Embed Size (px)

Citation preview

Borough of Brookville Strategic Management Planning Program Report

March 2021

Prepared By:

2

Borough of Brookville STMP

March 2021

ACKNOWLEGEMENTS

In 2020, the Pennsylvania Economy League Central Division (PEL) undertook an analysis of the financial condition of the borough of Brookville under the state’s Strategic Management Planning Program. The goals of the analysis were to determine the borough’s current and future overall financial condition.

PEL acknowledges and appreciates the full cooperation of all who contributed to the preparation of this study, including the Brookville elected officials, Borough Manager Dana Rooney and the rest of the borough staff. The analysis could not have been successfully completed without their assistance.

We would also like to thank our partners is this process: Cary Vargo of ARRO Consulting for his work on the management audit, W. Timothy Barry, Esq. for the labor and collective bargaining review and the Department of Community and Economic Development, including Local Policy Specialist, Terri Cunkle. PEL is Pennsylvania’s premier public policy think tank with offices in Harrisburg and Wilkes-Barre and affiliated organizations in Philadelphia and Pittsburgh. We are a 501(c)(3) educational and research organization formed in 1936.

Our mission includes:

• Independent. Insight. Information:

For 80+ years, we have provided objective, fact-based analysis to support good government,

serving as a trusted advisor to state and local officials

• Technical assistance to state and local government:

Our dedicated staff of expert policy professionals and consultants work with communities to

create fiscal sustainability and efficient public services

• Independent research on state and local issues impacting our communities:

Our non-partisan, data-driven research exposes government inefficiencies and provides

information that policy makers can use to design real solutions

• Civic education for local business, non-profit and government officials statewide:

We provide regional policy forums, expert testimony and more that give insight on emerging

policy issues and form coalitions of diverse partners

PEL’s financial analysis services served as a model for the state’s Strategic Management Planning Program (STMP), formerly the Early Intervention Program. PEL has completed over two dozen EIP/STMP plans in all types and sizes of municipalities.

3

Borough of Brookville STMP

March 2021

Table of Contents

CHAPTER 1 GOVERNMENT STRUCTURE AND DEMOGRAPHICS .......................................... 6

Government Overview................................................................................................................................... 6

Introduction ................................................................................................................................................. 6

Location and Government Structure ...................................................................................................... 7

Overview of Government Services, Staffing, Taxes, and Fees ........................................................... 7

Demographic Patterns .................................................................................................................................... 8

Introduction ................................................................................................................................................. 8

Population .................................................................................................................................................... 8

Population by Age Group ......................................................................................................................... 9

Births, Deaths, and Population Change 1990 through 2018 ............................................................... 9

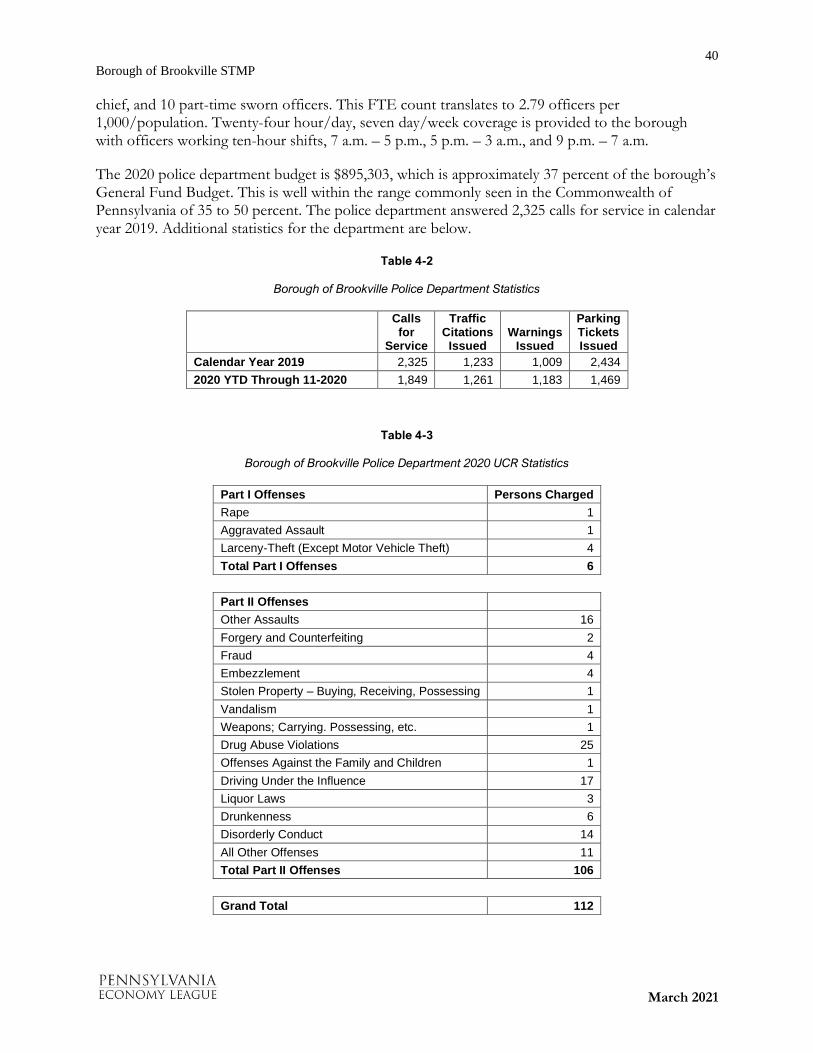

Housing Units ........................................................................................................................................... 10

Median Value of Owner-Occupied House........................................................................................... 11

Per Capita Income .................................................................................................................................... 12

Median Household Income .................................................................................................................... 12

Families Below Poverty Level................................................................................................................. 13

CHAPTER 2 HISTORICAL FINANCES ................................................................................................... 14

Introduction ................................................................................................................................................... 14

Methodology .................................................................................................................................................. 14

Financial Summary ........................................................................................................................................ 14

Total Revenues .............................................................................................................................................. 16

Assessed Value .......................................................................................................................................... 17

Tax Revenue .............................................................................................................................................. 18

Expenditures .................................................................................................................................................. 21

Departmental Expenditures .................................................................................................................... 21

Personnel and Non-Personnel Expenditures ...................................................................................... 22

2020 Estimated vs. 2020 Budget ................................................................................................................. 23

Property Tax Benchmarks ........................................................................................................................... 24

Other Funds ................................................................................................................................................... 26

The Brookville Municipal Authority .......................................................................................................... 27

CHAPTER 3 FINANCIAL PROJECTIONS ............................................................................................. 28

Introduction ................................................................................................................................................... 28

Revenue Assumptions.............................................................................................................................. 28

Expenditure Assumptions ....................................................................................................................... 28

4

Borough of Brookville STMP

March 2021

Capital Assumptions................................................................................................................................. 28

Financial Summary ........................................................................................................................................ 29

Total Revenues .............................................................................................................................................. 29

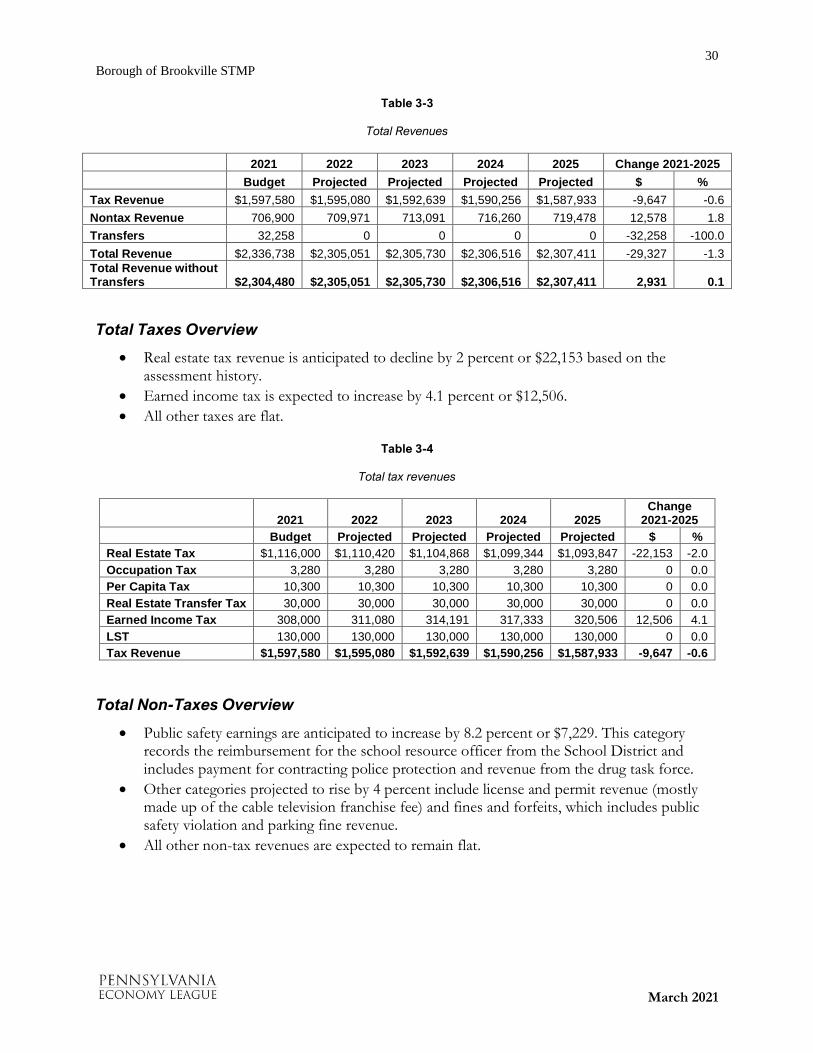

Total Taxes Overview .............................................................................................................................. 30

Total Non-Taxes Overview .................................................................................................................... 30

Expenditures .................................................................................................................................................. 31

Departmental Expenditures .................................................................................................................... 31

Personnel, Non-Personnel and Capital Expenditures ........................................................................ 32

Personnel Expenditures ........................................................................................................................... 32

CHAPTER 4 MANAGEMENT AUDIT .................................................................................................... 34

Introduction ................................................................................................................................................... 34

Administration and Finance (General Government) .............................................................................. 34

Recommendations Administration and Finance ................................................................................. 38

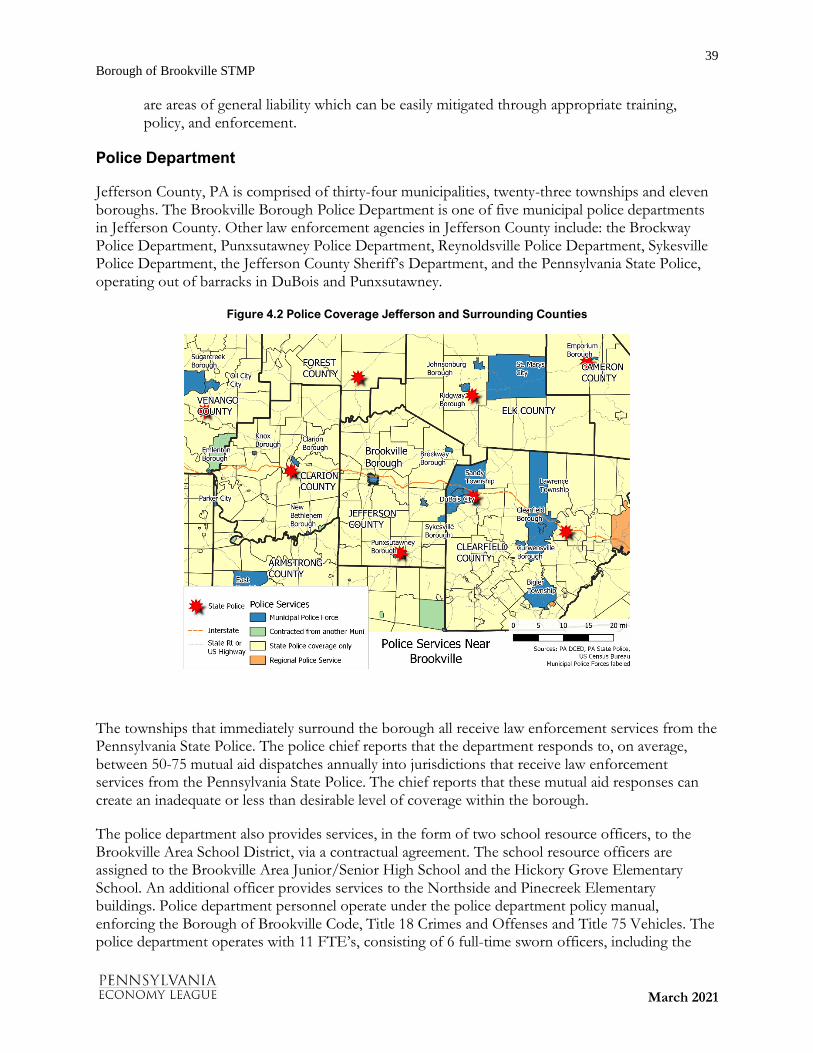

Police Department ........................................................................................................................................ 39

Recommendations – Police Department .............................................................................................. 41

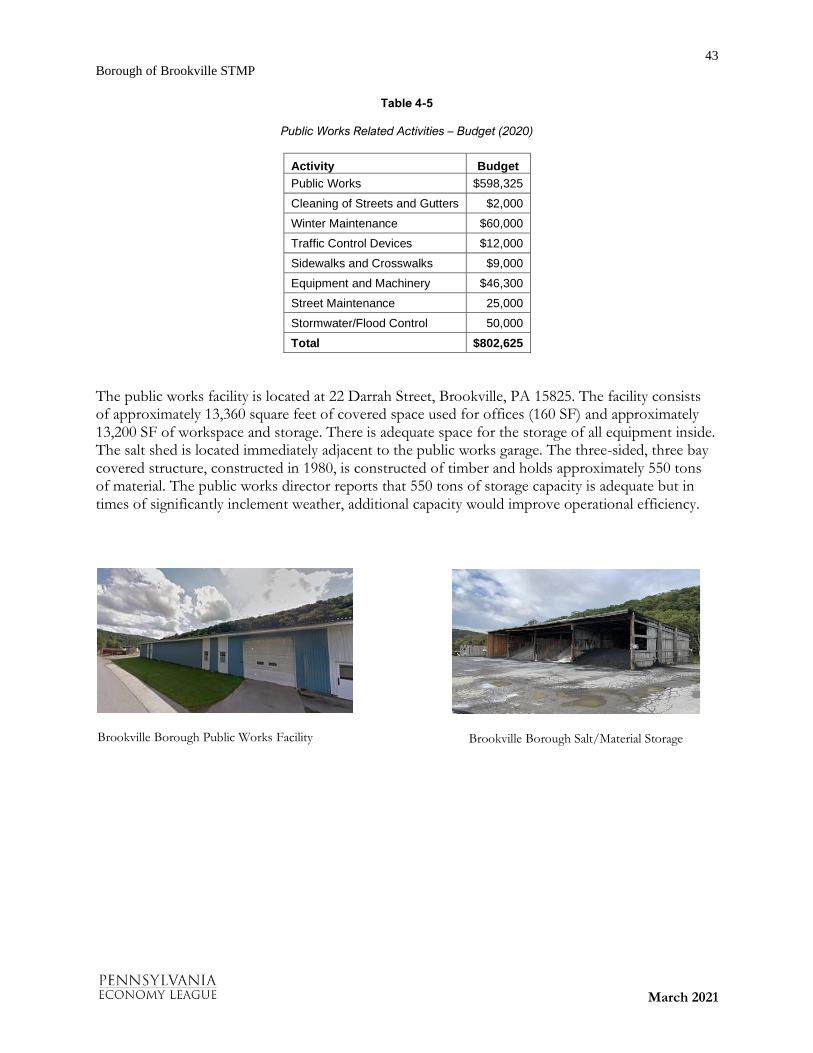

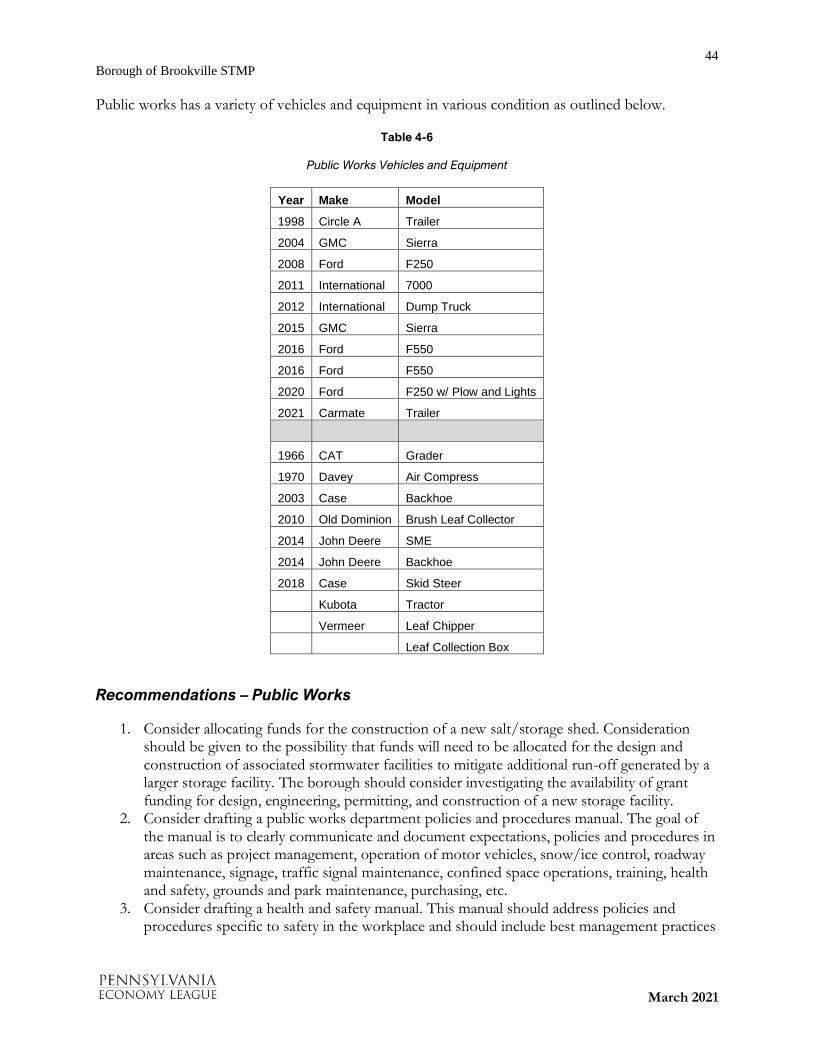

Public Works .................................................................................................................................................. 42

