Embed Size (px)

Citation preview

BP Amoco: Policy Statement on the Use of Project Finance

Case study made by:Ana-Maria Pase

Dan-Gabriel GrigorescuSergiu Alexandru Dragan

Structure of our presentation

• I) BP and Amoco: history, major investments, strategies and leaders, main markets

• II) Background and development of the project: Study on the advantages and disadvantages of

using project finance following the merger between the two companies

Answers to case study questions • III) Conclusions and opinions

I) Presentation of The British Petroleum Company (BP)

Founded in 1909 as the Anglo-Persian Oil Company by William Knox D’Arcy.

In 1923, it employs Winston Churchill (future British Prime-minister) as a consultant.

Becomes the Anglo-Iranian Oil Company (AIOC) in 1935.

In World War II, all three British armed services used oils and lubricating equipment from BP.

Assumes the name of BP in 1954.

In 1959, BP realizes its first major expansion of operations by investing in Alaska.

In 1965, BP becomes the first company to strike oil in the North Sea and discovers the hugely rich “Forties” oil field off the coast of Scotland.

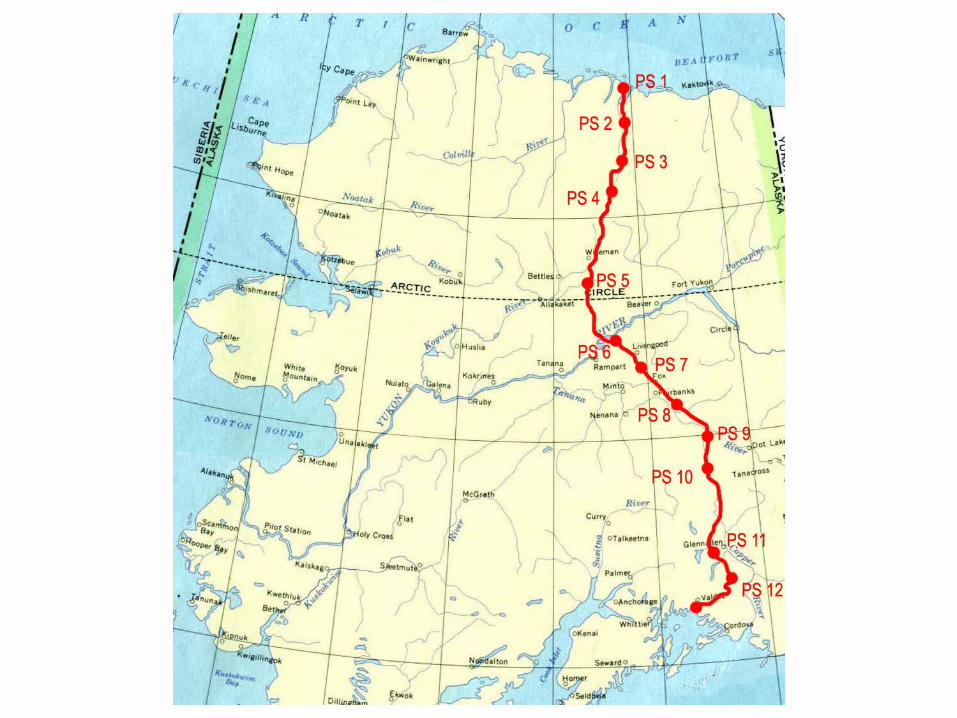

In 1975, the company finalizes one of its biggest challenges: the Trans-Alaska pipeline system, which was, at the time, the largest civil engineering project attempted in North America.

In 1987, BP becomes a fully privatized company, the British government having sold its last shares.

John Browne, who had been on the board as managing director since 1991, was appointed group chief executive in 1995.

