Embed Size (px)

Citation preview

MANAGERIAL AND DECISION ECONOMICS, VOL. 12, 57-66 (1991)

Bimodality in Diversification: an Efficiency and Effectiveness

Rationale Richard Reed

Washington State University, Pullman, WA, 99164-4726, USA

Various researchers have observed that the frequency distribution of firm diversification is bimodal The two modes are created by a majority of firms employing either very little or substantial amounts of diversification. Only a minority of firms opt for medium amounts of diversification. From theoretical discussion of the forces of efficiency and effectiveness in diversification, this work provides a rationale for the bimodality phenomenon. In turn, research implications arise regarding optimum degrees of diversification, what the impact of optimiza- tion is upon firm performance, and why the measurement of both type and degree of diversification is important.

INTRODUCTION

Bimodality in the distribution of diversification is important for two reasons. First, it is a phenom- enon that appears to be impervious to both time and national economic boundaries. Bimodality was reported for US firms by Wrigley (1970), for Cana- dian firms by Gorecki (1974) and for UK firms by Reed and Sharp (1987). As such, its continued existence demands attention.

Second, it has served as the basis for derivation of the Single-Dominant-Related-Unrelated (SDRU) system of classification (Wrigley, 1970). A sub- stantial literature has been built that discusses diversification using the SDRU system. Distinction between S, D, R and U starts with calculation of the Specialization Ratio (SR). The ratio describes the proportional contribution to total sales that is generated by a firm’s principal activity. S , D, R and U classifications are decided according to SR breakpoints occurring at 0.95 and 0.70. Thus, in the distribution of firms, a large number are found with consistent SRs between 1.00 and 0.95 (Single) and less than 0.70 (Related and Unrelated), but rela- tively few are found between 0.95 and 0.70 (Dom- inant).

Venkatraman and Grant (1986) criticized the SDRU system as not having been empirically val- idated. Soon after their review, empirical support for bimodality and authentication of the traditional

SR breakpoints of 0.70 and 0.95 was provided (Reed and Sharp, 1987). In line with Venkatraman and Grant’s broader criticisms of strategy research, however, the theoretical base of the classification system remains underdeveloped. This work seeks to provide a rationale for the existence of the bimodrl- ity phenomenon and thus addresses remaining criti- cisms. The work also considers the implications of the phenomenon for researchers and practitioners.

The organization of the paper is as follows. To start, the background to the bimodality issue is reviewed; this includes discussion on the measure- ment of diversification. Then, using theoretical deduction, it is argued that the combined effect of efficiency and effectiveness in degrees of diver- sification is responsible for bimodality. From this other issues are raised that, as yet, have received little or no attention within the research literature. These issues relate to optimal degrees of diversity, the largely ignored interrelationship between de- gree and type of diversification, and the impact upon performance. The implication for researchers is that a more comprehensive approach to the measurement of diversification is needed: notably, a multidimensional approach that describes type and degree, and thus permits an assessment of the most efficient and effective means of achieving given diversification goals. For practitioners, the bimod- ality phenomenon is consistent with the notion that there is a trade-off between efficiency and

0143-6570/91/’010057-10$05.00 0 1991 by John Wiley & Sons, Ltd.

58 R. REED

effectiveness in diversification. Large degrees of diversification may be effective, but they also mean inefficiency.

BACKGROUND TO BIMODALITY AND DIVERSIFICATION MEASUREMENT

Bimodality

Wrigley’s research considered growth strategies, based on core skills, in a 1967 sample of one hundred of the largest US firms. Wrigley attempted to order diversification on a simple linear scale with the proportion of output from the firm’s principal activity being 100%, 9070, . . . 10%. This attempt met with an unexpected problem. It appeared that managers preferred either low or high levels of diversification and shied away from medium levels, thus creating bimodality in the distribution of di- versification. To deal with the unexpected phenom- enon, Wrigley developed the basis of the Single, Dominant, Related and Unrelated system of classi- fication with which we are familiar today. Firms with low levels of diversification were a homogen- ous group, as were those in the less-preferred medium levels of diversification. Firms with high levels of diversification (less than 70% of sales from the primary product market) were heterogenous and had to be subdividea. Categories were devised to separate firms that had diversified on the basis of core skills from those that had diversified regardless of core skills. For a more detailed discussion of this, see Wrigley (1970); Channon (1973, pp. 8-13) and Rumelt (1974, pp. 14-16).

Channon’s (1973) work on diversification helped popularize the SDRU taxonomy. Rumelt’s (1974) work, which has had a major impact on diversi- fication research, used subdivisions of the SDRU categories to refine descriptive powers. Luffman and Reed (1984) and others have made additional refinements. Regardless of the various nuances and complexities that have been added, all variations of the classification system continue to be based on Wrigley’s (1970) seminal work and the original SDRU system and, consequently, on Wrigley’s ob- servation of managerial preferences for diversific- ation. They are thus all rooted in the concept of bimodality.

