Embed Size (px)

Citation preview

Bank of America Merrill Lynch 2014 Leveraged Finance Conference December 2, 2014

2

MTGA Overview • MTGA: Premier Tribal Gaming Operator

• High Quality “Built to Last” Gaming Assets • Leading Market Share/Fair Share/Operating Margins in its markets • Stable Governance, Transparent and Commercial • Mohegan Tribe is a Leader in Indian Country

• Focused Deleveraging Strategy and Cost Saving Initiatives • Focus on Deleveraging • Expiration of ~$50 million annual Relinquishment Payments in January 2015 • Strong Corporate Assets compared to other Tribal operators • Strategic Cost Saving Initiatives

• Diversification Through Capital-Light Growth Pipeline • Resorts Casino in Atlantic City – Margaritaville Brand • Mohegan Sun at The Concord in the Catskills, New York • Cowlitz Casino Development near Portland, Oregon • Internet Gaming – including PokerStars partnership

3

MTGA: Premier Tribal Gaming Operator

The Mohegan Tribe of Indians of Connecticut • Widely considered one of the strongest and most stable tribal

governments in the United States • Federally recognized Tribe with experienced leadership

• Elected 9-member Tribal Council governs the Tribe and acts as the Management Board of MTGA

• Staggered 4 year terms, next elections in August 2015 Mohegan Tribal Gaming Authority • One of the strongest management teams in Indian Country operating

three high-performing casinos • Mohegan Sun – on reservation land in Uncasville, CT • Pocono Downs – on commercial land in Wilkes-Barre, PA • Resorts in Atlantic City – on commercial land in Atlantic City, NJ

• SEC filer, values its lender relationships and has always complied with bank and bond covenants

• Mohegan Sun 1) is the highest grossing casino facility in the Western Hemisphere, 2) operates the highest grossing arena in the world of its size, and 3) is home to the Connecticut Sun WNBA and New England Black Wolves NLL franchises

• Well-known “Mohegan Sun” brand with 6 million+ high-value customers in Player Database

4

MTGA: Premier Regional Assets

5

Superior Win Efficiency

• Based on the fair share (number of slot machines offered), Mohegan Sun and Pocono Downs are in line with the competition

• However, both properties outperform the competition by 10-15% by measure of slot win efficiency

Results for LTM period ended October 31, 2014

Connecticut Northeastern PA

MSPD

Primary Competitor

Win Efficiency: 110%

(Fair Share: 55%)

Win Efficiency: 88%

(Fair Share: 45%)

Mohegan Sun

Primary Competitor

Win Efficiency: 112%

(Fair Share: 48%)

Win Efficiency: 89%

(Fair Share: 52%)

6

Near Term Expiration of Relinquishment Payments Relinquishment expiration means ~$50 million of incremental free cash flow per year

• In February 1998, MTGA and Trading Cove Associates ("TCA"), a development and financing partner of Mohegan Sun, agreed MTGA would pay 5% of gross revenues to TCA through January 2015

• Over the past few years, relinquishment payments have been $50 - $55 million per annum

• These payments expire in January 2015

• The total liability held on the balance sheet is now approximately $25 million

$385.4

$298.4

$230.7

$178.3

$120.8 $74.4

$25.2

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015E FY 2016E FY 2017E

$0

Relinquishment Liability over time

($ in millions)

Note: Relinquishment liability as of September 30, 2014 was $25.2 million.

$0 $0

7

MTGA: Financial Summary Overview

(1) Adjusted 2014 results adjusted for Massachusetts spending, normalized table hold and relinquishment payments (2) Cash flow for Financial Debt Service defined as Adj. EBITDA minus relinquishment payments, maintenance and development capital expenditure and distributions to the Tribe

• Termination of Mass spending, normalization of table hold in CT, and relinquishment payment expiration in January 2015 results in ~$80 million cash flow benefit in FY2015

Adjusted($ in mill ions) 2011A 2012A 2013A 2014A 2014 (1)

Net Revenues:

Mohegan Sun $1,115 $1,084 $1,042 $997 $1,007Pocono Downs 303 315 297 297 296Corporate and Other – – 1 1 1

Net Revenues $1,418 $1,399 $1,340 $1,294 $1,304

Adjusted EBITDA:

Mohegan Sun $285 $270 $281 $251 $261Pocono Downs 52 59 57 51 50Corporate and Other (15) (15) (24) (36) (13)

Adjusted EBITDA $322 $314 $313 $266 $298Adjusted EBITDA % margin 22.7% 22.4% 23.4% 20.6% 22.9%

Maintenance and development capex (46) (44) (66) (33) (33)Distributions to the Tribe (47) (53) (50) (50) (50)Relinquishment payments (55) (54) (51) (49) –

