Embed Size (px)

Citation preview

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

WELCOME!!

BONDS FORBEGINNERS

National Association of Local Housing Finance Agencies

PART I - Bonds & Yields

PART II - Credit Worthiness

PART III - Issuing Bonds

PART IV - Getting Best Rates

BONDS FORBEGINNERS

Think of an object that helps you describe your impression of the housing bond business.

BONDS FORBEGINNERS

National Association of Local Housing Finance Agencies

PART IBonds & Yields

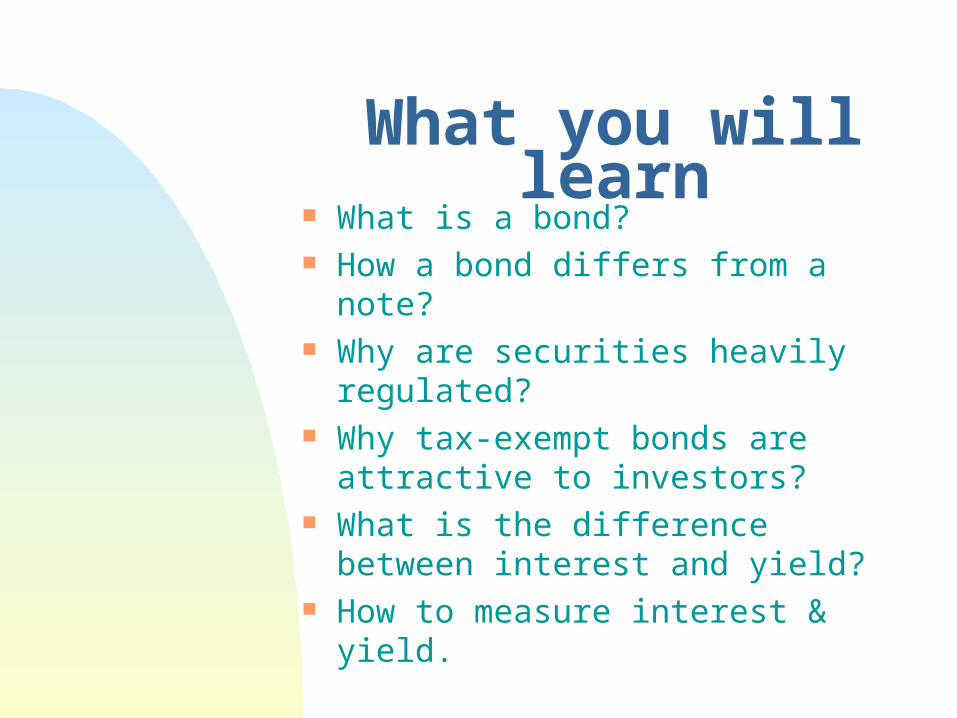

What you will learn What is a bond? How a bond differs from a note? Why are securities heavily

regulated? Why tax-exempt bonds are

attractive to investors? What is the difference between

interest and yield? How to measure interest & yield.

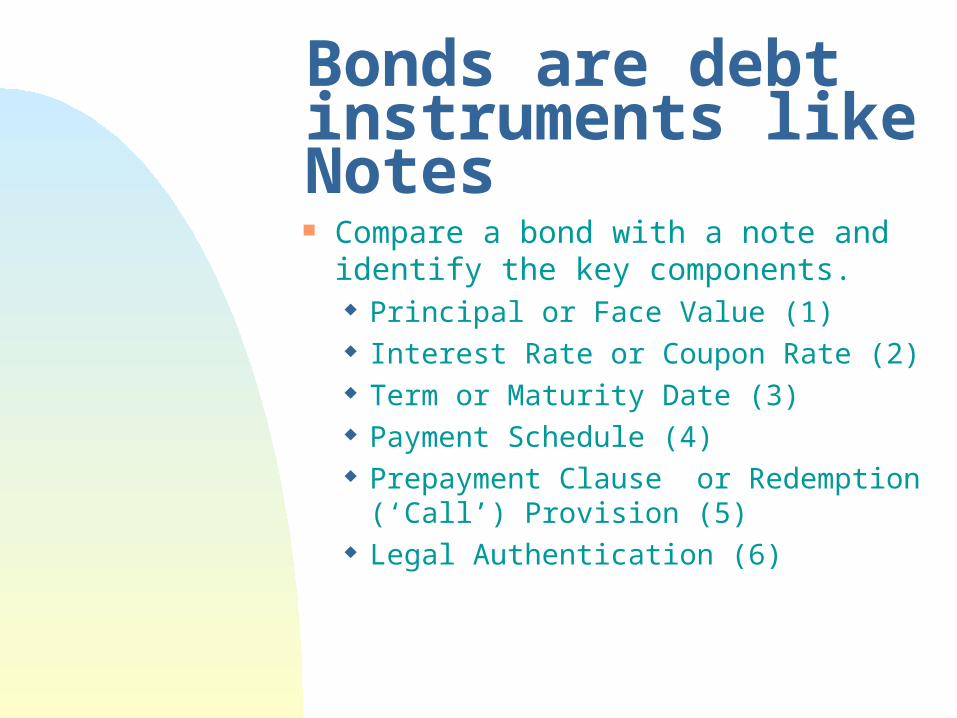

Bonds are debt instruments like Notes Compare a bond with a note and

identify the key components. Principal or Face Value (1) Interest Rate or Coupon Rate (2) Term or Maturity Date (3) Payment Schedule (4) Prepayment Clause or

Redemption (‘Call’) Provision (5) Legal Authentication (6)

Similarities betweenBonds & Notes

Both notes & bonds are

debt instruments

Both have face values, coupon rates, maturity dates, payment schedules & ‘call’ dates.

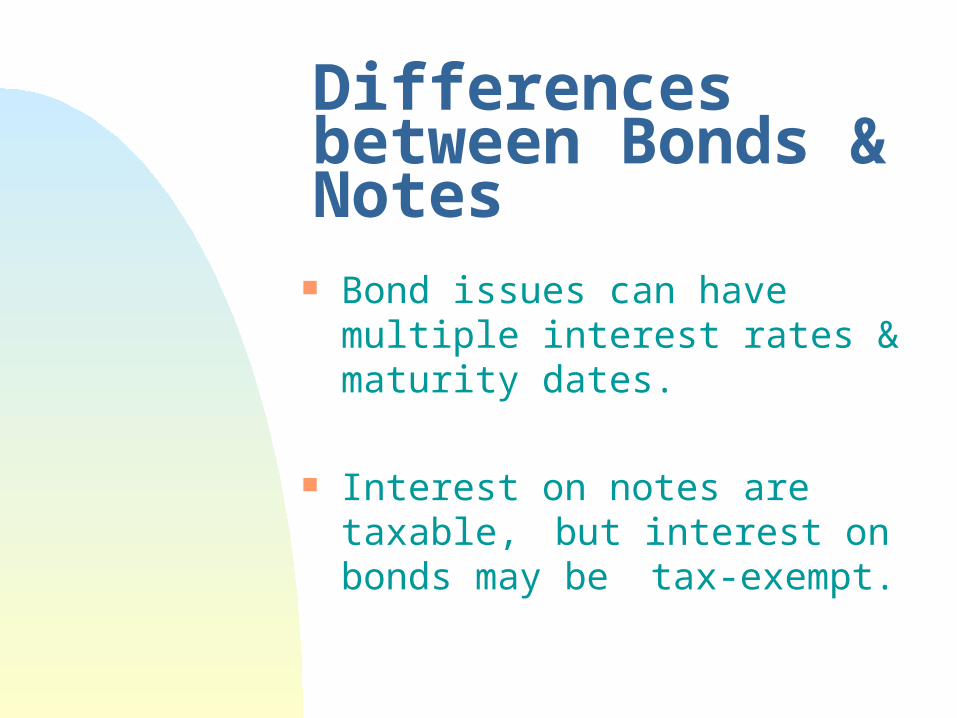

Differences between Bonds & Notes

Bond issues can have multiple interest rates & maturity dates.

Interest on notes are taxable, but interest on bonds may be tax-exempt.