While Wrigley (1970) can be ascribed with having discovered bimodality in diversification, the effects of the phenomenon were also observed by Gorecki

(1974) who found for Canadian industry that the D index frequency had a mode occurring in the 0.5M.59 range. Although Gorecki‘s employment- based explanation of the mode is arguably flawed, the observation of its existence remains valid. Un- like the SDRU system, the D index is a business- count type of measure, and validity for the bimodal- ity phenomenon is thus established through this alternative methodology.

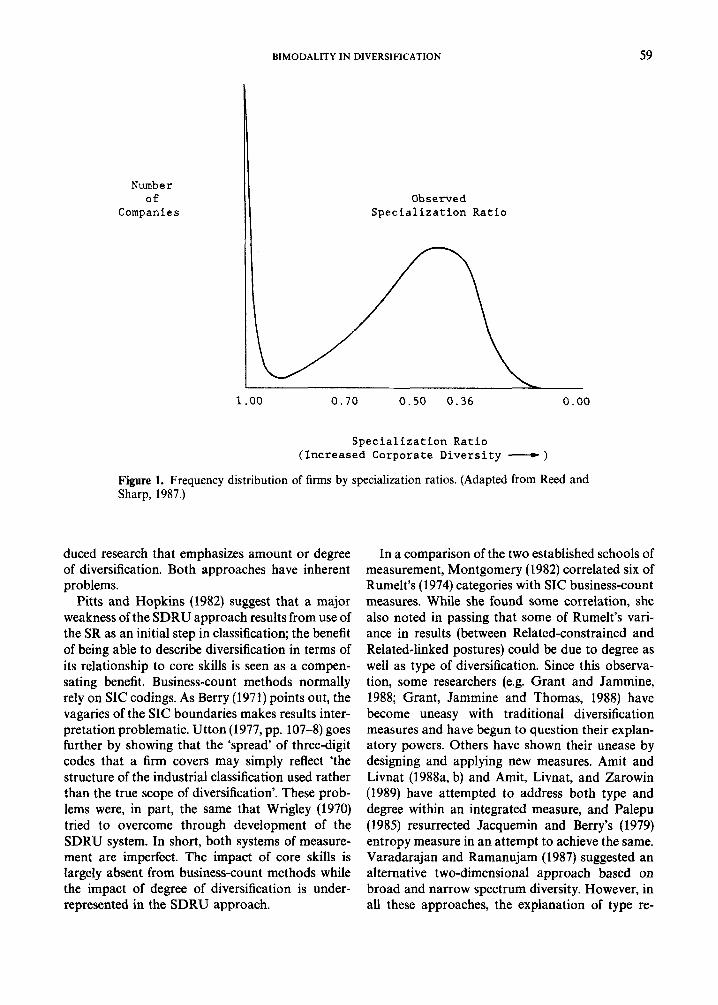

Using data from 496 British companies for the period 1970-80, Reed and Sharp (1987) used dy- namic modelling techniques to temporally extend observed diversification process operands. They found that the distribution of diversification had a definite bimodal profile (see Fig. l), and also con- firmed the authenticity of the traditionally accepted SR breakpoints of 0.95 and 0.70, finding a hitherto unsuspected SR breakpoint at 0.36. Firms whose diversification process continued to the degree where it pushed their SR below 0.36 exhibited a marked tendency to reverse the process. From this, it is apparent that there is a natural inclination for diversifying firms to center the degree of diver- sification within the relatively narrow SR range of 0.70-0.36. This conclusion remains compatible with Wrigley’s (1970) and Gorecki’s (1974) observations.

Some clues to bimodality in diversification exic t within the dynamics of the diversification process itself. Numerous researchers, in various countries (e.g. Channon, 1973, UK; Rumelt, 1974, USA; Suzuki, 1980, Japan), have observed an aggregate movement of large firms away from the Single posture towards more diversified postures. Luffman and Reed (1984) found the Dominant product posture to be a temporary stage as firms moved from Single product to more diversified postures in a continuous and often rapid process. While this describes movement in one direction, it does not explain the apparently opposing forces that make diversifying firms gravitate to the 0 .70 .36 SR range.

