

Not available

MPBIM 49

increase would be

25% of the

original SA or Rs

1, 00,000 which

ever is lower. SA

can be decreased

at any time.

Top ups Available. Minimum top

up amount is Rs 10000 in

multiples of 500.

Available.

Minimum top up

amount is 5000

Available

Switches 4 free switches per year,

with a minimum switch

amount being Rs

10000.all other switches

will be charged Rs100 per

switch.

3 free switches

every policy year.

Subsequent

switches would be

charged @1% of

the switch or Rs

100 whichever is

higher.

No free

switches. Cost

of switching 2%

of the fund

value.

Automatic

cover

continuance

Available after the 1st 3

yrs premiums have been

paid. Can be availed upto

a max of 2 yrs at a time in

the 1st 10 yr of the policy.

After the 10 yrs of the

policy the customer can

avail the cover

continuance without any

limits.

Premium holiday

or the cover

continues after

the payment 3 full

years premium.

the cover

continues till the

age of 70

Not avaliable

Charges

Initial charges

% Of premium allocation.

% Of premium

allocation.

MPBIM 50

18,000-35,999:

1st yr-81%; 2nd to5th yr-

96%; 6th to 10th yr-98%;

11th yr onwards-99%.

36,000-99,999:

1st yr-83%; 2nd to 5th yr-

96%; 6th to 10th yr-98%;

11th yr onwards-99%.

1,00,000-4,99,999:

1st yr-85%; 2nd to 5th yr-

96%; 6th to 10th yr-98%;

11th yr onwards-99%.

5,00,000++:

1st yr-88%; 2nd to 5th yr-

96%; 6th to 10th yr-98%;

11th yr onwards-99%.

allocation.

1st year -76%,

2nd year-97%,

3rd year-99%,

4th year

onwards100%

allocation is

made.

Allocation for top

ups is 100%

Admin charges Admin charges of Rs

60/month

Annual admin

charges of Rs 20

per

month,escalating

at 5%per annum

at the end of each

financial year.

This will be 1%

of the Fund per

annum, charged

on a weekly

basis

Riders Accident and disability

rider

Critical illness.

Major surgical assistance

benefit rider.

Accidental death

benefit.

Accidental

permanent

total/partial

disability.

Critical illness.

Inbuilt

accidental

benefit.

MPBIM 51

Hospital cash

benefit

Surrender value Acquires a surrender

value after 3 complete

years of the policy

provided 1st three

premium are been paid.

The surrender value is

100% of the investments.

Acquires a

surrender value

after 3 complete

years of the policy

provided 1st three

premium are been

paid. The

surrender value is

100% of the

investments.

Additional

allocation of

units

Declared as % of unit

value. Paid at the end of

4th, 8th &12th policy year.

The allocation of units

would be only made if the

annual contribution till

that date were made in

total.

<=75,000-5,00,000:0.15 %

75,001-5,00,000:0.2%

5,00,001-10,00,000:0.25%

10,00,001-50,00,000:0.30

50,00,001&above:0.35%

Not available Not available

MPBIM 52

ANALYSIS

From the above table it is very clear that the policies of the companies are

almost similar and it shows only minor differences between them making the product

more attractive from the customer’s viewpoint.

For Bajaj Allianz and ICICI the minimum age of entry is zero but in the case

of LIC ,policy starts only at the age of 18.hence LIC have to concentrate another

product for targeting the zero to 18 age group where as Bajaj and ICICI can cover

these groups with this policy. Naturally customer base for unit gain and unit gain plus

of Bajaj and life time of ICICI will be more compared to the LIC’s Bima plus.

The minimum premium when compared, ICICI has the highest premium, bajaj

allianz with Rs 15,ooo which cannot be affored by every one.

The minimum SA provided by all the companies is 5 times. But in case of

maximum sum assured, Bajaj Allianz is leading with 125 times coverage of annual

MPBIM 53

premium. On the other side ICICI is assuring only 50 times so we can predict that

Bajaj is giving more value to a person’s life. Bajaj allianz and ICICI pru provide

facility to increase or decrease the SA with or without increase in premium,but this

facility is not available in LIC.

