Embed Size (px)

Citation preview

BayernLB | Group InterIm report

fIrst half of 2013

fact

s |

fig

ure

s

BayernLB . Group Interim Report for the first half of 2013

›› 2

Contents

BayernLB . Group Interim Report for the first half of 2013

›› Contents 3

BayernlB Group – the first half of 2013 at a glance

selected business highlights in h1 2013

Board of managementForeword

Board of Management and responsibilities

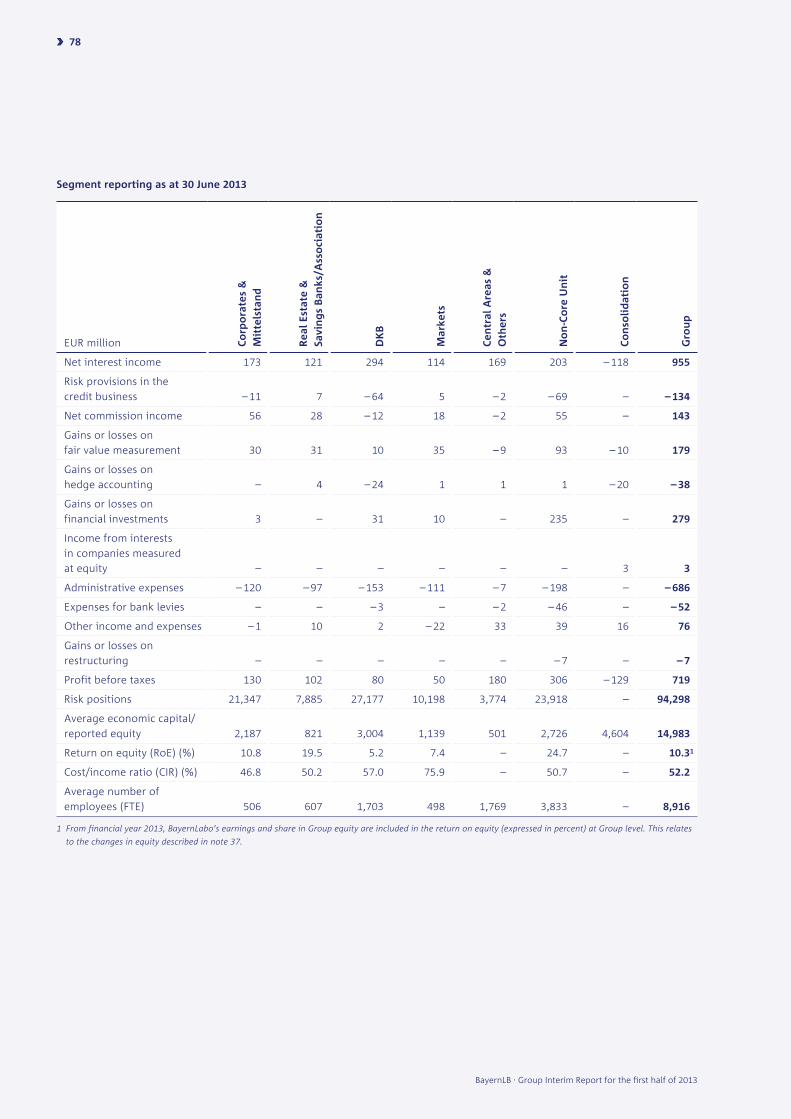

Group Interim management reportOverview

Financial position and financial performance

Segments

Events after the end of the reporting period

Outlook

Risk report

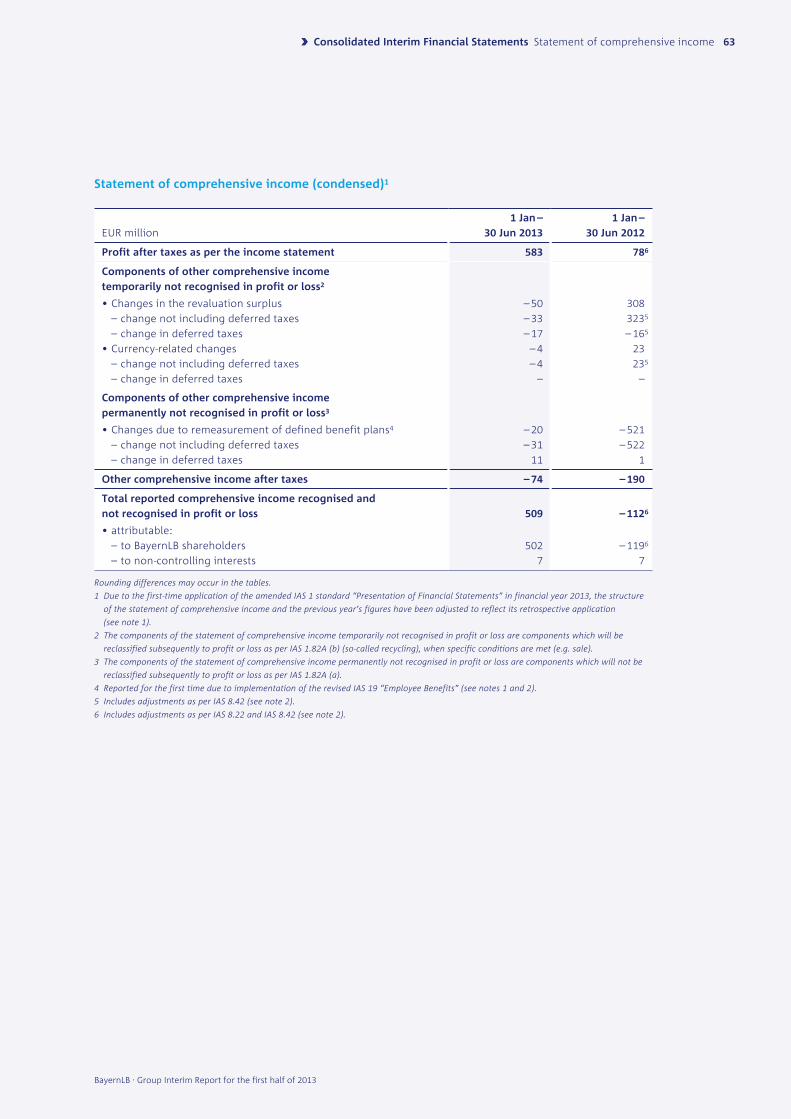

Consolidated Interim financial statementsStatement of comprehensive income

Income statement

Statement of comprehensive income

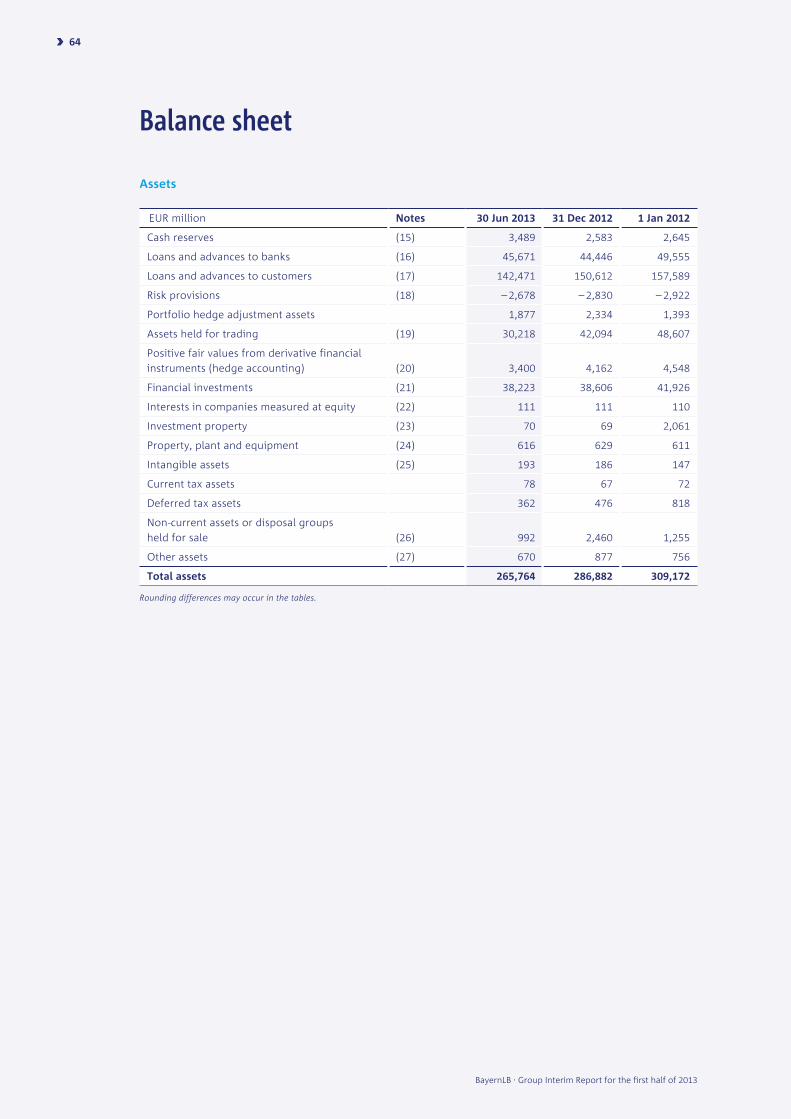

Balance sheet

Statement of changes in equity

Cash flow statement

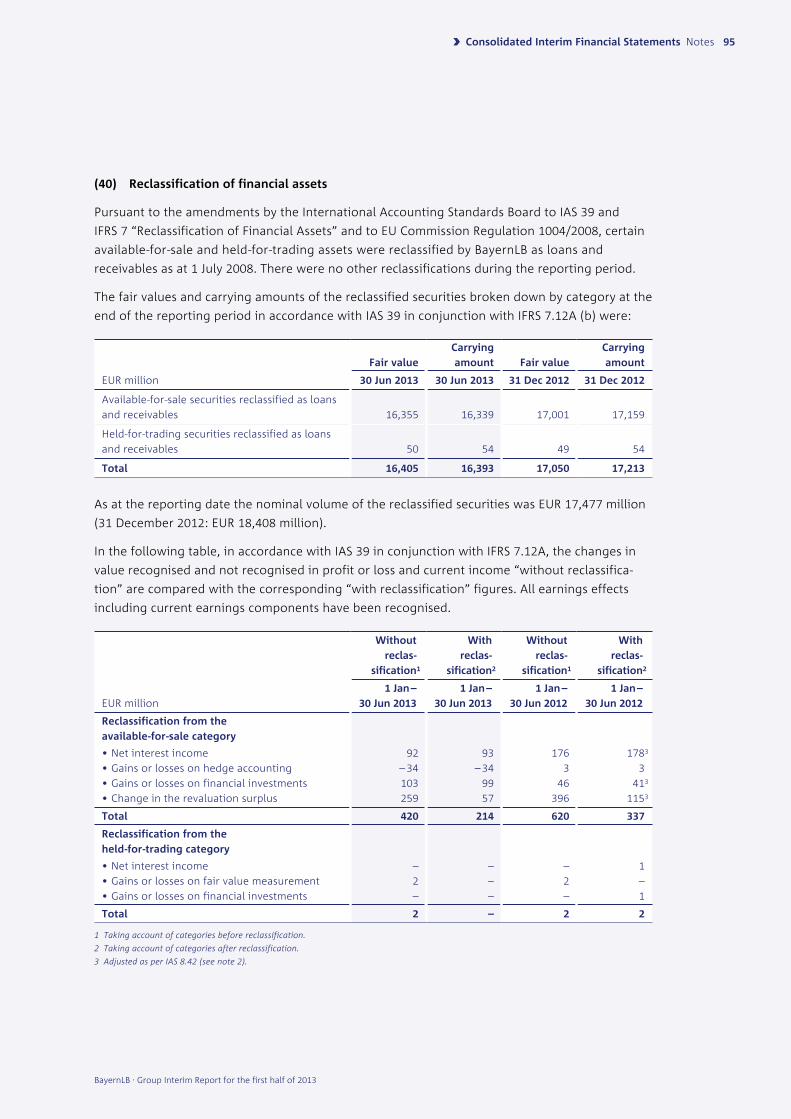

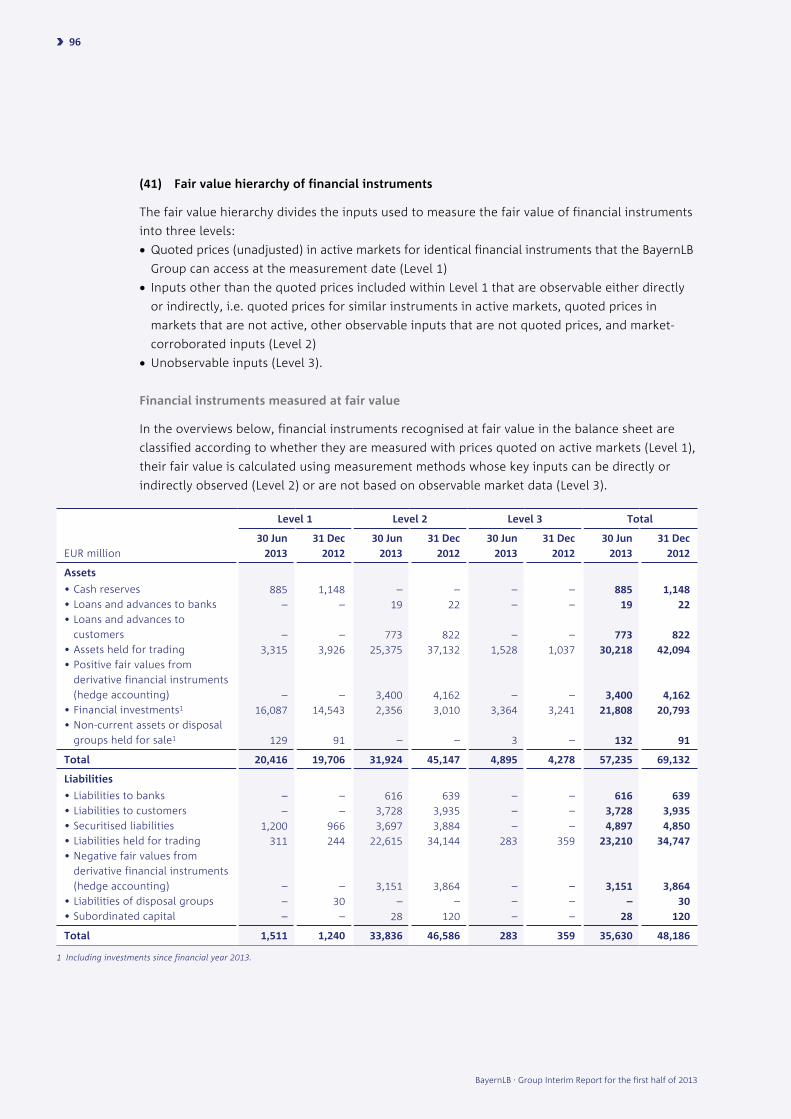

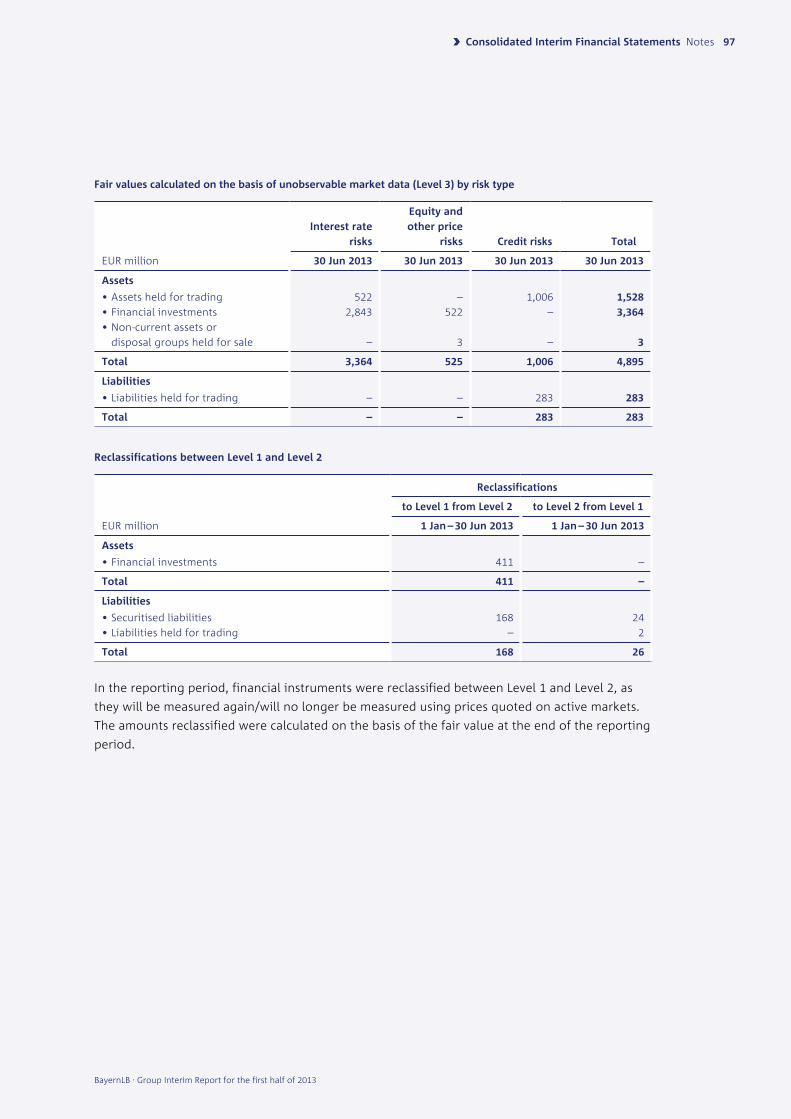

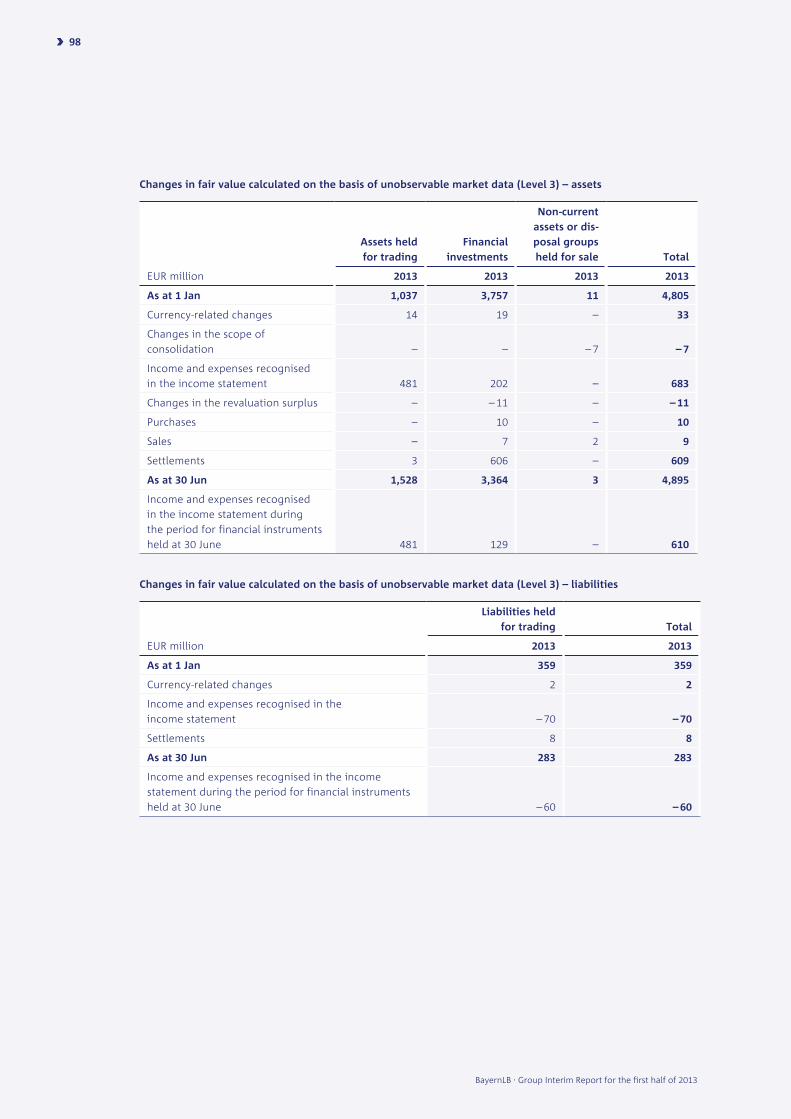

Notes

Responsibility statement by the Board of Management

Review Report

6

10

1214

18

2022

23

27

32

33

34

6062

62

63

64

66

68

69

106

107

The translation of consolidated interim financial statements – comprising the condensed state-ment of comprehensive income (including income statement), the balance sheet, statement of changes in equity, condensed statement of cash flows and selected explanatory notes – and the Group interim management report of the Bayerische Landesbank as well as the auditor’s review report is for convenience only; the German versions prevail.

BayernLB . Group Interim Report for the first half of 2013

›› 4

BayernLB Group – the first half

of 2013 at a glance

BayernLB . Group Interim Report for the first half of 2013

