Embed Size (px)

Citation preview

EXECUTIVE SUMMARY Palace Resources (ASX Code: PXR) is progressing due

diligence on the Lumpo coal project (“Lumpo Project”) in

West Sumatra, Indonesia in respect of which it has entered into a Memorandum of Understanding (MoU) to acquire 100% of Lumpo Resources Pte Ltd, a company incorporated in Singapore (“Lumpo Resources”). In turn, Lumpo Resources has entered into a binding MoU with PT Tambang Batubara Lumpo (TBL) to acquire a 65% joint venture (JV)

interest in the Lumpo Project, with TBL retaining 35%. A drilling program (1,800 metres; 30 holes) is planned to commence following the execution of the JV agreement. The Lumpo Project has the potential to produce high-quality premium Indonesia coal at low-to-moderate cost into the burgeoning Indonesian domestic thermal coal

market and the key export markets of China and India. Further, PXR believe that the acquisition of the Lumpo Project will help to establish the company’s presence in Indonesia, with PXR currently undertaking detailed negotiations on another coal project in Indonesia.

Due Diligence Progressing According to Plan PXR has four months (from the execution of the MoU) to complete the due diligence required to proceed with the JV. The company has already received a positive legal due diligence report, which now paves the way for PXR to commence planning for a drilling

program as part of the due diligence process. PXR is now focuses on undertaking technical due diligence on the Lumpo Project, and

to this end, have announced the appointment of a Competent Person (Mr Brett Gunter) to oversee Palace PXR‟s technical due diligence and to work towards the development of a JORC resource statement.

The vendor has undertaken drilling and test pits on a very small portion of the area being drilled (<3%) and made these available to PXR. These results indicate the potential for a mineable resource. PXR aims to confirm these figures through its own drilling program. Subject to the satisfactory completion of due diligence and

satisfaction of the conditions precedent under the Memorandum of Understanding, PXR aims to commence exploration programs in

the 1st quarter of 2012, with a view to developing a production plan for commencement in the 4th quarter of 2012.

PALACE RESOURCES LTD (PXR)

MMooUU EExxeeccuutteedd ttoo AAccqquuiirree HHiigghh--QQuuaalliittyy IInnddoonneessiiaann CCooaall PPrroojjeecctt

SPECULATIVE

7 October 2011

Important Disclosure Investors should be aware that Palace Resources Ltd is a corporate client of Alpha and that Alpha will receive a consultancy fee from Palace Resources Ltd for compiling this research report

Share Trading Info

ASX Code PXR

Current Share Price (cps) 3.1

Trading Low /High (Rolling Year) (cps) - $3.981.0 - 8.0

Mkt Captalisation (undiluted) $m 9.3

Issued Capital (m)

Total Ordinary Shares 301.5

Unlisted Options 160.3

Total Diluted Securities 461.8

Board of Directors*

Guy Le Page Non Executive Chairman

* Further details on Page 17

Major Shareholders

Spartan Nominees P/L 6.5%

Fay Holdings P/L 5.7%

Formaine P/L 3.7%

Ossart Holdings P/L 3.3%

John Wardman & Associates 2.9%

Ian Murie Non Executive Director

Nicholas Clark Managing Director

0

1,000

2,000

3,000

4,000

5,000

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Price (cps)Volume ('000)

PXR 6-month Price Chart

Price

Volume

Palace Resources (PXR)

Page 2 of 18

Potential Premium for High Quality Coal Several coal samples analysed by the vendor indicate the

presence of high-quality coal, underpinned by high calorific values ranging between 6,800 Kcal/kg and 8,000 Kcal/kg (averaging >7,200 Kcal/kg) and low moisture content. These figures are based on several verifiable samples provided by the vendor to PXR, with all samples results subject to due diligence.

The quality of coal also compares favourably with the specifications of typical Indonesian bituminous coal, as well as with the specifications of the Rio Tinto thermal coal blend.

The price for Lumpo Project coal - based on the indicative high coal quality and relatively lower moisture and ash content – may attract a premium above:

i) The benchmark for 6,500 Kcal/kg coal (currently around

US$122/tonne) and ii) The Indonesian coal reference price for 7,000 Kcal/kg

grade (US$132/tonne as at March 2011).

Favourable Project Infrastructure

The project area is located approximately 20 kilometres by sealed road from the stockpile and barge jetty at Painan giving it access

to export facilities. Indonesian export coals are typically loaded onto barges at either

river-based or coastal-sited loading facilities and transported to an offshore transfer point for loading onto ocean-going vessels or barged to a deep water coal terminal. Further, Indonesian coal is moved from mine to shipping points primarily via a combination of trucking and barging. At most Indonesian export thermal coal mines, coal is trucked

directly to a coal processing/barge-loading facility located on tidewater or on a barge-navigable river. For direct-haul operations, trucking distances typically vary from between 10 to 35 kilometres.

