Embed Size (px)

Citation preview

BAO6504Accounting for Management Lecture 1

An Introduction to Accounting

and Financial ReportingReference: Chapters 1 & 13

Dr chitra.desilva

Tel 9919 9469

2

INTRODUCTION TO ACCOUNTING

Primary function of accounting is to provide financial information for decision making that is Reliable Relevant

Accounting often referred to as ‘language of business’

3

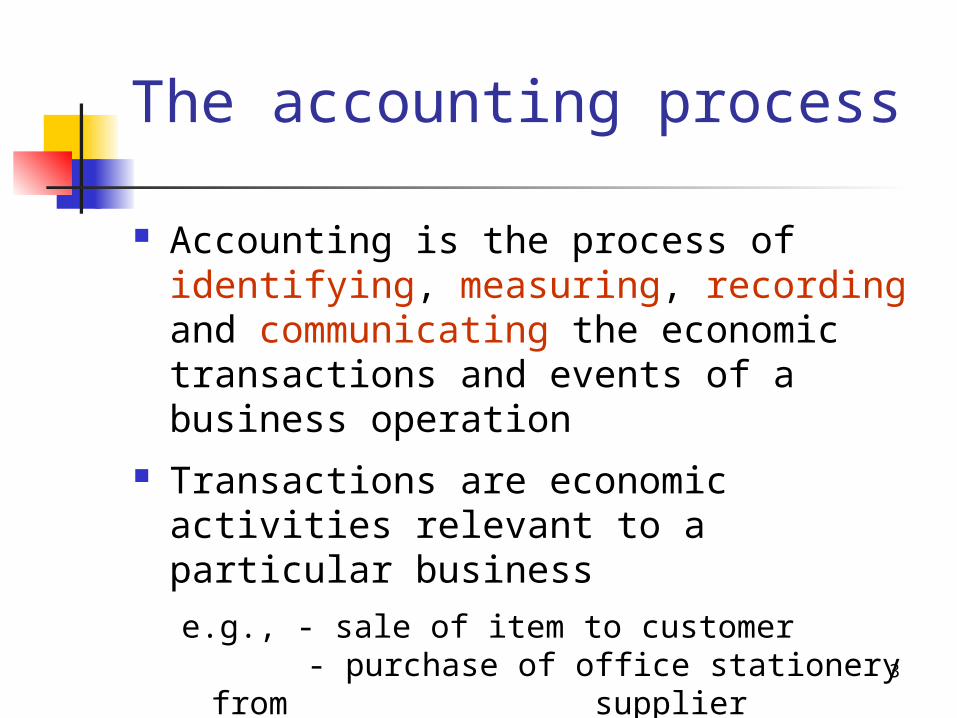

The accounting process

Accounting is the process of identifying, measuring, recording and communicating the economic transactions and events of a business operation