Recommendations – Public Works ....................................................................................................... 44

Parks and Recreation .................................................................................................................................... 45

Recommendations – Parks ...................................................................................................................... 46

Economic and Community Development ................................................................................................ 46

Recommendations – Economic and Community Development ..................................................... 47

Water and Wastewater .................................................................................................................................. 47

Recommendations Water and Wastewater ........................................................................................... 48

Planning and Economic Development ..................................................................................................... 48

Recommendations Planning and Economic Development .............................................................. 49

CHAPTER 5 REVIEW OF LABOR AGREEMENTS ............................................................................ 50

Introduction ................................................................................................................................................... 50

Methodology .................................................................................................................................................. 50

Police ............................................................................................................................................................... 50

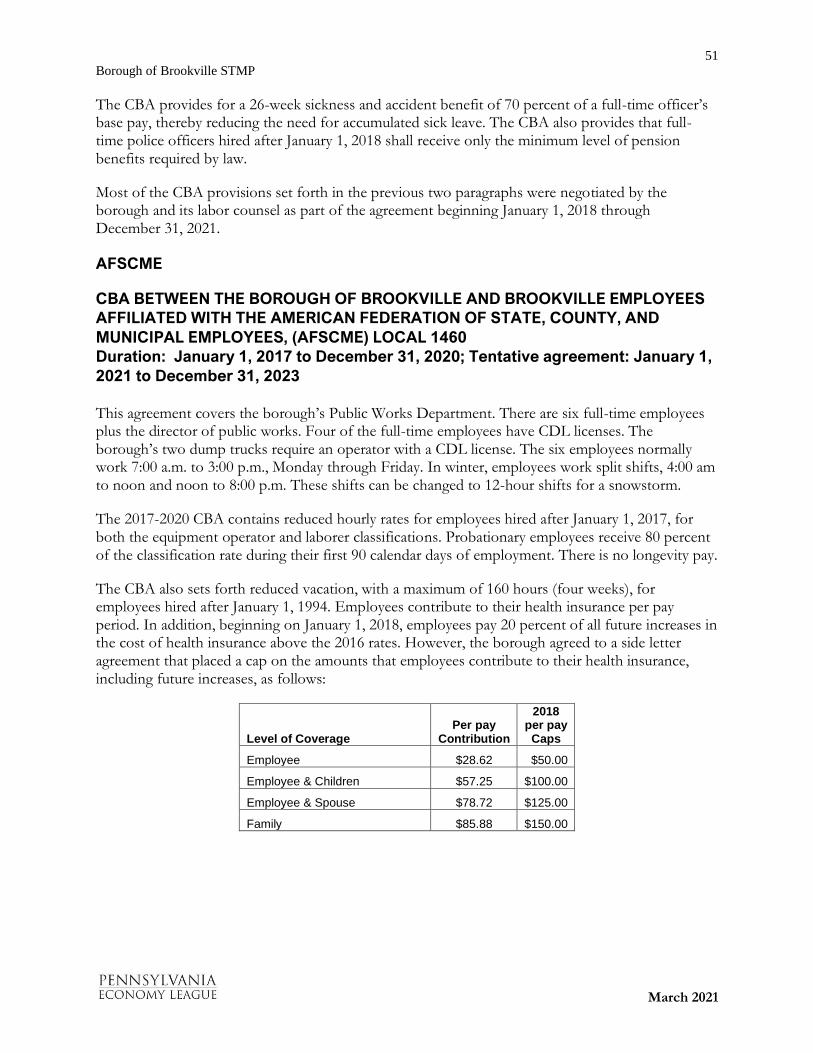

AFSCME ........................................................................................................................................................ 51

CHAPTER 6 OBSERVATIONS AND RECOMMENDATIONS ...................................................... 53

Introduction ................................................................................................................................................... 53

Recommendations ......................................................................................................................................... 54

Administration and Finance .................................................................................................................... 54

Economic Development ......................................................................................................................... 59

5

Borough of Brookville STMP

March 2021

Public Works ............................................................................................................................................. 59

Police ........................................................................................................................................................... 61

Parks ............................................................................................................................................................ 62

Water and Wastewater ............................................................................................................................. 63

Collective Bargaining ................................................................................................................................ 63

6

Borough of Brookville STMP

March 2021

CHAPTER 1

GOVERNMENT STRUCTURE AND DEMOGRAPHICS

In 2020, the Pennsylvania Economy League Central Division (PEL) undertook an analysis of the financial condition of the Borough of Brookville under the Commonwealth’s Strategic Management Planning Program. The goals of the analysis were to determine the borough’s current and future overall financial condition.

The current analysis involved a review of the borough’s financial reports, independent audits, debt payment schedules, pension obligations, the 2020 budget, other fiscal data, and additional relevant information and factors that may affect the current and future financial condition of the borough, including sociodemographic data. Furthermore, PEL staff participated in discussions with borough officials.

PEL acknowledges and appreciates the full cooperation of all who contributed to the preparation of this study, including the Brookville elected officials, Borough Manager Dana Rooney and the rest of the borough staff. The analysis could not have been successfully completed without their assistance.

During this project, PEL:

• Analyzed the borough’s financial history from 2014 through 2020 focusing on such factors as revenues, expenditures, tax base, operating positions and debt structure.

• Examined the historical data and the 2019 and 2020 budgets in relation to ongoing operations, salary and benefit requirements and other obligations of the borough.

• Reviewed all tax bases and revenues, major user fees and other revenue sources.

• Projected, to the extent possible based on known factors and available data, revenues, and expenditures for 2021 through 2025 assuming continuation of obligated levels of wages and operations, existing revenue patterns and other operating trends.

• Made recommendations to assist the borough in developing and improving its administration, public works and public safety services.

Government Overview

Introduction

The existence of municipal governments in Pennsylvania is authorized by the Pennsylvania Constitution and state law. All land within the commonwealth is incorporated by law as a municipality with its own government. There are three primary types or classifications of municipal governments: cities (of the first, second, second class A or third class), boroughs and townships (of the first or second class).

Municipal governments in Pennsylvania are the principal providers of direct public services to citizens. Services often include, among others, police and fire protection, construction and maintenance of roadways and bridges, street lighting, parks and recreation facilities and programs, planning and zoning activities, enforcement of building and related codes, water treatment and distribution, sewage collection and treatment, storm water management, solid waste collection and disposal, and recycling.

7

Borough of Brookville STMP

March 2021

Location and Government Structure

The town of Brookville was established and designated as the Jefferson County seat in 1830 and incorporated in 1843, although the first settlement dates to 1796 with the arrival of Joseph and Andrew Barnett and Samuel Scott in the area known as Port Barnett. During the nineteenth century, Brookville’s greatest growth resulted from the lumber industry. By the mid-1800s, there were 22 mills on the North Fork Creek and 20 mills on both Sandy Lick and Redbank creeks. With the coming of the railroad in 1873, industrial and commercial development grew and prospered during the late 19th and early 20th centuries. Of note was the Twyford Motor Car Company, which operated from 1905 to 1907 and produced the world’s first four-wheel drive automobile. During the 20th Century, residential, commercial and industrial development spread to the borough’s periphery, while the downtown revitalization program became a recognized award-winning model.

Brookville operates under Pennsylvania’s Borough Code. The form of government established by the code is characterized by a strong and dominant council and a weak executive in terms of duties, responsibilities and powers.

Brookville Council is comprised of seven members, who are elected at large to four-year staggered terms. The powers of council set forth in the Borough Code are broad and extensive covering virtually the whole range of municipal functions. The general supervision of borough affairs is in the hands of council, and many of the roles found in separate branches or levels of the state and federal governments are combined in the council members. Council serves as the legislative body by setting policy, enacting ordinances and resolutions, adopting budgets and levying taxes. Council may also perform executive functions, such as developing the budget, enforcing ordinances, approving expenditures and hiring employees. While council may also play a large role in administrative activities by overseeing the day-to-day operation of a borough government, that function is handled by an appointed borough manager.

The position of mayor is granted few statutory powers by the Borough Code. The mayor has no vote on council except to break ties; however, the mayor does have a defined veto power. Borough mayors retain limited administrative powers, chiefly centered on supervising the daily operations of the police department. The borough also has an elected tax collector and an appointed auditor, the latter being a certified public accountant firm.

Overview of Government Services, Staffing, Taxes, and Fees

The borough depicts its administration as the borough manager, the borough/municipal authority solicitor, borough/municipal authority engineer, the director of public works and the mayor, although the solicitor and engineer are employed by outside firms. Departments include finance/tax collection, fire and emergency services, health and code, planning and zoning, public works, and police, as well as the Brookville Municipal Authority, which is responsible for the water and wastewater systems and treatment for the borough and neighboring jurisdictions. Brookville has 15 full-time and 10 part-time employees, including its own police department with six full-time and eight part-time officers, and a volunteer fire department. The borough also functions with assistance from several committees, commissions and boards.

In 2020, Borough of Brookville real estate taxes are 16.915 mills, including 14.29 mills for general purpose, 1.5 mills for fire equipment and fire houses, 0.225 mills for library, and 0.9 mills for street

8

Borough of Brookville STMP

March 2021

lighting. The resident earned income tax is 1.0 percent, which is split with the Brookville Area School District. Other taxes include a $52 local services tax of which $5 goes to the school district, 0.5 percent realty transfer tax, 36 mill occupation tax, $60 mechanical devices tax, and $5 per capita tax.

Demographic Patterns

Introduction

Overall, Brookville’s population declined by 9.0 percent from 1970 to 2010, despite a 5.9 percent from 1970 to 1980. A 20.5 percent drop in persons under the age of 18 from 1990 to 2010 and disproportionate number of individuals in that age range in 2010 is consistent with the negative natural population change from 1990 through 2018, which could negatively affect the age 18 to 64 population. A mitigating factor may be that the negative natural population change exceeded the negative total population change, which revealed a net in-migration of 249 individuals for the 18-year period. The median number of owner-occupied homes somewhat decreased while the number of vacant units increased from 1990 to 2010, which may be attributed to the Great Recession coupled with an out-migration during the 2000 to 2010 decade. Wealth measures were positive for the borough from 1990 to 2010, with significant increases in median value of an owner-occupied house, median household income and per capita income, and a decrease in percentage of families below the poverty level. Overall, wealth measures for the borough were comparable to or better than the county, but not as good as the commonwealth.

Population

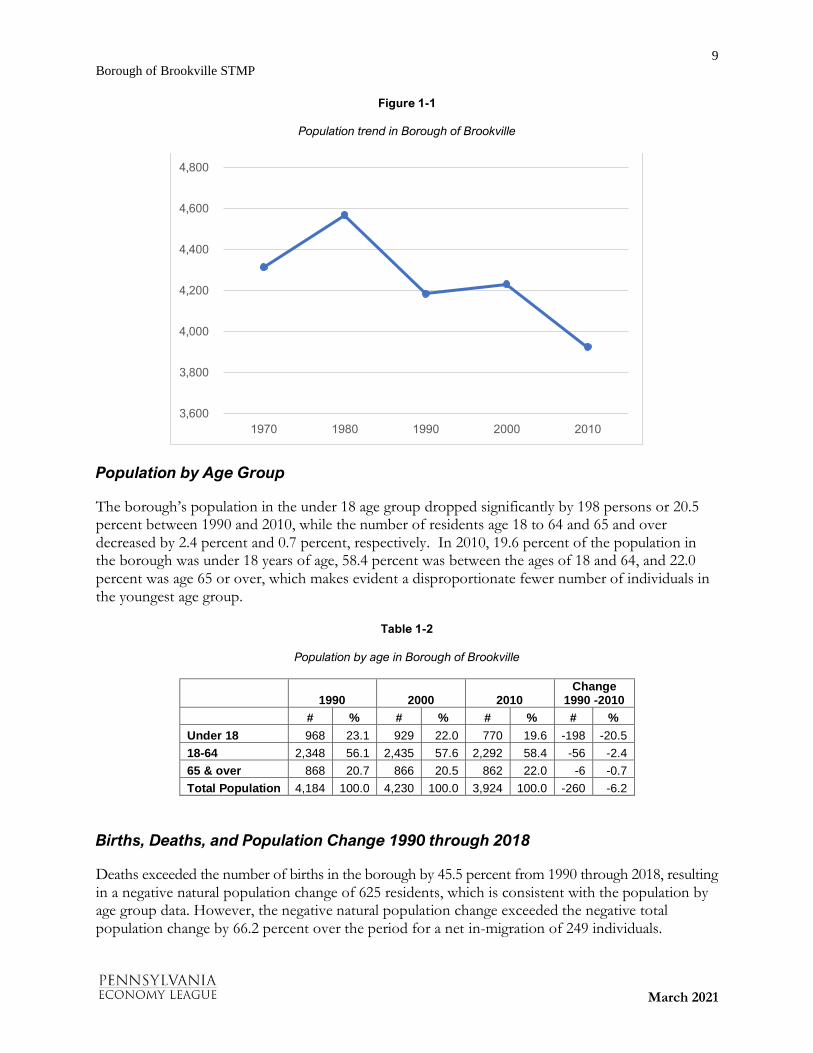

According to U.S. Census data, Brookville’s population decreased by 390 persons or 9.0 percent from 1970 to 2010 with an 8.4 percent decline from 1980 to 1990 and a 7.2 percent decline from 2000 to 2010, contrary to the 5.9 percent increase from 1970 to 1980. Jefferson County realized a 1,505 person or 3.4 percent gain in population from 1970 to 2010, although it was positive only because of the 10.5 percent increase from 1970 to 1980. The county lost population during each of the next three decades.

Table 1-1

Population trends

1970 1980 1990 2000 2010 Change

1970 to 2010

# %

Borough of Brookville 4,314 4,568 4,184 4,230 3,924 -390 -9.0

Jefferson County 43,695 48,303 46,083 45,932 45,200 1,505 3.4

9

Borough of Brookville STMP

March 2021

Figure 1-1

Population trend in Borough of Brookville

Population by Age Group

The borough’s population in the under 18 age group dropped significantly by 198 persons or 20.5 percent between 1990 and 2010, while the number of residents age 18 to 64 and 65 and over decreased by 2.4 percent and 0.7 percent, respectively. In 2010, 19.6 percent of the population in the borough was under 18 years of age, 58.4 percent was between the ages of 18 and 64, and 22.0 percent was age 65 or over, which makes evident a disproportionate fewer number of individuals in the youngest age group.

Table 1-2

Population by age in Borough of Brookville

1990 2000 2010 Change

1990 -2010

# % # % # % # %

Under 18 968 23.1 929 22.0 770 19.6 -198 -20.5

18-64 2,348 56.1 2,435 57.6 2,292 58.4 -56 -2.4

65 & over 868 20.7 866 20.5 862 22.0 -6 -0.7

Total Population 4,184 100.0 4,230 100.0 3,924 100.0 -260 -6.2

Births, Deaths, and Population Change 1990 through 2018

Deaths exceeded the number of births in the borough by 45.5 percent from 1990 through 2018, resulting in a negative natural population change of 625 residents, which is consistent with the population by age group data. However, the negative natural population change exceeded the negative total population change by 66.2 percent over the period for a net in-migration of 249 individuals.

