Embed Size (px)

Citation preview

Bill Boler

Director, Investment & Physical Regeneration

Business in the Community

Scottish Centre for RegenerationTown Centres and Local High Streets Learning Network

“Securing Private Sector Investment”

12th November 2009

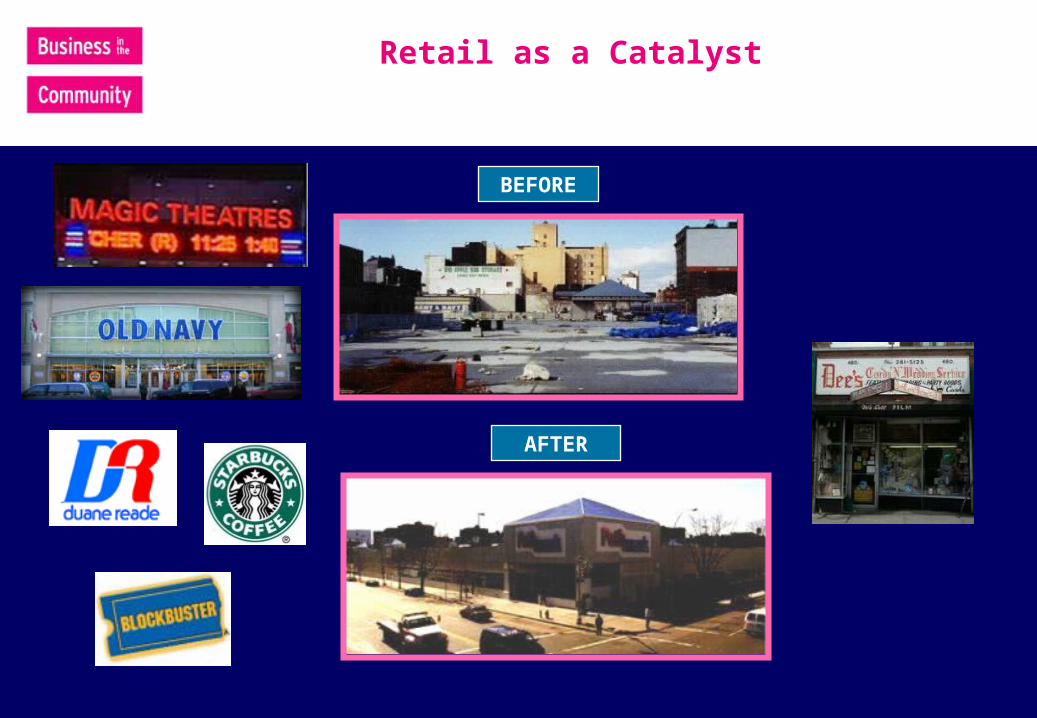

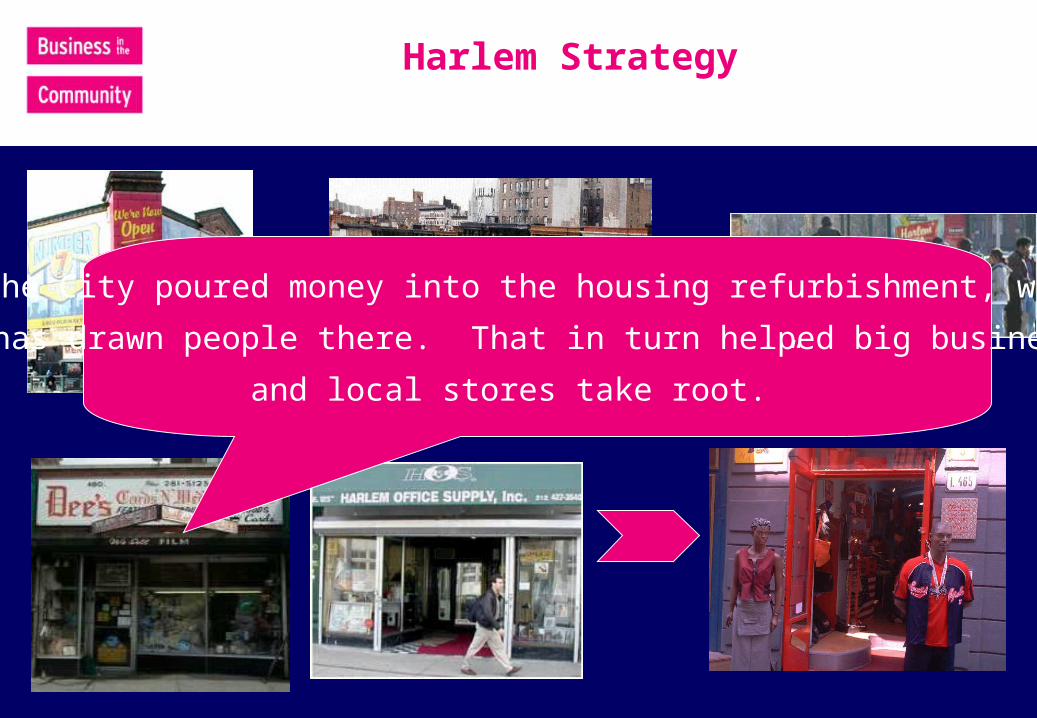

Harlem Strategy

“The City poured money into the housing refurbishment, which