Indonesia to lead Thermal Coal Export Growth

According to energy consultants Wood Mackenzie, Indonesia will lead global growth in thermal coal exports in the next decade with producers Bumi Resources and Adaro Energy becoming two of the top three coal exporting companies worldwide by 2015. Indonesia's coal export growth will also be fueled in large part by demand from China and India, with Chinese coal imports expected

to more than double by 2015. Wood Mackenzie estimates that China will produce an additional 1 billion tonnes through 2015 to meet that demand. Wood Mackenzie predicts that Indonesia will make up 39% of global increases in coal exports by 2015. By 2020, Indonesia's

annual production will be above 500 million tonnes.

Palace Resources (PXR)

Page 3 of 18

Strong Relationships in Indonesia PXR‟s Managing Director, Nicholas (Nick) Clark, has a vast amount

of experience of Indonesia. He was, born, raised and educated in Jakarta until the age of 11 and returned there in 1998 to work as a lawyer for an Indonesian commercial organisation. Mr Clark has also operated in China, a key potential market for PXR, and speaks both Bahasa and Mandarin. He has qualifications in Law, Economics and Accounting (CPA) and has a commercial and

financial background. Mr Clark‟s capability, contacts and understanding of Indonesia

have already enabled PXR to accelerate this opportunity and strengthen its commercial position. Legal due diligence undertaken by Jakarta-based layers have confirmed the „Clear and Clean‟ status of the IUP. Mr Clark is also utilising his network to identify

and secure additional Production Permits (IUPs) for PXR and his knowledge of US capital markets to join the OTCQX marketplace. PXR‟s Indonesian-based Geologist, Mr Mulyadi Hasan, has an extensive network of production permit holders and was instrumental in introducing the project to PXR. Mr Hasan is currently undertaking a site visit and has assisted in the review of

information provided by the vendor. Financial Position and Access to Capital

The cash balance as at 30 June 2011 was $1.53 million. PXR is currently in the process of listing on the OTCQX1 and has

appointed The Lebrecht Group as its principal liaison in the US, to provide guidance on the OTCQX International requirements and to advise PXR in relation to establishing its Level 1 American Depository Receipts (ADR‟s) program. The company has also appointed Spartan Securities, a privately-held, full-service investment banking firm based in St Petersburg,

Florida, as its sponsor for the OTCQX International application process. Spartan will also assist in introducing PXR to its extensive network of institutions and brokers in the US.

1 The premier tier of the US OTC market.

Palace Resources (PXR)

Page 4 of 18

11.. KKEEYY PPRROOJJEECCTT -- LLUUMMPPOO,, WWEESSTT SSUUMMAATTRRAA

1.1 Outline In August 2011, PXR announced that it had secured the rights to negotiate a JV interest on a prospective coal project (Lumpo Project) located in the resource-rich province of West Sumatra, Indonesia. On 6 October 2011, PXR announced that it had executed an agreement in which it will take a 65% JV interest in Lumpo Project.

The project area is situated at Lumpo - Painan in the Pesisir Selatan

District and is accessible by a well-sealed asphalt road from Padang. The project area, located very close to a stockpile and barge jetty at Painan, has access to developed roads and export areas. Figure 1: Location of Lumpo Project and Surrounding Infrastructure

Source: Google Earth, Alpha Securities

Palace Resources (PXR)

Page 5 of 18

1.1.1 Acquisition Terms Under the terms of the acquisition, PXR will acquire all of the issued

capital of Lumpo Resources Pte Ltd for the following consideration:

i. 75 million fully paid ordinary shares in PXR ii. Reimbursement of Lumpo Resources‟ investment in the Lumpo

Project up to a maximum of US$250,000; and iii. A royalty of US$10 per tonne from production.

Completion of the acquisition is subject to a number of conditions precedent, including financial and legal due diligence on Lumpo

Resources being completed by PXR and to PXR‟s satisfaction; and each party obtaining the required shareholder and regulatory approvals necessary for the acquisition. All conditions precedent must be satisfied or waived on or before 13 January 2012.

1.1.2 Due Diligence Process

In order to enable the company exercise its option2 to proceed with the joint venture, PXR has a 4-month period in which to undertake due diligence, which includes legal & accounting due diligence, and technical due diligence (which involves confirmation drilling and re-

sampling). A legal due diligence report has been received, confirming that the permit holder (i.e. vendor) with which PXR has executed a MoU has obtained an IUP3 for Operation and Production of coal at

Painan, West Sumatra and that the IUP is deemed valid, as it is listed with the Status „Clear and Clean‟ on the „List of Clear and Clean IUPs‟ published by the Directorate General of Minerals and Coal.

Accounting due diligence has commenced, with the company having at its disposal the majority of the 4-month period to complete the technical due diligence. Part of the due diligence process involves a program to confirm both previous drilling on the IUP and to test earlier reconnaissance rock chip

samples. The IUP covers an area of 922.7 hectares (ha), with all environmental and mining approvals in place. The license area allows production up to 10,000 tonnes per month immediately. To date, only 28ha (~3%) of the IUP has been explored by the current vendor and indicate the potential for a mineable resource4. PXR aims to confirm

these figures through their own drilling program.