3,600

3,800

4,000

4,200

4,400

4,600

4,800

1970 1980 1990 2000 2010

10

Borough of Brookville STMP

March 2021

Table 1-3

Resident births, deaths and population trend in Borough of Brookville

1990 to 1999

2000 to 2009

2010 to 2018

1990 to 2018

Births 459 496 420 1,375

Deaths 703 629 668 2,000

Natural Pop. Change -244 -133 -248 -625

Total Population (start) 4,184 4,230 3,924 4,184

Total Population (end) 4,230 3,924 3,808 3,808

Total Population Change 46 -306 -116 -376

Less Natural Change -244 -133 -248 -625

Net Migration 290 -173 132 249

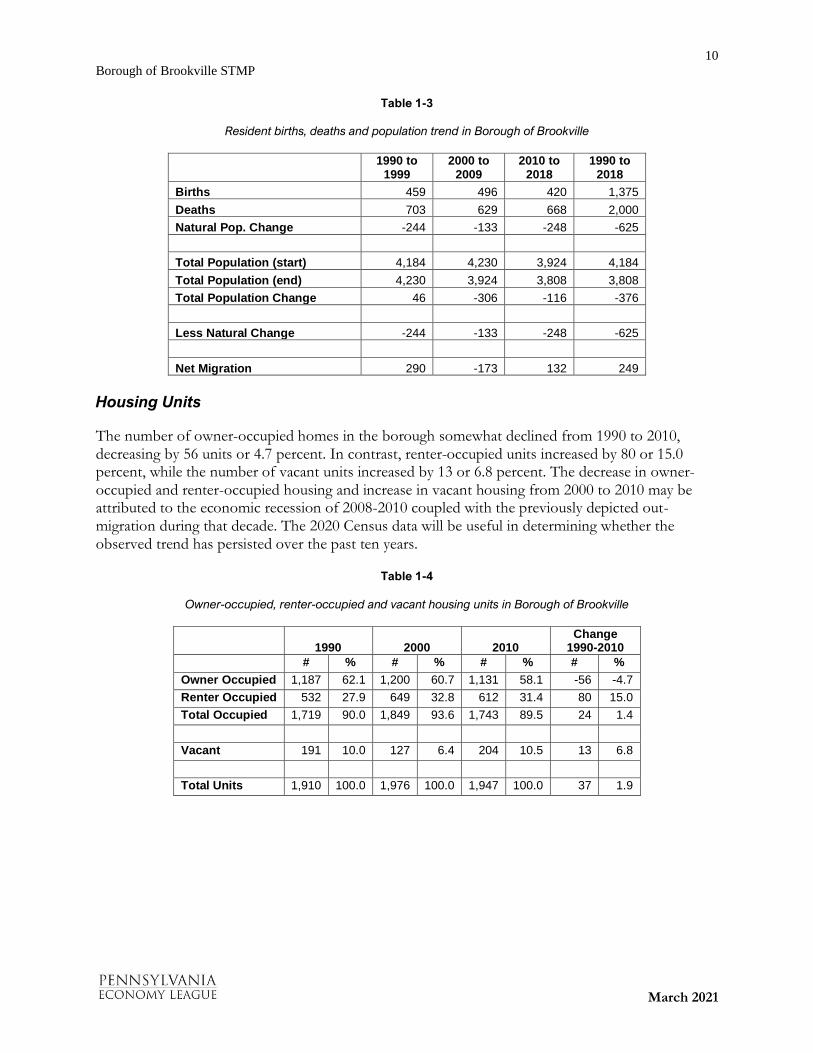

Housing Units

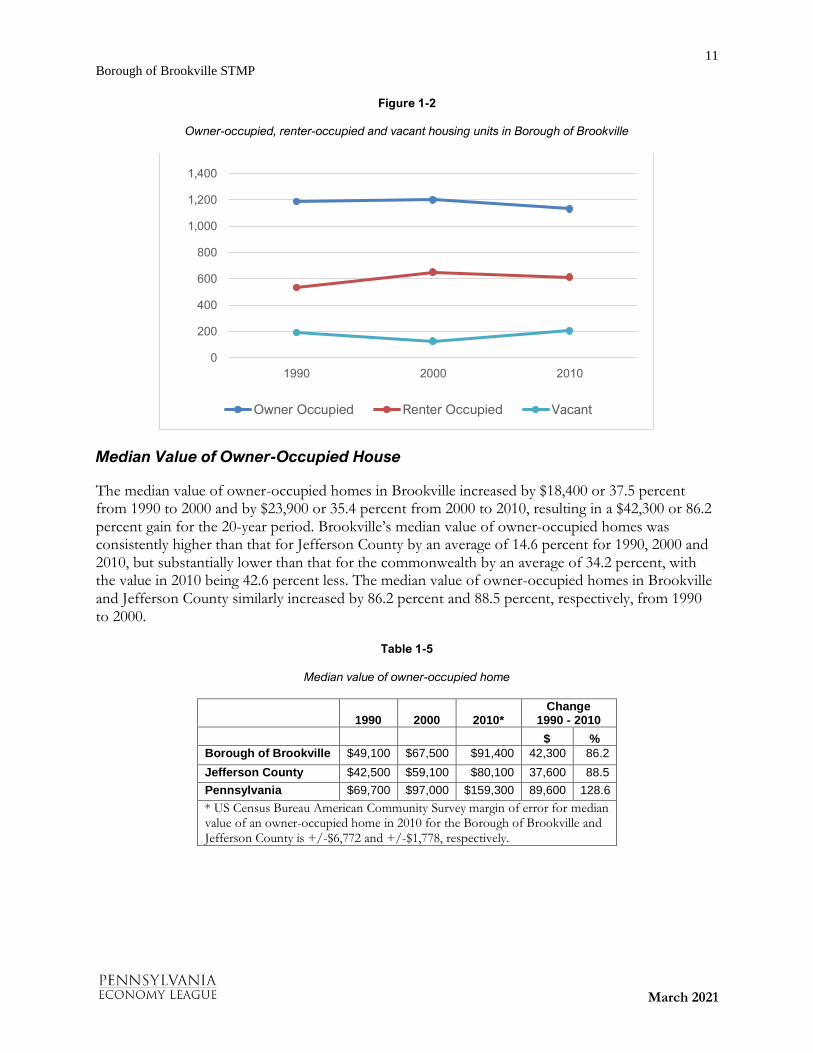

The number of owner-occupied homes in the borough somewhat declined from 1990 to 2010, decreasing by 56 units or 4.7 percent. In contrast, renter-occupied units increased by 80 or 15.0 percent, while the number of vacant units increased by 13 or 6.8 percent. The decrease in owner-occupied and renter-occupied housing and increase in vacant housing from 2000 to 2010 may be attributed to the economic recession of 2008-2010 coupled with the previously depicted out-migration during that decade. The 2020 Census data will be useful in determining whether the observed trend has persisted over the past ten years.

Table 1-4

Owner-occupied, renter-occupied and vacant housing units in Borough of Brookville

1990 2000 2010 Change

1990-2010 # % # % # % # %

Owner Occupied 1,187 62.1 1,200 60.7 1,131 58.1 -56 -4.7

Renter Occupied 532 27.9 649 32.8 612 31.4 80 15.0

Total Occupied 1,719 90.0 1,849 93.6 1,743 89.5 24 1.4

Vacant 191 10.0 127 6.4 204 10.5 13 6.8

Total Units 1,910 100.0 1,976 100.0 1,947 100.0 37 1.9

11

Borough of Brookville STMP

March 2021

Figure 1-2

Owner-occupied, renter-occupied and vacant housing units in Borough of Brookville

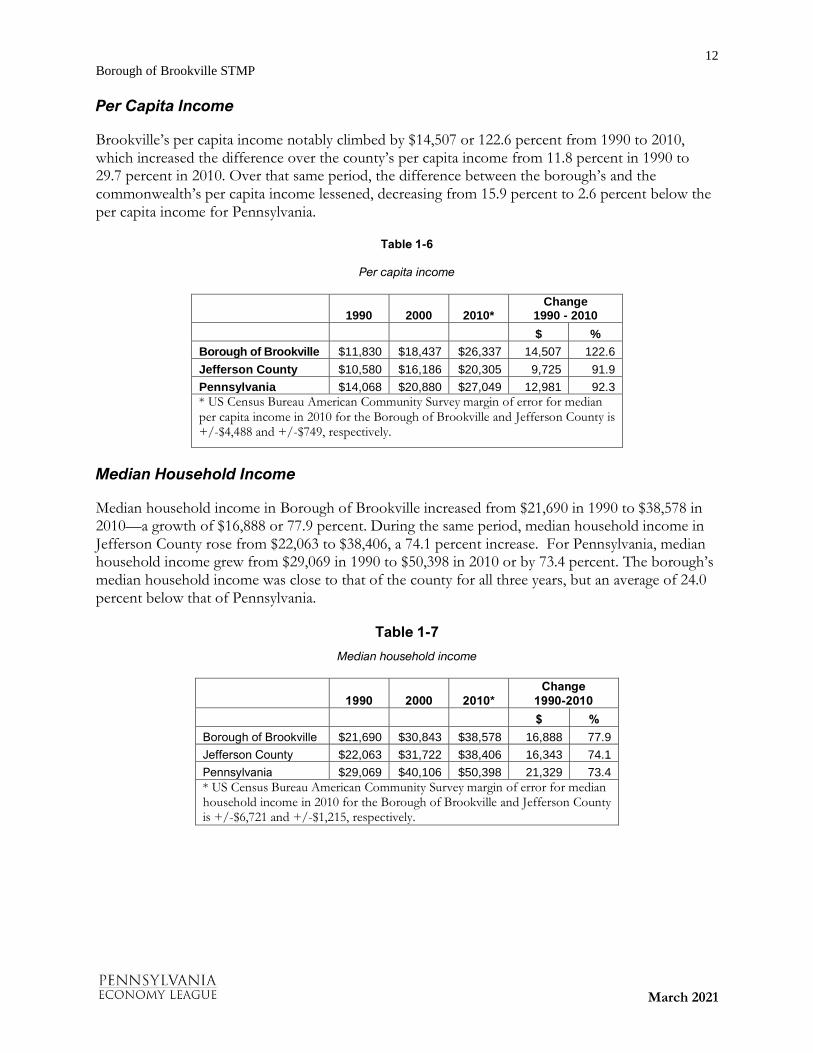

Median Value of Owner-Occupied House

The median value of owner-occupied homes in Brookville increased by $18,400 or 37.5 percent from 1990 to 2000 and by $23,900 or 35.4 percent from 2000 to 2010, resulting in a $42,300 or 86.2 percent gain for the 20-year period. Brookville’s median value of owner-occupied homes was consistently higher than that for Jefferson County by an average of 14.6 percent for 1990, 2000 and 2010, but substantially lower than that for the commonwealth by an average of 34.2 percent, with the value in 2010 being 42.6 percent less. The median value of owner-occupied homes in Brookville and Jefferson County similarly increased by 86.2 percent and 88.5 percent, respectively, from 1990 to 2000.

Table 1-5

Median value of owner-occupied home

1990 2000 2010* Change

1990 - 2010

$ %

Borough of Brookville $49,100 $67,500 $91,400 42,300 86.2

Jefferson County $42,500 $59,100 $80,100 37,600 88.5

Pennsylvania $69,700 $97,000 $159,300 89,600 128.6

* US Census Bureau American Community Survey margin of error for median value of an owner-occupied home in 2010 for the Borough of Brookville and Jefferson County is +/-$6,772 and +/-$1,778, respectively.

0

200

400

600

800

1,000

1,200

1,400

1990 2000 2010

Owner Occupied Renter Occupied Vacant

12

Borough of Brookville STMP

March 2021

Per Capita Income

Brookville’s per capita income notably climbed by $14,507 or 122.6 percent from 1990 to 2010, which increased the difference over the county’s per capita income from 11.8 percent in 1990 to 29.7 percent in 2010. Over that same period, the difference between the borough’s and the commonwealth’s per capita income lessened, decreasing from 15.9 percent to 2.6 percent below the per capita income for Pennsylvania.

Table 1-6

Per capita income

1990 2000 2010* Change

1990 - 2010

$ %

Borough of Brookville $11,830 $18,437 $26,337 14,507 122.6

Jefferson County $10,580 $16,186 $20,305 9,725 91.9

Pennsylvania $14,068 $20,880 $27,049 12,981 92.3

* US Census Bureau American Community Survey margin of error for median per capita income in 2010 for the Borough of Brookville and Jefferson County is +/-$4,488 and +/-$749, respectively.

Median Household Income

Median household income in Borough of Brookville increased from $21,690 in 1990 to $38,578 in 2010—a growth of $16,888 or 77.9 percent. During the same period, median household income in Jefferson County rose from $22,063 to $38,406, a 74.1 percent increase. For Pennsylvania, median household income grew from $29,069 in 1990 to $50,398 in 2010 or by 73.4 percent. The borough’s median household income was close to that of the county for all three years, but an average of 24.0 percent below that of Pennsylvania.

Table 1-7

Median household income

1990 2000 2010*

Change

1990-2010

$ %

Borough of Brookville $21,690 $30,843 $38,578 16,888 77.9

Jefferson County $22,063 $31,722 $38,406 16,343 74.1

Pennsylvania $29,069 $40,106 $50,398 21,329 73.4

* US Census Bureau American Community Survey margin of error for median household income in 2010 for the Borough of Brookville and Jefferson County is +/-$6,721 and +/-$1,215, respectively.

13

Borough of Brookville STMP

March 2021

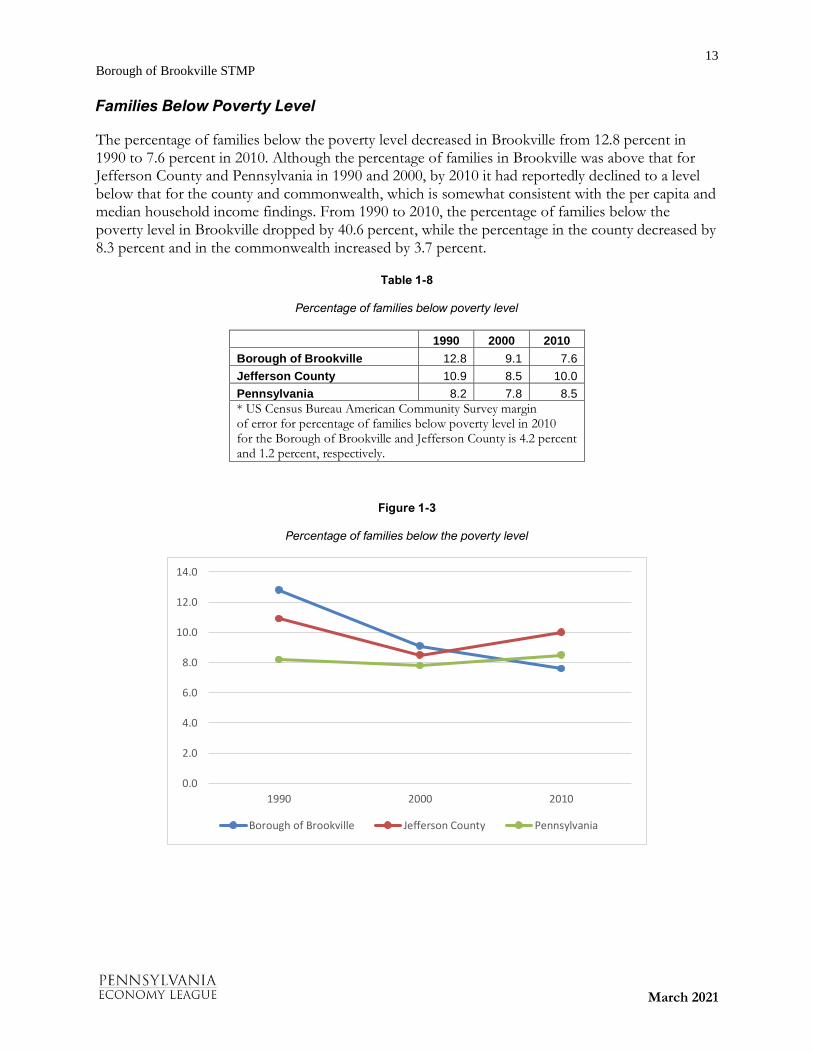

Families Below Poverty Level

The percentage of families below the poverty level decreased in Brookville from 12.8 percent in 1990 to 7.6 percent in 2010. Although the percentage of families in Brookville was above that for Jefferson County and Pennsylvania in 1990 and 2000, by 2010 it had reportedly declined to a level below that for the county and commonwealth, which is somewhat consistent with the per capita and median household income findings. From 1990 to 2010, the percentage of families below the poverty level in Brookville dropped by 40.6 percent, while the percentage in the county decreased by 8.3 percent and in the commonwealth increased by 3.7 percent.