Transactions are economic activities relevant to a particular business

e.g., - sale of item to customer - purchase of office stationery from supplier

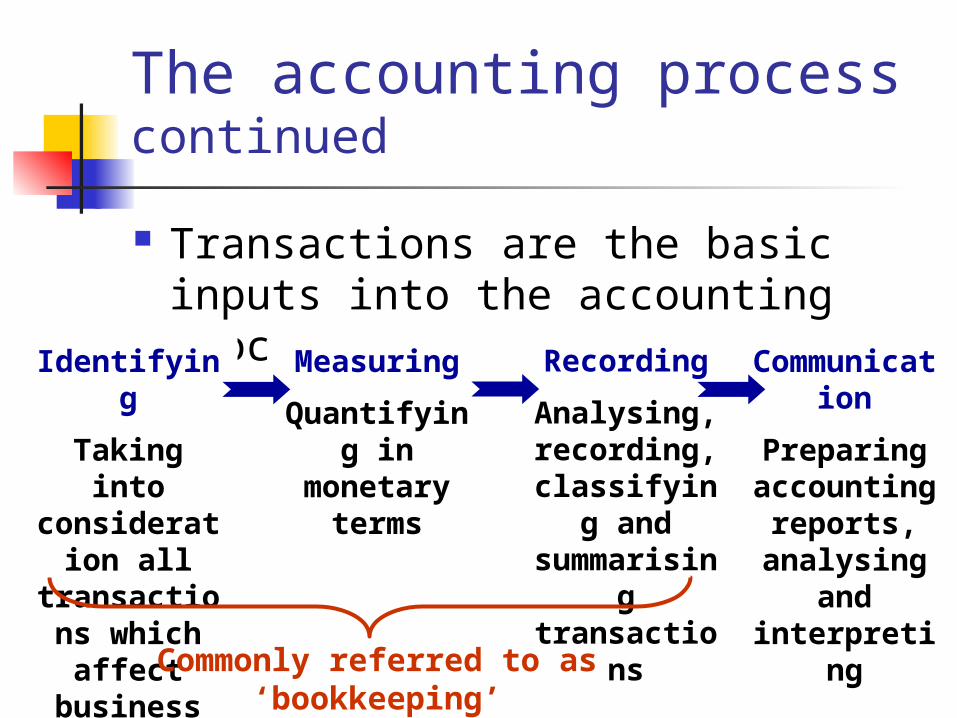

The accounting process continued

Transactions are the basic inputs into the accounting process

Identifying

Taking into consideration

all transactions which affect

business entity

Measuring

Quantifying in monetary terms

Recording

Analysing, recording,

classifying and summarising transactions

Communication

Preparing accounting

reports, analysing and

interpreting

Commonly referred to as ‘bookkeeping’

5

THE FINANCIAL REPORTING ENVIRONMENT

Australian Securities and Investments Commission

Financial Reporting Council Australian Accounting Standards

Board Urgent Issues Group Australian Stock Exchange Regulation in New Zealand Professional Accounting Bodies

6

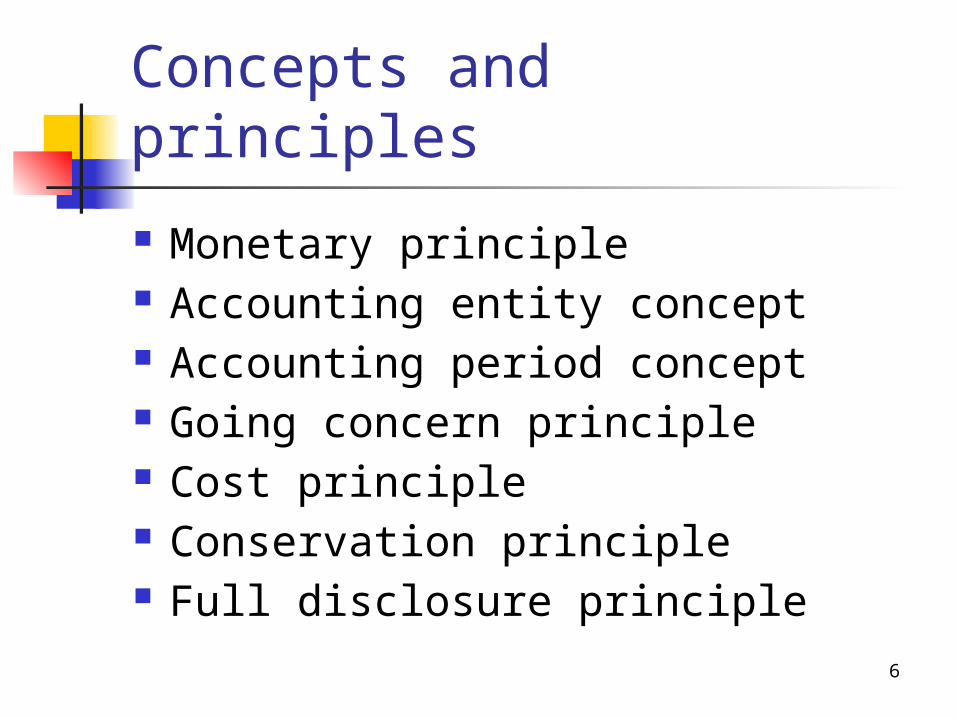

Concepts and principles

Monetary principle Accounting entity concept Accounting period concept Going concern principle Cost principle Conservation principle Full disclosure principle