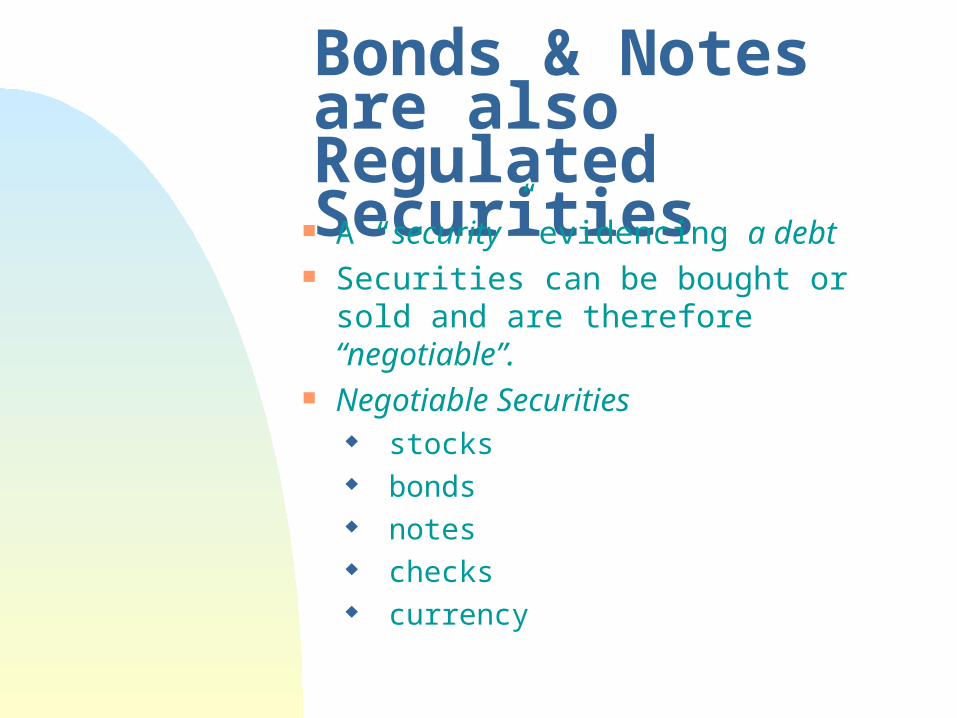

Bonds & Notes are also Regulated Securities

A “security” evidencing a debt Securities can be bought or sold

and are therefore “negotiable”. Negotiable Securities

stocks bonds notes checks currency

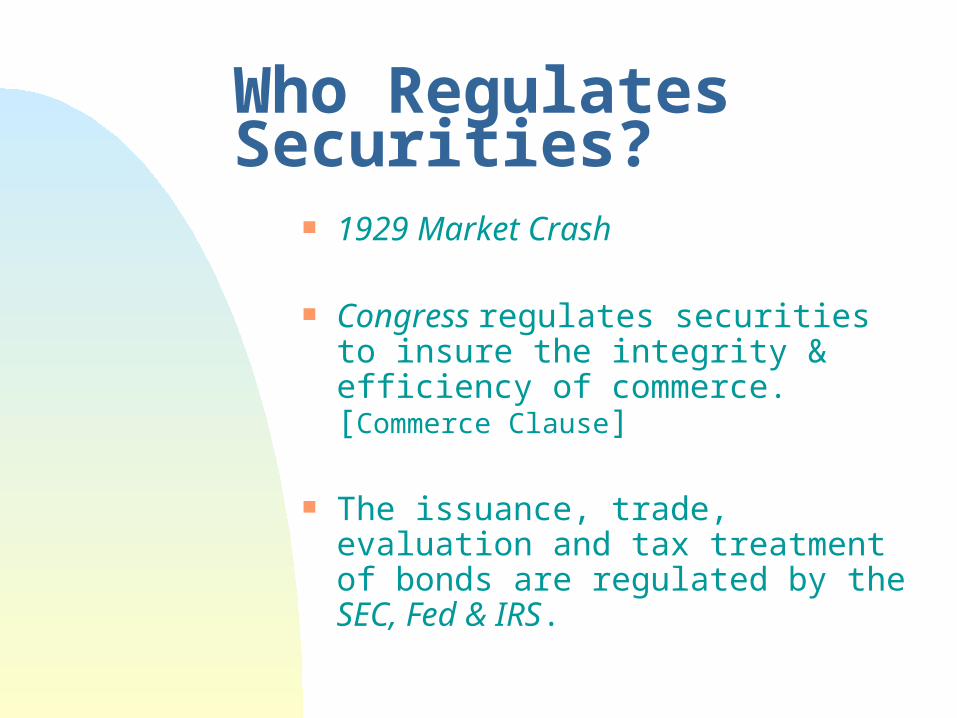

Who Regulates Securities?

1929 Market Crash

Congress regulates securities to insure the integrity & efficiency of commerce. [Commerce Clause]

The issuance, trade, evaluation and tax treatment of bonds are regulated by the SEC, Fed & IRS.

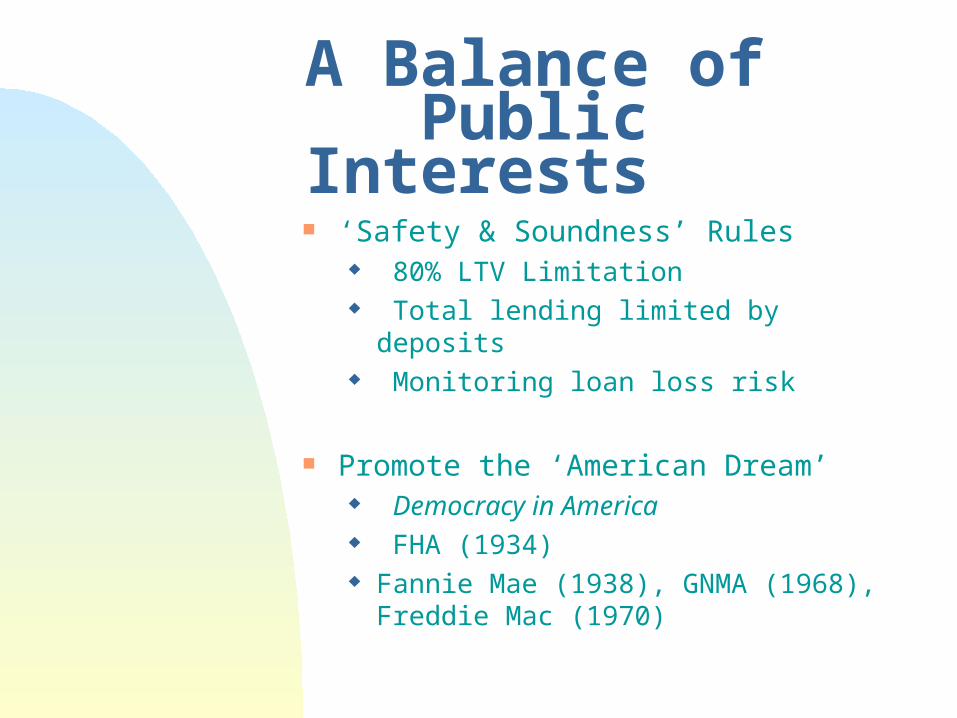

A Balance of Public Interests ‘Safety & Soundness’ Rules

80% LTV Limitation Total lending limited by deposits Monitoring loan loss risk

Promote the ‘American Dream’ Democracy in America FHA (1934) Fannie Mae (1938), GNMA (1968),

Freddie Mac (1970)

