Embed Size (px)

Citation preview

BASICS OF RISK

1-1

1-2

Agenda

• Meaning of Risk

• Chance of Loss

• Peril and Hazard

• Basic Categories of Risk

• Types of Pure Risk

• Burden of Risk on Society

• Methods of Handling Risk

1-3

Meaning of Risk

• Risk: Uncertainty concerning the occurrence of a loss

• Objective Risk vs. Subjective Risk– Objective risk is defined as the relative variation of actual loss from

expected loss• It can be statistically calculated using a measure of dispersion, such

as the standard deviation

– Subjective risk is defined as uncertainty based on a person’s mental condition or state of mind• Two persons in the same situation may have different perceptions of

risk• High subjective risk often results in conservative behavior

1-4

Chance of Loss

• Chance of loss: The probability that an event will occur

• Objective Probability vs. Subjective Probability– Objective probability refers to the long-run relative frequency of an

event assuming an infinite number of observations and no change in the underlying conditions• It can be determined by deductive or inductive reasoning

– Subjective probability is the individual’s personal estimate of the chance of loss • A person’s perception of the chance of loss may differ from the

objective probability

1-5

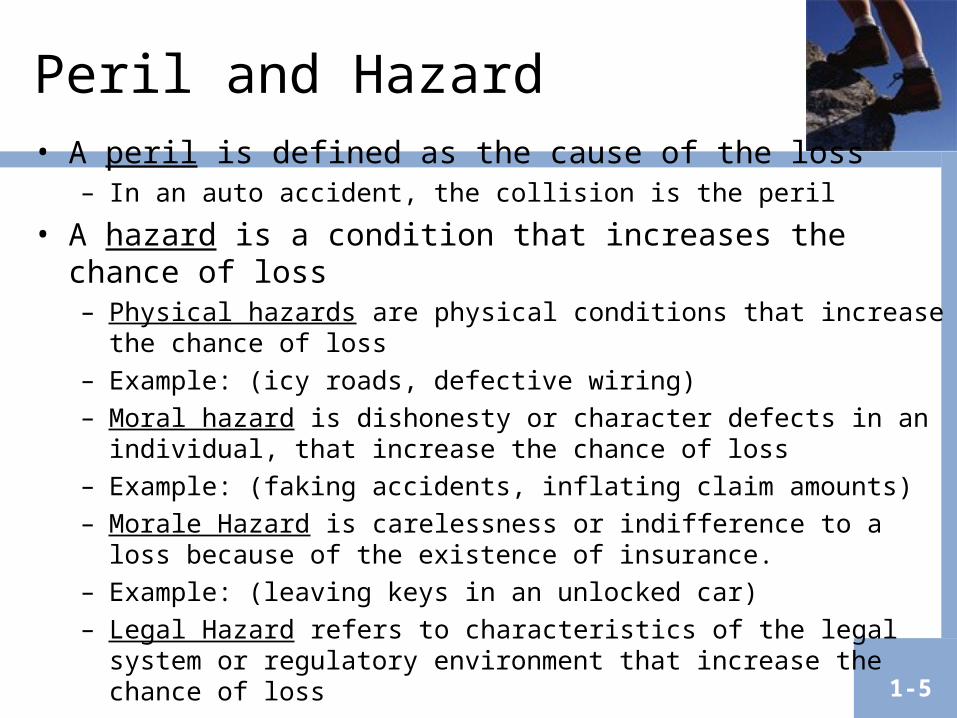

Peril and Hazard• A peril is defined as the cause of the loss

– In an auto accident, the collision is the peril

• A hazard is a condition that increases the chance of loss – Physical hazards are physical conditions that increase the chance of

loss– Example: (icy roads, defective wiring)– Moral hazard is dishonesty or character defects in an individual, that

increase the chance of loss– Example: (faking accidents, inflating claim amounts) – Morale Hazard is carelessness or indifference to a loss because of the

existence of insurance.– Example: (leaving keys in an unlocked car)– Legal Hazard refers to characteristics of the legal system or regulatory

environment that increase the chance of loss– Example: (large damage awards in liability lawsuits)