Measurement of Diversification

Measurement of diversification has been of interest to both strategy and economics (e.g. Wrigley, 1970; Berry, 1971; Gorecki, 1974; Rumelt, 1974; Hassid, 1975; Utton, 1977; Amit and Livnat, 1988a, b). The use of descriptive categories in strategy has led to research that is primarily concerned with the im- pact of diversification type (Related versus Un- related, constrained versus linked). In economics, indices based on SIC business counts have pro-

BIMODALITY IN DIVERSIFICATION 59

Number of

Companies Observed

Specialization Ratio

1 .oo 0.70 0.50 0.36 0 . 0 0

Specialization Ratio (Increased Corporate Diversity -)

Figure 1. Frequency distribution of firms by specialization ratios. (Adapted from Reed and Sharp, 1987.)

duced research that emphasizes amount or degree of diversification. Both approaches have inherent problems.

Pitts and Hopkins (1982) suggest that a major weakness of the SDRU approach results from use of the SR as an initial step in classification; the benefit of being able to describe diversification in terms of its relationship to core skills is seen as a compen- sating benefit. Business-count methods normally rely on SIC codings. As Berry (1971) points out, the vagaries of the SIC boundaries makes results inter- pretation problematic. Utton (1977, pp. 107-8) goes further by showing that the ‘spread’ of three-digit codes that a firm covers may simply reflect ‘the structure of the industrial classification used rather than the true scope of diversification’. These prob- lems were, in part, the same that Wrigley (1970) tried to overcome through development of the SDRU system. In short, both systems of measure- ment are imperfect. The impact of core skills is largely absent from business-count methods while the impact of degree of diversification is under- represented in the SDRU approach.

In a comparison of the two established schools of measurement, Montgomery (1982) correlated six of Rumelt’s (1974) categories with SIC business-count measures. While she found some correlation, she also noted in passing that some of Rumelt’s vari- ance in results (between Related-constrained and Related-linked postures) could be due to degree as well as type of diversification. Since this observa- tion, some researchers (e.g. Grant and Jammine, 1988; Grant, Jammine and Thomas, 1988) have become uneasy with traditional diversification measures and have begun to question their explan- atory powers. Others have shown their unease by designing and applying new measures. Amit and Livnat (1988a, b) and Amit, Livnat, and Zarowin (1989) have attempted to address both type and degree within an integrated measure, and Palepu (1985) resurrected Jacquemin and Berry’s (1979) entropy measure in an attempt to achieve the same. Varadarajan and Ramanujam (1987) suggested an alternative two-dimensional approach based on broad and narrow spectrum diversity. However, in all these approaches, the explanation of type re-

60 R. REED

mains linked to SIC classifications and thus the problems recognized by Berry (1971) and Utton (1977) arguably still exist.

Montgomery’s (1982) observation on type and degrees of diversification has an importance that is wholly out of proportion to its prominence in the literature. It indicates that while the SDRU-based classification systems give us type of diversification as an explanatory variable for performance, they ignore the explanatory variable of degree, and are therefore incomplete. Logically, diversifying firms will select not only the most appropriate type of diversification but also the most appropriate degree of diversification for achieving their goals with the least possible cost and effort.

EFFICIENCY AND EFFECTIVENESS IN DIVERSIFICATION

Bimodality and Motives for Diversification

Staudt (1954) identified 43 separate reasons for diversification but, according to Ansoff (1 965, pp. 113-14), the motives for diversification are far fewer in number. They include growth, defense and synergistic gain. Both Related and Unrelated types of diversification permit firms to achieve growth and defense, but only Related diversification facili- tates operational synergistic gains. Research con- tinues to show that the majority of firm diver- sifications are of the Related type (e.g. Channon, 1973; Rumelt, 1974; Luffman and Reed, 1984) and, therefore, the median diversified firm within the bimodal distribution is also Related, with all that that implies-a potential for growth, defense, syn- ergy and the need for inter-activity control (Porter, 1985; Jones and Hill, 1988). The following discus- sion on efficiency and effectiveness focuses on bi- modality and thus pertains to all diversifying firms. An aggregate motive for diversification has been assumed, but the emphasis is towards the median, Related-diversified type of firm.

Efficiency and Effectiveness

Definitions of effectiveness invariably state that the concept is governed by the success with which organizational goals are achieved (e.g. Fink, Jenks and Willets, 1983). In the context of diversification, effectiveness may be seen as reflecting the success with which firms achieve their goals for growth,

defense and synergy. Definitions of efficiency vary in detail, but the central theme remains constant- efficiency is the attainment of a desired outcome or goal with a minimum of effort, cost or waste. Within business, the notion of efficiency remains firmly linked to the effectiveness with which goals are achieved. Organizations can be somewhat effective while remaining inefficient, or they can be efficient without being particularly effective. However, for longer-term performance and success they need to be both efficient and effective. For example, highly efficient firms that are not effective in producing the goods and services demanded by customers do not survive. Equally, firms that are highly effective in the production of the requisite goods and services but have overly high costs, and thus are not effi- cient, do not survive. They are overtaken and re- placed by firms with better cost structures. This logic extends to all aspects of business, including strategy.

