Embed Size (px)

Citation preview

RESTR'ICT'ED

CIRCULATING COPY Report No. P-1062

TO BE RETURNED TO REPORTS DESK

- ~~~FILE C'OU"PYThis report is for official use only by the Bank Group and spccifically authorized organizations

or persons. It may not be -published, quoted or- cited-without Bartk Group-au:thcrization. The - -

Bank Group-does not accept responsibility fgr the accuracy or complctcness of the report.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED LOAN

TO

ISTANBUL GUBRE SANAYII ANONIM SIRKETI

GUARANTEED BY

THE REPUBLIC OF TURKEY

FOR AN

AMMONIA UREA MANUFACTURING PROJECT

April 28, 1972

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOYHENDATION OF THE PRESID ENTTO TIE EXECUTIVE DI.ECTORS ON A

PROPOSED LOAN TOISTANBUL GUB1E SANAYII ANONflI SIRKETIGUARANTEED BY THE REPUJBLIC OF TURKEY

FOR AN AMMONIA UREA MANUFACTURING PROJECT

1. *I submit the following report and recommendation on a proposedloan to Istanbul Gubre Sanayii Anonim Sirketi (IGSAS) with the guaranteeof the Republic of Turkey for the equivalent of $24 million to help financea fertilizer project designed to produce for sale 274,OOO tons per year ofurea and 90,000 tons of ammonia (other than ammornia produced and convertedinto urea). The loan would have a term of 15 years, including 4 years ofgrace, with interest at 7-1/4 percent per annum. A guarantee fee of 1-3/bpercent would be payable by IGSAS to the Republic of Turkey.

PART I - INTRODUCTION

2. The level of Bank Group operations in Turkey in past years hasbeen largely influenced by the almost chronic balance of payments diffi-culties and the heavy external debt service burden, the limited IDA re-sources which could be made available to Turkey and, to some extent, diffi-culties in project preparation. In 1968 the Bank and the Turkish authori-ties began discussions to establish a basis for a major increase and greatercontinuity in the level of lending. In the Bankts view, the main pre-requi-site for this was the institution of economic policies that would increaseTurkeyts capacity to borrow on Bank terms. This meant, in particular, im-proved extarnal debt management, introduction of reforms in the system oftrade and p3yments, and the provision of more resources and incentives forexport-oriented projects. Another important factor was a significant im-provement in the Government's capacity to identify and prepare projects.

3. By the end of 1970, the Government had made substantial progressin these fields. The goal of achieving external viability within a reason-able time period and the promotion of exports as the principal means of doingso had been accepted. In August 1970, a stabilization program was initiatedand the Turkish Lira was devalued. Parallel with these developments, theBank Group stepped up its assistance in project preparation, notably withadvice on project selection criteria and institution building. As a result,the volume of Bank/IDA lending reached $114 million in FY 1971, thus ex-ceeding the amount lent in the five preceding years.

- 2 -

4. Bank Group lending to Turkey aims at assisting the country inthree major tasks: (a) improving the foreign exchange position parti-cularly through export promotion; (b) institution building and reform inkey sectors including improved financial viability of the major StateEconomic Enterprises; and (c) the achievement of a better balance in ruraland urban development. Several projects financed by the Bank Group inrecent years or presently under discussion focus on the first task. Forinstance, emphasis was placed on export-oriented sub-projects in the lastloan (713-TU) made to the Industrial Development Bank of Turkey (TSKB) andin the Loan and Credit (762/257-TU) for the Fruit and Vegetable Export Pro-ject. Other projects for which lending is contemplated in coming years,especially for livestock, forestry and irrigation, are expected to enhanceTurkey's ability to earn foreign exchange, but attempts to assist the ex-pansion of tourism have not borne fruit so far for lack of a firm Govern-ment policy and of suitable projects. The objective of institution build-ing has been pursued chiefly in agriculture (including agricultural credit),power and transportation. The Bank has been instrumental in bringing abouta comprehensive reorganization of the power sector culminating in the es-tablishment of the Turkish power authority (TEK) to which a loan (763-TU)was made in 1971. It has also acted as executing agency for UNDP technicalassistance studies on transport coordination and on a railway investmentprogram, and a first railway project will be appraised in 1972. Finally,the two-pronged approach to agricultural development of the poorest partsof Central and Eastern Turkey and to urban development has been startedwith the Second Livestock Project and the proposed Urban Development andWater Supply Project for Greater Istanbul, the most rapidly growing urbancenter.

5. The industrial development that the Bank is seeking to encouragein Turkey aims primarily at improving the competitiveness of both the pri-vate and public enterprises which had for a long time been accustomed to arapid but inward-oriented growth behind a barrier of high tariffs and quan-titative restrictions. Given Turkey's natural resources and the emergenceduring the 1960's of a new class of industrial entrepreneurs, increasinglycapable and outward-looking, there appears now to be considerable scope forfurther growth both in export-oriented industries using domestic raw mate-rials(mining, food processing, forest products and textiles) and in judi-cious import replacement (particularly fertilizers and enginerring). PastBank industrial lending has been channeled through TSKB which has receivedsince 1950 eight loans totaling $128 million to assist private enterprises,covering the whole spectrum of industrial activities, but mostly for rela-tively small projects. The private sector has so far been unable to mobilizecapital resources on the scale required for large scale industrial operationswhich, as a result, have been left mostly to the Government. The proposedloan, like the one recently approved for the Erdemir Iron and Steel Companywhich was the first direct Bank lending operation to industry in Turkey,will help increase the flow of capital for industry, although a long runsclution has to be sought mainly through the development of the capitalmarket.

- 3 -

6. Recent Bank Group lending has concentrated predominantly on theagriculture and power sectors. In addition, attention has been given toindustry in the form of a series of loans to TSKB and lately to Erdemir,and to education. The execution of projects in Turkey has been generallysatisfactory apart from prolonged delays in achieving effectiveness forseveral recent loans (see my report on the Irrigation Rehabilitation andCompletion Project, dated January 6, 1972).