›› BayernLB Group – the first half of 2013 at a glance 5

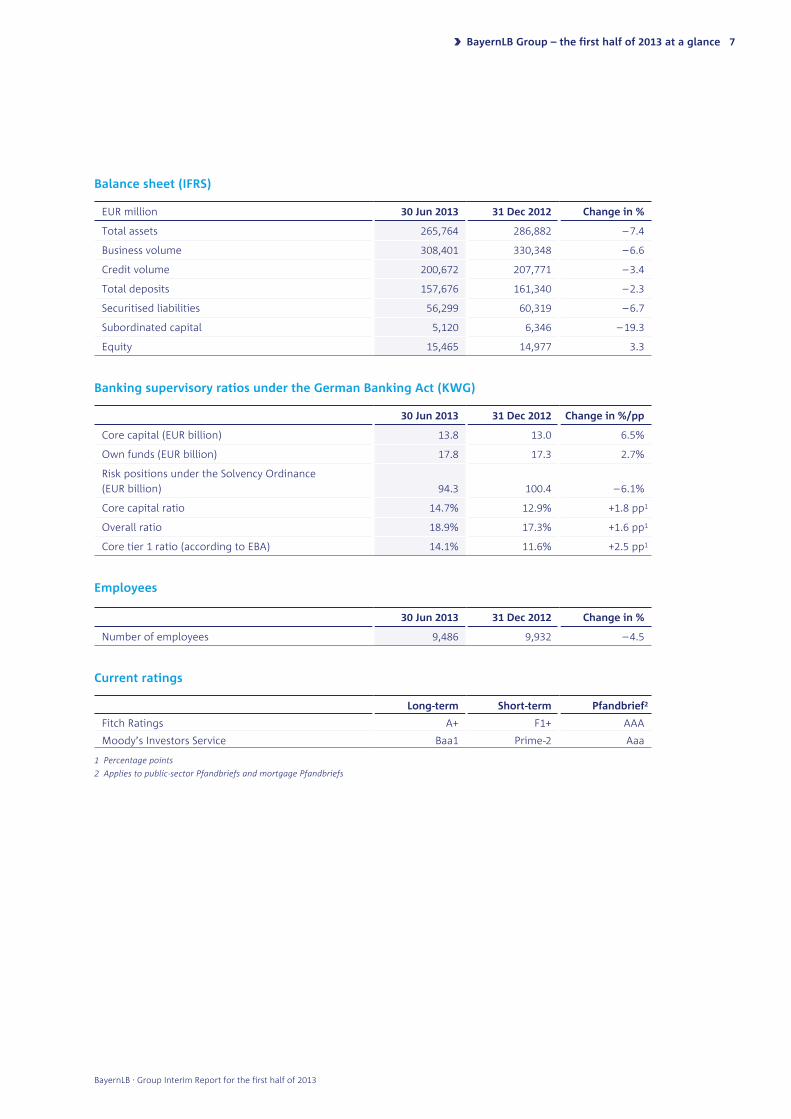

BayernLB Group – the first half of 2013 at a glance

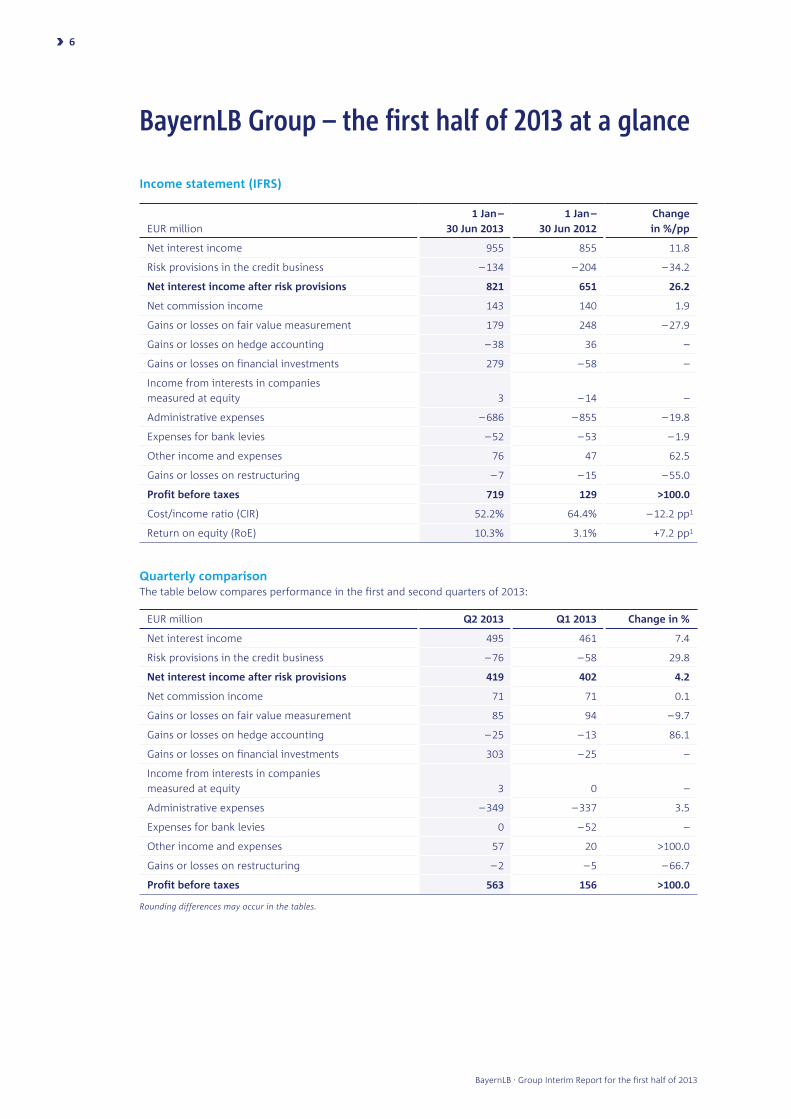

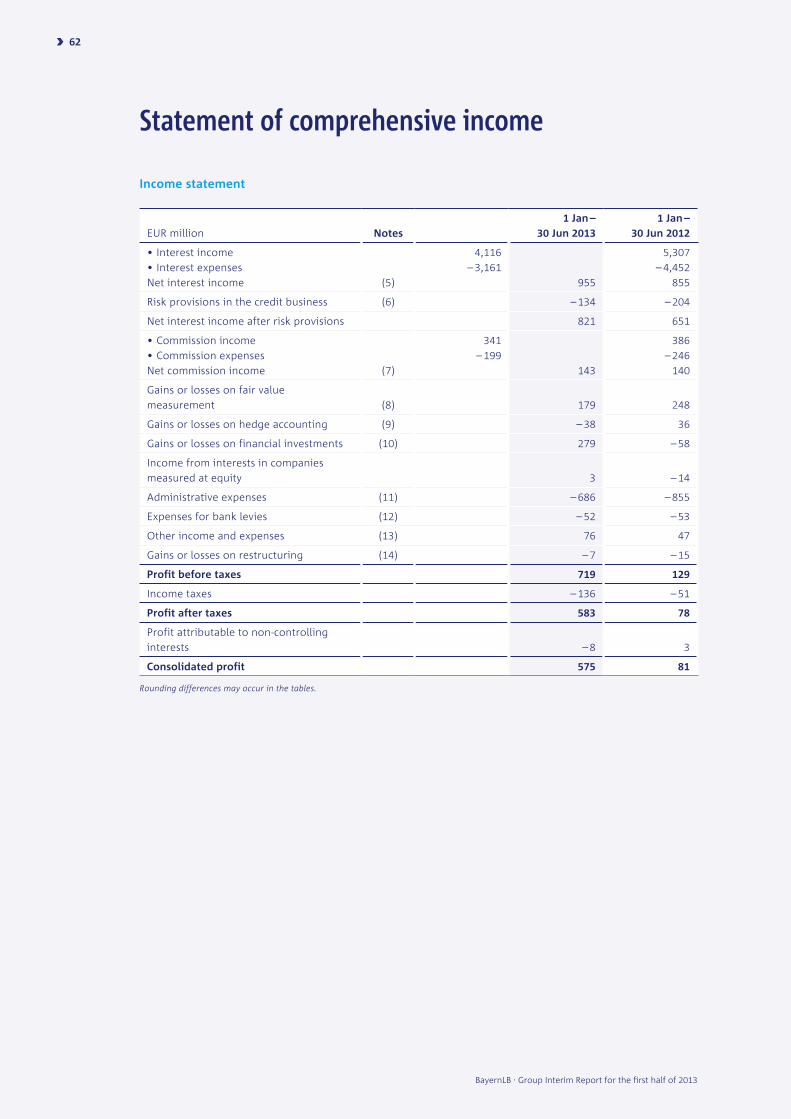

Income statement (IFrS)

EUR million

1 Jan –

30 Jun 2013

1 Jan –

30 Jun 2012

Change

in %/pp

Net interest income 955 855 11.8

Risk provisions in the credit business – 134 – 204 – 34.2

net interest income after risk provisions 821 651 26.2

Net commission income 143 140 1.9

Gains or losses on fair value measurement 179 248 – 27.9

Gains or losses on hedge accounting – 38 36 –

Gains or losses on financial investments 279 – 58 –

Income from interests in companies

measured at equity 3 – 14 –

Administrative expenses – 686 – 855 – 19.8

Expenses for bank levies – 52 – 53 – 1.9

Other income and expenses 76 47 62.5

Gains or losses on restructuring – 7 – 15 – 55.0

Profit before taxes 719 129 >100.0

Cost/income ratio (CIR) 52.2% 64.4% – 12.2 pp1

Return on equity (RoE) 10.3% 3.1% +7.2 pp1

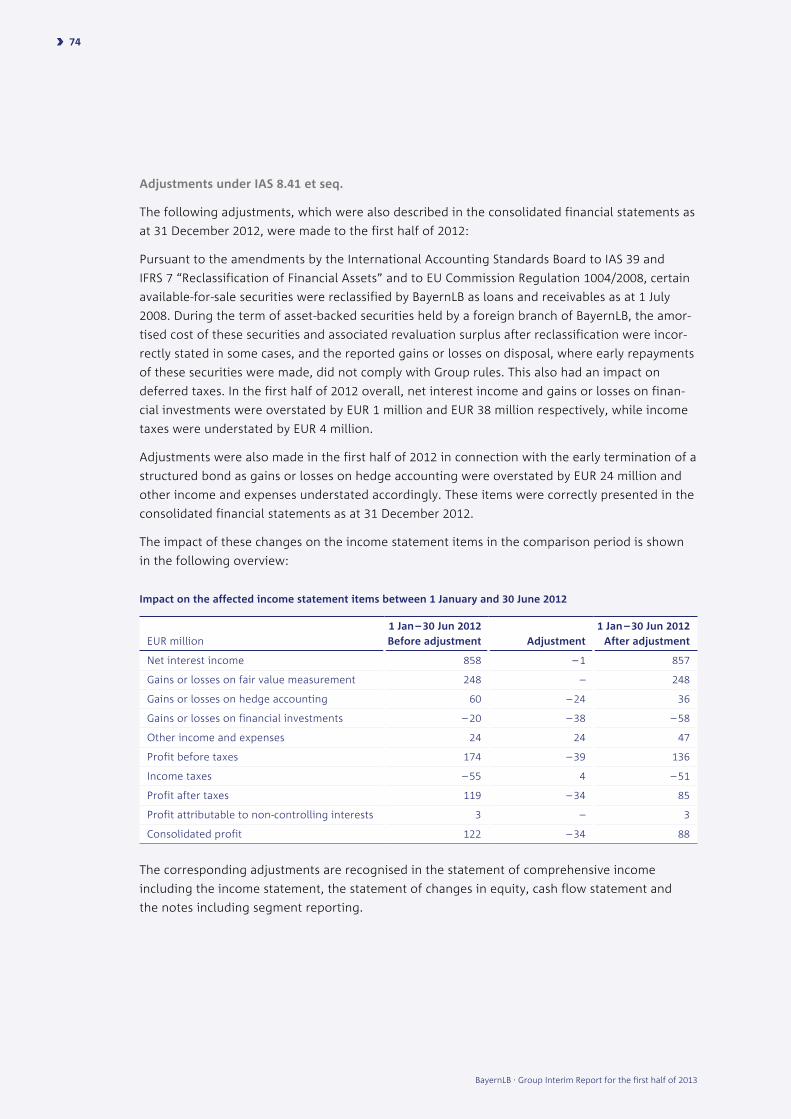

Quarterly comparisonThe table below compares performance in the first and second quarters of 2013:

EUR million Q2 2013 Q1 2013 Change in %

Net interest income 495 461 7.4

Risk provisions in the credit business – 76 – 58 29.8

net interest income after risk provisions 419 402 4.2

Net commission income 71 71 0.1

Gains or losses on fair value measurement 85 94 – 9.7

Gains or losses on hedge accounting – 25 – 13 86.1

Gains or losses on financial investments 303 – 25 –

Income from interests in companies

measured at equity 3 0 –

Administrative expenses – 349 – 337 3.5

Expenses for bank levies 0 – 52 –

Other income and expenses 57 20 >100.0

Gains or losses on restructuring – 2 – 5 – 66.7

Profit before taxes 563 156 >100.0

Rounding differences may occur in the tables.