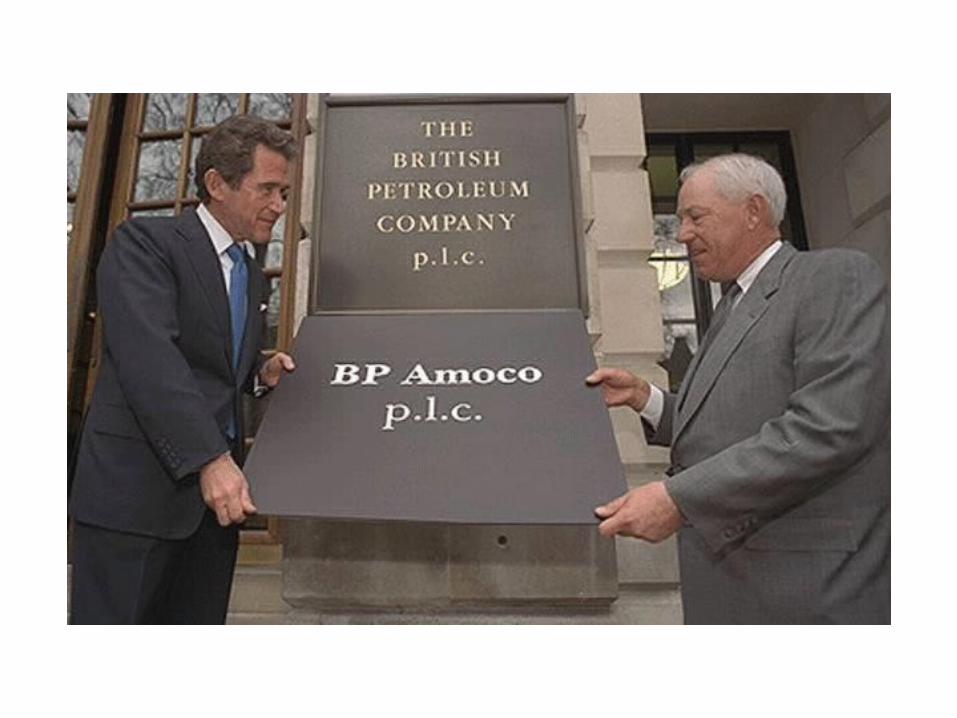

In 1998, with stiff competition in the energy industry setting off a string of prominent mergers, BP and Amoco joined to form BP Amoco.

Other important strategic moves followed and these included the expansion of the group by taking over ARCO, Castrol and Aral.

20th Century: Major long-term projects in Russia, the Gulf of Mexico, North America, Azerbaijan, Indonesia.

In 2000, BP unveiled a new, unified global brand. Its identifier was a green, yellow and white sunburst, symbolizing energy in all its dynamic forms.

To further strengthen this commitment, it created a new unit, BP Alternative Energy, devoted to making from all the various types of low-carbon energy – solar, wind, natural gas, bio-fuels – a viable, large-scale and profitable business.

We might say BP has become an organization that embodies energy in all its many forms.

American Oil Corporation (Amoco)Founded in 1889 under the name Standard Oil

Company (Indiana).By the early 1900’s it was the leading provider of

kerosene and gasoline in the Midwest. In 1930, company crews made their first huge discovery

when they struck oil at a large field in east Texas. During World War II, Amoco employees put much of

their energy into providing gasoline and other products to the American military.

Off the coast of Louisiana, Amoco explorers found the first off-shore oil field in the mid 1940’s.

The company’s research department followed on with some extraordinary breakthroughs, such as Hydrafrac, a hydraulic well fracturing process that increased industry production worldwide, and PTA, a chemical used in the production polyester fibres.

By the end of the century, it was the largest natural gas producer in North America, with a reach that stretched well beyond its home continent: exploration in 20 countries, production in 14 countries.

Standard Oil Company (Indiana) was officially renamed Amoco Corporation in 1985.

In 1998, Amoco and BP announced that they had merged, combining their worldwide operations into a single organization. Overnight, the new company, BP Amoco, became the largest producer of both oil and natural gas in the US.

At the start of the new millennium, Amoco service stations in the United States were rebranded BP, although Amoco gasoline continued to flow from the pumps.

II) Background and development of the project

• Reasons behind the merger:The main reason behind the BP-Amoco 1998 merger was

the desire to obtain economies of scale, in the belief that these would ensure future success, given the huge investments necessary in the oil and gas sector.

Another major reason, which derives from the first, was the expected cost savings, estimated to reach 2 billion USD annually.

Last but not least, synergies in both production and commercial operations were seen as another key factor in the merger.