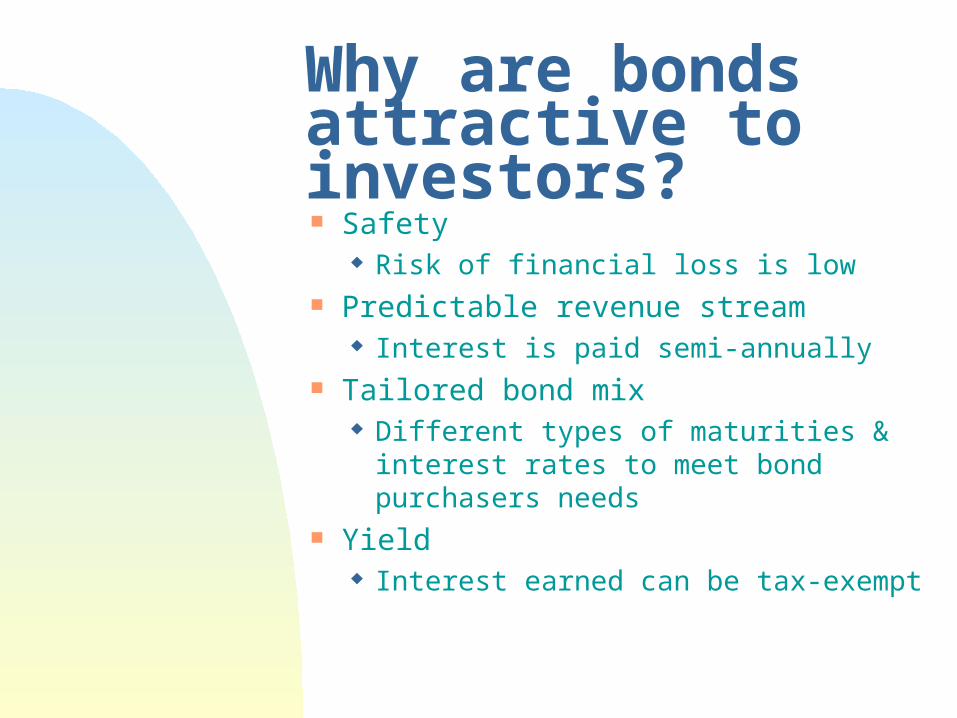

Why are bonds attractive to investors? Safety

Risk of financial loss is low Predictable revenue stream

Interest is paid semi-annually Tailored bond mix

Different types of maturities & interest rates to meet bond purchasers needs

Yield Interest earned can be tax-exempt

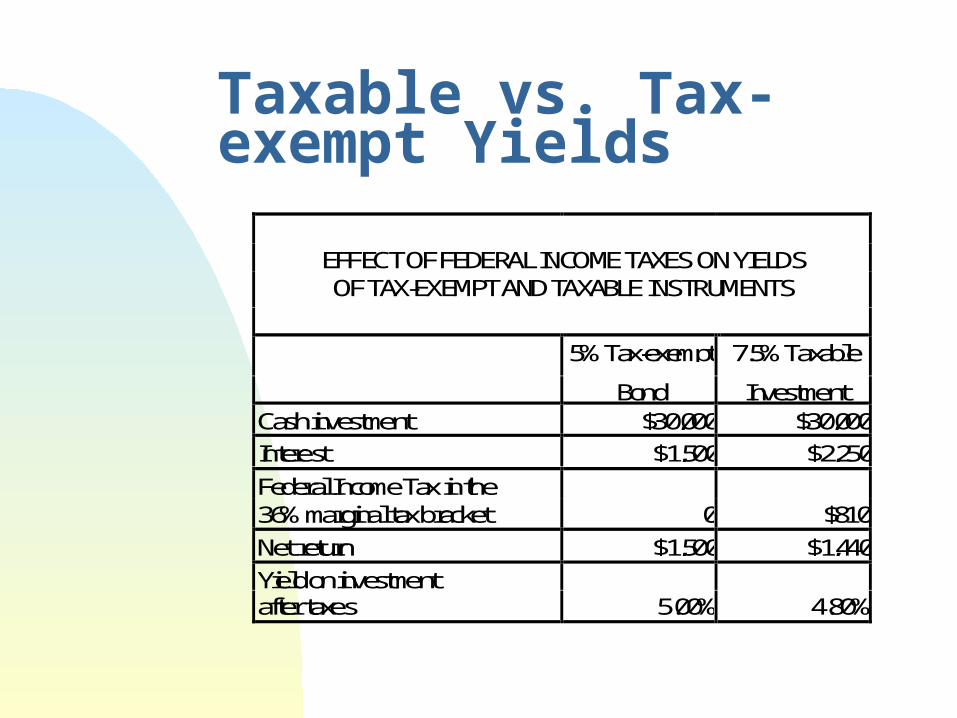

Taxable vs. Tax-exempt Yields

EFFECT OF FEDERAL INCOME TAXES ON YIELDSOF TAX-EXEMPT AND TAXABLE INSTRUMENTS

5% Tax-exempt 7.5% Taxable

Bond InvestmentCash investment $30,000 $30,000

Interest $1,500 $2,250

Federal Income Tax in the36% marginal tax bracket 0 $810

Net return $1,500 $1,440

Yield on investmentafter taxes 5.00% 4.80%

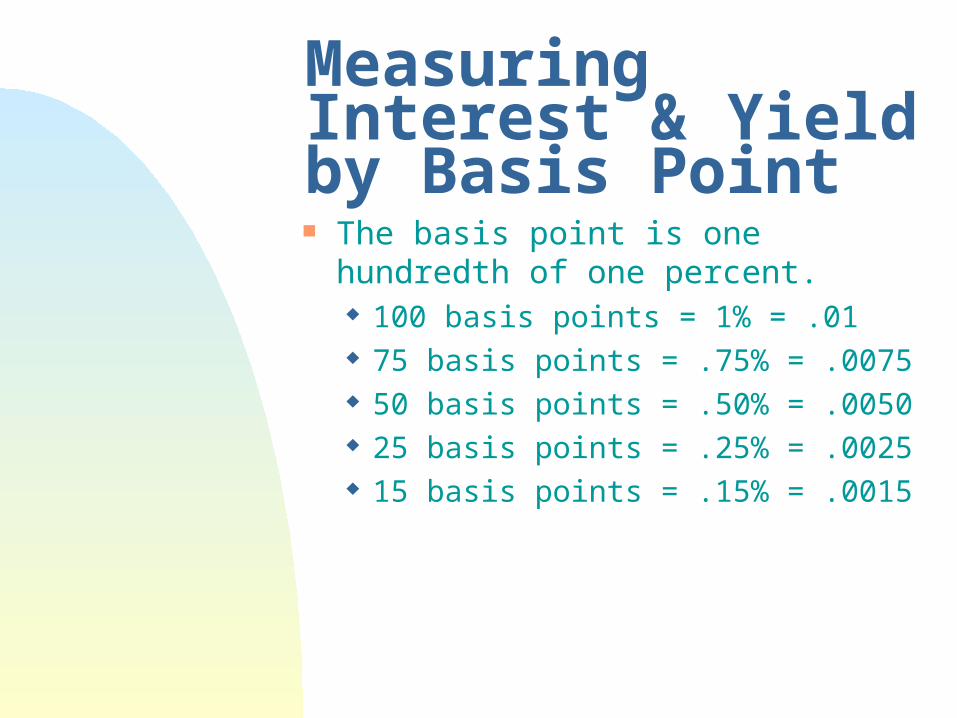

Measuring Interest & Yield by Basis Point The basis point is one hundredth of

one percent. 100 basis points = 1% = .01 75 basis points = .75% = .0075 50 basis points = .50% = .0050 25 basis points = .25% = .0025 15 basis points = .15% = .0015

What we have learned What is a bond? How a bond differs from a note? Why are securities heavily

regulated? Why tax-exempt bonds are

attractive to investors? What is the difference between

interest and yield? How to measure interest & yield.

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

PART IICredit Worthiness

What you will learn

What is credit worthiness & underwriting?

How to use the 5 C’s of credit worthiness analysis for a mortgage loan and for issuing bonds.

What are the key tools to enhance credit worthiness?

Credit Worthiness

Issuing bonds is taking out a loan for a public purpose.

Ever wonder how lenders decide on approval or denial of a loan?