has drawn people there. That in turn helped big business

and local stores take root.”

“Good vs. Bad” Local Business

“No People”

“What we need are more customers!”

Local Business View

“What we need are more customers!”

Harlem’s “High Street”

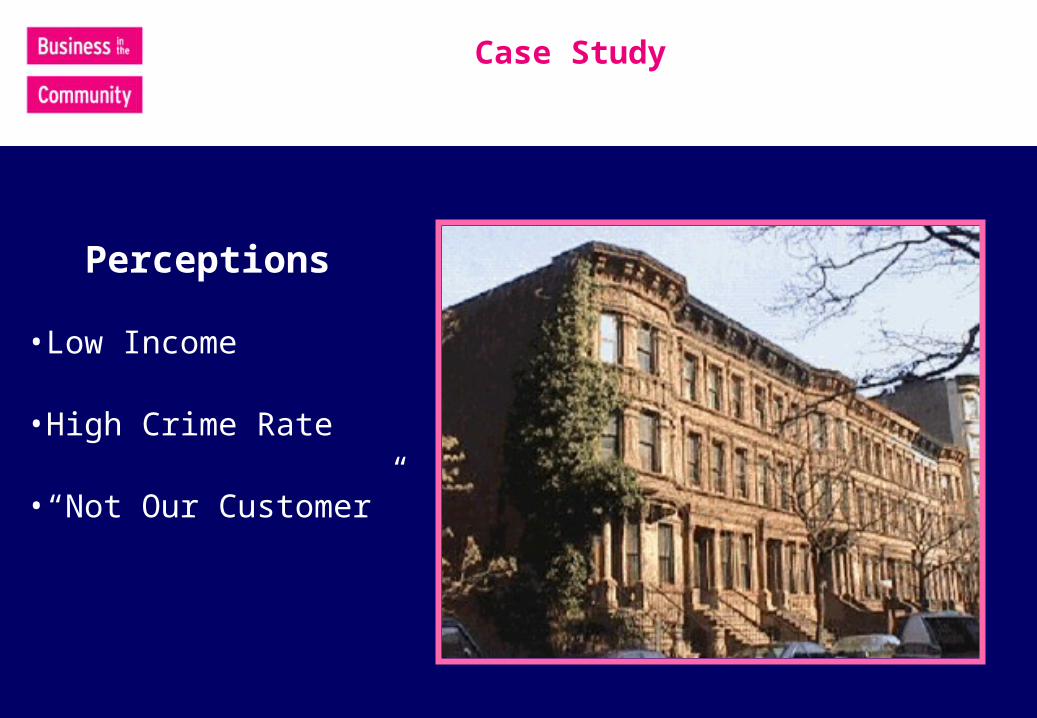

Case Study

Perceptions

•Low Income

•High Crime Rate

•“Not Our Customer”