PXR‟s technical team will undertake a further site visit in order to:

Survey and confirm the IUP boundaries; Identify previous drill holes and test pits and collect additional

samples for confirmatory analysis; Plan confirmatory drill holes;

Confirm the status of the stockpile and loading facilities at Painan Port and

Meet with locals and community elders, with whom PXR have a strong relationship.

2 PXR has secured an option to convert its interest into equity at a maximum value of US$10 million for 100%.

3 The abbreviation for Izin Usaha Pertambangan (i.e. Production Permit). The IUP gives the permit holder the right to conduct construction, production, haulage, sale and refining in the Mining Area. 4 To be confirmed by PXR through their own drilling program

Palace Resources (PXR)

Page 6 of 18

The vendor‟s analysis of several samples indicates the presence of a high-quality coal, underpinned by high calorific values5 of between 6,800 Kcal/kg and 8,000 Kcal/kg and low moisture content. Table 1

summarises the results for the samples analysed to date.

Table 1: Results from Coal Samples at Lumpo Project

arb - dried basis adb – air dried basis

Source: PXR

1.1.3 Details of Competent Person (Mr Brett Gunter) PXR has appointed Mr Brett Gunter to oversee technical due diligence of the Lumpo project and to work up to the development of a JORC-compliant resource statement.

Mr Gunter, a member of The Australian Institute of Mining and

Metallurgy (MAusIMM), has over 15 years experience of operating in Indonesia and has sufficient expertise relevant to the style and type of deposit under consideration. He is currently the President Director and Principal Consultant for PT GMT Indonesia, a geological consulting firm based in Jakarta.

Brett‟s activities include coal project generation and geological appraisals, geological modelling and resource estimation, exploration management, scoping and feasibility studies and assistance in AMDAL compilations. He has a wide range of experience across all of the major Indonesian coalfields and has managed the exploration and field operations of some large resource drilling programmes, including a 2-year 50,000 metre drilling program delineating in excess of two billion

tonnes of coal.

5 Calorific value is defined as the calories or thermal units contained in one unit of a substance and released when the substance is burned.

Unit Basis Range Average

Total Moisture % arb 1.4 - 3.6 2.3

Inherent Moisture % adb 1.4 - 2.5 1.9

Ash Content % adb 3.2 - 13.9 8.1

Volatile Matter % adb 5.2 - 14.4 9.2

Fixed Carbon % adb 75.9 - 87.0 80.8

Total Sulphur % adb 0.53 - 1.08 0.9

Calorific Value Kcal/Kg adb 6307 - 7999 7249.47

Palace Resources (PXR)

Page 7 of 18

1.2 Quality of Indonesian Coal

Export thermal coals in Indonesia are bituminous to sub-bituminous in quality, with widely varying ash, moisture, sulphur and volatile matter characteristics. In Indonesia, coal with calorific values in excess of 5,300 Kcal/kg is generally regarded as bituminous coals, while coal with calorific values of 4,100 to 5,300 Kcal/kg is classified as sub-bituminous coals. Table 2 outlines the typical coal quality specifications

for Indonesian export thermal coals.

Table 2: Typical Coal Specifications for Indonesian Export Thermal Coals

Source: World Coal Asia

The bituminous and higher calorific-value content sub-bituminous coals

produced from Indonesia are typically supplied to export markets, while the lower calorific-value content sub-bituminous coals are supplied to both export and domestic markets. Most of the lowest rank sub-

bituminous coals have gained acceptance in export markets due to their very low sulphur contents (typically <0.2%). Although Indonesian low-rank coal are typically low-to-very low in ash and sulphur content,

total moisture contents are generally greater than 40%. Domestic Indonesian customers are estimated to consume around one-quarter of Indonesia‟s total coal production, although an increasing share of Indonesia‟s total coal output is being consumed domestically, buoyed by growth in coal-fired power generation in Asia to combat growing energy demands and rising crude oil and natural gas prices.

Much of the increased production is likely to come from low-rank lignite and sub-bituminous coal deposits, with calorific values of about 3,700 Kcal/kg to 4,200 Kcal/kg.

1.3 Quality of Lumpo Coal Compared to Indonesian Coal

The sample results for Lumpo coal (outlined in Table 1) indicate that it compares very favourably with the figures for typical Indonesian

bituminous coal. In particular:

The average calorific value is well in excess of the 5,300 – 6,700 Kcal/kg range for typical Indonesian bituminous coal;

Total Moisture content for Lumpo coal is well below the range of 10-12% for typical Indonesian bituminous coal;

The ash content is within range and

The sulphur content is at the higher range for typical Indonesian bituminous coal.

Lumpo coal also compares favourably with the specifications for another cross reference 'benchmark' for thermal coal - the Rio Tinto thermal coal blend – illustrated in Table 3.