1-6

Basic Categories of Risk

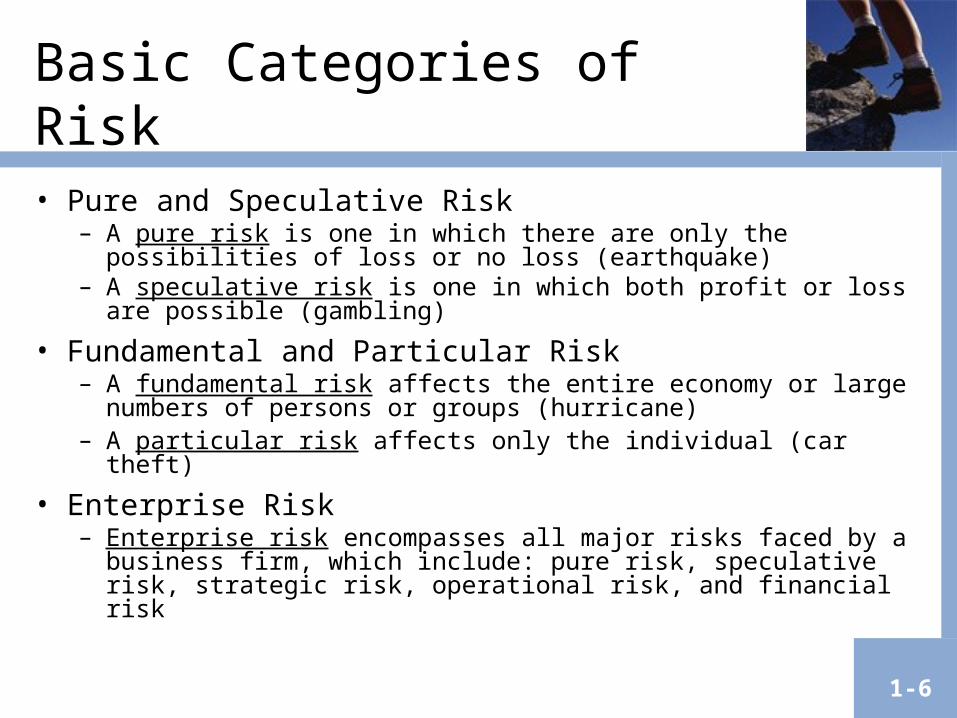

• Pure and Speculative Risk– A pure risk is one in which there are only the possibilities of loss or

no loss (earthquake)– A speculative risk is one in which both profit or loss are possible

(gambling)

• Fundamental and Particular Risk– A fundamental risk affects the entire economy or large numbers of

persons or groups (hurricane)– A particular risk affects only the individual (car theft)

• Enterprise Risk– Enterprise risk encompasses all major risks faced by a business

firm, which include: pure risk, speculative risk, strategic risk, operational risk, and financial risk

