Embed Size (px)

Citation preview

1

Bank of America UK Retirement Plan

Governance Statement

July 2021

2

DC Governance Statement Annual Chair’s Statement for the Bank of America UK Retirement Plan (the Plan), previously called

the Bank of America Merrill Lynch UK Pension Plan

A message from Peter Gibbs – Chair of the Trustee Board

As you will know, the Plan is established within a Trust and is governed by a Trust Deed and Rules which

set out the way in which the Plan operates. The Plan has a single Trustee, Bank of America Merrill Lynch UK

Pension Plan Trustees Limited (the Trustee), which has a Board of Trustee Directors.

The Trustee believes that good governance is key to ensuring that the Plan delivers good value and

outcomes for members. The Trustee regularly reviews and updates its governance processes and

procedures to make sure that they meet industry best practice.

This statement appears in the Plan's Annual Report and Financial Statements and sets out how the Trustee

is meeting the requirements and how it has complied with legislation and regulations relating to the

governance of the Defined Contribution (DC) arrangements within the Plan.

This statement covers governance and charges disclosures for the period from 1 January 2020 to

31 December 2020 in relation to:

• The default investment option into which contributions are paid for members who make no investment

choice – this is currently the Thames Flexible Lifestyle option (see the Plan Handbook available in the

“Resources” section of the Plan website for more details).

• The charges and transaction costs paid by Plan members.

• The Trustee's assessment of how the charges and transaction costs paid by Plan members represent

good value for members.

• How the Trustee ensures the prompt and accurate processing of core financial transactions within the

Plan, such as the investment of contributions, switching of funds and payment of benefits to members.

• How the Trustee Directors maintain the required knowledge and understanding of pensions issues and

use this knowledge, together with input from its advisers, to carry out the Trustee's duties.

As Chair of the Board I am pleased to confirm that the Plan meets, and in many areas exceeds the

standards set by the legislation. You can find more detail as required by legislation in the remainder of this

statement.

Peter Gibbs

Chair of Trustee Board

Date: 29 July 2021

3

The Default Investment Strategy

The Plan’s investment options

Plan members can choose between two different approaches to invest their Member Account – the ‘hands-

on’ Freestyle approach or the ‘hands-off’ Lifestyle approach.

Within the Lifestyle approach, the Plan offers members three options each with a different level of risk and

potential return ('Thames', 'Severn' and 'Tay'). For each of these Lifestyle options, members can also select

any one of three pre-retirement phase options. The three pre-retirement phase options target different

asset allocations at retirement that may be suitable for members seeking to either:

• purchase an annuity;

• move into a flexible drawdown product; or

• take the full amount as cash.

Members who join the Plan and do not make an active investment choice for their contributions are placed

into the Plan’s default investment strategy – the Thames Flexible Lifestyle strategy. The Plan is used as a

Qualifying Scheme for auto-enrolment.

About the Thames Flexible Lifestyle strategy

The Thames Flexible Lifestyle strategy is associated with a medium level of investment risk, and medium

potential investment return up to the point members use their benefits. The 'Flexible' Pre-retirement phase

represents the most neutral option regarding the member's choice of how to access their retirement

savings. It maintains a mix of investment assets, assuming the member has not made a specific choice to

align their Member Account to the options designed for those specifically targeting cash or an annuity.

The Trustee therefore views the Thames Flexible Lifestyle strategy as being the one most appropriate for

the majority of members who have not made a decision on how to invest their Member Account.

The Trustee has prepared a Statement of Investment Principles (SIP) in accordance with the Occupational

Pension Schemes (Investment) Regulations 2005, which governs decisions about investments. You can find

out more about the specific requirements of the default investment strategy and details of how the Lifestyle

options and Freestyle funds are currently invested in the SIP.

4

Monitoring the default investment strategy

The Trustee regularly monitors the funds made available to members as part of the Plan's fund range (both

freestyle funds and Lifestyle options), to ensure they are meeting their objectives and that their inclusion in

the fund range continues to be in members’ best interests.

A review of the default strategy was completed as part of the overall general review of the Plan's

investment strategy on 15 January 2020, within three years of the last strategy review on 28 September

2017. Strategic reviews are carried out on a triennial basis with the next such a review to be carried out no

later than 2023. The Trustee, with its investment adviser, initiated work on the implementation of changes

agreed following the strategy review during the year. However, due to the impact of Covid-19 on financial

markets at this time and to tie in with the transition of the pension administration services from Capita to

Willis Towers Watson, implementation of some of the proposed changes has been postponed until

2021/2022.

The 2020 investment strategy review took into account the Plan's membership profile, the needs of Plan

members as well as consideration of expected member outcomes at retirement and associated risks. The

Trustee took advice from their investment adviser on all of these aspects.

As a result of this review, the Trustee made some changes to the Equity Lifestyle Fund (ELF), which is used

as part of the Plan's default investment strategy, to ensure that it continues to meet the objectives for the

Plan. In particular, the Trustee reduced the UK Active Equity allocation, increased the Global Passive Equity

allocation and introduced currency hedging. The aim of the following changes was to achieve a lower level

of volatility with the fund while maintaining the same level of expected return:

▪ The weighting to the BlackRock Fundamental Weighted Index (hedged) was increased and the

weighting to the BlackRock Fundamental Weighted Index (unhedged) was reduced with the aim of

increasing exposure to global developed equities and to implement c.50% currency hedge within

the ELF.

▪ A significant portion of the BlackRock MSCI World Fund was replaced with an allocation to a

currency hedged version of the Fund, again with the aim of implementing c. 50% currency hedge

within the ELF.

▪ The Jupiter UK Growth Fund was removed as part of the intended strategic decrease in the UK

equities exposure.

▪ Weightings to the Schroder Global Emerging Markets and Lazard Emerging Markets Fund were

increased as part of the intended strategic increase in the emerging markets equities exposure.

The UK Equity Fund (Active) was also reviewed during the year, with the Jupiter UK Growth Fund being

removed and replaced with the Jupiter UK Special Situations Fund, following concerns regarding the

performance of the UK Equity Fund (Active).

The Trustee also made some changes to the Index-Linked Lifestyle Fund with the aim to reduce overall

duration from 18 to 15 years to better match expected member requirements.

• The allocation to the BlackRock Up to 5 Year Index-Linked Gilts Fund was increased;

• The allocation to the BlackRock Over 5 Year Index-Linked Gilts Fund was decreased.

5

Further to this, the Trustee reviewed the Diversified Lifestyle Fund and Diversified Growth Fund during the

year and decided to change the underlying asset allocation and introduce a Risk Parity Fund and Multi Asset

Credit Funds. These changes are to be implemented in 2021.

When carrying out the review, the Trustee took into account the impact of performance on different groups

of members and are satisfied that it is on target for all groups. Changes to the default investment strategy

resulting from the strategy review were implemented in 2020.

The SIP was reviewed and revised in August 2020 to reflect the above changes. A copy of the latest SIP for

the Plan can be requested from the Plan's administrators. The SIP is also attached to this statement in the

Annual Report and Financial Statements and is available on the Plan website.

The Trustee, with the help of their investment advisers, also undertakes a more in-depth review of the Plan's

underlying fund range on an annual basis. This is to:

• Consider the on-going suitability of the funds that make up the default and other Lifestyle options

and their adherence to their investment mandates;

• Ensure that the funds available to members continue to compare favourably with other funds

available in the market;

• Ensure costs and charges borne by members continue to represent good value to those members.

In addition, the performance of the default strategy and other investment options is regularly monitored

between each strategic review to ensure the funds and strategies are delivering as expected. The Trustee

is satisfied that over the year most of its funds and strategies performed in line with their aims and

objectives as set out in the SIP. The Trustee has in place performance monitoring metrics that brings any

underperforming funds to the attention of the Trustee.

A recent area of focus for the Trustee has been its policy on responsible investment and the relevant options

available to members. The Trustee believes that investing in companies which do not consider

Environmental, Social and Governance (ESG) issues creates an undesirable long-term investment risk.

Moreover, integrating ESG considerations into the governance of the Plan is both important and necessary

to members achieving the best retirement outcomes.

As part of the ongoing monitoring of the Plan's investment managers, the Trustee uses ESG ratings provided

by the Plan's investment advisers, where relevant and available, to monitor the level of the Plan's investment

managers' integration of ESG considerations on a quarterly basis. The Environmental, Social & Governance

Equity Fund (formerly "Ethical Global Equity Fund") is fully invested in the Impax Leaders Strategy Fund.

The Trustee concluded that this underlying fund is well placed to meet the objectives set for the Ethical

Global Equity Fund and is in members' best interests.

In addition, the Trustee have engaged directly with a number of their fund managers on these areas.

The SIP was also updated to take account of further regulatory changes which required the Trustee to

outline policies regarding how they incentivise asset managers to achieve their long-term objectives, their

policies on cost transparency, their policies on voting and stewardship, and how their policies align with

that of the sponsoring employer in relation to sustainability. The most recent SIP includes the changes

outlined here and was agreed and approved by the Trustee ahead of the 1 October 2020 statutory deadline.

6

Other default arrangements

As a result of the impact that the Covid-19 pandemic had on global financial markets, Threadneedle, the

fund manager responsible for the Plan's UK Property Fund, temporarily suspended trading in the fund

with immediate effect in March 2020. This was primarily due to the difficulty in providing an accurate

valuation of any of the Fund's property holdings during this period of heightened market uncertainty.

While these suspensions were in place, member contributions intended for this fund were redirected into

the Money Market Fund. This is in accordance with the Trustees decision to invest contributions

temporarily in a suitable, low risk alternative fund. This has led to the Money Market Fund being classified

as a default arrangement and having the same statutory requirements apply as the Plan's main default

arrangement. For the purpose of this reporting year the Trustee can confirm that the level of member

borne charges for the Money Market Fund did not exceed the regulatory charge cap of 0.75% p.a.

