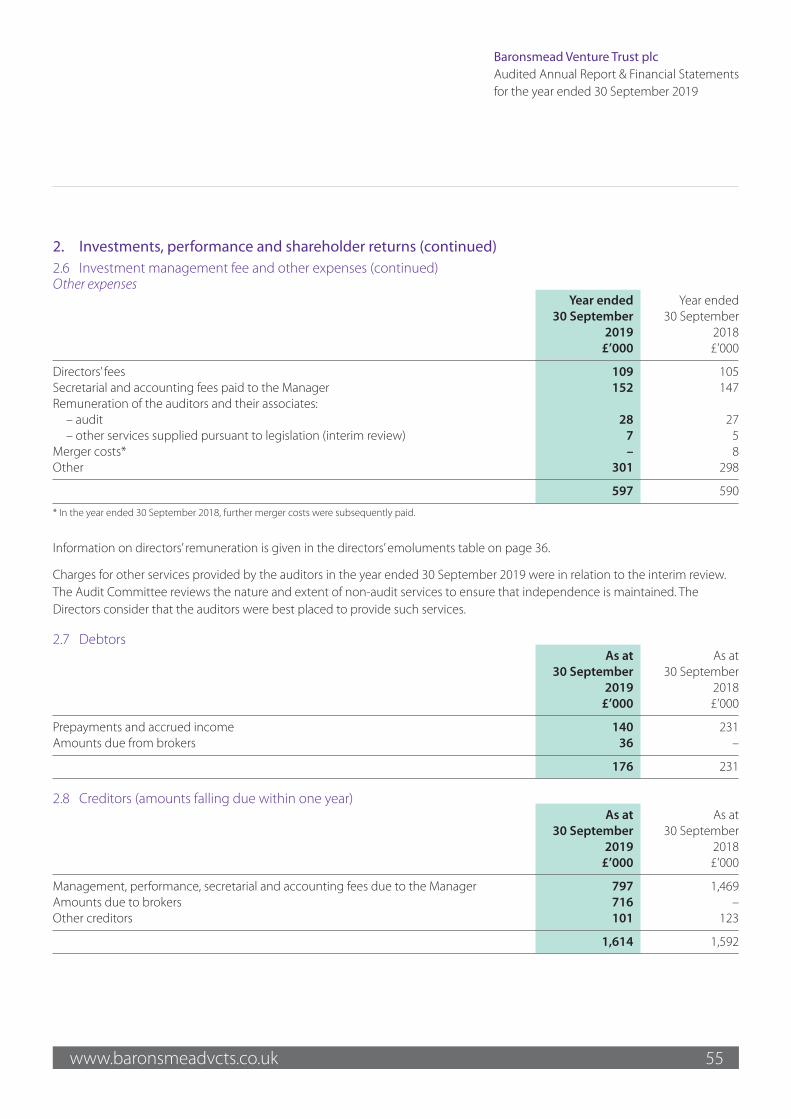

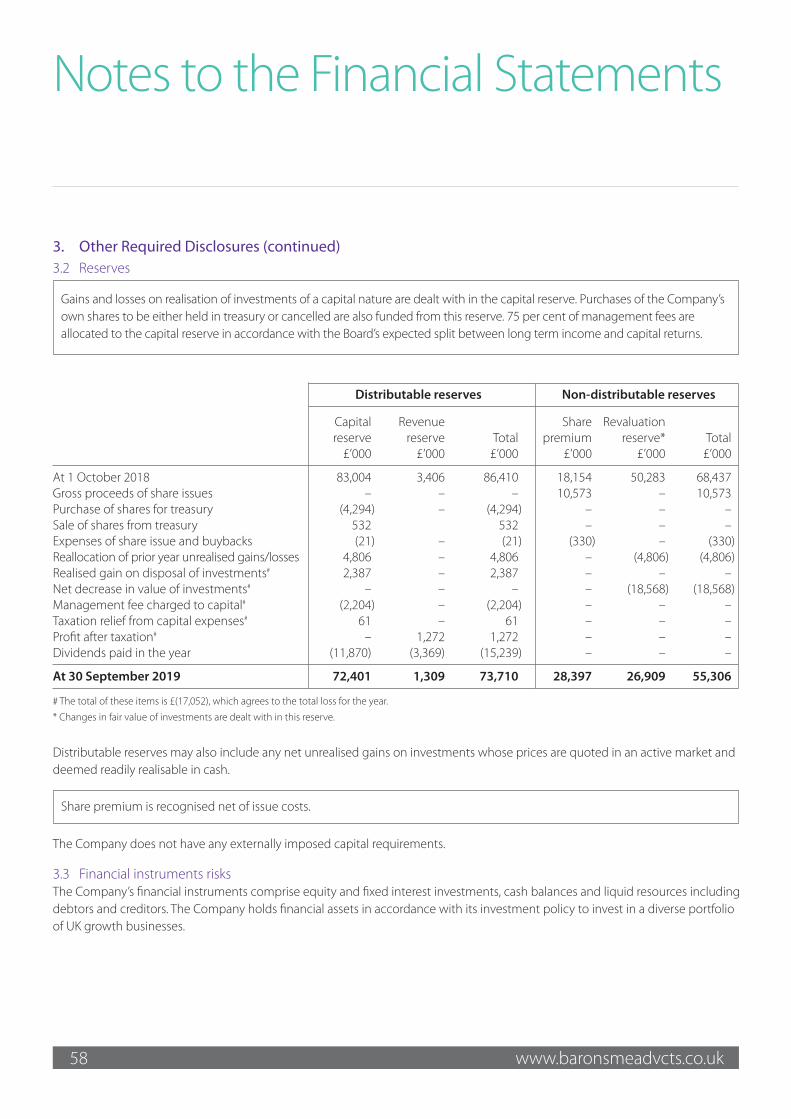

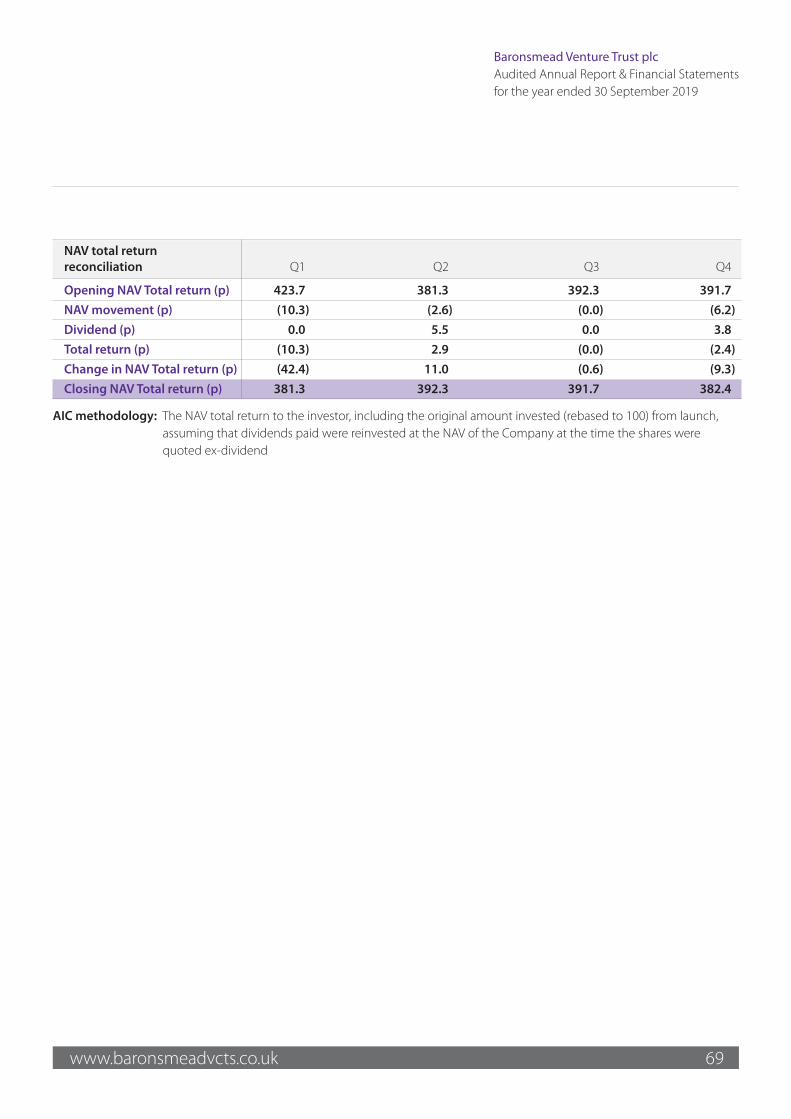

Embed Size (px)

Citation preview

2019Audited Annual Report and Financial Statements for the year ended 30 September 2019

Baronsmead Venture Trust plc

Baronsmead Venture Trust Cover 25/11/2019 07:56 Page a

www.baronsmeadvcts.co.uk

About Baronsmead Venture Trust plcOur Investment ObjectiveBaronsmead Venture Trust plc is a taxefficient listed company which aims toachieve long-term investment returns forprivate investors, including tax-freedividends.

Investment PolicyTo invest primarily in a diverseportfolio of UK growth businesses,whether unquoted or traded on AIM.

Investments are made selectivelyacross a range of sectors in companiesthat have the potential to grow andenhance their value.