1-7

Types of Pure Risks

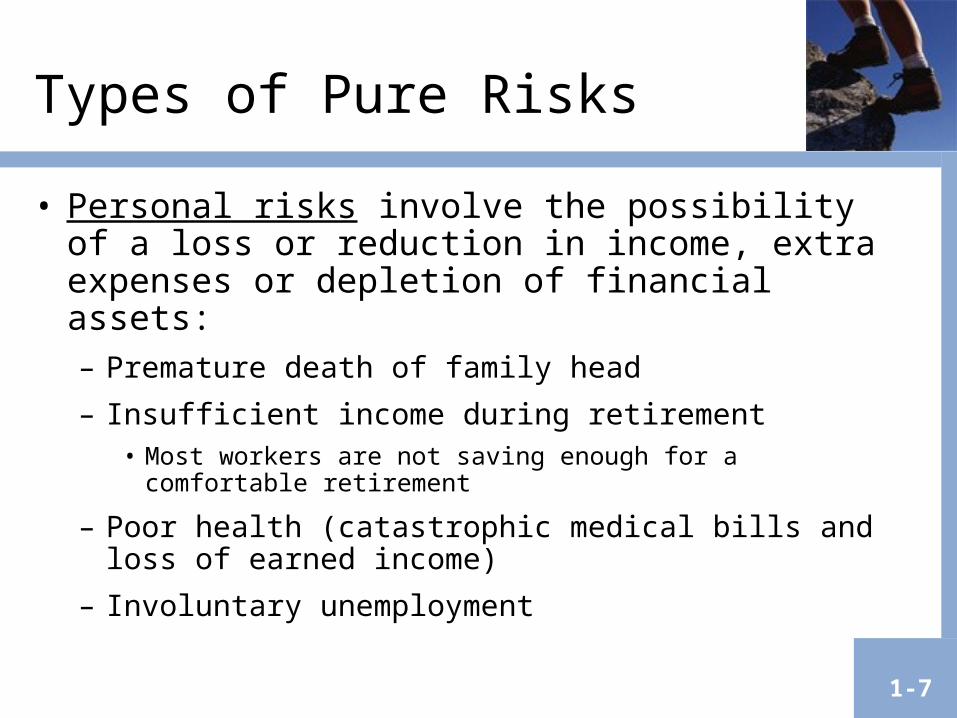

• Personal risks involve the possibility of a loss or reduction in income, extra expenses or depletion of financial assets:– Premature death of family head

– Insufficient income during retirement• Most workers are not saving enough for a comfortable

retirement

– Poor health (catastrophic medical bills and loss of earned income)

– Involuntary unemployment

1-8

Types of Pure Risks

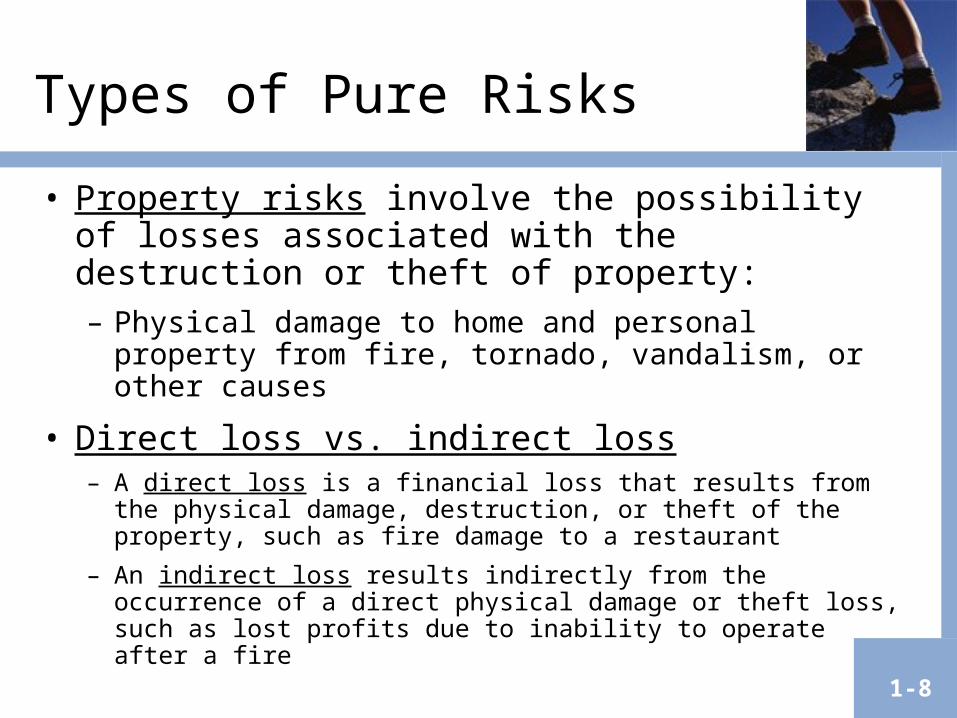

• Property risks involve the possibility of losses associated with the destruction or theft of property:– Physical damage to home and personal property from

fire, tornado, vandalism, or other causes

• Direct loss vs. indirect loss– A direct loss is a financial loss that results from the physical

damage, destruction, or theft of the property, such as fire damage to a restaurant

– An indirect loss results indirectly from the occurrence of a direct physical damage or theft loss, such as lost profits due to inability to operate after a fire

1-9

Types of Pure Risks

• Liability risks involve the possibility of being held liable for bodily injury or property damage to someone else– There is no maximum upper limit with respect to the

amount of the loss

– A lien can be placed on your income and financial assets

– Defense costs can be enormous

1-10

Burden of Risk on Society

• The presence of risk results in three major burdens on society:– In the absence of insurance, individuals would

have to maintain large emergency funds

– The risk of a liability lawsuit may discourage innovation, depriving society of certain goods and services

–Risk causes worry and fear

Larger Emergency Fund

• It is prudent to set aside the fund for emergency. However, in the absence of insurance individuals and business firms would have to increase the size of their emergency fund to pay for unexpected losses.