The fund suspension was lifted on 17th September 2020. Member contributions continued to be

redirected to the Money Market Fund and members were contacted and given the option to nominate an

alternative fund or funds to which they wish to redirect their future contributions.

Charges and transaction costs

The Trustee is required to assess the costs members have to pay in relation to the Plan, such as charges

and transaction costs.

Charges include the Annual Management Charge (AMC) which is the annual fee charged by the

investment manager for investing in a fund. Additional expenses such as trading fees or legal fees are

included in the Total Expense Ratio (TER), which is the total cost of investing in a fund.

Any relevant charges are deducted as a percentage of a member’s funds. You can find details about the

charges for each fund available in the Plan in the Plan Handbook available in the Resources section of the

Plan website.

Transaction costs are costs which are incurred within the day-to-day management of the assets by the

fund manager. This covers such things as the cost of buying and selling securities within a fund.

The requirement for fund managers to calculate and disclose transaction costs using a method prescribed

by the Financial Conduct Authority was introduced on 3 January 2018. Fund managers calculate

transaction costs at fund-level not scheme-level therefore the Trustee requested details of transaction

costs for the period 1 January 2020 to 31 December 2020 from the Plan's providers, Fidelity and Aviva.

Transaction costs are incurred on an on-going basis and are implicit within the performance of a fund.

The prescribed method of calculating transaction costs states the trading cost is arrived at by comparing

the price at which the transaction was actually executed, with the price when the order to transact

entered the market. So, when selling into a rising market or buying into a falling market, the calculation

produces a credit that may outweigh the other ‘explicit’ transaction costs, resulting in negative overall

transaction costs.

7

The Trustee has continued to seek to obtain information on these transaction costs from the fund

platform provider, Fidelity. However, the Trustee has not been provided with full transaction cost data

from all fund managers in respect of funds in which members were invested in during the year. The

Trustee continues to liaise with Fidelity to obtain the outstanding information and will provide further

information to members once this is available. The transaction cost details that have been received at this

stage are shown below.

TERs and transaction costs of the Lifestyle strategy

The table below shows the TERs and transaction costs of the Plan's default investment strategy (Thames

Flexible Lifestyle) and the other Lifestyle options available to members as at 31 December 2020.

Importantly, the TER range for the Plan's default strategy is below the charge cap set by the regulations

of 0.75% per year and therefore also satisfies this legal requirement.

Lifestyle option Pre-retirement

phase strategy

TER range

(% per year)*

Transaction costs

(%)

Thames

Flexible (default strategy) 0.380 – 0.539 0.100– 0.321

Cash 0.150 – 0.551 0.0 – 0.383

Annuity 0.128 – 0.551 0.038 – 0.383

Tay

Flexible 0.403 – 0.562 0.249 – 0.440

Cash 0.150 – 0.562 0.000 – 0.440

Annuity 0.128 – 0.562 0.038 – 0.440

Severn

Flexible 0.380 – 0.535 0.100 – 0.304

Cash 0.150 – 0.562 0.0 – 0.440

Annuity 0.128 – 0.562 0.038 – 0.440

*% per year of assets under management, depending on the combination of funds relating to each members' term to

Target Retirement Date.

The actual costs based on term to retirement during the year is shown in the Appendix.

8

TERs and transaction costs of the Freestyle funds

In addition to the Lifestyle strategies, the Plan also offers members a range of Freestyle funds. The table

below shows the TERs and transaction costs of the freestyle funds available to members as at

31 December 2020.

Fund TER

(% per year)

Transaction

costs (%)

Fidelity BoAML Asia Pacific (ex-Japan) Equity Fund - Passive 0.080% 0.020%

Fidelity BoAML Diversified Fund 0.560% 0.440%

Fidelity BoAML Emerging Market Equity Fund - Active 0.900% 0.240%

Fidelity BoAML European (ex-UK) Equity Fund - Passive 0.090% 0.0%

Fidelity BoAML Gilt Fund 0.09% 0.0%

Fidelity BoAML Global Equity Fund - Active 0.690% 0.130%

Fidelity BoAML Index Linked Gilts Fund 0.090% 0.0%

Fidelity BoAML Japanese Equity Fund - Passive 0.090% 0.0%

Fidelity BoAML Money Market Fund 0.150% 0.0%

Fidelity BoAML North American Equity Fund - Passive 0.090% 0.0%

Fidelity BoAML Pre-Retirement Fund 0.120% 0.810%

Fidelity BoAML Shariah Fund 0.330% 0.130%

Fidelity BoAML UK Corporate Bond - Passive Fund 0.090% 0.060%

Fidelity BoAML UK Corporate Bond -Active Fund 0.310% 0.020%

Fidelity BoAML UK Equity Fund - Active 0.550% 0.150%

Fidelity BoAML UK Equity Fund - Passive 0.090% 0.050%

Fidelity BoAML UK Property Fund 0.530% 0.080%

Fidelity BoAML Environmental, Social & Governance Global Equity Fund 0.650% 0.280%

The TER for the UK Equity Fund (Active) was reduced by 0.025% to an AMC of 0.512%, with effect from 1

March 2020. An increase in the transaction costs for the Diversified Fund, the Diversified Lifestyle Fund,

the Pre-Retirement Fund and the Pre-Retirement Lifestyle Fund was observed over the previous year’s

levels. Fidelity have reviewed the transaction costs with the underlying fund managers and have confirmed

that these are based on the actual transactions over the period and are accurate. The Pre-Retirement

Fund in particular had a higher number of transactions taking place over the period which has led to the

higher level of transaction costs.

Some components of the transaction costs for the Emerging Market Equity Fund, Diversified Fund, Ethical

Global Equity Fund and UK Equity Fund were not available. The Trustees and Aon continue to liaise with

Fidelity to obtain the outstanding information.

A floor of 0% p.a. has also been used for all transaction costs.

9

Illustration of the cumulative effect over time of costs and charges on member fund values

From 6 April 2018, the Occupational Pension Schemes (Administration and Disclosure) (Amendment)

Regulations 2018 introduced new requirements relating to the disclosure and publication of the level of

charges and transaction costs by the trustees and managers of a relevant scheme. These changes are

intended to improve transparency on costs. As part of the changes, the Trustee is required to illustrate

the cumulative effect over time of the application of transaction costs and charges on the value of a

member’s benefits.

The next few pages contain illustrations of the cumulative effect of costs and charges on the value of

member savings within the Plan over a period of time. The illustrations have been prepared having

regard to statutory guidance.

As each member has a different amount of savings within the Plan and the amount of any future

investment returns and future costs and charges cannot be known in advance, the Trustee has had to

make a number of assumptions about what these might be. The assumptions are explained in the notes

sections below the illustrations.

Members should be aware that such assumptions may or may not hold true, so the illustrations do not

promise what could happen in the future. This means that the information contained in this Chair’s

Statement is not a substitute for the individual and personalised illustrations which are provided to

members each year by the Plan.

The illustrations provided

Each of the charts and tables below illustrates the potential impact that costs and charges might have on

different investment options provided by the Plan. Not all investment options are shown in the

illustrations. The Trustee has chosen the following illustrations:

• charts showing the potential impact that costs and charges might have for 3 example members who

have assets invested in the Thames Flexible Lifestyle strategy (the default).

• under each chart, a table showing the potential impact that costs and charges might have if the

example member was charged a higher level of costs and charges on the default arrangement

compared to the one illustrated in the chart and a higher risk profile fund that also has a higher level

of costs and charges compared to the one illustrated in the chart.

We have produced the following illustrations to demonstrate the effect of the costs and charges set out

above for investment funds and strategies available through Fidelity on 3 different combinations of terms

to retirement, accumulated fund value, and both actively contributing and deferred members.

A large proportion of members are invested in the default Thames Flexible Lifestyle option which

automatically transitions members’ funds between the underlying funds as members approach retirement

age. We therefore chose this option for these illustrations. Members are also offered alternative lifestyle

options and a series of self-select funds which, as the tables on previous pages show, carry a variety of

TERs and transaction costs.

10

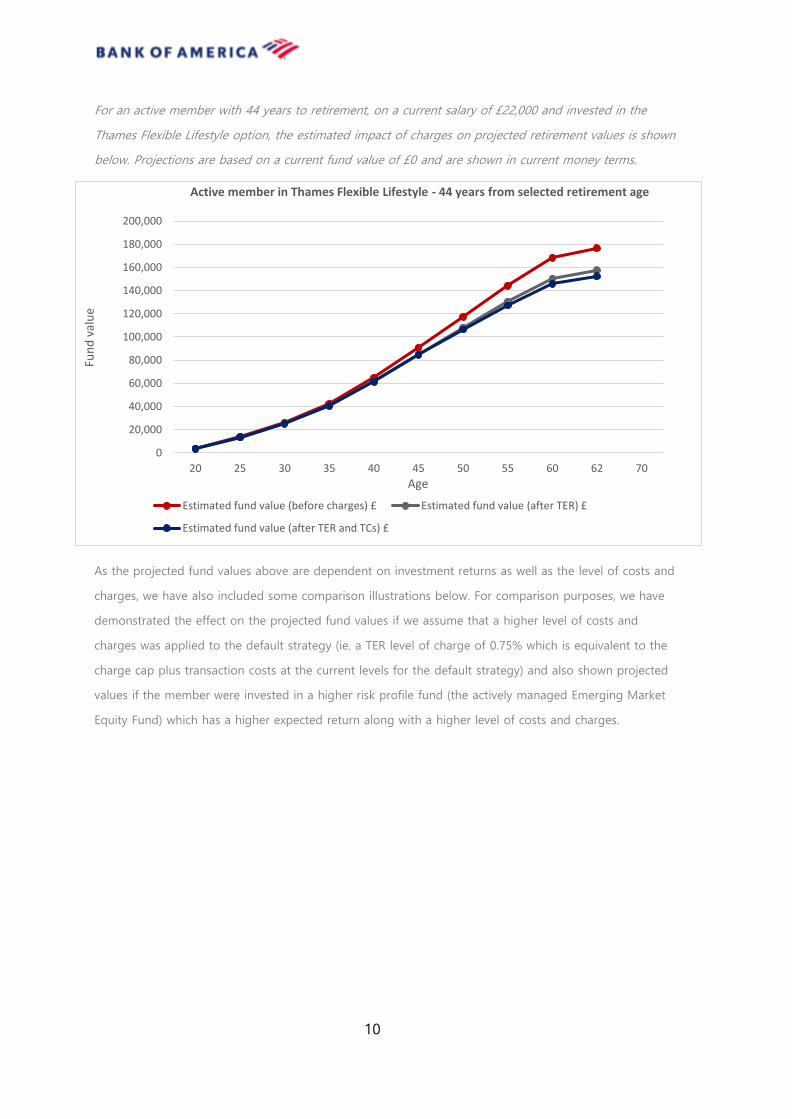

For an active member with 44 years to retirement, on a current salary of £22,000 and invested in the

Thames Flexible Lifestyle option, the estimated impact of charges on projected retirement values is shown

below. Projections are based on a current fund value of £0 and are shown in current money terms.