The customer has to pay the premium for the minimum period of 3 yrs in unit

gain plus. Hence the premium holiday can be extended till there are enough funds in

the policy to cover the risk of the policyholder. Where as in lifetime 2, the

policyholder has to pay premium for the first 3 years and can take premium holiday up

2 years then he has to continue paying the premium till the 10th year of the policy.

Hence unit gain plus is more beneficial to the customer than life time2.because the fear

of lapsation of the policy to the customer is reduced to a greater extent.

Customers can switch their money between funds according the market

situations. In this case ICICI is giving a more switches than bajaj and LIC. The

switching charges of LIC is higher than other 2 companies with no free switches.

The following table shows the fund allocations of different policies in different

years.

From the above table we can predict that for a investor of less than 5 years unit

gain plus is much better. For a long-term investment it is better to invest in Unit gain

why because after the 3 rd year it will invest 100 % premium to the funds.

All the policies are providing tax benefits to its customers. It is a main

advantage to the investors by comparing with mutual funds and other investment

year Unit gain plus Unit gain Life time

1st year 76% 30% 80%

2nd year 97% 98% 92.5%

3rd year 97% 99% 96%

4th year 97% 100% 96%

5th year onwards 97% 100% 96%

MPBIM 54

options. The tax benefits are given according to the section 10(10) D of Income Tax

Act and section 88.

�Unit-linked life insurance products are those where the benefits are expressed in terms

of number of units and unit price. They can be viewed as a combination of insurance and

mutual funds.

�7KH� DGYDQWDJH� RI� XQLW -linked plans is that they are simple, clear, and easy to

understand.

�7UDQVSDUHQF\�%HLQJ� WUDQVSDUHQW� WKH� SROLF\KROGHU� JHWV� WKH� HQWLUH� XSVLGH� RQ� WKH�performance of his fund.

�,QYHVWRUV�ZHOFRPH� WKHVH�SURGXFWV� DV� WKH\�SURYLGH�FDSLWDO�DSSUHFLDWLRQ�HYHQ�DV� WKH�yields on government securities have fallen below 6 per cent, which has made the

insurers slash payouts.

�7KH�LGHDO�WLPH�WR�EX\�D�XQLW -linked plan is when one can expect long-term growth

ahead. This is especially so if one also believes that current market values (stock

valuations) are relatively low.

�/LTXLGLW\��)OH[LELOLW\�

�The inherent strengths of ULIP make it adaptable to any and every other product

offering from the competition. The product is ‘all-in-one’ and can tackle every customer

need. The rider offerings namely Term, Critical Illness, Waiver of Premium and

Accidental Death & Dismemberment rider add to the attractiveness of the product, which

can provide various permutations and combinations.

�

MPBIM 55

CHILDREN PLANS:

Particulars\name of

the company

Bajaj Allianz Life Insurance, Co. Ltd ICICI Prudential LIC

Name of the

product

Child gain 21 or 24 Smart kid Komal jeevan

Minimum Term: 5 10 8

Maximum term 18 25 18

Minimum age of

entry(child)

0 0 0

Maximum age of

entry(child)

13 12 10

Max age of child at

maturity

21 or 24 22yrs to 25yrs 26

Minimum age of

entry(parent)

20 20yrs

MPBIM 56

entry(parent)

Maximum age of

entry(parent)

50 60yrs

Min sum assured Rs 1,00,000 Rs 1,00,000 1,00,000

Max sum assured Rs 50,00,000 Rs 30,00,000 25,00,000

Min premium

payment p.a

Rs 5,000 Rs 8,400 Policy will be issued only in

multiples of Rs.25, 000/-.

Death benefit 1. Future premium waived.

2. Family income benefit.

3. Guaranteed payouts.

4. Additional SA paid at the age of 21

or 24(as opted) of the child as “Start

Of Life Benefit” in case of Child gain

21 Plus and Child gain 24 Plus.

Sum assured +waiver of

premium+ periodic benefits

continue as it is

Sum Assured + Guaranteed

Additions + Loyalty Addition

if any

Survival benefit A guaranteed % of SA returned at

various ages and the vested bonus

along with the terminal bonus if any

will be given at the time of first cash

payout.

A guaranteed % of SA

returned at various terms and

the vested bonus if any will be

given at the time of first cash

payout.

SA + Guaranteed additions +

Loyalty Additions

Riders 1. Premium waiver benefit.