Table 1-8

Percentage of families below poverty level

1990 2000 2010

Borough of Brookville 12.8 9.1 7.6

Jefferson County 10.9 8.5 10.0

Pennsylvania 8.2 7.8 8.5

* US Census Bureau American Community Survey margin of error for percentage of families below poverty level in 2010 for the Borough of Brookville and Jefferson County is 4.2 percent and 1.2 percent, respectively.

Figure 1-3

Percentage of families below the poverty level

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1990 2000 2010

Borough of Brookville Jefferson County Pennsylvania

14

Borough of Brookville STMP

March 2021

CHAPTER 2

HISTORICAL FINANCES

Introduction

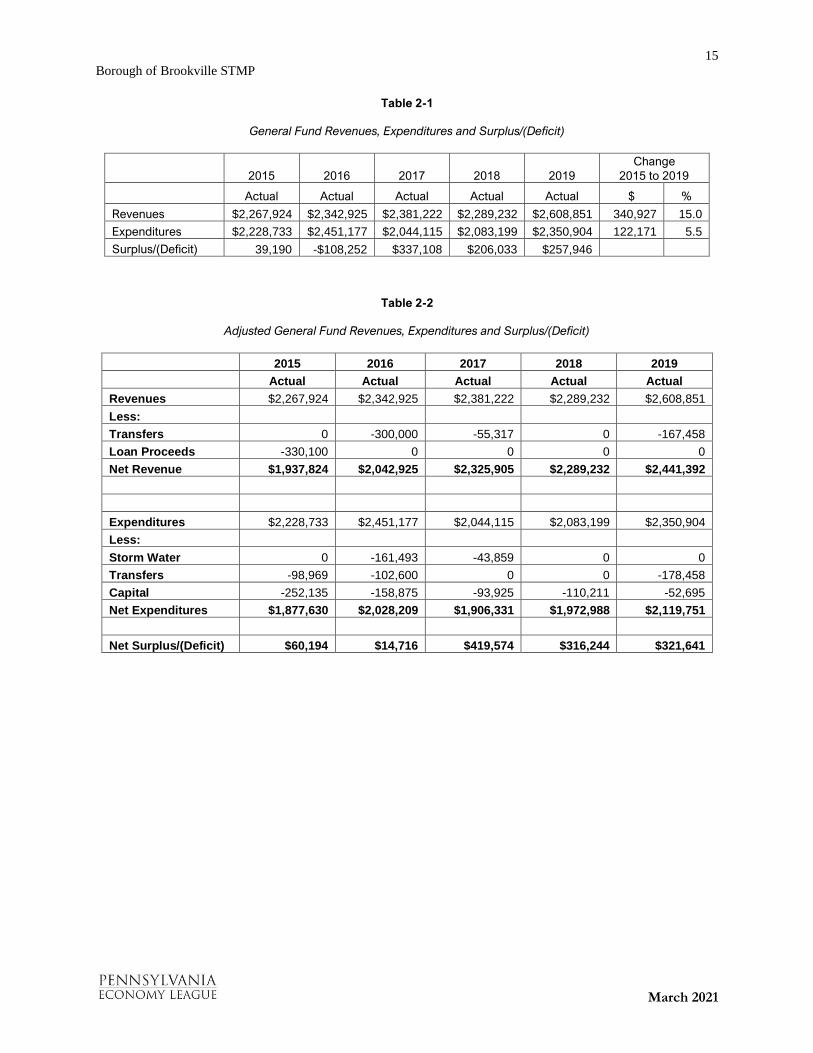

The borough of Brookville experienced surpluses in four out of five years during the historical review period from 2015 to 2019. During that time, the borough increased its general purpose property tax millage twice, with another millage hike in 2020. Brookville’s property tax revenue rose by over $200,000 or 26 percent as of 2019 because of the tax increases. In contrast, the taxable value of real estate, earned income and local services tax revenue showed little to no growth.

In terms of non-tax revenue, public safety earnings experienced the highest increase as the borough received reimbursements for its school resource officer. The largest sources of non-tax revenue are rents and royalties, which includes significant rental income for the borough complex. On the expenditure side, once transfers and capital expenditures are removed, the police department is the borough’s largest cost center.

In 2020, the borough experienced a surplus of almost $300,000, mostly due to reductions in budgeted expenditures.

Methodology

PEL compiled this historical review of the borough’s General Fund through analysis of year-end financial reports, independent audits, annual budgets, salary and benefit data, pension obligations and other financial obligations, as well as interviews with borough officials.

The borough operates on a cash basis with seven individual funds. The historical financial review concentrates on the General Fund, which is the borough’s primary operating fund. The General Fund operates on a cash basis of accounting. Other funds include liquid fuels, streetlights, fire protection, library, capital projects and the Walter Dick Park Endowment. Dedicated special purpose tax millage revenue for the respective services is recorded in the streetlights, fire protection and library funds.

Financial Summary

The borough’s General Fund experienced surpluses in four out of five years during the historical review period and one year of deficit as seen in Table 2-1. Revenues increased by 15 percent during that period reflecting general purpose tax increases in 2016 and 2017, and debt millage added in 2017. In contrast, expenditures grew by only 5.5 percent.

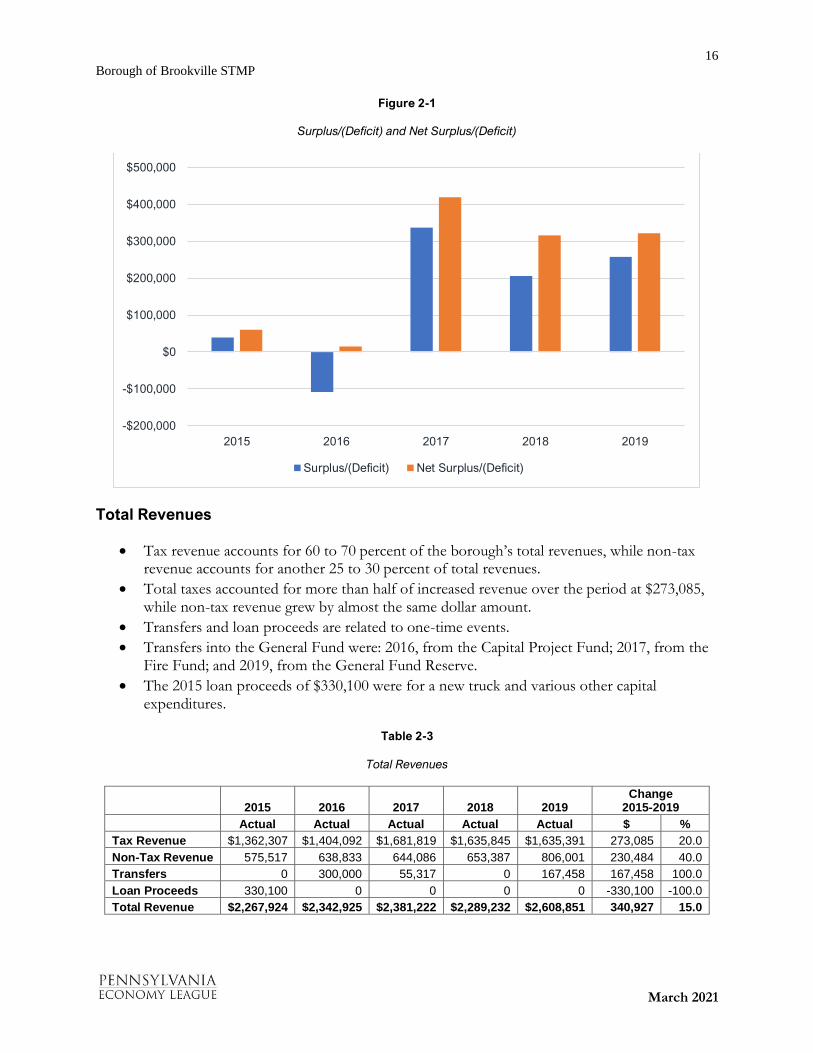

Table 2-2 eliminates one-time events from the General Fund including transfers, loan proceeds, storm water costs and capital expenditures. Removing these one-time events give a truer picture of the borough’s operational revenues and expenditures. The adjustment eliminates the 2016 deficit and results in larger annual surpluses. See Figure 2-1.

15

Borough of Brookville STMP

March 2021

Table 2-1

General Fund Revenues, Expenditures and Surplus/(Deficit)

2015 2016 2017 2018 2019

Change

2015 to 2019

Actual Actual Actual Actual Actual $ %

Revenues $2,267,924 $2,342,925 $2,381,222 $2,289,232 $2,608,851 340,927 15.0

Expenditures $2,228,733 $2,451,177 $2,044,115 $2,083,199 $2,350,904 122,171 5.5

Surplus/(Deficit) 39,190 -$108,252 $337,108 $206,033 $257,946

Table 2-2

Adjusted General Fund Revenues, Expenditures and Surplus/(Deficit)

2015 2016 2017 2018 2019

Actual Actual Actual Actual Actual

Revenues $2,267,924 $2,342,925 $2,381,222 $2,289,232 $2,608,851

Less:

Transfers 0 -300,000 -55,317 0 -167,458

Loan Proceeds -330,100 0 0 0 0

Net Revenue $1,937,824 $2,042,925 $2,325,905 $2,289,232 $2,441,392

Expenditures $2,228,733 $2,451,177 $2,044,115 $2,083,199 $2,350,904

Less:

Storm Water 0 -161,493 -43,859 0 0

Transfers -98,969 -102,600 0 0 -178,458

Capital -252,135 -158,875 -93,925 -110,211 -52,695

Net Expenditures $1,877,630 $2,028,209 $1,906,331 $1,972,988 $2,119,751

Net Surplus/(Deficit) $60,194 $14,716 $419,574 $316,244 $321,641

16

Borough of Brookville STMP

March 2021

Figure 2-1

Surplus/(Deficit) and Net Surplus/(Deficit)

Total Revenues

• Tax revenue accounts for 60 to 70 percent of the borough’s total revenues, while non-tax revenue accounts for another 25 to 30 percent of total revenues.

• Total taxes accounted for more than half of increased revenue over the period at $273,085, while non-tax revenue grew by almost the same dollar amount.

• Transfers and loan proceeds are related to one-time events.

• Transfers into the General Fund were: 2016, from the Capital Project Fund; 2017, from the Fire Fund; and 2019, from the General Fund Reserve.

• The 2015 loan proceeds of $330,100 were for a new truck and various other capital expenditures.

Table 2-3

Total Revenues

2015 2016 2017 2018 2019 Change

2015-2019

Actual Actual Actual Actual Actual $ %

Tax Revenue $1,362,307 $1,404,092 $1,681,819 $1,635,845 $1,635,391 273,085 20.0

Non-Tax Revenue 575,517 638,833 644,086 653,387 806,001 230,484 40.0

Transfers 0 300,000 55,317 0 167,458 167,458 100.0

Loan Proceeds 330,100 0 0 0 0 -330,100 -100.0

Total Revenue $2,267,924 $2,342,925 $2,381,222 $2,289,232 $2,608,851 340,927 15.0

-$200,000

-$100,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

2015 2016 2017 2018 2019

Surplus/(Deficit) Net Surplus/(Deficit)

17

Borough of Brookville STMP

March 2021

Assessed Value

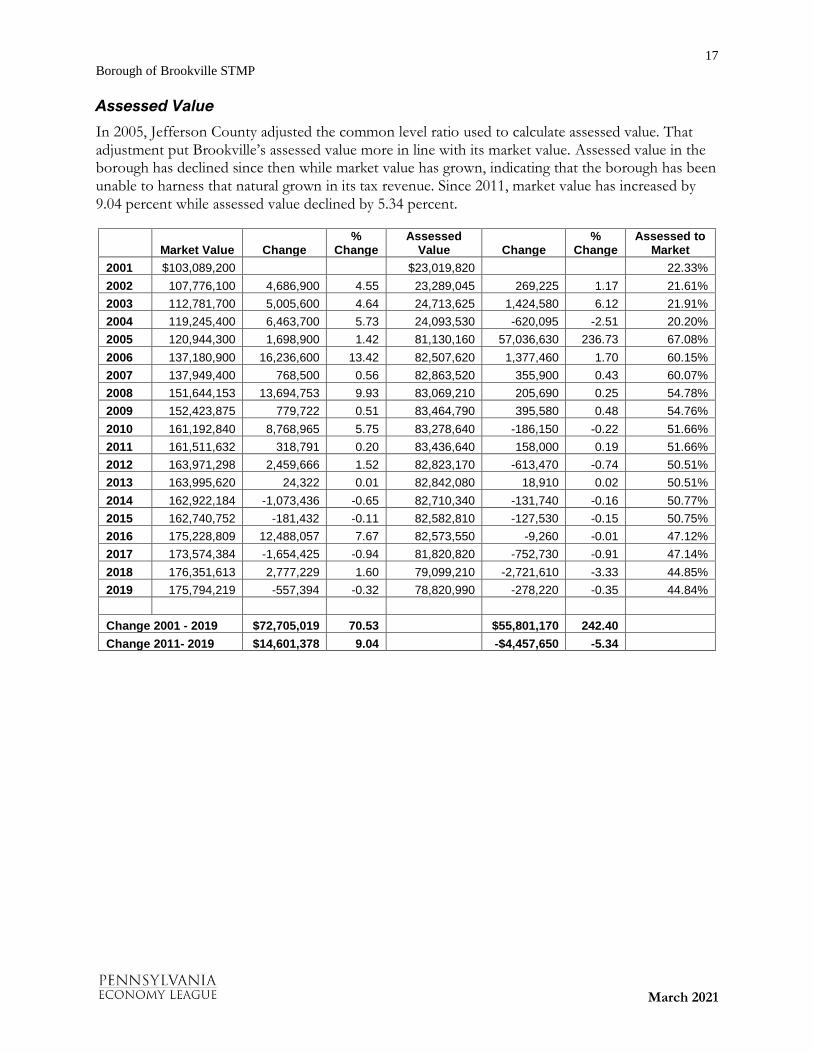

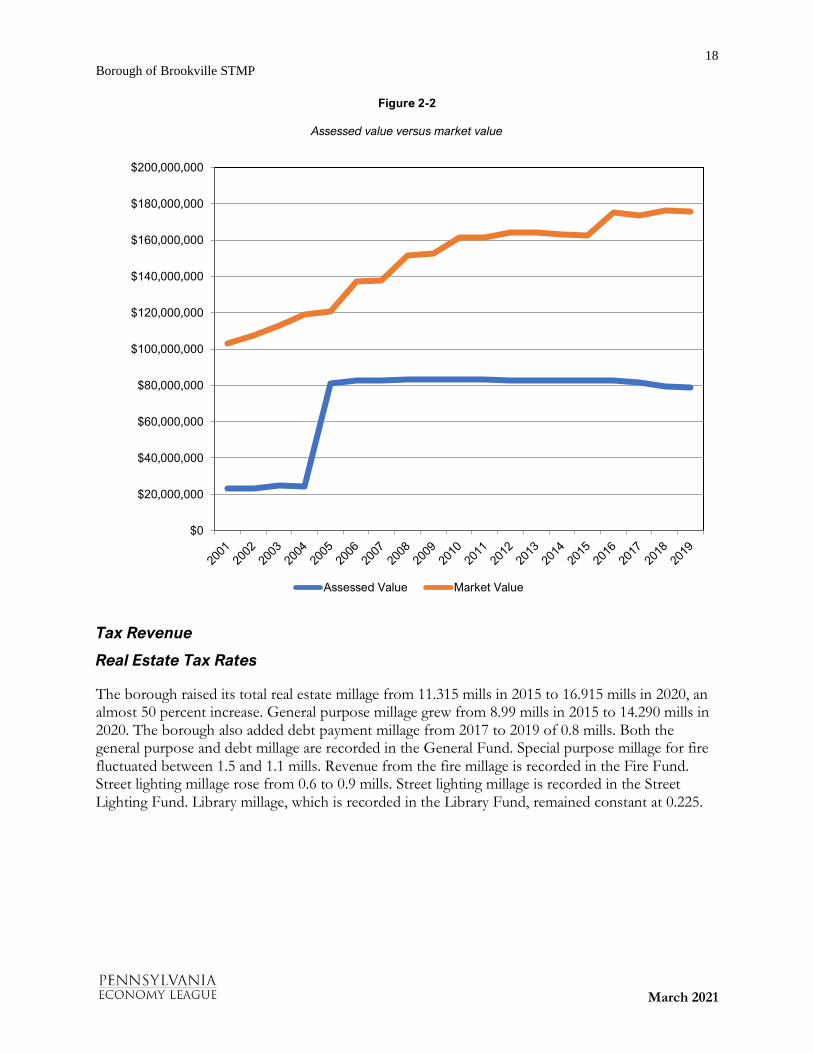

In 2005, Jefferson County adjusted the common level ratio used to calculate assessed value. That adjustment put Brookville’s assessed value more in line with its market value. Assessed value in the borough has declined since then while market value has grown, indicating that the borough has been unable to harness that natural grown in its tax revenue. Since 2011, market value has increased by 9.04 percent while assessed value declined by 5.34 percent.