As the projected fund values above are dependent on investment returns as well as the level of costs and

charges, we have also included some comparison illustrations below. For comparison purposes, we have

demonstrated the effect on the projected fund values if we assume that a higher level of costs and

charges was applied to the default strategy (ie. a TER level of charge of 0.75% which is equivalent to the

charge cap plus transaction costs at the current levels for the default strategy) and also shown projected

values if the member were invested in a higher risk profile fund (the actively managed Emerging Market

Equity Fund) which has a higher expected return along with a higher level of costs and charges.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

20 25 30 35 40 45 50 55 60 62 70

Fun

d v

alu

e

Age

Active member in Thames Flexible Lifestyle - 44 years from selected retirement age

Estimated fund value (before charges) £ Estimated fund value (after TER) £

Estimated fund value (after TER and TCs) £

11

Thames Flexible Lifestyle (Actual

charges)

Thames Flexible Lifestyle (TER = charge

cap 0.75% plus actual trans. costs)

Emerging Market Equity Fund (Actual

charges)

Age

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

20 3,603 3,585 18 3,603 3,576 27 3,603 3,569 34

25 13,812 13,564 248 13,812 13,446 366 13,812 13,355 457

30 26,001 25,185 816 26,001 24,802 1,199 26,001 24,510 1,491

35 42,356 40,511 1,845 42,356 39,656 2,700 42,356 39,011 3,345

40 64,837 61,262 3,575 64,837 59,625 5,212 64,837 58,399 6,438

45 90,848 84,490 6,358 90,848 81,715 9,133 91,680 80,499 11,181

50 117,359 106,554 10,805 117,359 102,467 14,892 123,731 105,692 18,039

55 144,077 127,352 16,725 144,077 121,752 22,325 161,999 134,409 27,590

60 168,332 145,948 22,384 168,332 138,261 30,071 207,690 167,144 40,546

62 176,791 152,432 24,359 176,791 143,729 33,062 228,360 181,486 46,874

12

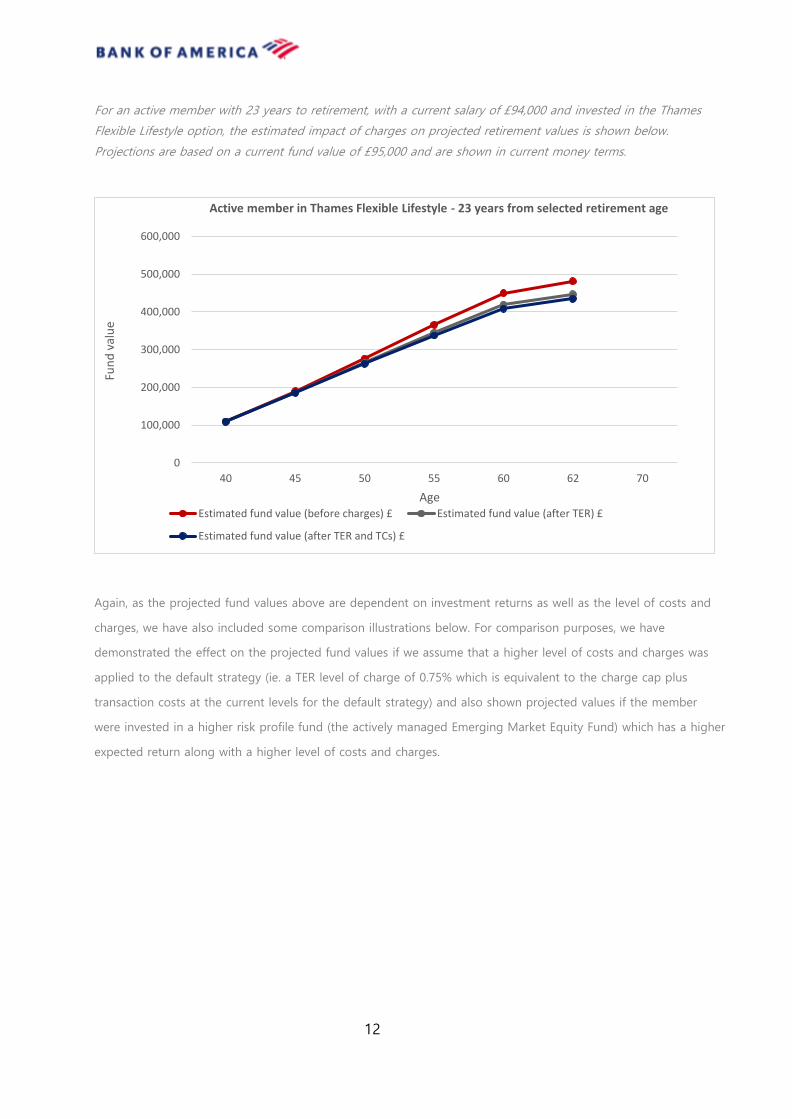

For an active member with 23 years to retirement, with a current salary of £94,000 and invested in the Thames

Flexible Lifestyle option, the estimated impact of charges on projected retirement values is shown below.

Projections are based on a current fund value of £95,000 and are shown in current money terms.

Again, as the projected fund values above are dependent on investment returns as well as the level of costs and

charges, we have also included some comparison illustrations below. For comparison purposes, we have

demonstrated the effect on the projected fund values if we assume that a higher level of costs and charges was

applied to the default strategy (ie. a TER level of charge of 0.75% which is equivalent to the charge cap plus

transaction costs at the current levels for the default strategy) and also shown projected values if the member

were invested in a higher risk profile fund (the actively managed Emerging Market Equity Fund) which has a higher

expected return along with a higher level of costs and charges.

0

100,000

200,000

300,000

400,000

500,000

600,000

40 45 50 55 60 62 70

Fun

d v

alu

e

Age

Active member in Thames Flexible Lifestyle - 23 years from selected retirement age

Estimated fund value (before charges) £ Estimated fund value (after TER) £

Estimated fund value (after TER and TCs) £

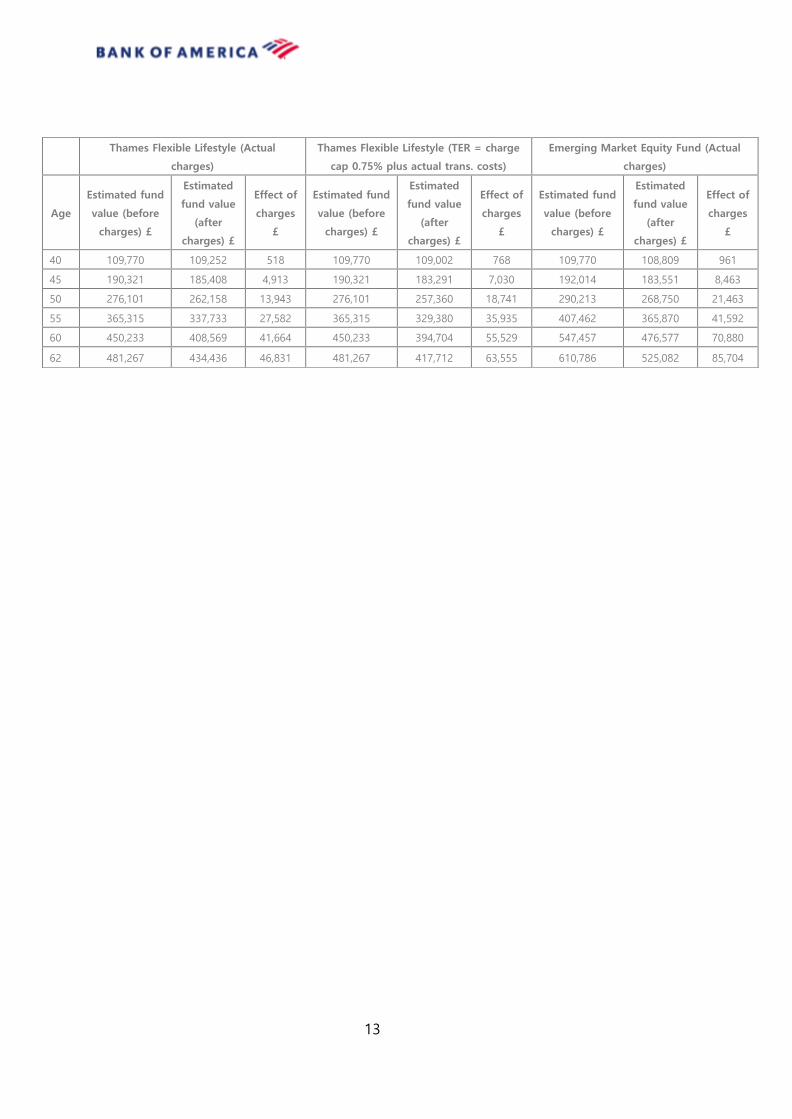

13

Thames Flexible Lifestyle (Actual

charges)

Thames Flexible Lifestyle (TER = charge

cap 0.75% plus actual trans. costs)