For diversification, the greatest efficiency and effectiveness arguably occurs when there is compat- ibility between diversification goals and the type and degree of diversification. For example, a Single- product company with an income seasonality prob- lem may require a defensive diversification into a counter-cyclical line of business to produce stability of earnings. Having decided upon the new type of business, a decision also has to be made on the degree of diversification. Adjusting the SR from 1.00 to 0.90 (Dominant) may be inadequate to produce smoothing, and a SR of 0.50 may be more appropri- ate. The firm would then be described as Related or Unrelated, depending upon the relationship be- tween the firm’s core skills and the diversification.

By definition, type of diversification describes the relationship between the firm’s core skills and the new activity, and is discrete in nature. Choices on type are thus relatively limited and the type of diversification is either the best available option and the most efficient and effective for achieving the firm’s goals or it is not. Degree describes amount of diversification and, unlike type, is continuous in nature. This poses a more complex problem of choice and interpretation.

Degree: a Deductive Analysis

Degrees of diversification are well described by any of the numerous indices developed in the economic literature. There is, for example, the Ash (1965) index, Gorecki’s (1975) T index, Hassids (1975) D index, and Utton’s (1977) W index. However,

BIMODALITY IN DIVERSIFICATION 61

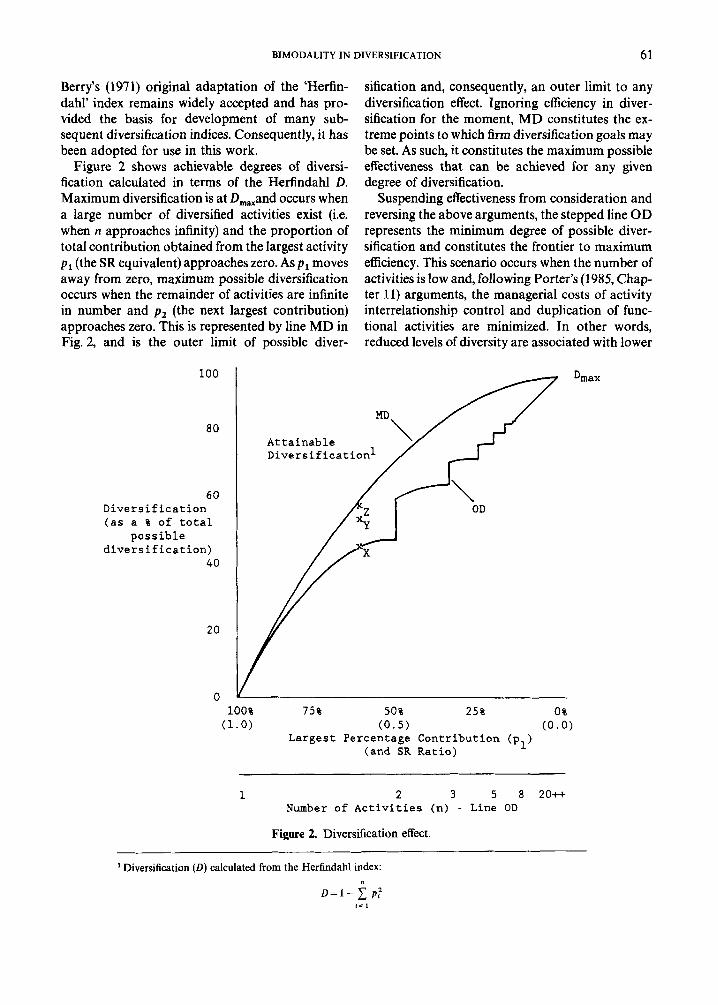

Berry’s (1971) original adaptation of the ‘Herfin- dahl’ index remains widely accepted and has pro- vided the basis for development of many sub- sequent diversification indices. Consequently, it has been adopted for use in this work.