BayernLB . Group Interim Report for the first half of 2013

›› 6

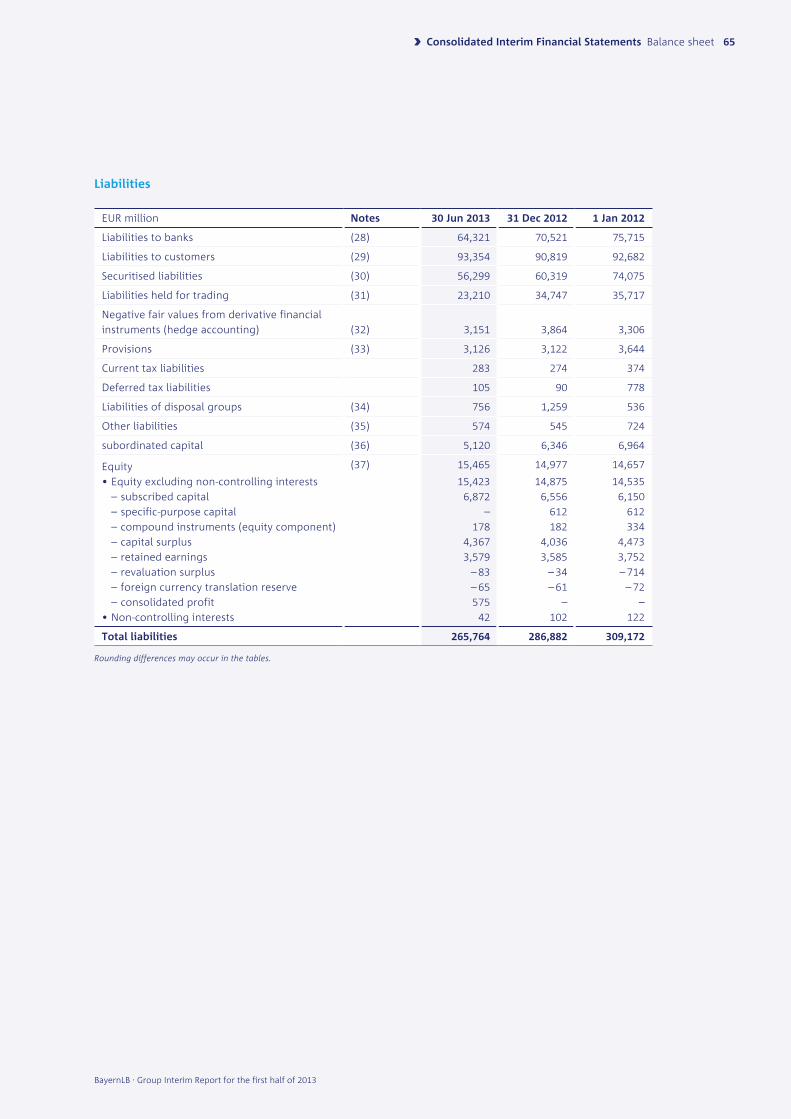

Balance sheet (IFrS)

EUR million 30 Jun 2013 31 Dec 2012 Change in %

Total assets 265,764 286,882 – 7.4

Business volume 308,401 330,348 – 6.6

Credit volume 200,672 207,771 – 3.4

Total deposits 157,676 161,340 – 2.3

Securitised liabilities 56,299 60,319 – 6.7

Subordinated capital 5,120 6,346 – 19.3

Equity 15,465 14,977 3.3

Banking supervisory ratios under the German Banking act (KWG)

30 Jun 2013 31 Dec 2012 Change in %/pp

Core capital (EUR billion) 13.8 13.0 6.5%

Own funds (EUR billion) 17.8 17.3 2.7%

Risk positions under the Solvency Ordinance

(EUR billion) 94.3 100.4 – 6.1%

Core capital ratio 14.7% 12.9% +1.8 pp1

Overall ratio 18.9% 17.3% +1.6 pp1

Core tier 1 ratio (according to EBA) 14.1% 11.6% +2.5 pp1

employees

30 Jun 2013 31 Dec 2012 Change in %

Number of employees 9,486 9,932 – 4.5

Current ratings

Long-term Short-term Pfandbrief2

Fitch Ratings A+ F1+ AAA

Moody’s Investors Service Baa1 Prime-2 Aaa

1 Percentage points

2 Applies to public-sector Pfandbriefs and mortgage Pfandbriefs

BayernLB . Group Interim Report for the first half of 2013

›› BayernLB Group – the first half of 2013 at a glance 7

›› 8

BayernLB , Group Interim Report for the first half of 2013

Selected business

highlights in H1 2013

BayernLB . Group Interim Report for the first half of 2013

›› Selected business highlights in H1 2013 9

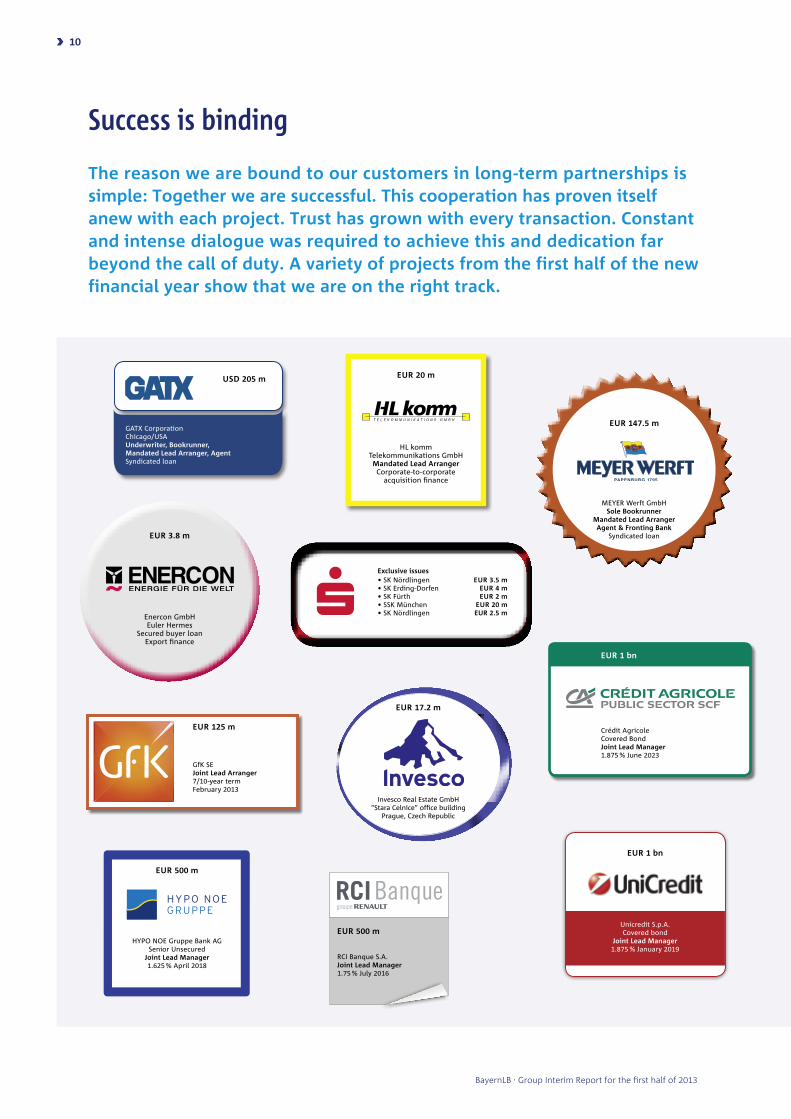

The reason we are bound to our customers in long-term partnerships is simple: Together we are successful. This cooperation has proven itself anew with each project. Trust has grown with every transaction. Constant and intense dialogue was required to achieve this and dedication far beyond the call of duty. a variety of projects from the first half of the new financial year show that we are on the right track.

Success is binding

Unicredit S.p.A.Covered bond

Joint Lead Manager1.875 % January 2019

EUR 1 bn

GfK SEJoint Lead Arranger 7/10-year term February 2013

EUR 125 m

GATX CorporationChicago/USAUnderwriter, Bookrunner,Mandated Lead Arranger, Agent Syndicated loan

USD 205 m

MEYER Werft GmbHSole Bookrunner

Mandated Lead Arranger Agent & Fronting Bank

Syndicated loan

EUR 147.5 m

• SK Nördlingen• SK Erding-Dorfen• SK Fürth• SSK München• SK Nördlingen

EUR 3.5 m EUR 4 m EUR 2 m EUR 20 m

EUR 2.5 m

Exclusive issues

Invesco Real Estate GmbH “Stara Celnice” office building

Prague, Czech Republic

EUR 17.2 m

HYPO NOE Gruppe Bank AG Senior Unsecured

Joint Lead Manager1.625 % April 2018

EUR 500 m

Crédit AgricoleCovered BondJoint Lead Manager1.875 % June 2023

EUR 1 bn

RCI Banque S.A.Joint Lead Manager 1.75 % July 2016

EUR 500 m

HL komm Telekommunikations GmbHMandated Lead ArrangerCorporate-to-corporate

acquisition finance

EUR 20 m

Enercon GmbHEuler Hermes

Secured buyer loanExport finance

EUR 3.8 m

BayernLB . Group Interim Report for the first half of 2013

›› 10

SEB ABCovered Bond

Joint Lead Manager1.50 % February 2020

EUR 1 bn

ThyssenKrupp AGJoint Lead Manager 4 % August 2018 February 2013

EUR 1.25 bn

SIMBA-DICKIE-GROUP GmbHFinancierCorporate-to-corporateacquisition finance

HOCHTIEF Solutions AGConstruction and operation of the Paul-Moor schoolNurembergPPP project

EUR 20 m

IKB Leasing GmbHLead Arranger

Securitisation of leasing receivables via the “Corelux” ABCP program

EUR 100 m

• SK Passau EUR 5 m (Bank share) acquistion Clothing sector

• SK Niederbayern-Mitte EUR 4 m (Bank share) increase in general credit limit Agricultural machinery sector

• SK Bad Neustadt an der Saale EUR 2.5 m (Bank share) capital expenditure finance Automotive supplier sector

Plafond loans

Jointly issued bond Nuremberg & Würzburg

Type: Bearer bondRating: n. r.

Joint Bookrunner: BayernLB

Deutsche Bank Helaba

UniCreditCoupon: 1.875 %

EUR 100 m issue volume

Immobilien KAGFinancing

Office/business premises“Ludwigpalais” Munich

Akelius GmbHFinancing of a residential portfolio5-year termVarious German citiesMarch 2013

EUR 103.5 m

Müller-Elmau GmbHFunding by KfW

Energy standard 20 % under EnEV 2009Construction finance for a hotel

Elmau, Germany

EUR 19 m in conjunction with Sparkasse

Garmisch-Partenkirchen

Grenzebach BSH GmbHExport finance

EU

R 4

4.6

m

BayernLB . Group Interim Report for the first half of 2013

›› Selected business highlights in H1 2013 11

BayernLB . Group Interim Report for the first half of 2013

›› 12

Board of Management

›› Vorstand 13

Foreword

Board of Management and responsibilities

14

18

Foreword

Ladies and gentlemen,

Dear customers and business partners,

The BayernLB Group posted an exceptionally good profit before taxes

of EUR 719 million in the first half of 2013. Our solid customer business,

focused on the Bavarian and German markets, was instrumental in the

results - delivering stable earnings while risk provisions were once again

moderate. This was due not least of all to the beneficial economic environ-

ment, particularly in the south of Germany. Another factor which had a

significant impact on earnings was the one-off income of EUR 351 million

from the sale of BayernLB’s stake in GBW AG in May. This positive effect

must be noted when making comparisons with the previous year’s earnings

(EUR 129 million), which were depressed by a one-off addition to pension

provisions. After adjusting for these special factors, it was still a good first

half of the year for BayernLB.

The Bank successfully met a broad range of challenges in the first six months.

On the one hand, it continued to set a strong pace in the Bank’s core

business, producing figures in the black in all customer-serving segments.

Examples include: 70 new large Mittelstand customers, six Schuldschein

note loan issues with a total volume of EUR 4.5 billion and new business

with commercial real estate customers totalling EUR 1 billion. Moreover,

BayernLB granted around 12,500 subsidised loans to customers of the

savings banks and its own customers, while DKB now serves just under

2.7 million online retail customers. All this is clear evidence of the new

BayernLB’s success in the customer business. Simultaneously, the staff

proceeded apace to further slim down the Bank by rapidly winding down

the non-core activities grouped in the Non-Core Unit (NCU) as profitably

as possible, while carrying out the painstaking process of disposing of

stakes in companies such as the recent sale of GBW AG. By 30 June 2013,

BayernLB . Group Interim Report for the first half of 2013

›› 14

total assets had been trimmed to EUR 265.8 billion. Just six months before

they were more than EUR 20 billion higher at just under EUR 287 billion.

At the mid point of 2013 BayernLB was still very much on track. This was

especially the case in regard to BayernLB’s extensive and sustained re-

structuring of its business activities, even though these are increasingly

under pressure from low interest rates, companies’ reluctance to spend

on capex and greater regulatory intervention. Furthermore, considerable

progress was made in meeting the conditions handed down in 2012 by the

European Commission in its ruling on the Bank’s state aid proceedings.

These included the sale of the holding in housing company GBW AG and

the disposal of an equity stake in Lufthansa at the beginning of the year.

BayernLB has even been paying the EUR 5 billion in state aid back to the

Free State of Bavaria ahead of schedule. By the mid point of the year, it had

paid a total of around EUR 1.1 billion. EUR 871 million was in aid payments;

the rest represents higher fees for the guarantee agreement on the ABS

portfolio. On 7 August of this year BayernLB transferred another tranche of

EUR 50 million. Since November 2012, taking into account the replenishment

of the silent partner contributions of the Free State of Bavaria and Bavarian

savings banks, BayernLB has paid EUR 1.6 billion to the owners.