Emerging Market Equity Fund (Actual

charges)

Age

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

40 109,770 109,252 518 109,770 109,002 768 109,770 108,809 961

45 190,321 185,408 4,913 190,321 183,291 7,030 192,014 183,551 8,463

50 276,101 262,158 13,943 276,101 257,360 18,741 290,213 268,750 21,463

55 365,315 337,733 27,582 365,315 329,380 35,935 407,462 365,870 41,592

60 450,233 408,569 41,664 450,233 394,704 55,529 547,457 476,577 70,880

62 481,267 434,436 46,831 481,267 417,712 63,555 610,786 525,082 85,704

14

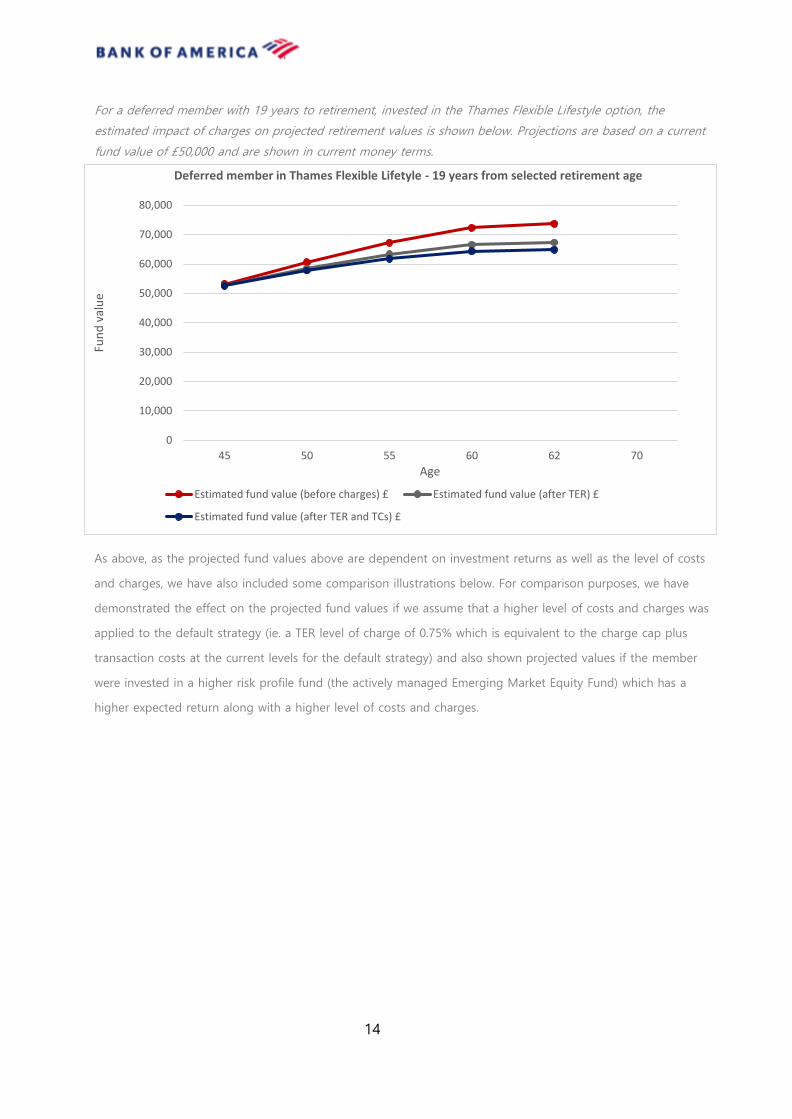

For a deferred member with 19 years to retirement, invested in the Thames Flexible Lifestyle option, the

estimated impact of charges on projected retirement values is shown below. Projections are based on a current

fund value of £50,000 and are shown in current money terms.

As above, as the projected fund values above are dependent on investment returns as well as the level of costs

and charges, we have also included some comparison illustrations below. For comparison purposes, we have

demonstrated the effect on the projected fund values if we assume that a higher level of costs and charges was

applied to the default strategy (ie. a TER level of charge of 0.75% which is equivalent to the charge cap plus

transaction costs at the current levels for the default strategy) and also shown projected values if the member

were invested in a higher risk profile fund (the actively managed Emerging Market Equity Fund) which has a

higher expected return along with a higher level of costs and charges.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

45 50 55 60 62 70

Fun

d v

alu

e

Age

Deferred member in Thames Flexible Lifetyle - 19 years from selected retirement age

Estimated fund value (before charges) £ Estimated fund value (after TER) £

Estimated fund value (after TER and TCs) £

15

Thames Flexible Lifestyle (Actual

charges)

Thames Flexible Lifestyle (TER = charge

cap 0.75% plus actual trans. costs)

Emerging Market Equity Fund (Actual

charges)

Age

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

Estimated fund

value (before

charges) £

Estimated

fund value

(after

charges) £

Effect of

charges

£

45 53,174 52,541 633 52,422 52,302 872 53,675 52,689 986

50 60,563 57,784 2,779 57,609 56,905 3,658 64,088 60,061 4,027

55 67,268 61,760 5,508 61,727 60,177 7,091 76,521 68,464 8,057

60 72,299 64,339 7,960 63,985 61,822 10,477 91,365 78,042 13,323

62 73,671 64,889 8,782 64,258 61,934 11,737 98,080 82,239 15,841

Members are advised to consider both the level of costs and charges and the expected return on assets

(ie. the risk profile of the strategy) in making investment decisions and not in isolation.

Assumptions for illustrations:

The following assumptions have been made for the purposes of the above illustrations:

• The assumed growth rates (gross of costs and charges) are as follows:

o Equity Lifestyle Fund 6.20%

o Diversified Lifestyle Fund 4.00%

o Pre-retirement Lifestyle Fund 0.80%

o Money Market Lifestyle Fund 0.30%

o Corporate Bond Lifestyle Fund 1.10%

o Index Linked Gilt Lifestyle Fund 0.00%

o Emerging Market Equity Fund – Active 6.20%

• The TERs and transaction costs for the funds underlying the Default Lifestyle are as follows:

TER Transaction costs

o Equity Lifestyle Fund 0.495% 0.100%

o Diversified Lifestyle Fund 0.562% 0.440%

o Pre-retirement Lifestyle Fund 0.12% 0.050%

o Money Market Lifestyle Fund 0.15% 0.000%

o Corporate Bond Lifestyle Fund 0.309% 0.020%

o Index Linked Gilt Lifestyle Fund 0.084% 0.010%

o Emerging Markets Equity Fund – Active 0.900% 0.240%

16

• The transaction costs have been averaged over a 3-year period based on information received from Fidelity. A

floor of 0% pa has been used for the transaction costs if these were negative in any year so as not to potentially

understate the effect of charges on fund values over time.

• Inflation (salary increase) is assumed to be 2.5% p.a.

• Retirement is assumed at the normal retirement age of 62.

• Total contributions of 8% of pensionable pay for the first 10 years of service and 12% thereafter.

• The average active member is assumed to have more than 10 years of service.

• The projected fund values shown are estimates for illustrative purposes only and are not guaranteed.

TERs of external AVC arrangements

AVC assets are also held outside of the Plan, in BlackRock Sub Investment accounts, a Common Investment Fund

and also with Equitable Life and Aviva.

BlackRock Sub Investment Accounts

Over recent years, the governance regulations applicable to Money Purchase arrangements have increased,

which have successively placed increasing requirements on trustees. In response to this, the Trustee regularly

reviews the Plan's Money Purchase arrangements to ensure they remain fit for purpose and are compliant with

the regulations. As part of this process, the Trustee reviewed the sub-investment accounts and decided that they

should be closed due to the increased governance requirements, the nature of the accounts and the lack of

Trustee involvement in the investment process. There is currently one remaining account which is still to be

closed.

At the time of writing, charges information for the BlackRock sub investment accounts was not available.

Common Investment Fund (CIF)

Historically, members of the DB section of the Plan were given the option to pay AVCs on a Money Purchase

basis into the DB section via a Common Investment Fund (CIF). These AVCs are attributed a value based on a

notional portfolio of assets. The CIF also offers a guaranteed investment return of 8% p.a. to some members on

a portion of their previous CIF contributions.

All contributions into the CIF AVC arrangement have now ceased. With regards to the notional funds in the CIF

AVC arrangement, these carry no explicit charges or direct transaction costs.

Equitable Life and Aviva

The Equitable Life and Aviva arrangements are both closed to new contributions.

In relation to Equitable Life, members were invested in With-Profits funds or unit-linked funds. With effect from 1

January 2020, the Equitable Life funds were transferred to Utmost Life and Pensions. The members invested in

the With-Profits Fund received a one off uplift in lieu of future investment guarantees and their funds were

subsequently invested in the Secure Cash fund with Utmost Life.

17

The Trustee took the decision, with advice from the investment advisers, to consolidate these funds and transfer

the holdings into the main Plan strategies. Members were given the option to select the investment strategy for

these funds from the Fidelity range of funds. Where members did not make a selection, funds were moved

during February 2020 to similar funds within the Fidelity range of funds, with the Secure Cash assets (ie. the

former With-Profits funds) being moved to the Thames Flexible Lifestyle arrangement (the Plan's default

strategy). The transition to the main Plan strategies was completed on 20 February 2020.