7

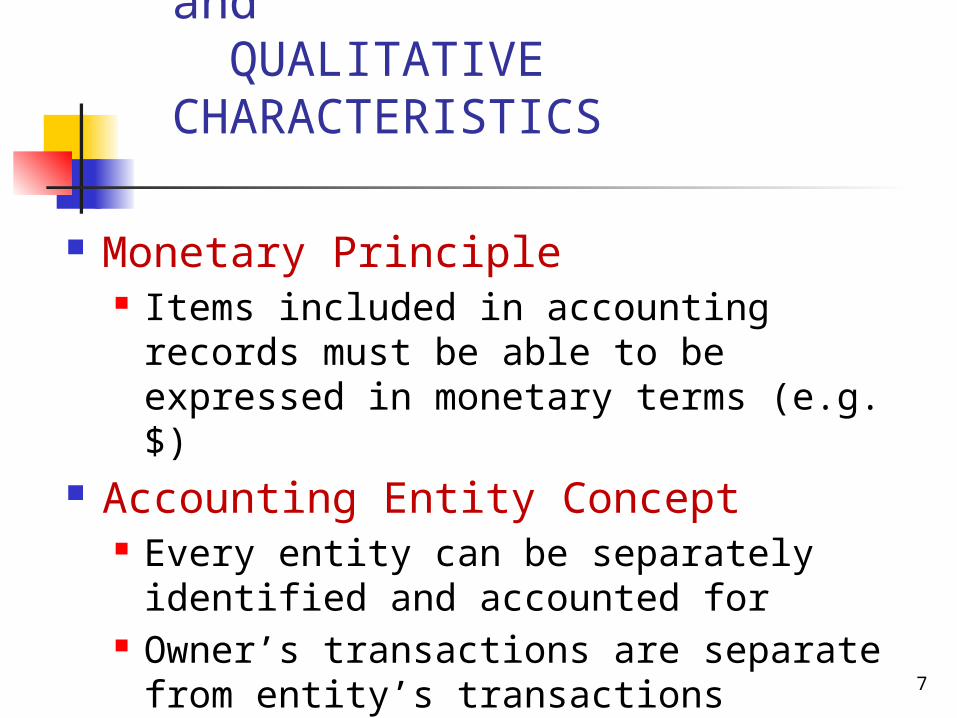

CONCEPTS , PRINCIPLES and QUALITATIVE CHARACTERISTICS

Monetary Principle Items included in accounting records

must be able to be expressed in monetary terms (e.g. $)