Dividend PolicyThe Board will, wherever possible, seekto pay two dividends to Shareholdersin each calendar year, typically aninterim in September and a finaldividend following the Annual GeneralMeeting in February/March;

The Board will use, as a guide, whensetting the dividends for a financialyear, a sum representing 7 per cent ofthe opening NAV of that financial year.

Key elements of the Business Model

Access to an attractive,diverse portfolioBaronsmead Venture Trust plc givesshareholders access to a diverse portfolioof growth businesses.

The Company will make investments ingrowth businesses, whether unquotedor traded on AIM, which are substantiallybased in the UK in accordance with theprevailing VCT legislation. Investmentsare made selectively across a range ofsectors.

The Manager’s approach toinvestingThe Manager endeavours to select thebest opportunities and applies adistinctive selection criteria based on:

Primarily investing in parts of theeconomy which are experiencing longterm structural growth

Businesses that demonstrate, or havethe potential for, market leadership intheir niche

Management teams that can developand deliver profitable and sustainablegrowth

Companies with the potential tobecome an attractive asset appealing toa range of buyers at the appropriatetime to sell

In order to ensure a strong pipeline ofopportunities, the Manager invests inbuilding deep sector knowledge andnetworks and undertakes significantproactive marketing to target companies inpreferred sectors. This approach generates anetwork of potentially suitable businesseswith which the Manager maintains arelationship ahead of possible investmentopportunities.

The Manager as aninfluential shareholderFor unquoted investments, the Manageris an engaged shareholder (on behalf ofthe Company) and representatives of theManager often join the investee boards.The role of the Manager with investees isto ensure that strategy is clear, thebusiness plan can be implemented andthe management resources are in placeto deliver profitable growth. The aim is tobuild on the business model and growthe company into an attractive targetwhich can be sold or potentially floatedin the medium term.

A more detailed explanation of how the investment policy and business model are applied is provided in the Other Matterssection of the Strategic Report on pages 18 to 22. The full investment policy can be found on page 63.

Baronsmead Venture Trust Cover 25/11/2019 07:56 Page b

www.baronsmeadvcts.co.uk 1

Baronsmead Venture Trust plcAudited Annual Report & Financial Statements for the year ended 30 September 2019Contents

Strategic Report

Financial Headlines 2Performance Summary 3Chairman’s Statement 4Manager’s Review 7Ten Largest Investments 12Principal Risks & Uncertainties 16Other Matters 18

Directors’ Report

Report of the Directors 23Board of Directors 23Corporate Governance 26Directors’ Remuneration Report 34Statement of Directors’ Responsibilities 38KPMG Independent Auditor’s Report 39

Financial Statements

Income Statement 45Statement of Changes in Equity 46Balance Sheet 47Statement of Cash Flows 48Notes to the Financial Statements 49

Appendices

Investment Policy 63Ten Year Dividend History 64Dividends Paid Since Launch 64Performance Record Since Launch 65Cash Returned to Shareholders Since Launch 65Full Investment Portfolio 66Glossary 68

Information

Shareholder Information and Contact Details 70Corporate Information 72

If you have sold or otherwise transferred all of your ordinary shares in Baronsmead Venture Trust plc, please forward thisdocument and the accompanying notice of Annual General Meeting and form of proxy as soon as possible to the purchaser ortransferee, or to the stockbroker, bank or other agent through whom the sale or transfer was, or is being, effected, for delivery tothe purchaser or transferee.

YappyYappy is an online personaliseddog product business foundedin 2018 and operating in the UKand US. The Manager hassuccessfully backed the founderof Yappy in a high growth,e-commerce businesspreviously. The platform offersa seamless customer experience,with each user having their ownpersonalised shop front witha large range of availableproducts all tailored to theindividual consumer.

Diaceutics Diaceutics is a data analyticsbusiness in the pharma sector.Diaceutics aggregates andcleanses multiple data pointsspecific to diagnostic testingfrom thousands of laboratoriesglobally. It then uses the dataand insights to help pharmacompanies either launchingnew drugs or acceleratinggrowth of existing drugs.

The Panoply HoldingsThe Panoply is a European ITservices company focused ondigital transformation in privatecompanies and the publicsector. Founded in 2016, ThePanoply is pursuing a buy-and-build strategy, initiallyconsolidating four companies atIPO. The Company provides arange of services includingconsultancy and softwaredevelopment which supportscustomers to digitally enhancetheir businesses.

Some examples of our recent investments

TravelLocalTravelLocal is a global onlinetravel marketplace, whichthrough its technology platformconnects consumers directly tovetted local travel experts tohelp design, organise anddeliver bespoke holidays;resulting in a more authenticand personal holiday experiencefor each consumer.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 1

2 www.baronsmeadvcts.co.uk

Financial Headlines

Strategic Report

Annual tax free dividend yield1,3

Annual tax free dividend yield based on 6.5p dividends(including proposed final dividend of 3.5p) and opening NAVof 87.0p.

7.5%

Net asset value total return1

Net Asset Value (“NAV”) total return to shareholders for every100.0p invested at launch (April 1998).

382.4p

New investmentsInvestments made into 13 new and 7 follow on opportunitiesduring the year.

£13.6m

Net asset value total return

Pence

0

100

200

300

400

500

201920182017

Net asset value per share1,2

NAV per share decreased 10.3 per cent to 78.1p in the12 months to 30 September 2019, before deductions ofdividends.

(10.3)%60

65

70

75

80

85

90

201920182017

Pence

* includes proposed !nal dividend of 3.5p

Dividends*Net asset value per share

0

2

4

6

8

10

2019*20182017

%

* includes proposed !nal dividend of 3.5p

£m

02468101214

201920182017

1 Alternative Performance Measures (“APM”) – pleaser refer to glossary on page 68 for definitions.2 Please refer to table on page 4 for breakdown of NAV per share movement.3 New APM in 2019.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 2

www.baronsmeadvcts.co.uk 3

Baronsmead Venture Trust plc Audited Annual Report & Financial Statements for the year ended 30 September 2019

Performance Summary

Ten Year Performance Record

Cash Returned to Shareholders by Date of Investment The chart below shows the cash returned to shareholders based on the subscription price and the income tax reclaimed on subscription.

Cash invested (p)

*Includes proposed final dividend of 3.5p

Income tax reclaim (p)

Pence

Cumulative dividends (p)*

0

20

40

60

80

100

120

140

160

180

200

2019(February)Ordinary

2017(October)Ordinary

2016(February)Ordinary

2014(March)Ordinary

2012(December)

Ordinary

2009(April)

Ordinary

2004(October)C Shares

2000(March)Ordinary

2000(February)Ordinary

1999(May)

Ordinary

1998(April)

Ordinary

** Net asset value total return (gross dividends reinvested) rebased to 100p.

** Net asset value increase following the merger of Baronsmead VCT plc & Baronsmead VCT2 plc in February 2016

Source: Gresham House Asset Management Ltd

Net asset value per share Share price (mid) Net asset value total return per share* Total net assets (£m)

Pence £m

50

100

150

200

250

300

350

400

450

201920182017201620152014201320122011201040

60

80

100

120

140

160

180

200

65.0m72.4m

75.8m83.1m 85.1m

150.6m**159.0m 175.5m

151.1m

63.7m

Baronsmead Venture Trust pp01-22.qxp 09/03/2020 13:54 Page 3

4 www.baronsmeadvcts.co.uk

During the year we have seen steady, positive progress from our unquotedinvestments including several successful realisations, although the quoted portfoliosuffered as a result of falling markets.

ResultsThe Company’s NAV per share decreased 10 percent from 87p to 78p before payments ofdividends during the year.

Pence per ordinary share

NAV as at 1 October 2018 (after final dividend) 87.0

Valuation decrease (10.3 per cent) (8.9)

NAV as at 30 September 2019 before dividends 78.1

Less:

Interim dividend paid on 27 September 2019 (3.0)

Proposed final dividend of 3.5p payable, after shareholder approval, on 6 March 2020 (3.5)

Illustrative NAV as at 30 September 2019 after dividends 71.6

Portfolio ReviewAt 30 September 2019, the Company’sinvestment portfolio was valued at £96 millionand comprised direct investments in a total of82 companies of which 28 are unquoted and54 are AIM-traded companies. The Company’sinvestments in the LF Gresham House UK MicroCap Fund (“Micro Cap”) and LF Gresham HouseUK Multi Cap Income Fund (“Multi Cap”) provideadditional diversity giving investment exposureto an additional 57 AIM-traded and fully listedcompanies and thus spreading investment riskacross some 139 companies.

During the 12 months to 30 September 2019,the underlying value of the unquoted portfolioincreased by 11 per cent.

It was disappointing to see a decrease in thevalue of the AIM-traded portfolio of 25 per cent.Performance was negatively impacted by thede-rating of the Trust’s holding in Staffline whichdowngraded profit expectations and undertooka dilutive equity fund raising to strengthen itsbalance sheet. Excluding this impact theremaining AIM-traded portfolio decreased by16 per cent. It should be noted that includingdivestments in previous years the Trust’sinvestment in Staffline has generated profits of£6.0 million, equivalent to 3.0p per share. Therewas also a decrease of 7 per cent in the MicroCap fund while the Multi Cap fund performancewas broadly flat over the period with a smallincrease of 1 per cent, following volatile tradingsince October 2018.

