Embed Size (px)

Citation preview

BHARAT Financial Inclusion Ltd

Prayaas se pragati

(Formerly known as 'SKS Microfinance Limited')

January 29, 2019

The General Manager, Department of Corporate Services BSE Limited Phiroze Jeejeebhoy Towers, Dalal Street, Fort, Mumbai - 400 001.

Dear Sir/Madam,

Head Office: 3rd Floor, My Home Tycoon, Block A, 6-3-1192, Kundanbagh Begumpet, Hyderabad - 500 016, Telangana, India T: +91 40 4452 6000

F: +91 40 4452 6001; [email protected] I www.bfil.co.in

Corporate Identity Number: L65999MH2003PLC250504

Registered Office: Unit No. 410, Madhava, Bandra-Kurla Complex Sandra (East), Mumbai - 400 051, Maharashtra, India T: +91 22 2659 2375

The Vice President - Listing Department The National Stock Exchange of India Limited Exchange Plaza, Bandra - Kurla Complex, Bandra (East) Mumbai - 400 051.

Sub: Approval of Audited Financial results for quarter/ nine months ended December 31, 2018

In compliance with Regulation 33 of the Securities and Exchange Board of India (Listing Obligations and

Disclosure Requirements) Regulations, 2015, we hereby inform you that the Board of Directors of Bharat

Financial Inclusion Limited at its meeting held on January 29, 2019 (commenced at 2.30 p.m. and

concluded at 5.30 p.m.) has approved Audited Financial Results for the quarter / nine months ended

December 31, 2018.

In relation to the above, we are enclosing herewith a copy of each of the following:

1. Audited Financial Results for the quarter / nine months ended December 31, 2018 along with the Auditor's Report thereon;

2. Earnings Update for the quarter / nine months ended December 31, 2018, which we plan to host

on our website www.bfil.co.in

We request you to take the same on record.

Thanking you,

Yours faithfully

For Bharat Financial Inclusion Limited

~ Rajendra Patil

Sr. Executive Vice President - Legal & Company Secretary

Encl: As above

January 29, 2019

Regional Offices: Ambala I Aurangabad I Bangalore I Bhagalpur I Bhopal I Bhubaneswar I Dharwad I Gulbarga I Hyderabad I Jaipur I Kechi Kolkata I Lucknow I Meerut I Nagpur I Patna I Pune I Raipur I Ranchi I Sambalpur I Siliguri I Varanasi I Vizag

B S R & Associates LLP Chartered Accountants

Salarpuria Knowledge City Orwell, B Wing, 6th Floor, Unit-3 Sy. No. 83/1, Plot No 2, Ra1durg Hyderabad-500081, India.

Telephone +91 40 7182 2000 Fax · +91 40 7182 2399

Independent Auditor's report on quarterly financial results and year-to-date results pursuant to Regulation 33 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 ('Listing Regulations')

To

The Board of Directors of Bharat Financial Inclusion Limited

1. We have audited the quarterly financial results of Bharat Financial Inclusion Limited ('the Company') for the quarter ended 31 December 2018 and the year-to-date financial results for the period from 1 April 2018 to 31 December 2018 ('financial results'), attached herewith, being submitted by the Company pursuant to the requirement of Regulation 33 of the Listing Regulations.

2. These quarterly financial results as well as the year-to-date financial results have been prepared on the basis of the interim financial statements, which are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial results based on our audit of such interim financial statements, which have been prepared in accordance with the recognition and measurement principles laid down in Indian Accounting Standard (Ind AS) for Interim Financial Reporting (Ind AS 34), prescribed under Section 133 of the Companies Act, 2013 and other accounting principles generally accepted in lndia and in compliance with Regulation 33 of Listing Regulation.

3. We conducted our audit in accordance with the auditing standards generally accepted in India. Those standards require that we plan and perform the audit to obtain reasonable assurance about . whether the financial results are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts disclosed as financial results. An audit also includes assessing the accounting principles used and significant estimates made by management. We believe that our audit provides a reasonable basis for our opinion.

B S R & Assocoa1es la paitnersh,p hrm with Registration No BA69226) convened ln!O B S R & Associates LLP (a litn1ted l.Ja~f1Y Pi>ranersh;p \•,,1h t. LP ~rstrat1on No MB-3182) with atteic.1 from OcloDer 14 1013"

Registered Office; 5th Floor, Lodha Excelus AJIDlo Mills Compoucd N M Joshi Marg, Mahalakshrn, Mumbai~ 400 011

B S R & Associates LLP

Bharat Financial Inclusion Limited Independent Auditor's Report (continued)

4. Based on our audit conducted as above, in our opinion and to the best of our information and according to the explanations given to us, these quarterly financial results as well as the year-todate results:

(i) are presented in accordance with the requirements of Regulation 33 of the Listing Regulations; and

(ii) give a true and fair view of the net profit and other comprehensive income and other financial information for the quarter ended 31 December 2018 as well as the year-to-date results for the period from I April 2018 to 31 December 2018.

Place: Mumbai Date: 29 January 2019

for B S R & Associates LLP Chartered Accountants

Firm's Registration Number: 116231 W/W-100024

2

Sriram Mahalingam Partner

Membership No: 049642

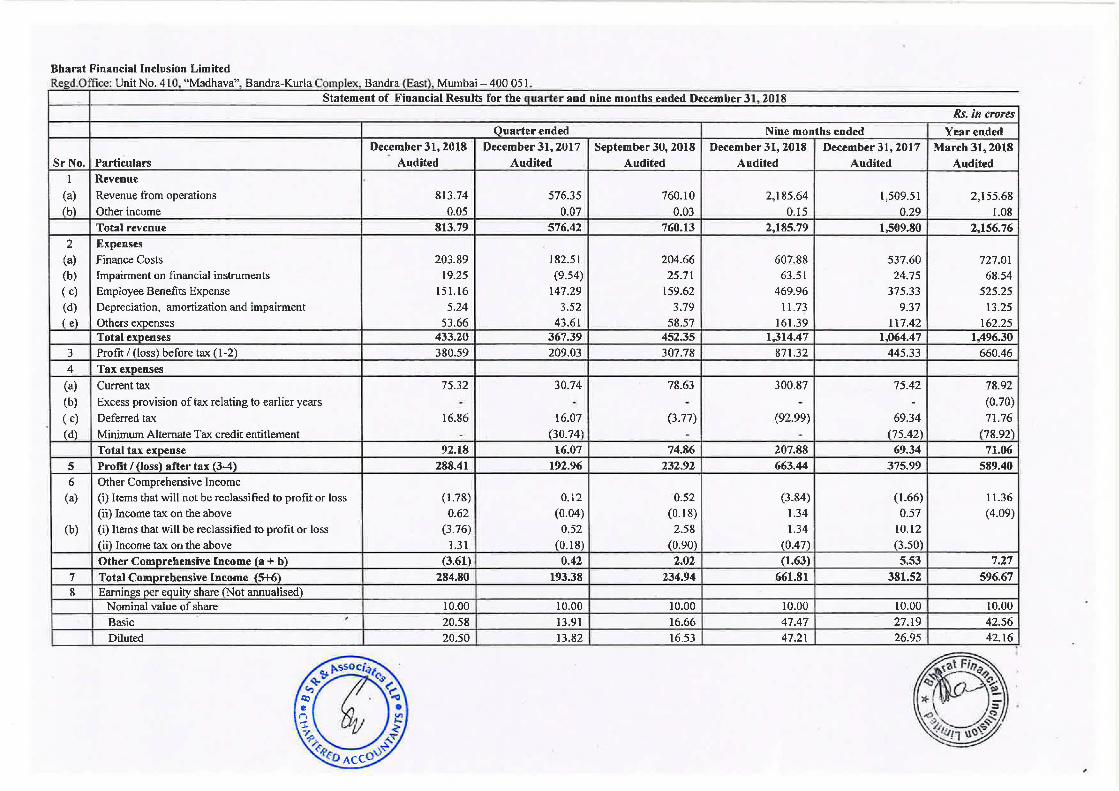

Bharat Financial Inclusion Limited Read.Office : Unit No. 410, "Madhava", Bandra-Kurla C . Bandra {East), Mumbai - 400 051

Statement of Financial Results for the quarter and nine months ended December 31, 2018 Rs. in crores

Quarter ended Nine months ended Year ended December 31, 2018 December 31, 2017 September 30, 2018 December 31, 2018 December 31, 2017 March 31, 2018

Sr No. Particulars Audited Audited Audited Audited Audited Audited 1 Revenue

(a) Revenue from operations 813.74 576.35 760.10 2,185.64 1,509.51 2,155.68 (b) Other income 0.05 0.07 0.03 0.15 0.29 1.08

Total revenue 813.79 576.42 760.13 2,185.79 1,509.80 2,156.76 2 Expenses

(a) Finance Costs 203.89 182.5 L 204.66 607.88 537.60 727.01 (b) Impairment on financial instruments 19.25 (9.54) 25.71 63.51 24.75 68.54 ( c) Employee Benefits Expense 151.16 147.29 159.62 469.96 375.33 525.25 (d) Depreciation, amortization and impairment 5.24 3.52 3.79 11.73 9.37 13.25 ( e) Others expenses 53.66 43.61 58.57 161.39 117.42 162.25

Total expenses 433.20 367.39 452.35 1,314.47 1,064.47 1,496.30 3 Profit/ (loss) before tax (l-2) 380.59 209.03 307.78 871.32 445.33 660.46

4 Tax expenses (a) Current tax 75.32 30.74 78.63 300.87 75.42 78.92

(b) Excess provision of tax relating to earlier years - - - - - (0.70)

( c) Deferred tax 16.86 16.07 (3. 77) (92.99) 69.34 71.76 (d) Minimum Alternate Tax credit entitlement . (30.74) - - (75.42) (78.92)

Total tax expense 92.18 16.07 74.86 207.88 69.34 71.06 5 Profit/ (loss) after tax (3-4) 288.41 192.96 232.92 663.44 375.99 589.40 6 Other Comprehensive Income

(a) (i) Items that will not be reclassified to profit or loss ( 1.78) 0.12 0.52 (3.84) (l.66) 11.36

(ii) Income tax on the above 0.62 (0.04) (0.18) 1.34 0.57 (4.09)

(b) (i) Items that will be reclassified to profit or loss (3.76) 0.52 2.58 1.34 10.12

(ii) Income tax on the above 1.31 (0.18) (0.90) (0.47) (3.50)

Other Comprehensive Income (a+ b) (3.61) 0.42 2.02 (l.63) 5.53 7.27

7 Total Comprehensive Income (5+6) 284.80 193.38 234.94 661.81 381.52 596.67 8 Earnings per equity share (Not annualised)

Nominal value of share 10.00 10.00 10.00 10.00 10.00 10.00

Basic ' 20.58 13.91 16.66 47.47 27.19 42.56

Diluted 20.50 13.82 16.53 47.21 26.95 42.16 •.

'?rn~ i,.ssoc;<l,;;:-, co ('_ e . ~ IJ • .).. V ..,, "Y.p t '<': ~"r'

.P,e ':<:' D ACCO\) . ~

BHARAT FINANCIAL INCLUSION LIMITED

Notes:

1. The Company has adopted Indian Accounting Standards ('Ind AS') notified under Section 133 of the Companies Act 2013 ('the Act') read with the Companies (Indian Accounting Standards) Rules, 2015 from 1 April 2018 and the effective date of such transition is 1 April 2017. Such transition has been carried out in line with the relevant exemptions provided under Ind AS 101 from the erstwhile Accounting Standards notified under the Act, read with relevant rules issued thereunder and guidelines issued by the Reserve Bank of India ('RBI') (collectively referred to as 'the previous GAAP').

Accordingly, the impact of transition has been recorded in the opening reserves as at 1 April 2017 and the corresponding figures presented in these results have been restated/ reclassified.

Any application guidance/ clarifications/ directions issued by RBI or other regulators will be implemented as and when they are issued/ applicable.

2. The above results have been reviewed by the Audit Committee and approved by the Board of Directors at their meetings held on January 29, 2019 in accordance with the requirement of Regulation 33 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

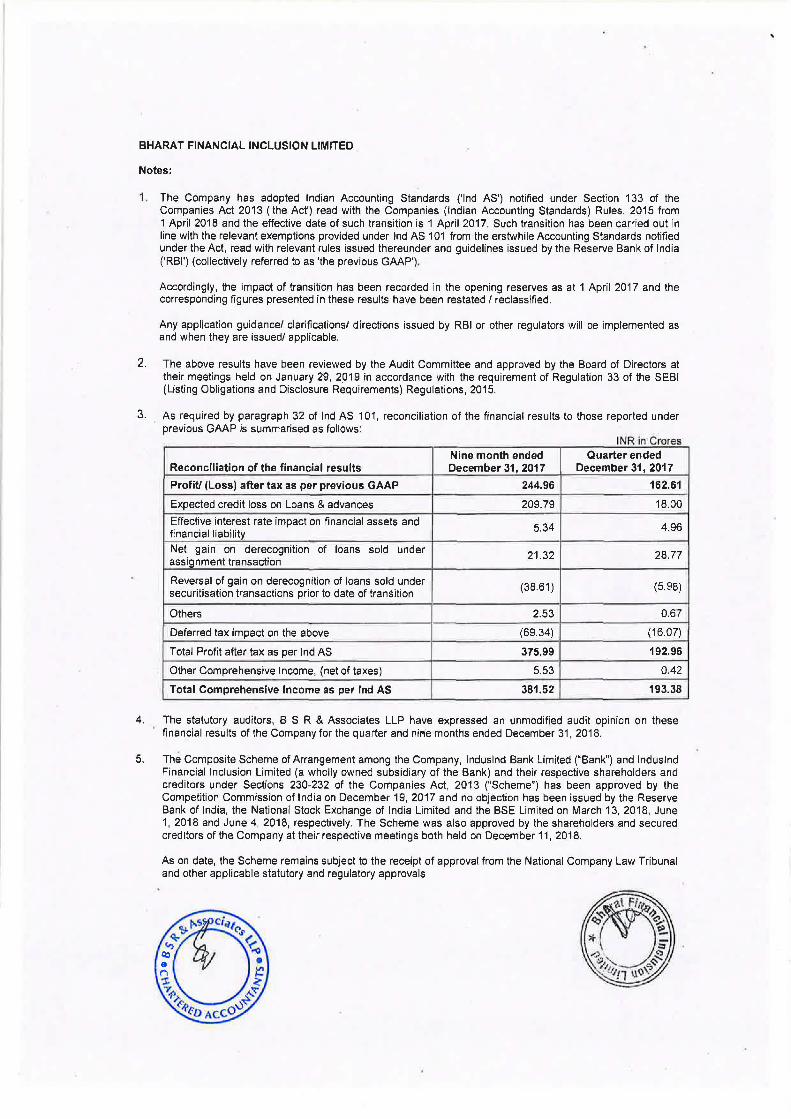

3. As required by paragraph 32 of Ind AS 101, reconciliation of the financial results to those reported under previous GAAP is summarised as follows:

INR in Crores Nine month ended Quarter ended

Reconciliation of the financial results December 31, 2017 December 31, 2017

Profit/ (Loss) after tax as per previous GAAP 244.96 162.61

Expected credit loss on Loans & advances 209.79 18.00

Effective interest rate impact on financial assets and 5.34 4.96

financial liability Net gain on derecognition of loans sold under 21.32 28.77 assignment transaction

Reversal of gain on derecognition of loans sold under (38.61) (598) securitisation transactions prior to date of transition

Others 2.53 0.67

Deferred tax impact on the above (69.34) (16.07)

Total Profit after tax as per Ind AS 375.99 192.96

Other Comprehensive Income, (net of taxes) 5.53 0.42

Total Comprehensive Income as per Ind AS 381.52 193.38

4. The statutory auditors, B S R & Associates LLP have expressed an unmodified audit opinion on these financial results of the Company for the quarter and nirie months ended December 31, 2018.

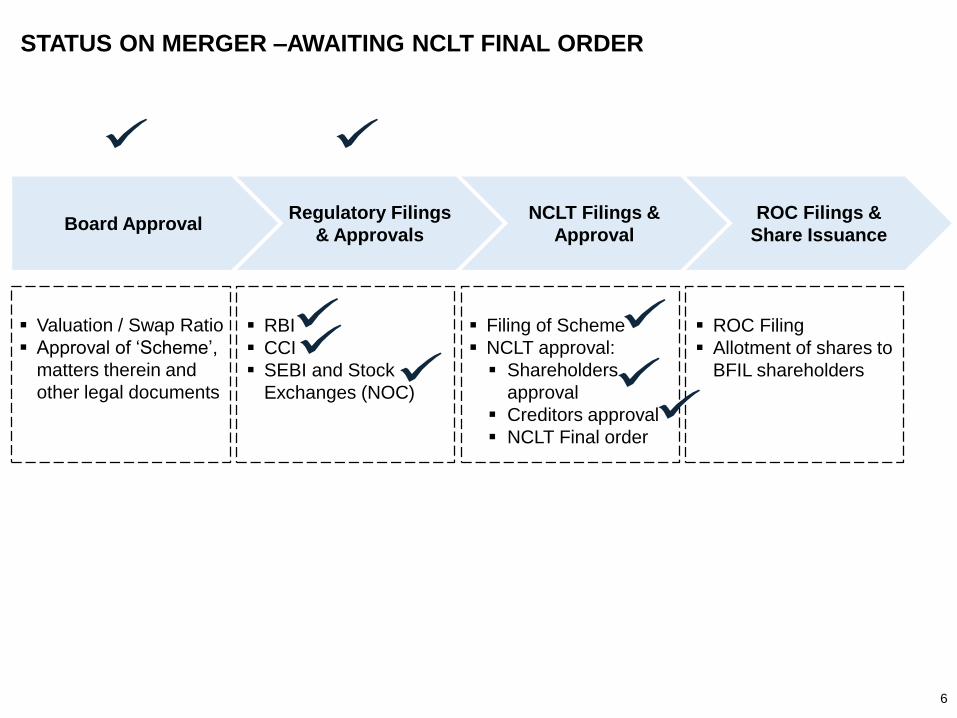

5. The Composite Scheme of Arrangement among the Company, lnduslnd Bank Limited ("Bank") and lnduslnd Financial Inclusion Limited (a wholly owned subsidiary of the Bank) and their respective shareholders and creditors under Sections 230-232 of the Companies Act, 2013 ("Scheme") has been approved by the Competition Commission of India on December 19, 2017 and no objection has been issued by the Reserve Bank of India, the National Stock Exchange of India Limited and the BSE Limited on March 13, 2018, June 1, 2018 and June 4, 2018, respectively. The Scheme was also approved by the shareholders and secured creditors of the Company at their respective meetings both held on December 11, 2018.

As on date, the Scheme remains subject to the receipt of approval from the National Company Law Tribunal and other applicable statutory and regulatory approvals

6. The Company is engaged primarily In the business of Micro- financing and accordingly there are no separate reportable segments as per Ind AS dealing with Operating Segment. The company operates in a single geographical segment l.e domestic.

Place: Hyderabad Date: January 29, 2019

EARNINGS UPDATE Q3FY19

BHARAT FINANCIAL INCLUSION LIMITED(Formerly known as ‘SKS Microfinance Limited’)BSE: 533228 ● NSE: BHARATFIN

Corporate Identity No. L65999MH2003PLC250504

www.bfil.co.in

This presentation is solely for viewing. No part of it may be circulated, quoted, or reproduced for distribution without prior written approval from BHARAT Financial Inclusion Limited.

JANUARY 2019

CONTENTS

Particulars Slide No.

Update on Merger 3

Executive Summary 7

Investment Hypothesis 9

Company Overview 12

Clarity on Major Uncertainties Post AP MFI Crisis 17

Growth Anatomy 22

Future Strategy 28

Pilot on Retail Distribution And Service Points (RDSP) 32

Update on Cashless Disbursement 36

Loans for Home Improvement & Two-Wheeler (Pilot) 38

Q3FY19 Performance Highlights 40

Operational Highlights 45

Industry Update On Credit Quality 51

Review of Financials 53

Financial Architecture 70

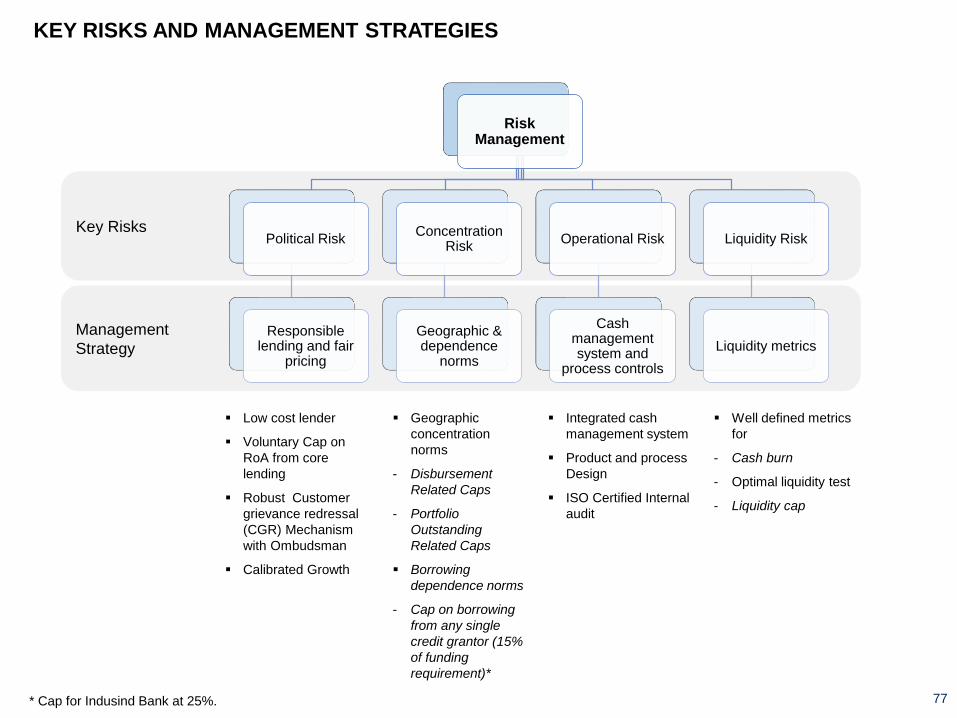

Risk Management 76

Capital Structure 78

Annexures 80

With effect from 1st April ,2018 , the company has adopted Indian Accounting Standards (Ind AS). Accordingly FY18 numbers

have been restated from previous GAAP to Ind AS to make them comparable.

Figures rounded off to the nearest digit across the presentation. Figures and ratios have been regrouped wherever necessary.2

3

UPDATE ON MERGER

3

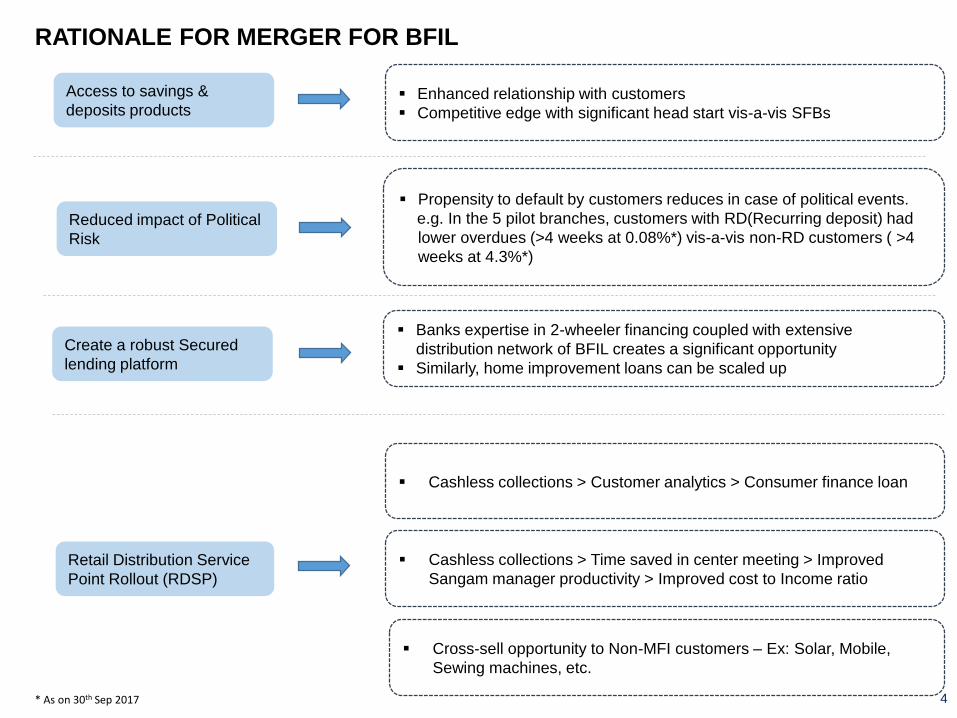

RATIONALE FOR MERGER FOR BFIL

4

Access to savings &

deposits products▪ Enhanced relationship with customers

▪ Competitive edge with significant head start vis-a-vis SFBs

Retail Distribution Service

Point Rollout (RDSP)

▪ Cashless collections > Customer analytics > Consumer finance loan

▪ Cross-sell opportunity to Non-MFI customers – Ex: Solar, Mobile,

Sewing machines, etc.