Accounting Entity Concept Every entity can be separately identified

and accounted for Owner’s transactions are separate from

entity’s transactions

8

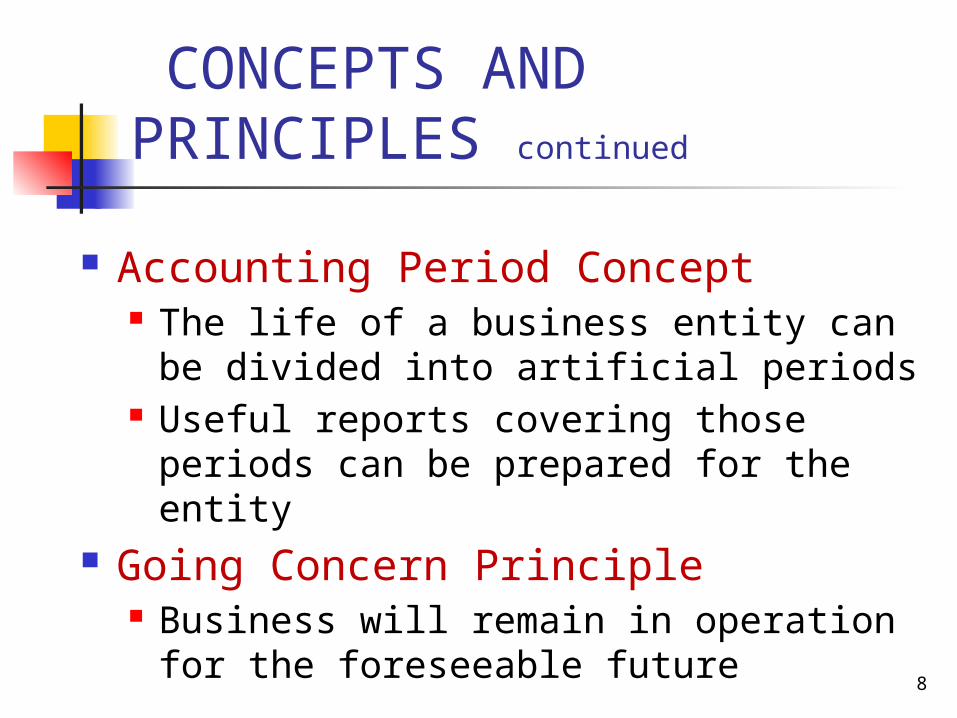

CONCEPTS AND PRINCIPLES continued

Accounting Period Concept The life of a business entity can be

divided into artificial periods Useful reports covering those periods

can be prepared for the entity Going Concern Principle

Business will remain in operation for the foreseeable future

9

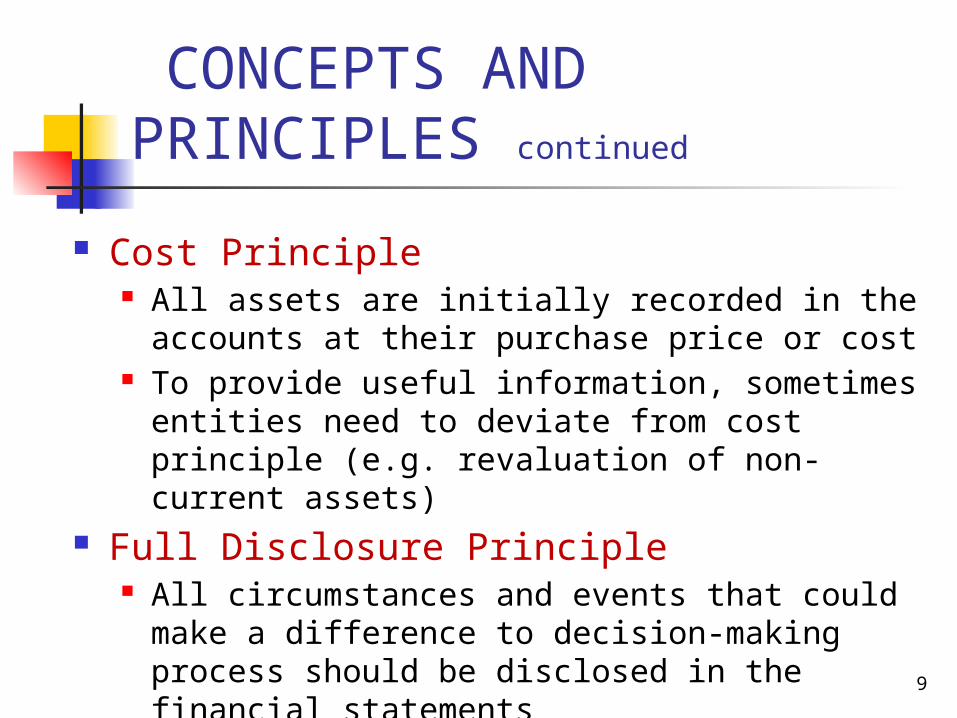

CONCEPTS AND PRINCIPLES continued

Cost Principle All assets are initially recorded in the accounts

at their purchase price or cost To provide useful information, sometimes

entities need to deviate from cost principle (e.g. revaluation of non-current assets)

Full Disclosure Principle All circumstances and events that could make a

difference to decision-making process should be disclosed in the financial statements