The quoted portfolios have been impacted bynegative sentiment towards the UK equitymarkets due to the uncertainty surroundingBrexit and wider economic conditions. SmallerUK listed companies, and domestically focusedbusinesses where your Trust’s investeecompanies typically sit, have underperformedtheir larger and more international peers sincethe referendum result in 2016. The Managerbelieves that the underlying health andprospects of the portfolio remain strong andvaluations are depressed. This view has beensupported by an elevated level of takeover offerswithin UK small cap companies during 2019coming from international trade as well asprivate equity buyers.

Peter LawrenceChairman

Strategic ReportThe Chairman’s Statement forms part of the Strategic Report.

Chairman’s Statement

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 4

www.baronsmeadvcts.co.uk 5

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

7.5% annualdividendyield(includingproposedfinal dividendof 3.5p)

£20.3mrealised fromfull andpartial salesduring theyear

NAV totalreturnof 382.4pper 100pinvestedfor foundershareholders

Investments and DivestmentsThe Manager has continued to build itsinvestment activity to focus on the provision ofdevelopment capital to earlier stage companies.The Board is pleased to report that theinvestment rate has continued to grow andduring the year the Company invested a total ofnearly £14 million in 20 companies. The newinvestments in earlier stage opportunities mayresult in greater volatility in returns over time.However, the more mature, established portfolioof existing investments should assist insustaining returns for shareholders as the newportfolio develops and grows.

There have been a number of strong realisationsduring the year. Firstly, from the unquotedportfolio, there was a total of £15 million realisedfrom full and partial sales. Full realisationsincluded a post-2015 investment, SymphonyVentures, a robotic process automationconsultancy business, resulting in a successfulreturn on cost of 2.4x. Other notable fullrealisations during the year were Create Healthfor 3.6x cost and Kirona for 3.1x cost. UpperStreet Events and IP Solutions were sold for 0.7xcost and 0.4x cost respectively.

Three quoted investments were fully realisedduring the period. Sanderson Group was realisedafter a takeover resulting in a return of 2.7x costand a partial divestment STM Group realised 0.9xcost. A notable additional success was the partialprofitable sale of shares in Bioventix. TheManager carefully reviews its larger quotedholdings and decided to crystallise some of thevalue in Bioventix, resulting in an outstandingreturn of 15.0x cost. Our investments inCrawshaw Group, a chain of butchers andParagon Entertainment were written off in theperiod, although the majority of the value ofthese investments had decreased in previousyears.

The Board is delighted to see realised capitalprofits being created to continue to fund currentand future dividends for shareholders.

Change of Dividend policyThe Board announced a change to the dividendpolicy on 23 September 2019. The previouspolicy was to sustain an annual dividend level atan average of 6.5p per ordinary share. The Boardbelieves this is no longer appropriate for tworeasons. Firstly, the number of shares hasincreased and will increase further throughfuture fundraisings and the absolute level of thisdividend may in time become too high tosustain consistently as a percentage of NAV.Secondly, as the proportion of investments inearlier stage companies increases, following theVCT rule changes in 2015, it is expected that thetiming of returns will be less predictable. TheBoard feels it is therefore prudent to adopta yield based dividend.

The new policy is as follows:

The Board will decide the annual dividends eachyear and the level of the dividends will dependon investment performance, the level of realisedreturns and available liquidity. The dividendpolicy guidelines below are not binding and theBoard retains the ability to pay higher or lowerdividends relevant to prevailing circumstancesand actual realisations. However, the Boardconfirms the following two guidelines thatshape its dividend policy:

The Board will, wherever possible, seek to•pay two dividends to Shareholders in eachcalendar year, typically an interim inSeptember and a final dividend followingthe AGM in February/March; and

The Board will use, as a guide, when setting•the dividends for a financial year, a sumrepresenting 7 per cent of the opening NAVof that financial year.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 5

Chairman’s Statement

6 www.baronsmeadvcts.co.uk

Strategic Report

Change of managerThe change of Investment Manager fromLivingbridge VC LLP (“Livingbridge”) to GreshamHouse Asset Management Ltd (“GreshamHouse”) on 30 November 2018 has been asmooth and well planned transition. The teamthat moved to Gresham House has continued towork in accordance with the terms of theoriginal investment management andco-investment agreements, with continuedsupport from Livingbridge partners, AndrewGarside and Sheenagh Egan.

The Board is pleased with the smooth and swiftintegration of the team into Gresham House andwith the high level of support and investmentprovided by our new Investment Manager.

FundraisingIn August 2019 the Board announced itsintention to raise new funds to enhance theCompany’s resources available for new andfollow on investments over the next two tothree years. Consequently, on 4 October 2019the Company launched an offer for subscriptionto raise £20 million (before costs). As at the dateof this statement there has been £11 millioninvested by shareholders and the offer remainsopen. We would like to thank existingshareholders for their continued support and towelcome new shareholders.

Annual General MeetingI look forward to meeting as many shareholdersas possible at the Annual General Meeting(“AGM”) to be held at 11.00am on 26 February2020, at Saddlers’ Hall, 40 Gutter Lane, London,EC2V 6BR. As usual I will present my own reviewof the year and will be joined by the Manager.We would be delighted if you would then join usfor lunch afterwards.

BrexitThe impact of the uncertainty caused by thelong-awaited Brexit deal has been most keenlyfelt in the volatile performance of our AIMportfolio over the year. The Board andInvestment Manager have considered the risksBrexit poses to the unlisted investments in theportfolio. The impact of changes in foreigncurrency exchange rates, the supply of labourand short-term fluctuations in demand has beenassessed across the portfolio of unlistedinvestments. The Board and the InvestmentManager continue to believe that theinvestment portfolio is robustly positioned towithstand the potential impact of Brexit.

The Investment Manager continues to considerthe risks and opportunities that Brexit maypresent in all new investment and portfoliomanagement decisions. The early stageinvestment arena remains highly active in the UKand Brexit does not appear to be reducingdemand for investment from young, innovativeand ambitious UK companies. The Board willcontinue to monitor Brexit developments asthey occur.

OutlookThere are macro-economic risks arising fromexternal factors including Brexit and trade warsand the quoted markets have experiencedvolatility this year. As always, the InvestmentManager endeavours to focus on fundamentalsof company performance and looks to the longterm, as the evergreen structure of your VCTfacilitates. Risk mitigation also comes in partfrom increasing diversity across a large portfolioof now 82 direct investees.

Peter LawrenceChairman

22 November 2019

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 6

Manager’s Review

www.baronsmeadvcts.co.uk 7

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

Ken WottonHead of Quoted Investments

Steve CordinerHead of Unquoted Investments

Bevan DuncanHead of Portfolio Management

Tania HayesDivisional Finance Director

During the year there were:

13 new and 7 follow on•investments in unquoted andquoted companies totalling £13.6m

11 realisations and 1 loan note•repayment that deliveredproceeds totalling £20.3m

Each quarter the direction of general trading and profitability of all investeecompanies is assessed so that the Board can monitor the overall health andtrajectory of the portfolio. At 30 September 2019, 85 per cent of the82 companies directly held in the portfolio (excluding the investments held byCollective Investment Vehicles) were progressing steadily or better.

The tables on pages 10 and 11 show the breakdown of new investments andrealisations over the course of the year and overleaf is commentary on some ofthe key highlights in both the unquoted and quoted portfolios.

It is disappointing to report a decline in the net asset value total return over the year. This has been driven by theunderperformance of the quoted portfolio primarily linked to the negative market sentiment towards UK small cap stocks. Wecontinue to believe that there is an attractive long-term investment case for the majority of the large quoted holdings. Theunquoted portfolio has seen steady performance with some strong realisations during the year helping offset some of thequoted portfolio decline.

PORTFOLIO REVIEWOverviewThe net assets of £151 million were invested as follows:

NAV % of Number of % return inAsset class (£m) NAV* investees the year**

Unquoted 42 28 28 11AIM-traded companies 54 36 54 (25)LF Gresham House UK Micro Cap Fund 26 17 45 (7)

LF Gresham House UK Multi Cap Income Fund 3 2 42 1

Liquid assets# 26 17 N/ATotals 151 100 169

* By value as at 30 September 2019.

** Return includes interest received on unquoted realisations during the year.# Represents cash, OEICs and net current assets.

Andrew HampshireGresham House

Chief Operating Officer

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 7

8 www.baronsmeadvcts.co.uk

Strategic Report

Manager’s Review

Investment Diversification at 30 September 2019Sector by value

Total assets by value

Time investments held by value

Business Services 27% Consumer Markets 14% Healthcare & Education 17% Technology, Media &

Telecommunications (“TMT”) 42%

Less than 1 year 12% Between 1 and 3 years 12% Between 3 and 5 years 14% Greater than 5 years Collective investment vehicles 62%

Unquoted – loan stock 14% Unquoted – equity 14% AIM 36%

31% Net current assets 5%

Investment Activity – Unquoted and QuotedDuring the year, £13.6 million was invested in 20 companiesincluding 13 new additions to the portfolio and 7 follow oninvestments. Below are descriptions of a selection of the newinvestments made;

Diaceutics plc (quoted) is a data analytics business in the•pharma sector.

Rockfish Group Limited (unquoted) is a chain of specialist•seafood restaurants based in Devon. Rockfish specialise inserving fresh local & sustainable seafood from their chain ofsix restaurants.

Storyshare Holdings Ltd (unquoted) provides learning and•employee engagement software for large businesses withmobile or international workforces

The Panoply Holdings plc (quoted) is an IT services•company focused on digital transformation in privatecompanies and the public sector. The Company providesa range of services including consultancy and softwaredevelopment which supports customers to digitallyenhance their businesses.