Create a robust Secured

lending platform

▪ Banks expertise in 2-wheeler financing coupled with extensive

distribution network of BFIL creates a significant opportunity

▪ Similarly, home improvement loans can be scaled up

▪ Cashless collections > Time saved in center meeting > Improved

Sangam manager productivity > Improved cost to Income ratio

Reduced impact of Political

Risk

▪ Propensity to default by customers reduces in case of political events.

e.g. In the 5 pilot branches, customers with RD(Recurring deposit) had

lower overdues (>4 weeks at 0.08%*) vis-a-vis non-RD customers ( >4

weeks at 4.3%*)

* As on 30th Sep 2017

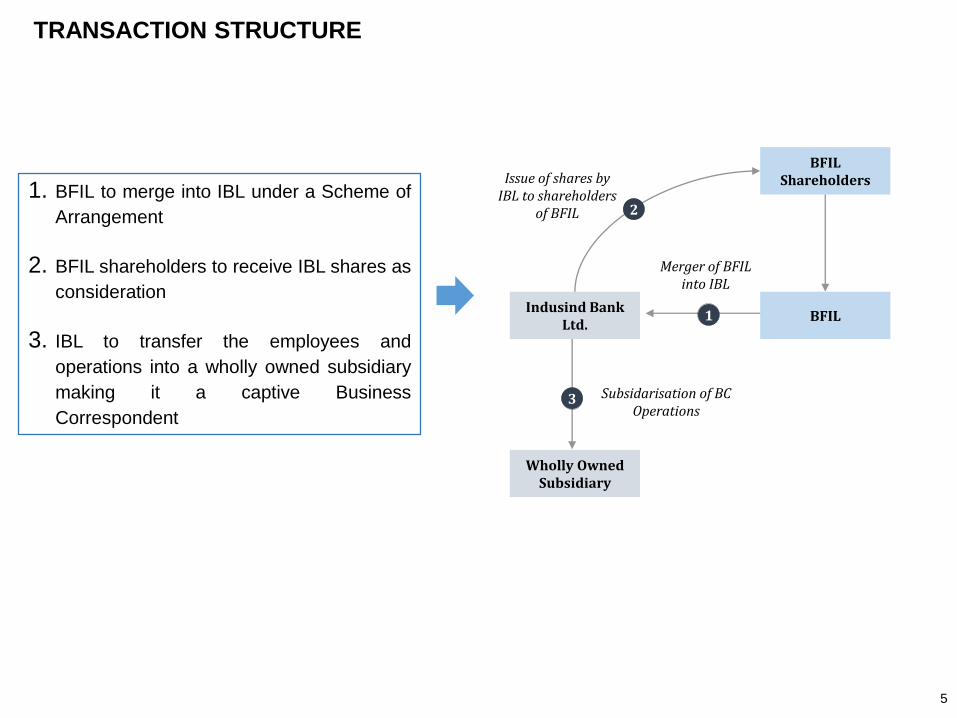

TRANSACTION STRUCTURE

5

1. BFIL to merge into IBL under a Scheme of

Arrangement

2. BFIL shareholders to receive IBL shares as

consideration

3. IBL to transfer the employees and

operations into a wholly owned subsidiary

making it a captive Business

Correspondent

Issue of shares by IBL to shareholders

of BFIL

BFILShareholders

BFILIndusind Bank

Ltd.1

Wholly Owned Subsidiary

3 Subsidarisation of BC Operations

2

Merger of BFIL into IBL

Board ApprovalRegulatory Filings

& Approvals

NCLT Filings &

Approval

ROC Filings &

Share Issuance

▪ Valuation / Swap Ratio

▪ Approval of ‘Scheme’,

matters therein and

other legal documents

▪ RBI

▪ CCI

▪ SEBI and Stock

Exchanges (NOC)

▪ Filing of Scheme

▪ NCLT approval:

▪ Shareholders

approval

▪ Creditors approval

▪ NCLT Final order

▪ ROC Filing

▪ Allotment of shares to

BFIL shareholders

STATUS ON MERGER –AWAITING NCLT FINAL ORDER

6

EXECUTIVE SUMMARY

7

8

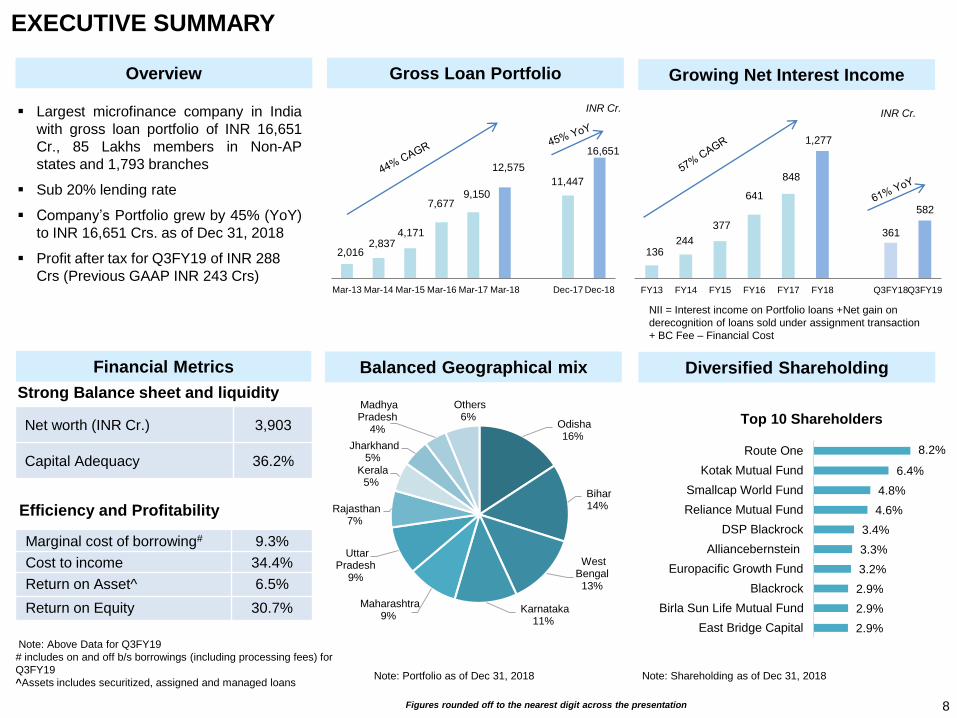

136 244

377

641

848

1,277

361

582

FY13 FY14 FY15 FY16 FY17 FY18 Q3FY18Q3FY19

2,016 2,837

4,171

7,677 9,150

12,575

11,447

16,651

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Dec-17 Dec-18

Overview Gross Loan Portfolio Growing Net Interest Income

Financial Metrics Balanced Geographical mix Diversified Shareholding

Marginal cost of borrowing# 9.3%

Cost to income 34.4%

Return on Asset^ 6.5%

Return on Equity 30.7%

EXECUTIVE SUMMARY

▪ Largest microfinance company in India

with gross loan portfolio of INR 16,651

Cr., 85 Lakhs members in Non-AP

states and 1,793 branches

▪ Sub 20% lending rate

▪ Company’s Portfolio grew by 45% (YoY)

to INR 16,651 Crs. as of Dec 31, 2018

▪ Profit after tax for Q3FY19 of INR 288

Crs (Previous GAAP INR 243 Crs)

Note: Shareholding as of Dec 31, 2018

Net worth (INR Cr.) 3,903

Capital Adequacy 36.2%

Note: Portfolio as of Dec 31, 2018

Strong Balance sheet and liquidity

Efficiency and Profitability

INR Cr.INR Cr.

NII = Interest income on Portfolio loans +Net gain on

derecognition of loans sold under assignment transaction

+ BC Fee – Financial Cost

Note: Above Data for Q3FY19

# includes on and off b/s borrowings (including processing fees) for

Q3FY19

^Assets includes securitized, assigned and managed loans

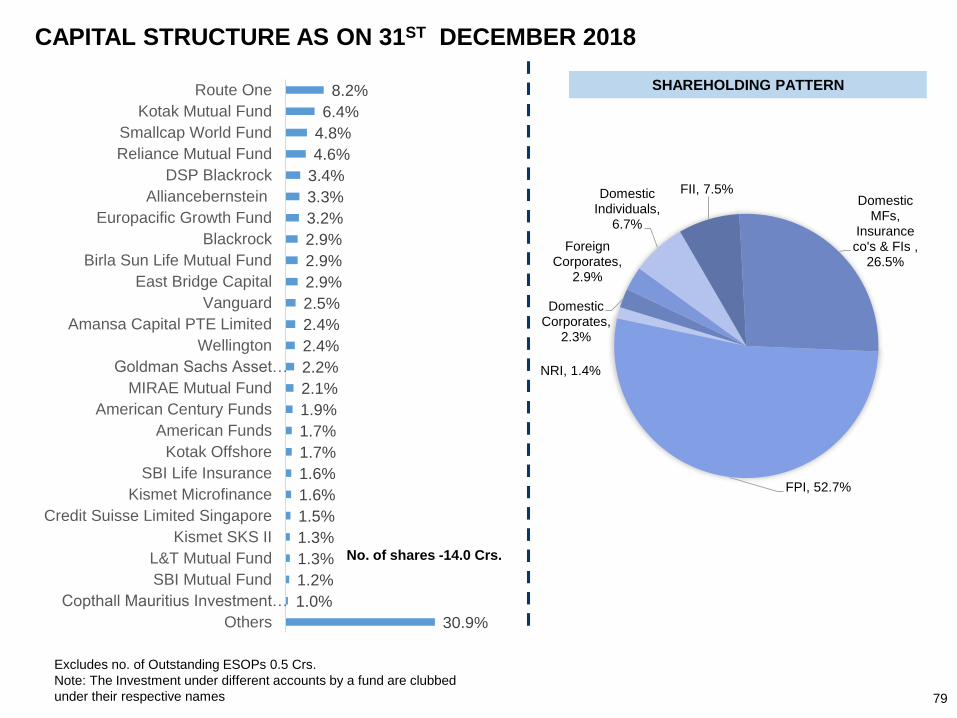

Odisha 16%

Bihar 14%

West Bengal 13%

Karnataka 11%

Maharashtra 9%

Uttar Pradesh

9%

Rajasthan 7%

Kerala 5%

Jharkhand 5%

Madhya Pradesh

4%

Others 6%

2.9%

2.9%

2.9%

3.2%

3.3%

3.4%

4.6%

4.8%

6.4%

8.2%

East Bridge Capital

Birla Sun Life Mutual Fund

Blackrock

Europacific Growth Fund

Alliancebernstein

DSP Blackrock

Reliance Mutual Fund

Smallcap World Fund

Kotak Mutual Fund

Route One

Top 10 Shareholders

Figures rounded off to the nearest digit across the presentation

9

INVESTMENT HYPOTHESIS

9

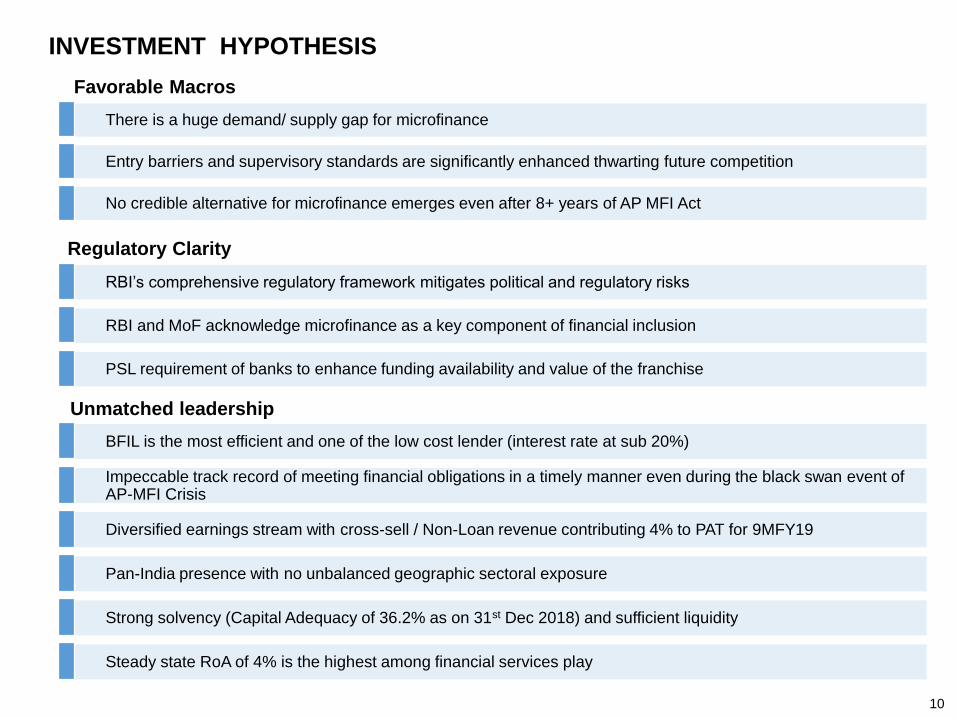

INVESTMENT HYPOTHESIS

BFIL is the most efficient and one of the low cost lender (interest rate at sub 20%)

Impeccable track record of meeting financial obligations in a timely manner even during the black swan event of AP-MFI Crisis

Diversified earnings stream with cross-sell / Non-Loan revenue contributing 4% to PAT for 9MFY19

Pan-India presence with no unbalanced geographic sectoral exposure

Strong solvency (Capital Adequacy of 36.2% as on 31st Dec 2018) and sufficient liquidity

Steady state RoA of 4% is the highest among financial services play

Favorable Macros

Unmatched leadership

There is a huge demand/ supply gap for microfinance

Entry barriers and supervisory standards are significantly enhanced thwarting future competition

No credible alternative for microfinance emerges even after 8+ years of AP MFI Act

Regulatory Clarity

RBI’s comprehensive regulatory framework mitigates political and regulatory risks

RBI and MoF acknowledge microfinance as a key component of financial inclusion

PSL requirement of banks to enhance funding availability and value of the franchise

10

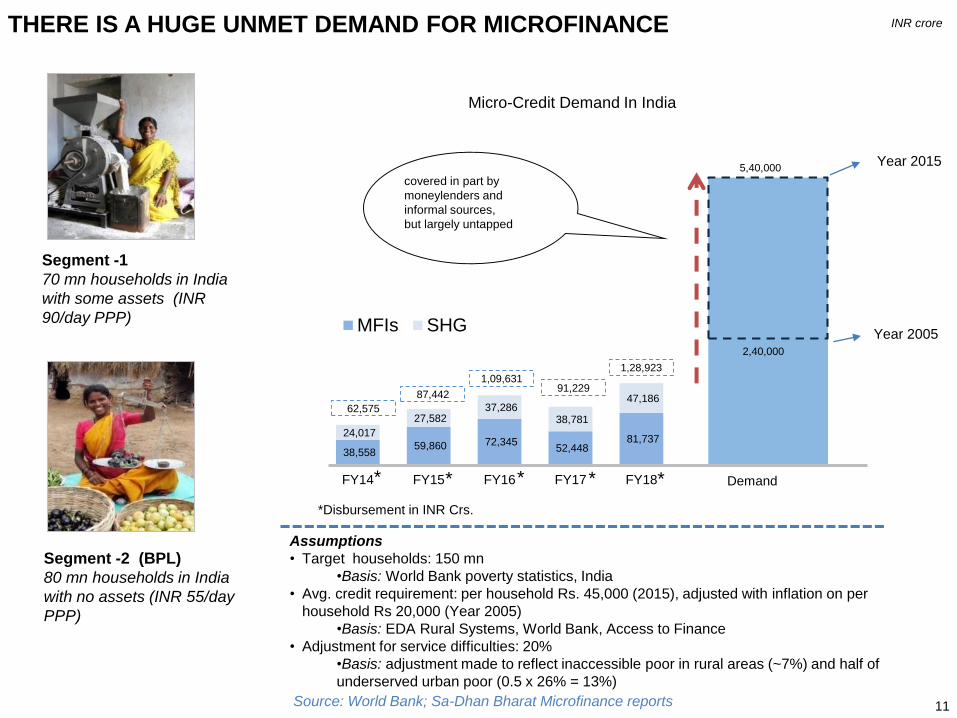

11

Segment -1

70 mn households in India

with some assets (INR

90/day PPP)

Segment -2 (BPL)

80 mn households in India

with no assets (INR 55/day

PPP)

THERE IS A HUGE UNMET DEMAND FOR MICROFINANCE

Assumptions

• Target households: 150 mn

•Basis: World Bank poverty statistics, India

• Avg. credit requirement: per household Rs. 45,000 (2015), adjusted with inflation on per

household Rs 20,000 (Year 2005)

•Basis: EDA Rural Systems, World Bank, Access to Finance

• Adjustment for service difficulties: 20%

•Basis: adjustment made to reflect inaccessible poor in rural areas (~7%) and half of

underserved urban poor (0.5 x 26% = 13%)

Source: World Bank; Sa-Dhan Bharat Microfinance reports

38,558 59,860 72,345

52,448 81,737

24,017

27,582 37,286

38,781

47,186

FY14 FY15 FY16 FY17 FY18

MFIs SHG

Micro-Credit Demand In India

covered in part by

moneylenders and

informal sources,

but largely untapped

*Disbursement in INR Crs.

Demand

2,40,000

* *

87,442

62,575

5,40,000

Year 2005

Year 2015

*

1,09,631 91,229

*

INR crore

1,28,923

*

12

COMPANY OVERVIEW

12

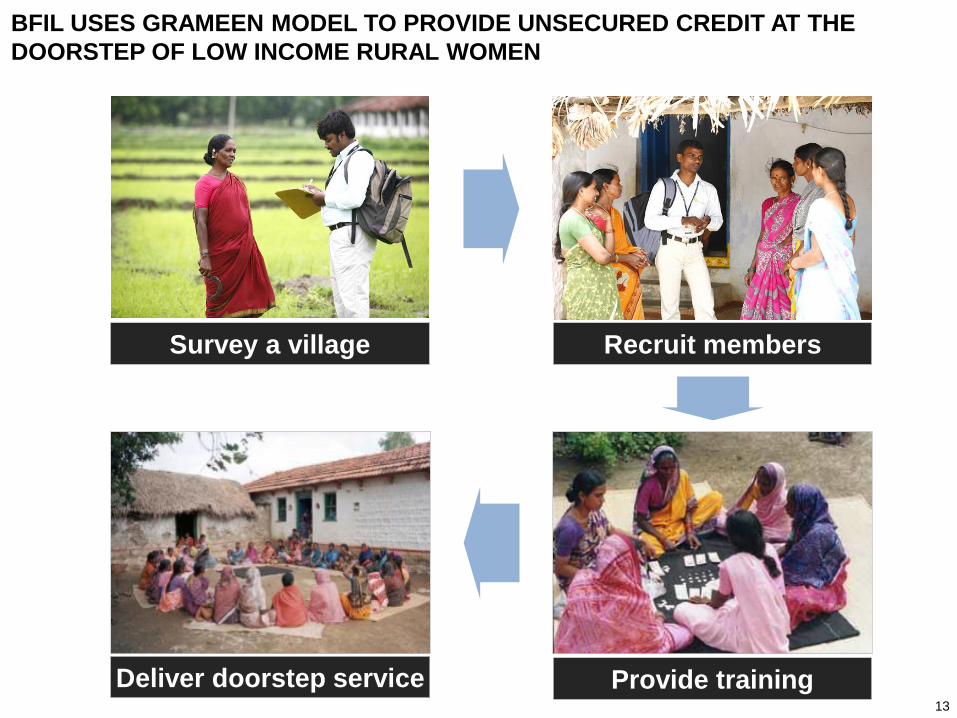

13

Survey a village Recruit members

Deliver doorstep service Provide training

BFIL USES GRAMEEN MODEL TO PROVIDE UNSECURED CREDIT AT THE

DOORSTEP OF LOW INCOME RURAL WOMEN

Put loan

officers pic

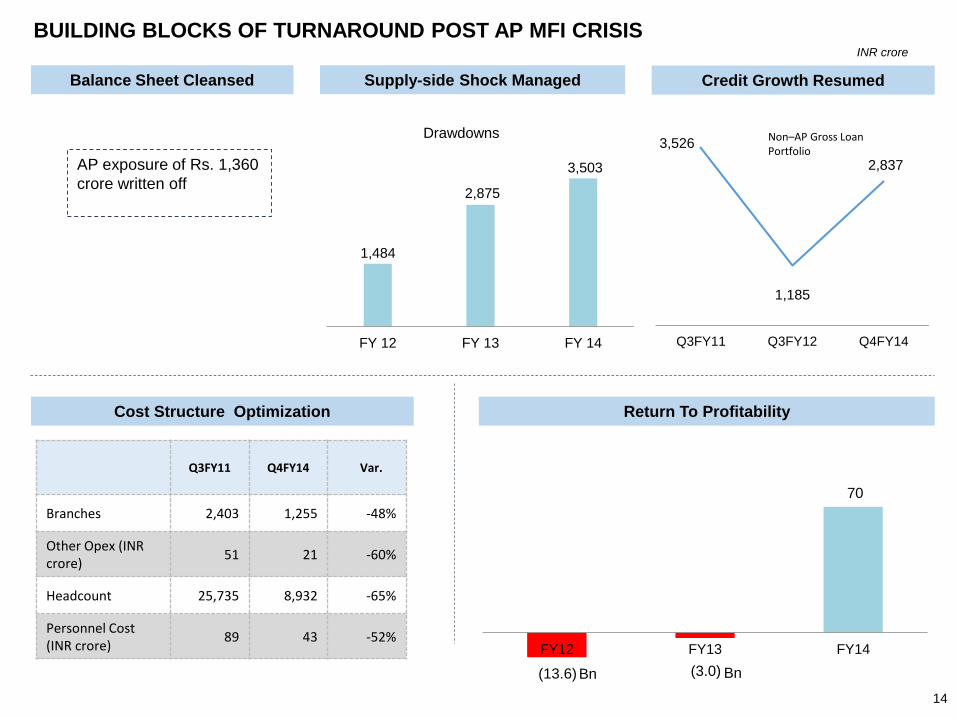

1,484

2,875

3,503

FY 12 FY 13 FY 14

Drawdowns

AP exposure of Rs. 1,360

crore written off

Q3FY11 Q4FY14 Var.

Branches 2,403 1,255 -48%

Other Opex (INR crore)

51 21 -60%

Headcount 25,735 8,932 -65%

Personnel Cost (INR crore)

89 43 -52%

3,526

1,185

2,837

Q3FY11 Q3FY12 Q4FY14

Non–AP Gross Loan Portfolio

(13.6) (3.0)

70

FY12 FY13 FY14

Return To Profitability

Bn Bn

INR crore

BUILDING BLOCKS OF TURNAROUND POST AP MFI CRISIS

Balance Sheet Cleansed Supply-side Shock Managed Credit Growth Resumed

Cost Structure Optimization

14

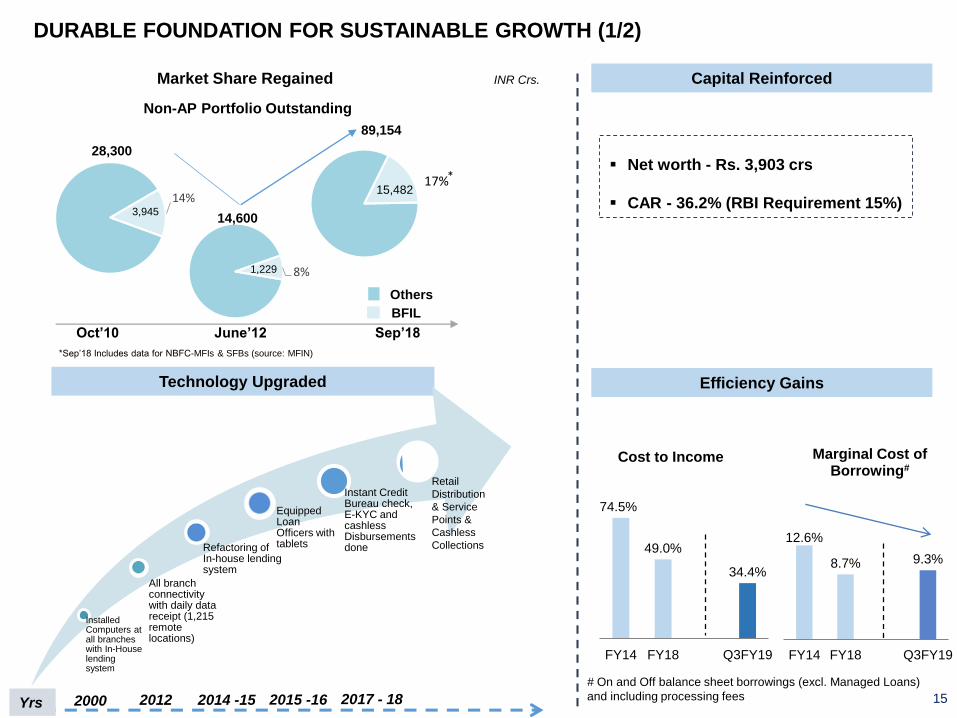

12.6%

8.7% 9.3%

FY14 FY18 Q3FY19

Marginal Cost of Borrowing#

74.5%

49.0%

34.4%

FY14 FY18 Q3FY19

Cost to Income

2000 2014 -152012Yrs

14%

8%1,229

Oct’10 June’12 Sep’18

28,300

14,600

Non-AP Portfolio Outstanding

3,945

BFIL

Others

INR Crs.

▪ Net worth - Rs. 3,903 crs

▪ CAR - 36.2% (RBI Requirement 15%)

# On and Off balance sheet borrowings (excl. Managed Loans)

and including processing fees 2015 -16

*Sep’18 Includes data for NBFC-MFIs & SFBs (source: MFIN)

17%15,482

89,154

DURABLE FOUNDATION FOR SUSTAINABLE GROWTH (1/2)

Market Share Regained

Technology Upgraded

Capital Reinforced

Efficiency Gains

Installed Computers at all branches with In-House lending system

All branch connectivity with daily data receipt (1,215 remote locations)

Refactoring of In-house lending system

Equipped Loan Officers with tablets

Instant Credit Bureau check, E-KYC and cashless Disbursements done

2017 - 18 15

*

Retail

Distribution

& Service

Points &

Cashless

Collections

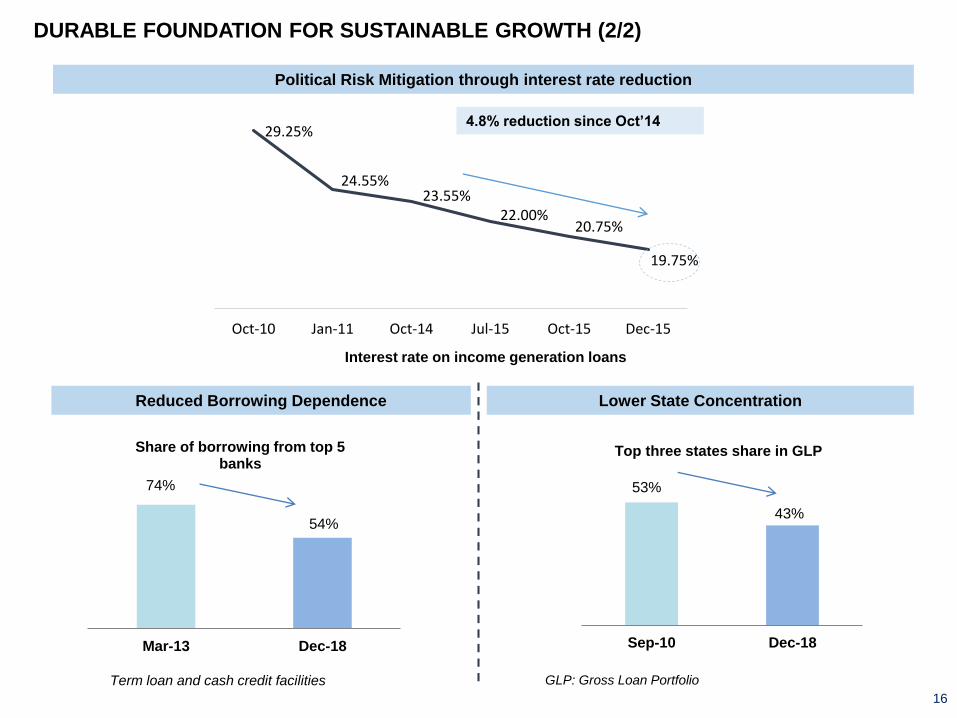

29.25%

24.55%23.55%

22.00%20.75%

19.75%

Oct-10 Jan-11 Oct-14 Jul-15 Oct-15 Dec-15

4.8% reduction since Oct’14

GLP: Gross Loan PortfolioTerm loan and cash credit facilities

Interest rate on income generation loans

74%

54%

Mar-13 Dec-18

Share of borrowing from top 5 banks

53%

43%

Sep-10 Dec-18

Top three states share in GLP

Political Risk Mitigation through interest rate reduction

Reduced Borrowing Dependence Lower State Concentration

DURABLE FOUNDATION FOR SUSTAINABLE GROWTH (2/2)

16

CLARITY ON MAJOR UNCERTAINTIES

POST AP MFI CRISIS

17

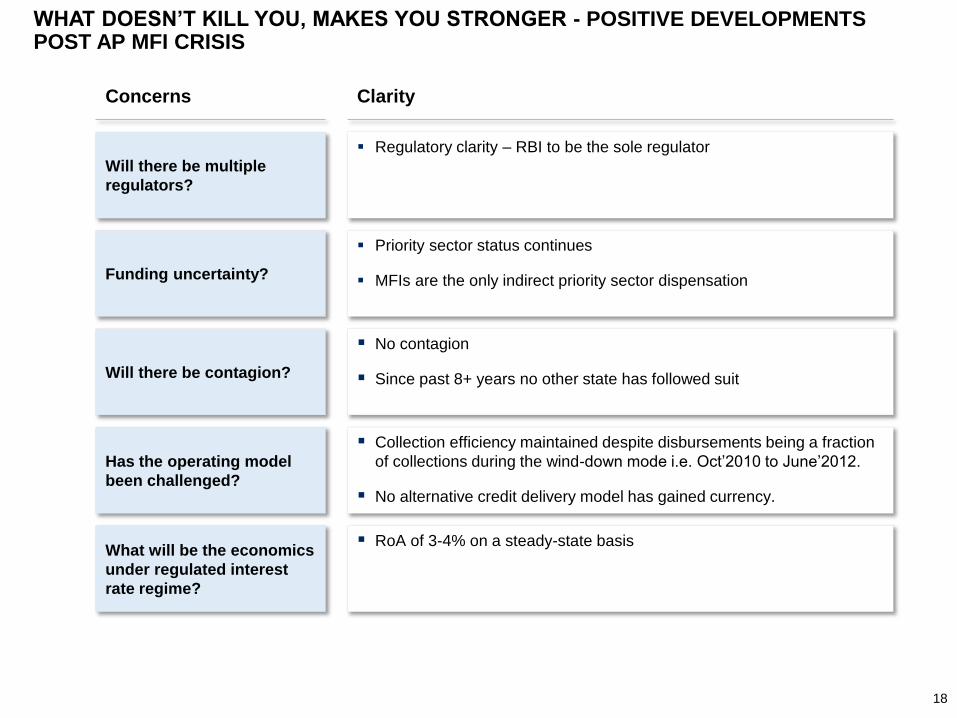

WHAT DOESN’T KILL YOU, MAKES YOU STRONGER - POSITIVE DEVELOPMENTS POST AP MFI CRISIS

Will there be multiple

regulators?

▪ Regulatory clarity – RBI to be the sole regulator

Funding uncertainty?

▪ Priority sector status continues

▪ MFIs are the only indirect priority sector dispensation

Will there be contagion?

▪ No contagion

▪ Since past 8+ years no other state has followed suit

Has the operating model

been challenged?