2. Family income benefit.

1. Accidental and disability

benefit.

2. Accident benefit rider.

3. Income benefit rider.

1. Premium waiver benefit.

2. Family benefit.

Additional benefits Start of life Rider(available in child

gain 21 plus & child gain 24 plus)

The policy holder can choose

between the 2 cash flow

payments or the periodic

benefits .

Cash flow intervals CHILD GAIN 21 & CHILD GAIN21

PLUS:

Policy anniversary following

completion of age

PERIODIC BENEFIT-1

T-7 : 20% OF SA

T-5 : 25% OF SA

T-2 : 25% OF SA

Age of the

child

MPBIM 57

completion of age

Policy

Term: 8-

21 years

Guarante

ed Payout

Policy Term:

8-21 years

Payout if

interest rates

are 7% at

the

beginning of

the payouts

18 20% +

Bonus*

20% +

Bonus*

19 25% 25%

20 25% 25%

21 35% 43%**

Total

payout

105% +

Bonus*

105% +

Bonus*

T : 30% OF SA+

Guaranteed additions @ 3.5%

compounded annually (for

first 4 years) + VB

PERIODIC BENEFIT-2

T-4 : 25% OF SA

T-3 : 20% OF SA

T-2 : 20% OF SA

T-1 : 20% OF SA

T : 20% OF SA+

Guaranteed additions @ 3.5%

compounded annually (for

first 4 years) + VB

child

18

20

22

24

26

CHILD GAIN 24 & CHILD GAIN 24

PLUS:

Policy anniversary following

completion of age

Policy

Term: 8-

21 years

Guarante

ed Payout

Policy

Term: 8-21

years

Payout if

interest

rates are

7% at the

beginning

of the

payouts

MPBIM 58

of the

payouts

18 20% +

Bonus*

25% +

Bonus*

20 25% 25%

22 25% 25%

24 35% 40%

Total

payout

105% +

Bonus*

115% +

Bonus*

Rebate Large sum assured discount:

Less than 2,00,000 : nil

2,00,000-4,99,999 :Re 1 per

1000

5,00,000 and above: Rs 2 per

1000

For yearly mode:2%of

premium

For half yearly mode:1%of

premium

Quarterly -No rebate

Sum Assured Rebates:

Sum Assured greater than or

equal to Rs.200000/- : Rs.1.00

per thousand Sum Assured

MPBIM 59

MPBIM 60

ANALYSIS

From the above comparison it can be found that,

1.The minimum payment term in Child gain is the least as

compared to that of Smart kid and Komal Jeevan. Because the

maximum age of entry in child gain is higher ie 13 yrs.

2. The minium SA for all the three products is the same but the

maximum SA is highest in case of child gain which inturn

benefits the customer the most.

3. The minimum premium is least in case of child gain, which

makes the policy more affordable by the customer.

4. All the products have almost same riders but the product Child

Gain plus has another benefit called “start of life” which means

the child is given another SA in case of death of the parents so

that the child can leads its life without many hurdles.

5. The total payout at maturity of the plan in case of Chid Gain and

smart kid is almost the same ie 105% but in case of Komal

Jeevan the payout at maturity is 100%

MPBIM 61

ENDOWMENT PLAN:

Particulars\name

of the company

Bajaj Allianz Life

Insurance, Co. Ltd

ICICI Prudential LIC

Name of the policy Invest gain Save N Protect Endowment

assurance plan(with

profits)

Minimum term 5 10 5

Maximum term 40 30 55

Min age at entry 0 0 12

Max age at entry 65 60 65

Max age at expiry 70 70 75

Min sum assured 50,000 50,000 20,000

Max sum assured No limit 1,00,00,000 No limit

Min premium 5,000 yearly 6,000yearly

Death benefit Sum assured +

bonuses

SA+GB+VG SA+VB

Maturity benefit Sum assured +

bonuses

SA+GB+VG SA+ VB+ final

additional bonus

Rider benefit • Family income

benefit.

• Comprehensive

accidental.

Protection.

• Accidental

death benefit.

• Accidental

permanent

total/ partial

disability

benefit.

• Accident&

disability

benefit

• Critical

illness

• Major

surgical

assistance

• Disability

benefit.

• Accident

benefit

• Waiver of

premium

benefit.