TravelLocal Ltd (unquoted) is an online travel agent that•differentiates itself from traditional bespoke holidayoperators by putting customers directly in touch with

experts who live in each country to help arrange itineraries,providing a more authentic and unique experience.

Vinoteca Ltd (unquoted) is a wine bar and restaurant•business built around an extensive wine choice andseasonal contemporary food. The company operates a chainof five wine bars and restaurants in London with a sixth sitecurrently in development in Birmingham.

Your Welcome (unquoted) supplies tablets and software•into vacation rental, Airbnb and corporate letting properties,with their proprietary software improving the guestexperience through an information portal, providing tipsand recommendations on the local area and a guestcommunication tool.

The company continues to execute its investment strategydeveloped since the November 2015 VCT rule changes. Thestrategy is to diversify investment across a number of smallerinvestments with the expectation of selectively providing followon funding as these companies grow to develop.

As Investment Manager we have a hands-on approach with eachinvestment company working with the management teams tohelp them accelerate growth. In addition to our in-houseportfolio team, we have a network of operating partners whohave deep experience of supporting investee companies and indelivering key business milestones and unlocking growth.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 8

www.baronsmeadvcts.co.uk 9

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

Unquoted PortfolioPerformanceThe unquoted portfolio has had a steady year of progress witha performance of 11 per cent increase over the course of the year.The portfolio is valued by the Board using a consistent valuationmethodology every quarter. The majority of the value createdby portfolio companies comes from trading and operationalimprovements including revenue and margin growth, rather thanfinancial leverage.

Divestments During the year the unquoted portfolio returned £15 million inproceeds following the full realisation of Create Health (3.6x cost),Kirona (3.1x cost) and Symphony Ventures (2.4x cost). Thisrepresents an excellent trio of realisations.

Along with the three successful realisations, two companies werefully realised at a loss. Upper Street Events was sold for 0.7x costand IP Solutions was fully realised for 0.4x cost. Armstrong Cravenmade a loan note repayment within the year and has now returned1.7x original invested cost over the course of our hold period. Therewas also a partial loan note write off in CMME as part of a balancesheet restructure.

After the year end the Company realised its investment in CR7 ata full loss.

Quoted Portfolio (AIM-traded investments)PerformanceThe quoted portfolio has had disappointing performance duringthe year with a decrease of 25 per cent as a result of difficultmarket conditions and stock specific factors.

The three top performers were Sanderson Group, a software andIT services business focused on digital retail technology andenterprise software to manufacturing, wholesale distribution andlogistics sectors, which was fully realised during the year afterannouncing a recommended cash offer by Aptean Limited;Bioventix, a manufacturer and supplier of sheep monoclonalantibodies for global diagnostic applications, driven by stronginterim results earlier in the year and Ixico, a pharma-focused dataanalytics and services business specialising in neurodegenerativediseases, after a strong trading update announcing contract winsand results expected to be materially ahead of expectations.

The major negative performer during the year was StafflineRecruitment Group after announcing a material profit warning inpart driven by Brexit uncertainty. Other detractors to performancewere Netcall, a customer engagement software provider whoissued a profit downgrade due to delayed contracts, LoopUpGroup, a conference calling solutions provider following a profitwarning due to lower activity in the existing customer base andDods Group, a provider of business intelligence, conference and

media services to the political, public sector and corporatemarkets, following a profit warning due to softer tradingconditions in the UK driven by political uncertainty towards theend of 2018.

While we have seen valuation decreases in a number of thecompanies in our quoted portfolio we believe the drop inperformance is largely due to market sentiment. We closely monitorour AIM portfolio with a rolling programme of independent reviewsof top AIM holdings and broadly continue to be positive on thelong-term investment prospects of these companies.

Divestments Proceeds totalled £5.3 million during the year following 3 full and2 partial realisations. Sanderson Group plc was fully realisedfollowing a takeover by Aptean Limited realising 2.7x cost whileCrawshaw Group and Paragon Entertainment were written off forzero proceeds during the year. The opportunity to crystallisesome profits was taken in two companies with proceeds of£2.0 million in Bioventix representing a 15.0x cost and a smallrealisation in STM Group realising 0.9x cost.

Collective Investment VehiclesLF Gresham House UK Micro Cap Fund (“Micro Cap”) had anegative return of 7 per cent over the year (2018, 19 per cent).At 30 September 2019, Baronsmead Venture Trust’s cumulative£7.0 million investment was valued at £25.8 million. As at30 September 2019, the Micro Cap fund held investments in45 AIM-traded and main market listed companies.

The investment in LF Gresham House UK Multi Cap Income Fund(“Multi Cap”) has had a modest increase of 1 per cent over theyear. At 30 September 2019, Baronsmead Venture Trust’sinvestment was valued at £2.8 million. As at 30 September 2019,the Multi Cap fund held investments in 41 AIM-traded and mainmarket listed companies.

Liquid assets (cash and near cash) Baronsmead Venture Trust plc had cash and liquidity OEICs ofapproximately £28 million at the year-end. This asset class isconservatively managed to take minimal or no capital risk.

OUTLOOKWe anticipate further periods of market volatility during theremainder of 2019 and into 2020, given the wider political andmacro-economic uncertainties. However, we continue to believethat in an uncertain market environment our focus on investing ina diverse portfolio of companies with strong fundamental attributeshas the potential to outperform over the cycle.

Gresham House Asset Management LtdInvestment Manager

22 November 2019

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 9

10 www.baronsmeadvcts.co.uk

Strategic Report

Investments in the year

Book costCompany Location Sector Activity £’000

Unquoted investmentsNew

IWP Holdings Ltd London Business Services Investment management advisory services 1,407

Vinoteca Ltd London Consumer Markets Chain of wine bars / restaurants 934

Samuel Knight International Ltd Newcastle Upon Business Services Global recruitment specialists 705Tyne

TravelLocal Ltd London Consumer Markets Online travel agent specialising in tailor-made 705holidays

Cisiv Ltd London TMT Pharmaceutical web-based software platform 700

Rainbird Technologies Ltd Norfolk TMT Decision support software with a focus on 700professional services and the financial services sector

RockFish Group Ltd Devon Consumer Markets Seafood restaurant chain 700

Tribe Digital Holdings Pty Ltd London TMT Influencer marketing interface 699

Storyshare Holdings Ltd London TMT Business App developer 536

Yappy Ltd Manchester Consumer Markets Supplier of customisable pet products 470

Follow on

Custom Materials Ltd (trading as London TMT Retailer of customisable products 782Moteefe)

Your Welcome Ltd London TMT Supplier of tablets and software for vacation 587rental properties

Equipsme (Holdings) Ltd London Business Services SME Health Insurance Plans Provider 140

SilkFred Ltd London Consumer Markets Online Fashion market place 115

Total unquoted investments 9,180

AIM-traded investmentsNew

Diaceutics plc Belfast Healthcare & Pharmaceutical data analytics and services 1,410Education

Entertainment AI plc London TMT Provides automated platform for analysis and 1,410monetisation of video content

The Panoply Holdings plc London TMT Information technology services company 585operating in the digital transformation sector

Follow on

CloudCall Group plc Leicestershire TMT Cloud based telephony platform 859

Collagen Solutions plc London Healthcare & Develops and manufactures medical grade 114Education collagen

Access Intelligence plc London Business Services Provider of corporate communications and 69reputation management software

Total AIM-traded investments 4,447

Total investments in the year 13,627

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 10

www.baronsmeadvcts.co.uk 11

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

Realisations in the year

First Original Overallinvestment book cost# Proceeds‡ multiple

Company date £’000 £’000 return*

Unquoted realisations

Create Health Ltd Trade sale Mar 13 556 4,923 3.6

Kirona Ltd Trade sale Dec 14 1,066 4,343 3.1

Symphony Ventures Ltd Trade sale Aug 17 1,575 3,502 2.4

Upper Street Events Ltd Trade sale Dec 14 1,906 1,203 0.7

Armstrong Craven Ltd Loan repayment Jun 13 606 934 1.7

IP Solutions Ltd Trade sale Dec 14 1,383 135 0.4

CMME Group Ltd Loan note restructure Apr 15 980 0 0.0

Total unquoted realisations 8,072 15,040

AIM-traded realisations

Sanderson Group plc Take over Dec 04 1,176 3,178 2.7

Bioventix plc Market sale Jun 13 134 2,004 15.0

STM Group plc Market sale Mar 08 124 109 0.9

Crawshaw Group plc Write Off Jul 14 400 0 0.0

Paragon Entertainment Ltd Write Off Dec 11 498 0 0.0

Total AIM-traded realisations 2,332 5,291

Total realisations in the year 10,404 20,331†

# Residual book cost at realisation date.

‡ Proceeds at time of realisation including interest.

* Includes interest/dividends received, loan note redemptions and partial realisations accounted for in prior periods.

† Deferred consideration of £20,000 was received in respect of Eque2 which had been sold in a prior period.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 11

12 www.baronsmeadvcts.co.uk

Ten Largest Investments

Strategic ReportThe top ten investments by current value at 30 September 2019 illustrate the diversity of investee companies within the portfolio. For consistency across the topten and based on guidance from the AIC, data extracted from the last set of published audited accounts is shown in the tables below. However, this may notalways be representative of underlying financial performance for several reasons. Published accounts lodged at Companies House are out of date and the Managerworks from up to date monthly management accounts and has access to draft but unpublished annual audited accounts. In addition, pre-tax profit in statutoryaccounts is often not a representative indicator of underlying profitability as it can be impacted by, for example, deductions of non-cash items such as amortisationthat relate to investment structures rather than operating performance.