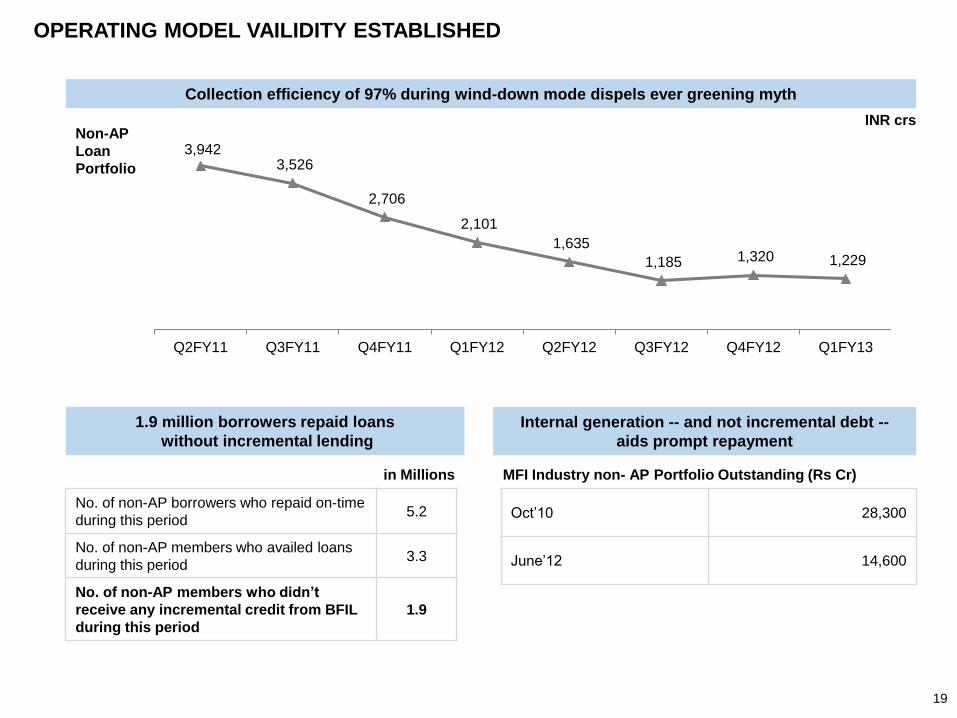

▪ Collection efficiency maintained despite disbursements being a fraction

of collections during the wind-down mode i.e. Oct’2010 to June’2012.

▪ No alternative credit delivery model has gained currency.

What will be the economics

under regulated interest

rate regime?

▪ RoA of 3-4% on a steady-state basis

Concerns Clarity

18

OPERATING MODEL VAILIDITY ESTABLISHED

3,942 3,526

2,706

2,101

1,635

1,185 1,320 1,229

Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13

Collection efficiency of 97% during wind-down mode dispels ever greening myth

Non-AP

Loan

Portfolio

No. of non-AP borrowers who repaid on-time

during this period5.2

No. of non-AP members who availed loans

during this period3.3

No. of non-AP members who didn’t

receive any incremental credit from BFIL

during this period

1.9

in Millions

1.9 million borrowers repaid loans

without incremental lending

INR crs

Internal generation -- and not incremental debt --

aids prompt repayment

MFI Industry non- AP Portfolio Outstanding (Rs Cr)

Oct’10 28,300

June’12 14,600

19

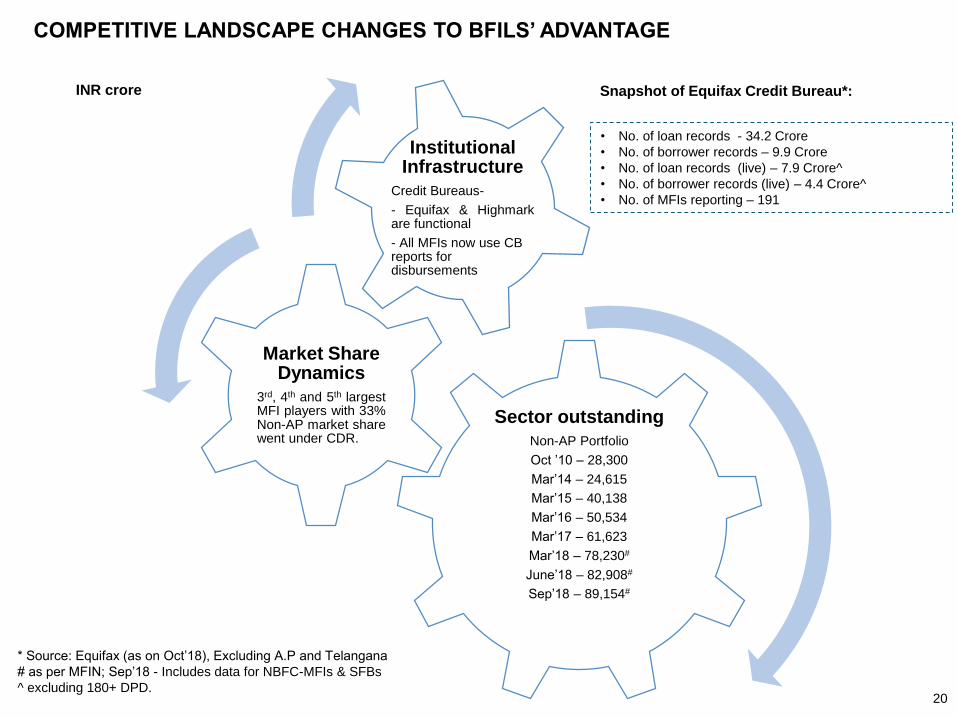

Sector outstanding

Non-AP Portfolio

Oct ’10 – 28,300

Mar’14 – 24,615

Mar’15 – 40,138

Mar’16 – 50,534

Mar’17 – 61,623

Mar’18 – 78,230#

June’18 – 82,908#

Sep’18 – 89,154#

Market Share Dynamics

3rd, 4th and 5th largestMFI players with 33%Non-AP market sharewent under CDR.

Institutional Infrastructure

Credit Bureaus-

- Equifax & Highmarkare functional

- All MFIs now use CB reports for disbursements

COMPETITIVE LANDSCAPE CHANGES TO BFILS’ ADVANTAGE

INR crore

• No. of loan records - 34.2 Crore

• No. of borrower records – 9.9 Crore

• No. of loan records (live) – 7.9 Crore^

• No. of borrower records (live) – 4.4 Crore^

• No. of MFIs reporting – 191

Snapshot of Equifax Credit Bureau*:

* Source: Equifax (as on Oct’18), Excluding A.P and Telangana

# as per MFIN; Sep’18 - Includes data for NBFC-MFIs & SFBs

^ excluding 180+ DPD.20

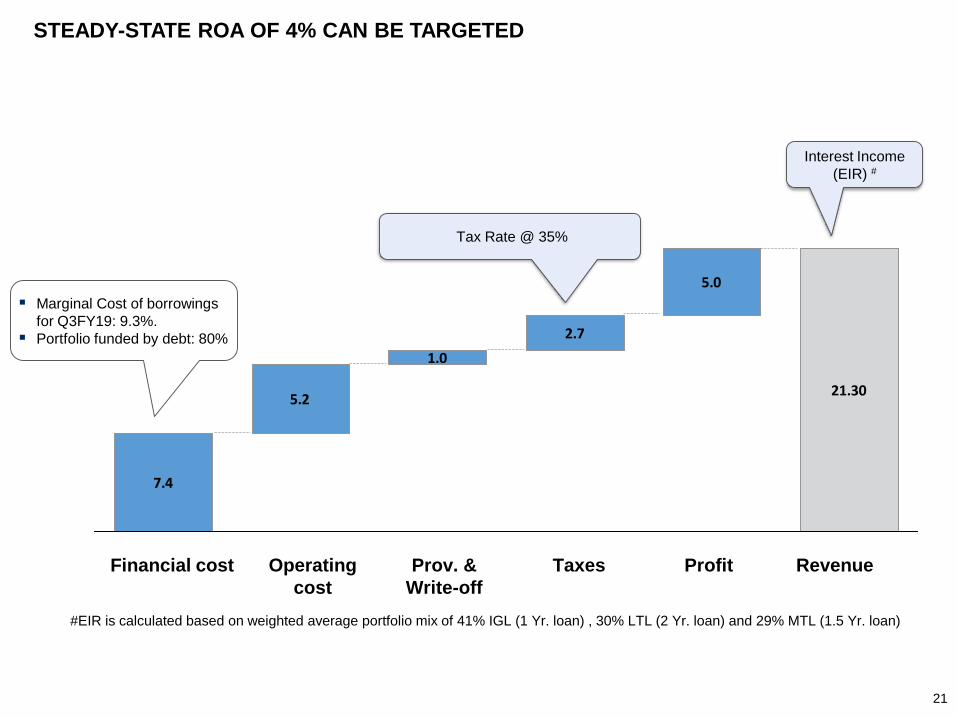

7.4

5.2

1.0

2.7

5.0

21.30

STEADY-STATE ROA OF 4% CAN BE TARGETED

RevenueProfitTaxesProv. &

Write-off

Operating

cost

Financial cost

▪ Marginal Cost of borrowings

for Q3FY19: 9.3%.

▪ Portfolio funded by debt: 80%

Tax Rate @ 35%

21

Interest Income

(EIR) #

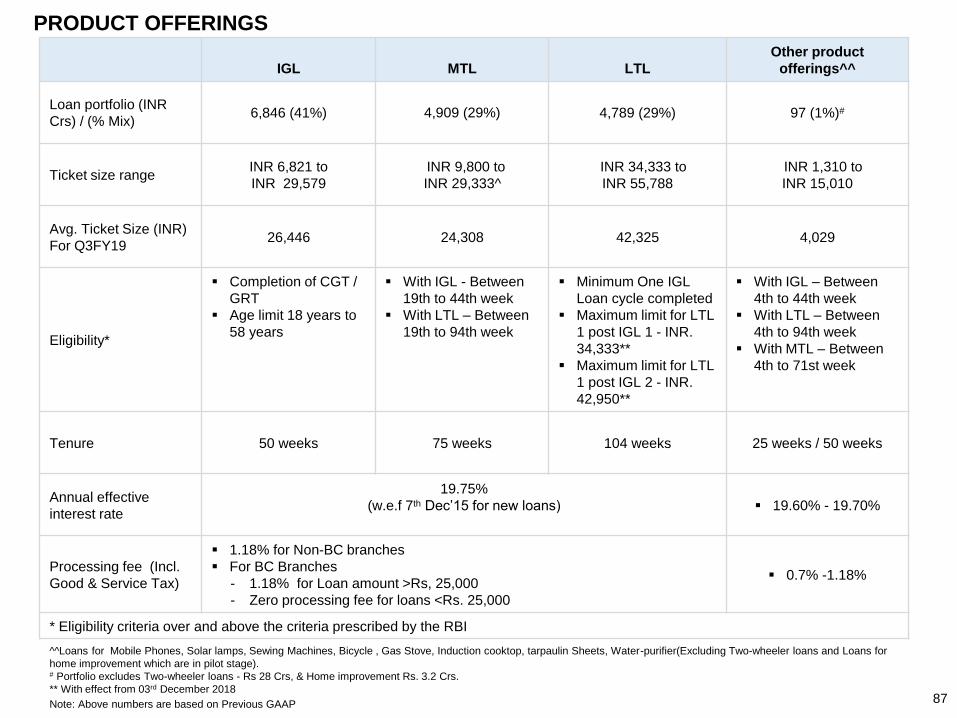

#EIR is calculated based on weighted average portfolio mix of 41% IGL (1 Yr. loan) , 30% LTL (2 Yr. loan) and 29% MTL (1.5 Yr. loan)

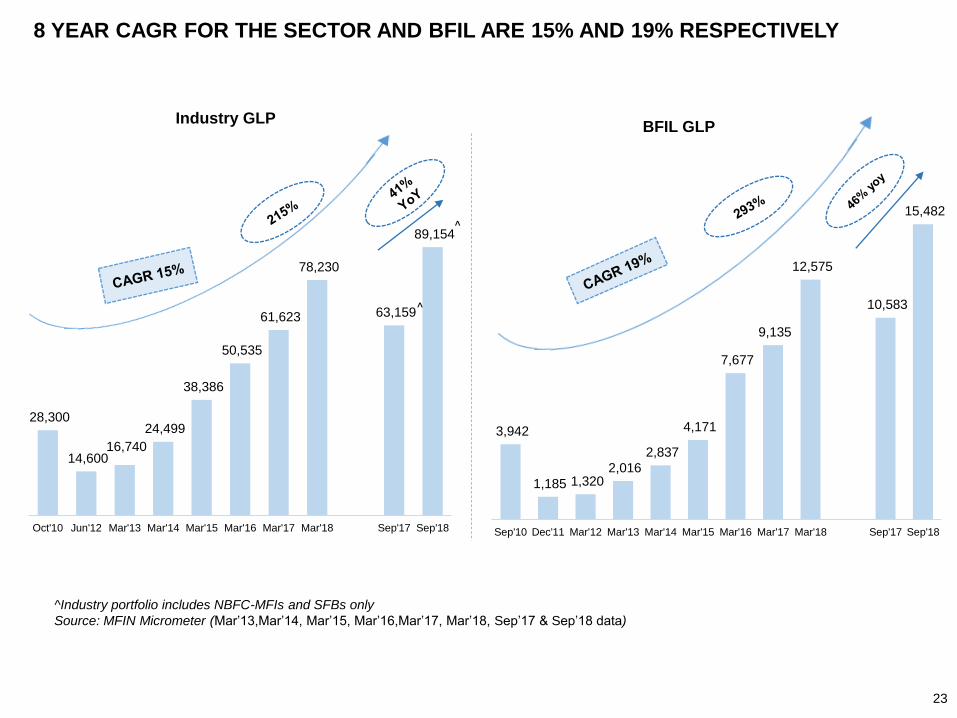

GROWTH ANATOMY

22

28,300

14,600 16,740

24,499

38,386

50,535

61,623

78,230

63,159

89,154

Oct'10 Jun'12 Mar'13 Mar'14 Mar'15 Mar'16 Mar'17 Mar'18 Sep'17 Sep'18

Industry GLP

3,942

1,185 1,320 2,016

2,837

4,171

7,677

9,135

12,575

10,583

15,482

Sep'10 Dec'11 Mar'12 Mar'13 Mar'14 Mar'15 Mar'16 Mar'17 Mar'18 Sep'17 Sep'18

BFIL GLP

8 YEAR CAGR FOR THE SECTOR AND BFIL ARE 15% AND 19% RESPECTIVELY

^Industry portfolio includes NBFC-MFIs and SFBs only

Source: MFIN Micrometer (Mar’13,Mar’14, Mar’15, Mar’16,Mar’17, Mar’18, Sep’17 & Sep’18 data)

23

^

^

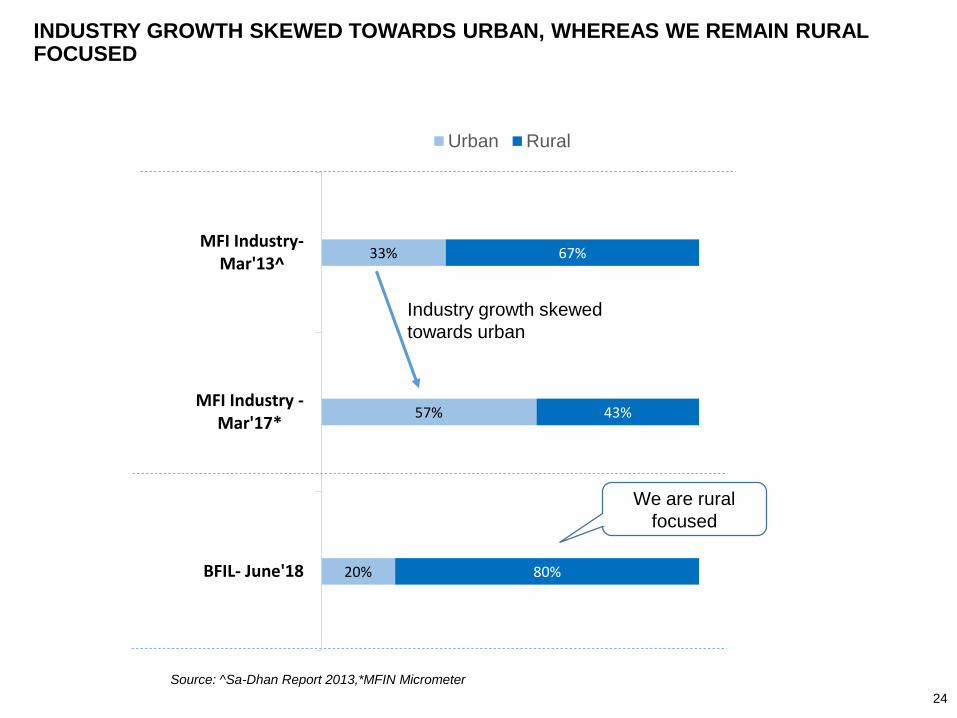

20%

57%

33%

80%

43%

67%

0% 20% 40% 60% 80% 100%

BFIL- June'18

MFI Industry -Mar'17*

MFI Industry-Mar'13^

Urban Rural

INDUSTRY GROWTH SKEWED TOWARDS URBAN, WHEREAS WE REMAIN RURAL FOCUSED

Industry growth skewed

towards urban

We are rural

focused

Source: ^Sa-Dhan Report 2013,*MFIN Micrometer

24

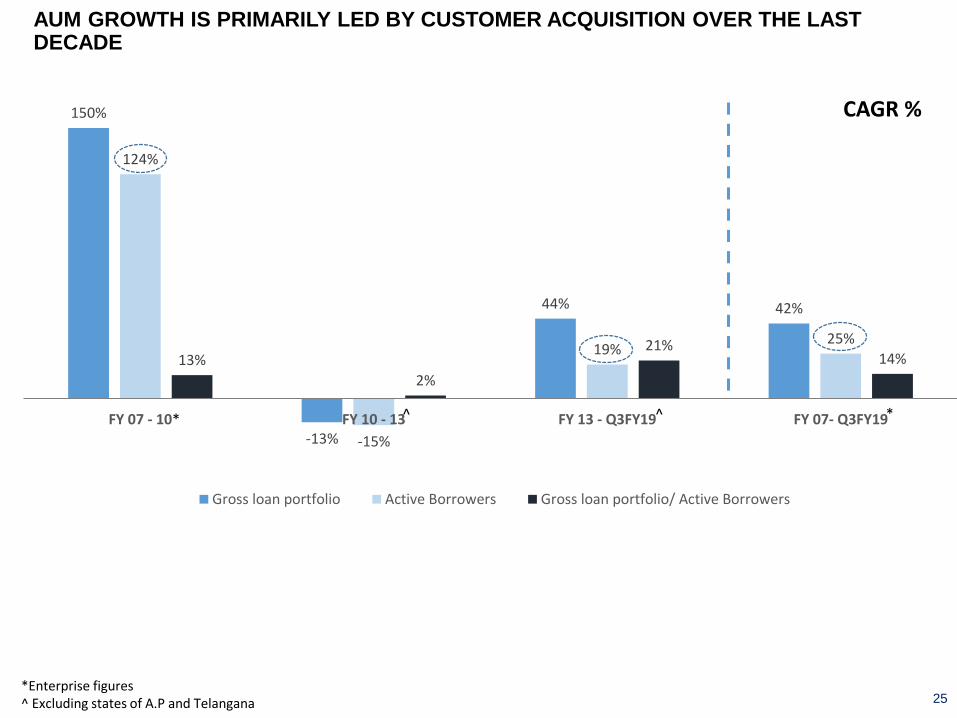

AUM GROWTH IS PRIMARILY LED BY CUSTOMER ACQUISITION OVER THE LAST DECADE

25

150%

-13%

44% 42%

124%

-15%

19%25%

13%

2%

21%14%

FY 07 - 10 FY 10 - 13 FY 13 - Q3FY19 FY 07- Q3FY19

Gross loan portfolio Active Borrowers Gross loan portfolio/ Active Borrowers

CAGR %

*

*Enterprise figures^ Excluding states of A.P and Telangana

^ ^ *

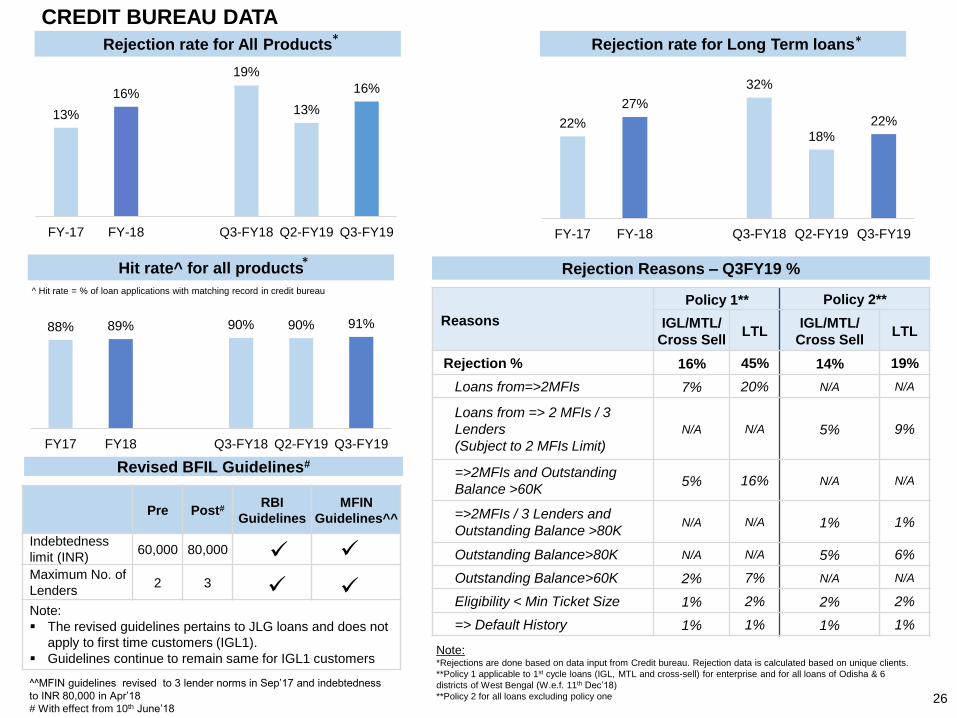

CREDIT BUREAU DATA

13%

16%

19%

13%

16%

FY-17 FY-18 Q3-FY18 Q2-FY19 Q3-FY19

22%

27%

32%

18%22%

FY-17 FY-18 Q3-FY18 Q2-FY19 Q3-FY19

Rejection rate for Long Term loansRejection rate for All Products

88% 89% 90% 90% 91%

FY17 FY18 Q3-FY18 Q2-FY19 Q3-FY19

Hit rate^ for all products

Hit rate = % of loan applications with matching record in credit bureau

Rejection Reasons – Q3FY19 %

26

Reasons

Policy 1** Policy 2**

IGL/MTL/

Cross SellLTL

IGL/MTL/

Cross SellLTL

Rejection % 16% 45% 14% 19%

Loans from=>2MFIs 7% 20% N/A N/A

Loans from => 2 MFIs / 3

Lenders

(Subject to 2 MFIs Limit)

N/A N/A 5% 9%

=>2MFIs and Outstanding

Balance >60K5% 16% N/A N/A

=>2MFIs / 3 Lenders and

Outstanding Balance >80KN/A N/A 1% 1%

Outstanding Balance>80K N/A N/A 5% 6%

Outstanding Balance>60K 2% 7% N/A N/A

Eligibility < Min Ticket Size 1% 2% 2% 2%

=> Default History 1% 1% 1% 1%

Note:*Rejections are done based on data input from Credit bureau. Rejection data is calculated based on unique clients.

**Policy 1 applicable to 1st cycle loans (IGL, MTL and cross-sell) for enterprise and for all loans of Odisha & 6

districts of West Bengal (W.e.f. 11th Dec’18)

**Policy 2 for all loans excluding policy one

* *

*

Pre Post#RBI

Guidelines

MFIN

Guidelines^^

Indebtedness

limit (INR)60,000 80,000

Maximum No. of

Lenders2 3

Note:

▪ The revised guidelines pertains to JLG loans and does not

apply to first time customers (IGL1).

▪ Guidelines continue to remain same for IGL1 customers

Revised BFIL Guidelines#

^^MFIN guidelines revised to 3 lender norms in Sep’17 and indebtedness

to INR 80,000 in Apr’18

# With effect from 10th June’18

✓

✓ ✓

✓

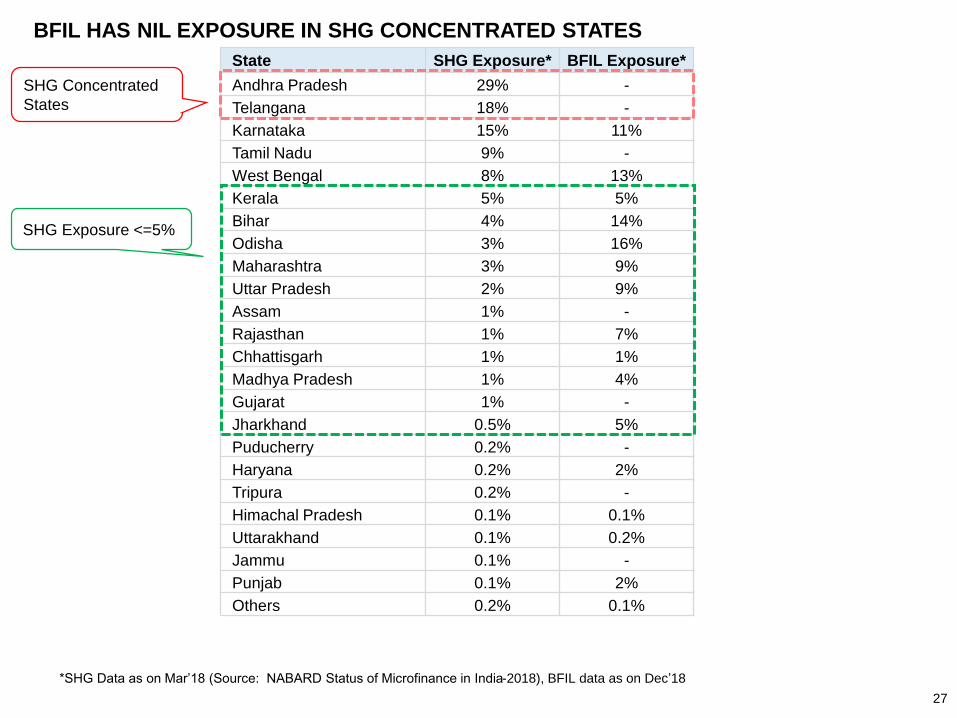

State SHG Exposure* BFIL Exposure*

Andhra Pradesh 29% -

Telangana 18% -

Karnataka 15% 11%

Tamil Nadu 9% -

West Bengal 8% 13%

Kerala 5% 5%

Bihar 4% 14%

Odisha 3% 16%

Maharashtra 3% 9%

Uttar Pradesh 2% 9%

Assam 1% -

Rajasthan 1% 7%

Chhattisgarh 1% 1%

Madhya Pradesh 1% 4%

Gujarat 1% -

Jharkhand 0.5% 5%

Puducherry 0.2% -

Haryana 0.2% 2%

Tripura 0.2% -

Himachal Pradesh 0.1% 0.1%

Uttarakhand 0.1% 0.2%

Jammu 0.1% -

Punjab 0.1% 2%

Others 0.2% 0.1%

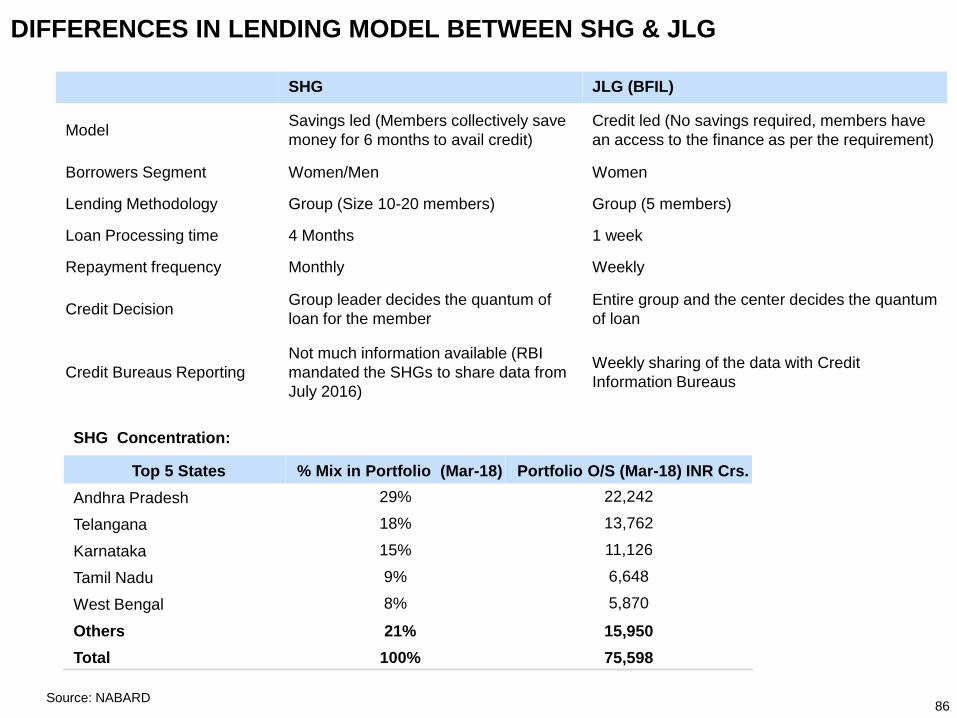

BFIL HAS NIL EXPOSURE IN SHG CONCENTRATED STATES

SHG Exposure <=5%

SHG Concentrated

States

*SHG Data as on Mar’18 (Source: NABARD Status of Microfinance in India-2018), BFIL data as on Dec’18