Key-aspects about the project

Bill Young, head of the new “Structured Finance” division of BP-Amoco, was tasked with:

reviewing the company’s policy with respect to the use of project finance

giving advice on project finance’s potential benefits and disadvantages in financing future capital investments

Project participants and stakeholders

Project “sponsors”: John Buchanan, new CFO of the BP-Amoco Group, David Watson, Treasurer and Group Vice-President in charge of Finance

Participants: Bill Young, Mike Wrenn (America Finance Group) and Adam Wilson (Specialized Finance Group-U.K.) made up the team in charge of the project

Stakeholders: The Board of Directors, the Finance Group, BP-Amoco as a whole, the governments of both the U.S. and the U.K.

Motivations behind the report

The assignment was crucial in the context of integrating the financial policies of both companies, following the merger.

Given the magnitude of the investments in fixed assets, the optimal way of financing such huge capital expenditures was of critical importance.

Project finance had been successfully used in the past by BP-Amoco’s competitors and thus was a viable financing option that had to be investigated by the team.

Major steps in implementing the project

Defining Project Finance in the team’s perceptionEstablishing the scope of the task at handUnderstanding the positions of both BP and Amoco

regarding Project FinanceGeneral Cost and Benefit analysis on the use of Project

Finance following the mergerStatement of exceptions to the general analysisConclusions and recommendations

Question 1Project Finance is a technique in which the financing of

a project is totally dependent on the future contracts which will be signed and cash-flows that will be generated by that independent project company.

The creditors will have to rely exclusively on the assets and profits of the project company in order to recuperate their loans and interest.

Therefore, most of the funds are provided by banks (or a syndicate of banks) and not from internal sources.

Differences between CF and PF In the case of PF, a new company is established (the

project company), which has no previous operational history and which will be entirely responsible for the successful implementation of the project. By contrast, in CF, no such company is created and the already established firm manages the project.

In PF, the capital structure of the project is highly-leveraged, the sponsors usually putting up about 30% of the funds, the remaining 70% being financed by external creditors (i.e. banks).

In CF, the company initiating the project has unlimited liability regarding debt repayment. On the other hand, on a PF basis, the project company has only limited liability concerning its debts, meaning that the risk is limited solely to the project’s own assets and cash-flows.

PF has a narrower field of use than CF. While the latter can be implemented in just about any rational investment on which the company decides, PF can only be used on large-scale projects (especially those who have a long life span).

Question 2

In Bill Young and his team’s opinion, CF is to remain the principal method of financing future investments at BP-Amoco. However, they consider that PF could be chosen under the following particular scenarios:

“Mega Projects”, meaning those projects so massive in size (financial requirements) that could jeopardize the well-being of the company as a whole.

Projects in Politically Volatile Areas, referring to those projects which are exposed to an increased political risk. Indeed, in these cases, the transfer of risk towards outside lenders was a major advantage deriving from the use of PF.

“Joint Ventures with Heterogeneous Partners”, meaning those situations when BP-Amoco needed to step in directly so as to compensate the insufficient financial capabilities of some of its partners.

Question 3

How and why does project finance create value? Hint: Think in terms of market imperfections. What are the costs associated with taxes, financial distress, information, incentives conflicts (agency), transaction, etc., and how does project finance increase or decrease the costs associated with these imperfections.

The costs of using PF In Bill Young’s opinion, the first major drawback of

using PF was the fact that BP-Amoco could obtain corporate debt at much lower costs than any newly created project company could. Otherwise said, Corporate Debt was much cheaper that Project Debt.

PF also results in substantial third-party costs: • High fees related to hiring financial advisors• Costs incurred because of having to draw up

engineering reports• Legal fees concerning operating contracts and loan

documentation

Time cost since PF takes longer than CF to arrange:• Decisions are delayed • This, in turn, leads to a lower project NPV• Opportunities could be missed all together because

of the extra-time neededLoss of managerial flexibility because of the strict

requirements placed on operations and reporting. This made adapting to changes during the project’s lifetime much more difficult for its sponsors.

High risk in using PF of “leaked” information due to the fact that greater disclosure is needed in this type of financing than in the case of using company funds exclusively.