Carousel Logistics LtdSittingbourneUnquoted

http://www.carousel.eu

Carousel Logistics based in Kent, designs and manages bespokesupply chain management solutions for clients with time critical,challenging or high touch customer care needs. Carousel has awide range of international clients for whom it delivers a completeintegrated service including e-fulfilment, procurement,warehousing, distribution, reverse logistics and internationalin-night services. Carousel acquired BDA in 2019, cementing itsposition as an industry leader underpinned by cutting edgetechnology. The acquisition increased company revenue by50 per cent.

1All funds managed by Gresham HouseFirst investment: October 2013Total original cost: £4,245,000Total equity held: 26.7%

Baronsmead Venture Trust onlyOriginal cost: £1,910,000Valuation: £8,028,000Valuation basis: Earnings MultipleIncome recognised in the year: £168,000% of equity held: 12.0%Voting rights: 12.9%

Year ended 31 December2018 2017

£ million £ millionSales: 38.5 31.8Pre-tax profits: (1.6) 0.0Net Assets: 2.3 1.8No. of Employees: 124 128

(Source: Carousel Logistics Limited Financial Statement31 December 2018.)

All funds managed by Gresham House†First investment: January 2013Total original cost: £3,000,000Total equity held: 5.0%

Baronsmead Venture Trust onlyOriginal cost: £1,350,000Valuation: £7,323,000Valuation basis: Bid PriceIncome recognised in the year: £13,000% of equity held: 2.3%Voting rights: 2.3%

Year ended 30 April2019 2018

£ million £ millionSales: 46.7 36.1Pre-tax profits: 1.4 1.4Net Assets: 73.7 50.5No. of Employees: 451 375

(Source: Ideagen plc, Annual Report & Accounts, 30 April 2019.)

Ideagen PlcNottinghamshireQuoted

www.ideagen.com

Ideagen is a governance, risk management and compliance (“GRC”)software and solutions business operating predominantly in thehealthcare, transport, aerospace & defence, manufacturing andfinancial services sectors. It provides content lifecycle solutions thatenable organisations to meet their regulatory and compliancestandards, helping them to reduce corporate risks and deliveroperational excellence. Its solutions cover enterprise and incidentrisk management, operational safety and quality management,audit risk management, as well as content and clinical solutions forthe NHS. Since the Baronsmead VCTs invested, the company hassuccessfully executed a buy-and-build strategy in the GRC softwaremarket to add capability and build on its market position.

2

† Excludes collective investment vehicles.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 12

www.baronsmeadvcts.co.uk 13

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

Happy Days Consultancy LtdCornwallUnquoted

www.happydaysnurseries.com

Happy Days is a leading child day care and early years educationprovider operating from 21 settings across the South West. Thebusiness focusses on delivering outstanding quality childcare inpremium settings within its target geographic markets.

The investment has enabled Happy Days to continue its UKexpansion strategy through supporting the funding to developnew leasehold nursery settings in attractive markets..

3All funds managed by Gresham HouseFirst investment: April 2012Total original cost: £7,600,000Total equity held: 57.2%

Baronsmead Venture Trust onlyOriginal cost: £3,420,000Valuation: £5,027,000Valuation basis: Earnings MultipleIncome recognised in the year: £Nil% of equity held: 25.7%Voting rights: 15.9%

Year ended 31 December2018 2017

£ million £ millionSales: 9.8 8.0Pre-tax profits: (1.9) (2.2)Net Assets: (8.2) (6.5)No. of Employees: 371 336

(Source: H. Days Holdings Limited Annual Report and FinancialStatements 31 December 2018.)

All funds managed by Gresham HouseFirst investment: May 2007Total original cost: £5,000,000Total equity held: 8.1%

Baronsmead Venture Trust onlyOriginal cost: £2,500,000Valuation: £4,892,000Valuation basis: Earnings MultipleIncome recognised in the year: £Nil% of equity held: 4.0%Voting rights: 4.0%

Year ended 31 January2019 2018*

£ million £ millionSales: 52.3 11.1Pre-tax profits: (15.1) (4.2)Net Assets: (56.1) (40.5)No. of Employees: 278 235

(Source: Glide Topco Ltd, Report and Financial Statements 31 January 2019.)* 3 month period ended 31 January 2018.

Glide LtdSomersetUnquoted

www.glidegroup.co.uk

Glide provides broadband and WiFi connections to studentaccommodation, build to rent properties and business parks, andutilities & bill-sharing to students and landlords. It delivers nicheconnectivity to harder-to-serve parts of the market. Glide acquiredits Shared Living division, focused on bill splitting, in May 2016 andWarwicknet in December 2016. The business reaches over 100,000premises and 350,000 students, and is active internationally, sellingin the UK, Ireland, Spain, Italy, Germany, Austria and TheNetherlands.

4

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 13

14 www.baronsmeadvcts.co.uk

Strategic Report

Cerillion PlcLondonQuoted

www.cerillion.com

7

Bioventix plcSurreyQuoted

www.bioventix.com

5

Pho Holdings LtdLondonUnquoted

www.phocafe.co.uk

6

Bioventix manufactures and supplies highaffinity sheep monoclonal antibodies for usein diagnostic applications such as clinicalblood testing. The company was founded in2003 as a biotechnology company and theirstrategy is to identify new or existingcommercial assays for which there is a needfor improved antibodies. They supplyantibodies to almost all of the globalmultinational immunodiagnostics companies.Since the Baronsmead VCTs first invested in2013, the company has tripled its revenuesand almost quadrupled profits.

All funds managed by Gresham House†First investment: June 2013Total original cost: £711,000Total equity held: 5.3%

Baronsmead Venture Trust onlyOriginal cost: £320,000Valuation: £4,514,000Valuation basis: Bid PriceIncome recognised in the year: £209,000% of equity held: 2.4%Voting rights: 2.4%

Year ended 30 June 2019 2018£ million £ million

Sales: 9.3 8.0Pre-tax profits: 7.0 6.9Net Assets: 10.8 11.0No. of Employees: 16 15(Source: Bioventix Plc, Annual Report and FinancialStatements, 30 June 2019.)

Pho is a fast casual restaurant chain servingVietnamese street food. Pho – a noodle soup –is the national dish of Vietnam. Pho also offer anarray of Vietnamese dishes and drinks.

Pho was founded in 2005 and now successfullyoperates from 29 sites in several differentchannels: London High St sites (e.g. Soho,Clerkenwell); regional sites (e.g. Brighton,Leeds); and food courts in shopping centres(e.g. Westfield). Sales through the home deliverychannel also continue to grow strongly.

* 52 week period ended 25 February 2018.** 52 week period ended 26 February 2017.

All funds managed by Gresham HouseFirst investment: July 2012Total original cost: £4,402,000Total equity held: 28.6%

Baronsmead Venture Trust onlyOriginal cost: £1,982,000Valuation: £4,411,000Valuation basis: Earnings MultipleIncome recognised in the year: £Nil% of equity held: 12.9%Voting rights: 12.9%

Year ended 25 February 2018* 2017**£ million £ million

Sales: 30.5 25.9Pre-tax profits: (1.0) 0.0Net Assets: 3.5 4.5No. of Employees: 605 540(Source: Pho 2012 Limited, Directors’ Report and FinancialStatements 25 February 2018.)

Cerillion provides carrier-grade enterpriseCRM and billing software to telecomscompanies globally. Cerillion’s core productprovides mission critical functionality toallow customers to manage their billing,charging, network provisioning, workflowand CRM processes, all of which are key froma business operations, revenue delivery andcustomer pipeline managementperspective. Currently Cerillion providesolutions to customers across 43 countries,which include their core product as well asCerillion Skyline, an industry agnosticsoftware-as-a-service billing application.

All funds managed by Gresham HouseFirst investment: November 2015Total original cost: £4,000,000Total equity held: 17.8%

Baronsmead Venture Trust onlyOriginal cost: £1,800,000Valuation: £4,074,000Valuation basis: Bid PriceIncome recognised in the year: £109,000% of equity held: 8.0%Voting rights: 8.0%

Year ended 30 September 2018 2017£ million £ million

Sales: 17.4 16.0Pre-tax profits: 1.8 2.0Net Assets: 14.4 13.8No. of Employees: 189 171(Source: Cerillion Plc, Annual Report and Accounts30 September 2018.)† Excludes collective investment vehicles

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 14

www.baronsmeadvcts.co.uk 15

Baronsmead Venture Trust plcAudited Annual Report & Financial Statements for the year ended 30 September 2019

† Excludes collective investment vehicles.

Custom Materials Ltd(trading as Moteefe)LondonUnquoted

www.moteefe.com

9

Inspired Energy plcLancashireQuoted

www.inspiredenergy.co.uk

10

Ten10 Group LtdLondonUnquoted

www.ten10.com

8 Ten10 is one of the leading independentprovider’s of quality assured technical testingservices in the UK onshore market. It achievesthis by offering a unique, seamless set ofdedicated testing services (with deepspecialism in agile environments) from staffaugmentation through managed delivery tooutsource all deliveries through the Ten10assurance wrapper (‘Tenology’).