27

FUTURE STRATEGY

28

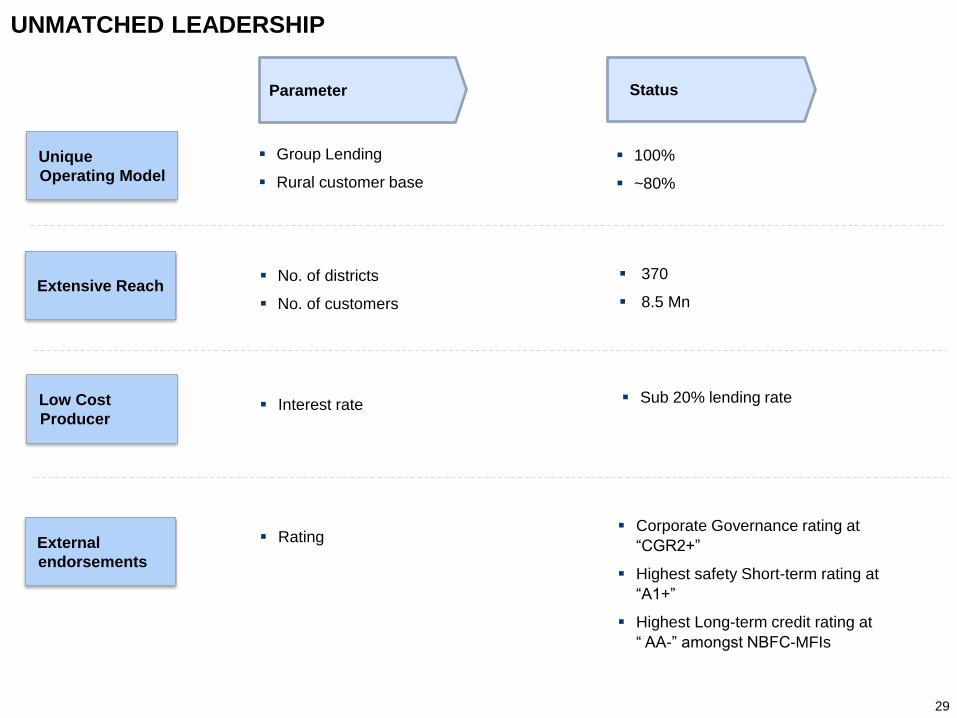

UNMATCHED LEADERSHIP

Unique

Operating Model

Extensive Reach

Low Cost

Producer

External

endorsements

Parameter

▪ Interest rate

▪ No. of districts

▪ No. of customers

▪ Group Lending

▪ Rural customer base

▪ Rating

Status

▪ 100%

▪ ~80%

▪ Sub 20% lending rate

▪ 370

▪ 8.5 Mn

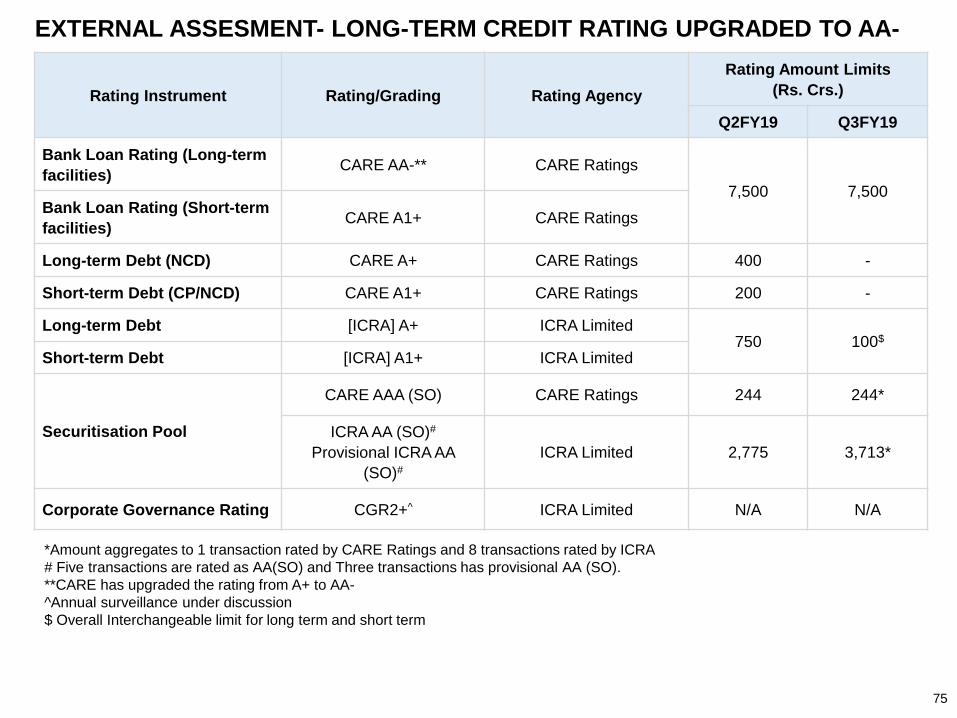

▪ Corporate Governance rating at

“CGR2+”

▪ Highest safety Short-term rating at

“A1+”

▪ Highest Long-term credit rating at

“ AA-” amongst NBFC-MFIs

29

THE MOST EFFICIENT MFI IN THE GLOBE

10

Metric

▪ Sub-20

Interest

Rate to

Borrower

▪ Cost to

Income

Ratio

▪ Balance sheet

strength

▪ Stellar

repayment

record

▪ Judicious

sources mix

▪ Technology

initiatives

▪ Scale

▪ AUM

growth

▪ Operating

leverage

▪ Non-Loan

revenue

Drivers

▪ Marginal

cost of

Borrowing

▪ Cumulative

next 2

years salary

increase to

field staff

Target %

▪ Annualised

earnings

growth

Medium Term Strategic Priorities:

20 30 40 50

▪ Low marginal

cost of borrowing

▪ Scale &

Efficiency

▪ Productivity &

Efficiency

Status –

Q3FY199.3* 19.75 - 34.4 49

*on and off b/s loans (including processing fees)

30

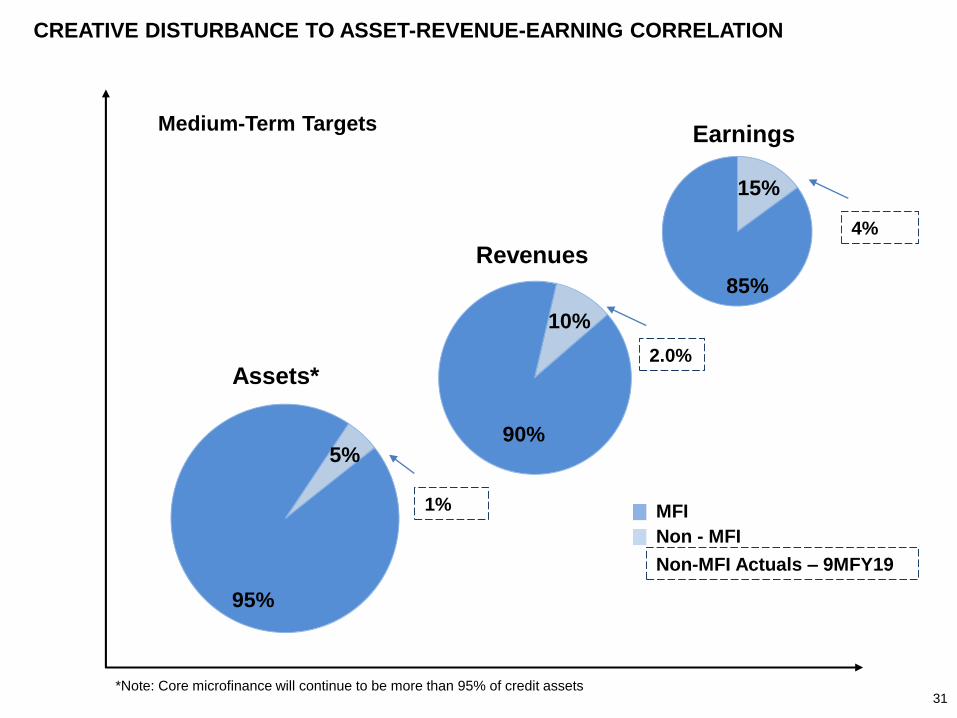

CREATIVE DISTURBANCE TO ASSET-REVENUE-EARNING CORRELATION

10%

90%

Revenues

5%

95%

Assets*

15%

85%

Earnings

*Note: Core microfinance will continue to be more than 95% of credit assets

Medium-Term Targets

MFI

Non - MFI

Non-MFI Actuals – 9MFY19

2.0%

1%

31

4%

PILOT ON RETAIL DISTRIBUTION

SERVICE POINTS (RDSP)

32

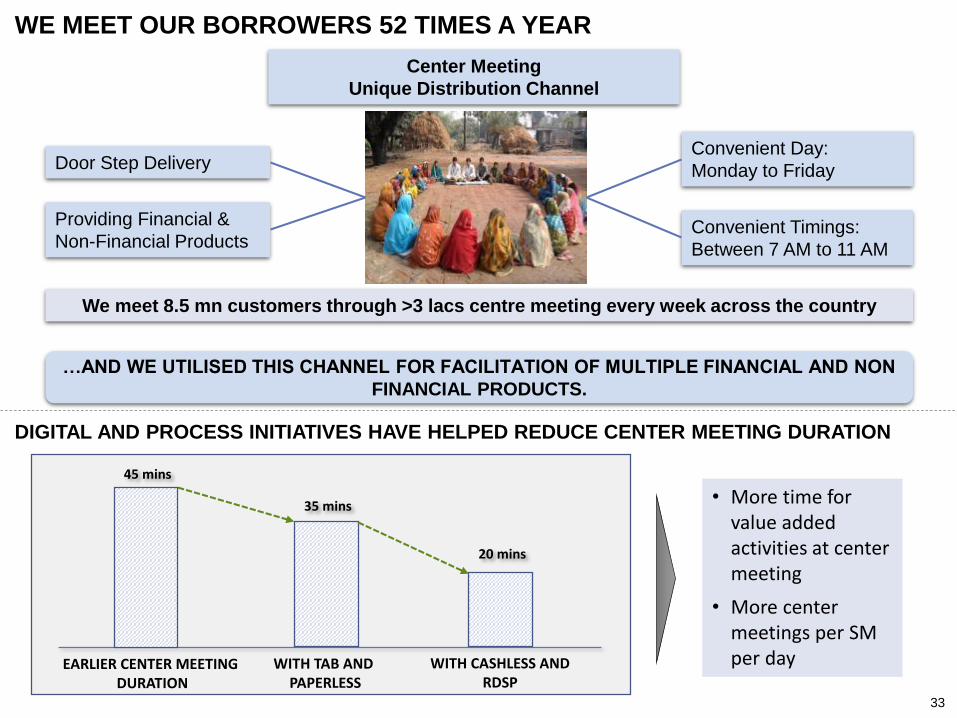

WE MEET OUR BORROWERS 52 TIMES A YEAR

Door Step Delivery

We meet 8.5 mn customers through >3 lacs centre meeting every week across the country

Center Meeting

Unique Distribution Channel

Convenient Day:

Monday to Friday

Convenient Timings:

Between 7 AM to 11 AM

Providing Financial &

Non-Financial Products

…AND WE UTILISED THIS CHANNEL FOR FACILITATION OF MULTIPLE FINANCIAL AND NON

FINANCIAL PRODUCTS.

33

DIGITAL AND PROCESS INITIATIVES HAVE HELPED REDUCE CENTER MEETING DURATION

EARLIER CENTER MEETINGDURATION

45 mins

WITH TAB AND PAPERLESS

35 mins

WITH CASHLESS AND RDSP

20 mins

• More time for value added activities at center meeting

• More center meetings per SM per day

Deposits and withdrawals point

Bill payments and recharges

Allied and OTC financial services

Cross sell and e-commerce

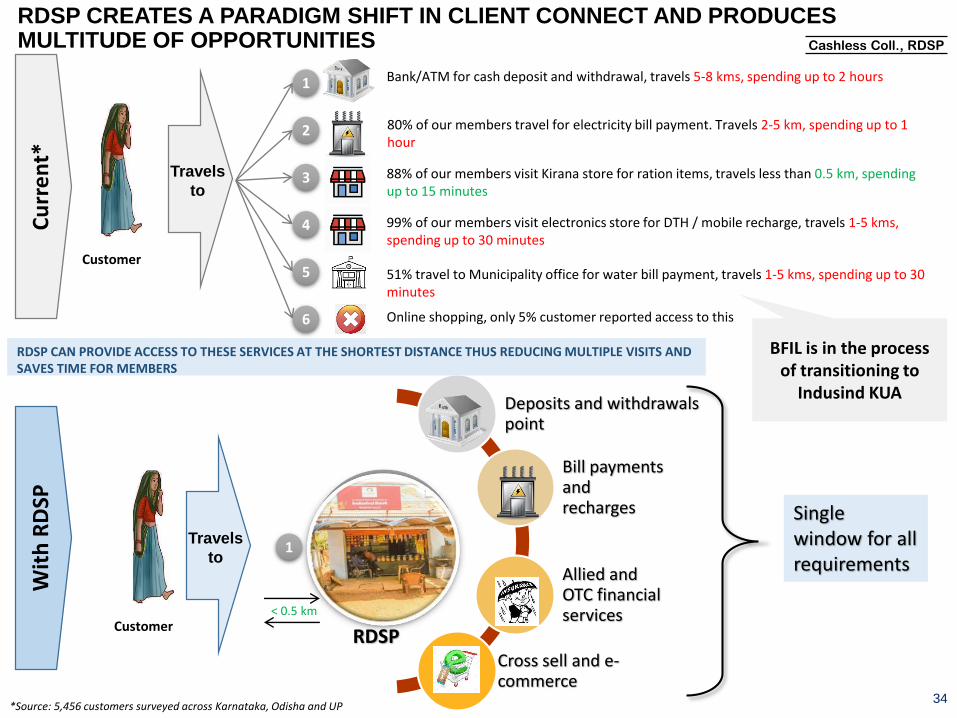

RDSP CREATES A PARADIGM SHIFT IN CLIENT CONNECT AND PRODUCES MULTITUDE OF OPPORTUNITIES

34

Customer

Cu

rre

nt*

Wit

h R

DSP

80% of our members travel for electricity bill payment. Travels 2-5 km, spending up to 1 hour

88% of our members visit Kirana store for ration items, travels less than 0.5 km, spending up to 15 minutes

Travels

to

99% of our members visit electronics store for DTH / mobile recharge, travels 1-5 kms, spending up to 30 minutes

51% travel to Municipality office for water bill payment, travels 1-5 kms, spending up to 30 minutes

Bank/ATM for cash deposit and withdrawal, travels 5-8 kms, spending up to 2 hours

Online shopping, only 5% customer reported access to this

1

2

3

4

5

6

Customer

Travels

to

RDSP

Single window for all requirements

< 0.5 km

1

RDSP CAN PROVIDE ACCESS TO THESE SERVICES AT THE SHORTEST DISTANCE THUS REDUCING MULTIPLE VISITS AND SAVES TIME FOR MEMBERS

*Source: 5,456 customers surveyed across Karnataka, Odisha and UP

Cashless Coll., RDSP

BFIL is in the process of transitioning to

Indusind KUA

RDSP PILOT

35

Leveraging distribution

strength

Last mile for leading retailers

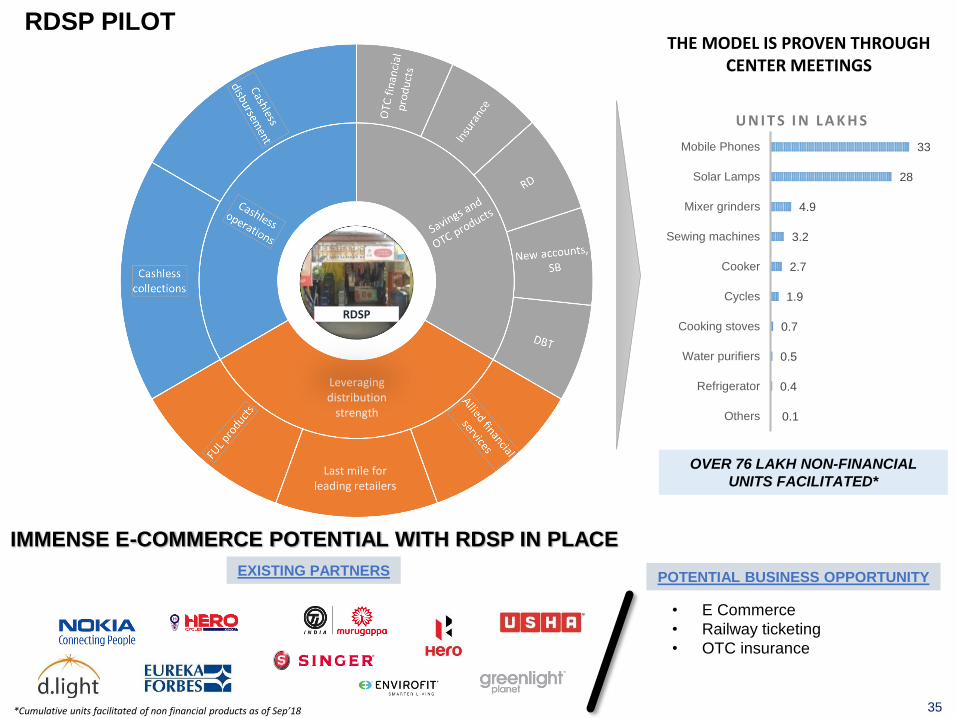

THE MODEL IS PROVEN THROUGH CENTER MEETINGS

IMMENSE E-COMMERCE POTENTIAL WITH RDSP IN PLACE

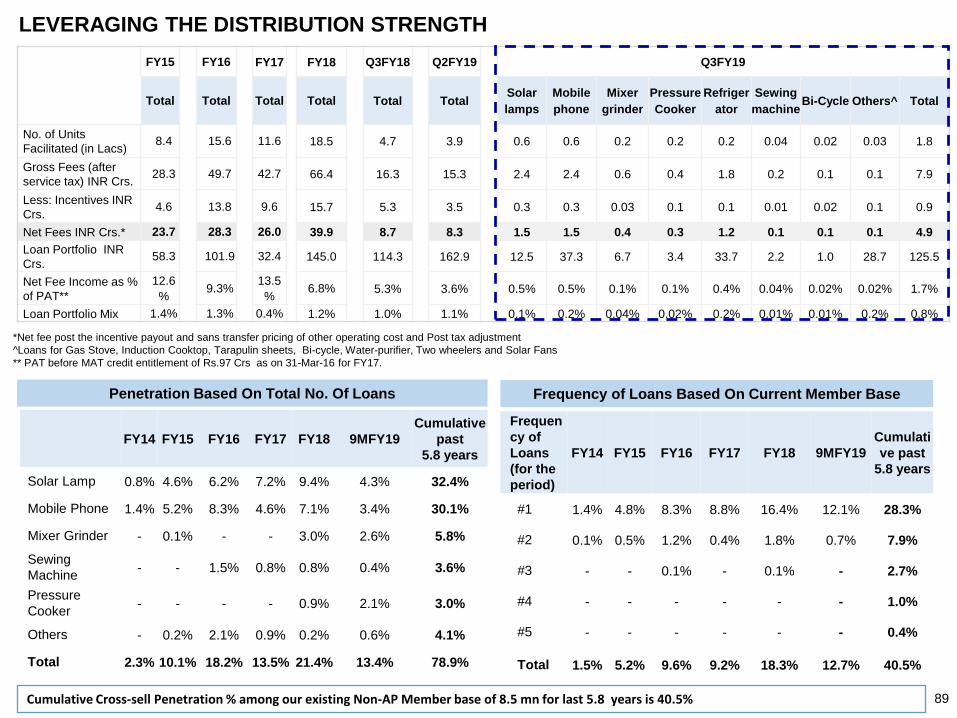

EXISTING PARTNERS POTENTIAL BUSINESS OPPORTUNITY

OVER 76 LAKH NON-FINANCIAL

UNITS FACILITATED*

*Cumulative units facilitated of non financial products as of Sep’18

RDSP

• E Commerce

• Railway ticketing

• OTC insurance

0.1

0.4

0.5

0.7

1.9

2.7

3.2

4.9

28

33

Others

Refrigerator

Water purifiers

Cooking stoves

Cycles

Cooker

Sewing machines

Mixer grinders

Solar Lamps

Mobile Phones

U N I T S I N L A K H S

UPDATE ON CASHLESS

DISBURSEMENT

36

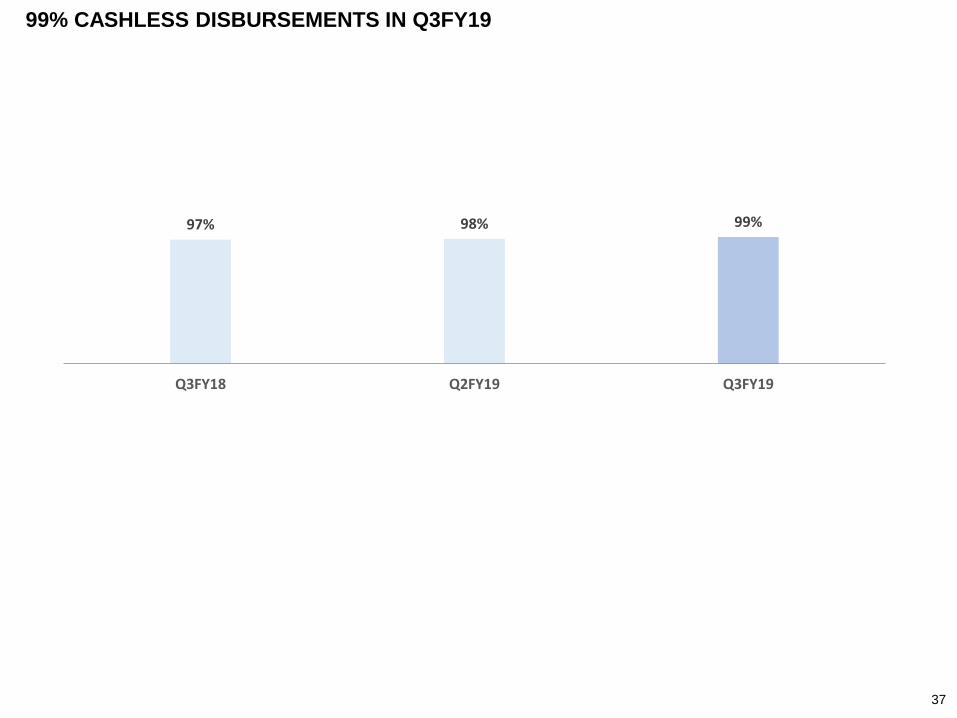

97% 98% 99%

0%10%20%30%40%50%60%70%80%90%

Q3FY18 Q2FY19 Q3FY19

37

99% CASHLESS DISBURSEMENTS IN Q3FY19

LOANS FOR HOME IMPROVEMENT &

TWO-WHEELER (PILOT)

38

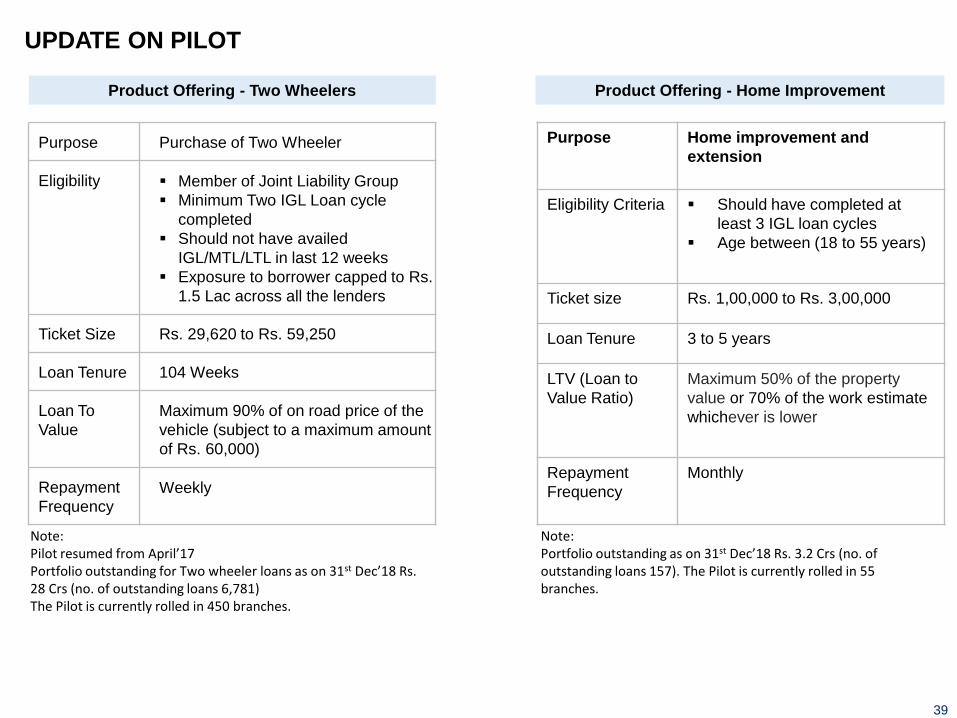

UPDATE ON PILOT

Purpose Purchase of Two Wheeler

Eligibility ▪ Member of Joint Liability Group

▪ Minimum Two IGL Loan cycle

completed

▪ Should not have availed

IGL/MTL/LTL in last 12 weeks

▪ Exposure to borrower capped to Rs.

1.5 Lac across all the lenders

Ticket Size Rs. 29,620 to Rs. 59,250

Loan Tenure 104 Weeks

Loan To

Value

Maximum 90% of on road price of the

vehicle (subject to a maximum amount

of Rs. 60,000)

Repayment

Frequency

Weekly

39

Note: Pilot resumed from April’17Portfolio outstanding for Two wheeler loans as on 31st Dec’18 Rs. 28 Crs (no. of outstanding loans 6,781)The Pilot is currently rolled in 450 branches.

Purpose Home improvement and

extension

Eligibility Criteria ▪ Should have completed at

least 3 IGL loan cycles

▪ Age between (18 to 55 years)

Ticket size Rs. 1,00,000 to Rs. 3,00,000

Loan Tenure 3 to 5 years

LTV (Loan to

Value Ratio)

Maximum 50% of the property

value or 70% of the work estimate

whichever is lower

Repayment

Frequency

Monthly

Product Offering - Home Improvement

Note: Portfolio outstanding as on 31st Dec’18 Rs. 3.2 Crs (no. of outstanding loans 157). The Pilot is currently rolled in 55 branches.