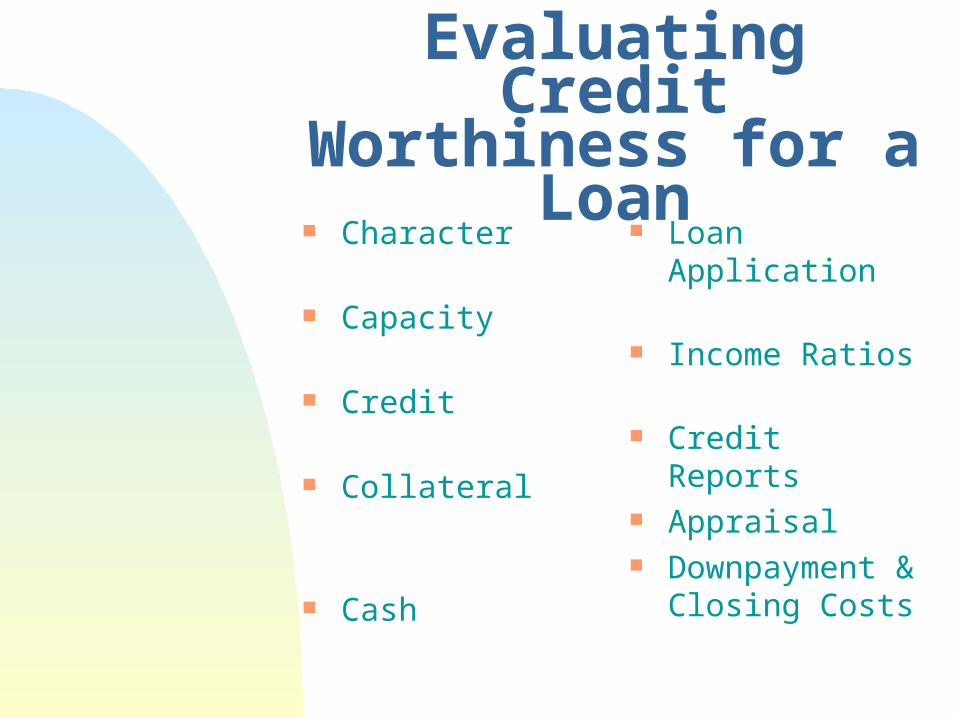

Evaluating Credit Worthiness for a Loan

Character

Capacity

Credit

Collateral

Cash

Loan Application

Income Ratios

Credit Reports

Appraisal

Downpayment & Closing Costs

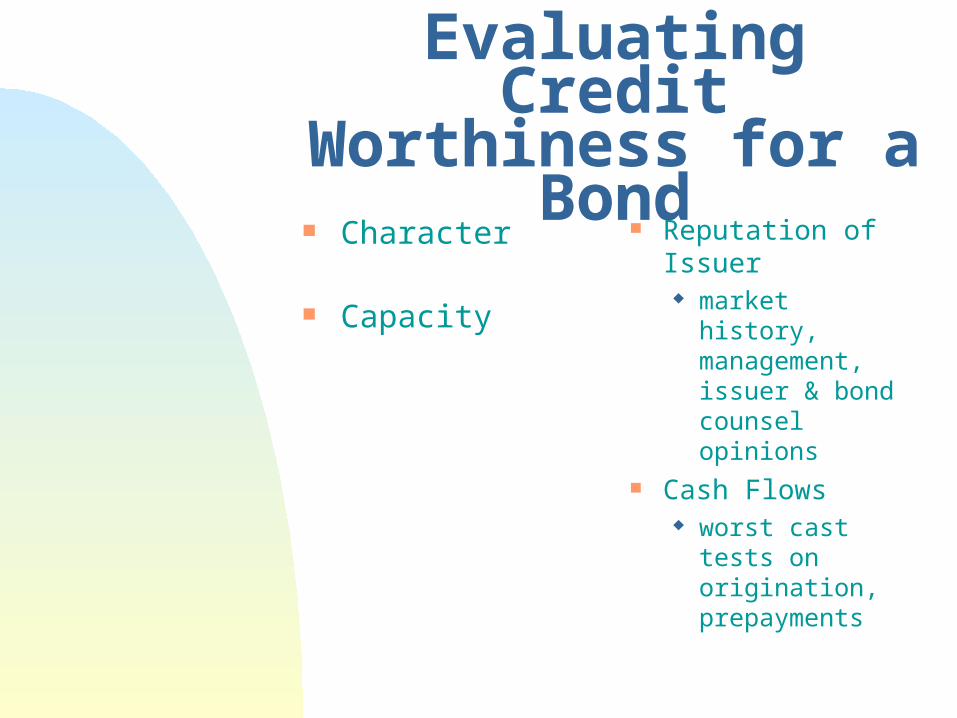

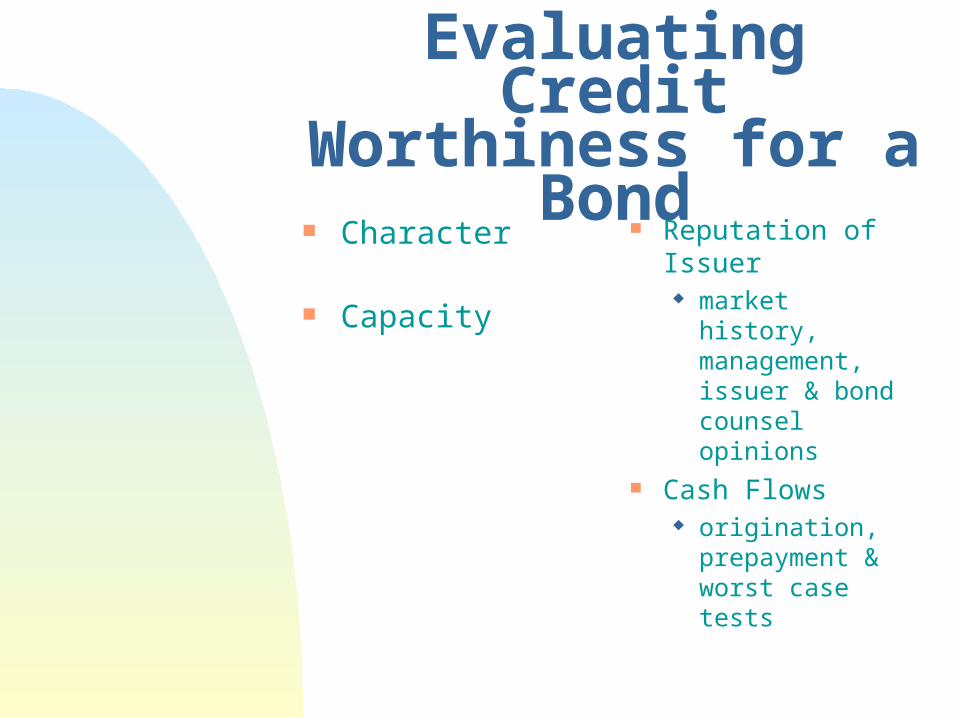

Evaluating Credit Worthiness for a Bond

Character

Capacity

Reputation of Issuer market history,

management, issuer & bond counsel opinions

Cash Flows worst cast tests

on origination, prepayments

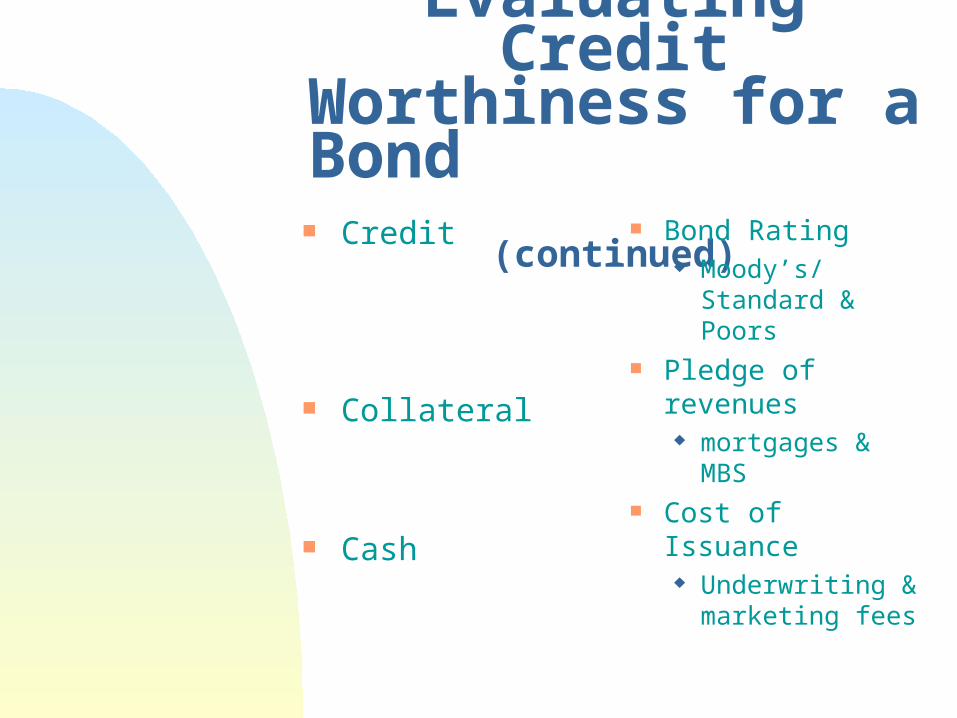

Evaluating Credit Worthiness for a Bond

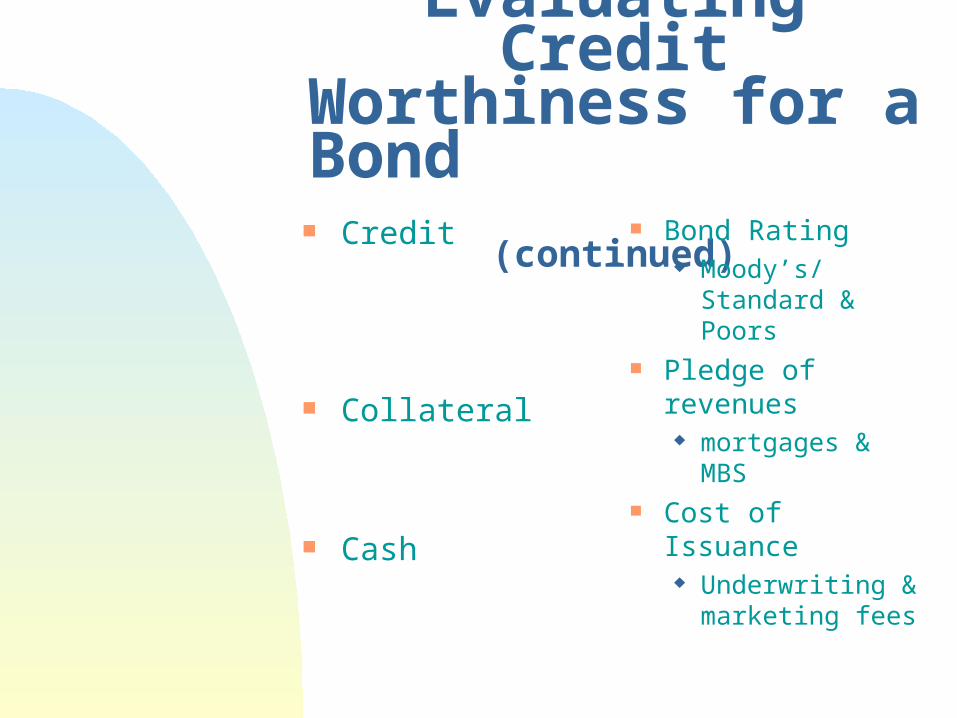

(continued) Credit

Collateral

Cash

Bond Rating Moody’s/

Standard & Poors

Pledge of revenues mortgages &

MBS Cost of Issuance

Underwriting & marketing fees

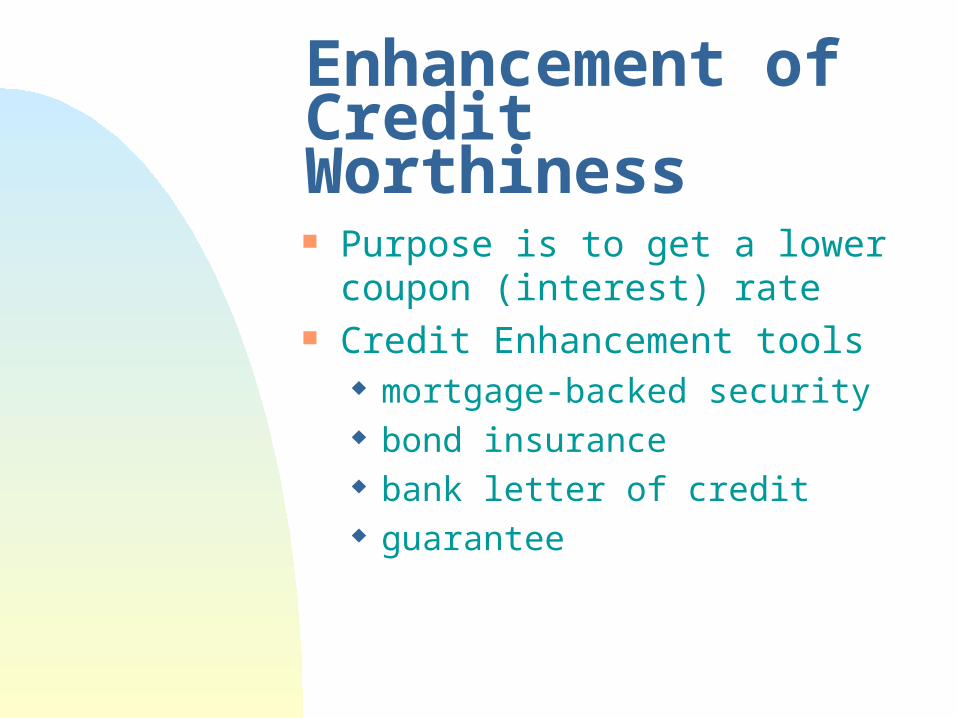

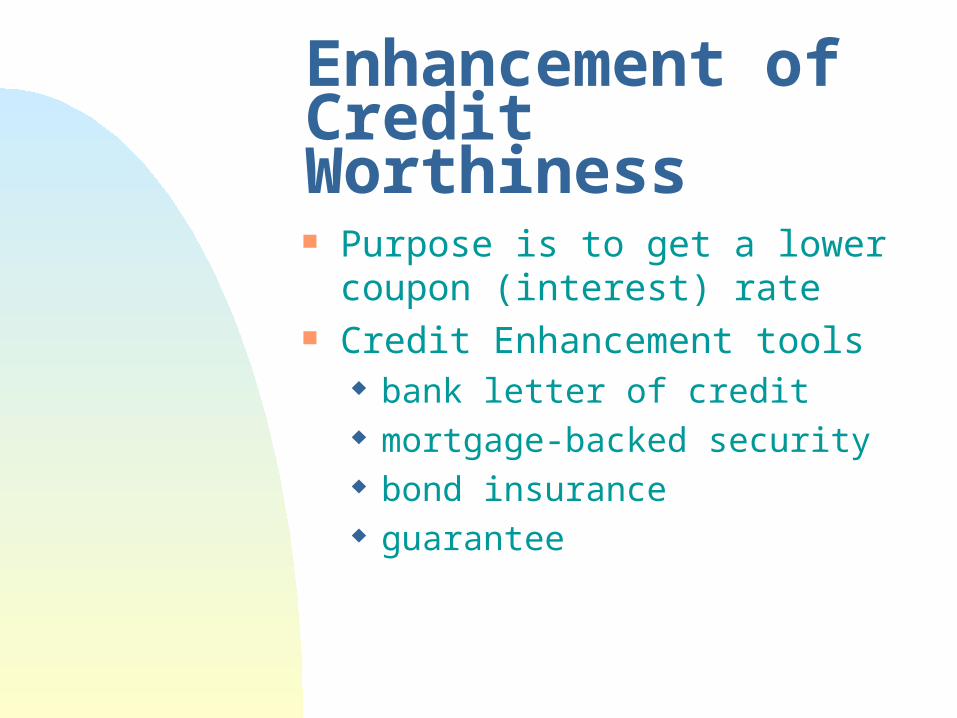

Enhancement of Credit Worthiness Purpose is to get a lower coupon

(interest) rate