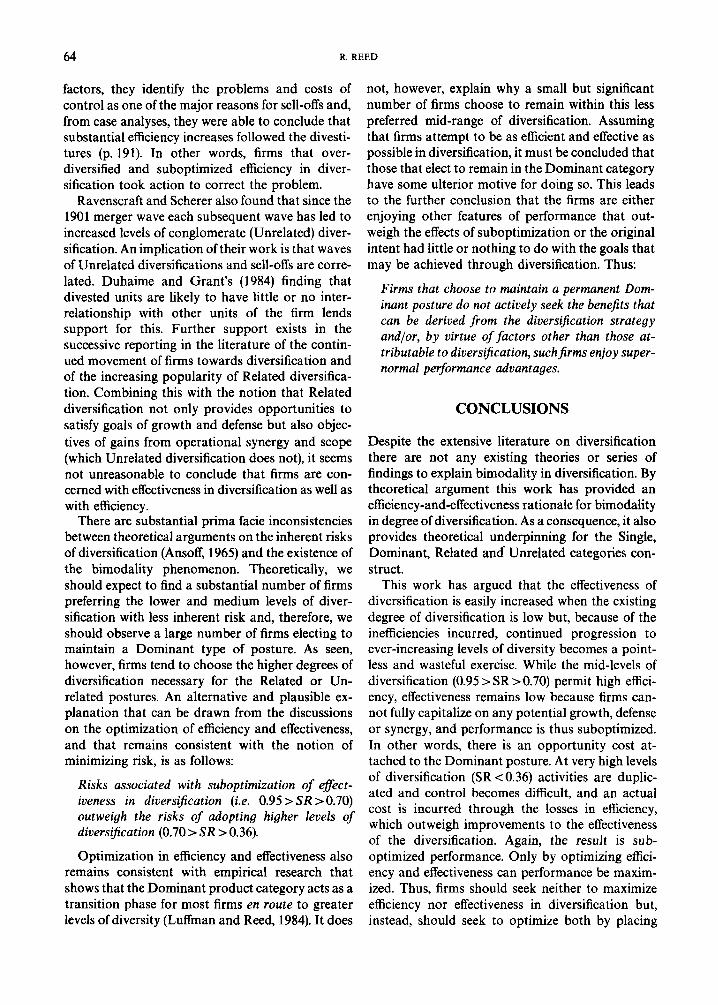

Figure 2 shows achievable degrees of diversi- fication calculated in terms of the Herfindahl D. Maximum diversification is at D,,,and occurs when a large number of diversified activities exist (i.e. when n approaches infinity) and the proportion of total contribution obtained from the largest activity p1 (the SR equivalent) approaches zero. As p1 moves away from zero, maximum possible diversification occurs when the remainder of activities are infinite in number and p 2 (the next largest contribution) approaches zero. This is represented by line MD in Fig. 2, and is the outer limit of possible diver-

sification and, consequently, an outer limit to any diversification effect. Ignoring efficiency in diver- sification for the moment, MD constitutes the ex- treme points to which firm diversification goals may be set. As such, it constitutes the maximum possible effectiveness that can be achieved for any given degree of diversification.

Suspending effectiveness from consideration and reversing the above arguments, the stepped line OD represents the minimum degree of possible diver- sification and constitutes the frontier to maximum efficiency. This scenario occurs when the number of activities is low and, following Porter’s (1985, Chap- ter 11) arguments, the managerial costs of activity interrelationship control and duplication of func- tional activities are minimized. In other words, reduced levels of diversity are associated with lower

100

ao

60 Diversification (as a % of total

possible diversification)

40

20

0 100% 75% 50% 25% 0% (1.0) (0.5) ( 0 . 0 )

Largest Percentage Contribution (p ) (and SR Ratio) 1

Dmax

Attainable Diversif icationl

1 2 3 5 8 20++ Number of Activities (n) - Line OD

Figure 2. Diversification effect.

Diversification (D) calculated from the Herfindahl index: n

D = 1 - c p ; i l l

62 R. REED

costs of control and, therefore, with improved effici- ency. Support for this is found in Ravenscraft and Scherer’s (1987, pp. 145, 191) work which identified the problem of the cost of control as being one of the reasons why highly diversified firms sold off many subsidiaries in the late 1970s and early 1980s in a bid to improve efficiency.

Further explanation of line OD is helped by reassociating efficiency and effectiveness. Taking the case ofjust two activities, p1 and p 2 , it is possible to obtain high efficiency, but any substantial imbal- ance between activity sizes (e.g. p1 =0.99 and p 2 = 0.01) limits the potential for diversification effect- iveness. Optimum efficiency and effectiveness is found when all percentage contributions are of equal size, i.e. where p1 = p 2 = 0.50, where p1 = p 2 = p 3 =0.3333, etc. Between these nodes, optimiza- tion of efficiency and effectiveness occurs when p1 is given and the remaining activities are all of equal

size (i.e. p z = p 3 = . . . p,,). Thus, calculation of line OD remains the same as that for MD, except that at each stage p,, is finite and known.