1-11

Loss of certain Goods and Services

• A second burden of risk is that society is deprived of certain goods and services. For example, because of the risk of a liability law suit, many corporation have discontinued manufacturing certain products. Some 250 companies in the world once manufactured child hood vaccine, today small number firms manufacture vaccine due in part to the treat of liability suit.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-12

Worry and fear

• A final burden of risk is that worry and fear are present. Numerous examples can illustrate the mental unrest and fear caused by risk. Some passengers in a commercial jet may become extremely nervous and fearful if the jet encounters severe turbulence during the flight. A college student who needs a grade of C in a course to graduate may enter the final examination room with a feeling of apprehension and fear

1-13

1-14

Methods of Handling Risk

• Avoidance• Loss control

– Loss prevention refers to activities to reduce the frequency of losses

– Loss reduction refers to activities to reduce the severity of losses

• Retention– An individual or firm retains all or part of a loss– Loss retention may be active or passive

• Noninsurance transfers– A risk may be transferred to another party through contracts,

hedging, or incorporation

• Insurance

Techniques/Methods for managing Risk

•Avoidance•Loss control•Retention•Noninsurance transfers•Insurance

1-15

avoidance

• Avoidance is one technique of managing the risk.

• A business firm can avoid the risk of being sued for a defective product by not producing the product.

• However, you can not avoid all the risk.

1-16

Loss Control

• Loss control is the another technique of managing the risk.

• Loss control consist of certain activities that reduces the frequency or severity of losses. Loss control has two major objectives:

• Loss prevention

• Loss reduction

1-17

Loss prevention

• Loss prevention aims at reducing the probability of loss so that the frequency of losses is reduced

• Auto accidents can be reduced if the motorists takes safe driving course and drive defensively.

• Loss prevention is also important for business firms.

1-18

Loss Reduction

• Strict loss prevention efforts can reduce the frequency of losses, yet some losses will inevitably occur.

• Thus, the second objective of loss control is to reduce the severity of a loss after it occurs.

• For example, a plant can be constructed with fire resistant material to minimize fire damage

1-19

Retention

• Retention means that an individual or business firm retains part of all the financial consequences of a given risk.

• Risk retention can be active or passive. Active retention means that an individuals consciously aware of the risk and deliberately plans to retain all or part of it.

• A motorist plan to take an insurance policy against the damage

1-20

• Passive retention means certain risk can be unknowingly retained because of ignorance, indifference or laziness.

• Passive retention is dangerous if the risk retained has the potential for destroying financially.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-21

Self Insurance

• It is a special form of planned retention by which part or all of a given loss exposure is retained by the firm. It is also called self funding.

1-22

Non Insurance Transfers

• Non Insurance Transfers are another technique of managing the risk.

• Here, the risk is transferred to a party other than insurance company.

• A risk can be transferred by several methods they are:

• Transfer risk by contracts

• Hedging price risk

• Incorporation of a business firm1-23

Insurance

• Insurance is the is the most practical method for handling the major risk.

• Although , private insurance have several characteristics, three major characteristic should be emphasized

• Risk transfer

• Pooling technique

• Law of large numbers

1-24

Model Questions

• What do you mean by risk?

• Explain different types of risk?

• Difference between objective probability and subjective probability?

• Define peril? give an example for peril

• Define hazards? Write an example for hazards

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-25

• What are the basic categories of risk?

• What are the different types of pure risk?

• What are the major burdens of risk on society?

• Explain the different risk handling techniques? Or methods of risk management

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-26

• ----------------involve the possibility of a loss or reduction in income, extra expenses or depletion of financial assets.

• ------------------means that an individual or business firm retains part of all the financial consequences of a given risk.

• ----------------necessitate individuals and business firms would have to increase the size of their emergency fund to pay for unexpected losses.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-27

• --------------is defined as the cause of the loss

• -------------------------involve the possibility of being held liable for bodily injury or property damage to someone else

• ----------------------------consist of certain activities that reduces the frequency or severity of losses

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 1-28