Product Offering - Two Wheelers

Q3FY19

PERFORMANCE HIGHLIGHTS

40

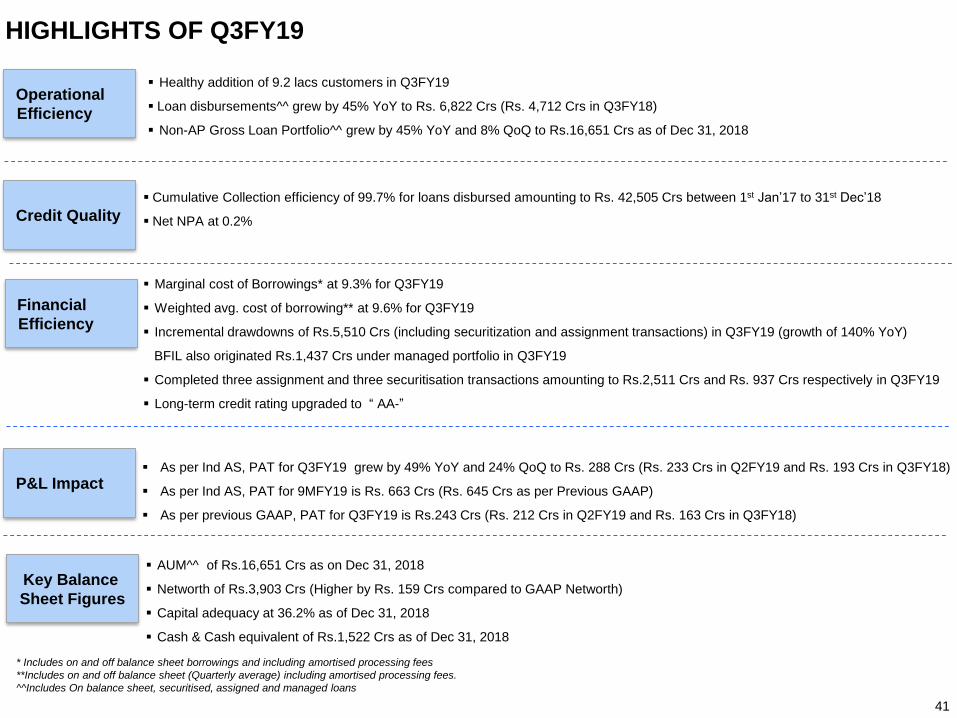

Operational

Efficiency

Financial

Efficiency

P&L Impact

Key Balance

Sheet Figures

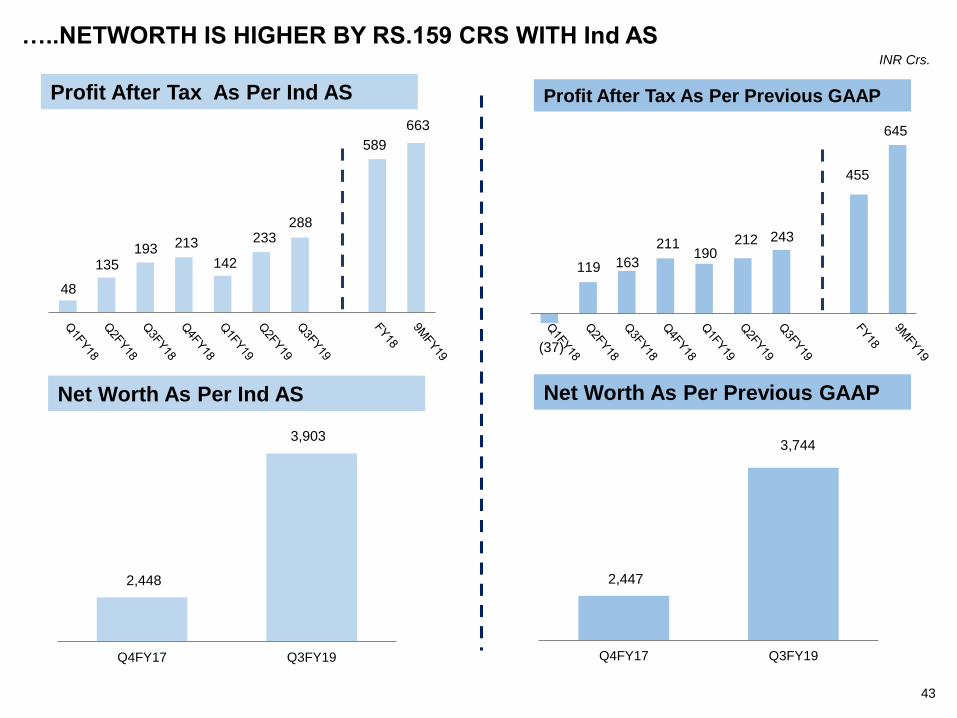

▪ As per Ind AS, PAT for Q3FY19 grew by 49% YoY and 24% QoQ to Rs. 288 Crs (Rs. 233 Crs in Q2FY19 and Rs. 193 Crs in Q3FY18)

▪ As per Ind AS, PAT for 9MFY19 is Rs. 663 Crs (Rs. 645 Crs as per Previous GAAP)

▪ As per previous GAAP, PAT for Q3FY19 is Rs.243 Crs (Rs. 212 Crs in Q2FY19 and Rs. 163 Crs in Q3FY18)

▪ Marginal cost of Borrowings* at 9.3% for Q3FY19

▪ Weighted avg. cost of borrowing** at 9.6% for Q3FY19

▪ Incremental drawdowns of Rs.5,510 Crs (including securitization and assignment transactions) in Q3FY19 (growth of 140% YoY)

BFIL also originated Rs.1,437 Crs under managed portfolio in Q3FY19

▪ Completed three assignment and three securitisation transactions amounting to Rs.2,511 Crs and Rs. 937 Crs respectively in Q3FY19

▪ Long-term credit rating upgraded to “ AA-”

▪ Healthy addition of 9.2 lacs customers in Q3FY19

▪ Loan disbursements^^ grew by 45% YoY to Rs. 6,822 Crs (Rs. 4,712 Crs in Q3FY18)

▪ Non-AP Gross Loan Portfolio^^ grew by 45% YoY and 8% QoQ to Rs.16,651 Crs as of Dec 31, 2018

▪ AUM^^ of Rs.16,651 Crs as on Dec 31, 2018

▪ Networth of Rs.3,903 Crs (Higher by Rs. 159 Crs compared to GAAP Networth)

▪ Capital adequacy at 36.2% as of Dec 31, 2018

▪ Cash & Cash equivalent of Rs.1,522 Crs as of Dec 31, 2018

41

* Includes on and off balance sheet borrowings and including amortised processing fees

**Includes on and off balance sheet (Quarterly average) including amortised processing fees.

^^Includes On balance sheet, securitised, assigned and managed loans

HIGHLIGHTS OF Q3FY19

Credit Quality

▪ Cumulative Collection efficiency of 99.7% for loans disbursed amounting to Rs. 42,505 Crs between 1st Jan’17 to 31st Dec’18

▪ Net NPA at 0.2%

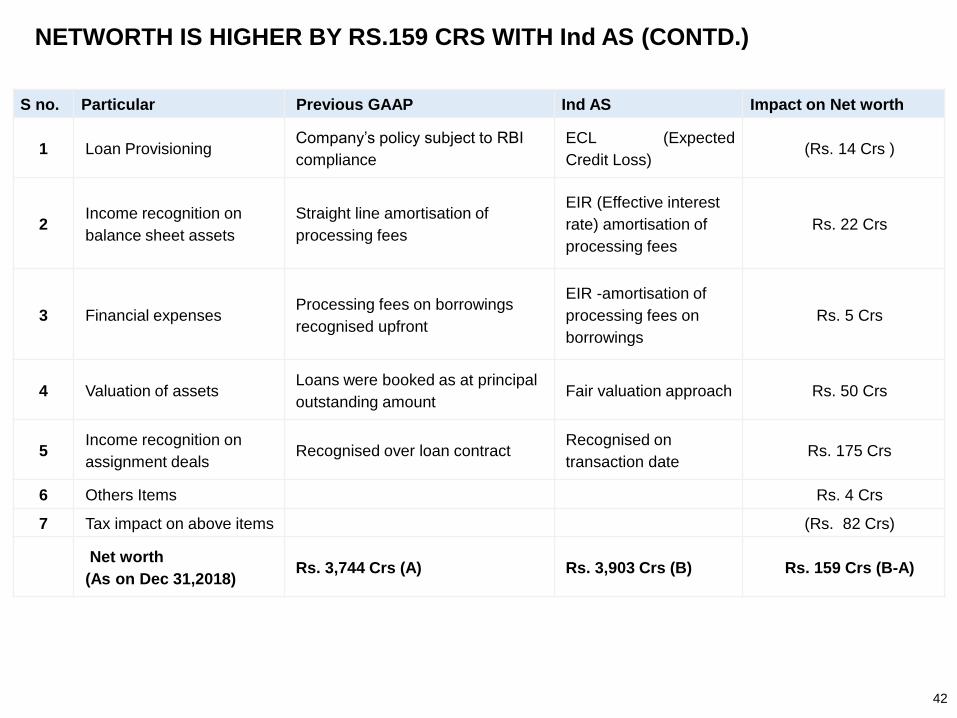

NETWORTH IS HIGHER BY RS.159 CRS WITH Ind AS (CONTD.)

42

S no. Particular Previous GAAP Ind AS Impact on Net worth

1 Loan Provisioning Company’s policy subject to RBI

compliance

ECL (Expected

Credit Loss)(Rs. 14 Crs )

2Income recognition on

balance sheet assets

Straight line amortisation of

processing fees

EIR (Effective interest

rate) amortisation of

processing fees

Rs. 22 Crs

3 Financial expenses Processing fees on borrowings

recognised upfront

EIR -amortisation of

processing fees on

borrowings

Rs. 5 Crs

4 Valuation of assetsLoans were booked as at principal

outstanding amountFair valuation approach Rs. 50 Crs

5Income recognition on

assignment dealsRecognised over loan contract

Recognised on

transaction dateRs. 175 Crs

6 Others Items Rs. 4 Crs

7 Tax impact on above items (Rs. 82 Crs)

Net worth

(As on Dec 31,2018)Rs. 3,744 Crs (A) Rs. 3,903 Crs (B) Rs. 159 Crs (B-A)

2,447

3,744

Q4FY17 Q3FY19

…..NETWORTH IS HIGHER BY RS.159 CRS WITH Ind AS

43

Profit After Tax As Per Previous GAAPProfit After Tax As Per Ind AS

INR Crs.

Net Worth As Per Previous GAAPNet Worth As Per Ind AS

(37)

119 163

211 190

212 243

455

645

48

135 193 213

142

233 288

589

663

2,448

3,903

Q4FY17 Q3FY19

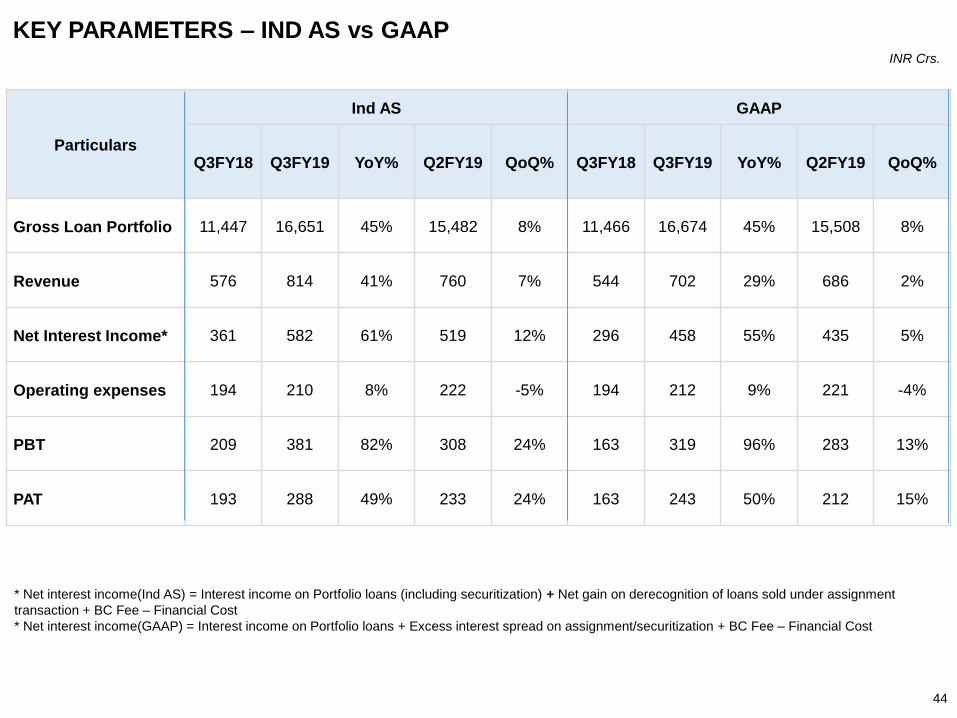

KEY PARAMETERS – IND AS vs GAAP

44

* Net interest income(Ind AS) = Interest income on Portfolio loans (including securitization) + Net gain on derecognition of loans sold under assignment

transaction + BC Fee – Financial Cost

* Net interest income(GAAP) = Interest income on Portfolio loans + Excess interest spread on assignment/securitization + BC Fee – Financial Cost

INR Crs.

Particulars

Ind AS GAAP

Q3FY18 Q3FY19 YoY% Q2FY19 QoQ% Q3FY18 Q3FY19 YoY% Q2FY19 QoQ%

Gross Loan Portfolio 11,447 16,651 45% 15,482 8% 11,466 16,674 45% 15,508 8%

Revenue 576 814 41% 760 7% 544 702 29% 686 2%

Net Interest Income* 361 582 61% 519 12% 296 458 55% 435 5%

Operating expenses 194 210 8% 222 -5% 194 212 9% 221 -4%

PBT 209 381 82% 308 24% 163 319 96% 283 13%

PAT 193 288 49% 233 24% 163 243 50% 212 15%

OPERATIONAL HIGHLIGHTS

45

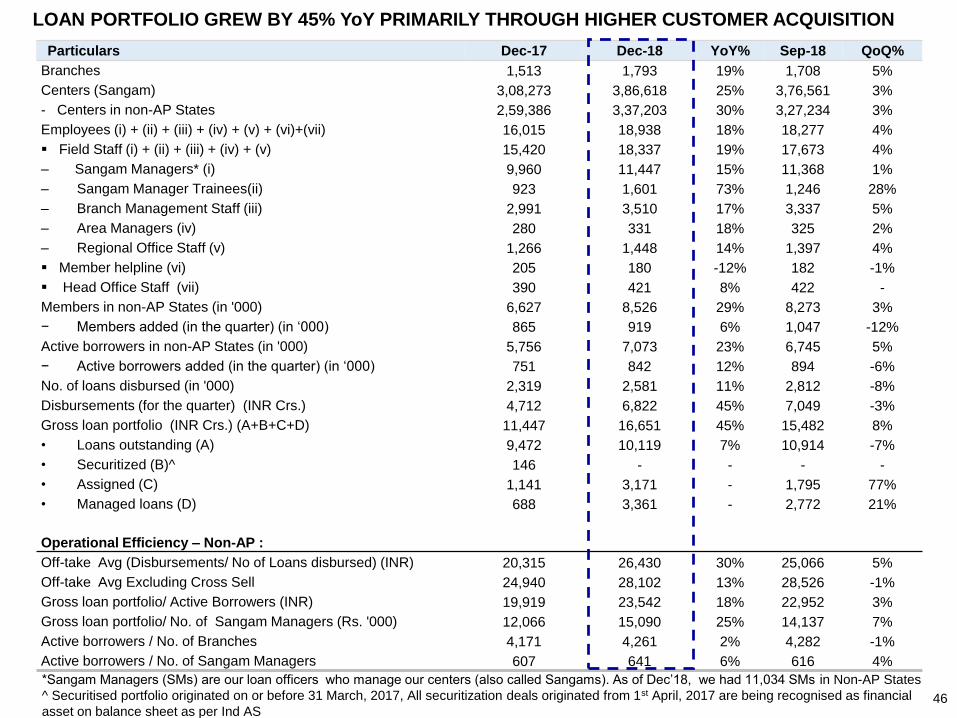

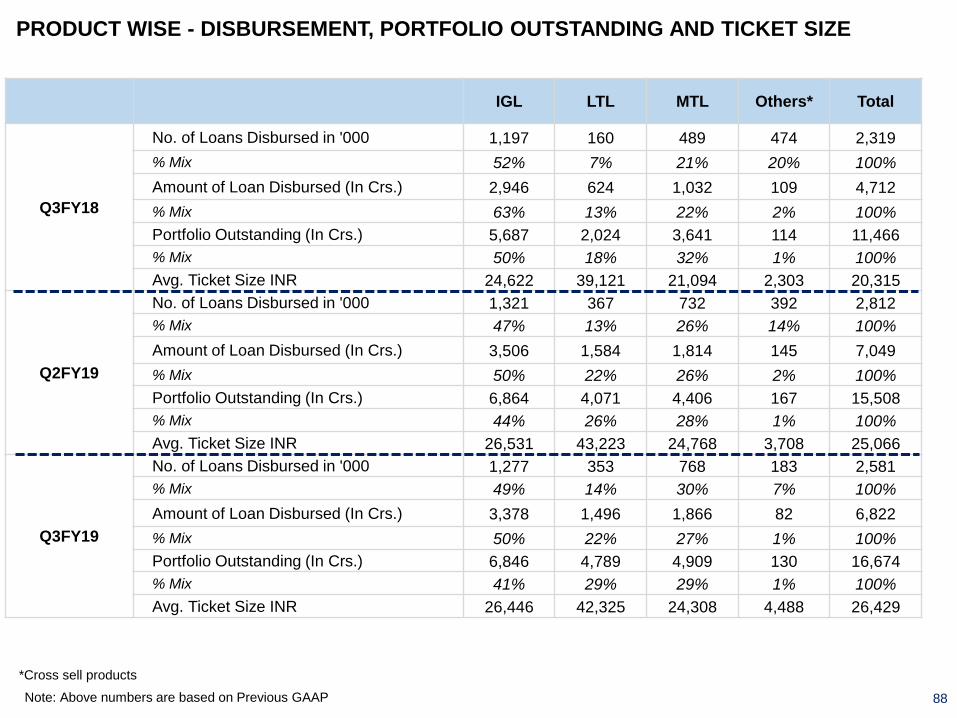

LOAN PORTFOLIO GREW BY 45% YoY PRIMARILY THROUGH HIGHER CUSTOMER ACQUISITION

Particulars Dec-17 Dec-18 YoY% Sep-18 QoQ%

Branches 1,513 1,793 19% 1,708 5%

Centers (Sangam) 3,08,273 3,86,618 25% 3,76,561 3%

- Centers in non-AP States 2,59,386 3,37,203 30% 3,27,234 3%

Employees (i) + (ii) + (iii) + (iv) + (v) + (vi)+(vii) 16,015 18,938 18% 18,277 4%

▪ Field Staff (i) + (ii) + (iii) + (iv) + (v) 15,420 18,337 19% 17,673 4%

– Sangam Managers* (i) 9,960 11,447 15% 11,368 1%

– Sangam Manager Trainees(ii) 923 1,601 73% 1,246 28%

– Branch Management Staff (iii) 2,991 3,510 17% 3,337 5%

– Area Managers (iv) 280 331 18% 325 2%

– Regional Office Staff (v) 1,266 1,448 14% 1,397 4%

▪ Member helpline (vi) 205 180 -12% 182 -1%

▪ Head Office Staff (vii) 390 421 8% 422 -

Members in non-AP States (in '000) 6,627 8,526 29% 8,273 3%

− Members added (in the quarter) (in ‘000) 865 919 6% 1,047 -12%

Active borrowers in non-AP States (in '000) 5,756 7,073 23% 6,745 5%

− Active borrowers added (in the quarter) (in ‘000) 751 842 12% 894 -6%

No. of loans disbursed (in '000) 2,319 2,581 11% 2,812 -8%

Disbursements (for the quarter) (INR Crs.) 4,712 6,822 45% 7,049 -3%

Gross loan portfolio (INR Crs.) (A+B+C+D) 11,447 16,651 45% 15,482 8%

• Loans outstanding (A) 9,472 10,119 7% 10,914 -7%

• Securitized (B)^ 146 - - - -

• Assigned (C) 1,141 3,171 - 1,795 77%

• Managed loans (D) 688 3,361 - 2,772 21%

Operational Efficiency – Non-AP :

Off-take Avg (Disbursements/ No of Loans disbursed) (INR) 20,315 26,430 30% 25,066 5%

Off-take Avg Excluding Cross Sell 24,940 28,102 13% 28,526 -1%

Gross loan portfolio/ Active Borrowers (INR) 19,919 23,542 18% 22,952 3%

Gross loan portfolio/ No. of Sangam Managers (Rs. '000) 12,066 15,090 25% 14,137 7%

Active borrowers / No. of Branches 4,171 4,261 2% 4,282 -1%

Active borrowers / No. of Sangam Managers 607 641 6% 616 4%

*Sangam Managers (SMs) are our loan officers who manage our centers (also called Sangams). As of Dec’18, we had 11,034 SMs in Non-AP States

^ Securitised portfolio originated on or before 31 March, 2017, All securitization deals originated from 1st April, 2017 are being recognised as financial

asset on balance sheet as per Ind AS46

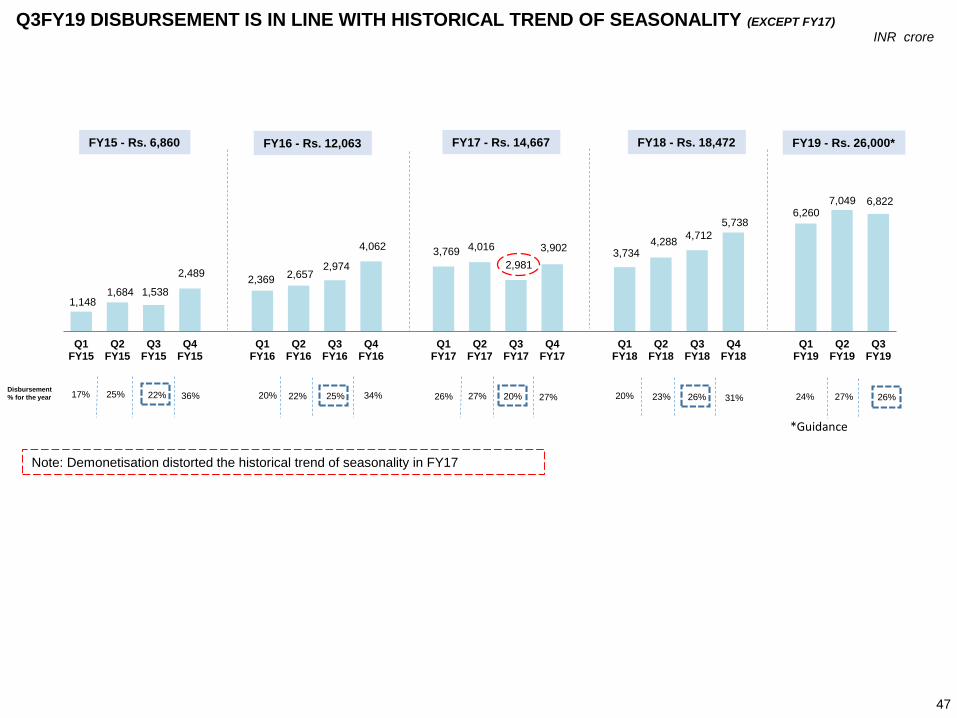

47

INR crore

1,148 1,684 1,538

2,489 2,369

2,657 2,974

4,062 3,769 4,016

2,981

3,902 3,734

4,288 4,712

5,738 6,260

7,049 6,822

Q1FY15

Q2FY15

Q3FY15

Q4FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Q1FY19

Q2FY19

Q3FY19

Disbursement

% for the year 17% 25% 22% 36%

FY16 - Rs. 12,063

Q3FY19 DISBURSEMENT IS IN LINE WITH HISTORICAL TREND OF SEASONALITY (EXCEPT FY17)

FY15 - Rs. 6,860 FY18 - Rs. 18,472FY17 - Rs. 14,667

20% 22% 25% 34% 26% 27% 20% 27% 20%

Note: Demonetisation distorted the historical trend of seasonality in FY17

23% 26%

FY19 - Rs. 26,000*

31% 24%

*Guidance

27% 26%

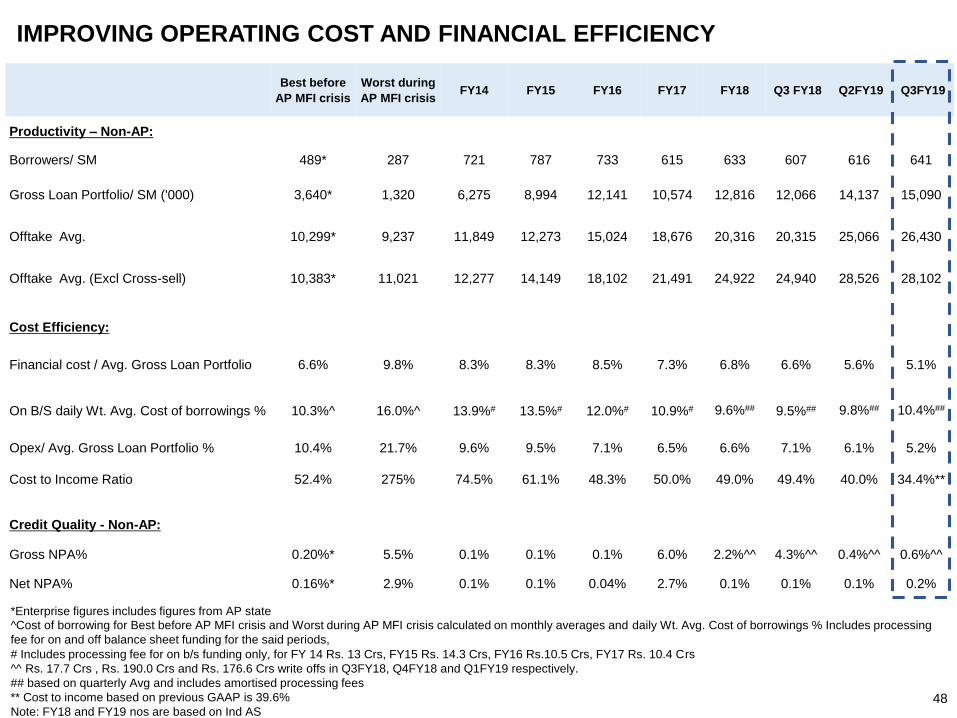

IMPROVING OPERATING COST AND FINANCIAL EFFICIENCY

Best before

AP MFI crisis

Worst during

AP MFI crisisFY14 FY15 FY16 FY17 FY18 Q3 FY18 Q2FY19 Q3FY19

Productivity – Non-AP:

Borrowers/ SM 489* 287 721 787 733 615 633 607 616 641

Gross Loan Portfolio/ SM ('000) 3,640* 1,320 6,275 8,994 12,141 10,574 12,816 12,066 14,137 15,090

Offtake Avg. 10,299* 9,237 11,849 12,273 15,024 18,676 20,316 20,315 25,066 26,430

Offtake Avg. (Excl Cross-sell) 10,383* 11,021 12,277 14,149 18,102 21,491 24,922 24,940 28,526 28,102

Cost Efficiency:

Financial cost / Avg. Gross Loan Portfolio 6.6% 9.8% 8.3% 8.3% 8.5% 7.3% 6.8% 6.6% 5.6% 5.1%

On B/S daily Wt. Avg. Cost of borrowings % 10.3%^ 16.0%^ 13.9%# 13.5%# 12.0%# 10.9%# 9.6%## 9.5%## 9.8%## 10.4%##

Opex/ Avg. Gross Loan Portfolio % 10.4% 21.7% 9.6% 9.5% 7.1% 6.5% 6.6% 7.1% 6.1% 5.2%

Cost to Income Ratio 52.4% 275% 74.5% 61.1% 48.3% 50.0% 49.0% 49.4% 40.0% 34.4%**

Credit Quality - Non-AP:

Gross NPA% 0.20%* 5.5% 0.1% 0.1% 0.1% 6.0% 2.2%^^ 4.3%^^ 0.4%^^ 0.6%^^

Net NPA% 0.16%* 2.9% 0.1% 0.1% 0.04% 2.7% 0.1% 0.1% 0.1% 0.2%

*Enterprise figures includes figures from AP state

^Cost of borrowing for Best before AP MFI crisis and Worst during AP MFI crisis calculated on monthly averages and daily Wt. Avg. Cost of borrowings % Includes processing

fee for on and off balance sheet funding for the said periods,

# Includes processing fee for on b/s funding only, for FY 14 Rs. 13 Crs, FY15 Rs. 14.3 Crs, FY16 Rs.10.5 Crs, FY17 Rs. 10.4 Crs

^^ Rs. 17.7 Crs , Rs. 190.0 Crs and Rs. 176.6 Crs write offs in Q3FY18, Q4FY18 and Q1FY19 respectively.