7. Five Bank/IDA operations are planned for FY 1972. A $18 millioncredit for the Irrigation Rehabilitation and Completion Project was signedon January 25, 1972; a $76 million loan for the Erdemir Steel Plant Expan-sion Project was approved on March 14, 1972; and a $16 million Credit forthe Second Livestock Development Project was approved on April 4., 1972.The Istanbul Urban Development and Water Supply Project has been appraisedand is planned for negotiations in the second quarter of 1972. A summaryof Bank loans, IDA Credits and IFC Investments as of March 31, 1972 isattached as Annex I. If the Erdemir Expansion and Second Livestock pro-jects approved but not signed are included, total Bank Group lending inTurkey to date amounts to $314.7 million in loans and $145.8 million incredits. A number of projects have been identified and preparation isunderway for Bank Group lending in FY 1973 including a multipurpose powerand irrigation project, a further loan to TSKB and the first Bank financedoperation proposed in the transportation sector, for railway improvement.

8. IFC has been active in Turkey, having participated in industrialinvestments for nylon yarn, pulp and paper, glass and aluminium. Totalcommitments so far amount to $29 million. IC is currently investigatinga number of new investment opportunities in various sectors including mining,special steel and cement.

9. The Ammonia-Urea Manufacturing Project was first appraised by aBank mission in December 1970 and was reappraised in November/December 1971following several project changes introduced by the Sponsors. During nego-tiations in Washington from February 22 to Iiarch 10, the Government of Turkeywas represented by Mr. Ahmet Tufan GMl, Chief Commercial and Economic Counselor,l1r. Teoman Koproluler, Counselor and Mr. Alaeddin Yoruk, Financial Attach6,all of the Turkish Embassy, Washington, D.C., and Mr. Yusuf Ergun, Ministry ofAgriculture; the Borrower was represented by Kr. Selahattin Ozkan, Presidentof Turkiye Petrolleri Anonim Ortakligi (TPAO), Mir. Hassan Cil, Vice Presidentof TPAO, Fir. Erdal Kutlug and Mr. Mehmet Adanali of TPAO, Mr. Turgut Ogmen,Refinery Manager of Istanbul Petrol Rafinerisi Anonim Sirketi (IPRAS) andYMr. Kaya Uysal, Legal Adviser of IPRAS. The Agricultural Bank of Turkey wasrepresented by its Secretary General, Mr. Nesit Parman.

- 4 -

PART II - THE EnONOMY

10. A report entitled "The Development Prospects of Turkey" (EMA-30a)dated February 1, 1971, was distributed to the Executive Directors on February4, 1971. This was updated by a memorandum entitled "Current Economic Positionand Prospects of Turkey" (EMA-40a) dated July 19, 1971, which was distributedon July 26, 1971. A Bank economic mission visited Turkey in April 1972 anda new report will be distributed in the fall of 1972. A country data sheetis attached as Annex II.

11. Following the 1969 elections, which confirmed the Justice Party inpower, the Government under Prime Minister Demirel faced a constant erosionof its majority in the National Assembly. At the same time, violence bygroups of extremist students and unrest among workers were on the rise andpersisted through 1970 into the early months of 1971. In March 1971, theArmed Forces intervened, the Government resigned and a new "above-party andreformist" government was formed under Prime Minister Erim.

12. The new government's program called for the restoration of lawand internal security, more rational.management of the economy, and longoverdue wide-ranging structural reforms. These reforms included: land andeducational reform; far-reaching reorganization of the government, includingState Economic Enterprises (SEEs) and external trade agencies; nationali-zation of private enterprise in mining, petroleum arid forestry industries;and stricter enforcement of the conditions for foreign capital investment,including Turkish majority participation.

13. In its eight months in office, the Government largely restoredlaw and order and, on the economic side, introduced some administrativechanges, sub:stantially raised prices of several SEE products and presentedseveral reform bills to Parliament but was not yet able to translate itslong-range economic policies into detailed measures and decrees. It wasalso unable to bring under control the serious fiscal iibalance and therapid increase in prices, both of which were aggravated by the salaryrises introduced as part of the Personnel Reform Law by the previous Govern-ment. Growing opposition from Parliament and the private sector to someadministrative changes and reform proposals brought about the resignationof a large group of technocratic.ministers in December 1971. A new coali-tion Government, headed again by Prime M1inister Erim, was then formed witha large nurmber of representatives of the political parties.

lb. The second Erim Governmentts program reiterated the urgency ofexecuting-major structural reforms, emphasized the importance of the survival.of democratic procedures in Tur key, and appeared to be conciliatory both intone and in the choice of key ministers towards Parliament and the privatesector. In the program and in subsequent public statements, the role of theprivate sector was stressed. Since then several administrative features of

- 5 -

the original program of April 1971 affecting the private sector have beenmodified and policies affecting domestic and foreign private investors havebeen under review. i/

15. Economic growth in 1970 was influenced by factors associated withcivil unrest, the growing balance of payments problems, devaluation, and un-favorable weather affecting the 1969-70 harvest. GNP grew by 5.6 percent atconstant prices, compared with an average of 6.6 percent in the precedingeight years. Industrial growth slowed down to 3 percent from 10 percent in1969, and agricultural output rose by only 1 percent. However, the rest ofthe economy grew at a rate of 7 percent.

16. In 1971, economic growith, buoyed by a sharp improvement in theoverall balance of payments position following devaluation, rebounded to arecord rate provisionally estimated at about 9 percent. This performancereflected a record increase in agricultural output for the 1970-71 cropyear estimated at over B percent and a recovery in industrial output, whichis estimated to have i.ncreased by about 9 percent.

17. Other aspects of economic performance in 1971 were less encoura-ging. Growth of investment slowed down considerably, with public invest-ment actually decreasing in real terms, and private investment increasing

.only moderately. The decrease in public investment wTas due to the drop inpublic savings, which was largeLy the result of the high cost of the PersonnelReform Law and the poor performance of the SEEs. The overall savings ratioincreased from 15.1 percent of G-MP at constant prices in 1967 to 16.6 percentin 1970, but according to preliminary estimates, did not improve further in1971. Viholesale prices increased by more than 20 percent as a result of thecombined pressure of increased wage settlements under the Personnel ReformLaw, the efect of the 66 percent devaluation on import prices, and thesubstantial increases in SE3s prices.