Also related to the outcome of the state aid proceedings was a reshuffling

of the Bank’s ownership structure. On 25 June 2013, the Bavarian savings

banks increased their equity in BayernLB Holding AG by around EUR 830

million, thus raising their indirect stake in Bayerische Landesbank to ap-

proximately 25 percent. This means that BayernLB once again has a second

strong owner in addition to the Free State of Bavaria. This relationship is

reflected in the fact that the Bavarian savings banks appoint the deputy

chairperson of BayernLB’s new Supervisory Board. The Supervisory Board

was established on 4 July and replaces the Board of Administration. The

new board no longer includes any politicians from the Bavarian government

BayernLB . Group Interim Report for the first half of 2013

›› Board of Management Foreword 15

as ex officio board members. The transformation of the supervisory

board was also one of the conditions in the EU ruling.

BayernLB is well positioned for the second half of the year. BayernLB’s Board

of Management anticipates full-year results will be solid. But there will

not be a continuation of the performance in the first half, as the one-off

gains, of course, cannot be repeated. Political and regulatory uncertainty

will also cloud the picture. The banking industry is being hamstrung over

the long term by the European Central Bank’s (ECB) monetary policy, which is

hoping to cajole capital into flowing from the north to the south of Europe

through low interest rates. German savers are among the losers here as is

bank profitability, which is also being squeezed by the proliferation of

regulations from national and international supervisors that are driving up

labour and operating costs. Critical steps by regulators are often not co-

ordinated internationally and in some cases even contradict each other.

Developments in Hungary are of key importance for BayernLB. The country’s

government is toying with the idea of fresh political intervention on

foreign currency loans which could severely test the business of banks

operating there. BayernLB’s MKB subsidiary, which we are still restructuring

from the ground up for the long term, may then take another knock.

BayernLB is faced with several key challenges. The Bank needs to maintain

its equity ratios close to the very high levels it now has even after payouts

to owners and investors. Currently the core tier 1 ratio as defined by the

European Banking Authority (EBA) is 14.1 percent. Over the next five years

it is due to return another EUR 4 billion of core tier 1 capital to the Free

State of Bavaria. To meet these challenges, BayernLB will proceed along

two tracks at the same time. It will invest in its sales force, while simulta-

neously scrutinising the Bank’s cost structures. The goal is to grow the

customer business even more, while keeping production costs competitive

and making scant capital resources go further.

After reducing its total assets by around EUR 160 billion in the past four

years, BayernLB is the size it was at the end of the 1990s. Its infrastructure

in many cases, though, is more in keeping with that of a much larger bank.

Red tape has also raised platform costs. BayernLB will therefore be seeking

BayernLB . Group Interim Report for the first half of 2013

›› 16

to cut costs and improve efficiency. At the end of March it announced ad-

ministrative expenses at BayernLB (excluding its subsidiaries) will be reduced

by 15 percent by 2017. The Bank has started making good progress in

further downsizing its New York and London branches for example.

In the second half of the year the new BayernLB will continue to work

hard at achieving its goal of becoming a normal bank. We will continue

to trust in the loyalty of our customers and the dedication of our staff

and would like to offer a big thank you to them all.

Sincerely,

The Board of Management

Gerd Haeusler, CEO

Marcus Kramer, Member of the Board of Management

Dr. Edgar Zoller, Deputy CEO

Michael Bücker, Member of the Board of Management

Nils Niermann, Member of the Board of Management

Stephan Winkelmeier, Member of the Board of Management

BayernLB . Group Interim Report for the first half of 2013

›› Board of Management Foreword 17

The Board of Management

Corporate CenterDeutsche Kreditbank aG

Gerd Haeusler Ceo

real estate & Savings Banks/association Bayerische Landesbodenkreditanstalt

Human resources

Dr edgar Zoller Deputy Ceo

risk Officerestructuring UnitGroup Compliance

Marcus Kramer member of the Board of management Cro

Responsibilities as at 1 August 2013

BayernLB . Group Interim Report for the first half of 2013

›› 18

The Board of Management

Corporates, Mittelstand & Financial Institutions

Michael Bücker member of the Board of management

Markets Banque LBLux S. a. BayernInvest Kapitalanlagegesellschaft mbH

nils niermann member of the Board of management

Stephan Winkelmeier member of the Board of management Cfo/Coo

Financial Office Operating OfficeMKB Bank Zrt.

BayernLB . Group Interim Report for the first half of 2013

›› Board of Management 19

BayernLB . Group Interim Report for the first half of 2013

›› 20

Group Interim Management

report

BayernLB . Group Interim Report for the first half of 2013

Overview

Financial position and financial performance

Segments

Events after the end of the reporting period

Outlook

Risk report

22

23

27

32

33

34

Overview

After a weak start to 2013, when the weather brought a noticeable chill, the German economy

made a strong comeback in spring. Although some of this was undoubtedly due to pent-up

demand, the recovery went beyond just that. Despite the weather, total economic output in the

first half of 2013 was slightly up on the second half of 2012. The labour market remained buoy-

ant. Severe flooding in May and June had no significant dampening effect on employment as

companies in the affected regions made greater use of short-time working. Coupled with recent

higher wage increases and moderate inflation in consumer prices, the improved situation on the

labour market boosted private consumption. Interest rates remained low, supporting the building

sector. Although the spell of unusually cold weather put the brakes on construction at the start of

the year, the impact is likely to have been reversed in spring when the economy came storming

back. Spending on plant and equipment as well as exports was, however, disappointing in the

first half. The uncertainty caused by the sovereign debt crisis continued to hold back capital

expenditure. And companies in Germany will not loosen the purse strings again until uncertainty

eases for good and earnings outlooks are more stable. The financing conditions for this remain

favourable. Falling demand for German exports from the crisis-hit countries in the eurozone was

not offset by growth in orders from the rest of the world. The temporary dip in the US economy

in October- March and the flattening out of economic momentum in China also played a major

role in this.

Although the European sovereign debt crisis eased once again in the first half of 2013, it is by

no means over. The risk of fresh financial market turmoil is no longer so acute as the European

Central Bank is ready to intervene on the government bond market (OMT programme). But the

countries in crisis still have a long hard road of structural adjustments ahead of them before they

bring public and private debt down to sustainable levels, stabilise their banking systems and

improve their competitiveness. The ECB’s assurances have bought national and EU politicians

time to implement reforms. But the pace of structural reform and budgetary spring cleaning has

slowed in some cases. And even the European Union has been pressured by the crisis-hit coun-

tries into extending the timeframe for the fiscal adjustment path. Not enough progress has been

made in creating a fiscal and banking union either. The uncertainty over the political stability of

Greece, Portugal and Italy is proof once again of the major risks on the path to achieving a stable

currency union.

Financial markets rallied in the first half of 2013. The highly expansionary policy of central banks

in the eurozone, US, UK and Japan has kept interest rates very low and resulted in major shifts in

portfolio assets (into equities and real estate). In May, the blue-chip DAX index hit a new all-time

high on the German stock exchange, though this was followed soon after by a short correction.

Altogether, Germany’s leading index gained 4.6 percent in the first half. Bond market yields had

trended to historic lows by the start of May. But a reversal set in in late spring, after the Federal

Reserve announced its exit from the current bond buyback programme. The euro-dollar exchange

rate moved sideways during the first half and was highly volatile at times. Based on weekly aver-

ages, at the end of June, the pair was trading at almost exactly the same rate as it was at the start

of the year.

Please refer to the Group management report and financial statements for 2012 for information

on BayernLB’s business model and strategy and also its organisation and structure.

BayernLB . Group Interim Report for the first half of 2013

›› 22

Financial position and financial performance

In the first half of 2013, earnings from the BayernLB Group’s core businesses were very satisfac-

tory. A high one-off effect in the non-core business inflated total profit before taxes. When com-

paring this year’s figure with the previous year’s, it should be noted that earnings for the first half

of 2012 were depressed by a one-off addition to pension provisions. Core business generated

profit before taxes of EUR 419 million (H1 2012: EUR 96 million). The deconsolidation gain of

EUR 351 million from the sale of the holding in GBW AG, Munich (GBW) was recognised in non-

core business. As a result, non-core business reported profits before taxes of EUR 300 million

(H1 2012: EUR 33 million). Total profit before taxes for the BayernLB Group therefore amounted

to EUR 719 million (H1 2012: EUR 129 million).

In addition to disposing of GBW, BayernLB completely sold its equity stake in Deutsche Lufthansa AG,

Cologne in the first half of 2013, thus fulfilling another condition of the European Commission’s

ruling. Two payments, one in February and one in May 2013, bring the total amount of state aid

repaid to the Free State of Bavaria to EUR 871 million as at 30 June 2013. The total amount that

has to be repaid under the EU’s ruling has thus fallen from around EUR 5 billion to approximately

EUR 4.1 billion.

Supervisory equity ratios improved again as a result of further winding down of risk positions in

the non-core business and the replenishment of silent partner contributions to their nominal

value reported in the 2012 annual financial statements. The core capital ratio as at 30 June 2013

was 14.7 percent (31 December 2012: 12.9 percent) and the own funds ratio 18.9 percent

(31 December 2012: 17.3 percent).

Income statement

The figures for the same period in 2012 include income from LBS Bayerische Landesbausparkasse

(LBS Bayern) which was sold on 31 December 2012. In the first half of 2012, LBS Bayern contri-

buted EUR 14 million to profit before taxes. The previous year’s figures were not adjusted.

Even without the EUR 93 million contribution to net interest income from LBS Bayern in H1 2012,

net interest income rose by 11.8 percent to EUR 955 million. A large share of the gain resulted

from a switch in Deutsche Kreditbank AG, Berlin (DKB)’s hedge accounting, but BayernLB also

increased earnings from interest rate hedges as a result of changes in market rates.

risk provisions in the credit business were EUR 134 million (H1 2012: EUR 204 million). These

largely related to DKB (EUR 68 million) and MKB Bank Zrt., Budapest (MKB) (EUR 94 million).

BayernLB saw a net release of provisions. Total risk provisions are significantly below target and,

going by previous trends, will increase in the second half of the year.

Commission income in the credit business remains behind the previous year due to the

targeted winding down of business. The increase in net commission income by EUR 3 million

to EUR 143 million is due to the sale of LBS Bayern, which weighed on net commission income

by EUR 13 million in the first half of 2012.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Overview · Financial position and financial performance 23

Gains or losses on fair value measurement (including gains or losses on hedge accounting) were

EUR 141 million altogether and therefore significantly below the EUR 284 million of the previous-

year period. But the previous year’s high figure was offset by negative items of nearly the same

amount in net interest income, gains or losses on financial investments and other income and

expenses. There was a total negative contribution of EUR – 38 million (H1 2012: EUR – 167 million)

from the measurement of and current income from cross-currency swaps and own credit spreads

in H1 2013. Besides the customer margin of EUR 84 million (H1 2012: EUR 89 million), a large

contribution to the positive overall result came from impairment reversals in the ABS portfolio of

EUR 67 million (H1 2012: EUR 92 million) and reversals of fair value adjustments of EUR 46 million

(H1 2012: EUR 85 million).

The sale of GBW produced a deconsolidation gain of EUR 351 million, which is recognised in

gains or losses on financial investments. Including income from interests in companies

measured at equity, gains and losses on financial investments were EUR 282 million (H1 2012:

EUR – 72 million) in the first half of 2013. The valuation of the Umbrella guarantee agreement led

to a negative item of EUR – 124 million (H1 2012: EUR – 118 million) which was offset to a degree

by EUR 67 million in gains or losses on fair value measurement. The aim of the umbrella is to off-

set losses and measurement changes in the ABS portfolio, whereby for measurement reasons,

earnings are reported in different periods and interdependencies with the gains or losses on fair

value measurement arise.

administrative expenses amounted to EUR 686 million which was 19.8 percent lower than the

year before. It should be noted here that EUR 133 million of additions to the pension provisions

needed to be made as a result of the ruling by the German Federal Employment Court on retire-

ment benefits in the first half of 2012. Adjusted for this and the sale of LBS Bayern, administrative

expenses were on par with the previous year.

Other income and expenses covers both the activities of the real estate subsidiaries and the

gains or losses from buying back own issues, and amounted to EUR 76 million in the first half of

2013 (H1 2012: EUR 47 million).

expenses for bank levies were EUR 52 million (H1 2012: EUR 53 million). Of this, EUR 46 million

related to MKB, EUR 3 million to DKB and EUR 3 million to BayernLB.

restructuring expenses at the BayernLB Group fell to EUR 7 million (H1 2012: EUR 15 million).

return on equity (roe)1 was 10.3 percent (H1 2012: 3.1 percent). The cost/income ratio (CIr)2

was 52.2 percent (H1 2012: 64.4 percent).

1 Profit before taxes excluding non-controlling interests, bank levy expenses and gains or losses on restructuring/

subscribed capital + compound instruments (equity component) + capital surplus and retained earnings. Up to and

including 2012, excludes the share of earnings and equity from BayernLabo which is a non-competitive business.

2 CIR = administrative expenses/net interest income + net commission income + gains or losses on fair value

measurement + gains or losses on hedge accounting + other income and expenses

BayernLB . Group Interim Report for the first half of 2013

›› 24

Balance sheet items

Total assets fell to EUR 265.8 billion as at 30 June 2013, a fall of 7.4 percent on the end of 2012.

The steepest declines were in assets and liabilities held for trading, which were each around

EUR 12 billion lower. This was due to changes in interest rates and portfolio optimisation through

the termination and closing out of redundant swap transactions.

Loans and advances to customers saw another drop of EUR 8.1 billion to EUR 142.5 billion. Loans

and advances to foreign customers decreased by 11.7 percent to EUR 32.4 billion, while loans and

advances to domestic customers contracted by 3.4 percent to EUR 110.1 billion.

The three major pillars of the BayernLB Group’s funding are: liabilities to customers, liabilities to

banks and securitised liabilities; liabilities to customers rose again by 2.8 percent to EUR 93.4 bil-

lion. As funding needs were lower on the whole, liabilities to banks fell by EUR – 6.2 billion to

EUR 64.3 billion, and securitised liabilities by EUR – 4.0 billion to EUR 56.3 billion.

Subordinated capital went down by EUR 1.2 billion to EUR 5.1 billion as instruments fell due.

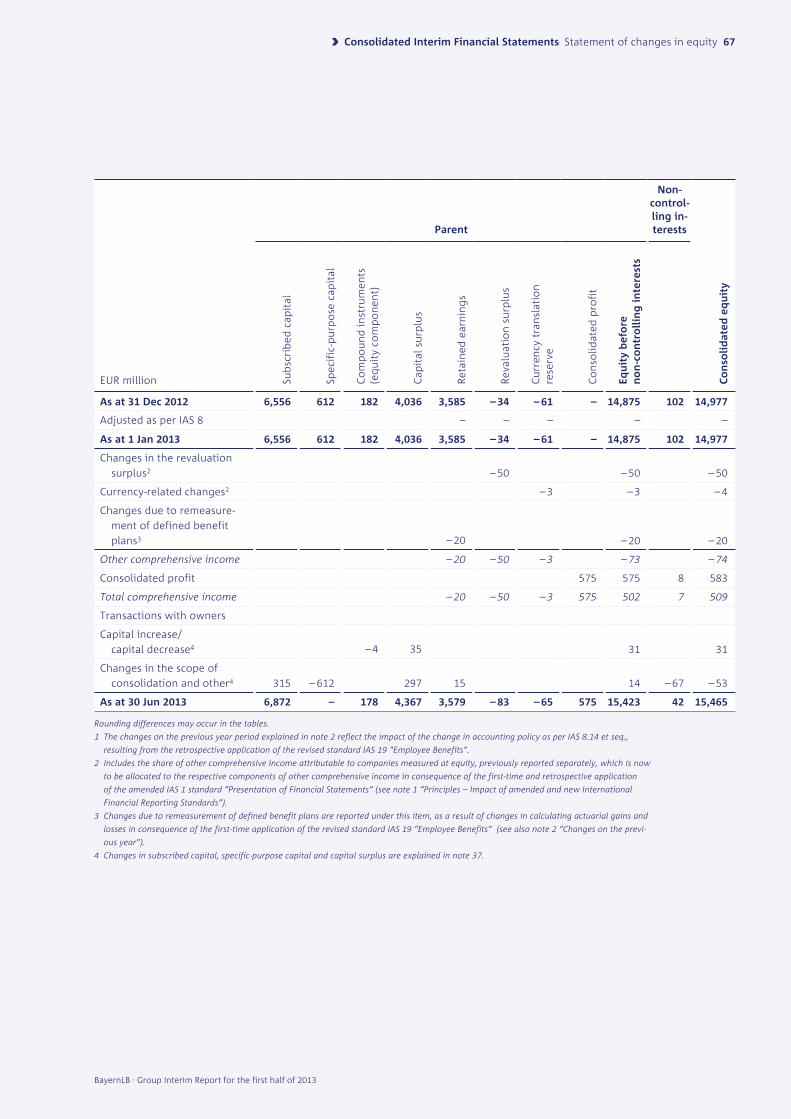

equity rose slightly by EUR 0.5 billion to EUR 15.5 billion.