From the above arguments, it can be deduced that efficiency and effectiveness are counterposing forces within degrees of diversification. Effect- iveness increases with movement towards D,,,and boundary MD, while efficiency increases with movement towards the origin and boundary OD. The shape of the line MD suggests that effectiveness in diversification is subject to laws of diminishing return. While benefits are quick to accrue with large values of p l , the proportional increase in benefits quickly diminishes as p1 decreases. Decreased step sizes on line OD point to geometric reductions in p1 being required for linear gains in diversification effect. Because p1 is always the largest activity, this principle translates directly into increases in the number of other activities, p 2 . . . p,,. In keeping with

Efficiency Effectiveness

Efficiency and

Effectiveness

BIMODALITY IN DIVERSIFICATION 63

Blau (1970) and Jones and Hill (1988), the costs of managing separate activities accumulate at a geo- metric rate and, therefore, linear gains in diver- sification mean that efficiency decreases at a geo- metric rate. The corollary argument to this is that for a given p 1 and an increasing value of n, pro rata gains in effectiveness become correspondingly diffi- cult to achieve. To illustrate this point further, points X, Y and Z (Fig. 2) all occur at p 1 =0.60, but where X has two activities with pz contributing 40% and Y has three activities with p2 and p3 contributing 20% each, Z has nine activities with p2 to p9 contributing only 5% each.

From the above discussions, and bearing in mind the interrelatedness of efficiency and effectiveness, the efficiency curve is logically a mirror image of the effectiveness curve (see Fig. 3). At one extreme effici- ency is high but effectiveness is minimal, while at the other extreme effectiveness is high but so too are inefficiencies. From this it can be deduced that both efficiency and effectiveness are unlikely to be max- imized in the degree of adopted diversification. Between the extremes both curves are subject to laws of diminishing returns. Increases in diver- sification at low levels of diversity (high values of p i ) result in substantial improvements in effectiveness, but only limited decreases in efficiency. At high levels of diversity (low values of p l ) , the reverse is true. It is only at the mid-levels that the trade-off between efficiency and effectiveness is directly pro- portional. Therefore it seems fair to conclude that optimization will occur somewhere in the middle of the p 1 or SR range, where efficiency and effect- iveness are in balance.

In summary, observed bimodality in diversifica- tion can be explained by theory. The first mode, which occurs in the SR range of 1.00-0.95, is consistent with Ansoff s (1965) original arguments which suggest that firms should, where possible, avoid the inherent risks involved in substantial diversification. Firms should not adopt large or radical diversifications unless they need to do so. The second mode, which occurs between SR values of 0.70 and 0.36, is consistent with the notion of optimization and is produced by firms balancing efficiency and effectiveness in the degree of diver- sification.

DISCUSSION

Prahalad and Bettis (1986) pointed out when com- menting upon existing analyses of diversification

and performance that if we are to enhance our understanding of the strategy, further conceptual developments are needed. This work addresses that sentiment and has, in effect, generated a new theory on the optimization of efficiency and effectiveness within degrees of diversification. The following discussion draws on that theory and, by synthesi- zing it with the complementary findings of other research, makes new observations on firm diver- sification.

Through an examination of the interrelated but counterposing forces of efficiency and effectiveness, arguments have been made that support the notion of bimodality and Wrigley’s (1970) supposition that managers prefer either little or no diversification, or substantial amounts of diversification. It has been theorized that the benefits to be gained from ex- tremes of diversification (very low SR values) are greatly outweighed by the inefficiencies incurred. This is compatible with the observations of Reed and Sharp (1987), who noted that firms that went to extremes of diversification tended to reverse the process. Also, the above discussions on diminishing returns have suggested that there are only small efficiency-cost differentials between diversification at the mid-levels (SR 0.95-0.70, Dominant product range) and diversification at the higher levels (0.70 > SR > 0.36, Related and Unrelated product range), while gains in effectiveness are large. Together, these arguments fit neatly with the find- ings of Grant et al. (1988), who observed a quadratic form of relationship between diversity (measured by a Herfindahl type index) and profitability. The higher but not extreme levels of diversification resulted in superior performance. Thus it can be deduced that:

Firms seek neither maximum effectiveness nor maximum eficiency in diversijication. Instead, they actively seek to optimize both eficiency and effect- iveness in a mid-range specialization ratio (0.36 < SR c 0.70). Further, for any given SR value within that range, firms seek optimization by pla- cing themselves nearer line OD than line M D (Fig. 2).

Recent evidence on merger waves and the sub- sequent increases in divestment activity provides support for the contention that firms seek to optim- ize efficiency and effectiveness in diversification. Ravenscraft and Scherer (1987) found a significant increase in the number of divestments following the merger waves of both 1968 and 1981. Among other

64 R. REED

factors, they identify the problems and costs of control as one of the major reasons for sell-offs and, from case analyses, they were able to conclude that substantial efficiency increases followed the divesti- tures (p. 191). In other words, firms that over- diversified and suboptimized efficiency in diver- sification took action to correct the problem.