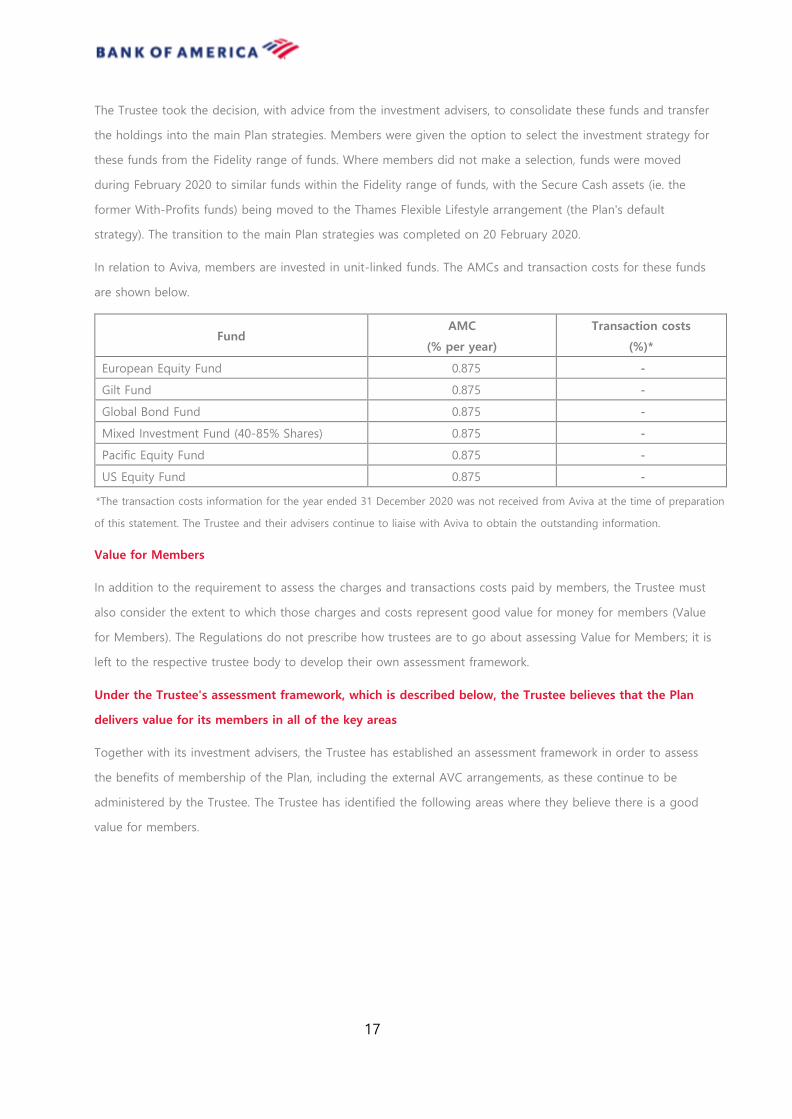

In relation to Aviva, members are invested in unit-linked funds. The AMCs and transaction costs for these funds

are shown below.

Fund AMC

(% per year)

Transaction costs

(%)*

European Equity Fund 0.875 -

Gilt Fund 0.875 -

Global Bond Fund 0.875 -

Mixed Investment Fund (40-85% Shares) 0.875 -

Pacific Equity Fund 0.875 -

US Equity Fund 0.875 -

*The transaction costs information for the year ended 31 December 2020 was not received from Aviva at the time of preparation

of this statement. The Trustee and their advisers continue to liaise with Aviva to obtain the outstanding information.

Value for Members

In addition to the requirement to assess the charges and transactions costs paid by members, the Trustee must

also consider the extent to which those charges and costs represent good value for money for members (Value

for Members). The Regulations do not prescribe how trustees are to go about assessing Value for Members; it is

left to the respective trustee body to develop their own assessment framework.

Under the Trustee's assessment framework, which is described below, the Trustee believes that the Plan

delivers value for its members in all of the key areas

Together with its investment advisers, the Trustee has established an assessment framework in order to assess

the benefits of membership of the Plan, including the external AVC arrangements, as these continue to be

administered by the Trustee. The Trustee has identified the following areas where they believe there is a good

value for members.

18

These benefits can be financial or non-financial in nature.

• Member communications and engagement (including support at retirement)

- The Plan provides effective communications that are accurate, clear, informative and timely.

- The use of a variety of communication media, including access to well-developed online tools and helpful

information around retirement planning via the Plan website.

- Members can access help to support them in their decision making in the form of decision trees,

factsheets and case studies.

• Investment choices

- The Plan offers a variety of lifestyle strategies and freestyle funds covering a range of member risk profiles

and asset classes. The investment funds available have been designed, following advice from the Plan's

investment adviser, with the specific needs of members in mind.

• Flexible contributions

- The Plan has a flexible employee contribution structure, paid by salary sacrifice, which allows members to

set their own level of contributions and change their level of contributions at any time with ease.

Employees can also pay extra contributions in the form of Additional Voluntary Contributions and/or

special lump sums.

• Sound administration

- Capita provided administration services to the Plan during the period of review and the Trustee is satisfied

that Capita has sufficient checks in place to monitor and report on the standard of the administration

service and to ensure that when administrative errors do occur, members are not disadvantaged as a

result.

• Plan governance

- Plan governance covers the time spent by the Trustee to ensure the Plan is run in compliance with the

law and regulation, including taking account of the interests of its members.

- The Trustee believes that good governance is key to ensuring that a framework exists and is actively in

use to help deliver better member outcomes. The Trustee regularly reviews and updates its governance

processes and procedures to make sure that these meet industry best practice.

19

Processing of Core Financial Transactions

The Trustee has a specific duty to ensure that core financial transactions are processed promptly and accurately.

These transactions include, but are not limited to:

• investment of contributions to the Plan;

• transfer of member assets into and out of the Plan;

• transfers between different investments within the Plan; and

• payments to and in respect of members.

Accurate and timely processing of Plan transactions

Bank of America is responsible for ensuring that contributions are paid over to the Plan promptly, and that the

timing of such payments is monitored through regular reports submitted by the Plan's Administrator, Capita

Employee Benefits (Capita).

Capita carry out the bulk of the above listed core financial transactions. The Trustee has received assurance from

Capita and has taken steps to try and ensure that there are adequate internal controls to ensure that core

financial transactions relating to the Plan are processed promptly and accurately. The Plan has a service level

agreement (“SLA”) in place with the administrator which covers the accuracy and timeliness of all core financial

transactions. Along with other key aspects of administration and performance against the agreed service levels,

Capita report to the Trustee quarterly. The service levels reported by the administrator were generally high over

the period (generally above 90%). Considering the general impact of the COVID 19 pandemic, Capita were

requested to confirm immediately if any issues were experienced that put in jeopardy that members benefits

might not be paid so that the Trustee and Capita can jointly consider how to mitigate the situation. A spike in

workload received in June, along with internet connectivity problems for staff working from home, meant that

the SLA for Capita was affected, and was down to about 72% over the summer. This did stabilise from

September onwards increasing to 91% and to 96% by October. Capita have concentrated on disclosure cases to

ensure regulatory deadlines are met. Wireless dongles were also provided to the team in the event of further

connectivity problems.

The administration service is also independently reviewed and verified by Silverwolf.

The key processes adopted by the administrator to help it meet the SLA are as follows:

• as part of their checking process, Capita carry out monthly checks, in addition to daily reconciliation of the

Trustee's bank account.

• all investment and banking transactions are also checked and verified before being processed.

• all work processes are documented and subject to a peer review process, with work being calculated and

independently checked by another member of the team.

• Capita provides quarterly core financial transaction metrics to the Trustee, compared to target processing

times in accordance with the SLA.

20

• Capita also provide confirmation to the Trustees regarding the current position on common and conditional

data as well as any amendments which may be required to rectify gaps in the data. The raw score for new

data is currently below the regulator's requirement and the Trustee has liaised with the administrator

regarding improving this data.

As an additional level of scrutiny, Capita also have an internal reconciliations team who independently carry out

monthly checks, in addition to daily reconciliation of the Trustee bank account.

The Trustee has reviewed the processes and controls implemented by Capita and consider them to be suitably

designed and meeting required levels. Controls around administration and the processing of transactions are

documented in the Plan risk register, which is regularly reviewed.

The Trustee is pleased to report there have been no administration service issues with respect to core financial

transactions which need to be reported.

The Trustee is satisfied that over the period covered by this statement:

• the administrator was operating appropriate procedures, checks and controls and operating within the

agreed SLA;

• there have been no material administration errors in relation to processing core financial transactions; and

• all core financial transactions have been processed promptly and accurately during the Plan year.

The Trustee has also recently completed an administrator provider review. The decision was taken to change the

administrator to Willis Towers Watson (WTW). The Trustee and their advisers are working with WTW and Capita

to ensure that the transition to the new administrator is completed smoothly with minimal impact for members.

The Trustee have considered and reviewed WTW's process and procedures as part of the provider review and

have confidence in the level of service that WTW will be able to deliver to members. As was the case with

Capita, regular reporting will be available from WTW to enable the Trustee to monitor that level of service.

External AVC arrangements

AVC assets are also held outside of the Plan, in BlackRock Sub Advisory accounts, as member balances within a

Common Investment Fund and with Aviva.

BlackRock Sub Investment Accounts

At the time of writing, information relating to core financial transactions for this arrangement was not available.

Given the increasing governance requirements being placed on the Trustee, the nature of the sub-investment

accounts and the lack of Trustee involvement in the investment process, the Trustee decided that it is no longer

able to support the operation of these accounts and is in the process of closing one remaining account.

Common Investment Fund

The units held by members in this arrangement are administered by Capita. As there are no contributions being

paid into this arrangement, any core financial transactions are restricted to 'transfers out/disinvestments' or

21

'payments in respect of members' from the above list. As per the core financial transactions processed by Capita

for the main assets of the Plan, the Trustee is satisfied that there are clear processes in place to ensure that all

core Plan transactions are processed in an accurate and timely manner.

Aviva

As with the Common Investment Fund, there are no contributions being paid into this arrangement and any core

financial transactions are restricted to 'transfers out' or 'payments in respect of members'.

The Trustee has requested information relating to these core financial transactions from the provider. As at the

time of writing, the requested information was still awaited.

Aviva has published a full Corporate Governance Statement in their Annual Report and Accounts to 31

December 2020, which includes information on their systems of internal controls and risk management. The

Trustee will continue to request management information relating to the core financial transactions, although the

Governance reports do confirm that Aviva have established processes and procedures in place to ensure that

these transactions are processed promptly and accurately.