Unit Basis Bituminous Sub-Bituminous

Coals Coals

Total Moisture % arb 10 - 12 24 - 38

Ash Content % adb 2 - 12 1.5 - 7.5

Volatile Matter % adb 31 - 42 28 - 37

Total Sulphur % adb 0.10 - 0.95 0.07 - 0.90

Calorific Value Kcal/Kg adb 5300 - 6700 4100 - 5200

Palace Resources (PXR)

Page 8 of 18

Table 3: Quality of Lumpo Coal vs Rio Tinto Thermal Coal Blend

1.4 Expected Pricing for Lumpo Coal

Recent coal prices for Indonesia coal, provided for 6,500 Kcal/kg grade

is considered an appropriate reference price for Lumpo coal. Figure 2 below highlights to prices over the last three months for 6,500 Kcal/kg,

5,800 Kcal/kg and 5,000 Kcal/kg grades and shows the benchmark for 6,500 Kcal coal at around US$122/tonne.

Figure 2: Recent Prices for Indonesian Coal Grades (US$/tonne)

Source: Argus/Coalindo Indonesian Coal Index Report, 2 September 2011

In comparison, mid-range coal samples from the Lumpo Project are in excess of 7,000 Kcal/kg, although the better coal quality from the Lumpo Project does not in itself suggest that Lumpo coal should attract

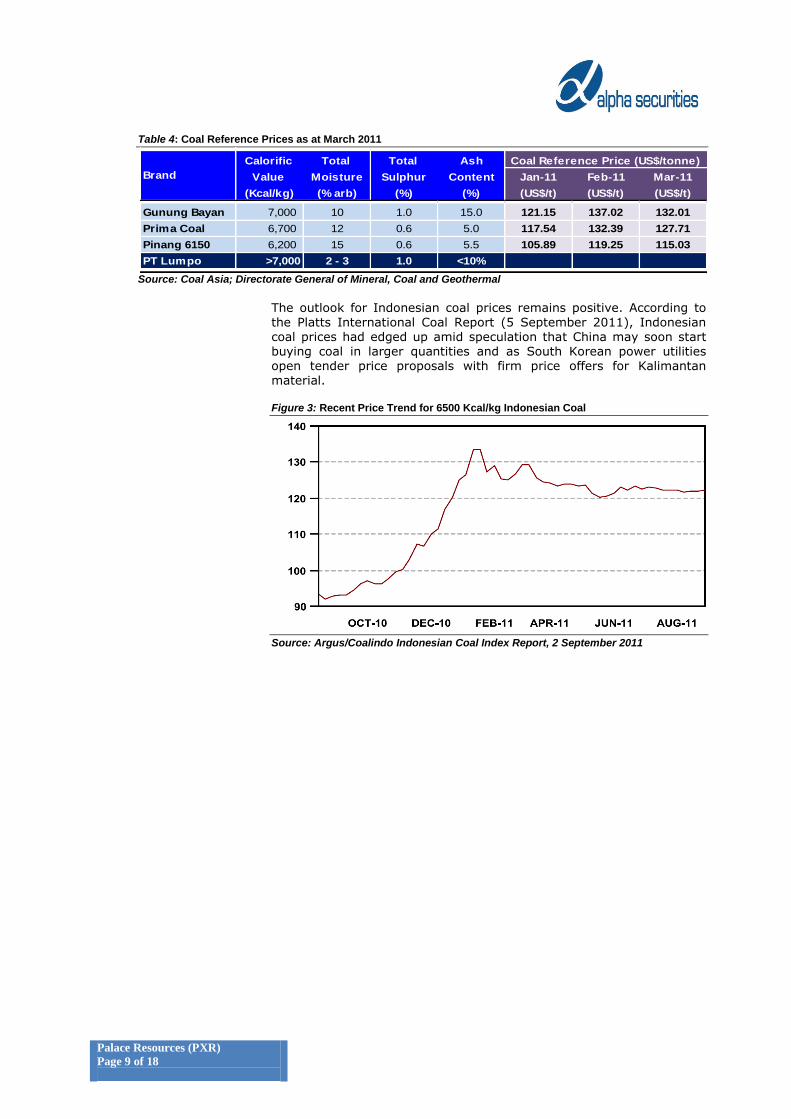

a premium over this benchmark price. To this end, it is worth noting that Lumpo coal with specifications of >7,000 Kcal/kg; total moisture around 2-3%; ash content <10% and sulphur content of 1% would support the argument for a premium price. To illustrate, the Indonesia Coal Reference Price (HBA) for March 2011 for Gunung Bayan (with a 7,000 Kcal/kg grade) was US$132/tonne.

In comparison to the coal samples for the Lumpo Project, Gunung Bayan coal had a total moisture content of 10%, ash content of 15% and sulphur content of 1%. This is illustrated in Table 4, together with the coal reference prices for coal brands. Given the superior quality of Lumpo coal (in comparison to Gunung Bayan), it could justify a

premium above the US$132/tonne achieved for Gunung Bayan in March 2011, as the Lumpo coal‟s ash and moisture content is lower.