Market Value Change %

Change Assessed

Value Change %

Change Assessed to

Market

2001 $103,089,200 $23,019,820 22.33%

2002 107,776,100 4,686,900 4.55 23,289,045 269,225 1.17 21.61%

2003 112,781,700 5,005,600 4.64 24,713,625 1,424,580 6.12 21.91%

2004 119,245,400 6,463,700 5.73 24,093,530 -620,095 -2.51 20.20%

2005 120,944,300 1,698,900 1.42 81,130,160 57,036,630 236.73 67.08%

2006 137,180,900 16,236,600 13.42 82,507,620 1,377,460 1.70 60.15%

2007 137,949,400 768,500 0.56 82,863,520 355,900 0.43 60.07%

2008 151,644,153 13,694,753 9.93 83,069,210 205,690 0.25 54.78%

2009 152,423,875 779,722 0.51 83,464,790 395,580 0.48 54.76%

2010 161,192,840 8,768,965 5.75 83,278,640 -186,150 -0.22 51.66%

2011 161,511,632 318,791 0.20 83,436,640 158,000 0.19 51.66%

2012 163,971,298 2,459,666 1.52 82,823,170 -613,470 -0.74 50.51%

2013 163,995,620 24,322 0.01 82,842,080 18,910 0.02 50.51%

2014 162,922,184 -1,073,436 -0.65 82,710,340 -131,740 -0.16 50.77%

2015 162,740,752 -181,432 -0.11 82,582,810 -127,530 -0.15 50.75%

2016 175,228,809 12,488,057 7.67 82,573,550 -9,260 -0.01 47.12%

2017 173,574,384 -1,654,425 -0.94 81,820,820 -752,730 -0.91 47.14%

2018 176,351,613 2,777,229 1.60 79,099,210 -2,721,610 -3.33 44.85%

2019 175,794,219 -557,394 -0.32 78,820,990 -278,220 -0.35 44.84%

Change 2001 - 2019 $72,705,019 70.53 $55,801,170 242.40

Change 2011- 2019 $14,601,378 9.04 -$4,457,650 -5.34

18

Borough of Brookville STMP

March 2021

Figure 2-2

Assessed value versus market value

Tax Revenue

Real Estate Tax Rates

The borough raised its total real estate millage from 11.315 mills in 2015 to 16.915 mills in 2020, an almost 50 percent increase. General purpose millage grew from 8.99 mills in 2015 to 14.290 mills in 2020. The borough also added debt payment millage from 2017 to 2019 of 0.8 mills. Both the general purpose and debt millage are recorded in the General Fund. Special purpose millage for fire fluctuated between 1.5 and 1.1 mills. Revenue from the fire millage is recorded in the Fire Fund. Street lighting millage rose from 0.6 to 0.9 mills. Street lighting millage is recorded in the Street Lighting Fund. Library millage, which is recorded in the Library Fund, remained constant at 0.225.

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

$160,000,000

$180,000,000

$200,000,000

Assessed Value Market Value

19

Borough of Brookville STMP

March 2021

Table 2-3

Real estate tax rates

Tax 2015 2016 2017 2018 2019 2020

Real Estate - General Purpose (mills) 8.990 9.990 13.490 13.490 13.490 14.290

Real Estate - Fire Equipment & Firehouses (mills) 1.500 1.500 1.100 1.100 1.100 1.500

Real Estate - Library (mills) 0.225 0.225 0.225 0.225 0.225 0.225

Real Estate - Street Lighting (mills) 0.600 0.600 0.600 0.900 0.900 0.900

Real Estate - Debt Payment (mills) 0.000 0.000 0.800 0.800 0.800 0.000

Real Estate Total 11.315 12.315 16.215 16.515 16.515 16.915

Percent Change from Prior Year 3.66% 8.84% 31.67% 1.85% 0.00% 2.42%

Total Taxes Overview

• Real estate tax revenue for general purposes grew over the period by over $200,000 or 26.4 percent as the result of property tax increases, accounting for most of the growth in total taxes.

• Debt service millage was levied for a new truck and various capital expenditures and ended after 2019.

• Earned income at 0.5 percent is the borough’s second most productive tax but showed little growth over the historical review period, increasing by only 1.3 percent.

• Local services tax at $47 annually, which reflects employment within the borough, declined slightly.

• The per capita tax is $5 while the occupation tax is $36; neither is a significant source of income.

• The real estate transfer tax of 0.5 percent fluctuates with real estate activity within the borough.

Table 2-4

Total tax revenues

2015 2016 2017 2018 2019 Change

2015-2019

Actual Actual Actual Actual Actual $ %

Real Estate $810,205 $880,559 $1,099,300 $1,042,881 $1,024,017 213,812 26.4

Earned Income 347,922 333,635 332,845 355,558 352,537 4,615 1.3

Local Services 140,489 136,649 131,993 134,483 140,292 -197 -0.1

Debt Service 0 0 59,802 60,857 59,895 59,895 100.0

Real Estate Transfer 49,295 39,271 43,379 28,716 43,495 -5,800 -11.8

Per Capita 11,165 10,694 11,182 10,490 12,006 841 7.5

Occupation 3,230 3,284 3,318 2,862 3,149 -81 -2.5

Tax Revenue $1,362,307 $1,404,092 $1,681,819 $1,635,845 $1,635,391 273,085 20.0

20

Borough of Brookville STMP

March 2021

Total Non-Taxes Overview

• Rents and royalties are the largest non-tax revenue category and mostly include fees for rent of the borough complex.

• State shared revenues is primarily from state aid for pension and fire with a small amount for Act 13 impact fees. It is the borough’s second largest non-tax revenue category and has growth of almost $40,000 or 33 percent.

• Cable franchise fee revenue accounts for the bulk of license and permit revenue.

• Fines and forfeits include public safety violations and parking fine revenue. The category was flat.

• Highway and streets earnings include parking revenue with meter revenue ranging from $37,500 to $39,000 annually and parking lot permit revenue of approximately $12,000 annually. Meters are 5 cents for 15 minutes and permit costs are $300 a year or $30 a month. Also included is revenue received from PennDOT for snow plowing. This category spiked in 2019 due to the sale of a dump truck.

• Public safety earnings record the reimbursement for the school resource officer from the School District starting at $15,500 in 2018 and growing to $71,900 in 2019. This category also includes payment for contracting police protection and revenue from the drug task force.

• General government earnings include fees associated with zoning and code enforcement, reimbursements and various miscellaneous revenue.

Table 2-5

Non-tax revenues

2015 2016 2017 2018 2019 Change

2015-2019

Actual Actual Actual Actual Actual $ %

Rents & Royalties $227,747 $222,106 $221,460 $230,824 $233,998 6,251 2.7

State Shared Revenue 119,641 131,130 142,553 138,646 159,005 39,364 32.9

Highway/Street Earnings 48,369 59,722 53,848 55,829 105,264 56,896 117.6

Public Safety Earnings 13,537 49,521 25,044 49,427 100,437 86,900 642.0

Licenses & Permits 60,538 67,633 71,793 67,768 66,927 6,390 10.6

Fines & Forfeits 51,722 47,738 52,018 51,740 57,036 5,314 10.3

General Gov Earnings 50,663 17,903 43,767 37,481 46,323 -4,340 -8.6

Interest 783 1,360 1,883 9,868 27,958 27,175 3,471.0

Miscellaneous Revenue 488 724 44 55 7,092 6,604 1,351.9

PURTA 0 0 1,609 1,824 1,611 1,611 100.0

Culture/Recreation Earnings 2,030 40,995 30,068 9,924 350 -1,680 -82.8

Non-Tax Revenue $575,517 $638,833 $644,086 $653,387 $806,001 230,484 40.0

21

Borough of Brookville STMP

March 2021

Expenditures

Departmental Expenditures

• General Government expenditures appear to have risen the most, but actual operating costs are masked by one-time transfers that were made to the Liquid Fuels, Capital, Streetlight and CD funds as shown in Table 2-7. In addition, HVAC repairs in 2019 were approximately $100,000 higher than the historical average.

• General Government includes elected officials, administration, solicitor, IT, engineering, buildings, zoning, codes, debt service and tax collections. Administration costs rose by $29,073 or 20.8 percent from 2015 to 2019.

• Public Works appears to have grown the least among departments, but the change from 2015 to 2019 is skewed by over $200,000 in 2015 capital expenditures.

• Salaries and wages in Public Works increased from $195,084 in 2015 to $260,457 in 2019. Overall, personnel costs in the department rose from $443,116 in 2015 to $460,868 in 2019.

• Costs for part-time police officers increased in 2018 and 2019, appearing to put a check on full time officer wages that were starting to climb in 2016 and 2017. Still, personnel costs in the Police Department rose from $622,512 in 2015 to $753,703 in 2019. Overall department expenditures increased by over 12 percent.

• Police expenditures include costs for new vehicles in four out of five years and for technology in 2015 and 2019.

• Spending in culture and recreation fluctuated considerably during the historical review period with significant changes in personnel costs and a capital expenditure in 2016.

Table 2-6

Departmental expenditures

2015 2016 2017 2018 2019 Change

2015 to 2019

Actual Actual Actual Actual Actual $ %

General Government $565,798 $731,732 $560,148 $523,898 $841,920 276,121 48.8

Police 759,441 737,736 707,518 848,115 855,721 96,280 12.7

Fire 33,443 34,073 90,095 33,614 33,301 -142 -0.4

Public Works 845,982 877,153 642,453 666,102 609,457 -236,525 -28.0

Culture/Recreation 24,069 70,483 43,901 11,471 10,506 -13,563 -56.3

Total Expenditures $2,228,733 $2,451,177 $2,044,115 $2,083,199 $2,350,904 122,171 5.5

Table 2-7

General Government Transfers

2015 2016 2017 2018 2019

Actual Actual Actual Actual Actual

Transfer to CD $0 $0 $0 $0 $167,458

Transfer to Street Light Fund 0 24,610 0 0 6,000

Transfer to Capital Fund 0 0 0 0 5,000

Transfer to Liquid Fuels Fund 98,969 77,990 0 0 0

Total $98,969 $102,600 $0 $0 $178,458

22

Borough of Brookville STMP

March 2021

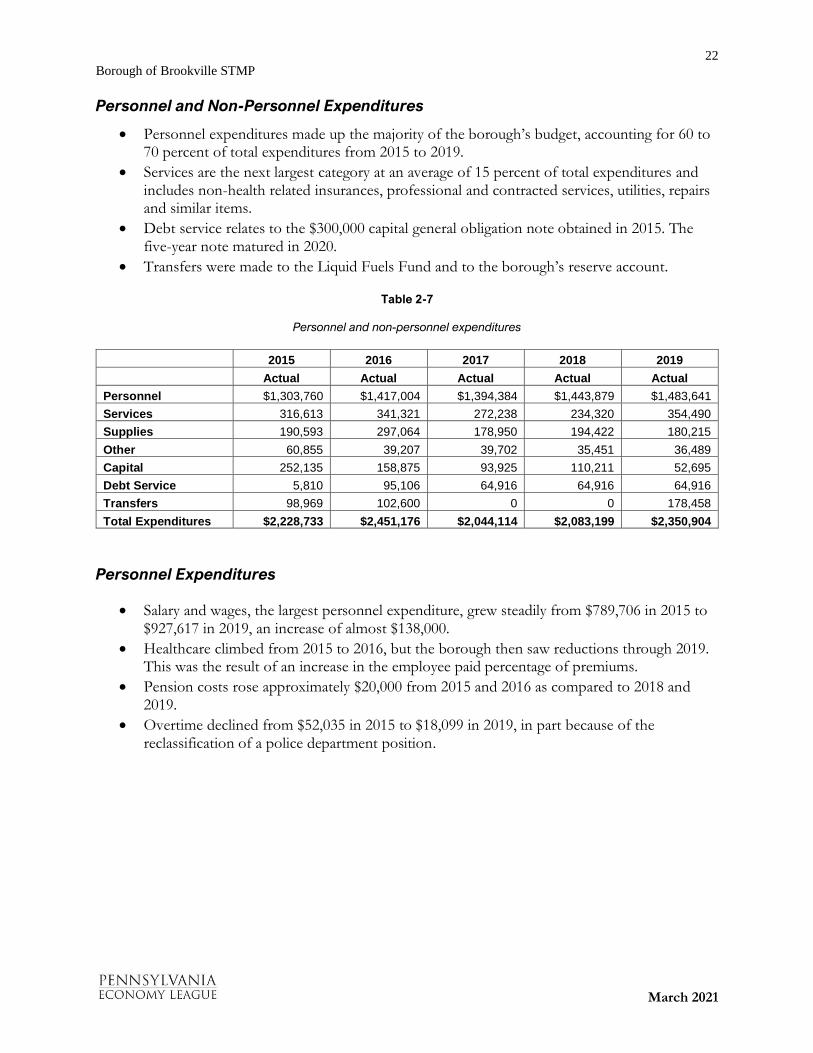

Personnel and Non-Personnel Expenditures

• Personnel expenditures made up the majority of the borough’s budget, accounting for 60 to 70 percent of total expenditures from 2015 to 2019.

• Services are the next largest category at an average of 15 percent of total expenditures and includes non-health related insurances, professional and contracted services, utilities, repairs and similar items.

• Debt service relates to the $300,000 capital general obligation note obtained in 2015. The five-year note matured in 2020.

• Transfers were made to the Liquid Fuels Fund and to the borough’s reserve account.

Table 2-7

Personnel and non-personnel expenditures

2015 2016 2017 2018 2019

Actual Actual Actual Actual Actual

Personnel $1,303,760 $1,417,004 $1,394,384 $1,443,879 $1,483,641

Services 316,613 341,321 272,238 234,320 354,490

Supplies 190,593 297,064 178,950 194,422 180,215

Other 60,855 39,207 39,702 35,451 36,489

Capital 252,135 158,875 93,925 110,211 52,695

Debt Service 5,810 95,106 64,916 64,916 64,916

Transfers 98,969 102,600 0 0 178,458

Total Expenditures $2,228,733 $2,451,176 $2,044,114 $2,083,199 $2,350,904

Personnel Expenditures

• Salary and wages, the largest personnel expenditure, grew steadily from $789,706 in 2015 to $927,617 in 2019, an increase of almost $138,000.

• Healthcare climbed from 2015 to 2016, but the borough then saw reductions through 2019. This was the result of an increase in the employee paid percentage of premiums.

• Pension costs rose approximately $20,000 from 2015 and 2016 as compared to 2018 and 2019.

• Overtime declined from $52,035 in 2015 to $18,099 in 2019, in part because of the reclassification of a police department position.