Trustee's knowledge and understanding

The Regulations require the Trustee to have appropriate knowledge and understanding of relevant topics to run

the Plan effectively. The Trustee recognises the importance of training and development and has put in place

arrangements for ensuring that the Trustee Directors, who together form the Trustee, take personal responsibility

for keeping themselves up to date with relevant developments and undertaking a self-assessment of training

needs.

All Trustee Directors receive onboarding as well as regular training. Training logs, which record all relevant

training completed by each member of the Trustee Board, are maintained for the Trustee Directors and these are

reviewed and updated regularly. Trustee Directors are also encouraged to complete the Pensions Regulator's

Toolkit training online and gain the Pensions Management Institute (PMI) certificate in Trusteeship. Six of the

Trustee Directors have completed the PMI’s certificate in Trusteeship and the Trustee Board includes two

professional Trustee Directors who are accredited members of the Association of Professional Pension Trustees

(APPT). There was one new Trustee Director who joined the Board during the year, Andrew Hackling, who had a

previous role within the Pensions Team at the Bank, meaning he already had a sound understanding of the Plan

and its governing documents. Andrew has completed the Trustee Toolkit which is an online training course

provided by the Pensions Regulator that covers various topics such as pension law, scheme governance and DC

specific modules. Andrew has also completed the PMI’s certificate in Trusteeship. Based on his previous role

within the Pensions Team, Andrew is familiar with the Plan’s Trust Deed and Rules, Statement of Investment

Principles, Trustee Report and Accounts and other Plan documents.

The Trustee Directors are conversant with governing documents for the Plan and can access them through an

electronic data repository.

22

During the Plan year, the Trustee has, amongst other things:

• implemented a number of changes from the investment strategy and performance reviews. The Statement of

Investment Principles (SIP) was reviewed and amended in light of the agreed strategy changes and to reflect

the Trustee's approach and policies in respect of responsible investing. The Trustee received training on

Responsible Investment (RI), covering financial and non-financial factors, climate risks including physical risks,

regulatory factors, members' perspectives on RI, and developments in the wider market in relation to pension

funds' considerations of these areas. The Trustee training also covered the risk that the Environmental, Social

and Governance factors, including climate change, negatively impact the value of investments held if not

understood and evaluated property (demonstrating the Regulator's requirement to understand the principles

relating to the funding and investment of occupational DC schemes and to have a working knowledge of the

current SIP).

• reviewed and discussed several of the Regulator's guides linked to the DC Code of practice in the context of

the Trustee's existing policies in these areas. The Trustee also received training on cyber security and on

updating the data protection checks, policies and privacy notice (demonstrating the Regulator's requirement

to have a working knowledge of the documents setting out the Trustee's current policies and to have

knowledge and understanding of the law relating to pensions and trusts).

• undertook a review of the Plan administrator, with an external independent adviser, during the year and

decided to transition to a new administrator in 2021 (demonstrating the Regulator's requirement for effective

scheme management and providing value for members).

• considered non-financial investment strategy considerations, specifically in respect of Environmental, Social

and Governance factors.

• Completed a full strategy review of the investment options and the AVC investment providers and funds

(demonstrating the Regulator's requirement to understand the principles relating to the funding and

investment of occupational DC schemes).

• reviewed and updated the Member Nominated Director selection process to better represent that Plan's

population (demonstrating the Regulator's requirement of effective scheme management).

The Trustee board has a range of skills and experiences including a mixture of Member Nominated and

Company Nominated directors with varying backgrounds.

The Chair of the Trustee is scheduled, as noted in the Plan’s risk register, to carry out an annual assessment of

each Trustee Director by way of an informal catch up.

The Trustee previously completed a Trustee Knowledge Gap analysis (in the form of a survey) which compared

the current level of knowledge of the Trustee Directors (based on the completion of the survey by seven Trustee

Directors) against the Pensions Regulator’s Trustee Knowledge and Understanding (TKU) framework. It showed

how well the Trustee Directors believe they have met each of the Pensions Regulator's specific knowledge

requirements.

The analysis showed that overall; the Trustee Directors possessed a good understanding of relevant topics.

23

There is currently no plan to undertake another Trustee Knowledge gap analysis, however the Pensions Team

does undertake an annual review of training logs to determine training needs and advisers are regularly invited

to Administration and Governance Sub-Committee (AGSC) meetings to deliver specific training. During 2020, this

included training delivered by Aon on Manager selection and responsible investment.

In addition to the skills within the Trustee Board, the Trustee works closely with its appointed professional

advisers throughout the year to ensure that it runs the Plan and exercises its functions properly. Its professional

advisers also attend all Trustee's meetings.

Considering the training activities completed by the Trustee Board together with the professional advice

available to the Trustee, the Trustee considers that it meets the Pension Regulator's TKU requirements (as set out

under Code of Practice No 7) and is confident that the combined knowledge and understanding of the Trustee

Board, together with the input from its specialist advisers, enables it to properly exercise its functions as the

Trustee of the Plan. Each Trustee Director is encouraged to complete and record in their training log 15 hours a

year of continuous professional development.

In conclusion

Overall, the Trustee is confident that all requirements of the Regulations are being met and, in many areas, even

exceeded, in the interests of members of the Plan.

Signed on behalf of the Trustee of the Bank of America UK Retirement Plan

----------------------------------------------------------

Peter Gibbs

Chairman of the Trustee

Date: 29 July 2021

24

Addendum: Actual costs for the period based on term to retirement for lifestyles

Severn Annuity

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a.

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50 0.50 0.51 0.52 0.54 0.55 0.56 0.47 0.39 0.30 0.21 0.13

Transaction costs %

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.17

0.24

0.30

0.37

0.44 0.36 0.28 0.20 0.12 0.04

Total costs %

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60 0.60 0.68 0.76 0.84 0.92 1.00 0.84 0.67 0.50 0.33 0.17

Severn Cash

Severn Flexible

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.51

0.52

0.54

0.52

0.49

0.47

0.45

0.43

0.40

0.38

Transaction costs % 0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10 0.17 0.24 0.30 0.29 0.27 0.24 0.21 0.18 0.16 0.13

Total costs % 0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60 0.68 0.76 0.84 0.81 0.76 0.71 0.66 0.61 0.56 0.51