Unit Basis PT Lumpo Rio Tinto

Coal (Avg) Thermal Blend

Ash Content % adb 8.1 13.5

Total Sulphur % adb 0.9 0.55

Calorific Value Kcal/Kg adb >7200 6850

122.5 122.6 121.9

103.5 102.8 101.0

83.5 82.4 80.5

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Jun 2011 Jul 2011 Aug 2011

6500 Kcal

5800 Kcal

5000 Kcal

Palace Resources (PXR)

Page 9 of 18

Table 4: Coal Reference Prices as at March 2011

Source: Coal Asia; Directorate General of Mineral, Coal and Geothermal

The outlook for Indonesian coal prices remains positive. According to

the Platts International Coal Report (5 September 2011), Indonesian coal prices had edged up amid speculation that China may soon start buying coal in larger quantities and as South Korean power utilities open tender price proposals with firm price offers for Kalimantan material.

Figure 3: Recent Price Trend for 6500 Kcal/kg Indonesian Coal

Source: Argus/Coalindo Indonesian Coal Index Report, 2 September 2011

Calorific Total Total Ash Coal Reference Price (US$/tonne)

Value Moisture Sulphur Content Jan-11 Feb-11 Mar-11

(Kcal/kg) (% arb) (%) (%) (US$/t) (US$/t) (US$/t)

Gunung Bayan 7,000 10 1.0 15.0 121.15 137.02 132.01

Prima Coal 6,700 12 0.6 5.0 117.54 132.39 127.71

Pinang 6150 6,200 15 0.6 5.5 105.89 119.25 115.03

PT Lumpo >7,000 2 - 3 1.0 <10%

Brand

Palace Resources (PXR)

Page 10 of 18

22.. RROOBBUUSSTT DDEEMMAANNDD FFOORR IINNDDOONNEESSIIAANN CCOOAALL

2.1 Overview of Indonesia

Indonesia comprises over 13,000 islands between Asia and Australia and 33 provinces. With over 237.6 million people6, it is the world's fourth most populous country, and has the world's largest Muslim population. Ethnically it is highly diverse, with more than 300 local languages. The

population ranges from rural hunter-gatherers to modern urban elite.

Approximately two-thirds of the population is rural, but there is a substantial urban migration that is leading to increasing demands for electricity, much of which will be generated by coal-fired power stations. Indonesia is one of the emerging market economies of the world and a

member of Group of 20 (G20) major economies. Economic growth this year is the highest it has been since the 1998 Asian crisis, supported by investment, exports and private consumption. The Indonesian government expects GDP to grow 6.5% in 2011 and 6.7% in 2012, after expanding 6.1% in 2010, when it was among the best performing economies in the Group of 20 nations.

Indonesia is one step away from its first investment-grade credit rating in more than a decade as President Susilo Bambang Yudhoyono targets

growth of as much as 6.6% on average through the remainder of his term ending in 2014. In contrast to the Indonesian Government‟s GDP growth forecasts for

this year and next, the Indonesian Chamber of Commerce expects GDP to grow to by 6.8%-7.0% this year and 7.5% in 2012, underpinned by evidence of robust domestic consumption and global demand for natural resources. According to Bloomberg, the Indonesian government earned 35% of its revenue from the oil, gas and minerals industry, and of that, 4-5% came from minerals.

The recently-announced budget for 2012 pledged to increase infrastructure spending in order to redress an infrastructure shortfall and also contains plans to cut the budget deficit to 1.5% of GDP from a

targeted 2.1% (of GDP) this year. Indonesia has also recently announced plans to introduce 5-year tax breaks in order to attract foreign investment. The tax breaks are to apply to international companies that invest more than US$120 million in Indonesia.

6 According to the National Census in 2010

Palace Resources (PXR)

Page 11 of 18

Figure 4: Main Indonesian Export Partners (As at 2009)

Source: Federation of International Trade Association

Figure 5: Main Indonesian Import Partners (As at 2009)

Source: Federation of International Trade Association

Japan, 15.9%

China, 9.9%

US, 9.3%

Singapore, 8.8%

South Korea, 7.0%

India , 6.4%

Malaysia, 5.5% Australia, 2.8%

Japan China US Singapore South Korea India Malaysia Australia

Singapore, 16.1%

China, 14.5%

Japan, 10.2%

US, 7.3%

Malaysia, 5.9%

South Korea, 4.9%

Thailand, 4.8% Australia, 3.5%

Saudi Arabia, 3.2%

Singapore China Japan US Malaysia South Korea Thailand Australia Saudi Arabia

Palace Resources (PXR)

Page 12 of 18

2.2 Indonesian Coal Production

Indonesia currently produces thermal coal from more than 40 different mines in East Kalimantan, South Kalimantan and Sumatra. About two-thirds of the country‟s export thermal coal is currently produced from around two dozen mines in East Kalimantan, with nine mines in South Kalimantan accounting for most of the remaining exports. The larger producers dominate the supply of export coal, with the four largest

suppliers accounting for more than two-thirds of total Indonesian thermal coal exports in 2007. International markets have traditionally been the principal destination

for Indonesian thermal coals, with more than 75% of the country‟s total thermal coal production being exported. Major export markets for

Indonesian thermal coals include Japan, Taiwan, South Korea, Hong Kong, India, other Southeast Asian countries and Western Europe. Over an 8-year period from 2000 to 2007, Indonesia‟s thermal coal exports almost tripled, from 56 million tonnes in 2000 to nearly 165 million tonnes in 2007.