## based on quarterly Avg and includes amortised processing fees

** Cost to income based on previous GAAP is 39.6%

Note: FY18 and FY19 nos are based on Ind AS48

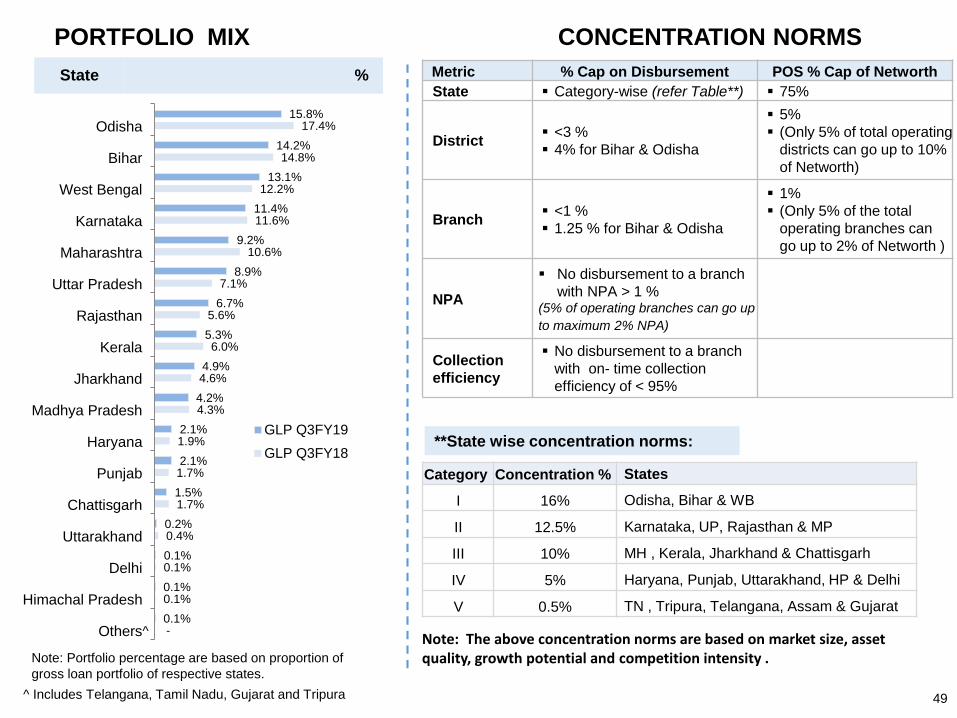

PORTFOLIO MIX CONCENTRATION NORMS

Metric % Cap on Disbursement POS % Cap of Networth

State ▪ Category-wise (refer Table**) ▪ 75%

District ▪ <3 %

▪ 4% for Bihar & Odisha

▪ 5%

▪ (Only 5% of total operating

districts can go up to 10%

of Networth)

Branch ▪ <1 %

▪ 1.25 % for Bihar & Odisha

▪ 1%

▪ (Only 5% of the total

operating branches can

go up to 2% of Networth )

NPA

▪ No disbursement to a branch

with NPA > 1 %(5% of operating branches can go up

to maximum 2% NPA)

Collection

efficiency

▪ No disbursement to a branch

with on- time collection

efficiency of < 95%

State %

49

Category Concentration % States

I 16% Odisha, Bihar & WB

II 12.5% Karnataka, UP, Rajasthan & MP

III 10% MH , Kerala, Jharkhand & Chattisgarh

IV 5% Haryana, Punjab, Uttarakhand, HP & Delhi

V 0.5% TN , Tripura, Telangana, Assam & Gujarat

**State wise concentration norms:

Note: The above concentration norms are based on market size, asset quality, growth potential and competition intensity .Note: Portfolio percentage are based on proportion of

gross loan portfolio of respective states.

^ Includes Telangana, Tamil Nadu, Gujarat and Tripura

-

0.1%

0.1%

0.4%

1.7%

1.7%

1.9%

4.3%

4.6%

6.0%

5.6%

7.1%

10.6%

11.6%

12.2%

14.8%

17.4%

0.1%

0.1%

0.1%

0.2%

1.5%

2.1%

2.1%

4.2%

4.9%

5.3%

6.7%

8.9%

9.2%

11.4%

13.1%

14.2%

15.8%

Others

Himachal Pradesh

Delhi

Uttarakhand

Chattisgarh

Punjab

Haryana

Madhya Pradesh

Jharkhand

Kerala

Rajasthan

Uttar Pradesh

Maharashtra

Karnataka

West Bengal

Bihar

Odisha

GLP Q3FY19

GLP Q3FY18

^

*As of Dec’18

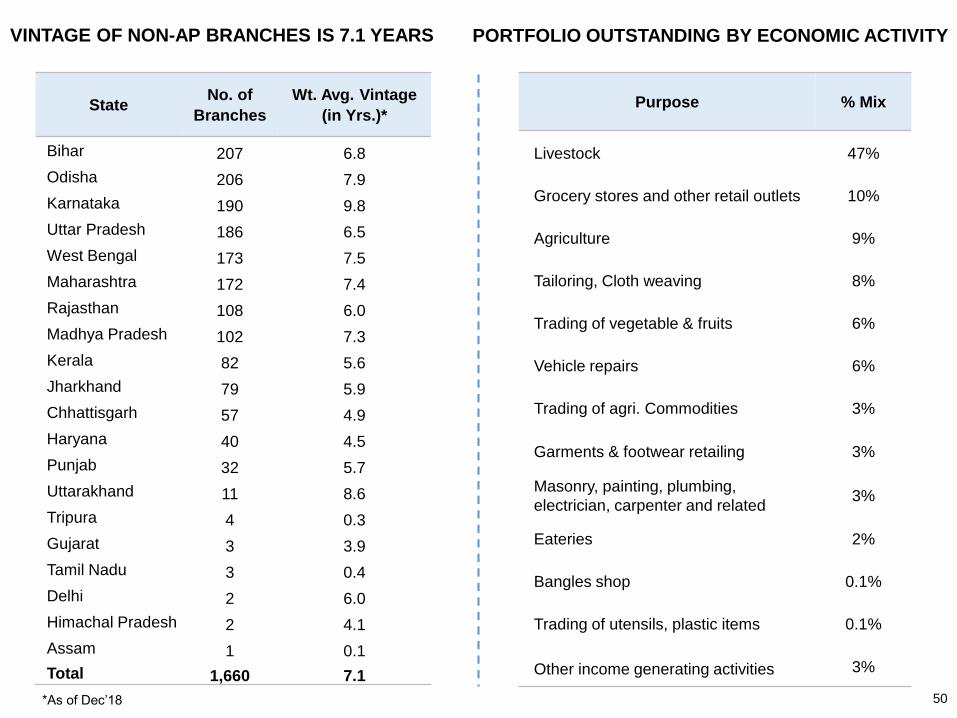

VINTAGE OF NON-AP BRANCHES IS 7.1 YEARS PORTFOLIO OUTSTANDING BY ECONOMIC ACTIVITY

StateNo. of

Branches

Wt. Avg. Vintage

(in Yrs.)*

Bihar 207 6.8

Odisha 206 7.9

Karnataka 190 9.8

Uttar Pradesh 186 6.5

West Bengal 173 7.5

Maharashtra 172 7.4

Rajasthan 108 6.0

Madhya Pradesh 102 7.3

Kerala 82 5.6

Jharkhand 79 5.9

Chhattisgarh 57 4.9

Haryana 40 4.5

Punjab 32 5.7

Uttarakhand 11 8.6

Tripura 4 0.3

Gujarat 3 3.9

Tamil Nadu 3 0.4

Delhi 2 6.0

Himachal Pradesh 2 4.1

Assam 1 0.1

Total 1,660 7.1

Purpose % Mix

Livestock 47%

Grocery stores and other retail outlets 10%

Agriculture 9%

Tailoring, Cloth weaving 8%

Trading of vegetable & fruits 6%

Vehicle repairs 6%

Trading of agri. Commodities 3%

Garments & footwear retailing 3%

Masonry, painting, plumbing,

electrician, carpenter and related3%

Eateries 2%

Bangles shop 0.1%

Trading of utensils, plastic items 0.1%

Other income generating activities 3%

50

INDUSTRY UPDATE ON CREDIT

QUALITY

51

0.6%

0.3%

30+ DPD 60+ DPD

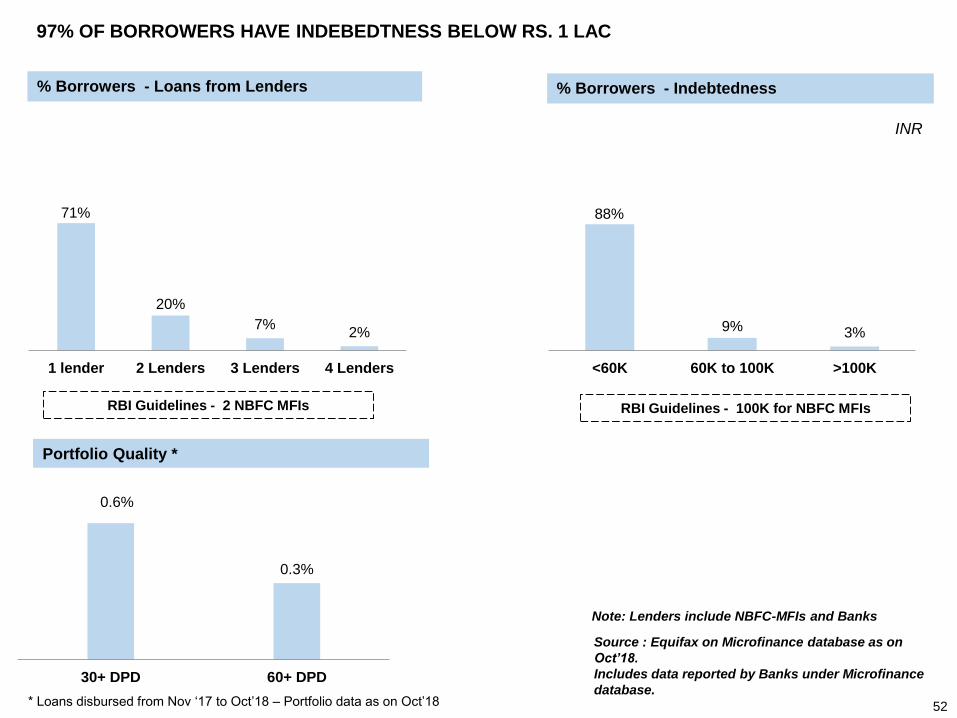

97% OF BORROWERS HAVE INDEBEDTNESS BELOW RS. 1 LAC

% Borrowers - Indebtedness

Portfolio Quality *

% Borrowers - Loans from Lenders

52

71%

20%

7%2%

1 lender 2 Lenders 3 Lenders 4 Lenders

Source : Equifax on Microfinance database as on

Oct’18.

Includes data reported by Banks under Microfinance

database.

88%

9% 3%

<60K 60K to 100K >100K

RBI Guidelines - 2 NBFC MFIs RBI Guidelines - 100K for NBFC MFIs

Note: Lenders include NBFC-MFIs and Banks

INR

* Loans disbursed from Nov ‘17 to Oct’18 – Portfolio data as on Oct’18

REVIEW OF FINANCIALS

53

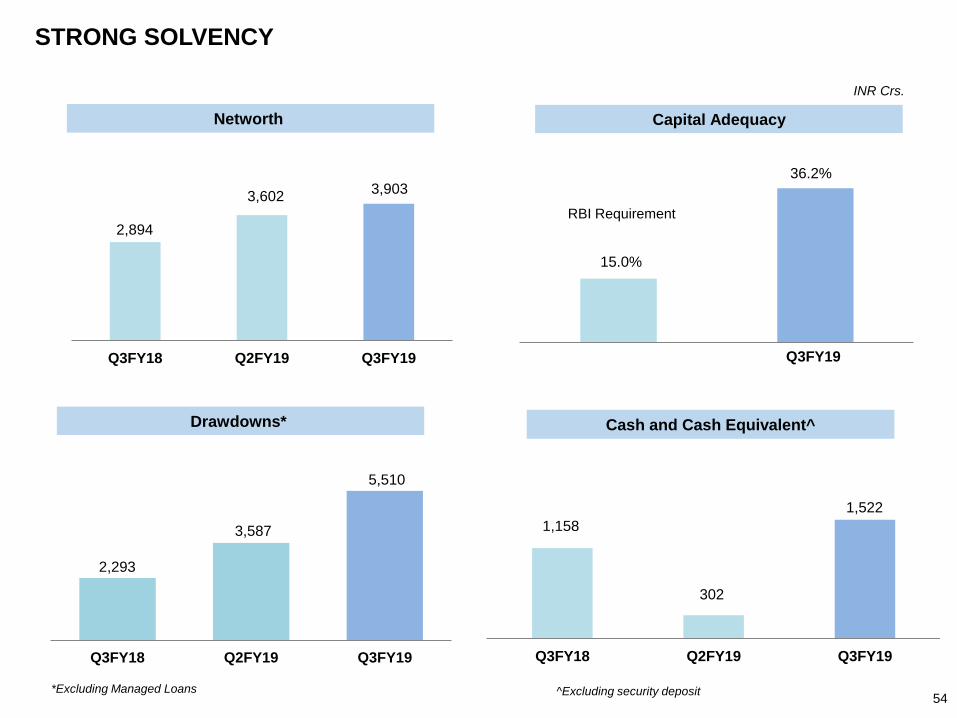

STRONG SOLVENCY

INR Crs.

Capital AdequacyNetworth

Cash and Cash Equivalent^Drawdowns*

^Excluding security deposit

15.0%

RBI Requirement

Q3FY19

36.2%

2,293

3,587

5,510

Q3FY18 Q2FY19 Q3FY19

2,894

3,602 3,903

Q3FY18 Q2FY19 Q3FY19

*Excluding Managed Loans

1,158

302

1,522

Q3FY18 Q2FY19 Q3FY19

54

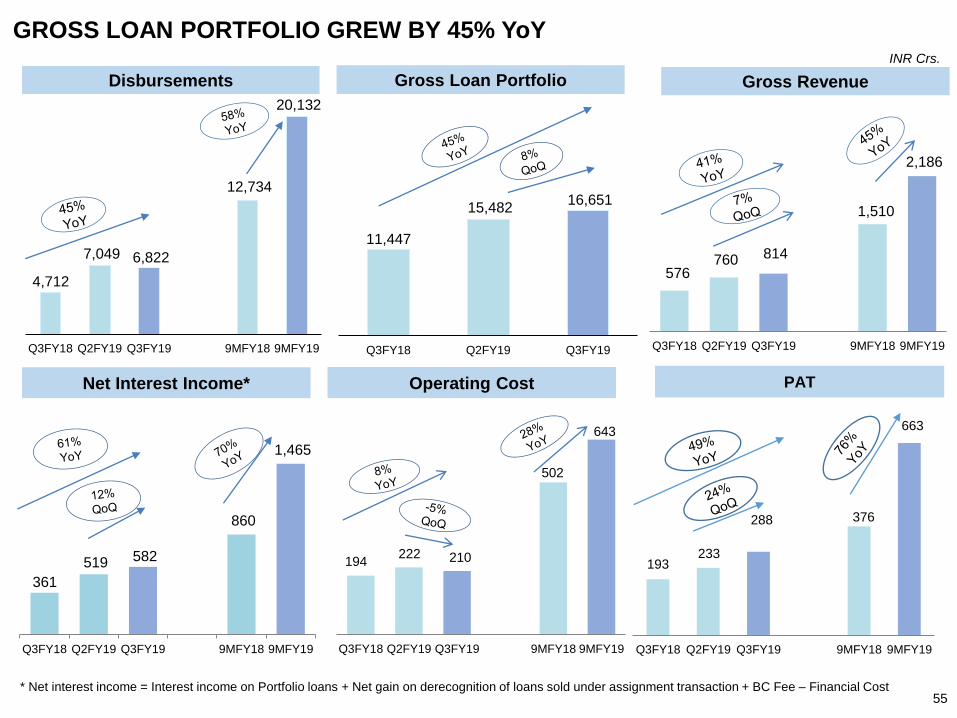

4,712

7,049 6,822

12,734

20,132

Q3FY18 Q2FY19 Q3FY19 9MFY18 9MFY19

193 233

288 376

663

Q3FY18 Q2FY19 Q3FY19 9MFY18 9MFY19

194 222 210

502

643

Q3FY18 Q2FY19 Q3FY19 9MFY18 9MFY19

GROSS LOAN PORTFOLIO GREW BY 45% YoY

55

PATOperating CostNet Interest Income*

* Net interest income = Interest income on Portfolio loans + Net gain on derecognition of loans sold under assignment transaction + BC Fee – Financial Cost

Disbursements Gross Loan Portfolio Gross Revenue

INR Crs.

11,447

15,482 16,651

Q3FY18 Q2FY19 Q3FY19

576 760 814

1,510

2,186

Q3FY18 Q2FY19 Q3FY19 9MFY18 9MFY19

361

519 582

860

1,465

Q3FY18 Q2FY19 Q3FY19 9MFY18 9MFY19

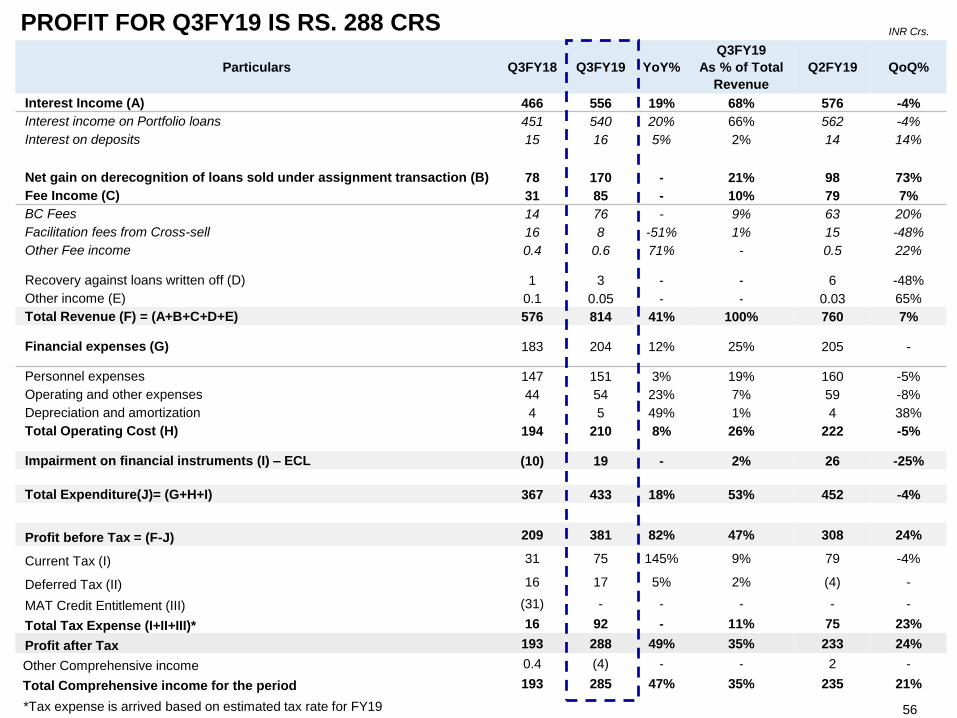

Particulars Q3FY18 Q3FY19 YoY%

Q3FY19

As % of Total

Revenue

Q2FY19 QoQ%

Interest Income (A) 466 556 19% 68% 576 -4%

Interest income on Portfolio loans 451 540 20% 66% 562 -4%

Interest on deposits 15 16 5% 2% 14 14%

Net gain on derecognition of loans sold under assignment transaction (B) 78 170 - 21% 98 73%

Fee Income (C) 31 85 - 10% 79 7%

BC Fees 14 76 - 9% 63 20%

Facilitation fees from Cross-sell 16 8 -51% 1% 15 -48%

Other Fee income 0.4 0.6 71% - 0.5 22%

Recovery against loans written off (D) 1 3 - - 6 -48%

Other income (E) 0.1 0.05 - - 0.03 65%

Total Revenue (F) = (A+B+C+D+E) 576 814 41% 100% 760 7%

Financial expenses (G) 183 204 12% 25% 205 -

Personnel expenses 147 151 3% 19% 160 -5%

Operating and other expenses 44 54 23% 7% 59 -8%

Depreciation and amortization 4 5 49% 1% 4 38%

Total Operating Cost (H) 194 210 8% 26% 222 -5%

Impairment on financial instruments (I) – ECL (10) 19 - 2% 26 -25%

Total Expenditure(J)= (G+H+I) 367 433 18% 53% 452 -4%

Profit before Tax = (F-J) 209 381 82% 47% 308 24%

Current Tax (I) 31 75 145% 9% 79 -4%

Deferred Tax (II) 16 17 5% 2% (4) -

MAT Credit Entitlement (III) (31) - - - - -

Total Tax Expense (I+II+III)* 16 92 - 11% 75 23%

Profit after Tax 193 288 49% 35% 233 24%

Other Comprehensive income 0.4 (4) - - 2 -

Total Comprehensive income for the period 193 285 47% 35% 235 21%

INR Crs.

56

PROFIT FOR Q3FY19 IS RS. 288 CRS

*Tax expense is arrived based on estimated tax rate for FY19

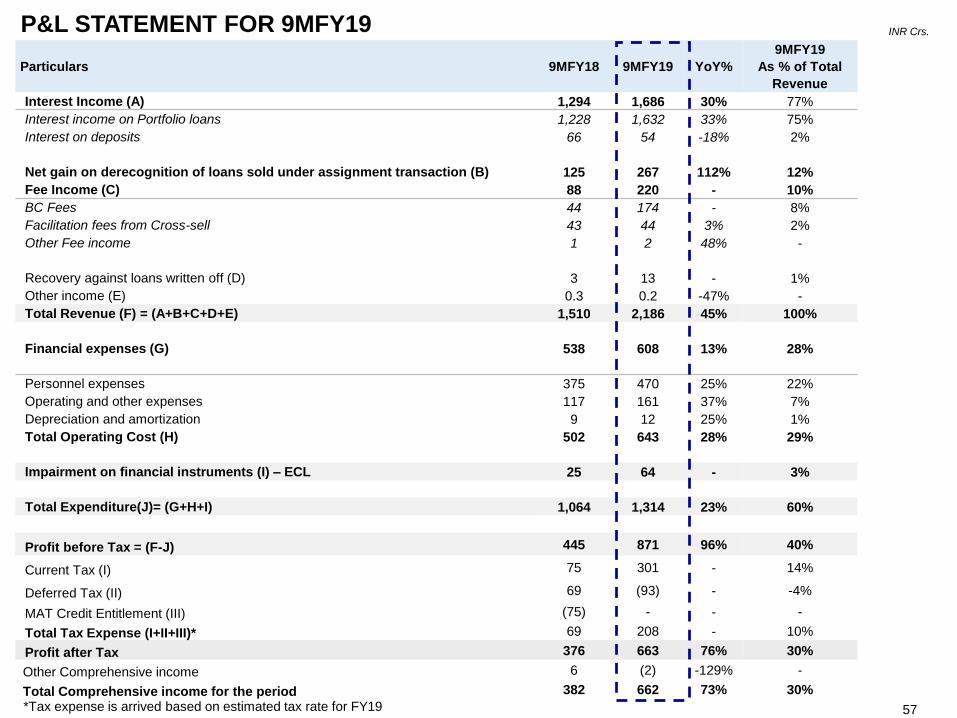

Particulars 9MFY18 9MFY19 YoY%

9MFY19

As % of Total

Revenue

Interest Income (A) 1,294 1,686 30% 77%

Interest income on Portfolio loans 1,228 1,632 33% 75%

Interest on deposits 66 54 -18% 2%

Net gain on derecognition of loans sold under assignment transaction (B) 125 267 112% 12%

Fee Income (C) 88 220 - 10%

BC Fees 44 174 - 8%

Facilitation fees from Cross-sell 43 44 3% 2%

Other Fee income 1 2 48% -

Recovery against loans written off (D) 3 13 - 1%

Other income (E) 0.3 0.2 -47% -

Total Revenue (F) = (A+B+C+D+E) 1,510 2,186 45% 100%

Financial expenses (G) 538 608 13% 28%

Personnel expenses 375 470 25% 22%

Operating and other expenses 117 161 37% 7%

Depreciation and amortization 9 12 25% 1%

Total Operating Cost (H) 502 643 28% 29%

Impairment on financial instruments (I) – ECL 25 64 - 3%

Total Expenditure(J)= (G+H+I) 1,064 1,314 23% 60%

Profit before Tax = (F-J) 445 871 96% 40%

Current Tax (I) 75 301 - 14%

Deferred Tax (II) 69 (93) - -4%

MAT Credit Entitlement (III) (75) - - -

Total Tax Expense (I+II+III)* 69 208 - 10%

Profit after Tax 376 663 76% 30%

Other Comprehensive income 6 (2) -129% -

Total Comprehensive income for the period 382 662 73% 30%

INR Crs.