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.50

0.51

0.52

0.54

0.55

0.56

0.47

0.39

0.31

0.23

0.15

Transaction costs % 0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10

0.10 0.17

0.24 0.30 0.37 0.44 0.36 0.28 0.19 0.09 0.00

Total costs %

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60

0.60 0.60 0.68 0.76 0.84 0.92 1.00 0.84 0.67 0.50 0.32 0.15

25

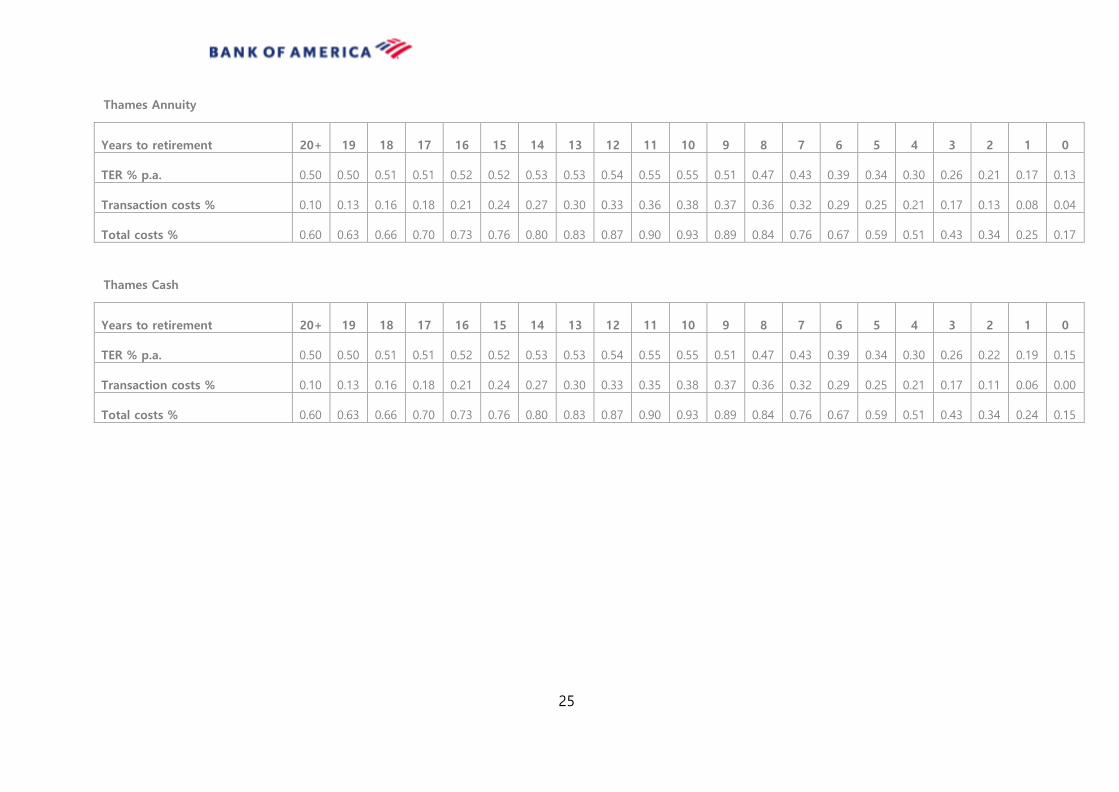

Thames Annuity

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.50

0.50

0.51

0.51

0.52

0.52

0.53

0.53

0.54

0.55

0.55

0.51

0.47

0.43

0.39

0.34

0.30

0.26

0.21

0.17

0.13

Transaction costs % 0.10

0.13

0.16

0.18

0.21

0.24

0.27

0.30

0.33

0.36

0.38

0.37 0.36 0.32 0.29 0.25 0.21 0.17 0.13 0.08 0.04

Total costs % 0.60

0.63

0.66

0.70

0.73

0.76

0.80

0.83

0.87

0.90 0.93 0.89 0.84 0.76 0.67 0.59 0.51 0.43 0.34 0.25 0.17

Thames Cash

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.50

0.50

0.51

0.51

0.52

0.52

0.53

0.53

0.54

0.55

0.55

0.51

0.47

0.43

0.39

0.34

0.30

0.26

0.22

0.19

0.15

Transaction costs % 0.10

0.13

0.16

0.18

0.21

0.24

0.27

0.30

0.33

0.35 0.38 0.37 0.36 0.32 0.29 0.25 0.21 0.17 0.11 0.06 0.00

Total costs % 0.60

0.63

0.66

0.70

0.73

0.76

0.80

0.83

0.87

0.90 0.93 0.89 0.84 0.76 0.67 0.59 0.51 0.43 0.34 0.24 0.15

26

Tay Annuity

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.56

0.56

0.56

0.56

0.56

0.56

0.55

0.54

0.52

0.51

0.50

0.49

0.48

0.47

0.46

0.45

0.40

0.36

0.28

0.20

0.13

Transaction costs % 0.44

0.44

0.44

0.44

0.44

0.44

0.42

0.41

0.39

0.37 0.36 0.34 0.33 0.32 0.30 0.29 0.26 0.23 0.17 0.10 0.04

Total costs % 1.00

1.00

1.00

1.00

1.00

1.00

0.97

0.94

0.91

0.88 0.86 0.83 0.81 0.78 0.76 0.74 0.67 0.59 0.45 0.31 0.17

Tay Cash

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.56

0.56

0.56

0.56

0.56

0.56

0.55

0.54

0.52

0.51

0.50

0.49

0.48

0.47

0.46

0.45

0.44

0.43

0.34

0.24

0.15

Transaction costs % 0.44

0.44

0.44

0.44

0.44

0.44

0.42

0.41

0.39

0.37

0.36 0.34 0.33 0.32 0.30 0.29 0.28 0.27 0.18 0.09 0.00

Total costs % 1.00

1.00

1.00

1.00

1.00

1.00

0.97

0.94

0.91

0.88 0.86 0.83 0.81 0.78 0.76 0.74 0.72 0.70 0.52 0.33 0.15

Tay Flexible

Years to retirement

20+

19

18

17

16

15

14

13

12

11 10 9 8 7 6 5 4 3 2 1 0

TER % p.a. 0.56

0.56

0.56

0.56

0.56

0.56

0.55

0.54

0.52

0.51

0.50

0.49

0.48

0.47

0.46

0.45

0.44

0.43

0.42

0.41

0.40

Transaction costs % 0.44

0.44

0.44

0.44

0.44

0.44

0.42

0.41

0.39

0.37 0.36 0.34 0.33 0.32 0.30 0.29 0.28 0.27 0.27 0.26 0.25

Total costs % 1.00

1.00

1.00

1.00

1.00

1.00

0.97

0.94

0.91

0.88 0.86 0.83 0.81 0.78 0.76 0.74 0.72 0.70 0.69 0.67 0.65

27

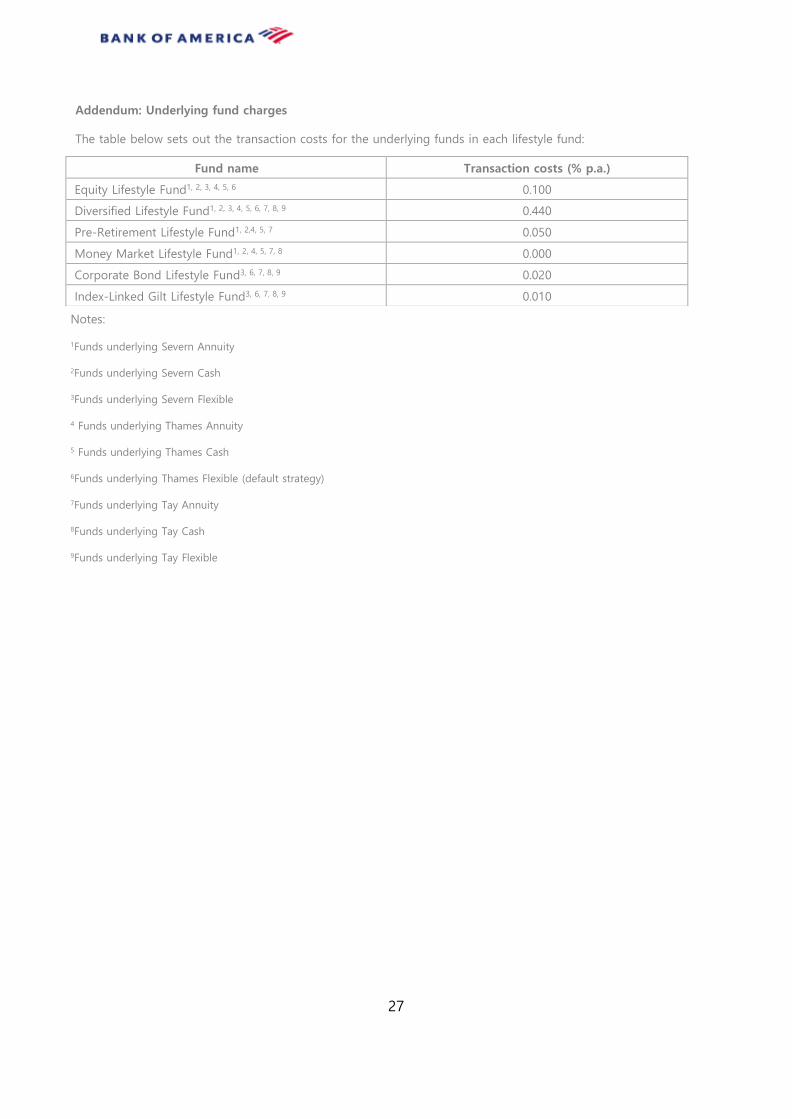

Addendum: Underlying fund charges

The table below sets out the transaction costs for the underlying funds in each lifestyle fund:

Fund name Transaction costs (% p.a.)

Equity Lifestyle Fund1, 2, 3, 4, 5, 6 0.100

Diversified Lifestyle Fund1, 2, 3, 4, 5, 6, 7, 8, 9 0.440

Pre-Retirement Lifestyle Fund1, 2,4, 5, 7 0.050

Money Market Lifestyle Fund1, 2, 4, 5, 7, 8 0.000

Corporate Bond Lifestyle Fund3, 6, 7, 8, 9 0.020

Index-Linked Gilt Lifestyle Fund3, 6, 7, 8, 9 0.010

Notes:

1Funds underlying Severn Annuity

2Funds underlying Severn Cash

3Funds underlying Severn Flexible

4 Funds underlying Thames Annuity

5 Funds underlying Thames Cash

6Funds underlying Thames Flexible (default strategy)

7Funds underlying Tay Annuity

8Funds underlying Tay Cash

9Funds underlying Tay Flexible

28

Statement of Investment Principles

This Statement of Investment Principles (‘SIP’) covers both the defined benefit (also known as ‘final salary’) and

the defined contribution (also known as ‘money purchase’) sections of the Bank of America UK Retirement Plan

(the ‘Plan’). Each of the two sections of the Plan are covered individually below. This SIP also covers the Trustee’s

policy on issues that apply equally to both sections.

Details of the appointed managers can be found in a separate document produced by the Trustee entitled

“Summary of Investment Arrangements”.

Defined Benefit Section

1. Investment Objective

The Trustee aims to invest the assets of the Plan prudently to ensure that the benefits promised to Plan

members are provided. In setting the Plan’s investment strategy, the Trustee took advice from its

investment adviser and consulted with the sponsoring employer. The asset allocation strategy selected is

designed to achieve a higher return than the lowest risk strategy while maintaining a prudent approach to

meeting the Plan’s liabilities.

2. Strategy

The current planned asset allocation strategy chosen to meet the objective above is set out in the table

below. In addition to the assets detailed below the Trustee has purchased an annuity policy designed to

pay the benefits of the pensioner membership covered in the policy. The annuity policy provides protection,

however the Trustee does not target a specific allocation to annuity policies. Instead the Trustee considers

opportunities to purchase annuity policies as and when pricing and the Plan's circumstances permit. The

strategic allocation set out in the table below therefore excludes the allocation to any annuity policies.

Based on the Trustee's Gilts +0% basis, the value of the Plan's annuity policies was c.£408m as at 31 March

2020 (calculated using December 2019 membership data. At 31 March 2020 this c.£408m valuation was out

of total assets of c.£1,696m i.e. 24% of total assets. This percentage of total assets will vary over time).

This Statement of Investment Principles is produced to meet the requirements of the Pensions

Acts 1995 & 2004, the Occupational Pension Schemes (Investment) Regulations 2005 and to

reflect the Government's Voluntary Code of Conduct for Institutional Investment in the UK.

The Trustee also complies with the requirements to maintain and take advice on the Statement

and with the disclosure requirements.

29

Section / Asset Class

Target

Weight (ex.

buy-in) (%) Benchmark

Performance

Target (p.a)

Returns Section 30 Composite

Beta 10

*Property IPD All Balanced Funds +1%

Cash Plus 20

Loans 3 Month LIBOR +4%

Property Debt

Unconstrained Bonds

Protection Section 70 Plan specific liability benchmark

Absolute Return Bond Investments (ARBIs)

3 Month LIBOR +2%

Asset Backed Securities 3 Month LIBOR +2%

Cash/Money Market 7 Day LIBID +0.5%

LDI Plan specific liability benchmark

*As and when an opportunity at what the Trustee considers a fair price is available, the Trustee intends to redeem from the

Property allocation and replace it with something more liquid but providing a similar contribution to total expected return.

• The Returns section consists of a 'Beta' subsection and 'Cash Plus' subsection. 'Beta' mandates are those

where performance is expected to be determined largely by market returns. 'Cash Plus' mandates are those

where performance is expected to be determined largely by manager skill.