In December 2015, Centre4Testing merged withThe Test People and the combined organisationwas rebranded as Ten10. Now, Ten10 hasoffices in both London and Leeds with over200 specialists working alongside Enterpriseand mid-market clients and helping to solvesome of their most critical technical challenges.

All funds managed by Gresham HouseFirst investment: February 2015Total original cost: £4,237,000Total equity held: 20.8%

Baronsmead Venture Trust onlyOriginal cost:: £1,908,000Valuation: £3,424,000Valuation basis: Earnings MultipleIncome recognised in the year: £636,000% of equity held: 9.3%Voting rights: 8.4%

Year ended 30 April 2019 2018

£ million £ millionSales: 24.9 20.8Pre-tax profits: (0.4) (2.2)Net Assets: (0.1) 0.6No. of Employees: 228 195(Source: Ten10 Group Limited, Annual Report and FinancialStatements 30 April 2019.)

Moteefe, based in London and Lisbon, isa technology company which provides anonline platform for retailers, online and offlinebusinesses of all sizes to design, market andsell products on demand into socialcommerce globally using print on demandtechnology.

Moteefe provides an end to end solution formerchants including product range, printsupply network, logistics and payment, anda suite of marketing analytics for how amerchants campaigns are performing withlittle to no upfront cost or investment.Currently the business operates three B2B2Cbrands focussed on different internationalmarkets and target merchant segments.

All funds managed by Gresham HouseFirst investment: March 2017Total original cost: £3,550,000Total equity held: 16.1%

Baronsmead Venture Trust onlyOriginal cost: £1,598,000Valuation: £2,998,000Valuation basis: Rebased CostIncome recognised in the year: £Nil% of equity held: 7.2%Voting rights: 7.2%

Year ended 31 December2018 2017

£ million £ millionNet Assets: 1.9 0.5(Source: Custom Materials Ltd, Unaudited FinancialStatements 31 December 2018.)

A full set of accounts is not publicly available.

All funds managed by Gresham House†First investment: November 2011Total original cost: £1,437,000Total equity held: 6.4%

Baronsmead Venture Trust onlyOriginal cost: £574,000Valuation: £2,755,000Valuation basis: Bid PriceIncome recognised in the year: £119,000% of equity held: 2.6%Voting rights: 2.6%

Year ended 31 December 2018 2017£ million £ million

Sales: 32.7 26.4Pre-tax profits: 4.2 3.0Net Assets: 45.3 24.6No. of Employees: 332 257(Source: Inspired Energy Plc, Annual Report and Accounts 2018.)

Inspired Energy is an energy consultancy businessfor commercial and industrial clients, providingenergy procurement, management and advisoryservices to optimise energy costs and carbonemissions. Established in 2000, the company nowhas a team of 240 energy professionals who adviseand manage over 11,500 clients. The corporatedivision comprises five subsidiaries and providesreview, analysis and negotiation of gas andelectricity contracts on behalf of corporate clients;the SME division offers reduced tariffs andcontracts based on unique customer situation. TheBaronsmead VCTs first invested as cornerstoneinvestors in the 2011 IPO and since then InspiredEnergy has grown revenues 11.4x both organicallyand by acquisitions.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 15

16 www.baronsmeadvcts.co.uk

Strategic Report

Principal Risks & UncertaintiesThe Board has included below details of the principal risks & uncertainties facing the Company and the appropriate measures taken in order to mitigate these risksas far as practicable.

Principal Risk Context Specific risks we face

The financial risks faced by the Company are covered within the Notes to the Financial Statements on pages 58 to 61.

Loss of approval asa Venture CapitalTrust

The Company must comply with section 274 of the Income TaxAct 2007 which enables its investors to take advantage of taxrelief on their investment and on future returns.

Breach of any of the rules enabling the Company to holdVCT status could result in the loss of that status.

Legislative VCTs were established in 1995 to encourage private individualsto invest in early stage companies that are considered to berisky and therefore have limited funding options. In return thestate provides these investors with tax reliefs which fall underthe definition of state aid.

A change in government policy regarding the funding ofsmall companies or changes made to VCT regulations tocomply with EU State Aid rules could result in a cessation ofthe tax reliefs for VCT investors or changes to the reliefs thatmake them less attractive to investors.

Investmentperformance

The Company invests in small, mainly UK based companies,both unquoted and quoted. Smaller companies often havelimited product lines, markets or financial resources and maybe dependent for their management on a smaller number ofkey individuals and hence tend to be riskier than largerbusinesses.

Investment in poor quality companies with the resultant riskof a high level of failure in the portfolio.

Economic, politicaland other externalfactors

Whilst the Company invests in predominantly UK businesses,the UK economy relies heavily on Europe as one of its largesttrading partners. This, together with the increase inglobalisation, means that economic unrest and shocks in otherjurisdictions, as well as in the UK, can impact on UK companies,particularly smaller ones that are more vulnerable to changes intrading conditions. In addition the potential impact of leavingthe European Union remains uncertain.

Events such as fiscal policy changes, Brexit, economicrecession, movement in interest or currency rates, civilunrest, war or political uncertainty or pandemics canadversely affect the trading environment for underlyinginvestments and impact on their results and valuations.

Regulatory &Compliance

The Company is authorised as a self managed AlternativeInvestment Fund Manager (“AIFM”) under the AlternativeInvestment Fund Managers Directive (“AIFMD”) and is alsosubject to the Prospectus and Transparency Directives. It isrequired to comply with the Companies Act 2006 and theUKLA Listing Rules.

Failure of the Company to comply with any of its regulatoryor legal obligations could result in the suspension of itslisting by the UKLA and/or financial penalties and sanctionby the regulator or a qualified audit report.

Operational The Company relies on a number of third parties, in particularthe Investment Manager, to provide it with the necessaryservices such as registrar, sponsor, custodian, receiving agent,lawyers and tax advisers.

The risk of failure of the systems and controls of any of theCompany’s advisers leading to an inability to serviceshareholder needs adequately, to provide accuratereporting and accounting and to ensure adherence to allVCT legislation rules.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 16

www.baronsmeadvcts.co.uk 17

Baronsmead Venture Trust plcAudited Annual Report & Financial Statements for the year ended 30 September 2019

Possible impact Mitigation

The loss of VCT status would result in shareholderswho have not held their shares for the designatedholding period having to repay the income taxrelief they had already obtained and futuredividends and gains would be subject to incometax and capital gains tax.

The Board maintains a safety margin on all VCT tests to ensure that breaches are unlikely to be caused byunforeseen events or shocks. The Investment Manager monitors all of the VCT tests on an ongoing basisand the Board reviews the status of these tests on a quarterly basis. Specialist advisors review the tests ona bi-annual basis and report to the audit committee on their findings.

The Company might not be able to maintain itsasset base leading to its gradual decline andpotentially an inability to maintain either its buyback or dividend policies.

The Board and the Investment Manager engage on a regular basis with HMT and industryrepresentative bodies to demonstrate the cost benefit of VCTs to the economy in terms ofemployment generation and taxation revenue. In addition, the Board and the Investment Managerhave considered the options available to the Company in the event of the loss of tax reliefs to ensurethat it can continue to provide a strong investment proposition for its shareholders despite the loss oftax reliefs.

Reduction in both the capital value of investorsshareholdings and in the level of incomedistributed.

The Company has a diverse portfolio where the cost of any one investment is typically less than5 per cent of NAV thereby limiting the impact of any one failed investment. The InvestmentManagement team has a strong and consistent track record over a long period. The Investment Managerundertakes extensive due diligence procedures on every new investment and reviews the portfoliocomposition maintaining a wide spread of holdings in terms of financing stage and industry sector.

Reduction in the value of the Company’s assetswith a corresponding impact on its share price mayresult in the loss of investors through buy backsand may limit its ability to pay dividends.

The Company invests in a diversified portfolio of companies across a number of industry sectors, whichprovides protection against shocks as the impact on individual sectors can vary depending upon thecircumstances. In addition, the Manager uses a limited amount of bank gearing in its investments whichenables its investments to continue trading through difficult economic conditions. The Company alwaysmaintains healthy cash balances so that it can support portfolio companies with further investmentshould the investment case support it. The Board reviews the make up and progress of the portfolio eachquarter to ensure that it remains appropriately diversified and funded.

The Company’s performance could be impactedseverely by financial penalties and a loss ofreputation resulting in the alienation ofshareholders, a significant demand to buy backshares and an inability to attract future investment.The suspension of its shares would result in the lossof its VCT taxation status and most likely theultimate liquidation of the Company.

The Board and the Investment Manager employ the services of leading regulatory lawyers, sponsors,auditors and other advisers to ensure the Company complies with all of its regulatory obligations.The Board has strong systems in place to ensure that the Company complies with all of its regulatoryresponsibilities. The Investment Manager has a strong compliance culture and employs dedicatedcompliance specialists within its team who support the Board in ensuring that the Company iscompliant.

Errors in shareholders records or shareholdings,incorrect marketing literature, non compliance withlisting rules, loss of assets, breach of legal dutiesand inability to provide accurate reporting andaccounting all leading to reputational risk and thepotential for litigation.