18. Following the devaluation in August 1970, Turkey's current accountdeficit declined sharply to roughly $100 million in 1971, compared with $172million in 1970 and $221 million in 1969. This improvement occurred despitea widening of the trade deficit in both 1970 and 1971 when steadily risingexports were outstripped by more rapid increases in imports. The main off-setting factor was a jump in workers' remittances from $1L1 million in 1969to $273 million in 1970 and an estimated $b75 million in 1971.29. Although private and public capital inflows appear to have declinedsomewhat in 1971 after a substantial increase in 1970, the growth in remit-tances was strong enough to push up the level of official foreign reservesto a record M772 rillion at the end of 1971, a trend which has continued inearly 1972. Turkey's net foreign assets, which were negative in 1968, roseto $411 million by the end of 1971. This relatively high level of reservesshould help Turkey protect its new rate of exchange, cushion any sudden dropin remittances, wshich are vulnerable to conditions in Europe, and possiblysupport a larger degree of import liberalisation. Following the changesintroduced in the relationships among the major world currencies in December1971, Turkey established a central rate of 1L Turkish lira to the the USdollar (replacing the previous parity of TL 15 to the dollar).

Y/ The secorld Erim Cabinet resigned on April 17, 1972.

- 6 -

20. Provisional estimates for 1971 indicate a significant increase inthe budget deficit over 1970. Although total domestic revenues increasedsubstantially to an estimated ¶TL 37 billion in 1971, as compared to aboutTL 29 billion in 1970, expenditures rose more rapidly to an estimated TL 43billion fran about TL 32 billion in 1970 (mainly due to the increase inpersonnel costs). As a result, whereas the deficit in 1970 was virtuallyall covered by conterpart financing, in 1971 the estimated deficit necessi-tated substantial short-term borrowing from the Central Bank.

21. In summary, the economic situation in 1971 could be regarded astransitional, showing the first effects of the major adjustments in theexchange rate, salaries, and SEE prices, and the clearing of the backlog ofimports. The budget is being severely strained by the heavy cost of thePersonnel Reform Law and faces probable continued pressure from the weakfinancial position of some of the SEEs and from the need to step up invest-ment expenditures. In the private sector too, wage-price inflationarypressures appear to be substantial. Consequently, measures are needed tocontain aggregate demand whilst at the same time additional resources haveto be mobilized to step up investment in both the public and private sectors.The new Government's economic program attaches therefore special importanceto the efficient utilization of existing capacity, investment in quick-yielding projects, and completion of on-going ones. It calls for a majorrise in taxation to finance an increase of 30 percent in the level ofpublic investment expenditures in 1972 and to do so within a balancedbudget. In the 1972 budget, tax revenues are targeted to increase by46 percent compared to the estimated actual in 1971. Howvever, new taxbills necessary to realize the increase in revenues had not been passedby Parliament by March 1972. These measures, which in themselves willtest the strength of the new Government, will need to be supplementedby other actions aimed more specifically at checking the wage and priceincrease in both the public and the private sectors.

22. For the longer term, if the country remains politically stable,and if the Government can carry out at least a modified reform program inseveral essential fields and promote exports and investments, the prospectsfor continued growth will be promising. However, to maintain an adequaterate of investment Turkey will continue to need substantial amounts of ex-ternal assistance. The main sources of foreign aid to Turkey have so farbeen the members of the OECD Consortium. Of total disbursements of offi-cial external assistance estimated at $L,17 million in 1970, a total of$306 million was provided by Consortium members. The United States providedthe largest amount ($78 mil'lion); followed by the EMA ($75 million);Germany ($41 million); the Bank Group, including IFC ($28 million); theEuropean Investment Bank ($26 million); and France ($22 million). Othercountries provided smaller amounts. Preliminary estimates indicate thatin 1971, of the total disbursements of official external assistance ofabout $l00 million, the Consortium members provided about $290 million.

- 7 -

In the future, the proportionate share of the Bank Group's disbursementswill rise significantly since the level of Bank Group commitments has goneup markedly in the past two years.

23. As a result of successive debt reschedulings and arrangements fordebt relief together with increased remittancesp the debt service ratio waslower than expected in 1971, and is provisionally estimated at about 15 per-cent of total foreign exchange earnings. In the ne:t five years, with ananticipated gross inflow of external assistance of about *$4b.million peryear and gradually hardening terms, the debt service ratio can be expectedto fluctuate around 15 percent provided exports and remittances continue togrow. Turkey's borrowing capacity will need to be kept under review in thelight of balance of payments developments and the Government should continueto seek a part of future external aid on concessionary terms.

PART III - THE FERTILIZER SECTOR

24. Reports on the Turkish industrial and agricultural sectors weredistributed to the Dcecutive Directors as Annexes to the.main economic re-port entitled "The Developiaent Prospects of Turkey" (MEA-30a dated February 1,1971). They include "The Manufacturing Industries" (Volume V, Annex III,dated December 10, 1971 - see paras 86 tlhrough 96) and "Agricultural Policiesand Problems" (Volume III, Annex I dated Ilarch 10, 1971 - see paras 35 through38 and para 111).

25. Turkish manufacturing outpu-t grew by about 10 percent per year inthe 1960's with industries like machinery and equipment, steel and chemicalsproviding.much of the impetus for growth. Industrialisation has reached alevel of sophistication and diversity which now includes aluminium, motorvehicles, dturable consumer goods, syn-thetic fibres and major chemical inter--mediates. P-ioduction of all types of fertilizer reached 200,000 tons in 1971and includes both nitrogenous and phosphate fertilizers. As a result indus-try now represents about 20 percent of net domestic product, as comparedwith about 16 percent in 1962. But this rapid growth has often been motivatedby Turkish foreign exchange constraints and a consequent desire for importsubstitution, even when competitive cost production was not possible.

26. Agriculbure continues to be the largest sector in the econo.my,providing about 30 percent of the net domestic product and about 70 percentemployment in 1970, supplying .uch of the raw.material for industry andaccounting for the bulk of the commodity exports. Turkish agriculture isconcentrated on cereals (mainly wheat) and livestock, but fruits, nuts andindustrial crops also represent a large share of agricultural production.In recent years, the agricultural sector has lagged behind the rest of theeconomy growing at about 3.1 percent per year during 1965-70. lIuch of thedisappointing performance, apart from unfavorable wieather conditions whichhave had an adverse effect particularly on wheat production, has been dueto insufficient utilizationof existing irrigation projects, inadequate con-centration on fruit and vegetable, livestock and forest development and

- 8 -

lack of inputs and supporting services. Several projects financed by theBank Group during the last year or presently under discussion focus onthese problems in an attempt to reduce these constraints, e.g. irrigationrehabilitation, fruit and vegetables and livestock.