Figure 6: Historical Indonesian Thermal Coal Production (Mtpa)

Source: Worldcoal.com: World Coal Asia Special, 2009

2.3 Global Outlook for Thermal Coal Export Growth The demand for thermal coal demand has increased in line with the global capacity for steam power plants and has continued to grow for the last several years.

As the most widely-utilised energy resource apart from oil, the ever-

increasing demand for coal is due to its utilisation in power plants. The International Energy Agency (IEA) affirms that between 2006 and 2030, world coal consumption is predicted to increase by 49% from 127.5 billion tonnes in 2006 to 190.2 billion in 2030. IEA also forecasts a growth trend in coal consumption between 2005 and 2015, with an average rate of 2.6% per annum, after which the growth will decelerate

to 1.7% per annum between 2015 and 2030.

22 27 29 31 36 41 45 48

56 56

75

94

109

124

146

164

-

25

50

75

100

125

150

175

200

2000 2001 2002 2003 2004 2005 2006 2007

Exports Domestic Consumption

Palace Resources (PXR)

Page 13 of 18

2.3.1 China

In order to boost the production of steel and power plants, China‟s total consumption for coal (both thermal and coking) from 2006 to 2008 had increased to 6.8% or 1.4 billion tonnes - equivalent to 42.6% of the world‟s total coal consumption. This demand has exceeded domestic production capacity and has forced China to import both types of coal. In 2009, China increased imports of thermal coal and coking coal by

167% and 400% respectively, in contrast to the previous year, 2008. As an outline, in the nine months from September 2008, China

exported just 5.9 million tonnes of thermal coal. Due to the decline in production capacity and the pressure from the high demand by power plants, by September 2009, China had become the world‟s largest thermal coal importer at 46.4 billion tonnes. It is estimated that China‟s

demand will be 60 million tonnes in 2015. In August 2010, China's sovereign wealth fund, China Investment Corporation (CIC) announced that, in order to secure more resources in Southeast Asia and benefit from increasing trade in the region, it would invest US$2 billion into coal, electricity and port projects in Indonesia. No time limit was given for fulfilling these objectives, but CIC said it

was interested specifically in three Indonesian state firms: the coal mine company PT Tambang Batubara Bukit Asam; the state electricity company, PLN; and port operator, Pelindo.

2.3.2 India

A similar situation has also eventuated in India. In 2008, India‟s total coal consumption increased by 8.4% to 231 million tonnes or equivalent to 7% of the world‟s total coal consumption. The insufficiency of domestic coal supply has increased the import of coal. Between 2003 and 2008, India‟s coal import growth was 17.1%. Meanwhile, India‟s coal export suffered a drop with CAGR of -0.1%. In

order to maintain productivity, India‟s steel mills imported approximately 50% of their coal supply. By July 2009, India had imported 32.6 million tonnes of thermal coal, or 55% higher compared to July 2008. India‟s increase in demand has been forecast to continue in the next few years. In 2015, India‟s thermal coal demand is forecast

to 108 million tonnes.

2.3.3 Indonesia to lead thermal coal export growth

According to energy consultants Wood Mackenzie, Indonesia will lead global growth in thermal coal exports in the next decade with producers Bumi Resources and Adaro Energy becoming two of the top three coal exporting companies worldwide by 2015.

Wood Mackenzie predicts that Indonesia will make up 39% of global increases in coal exports by 2015, with Australia coming in a close second, accounting for 36% of export growth. By 2020, Indonesia's annual production will be above 500 million tonnes, a more than 50% increase from last year's production of 320 million tonnes. About a

quarter of that, some 130 million tonnes, will be from new greenfield

projects, and about 60% of which will be exported. Underpinning the strong growth rate in thermal coal exports for Indonesia is the fact that Bumi Resources and Adaro Energy each own mines at the top of the 10 largest mine expansions for thermal exports

Palace Resources (PXR)

Page 14 of 18

in the world, with Wood Mackenzie adding that six of the 10 largest mine expansions globally will be in Indonesia.