Please consult the risk report for further information on the financial position.

Banking supervisory capital and ratios

In the first half of 2013, risk positions pursuant to the Solvency Ordinance, consisting of credit

and market risk positions and operational risks, were wound down by a further 6.1 percent to

EUR 94.3 billion.

Several measures were implemented in the first half of 2013 in connection with the conditions of

the European Commission’s state aid ruling and to ensure that BayernLB’s capital meets the forth-

coming requirements under CRR/CRD IV for classification as core equity tier 1. On 1 January 2013,

for example, the contractual provisions relating to specific-purpose capital were amended in line

with CRR/CRD IV requirements. The restructured capital instrument has been reported as a capital

contribution since the start of the year.

At the level of BayernLB Holding AG, the Bavarian savings banks subscribed to a capital increase

of around EUR 832 million through the Association of Bavarian Savings Banks (SVB). This took

effect on 25 June 2013 when it was recorded in the Commercial Register. The SVB’s indirect

equity interest in BayernLB rose to around 25 percent as a result with the Free State of Bavaria’s

stake falling correspondingly to around 75 percent. Besides cash, the capital increase was funded

by a contribution in kind of all the perpetual silent partner contributions of the Bavarian savings

banks in the amount of EUR 797 million. The capital raised was transferred directly by BayernLB

Holding AG into BayernLB’s capital surplus.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Financial position and financial performance 25

Core capital under the Solvency Ordinance was EUR 13.8 billion (up EUR 0.8 billion from

31 December 2012). One factor in this increase was the replenishment of silent partner contri-

butions to their nominal value reported in the 2012 annual financial statements.

Partly as a result of the sharp drop in risk positions in the non-core business, capital ratios

improved further. The core capital ratio was a solid 14.7 percent (31 December 2012: 12.9 percent),

while the own funds ratio was 18.9 percent (31 December 2012: 17.3 percent).

The BayernLB Group’s stable capital base is also reflected in the EBA ratio. As at 30 June 2013, the

core tier 1 ratio (CET 1 ratio) as defined by the European Banking Authority (EBA) was 14.1 percent

(31 December 2012: 11.6 percent). Besides the fall in risk positions, the increase is due to a capi-

tal increase by the Bavarian savings banks of around EUR 832 million, as the silent partner contri-

butions of the savings banks used for the capital increase are not included in the calculation of

the CET 1 ratio.

The BayernLB Group’s financial position and financial performance is sound.

BayernLB . Group Interim Report for the first half of 2013

›› 26

Segments

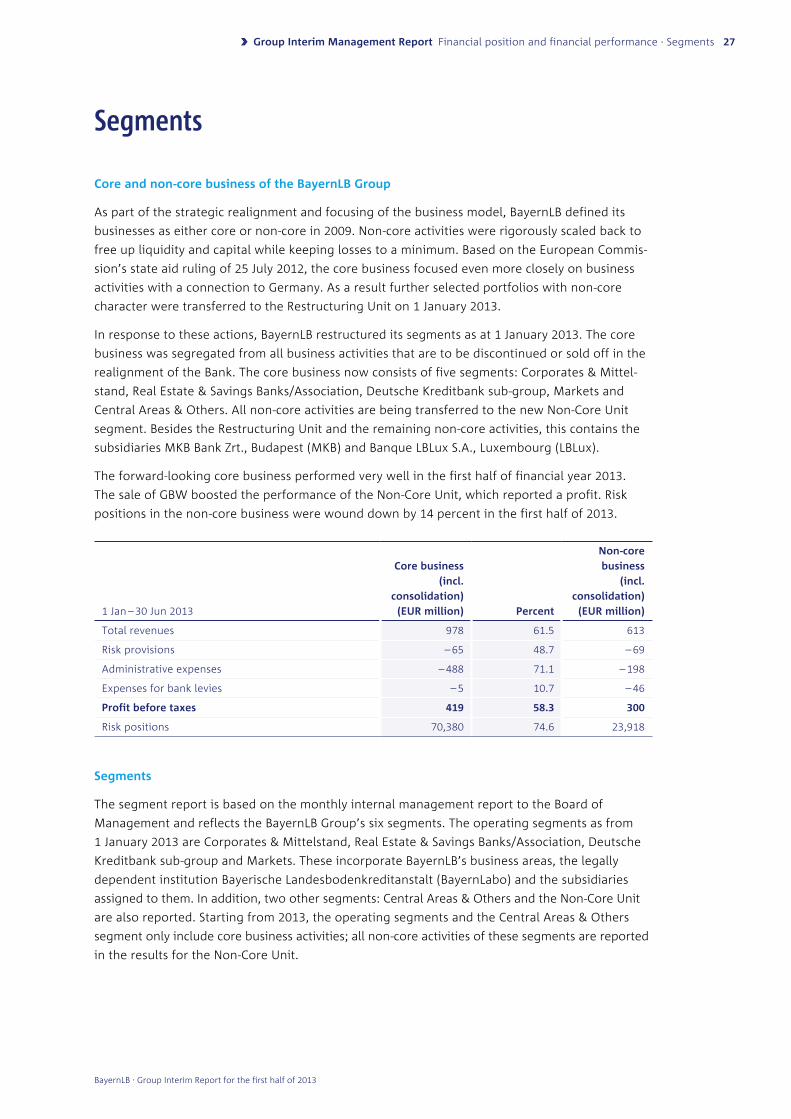

Core and non-core business of the BayernLB Group

As part of the strategic realignment and focusing of the business model, BayernLB defined its

businesses as either core or non-core in 2009. Non-core activities were rigorously scaled back to

free up liquidity and capital while keeping losses to a minimum. Based on the European Commis-

sion’s state aid ruling of 25 July 2012, the core business focused even more closely on business

activities with a connection to Germany. As a result further selected portfolios with non-core

character were transferred to the Restructuring Unit on 1 January 2013.

In response to these actions, BayernLB restructured its segments as at 1 January 2013. The core

business was segregated from all business activities that are to be discontinued or sold off in the

realignment of the Bank. The core business now consists of five segments: Corporates & Mittel-

stand, Real Estate & Savings Banks/Association, Deutsche Kreditbank sub-group, Markets and

Central Areas & Others. All non-core activities are being transferred to the new Non-Core Unit

segment. Besides the Restructuring Unit and the remaining non-core activities, this contains the

subsidiaries MKB Bank Zrt., Budapest (MKB) and Banque LBLux S.A., Luxembourg (LBLux).

The forward-looking core business performed very well in the first half of financial year 2013.

The sale of GBW boosted the performance of the Non-Core Unit, which reported a profit. Risk

positions in the non-core business were wound down by 14 percent in the first half of 2013.

1 Jan – 30 Jun 2013

Core business

(incl.

consolidation)

(eUr million) Percent

non-core

business

(incl.

consolidation)

(eUr million)

Total revenues 978 61.5 613

Risk provisions – 65 48.7 – 69

Administrative expenses – 488 71.1 – 198

Expenses for bank levies – 5 10.7 – 46

Profit before taxes 419 58.3 300

Risk positions 70,380 74.6 23,918

Segments

The segment report is based on the monthly internal management report to the Board of

Management and reflects the BayernLB Group’s six segments. The operating segments as from

1 January 2013 are Corporates & Mittelstand, Real Estate & Savings Banks/Association, Deutsche

Kreditbank sub-group and Markets. These incorporate BayernLB’s business areas, the legally

dependent institution Bayerische Landesbodenkreditanstalt (BayernLabo) and the subsidiaries

assigned to them. In addition, two other segments: Central Areas & Others and the Non-Core Unit

are also reported. Starting from 2013, the operating segments and the Central Areas & Others

segment only include core business activities; all non-core activities of these segments are reported

in the results for the Non-Core Unit.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Financial position and financial performance · Segments 27

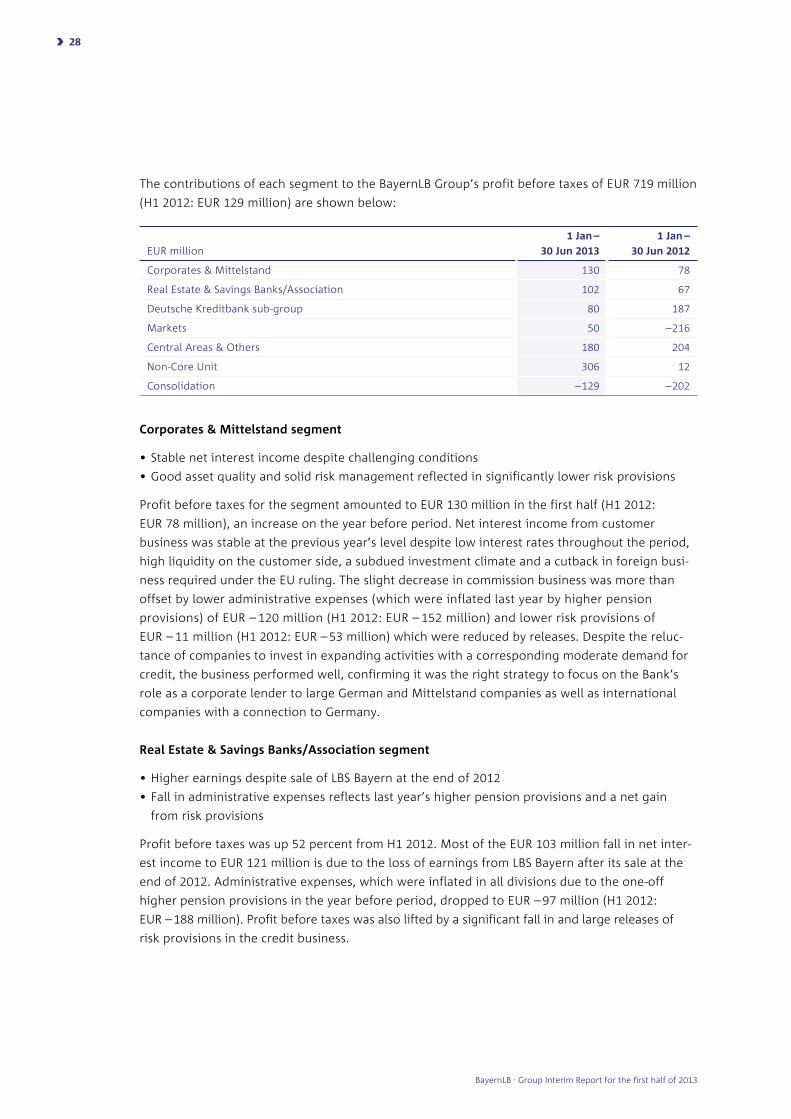

The contributions of each segment to the BayernLB Group’s profit before taxes of EUR 719 million

(H1 2012: EUR 129 million) are shown below:

EUR million

1 Jan –

30 Jun 2013

1 Jan –

30 Jun 2012

Corporates & Mittelstand 130 78

Real Estate & Savings Banks/Association 102 67

Deutsche Kreditbank sub-group 80 187

Markets 50 – 216

Central Areas & Others 180 204

Non-Core Unit 306 12

Consolidation – 129 – 202

Corporates & Mittelstand segment

• Stable net interest income despite challenging conditions

• Good asset quality and solid risk management reflected in significantly lower risk provisions

Profit before taxes for the segment amounted to EUR 130 million in the first half (H1 2012:

EUR 78 million), an increase on the year before period. Net interest income from customer

business was stable at the previous year’s level despite low interest rates throughout the period,

high liquidity on the customer side, a subdued investment climate and a cutback in foreign busi-

ness required under the EU ruling. The slight decrease in commission business was more than

offset by lower administrative expenses (which were inflated last year by higher pension

provisions) of EUR – 120 million (H1 2012: EUR – 152 million) and lower risk provisions of

EUR – 11 million (H1 2012: EUR – 53 million) which were reduced by releases. Despite the reluc-

tance of companies to invest in expanding activities with a corresponding moderate demand for

credit, the business performed well, confirming it was the right strategy to focus on the Bank’s

role as a corporate lender to large German and Mittelstand companies as well as international

companies with a connection to Germany.

real estate & Savings Banks/association segment

• Higher earnings despite sale of LBS Bayern at the end of 2012

• Fall in administrative expenses reflects last year’s higher pension provisions and a net gain

from risk provisions

Profit before taxes was up 52 percent from H1 2012. Most of the EUR 103 million fall in net inter-

est income to EUR 121 million is due to the loss of earnings from LBS Bayern after its sale at the

end of 2012. Administrative expenses, which were inflated in all divisions due to the one-off

higher pension provisions in the year before period, dropped to EUR – 97 million (H1 2012:

EUR – 188 million). Profit before taxes was also lifted by a significant fall in and large releases of

risk provisions in the credit business.

BayernLB . Group Interim Report for the first half of 2013

›› 28

The customer business in the Real Estate division was again buoyant in the period under review.

Despite the withdrawal from foreign business with no connection to Germany, net interest

income and net commission income rose thanks to higher margin new business. While there was

a pleasing increase in total revenues, the jump in profit before taxes to EUR 56 million (H1 2012:

EUR 21 million) was largely due to a fall in administrative expenses and a turnaround in risk

provisions to a positive EUR 6 million (H1 2012: EUR – 9 million), driven by releases.

Total revenues in the Savings Banks & Association division fell, however, despite the productive

and close collaboration with the savings banks and the public sector. This was primarily due to

fewer sales of BayernLB’s own issues thanks to the Bank’s good liquidity at the moment. Despite

this, earnings rose to EUR 7 million (H1 2012: EUR 4 million), with a major contribution coming

from the decrease in administrative expenses.

Low interest rates and lower volumes weighed on BayernLabo’s total revenues. However, this

was offset by a significant rise in gains or losses on fair value measurement from interest rate

hedges and a fall in administrative expenses. Profit before taxes rose to EUR 35 million (H1 2012:

EUR 22 million) as a result.

Deutsche Kreditbank sub-group segment

• Persistent low interest rates weigh on earnings

• Risk provisions virtually unchanged on the previous year

• Customer deposits rise to EUR 42 billion

DKB’s business performed well in all customer groups. In the reporting period the credit business

grew by EUR 0.7 billion to EUR 55.9 billion despite customers taking advantage of low interest

rates to repay loans early or make large repayments and intense competition for customers

with good credit ratings. Customer deposits, which are an important source of funding, grew by

5.8 percent to EUR 42 billion. In addition to DKB’s success in positioning itself as “Your bank on

the web” reflected in its 2.7 million retail customers, there were also higher inflows of customers’

funds into the infrastructure and corporate customers segments. Nonetheless, profit before taxes

fell to EUR 80 million (H1 2012: EUR 187 million). Besides the one-off income in 2012 from the

sale of DKB Immo and fair value measurement, this was primarily due to the low interest rate

environment. When comparing net interest income with the previous year, it should be noted

that a change was made in the disclosure of interest rate hedges. Administrative expenses and

risk provisions were essentially unchanged on the previous year. Given current economic condi-

tions, DKB’s business has performed well overall.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Segments 29

Markets segment

• Significant increase in earnings, largely due to optimised net interest income and the dissolu-

tion of the valuation reserve for bid-ask spreads

• Good customer business

In the first half of 2013, the Markets segment earned profit before taxes of EUR 50 million

(H1 2012: EUR – 216 million), a significant year-on-year increase. The strong swing in earnings is

largely due to the gains or losses on fair value item. The negative figure in the year before was

mainly due to cross-currency swaps, own credit spreads and securities held in the strategic liquid-

ity reserve used to manage risks at BayernLB - Bank level. The optimisation of net interest income

by Asset Liability Management and the dissolution of the valuation reserve for bid-ask spreads

also contributed to the postive results. The fall in administrative expenses is due to the one-time

addition to the pension provisions in the previous year. Earnings from customers in the Corpo-

rates & Mittelstand and Real Estate segments were healthy and partly offset the weaker business

with savings banks and banks. Unexpected repayments of loans to banks also contributed to the

net gain from risk provisions.