Credit Enhancement tools mortgage-backed security bond insurance bank letter of credit guarantee

What you have learned

What is underwriting? What are the 5 C’s of credit

worthiness? How do underwriters make sure

the bond issue is credit worthy? What are the key tools to enhance

credit worthiness?

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

PART IIIIssuing Bonds

What you will learn

What is the difference between a GO bond and a revenue bond?

What is the private activity volume cap?

How does a public agency issue & sell bonds?

Who are the key professionals used to issue bonds?

What is the basic Flow of Funds?

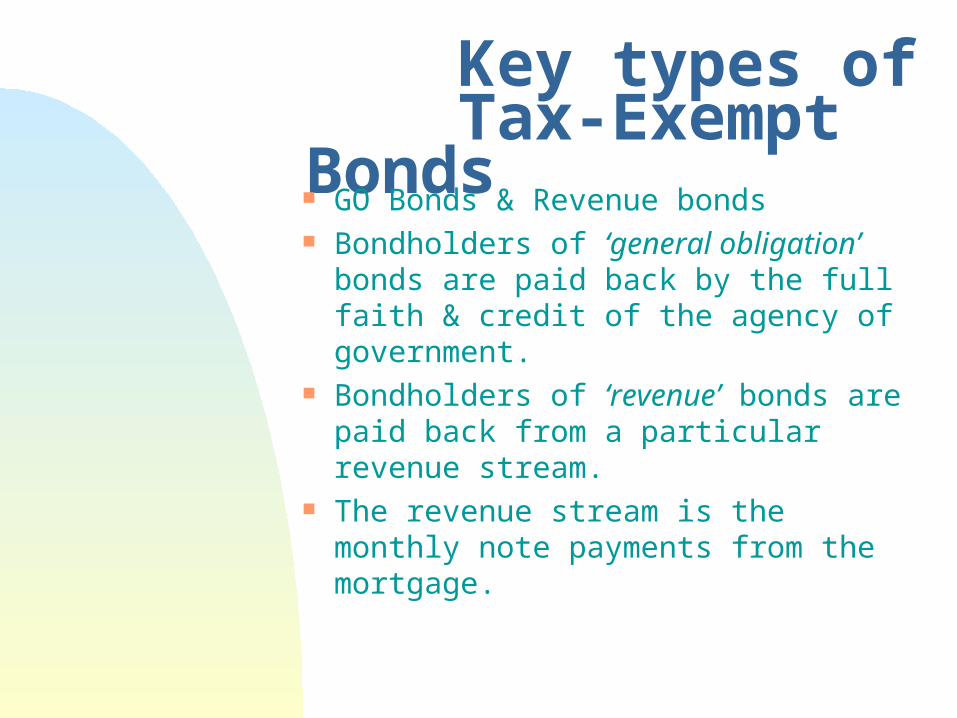

Key types of Tax-Exempt Bonds GO Bonds & Revenue bonds Bondholders of ‘general obligation’

bonds are paid back by the full faith & credit of the agency of government.

Bondholders of ‘revenue’ bonds are paid back from a particular revenue stream.

The revenue stream is the monthly note payments from the mortgage.