The Board has appointed an audit committee who review the internal control (“ISAE3402”) and/orinternal audit reports from all significant third party service providers, including the Investment Manager,on a bi-annual basis to ensure that they have strong systems and controls in place including BusinessContinuity Plans. The Board regularly reviews the performance of its service providers to ensure that theycontinue to have the necessary expertise and resources to provide a high class service and always wherethere has been any changes in key personnel or ownership.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 17

18 www.baronsmeadvcts.co.uk

Strategic Report

Other Matters

Applying the Business ModelThis section of the Strategic Report sets out the practical stepsthat the Board has taken in order to apply the business model,achieve the investment objective, and adhere to theinvestment policy. The investment policy, which is set out infull on page 63, is designed to ensure that the Companycontinues to qualify and is approved, as a VCT byHM Revenue and Customs.

Investing in the Right CompaniesInvestments are primarily made in companies which aresubstantially based in the UK, although many of theseinvestees may have some trade overseas. Investments areselected in the expectation that the application of privateequity disciplines, including an active management style forunquoted companies, will enhance value and enable profits tobe realised from planned exits.

The Board has delegated the management of the investmentportfolio to Gresham House. The Manager has adopted a‘top-down, macro economic and sector-driven’ approach toidentifying and evaluating potential investment opportunities,by assessing a forward view of firstly the broader businessenvironment, then the sector and finally the specific potentialinvestment opportunity.

Based on its research, the Manager has selected a number ofsectors that it believes will offer attractive growth prospectsand investment opportunities. Diversification is also achievedby spreading investments across different asset classes andmaking investments for a variety of different periods.

The Manager’s Review on pages 7 to 9 provides a review of theinvestment portfolio and of market conditions during the year,including the main trends and factors likely to affect the futuredevelopment, performance and position of the business.

Risk is spread by investing in a number of different businesseswithin different qualifying industry sectors using a mixture ofsecurities. The maximum the Company will invest in a singlecompany (including a collective investment vehicle) is 15 percent of its investments by value of its investments calculatedin accordance with Section 278 of the Income Tax Act 2007

(as amended) (“VCT Value”). The value of an individualinvestment is expected to increase over time as a result oftrading progress and a continuous assessment is made of itssuitability for sale.

The Company invests in a range of securities including, butnot limited to, ordinary and preference shares, loan stocks,convertible securities and permitted non qualifyinginvestments as well as cash. Unquoted investments are usuallystructured as a combination of ordinary shares and loan stocksor preference shares, while AIM-traded investments areprimarily held in ordinary shares. Pending investment in VCTqualifying investments, the Company’s cash and liquid fundsare held in permitted non qualifying investments.

VCTs are required to comply with a number of differentregulations and the Company has appointedPricewaterhouseCoopers (“PwC”) as VCT Tax Status Advisers toadvise it on compliance with VCT requirements. PwC reviewsnew investment opportunities, as appropriate, and regularlyreviews the investment portfolio of the Company. PwC worksclosely with the Manager and reports directly to the Board.

Environmental, Human Rights, Employee, Socialand Community IssuesThe Company seeks to conduct its affairs responsibly and theManager is encouraged to consider environmental, humanrights, social and community issues, where appropriate, withregard to investment decisions.

The Company is required, by company law, to provide detailsof environmental (including the impact of the Company’sbusiness on the environment), employee, human rights, socialand community issues; including information about anypolicies it has in relation to these matters and the effectivenessof these policies. The Company does not have any employeesand as a result does not maintain specific policies in relation tothese matters.

As a signatory to the UN-supported Principles for ResponsibleInvestment, Gresham House is committed to operatingresponsibly and sustainably, and believes its strategy of takingthe long view in delivering sustainable investment solutions

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 18

www.baronsmeadvcts.co.uk 19

Baronsmead Venture Trust plcAudited Annual Report & Financial Statementsfor the year ended 30 September 2019

will continue to be a growing factor in the strength of itsmarket position.

Gresham House has an Environmental, Social and Governance(“ESG”) policy.

The six principles of the Gresham House policy are:

1) Encourage a work environment which values and respectsall employees.

2) Adopt a responsible and ethical approach to governance.

3) Incorporate ESG considerations into all investment analysisand decision-making processes where relevant.

4) Ensure Group-wide awareness of ESG issues andcompliance with the Group ESG policy.

5) Promote awareness and adoption of ESG considerations.

6) Inform our investors of this ESG policy and provide themwith information on our approach to ESG issues.

Within the Strategic Equity division of Gresham House, ourinvestment teams judge sound corporate governance to bea significant factor in a company’s ability to create and sustainlong-term shareholder value. ESG considerations areintegrated into our investment processes. Gresham Housesupports the UK Stewardship Code and complies with itsguidelines regarding proxy voting and engagement. GreshamHouse is currently undertaking a review looking at how it canfurther integrate ESG considerations across all aspects of theinvestment lifecycle. As part of that, Gresham House isimplementing tailored versions of its overarching policy foreach asset class. Within those policies it is looking at how itsapproach to Sustainable Investing will contribute towards theUN Sustainable Development Goals alongside improvementsto the reporting and engagement with investee companieson the subjects of governance, social impact, the environmentand climate change where appropriate.

Global Greenhouse Gas EmissionsThe Company has no greenhouse gas emissions to reportfrom the operations of the Company, nor does it haveresponsibility for any other emissions producing sourcesunder the Companies Act 2006 (Strategic Report and Directors’Reports) Regulations 2013, including those within itsunderlying investment portfolio.

Gender DiversityThe Board of Directors of the Company comprises two femaleand two male Directors.

Appointment of the ManagerThe Board expects the Manager to deliver a performancewhich meets the objective of achieving long-term investmentreturns, including tax free dividends. A review of the Company’sperformance during the financial year, the position of theCompany at the year end and the outlook for the coming yearis contained within the Chairman’s Statement on pages 4 to 6.The Board assesses the performance of the Manager inmeeting the Company’s objective against the KPIs highlightedon page 2 of the report.

The management agreementUnder the management agreement, the Manager receivesa fee of 2.0 per cent per annum of the net assets of theCompany. In addition, the Manager is responsible forproviding all secretarial, administrative and accountingservices to the Company for an additional fee. The Managerhas appointed Link Alternative Fund Administrators Ltd toprovide these services to the Company on its behalf. TheCompany is responsible for paying the fee charged by LinkAlternative Fund Administrators Ltd to the Manager in relationto the performance of these services.

Annual running costs are capped at 3.5 per cent of the netassets of the Company (excluding any performance feepayable to the Manager and irrecoverable VAT), any excessbeing refunded by the Manager by way of an adjustment toits management fee. The running cost as at 30 September2019 was 2.2 per cent.

The management agreement may be terminated at any dateby either party giving 12 months’ notice of termination and, ifterminated, the Manager is only entitled to the managementfees paid to it and any interest due on unpaid fees.

Performance feesA performance fee will be payable to the Manager once thetotal return on shareholders’ funds exceeds an annualthreshold of the higher of 4 per cent or base rate plus 2 percent calculated on a compound basis. To the extent that thetotal return exceeds the threshold over the relevant periodthen a performance fee of 10 per cent of the excess will be

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 19

20 www.baronsmeadvcts.co.uk

Strategic Report

paid to the Manager. The amount of any performance feewhich is paid in an accounting period shall be capped at5 per cent of shareholders’ funds for that period.

No performance fee is payable for the year to 30 September2019 (2018: £548,000).

Management retentionThe Board is keen to ensure that the Manager continues tohave one of the best investment teams in the VCT and privateequity sector. A VCT incentive scheme was introduced inNovember 2004 under which members of the Manager’sinvestment team invest their own money into a proportion ofthe ordinary shares of each eligible unquoted investmentmade by the Baronsmead VCTs. The Board regularly monitorsthe VCT incentive scheme arrangements but considers thescheme to be essential in order to attract, retain andincentivise the best talent. The scheme is in line with currentmarket practice in the private equity industry and the Boardbelieves that it aligns the interests of the Manager with thoseof the Baronsmead VCTs.

Executives have to invest their own capital in every eligibleunquoted transaction and cannot decide selectively whichinvestments to participate in. In addition, the VCT incentivescheme only delivers a return after each VCT has realiseda priority return built into the structure. The shares held by themembers of the VCT incentive scheme in any portfoliocompany can only be sold at the same time as the investmentheld by the Baronsmead VCTs is sold. Any prior rankingfinancial instruments, such as loan stock, held by theBaronsmead VCTs have to be repaid in full together with theagreed priority annual return before any gain accrues to theordinary shares. This ensures that the Baronsmead VCTsachieve a good priority return before profits accrue to the VCTincentive scheme.

Prior to January 2017, executives participating in the VCTincentive scheme subscribed jointly for a proportion (12 percent) of the ordinary shares (but not the prior ranking financialinstruments) available to the Baronsmead VCTs in each eligibleunquoted investment. The level of participation was increasedfrom 5 per cent in 2007 when the Manager’s performance feewas reduced from 20 per cent to its current level of 10 percent. With effect from January 2017, an additional limb wasadded to the VCT incentive scheme to accommodate the

increasing number of “permanent equity” investments beingmade by the Baronsmead VCTs. “Permanent equity”investments are those in which the Baronsmead VCTs holda relatively lower proportion of prior ranking instruments(if any at all) and a higher proportion of permanent equity orordinary shares. This means that there is less prior rankinginstruments yielding a priority return for the Baronsmead VCTsbefore any gain accrues to the ordinary shares, hence thisadditional limb to create a hurdle described below. The cut offto define a “permanent equity” investment is one wherepermanent equity is greater than 25 per cent of the total orwhere permanent equity is greater than £250,000.