Cash Flow for Financial Debt Service (2) $173 $163 $146 $134 $215

FY15 Cash Flow Benefit $81

FYE September 30,

8

Proactive Cost Saving Initiatives

Disciplined approach to cost containment, while maintaining superior service and customer experience

• Right sizing of workforce at Mohegan Sun and Pocono Downs

• Changes to the slot mix on the gaming floor, increasing slot win with the same overhead costs

• Modification to medical benefits

• Costs savings through in-house purchase of prescription drugs via government program

• Replacement of Mohegan Sun-owned or operated food and beverage outlets with 3rd-party operators

Cost saving initiatives reflect continued focus on increasing Adjusted EBITDA and margins

• Consolidated property operating costs and expenses for Q4 FY14 decreased by approximately $9.3 million from prior year, which equates to approximately $37 million of cost savings on an annualized basis

• Cost saving initiatives are ongoing and expected to continue over the next few years

9

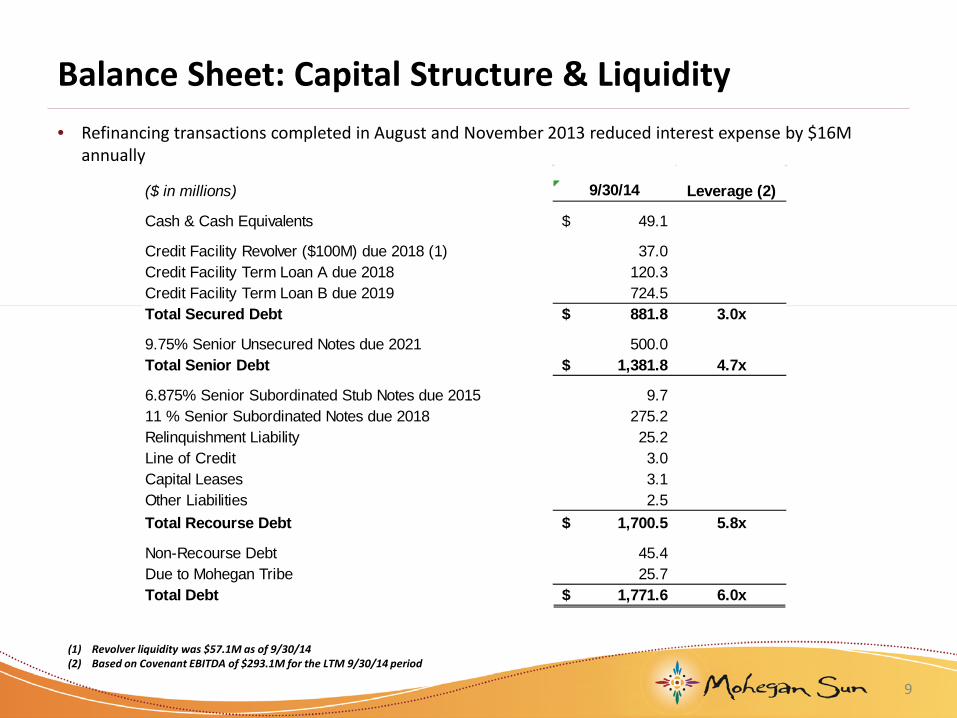

Balance Sheet: Capital Structure & Liquidity

(1) Revolver liquidity was $57.1M as of 9/30/14 (2) Based on Covenant EBITDA of $293.1M for the LTM 9/30/14 period

• Refinancing transactions completed in August and November 2013 reduced interest expense by $16M annually

($ in millions) 9/30/14 Leverage (2)

Cash & Cash Equivalents 49.1$

Credit Facility Revolver ($100M) due 2018 (1) 37.0 Credit Facility Term Loan A due 2018 120.3 Credit Facility Term Loan B due 2019 724.5 Total Secured Debt 881.8$ 3.0x

9.75% Senior Unsecured Notes due 2021 500.0 Total Senior Debt 1,381.8$ 4.7x

6.875% Senior Subordinated Stub Notes due 2015 9.7 11 % Senior Subordinated Notes due 2018 275.2 Relinquishment Liability 25.2 Line of Credit 3.0 Capital Leases 3.1 Other Liabilities 2.5 Total Recourse Debt 1,700.5$ 5.8x