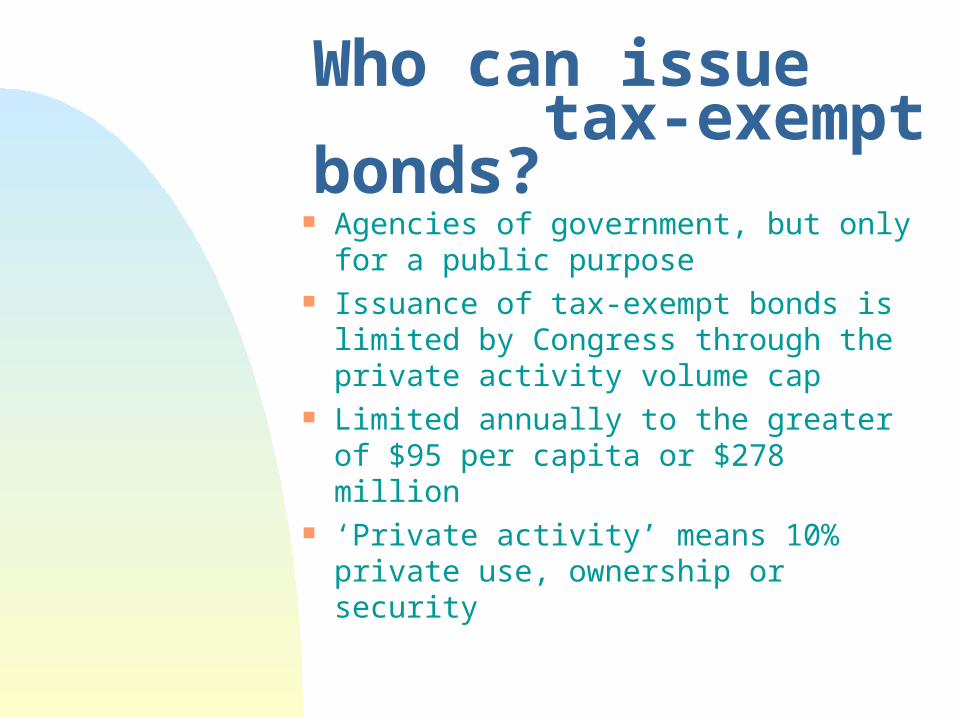

Who can issue tax-exempt bonds?

Agencies of government, but only for a public purpose

Issuance of tax-exempt bonds is limited by Congress through the private activity volume cap

Limited annually to the greater of $95 per capita or $278 million

‘Private activity’ means 10% private use, ownership or security

Cooking with Bonds

Due Diligence

Testing the Ingredients

Professionals

Associate Chefs

Legal Actions

Shaking & Baking

Market Bonds

Adding Seasoning

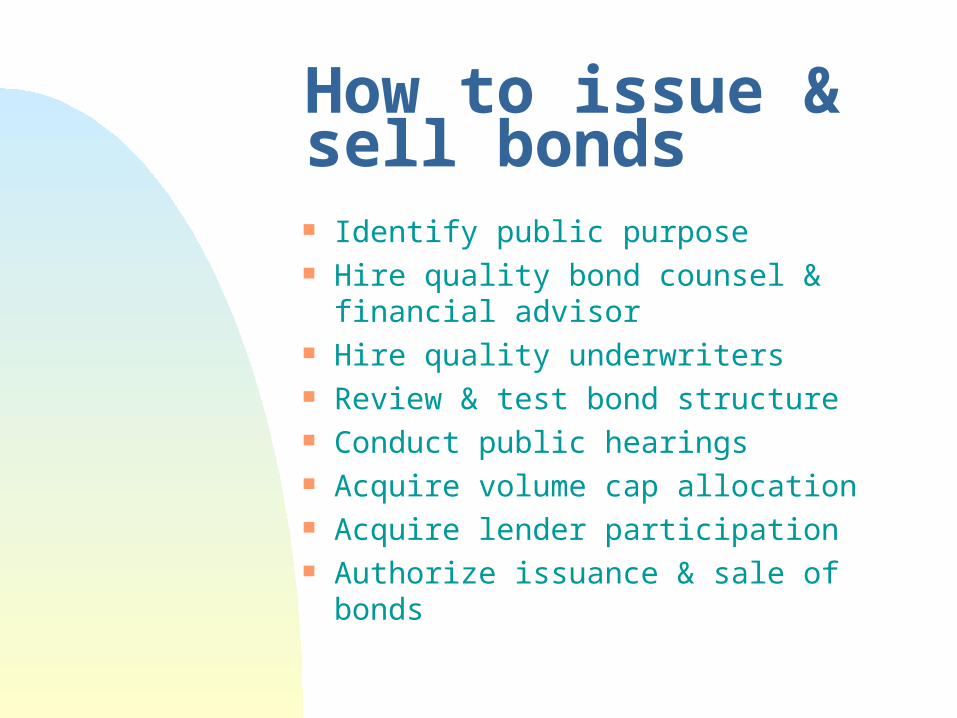

How to issue & sell bonds Identify public purpose Hire quality bond counsel & financial

advisor Hire quality underwriters Review & test bond structure Conduct public hearings Acquire volume cap allocation Acquire lender participation Authorize issuance & sale of bonds

How to issue & sell bonds (continued)

Hire Trustee, bond insurer & GIC Acquire credit enhancement Acquire bond rating Execute Bond Closing Documents Monitor the origination of loan and

repayment of principal & interest to bondholders

Perform continuing SEC disclosure, IRS rebate calculations, and cash flow analysis

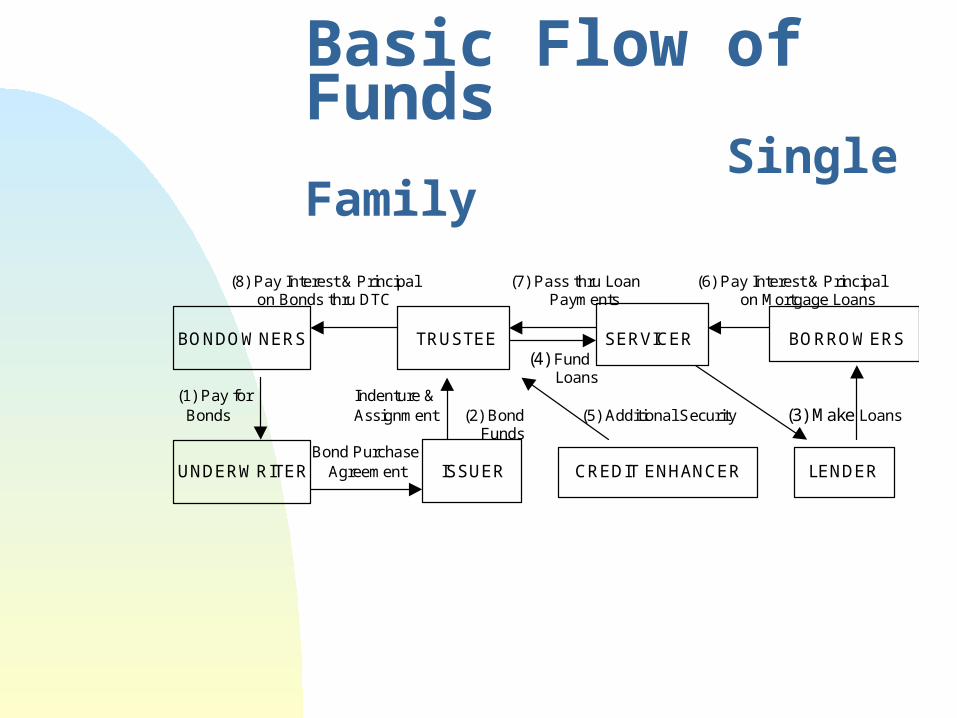

Basic Flow of Funds Single Family

(8) Pay Interest & Principal (7) Pass thru Loan (6) Pay Interest & Principal on Bonds thru DTC Payments on Mortgage Loans

BONDOWNERS TRUSTEE SERVICER BORROWERS (4) Fund

Loans (1) Pay for Indenture & Bonds Assignment (2) Bond (5) Additional Security (3) Make Loans Funds