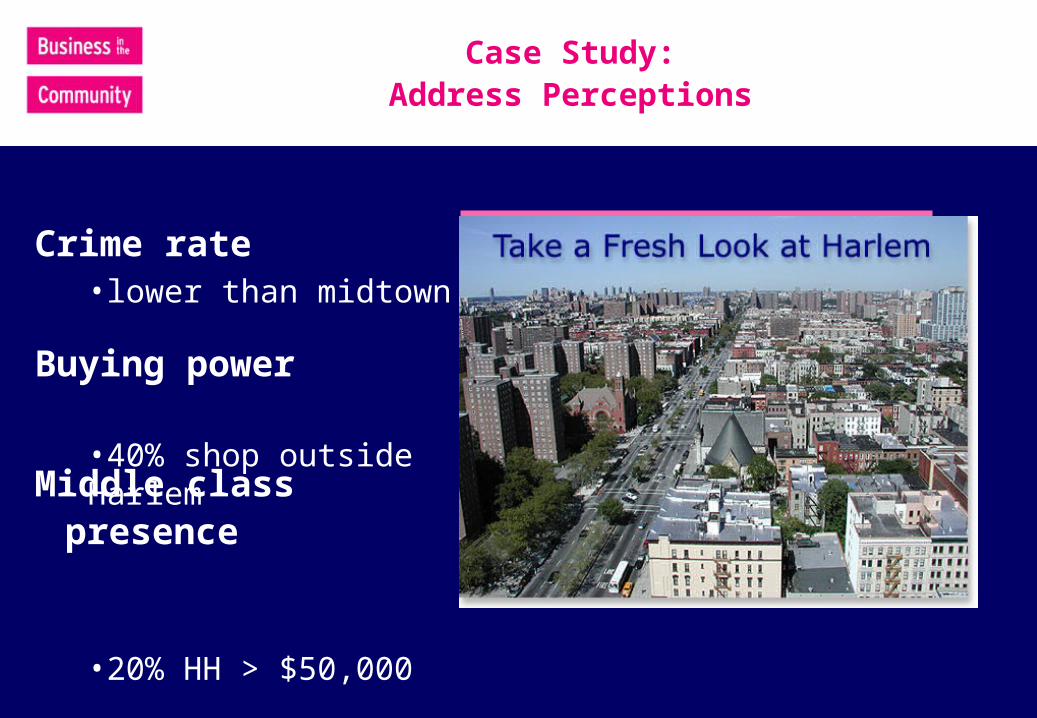

Crime rate

Buying power

Middle class presence

•lower than midtown

•40% shop outsideHarlem

•20% HH > $50,000

Case Study:Address Perceptions

New market information

Cash Economy

‘Street’ Retailers

‘Cheques Cashed’ shops

% 1st generation immigrants

Income/Spend ratios

20% additional Household Income

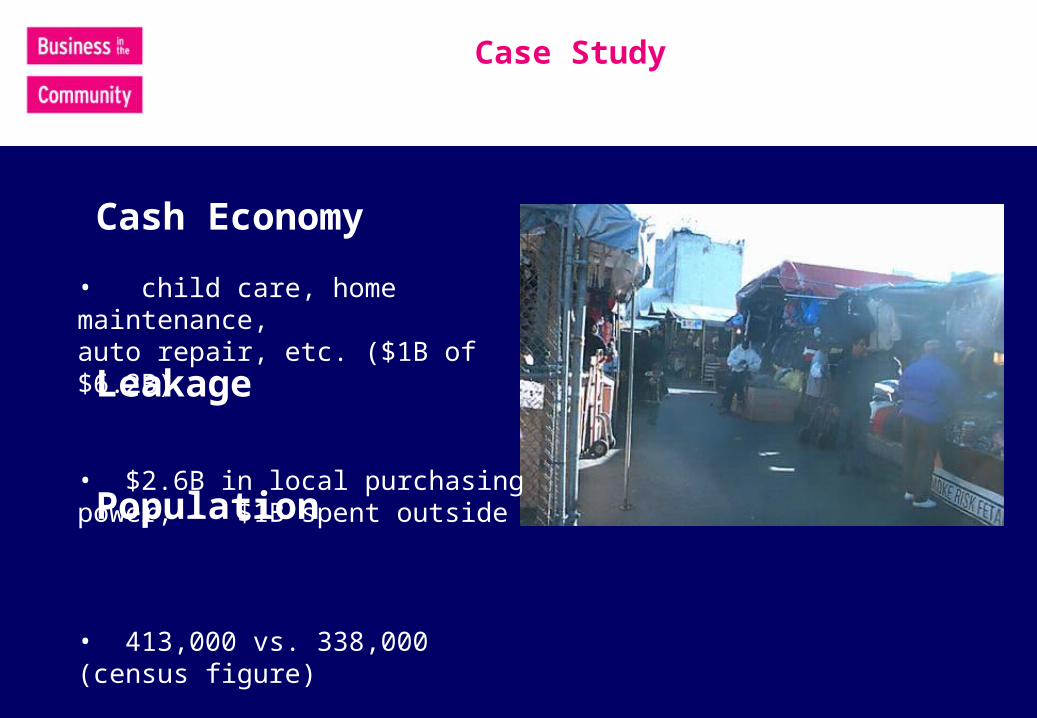

Case Study

Cash Economy

Leakage

Population

• child care, home maintenance,auto repair, etc. ($1B of $6.2B)

• $2.6B in local purchasing power, $1B spent outside

• 413,000 vs. 338,000 (census figure)

“The US isn’t the UK/Europe”

=

Are there any lessons?