27. The use of farm inputs grew rapidly in the sixties. Fertilizerconsumptionincreased from 20,000 tons of nutrient in 1960 to 463,000 tonsin 1971, i.e. an average annual increase of 33 percent. The rapid increasein fertilizer consumption was due to a well conceived extension program bythe Food and Agriculture Organization (FAO), a distribution system w^hich,until recently, provided adequate supplies of fertilizer where needed and theprovision of sufficient credit by the Agricultural Bank of Turkey (ABT) onliberal terms. IHowever, in 1970 and 1971 consumption stagnated. This wasdue mainly to supply constraints: in particular shortage of foreign exchangeand insufficient credit for the procurement and storage by distributors andretail buying by farmers. The credit stringency was due to cash shortagesin the ABT Fertilizer Financing Fund (which provides 80-85 percent of allfertilizer credits), primarily caused by inability of the farmers to repayloans after the poor harvests in 1969 and 1970. It is estimated that iffertilizers and credit are available in sufficient quantity and on time,farmer's demand would be 20 percent above the ac-ual consumption in 1971 of463,000 tons of nutrient. The slowdown of consumption growth since 1969therefore does not indicate weaker demand for fertilizer use, but is pri-marily due to shortages of foreign exchange and domestic credit. Thegenerally healthier situation of the Turkish balance of payments (see paras18 and 19) and the specific provisions in the project (see para LO (c))should ease the foreign exchange constraint. The Fruit and VegetableExport Project (762/257-TU) includes a study of the ABT with the objectiveof improving the supply of domestic credit. Depending on the results ofthe study, there may be Bank Group lending for agricultural credit in thefuture.

28. Procurement and distribution of domestic and imported fertilizersare carried out by three major State Economic Enterp-ises (the AgriculturalSupply Organization, the Association of Agricultural Credit Cooperativesand the Sugar Factories Corporation) and, to a lesser extent, by productionand sales cooperatives and private dealers. The limitations on imports offertilizers and credit shortages after 1969 created a number of bottlenecksin the distribution system which, due to lack of coordination among thesevarious agencies, resulted in shortages of' fertilizer in some regions andexcess stocks in others. Capacity for fertilizer storage is adequate, butimproved planning and coordination between storage points is required. Tohelp coordinate fertilizer production and distribution, the Government hasset up a Fertilizer Committee under the 1Iinistry of Agriculture, on whichall agencies and Government Departments concerned are represented.

- 9 -

29. The distribution of fertilizer is controlled by the Governmentthrough a system of import licensing and by setting prices for both ex-factory and retail sales to farmers. In the case of domestic fertilizers,distributors' margins are fixed. At present, losses on the sale of domes-tic fertilizers are made up by profits on the distribution of importedfertilizers (because c.i.f. prices are lower) and, where Government con-trolled distributors are concerned, through budget subsidies. As a resultof this pricing policy and the decision to restrict import allocations in1970, government-owned agencies are presently the prirrmary means for ferti-lizer distribution.

30. Comparison with other countries suggests that fertilizer consump-tion in Turkey will continue to grow but, partly due to the supply constraintsnoted above, growth rates are unlikely to be as high as they were in the1960's. The Bank estimates growth of nitrogen c6nsumption to average about15 percent during 1971-75 slowing to 10 percent during 1975-80, althoughthese figures may be regarded as conservative. Urea was introduced inTurkey only recently and urea consumption has developed rapidly in the pasttwo years to 63,ooo tons in 1971. Urea enjoys a considerable advantage overother forms of nitrogen fertilizer in that it is relatively concentrated(146 percent nitrogen content) and thus more economical to handle. To obtainsatisfactory results, however, it must be used carefully and this requiresintensive research and demonstration to farmers of the correct methods ofapplication. Assuming these measures are adequately carried out, the Bankbelieves that consumption of nitrogen in the form of urea could continue toexpand rapidly.

PART IV - THE PROJECT

31. A detailed description of the proposed project is given in thereport entitled "Appraisal of the IGSAS Ammonia-Urea M'Ianufacturing Project"(PI-6a) dated.April 12, 1972, which is being distributed separatelyA Loan and Project Summary is attached as Annex III.

32. The Project. The proposed project consists of the construction ofa fertilizer plant to produce for sale 2711,000 tons per year of urea and90,000 tons per year of ammonia (other than ammonia produced and convertedinto urea). The plant is to be located at Izmit (see map) about 80 km fromIstanbul on the Asian shore of the Marmara Sea, adjacent to an existing oilrefinery which would provide feedstock and fuel for the project. Urea wouldbe sold for consumption in Turkey as a fertilizer. Ammonia would be sold inpart (38,000 tons per year) to a petrochemical plant manufacturing capro-lactam (the raw material for nylon) and in part (52,000 tons per year) toa plant manufacturing diammonium phosphate fertilizer. The project includesthe purchase and installation of a 750 ton per day single stream ammoniaplant, a 830 ton per day single stream urea plant, construction of buildingsand related civil works and the provision of engineering consultant services.

- 10 -

Auxiliary facilities such as roads, office space, laboratories and utilitysystems would be shared with the neighbouring refinery with only minor addi-tions needed as part of the project.

33. A new Company, Istanbul Gubre Sanayii Anonim Sirketi (IGSAS) hasbeen formed to build and operate the plant. The Company will be run as aprivate enterprise under the Turkish Commercial Code. The equity of IGSASwill amount to TL 330 million and will be subscribed by TPAO (Turkiye Petrol-leri Anonim Ortald igi, an oil company controlled by the Turkish Government)and IPRAS (Istanbul Petrol Rafinerisi Anonim Sirketi, a subsidiary of TPAO)in the proportion of 60:40. Engineering consultants will be employed by theCompany, following Bank approved procedures, to assist the management of theCompany in all technical phases of its work including the initial period ofoperation until local staff is sufficiently trained.