Indonesia's coal export growth will be fueled in large part by China and India, where power demand is expected to lift coal imports significantly over the next five years. Trading house Noble Group has predicted that Chinese coal imports could more than double by 2015. Wood Mackenzie estimates that China, the world's largest producer and consumer of coal, will produce an additional 1 billion tonnes through 2015 to meet

that demand. Wood Mackenzie believes that Indonesia is relatively well placed to

attract investment, as a reduction in royalties has encourages more investment into Indonesia. In addition, the tax rate has also reduced for producers of coal from previous years to the current system.

2.3.4 Transportation & Infrastructure Considerations in Indonesia There are only two known export coal operations in Indonesia that are capable of loading coal product directly onto ocean-going vessels - Pinang Mine (Bumi Resources) and Indominco-Bantang Mine (Banpu Public Company). Other Indonesian export coals are typically loaded onto barges at either river, or coastal-sited loading facilities and

transported to an offshore transfer point for loading onto ocean-going vessels or barged to a deep water coal terminal, such as the Balikpapan Coal Terminal, Indonesian Bulk Terminal or Arutmin‟s North Pulau Laut

Coal Terminal. Indonesian coal moves from mines to shipping points primarily via a

combination of trucking and barging (typically performed by contractors); however, some inland coal transportation is by rail and conveyor. At most Indonesia export thermal coal mines, coal is trucked directly to a coal processing/barge-loading facility located on tidewater or on a barge-navigable river. For direct-haul operations, trucking distances typically range from

between 10 kilometres to 35 kilometres, with a few mines experiencing longer hauls of up to 75 kilometres. Crushed coal is generally stockpiled and then loaded into barges and transported offshore for transfer to ocean-going vessels7. Coal destined for the Indonesian domestic market and some nearby export destinations, such as

Malaysia, is barged directly from Kalimantan or Sumatra to end users.

7 This process is known as transhipping.

Palace Resources (PXR)

Page 15 of 18

33.. OOTTHHEERR IINNTTEERREESSTTSS

3.1 West Papua Mining Project, Indonesia

3.1.1 Background

In October 2010, PXR announced the proposed acquisition of a 75% stake in 1,970km2 of tenements in the West Papua province of

Indonesia. The acquisition was to be undertaken by the acquisition of Primecity Holdings P/L (Primecity), which has the right to acquire the 75% interest in the three projects.

The tenements are immediately along strike from extensive coal outcrop on neighbouring tenements, including a 2.5 metre outcrop of

high-grade, semi-soft metallurgical coal. The area is considered by PXR to be prospective for high-grade and high calorific coal content, based on reconnaissance exploration results in the region. The tenements are located (from an infrastructure viewpoint) close to existing roads (from 0 to 30 kilometres by road from a deepwater harbor) and an existing operational port and (from a geographical

viewpoint) towards the northern tip of West Papua, approximately 300 kilometres south of the township of Manokwari. Basic road infrastructure is reasonable throughout the majority of the prospects, but requires upgrading in order to permit the movement of heavy

mining equipment should a future mining operation take place. Primecity entered into an MoU with the Regional Government of

Manokwari in November 2010 to develop a dedicated coal terminal at the port of Mumiwaren. A scoping study on the suitability of the port of Mumiwaren concluded that a conceptual port design of an export coal handling terminal, including the necessary support facilities, utilising approved port-marine infrastructure, is capable of being developed.

The conceptual port will be an open-access port capable of exporting a minimum of 10mtpa of coal products, together with the option of investigating ramp-up options of 2mtpa, moving to 5mtpa and then to 10mtpa.

3.1.2 Current Status

The due diligence process, which commenced shortly after the announcement of the proposed acquisition, has yet to be completed to PXR‟s satisfaction. Primecity have yet to verify all of the permits granted to the vendors, as well as compliance to the terms and conditions of any and all of the permits granted to the vendors as well as the prevailing laws and regulations.

If and when the due diligence process is completed to PXR‟s satisfaction, the company envisage an aggressive drilling program to be undertaken with a view to obtaining a maiden JORC resource within 6-9 months.

Palace Resources (PXR)

Page 16 of 18

3.2 Tanami Project, NT

PXR has JV with Excalibur Mining Ltd (ASX Code: EXM) to explore the Tanami region of the Northern Territory. Excalibur has the right to earn a 90% JV interest in project EL 25207. During the September 2010 quarter, EXM completed a wide-spaced drilling program at EXM‟s Browns Range project on EL 25207 (over

1,400km2), to follow up airborne geophysical analysis which identified a number of targets. The tenements are considered prospective for an unconformity style gold and/or uranium mineralisation similar to deposits in the East Alligator region of the Northern Territory. A total of

4,686 metres were drilled in the quarter completing the program of 8,760 metres in 267 holes across a total of nine targets.

Results from the assays from drilling undertaken in 2010 did not indicate any obvious anomalous results. However, further analysis and review is required to consider the potential of the area and any appropriate follow up field work. EXM has subsequently relinquished the southern portion of EL 25207,

which has deeper cover and is considered less prospective. EXM has also applied for an additional exploration tenement (EL 28565) which is contiguous with EL 25207 and in an area considered more likely for exploration success based on the drilling work completed in 2010.