57

P&L STATEMENT FOR 9MFY19

*Tax expense is arrived based on estimated tax rate for FY19

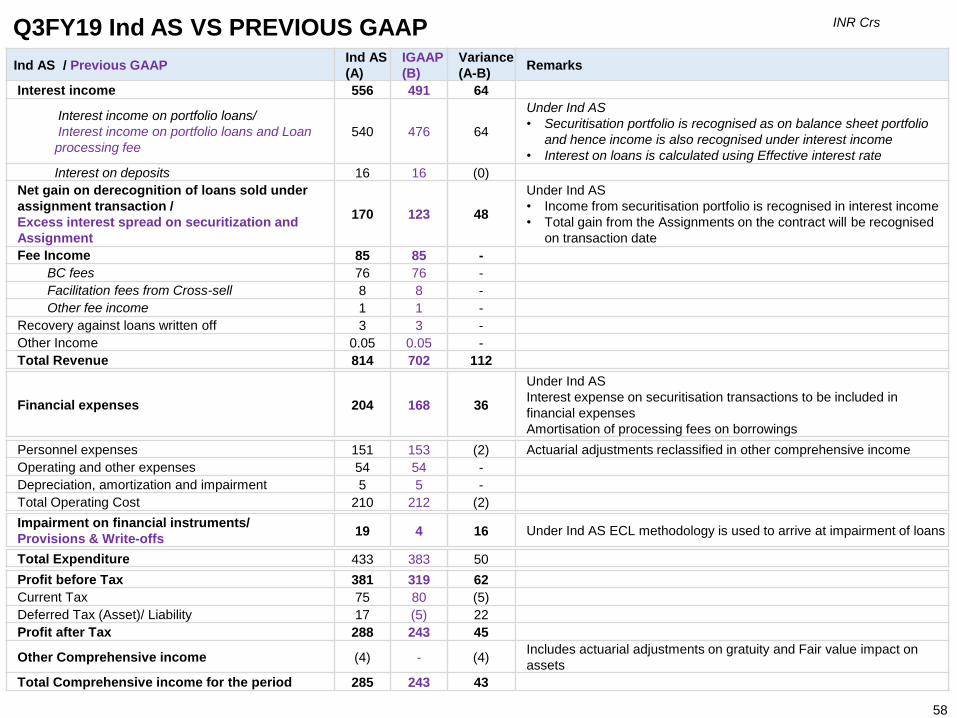

Q3FY19 Ind AS VS PREVIOUS GAAP

58

Ind AS / Previous GAAPInd AS

(A)

IGAAP

(B)

Variance

(A-B)Remarks

Interest income 556 491 64

Interest income on portfolio loans/

Interest income on portfolio loans and Loan

processing fee

540 476 64

Under Ind AS

• Securitisation portfolio is recognised as on balance sheet portfolio

and hence income is also recognised under interest income

• Interest on loans is calculated using Effective interest rate

Interest on deposits 16 16 (0)

Net gain on derecognition of loans sold under

assignment transaction /

Excess interest spread on securitization and

Assignment

170 123 48

Under Ind AS

• Income from securitisation portfolio is recognised in interest income

• Total gain from the Assignments on the contract will be recognised

on transaction date

Fee Income 85 85 -

BC fees 76 76 -

Facilitation fees from Cross-sell 8 8 -

Other fee income 1 1 -

Recovery against loans written off 3 3 -

Other Income 0.05 0.05 -

Total Revenue 814 702 112

Financial expenses 204 168 36

Under Ind AS

Interest expense on securitisation transactions to be included in

financial expenses

Amortisation of processing fees on borrowings

Personnel expenses 151 153 (2) Actuarial adjustments reclassified in other comprehensive income

Operating and other expenses 54 54 -

Depreciation, amortization and impairment 5 5 -

Total Operating Cost 210 212 (2)

Impairment on financial instruments/

Provisions & Write-offs19 4 16 Under Ind AS ECL methodology is used to arrive at impairment of loans

Total Expenditure 433 383 50

Profit before Tax 381 319 62

Current Tax 75 80 (5)

Deferred Tax (Asset)/ Liability 17 (5) 22

Profit after Tax 288 243 45

Other Comprehensive income (4) - (4)Includes actuarial adjustments on gratuity and Fair value impact on

assets

Total Comprehensive income for the period 285 243 43

INR Crs

Q2FY19 Ind AS VS Previous GAAP

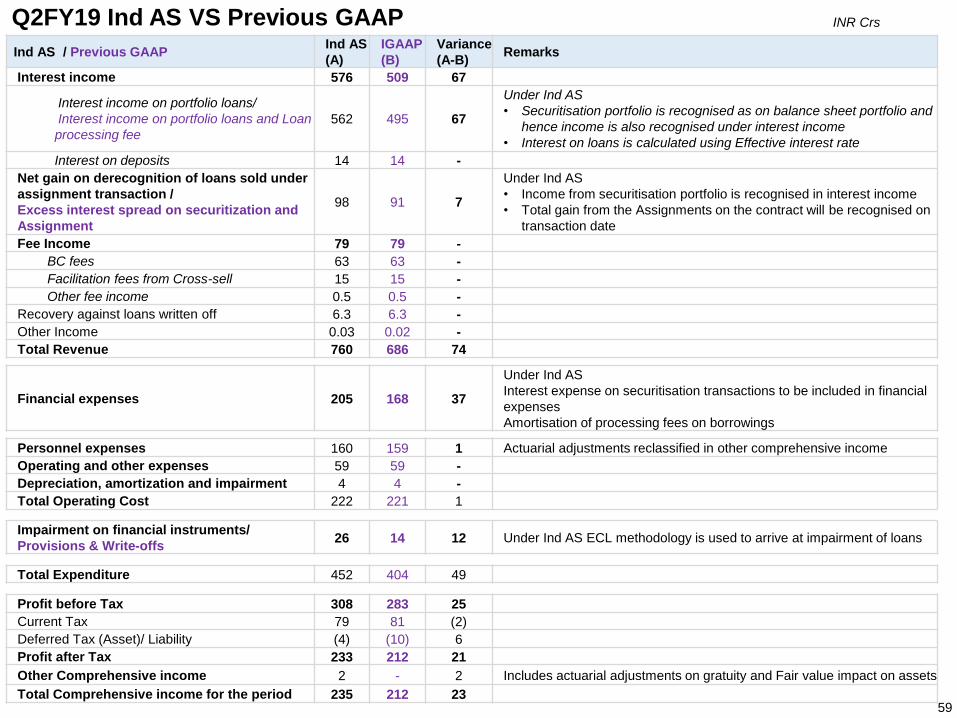

59

Ind AS / Previous GAAPInd AS

(A)

IGAAP

(B)

Variance

(A-B)Remarks

Interest income 576 509 67

Interest income on portfolio loans/

Interest income on portfolio loans and Loan

processing fee

562 495 67

Under Ind AS

• Securitisation portfolio is recognised as on balance sheet portfolio and

hence income is also recognised under interest income

• Interest on loans is calculated using Effective interest rate

Interest on deposits 14 14 -

Net gain on derecognition of loans sold under

assignment transaction /

Excess interest spread on securitization and

Assignment

98 91 7

Under Ind AS

• Income from securitisation portfolio is recognised in interest income

• Total gain from the Assignments on the contract will be recognised on

transaction date

Fee Income 79 79 -

BC fees 63 63 -

Facilitation fees from Cross-sell 15 15 -

Other fee income 0.5 0.5 -

Recovery against loans written off 6.3 6.3 -

Other Income 0.03 0.02 -

Total Revenue 760 686 74

Financial expenses 205 168 37

Under Ind AS

Interest expense on securitisation transactions to be included in financial

expenses

Amortisation of processing fees on borrowings

Personnel expenses 160 159 1 Actuarial adjustments reclassified in other comprehensive income

Operating and other expenses 59 59 -

Depreciation, amortization and impairment 4 4 -

Total Operating Cost 222 221 1

Impairment on financial instruments/

Provisions & Write-offs26 14 12 Under Ind AS ECL methodology is used to arrive at impairment of loans

Total Expenditure 452 404 49

Profit before Tax 308 283 25

Current Tax 79 81 (2)

Deferred Tax (Asset)/ Liability (4) (10) 6

Profit after Tax 233 212 21

Other Comprehensive income 2 - 2 Includes actuarial adjustments on gratuity and Fair value impact on assets

Total Comprehensive income for the period 235 212 23

INR Crs

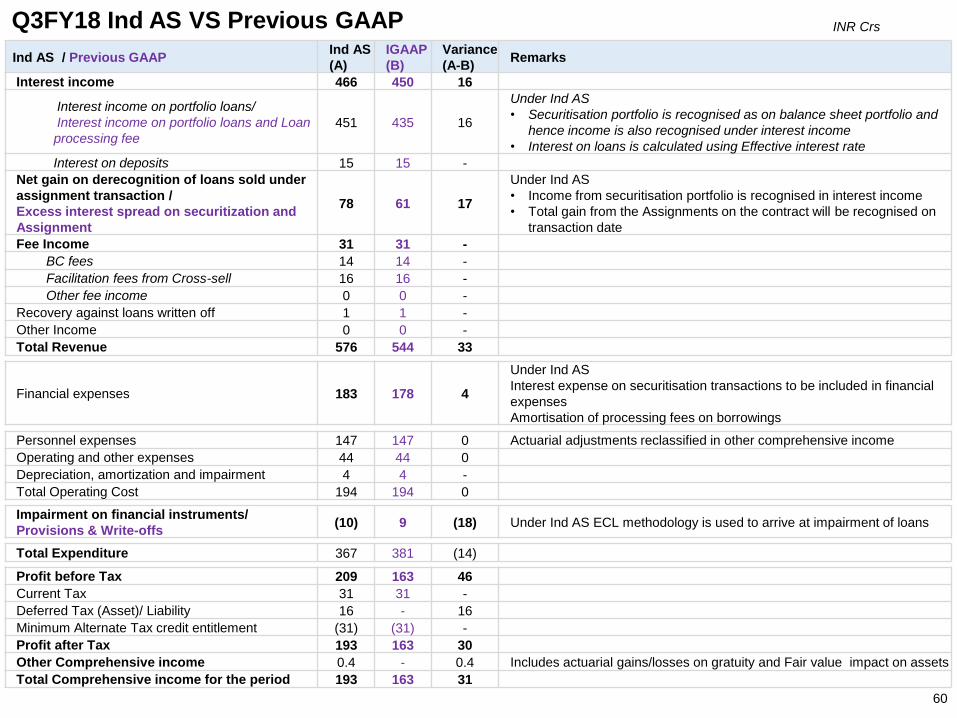

Q3FY18 Ind AS VS Previous GAAP

60

Ind AS / Previous GAAPInd AS

(A)

IGAAP

(B)

Variance

(A-B)Remarks

Interest income 466 450 16

Interest income on portfolio loans/

Interest income on portfolio loans and Loan

processing fee

451 435 16

Under Ind AS

• Securitisation portfolio is recognised as on balance sheet portfolio and

hence income is also recognised under interest income

• Interest on loans is calculated using Effective interest rate

Interest on deposits 15 15 -

Net gain on derecognition of loans sold under

assignment transaction /

Excess interest spread on securitization and

Assignment

78 61 17

Under Ind AS

• Income from securitisation portfolio is recognised in interest income

• Total gain from the Assignments on the contract will be recognised on

transaction date

Fee Income 31 31 -

BC fees 14 14 -

Facilitation fees from Cross-sell 16 16 -

Other fee income 0 0 -

Recovery against loans written off 1 1 -

Other Income 0 0 -

Total Revenue 576 544 33

Financial expenses 183 178 4

Under Ind AS

Interest expense on securitisation transactions to be included in financial

expenses

Amortisation of processing fees on borrowings

Personnel expenses 147 147 0 Actuarial adjustments reclassified in other comprehensive income

Operating and other expenses 44 44 0

Depreciation, amortization and impairment 4 4 -

Total Operating Cost 194 194 0

Impairment on financial instruments/

Provisions & Write-offs(10) 9 (18) Under Ind AS ECL methodology is used to arrive at impairment of loans

Total Expenditure 367 381 (14)

Profit before Tax 209 163 46

Current Tax 31 31 -

Deferred Tax (Asset)/ Liability 16 - 16

Minimum Alternate Tax credit entitlement (31) (31) -

Profit after Tax 193 163 30

Other Comprehensive income 0.4 - 0.4 Includes actuarial gains/losses on gratuity and Fair value impact on assets

Total Comprehensive income for the period 193 163 31

INR Crs

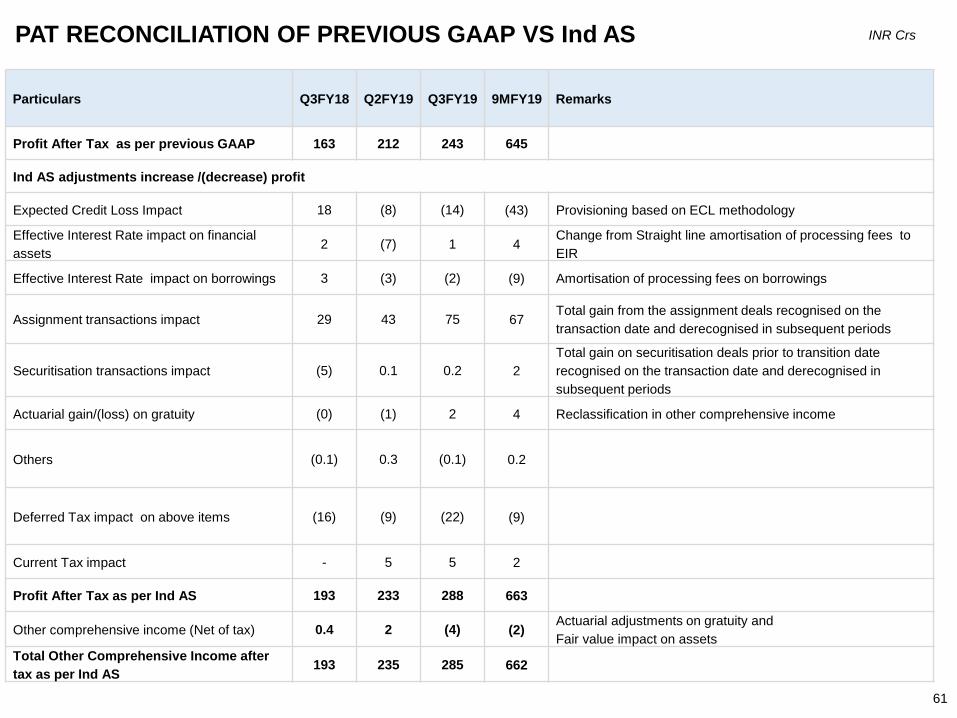

PAT RECONCILIATION OF PREVIOUS GAAP VS Ind AS

61

Particulars Q3FY18 Q2FY19 Q3FY19 9MFY19 Remarks

Profit After Tax as per previous GAAP 163 212 243 645

Ind AS adjustments increase /(decrease) profit

Expected Credit Loss Impact 18 (8) (14) (43) Provisioning based on ECL methodology

Effective Interest Rate impact on financial

assets2 (7) 1 4

Change from Straight line amortisation of processing fees to

EIR

Effective Interest Rate impact on borrowings 3 (3) (2) (9) Amortisation of processing fees on borrowings

Assignment transactions impact 29 43 75 67Total gain from the assignment deals recognised on the

transaction date and derecognised in subsequent periods

Securitisation transactions impact (5) 0.1 0.2 2

Total gain on securitisation deals prior to transition date

recognised on the transaction date and derecognised in

subsequent periods

Actuarial gain/(loss) on gratuity (0) (1) 2 4 Reclassification in other comprehensive income

Others (0.1) 0.3 (0.1) 0.2

Deferred Tax impact on above items (16) (9) (22) (9)

Current Tax impact - 5 5 2

Profit After Tax as per Ind AS 193 233 288 663

Other comprehensive income (Net of tax) 0.4 2 (4) (2)Actuarial adjustments on gratuity and

Fair value impact on assets

Total Other Comprehensive Income after

tax as per Ind AS193 235 285 662

INR Crs

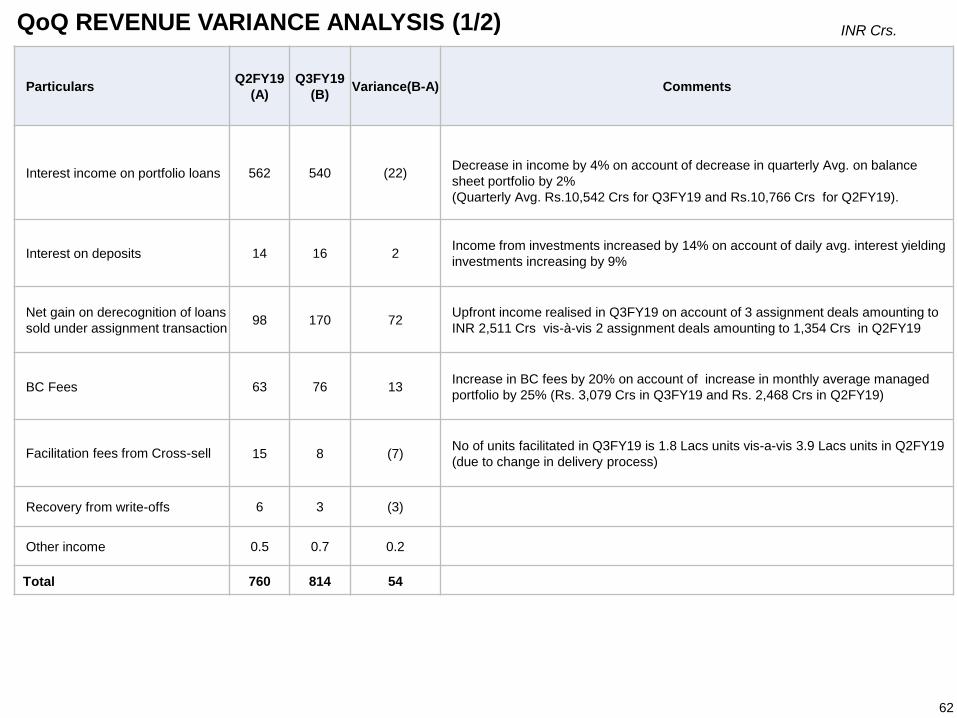

QoQ REVENUE VARIANCE ANALYSIS (1/2)

62

ParticularsQ2FY19

(A)

Q3FY19

(B)Variance(B-A) Comments

Interest income on portfolio loans 562 540 (22)Decrease in income by 4% on account of decrease in quarterly Avg. on balance

sheet portfolio by 2%

(Quarterly Avg. Rs.10,542 Crs for Q3FY19 and Rs.10,766 Crs for Q2FY19).

Interest on deposits 14 16 2Income from investments increased by 14% on account of daily avg. interest yielding

investments increasing by 9%

Net gain on derecognition of loans

sold under assignment transaction98 170 72

Upfront income realised in Q3FY19 on account of 3 assignment deals amounting to

INR 2,511 Crs vis-à-vis 2 assignment deals amounting to 1,354 Crs in Q2FY19

BC Fees 63 76 13Increase in BC fees by 20% on account of increase in monthly average managed

portfolio by 25% (Rs. 3,079 Crs in Q3FY19 and Rs. 2,468 Crs in Q2FY19)

Facilitation fees from Cross-sell 15 8 (7)No of units facilitated in Q3FY19 is 1.8 Lacs units vis-a-vis 3.9 Lacs units in Q2FY19

(due to change in delivery process)

Recovery from write-offs 6 3 (3)

Other income 0.5 0.7 0.2

Total 760 814 54

INR Crs.

ParticularsQ2FY19

(A)

Q3FY19

(B)

Variance

(B-A)Comments

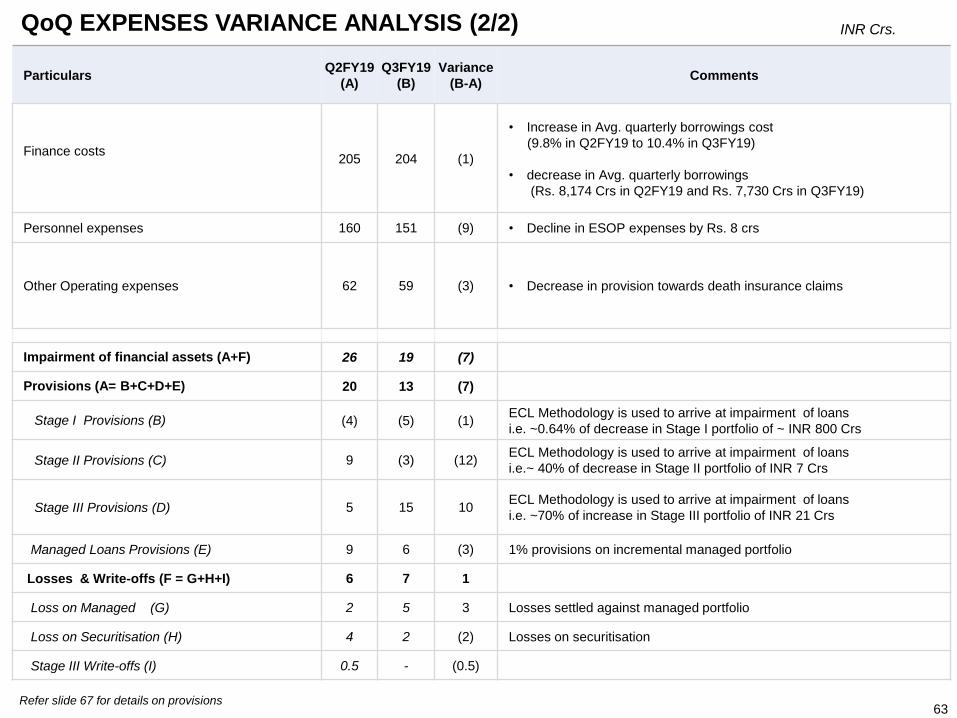

Finance costs 205 204 (1)

• Increase in Avg. quarterly borrowings cost

(9.8% in Q2FY19 to 10.4% in Q3FY19)

• decrease in Avg. quarterly borrowings

(Rs. 8,174 Crs in Q2FY19 and Rs. 7,730 Crs in Q3FY19)

Personnel expenses 160 151 (9) • Decline in ESOP expenses by Rs. 8 crs

Other Operating expenses 62 59 (3) • Decrease in provision towards death insurance claims

Impairment of financial assets (A+F) 26 19 (7)

Provisions (A= B+C+D+E) 20 13 (7)

Stage I Provisions (B) (4) (5) (1)ECL Methodology is used to arrive at impairment of loans

i.e. ~0.64% of decrease in Stage I portfolio of ~ INR 800 Crs

Stage II Provisions (C) 9 (3) (12)ECL Methodology is used to arrive at impairment of loans

i.e.~ 40% of decrease in Stage II portfolio of INR 7 Crs

Stage III Provisions (D) 5 15 10ECL Methodology is used to arrive at impairment of loans

i.e. ~70% of increase in Stage III portfolio of INR 21 Crs

Managed Loans Provisions (E) 9 6 (3) 1% provisions on incremental managed portfolio

Losses & Write-offs (F = G+H+I) 6 7 1

Loss on Managed (G) 2 5 3 Losses settled against managed portfolio

Loss on Securitisation (H) 4 2 (2) Losses on securitisation

Stage III Write-offs (I) 0.5 - (0.5)

QoQ EXPENSES VARIANCE ANALYSIS (2/2)

63

INR Crs.

Refer slide 67 for details on provisions

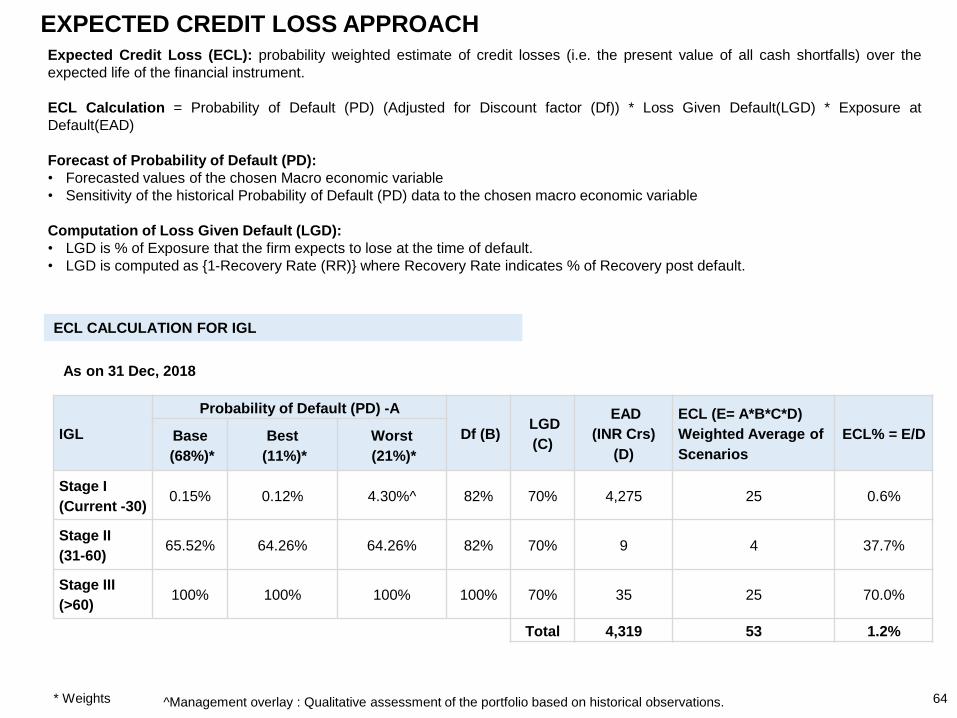

EXPECTED CREDIT LOSS APPROACH

64

Expected Credit Loss (ECL): probability weighted estimate of credit losses (i.e. the present value of all cash shortfalls) over the

expected life of the financial instrument.

ECL Calculation = Probability of Default (PD) (Adjusted for Discount factor (Df)) * Loss Given Default(LGD) * Exposure at

Default(EAD)

Forecast of Probability of Default (PD):

• Forecasted values of the chosen Macro economic variable

• Sensitivity of the historical Probability of Default (PD) data to the chosen macro economic variable

Computation of Loss Given Default (LGD):

• LGD is % of Exposure that the firm expects to lose at the time of default.

• LGD is computed as {1-Recovery Rate (RR)} where Recovery Rate indicates % of Recovery post default.

ECL CALCULATION FOR IGL

As on 31 Dec, 2018

IGL

Probability of Default (PD) -A

Df (B)LGD

(C)

EAD

(INR Crs)

(D)

ECL (E= A*B*C*D)

Weighted Average of

Scenarios

ECL% = E/DBase

(68%)*

Best

(11%)*

Worst

(21%)*

Stage I

(Current -30)0.15% 0.12% 4.30%^ 82% 70% 4,275 25 0.6%

Stage II

(31-60)65.52% 64.26% 64.26% 82% 70% 9 4 37.7%

Stage III

(>60)100% 100% 100% 100% 70% 35 25 70.0%

Total 4,319 53 1.2%

^Management overlay : Qualitative assessment of the portfolio based on historical observations.* Weights

65

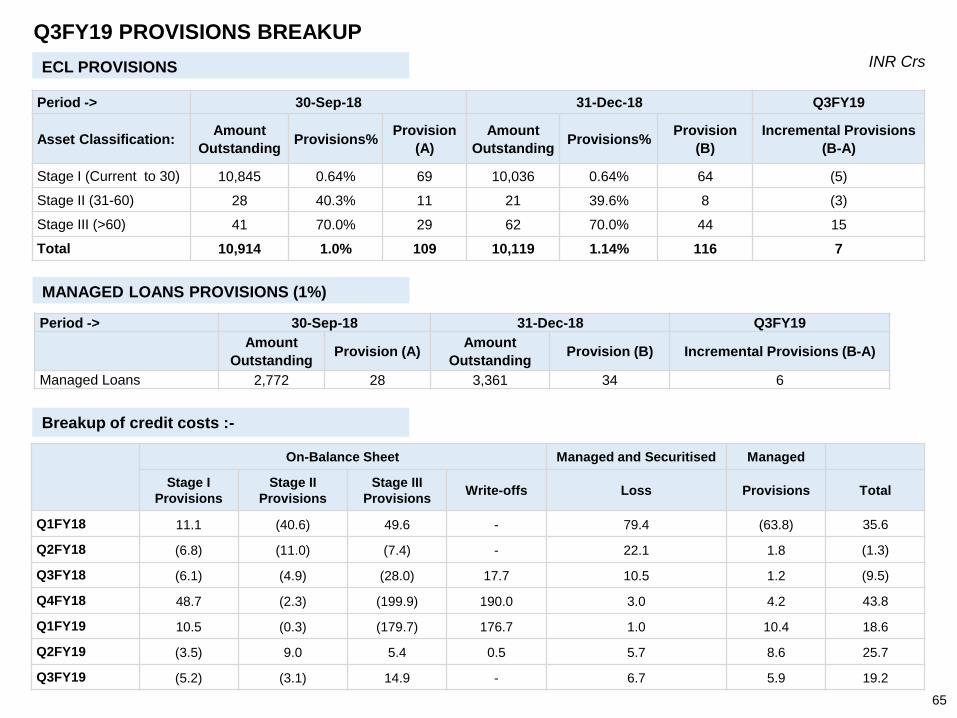

Period -> 30-Sep-18 31-Dec-18 Q3FY19

Asset Classification:Amount

OutstandingProvisions%

Provision

(A)

Amount

OutstandingProvisions%

Provision

(B)

Incremental Provisions

(B-A)

Stage I (Current to 30) 10,845 0.64% 69 10,036 0.64% 64 (5)

Stage II (31-60) 28 40.3% 11 21 39.6% 8 (3)

Stage III (>60) 41 70.0% 29 62 70.0% 44 15

Total 10,914 1.0% 109 10,119 1.14% 116 7

INR Crs

Q3FY19 PROVISIONS BREAKUP

Period -> 30-Sep-18 31-Dec-18 Q3FY19

Amount

OutstandingProvision (A)

Amount

OutstandingProvision (B) Incremental Provisions (B-A)

Managed Loans 2,772 28 3,361 34 6

ECL PROVISIONS

MANAGED LOANS PROVISIONS (1%)

On-Balance Sheet Managed and Securitised Managed

Stage I

Provisions

Stage II

Provisions

Stage III

ProvisionsWrite-offs Loss Provisions Total

Q1FY18 11.1 (40.6) 49.6 - 79.4 (63.8) 35.6

Q2FY18 (6.8) (11.0) (7.4) - 22.1 1.8 (1.3)

Q3FY18 (6.1) (4.9) (28.0) 17.7 10.5 1.2 (9.5)

Q4FY18 48.7 (2.3) (199.9) 190.0 3.0 4.2 43.8

Q1FY19 10.5 (0.3) (179.7) 176.7 1.0 10.4 18.6

Q2FY19 (3.5) 9.0 5.4 0.5 5.7 8.6 25.7

Q3FY19 (5.2) (3.1) 14.9 - 6.7 5.9 19.2

Breakup of credit costs :-

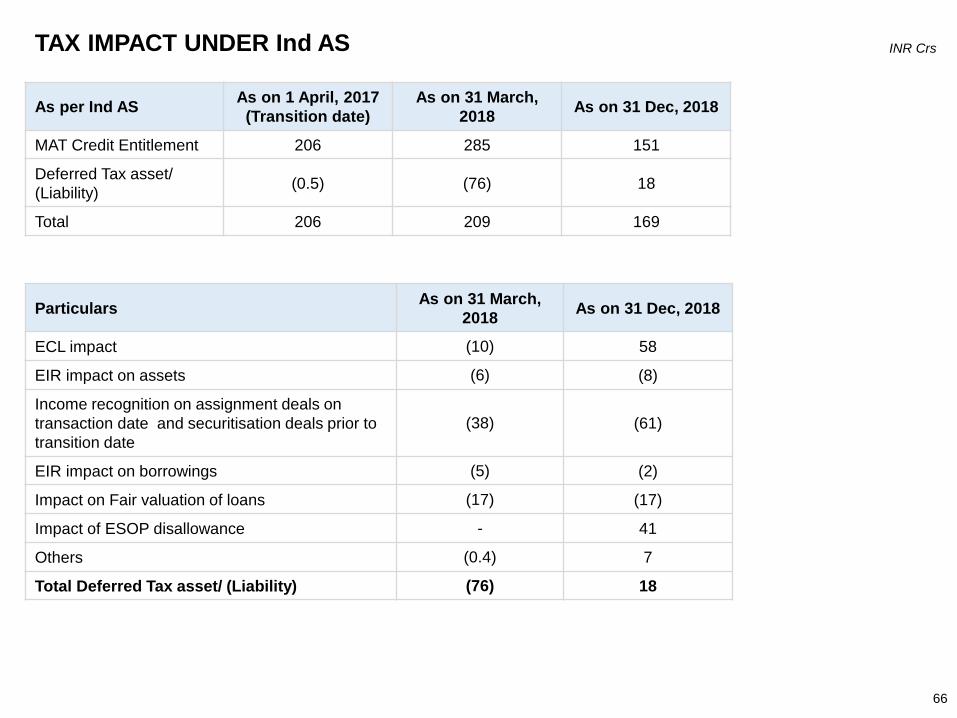

TAX IMPACT UNDER Ind AS

66

As per Ind ASAs on 1 April, 2017

(Transition date)