34. Cap Cost and Financtn. The total cost of the project, inclu-ding initial working capital, is estimated at $57.8 million equivalent, ofwhich the foreign exchange component is $32.0 million. This estimate takesinto account the probable effects of the latest currency realignments andalso includes contingency and price escalation allowances amounting to $10.2million. TPAO and IPRAS have given an undertaking to provide the Companywith additional funds that may be required to meet any project capital costoverrun. Financing will be provided from the following sources:

Local Foreign Total(US$ million equivalent)

Long Term Debt

IBRD - 24.0 24.0

State Investment Bank (SIB) 2.2 8.0 10.2

Equity

TPAO (60%) 1L.2 - 12

IPRAS (bol) 9.L - 9. 4

Total 25.3 32.0 57.8

35. SIB has given a commitment to provide a loan of TL 1!;2.5 millionto the Company. The loan will be at 10-1/2 percent interest and have a termof 15 years. The Company will have an initial long term debt equity ratioof about 60:40. Debt service coverage is estimated at 1.5 in 1975 rising to2.0 by 1979 and gradually increasing thereafter. Payment of dividends andother borrowings by the Company are restricted to protect the Company's cashposition.

- 11 -

36. The Bank loan of $24 million will be repayable over 15 yearsincluding a l4 year period of grace and will be guaranteed both by theGovernment of Turkey and jointly anld severally by TPAO and IPRAS. TheGovernment of Turkey will charge the Company a 1-3/4 percent guaranteefee on the amount of the Bank loan, which will bring the effective inte-rest rate payable by the Company to 9 percent. This is lower than thecurrent interest rate for industrial borrowing in Turkey which normallyvaries from 10-1/2 percent to 11-1/2 percent depending on the status ofthe borrower. The exchange risk on the Bank loan will be borne by theCompany.

37. The ability of TPAO and ILRAS to provide their share of thefinancing has been given particular attention by the Bank in view of themagnitude of the sum involved and the tight liquidity situation of thesetwo Companies. At the Bank's request, the Government of Turkey has there-fore agreed that, whenever there is reasonable cause to believe that thefunds available to TPAO and IPRAS would be inadequ&te to cover their equitycontributions or to honor the cost overrun conmitment, the Government wouldmake arrangements, satisfactory to the Bank, to cause the necessary fundsto be provided.

38. Procurement and Disbursement. The Bank proposes to finance theforeign exchange cost of specific items of equipment machinery and spareparts for the proposed project (see Annex III). Tnese items will be procuredon the basis of international competition. Goods and services to be finan-ced by the Borrower out of local uLnds including all civil works, which areexpected to be provided by Turkish contractors, will be procured under pro-cedures which will ensure a reasonable degree of competition. It is expectedthat disbursement of the Bank loan would take place over the three year cons-turction period of the project commencing June 1972. IGSAS is exempt fromimport duties on goods required for the project and bids will be evaluatedon a net of-duty basis.

39. Technology. The complexity of ammonia-urea plants entails certaintechnical risks which can lead to delays in construction and start up of ope-rations. As far as the project is concerned, these risks will be limitedthrough the employment by the Company of an engineering consulting firm(see para 33) and the fact that the relatively small size of the plant willnot give rise to major technical difficulties in process design and equip-ment.

ho. Thie handling of effluents by urea and ammonia plants is still inthe experimental stage. However, both TPAO and IPRAS are well aware of publicconcern over water and air pollution and plan to keep abreast of the latestdevelopments for pollution control. The project cost estimates include itemsof equipment for the treatment of liquid effluent and sanitary waste and alsoallow a margin for any additional expenditure that may be required. Themethods to be adopted for handling plant effluents will depend on the ammoniaand urea processes finally selected and the Company has agreed to solve theseproblems to the satisfaction of the Bank.

- 12 -

41. Marketing and Distribution. As urea is a relatively new productin Turkey, particular attention has been given in project preparation tominimize the conmmercial risks. The success of the project depends to alarge extent on the efficiency of the marketing and distribution arrange-ments and the rate at which farmers' interest in using increasing quanti-ties of fertilizer in general, and urea in particular. can be developedand maintained. The Government of Turkey and the Company have given thefollowing assurances which will help develop the market for urea in anti-cipation of the level of demand required at the time the project comesinto production in the mid 1970's and will help provide the necessaryincentives for the expansion of fertilizer production and consumption inthe future:

(a) The Goverrnment of Turkey has agreed to appoint IGSAS to carryout a comprehensive marketing study for urea to be completedby March 31, 1973. Detailed terms of reference and suggestedstaffing, which.may include consultants for certain aspectsof the study, are being drawn up by IGSAS and will be reviewedby the Government and the Barik. IGSAS will be responsible forimplementation of the study after its recommendations havebeen approved by the Government.

(b) Agreement has been reached with the MIinistry of Agricultureand the Ministry of Rural Affairs concerning the establishmentof urea trials and with the MIinistry of Agriculture ExtensionService on increasing extension work to promote the properuse of urea.

(c) The Government has agreed to continue issuing import licensesfor urea with the intention of developing a market for at least160,000 tons of urea per year by 1975, when IGSAS is scheduledto come into production. After this period, the Bank estimatesthat the.market demand for urea would be met by IGSAS for so-meyears to come. In order to avoid the possibility of over-production from existing or future plants producing urea andnitrogen fertilizers, the Government has undertaken to with-hold the provision of incentives or finance for the establish-ment of plants to produce and sell urea and other nitrogenfertilizers unless additional production capacity is requiredto.meet Turkey's projected agricultural development needs.

(d) Fertilizer credit requirements, appropriate policies, capitalsources and institutional and procedural arrangements forsupplying these requirements, will be studied under the CreditSurvey for which Bank/IDA financing is being provided as partof the Fruit and Vegetable Export Project (762/257-TU). Creditneeds for distribution and sale of urea will also be examinedunder the Urea Iiarketing Study to be carried out by IGSAS incoordination with the Credit Survey. In the meantime, theGovernment has undertaken to provide, through the AgriculturalBank of Turkey, appropriate credit facilities to enable eligi-ble farmers to purchase urea under the existing fertilizerpurchasing credit system.