Non-Recourse Debt 45.4 Due to Mohegan Tribe 25.7 Total Debt 1,771.6$ 6.0x

10

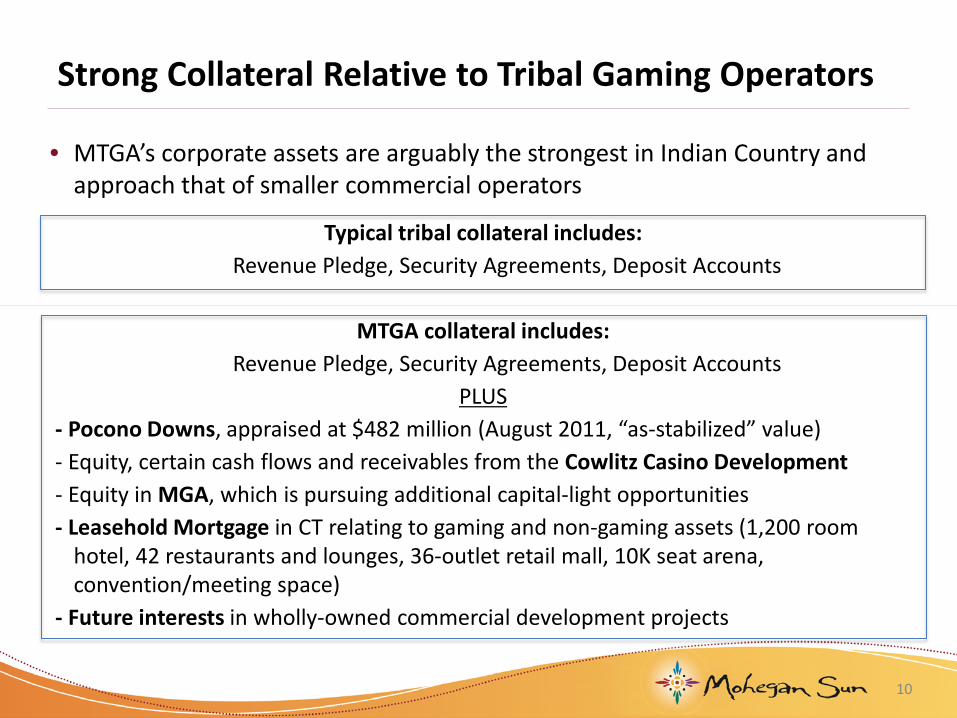

Strong Collateral Relative to Tribal Gaming Operators

• MTGA’s corporate assets are arguably the strongest in Indian Country and approach that of smaller commercial operators

Typical tribal collateral includes: Revenue Pledge, Security Agreements, Deposit Accounts

MTGA collateral includes:

Revenue Pledge, Security Agreements, Deposit Accounts PLUS

- Pocono Downs, appraised at $482 million (August 2011, “as-stabilized” value) - Equity, certain cash flows and receivables from the Cowlitz Casino Development - Equity in MGA, which is pursuing additional capital-light opportunities - Leasehold Mortgage in CT relating to gaming and non-gaming assets (1,200 room

hotel, 42 restaurants and lounges, 36-outlet retail mall, 10K seat arena, convention/meeting space)

- Future interests in wholly-owned commercial development projects

Estimated First Lien Collateral Coverage

11

$482

$882

$201

$199

$18 $39

– $100 $200 $300 $400 $500 $600 $700 $800 $900

$1,000

PoconoDowns

CT Hotel CT Mall GolfCourse

CowlitzReceivable

First LienDebt

$955 (fully-drawn

revolver)

• First lien debt as of September 30, 2014 was covered by MTGA’s collateral package, which has an estimated value of $939 million

($ in millions)

12

Capital-Light Growth Strategy

• Illustrative 3-year Timeline (Estimated)

Project / Expansion Location Primary Market

Population (1) Ownership Structure

Est. Opening

Pocono Downs Hotel Wilkes-Barre, PA NA 100% equity,

Non-recourse debt Completed Open

Mohegan Sun Hotel Expansion Uncasville, CT NA Third-party

financing 2016

Cowlitz Casino Development La Center, WA 2.3 Management

contract 2017

Resorts Casino Management Atlantic City, NJ 1.4 10% equity Completed Open

Status

Advanced planning

Pending litigation

New Jersey Internet Gaming

10% equity Advanced planning

2015

Benefit to MTGA

• Profits after lease payment

• 100% of equity

Profits after lease payment

• Development fee • Management fee • ~$40m receivable

Through MGA (2)

Mohegan Sun at The Concord Catskills, NY JV, 50% equity Pending RFP

application 2016 Through MGA (2)

Through MGA (2)

(1) In millions. Represents population within 60 minute drive time or MSAs and state population from US Census (2) Mohegan Gaming Advisors, LLC (“MGA”) is an unrestricted subsidiary that is wholly-owned by MTGA

• Expiration of Relinquishment Payments • Internet Gaming • Cowlitz Casino Receivables

2015 • Mohegan Sun Hotel Expansion • Cowlitz Casino Development Fees • Mohegan Sun at The Concord