23

Borough of Brookville STMP

March 2021

Table 2-8

Personnel expenditure detail

2015 2016 2017 2018 2019

Actual Actual Actual Actual Actual

Salary & Wages $789,706 $863,976 $851,315 $891,989 $927,617

Longevity 6,427 8,485 9,910 0 18,063

Overtime 52,035 32,652 36,364 23,901 18,099

FICA 40,601 44,881 42,012 46,065 47,942

Healthcare 208,048 265,351 262,867 245,260 239,355

Life Insurance 7,724 8,315 7,194 7,780 10,971

Pension 128,375 127,791 115,788 151,095 146,013

Unemployment Comp 7,074 6,829 6,324 7,205 7,711

Uniform Allowance 6,035 7,594 3,750 9,297 8,377

Workers Comp 57,733 51,129 58,862 61,286 59,493

Personnel Expenditures $1,303,760 $1,417,004 $1,394,384 $1,443,879 $1,483,641

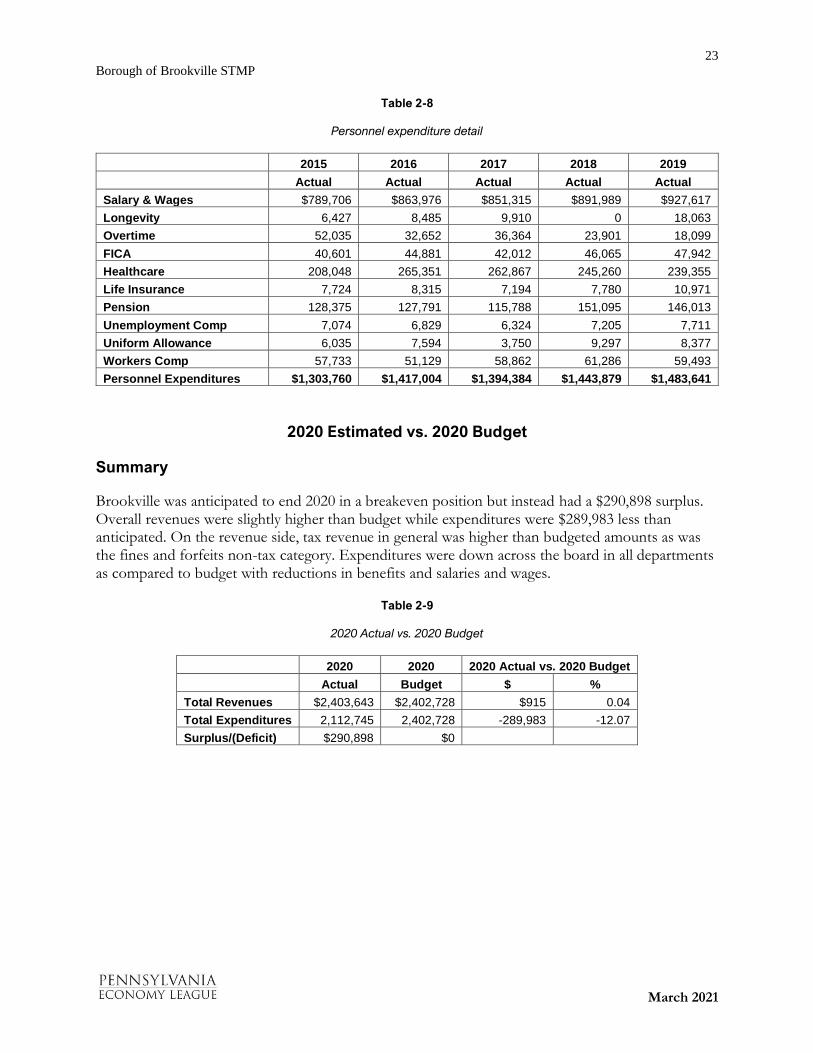

2020 Estimated vs. 2020 Budget

Summary

Brookville was anticipated to end 2020 in a breakeven position but instead had a $290,898 surplus. Overall revenues were slightly higher than budget while expenditures were $289,983 less than anticipated. On the revenue side, tax revenue in general was higher than budgeted amounts as was the fines and forfeits non-tax category. Expenditures were down across the board in all departments as compared to budget with reductions in benefits and salaries and wages.

Table 2-9

2020 Actual vs. 2020 Budget

2020 2020 2020 Actual vs. 2020 Budget

Actual Budget $ %

Total Revenues $2,403,643 $2,402,728 $915 0.04

Total Expenditures 2,112,745 2,402,728 -289,983 -12.07

Surplus/(Deficit) $290,898 $0

24

Borough of Brookville STMP

March 2021

Table 2-10

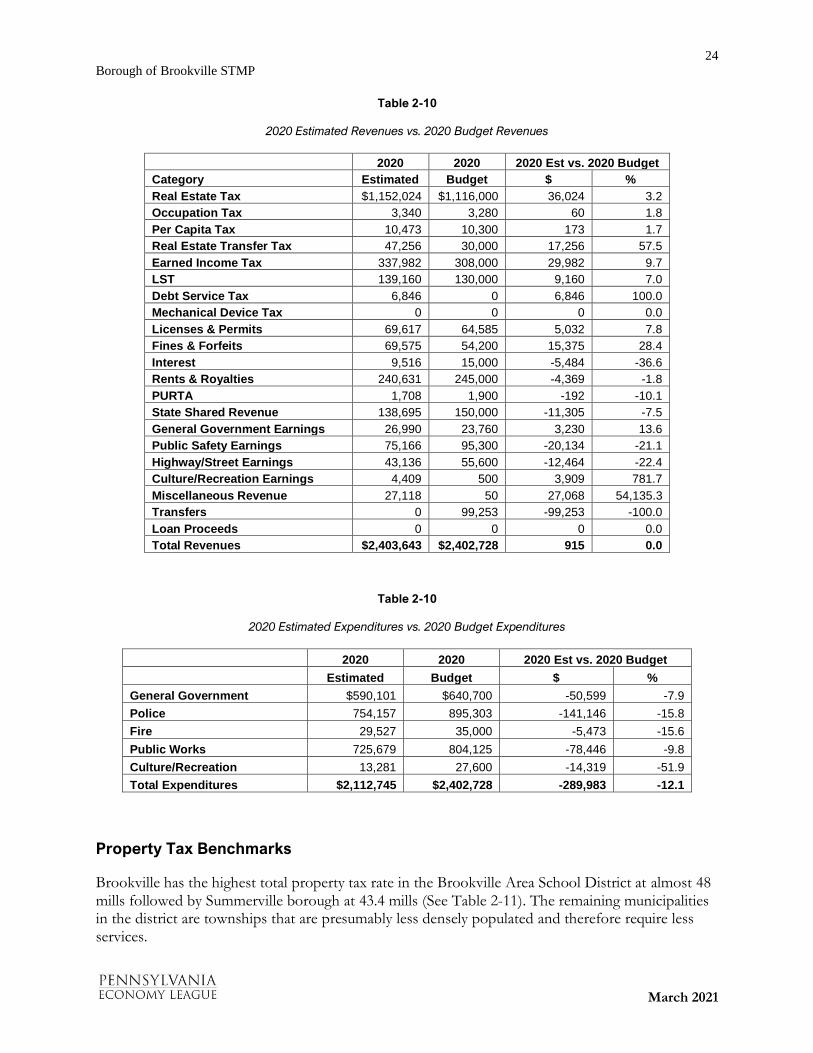

2020 Estimated Revenues vs. 2020 Budget Revenues

2020 2020 2020 Est vs. 2020 Budget

Category Estimated Budget $ %

Real Estate Tax $1,152,024 $1,116,000 36,024 3.2

Occupation Tax 3,340 3,280 60 1.8

Per Capita Tax 10,473 10,300 173 1.7

Real Estate Transfer Tax 47,256 30,000 17,256 57.5

Earned Income Tax 337,982 308,000 29,982 9.7

LST 139,160 130,000 9,160 7.0

Debt Service Tax 6,846 0 6,846 100.0

Mechanical Device Tax 0 0 0 0.0

Licenses & Permits 69,617 64,585 5,032 7.8

Fines & Forfeits 69,575 54,200 15,375 28.4

Interest 9,516 15,000 -5,484 -36.6

Rents & Royalties 240,631 245,000 -4,369 -1.8

PURTA 1,708 1,900 -192 -10.1

State Shared Revenue 138,695 150,000 -11,305 -7.5

General Government Earnings 26,990 23,760 3,230 13.6

Public Safety Earnings 75,166 95,300 -20,134 -21.1

Highway/Street Earnings 43,136 55,600 -12,464 -22.4

Culture/Recreation Earnings 4,409 500 3,909 781.7

Miscellaneous Revenue 27,118 50 27,068 54,135.3

Transfers 0 99,253 -99,253 -100.0

Loan Proceeds 0 0 0 0.0

Total Revenues $2,403,643 $2,402,728 915 0.0

Table 2-10

2020 Estimated Expenditures vs. 2020 Budget Expenditures

2020 2020 2020 Est vs. 2020 Budget

Estimated Budget $ %

General Government $590,101 $640,700 -50,599 -7.9

Police 754,157 895,303 -141,146 -15.8

Fire 29,527 35,000 -5,473 -15.6

Public Works 725,679 804,125 -78,446 -9.8

Culture/Recreation 13,281 27,600 -14,319 -51.9

Total Expenditures $2,112,745 $2,402,728 -289,983 -12.1

Property Tax Benchmarks

Brookville has the highest total property tax rate in the Brookville Area School District at almost 48 mills followed by Summerville borough at 43.4 mills (See Table 2-11). The remaining municipalities in the district are townships that are presumably less densely populated and therefore require less services.

25

Borough of Brookville STMP

March 2021

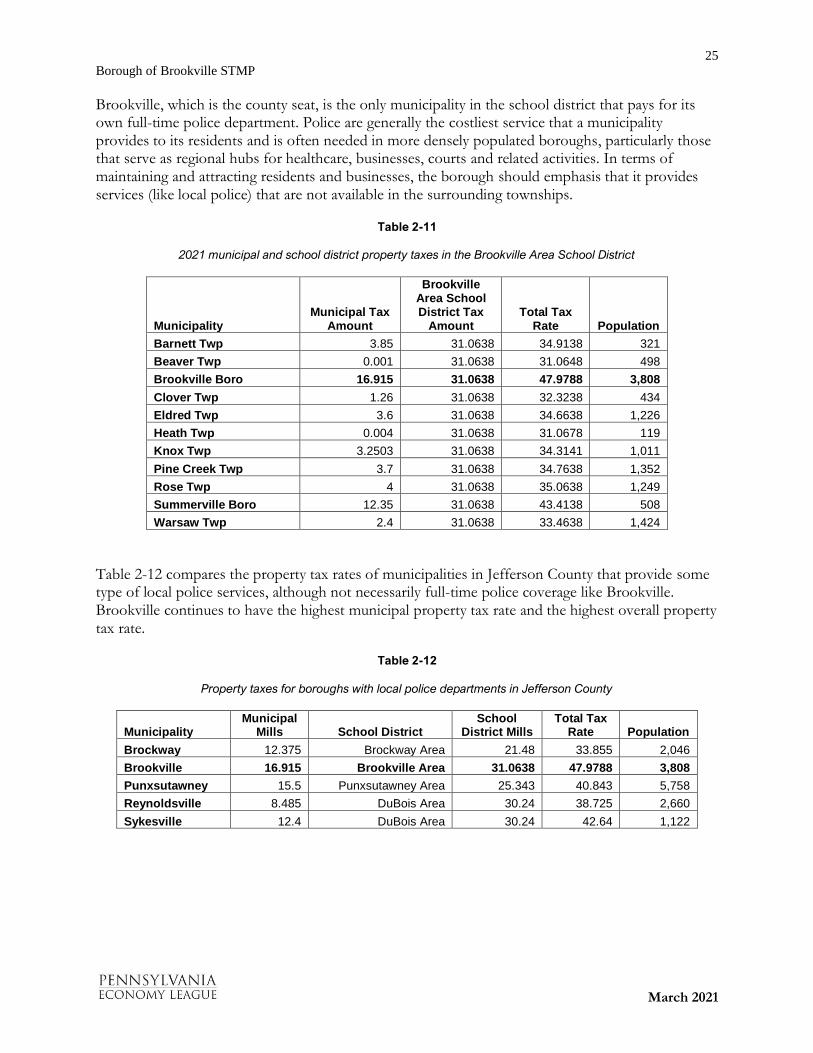

Brookville, which is the county seat, is the only municipality in the school district that pays for its own full-time police department. Police are generally the costliest service that a municipality provides to its residents and is often needed in more densely populated boroughs, particularly those that serve as regional hubs for healthcare, businesses, courts and related activities. In terms of maintaining and attracting residents and businesses, the borough should emphasis that it provides services (like local police) that are not available in the surrounding townships.

Table 2-11

2021 municipal and school district property taxes in the Brookville Area School District

Municipality Municipal Tax

Amount

Brookville Area School District Tax

Amount Total Tax

Rate Population

Barnett Twp 3.85 31.0638 34.9138 321

Beaver Twp 0.001 31.0638 31.0648 498

Brookville Boro 16.915 31.0638 47.9788 3,808

Clover Twp 1.26 31.0638 32.3238 434

Eldred Twp 3.6 31.0638 34.6638 1,226

Heath Twp 0.004 31.0638 31.0678 119

Knox Twp 3.2503 31.0638 34.3141 1,011

Pine Creek Twp 3.7 31.0638 34.7638 1,352

Rose Twp 4 31.0638 35.0638 1,249

Summerville Boro 12.35 31.0638 43.4138 508

Warsaw Twp 2.4 31.0638 33.4638 1,424

Table 2-12 compares the property tax rates of municipalities in Jefferson County that provide some type of local police services, although not necessarily full-time police coverage like Brookville. Brookville continues to have the highest municipal property tax rate and the highest overall property tax rate.

Table 2-12

Property taxes for boroughs with local police departments in Jefferson County

Municipality Municipal

Mills School District School

District Mills Total Tax

Rate Population

Brockway 12.375 Brockway Area 21.48 33.855 2,046

Brookville 16.915 Brookville Area 31.0638 47.9788 3,808

Punxsutawney 15.5 Punxsutawney Area 25.343 40.843 5,758

Reynoldsville 8.485 DuBois Area 30.24 38.725 2,660

Sykesville 12.4 DuBois Area 30.24 42.64 1,122

26

Borough of Brookville STMP

March 2021

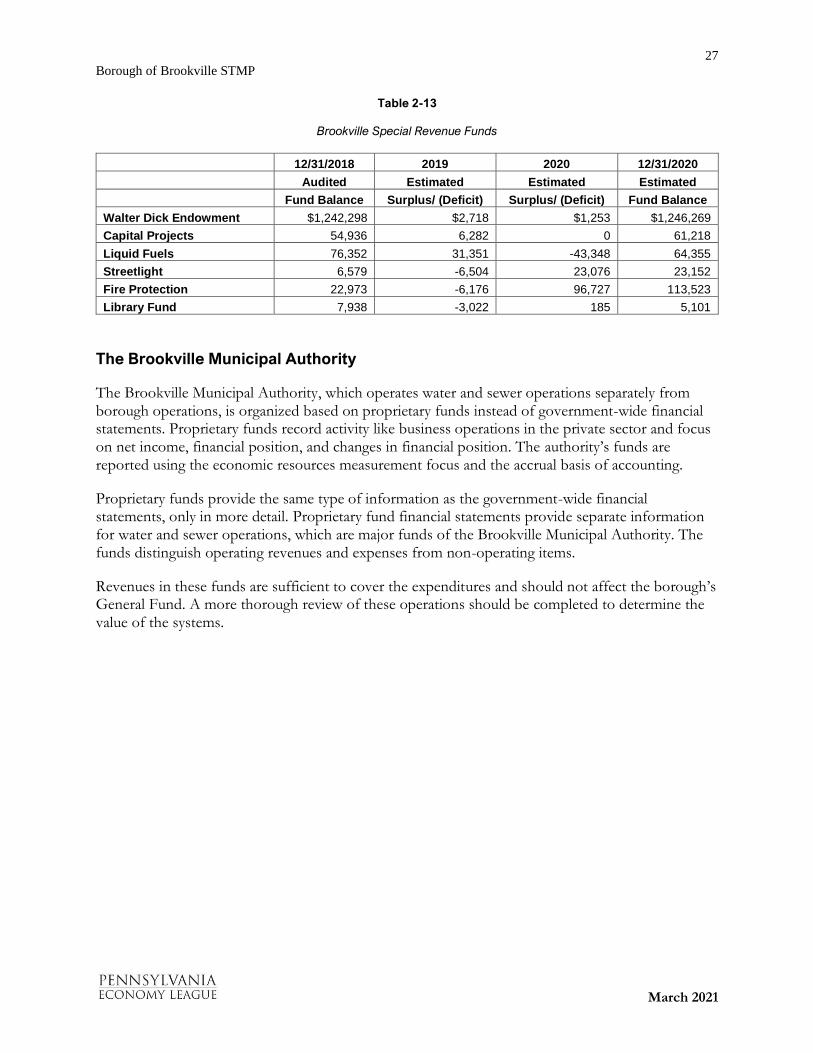

Other Funds

As noted previously, Brookville maintains seven government funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the General Fund and the Walter Dick Park Endowment Fund, which are considered major funds.

• General Fund - The General Fund is the primary operating fund of the borough and is always classified as a major fund. It is used to account for and report all activities of the borough except those legally or administratively required to be accounted for in other funds.

• Special Revenue Funds - Special Revenue Funds are used to account for and report the proceeds of specific revenue sources that are restricted or committed to expenditures for specified purposes other than debt service or capital projects.

Brookville includes the following Special Revenue Funds, all of which are reported as nonmajor funds:

• Liquid Fuel Fund - Accounts for revenues received from the Commonwealth of Pennsylvania from the State Liquid Fuels Tax Fund and the related expenditures for building, improving or maintaining local roads and bridges.

• Street Light Fund - Accounts for local tax revenues and expenditures to provide street lighting within the borough.

• Fire Protection Fund - Accounts for local tax revenues and expenditures to provide fire protection services to the borough.

• Library Fund - Accounts for local tax revenues and expenditures to assist the local library to provide services to the residents of the borough.