Ravenscraft and Scherer also found that since the 1901 merger wave each subsequent wave has led to increased levels of conglomerate (Unrelated) diver- sification. An implication of their work is that waves of Unrelated diversifications and sell-offs are corre- lated. Duhaime and Grant's (1984) finding that divested units are likely to have little or no inter- relationship with other units of the firm lends support for this. Further support exists in the successive reporting in the literature of the contin- ued movement of firms towards diversification and of the increasing popularity of Related diversifica- tion. Combining this with the notion that Related diversification not only provides opportunities to satisfy goals of growth and defense but also objec- tives of gains from operational synergy and scope (which Unrelated diversification does not), it seems not unreasonable to conclude that firms are con- cerned with effectiveness in diversification as well as with efficiency.

There are substantial prima facie inconsistencies between theoretical arguments on the inherent risks of diversification (Ansoff, 1965) and the existence of the bimodality phenomenon. Theoretically, we should expect to find a substantial number of firms preferring the lower and medium levels of diver- sification with less inherent risk and, therefore, we should observe a large number of firms electing to maintain a Dominant type of posture. As seen, however, firms tend to choose the higher degrees of diversification necessary for the Related or Un- related postures. An alternative and plausible ex- planation that can be drawn from the discussions on the optimization of efficiency and effectiveness, and that remains consistent with the notion of minimizing risk, is as follows:

Risks associated with suboptimization of efect- iveness in diversijication (i.e. 0.95 > SR > 0.70) outweigh the risks of adopting higher levels of diversijication (0.70 > SR > 0.36).

Optimization in efficiency and effectiveness also remains consistent with empirical research that shows that the Dominant product category acts as a transition phase for most firms en route to greater levels of diversity (Luffman and Reed, 1984). It does

not, however, explain why a small but significant number of firms choose to remain within this less preferred mid-range of diversification. Assuming that firms attempt to be as efficient and effective as possible in diversification, it must be concluded that those that elect to remain in the Dominant category have some ulterior motive for doing so. This leads to the further conclusion that the firms are either enjoying other features of performance that out- weigh the effects of suboptimization or the original intent had little or nothing to do with the goals that may be achieved through diversification. Thus:

Firms that choose to maintain a permanent Dom- inant posture do not actively seek the benefits that can be derived from the diversijication strategy andlor, by virtue of factors other than those at- tributable to diversijication, suchfrms enjoy super- normal performance advantages.

CONCLUSIONS

Despite the extensive literature on diversification there are not any existing theories or series of findings to explain bimodality in diversification. By theoretical argument this work has provided an efficiency-and-effectiveness rationale for bimodality in degree of diversification. As a consequence, it also provides theoretical underpinning for the Single, Dominant, Related and' Unrelated categories con- struct.

This work has argued that the effectiveness of diversification is easily increased when the existing degree of diversification is low hut, because of the inefficiencies incurred, continued progression to ever-increasing levels of diversity becomes a point- less and wasteful exercise. While the mid-levels of diversification (0.95 > SR > 0.70) permit high effici- ency, effectiveness remains low because firms can- not fully capitalize on any potential growth, defense or synergy, and performance is thus suboptimized. In other words, there is an opportunity cost at- tached to the Dominant posture. At very high levels of diversification (SR < 0.36) activities are duplic- ated and control becomes difficult, and an actual cost is incurred through the losses in efficiency, which outweigh improvements to the effectiveness of the diversification. Again, the result is sub- optimized performance. Only by optimizing effici- ency and effectiveness can performance be maxim- ized. Thus, firms should seek neither to maximize efficiency nor effectiveness in diversification but, instead, should seek to optimize both by placing

BIMODALITY IN DIVERSIFICATION 65

themselves within the mid-range of the specializa- tion ratio (0.70>SR>0.36). This logic is com- mensurate with the observed second mode in the bimodal frequency distribution of diversified firms.

Exploration of the bimodality issue has not only led to the generation of new theory on the optimiza- tion of efficiency and effectiveness in degrees of diversification but it has also pointed to some shortcomings for traditional forms of diversific- ation measurement. There is both a need to test the theory developed here and, just as importantly, to reassess the whole approach to the measurement issue. The continued mutual exclusivity of diver- sification type and degree, between strategy and economics research streams, is probably a prime reason why the implications of bimodality have remained obscured. Because both type and degree arguably have explanatory power for performance, it may also be a reason why existing work on diversification and performance remains largely mixed in observed results and, in aggregate, in- conclusive in findings. Some recent research (e.g. Palepu, 1985; Amit and Livnat, 1988a, b; Amit et al., 1989) has attempted to address the measurement problem through the development of new, SIC- based measures. However, there are long-recog- nized problems with the SIC approach (Berry, 1971, Utton, 1977) and, after all, this was a prime reason why the core skill-based SDRU system was de- veloped (Rumelt, 1974, pp. 12-14).The strategy of diversification is multidimensional and, as argued within this article, diversifying firms decide upon both the appropriate type and the appropriate degree of diversification. Surely, then, research should reflect this by utilizing an appropriate multi- dimensional measure. Such a measure should in- corporate the judgmental aspects of the SDRU system necessary for favoring ‘relevancy over ex- actness’ (Rumelt, 1974, p. 14) in the identification of type, and incorporate the objectivity of the busi- ness-count methods in the measurement of degree.