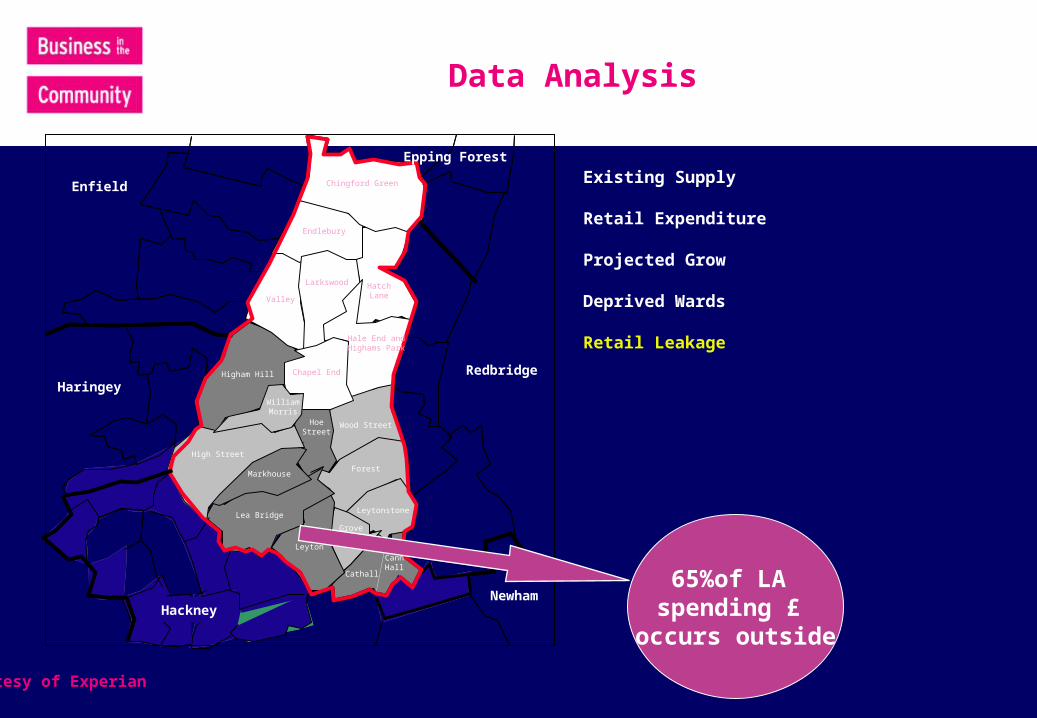

Cathall

Chapel End

Chingford Green

Endlebury

Cann Hall

Forest

Grove Green

Hale End and Highams Park

Hatch Lane

High Street

Higham Hill

Hoe Street

Larkswood

Lea Bridge

Leyton

Leytonstone

Markhouse

Valley

William Morris

Wood Street

Redbridge

Enfield

Haringey

Hackney

Epping Forest

Newham

Courtesy of Experian

Existing Supply

Retail Expenditure

Projected Grow

Deprived Wards

Retail Leakage

Data Analysis

65%of LA spending £

occurs outside

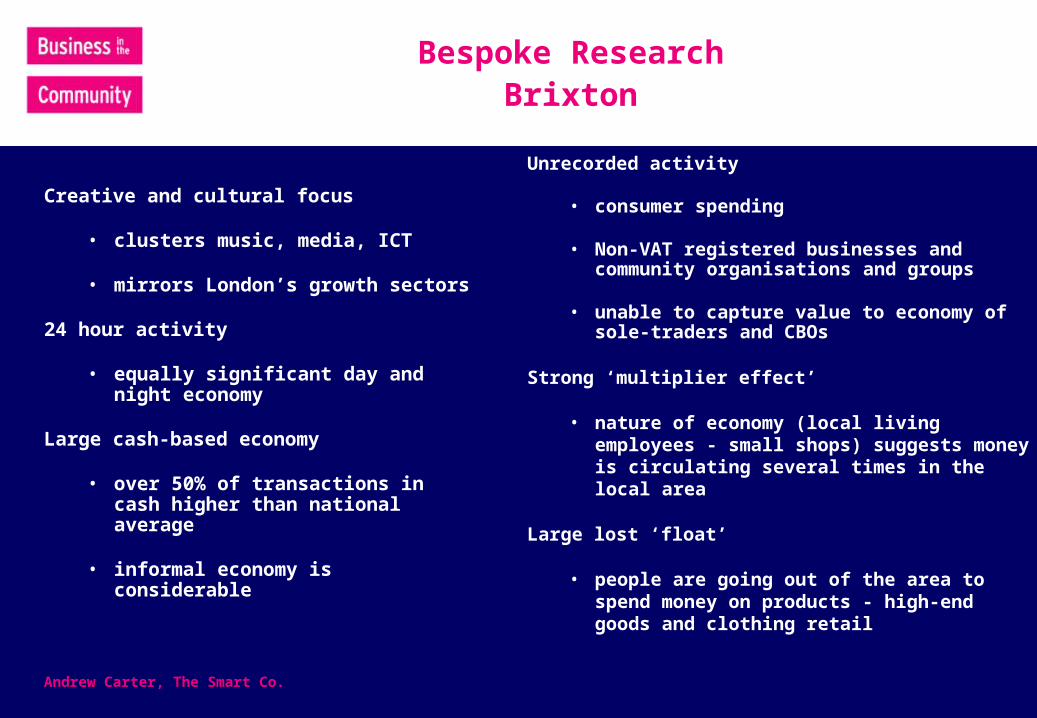

Creative and cultural focus

• clusters music, media, ICT

• mirrors London’s growth sectors

24 hour activity

• equally significant day and night economy

Large cash-based economy

• over 50% of transactions in cash higher than national average

• informal economy is considerable

Andrew Carter, The Smart Co.

Unrecorded activity

• consumer spending

• Non-VAT registered businesses and community organisations and groups

• unable to capture value to economy of sole-traders and CBOs

Strong ‘multiplier effect’

• nature of economy (local living employees - small shops) suggests money is circulating several times in the local area

Large lost ‘float’

• people are going out of the area to spend money on products - high-end goods and clothing retail