• Capital Projects Fund - Capital Projects Funds are used to account for and report financial resources that are restricted, committed, or assigned for the acquisition or construction of specific capital projects or items. Brookville has one Capital Projects Fund which accounts for contributions and specific revenues and transfers from the borough’s General Fund and expenditures for various capital acquisitions as the borough council may designate. The fund is reported as a nonmajor fund.

• Permanent Fund - Permanent Funds are used to account for resources that are legally restricted to the extent that only earnings, and not principal, may be used for purposes that support the reporting government programs. Brookville has one Permanent Fund, the Walter Dick Park Endowment Fund, which accounts for contributions and other revenues to be used to provide funds for the maintenance and upkeep of the Walter Dick Memorial Park. This fund is reported as a major fund.

Table 2-13 shows that these funds have sufficient balances so that they should not impact the balance in the borough’s General Fund.

27

Borough of Brookville STMP

March 2021

Table 2-13

Brookville Special Revenue Funds

12/31/2018 2019 2020 12/31/2020

Audited Estimated Estimated Estimated

Fund Balance Surplus/ (Deficit) Surplus/ (Deficit) Fund Balance

Walter Dick Endowment $1,242,298 $2,718 $1,253 $1,246,269

Capital Projects 54,936 6,282 0 61,218

Liquid Fuels 76,352 31,351 -43,348 64,355

Streetlight 6,579 -6,504 23,076 23,152

Fire Protection 22,973 -6,176 96,727 113,523

Library Fund 7,938 -3,022 185 5,101

The Brookville Municipal Authority

The Brookville Municipal Authority, which operates water and sewer operations separately from borough operations, is organized based on proprietary funds instead of government-wide financial statements. Proprietary funds record activity like business operations in the private sector and focus on net income, financial position, and changes in financial position. The authority’s funds are reported using the economic resources measurement focus and the accrual basis of accounting.

Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. Proprietary fund financial statements provide separate information for water and sewer operations, which are major funds of the Brookville Municipal Authority. The funds distinguish operating revenues and expenses from non-operating items.

Revenues in these funds are sufficient to cover the expenditures and should not affect the borough’s General Fund. A more thorough review of these operations should be completed to determine the value of the systems.

28

Borough of Brookville STMP

March 2021

CHAPTER 3

FINANCIAL PROJECTIONS

Introduction

Based on historical patterns of reductions in assessment value, the borough’s annual General Fund revenues will not be able to support General Fund expenditures starting in 2023. While earned income taxes are expected to grow, property tax revenue is anticipated to decline and revenue from other taxes is projected to remain flat. Personnel costs are projected to increase by 5.8 percent from $1.55 million to $1.64 million. In a continuation of historical patterns, the police department remains the largest departmental expense.

Revenue Assumptions

• The 2021 budget serves as the baseline

• Tax rates and fees remain at 2021 levels

• Real estate tax revenue reduced 0.5 percent per year based on assessment history

• Earned income tax revenue annual growth of 1.0 percent

• Licenses & permits, fines & forfeits and interest revenue annual growth of 1.0 percent

• Rents & royalties grow 1.5 percent annually

• State Aid for pensions and Act 13 revenue remain at 2021 levels.

• Other revenues held at 2021 levels

Expenditure Assumptions

• The 2021 budget serves as the baseline

• Employee count remains at 2021budgeted levels

• No new debt incurred; existing debt service based on amortization schedules

• Union employee wages and salaries were increased at the annual contractual rate:

• Other employee wages and salaries were increased 2 percent annually; union wages were increased at 2 percent annually following CBA expiration

• Pension annual obligation was increased by rate of annual wage increases including longevity and step movement

• Health insurance expense was increased by 5.5 percent annually

• Other expenditure growth based on the Core Personal Consumer Index (CBO August 2019)

Capital Assumptions

• 2021 budget

• Transfer from Reserve reduced to $0 for 2022- 2025

• Department Improvements reduced to $5,000 annually, 2022 -2025

• Police Vehicle - 2021, 2023, 2025 $45,000

• DPW Vehicle – 2021,2024 -$55,000

29

Borough of Brookville STMP

March 2021

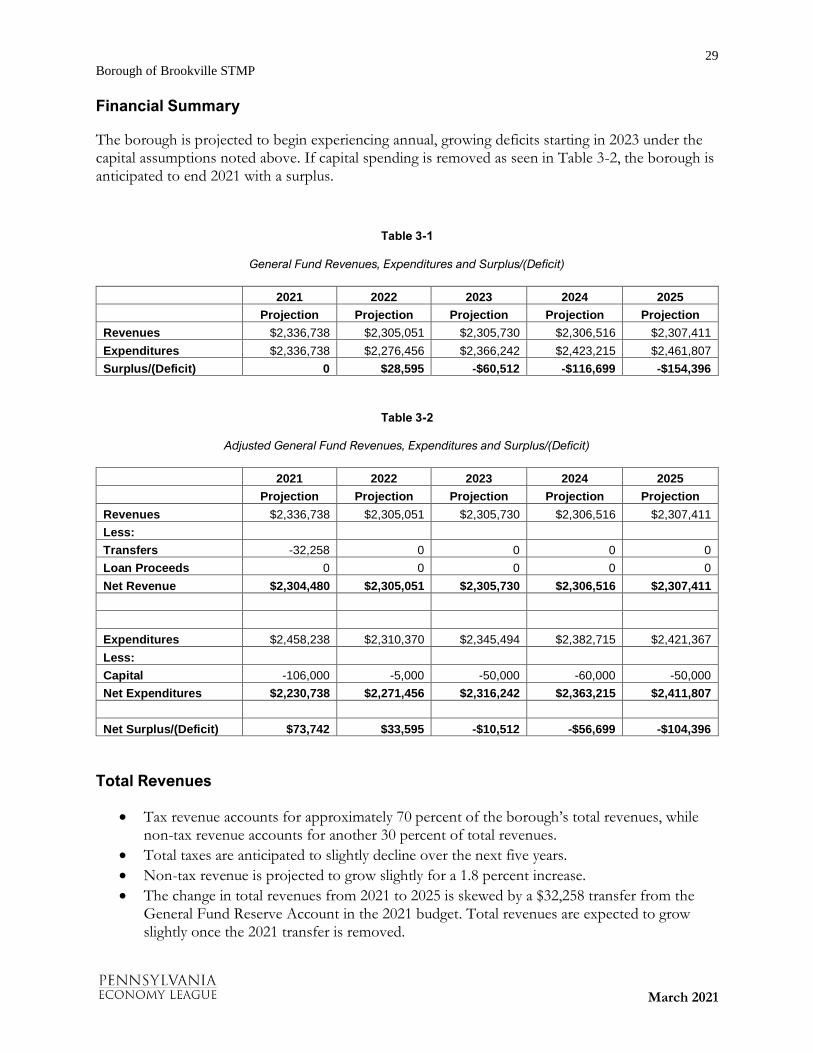

Financial Summary

The borough is projected to begin experiencing annual, growing deficits starting in 2023 under the capital assumptions noted above. If capital spending is removed as seen in Table 3-2, the borough is anticipated to end 2021 with a surplus.

Table 3-1

General Fund Revenues, Expenditures and Surplus/(Deficit)

2021 2022 2023 2024 2025

Projection Projection Projection Projection Projection

Revenues $2,336,738 $2,305,051 $2,305,730 $2,306,516 $2,307,411

Expenditures $2,336,738 $2,276,456 $2,366,242 $2,423,215 $2,461,807

Surplus/(Deficit) 0 $28,595 -$60,512 -$116,699 -$154,396

Table 3-2

Adjusted General Fund Revenues, Expenditures and Surplus/(Deficit)

2021 2022 2023 2024 2025

Projection Projection Projection Projection Projection

Revenues $2,336,738 $2,305,051 $2,305,730 $2,306,516 $2,307,411

Less:

Transfers -32,258 0 0 0 0

Loan Proceeds 0 0 0 0 0

Net Revenue $2,304,480 $2,305,051 $2,305,730 $2,306,516 $2,307,411

Expenditures $2,458,238 $2,310,370 $2,345,494 $2,382,715 $2,421,367

Less:

Capital -106,000 -5,000 -50,000 -60,000 -50,000

Net Expenditures $2,230,738 $2,271,456 $2,316,242 $2,363,215 $2,411,807

Net Surplus/(Deficit) $73,742 $33,595 -$10,512 -$56,699 -$104,396

Total Revenues

• Tax revenue accounts for approximately 70 percent of the borough’s total revenues, while non-tax revenue accounts for another 30 percent of total revenues.

• Total taxes are anticipated to slightly decline over the next five years.

• Non-tax revenue is projected to grow slightly for a 1.8 percent increase.

• The change in total revenues from 2021 to 2025 is skewed by a $32,258 transfer from the General Fund Reserve Account in the 2021 budget. Total revenues are expected to grow slightly once the 2021 transfer is removed.

30

Borough of Brookville STMP

March 2021

Table 3-3

Total Revenues

2021 2022 2023 2024 2025 Change 2021-2025

Budget Projected Projected Projected Projected $ %

Tax Revenue $1,597,580 $1,595,080 $1,592,639 $1,590,256 $1,587,933 -9,647 -0.6

Nontax Revenue 706,900 709,971 713,091 716,260 719,478 12,578 1.8

Transfers 32,258 0 0 0 0 -32,258 -100.0

Total Revenue $2,336,738 $2,305,051 $2,305,730 $2,306,516 $2,307,411 -29,327 -1.3

Total Revenue without Transfers $2,304,480 $2,305,051 $2,305,730 $2,306,516 $2,307,411 2,931 0.1

Total Taxes Overview

• Real estate tax revenue is anticipated to decline by 2 percent or $22,153 based on the assessment history.

• Earned income tax is expected to increase by 4.1 percent or $12,506.

• All other taxes are flat.

Table 3-4

Total tax revenues

2021 2022 2023 2024 2025 Change

2021-2025

Budget Projected Projected Projected Projected $ %

Real Estate Tax $1,116,000 $1,110,420 $1,104,868 $1,099,344 $1,093,847 -22,153 -2.0

Occupation Tax 3,280 3,280 3,280 3,280 3,280 0 0.0

Per Capita Tax 10,300 10,300 10,300 10,300 10,300 0 0.0

Real Estate Transfer Tax 30,000 30,000 30,000 30,000 30,000 0 0.0

Earned Income Tax 308,000 311,080 314,191 317,333 320,506 12,506 4.1

LST 130,000 130,000 130,000 130,000 130,000 0 0.0

Tax Revenue $1,597,580 $1,595,080 $1,592,639 $1,590,256 $1,587,933 -9,647 -0.6

Total Non-Taxes Overview

• Public safety earnings are anticipated to increase by 8.2 percent or $7,229. This category records the reimbursement for the school resource officer from the School District and includes payment for contracting police protection and revenue from the drug task force.

• Other categories projected to rise by 4 percent include license and permit revenue (mostly made up of the cable television franchise fee) and fines and forfeits, which includes public safety violation and parking fine revenue.

• All other non-tax revenues are expected to remain flat.

31

Borough of Brookville STMP

March 2021

Table 3-5

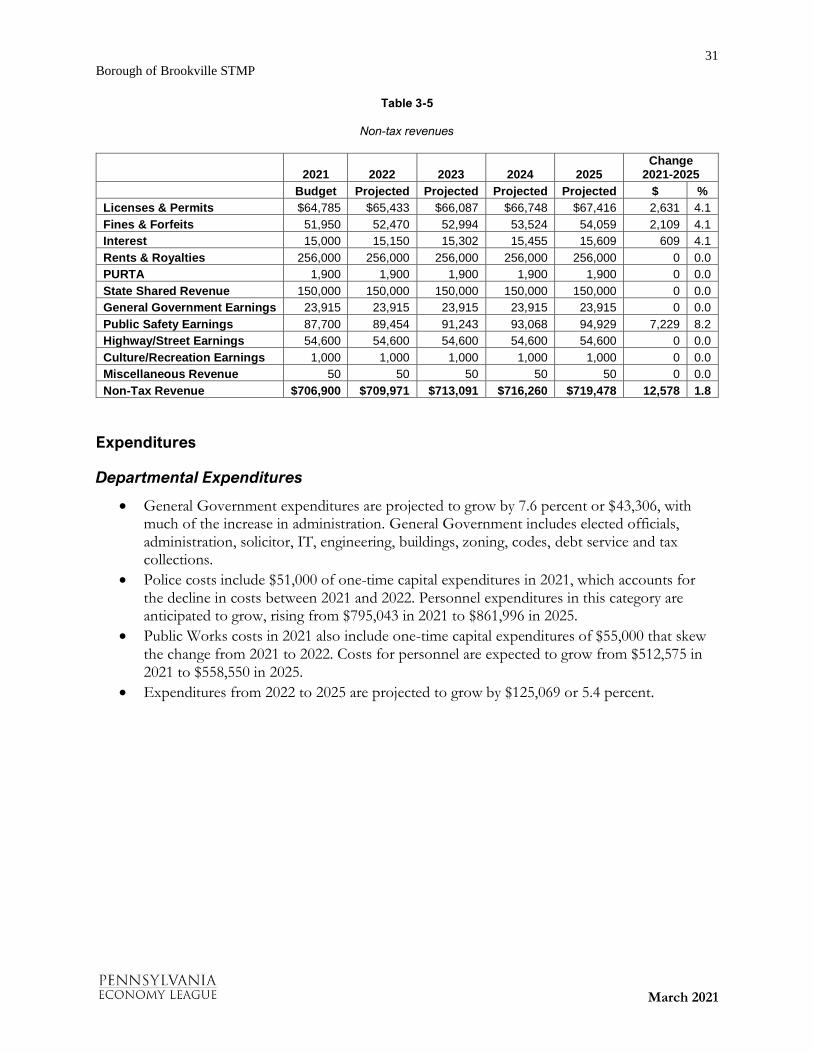

Non-tax revenues

2021 2022 2023 2024 2025 Change

2021-2025

Budget Projected Projected Projected Projected $ %

Licenses & Permits $64,785 $65,433 $66,087 $66,748 $67,416 2,631 4.1

Fines & Forfeits 51,950 52,470 52,994 53,524 54,059 2,109 4.1

Interest 15,000 15,150 15,302 15,455 15,609 609 4.1

Rents & Royalties 256,000 256,000 256,000 256,000 256,000 0 0.0

PURTA 1,900 1,900 1,900 1,900 1,900 0 0.0

State Shared Revenue 150,000 150,000 150,000 150,000 150,000 0 0.0

General Government Earnings 23,915 23,915 23,915 23,915 23,915 0 0.0

Public Safety Earnings 87,700 89,454 91,243 93,068 94,929 7,229 8.2

Highway/Street Earnings 54,600 54,600 54,600 54,600 54,600 0 0.0

Culture/Recreation Earnings 1,000 1,000 1,000 1,000 1,000 0 0.0

Miscellaneous Revenue 50 50 50 50 50 0 0.0

Non-Tax Revenue $706,900 $709,971 $713,091 $716,260 $719,478 12,578 1.8

Expenditures

Departmental Expenditures

• General Government expenditures are projected to grow by 7.6 percent or $43,306, with much of the increase in administration. General Government includes elected officials, administration, solicitor, IT, engineering, buildings, zoning, codes, debt service and tax collections.

• Police costs include $51,000 of one-time capital expenditures in 2021, which accounts for the decline in costs between 2021 and 2022. Personnel expenditures in this category are anticipated to grow, rising from $795,043 in 2021 to $861,996 in 2025.

• Public Works costs in 2021 also include one-time capital expenditures of $55,000 that skew the change from 2021 to 2022. Costs for personnel are expected to grow from $512,575 in 2021 to $558,550 in 2025.

• Expenditures from 2022 to 2025 are projected to grow by $125,069 or 5.4 percent.