- 13 -

(e) The pricing policies to be adopted by the Government for ureaand for fertilizers generally will be examined as part of theUrea Marketing Study mentioned above. IGSAS has agreed toconsult the Bank before establishing the prices or alteringthe prices charged for its products.

(f) At present responsibility for programming supplies of ferti-lizer and procurement of imports, distribution and allocationof fertilizers to distributors and other agencies, statistical,research and other services are shared by a number of inistriesand Government agencies, which makes coordination difficult toachieve. An attempt at better coordination is being made throughthe Fertilizer Committee established in 1970 and chaired bythe Ministry of Agriculture on which all concerned are represen-ted. The Government has agreed to appoint IGSAS to this Commit-tee.

42. Benefits. At full production the annual output of ammonia and ureafrom the project measured in terms of current world market prices will amountto about $18.9 million per year. The savings in foreign exchange, after allow-ing for foreign debt service and imported materials used in production, willbe $7 - 8 million per year.

43. Potential returns from increased application of urea fertilizer arehigh. Fertilizer is recognized as one of the major requirements for an ex-pansion of Turkish agricultural output. Increased use of fertilizer uill bothhelp reduce Turkey's reliance on cereal imports in bad years and further thedevelopment of fruit and vegetable groVing for export, a promising activitywhich is already receiving Bank Group support. The ex-factory selling priceof urea mill be fixed after consultations between IOSAS and the Bank and isexpected to be close to the $62 per ton level presently proposed by IGSAS.This is about 12 percent less on a nutrient basis than the current price ofdomestic nitrogen fertilizer but about 114 percent more than the c.i.f. priceof imported urea forecast for the mid 1970's (US$55 per ton). The ex-factoryprice of ammonia is estimated at $47 per ton for the 38,000 tons per year soldto the caprolactam plant and $52 per ton for the 52,000 tons per year sold tothe diammonium phosphate plant, the price difference being accounted for bythe additional expense of shipping ammonia to the latter plant. The 1974-75import price of ammonia may be considerably lower than these levels for largebulk deliveries but not for the small quantities that ]DSAS expects to sell.

1414. At these price levels, the internal economic return of the projectis estimated at 15.4 percent, the internal financial return before tax at14.7 percent and after tax at 13.0 percent. The financial projections showthat after the first two years of operation of the plant, it would be possibleto reduce the ex-factory selling prices of urea and ammonia to levels compa-rable with current world market prices and the Company vould still show anacceptable rate of return. Higher prices in the first two years are necessi-tated by the low debt service coverage in these years. The Government would

- 14 -

thus have some flexibility, after the first few years of operation of theplant, to achieve a better balance between the prices charged by the industryand world market prices. It is expec-ted that the price paid by the farmerfor urea would not be affected by the change-over from imported to domesticproduction urea. in the longer run however the farmer stands to benefitdirectly by any price reductions that can be achieved.

PART V - LEGAL UISTMENTS AND AUTHORITY

6.5 The draft Loan Agreement between the Bank, Istanbul Gubre SanayiiAnonim Sirketi, Turkiye Petrolleri Anonim Ortakligi and Istanbul PetrolRafinerisi Anonim Sirketi, the draft Guarantee Agreement between the Republicof Turkey and the Bank, the Report of the Committee provided for in Article III,Section 4 (iii) of the Articles of Agreement and the text of the Resolutionapproving the proposed loan are being distributed to the Executive Directorsseparately.

46. The Executive Directors' attention is drawn to the following cove-nantsin (a) the draft Loan Agreement relating to : changes in the Company'sArticles of Association Which require the Bank's consent (Section 3.10);the urea marketing study to be carried out by the Company (Section 3.12);consultation on ammonia and urea prices (Section 3.13); joint and severalguarantee by TPAO and IPRAS of the Bank loan (Section 4.04); provision ofequity (Section L.05); cost overrun commitment by TPAO and IPRAS (Section4.06); and (b) the draft Guarantee Agreement relating to : the back-upcomnitment by the Republic of Tarkllcey to provide funds for the project(Section 2.03); payment of the guarantee fee (Section 3.02); the coordi-nation of expansion of nitrogen fertilizer production capacity in Turkey(Section 3.04); and the provision of credit facilities (Section 3.05).

47. I am satisfied that the proposed loan would comply with theArticles of Agreement of the Bank.

PARLT VI - RECO142NDATION

l!8. I recommend that the Executive Directors approve the proposed loan.

Attachments Robert S. HIcNamaraPresident

April 28, 1972

ANNEX I

STATEMENT OF BANK LOANS AND IDA CREDITS TO page 1TURKEY AT MARCH 31, 1972 *

Loan or (US$ million)Credit Amount Undis-Number Year Borrower Purpose Bank IDA bursed

Seven loans and seven credits fully disbursed 70.7 80.3 -

568-TU 1968 Republic of Turkey Keban TransmissionLines 25.0 - 6.9

587-TU 1969 - - Seyhan IrrigationStage II 12.0 - 11.8

143-TU 1969 _ n _ Seyhan IrrigationStage II - 12.0 2.9

589-Tu 1969 T.S.K.B. Industry 25.0 1.9

623-TU 1969 Republic of Turkey Third Cukurova Power 11.5 - 4.4

713-TU 1970 T.S.K.B. Industry W0.0 - 3b.6

236-TU 1971 Republic of Turkey Livestock I - 4.5 4 5

748-TU 1971 - i - Education 13.5 - 13.5

257-TU** 1971 - tt _ Fruit and Vegetable - 15.0 15.0

762-TU-X-K 1971 - - Fruit and Vegetable 10.0 - 10.0

763-TU 1971 T.E.K. Power Transmission 2L.0 - 24.o

775-TU 1971 Republic of Turkey Fourth Cukurova Power 7.0 - 7.0

281-TU**- 1972 - - IrrigationRehabilitation - 18.0 18.0

Total (less cancellations) 238.7 129.8

of which has been repaid it9.3

Total now outstanding 189.L

Amount sold 1.2of which has been repaid 0.7 0.5

Total now held by Bank and MDA 188.9 129.8

Total undisbursed 11IL.1 Lo.L 154.5

* Excluding $76 million loan for Erdemir Steel Expansion and t16 million credit for

Second Livestock Project approved but not signed.** Not yet effective.