• Target weights are in respect of total assets excluding the annuity policy.

The Plan has a Liability Driven Investment (LDI) allocation within the Protection section. The value of the LDI

allocation will vary over time in line with its objective of mitigating the interest rate and inflation risks faced by

the Plan (excluding those already hedged by the annuity policy).

The Trustee monitors the actual asset allocation versus the target weights listed in the asset allocation strategy

on a quarterly basis. The Trustee considers rebalancing the assets back towards the target weights should the

asset allocations deviate significantly from the target.

The current investment strategy was determined with regard to:

• The actuarial characteristics of the Plan, i.e. the nature and timing of the Plan’s expected future liability cash

flows. These characteristics were considered when designing the Plan’s LDI mandate.

• The strength of the current funding position and sponsoring employer’s covenant (the direct covenant rests

with the sponsoring employers of the Plan: MLI and MLIH).

• The sponsoring employer’s contribution policy.

The Trustee’s policy is to make the assumption that return seeking asset classes will outperform the Plan's

liabilities over the long term. The Trustee also assumes that active fund management can be expected to add

value. However, the Trustee recognises the potential volatility in return seeking assets relative to the present

value of the Plan’s liabilities.

Prior to setting the current investment strategy, the Trustee considered written advice from its investment adviser

and in doing so addressed the following:

• The need to consider a full range of asset classes including private equity, property and other alternative

30

assets.

• The overall risks and expected returns of a range of alternative asset allocation strategies.

• The suitability of each asset class.

• The need for appropriate diversification.

The Trustee also consulted with the sponsoring employer when setting the Plan’s investment strategy.

3. Risk Measurement and Management

The Trustee maintains a ‘Statement of Funding Principles’ which specifies that the funding objective is to have

sufficient assets so as to make provision for 100% of the Plan’s liabilities as determined by an actuarial

calculation.

The Trustee recognises that the key risk to the Plan is that it has insufficient assets to make provisions for 100%

of its liabilities (‘funding risk’). The Trustee has identified a number of risks which have the potential to cause a

deterioration in the Plan’s funding level and therefore contribute to funding risk. These are as follows:

• The risk of a significant difference in the sensitivity of asset and liability values to changes in financial and

demographic factors (‘mismatching risk’). The Trustee and its advisers considered this mismatching risk when

setting the investment strategy and have specifically structured the Plan’s assets so as to mitigate this risk.

• The risk of a shortfall of liquid assets relative to the Plan’s immediate liabilities (‘cash flow risk’). The Trustee

and its advisers will manage the Plan’s cash flows taking into account the timing of future payments in order

to minimise the probability that this occurs.

• The failure by the fund managers to achieve the performance targets set by the Trustee relative to the

benchmark (‘manager risk’). This risk is considered by the Trustee and its advisers both upon the initial

appointment of the fund managers and on an ongoing basis thereafter.

• The failure to spread investment risk (‘risk of lack of diversification’). The Trustee and its advisers considered

this risk when setting the Plan’s investment strategy and when appointing multi asset fund managers.

• The possibility of failure of the Plan’s sponsoring employer (‘covenant risk’). The Trustee and its advisers

considered this risk when setting investment strategy and consulted with the sponsoring employer as to the

suitability of the proposed strategy. The Trustee has appointed a covenant adviser to monitor the covenant

on an ongoing basis.

• The risk of fraud, poor advice or acts of negligence (‘operational risk’). The Trustee has sought to minimise

such risk by ensuring that all advisers and third-party service providers are suitably qualified and

experienced and that suitable liability and compensation clauses are included in all contracts for professional

services received.

Due to the complex and interrelated nature of these risks, the Trustee considers the majority of these risks in a

qualitative rather than quantitative manner as part of each formal investment strategy review (normally

triennially). Some of these risks may also be modelled explicitly during the course of such reviews.

The Trustee’s policy is to monitor, where possible, these risks quarterly. The Trustee receives quarterly reports

showing:

• Estimated current funding level versus the Plan’s specific funding objective.

• Performance of the Plan’s assets versus the overall investment objective.

• Performance of individual fund managers versus their respective targets.

31

• Evaluative comments and any significant issues regarding the Plan’s current fund managers.

• Performance of the Plan’s LDI mandate and its success at reducing mismatching risk.

• Projected risk attribution for the Plan's assets relative to the liabilities.

More broadly the Trustee maintains a risk register which looks at the whole range of risks to which the Plan may

be subject. This includes the risks described above.

4. Implementation

The Plan’s strategy is implemented largely through investment in pooled funds (at the time of writing the only

exception is the segregated LDI mandate). The fund managers are monitored and may change from time to time.

The investment objectives of each mandate and its alignment with the Plan’s strategy is considered at inception

and on an ongoing basis.

The Plan’s LDI mandate has been implemented through a portfolio of physical gilts and gilt derivatives of various

maturities. The LDI mandate is not designed to achieve a profit for the Plan. Instead, it has been implemented to

try and reduce the volatility of the Plan’s overall funding level through time. Movements in long-term interest

rates and inflation expectations affect the present value of the Plan’s expected future liabilities. The LDI mandate

hedges the Plan against these movements.

32

Defined Contribution Section

1. Investment Objective

The Trustee is responsible for providing an appropriate range of investment options to members. Its key aim is

to provide a range of investments that are suitable for meeting members' long and short-term investment

objectives. It has taken into account members' circumstances, in particular the range of members' attitudes to

risk and term to retirement.

2. Strategy

The Trustee's policy is to provide suitable information for members so that they can make appropriate

investment decisions. The range of funds was chosen by the Trustee after taking expert advice from the Trustee's

investment advisers. In choosing the Plan's investment options, it is the Trustee's policy to consider:

• A wide range of asset classes.

• The suitability of each asset class for a defined contribution plan.

• The need for appropriate diversification of asset classes.

• The suitability of the possible styles of investment management and the need for manager diversification.

In addition, the Trustee will consider the characteristics of various member types or groups and the potential

differences between these in relation to attitude to risk over the period of their membership in the Plan, and the

different ways in which benefits may be taken at retirement.

The Trustee expects the long-term return on the investment options that invest predominantly in equities to

exceed price inflation and general salary growth. The long-term returns on the bond and cash options are

expected to be lower than returns on predominantly equity options. However, bond funds have the potential to

broadly offset changes in the price of annuities, giving some protection to the amount of pension that can be

secured by members choosing to purchase an annuity at retirement. Cash funds are expected to provide

protection against changes in short-term capital values.

2.1 Investment options

The investment options for members of the defined contribution section of the Plan comprise nineteen freestyle

and three risk-differentiated lifestyle strategies.

The three Lifestyle strategies each have options aligned to the at retirement access choices of: flexible

drawdown, annuity or cash.

The Lifestyle options are designed based on analysis of the demographics of the Plan’s membership to provide a

range of options offering members a choice of investment risk and potential for growth. These will be reviewed

on an ongoing basis to ensure they remain appropriate for a broad range of the membership.

The Lifestyle options are designed using a retirement age that can be pre-selected by the member, otherwise a

default age is used. The Trustee recognises that the Lifestyle options may be less suitable for members who

retire earlier or later than their chosen, or the Plan's, default age, and communicates this issue to members.

The Freestyle fund range has been designed to enable members to create a diversified investment portfolio; the

range comprises both single-manager funds and multi-manager ‘blended’ funds, with blending used where it is

33

felt that manager diversification and/or style differentiation could enhance member outcomes. The range

contains a number of passively managed options as well as actively managed funds, offering the member the

option of paying a lower level of fees for index-tracking, or higher fees in seeking the potential of additional

returns. Actively managed funds have the objective to outperform the index net of fees to ensure that active

management is delivering value for members. The Plan also makes available a Shariah Fund and an

Environmental, Social & Governance Global Equity Fund for those wishing to invest in line with the specific

objectives of these funds.

The Trustee does not allow members to have simultaneous investments in both Freestyle and Lifestyle options. A

member must invest solely either in Freestyle options or in one of the Lifestyle options.

2.2 Default strategy

The Trustee has chosen the Thames Flexible Lifestyle option as the default investment for the Plan. This is the

strategy that has the most balanced approach to risk and return of the three Lifestyle options available and the

Trustee therefore views it as being the one most appropriate for the majority of members who have not made a

decision on where to invest.

The ‘Flexible’ pre-retirement option has been chosen as the Trustee expects, based on analysis of the

membership and in particular the projected longer-term average value of members’ funds at retirement, that

many would potentially look for income drawdown in retirement. Importantly in selecting this as the default, this

strategy also reflects in its design that there will be members who choose alternative options such as annuity or

cash at retirement.

2.3 Ongoing monitoring and review

The Trustee has a policy in place to review the funds within both the Lifestyle and Freestyle funds on an on-

going basis. Where it is deemed that a manager or fund is no longer appropriate, the Trustee has operational

procedures in place to remove and replace the manager or fund from the fund range. To support this process,

the Trustee has created a number of blended ‘white labelled’ funds which allow the replacement of

underperforming managers or funds to be carried out in a timely manner to the benefit of members

3. Risk Measurement and Management

The Trustee recognises the key risk is that members will have insufficient income in retirement or an income that

does not meet their expectations. The Trustee considered this risk when setting the investment options and

strategy for the Plan. The Trustee’s policy in respect of risk measurement methods and risk management processes

is set out below.

The Trustee considers the following sources of risk:

• Risk of not meeting the reasonable expectations of members, bearing in mind members’ contributions and

fund choices.

• Risk of fund managers not meeting their objectives (‘manager risk’). This risk is considered by the Trustee

and its advisers both upon the initial appointment of the fund manager and on an ongoing basis thereafter.

• Risk of asset classes not delivering the anticipated rate of return over the long term.

• Risk of the Lifestyle options being unsuitable for the requirements of some members.

34

• The risk of fraud, poor advice or acts of negligence (‘operational risk’). The Trustee has sought to minimise

such risk by ensuring that all advisers and third-party service providers are suitably qualified and experienced