32

Borough of Brookville STMP

March 2021

Table 3-6

Departmental expenditures

2021 2022 2023 2024 2025 Change

2021-2025

Budget Projected Projected Projected Projected $ %

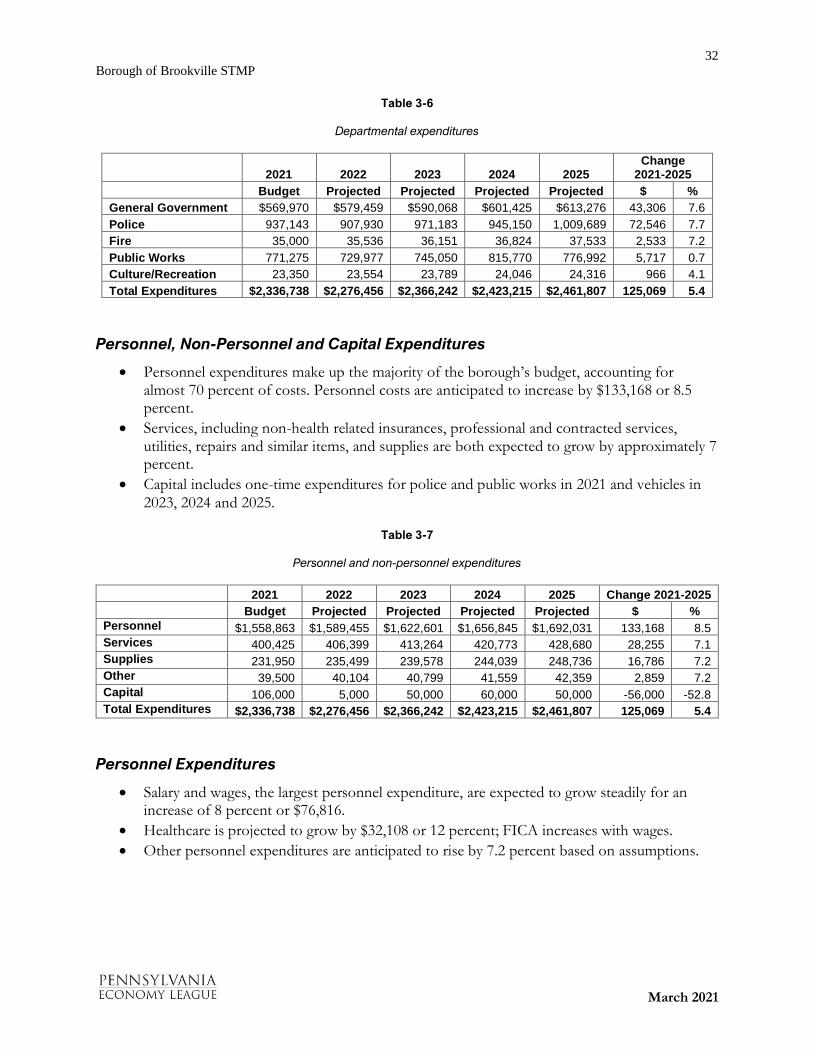

General Government $569,970 $579,459 $590,068 $601,425 $613,276 43,306 7.6

Police 937,143 907,930 971,183 945,150 1,009,689 72,546 7.7

Fire 35,000 35,536 36,151 36,824 37,533 2,533 7.2

Public Works 771,275 729,977 745,050 815,770 776,992 5,717 0.7

Culture/Recreation 23,350 23,554 23,789 24,046 24,316 966 4.1

Total Expenditures $2,336,738 $2,276,456 $2,366,242 $2,423,215 $2,461,807 125,069 5.4

Personnel, Non-Personnel and Capital Expenditures

• Personnel expenditures make up the majority of the borough’s budget, accounting for almost 70 percent of costs. Personnel costs are anticipated to increase by $133,168 or 8.5 percent.

• Services, including non-health related insurances, professional and contracted services, utilities, repairs and similar items, and supplies are both expected to grow by approximately 7 percent.

• Capital includes one-time expenditures for police and public works in 2021 and vehicles in

2023, 2024 and 2025.

Table 3-7

Personnel and non-personnel expenditures

2021 2022 2023 2024 2025 Change 2021-2025

Budget Projected Projected Projected Projected $ %

Personnel $1,558,863 $1,589,455 $1,622,601 $1,656,845 $1,692,031 133,168 8.5

Services 400,425 406,399 413,264 420,773 428,680 28,255 7.1

Supplies 231,950 235,499 239,578 244,039 248,736 16,786 7.2

Other 39,500 40,104 40,799 41,559 42,359 2,859 7.2

Capital 106,000 5,000 50,000 60,000 50,000 -56,000 -52.8

Total Expenditures $2,336,738 $2,276,456 $2,366,242 $2,423,215 $2,461,807 125,069 5.4

Personnel Expenditures

• Salary and wages, the largest personnel expenditure, are expected to grow steadily for an increase of 8 percent or $76,816.

• Healthcare is projected to grow by $32,108 or 12 percent; FICA increases with wages.

• Other personnel expenditures are anticipated to rise by 7.2 percent based on assumptions.

33

Borough of Brookville STMP

March 2021

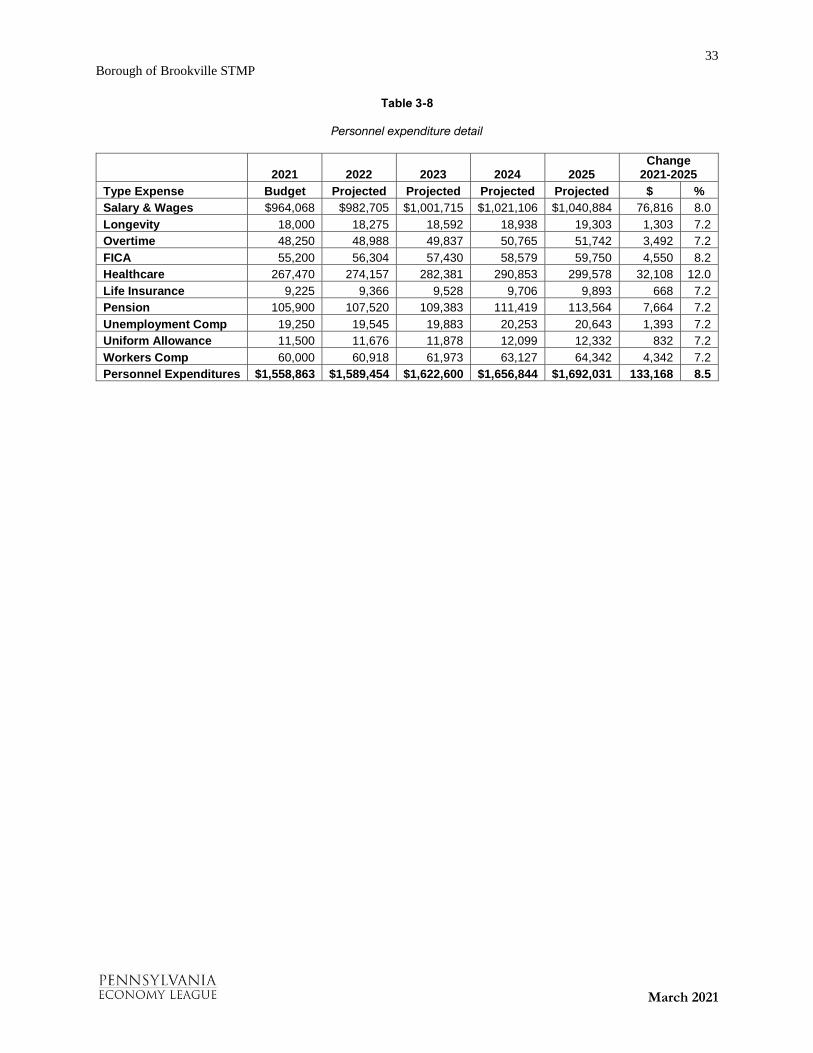

Table 3-8

Personnel expenditure detail

2021 2022 2023 2024 2025 Change

2021-2025

Type Expense Budget Projected Projected Projected Projected $ %

Salary & Wages $964,068 $982,705 $1,001,715 $1,021,106 $1,040,884 76,816 8.0

Longevity 18,000 18,275 18,592 18,938 19,303 1,303 7.2

Overtime 48,250 48,988 49,837 50,765 51,742 3,492 7.2

FICA 55,200 56,304 57,430 58,579 59,750 4,550 8.2

Healthcare 267,470 274,157 282,381 290,853 299,578 32,108 12.0

Life Insurance 9,225 9,366 9,528 9,706 9,893 668 7.2

Pension 105,900 107,520 109,383 111,419 113,564 7,664 7.2

Unemployment Comp 19,250 19,545 19,883 20,253 20,643 1,393 7.2

Uniform Allowance 11,500 11,676 11,878 12,099 12,332 832 7.2

Workers Comp 60,000 60,918 61,973 63,127 64,342 4,342 7.2

Personnel Expenditures $1,558,863 $1,589,454 $1,622,600 $1,656,844 $1,692,031 133,168 8.5

34

Borough of Brookville STMP

March 2021

CHAPTER 4

MANAGEMENT AUDIT

Introduction

Brookville’s operations are generally well-run with no major deficiencies. Most operations recommendations for Brookville center on best practice improvements for policies and procedures, training and other human resources functions as well as a focus on long-term and capital planning. The borough should also concentrate on economic and community development efforts that serve to maintain and strengthen the tax base including potential investments in community parks. In addition, Brookville should consider appropriate upgrades to information technology to improve operations and increase staff capacity.

Methodology

Interviews were conducted with the borough manager, police chief, public works director, water & wastewater commissioner, three elected council members, and additional borough staff. This study included an analysis of administration and finance, the police department, the public works department and parks.

Reviews were also conducted of existing studies and plans that could be used to advance organizational and community goals such as planning, recreation, and economic development. The borough provides administration and finance functions, tax collection, utility billing, human resources, law enforcement, codes and zoning, and public works. Brookville has an FTE count of 22 including, 17 full-time employees and 10 part-time employees.

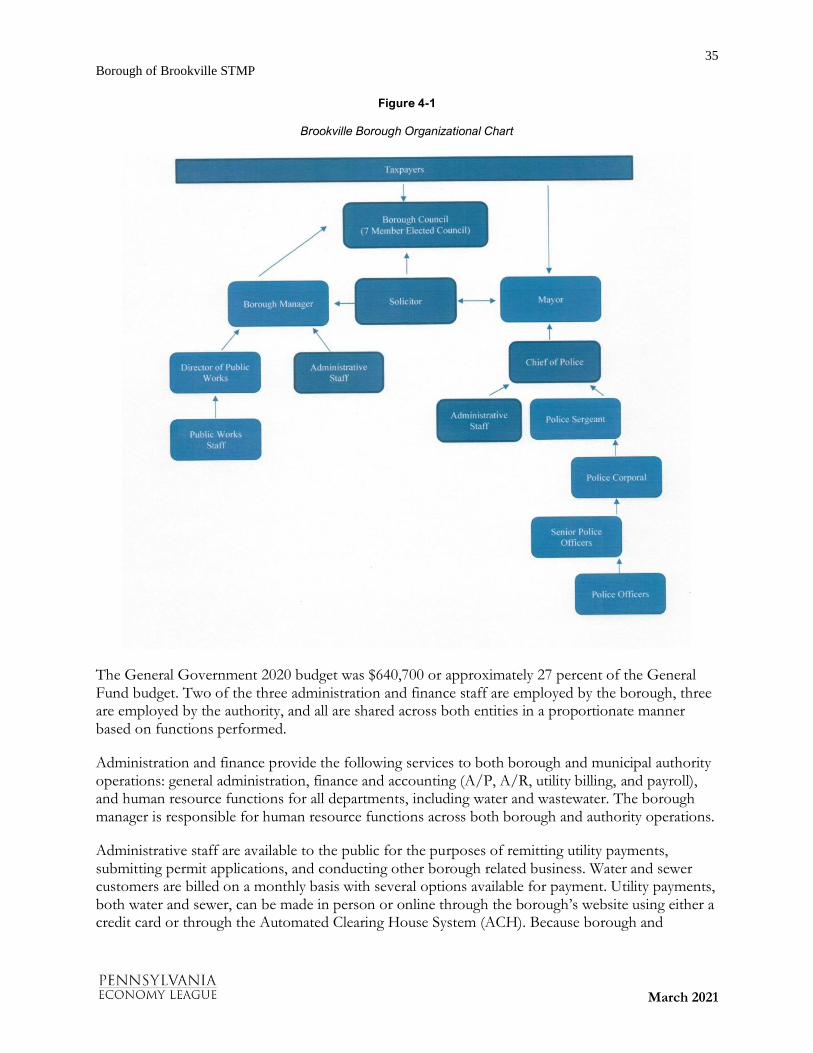

Administration and Finance (General Government)

Borough administration and finance is staffed by five full-time employees, including the borough manager, who also serves as the administrative manager for the municipal authority. Management reports that current staffing levels are appropriate for the expected level of service delivery by both the borough and the municipal authority. The administrative and finance staff report to the borough manager. The borough manager, per Borough Code, is the Chief Administrative Officer of the borough and is responsible to council for the proper and efficient administration of the affairs of the borough. Additional detail on the borough manager position such as qualifications, appointment and removal, and duties can be found in Chapter 31, Article V of the Brookville Borough Code.

35

Borough of Brookville STMP

March 2021

Figure 4-1

Brookville Borough Organizational Chart

The General Government 2020 budget was $640,700 or approximately 27 percent of the General Fund budget. Two of the three administration and finance staff are employed by the borough, three are employed by the authority, and all are shared across both entities in a proportionate manner based on functions performed.

Administration and finance provide the following services to both borough and municipal authority operations: general administration, finance and accounting (A/P, A/R, utility billing, and payroll), and human resource functions for all departments, including water and wastewater. The borough manager is responsible for human resource functions across both borough and authority operations.

Administrative staff are available to the public for the purposes of remitting utility payments, submitting permit applications, and conducting other borough related business. Water and sewer customers are billed on a monthly basis with several options available for payment. Utility payments, both water and sewer, can be made in person or online through the borough’s website using either a credit card or through the Automated Clearing House System (ACH). Because borough and

36

Borough of Brookville STMP

March 2021

authority personnel are shared, the two entities should consider drafting a management and operations agreement, formally memorializing the relationship between the two entities.

The borough property tax rate is 16.915 mills and is collected by an elected tax collector. The tax collector has office hours in the borough complex, accepting tax payments on Wednesday (12:00 p.m. – 3:00 p.m.), Thursday and Friday (9:30 a.m. – 12:00 p.m. and 1:00 p.m. – 4:00 p.m.) for a total of fourteen hours/weekly. There is a secure drop box available for payments at the entrance of Borough Hall. Tax payments can be made using either cash or check. The borough’s earned income tax and local services tax are collected by Berkheimer Associates.

The borough manager is also responsible for the activities of all borough departments except for the Police Department. Departments under the purview of the borough manager include administration and finance and public works. Per Borough Code, the borough manager is also responsible for coordinating the activities of borough council, the municipal authority (water and wastewater), the zoning hearing board, and the planning commission.

Responsibilities for permitting (building and zoning) lie with the borough manager and administrative staff. The borough refers permits to a third-party consultant for review, when necessary. Residents wishing to apply for building and/or zoning permits do so in person at the Borough Hall complex. The borough manager and police chief assumed code enforcement and zoning duties in May 2020 due to personnel and performance issues. According to the borough manager, there are no plans to alter the current status of codes and zoning activities through the addition of personnel or third-party consultants. Activities specific to codes enforcement include notification and enforcement in areas such as abandoned vehicles, grass complaints, property blight, littering, etc.

Table 4-1

Borough of Brookville Permitting, Codes & Zoning Statistics

Year Building Permits Issued Zoning Permits Issued Code Complaints Received/Addressed

2019 36 1 72

2020 24 1 265

The borough manager reports that facilities are appropriate, allowing for adequate space for staff, equipment, and storage. There are no security measures noted, i.e., cameras, key fob systems, etc., that can be used to restrict access and monitor and document activity within and outside of the borough administrative campus.

Borough operations uses standard software, i.e., the Microsoft suite of Office products. IT support is provided by a third party contracted provider on an on-call, as needed basis. The borough’s server was last updated in 2013 and is currently running on Windows Server 2011. The server was easily accessed, located in an unsecured meeting room. The useful life of standard server hardware is approximately 3-5 years with maintenance costs and the probability of failure increasing with the passage of time.

37

Borough of Brookville STMP

March 2021

Standard cyber-security practices would recommend upgrading hardware and locating the server in a secure, environmentally controlled location. Consideration should also be given to redundancy in the area of data back-up; possibly implementing both onsite and cloud-based back-up procedures. Software platforms needed for service delivery, i.e., accounting, billing, GIS, will continue to transition to cloud based solutions.

Based on the availability of high-speed internet infrastructure, the borough should monitor the availability of high-speed internet access. Continuity of operations will be discussed later in this report. A VOIP phone system facilitates continuity of operations in all departments. The borough should consider investigating VOIP phone systems, or an appropriate alternative.

The borough operates on a modified cash basis of accounting, using a total of seven funds (activity groups) which include the General Fund, the Walter Dick Park Endowment Fund, Liquid Fuels Fund, Street Light Fund, Fire Protection Fund, Library Fund, and the Capital Projects Fund. Detailed financial statements are completed and audited annually for both the borough and the Municipal Authority.

The borough should consider issuing a Comprehensive Annual Financial Report. The statistics section contained in the report would be useful in ongoing economic development efforts. Both the borough manager and staff accountant report that the finance and billing software was upgraded to Abila/Diversified Technologies in 2018. Management and staff report that the accounting software is appropriate for the functions for which it is being used (accounts payable, accounts receivable, water (2,672 customers) and wastewater (2,241 customers) utility billing, and payroll).

The general liability, property, and workers compensation insurance products are evaluated on an annual basis for adequacy and cost.