Acknowledgements

While responsibility for the content of this paper remains with the author, he wishes to thank Michael Lubatkin, University of Connecticut, for his helpful comments and suggestions on earlier versions.

REFERENCES

R. Amit and J. Livnat (1988a). Diversification and the risk-return trade-off. Academy of Management Journal 31, 154-46.

R. Amit and J. Livnat (1988b). Diversification strategies, business cycles and economic performance. Strategic Management Journal 9, 99-1 10.

R. Amit, J. Livnat and P. Zarowin (1989). The mode of corporate diversification: Internal versus acquisitions. Managerial and Decision Economics 10, 89-100.

H. I. Ansoff (1965). Corporate Strategy: An Analytical Approach to Business Policy for Growth and Expansion, New York: McGraw-Hill.

R. Ash (1965). Information Theory, New York: Inter- science.

C. H. Berry (1971). Corporate growth and diversification. Journal of Law and Economics 14, 371-8.

P. M. Blau (1970). A formal theory of differentiation in organizations. American Sociological Review 35,

D. F. Channon (1973). The Strategy and Structure of British Enterprise, London: Macmillan.

I. M. Duhaime and J. H. Grant (1984). Factors influ- encing divestment decision-making. Strategic Manage- ment Journal 5, 301-18.

S. L. Fink, R. S. Jenks and R. D. Willets (1983). Designing and Managing Organizations, Homewood, IL: Irwin.

P. K. Gorecki (1974). The measurement of enterprise diversification. Review of Economics and Statistics 56, 399401.

P. K. Gorecki (1975). An inter-industry analysis of diver- sification in U.K. manufacturing industry. Journal of Industrial Economics 24, 13146.

R. M. Grant and A. P. Jammine (1988). Performance differences between the Wrigley/Rumelt strategic cat- egories. Strategic Management Journal 9, 33346.

R. M. Grant, A. P. Jammine and H. Thomas (1988). Diversity, diversification and profitability among British manufacturing companies, 1972-84. Academy of Management Journal 31, 771-801.

J. Hassid (1 975). Recent evidence on conglomerate diver- sification in U.K. manufacturing industry. Manchester School of Economic and Social Studies 43, 384-7.

A. P. Jacquemin and C. H. Berry (1979). Entropy meas- ures of diversification and corporate growth. Journal of Industrial Economics 27, 359-69.

G. R. Jones and C. W. L. Hill (1988). Transaction cost analysis of strategy-structure choice. Strategic Management Journal 9, 159-72.

G. A. Luffman and R. Reed (1984). The Strategy and Performance of British Industry, 197Ck80, London: Macmillan.

C. A. Montgomery (1982). The measurement of firm diversification: some new empirical evidence. Academy of Management Journal 25, 299-307.

K. Palepu (1985). Diversification strategy, profit per- formance and the entropy measure. Strategic Manage- ment Journal 6, 239-55.

R. A. Pitts and H. D. Hopkins (1982). Firm diversity: conceptualization and measurement. Academy of Man- agement Review 7, 420-29.

M. E. Porter (1985). Competitive Advantage, New York: Free Press.

C. K. Prahalad and R. A. Bettis (1984). The dominant logic: a new linkage between diversity and per- formance. Strategic Management Journal 7, 485-501.

D. J. Ravenscraft and F. M. Scherer (1987). Mergers, Sell-

201-18.

66 R. REED

offs, and Economic Theory, Washington, DC: The Brookings Institution.

R. Reed and J. A. Sharp (1987). Confirmation of the specialization ratio. Applied Economics 19, 393-405.

R. P. Rumelt (1974). Strategy, Structure and Economic Performance, Boston, MA: Harvard Business School (Division of Research).

T. A. Staudt (1954). Program for product diversification. Harvard Business Review 32, 6, 121-31.

Y. Suzuki (1980). The strategy and structure of the top 100 Japanese industrial enterprises, 1950-70. Strategic Management Journal 1, 265-91.

M. A. Utton (1977). Large firm diversification in British

manufacturing industry. The Economic Journal 87,

N. Venkatraman and J. H. Grant (1986). Construct measurement in organizational strategy research a critique and proposal. Academy of Management Review

P. Varadarajan and V. Ramanujam (1987). Diversific- ation and performance: a reexamination using a new two-dimensional conceptualization of diversity in firms. Academy of Management Journal 30, 38&93.

L. Wrigley (1970). Divisional autonomy and diversific- ation. Harvard: Unpublished doctoral dissertation.

345, 96-113.

11, 71-87.