Under the terms of the amended VCT incentive scheme, incircumstances where the Baronsmead VCTs hold a sufficientnumber of prior ranking financial instruments (a “TraditionalStructure”), the terms are identical to those set out above.However, in circumstances where the Baronsmead VCTs makea “permanent equity” investment, the executives participatingin the incentive scheme are required to coinvest pari passualongside the Baronsmead VCTs for a proportion (currently0.75 per cent) of all instruments available to the BaronsmeadVCTs and they also receive an option over a further proportion(currently 12 per cent) of the ordinary shares available to theBaronsmead VCTs. The ordinary shares can only be sold andthe option can only be exercised by the scheme participantswhen the investment held by the Baronsmead VCTs is sold.The option exercise price has a built in hurdle rate to ensurethat the options are only “in the money” if the BaronsmeadVCTs achieve a good return (equivalent to the priority returnthey would have to achieve prior to any value accruing to theordinary shares in a Traditional Structure).

Since the formation of the scheme in 2004, 82 executives haveinvested a total of £1,033,000 in 67 companies. At 30 September2019, 42 of these investments have been realised generatingproceeds of £338,000,000 for the Baronsmead VCTs and£18,000,000 for the VCT incentive scheme. For BaronsmeadVenture Trust the average money multiple on these42 realisations was 1.8 times cost. Had the VCT incentivescheme shares been held instead by the Baronsmead VCTs, theextra return to shareholders would have been the equivalent of4.4p a share over 15 years (based on the current number ofshares in issue). The Board considers this small cost to retainquality people to be in the best interests of shareholders.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 20

www.baronsmeadvcts.co.uk 21

Baronsmead Venture Trust plcAudited Annual Report & Financial Statements for the year ended 30 September 2019

Advisory and Directors’ feesDuring October and November 2018, Livingbridge VC LLPreceived £Nil (2018: £14,000) advisory fees, £55,000 (2018:£292,000) directors’ fees for services provided to companies inthe investment portfolio and incurred abort costs of £42,000(2018: £34,000) with respect to investments attributable toBaronsmead Venture Trust plc.

For the remainder of the year, Gresham House AssetManagement Ltd received £107,000 (2018: £Nil) advisory fees,£206,000 (2018: £Nil) directors’ fees for services provided tocompanies in the investment portfolio and incurred abort costsof £23,000 (2018: £Nil) with respect to investments attributableto Baronsmead Venture Trust plc.

Alternative Investment Fund Manager’s Directive (“AIFMD”)The AIFMD regulates the management of alternativeinvestment funds, including VCTs. On 22 July 2014 theCompany was registered as a Small UK registered AIFM underthe AIFMD.

Viability StatementIn accordance with principle 21 of the Association ofInvestment Companies Code of Corporate Governance (“AICCode”), the Directors have assessed the prospects of theCompany over the three year period to 30 September 2022.This period is used by the Board during the strategic planningprocess and is considered reasonable for a business of ournature and size.

The three year period is considered the most appropriategiven the forecasts that the Board require from the Managerand the estimated timeline for finding, assessing andcompleting investments.

In making this statement the Board carried out a robustassessment of the principal risks facing the Company,including those that might threaten its business model, futureperformance, solvency, or liquidity. The Directors haveconsidered the ability of the Company to comply on anongoing basis with the conditions for maintaining VCTapproval status.

The Board also considered the ability of the Company to raisefinance and deploy capital. Their assessment took account ofthe availability and likely effectiveness of the mitigatingactions that could be taken to avoid or reduce the impact of

the underlying risks, and the large listed portfolio that couldbe liquidated if necessary.

This review has considered the principal risks as outlined onpages 16 and 17. The Board concentrated its efforts on themajor factors which affect the economic, regulatory andpolitical environment. The Board also paid particular attentionto the importance of its close working relationship with theManager, Gresham House.

The Directors have also considered the Company’s incomeand expenditure projections and find these to be realisticand sensible.

Based on the Company’s processes for monitoring costs, shareprice discount, the Manager’s compliance with the investmentobjective, policies and business model, asset allocation andthe portfolio risk profile, the Directors have concluded thatthere is a reasonable expectation that the Company will beable to continue in operation and meet its liabilities as they falldue over the three year period to 30 September 2022.

Returns to InvestorsDividend policyThe Board will decide the annual dividends each year and thelevel of the dividends will depend on investmentperformance, the level of realised returns and availableliquidity. The dividend policy guidelines below are not bindingand the Board retains the ability to pay higher or lowerdividends relevant to prevailing circumstances and actualrealisations. However, the Board confirms the following twoguidelines that shape its dividend policy:

The Board will, wherever possible, seek to pay two•dividends to Shareholders in each calendar year, typicallyan interim in September and a final dividend followingthe AGM in February/March; and

The Board will use, as a guide, when setting the dividends•for a financial year, a sum representing 7 per cent of theopening NAV of that financial year.

Shareholder choiceThe Board wishes to provide shareholders with a number ofchoices that enable them to utilise their investment inBaronsmead Venture Trust in ways that best suit their personalinvestment and tax planning and in a way that treats allshareholders equally.

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 21

22 www.baronsmeadvcts.co.uk

Strategic Report

Fund raising | From time to time the Company seeks to•raise additional funds by issuing new shares at apremium to the latest published net asset value toaccount for costs. The Company currently has an Offeropen to raise up to £20 million.

Dividend Reinvestment Plan | The Company offers•a Dividend Reinvestment Plan which enablesshareholders to purchase additional shares through themarket in lieu of cash dividends. Approximately1,934,000 shares were bought in this way during the yearto 30 September 2019.

Buy back of shares | From time to time the Company•buys its own shares through the market in accordancewith its share price discount policy. Subject to the likelyimpact on shareholders as a whole, the fundingrequirements of the Company and market conditions atthe time, the Company seeks to maintain a mid shareprice discount of approximately 5 per cent to net assetvalue where possible. However shareholders should notethis discount may widen during periods of marketvolatility.

Secondary market | The Company’s shares are listed on•the London Stock Exchange and can be bought usinga stockbroker or authorised share dealing service in thesame way as shares of any other listed company.Approximately 792,000 shares were bought by investorsin the Company’s existing shares in the year to30 September 2019.

On behalf of the BoardPeter LawrenceChairman

22 November 2019

Baronsmead Venture Trust pp01-22.qxp 25/11/2019 07:27 Page 22

www.baronsmeadvcts.co.uk 23

Report of the DirectorsThe Chairman’s Statement on pages 4 to 6, the Corporate Governance Statement on pages 26 to 33 and the StrategicReport on pages 2 to 22 forms part of the Report of the Directors.

Baronsmead Venture Trust plcAudited Annual Report & Financial Statements for the year ended 30 September 2019

Board of Directors

Peter Lawrence Chairman

Appointed: 8 February 2016

Past experience Peter was until the Merger on 8 February 2016 a non-executive director of Baronsmead VCT plchaving been appointed in November 1999 and becoming Chairman in 2009. Peter was also a priorChairman of Baronsmead VCT 5 plc before retiring in 2010. Peter was formerly chairman of ECOAnimal Health Group plc, an Aim-traded company which he founded in 1972.

Other appointments Peter is currently the chairman of Amati AIM VCT plc and the chairman of Anpario plc, which istraded on AIM.

Beneficial Shareholding 371,928 Ordinary Shares

Les Gabb Non-Executive Director and Audit Committee Chairman

Appointed: 8 February 2016

Past experience Les served as a director of Baronsmead VCT plc from May 2014 until the Merger on 8 February 2016.He studied biochemistry at Oxford University and subsequently qualified as a Chartered Accountantat KPMG in 1987. For 10 years Les was the managing director of the London subsidiary of the Bankof Bermuda with responsibility for the finance function of the Bank’s European group.

Other appointments Since 2015 Les has been finance partner at Felix Capital Partners and previously from 2000 held asimilar role at Advent Venture Partners. Les is an ACA and an Associate of the Institute of Taxation,and a previous member of the BVCA Legal and Technical committee and the EVCA Venture CapitalCouncil.

Beneficial Shareholding 85,660 Ordinary Shares

Valerie Marshall Senior Independent Director and Nomination Committee Chair

Appointed: 8 February 2016

Past experience Valerie served as a director of Baronsmead VCT plc from November 2009 until the Merger on8 February 2016. Previously, she was corporate finance director at stockbrokers Greig Middleton &Co Ltd, and formerly invested in growing companies with both 3i plc and the ScottishDevelopment Agency. She has been chair of the Council of the University of Kent and deputy chairof the Committee of University Chairs. She was also Treasurer and Trustee of the British ScienceAssociation, established by Royal Charter. Valerie has recently retired as CEO of Stratagem CorporateFinance and Strategy Ltd.

Other appointments Valerie is the appointed Senior Independent Director of BVT and a director of Marshall Capital Limited.Valerie is also a non-executive director of Town and Country Housing Group and an investmentcommittee member of the Angel Co-Investment Fund.

Beneficial Shareholding 77,224 Ordinary Shares

Susannah Nicklin Non-Executive Director and Management Engagement & Remuneration Committee Chairman

Appointed: 21 February 2018

Past experience Susannah Nicklin is an investment and financial services professional with 25 years of experience inexecutive roles at Goldman Sachs and Alliance Bernstein in the US, Australia and the UK. She has alsoworked in the social impact private equity sector with Bridges Ventures, the Global Impact InvestingNetwork and Impact Ventures UK. Susannah was previously a director of Baronsmead VCT Plc.