Palace Resources (PXR)

Page 17 of 18

44.. BBOOAARRDD OOFF DDIIRREECCTTOORRSS

DIRECTOR

INTEREST

IN PXR

BACKGROUND

Guy Le Page Non Executive Chairman

NIL

Mr Le Page is currently a Director & Corporate Adviser of RM Corporate Finance specialising in resources. He is actively involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting and corporate advisory roles. He was formerly Head of Research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July of 1998 and has also worked as a Resources Analyst. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada and the US. His experience spans gold and base metal exploration and mining geology, and he has acted as a consultant to private and public companies. This professional experience included the production of both technical and valuation reports for resource companies. Mr Le Page holds a Bachelor of Arts, a Bachelor of Science and a Masters Degree in Business Administration from the University of Adelaide, a Bachelor of Applied Science (Hons) from the Curtin University of Technology and a Graduate Diploma in Applied Finance and Investment from the Securities Institute of Australia.

Nicholas Clark Managing Director

NIL

Mr Clark was appointed to the role of Managing Director in August 2011. His career extends over 18 years including extensive periods in the US and China. He comes from a Commercial, Institutional Relations, Investor Relations and Strategic Management background as a senior and executive leader. Critically for Palace, Mr Clark has a vast amount of

experience in Indonesia, having been born and raised in Indonesia up until the age of 11. He has also worked in Indonesia and speaks both Bahasa and Mandarin. His qualifications include a Bachelor of Economics & Bachelor of Law, Masters in Business Administration (MBA) as well as being a CPA (AI), a Fellow with the Financial Services Institute of Australia (FINSIA) and an Associate Fellow for the Australian Institute of Management (AIM).

Ian Murie Non Exec Director

2.92m ord shares; 106,666 unlisted

options

Mr Murie, who was appointed to the Board in April 2011, has 30 years experience as a commercial lawyer providing services to various clients, including ASX-listed and unlisted companies. His areas of expertise include corporate governance advisory roles to managed investment schemes. Mr Murie is a director of Acuvax Limited and is a Non Executive Director of Olea Australia Limited and was formerly Non Executive director of Excalibur Mining Corporation Ltd from 2005 to 2009. Mr Murie holds a Bachelor of Law and a Bachelor of Jurisprudence and is a public notary.

Palace Resources (PXR)

Page 18 of 18

DIRECTORY – ALPHA SECURITIES Corporate

George Karantzias

0401 670 620

Research Analyst

John Haddad

[email protected] 0407 219 222

Disclaimer This report is not for distribution and is not directed to, nor intended for distribution or use by,

any person or entity in any jurisdiction or country where the publication or availability of this report or such distribution or use would be contrary to local law or regulation. This document has been prepared (in Australia) by Alpha Securities Pty Ltd ABN 94 073 633 664 (“Alpha”), who holds an Australian Financial Services License (License number 330757). Alpha has made every effort to ensure that the information and material contained in this report is accurate and correct and has been obtained from reliable sources. However, Alpha makes no representation and gives no warranties about the accuracy or completeness of the information and material, including any forward looking statements and forecasts made by Palace Resources Ltd to Alpha, and it should not be relied upon as a substitute for the exercise of independent judgment. Except to the extent required by law, Alpha does not accept any liability, including negligence, for any loss

or damage arising from the use of, or reliance on, the material contained in this report, or as a result of errors or omissions on the part of Alpha or by any of their respective officers, employees or agents. This report is for information purposes only and is not intended as an offer or solicitation with respect to the sale or purchase of any securities. The securities recommended by Alpha carry no guarantee with respect to return of capital or the market value of those securities. There are general risks associated with any investment in securities. Investors should be aware that these risks might result in loss of income and capital invested. Neither Alpha nor any of its associates guarantees the repayment of capital. This report and any communication transmitted with it are confidential and are intended solely for the use of the individual or entity to which they are addressed. If you have received this email in error please notify

the sender. If you no longer wish to receive communication from Alpha, please contact Alpha requesting to be unsubscribed from future communications. General Advice Warning This report may contain general securities advice or recommendations, which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This report does not contain specific securities advice and does not take into account particular investment objectives, financial situation and needs of any particular person. You should carefully assess whether such information is appropriate in light of your individual circumstances before acting on it.

Disclosure

Alpha, its Directors and associates declare that they may have a relevant interest in the securities mentioned herein. This position can change at any time. Alpha also receives fees for advisory services. Alpha does and seeks to do business with companies covered in its research reports and investors should be aware that Alpha received a consultancy fee from Palace Resources Ltd for compiling this research report.

![[Ringkasan] Praktik tambang batubara meracuni air di kalimantan selatan](https://img.pdfslide.net/doc/110x75/568ca7f31a28ab186d9764c3/ringkasan-praktik-tambang-batubara-meracuni-air-di-kalimantan-selatan.jpg)