Bond Purchase UNDERWRITER Agreement ISSUER CREDIT ENHANCER LENDER

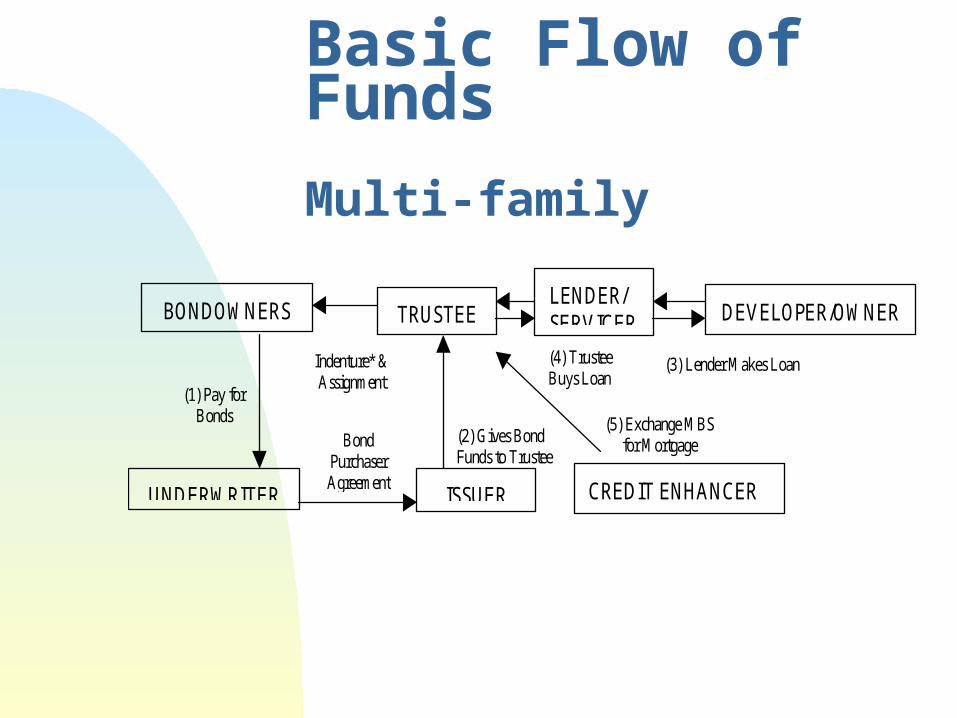

Basic Flow of Funds Multi-family

(3) Lender Makes Loan

BONDOWNERS TRUSTEE DEVELOPER/OWNER

UNDERWRITER ISSUER CREDIT ENHANCER

(4) TrusteeBuys Loan

(5) Exchange MBSfor Mortgage(2) Gives Bond

Funds to Trustee

Indenture* &Assignment

BondPurchaserAgreement

(1) Pay forBonds

LENDER/SERVICER

What you have learned What is the difference between a

GO bond and a revenue bonds Who can issue tax-exempt bonds? What is the private activity volume

cap? What are key steps to issue & sell

bonds? Who are the key professionals

used to issue bonds? What is the basic Flow of Funds?

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

PART IVSelling Safety & Quality

Adding Seasonings

What you will learn

How to get a better rate by reducing perceived risk.

How to reduce common risk factors Why the Official Statement is so

important. What are the key due diligence

requirements. Needed credit enhancements

What do bond purchasers want?

Bond purchasers want a secure & quality yield.

The lower the perceived risk, the lower the expected return (interest).

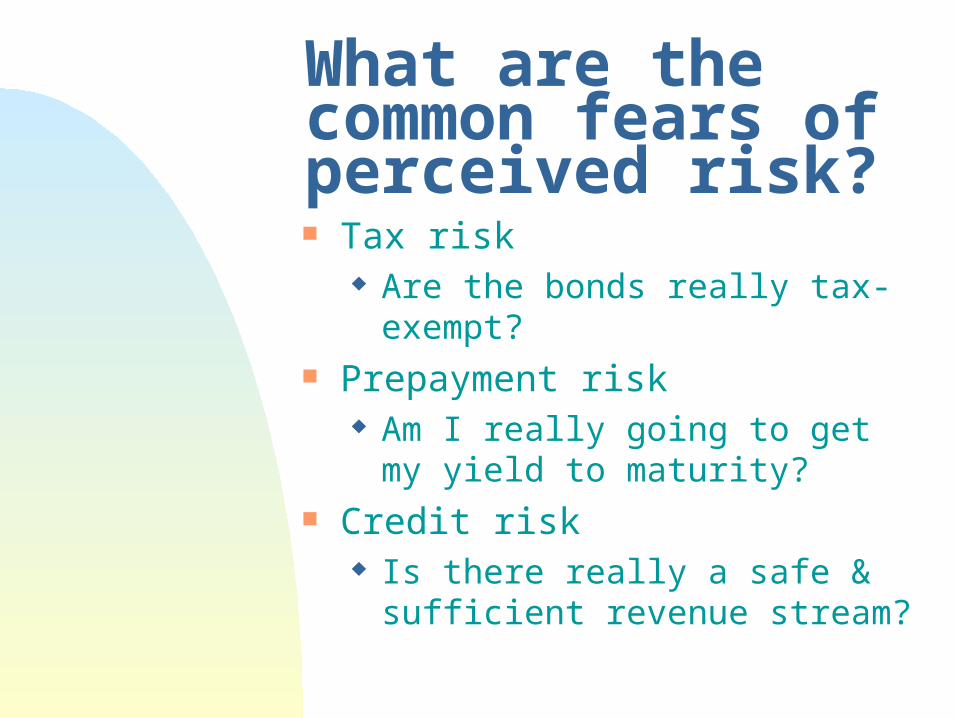

What are the common fears of perceived risk? Tax risk

Are the bonds really tax-exempt? Prepayment risk

Am I really going to get my yield to maturity?

Credit risk Is there really a safe & sufficient

revenue stream?

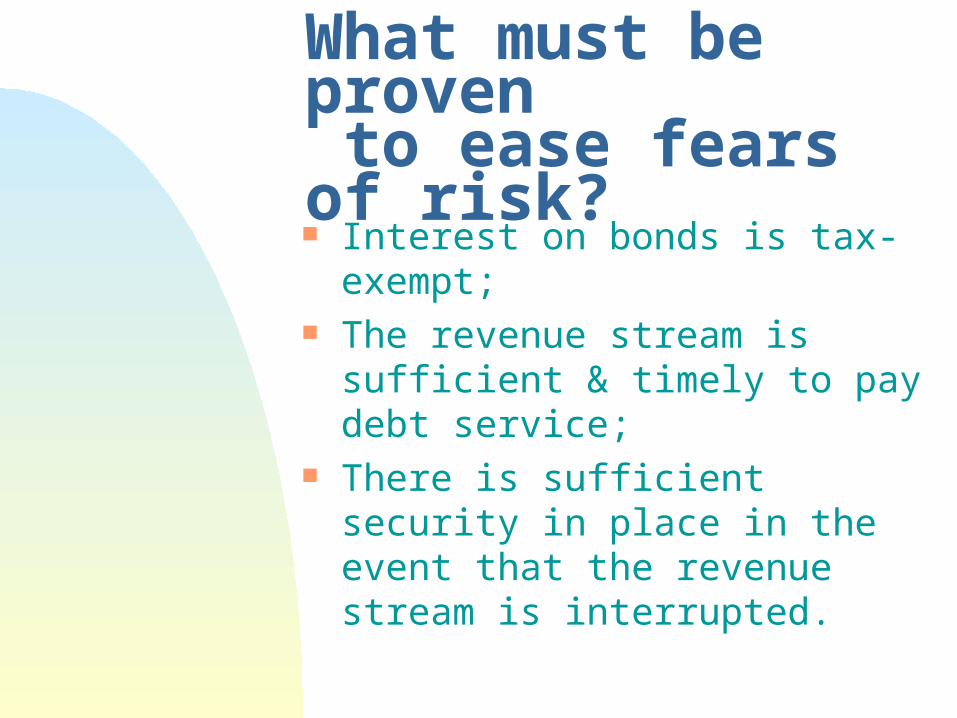

What must be proven to ease fears of risk? Interest on bonds is tax-exempt; The revenue stream is sufficient &

timely to pay debt service; There is sufficient security in place

in the event that the revenue stream is interrupted.

How does the Agency prove bond quality to the bond purchaser?

Credit Enhancement

Due Diligence

Disclosure

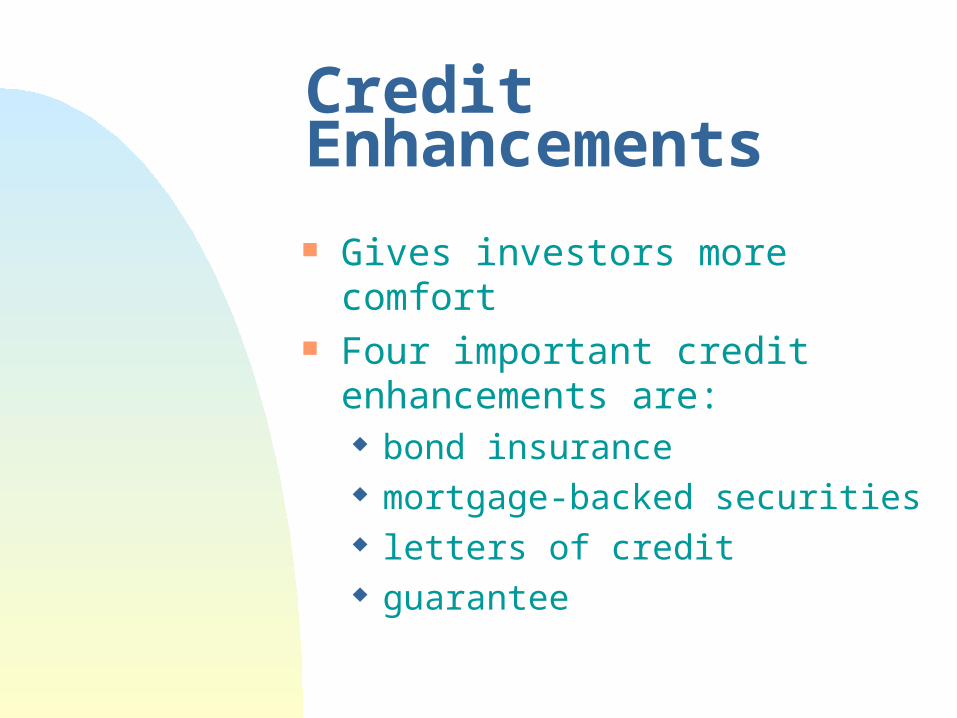

Credit Enhancements

Gives investors more comfort

Four important credit enhancements are: bond insurance mortgage-backed securities letters of credit guarantee

Mortgage-backed security Mortgages are pooled by master

servicer; Pool of mortgages are exchanged

for pass-through certificates; The certificates are backed by the

full faith & credit of Fannie Mae, Freddie Mac and/or Ginnie Mae.