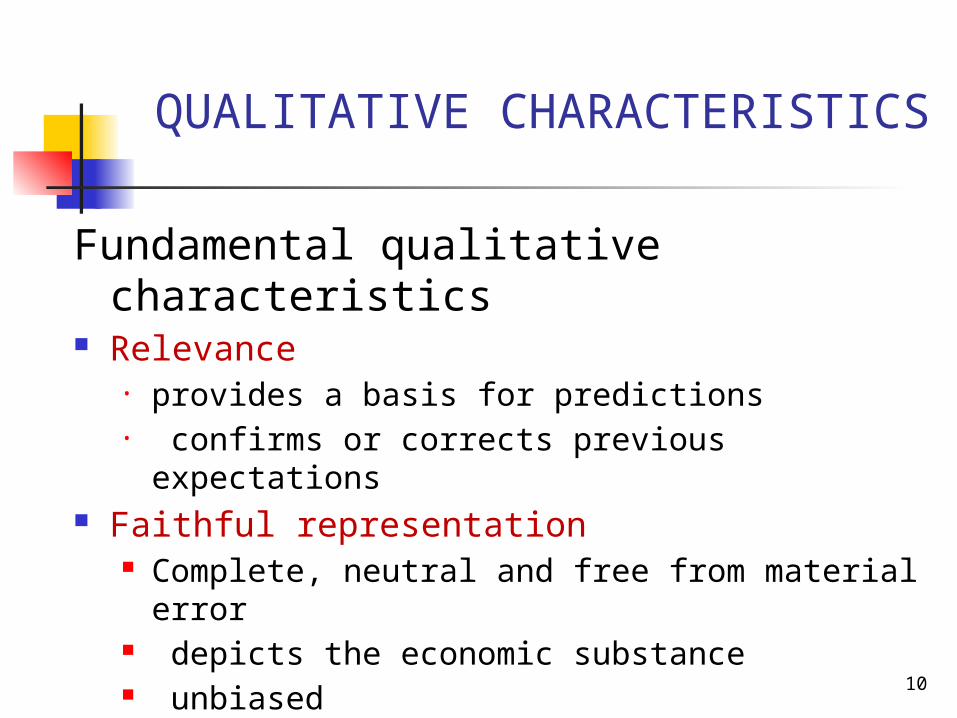

QUALITATIVE CHARACTERISTICS

Fundamental qualitative characteristics Relevance

• provides a basis for predictions• confirms or corrects previous expectations

Faithful representation Complete, neutral and free from material error depicts the economic substance unbiased judgements and estimates reflect best

available information 10

QUALITATIVE CHARACTERISTICS

Enhancing qualitative characteristics Comparability

between different companies between different years of the same company

Verifiability Independent observer consensus

Timeliness Preparers should not take so long to prepare financial

reports that the reported information loses its relevance Understandability

able to be understood by proficient users

11

CONSTRAINTS OF FINANCIAL REPORTING

Costs versus benefits Costs of preparing financial reports should not

exceed the benefits to be derived from the reports

12

13

FORMS OF BUSINESS ORGANISATION

Sole Proprietorship Owned by one person e.g. restaurants, dentist, panel beaters

Partnership Owned by more than one partner e.g. accountants, solicitors, doctors

Corporation organised as a separate legal entity and owned by

shareholders BHP, CSR, Westpac, RM Williams

14

USERS AND USES OF FINANCIAL INFORMATION

Primary users of general purpose financial reports are the resource providers

Resource providers are equity investors, lenders and other creditors

Equity investors contribute resources usually cash for a return include shareholders (existing and potential), holders of partnership interests

Lenders contribute by lending resources for the purpose of receiving a return in form of interest

Other creditors provide resources in the form of credit ; eg suppliers, employees

15

USERS AND USES OF FINANCIAL INFORMATION continued

Other Users Recipients of goods and services

e.g. customers, beneficiaries Parties performing a review or oversight

function e.g. regulatory agencies, media,

governments, trade unions, special interest groups

USERS AND USES OF FINANCIAL INFORMATION continued

Internal Users Managers who plan, organise and run

the business e.g. production supervisors, marketing

managers, and directors

16

GENERAL PURPOSE FINANCIAL REPORTS

General purpose financial reports are the published financial statements of an entity prepared in accordance with applicable accounting standards

External users have an interest in 3 main types of activities financing investing and operating

17

18

GENERAL PURPOSE FINANCIAL REPORTS continued

Financing Activities Outside sources of funds

Borrowing (debt funding) from banks or investors by debt securities

Unsecured notes Debentures

Selling shares to investors Payments to shareholders are called dividends

19

GENERAL PURPOSE FINANCIAL REPORTS continued

Investing Activities Acquisition or sale of resources/assets

needed to operate the business Examples:

Purchase or sale of property plant and equipment

Purchase of investments

20

GENERAL PURPOSE FINANCIAL REPORTS continued

Operating Activities Results from operational activities

undertaken to earn income: Revenue (sale of goods, provision of

services, return from investments)LESS

Expenses (cost of resources/assets consumed or services used)

SUSTAINABILITY REPORTING

Sustainability -making sure the social, economic and environmental needs of our community are met and kept healthy for future generations

Concerned 3 main areas Economic Environmental Social

21

THE ANNUAL REPORT

Go to

www.ibm.com/investor/help

Provided is a guide on the parts of an Annual Report prepared by companies to communicate to investors, creditors and management the health of the organisation.

22