The benefits of using PFThe main benefit identified by Bill Young and his team

was risk sharing. BP-Amoco basically sacrificed the majority stake (and therefore potential profits) in a project but also transferred most of the risk to external creditors (potential losses and default of the project company).

“Artificial” expansion of BP-Amoco’s debt capacity if project assets or liabilities were not required to appear on its balance sheet.

PF generates additional tax shields because of the much higher leverage ratios used for projects (typically financed by debt in proportion of 70%).

Additional tax benefits could be generated by PF for particular projects, when certain governments could be prepared to offer reduced/no taxes in order to attract investments to their countries.

PF also generates value by better allocating the risk of the project between all the parties involved.

PF provides a lot of benefits for companies who engage in first-time investments (high risk involved).

PF combats information asymmetry on the markets and thus creates value by making them more transparent.

Question 4Do you agree with the recommended

policy? Which parts? Is anything missing?

Further to the assessment of choosing PF versus CF, the assigned team concluded that corporate funds for new projects were more popular than external funds among both companies before the merger, and that it should continue to remain as such for the combined firm, BP-Amoco.

Additionally, project finance would be used solely in three very particular circumstances, as already mentionned:

Mega projectsProject in politically volatile areasJoint ventures with heterogeneous partners

Considering the above, we do not fully agree with the recommended policy, as per the following arguments:

The areas and circumstances chosen by Young’s team for the use of project finance were too narrow and restrictive.

Bill Young underestimated the advantages of PF, considering most of them to be fictitious or absent.

The team focused more on the disadvantages of project finance at the level of BP Amoco, neglecting the advantages arising from its use and, therefore, resulting in a negative impact within the final decision.

Question 5

Study Exhibit 7. How is project finance like holding a portfolio of call options on project assets? How is corporate finance like holding a call option on a portfolio of assets?

By examining exhibit 7, we are able to draw some conclusions as to how PF might affect the overall corporate entity when it is utilized. As described above, using PF, each sponsor has limited liability towards the project; its liability is concentrated to the funds he has initially brought into the project.

Therefore, each project which is financed through PF can be thought of as a single callable option. If the project doesn’t go well, the company can simply walk away, incurring a loss, which is limited to the initial funds it has invested in the project. Therefore, a project-based company can consider its overall project portfolio as a sum of callable options, the initial investment representing the premium on the call option.

This representation serves many purposes, but the main one is that the company is able to mitigate the risk of default.

In the case of corporate finance such a thing is not possible.

If the company decides to invest in certain projects using internal funds, it has sole ownership of both assets and liabilities resulting from the new investments.

Therefore, the company will gain all the potential profits but will also incur all the losses, without any option to walk away, if the investment decision wasn’t a sound one. The only actual call option the firm has is to declare bankruptcy and discontinue its operations.

Thus, in the case of CF, the company has a portfolio of assets/projects, on which it can exercise a single global option: to operate or not.

After having discussed the above, the stand which Bill Young and his team took, regarding project finance for BP Amoco is somewhat understandable, since except on the three circumstances described, they do not see a plausible risk of default given the size and financial strength of BP Amoco.

Bill Young’s conclusions

Both BP and Amoco indeed shared a common preference to use CF in financing new projects.

Excluding the three major exceptions, CF would remain the principal way to finance new projects at BP-Amoco, with PF relegated to only a marginal use.

Identification of two types of NPV: “Investment NPV” and “Financing NPV” (the latter being typically negative).

If the sum of these two NPV’s was positive, a possible recommendation for using PF in order to finance the new endeavor could follow.

Personal conclusions and opinionsIn our view, BP-Amoco places a too great emphasis

on CF than it should. Indeed, the analysis performed was not entirely objective and had been deeply influenced by the financing philosophies of both companies prior to the merger: BP almost never used PF and Amoco employed it only in a secondary role.

As a result of this common preference towards CF, the team lead by Bill Young focused mostly on the advantages of CF, while in the mean time highlighting the drawbacks of PF.

We consider that the separation between the two types of NPV was founded on a largely arbitrary statement that the ideal debt-to-capitalization ratio of the company should be 30%.

To sum up, we believe that the merits of PF were grossly underestimated. Even in the three exceptional cases presented, its use could ultimately be rejected in favor of internal funds because of questionable corporate beliefs.