Central areas & Others segment

This segment includes the central areas and business transactions executed in the overall inter-

ests of the Bank or Group and therefore not allocated to the business segments. Profit before

taxes in the first half of 2013 was a solid EUR 180 million (H1 2012: EUR 204 million).

non-Core Unit segment

• Earnings boosted by sale of GBW

• Measurement of umbrella guarantee agreement weighs on Restructuring Unit’s results

• MKB’s profits hit once again by the tough economic and political environment – focus on

repositioning and optimising costs

• Satisfactory earnings contribution from LBLux

Since the beginning of 2013, all non-core activities have been pooled in the segment. The sizeable

profit before taxes of EUR 306 million (H1 2012: EUR 12 million) was largely due to one-off

income from the sale of GBW, which easily offset the decreased earnings in the Restructuring

Unit and also losses at MKB.

BayernLB . Group Interim Report for the first half of 2013

›› 30

All domestic and foreign portfolios to be wound down as a result of the EU state aid proceedings

in the Real Estate, Corporates, Structured Finance and Public Sector divisions have now also been

transferred to the Restructuring Unit since the start of the year. The volume of all portfolios

including the non-core securities holdings fell by a total of EUR 5.4 billion over the reporting

period due to scheduled and early repayments, sales and restructuring. Profit before taxes of

EUR 27 million (H1 2012: EUR 61 million) was significantly below the year before period largely

due to a sharp fall in net interest and net commission income caused by the reduction in credit

volumes, and also a negative measurement result on the ABS portfolio hedge (Umbrella measure-

ment). Contributing to earnings were lower administrative expenses (due to the one-off effect on

pension provisions in the previous year), the net gain in risk provisioning and one-off income

from a sale of equity investments.

MKB once again reported a large loss before taxes of EUR – 108 million in the first half (H1 2012:

EUR – 66 million). The continuing losses are largely attributable to the ongoing difficult economic

and political environment in Hungary. In addition to a EUR 46 million expense for Hungary’s bank

levy, the introduction of a financial transaction tax in 2013 also weighed on earnings in the

amount of EUR 26 million. Also weighing on operating earnings were the country’s spluttering

economic recovery and a subdued climate for consumption and capital expenditure. However,

net interest income and net commission income rose slightly on the previous year period due to

one-off income from the payments business. Gains or losses on fair value measurement fell by

EUR 26 million due to mark to market losses on government and central bank bonds in the wake

of a sharp fall in the key interest rate and on FX swaps. Furthermore, the continued tough situa-

tion on the Hungarian real estate market means that additional high writedowns on the commer-

cial and private real estate portfolios had to be taken, resulting in an EUR 25 million addition to

risk provisions. Administrative expenses were, however, cut by a sizeable EUR 9 million thanks to

the systematic restructuring of MKB.

Although customer business in corporate banking and private banking remains subdued, LBLux

reported profit before taxes of EUR 18 million (H1 2012: EUR 19 million) thereby making a solid

contribution to the segment’s performance.

Since the start of the year, the non-core activities of DKB, additional non-core investments not

assigned to the divisions referred to above and business transactions in non-core business exe-

cuted in the overall interests of the Bank or Group are shown in the non-organisational Other

NCU division. Profit before taxes in the reporting period was EUR 362 million (H1 2012:

EUR 19 million), primarily due to the proceeds from the sale of GBW.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Segments 31

Events after the end of the reporting period

In December 2012 Hypo Alpe-Adria-Bank International AG, Klagenfurt, the respondent,

announced that until further notice it would make no more payments of principal and interest

on loans it has been granted as it is of the opinion that these loans granted after 2008 must be

classified as substitute equity instead. On 4 July 2013, in the legal dispute between Bayerische

Landesbank and the respondent to determine if an obligation to repay the loan exists, Munich

District Court I issued a preliminary opinion that the clause in the loan agreement defining the

place of jurisdiction as Munich was valid. Based on the respondent’s own submission, the court

has concluded that the respondent must argue and provide proof that the “capital replacement

provisions” apply and is of the opinion that the report submitted in evidence of this, which con-

tains only anonymised information, fails to do so. It is also doubtful whether the method selected

by an outside expert is suitable for determining the status of the respondent’s capital in the rele-

vant period of time.

The European Commission’s ruling called for certain changes to be made in respect of corporate

governance. In the constituent meeting of 4 July 2013, the former Board of Administration of

BayernLB was reconfigured into the Supervisory Board. The new board no longer includes any

politicians from the Bavarian government as ex officio board members.

On 15 August 2013, MKB signed a sales agreement to fully dispose of its Bulgarian subsidiary

MKB Unionbank. The sales agreement must be approved by the Bulgarian central bank and the

Bulgarian anti-trust authority before it can take effect. The process could take several months.

The transaction is expected to result in a deconsolidation loss in the middle double-digit millions

of euros range.

BayernLB . Group Interim Report for the first half of 2013

›› 32

Outlook

In the second half of 2013, the German economy should generally continue to expand. The

gradual shift from foreign trade to the domestic economy as drivers of activity is likely to con-

tinue. So private consumption should give the economy an additional leg up, and the very low

cost of borrowing will encourage businesses to expand. Foreign trade will probably provide only

limited stimulus as momentum in key emerging markets has started to flag.

The main assumption is that the eurozone debt crisis will not escalate again and seriously rattle

financial markets. Persistently high risk aversion is keeping interest rates very low. But Bund

yields should tend to tick upwards. Subdued corporate earnings mean that the stock market has

limited upside potential. The Federal Reserve’s announcement of an exit from the bond buyback

programme should nudge the euro south initially.

In “year one” following the EU ruling, BayernLB’s strategic focus as a corporate and real estate

lender and partner to the savings banks has paid off once again with good results reported in all

core businesses in the first two quarters of 2013. However, in its ruling in 2012, the European

Commission has placed a number of ambitious conditions on the Bank that will constrain its free-

dom of action over the coming years. For example, the Bank must shrink to around half of its size

at the end of 2008 and repay around EUR 5 billion in capital to the Free State of Bavaria by 2019.

Given the increasingly restrictive regulatory environment and consequent increase in capital

requirements, these capital repayments will be the biggest challenge in the next several years.

BayernLB has already made good progress this year in meeting the EU conditions. This was and

will continue to be regularly checked in detail by an independent monitoring trustee (audit

firm RBS RoeverBroennerSusat) on behalf of the Commission. The Bank is still resizing and it will

continue to drive this process forward. To further downsize the investment portfolio by a large

amount, the sale of MKB and LBLux is a key item on the agenda under the EU ruling. In the

medium term BayernLB will continue to hold equity stakes that for the duration will underpin its

business model as a corporate and real estate lender and partner to the savings banks focused on

the domestic market of Germany.

Besides implementing the EU’s conditions, the Bank, as a systemically important institution in

Germany, still faces the challenge of complying with the burgeoning volume of regulations,

particularly CRR/CRD IV, which comes into effect on 1 January 2014, and implementing the

Minimum Requirements for Recovery Plans for Financial Institutions (MaSan).

The BayernLB Group expects full-year 2013 earnings to be positive. However, it is faced with

contingencies, particularly as the economic and political environment in eastern Europe remains

challenging. Developments in Hungary are of key importance for BayernLB. The country’s govern-

ment is toying with the idea of fresh political intervention on foreign currency loans which could

severely test the business of banks operating there. MKB, which is still being restructured from

the ground up, may then take another knock.

BayernLB’s funding situation is still very good. There is a significant surplus of liabilities in the

banking book available for future lending. Corporate deposits went up in the first half of 2013.

Funding needs for the whole of 2013 have largely been covered.

The statements made in this outlook section should be read in conjunction with the outlook

given in the 2012 annual report. Changes in the general economic situation may have a

corresponding impact on the BayernLB Group.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Events after the end of the reporting period · Outlook 33

Risk report

The information provided in the risk report of the Group interim report relates mainly to the

changes in the first half of 2013. The risk report in the 2012 Group management report gives a

detailed description both of the principles, methods, procedures and organisational structures of

the risk management used within the BayernLB Group and of the internal control and risk man-

agement system for ensuring the accounts have been properly prepared and are reliable.

Rounding differences may occur in the tables in the last digit to the right.

Key developments in the first half of 2013 and outlook

• Risk profile remained stable

• Core business expanded in line with strategy

• Progress in winding down non-core business

• Risk-bearing capacity maintained at all times

• Increase in market risk predominantly due to accounting policies

• Comfortable levels of liquidity

The BayernLB Group’s risk profile was stable overall in the first half of 2013.

The business model of the Group as a corporate and real estate lender and partner to the savings

banks with a regional focus on Bavaria and Germany is increasingly reflected in the portfolio

structure.

The standards set in the strategy were adhered to and significant progress made in building up

core and winding down non-core businesses.

The gross credit volume fell by a total of EUR 11.5 billion to EUR 289.9 billion as a result.

The share of the portfolio in Germany, the core market of BayernLB and Deutsche Kreditbank AG,

rose once again to 74 percent overall.

The foreign portfolio experienced a sharp fall. Gross credit volumes fell significantly, particularly

in western Europe (the United Kingdom, France and the GIIPS countries: Greece, Italy, Ireland,

Portugal and Spain).

The largest winding down by volume was in the Financial Institutions sub-portfolio (incl. ABSs).

In the Corporate Customers sub-portfolio, the winding down was centred on foreign business,

while in the Commercial Real Estate sub-portfolio, it was mainly exposures with low credit ratings

that were run down.

Portfolio quality was boosted by new business in core business areas, favourable business and

economic conditions in Germany and the reduction in volumes.

The investment grade share rose back up to 76.4 percent, while the non-performing ratio fell

to 3.2 percent compared with the 3.4 percent as at 31 December 2012. Risk provisions were

markedly lower in the first half of 2013 compared with the same period of the previous year.

BayernLB . Group Interim Report for the first half of 2013

›› 34

Risk-bearing capacity was maintained throughout the first half of 2013 as the provision of risk

capital was solid. The increase in risk capital requirements due to adjustments in methodology

for market risk did not impair risk-bearing capacity at any time. The BayernLB Group continued

to enjoy comfortable levels of liquidity.

The previous forecasts for risk trends therefore remain unchanged overall.

As before, factors which could affect the accuracy of the forecasts presented in the 2012 consoli-

dated financial statements include the difficult economic and political situation in Hungary, which

is the domestic market of subsidiary MKB, and the ongoing crisis affecting some financially

weaker EMU countries.

risk-bearing capacity

Risk-bearing capacity is monitored using the Internal Capital Adequacy Assessment Process

(ICAAP) at BayernLB level, the subsidiaries DKB, MKB and LBLux, and at Group level. The ICAAP

assesses whether the available risk cover funds fully cover the risks taken on or planned.

The method for calculating risk-bearing capacity is assessed and refined on a regular basis to

ensure it takes adequate account of external factors and internal strategic goals. BayernLB’s

ICAAP approach is designed to protect senior creditors in case of liquidation. This is computed

using internal target standards for the precision of risk measurement. This corresponds to a

confidence level of 99.95 percent and a rating score of A2 on Moody’s rating scale.

risk capital requirements

EUR million 30 Jun 2013 31 Dec 2012

risk capital requirements

• credit risk and country risk (counterparty risk)

• credit risk (specific interest rate risk)

• market risk*

• operational risk

• investment risk

5,331

2,639

1,990

533

169

4,717

2,776

493

493

664

291

* As from 30 April 2013 this includes specific interest rate risk.

The increase in market risk is largely due to the adjustments in methodology that were imple-

mented on 30 April 2013. To harmonise the holding period assumptions for market risk positions

with the risk observation horizons of the other risk types in the risk-bearing capacity, they were

set at a uniform 250 days Group-wide. This has resulted in much more conservative assumptions

of market risk in risk-bearing capacity. In this context and taking account of correlation effects,

general market risks and specific interest rate risks, which had been reported separately, were

merged into the single risk type “market risk”.

As a result of the adjustments in methodology, most of the increase in risk capital requirements

was due to market risk and specific interest rate risks. To a lesser extent, the rise was due to

higher interest rate volatility over the observation period.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Risk report 35

The BayernLB Group holds sufficient available economic capital (EUR 17.2 billion) to cover risk

capital requirements. The BayernLB Group had adequate risk-bearing capacity in the first half of

the year.

The possibility of a severe economic downturn (ICAAP stress scenario) arising is calculated in a

stress scenario. The risk capital requirement for the individual risk types in this case totals

EUR 11.1 billion. The BayernLB Group is adequately capitalised also for this scenario.

Management of the individual risk types in the Group

Credit risk

In accordance with its business model as a corporates and real estate lender and partner to the

savings banks with a regional focus on Bavaria and Germany, the largest risk for the BayernLB

Group in terms of amount is credit risk.

At the end of the first half of 2013, no significant changes had been made in the instruments and

methods for measuring, managing and monitoring credit risks as described in the risk report in

the 2012 consolidated financial statements.

Noteworthy upgrades were made in the internal rating procedures approved by supervisory

authorities, particularly the rating module for banks and corporate customers. In partnership

with RSU Rating Service Unit GmbH & Co. KG, bank default forecasts were further improved by

including additional market factors, while the balance-sheet rating and market data-based

models of the corporate customer rating module were redesigned. Further information on the

overall internal rating procedures is published in the 2012 disclosure report.

The following account uses both the management approach, which is based on the figures used

for internal reporting, and the balance sheet approach, which is based on balance sheet figures

and focuses on the value of the assets shown in the statement of financial position.

For the purposes of internal risk management and risk reporting to the Board of Management

and the risk committee of the Supervisory Board, credit volume is defined differently in certain

respects to how it is defined for balance sheet purposes (e.g. only irrevocable credit commit-

ments are included). Similarly, the materiality thresholds for including subsidiaries in the MaRisk

risk inventory for internal risk management may differ from those used to determine the scope

of consolidation. The figures under the management approach may therefore differ from those

under the balance sheet approach.

BayernLB . Group Interim Report for the first half of 2013

›› 36

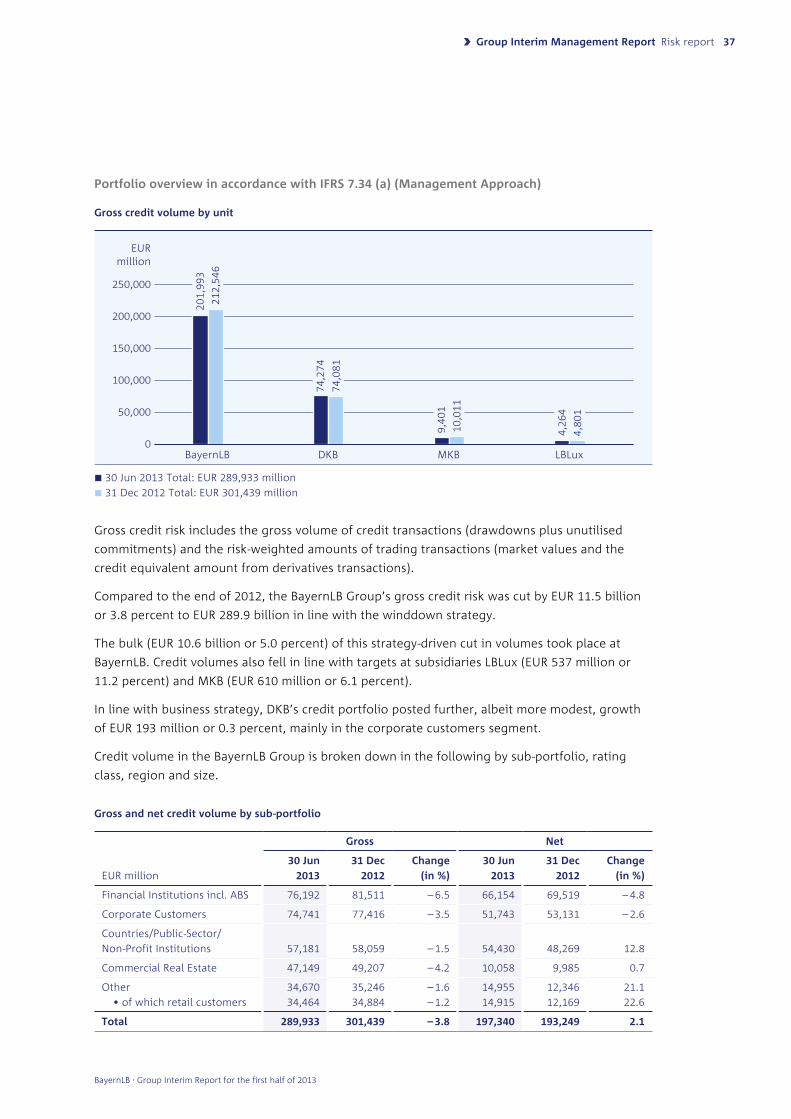

Portfolio overview in accordance with IFrS 7.34 (a) (Management approach)

Gross credit volume by unit

30 Jun 2013 Total: EUR 289,933 million

31 Dec 2012 Total: EUR 301,439 million

Gross credit risk includes the gross volume of credit transactions (drawdowns plus unutilised

commitments) and the risk-weighted amounts of trading transactions (market values and the

credit equivalent amount from derivatives transactions).