Bespoke ResearchBrixton

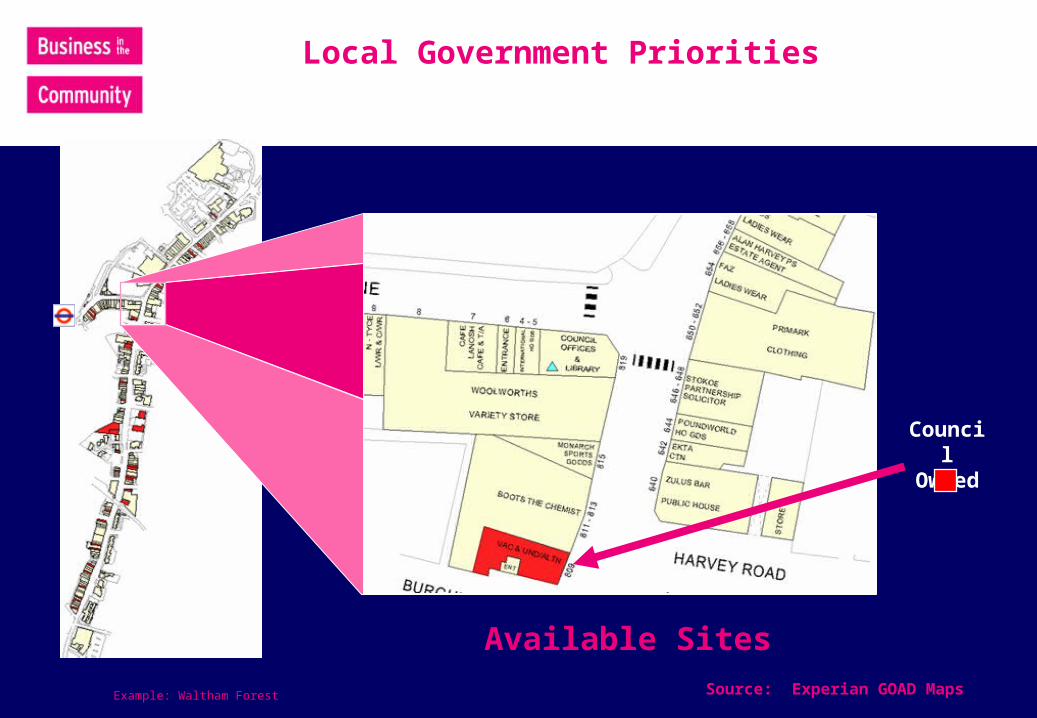

Source: Experian GOAD Maps

Available Sites

Local Government Priorities

Example: Waltham Forest

Council Owned

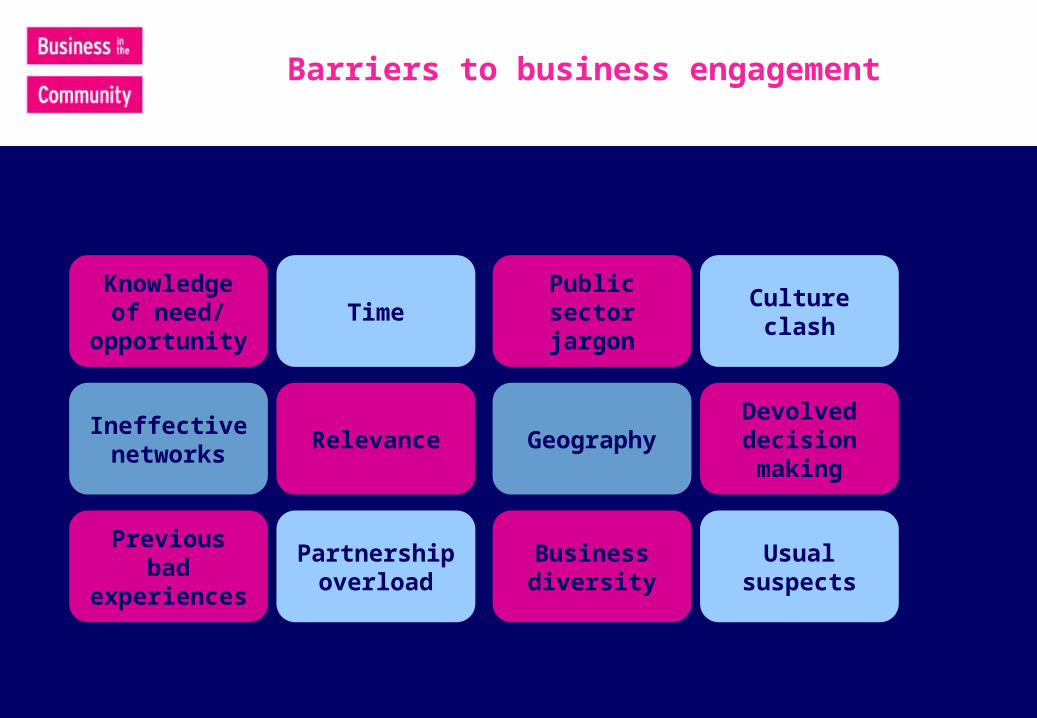

Knowledge of need/

opportunityTime

Public sectorjargon

Culture clash

Ineffective networks

Relevance GeographyDevolved decision making

Previous bad experiences

Partnership overload

Business diversity

Usual suspects

Barriers to business engagement

Strategy: Focus on “Catalyst” Investors

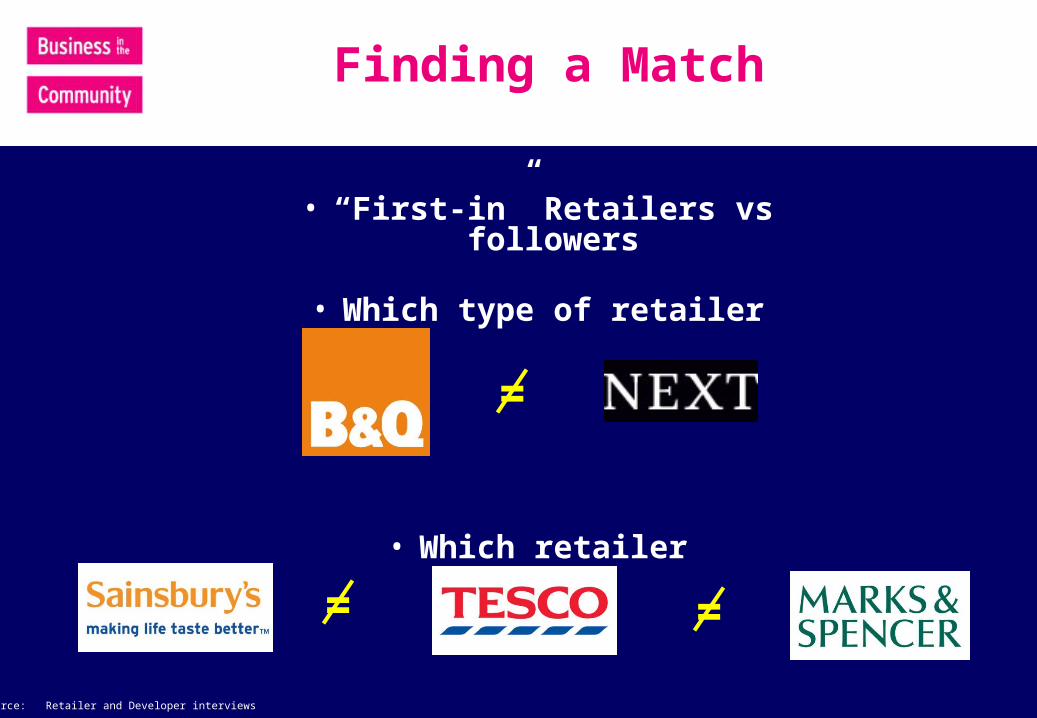

Finding a Match

• “First-in” Retailers vs followers

• Which type of retailer

• Which retailer

Source: Retailer and Developer interviews

= =

=

Learn how Retail thinks

• Competitive Offer: “If we have a choice between an untried market or area and a good site in say Oxfordshire, we would bias the latter”

Investment in challenged areas is viewed relative to other investment options

• Overall retailers focus on areas where they have no outlets or existing outlets are small, competitors are few and the level of affluence is adequate

Time and lack of certainty of planning process discourages investors from looking at deprived areas

Source: Retailer and Developer interviews

Learnings: Private Sector

Preference to be part of larger transformation project

Key business considerations include:

• ability to implement required business/format model (i.e. site availability, accessibility, parking);

• ability to achieve needed operating performance (i.e. crime, employee availability);

Local Government

Local Authorities vary in their level of understanding and ability to engage retailers on these issues;

Many have retail in a “silo” and struggle to link or include a retail strategy with other initiatives

For deprived areas in non-town centre locations, many local authorities struggle to balance the need to promote investment and the intentions of national planning policy;

Many still question whether brand retail can bring real benefits, and not destroy the existing fabric