ANNEX IPage 2

STAT3MENT CF IFC INVESTHENTS IN TURKEY AT MARCH 31, 1972

Commitments(Net of Exchange Ad4ustnents)

Calendar (US$ millions)Tear Company Loan quity Total

1963 Industrial Development Bank of Turkey - 0.92 0.92(TSKB)

1966 SIFAS I (Nylon yarn) 0.90 0.47 1.37

1967 Industrial Development Bank of Turkey - 0.34 0.34(TSKB)

1969 Industrial Development Bank of Turkey - 0.41 0.41(TSKB)

1969 SIFAS II (Nylon yarn) 1.50 0.43 1.93

1969 Viking I (Pulp and paper) 2.50 0.62 3.12

1970 A.C.S. (Glass) 10.00 1.58 11.58

1970 NASAS (Aluminum Sheet and Foil) 7.00 1.37 8.37

1970 SIFAS III (Nylon yarn) 0.75 - 0.75

1971 Viking II (Pulp and Paper) - 0.05 0.05

1971 SIFAS IV (Nylon yarn) _0.52 0.52

Total commitments 22.65 6.71 29.36

Less cancellations,sales,and repayments 5.X; 0.37 5.51

Total held 17.51 6.34 23.85

Undisbursed balance 11.29

ADNNEX II

page 1

TURKEY - COUNTRY DATA

Area 780,000 sq. km.

Population (1970) 35.5 million

Rate of growth 2.6 percent per annum

Density 46 per sq.km.

Gross National Produnt

1970 (current markec prices) TL 144.5 billion

Annual Rate of growth (constant prices) 1963-67 = 6.9N1969 = 6.4%1970 = 5.65.

GNP at factor cost (1970 current prices) TL 127.7 billion

GNP per capita at factor cost (1970) TL 3,597 /

Industrial Origin of NDP(% of NDP at constant prices) 1962 1970

Agriculture and forestry 39.7 29.6

lianufacturing, mining and power 16.2 19.5Construction 6.3 7.4

Transport and Communications 7.2 8.0

Trade 8.1 9.0

Housing 4.8 5.5

Government services 9.7 11.1Financial institutions and other services 8.1 9.9

Expenditure of GNP (% of GNIP at constant prices)

Private Consumption 7L.1 70.7Public Consumption 15.4 12.7

Gross fixed investment 14.8 19.5Net imports of goods and services 3.6 3.8

Net factor income from abroad -0.6 0.9

Gross National Saving 10.5 16.61969/1970

Public Finance (Billion TL) 1969 1970 Growth Rate 5

Current Receipts 21.6 28.6 32.4

Current expenditures 15.6 20.3 30.1

Capital transfer 3.) 4.8 41.2Surplus, net of transfer 2.6 3.5 34.6

Investment expenditures o.9 7.0 1.h

~/ $257 at the new central rate of TL 14 = US$1.

ANNEX IIpage 2

1969/1970Money, Credit and Prices (Billion TL) 1969 1970 Growth Rate %

Total money supply, including sightand saving deposits 30.1 35.1 16.6

Total central credits and advances 12.9 14.6 13.2Total commercial bank credits 33.2 37.2 12.0Change of wholesale price index 6.0% 5.8%Change of consumer price index (Istanbul) 4.3% 7.6%

Balance of Payments (Million $) 1962 1969 1970

Imports of goods 622 801 948Exports of goods 381 537 588Net invisibles (including NATO receipts) - 1 43 188Current Account Deficit -242 -221 -172

Commodity Concentration of Exports (%) 1962 1970

Cotton 17 29Tobacco 25 13Hazelnuts 17 15Fruits and vegetables 7 9

External Public Debt (million $) 1969 1970

Total outstanding debt (end of calendar 2,196.7 2,1442.9year)

Debt service 134.1 160.4Debt service ratio (% of exports of 25 27

goods)(% of exports ofgoods & services,gross) 20 22

(% of goods & ser-vices, incl. workers'remittances) 16.7 15.6

IBRD/IDA Operations (Million $) 1968 1969 1970 1971

(Cumulative - end of calendar year)Total loans- IBRD 98.4 146.9 186.9 238.7

- IDA 80.7 92.7 92.7 111.8Repayments - IBRD 39.9 42.2 45.1 48.3Total loans outstanding - IBRD 55.8 102.0 139.1 189.2

- IDA 80.5 92.5 92.3 111.8

ANNEX IIpage 3

J2. Position (Iiillion $) 1968 1969 1970 1971

Quota 108 108 151 16h-Net fIF drawings 27 - 12 48 - 12SDR drawings - - 18 16.