Compared to the end of 2012, the BayernLB Group’s gross credit risk was cut by EUR 11.5 billion

or 3.8 percent to EUR 289.9 billion in line with the winddown strategy.

The bulk (EUR 10.6 billion or 5.0 percent) of this strategy-driven cut in volumes took place at

BayernLB. Credit volumes also fell in line with targets at subsidiaries LBLux (EUR 537 million or

11.2 percent) and MKB (EUR 610 million or 6.1 percent).

In line with business strategy, DKB’s credit portfolio posted further, albeit more modest, growth

of EUR 193 million or 0.3 percent, mainly in the corporate customers segment.

Credit volume in the BayernLB Group is broken down in the following by sub-portfolio, rating

class, region and size.

Gross and net credit volume by sub-portfolio

EUR million

Gross net

30 Jun

2013

31 Dec

2012

Change

(in %)

30 Jun

2013

31 Dec

2012

Change

(in %)

Financial Institutions incl. ABS 76,192 81,511 – 6.5 66,154 69,519 – 4.8

Corporate Customers 74,741 77,416 – 3.5 51,743 53,131 – 2.6

Countries/Public-Sector/

Non-Profit Institutions 57,181 58,059 – 1.5 54,430 48,269 12.8

Commercial Real Estate 47,149 49,207 – 4.2 10,058 9,985 0.7

Other

• of which retail customers

34,670

34,464

35,246

34,884

– 1.6

– 1.2

14,955

14,915

12,346

12,169

21.1

22.6

Total 289,933 301,439 – 3.8 197,340 193,249 2.1

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Risk report 37

BayernLB DKB MKB LBLux

EUR million

250,000

200,000

150,000

100,000

50,000

0

20

1,9

93

74

,27

4

9,4

01

4,2

64

21

2,5

46

74

,08

1

10

,01

1

4,8

01

Net credit risk is calculated by deducting the value of collateral, outplaced business and risk-free

transactions (transactions for account of a third party). The following analyses relate to gross

credit risk.

Financial Institutions sub-portfolio

Reductions in the BayernLB Group were concentrated in the Financial Institutions sub-portfolio,

which was cut by EUR 5.3 billion or 6.5 percent.

The credit volume with banks/savings banks fell in Germany, North America and the United

Kingdom in particular. The ABS portfolio continued to shrink (by more than 10 percent), largely

due to ongoing repayments. The volume in the insurance sector was, however, stable.

Germany’s share rose slightly from 64.8 to 65.3 percent, while the investment grade share

climbed from 86.6 to 87.7 percent.

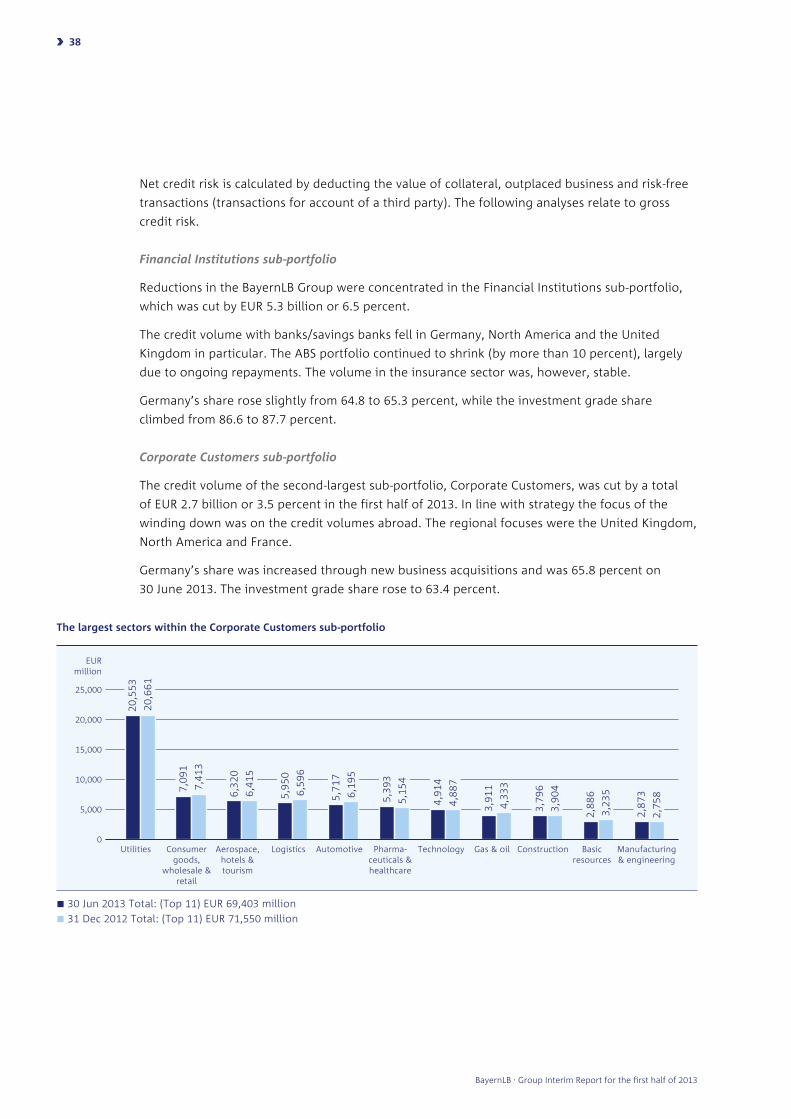

Corporate Customers sub-portfolio

The credit volume of the second-largest sub-portfolio, Corporate Customers, was cut by a total

of EUR 2.7 billion or 3.5 percent in the first half of 2013. In line with strategy the focus of the

winding down was on the credit volumes abroad. The regional focuses were the United Kingdom,

North America and France.

Germany’s share was increased through new business acquisitions and was 65.8 percent on

30 June 2013. The investment grade share rose to 63.4 percent.

The largest sectors within the Corporate Customers sub-portfolio

30 Jun 2013 Total: (Top 11) EUR 69,403 million

31 Dec 2012 Total: (Top 11) EUR 71,550 million

Utilities Consumer goods,

wholesale & retail

Aerospace, hotels & tourism

Logistics Automotive Pharma-ceuticals & healthcare

Technology Gas & oil Construction Basic resources

Manufacturing & engineering

EUR million

25,000

20,000

15,000

10,000

5,000

0

20

,55

3

7,0

91

6,3

20

5,9

50

5,7

17

5,3

93

4,9

14

3,9

11

3,7

96

2,8

86

2,8

73

20

,66

1

7,4

13

6,4

15

6,5

96

6,1

95

5,1

54

4,8

87

4,3

33

3,9

04

3,2

35

2,7

58

BayernLB . Group Interim Report for the first half of 2013

›› 38

Among the sectors, the main increases in credit volume took place in the core pharmaceuticals

and healthcare and manufacturing & engineering sectors. Most new business in these sectors

was acquired in Germany, increasing the country’s share further to 89.8 and 87.1 percent

respectively.

The largest reduction in volume took place in the logistics and automotive sectors.

Country/Public-Sector/Non-Profit Institutions sub-portfolio

In the Country/Public-Sector/Non-Profit Institutions sub-portfolio, the third-largest sub-portfolio,

credit volumes were reduced by EUR 878 million or 1.5 percent. Most of the fall resulted from

redemptions by German states and in Spain and Hungary.

Germany’s share of this sub-portfolio remained high at 79.7 percent.

Commercial Real Estate sub-portfolio

The fall in the gross credit volume in the Commercial Real Estate sub-portfolio totalling

EUR 2.1 billion or 4.2 percent took place in all Group units.

Most of this related to non-core business in BayernLB’s Restructuring Unit. Credit volumes at MKB

and LBLux were run down by a total of EUR 356 million in line with strategy.

New business was mainly acquired in Germany. Germany’s share of the sub-portfolio rose from

76.1 to 78.1 percent.

Portfolio quality was improved through a significant ratings upgrade and targeted volume reduc-

tions in the non-investment grade and non-performing areas. This was clearly evident in the

increase in the investment grade share from 65.4 to 69.8 percent and the lower non-performing

ratio.

Retail Customers/Other sub-portfolio

The slight fall in gross credit volume in the Retail Customers/Other sub-portfolio of EUR 576 million

or 1.6 percent is due to the contraction in BayernLB’s retail customer business and repayment of

retail residential construction loans at DKB.

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Risk report 39

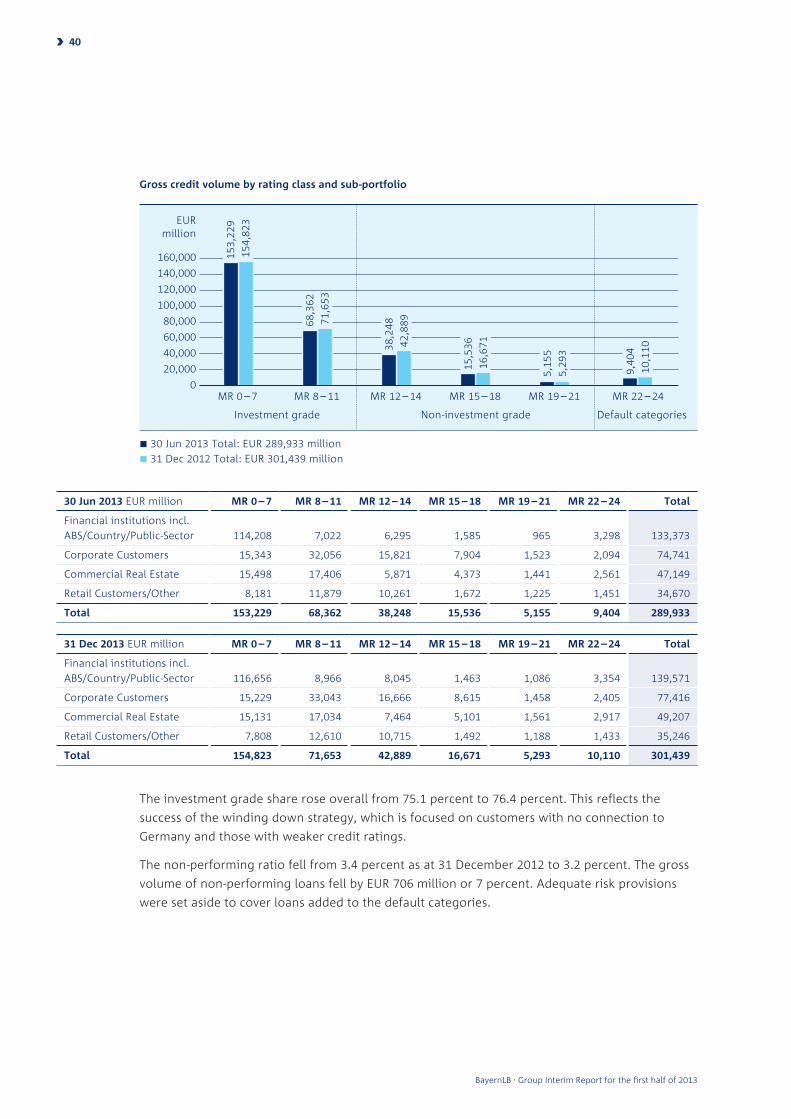

Gross credit volume by rating class and sub-portfolio

30 Jun 2013 Total: EUR 289,933 million

31 Dec 2012 Total: EUR 301,439 million

30 Jun 2013 EUR million MR 0 – 7 MR 8 – 11 MR 12 – 14 MR 15 – 18 MR 19 – 21 MR 22 – 24 Total

Financial institutions incl.

ABS/Country/Public-Sector 114,208 7,022 6,295 1,585 965 3,298 133,373

Corporate Customers 15,343 32,056 15,821 7,904 1,523 2,094 74,741

Commercial Real Estate 15,498 17,406 5,871 4,373 1,441 2,561 47,149

Retail Customers/Other 8,181 11,879 10,261 1,672 1,225 1,451 34,670

Total 153,229 68,362 38,248 15,536 5,155 9,404 289,933

31 Dec 2013 EUR million MR 0 – 7 MR 8 – 11 MR 12 – 14 MR 15 – 18 MR 19 – 21 MR 22 – 24 Total

Financial institutions incl.

ABS/Country/Public-Sector 116,656 8,966 8,045 1,463 1,086 3,354 139,571

Corporate Customers 15,229 33,043 16,666 8,615 1,458 2,405 77,416

Commercial Real Estate 15,131 17,034 7,464 5,101 1,561 2,917 49,207

Retail Customers/Other 7,808 12,610 10,715 1,492 1,188 1,433 35,246

Total 154,823 71,653 42,889 16,671 5,293 10,110 301,439

The investment grade share rose overall from 75.1 percent to 76.4 percent. This reflects the

success of the winding down strategy, which is focused on customers with no connection to

Germany and those with weaker credit ratings.

The non-performing ratio fell from 3.4 percent as at 31 December 2012 to 3.2 percent. The gross

volume of non-performing loans fell by EUR 706 million or 7 percent. Adequate risk provisions

were set aside to cover loans added to the default categories.