The certificates act as additional security for the bondholders.

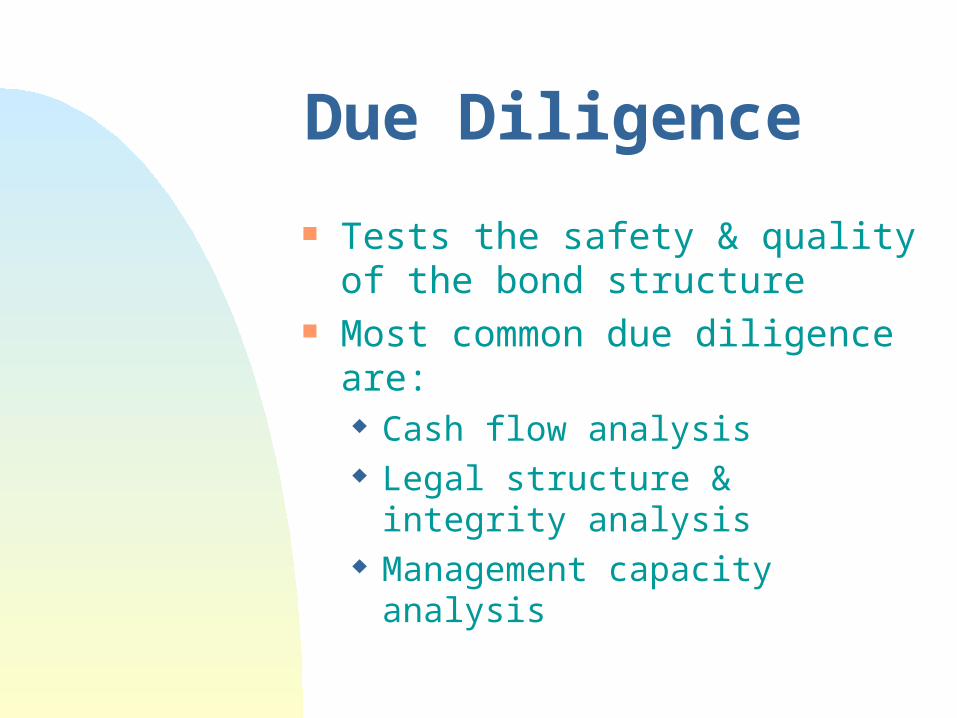

Due Diligence

Tests the safety & quality of the bond structure

Most common due diligence are: Cash flow analysis Legal structure & integrity analysis Management capacity analysis

Duty to Disclose

The SEC places the responsibility & liability on the Agency for accurate & complete disclosure.

The primary instrument of disclosure is the Official Statement.

The Official Statement

Gives all the information that investors would reasonably need in evaluating the merits, as well as the risks, of buying the Agency’s bonds.

Prepared by the underwriter. Underwriter’s counsel issues SEC

10b-5 opinion. SEC wants approval by issuer.

What’s in the Official Statement ? States yields & offering prices Identifies payment terms Reveals redemption provisions States method of bond registration Describes the Agency & its

management Explains the flow of funds How fund balances will be invested Summarizes the trust indenture

What you have learned

What are the common perceived fears of the bond purchasers?

How are the common fears reduced? Name the key credit enhancements. What are the key due diligence

requirements. Why the Official Statement is so

important.

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

THANK YOU VERY MUCH!!

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

THANK YOU VERY MUCH!!

BONDS FOR BEGINNERS

National Association of Local Housing Finance Agencies

THANK YOU VERY MUCH!!

BONDS FOR BEGINNERS

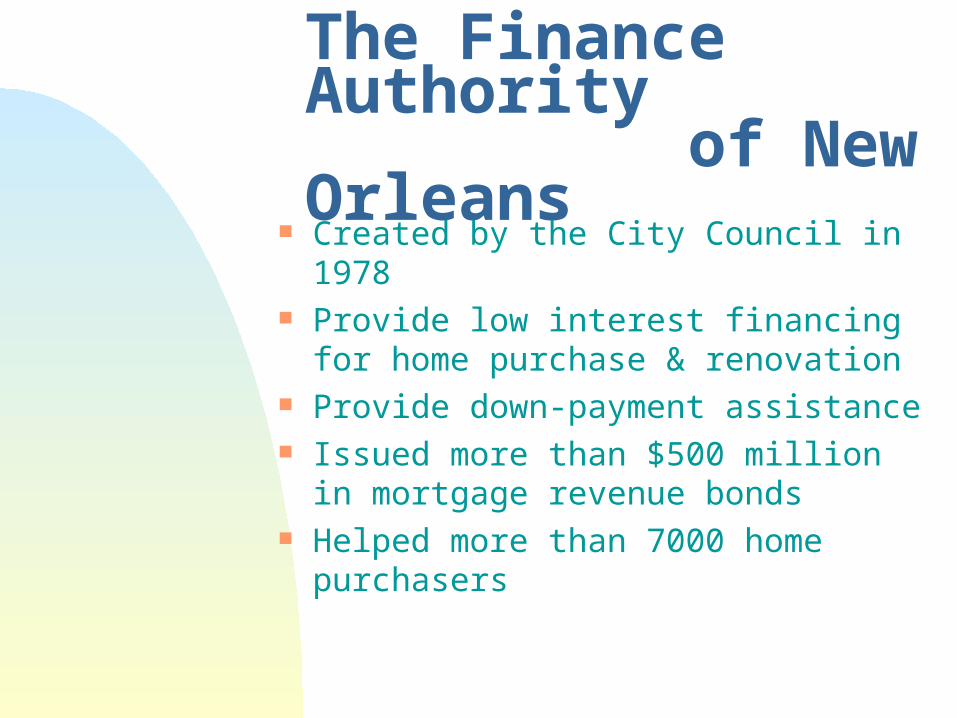

The Finance Authority

of New Orleans

Mtumishi St. Julien Executive Director

The Finance Authority of New Orleans

Created by the City Council in 1978 Provide low interest financing for

home purchase & renovation Provide down-payment assistance Issued more than $500 million in

mortgage revenue bonds Helped more than 7000 home

purchasers

BONDS FORBEGINNERS

The Finance Authority

of New Orleans

PART IBonds & Yields

BONDS FORBEGINNERS

The Finance Authority

of New Orleans

PART IICredit Worthiness

Credit Worthiness

Ever wonder how lenders decide on approval or denial of a loan?

Evaluating Credit Worthiness for a Loan

Character

Capacity

Credit

Collateral

Cash

Loan Application

Income Ratios

Credit Reports

Appraisal

Downpayment & Closing Costs

Evaluating Credit Worthiness for a Bond

Character

Capacity

Reputation of Issuer market history,

management, issuer & bond counsel opinions

Cash Flows origination,

prepayment & worst case tests

Evaluating Credit Worthiness for a Bond

(continued) Credit

Collateral

Cash

Bond Rating Moody’s/

Standard & Poors

Pledge of revenues mortgages &

MBS Cost of Issuance

Underwriting & marketing fees

Enhancement of Credit Worthiness Purpose is to get a lower coupon

(interest) rate

Credit Enhancement tools bank letter of credit mortgage-backed security bond insurance guarantee

BONDS FORBEGINNERS

The Finance Authority

of New Orleans

PART IIIIssuing Bonds

BONDS FOR BEGINNERS

The Finance Authority

of New Orleans

PART IVSelling Safety & Quality

Adding Seasonings

BONDS FOR BEGINNERS

The Finance Authority

of New Orleans

Thank You