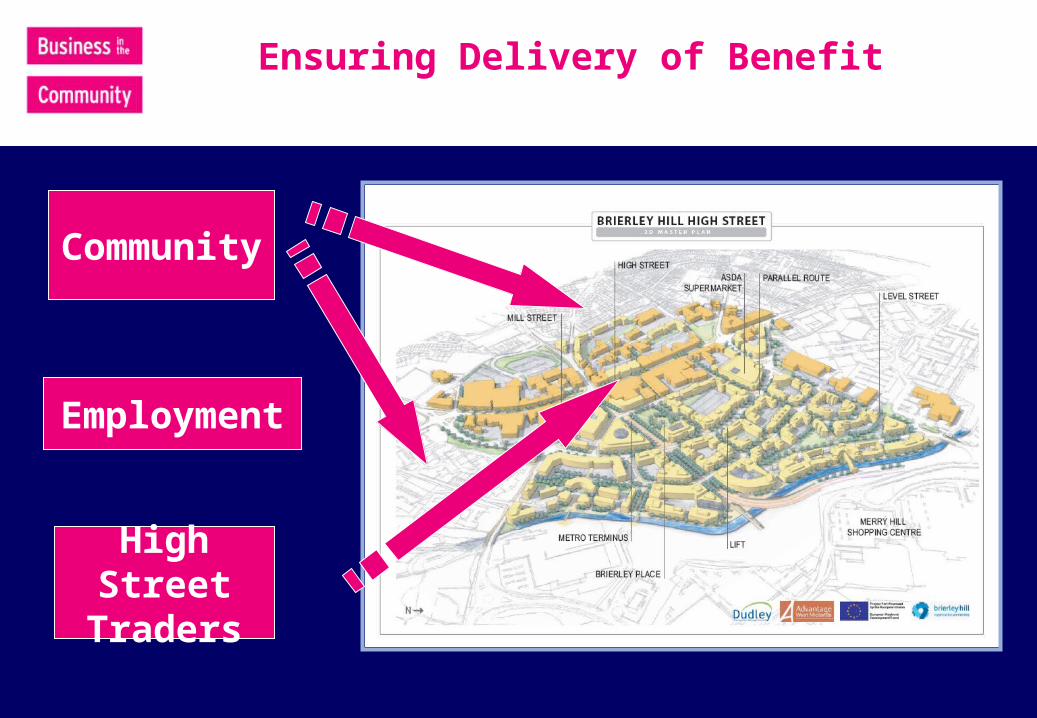

Ensuring Delivery of Benefit

Employment

Community

High Street Traders

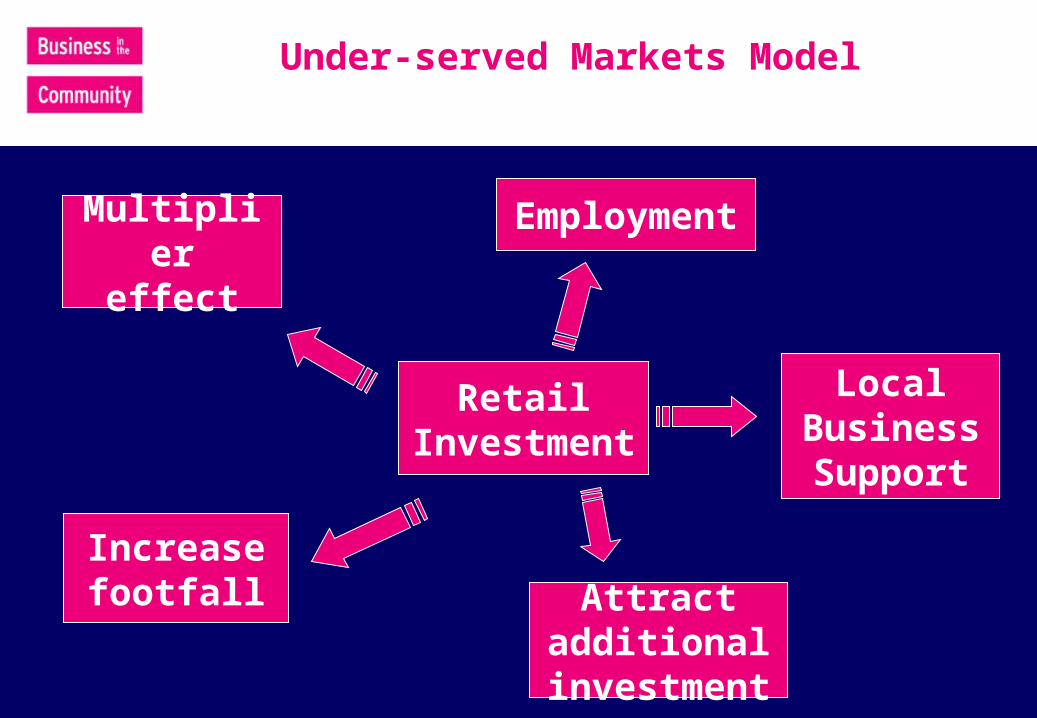

Under-served Markets Model

Retail Investment

Employment

LocalBusiness Support

Increase footfall Attract

additional investment

Multiplier effect

James BrownHot Pants Pt 1 (1971)

“You got to use what you got to get what you want!”

Final Thoughts