MR 0 – 7 MR 8 – 11 MR 12 – 14 MR 15 – 18 MR 19 – 21 MR 22 – 24

Default categoriesInvestment grade Non-investment grade

EUR million

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

15

4,8

23

71

,65

3

42

,88

9

16

,67

1

5,2

93

10

,11

0

15

3,2

29

68

,36

2

38

,24

8

15

,53

6

5,1

55

9,4

04

BayernLB . Group Interim Report for the first half of 2013

›› 40

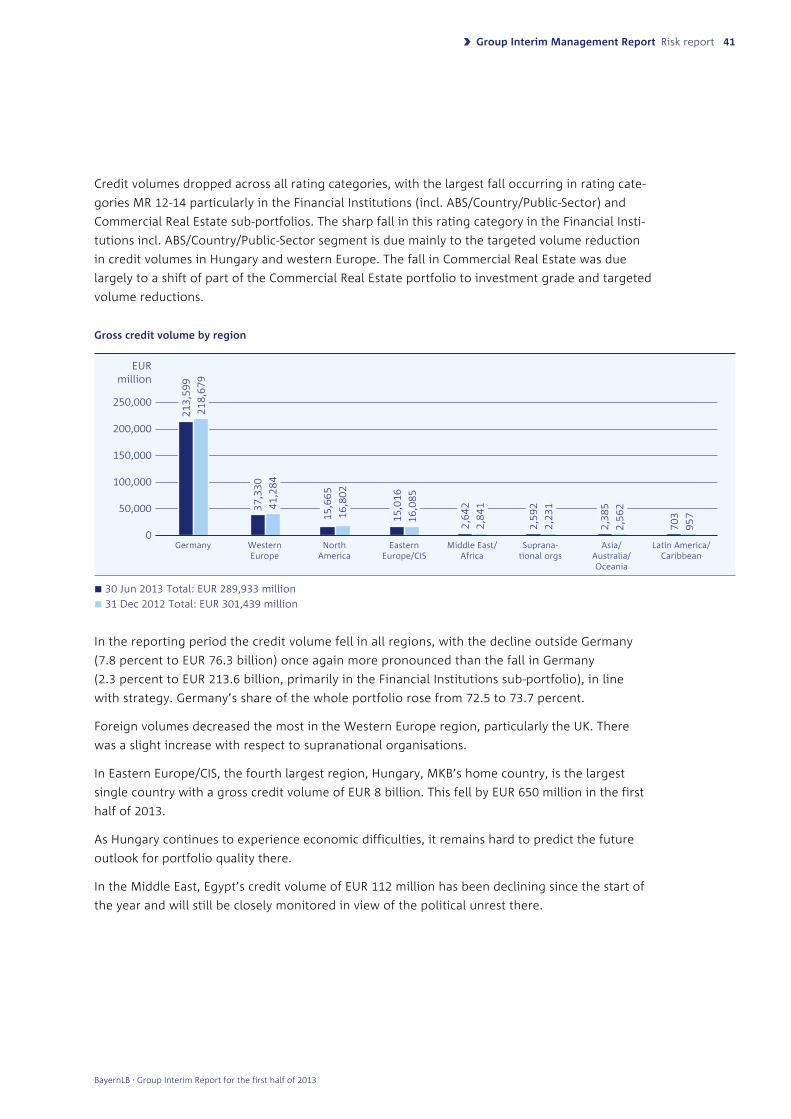

Credit volumes dropped across all rating categories, with the largest fall occurring in rating cate-

gories MR 12-14 particularly in the Financial Institutions (incl. ABS/Country/Public-Sector) and

Commercial Real Estate sub-portfolios. The sharp fall in this rating category in the Financial Insti-

tutions incl. ABS/Country/Public-Sector segment is due mainly to the targeted volume reduction

in credit volumes in Hungary and western Europe. The fall in Commercial Real Estate was due

largely to a shift of part of the Commercial Real Estate portfolio to investment grade and targeted

volume reductions.

Gross credit volume by region

30 Jun 2013 Total: EUR 289,933 million

31 Dec 2012 Total: EUR 301,439 million

In the reporting period the credit volume fell in all regions, with the decline outside Germany

(7.8 percent to EUR 76.3 billion) once again more pronounced than the fall in Germany

(2.3 percent to EUR 213.6 billion, primarily in the Financial Institutions sub-portfolio), in line

with strategy. Germany’s share of the whole portfolio rose from 72.5 to 73.7 percent.

Foreign volumes decreased the most in the Western Europe region, particularly the UK. There

was a slight increase with respect to supranational organisations.

In Eastern Europe/CIS, the fourth largest region, Hungary, MKB’s home country, is the largest

single country with a gross credit volume of EUR 8 billion. This fell by EUR 650 million in the first

half of 2013.

As Hungary continues to experience economic difficulties, it remains hard to predict the future

outlook for portfolio quality there.

In the Middle East, Egypt’s credit volume of EUR 112 million has been declining since the start of

the year and will still be closely monitored in view of the political unrest there.

Germany Western Europe

North America

Suprana-tional orgs

Middle East/Africa

Eastern Europe/CIS

Asia/ Australia/Oceania

Latin America/Caribbean

EUR million

250,000

200,000

150,000

100,000

50,000

0

21

3,5

99

37

,33

0

15

,66

5

2,5

92

2,6

42

15

,01

6

2,3

85

70

3

21

8,6

79

41

,28

4

16

,80

2

2,2

31

2,8

41

16

,08

5

2,5

62

95

7

BayernLB . Group Interim Report for the first half of 2013

›› Group Interim Management report Risk report 41

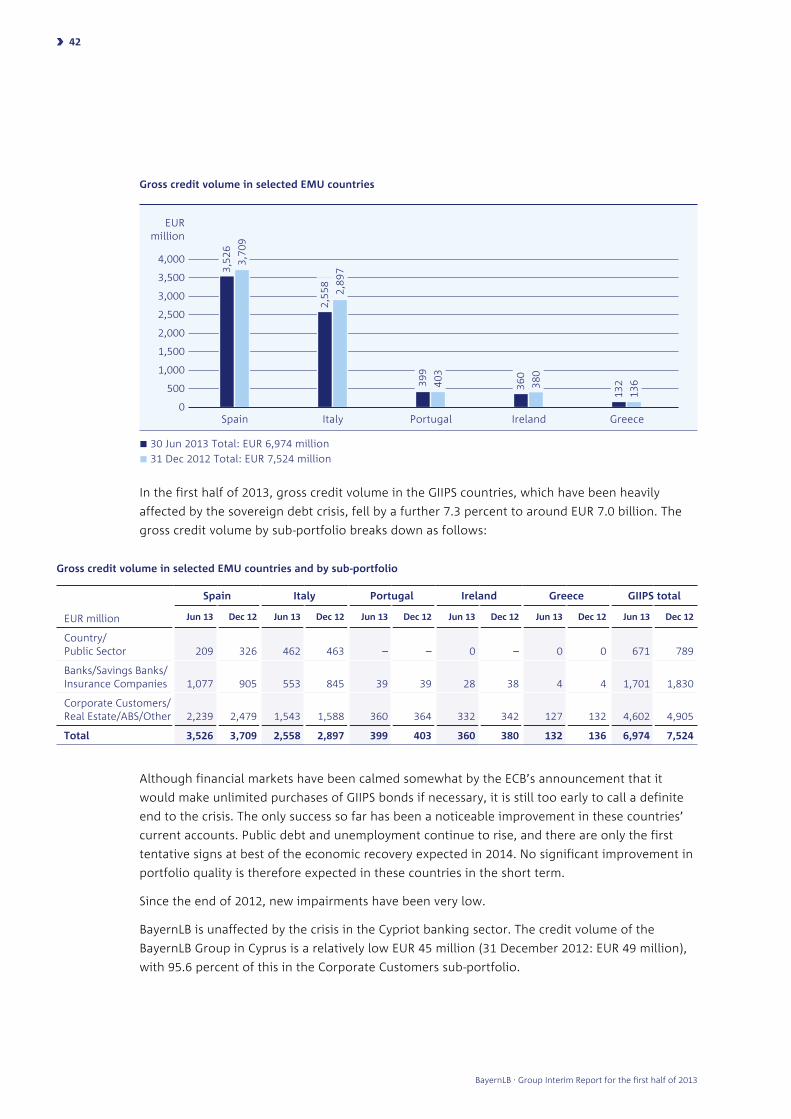

Gross credit volume in selected eMU countries

30 Jun 2013 Total: EUR 6,974 million

31 Dec 2012 Total: EUR 7,524 million

In the first half of 2013, gross credit volume in the GIIPS countries, which have been heavily

affected by the sovereign debt crisis, fell by a further 7.3 percent to around EUR 7.0 billion. The

gross credit volume by sub-portfolio breaks down as follows:

Gross credit volume in selected eMU countries and by sub-portfolio

EUR million

Spain Italy Portugal Ireland Greece GIIPS total

Jun 13 Dec 12 Jun 13 Dec 12 Jun 13 Dec 12 Jun 13 Dec 12 Jun 13 Dec 12 Jun 13 Dec 12

Country/ Public Sector 209 326 462 463 – – 0 – 0 0 671 789

Banks/Savings Banks/Insurance Companies 1,077 905 553 845 39 39 28 38 4 4 1,701 1,830

Corporate Customers/ Real Estate/ABS/Other 2,239 2,479 1,543 1,588 360 364 332 342 127 132 4,602 4,905

Total 3,526 3,709 2,558 2,897 399 403 360 380 132 136 6,974 7,524

Although financial markets have been calmed somewhat by the ECB’s announcement that it

would make unlimited purchases of GIIPS bonds if necessary, it is still too early to call a definite

end to the crisis. The only success so far has been a noticeable improvement in these countries’

current accounts. Public debt and unemployment continue to rise, and there are only the first

tentative signs at best of the economic recovery expected in 2014. No significant improvement in

portfolio quality is therefore expected in these countries in the short term.

Since the end of 2012, new impairments have been very low.

BayernLB is unaffected by the crisis in the Cypriot banking sector. The credit volume of the

BayernLB Group in Cyprus is a relatively low EUR 45 million (31 December 2012: EUR 49 million),

with 95.6 percent of this in the Corporate Customers sub-portfolio.

EUR million

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

3,5

26

2,5

58

39

9

36

0

13

2

3,7

09

2,8

97

40

3

38

0

13

6

Spain Italy Portugal Ireland Greece

BayernLB . Group Interim Report for the first half of 2013

›› 42

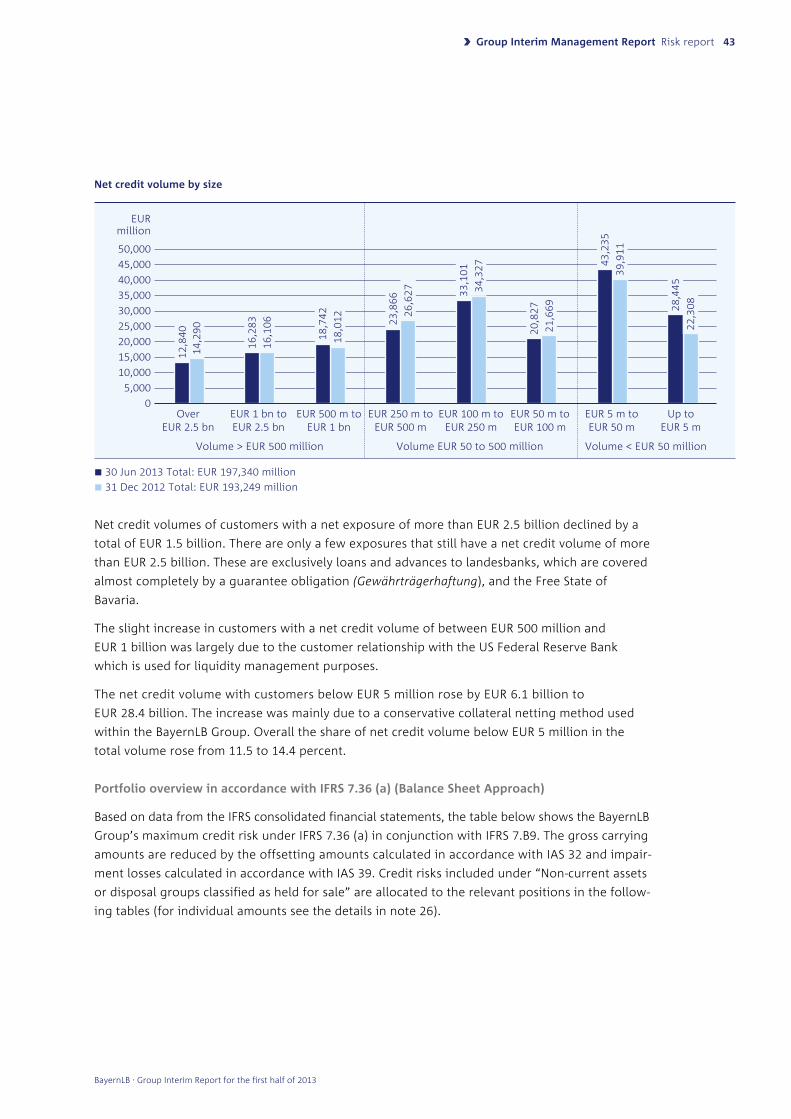

net credit volume by size

30 Jun 2013 Total: EUR 197,340 million

31 Dec 2012 Total: EUR 193,249 million

Net credit volumes of customers with a net exposure of more than EUR 2.5 billion declined by a

total of EUR 1.5 billion. There are only a few exposures that still have a net credit volume of more

than EUR 2.5 billion. These are exclusively loans and advances to landesbanks, which are covered

almost completely by a guarantee obligation (Gewährträgerhaftung), and the Free State of

Bavaria.

The slight increase in customers with a net credit volume of between EUR 500 million and

EUR 1 billion was largely due to the customer relationship with the US Federal Reserve Bank

which is used for liquidity management purposes.

The net credit volume with customers below EUR 5 million rose by EUR 6.1 billion to

EUR 28.4 billion. The increase was mainly due to a conservative collateral netting method used

within the BayernLB Group. Overall the share of net credit volume below EUR 5 million in the

total volume rose from 11.5 to 14.4 percent.

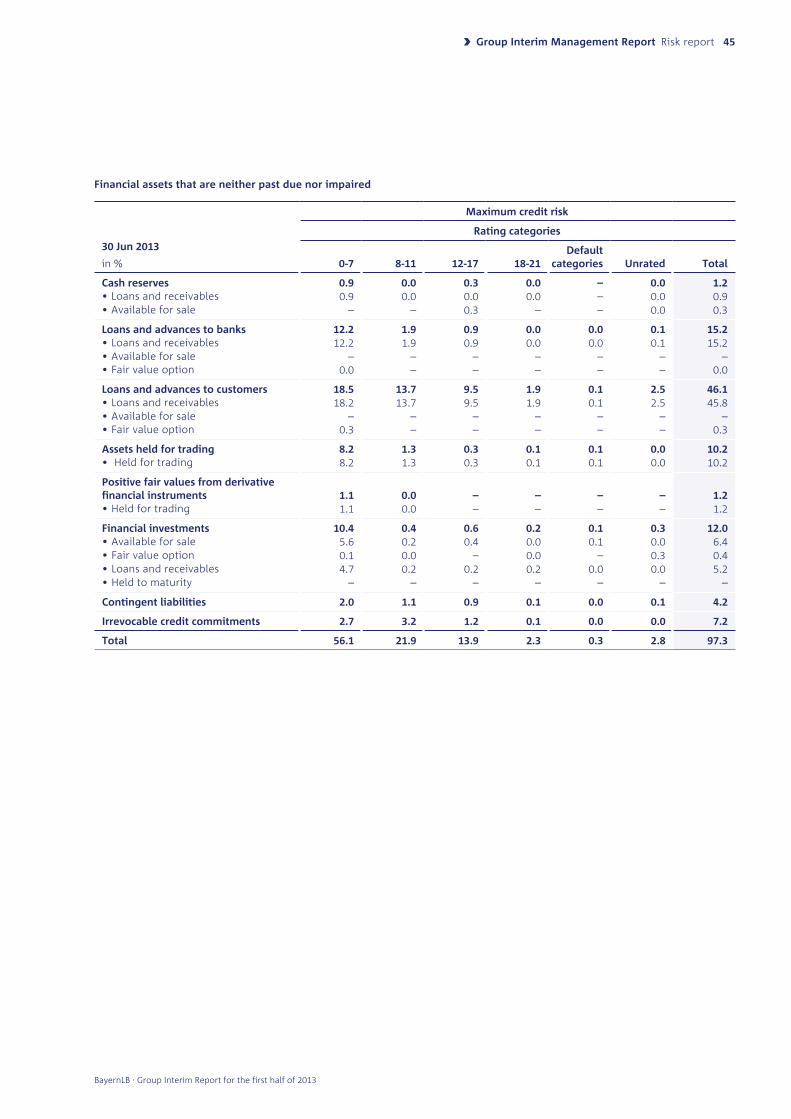

Portfolio overview in accordance with IFrS 7.36 (a) (Balance Sheet approach)

Based on data from the IFRS consolidated financial statements, the table below shows the BayernLB

Group’s maximum credit risk under IFRS 7.36 (a) in conjunction with IFRS 7.B9. The gross carrying

amounts are reduced by the offsetting amounts calculated in accordance with IAS 32 and impair-

ment losses calculated in accordance with IAS 39. Credit risks included under “Non-current assets

or disposal groups classified as held for sale” are allocated to the relevant positions in the follow-

ing tables (for individual amounts see the details in note 26).

EUR million

50,000

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

22

,30

8

28

,44

5

39

,91

1

43

,23

5

21

,66

9

20

,82

7

34

,32

7