MPBIM 62

permanent

total/ partial

disability

benefit.

• Waiver of

premium

benefit.

• Critical illness

benefit.

• Hospital cash

benefit.

• Accident

rider

benefit

Rebate For every Rs 10,000

SA above Rs 50,000

For yearly:3%

Half year:1.5%

SA 25000 to 49000: 1

SA 50000 & above:2

Loan Can avail loan upto

90% of the surrender

value.

Can avail loan

upto 90% of the

surrender value.

No loans granted

Surrender After 3 full policy year After 3 full policy

year

After 3 full policy

year

Additional

features

Flexibility to change

the packages at each

policy anniversary.

Addl risk cover of

50% of SA on

marriage, birth of 1st

child & birth of 2nd

child.

Extra insurance

cover for 5 years

after maturity of

the policy for 50%

of the sum

assured.

Premium

discounts for

females equal to 2

yr younger male

on base plan.

MPBIM 63

child.

Discount for females-

equal to 2 yr younger

male on base pack

discounts for

females equal to 2

yr younger male

on base plan.

Plans Economy –the basic

package.

Gold –with triple

protection

Diamond- with triple

protection

Platinum- with

quadruple protection

MPBIM 64

REFERENCES

BOOKS

• Insurance chronicle-ICFAI publications

• Outlook money –magazine

WEBSITES

• www.google.com

• www.bajajallianz.co.in

• www.iciciprulife.com

• www.in.insuranceyahoo.com

• www.moneycontrol.com

• www.bimaonline.com

• www.irdaindia.org

• www.licindia.com

• www.outlookmoney.com

OTHERS

• Broachers of different products considered for

comparison

• Product manuals

MPBIM 65

PERFORMANCE OF DIFFERENT

INSURERS IN 2004-2005

Total No. of Total Premium u/w

Policies Issued Market Share based on

Sl. No. Insurer

March Apr.- Mar March Apr.- Mar Premium Policy

1 TATA AIG 4738.99 30022.07 31148 228894 1.18 0.87

2

KOTAK MAHINDRA OLD MUTUAL 23313.41 37475.21 14975 63468 1.48 0.24

3 BIRLA SUNLIFE 13673.42 62128.31 41710 198370 2.45 0.76

4 MAX NEW YORK 4208.25 22469.01 33608 216671 0.89 0.83

5 ING VYSYA 18478.59 28162.46 26088 111141 1.11 0.42

6 HDFC STANDARD 19771.79 48615.08 58695 206320 1.92 0.79

7 MET LIFE 1048.10 5603.71 9579 46682 0.22 0.18

8 BAJAJ ALLIANZ 36596.63 86001.80 83017 288191 3.39 1.10

9 ICICI PRUDENTIAL 42942.95 158408.46 96352 614673 6.25 2.34

10 SBI 8690.23 48293.56 43271 129974 1.91 0.49

11 AVIVA 4248.50 19229.27 13989 83209 0.76 0.32

12 AMP SANMAR 870.99 9118.44 6378 35268 0.36 0.13

MPBIM 66

13 SAHARA LIFE 131.86 167.09 7146 10214 0.01 0.04

PRIVATE TOTAL 178713.70 555694.47 465956 2233075 21.93 8.50

14 LIC 634300.31 1978593.20 7061742 24027393 78.07 91.50

MPBIM 67

S.NO

Company Premium Premium market share%

Growth rate

Up to FEB 2005

Up to FEB 2005

Up to FEB 2005

1 Bajaj Allianz 49405.12 2.86 333.50 2 ING Vysya 9684.14 .56 114.39 3 AMP Sanmar 8247.45 0.48 292.72 4 SBI Life 39603.33 2.29 240.90 5 Tata AIG 25283.08 1.46 76.96 6 HDFC Standard 33533.73 1.94 123.53 7 ICICI Prudential 115465.48 6.69 100.06 8 Birla Sunlife 48454.48 2.81 95.76 9 Aviva 14980.78 0.87 152.40 10 Kotak Mahindra 14398.02 0.83 106.85 11 Max New York 18260.76 1.06 73.61 12 Met Life 4555.62 0.26 149.18 13 Sahara Life 35.23 0.00 0.00 Private 381907.65 22.12 129.20