As on 31 March,

2018As on 31 Dec, 2018

MAT Credit Entitlement 206 285 151

Deferred Tax asset/

(Liability)(0.5) (76) 18

Total 206 209 169

INR Crs

ParticularsAs on 31 March,

2018As on 31 Dec, 2018

ECL impact (10) 58

EIR impact on assets (6) (8)

Income recognition on assignment deals on

transaction date and securitisation deals prior to

transition date

(38) (61)

EIR impact on borrowings (5) (2)

Impact on Fair valuation of loans (17) (17)

Impact of ESOP disallowance - 41

Others (0.4) 7

Total Deferred Tax asset/ (Liability) (76) 18

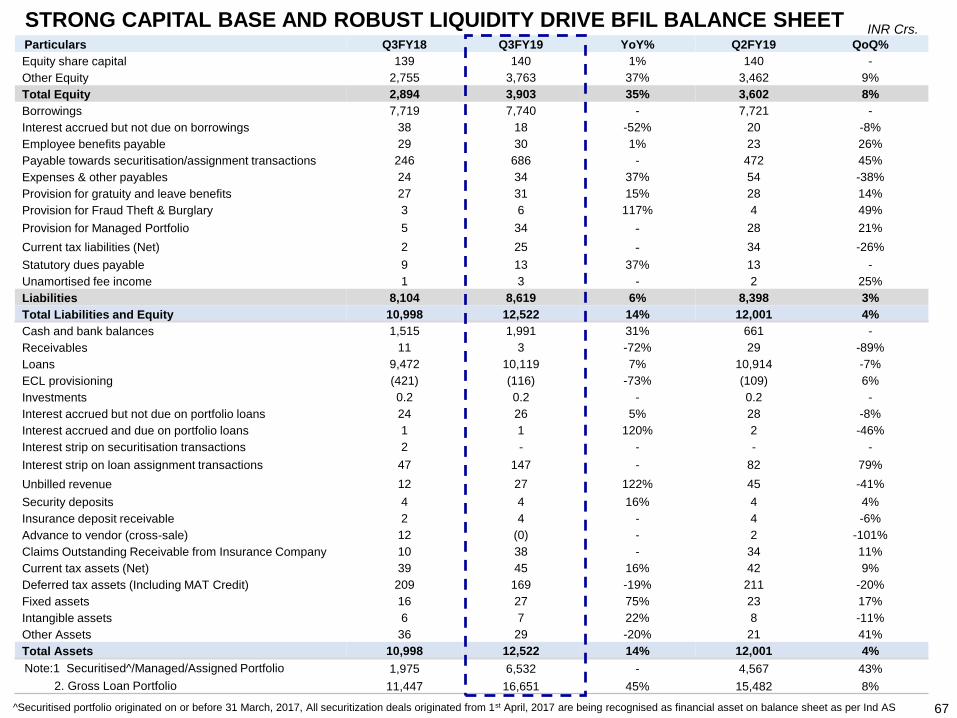

STRONG CAPITAL BASE AND ROBUST LIQUIDITY DRIVE BFIL BALANCE SHEETParticulars Q3FY18 Q3FY19 YoY% Q2FY19 QoQ%

Equity share capital 139 140 1% 140 -

Other Equity 2,755 3,763 37% 3,462 9%

Total Equity 2,894 3,903 35% 3,602 8%

Borrowings 7,719 7,740 - 7,721 -

Interest accrued but not due on borrowings 38 18 -52% 20 -8%

Employee benefits payable 29 30 1% 23 26%

Payable towards securitisation/assignment transactions 246 686 - 472 45%

Expenses & other payables 24 34 37% 54 -38%

Provision for gratuity and leave benefits 27 31 15% 28 14%

Provision for Fraud Theft & Burglary 3 6 117% 4 49%

Provision for Managed Portfolio 5 34 - 28 21%

Current tax liabilities (Net) 2 25 - 34 -26%

Statutory dues payable 9 13 37% 13 -

Unamortised fee income 1 3 - 2 25%

Liabilities 8,104 8,619 6% 8,398 3%

Total Liabilities and Equity 10,998 12,522 14% 12,001 4%

Cash and bank balances 1,515 1,991 31% 661 -

Receivables 11 3 -72% 29 -89%

Loans 9,472 10,119 7% 10,914 -7%

ECL provisioning (421) (116) -73% (109) 6%

Investments 0.2 0.2 - 0.2 -

Interest accrued but not due on portfolio loans 24 26 5% 28 -8%

Interest accrued and due on portfolio loans 1 1 120% 2 -46%

Interest strip on securitisation transactions 2 - - - -

Interest strip on loan assignment transactions 47 147 - 82 79%

Unbilled revenue 12 27 122% 45 -41%

Security deposits 4 4 16% 4 4%

Insurance deposit receivable 2 4 - 4 -6%

Advance to vendor (cross-sale) 12 (0) - 2 -101%

Claims Outstanding Receivable from Insurance Company 10 38 - 34 11%

Current tax assets (Net) 39 45 16% 42 9%

Deferred tax assets (Including MAT Credit) 209 169 -19% 211 -20%

Fixed assets 16 27 75% 23 17%

Intangible assets 6 7 22% 8 -11%

Other Assets 36 29 -20% 21 41%

Total Assets 10,998 12,522 14% 12,001 4%

Note:1 Securitised^/Managed/Assigned Portfolio 1,975 6,532 - 4,567 43%

2. Gross Loan Portfolio 11,447 16,651 45% 15,482 8%

INR Crs.

67^Securitised portfolio originated on or before 31 March, 2017, All securitization deals originated from 1st April, 2017 are being recognised as financial asset on balance sheet as per Ind AS

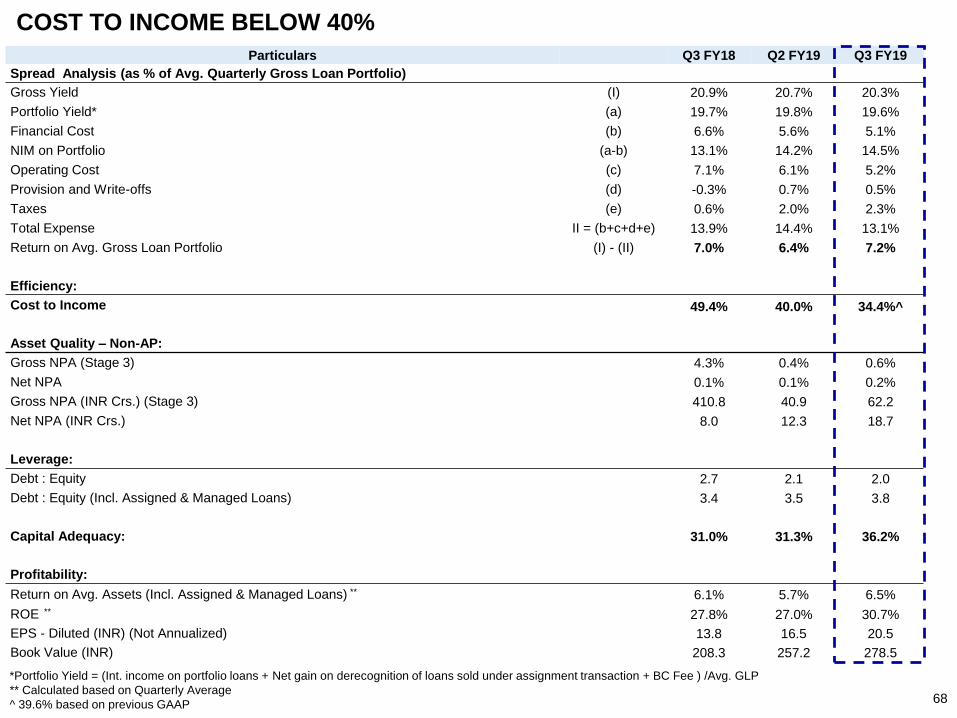

COST TO INCOME BELOW 40%

Particulars Q3 FY18 Q2 FY19 Q3 FY19

Spread Analysis (as % of Avg. Quarterly Gross Loan Portfolio)

Gross Yield (I) 20.9% 20.7% 20.3%

Portfolio Yield* (a) 19.7% 19.8% 19.6%

Financial Cost (b) 6.6% 5.6% 5.1%

NIM on Portfolio (a-b) 13.1% 14.2% 14.5%

Operating Cost (c) 7.1% 6.1% 5.2%

Provision and Write-offs (d) -0.3% 0.7% 0.5%

Taxes (e) 0.6% 2.0% 2.3%

Total Expense II = (b+c+d+e) 13.9% 14.4% 13.1%

Return on Avg. Gross Loan Portfolio (I) - (II) 7.0% 6.4% 7.2%

Efficiency:

Cost to Income 49.4% 40.0% 34.4%^

Asset Quality – Non-AP:

Gross NPA (Stage 3) 4.3% 0.4% 0.6%

Net NPA 0.1% 0.1% 0.2%

Gross NPA (INR Crs.) (Stage 3) 410.8 40.9 62.2

Net NPA (INR Crs.) 8.0 12.3 18.7

Leverage:

Debt : Equity 2.7 2.1 2.0

Debt : Equity (Incl. Assigned & Managed Loans) 3.4 3.5 3.8

Capital Adequacy: 31.0% 31.3% 36.2%

Profitability:

Return on Avg. Assets (Incl. Assigned & Managed Loans) ** 6.1% 5.7% 6.5%

ROE ** 27.8% 27.0% 30.7%

EPS - Diluted (INR) (Not Annualized) 13.8 16.5 20.5

Book Value (INR) 208.3 257.2 278.5

*Portfolio Yield = (Int. income on portfolio loans + Net gain on derecognition of loans sold under assignment transaction + BC Fee ) /Avg. GLP

** Calculated based on Quarterly Average

^ 39.6% based on previous GAAP 68

*Portfolio Yield = (Int. income on portfolio loans + Net gain on derecognition of loans sold under assignment transaction + BC Fee ) /Avg. GLP

** Calculated based on Quarterly Average

^ 42.9% based on previous GAAP

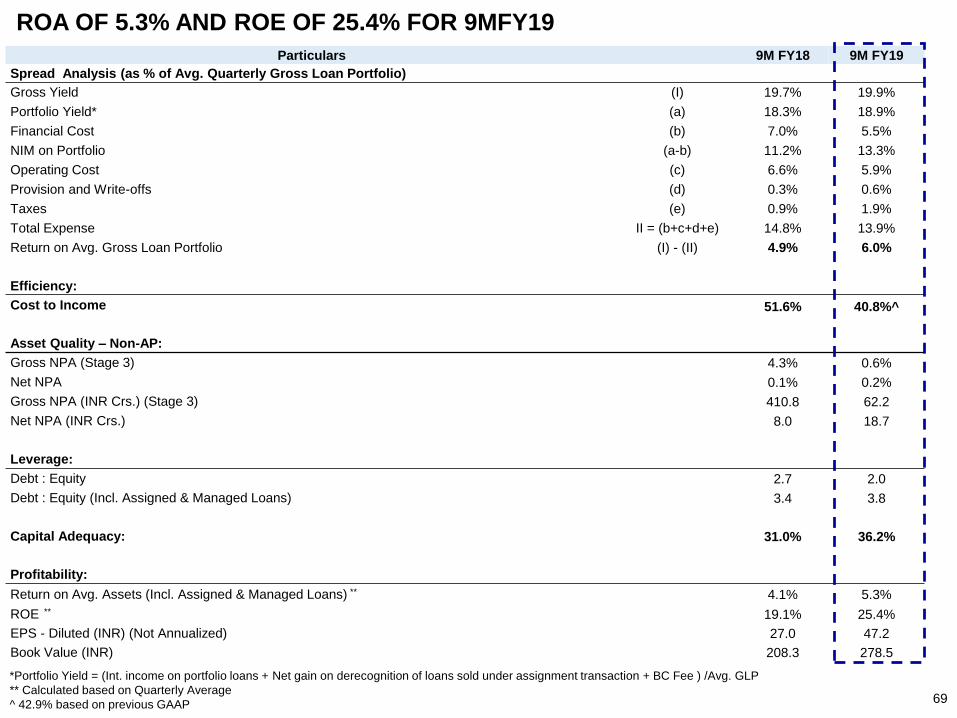

ROA OF 5.3% AND ROE OF 25.4% FOR 9MFY19

Particulars 9M FY18 9M FY19

Spread Analysis (as % of Avg. Quarterly Gross Loan Portfolio)

Gross Yield (I) 19.7% 19.9%

Portfolio Yield* (a) 18.3% 18.9%

Financial Cost (b) 7.0% 5.5%

NIM on Portfolio (a-b) 11.2% 13.3%

Operating Cost (c) 6.6% 5.9%

Provision and Write-offs (d) 0.3% 0.6%

Taxes (e) 0.9% 1.9%

Total Expense II = (b+c+d+e) 14.8% 13.9%

Return on Avg. Gross Loan Portfolio (I) - (II) 4.9% 6.0%

Efficiency:

Cost to Income 51.6% 40.8%^

Asset Quality – Non-AP:

Gross NPA (Stage 3) 4.3% 0.6%

Net NPA 0.1% 0.2%

Gross NPA (INR Crs.) (Stage 3) 410.8 62.2

Net NPA (INR Crs.) 8.0 18.7

Leverage:

Debt : Equity 2.7 2.0

Debt : Equity (Incl. Assigned & Managed Loans) 3.4 3.8

Capital Adequacy: 31.0% 36.2%

Profitability:

Return on Avg. Assets (Incl. Assigned & Managed Loans) ** 4.1% 5.3%

ROE ** 19.1% 25.4%

EPS - Diluted (INR) (Not Annualized) 27.0 47.2

Book Value (INR) 208.3 278.5

69

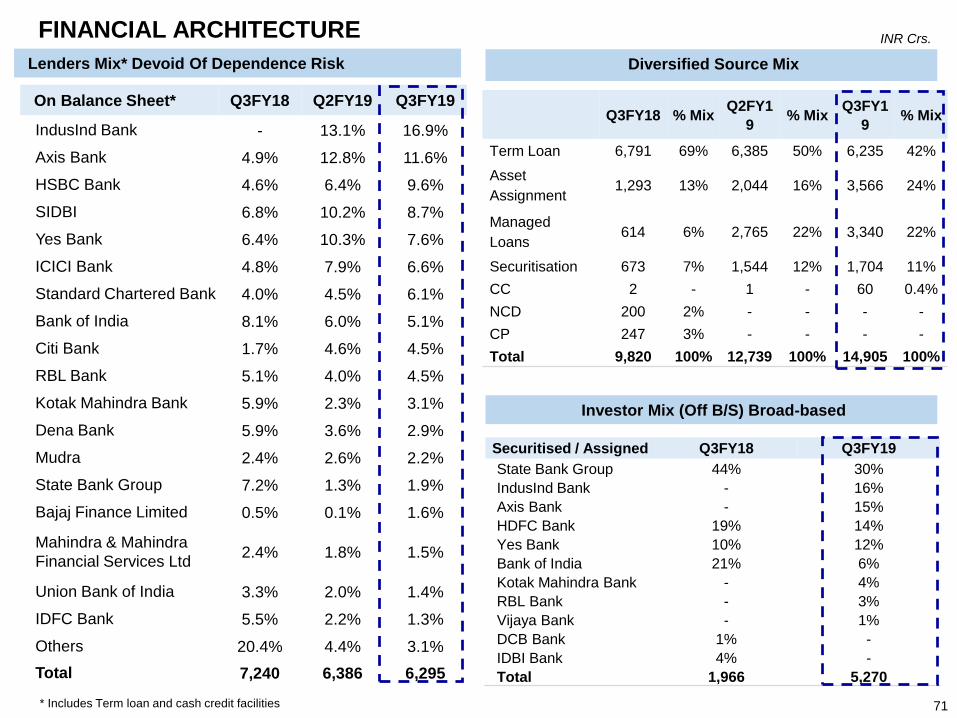

FINANCIAL ARCHITECTURE

70

Q3FY18 % MixQ2FY1

9% Mix

Q3FY1

9% Mix

Term Loan 6,791 69% 6,385 50% 6,235 42%

Asset

Assignment1,293 13% 2,044 16% 3,566 24%

Managed

Loans614 6% 2,765 22% 3,340 22%

Securitisation 673 7% 1,544 12% 1,704 11%

CC 2 - 1 - 60 0.4%

NCD 200 2% - - - -

CP 247 3% - - - -

Total 9,820 100% 12,739 100% 14,905 100%

On Balance Sheet* Q3FY18 Q2FY19 Q3FY19

IndusInd Bank - 13.1% 16.9%

Axis Bank 4.9% 12.8% 11.6%

HSBC Bank 4.6% 6.4% 9.6%

SIDBI 6.8% 10.2% 8.7%

Yes Bank 6.4% 10.3% 7.6%

ICICI Bank 4.8% 7.9% 6.6%

Standard Chartered Bank 4.0% 4.5% 6.1%

Bank of India 8.1% 6.0% 5.1%

Citi Bank 1.7% 4.6% 4.5%

RBL Bank 5.1% 4.0% 4.5%

Kotak Mahindra Bank 5.9% 2.3% 3.1%

Dena Bank 5.9% 3.6% 2.9%

Mudra 2.4% 2.6% 2.2%

State Bank Group 7.2% 1.3% 1.9%

Bajaj Finance Limited 0.5% 0.1% 1.6%

Mahindra & Mahindra

Financial Services Ltd2.4% 1.8% 1.5%

Union Bank of India 3.3% 2.0% 1.4%

IDFC Bank 5.5% 2.2% 1.3%

Others 20.4% 4.4% 3.1%

Total 7,240 6,386 6,295

Lenders Mix* Devoid Of Dependence Risk

* Includes Term loan and cash credit facilities

FINANCIAL ARCHITECTURE

Diversified Source Mix

Investor Mix (Off B/S) Broad-based

INR Crs.

71

Securitised / Assigned Q3FY18 Q3FY19

State Bank Group 44% 30%

IndusInd Bank - 16%

Axis Bank - 15%

HDFC Bank 19% 14%

Yes Bank 10% 12%

Bank of India 21% 6%

Kotak Mahindra Bank - 4%

RBL Bank - 3%

Vijaya Bank - 1%

DCB Bank 1% -

IDBI Bank 4% -

Total 1,966 5,270

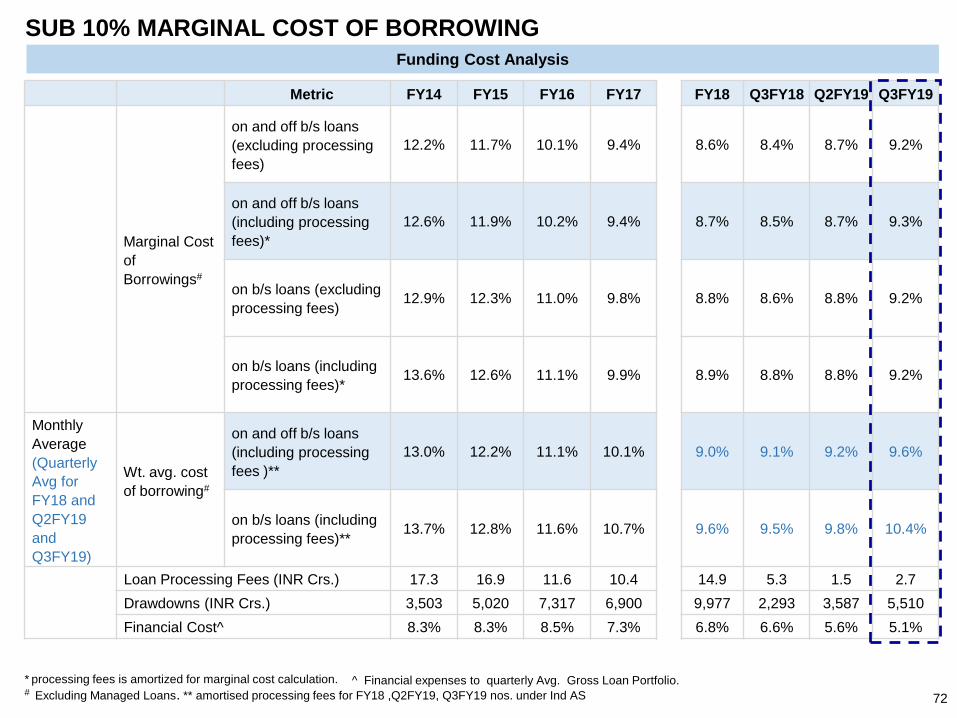

SUB 10% MARGINAL COST OF BORROWING

* processing fees is amortized for marginal cost calculation.# Excluding Managed Loans. ** amortised processing fees for FY18 ,Q2FY19, Q3FY19 nos. under Ind AS

Metric FY14 FY15 FY16 FY17 FY18 Q3FY18 Q2FY19 Q3FY19

Marginal Cost

of

Borrowings#

on and off b/s loans

(excluding processing

fees)

12.2% 11.7% 10.1% 9.4% 8.6% 8.4% 8.7% 9.2%

on and off b/s loans

(including processing

fees)*

12.6% 11.9% 10.2% 9.4% 8.7% 8.5% 8.7% 9.3%

on b/s loans (excluding

processing fees)12.9% 12.3% 11.0% 9.8% 8.8% 8.6% 8.8% 9.2%

on b/s loans (including

processing fees)*13.6% 12.6% 11.1% 9.9% 8.9% 8.8% 8.8% 9.2%

Monthly

Average

(Quarterly

Avg for

FY18 and

Q2FY19

and

Q3FY19)

Wt. avg. cost

of borrowing#

on and off b/s loans

(including processing

fees )**

13.0% 12.2% 11.1% 10.1% 9.0% 9.1% 9.2% 9.6%

on b/s loans (including

processing fees)**13.7% 12.8% 11.6% 10.7% 9.6% 9.5% 9.8% 10.4%

Loan Processing Fees (INR Crs.) 17.3 16.9 11.6 10.4 14.9 5.3 1.5 2.7

Drawdowns (INR Crs.) 3,503 5,020 7,317 6,900 9,977 2,293 3,587 5,510

Financial Cost^ 8.3% 8.3% 8.5% 7.3% 6.8% 6.6% 5.6% 5.1%

Funding Cost Analysis

^ Financial expenses to quarterly Avg. Gross Loan Portfolio.

72

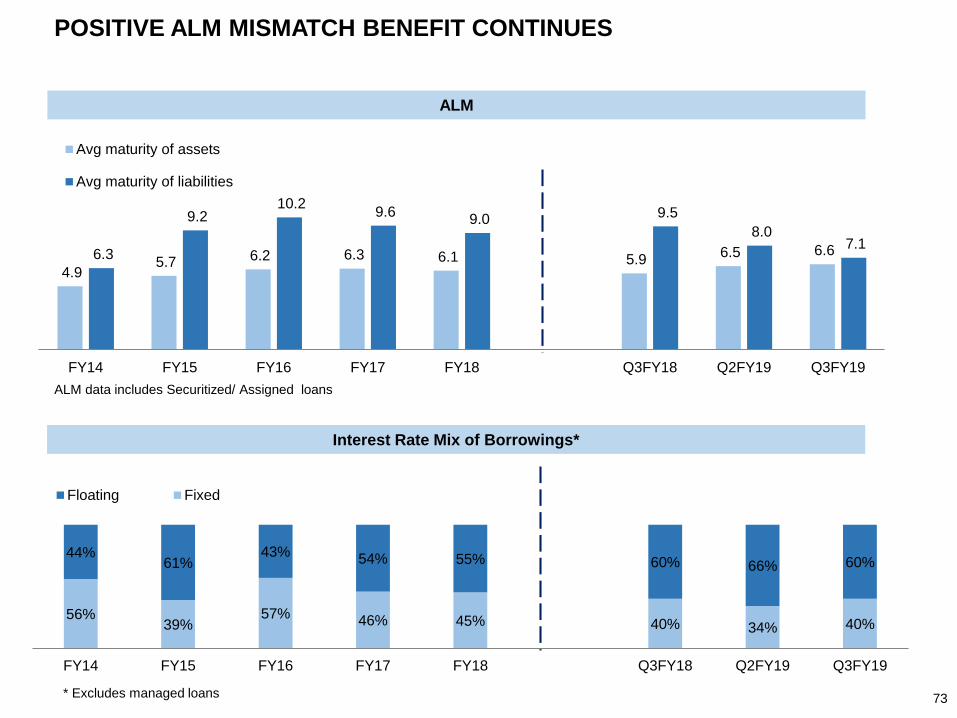

POSITIVE ALM MISMATCH BENEFIT CONTINUES

56%39%

57% 46% 45% 40% 34% 40%

44%61%

43%54% 55% 60% 66% 60%

FY14 FY15 FY16 FY17 FY18 Q3FY18 Q2FY19 Q3FY19

Floating Fixed

* Excludes managed loans

ALM data includes Securitized/ Assigned loans

ALM

4.9 5.7 6.2 6.3 6.1 5.9

6.5 6.6 6.3

9.2 10.2

9.6 9.0 9.5

8.0 7.1

FY14 FY15 FY16 FY17 FY18 Q3FY18 Q2FY19 Q3FY19

Avg maturity of assets

Avg maturity of liabilities

Interest Rate Mix of Borrowings*

73

74

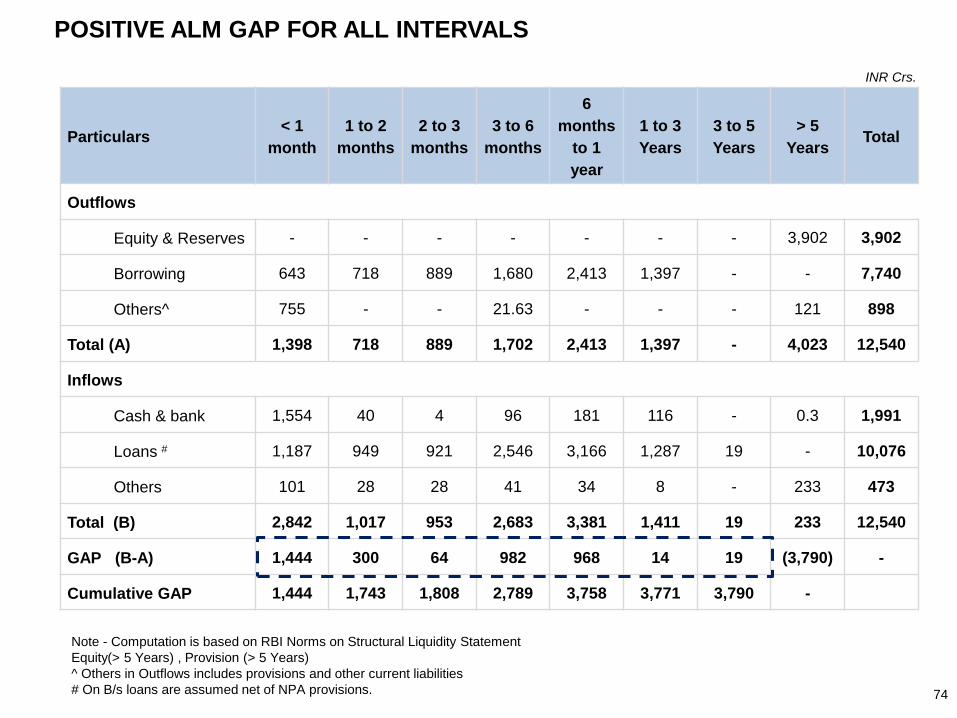

POSITIVE ALM GAP FOR ALL INTERVALS

Particulars< 1

month

1 to 2

months

2 to 3

months

3 to 6

months

6

months

to 1

year

1 to 3

Years

3 to 5

Years

> 5

YearsTotal

Outflows

Equity & Reserves - - - - - - - 3,902 3,902

Borrowing 643 718 889 1,680 2,413 1,397 - - 7,740

Others^ 755 - - 21.63 - - - 121 898

Total (A) 1,398 718 889 1,702 2,413 1,397 - 4,023 12,540

Inflows

Cash & bank 1,554 40 4 96 181 116 - 0.3 1,991

Loans # 1,187 949 921 2,546 3,166 1,287 19 - 10,076