• Cowlitz Casino Management Fees • Mohegan Sun Retail Expansion

2017 2016

PokerStars, Resorts, and Mohegan Sun skins

8.8

0.8

Mohegan Sun Retail Expansion Uncasville, CT NA Third-party

financing 2017 Planning

stage • Rental income • Management fee

13

Mohegan Gaming Advisors: Resorts in Atlantic City • In October 2012, MGA acquired 10% of

Resorts in Atlantic City for $5 million and entered into management agreement

• MGA directed $60M+ expansion: • May 2013 – Room remodel complete • Memorial Day/June 2013 –

• Jimmy Buffett’s Margaritaville • LandShark Bar & Grill (AC’s only

year-round beach bar) • 5 O’Clock Somewhere Bar

• Spring 2014 – New Food Court opened

• Drive significant additional revenue to Resorts by moving thousands of Mohegan customer Atlantic City trips to Resorts from other Atlantic City casinos

• For LTM September 2014, Resorts has outpaced the market in GGR growth

14

Mohegan Sun Hotel Project

• Advanced construction drawings and financing documentation ongoing on $120 million, 400-room, third-party financed hotel

• 4 star, full-service price point rooms • Direct connection with Mohegan Sun

casino and Mohegan Sun Winter Garage • Anticipated groundbreaking by early 2015,

anticipated opening in mid-2016 • 93%+ occupancy at existing 1,175 room

AAA Four-Diamond luxury Sky hotel over each of the last 9 years; 480,000 annual turnaways

• Existing hotel turns away ~1,200 rooms per night on weekdays; over 1,600 on weekends

15

Pocono Hotel Progress – Monthly Occupancy %

80.1%

88.1%

91.6%

90.3%

93.9%

95.9% 94.7%

96.1% 96.1%

92.2% 92.8%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

16

Pocono Hotel Progress – Monthly Transient ADR Rate

$127 $118

$159 $159

$153

$174

$197 $195 $207

$173 $182

$-

$50

$100

$150

$200

$250

17

Cowlitz Project Overview

Economic Summary • MTGA is a 49% equity partner in Salishan-Mohegan,

the management company for the Cowlitz casino • Reimbursement of all MTGA invested capital,

approximately $40 million to date • Development Fee – 3% of Project Costs (MTGA

will receive 100%) • Management Fee – 24% of net revenues (as

defined by the NIGC) for 7 years to credit group

Project Background • On Oct 22, 2014 U.S. District Court received notice that

DOI will place land in trust the earlier of January 21, 2015 or 30 days following favorable ruling by Court

• Project financing and development efforts ramping up • Proposed casino would be closest large-scale gaming

facility to Portland, Oregon • Underserved market with approximately 2.3 million

people within a 60 minute drive • Full gaming (slots, tables and poker), effective gaming

tax rate of approximately 4% Proposed Site

18

Cowlitz Project Proposed Site

19

Connecticut Properties: Geographic Makeup

• Although only ~9 miles apart, the geographic makeup of customers at the two Connecticut properties differ due to varying highway access and other factors

52.9%

18.6%

17.6%

3.2% 7.8%

Mohegan Sun

CT

NY

MA

RI Other

Source: Mohegan Sun (Results for LTM Period Ended October 31, 2014)

38.0%

9.8% 32.1%

11.7%

8.4%

Primary Competitor

RI

Other

CT

NY

MA

Source: UMASS Dartmouth Center for Policy Analysis (2013 New England Casino Update)

Expectations for MA Casinos’ Impact on Mohegan Sun

20

• Similar number of machines caused an approximately 6% reduction in NY exposure, or approximately one-quarter of previous business

• Mohegan has less exposure to MA than it did to NY in 2006

• No smoking allowed in MA casinos

• Roll-off of ~$50mm annual relinquishment liability and cash flows from capital light projects likely to offset MA impact

Number of Facilities

Number of Slot Machines

Estimated Opening Date

Gaming Tax Rate

Drive Time to Key Locations

Smoking

Revenues Exposure Before Competition

Revenues Exposure After Competition

Difference

New York Massachusetts

• 2 • 4

• ~10,000 • ~10,000

• Empire City: Oct 2006 • Resorts World: Oct 2011

• Racino: mid 2015 • Casinos: 2018 and later

• 69% effective • 25%

• Empire City: 2 hours • Resorts World: 2.25 hours

• Springfield: 1.25 hours • Boston: 1.75 hours

• No • No

• 24.8% (LTM Sept 2006)

• 17.6% (LTM Oct 2014)

• 18.6% (LTM Oct 2014)

• TBD

• ~ 6.0% or ~1/4 of previous business • TBD

Thank You and Q&A