Foreign Extchange ReservesCHillion $)Gold and convertibleforeign exchange, gross 123 245 431 773Net foreign assets - 6 13 10 411Inconvertible currencies 92 125 151 159

Exchange Rate

December 1971: Turkey established a central rate of US $ 1 = TL 14.00

August 9, 1970 to December 1971 US $ 1 = TL 15.00

Prior to August 9, 1970: US $ 1 = TL 9.00

Social Indicators Unit 1950 1960 1965 1970

Population Growth rate % 2.7 2.9 2.5 2.6Urban Population

growth rate % 6.2 5.4School enrollment: , school 33.0 47.0 54.0 56.0 2/

Primary and ageSecondary adjusted popln

Literacy rate -' adu].t 32.0 38.0popln

Unemployment rate 5. labor force 9.0 iPopulation per hospitalbed (public andprivate) Number 659 600 576 /

i 1967

i 1969

April 2.R, 1972

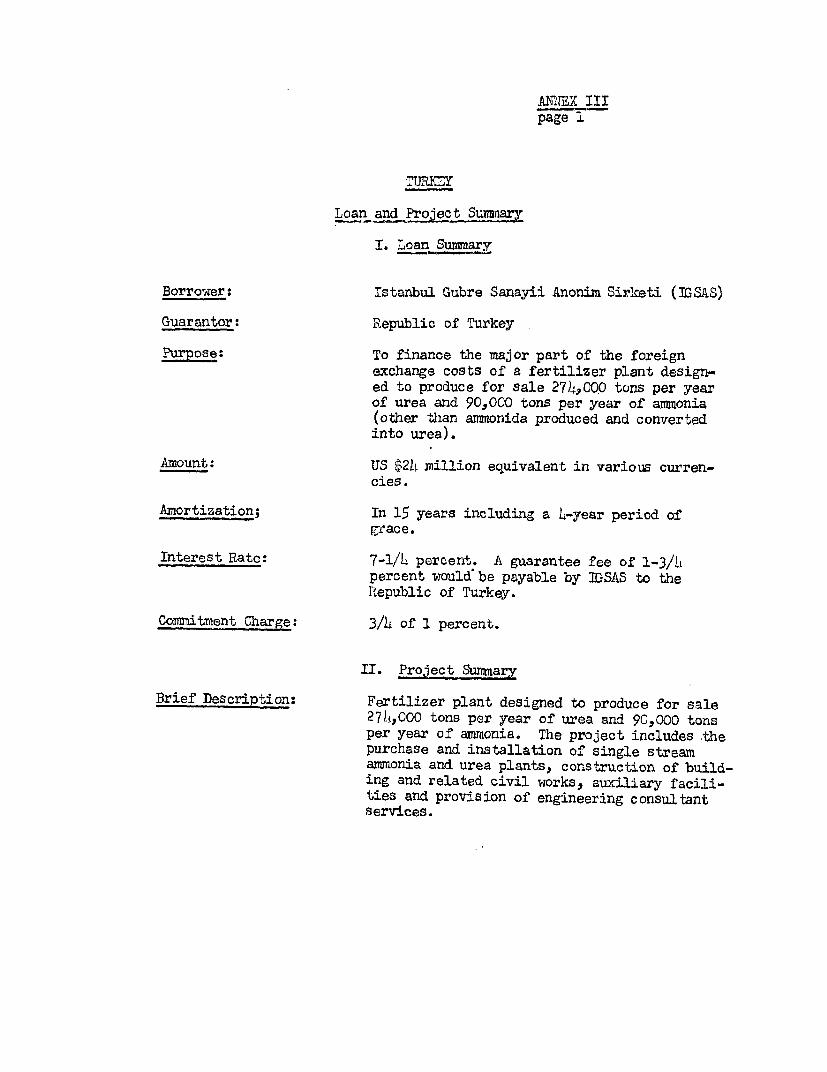

ANNEX IIIpage 1

I. Loan Summar

Borrower: Istanbul Gubre Sanayii Anonim Sirketi (IGSAS)

Guarantor: Republic of Turkey

Purpose: To finance the major part of the foreignexchange costs of a fertilizer plant design-ed to produce for sale 27)h.0O tons per yearof urea and 90,000 tons per year of ammonia(other than ammonida produced and convertedinto urea).

Amount: us $2h nillion equivalent in various curren-cies.

Amortization; In 15 years including a 4-year period ofgcace.

Interest Rate: 7-1/4 percent. A guarantee fee of 1-3/)4percent would' be payable by 2bSAS to thePRepublic of Turkey.

Commitment Charge: 3/4 of 1 percent.

II. Project Summary

Brief Description: Fertilizer plant designed to produce for sale274,000 tons per year of urea and 90,000 tonsper year of ammonia. The project includes thepurchase and installation of single streamammonia and urea plants, construction of build-ing and related civil works, auxiliary facili-ties and provision of engineering consultantservices.

AINNEX IIIpage 2

Cost of the Project:Local ForeiGn Total

c ;million)

Engineering 1.5 3.2 4.7Buildings and

Civil Works 4.2 - 4.2Equipment and Spares 2.8 17.9 20.7Freight, Insurance,

Erection 5.0 2.4 7.4Pre-operating Ex-

penses 1.7 0.6 2.3Contingencies and

Escalation 4.6 5.6 10.2Total 19.6 29.7 49.5

Interest duringconstruction,guarantee andcommitment fees 2.1 2.3 4.4

Working Capital 3.9 - 3.9

25.8 32.0 57.8

Financing P.an: Local Forein Total(illion of US$ equivalent V

Long Term Debt

IBRD _ 24.0 24.0State InvestmentBank 2.2 8.0 10.2

Equity

TPAO (60%) 14.2 - 14.2IGSAS (40%) .42 -9.

25.8 32.0 57.8

ANNE IIIPage 3

Ecpenditures tobe financed byBank Loan: (a) Ammonia process unit $ 2$150,000

(b) Urea process unit 3,950o,0o0(c) Utility Systems 1,200,000(d) Catalysts and Chemicals 500,000(e) Spare Parts 1,800,000(f) Engineering Services 3,200,000(g) Interest and other charges on

the Loan 1,800,000(h) Escalation, contingencies and

unallocated 2 ,X001000Total °°°°°000

Procurement Bank financed items will be procured following inter-national competition. For certain critical items ofequipment, bidding may be restricted with Bank consent tomanufacturers of proven capability. Goods and servicesto be financed out of local funds, including civil worksexpected to be provided by Turkish contractors, will beprocured under procedures which will ensure a reasonabledegree of competition.

Estimated Dis- $ 4illionbursements: CY 1972 1973 1974 1977

1.0 6.o 11.0 6.0

Consultants: Engineering Consultants financed in part by the Bank.

Economic Rat- ofReturn on theProject: 15.4 percent.

Financial Rate ofReturn on thePro,ject'.(before tax): 11!.7 percent.

Financial Rate ofReturn on theProject(after tax): 13.0 percent.

Estimated ProjectCompletion Date: June 30, 1975

Appraisal Report: Report No.PI-6a dated April 12, 1972Industrial Projects Department

TURKEY

AGRICULTURAL REGIONS & LOCATION OF FERTILIZER PLANTS

(? & X~~~~z~~=L,- ~~TA TVZON

&m fl~ ~ ~ ~ ~~~~~~~f* 9R . IRES TORALBZOUNDREKI

AII411~~ ~ IIlU GIRESUNIOSICLOOTR

-: T

4R~~~~~~~A ~~~~1~~~EirD.~NKRARA

APRIL 1972 lORD 33950N